Embed Size (px)

Citation preview

© The McGraw-Hill Companies, Inc., 1999 12.1Irwin/McGraw-Hill

Chapter Outline

12.1 Risk Identification and Evaluation

Identifying Exposures

Property Loss Exposures

Liability Losses

Losses to Human Capital

Losses from External Economic Forces

Evaluating the Frequency And Severity of Loss

Frequency

Severity

Expected Loss and Standard Deviation

© The McGraw-Hill Companies, Inc., 1999 12.2Irwin/McGraw-Hill

Chapter Outline

12.2 Retention and Insurance Revisited

Benefits of Increased Retention

Savings on Premium Loadings

Reducing Exposure to Insurance Market Volatility

Reducing Moral Hazard

Avoiding High Premiums Caused by Asymmetric Information

Avoiding Implicit Taxes due to Insurance Price Regulation

Maintaining Use of Funds

Costs of Increased Retention

Closely-held vs. Publicly-Traded Firms with Widely Held Stock

Firm Size and Correlation Among Losses

Correlation of Losses with Other Cash Flows and with

Investment Opportunities

Financial Leverage

A Basic Guideline for Optimal Retention

© The McGraw-Hill Companies, Inc., 1999 12.3Irwin/McGraw-Hill

Chapter Outline

12.3 Benefits and Costs of Loss Control

Basic Cost-Benefit Tradeoff

Examples of Identifying Benefits and Costs

Installation of Automatic Sprinkler System

Installation of Safety Guards

Child-Resistant Packaging of Non-Prescription Drugs

Qualitative vs. Quantitative Decision-Making

12.4 Statistical Analysis in Risk Management

Approximating Loss Distributions with the Normal Distribution

Illustration

Problems and Limitation

Computer Simulation of Loss Distributions

Illustration

Comparison of Results to Assuming the Normal Distribution

Limitations of Computer Simulation

© The McGraw-Hill Companies, Inc., 1999 12.4Irwin/McGraw-Hill

Chapter Outline

12.5 Use of Discounted Cash Flow Analysis

The Net Present Value Criterion

Example: Forming a Captive Insurer

The Appropriate Cost of Capital

12.6 Summary

© The McGraw-Hill Companies, Inc., 1999 12.5Irwin/McGraw-Hill

Identifying Exposures

● Types of Exposures

• Property• Liability

• Human resource

• External economic factors (e.g., price changes)

● Methods of identification

• Lists

• Understanding business

© The McGraw-Hill Companies, Inc., 1999 12.6Irwin/McGraw-Hill

Assessing Loss Exposures

• Ideally, a risk manager would have information about the probability distribution of losses

• Then assess how different risk management approaches would change the distribution

• Summary measures of probability distributions:

• frequency• severity• expected loss• standard deviation

© The McGraw-Hill Companies, Inc., 1999 12.7Irwin/McGraw-Hill

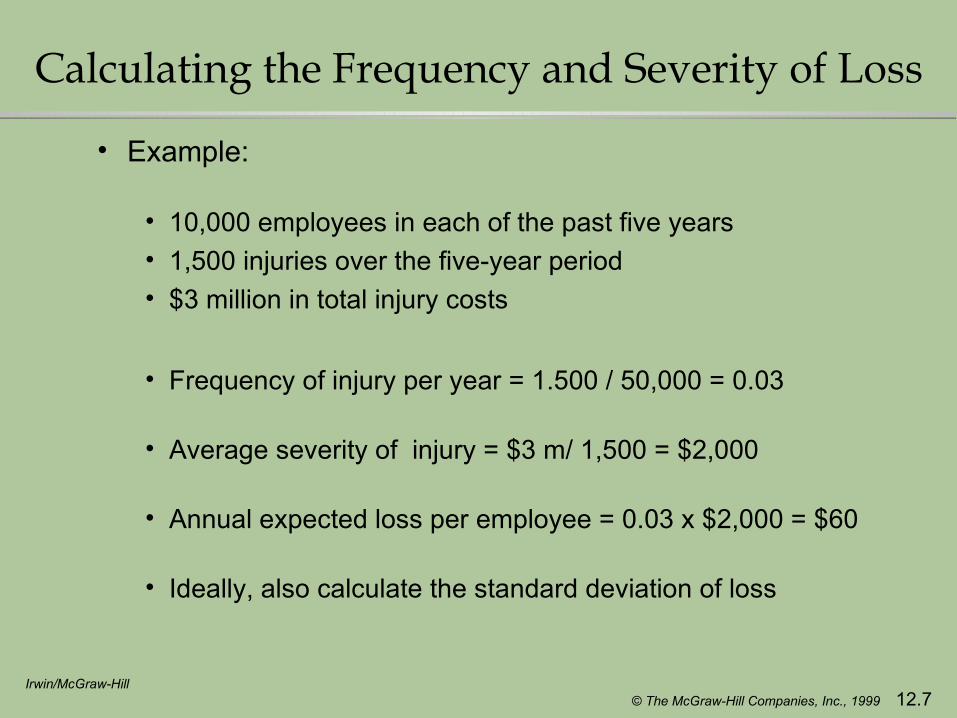

Calculating the Frequency and Severity of Loss

• Example:

• 10,000 employees in each of the past five years

• 1,500 injuries over the five-year period

• $3 million in total injury costs

• Frequency of injury per year = 1.500 / 50,000 = 0.03

• Average severity of injury = $3 m/ 1,500 = $2,000

• Annual expected loss per employee = 0.03 x $2,000 = $60

• Ideally, also calculate the standard deviation of loss

© The McGraw-Hill Companies, Inc., 1999 12.8Irwin/McGraw-Hill

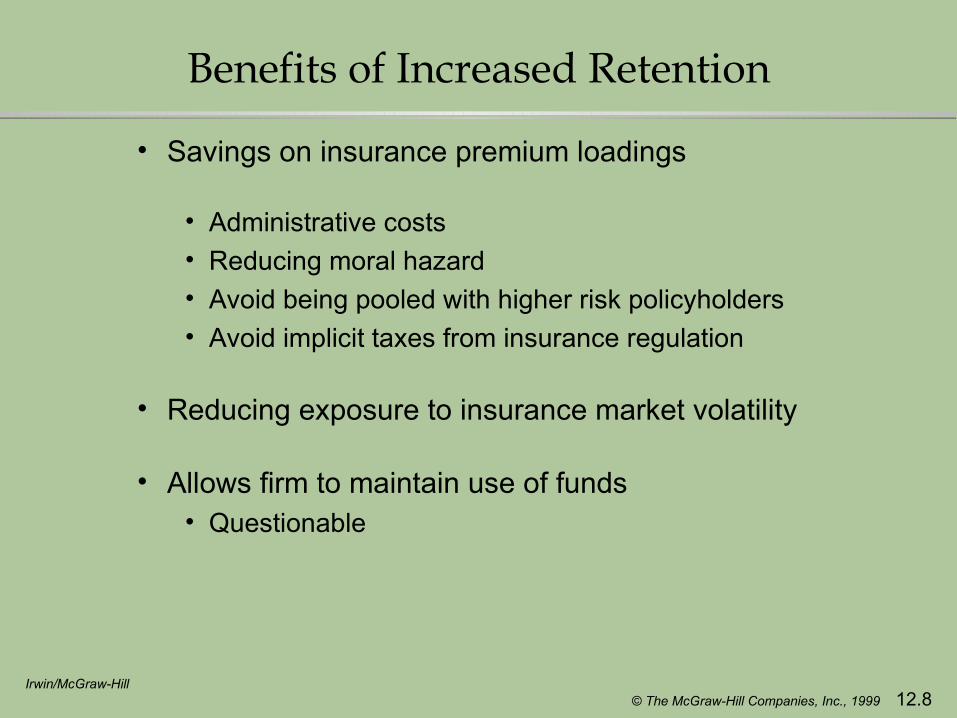

Benefits of Increased Retention

• Savings on insurance premium loadings

• Administrative costs

• Reducing moral hazard

• Avoid being pooled with higher risk policyholders

• Avoid implicit taxes from insurance regulation

• Reducing exposure to insurance market volatility

• Allows firm to maintain use of funds• Questionable

© The McGraw-Hill Companies, Inc., 1999 12.9Irwin/McGraw-Hill

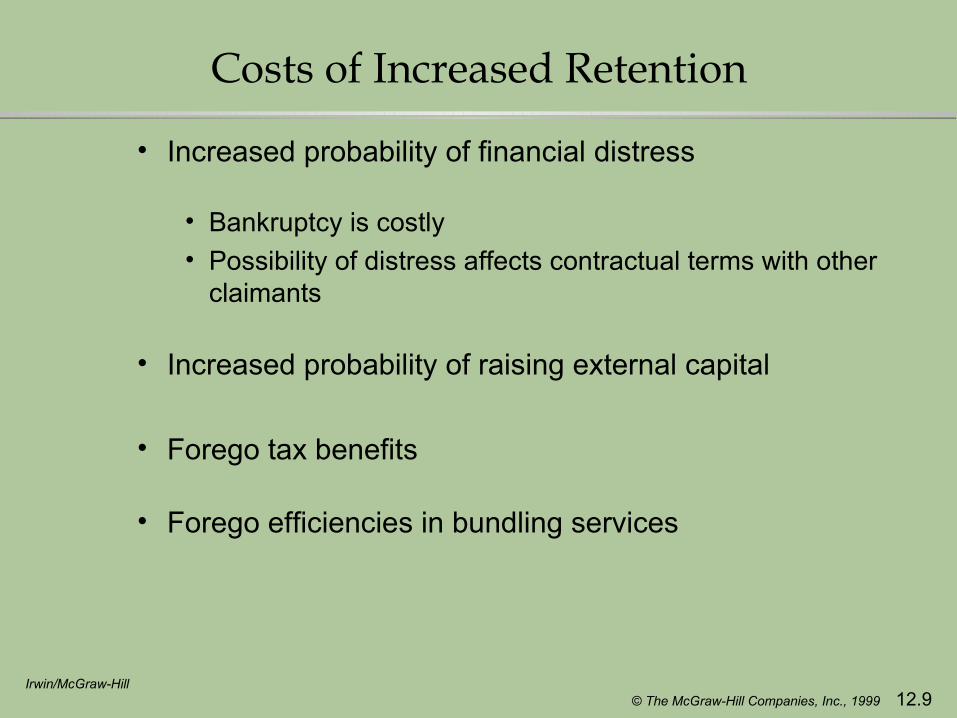

Costs of Increased Retention

• Increased probability of financial distress

• Bankruptcy is costly

• Possibility of distress affects contractual terms with other claimants

• Increased probability of raising external capital

• Forego tax benefits

• Forego efficiencies in bundling services

© The McGraw-Hill Companies, Inc., 1999 12.10Irwin/McGraw-Hill

Factors Affecting Costs of Increased Retention

• Ownership structure (closely-held vs. widely-held firms)

• Firm size

• Correlation among losses

• Correlation of losses with other cash flows

• Correlation of losses with investment opportunities

• Financial leverage

© The McGraw-Hill Companies, Inc., 1999 12.11Irwin/McGraw-Hill

Basic Guideline for Optimal Retention

● Retain reasonably predictable losses and insure potentially large disruptive losses

• Not always right (BP case)

• But often is

© The McGraw-Hill Companies, Inc., 1999 12.12Irwin/McGraw-Hill

British Petroleum Case

● British Petroleum

• Perspective

• risk management strategy• 1990

• Basic Businesses

• Exploration• Oil Refining, Distribution, and Retailing• Chemicals (small)• Nutrition (small)

© The McGraw-Hill Companies, Inc., 1999 12.13Irwin/McGraw-Hill

British Petroleum Case

● Financial Data

• Capital Structure

• Equity = $35 billion • Debt = $15 billion

• After-tax profit

• average = $1.9 billion• standard deviation = $1.1 billion

• Assets

• Diversified: 13,000 service stations in 50 countries • Undiversified: oil production

© The McGraw-Hill Companies, Inc., 1999 12.14Irwin/McGraw-Hill

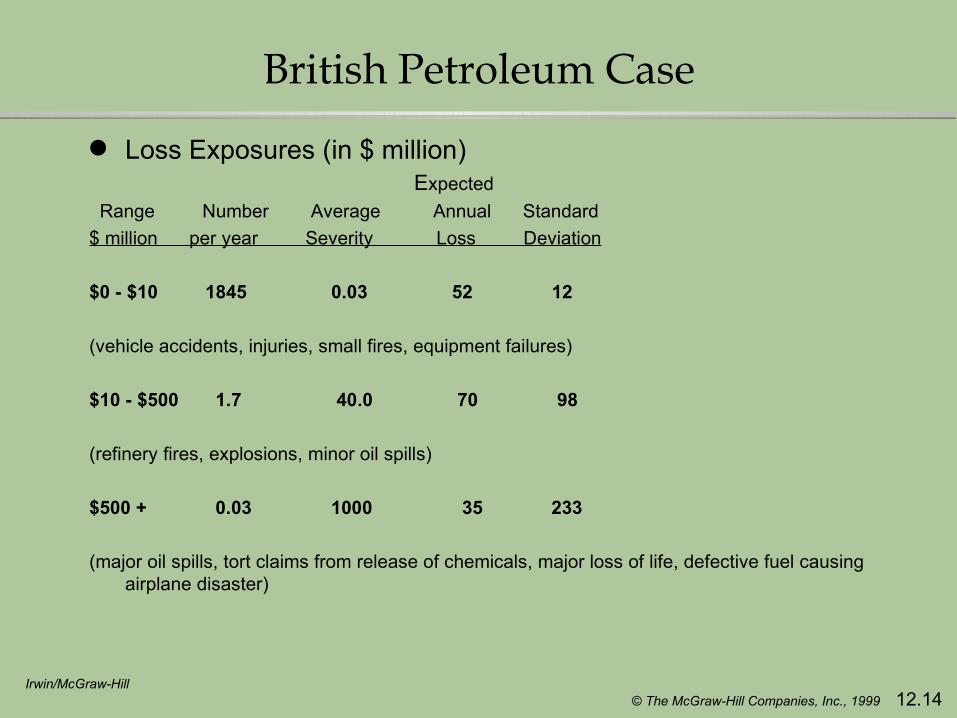

British Petroleum Case

● Loss Exposures (in $ million) Expected

Range Number Average Annual Standard

$ million per year Severity Loss Deviation

$0 - $10 1845 0.03 52 12

(vehicle accidents, injuries, small fires, equipment failures)

$10 - $500 1.7 40.0 70 98

(refinery fires, explosions, minor oil spills)

$500 + 0.03 1000 35 233

(major oil spills, tort claims from release of chemicals, major loss of life, defective fuel causing airplane disaster)

© The McGraw-Hill Companies, Inc., 1999 12.15Irwin/McGraw-Hill

British Petroleum Case

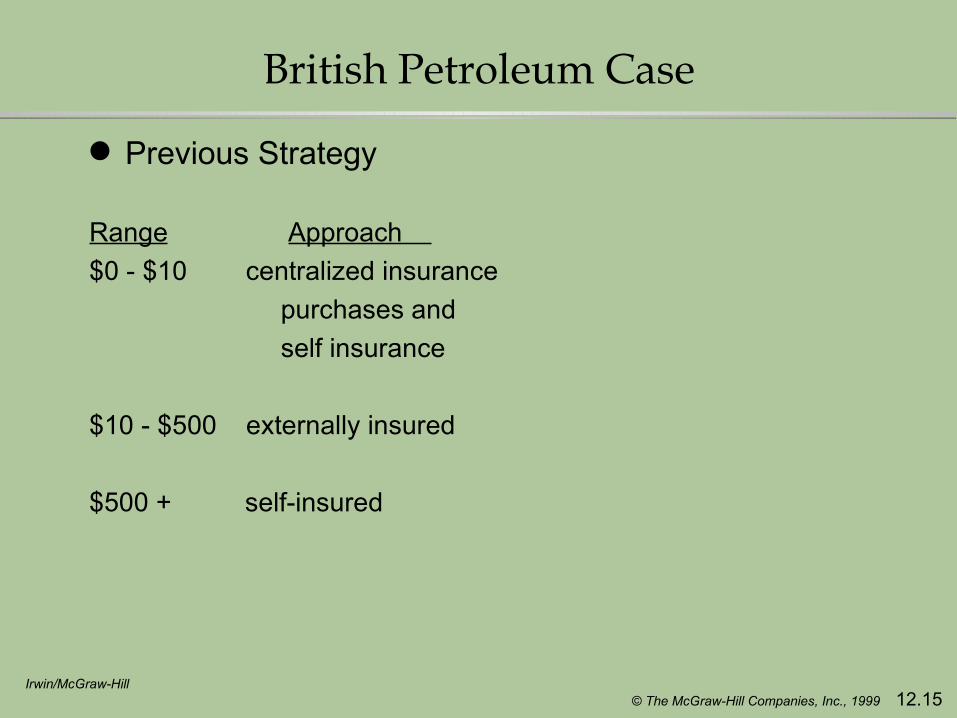

● Previous Strategy

Range Approach

$0 - $10 centralized insurance

purchases and

self insurance

$10 - $500 externally insured

$500 + self-insured

© The McGraw-Hill Companies, Inc., 1999 12.16Irwin/McGraw-Hill

British Petroleum Case

● Conclusions for First Range of Exposures

• Decentralize insurance decisions

• More insurance (Why?)

• local insurers are more efficient in • loss control

• claims processing

• insurance markets are competitive

• insurer insolvency not a concern

© The McGraw-Hill Companies, Inc., 1999 12.17Irwin/McGraw-Hill

British Petroleum Case

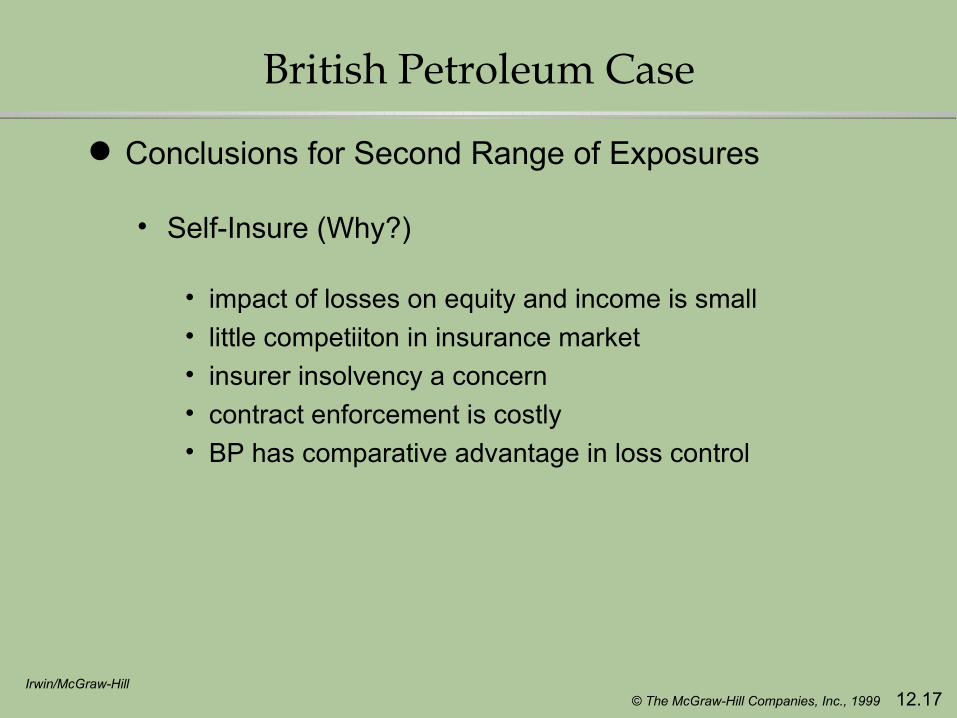

● Conclusions for Second Range of Exposures

• Self-Insure (Why?)

• impact of losses on equity and income is small• little competiiton in insurance market• insurer insolvency a concern• contract enforcement is costly• BP has comparative advantage in loss control

© The McGraw-Hill Companies, Inc., 1999 12.18Irwin/McGraw-Hill

British Petroleum Case

● Conclusions for Third Range of Exposures

• Continue to Self-Insure

• insurance is not availability (not credible)

© The McGraw-Hill Companies, Inc., 1999 12.19Irwin/McGraw-Hill

Making Loss Control Decisions

● Ideally, calculate the present value of the benefits and costs of loss control

• Primary benefit = reduction in expected loss

• Primary costs = cost of loss control device

● Other harder to quantify effects of loss control:

• Lost productivity• Improved contractual terms with employees, etc.

● Quantitative versus qualitative decision making

© The McGraw-Hill Companies, Inc., 1999 12.20Irwin/McGraw-Hill

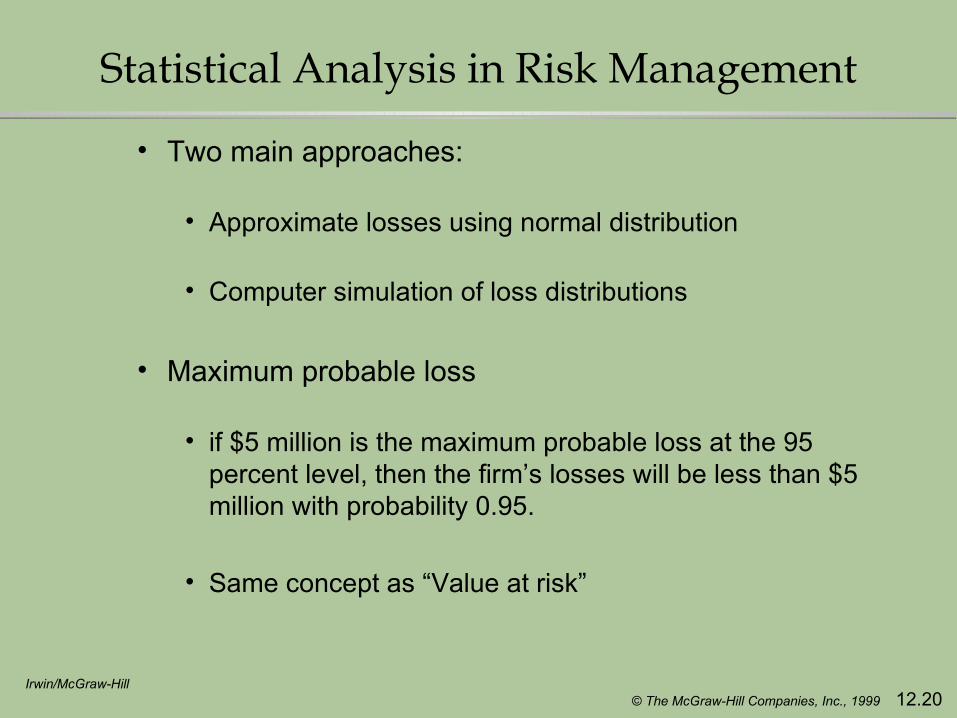

Statistical Analysis in Risk Management

• Two main approaches:

• Approximate losses using normal distribution

• Computer simulation of loss distributions

• Maximum probable loss

• if $5 million is the maximum probable loss at the 95 percent level, then the firm’s losses will be less than $5 million with probability 0.95.

• Same concept as “Value at risk”

© The McGraw-Hill Companies, Inc., 1999 12.21Irwin/McGraw-Hill

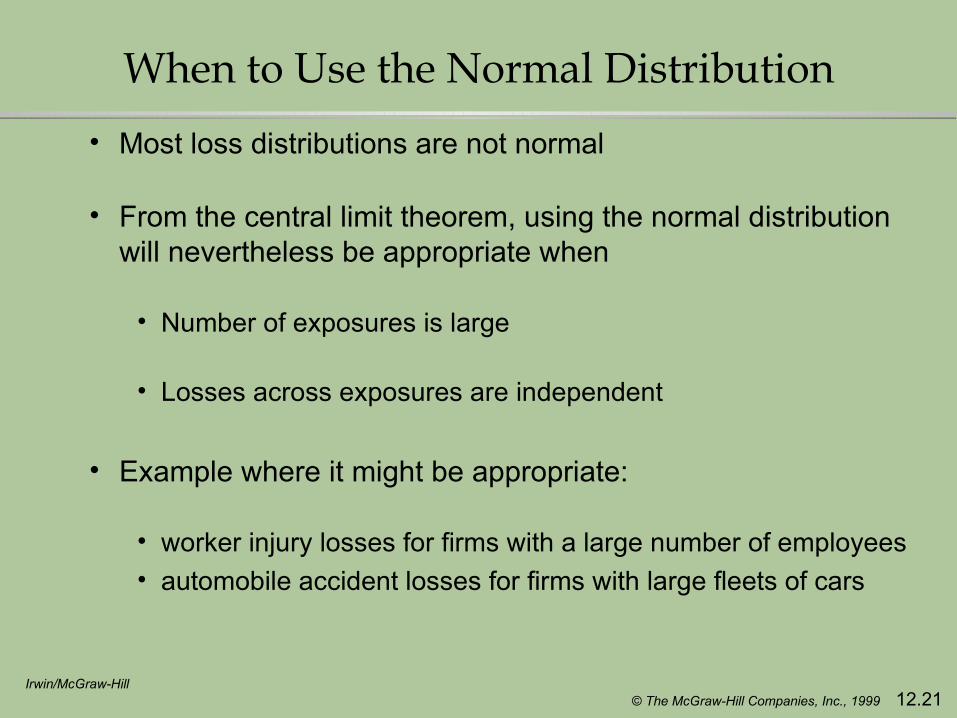

When to Use the Normal Distribution

• Most loss distributions are not normal

• From the central limit theorem, using the normal distribution will nevertheless be appropriate when

• Number of exposures is large

• Losses across exposures are independent

• Example where it might be appropriate:

• worker injury losses for firms with a large number of employees• automobile accident losses for firms with large fleets of cars

© The McGraw-Hill Companies, Inc., 1999 12.22Irwin/McGraw-Hill

Using the Normal Distribution

● Important property

• If Losses are normally distributed with

• mean = m • standard deviation = s

• Then

• Probability (Loss < m + 1.645 s) = 0.95

• Probability (Loss < m + 2.33 s) = 0.99

© The McGraw-Hill Companies, Inc., 1999 12.23Irwin/McGraw-Hill

Using the Normal Distribution - An Example

• Worker compensation losses for Stallone Steel

• sample mean loss per worker = $300

• sample standard deviation per worker = $20,000

• number of workers = 10,000

• Assume total losses are normally distributed with• mean = $3 million

• standard deviation = 100 x $20,000 = $2million

• Then maximum probable loss at the 95 percent level is

• $3 million + 1.645 ($2 million) = $6.3 million

© The McGraw-Hill Companies, Inc., 1999 12.24Irwin/McGraw-Hill

A Limitation of the Normal Distribution

● Applies only to aggregate losses, not individual losses

● Thus, it cannot be used to analyze decisions about per occurrence deductibles and limits

© The McGraw-Hill Companies, Inc., 1999 12.25Irwin/McGraw-Hill

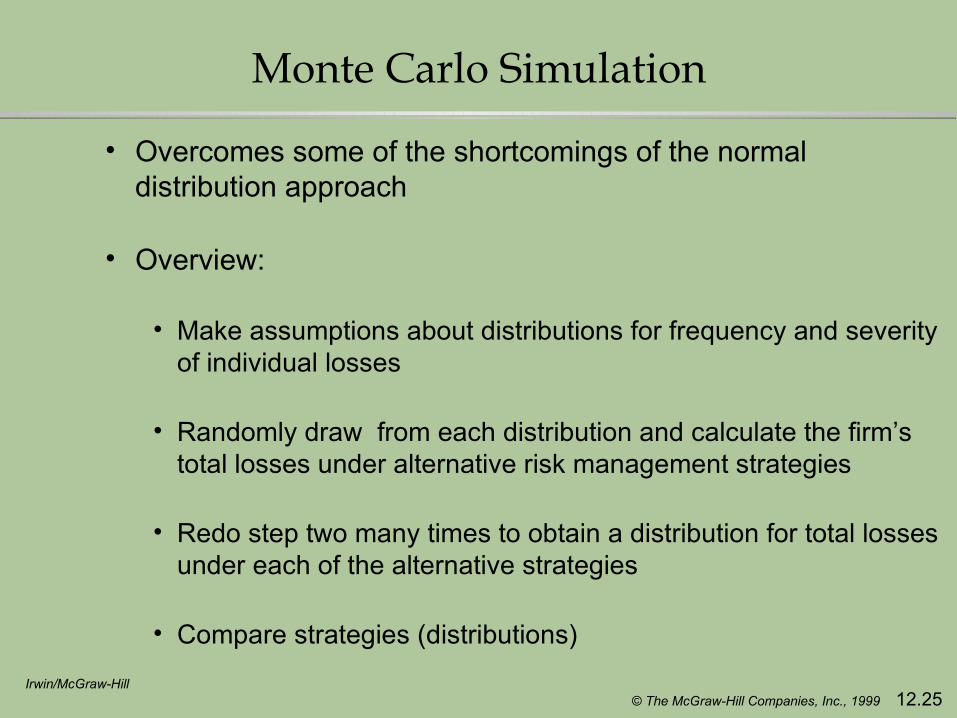

Monte Carlo Simulation

• Overcomes some of the shortcomings of the normal distribution approach

• Overview:

• Make assumptions about distributions for frequency and severity of individual losses

• Randomly draw from each distribution and calculate the firm’s total losses under alternative risk management strategies

• Redo step two many times to obtain a distribution for total losses under each of the alternative strategies

• Compare strategies (distributions)

© The McGraw-Hill Companies, Inc., 1999 12.26Irwin/McGraw-Hill

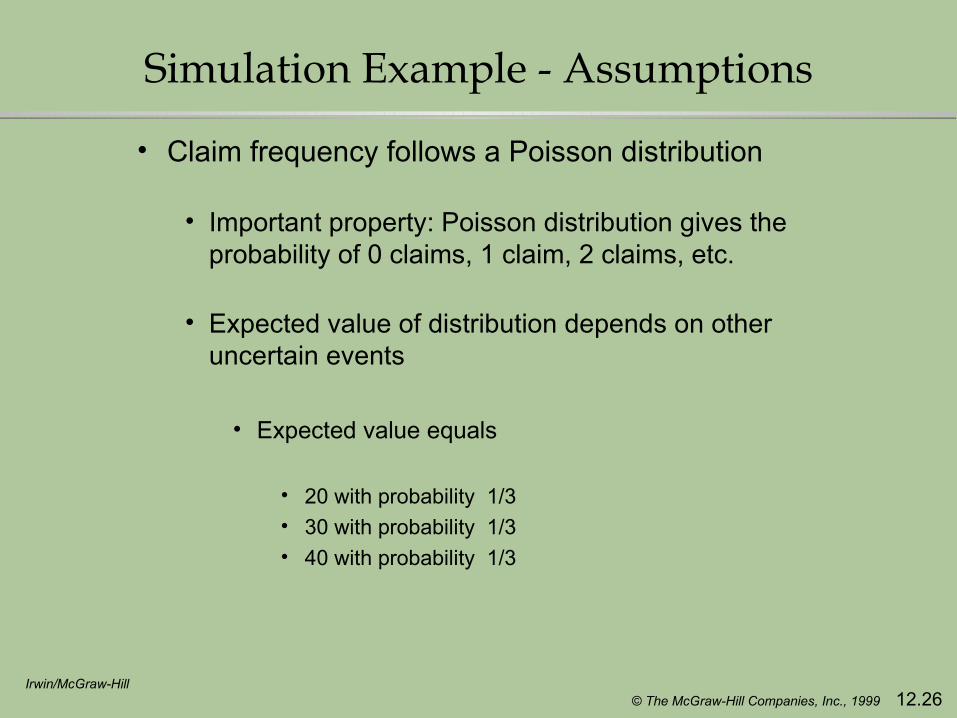

Simulation Example - Assumptions

• Claim frequency follows a Poisson distribution

• Important property: Poisson distribution gives the probability of 0 claims, 1 claim, 2 claims, etc.

• Expected value of distribution depends on other uncertain events

• Expected value equals

• 20 with probability 1/3• 30 with probability 1/3• 40 with probability 1/3

© The McGraw-Hill Companies, Inc., 1999 12.27Irwin/McGraw-Hill

Simulation Example - Assumptions

• Claim severity follows a Lognormal distribution with

• expected value = $100,000

• standard deviation = $300,00

• note skewness

© The McGraw-Hill Companies, Inc., 1999 12.28Irwin/McGraw-Hill

Simulation Example - Assumptions Frequency Distribution with Expected Value

Equal to 30

0

0.05

0.1

0.15

0.2

0.25

0 6

12

18

24

30

36

42

48

54

Number of Claims

PR

OB

AB

ILIT

Y Sample Frequency Distribution with Uncertain

Expected Value (1000 trials)

0

0.05

0.1

0.15

0.2

0.25

0 6

12

18

24

30

36

42

48

54

Number of Claims

PR

OB

AB

ILIT

Y

Sample Loss Severity Distribution(1000 trials)

0

0.02

0.04

0.06

0.08

0.1

0.12

0.0075 0.6 1.2 1.8 2.4 3

Loss in Millions

PR

OB

AB

ILIT

Y

© The McGraw-Hill Companies, Inc., 1999 12.29Irwin/McGraw-Hill

Simulation Example - Alternative Strategies

Policy 1 2 3

Per Occurrence Deductible $500,000 $1,000,000 none

Per Occurrence Policy Limit $5,000,000 $5,000,000 none

Aggregate Deductible none none $6,000,000

Aggregate Policy Limit none none $10,000,000

Premium $780,000 $415,000 $165,000

© The McGraw-Hill Companies, Inc., 1999 12.30Irwin/McGraw-Hill

Simulation Example - Results

No Insurance

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.20 1. 5 3 4. 5 6 7. 5 9 10 .5 12

13 .5

Values in Millions

PR

OB

AB

ILIT

Y $500,000 per Occurrence Retention

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0 1. 5 3 4. 5 6 7. 5 9 10 .5 12

13 .5

Values in Millions

PR

OB

AB

ILIT

Y

$6 Million Aggregate Annual Retention

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0 1. 5 3 4. 5 6 7. 5 9 10 .5 12

13 .5

Values in Millions

PR

OB

AB

ILIT

Y

$1 Million per Occurrence Retention

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

0 1. 5 3 4. 5 6 7. 5 9 10 .5 12

13 .5

Values in Millions

PR

OB

AB

ILIT

Y

© The McGraw-Hill Companies, Inc., 1999 12.31Irwin/McGraw-Hill

Simulation Example - Results

Statistic Policy 1: Policy 2: Policy 3: No insurance

Mean value of retained losses $2,414 $2,716 $2,925 $3,042

Standard deviation of retained losses 1,065 1,293 1,494 1,839

Maximum probable retained loss at 95% level 4,254 5,003 6,000 6,462

Maximum value of retained losses 11,325 12,125 7,899 18,898

Probability that losses exceed policy limits 1.1% 0.7% 0.1% n.a.

Probability that retained losses ≤ $6 million 99.7% 98.7% 99.9% 92.7%

Premium $780 $415 $165 $0

Mean total cost 3,194 3,131 3,090 3,042

Maximum probable total cost at 95% level 5,034 5,418 6,165 6,462

© The McGraw-Hill Companies, Inc., 1999 12.32Irwin/McGraw-Hill

Discounted Cash Flow (DCF) Analysis

• When risk management decisions affect cash flows over multiple periods, the effect on value should be calculated using DCF analysis

• Calculate the Net Present Value (NPV) of the alternative decisions

• NPV =

• where • NCFt == net cash flow in year t

• r = opportunity cost of capital (reflects the risk of the cash flows)

∑+=

n

0ttt

)r1(

)NCF(E