Embed Size (px)

Citation preview

1

Status of Global Wind Power

World Energy Solutions ConferenceSao Paulo

23 November 2007

Steve SawyerSecretary General

Global Wind Energy Council

2

GWEC: Uniting the Global Wind Industry

Associations:

Companies:

3

Overview

• Massive investment in renewables globally; wind getting the lion’s share of asset investment;

• Wind power growth rate globally continues very strong – at the upper range (or above) projections;

• Industry becoming global – European dominance lessening

• Massive investment in new manufacturing capacity – China and the US - but supply still lags demand;

• Climate Imperative – eyes on 2020

4

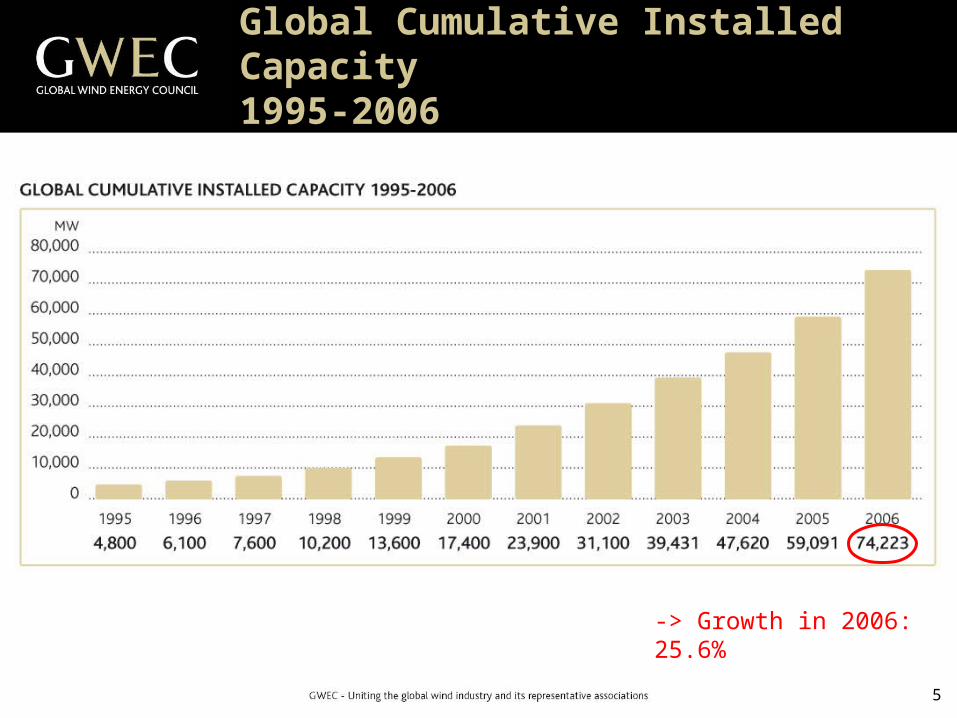

Global Cumulative Installed Capacity 1995-2006

5

Global Cumulative Installed Capacity 1995-2006

-> Growth in 2006: 25.6%

6

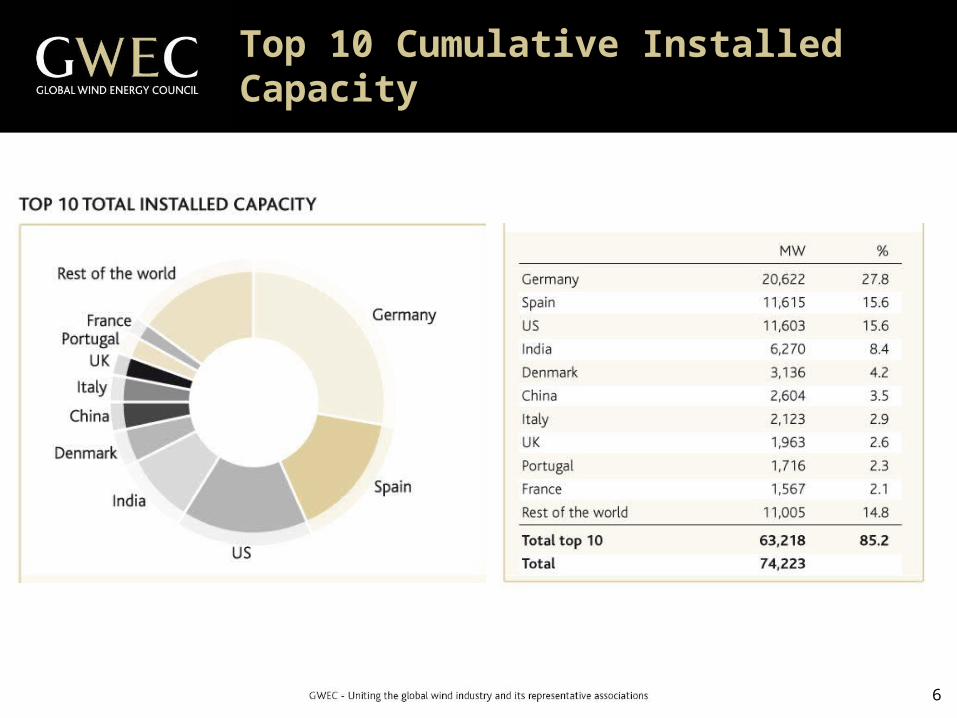

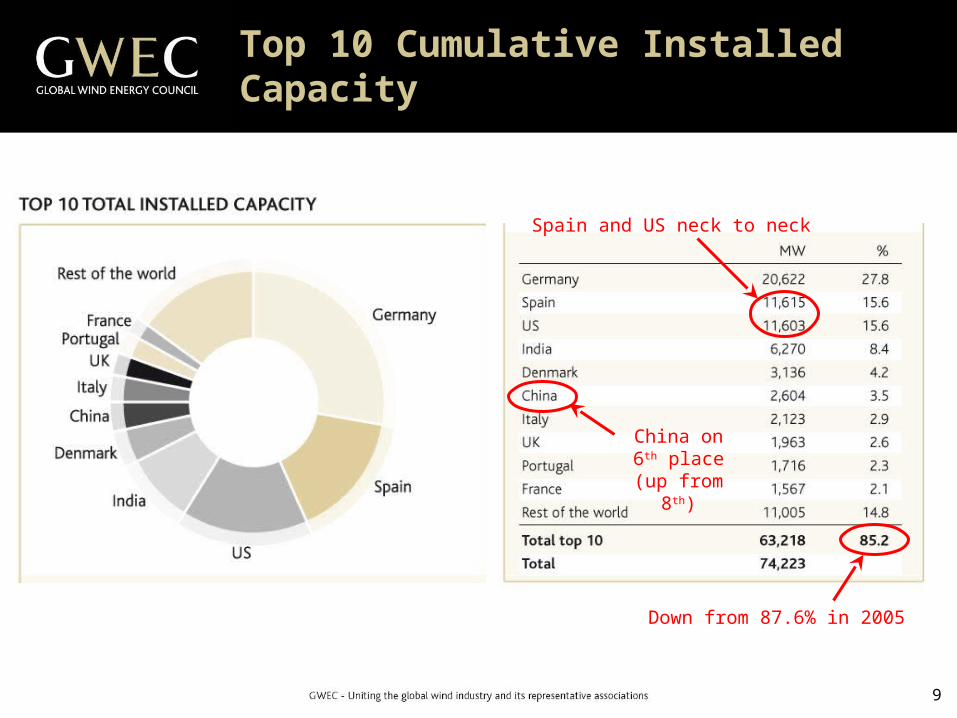

Top 10 Cumulative Installed Capacity

7

Top 10 Cumulative Installed Capacity

Spain and US neck and neck

8

Top 10 Cumulative Installed Capacity

Spain and US neck and neck

China on 6th place (up from

8th)

9

Top 10 Cumulative Installed Capacity

Down from 87.6% in 2005

Spain and US neck to neck

China on 6th place (up from

8th)

10

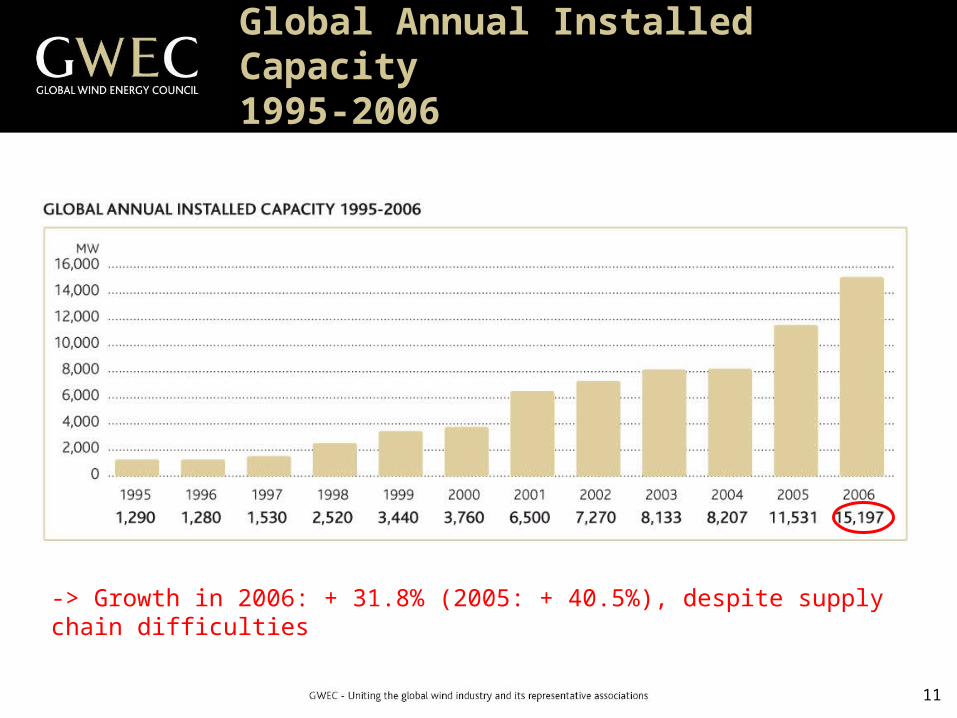

Global Annual Installed Capacity 1995-2006

11

Global Annual Installed Capacity 1995-2006

-> Growth in 2006: + 31.8% (2005: + 40.5%), despite supply chain difficulties

12

Top 10 New Installed Capacity 2006

13

Top 10 New Installed Capacity 2006

New in top 10

China 2nd in 2007?

Down from 86.9% in 2005

14

Annual Installed Capacity by Region

50.1%

21.3%

1.9% 1.3% 0.7%

24.2%

15

Global Development to 2050

16

% of Global Electricity Supply

1500 million tonnes of CO2/annum

After 2 years, actual performance is ahead of

Advanced Scenario

17

Conclusions

• Advanced Scenario is closest to reality at the moment; 2006/07 ahead of advanced scenario;

• Growth rates since 2000 have averaged 28%.

• Capital costs: demand and commodity markets driving prices up…and will continue to as long as there’s very high demand and more investor interest than available projects;

• China and US becoming major markets – US firmly in place as market leader – expected to install 4 GW in 2007; China exceeding advanced scenario, will meet its 2010 target this year;

• Three dominant markets: China, US, Europe.

18

Conclusions (2)

Impact of Climate Policy:

• Imperative for global emissions peak prior to 2020;• Power sector is largest source of emissions - 38% of

CO2, and about 25% of overall emissions;• In practical terms, there are 3 options for making major

emissions reductions in the power sector out to 2020: Efficiency; Fuel switching from coal to gas; and Wind Power;

• Wind energy is most cost-effective and timely option on the supply side out to 2020;

• Post 2012 carbon market design will have major impact;• Will 2600 Twh/year be sufficient?