Embed Size (px)

Citation preview

© The McGraw-Hill Companies, Inc., 2004

Slide 13-1

McGraw-Hill/Irwin

Chapter Thirteen

Accounting for Accounting for Legal Legal

Reorganizations Reorganizations and Liquidationsand Liquidations

© The McGraw-Hill Companies, Inc., 2004

Slide 13-2

McGraw-Hill/Irwin

Bankruptcy

A basic assumption of accounting theory is that a business is a going concern.

Occasionally, a business becomes insolvent; i.e., unable to pay its bills.

An insolvent business can either cease to exist, or can seek a legal remedy called bankruptcy.

A basic assumption of accounting theory is that a business is a going concern.

Occasionally, a business becomes insolvent; i.e., unable to pay its bills.

An insolvent business can either cease to exist, or can seek a legal remedy called bankruptcy.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-3

McGraw-Hill/Irwin

What happens to a business when it fails?

Who gets the

assets?

Who gets the

assets?

Are the creditors

protected?

Are the creditors

protected?

How it the business

failure reported?

How it the business

failure reported?

If the assets are sold, who

gets the money?

If the assets are sold, who

gets the money?

© The McGraw-Hill Companies, Inc., 2004

Slide 13-4

McGraw-Hill/Irwin

Bankruptcy Reform Act of 1978

Strives to achieve two goals in connection with

insolvency cases: the fair distribution of

assets to creditors, and the discharge of an

honest debtor from debt.

Strives to achieve two goals in connection with

insolvency cases: the fair distribution of

assets to creditors, and the discharge of an

honest debtor from debt.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-5

McGraw-Hill/Irwin

Bankruptcy Reform Act of 1978

Two basic forms of Two basic forms of filings filings

Two basic forms of Two basic forms of filings filings

Voluntary Voluntary BankruptcyBankruptcyVoluntary Voluntary

BankruptcyBankruptcyInvoluntary Involuntary BankruptcyBankruptcyInvoluntary Involuntary BankruptcyBankruptcy

© The McGraw-Hill Companies, Inc., 2004

Slide 13-6

McGraw-Hill/Irwin

Voluntary Bankruptcy The company files the

petition with the court requesting bankruptcy.

When facing the prospect severe losses or a difficult operating environment, companies will seek voluntary Chapter 11.

Voluntary Bankruptcy The company files the

petition with the court requesting bankruptcy.

When facing the prospect severe losses or a difficult operating environment, companies will seek voluntary Chapter 11.

Bankruptcy Reform Act of 1978

© The McGraw-Hill Companies, Inc., 2004

Slide 13-7

McGraw-Hill/Irwin

Involuntary Bankruptcy The company’s

creditors file the petition with the court.

This can result in the company being forced into liquidation under Chapter 7 or receiving protection under Chapter 11.

Involuntary Bankruptcy The company’s

creditors file the petition with the court.

This can result in the company being forced into liquidation under Chapter 7 or receiving protection under Chapter 11.

Bankruptcy Reform Act of 1978

© The McGraw-Hill Companies, Inc., 2004

Slide 13-8

McGraw-Hill/Irwin

Criteria for Forcing Involuntary Bankruptcy

© The McGraw-Hill Companies, Inc., 2004

Slide 13-9

McGraw-Hill/Irwin

Court Response to the Involuntary Petition

If the petition is not rejected by the court, an order of relieforder of relief is issued.

The order of relief halts all actions against the debtor.

A trustee is appointed to oversee the bankruptcy process.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-10

McGraw-Hill/Irwin

Fully Secured

Partially Secured

Unsecured With Priority

Unsecured

Top Priority

Classification of Creditors

Common and preferred

stockholders get what’s left

over.

Each level must be paid in full prior to

making distributions to the next level.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-11

McGraw-Hill/Irwin

Administrative costs related to liquidating the company.

Administrative costs related to liquidating the company.

Debts arising between the filing date and the issuance of an order of relief.

Debts arising between the filing date and the issuance of an order of relief.

Employee claims for wages earned during the 90 days prior to filing. Limited to $4,650 per

employee.

Employee claims for wages earned during the 90 days prior to filing. Limited to $4,650 per

employee.

Employee benefit plan claims during the 180 days prior to filing. Limited to $4,650 per

employee.

Employee benefit plan claims during the 180 days prior to filing. Limited to $4,650 per

employee.

Customer deposits. Limited to $2,100 per customer.

Customer deposits. Limited to $2,100 per customer.

Government claims for unpaid taxes. Government claims for unpaid taxes.

Unsecured Creditors with Priority

© The McGraw-Hill Companies, Inc., 2004

Slide 13-12

McGraw-Hill/Irwin

Assets labeled as: Pledged with fully secured creditors. Pledged with partially secured

creditors. Available for priority liabilities and

unsecured creditors.

Assets labeled as: Pledged with fully secured creditors. Pledged with partially secured

creditors. Available for priority liabilities and

unsecured creditors.

Debts labeled as:Debts labeled as: Liabilities with priority.Liabilities with priority. Fully secured creditors.Fully secured creditors. Partially secured creditors.Partially secured creditors. Unsecured creditors.Unsecured creditors.

Debts labeled as:Debts labeled as: Liabilities with priority.Liabilities with priority. Fully secured creditors.Fully secured creditors. Partially secured creditors.Partially secured creditors. Unsecured creditors.Unsecured creditors.

Statement of Financial Affairs

Prepared at the start of the proceedings.Prepared at the start of the proceedings. Helps the creditors to decide whether to push Helps the creditors to decide whether to push

for reorganization or liquidation.for reorganization or liquidation.

Prepared at the start of the proceedings.Prepared at the start of the proceedings. Helps the creditors to decide whether to push Helps the creditors to decide whether to push

for reorganization or liquidation.for reorganization or liquidation.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-13

McGraw-Hill/Irwin

Liquidation - A Chapter 7 Bankruptcy

Interim Trustee Interim Trustee is appointed by is appointed by

the court.the court.

Interim Trustee Interim Trustee is appointed by is appointed by

the court.the court.

Changes locks. Posts notices. Notifies U.S. Post

Office to forward all mail to trustee.

Opens a new bank acount (in the trustee’s name).

Compiles all financial records.

Obtains possession of all corporate records.

Changes locks. Posts notices. Notifies U.S. Post

Office to forward all mail to trustee.

Opens a new bank acount (in the trustee’s name).

Compiles all financial records.

Obtains possession of all corporate records.

An advisory An advisory committee of 3 - 11 committee of 3 - 11

unsecured unsecured creditors is creditors is appointed.appointed.

An advisory An advisory committee of 3 - 11 committee of 3 - 11

unsecured unsecured creditors is creditors is appointed.appointed.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-14

McGraw-Hill/Irwin

Appointed by the court;

approved by the creditors.

Appointed by the court;

approved by the creditors.

Has possession and control of the debtor’s

assets.

Has possession and control of the debtor’s

assets.

Can void property transfers made 90 days prior to the

petition filing.

Can void property transfers made 90 days prior to the

petition filing.

Prepares the statement of

realization and liquidation.

Prepares the statement of

realization and liquidation.

Role of the Trustee

© The McGraw-Hill Companies, Inc., 2004

Slide 13-15

McGraw-Hill/Irwin

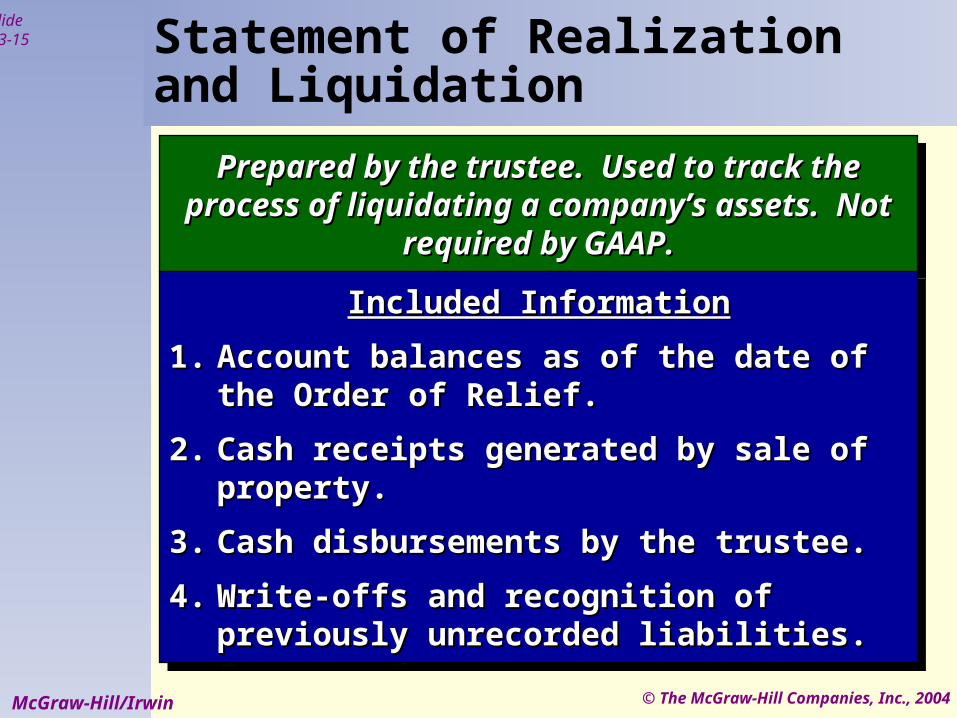

Prepared by the trustee. Used to track the Prepared by the trustee. Used to track the process of liquidating a company’s assets. Not process of liquidating a company’s assets. Not

required by GAAP.required by GAAP.

Prepared by the trustee. Used to track the Prepared by the trustee. Used to track the process of liquidating a company’s assets. Not process of liquidating a company’s assets. Not

required by GAAP.required by GAAP.

Statement of Realization and Liquidation

Included InformationIncluded Information

1.1. Account balances as of the date of the Order Account balances as of the date of the Order of Relief.of Relief.

2.2. Cash receipts generated by sale of property.Cash receipts generated by sale of property.

3.3. Cash disbursements by the trustee.Cash disbursements by the trustee.

4.4. Write-offs and recognition of previously Write-offs and recognition of previously unrecorded liabilities.unrecorded liabilities.

Included InformationIncluded Information

1.1. Account balances as of the date of the Order Account balances as of the date of the Order of Relief.of Relief.

2.2. Cash receipts generated by sale of property.Cash receipts generated by sale of property.

3.3. Cash disbursements by the trustee.Cash disbursements by the trustee.

4.4. Write-offs and recognition of previously Write-offs and recognition of previously unrecorded liabilities.unrecorded liabilities.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-16

McGraw-Hill/Irwin

A legal way to “salvage” a company rather than to liquidate it.

A legal way to “salvage” a company rather than to liquidate it.

ReorganizationChapter 11 Bankruptcy

The company is temporarily protected from its creditors.

Creditors are encouraged to negotiate new terms with the company.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-17

McGraw-Hill/Irwin

ReorganizationChapter 11 Bankruptcy

Workers get to keep their jobs.

Suppliers get to keep their customer.

Customers get to maintain their source of supply.

A legal way to “salvage” a company rather than to liquidate it.

A legal way to “salvage” a company rather than to liquidate it.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-18

McGraw-Hill/Irwin

ReorganizationChapter 11 Bankruptcy

A plan of reorganization must be put forth within 120 days

and approved within 180 days by the debtor in possession.

Examples include: Plans proposing changes in the

company’s operations. Plans for getting additional

monetary resources. Plans for changes in management of

the company. Plans to settle debts that existed

when the order of relief was issued.

A plan of reorganization must be put forth within 120 days

and approved within 180 days by the debtor in possession.

Examples include: Plans proposing changes in the

company’s operations. Plans for getting additional

monetary resources. Plans for changes in management of

the company. Plans to settle debts that existed

when the order of relief was issued.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-19

McGraw-Hill/Irwin

ReorganizationChapter 11 Bankruptcy

Acceptance of a reorganization plan requires approval of: 2/3 of the $ amount and more than

1/2 of the creditors 2/3 of each class of stockholders

If plan is turned down, the court can force its acceptance in a “cram down”.

As a final alternative, the court can convert a Chapter 11 Bankruptcy to a Chapter 7 Liquidation at any time.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-20

McGraw-Hill/Irwin

ReorganizationChapter 11 Bankruptcy

Financial Reporting During Reorganization

Gains/losses, revenues/expenses resulting from the reorganization process are reported separately.

Liabilities are restated. Current/noncurrent

classification not applicable.

Financial Reporting During Reorganization

Gains/losses, revenues/expenses resulting from the reorganization process are reported separately.

Liabilities are restated. Current/noncurrent

classification not applicable.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-21

McGraw-Hill/Irwin

Fresh Start Accounting

Per SOP 90-7, when a company emerges from Chapter 11, fresh start

accounting can be used if 2 conditions are met:

The FMV of the assets < the total of the allowed claims as of the order of relief.

The original owners are left with < 50% of the voting stock.

Per SOP 90-7, when a company emerges from Chapter 11, fresh start

accounting can be used if 2 conditions are met:

The FMV of the assets < the total of the allowed claims as of the order of relief.

The original owners are left with < 50% of the voting stock.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-22

McGraw-Hill/Irwin

Fresh Start Accounting

Fresh Start Accounting Assets are restated to FMV. Liabilities are stated at

discounted present value. R/E is stated at zero. A balancing account is used;

called Reorganization value in excess of amounts allocable to identifiable assets.

Fresh Start Accounting Assets are restated to FMV. Liabilities are stated at

discounted present value. R/E is stated at zero. A balancing account is used;

called Reorganization value in excess of amounts allocable to identifiable assets.

© The McGraw-Hill Companies, Inc., 2004

Slide 13-23

McGraw-Hill/Irwin

Reorganize this, Hu-mon!

End of Chapter 13