Embed Size (px)

Citation preview

2

7

-1

NP Paper

Group

Revenue CAGR %

(2011 – LTM Q115)

11

8

NP Paper

Group

EBIT Margins %

(LTM Q115)

10

6

NP Paper

Group

Return on Capital %

(2014)

When it delivers

strong, consistent

top & bottom line

growth

With attractive

profit margins

..and a sustainable

double digit Return

on Capital

3

Two primary business segments:

• Performance-based TECHNICAL PRODUCTS

• Image-oriented FINE PAPER & PACKAGING

> 2,500 employees worldwide

Publicly traded on NYSE/Euronext (NP)

Market cap ~US$1 billion

Headquartered in Alpharetta (Atlanta), GA

Sales in more than 80 countries

Global manufacturing base:

U.S. (14 sites)

Germany (3 sites), U.K. and India (small JV)

> $1 bn sales

55% Technical Products

45% Fine Paper & Pkg

Enhance leading positions in high value, core categories

Expand our geographic presence in transportation filtration

Build off our global base in performance backings

Leverage our strong market position in fine paper & packaging

Invest to grow in targeted niche markets that are profitable and

defensible and where our capabilities are valued

Focused on filtration, premium packaging and performance materials

Prioritize organic growth and supplement with value-adding acquisitions

Deliver consistent, attractive returns

Disciplined capital deployment and double-digit Return on Capital

An attractive dividend part of a meaningful return to shareholders

4

5

On August 1, 2015, Neenah acquired FiberMark, a specialty coating and

finishing company, for $120 million

Over $160 million in revenue, with EBITDA of ~$18 million • Added revenue approximately evenly split between both segments

7 operating facilities (with more than 100 assets focused on converting)

Almost 600 employees

Strategic fit with targeted growth areas

Expands presence in premium packaging

Overlapping presence in tapes, décor and other technical products

Extends and deepens our ability to drive future growth through new

coating/converting/laminating, heavyweight papers and prototyping

Delivers attractive financial returns

Annual synergies of >$6 million by year three; mid-teen IRR

Not-dilutive to Neenah’s (mid-teen) EBITDA margins

Ongoing accretion of >$0.40/share (and accretive in year one)

Filtration 40%

Backings 25%

Specialties 35%

6

Filtration

Specialties:

Backings:

High-performance

filtration media for

transportation,

water and other

markets Includes security

papers, decorative

coverings, label,

and others

Saturated and

coated backings for

specialty abrasives

and tapes

* adjusted to reflect FiberMark acquisition

~ $550 million

net sales*

7

Technical

Products Top-line reflects growing markets

and share gains, including 2014

acquisition

Margin expansion through higher

value mix, volume-driven growth

and cost efficiencies

Filtration a key driver, with faster

growth and attractive margins

Further opportunities to expand in

new markets and geographies,

both organically & through M&A

$421 $407

$416

$467 $471

8.0%

9.2% 9.3%

10.1%

10.9%

5.0 %

6.0 %

7.0 %

8.0 %

9.0 %

10. 0%

11. 0%

12. 0%

13. 0%

14. 0%

15. 0%

$320

$340

$360

$380

$400

$420

$440

$460

$480

$500

$520

2011 2012 2013 2014 LTM

Q215

Net Sales

EBIT %

Adj. for currency $505

8

Key technologies

Multi-fiber forming

capabilities

Polymer chemistries

Saturation, coating

and surface treatments

R&D facilities in U.S.

and Germany

Ability to Meet

Specialized Performance Requirements

Customer Intimacy

and Qualification

Long-standing relationships

Global market-leading

customers

Intricate qualification

requirements

Ongoing joint product

development

11%

14% 16%

16% 16%

2011 2012 2013 2014 LTM

Q215

Innovative New Next

Generation Products

New Product Sales (% of total sales of new products launched within past 36 months)

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14

Asia NAFTA Europe RoW

Other

NP

H&V

Ahlstrom

Global Transportation Filtration Market Size and Share Global Market ~ US $1 billion

Growing global market

Global market growing ~4%/year with sales split: 30% OEMs/ 70% aftermarket

Filter needs continuing to become more demanding (fuel, oil, engine & cabin air)

Neenah growing twice the market with share gains due to advanced technology, innovation and focus on higher value mix

Expansion Opportunity- U.S.

Current operations based in Germany; existing capacity likely consumed in 2016

Historical constraint on US entry expired; project underway for capital-efficient repurposing of fine paper asset

Customers supporting expansion

Proven success vs. NAFTA competitors

Start-up early 2017; attractive mid-teen IRR

9

Net Sales

CAGR 8%

Source: company estimates

10

Beverage Filtration Micro/Ultrafiltration

(6-12% growth)

Water Filtration Reverse Osmosis (RO)

(8-10% growth)

Environmental (4-5% growth)

Energy Management (3-4% growth)

Thermal & Acoustical Insulation

(2-3% growth)

Important fast-growing markets

Currently represent ~ 25% of filtration sales

Products employ a variety of technologies,

including cellulose and synthetic wet laid nonwovens, glass and melt blown substrates

Bolstered by July 2014 acquisition of specialty No. American filtration business from Crane

11

Backings

Sizeable global category with primary end uses including tapes and abrasives

Markets generally growing with global GDP

Focused on performance niches requiring downstream applications

Specialties

Smaller specialized markets including security, medical packaging, labels, décor, and others

Markets generally growing at above GDP rates with attractive margins

Similarly employ saturating and coating to impart unique characteristics

12

Graphic Imaging

Premium Packaging

Unique colors,

textures and finishes

for high-end

commercial printing

and consumer needs

Image-enhancing

colors and textures

of premium folded

cartons, curved box

wrap, bags, & labels

Graphic Imaging

78%

Packaging 15%

Folder/ Office

7%

~ $480 million

net sales*

* adjusted to reflect FiberMark acquisition

Filing/Office Premium boards with a

variety of colors and

properties. Used for

records mgmt,

classification, binder

covers, and other

professional applications

13

$275

$373 $402 $409 $401

14.4% 15.0% 15.0% 15.0%

16.3%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

-20

30

80

130

180

230

280

330

380

430480

2011 2012 2013 2014 LTM

Q215

Net Sales

EBIT % Growing organically via share gains,

new revenue streams and premium

packaging. Supplemented by highly

accretive consolidating acquisitions.

Consistently attractive margins, with

strong brand equity supporting

pricing power

Capital efficient, with strong cash

flows and high returns on capital

Fine Paper

& Packaging

14

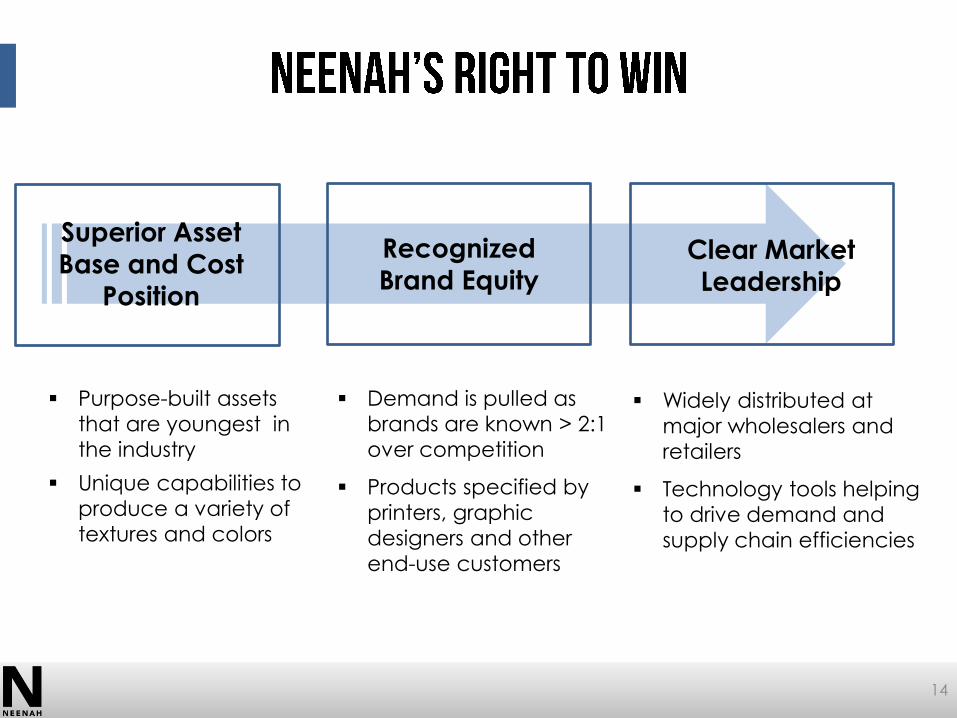

Demand is pulled as

brands are known > 2:1

over competition

Products specified by

printers, graphic

designers and other

end-use customers

Purpose-built assets

that are youngest in

the industry

Unique capabilities to

produce a variety of

textures and colors

Recognized

Brand Equity

Superior Asset

Base and Cost Position

Clear Market

Leadership

Widely distributed at

major wholesalers and

retailers

Technology tools helping

to drive demand and

supply chain efficiencies

Neenah 65% Mohawk

25%

Others 10%

Market Share Commercial Channel

~$500 million

Neenah 55% Others

45%

Market Share Retail Channel ~$150 million

NA Printing & Writing

$20+ bn

Uncoated Free sheet

$10 bn

15

Premium Fine Paper ~ $650 mm

Graphic Imaging

Niche market focused on high

quality, textured and colored

papers

End uses include premium

printing, marketing collateral

and advertising, and specialty

retail products

Market is growth-challenged;

we have increased organically

and through highly accretive

consolidating acquisitions

Clear leader in commercial

and retail channels

US-based operations and sales

Cosmetics &

Fragrance

Spirits

Food

Electronics

Retail

Global Pkg Mkt

$42 bn

Premium Market

$2 bn (5%)

Near Term Targeted $450 mm

(<1%)

16

Premium Packaging

Global market, growing 3-5% annually

Fragmented category with no clear market leader

Leverages strength of our high end color and texture capabilities

$450 million targeted market focused in high value niche areas

17

Consistent and profitable growth

High Return on Capital and Return on Equity

Flexible and prudent capital structure

Attractive shareholder returns, including a

meaningful cash component

18

$ millions 2011 2012

2013 2014

LTM Q2’15

% 15 vs. 14

Sales $ 696 $ 809 $ 845 $ 903 $ 899 (0.4%)

Adj. EBIT1 59 80 85 94 101 8%

% ROS 8.5% 9.9% 10.1% 10.4% 11.3%

Adj. E.P.S.1 $ 1.91 $ 2.78 $ 2.93 $ 3.28 $ 3.50 7%

(1) Excludes integration costs, tax credits and other items noted in GAAP table

Five-year annual mid single digit top line and

double-digit bottom line growth with share gains,

new products, price/mix improvement and

acquisitions

Continued margin improvement

* 2015 YTD reflects currency impacts from a weaker euro

of $30 million. YTD constant currency growth 6%

$1.91

$2.78 $2.93 $3.28

$3.50

2011 2012 2013 2014 LTM

Q2'15

Adjusted

E.P.S.

7%

15%

16%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Sales Adj. EBIT Adj. E.P.S

% Annual Growth

2011-2015

* *

9%

11% 12% 13% 13%

2011 2012 2013 2014 LTM

Q2'15

19

Delivering improvements through:

Profitable growth/margin expansion

Management focus on asset efficiency

Disciplined organic capital spending/good returning projects

Value-adding acquisitions

WACC

~ 8%

Primary measure to evaluate investments, judge business performance

- also a key metric in management compensation plans

$186 $182

$212

$234 $216

2.0x

1.6x

1.8x 1.8x

1.6x

1

1.5

2

2.5

3

3.5

0

50

100

150

200

250

300

350

Dec 11 Dec 12 Dec 13 Dec 14 Jun 15

20

$ millions

Dec

2011

Dec

2012

Dec

2013

Dec

2014

Jun

2015

Bonds 5.25% (due Nov. 2021)

$ 158 $ 90 $ 175 $ 175 $ 175

Global ABL Rate Libor +125

- 56 - 50 32

Other 28 36 37 9 9

Total Debt $ 186 $ 182 $ 212 $ 234 $ 216

Cash $ 13 $ 8 $ 73 $ 73 $ 78

Balance sheet providing financial strength and capacity for growth

Currently below targeted range of 2 – 3 x Debt/EBITDA

Attractive bonds with debt rating of Ba3/BB and low coupon rate

Global ABL sized at $200 million providing added flexibility/borrowing capacity

Debt ($ millions)

Targeted Debt/EBITDA

Range 2.0x – 3.0x

Actual Debt/EBITDA

21

Pro Forma Cash Flow ($ millions)

EBITDA $ 155

Interest Expense (11)

Other (tax, wkg cap, pension, etc.) (35 - 40)

Cash From Operations $ 105 – 115

Capital Spending (3-5% sales) (35 - 55)

Free Cash Flow $ 60 – 85

FCF/Share $3.50 - $5.00

Cash Deployment

Priority on highest returning investments o Organic initiatives

o Value-adding M&A

Authorized $25 mm

stock repurchase plan

Committed to cash returns via attractive and growing dividend

Cash Generation

Strong operating cash flows

Efficient asset base; maintenance cap-

ex of < $15 mm/year

Pension plan well funded, significant US R&D tax credits

$0.44 $0.48

$0.70

$1.02 $1.20

0

0.5

1

1.5

2011 2012 2013 2014 2015

Cash Dividends Paid

(per share)

* excludes one-time costs for acquisition accounting and other items

$57 $66

$84 $95

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014

Cash From Operations

*

Adjusted for FiberMark acquisition

22

Performance-based and aligned with shareholders

All incentive plans are tied to performance achievement

50% cash, based on growth in business profit/EBITDA

50% equity, based (options and performance shares)

Performance shares based on:

Return on Capital improvement

Revenue growth

Free cash flow (as a % of sales)

Total Shareholder Return (vs. Russell 2000 index)

Management required to hold a multiple of salary in Neenah

stock (for example CEO = 6x)

Active and disciplined process with dedicated

resources

Targeting growing, profitable niche markets

(filtration, performance materials, premium pkg,

etc…) with a strategic linkage

Most targets sized between $50 and $250 million

of sales

Demonstrated track record and competency in deal execution and integration to capture value

Strategic Growth

Touch points

Geographies

Technologies Products/

End Markets

Customers

23

FiberMark (Germany)

2006

Fox River 2007

Wausau brands 2012

Southworth brand 2013

Crane 2014

FiberMark (US) 2015

With leading positions in defensible and profitable niche markets

With catalysts to enhance our growth profile in filtration, premium packaging and other targeted markets

With financial strength and a double-digit Return on Invested Capital

With a clear track record of value-adding capital deployment and generating attractive financial returns

24

Transportation filtration Performance Materials Fine paper

U.S. transp. filtration expansion Premium packaging Adjacent filtration markets

Strong cash flow generation Low debt/financial flexibility

Double-digit Return on Capital Top quartile shareholder returns Dividend tripled over last 5 years

25

For more information

visit our website: www.neenah.com

email: [email protected]

Investor Relations

Bill McCarthy

VP, Financial Planning and Analysis &

Investor Relations

3460 Preston Ridge Rd., Suite 600

Alpharetta, GA 30005

Phone: (678) 518-3278

Email: [email protected]

26

Continuing Operations

$ millions 2011 2012

2013

2014 LTM

Q2 2015

EBIT (Operating Income) $ 57 $ 70 $ 84 $ 87 $ 95

Acquisition integration costs 6 1 3 4

Other1 2 4 4 2

Adjusted EBIT $ 59 $ 80 $ 85 $ 94 $ 101

Depreciation & Amortization 30 28 29 30 31

Amort. Equity-Based Compensation 4 5 5 5 5

Adjusted EBITDA $ 93 $ 113 $ 119 $ 129 $ 137

Earnings (Loss) per Share $ 1.82 $ 2.41 $ 2.96 $ 4.03 $ 4.29

Acquisition integration costs 0.22 0.02 0.11 0.07

R&D Tax Credit (0.08) (1.00) (1.00)

Other1 0.09 0.15 0.03 0.14 0.14

Adjusted Earnings per Share $ 1.91 $ 2.78 $ 2.93 $ 3.28 $ 3.50

1 Results for year ended December 31, 2011, includes $2.4 million of costs related to the early extinguishment of debt, results for the year ended

December 31, 2012, include a supplemental executive pension plan settlement charge of $3.5 million and costs related to the early extinguishment of debt of $0.6 million, results for the year ended December 31, 2013, include integration and restructuring costs of $0.6 million, a post-retirement

benefit plan settlement charge of $0.2 million and costs related to the early extinguishment of debt of $0.5 million, results for the year ended

December 31, 2014, include integration and restructuring costs of $2.9 million, a post-retirement benefit plan settlement charge of $3.5 million and

costs related to the early extinguishment of debt of $0.2 million.

EBITDA, Adjusted EBITDA and Free Cash Flow as presented in these slides, are supplemental measures of our performance, and Net Debt, as presented in these slides, is a supplemental measure of our financial position. In each case, these measures are not required by, or presented in accordance with, generally accepted accounting principles in the United States (‘‘GAAP’’). EBITDA, Adjusted EBITDA and Free Cash Flow are not measurements of our financial performance or financial position under GAAP and should not be considered as alternatives to net sales, net income (loss), operating income or any other performance measures derived in accordance with GAAP or as alternatives to cash flow from operating activities as a measure of our liquidity.

Adjusted EBITDA consists of operating income plus depreciation, amortization and stock-based compensation expense. We also exclude acquisition-related costs, gain (loss) on sale of fixed assets, SERP settlement charge and costs related to early retirement of debt, as these amounts are not considered as part of usual business operations. Our management considers EBITDA, Adjusted EBITDA and Free Cash Flow to be measurements of performance which provide useful information to both management and investors. Because EBITDA, Adjusted EBITDA and Free Cash Flow are not calculated identically by all companies, our measurements of EBITDA, Adjusted EBITDA and Free Cash Flow may not be comparable to similarly titled measures reported by other companies. All amounts in USD unless otherwise noted.

EBITDA, Adjusted EBITDA and Free Cash Flow, as presented herein, are non-GAAP financial measures as defined by SEC regulations. As required by those regulations, a reconciliation of these measures to what management believes are the most directly comparable GAAP measures is included as an appendix to this presentation.

27

Statements in this presentation which are not statements of historical fact are “forward-looking statements” within the “safe harbor”' provision of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on the information available to, and the expectations and assumptions deemed reasonable by, Neenah Paper, Inc. at the time this presentation was made. Although Neenah Paper believes that the assumptions underlying such statements are reasonable, it can give no assurance that they will be attained. Factors that could cause actual results to differ materially from expectations include the risks detailed in the section “Risk Factors” in the Company’s most recent Form 10-K and SEC filings.

In addition, the company may use certain figures in this presentation that include non-GAAP financial measures as defined by SEC regulations. As required by those regulations, a reconciliation of these measures to what management believes are the most directly comparable GAAP measures would be included as an appendix to this presentation and posted on the company’s web site at www.neenah.com

28