Embed Size (px)

Citation preview

© 2007 Thomson South-Western

Chapter 24Mergers, Corporate Control, and Corporate Governance

Professor XXXCourse Name/Number

2

Corporate Control Defined

What is Corporate Control?Monitoring, supervision and direction of a

corporation or other business organization

Changes in corporate control occur through:Acquisitions (purchase of additional resources by a

business enterprise):1. Purchase of new assets

2. Purchase of assets from another company

3. Purchase of another business entity (merger)

Consolidation of voting power DivestitureSpinoff

3

Corporate Control Transactions

Statutory: Acquired firm is consolidated into acquiring firm with no further separate identity.

Subsidiary: Acquired firm maintains its own former identity.

Consolidation: Two or more firms combine into a new corporate identity.

4

LBOs, MBOs, and Dual-Class Recapitalization

Going Private TransactionsLBOs (public shares of a firm are bought

and taken private through the use of debt) MBOs (an LBO initiated by the firm’s

management)

Dual-Class Recapitalization

5

Methods of Acquisition

Negotiated MergersContact is initiated by the potential acquirer or by

target firm.

Open Market PurchasesBuy enough shares on the open market to obtain

controlling interest without engaging in a tender offer

Proxy FightsProxy for directors: attempt to change management

through the votes of other shareholdersProxy for proposal: attempt to gain voting control over

corporate control, antitakeover amendments (shark repellents, golden parachutes, white knights, poison pills

6

Methods of Acquisition (Continued)

Tender Offers: an open and public solicitation for shares

Open Market Purchases, Tender Offers and Proxy Fights could be combined to launch a “surprise attack”Acquirer accumulates a number of shares

(‘foothold”) without having to file 13-d form with SEC

7

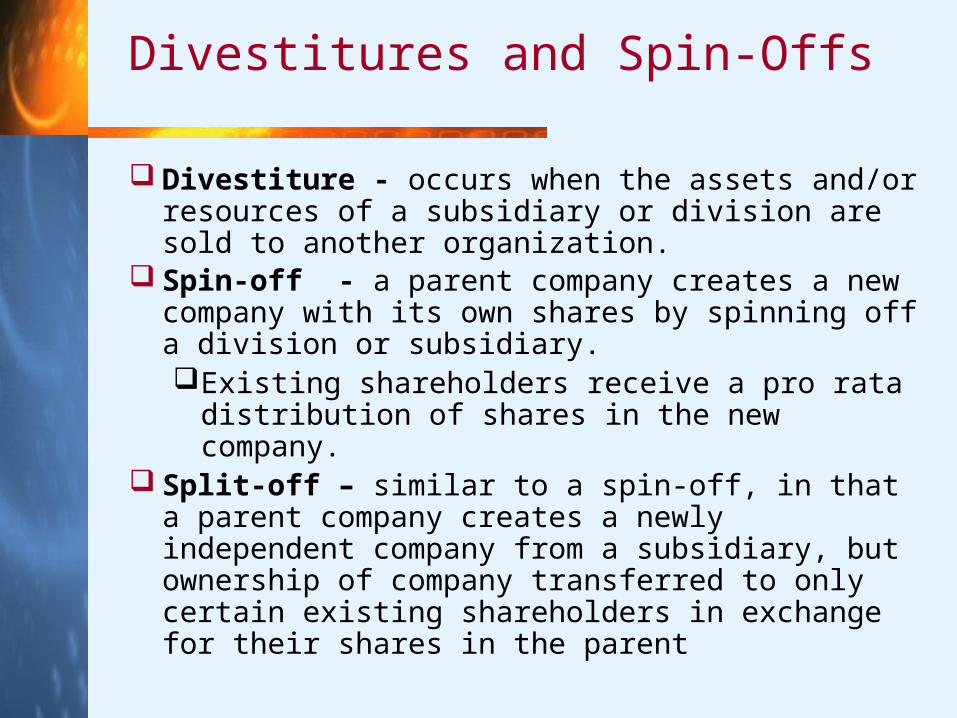

Divestitures and Spin-Offs

Divestiture - occurs when the assets and/or resources of a subsidiary or division are sold to another organization.

Spin-off - a parent company creates a new company with its own shares by spinning off a division or subsidiary. Existing shareholders receive a pro rata

distribution of shares in the new company. Split-off – similar to a spin-off, in that a parent

company creates a newly independent company from a subsidiary, but ownership of company transferred to only certain existing shareholders in exchange for their shares in the parent

8

Mergers by Business Concentration

Horizontal: between former intra-industry competitors Attempt to gain efficiencies of scale/scope and benefit from

increased market power Susceptible to antitrust scrutiny Market extension merger

Vertical: between former buyer and seller Forward or backward integration Creates an integrated product chain

Conglomerate: between unrelated firms Product extension mergers vs. pure conglomerate mergers Popular in the 60’s as the idea of portfolio diversification was

applied to corporations

9

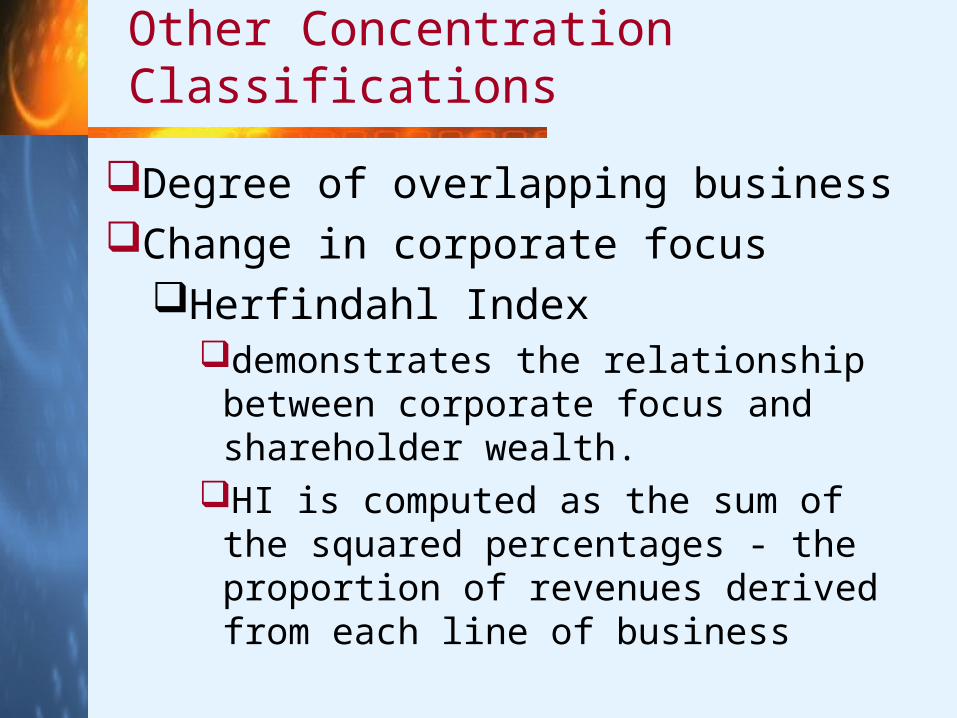

Other Concentration Classifications

Degree of overlapping business Change in corporate focus

Herfindahl Indexdemonstrates the relationship between

corporate focus and shareholder wealth. HI is computed as the sum of the

squared percentages - the proportion of revenues derived from each line of business

10

Merger and Acquisition Transaction Characteristics

Method of payment used to finance a transaction Pure stock exchange merger: issuance of new shares of common

stock in exchange for the target’s common stock Mixed offerings: a combination of cash and securities

Attitude of target management to a takeover attempt Friendly Deals vs. Hostile Transactions

Accounting treatment used for recording a merger With the implementation of FASB Statements 141 and 142, one

standard method of accounting for mergersTarget liabilities remain unchanged, but target assets are “written up”

to reflect current market values, and the equity of the target is revised upward to incorporate the purchase price paid.

The revised values are then carried over to the surviving firm’s financial statements.

Goodwill is created if the restated values of the target lead to a situation in which its assets are less than its liabilities and equity

11

Merger and Intangible Assets Accounting

Target firm has 3.2 million shares at $25 per share. Acquirer pays a 20% premium ($30 per share) to expand in the

geographic area where target firm operates. Transaction value 3.2 million shares x $30/share = $96,000,000. Net asset value of target company is $72,000,000.

Current Assets $22,000,000

Restated fixed assets $120,000,000less liabilities $70,000,000

Net Asset Value $72,000,000

Acquirer pays $24,000,000 for intangible assets.

Purchase price paid $96,000,000less Net asset value $72,000,000

Goodwill $24,000,000

Goodwill will remain on the balance sheet as long as the firm can demonstrate that is fairly valued.

12

Shareholder Wealth Effects and Transaction Characteristics

Target returns – stockholders almost always experience substantial wealth gains

Acquirer returns – less conclusive than those for target shareholders

Combined returns Mode of payment

Cash transactionsStock transactionsTax hypothesis: target shareholders must be awarded a

capital gains tax premium in cash offers, which is not required in a stock offer.

Preemptive bidding hypothesis: acquirers wishing to ward off other potential bidders for a target offer a substantial initial takeover premium in the form of cash.

13

Returns to Other Security Holders

BondsConvertibleNonconvertible

Preferred stockConvertibleNonconvertible

14

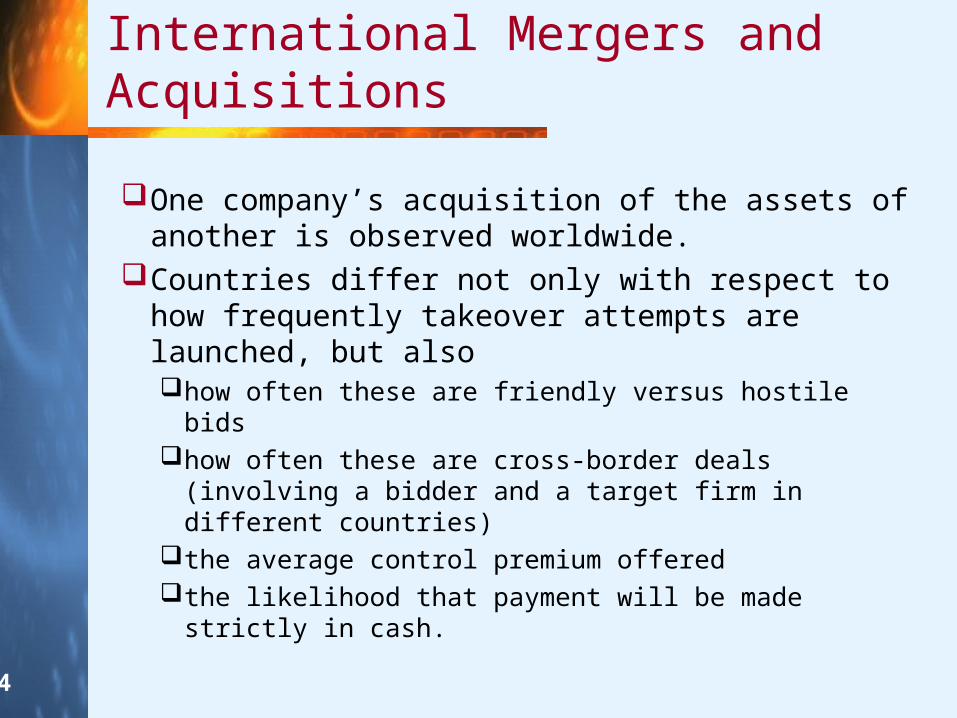

International Mergers and Acquisitions

One company’s acquisition of the assets of another is observed worldwide.

Countries differ not only with respect to how frequently takeover attempts are launched, but also how often these are friendly versus hostile bidshow often these are cross-border deals (involving a

bidder and a target firm in different countries)the average control premium offeredthe likelihood that payment will be made strictly in

cash.

15

Geographic Distribution of WorldwideAnnounced Mergers and Acquisitions, 2004 v. 2003

16

Industrial Distribution of Worldwide Announced Mergers and Acquisitions, Value in $ Millions, 2004 v. 2003

17

Value Maximizing Strategies

Geographic (internal and international) expansion in markets with little competition may increase shareholders’ wealth.External expansion provides an easier approach to

international expansion.Joint ventures and strategic alliances give

alternative access to foreign markets. Profits are shared.

Synergy, market power, and strategic mergersOperational, managerial and financial merger-

related synergies

18

Operational Synergies

Economies of scale: Merger may reduce or eliminate overlapping resources 1995 merger between Chemical Bank and Chase Manhattan

Bank resulted in elimination of 12,000 positions.

Economies of scope: involve some activities that are possible only for a certain company size. The launch of a national advertising campaign Economies of scale/scope most likely to be realized in

horizontal mergers.

Resource complementarities: Merging firms have operational expertise in different areas. One company has expertise in R&D, the other in marketing. Successful in both horizontal and vertical mergers

19

Managerial Synergies and Financial Synergies

Managerial synergies are effective when management teams with different strengths are combined.For example, expertise in revenue growth and

identifying customer trends paired with expertise in cost control and logistics

Financial synergies occur when a merger results in less volatile cash flows, lower default risk, and a lower cost of capital.

20

Managerial Synergies and Financial Synergies

Market power is a benefit often pursued in horizontal mergers.Number of competitors in industry declinesIf the merger creates a dominant firm, as in the

Office Depot-Staples merger’s attempt to create market power and set prices

Other strategic reasons for mergers:Product quality in vertical mergersDefensive consolidation in a mature or declining

industry: consolidation in the defense industry

21

Cash Flow Generation and Financial Mergers

Acquirer sees target undervalued. Many junk bond-financed deals of the 1980s had one of the

following two outcomes: “Busting up” the target for greater value than acquisition priceRestructuring the target to increase corporate focus. Sell non-core

businesses to pay acquisition cost

Tax-considerations for the merger: Tax loss carry-forward of the target company used to offset

future taxes; resulting in increased cash flow. 1986 change in tax code limits the use of tax loss carry-

forward. Merging may yield lower borrowing costs for the

merged company. Cash flows of the two businesses are less risky when

combined, leading to lower probability of bankruptcy and lower default risk premium

22

Non-Value-Maximizing Motives

Agency problems: Management’s (disguised) personal interests are often driver of mergers and acquisitions.Managerialism theory of mergers: Managerial

compensation often tied to corporation sizeFree cash flow theory of mergers: Managers invest in

projects with negative NPV to build corporate empires.

Hubris hypothesis of corporate takeovers: Management of acquirer may overestimate capabilities and overpay for target company in belief they can run it more efficiently.

Agency cost of overvalued equity

23

Non-Value-Maximizing Motives

DiversificationCoinsurance of debt: the debt of each

combining firm is now insured with cash flows from two businesses

Internal capital markets: created when the high cash flows (cash cow) businesses of a conglomerate generate enough cash flow to fund the “rising star” businesses

24

History of Merger Waves

Five merger waves in the U.S. history Merger waves positively related to high economic growth. Concentrated in industries undergoing changes Regulatory regime determines types of mergers in each wave. Usually ends with large declines in stock market values

First wave (1897-1904): period of “merging for monopoly”. Horizontal mergers possible due to lax regulatory environment Ended with the stock market crash of 1904

Second wave (1916-1929): period of “merging for oligopoly” Antitrust laws from early 1900 made monopoly hard to achieve. Just like first wave, intent to create national brands Ended with the 1929 crash

25

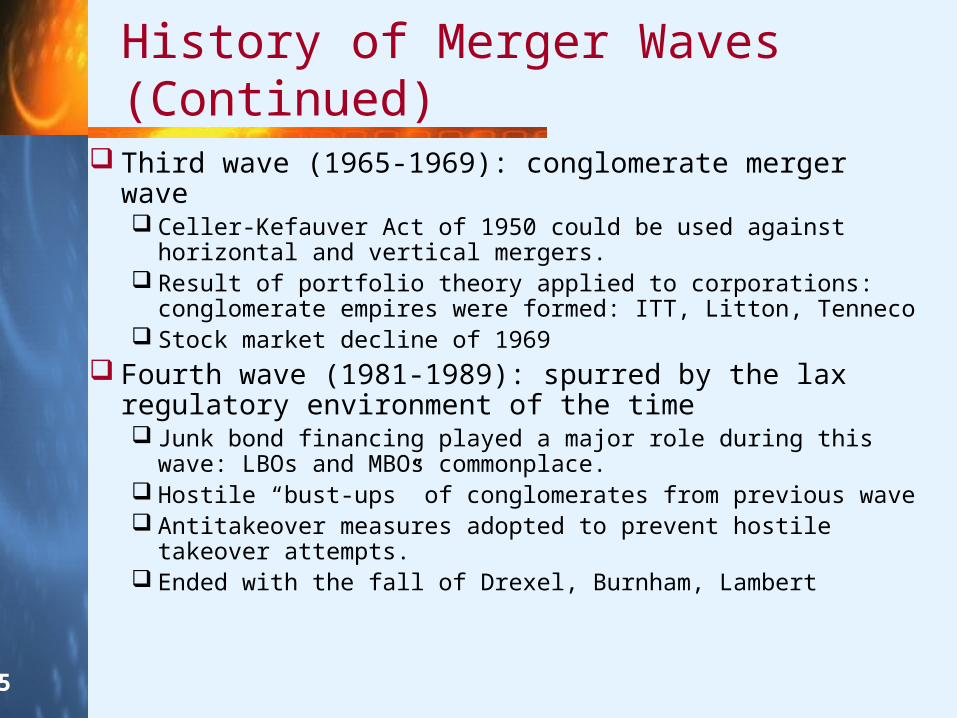

History of Merger Waves (Continued)

Third wave (1965-1969): conglomerate merger wave Celler-Kefauver Act of 1950 could be used against horizontal

and vertical mergers. Result of portfolio theory applied to corporations: conglomerate

empires were formed: ITT, Litton, Tenneco Stock market decline of 1969

Fourth wave (1981-1989): spurred by the lax regulatory environment of the time Junk bond financing played a major role during this wave: LBOs

and MBOs commonplace. Hostile “bust-ups” of conglomerates from previous wave Antitakeover measures adopted to prevent hostile takeover

attempts. Ended with the fall of Drexel, Burnham, Lambert

26

Fifth Merger Wave

Fifth wave (1993 – 2001): characterized by friendly, stock-financed mergers Relatively lax regulatory environment: still open to horizontal

mergers Consolidation in non-manufacturing service sector:

healthcare, banking, telecom, high tech Explained by industry shock theory: Deregulation influenced

banking mergers and managed care affected health care

industry. Merger activity: unprecedented transaction value for

both US and non-US mergers In 2000, aggregate merger value hit $3.4 trillion: $1.8 trillion in

US and $1.6 trillion outside US. Declined in 2001 to $1.7 trillion and only $1.2 trillion in 2002

27

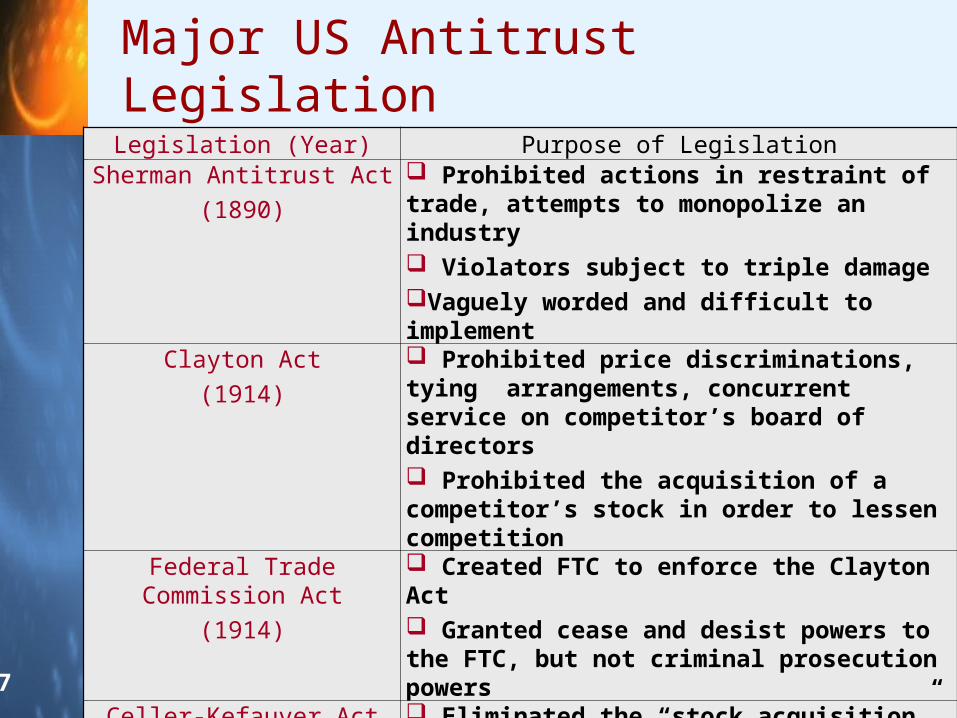

Major US Antitrust Legislation

Legislation (Year) Purpose of LegislationSherman Antitrust Act

(1890)

Prohibited actions in restraint of trade, attempts to monopolize an industry Violators subject to triple damageVaguely worded and difficult to implement

Clayton Act

(1914)

Prohibited price discriminations, tying arrangements, concurrent service on competitor’s board of directors Prohibited the acquisition of a competitor’s stock in order to lessen competition

Federal Trade Commission Act

(1914)

Created FTC to enforce the Clayton Act Granted cease and desist powers to the FTC, but not criminal prosecution powers

Celler-Kefauver Act

(1950)

Eliminated the “stock acquisition” loophole in the Clayton Act Severely restricts approval for horizontal mergers

Hart-Scott-Rodino Act

(1976) FTC and DOJ can rule on the permissibility of a merger prior to consummation.

28

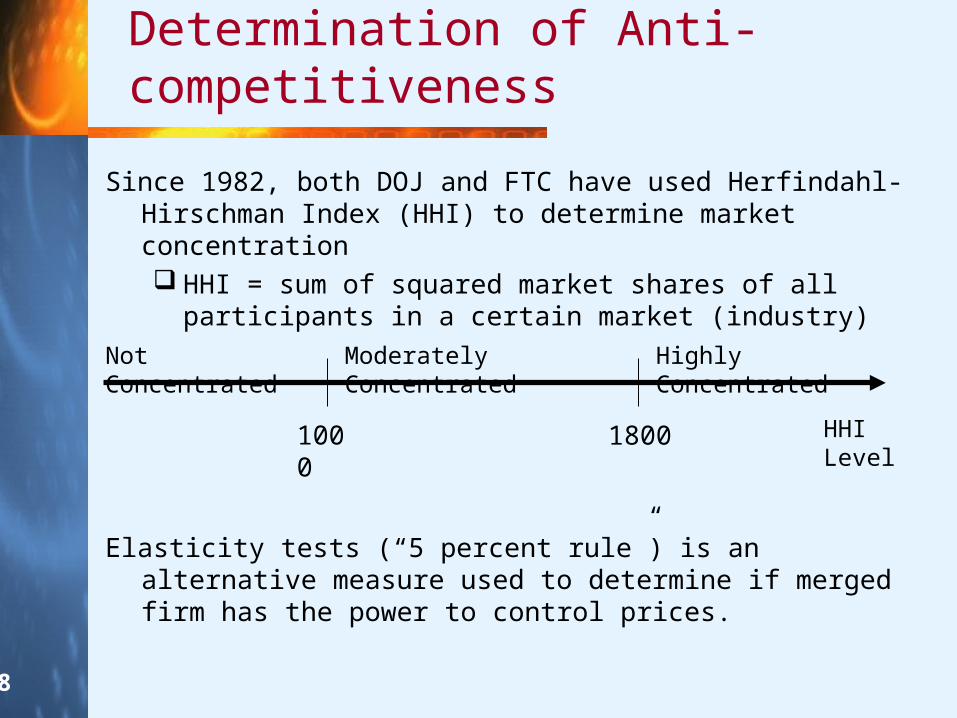

Determination of Anti-competitiveness

Since 1982, both DOJ and FTC have used Herfindahl-Hirschman Index (HHI) to determine market concentration HHI = sum of squared market shares of all participants in a

certain market (industry)

Elasticity tests (“5 percent rule”) is an alternative measure used to determine if merged firm has the power to control prices.

1000 1800 HHI Level

Not Concentrated Moderately Concentrated Highly Concentrated

29

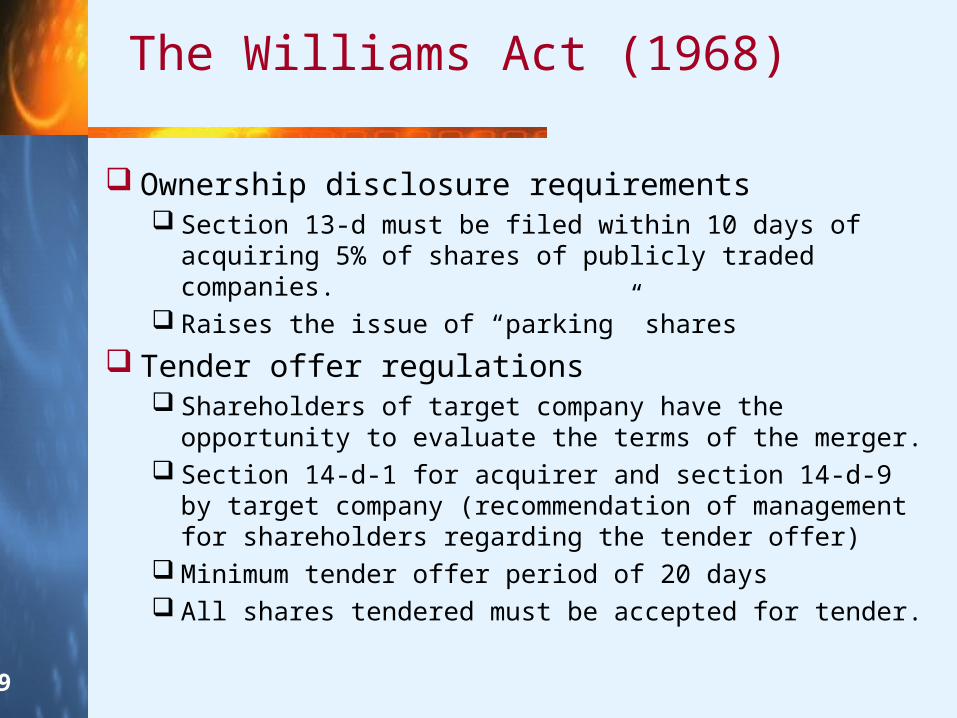

The Williams Act (1968)

Ownership disclosure requirements Section 13-d must be filed within 10 days of acquiring 5% of

shares of publicly traded companies. Raises the issue of “parking” shares

Tender offer regulations Shareholders of target company have the opportunity to

evaluate the terms of the merger. Section 14-d-1 for acquirer and section 14-d-9 by target

company (recommendation of management for shareholders regarding the tender offer)

Minimum tender offer period of 20 days All shares tendered must be accepted for tender.

30

Other Legal Issues

Sarbanes-Oxley Act of 2002 primarily targeted accounting practices, it also mandated

significant changes in how, and how much, information companies must report to investors.

Laws Affecting Corporate Insiders SEC rule 10-b-5 outlaws material misrepresentation of

information for sale or purchase of securities. Rule 14-e-3 addresses trading on inside information in tender

offers. The Insider Trading Sanctions Act, 1984 awards triple

damages. Section 16 of Securities and Exchange Act

Requires insiders to report any transaction in shares of their affiliated corporations.

31

Other Legal Issues

State Antitrust LawsInclude anti-takeover and anti-bust up

provisionsFair price provisions disallow two-tiered tender

offers. All shareholders receive the same price for their shares, regardless of when they are tendered.

Cash-out statutes forbid partial tender offers.

Provisions usually used in conjunction with each other

32

Corporate Governance

Law and financeEfficient capital markets promote rapid

economic growthPrivatization’s impact on stock and bond

market development