Embed Size (px)

Citation preview

2015 SOLAR SUMMITGEORGIA PROPERTY TAX CHALLENGES

September 10, 2015

John L. Gornall, Esq.Arnall Golden Gregory [email protected]

8030009

Mark A. Gould, Jr., Esq.Arnall Golden Gregory [email protected]

2

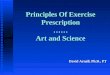

AD VALOREM PROPERTY TAX IN GEORGIA

(a) County Tax

(b) City Tax

(c) School District

(d) State

(e) Other Taxing District, such as a Fire District

3

EXPRESSED AS A MILLAGE RATE

$1 / $1000 OF ASSESSED VALUE

ASSESSED VALUE IS 40% OF FAIR MARKET VALUE

4

Article 7, Section 1, Paragraph 3 of the Georgia Constitution

Uniformity; classification of property; assessment of agricultural land; utilities

(a) All taxes shall be levied and collected under general laws and for public purposes only. Except as otherwise provided in subparagraphs (b), (c), (d), (e), and (f) of this Paragraph, all taxation shall be uniform upon the same class of subjects within the territorial limits of the authority levying the tax.

5

None of the Enumerated Exceptions apply to

Solar Generation Facilities

6

Article 7, Section 2, Paragraph 1Section II. Exemptions from Ad Valorem Taxation

Unauthorized Tax exemptions void.

Except as authorized in or pursuant to this Constitution, all laws exempting property from ad valorem taxation are void.

7

Article 7, Section 2, Paragraph 2(a)(1)

Exemptions from taxation of property

(a)(1) Except as otherwise provided in this Constitution, no property shall be exempted from ad valorem taxation unless the exemption is approved by two-thirds of the members elected to each branch of the General Assembly in a roll-call vote and by a majority of the qualified electors of the state voting in a referendum thereon.

8

Article 7, Section 2, Paragraph 3(a)(1) - Provides

Exemptions which may be authorized locally.

(a)(1) The governing authority of any county or municipality, subject to the approval of a majority of the qualified electors of such political subdivision voting in a referendum thereon, may exempt from ad valorem taxation, including all such taxation levied for educational purposes and for state purposes, inventories of goods in the process of manufacture or production, and inventories of finished goods.

The “Freeport” Exemption.

9

Articles 9, Section 2, Paragraph 7(c)

Enterprise Zones

(c) The General Assembly is authorized to provide by general law for the creation of enterprise zones by counties or municipalities, or both. Such law may provide for exemptions, credits, or reductions of any tax or taxes levied within such zones by the state, a county, a municipality, or any combination thereof. Such exemptions shall be available only to such persons, firms, or corporations, which create job opportunities within the enterprise zone for unemployed, low, and moderate income persons in accordance with the standards set forth in such general law.

10

Enterprise Zones (cont’d)

Such general law shall further define enterprise zones so as to limit such tax exemptions, credits, or reductions to persons and geographic areas which are determined to be underdeveloped as evidenced by the unemployment rate and the average personal income in the area when compared to the remainder of the state. The General Assembly may by general law further define areas qualified for creation of enterprise zones and may provide for all matters relative to the creation, approval, and termination of such zones.

11

Georgia Code Section 36-88-8 permits a City or County

to grant a limited property tax abatement for property

in an “Enterprise Zone" as defined in Section 36-88-6.

12

The “Enterprise Zone” area has to meet 3 of 5 criteria:

1. Pervasive Poverty – at least15% of residents with less than poverty level income;

2. Unemployment – at least 10% higher than state average or significant dislocation;

3. General Distress – as evidenced by population decline, health and safety issues, etc.;

4. Underdevelopment – as evidenced by lack of building permits, business licenses, land disturbance permits, etc.; or

5. General Blight – as evidenced by the inclusion of any portion of the nominated area in an urban redevelopment area.

13

Georgia Code Section 36-88-8(a) Property Tax Exemption

(a)(1) The governing body of a local government or governments creating an enterprise zone shall include in the creating ordinance a provision to exempt qualifying business and service enterprises from state, county, and municipal ad valorem taxes that would otherwise be levied on the qualifying business and service enterprises not to exceed the following schedule:

(A) One hundred percent of the property taxes shall be exempt for the first five years;

(B) Eighty percent of the property taxes shall be exempt for the next two years;

(C) Sixty percent of the property taxes shall be exempt for the next year;

(D) Forty percent of the property taxes shall be exempt for the next year; and

(E) Twenty percent of the property taxes shall be exempt for the last year.

14

Georgia Code Section 36-88-9(a) permits exemption or

abatement from local occupation taxes, regulatory fees,

building inspection fees and other fees that would

otherwise be imposed on a business.

15

36-88-9. Other tax incentives; reporting.

(a) In addition to other incentives, the local governing body or bodies creating an enterprise zone may include in the creating ordinance an exemption or abatement from occupation taxes, regulatory fees, building inspection fees, and other fees that would otherwise have been imposed on a qualifying business. Such governing bodies may grant any of these incentives either when the enterprise is initially created or by subsequent resolution making such incentives applicable to an existing enterprise zone.

16

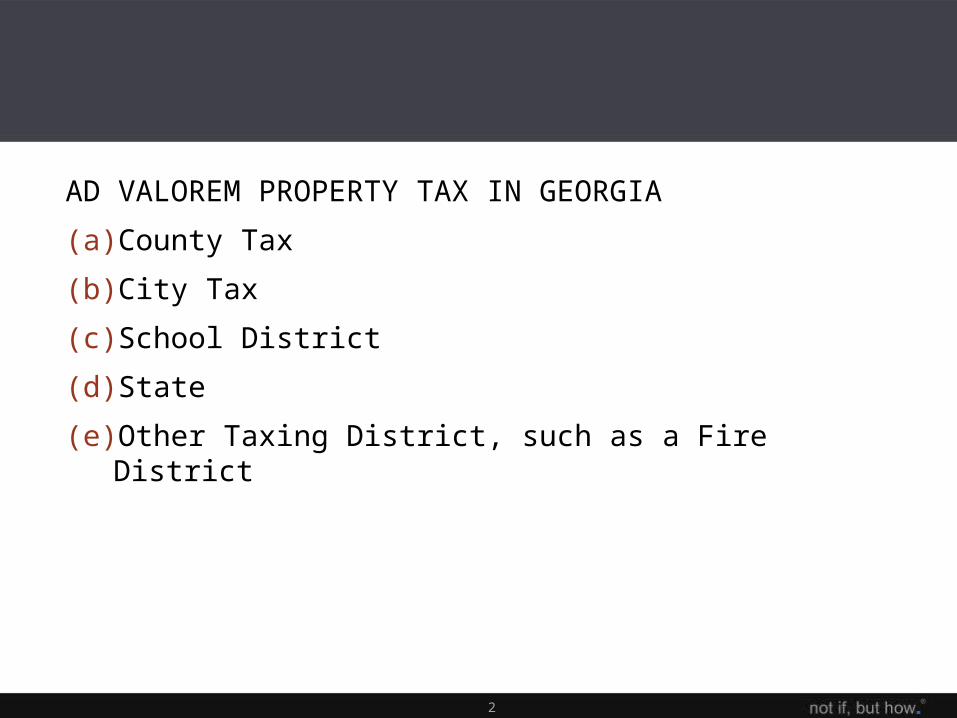

The County or City wishing to designate

an area as an Enterprise Zone must apply to the

Georgia Department of Community Affairs

17

Enterprise Zones are sometimes referred to as a

“Poor Man’s Bond for Title.”

18

A resolution from the relevant local government confirming the benefits available under its Enterprise Zone Program and that a Taxpayer is eligible to participate is usually sufficient for Investors and Lenders

19

If an Enterprise Zone is not available, then all paths lead to a local authority, usually a Development Authority

20

Typically the justification for time limited, performance based property tax reduction is a sale-lease back transaction with a Development Authority in which Bonds are issued

21

BONDS FOR TITLE STRUCTURE

22

• The Company pays rent to the Development Authority.

• The Company receives payments of principal and interest as Bondholder.

23

• The Lease will include an Option provision under which the Company can tender, at any time the Company chooses, the Bonds to the Development Authority as payment for the “purchase” of the Project. The Development Authority would then transfer the Project to the Company. The Bonds would be cancelled.

24

Development Authorities are exempt from Tax, including Georgia Property Tax

25

However, Georgia Property Tax often applies to a Lessee’s “Estate for Years.”

26

Best solution: A Bond-for-Title transaction with a Constitutional Development Authority with property tax exemption language in the Constitutional Amendment language that created the Development Authority

27

Development Authorities may no longer be created by Constitutional Amendment

28

Other Solutions:

1. Lease interest of Taxpayer/Lessee is an Usufruct, an interest in real estate not subject to property tax

29

2. Valuation of Leasehold/Estate for Years of Taxpayer/Lessee

30

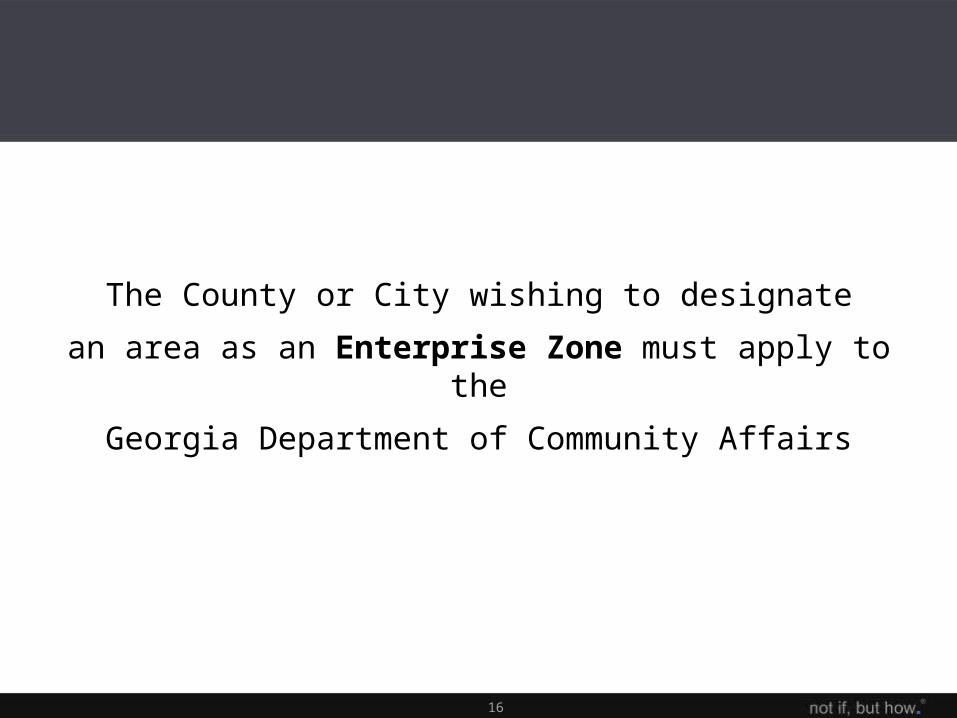

A typical Leasehold Valuation Agreement between Taxpayer/Lessee and Local Government through the Development Authority might be:

31

Lease Year Valuation of Lessee’s Leasehold

Year 1 0% of Fair Market Value

Year 2 10% of Fair Market Value

Year 3 20% of Fair Market Value

Year 4 30% of Fair Market Value

Year 5 40% of Fair Market Value

32

Lease Year Valuation of Lessee’s Leasehold

Year 6 50% of Fair Market Value

Year 7 60% of Fair Market Value

Year 8 70% of Fair Market Value

Year 9 80% of Fair Market Value

Year 10

Year 11

90% of Fair Market Value

100% of Fair Market Value

33

Development Authorities (“DAs”) are now created by a General Statute (so-called “Statutory DAs”) or Local Statute. Previously they were created by Constitutional Amendment

34

Statutory DAs have a board of 7 appointed to staggered 4 year terms by the relevant County Commission or City Council

35

Many DAs hold regular meetings once a month

Many have an Executive Director

36

Most DAs now often give more weight to new Full-Time Jobs created than to the Investment Amount in decisions about Property Tax Reduction

37

Some Solar Projects have been offered no Property Tax Reduction because they create no or almost no permanent Full-Time Jobs

38

EXAMPLE

Assume a 10 MGW project that costs $20 million

Assume a total millage rate of 25 mills

39

Over 30 years, the total property tax would be approximately $2.5 million

40

How long does it take to put a Bond-for-Title structure in place once the DA and relevant Taxing Authorities say yes?

60-90 days

41

WHY?

1. Agreeing on the Bond-for-Title Documents, giving the required public notice of a meeting of the DA to approve the Documents and holding the public meeting of the DA typically requires at least 30 days

42

2. Most Lessees/Taxpayers want the advantages of issuing Bonds and a Judicial Validation Order

43

Judicial validation of Bonds means the validity of the Bonds and agreements supporting payment of the Bonds cannot thereafter be contested.

44

Take the position that the Leasehold Valuation Agreement is such an agreement

45

Judicial validation requires a lawsuit, publication of the proposed issuance of Bonds and a Validation Hearing before a Superior Court Judge

46

This typically requires at least 30 days

47

Then the Project is transferred to the DA and the Project is leased back to the Lessee/Taxpayer

48

The Lessee/Taxpayer is typically required to file an annual Company Report with the DA, the County Board of Assessors and the County Tax Commissioner on or before April 1, reporting cumulative investment and new Full-Time Jobs for the prior Tax Year

49

The Lessee/Taxpayer also files a Property Tax Return for the prior year on or before April 1

50

Some Tax Assessors put the Project on the Tax Digest as “Exempt”

51

Some Tax Assessors put the Project on the Property Tax Digest at the agreed valuation under the Leasehold Valuation Agreement

52

For income tax and financial reporting purposes, the Lessee in a Bond-for-Title structure is treated as the owner of the Project

53

Instead of using a Bond-for-Title structure, why not amend the Georgia Constitution?

54

A Resolution proposing such an amendment would not likely receive the required 2/3rds vote in the Georgia House and Senate

55

It would not likely reach the floor of either Chamber for a vote

56

Such an Amendment would not likely be approved by a majority of voters in a Public Referendum

57

Deal with the local politics and public. Don’t assume if the DA Board approves the Property Tax Structure, you are done.

58

Any resident of the Jurisdiction which created or activated the DA may intervene in the Bond Validation Hearing

59

Intervention is rare. My experience is that interventions are often motivated by something other than the particular proposed Property Tax Reduction

60

PREPARATION FOR THE TAX ABATEMENT PITCH

A. Talk to Executive Director of the County Development Authority

61

B. Name of the Chief Appraiser and how many years ofexperience?

Years of experience in the County?

62

C. What property taxes were paid for the Project property for the past 3 years?

63

D. Do the Local Governments and School District have a Property Tax abatement policy?

64

E. Who are the attorneys for the County, Board of Tax Assessors and the Development Authority?

65

F. Are there any Solar Projects in the County? Did they receive Property Tax abatement?

66

The TREND for awarding Incentives such as Property Tax Abatement has been to stress:

• Permanent Full Time Jobs and

• Average Wages,

• Not Investment.

67

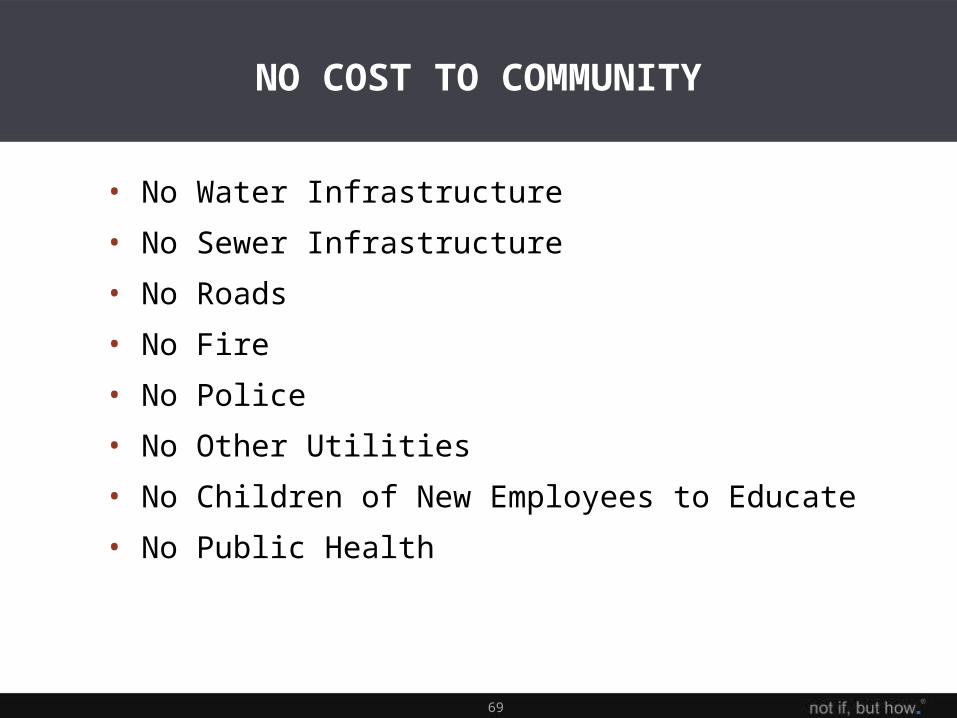

SOLAR PROJECT SELLING POINTS

A. No Costs to the Local Governments and the School District

68

• Compare to the high costs to Local Government of a manufacturing plant

69

NO COST TO COMMUNITY

• No Water Infrastructure

• No Sewer Infrastructure

• No Roads

• No Fire

• No Police

• No Other Utilities

• No Children of New Employees to Educate

• No Public Health

70

• Compare the Proposed Abated Property Tax Revenue to the Property Tax Revenue currently received for the Property – Calculate ROI for the Local Governments and School District

• Agree to pay roughly X times the currently received Property Tax Revenue

71

• Calculate the project’s expenditures:

labor, lodging, gasoline, food, etc. and the local tax revenue generated by Sales Tax for the

Governments and the School District

72

Spread Sheets are an Excellent Tool for

Presentations and Negotiations

73

Consider obtaining an Inducement Resolution from and an Inducement Agreement with the relevant Development Authority before award of the Solar Project.

74

If you have questions or comments, please contact:John L. Gornall, Jr.

ARNALL GOLDEN GREGORY LLP171 – 17th Street NW, Suite 2100

Atlanta, Georgia 30363-1031Phone: 404-873-8650

Email: [email protected] Website: www.agg.com

Mark A. Gould, Jr.ARNALL GOLDEN GREGORY LLP

171 – 17th Street NW, Suite 2100Atlanta, Georgia 30363-1031

Phone: 404-873-8782Email: [email protected]

Website: www.agg.com