Embed Size (px)

Citation preview

FOCUS ON IMPROVING OPERATIONS 2014 Investor Days

DISCLAIMER

This document has been prepared by Klepierre (the “Company”) solely for use at the presentation of June 13, 2014. This document is not

to be reproduced nor distributed, in whole or in part, by any person other than the Company. The Company takes no responsibility for the

use of these materials by any person.

The information contained in this document has not been subject to independent verification and no representation, warranty or

undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness

of the information or opinions contained herein. None of the Company, its shareholders, its advisors or representatives nor any other

person shall have any liability whatsoever for any loss arising from any use of this document or its contents or otherwise arising in

connection with this document.

This document does not constitute an offer to sell or an invitation or solicitation of an offer to subscribe for or purchase any securities, and

this shall not form the basis for or be used for any such offer or invitation or other contract or engagement in any jurisdiction.

Participants are invited to read the registration document (“document de reference”) of the Company filed with the AMF on March 10, 2014

and the risk factors described in the Risk Factors section from page 109 to 116 of the registration document. The registration document is

made available free of charge at the headquarters of the Company (Klepierre), on the Internet site of the AMF (http://www.amf-france.org)

and on the website of the Company (http://www.Klepierre.com).

Certain statements included in the registration document contain forward-looking statements with respect to future events, trends, plans or

objectives. The information, assumptions and estimates that were used to determine these objectives are subject to change or

modification due to economic, financial and competitive uncertainties. Furthermore, it is possible that some of the risks described in the

aforementioned section of the registration document could have an impact on the Company’s ability to achieve these objectives.

Accordingly, the Company cannot give any assurance as to whether it will achieve the objectives described, and makes no commitment or

undertaking to update or otherwise revise this information.

No assurance is given as to the fairness, accuracy, completeness or correctness of the information or opinions contained in this document.

In case of any discrepancies between the information contained in this document and the registration document, the latter will prevail.

06/13/2014 2014 INVESTOR DAYS 2

2014 Investor Days

FROM VISION TO

OPERATIONAL

EXCELLENCE

1

4 2014 INVESTOR DAYS 06/13/2014

OUR VISION

• To develop and operate quality and superior

retail destinations in major cities

Highly productive and sales intensive

With strong franchise value

Able to attract leading retail brands

5 2014 INVESTOR DAYS 06/13/2014

OUR CUSTOMER-CENTRIC KNOWHOW

• By understanding our customers we create

and transform their experience at our centers

in order to:

Attract more customers

Encourage them to come more often and stay

longer

Develop a deeper relationship with the

community

6 2014 INVESTOR DAYS 06/13/2014

OUR FOCUS

• From “shoppers” to “style-conscious guests”: provide a

distinctive and image-enhancing combination of

Modern and fashion shopping

The best in casual and fine dining (with gourmet grocery and artisan

shops)

Entertainment and unforgettable performances and activities

• From “retailers” to “partners”: offer an unparalleled

opportunity to thrive in the best real estate with new

locations, an adapted format and a more consistent

merchandizing mix

• From “market places” to “connected places”: use technology

to better connect retailers with consumers

• Uncompromising asset selection with good fundamentals

• Consistent and comprehensive deployment of the vision

with each and every property

• Talented, motivated, passionate, and empowered teams

focused on creating mutually-beneficial opportunities and

relationships with partners

“Be creative, collaborative and connected”

7 2014 INVESTOR DAYS 06/13/2014

OUR RESOURCES

KLEPIERRE’S OPERATIONAL FOCUS

8 2014 INVESTOR DAYS 06/13/2014

1. ANTICIPATE TRENDS TO ACCELERATE RE

TENANTING

2. IMPROVE SHOPPERS’ EXPERIENCE

Club Store®

3. ENHANCE MARKETING POSITIONNING

Let’s play®

4. OPTIMIZE OPERATING COSTS AND

SUSTAINABLE FOOTPRINT

Good Choices®

Shopping center analysis

- Footfall analysis

- Retailer sales

- OCR by tenant

- KPI by tenant and benchmark

- Merchandising mix

- Competition

- Catchment area

- Customer profile

9 2014 INVESTOR DAYS 06/13/2014

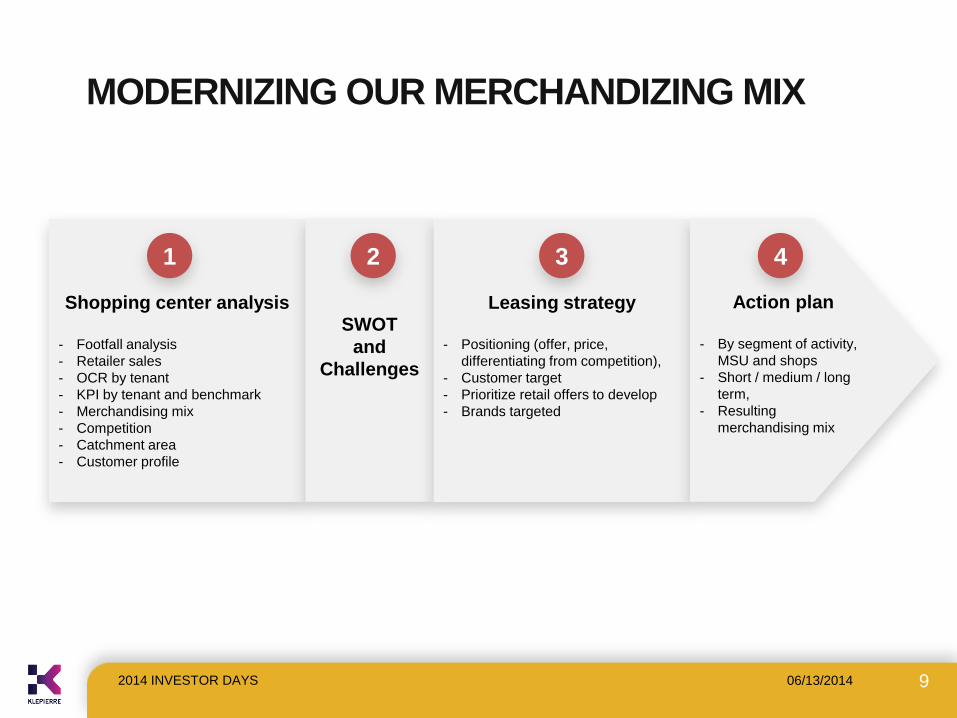

MODERNIZING OUR MERCHANDIZING MIX

1

SWOT

and

Challenges

2

Leasing strategy

- Positioning (offer, price,

differentiating from competition),

- Customer target

- Prioritize retail offers to develop

- Brands targeted

3

Action plan

- By segment of activity,

MSU and shops

- Short / medium / long

term,

- Resulting

merchandising mix

4

10 2014 INVESTOR DAYS 06/13/2014

THE LEASING AND MERCHANDIZING MIX

ACTION PLAN TOOL

ANTICIPATE

TRENDS

TO ACCELERATE

RE-TENANTING

2

2014 Investor Days

12 2014 INVESTOR DAYS 06/13/2014

ILLUSTRATIVE EXAMPLES

L’Esplanade (Belgium) Leveraging a large renewal campaign as an opportunity to

optimize the center’s retail mix and consolidate its leadership

Créteil Soleil Rejuvenating and upgrading the offer of a well-

established and high performing historical regional mall

Belle Epine Upgrading the customer path through re-

tenanting and mall design via the ClubStore®

Les Passages - Boulogne A city-center mall recently repositioned through a renovation

scheme combined with a renewal/re-tenanting campaign

A large re-tenanting and renewal campaing to be followed in the

medium term by an extension scheme

L’ESPLANADE – LEADERSHIP CONSOLIDATION

13 2014 INVESTOR DAYS 06/13/2014

Key figures (2013):

56,000 sq.m. GLA

Footfall : 8M

MGR : 14.4M€

Av. OCR (shops): 12.2%

2005: shopping center

opens

2014: renewal campaign

involving around 80 leases

14 2014 INVESTOR DAYS 06/13/2014

1. LEADERSHIP CONSOLIDATION THROUGH

RE-TENANTING

• Objectives

Maintain well-performing retailers with a

significant increase in rents

Negotiate out underperforming tenants

and replace them with attractive

international prospects

• “Move” Belgium market practices

Differentiate from competition new

retailers for the region

Adapted to catchment area: families with

high income and students

• Outcome

Re-tenanting: rental uplift of +49% vs

former MGR

Renewals: +22% vs former MGR

15 2014 INVESTOR DAYS 06/13/2014

2. L’ESPLANADE EXTENSION PROJECT – 2018

Pipeline status: controlled

Floor area: +18,000 sq.m.

A mall that is continuous with the existing

mall,

Connected to its vicinity and the

Park&Ride at the upper level

Expand the retail offer in line with the

growth outlook for the catchment area:

• Brabant Wallon population expected to grow by 7%, i.e., 30 000 inhabitants by 2015 (vs population growth of 3.6% in five years for Belgium)

• Strong development of the Louvain area, partly due to the arrival of the regional rail system in 2016

Strengthen the retail mix with additional

high performing brands, new to the region

Transforming the shopping center into a large regional shopping mall

Fashion mall upgraded by resizing concepts, renewing retail mix and

improving customer path

CRETEIL SOLEIL - REJUVENATE A WELL-

ESTABLISHED, WELL-PERFORMING REGIONAL MALL

16 2014 INVESTOR DAYS 06/13/2014

Key figures (end Q1 2014):

119,000 sq,m, GLA

220 shops

Footfall : 18M

MGR : 37.4M€

Av. OCR (shops) : 16.5%

#1 asset in Klépierre’s

portfolio in value terms

1974 :center opens

2000 : Extension (Level 3

: food court)

2014 : Renovation of the

parking area and main

entrance (Porte 23)

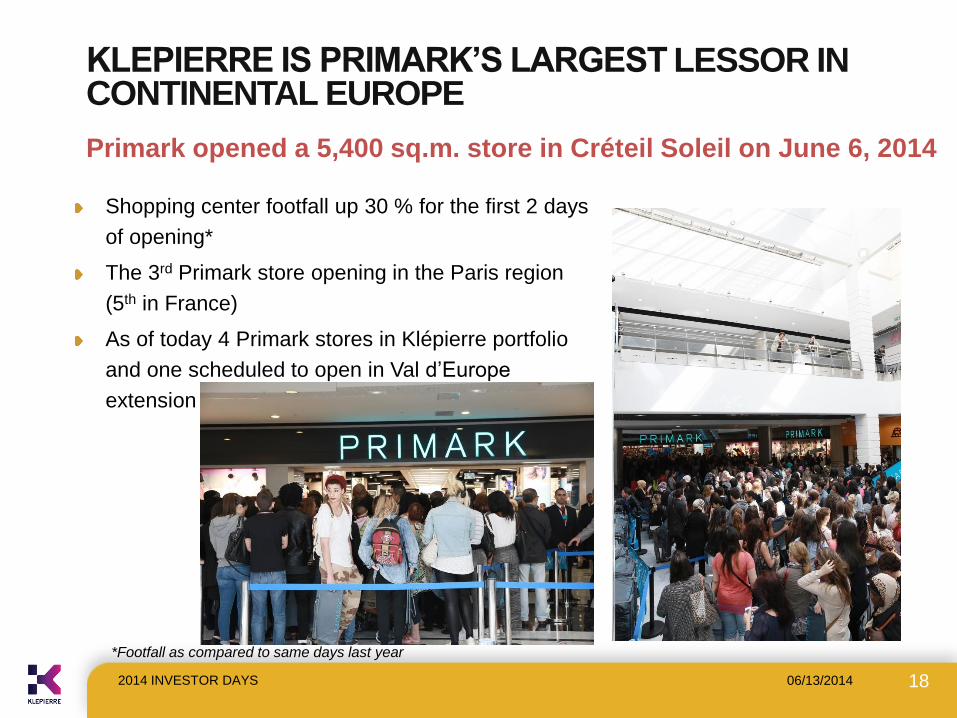

=> Primark opened on June 6, 2014 on 5.406 sqm

Zara on its best format (3.200m²) in replacement of Boulanger

=> Targeted brands

17 2014 INVESTOR DAYS 06/13/2014

1. CRETEIL-SOLEIL : REJUVENATING THE RETAIL

MIX • Staged re-tenanting plan is ongoing

Today: a mass-market retail offer

Lacks innovative and dynamic retailers

• Development of a complete fashion mall

following the arrival of Primark arrival

and extension of Zara stores

Resizing a few existing concepts

Attracting new ones

• Similar plans to extend Zaraland in

Annecy, Boulogne, Jaude, Emporia

18 2014 INVESTOR DAYS 06/13/2014

Primark opened a 5,400 sq.m. store in Créteil Soleil on June 6, 2014

KLEPIERRE IS PRIMARK’S LARGEST LESSOR IN CONTINENTAL EUROPE

*Footfall as compared to same days last year

Shopping center footfall up 30 % for the first 2 days

of opening*

The 3rd Primark store opening in the Paris region

(5th in France)

As of today 4 Primark stores in Klépierre portfolio

and one scheduled to open in Val d’Europe

extension

• Optimize the customer path

Renovate main entrance from

metro line – “Porte (Gate) 23”

Improve visibility of stores

Digital screens

Accessibility

• First phase of a large extension-refurbishment program designed to leverage a powerful retail hub

Floor area: + 7,500 sq.m. of

stores

Partial renovation of existing mall

Restructured food court: link mall

to subway line and location near

the movie theaters

19 2014 INVESTOR DAYS 06/13/2014

2. CRETEIL-SOLEIL : MORE TO COME

Extension project

Main entrance

Porte « 23 » renovation

Project perspective

Renovation for deployment of Club Store® concept and the arrival of

anchors’ latest concepts

BELLE EPINE – UPGRADING SHOPPING EXPERIENCE

20 2014 INVESTOR DAYS 06/13/2014

Key figures:

134.000 sq.m. GLA

220 shops

Footfall : 17M

1971 : Shopping center

opens

1993 : Extension

2014 : Ongoing

renovation

Tati comeback with its new concept on a 4,000 sq.m. store

Uniqlo (1,200 sq.m.) opening in sept 2014

Latest arrivals and new concepts

21 2014 INVESTOR DAYS 06/13/2014

1. BELLE EPINE: REAFFIRM RETAIL LEADERSHIP

Intense, ongoing re-tenanting campaign

to modernize a mall with a long history,

including aging retailers

• Re-tenanting opportunities exploited to

attract international premium anchor stores

Virgin departure Flagship 4,000

sq.m. H&M store combining 2 existing

floor spaces, with H&M Home added

Uniqlo to replace OVS

• Expand the offer to encompass under-

represented segments for the catchment

area

• Install latest brand concepts, with attention

to design and shop windows

• Around 20% of leases up for renewal by

end 2016

BELLE EPINE, 2014

BELLE EPINE - RETAILERS

22 2014 INVESTOR DAYS 06/13/2014

• Complete refurbishment of the center launched

• Customers will discover the Cosmopolis

Club Store® by Fall 2014

Mall design

Services

Image and Brand revisited

• Buzz to boost traffic and visibility

Brand roadshows, e.g., Nespresso

Virtual fitting rooms: an innovative

interactive digital experience via the digital

display panels of Clear Channel.

•Food offer reinforced

23 2014 INVESTOR DAYS 06/13/2014

2. BELLE EPINE: ENHANCE ATTRACTIVITY

An illustration of Klepierre’s knowhow in brownfield development

LES PASSAGES (BOULOGNE) - CITY CENTER

RENEWAL

24 2014 INVESTOR DAYS 06/13/2014

Key figures (end Q1 2014):

23,000 sq.m. GLA

58 shops

Footfall : 6M

MGR : 11.7M€

Av. OCR (shops) : 12.7%

2001 : center opens

2013: Launch of the

“Original Club Store”

2014 : Renewal campaign

completed

LES PASSAGES

A COZY MALL – NEW IDENTITY AND WELCOME DESK

25 2014 INVESTOR DAYS 06/13/2014

2012 2014

Zara upgrade and opening of Zara

Men in 908 sq.m. space displaying

the full concept

Ongoing re-tenanting with best

performers and exclusive brands

26 2014 INVESTOR DAYS 06/13/2014

1. REPOSITIONING OF LES PASSAGES : AN

UPSCALE RETAIL OFFER • A unique shopping experience in the

West of Paris

Boulogne is the gateway to Paris for its

western suburbs, a very convenient stop

and shop center

• Extensive re-tenanting campaign

started in 2012, still underway

44 leases out of 62 expired in 2013

Enrich the retail offer with specific focus

on differentiating brands

• Outcome

2013 reversion: +36%

Re-tenanting: rental uplift of +45% vs

former MGR

Renewals: +35% vs former MGR

OCR for small shops above 14.5% at

year-end 2013

• Club Store® creates a unique feeling of cozy

and chic shopping in all areas of the mall

• Passages brand and identity reinvented to

align with redefined positioning

27 2014 INVESTOR DAYS 06/13/2014

2. REPOSITIONING OF LES PASSAGES : A NEW

AND VIBRANT COZY MALL

May 2014: +7.5% rise in footfall vs May 2013

• Natural attractivity of the

center reinforced

Total investment for the 2013

refurbishment less than 1% of

the asset’s value

2014 Investor Days

IMPROVE

SHOPPERS’

EXPERIENCE -

CLUB STORE®

3

AS FASHION PLACES BRANDS COLLECTION SHOP-IN-SHOP FOOD MEETING POINTS MASS PREMIUM

29

KLEPIERRE REDEFINES

SHOPPING CENTERS

THE CLUB STORE® MODEL

CLUB STORE® CHALLENGES

1. Upgrade the customer path

2. Improve sense of well-being

3. Provide a unique recreational atmosphere

4. Extend customer visits

2014 INVESTOR DAYS

WOW

EFFECT

WINK

LIGHTING

GREENERY

SHOWCASE

EVENT

PLACE

MAIN

ANCHOR

ACCESS

HOST

FOCUSED

(approach)

HOST

FOCUSED

(langage)

CLUB

LOUNGE

BREAK

SPOT

WIFI

SOCIAL

LINK

REFRESH

KIDS

LABEL

CURIOSITY

ROOM

ECO

SIGNAGE

PARKING

30

EACH POINT OF CONTACT IS PEOPLE ORIENTED

1. UPGRADED CUSTOMER PATH

2014 INVESTOR DAYS

*Club Store Les Passages insight – 14/04/2014. 150 interviews on line

2. IMPROVED SENSE OF WELL-BEING

THE CLUB LOUNGE DIRECT RELATIONSHIPS WITH CUSTOMERS

BREAK AND MINI-BREAK HOME FEELING

72% use the areas for a break during shopping

time

The design is detail-oriented for 90%

The furniture is high-quality for 86%

The areas are soothing for 79%

The place is welcoming for 76%

58% see it as a meeting point

57% say their questions are answered

Book sharing is an enriching service for 64%

31

ClubStore

Les Passages

Insight*

2014 INVESTOR DAYS

3. UNIQUE RECREATIONAL ATMOSPHERE

INTERACTIVE FLOOR CHILDREN ARE BUSY

THE CURIOSITY ROOM EXCLUSIVE CONCEPT

The restrooms at Les Passages are

clean for 92%, comfortable for 82%,

surprising for 77%

WINK

Entertaining for 71%

The MUSICAL STAIRS

Never seen before for 71%

*Club Store Les Passages insight – 14/04/2014. 150 interviews on line

32

ClubStore

Les Passages

Insight*

2014 INVESTOR DAYS

*Club Store Les Passages insight – 14/04/2014. 150 interviews on line

18%

25% 27%

18%

12%

Fully agree Stronglydisagree

43% OF RESPONDENTS

DECLARE THAT THEY ARE

SPENDING MORE TIME AT LES

PASSAGES AFTER

REFURBISHMENT

43%

4. EXTENDED CUSTOMER VISITS

33

ClubStore

Les Passages

Insight*

2014 INVESTOR DAYS

OPERATING COSTS

AND SUSTAINABLE

FOOTPRINT -

GOOD CHOICES ®

4

2014 Investor Days

35 2014 INVESTOR DAYS 06/13/2014

ROADMAP

Shopping

centers - 2013

yoy growth*

Gross

rents

Net

rents

France-

Belgium

+5.0% +5.0%

Scandinavia +3.5% +7.1%

Italy +1.3% +1.6%

Central Europe +2.0% +5.3%

Iberia -3.7% -4.5%

* Proforma the disposal of the €2.0Bn portfolio

of retail galleries completed in April 2014

• Optimize costs - Good Choices®, a

comprehensive approach

Generalized approach to CAM* expenses:

a centralized procurement function

Improved environmental performance,

particularly in terms of energy use and

waste recycling

• Reduce vacancy costs and net service

charges

Short-term leases

• Capex : recurring maintenance and upgrade or refurbishment of malls

Help attract must-have, exclusive or differentiating retailers

Control costs through the centralized procurement function

• Optimize services and marketing actions throughout the portfolio

* CAM: Common Area Maintenance

Operating costs and sustainable

footprint

PROCUREMENT

FUNCTION

Guarantee management of operational risks and optimize group results by:

Optimizing the procurement process

Contributing to group’s net income

Steering procurement performance

Securing and monitoring supplier market

Paying particular attention to responsible and sustainable

procurement

2 principles:

Neutrality: a process that guarantees objectivity, equity, ethics

and transparency

TCO (Total Cost of Ownership) Vision

37 2014 INVESTOR DAYS 06/13/2014

PROCUREMENT FUNCTION OBJECTIVES

38 2014 INVESTOR DAYS 06/13/2014

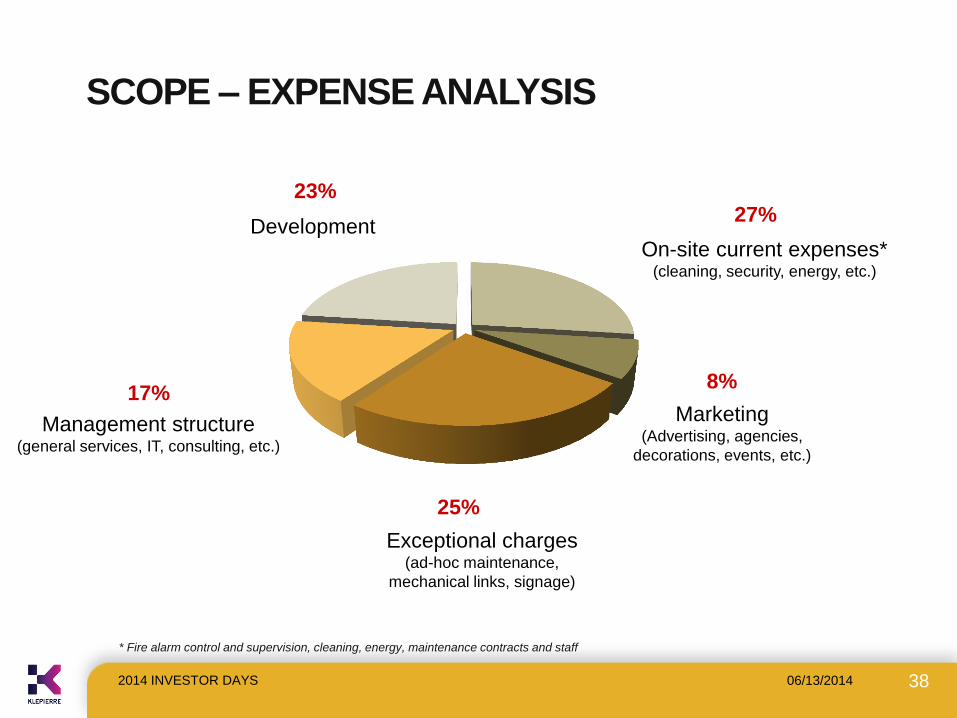

* Fire alarm control and supervision, cleaning, energy, maintenance contracts and staff

SCOPE – EXPENSE ANALYSIS

Development

Management structure (general services, IT, consulting, etc.)

On-site current expenses* (cleaning, security, energy, etc.)

Marketing (Advertising, agencies,

decorations, events, etc.)

Exceptional charges (ad-hoc maintenance,

mechanical links, signage)

23% 27%

17% 8%

25%

39 2014 INVESTOR DAYS 06/13/2014

APPROACH

Capture rate

Cover rate 60%

[x]%

TOTAL scope of

expenses incurred with

goods/services suppliers

100%

100%

50%

Com

plia

nce r

ate

• Identify addressable

procurement scope

• Capture rate as a key

measure for identifying

potential for optimization

• Asset-by-asset analysis

Scope – Supplier selection

80% of expenses

incurred with 3% of

active suppliers

identified

Segment purchasing: 15

categories

5 of which account for

82% of current

expenses

Define potential target for

reducing/optimizing expenses

Illustrative example of current expenses

Monitoring performance and management of supplier risks

An executive management dashboard for tracking performance,

with measurable, factual financial objectives

Supplier risk mapping to help manage financial health,

dependency rate, undeclared workers

Professionalizing the procurement function

A procurement tool (native SAP) to manage, optimize and

secure contractual data

Mission statements clearly established with measurable

qualitative and financial objectives

Dedicated resources

Reporting directly to Operations Department, France, and close

to the field

40 2014 INVESTOR DAYS 06/13/2014

IMPLEMENTATION AND MONITORING

41 2014 INVESTOR DAYS 06/13/2014

AN EVOLVING STRATEGY

2014 - 2017

X M€ X M€ X M€ X M€ X M€

2014 2017

Cover rate

New centers

opening Extent of cover

rate

Extend standard

contracts Sourcing Improve existing

conditions

Benchmarks per

category

New supply

sources

Mgr category

FRANCE

ITALY SCANDINAVIA

Operating costs and sustainable

footprint

ENERGY AND

WASTE

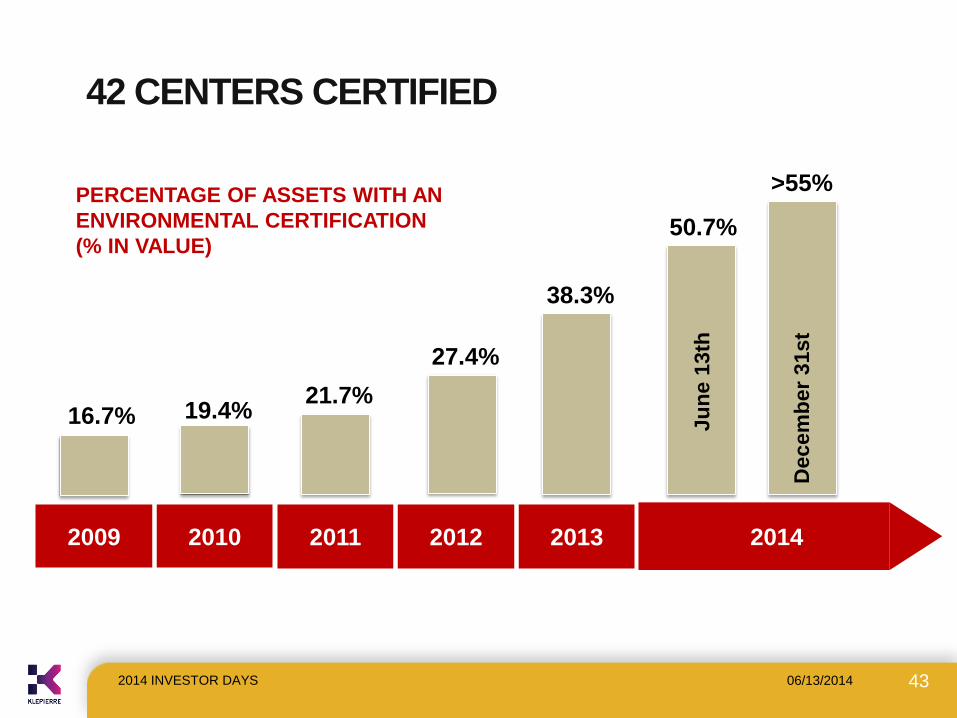

43

42 CENTERS CERTIFIED

PERCENTAGE OF ASSETS WITH AN

ENVIRONMENTAL CERTIFICATION

(% IN VALUE)

2009 2010 2011 2012 2013 2014

16.7% 19.4% 21.7%

27.4%

38.3%

50.7%

>55%

Ju

ne 1

3th

Decem

ber

31st

2014 INVESTOR DAYS 06/13/2014

44

A STRONG INVESTMENT IN OUR INDUSTRY

Publication of the

1st guide to sustainability

reporting principles

Gold Award

For the quality of its

sustainability

reporting

Main missions for

2013/2014

• Environmental

dialogue between

lessors and lessees

• Certifications

Member of the

GRESB User Group,

whose mission is to

devise tools for sectorial

benchmarking

2014 INVESTOR DAYS 06/13/2014

45

RESULTS AND AMIBITIONS HIGHLIGHTED BY

MAIN ESG RATINGS AND AGENCIES

Main ratings

Score 2013

/ 100

Improvement

vs. last rating Distinction

RobecoSAM 74/100 + 17 % DJSI World & Europe

Vigeo 57/100 + 30 % Euronext Vigeo

- France 20

- Eurozone 120

- Europe 120

- World 120

GRESB 67/100 + 16 % Green Star

Carbon Disclosure Project 72/100 - B + 26 % -

2014 INVESTOR DAYS 06/13/2014

www.klepierre.com

Thank you

2014 INVESTOR DAYS

![Investor Relations - hanatourcompany.comInvestor Relations 1 Investor Relations ... •5 days school-week - twice a month since 2006 ... Pro-Forma Income Statement (W bn) ...hanatour]ir... ·](https://img.dokumen.tips/doc/110x75/5a7180837f8b9ab6538ccec5/investor-relations-hanatourcompanycominvestor-relations-1-investor-relations.jpg)