Embed Size (px)

Citation preview

1

Opportunities for Investment in the current Canadian power climate

Bob Livet, P.Eng.Vice President Energy OperationsAMEC Americas Limited

Presented to

The Canada Europe Energy Round Table for BusinessThe 2004 Energy Round Table

September 20, 2004

Regulatory Framework

Electricity is a Provincial Jurisdiction

Among Major Utilities:

• 10 have Provincial / Territorial Ownership• 6 are Investor Owned• 2 have Municipal Ownership

Utility Industry is Vertically Integrated

Canada signed Kyoto Protocol in 2003

• Federal and Provincial Government Negotiate CO2 Targets

• Federal Government Establishes Renewable Energy Credits

• Some Provinces Provide Further Tax Incentives

• Has Stimulated a Demand for Renewable Energy

3

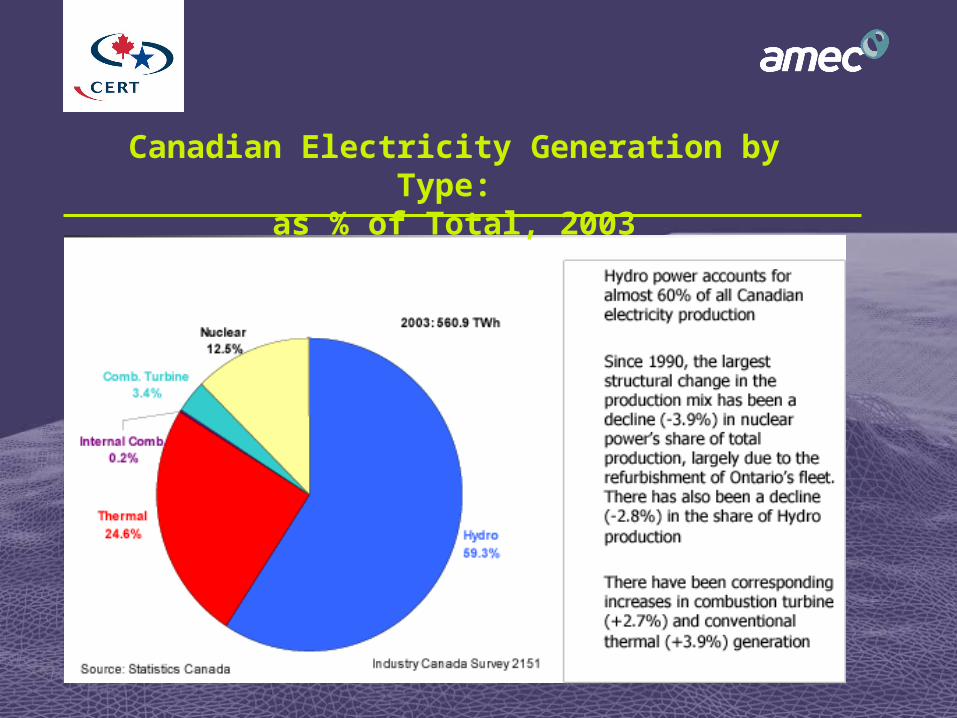

Canadian Electricity Generation by Type: as % of Total, 2003

4

Canadian Electricity Generation by Region and Type TWH, 2003

5

Canada – U.S. Electricity Trade: TWh, 1991 to 2003

6

Canadian Net Exports by Province: GWh, 2003

7

CEA (2001) Electricity Demand ProjectionTWh, 2000 - 2020

New demand, plant replacements and export requires significant new capacity over the next 20 years

By 2020, demand will be 670 TWh, coming from new plants – 35% of year 2000 production

New investments of over 20,000 MW per decade to 2020

$ 150 Billion Cdn in investment needed.

8

Emerging Renewables and Alternatives:Generation Capacity, 2002

Emerging renewables and alternatives include:

• wind, solar, tidal, biomass, bio-gas, solid waste

More than 7000 GWh were generated in 2002 by Emerging Renewable and Alternative Energy sources

Source: CIEECAC Annual Renewable Energy Review, March 2003

9

Renewable Energy

Positive Public Acceptance

Tax and Cash Incentives• Wind Power Production Incentive (WPPI)• Class 43.1 Accelerated Write Off• Canadian Renewable & Conservation Expenses (CRCE)• Municipal Funding Sources• Retail Tax Credits (some Provinces)

Wind Power Coupled with Hydro Electric Power makes Economic Sense

Transmission Grid Stability / Upgrades

10

Recent Structural Changes

Nova Scotia has Privatized its Electric Utility

British Columbia, Quebec and New Brunswick have implemented limited restructuring

Alberta and Ontario have opened their electricity markets to competition

11

Experience with Restructuring

Alberta opened its market to competition in 2001• Resultant consumer price spikes caused government to intervene

with price subsidies

Ontario followed in May 2002• Unusually hot weather and supply shortages caused price spikes

and government reacted by freezing retail electricity rates

12

REVIEW OF MAJOR CANADIAN POWER GENERATION MARKETS

Alberta

Ontario

Quebec

13

Alberta – Current Status

Open Market for Wholesale and Retail Electricity Suppliers

Market administered through the AESO and EUB

• AESO is responsible for Transmission Planning

Generators can sell:

• Bid to the Pool• Pool Pricing based on merit order dispatch• Firm Capacity under Contract • Can export power to Other Jurisdiction

Application for new Generation Facilities made to EUB

Alberta is net importer of power

• (312 GWHR 2002) (257 GWNR 2003)

14

Alberta – Growth Activity

First supercritical coal fired plant in Canada under construction (450 MW)

Addition of cogeneration facilities from oil sand developments

Opportunities for Renewable Energy Projects

• Mandated Green Energy Mix (3.5% Target)• CO2 Emission Credits• Consumers willing to pay more • Government recognizes need for improving grid capacity

15

Ontario – Current Status

New Government (2003) lifted price freeze

Stated goal to shut down all coal fired plants by Dec 07 (7500 MW)

Proposes a Mixed Market Arrangement (Bill 100)

• Regulate Power Sales from Heritage Assets (OPG)• Free Market Pricing for other Generators based on

Merit Order Dispatch• Regulated Retail Price to Small Consumers

(<250,000 kWhr/ year)

16

Ontario – Electricity Supply

Forecast

17

OntarioObjectives - Renewables

Established Renewable Energy Targets • 1,350 MW by 2007 • 3,000 MW by 2011

Qualifying facilities are:• Wind Energy Centers• Water Power Facilities• Energy Projects using Biomass, Bio Fuel, Bio Gas or Landfill Gas• Minimum Capacity of 0.5 MW

18

OntarioObjective - Renewables

First Solicitation for 300 MW closed Aug.27,04• Successful Bidders Announced Jan.05• Further Call for Proposals expected next year

Requirements for participation:• Own or Lease the Site• Proponent Team to have Prior Experience• Commit to all technical & financial requirements of the RFP• Responsible for Environmental Approval & Permitting• Bears All Cost for System Connection and Upgrades

19

Ontario – Other RFP

Seeks proposals for 2500 MW of:• New Clean Intermediate Generation (Gas as Primary Fuel)• Demand Reduction Projects• DSM Projects• Minimum 5 MW Capacity

Time Line:• Pre-qualification of Proponents – Sep. 04 • Issue Request for Proposals – Sep. 04• Submission of Bids – Nov. 04• Announcement of Successful Bidders – Jan. 05

20

Quebec – Current Status

Quebec Energy Board • Responsible for Regulatory Supervision of Transmission and

Distribution

Hydro Quebec remains a Crown Corporation divided into 4 Divisions:• HQ Distribution (Responsible for Generation Planning) • HQ Production• HQ Equipment• HQ Trans Energy (Responsible for Transmission)

Substantial North American Market Access via its Transmission System)

21

Quebec – Current Status cont’d

HQ Distribution is mandated to call tenders for New Generation Requirements.• Proponent enters into a Power Purchase Agreement (20-25 Yr)

HQ Production can sign Power Purchase Agreements

Quebec is a major Exporter of Energy to US Markets

Peak Demand has reached Capacity

22

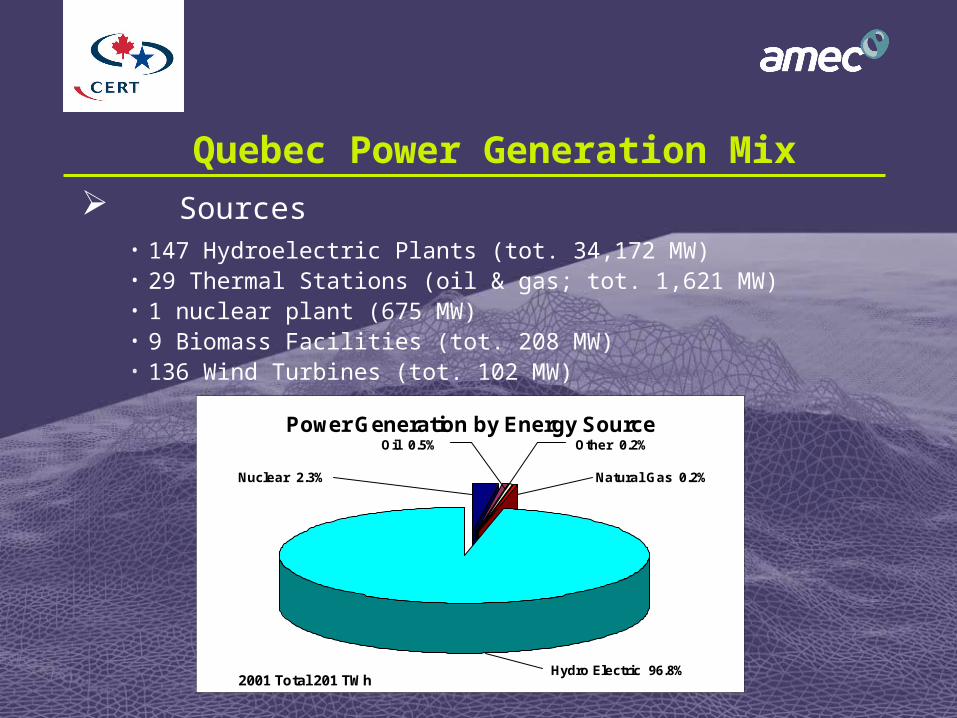

Quebec Power Generation Mix

Power Generation by Energy Source

Nuclear 2.3%

Oil 0.5% Other 0.2%

Natural Gas 0.2%

Hydro Electric 96.8%2001 Total 201 TWh

Sources• 147 Hydroelectric Plants (tot. 34,172 MW)• 29 Thermal Stations (oil & gas; tot. 1,621 MW)• 1 nuclear plant (675 MW) • 9 Biomass Facilities (tot. 208 MW)• 136 Wind Turbines (tot. 102 MW)

23

Quebec - Objectives

Development of Renewable Energy • Substantial Hydro Storage Capacity encourages Development of

Wind Energy Projects

Recent tender calls:• 600 MW of gas fired generation

• 1000 MW of Wind Power Projects (Award in Sep 04)

Expected future tender calls: • 600 MW Gas Fired Cogeneration (late 2004)

• Small Hydro Developments (<50 MW)

• 1000 MW of new Wind Power Projects

24

Investment Opportunities in Other Provinces

Nova Scotia• Ageing Coal fired plants require investment in pollution control

equipment

New Brunswick • Market opens to Wholesalers & Large Industrial Users Oct. 1, 04 • Refurbishment of Pt. Lepreau or 600 MW of Replacement Capacity by

2009• Seeking private investor

British Columbia• Wind / Hydraulic Benefit • Base Load growing in GVRD

25

Summary – Canadian Power Market

Provinces take different approaches to Open Electricity Market

Large Investment required till 2020 (Cdn $ 150 B)• Private Funding Sources Required

Renewable Energy has Broad Political and Public Support

• Good Opportunities in several Provinces• Federal and Provincial Incentives Available• Market for Emission Credits being developed

26

International Project Management and Services Company

Office network across the Americas, Continental Europe and Asia

AMEC Manages Projects Worldwide

Annual Revenues of CAD 10.4 Billion in 2003

Employs 45,000 People in over 40 Countries

In Canada AMEC has 4000 Employees and 78 Offices

Sectors: Transport, Oil & Gas, Power, Infrastructure and Industry and Commerce

Designs and Implements Power Generation and Transmission Facilities since 1907

www.amec.com

AMEC