Embed Size (px)

Citation preview

2015 GLOBAL MACRO OUTLOOK &ANALYSISNaufal Sanaul lahCharles ChenAaron Murphy

OVERVIEW

THEMES

• Real wage acceleration and more dispersed growth across income & wealth classes in the US

• Energy price crash = progressive tax cut helping lower-income & lower-age consumer cohorts

• H1 cyclical rebound in the Eurozone trumping ambiguous impact of further ECB easing

• Important tests of monetary easing efficacy in Japan & China (Chinese RRR vs M2 r2 has gone from -0.9 to -0.1 since end-2012)

• Energy price crash having spillover effect in Canada & Australia, including on labor & housing markets

• Transition to new vol & risk premia regimes

• Divergence (or re-convergence) between real economy & financial asset performance

POLICY

• 2014 = divergent G3 monetary policy:– BoJ expanding QQE– ECB signaled asset purchases & lower-for-

longer– Fed signaled liftoff

• 2015 = divergent policy efficacy & inflation:– BoJ & ECB fighting low monetary transmission– Fed reacting to pass-through of lower

commodities prices into consumer FCF– Time for ECB QE front-running to get tested

• FOMC taper & liftoff signaling persisted despite inflation deceleration

• This ignited a broad-based USD rally• Bernanke correctly identified post-QE2

inflation as “transient”• Decline in B/E’s this year is also likely to be

transient• Core inflation differentials will matter more

than divergent CB guidance in 2015• We expect the passive tightening from USD

appreciation to push back liftoff to September

Number of months to first Fed hike

Source: Bloomberg

MACRO

UNITED STATES

• Our assessment of US macro in 2015 is informed by three conceptual frameworks:– Cornerstone Macro’s consumer free cash

flow framework– Jan Hatzius’s personal savings rate model– Michael Pettis’s trade intervention mechanics

• The above frameworks inform the following conclusions:– Real US incomes will accelerate– These increased surpluses will be spent, rather

than saved– USD appreciation supports the above two

theses

US consumer free cash flow

• Consumer FCF = (DPI – F&E – FO) / DPI– DPI = disposable personal income– F&E = food & energy spending– FO = financial obligations

• Over 73% of current disposable income is free cash flow for consumers higher real spending

• Tailwinds for all three have supported CFCF:– Stronger labor markets feeding higher DPI– Commodities price crash driving lower F&E– ECB & BoJ easing and US curve flattening driving

lower FO

US consumer free cash flow

1982 1986 1990 1994 1998 2002 2006 2010 201465

66

67

68

69

70

71

72

73

74

% o

f dis

posa

ble

inco

me

Source: Federal Reserve, Cornerstone Macro

Personal savings rate

• Goldman’s Jan Hatzius savings rate model regresses against:– Household wealth– Consumer lending standards– Labor market

• All three are providing positive impulses, supporting GS Global Investment Research’s forecast of a 3% PSR by end-2015

• This suggests that increased consumer real income will be spent, rather than saved, suggesting a delayed inflationary impulse rather than deflationary risk

• The 32% YoY increase in pick-up truck sales (which have a strong inverse correlation to gas prices) supports this

Personal savings rate

Source: Goldman Sachs

Currency appreciation

• Michael Pettis’s trade intervention mechanics explain how currency appreciation impacts the current account:– It is not by a direct pass-through of lower import prices into a

negative impulse on the trade balance; but rather– Currency appreciation driving higher real incomes, driving

higher real spending and lower real production; and thus– A lower savings rate, which drives the savings/investment

imbalances that fuel a negative impulse on the trade balance

• Thus, so long as the savings rate declines commensurate to increased real incomes, the impact of USD appreciation is likely to be a consumer tailwind

Real GDP decomposition

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014-10

-8

-6

-4

-2

0

2

4

6

Consumption Investment GovernmentTrade GDP

% Q

oQ

SA

AR

Source: Federal Reserve

Real GDP decomposition

• With real incomes accelerating & 2011-2014 fiscal drag turning into a positive impulse, consumers & government will be providing a tailwind to growth

• Slowing exports will weigh on growth, exacerbated by the impact from USD appreciation

• Fixed investment acceleration will be key to driving further money velocity & credit expansion

• Capex has accelerated since 2012, as forecast in previous macrobeat decks, albeit slowly

• As energy-related capex slows, housing will be key to fixed investment in 2015

Housing

• Housing explains the majority of the variance of the business cycle; it’s more aptly titled the “housing cycle” or “fixed investment cycle”

• The current cycle only began in 2011, so we are less than four years into it so far

• Housing starts are still very low, particularly for single-family homes, a reflection of labor market headwinds for Millennials thus far

• For age 23-34, the homeownership rate have declined substantially for overall single people, but for full-time employees it is actually much higher than in 1970-1990

• Meanwhile, aggregate vacancy rates are back to normalized levels and renting is half as affordable as buying in the US

Housing

• Survey-based measures don’t suggest Millennials have a generational aversion to homebuying

• Headship rates continue to be correlated to lower age-cohort unemployment rates

• The strengthening of the labor market is now disproportionately favoring younger, higher-MPC cohorts, as does the oil crash

• The share of 18-34 year olds living with their parents peaked in 2013 and began reversing down in 2014

• With mortgage rates near record-lows and excess housing supply unwound, housing starts should pick up in 2015

• Continued housing investment weakness despite these tailwinds will be very strong support for “secular stagnation” themes

Home vacancy rates

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 20141.0

1.5

2.0

2.5

3.0

Source: Federal Reserve

Godley sectoral financial balances

• Wynne Godley’s sectoral balances model decomposes financial net surpluses & deficits into the household, corporate, government, and foreign (inverse current account) sectors

• With wage disbursements now growing faster than NGDP, household & government (tax revenue) financial balances have a tailwind at the expense of foreign financial balances

• Corporate profits/GDP & margins are likely peaking, even as aggregate profits are likely to continue growing

Godley sectoral financial balances

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005-15

-10

-5

0

5

10

15

Household Business Government Foreign

% G

NP

Source: Federal Reserve, BEA

Kalecki-Levy profits decomposition

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010-15

-10

-5

0

5

10

15

20

Household investment Business investment Government investment Household saving

Government saving Foreign saving Dividends Statistical disrepancy

Profits Kalecki

% G

NP

Source: Federal Reserve, BEA

EUROPE

• Market has already priced-in the “Japanification” of Europe in long forwards

• Monetary aggregates suggest PMIs are nearing a cyclical low

• We expect dispersion in the periphery:– France & Italy facing idiosyncratic headwinds

– Greece, Ireland, & Portugal seeing credit multipliers returning

• Political risk remains the real upheaval risk, and longer-term break-up risk is underpriced

• Sovereign QE efficacy over-hyped & market over-positioned

• We are more concerned about European macro in H2

European H1 cyclical rebound?

Source: Nordea Markets, Macrobond, Aurelija Augulyte

ASSET CLASSES

Some market calls for 2015• Lower-for-longer + curve steepening in US

• US breakevens bottoming in H1, rising in H2

• Bunds & USD peak around late-January ECB/FOMC/Greek elections

• EDZ5-Z6 steepening

• 2s5s30s fly heading back down

• Australian duration outperforming US

• Gold vol-adjusted outperformance vs US credit

• EUR/USD rising in H1 and GBP, MXN outperforming CAD, NZD in 2015

• US equity chop and Indian equities outperforming US & Chinese

• Tail risks from JPY appreciation and OAT & US HY spread widening

• Outperformance of US banks vs US utilities and Canadian & Aussie banks

• Outperformance of US consumer finance & asset-sensitive bank stocks

RATES

ACM UST term premia

2004 2006 2008 2010 2012 2014-1

0

1

2

3

2yr 5yr 10yrSource: Federal Reserve

ACM UST risk-neutral yield

2004 2006 2008 2010 2012 2014-1

0

1

2

3

4

5

6

2yr 5yr 10yrSource: Federal Reserve

What explains low UST risk premia?

• Global imbalances– “Euroglut” this cycle– OPEC/China last cycle

• Risk parity & global asset allocators– European rates have been “Japanified”– US rates offer optically-better vol-adjusted returns after USD

appreciation & US disinflation

• Global monetary easing– BoJ QQE– ECB negative deposit rates, TLRTO, ABPFF

• Secular stagnation/“policy error” theses– Expected terminal short rate lower than Fed estimate/“dots”– 5y1mo OIS forward rates (a measure of expected terminal short rate) &

their spread to 10yr yields (a measure of embedded risk premia in bonds) back to pre-“taper tantrum” levels

Lower expected terminal rate

2007 2008 2009 2010 2011 2012 2013 2014 20151

2

3

4

5

6

5y1mo OIS 10yr yieldSource: Federal Reserve, Bloomberg, Matthew Boesler

FX

USD appreciation extended

• Driven by stable liftoff path FOMC communication despite commodities crash

• Exacerbated by capital flows fleeing ECB NIRP & BoJ QQE and nominal rate spreads

• But drivers of sustained inflation trends (wages & shelter) highlight importance of real vs nominal, especially going forward

• We see upside risk to USD returning only in the back half of the year

USD appreciation extended

2011 2012 2013 2014 2015-1

-0.5

0

0.5

1

1.5

2

1.15

1.2

1.25

1.3

1.35

1.4

1.45

1.5

R2 = 0.70

2yr DE-US real spread EUR/USDSource: Federal Reserve, Bloomberg, Jeremy Wilkinson-Smith

EQUITIES

New volatility regime?

• Diversifying against volatility in 2015 = cash allocations

• During volatility periods in 2013 (May/Jun) and 2014 (Sep/Oct), all of the following declined in value (as per Columbia Management):– US/world/EAFE/EM equities– IG, HY, & REITs– USTs– Commodities

New volatility regime?

• The global “lowflation” theme is ripe for challenging in H2

• Commodities crash impact on US B/E’s has driven inflation risk premium & short rate path uncertainty risk premium to very low levels

• These risk premia rising set the stage for a new, higher vol regime, which has started being reflected in H2 2014 VIX trend & credit spreads (as BGC’s Jared Woodward has written about)

COMMODITIES

Core vs headline inflation correlations

Source: Cornerstone Macro

• Why did oil crash?– OPEC pricing power breakdown

– USD appreciation

– Weakening European & Chinese demand

– Excessively net long speculative positioning

• What matters going forward?– Nonlinear impact to output from shale being

“priced out”

– Large debt overhangs preventing rapid output cuts and rebalancing

– Direction of USD

– Chinese credit elasticity

OPEC pricing power breakdown

• US shale boom put pressure on Saudi

• Since at least 2012’s secret negotiations with Putin, Saudi shifted its emphasis from market prices to market share, due to recognition of:– Persistence of weak European demand

– Peak Chinese fixed investment/GDP

– High-cost producer output boom

• Syrian War = Iran/Russia vs Saudi/Qatar/GCC

OPEC pricing power breakdown

• After 2012 Ghouta chemical weapons attack, Saudi sent intelligence minister Bandar bin Sultan to Putin to try forging a Saudi-Russian alliance

• Russia would stop backing Assad in exchange for a Russian-Saudi monopolization of European energy markets

• Putin declined, bin Sultan was fired, and Saudi was forced into a bind: its market share would be under threat at prevailing prices

• This led to an internal breakdown of incentives within OPEC and its loss of pricing power, culminating in Saudi’s lack of output cuts in the most recent OPEC meeting

USD appreciation

• The policy divergence theme sparked off a passive tightening in the US via FX rather than rates

• This USD appreciation ignited feedback loops due to legacy EM cross-border borrowing

• This in turn exacerbated commodities price declines, driving US breakevens lower and continuing the policy divergence theme

Chinese FAI/GDP vs Brent oil

Source: Cornerstone Macro

Speculative positioning washout

Source: Guillermo Roditi Dominguez/New River Investments, Bloomberg

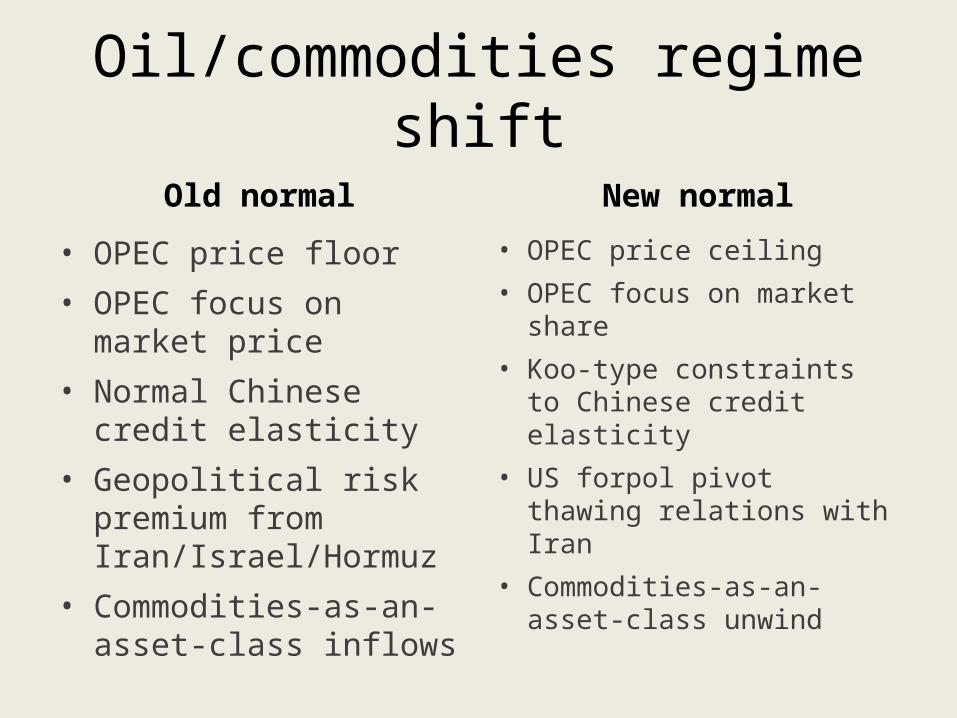

Oil/commodities regime shift

Old normal

• OPEC price floor

• OPEC focus on market price

• Normal Chinese credit elasticity

• Geopolitical risk premium from Iran/Israel/Hormuz

• Commodities-as-an-asset-class inflows

New normal

• OPEC price ceiling

• OPEC focus on market share

• Koo-type constraints to Chinese credit elasticity

• US forpol pivot thawing relations with Iran

• Commodities-as-an-asset-class unwind

THANK YOU FOR VIEWING

C o m m e n t s & c r i t i q u e w e l c o m e :

n a u f a l @ m a c ro b e a t . c o m

![[Naufal] Isi Laporan Acara 1](https://img.dokumen.tips/doc/110x75/5695d3bb1a28ab9b029ef97f/naufal-isi-laporan-acara-1.jpg)