Embed Size (px)

Citation preview

Capital Market Story

August 2013

Cleaner & better energy

Strategic priorities

Target positive free cash flow by 2015

Reduce capex and improve capital management

Drive efficiency

Return to 50-60% payout ratio policy for dividends

Restructure depressed European commodity businesses

Focus on capability-driven business approach

Direct discretionary capex towards priority areas Renewables Distributed energy Outside Europe

Distribution networks as portfolio stabilizers and enablers of new business models

Complete ~€20bn of targeted disposals

Rebalance portfolio and expedite transformation

Increased focus on cash and profitability

2

EuropeRestructuring

& New business models

OutsideEurope

Profitable growth

PerformanceEfficiency & Capabilities

Cleaner & better energy

InvestmentLess capital, more value

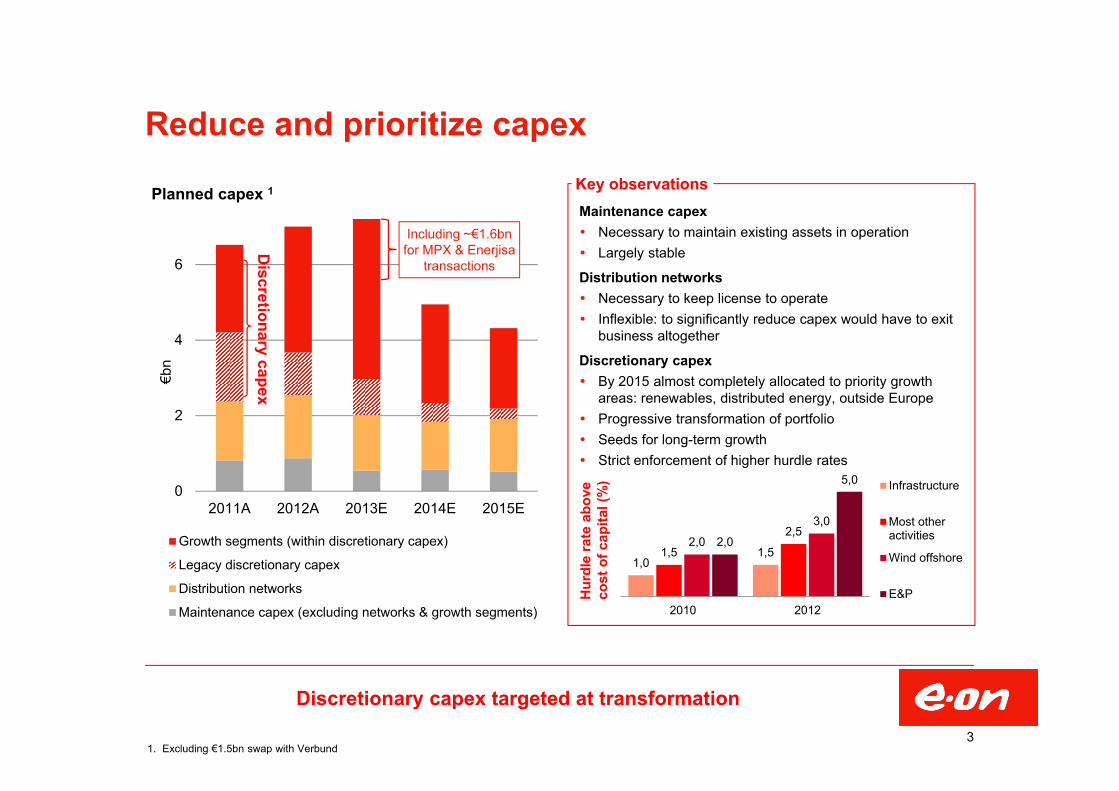

Reduce and prioritize capex

Discretionary capex targeted at transformation

3

Maintenance capex Necessary to maintain existing assets in operation Largely stable

Distribution networks Necessary to keep license to operate Inflexible: to significantly reduce capex would have to exit

business altogether

Discretionary capex By 2015 almost completely allocated to priority growth

areas: renewables, distributed energy, outside Europe Progressive transformation of portfolio Seeds for long-term growth Strict enforcement of higher hurdle rates

Key observations

0

2

4

6

2011A 2012A 2013E 2014E 2015E

€bn

Growth segments (within discretionary capex)

Legacy discretionary capex

Distribution networks

Maintenance capex (excluding networks & growth segments)

Discretionary capex

Planned capex 1

1,01,51,5

2,52,0

3,0

2,0

5,0

2010 2012

Infrastructure

Most otheractivities

Wind offshore

E&PHur

dle

rate

abo

ve

cost

of c

apita

l (%

)

Including ~€1.6bnfor MPX & Enerjisa

transactions

1. Excluding €1.5bn swap with Verbund

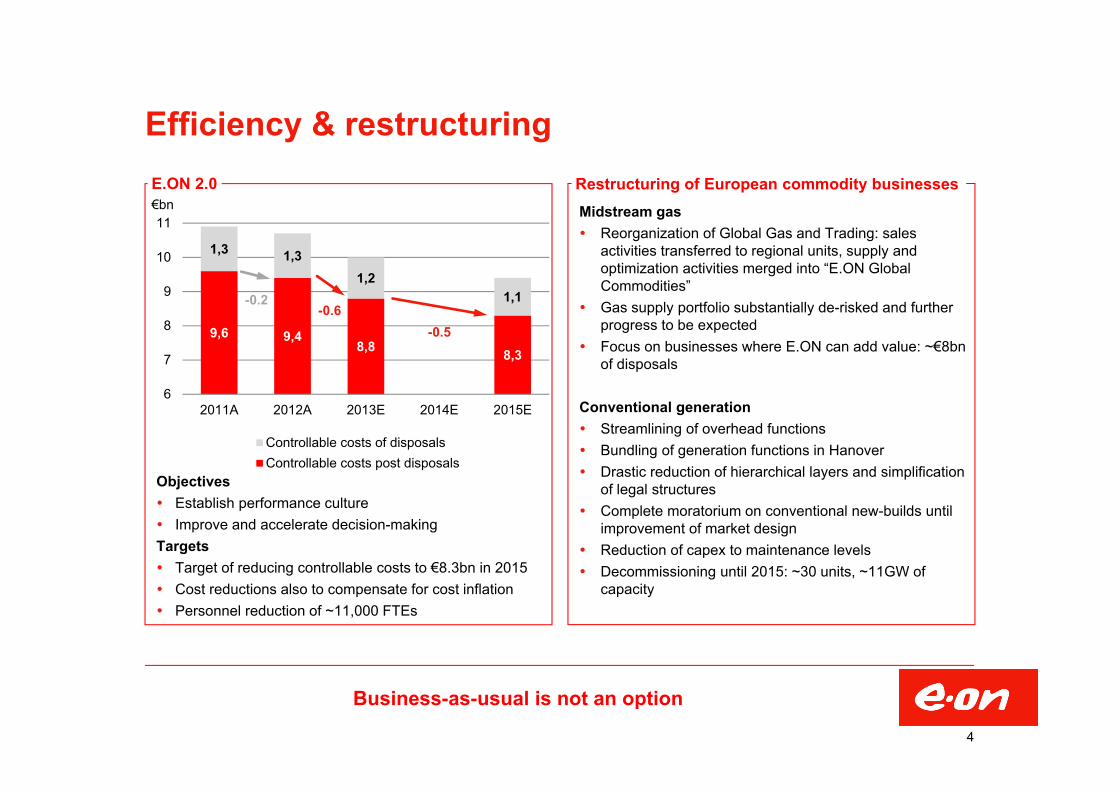

Objectives Establish performance culture Improve and accelerate decision-makingTargets Target of reducing controllable costs to €8.3bn in 2015 Cost reductions also to compensate for cost inflation Personnel reduction of ~11,000 FTEs

9,6 9,48,8 8,3

1,3 1,31,2

1,1

6

7

8

9

10

11

2011A 2012A 2013E 2014E 2015E

€bn

Controllable costs of disposalsControllable costs post disposals

Efficiency & restructuring

Midstream gas Reorganization of Global Gas and Trading: sales

activities transferred to regional units, supply and optimization activities merged into “E.ON Global Commodities”

Gas supply portfolio substantially de-risked and further progress to be expected

Focus on businesses where E.ON can add value: ~€8bn of disposals

Conventional generation Streamlining of overhead functions Bundling of generation functions in Hanover Drastic reduction of hierarchical layers and simplification

of legal structures Complete moratorium on conventional new-builds until

improvement of market design Reduction of capex to maintenance levels Decommissioning until 2015: ~30 units, ~11GW of

capacity

Business-as-usual is not an option

-0.2-0.6

-0.5

4

Restructuring of European commodity businessesE.ON 2.0

Monetize important pipeline and unique skills

Renewables Project pipeline (GW)*

3.6

50%

8.7

85%Construction

2.3

Total

21.5

Europe63%

NorthAmerica37%

Origination

6.6

25%

0.3

Speed up capital rotation Free up capital to further develop pipeline

Sell stakes of selected assets post commissioning

Offer continued, world-class O&M services

Aim to recycle at least €300m p.a.

Important unique selling points Expertise in development and construction

Wind fleet approach and O&M strategy

Unique offshore experience with pioneering advantage

Further opportunities in E.ON group context Biomass conversion

Leverage know how for outside Europe markets

Leverage pipeline and competencies

5

Development

* Project pipeline in GW as of 30th September 2012

Total attributable capacity by technology (GW)

Distributed energy

Well-established track record in distributed energy

6

0,4 0,4 0,4

0,2 0,2 0,2

0,0

0,1

0,2

0,3

0,4

2010 2011 2012

EBITDA

EBIT

Focus of activities on district heating and industrial CHP Most important regions Sweden, Germany, UK, and NL Sweden: 2nd biggest market player in integrated heat

business (13% market share) with ~50 district heating networks

Germany: ~4,000 distributed energy assets with installed capacity of 5,100MW heat and 1,200MW power

Sizeable mainly long-term contracted business Trustful relationships with numerous European

municipalities

0,3 0,3

0,45 0,45 0,45

0,0

0,1

0,2

0,3

0,4

0,5

2011 2012 2013 2014 2015

Higher capex level from 2013 onwards

Strong investment focus on Germany to seize opportunities from the energy system transformation Special emphasis on mini-midi CHP (10kW – 10MW)

and contracting business with industrial CHP (>10MW)

Additional priority area: Sweden Development opportunity in attractive Stockholm area

with growing heat demand

UK: growth in low carbon heat networks for municipalities Develop project pipeline of up to 20 projects

E.ON Connecting Energies: partnership with Metro

Distributed energy EBIT(DA) 2010-2012 (€bn) Distributed energy capex plan (€bn)

Step-up of ~50%

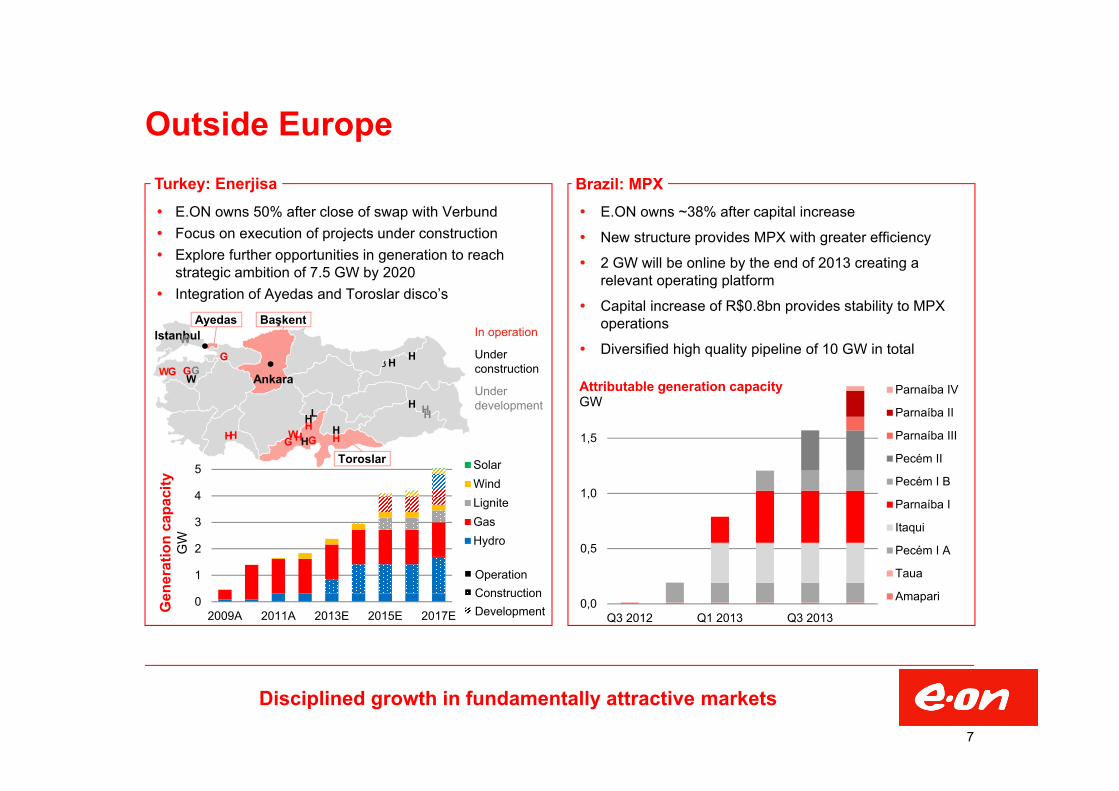

E.ON owns 50% after close of swap with Verbund Focus on execution of projects under construction Explore further opportunities in generation to reach

strategic ambition of 7.5 GW by 2020 Integration of Ayedas and Toroslar disco’s

E.ON owns ~38% after capital increase

New structure provides MPX with greater efficiency

2 GW will be online by the end of 2013 creating a relevant operating platform

Capital increase of R$0.8bn provides stability to MPX operations

Diversified high quality pipeline of 10 GW in total

Outside EuropeTurkey: Enerjisa Brazil: MPX

Disciplined growth in fundamentally attractive markets

2.3Ankara

IstanbulH

HHHH

H

H

HH

H H

H

H

GG

GGG

G

W

W

W

W

L

7

In operation

Under construction

Underdevelopment

Gen

erat

ion

capa

city

GW

BaşkentAyedas

Toroslar

0

1

2

3

4

5

2009A 2011A 2013E 2015E 2017E

SolarWindLigniteGasHydro

OperationConstructionDevelopment 0,0

0,5

1,0

1,5

Q3 2012 Q1 2013 Q3 2013

Attributable generation capacityGW

Parnaíba IV

Parnaíba II

Parnaíba III

Pecém II

Pecém I B

Parnaíba I

Itaqui

Pecém I A

Taua

Amapari

2.9 2.8 3.0

0

1

2

3

2010 2011 2012

Distribution contributes roughly 30% of E.ON‘s total group EBITDA

Adjusted for disposals, the EBITDA contribution of the segment has been very robust amid turbulent times

Due to its regulated nature, distribution is only temporarily exposed to volume risks resulting from the weak general economy

No commodity price exposure

Exposed to regulatory risk (notably Hungary and Spain), but broad geographical footprint (7 countries with different regulatory regimes) provides certain hedge for regulatory reviews next regulatory milestone: German power distribution in 2014

Additional distribution activities in Turkey via Enerjisa

E.ON‘s business backbone

Robust earnings base and potential enabler for new business models

8

Excluding contribution of Central Networks, E.ON Rete (both sold in 2011), and E.ON Bulgaria (sold in 2012)

In general, RABs between different regulatory regimes are not directly comparable due to significant methodical differences

In Sweden for example, RAB is based on replacement value of all physically existing assets irrespective of the actual age of the assets

2011/2012 Regulated asset base1 (€bn)

Distribution networks €b

nPro forma EBITDA

Germany ~13Sweden ~8.8Spain N.A.2

Hungary ~1.5Czech Republic ~1.3

Romania ~0.7Slovakia ~0.63

1. 2012 for Sweden and Slovakia. Exchange rates as of 25 Jan 20132. System based on indexed regulatory revenue allowance.3. RAB for 100% of ZSE (E.ON-share 49%)

Mid-term portfolio target

Regional Units Networks to remain stabilizer of portfolio: stable or

slightly growing earnings and positive free cash flow generation

Forge customer-based business models around distributed energies

Renewables & Non-EU countries Earnings to compensate for declining businesses Required to move into positive free cash flow

territory and to become self-supporting

European commodity businesses Not counting on recovery of European markets Restructure businesses and push for more

sustainable market design Prepare for cash-out from decommissioning

Key drivers

Ensure positive free cash flows and sustainable earnings prospects

9

Free cash flow generation

Earn

ings

pro

spec

ts

+--

+

NetworksE&P

Fossil

Rus-sia

ECR1

Sales

Hydro

Nuclear

EGC1

DE1

BrazilTurkey

Bubble sizes representsEBITDA contribution

1. ECR = E.ON Climate & Renewables; DE = Distributed energy;EGC = E.ON Global Commodities

0

1

2

3

4

2010 2011 2012 … Target

Debt factor

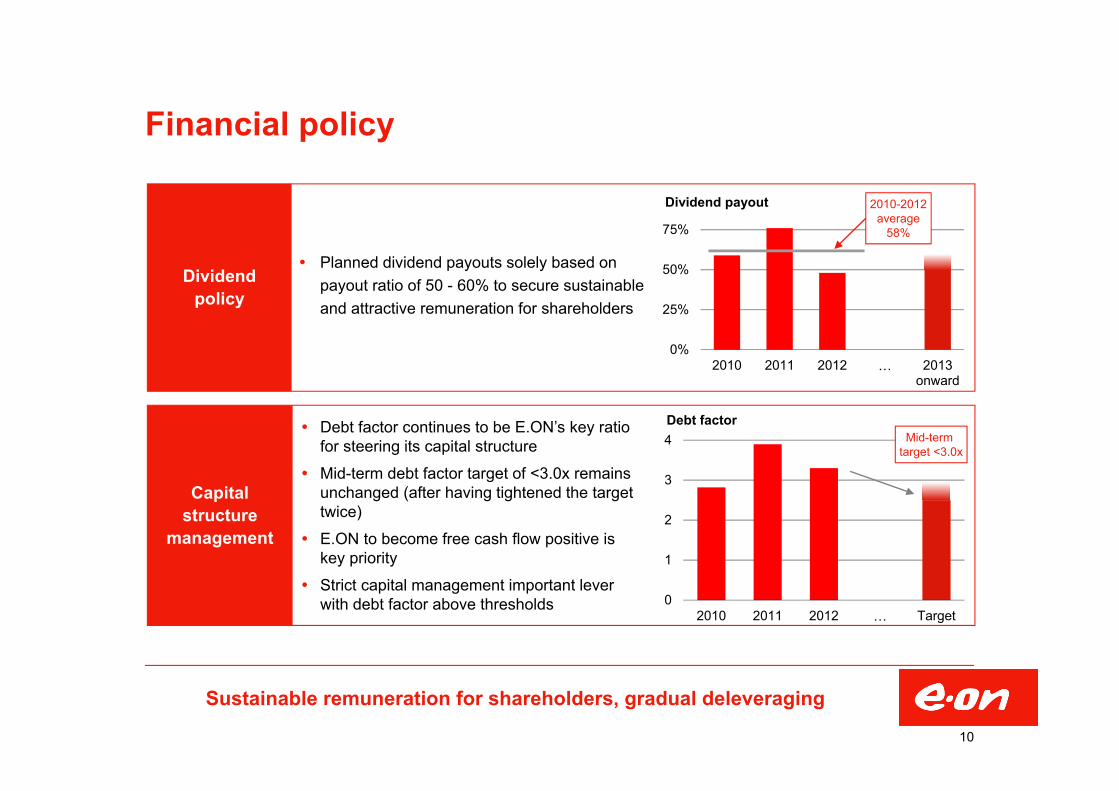

Financial policy

Sustainable remuneration for shareholders, gradual deleveraging

10

Debt factor continues to be E.ON’s key ratio for steering its capital structure

Mid-term debt factor target of <3.0x remains unchanged (after having tightened the target twice)

E.ON to become free cash flow positive is key priority

Strict capital management important lever with debt factor above thresholds

Capital structure

management

Mid-term target <3.0x

Dividend policy

Planned dividend payouts solely based on payout ratio of 50 - 60% to secure sustainable and attractive remuneration for shareholders

0%

25%

50%

75%

2010 2011 2012 … 2013onward

Dividend payout 2010-2012average

58%

Conclusion

Continuing E.ON’s transformation to face the industry’s game changers

11

Business profile

Financialprofile

E.ON has continuously delivered on its strategy via A highly successful portfolio streamlining

Substantially improving efficiency

Successful expansion in profitable growth areas

Using less capital and creating more value

E.ON will continue its transformation by Restructuring its businesses in depressed European markets

Pursuing selected growth in renewables, distributed energy and outside Europe

Benefiting from networks as a key stabilizer

Investor interest remains a key part of E.ON’s financial policy given Portfolio optimization and debt reduction (well advanced)

Strict capex discipline

Target to become free cashflow positive by 2015 at latest

12

Backup Financials Outlook FY 2012 and H1 2013 financials

Overall trends Key segment topics Generation Renewables Exploration & Production Global Commodities Germany Other EU Countries Non-EU Countries

IR team and calendar

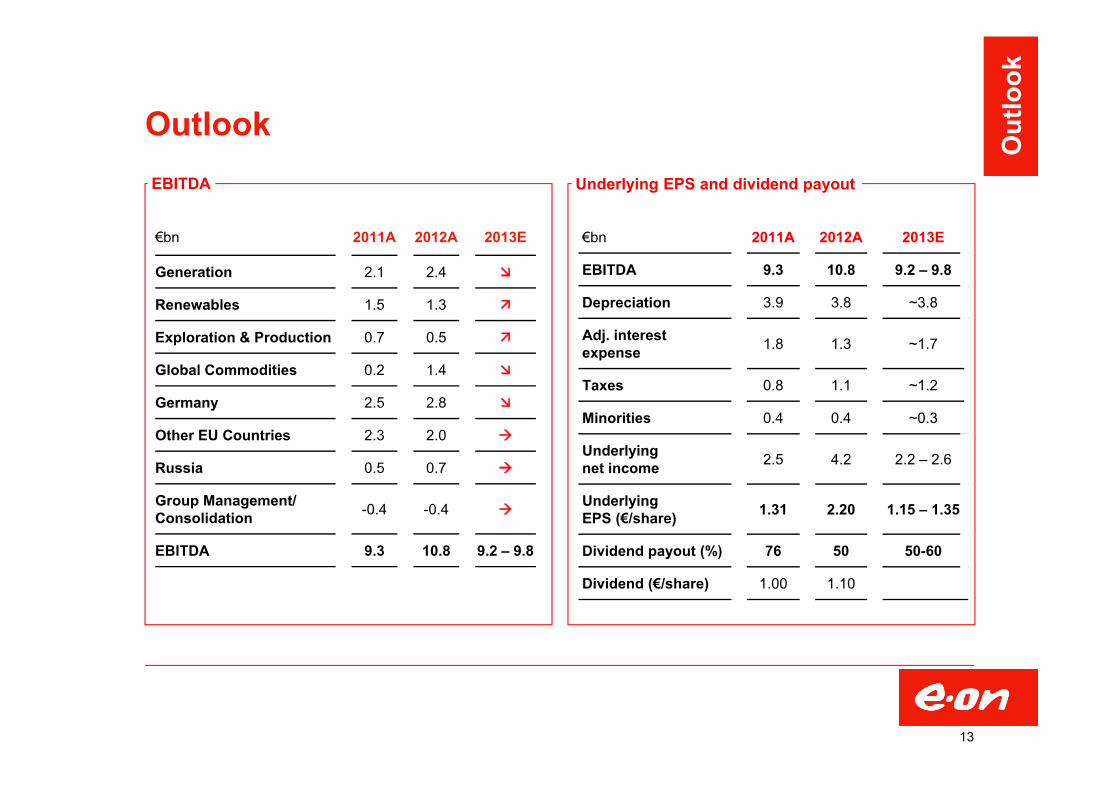

Outlook EBITDA Underlying EPS and dividend payout

13

€bn 2011A 2012A 2013E

Generation 2.1 2.4

Renewables 1.5 1.3

Exploration & Production 0.7 0.5

Global Commodities 0.2 1.4

Germany 2.5 2.8

Other EU Countries 2.3 2.0

Russia 0.5 0.7

Group Management/Consolidation -0.4 -0.4

EBITDA 9.3 10.8 9.2 – 9.8

€bn 2011A 2012A 2013E

EBITDA 9.3 10.8 9.2 – 9.8

Depreciation 3.9 3.8 ~3.8

Adj. interest expense 1.8 1.3 ~1.7

Taxes 0.8 1.1 ~1.2

Minorities 0.4 0.4 ~0.3

Underlyingnet income 2.5 4.2 2.2 – 2.6

UnderlyingEPS (€/share) 1.31 2.20 1.15 – 1.35

Dividend payout (%) 76 50 50-60

Dividend (€/share) 1.00 1.10

Out

look

Key drivers for 2013 vs. 2012 EBITDA1 and EPS1

Underlying EPS1 (in € per share)EBITDA1 (in €bn)

EPS stronger down than EBITDA

14

2012 EBITDA1 10.8

E&P volumes

Revaluation one-off 2012

Power portfolio

CO2 certificates

Gas midstream

Disposals

2013 EBITDA range1 9.2 - 9.8

Other

Controllable costs

Renewables

1. Adjusted for extraordinary effects

Interest

Depreciation

Other EBITDA effects

E&P

Disposals

Underlying EPS 20121 ~2.2

2013 EPS range1 1.15 – 1.35

Tax

Out

look

26%

3%5%

30%

26%

10% GenerationRenewablesGlobal CommoditiesGermanyOther EU countriesOther

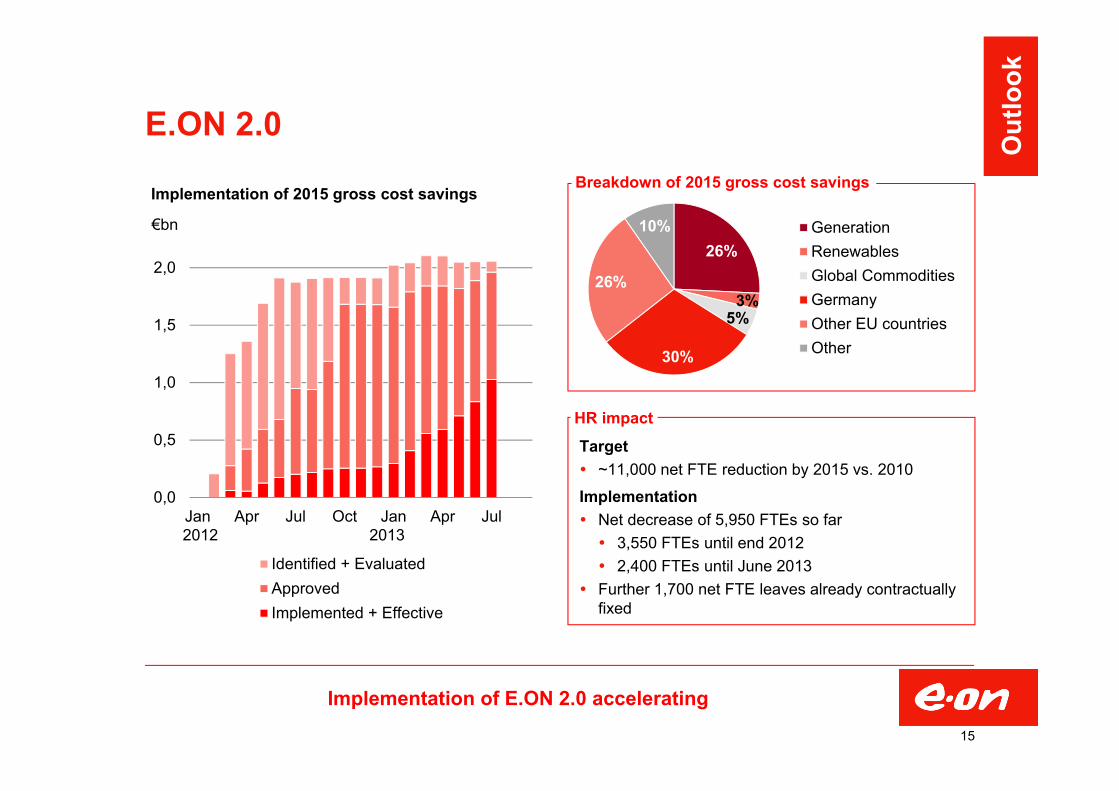

E.ON 2.0

Target ~11,000 net FTE reduction by 2015 vs. 2010

Implementation Net decrease of 5,950 FTEs so far 3,550 FTEs until end 2012 2,400 FTEs until June 2013

Further 1,700 net FTE leaves already contractually fixed

Implementation of 2015 gross cost savings

HR impact

Breakdown of 2015 gross cost savings

Implementation of E.ON 2.0 accelerating

0,0

0,5

1,0

1,5

2,0

Jan Apr Jul Oct Jan Apr Jul

€bn

Identified + EvaluatedApprovedImplemented + Effective

2012 2013

15

Out

look

Disposal proceeds and dilution overview

Gazprom €3.4bn Central Networks €4.8bn Open Grid Europe €2.9bn 50% of Horizon €0.4bn E.ON Rete €0.3bn HSE Shares €0.3bn Other transactions €1.4bnClosed transactions per end 2012: €13.5bn

50% of 3 US wind farms E.ON Energy from Waste 53% E.ON Thüringer Energie 25% in SPP 44% in JMP 63% E.ON Westfalen Weser Other transactionsClosed transactions in H1 2013 €4.0bn

E.ON Földgáz Trade & Storage E.ON FinlandSigned and expected to close in H2: ~€0.9bn

E.ON Mitte UrencoPlanned and not signed: >€1.6bn

Disposal proceeds 1,2

€17.5bn of disposal proceeds already materialized (expected total ~€20bn)

161. Disposal proceeds illustrate the Economic Net Debt impact.2. Not considered are the assets transferred to Verbund valued at €1.5bn (in exchange of Verbund’s Enerjisa shareholding)

EBITDA effect of disposals in 2013 and 2014 (€bn)

0,0

0,3

0,6

0,9

1,2

0,0

0,2

0,4

0,6

EGC Germany Other

Deals closedin 2012

Deals closedin H1 2013

Deals planned toclose after H1 2013

Disposal impact 2013 Disposal impact 2014

Out

look

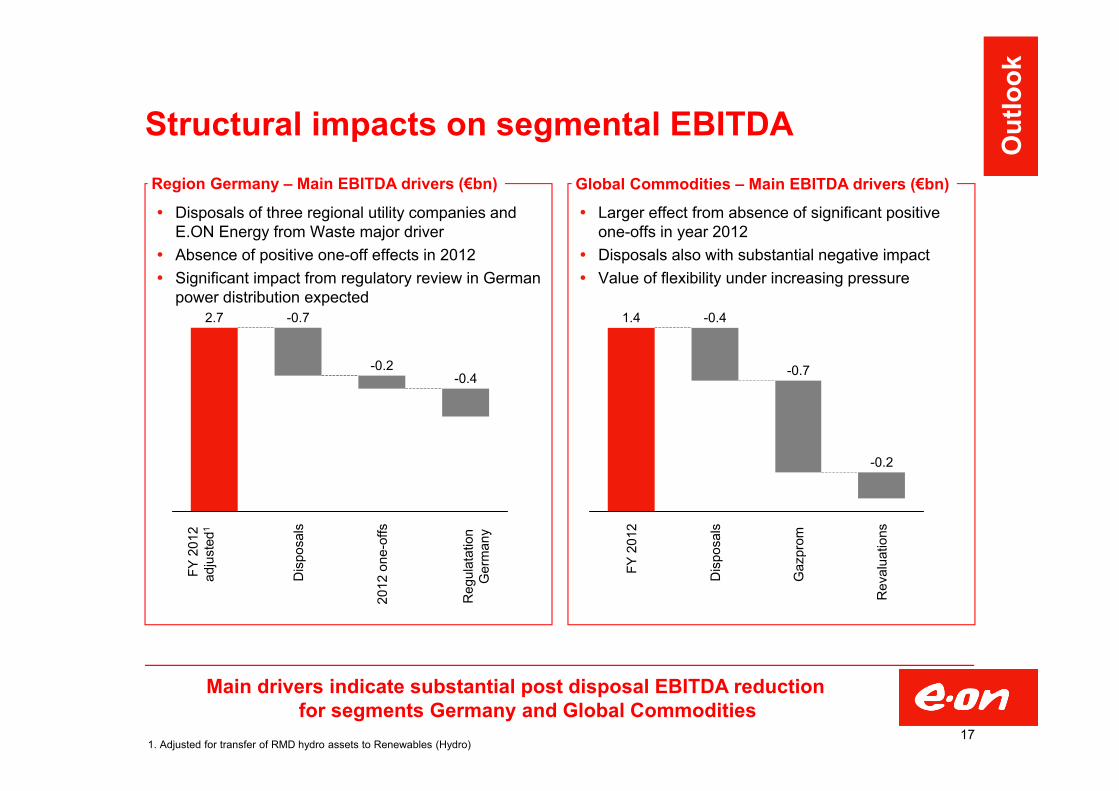

Structural impacts on segmental EBITDA

Disposals of three regional utility companies and E.ON Energy from Waste major driver

Absence of positive one-off effects in 2012 Significant impact from regulatory review in German

power distribution expected

Larger effect from absence of significant positive one-offs in year 2012

Disposals also with substantial negative impact Value of flexibility under increasing pressure

Region Germany – Main EBITDA drivers (€bn) Global Commodities – Main EBITDA drivers (€bn)

Main drivers indicate substantial post disposal EBITDA reduction for segments Germany and Global Commodities

2012

one

-offs

Dis

posa

ls2.7

-0.4

-0.7

-0.2

Rev

alua

tions

Gaz

prom

Dis

posa

ls

FY 2

012

1.4

-0.2

-0.4

-0.7

Reg

ulat

atio

nG

erm

any

FY 2

012

adju

sted

1

1. Adjusted for transfer of RMD hydro assets to Renewables (Hydro)17

Out

look

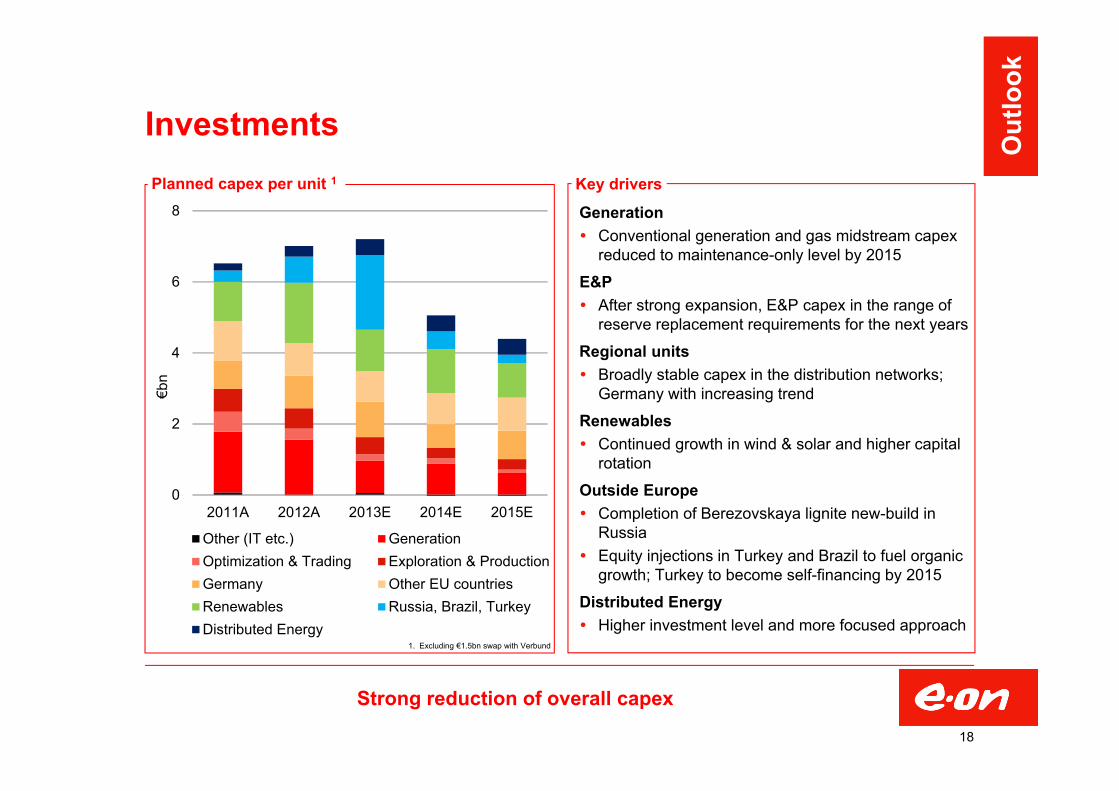

Investments

Strong reduction of overall capex

18

Generation Conventional generation and gas midstream capex

reduced to maintenance-only level by 2015

E&P After strong expansion, E&P capex in the range of

reserve replacement requirements for the next years

Regional units Broadly stable capex in the distribution networks;

Germany with increasing trend

Renewables Continued growth in wind & solar and higher capital

rotation

Outside Europe Completion of Berezovskaya lignite new-build in

Russia Equity injections in Turkey and Brazil to fuel organic

growth; Turkey to become self-financing by 2015

Distributed Energy Higher investment level and more focused approach

0

2

4

6

8

2011A 2012A 2013E 2014E 2015E

€bn

Other (IT etc.) GenerationOptimization & Trading Exploration & ProductionGermany Other EU countriesRenewables Russia, Brazil, TurkeyDistributed Energy

Planned capex per unit 1 Key drivers

Out

look

1. Excluding €1.5bn swap with Verbund

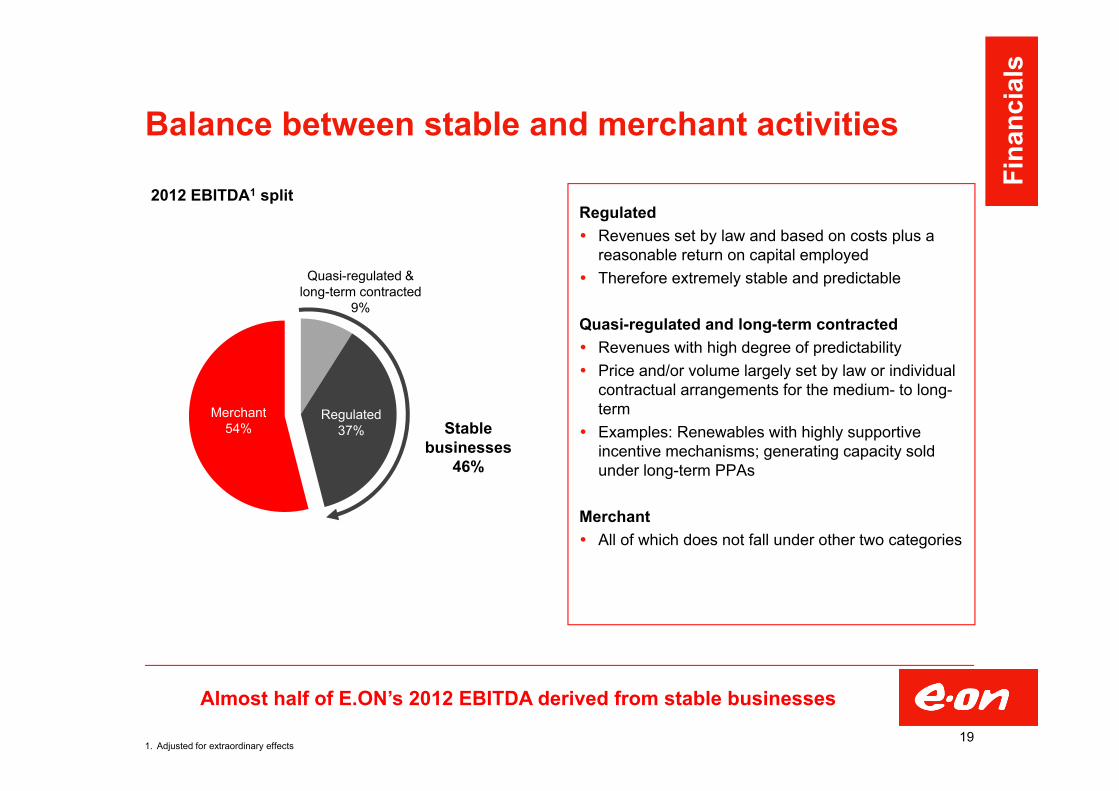

Balance between stable and merchant activities

Regulated Revenues set by law and based on costs plus a

reasonable return on capital employed Therefore extremely stable and predictable

Quasi-regulated and long-term contracted Revenues with high degree of predictability Price and/or volume largely set by law or individual

contractual arrangements for the medium- to long-term

Examples: Renewables with highly supportive incentive mechanisms; generating capacity sold under long-term PPAs

Merchant All of which does not fall under other two categories

Almost half of E.ON’s 2012 EBITDA derived from stable businesses

19

Merchant54%

Regulated37%

Quasi-regulated & long-term contracted

9%

Stable businesses

46%

Fina

ncia

ls

2012 EBITDA1 split

1. Adjusted for extraordinary effects

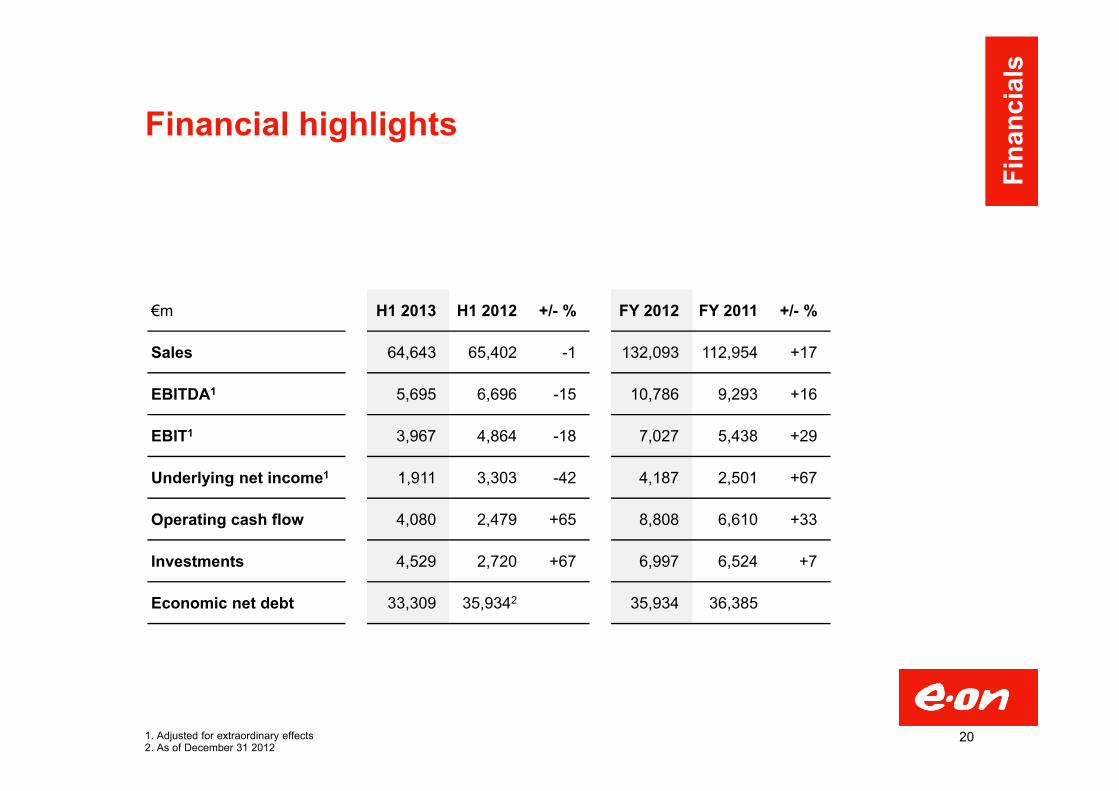

Financial highlights

20

€m H1 2013 H1 2012 +/- % FY 2012 FY 2011 +/- %

Sales 64,643 65,402 -1 132,093 112,954 +17

EBITDA1 5,695 6,696 -15 10,786 9,293 +16

EBIT1 3,967 4,864 -18 7,027 5,438 +29

Underlying net income1 1,911 3,303 -42 4,187 2,501 +67

Operating cash flow 4,080 2,479 +65 8,808 6,610 +33

Investments 4,529 2,720 +67 6,997 6,524 +7

Economic net debt 33,309 35,9342 35,934 36,385

Fina

ncia

ls

1. Adjusted for extraordinary effects2. As of December 31 2012

FY 2012 – EBITDA1 and EBIT1 by unit

21

€m EBITDA1 EBIT1

FY 2012 FY 2011 +/- % FY 2012 FY 2011 +/- %

Generation 2,403 2,114 +14 1,442 1,128 +28

Renewables 1,271 1,459 -13 877 1,088 -19

Optimization & Trading 1,421 160 - 1,163 -134 -

Exploration & Production 523 727 -28 293 481 -39

Germany 2,819 2,457 +15 1,851 1,499 +23

Other EU countries 2,032 2,259 -10 1,345 1,491 -10

Russia 729 553 +32 546 398 +37

Group Management / Consolidation -412 -436 - -490 -513 -

Group total 10,786 9,293 +16 7,027 5,438 +29

Fina

ncia

ls

1. Adjusted for extraordinary effects

FY 2012 - Key drivers of EBITDA1 developmentIn €bn

Large one-off effects driving 2012 EBITDA growth

EBITDA FY 2011

EBITDA FY 2012

-0.2

E&P -0.2Nuclear tax -0.2Power: Price and volume effect -0.3Region Russia: Increased generation capacity 0.2

10.8

-0.3UK: Retail + Central Networks -0.2Trading: Gas optimization -0.2

Other

Gas: Lower storage optimization -0.2

Gas: Open Grid Europe disposal

E.ON 2.0: Controllable cost reduction 0.2

Gas: Revaluation of participations 0.2

Gas: Wholesale 1.2

Generation: Nuclear exit cost in 2011 1.5

9.3

221. Adjusted for extraordinary effects

Fina

ncia

ls

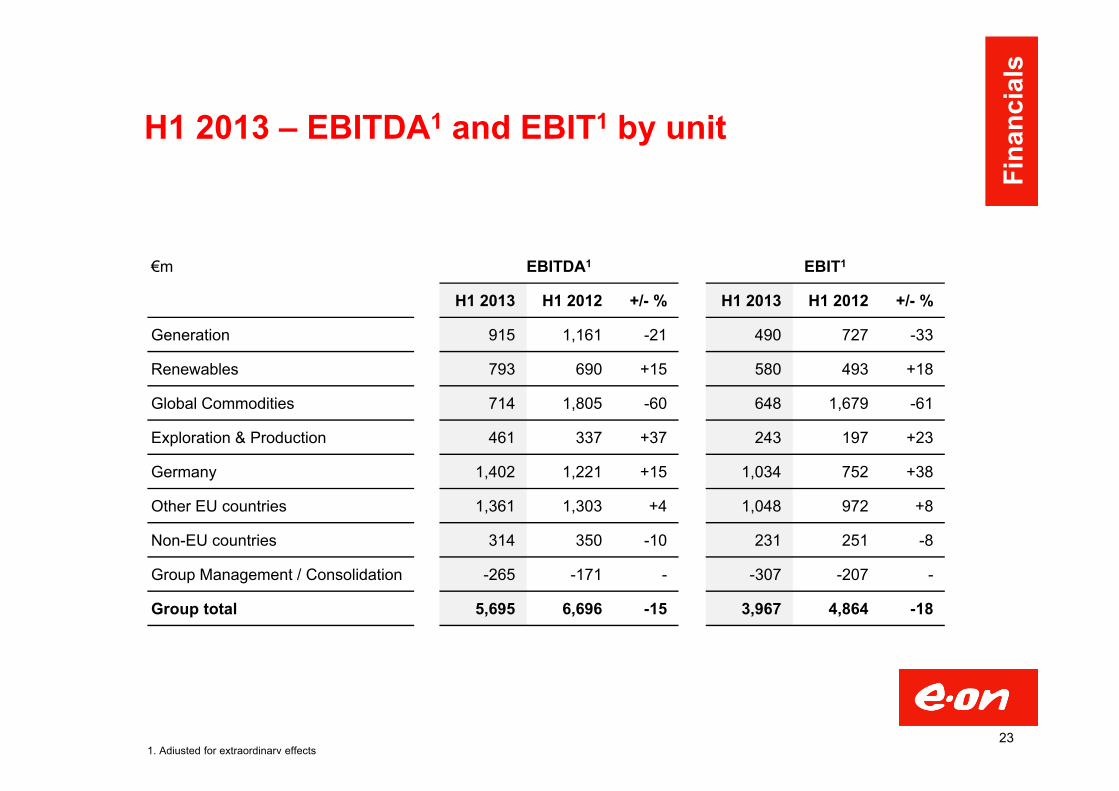

€m EBITDA1 EBIT1

H1 2013 H1 2012 +/- % H1 2013 H1 2012 +/- %

Generation 915 1,161 -21 490 727 -33

Renewables 793 690 +15 580 493 +18

Global Commodities 714 1,805 -60 648 1,679 -61

Exploration & Production 461 337 +37 243 197 +23

Germany 1,402 1,221 +15 1,034 752 +38

Other EU countries 1,361 1,303 +4 1,048 972 +8

Non-EU countries 314 350 -10 231 251 -8

Group Management / Consolidation -265 -171 - -307 -207 -

Group total 5,695 6,696 -15 3,967 4,864 -18

H1 2013 – EBITDA1 and EBIT1 by unit

1. Adjusted for extraordinary effects23

Fina

ncia

ls

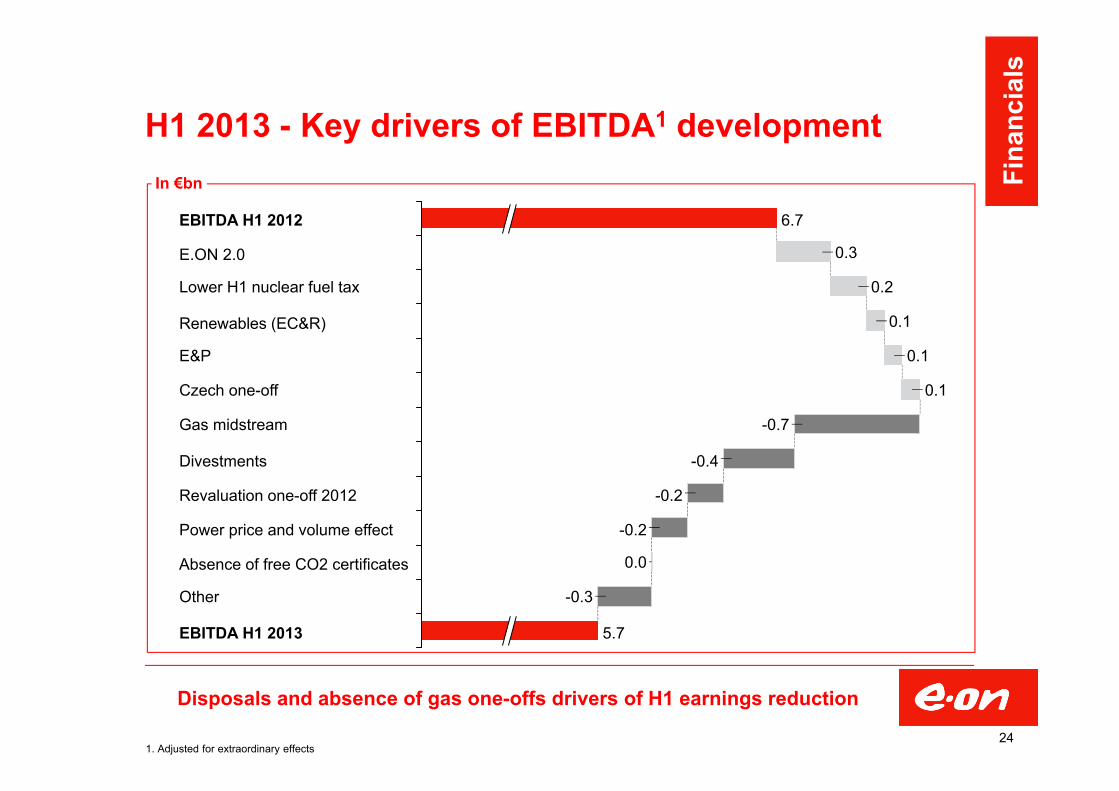

H1 2013 - Key drivers of EBITDA1 development

Disposals and absence of gas one-offs drivers of H1 earnings reduction

1. Adjusted for extraordinary effects

EBITDA H1 2013 5.7

Absence of free CO2 certificates

Other

-0.4

-0.2

0.0

Power price and volume effect

-0.3

Revaluation one-off 2012 -0.2

Gas midstream -0.7

E&P 0.1

Renewables (EC&R) 0.1

Lower H1 nuclear fuel tax

Divestments

E.ON 2.0 0.3

EBITDA H1 2012 6.7

0.1Czech one-off

0.2

In €bn

24

Fina

ncia

ls

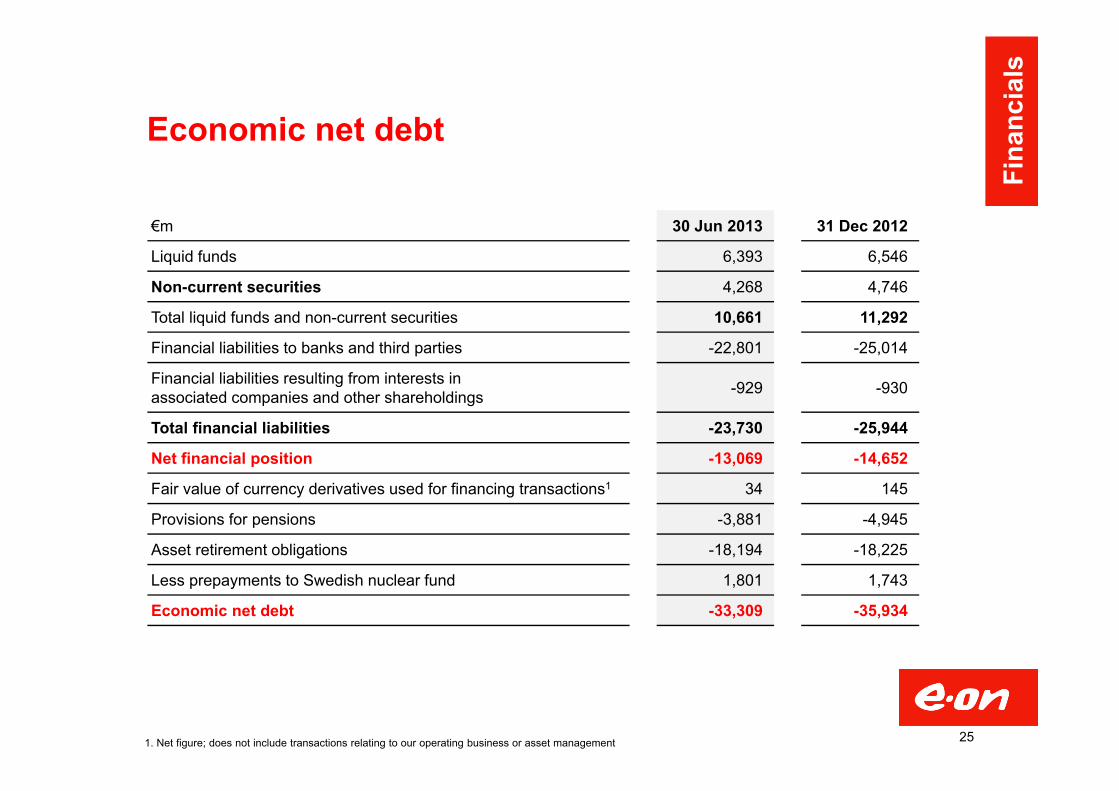

Economic net debt

25

€m 30 Jun 2013 31 Dec 2012

Liquid funds 6,393 6,546

Non-current securities 4,268 4,746

Total liquid funds and non-current securities 10,661 11,292

Financial liabilities to banks and third parties -22,801 -25,014

Financial liabilities resulting from interests inassociated companies and other shareholdings -929 -930

Total financial liabilities -23,730 -25,944

Net financial position -13,069 -14,652

Fair value of currency derivatives used for financing transactions1 34 145

Provisions for pensions -3,881 -4,945

Asset retirement obligations -18,194 -18,225

Less prepayments to Swedish nuclear fund 1,801 1,743

Economic net debt -33,309 -35,934

1. Net figure; does not include transactions relating to our operating business or asset management

Fina

ncia

ls

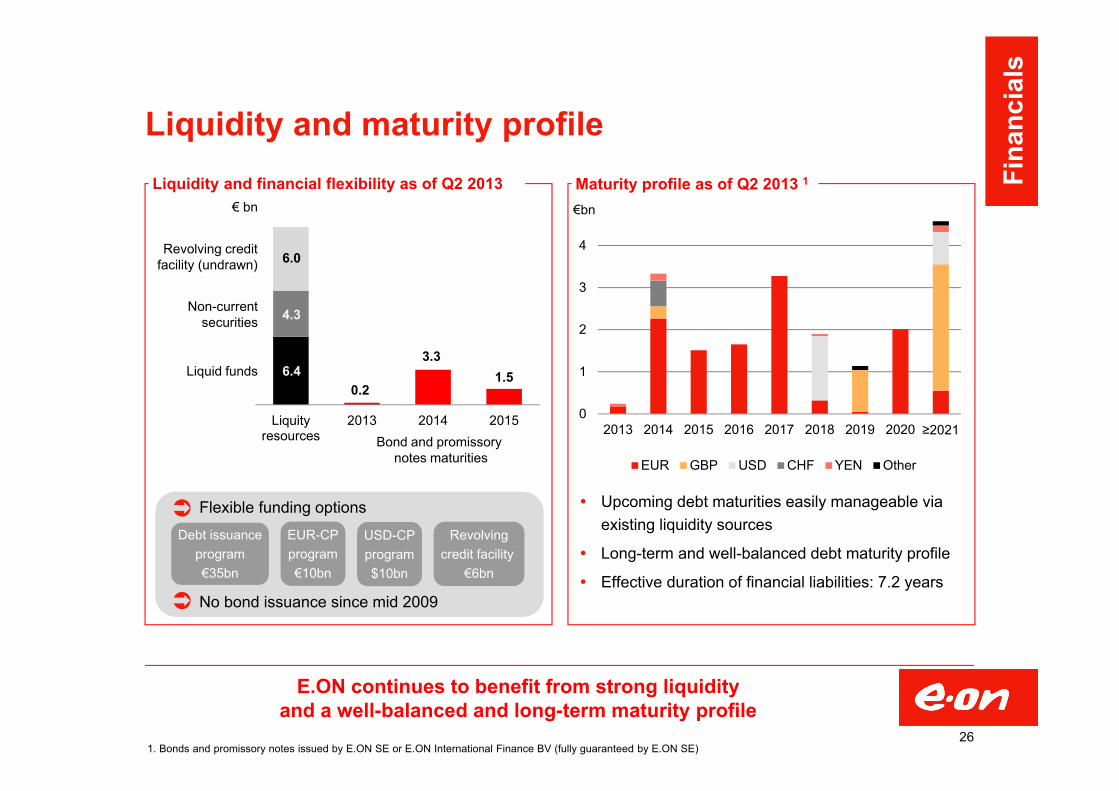

Upcoming debt maturities easily manageable via existing liquidity sources

Long-term and well-balanced debt maturity profile

Effective duration of financial liabilities: 7.2 years

Liquityresources

2013 2014 2015

Liquidity and maturity profileLiquidity and financial flexibility as of Q2 2013 Maturity profile as of Q2 2013 1

E.ON continues to benefit from strong liquidityand a well-balanced and long-term maturity profile

261. Bonds and promissory notes issued by E.ON SE or E.ON International Finance BV (fully guaranteed by E.ON SE)

Flexible funding optionsDebt issuance

program€35bn

EUR-CPprogram€10bn

USD-CPprogram$10bn

Revolvingcredit facility

€6bn

No bond issuance since mid 2009

0

1

2

3

4

2013 2014 2015 2016 2017 2018 2019 2020 ≥2021

€bn

EUR GBP USD CHF YEN Other

Revolving creditfacility (undrawn)

Bond and promissorynotes maturities

0.2

3.31.5

6.0

4.3

6.4

€ bn

Liquid funds

Non-currentsecurities

Fina

ncia

ls

4500

5000

5500

6000

2000 2005 2010

TWh

2500

2750

3000

3250

2000 2005 2010

TWh

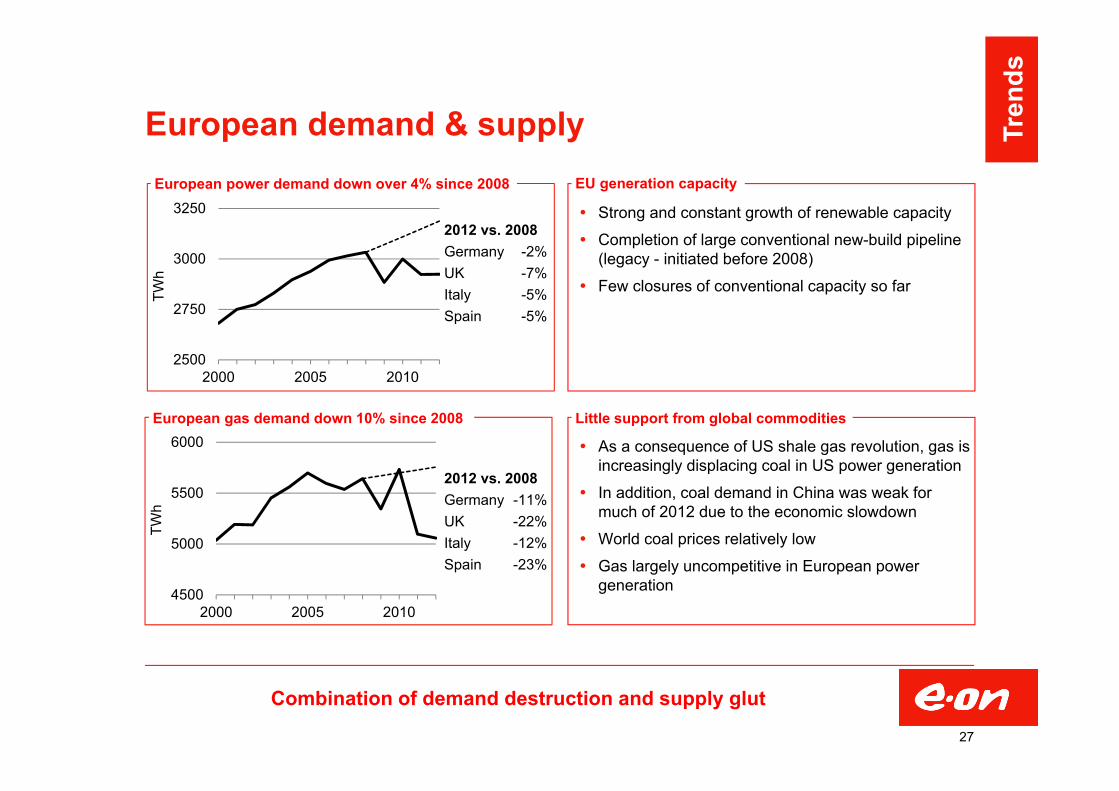

European demand & supply

Strong and constant growth of renewable capacity

Completion of large conventional new-build pipeline (legacy - initiated before 2008)

Few closures of conventional capacity so far

As a consequence of US shale gas revolution, gas is increasingly displacing coal in US power generation

In addition, coal demand in China was weak for much of 2012 due to the economic slowdown

World coal prices relatively low

Gas largely uncompetitive in European power generation

Combination of demand destruction and supply glut

27

2012 vs. 2008Germany -2%UK -7%Italy -5%Spain -5%

2012 vs. 2008Germany -11%UK -22%Italy -12%Spain -23%

European power demand down over 4% since 2008

European gas demand down 10% since 2008 Little support from global commodities

EU generation capacity

Tren

ds

Inefficient carbon policies

-10

0

10

20

30

40

-250

0

250

500

750

1.000

2005 2008 2011 2014 2017 2020

€/t CO2mt CO2 2005-20072008-20122013-2020CO2price

0

5

10

15

20

25

1998 2001 2004 2007 2010 2013

€cts/kWh RES support

Other charges

VAT

Transport & Sales

Generation

Generation,Transport & Sales

Steep increase in consumer prices

Main incentive scheme bust

Massive collateral damage

28

Expected carbon surplus/deficit of EU ETS

Electricity price for German residential customers

30

35

40

45

50

55

00:00 04:00 08:00 12:00 16:00 20:00

GWJuly2010

July2012

July2016

Market value of flexible energy eroded

Hourly load factor of peak capacity

0

100

200

300

400

2000 2002 2004 2006 2008 2010 2012

TWh

Solar

WindOffshore

WindOnshore

OtherRenewables

Strong renewables growth in Europe

Tren

ds

Generation – Business snapshot

3,8

2,12,4

2,8

1,11,5

0,00,51,01,52,02,53,03,54,0

2010 2011 2012EBITDA EBIT

2013:(+) E.ON 2.0(-) Absence of free allocation of CO2 allowances(-) Lower transfer prices / spreads(-) Political interventions

Post 2013:(+) Additional E.ON 2.0 impact(+) First time consolidation Maasvlakte(-) Lower outright prices

0,7 0,7 0,5 0,5 0,4

1,0 0,8

0,4 0,30,2

0,00,20,40,60,81,01,21,41,61,8

2011 2012 2013 2014 2015Non-maintenance Maintenance

Segment capex plan (€bn)

Key earnings drivers – 2013 and beyond

Further downward pressure from outright prices and spreads

29

(+) Absence of prior yearnuclear one-off

(-) Price/volume effect

(-) Higher nuclear tax payments

Maasvlakte III Planned COD: 2014 Total capex: €1.7bn

Maintenance at minimum by 2015

Moratorium on new build projects

Streamline power plant portfolio to adapt to market conditions

Improve profitability of power plant assets by extensive costs reduction program

Very selective development activities to be prepared for potential opportunities driven by new market designs

Strategic priorities

EBIT(DA) – Main drivers 2012 vs. 2011 (€bn) Gen

erat

ion

0

2

4

6

Q4 2012 Q1 2013 Q2 2013

GWTavazzano 8

Staudinger 1

Shamrock 1-4

Provence 4

Hornaing 3

Kingsnorth

Fiume Santo 5-6

Escucha

Ostiglia 4

Veltheim 2 & 4

Staudinger 3

Ironbridge 1-2

Grain 1 & 4

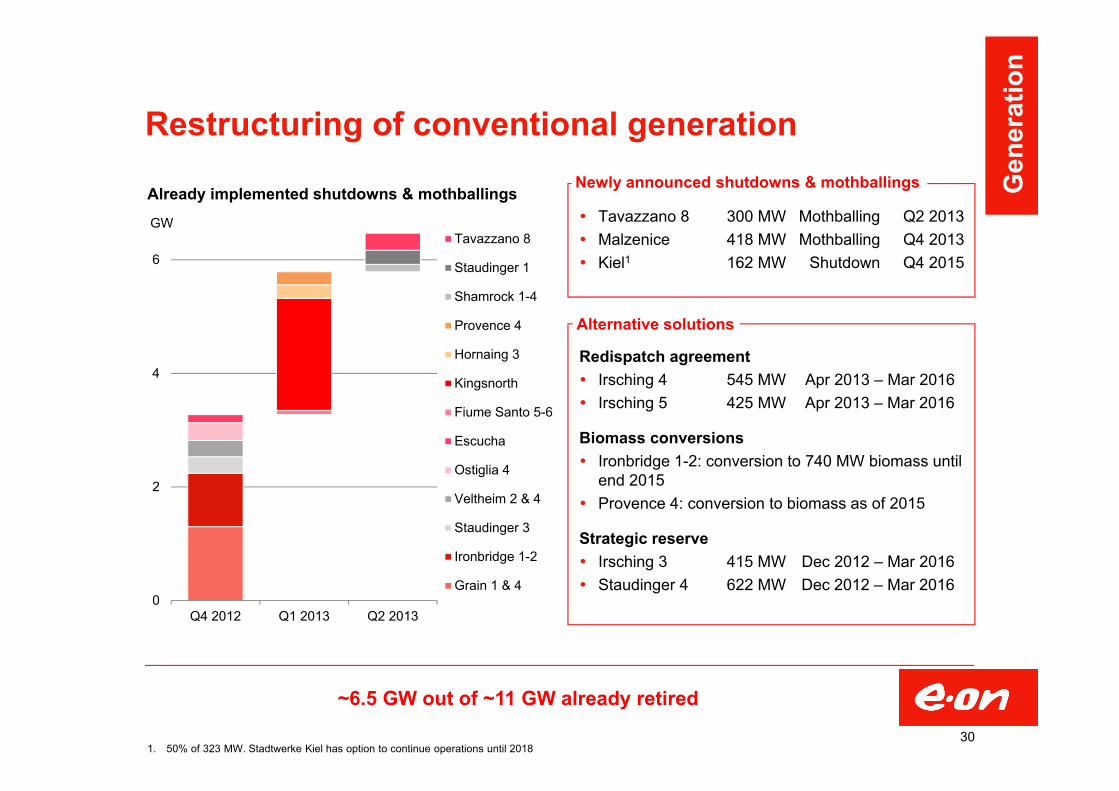

Restructuring of conventional generation

Tavazzano 8 300 MW Mothballing Q2 2013 Malzenice 418 MW Mothballing Q4 2013 Kiel1 162 MW Shutdown Q4 2015

Redispatch agreement Irsching 4 545 MW Apr 2013 – Mar 2016 Irsching 5 425 MW Apr 2013 – Mar 2016

Biomass conversions Ironbridge 1-2: conversion to 740 MW biomass until

end 2015 Provence 4: conversion to biomass as of 2015

Strategic reserve Irsching 3 415 MW Dec 2012 – Mar 2016 Staudinger 4 622 MW Dec 2012 – Mar 2016

Already implemented shutdowns & mothballings

Alternative solutions

~6.5 GW out of ~11 GW already retired

30

Newly announced shutdowns & mothballings

1. 50% of 323 MW. Stadtwerke Kiel has option to continue operations until 2018

Gen

erat

ion

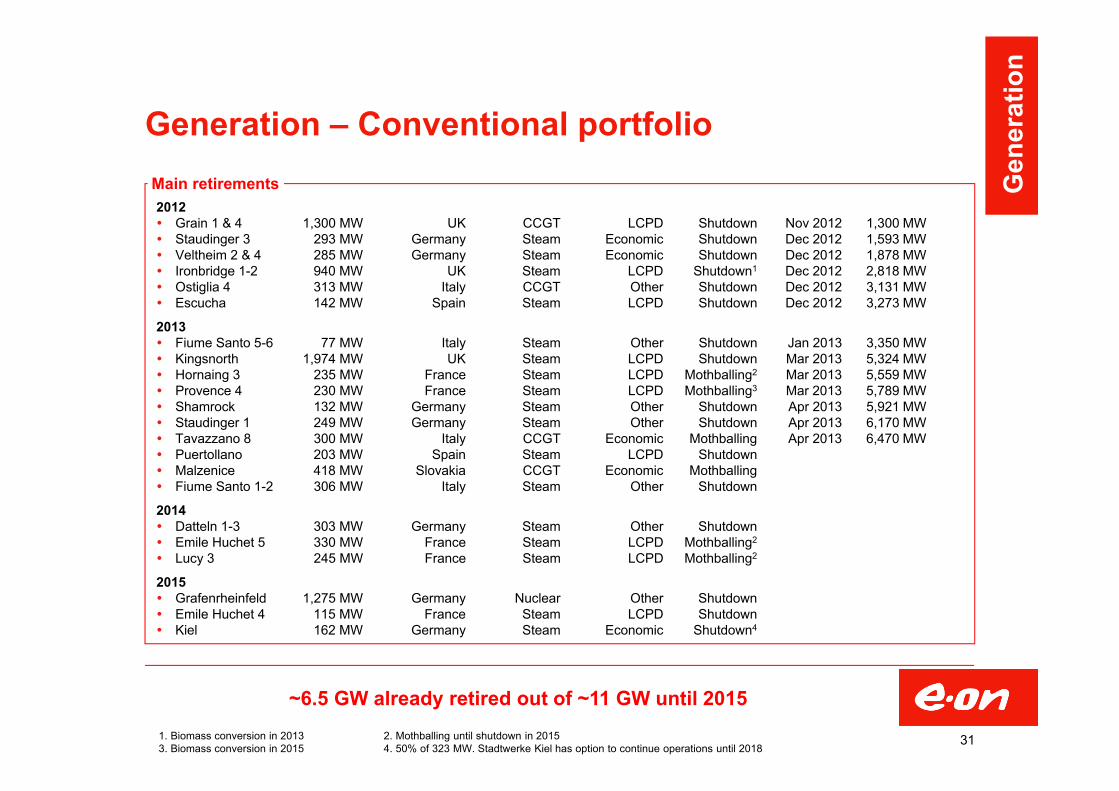

2012 Grain 1 & 4 1,300 MW UK CCGT LCPD Shutdown Nov 2012 1,300 MW Staudinger 3 293 MW Germany Steam Economic Shutdown Dec 2012 1,593 MW Veltheim 2 & 4 285 MW Germany Steam Economic Shutdown Dec 2012 1,878 MW Ironbridge 1-2 940 MW UK Steam LCPD Shutdown1 Dec 2012 2,818 MW Ostiglia 4 313 MW Italy CCGT Other Shutdown Dec 2012 3,131 MW Escucha 142 MW Spain Steam LCPD Shutdown Dec 2012 3,273 MW

2013 Fiume Santo 5-6 77 MW Italy Steam Other Shutdown Jan 2013 3,350 MW Kingsnorth 1,974 MW UK Steam LCPD Shutdown Mar 2013 5,324 MW Hornaing 3 235 MW France Steam LCPD Mothballing2 Mar 2013 5,559 MW Provence 4 230 MW France Steam LCPD Mothballing3 Mar 2013 5,789 MW Shamrock 132 MW Germany Steam Other Shutdown Apr 2013 5,921 MW Staudinger 1 249 MW Germany Steam Other Shutdown Apr 2013 6,170 MW Tavazzano 8 300 MW Italy CCGT Economic Mothballing Apr 2013 6,470 MW Puertollano 203 MW Spain Steam LCPD Shutdown Malzenice 418 MW Slovakia CCGT Economic Mothballing Fiume Santo 1-2 306 MW Italy Steam Other Shutdown

2014 Datteln 1-3 303 MW Germany Steam Other Shutdown Emile Huchet 5 330 MW France Steam LCPD Mothballing2

Lucy 3 245 MW France Steam LCPD Mothballing2

2015 Grafenrheinfeld 1,275 MW Germany Nuclear Other Shutdown Emile Huchet 4 115 MW France Steam LCPD Shutdown Kiel 162 MW Germany Steam Economic Shutdown4

Generation – Conventional portfolioMain retirements

~6.5 GW already retired out of ~11 GW until 20151. Biomass conversion in 2013 2. Mothballing until shutdown in 20153. Biomass conversion in 2015 4. 50% of 323 MW. Stadtwerke Kiel has option to continue operations until 2018

31

Gen

erat

ion

E.ON’s nuclear fleet in Germany

32

Start-up date E.ON share(%)

Capacity(MW)

2012 output(TWh)

2012 remainingvolumes (TWh)1

Shutdown date

Isar 1 1979 100.0 878 0.0 2 2011

Unterweser 1979 100.0 1,345 0.0 11 2011

Brunsbüttel 1977 33.3 771 0.0 11 2011

Krümmel 1984 50.0 1,346 0.0 88 2011

Grafenrheinfeld 1982 100.0 1,275 10.0 23 31 Dec 2015

Gundremmingen B 1984 25.0 1,284 9.9 30 31 Dec 2017

Gundremmingen C 1985 25.0 1,288 10.1 39 31 Dec 2021

Grohnde 1985 83.3 1,360 11.0 61 31 Dec 2021

Brokdorf 1986 80.0 1,410 10.2 74 31 Dec 2021

Isar 2 1988 75.0 1,410 11.4 82 31 Dec 2022

Emsland 1988 12.5 1,329 10.8 87 31 Dec 2022

1. Source: Bundesamt für Strahlenschutz, Tabelle der erzeugten Strommengen und verbleibenden Reststrommengen

Gen

erat

ion

Generation - Addressing the CCGT issue

Reduce maintenance costs

Maintenance intervals lengthened due to lower utilization

Maintenance costs lowered through restructuring of long-term service agreements

Reduce fixed costs Switch from CCGT mode to OCGT mode

Permanent connections to gas network contribute strongly to fixed costs (10-30 €/kW out of 30-40 €/kW):

Switch from permanent to occasional connection (e.g. when called by TSOs for ancillary services): higher variable connection costs compensated by high prices

Switch fuel from gas to oil: higher variable fuel costs compensated by much lower fixed costs

Mothball / close sustainably cash-negative units

Response

Turning every stone

33

0

10

20

30

40

2011 2012 2013

€/kW

Classic spark spread Dispatched spark spread

CCGTs not dispatched when spreads negative

Dispatched spark spreads take this into account, unlike classic spark spreads

Dispatched spark spreads have fallen even more than classic spark spreads

CCGTs certainly not earning their cost of capital, in fact barely earning their fixed costs

Strong deterioration of CCGT economics Gen

erat

ion

1,2

1,51,3

0,91,1

0,9

0,00,20,40,60,81,01,21,41,6

2010 2011 2012EBITDA EBIT

0,2 0,3 0,3 0,20,70,3

0,60,1

0,2

0,3

0,10,1

0,4

0,6

0,8 1,0 0,3

0,00,20,40,60,81,01,21,41,61,82,0

2011 2012 2013 2014 2015Offshore EU Onshore EUOnshore US Other/unallocated

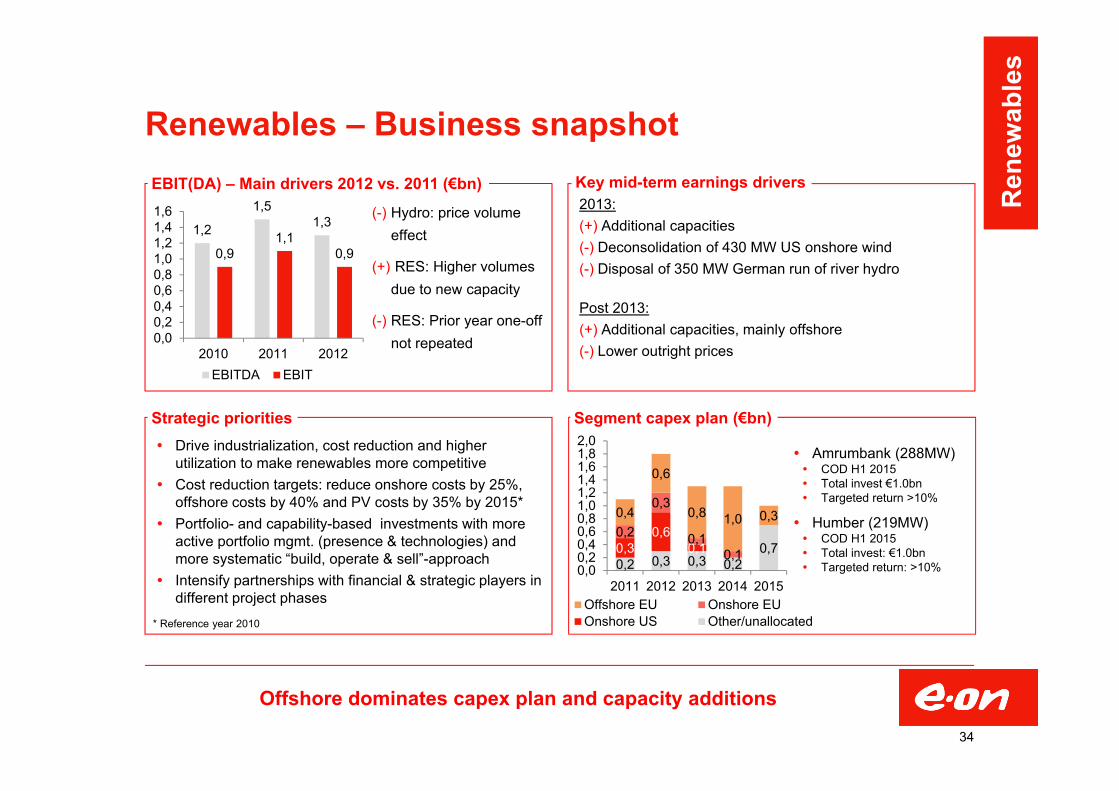

Renewables – Business snapshot

Offshore dominates capex plan and capacity additions

34

(-) Hydro: price volume effect

(+) RES: Higher volumes due to new capacity

(-) RES: Prior year one-off not repeated

Amrumbank (288MW) COD H1 2015 Total invest €1.0bn Targeted return >10%

Humber (219MW) COD H1 2015 Total invest: €1.0bn Targeted return: >10%

Segment capex plan (€bn)

2013:(+) Additional capacities(-) Deconsolidation of 430 MW US onshore wind(-) Disposal of 350 MW German run of river hydro

Post 2013:(+) Additional capacities, mainly offshore(-) Lower outright prices

Drive industrialization, cost reduction and higher utilization to make renewables more competitive

Cost reduction targets: reduce onshore costs by 25%, offshore costs by 40% and PV costs by 35% by 2015*

Portfolio- and capability-based investments with more active portfolio mgmt. (presence & technologies) and more systematic “build, operate & sell”-approach

Intensify partnerships with financial & strategic players in different project phases

Strategic priorities

EBIT(DA) – Main drivers 2012 vs. 2011 (€bn) Key mid-term earnings drivers

* Reference year 2010

Ren

ewab

les

0% 20% 40% 60% 80% 100%Turbine Foundation InstallationElectrics Contingency / other

0,0

2,0

4,0

6,0

2010 2011 2012 2013 2014 2015

Solar andotherBiomass

OffshoreEuropeOnshore US

OnshoreEurope

-0,4

0,0

0,4

0,8

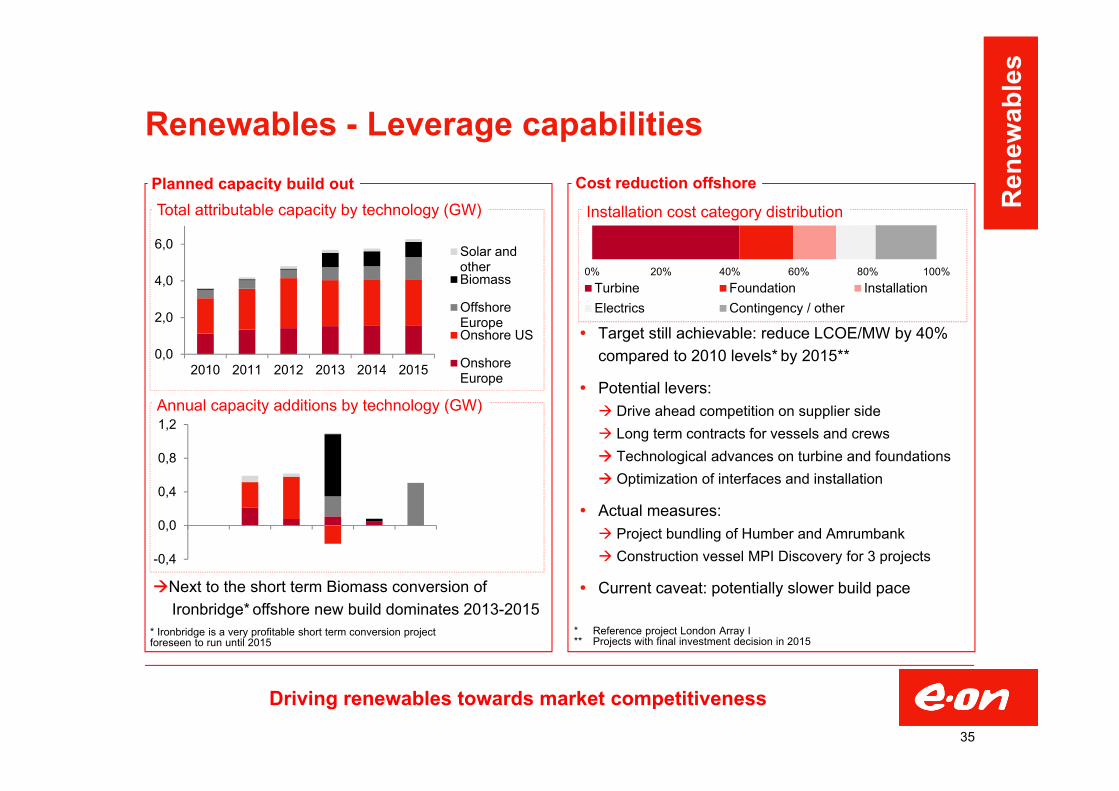

1,2

Target still achievable: reduce LCOE/MW by 40% compared to 2010 levels* by 2015**

Potential levers: Drive ahead competition on supplier side Long term contracts for vessels and crews Technological advances on turbine and foundations Optimization of interfaces and installation

Actual measures: Project bundling of Humber and Amrumbank Construction vessel MPI Discovery for 3 projects

Current caveat: potentially slower build pace

Renewables - Leverage capabilities Planned capacity build out Cost reduction offshore

Driving renewables towards market competitiveness

35

Installation cost category distribution

Next to the short term Biomass conversion of Ironbridge* offshore new build dominates 2013-2015

Annual capacity additions by technology (GW)

* Ironbridge is a very profitable short term conversion project foreseen to run until 2015

* Reference project London Array I** Projects with final investment decision in 2015

Total attributable capacity by technology (GW) Ren

ewab

les

0,1 0,1

0,30,2

0,1 0,1 0,1

0,2

0,00,10,20,30,40,50,60,7

2011 2012 2013 2014 2015Other Gas Storage

2,5

0,2

1,4

2,2

-0,2

1,2

-0,50,00,51,01,52,02,53,0

2010 2011 2012

EBITDA EBIT

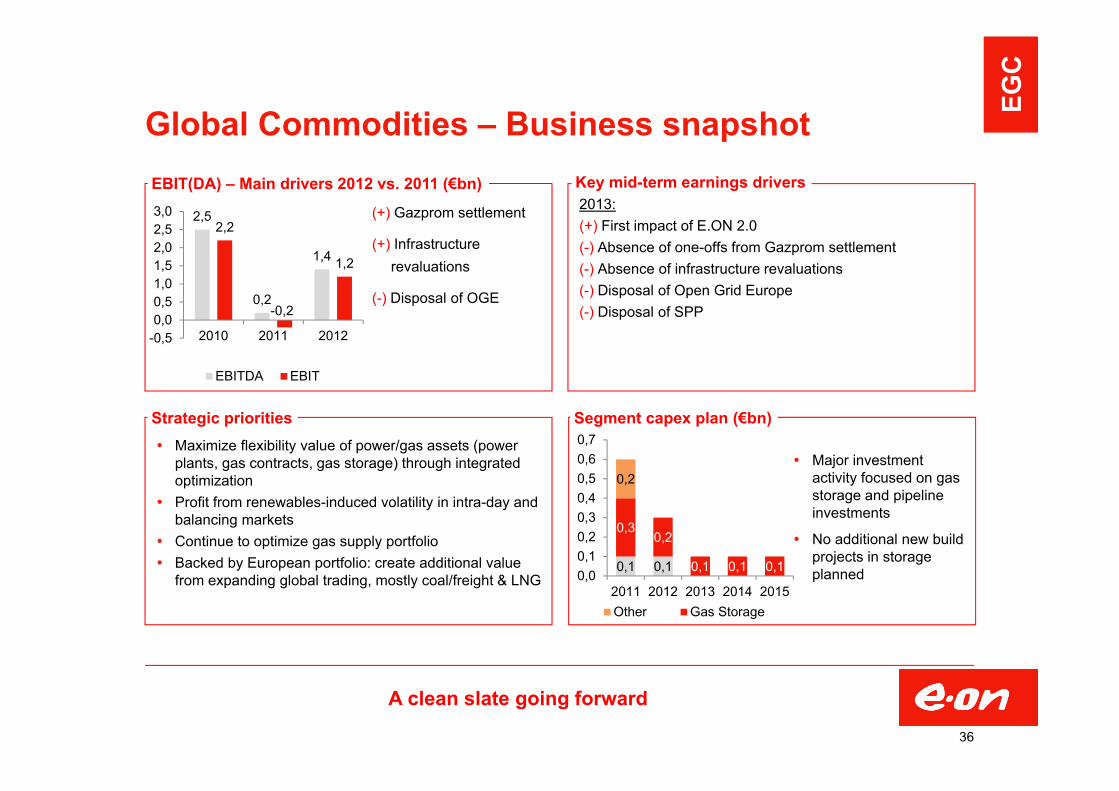

Global Commodities – Business snapshotEBIT(DA) – Main drivers 2012 vs. 2011 (€bn)

A clean slate going forward

36

(+) Gazprom settlement

(+) Infrastructure revaluations

(-) Disposal of OGE

Major investment activity focused on gas storage and pipeline investments

No additional new build projects in storage planned

Segment capex plan (€bn)

2013:(+) First impact of E.ON 2.0 (-) Absence of one-offs from Gazprom settlement(-) Absence of infrastructure revaluations(-) Disposal of Open Grid Europe(-) Disposal of SPP

Key mid-term earnings drivers

Maximize flexibility value of power/gas assets (power plants, gas contracts, gas storage) through integrated optimization

Profit from renewables-induced volatility in intra-day and balancing markets

Continue to optimize gas supply portfolio Backed by European portfolio: create additional value

from expanding global trading, mostly coal/freight & LNG

Strategic priorities

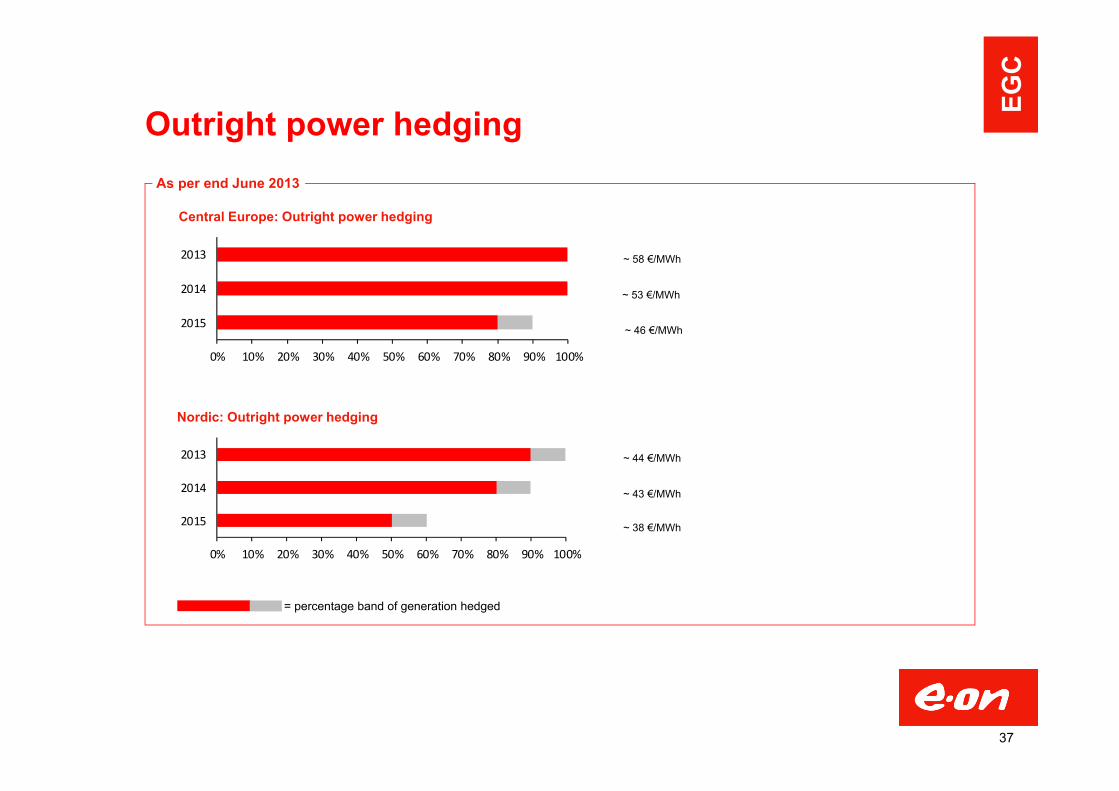

EGC

Outright power hedgingAs per end June 2013

~ 58 €/MWh

~ 53 €/MWh

~ 44 €/MWh

~ 43 €/MWh

Nordic: Outright power hedging

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2015

2014

2013

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2015

2014

2013

= percentage band of generation hedged

Central Europe: Outright power hedging

~ 46 €/MWh

~ 38 €/MWh

37

EGC

0

2

4

6

2010 2011 2012 2013

€/MWh

2013/142014/15

0%

20%

40%

60%

2010 2011 2012 2013

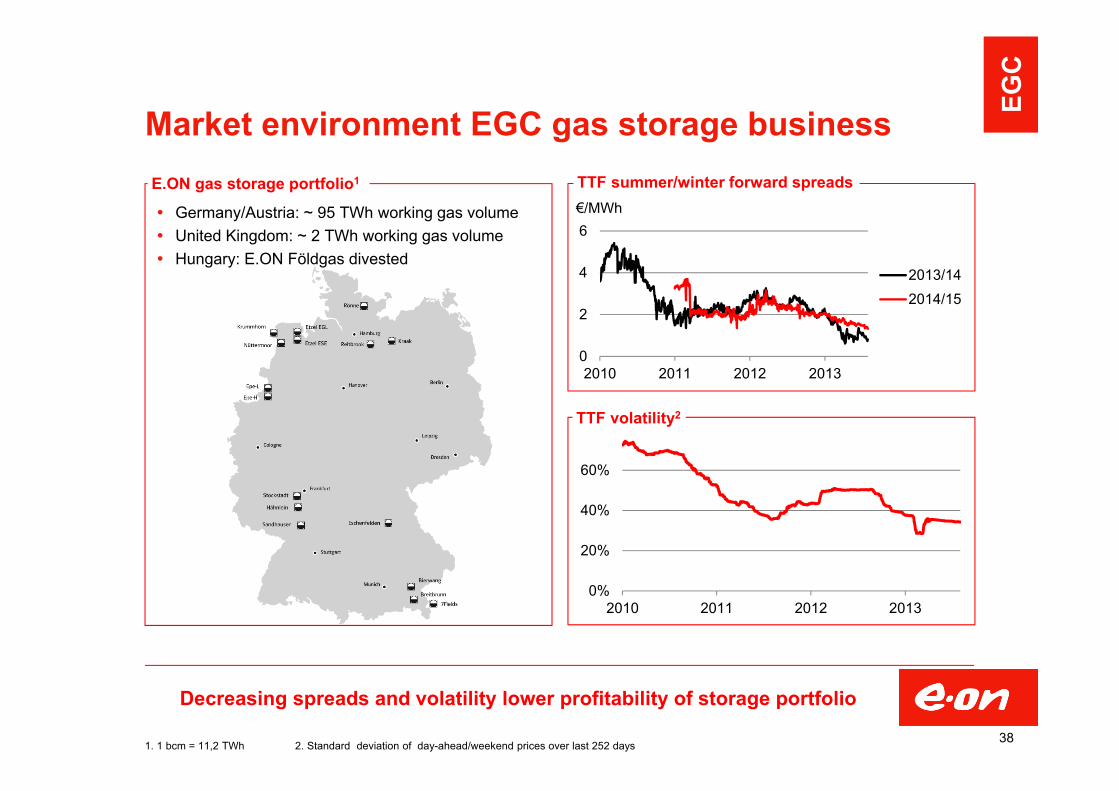

Market environment EGC gas storage business

Germany/Austria: ~ 95 TWh working gas volume United Kingdom: ~ 2 TWh working gas volume Hungary: E.ON Földgas divested

E.ON gas storage portfolio1

TTF volatility2

TTF summer/winter forward spreads

Decreasing spreads and volatility lower profitability of storage portfolio

1. 1 bcm = 11,2 TWh 2. Standard deviation of day-ahead/weekend prices over last 252 days38

EGC

0.1 0.1 0.1

0,5 0,5 0,2 0,1 0,1

0,1 0,1

0,2

0,1 0,1

0,0

0,2

0,4

0,6

0,8

2011 2012 2013 2014 2015UK Norway Other

0,7 0,7

0,50,4

0,5

0,3

0,00,10,20,30,40,50,60,70,8

2010 2011 2012EBITDA EBIT

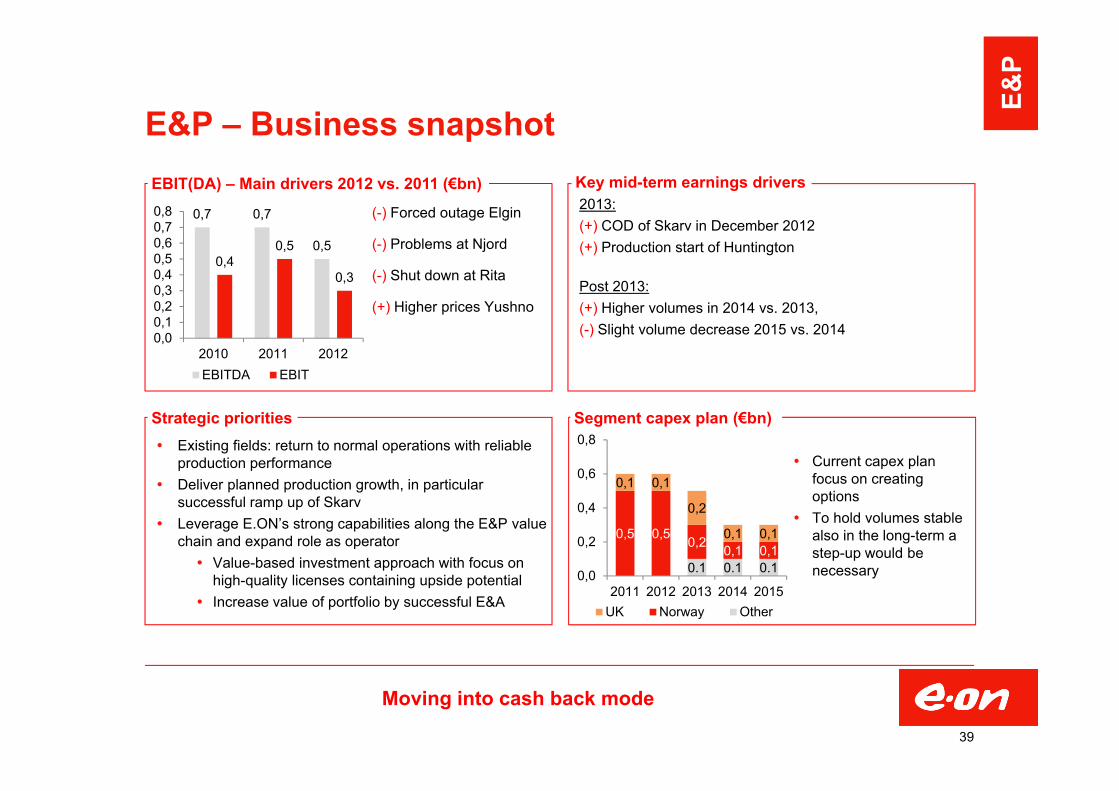

E&P – Business snapshot

Moving into cash back mode

39

(-) Forced outage Elgin

(-) Problems at Njord

(-) Shut down at Rita

(+) Higher prices Yushno

Current capex plan focus on creating options

To hold volumes stable also in the long-term a step-up would be necessary

Segment capex plan (€bn)

2013:(+) COD of Skarv in December 2012(+) Production start of Huntington

Post 2013:(+) Higher volumes in 2014 vs. 2013, (-) Slight volume decrease 2015 vs. 2014

Existing fields: return to normal operations with reliable production performance

Deliver planned production growth, in particular successful ramp up of Skarv

Leverage E.ON’s strong capabilities along the E&P value chain and expand role as operator Value-based investment approach with focus on

high-quality licenses containing upside potential Increase value of portfolio by successful E&A

Strategic priorities

EBIT(DA) – Main drivers 2012 vs. 2011 (€bn) Key mid-term earnings drivers

E&P

2011A 2012A 2013E 2014E 2015E

Other RitaBabbage Elgin FranklinHuntington NjordSkarv Yuzhno Russkoye

E&P - Near term production outlook

Skarv – Norway Skarv on stream since December 2012 Production ramp-up in 2013

Njord – Norway Infill well drilling ongoing Satellite field Hyme in production in 2013

Elgin Franklin – UK Back in production in 2013

Huntington – UK Production commenced in April 2013

Yuzhno Russkoye – Russia Stable production

2013 production expected to range between 55m boe and 59m boe

40

Productionm boe

18-22

26-3024-28

~37 ~37~37Production drivers

E&P

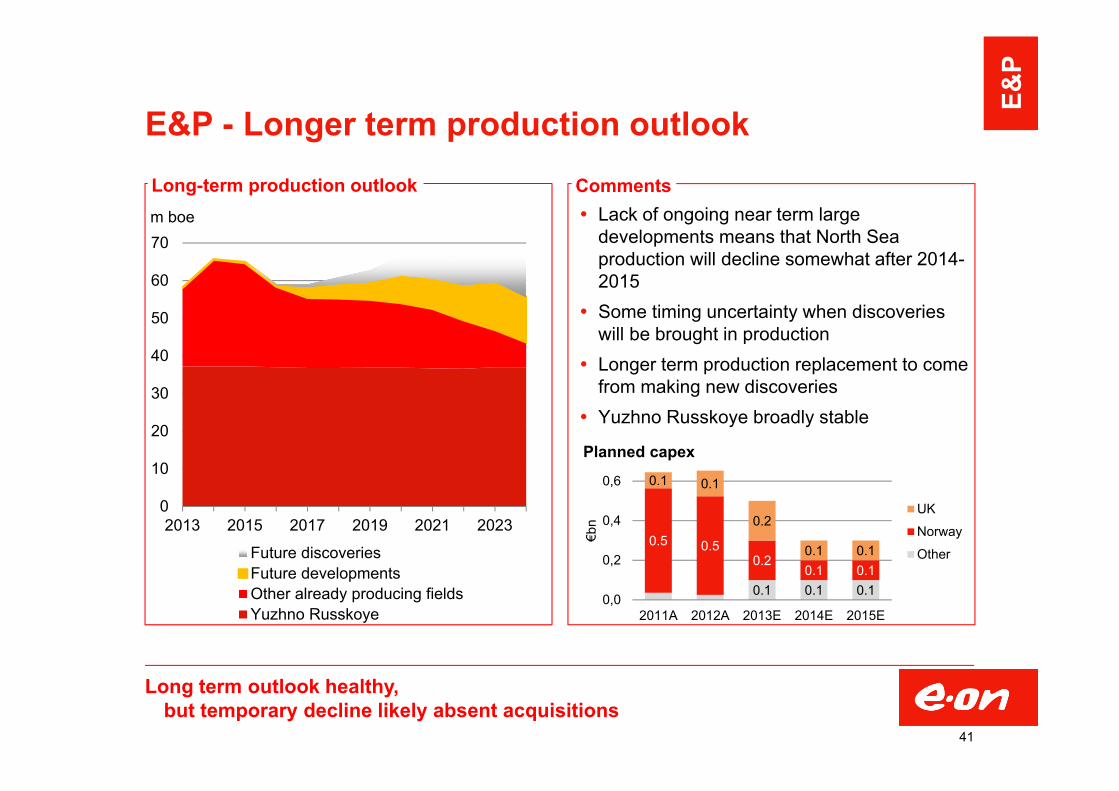

E&P - Longer term production outlook

Long term outlook healthy,but temporary decline likely absent acquisitions

41

0

10

20

30

40

50

60

70

2013 2015 2017 2019 2021 2023

m boe

Future discoveriesFuture developmentsOther already producing fieldsYuzhno Russkoye

Lack of ongoing near term large developments means that North Sea production will decline somewhat after 2014-2015

Some timing uncertainty when discoveries will be brought in production

Longer term production replacement to come from making new discoveries

Yuzhno Russkoye broadly stable

Long-term production outlook Comments

0.1 0.1 0.1

0.5 0.50.2

0.1 0.1

0.1 0.1

0.2

0.1 0.1

0,0

0,2

0,4

0,6

2011A 2012A 2013E 2014E 2015E

€bn

Planned capex

UK

Norway

Other

E&P

No hedging of Norwegian production No hedging of Russian production Some hedging of UK oil and gas production

74

96 99

1823

26

10

20

30

40

50

0

30

60

90

120

2010 2011 2012

€/M

Wh

$/bb

l

Liquids - LHS Brent - LHS

Gas - RHS NBP - RHS

E&P - 2010-2012 financialsEarnings North Sea / North Africa / Other

Earnings Russia

North Sea / North Africa moving to another scale in 2013

42

€m 2010A 2011A 2012A

Net sales 641 607 362

Opex -228 -335 -357

EBITDA 413 272 5

DD&A -184 -126 -110

EBIT 230 146 -105

Net interest -28 -31 1

Taxes -73 -46 108

Net income 129 70 4

€m 2010A 2011A 2012A

EBITDA 296 455 518

DD&A -120 -120 -120

EBIT 176 335 398

Achieved prices North Sea production

E&P

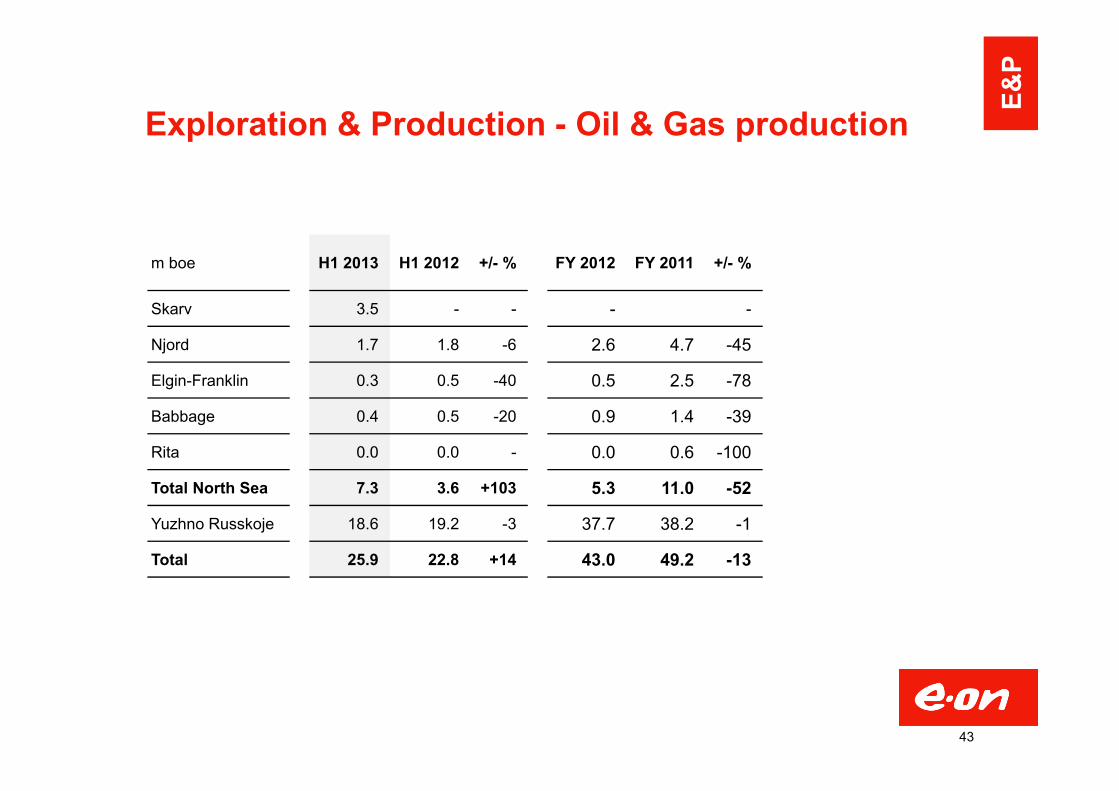

Exploration & Production - Oil & Gas production

43

m boe H1 2013 H1 2012 +/- % FY 2012 FY 2011 +/- %

Skarv 3.5 - - - -

Njord 1.7 1.8 -6 2.6 4.7 -45

Elgin-Franklin 0.3 0.5 -40 0.5 2.5 -78

Babbage 0.4 0.5 -20 0.9 1.4 -39

Rita 0.0 0.0 - 0.0 0.6 -100

Total North Sea 7.3 3.6 +103 5.3 11.0 -52

Yuzhno Russkoje 18.6 19.2 -3 37.7 38.2 -1

Total 25.9 22.8 +14 43.0 49.2 -13

E&P

2,5 2,42,8

1,5 1,51,9

0,00,51,01,52,02,53,0

2010 2011 2012EBITDA EBIT

0,81,0

0,80,6 0,7

0,1

0,20,2

0,10,1

0,00,20,40,60,81,01,21,4

2011 2012 2013 2014 2015Other Distribution

Region Germany – Business snapshot EBIT(DA) 2012 vs. 2011 – Main drivers (€bn)

Disposal impact on EBITDA, but also on capex

44

(+) Higher grid revenues

(+) First impact E.ON 2.0

(+) Provision release inunregulated business

Capex flexibility fully used

High share of distribution capex

~€0.2bn of distribution capex foregone with disposals

Segment capex plan (in €bn)

2013:(+) Further E.ON 2.0 contribution(-) Disposal of regional distribution companies(-) Disposal of Energy from Waste(-) Absence of one-off provision release

Post 2013:(+/-) Uncertainty regarding outcome of regulatory review for power distribution

Key mid-term earnings drivers

Capture opportunities from German “Energiewende”: Profitable growth in distributed energy (e.g. CHP) Innovative sales propositions beyond pure commodity Develop distribution networks according to new requirements

(integration of renewables, smart technologies, etc.) Secure concession renewals in distribution networks Continuously drive operational excellence & performance Actively contribute to the discussion about an optimized

legal/regulatory framework enabling the “Energiewende”

Strategic priorities

EU re

gion

s

0,8 0,7 0,7 0,7 0,7

0,40,4 0,4 0,4 0,4

0,00,20,40,60,81,01,21,4

2011 2012 2013 2014 2015Other Distribution

2,62,3

2,01,7 1,5 1,3

0,00,51,01,52,02,53,0

2010 2011 2012EBITDA EBIT

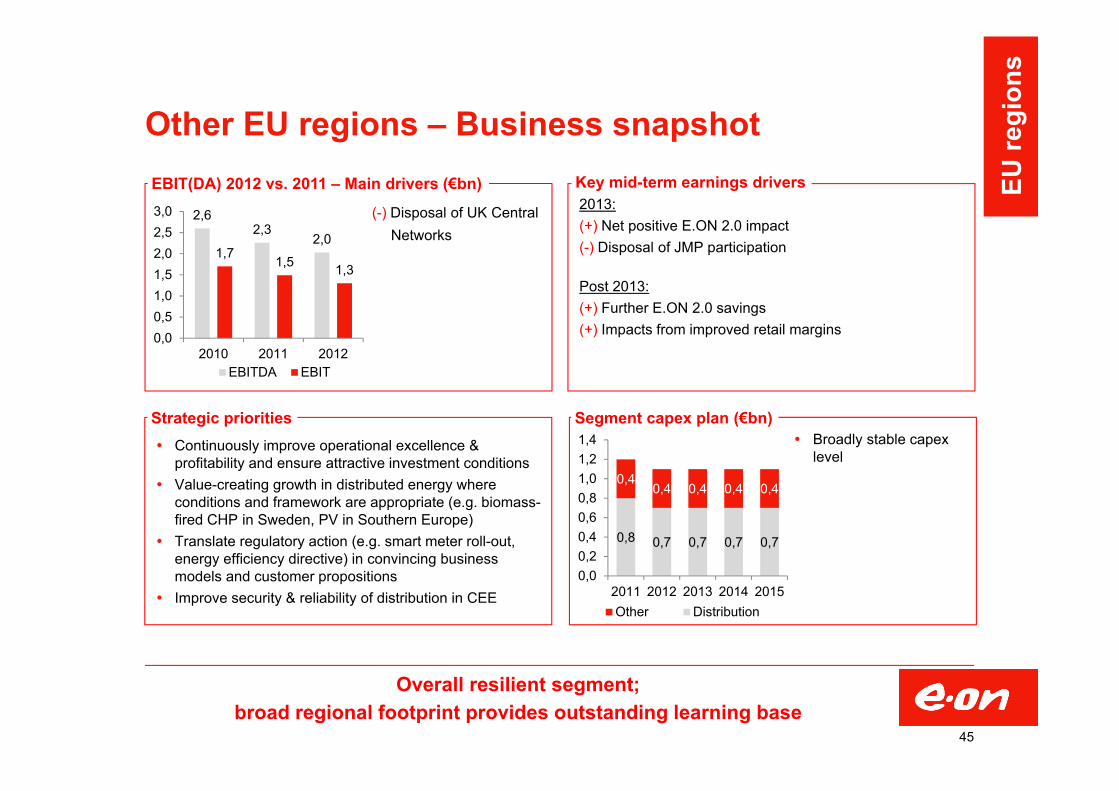

Other EU regions – Business snapshot

Overall resilient segment;broad regional footprint provides outstanding learning base

45

(-) Disposal of UK Central Networks

Broadly stable capex level

Segment capex plan (€bn)

2013:(+) Net positive E.ON 2.0 impact(-) Disposal of JMP participation

Post 2013:(+) Further E.ON 2.0 savings(+) Impacts from improved retail margins

Key mid-term earnings driversEBIT(DA) 2012 vs. 2011 – Main drivers (€bn)

Continuously improve operational excellence & profitability and ensure attractive investment conditions

Value-creating growth in distributed energy where conditions and framework are appropriate (e.g. biomass-fired CHP in Sweden, PV in Southern Europe)

Translate regulatory action (e.g. smart meter roll-out, energy efficiency directive) in convincing business models and customer propositions

Improve security & reliability of distribution in CEE

Strategic priorities

EU re

gion

s

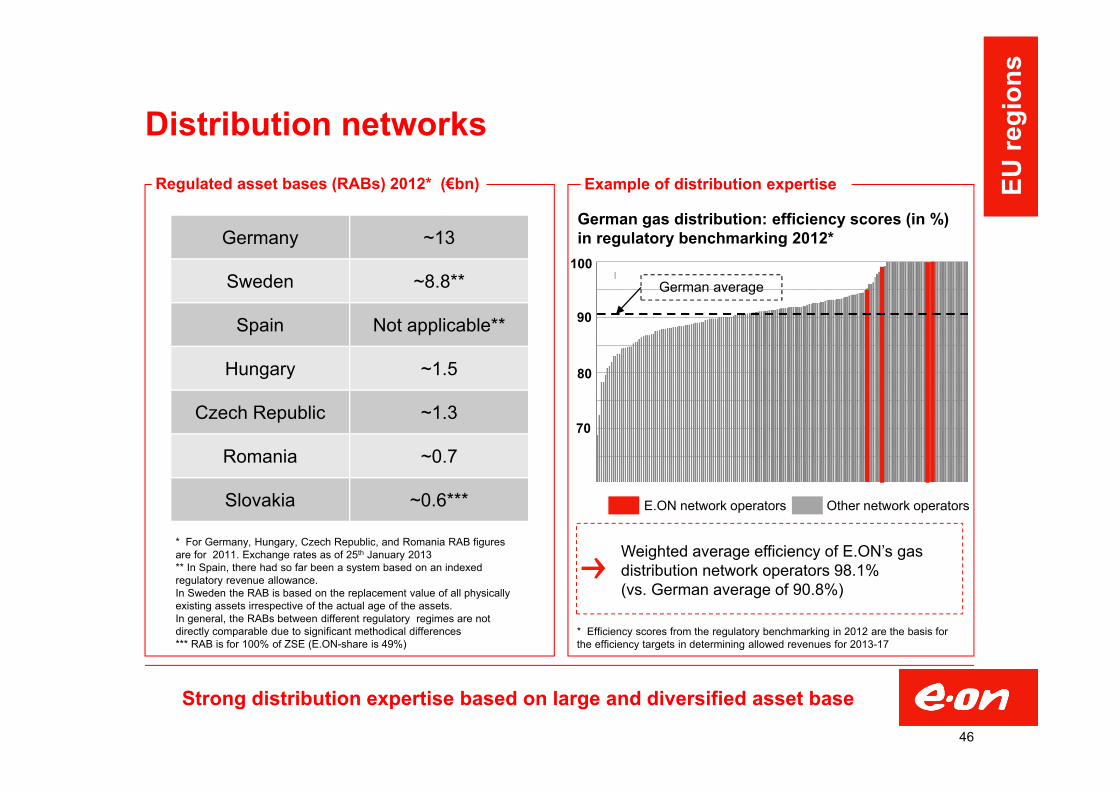

Strong distribution expertise based on large and diversified asset base

Regulated asset bases (RABs) 2012* (€bn)

* For Germany, Hungary, Czech Republic, and Romania RAB figures are for 2011. Exchange rates as of 25th January 2013** In Spain, there had so far been a system based on an indexed regulatory revenue allowance.In Sweden the RAB is based on the replacement value of all physically existing assets irrespective of the actual age of the assets.In general, the RABs between different regulatory regimes are not directly comparable due to significant methodical differences*** RAB is for 100% of ZSE (E.ON-share is 49%)

Germany ~13

Sweden ~8.8**

Spain Not applicable**

Hungary ~1.5

Czech Republic ~1.3

Romania ~0.7

Slovakia ~0.6***

Example of distribution expertise

Distribution networks

German gas distribution: efficiency scores (in %) in regulatory benchmarking 2012*

E.ON network operators Other network operators

Weighted average efficiency of E.ON’s gas distribution network operators 98.1%(vs. German average of 90.8%)

* Efficiency scores from the regulatory benchmarking in 2012 are the basis for the efficiency targets in determining allowed revenues for 2013-17

100

80

90

70

German average

EU re

gion

s

46

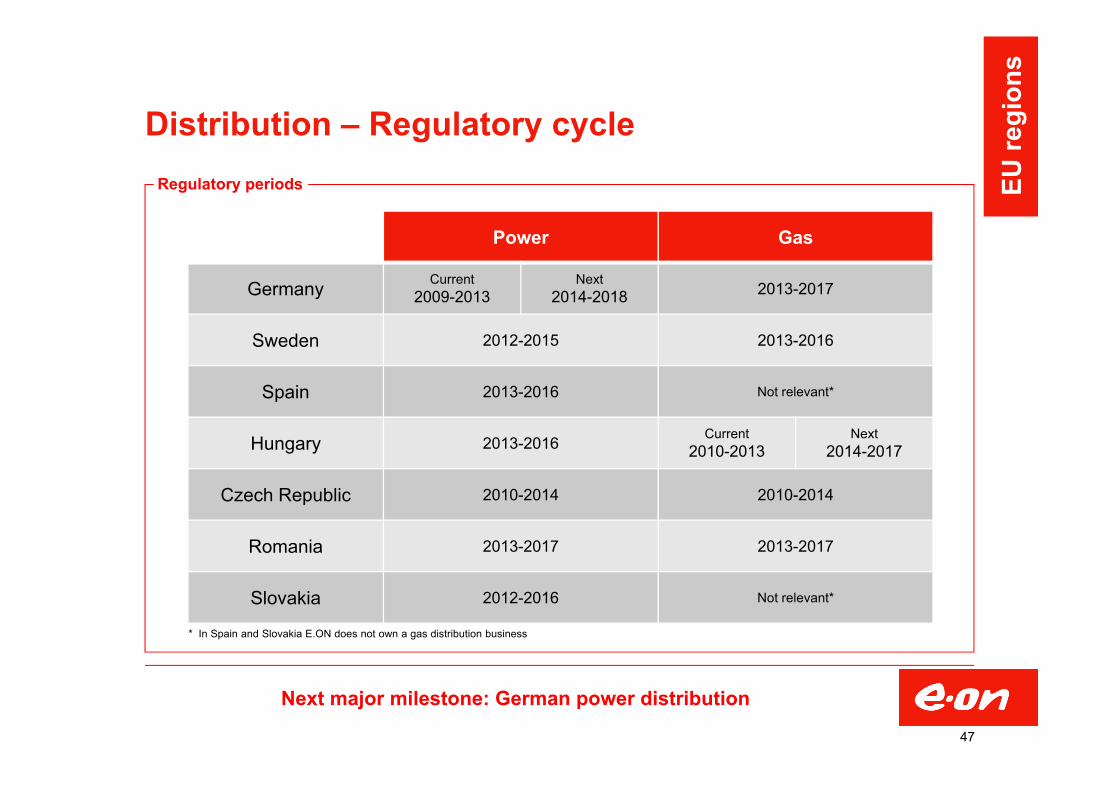

Distribution – Regulatory cycle

Power Gas

Germany Current2009-2013

Next2014-2018 2013-2017

Sweden 2012-2015 2013-2016

Spain 2013-2016 Not relevant*

Hungary 2013-2016 Current2010-2013

Next2014-2017

Czech Republic 2010-2014 2010-2014

Romania 2013-2017 2013-2017

Slovakia 2012-2016 Not relevant*

47

Regulatory periods

* In Spain and Slovakia E.ON does not own a gas distribution business

Next major milestone: German power distribution

EU re

gion

s

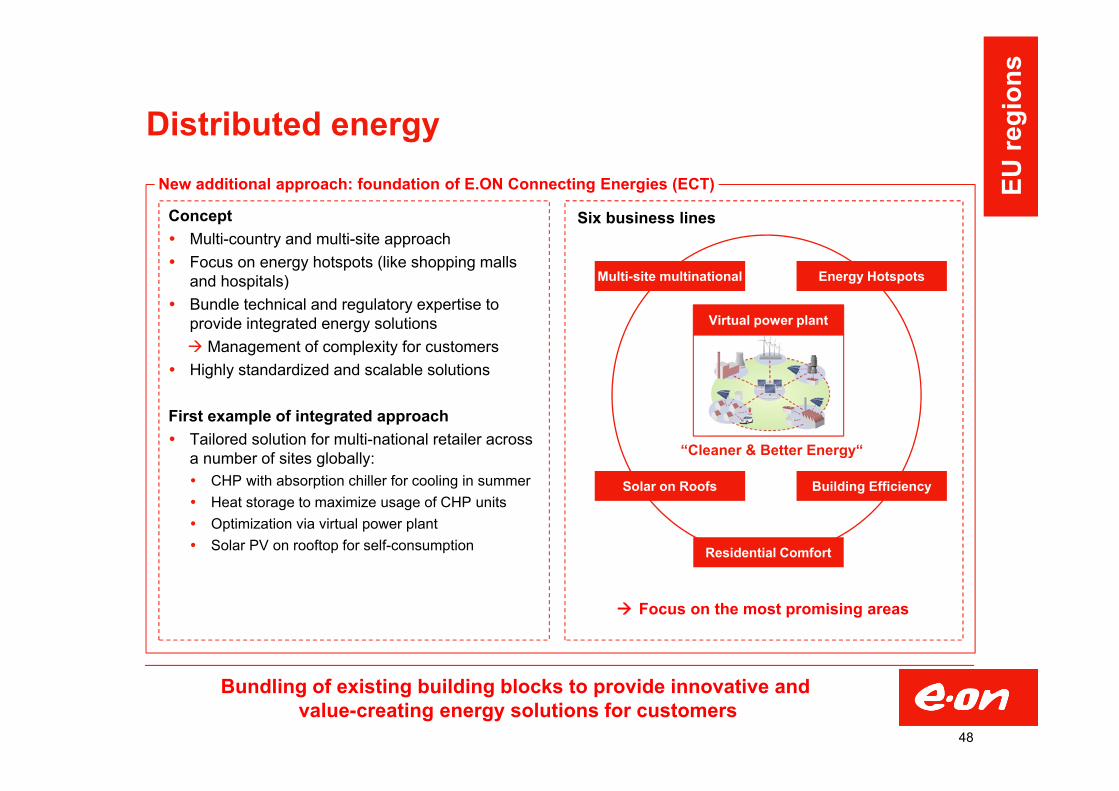

Distributed energy

48

New additional approach: foundation of E.ON Connecting Energies (ECT)

Bundling of existing building blocks to provide innovative and value-creating energy solutions for customers

Concept Multi-country and multi-site approach Focus on energy hotspots (like shopping malls

and hospitals) Bundle technical and regulatory expertise to

provide integrated energy solutions Management of complexity for customers

Highly standardized and scalable solutions

First example of integrated approach Tailored solution for multi-national retailer across

a number of sites globally: CHP with absorption chiller for cooling in summer Heat storage to maximize usage of CHP units Optimization via virtual power plant Solar PV on rooftop for self-consumption

Six business lines

“Cleaner & Better Energy“

Virtual power plant

Residential Comfort

Energy HotspotsMulti-site multinational

Building EfficiencySolar on Roofs

Focus on the most promising areas

EU re

gion

s

0,1 0,1 0,1 0,1 0,1

0,30,2

0,40,3

0,1

0,0

0,1

0,2

0,3

0,4

0,5

0,6

2011 2012 2013 2014 2015Non-maintenance Maintenance

0,4

0,6

0,7

0,3

0,40,5

0,0

0,2

0,4

0,6

0,8

2010 2011 2012EBITDA EBIT

Russia – Business snapshot

From growth driver to cash provider

49

Mainly driven by higher volumes (full year contribution from new plants with COD 2011)

Berezovskaya (lignite) COD: 2014 Total capex: €1.1bn Targeted IRR >10%

Maintenance at minimum by 2015

No additional new build projects planned

Segment capex plan (€bn)

2013:(+) Efficiency improvements(-) Lower spreads

Post 2013:(+) First time contribution from new build Berezovskaya

Key mid-term earnings driversEBIT(DA) 2012 vs. 2011 – Main drivers (€bn)

Maintain and improve top-line operational performance among Russian power generators

Complete Berezovskaya new-build project and ensure full financial contribution to E.ON earnings

Assess options to further solidify E.ON Russia’s position as leading independent generator in the Russian power market

Strategic priorities

Non

-EU

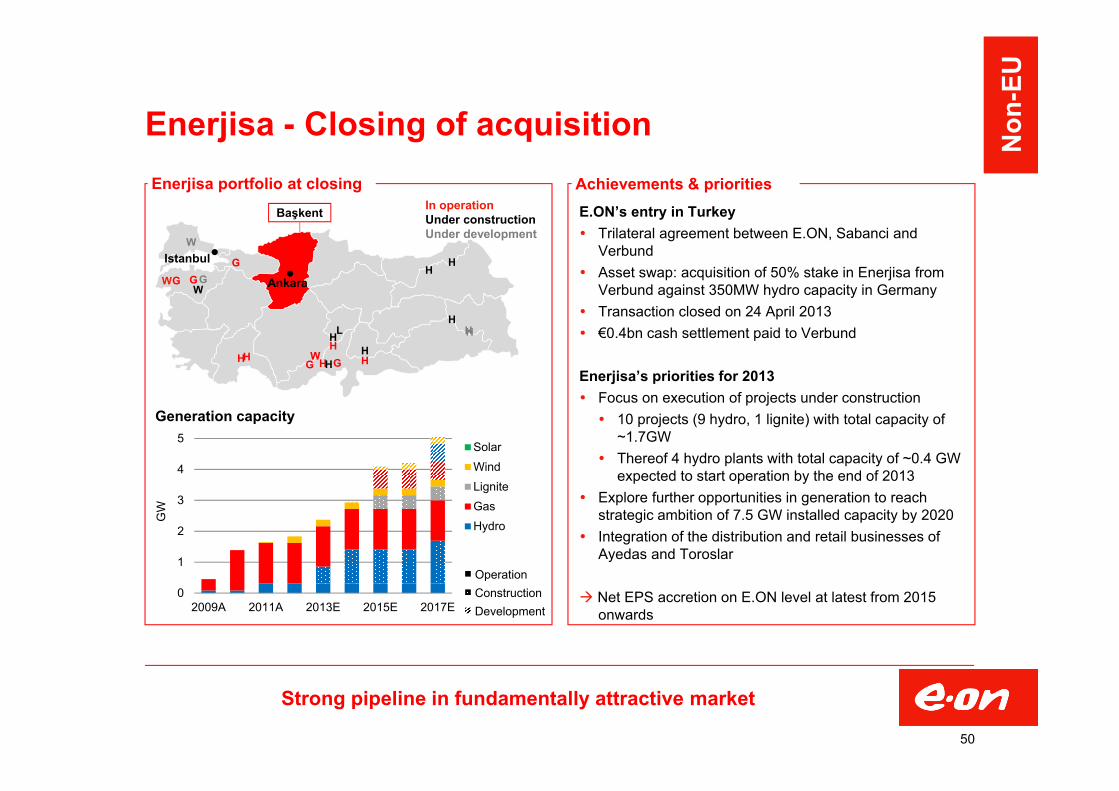

Enerjisa - Closing of acquisition

E.ON’s entry in Turkey Trilateral agreement between E.ON, Sabanci and

Verbund Asset swap: acquisition of 50% stake in Enerjisa from

Verbund against 350MW hydro capacity in Germany Transaction closed on 24 April 2013 €0.4bn cash settlement paid to Verbund

Enerjisa’s priorities for 2013 Focus on execution of projects under construction 10 projects (9 hydro, 1 lignite) with total capacity of

~1.7GW Thereof 4 hydro plants with total capacity of ~0.4 GW

expected to start operation by the end of 2013 Explore further opportunities in generation to reach

strategic ambition of 7.5 GW installed capacity by 2020 Integration of the distribution and retail businesses of

Ayedas and Toroslar

Net EPS accretion on E.ON level at latest from 2015 onwards

Enerjisa portfolio at closing Achievements & priorities

Strong pipeline in fundamentally attractive market

0

1

2

3

4

5

2009A 2011A 2013E 2015E 2017E

GW

SolarWindLigniteGasHydro

2.3Ankara

Istanbul

H HHHH

H

H

HH

HH

H

H

GG

GGG

G

W

W

W

W

L

In operationUnder constructionUnder development

Başkent

Generation capacity

OperationConstructionDevelopment

50

Non

-EU

Enerjisa - Win of Ayedas and Toroslar privatizations

Strong organic growth thanks to population and econo-mic growth, and reduction of average household size

Potential to improve operational performance by leveraging … Enerjisa’s experience with Baskent Disco since 2009 E.ON’s expertise in running various distribution

businesses

Distribution as portfolio stabilizer and potential enabler of new business models in distributed energy

Acquisition of 100% of the shareholders’ equity of the Ayedas and of the Toroslar distribution and retail companies

Transaction equity values1

Ayedas: $1,227m (€0.9bn, 2.2bn TRY) Toroslar: $1,725m (€1.3bn, 3.1bn TRY)

Transaction enterprise value close to equity value

Transaction financing: 40% of purchase price to be paid at closing Remainder of purchase price to be paid in 3 equal

yearly installments Target of 50-60% gearing in medium term

Financial impact for E.ON €0.5-0.6bn of equity injections in Enerjisa in 2013 to

fund Ayedas and Toroslar acquisitions Potential acquisition of one distribution company by

Enerjisa already considered in E.ON’s 2013-15 investment plan

Transaction rationale Transaction parameters

Attractive distribution portfolio to complement generation development

1.Assuming 1.30 $/€ and 2.35 TRY/€

Subscribers: 3.6 mConsumption: 11 TWh

Subscribers: 2.9 m Consumption: 14 TWh

Başkent

Toroslar

Subscribers: 2.5 mConsumption: 8 TWh

Ayedas

51

Non

-EU

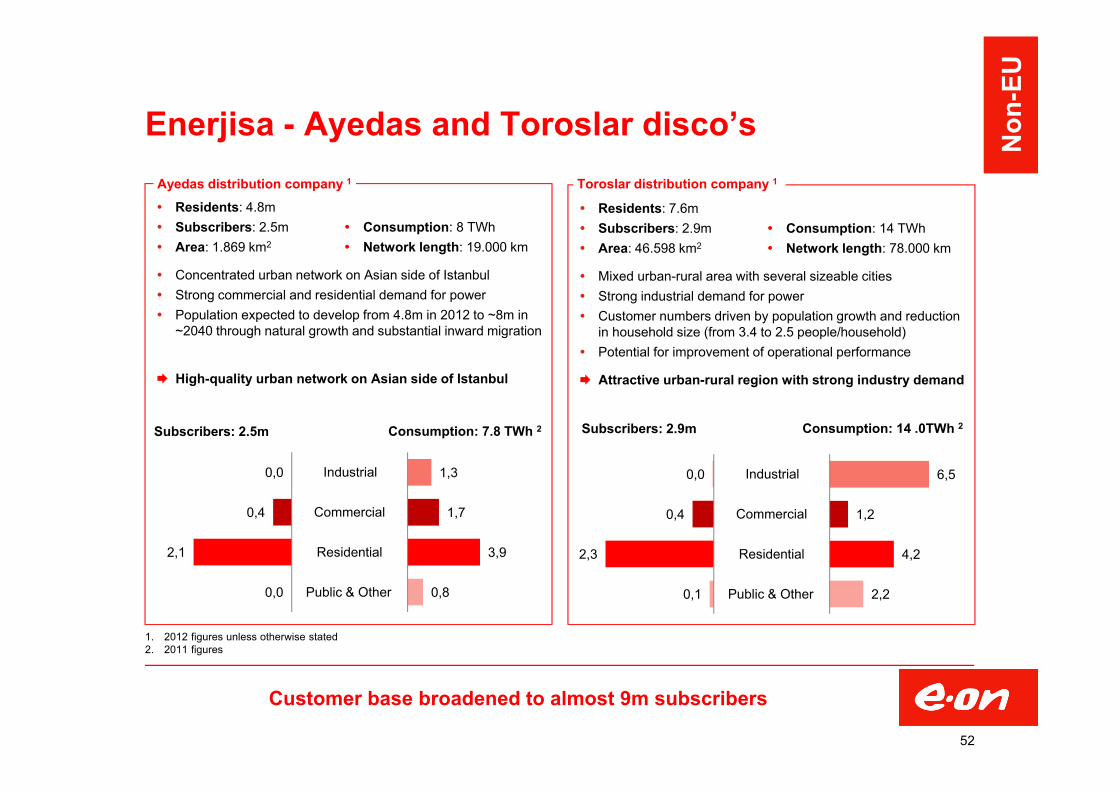

Enerjisa - Ayedas and Toroslar disco’s

Residents: 4.8m Subscribers: 2.5m Consumption: 8 TWh Area: 1.869 km2 Network length: 19.000 km

Concentrated urban network on Asian side of Istanbul Strong commercial and residential demand for power Population expected to develop from 4.8m in 2012 to ~8m in

~2040 through natural growth and substantial inward migration

High-quality urban network on Asian side of Istanbul

Residents: 7.6m Subscribers: 2.9m Consumption: 14 TWh Area: 46.598 km2 Network length: 78.000 km

Mixed urban-rural area with several sizeable cities Strong industrial demand for power Customer numbers driven by population growth and reduction

in household size (from 3.4 to 2.5 people/household) Potential for improvement of operational performance

Attractive urban-rural region with strong industry demand

Ayedas distribution company 1

Customer base broadened to almost 9m subscribers

0,0

0,4

2,1

0,0

1,3

1,7

3,9

0,8

Industrial

Commercial

Residential

Public & Other

Subscribers: 2.5m Consumption: 7.8 TWh 2

1. 2012 figures unless otherwise stated2. 2011 figures

Toroslar distribution company 1

0,0

0,4

2,3

0,1

6,5

1,2

4,2

2,2

Industrial

Commercial

Residential

Public & Other

Subscribers: 2.9m Consumption: 14 .0TWh 2

52

Non

-EU

MPX - Transaction summary

Expected outcome after 3 transactions E.ON achieves ~38% direct share in MPX EBX / Eike Batista reduces interest in MPX to ~24% Early capital injection in MPX and JV reintegrated into MPX

MPX becomes E.ON’s expansion vehicle in Brazil MPX becomes E.ON’s main vehicle for expansion in Brazil,

instead of JV with MPX MPX capital increase of R$0.8bn provides stability to MPX

operations

Ownership and governance Simplification of ownership and governance structures Shareholders agreement and by-laws create “joint-control”

concept within Board of Directors and Executive Committee New Board of Directors and Executive Committee in place MPX has already relocated its headquarters, and will also be

renamed

Targeted structure

Current structure

Enhancement of E.ON’s position in MPX

MPX

MPX-E.ON JV

E.ON

11.7%

50% 50%

EBX / EikeBatista

Others

53.5% 34.8%

MPX

E.ON

~38%

EBX / EikeBatista

Others

~24% ~38%

53

Non

-EU

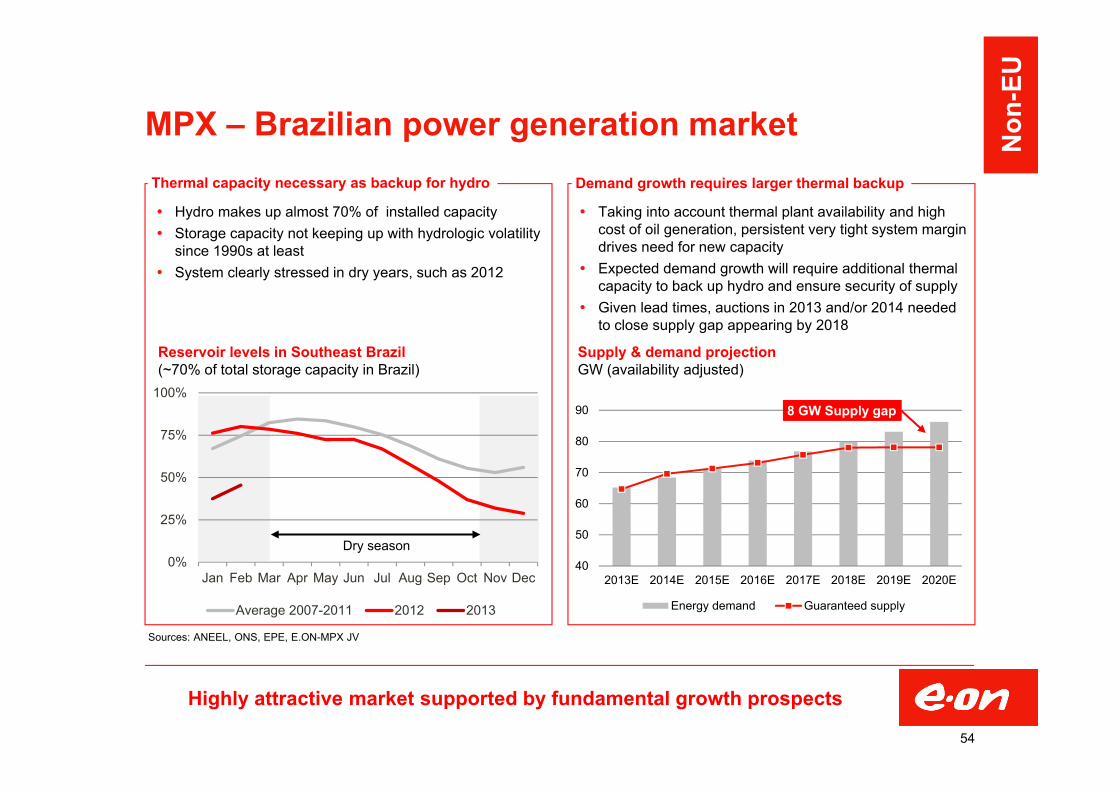

MPX – Brazilian power generation market

Hydro makes up almost 70% of installed capacity Storage capacity not keeping up with hydrologic volatility

since 1990s at least System clearly stressed in dry years, such as 2012

Taking into account thermal plant availability and high cost of oil generation, persistent very tight system margindrives need for new capacity

Expected demand growth will require additional thermal capacity to back up hydro and ensure security of supply

Given lead times, auctions in 2013 and/or 2014 needed to close supply gap appearing by 2018

Thermal capacity necessary as backup for hydro Demand growth requires larger thermal backup

Highly attractive market supported by fundamental growth prospects

40

50

60

70

80

90

2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

Energy demand Guaranteed supply

Reservoir levels in Southeast Brazil(~70% of total storage capacity in Brazil)

0%

25%

50%

75%

100%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Average 2007-2011 2012 2013

Dry season

Supply & demand projectionGW (availability adjusted)

Sources: ANEEL, ONS, EPE, E.ON-MPX JV

8 GW Supply gap

54

Non

-EU

0,0

0,5

1,0

1,5

Q3 2012 Q1 2013 Q3 2013

Parnaíba IV

Parnaíba IIopen cycleParnaíba IIINova VeneciaPecém II

Pecém I B

Parnaíba I

Itaqui

Pecém I A

Taua

Amapari

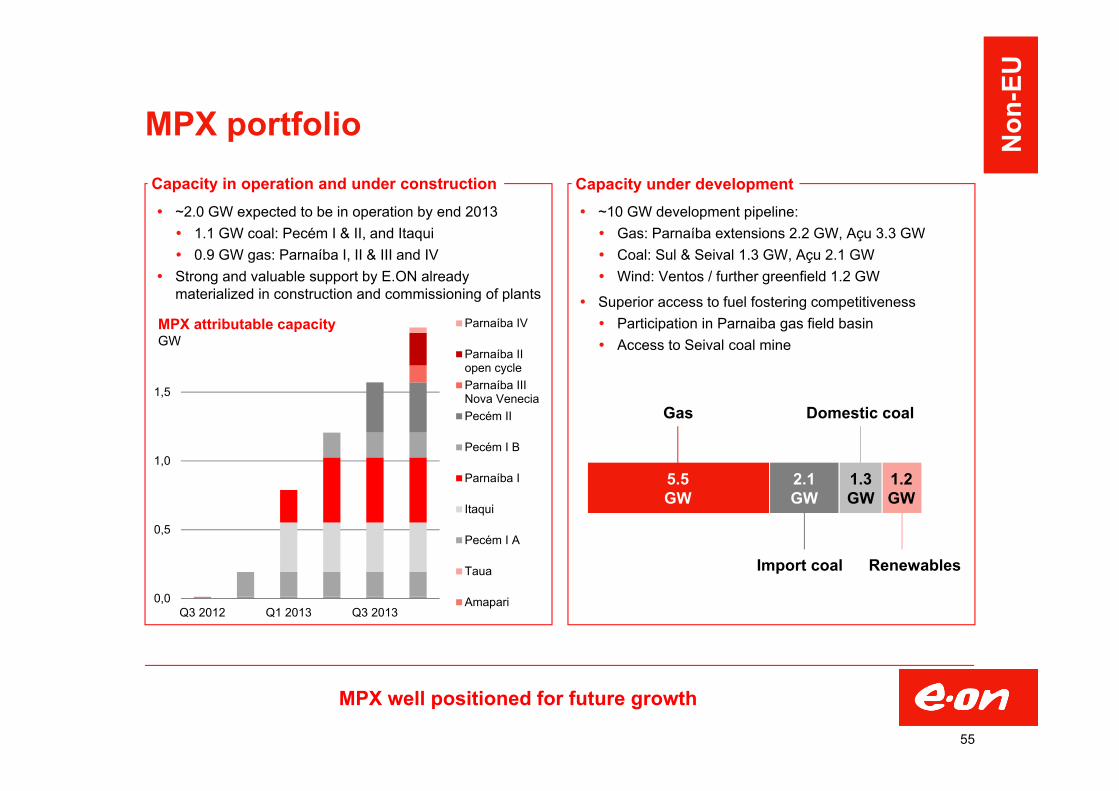

~2.0 GW expected to be in operation by end 2013 1.1 GW coal: Pecém I & II, and Itaqui 0.9 GW gas: Parnaíba I, II & III and IV

Strong and valuable support by E.ON already materialized in construction and commissioning of plants

MPX portfolio

~10 GW development pipeline: Gas: Parnaíba extensions 2.2 GW, Açu 3.3 GW Coal: Sul & Seival 1.3 GW, Açu 2.1 GW Wind: Ventos / further greenfield 1.2 GW

Superior access to fuel fostering competitiveness Participation in Parnaiba gas field basin Access to Seival coal mine

Capacity in operation and under construction Capacity under development

MPX well positioned for future growth

MPX attributable capacityGW

55

Non

-EU

Gas

Import coal

Domestic coal

Renewables

5.5GW

2.1GW

1.3GW

1.2GW

56

Dr. Marc SpiekerHead of IR T+49 2 11-45 79-3 45

[email protected] BlankenhornRegions/Sales, SRI, Retail, T +49 2 11-45 79-4 81Facts & Figures [email protected]

François PoulletGeneration, Gas T +49 2 11-45 79-3 32

Marc KoebernickRenewables, Trading T +49 2 11-45 79-2 39

Dr. Stephan SchönefußPolitics & Regulation, Regions/Distribution T +49 2 11-45 79-48 08

Carmen SchneiderTechnology & Innovation, Roadshow planning & management, T +49 2 11-45 79-3 45Shareholder ID & Targeting [email protected]

E.ON Investor Relations Contact

E.ON IR - Reporting calendar & important links

Date Event

November 13, 2013 Interim Report III: January – September 2013

March 12, 2014 Annual Report 2013

April 30, 2014 2014 Annual Shareholders Meeting

May 2, 2014 Dividend Payout

May 13, 2014 Interim Report I: January – March 2014

August 13, 2014 Interim Report II: January – June 2014

Content Link

Equity Story http://www.eon.com/en/investors/26658.jsp

Segment Stories http://www.eon.com/en/investors/42341.jsp

Annual Report http://www.eon.com/en/corporate/19886.jsp

Interim Reports http://www.eon.com/en/corporate/1022.jsp

Facts & Figures http://www.eon.com/en/corporate/1029.jsp

Creditor Relations http://www.eon.com/de/investoren/dialog/creditor-relations.htm

Important links

Reporting calendar

57

This presentation may contain forward-looking statements based on current assumptions and forecasts madeby E.ON Group management and other information currently available to E.ON. Various known and unknownrisks, uncertainties and other factors could lead to material differences between the actual future results,financial situation, development or performance of the company and the estimates given here. E.ON SE doesnot intend, and does not assume any liability whatsoever, to update these forward-looking statements or toconform them to future events or developments.

Disclaimer