Embed Size (px)

Citation preview

2016/04/05

1

Welcome to ACLTeam collaboration, remote work and continuous monitoring for the most sought-after teams

Dominic NelDominic NelDominic NelDominic NelHead of ACL South Africa

“Data analytics analyses data immediately. Identifying errors within the organization,

allowing companies to quickly react and mitigate the issue.”

2013

Who do we service

32of countries across Africa

4000happy customers across Africa

98%of the fortune 500

15 000happy customers across the globe

32of countries across Africa

4000happy customers across Africa

15 000happy customers across the globe

Risk Based AuditsRisk Based AuditsRisk Based AuditsRisk Based AuditsAre they assisting municipalities to deliver sustainable services?

“How many mistakes does it take before we consider something to be broken? Is 1%

inaccuracy sufficient? Would you be happy if 99% of your debtors paid you accurately?”

2016

King ll & King lll Reflection

King ll acknowledged the important role of an effective internal audit function

in good corporate governance.

King lll emphasizes that internal audit should follow a risk-based approach to

it’s plan. This is consistent with Section 165 (2) a of the MFMA (Municipal

Finance Management Act) which requires internal audit to prepare a risk-

based audit plan for each financial year.

King lll expects that the CAE or Head of Internal Audit’s, should:

1. Provide a constant assessment of the municipality's control environment

2. Discuss the adequacy of the resources and skills available to the CAE and Audit Committee

3. Internal audit planning and approach should be risk based rather than compliance based.

Clean audit

outcome

Financially

unqualified

audit opinion

Qualified audit

opinion

Adverse audit

opinion

Auditor General outcomes:

The financial statements are free from material misstatements and there are no

material findings or non-compliance with legislation.

Understanding Audit Compliance

2016/04/05

2

24% Financially unqualified

audit opinion41% Qualified or Adverse

audit opinions

Who got clean audits 2013/2014

2

4

013

0

2

2

0

17

Round of Applause!

City of Cape Town Metro

Cape Winelands District

Eden District West Coast District

Bitou

Breede Valley

Cape Agulhas

Drakenstein

George

Hessequa

Knysna

Langeberg

Mossel Bay

Overstrand

Swartland

Theewaterskloof

Witzenberg

Centralization. Automation. Predefined best practice.

How does ACL assist Municipalities?

2016/04/05

3

Objectives

Provide assurance

Process improvement

Add value to business

Manage exceptions

Reality

Request data from IT

Import, sort, format, normalize

Analyze data and identify

Report findings

Make Audit Valuable

VSVSLower Cost

Increase Coverage

Maturity Level 2 Maturity Level 3

Number of Tests

Time

Maturity Level 1

MANUAL(PROCESS &RISK BASED)

AUTOMATE

Adhoc Testing

MANUALMANUALMANUALMANUAL(RISK BASED)(RISK BASED)(RISK BASED)(RISK BASED)

AUTOMATED(PROCESS BASED)(PROCESS BASED)(PROCESS BASED)(PROCESS BASED)

Continuous Auditing

MANUALMANUALMANUALMANUAL(RISK BASED)(RISK BASED)(RISK BASED)(RISK BASED)

AUTOMATED(PROCESS BASED)(PROCESS BASED)(PROCESS BASED)(PROCESS BASED)

Continuous Monitoring

How has audit technology evolved

Continuous Auditing and MonitoringContinuous Auditing and MonitoringContinuous Auditing and MonitoringContinuous Auditing and MonitoringHow does Kobus feel about this?

“Data access is a hassle for analysts and a nuisance for IT. Stop having to be a pest. Build

trusted connections and test entire datasets during non-production hours.”

The Truth

What are our current challenges

Independent access to data Knowledge

Skills

Time

Type of technology

2016/04/05

4

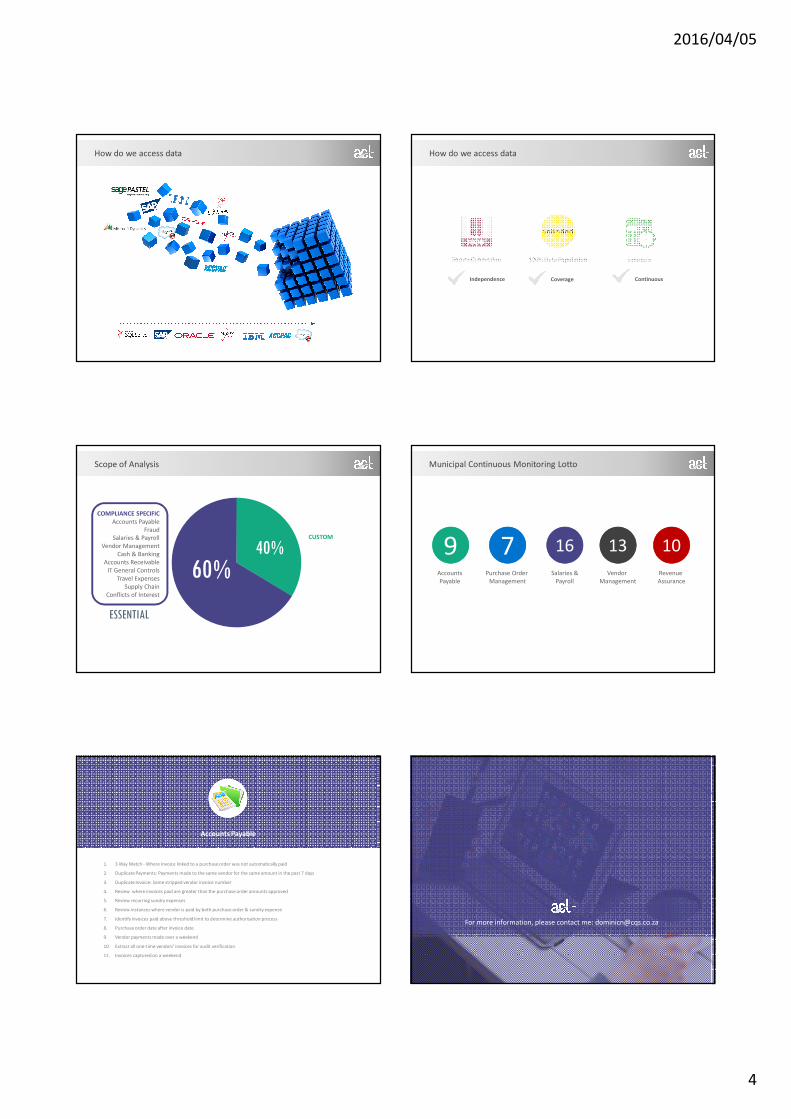

How do we access data How do we access data

Secure Connection 100% Data Population Schedule

Independence Coverage Continuous

Scope of Analysis

CUSTOM

40%

COMPLIANCE SPECIFIC

Accounts Payable

Fraud

Salaries & Payroll

Vendor Management

Cash & Banking

Accounts Receivable

IT General Controls

Travel Expenses

Supply Chain

Conflicts of Interest

60%

ESSENTIAL

Municipal Continuous Monitoring Lotto

9Accounts

Payable

7Purchase Order

Management

16

Salaries &

Payroll

13

Vendor

Management

10

Revenue

Assurance

Accounts Payable

1. 3 Way Match - Where Invoice linked to a purchase order was not automatically paid

2. Duplicate Payments: Payments made to the same vendor for the same amount in the past 7 days

3. Duplicate Invoice: Same stripped vendor invoice number

4. Review where invoices paid are greater than the purchase order amounts approved

5. Review recurring sundry expenses

6. Review instances where vendor is paid by both purchase order & sundry expense

7. Identify invoices paid above threshold limit to determine authorisation process

8. Purchase order date after invoice date

9. Vendor payments made over a weekend

10. Extract all one-time vendors’ invoices for audit verification

11. Invoices captured on a weekend

For more information, please contact me: [email protected]