Embed Size (px)

Citation preview

1

2014 Investor Presentation Final version 3.2

read disclaimers on the final page

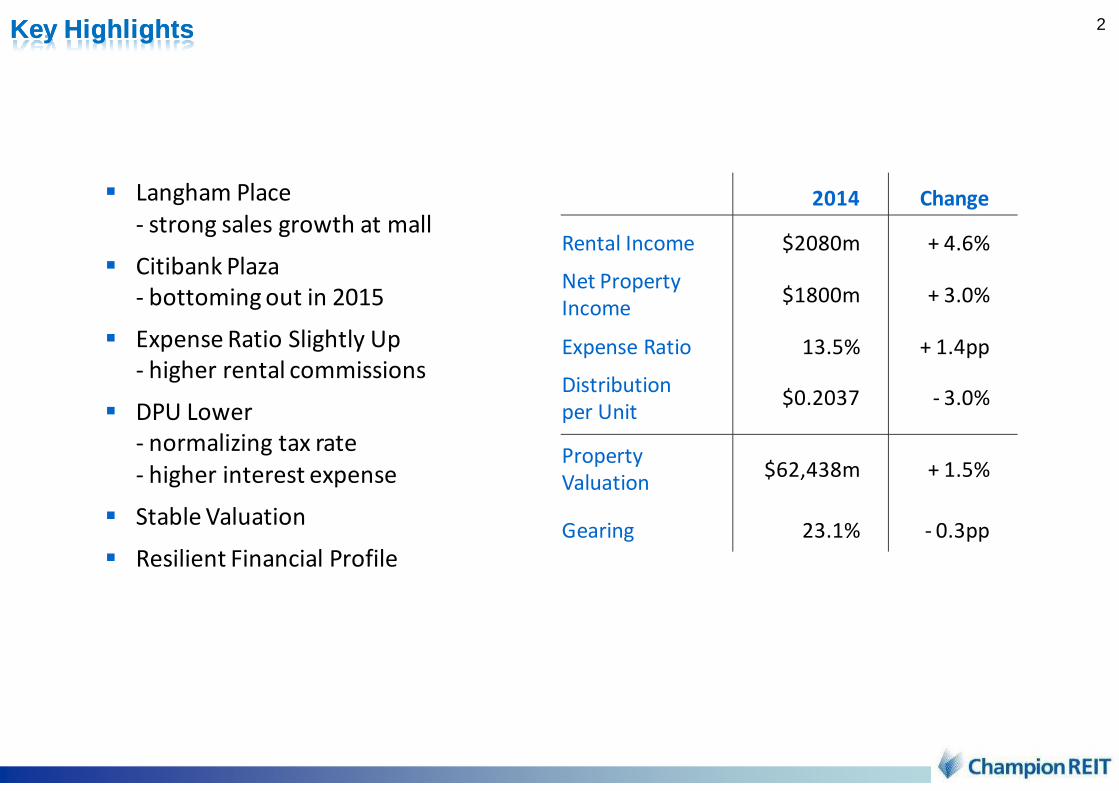

2Key HighlightsKey Highlights

� Langham Place

- strong sales growth at mall

� Citibank Plaza

- bottoming out in 2015

� Expense Ratio Slightly Up

- higher rental commissions

� DPU Lower

- normalizing tax rate

- higher interest expense

� Stable Valuation

� Resilient Financial Profile

2014 Change

Rental Income $2080m + 4.6%

Net Property

Income$1800m + 3.0%

Expense Ratio 13.5% + 1.4pp

Distribution

per Unit$0.2037 - 3.0%

Property

Valuation$62,438m + 1.5%

Gearing 23.1% - 0.3pp

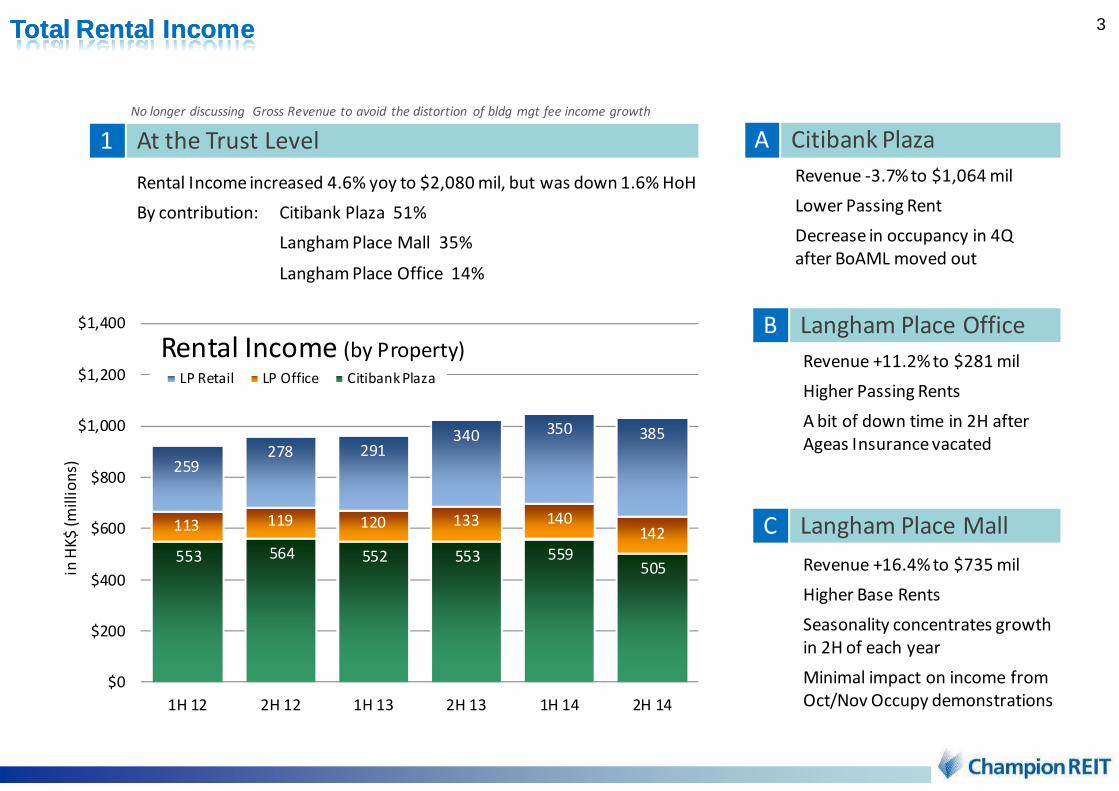

3Total Rental IncomeTotal Rental Income

Rental Income increased 4.6% yoy to $2,080 mil, but was down 1.6% HoH

By contribution: Citibank Plaza 51%

Langham Place Mall 35%

Langham Place Office 14%

At the Trust Level1

Langham Place OfficeB

Langham Place MallC

Revenue -3.7% to $1,064 mil

Lower Passing Rent

Decrease in occupancy in 4Q

after BoAML moved out

Citibank PlazaA

Revenue +11.2% to $281 mil

Higher Passing Rents

A bit of down time in 2H after

Ageas Insurance vacated

Revenue +16.4% to $735 mil

Higher Base Rents

Seasonality concentrates growth

in 2H of each year

Minimal impact on income from

Oct/Nov Occupy demonstrations

No longer discussing Gross Revenue to avoid the distortion of bldg mgt fee income growth

553 564 552 553 559 505

113 119 120 133 140142

259278 291

340 350 385

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1H 12 2H 12 1H 13 2H 13 1H 14 2H 14

in H

K$

(m

illi

on

s)

Rental Income (by Property) LP Retail LP Office Citibank Plaza

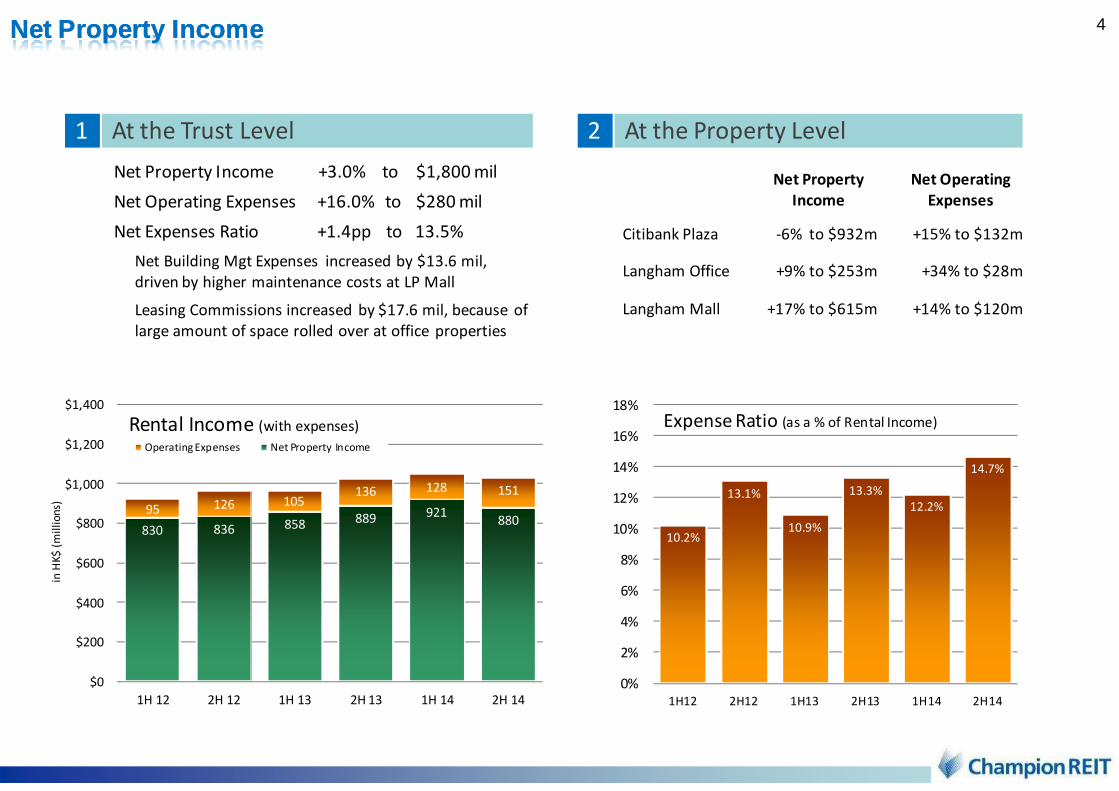

4Net Property IncomeNet Property Income

Net Property Income +3.0% to $1,800 mil

Net Operating Expenses +16.0% to $280 mil

Net Expenses Ratio +1.4pp to 13.5%

Net Building Mgt Expenses increased by $13.6 mil,

driven by higher maintenance costs at LP Mall

Leasing Commissions increased by $17.6 mil, because of

large amount of space rolled over at office properties

At the Trust Level1 At the Property Level2

Net Property

Income

Net Operating

Expenses

Citibank Plaza -6% to $932m +15% to $132m

Langham Office +9% to $253m +34% to $28m

Langham Mall +17% to $615m +14% to $120m

830 836 858 889 921880

95 126 105136 128 151

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

1H 12 2H 12 1H 13 2H 13 1H 14 2H 14

in H

K$

(m

illi

on

s)

Rental Income (with expenses)

Operating Expenses Net Property Income

10.2%

13.1%

10.9%

13.3%

12.2%

14.7%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1H12 2H12 1H13 2H13 1H14 2H14

Expense Ratio (as a % of Rental Income)

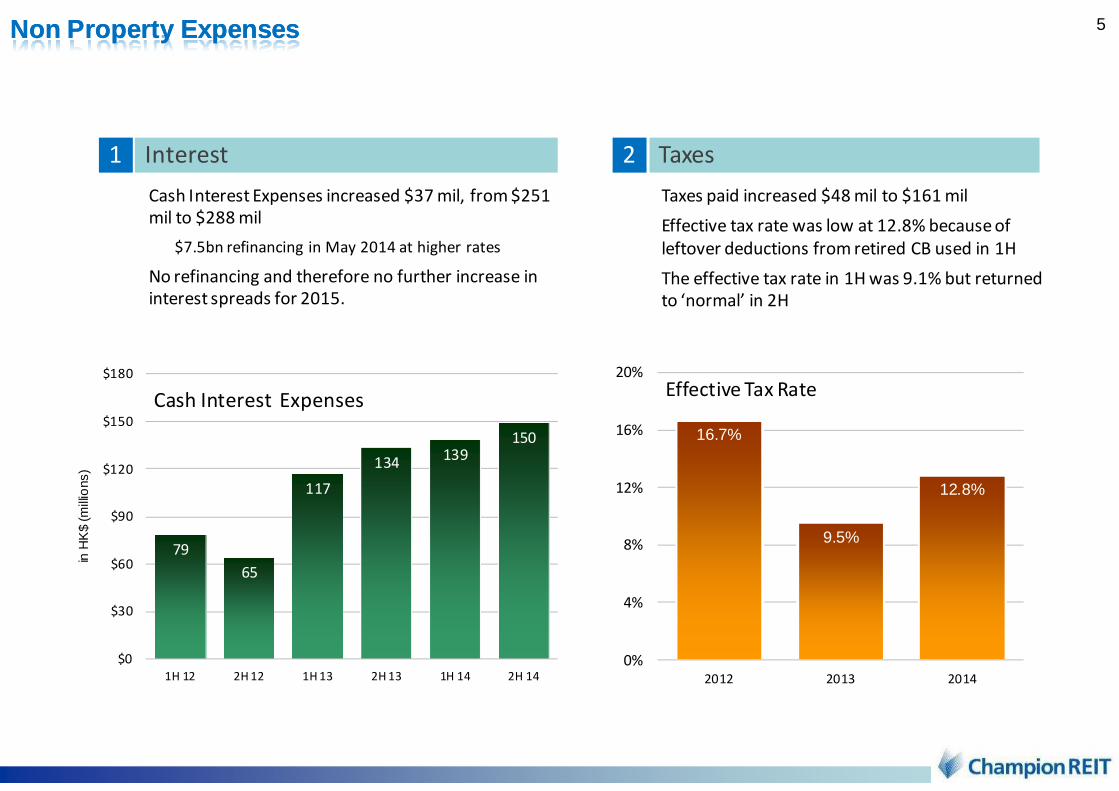

5

Cash Interest Expenses increased $37 mil, from $251

mil to $288 mil

$7.5bn refinancing in May 2014 at higher rates

No refinancing and therefore no further increase in

interest spreads for 2015.

Interest1

Taxes paid increased $48 mil to $161 mil

Effective tax rate was low at 12.8% because of

leftover deductions from retired CB used in 1H

The effective tax rate in 1H was 9.1% but returned

to ‘normal’ in 2H

Taxes 2

Non Property ExpensesNon Property Expenses

79

65

117

134139

150

$0

$30

$60

$90

$120

$150

$180

1H 12 2H 12 1H 13 2H 13 1H 14 2H 14

in H

K$

(mill

ions

)

Cash Interest Expenses

16.7%

9.5%

12.8%

0%

4%

8%

12%

16%

20%

2012 2013 2014

Effective Tax Rate

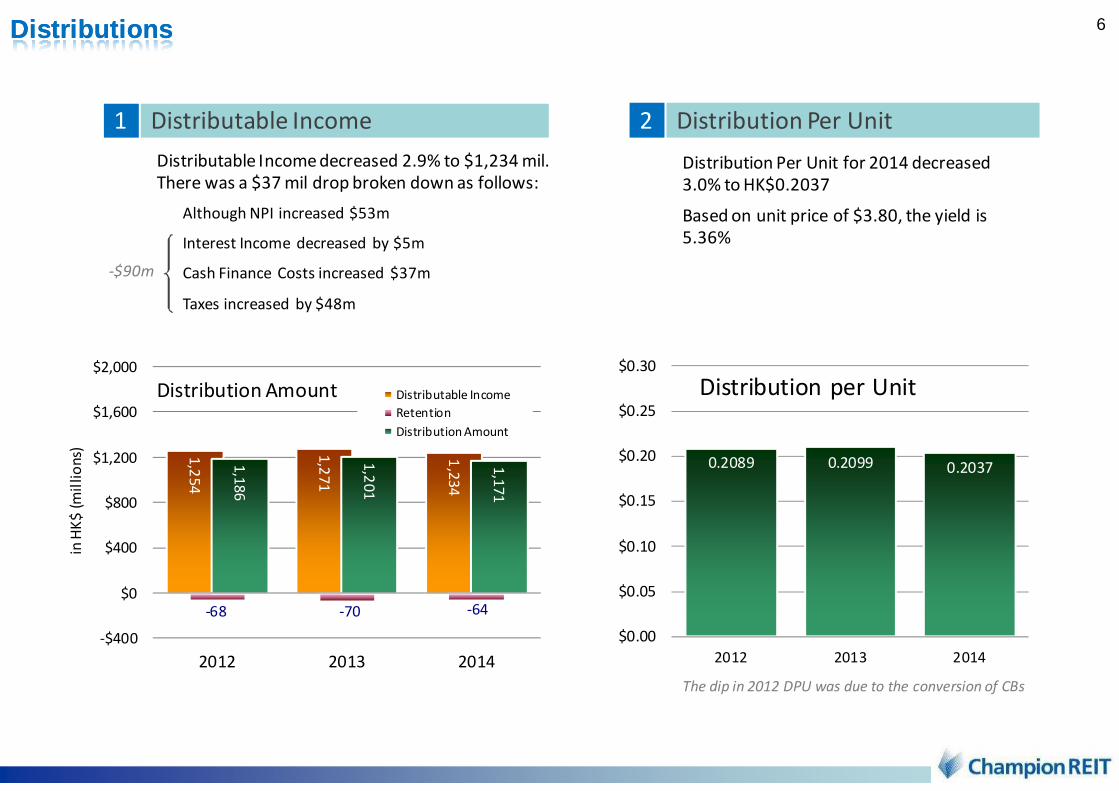

6DistributionsDistributions

Distributable Income decreased 2.9% to $1,234 mil.

There was a $37 mil drop broken down as follows:

Although NPI increased $53m

Interest Income decreased by $5m

Cash Finance Costs increased $37m

Taxes increased by $48m

Distributable Income1

Distribution Per Unit for 2014 decreased

3.0% to HK$0.2037

Based on unit price of $3.80, the yield is

5.36%

-$90m

The dip in 2012 DPU was due to the conversion of CBs

Distribution Per Unit2

1,2

54

1,2

71

1,2

34

-68 -70 -64

1,1

86

1,2

01

1,1

71

-$400

$0

$400

$800

$1,200

$1,600

$2,000

2012 2013 2014

in H

K$

(m

illi

on

s)

Distribution Amount Distributable Income

Retention

Distribution Amount

0.2089 0.2099 0.2037

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

2012 2013 2014

Distribution per Unit

7

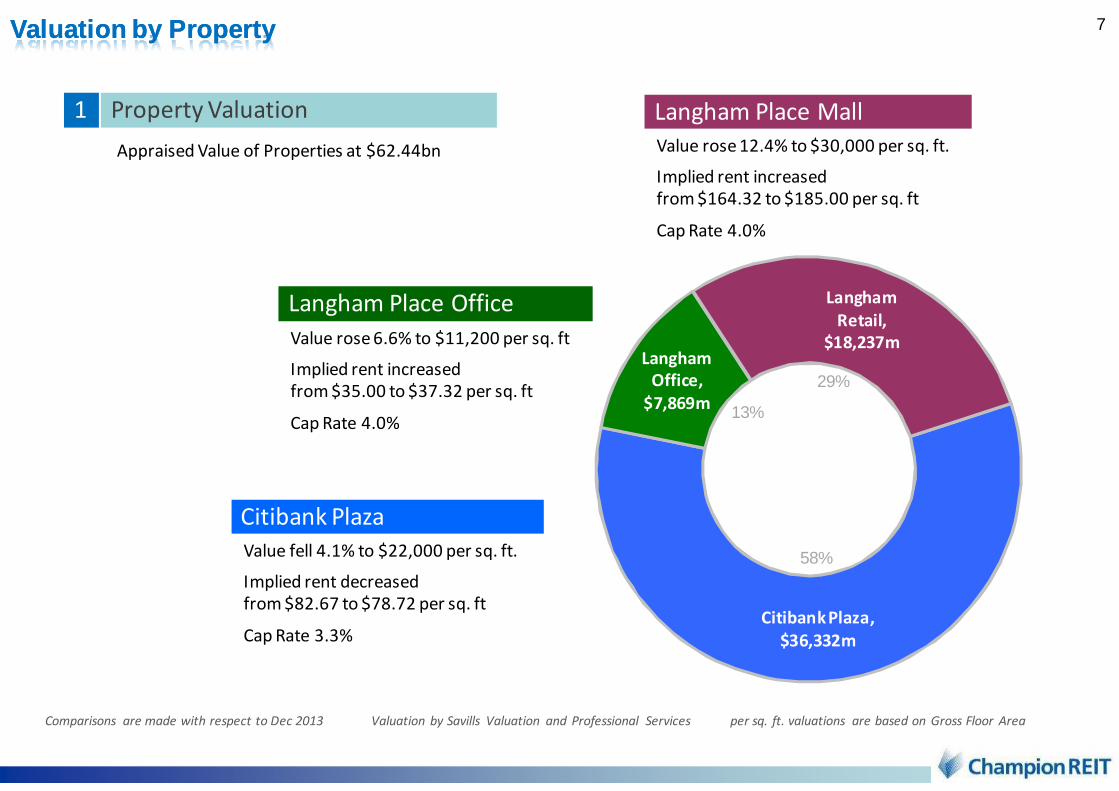

Citibank Plaza,

$36,332m

Langham

Office,

$7,869m

Langham

Retail,

$18,237m

Valuation by Property Valuation by Property

58%

29%

13%

Value fell 4.1% to $22,000 per sq. ft.

Implied rent decreased

from $82.67 to $78.72 per sq. ft

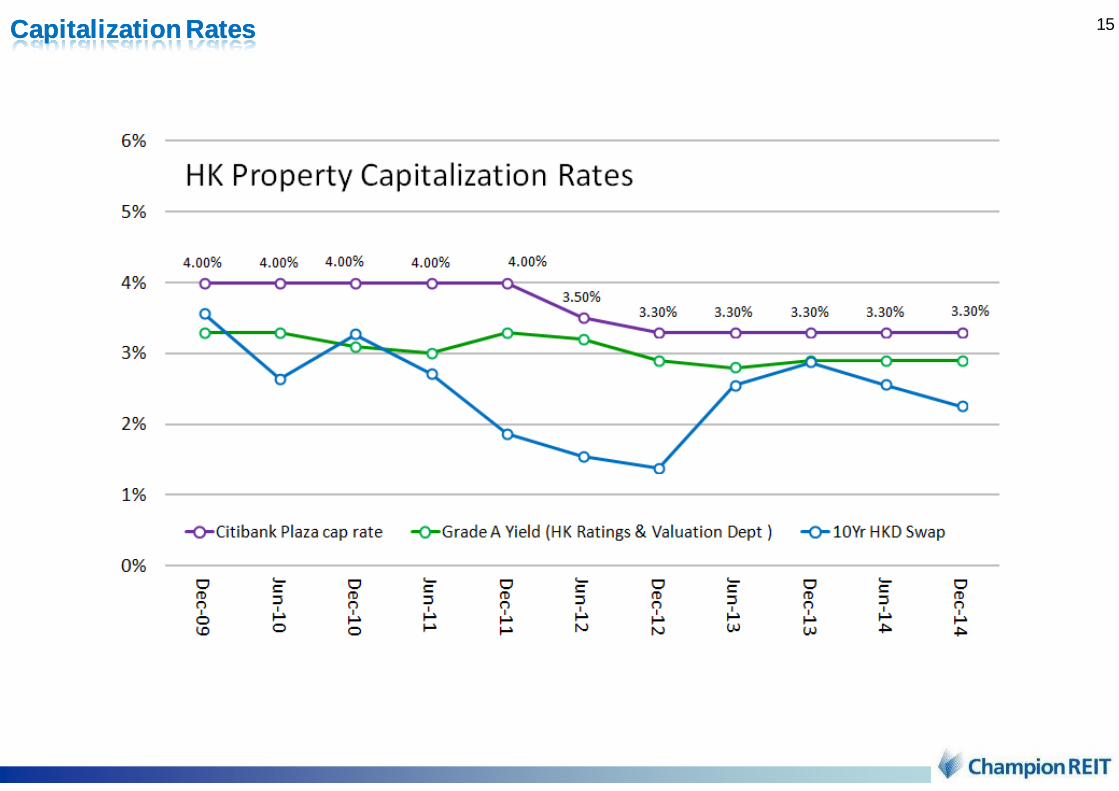

Cap Rate 3.3%

Citibank Plaza

Langham Place Mall

Langham Place Office

Comparisons are made with respect to Dec 2013 Valuation by Savills Valuation and Professional Services per sq. ft. valuations are based on Gross Floor Area

Value rose 6.6% to $11,200 per sq. ft

Implied rent increased

from $35.00 to $37.32 per sq. ft

Cap Rate 4.0%

Value rose 12.4% to $30,000 per sq. ft.

Implied rent increased

from $164.32 to $185.00 per sq. ft

Cap Rate 4.0%

Appraised Value of Properties at $62.44bn

Property Valuation1

8

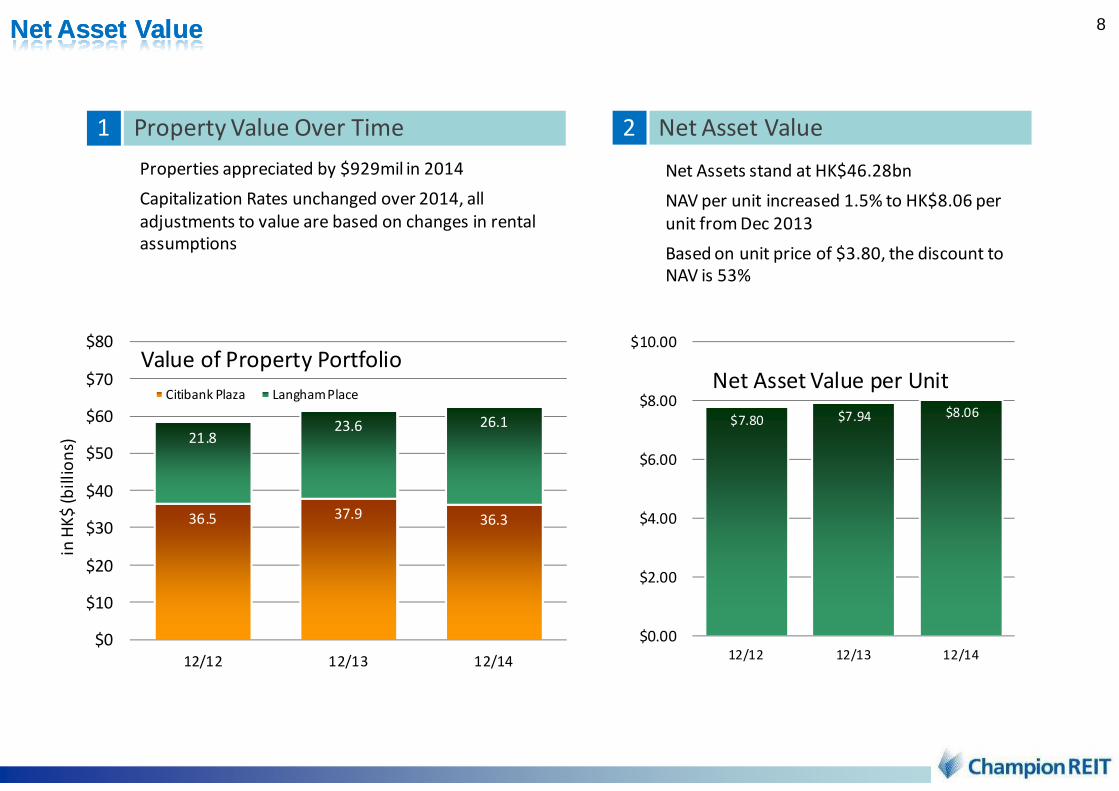

Properties appreciated by $929mil in 2014

Capitalization Rates unchanged over 2014, all

adjustments to value are based on changes in rental

assumptions

Property Value Over Time1 Net Asset Value2

Net Assets stand at HK$46.28bn

NAV per unit increased 1.5% to HK$8.06 per

unit from Dec 2013

Based on unit price of $3.80, the discount to

NAV is 53%

Net Asset ValueNet Asset Value

$7.80 $7.94 $8.06

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

12/12 12/13 12/14

Net Asset Value per Unit

36.5 37.9 36.3

21.823.6 26.1

$0

$10

$20

$30

$40

$50

$60

$70

$80

12/12 12/13 12/14

in H

K$

(b

illi

on

s)

Value of Property Portfolio

Citibank Plaza Langham Place

9

22

00 3

70

0

19

00

38

00

31

04

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

2015 2016 2017 2018 2019 2020 2021 2022 2023

HK

$ m

illi

on

s

Debt MaturityBank Loans MTN

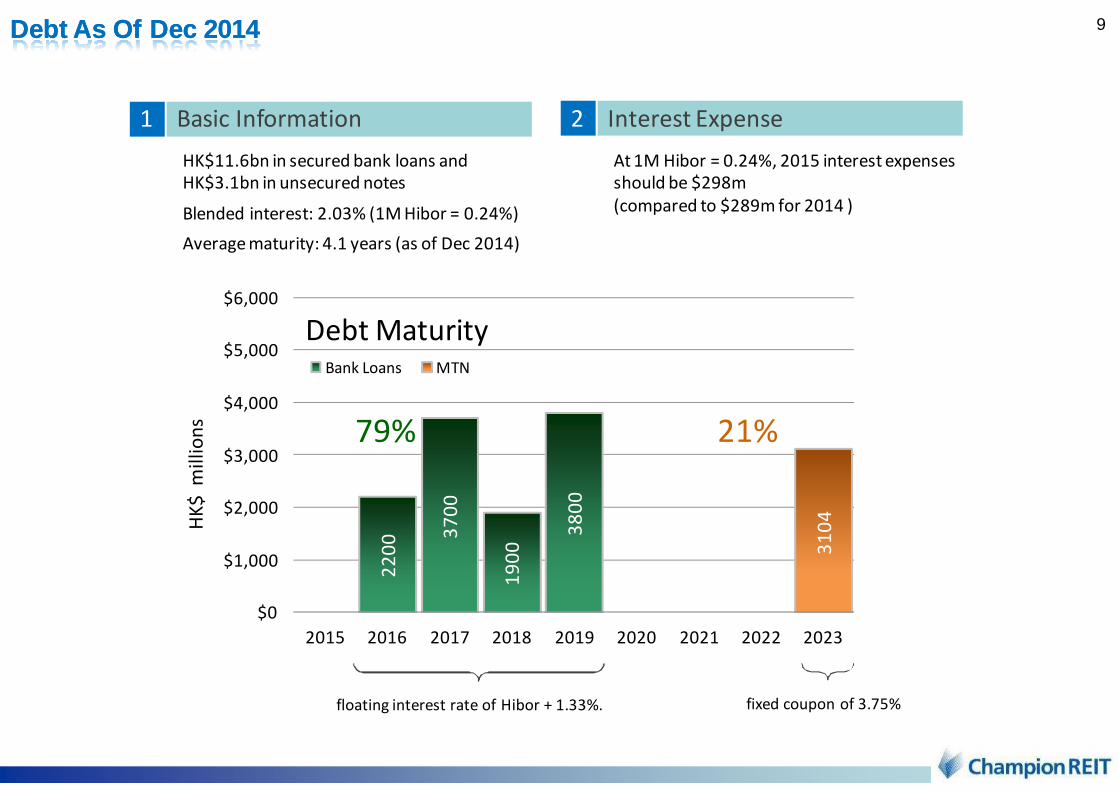

HK$11.6bn in secured bank loans and

HK$3.1bn in unsecured notes

Blended interest: 2.03% (1M Hibor = 0.24%)

Average maturity: 4.1 years (as of Dec 2014)

Interest Expense2

floating interest rate of Hibor + 1.33%. fixed coupon of 3.75%

79% 21%

Debt As Of Dec 2014 Debt As Of Dec 2014

Basic Information1

At 1M Hibor = 0.24%, 2015 interest expenses

should be $298m

(compared to $289m for 2014 )

10

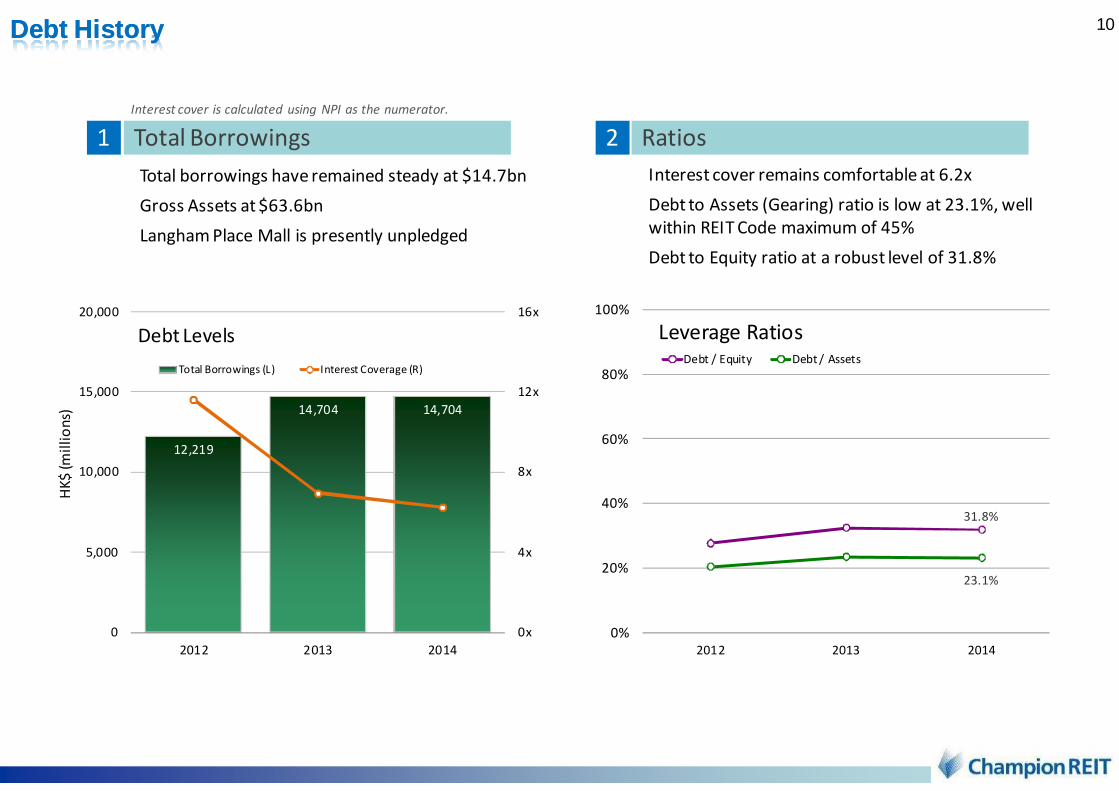

Total borrowings have remained steady at $14.7bn

Gross Assets at $63.6bn

Langham Place Mall is presently unpledged

Total Borrowings1

Interest cover remains comfortable at 6.2x

Debt to Assets (Gearing) ratio is low at 23.1%, well

within REIT Code maximum of 45%

Debt to Equity ratio at a robust level of 31.8%

Ratios 2

Debt HistoryDebt History

Interest cover is calculated using NPI as the numerator.

12,219

14,704 14,704

0x

4x

8x

12x

16x

0

5,000

10,000

15,000

20,000

2012 2013 2014

HK

$ (m

illi

on

s)

Debt Levels

Total Borrowings (L) Interest Coverage (R)

31.8%

23.1%

0%

20%

40%

60%

80%

100%

2012 2013 2014

Leverage RatiosDebt / Equity Debt / Assets

11

OFFICE MARKET UPDATEOFFICE MARKET UPDATE

12

$0

$20

$40

$60

$80

$100

$120

$140

$H

K p

er

sq.

ft.

Index rebased from original data series to the approximate equivalent rental levels

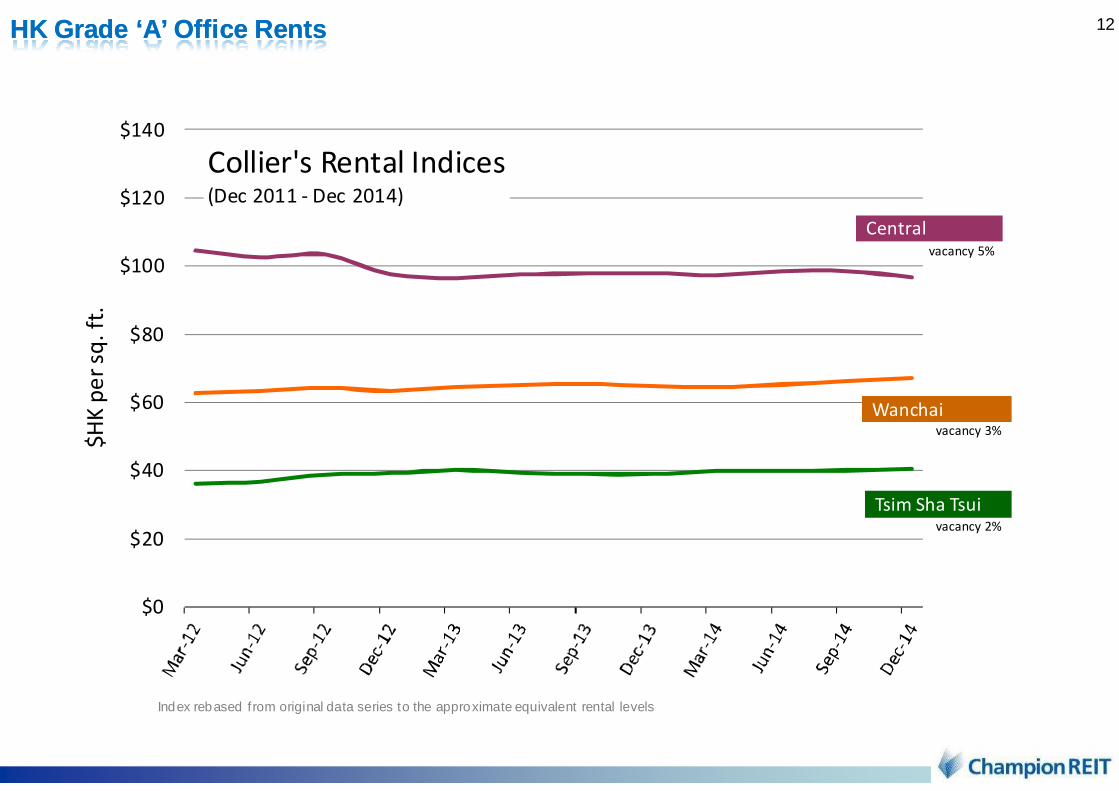

Collier's Rental Indices(Dec 2011 - Dec 2014)

Wanchai

Central

Tsim Sha Tsui

HK HK Grade ‘A’ Office Rents Grade ‘A’ Office Rents

vacancy 5%

vacancy 3%

vacancy 2%

13

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

NE

T F

LOO

R A

RE

A (

mill

ion

sq

ft)

HONG KONG CENTRAL GRADE A OFFICE SUPPLY (1986 - 2016)

Grade Grade ‘A’ Office ‘A’ Office Supply Supply -- Central Central

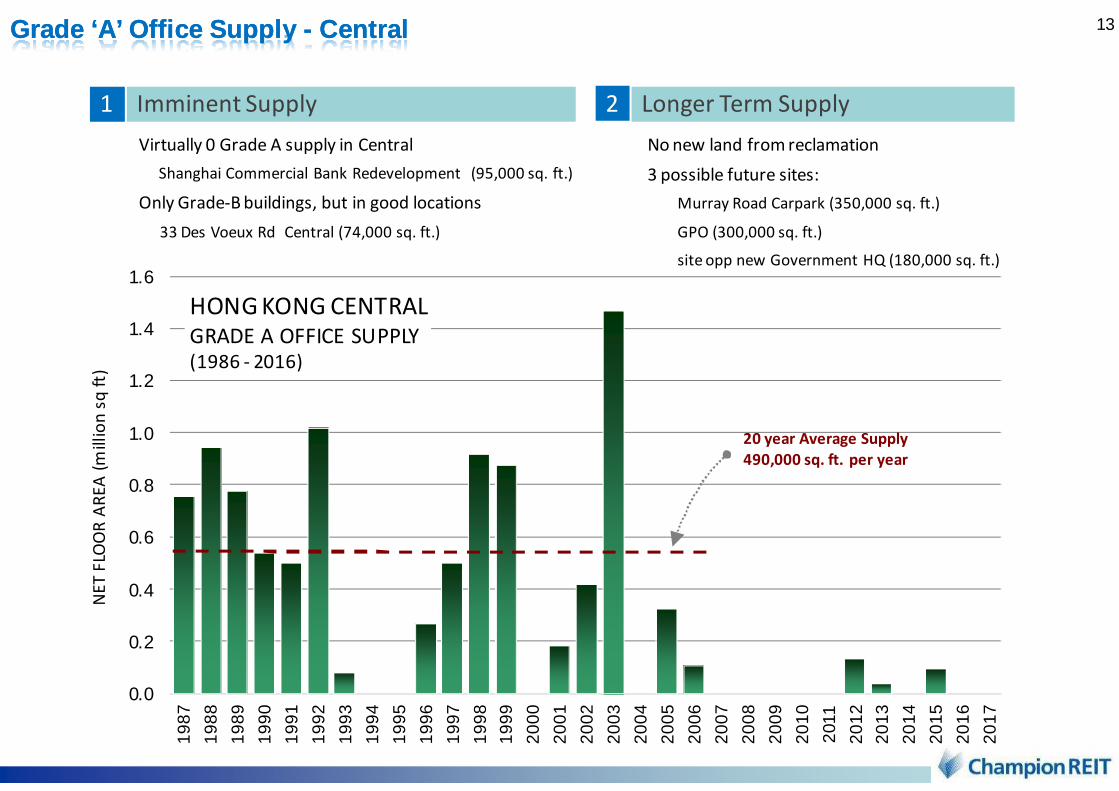

No new land from reclamation

3 possible future sites:

Murray Road Carpark (350,000 sq. ft.)

GPO (300,000 sq. ft.)

site opp new Government HQ (180,000 sq. ft.)

Longer Term Supply2

Virtually 0 Grade A supply in Central

Shanghai Commercial Bank Redevelopment (95,000 sq. ft.)

Only Grade-B buildings, but in good locations

33 Des Voeux Rd Central (74,000 sq. ft.)

Imminent Supply1

20 year Average Supply

490,000 sq. ft. per year

14

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

198

7

198

8

198

9

199

0

199

1

199

2

199

3

199

4

199

5

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

2011

201

2

201

3

201

4

201

5

201

6

201

7

NE

T FL

OO

R A

REA

(mill

ion

sq

ft)

HONG KONG SAR GRADE A OFFICE SUPPLY (1986 - 2016)

Central Rest of HKSAR

Grade Grade ‘A’ Office ‘A’ Office Supply Supply -- HKSARHKSAR

20 year Average Supply

2,470,000 sq. ft. per year

2016 Supply2

550k sq. ft. - 2 projects in Shatin

710k sq. ft. - 2 projects in Kwln E

240k sq. ft. - project in Island E

600k sq. ft. - Somerset Hse in Island E

180k sq. ft. - Sunning Plaza in CWB

240k sq. ft. - Asia House in CWB

Recent Demolitions3 2015 Supply1

2.3m sq. ft. - 5 projects in Kwln E

250k sq. ft - Octagon in Tsuen Wan

120k sq. ft. - Observatory Rd in TST

15Capitalization RatesCapitalization Rates

16

CITIBANK PLAZACITIBANK PLAZA

17

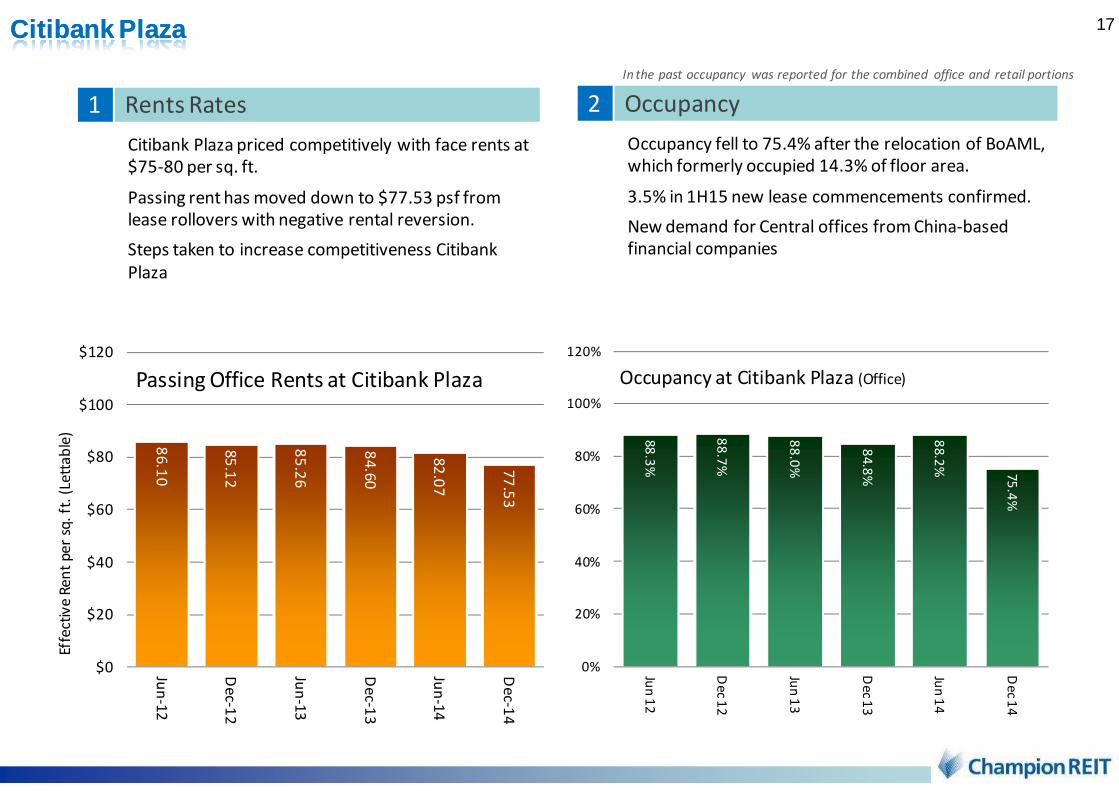

Citibank Plaza priced competitively with face rents at

$75-80 per sq. ft.

Passing rent has moved down to $77.53 psf from

lease rollovers with negative rental reversion.

Steps taken to increase competitiveness Citibank

Plaza

Rents Rates1

Citibank Plaza Citibank Plaza

Occupancy fell to 75.4% after the relocation of BoAML,

which formerly occupied 14.3% of floor area.

3.5% in 1H15 new lease commencements confirmed.

New demand for Central offices from China-based

financial companies

Occupancy 2

86

.10

85

.12

85

.26

84

.60

82

.07

77

.53

$0

$20

$40

$60

$80

$100

$120

Jun

-12

De

c-12

Jun

-13

De

c-13

Jun

-14

De

c-14

Effe

ctiv

e R

en

t p

er

sq.

ft.

(Le

tta

ble

)

Passing Office Rents at Citibank Plaza

88

.3%

88

.7%

88

.0%

84

.8%

88

.2%

75

.4%

0%

20%

40%

60%

80%

100%

120%

Jun

12

De

c 12

Jun

13

De

c 13

Jun

14

De

c 14

Occupancy at Citibank Plaza (Office)

In the past occupancy was reported for the combined office and retail portions

18Citibank Plaza Citibank Plaza

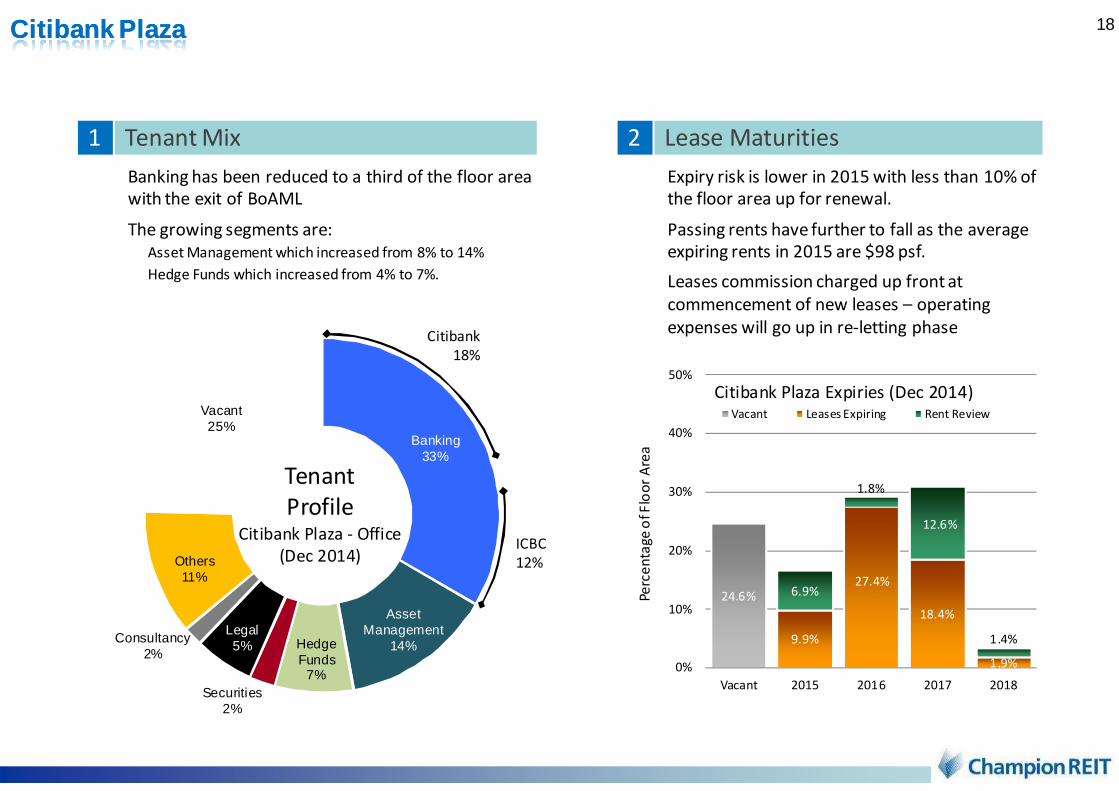

Expiry risk is lower in 2015 with less than 10% of

the floor area up for renewal.

Passing rents have further to fall as the average

expiring rents in 2015 are $98 psf.

Leases commission charged up front at

commencement of new leases – operating

expenses will go up in re-letting phase

Lease Maturities 2 Tenant Mix 1

Banking has been reduced to a third of the floor area

with the exit of BoAML

The growing segments are:

Asset Management which increased from 8% to 14%

Hedge Funds which increased from 4% to 7%.

Banking33%

Asset Management

14%Hedge Funds

7%Securities

2%

Legal5%

Consultancy2%

Others11%

Vacant25%

Tenant

ProfileCitibank Plaza - Office

(Dec 2014)

Citibank

18%

ICBC

12%

24.6%

9.9%

27.4%

18.4%

1.9%

6.9%

1.8%

12.6%

1.4%

0%

10%

20%

30%

40%

50%

Vacant 2015 2016 2017 2018

Perc

en

tage

of F

loo

r A

rea

Citibank Plaza Expiries (Dec 2014)Vacant Leases Expiring Rent Review

19Asset EnhancementAsset Enhancement

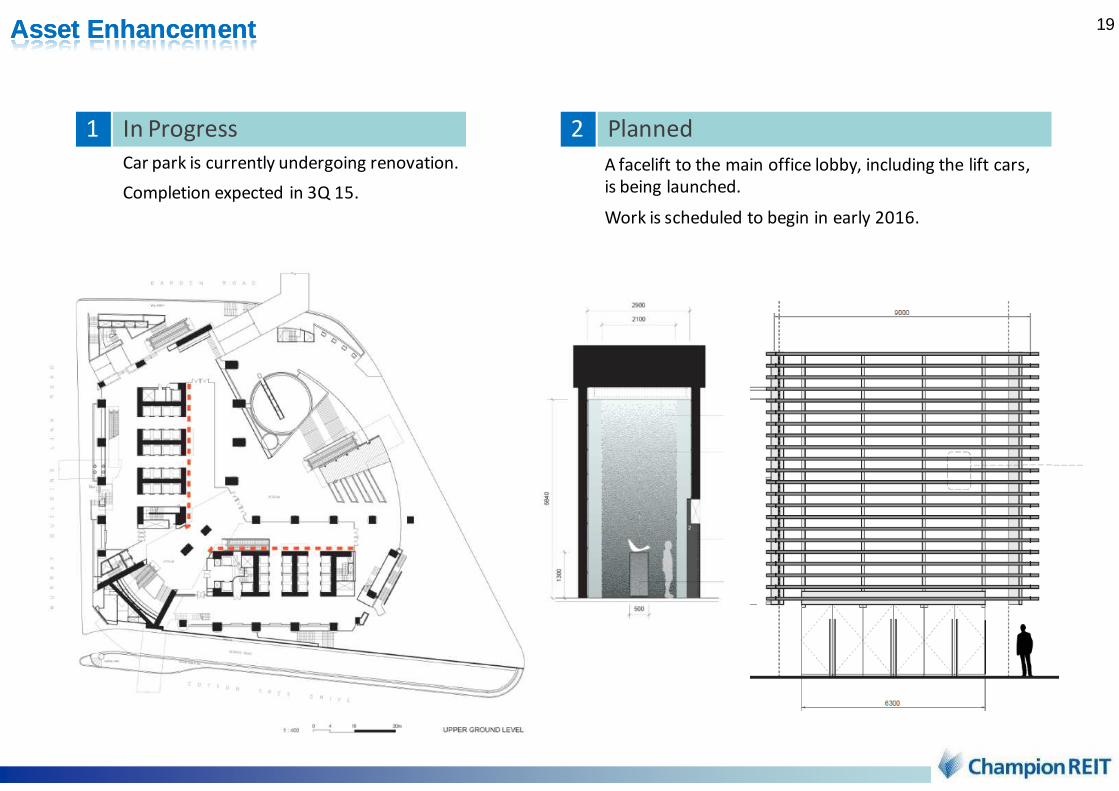

Planned2 In Progress1

Car park is currently undergoing renovation.

Completion expected in 3Q 15.

A facelift to the main office lobby, including the lift cars,

is being launched.

Work is scheduled to begin in early 2016.

20

SUPPLIMENTARY MATERIALSSUPPLIMENTARY MATERIALS

LANGHAM PLACE LANGHAM PLACE

21

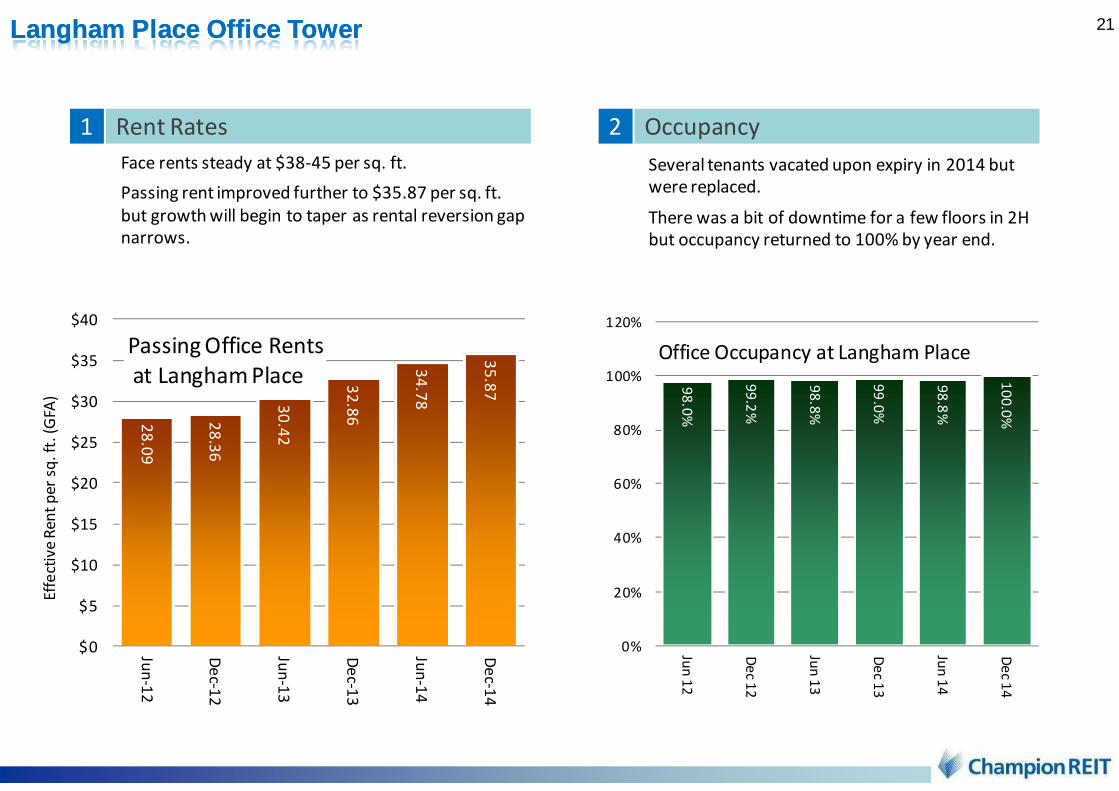

Face rents steady at $38-45 per sq. ft.

Passing rent improved further to $35.87 per sq. ft.

but growth will begin to taper as rental reversion gap

narrows.

Rent Rates 1

LanghamLangham Place Office TowerPlace Office Tower

Several tenants vacated upon expiry in 2014 but

were replaced.

There was a bit of downtime for a few floors in 2H

but occupancy returned to 100% by year end.

Occupancy2

28

.09

28

.36

30

.42

32

.86

34

.78

35

.87

$0

$5

$10

$15

$20

$25

$30

$35

$40

Jun

-12

De

c-12

Jun

-13

De

c-13

Jun

-14

De

c-14

Eff

ect

ive

Re

nt

pe

r sq

. ft

. (G

FA)

Passing Office Rents

at Langham Place 98

.0%

99

.2%

98

.8%

99

.0%

98

.8%

10

0.0

%

0%

20%

40%

60%

80%

100%

120%

Jun

12

De

c 12

Jun

13

De

c 13

Jun

14

De

c 14

Office Occupancy at Langham Place

22

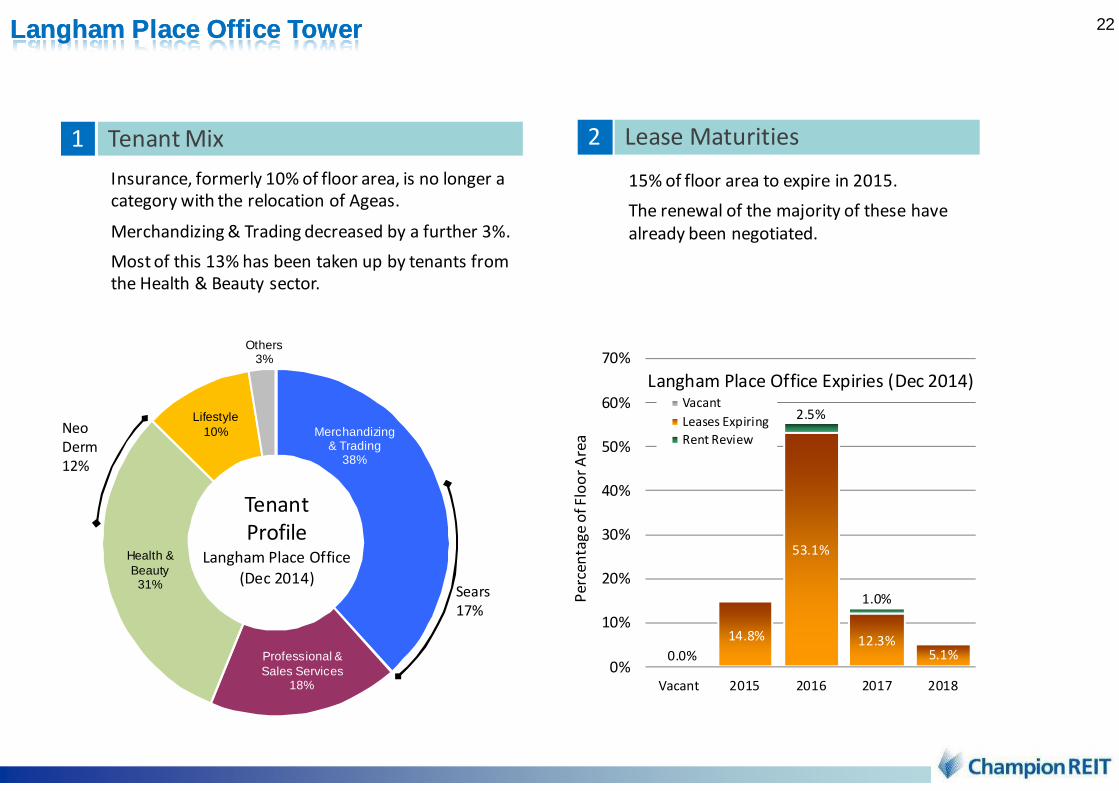

Insurance, formerly 10% of floor area, is no longer a

category with the relocation of Ageas.

Merchandizing & Trading decreased by a further 3%.

Most of this 13% has been taken up by tenants from

the Health & Beauty sector.

Tenant Mix 1

LanghamLangham Place Office TowerPlace Office Tower

Lease Maturities2

15% of floor area to expire in 2015.

The renewal of the majority of these have

already been negotiated.

Merchandizing& Trading

38%

Professional & Sales Services

18%

Health & Beauty

31%

Lifestyle10%

Others3%

Tenant

ProfileLangham Place Office

(Dec 2014)

0.0%

14.8%

53.1%

12.3%5.1%

2.5%

1.0%

0%

10%

20%

30%

40%

50%

60%

70%

Vacant 2015 2016 2017 2018

Pe

rce

nta

ge

of

Flo

or

Are

a

Langham Place Office Expiries (Dec 2014) Vacant

Leases Expiring

Rent Review

Sears

17%

Neo

Derm

12%

23Some 2014 LP Mall EventsSome 2014 LP Mall Events

24

Fashion & Accessories

44%

Health &Beauty10%

Entertainment16%

Food & Beverage

20%

Others10%

Tenant

ProfileLangham Place Mall

(Dec 2014)

LanghamLangham Place MallPlace Mall

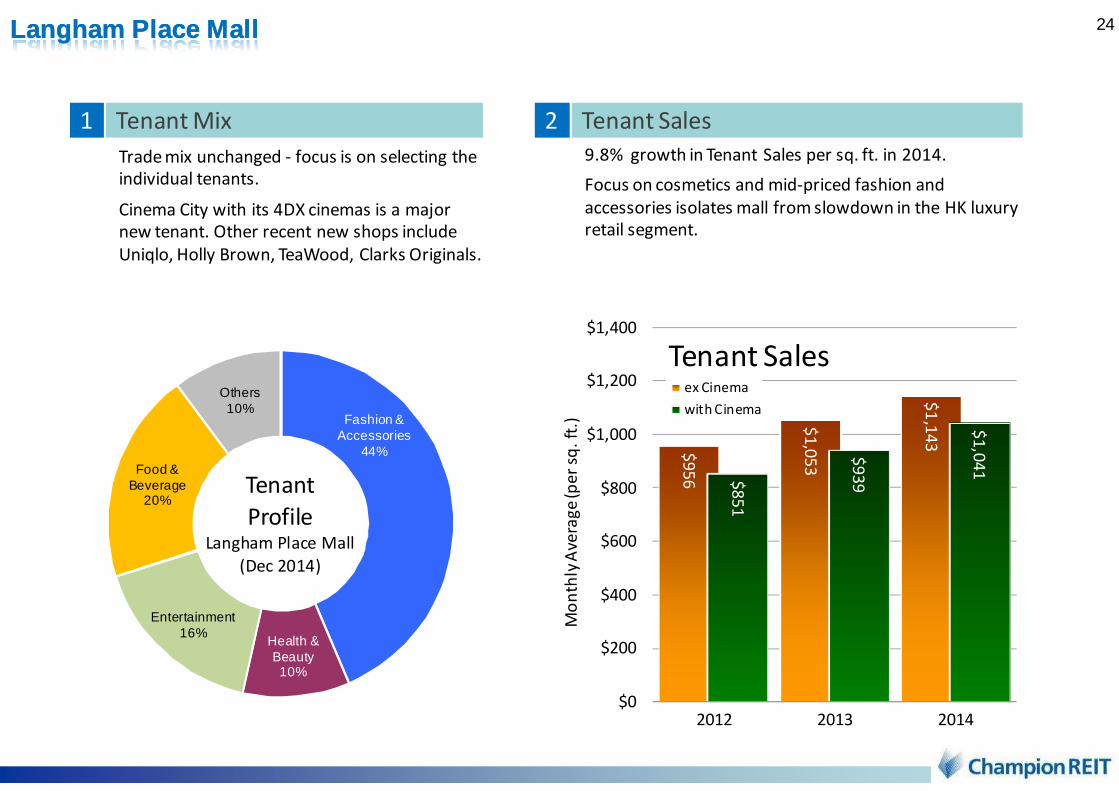

9.8% growth in Tenant Sales per sq. ft. in 2014.

Focus on cosmetics and mid-priced fashion and

accessories isolates mall from slowdown in the HK luxury

retail segment.

Tenant Sales2

Trade mix unchanged - focus is on selecting the

individual tenants.

Cinema City with its 4DX cinemas is a major

new tenant. Other recent new shops include

Uniqlo, Holly Brown, TeaWood, Clarks Originals.

Tenant Mix 1

$9

56

$1

,05

3

$1

,14

3

$8

51

$9

39

$1

,04

1

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

2012 2013 2014

Mo

nth

ly A

vera

ge

(pe

r sq

. ft

.)

Tenant Salesex Cinema

with Cinema

25

10

2.6

5

11

4.8

9

11

8.7

1

14

4.2

6

14

6.0

1

16

5.4

4

$0

$40

$80

$120

$160

$200

Jun

-12

De

c-12

Jun

-13

De

c-13

Jun

-14

De

c-14

Effe

ctiv

e R

en

t p

er s

q.

ft.

(Let

tab

le)

Passing Retail Rents at Langham Place

(exclusive of turnover rent)

LanghamLangham Place MallPlace Mall

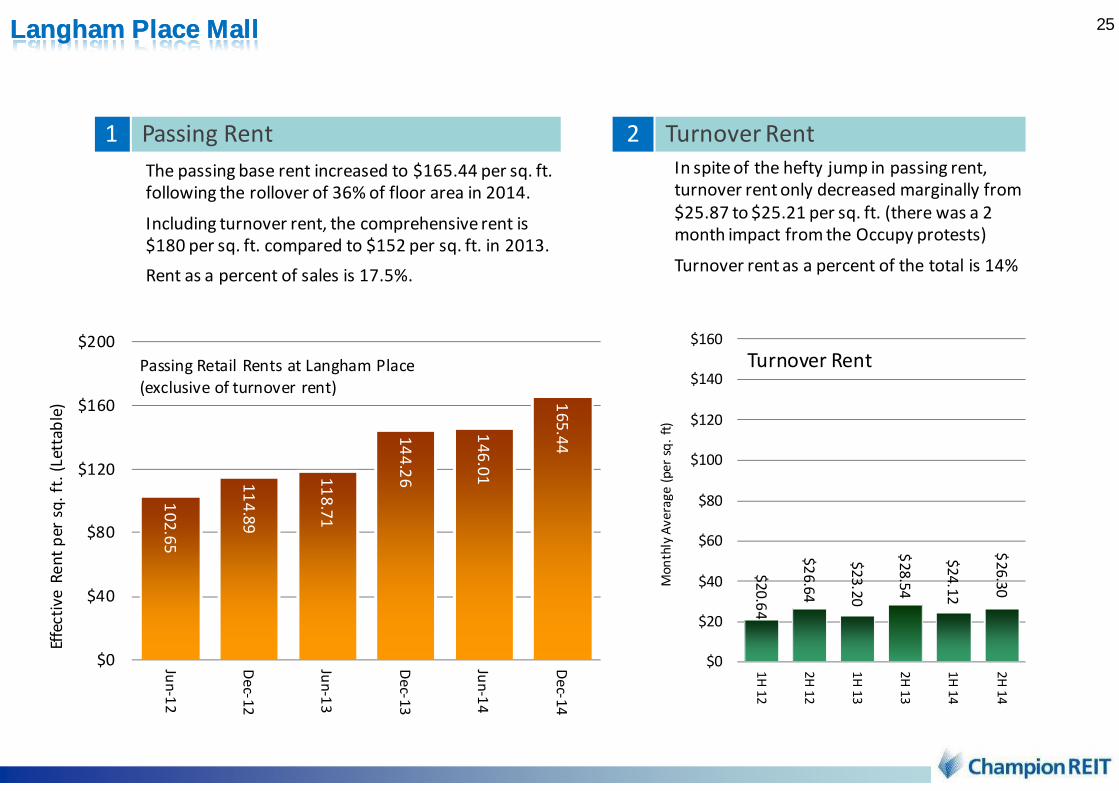

The passing base rent increased to $165.44 per sq. ft.

following the rollover of 36% of floor area in 2014.

Including turnover rent, the comprehensive rent is

$180 per sq. ft. compared to $152 per sq. ft. in 2013.

Rent as a percent of sales is 17.5%.

Passing Rent1

In spite of the hefty jump in passing rent,

turnover rent only decreased marginally from

$25.87 to $25.21 per sq. ft. (there was a 2

month impact from the Occupy protests)

Turnover rent as a percent of the total is 14%

Turnover Rent2

$2

0.6

4

$2

6.6

4

$2

3.2

0

$2

8.5

4

$2

4.1

2

$2

6.3

0

$0

$20

$40

$60

$80

$100

$120

$140

$1601

H 1

2

2H

12

1H

13

2H

13

1H

14

2H

14

Mo

nth

ly A

ve

rag

e (

pe

r sq

. ft

)

Turnover Rent

26

0.0%

25.8%24.1%

17.4%14.1%

4.7%

2.2%

0%

10%

20%

30%

40%

50%

Vacant 2015 2016 2017 2018

Pe

rce

nta

ge

of

Flo

or

Are

a

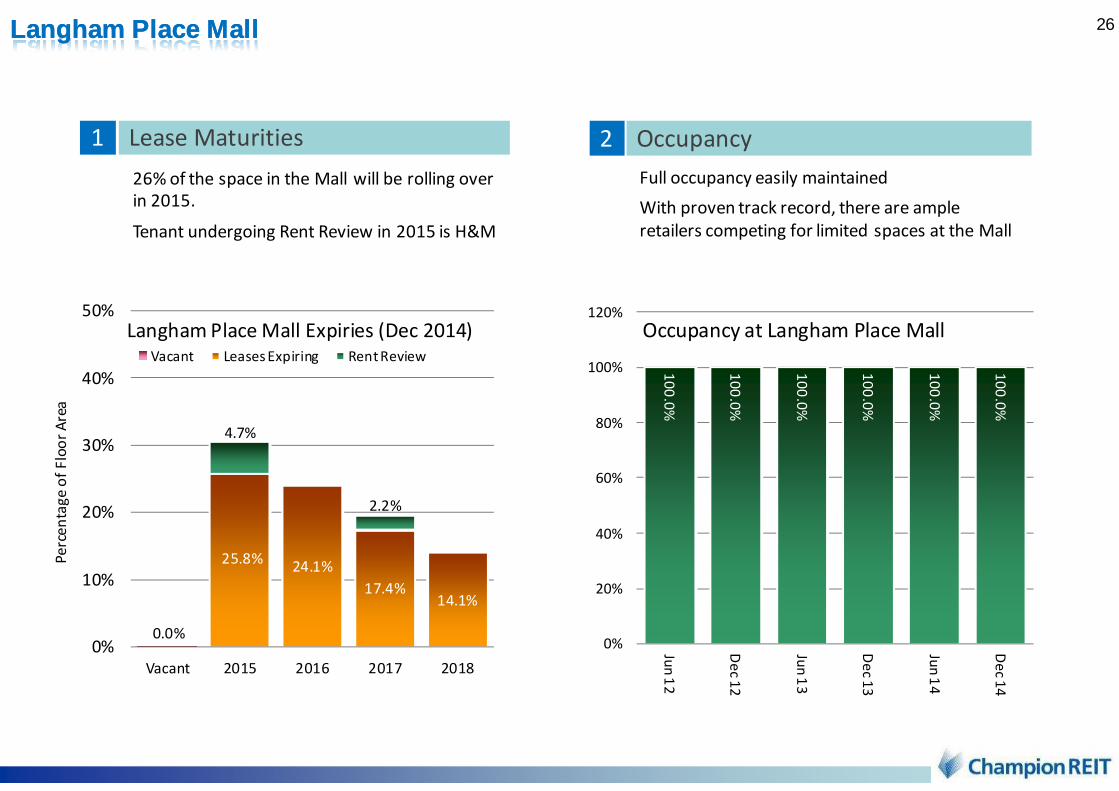

Langham Place Mall Expiries (Dec 2014)Vacant Leases Expiring Rent Review

LanghamLangham Place MallPlace Mall

Full occupancy easily maintained

With proven track record, there are ample

retailers competing for limited spaces at the Mall

Occupancy2

26% of the space in the Mall will be rolling over

in 2015.

Tenant undergoing Rent Review in 2015 is H&M

Lease Maturities1

10

0.0

%

10

0.0

%

10

0.0

%

10

0.0

%

10

0.0

%

10

0.0

%

0%

20%

40%

60%

80%

100%

120%

Jun

12

De

c 12

Jun

13

De

c 13

Jun

14

De

c 14

Occupancy at Langham Place Mall

27ConclusionConclusion

At the operational level the strong performance of Langham Place will not be able to offset the

expected fall in Citibank Plaza income as it did in 2014.

Distributions, which will also be affected by a slightly higher effective tax rate, are expected to be

lower in 2015

the REIT3

Lower average occupancy and lower passing rent in 2015. Rental rates will continue to be under

pressure this year as we focus on rebuilding occupancy.

While there has been some progress in reducing vacancy in 1Q15, income from Citibank Plaza is

expected to decline this year.

Citibank Plaza1

Office Rents are firm, there should continue to be positive rental reversion but only 15% of the

building is expiring in 2015.

Retail Rental Income should continue to increase in 2015 but the increase will depend on the pace of

tenant sales growth in 1H 15.

Langham Place2

28

the END the END

29

This presentation may contain information which is proprietary, confidential and/or legally privileged and has been prepared by Eagle AssetManagement (CP) Limited, in its capacity as the manager (the “REIT Manager”) of Champion Real Estate Investment Trust (the “Trust”). Thispresentation is being communicated for information purposes only and its intended recipients are professional investors in Hong Kong (asdefined by Part 1 of Schedule 1 to the Securities and Futures Ordinance(Cap.571)) and professional investors outside of Hong Kong to whomit is lawful to communicate the presentation. Any other persons should not rely or act upon this presentation or any of its contents.

The information contained in this document, including any obtained from external data sources, has not been verified. The information andopinions in this presentation are subject to change without notice and the REIT Manager is under no obligation to update or keep current theinformation contained in this presentation. No representation or warranty, express or implied is made as to, and no reliance should be placedon, the fairness, accuracy, completeness or correctness of the information or opinions contained herein. It is not the intention to provide, andyou may not rely on this document as providing, a complete or comprehensive analysis of the Trust’s financial or operational position.Furthermore, this presentation should not be construed as legal, tax, investment, or other advice. None of the REIT Manager, the Trust, norany of their respective affiliates, advisors or representatives shall be held liable for any damages, losses or expenses of any kind, whetherdirect, indirect, special, consequential or incidental, arising out of or in connection with the presentation. In this regard, all warranties orrepresentations of any kind, whether expressed or implied by law, equity or statutes, are excluded to the extent permissible under theapplicable law. All liabilities whatsoever arising from or incidental to the document are hereby expressly disclaimed.

Certain information and statements made in this presentation contain forward-looking statements. All forward-looking statements are based oncurrent expectation of future events and are subject to a number of factors that could cause actual results to differ materially from thosedescribed in the forward-looking statements. Caution should be taken with respect to such statements and you should not place unduereliance on any such forward-looking statements.

This document does not constitute a prospectus, notice, circular, brochure or advertisement offering to sell or inviting offers to acquire,purchase or subscription for any units (“Units”) or other securities of the Trust. The value of Units and the income from them, if any, may fall aswell as rise from time to time. Units are not obligations of, deposits in, or guaranteed by the REIT Manager, the Trust, nor any of theirrespective affiliates, advisors or representatives. An investment in Units or other securities of the Trust is subject to investment risks, includingthe possible loss of the principal amount invested. It is intended that holders of Units may only deal in their Units through trading on the StockExchange of Hong Kong and investors have no right to request the REIT Manager to redeem their Units. Listing status does not guarantee aliquid market for the Units.

All copyright, patent, intellectual and other property rights in information contained herein is owned by the REIT Manager or other third parties.No rights of any kind are licensed or assigned or shall otherwise pass to persons accessing such information. Without the expressed writtenpermission of the REIT Manager under no circumstances should information contained herein or any part of it be quoted, reproduced,redistributed or transmitted in any form, by any means, electronic or otherwise.

Important Notice