Embed Size (px)

Citation preview

1

Forecasting forFinancial Planning

2

Learning ObjectivesLearning Objectives

The importance of forecasting to business success.

The financial forecasting process.Preparation of pro forma financial

statements.The importance of analyzing forecasts.

3

Why is forecasting important?Why is forecasting important?

– If you produce too much of a product, or a product that no one wants to buy, you still must pay for materials, labor, and storage.

– If you produce too little of a product, you will lose sales and possibly market share.

Mistakes are costly:

4

Forecasting ApproachesForecasting Approaches

ExperienceProbabilityCorrelation

Financial managers concentrate on

three general approaches to financial

forecasting:

5

ExperienceExperience

Managers who have been in the business for a long time have developed a sense for the patterns in sales, expenses, consumer demand factors, etc.– Example: Editors who work for book

publishers regularly read submitted manuscripts and make judgements about whether their company should buy the rights to publish the books.

6

ProbabilityProbability

Past history often tells us a lot about what will happen in the future.

Managers can use this information to estimate the future.– Example: In the past, a 7-11 manager

has found that she will lose 1% of candy inventory to shoplifters. She can use this information to estimate future losses and also to design better controls.

7

CorrelationCorrelation

Correlation is a measure of the relative movement of two variables relative to each other. – Example: If interest rates go up, a real estate

agent knows that home sales will tend to fall (because the higher cost of financing makes it harder for buyers to qualify for mortgages).

– Example: Sales of umbrellas are higher in rainy seasons.

8

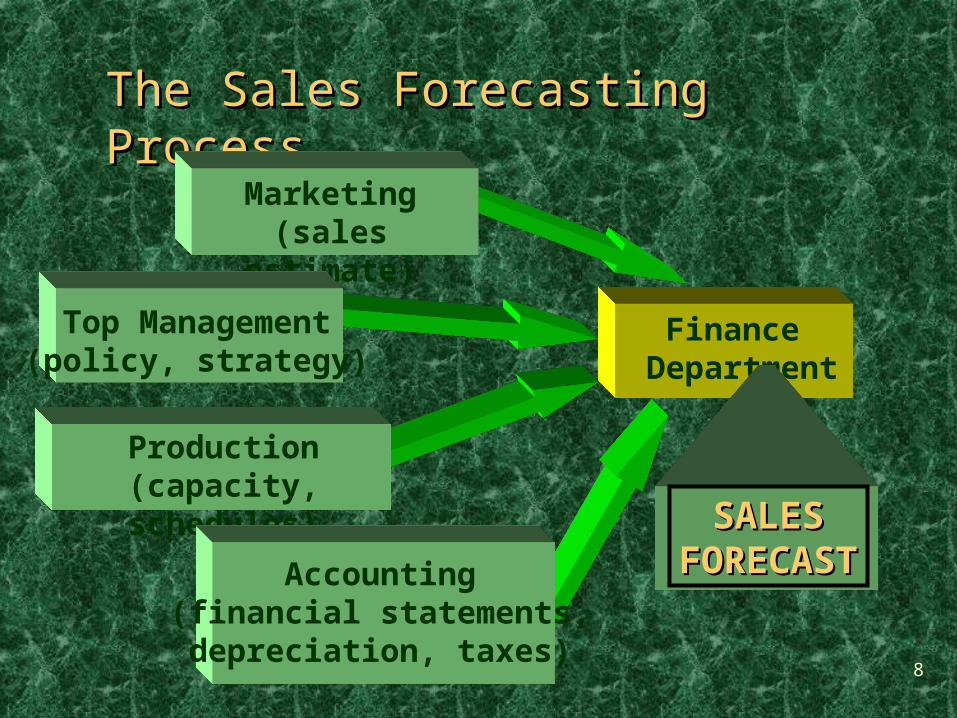

Finance Department

The Sales Forecasting ProcessThe Sales Forecasting Process

Marketing(sales estimate)

Top Management(policy, strategy)

Production(capacity, schedules)

Accounting(financial statements,depreciation, taxes)

SALESSALESFORECASTFORECAST

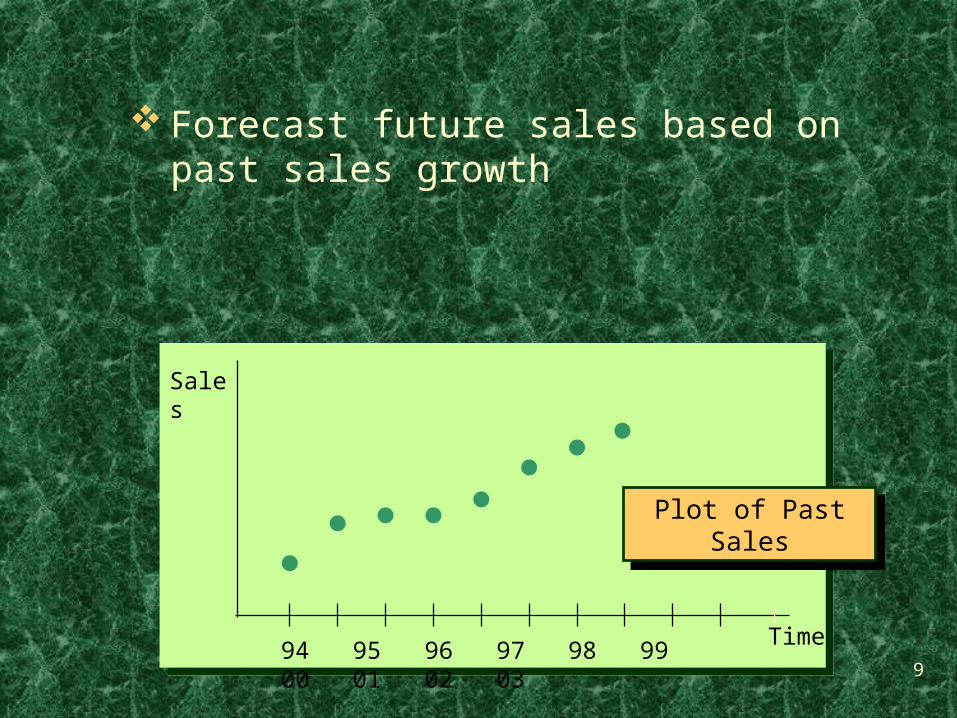

994 95 96 97 98 99 00 01 02 03

Time

Sales

Plot of Past SalesPlot of Past Sales

Forecast future sales based on past sales growth

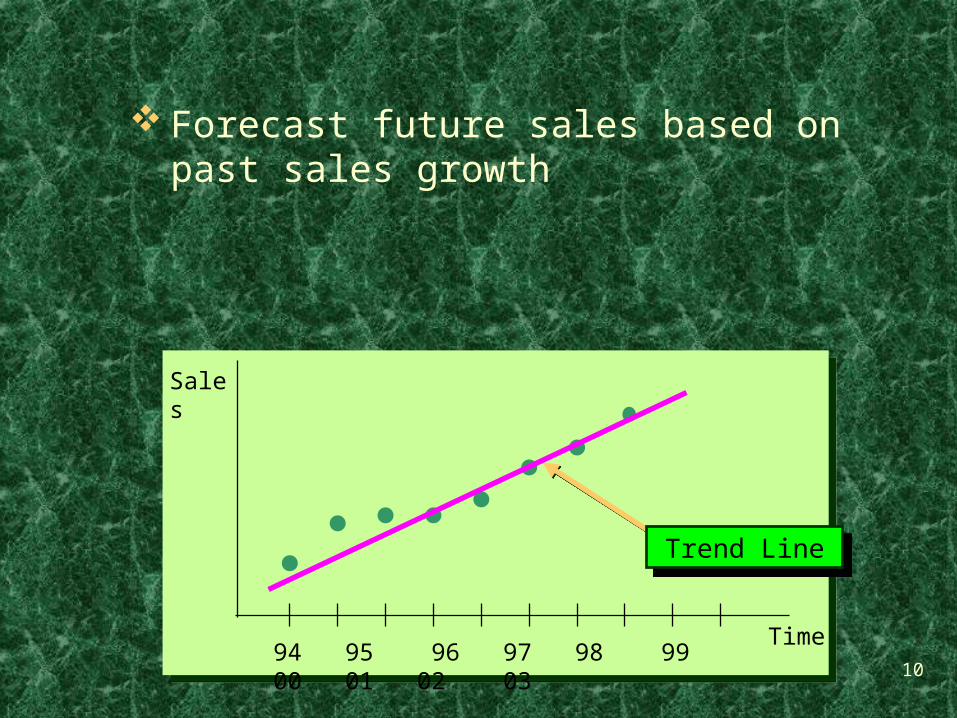

1094 95 96 97 98 99 00 01 02 03

Time

Sales

Forecast future sales based on past sales growth

Trend LineTrend Line

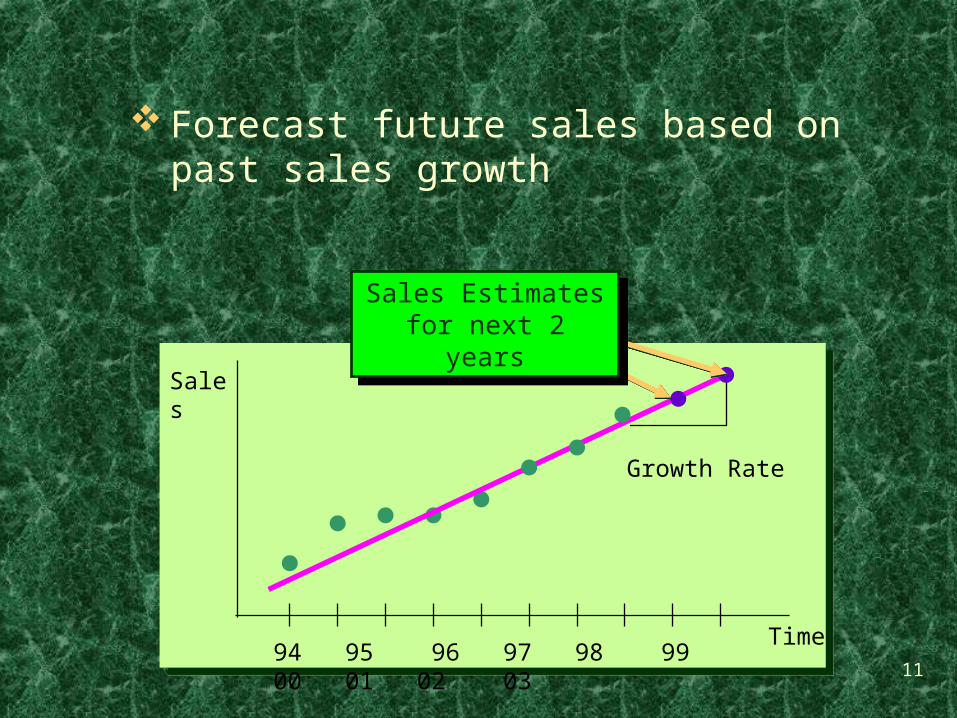

1194 95 96 97 98 99 00 01 02 03

Time

Sales

Growth Rate

Forecast future sales based on past sales growth

Sales Estimates for next 2 years

Sales Estimates for next 2 years

1294 95 96 97 98 99 00 01 02 03

Time

Sales

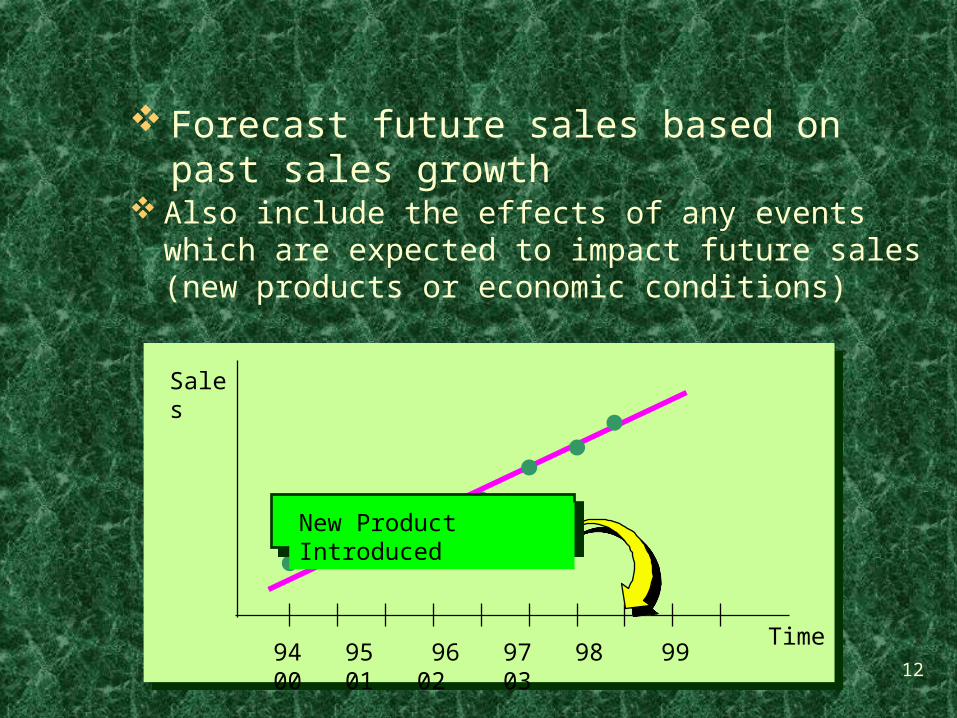

Also include the effects of any events which are expected to impact future sales (new products or economic conditions)

Forecast future sales based on past sales growth

New Product Introduced

1394 95 96 97 98 99 00 01 02 03Time

Sales

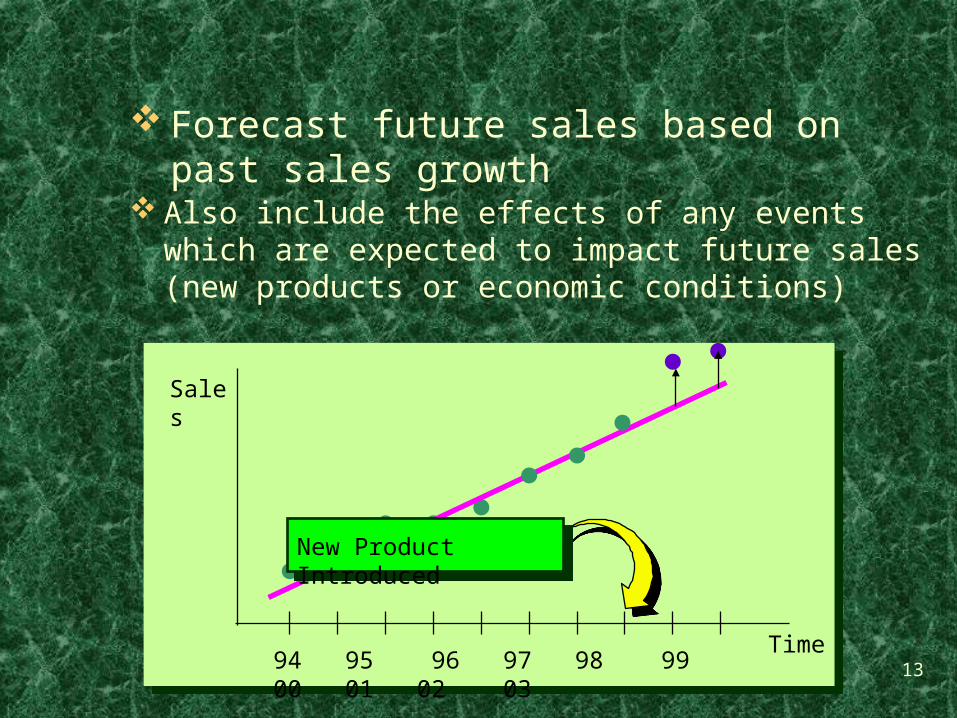

Also include the effects of any events which are expected to impact future sales (new products or economic conditions)

Forecast future sales based on past sales growth

New Product Introduced

14

– Current Assets: Inventory, A/R, Cash– Fixed Assets: Plant and Equipment

2002200220032003

Sales Growth Imposes Costs on the FirmSales Growth Imposes Costs on the Firm

Will require additional resources

15

Pro Forma Financial StatementsPro Forma Financial Statements

Pro forma financial statements are forecasts of the firm’s future financial statements based on a certain set of assumptions about sales trends and the relationships between sales and various financial variables, and between other financial statement variables relative to each other.

16

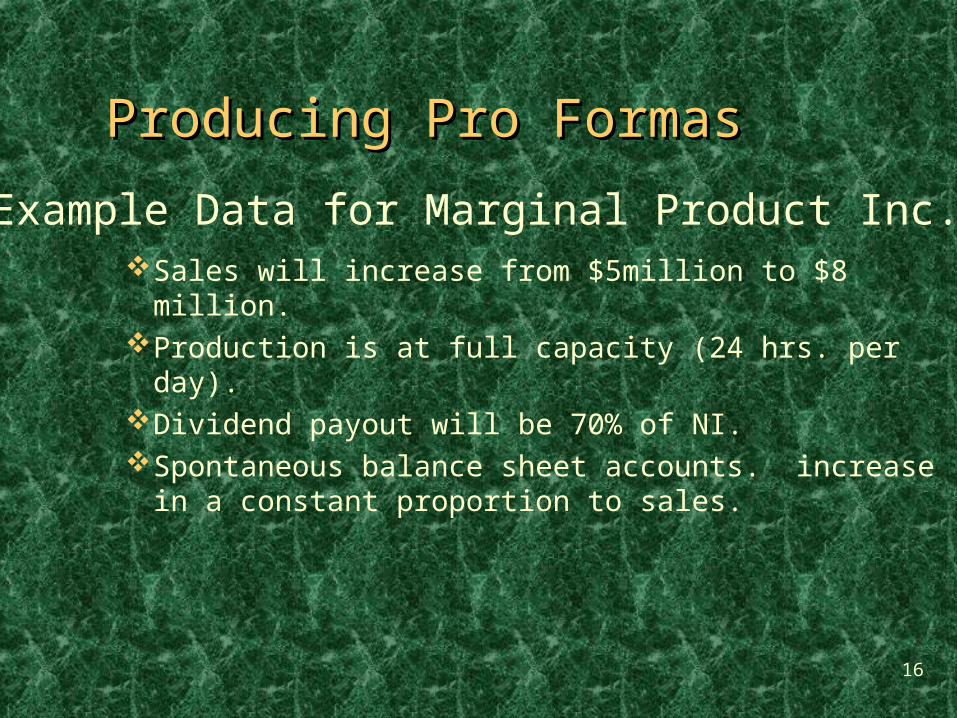

Producing Pro FormasProducing Pro Formas

Sales will increase from $5million to $8 million.Production is at full capacity (24 hrs. per day).Dividend payout will be 70% of NI.Spontaneous balance sheet accounts.

increase in a constant proportion to sales.

Example Data for Marginal Product Inc.

17

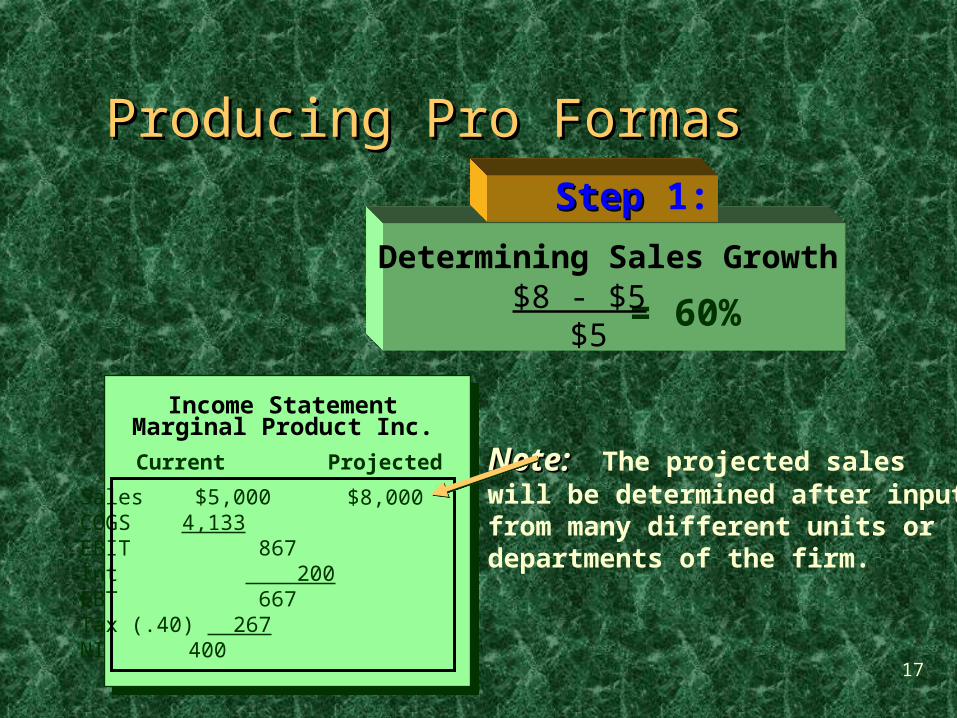

Producing Pro FormasProducing Pro Formas

Note:Note: The projected saleswill be determined after inputfrom many different units ordepartments of the firm.

Determining Sales Growth

= 60%$8 - $5 $5

StepStep 1:

Income StatementMarginal Product Inc.

Sales $5,000 COGS 4,133 EBIT 867Int 200EBT 667Tax (.40) 267NI 400

Current Projected

$8,000

18

Calculate projected Net Income. New COGS =Old COGS x 1.6 = 6,613

Producing Pro FormasProducing Pro Formas

Note:Note: There is no increase yetin the interest charges sinceMarginal Product’s managershave not yet decided how theywill finance the growth.

StepStep 2:

Income StatementMarginal Product Inc.

Sales $5,000 $8,000COGS 4,133 6,613EBIT 867 1,387Int 200 200EBT 667 1,187Tax (.40) 267 475NI 400 712

Current Projected

19

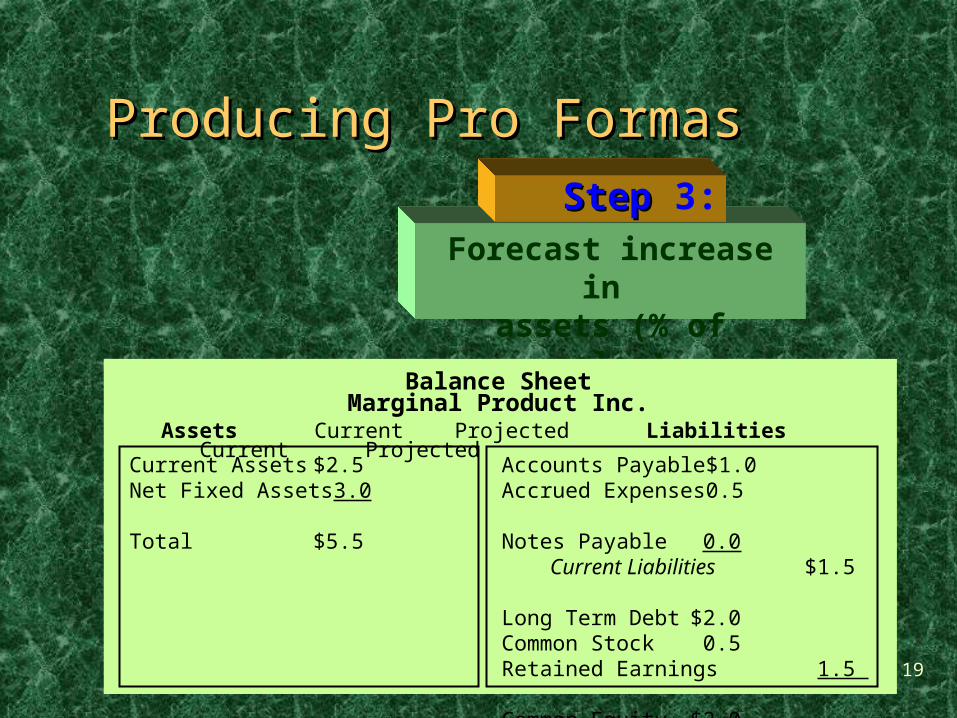

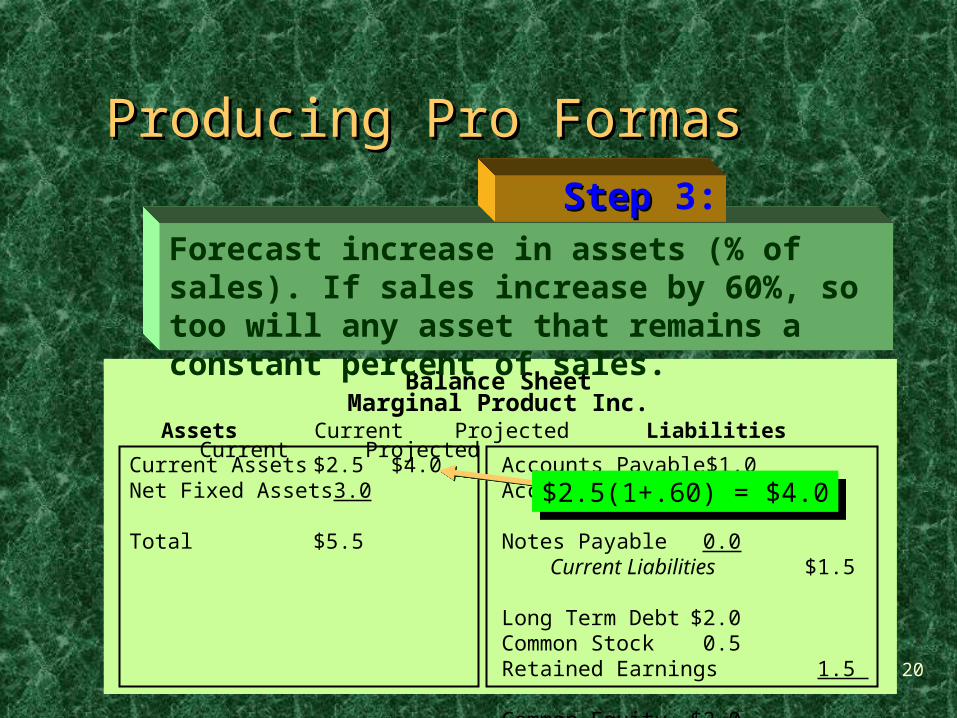

Producing Pro FormasProducing Pro Formas

Forecast increase in assets (% of sales)

StepStep 3:

Balance SheetMarginal Product Inc.

Current Assets $2.5 Accounts Payable $1.0 Net Fixed Assets 3.0 Accrued Expenses 0.5 Total $5.5 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected

20

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 Net Fixed Assets 3.0 Accrued Expenses 0.5 Total $5.5 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected

Producing Pro FormasProducing Pro Formas

Forecast increase in assets (% of sales). If sales increase by 60%, so too will any asset that remains a constant percent of sales.

StepStep 3:

$2.5(1+.60) = $4.0$2.5(1+.60) = $4.0

21

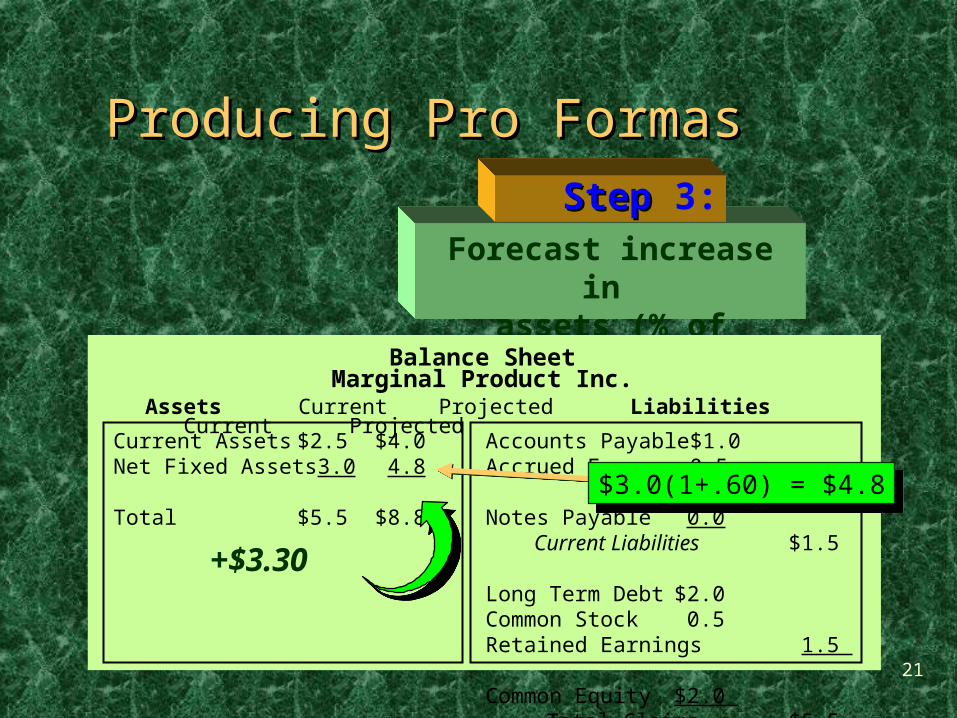

Producing Pro FormasProducing Pro Formas

Forecast increase in assets (% of sales)

StepStep 3:

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 Total $5.5 $8.8 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected

+$3.30

$3.0(1+.60) = $4.8$3.0(1+.60) = $4.8

22

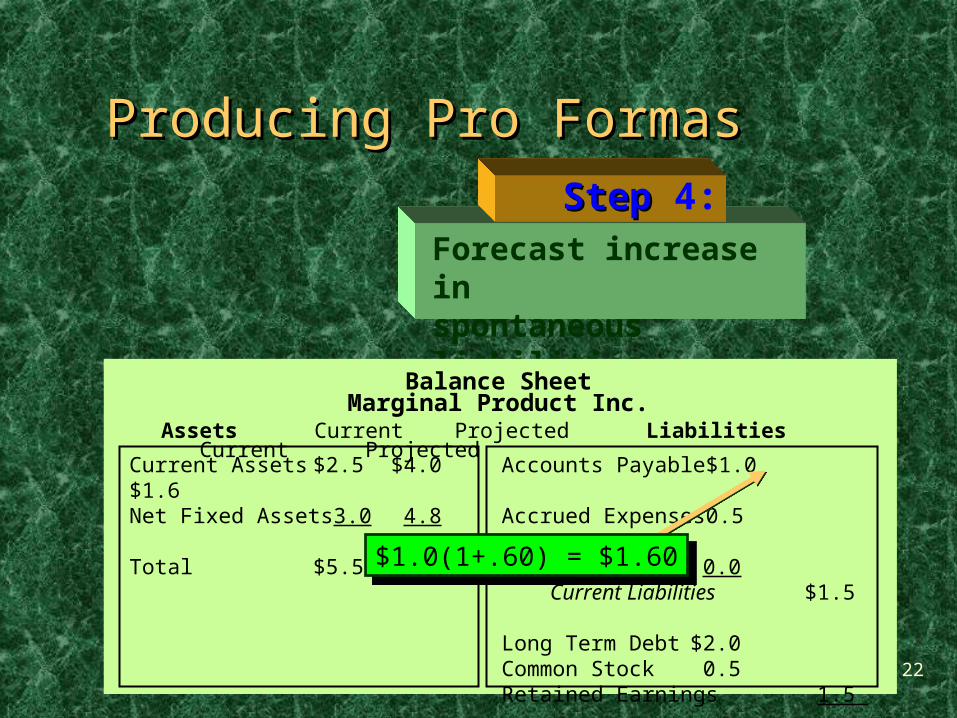

Producing Pro FormasProducing Pro Formas

Forecast increase inspontaneous liabilities.

StepStep 4:

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 Total $5.5 $8.8 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected

$1.0(1+.60) = $1.60$1.0(1+.60) = $1.60

23

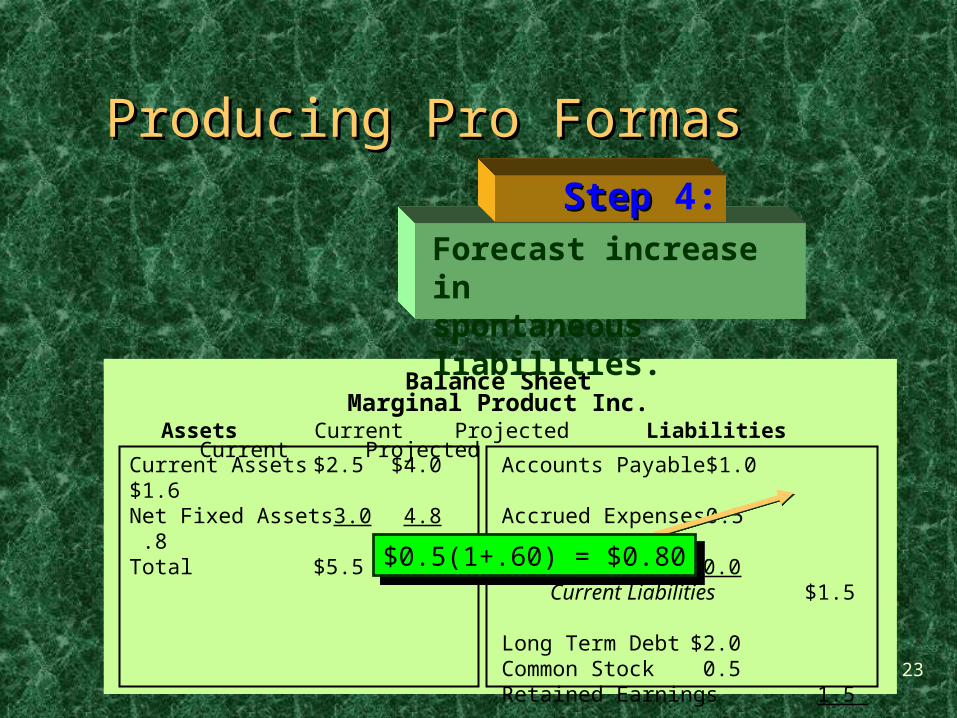

Producing Pro FormasProducing Pro Formas

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 .8Total $5.5 $8.8 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected

$0.5(1+.60) = $0.80$0.5(1+.60) = $0.80

Forecast increase inspontaneous liabilities.

StepStep 4:

24

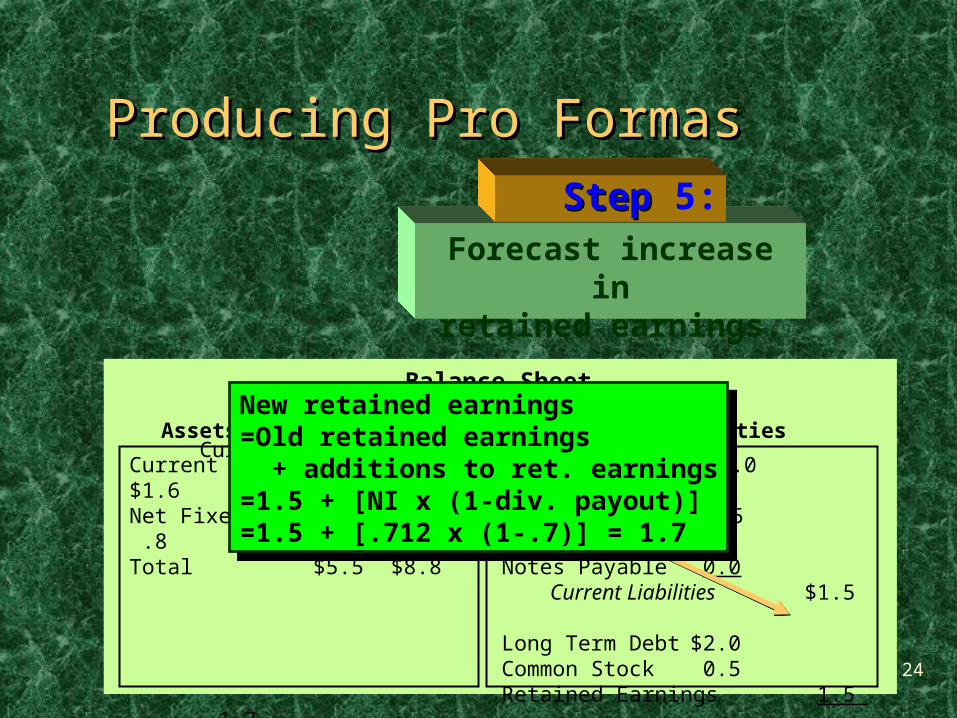

Producing Pro FormasProducing Pro Formas

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 .8Total $5.5 $8.8 Notes Payable 0.0

Current Liabilities $1.5 Long Term Debt $2.0 Common Stock 0.5 Retained Earnings 1.5 1.7Common Equity $2.0 Total Claims $5.5

Assets Current Projected Liabilities Current Projected New retained earnings =Old retained earnings + additions to ret. earnings=1.5 + [NI x (1-div. payout)]=1.5 + [.712 x (1-.7)] = 1.7

New retained earnings =Old retained earnings + additions to ret. earnings=1.5 + [NI x (1-div. payout)]=1.5 + [.712 x (1-.7)] = 1.7

Forecast increase inretained earnings.

StepStep 5:

25

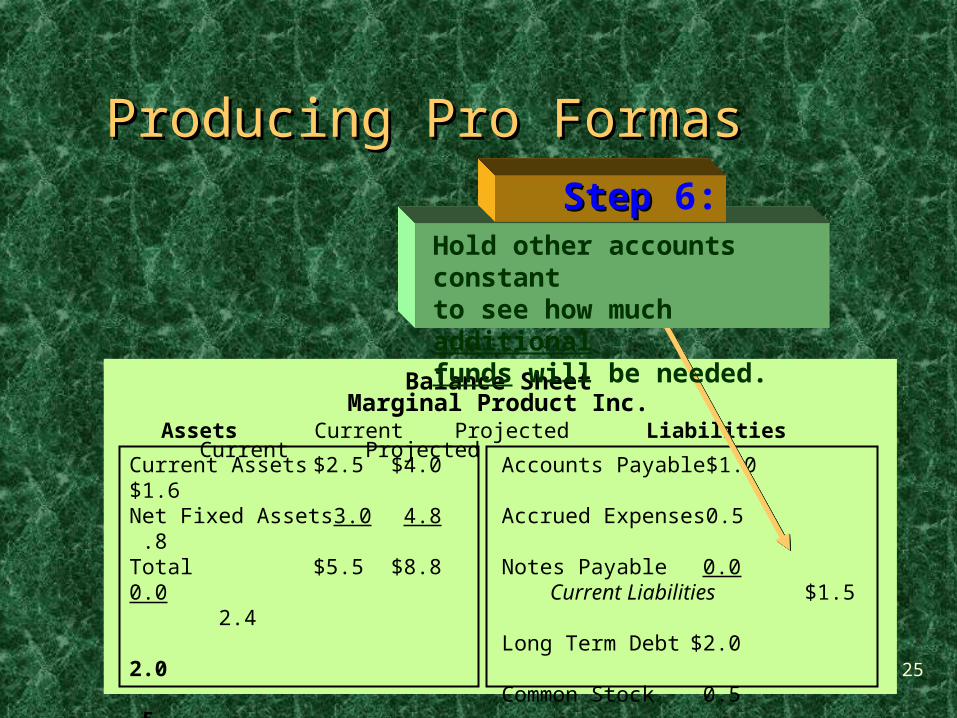

Producing Pro FormasProducing Pro Formas

Balance SheetMarginal Product Inc.

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 .8Total $5.5 $8.8 Notes Payable 0.0 0.0

Current Liabilities $1.5 2.4Long Term Debt $2.0 2.0Common Stock 0.5 .5Retained Earnings 1.5 1.7Common Equity $2.0 2.2Total Claims $5.5 $6.6

Assets Current Projected Liabilities Current Projected

Hold other accounts constant to see how much additionalfunds will be needed.

StepStep 6:

26

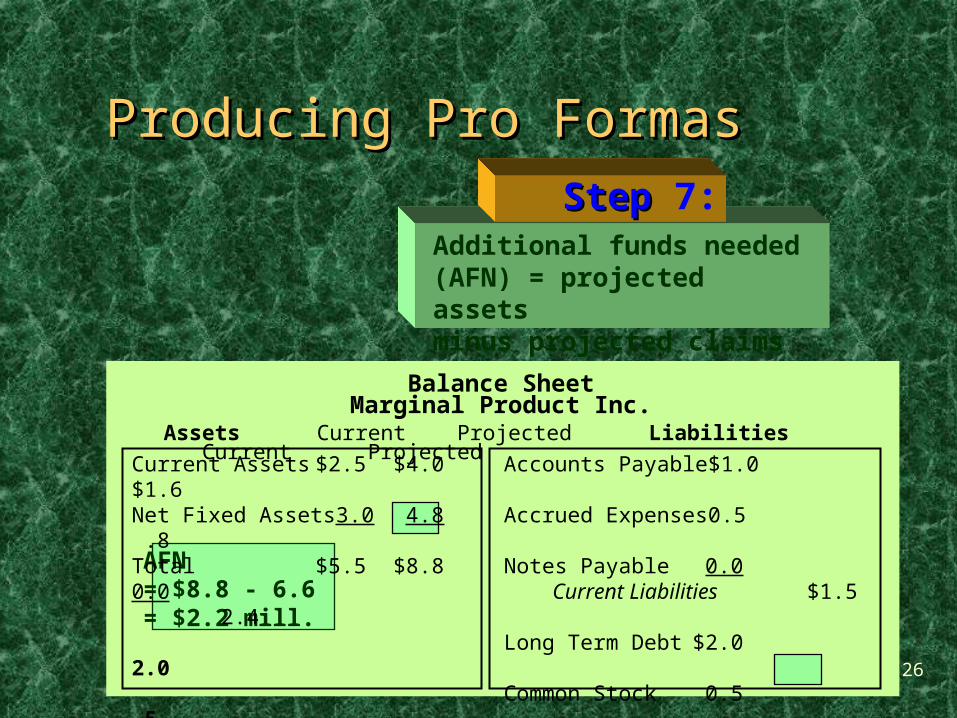

Balance SheetMarginal Product Inc.

Assets Current Projected Liabilities Current Projected

AFN = $8.8 - 6.6 = $2.2 mill.

Producing Pro FormasProducing Pro Formas

Additional funds needed (AFN) = projected assetsminus projected claims

StepStep 7:

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 .8Total $5.5 $8.8 Notes Payable 0.0 0.0

Current Liabilities $1.5 2.4Long Term Debt $2.0 2.0Common Stock 0.5 .5Retained Earnings 1.5 1.7Common Equity $2.0 2.2Total Claims $5.5 $6.6

27

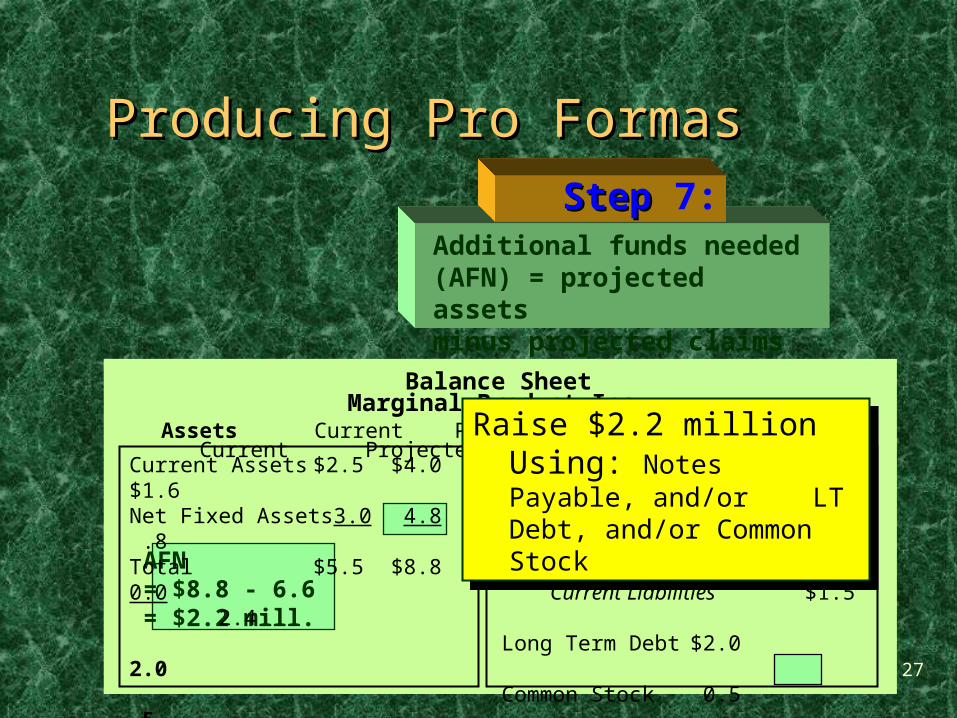

Producing Pro FormasProducing Pro Formas

Balance SheetMarginal Product Inc.

Assets Current Projected Liabilities Current Projected

AFN = $8.8 - 6.6 = $2.2 mill.

Current Assets $2.5 $4.0 Accounts Payable $1.0 $1.6Net Fixed Assets 3.0 4.8 Accrued Expenses 0.5 .8Total $5.5 $8.8 Notes Payable 0.0 0.0

Current Liabilities $1.5 2.4Long Term Debt $2.0 2.0Common Stock 0.5 .5Retained Earnings 1.5 1.7Common Equity $2.0 2.2Total Claims $5.5 $6.6

Raise $2.2 million Using: Notes Payable, and/or LT Debt, and/or Common Stock

Raise $2.2 million Using: Notes Payable, and/or LT Debt, and/or Common Stock

Additional funds needed (AFN) = projected assetsminus projected claims

StepStep 7:

28

Producing Pro Formas - SummaryProducing Pro Formas - Summary

Determine sales growth.Calculate projected net income.Project assets needed to support the new

sales level.Project increases in spontaneous asset

and liability accounts.Project addition to retained earnings.Determine the difference between

projected assets and projected liabilities & equity.

29

Financing feedbackFinancing feedback

If outside financing is required, the new debt or equity may affect your original projections of the amount of the addition to retained earnings (due to increased interest or dividends on the income statement).

In this case, the pro forma should be recast with the new information to make final projections of AFN.