Embed Size (px)

Citation preview

Integration of Renewables into the Grid

About Us

SEPA’s mission is to facilitate the utility industry’s smart transition to a clean energy future through

education, research, and collaboration.

www.sepapower.org

www.sepapower.org

Neutral Platform for Stakeholder Collaboration

Words most frequently used to

describe SEPA:

• Trustworthy• Balanced• Strategic

• Collaborative• Accessible

• Informational• Knowledgeable

• Friendly

2015 survey with 800 member and non-member responses

www.sepapower.org

The “Smart” Transition

Solar Snapshot

www.sepapower.org

Solar grows;utilities respond

Mainstream Utility Solar Strategies:

• Large Scale Solar PV in IRPs

• Redesigning Rate Structures

• Exploring Community Solar

www.sepapower.org

2015 Pricing

Sources: SEPA “2015 Utility Solar Marketplace Snapshot,” Data from EnergySage & Mercatus

US pricing varies significantly by state, and is generally higher than many countries by as much as 50% in the residential market

• Residential pricing has been quoted as low as $2.50/W

• FirstSolar expects $1/W for large scale by 2017

www.sepapower.org

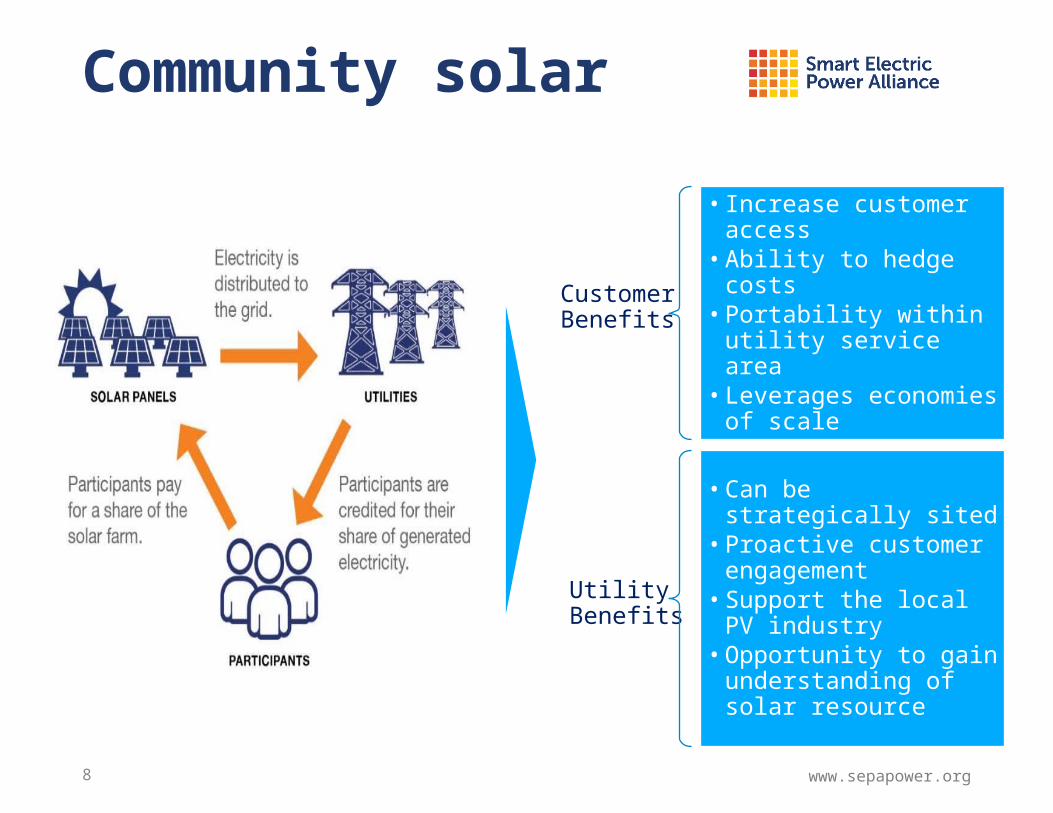

Community solar

8

Customer Benefits

Utility Benefits

• Increase customer access

• Ability to hedge costs• Portability within utility

service area• Leverages economies of

scale

• Can be strategically sited• Proactive customer

engagement• Support the local PV

industry• Opportunity to gain

understanding of solar resource

www.sepapower.org

Rate Reform Strategies

Continued Storage Growth

www.sepapower.org

Storage: Multiple Values

www.sepapower.org

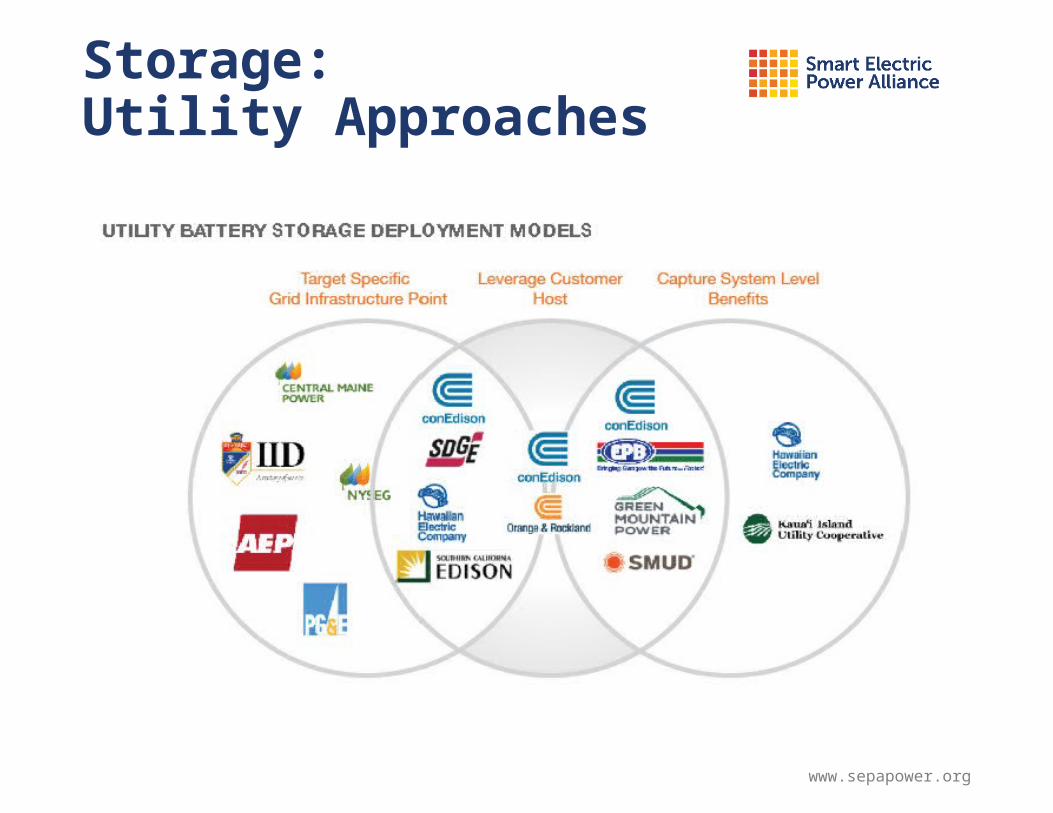

Storage: Utility Approaches

Business Model Evolution

Julia Hamm

202-559-2025

HEADQUARTERS

Smart Electric Power Alliance

1220 19th St NW, Suite 800

Washington, DC 20036

Contact Info

SEPA is an educational non-profit (501 c3)

Membership

Our unique mission is aimed at supporting utilities integration of solar, and other distributed energy resources, through educational events, research publications, & tailored consultations.

550+ Utility

> 90% of

installed solar

capacity550+

solar industry & stakeholder

About SEPA

Education

SEPA Products & Services

Research

Advisory

Our Work

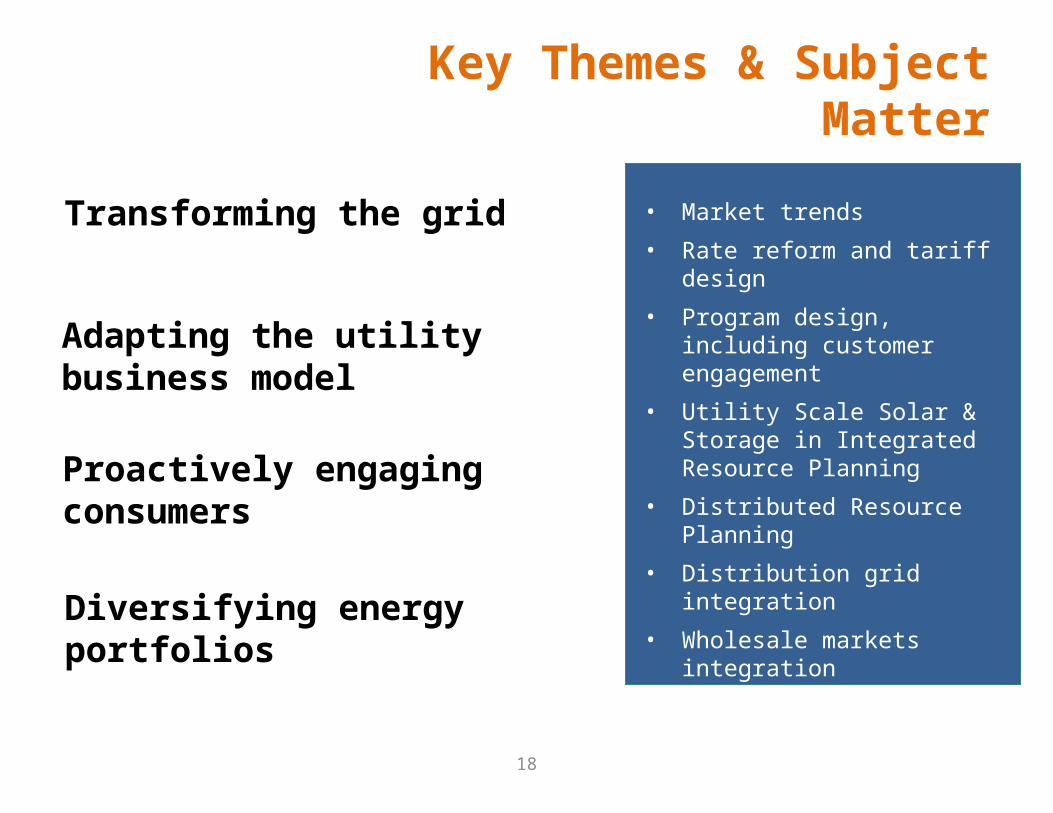

Transforming the grid

Key Themes & Subject Matter

18

• Market trends• Rate reform and tariff design• Program design, including

customer engagement• Utility Scale Solar & Storage in

Integrated Resource Planning• Distributed Resource Planning• Distribution grid integration• Wholesale markets integration• Asset management• Energy analytics • Clean Power Plan Implementation

Adapting the utility business model

Proactively engaging consumers

Diversifying energy portfolios

Market TrendsSolar’s Big Decade

• In the past ten years, the cost of solar has fallen by about 80% and worldwide growth has boomed.

• In the U.S., solar capacity has expanded from approximately 500 MW in 2005 to about 23 GW in 2015, and an estimated 60-70 GW by 2020.

19

20156,193

Source: SEPA, GTM Research

Cumulative: 22,488 MW

Solar Growth

Installed PV Costs – 2014-2015

21

Cost of Residential PV in Selected States

22Source: Energy Sage

Strong solar policy does not equate to lower costs to the consumer

How Competitive Is Solar?

23Source: “Lazard’s LCOE Analysis – Version 9.0” (November 2015)

Forecasts of Customer-sited PV Costs

24Source: Lazard's Levelized Cost of Energy Analysis - Version 8.0 (Nov 2014)

42% price decline projected28% price decline projected

Source: Sioux Valley Energy

Solar: Not The Perfect Utility Resource…

All Solar Markets are Growing

26

Source: SEPA 2014 Solar Market Snapshot www.sepatop10.org

Where Utilities Are Active in Solar

27

Community Solar (maturing)

Utility scale in generation

portfolio (maturing)

Customer-sited (emerging)

Source: GTM Research, SEPA Analysis

• ~80% of customers interested in solar ownership are precluded due to non-policy constraints.

• Suggests 50 GW of demand unmet1

1 10 GW met demand / (20% met demand/total market ) = 50 GW

Community Solar An Alternative To Rooftop PV

Example:Orlando Utilities Commission

29

• 1 kW blocks, up to 15 kW at $0.13/kWh fixed based on actual plant generation; net metered $.025/kWh (residential) or $.015/kWh (commercial) more than current rates

• Term: 25 years• No performance guarantee• Customers pay a $50 deposit

(refundable after 2 years)

• Phase I: 400 KW

• Fully subscribed in 6 days

Offer

Response

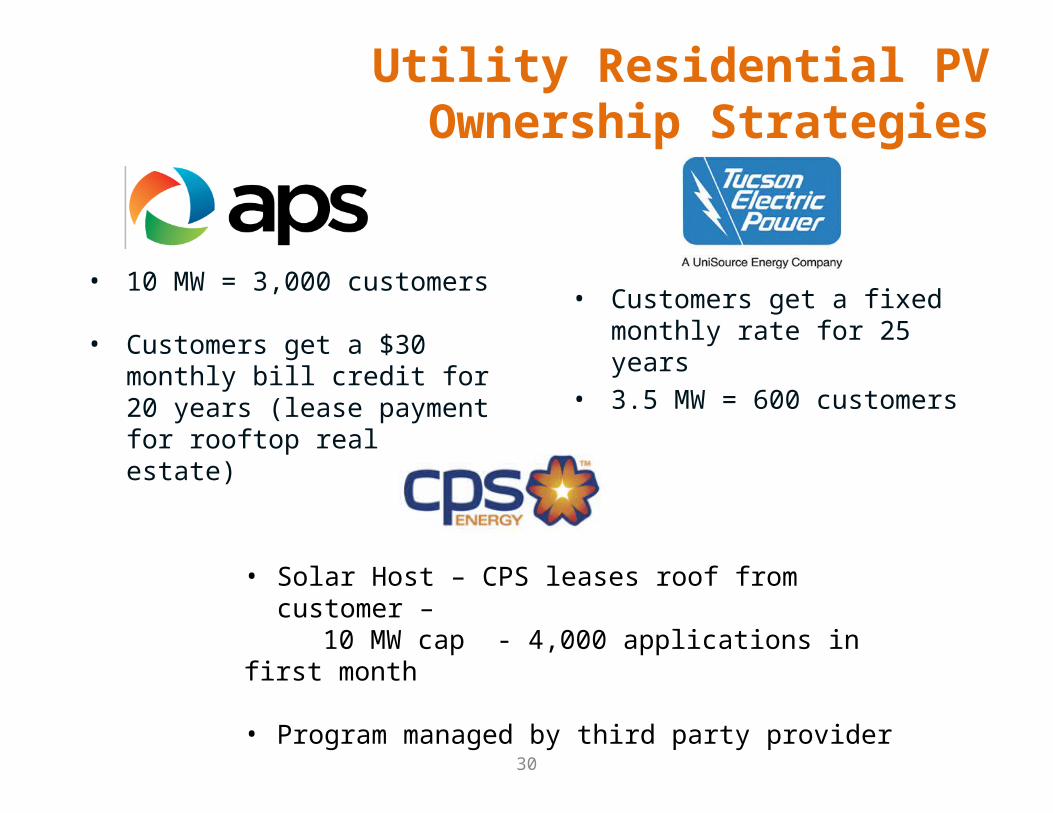

Utility Residential PV Ownership Strategies

30

• 10 MW = 3,000 customers

• Customers get a $30 monthly bill credit for 20 years (lease payment for rooftop real estate)

• Customers get a fixed monthly rate for 25 years

• 3.5 MW = 600 customers

• Solar Host – CPS leases roof from customer – 10 MW cap - 4,000 applications in first month

• Program managed by third party provider

Examples of Utilities Venturing into “Solar Plus”

• San Diego Gas & Electric solar plus storage microgrid boosts system reliability

• Steele-Waseca Co-op Electric – Community Solar + Load Management + Load Growth!

• Green Mountain Power – offering customers purchase or lease of Tesla Powerwall (goal: peak demand reduction)

31

Where We Are Today

32

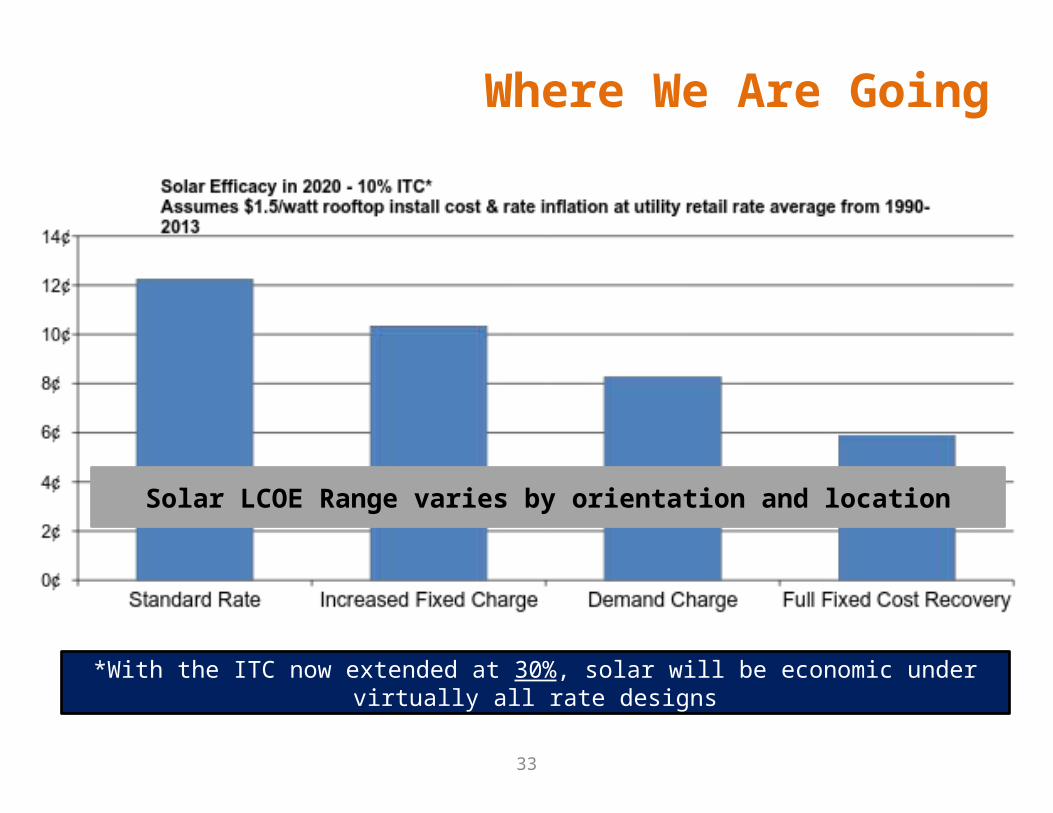

At today’s costs, modifying retail rate design can impact solar deployment economics

Solar LCOE Range varies by orientation and location

Where We Are Going

33

*With the ITC now extended at 30%, solar will be economic under virtually all rate designs

Solar LCOE Range varies by orientation and location

Increased Expectations of Utilities

34

LegacyExpectations

● Safe● Reliable● Low Cost● Enabling Economic Development● Stable and Predictable Costs

35

LegacyExpectations

NewDemands

● Safe● Reliable● Low Cost● Enabling Economic Development● Stable and Predictable Cost

● Greater Grid Resiliency● Proactive Environmental Stewardship● Support for Consumer Choice, including Self Generation

(Solar)● Support for Electric Vehicles

Increased Expectations of Utilities

Public Expectations of Utility are Increasing

36

LegacyExpectations

NewDemands

OftenForgotten

● Safe● Reliable● Low Cost● Enabling Economic Development● Stable and Predictable Cost

● Resilient● Support for DSM● Proactive Environmental Stewardship● Support for Consumer Choice, including Self

Generation● Support for Transportation Infrastructure

● Obligation to serve● Existing (& Unquestioned) Cross-Subsidization● Impact on Capital Cost & Availability● Data Availability, Security, & Ownership

A Proactive Utility Strategy

Passive Player Trusted Energy Advisor

Trusted Energy Partner

37

Transitioning from a passive player …

…to a proactive partner for customers adopting solar and other DER

Solar Is Pushing Change

38

SEPA’s 51st State

Created to provide a collaborative platform across the power sector to discuss the future of the electric industry. Designed as an alternative to today’s contentious debates.

The 51st State is a safe space for experts and industry leaders to present, sound out, and provide feedback on utility sector evolution.

39

40

2015 Concepts

Incremental Movement● Refresh the regulatory construct● Shift towards innovative rate

designs● Clearly articulate the roles of the

monopoly utility● Focus on enabling customer

adoption through:1. Improved interconnection

standards 2. Real-time information for

consumers

Paradigm Shift● Create a platform to connect

consumer-sited assets● Shift the role of utilities to grid

investment and maintenance● Place an independent third party

in charge of planning and operations

● Include societal impacts in cost-benefit calculations

● Turn customers from passive “takers” to proactive decision-makers in the electricity marketplace (“prosumers”)

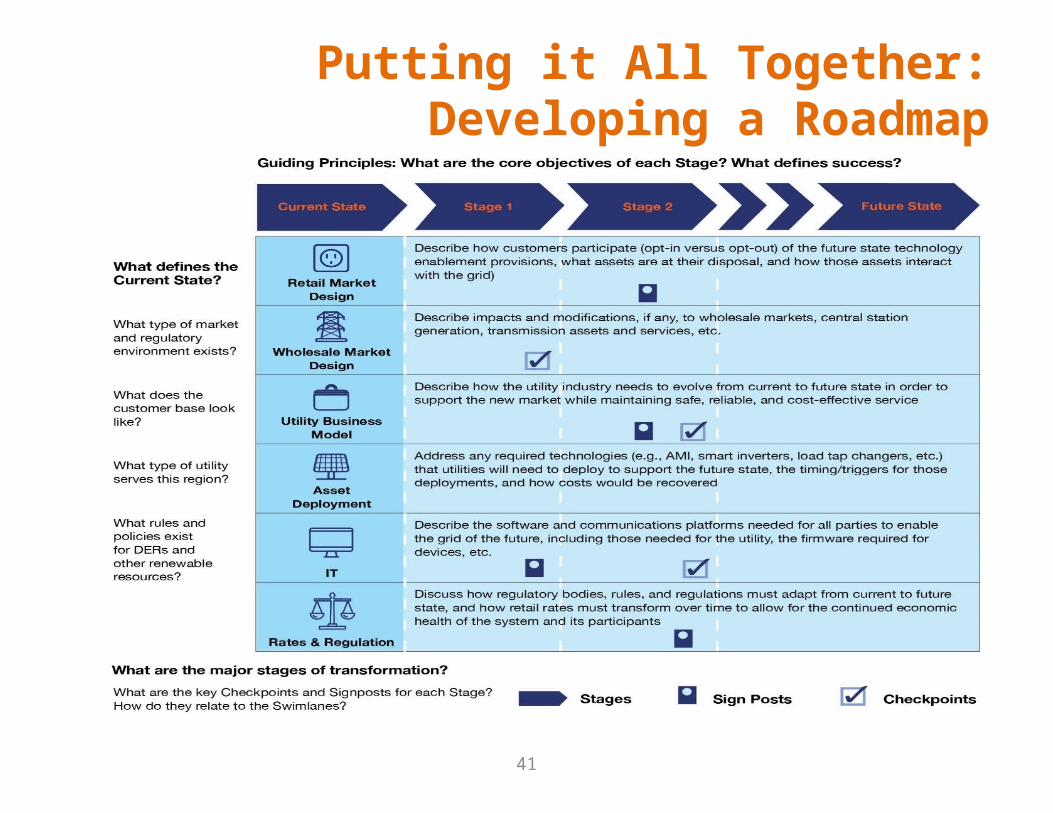

Putting it All Together:Developing a Roadmap

41

In Conclusion

• Solar growth will continue, based on increasingly compelling economics, across all market types. But solar won’t be a mature and truly valuable power resource until it becomes smart…

• The next constraint facing solar adoption will be integration challenges – engineering and economic.

• Utilities are learning how to turn this “threat” into an opportunity – for both customers and shareholders.

• Solar PV will be one part of a clean energy portfolio, which will include a mix of bulk power and distribution system scale resources.

42

Thank You!

43

Jennifer SzaroSenior Director of ProgramsSmart Electric Power Alliancejszaro@sepapower.orgwww.sepapower.orgwww.sepatop10.orgwww.sepa51.org

•Step 1 –Identify Service

Type

•Step 2–Evaluate existing

Service Capacity for PV Export

•Step 3 –Identify Local Area

Network’s Minimum Load Condition

NYC Grid Ready Project

Upcoming Initiatives - CECONY CUNY NY Solar Map

Grid Ready ProjectSummaryThis building is on a spot or isolated

network. In order to install the PV system size analyzed in Grid Ready,

grid upgrades may be required to accommodate potential solar export.

Please review the NYC Grid Ready Fact Sheet for more information on spot networks and average costs

incurred by the customer/developer to install a PV system.

49 5th Avenue,

Manhattan, NY 10003

Solar Potential Analyzed275 kW

Is the building on a Spot or Isolated Network?

Is the building’s service capacity too small to accommodate potential PV export?

Is the minimum load in the surrounding area too small to accommodate potential PV

export?

Interconnection Preliminary Review

45

UTILITY INTERVIEW FINDINGS

46

UTILITY TRENDS

47

1. Solar PV (and smart inverters)2. Energy Storage3. Electric Vehicles4. Demand Response5. Non-Solar DG6. Energy Efficiency

Technologies of Concern

• Traditional siloes with some cross-functional coordination vs. dedicated DER planning departments

• Distribution engineer responsibilities becoming more complex

• Most utilities are short-staffed in this area

Organizational Structure

EXTERNAL PRESSURES

48

Customers/Developers

Maintain Grid Reliability

Faster Interconnection

Times

Ease Penetration Limits

Compensation for Grid Services

Regulators

Maintain Grid Reliability: Mandates

Interconnection Timelines

DER Plan Mandates

Market/Rate Restructuring

UTILITY DER INTERCONNECTION PROCESSES

Receive paper interconnection applications

Apply basic screens (“rules of thumb”)

Allow/reject interconnections one at a time

Upgrade equipment (if needed)

49

Conventional Approach

Emerging Approach

Provide map of preferred interconnection locations

Receive online interconnection

applications

Run full distribution grid model for DER

“clusters”

Plan for optimal mix of mitigation solutions

SOFTWARE AND IT SYSTEMS

•EMS, DMS, OMS, DRMS, DERMS

•SCADA data, customer AMI data, DER meter data (MDMS)

•Traditional static tools vs. emerging dynamic tools

•Details on DERs, transformers, capacitor banks, etc. (GIS)

Distribution Infrastructure

Data

Distribution Modeling Software

Real-Time Management

SystemsInterval Metering

Data

50• Difficult to fully integrate all these components

DER Forecasting Tools

INDUSTRY GAPS

51

Methodology

Standard approach for distribution planning, taking DER deployment into account (how to

define “optimal”?)

Best practices for modeling (timescale, which impacts, which

mitigation solutions, etc.)

What level of DER control/aggregation is

appropriate?

Tools

Comprehensive time-series distribution system models that are easy to use and automated

Accurate DER device-level models (e.g., smart inverters)

Financial/rate models tied to distribution/DER planning

Solutions for widespread DER monitoring/control

• Planning vs. Operations• Most utilities struggling to meet operational needs and

comply with regulations• Most are not developing comprehensive plans or

streamlining processes for the future• Data/Modeling/IT

• Gathering/updating distribution system data• Ensuring accurate DER modeling• Integrating software/IT systems

• Coordination/Collaboration with Customers/Developers• Guiding projects to preferred interconnection locations• DER project design to minimize grid impacts

TOP CHALLENGES

52

SUMMARY OF DER PLANNING PROCESSES

53

Utility 1 Utility 2 Utility 3 Utility 4 Utility 5

Key Drivers

Regulatory Compliance

Regulatory DER Mandates

PUC DER Mandates

PUC DER & Reliability Mandates

Reliability Mandates None

Operational Necessity

Inter-connections

Inter-connections

Reliability; Inter-connections

Reliability; Inter-connections

Inter-connections

Methodology

Timeline for DER planning

Short-termEarly 2016

Short-termJuly 2015 Short-term Mixed Not set

Incentivizing preferred

interconnection locations

Somewhat Somewhat Yes Somewhat No

Cost recovery/rate restructuring

Under consideration Yes Under

consideration No specific plans Under consideration

Tools

Maps of preferred

interconnection locations

Somewhat Yes No Somewhat No

Advanced DER modeling tools Most Developed Some

DevelopmentSome

Development Most Developed Some Development

Active DER management Pilots Most Advanced Demo-stage Most Advanced Demo-stage

DETAILS OF DER PLANNING PROCESSES (1)

54

Utility 1 Utility 2 Utility 3 Utility 4 Utility 5

Key Drivers

Regulatory Compliance

Regulatory DER Mandates

PUC DER Mandates

PUC DER & Reliability Mandates

Reliability Mandates None

Operational Necessity Interconnections Interconnections Reliability;

InterconnectionsReliability;

Interconnections Interconnections

Methodology

Timeline for DER planning

Short-termEarly 2016

Short-termBy July 1, 2015

Short-termWill submit DER plan under PUC

proceeding in the near future

MixedJurisdictions have different planning

requirements, some include DERs

Not setNo specific

timeline

Incentivizing preferred

interconnection locations

SomewhatInterconnection

studies differentiate costs

by location (indirect guidance

for customers)

SomewhatProvides maps of

preferred interconnection

locations

YesStrategic Solar Locations come

with extra incentives

SomewhatCurrently provides

maps of "restricted" circuits; may provide more

detailed guidance in the future

NoDoes not provide

any specific guidance on

interconnection locations

Cost recovery/rate restructuring

Under consideration

Conscious of DER rate impacts and

considering future rate design

options

YesNEM 2.0

proceeding underway

Under consideration

Rate restructuring likely under PUC

proceeding

No specific plansNEM tariff is only

rate structure currently for

behind-the-meter DERs

Under consideration

Assessing current rate structure and

design

DETAILS OF DER PLANNING PROCESSES (2)

55

Utility 1 Utility 2 Utility 3 Utility 4 Utility 5

Tools

Maps of preferred interconnection

locations

SomewhatRecent RFO

identifies optimal solar

interconnection locations

YesPreferred

interconnection location maps

publicly available

NoThird-party

provides solar installation

mapping for public view; but contains no interconnection

info

SomewhatPublic can view

distribution mapping of

restricted circuits; working on further

guidance

No

Advanced DER modeling tools

Most DevelopedSystem-wide

distribution model; tools for measuring

and forecasting solar output

Some DevelopmentDoes T&D

modeling, but no system-wide

distribution model; uses static

distribution modeling tools

Some DevelopmentNo DER forecasting;

sophisticated internal modeling

tools but no system-wide

distribution model and tools need to

be integrated better

Most Developed System-wide

distribution model and DER forecasting tools; DOE grant for modeling advanced

voltage reg. strategies and

upgraded control schemes

Some DevelopmentRuns offline GIS/DMS for

interconnection studies in some

cases;conducting high

solar penetration impact studies on

bulk generation and T&D system-wide

Active DER management

Demo-stageMultiple storage

demos; establishing EV plans; testing IT systems to better

integrate DER data

Most AdvancedSmart inverter

standards; substation-level

energy storage; EV and demand

response integration; DERMS

Demo-stageMicrogrid projects;

AMI pilot

Most AdvancedPlanning auto-sectionalizing /

restoration schemes w/ all customer DER

mapped; testing smart inverter

functions

Demo-stageDeveloping DER interoperability

standards; adapting DMS to handle DER

PROACTIVE DER PLANNING FRAMEWORK

56

Does not take DER deployment into account

Forecast Load Growth

Model Circuit Impacts (Static)

Implement Lowest-Cost Solutions

Calculate Rate Impacts

STATUS QUO FOR UTILITY DISTRIBUTION PLANNING

57

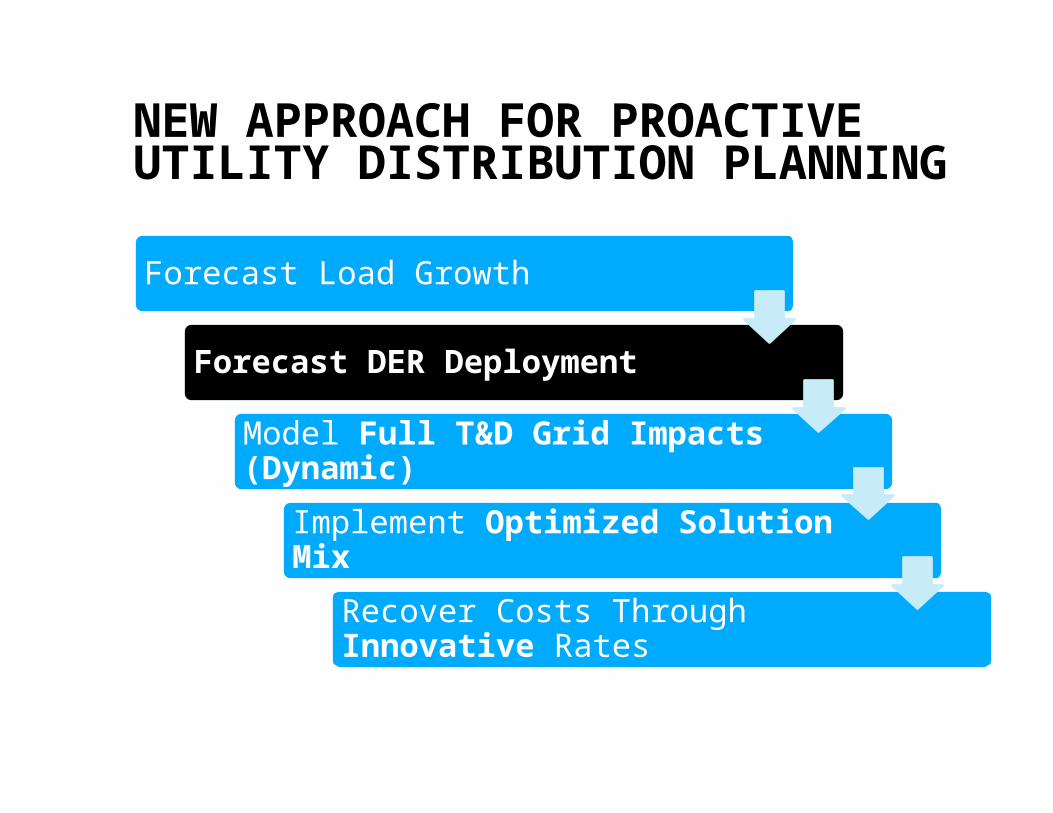

Forecast Load Growth

Forecast DER Deployment

Model Full T&D Grid Impacts (Dynamic)

Implement Optimized Solution Mix

Recover Costs Through Innovative Rates

NEW APPROACH FOR PROACTIVE UTILITY DISTRIBUTION PLANNING

58

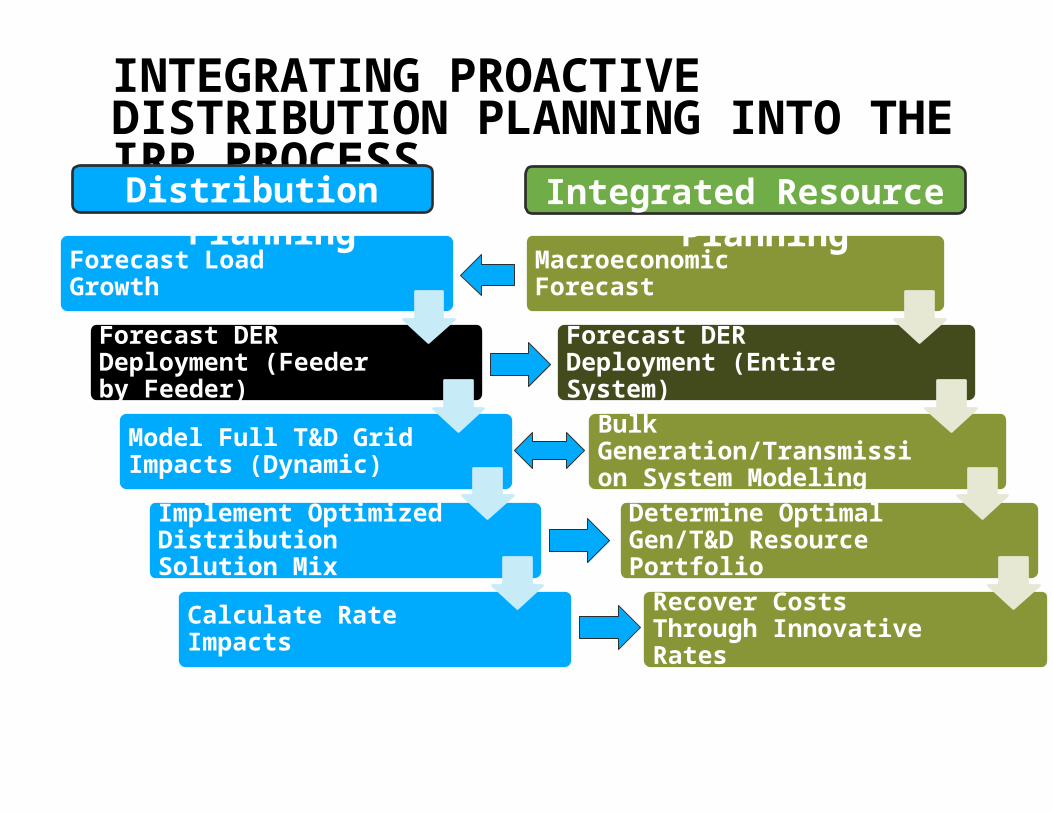

Forecast Load Growth

Forecast DER Deployment (Feeder by Feeder)

Model Full T&D Grid Impacts (Dynamic)

Implement Optimized Distribution Solution Mix

Calculate Rate Impacts

INTEGRATING PROACTIVE DISTRIBUTION PLANNING INTO THE IRP PROCESS

59

Macroeconomic Forecast

Forecast DER Deployment (Entire System)

Bulk Generation/Transmission System Modeling

Determine Optimal Gen/T&D Resource Portfolio

Recover Costs Through Innovative Rates

Distribution Planning Integrated Resource Planning

GRID MODELING HAS THREE PARTS

6 May 2015

60

Power FlowState Estimation

T, D Asset Model

Analytics Optimization

GIS

SCADALoad Research

AMIMonitoring & Sensors

Existing Models

Scenarios

GRID MODELING THEN & NOW

6 May 2015

61

T and DPlanningOperationsDynamicOptimizationFull systemFull DER

T or DEngineeringDesignSnapshotsHeuristicFeedersLimited DER

DMS Grid ModelsOperationsOracle, GE, Schneider/Telvent

Find out how utilities are rethinking everything to embrace a new distributed energy grid.

Download at: one.btm.report

Beyond the MeterThe Potential for a New Customer-Grid Dynamic

Discover our methodology for quantifying the locational value of deployed DER grid assets.

Download at: two.btm.report

Beyond the MeterAddressing the Locational Valuation Challenge for Distributed Energy Resources

www.sepapower.org

What the Community Solar Customer Wants

Based on a survey of 2,000 customers and over 250 small businesses, we uncover what community solar customers really want out of their program.

Download at: communitysolar.report

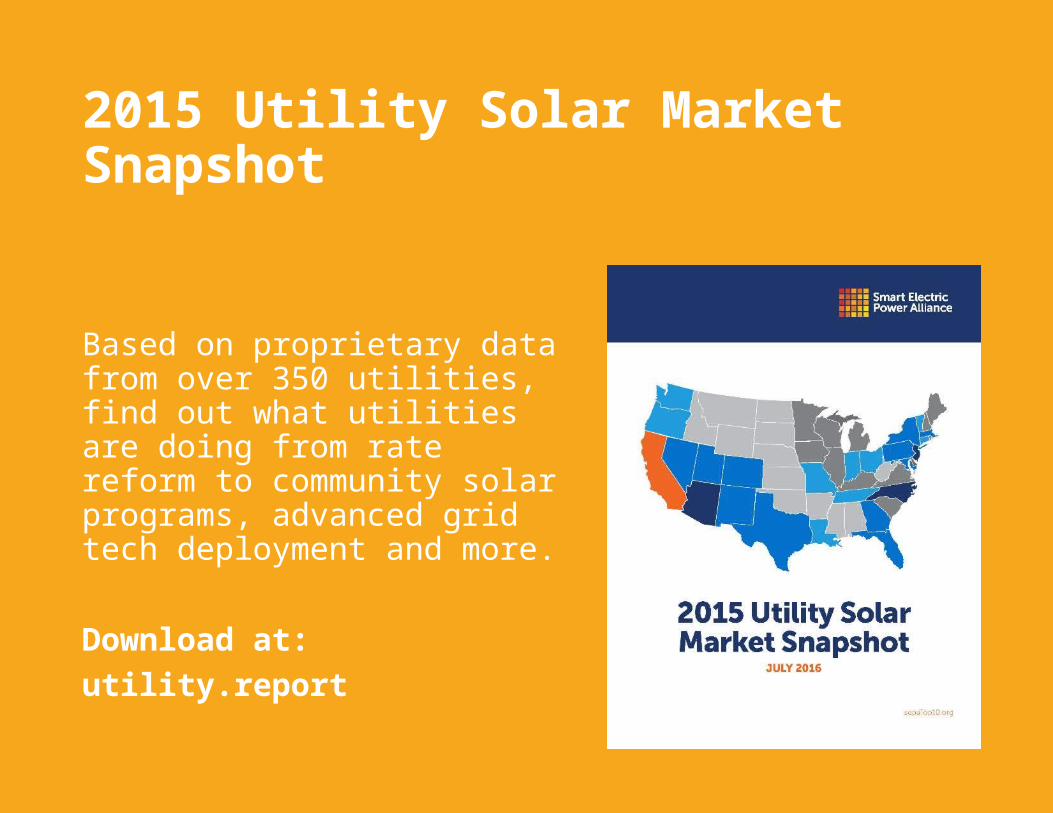

2015 Utility Solar Market Snapshot

Based on proprietary data from over 350 utilities, find out what utilities are doing from rate reform to community solar programs, advanced grid tech deployment and more.

Download at: utility.report

www.sepapower.org

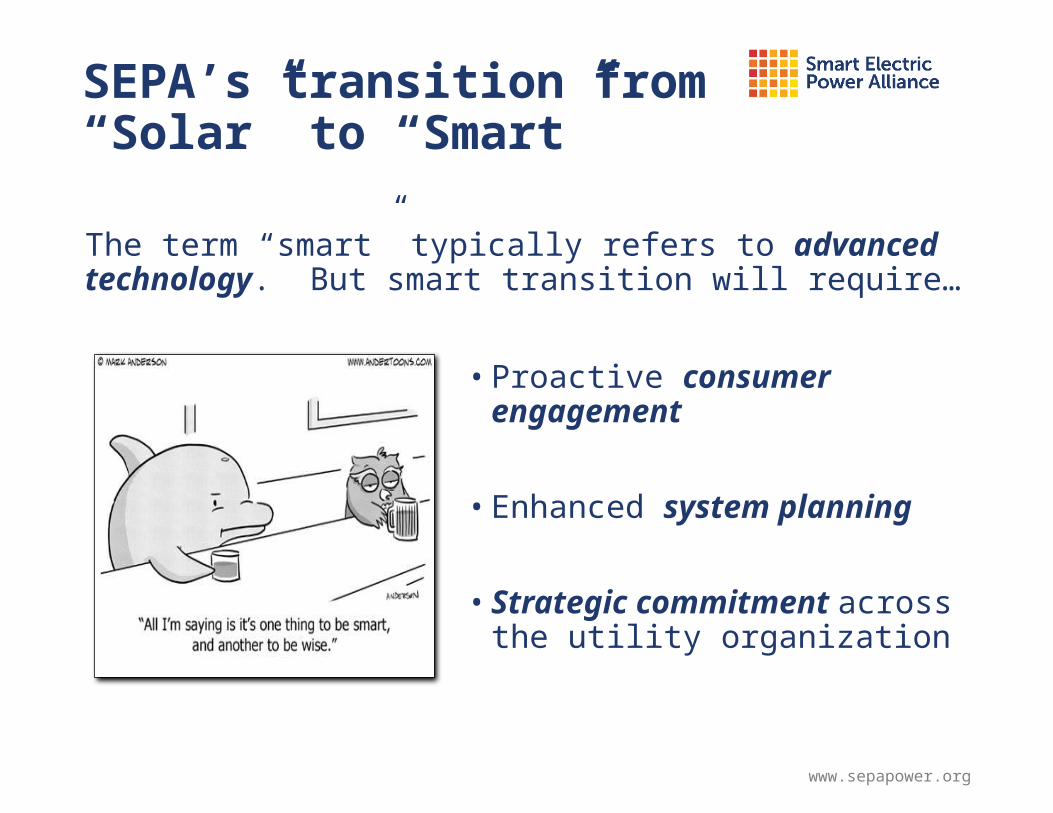

SEPA’s transition from “Solar” to “Smart”The term “smart” typically refers to advanced technology. But smart transition will require…

• Proactive consumer engagement

• Enhanced system planning

• Strategic commitment across the utility organization

www.sepapower.org

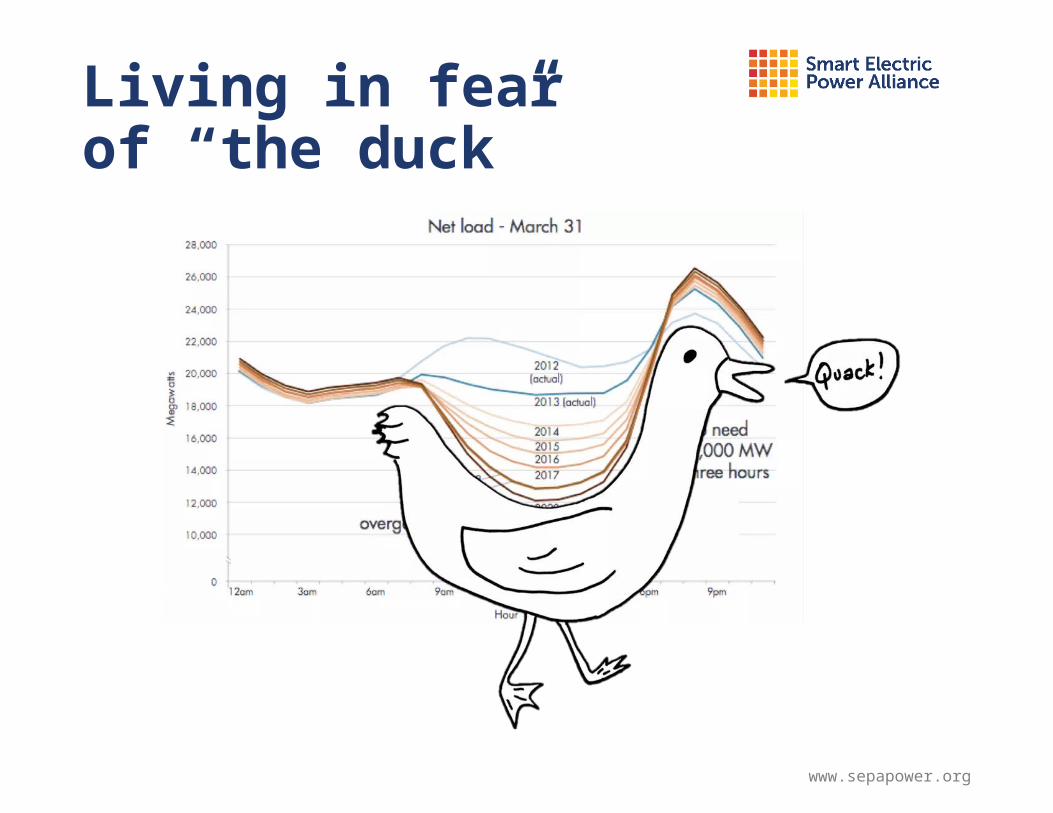

Living in fear of “the duck”

www.sepapower.org

Advanced grid tech deployments underway

Source: 2015 Solar Market Snapshot, SEPA

www.sepapower.org

A proactive DER planning approach

Source: Planning the Distributed Energy Future, SEPA and Black & Veatch

www.sepapower.org

DER capabilities

Source: Distributed Energy Resources Capabilities Guide, SEPA

www.sepapower.org

Valuation of DER of Distribution Assets

Source: Addressing the Locational Valuation Challenge for Distributed Energy Resources, SEPA and Nexant

www.sepapower.org

Utilities thinking “Beyond the Meter”

Source: Beyond the Meter: The Potential for a New Customer-Grid Dynamic, SEPA

Aligning Solar and UtilitiesSampling of Utility Members

74

Aligning Solar and UtilitiesSampling of Non-Utility Members

75

SEPA Events, Products, & Services

76

77

Planning for an Uncertain Future

The future of the utility industry is

uncertain; whether current conditions continue or a push

towards a greener or more interactive

future awaits, utilities must plan and

prepare for tomorrow

NREL’s Electric System of the Future

78

SEPA / NREL Collaboration• SEPA and NREL have partnered on a research

initiative to dive into how a utility’s functions across the organization are impacted by this future uncertainty

• Focus on Rapid Growth of DER Future• Provides distinct operational challenges compared to

Business as Usual• Being experienced today in many jurisdictions

• Goal: identify steps that can be taken today to prepare for the future, regardless of what that may entail

• Expected publication at end of month• Publicly available on both SEPA and NREL websites

Solar Impact Areas

79

Sola

r Im

pact

Are

as

Long-Term PlanningImpact to generation, transmission, and distribution long-term planning

processes, including net load impacts

OperationsImpact to generation, transmission,

and distribution real-time operations and technology deployment

IT, Data, & CommunicationsImpact to data systems, including

information technology, data gathering, data processing,

communications, etc.

Utility Interactions with Customers

Impact to systems, processes, and procedures used to interact with

customers, both as ratepayers and potentially as self-generators

Utility Business ModelsImpact to how utilities run their

business, including which products and services are offered to

customers, and how utilites collect $

Distributed Solar impacts utilities in many ways…

80

Utility Impact Areas…across a host of different utility functions, roles, and responsibilities

81

Integration of Planning & Operations

• Increasing integration within the utility can lead to stronger long-term planning processes that better account for the impacts of DERs

• Proactive planning can lead to better operational visibility at the edge of the grid• Operational visibility translates into prevention of system issues before they

happen, and quicker resolution when issues do arise• Constant feedback loop

82

Least Regrets StrategiesLong-Term Planning

Develop supply- and demand-based distribution plans that roll up into the IRP

Treat DERs as both fixed inputs and as selectable resources in the IRP

Integrate Supply, Demand, Transmission, and Distribution planning processes into an

overarching process

Discuss a long-term distribution system investment plan with regulators

83

Least Regrets StrategiesOperations

Update standard equipment list to support distribution integration needs and

infrastructure requirements

Deploy advanced inverters system-wide

Deploy sub-meters for distributed generation resources

84

Least Regrets StrategiesIT, Data, & Communications

Develop a long-term IT, data, and communications plan that is tied into other planning processes

Strategically deploy real-time communications infrastructure, AMI, etc.

Move towards automated data management and analytics

85

Least Regrets StrategiesUtility Interactions with Customers

Create a “green team” for the customer call center

Enable sophisticated customer energy portals

Investigate new rate and pricing models

Create routine customer workshops on energy consumption, new in-home technologies, and

other topics of interest

86

Least Regrets StrategiesUtility Business Models

Move towards holistic customer program design

Create employee training initiatives around the changing grid

Balance rate cases with multi-year rate reform plans

SignpostsIdentifying the Speed and Direction of Change

• Industry Trends• Cost trends• Technology

advancements• Codes & standards

• Utility Metrics• Peer activities• Feeder characteristics• Interconnection volume

• Customer Activities• Load shape changes• Energy portal utilization

88

The Flexible Utility

The Flexible Utility

Prepares for a variety of

potential futures

Focuses strategic

thinking on a future where

DERs are commonplace

Proactively integrates

planning and operations activities

Identifies and monitors DER

signposts regularly

Leverages Least Regrets

strategies

89

The 51st State Phase II

www.sepa51.org

RenewablesTransmission Connected RenewablesSmart inverter control; Generation Management

Distribution Connected RenewablesSmart inverter control

Rooftop SolarSmart inverter control

Smart Inverter Control

PF, Volt-varVolt-Watt, Watt-FreqPower export limit L/HVRT, L/HFRT

Primary Voltage

0.9

0.925

0.95

0.975

1

1.025

1.05

0 4 8 12 16 20

Hour

Vol

tage

(pu)

Baseline – No PV

20% PV20% PV withvolt/var control

24 Hour Simulation%

Ava

ilabl

e Va

rs

% voltage

100%

0.95

1.05

-100%

1.0V

Control Settings

Energy Storage

Bulk Storage Peaking and ramping service; Grid flexibility

Distribution Storage

Power flow control; Load peak shaving

Customer-Sited StorageDemand & energy savings; Resiliency Vehicle-to-Grid

(V2G)

Virtual Power Plant (VPP)

Load Management

Industrial Demand ResponseFrequency Regulation; Reserve; Capacity

Residential Demand ResponseDemand & energy savings;Energy services (aggregate)

-1.5

-1

-0.5

0

0.5

1

1.5

8:00 10:00 12:00 14:00 16:00 18:00 20:00 22:00 0:00

Load

Red

uctio

n (k

W)

Customer Control

Utility Control (4hr Event)

Utility Control (6hr event)

Load Reduction

“Snapback”

Demand Response Characteristics

DER - Reshaping the Power System

Sharing the same power system – need more coordination and shared responsibility

• Consumers becoming energy producers

• Loads becoming more interactive and dynamic

• Generation becoming more flexible

• T&D becoming more controllable and resilient

Beneficial Integration of DER

Making grid ready for seamless integration of DER to support customer choice

Making DER more operationally integrated in cost competitive manner

Extending DER benefits beyond

customer premises

System Controller

Local Controller #1

Local DER

….

Integrated DER

Distribution System Controllable Equipment

(cap banks, LTCs, etc.)

Local Controller #2

Local DER

Local Controller #N

Local DER

Integrated Solution

Non-integrated DERIntegrated DER Integrated DER

Grid Issues with High Penetration of PVVoltage• Overvoltage• Voltage variations

Equipment Operation• Feeder regulators, • Load tap changers• Switched capacitor banks

Demand/Energy• “Masking” peak demand• Unbalancing supply and demand

System Protection• Relay desensitization, networks• Breaker reduction of reach• Unintentional islanding

Power Quality• Harmonic generation• Flicker worries

1 2 3 4 5

6 7 8 9 10 11 12

13 14 15 16 17 18 19

20 21 22 23 24 25 26

27 28 29 30

Tue Wed Thu Fri SatSun MonApril 2014

Variability Conditions: AZ

Variability Conditions: NM Variability Conditions: NJ

Q2 2012 Q3 2012 Q4 2012 Q1 20130

20

40

60

80

100

Perc

enta

ge o

f Day

s (%

)

Season

Variability Conditions: TN

Q2 2012 Q3 2012 Q4 2012 Q1 20130

20

40

60

80

100

Perc

enta

ge o

f Day

s (%

)

Season

Q2 2012 Q3 2012 Q4 2012 Q1 20130

20

40

60

80

100

Perc

enta

ge o

f Day

s (%

)

Season

Q2 2012 Q3 2012 Q4 2012 Q1 20130

20

40

60

80

100

Perc

enta

ge o

f Day

s (%

)

Season

Understanding Distribution Circuit’s DER Hosting CapacityWhat matters most Regarding Hosting Capacity?• DER technology and impacts• DER size and location• Feeder construction and operation

Impact Below

Threshold

Impact Depends

Impact Above

ThresholdVoltage

Protection coordination

Thermal capacity

Safety/ Reliability

DER Distribution Impacts

DER Size and Location Feeder Construction and Operation

Improving Analytics• Grid/DER modeling

• Planning methods

• Improving Planning Tools

Proactive Planning• DER locational value

Integrating New Technologies

• Smart inverters

• Automation and dispatchable resources

Advancing Distribution Planning and Analysis

Substation

EV/PHEV

Demand Response

Distributed Var control

Energy Storage

Primary Voltage

0.9

0.925

0.95

0.975

1

1.025

1.05

0 4 8 12 16 20

Hour

Vol

tage

(pu)

Baseline – No PV

20% PV20% PV withvolt/var control

24 Hour Simulation

Substation-level Hosting Capacity

Feeder-levelHosting Capacity

Adopting Open Standards and Protocols

VoltageManagement

BulkSystemSupport

Comm. & Interactivity

• Fixed Power Factor• Volt-VAR Control• Volt-Watt Control

• Voltage Ride-through• Freq Ride-through• Freq-Watt Control

• Configuration• Coordination• R/T Feedback

Architecture for DER Integration

DERMS = Distributed Energy Resource Management System

DERMS

SOLAR BATTERY PEV

MDMS OMS

Enterprise Integration

GIS Etc.

DRASDMS

AD

MS

GAP Area

Maturing, Well Defined Interfaces

DER Integration Challenges …

Grid SupportIncentivized or

grid-code

AuthorityUtility resource vs. customer owned Control &

CommunicationAutonomous or configurable

Co-ordinationOpen standards and Protocols

Transmission and DistributionPlanning and operation