Embed Size (px)

Citation preview

www.keglerbrownGlobal.com

@KeglerGlobal

Luis Alcalde & David M. Wilson, Kegler

Brown

PREPARING FOR

SUCCESS IN BRAZIL,

COLOMBIA & CHILE

Methods of Entry

Import / ExportAgency,

Distributorships & Labor

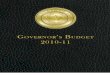

3 Issues that can Make or Break

Your Latin America Business

Strategy

Agency, Distributorships &

Labor-Creation

-Termination

3. Labor

Methods of Entry-Strategic Considerations

-Available Organizational &

Entity Structures

-Features

1. Entry Method &

Organizational

Structure

Import/Export-Process

-Taxes

-Free Trade Zones &

Treaties

2. Regulation & Tax

Methods of Entry

Import / ExportAgency,

Distributorships & Labor

Entry Method & Organizational

Structure Strategic Considerations

Available Organizational & Entity Structures

Features

Methods of Entry

Import / ExportAgency,

Distributorships & Labor

Entry Method & Organizational

Structure

Political The ability of government to respond to and NOT create political

risk

Economic Macro trends, Currency risks

Social The ability of stakeholders to identify vulnerabilities & apply

pressure to the company to change its behavior

Technological Infrastructure, IP Protection, Government Incentives

P E S T

What are the Political, Economic, Social and Technological

reasons to enter Brazil, Colombia or Chile?

export, manufacture, distribute, design . . .

Methods of Entry

Import / ExportAgency,

Distributorships & Labor

Entry Method & Organizational

Structure P E S T

Methods of Entry

Import / ExportAgency,

Distributorships & Labor

0

10

20

30

40

50

60

70

80

90

100

PDI IDV MAS UAI LTO

Chile

Chile

0

10

20

30

40

50

60

70

80

PDI IDV MAS UAI LTO

Brazil

Brazil

Geert Hofstede’s Cultural Dimensions

Power Distance

Individualism

Masculinity

Uncertainty Avoidance

Long-Term Orientation

www.geert-hofstede.com

0

10

20

30

40

50

60

70

80

90

PDI IDV MAS UAI LTO

Colombia

Colombia

0

10

20

30

40

50

60

70

80

90

PDI IDV MAS UAI LTO

Latin America

Latin America

Entry Method & Organizational

Structure P E S T

Geert Hofstede’s Cultural Dimensions

Power Distance

Individualism

Masculinity

Uncertainty Avoidance

Long-Term Orientation

www.geert-hofstede.comMethods of Entry Import / Export

Agency, Distributorships & Labor

0

10

20

30

40

50

60

70

80

90

100

PDI IDV MAS UAI LTO

US

Brazil

Colombia

Chile

Latin America

0

10

20

30

40

50

60

70

80

PDI IDV MAS UAI LTO

Brazil

Brazil

Entry Method & Organizational

Structure

Direct sale from US using freight forwarder

Non-Equity Alliance Distribution agreements

Licensing agreements

Franchising agreements

Supply agreements

Joint venture

Equity Alliance Joint venture

Joint company

Wholly Owned Subsidiaries Greenfield operations

Methods of Entry Import / ExportAgency, Distributorships

& Labor

May also require

a small wholly

owned subsidiary

holding company

presence in

country

Entry Method & Organizational

Structure

Joint Venture

May be created with or without a full joint company

Contractual joint ventures between subsidiary company and a partner company

Low cost entry and exit to new markets, industries and industry segments

Opportunity for learning

Provides a “contractual” framework for operations without generating many issues associated with an agency relationship

Enables each party to take full responsibility for its contribution to the venture while minimizing the issues associated with exclusivity

Enables low cost entry and exit

May later evolve into full equity allianceMethods of Entry Import / Export

Agency, Distributorships & Labor

Entry Method & Organizational

Structure

Methods of Entry Import / ExportAgency, Distributorships

& Labor

Similar to US

LLC

Similar to US

Corporation

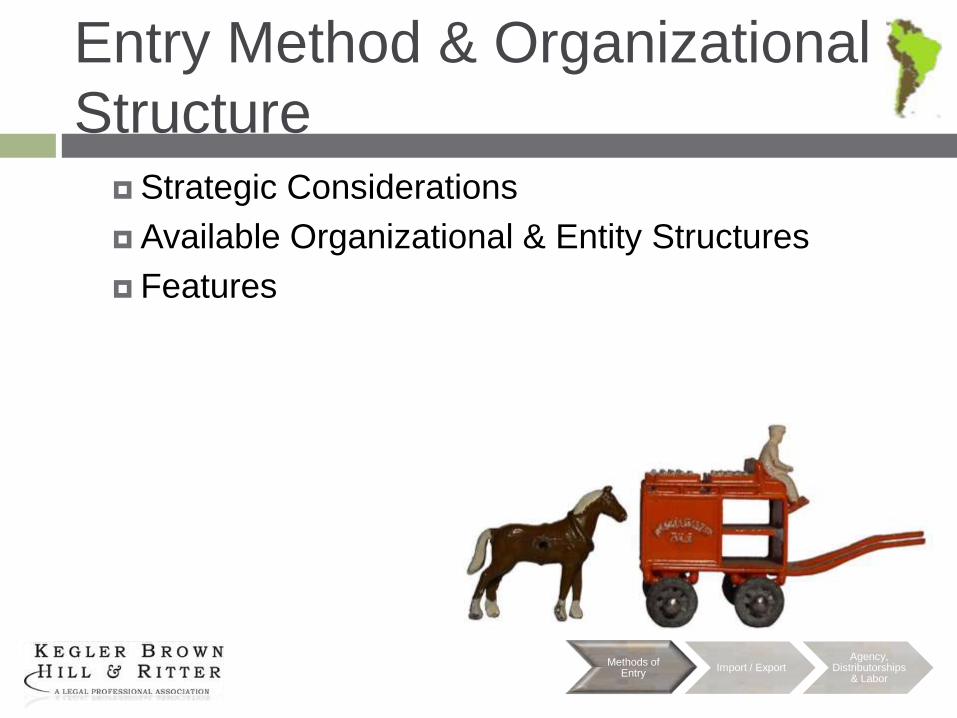

Sociedade Limitada (LTDA)

Sociedade Anônima (SA)

Sociedad por Acciones Simplificada

(SAS)

Sociedad Anónima (SA)

Sociedades de Responsabilidad Limitada (SRL)

Sociedades Anónima (SA)

Entry Method & Organizational

Structure

Methods of Entry Import / ExportAgency, Distributorships

& Labor

-No restrictions on foreign ownership*

-No minimum or maximum capital requirements*

-Partner & parent company liability limited to capital contributions

-Product Liability: Yes

-No restrictions on foreign ownership*

-No minimum or maximum capital requirements*

-Partner and parent company liability is limited to capital contributions ** In insolvency PC is responsible for subsidiary liabilities if PC caused the subsidiary’s liquidation

-Product Liability: Yes

-No restrictions on foreign ownership*

-No minimum or maximum capital requirements*

-Partner and parent company liability is limited to capital contributions

-Product Liability: Yes

LTDA / SAS / SRL

&

SA Common Features

Import / Export

Import Export Process

Associated Taxes & Duties

Free Trade Zones & Treaties

Methods of Entry Import / ExportAgency, Distributorships

& Labor

Import / Export

Methods of Entry Import / ExportAgency, Distributorships

& Labor

17 Days

-Document Preparation (8 days)

-Customs clearance and technical control (4 days)

-Ports and terminal handling (3 days)

-Inland transportation and handling (2 days)

13 Days

-Document Preparation (6 days)

-Customs clearance and technical control (2 days)

-Ports and terminal handling (2 days)

-Inland transportation and handling (3 days)

20 Days

-Document Preparation (12 days)

-Customs clearance and technical control (2 days)

-Ports and terminal handling (4 days)

-Inland transportation and handling (2 days)

General Import Process

& Timeline

Source: World Bank, Doing Business

2012

Importing a container of

goods to Brazil requires 8

documents, takes 17 days

and costs $2,275

Importing a container of

goods to Colombia requires

6 documents, takes 13 days

and costs $2,830

Importing a container of goods

to Chile requires 6

documents, takes 20 days and

costs $795

Baseline:

-medium size business

-ship to economy’s

largest business city

-private, LLC

-non hazardous goods

-dry cargo, 20-foot full

container

* All US exports are also subject to US export

controls *

Import / Export

Methods of Entry Import / ExportAgency, Distributorships

& Labor

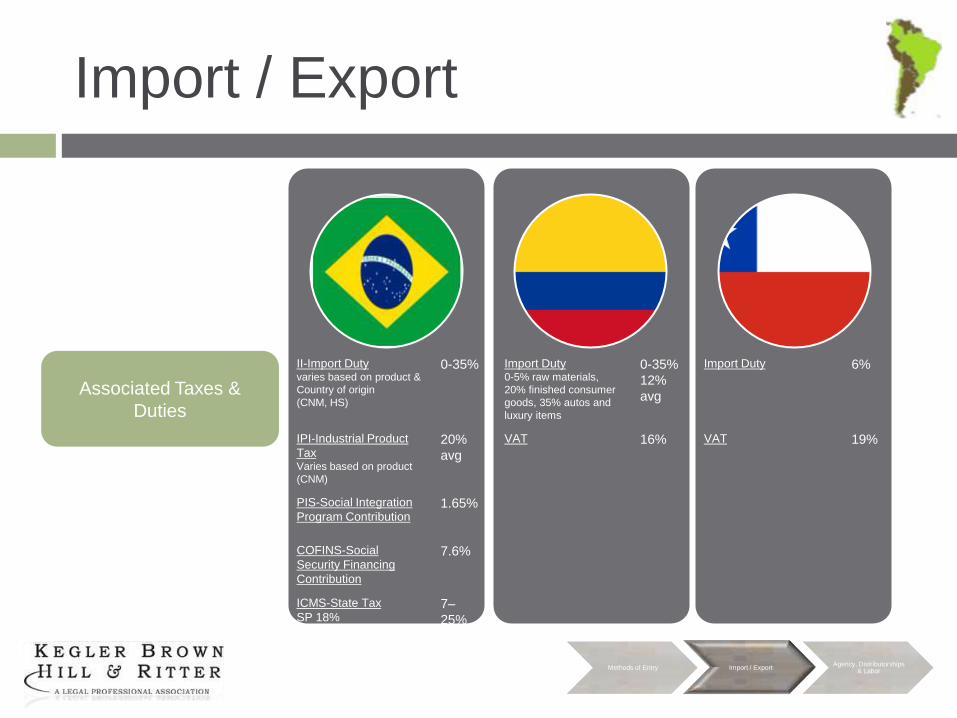

Associated Taxes &

Duties

II-Import Dutyvaries based on product &

Country of origin

(CNM, HS)

0-35% Import Duty0-5% raw materials,

20% finished consumer

goods, 35% autos and

luxury items

0-35%

12%

avg

Import Duty 6%

IPI-Industrial Product

TaxVaries based on product

(CNM)

20%

avg

VAT 16% VAT 19%

PIS-Social Integration

Program Contribution1.65%

COFINS-Social

Security Financing

Contribution

7.6%

ICMS-State Tax

SP 18%7–

25%

Import / Export

Methods of Entry Import / ExportAgency, Distributorships

& Labor

-Importer must register with Brazilian Ministry of Development, Industry and Commerce

-No payment for the product may be made by a Brazilian entity

-Exemption from II (Import Duty)

-No license required for samples & promotional products outside of prior license list

-Maximum of 10 samples

-Max value of US $50 per sample

-If over 10 samples but less than US $1,000 value packing must state “merchandize with no commercial value"

-Subject to applicable custom duties

-Under the terms of the US / Chile FTA

-Professional equipment necessary for carrying out business may receive temporary duty-free admission

-This is intended for display or demonstration of commercial samples

-Temporary admission of food samples require additional consideration

Samples / Tradeshow

exceptions

Import / Export

Methods of Entry Import / ExportAgency, Distributorships & Labor

Additional Tax

Considerations

Corporate TaxPlus 10% on taxable

income over R$240,000

15% Corporate Tax 33% Corporate Tax 17%

Transfer Price

ConsiderationsYes Transfer Price

ConsiderationsYes Transfer Price

ConsiderationsYes

On average, firms make 9

tax payments per year and

spend 2600 hours per year

filing, preparing and paying

taxes and pay total taxes

amounting to 22.4% of profit

On average, firms make 9

tax payments per year and

spend 193 hours per year

filing, preparing and paying

taxes and pay total taxes

amounting to 18.9% of

profit

On average, firms make 9

tax payments per year and

spend 316 hours per year

filing, preparing and paying

taxes and pay total taxes

amounting to 18% of profit

Baseline:

-medium size business

-began operations 1/1/2009

-taxes & mandatory

contributions are measured

at all levels of government

-a range of standard

deductions & exemptions is

also factored

Source: World Bank, Doing Business

2012

Import / Export

Methods of Entry Import / ExportAgency, Distributors

hips & Labor

Free Trade Agreements

and Memberships

Double Tax Treaties

US

Colombia

Chile

NO

NO

YES

Double Tax Treaties

US

Brazil

Chile

YES

NO

YES

Double Tax Treaties

US

Brazil

Colombia

YES

YES

YES

MembershipMercosur (Argentina,

Uruguay, Paraguay,

Bolivia, Chile, Colombia,

Ecuador, Peru)

Latin American

Integration Association

LAIA (Argentina, Brazil,

Mexico, Chile, Paraguay,

Uruguay, El Salvador,

Costa Rica,

Guatemala, Nicaragua,

Honduras, Cuba)

MembershipMercosur

Latin American

Integration Association

LAIA

Andean Community of

Nations CAN (Ecuador,

Bolivia, Venezuela – Peru

withdrew)

G-3 (Mexico, Venezuela)

Membership

Mercosur

Latin American

Integration Association

LAIA

Import / Export

Methods of Entry Import / ExportAgency,

Distributorships & Labor

-Manaus ZFM

-Areas de livre Comercio ALC (4)

-Amazonia Ocidental

-Permanent Free Trade Zones (23)

-Special Enterprise Free Trade Zones (40)

-Transitory Free Trade Zones

-Inquique

-Punta Arenas

Free Trade Zones: The

basics

Reduced/Exempte

d

II, PIS & COFINS

Reduced/Exempt

ed

II & VAT

Reduced/Exempt

ed

II & VAT

Import / Export

US / Colombia Free Trade Agreement

18 to 24 months to implement

Will Reduce tariffs on 80% of US imports

Other tariffs reduced over 10 years

Colombia to implement new domestic legislation in a

number of areas:

sales agents, intellectual property, provide greater access

to several sectors in financial services and

telecommunications investments

Methods of Entry Import / ExportAgency, Distributorships & Labor

Agency, Distributorships &

Labor Agency, Distributorships & Labor

Creation

Termination

Methods of Entry Import / ExportAgency, Distributorships

& Labor

Agency, Distributorships &

Labor

Methods of Entry Import / ExportAgency, Distributorships & Labor

Creation:

-If written contract does not exist, one may be implied

-Contract should contain limitations, termination events, territory, products or goods, commission structure and time of payment

-Exclusivity is not presumed

Termination:

Upon termination, without cause, agent entitled to:

-1/12 of the total compensation during the time of agency

-If a specific agency term , then the average monthly compensation for half of the months remaining in the contract. If $3,000 per month and 12 months into a 36 month contract, then agent would receive $3,000 x 12 = $36,000

-Expenses related to promoting the brand and opening the market

Creation:

-Written registered contract subject to Colombian law

-Contract should contain limitations, termination events & territory

Termination:

-Upon termination agent entitled to 1/12 of the average commission of the last three years

-Without cause termination agent entitled to damages for opening market & promoting product

Creation:

-In Chile, agency, distribution and franchise agreements are not specifically regulated. However, case law has provided some useful guidance

-Their validity, binding nature and enforceability has been recognized by the civil and anti-trust courts

-Relationship is contractual

Termination:

-Chilean civil and anti-trust courts provide precedents for termination and have established circumstances in which they are null and void

-Relationship is contractual

-Contract subject to anti-trust, consumer and general commercial contract law principals

Sales Agent / Distributor

Creation & Termination

Agency, Distributorships &

Labor

Methods of Entry Import / ExportAgency, Distributorships

& Labor

General Labor

Considerations

-Labor law is rooted deeply

-Written contract not required, employment relationship

may be implied

-Termination without cause will likely require provision of

wages, holiday compensation and other benefits

www.keglerbrownGlobal.com

@KeglerGlobal

Luis Alcalde & David M. Wilson, Kegler

Brown

PREPARING FOR

SUCCESS IN BRAZIL,

COLOMBIA & CHILE

Methods of Entry Import / ExportAgency, Distributor

ships & Labor

Additional Sources

Doing Business 2012, Doing Business in a More Transparent World, World Bank Report, October 20, 2011

UBS Investment Research: Emerging Economic Focus, UBS, August 29, 2011

A Closer Look at Brazil’s Credit Boom, Deutsche Bank EM Special Publication, July 22, 2011

Anchoring, De-Anchoring, Re-Anchoring, Bradesco Corretora Economics BBI Equity Research, September 6, 2011

Economic Outlook: Brazil, BBVA, Third Quarter 2011

Brazil Auctions Rights to Airport, WSJ, August 23, 2011

The Geopolitics of Brazil: An Emergent Power’s Struggle with Geography, STRATFOR, July 14, 2011

The Aging World, Ned Davis Research Inc, July 21, 2011

Japanese Dump Real Funds at Fastest Pace Since Earthquake: Brazil Credit, Bloomberg, September, 30, 2011

First they went for the currency, now for the land, The Economist, September 24, 2011

Gaining & Sustaining Competitive Advantage Third Edition, Jay B. Barney, 2007

Privatization and the Distribution of Assets and Income in Brazil, Economic Reform Project: Global Policy Program, July, 2000