Embed Size (px)

Citation preview

MARKET OUTLOOK PT Trimegah Securities Tbk - www.trimegah.com 1

Global factors adding to uncertainty level...

Mr. Trump is entering US presidential office with a promise to expand

fiscal stimulus that may prompt the Fed to raise rates more often than

previously expected, and we continue to expect volatility in Europe next

year given elections in Germany and France. Higher expectation for US

growth and a stronger Dollar are usually negative for emerging markets

overall. Foreign investors have recorded USD851mn of net sell in Indo-

nesian equity in Nov with risk of another USD500mn—1bn if Fed indeed

indicates plans to be more aggressive.

...but domestic economy is actually better than six months ago

We track seven micro indicators and found recent economic momentum

more encouraging, raising our stance from neutral to slight positive. Our

proprietary survey (see p.63) also suggests that Indonesians plan to

spend more on property, autos and travelling although less on gadgets

and luxury items. A signal that economy is still recovering on a U-curve

trajectory.

JCI: downside to 5053 near-term, upside to 5964 by end-2017

With 4% downside and 14% upside from index level of 5246 (last clos-

ing before report publication) and a 27% expected earnings growth next

year should be able to cushion the downside, we remain cautious near-

term but more constructive medium-term, especially from end 1Q on-

ward.

Portfolio: tilting towards defensives and commodities for now

We populate our model portfolio with more defensives (MIKA, GGRM,

ROTI) and commodities (DOID, PTBA, PGAS). We also add WSKT (a low

beta construction company that has de-rated) and MAPI (attractive

bottom-up catalyst of Vietnam expansion).

2017 Indonesia market outlook Plenty of earnings growth ahead

2017 market outlook

5 December 2016

JCI Index Target:

JCI Index (as of 28 Nov16) 5,115

End-2016 5,053

1Q-2017 5,229

2Q-2017 5,598

End-2017 5,964

Sebastian Tobing

Rovandi

Trimegah research team

Trimegah’s model portfolio

Source: Trimegah Research, Bloomberg

Note: Given the time required to prepare the report, all index and stock prices in this report are as at end of 28 Nov 2016.

Top

picks

Price (Rp)

Mkt. Cap

TP Rec

EPS growth

P/E (x) EV/EBITDA

(x) P/BV (x)

Divd yield

Beta Upside

28-Nov (Rptrn) 2017 2017 2017 2017 2017 2yr

weekly

DOID 515 4.3 800 55% Buy 99% 4.4 3.4 1.6 0% 1.3

PTBA 11,550 26.6 16,000 39% Buy 125% 6.5 4.3 1.9 2% 1.6

PGAS 2,620 63.5 3,300 26% Buy 12% 9.1 6.0 1.3 3% 1.2

WSKT 2,270 30.8 2,910 28% Buy 81% 14.5 9.5 2.5 1% 0.6

MAPI 4,870 8.1 7,200 48% Buy 109% 16.0 6.2 2.2 0% 0.9

MIKA 2,580 37.2 3,000 16% Buy 11% 47.9 36.1 9.7 1% 0.4

GGRM 62,775 120.8 82,000 31% Buy 19% 15.3 10.0 2.8 4% 0.8

ROTI 1,455 7.4 1,900 31% Buy 22% 22.5 10.1 4.4 1% 0.9

Simple average 34% 60% 17.0 10.7 3.3 2% 0.96

Note: Given the time required to pre-

pare the report, all share prices in this

report are as at end of 28 Nov 2016.

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 2

Table of contents

Economic outlook 3

- Global factors 3

- Indonesia's economy 7

Investment themes 12

Equity strategy 15

Sector and company pages 20

- Bank sector 20

- Automotive sector 50

- Consumer sector (staples, retail, healthcare) 60

- Telecommunication sector 100

- Media sector 120

- Construction sector 130

- Property sector 147

- Cement sector 172

- Coal sector 182

- Others (companies not in a specific sector) 200

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 3

Global factors have raised uncertainty levels

Higher global interest rates is becoming a real concern

Mr. Trump’s win in US presidential election has changed US growth and global interest rate expectations over-

night. We are likely to see larger fiscal stimulus plan in the US (Trump has mentioned USD1trn stimulus plan or

6% of GDP), stronger USD, and higher yields. With upcoming fiscal stimulus and already rising inflation, expect

US Fed to accelerate its interest rate hike. We think expectation was for a 50bps increase next year before Mr.

Trump’s win, but there is higher likelihood of a 100bps increase now. US 10 year treasury yield has risen by

~400bps (basis points) to 2.3% and the US rate curve has steepened in the process with 10-2yr treasury yield

rising by 20bps to 1.2% since Mr. Trump’s win.

How high can US Fed rate go?

We think a 25bps US Fed rate increase in December to 75bps was already a high likelihood even if Mr. Trump

had not won the US presidential election. The question is, how much will the Fed increases its rate next year?

Currently Fed rate is at 0.5% with a –1.1% spread over inflation Versus 0.9% long-term spread (30 years histor-

ical average). Assuming the spread over inflation returns to its historical average, Fed rate should rise by 2.0%

to 2.5%. History suggests that Fed rate’s return to normalcy usually takes about two years or on average 25bps

per quarter. Note however, that inflation is also a moving statistic. US inflation swap forward currently stands at

2.5% (a hedging instrument that indicates market’s inflation expectation). If we use this as US inflation bench-

mark, we are looking at Fed rate rising by 2.9% (290 bps) to 3.4%. To put this in perspective, the last time Fed

rate was 3% was in March 2008 before global financial crisis hit its peak.

Figure 1. Fed rate and spread over inflation

Source: Bloomberg, Trimegah Research

Figure 2. Fed rate, inflation, and inflation swap forward

Source: Bloomberg, Trimegah Research

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US Inflation Swap Forward US Inflation Fed Rate

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Fed RateUS InflationFed spread over US inflation

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

Fed spread over US inflation

Average spread in last 30 years

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 4

How does an accelerated interest rate hike in the US affect Indonesia?

In order to do an analysis with longer historical data, we use adjusted BI rate, which is calculated by assuming

same rate cut to BI rate as recent 7-days repo rate. Current adjusted BI rate is 6.0% (BI has cut by 50bps after

switching benchmark rate to 7-days repo rate). Based on latest inflation rate of 3.3%, BI real rate is at 2.7%

and the current spread over Fed real rate is at 3.8% versus average historical spread of 2.7%. This implies that

BI has room of 1.1% before having to increase its rate. It also means there is a risk of 0.9-1.8% increase in BI

rate based on our earlier calculation of a 2.0-2.9% risk of increase in Fed rate over the next two years.

Indonesia’s 10yr govt bond yield is currently 8.2% and US 10yr treasury at 2.4%, implying a 5.8% nominal

spread Vs. historical average of 5.1%. Indonesia’s real rate (taking into account current inflation) is 4.9% and

US at 0.8%, implying 4.1% real spread Vs. historical average of 1.3%. This implies that judging by nominal rate,

there is a risk we could see Indonesia’s 10yr bond yield rising to as high as 9.4% based on US inflation forward

swap currently at 2.5%. Judging by average historical real yield at only 1.3%, Indonesia’s 10yr bond yield could

be as low as 7.0%. The mid-point of the 7.0-9.4% range is 8.2%, exactly where current Indonesia’s 10yr bond

yield is.

Figure 3. BI adjusted real rate currently at 3.8% above Fed real rate Vs. 2.7% average

Source: Bloomberg, Trimegah Research

Figure 4. Indonesia’s nominal and real 10 yr govt bonds spread over US 10 year treasury bonds

Source: Bloomberg, Trimegah Research

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

2010 2011 2012 2013 2014 2015 2016

BI real rate spread over Fed real rate Average real spread

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Indo 10yr nominal spread over US treasury

Average nominal spread

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2010 2011 2012 2013 2014 2015 2016

Indo 10yr real spread over US treasury

Average real spread

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 5

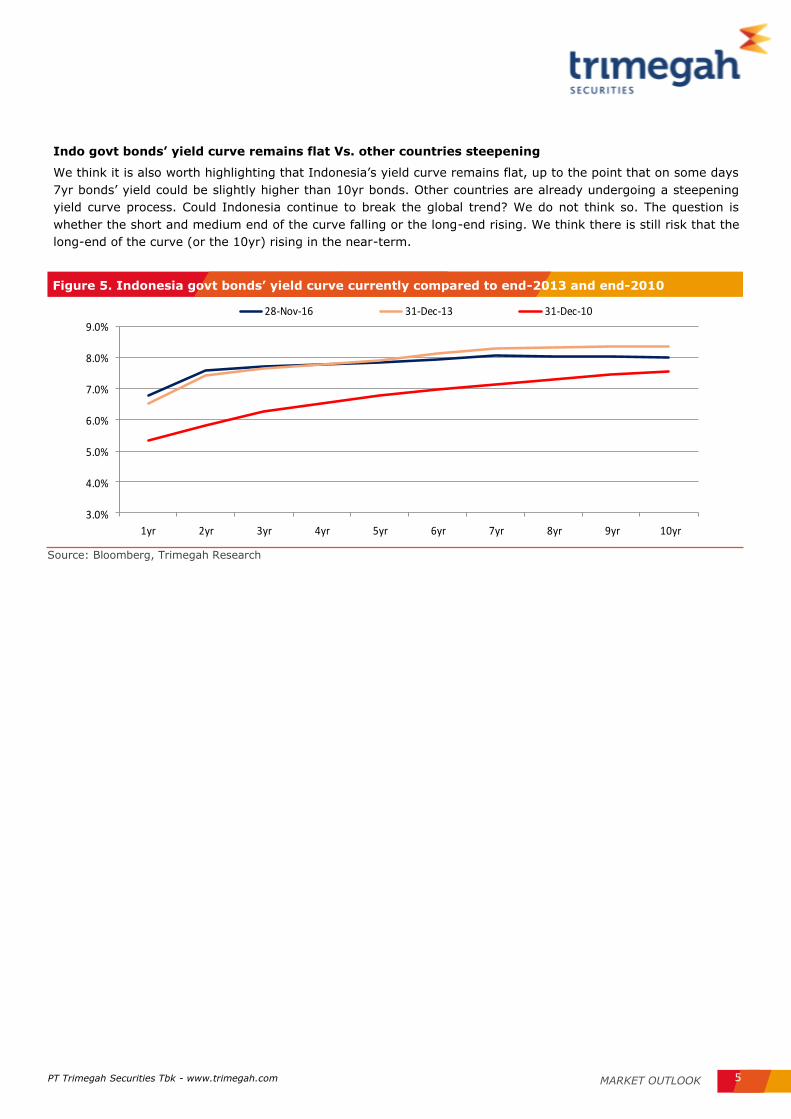

Indo govt bonds’ yield curve remains flat Vs. other countries steepening

We think it is also worth highlighting that Indonesia’s yield curve remains flat, up to the point that on some days

7yr bonds’ yield could be slightly higher than 10yr bonds. Other countries are already undergoing a steepening

yield curve process. Could Indonesia continue to break the global trend? We do not think so. The question is

whether the short and medium end of the curve falling or the long-end rising. We think there is still risk that the

long-end of the curve (or the 10yr) rising in the near-term.

Figure 5. Indonesia govt bonds’ yield curve currently compared to end-2013 and end-2010

Source: Bloomberg, Trimegah Research

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

1yr 2yr 3yr 4yr 5yr 6yr 7yr 8yr 9yr 10yr

28-Nov-16 31-Dec-13 31-Dec-10

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 6

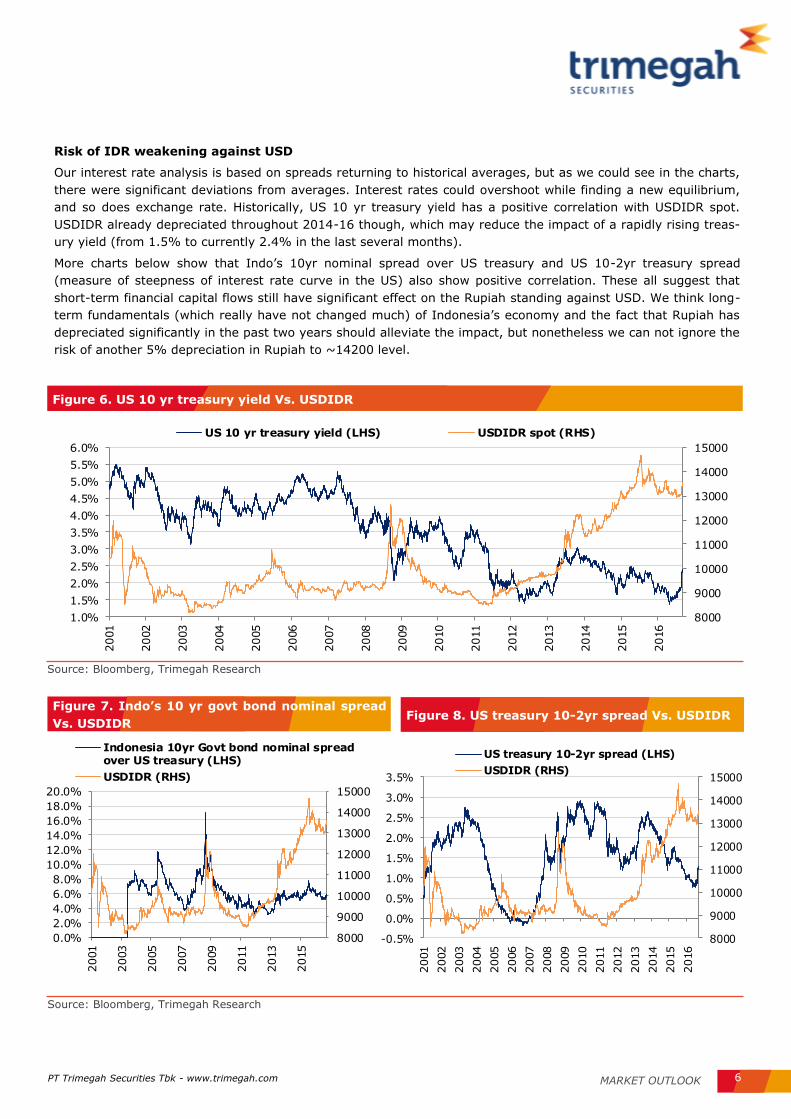

Risk of IDR weakening against USD

Our interest rate analysis is based on spreads returning to historical averages, but as we could see in the charts,

there were significant deviations from averages. Interest rates could overshoot while finding a new equilibrium,

and so does exchange rate. Historically, US 10 yr treasury yield has a positive correlation with USDIDR spot.

USDIDR already depreciated throughout 2014-16 though, which may reduce the impact of a rapidly rising treas-

ury yield (from 1.5% to currently 2.4% in the last several months).

More charts below show that Indo’s 10yr nominal spread over US treasury and US 10-2yr treasury spread

(measure of steepness of interest rate curve in the US) also show positive correlation. These all suggest that

short-term financial capital flows still have significant effect on the Rupiah standing against USD. We think long-

term fundamentals (which really have not changed much) of Indonesia’s economy and the fact that Rupiah has

depreciated significantly in the past two years should alleviate the impact, but nonetheless we can not ignore the

risk of another 5% depreciation in Rupiah to ~14200 level.

Figure 6. US 10 yr treasury yield Vs. USDIDR

Source: Bloomberg, Trimegah Research

Figure 7. Indo’s 10 yr govt bond nominal spread

Vs. USDIDR

Source: Bloomberg, Trimegah Research

Figure 8. US treasury 10-2yr spread Vs. USDIDR

8000

9000

10000

11000

12000

13000

14000

15000

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

US 10 yr treasury yield (LHS) USDIDR spot (RHS)

8000

9000

10000

11000

12000

13000

14000

15000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

2001

2003

2005

2007

2009

2011

2013

2015

Indonesia 10yr Govt bond nominal spreadover US treasury (LHS)

USDIDR (RHS)

8000

9000

10000

11000

12000

13000

14000

15000

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

US treasury 10-2yr spread (LHS)

USDIDR (RHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 7

Indonesia’s economy is still on a path of gradual recovery

Micro indicators are actually improving

We track seven micro indicators ranging from auto sales volume to banking system’s loan and deposit growth.

Compared to our last assessment in May16, three out of seven indicators have improved and the economic sig-

nal indicated by these factors has improved from “neutral” in May16 to currently “slight positive” (most of these

indicators latest data point is Oct16).

The big question of course, is whether a combination of likely higher interest rates and further Rupiah deprecia-

tion in the short-term could halt economic progress. Our recent conversations with the real sector (IDR revenue)

suggest they are still digesting the impact of Mr. Trump’s win and have not made significant changes to their

plans other than reviewing USD costs and capex. The nature of a potential further depreciation is also important.

A swift depreciation (and likely overshooting) would have a larger negative psychological and real effect than a

gradual depreciation.

We think rising interest rate is unlikely to have significant effect on loan growth and the economy either, espe-

cially as we see little risk of BI raising benchmark rate significantly. Indonesian banks only registered 3.8% YoY

loan growth year-to-date, far below 10.4% in 2015 and 11.6% in 2014.

Hence, despite risk of a depreciating Rupiah and rising interest rate, we still expect GDP growth of 5.1%, similar

to this year. There is upside risk if coal price remains at current level of USD90/ton versus our forecast of

USD75/ton for next year. Kalimantan and South Sumatra combined is 28% of Indonesia’s GDP but the ripple

effect can be larger than Kalimantan’s and South Sumatra’s contribution to Indonesia GDP suggests.

Figure 9. Micro indicators are improving

Source: Trimegah research

Economic indicators May-16 Nov-16

Auto sales volume Positive Positive

Property marketing sales Neutral Neutral

Cement consumption Negative Negative

Retail SSSG Neutral Neutral

Imports growth Negative Positive

SOE construction order book Neutral Positive

Loan and deposit growth Negative Negative

Overall Neutral Slight Positive

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 8

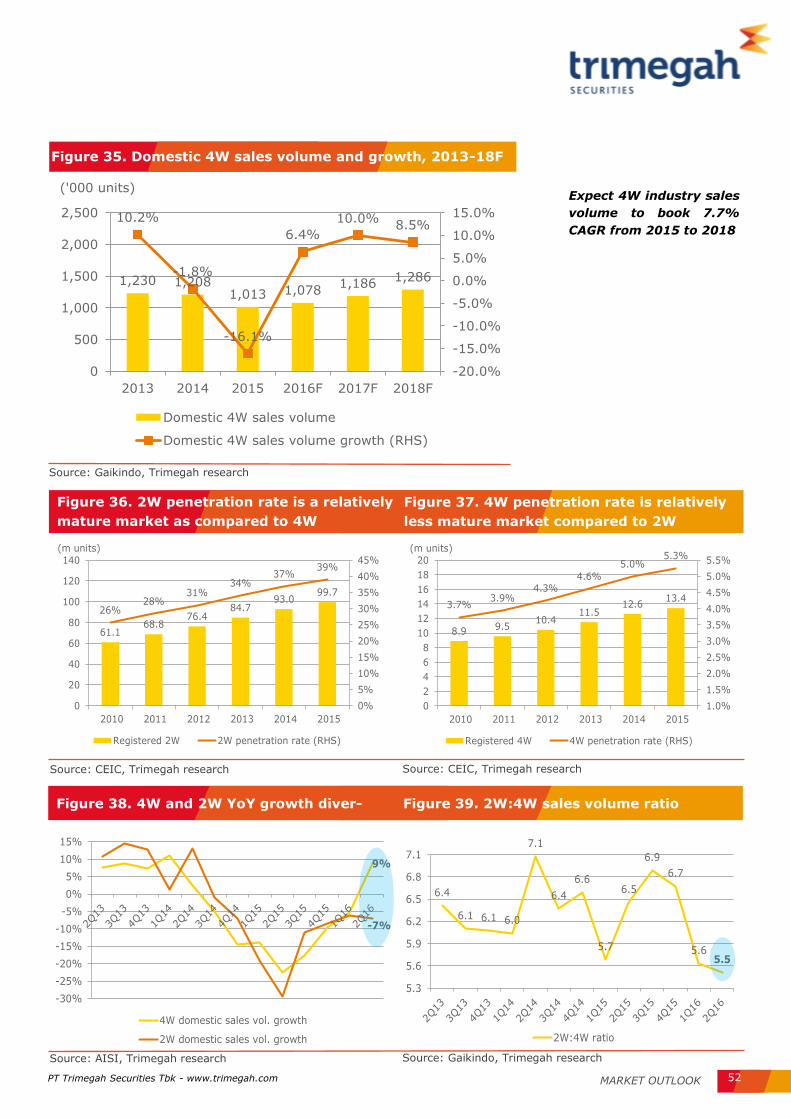

Indicator #1: Auto sales momentum remain positive

The positive 4W sales volume momentum that started rebounding in Aug15 has continued its positive trajectory

and we remain upbeat on next year’s 4W volume, expecting ~10% growth, an improvement over this year’s 3%

growth pace (Jan-Oct YoY). 2W sales volume growth remains in negative territory, but at least has stopped

worsening. We are less optimistic on 2W volume as penetration has already reached 40% in 2W (versus 5% for

4W) and expect a structural change in marketing strategy whereby 2W distributors would focus more on increas-

ing ASP by launching higher-end new models (some of recent models are priced at IDR 50mn versus normally

~IDR 15mn).

We have also noticed higher volume of upper-end 4W, which signals higher propensity to spend by upper-end

consumers.

Figure 10. Indonesia 4W sales volume growth YoY

Source: Bloomberg, TRIM Research

Figure 11. Indonesia 2W sales volume growth YoY

Source: Bloomberg, TRIM Research

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Aug-0

6

Dec-

06

Apr-

07

Aug-0

7

Dec-

07

Apr-

08

Aug-0

8

Dec-

08

Apr-

09

Aug-0

9

Dec-

09

Apr-

10

Aug-1

0

Dec-

10

Apr-

11

Aug-1

1

Dec-

11

Apr-

12

Aug-1

2

Dec-

12

Apr-

13

Aug-1

3

Dec-

13

Apr-

14

Aug-1

4

Dec-

14

Apr-

15

Aug-1

5

Dec-

15

Apr-

16

Aug-1

6

GDP YoY (LHS) Indo Car Sales YoY (RHS)

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Au

g-0

7

Jun

-08

Ap

r-0

9

Feb

-10

De

c-10

Oct

-11

Au

g-1

2

Jun

-13

Ap

r-1

4

Feb

-15

De

c-15

Oct

-16

GDP YoY (LHS) Indo 2W sales volume growth YoY (RHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 9

Indicator #2: Cement growth momentum remains negative

After rising in June to August, cement domestic consumption 3M Average volume YoY growth slowed down in

September and October. Although cement companies are more optimistic on next year’s volume growth i.e. INTP

expects 5% domestic cement consumption growth next year Vs. 3% YoY growth year-to-date, we choose to be

conservative and maintain negative consumption.

Indicator #3: raising construction SOEs’ new contract growth momentum from neutral to positive

SOE construction companies’ new contract book has improved, currently over 150% growth versus slightly over

100% YoY growth in May (with negative momentum). Given higher base, we expect new contract value to be flat

next year, but total order book would still grow by 31% next year. Under finance minister Ms. Sri Mulyani, the

government has been more prudent and careful in spending, but we remain optimistic that government will stay

committed when it comes to infrastructure, which is the sort of productive spending that Ms. Sri Mulyani likes.

Figure 12. Cement domestic consumption 3M Average Volume and YoY growth

Source: Bloomberg, Trimegah research

Figure 13. Construction SOEs’ cumulative YoY growth

Source: Bloomberg, TRIM Research

Note: Data includes monthly data for PTPP, ADHI, and WSKT as WIKA has not published Oct16 new contract numbers

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Mar-

11

Jul-11

Nov-1

1

Mar-

12

Jul-12

Nov-1

2

Mar-

13

Jul-13

Nov-1

3

Mar-

14

Jul-14

Nov-1

4

Mar-

15

Jul-15

Nov-1

5

Mar-

16

Jul-16

'000 tons3M Avg. Volume (LHS) 3M Avg. Volume YoY Growth (RHS)

0%

50%

100%

150%

200%

250%

300%

350%

400%

450%

2M

15

3M

15

4M

15

5M

15

6M

15

7M

15

8M

15

9M

15

10M

15

11M

15

12M

15

1M

16

2M

16

3M

16

4M

16

5M

16

6M

16

7M

16

8M

16

9M

16

10M

16

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 10

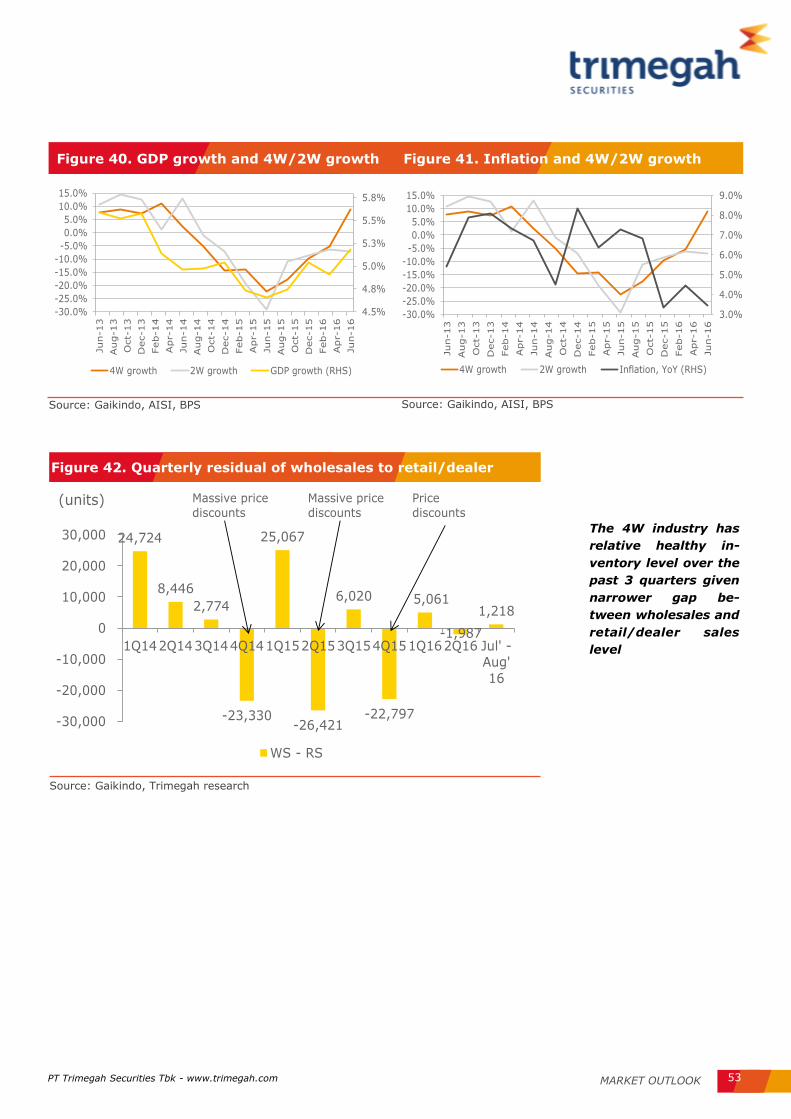

Figure 15. Indonesia GDP versus Imports YoY growth

Source: Companies data, Trimegah research

Indicator # 4: ACES and RALS’ YoY SSSG momentum is neutral

Both RALS (Ramayana Dept Store), which target low to mid-end consumers, and ACES, which target higher end

consumers, show some signs of recovery. However, we still assign a neutral momentum for retail sector as

RALS’ recent strong SSSG could be driven by higher market share as management has improved its product of-

ferings. We also want to wait for 2-3 more months of further recovery in ACES before we are more confident in

calling for a retail recovery.

Indicator # 5: Monthly imports shows positive momentum

Monthly import is another statistic that historically has high correlation with GDP. Imports YoY growth is finally

rebounding and should reach positive YoY growth soon.

Figure 14. Retail stores (ACES and RALS)’ YoY growth (3months MA)

Source: Bloomberg, Trimegah research

-30

-20

-10

0

10

20

30

40

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

Sep-1

2

Mar-

13

Sep-1

3

Mar-

14

Sep-1

4

Mar-

15

Sep-1

5

Mar-

16

Sep-1

6

%ACES (Ace Hardware) RALS (Ramayana Dept. Store)

-40%

-20%

0%

20%

40%

60%

80%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

Jun-09 Feb-10 Oct-10 Jun-11 Feb-12 Oct-12 Jun-13 Feb-14 Oct-14 Jun-15 Feb-16 Oct-16

GDP YoY (LHS) Imports YoY (RHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 11

Figure 16. Total marketing sales

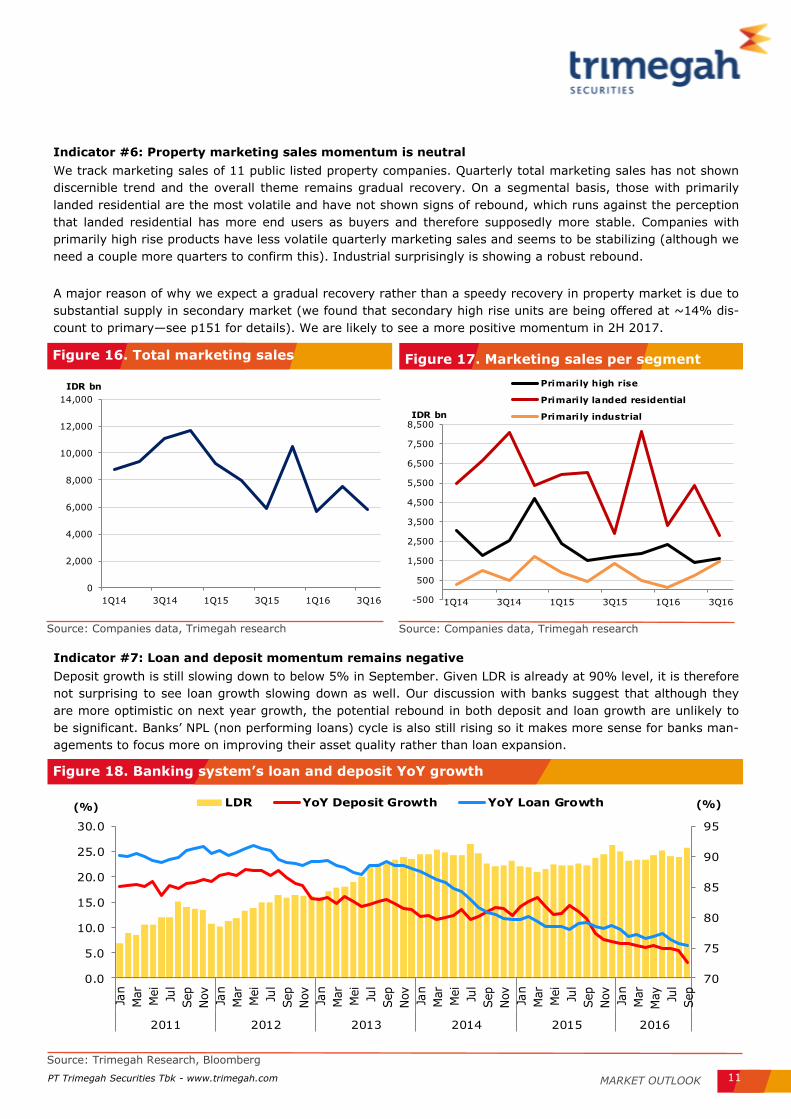

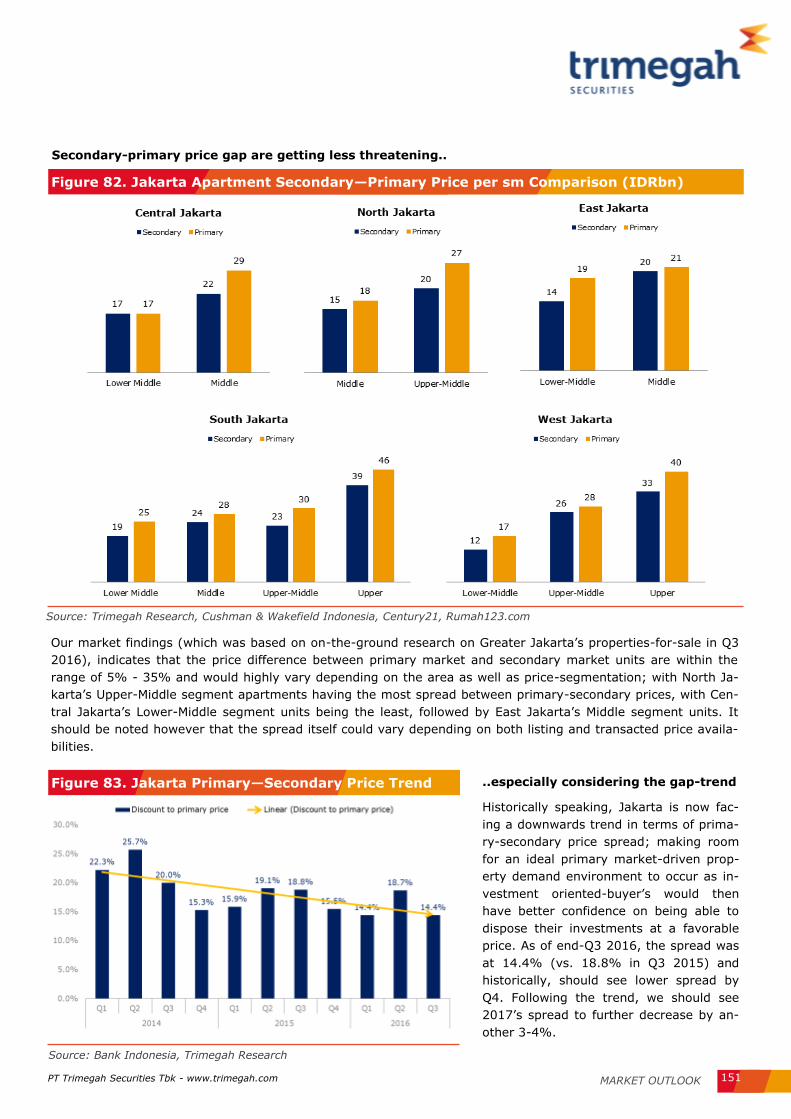

Indicator #6: Property marketing sales momentum is neutral

We track marketing sales of 11 public listed property companies. Quarterly total marketing sales has not shown

discernible trend and the overall theme remains gradual recovery. On a segmental basis, those with primarily

landed residential are the most volatile and have not shown signs of rebound, which runs against the perception

that landed residential has more end users as buyers and therefore supposedly more stable. Companies with

primarily high rise products have less volatile quarterly marketing sales and seems to be stabilizing (although we

need a couple more quarters to confirm this). Industrial surprisingly is showing a robust rebound.

A major reason of why we expect a gradual recovery rather than a speedy recovery in property market is due to

substantial supply in secondary market (we found that secondary high rise units are being offered at ~14% dis-

count to primary—see p151 for details). We are likely to see a more positive momentum in 2H 2017.

Source: Companies data, Trimegah research

Figure 17. Marketing sales per segment

Source: Companies data, Trimegah research

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1Q14 3Q14 1Q15 3Q15 1Q16 3Q16

IDR bn

-500

500

1,500

2,500

3,500

4,500

5,500

6,500

7,500

8,500

1Q14 3Q14 1Q15 3Q15 1Q16 3Q16

IDR bn

Primarily high rise

Primarily landed residential

Primarily industrial

Figure 18. Banking system’s loan and deposit YoY growth

Indicator #7: Loan and deposit momentum remains negative

Deposit growth is still slowing down to below 5% in September. Given LDR is already at 90% level, it is therefore

not surprising to see loan growth slowing down as well. Our discussion with banks suggest that although they

are more optimistic on next year growth, the potential rebound in both deposit and loan growth are unlikely to

be significant. Banks’ NPL (non performing loans) cycle is also still rising so it makes more sense for banks man-

agements to focus more on improving their asset quality rather than loan expansion.

Source: Trimegah Research, Bloomberg

70

75

80

85

90

95

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan

Mar

Mei

Jul

Sep

Nov

Jan

Mar

Mei

Jul

Sep

Nov

Jan

Mar

Mei

Jul

Sep

Nov

Jan

Mar

Mei

Jul

Sep

Nov

Jan

Mar

Mei

Jul

Sep

Nov

Jan

Mar

May

Jul

Sep

2011 2012 2013 2014 2015 2016

LDR YoY Deposit Growth YoY Loan Growth(%) (%)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 12

Four Investment themes for 2017

Theme 1: Companies with bottom-up catalysts

In a search for alpha, we have identified companies with secular earnings improvement that should alleviate the

volatility caused by changes in macro outlook. MAPI, DOID, and MPMX benefit from expected improvement in

operations and balance sheet while RALS benefits from expected improvement only. Of these, RALS and DOID

are turnaround stories that are already visible in recent quarterly results, while MAPI and MPMX are arguably

more forward-looking calls and should be less “crowded” trades.

Figure 19. Stocks with clear bottom-up catalysts

Source: Trimegah research, Bloomberg

Ticker Comment 2017 PE 2017 EPS

growth

2017

EV/EBITDA

2017EBITD

A growth

MAPI

We believe MAPI's expansion into Vietnam will be more suc-

cessful than market expects and it will be an important

growth driver for the company. Company has also been able

to reduce debt burden from 1.7 to 1.5 net debt to EBITDA.

18.5 123% 6.2 22%

RALS

RALS has undergone transformation in product line-up that

will still bear fruits in the coming years. We expect the com-

pany to add more celebrities related products and revamps

its kids' clothing line-up to drive sales next year.

15.3 22% 10 18%

DOID

DOID recently obtained sizable long-term contract that in-

creases its EBITDA backlog to ~USD1bn. Despite this year's

strong performance in share price, it is still trading at 3.4x

2017 EV/EBITDA, a 28% discount to closest competitor

UNTR.

4.5 99% 3.4 26%

MPMX

New management is focused on transforming the company

to increase cross-selling between divisions, reduce capex

and to be more cost efficient. We expect write-off for its

financing business to have peaked, something that is not yet

reflected in current share price.

9.7 21% 6.6 10%

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 13

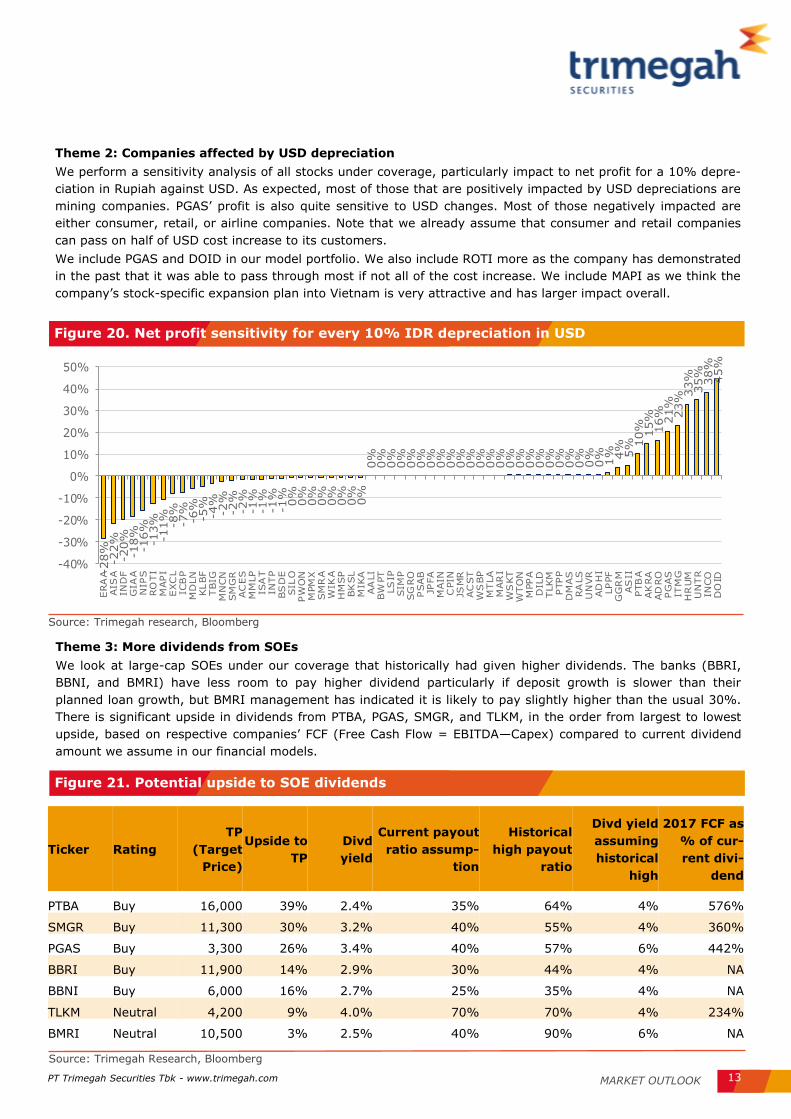

Figure 20. Net profit sensitivity for every 10% IDR depreciation in USD

Theme 2: Companies affected by USD depreciation

We perform a sensitivity analysis of all stocks under coverage, particularly impact to net profit for a 10% depre-

ciation in Rupiah against USD. As expected, most of those that are positively impacted by USD depreciations are

mining companies. PGAS’ profit is also quite sensitive to USD changes. Most of those negatively impacted are

either consumer, retail, or airline companies. Note that we already assume that consumer and retail companies

can pass on half of USD cost increase to its customers.

We include PGAS and DOID in our model portfolio. We also include ROTI more as the company has demonstrated

in the past that it was able to pass through most if not all of the cost increase. We include MAPI as we think the

company’s stock-specific expansion plan into Vietnam is very attractive and has larger impact overall.

Source: Trimegah research, Bloomberg

Figure 21. Potential upside to SOE dividends

Theme 3: More dividends from SOEs

We look at large-cap SOEs under our coverage that historically had given higher dividends. The banks (BBRI,

BBNI, and BMRI) have less room to pay higher dividend particularly if deposit growth is slower than their

planned loan growth, but BMRI management has indicated it is likely to pay slightly higher than the usual 30%.

There is significant upside in dividends from PTBA, PGAS, SMGR, and TLKM, in the order from largest to lowest

upside, based on respective companies’ FCF (Free Cash Flow = EBITDA—Capex) compared to current dividend

amount we assume in our financial models.

Source: Trimegah Research, Bloomberg

Ticker Rating

TP

(Target

Price)

Upside to

TP

Divd

yield

Current payout

ratio assump-

tion

Historical

high payout

ratio

Divd yield

assuming

historical

high

2017 FCF as

% of cur-

rent divi-

dend

PTBA Buy 16,000 39% 2.4% 35% 64% 4% 576%

SMGR Buy 11,300 30% 3.2% 40% 55% 4% 360%

PGAS Buy 3,300 26% 3.4% 40% 57% 6% 442%

BBRI Buy 11,900 14% 2.9% 30% 44% 4% NA

BBNI Buy 6,000 16% 2.7% 25% 35% 4% NA

TLKM Neutral 4,200 9% 4.0% 70% 70% 4% 234%

BMRI Neutral 10,500 3% 2.5% 40% 90% 6% NA

-28%

-22%

-20%

-18%

-16%

-13%

-11%

-8%

-7%

-6%

-5%

-4%

-2%

-2%

-2%

-1%

-1%

-1%

-1%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

0%

1% 4%

5% 1

0% 15%

16%

21%

23%33%

35%

38%

45%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

ERA

AAIS

AIN

DF

GIA

AN

IPS

RO

TI

MAPI

EXC

LIC

BP

MD

LN

KLBF

TBIG

MN

CN

SM

GR

AC

ES

MM

LP

ISA

TIN

TP

BS

DE

SIL

OPW

ON

MPM

XSM

RA

WIK

AH

MSP

BK

SL

MIK

AAA

LI

BW

PT

LS

IPSIM

PSG

RO

PSAB

JPFA

MAIN

CPIN

JSM

RAC

ST

WS

BP

MTLA

MAR

IW

SKT

WTO

NM

PPA

DIL

DTLKM

PTPP

DM

AS

RA

LS

UN

VR

AD

HI

LPPF

GG

RM

AS

IIPTB

AAK

RA

AD

RO

PG

AS

ITM

GH

RUM

UN

TR

INCO

DO

ID

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 14

Theme 4: A rebound in commodities prices

We view that our coal price average of USD75/ton for 2017 (+16% YoY) and oil price of USD60/barrel (+39.5%

YoY; ~30% of coal miners’ production cost) is a fair level to safeguard a disciplined supply level and is a fair lev-

el to align and share a relatively even profitability among the upstream (coal miners & contractors) and down-

stream (power plants) value chain. Large mining contractors and large miners in Indonesia and China are pro-

posing to hedge contracts under a favorable price of above USD65/ton, which benefits the well-established/large

players in the coal market. This creates a healthy cycle for the big coal miners and contractors in our view.

DOID, PTBA and ADRO are our top picks. 3 of these companies share a similarity which is relatively strong earn-

ings predictability. This is an important factor which should be more emphasized in the commodity market in our

view knowing that coal price rally is expected to be short lived (rally is mainly driven by China’s supply cut policy

rather than from demand side). Note that DOID is able to secure USD3bn worth of contracts from a single miner

(BRAU COAL) until 2025, PTBA is able to secure attractive domestic price contracts for 2017 using 4Q16’s Indo-

nesia coal benchmark (HBA) price average and ADRO has been proven to have the highest flexibility in adjusting

stripping ratios in order to maintain margins.

Figure 22. Trimegah coal price forecast

Source: Bloomberg, Trimegah Research

Coal price to normal-

ize at USD75/tonne

in 2017 and will

gradually fall to

USD65/ton by 2021

and will be used as

o u r l o n g - t e r m

benchmark price

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 15

Figure 23. Earnings growth per sector

JCI’s earnings growth to rebound in 2017

Based on our analysts’ bottom-up projections, we expect JCI to post a strong 27% earnings growth, driven by

commodities, construction, banks, and retail. Commodities is driven by expected rebound in commodities prices

and already assuming coal price to fall from current level of USD92/ton (Newcastle generic 1 month contract) to

average USD75/ton next year, which is still a 16% growth versus this year’s average coal price. Banks’ earnings

growth is driven by lower provisioning, which has caused a 2% earnings decline this year. Retail is driven by

earnings recovery in several companies i.e. MPPA, MAPI, ERAA, which have suffered this year.

Largest risk to our JCI earnings growth forecast lies with banks and commodities sectors, which are driven by

banks’ NPL and coal price, respectively. Banks’ earnings growth contributes 46% of JCI’s absolute earnings

growth and commodities sector’s earnings growth contributes 25% of JCI’s absolute earnings growth.

Source: Trimegah research, Bloomberg

-5%

5%10% 14% 16% 18%

24% 27% 27%31%

45%

68%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Pro

pert

y

Cem

ent

Media

Consu

mer

sta

ple

s

Tele

com

Healthca

re

Auto

motive

JCI

Reta

il

Banks

Const

ruct

ion

Com

moditie

s

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 16

Figure 24. JCI PE band

JCI trajectory: near-term flattish (with downside to 5053 level) before up-

ward momentum accelerates

In the short-term, we remain concerned of emerging market outflow affecting Indonesia. Despite a USD850mn

outflow in Nov, Indonesia still registers USD1.6bn in-flow year-to-date and remain prone for more outflow in the

near-term. We expect more outflow leading up to Fed’s decision to increase rate and as Mr. Trump clarifies his

agenda in the coming weeks (we expect Mr. Trump to focus more on fiscal stimulus rather than trade protection-

ism).

Having said that, a 27% earnings growth should be able to attract or at least reduce the outflows and we expect

index to perform better from end-1Q17 onward. Our index targets are 5053 (-1% downside) at end of 2016,

5229 (2% upside) by 1Q17, 5598 (9% upside) by 2Q17, and 5964 (17% upside) at end of 2017. Upside/

downsides are based on index at 5115 on 28 Nov (we have to use delayed prices and index levels given the time

needed for a report this size to be ready for publication).

Our end-2016 and 1Q17 index targets are based on 15.4x PE, slightly lower than 15.9x historical average. Our

2Q17 and end-2017 index targets are based on 15.9x historical average, as we assume a slight re-rating in the

index.

Source: Trimegah Research, Bloomberg

Figure 25. Foreign fund flows in JCI

96435

8731,168

2,126

-1,732

1,942

3,600

1,753

1,292

2,353

2,956

1,712

-1,806

3,830

-1,456

1,611

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016 Y

tD

USD mn

Source: Trimegah Research, Bloomberg

10

12

14

16

18

20

Jan/1

1

Mar/

11

May/1

1

Jul/11

Sep/1

1

Nov/1

1

Jan/1

2

Mar/

12

May/1

2

Jul/12

Sep/1

2

Nov/1

2

Jan/1

3

Mar/

13

May/1

3

Jul/13

Sep/1

3

Nov/1

3

Jan/1

4

Mar/

14

May/1

4

Jul/14

Sep/1

4

Nov/1

4

Jan/1

5

Mar/

15

May/1

5

Jul/15

Sep/1

5

Nov/1

5

Jan/1

6

Mar/

16

May/1

6

Jul/16

Sep/1

6

Nov/1

6

Forward PE of 15.9x, Avg PE of 15.9x, +1 StDev of 18.1, -1 StDev of 13.8x

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 17

Figure 26. Trimegah’s model portfolio

Model portfolio

We think a portfolio that best captures the short-term risk of outflows or depreciating Rupiah and medium-term

bullish earnings growth outlook is a combination of: 1) Stocks that benefit or less affected by potential short-

term Rupiah depreciation or increase in yields, 2) Bottom-up picks with stock specific catalysts that should be

attractive long-term holdings despite macro turbulence, and 3) Low beta companies with relatively defensive

earnings. Hence, we populate our model portfolio with coal stocks with strong earnings growth (DOID, PTBA),

under-owned forgotten utilities with upstream oil holdings (PGAS), a cheap construction company with strong

growth and plenty of contracts secured (WSKT), a retail company with stock-specific turnaround story (MAPI),

three consumer companies with relatively lower beta and higher earnings growth compared to the sector (GGRM,

ROTI), and a healthcare company with very low beta and defensive earnings (MIKA).

We intentionally try to keep our portfolio beta lower than 1.0 and exclude cyclicals (although we prefer ASII to

banks among cyclicals) as we remain concerned over possibility of a rise in yield in the near-term. Currently Indo

govt yield is very flat with risk of long-end rising.

One notable exclusion from our model portfolio is TLKM, which despite market’s perception as a defensive stock,

we think would behave more as a beta stock now due to its valuation (8x 2017 EV/EBITDA, near historical high)

and risk of heightening competition among telecoms next year.

Source: Trimegah Research, Bloomberg

Top

picks

Price (Rp)

Mkt. Cap

TP Rec

EPS growth

P/E (x) EV/

EBITDA (x)

P/BV (x)

Divd yield

Beta

Upside

28-Nov (Rptrn) 2017 2017 2017 2017 2017 2yr

weekly

DOID 515 4.3 800 55% Buy 99% 4.4 3.4 1.6 0% 1.3

PTBA 11,550 26.6 16,000 39% Buy 125% 6.5 4.3 1.9 2% 1.6

PGAS 2,620 63.5 3,300 26% Buy 12% 9.1 6.0 1.3 3% 1.2

WSKT 2,270 30.8 2,910 28% Buy 81% 14.5 9.5 2.5 1% 0.6

MAPI 4,870 8.1 7,200 48% Buy 109% 16.0 6.2 2.2 0% 0.9

MIKA 2,580 37.2 3,000 16% Buy 11% 47.9 36.1 9.7 1% 0.4

GGRM 62,775 120.8 82,000 31% Buy 19% 15.3 10.0 2.8 4% 0.8

ROTI 1,455 7.4 1,900 31% Buy 22% 22.5 10.1 4.4 1% 0.9

Simple average 34% 60% 17.0 10.7 3.3 2% 0.96

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 18

Figure 27. Sector weighting and valuations

Sectoral outlook on 2017

Bullish on coal

We have overweight on coal, supported by healthier coal price level of USD75/72.5/70 per tonne in 2017/18/19

as well as a new healthy and sustainable up-cycle era of the sector. This up-cycle era can be seen from stronger

2017-18 earnings growth, due to coal price recovery and better cost structure–due to low fuel cost, as fuel

makes up ~30% of mining cost. Additionally, we also see healthier supply side, as major companies are

providing conservative production plans. Our top picks are PTBA (Buy, TP IDR16,000), ADRO (Buy, TP

IDR2,000), DOID (Buy, TP IDR800).

Bullish on consumers (staples, retail, healthcare)

We also have overweight on consumers, with more inclination towards discretionary vs. staples, on the back of

higher confidence on consumer purchasing power next year. We believe higher consumer purchasing power is

supported by improvement on overall economic conditions (benign inflation, higher GDP growth, post tax

amnesty and rising commodity prices). Moreover, our belief is further reinforced by our proprietary survey,

which shows more aggressive spending outlook post tax amnesty. However, we are also aware of downside risk

in electricity subsidy removal and exchange rate volatility that might disrupt overall consumer spending. Hence,

we advise investors to look more through bottom-up approach rather than top-down, as reflected in our

preference for companies with higher sales growth, margin expansion, and undemanding valuation. Our top

picks thus include: MAPI (Buy, TP IDR7,200), RALS (Buy, TP IDR1,900), GGRM (Buy, TP IDR82,000).

We are less bullish on interest-rate sensitive sectors except automotive

We have neutral on banks on risk of higher interest rate risk and as NPL risk remains (likely to peak in 1H). We

are also neutral on property as we see only a gradual recovery in price momentum as there is still plenty of sup-

ply in the secondary market. The only exception is automotive, where we see lower risk to our earnings growth

relative to other interest-rate sensitive sectors. It also helps that the largest automotive company, ASII, is a

conglomerate with ~30% of its earnings contributed by commodities businesses.

Source: Trimegah Research, Bloomberg

Sector Weighting 2017 PE 2017 earnings

growth 2017 PBV

Banks Neutral 10.0 31% 1.5

Automotive Overweight 15.3 24% 2.5

Commodities Overweight 9.5 68% 1.5

Property Neutral 18.3 -5% 1.6

Construction Neutral 16.1 45% 2.0

Telecom Neutral 19.5 16% 3.8

Media Neutral 14.2 10% 2.3

Consumer staples Overweight 26.1 14% 7.1

Retail Overweight 17.4 27% 4.1

Healthcare Overweight 31.2 18% 5.7

Cement Neutral 13.9 5% 1.8

JCI 14.8 27% 2.5

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 19

Neutral on construction

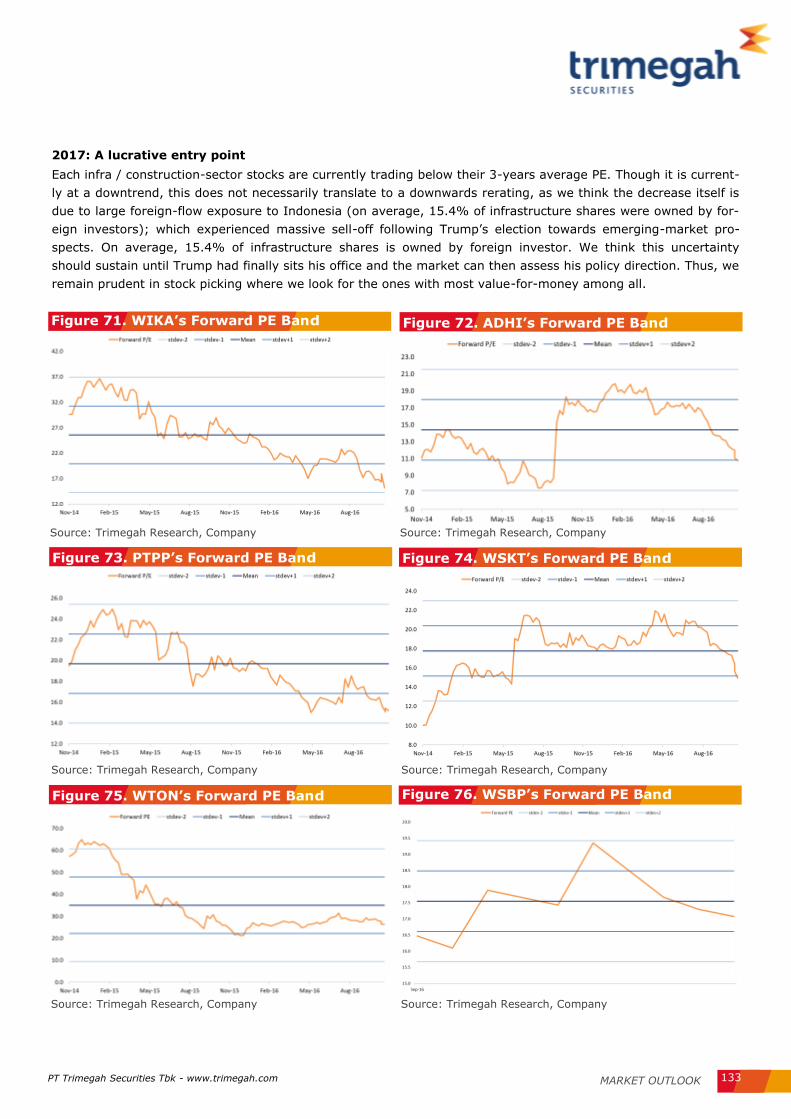

We have neutral on construction as macro outlook for 2017 seems to have mixed impact on infrastructure SOE.

We foresee budget cut for ministries that might adversely affect SOE contractors. However, looking at

government priority projects, we expect higher portion of oil refinery projects, which should benefit several

companies as these projects give higher gross margin. However, with current valuation, we view the stocks to be

cheap for the time being, as they are currently trading below their 3-years average PE, largely due to massive

foreign selloff caused by uncertainty on emerging market post-US election. We therefore screen our stocks over

their PE ratio, EV to new contract, and potential earnings growth, with WSKT (Buy, TP IDR2,910) and WIKA

(Buy, TP IDR2930) as our top picks.

Neutral on telecommunications and media

We have neutral on telecommunications, as we expect more competitive environment, resulting in prolonged

price war, though not to the extent of 2008-12 price war. Moreover, we also expect slower growth from cellular

business’ EBITDA, mainly due to lower margin. Tower industry outlook is also quite bleak, as we expect lower

demand due to possibility of network sharing regulation change. Likewise, we also have neutral on media as

despite expected higher revenue growth from consumer companies’ expected higher spending, we still assume

rather slow earnings growth. Our top pick for the sector is MARI (Buy, TP IDR1,100).

Neutral on cement

We have neutral on cement, as we expect lingering oversupply condition, potential demand growth slowdown,

prolonged decline in ASP, as well as increase in cost from rising coal price (coal composes ~16-20% of SMGR

and INTP’s COGS). However, the cement companies have put in place cost-efficiency measures, which have

enabled them to protect their market share as well as their margins. Furthermore, we expect slower rate of

decline of ASP in 2017, compared to 2016. Our top pick remains with SMGR (Buy, TP IDR11,300), as we believe

the company will outperform in terms of demand growth, due to it holding the largest market share in areas with

positive demand growth (outside Java).

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 20

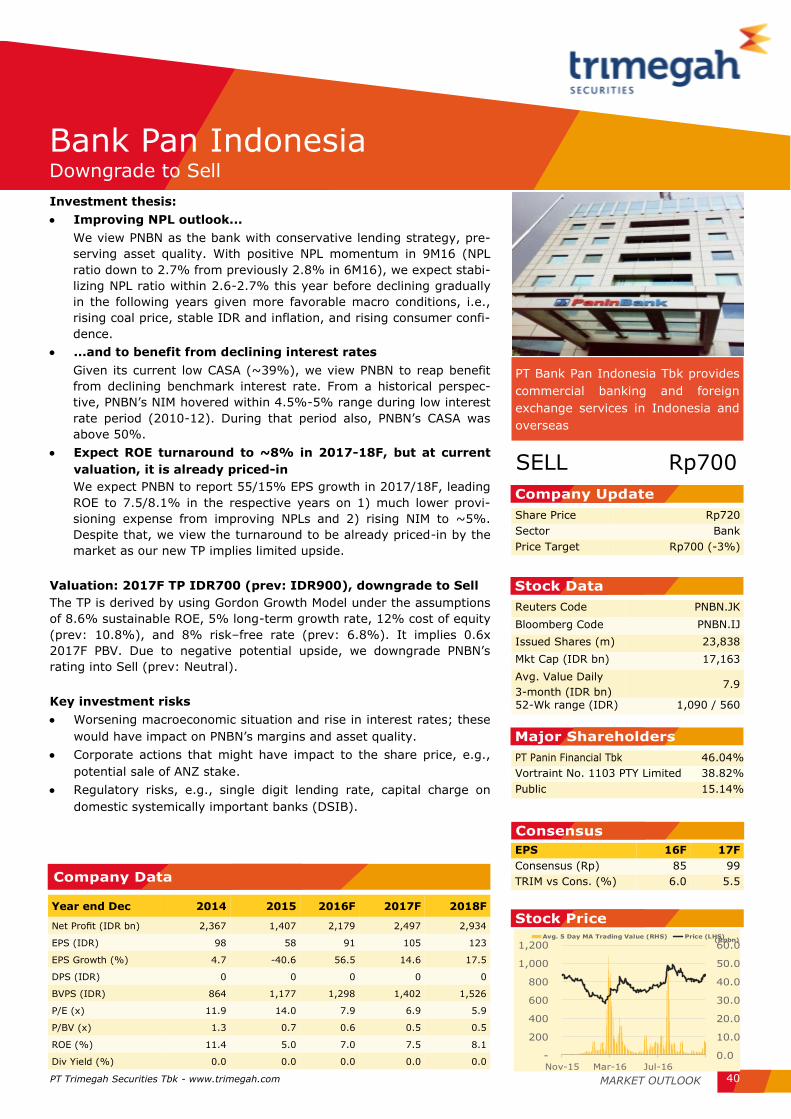

Bank Sector

MARKET OUTLOOK PT Trimegah Securities Tbk - www.trimegah.com 21

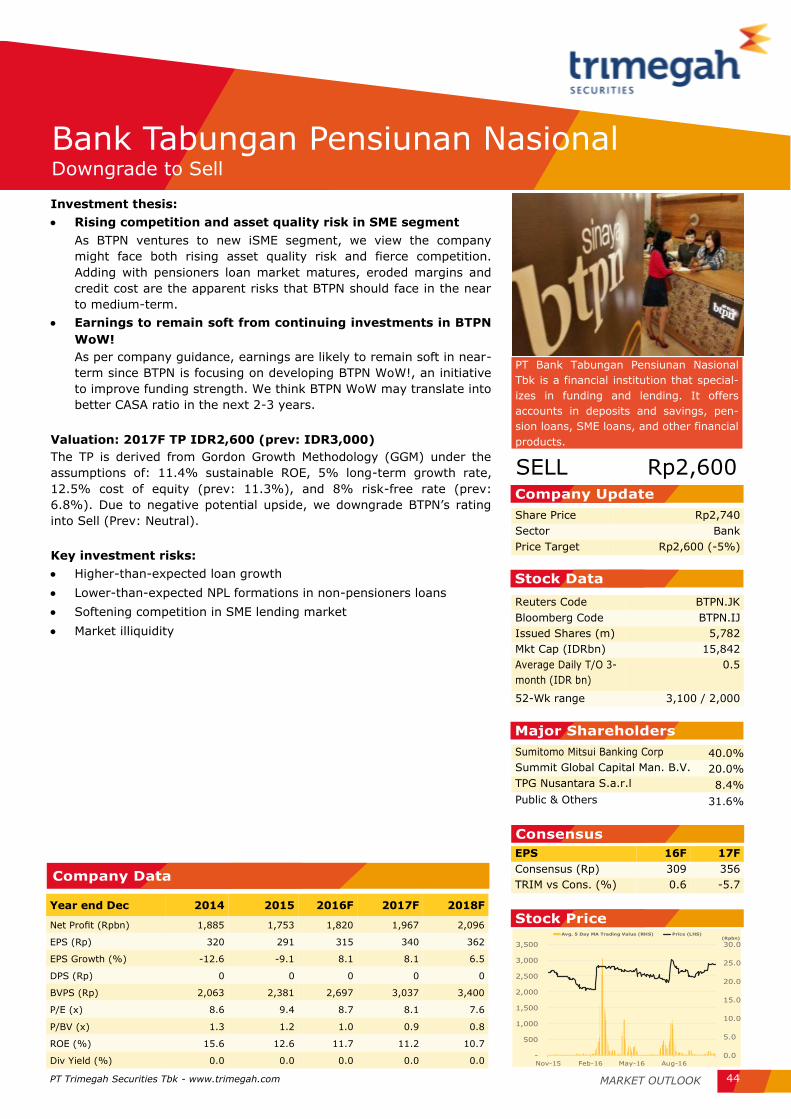

High risk-free rate environment. Downgrade the sector tactically into Neutral (prev: Overweight) The recent developments in the share price of JCI stocks made us realign-ing the strategy toward Indonesian banks stocks. We now assume higher

risk-free rate of 8% as in-line with the current 10-yr Indonesian govt bond yield (~8.3%). As a result, the target prices of banks under our coverage are cut, leaving 4 Buys, 3 Neutrals, and 5 Sells. We therefore downgraded the sector rating tactically into Neutral (prev: Overweight). But, there is an upside risk from higher coal price... Since our coal analyst expects USD75/ton coal price in 2017F, it is fair to

expect improvement in coal debtors’ repayment capability. Anecdotal evidence suggest increasing interest coverage ratios of several publicly listed coal firms, which is an early signs of the improvement in the system-wide NPL ratio, in our view. Our checks with BBNI and BNLI revealed some of their coal-related debtors that went NPL have started to repay the interests and instalments again. We therefore expect NPL ratio in all

banks to start gradually declining in 2017F onwards. ...and also rising consumer confidence The declining interest rate environment combined with low inflation and rising consumer confidence index should bode well with consumer loan growth. Historical data suggests positive correlation between consumer loan growth and consumer confidence index. The rising consumer confi-

dence is evidenced by our consumer team survey, revealing more buying appetite in the next 12 months, especially in property products. This, in our view, should lead to higher consumer loan growth. Our top picks now: BBNI, BBTN, and BNLI

We favor BBNI since it is now valued cheap and its asset quality is not as worse as we think. Besides, it is relatively under-owned now since nega-

tive sentiments surrounded the company post the announcement of it providing loans to VIVA (a Bakrie company). We view VIVA to be credit-worthy instead, since it showed an improvement in interest coverage ratio this year. BBTN is also favored for its high earnings visibility from govt public housing program. We think the potential impact from govt funding scheme change into 60:40 (vs. current 90:10) would be muted as BBTN

still have a room for 50bps TD rate cut. Lastly, we recommend to own BNLI as it is expected to benefit greatly from higher coal price.

Banks Tactical Downgrade to Neutral

Companies Data

TICKER

Price

(IDR) Mkt. Cap

TP Ups.

Rec. EPS Growth(%) ROE(%) P/BV (X)

28-Nov (IDR bn) (%) 2016 2017 2016 2017 2016 2017

BBRI 10,475 255,825 11,900 13.6 Buy (2.5) 7.3 18.6 17.5 1.9 1.7

BBNI 5,075 93,696 6,000 18.2 Buy 11.2 38.5 11.8 16.5 1.1 1.1

BBTN 1,600 16,775 1,850 15.6 Buy 29.5 19.2 12.6 13.4 0.9 0.8

BNLI 530 11,722 600 13.2 Buy NM NM (4.3) 7.1 0.5 0.5

BBCA 14,375 350,872 15,000 4.3 Neutral 5.8 15.1 18.3 18.0 3.4 2.9

BMRI 10,150 234,465 10,500 3.4 Neutral (28.1) 74.3 9.6 17.4 1.5 1.6

BNGA 785 19,531 800 1.9 Neutral 250.6 128.3 4.9 10.0 0.6 0.6

BDMN 3,290 31,218 2,000 (39.2) Sell 37.3 10.9 9.0 9.3 0.9 0.8

PNBN 720 17,163 700 (2.8) Sell 54.9 14.6 7.0 7.5 0.6 0.5

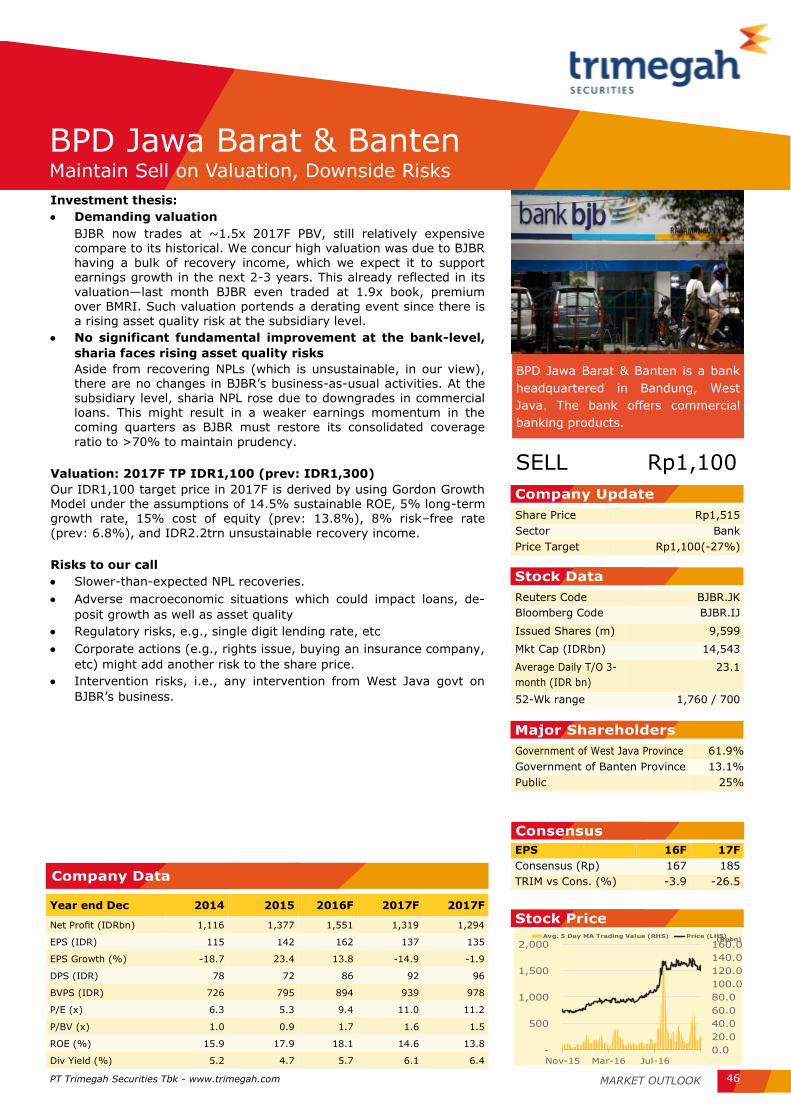

BJBR 1,515 14,543 1,100 (27.4) Sell 12.6 (14.9) 18.1 14.6 1.7 1.6

BTPN 2,740 15,842 2,600 (5.1) Sell 3.8 8.1 11.7 11.2 1.0 0.9

BJTM 505 7,472 420 (16.8) Sell 12.7 7.0 15.0 15.1 1.1 1.1

Angga Aditya Assaf

Neutral

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 22

Source: Bloomberg. Companies. Trimegah Research

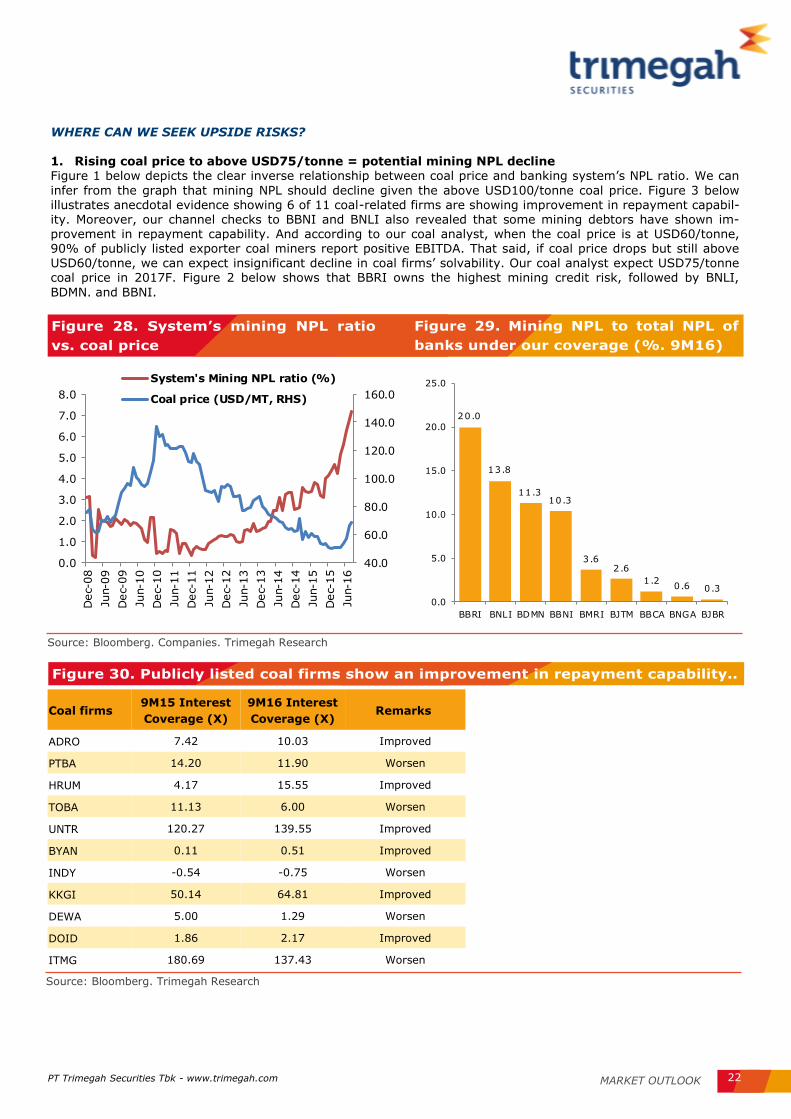

WHERE CAN WE SEEK UPSIDE RISKS? 1. Rising coal price to above USD75/tonne = potential mining NPL decline Figure 1 below depicts the clear inverse relationship between coal price and banking system’s NPL ratio. We can

infer from the graph that mining NPL should decline given the above USD100/tonne coal price. Figure 3 below illustrates anecdotal evidence showing 6 of 11 coal-related firms are showing improvement in repayment capabil-ity. Moreover, our channel checks to BBNI and BNLI also revealed that some mining debtors have shown im-provement in repayment capability. And according to our coal analyst, when the coal price is at USD60/tonne, 90% of publicly listed exporter coal miners report positive EBITDA. That said, if coal price drops but still above

USD60/tonne, we can expect insignificant decline in coal firms’ solvability. Our coal analyst expect USD75/tonne coal price in 2017F. Figure 2 below shows that BBRI owns the highest mining credit risk, followed by BNLI,

BDMN. and BBNI.

Figure 28. System’s mining NPL ratio

vs. coal price

Figure 29. Mining NPL to total NPL of

banks under our coverage (%. 9M16)

Source: Bloomberg. Trimegah Research

Figure 30. Publicly listed coal firms show an improvement in repayment capability..

Coal firms 9M15 Interest

Coverage (X)

9M16 Interest

Coverage (X) Remarks

ADRO 7.42 10.03 Improved

PTBA 14.20 11.90 Worsen

HRUM 4.17 15.55 Improved

TOBA 11.13 6.00 Worsen

UNTR 120.27 139.55 Improved

BYAN 0.11 0.51 Improved

INDY -0.54 -0.75 Worsen

KKGI 50.14 64.81 Improved

DEWA 5.00 1.29 Worsen

DOID 1.86 2.17 Improved

ITMG 180.69 137.43 Worsen

40.0

60.0

80.0

100.0

120.0

140.0

160.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

Dec-

08

Jun-0

9

Dec-

09

Jun-1

0

Dec-

10

Jun-1

1

Dec-

11

Jun-1

2

Dec-

12

Jun-1

3

Dec-

13

Jun-1

4

Dec-

14

Jun-1

5

Dec-

15

Jun-1

6

System's Mining NPL ratio (%)

Coal price (USD/MT, RHS)

20.0

13.8

11.310.3

3.62.6

1.20.6 0.3

0.0

5.0

10.0

15.0

20.0

25.0

BBRI BNLI BDMN BBNI BMRI BJTM BBCA BNGA BJBR

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 23

Source: BI. OJK. Trimegah Research

WHERE CAN WE SEEK UPSIDE RISKS? … (CONT’D) 2. Rising CCI provides growth opportunity for consumer loans As illustrated in the Figure 4 and 5 below, we are seeing potential reversal in consumer loans growth from: 1)

rising consumer confidence index (CCI), and 2) declining interest rates: in general, consumer loans correlate negatively with benchmark interest rate during the past 3 years. Subsequently. Figure 6 complements the argu-ment that there will be potential uptick in vehicle loan growth given the recent uptick in 4W and 2W sales growth. Note that based on the graph presented, automotive sales growth tend to move ahead of vehicle loan growth.

102

104

106

108

110

112

114

116

118

Dec-1

5

Jan-1

6

Feb-1

6

Mar-

16

Apr-

16

May-1

6

Jun-1

6

Jul-

16

Aug-1

6

Sep-1

6

Oct-

16

Figure 31. Consumer Confidence Index

(CCI)

Figure 32. BI Rate vs. consumer loans

growth trend (%)

Source: Gaikindo. Trimegah Research

Figure 33. Auto sales growth trend vs. vehicle loan YoY growth

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

5.5

6.0

6.5

7.0

7.5

8.0

Aug-12 Aug-13 Aug-14 Aug-15

BI Rate (LHS) Mortgage

Vehicles Multipurpose + others

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

Aug-1

2

Oct-

12

Dec-

12

Feb-1

3

Apr-

13

Jun-1

3

Aug-1

3

Oct-

13

Dec-

13

Feb-1

4

Apr-

14

Jun-1

4

Aug-1

4

Oct-

14

Dec-

14

Feb-1

5

Apr-

15

Jun-1

5

Aug-1

5

Oct-

15

Dec-

15

Feb-1

6

Apr-

16

Jun-1

6

4W sales YoY growth 2W sales YoY growth Vehicle loan growth (YoY, RHS))

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 24

STOCKS TO PICK… BBNI (Buy, TP IDR5,900) Reason: share price had been under punishment in the recent months due to asset quality concerns and negative

market perception about loan to VIVA, a Bakrie company. However. our recent meeting with the management revealed that the majority of small and medium debtors are having collateral with >3x interest coverage, which should restore investors confidence. We therefore concur that BBNI may report good earnings momentum in the coming quarters, with valuation remains the cheapest among big cap banks. poising to outperform BMRI and

BBCA in the near-term. In addition, VIVA is fundamentally sound now as shown by 1.2x interest coverage ratio (vs. 0.9x in 9M15). Therefore, the weak share price is more sentiment-related than fundamental.

BBTN (Buy, TP IDR1,850) Reason: the company is expected to report ~20% EPS growth in 2017-18F on the back of the continuous govt public housing program. We have already accounted the potential funding change scheme into 60:40 but we believe the management would encounter the impact by cutting TD rate by 50bps. therefore less NIM concerns. Currently, BBTN trades at 0.8x 2017F PBV. undemanding enough for the stock that offers 13-14% ROE in the next couple of years (vs. 11.9% in 9M16).

BNLI (Buy, TP IDR600) Reason: We admit that this a quite exotic stock to pick. BNLI is relatively under-owned due to its asset quality

problems. However, we see BNLI’s earnings to start turning around in 2017F from gradual NPL improvement. Based on its latest disclosure, BNLI owns the highest mining credit risk among small banks. Therefore, the im-provement in coal price should have a positive impact toward earnings and share price. Our recent talk with the company suggests that some of its mining debtors have shown an improved repayment capability. Thus, we may

see more loan upgrades next year. We also tactically upgrade BBRI to Buy (TP: IDR11,900) as share price have weaken in the past few days, opening 13% potential upside to our TP. However, downside risks remain on govt to lower KUR lending rate to 7% while at the same time, there is a possibility of kitchen-sinking event as current CEO will depart in 1Q17—the same event occurred in BBNI and BMRI post CEO changes.

Risks to our call

1). Sharp increase in Fed Fund Rate (FFR). 2) tightening in liquidity. 3) coal price drop to below USD60/tonne level. and 4) any adverse macroeconomic changes.

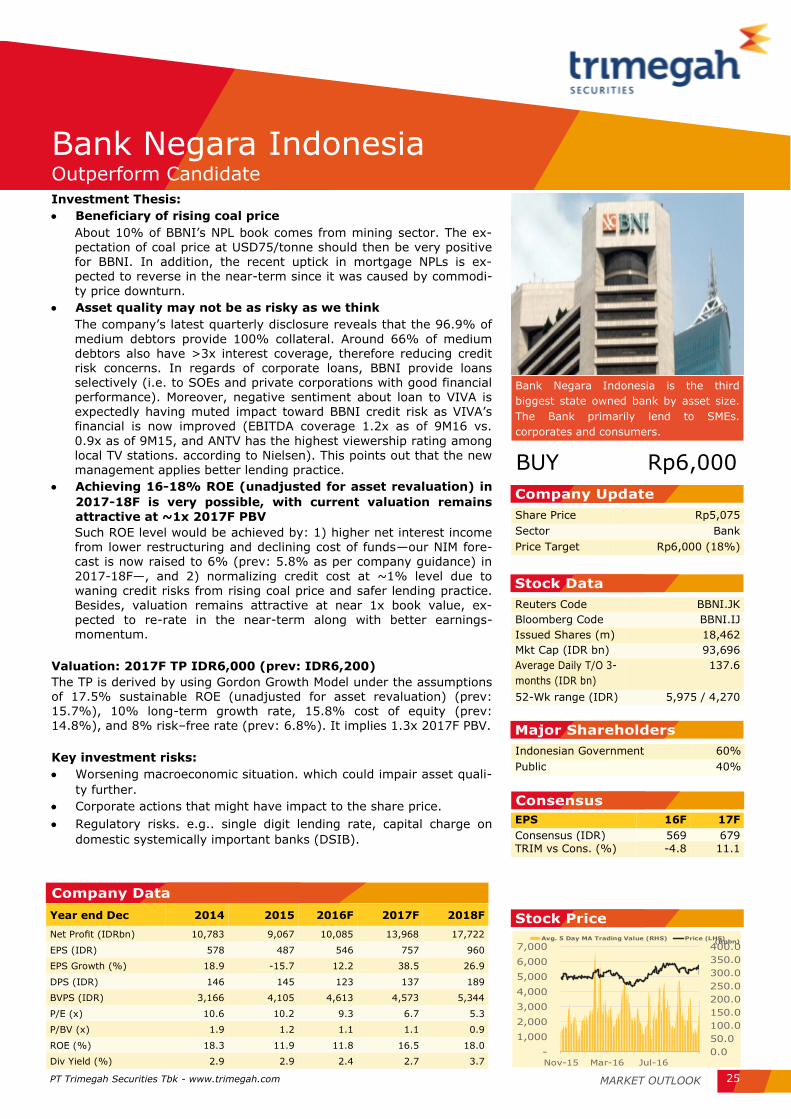

MARKET OUTLOOK PT Trimegah Securities Tbk - www.trimegah.com 25

Investment Thesis:

Beneficiary of rising coal price

About 10% of BBNI’s NPL book comes from mining sector. The ex-pectation of coal price at USD75/tonne should then be very positive

for BBNI. In addition, the recent uptick in mortgage NPLs is ex-pected to reverse in the near-term since it was caused by commodi-

ty price downturn.

Asset quality may not be as risky as we think

The company’s latest quarterly disclosure reveals that the 96.9% of

medium debtors provide 100% collateral. Around 66% of medium debtors also have >3x interest coverage, therefore reducing credit risk concerns. In regards of corporate loans, BBNI provide loans selectively (i.e. to SOEs and private corporations with good financial performance). Moreover, negative sentiment about loan to VIVA is expectedly having muted impact toward BBNI credit risk as VIVA’s financial is now improved (EBITDA coverage 1.2x as of 9M16 vs.

0.9x as of 9M15, and ANTV has the highest viewership rating among local TV stations. according to Nielsen). This points out that the new management applies better lending practice.

Achieving 16-18% ROE (unadjusted for asset revaluation) in

2017-18F is very possible, with current valuation remains

attractive at ~1x 2017F PBV

Such ROE level would be achieved by: 1) higher net interest income from lower restructuring and declining cost of funds—our NIM fore-cast is now raised to 6% (prev: 5.8% as per company guidance) in

2017-18F—, and 2) normalizing credit cost at ~1% level due to waning credit risks from rising coal price and safer lending practice. Besides, valuation remains attractive at near 1x book value, ex-

pected to re-rate in the near-term along with better earnings-momentum.

Valuation: 2017F TP IDR6,000 (prev: IDR6,200)

The TP is derived by using Gordon Growth Model under the assumptions of 17.5% sustainable ROE (unadjusted for asset revaluation) (prev: 15.7%), 10% long-term growth rate, 15.8% cost of equity (prev: 14.8%), and 8% risk–free rate (prev: 6.8%). It implies 1.3x 2017F PBV.

Key investment risks:

Worsening macroeconomic situation. which could impair asset quali-

ty further.

Corporate actions that might have impact to the share price.

Regulatory risks. e.g.. single digit lending rate, capital charge on

domestic systemically important banks (DSIB).

Bank Negara Indonesia is the third

biggest state owned bank by asset size.

The Bank primarily lend to SMEs.

corporates and consumers.

Share Price Rp5,075

Sector Bank

Price Target Rp6,000 (18%)

Year end Dec 2014 2015 2016F 2017F 2018F

Net Profit (IDRbn) 10,783 9,067 10,085 13,968 17,722

EPS (IDR) 578 487 546 757 960

EPS Growth (%) 18.9 -15.7 12.2 38.5 26.9

DPS (IDR) 146 145 123 137 189

BVPS (IDR) 3,166 4,105 4,613 4,573 5,344

P/E (x) 10.6 10.2 9.3 6.7 5.3

P/BV (x) 1.9 1.2 1.1 1.1 0.9

ROE (%) 18.3 11.9 11.8 16.5 18.0

Div Yield (%) 2.9 2.9 2.4 2.7 3.7

Bank Negara Indonesia Outperform Candidate

BUY Rp6,000

Reuters Code BBNI.JK

Bloomberg Code BBNI.IJ

Issued Shares (m) 18,462

Mkt Cap (IDR bn) 93,696

Average Daily T/O 3-

months (IDR bn)

137.6

52-Wk range (IDR) 5,975 / 4,270

Indonesian Government 60%

Public 40%

EPS 16F 17F

Consensus (IDR) 569 679

TRIM vs Cons. (%) -4.8 11.1

Company Update

Stock Data

Major Shareholders

Consensus

Stock Price

Company Data

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Nov-15 Mar-16 Jul-16

(Rpbn)Avg. 5 Day MA Trading Value (RHS) Price (LHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 26

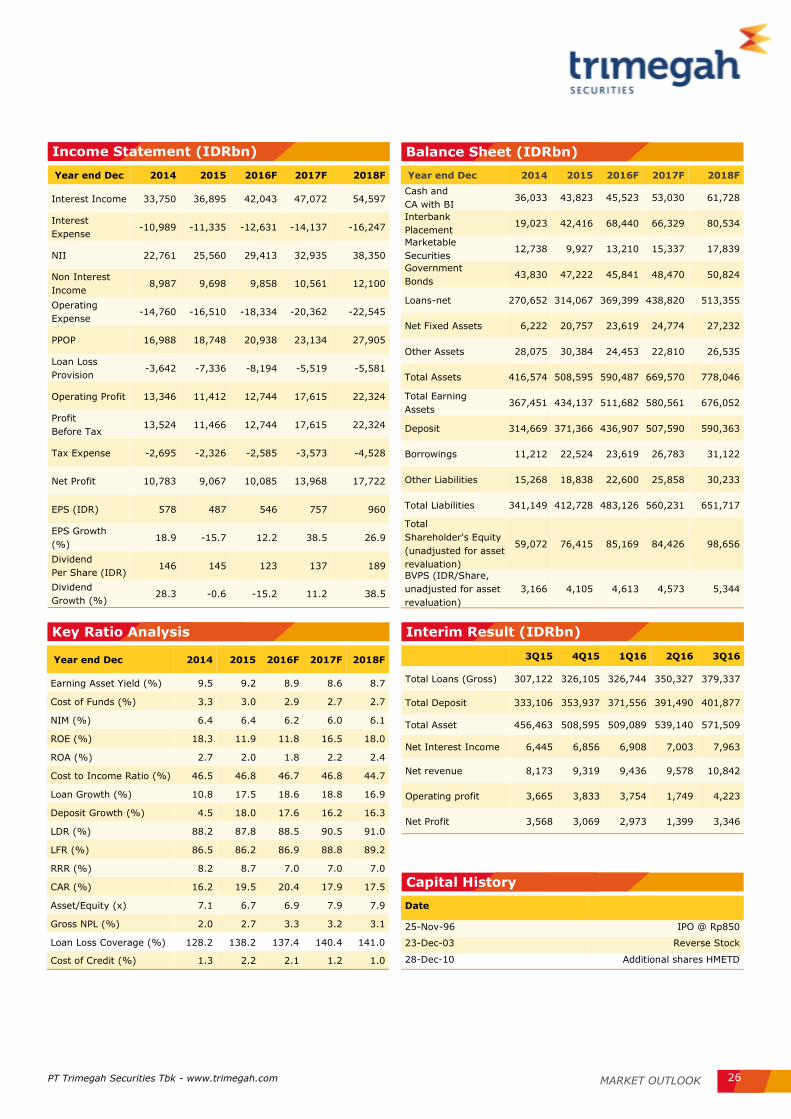

Income Statement (IDRbn)

Year end Dec 2014 2015 2016F 2017F 2018F

Interest Income 33,750 36,895 42,043 47,072 54,597

Interest

Expense -10,989 -11,335 -12,631 -14,137 -16,247

NII 22,761 25,560 29,413 32,935 38,350

Non Interest

Income 8,987 9,698 9,858 10,561 12,100

Operating

Expense -14,760 -16,510 -18,334 -20,362 -22,545

PPOP 16,988 18,748 20,938 23,134 27,905

Loan Loss

Provision -3,642 -7,336 -8,194 -5,519 -5,581

Operating Profit 13,346 11,412 12,744 17,615 22,324

Profit

Before Tax 13,524 11,466 12,744 17,615 22,324

Tax Expense -2,695 -2,326 -2,585 -3,573 -4,528

Net Profit 10,783 9,067 10,085 13,968 17,722

EPS (IDR) 578 487 546 757 960

EPS Growth

(%) 18.9 -15.7 12.2 38.5 26.9

Dividend

Per Share (IDR) 146 145 123 137 189

Dividend

Growth (%) 28.3 -0.6 -15.2 11.2 38.5

Balance Sheet (IDRbn)

Year end Dec 2014 2015 2016F 2017F 2018F

Cash and

CA with BI 36,033 43,823 45,523 53,030 61,728

Interbank

Placement 19,023 42,416 68,440 66,329 80,534

Marketable

Securities 12,738 9,927 13,210 15,337 17,839

Government

Bonds 43,830 47,222 45,841 48,470 50,824

Loans-net 270,652 314,067 369,399 438,820 513,355

Net Fixed Assets 6,222 20,757 23,619 24,774 27,232

Other Assets 28,075 30,384 24,453 22,810 26,535

Total Assets 416,574 508,595 590,487 669,570 778,046

Total Earning

Assets 367,451 434,137 511,682 580,561 676,052

Deposit 314,669 371,366 436,907 507,590 590,363

Borrowings 11,212 22,524 23,619 26,783 31,122

Other Liabilities 15,268 18,838 22,600 25,858 30,233

Total Liabilities 341,149 412,728 483,126 560,231 651,717

Total

Shareholder's Equity

(unadjusted for asset

revaluation)

59,072 76,415 85,169 84,426 98,656

BVPS (IDR/Share,

unadjusted for asset

revaluation)

3,166 4,105 4,613 4,573 5,344

Key Ratio Analysis

Year end Dec 2014 2015 2016F 2017F 2018F

Earning Asset Yield (%) 9.5 9.2 8.9 8.6 8.7

Cost of Funds (%) 3.3 3.0 2.9 2.7 2.7

NIM (%) 6.4 6.4 6.2 6.0 6.1

ROE (%) 18.3 11.9 11.8 16.5 18.0

ROA (%) 2.7 2.0 1.8 2.2 2.4

Cost to Income Ratio (%) 46.5 46.8 46.7 46.8 44.7

Loan Growth (%) 10.8 17.5 18.6 18.8 16.9

Deposit Growth (%) 4.5 18.0 17.6 16.2 16.3

LDR (%) 88.2 87.8 88.5 90.5 91.0

LFR (%) 86.5 86.2 86.9 88.8 89.2

RRR (%) 8.2 8.7 7.0 7.0 7.0

CAR (%) 16.2 19.5 20.4 17.9 17.5

Asset/Equity (x) 7.1 6.7 6.9 7.9 7.9

Gross NPL (%) 2.0 2.7 3.3 3.2 3.1

Loan Loss Coverage (%) 128.2 138.2 137.4 140.4 141.0

Cost of Credit (%) 1.3 2.2 2.1 1.2 1.0

Interim Result (IDRbn)

3Q15 4Q15 1Q16 2Q16 3Q16

Total Loans (Gross) 307,122 326,105 326,744 350,327 379,337

Total Deposit 333,106 353,937 371,556 391,490 401,877

Total Asset 456,463 508,595 509,089 539,140 571,509

Net Interest Income 6,445 6,856 6,908 7,003 7,963

Net revenue 8,173 9,319 9,436 9,578 10,842

Operating profit 3,665 3,833 3,754 1,749 4,223

Net Profit 3,568 3,069 2,973 1,399 3,346

Capital History

Date

25-Nov-96 IPO @ Rp850

23-Dec-03 Reverse Stock

28-Dec-10 Additional shares HMETD

MARKET OUTLOOK PT Trimegah Securities Tbk - www.trimegah.com 27

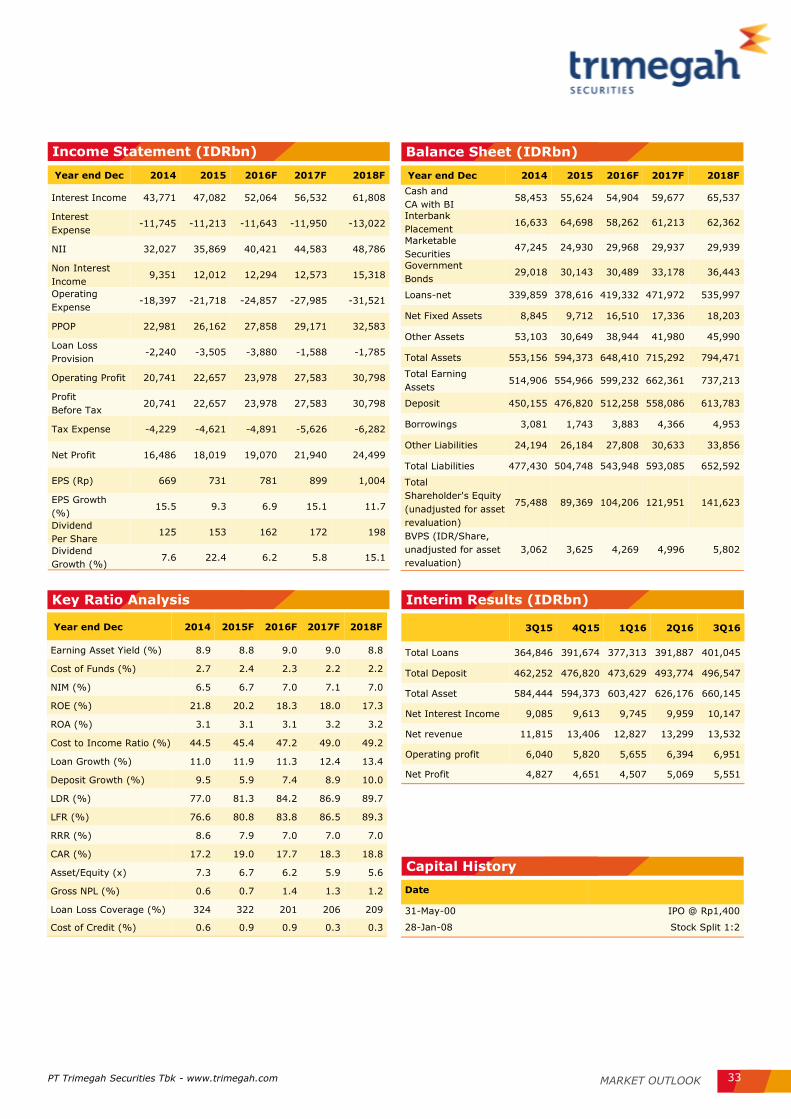

Investment thesis:

Lowering 2016F EPS by 16% on rising NPL outlook in 4Q16.

Recently, CEO mentioned in the news that BMRI will raise FY16

provisioning estimates to IDR22trn (vs. our previous estimates of

IDR18.3trn). We also raised our 2016F NPL assumption to 4.2%

(prev: 3.9%) and write-off to IDR11trn (prev: IDR8.8trn) according-

ly as per company confirmation. As a result, our 2016F EPS esti-

mates is lowered by 16% and our 2017F TP is cut to IDR10,500.

Valuation: 2017F TP IDR10,500 (prev: IDR12,000)

The TP is derived by using Gordon Growth Model under the assumptions

of 17.7% sustainable ROE (unadjusted for asset revaluation) (prev:

15.3%), 10% long-term growth rate, 14.6% cost of equity (prev:

13.3%), and 8% risk–free rate (prev: 8%). Leaving only 3% potential

upside to our TP, we therefore downgrade BMRI’s rating into Neutral

(prev: Buy).

Key investment risks:

Worsening macroeconomic situation, which could impair asset quali-

ty further.

Corporate actions that might have impact to the share price. distrib-

uting special dividends, etc.

Regulatory risks. e.g., single digit lending rate, capital charge on

domestic systemically important banks (DSIB).

Bank Mandiri is Indonesia’s biggest

bank by assets. The state owned

bank is focused on wholesale and re-

tail lending and funding

Share Price Rp10,150

Sector Bank

Price Target Rp10,500 (3%)

Year end Dec 2014 2015 2016F 2017F 2018F

Net Profit (IDRbn) 19,872 20,335 14,625 25,485 30,638

EPS (IDR) 852 872 633 1,103 1,326

EPS Growth (%) 9.2 2.3 -27.4 74.3 20.2

DPS (IDR) 234 213 264 253 276

BVPS (IDR) 4,400 5,017 6,609 6,336 7,387

P/E (x) 12.7 10.6 16.0 9.2 7.7

P/BV (x) 2.4 1.8 1.5 1.6 1.4

ROE (%) 19.4 17.4 9.6 17.4 18.0

Div Yield (%) 2.3 2.1 2.6 2.5 2.7

Bank Mandiri Poor Earnings Momentum in the Near-term

NEUTRAL Rp10,500

Reuters Code BMRI.JK

Bloomberg Code BMRI.IJ

Issued Shares (m) 23,100

Mkt Cap (IDRbn) 234,465

Avg. Value Daily

3-month (IDRbn)

243.6

52-Wk range (IDR) 11,950 / 8,175

Indonesian Government 60%

Public 40%

EPS 16F 17F

Consensus (Rp) 739 927

TRIM vs Cons. (%) 1.0 16.1

Company Update

Stock Data

Major Shareholders

Consensus

Stock Price

Company Data

0.0

100.0

200.0

300.0

400.0

500.0

600.0

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Nov-15 Mar-16 Jul-16

(Rpbn)Avg. 5 Day MA Trading Value (RHS) Price (LHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 28

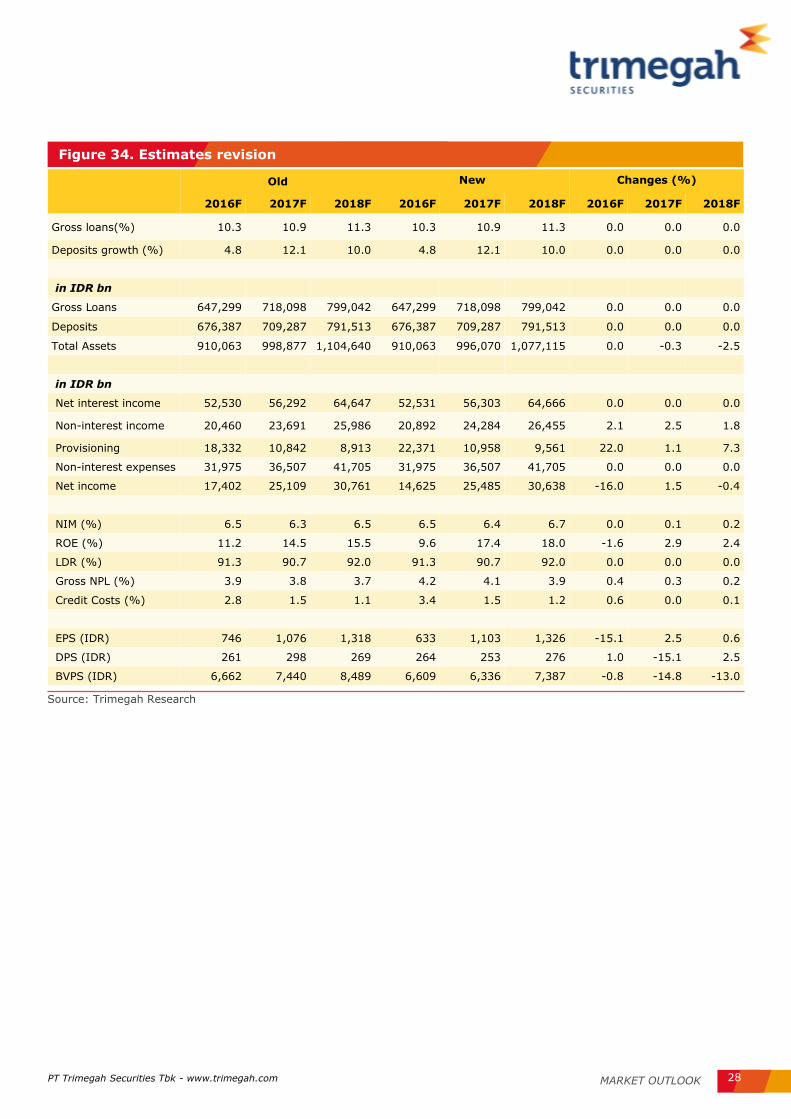

Old New Changes (%)

2016F 2017F 2018F 2016F 2017F 2018F 2016F 2017F 2018F

Gross loans(%) 10.3 10.9 11.3 10.3 10.9 11.3 0.0 0.0 0.0

Deposits growth (%) 4.8 12.1 10.0 4.8 12.1 10.0 0.0 0.0 0.0

in IDR bn

Gross Loans 647,299 718,098 799,042 647,299 718,098 799,042 0.0 0.0 0.0

Deposits 676,387 709,287 791,513 676,387 709,287 791,513 0.0 0.0 0.0

Total Assets 910,063 998,877 1,104,640 910,063 996,070 1,077,115 0.0 -0.3 -2.5

in IDR bn

Net interest income 52,530 56,292 64,647 52,531 56,303 64,666 0.0 0.0 0.0

Non-interest income 20,460 23,691 25,986 20,892 24,284 26,455 2.1 2.5 1.8

Provisioning 18,332 10,842 8,913 22,371 10,958 9,561 22.0 1.1 7.3

Non-interest expenses 31,975 36,507 41,705 31,975 36,507 41,705 0.0 0.0 0.0

Net income 17,402 25,109 30,761 14,625 25,485 30,638 -16.0 1.5 -0.4

NIM (%) 6.5 6.3 6.5 6.5 6.4 6.7 0.0 0.1 0.2

ROE (%) 11.2 14.5 15.5 9.6 17.4 18.0 -1.6 2.9 2.4

LDR (%) 91.3 90.7 92.0 91.3 90.7 92.0 0.0 0.0 0.0

Gross NPL (%) 3.9 3.8 3.7 4.2 4.1 3.9 0.4 0.3 0.2

Credit Costs (%) 2.8 1.5 1.1 3.4 1.5 1.2 0.6 0.0 0.1

EPS (IDR) 746 1,076 1,318 633 1,103 1,326 -15.1 2.5 0.6

DPS (IDR) 261 298 269 264 253 276 1.0 -15.1 2.5

BVPS (IDR) 6,662 7,440 8,489 6,609 6,336 7,387 -0.8 -14.8 -13.0

Figure 34. Estimates revision

Source: Trimegah Research

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 29

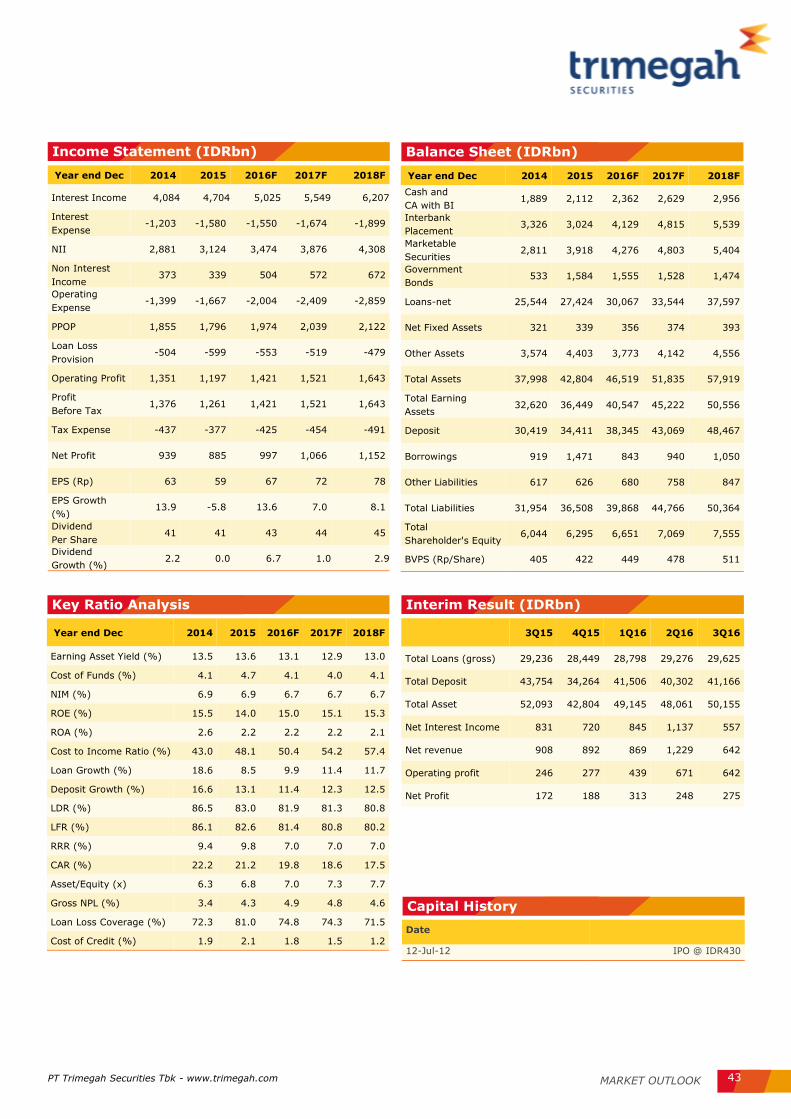

Income Statement (IDRbn)

Year end Dec 2014 2015 2016F 2017F 2018F

Interest Income 62,638 71,570 78,347 83,520 94,659

Interest

Expense -23,506 -26,207 -25,816 -27,217 -29,992

NII 39,132 45,363 52,531 56,303 64,666

Non Interest

Income 17,749 21,773 20,892 24,284 26,455

Operating

Expense -25,374 -28,755 -31,975 -36,507 -41,705

PPOP 31,507 38,382 41,448 44,080 49,416

Loan Loss

Provision -5,529 -12,043 -22,371 -10,958 -9,561

Operating Profit 25,978 26,339 19,078 33,123 39,855

Profit

Before Tax 26,008 26,369 18,992 33,095 39,786

Tax Expense -5,353 -5,217 -3,757 -6,548 -7,871

Net Profit 19,872 20,335 14,625 25,485 30,638

EPS (IDR) 852 872 633 1,103 1,326

EPS Growth

(%) 9.2 2.3 -27.4 74.3 20.2

Dividend

Per Share 234 213 264 253 276

Dividend

Growth (%) 17.4 -9.0 24.0 -4.1 8.9

Balance Sheet (IDRbn)

Year end Dec 2014 2015 2016F 2017F 2018F

Cash and

CA with BI 71,303 81,423 72,195 79,995 88,133

Interbank

Placement 70,101 47,473 82,956 83,030 102,638

Marketable

Securities 40,465 43,642 48,806 50,399 55,369

Government

Bonds 86,154 103,869 81,559 87,744 88,475

Loans-net 505,395 564,394 612,345 680,039 758,291

Net Fixed Assets 8,929 9,762 36,762 37,497 37,872

Other Assets 72,692 59,501 61,447 58,412 58,803

Total Assets 855,040 910,063 996,070 1,077,115 1,189,581

Total Earning

Assets 728,519 768,560 836,654 913,207 1,017,832

Deposit 636,382 676,387 709,287 791,513 868,988

Borrowings 24,227 33,765 35,762 36,535 40,690

Other Liabilities 89,586 80,420 95,934 100,279 106,847

Total Liabilities 750,195 790,572 840,983 928,327 1,016,526

Total

Shareholder's Equity

(unadjusted for

asset revaluation)

102,658 117,070 152,665 146,367 170,634

BVPS (IDR/Share,

unadjusted for asset

revaluation)

4,400 5,017 6,609 6,336 7,387

Key Ratio Analysis

Year end Dec 2014 2015 2016F 2017F 2018F

Earning Asset Yield (%) 9.2 9.6 9.8 9.5 9.8

Cost of Funds (%) 3.7 3.7 3.4 3.3 3.3

NIM (as calculated, in%) 5.8 6.1 6.5 6.4 6.7

ROE (%) 19.4 17.4 9.6 17.4 18.0

ROA (%) 2.3 2.2 1.5 2.4 2.6

Cost to Income Ratio (%) 44.6 42.8 43.5 45.3 45.8

Loan Growth (%) 12.0 12.2 10.3 10.9 11.3

Deposit Growth (%) 14.6 6.7 4.8 12.1 10.0

LDR (%) 82.2 86.7 91.3 90.7 92.0

LFR (%) 81.9 86.4 90.1 89.3 90.4

RRR (%) 8.7 9.0 7.0 7.0 7.0

CAR (%) 16.3 18.0 21.4 21.5 21.3

Asset/Equity (x) 8.3 7.8 6.5 7.4 7.0

Gross NPL (%) 2.2 2.6 4.2 4.1 3.9

Loan Loss Coverage (%) 157 145 128 129 132

Cost of credit (%) 1.0 2.0 3.4 1.5 1.2

Interim Result (IDRbn)

3Q15 4Q15 1Q16 2Q16 3Q16

Total Loans (Gross) 552,660 586,675 564,705 597,015 637,500

Total Deposit 602,656 622,332 655,063 691,359 690,507

Total Asset 905,759 910,063 906,739 971,444 975,163

Net Interest Income 11,252 12,911 12,331 11,912 14,413

Net revenue 17,512 19,086 17,225 17,525 20,163

Operating profit 5,800 7,455 5,071 4,390 6,501

Net Profit 4,658 5,752 3,817 3,263 4,933

Capital History

Date

14-Jul-03 IPO @ IDR675

01-Mar-11 Additional Share HMETD

MARKET OUTLOOK PT Trimegah Securities Tbk - www.trimegah.com 30

Investment thesis:

Current CEO is departing, kitchen-sinking event is possible

The company will replace its current CEO, Mr, Asmawi Syam, who will end his term at around 1Q17, Thus, there is a possibility of

kitchen-sinking event next year, as also occured in BBNI and BMRI, Despite its highest upside risk from rising coal price (BBRI’s mining

NPL accounts for 20% of total NPL book), market is likely to expect larger downgrades in 2017F. We conservatively raised our credit cost estimates by 60bps next year, translated into dropping ROE to 17.5%, There is further downside risk if turns out that 2017F NPL ratio is higher than our expectation (2.3%),

There is also a risk that KUR lending rate to be set at 7% (vs,

currently 9%)

With KUR interest subsidy budget being cut to IDR9,5trn while na-tion-wide disbursement target increased to IDR120trn (vs, this

year’s IDR100trn), there is NIM pressure risk in our view. We con-servatively forecasted lower NIM in 2017F (8.1%) from currently 8.3%. However, if govt stops KUR program in 2018F, then NIM will likely to go up again above 8.3% as we assume BBRI would return

to conventional micro loans as its main engine of growth.

Valuation: 2017F TP IDR11,900 (unchanged), tactical upgrade to Buy

The TP is derived by using Gordon Growth Model under the assumptions of 19.4% sustainable ROE (unadjusted for asset revaluation) (prev: 18%), 10% long-term growth rate, 15.8% cost of equity (prev: 14.6%),

and 8% risk–free rate (prev: 6.8%). Due to 14% potential upside to our

TP, we therefore upgrade BBRI rating into Buy (prev: Neutral).

Key investment risks:

Worsening macroeconomic situation, which could impair asset quali-

ty further,

Corporate actions that might have impact to the share price,

Regulatory risks, e,g,, single digit lending rate, capital charge on

domestic systemically important banks (DSIB),

BBRI is Indonesia’s biggest MSME lender

with the most extensive network of

branches and outlets throughout the

country, The bank also offers corporate

and consumer loans,

Share Price Rp10,475

Sector Bank

Price Target Rp11,900 (14%)

Year end Dec 2014 2015 2016F 2017F 2018F

Net Profit (IDRbn) 24,215 25,398 24,772 26,585 35,271

EPS (IDR) 983 1,030 1,014 1,089 1,444

EPS Growth (%) 13.6 4.9 -1.6 7.3 32.7

DPS (IDR) 258 258 298 304 272

BVPS (IDR) 3,959 4,578 5,453 6,237 7,409

P/E (x) 11.9 11.1 10.0 9.3 7.0

P/BV (x) 2.9 2.5 1.9 1.6 1.4

ROE (%) 24.8 22.5 18.6 17.5 19.5

Div Yield (%) 2.5 2.5 2.9 3.0 2.7

Bank Rakyat Indonesia Tactical Upgrade into Buy

BUY Rp11,900

Reuters Code BBRI,JK

Bloomberg Code BBRI,IJ

Issued Shares (m) 24,422

Mkt Cap (IDRbn) 255,825

Avg, Value Daily

3-month (IDRbn)

266.4

52-Wk range (IDR) 12,975 / 9,525

Indonesian Government 57.8%

Public 42.2%

EPS 16F 17F

Consensus (Rp) 1,037 1,173

TRIM vs Cons, (%) -2.3 -6.7

Company Update

Stock Data

Major Shareholders

Consensus

Stock Price

Company Data

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Nov-15 Mar-16 Jul-16

(Rpbn)Avg. 5 Day MA Trading Value (RHS) Price (LHS)

PT Trimegah Securities Tbk - www.trimegah.com MARKET OUTLOOK 31

Income Statement (IDRbn)

Year end Dec 2014 2015 2016F 2017F 2018F

Interest Income 75,122 85,434 94,200 103,772 120,000

Interest

Expense -23,680 -27,154 -27,796 -29,412 -32,926

NII 51,442 58,280 66,404 74,361 87,074

Non Interest

Income 9,299 12,398 13,559 14,422 16,304

Operating

Expense -26,715 -31,265 -36,293 -41,579 -47,647

PPOP 34,026 39,413 43,670 47,203 55,731

Loan Loss

Provision -5,719 -8,900 -12,977 -13,191 -10,611

Operating Profit 28,307 30,513 30,693 34,012 45,120

Profit

Before Tax 30,804 32,494 31,693 34,012 45,120

Tax Expense -6,578 -7,083 -6,909 -7,414 -9,835

Net Profit 24,215 25,398 24,772 26,585 35,271

EPS (IDR) 983 1,030 1,014 1,089 1,444

EPS Growth

(%) 13.6 4.9 -1.6 7.3 32.7

Dividend

Per Share 258 258 298 304 272

Dividend

Growth (%) 14.4 0.0 15.6 2.2 -10.6

Balance Sheet (IDRbn)

Year end Dec 2014 2015F 2016F 2017F 2018F

Cash and

CA with BI 73,654 90,489 80,826 92,639 107,473

Interbank

Placement 62,035 49,835 80,420 119,277 169,703

Marketable

Securities 84,168 124,874 76,984 88,178 92,177

Government

Bonds 4,304 3,816 4,453 5,109 4,953

Loans-net 479,211 547,318 626,027 695,870 795,461

Net Fixed Assets 5,917 8,039 24,936 26,143 27,687

Other Assets 92,665 54,055 103,776 109,442 120,976

Total Assets 801,955 878,426 997,422 1,136,658 1,318,430

Total Earning

Assets 694,877 751,955 861,738 983,776 1,143,718

Deposit 622,322 668,995 763,458 874,676 1,016,078

Borrowings 24,987 35,480 42,168 47,018 49,510

Other Liabilities 56,909 60,823 58,330 62,344 71,598

Total Liabilities 704,218 765,299 863,956 984,038 1,137,186

Total

Shareholder's

Equity

(unadjusted for

asset revalua-

97,560 112,833 133,172 152,325 180,950

BVPS (IDR/

Share, unadjust-

ed for asset

revaluation)

3,959 4,578 5,453 6,237 7,409

Key Ratio Analysis

Year end Dec 2013 2014 2015F 2016F 2017F

Earning Asset Yield (%) 12.2 11.9 11.7 11.2 11.3

Cost of Funds (%) 3.9 3.9 3.6 3.3 3.2

NIM (%) 8.3 8.1 8.2 8.1 8.2

ROE (%) 24.8 22.5 18.6 17.5 19.5

ROA (%) 3.4 3.0 2.6 2.5 2.9

Cost to Income Ratio (%) 44.0 44.2 45.4 46.8 46.1

Loan Growth (%) 14.0 14.0 14.9 11.5 14.1