Embed Size (px)

Citation preview

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 1/72

GLOBAL WIND

2007 REPORT

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 2/72

Table of conTenTs

Few 1

The gaisatin the win inust 2

The status ga win we in 2007 6

Maket ecast 2008-2012 11

Instae caacit egin 15

Cunt et

Australia 20Brazil 22

Canada 24Chile 26China 28Egypt 32European Union 34France 36Germany 38India 40Iran 42Italy 44 Japan 46

Mexico 48Morocco 50New Zealand 52Poland 54Republic o Korea 56Spain 58Turkey 60United Kingdom 62U n i t e d S t a t e s 6 4

Cncusin 66

Aut GWEC 68

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 3/72

1GWEC – GLOBAL WIND 2007 REPORT

Frewr2007 was yet another banner year or the wind industry,with a 27% increase in installed capacity, bringing the globaltotal to more than 94,000 MW The increasingly mature andglobal industry installed more than 20,000 MW o clean,emissions ree wind energy capacity in the course o the year, representing about€ 25 billion (about $US 37 billion)o investment, and by the time this publication is released,the total global capacity will no doubt have passed the100,000 MW mark

With the price o oil hovering around $US 100 per barrel,and the price o coal and gas at historically high levels,the advantages o an energy source independent rom thevagaries o the international commodities markets has neverbeen clearer ‘Resource depletion’ will never be a problem orwind power We have only just begun to scratch the suraceo its potential

This is good news not only or energy planners seekingto achieve security o supply, but also or politicians and

diplomats searching or solutions to the global crisis ohuman-induced climate change As governments ranticallynegotiate a new agreement or the period ater 2012, thewind industry stands ready to make a very substantialcontribution to solving what most now acknowledge is thegreatest long term threat to our civilization

The wind energy industry is also playing a major role inanother kind o boom: regional economic (re)developmentFrom the Texas Panhandle to Inner Mongolia, and romSchleswig-Holstein to Andalucía, the wind industry is

building new actories, expanding local tax bases and creatingthousand o new ‘green collar’ jobs at an ever-expanding rateAt the local, regional, and national level as well as globally,wind power is more and more oten the answer to questionsabout our energy uture

2007 will be remembered as the year when the globalcommunity nally started to get to grips with the climateissue Most notably, the release o the IPCC’s 4th AssessmentReport put all reasonable doubts to rest about the natureand causes o climate change The thousands o scientists,

reviewers and editors who volunteer their time to make upthe Panel were the much deserved recipients o the Nobel

Peace Prize, shared with ormer US vide-President Al Gore orhis lm ‘An Inconvenient Truth’

One clear ‘take home’ message rom the IPCC report is thatregardless o long term targets, i we are going to have anychance o avoiding the worst ravages o climate change, thenthe one thing we must do is to stop increasing greenhousegas emissions: they must peak and begin to decline globallybeore the end o the next decade.

While the power sector is ar rom being the only culpritwhen it comes to climate change, it is the largest singlesource o emissions, accounting or about 38% o CO2 emissions, and about 25% o overall emissions Our optionsor making major emissions reductions in the power sectorbetween now and 2020 are basically three: energy eciencyand conservation; uel switching rom coal to gas; andrenewable energy, primarily wind power

As policy makers become more aware o this reality, they

appreciate more and more wind power’s technologicalmaturity, widespread availability, speed o deployment, andthe act that there is a robust, growing industry becomingmore and more global with every passing year The windindustry is ready, willing and able to ulll these growingexpectations and responsibilities

This is the third annual report on the status o the globalwind industry by the Global Wind Energy Council, and itprovides a comprehensive snapshot o this global industry,which is now present in more than 70 countries The data

and country proles or this report have been collectedthrough GWEC’s member associations around the world andadditional government and industry contacts The Councilwishes to thank the contributors and is looking orward to anequally ruitul cooperation or uture editions

Arthouros Zervos

ChairmanGlobal Wind Energy Council

Steve Sawyer

Secretary GeneralGlobal Wind Energy Council

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 4/72

2 GWEC – GLOBAL WIND 2007 REPORT

The last ew years have witnessed a sea change in boththe scale and extent o the international wind industry’soperations Individual wind arms have grown in size rom aew dozen megawatts capacity up to several hundred Outat sea, giant wind parks o 1,000 MW capacity or more are

now waiting or construction Successul wind turbine modelsare pouring out rom manuacturing acilities much likeother mass produced hardware And the continued growth indemand or clean, emissions-ree wind power has outstrippedthe available supply, creating a demand or very largeinvestments in manuacturing capacity, long term equipmentpurchase arrangements and project development

The structural changes which have accompanied thisexpansion have concentrated around two key trends One

The glbalisatin the wininustry

has been the involvement in the business o companiesrom outside the traditional wind turbine manuacturingand project development community The other has beenthe spread o the wind power market well beyond its coregeographical centres o Europe and the United States

Signicantly, the two trends have overlapped with eachother

Increasing involvement o new players in the market is in parta refection o wind power’s success This is now a businessrom which it is clearly possible to make a secure andprotable return In most countries where the technologyhas been successul there is a structural ramework inplace which supports renewable energy because o theenvironmental benets it brings, especially in the battleagainst climate change They also help counter the eects

o the massive subsidies over many decades to conventionalenergy generation These rameworks have in some casesstood the test o time over a number o years

An additional actor is the pressure rom some nationalgovernments to place an obligation on energy producersto source an increasing percentage o their electricity romrenewables This is the case or instance in the UnitedKingdom, with its Renewables Obligation, and in the UnitedStates, with its state by state Renewable Portolio StandardsAt an international level, the European Union has led the way

by introducing a legally binding target or 20% o the region’senergy to come rom renewable sources by 2020

These twin encouragements have generated a surge ointerest in renewable energy, and particularly wind power,rom companies whose previous investment portolio hadbeen mainly concentrated in ossil uels or nuclear or evenoutside the energy sector Most importantly, these newerentrants have both the advantage o the available balancesheet to consider large investments and the incentive todiversiy away rom increasingly uncertain traditional power

sourcesSottevast wind arm, Manche, France© Pascal Lecoeur

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 5/72

3GWEC – GLOBAL WIND 2007 REPORT

Changing wneshi

The result has been a shit in the type o companiesdeveloping and owning wind arms - rom relatively smallindependent project developers towards general powergeneration and supply companies (utilities) and largeIPPs (Independent Power Producers), oten nanced byinvestment banks At the same time there has been animportant commitment to wind energy rom a number othe largest multinational oil companies, most notably Shelland BP Shell, or example, is a partner in the proposed 1,000MW London Array oshore wind arm in the UK’s ThamesEstuary as well as an even larger project in the US state

o Texas According to market analysts Emerging EnergyResearch, seven o the top ten global owners o operatingwind power capacity are now either European utilities or IPPs

The most prominent example rom Europe o utilityinvolvement is the Spanish electricity company Iberdrola,which had previously concentrated on its gas, nuclear andhydro generation businesses Starting less than ten years agoit began to invest seriously in wind, mainly in Spain using thedomestically produced Gamesa turbines

Last year Iberdrola merged with the Scottish utility ScottishPower, which owned a number o wind arms in the UK aswell as the US wind developer PPM Energy It has since madeurther US acquisitions By the end o 2007 the company hadreached a total o 7,704 MW o renewable capacity,7,362 MW o which was wind power This made it the worldleader in wind capacity Its current target is to increasethis at a rate o 2,000 MW a year, reaching 13,600 MW orenewables by the end o the decade

Other large utilities which have moved into wind in a serious

way, by investing in large project development, are FloridaPower and Light (FPL) in the United States, the ormerstate power company Energias de Portugal (EdP), Endesarom Spain, DONG rom Denmark, Vattenall rom Sweden,Enel rom Italy, EdF rom France and EON and RWE romGermany

On the manuacturing side, the increase in the size o themarket and the requirement or a substantial investment inexpanded production acilities has also brought new playerson board The rst major example was General Electric, which

purchased the Enron Wind business, with assembly plantsin both Germany and the US GE Energy is now the third

largest supplier o wind turbines Three years ago, the giantengineering company Siemens acquired Bonus, one o theoriginal Danish turbine makers Siemens is currently the mostsuccessul supplier o turbines or the oshore market

An indication o how successul these acquisitions have beenwas the conrmation rom General Electric at the beginningo 2008 that it would increase its investment in renewablesto $6 billion by 2010 The majority o that is likely to go

into wind This gure represents about a quarter o thecorporation’s total investment in energy and water assets

More recently, with the oshore market beginning toseriously take o, the French energy/nuclear company Arevaacquired a majority shareholding in Multibrid, a German-based manuacturer developing a 5 MW turbine specicallydesigned or operating out at sea Engineering giant Alstomhas meanwhile taken over Ecotecnia, the Spanish turbinemanuacturer with a long and impressive track record Thesemoves are seen as signicant examples o broader industrial

conglomerates wanting to gain a toehold in the attractivewind market

Wind park, Germany

© Bundesverbansd WindEnergie e.V.

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 6/72

4 GWEC – GLOBAL WIND 2007 REPORT

Another actor which has encouraged the involvement olarger companies is the current shortage o turbines, a result

o the global boom in wind power development Projectdevelopers now need to make orders or their turbinesin large blocks up to several years in advance, requiring asubstantial nancial commitment in order to ensure a rmdelivery date rom the manuacturers At the same time themanuacturers themselves are having to invest large sums toexpand their production acilities so that they can meet thesoaring demand

Geate gaisatin

The involvement o these larger players has in turnencouraged a greater globalisation o the industry, althoughother actors are involved here as well as the simple drive toexploit new markets In the US, or example, the explosiono the wind power market has been driven by a mixtureo attractive state and ederal incentives, encouraging the

supply o green energy, and the competitiveness o windcompared with increasingly expensive gas There is also much

more space or large projects than in the more crowdedEuropean landscape

In Asia, on the other hand, the market has been spurred asmuch by the sheer growth in demand or more electricity toeed new industries as by wind’s environmental credentialsIndian businesses are also investing in their own windgenerators as a more reliable source o power than the over-stretched and temperamental grid

As a result, both Asia and the United States have witnessed

a recent burst o activity by mainly Europe-based companiesto gain a slice o their burgeoning wind markets In the USthis has seen Energias de Portugal acquire the developerHorizon Wind Power and EON buy developer Airtricity’sNorth American assets In Asia the activity has mainlybeen in the orm o joint ventures established by Europeanand US turbine manuacturers with Chinese companies toestablish local production acilities Under its bidding rulesor development sites the Chinese government has decreedthat 70% o the hardware used in any commercial windarm built in the country must be sourced rom a domestic

manuacturer

Many observers believe that Asia, and China in particular, willbe central to the uture o the global wind energy marketNot only does China have an insatiable demand or energy, italso has the industrial inrastructure and manpower to createa major powerhouse or turbine production More than40 companies are now involved in turbine manuacture Last year they increased their share to 56% o the almost3,500 MW o new capacity installed

Most o the Chinese manuacturers have used European orUS technology as the basis or their designs Goldwind, orinstance, the market leader, has relied on German companiesREpower and Vensys Among other oreign companies whichhave already gained a oothold in the Chinese market areAcciona, Nordex, Vestas, Gamesa, Suzlon and General ElectricBut the trac is beginning to reverse One Chinese company,MingYang Wind Power Technology, recently signed a deal tosupply its turbines to the United States An agreement withdeveloper GreenHunter means that all the company’s initialproduction o up to 900 MW capacity will cross the Pacic

Ocean

Dabancheng wind arm, Dabancheng, Urumqi, Xinjiang

© Greenpeace.

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 7/72

5GWEC – GLOBAL WIND 2007 REPORT

Meges an acquisitins

At the same time, wind developers and manuacturers havebeen expanding their international horizons through a serieso mergers and acquisitions Spanish group Acciona andItalian utility Enel, or example, jointly bought Spanish utilityEndesa during 2007, dividing up its wind power assets

The most dramatic example has been that o Suzlon, the

Indian wind turbine manuacturer created in 1994 by TulsiTanti, then running a amily textile business Ater achievinga strong position in the Indian wind market using importedGerman technology, Suzlon moved abroad, opening newheadquarters in Denmark and manuacturing capacity inthe US In 2005 it acquired the Belgian gearbox companyHansen Transmissions, which has about 30% o the windpower market, and last year took over German turbinemanuacturer REpower It is now knocking on the door othe world’s top ve turbine suppliers

Melanchton wind arm in Shelburne, Ontario

© CanWEA

On the project development side, according to Danishconsultants MAKE Consulting, “large IPPs and utilities areaggressively seeking to increase their own portolios owind power by acquiring smaller developers The end resultwill be seen in a couple o years’ time, when the number ocompanies active in project development will be reduced, asthe market is moving towards ewer, but larger, players”

But whilst current trends might point to North America and

Asia as the ront-runners in the globalisation o wind, othermarkets are certain to emerge soon Within Europe, investorsare turning to the potential o the new EU member states,especially in Eastern Europe, with Turkey another giant marketon Europe’s doorstep In South America, a number o countriesare on the verge o take-o, including Brazil and MexicoMeanwhile, with a new government elected on a mandateto sign up to the Kyoto Protocol, Australia could soon see itsmassive wind power opportunities nally realised What iscertain is that the changes o the last ew years mean that agrowing list o large globalised companies are ready, waiting

and have the nancial muscle to exploit these new markets assoon as the starting gun is red

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 8/72

6 GWEC – GLOBAL WIND 2007 REPORT

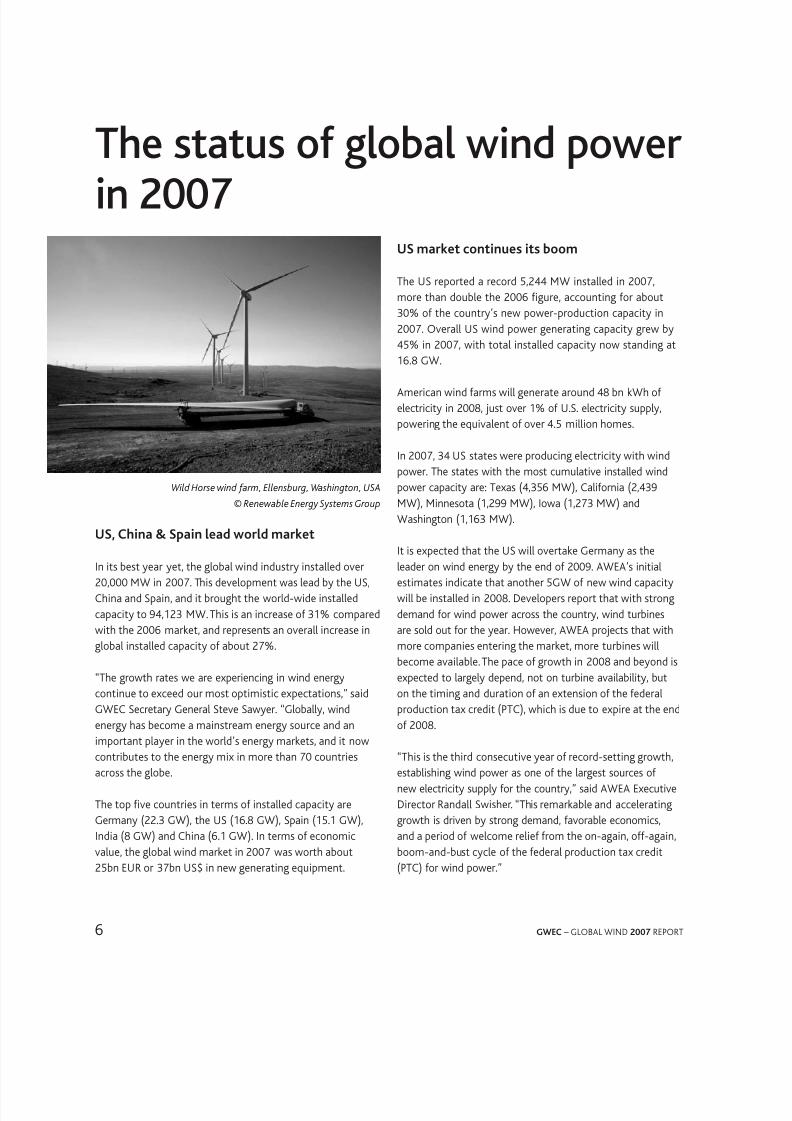

The status glbal win pwerin 2007

US, China & Sain ea w maket

In its best year yet, the global wind industry installed over20,000 MW in 2007 This development was lead by the US,China and Spain, and it brought the world-wide installedcapacity to 94,123 MW This is an increase o 31% comparedwith the 2006 market, and represents an overall increase inglobal installed capacity o about 27%

“The growth rates we are experiencing in wind energy

continue to exceed our most optimistic expectations,” saidGWEC Secretary General Steve Sawyer “Globally, windenergy has become a mainstream energy source and animportant player in the world’s energy markets, and it nowcontributes to the energy mix in more than 70 countriesacross the globe

The top ve countries in terms o installed capacity areGermany (223 GW), the US (168 GW), Spain (151 GW),India (8 GW) and China (61 GW) In terms o economicvalue, the global wind market in 2007 was worth about

25bn EUR or 37bn US$ in new generating equipment

US maket cntinues its m

The US reported a record 5,244 MW installed in 2007,more than double the 2006 gure, accounting or about30% o the country’s new power-production capacity in2007 Overall US wind power generating capacity grew by

45% in 2007, with total installed capacity now standing at168 GW

American wind arms will generate around 48 bn kWh oelectricity in 2008, just over 1% o US electricity supply,powering the equivalent o over 45 million homes

In 2007, 34 US states were producing electricity with windpower The states with the most cumulative installed windpower capacity are: Texas (4,356 MW), Caliornia (2,439MW), Minnesota (1,299 MW), Iowa (1,273 MW) and

Washington (1,163 MW)

It is expected that the US will overtake Germany as theleader on wind energy by the end o 2009 AWEA’s initialestimates indicate that another 5GW o new wind capacitywill be installed in 2008 Developers report that with strongdemand or wind power across the country, wind turbinesare sold out or the year However, AWEA projects that withmore companies entering the market, more turbines willbecome available The pace o growth in 2008 and beyond isexpected to largely depend, not on turbine availability, but

on the timing and duration o an extension o the ederalproduction tax credit (PTC), which is due to expire at the endo 2008

“This is the third consecutive year o record-setting growth,establishing wind power as one o the largest sources onew electricity supply or the country,” said AWEA ExecutiveDirector Randall Swisher “This remarkable and acceleratinggrowth is driven by strong demand, avorable economics,and a period o welcome relie rom the on-again, o-again,boom-and-bust cycle o the ederal production tax credit

(PTC) or wind power”

Wild Horse wind arm, Ellensburg, Washington, USA

© Renewable Energy Systems Group

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 9/72

7GWEC – GLOBAL WIND 2007 REPORT

“The extension o the production tax credit (PTC) is urgentlyneeded to protect tens o thousands o US manuacturing

and construction jobs and create tens o thousands more,and to keep investment fowing into one o the astest-growing and brightest sectors o our economy: renewableelectricity,” he adds

China sees uing annua maket - again

China added 3,449 MW o wind energy capacity during 2007,representing market growth o 156% over 2006, and nowranks th in total installed wind energy capacity with over

6,000 MW at the end o 2007 However, experts estimatethat this is just the beginning, and that the real growth inChina is yet to come Based on current growth rates, theChinese Renewable Energy Industry Association (CREIA)orecasts a capacity o around 50,000 MW by 2015 Theregions with the best wind regimes are located mainly alongthe South-East coast and Inner Mongolia, Xinjiang, GansuProvince’s Hexi Corridor and in some parts o North-EastChina, North-West China, Northern China and the Qinghai-Tibetan Plateau

The wind manuacturing industry in China is booming Whilein the past, imported wind turbines dominated the Chinesemarket, this is changing rapidly as the growing wind powermarket and the clear policy direction have encourageddomestic production

At the end o 2007, they were 40 Chinese manuacturersinvolved in wind energy, accounting or about 56% o theequipment installed during the year, up rom 41% in 2006

“This percentage is expected to increase substantially in the

uture Total domestic manuacturing capacity is now about5,000 MW, and is expected to reach 10-12 GW by 2010,”predicts GWEC President Pro Arthouros Zervos Establishedmajor Chinese manuacturers are Goldwind, Sinovel Windtec,Windey and Dongeng Electrical

While in 2006, only about 400 MW o new capacity wasmanuactured by Chinese manuacturers, in 2007, thetop two Chinese companies (Gold Wind and Sinovel)alone accounted or 1,460 MW o the new installedcapacity,representing about 42% o the annual market This

compares to only 37% provided by the top three oreignmanuacturers (Gamesa, Vestas and GE)

Natina gwth incnsistent in Eue, Saineaing the wa

The capacity o new wind turbines brought on line acrossEurope last year was 8,662 MW Total wind power capacity

installed by the end o 2007 reached 57,135 MW, which willavoid about 90 million tonnes o CO2

annually and produce119 TWh in an average wind year Wind energy is nowincreasing more than any other power technology in Europe,making up 40% o total new power installations in 2007,according to EWEA

The big surprise in the European market was Spain with3,522 MW o new capacity installed in 2007, the highestamount o any European country ever, earning it secondplace globally ater the US Total installed wind energy

capacity now stands at over 15 GW in Spain There was alsosustained growth in France with 888 MW o added capacityto reach 2,454 MW and Italy, with 603 MW added or a totalo 2,726 MW The new Member States perormed well andincreased installed capacity by 60%, with Poland, the mostsuccessul, reaching a total o 276 MW The Czech Republicinstalled 63 MW, its best year ever, and Bulgaria 34 MW

Nevertheless, a handul o markets pulled in the oppositedirection, including Germany, whose annual market shrank by25% compared to 2006 Portugal and the UK also slumped

As a result, the overall annual market growth in Europe in2007 o 11% was not what the industry had hoped or

Druiberg wind arm, Sachsen-Anhalt, Germany

© Energiepark Druiberg

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 10/72

8 GWEC – GLOBAL WIND 2007 REPORT

Mait new instaatins in 2007 utsie Eue

While Europe remains the leading market or wind energy,new installations represented just 43% o the global total,down rom nearly 75% in 2004 For the rst time in decades,more than 50% o the annual wind market was outsideEurope, and this trend is likely to continue into the uture

While Europe, North America and Asia continue to see themost important additions to their wind energy capacity, theMiddle East/North Arica region increased its wind powerinstallations by 42%, reaching 538 MW at the end o 2007

New capacity was added in Egypt, Morocco and Iran

Growth in the Pacic region was led by New Zealand with151 MW in new capacity, which nearly doubled the country’s

total installations, reaching 322 MW While Australia had anexceptionally weak year with only 7 MW o new installations,the change in government at the end o 2007 spurs hopesor a brighter uture or wind energy Within hours o beingsworn in to oce, the new Labour Prime Minister Kevin Ruddsigned the ratication o the Kyoto Protocol, and the newgovernment is now making good on its promise o a targeto 20% power production by renewables by 2020 This islikely to have positive long-term impacts or wind energydevelopment on the continent

MW %

US 5,244 261

Spain 3,522 175

China 3,449 172

India 1,730 86

Germany 1,667 83

France 888 44

Italy 603 30

Portugal 434 22

UK 427 21

Canada 386 19

Rest o world 1,726 86

Tta t 10 18,350 914

Tta 20,076 1000

Top 10 NEW CApACITy

MW %

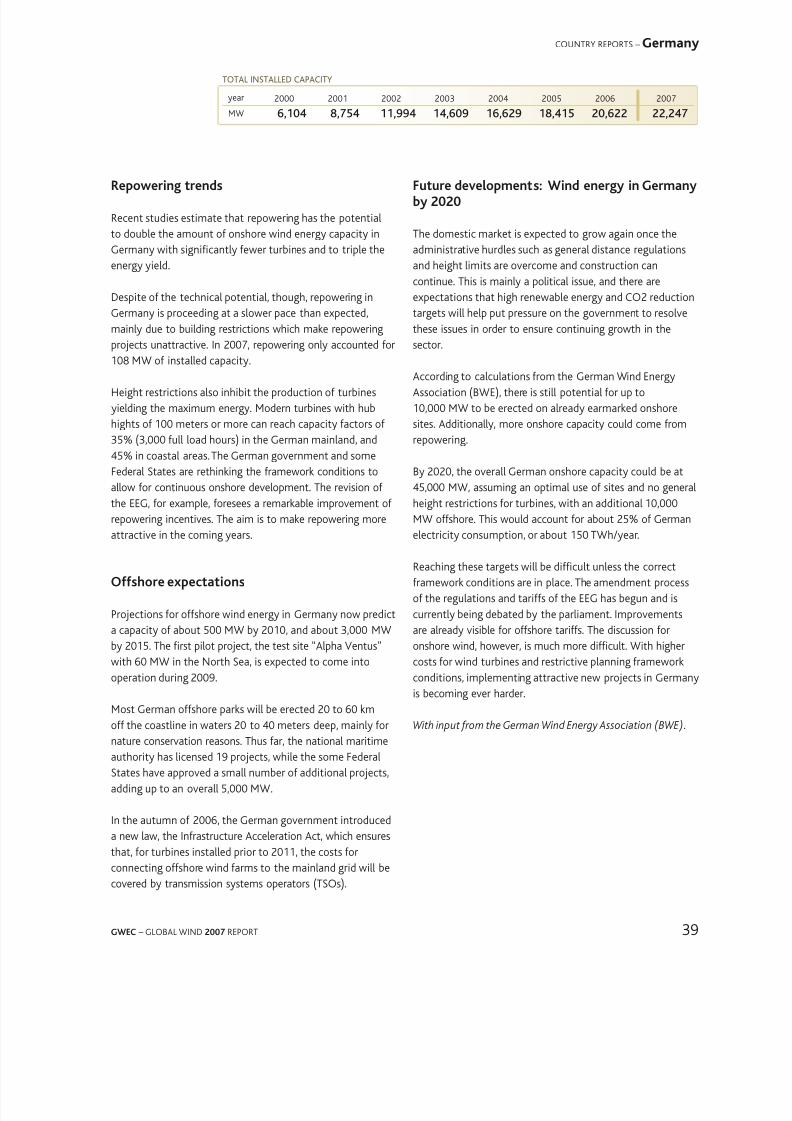

Germany 22,247 236

US 16,818 179

Spain 15,145 161

India 8,000 85

China 6,050 64

Denmark 3,125 33

Italy 2,726 29

France 2,454 26

UK 2,389 25

Portugal 2,150 23

Rest o world 13,019 138

Tta t 10 81,104 862

Tta 94,123 1000

Top 10 ToTAl INSTAllEd CApACITy

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 11/72

9GWEC – GLOBAL WIND 2007 REPORT

GlobAl CUMUlATIvE INSTAllEd CApACITy 1996-2007

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 20076,100 7,600 10,200 13,600 17,400 23,900 31,100 39,431 47,620 59,091 74,141 94,123

90,00080,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

20,000

18,000

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

ANNUAl INSTAllEd CApACITy by rEGIoN 2003-2007

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

1,280 1,530 2,520 3,440 3,760 6,500 7,270 8,133 8,207 11,531 15,318 20,076

GlobAl ANNUAl INSTAllEd CApACITy 1996-2007

MW

MW

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Europe Latin America Africa & Middle East Pacic

20032004

2005

2006

2007

MW

AsiaNorth America

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 12/72

10 GWEC – GLOBAL WIND 2007 REPORT

GlobAl INSTAllEd WINd poWEr CApACITy (MW) – rEGIoNAl dISTrIbUTIoN

1 Cape Verde, Israel, Jordan,Nigeria, South Arica;

2 Bangladesh, Indonesia,Sri Lanka;

3 Bulgaria, Croatia, Cyprus,Czech Republic, Estonia,Faroe Islands, Finland,Hungary, Iceland, Latvia,Liechtenstein, Lithuania,Luxembourg, Malta, Norway,Romania, Russia, Slovakia,

Slovenia, Switzerland,Ukraine;4 Austria, Belgium, Bulgaria,

Cyprus, Czech Republic,Denmark, Estonia, Finland,France, Germany, Greece,Hungary, Ireland, Italy, Latvia,Lithuania, Luxembourg,Malta, Netherlands, Poland,Portugal, Romania, Slovakia,Slovenia, Spain, Sweden, UK;

Please note: project

decommissioning o 93 MW and

rounding aect the fnal sums

*These numbers are provisional

and are awaiting nalconrmation

Source: GWEC

AFRICA & MIDDLE EAST

ASIA

EUROPE

LATIN AMERICA

& CARIBBEAN

NORTH AMERICA

PACIFIC REGION

Revised end 2006 New 2007 Total end 2007

Egypt 230 80 310

Morocco 64 60 124

Iran 48 19 67Tunisia 20 0 20

Other 1 16 1 17

Tta 378 160 538

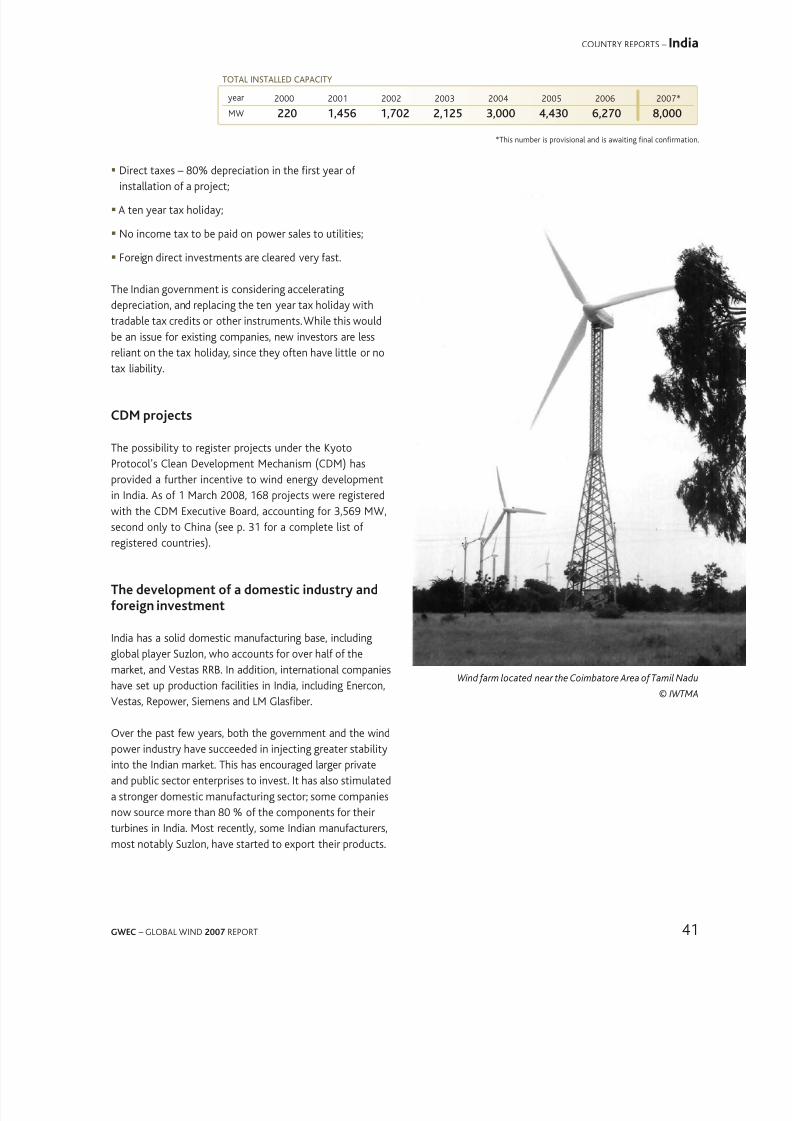

India 6,270 1,730 * 8,000 *

China 2,604 3,449 * 6,050 *

Japan 1,394 139 1,538

Taiwan 188 100 282

South Korea 173 18 191

Philippines 25 0 25

Other 2 5 0 5

Tta 10,659 5,436 16,091

Germany 20,622 1,667 22,247

Spain 11,623 3,522 15,145

Denmark 3,136 3 3,125

Italy 2,123 603 2,726

France 1,567 888 2,454

UK 1,962 427 2,389

Portugal 1,716 434 2,150

Netherlands 1,558 210 1,746

Austria 965 20 982

Greece 746 125 871

Ireland 746 59 805

Sweden 571 217 788

Norway 325 8 333Belgium 194 93 287

Poland 153 123 276

Rest o Europe 3 556 263 812

Tta Eue 48,563 8,662 57,136

o which EU-27 4 48,069 8,554 56,535

Brazil 237 10 247

Mexico 87 0 87

Costa Rica 74 0 74

Caribbean (w/o Jamaica) 35 0 35

Argentina 27 2 29

Colombia 20 0 20

Jamaica 20 0 20Chile 2 18 20

Cuba 5 0 5

Tta 507 30 537

USA 11,575 5,244 16,818

Canada 1,460 386 1,846

Tta 13,035 5,630 18,664

Australia 817 7 824

New Zealand 171 151 322

Pacic Islands 12 0 12

Tta 1,000 158 1,158

W tta 74,141 20,076 94,123

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 13/72

11GWEC – GLOBAL WIND 2007 REPORT

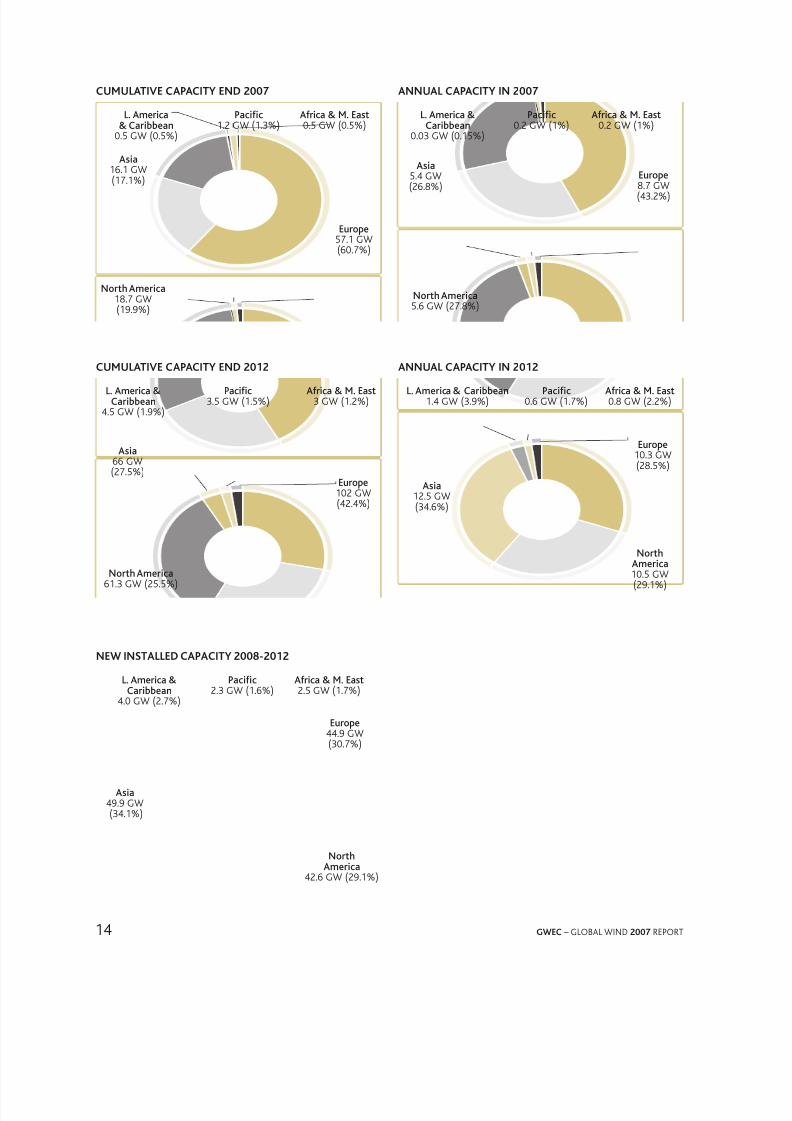

GWEC is predicting the global wind market to grow byover 155% rom its current size to reach 240 GW o totalinstalled capacity by the year 2012 This would represent

an addition o 146 GW in 5 years, equaling an investmento over 180bn EUR (277 bn US$, both in 2007 value) Theelectricity produced by wind energy will reach over 500 TWhin 2012 (up rom 200 TWh in 2007), accounting or around3% o global electricity production (up rom just over 1% in2007)

The main areas o growth during this period will be NorthAmerica and Asia, and more specically the US and China

This orecast exceeds previous estimates by GWEC, and the

total installed capacity or 2010 has been corrected upwardsto reach 1719 GW (rom 1495 GW) These gures also lie

above GWEC’s most ambitious scenario as outlined in theGlobal Wind Energy Outlook in 2006, which orecast a totalglobal installed capacity o 221 GW in 2012, ie 193 GW

below the current estimate

The reasons or this adjustment are twoold: Firstly, boththe US and the Chinese market have been growing andwill continue to grow at a much aster rate than expectedeven a year ago Secondly, the emergence o signicantmanuacturing capacity in China will have a more importantimpact on the growth o the global markets than originallythought While tight production capacity is going to remainthe main limiting actor o urther market growth, machines‘made in China’ will help take some o the strain out o the

current supply situation

Market recast r 2008-2012

Fujian Dongshan Wujiao Wan wind arm, Dongshan, Fujian, China

© Greenpeace

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 14/72

12 GWEC – GLOBAL WIND 2007 REPORT

The average growth rates during this ve year period interms o total installed capacity are expected to be 206%,compared with 234% during 2003-2007 In 2012, Europewill continue to host the largest wind energy capacity, withthe total reaching 102 GW, ollowed by Asia with 66 GW andNorth America with 613 GW

The additions in installed capacity every year are predicted

to grow rom 20 GW in 2007 to 361 MW in 2012, withan average growth rate o 124% Considering that annualmarkets have been increasing by an average o 247% overthe last 5 year, growth could be much stronger also in theuture, were it not or continuing supply chain dicultieswhich considerably limit the growth o annual marketsor the next two years This problem should be overcomeby 2010, and along with the development o the oshoremarket, growth rates are expected to recover in the nextdecade

Asia is predicted to overtake Europe as the biggest annualmarket, with as much as 125 GW o new wind generatingcapacity installed during the year 2012, up rom 54 GWin 2007 This growth will be mainly led by China, whichhas since 2004 doubled its total capacity every year,thereby consistently exceeding even the most optimisticpredictions

By 2010, China is expected to be the biggest national annualmarket globally This development is underpinned by a rapidlygrowing number o domestic manuacturers operating in the

Chinese market, delivering home made turbines to large scalewind energy projects Already in 2007, 40 domestic suppliers

supplied 56% o the new installations in the domesticmarket, up rom 41% in 2006

While China will emerge as the continental leader in Asia,sustained growth is also oreseen in India, while other marketssuch as Japan, South Korea and Taiwan will also contribute tothe development o wind energy on the continent

The European market will by 2012 have allen to third placein terms o annual installations (103 GW), behind NorthAmerica (105 GW) Overall, this means that over 71% onew installations will occur outside o Europe in 2012, uprom 28% in 2004 and 57% in 2007 While in terms o totalinstalled capacity, Europe will continue to be the biggestregional market, its share will have allen to 424%

The large scale development o oshore wind energy isurther delayed and will only start to have a signicantimpact on European market growth towards the end o the

time period under consideration However, it is expected thatoshore development will lend new momentum to growth inEurope during the next decade

In Europe, Germany and Spain will remain the leadingmarkets, but their relative weight will decrease as a largernumber o national markets emerge on the scene While thespectacular growth o the Spanish market in 2007 with over35 GW o new installations will not be sustained, a stablepace o 2-25 GW per year on average can be expected,enabling Spain to reach the government’s 2010 target o

20 GW The size o the German annual market will continueto decrease, but it will remain the second strongest European

Tauern wind park Oberzeiring

© Vestas

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 15/72

13GWEC – GLOBAL WIND 2007 REPORT

ANNUAl INSTAllEd CApACITy 2008 - 2012

2008 2009 2010 2011 2012

14.4 % 12.6 % 11.6 % 11.8 % 11.8 %

23259

289

323

36140

35

30

25

20

15

10

5

0

GW

Growth rate

CUMUlATIvE CApACITy 2008 - 2012

2008 2009 2010 2011 2012

24.4 % 22.1 % 20.2 % 18.8 % 17.7 %

1173

143

1719

2042

2403300

250

200

150

100

50

0

GW

Growth rate

market or the 2008-2012 period, and the biggest in termso total installed capacity By 2010, oshore developments

will give new impetus to the German market, resulting instronger growth Other important markets in Europe willbe France and the United Kingdom, each increasing by anaverage o 1 GW per year

The North American market will grow even stronger thanpreviously thought, led by signicant growth in the US, aswell as sustained development o the Canadian market Intotal, North America will see an addition o 426 GW in thenext ve years, reaching 613 GW o total capacity in 2012This represents an average o 85 GW o new capacity added

every year, the bulk o which will be in the US

These gures assume that the US Production Tax Credit (PTC)will continue to be renewed in time or the current stronggrowth to continue Moreover, high level engagement o anincreasing number o US states, 24 o which have alreadyintroduced Renewable Portolio Standards, will also assuresustained growth A change in US administration may urtherunderpin this development

Latin America is expected to contribute to the global total in

a more substantial way in the uture, mainly driven by Brazil,Mexico and Chile By 2012, the total installed capacity inLatin America and the Caribbean will increase 8-old to reach

45 GW, with an annual market o 14 GW However, despiteits tremendous potential, Latin America is likely to remain a

small market until the end o the period under consideration,progressing towards more signicant development in thenext decade

The Pacic region will see around 23 GW o newinstallations in 2008-2012, bringing the total up to 35 GWWhile in Australia, wind energy development slowed downconsiderably in 2006 and 2007, the outlook or the utureis more optimistic, mainly thanks to the change in ederalgovernment at the end o 2007, the ratication o the KyotoProtocol and the pledge to implement a new target or

20% o electricity to come rom renewables by 2020 NewZealand, however, got new impetus with 151 MW o newinstallations, and many more projects are at various stages odevelopment

Arica and the Middle East will remain the region with thesmallest wind energy development, with a total installedcapacity o 3 GW by 2012, up rom 500 MW in 2007However, it is expected that market growth will pick up inthe coming ve years, with annual additions reaching around800 MW by 2012 This development will be driven by Egypt

and Morocco, with some development also predicted in otherNorth Arican and Middle Eastern countries

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 16/72

14 GWEC – GLOBAL WIND 2007 REPORT

CUMUlATIvE CApACITy ENd 2007 ANNUAl CApACITy IN 2007

L. America& Caribbean

05 GW (05%)

Asia

161 GW(171%)

Pacifc12 GW (13%)

Arica & M. East05 GW (05%)

Pacifc02 GW (1%)

Arica & M. East02 GW (1%)

Eurpe87 GW(432%)

L. America &Caribbean

003 GW (015%)

Asia

54 GW(268%)

Nrth America56 GW (278%)

Eurpe571 GW(607%)

Nrth America187 GW(199%)

CUMUlATIvE CApACITy ENd 2012 ANNUAl CApACITy IN 2012

L. America &Caribbean

45 GW (19%)

Pacifc35 GW (15%)

Arica & M. East3 GW (12%)

L. America & Caribbean14 GW (39%)

Pacifc06 GW (17%)

Arica & M. East08 GW (22%)

Eurpe103 GW(285%)

NrthAmerica105 GW(291%)

Asia125 GW(346%)

Eurpe102 GW(424%)

Nrth America613 GW (255%)

Asia66 GW(275%)

NEW INSTAllEd CApACITy 2008-2012

L. America &Caribbean

40 GW (27%)

Pacifc23 GW (16%)

Arica & M. East25 GW (17%)

Eurpe449 GW(307%)

Nrth

America426 GW (291%)

Asia499 GW(341%)

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 17/72

15GWEC – GLOBAL WIND 2007 REPORT

Installe capacity by regin

Eue

>5,000 MW

2,000 - 5,000 MW

500 - 2,000 MW

50 - 500 MW

<49 MW

0 MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 18/72

16 GWEC – GLOBAL WIND 2007 REPORT

Nth Ameica, latin Ameica & Caiean

>5,000 MW

2,000 - 5,000 MW

500 - 2,000 MW

50 - 500 MW

<49 MW

0 MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 19/72

17GWEC – GLOBAL WIND 2007 REPORT

CAPACITY BY REGION

Asia & pacifc regin

>5,000 MW

2,000 - 5,000 MW

500 - 2,000 MW

50 - 500 MW

<49 MW

0 MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 20/72

18 GWEC – GLOBAL WIND 2007 REPORT

Aica & Mie East

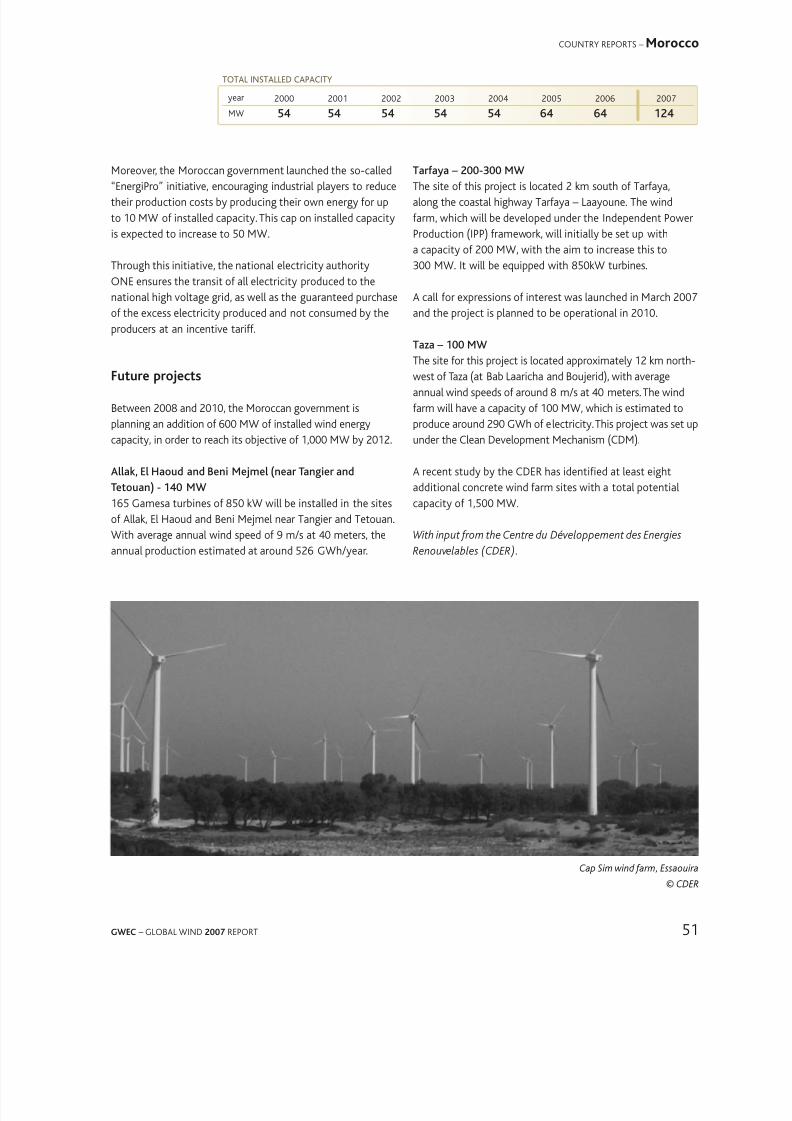

>5,000 MW

2,000 - 5,000 MW

500 - 2,000 MW

50 - 500 MW

<49 MW

0 MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 21/72

19GWEC – GLOBAL WIND 2007 REPORT

CAPACITY BY REGION

Cuntry reprts

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 22/72

20 GWEC – GLOBAL WIND 2007 REPORT

AustraliaWith some o the world’s best wind resources, Australia is aprime market or wind energy The growing industry can takeadvantage o a stable, growing economy, good access to gridinrastructure and well organised nancial and legal servicesA change in government in late 2007 signalled a majorshit or climate change policy – placing the Australian windindustry in a strong position with a very positive outlook orgrowth in 2008 and beyond

The ic eninment

2007 was a watershed year in terms o Australia’s approachto climate change policy that will result in positive long-termimpacts or the wind industry

Bipartisan acceptance o the need or strong supportivepolicies or technology deployment, not just researchand development programs, is a major shit in the policylandscape and will drive deployment in the near term toensure the lowest cost in the long-term to meet emissionstargets

Despite little movement in ederal policy or most o 2007 –particularly in relation to extending the national MandatoryRenewable Energy Target (MRET) – momentum to supportrenewable energy deployment was building at the stateand territory level By August 2007, the states o Victoria,New South Wales, Queensland, Western Australia and theAustralian Capital Territory were all at various stages oimplementing state-based mandatory renewable energydeployment schemes

There were initial ears that the previous Liberal Governmentwould move to wind-up technology deployment policiessuch as MRET and attempt to abolish state schemes,including the Victorian Renewable Energy Target However, inSeptember they surprised many by announcing that ratherthan scrapping all renewable energy deployment schemesthey would consolidate all schemes into a national CleanEnergy Target scheme o 15% o electricity coming rom ‘lowemissions technologies’

However, the overwhelming breakthrough o the year or the

Australian wind industry came during the election campaignwhen the Labor Party, now the new government, met one o

the key asks o the Clean Energy Council – committing to anexpanded national target o 20% o electricity coming romrenewable energy by 2020 The new renewable energy targetwill underpin a strong and consistent growth in renewableenergy projects over the coming decade

Bipartisan support or a domestic emissions trading systememerged in 2007, with both major parties going into theederal election pledging to implement a domestic emissionstrading program The Labour Party had also announced itscommitment to a long term emissions reduction target o60% (compared with year 2000 levels) by 2050 as part otheir campaign These policies will gradually begin to levelthe playing eld between wind and other renewable energyand coal power, which holds a 77 per cent share o Australia’selectricity generation

2007 also saw the amalgamation o the Australian WindEnergy Association (Auswind) and the Australian BusinessCouncil or Sustainable Energy to orm the Clean EnergyCouncil - a single powerul industry voice or the cleanenergy sector in Australia

It is expected that 2008 is going to be an exciting andchallenging year The Clean Energy Council is ocussing onensuring that the details o the RE support scheme deliverinvestment certainty to wind and clean energy developersKey issues include: the build-up o electricity retailer liabilities

(ie the amount o renewable energy each retailer must buyand surrender under the scheme); project eligibility (ie which

Cathedral Rocks wind arm, South Australia

© Roaring 40s

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 23/72

21GWEC – GLOBAL WIND 2007 REPORT

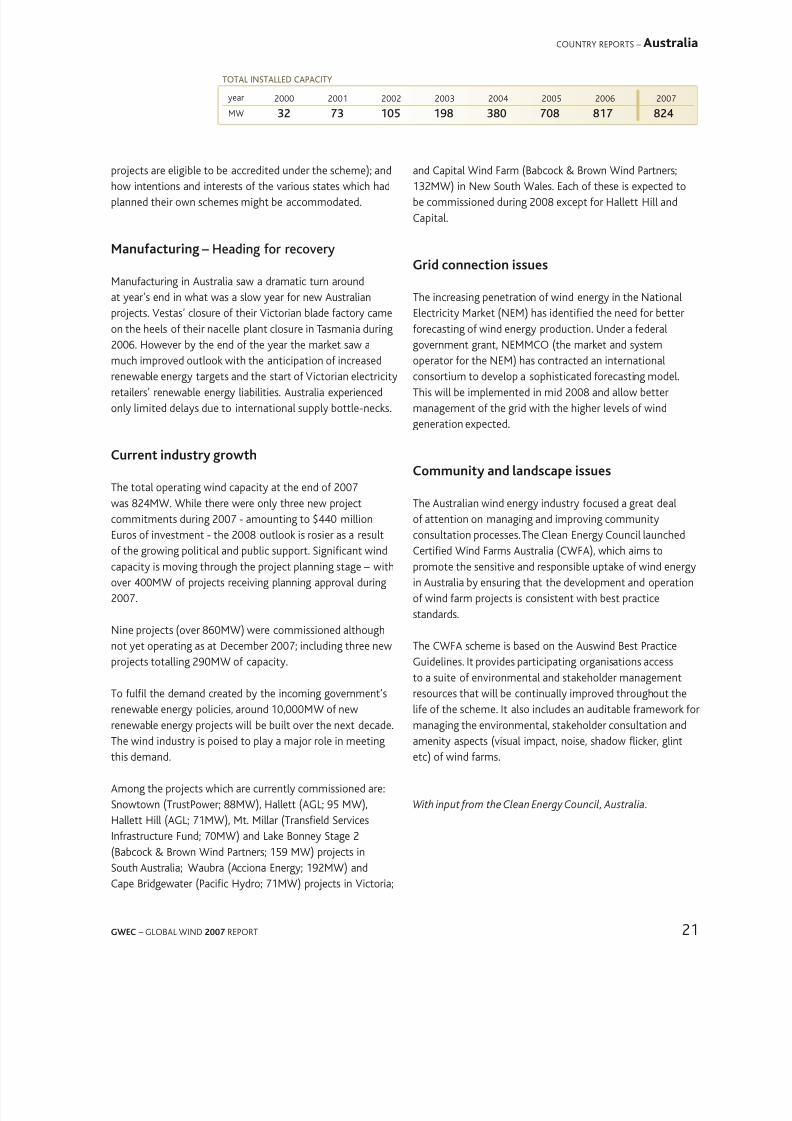

2000 2001 2002 2003 2004 2005 2006 2007

32 73 105 198 380 708 817 824

year

MW

ToTal InsTalleD caPacITY

COUNTRY REPORTS – Australia

projects are eligible to be accredited under the scheme); andhow intentions and interests o the various states which hadplanned their own schemes might be accommodated

Manuactuing – Heaing r recvery

Manuacturing in Australia saw a dramatic turn aroundat year’s end in what was a slow year or new Australianprojects Vestas’ closure o their Victorian blade actory cameon the heels o their nacelle plant closure in Tasmania during

2006 However by the end o the year the market saw amuch improved outlook with the anticipation o increasedrenewable energy targets and the start o Victorian electricityretailers’ renewable energy liabilities Australia experiencedonly limited delays due to international supply bottle-necks

Cuent inust gwth

The total operating wind capacity at the end o 2007was 824MW While there were only three new project

commitments during 2007 - amounting to $440 millionEuros o investment - the 2008 outlook is rosier as a resulto the growing political and public support Signicant windcapacity is moving through the project planning stage – withover 400MW o projects receiving planning approval during2007

Nine projects (over 860MW) were commissioned althoughnot yet operating as at December 2007; including three newprojects totalling 290MW o capacity

To ull the demand created by the incoming government’srenewable energy policies, around 10,000MW o newrenewable energy projects will be built over the next decadeThe wind industry is poised to play a major role in meetingthis demand

Among the projects which are currently commissioned are:Snowtown (TrustPower; 88MW), Hallett (AGL; 95 MW),Hallett Hill (AGL; 71MW), Mt Millar (Transeld ServicesInrastructure Fund; 70MW) and Lake Bonney Stage 2(Babcock & Brown Wind Partners; 159 MW) projects in

South Australia; Waubra (Acciona Energy; 192MW) andCape Bridgewater (Pacic Hydro; 71MW) projects in Victoria;

and Capital Wind Farm (Babcock & Brown Wind Partners;132MW) in New South Wales Each o these is expected tobe commissioned during 2008 except or Hallett Hill andCapital

Gi cnnectin issues

The increasing penetration o wind energy in the NationalElectricity Market (NEM) has identied the need or betterorecasting o wind energy production Under a ederal

government grant, NEMMCO (the market and systemoperator or the NEM) has contracted an internationalconsortium to develop a sophisticated orecasting modelThis will be implemented in mid 2008 and allow bettermanagement o the grid with the higher levels o windgeneration expected

Cmmunit an anscae issues

The Australian wind energy industry ocused a great deal

o attention on managing and improving communityconsultation processes The Clean Energy Council launchedCertied Wind Farms Australia (CWFA), which aims topromote the sensitive and responsible uptake o wind energyin Australia by ensuring that the development and operationo wind arm projects is consistent with best practicestandards

The CWFA scheme is based on the Auswind Best PracticeGuidelines It provides participating organisations accessto a suite o environmental and stakeholder management

resources that will be continually improved throughout thelie o the scheme It also includes an auditable ramework ormanaging the environmental, stakeholder consultation andamenity aspects (visual impact, noise, shadow ficker, glintetc) o wind arms

With input rom the Clean Energy Council, Australia.

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 24/72

22 GWEC – GLOBAL WIND 2007 REPORT

Brazil

Mucuripe wind arm, Ceará

© A WOBBEN WINDPOWER Ind. e Com. Ltda

The power generation mix in Brazil consists o 84%renewables (mainly hydropower), and renewables willcontinue to play an important role in the country’selectrication plans As high oil prices, electrical shortagesand air pollution problems are putting pressure on theauthorities to provide sustainable solutions, biomass,hydroelectricity, wind and solar power generation are in astrong position to be the main sources or rural electricationprojects

According to a wind atlas published by the Brazilian Wind

Energy Centre (CBEE) the total wind potential in Brazil isestimated to be about 143,500 MW However, at this stage,wind still plays a secondary role in Brazil Areas with thegreatest wind energy potential are in the North Eastern,Southern and South Eastern regions

Between 1999 and 2005, wind energy capacity in Brazilincreased only in very small increments, until in 2006, when208 MW were installed in one year, bringing the total to237 MW In 2007, only one wind arm o 102 MW cameonline: Eólica Millennium, a project acquired by Pacic Hydro

rom local company Bioenergy The total now stands at247 MW

The main obstacles to Brazilian wind power are signicantimport duties and taxes making projects less protable,unless complete local production and sourcing areestablished Also, the country has prioritised the developmento its biomass potential in the past ew years Wind power,however, is expected to grow substantially in the near uture

The proINFA gamme

Due to the high dependency on Brazil’s large but alreadymostly exploited hydro resources, the country aced a powershortage in 2001 In order to remedy the situation and avoidmore severe power crises in the uture, the governmentlaunched incentive programmes to encourage thermal andrenewable power generation

In 2002, the Brazilian government passed a programme calledPROINFA to stimulate the development o biomass, wind

and small hydro power generation This law was revised inNovember 2003

In the rst stage (up to 2008), the programme guaranteedpower sale contracts o 3,300 MW o projects using thesetechnologies The Brazilian state-controlled electricityutility Eletrobrás will buy power produced by RES underpower purchase agreements (PPAs) o 20 years at pre-setpreerential prices

As some projects under construction at the present stagemay not reach the PROINFA time limit o 2008, Eletrobrás isconsidering the possibility o extending the deadline to June

2009

The incremental costs o the RES power will be passed on tothe end-use consumers The Brazilian National DevelopmentBank (BNDES) will make special nancing programmesavailable or renewables projects that are eligible orPROINFA

PROINFA stipulates that a minimum o 60% o constructioncosts have to be spent domestically As a result, thegovernment expects the programme to generate 150,000

jobs and to attract private investments worth some26bn USD

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 25/72

23GWEC – GLOBAL WIND 2007 REPORT

2002 2003 2004 2005 2006 2007

22 29 29 29 237 247

ToTal InsTalleD caPacITY

COUNTRY REPORTS – Brazil

Originally, a second stage o PROINFA was oreseen once the3,300 MW objective had been met, with the aim to increasethe share o the three renewable sources to 10% o annualelectricity consumption within 20 years Renewable energygenerators would then have been required to issue a numbero Renewable Energy Certicates proportional to the amounto clean energy produced

However, despite the high expectations raised by the PROINFAprogramme, the scheme has to date ailed to deliver the greatnumber o wind projects the government had aimed or As

a result, the current government is showing little interestin taking PROINFA to its second stage, and is consideringreplacing it with an auction system The Brazilian Wind PowerAssociation (ABEEolica) is lobbying to proceed with PROINFA IIwhile at the same time introducing an auction process

Predictions or 2008 are quite optimistic: there are 14 windenergy plants under construction nanced by the PROINFAprogramme, amounting to 1073 MW o installed capacityIn addition, experts estimate that another 27 wind armsrepresenting 90129 MW could be added to the grid in 2009,

provided that PROINFA is extended until the rst semestero 2009

Ke aes in the baiian maket

In 2008, the largest players are expected to be Ventos do SulEnergia (SPC), Energias Renováveis do Brasil and SIIF Énergiesdo Brasil All players are in the process o constructing largewind arms in the regions o Rio Grande do Sul, Rio Grandedo Norte and Ceará SIIF Energies do Brasil intends to install

928 MW o wind energy by 2010

There are also a number o oreign groups looking orproject development opportunities as well as acquisitiono developed projects Fortuny intends to install 223 MWo wind energy in the south by 2011 Enercon is the largestsupplier o wind generators in Brazil, while Suzlon enteredthe market in 2007, signing two large contracts or a totalo 350 MW (or ‘nationalisation’ requirements, tower andother components will be bought rom Brazilian actories)Argentinean Impsa has also started building a actory in

Pernambuco to produce Vensys turbines, and is planning tomanuacture its own machines in the uture

Financing is typically done via the National Economic &Social Development Bank (BNDES), the Development Agencyo the Northeast (ADENE) and the Bank o the Northeast(BNB), all o which ocus on ethical and environmentallyriendly projects Furthermore the PROINFA also assures low-interest loans rom BNDES

Grid operators include Centrais Elétricas Brasileiras(Eletrobras) and Operador Nacional do Sistema Elétrico(ONS)

More than 5,000 MW o wind energy projects have alreadybeen registered with Brazilian Electricity RegulatoryAgency (ANEEL), awaiting approval or supply contractswith utilities in order to move orward with planning andconstruction These projects are non-PROINFA, but they arebeing developed in the anticipation o an auctions scheme,despite the act that the conditions o this scheme are as yetunknown

WINd FArMS IN brAzIl

Win pakrate pwe

(MW)

1 Eólica de Prainha 10

2 Eólica de Taíba 5

3 Eólica-Elétrica Experimental do Morro do Camelinho 1

4 Eólio - Elétrica de Palmas 25

5 Eólica de Fernando de Noronha 0225

6 Mucuripe 24

7 Rio do Fogo 493

8 Eólica de Bom Jardim 06

9 Eólica Olinda 0225

10 Parque Eólico do Horizonte 48

11 Macau 18

12 Eólica Água Doce 9

13 Parque Eólico de Osório 50

14 Parque Eólico Sangradouro 50

15 Parque Eólico dos Índios 50

16 Eólica Millennium 102

Tta 24710

With input rom AEEolica and Greenpeace Brazil.

year

MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 26/72

24 GWEC – GLOBAL WIND 2007 REPORT

Canaa

Melanchton wind arm in Shelburne, Ontario

© CanWEA

Canada’s wind energy market experienced its second best year ever in 2007 A total o 386 MW o new wind energycapacity was installed in 2007, increasing Canada’s total by26% Canada now has 1,846 MW o installed wind energycapacity

2007 pects

Ten wind energy projects were commissioned in 2007 in vedierent Canadian provinces

Alberta led all provinces in 2007, installing three newprojects totaling 139 MW Alberta is now Canada’s leading jurisdiction or wind energy with 524 MW

The largest wind energy project commissioned in Canada in2007 was the 1005 MW Anse-a-Valleau project in Quebec,the second project to be commissioned rom Hydro-Quebec’s earlier 1,000 MW request or proposals

Two new projects, totaling 776 MW were commissionedin Ontario These two projects brought Ontario’s totalinstalled capacity to 491 MW

Three smaller projects, totaling 59 MW, were installed inCanada’s smallest province, Prince Edward Island (PEI) Theinstallation o these acilities means that PEI has now metits target to produce wind energy equivalent to 15% o itstotal electricity demand three years ahead o schedule

One new 10 MW project was commissioned in Nova Scotia

Turbines or these projects were provided by threemanuacturers: Enercon (169 MW), Vestas (1164 MW) andGE (1005 MW)

Futue Gwth psects

Canada enters 2008 with signed contracts in place or theinstallation o an additional 2,800 MW o wind energy, mosto which is to be installed by 2010

In addition, several new competitive tendering processes orwind energy were launched in 2007 in Manitoba, Quebec,New Brunswick and Nova Scotia and in early 2008, this is

expected to lead to the signing o an additional 2,800 MW ocontracts or new wind energy development in Canada

In 2008, Ontario is planning to issue a call or another500 MW o renewable energy (most o which is likely to besupplied by wind), Quebec will issue calls or another500 MW o wind energy and British Columbia will issue amajor new call or clean power

Moreover, the removal o the 900 MW threshold on windenergy development in Alberta in late 2007, accompaniedby new investments in transmission resources, is likely tostimulate signicant new wind energy investment in thatprovince

Finally, several o Canada’s provincial governments (eg,Saskatchewan, Manitoba, Ontario) have made commitmentsto signicant additional uture procurements o wind /renewable energy, although these will take place ater 2008

I all o Canada’s provincial governments / utilities meet theirstated targets or wind / renewable energy development, it isanticipated that Canada will have a minimum o 12,000 MWo installed wind energy capacity by 2016

12,000 MW o installed wind energy capacity would producearound 31,200 GWh, enough to meet about 4% o totalCanadian electricity demand in 2016 However, the newwind energy acilities constructed in Canada between 2005and 2015 would produce enough electricity to meet 21% oCanada’s projected increase in electricity demand over that

period

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 27/72

25GWEC – GLOBAL WIND 2007 REPORT

2000 2001 2002 2003 2004 2005 2006 2007

137 198 236 322 444 684 1,460 1,846

ToTal InsTalleD caPacITY

COUNTRY REPORTS – Canada

Canaa’s pic Famewk

Canada’s ederal and provincial governments have bothdeveloped policy rameworks to support the deployment owind energy in Canada The Federal Government’s ecoEnergyRenewable Power Program provides a production incentiveo 1 cent / kWh or the rst 10 years o production at a windenergy acility

Provincially, most governments have either legislatedrenewable portolio standards, or simply directed government

owned utilities to meet wind / renewable energy targetsProcurement to meet these targets is usually conductedthrough a competitive tendering (request or proposalsprocess), although Ontario has implemented a StandardOer Contract (ie eed-in tari) program or projects o10 MW or less and similar programs are under considerationin other provinces The only exception is Alberta, where aderegulated market means that wind developers must buildplants on a merchant basis

It also appears likely that wind energy projects will be able to

create greenhouse gas emission osets within both Federaland Albertan greenhouse gas emission regulatory rameworksthat are to be put in place in 2008, providing an opportunityor wind energy projects to obtain some value or theirenvironmental attributes in a domestic carbon market

Emeging Chaenges

While the prospects or wind energy in Canada are extremelypositive, the industry does ace a number o challenges that

must be addressed i Canada is to maximize the economicand environmental benets o its massive wind energypotential

On the policy ront, the ederal ecoEnergy Renewable PowerProgram is likely to have ully allocated its unds in 2009and it is not yet clear what orm uture ederal support willtake At the same time, several provinces have now procuredenough wind energy to meet their initial wind / renewableenergy targets and subsequent targets still need to beestablished Permitting and approval processes can still be

made more ecient and streamlined, particularly at themunicipal level

The availability o transmission capacity is also an emergingissue There are already some areas o Canada where winddevelopers must await the completion o major transmissionupgrades beore work can proceed More generally, Canadaexpects to make signicant investments in new transmissionover the next decade, but it remains to be determined howmuch o this will be designed to acilitate both access towind resources and greater wind integration

While public opposition to wind energy projects is still anissue with respect to a minority o projects in Canada, such

opposition is gaining a higher prole in light o the rapidexpansion o the industry Finally, increased turbine costs andissues related to turbine availability are having an impact onthe marketplace

None o these challenges are insurmountable In act, it isincreasingly the case that government, electricity sectorstakeholders and the wind energy industry are workingtogether to address these issues Accordingly, the utureor Canada’s wind industry looks bright with stable andsustainable growth oreseen or the next several years

With input rom the Canadian Wind Energy Association

(CanWea)

Mount Copper wind arm in Murdochville, Quebec© 3Ci and Creststreet Asset Management Ltd

year

MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 28/72

26 GWEC – GLOBAL WIND 2007 REPORT

Chile

Canela wind arm

©EndesaEco

At the end o 2007, the rst wind park was connected tothe main grid system in Chile, adding 182 MW o powergenerating capacity There is another small wind park inthe ar south o the country Since May 2006, anothersix projects totalling 257 MW are being evaluated by theenvironmental authorities The construction o three o themhas already been approved and the rest are waiting or ananswer

renewae eneg icies in Chie

President Bachelet has committed her government to atarget or 15% o new power capacity to come rom newrenewable energy between 2006 and 2010

The previous government already eliminated some o thebarriers to renewable energy in 2004 and 2005:

the right to provide renewable energy to distributors whosupply small consumers;

the obligation o the distribution operators to allow the

connection o small power stations to their networks;

the elimination o the obligation to pay dispatching coststo the system operator;

priority access to the grid without a specic generationrequirement;

the partial exemption rom transmission costs; thisexemption applies only i small generators o renewableenergy do not exceed 5% o the total demand o smallconsumers, who are regulated separately A distinction is

also made between power stations smaller than 9 MW thathave the ull exemption and power stations smaller than20 MW that can claim partial exemption

These changes in legislation have encouraged the study oseveral wind power stations, supported by a und establishedby the government, which provides support o up to150,000 dollars per project To speed up the development onew renewable energy projects, the government introduceda new modication o the law governing electricity at thebeginning o 2007

This law, which is currently still being discussed, obliges thebig power companies to purchase 5% renewable energyby the end o 2010 until the year 2035; this percentageobligation will increase gradually, by 0,5% each year, until itreaches 10%

Failure to ull this requirement will invoke a ne o about30 USD or each MWh that was not purchased each yearThese nes will be turned over to the consumers who buypower rom companies that did ull the requirement

baies t win eneg eement

These legal modications are insucient support topromoters and investors in new renewable energy, asthis law does not incorporate mechanisms or xing orsupporting taris, which would increase certainty orinvestors Furthermore the new renewables generatorshave the same obligations in their supply contracts as a bigthermal or hydroelectric power stations; they have to pay

the transmission costs which are highly variable but can bevery substantial, and are obliged to assume the costs o gridconnection

Another barrier to the development o wind energy is thelack o good publicly available resource mapping Mostmeasurements have been done on a commercial basis andare thereore not available or public planning purposes Thegovernment is looking to do resource assessment in thoseareas that have been identied as suitable: the coastal zoneso the regions o Atacama, Coquimbo and Maule Other areas

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 29/72

27GWEC – GLOBAL WIND 2007 REPORT

Alto Baguales wind arm, Aysen© Alejandro Medina B

2000 2001 2002 2003 2004 2005 2006 2007

0 2 2 2 2 2 2 20

ToTal InsTalleD caPacITY

COUNTRY REPORTS – Chile

with potential include Calama and the high plateau zones inthe region o Antoagasta, and around the headlands alongthe entire coast o the north and central zones

The real trigger or new wind projects in Chile is thecurrent energy crisis because o gas supply disruptionsrom Argentina, which has caused acute shortages or longperiods In addition, 2007 was a very dry year, with a notabledecrease in spring runo, which is a major contributor to thefow in most Chilean rivers

This crisis, which oreshadows energy rationing or 2008, hascaused an abrupt change in the energy supply o the countryUp until 2006, 75% o the electricity generated was based onhydro resources and natural gas This was reduced to 50% in2007, when it was largely replaced by diesel generators (22%o the total) The skyrocketing o the price o energy wasinevitable, reaching 140 USD per MWh in November o 2007,practically double the price established by the authorities inApril o 2007

Existing win aks in Chie

Parque Alto Baguales.Operated by PSEG Energy Holdingsand located in the extreme south o the country in the regiono Aysén With its 2 MW o power it has been supplying thecity o Coyhaique since 2001 They are planning to increasethe capacity o this project in 2008 by installing an additional198 MW

Parque Eólico Canela. Operated by Endesa and locatedin the region o Coquimbo, this station was connected tothe grid in November 2007 With an investment o USD 35million, its capacity is 1815 MW, and will avoid about 30,000tons o C0

2in an average year The second phase o the park

will add an additional 70 MW and will be operational in2009, ater an investment o USD 120 million

Futue utk

257 MW o wind projects are under consideration by theenvironmental authorities, including projects proposed byAcciona, GHF mbH, Eólica Navarra, Barrick Gold, SeaWindand SN Power In addition, there are other projects underdevelopment, including by: Iberdrola (150 MW), BHP Billitonwith Pacic Hydro (100 MW) and Ecopower (140 MW)

These projects are competing with new conventionalsupply projects that have been presented to environmentalauthorities, including: diesel (21 new projects with a capacityo 1,626 MW); coal (11 projects with a total o 5,515 MW);

and hydroelectricity (11 projects with a total o 1286 MW)This is in addition to the large dam project in Aysén beingdeveloped by Endesa/Colbún, which is expected to deliver anadditional 2800 MW

All o this is happening in a system with a total o 13,000MW o installed capacity, where part o the recently installedgas generation capacity needs to be replaced, and there is aneed or 700 MW o new power capacity annually to coverthe increasing demand

Chile doesn’t have a local wind industry and it doesn’thave any national experience in the development o thisindustry However, the current changes are opening up newpossibilities Wind energy, small hydro and geothermal energycan add to the diversity o the electricity supply network,which is one o the objectives o the government This willrequire the cooperation o government and society in theestablishment o a long term energy development plan,rather than just reacting to short term market orces

With input rom Cooperativa Potencia Verde

year

MW

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 30/72

28 GWEC – GLOBAL WIND 2007 REPORT

China

The w’s astest gwing win enegmaket

China is the world’s astest growing wind energy market,with an average annual growth rate o 56% in the pastseven years The country has now reached the th placeor installed wind energy capacity, with over 6 GW at theend o 2007 However, experts estimate that this is just thebeginning, and that the real growth in China is yet to comeBased on the current growth rates, the Chinese RenewableEnergy Industry Association (CREIA) orecasts a capacity o

around 50 GW by 2015

With its large land mass and long coastline, China isexceptionally rich in wind energy potential In 2007, nationalresearch showed that the on-shore technically easible windresource in China is around 1,000 GW In addition to that,the o-shore potential is estimated at around 300 GW Theregions with the best wind regimes are located mainly alongthe South-East coast and Inner Mongolia, Xinjiang, GansuProvince’s Hexi Corridor and in some parts o North-EastChina, North-West China, Northern China and the Qinghai-

Tibetan Plateau

The rst Chinese wind arm went online in 1986 as ademonstration project, ollowed by urther projects nancedby oreign grants or sot loans In 1994, the ormer Ministryo Electric Power took the decision to develop wind energy asa new clean power source or the country Regulations wereissued to address issues o grid connection and paymentmechanisms

The main ies win eneg

Satisying rocketing electricity demand and reducing airpollution are the main driving orces behind the developmento wind energy in China However, given the country’ssubstantial coal resources and the still relatively low costo coal-red generation, cost reduction o wind poweris a crucial issue, which is being addressed through thedevelopment o large scale projects and boosting localmanuacturing o wind turbines

The Chinese government estimates that the localisationo wind turbine manuacturing brings benets to the local

economy and helps keep costs down Moreover, since mostgood wind sites are located in remote and poorer rural areas,wind arm construction benets the local economy through

the annual income tax paid to county governments, whichrepresents a signicant proportion o their budget Otherbenets include grid extension or rural electrication as wellas employment in wind arm construction and maintenance

The gwth the mestic inust

The wind manuacturing industry in China is booming Whilein the past, imported wind turbines dominated the Chinesemarket, this is changing rapidly as the growing wind power

market and the clear policy direction have encourageddomestic production

Fujian Dongshan Wujiao Wan wind arm, Dongshan, Fujian

© Greenpeace

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 31/72

29GWEC – GLOBAL WIND 2007 REPORT

2000 2001 2002 2003 2004 2005 2006 2007*

346 402 469 567 764 1,260 2,604 6,050

ToTal InsTalleD caPacITY

COUNTRY REPORTS – China

At the end o 2007, they were 40 Chinese manuacturersinvolved in wind energy, accounting or about 56% o theequipment installed during the year, up rom 41% in 2006This percentage is expected to increase substantially in theuture

companies operating in China include GE, Gamesa, Vestasand Suzlon

pic sut win eneg

In order to promote the development o renewable energytechnologies, the Chinese government published its

Renewable Energy Law in February 2005, and it enteredinto orce on 1 January 2006 This law was complementedby two regulations dening the pricing and cost sharing orenewable energy power and promoting renewable powergrid connection While the law set a target or renewableenergy development in China, the regulations introduced abidding procedure to determine the price, which then hasto be approved by the government The additional cost orenewable energy or power and the grid connection cost areshared by all electricity users

In September 2007, the National Plan or Renewable EnergyDevelopment was issued The Plan set out the nationaltarget and a mandated market share (MMS) system orthe development o renewable energy This plan ociallyconrms the target to increase the share o renewable energyin the country’s total primary energy consumption to 10%by 2010, and to 15% by 2020 Moreover, it aims to have5GW o grid-connected wind capacity installed by 2010(although this gure was already exceeded in 2007), and tohave about thirty 100 MW-scale wind arms established,mainly in the eastern coastal areas and “Sanbei Region”

(“Three Norths Region”), thus building up three 1 GW-scalewind arm bases in Jiangsu, Hebei, and Inner Mongolia,respectively In addition, one or two 100 MW-scale pilotoshore wind projects will be set up

The plan also conrmed the target to reach 30 GW oinstalled wind capacity by 2020 Rich wind energy resourcesin provinces such as Guangdong, Fujian, Jiangsu, Shandong,Hebei, Inner Mongolia, Liaoning, and Jilin, will be exploitedin adjacent swaths, thus establishing a backbone o majorwind provinces, each with over 2 GW o capacity installed

Six wind arm bases (Dabancheng in Xinjiang, Yumen inGansu, the eastern coastal area around Jiangsu and Shanghai,

Source: 2007 China Wind Power Report (Li Juneng, Gao Hu); CREIA

ANNUAl INSTAllEd CApACITy 2008 - 2012

2004 2005 2006 2007

75%

25%

70%

30%

551%

422%

559%

16%

413%

37%

80

60

40

20

0

Foreign Domestic Joint Venture

%

While in 2006, around 400 MW o new installations weremanuactured in China, in 2007, the top two Chinesemanuacturers (Gold Wind and Sinovel) alone accounted or

1,460 MW o the new installed capacity, which representedabout 42% o the annual market This compares to only 37%provided by the top three oreign manuacturers (Gamesa,Vestas and GE)

Total domestic manuacturing capacity has now approached5,000 MW, and is expected to reach 10-12 GW by 2010with 50% (about 6 GW) o the capacity coming rom thebig domestic manuacturers including Sinovel Windtec,Goldwind and Dongeng Electrical Machinery Joint venturesin the Chinese market include Nantong CASC Wanyuan Wind

Acciona Wind Turbine Manuacture, REpower North, Nordex(Yinchuan) and Hunan Hara XEMC Windpower Foreign

year

MW

*This number is provisional and is awaiting nal conrmation

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 32/72

30 GWEC – GLOBAL WIND 2007 REPORT

Huitengxile in Inner Mongolia, the Zhangbei Region o Hebei,and Baicheng in Jilin) will be developed each with a GW-level

installed capacity In addition, 1 GW oshore wind capacitywill be installed

In December 2007, a White Paper Council on energyconditions and policies by the Oce o the State did not, asexpected, emphasise coal as the main energy source or thecountry, but ocused on energy diversication, environmentalprotection and clean energy

Cncessin ects

Encouraging large scale commercial development o thedomestic wind power industry is a priority or the Chinesegovernment, and wind power projects larger than 50 MW areapproved by the national government through the National

Development and Reorm Commission (NDRC) The NDRCevaluates submissions according to the price per kWh o

power produced and the share o domestic components used

The main elements or wind power concession projects are: Each project should be 100MW and the turbines no smaller

than 600kW

Project investors are selected by public bidding, with thelowest eed-in tari (price per kWh) obtaining the contractThe length o the contract is 25 years

Ater the rst 30,000 ull load hours o operation or aturbine, the eed-in tari is reduced to the average or the

power market at that timeAll electricity produced by the project must be purchased

by the provincial power grid company

The dierence between the wind power price and theconventional power price is shared among the provincialgrids

70% o the wind turbine components should be made inChina

Local authorities are responsible or building access roads

to the wind arm sub-station, and the grid company ortransmission lines to the sub-station

In 2003-2006, our rounds o wind concession tenderingprogrammes have been conducted and by the end o 2006,teen projects were approved, accounting or 255GWo wind energy capacity All the projects have startedconstruction, but only 25% o them have been completedFull completion should be achieved by 2009 A urther3,000 MW have been approved by the local wind biddingprocedures based on the same principles as the wind

concession programme

The aim o the concession scheme has been to encourage areduction in the price o wind power within China’s reormedelectricity industry As a result, the taris oered by winningconcessions have been extremely low, causing the biddersto either overestimate the power output o their project orunderestimate the costs involved It is signicant to notethat successul bidders have been predominantly Chinesestate-run companies prepared to sacrice the short-termprotability o their projects For international market

entrants, however, this provided little incentive or urtherinvestment Jieyuan Yumen wind arm, Yumen, Gansu

© Greenpeace

8/3/2019 03GWEC - Global Wind 2007

http://slidepdf.com/reader/full/03gwec-global-wind-2007 33/72

31GWEC – GLOBAL WIND 2007 REPORT

To remedy this situation, changes were made to theconcession bidding process in the 5th round o tendering

in 2007 with the aim to discourage bidders rom usingan unreasonably low price or their bid The weight o thebidding price is 25% and those bidders with the bidding priceclosest to the average bidding price score the highest

Another major adjustment relates to the specic regulationor wind power equipment manuacturers As a supplier joining the bidding, one manuacturer can sign supplycontracts or a single type o wind turbine with up to threedevelopers In the rst our rounds, a supplier contract hadto be exclusively with one developer This adjustment means

that developers have more choice o turbines, therebyimproving the technical quality o the project plan