Embed Size (px)

Citation preview

IPO trends worldwide and experiences from the

Warsaw Stock Exchange

Tomasz Konieczny

2 July 2010

PricewaterhouseCoopers Page 2

Agenda

Recent IPO trends

Experiences from Warsaw

Privatisation through the WSE

PricewaterhouseCoopers Page 3

Agenda

Recent IPO trends

Experiences from Warsaw

Privatisation through the WSE

PricewaterhouseCoopers Page 4

Source: PricewaterhouseCoopers – IPO Watch Europe

Number and value of IPOs on the European markets 2003-2009

149

433

573

295

126

771806

0

150

300

450

600

750

900

2003 2004 2005 2006 2007 2008 2009

Nu

mb

er

of

IPO

s

0

20,000

40,000

60,000

80,000

100,000

Valu

e o

f IP

Os (

€m

)

Number of IPOs Value of IPOs (€m)

Recent IPO trends

PricewaterhouseCoopers Page 5

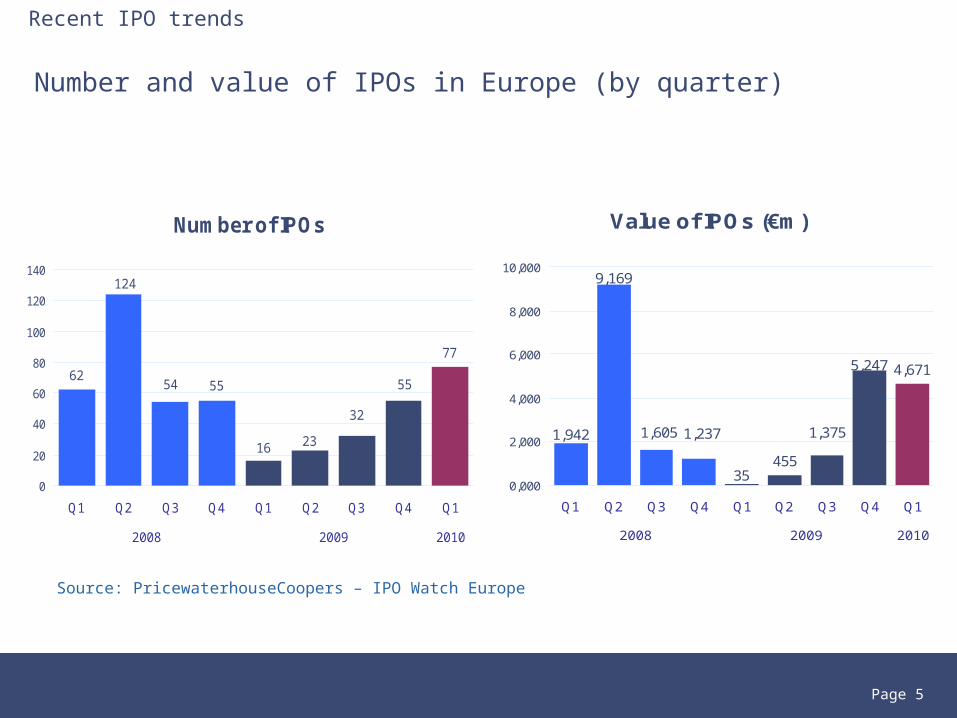

Number and value of IPOs in Europe (by quarter)

Source: PricewaterhouseCoopers – IPO Watch Europe

Value of IPOs (€m)

455

4,671

1,375

5,247

9,169

35

1,6051,942 1,237

0,000

2,000

4,000

6,000

8,000

10,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2008 2009 2010

Number of IPOs

62

77

124

55

32

16 23

54 55

0

20

40

60

80

100

120

140

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2008 2009 2010

Recent IPO trends

PricewaterhouseCoopers Page 6

Number and value of IPOs on main EU regulated markets in 2009

12

9

6

0

2

4

6

8

10

12

Warsaw London Euronext

Number of IPOs

Source: PricewaterhouseCoopers – IPO Watch Europe

1 584

620

1 907

0.000

0.500

1.000

1.500

2.000

Warsaw London Euronext

Value of IPOs (€m)

Recent IPO trends

PricewaterhouseCoopers Page 7

Number and value of IPOs on main exchange regulated markets in 2009

26

14

28

0

5

10

15

20

25

30

Warsaw (NewConnect) London (AIM) Euronext (Marche Libre)

Number of IPOs

Source: PricewaterhouseCoopers – IPO Watch Europe

10

655

10

200

400

600

Warsaw (NewConnect)

London (AIM) Euronext (Marche Libre)

Value of IPOs (€m)

Recent IPO trends

PricewaterhouseCoopers Page 8

Agenda

Recent IPO trends

Experiences from Warsaw

Privatisation through the WSE

PricewaterhouseCoopers Page 9

Warsaw Stock Exchange (WSE)

• WSE runs several markets:

- Main Market – EU regulated

- alternative markets (New Connect for equities, Catalyst for debt) – exchange regulated

• According to FESE data, WSE market capitalisation at the end of May 2010 was EUR 118,224 million

• As of 18 June 2010 there were:

- 381 companies listed on the WSE Main Market, 23 of which were non-domestic (including two Estonian entities)

- 135 companies listed on the NewConnect market, 2 of which were non-domestic

Experiences from Warsaw

PricewaterhouseCoopers Page 10

020 00040 00060 00080 000

100 000120 000140 000160 000

Market capitalisation of mid-size European marketsas of May 2010

Source: FESE

Experiences from Warsaw

€ ‘000

PricewaterhouseCoopers Page 11

WSE and selected other regional exchanges

Stock exchange

Market capitalisation

(€m)

Number of companies

(main + alternative)

WSE 118.2 508

Vienna 76.9 113

Prague 32.8 26

Budapest 21.1 46

Source: FESE, May 2010

Experiences from Warsaw

PricewaterhouseCoopers Page 12

Number and average offering value of domestic IPOs on the WSE main market by total assets and revenue of issuers (2006-2009)*

0-12 12-37 37-61 61-243 >243 Total

0-12 58 (€5.1m) 16 (€8.0m) - 1 (€1.5m) - 75 (€5.8m)

12-73 6 (€9.0m) 19 (€10.9m) 7 (€12.2m) 6 (€11.9m) - 38 (€10.9m)

37-61 1 (€6.8m) 3 (€20.2m) 2 (€12.2m) 3 (€25.6m) - 9 (€18.7m)

61-243 1 (€258.0m) 2 (€41.6m) 3 (€100.0m) 7 (€89.1m) 2 (€36.8m) 15 (€89.3m)

>243 - - - - 5 (€435.5m) 5 (€435.5m)

Total 66 (€9.2m) 40 (€11.9m) 12 (€34.1m) 17 (€45.4m) 7 (€321.6m) 142 (€31.9m)

Revenue (EUR million)

To

tal a

ss

ets

(E

UR

mill

ion

)

Experiences from Warsaw

Source: PricewaterhouseCoopers, prospectuses and current reports of listed companies

* Translated from PLN to EUR using 4.1082 PLN/1€ exchange rate (end-December 2009 exchange rate)

PricewaterhouseCoopers Page 13

Number of domestic IPOs on the WSE main market by % of equity offered (2006-2009)

43

40

24

15

2 1

0

5

10

15

20

25

30

35

40

45

0-20 20-30 30-40 40-50 50-60 >60

Nu

mb

er o

f IP

Os

% of equity offered

Experiences from Warsaw

Source: PricewaterhouseCoopers, prospectuses and current reports of listed companies

PricewaterhouseCoopers Page 14

Average cost of domestic IPOs on the WSE main market by offering value (2006-2009)*

6.3%

3.8%

3.2%

2.5%

1.0%

0%

1%

2%

3%

4%

5%

6%

7%

0-12 12-37 37-61 61-243 >243

Offering value (EUR million)

Experiences from Warsaw

Source: PricewaterhouseCoopers, prospectuses and current reports of listed companies

* Translated from PLN to EUR using 4.1082 PLN/1€ exchange rate (end-December 2009 exchange rate), does not include underwriting fees (if any)

PricewaterhouseCoopers Page 15

WSE key success factors

• Strong market institutions and regulations

• Pension funds in Poland invest up to 40% of their assets in equities of the companies listed on the regulated market

• Large individual investor base

• Privatisation of the biggest state-owned enterprises through an IPO

• Relatively large internal market

• Ability to compete with London and other exchanges for the biggest CEE companies

• Poland’s resilient economy

Experiences from Warsaw

PricewaterhouseCoopers Page 16

Agenda

Recent IPO trends

Experiences from Warsaw

Privatisation through the WSE

PricewaterhouseCoopers Page 17

Privatisation through the Warsaw Stock Exchange (WSE)

Ciech, KGHM, PKN Orlen, PKO BP, PZU, …..

• Interesting examples where the Treasury managed to:

• increase management effectiveness through privatisation

• reduce the Treasury’s ownership below 50%

• ensure high free float

• retain control over the strategically important companies

• ensure high transparency

• As a result of the privatisation process:

• The WSE helped the Treasury privatise companies

• The Treasury helped the WSE increase its capitalisation and attract domestic and foreign investors

Experiences from Warsaw

PricewaterhouseCoopers

Treasury’s ownership of selected companies privatised through the WSE

Page 18

Company Shareholder Ownership (% of capital)

PKN Orlen AVIVA OFE 5.08%

Oil&gas ING OFE 5.17%

Treasury 27.52%

Free-float 62.23%

KGHM Treasury 31.79%

Mining Free-float 68.21%

PKO BP BGK Bank (state-owned) 10.25%

Banks Treasury 40.99%

Free-float 48.76%

PZU EUREKO B.V. 12.99%

Insurance Treasury 45.19%

Free-float 41.82%

Ciech PZU OFE 6.12%

Chemicals Pioneer Pekao Investment Management SA 19.64%

Treasury 36.68%

Free-float 37.56%

Source: WSE, valid as of 17.05.2010

Experiences from Warsaw

PricewaterhouseCoopers

Privatisation of banks through the WSE

• The government’s strategy was to:• privatise the banks• ensure that banks will go public and stay listed on the WSE• sell strategic stakes to foreign banking groups to ensure the

transfer of know-how

• The aim was to:• increase the banks’ efficiency• open up a new source of capital• ensure high transparency of banks (acting as public companies)• limit the ability to transfer of funds (e.g. during crisis) to foreign

headquarters, due to the transparency and rules applicable to public companies

• promote corporate governance

Page 19

Experiences from Warsaw

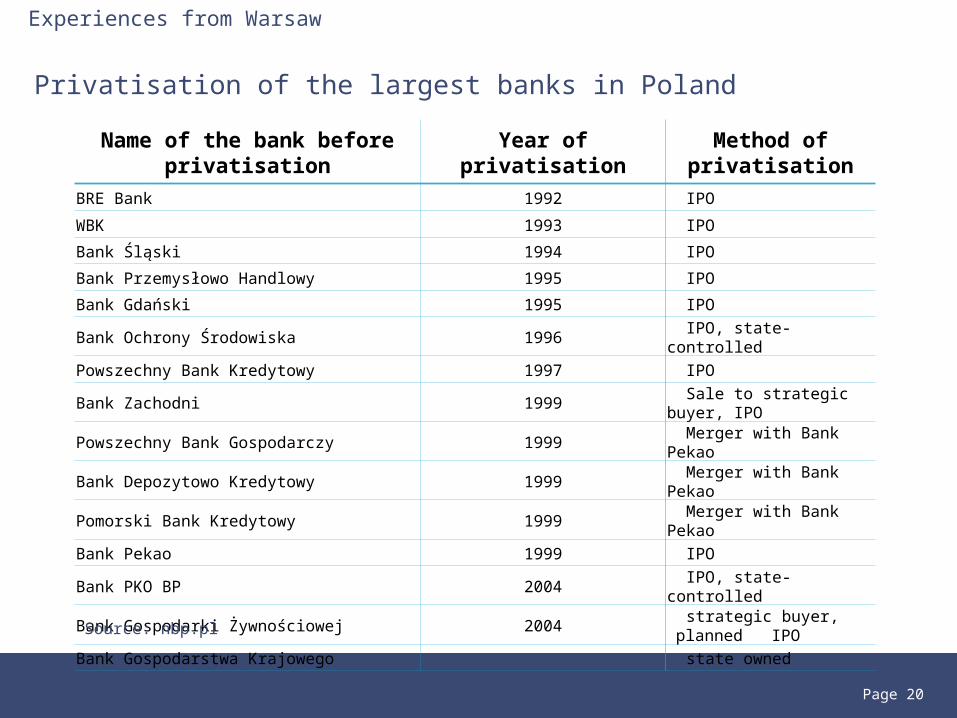

PricewaterhouseCoopers Page 20

Privatisation of the largest banks in Poland

Experiences from Warsaw

Name of the bank before privatisation

Year of privatisationMethod of

privatisation

BRE Bank 1992 IPO

WBK 1993 IPO

Bank Śląski 1994 IPO

Bank Przemysłowo Handlowy 1995 IPO

Bank Gdański 1995 IPO

Bank Ochrony Środowiska 1996 IPO, state-controlled

Powszechny Bank Kredytowy 1997 IPO

Bank Zachodni 1999 Sale to strategic buyer, IPO

Powszechny Bank Gospodarczy 1999 Merger with Bank Pekao

Bank Depozytowo Kredytowy 1999 Merger with Bank Pekao

Pomorski Bank Kredytowy 1999 Merger with Bank Pekao

Bank Pekao 1999 IPO

Bank PKO BP 2004 IPO, state-controlled

Bank Gospodarki Żywnościowej 2004 strategic buyer, planned

IPO

Bank Gospodarstwa Krajowego state owned

Source: nbp.pl

Thank you!

Tomasz KoniecznyPartner

[email protected]+48 502 18 42 85+48 22 523 42 85

© 2010 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers LLP (US).

![[piotr konieczny] google hacking](https://img.dokumen.tips/doc/110x75/552952e34a7959cc158b46e7/piotr-konieczny-google-hacking.jpg)