Embed Size (px)

Citation preview

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 1/76

United House, 10 Gulshan Ave, Gulshan-1 Dhaka-1212 BangladeshPhone: +880 2 88337-52 up to 66 Fax: +880 2 8833495

BICF is managed and executed by the IFC and funded bythe U.K. Department for International Development and the European Commission

Pre-feasibility Study for Sylhet Economic Zone

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 2/76

1

About IFC BICF

The IFC Bangladesh Investment Climate Fund was established in January 2007 with the keyobjective of addressing some of the main investment constraints in Bangladesh including an unduly

high administrative burden, poor infrastructure and corruption.

IFC BICF is funded by the UK Government’s Department for International Development (DFID)and the European Commission for a total of US54.8 million over eight years. It will consist of twofour-year phases, with the implementation of Phase II dependent on the success of Phase I.

IFC BICF’s primary objective is to provide advisory services to the Government of Bangladesh inits efforts to improve the country’s investment climate, whilst also working with other stakeholders within the private sector, civil society and the media. IFC BICF’s main counterpart in Governmentis the Board of Investment.

IFC BICF targets three reform areas: improving overall business regulations through a dedicatedbody within the Government; improving the regulatory framework for private participation andenvironmental/social compliance practices in economic zones; and, strengthening institutional andcivil service capacity to promote private sector development reforms, while improving advocacycapacity among all stakeholders.

Disclaimer

IFC, through IFC BICF, endeavors, using its best efforts in the time available, to provide highquality services hereunder and have relied on information provided to them by a wide range of other

sources. However, IFC makes no express or implied representation or warranty as to the accuracy,completeness or sufficiency of this report and its analyses.

Consequently, IFC shall not be liable for any loss, damage or liability that the Client or any otherthird party may suffer or incur as a result of (i) this report prepared by IFC or (ii) any advice orrecommendation given or made by IFC in this report, unless a court of competent jurisdictiondetermines by final judgment that such loss, damage or liability was the result of gross negligence or willful misconduct on the part of IFC.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 3/76

2

Foreword – Acknowledgements

In the past three decades, Bangladesh has made wide use of Export Processing Zones (EPZs) as atool for economic growth and job creation. Industrial estates have also been established in most of

the 64 districts of Bangladesh, and the Government of Bangladesh (GoB) is also contemplatingpaving the way for a variety of other kinds of economic zones in the country. The zones haveproven to be effective tools in setting aside and allocating land for industrial use and in creating jobs.

With a view to reaping the benefits of an economic zone in the northeast division of Sylhet, in 2005the Sylhet Chamber of Commerce & Industry (SCCI) commissioned a pre-feasibility study for aproposed economic zone in Sylhet to a local consulting company, Young Consultants. A major aimof the proposed project was to attract investment from non-resident Bangladeshis, primarily thoseof Sylheti origin, now residing in the U.K. and enjoying a great deal of economic success. The first version of the study completed in August 2007 contained much useful information, however, theBoard of Investment (BOI), which was assigned responsibility for the project by the GoB felt that

the study could be enriched by bringing in international expertise to complete the financial andeconomic models and to benchmark the site against other international zone projects.

The following pre-feasibility study was the result of a joint effort by Young Consultants and severalinternational experts brought in to Bangladesh between November 2007 and May 2008. There werenumerous trips to Sylhet by the consultants and the IFC BICF staff, as well as vast amounts ofinformation gathered both about Sylhet and Bangladesh and information about industries worldwidefor the benchmarking exercise.

Various people assisted us with information and logistics in the course of performing this study. We would like to thank the Sylhet Chamber of Commerce for the original impetus for the project andfor providing extensive information on the project during our visits.

We would also like to thank the Board of Investment for making the request for the study of theIFC BICF and especially Mr. M. Emdad-ul Haque, Deputy Director, Board of Investment in Sylhet,for personally accompanying us on each of the trips to Sylhet. We also appreciate and thank theSylhet and Dhaka branches of the Board of Investment for providing the international and localexperts with data and background material for the study.

We extend thanks both to Mr. Haque and to the Sylhet Chamber of Commerce for assisting withthe organization of a mid-project presentation of the study’s findings in Sylhet on February 25, 2008,reserving the venue, and inviting the approx. one hundred stakeholders who were at the event.

The Bangladesh Export Processing Zones Authority (BEPZA) also provided important informationabout the EPZs of the country that gave a picture of the role of economic zones in Bangladesh andenabled the consultants to benchmark the proposed site in Sylhet against the other zone projects inBangladesh.

And lastly, we would like to extend our appreciation to the private sector in Dhaka, Sylhet,Chittagong and elsewhere across Bangladesh who have worked with us and have providedinvaluable insight to the needs of companies.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 4/76

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 5/76

4

Employment Forecast ............................................................................................................................ 41

Utility Forecast ........................................................................................................................................ 41

Demand Forecast Summary ...................................................................................................................... 42

VI. Financial Analysis ...................................................................................................................................... 44

Methodology ................................................................................................................................................ 44

Assumptions................................................................................................................................................. 45

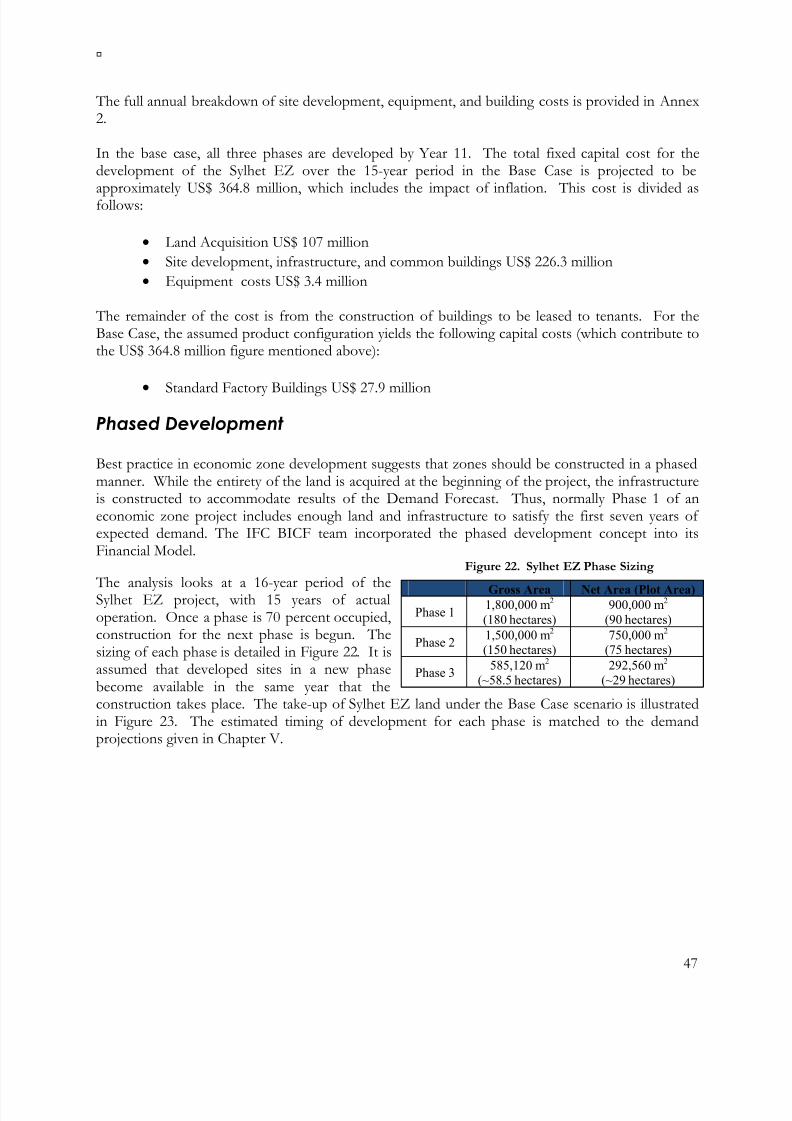

Capital Costs............................................................................................................................................ 46

Phased Development ............................................................................................................................. 47

Operating Costs ...................................................................................................................................... 48

Product Configuration ........................................................................................................................... 49

Prices......................................................................................................................................................... 49

Capital Structure...................................................................................................................................... 50

Public Private Partnership Structure.................................................................................................... 50

Net Present Value................................................................................................................................... 52

Results........................................................................................................................................................... 53

Sensitivity to Capital Costs and Prices................................................................................................. 54

Financial Conclusions................................................................................................................................. 55

VII. Economic Analysis .................................................................................................................................. 56 Scenario 1: 100% Private Sector Project ............................................................................................. 57

Scenario 2: Government Develops Phase 1 Infrastructure.............................................................. 57

Scenario 3: Government Acquires Land............................................................................................. 57

Scenario 4: Government Acquires Land and Develops Phase 1..................................................... 57

Economic Analysis Summary .................................................................................................................... 57

VIII. Recommendations ................................................................................................................................. 59

Annex 1: Demand Forecast............................................................................................................................ 60

Aggressive Case Demand........................................................................................................................... 60

Base Case Demand...................................................................................................................................... 64

Annex 2: Financial Analysis............................................................................................................................ 68

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 6/76

5

Acronyms, Abbreviations, and Initials

BEPZA Bangladesh Export Processing Zone Authority

BICF Bangladesh Investment Climate FundBOI Board of InvestmentBPO Business process outsourcingBSCIC Bangladesh Small and Cottage Industries CorporationEPZ Export processing zoneEZ Economic ZoneHEPZA Ho Chi Minh City Export Processing Zone AuthorityICT Inland container terminalID Industrial districtIFC International Finance CorporationIRR Internal rate of return

IZ Industrial zoneLtd. LimitedKg. KilogramKVA Kilovolt ampereKW/h Kilowatt hourM2 Square metersM3 Cubic metersMo. MonthNA Not availableNRS Non-resident SylhetisPPP Public-private partnership

RMG Ready-made garmentSCCI Sylhet Chamber of Commerce and IndustrySFB Standard factory buildingSq. Square Tk. TakaU.N. United Nations VAT Value-added tax Yr. Year

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 7/76

6

I. Executive Summary

Introduction

In 2007, the Board of Investment (BOI) of Bangladesh commissioned a pre-feasibility study todevelop a site for an economic zone in Sylhet. The study was funded by the International FinanceCorporation (IFC)-Bangladesh Investment Climate Fund (BICF) and was undertaken by aninternational specialist and the local firm, Young Consultants, which had carried out the original pre-feasibility study from 2006 to 2007. The following pre-feasibility study includes: i) a brief site reviewand an environmental and social assessment, ii) a market analysis, iii) a demand forecast, iv) anenvironmental and social assessment, v) a financial analysis, and vi) an economic analysis.

The Site

The Economic Zone site is situated 5 kilometers south of Sylhet, bounded by the Sylhet-FenchuganjRoad to the south, the Sylhet-Tamabil Bypass to the north, and the rural community of DakhinSuma to the south and east. The total area of the site is 389 hectares (961 acres) and these lands arecomprised of lowlands, wetlands, and gently rolling hills, as well as a lake and four rivers.

The advantage of the site’s location is:• It is located near an existing urban area, on the outskirts of Sylhet;• It has direct highway access to roads leading to India and Chittagong;• It is in close proximity to a railroad corridor that leads to Chittagong, which could be

connected to the economic zone through a spur;• The land is occupied by approximately 30 families, which means that there are few

resettlement issues;• It is adjacent a new residential/commercial community, which will provide an international

level of living to potential investors and their senior staff.

The disadvantage of the location is:• The government will have to acquire 90 percent of the land, which may mean delays in

beginning the project;• The land contains 4 rivers and a lake, which may present major master planning,

infrastructure and environmental challenges as well as increase the cost of developmentsignificantly;

• The mix of lowlands and wetlands on the site will mean that the land will have to be filled(15-20 feet)—possibly using sand dredged from the adjacent river—and may take up to two

years to settle;• The land is currently used for sustenance farming, so livelihoods will be lost;• The proximity to the urban area of Sylhet may be a liability as the city grows and encroaches

on the site;• Most of the farm workers are women, which may mean an unbalanced impact of the project

on women.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 8/76

7

In addition, there are some critical environmental and social issues related to Sylhet in general, which will significantly impact the financial and economic analysis of the site. Key concerns are:

• Availability of water in the region is uncertain (Sylhet regional issue). Sylhet’s existinggroundwater table is unlikely to be able to support the EZ. A detailed hydrology study is

necessary to determine the medium and long-term water availability for the EZ and theSylhet region as a whole.

• The EZ is in an area of high seismic risk (Sylhet regional issue). Bangladesh is locatedin a seismic zone, and the north-eastern part of Bangladesh is an area of high seismic risk. The main concern for the EZ is that the fill, which is needed to raise the lands above theflood level, will have enough time to properly settle before construction is started. This isnecessary so the lands can support construction.

The above is true for the entire Sylhet Region therefore this applies to any site selected in Sylhet.

The rest of the concerns listed below only apply to the proposed site.

• Flood retention capacity of the site must not be reduced (Issue related to the proposed site). According to the Department of Public Health Engineering (DPHE), it iscritical that development of the site for an EZ not affect or reduce the site’s current floodretention capacity. A study and drainage management plan will need to be developed. This will affect the master planning of the site and reduce the area which can be developed.

• Location of the EZ may be too close to the city of Sylhet (Issue related to the proposed site). If Sylhet continues to grow at a rapid pace, the EZ site will be surroundedby residential communities. Although the land is currently zoned for industrial purposes, if

development is postponed, there will be pressure to rezone the lands to residential use in thefuture. An EZ commitment should be obtained from the Government to ensure thedevelopment of a zone in whichever site is chosen. An EIA should also be done quickly, ifdevelopment of this site is selected, in order to obtain an Environmental ClearanceCertificate.

• Effluent Management is required for the EZ (Issue related to the proposed site). Aneffluent management plan is required for the EZ, which includes: i) the installation of acentral sewage and effluent treatment plant (ETP), ii) pretreatment of effluents by tenantindustries if they do not meet ETP influent requirements, and iii) an emergency response inthe event of an ETP breakdown.

• Land and resettlement may be more costly than previously estimated (Issue relatedto the proposed site) If the Acquisition and Requisition of Immovable Property Ordinanceof 1982 is utilitzed, land expropriation costs will increase to 7,478,484,000 Tk, which is2,492,828,000 Tk more than anticipated. In addition, if resettlement is carried out inconformity with the IFC’s Performance Standards then costs will be increased to pay for there-establishment of lost livelihoods.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 9/76

8

Market Analysis

An analysis of the business climate and economic market in Sylhet was undertaken to help forecastthe market demand in the new EZ. They types of industry sectors proposed for the site are: i) Foodand beverage processing, ii) Garments and textiles, iii) Ceramic and mineral products, iv) Chemicals,

soaps, pharmaceuticals, v) Metalworking, vi) Electronics and electrical appliances, vii) Software andBPO, viii) Rubber and plastic products, ix) Warehousing, and x) Manufacturing.

The following conclusions were determined from the market assessment:

• Sylhet is a competitive location. When benchmarked against Dhaka (Bangladesh),Kathmandu (Nepal), Visakhapatnam and New Delhi (India), Ho Chi Minh City (Vietnam),Colombo (Sri Lanka), Karachi (Pakistan), and Guangzhou (China), Sylhet fares well, as itdelivers a low cost framework for doing business. Worker wages and salaries in Sylhet areamong the lowest in South Asian region. This is positive for companies with labor-intensiveproduction processes. However, the Sylhet labor force also lacks skills necessary for

industrial production or service-oriented exports.

• Sylhet is not in the favored location for investment along the Dhaka-Chittagongcorridor. Bangladesh has experienced an increase in exports in a variety of sectors such asapparel, leather, textiles, metal products, fish, footwear, mineral products (ceramics), andothers. Although Sylhet can attract a small fraction of these investments, business ownersstill favor locations along the Dhaka-Chittagong corridor.

• The location may only attract local investors selling to a local market. Most of thecompanies that will locate in the proposed Sylhet economic zone will be local firmsproducing goods and products for the local market. Some firms may also distribute goods

nationally, or export some items to northeast India.

• NRS capital is high but they lack local industry knowledge. The non-resident Sylheti(NRS) community has shown great interest in locating ventures in the Sylhet economic zone.However, they generally lack industrial expertise, and require local investment partners withsuch knowledge.

Demand Forecast

The Demand Forecast serves the dual purposes of determining the most likely mix of industries inthe zone, and estimating the numbers of new tenants that will locate in the economic zone each

year. Demand for land in the zone was estimated in two scenarios—a Base Case and AggressiveCase. Figure 1 illustrates the potential number of tenants the Sylhet Economic Zone will have undereach scenario over the course of 15 years. In the Base Case, 160 firms will likely locate in the zoneby Year 15. This expands to 290 firms in the Aggressive Scenario (see Annex 1 for demand forecastnumbers).

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 10/76

9

Figure 1. Number of Tenants

Number of Tenants

0

50

100

150

200

250

300

350

Year

1

Year

2

Year

3

Year

4

Year

5

Year

6

Year

7

Year

8

Year

9

Year

10

Year

11

Year

12

Year

13

Year

14

Year

15

C u m u l a t i v e N u m b e r o f T e n a n t s

Aggressive

Base Case

Financial Analysis

The IFC BICF developed a Financial Model which was developed using the base-case scenario toassess the viability of the zone project from the perspective of a private sectorowner/developer/operator under four PPP scenarios.

• Scenario 1: Full Private Sector Acquisition, Development, and Operation of the Sylhet EZ

• Scenario 2: Public Sector Develops Phase 1 Infrastructure; and Private Sectors AcquiresLand and Develops Subsequent Phases of the Sylhet EZ

• Scenario 3: Public Sector Acquires Land; and Private Sector Develops and Operates theSylhet EZ

• Scenario 4: Public Sector Acquires Land and Develops Phase 1 Infrastructure; and PrivateSector Develops Subsequent Phases of the Sylhet EZ.

A summary of the financial model results is shown below.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 11/76

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 12/76

11

projects, and decisions on similar projects have not always been based on a thorough cost-benefitanalysis.

Recent trends in Bangladesh are to move away from wholly government funded economic zoneprojects to projects that include some degree of private sector participation. There are a number of

reasons for this including: i) the need for master planning for new zones, ii) the lack of governmentfunding for such projects and iii) the recognition that the private sector does a better job ofmanaging zones while the public sector does a better job of regulating them.

Therefore, the goal of public sector stakeholders in the Sylhet Economic Zone should be to makethe zone profitable to a private sector owner/developer/operator under a PPP situation whileensuring a positive economic impact as well. The IFC BICF team has demonstrated four possiblePPP scenarios in this pre-feasibility study. None of these scenarios is likely to generate the kind ofIRR necessary to attract a private investor if the current site is developed. A suitable IRR could begenerated if the public sector were to provide almost all of the capital required to develop the zone(Scenario 4), but the economic returns to the public sector would fall proportionately. In thisscenario, the financial structure would more closely resemble a no-risk gift to the private sector

developer rather than a true PPP in which both risk and reward are shared.

For the Sylhet EZ, the high capital costs of the project make it unfeasible for any kind of privatedeveloper. Given that the Government of Bangladesh has stated its preference for involving theprivate sector in future EZs, the current site is not suitable and thus does not require a full-scaleeconomic analysis to justify public sector involvement. If a suitable site is found in the future, a full-scale economic model should be used to justify any public contribution to the PPP.

If a new site is identified for development, the government should only participate in the initialcapital development stages of the zone, rather than subsidize zone operations or hold equity in thezone itself. The government can specifically discuss the fine details of its involvement once a new

site has been selected and a private owner/developer/operator has been identified.

Recommendations

1. After a detailed environmental and social review of the site was completed and the newinformation was added to the financial model, it was determined that the development costs forthe Sylhet site would not allow for a profitable PPP structure. This is due to the significantplanning and environmental mitigation costs associated with the site.

2. Demand for an EZ in Sylhet does exist, so a new site should be considered.

3. If an alternative site is investigated in Sylhet, access to water for the industrial facility will needto be examined further, as there is a water supply problem in the area, which needs to beaddressed at a regional level.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 13/76

12

II. Introduction

This study was commissioned by the International Finance Corporation’s Bangladesh InvestmentClimate Fund (IFC BICF) to determine the market demand and financial viability of establishing an

economic zone in Sylhet, Bangladesh. The IFC- BICF is a technical assistance program designed tocreate a better environment for businesses in Bangladesh.

Purpose of the Study

Export processing zones (EPZs) and industrial estates in Bangladesh have historically beendeveloped by the government with little bearing on the actual demand for serviced industrial land. This has yielded “successful” EPZs in population and transportation centers such as Dhaka andChittagong, but less successful ones in places such as Ishwardi. Traditional EPZs—and theirassociated fiscal benefits—have also been off limits to firms that do not have an export-orientedbusiness model.

The government of Bangladesh is no longer willing to expend public funds for new EPZ projects.Current EPZs are heavily subsidized, and do not reflect the market value of serviced industrial land. There thus exists a need for private commercial funding for new economic zones, including ways todetermine market demand and financial viability of such projects.

The IFC BICF is providing guidance to the Bangladesh Export Processing Zone Authority(BEPZA) on evaluating new economic zones projects using internationally accepted methods ofmarket analysis, financial and economic modeling, and private sector participation in economic zoneownership, development, and operation. In parallel, BICF is also training Bangladeshi companiesand non-profit organizations to conduct market demand-based feasibility studies.

This study is in response to government and private sector interest in establishing an economic zonein Sylhet. In a demonstration of international best practices, IFC BICF commissioned this pre-feasibility study to examine the market demand for serviced industrial infrastructure in Sylhet. This will suggest, in part, the recommended mix of public and private sector participation in the projectsufficient to yield a positive internal rate of return (IRR) for private sector stakeholders. This typeof feasibility analysis is what has traditionally been lacking in past BEPZA and BSCIC industrialzone and estate developments.

SCCI-Commissioned Feasibility Study

The analysis contained in this report builds upon the October 2007 Feasibility Report on Special Economic Zone & Industrial Park in and around Sylhet prepared by Young Consultants. That study wascommissioned in 2005 by the Sylhet Chamber of Commerce and Industry (SCCI) with the beliefthat an economic zone was necessary for spurring manufacturing and economic development inSylhet—including investment by non-resident Sylhetis (NRSs), local entrepreneurs, and foreignfirms alike.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 14/76

13

The study undertaken for SCCI did not include a market demand forecast, a land assessment, anenvironmental evaluation, or a financial and economic analysis. It did, however provide an overviewof the socioeconomic climate in Sylhet, including local community and business support for aneconomic zone, availability of productive resources for viable industries, location advantages ofSylhet, location alternatives for an economic zone, and options for ownership and financing of such

a project.

Sylhet is a prosperous district in northeast Bangladesh, owing in significant part to the largeremittances sent by Sylhetis who have emigrated abroad. In 2006/2007, Sylhetis received BDT 5.7billion (approximately US$ 80 million) in remittance earnings. The feasibility study commissionedby SCCI showed, however, that these remittances have not translated into significant investments orloans—particularly for industrial ventures of the type that would locate in an economic zone.Rather, NRS remittances have been plowed primarily into savings, consumption, and real estate. The result is a demand for consumer goods and construction materials that is higher in Sylhet thanmany other districts outside Dhaka.

A survey of remittance receivers did find a willingness among them to invest in an economic zone in

Sylhet, primarily through the purchase of equity bonds for the zone construction. Surveys by YoungConsultants also unveiled some interest by existing business owners—as well as some NRSs— toexpand, relocate, or open new ventures in the proposed zone. These ventures would likely includeproduction of consumer products such as processed foods, plastic and rubber products, handicrafts,mineral-based items, and products to sell in expatriate niche markets.

Investments outside of real estate have been slow to materialize for several reasons, according to theSCCI-commissioned study. Business formation has been limited by the following:• Scarcity of serviced industrial infrastructure• Bureaucratic hassles of obtaining land, permits, registrations, and venture capital• Lack of technically skilled labor

• Little experience among local and NRS entrepreneurs and investors in operating industrial ventures

The SCCI anticipates that an economic zone in Sylhet will ease constraints caused by the scarcity ofland, as well as improve the business climate through reduction of bureaucratic hurdles andcorruption. Provided that is the case, Sylhet does have some positive location attributes, whichinclude the following:• Inexpensive labor• Relatively wealthy local consumer market• Potential to tap consumer markets in northeast India• Good road, rail, and water transportation connectivity to Dhaka and Chittagong Port•

International airport• Abundance of agricultural and mineral-based resources

A site audit was also conducted for the SCCI-sponsored report. It compared potential locations foran economic zone within Sylhet. A location just outside Sylhet Sadar (city) ranked the highest, basedon criteria such as access to utilities, labor, transportation infrastructure, traffic congestion, andnatural resources. The IFC BICF Sylhet Prefeasibility Study will base its analysis and financial andeconomic calculations on that site.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 15/76

14

The IFC BICF Study

The IFC BICF Pre-feasibility Study for Sylhet is comprised of 5 components: i) a site assessmentincluding an environmental and social evaluation, ii) a market analysis, iii) a demand forecast, iv) afinancial model, and vi) an economic benefit review. The critical element of this study is a market

and land demand forecast for local, NRS, and foreign firms in Sylhet. This analysis was fed directlyinto a financial and economic model to determine the IRR of the project.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 16/76

15

III. The Site

This chapter provides an overview of the proposed site, its location, ownership, and theenvironmental and social issues key to the development of the lands. This data will be used in the

financial model to help determine the feasibility of the site.

Site Location

The proposed zone site is situated 5 kilometers south of Sylhet, bounded by the the Sylhet-Fenchuganj road to the south, the Sylhet-Tamabil Bypass to the north, and the rural community ofDakhin Suma to the south and east. The Bypass leads to the Sylhet Airport, as well as the Tamabil-Dowki border of India, which is considered the gateway to Meghalaya and Assam. The Sylhet-Fenchuganj road runs south through the country ending in Chittagong. Adjacent the property is the Akhaura-Chittagong railway line running from Akhaura to Chittagong. Although the railway runsparallel to the site, there is an opportunity to develop a rail spur with direct connection into the siteto improve rail access.

Site Description

The site is 389 hectares or 961 acres in size. The lands are comprised of a mix of lowlands, wetlands,and gently rolling hills. There is a lake and four rivers running through the property. In the centre ofthe site is a small bridge. A few areas within the site contain trees and low lying vegetation, thoughthe majority of the property is flat and unencumbered as it is currently being utilized for crops,fishing, and grazing. During the monsoon season these lands flood, hence to make these lands viablefor development, the lands must be raised approximately 15-18 feet in height.

Land Use Designation

The site and its surrounding area is deemed “agricultural land” by the planning department. In closeproximity to the economic zone are three (3) large-scale housing projects, (recently approved by themunicipality), which will change the existing land use designation in this area from agriculture tomixed use. The Royal, which is the nearest to the economic zone lands, (directly across thehighway), contains 3,000 residential units with schools, community centers, commercial complexes,mosques, and a range of support amenities. East of the site is an amusement park, which has a sitespecific land use designation, and south of the site is a new government office building, which isdesignated as institutional.

Ownership

Only 10 percent of the land is currently owned by the Government of Bangladesh. Hence theremainder of the land will need to be assembled through expropriation, which may take 1 to 2 years. There are a large number of land parcels that need to be acquired. Currently, the land is divided into very small plots, which are used for sustenance farming.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 17/76

16

Access

The site has good road and rail access, which makes its location desirable. It is situated at theintersection of roads leading to Dhaka, Sylhet, India, and Fenchuganj. The existing roads are dualcarriageways and paved but not always lit. They do however currently handle heavy truck transport.

Because the proposed site is adjacent these key transportation corridors, it does reduce potentialtransportation problems. Access points onto the existing roads and byways should be investigatedfurther in the feasibility study. In addition, it is anticipated that the highways will need to be widenedin the future to accommodate traffic flows from both the industrial and residential intensificationproposed for the area. There is however, land on both sides of the road to accommodate thisincrease.

Utilities

The economic zone will need its own water and power supply as there is not enough water or power

in the region to support the industrial facility to the standards needed to attract both local andinternational investors. There is an opportunity here to develop environmentally-friendly options.

Presently there is a high-pressure gas line, which runs through the economic zone site. When the siteis being designed, this must be taken into consideration. It will be important to provide an easementand mandatory setbacks over this high-pressure pipeline to provide access in case of an emergencyor breakage. The connection point to this gas line is located in close proximity but off site. This doesnot create any problem for hook up however.

To conform to best practices, there is a 100-meter setback from the railway line. This setbackencroaches on the perimeter of the site by approximately 25 feet. This land however, is targeted for

highway widening. Within this encroachment is also a low watt power line following the side of thehighway. At this point, there is a 15-20-foot dip from the highway level to the level of the site.

Environmental and Social Assessment

The site has environmental and social concerns, which need to be further investigated in order todetermine if they are fatal flaws for the project. Key issues are as follows:

Availability of water in the region is uncertain. (Sylhet Regional Issue- Potential Fatal Flaw).• The groundwater table in Sylhet is dropping rapidly and available groundwater resources are

unlikely to be able to support the EZ (Water demand for the EZ is estimated at a minimum of

280,235 cubic meters-m3

-in year five of the base case scenario to a maximum of 1,056,580 m3

inyear fifteen of the aggressive scenario).

• Surface water resources from the Surma River are not sufficient in the dry season, and although water could be piped from the Kushiyara River in the dry season, there is no certainty as to theavailability of surface water from this river in the medium to long term, which will be affected bya planned irrigation project upstream of Fenchuganj. If the Tipaimukh Dam on the Barak Riverin India is constructed it could severely constrain downstream water supply in Bangladesh inboth the Surma and Kushiyara Rivers, which are distributaries of the Barak River.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 18/76

17

• A detailed hydrological study is necessary to determine water availability in the medium and longterm water for municipal users, the proposed EZ, other industrial users and for environmentalinstream flow requirements for both the Kushiyara and Surma Rivers.

The EZ is in an area of high seismic risk (Sylhet Regional Issue)

• Bangladesh is located in a seismic zone, and the north-eastern part of Bangladesh is an area ofhigh seismic risk. The main concern here is the liquefaction of soils during a seismic event.Hence, it will be important that the site, once filled, rests for an appropriate amount of time tolet the land settle properly in order for it to be able to support construction.

• International earthquake building standards should be utilized when constructing infrastructureand buildings on this site.

The above is true for the entire Sylhet Region therefore this applies to any site selected in Sylhet. The rest of the concerns listed below only apply to the proposed site.

Flood retention capacity of the site must not be reduced (Issue related to the proposed site)• The Department of Public Health Engineering (DPHE) has indicated that the site’s current

flood retention capacity can not be reduced by the development of the EZ. A study needs to becarried out to see if it is viable to build an EZ in this location if current drainage and floodretention levels must be maintained.

• A Drainage Management Plan with baseline flood levels and drainage requirements is needed todetermine the amount of land, which is left available for development. This will affect the designof the Master Plan and phasing of the project.

Location of the EZ may be too close to the city of Sylhet (Issue related to the proposed site)

• If the rapid expansion of residential areas on the outskirts of Sylhet continues, the EZ site will,in the coming years, be surrounded by urban sprawl.

• While the Department of Environment currently has no objection to an EZ on the proposedsite, delayed development could lead to a rezoning the area to a residential designation, which would prohibit the development of the EZ in this location.

• To show good will, if a feasibility study recommends the development of the EZ in this location,a full environmental impact assessment (EIA) should be undertaken immediately so the siteobtains an Environmental Clearance Certificate. An EIA is a lengthy process and must becompleted before construction is permitted. A commitment from the Department ofEnvironment will also be needed so they do not revoke the certificate at a later date.

Effluent Management is required for the EZ (Issue related to the proposed site)

• An effluent management plan is required for the EZ, which includes: i) the installation of acentral sewage and effluent treatment plant (ETP), ii) pretreatment of effluents by tenantindustries if they do not meet ETP influent requirements, and iii) an emergency response in theevent of an ETP breakdown.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 19/76

18

Land and resettlement may be more costly than previously estimated (Issue related to the

proposed site)

• Land acquisition costs are estimated at 4,985,656,000 Tk. based on an average market value of1,300 Tk/m2. Under the Acquisition and Requisition of Immovable Property Ordinance (1982),the Deputy Commissioner must award a sum of 50 percent of the land’s market value in

addition to the market value itself for any expropriation. This would increase the land acquisitioncosts to 7,478,484,000 Tk.

• If resettlement of the site is carried out in conformity with the IFC's Performance Standards,then resettlement costs may be more expensive than initially anticipated because displacedpersons would also be paid in order to re-establish their livelihoods.

Site Summary

Like most development sites, this location for the Economic Zone has a number of advantages anddisadvantages. In summary, the advantages are:

i) It is located near an existing urban area on the outskirts of Sylhet;ii) It has excellent highway access to roads leading to India and Chittagong, the major port

of Bangladesh;iii) It has close proximity to a railroad link that leads to Chittagong and which could be

connected directly to the economic zone through a spur;iv) The land is occupied by approximately 30 families which, for a site of 961 acres, is

relatively few and will present fewer resettlement issues than might otherwise be thecase;

v) Three residential developments are located directly outside the zone and have been builtaccording to UK-standards with full recreational facilities. This will provide attractive

living accommodations to potential investors and their relocating staff.

The disadvantages are:

i) The government will have to acquire 90 percent of the land which may mean initialdelays in beginning the project;

ii) The land includes 4 rivers and a lake, which may present major challenges forconstruction. This will reduce the amount of land for development and constructionmay be significantly more expensive because development must preserve the rivers andlake;

iii) The land must remain as a floodwater catchment area for the surrounding region;iv) The mix of lowlands and wetlands on the site will mean that the land must be raised, and

the materials used will most likely take a significant amount of time to settle; v) The land is livelihood property, which includes sustenance agriculture and raising of

cattle. Resettlement costs may be more than expected; vi) The proximity to Sylhet may be a liability as the city grows and encroaches on the site; vii) There are water constraints in the region and water may be a fatal flaw to the project; viii) Most of the farm workers observed were women, which may mean a potential impact on

gender issues.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 20/76

19

IV. Market Analysis

This chapter examines the past and present market conditions in Sylhet and in Bangladesh. Thisincludes an analysis of trade and investment data, industry trends, and comparative cost of doing

business in Sylhet and other locations in the region. This Market Analysis is meant as a supplementto the findings of the Feasibility Report prepared for the SCCI in November 2007.2

Methodology

An analysis of the business climate and economic market provided the keystone to forecasting thedemand for serviced industrial land in Sylhet. The IFC BICF team examined the business trends andthe competitiveness of the Sylhet market from several different angles. This allowed the team tomake realistic assumptions about the types of industries and numbers of companies that wouldlocate in the zone each year, and the land, utility, and employment requirements of such firms. The

market was analyzed in the following manner:

• Competitiveness benchmarking. The cost and quality of doing business in Sylhet wascompared to those of other locations in Bangladesh and Asia where investors might locate afactory. This helped gauge the attractiveness of Sylhet as a place to do business.

• Trade trends. The team examined recent import and export data to gauge the strength of various industries in Bangladesh. This helped narrow the types of companies most likely tolocate in Sylhet in the near term.

• Investment trends. Data on new company registrations and investor inquiries was sourcedfrom BOI, BSCIC, and BEPZA to determine the numbers of new companies in various sectorsthat have invested throughout Bangladesh in the last five to seven years. Additionally, the teamsurveyed existing investors to gauge their perceptions of future business trends. This data was

used to narrow the types of investors likely to locate in Sylhet, as well as predict the futurenumbers of new companies in the Sylhet Economic Zone.

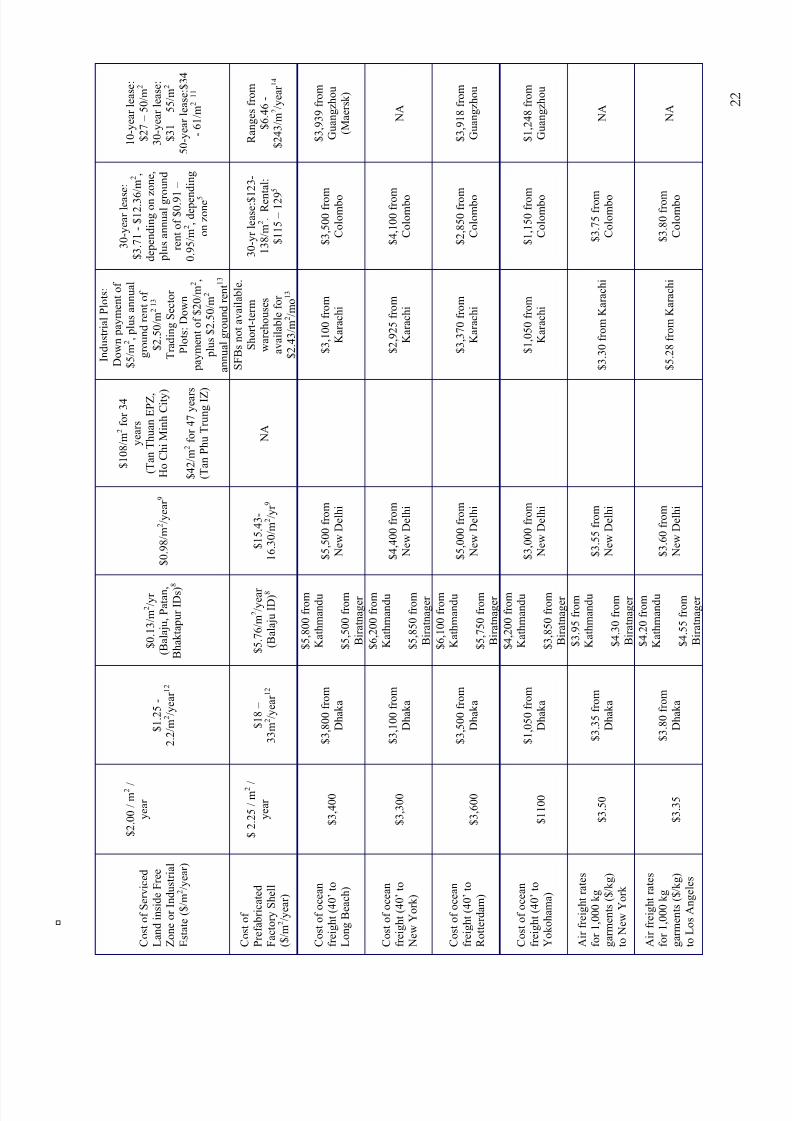

Competitiveness Benchmarking

The team examined the operating costs and quality conditions associated with doing business inSylhet, and compared them to those of seven other locations—Dhaka (Bangladesh), Kathmandu(Nepal), Visakhapatnam and New Delhi (India), Ho Chi Minh City (Vietnam), Colombo (Sri Lanka),Karachi (Pakistan), and Guangzhou (China). These locations were selected for the followingreasons.

• They compete for foreign investment in South Asia• They are home to some foreign investors in Bangladesh• They were cited by existing companies in Bangladesh as being competitive locations to produce

products and/or services

2 See Feasibility Report on Special Economic Zone & Industrial Park in and around Sylhet , Young Consultants, October 2007,namely Chapter 3 “Findings of the Field Surveys on Industrial Park/Economic Zone” and Chapter 4 “Availability ofRaw Materials in and around Sylhet”.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 21/76

20

Investment Priorities

0 2 4 6 8 10 12 14

Cost of Labor

Tax Benefits

Availability of Labor

Access to Markets

Cost of Operations

Close to Residence

Availability of Specialty Skills

Availability of Raw Materials and Supplies

Availability of Utilities

Availability of Supporting Industries

Cost of Utilities

Few Unions

Access to Seaport

Availability of Transportation

Security

Cost of Land

Availability of Buildings

Cost of Transportation

Political Stability

Duty Rebate

Availability of Land

Policy SupportRecreation and Lodging Opportunities

Software

Number of Responses

Figure 3. Investment Priorities

Figure 4 compares important operating costs such as labor, land, utilities, taxation, and freight

transportation, along with some common quality benchmarks such as the rigidity of the labor regimeand administrative burden in paying taxes. The IFC BICF team surveyed over 30 companies inSylhet, Dhaka, and other locations to learn more about what their actual priorities are when choosingan investment location. In an interview setting, firms were asked to describe their top fiveinvestment priorities when choosing a location for a new facility. The results of this survey, shownabove in Figure 3, provide a sense of the relative importance that companies place on eachbenchmarked factor.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 22/76

2 1

F i g u r e 4

S y l h e t

D h a k a

N e p a l

I n d i a

V i e t n a m

P a k i s t a n

S r i L a n k a

C h i n a ( G u a n g z h o u )

M o n t h l y S a l a r y —

M i d - L e v e l M a n a g e r

$ 2 0 1 / m o n t h

3

$ 3 0 5 / m o n t h 3

$ 3 3 3 / m o n t h 1

$ 1 , 6 3 9 / m o n t h 2

$ 5 0 0 -

7 0 0 / m o n t h 1 9

$ 5 7 5 –

1 , 7 2 5 / m o n t h 4

$ 1 6 0 – 3 0 0 / m o n t h 5

5 2 0 / m o n t h 6

M o n t h l y S a l a r y —

S k i l l e d / T e c h n i c a l

W o r k e r

$ 7 2 - 1 4 0 / m o n

t h 3

$ 7 7 - 2 2 6 / m o n t h 3

$ 2 2 5 / m o n t h 1

$ 3 5 4 / m o n t h 2

$ 6 8 - 2 8 0 / m o n t h 1 9

$ 1 1 5 – 2 8 7 / m o n t h 4

$ 6 4 – 3 0 0 / m o n

t h 5

2 5 0 / m o n t h 6

M o n t h l y S a l a r y —

U n s k i l l e d W o r k e r

$ 2 7 / m o n t h

3

$ 4 1 / m o n t h 3

$ 7 1 / m o n t h 1

$ 1 0 2 / m o n t h 2

$ 6 3 / m o n t h 1 9

$ 7 7 - 1 0 5 / m o n t h 4

$ 4 5 / m o n t h 5

1 3 5 / m o n t h 6

R i g i d i t y o f

E m p l o y m e n t

( C o m p o s i t e I n d e x )

3 5

3 5

5 2

3 0

2 7

4 3

2 7

2 4

D i f f i c u l t y H i r i n g

I n d e x

4 4

4 4

6 7

0

0

7 8

0

1 1

R i g i d i t y o f W o r k i n g

H o u r s I n d e x

2 0

2 0

2 0

2 0

4 0

2 0

2 0

2 0

D i f f i c u l t y F i r i n g

I n d e x

4 0

4 0

7 0

7 0

4 0

6 0

6 0

4 0

F i r i n g C o s t s ( W e e k s

W a g e s )

1 0 4 . 3

1 0 4 . 3

9 0

5 5 . 9

8 7

1 6 9

1 6 9

9 1

N o n - W a g e L a b o r

C o s t ( % S a l a r y )

0

0

1 0

1 7

1 7

1 5

1 5

4 4

C o s t o f E l e c t r i c i t y

U s a g e ( $ / k w h )

$ 0 . 0 5 9 K w h

$ 0 . 0 5 9 7 ( D h a k a

E P Z ) 1 0

$ 0 . 0 8 9 8 / k w h 8

$ 0 . 0 7 6 / k w h 9

$ 0 . 0 7 5 / k w h 1 8

I n d u s t r i a l O f f - P e a k :

$ 0 . 0 5 8 / k w h

I n d u s t r i a l P e a k :

$ 0 . 0 8 3 / k w h 4

O f f - P e a k :

$ 0 . 0 5 9 / k w h

P e a k : $ 0 . 1 3 3 / k w h 5

O f f - P e a k :

$ 0 . 0 3 9 / k w h

P e a k : $ 0 . 1 1 8 / k w h 1 1

C o s t o f E l e c t r i c i t y

C a p a c i t y D e m a n d

( $ / K V A / m o n t h )

N / A

N / A

$ 2 . 8 9 2 / K V A /

m o 8

$ 4 . 2 4 -

$ 6 . 5 2 K V A / m o .

9

N o n e

N o n e

$ 3 . 4 4 0 / K V A / m o n t h

f o r b u l k c u s t o m

e r s

d e m a n d i n g > 4

2

K V A 5

V o l u m e o f

t r a n s f o r m e r :

$ 2 . 4 3 / K V A / m o n t h

B a s i c F e e :

$ 3 . 6 4 / K V A / m o 1 1

C o s t o f P i p e d W a t e r

( $ / m 3 )

$ 0 . 3 1

$ 0 . 2 5 3 ( D h a k a

E P Z ) 1 0

$ 0 . 2 0 / m

3

( H e t a u d a I D )

$ 0 . 0 7 6 / m 3

( K a t h m a n d u

V a l l e y f o r

c u s t o m e r s u s i n

g

> 1 0 m

3 / m o . ) 8

$ 0 . 5 2 / m

3 9

$ 0 . 2 4 / m

3 1 8

S e w e r a g e :

A p p r o x i m a t e l y

$ 0 . 1 9 / m

3

$ 0 . 2 6 1 / m 3

S e w e r a g e :

$ 0 . 0 6 5 / m 3 4

$ 0 . 4 7 1 / m 3 5

$ 0 . 1 6 8 / m 3 1 1

N a t u r a l G a s

$ 0 . 0 8 2

$ 0 . 0 7 / m

3 1 0

$ 0 . 1 0 2 / m 3 9

$ 0 . 0 7 2 / M M B T U 4

$ 0 . 1 5 4 / m 3

$ 0 . 1 2 6 / m 3 1 1

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 23/76

2 2

C o s t o f S e r v i c e d

L a n d i n s i d e F r e e

Z o n e o r I n d u s t r i a l

E s t a t e ( $ / m 2 / y e a r )

$ 2 . 0 0 / m 2 /

y e a r

$ 1 . 2 5 -

2 . 2 / m

2 / y e a r

1 2

$ 0 . 1 3 / m

2 / y r

( B a l a j u , P a t a n ,

B h a k t a p u r I D s )

8

$ 0 . 9 8 / m

2 / y e a r

9

$ 1 0 8 / m 2 f o r 3 4

y e a r s

( T a n T h u a n E P Z ,

H o C h i M i n h C i t y )

$ 4 2 / m

2 f o r 4 7 y e a r s

( T a n P h u T r u n g I Z )

I n d u s t r i a l P l o t s :

D o w n p a y m e n t o f

$ 5 / m 2 , p l u s a n n u a l

g r o u n d r e n t o f

$ 2 . 5 0 / m

2 1 3

T r a d i n g S e c t o r

P l o t s : D o w n

p a y m e n t o f $ 2 0 / m

2 ,

p l u s $ 2 . 5 0 / m

2

a n n u a l g r o u n d r e n t

1 3

3 0 - y e a r l e a s e :

$ 3 . 7 1 - $ 1 2 . 3 6

/ m 2 ,

d e p e n d i n g o n z

o n e ,

p l u s a n n u a l g r o u n d

r e n t o f $ 0 . 9 1

–

0 . 9 5 / m 2 , d e p e n

d i n g

o n z o n e

5

1 0 - y e a r l e a s e :

$ 2 7 – 5 0 / m 2

3 0 - y e a r l e a s e :

$ 3 1 – 5 5 / m 2

5 0 - y e a r l e a s e : $ 3 4

- 6 1 / m 2 1 1

C o s t o f

P r e f a b r i c a t e d

F a c t o r y S h e l l

( $ / m 2 / y e a r )

$ 2 . 2 5 / m

2 /

y e a r

$ 1 8 –

3 3 m

2 / y e a r

1 2

$ 5 . 7 6 / m

2 / y e a r

( B a l a j u I D ) 8

$ 1 5 . 4 3 -

1 6 . 3 0 / m

2 / y r

9

N A

S F B s n o t a v a i l a b l e .

S h o r t - t e r m

w a r e h o u s e s

a v a i l a b l e f o r

$ 2 . 4 3 / m

2 / m o 1 3

3 0 - y r l e a s e : $ 1

2 3 -

1 3 8 / m

2 . R e n t a l :

$ 1 1 5 – 1 2 9

5

R a n g e s f r o m

$ 6 . 4 6 -

$ 2 4 3 / m 2 / y e a r

1 4

C o s t o f o c e a n

f r e i g h t ( 4 0 ’ t o

L o n g B e a c h )

$ 3 , 4 0 0

$ 3 , 8 0 0 f r o m

D h a k a

$ 5 , 8 0 0 f r o m

K a t h m a n d u

$ 5 , 5 0 0 f r o m

B i r a t n a g e r

$ 5 , 5 0 0 f r o m

N e w D e l h i

$ 3 , 1 0 0 f r o m

K a r a c h i

$ 3 , 5 0 0 f r o m

C o l o m b o

$ 3 , 9 3 9 f r o m

G u a n g z h o u

( M a e r s k )

C o s t o f o c e a n

f r e i g h t ( 4 0 ’ t o

N e w Y o r k )

$ 3 , 3 0 0

$ 3 , 1 0 0 f r o m

D h a k a

$ 6 , 2 0 0 f r o m

K a t h m a n d u

$ 5 , 8 5 0 f r o m

B i r a t n a g e r

$ 4 , 4 0 0 f r o m

N e w D e l h i

$ 2 , 9 2 5 f r o m

K a r a c h i

$ 4 , 1 0 0 f r o m

C o l o m b o

N A

C o s t o f o c e a n

f r e i g h t ( 4 0 ’ t o

R o t t e r d a m )

$ 3 , 6 0 0

$ 3 , 5 0 0 f r o m

D h a k a

$ 6 , 1 0 0 f r o m

K a t h m a n d u

$ 5 , 7 5 0 f r o m

B i r a t n a g e r

$ 5 , 0 0 0 f r o m

N e w D e l h i

$ 3 , 3 7 0 f r o m

K a r a c h i

$ 2 , 8 5 0 f r o m

C o l o m b o

$ 3 , 9 1 8 f r o m

G u a n g z h o u

C o s t o f o c e a n

f r e i g h t ( 4 0 ’ t o

Y o k o h a m a )

$ 1 1 0 0

$ 1 , 0 5 0 f r o m

D h a k a

$ 4 , 2 0 0 f r o m

K a t h m a n d u

$ 3 , 8 5 0 f r o m

B i r a t n a g e r

$ 3 , 0 0 0 f r o m

N e w D e l h i

$ 1 , 0 5 0 f r o m

K a r a c h i

$ 1 , 1 5 0 f r o m

C o l o m b o

$ 1 , 2 4 8 f r o m

G u a n g z h o u

A i r f r e i g h t r a t e s

f o r 1 , 0 0 0 k g

g a r m e n t s ( $ / k g )

t o N e w Y o r k

$ 3 . 5 0

$ 3 . 3 5 f r o m

D h a k a

$ 3 . 9 5 f r o m

K a t h m a n d u

$ 4 . 3 0 f r o m

B i r a t n a g e r

$ 3 . 5 5 f r o m

N e w D e l h i

$ 3 . 3 0 f r o m K a r a c h i

$ 3 . 7 5 f r o m

C o l o m b o

N A

A i r f r e i g h t r a t e s

f o r 1 , 0 0 0 k g

g a r m e n t s ( $ / k g )

t o L o s A n g e l e s

$ 3 . 3 5

$ 3 . 8 0 f r o m

D h a k a

$ 4 . 2 0 f r o m

K a t h m a n d u

$ 4 . 5 5 f r o m

B i r a t n a g e r

$ 3 . 6 0 f r o m

N e w D e l h i

$ 5 . 2 8 f r o m K a r a c h i

$ 3 . 8 0 f r o m

C o l o m b o

N A

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 24/76

2 3

( 1 ) S o u r c e : I F C s u r v e y ; ( 2 ) S o u r c e : I F C S u r v e y ; ( 3 ) S o u r c e : I F C B I C F S u r v e y ; ( 4 ) S o u r c e : P a k i s t a n B O I ; ( 5 ) S o u r c e : S r i L a n k a B O I ; ( 6 ) S o u r c e : I F C S u r v e y ; ( 7 )

S o u r c e : D o i n g B u s i n e s s

2 0 0 8 , I F C , W o r l d B a n k G r o u p

; ( 8 ) S o u r c e : I n d u s t r i a l D i s t r i c t s M a n a g e m e n t L i m i t e d ; ( 9 ) S o u r c e : V i s a k h a p a t n a m S p e c i a l E c o n o m i c Z o n e a n d M a d r a s E x p o r t P r o c e s s i n g Z o n e ; ( 1 0 )

S o u r c e : B a n g l a d e s h E x p o r t P r o c e s s i n g Z o n e A u t h o r i t y ( B E P Z A ) ; ( 1 1 ) S o u

r c e : G u a n g z h o u E c o n o m i c a n d T e c h n o l o g

i c a l D e v e l o p m e n t D i s t r i c t ; ( 1 2 ) S o u r c e : I F C S u r v e y ; ( 1 3 ) S o u r c e :

P a k i s t a n E x p o r t P r o c e s s i n g Z o n e A u t h o r i t y ; ( 1 4 ) S h e n z h e n G o v e r n m e n t O

n l i n e h t t p : / / e n g l i s h . s z . g o v . c n ; ( 1 5 ) S o u r c e : G a n

e s h A i r C a r g o , N e p a l , e x c e p t C h i n a . C h i n

a S o u r c e : M a e r s k . S e a

f r e i g h t r a t e s a r e f r o m p o r t t o p o

r t , a n d d o n o t i n c l u d e a n y f o b c h a r g e s a n d

p i c k - u p . D o e s n o t i n c l u d e i n s u r a n c e . A i r f r e i g h t r a t e s a r e i n c l u s i v e o f s e c u r i t y s u r c h a r

g e a n d f u e l s u r c h a r g e .

R a t e s a r e f r o m a i r p o r t t o a i r p o r t , a n d d o n o t i n c l u d e f o b c h a r g e s . ( 1 6 ) T a x

o n p r o f i t s f o r a t y p i c a l m e d i u m - s i z e d e n t e r p r i s e . S o u r c e : D o i n g B u s i n e s s 2 0 0 8 , I F C , W o r l d B a n k G r o u p ; ( 1 7 )

T a x c a l c u l a t e d a f t e r a l l o w i n g f o r t y p i c a l d e d u c t i o n s a n d e x e m p t i o n s o f a m e d i u m - s i z e d c o m p a n y . S o u r c e : D o i n g B u s i n e s

s 2 0 0 8 , I F C , W o r l d B a n k G r o u p ; ( 1 8 ) S o u r

c e : H o C h i M i n h C i t y

E x p o r t P r o c e s s i n g Z o n e A u t h o

r i t y ( H E P Z A ) ; ( 1 9 ) S o u r c e : “ V i e t n a m — O p

e n f o r B u s i n e s s ” i n w w w . b u s i n e s s - i n - a s i a . c o m ,

a n d “ O f f s h o r e S a l a r i e s : V i e t n a m i s C h e a p e

s t , B u t I n d i a I s S t i l l a

B a r g a i n ” i n w w w . i n f o r m a t i o n w e e k . c o m . ( 2 0 ) S o u r c e : B i m a n B a n g l a d e s h A i r l i n e s , F e d r e a l C a r g o S e r v i c e s L t d . A n d F T I C a r g

o S e r v i c e s , L t d . ; ( 2 1 ) S o u r c e : F e d e r a l C a r g o

S e r v i c e L t d . A n d F T I

C a r g o S e r v i c e s L t d .

A i r f r e i g h t r a t e s

f o r 1 , 0 0 0 k g

g a r m e n t s ( $ / k g )

t o A m s t e r d a m

$ 2 . 3 5

$ 3 . 1 0 f r o m

D h a k a

$ 2 . 7 7 f r o m

K a t h m a n d u

$ 3 . 1 2 f r o m

B i r a t n a g e r

$ 2 . 9 0 f r o m

N e w D e l h i

$ 2 . 7 0 f r o m K a r a c h i

$ 2 . 9 0 f r o m

C o l o m b o

N A

A i r f r e i g h t r a t e s

f o r 1 , 0 0 0 k g

g a r m e n t s ( $ / k g )

t o T o k y o

$ 2 . 2 0

$ 3 . 2 0 f r o m

D h a k a

$ 3 . 9 5 f r o m

K a t h m a n d u

$ 4 . 3 5 f r o m

B i r a t n a g e r

$ 2 . 4 0 f r o m

N e w D e l h i

$ 2 . 7 5 f r o m K a r a c h i

$ 2 . 6 0 f r o m S

r i

L a n k a

N A

S t a t u t o r y

C o r p o r a t e I n c o m e

T a x R a t e 1 6

4 0 %

( 3 0 % f o r

p u b l i c l y t r a d e

d

c o m p a n i e s ,

a c c o r d . N a t ’ l

B o a r d o f

R e v e n u e )

4 0 %

( 3 0 % f o r p u b l i c l y

t r a d e d

c o m p a n i e s ,

a c c o r d . N a t ’ l

B o a r d o f

R e v e n u e )

2 0 %

3 3 . 7 %

2 8 %

3 5 %

3 5 %

3 3 %

T o t a l C o r p o r a t e

I n c o m e T a x

R a t e 1 7

2 7 . 3 %

2 7 . 3 %

1 8 . 6 %

1 7 . 2 %

2 0 . 1 %

2 5 . 8 %

2 6 . 3 %

1 9 . 4 %

V A T 7

1 5 %

1 5 %

1 3 %

4 % ( C e n t r a l

S a l e s T a x )

1 2 . 5 % ( S t a t e

V A T )

1 0 %

1 5 %

1 5 %

1 7 %

A d m i n i s t r a t i v e

b u r d e n s p e n t

p a y i n g t a x e s

( H o u r s p e r y e a r ) 7

4 0 0

4 0 0

4 0 8

2 7 1

1 , 0 5 0

5 6 0

2 5 6

8 7 2

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 25/76

24

Benchmarking Results

The benchmarking exercise illustrated that Sylhet compares favorably to most locations in terms ofthe basic costs associated with doing business. Labor costs—the most frequently mentioned

investment priority—were generally lower than all other surveyed locations. The Sylhet district alsohas important natural resources such as agricultural products and minerals. However, the availabilityof some important factors of production—such as skilled work force, reliable utilities, and presenceof suppliers and supporting industries—are currently lacking.

Most factory, software, and BPO business owners in Sylhet chose their locations because they arefrom the Sylhet district, and understand the tastes and purchasing power of residents in the district. There are numerous Sylhetis and NRSs, however, who chose to locate their enterprises in Dhaka,Comilla, or Chittagong. Like other Bangladeshis and foreign business owners, they want to takeadvantage of the synergies associated with existing industry clusters, and better air and seatransportation options—currently not available in Sylhet.

Company owners and managers interviewed for this analysis stated that the main deterrents tolocating a business in Sylhet were the following:

• Lack of serviced industrial land. Most BSCIC industrial estates in the vicinity of Sylhet cityhave reached full occupancy.

• Bureaucratic conditions associated with opening and operating a business. One investornoted that he had to write over 1,000 letters just to open his single factory in the Sylhet division.

• Inadequate power, water, and other necessary utilities. Use of expensive generators isrequired, and most firms must dig their own wells or have water delivered to their facilities

• Lack of skilled workforce in Sylhet area. In general, the workforce in Sylhet is well-educated,but not experienced with industrial manufacturing; though the service sector—software,

hospitality—is more developed.• Lack of industrial base and industry clusters in Sylhet area. Network of suppliers and

industry-specific support services do not exist in Sylhet, as they do in Dhaka, Chittagong,Guangzhou, and other surveyed areas.

• Unfamiliarity of Sylhet with foreign investors. The City of Sylhet is currently not on theradar screen of foreign investors, and although Sylhet is a large city, it is not accustomed todealing with foreigners and international corporations.

• Not a preferred location by NRSs. Sylhet is far from the community of risk-taking industrialBangladeshi entrepreneurs who are centered along the Dhaka-Chittagong corridor.

Most interviewed firms located in the Dhaka-Chittagong corridor were generally pleased with the

infrastructure provided by BEPZA or other industrial areas, rating it from ‘good’ to ‘excellent’. They noted recent improvements in the types of modern building facilities available, but also desirednecessary upgrades in utilities. Their primary reasons for locating there were the availability ofskilled labor, access to markets in Dhaka, and good transportation connections.

The IFC BICF team is optimistic about the low operating costs associated with doing business inSylhet. An economic zone in Sylhet will address and alleviate the top three concerns ofentrepreneurs—namely, i) lack of land, ii) troublesome bureaucracy, and iii) poor quality of utilities.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 26/76

25

However, the most attractive investment locations in Bangladesh, according to business owners, arealong the Dhaka-Chittagong corridor, where freight and air transportation options are moreestablished and worker skills, suppliers, and specialty services already exist for a variety of industries. As long as industrial land and skilled labor continues to exist along this corridor, demand for land inSylhet will remain somewhat depressed in the near to medium term.

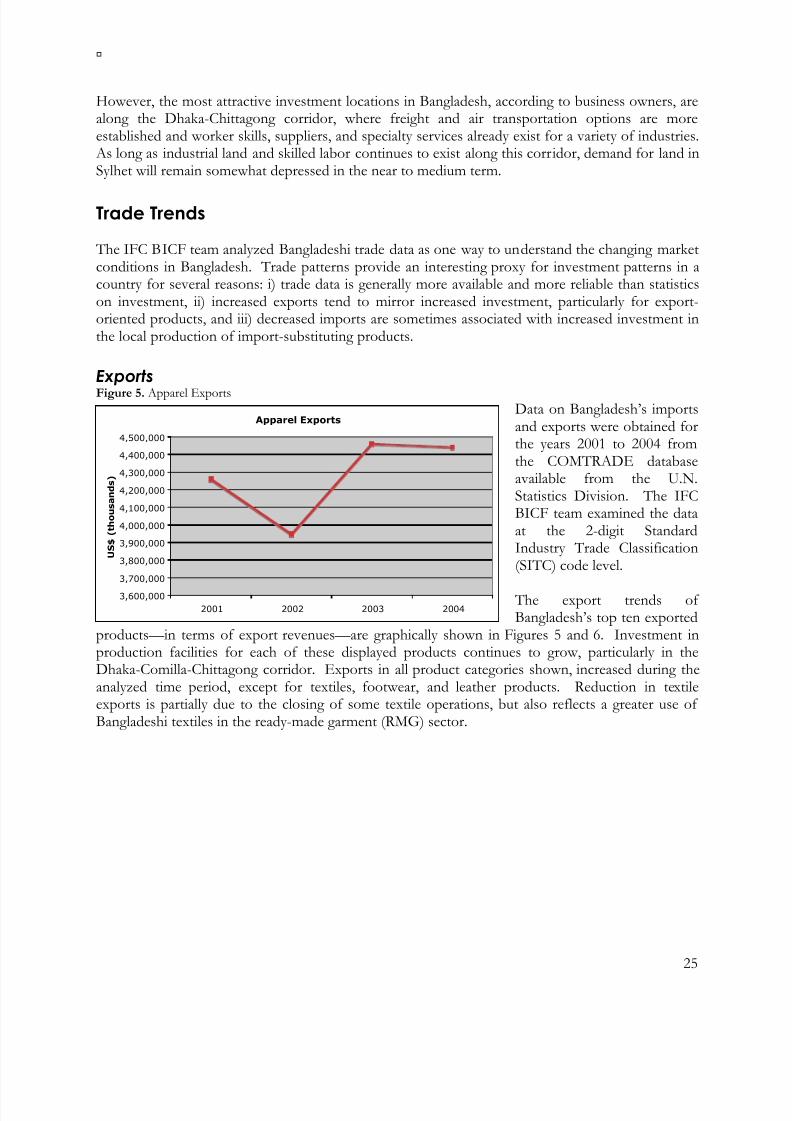

Trade Trends

The IFC BICF team analyzed Bangladeshi trade data as one way to understand the changing marketconditions in Bangladesh. Trade patterns provide an interesting proxy for investment patterns in acountry for several reasons: i) trade data is generally more available and more reliable than statisticson investment, ii) increased exports tend to mirror increased investment, particularly for export-oriented products, and iii) decreased imports are sometimes associated with increased investment inthe local production of import-substituting products.

ExportsFigure 5. Apparel Exports

Data on Bangladesh’s importsand exports were obtained forthe years 2001 to 2004 fromthe COMTRADE databaseavailable from the U.N.Statistics Division. The IFCBICF team examined the dataat the 2-digit StandardIndustry Trade Classification(SITC) code level.

The export trends ofBangladesh’s top ten exported

products—in terms of export revenues—are graphically shown in Figures 5 and 6. Investment inproduction facilities for each of these displayed products continues to grow, particularly in theDhaka-Comilla-Chittagong corridor. Exports in all product categories shown, increased during theanalyzed time period, except for textiles, footwear, and leather products. Reduction in textileexports is partially due to the closing of some textile operations, but also reflects a greater use ofBangladeshi textiles in the ready-made garment (RMG) sector.

Apparel Exports

3,600,000

3,700,000

3,800,000

3,900,000

4,000,000

4,100,000

4,200,000

4,300,000

4,400,000

4,500,000

2001 2002 2003 2004

U S $ ( t h o u s a n d s )

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 27/76

26

Figure 6: Top Exported Products (Excluding Apparel)

Top Exported Products (Excluding Apparel)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

2001 2002 2003 2004

U S $ ( t h o u s a n d s )

Fish Products

Textiles

Leather Products

Textile Fibers

Footwear

Mineral and glass products

Petroleum products

Tobacco and products

Metal products

Imports

Examination of import flows can provide clues as to consumer goods demanded by Bangladeshis, as well as the capital equipment, raw materials, and intermediate goods required by the country’sindustrial sector. There are often clues as to what import substituting industrial are currentlyarising—or could arise—throughout Bangladesh.

Figure 7. Top Increasing Import Items

Top Increasing Imports

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

2001 2002 2003 2004

U S $ ( t h o u s a n d s ) 32 Coal

07 Coffee, chocolate, spices

23 Rubber materials

05 Fruit and vegetable products

08 Animal feed

28 Ores

25 Paper pulp

33 Petroleum products

24 Rough wood

72 Specialty machinery

Bangladesh imports a wide variety of products—some in very small quantities; others in large volumes. The Team analyzed products with import volumes in excess of US$ 10 million per year.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 28/76

27

The team then examined the sectors in which import volumes were most rapidly increasing (Figure7), and most rapidly decreasing (Figure 8).

Products with rapidly rising imports tend to be in raw material and natural resource sectors such ascoal, rubber, ore, paper pulp, petroleum, and wood, or capital inputs such as factory machinery.

Due to the complexion of these imports, these sectors are not good proxies for increased import-substituting investment. One exception, however, could be in the manufacturing of fruit and vegetable products, imports of which increased 92 percent between 2001 and 2002.

Examination of sectors where imports are decreasing can provide clues as to import-substitutinginvestment trends in Bangladesh. Figure 8 illustrates products with greater than US$ 10 million inannual imports, in which levels of imports have most rapidly decreased between 2001 and 2003.

Figure 8. Top Decreasing Import Items

Top Decreasing Imports

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

2001 2002 2003 2004

U S $ ( t h o u s a n d s ) Metal products

Boilers and non-electric engines

Other manufactured items, n.e.s.

Apparel

Metalworking tools and machinery

Dairy

Pharmaceuticals

Basic plastic products

Instruments and meters, n.e.s.

Steel base metal products

Some of the products depicted in Figure 8—namely, apparel and metal products—have becomeexport leaders in Bangladesh. Local entrepreneurs and non-resident Bangladeshis (NRBs) have alsoincreasingly invested in factories to produce the above products specifically for the domestic market. This mirrors the existing types of industrial ventures currently seen in and around Sylhet—foodprocessing, agricultural machinery, pharmaceuticals, plastic products, metalworking, and otherfactories.

Investment Trends

When estimating the demand for serviced industrial land, it is helpful to understand recentinvestment trends. This helps determine the following:• Types of companies that locate in serviced industrial estates, free zones, and/or export

processing zones• Levels of investment over the past five years• Infrastructure requirements of companies in economic zones

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 29/76

28

• Degree of satisfaction that current tenants of such zones have with the infrastructure andservices provided

To assess the above factors, the IFC BICF team accessed investment data from BEPZA, BSCIC,and BOI and interviewed approximately 30 companies located in Sylhet, Dhaka, and Comilla. The

team also referred to surveys undertaken by Young Consultants for its report to the SCCI inNovember 2007.

Export-Oriented Investments

Figure 9, below illustrates the trend of new tenants locating in BEPZA’s EPZs each year between2003 and 2007.

Figure 9. New EPZ Tenants3

New EPZ Tenants

0

5

10

15

20

25

2003 2004 2005 2006 2007

(up to Sep.)

N u m b e r o f N e w

T e n a n t s

Garments/Knitting Garments Accessories

Agro products TextileMetal/Steel industry Plastic industry

Elect ronics & Electr ical Goods Power Industry

Footwerar & Leather Furniture industry

Paper industry Service Industry

Chemical & Fertilizer Tent

Misc.

Figure 9 shows that roughly 10 to 20 new RMG companies have located in Bangladeshi EPZs eachyear over the past five years. There are also about five to ten garment accessory firms, andapproximately five each of agro products, plastics, and metalworking firms locating in EPZs eachyear. This examination is useful for gauging the possibilities of export-oriented investments on anational scale. For instance, if the trend is for an average of 15 export-oriented RMG factories tolocate in economic zones each year, it is possible for an economic zone in Sylhet to attract a fraction of this. In the near and medium terms, this may be a small fraction, however, based on the tendencyof RMG operations to locate in clusters where forward and backward linkages are strong.

3 Source: IFC BICF aggregation of BEPZA data.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 30/76

29

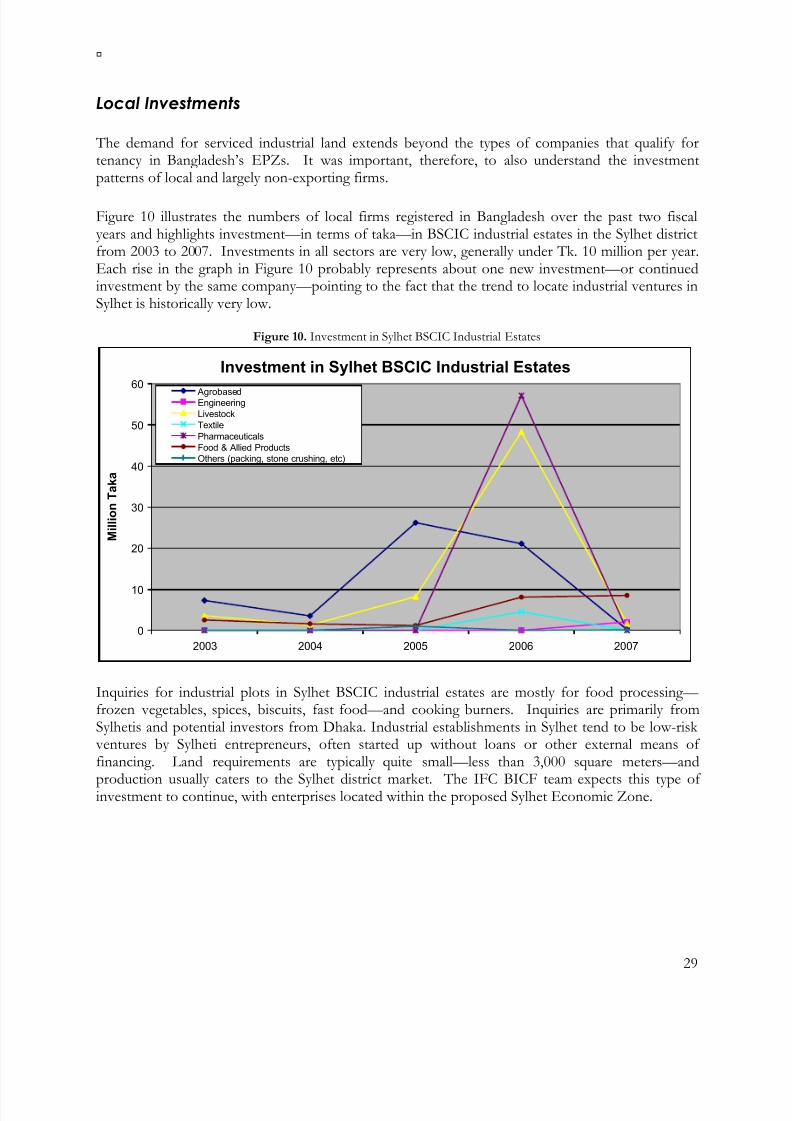

Local Investments

The demand for serviced industrial land extends beyond the types of companies that qualify fortenancy in Bangladesh’s EPZs. It was important, therefore, to also understand the investmentpatterns of local and largely non-exporting firms.

Figure 10 illustrates the numbers of local firms registered in Bangladesh over the past two fiscalyears and highlights investment—in terms of taka—in BSCIC industrial estates in the Sylhet districtfrom 2003 to 2007. Investments in all sectors are very low, generally under Tk. 10 million per year.Each rise in the graph in Figure 10 probably represents about one new investment—or continuedinvestment by the same company—pointing to the fact that the trend to locate industrial ventures inSylhet is historically very low.

Figure 10. Investment in Sylhet BSCIC Industrial Estates

Investment in Sylhet BSCIC Industrial Estates

0

10

20

30

40

50

60

2003 2004 2005 2006 2007

M i l l i o n T a k a

AgrobasedEngineering

Livestock

Textile

Pharmaceuticals

Food & Allied Products

Others (packing, stone crushing, etc)

Inquiries for industrial plots in Sylhet BSCIC industrial estates are mostly for food processing— frozen vegetables, spices, biscuits, fast food—and cooking burners. Inquiries are primarily fromSylhetis and potential investors from Dhaka. Industrial establishments in Sylhet tend to be low-risk ventures by Sylheti entrepreneurs, often started up without loans or other external means offinancing. Land requirements are typically quite small—less than 3,000 square meters—and

production usually caters to the Sylhet district market. The IFC BICF team expects this type ofinvestment to continue, with enterprises located within the proposed Sylhet Economic Zone.

8/10/2019 (2008.08) Pre-Feasibility Study for Sylhet Economic Zone

http://slidepdf.com/reader/full/200808-pre-feasibility-study-for-sylhet-economic-zone 31/76

30

Industries Experiencing Positive Trends

0 1 2 3 4 5 6 7

Food Processing

Garments

Leather

Textiles

Shoes

Packaging

Pharmaceuticals

Glass and Ceramics

Plastics

Agriculture Equipment

Toiletries

Software

Metalworking

Logistics Services

Electronics

Number of Responses

Figure 11. BOI Registered Local Industries

In the near term, additionalinvestments may be seen by NRSinvestors, if they judge the risk ofinvesting to be lowered by theexistence of the zone. NRSs havetraditionally been opposed to risky ventures or ventures with longpayback periods. One-stop provisionof bureaucratic services would assistimmensely in this regard by loweringinvestment risk. Investments inexport-oriented ventures, orcompanies established by non-Sylhetismight be possible once thetransportation corridor between