Embed Size (px)

DESCRIPTION

2003 Analyst/ Investor Conference Savannah, Georgia November 17-19, 2003. Forward-Looking Statements. - PowerPoint PPT Presentation

Citation preview

2003 Analyst/Investor Conference

Savannah, Georgia

November 17-19, 2003

2003 Analyst/Investor Conference 2

Forward-Looking Statements

Statements contained in this presentation that include company expectations or predictions of the future are forward-looking statements intended to be covered by the safe harbor provisions of the Securities Act of 1933 and the Securities Exchange Act of 1934. It is important to note that the actual results of company earnings could differ materially from those projected in any forward-looking statements. For additional information refer to AGL Resources’ Securities and Exchange Commission filings.

Seeking Value…Every Day

Paula G. RosputChairman, President and Chief Executive Officer

2003 Analyst/Investor Conference 4

We Set Four Goals for 2003

• Strengthen ATG financially

• Grow around existing assets

• Execute flawlessly

• Demonstrate compelling proposition for all stakeholders

2003 Analyst/Investor Conference 5

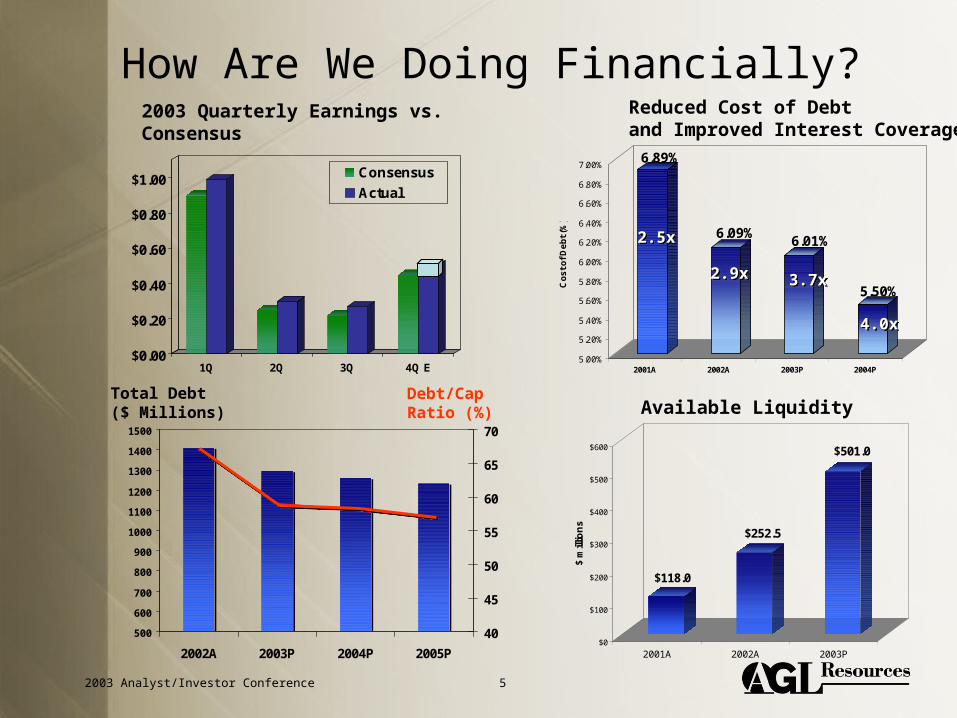

How Are We Doing Financially?

500

600

700

800

900

1000

1100

1200

1300

1400

1500

2002A 2003P 2004P 2005P

40

45

50

55

60

65

70

Total Debt($ Millions)

Debt/CapRatio (%)

6.89%

6.09%6.01%

5.50%

5.00%

5.20%

5.40%

5.60%

5.80%

6.00%

6.20%

6.40%

6.60%

6.80%

7.00%

Co

st

of

De

bt

(%)

2001A 2002A 2003P 2004P

Reduced Cost of Debt and Improved Interest Coverage

$118.0

$252.5

$501.0

$0

$100

$200

$300

$400

$500

$600

$ m

illio

ns

2001A 2002A 2003P

Available Liquidity

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

1Q 2Q 3Q 4Q E

Consensus

Actual

2003 Quarterly Earnings vs. Consensus

2.5x2.5x

2.9x2.9x 3.7x3.7x

4.0x4.0x

2003 Analyst/Investor Conference 6

Asset Rationalization

• Sale of former headquarters property

• Purchase of Dynegy’s interest in SouthStar

• Sale of Heritage/US Propane interests

2003 Analyst/Investor Conference 7

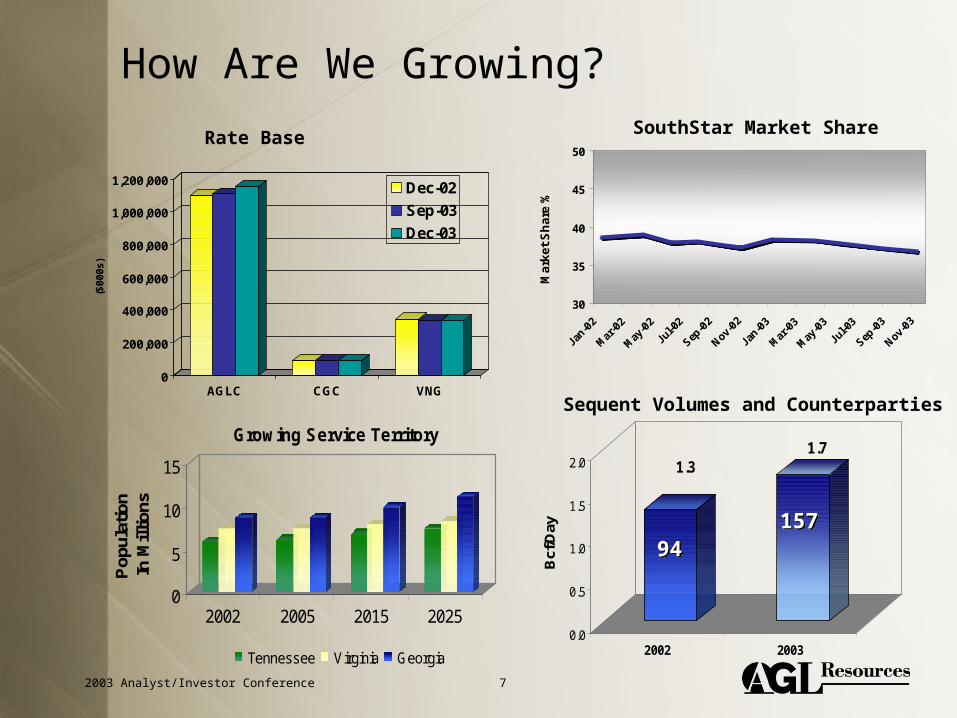

How Are We Growing?

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

($0

00

s)

AGLC CGC VNG

Dec-02

Sep-03

Dec-03

Rate Base SouthStar Market Share

1.31.7

0.0

0.5

1.0

1.5

2.0

Bcf

/Day

2002 2003

0

5

10

15

Pop

ulat

ion

In

Mill

ions

2002 2005 2015 2025

Growing Service Territory

Tennessee Virginia Georgia

Sequent Volumes and Counterparties

9494157157

30

35

40

45

50

Jan-0

2

Mar

-02

May

-02

Jul-0

2

Sep-0

2

Nov-0

2

Jan-0

3

Mar

-03

May

-03

Jul-0

3

Sep-0

3

Nov-0

3

Ma

rke

t S

ha

re %

2003 Analyst/Investor Conference 8

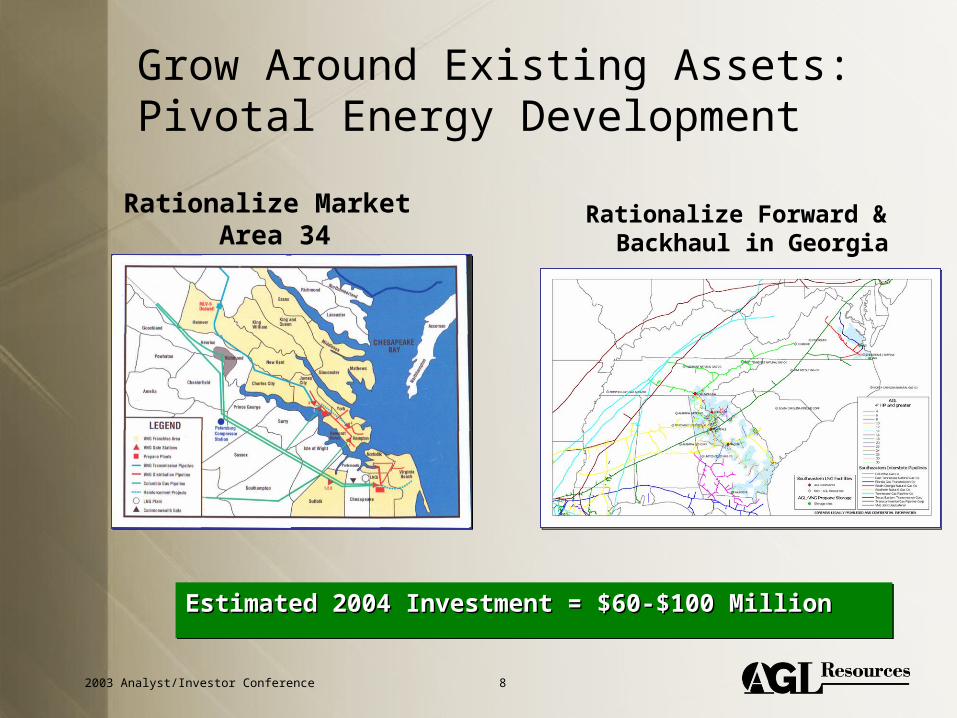

Grow Around Existing Assets:Pivotal Energy Development

Rationalize Market Area 34

Rationalize Forward & Backhaul in Georgia

Estimated 2004 Investment = $60-$100 MillionEstimated 2004 Investment = $60-$100 MillionEstimated 2004 Investment = $60-$100 MillionEstimated 2004 Investment = $60-$100 Million

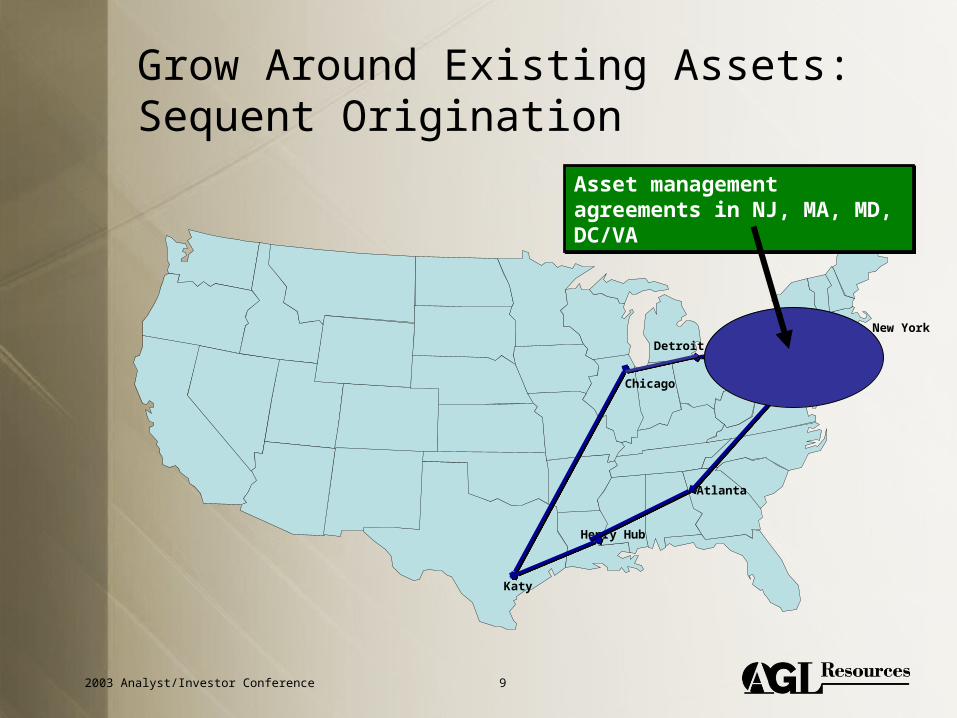

2003 Analyst/Investor Conference 9

New York

Henry Hub

Chicago

Atlanta

Katy

Grow Around Existing Assets:Sequent Origination

Asset management agreements in NJ, MA, MD, DC/VAAsset management agreements in NJ, MA, MD, DC/VA

Detroit

2003 Analyst/Investor Conference 10

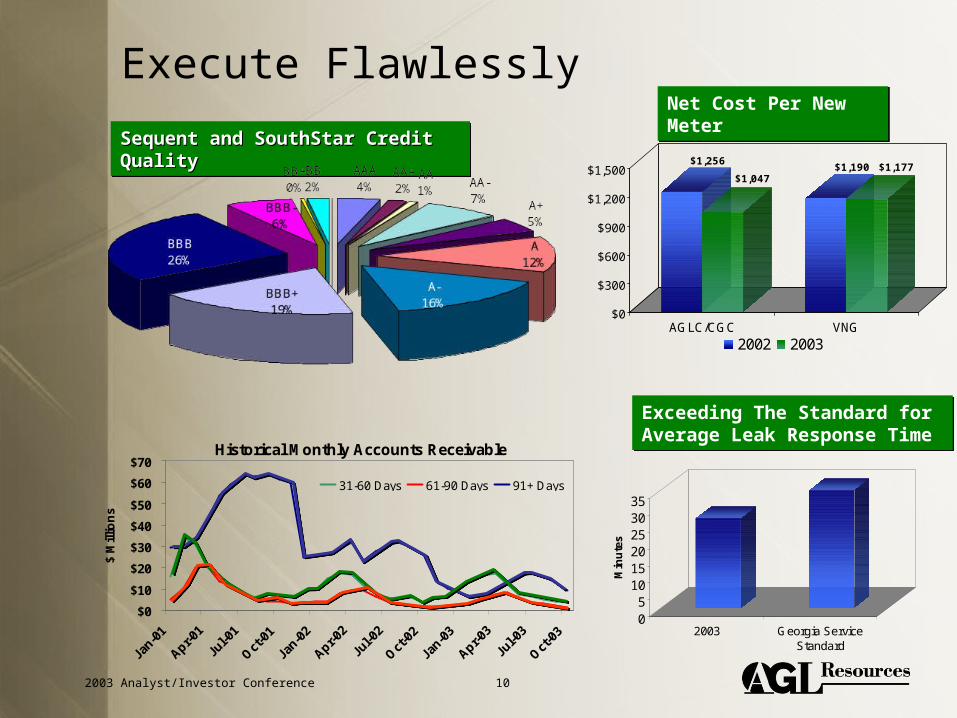

Execute Flawlessly

$1,256

$1,047$1,190 $1,177

$0

$300

$600

$900

$1,200

$1,500

AGLC/CGC VNG

2002 2003

Net Cost Per New MeterNet Cost Per New Meter

Sequent and SouthStar Credit QualitySequent and SouthStar Credit QualitySequent and SouthStar Credit QualitySequent and SouthStar Credit Quality

05

101520253035

Min

ute

s2003 Georgia Service

Standard

Exceeding The Standard for Average Leak Response TimeExceeding The Standard for Average Leak Response Time

Historical Monthly Accounts Receivable

$0

$10

$20

$30

$40

$50

$60

$70

Jan-0

1

Apr-01

Jul-0

1

Oct

-01

Jan-0

2

Apr-02

Jul-0

2

Oct

-02

Jan-0

3

Apr-03

Jul-0

3

Oct

-03

$ M

illio

ns

31-60 Days 61-90 Days 91+ Days

2003 Analyst/Investor Conference 11

What A Difference A Great Board Makes

• Capital Markets Experience (8)

• Energy Industry Experience (3)

• Public Company Experience (7)

• Capital Markets Experience (8)

• Energy Industry Experience (3)

• Public Company Experience (7)

Good Board => Good GovernanceGood Board => Good GovernanceGood Board => Good GovernanceGood Board => Good Governance

2003 Analyst/Investor Conference 12

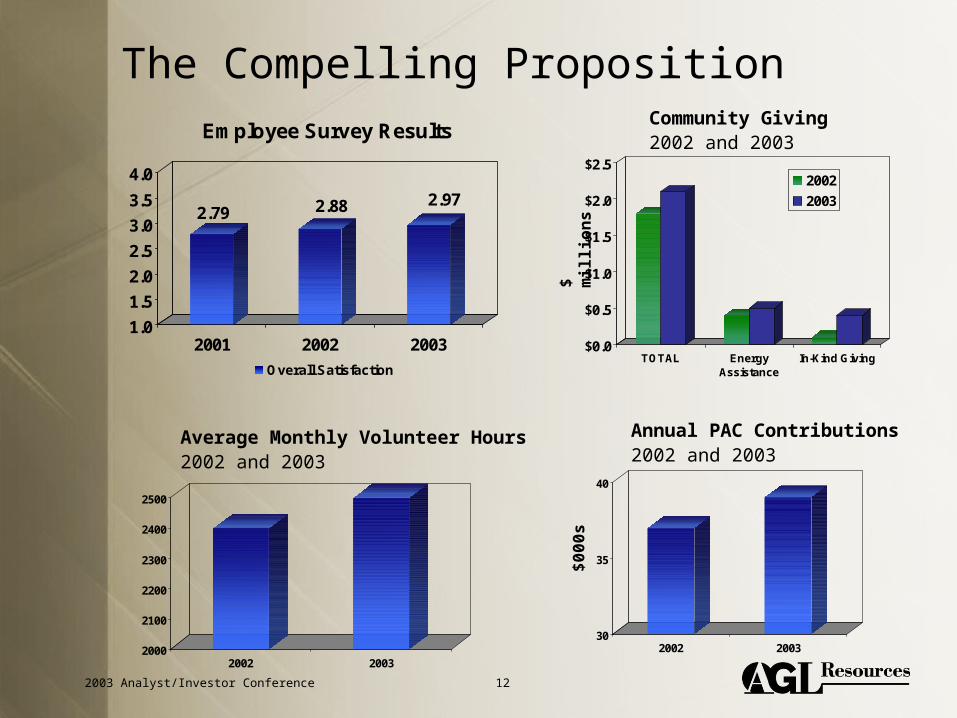

The Compelling Proposition

Average Monthly Volunteer Hours2002 and 2003

Community Giving 2002 and 2003

2000

2100

2200

2300

2400

2500

2002 2003

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

TOTAL EnergyAssistance

In-Kind Giving

2002

20032.79 2.88 2.97

1.0

1.5

2.0

2.5

3.0

3.5

4.0

2001 2002 2003

Employee Survey Results

Overall Satisfaction

30

35

40

2002 2003

Annual PAC Contributions2002 and 2003

$ m

illi

on

s$

00

0s

2003 Analyst/Investor Conference 13

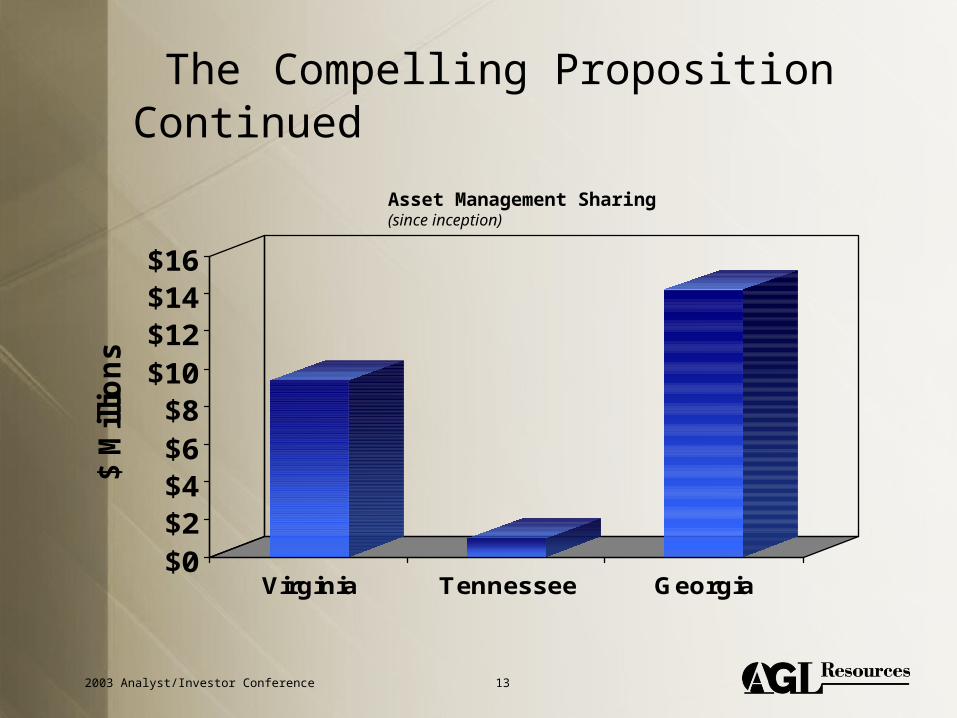

The Compelling Proposition Continued

$0$2$4$6$8

$10$12$14$16

$ M

illio

ns

Virginia Tennessee Georgia

Asset Management Sharing(since inception)

2003 Analyst/Investor Conference 14

Current Environment

• Push/pull of costs

• Volatility of product

• Next wave of productivity

• Future deal flow

2003 Analyst/Investor Conference 15

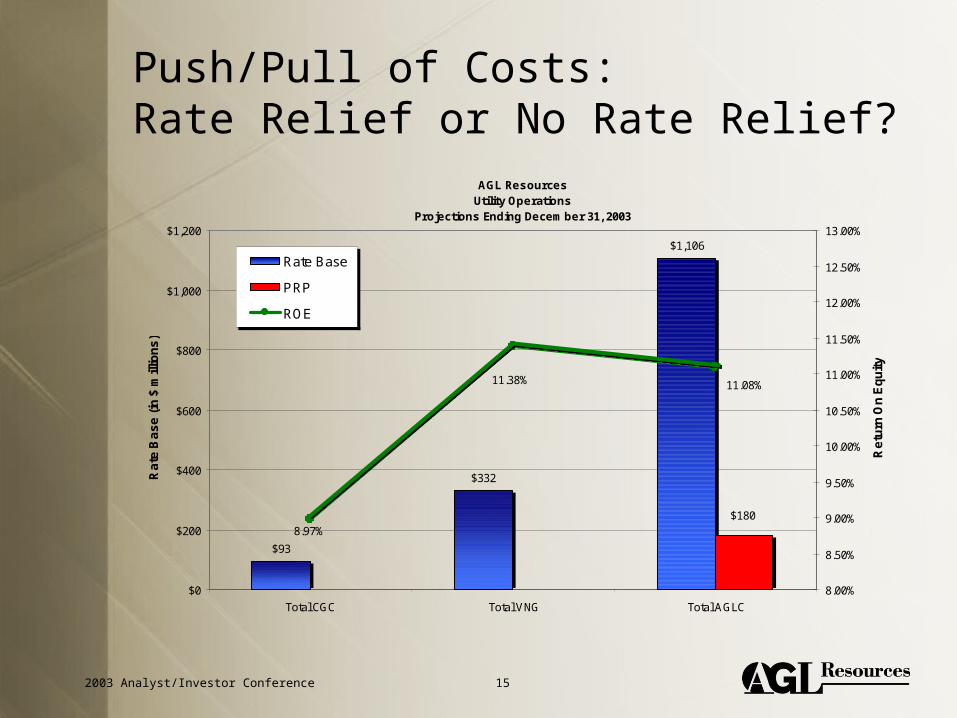

Push/Pull of Costs: Rate Relief or No Rate Relief?

AGL Resources Utility Operations

Projections Ending December 31, 2003

$93

$332

$1,106

$180

11.08%11.38%

8.97%

$0

$200

$400

$600

$800

$1,000

$1,200

Total CGC Total VNG Total AGLC

Ra

te B

as

e (

in $

mill

ion

s)

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

11.00%

11.50%

12.00%

12.50%

13.00%

Re

turn

On

Eq

uit

y

Rate Base

PRP

ROE

2003 Analyst/Investor Conference 16

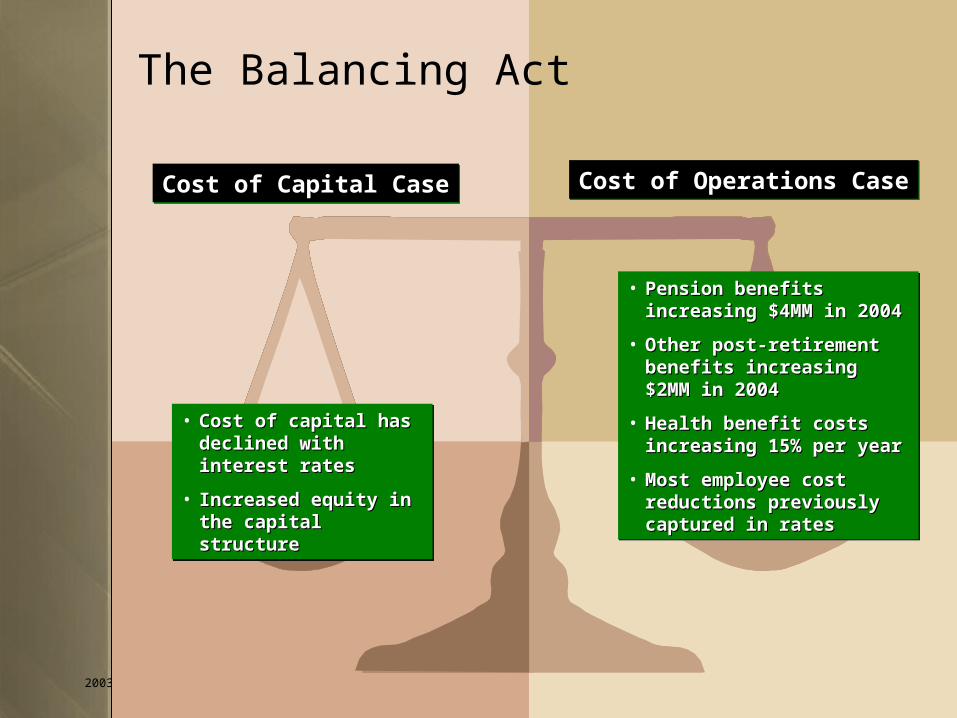

The Balancing Act

• Cost of capital has Cost of capital has declined with interest declined with interest ratesrates

• Increased equity in the Increased equity in the capital structurecapital structure

• Cost of capital has Cost of capital has declined with interest declined with interest ratesrates

• Increased equity in the Increased equity in the capital structurecapital structure

• Pension benefits increasing Pension benefits increasing $4MM in 2004$4MM in 2004

• Other post-retirement Other post-retirement benefits increasing $2MM in benefits increasing $2MM in 20042004

• Health benefit costs Health benefit costs increasing 15% per yearincreasing 15% per year

• Most employee cost Most employee cost reductions previously reductions previously captured in ratescaptured in rates

• Pension benefits increasing Pension benefits increasing $4MM in 2004$4MM in 2004

• Other post-retirement Other post-retirement benefits increasing $2MM in benefits increasing $2MM in 20042004

• Health benefit costs Health benefit costs increasing 15% per yearincreasing 15% per year

• Most employee cost Most employee cost reductions previously reductions previously captured in ratescaptured in rates

Cost of Capital CaseCost of Capital Case Cost of Operations CaseCost of Operations Case

2003 Analyst/Investor Conference 17

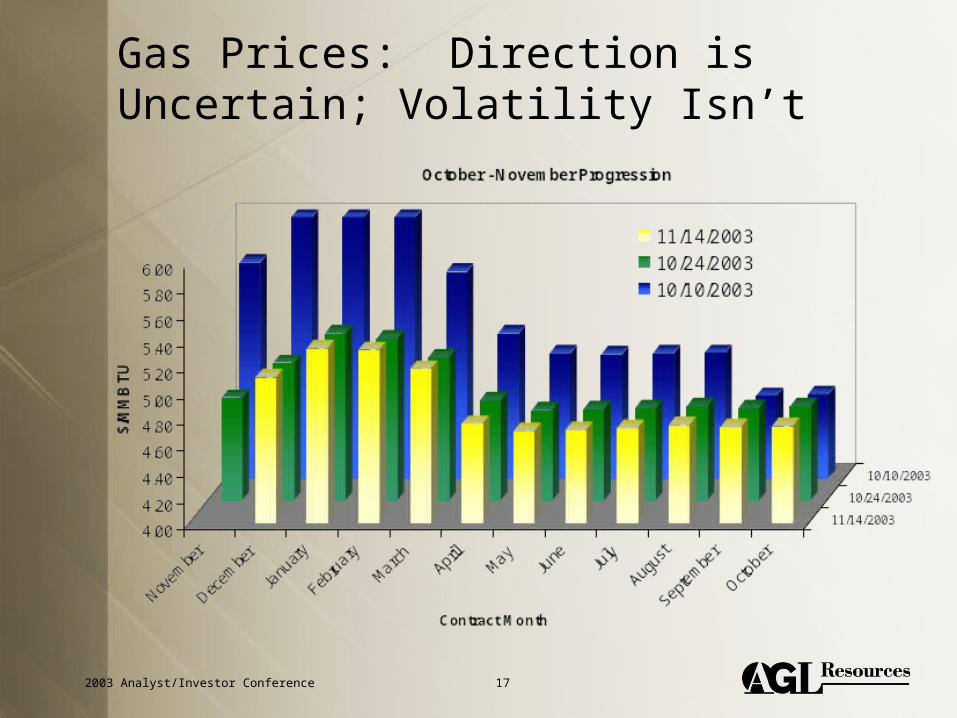

Gas Prices: Direction is Uncertain; Volatility Isn’t

2003 Analyst/Investor Conference 18

Implications

• Must meet the challenge of retail market communications

• Validates SouthStar’s fixed-charge strategy

• Supports Pivotal incremental approach; cautious outreach on LNG and storage investment

• Sequent’s services have value; storage arbitrage strategy is robust

2003 Analyst/Investor Conference 19

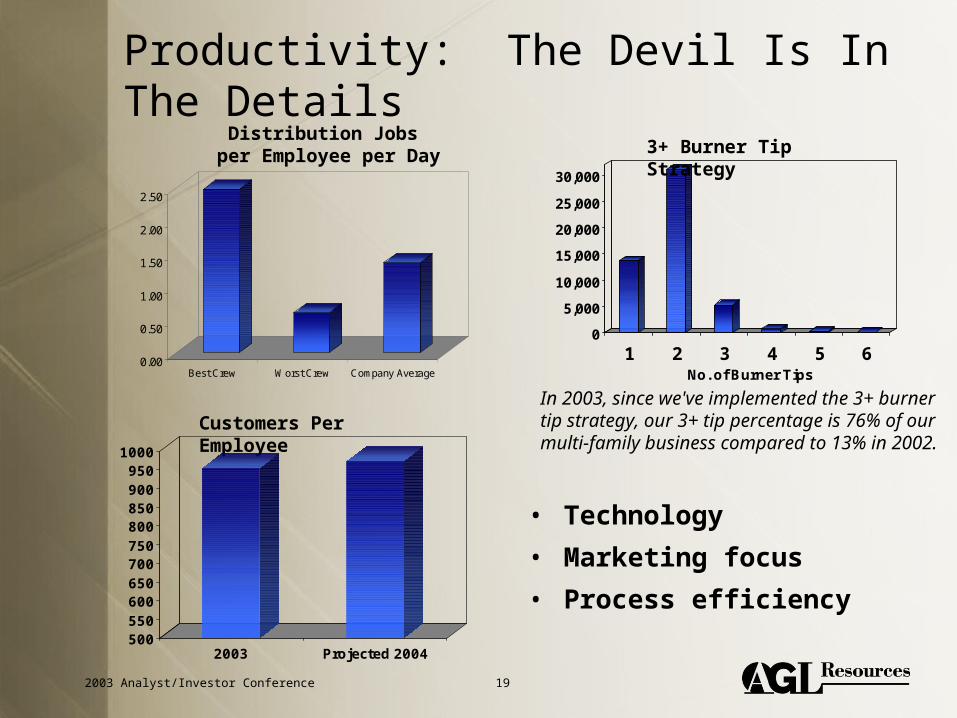

Productivity: The Devil Is In The Details

0

5,000

10,000

15,000

20,000

25,000

30,000

1 2 3 4 5 6No. of Burner Tips

In 2003, since we've implemented the 3+ burner tip strategy, our 3+ tip percentage is 76% of our multi-family business compared to 13% in 2002.

0.00

0.50

1.00

1.50

2.00

2.50

Best Crew Worst Crew Company Average

• Technology

• Marketing focus

• Process efficiency

Distribution Jobs per Employee per Day

Customers Per Employee

500550600650700750800850900950

1000

2003 Projected 2004

3+ Burner Tip Strategy

2003 Analyst/Investor Conference 20

Future Deal Flow

• Best buyer

• Capital structure optimization

• Regulatory ease

• Earnings accretion

2003 Analyst/Investor Conference 21

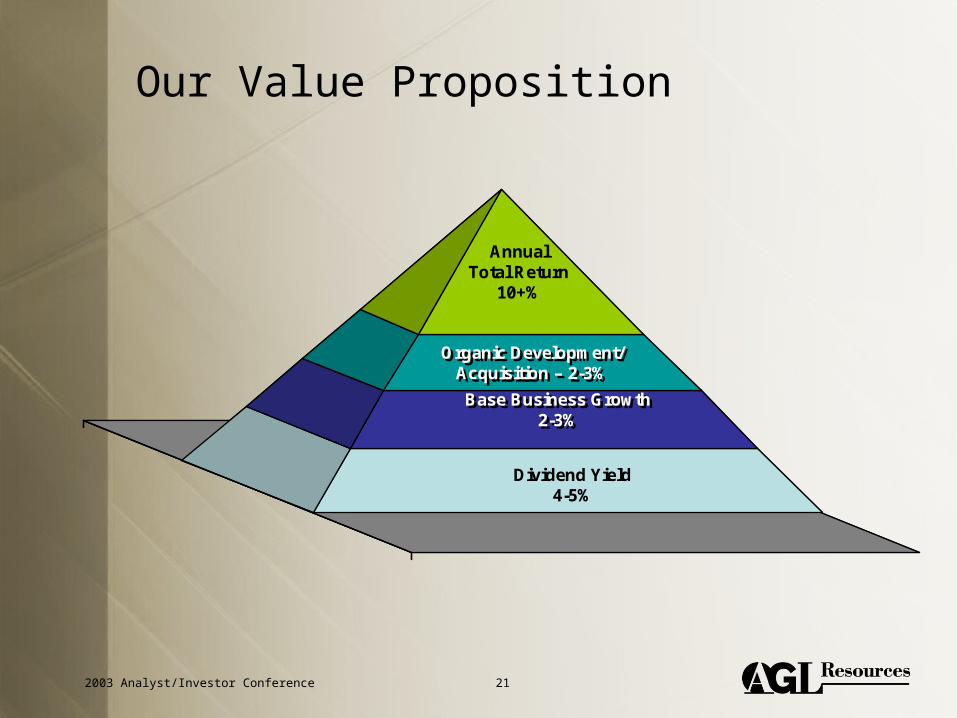

Our Value Proposition

Annual Total Return

10+%

Organic Development/Acquisition – 2-3%

Organic Development/Acquisition – 2-3%

Base Business Growth2-3%

Base Business Growth2-3%

Dividend Yield4-5%

Annual Total Return

10+%

Organic Development/Acquisition – 2-3%

Organic Development/Acquisition – 2-3%

Base Business Growth2-3%

Base Business Growth2-3%

Dividend Yield4-5%

2003 Analyst/Investor Conference 22

2004 Goals

• We will sustain superior financial and operating performance

• We will reconfigure the gas delivery system to save money for our customers – and invest in our own infrastructure

• We will market our products and services as never before

• We will change our business process and culture by driving technology through everything we do

2003 Analyst/Investor Conference 23

Our Culture

generosityof spirit

generosityof spirit

inside

the

lines

inside

the

lines

honestyhonesty

valueseekingvalueseeking

Our Values

2003 Analyst/Investor Conference 24

Our Promise

• The Value Is Here

• The Value is Still Here

• Every Day, We Seek Value For You

2001

2002