Embed Size (px)

Citation preview

1

MF-852 Financial Econometrics

Lecture 2

Matrix Operations in Econometrics, Optimization with Excel

Roy J. EpsteinFall 2003

2

Matrix Application in Excel: Curve Fitting Data for 3 different years as

follows:Year Value1 157 4525 60

Fit a smooth curve through these points using a quadratic (2nd degree) polynomial. Why does a parabola work?

3

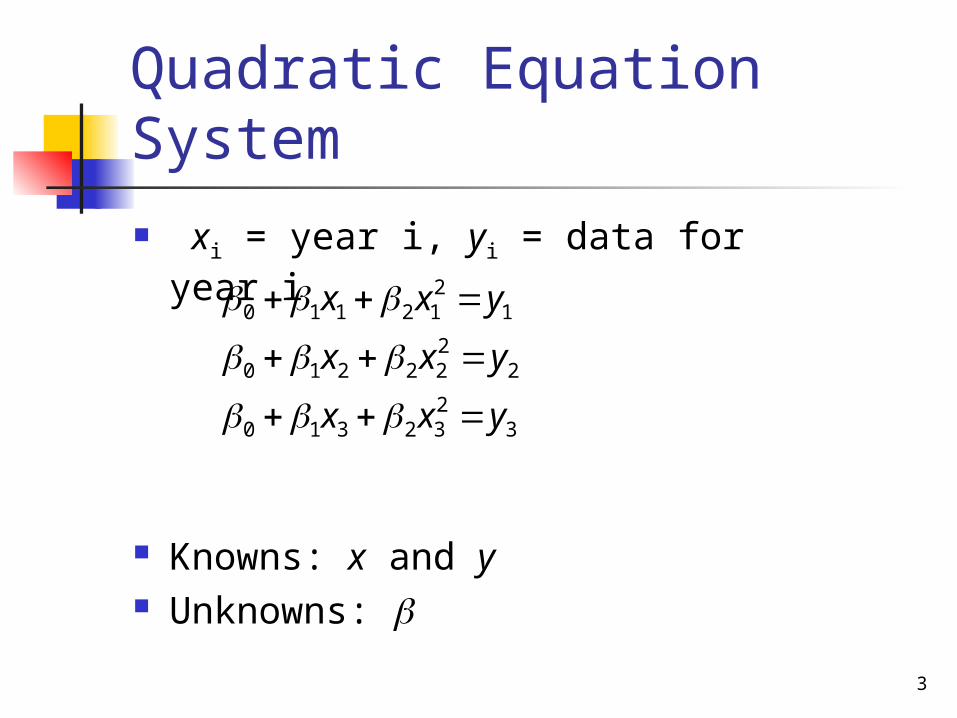

Quadratic Equation System xi = year i, yi = data for year i

Knowns: x and y Unknowns:

3232310

2222210

1212110

yxx

yxx

yxx

4

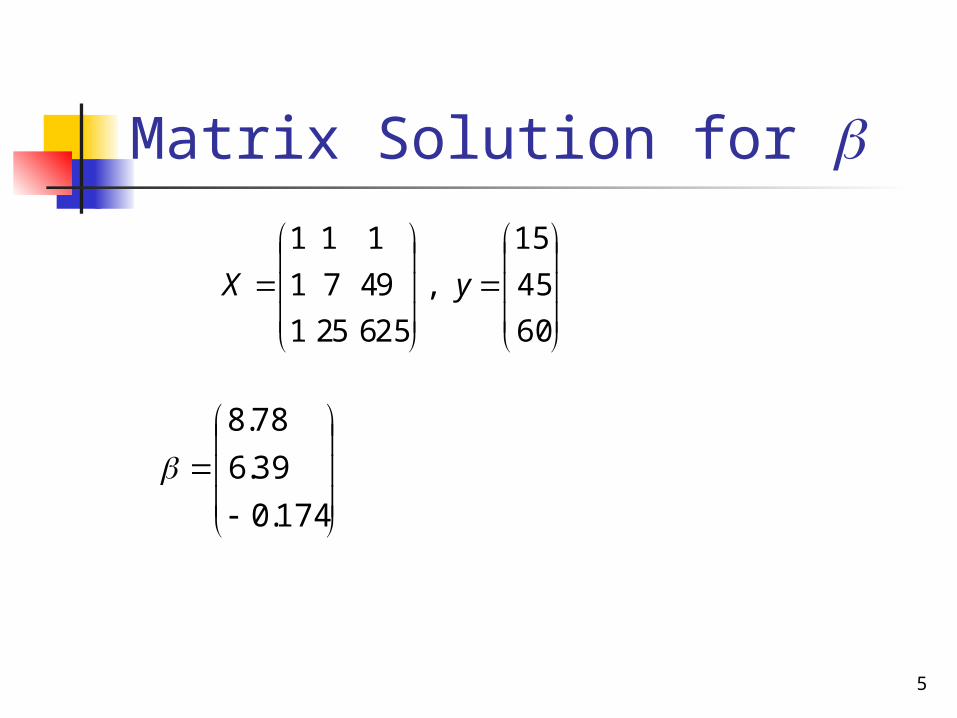

Matrix Solution for

Can solve when X has an inverse! Must be square, non-singular matrix

3

2

1

2

1

0

233

222

211

, ,

1

1

1

y

y

y

y

xx

xx

xx

X

Xy

yX 1

5

Matrix Solution for

60

45

15

,

256 52 1

94 7 1

1 1 1

yX

174.0

39.6

78.8

6

Excel GraphQuadratic Fit with 3 Data Points

0

10

20

30

40

50

60

70

80

0 5 10 15 20 25 30

X

Y

7

Sum of Squares Suppose

Then

mb

b

b

b

2

1

n

ibbb1

2

8

Cross-Products Matrix Suppose m > n and

Does X –1 exist?

XX is the cross-products matrix.

mnmm

n

n

xxx

xxx

xxx

X

2 1

2 22 21

1 12 11

9

Cross-Products Matrix XX =

Can (XX )–1 exist?

m

inin

m

iin

m

iin

m

ini

m

ii

m

ii

m

ini

m

ii

m

ii

xxxxxx

xxxxxx

xxxxxx

1

12

11

12

122

112

11

121

111

10

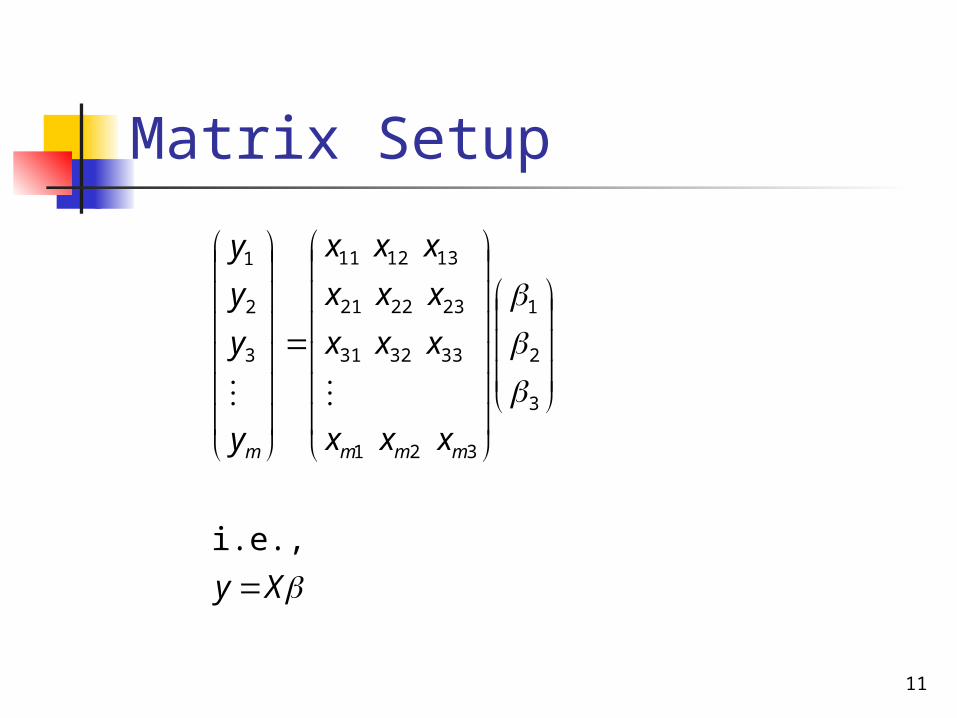

Exact Linear Model y is dependent variable (a vector). 3 independent variables: x1, x2, x3

(each is a vector). Each observation is of the form

The ’s are unknown and have to be estimated from the data.

332211 iiii xxxy

11

Matrix Setup

Xy

xxx

xxx

xxx

xxx

y

y

y

y

mmmm

i.e.,

3

2

1

321

333231

232221

131211

3

2

1

12

Model Dimensionality Model is y = X . How many equations? How many unknowns? Is there a solution?

13

Solution to Linear Model

Multiply through by XX y = X X

How many equations, how many unknowns?

Solution is = (X X )–1X y

14

Linear Regression Model Each observation is of the form

ei is “noise” or an “error” term. Why would a model contain an

error term?

eXy

exxxy iiiii

so

332211

15

Solution to Regression Model Multiply through by X

X y = X X + X e

Suppose X e = 0. What are the implications?

Then solution is = (X X )–1X y

16

Regression Example RR: Dataset data4-1

Model of housing prices as function of house characteristics

Price = f(sq. ft., # bedrooms, # baths)

17

Constrained Optimization We often need to maximize (or

minimize) a function subject to constraints on the function’s arguments.

E.g. Maximize a1x1 + a2x2 + a3x3 subject to b11x1 + b12x2 + b13x3 c1

b21x1 + b22x2 + b23x3 c2

Knowns: ai , bi , ci

Unknowns: xi

18

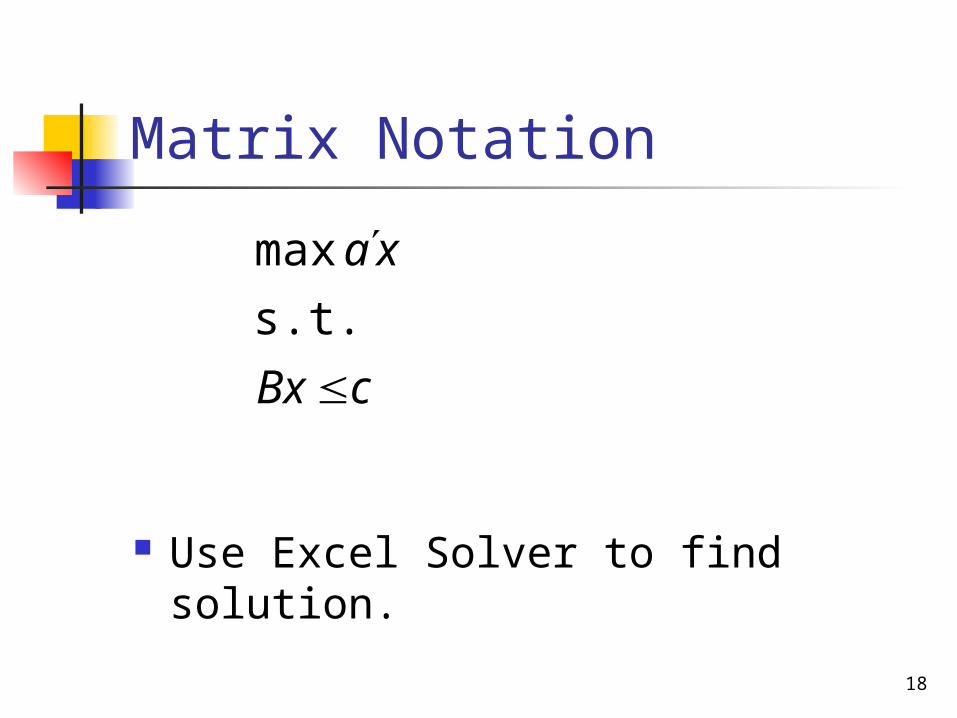

Matrix Notation

Use Excel Solver to find solution.

cBx

xa

s.t.

max

19

Example — Bond Portfolio Maximize expected after-tax return subject to

constraints on portfolio characteristics

Instrument After-tax yield MaturityT-bill 4.85% 0.5T-bond 6.88% 18.5State bond 8.05% 19.4Local bond 7.65% 7.3Corporates 7.34% 24.4

20

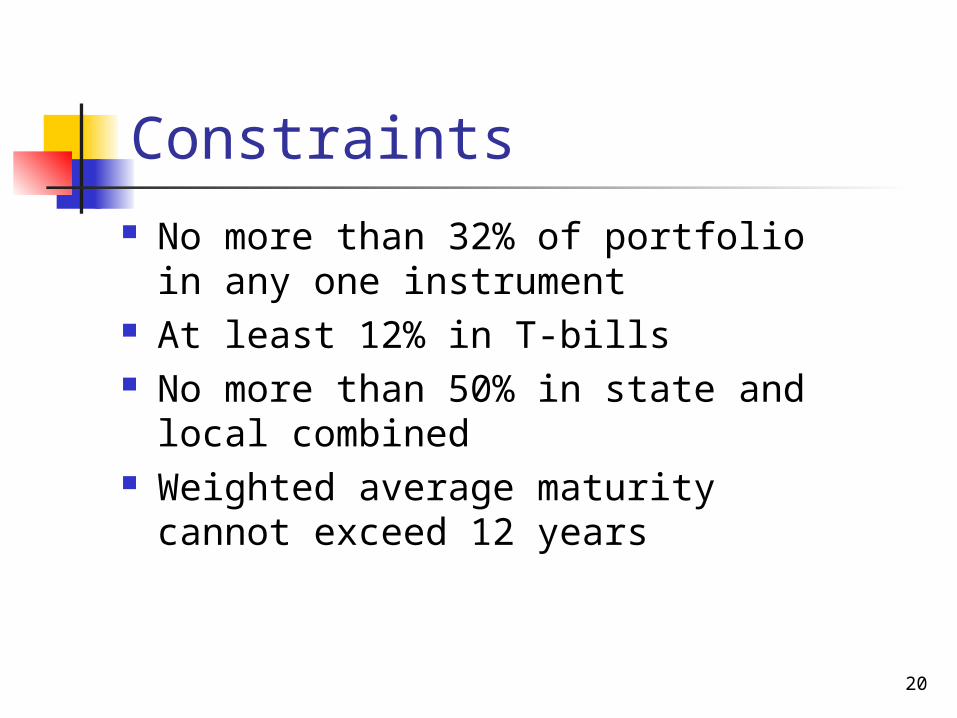

Constraints No more than 32% of portfolio in

any one instrument At least 12% in T-bills No more than 50% in state and

local combined Weighted average maturity

cannot exceed 12 years

21

Problem Set-Up Max .0485x1 + .0688x2 + .0805x3 + .0765x4

+ .0734x5

s.t.x1 + x2 + x3 + x4 + x5 = 1

x1 0.32

x2 0.32

x3 0.32

x4 0.32

x5 0.32

x3 + x4 0.50

0.5x1 + 18.5x2 + 19.4x3 + 7.3x4 + 24.4x5 12

x1 0.12

22

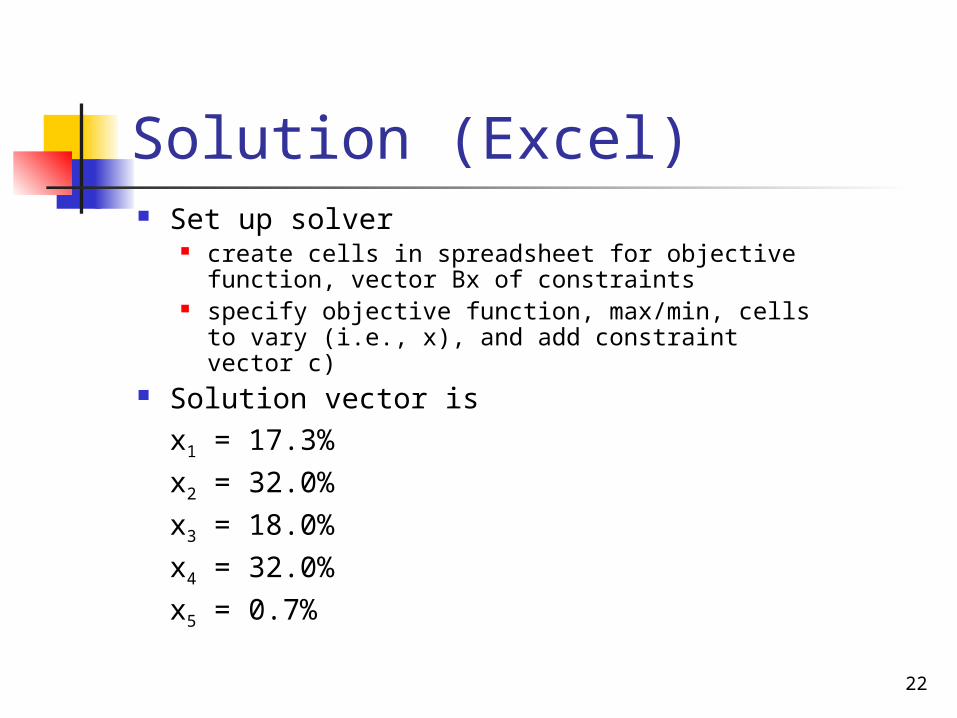

Solution (Excel) Set up solver

create cells in spreadsheet for objective function, vector Bx of constraints

specify objective function, max/min, cells to vary (i.e., x), and add constraint vector c)

Solution vector isx1 = 17.3%

x2 = 32.0%

x3 = 18.0%

x4 = 32.0%

x5 = 0.7%