Embed Size (px)

Citation preview

1

LEGAL & ETHICAL ASPECTS OF GOVERNANCE

LEGAL & ETHICAL ASPECTS OF GOVERNANCE

Edward Chr Kieswetter

SARS: Deputy Commissioner

2

PRESENTATION CONTENT

1. Law vs. Ethics

2. The Cost of Questionable Ethics

3. Experiences from SARS

Our Approach Our Experience Some Results

4. Conclusion

• Slavery in the USA up to1865• Women’s suffrage denied deep onto the 20th

century in many “developed countries”• No German citizenship for German Jews up

to about 60 years ago• Black South Africans denied the vote in their

own country only 16 years ago

3

YOU MAY RECALL THAT IT WASPERFECTLY LEGAL…

…BUT IS IT RIGHT SIMPLY BECAUSE ITS LEGAL?

EQUALLY…

From a legal standpoint…

• You have no obligation to stop a drunk from driving his car

• A witness at the scene of a crime bear no responsibility to intervene

• Johnson & Johnson did not have to withdraw 31 million bottles of Tylenol when 7 people died in1982

• You will not be prosecuted for allowing someone to drown, even if you could help

4

…YET IN EACH INSTANCE IT WOULD BE CONSIDERED TO BE RIGHT/REQUIRED/EXPECTED TO DO SOMETHING!

LIMITATIONS OF THE LAW

In prescribing a set of generally accepted, widely published, and generally enforced rules, laws are meant to provide us with:

• A broad framework for acceptable behaviour• Prescriptions on how to conduct specific

relationships within society• A reference for holding individuals and groups

accountable for social order

5

YET LAWS, WHILST INDISPENSABLE, ARE NOT SUFFICIENT AS A COMLPETE REFERENCE TO GOVERN BEHAVIOUR!

IN THE HIGHLY CONTESTED SPACE OFGOVERNMENTS, CIVIL SOCIETY AND BUSINESS

• Where not everything which is allowed is necessarily right or good

• Where narrow self interests are often pursued at the expense of greater social good

• Where not every eventuality can be always fully anticipated

• Where the eventual impact of leadership decisions may have far-reaching consequences beyond its immediacy

6

LEGAL PRINCIPLES HAVE TO CO-EXIST WITH ETHICAL VALUES

SO WHAT EXACTLY IS ETHICS?

7

ETHICS….

• Greek derivative – ethos or character

• Having, and acting on a sense of what is right

• An awareness of consequences: intended, unintended, immediate, extended…

• Doing the right thing, all the time, even when no-one is watching

• One’s view on morality (mores –latin) informs what is ethical for you!

8

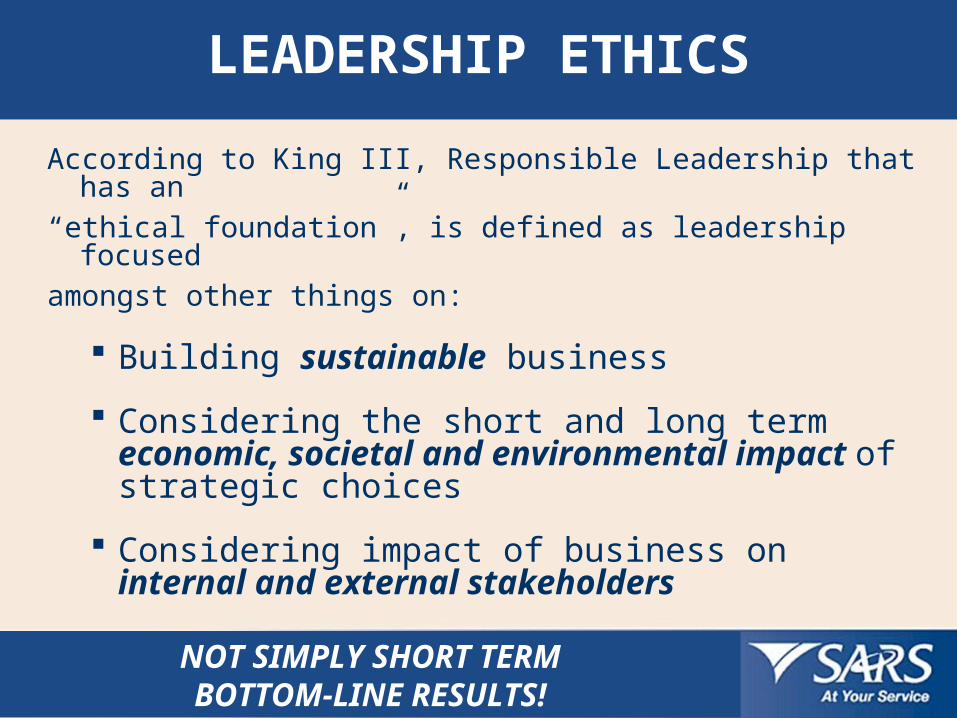

LEADERSHIP ETHICS

According to King III, Responsible Leadership that has an

“ethical foundation”, is defined as leadership focused

amongst other things on:

Building sustainable business

Considering the short and long term economic, societal and environmental impact of strategic choices

Considering impact of business on internal and external stakeholders

9NOT SIMPLY SHORT TERMBOTTOM-LINE RESULTS!

A QUICK LOOK AT CONTEXT AND THE COST OF

QUESTIONABLE ETHICS

10

11

A QUEST FOR THE CORRECT MODEL

“We must reject the idea – well intentioned, but dead wrong – that the

primary path to greatness in social sectors is to become “more like a

business.”

Most businesses fall somewhere between mediocre and good. Few are great!

Jim Collins, 2006

12

EXAMPLES OF ORGANISATIONS WHERE QUESTIONS ABOUT LEADERSHIP ETHICS CAN BE ASKED

• Enrons, Worldcoms, Parmalat, etc,

• And on our doorstep

Leisurenet

Saambou

Fidentia

and many more examples of fraud, insider trading, colluding, price fixing, etc

13

CAPITALISM vs CAPITALIST

“Are we dealing with a crisis of capitalism or a crisis caused by

capitalists?

Sir Martin Sorrel (CEO: WPP) believes that a few misguided capitalists are to blame for the current financial crisis that

precipitated the subsequent economic crisis in the world today – he singled out amongst chief contributory factors, the perverse

incentives, for example of “pariah merchant bankers”

Its about the greed of people!

14

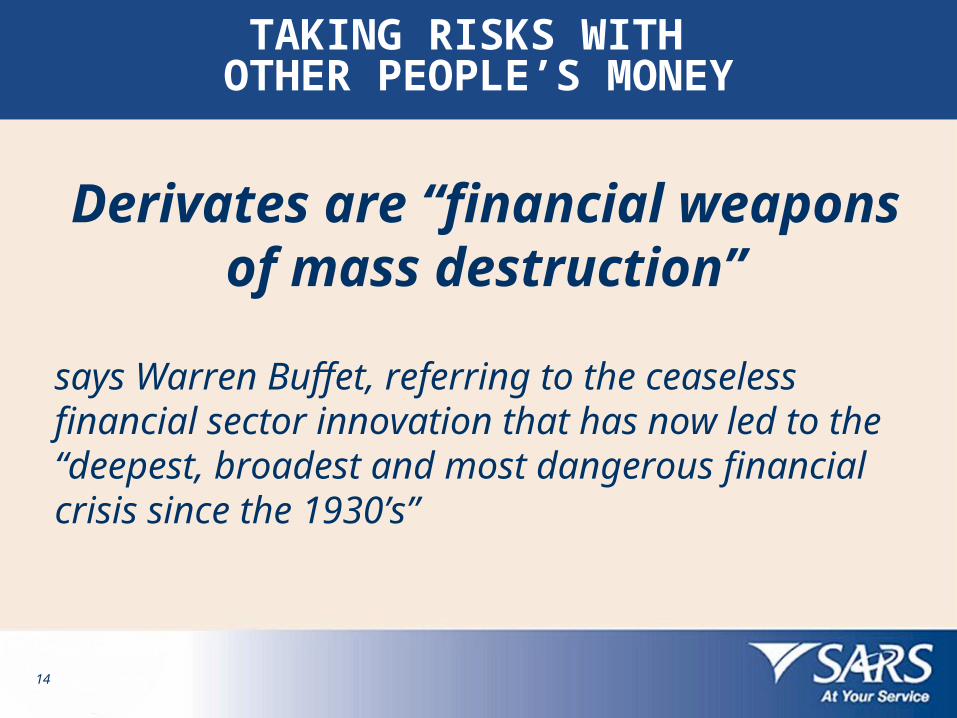

TAKING RISKS WITH OTHER PEOPLE’S MONEY

Derivates are “financial weapons of mass destruction”

says Warren Buffet, referring to the ceaseless financial sector innovation that has now led to the “deepest, broadest and most dangerous financial crisis since the 1930’s”

15

PRUDENCE: CAPITAL/ASSET RATIOS

European Banks:

•100 years ago – 4:1

• 1970’s – 10:1

US leverage ratios 2002 – 2006:

Morgan Stanley 21 - 33

Goldman Sachs 24 - 26

Merrill Lynch 27 – 32

Bear Sterns 32 - 34

In September 2008, the Bank of America’s leverage ratio was 73.7:1

HBR, July – Aug 2009

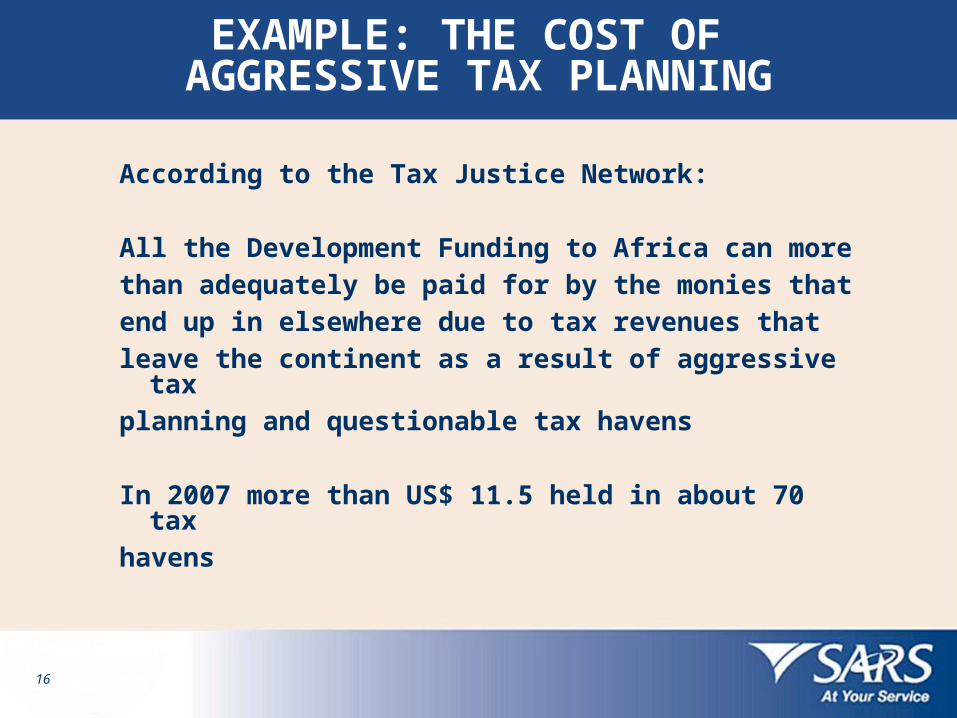

EXAMPLE: THE COST OF AGGRESSIVE TAX PLANNING

According to the Tax Justice Network:

All the Development Funding to Africa can more

than adequately be paid for by the monies that

end up in elsewhere due to tax revenues that

leave the continent as a result of aggressive tax

planning and questionable tax havens

In 2007 more than US$ 11.5 held in about 70 tax

havens

16

POSSIBLE RESPONSES?

• Regulation: How much?

• Government Intervention: Appropriate level?

• Protectionism: Can it be justified?

• Quick Fix vs. Sustainable Solutions?

• Current “Fix” vs. Future “Cost”

17

18

LETTER vs SPIRIT

“I’ve lived my life in a society where there was no rule of law, and that’s a

terrible existence. But a society where the rule of law is the only standard of ethical behaviour is

equally bad”Kevin Rollins

(President of Dell Computer Corporation paraphrasing Aleksander Solzhenitsyn)

EXPERIENCES FROM THE

SOUTH AFRICAN REVENUE SERVICE

19

20

WE EXPECT OF OURSELVES….

TO DO THE RIGHT THING

ALL THE TIME

EVEN IF NO ONE IS

WATCHING

SARS’ APPROACH TO ETHICAL LEADERSHIP

21

ETHICAL LEADERSHIP IS ABOUT…

• Building an effective corporate culture at SARS that is more than conforming to what is legal or as set out in the King recommendations

• Ethical and moral standards go beyond the law and the language of ‘thou shall not’

• SARS duty arises out of respect for the worth and dignity of individuals who devote their energies to the organisation and depend on SARS for their economic wellbeing

22

ETHICAL LEADERHIP IN PRACTICE

Requires:

• Absolute clarity about what values we want to promote at SARS

• Relentlessly reinforcing behaviours that support our desired values

• Visibly sanction behaviours that detract from our desired values

• Fair & Consistent Enforcement

23

CULTURE AND ETHICS

• Whilst organizational structure, policies & procedures may help, it will not ensure a sustainable ethical environment.

• There is a strong link between the organizational culture and ethics

• You have to get it into the DNA!

24

THE SARS EXPERIENCE

Elaborating on the SARS experience

• Our commitment to the public

• Our commitment to our staff

• Institutional arrangements

• Some Results at a glance

OUR COMMITMENT TO THE PUBLIC

25

26

SARS PURPOSE STATEMENT

We will contribute to South Africa’s development as a globally competitive economy by facilitating legitimate trade, tax payment and

economic growth and by eliminating illegal trade and tax evasion.

We administer an efficient tax system and reduce the compliance burden by advocating the value of compliance and creating a culture of

good citizenship across all sectors of society and the economy

A successful South Africa will improve the prosperity of its people and that of Africa

SARS THEORY OF COMPLIANCE

Rationale: Clarity & Simplicity

“The easier we make it for honest taxpayers to comply, and the earlier we detect non-compliance, the higher the levels of compliance is likely to be ”

We therefore aspire to:

• Reach out and educate

• Provide world-class service

• Enforcement responsibly

Service CharterYou are entitled to expect SARS:

To help you through• self-explanatory leaflets and booklets as well as our website• courteous and professional service at all times• providing clear, accurate and helpful responses• making clear what action you need to take and by when• being accessible via our call centre and walk-in centres• listening to your suggestions

To be fair by• expecting you to pay only what is due under law• treating everyone equally• ensuring everyone pays their fair share

To respect your constitutional rights and privacy by• keeping your private affairs strictly confidential• furnishing you with reasons for decisions taken• applying the law consistently and impartially

If you are not satisfied, you may• request that your tax affairs be re-examined• exercise your right to object and appeal• request that we advise you of the procedures to be followed in our alternative Dispute Resolution (ADR) process• lodge a formal complaint at any of our offices• lodge a complaint with the SARS Service Monitoring Office (SSMO)

In return, your obligations are to• be honest• submit full and accurate information on time• pay your tax and/or duties on time and in full• encourage others to pay their tax and/or duties• report others who are not paying their fair share• not encourage or be party to bribery or fraud in any form

OUTREACH TO TAXPAYERS

BALANCE: SERVICE & ENFORCEMENT

OUR COMMITMENT TO OUR STAFF

31

SARS Leadership Model

32

33

ADDRESSING DYSFUNCTIONAL ISSUES OR RESTRAINING FORCES THAT ACT AGAINST DRIVING

FORCES FROM SARS MANAGEMENT

You can not demand ethical behaviour until you deal with the basics

Examples for us:

• Dissatisfaction relating to Grades and Salaries

• Career Development Program

• Recruitment and Selection Practices

• Level & Quality of Communication

• Double Standards, mixed messages and inconsistent behaviour

INSTITUTIONAL ARRANGEMENTS

34

35

STRUCTURE FOLLOWS STRATEGY

SARS established an Ethics Office at the end of 2004 comprising the following units:• Integrity Unit: pre-employment screening and

security vetting

• Ethics Awareness Unit: ethics training and advice to SARS personnel

• Anti-Corruption Unit: eradicating fraud and corruption within the organization

• Other Stakeholders: FIC, SARB, SAPS, NPA, etc

36

LESSONS FOR ETHICAL LEADERSHIP

37

SOME TELL−TALE SIGNS OF UNETHICAL LEADERSHIP BEHAVIOUR

• Power-driven people

• Pursuit of narrow self-interest

• Nepotistic behaviour

• Discourage open and challenging conversations

• Focus on short term gain at the expense of long term integrity

38

IN SUMMARY

• Clear ethical expectations

• Leadership visibility & behaviour

• Substantive ethical training

• Vigilance & Relentless monitoring

• Visible rewards and sanctions

• Create a Safe environment – for frank conversation, for bad news, for learning

39

ETHICS CANNOT BE ROLE PLAYED!

Ethics in fact is:

• More than “leadership saying”

• More than “leadership doing”

• It is about “leadership being”

SOME RESULTS AT A GLANCE

40

STRIVING FOR SERVICE EXCELLENCE

41

Metric 2004 – 2006(1st 3 years)

2007 – 2009(2nd 3 years)

Registered users ±500k ±5m

Number of returns ±1.5m p.a. ±7m p.a.

% of eFiled returns to total returns

±8% Approaching 50%

Value of Assessment processed via eFiling

±R100bn ±R382bn

Payments processed via eFilling

±R55bn ±R343bn

% Payments to Total Revenue

±13% ±55%

41

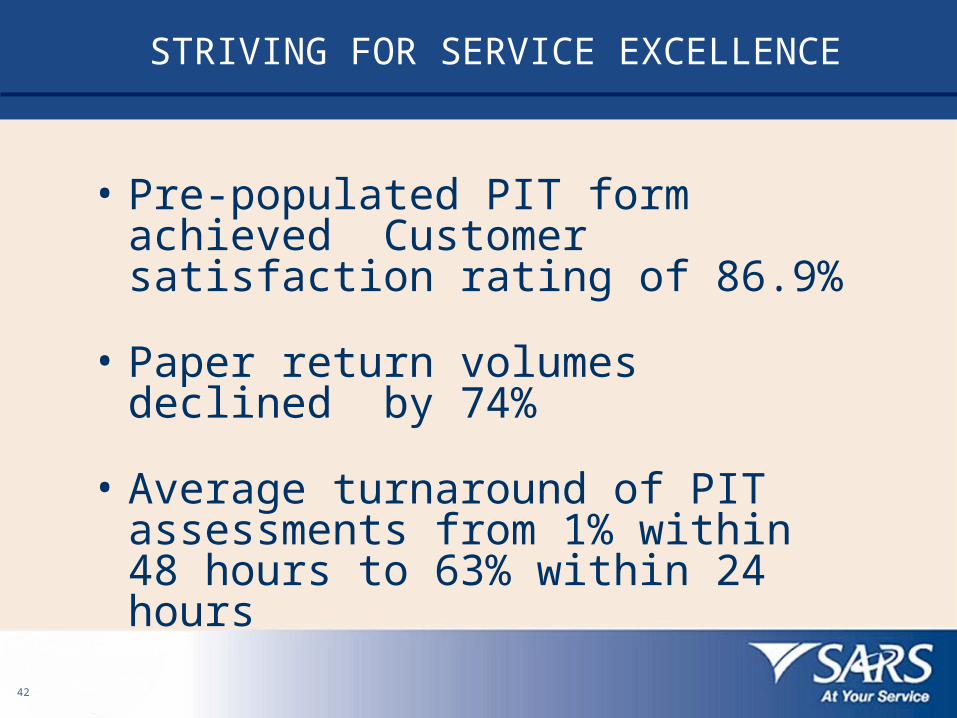

Introduction of Electronic Filing

• Pre-populated PIT form achieved Customer satisfaction rating of 86.9%

• Paper return volumes declined by 74%

• Average turnaround of PIT assessments from 1% within 48 hours to 63% within 24 hours

42

STRIVING FOR SERVICE EXCELLENCE

TOWARDS A CULTURE OF VOLUNTARY COMPLIANCE

• 31% improvement on PAYE submissions

• 518 guilty verdicts attained

• 73k audits - average yield of ~R70k

per case

• R13.4b debt collected last year

43

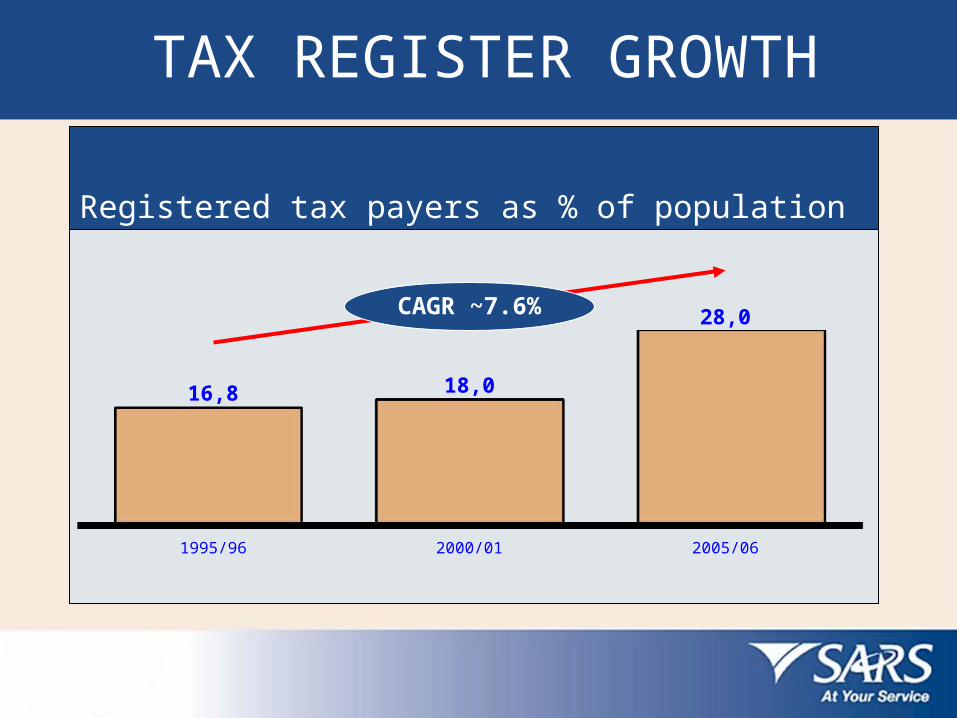

TAX REGISTER GROWTH

Registered tax payers as % of population

16,8

1995/96

18,0

2000/01

28,0

2005/06

CAGR ~7.6%

Revenue

• Revenue growth from R184b to R625b over past 10 years (CAGR ~ 13%)

• Revenue increased from R572.8b to R625 b

45

COST AS PERCENTAGE OF REVENUE

LASTLY…

BY OUR OWN ASSESSMENT SARS, DESPITE ITS RELATIVE

SUCCESSES STILL HAVE MANY CHALLENGES AHEAD, REMAIN COMMITTED TO THIS JOURNEY

47

48

CONCLUSION

“The ultimate measure of a man is not where he stands in moments of

comfort and convenience, but where he stands at times of challenge and controversy”

Martin Luther King, Jr.