Embed Size (px)

Citation preview

© 2012 IBM Corporation

WELCOMEWELCOME to theIBM Business Partner 2012 Business Strategy Update Event

IBM Business Partner Organisation

© 2012 IBM Corporation

IBM Business Partner 2012 Business Strategy UpdateRichard Potts, VP IBM BPO & MM UKI

IBM Business Partner Organisation

© 2012 IBM Corporation

Roy Struthers

Director, Systems and Technology GroupUK & Ireland

Systems and Technology Group, UK & Ireland

© 2012 IBM Corporation

Look back at 2011

STG Strategy

Coverage Model and Organisation

What does it mean for our partners ?

Systems and Technology Group, UK & Ireland

Agenda

© 2012 IBM Corporation

A look back at 2011 for STG in UK and IrelandSystems and Technology Group, UK & Ireland

Platforms

Storage, RSS and Mainframe

System X

Power Systems

Growth Initiatives

Competitive Winback

Midmarket

Software/Analytics/Cloud/HPC

Execution

Market Share

End of quarter deal slippage

Revenue decline in major accounts

Inefficient go to market/coverage

© 2012 IBM Corporation

STG Strategic Initiatives

TransformGo to Market

Invest in Growth

Exploit new routes

– Expand business partner channel

– Systems Integrators & ISVs Focus on solutions

– Strengthen Solution selling skills

– Go-to-market teaming with software

Expand the client base

– Competitive migrations

– Expansion in Growth Markets

Scale Smarter Computing

– Accelerate adoption

– Deliver proof points

IBM Growth Priorities

– Business Analytics and Optimization

– Cloud

– Smarter Planet

– Growth Markets

STG-led Growth Plays

– Systems Software

– Systems Networking

Deliver TechnologyInnovation

Systems optimization– Semiconductor to

middleware – Integration across

server, storage and networks

Storage differentiation– Storage efficiency – Data protection

Acquisitions

Systems and Technology Group, UK & Ireland

© 2012 IBM Corporation

The STG 2012 Coverage Model

BP fulfillment

BP Sell and Fulfill

Whitespace accounts

From general account alignment…

Engaging en-mass with inconsistent roles

Overly focused on Core Accounts

… to alignment dictated by OO-lead on each account

IBM leads saleIBM or BP fulfills

IBM Core Account Brand Sales Specialists

BP leads sale BP fulfills

IBM Channel Account Brand Sales Specialists

IBM or BP leads saleIBM or BP fulfills

IBM Invest Account Brand Sales Specialists

STG Core Accounts STG Channel Growth Accounts

STG Invest Accounts

Systems and Technology Group, UK & Ireland

© 2012 IBM Corporation

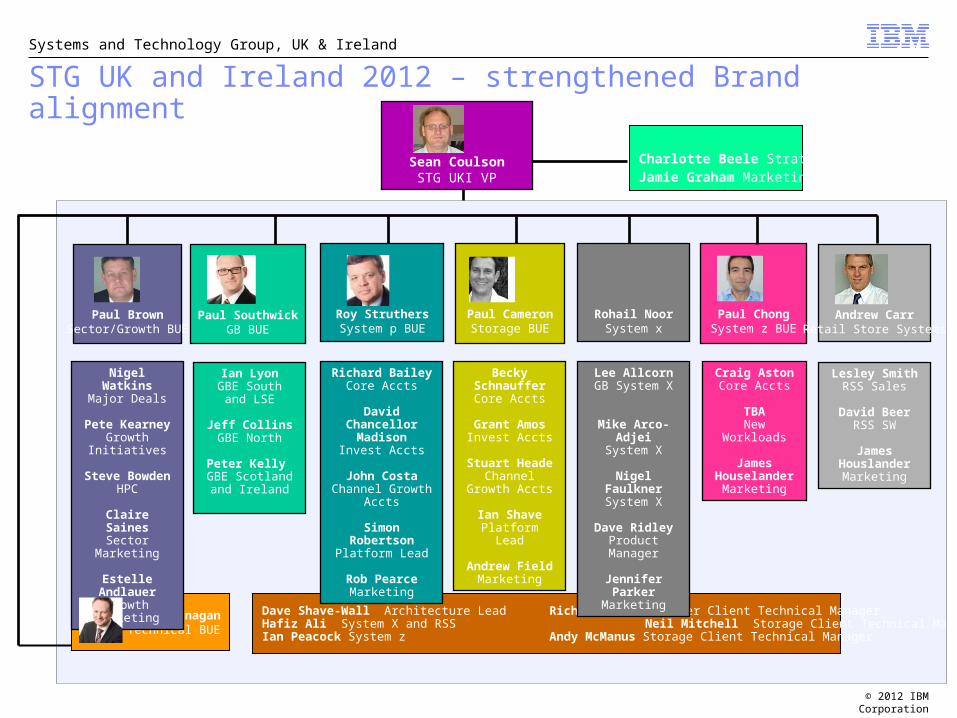

Sean CoulsonSTG UKI VP

Dave Shave-Wall Architecture Lead Richard Wilson Power Client Technical ManagerHafiz Ali System X and RSS Neil Mitchell Storage Client Technical Manager Ian Peacock System z Andy McManus Storage Client Technical Manager

Sean FlanaganTechnical BUE

Charlotte Beele StrategyJamie Graham Marketing

STG UK and Ireland 2012 – strengthened Brand alignment

Paul ChongSystem z BUE

Paul CameronStorage BUE

Roy StruthersSystem p BUE

Richard BaileyCore Accts

David Chancellor Madison

Invest Accts

John CostaChannel Growth

Accts

Simon RobertsonPlatform Lead

Rob PearceMarketing

Paul BrownSector/Growth BUE

Paul SouthwickGB BUE

Systems and Technology Group, UK & Ireland

Becky SchnaufferCore Accts

Grant AmosInvest Accts

Stuart HeadeChannel Growth

Accts

Ian ShavePlatform Lead

Andrew FieldMarketing

Craig AstonCore Accts

TBANew Workloads

James Houselander

Marketing

Lee AllcornGB System X

Mike Arco-AdjeiSystem X

Nigel FaulknerSystem X

Dave RidleyProduct Manager

Jennifer ParkerMarketing

Rohail NoorSystem x

Nigel WatkinsMajor Deals

Pete KearneyGrowth Initiatives

Steve BowdenHPC

Claire SainesSector Marketing

Estelle Andlauer

Growth Marketing

Ian LyonGBE South and

LSE

Jeff CollinsGBE North

Peter Kelly GBE Scotland

and Ireland

Lesley SmithRSS Sales

David BeerRSS SW

James HouslanderMarketing

Andrew CarrRetail Store Systems

© 2012 IBM Corporation

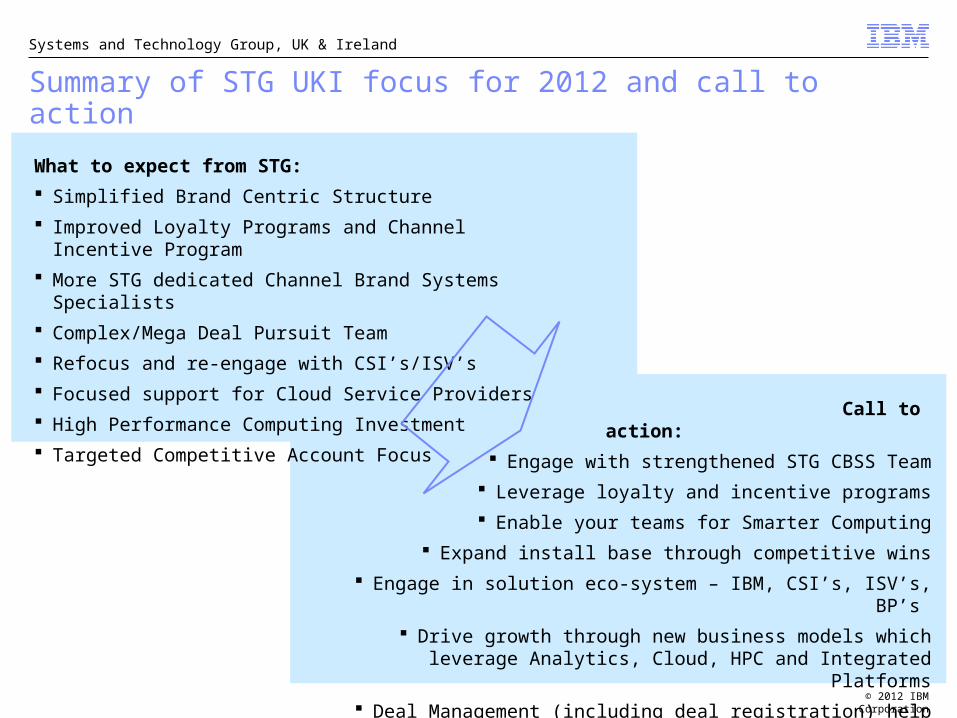

Summary of STG UKI focus for 2012 and call to action

What to expect from STG:

Simplified Brand Centric Structure

Improved Loyalty Programs and Channel Incentive Program

More STG dedicated Channel Brand Systems Specialists

Complex/Mega Deal Pursuit Team

Refocus and re-engage with CSI’s/ISV’s

Focused support for Cloud Service Providers

High Performance Computing Investment

Targeted Competitive Account Focus

Systems and Technology Group, UK & Ireland

Call to action:

Engage with strengthened STG CBSS Team

Leverage loyalty and incentive programs

Enable your teams for Smarter Computing

Expand install base through competitive wins

Engage in solution eco-system – IBM, CSI’s, ISV’s, BP’s

Drive growth through new business models which leverage Analytics, Cloud, HPC and Integrated Platforms

Deal Management (including deal registration) help us to help you

© 2012 IBM Corporation

Cloud … Enabling a smarter future Doug Clark, IBM Cloud Leader UK and IrelandTwitter: cloudstuff

IBM Business Partner Organisation

© 2012 IBM Corporation

“Cloud” is a service-based on-demand consumption and delivery model for IT

Cloud is enabled by

Ubiquitous network access Pooling and virtualization of resources Automation of service management Standardization of workloads

Cloud enables Self-service Location independence Sourcing options Flexible payment models Economies-of-scale

© 2012 IBM Corporation

• Expect significant increase in substantial change resulting from cloud

41%13%

• Expect to reinvent their customer value propositions with cloud

29%10%

• Expect to create / transform value chain through cloud

• Shift focus to driving substantial impact on customer relationships

57%

16%

14%

*Source: Institute for Business Value / The Economist study 2011

Recognition of the direction of travel..

43%

© 2012 IBM Corporation

2012Smarter Planet

The 2012 IBM HorizonWatch Technology Trends To Watch identifies the technology building blocks of a Smarter Planet

13 HorizonWatch: Top Technology Trends To Watch In 2012January 11, 2012

1. Cloud Computing

2. Virtualization

3. Social Business

4. Mobile Computing

5. Big Data

6. Analytics

7. IBM Watson

8. Human / Computer Interaction

9. Security

10. Sustainability & Green IT

11. Consumerization of IT

Top Trends - 2012

Amount of Data Collected and Stored

© 2012 IBM CorporationHorizonWatch: Top Technology Trends To Watch In 2012January 11, 2012

These trends interact…particularly cloud

Source: David Jarvis, Bill Chamberlin

14

Cloud Computing Virtualization

Social Business

Mobile Computing

Big Data

IBM Watson

Security

Sustainability & Green IT

Analytics

Consumerization of IT

Human / Computer Interaction

© 2012 IBM Corporation

Speed / Adaptability

Reduced Complexity

Cost flexibility

Scalability / ElasticityEnhanced collaboration

Faster time to marketRapid prototyping, development, deployment

Tap into new, innovative solutionsAdaptability to competitor response

Shift capex to opexFaster ROI or time to value

Pay-per-use software and servicesProcurement of fine-grained services

Creation of new value nets including SMEsShared infrastructure and services from cloud service providers

Enhanced productivity through customer / partner interaction

On demand computing power, software and servicesScale rapidly up or down

Limitless peakingAddress highly volatile, unpredictable resource demands

Complexity hidden from end-userUser independence from IT or other operational issues

Strict separation of concerns between provider and consumer

Standardization

Browser-based accessEasy provisioning of services

Promotes standardized resources & processesEncourages collaboration and device agnostic mobility

1

2

3

4

5

6

Cloud enables..

Six business benefits of cloud

© 2012 IBM Corporation

Server / Storage Utilization 10-20%

Self service None

Test Provisioning Weeks

Change Management Months

Release Management Weeks

Metering/Billing Fixed cost model

Standardization Complex

Payback period for new services Years

70-90%

Unlimited

Minutes

Days/Hours

Minutes

Granular

Self-Service

MonthsLegacyenvironments

Cloud enabled enterprise

Cloud accelerates business value across a wide variety of domains.

Capability From To

VIRTUALIZATION

AUTOMATION

STANDARDIZATION

..being manifested in step-change improvements

Cost Flexibility

© 2012 IBM Corporation

Creating new business models Enabling speed and innovation Re-engineering business processes Supporting new levels of collaboration Unleashing the end user productivity

Reinvent Business

Changing the economics of IT Automation of service delivery IT governance and policies Radically exploiting standardization Rapidly deploying new capabilities

Rethink IT

Tran

sform

ation

Eff

icie

nc

y

..with the major prize being transformation and smarter business

© 2012 IBM Corporation

Del

iver

y M

od

el

• Single Enterprise• Commodity, Core and

Specialist Services• Secure Hosted inside

client firewall.

Ser

vice

Mo

del

Single Enterprise

Enterprise EnterpriseEnterpriseEnterprise

• Shared process and Shared data across many Enterprises

• Core, Commodity and Specialist Services

• Club Cloud Model• Secure access to

PAYG service.

Regional ‘Club’ Clouds

• Extended Club and affiliate Model

• Shared services or traded services on a PAYG basis

• More focus on specialist services e.g. weather/ crime/ retail.

Common Interest ‘Club’ Clouds

• Commodity Services only• Create stickiness and

customer retention with ‘club’ look and feel

• Security and Data privacy is harder.

Public Clouds

1 2 3 4

Federated/Collegiate Centralised & Endorsed

User DUser A

User BUser CUser DUser A

User BUser C

Hybrid (Public/ Private) Cloud

Services

Public Cloud Services

..across different cloud models

Provider owned and operated

Hosted Private Cloud

Hybrid (Public/ Private) Cloud

Services

© 2012 IBM Corporation

Cloud is already ‘enabling a smarter future’ The unpredictable nature of a sporting event

demands a dynamic infrastructureThe unpredictable nature of a sporting event

demands a dynamic infrastructure

© 2012 IBM Corporation

Behind the scenes: Wimbledon 2011

Common business challenges

Rising global energy prices

Squeeze on IT budgets

Constraints on IT growth

High density server systems

Exploding power & cooling cost

Ageing data centers

Special challenges:

Unforeseeable spikes in demand

Services cannot be easily moved to match availability of system resources

Over-provisioning to ensure capacity and redundancy at peak

© 2012 IBM Corporation21

Allows dynamic provisioning/de-provisioning of resources for changing requirements across year.

Is highly optimised - achieve more with less – huge user growth yet the cost per user reduced.

Ensures continuous availability using 3-Active architecture.

Uses virtualisation, energy efficiency, standardisation and automation to free up operational budget for new investment.

Increases flexibility, improves resilience, lowers cost and improves time-to-market.

Deals with tremendous year to year growth in traffic and increased user demand – affordably.

The Infrastructure behind Wimbledon.com

© 2012 IBM Corporation22

The Infrastructure behind Wimbledon.com……RESONATES!

© 2012 IBM Corporation

IBM PointStream:

Gives 3 “Keys to the Match”, using predictive analytics technology in the Cloud: IBM’s SPSS as a Analytics as a Service on the Cloud

Wimbledon.com – analytics makes the experience more engaging for users

Analyzes over 5 years of Grand Slam Tennis data (>39 million data points) for patterns and styles, Applied knowledge against an opponents patterns gives the “Keys to the Match" Dashboard updated in real-time

© 2012 IBM Corporation

Or….Australian Open – Slam Tracker!

© 2012 IBM Corporation25

Behind the scenes: Australian Open 2012

© 2012 IBM Corporation

Wimbledon 2011 Users increased 36% to 15.6M

Wimbledon 2011 Page Views increased 37% to 451M

Plus….

Energy consumption has been reduced by 38% and cooling demand reduced by 48%.

Floor space has been reduced by 54% due to the migration to the Leadership Data Center

2011: Business Outcomes…across the “majors”

*These results reflect the traffic to the Infrastructure that hosts the Four Tennis Grand Slams, Tony Awards, The Masters and US Open Golf .

© 2012 IBM Corporation

Cloud Components

CloudServices

“Consume over Internet”“Design and Build Private

Clouds or Service Provider Clouds”

IBM Cloud Portfolio - mapped

Platform as a Service Technologies

Infrastructure as a Service Technologies

InfrastructurePlatform

Usage and Accounting

Availability and Performance

Managementand Administration

Security and Compliance

Application Lifecycle

Application Resources

Application Environments

Application Management

Integration

Platform as a Service Technologies

Infrastructure as a Service Technologies

InfrastructurePlatform

Usage and Accounting

Availability and Performance

Managementand Administration

Security and Compliance

Application Lifecycle

Application Resources

Application Environments

Application Management

Integration

Smarter Cities

Social Business

Smarter Commerce

Business Analytics and Optimization

Business Process as a ServiceSoftware as a Service

Consulting &Implementation

Services

IaaS

PaaS

BPaaSSaaS

“Design my cloud”

IaaS

PaaS

SaaS

BPaaS

CloudStrategy

© 2012 IBM Corporation

We are seeing new cloud partner types emerge that blur traditional partner definitions and models

The IBM Cloud Specialties

Cloud BuildersCreating customized private cloud solutions for client and provider infrastructures

Cloud Infrastructure ProvidersLeveraging the IBM Cloud to provide IaaS/PaaS capabilities

Cloud Technology ProvidersExtending the function and value of IBM SmartCloud

Cloud Application ProvidersDelivering standardized SaaS solutions on IBM SmartCloud

© 2012 IBM Corporation

“ organisations who are able to meet the changing needs of customers and

through partnerships establish themselves as

differentiated service providers in cloud-enabled

markets can win.. ”

Read all about it

© 2012 IBM Corporation

$100m +Announced IBM cloud investments in 2011

$100m +Announced IBM cloud investments in 2011

IBM and cloud..

2000Cloud engagements in first half of 2011

2000Cloud engagements in first half of 2011

4.5mDaily client transactions through public cloud

4.5mDaily client transactions through public cloud

1mManaged virtual machines

1mManaged virtual machines

80%Fortune 500 utilising IBM cloud capability

80%Fortune 500 utilising IBM cloud capability

19mIBM Saas users

19mIBM Saas users

6bnConsumer interactions managed in 2010 on IBM SmartCloud

6bnConsumer interactions managed in 2010 on IBM SmartCloud

200IBM researchers working on cloud security and privacy

200IBM researchers working on cloud security and privacy

13bnSecurity events managed per day for 4000+ clients

13bnSecurity events managed per day for 4000+ clients

$7bnIBM cloud revenue by 2015

$7bnIBM cloud revenue by 2015

© 2012 IBM Corporation

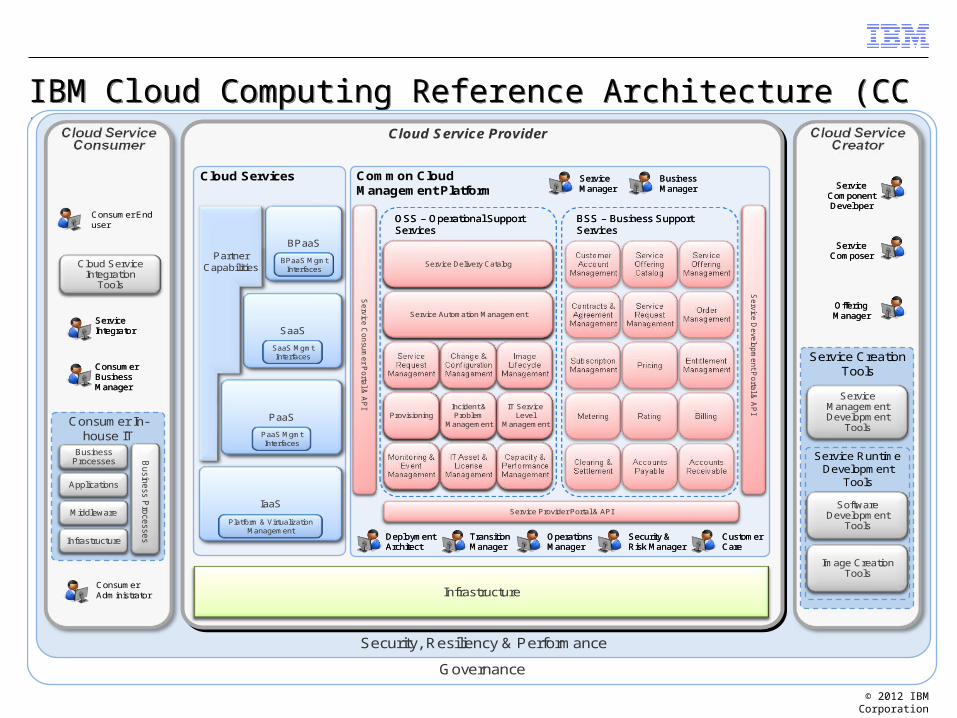

IBM Cloud Computing Reference Architecture (CC RA)IBM Cloud Computing Reference Architecture (CC RA)

Governance

Security, Resiliency & Performance

Cloud Service Provider

Cloud Services

IaaSIaaS

PaaSPaaS

SaaSSaaS

BPaaSBPaaSPartner

CapabilitiesPartner

Capabilities

Common CloudManagement Platform

Cloud Service Integration

Tools

Cloud Service Integration

Tools

Consumer In-house IT

InfrastructureInfrastructure

MiddlewareMiddleware

ApplicationsApplications

Business ProcessesBusiness

Processes

OSS – Operational Support ServicesOSS – Operational Support Services

Platform & Virtualization Management

Platform & Virtualization Management

ProvisioningIncident & Problem

Management

IT Service Level

Management

Service Automation Management

Service Delivery Catalog

ProvisioningIncident & Problem

Management

IT Service Level

ManagementProvisioningProvisioning

Incident & Problem

Management

Incident & Problem

Management

IT Service Level

Management

IT Service Level

Management

Service Automation Management

Service Delivery Catalog

Service Automation ManagementService Automation Management

Service Delivery CatalogService Delivery Catalog

BSS – Business Support ServicesBSS – Business Support Services

TransitionManager TransitionManager

DeploymentArchitectDeploymentArchitect

OperationsManager OperationsManager

Service Provider Portal & APIService Provider Portal & API

Consumer Administrator

Consumer BusinessManager

Consumer BusinessManager

Consumer End user

Service Creation Tools

Service Management Development

Tools

Service Management Development

Tools

Service Runtime Development

Tools

Software Development

Tools

Software Development

Tools

Image Creation Tools

Image Creation Tools

Service Component Developer

Service Component Developer

InfrastructureInfrastructure

PaaS MgmtInterfaces

PaaS MgmtInterfaces

SaaS MgmtInterfaces

SaaS MgmtInterfaces

BPaaS MgmtInterfaces

BPaaS MgmtInterfaces

Security &Risk Manager Security &Risk Manager

CustomerCareCustomerCare

ServiceManager ServiceManager

BusinessManager BusinessManager

Service Composer

Service Composer

OfferingManagerOfferingManager

ServiceIntegratorServiceIntegrator

Busin

ess P

roce

sses

Busin

ess P

roce

sses

Se

rvice C

on

sum

er P

orta

l & A

PI

Se

rvice C

on

sum

er P

orta

l & A

PI

Se

rvice D

eve

lopm

en

t Po

rtal &

AP

IS

ervice

De

velo

pm

en

t Po

rtal &

AP

I

© 2012 IBM Corporation

IBM’s uses cloud across the organization to transform business

•109,000 IBM employees use Blue Insight, the world’s largest business analytics private cloud.

•1,800 IBM marketers across 6 continents utilize IBM cloud-based Marketing Operations daily.

•6,000 IBM users of Blueworks Live to improve internal business processes

•200 million minutes of IBM web conferencing with LotusLive Meetings.

•Avoiding over $20M in expenses over 5 years with our private analytics cloud

•1,200 users in IBM China development labs, plus IBM Call Center teams in the United States and India, have migrated to a desktop cloud environment.

32

© 2012 IBM Corporation

IBM Software – the perfect time to engage

Paul Shackleton

Software Group Midmarket Sales Leader - Europe

23rd January 2012

© 2012 IBM Corporation

Agenda

IBM commitment to software

2012 Priorities

Business Partner Led Model

© 2012 IBM Corporation35 IBM Investors Briefing April 2011; Segment pre-tax Income

IBM – Investing in Software

Profit: Software and Services driving IBM growth

Hardware/financing

45%

38%

16%

40%

37%

23%

25%

40%

35%

2000 2006 2010

Software Services

Recent IBM Software Investment:

• More than US$14 billion in acquisitions since 2005

• 70 software acquisitions since 2001; US$20 billion in future acquisitions

• More than US$9 billion in R&D from 2007

• 40 innovations centers, 80 R&D labs, 33,000 developers, more than 16,000 active IBM Business Partners and ISVs

• Strategic focus on software solutions and business process transformation

IBM Key Objectives: 2015 Roadmap• $100B in free cash flow• $70B of capital returned to shareholders• Software becomes approx half of segment profit• $20B spending made available for acquisitions• Growth markets approach 30% of Geo revenue

IBM Key Objectives: 2015 Roadmap• $100B in free cash flow• $70B of capital returned to shareholders• Software becomes approx half of segment profit• $20B spending made available for acquisitions• Growth markets approach 30% of Geo revenue

© 2012 IBM Corporation

Acquisitions

© 2011 IBM Corporation3636

Autonomic Operations

Developer Productivity

Deep Compression

pureXML

pureScale

Pervasive Content

Stream Computing

Content Analytics

Advanced Case Management

Workload Optimized Systems

Social Analytics/Consumer Insight

2011

2005

Decision Management

• 100+ acquisitions since 2000

• More than $14B spent in acquisitions since 2005

• More than 10,000 Technical Professionals

• More than 7,500 Dedicated Consultants

• More than 27,000 Business Partner Certifications

1The completion of the transaction is subject to closing conditions including any required regulatory approvals.

1The completion of the transaction is subject to closing conditions including any required regulatory approvals.

www.ibm.com/partnerworld/acquisitionswww.ibm.com/partnerworld/acquisitions

Recently announced: i2, Algorithmics, Q1 Labs, Curam Software, DemandTec, Green Hat, Emptoris Inc.1

Key Component for IBM Software Growth

© 2012 IBM Corporation

$1B opportunity & growing faster than the Enterprise segment, the fastest growing software market is Business Analytics.

Source: 4Q11 GMV Internal Div Forecast v2. Market opportunity for Software sub-brands in the Midmarket is highly modeled, and at this level of granularity it should only be used as a rough guide.

AIM9% Collaborative

Solutions8%

Rational7%

Tivoli27%

Information Management

27%

Business Analytics

14%

Industry Solutions

8%

Share of MM opportunity by brandIn UK & Ireland, 2012, total = $1.02B

2012-2015 MM opportunity growthIn UK & Ireland, 2012-2015 CAGR

BrandGrowth ’12-’15

Business Analytics 8.0%

Industry Solutions 6.2%

Tivoli 6.1%

Information Management 5.6%

AIM 5.6%

Collaborative Solutions 4.9%

Rational 1.9%

Total 5.8%

UK & Ireland Software Opportunity (Midmarket Only) 2012 to 2015UK & Ireland Software Opportunity (Midmarket Only) 2012 to 2015

© 2012 IBM Corporation

Software Portfolio

Solving Business & IT Issues

© 2012 IBM Corporation

e.g. Selling Storage but potential for Systems Management

e.g. Adding Security speciality to your portfolio

e.g. Customers looking for business insights from their data

Examples: IBM Software solutions for alI Partner portfolios

A: Cognos Express - Business intelligence and planning software for midsize companies

A: Tivoli End Point Mgr End point management software for servers, desktops, laptops, and specialized equipment

A: Tivoli & Q1 Labs - Stop internet threats with advanced threat detection and prevention

e.g. Disaster Recovery and Business Continuity

A: Tivoli Storage FastBack - Data protection & recovery for Windows and Linux servers connected to storage platforms

Q: Fulfilling Software but have an opportunity to enhance customer solution?

Q: Already selling some IBM Software today but want to widen the portfolio?

Q: Selling software (but not IBM Software) interested in expanding / complimenting existing products and solutions?

Q: Selling some IBM Software but want to expand within that portfolio?

© 2012 IBM Corporation

2011 IBM Cost Buster Solutions for Small Deals

Sample solution bundles, delivered by IBM Business Partners to solve a business problem and are wrapped with financing from IBM Global Financing, making them affordable and accessible.

Configurations are provided for 100 employee size businesses, financed for 36 months. Country Localization may allow financing for 48 or 60 months (4 or 5 years). Solutions can scale beyond 100 end users, there is no hard restriction.

IBM Global Financing provides qualified clients with financing for the total solution including hardware, software and services for both IBM and non-IBM, in one contract with one predictable payment for transactions starting at $5K USD.

Create your specific IBM Cost Buster Solution by working with your local IBM VAD

Highlights:

Customer business needs based approach

Solutions starting at $5K USD

29 New & Refreshed IBM Solutions

Simple ‘per user’ based financing options

End-to-end execution via online tools

Customer Solution Case Study available

Tested with IDC & SMB Group Analysts

Customer deliverables coming to ibm.com

Solutions Built On Business Needs: Turning Information Into Insights Drive Business Integration and Optimization Connect and Collaborate Enable Product & Service Inn. Manage Risk Security and Compliance Optimize the impact of Infrastructures and Services

Exclusively focused on small and midsize businesses bringing affordable financed IBM solutions to address current business needs

Visit Link

© 2012 IBM Corporation

Invest and Grow with IBM Software

Accelerate the expansion of your business. Benefit from the market growth in Smarter Computing, Business and Environment requirements that can be delivered through IBM Systems, Solutions, Software and Financing

Add additional value and margin to each sale. IBM Software will enhance the value proposition to your customers and considerably increase your profit margins on each sale.

Broaden the skills set in your business....and the value of your employees. We will support you in obtaining these skills (You pass we Pay). Customers value these skills and will pay for them. Your staff will achieve enhanced job satisfaction and career development.

Offer additional services to your customers. The expanded skills of your staff will enable you to offer a higher, deeper and broader level of service to your customers. You can demand higher chargeable day rates. Software sales can produce a multiple of over seven times services revenue.

Offer additional value to your customers...through attractive financing. Industry leading financing options reduce your receivable's risk. Customers can spread payments and in selective cases benefit from 0% financing through our Costbuster program.

Retain and secure your client base by offering a complete solution. You can become the sole supplier to your customer and also advise them on future direction, including Cloud, Analytics, Smarter Computing and Smarter Business. Be a trusted advisor.

Increase your customer base. IBM’s customer base continues to expand generically and through acquisition. IBM SWG has acquired over 80 businesses in the last 10 years…you can be part of this great market development.

© 2012 IBM Corporation

SWG Channel Focus in 2012

Increase Channel Engagement & Incentives

• BPLM Launch with Midmarket focus

• Drive solutions with key partners – VARs, MSPs, ISVs, SIs…

• Software Renewal Value Incentive

• Expand focus on acquired offerings

Drive more opportunities with Business Partners

• Significant increase in co marketing funds available

• Accelerated Lead Passing Expansion

• All leads below 100k to be passed to Channel

Program simplification

• SVI claiming process reduced

• SVI Fastpath for Small Deals

© 2011 IBM Corporation42

© 2012 IBM Corporation

Business Partner Led Model

Link to BPLM page in PartnerWorldLink to BPLM page in PartnerWorld

© 2012 IBM Corporation

Business Partner Led Model - Introduction

What is the IBM Software Group BPLM?

A growth initiative designed to expand coverage, accelerate market penetration and increase revenue

A new coverage segmentation which utilises BPs as the lead SWG Route to Market

A BPLM is defined by IBM as either a defined territory, a defined set of accounts, a geographical coverage area or a defined set of products in a brand, for example:

– All Midmarket customers in London & South East Territory – Business Analytics Portfolio for North Region– All sectors Ireland

Why have IBM implemented this approach?

Market opportunity exists and is not being covered by IBM Sales force effectively

Great opportunity to increase Channel participation and increase investment by Business Partners

Recognition that Business Partners have more expertise in those brands / industries / territories

Major Software Group investment to succeed in Midmarket

Who can enrol in an IBM BPLM?

BPLM is open to any partners wishing to meet the program criteria

ASL Business Partner revenue is ineligible

© 2012 IBM Corporation

BPLM – Key Details

How does a SWG BPLM work?

A BPLM is defined in country

A dedicated revenue plan is assigned to IBM Software BPLM Manager to be executed exclusively through Business Partners

Business Partners will need to register but must meet simple Program criteria to enrol

Business Partner commits to an annual target for each BPLM they wish to enrol for

Business Partner creates business plan and commits to regular sales & marketing interlock

IBM commitment to the BPLM is established for minimum 2 years

What are the benefits to a BPLM Business Partner? No competing IBM resources or Channel conflict

Competitive advantage versus other BPs (incremental incentive is applied to your normal SW margins)– Additional 8% rebate is applied for performance of up to 100% of target – An additional 7% rebate is applied once BP is above 100% of target (Commercial Accounts only)

Dedicated IBM resources and focus provided– BPLM Manager assigned– Priority SWG Technical Support– Priority Marketing Support (Co Marketing Funds & Lead Allocation)

Increased opportunity with IBM– New whitespace accounts– Upsell opportunity with existing customers in that BPLM– Services growth

© 2012 IBM Corporation

UKI – Planned BPLM Structure & Coverage

1. Business AnalyticsLondon South East Region

1. Business AnalyticsLondon South East Region

2. Business AnalyticsNorth / South Regions2. Business AnalyticsNorth / South Regions

3. ICS (Lotus)LSE / North / South Regions

3. ICS (Lotus)LSE / North / South Regions

4. RationalLSE / North / South Regions

4. RationalLSE / North / South Regions

5. TivoliLSE / North / South Regions

5. TivoliLSE / North / South Regions

6. All SWG BrandsIreland

6. All SWG BrandsIreland

• 6 x BPLMs covering UKI and Ireland will be launched for Midmarket (excludes MM

customers in Public Sector & Health Auth.)• Planned implementation and enrolment NOW = January 2012• BPLMs for Scotland being finalised• BPLMs for Information Mgmt and WebSphere under consideration

• 6 x BPLMs covering UKI and Ireland will be launched for Midmarket (excludes MM

customers in Public Sector & Health Auth.)• Planned implementation and enrolment NOW = January 2012• BPLMs for Scotland being finalised• BPLMs for Information Mgmt and WebSphere under consideration

© 2012 IBM Corporation

BPLM – Partner Enrolment Criteria

Business Partners are requested to meet the following requirements:

Be a member of IBM PartnerWorld

Have the Software Value Plus (SVP) authorisation(s) to resell the Software Product Group(s) for which you apply

Designate an individual from your Business Partner firm to be the primary contact

Have an approved BPLM Business Plan, including sales and marketing / demand generation activities, to reach the annual revenue target commitment published for the BPLM Coverage Group to which the Business Partner is applying

Complete and submit the application to the BPLM offering, acknowledging the corresponding annual revenue target published for that BPLM (applicable for resellers only)

Once the application is approved, accept the terms and conditions of the Attachment for Business Partner-Led Model in the Partnerworld Web site

Business Partners are requested to meet the on-going requirements:

Satisfactory marketing reviews (one per quarter)

Satisfactory sales reviews (four each quarter)

Achieve at least 75% of the BPLM Coverage Group annual revenue target

© 2012 IBM Corporation

IBM Software – Business Partner Incentives

Software Incentives can include a mix of the following:

Base Discount:– Calculated from end-user entitled/special bid price

Enterprise / General Business / Midmarket Rebates:– Different discounts applied to each account set

Value Advantage Plus (VAP):– New license revenue, instant rebate

Solution Value Incentive (SVI) Sales & Solution Incentives:– Identification + Sell Incentive– SVI Solution Incentives

• Industry Solution and Capability Solution• Fees in commercial accounts, instant rebate in Government accounts

– SVI x2 Competitive Incentive Fee

Business Partner Led Model (BPLM) rebates- initial base incentive- Additional incentive

© 2011 IBM Corporation48

Significant margins exist – contact your VAD for details on what you can earn on IBM SoftwareSignificant margins exist – contact your VAD for details on what you can earn on IBM Software

0%0%

Potential to earnup to 70%

Potential to earnup to 70%

© 2012 IBM Corporation

$2.5B annual investment in Business Partners

Longstanding commitment to collaboration

Software will drive 50% of IBM’s profits by 2015

Capabilities to help build a Smarter Planet

Industry Leading Products, Solutions

and Services

Exceptional Profit Model for

Business Partners

Worldclass Enablement and Go-to-Market Support

Why invest in IBM Software?

The Roadmap to Smarter Profits

© 2012 IBM Corporation

David CornickVice President Europe, Business Partners & Midmarket

January 23, 2012

IBM Business Partner Organisation – David Cornick – IBM

© 2012 IBM Corporation

Executive Summary

Home to 180+ Global Fortune 500 and other progressive companies

109 of the top 600 cities by GDP

GDP nearly $16T growing at 1.9% in 2012

Notes: GDP = gross domestic product , * 20 countries exclude , channel Islands, Gibraltar, Isle of Man, St. Helena, Greenland, Iceland, Faeroe Islands, Liechtenstein, San Marino, Vatican CityAndorra, French Guiana, French Polynesia, Guadeloupe, Martinique, Mayotte, Monaco, New Caledonia, Reunion, Wallis & Futuna, Comoros

2012: The European Opportunity

Focus on driving VALUE CREATION and long-term business development

Europe IT opportunity is 235 Billion in 2012, more than 2/3 in Services & Solutions

© 2012 IBM Corporation

Total IT at Constant Currency

-10%

-5%

0%

5%

10%

15%

20%

25%

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

Major Mkts Growth Mkts Total

Growth Markets

Major Markets

’09-’15 CGR

9.0%

4.4%3.1%

Source: IBM Market Insights analysis, using GMV2H10 (July 2010) and QMV4Q10 (October 2010)

% Growth

IT Industry growth is slowing recovering, at two speeds

IBM 2011 Results:

Growth market: +11% y/yMajor market: +2% y/y with EMEA at +2%

© 2012 IBM Corporation

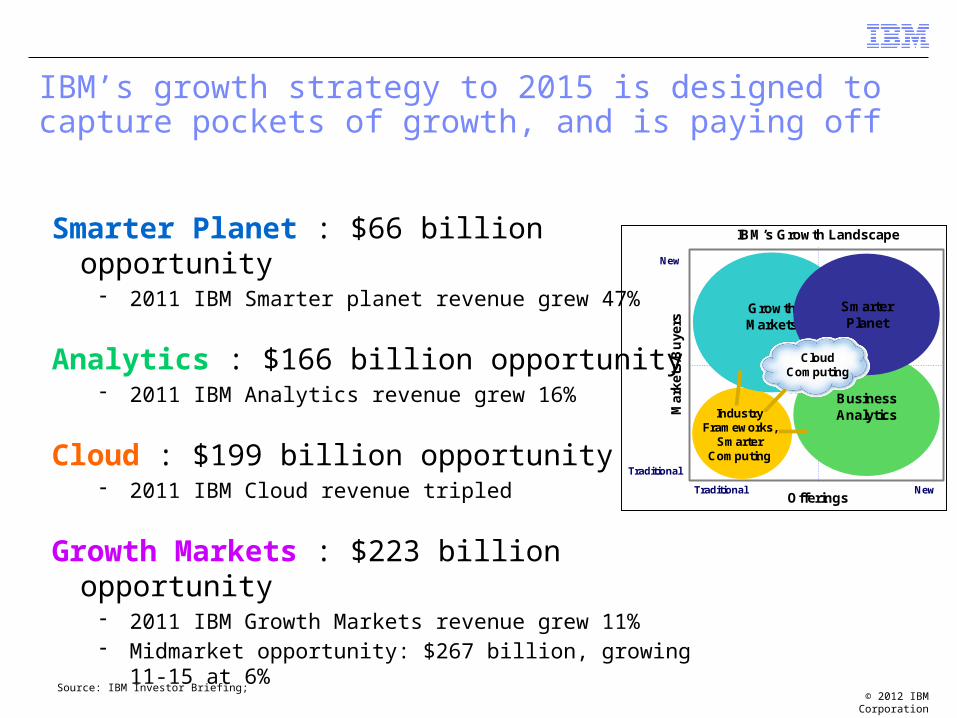

IBM’s growth strategy to 2015 is designed to capture pockets of growth, and is paying off

Smarter Planet : $66 billion opportunity 2011 IBM Smarter planet revenue grew 47%

Analytics : $166 billion opportunity 2011 IBM Analytics revenue grew 16%

Cloud : $199 billion opportunity 2011 IBM Cloud revenue tripled

Growth Markets : $223 billion opportunity 2011 IBM Growth Markets revenue grew 11% Midmarket opportunity: $267 billion, growing 11-15 at 6%

Source: IBM Investor Briefing; M

arke

ts/B

uye

rs

Traditional

New

Offerings

IBM’s Growth Landscape

New

GrowthMarkets

BusinessAnalytics

SmarterPlanet

Cloud Computing

Traditional

IndustryFrameworks,

Smarter Computing

© 2012 IBM Corporation

We have remixed our business to higher value areas and are reaping rewards of transformational change

© 2012 IBM Corporation

IBM’s channel strategy: Clarity, Consistency and Predictability to seize the opportunities to Grow together

Continue to focus and grow our base business while aligning the channel to take advantage ofIBM’s 2015 strategic priorities:

Smarter Planet

Business Analytics

Cloud Computing

Midmarket

CLARITY

CONSISTENCY

PREDICTABILITY

© 2012 IBM Corporation56

2012: we are further creating opportunities to Grow together

Business Solutions

•Client / ISV / vertical middleware applications

•Business Process

Traditional Infrastructure• Servers/storage• Middleware• Implementation services• Helpdesk• Financing

Appliance• Application Platform• Industry Solution Reseller• Industry Solution Integrator

Provider Model•Public Cloud Offerings•Private Cloud Solutions•Business Model Transformation

Business Services•Business Process / IT Consulting

• Integration Services

Embedded Software Solutions• Analytics• Database• Portal

Business Partner Value creation models

© 2012 IBM Corporation

Working together is critical to our mutual success

Industry-leading technology and vision– Smarter planet strategy

– $6B in research and development

– Industry-leading systems, software,services and financing offerings for the channel

Business Partner-led business model for midmarket

Investment in skills

Significant earnings opportunities– Partner incentives, end-user incentives,

Business Partner seller incentives and strategic investment

Consistency in our commitment to our Business Partner ecosystem

IBM is deeply committed to the success of its Business Partners

© 2012 IBM Corporation

Business Partner actions for 2012

Take advantage of IBM’s 2015 strategic imperatives

Significantly Grow Run-rate/autonomous business

Expand Channel Software and Services portfolio

sell the total package

Seize the Midmarket opportunity

Invest in new skills and IBM certifications

© 2012 IBM Corporation5959

© Copyright IBM Corporation 2012 All rights reserved. The information contained in these materials is provided for informational purposes only, and is provided AS IS without warranty of any kind, express or implied. IBM shall not be responsible for any damages arising out of the use of, or otherwise related to, these materials. Nothing contained in these materials is intended to, nor shall have the effect of, creating any warranties or representations from IBM or its suppliers or licensors, or altering the terms and conditions of the applicable license agreement governing the use of IBM software. References in these materials to IBM products, programs, or services do not imply that they will be available in all countries in which IBM operates. Product release dates and/or capabilities referenced in these materials may change at any time at IBM’s sole discretion based on market opportunities or other factors, and are not intended to be a commitment to future product or feature availability in any way. IBM, the IBM logo, Cognos, the Cognos logo, and other IBM products and services are trademarks of the International Business Machines Corporation, in the United States, other countries or both. Other company, product, or service names may be trademarks or service marks of others.