Embed Size (px)

Citation preview

1

Introduction to the Cross Media Optimization Study

Introduction to the Cross Media Optimization Study

Robert AcquaottaDirector, Advertiser Relations

2

Landmark study methodology assesses “Cost Effectiveness”

of each Medium

Scientifically evaluates real world, in-market

campaigns

Marketers carefully considered

methodology

Largest Cross Media Study Ever ConductedLargest Cross Media Study Ever Conducted

3

Introducing the ParticipantsIntroducing the Participants

IAB:IAB: The organizing Association

Marketing Evolution/Rex Briggs:Marketing Evolution/Rex Briggs: Developed landmark study methodology and executed the studies

Dynamic Logic:Dynamic Logic: Applied AdIndex® product to collect consumer views and behavior

ARF (Advertising Research Foundation):ARF (Advertising Research Foundation): Reviewed the study methodology

Forrester Research:Forrester Research: Full analysis & review

4

State of The Union:

Interactive Medium

State of The Union:

Interactive Medium

5

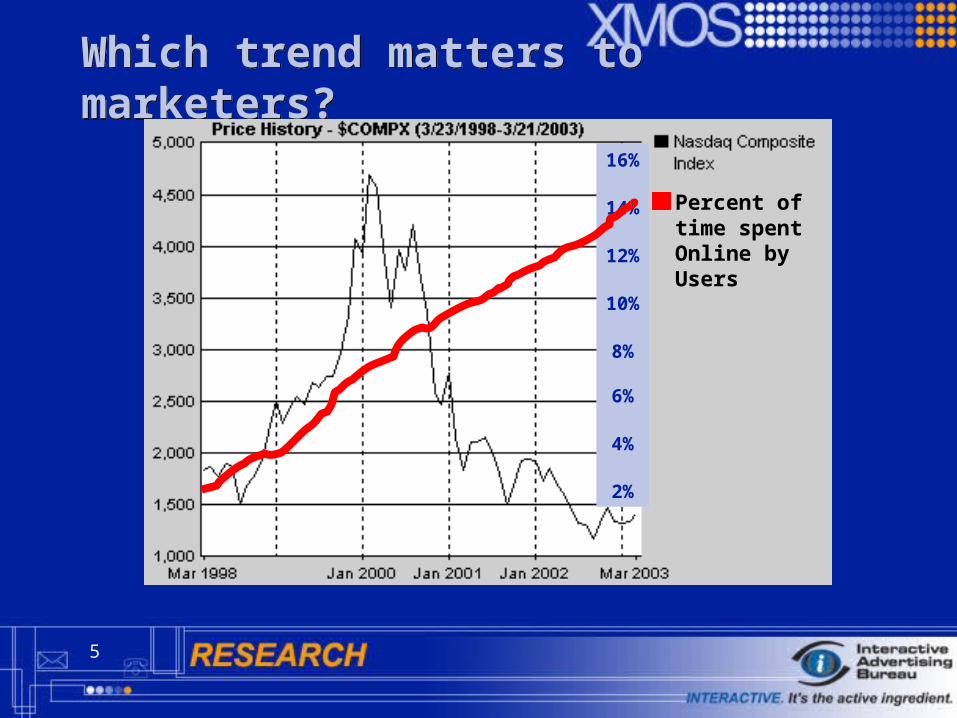

Which trend matters to marketers?Which trend matters to marketers?

Percent of time spent Online by Users

16%

14%

12%

10%

8%

6%

4%

2%

6

Online Delivers the AudienceOnline Delivers the Audience

66%

34%

Source: Harris Interactive, April 2002

Fully Two Thirds of the

Adult U.S. Population is Now Online

137 Million Consumers Online

137 Million Consumers Online

Source: Harris Interactive, April 2002

7

…And their Usage Doubles Over Time…And their Usage Doubles Over Time

6.57.5

8.8

11.1

13.2

0

2

4

6

8

10

12

14

Ho

urs

Per

Wee

k

<1 year 1-2 years 2-4 years 4-5 years 5+ years

The longer online, the more they use & engage

Source: eMarketer; UCLA Center for Communications Policy, November, 2001

8

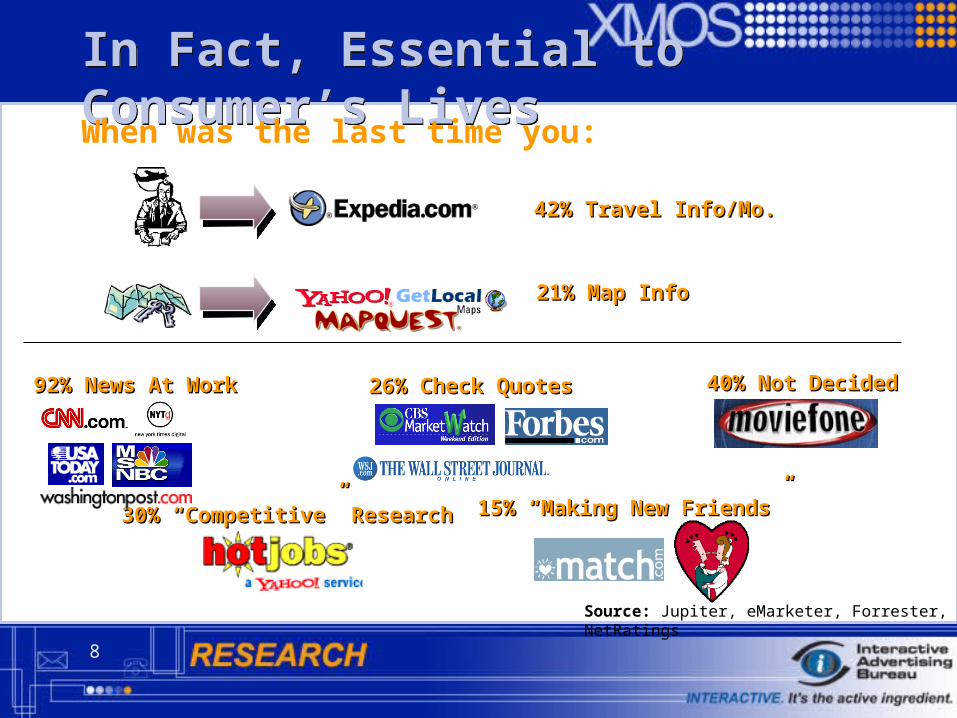

In Fact, Essential to Consumer’s LivesIn Fact, Essential to Consumer’s LivesWhen was the last time you:

Source: Jupiter, eMarketer, Forrester, NetRatings

40% Not Decided40% Not Decided

42% Travel Info/Mo.42% Travel Info/Mo.

21% Map Info21% Map Info

92% News At Work92% News At Work

30% “Competitive” Research30% “Competitive” Research 15% “Making New Friends”15% “Making New Friends”

26% Check Quotes26% Check Quotes

9

The Media Landscape Has ChangedThe Media Landscape Has Changed

34%

24%

13%9%

0%

5%

10%

15%

20%

25%

30%

35%

% D

ay A

fter

TV

Rec

all

1965 1974 1981 2000

Source: NAB (1965-1986); Nielsen (2000)

Percent of adult evening viewers who can name a brand advertised watched

Make bars in same colors

10

Perhaps you have questions about the

Effectiveness of Online advertising…

Perhaps you have questions about the

Effectiveness of Online advertising…

11

1,000+ Ads Tested – Online Advertising Works!1,000+ Ads Tested – Online Advertising Works!

0% 20% 40% 60% 80%

PurchaseIntent

BrandFavorability

MessageAssociation

Aided BrandAwareness

Exposed

Control

Mean Changes for Four Measures of EffectivenessSource: Dynamic Logic MarketNorms – Database of 400 campaigns

*All measures statistically significant at 99%; n=campaigns; between 375 and 416

+3.7+3.7

+5.9+5.9

+2.0+2.0

+2.1+2.1

12

The New Marketing QuestionThe New Marketing Question

No longer talking about WhyWhy Online

HowHow to integrate

Specifically, how to integrate to

maximize:• Brand Awareness• Brand Image • Purchase Intent & Sales

13

Key Findings from XMOSKey Findings from XMOSThe major findings of the Study to date

14

The Key Finding of the StudyThe Key Finding of the Study

Same budget Same budget Better resultsBetter results

15

Why does Increasing Online produce better results within the same budget?Why does Increasing Online produce better results within the same budget?

Online advertising affects branding metrics

Online advertising is typically more cost efficient at producing branding gains

Online reaches those who would otherwise not get the advertising message

CoverageCoverage

EffectivenessEffectiveness

ValueValue

16

CoverageCoverage

Media Media potholespotholesCoverageCoverage

17

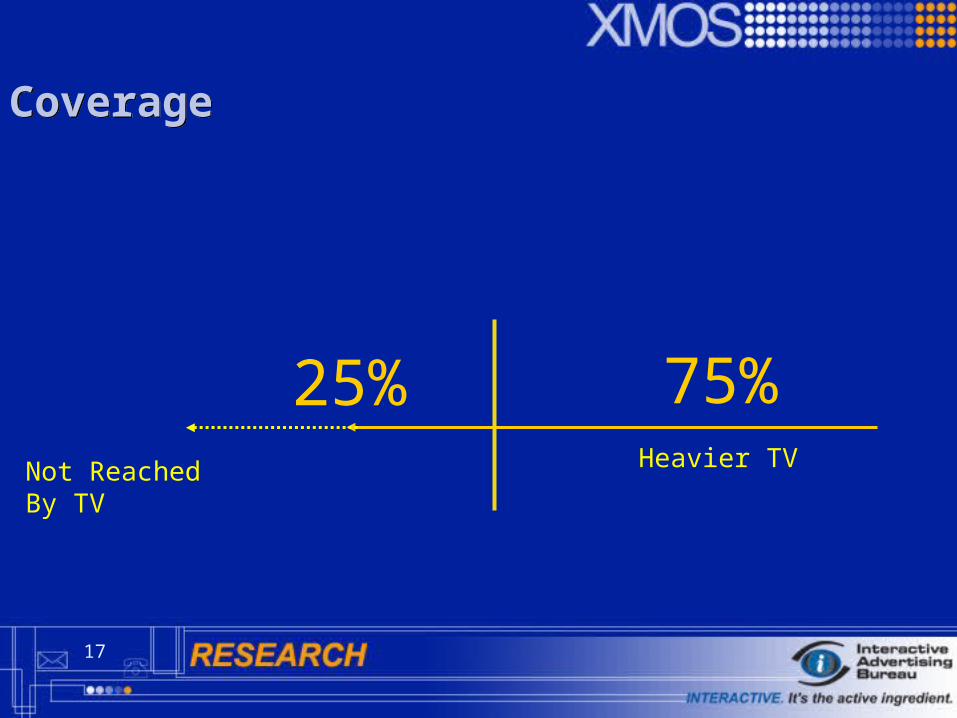

CoverageCoverage

Heavier TV Not Reached

By TV

25% 75%

18

Frequency Does Not Fall EvenlyFrequency Does Not Fall Evenly

2.4

4.3

7.6

16.4

1.0

V IV III II I

HEAVIESTLIGHTEST

Avg

. F

req

by

Qu

inti

le Frequency considered

wasteful

Frequency considered not helpful

15%

19

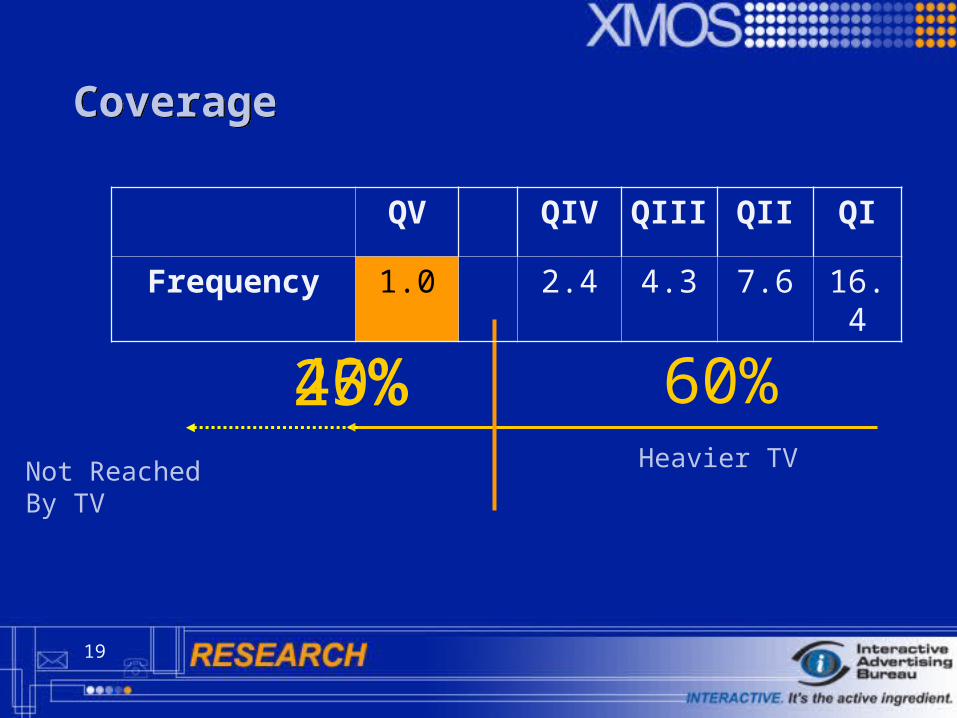

CoverageCoverage

Heavier TV Not Reached

By TV

25%

QV QIV QIII QII QI

Frequency 1.0 2.4 4.3 7.6 16.4

60% 40%

20

CoverageCoverage

Media Media potholes!potholes!

21

Effectiveness

and ValueEffectiveness

and Value

22

Effectiveness and valueEffectiveness and value

*OTS = Opportunity to see advertisement based on GRP levels

% P

urch

ase

inte

nt

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10

Frequency: Number of OTS* ad exposures

Diminishing returns

23

Bra

n din

g e f

f ect

Marketing spend

Television

Internet

Effectiveness and valueEffectiveness and value

24

CoverageCoverage

EffectivenessEffectiveness

ValueValue

• Brand Awareness

• Brand Image

• Purchase preference

25

Growing Brand Awareness Growing Brand Awareness The major findings of the Study to date

26

Growing Brand AwarenessGrowing Brand Awareness

Increasing Online is more cost effective way to build brand awareness

27

Product AwarenessProduct AwarenessAided awareness: Grilled chicken flatbread sandwich

*4 day moving average (for greater sample size stability)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

6/3 6/5 6/7 6/9 6/11 6/13 6/15 6/17 6/19

Broadcast Only

28

Online builds brand awareness Online builds brand awareness

That’s a 3pt incremental That’s a 3pt incremental branding gain for same branding gain for same budgetbudget

10.0%10.0%

20.0%20.0%

30.0%30.0%

40.0%40.0%

50.0%50.0%

60.0%60.0%

0.0%0.0%

*Online advertising:

• 60% reach/2.0 frequency

• TV TRPs trimmed by approximately 20%13.6%13.6%

Of budgetOf budget

Point of diminishing returns

29

Optimizing for Brand BuildingOptimizing for Brand Building

Recommendation

Intern

etIn

ternet R

eachR

each

60%60%

or66 MillionMillion

More More Consumers Consumers Aware of the Aware of the

Product!Product!The AffectThe Affect

==

Aw

areness

Aw

areness

30

CoverageCoverage

EffectivenessEffectiveness

ValueValue

31

Positioning the Brand Brand ImagePositioning the Brand Brand Image

The major findings of the Study to date

32

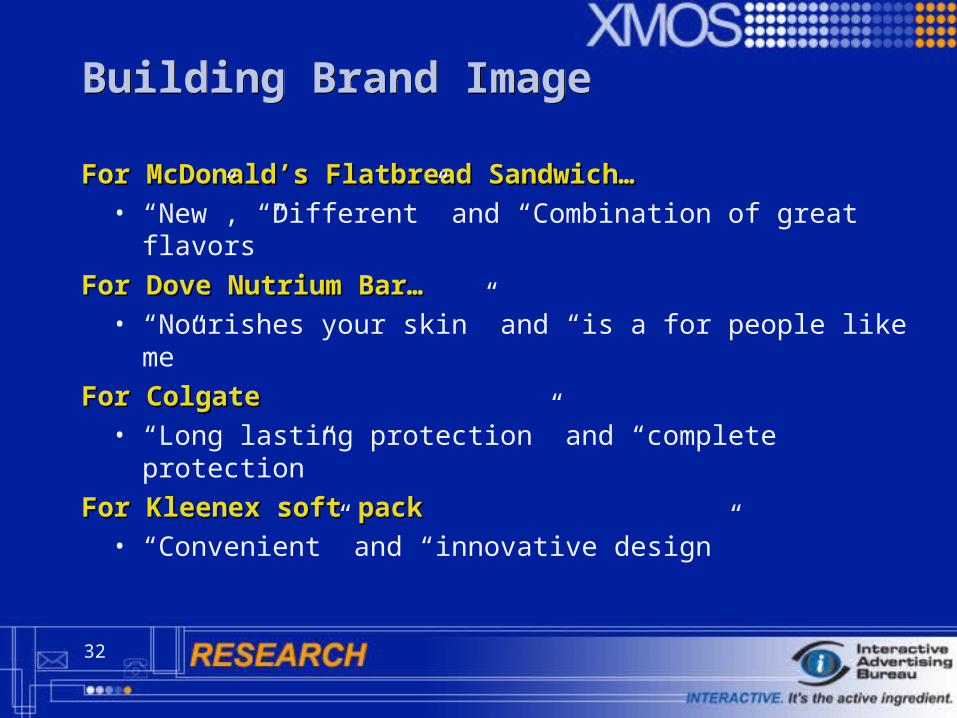

Building Brand ImageBuilding Brand Image

For McDonald’s Flatbread Sandwich…For McDonald’s Flatbread Sandwich…• “New”, “Different” and “Combination of great flavors”

For Dove Nutrium Bar…For Dove Nutrium Bar… • “Nourishes your skin” and “is a for people like me”

For ColgateFor Colgate• “Long lasting protection” and “complete protection”

For Kleenex soft packFor Kleenex soft pack• “Convenient” and “innovative design”

33

Cross-media synergy

Creative reinforced the Creative reinforced the core message across mediacore message across media

34

“Surround Sound Marketing”“Surround Sound Marketing”

““ Just as each speaker accomplishes Just as each speaker accomplishes the same goal by exploiting its unique the same goal by exploiting its unique position and strength, each element position and strength, each element of the marketing mix must find its of the marketing mix must find its strength and leverage it to surround strength and leverage it to surround the consumer with a synergistic and the consumer with a synergistic and consistent message.”consistent message.”

35

What about the

40% of your target that are not reached by TV?

What about the

40% of your target that are not reached by TV?

36

The Kleenex® TV campaignThe Kleenex® TV campaign

37

Campaign over 8 weeksCampaign over 8 weeks

Heavier TV Lighter TV Not Reached

By TV

40% 60% 25%

Heavier Online Heavier Online

Lighter Online Lighter Online Not Reached Not Reached By Online By Online

38

39

Summary of branding gains among lightly reached / not reached TV audienceSummary of branding gains among lightly reached / not reached TV audience

Positive Brand association Positive Brand association

(top box average) (top box average)

35%

39%

39%

42%

10% 15% 20% 25% 30% 35% 40% 45%

No Mag or OnlineNo Mag or Online

Online (no mag)Online (no mag)

Magazine (no online)Magazine (no online)

Magazine and OnlineMagazine and Online

40

CoverageCoverage

EffectivenessEffectiveness

ValueValue

41

Purchase Intent & SalesPurchase Intent & Sales

The major findings of the Study to date

42

Results in a 14% increase in purchase intent

Same Budget, Same Budget, Better ResultsBetter Results

Results in a 14% increase in purchase intent

Same Budget, Same Budget, Better ResultsBetter Results

Optimizing OnlineOptimizing Online

43

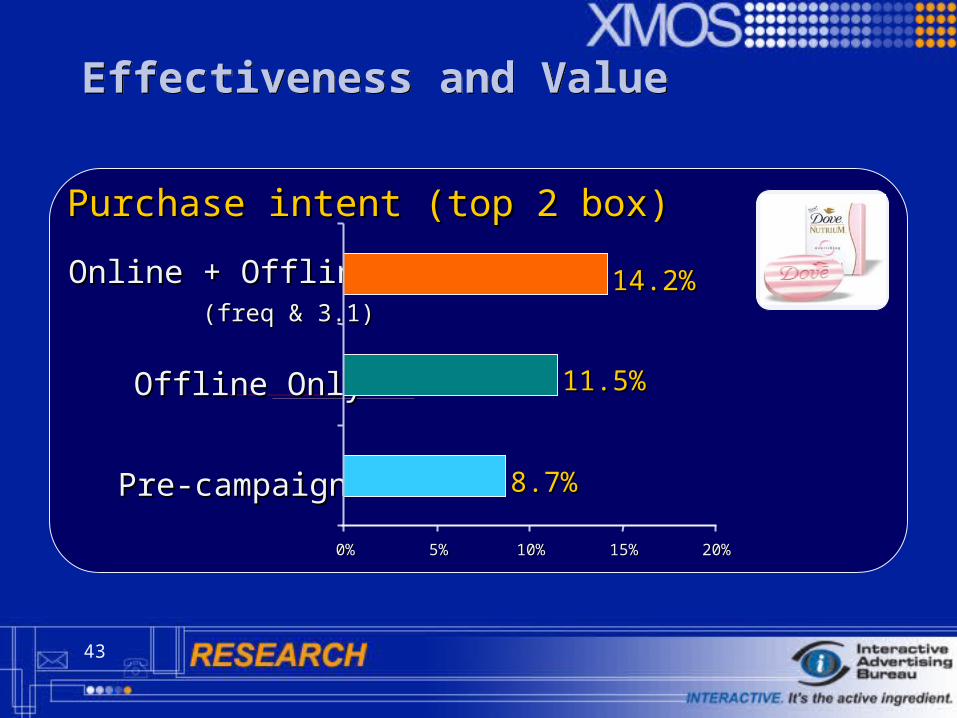

Effectiveness and Value Effectiveness and Value

Purchase intent (top 2 box)Purchase intent (top 2 box)

8.7%8.7%

11.5%11.5%

14.2%14.2%

0%0% 5%5% 10%10% 15%15% 20%20%

Pre-campaignPre-campaign

Offline OnlyOffline Only

Online + OfflineOnline + Offline ((freq & freq & 3.1)3.1)

44

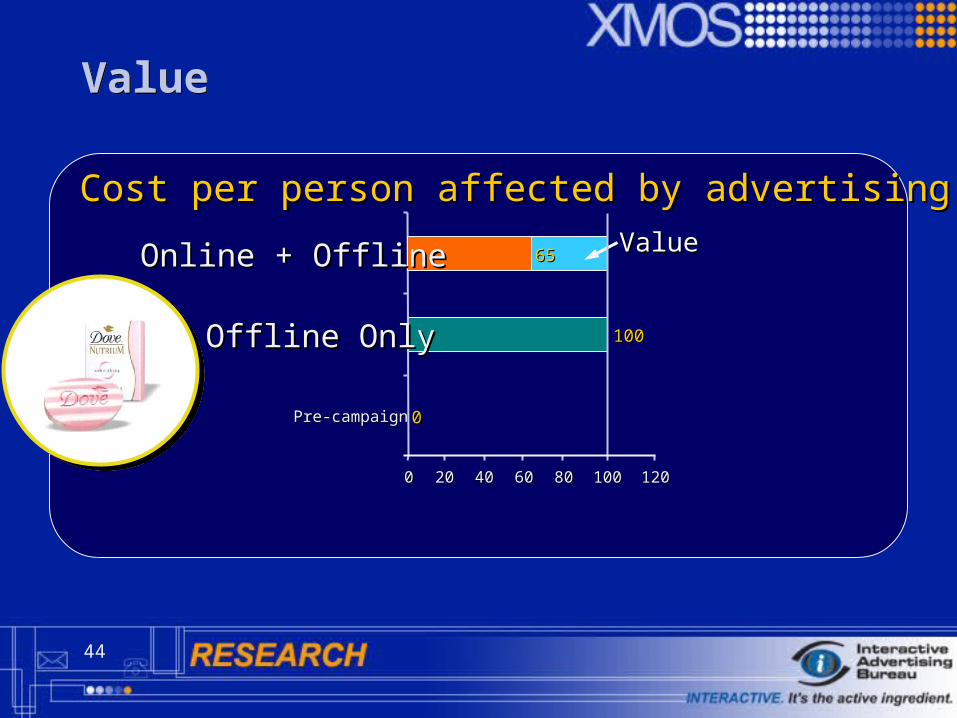

ValueValue

ValueValue

Cost per person affected by advertisingCost per person affected by advertising

00

100100

00 2020 4040 6060 8080

Pre-campaignPre-campaign

100100 120120

6565

Offline OnlyOffline Only

Online + OfflineOnline + Offline

45

All Media Demonstrate Diminishing ReturnsAll Media Demonstrate Diminishing Returns

Number of advertising exposures

Ave

rag

e o

f B

ran

din

g M

etri

cs (

%)

MagazineMagazineOnlineOnline

TelevisionTelevision

20%

25%

30%

35%

40%

45%

0 2 4 6 8 10 12 14 16Frequency

46

Optimizing the Dove Plan for Brand BuildingOptimizing the Dove Plan for Brand Building

2.0 impressions(down from 2.6)

5.5 impressions (down from 6.0)

TV

3.1 Impressions(up from 1.7)

Inte

rnet

TV Print

85%

50%

10%

10% in Original

Plan

Reach Frequency

Inte

rnet

60%

47

Colgate Total ToothpasteColgate Total Toothpaste

48

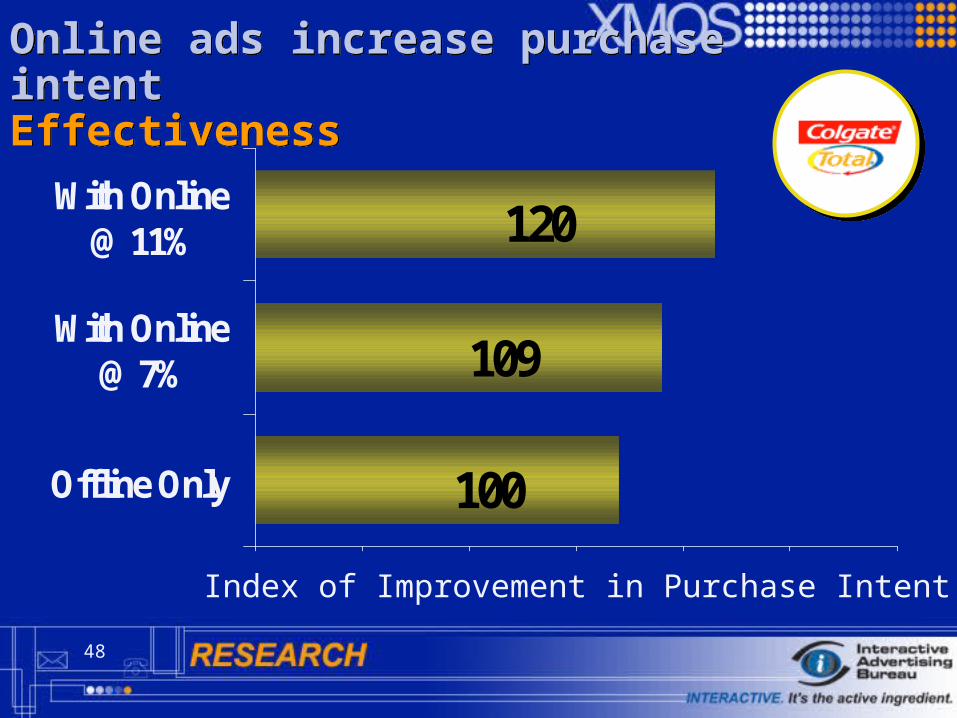

Online ads increase purchase intentEffectivenessOnline ads increase purchase intentEffectiveness

120

109

100

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

Offline Only

With Online@ 7%

With Online@ 11%

Index of Improvement in Purchase Intent

49

Online is More Cost Effective than Other MediaOnline is More Cost Effective than Other Media

Effective TV and Print CPMs are compared and indexed to this number.

Online TV Magazine

(100) (123) (184)

Purchase Intent Purchase Intent

Cost of Change by Other Media Indexed to Online

50

Overall, Online is the most cost efficient mediaOverall, Online is the most cost efficient media

Cost per impact

Media CombinationsOnline only Most cost efficient

Magazine & Online

All media combined

Broadcast Only

Magazine Only Least cost efficient

Point gain over baseline is calculated by measuring the post branding level and subtracting the pre-campaign level (linear regression used to measure underlying trend). Costs per person impacted indexed against online advertising only and rank ordered.

51

Recap: Topline Brand ResultsRecap: Topline Brand Results

Base %Base %Online:Online:

Reco %Reco %Online:Online:

Resu

lts

And more to come…And more to come…

2%2%2%2%

15%15%

+14%

1%1%1%1%

13%13%

+8%

7%7%7%7%

11%11%

+20%

+34%

2%2%2%2%

10%10%

+7%

Purchase Intent

Brand Image

Awareness

52

CoverageCoverage

EffectivenessEffectiveness

ValueValue

53

Key TakeawaysKey Takeaways

Same budget Same budget Better resultsBetter results

54

Thank YouThank You