Embed Size (px)

Citation preview

131

HANSEN & MOWENHANSEN & MOWEN

Cost ManagementCost ManagementACCOUNTING AND CONTROLACCOUNTING AND CONTROL

132

The Balanced Scorecard: The Balanced Scorecard: Strategic-Based ControlStrategic-Based Control

13

133

The activity-based system adds a process

perspective to the financial perspective of

the functional-based responsibility accounting

system.

The activity-based system adds a process

perspective to the financial perspective of

the functional-based responsibility accounting

system.A strategy-based

responsibility accounting system translates the

strategy of the organization into

operational objectives and measures.

A strategy-based responsibility accounting

system translates the strategy of the

organization into operational objectives

and measures.

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

134

The Balanced Scorecard is a strategic-

based performance management system that typically identifies

objectives and measures for four

different perspectives.

The Balanced Scorecard is a strategic-

based performance management system that typically identifies

objectives and measures for four

different perspectives.

The financial perspective

The customer perspective

The process perspective

The learning and growth perspective

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

135

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

Responsibility Assignments ComparedResponsibility Assignments ComparedResponsibility Assignments ComparedResponsibility Assignments Compared

136

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

Performance Measures ComparedPerformance Measures ComparedPerformance Measures ComparedPerformance Measures Compared

137

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

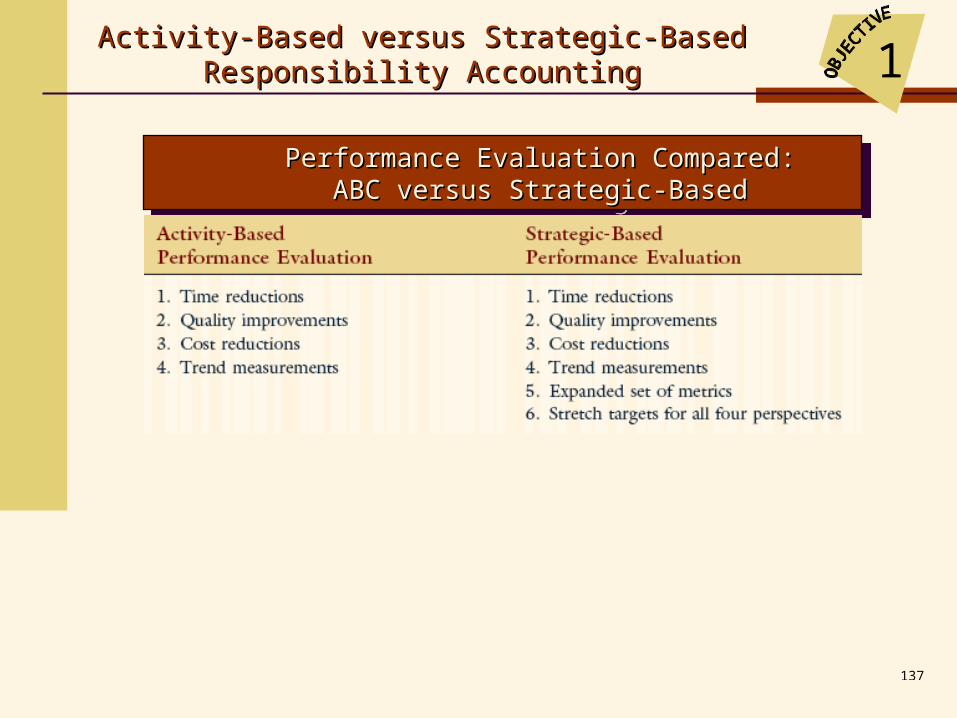

Performance Evaluation Compared: Performance Evaluation Compared: ABC versus Strategic-BasedABC versus Strategic-Based

Performance Evaluation Compared: Performance Evaluation Compared: ABC versus Strategic-BasedABC versus Strategic-Based

138

Activity-Based versus Strategic-Based Activity-Based versus Strategic-Based Responsibility AccountingResponsibility Accounting 1

Rewards ComparedRewards ComparedRewards ComparedRewards Compared

139

Strategy is choosing the market and customer segments the business unit

intends to service, identifying the critical internal and business processes that the

unit must excel at to deliver the value propositions to customers in the targeted

market segments, and selecting the individual and organizational capabilities required for the internal, customer, and

financial objectives.

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1310

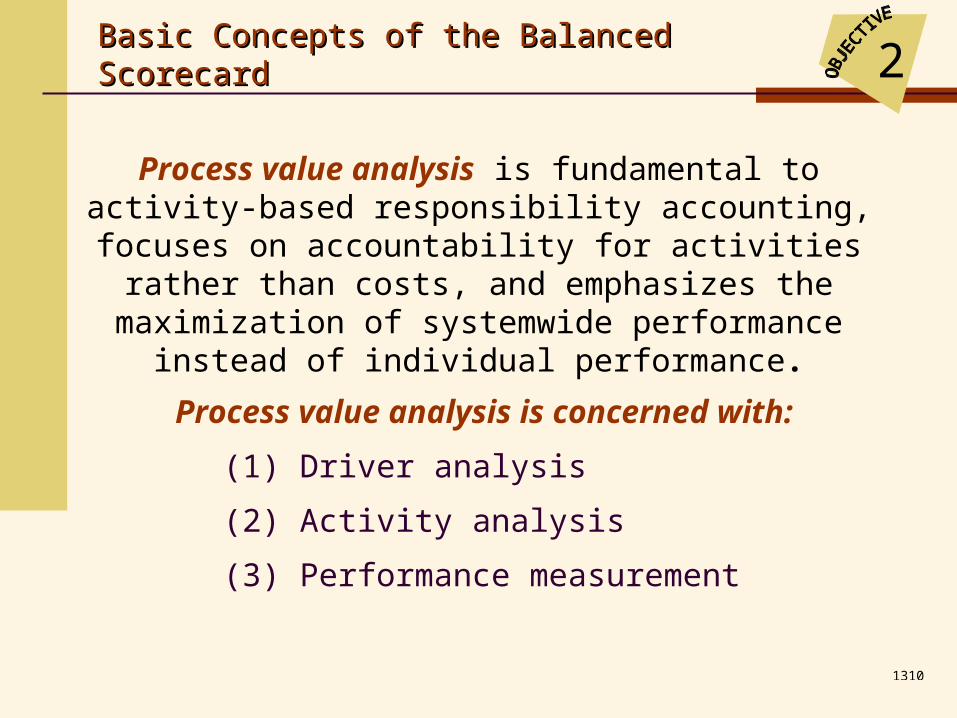

Process value analysis is fundamental to activity-based responsibility accounting, focuses on

accountability for activities rather than costs, and emphasizes the maximization of systemwide

performance instead of individual performance.

Process value analysis is concerned with:

(1) Driver analysis

(2) Activity analysis

(3) Performance measurement

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1311

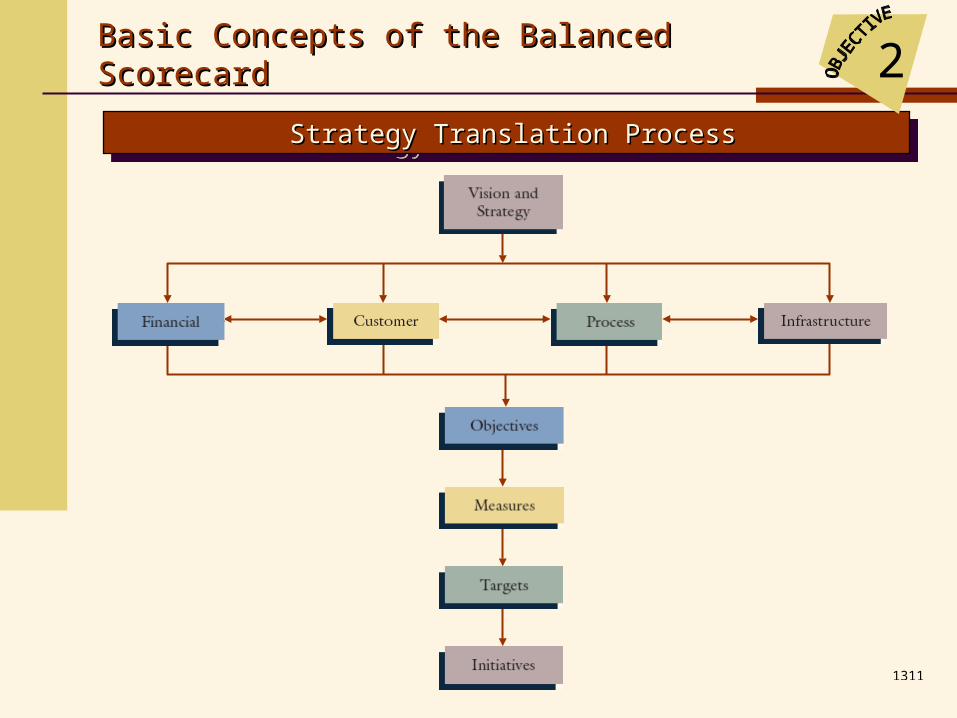

Strategy Translation ProcessStrategy Translation ProcessStrategy Translation ProcessStrategy Translation Process

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1312

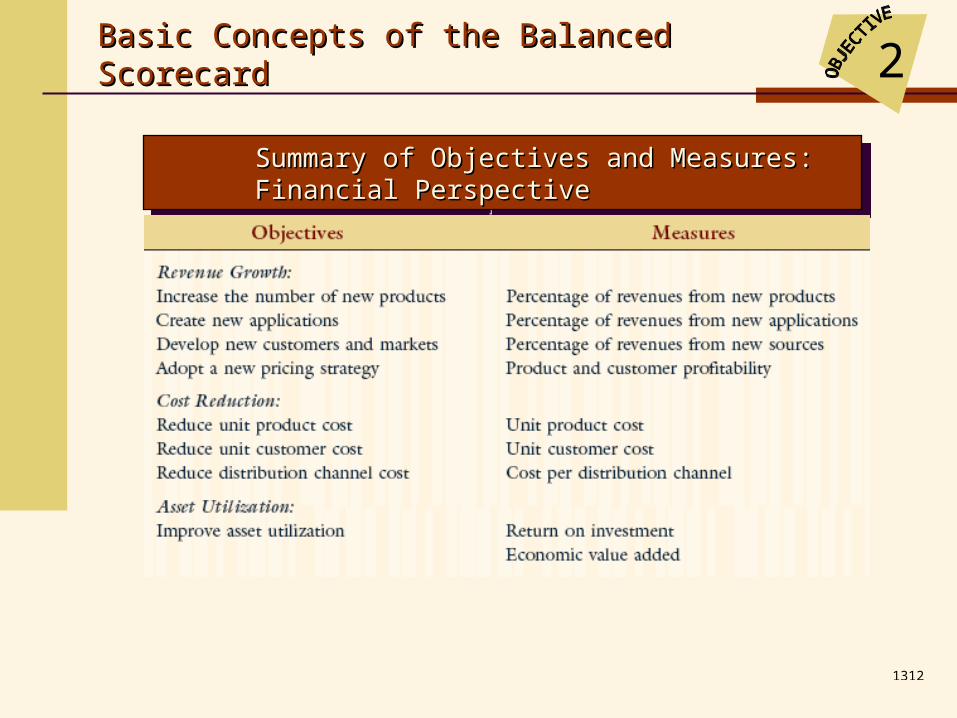

Summary of Objectives and Measures: Summary of Objectives and Measures: Financial PerspectiveFinancial Perspective

Summary of Objectives and Measures: Summary of Objectives and Measures: Financial PerspectiveFinancial Perspective

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1313

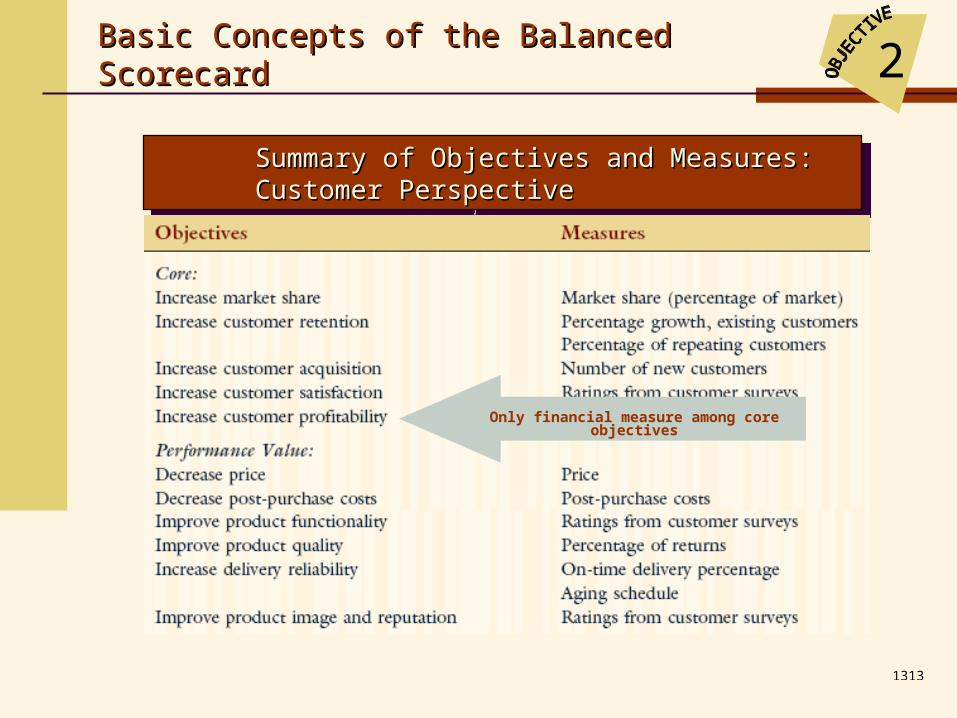

Summary of Objectives and Measures: Summary of Objectives and Measures: Customer PerspectiveCustomer Perspective

Summary of Objectives and Measures: Summary of Objectives and Measures: Customer PerspectiveCustomer Perspective

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

Only financial measure among core objectives

1314

Customer value is the difference between realization and sacrifice, where realization is what the customer receives and sacrifice

is what is given up.

Customer value is the difference between realization and sacrifice, where realization is what the customer receives and sacrifice

is what is given up.

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1315

The time it takes a company to respond to

a customer order is referred to as

responsiveness.

The time it takes a company to respond to

a customer order is referred to as

responsiveness.

Cycle time and velocity are two

operation measures of responsiveness.

Cycle time and velocity are two

operation measures of responsiveness.

Cycle time (manufacturing) is the length of time it takes to

produce a unit of output from the time materials are received until the good is delivered to finished

goods inventory.

Cycle time (manufacturing) is the length of time it takes to

produce a unit of output from the time materials are received until the good is delivered to finished

goods inventory.Velocity is the number of units of output that an be produced in a

given period of time.

Velocity is the number of units of output that an be produced in a

given period of time.

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1316

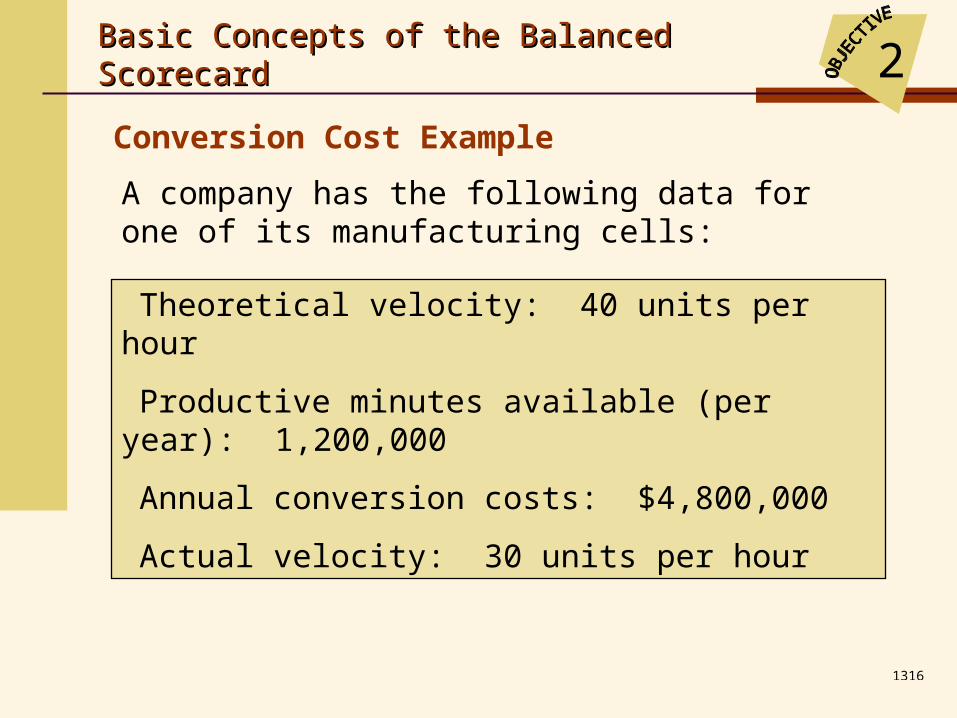

A company has the following data for one of its manufacturing cells:

Theoretical velocity: 40 units per hour

Productive minutes available (per year): 1,200,000

Annual conversion costs: $4,800,000

Actual velocity: 30 units per hour

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

Conversion Cost Example

1317

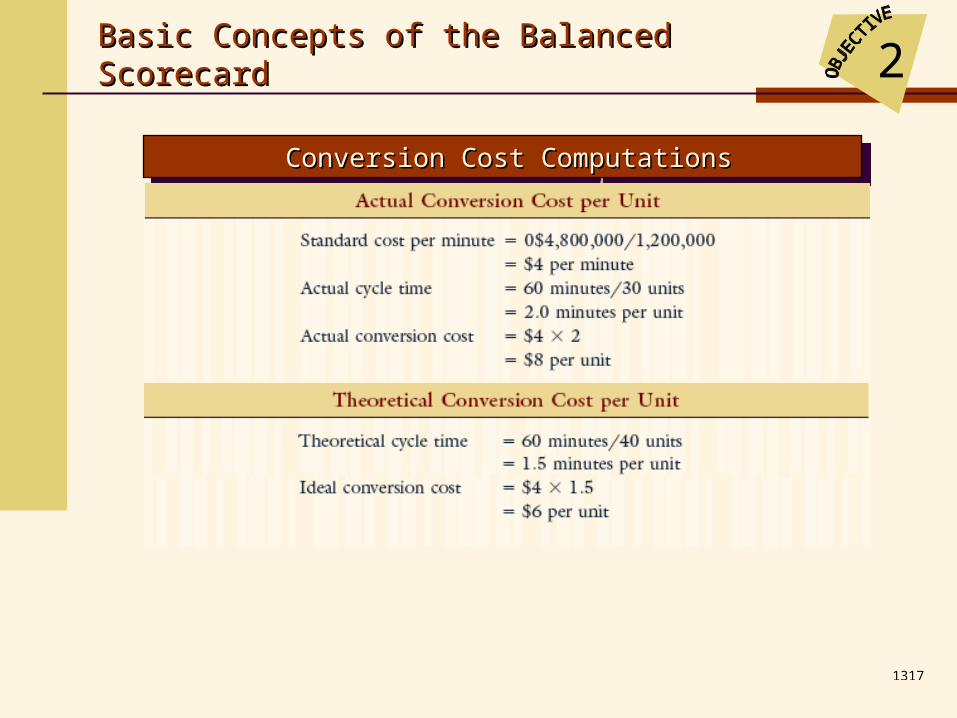

Conversion Cost ComputationsConversion Cost ComputationsConversion Cost ComputationsConversion Cost Computations

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1318

Summary of Objectives and Measures: Summary of Objectives and Measures: Process PerspectiveProcess Perspective

Summary of Objectives and Measures: Summary of Objectives and Measures: Process PerspectiveProcess Perspective

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1319

Summary of Objectives and Measures: Summary of Objectives and Measures: Learning and Growth PerspectiveLearning and Growth Perspective

Summary of Objectives and Measures: Summary of Objectives and Measures: Learning and Growth PerspectiveLearning and Growth Perspective

Basic Concepts of the Balanced Basic Concepts of the Balanced ScorecardScorecard 2

1320

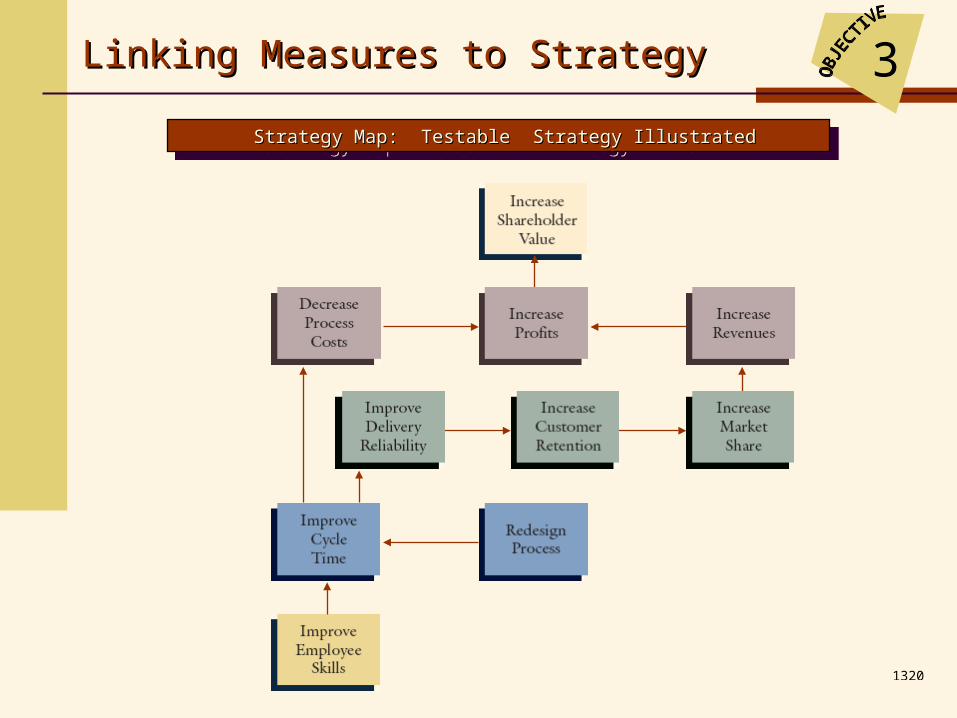

3Linking Measures to StrategyLinking Measures to Strategy

Strategy Map: Testable Strategy IllustratedStrategy Map: Testable Strategy IllustratedStrategy Map: Testable Strategy IllustratedStrategy Map: Testable Strategy Illustrated

1321

Strategic AlignmentStrategic Alignment 4

ABM Implementation ModelABM Implementation ModelABM Implementation ModelABM Implementation Model

1322

End of End of Chapter 13Chapter 13