Embed Size (px)

Citation preview

1IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Transfer Pricing:

Comparing the Indian Approach with the OECD Transfer Pricing Guidelines

2IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Panel

Chairman:• Gautam Doshi, Joint Managing Director, Reliance

Anil Dhirubhai Ambani Group.

Speakers:• Shyamal Mukherjee, PricewaterhouseCoopers India• Rupak Saha, GE India• Caroline Silberztein, OECD

3IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Agenda

• Implementation of the arm’s length principle in India: selected issues:– Comparability and TP documentation

– Lack of guidance for certain transactions

– Dispute resolution and dispute prevention

– Transfer pricing and customs valuation of related party transactions

• Conclusion: what does the future hold?

4IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Implementation of the arm’s length principle in India: selected issues

5IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Access to comparables information

• Indian Rules permit use of public data- supported by authentic documents,

illustrative list of documents suggest comparable data to be maintained by the

taxpayer must be published data and available in public domain [Rule 10D(3)]

• OECD guidance on documentation: taxpayer to determine transfer pricing based

upon information reasonably available at the time of determination [Para 5.3

OECD Guidelines (“TPG”)]

6IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

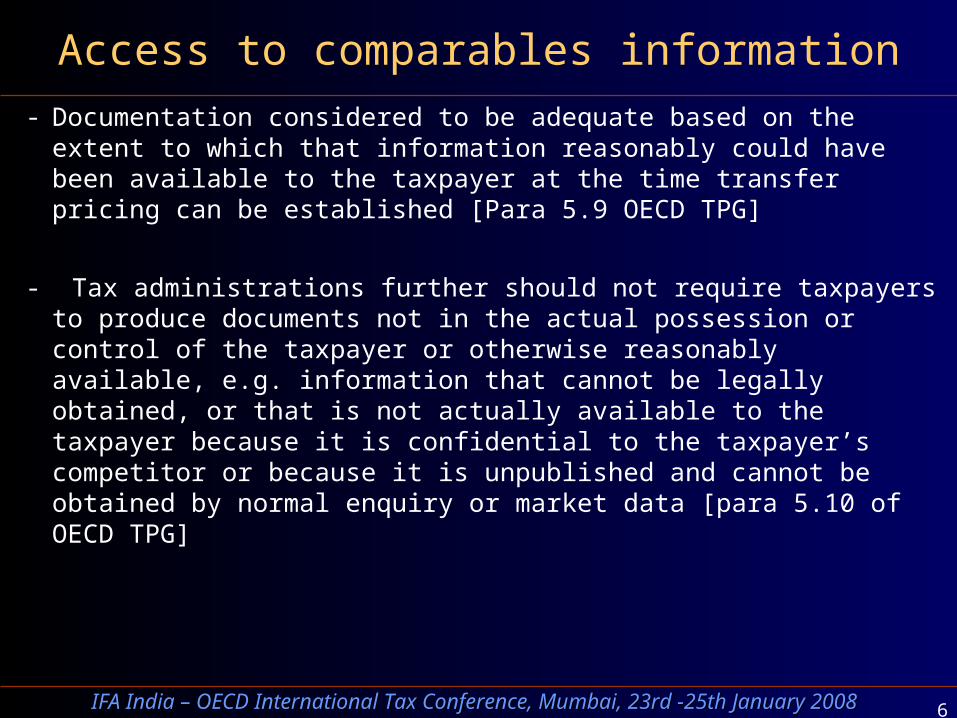

Access to comparables information

- Documentation considered to be adequate based on the extent to which that information reasonably could have been available to the taxpayer at the time transfer pricing can be established [Para 5.9 OECD TPG]

- Tax administrations further should not require taxpayers to produce documents not in the actual possession or control of the taxpayer or otherwise reasonably available, e.g. information that cannot be legally obtained, or that is not actually available to the taxpayer because it is confidential to the taxpayer’s competitor or because it is unpublished and cannot be obtained by normal enquiry or market data [para 5.10 of OECD TPG]

7IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Access to comparables information – OECD perspective

- Sources of information: commercial database; taxpayer’s knowledge of competitors or comparables; industry analyses; etc.

- How detailed / transactional are public data?

- Non-domestic comparables

- Increased focus on functional comparability for integrated industries

8IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

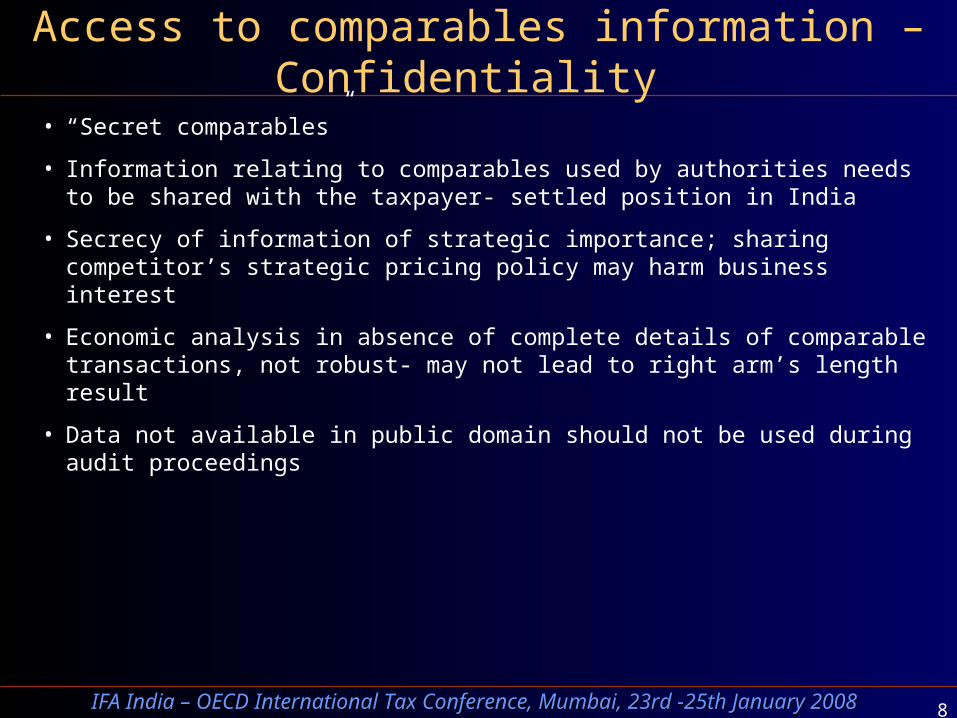

Access to comparables information – Confidentiality

• “Secret comparables”

• Information relating to comparables used by authorities needs to be shared with the taxpayer- settled position in India

• Secrecy of information of strategic importance; sharing competitor’s strategic pricing policy may harm business interest

• Economic analysis in absence of complete details of comparable transactions, not robust- may not lead to right arm’s length result

• Data not available in public domain should not be used during audit proceedings

9IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Data for Comparability Analysis: timing issues

• Contemporaneous documentation required [Rule 10D(4)]

• Preference for current year data for comparability analysis

[Rule 10B(4)]

• Use of past 2 years data permitted – only in certain

circumstances

• Multiple year analysis more robust - allowed globally

• Paras 1.49, 1.50 and 3.44 of the OECD TPG

10IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Data for Comparability Analysis

• Fresh search for updated data at the time of audit - such data

not available with the taxpayer while setting arm’s length

prices (Paras 5.3 and 5.9 of the OECD TPG)

• Data available with taxpayer at the time of documentation

should be acceptable and used in audits

11IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

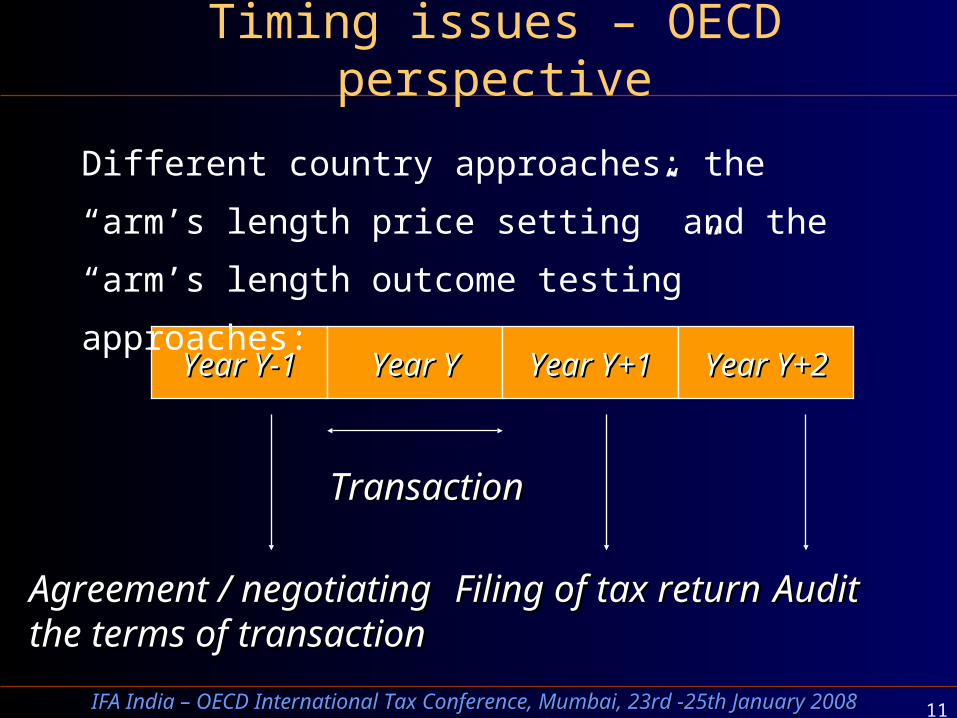

Timing issues – OECD perspective

Agreement / negotiatingAgreement / negotiatingthe terms of transactionthe terms of transaction

TransactionTransaction

Filing of tax returnFiling of tax return AuditAudit

Year Y-1Year Y-1 Year YYear Y Year Y+1Year Y+1 Year Y+2Year Y+2

Different country approaches: the “arm’s length price

setting” and the “arm’s length outcome testing”

approaches:

12IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Timing issues – OECD perspective

• OECD TPG paragraph 1.51:

“Data from years following the year of the transaction may also be relevant to the analysis of transfer prices, but care must be taken by tax administrations to avoid the use of hindsight. For example, data from later years may be useful in comparing product life cycles of controlled and uncontrolled transactions […]. Subsequent conduct by the parties will also be relevant in ascertaining the actual terms and conditions that operate between the parties.”

13IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Data for Comparability Analysis: multiple year data

• Average data analysis more robust

– Better comparability analysis

– Evens out product/ business life cycles, short term

economic conditions etc.

• Indian Regulations should unconditionally permit use of past

years data

14IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

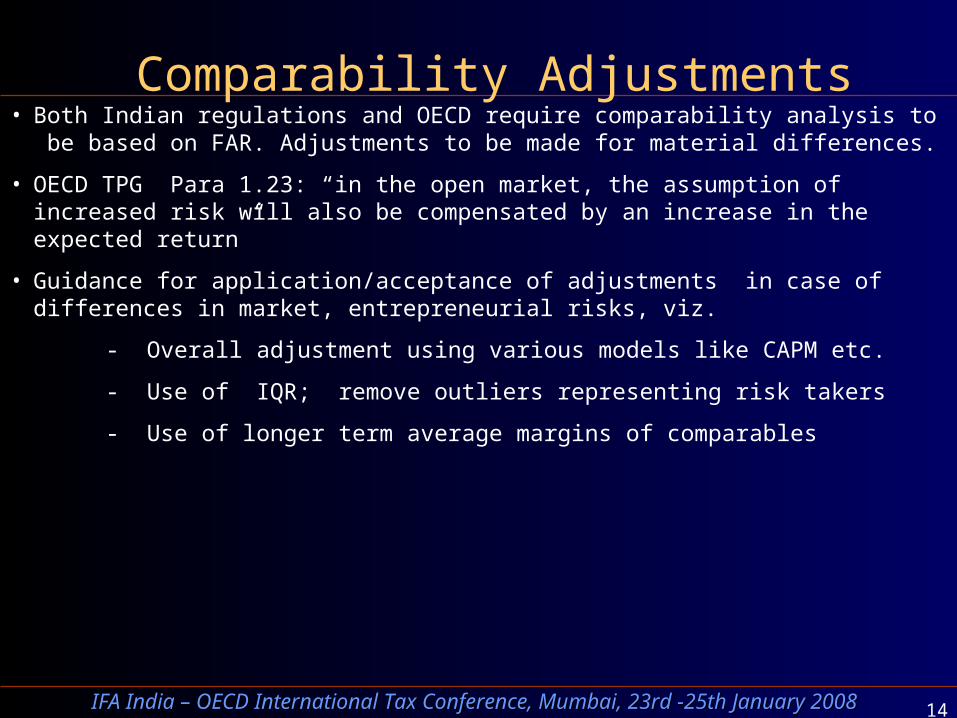

Comparability Adjustments• Both Indian regulations and OECD require comparability analysis to be based on FAR.

Adjustments to be made for material differences.

• OECD TPG Para 1.23: “in the open market, the assumption of increased risk will also be compensated by an increase in the expected return”

• Guidance for application/acceptance of adjustments in case of differences in market, entrepreneurial risks, viz.

- Overall adjustment using various models like CAPM etc.

- Use of IQR; remove outliers representing risk takers

- Use of longer term average margins of comparables

15IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Comparability Adjustments• Indian TP authorities have expected limited risk captives to earn

margins comparable to entrepreneurs; disregard of the risk and asset profile of the taxpayer vis-à-vis comparables

• Indian authorities have in most cases accepted adjustment made to comparables primarily for working capital differences

• More guidance for application/ acceptance of other adjustments:

– Excess capacity adjustments - Credit risk adjustments

– Adjustment for non-comparable functions, pass through costs etc.

– Adjustment for R&D activities - Other adjustments

16IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Acceptability of Business Strategies and Economic Principles

• OECD recommends consideration of business strategies for determining comparability [TPG para 1.31 to para 1.35]

• Acceptability of business strategies adopted by taxpayer:

– Start-up companies - Market penetration strategies; initial/interim losses as part of bigger strategy

– Intentional set-offs - Use of budgets and forecasts

– Other business and commercial practices

• Acceptability of economic techniques and methods

• Business realities and commercial considerations should be

recognized and accepted; documentation guidelines

17IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Acceptability of Business Strategies and Economic Principles - Losses

• Indian TP authorities may not appreciate business dynamics and strategies while conducting audits; profit position of the taxpayer is the prime focus

• General resistance to losses earned by taxpayers as well as loss comparables

• Cherry picking of profitable companies for comparison purposes

• Losses justified, if part of business strategy [para 1.52 and 1.54 of the OECD TPG]

18IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Losses – OECD perspective

• No reason to systematically exclude loss-making comparables.

No cherry picking.

• But: re-examine whether the selection of comparables was well

done. What are the reasons for the comparable to be loss-

making ? Is it because of a different risk profile (e.g. if tested

party is risk-less and loss making comparable is full-risk).

• In addition, many countries reject long-term loss making

distributors.

19IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Transactional/ segment-level analysis

• OECD TPG permit aggregated analysis if transactions are closely interlinked [paras 1.42 to 1.44]

• Indian TP authorities: preference for transactional or product-wise analysis over overall, aggregated company-level analysis disregarding:

– principles of aggregation and materiality of transactions

– taxpayer may adopt basket of products approach to manage business dynamics and achieve sustainability on a consistent basis, organize their business into various baskets or product portfolios

• Typically have sought “product-wise” profitability. Guidance needed.

20IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Transactional / aggregated analysis: OECD perspective

• Need balance between theoretical soundness and workability: transactional focus of all methods, but recognise that third party data often not transactional

• Difference between:– Taxpayer data: segmentation possible according to

coherent parts, e.g. product or business line– Third party comparables: company-wide data

acceptable if most reliable data available and reasonably homogeneous

=> Segmented taxpayer data often compared to several sets of company-wide third party data

21IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Intentional set-off

• Intentional set-offs are consistent with the arm’s length

principle [para 1.60 and 1.62 of the OECD TPG]

• Such approach reflects commercial realities of a

business/transactions

• No specific guidance on intentional set-off in the Indian TP

regulations

• Guidance (including documentation) needs to be included,

drawing support from the OECD TPG

22IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Arm’s Length Range

• Indian regulations permit limited 5% variation from Arm’s

Length Price (ALP) [proviso to Section 92C(2)]

• ALP computed as mean of comparable prices

• OECD Guidelines permit use of complete arm’s length range-

entire range of outcomes obtained by application of most

appropriate method; all such results are considered relatively

equally reliable [para 1.45 of the OECD TPG]

• Recent Indian Tribunal Ruling – step in the right direction

23IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Arm’s Length Range

• Many countries allow use of Inter Quartile Range (IQR)

• Limited flexibility in view of the mean and 5% tolerance

band- leads to mathematical approach and cherry picking of

comparables

• Indian rules should recognize the concept of range/ IQR and

replace “mean” with “median”

24IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Lack of guidance for certain transactions

• Lack of guidance in the Indian TP regulations on transactions

like:

– Transfer of intangibles

– Cost contribution agreements

– Other complex transactions

• OECD TPG Chapters VI & VIII

• Guidance/ Rules required in Indian Regulations

Dispute resolution: elimination of double taxation

Dispute prevention: APAs

26IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Secondary adjustments

• Refund of withholding tax not allowed in case of expense

adjustments to paying Indian entities [second proviso to

Section 92C(4)]

• Results in double taxation of group profits – against basic

principles of taxation

• Corresponding adjustment should be permitted

27IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

MAPs and Arbitration – OECD perspective

• Next panel: Resolution of Tax Treaty Disputes

• Transfer pricing disputes are among the most costly and complex international tax disputes

• Essential to have efficient mechanisms to eliminate double taxation

28IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Advance Pricing Arrangements

• “Arm’s Length” – an abstract concept

• APA’s – allowed globally

• Need for comprehensive procedure to obtain APA

• Adequate mechanism for negotiating bilateral and multilateral

APA’s required

• Need to introduce APA mechanism in domestic tax law

29IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

APAs: the OECD perspective• APAs involve a lengthy and resource intensive process (especially for bilateral

ones),but one which is remarkably short compared with TP examinations + litigation + mutual agreement procedure to resolve double taxation

• They cannot be a wide scale solution and in particular they cannot be a substitute for the legal certainty provided by clear regulations.

• But APAs can be part of a more constructive dialogue between taxpayers and tax authorities and be instrumental in limiting double taxation issues.

30IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

APAs: the OECD perspective

• Voluntary process

• Non controversial (each party can withdraw at any time)

• In advance of the transactions => not an archive digging

• Only transfer pricing, agreed scope of selected transactions => more focused than examinations in general

• If bilateral or multilateral: eliminate risk

of double taxation

• Can provide certainty for up to 5 years

(renewable)

31IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

APAs: the OECD perspective

• APA programmes can be adapted to the economic realities of the country:

• Mexico: extensive APA programme developed mostly for the maquiladora industry (unilateral and bilateral APAs)

• China introduced the APA concept in its transfer pricing regulations in 1998. In 1998-2007: approx. 160 unilateral APAs completed in China. In 2005: first bilateral APA between China and Japan; 2007: first bilateral APA between China and the United States and first bilateral APA between China and Korea.

• Russia has indicated willingness to implement APAs in 2010

Transfer pricing and customs valuation of related party

transactions

33IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008

Jurisdiction Exporting Country Importing Country

Authority Customs Department

Tax Department Customs Department

Tax Department

Primary Objective

Prevent money laundering

Maximize taxable income

Maximize import duty

Maximize taxable income

Achieving the Objective

Determine correct export

value

Maximize export value

Maximize import value

Minimize import value

AssesseeAssessee

Higher price for Higher price for higher customs dutyhigher customs duty

Lower price for Lower price for higher taxable higher taxable

incomeincome

Income Tax Income Tax DepartmentDepartment

Customs Customs DepartmentDepartment

Approach To Valuation Approach To Valuation Under Customs and Income Tax LawsUnder Customs and Income Tax Laws

34IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Global Convergence InitiativesGlobal Convergence Initiatives

• Many countries have initiated processes to increase interaction between the Customs and Transfer Pricing authorities

• Various governments have issued guidelines to resolve the Customs / TP conflicts

• Review of TP Studies, Advance Pricing Arrangements and other TP documentation for determining customs value

• WCO/OECD Conference on TP and Customs Valuation in Brussels

• Indian Government’s initiative - Customs Circular No. 20/2007 dt. 8th May, 07

35IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

• Implementation of the recommendations of the Joint Working Group, on transfer pricing, comprising officers from Income-tax and Customs

- Two – Tier co-operation through recommended ‘Bi-monthly’ and ‘Six-monthly’ joint meetings

- Exchange of information on specific-cases

- Sharing of ‘Related Party’ information on a ‘Need to Know’ basis

- Training programs for officers of both Departments

Indian Initiative …/…Indian Initiative …/…

36IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

• Questionnaire issued by Chief Commissioner of Customs to various institutions to gather information on several issues surrounding valuation

• Aim to increase the co-ordination and exchange of information between the Customs and Income Tax Authorities on Transfer Pricing matters

• Transfer Pricing Officers (TPOs) have started focusing on Customs Valuation to evaluate the appropriateness of transfer prices

Indian Initiative (cont’d)Indian Initiative (cont’d)

37IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008

Key Aspects

Transfer Pricing Customs

Methods Specified

Comparable Uncontrolled Price (CUP)

Using exact comparables

Using inexact comparables (with appropriate adjustments)

Transaction Value of

Identical goods

Similar goods

Resale Price Deductive Value

Cost plus method Computed Value

Profit split / TNMM Residual method

Customs and TP: Common Objective, Customs and TP: Common Objective, Differing Approach…Contd.Differing Approach…Contd.

38IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008

Key Aspects Transfer Pricing Customs

Choice of valuation methodology

Arm’s-length Price – Based on the choice of the ‘Most Appropriate Method’.

No Priority to any Methods.

Based on the concept of “Arithmetic mean”.

Transaction Value (TV) based on the specified methods

Upon rejection of the assessee determined TV, the hierarchy of the valuation methods followed to re-determine the price.

Deviation from ALP

Deviation of + / - 5% Range from the ALP is permissible

No such range specified

Documentation requirements

Enterprise and Transaction wise “Contemporaneous Documentation” to be maintained by the company. Specified in Rule 10D.

No requirements specified by the legislation.

Customs and TP: Common Objective, Customs and TP: Common Objective, Differing Approaches…Contd.Differing Approaches…Contd.

39IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23th -25th January 2008

Key Aspects Transfer Pricing Customs

Adjustments to the book value of imports

No legislated adjustments specified. Reasonable adjustments may be made by the Assessee or the TPO, to eliminate material effect

Mandatory adjustments provided under Rule 9 of Customs Valuation Rules (CVR). For eg: Commission and brokerage, container costs, packing costs, assists, royalties and license fees, etc.

Time period for which data used

TP allows for usage of data upto 2 years prior to the relevant financial year

3-6 months

Timing of audit and Validity of the order

The TP audit concluded within a period of 31 months from the end of the relevant assessment year

TP order valid for the year for which the audit takes place

The Customs audit is conducted on need basis (limitation period 6 months - 5 years)

SVB order is valid for three years if no change in the facts (relationship / product, etc.)

Customs and TP: Common Objective, Customs and TP: Common Objective, Differing ApproachesDiffering Approaches

40IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

• Divergence of definitions and other requirements specified in the Income Tax Act and the CVR

• Effective ground level administrative coordination between tax and customs authorities to achieve the same price for Transfer Pricing and Customs

• Applicability of prices established under customs valuation methods for income tax purposes (and vice versa)

• Reconciliation of ‘Aggregate Profit Level’ adjustments in Transfer Pricing to the ‘Individual Transaction Level’ used in Customs

• Mechanism for refund of customs duty due to subsequent TP Adjustments

Issues and ChallengesIssues and Challenges

Conclusion:what does the future hold?

42IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Arm’s Length Standard As The International Consensus In Theory

• Follows separate entity approach that approximates Follows separate entity approach that approximates economic realities and market forceseconomic realities and market forces

• Relies on comparables’ analysis for verificationRelies on comparables’ analysis for verification

• Substantial shared international experience minimizes Substantial shared international experience minimizes double taxationdouble taxation

43IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

But Is Arm’s Length simplistic in a complex business environment ?

((1) Difficulties to a separate entity approach 1) Difficulties to a separate entity approach

Outsourcing and integrated functions/ matrixed organizations/ Outsourcing and integrated functions/ matrixed organizations/ isolation of functions and risks…changing business modelsisolation of functions and risks…changing business models(2) In practice, do true comparables exist for various common (2) In practice, do true comparables exist for various common transactions?transactions?Bundled transactions/ Specialized captive services/ embedded Bundled transactions/ Specialized captive services/ embedded intangibles and unique value driversintangibles and unique value drivers(3) Recent International Experience (3) Recent International Experience Few examples of aggressive assertions of source based taxation Few examples of aggressive assertions of source based taxation (permanent establishment, location savings, local marketing (permanent establishment, location savings, local marketing intangibles) seek to re-allocate residual profitsintangibles) seek to re-allocate residual profits

More prescriptive guidance on adjustments More prescriptive guidance on adjustments by revenue authorities a mustby revenue authorities a must

44IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Concerns on Arm’s length Standard ..

-- -- Uncertainty and disputes on subjective matters of Uncertainty and disputes on subjective matters of comparable analysis on a steep risecomparable analysis on a steep rise

-- Instances of formulatory apportionment in recent -- Instances of formulatory apportionment in recent judicial precedentsjudicial precedents

-- Consideration of Common Consolidated Corporate Tax -- Consideration of Common Consolidated Corporate Tax Base (“CCCTB”) in the EUBase (“CCCTB”) in the EU

-- Continued urge for reform for certainty and -- Continued urge for reform for certainty and administrative ease of compliance administrative ease of compliance

45IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

Other Alternatives ?

• Arm’s length methodologies could be re-evaluated:Arm’s length methodologies could be re-evaluated:-- -- Transactional Net Margin Method to be Transactional Net Margin Method to be

elevated from the method of last resortelevated from the method of last resort-- Profit split approach ideal for integrated -- Profit split approach ideal for integrated

transactions…but greater guidance required for its transactions…but greater guidance required for its applicationapplication

• Global formulary apportionment … unrealistic … Global formulary apportionment … unrealistic … requires international agreement of formulae for each requires international agreement of formulae for each transaction to be successfultransaction to be successful

-- De Minimis rules and Safe Harbors … potential tools to -- De Minimis rules and Safe Harbors … potential tools to contain disputes, and add certainty to taxpayerscontain disputes, and add certainty to taxpayers

Need for reforms to increase certainty to taxpayers while staying Need for reforms to increase certainty to taxpayers while staying within the Arm’s Length frameworkwithin the Arm’s Length framework

46IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

The future of TP: the OECD perspective

Today the arm’s length principle is confronted with difficult challenges, among which:

•Scarcity of comparables in integrated industries (few comparable independents)

•MNEs implement transactions and business models that are hardly found between independents (e.g. global business models)

•Need more consistency in implementation of the arm’s length principle by countries

47IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

The future of TP: the OECD perspective

In theory, 2 possible responses:• Replace the arm’s length principle with a

different system which would provide theoretically sound allocation of tax bases, as large an international consensus, and be more practical: but what are the viable options?

• Improve the arm’s length principle => the OECD’s choice so far

48IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008IFA India – OECD International Tax Conference, Mumbai, 23rd -25th January 2008

The future of TP: the OECD perspective

• Review and update the 1995 TP Guidelines• Promote risk assessment techniques and better

use of taxpayers’ and tax administrations’ resources

• Provide more certainty: clearer guidance, more guidance, more efficient dispute prevention and dispute resolution mechanisms

• Improve consistency of application across countries

Thank You !

![OECD Transfer Pricing Guidelines for OECD Transfer Pricing ... · OECD Transfer Pricing Guidelines and the involvement of the business community [DAFFE/CFA/WD(97)11/REV1], adopted](https://img.dokumen.tips/doc/110x75/5e02ef38d9e2ea2f2040f98f/oecd-transfer-pricing-guidelines-for-oecd-transfer-pricing-oecd-transfer-pricing.jpg)