Embed Size (px)

Citation preview

Venture Capitalists’ and Entrepreneurs’ Knowledge in New Venture Internationalization

Joseph LiPuma* Christiane Prange Sarah Park Affiliate Professor of Associate Professor of Ph.D. Student

Entrepreneurship International Strategy & Marketing Strategy

[email protected] [email protected] [email protected]

All:

EMLYON Business School

23 avenue Guy de Collongue

F-69134 Ecully

*corresponding author Tel: +33-(0) 4 78 33 64 31

ABSTRACT

Explanations of internationalization focus on knowledge and experience accumulation over time.

Research on international new ventures (INVs) suggests that young companies may follow an

accelerated expansion strategy, mainly based on the knowledge of the entrepreneur or that of

associated outsiders. Research on the role of venture capitalists‟ knowledge in the

internationalization process has been sparse, despite their acknowledged role as providers of

knowledge and networks in addition to financial capital. By deconstructing knowledge types

relevant to internationalization, we explore their source in the entrepreneur-venture capitalist

dyad. We utilize the literature on ambidexterity as a lens through which we examine potential

substitution effects, and suggest a number of propositions as a basis for future empirical research.

2

Venture Capitalists’ and Entrepreneurs’ Knowledge in New Venture Internationalization

In an increasingly global economy, internationalization is a cornerstone of

competitiveness. While many companies postpone their cross-border engagement until they have

accumulated sufficient domestic experience and success, others pursue internationalization at or

near inception. These divergent strategies are reflected in different streams of the international

business literature. The Uppsala model of internationalization explains incremental foreign

market engagement as a sequential process of experience and knowledge accumulation to reduce

the risks of internationalization (Johanson & Vahlne, 1977; Johanson & Wiedersheim-Paul,

1975). Companies typically enter foreign markets when they are older and sufficiently

experienced in overcoming the threats posed by cultural distance and foreign business practices.

In contrast, the international new ventures (INVs) or born global (BG) streams of research draw

attention to the fact that companies may internationalize rapidly at a young age and experience

high international growth, despite being constrained by resource scarcity and by liabilities of

foreignness and newness (Oviatt & McDougall 1994; Knight & Cavusgil, 2005).

While different, both internationalization strategies assume that knowledge plays a

central role in a company‟s internationalization process (Autio, Sapienza & Almeida, 2000;

Casillas, Moreno, Acdeo, Gallego & Ramos, 2009). Late internationalizers follow a process of

internationalization based on existing know-how from the domestic market that is extended by

direct experiences through gradually increasing market commitment. These companies use firm-

level knowledge acquired via their internationalization experiences. In contrast, young and

rapidly internationalizing ventures enter and intensify foreign activities by largely capitalizing on

the entrepreneur‟s existing knowledge base (McDougall, Shane & Oviatt, 1994; Oviatt &

McDougall,1994).

3

Recent studies from both perspectives have focused on different dimensions of

knowledge related to internationalization, such as knowledge domains (market, institutional or

competitor knowledge), processes of knowledge development (experiential learning, learning by

imitating), or levels of analysis (individual, firm or network knowledge) (Casillas et al., 2009;

Eriksson, Johanson, Majkgard & Sharma, 1997; Eriksson, Majkgard & Sharma, 2000).

Strikingly, the source of knowledge has often been neglected but is likely to affect perceptions

about knowledge usability (Shi, Sia, Banrjee, Luo, Tan & Chen, 2009), applicability (Peili &

Zhonghong, 2006) or judgement as to its relevance (Nguyen & Barrett, 2006). These aspects are

relevant to internationalization but have not, to our knowledge, been addressed.

For example, while external equity investment such as venture capital (VC) is important

for the financing of young companies, its relevance for knowledge development has received

scant attention (Fernhaber & McDougall-Covin, 2009; Fernhaber, McDougall-Covin &

Shepherd, 2009). This is despite the recognition of VC as a bundle of resources, including

knowledge that is used for advice (Rosenstein, Bruno, Bygrave & Taylor, 1993), assistance with

decision making (Maula, Autio & Murray, 2005) and strategy formulation (Rosenstein, 1988).

Moreover, there is little conceptual and empirical clarity on the different types of knowledge,

roles of entrepreneurs and venture capitalists (VCs), and their respective knowledge bases as a

foundation for a venture‟s internationalization.

The goal of this paper is to analyze types of individual knowledge, their sources, and

their impact on new ventures‟ internationalization. We investigate the role of individual

knowledge in new ventures. Extending previous research, we offer two contributions. First, we

identify different types of knowledge in a young venture that are relevant to internationalization.

Second, we investigate interplays between different types of knowledge that entrepreneurs and

VCs possess relative to new venture internationalization. We investigate the potential

4

complementarity between entrepreneurs‟ knowledge and VCs‟ knowledge that facilitates INV

internationalization speed and performance. We propose that the respective stocks of knowledge

possessed by each partner in the entrepreneur-VC dyad are dynamic and vary relative to each

other during the venture‟s development. These contributions suggest a variety of future research

directions as well as important insights for managers and investors in their financing strategies

and their internationalization policies.

KNOWLEDGE AND NEW VENTURE INTERNATIONALIZATION

Studies of internationalization processes have traditionally focused on an incremental

approach (Johanson & Vahlne 1977; Johanson & Wiedersheim-Paul 1975). Behind the

incremental and gradual market entry process lies the step-wise accumulation of knowledge used

to mitigate uncertainty and perceived risks of international operations. Recent research has

criticized this approach as being too eclectic and mechanistic as companies may skip several

stages or internationalize more quickly (Moen & Servais, 2002; Pla-Barber & Escribá-Esteve,

2006). The growing literature on international new ventures or born globals illustrates that

companies may internationalize in an accelerated way, and do so at or near inception.

International new ventures (also referred to as born globals1 (Knight & Cavusgil, 2005) are

defined as companies “that, from inception, seek to derive significant competitive advantage

from the use of resources and sale of outputs in multiple countries” (Oviatt & McDougall, 1994:

49).

The distinguishing feature of INVs is their international origins, as demonstrated by

management‟s global focus and the concomitant commitment of resources to international

1 The terms “international new venture” and “born global” are used in the literature to describe internationalization

at or near inception. While some differences may exist in their definitions based on venture age, age at

internationalization and international intensity, we use the term international new venture (INV) in this document to

describe both with no bias or loss of generalizability.

5

activities (Knight, Madsen & Servais, 2004; Kuemmerle, 2002). Since most lack the tangible

resources of large multinationals, INVs capitalize on other, perhaps more fundamental and tacit

resources like knowledge and learning capability (Kundu & Katz, 2003; Zahra, Matherane &

Carleton , 2003). Indeed, it is the knowledge of entrepreneurs with a strong international outlook

based on previous industry and/or country experiences that facilitates foreign expansion from

inception (Harveston, Kedia & Davis, 2000; McDougall et al,. 1994; Nummela, Saarenketo &

Puumalainen, 2004). Thus, the internationalization process of INVs renders the assumption of

incremental knowledge accumulation in stage models obsolete since international knowledge is

potentially less of a barrier in global industries and therefore affords a faster internationalization

process (Andersen, 1993; Brennan & Garvey 2009; Eriksson et al., 1997). Knowledge is thus a

most precious resource for INVs but this knowledge need not exclusively come from the

entrepreneurs themselves; it may also come from external stakeholders such as venture

capitalists (Coviello & Munro, 1995; Fernhaber et al., 2009; Reuber & Fischer, 1997; Sharma &

Blomstermo, 2003).

Definitions of International Knowledge

International knowledge is “any information, belief, or skill that the organization can

apply to its [international] activities” (Anand, Glick & Manz, 2002: 88). More dynamic views

acknowledge that knowledge relates to the founders‟ experience prior to launching a new venture

(Kundu & Katz, 2003; Reuber & Fischer, 1997; Zahra, 2005), or to the accumulation of learning

and experience during the venture‟s life (De Clercq, Sapienza & Crijns, 2005; Zahra & Hayton,

2008). As INVs enter foreign markets early, their initial endowment of relevant knowledge

seems to be more important than later learning experiences (Cooper, Gimeno-Gascon & Woo,

1997). The specificity of experience may be important: for example, founders‟ human capital in

the form of technical experience in the industry and managerial training positively affect

6

company growth (Colombo & Grilli, 2005). After inception, experience accumulation and

continuous learning also impact internationalization performance (De Clercq et al,. 2005; Kundu

& Katz, 2003).

Social Capital and Human Capital

The literature further distinguishes between human and social capital (or knowledge).

Human capital, the knowledge and skills acquired by an individual in the course of training and

experience (Becker, 1964) has long been identified as a strategic resource for new ventures

(Eisenhardt & Schoonhoven, 1990). Individual assets are emphasized since they help

entrepreneurs to recognize opportunities and assemble resources (Alvarez & Busenitz, 2001).

Ruzzier, Hisrich & Antoncic (2006) argue that entrepreneurs‟ personal factors, as the individual

dimension of human capital, are predictors of small/medium sized enterprise (SME)

internationalization. Social capital (“friends, colleagues, and more general contacts through who

you receive opportunities to use your financial and human capital” (Burt 1992: 9); who they

know) helps entrepreneurs to decipher what they know and how to apply it in a foreign context.

Entrepreneurs and top management teams (TMTs) with high levels of social knowledge know

who to contact to get relevant information. TMTs may include venture capitalists as boundary-

spanning governors (Zahra, Ucbasaran & Newey, 2009).

Tacit Knowledge and Explicit Knowledge

A more in-depth analysis of knowledge in the internationalization process can identify

ways in which knowledge manifests itself in the INV. One basic distinction is tacit and explicit

(or codified) knowledge (Nonaka, 1994). Tacit knowledge is hard to replicate as it pertains to the

skills, abilities, and practices that can only be made explicit and transferred to others at high

costs (Polanyi, 1966). Tacit knowledge is typically content-bound and embedded within people,

thus requiring intense interaction to be shared. In contrast, explicit knowledge, stored on data

7

carriers such as books or computers, is easily transmissible but understanding in different

contexts may vary. Because organizational knowledge is created by individuals but utilized by

organizations (Nonaka & Takeuch, 1995, the sharing and transfer of knowledge are critical

processes in organizations. Thus, understanding knowledge sharing is about understanding the

individual who possesses and provides the knowledge and how this manifests itself at the

organizational level (Freeman, Hutchings, Lazaris & Zyngier, 2009).

Types of Knowledge

Knowledge types most pertinent for INVs are know-what, know-why, know-how, and

know-who (Bertoin-Antal, 2000; Lubatkin, Florin & Lane, 2001; OECD, 2000; Zook, 2004).

Know-what is declarative knowledge that relates to knowing the facts required to make a

decision or complete a task (Anderson, 1983). It is knowledge individuals often apply

subconsciously and use when they first become familiar with a particular information domain.

Know-why is axiomatic knowledge that relates to strategic insight - the "big picture" view of

things. It is the knowledge that is drawn to explain why things happen and refers to the reasons

and explanation of final causes (Sackman, 1992). Typically, questions like “why are we doing

this?” and “where are we trying to go?” relate to this type of knowledge, which provides the

„dominant logic‟ (Prahalad & Bettis, 1986) for executing tasks.

Know-how relates to procedural knowledge and captures the processes, activities,

techniques and tools one uses to get something done (Anderson, 1983). Know-how usually

implies the ability to articulate cause and effect relationships and can be obtained from learning

via experience accumulation. It is largely tacit and cannot be easily separated from a person or an

organization. Finally, know-who relates to personal networks of people, and the degree to which

it can be accessed will be a reflection of an organization‟s culture. Know-who is a way to obtain

relevant knowledge as it often relates to expert knowledge with high interconnectedness.

8

The four knowledge types are related to each other and the boundaries between the

categories are likely to blur somewhat in practice (Bertoin-Antal, 2000). This knowledge

typology promotes a better understanding of different roles of knowledge in internationalization,

and conveys a more realistic picture of the world.

DEVELOPMENT OF THEORETICAL FRAMEWORK

The Role of Entrepreneurs’ Knowledge in Venture Internationalization

Research on INVs finds that entrepreneurs may possess relevant knowledge from

individual international experience (Casillas et al., 2009; Fernandez-Ortiz & Lombardo, 2009;

Kundu & Katz, 2003; Schwens & Kabst, 2009) and through international exploration during the

venture‟s early stages (Kuemmerle, 2002).

Entrepreneurs’ Internationalization Knowledge Types

At the individual level, studies on knowledge in the new venture internationalization

process have focused largely on the entrepreneur‟s knowledge (Andersson, 2000; Lindsay,

Chadee, Mattson, Johnston & Millett, 2003). Although these studies view internationalization

knowledge as a bundle without distinguishing different relevant types, a variety of knowledge

types are often implicitly employed. Different types of know-what that entrepreneurs possess,

including foreign market knowledge (Zhou, 2007) and foreign language knowledge (Fernandez-

Ortiz & Lombardo, 2009), influence new venture internationalization via the timing and the level

of international diversification (know-how). This is relevant for INVs that enter foreign markets

quickly, as this type of knowledge is associated with early venture internationalization success

(Schwens & Kabst, 2009) and higher levels of international diversification (Fernandez-Ortiz &

Lombardo 2009). Many INVs are technology-based and knowledge intensive (Coviello &

Munro, 1995; Johnson, 2004), requiring high up-front costs related to industry drivers or the

technological savvyness (know-why) that may require entrepreneurs to rapidly enter foreign

9

markets and quickly expand (Brennan & Garvey, 2009; Johnson, 2004). Prior international

experience of entrepreneurs, by decreasing the venture‟s liability of foreignness facilitates

market expansion and early internationalization (Schwens & Kabst, 2009) and may serve as a

proxy for the reduction of uncertainty and as a surrogate for accumulating cultural knowledge

(Daily, Certo & Dalton, 2000). It is here that internationalization know-what, know-why and

know-how closely intersect. Initially, it may be the international experience of the management

team that provides better understanding of foreign markets, making it easier for managers to

recognize international opportunities (know-why) and diversify internationally (Fernandez-Ortiz

& Lombardo, 2009). At later stages, entrepreneurs‟ social knowledge (know-who) positively

influences the scope of the INV‟s international activities (Zahra et al. 2009), establishing

legitimacy and acquiring trust, information and resources.

The Role of Venture Capitalist Knowledge in Venture Internationalization

Studies of the impact of entrepreneurs‟ international knowledge or that of venture

capitalists‟ on new venture internationalization are few (Fernhaber & McDougall-Covin 2009;

George, Wiklund & Zahra, 2005). Those that do exist suggest a positive relationship between

venture capitalist support and new venture internationalization (Carpenter, Pollock & Leary,

2003; Fernhaber & McDougall-Covin, 2009). Research has demonstrated the role of VCs as

catalysts in new venture internationalization based primarily on their combined provision of

knowledge and reputational resources (Fernhaber & McDougall-Covin, 2009). Venture capital

may be a solution to resource constraints that retard new venture internationalization

(Bloodgood, Sapienza & Almeida, 1996; Oviatt & McDougall, 1994). Many VCs are actively

involved in the venture (Baum & Silverman, 2004) and are willing to share their knowledge and

increase legitimacy. They can facilitate the venture‟s internationalization by expanding its

resource base and by influencing the strategic direction towards internationalization (Fernhaber

10

& McDougall-Covin, 2009), providing access to additional information related to

internationalization (Sapienza, 1992).

The study by Fernhaber et al. (2009) investigated the moderating effect of TMT

knowledge on the impact VC's knowledge has on new venture internationalization, but their

study also adopted a bundled view of knowledge and focused on the level of new venture

internationalization. This paper distinguishes among VCs‟ different knowledge types and

postulates the effect of interplays between types of knowledge of entrepreneurs and venture

capitalists on new venture internationalization.

Venture Capitalists’ Internationalization Knowledge Types

Venture capitalists‟ advice takes various forms based on their knowledge and their

portfolio company‟s needs.

Know-what. Venture capital represents a bundle of resources, comprised of financial, human

and social capital of the investing venture capitalist. Human capital is provided in the form of

knowledge and advice (Sapienza, 1992) that is used by the entrepreneur for development and

execution of strategies. Such knowledge may include in-depth insights into industry

developments, customer and demand analyses, or business strategies for specific countries. In the

past decade, VC providers have internationalized their activities significantly (Forer &

Haemmig, 2007; Wright, Pruthi & Lockett, 2005) by financing foreign ventures, syndicating

with foreign investors and partnering with foreign VC firms. They have thus extended their

networks, increased their knowledge base and broadened their insights into the environmental

conditions of foreign investments. Venture capitalists‟ internationalization knowledge can aid

entrepreneurs by reducing uncertainty and facilitating the development and selection of foreign

markets and reduce costs associated with searching for foreign partners willing to provide market

data and customer information. Know-what is largely experience-based, and prior international

11

experience of board members, which may include VCs, increases foreign market knowledge. In

addition to reducing uncertainty, foreign experience provides cultural knowledge and may also

be inimitable and non-substitutable (Daily et al., 2000).

Know-why. Technology-based ventures often require significant investment to develop

intellectual property and products. High upfront investment requirements may force these

ventures to rapidly enter foreign markets, potential requiring the use of VC funds to finance

foreign market entry. Technology-based ventures also exhibit high levels of information

asymmetries due to their highly specialized and knowledge-intensive activities (Gompers &

Lerner, 1999). Such ventures are likely to adopt early foreign market entry strategies due to short

product lifecycles and quick market expansion to recover high investment costs (Johnson, 2004).

Venture capital firms who typically seek to exit the investment in five to seven years may push

for rapid international expansion of ventures in which they invest. Thus, entry speed and timing

may be facilitated through VCs‟ previous experiences. Additionally, it may be the VCs‟ in-depth

affiliation with industry trends that further helps to detect valuable internationalization

trajectories and implement expansion strategies that may otherwise be outside the scope of the

entrepreneurs, or have even prevented them from internationalizing.

Know-how. Cross-border VC investments are increasing (Wright et al., 2005), as are

investments in INVs. This provides investors with relevant experience in governing

internationalized ventures and knowledge about how to internationalize. Their experience and

knowledge may promote the creation of early routines for serving demand or analyzing foreign

data as well as procedures for initiating relevant relations and involvement with governmental

bodies. Thus, VCs that have invested in foreign ventures or in INVs possess knowledge that can

be used by their portfolio companies to re-think existing routines and capabilities to conform to

foreign market requirements. Foreign market entry modes vary in degree of control, the need for

12

which is related to the degree of understanding of processes (e.g., for internationalizing or for

operations). Relevant know-how on different internationalization modes (e.g., exporting or

licensing) may thus affect entry mode choice (Anderson & Gatignon, 1986) as a specific variant

of know-why. The pace, rhythm and scope of internationalization (Vermeulen & Barkema,

2002) may be affected by the knowledge of VCs, who may act by exercising control rights to

ensure that the entrepreneur does not overextend his capabilities in an attempt to internationalize.

Know-who. The process of internationalization reflects an opportunistic, reactive and varied

approach based on network knowledge (Coviello & Munro, 1995). In a new venture, one of the

major assets is the entrepreneur‟s social capital, an intangible asset developed over time. The

social capital of VC providers offers access to a network of other ventures, potential capital

providers, and foreign customers (Maula et al., 2005). The embeddedness of the entrepreneur

and of the VC in their respective networks provides access to additional trust-based resources

and opportunities (Uzzi, 2000) that can be exchanged and mutually deployed. Quite often, these

relationships develop over time and it is the VCs propensity of accelerating the use and

implementation of relationships (to hasten a successful exit) that helps the entrepreneur to realize

high speed to market. This knowledge is also impacted by certain elements of know-what related

to cultural knowledge, which may prioritize relational over contractual ties.

The preceding suggests that VCs possess different types of knowledge that may be used

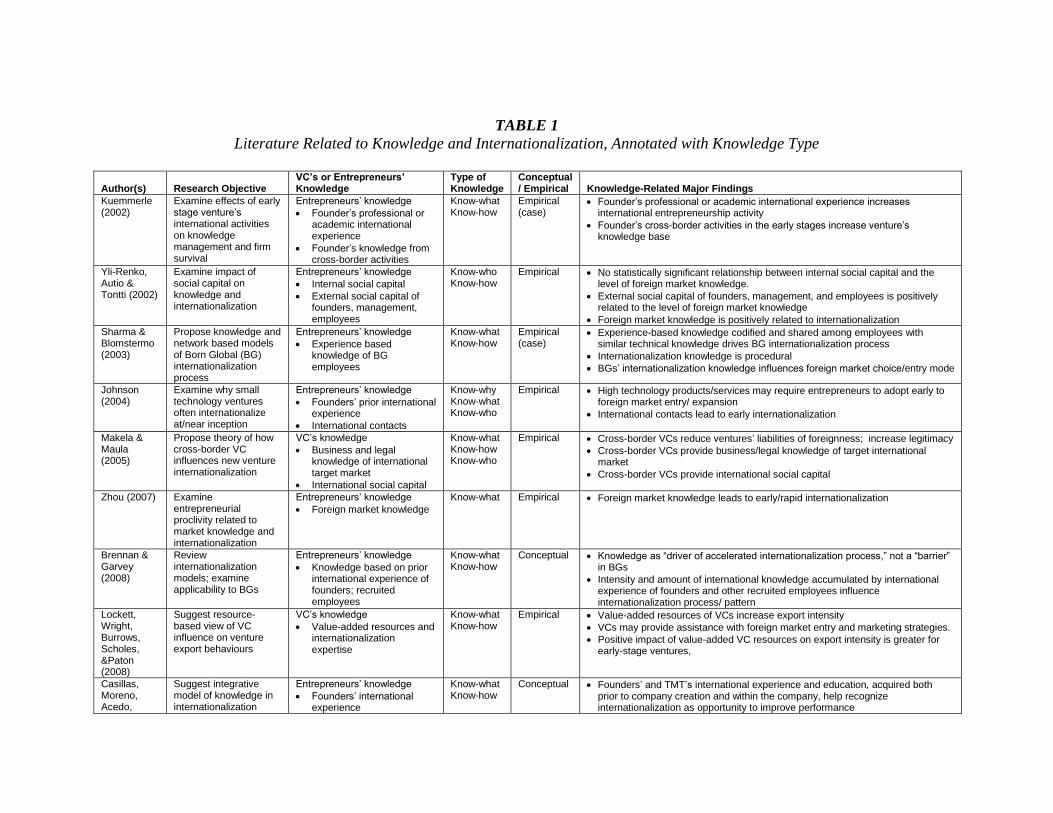

to aid the internationalization process of ventures in which they invest. Table 1 provides a

summary of different knowledge types found in the internationalization literature.

--------------------------------

Insert Table 1 about here

--------------------------------

13

PROPOSITIONS

Much of the research investigating new venture internationalization is built around the

assumption that the entrepreneur is responsible for providing knowledge and the venture

capitalist is responsible for providing funds. While this reduced role of the venture capitalist has

been recently challenged, investigations of the complementarity of internationalization

knowledge of entrepreneurs and venture capitalists are few, and none exist which “unbundles”

knowledge into its various types. We analyze this dyadic knowledge relationship by adopting an

ambidexterity perspective that examines the balance of conflicting activities or knowledge

complementarity (e.g. Raisch & Birkinshaw, 2008; Simsek, Heavey, Veiga & Souder, 2009). On

the individual level, ambidexterity is related to managers engaging in seemingly conflicting

tasks, either sequentially or simultaneously (Mom, van den Bosch & Volberda, 2009). Here,

ambidexterity refers to combinations of knowledge from two different, and sometimes

conflicting, sources. We examine the dominant source for different types of knowledge and

consider interplays between different types of knowledge that entrepreneurs and VCs possess

and their effect on venture internationalization. Relevant internal knowledge may be substituted

by external venture capitalist knowledge. This, in turn, may impact the governance structure of

the venture as VCs may use knowledge to take more active roles in ventures, potentially to the

detriment of internal knowledge development. On the other hand, the different types and sources

of knowledge may be reinforcing, so that combining them could enhance the venture‟s

internationalization through the generation of a larger pool of knowledge that may be leveraged

(Cao, Gedajlovic & Zheng, 2009).

Entrepreneurs as Dominant Source of Knowledge

Know-Why. Entrepreneurs typically first utilize their own knowledge, since it is their own

idea(s) that gave rise to the venture‟s formation, while they may search for knowledge from

14

external stakeholders. Know-why is the very reason for the existence of the venture and why the

founders rapidly adopt an international strategy. It relates the founders‟ interest and conviction in

foreign business as a viable and valuable undertaking. Thus, entrepreneurs generally possess

know-why and develop this knowledge further before advancing with the services of an investor.

Subsequently, the knowledge of the venture capitalist may serve to reduce the uncertainty

relating to the internationalization strategy, as entrepreneurs‟ may not have a sufficient overview

on how the „big picture‟ could work abroad and why internationalization will provide value.

Early internationalization often results in lower survival rates than later internationalization

(Sapienza et al., 2006) as resource endowments are limited and INVs face liabilities of newness

(Stinchcombe, 1965) and liabilities of foreignness (Zaheer, 1995). As wider scope know-why of

the venture capitalist complements entrepreneurs‟ know-why, a new venture‟s

internationalization process may be facilitated. In making use of the venture capitalist‟s know-

why from previous INV involvement, the process of early internationalization may be subjected

to tests of relevance (i.e., the likelihood of success abroad) and stimulated with the VC‟s support.

Complementary know-why can enhance strategies, increase efficiency and decrease agency-

related issues. Building on these insights, we propose:

P1a: The complementarity of know-why between the entrepreneur and the VC is positively

related to the speed of INV internationalization.

P1b: The complementarity of know-why between the entrepreneur and the VC is positively

related to INV international survival.

Know-what. Know-what is closely related to know-why, and is the easiest to acquire as it

normally exists in codified form and is thus more accessible. Through entrepreneurial

opportunity seeking activities (Stevenson & Jarillo, 1990) are linked to the entrepreneur‟s core

competencies, knowledge about potential demand in foreign markets can be acquired from

15

market research agencies and cost figures can be drawn from public sources. Entrepreneurs‟

know-what from their experience in domestic markets or their international experience may

increase absorptive capacity (Cohen & Levinthal, 1990), facilitating the integration of VC

knowledge. However, if the complementarity of know-what between the entrepreneur and the

VC is too low, knowledge integration may be impeded due to a lack of shared routines and

mutual understanding. Likewise, if the VC‟s know-what is contradictory to the entrepreneur‟s

know-what, different interpretations may lead to different views of the know-why, leading to

dissonance and little contribution to venture internationalization.

P2a: The complementarity of know-what between the entrepreneur and the VC is positively

related to the speed of INV internationalization.

P2b: The complementarity of know-what between the entrepreneur and the VC is positively

related to INV international survival.

Venture Capitalists as Dominant Source of Knowledge

The dominance of the investor‟s role concerning know-who and know-how underscores

their role as tacit knowledge brokers (Zook, 2004). In this view, it is the difficulty in acquiring

knowledge that makes it a key strategic resource for the entrepreneur. Its tacitness, stickiness and

local nature permit venture capitalists to act as catalysts for internationalization.

Know-who. During the early phase of the venture‟s formation and internationalization,

entrepreneurs particularly need to mobilize social resources because of liabilities due to size, lack

of foreign market knowledge and newness (Sharman, Gray & Yan, 1991). While entrepreneurs

may have selective personal relationships, VCs‟ membership in valuable networks and their

imperfectly imitable knowledge and experience (Maula et al., 2005) can be invaluable in

facilitating new venture internationalization. Indeed, differences in social networks that VCs

provide in their roles as “relationship investors” (Fried & Hisrich, 1995) may give rise to

16

different value-adding services and attract local and foreign customers, key executives and

partners from countries abroad. Venture capitalists also aid in identifying and hiring key

executives in foreign markets to facilitate growth (Sapienza, Manigart & Vermeir, 1996).

Knowledge sharing, particularly cross-culturally, is less likely to occur in the absence of

insider trust relationships (Hutchings & Michailova, 2006). Research shows that changes in TMT

composition are key factors influencing incrementally internationalizing companies to change

strategies and embark on rapid internationalization (Bell, McNaughton, Young & Crick, 2003).

Venture capitalists who serve on portfolio company boards may have prior international

experience that increases awareness of foreign opportunities, expands entrepreneurs‟ networks,

and accelerates internationalization (Bloodgood et al., 1996).

P3a: The complementarity of know-who between the entrepreneur and the VC is positively

related to the speed of INV internationalization.

P3b: The complementarity of know-who between the entrepreneur and the VC is positively

related to INV international survival.

Know-how. As with know-who, VCs may represent a dominant source of INV‟s know-how,

which may include the intricate routines that help a venture to internationalize and better cope

with liabilities of foreignness. Although venture capitalists act to decrease the information

asymmetries between entrepreneurs and investors, they rarely possess all the technical and

market knowledge of the entrepreneur. Yet, VCs may possess know-how that entrepreneurs

often do not have. Closely linked to their role as investor, VCs have knowledge on how to best

raise additional financing, how to signal legitimacy to the market and to relevant stakeholders,

and how to collect and interpret strategic information (Pinch & Sunley, 2009). This knowledge,

often referred to as internationalization capabilities, supports the maintenance of efficiently

operating management procedures abroad and is related “to the ability of the firm to organize so

17

as to function competitively in different contexts” (Tallman & Fadmore-Lindquist, 2002: 120).

Because INVs need these critical capabilities that take their time to develop, they may acquire

them via vicarious learning, since know-how needed to build these capabilities are mainly tacit

(Gioa & Manz, 1985). Even though time compression diseconomies (Dierickx & Cool, 1989)

cannot be completely overcome, new venture internationalization can be accelerated by tapping

the VC‟s know-how.

P4a: The complementarity of know-how between the entrepreneur and the VC is positively

related to the speed of INV internationalization.

P4b: The complementarity of know-how between the entrepreneur and the VC is positively

related to INV international survival.

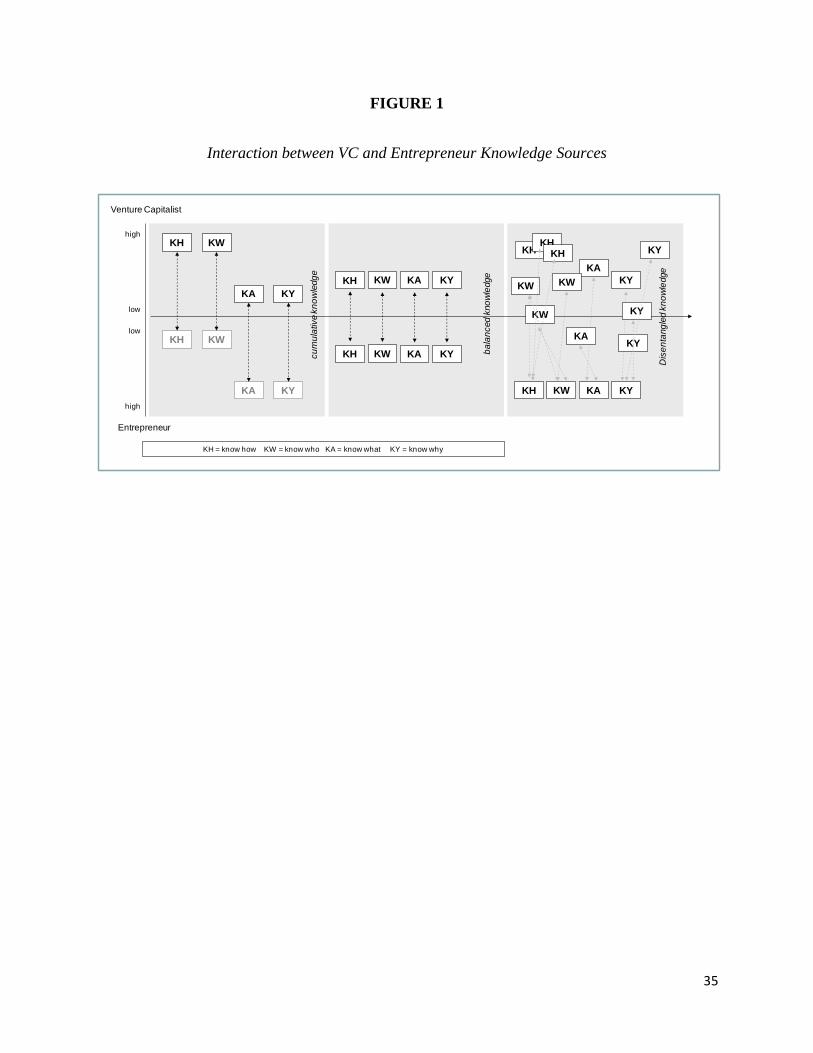

Knowledge Interaction between Entrepreneur and Venture Capitalist

While the general complementarity of knowledge is seen as a driver of increasing survival it may

not be equally supportive of foreign growth rates. When companies continuously maintain a high

speed in market entry, they explore a variety of options but lack the time to consolidate previous

experience and knowledge. Thereby, entrepreneurs may become too dependent on VC

knowledge. We argue in the following section that the relative magnitude of incorporated

knowledge provided by either the VC or the entrepreneur is subject to change if a company

wants to increase both elements of its internationalization performance, i.e., survival and growth.

We focus on potential substitution effects of dyadic knowledge, as different knowledge

configurations may differentially influence internationalization performance. The literature often

refers to different phases of the investor-entrepreneur relationship, although a focus on

internationalization is largely missing. First, VCs have to deal with usually talented but

inexperienced entrepreneurs (Bygrave & Timmons, 1992) and need to share critical knowledge

so as to improve the venture‟s initial survival chances. In doing so, VCs may take on strategic

18

and interpersonal coaching roles (Sapienza et al., 1996). Second, entrepreneurs learn through

both experiential learning and vicarious learning from the VC and their environment, and

upgrade their knowledge portfolio. Here, they can make optimal use of mutual knowledge

exchange given increasing knowledge overlap and relational quality improvements (De Clercq &

Sapienza, 2001). The last phase relates to VCs exit expectations (nominally 5-7 years post

investment) to time an exit when market conditions are most favourable (Gompers & Lerner,

1999). This focus on the timing and conditions that affect exit performance (know-how)

enhances their knowledge of the timing of certain critical actions of portfolio companies but

reduces their input in terms of other critical knowledge resources. Indeed, it is in the interest of

the entrepreneurs to further liberate themselves from the shackles of VC-knowledge dominance

and instead tap all other sources of available knowledge to enrich their own portfolio. These

three stages of the new venture internationalization process can be related to the types of

knowledge as introduced above (Figure 1).

--------------------------------

Insert Figure 1 about here

--------------------------------

Cumulative knowledge

In the first phase, entrepreneurial and VC knowledge are differentially linked. Entrepreneurs

dominate know-why and know-what whereas VCs have a driving role in providing know-who

and know-how. While this perspective has some support in the literature (Maula et al., 2005;

Politis, 2008), insights into how these knowledge components may be combined have remained

scarce. If, for instance, „higher‟ knowledge input of one of the partners is generally more

desirable, do missing knowledge components compensate or cannibalize each other? More

insight to this question can be drawn from referring to the literature on organizational

ambidexterity, which distinguishes between balanced or combined outputs of activities (Cao et

19

al., 2009). The combined dimension (CD) refers to the additively or multiplicatively cumulated

magnitude of activities, or knowledge types in this case. It has been argued that CD enhances a

company‟s performance through the generation of a greater pool of complementary knowledge.

Indeed, VCs‟ knowledge concerning know-how and know-who can support what the

entrepreneur already knows. In turn, entrepreneurial command of know-what and know-why

may elicit additive VC knowledge, providing a richer, more coherent and more complete

knowledge portfolio. Thus, each knowledge component, irrespective of source, may leverage the

effects of others. It has also been argued that a company will become more capable of initiating

various reconfigurations of already absorbed knowledge (Kogut & Zander, 1992), which is

especially pertinent for INVs that need to adjust their internationalization trajectories and

resource base over time. This need typically manifests itself early in a new venture‟s

internationalization process, when critical performance output often relates to survival rather

than growth and cumulatively available knowledge (Delios & Beamish, 2001). Consequently, we

propose the following:

P5: INVs that have a high combined magnitude, i.e., high levels of all types of knowledge

sources, have higher survival rates in the early phases than those who do not.

Balanced knowledge

In the second phase of VC-entrepreneur knowledge interaction, initial relationship and mutual

knowledge-building and sharing have already started. Building personal relationships between

VCs and entrepreneurs is vital to the ongoing growth of the INV as these act as channels for

knowledge dissemination (Powell, Koput, Boiw & Smith-Doerr, 2002). Entrepreneurs can make

fuller use of the VC‟s value-adding capabilities if they build sufficient knowledge receptivity

and increase knowledge, thereby strengthening their absorptive capacity “to better recognize the

value of new, external information, assimilate it, and apply it to commercial ends” (Cohen &

20

Levinthal, 1990: 128). On the individual level, the cognitive basis of an individual‟s capacity is

related to prior knowledge and related backgrounds. The importance of close interactions among

experienced entrepreneurs, venture capitalists, and other experts is underscored by integrative

mechanisms for combining relevant knowledge from various networks to steer research and

commercialization (Collinson & Gregson, 2003). In linking the absorptive capacity of

entrepreneurs with the balanced dimension (BD) of ambidexterity, we arrive at a variety of new

insights. A balanced view of knowledge sources implies that a closer match in the relative

magnitude contributes to the INV‟s performance through higher absorptive capacity that

facilitates the integration of VC knowledge and more structured control based on similar

knowledge capacities. A great imbalance in this phase may put both the investor‟s and the

entrepreneur‟s objectives at risk as the former wants to obtain rapid returns from

internationalizing and the latter wants to build a sustainable and independent business, which

requires high growth rates. When the knowledge input of the investor exceeds that of the

entrepreneur in all knowledge types, independence may not be advancing. In turn, when the

entrepreneur‟s knowledge exceeds that of the investor in all categories, VCs may be able to add

little value beyond financial capital, become less involved and limit access to other potential

investors, endangering growth when early investments do not initially yield profitability (Zott,

2003). Thus, we propose the following:

P6: INVs that have higher balanced availability of all knowledge types vis-à-vis their

investors have higher growth rates in the expansion phase than those who have a lower

availability.

Disentangled knowledge

In the later stage of the VC-entrepreneur relationship, knowledge interaction reaches again a

novel constellation, which is driven by mutually diverging goals. The investor has shared most of

21

the available, relevant knowledge and is seeking a return from exit. The entrepreneur wants to

gain more independence and improve his position in the knowledge dyad. These opposing

objectives make it rather unlikely that knowledge is further developed in a cumulative or

balanced way as in the previous stages. More so, the same bonds that facilitated knowledge

sharing in earlier stages may now turn into a filter for information and perception, resulting in a

„cognitive lock-in‟ or „relational inertia‟ (Gargiulo & Benassi, 2000) with potentially blinding

effects. As the extent to which the INV managers can learn from their ongoing international

operations may be influenced directly by the diversity of knowledge acquired before, the

successful completion of the two previous knowledge exchange stages may be important. Even

more so in the later stage of interaction, it becomes vital for the entrepreneur to tap different and

various sources of knowledge to decrease dependency. At the same time, more diverse

knowledge sources help to increase the strengths of weak ties (Granovetter, 1985) that may not

have existed in the close relationship with the VC who now wants to move on to other projects.

Thus, we formally propose:

P7: INVs that have disentangled all knowledge types from VCs have both higher survival

and higher growth rates in the late phases than those who have not.

In summary, the level, type and source of knowledge possessed by the members of a new

venture/investor dyad affect the internationalization, performance, and survival of new ventures.

DISCUSSION

While the literature on the role of knowledge in the internationalization process is growing,

much of it focuses on knowledge acquisition or internalization (e.g. Knight & Liesch, 2002).

Learning is a key element in such literatures, and the “learning advantage of newness” (Sapienza,

Autio, George & Zahra, 2006) is a key consideration for why international new ventures thrive.

22

Yet there is a void in the discussion as to what type of knowledge is learned in these ventures,

and who contributes to the knowledge upon which the learning is based.

The use of a typology of knowledge based on the OECD (2000) framework permits a fine

grained examination of the nature of the knowledge learned and its value to the

internationalization processes. It further helps to analyze which type of knowledge may be more

important in individual stages of the interaction with the VC for INVs as well as if and how they

may be complements or substitutes (Fernhaber et al., 2009).

The examination of the knowledge types possessed by two of the main actors in the

internationalization of new ventures, the entrepreneur and the venture capitalist, extends the

work done by many on the overall value of venture capital (e.g. Sapienza, 1992) and its value to

venture internationalization (e.g., Fernhaber & McDougall-Covin, 2009; Maula et al., 2005;

Maula & Murray, 2002). While it is clear that venture capital provides value over and above that

of the financial capital invested, and that the value is often bound up in the advice provided to

the new venture, the knowledge intrinsic to this advice has been largely ignored, as has the fact

that knowledge taken in by a new venture must first be absorbed by a person (e.g., the

entrepreneur, founder or TMT member) before it may be used on the company‟s behalf. Thus

the nature of the knowledge, the background of both the sender and receiver and the absorptive

capacity of the receiver are most important.

This model and subsequent empirical investigation of the propositions in this paper have a

number of implications for research. They will help to further strengthen the evidence on the

value that VCs provide to the ventures. They also permit analyses by using more detailed data on

knowledge related to internationalization, which may impact established companies in addition

to nascent ventures.

23

The framework may also help to analyze knowledge related to internationalization under

different contingencies. For example, are different types of knowledge more or less important

based on psychic or geographic distance? Are different types of knowledge configurations

between the investor and entrepreneur more valuable when entering transition economies?

Further, as we concentrated on individual knowledge, it may be worthwhile to investigate how

individual knowledge translates into social knowledge and how the interplay between tacit and

explicit knowledge components is managed by the venture.

For practitioners, a clearer understanding of venture capitalists‟ knowledge and its

prerequisites may make the selection process more informed. While receipt of VC is still rare,

those who do receive it generally have multiple offers from which to choose. Thus, an

entrepreneur may more carefully screen potential investors for the type of knowledge they hold

that is most relevant to internationalization based on the entrepreneur‟s knowledge regarding

foreign markets and their international objectives. This may avoid potential subsequent power

struggles if both the entrepreneur and investor possess inconsistent knowledge of the same type –

a situation in which venture capitalists‟ knowledge may be detrimental. This research may also

help to sensitize the venture capitalist to his role as a knowledge contributor, and not just an

advice-giver, fostering more constructive dialog. Additionally, as the VC industry is

internationalizing, venture capitalists may need to take into account the knowledge stock of

potential foreign VC alliance partners to better support internationalization of the portfolio

companies in which they invest.

This paper presents a conceptual model of knowledge of investors and entrepreneurs related

to internationalization. While its lack of empirical analyses may be considered a limitation, it

has permitted us to more patiently examine this important gap in the literature while building a

foundation for subsequent empirical analysis. It is clear that our focus on individual‟s knowledge

24

and not on the venture‟s embedded knowledge and capabilities may cause us to ignore dynamic

aspects of knowledge internalization and capabilities development necessary for

internationalization. Finally, while the attention to the value of networks in new venture

internationalization is highlighted in the literature, our seeming neglect of networks other than

knowing-who again permits us to look at the knowledge aspect of the network and not the

network aspect of the knowledge mainly presented in the network literature.

REFERENCES

Alvarez, S.A., Busenitz, L.W., 2001. The entrepreneurship of resource-based theory. Journal of

Management 27(6), 755-775.

Anand, V., Glick, W.H., Manz, C.C., 2002. Thriving on the knowledge of outsiders: Tapping

organizational social capital. The Academy of Management Executive 16(1), 87–101.

Andersen, O., 1993. On the internationalization process of firms: A critical analysis. Journal of

International Business Studies 24(2), 209-231.

Anderson, E., Gatignon, H., 1986. Modes of foreign entry: A transaction cost analysis and

propositions. Journal of International Business Studies 17, 1–26.

Anderson, J.R., 1983. The Architecture of Cognition. Harvard University Press, Cambridge, MA.

Andersson, S. 2000. The internationalization of the firm from an entrepreneurial perspective.

International Studies of Management and Organization, 30(1), 63-92.

Autio, E., Sapienza, H.J., Almeida, J., 2000. Effects of age at entry, knowledge intensity, and

imitability on international growth. Academy of Management Journal 43(5), 909–924.

Baum, J.A., Silverman, B.S., 2004. Picking winners or building them? Alliance, intellectual, and

human capital as selection criteria in venture financing and performance of biotechnology

startups. Journal of Business Venturing 19(3), 411–436.

25

Becker, G.S., 1964. Human Capital: A Theoretical Analysis with Special Reference to

Education. National Bureau for Economic Research, Columbia University Press, New

York and London.

Bell, J., McNaughton, R.B., Young, S., Crick, D., 2003. Towards an integrative model of small

firm internationalization. Journal of International Entrepreneurship 1(4), 339-364.

Bertoin-Antal, A., 2000. Types of knowledge gained by expatriate managers. Journal of General

Management 26(2), 32-51.

Bloodgood, J.M., Sapienza, H.J., Almeida, J.G., 1996. The Internationalization of new

high-potential US ventures: Antecedents and outcomes. Entrepreneurship: Theory and

Practice 20(4), 61-76.

Brennan, L., Garvey, D., 2009. The role of knowledge in internationalization. Research in

International Business and Finance 23(2), 120–133.

Burt, R.S., 1992. Structural Holes. Harvard University Press, Cambridge, MA.

Bygrave, W.D., Timmons, J.A., 1992. Venture Capital at the Crossroads. Harvard Business

School Press, Boston, MA.

Cao, Q., Gedajlovic, E., Zhang, H., 2009. Unpacking organizational ambidexterity: Dimensions,

contingencies, and synergistic effects. Organization Science 20(4), 781–796.

Carpenter, M.A., Pollock, T.G., Leary, M.M., 2003. Testing a model of reasoned risk-taking:

Governance, the experience of principals and agents, and global strategy in high-

technology IPO firms. Strategic Management Journal 24(9), 803–820.

Casillas, J.C., Moreno, A.M., Acedo, F J., Gallego, M.A., Ramos, E., 2009. An integrative model

of the role of knowledge in the internationalization process. Journal of World Business

44(3), 311–322.

26

Caves, R.E., 1996. Multinational Enterprise and Economic Analysis. Cambridge University

Press, Cambridge, MA.

Chung, W., Alcácer, J., 2002. Knowledge seeking and location choice of foreign direct

investment in the United States. Management Science 48(12), 1534–1554.

Cohen, W.M., Levinthal, D.A., 1990. Absorptive capacity: A new perspective on learning and

innovation. Administrative Science Quarterly 35(1), 128-152.

Collinson, S., Gregson, G., 2003. Knowledge networks for new technology-based firms: an

international comparison of local entrepreneurship promotion. R&D Management 33(2),

189-208.

Colombo, M.G., Grilli, L., 2005. Founders‟ human capital and the growth of new technology-

based firms: A competence-based view. Research Policy 34(6), 795–816.

Cooper, A., Gimeno-Gascón, F., Woo, C.Y., 1997. Initial human and financial capital as

predictors of new venture performance. The Journal of Private Equity 1(2), 13–30.

Coviello, N. E., Munro, H.J., 1995. Growing the entrepreneurial firm. European Journal of

Marketing 29(7), 49–61.

Daily, C.M., Certo, S.T., Dalton, D.R., 2000. International experience in the executive suite: the

path to prosperity? Strategic Management Journal 21(4), 515–523.

De Clercq, D., Sapienza, H.J., Crijns, H., 2005. The internationalization of small and medium-

sized firms: The role of organizational learning effort and entrepreneurial orientation.

Small Business Economics 24(4), 409–419.

De Clercq, D., Sapienza, H.J., 2001. The creation of relational rents in venture capital

entrepreneurial dyads. Venture Captial 3, 107-127.

27

Delios, A., Beamish, P.W., 2001. Survival and profitability: The roles of experience and

intangible assets in foreign subsidiary performance. The Academy of Management

Journal 44(5), 1028–1038.

Dierickx, I., Cool, K., 1989. Asset stock accumulation and sustainability and competitive

advantage. Management Science 35, 1504-1511.

Eisenhardt, K.M., Schoonhoven, C.B., 1990. Organizational growth: Linking founding team,

strategy, environment, and growth among US semiconductor ventures, 1978-1988.

Administrative Science Quarterly 35(3), 504–529.

Eisenhardt, K.M., Schoonhoven, C.B., 1996. Resource-based view of strategic alliance

formation: Strategic and social effects in entrepreneurial firms. Organization Science

7(2), 136–150.

Eriksson, K., Johanson, J., Majkgard, A., Sharma, D., 1997. Experiential knowledge and cost in

the internationalization process. Journal of International Business Studies 28(2), 337-360.

Eriksson, K., Majkgard, A., Sharma, D.D., 2000. Path dependence and knowledge development

in the internationalization process. Management International Review 40(4), 307–328.

Fernandez-Ortiz, R., Lombardo, G.F., 2009. Influence of the capacities of top management on

the internationalization of SMEs. Entrepreneurship and Regional Development 21(2),

131–154.

Fernhaber, S.A., McDougall-Covin, P.P., 2009. Venture capitalists as catalysts to new venture

internationalization: The impact of their knowledge and reputation resources.

Entrepreneurship Theory and Practice 33(1), 277–295.

Fernhaber, S.A, McDougall-Covin, P.P., Shepherd, D.A. 2009. International entrepreneurship:

Leveraging internal and external knowledge. Strategic Entrepreneurship Journal 3(4),

297-320.

28

Forer, G., Haemming, M., 2007. Global Venture Capital Insights Report, Ernst and Young.

Freeman, S., Hutchings, K., Lazaris, M., Zyngier, S., 2009. A model of rapid knowledge

development: The smaller born-global firm. International Business Review 19(1), 70-84

Fried, V.H., Hisrich, R.D., 1995. The venture capitalist: A relationship investor. California

Management Review 37(2), 101-113.

Gargiulo, M., Benassi, M., 2000. Trapped in your own net? Network cohesion, structural holes,

and the adaption of social capital. Organization Science 11(2), 183-196.

George, G., Wiklund, J., Zahra, S.A., 2005. Ownership and the internationalization of small

firms. Journal of Management 31(2), 210-233.

Gioa, D.A., Manz, C.C., 1985. Linking cognition and behavior: A script processing

interpretation of vicarious learning. Academy of Management Review 10(3), 527-539.

Gompers, P.A., Lerner, J., 1999. The Venture Capital Cycle. The MIT Press, Cambridge, MA.

Granovetter, M., 1985. Economic action and social structure: the problem of embeddedness.

American Journal of Sociology 91, 481–510.

Harveston, P.D., Kedia, B.L., Davis, P.S., 2000. Internationalization of born global and gradual

globalizing firms: the impact of the manager. Advances in Competitiveness Research

8(1), 92–99.

Hellmann, T., Puri, M., 2002. Venture capital and the professionalization of start-up firms:

Empirical evidence. Journal of Finance 57(1), 169–197.

Hutchings, K., Michailova, S., 2006. The impact of group membership on knowledge sharing

in Russia and China. International Journal of Emerging Markets 1(1), 21–34.

Ibarra, H., 1990. Personal networks of women and minorities in management: A conceptual

Framework. Academy of Management Review 18(1), 56-87.

29

Javernick-Will, A.M., 2009. Organizational learning during internationalization: acquiring local

institutional knowledge. Construction Management and Economics 27(8), 783–797.

Johanson, J., Vahlne, J.E., 1977. The internationalization process of the firm-a model of

knowledge development and increasing foreign market commitments. Journal of

International Business Studies 8, 23–32.

Johanson, J., Wiedersheim-Paul, F., 1975. The internationalization of the firm – Four Swedish

cases. Journal of Management Studies 12(3), 305–323.

Johnson, J.E., 2004. Factors influencing the early internationalization of high technology start-

ups: US and UK evidence. Journal of International Entrepreneurship 2(1), 139–154.

Knight, G.A., Cavusgil, S.T., 2005. A taxonomy of born-global firms. Management International

Review 45(3), 15–35.

Knight, G.A., Liesch, P.W., 2002. Information internalisation in internationalising the firm.

Journal of Business Research 55(12), 981–995.

Knight, G., Madsen, T.K., Servais, P., 2004. An inquiry into born-global firms in Europe and the

USA. International Marketing Review 21(6), 645–665.

Kogut, B., Zander, U., 1992. Knowledge of the firm, combinative capabilities, and the

replication of technology. Organization science 3(3), 383–397.

Kuemmerle, W., 2002. Home base and knowledge management in international ventures. Journal

of Business Venturing 17(2), 99–122.

Kundu, S. K., Katz, J.A., 2003. Born-international SMEs: BI-level impacts of resources and

intentions. Small Business Economics 20(1), 25–47.

Lindsay, V., Chadee, D., Mattson, J., Johnston, R., Millett, B. 2003. Relationships, the role of

individuals and knowledge flows in the internationalisation of service firms. International

Journal of Service Industry Management 14(1), 7-35.

30

Lubatkin , M., Florin, J., Lane, P., 2001. Learning together and apart: A model of reciprocal

interfirm learning. Human Relations 54(10), 1353-1382.

Mäkelä, M., Maula, M., 2005. Cross-border venture capital and new venture internationalization:

An isomorphism perspective. Venture Capital 7(3), 227–257.

Maula, M., Autio, E., Murray, G., 2005. Corporate venture capitalists and independent venture

capitalists: What do they know, who do they know, and should entrepreneurs care?

Venture Capital 7, 3-21.

Maula, M., Murray, G.C., 2002. Corporate venture capital and the creation of US public

companies: the impact of sources of venture capital on the performance of portfolio

companies, in: Hitt, M.A., Amit, R., Lucrier, C., Nixon, R. (Eds.), Creating value:

Winners in the New Business Environment, Wiley-Blackwell, Oxford, pp.164–187.

McDougall, P., Shane, S., Oviatt, B., 1994. Explaining the formation of international new

ventures: The limits of theories from international business research. Journal of Business

Venturing 9(6), 469–487.

Moen, O., Servais, P., 2002. Born global or gradual global? Examining the export behavior of

small and medium-sized enterprises. Journal of International Marketing 10(3), 49–72.

Mom, T.J.M., van den Bosch, F.A.J., Volberda, H.W. 2009. Understanding variation in

managers' ambidexterity: Investigating direct and interaction effects of formal structural

and personal coordination mechanisms. Organization Science 20(4), 812-828.

Nguyen, T., Garrett, N., 2006. Internet-based knowledge internationalization and firm inter-

nationalization in transition markets. Advances in International Marketing 17, 369-394.

Nonaka, I., 1994. A dynamic theory of organizational knowledge creation. Organization Science

5(1), 14–37.

31

Nonaka, I.A., Takeuchi, H.A., 1995. The Knowledge-Creating Company: How Japanese

Companies Create the Dynamics of Innovation. Oxford University Press, New York.

Nummela, N., Saarenketo, S., Puumalainen, K., 2004. A global mindset- a prerequisite for suc-

cessful internationalization? Canadian Journal of Administrative Sciences 21(1), 51–64.

OECD, 2000. Knowledge Management in the Learning Economy: Education and Skills. OECD.

Oviatt, B.M., McDougall, P.P., 1994. Toward a theory of international new ventures. Journal of

International Business Studies 25(1), 45-64.

Peili, Y., Zhonghong, F. 2006. Knowledge stickiness in the process of integrated innovation:

Performance and countermeasures. IAMOT-conference, 2006.

Pinch, S., Sunley, P., 2009. Understanding the role of venture capitalists in knowledge

dissemination in high-technology agglomerations: a case study of the University of

Southampton spin-off cluster. Venture Capital 11(4), 311-333.

Pla-Barber, J., Escriba-Esteve, A., 2006. Accelerated internationalisation: evidence from a late

investor country. International Marketing Review 23(3), 255–278.

Polanyi, M., 1966. The Tacit Dimension, Doubleday, Garden City, NY.

Politis, D., 2008. Business angels and value added: what do we know and where do we go?

Venture Capital 10(2), 127-147.

Powell, W.W., Koput, K., Boiw, J., Smith-Doerr, L., 2002. The spatial clustering of science and

capital: Accounting for biotech firm-venture capital relationships. Regional Studies 36,

291-305.

Prange, C., Verdier, S., 2011. Dynamic capabilities, internationalization processes, and

performance. Journal of World Business, forthcoming.

Raisch, S., and Birkinshaw, J. 2008. Organizational ambidexterity: Antecedents, outcomes, and

moderators. Journal of Management, 34(3): 375.

32

Reuber, A.R., Fischer, E., 1997. The influence of the management team's international

experience on the internationalization behaviors of SMEs. Journal of International

Business Studies 28(4), 807-825.

Rosenstein, J., 1988. The board and strategy: Venture capital and high technology. Journal of

Business Venturing 3(2), 159-170.

Rosenstein, J., Bruno, A.V., Bygrave, W.D., Taylor, N.T., 1993. The CEO, venture capitalists,

and the board. Journal of Business Venturing 8(2), 99-113.

Ruzzier, M., Hisrich, R.D., Antoncic, B., 2006. SME internationalization research: past, present,

and future. Journal of Small Business and Enterprise Development 13(4), 476-497.

Sackman, S.A., 1992. Culture and subcultures: An analysis of organizational knowledge.

Administrative Science Quarterly 37(1), 140-161.

Sapienza, H.J., 1992. When do venture capitalists add value? Journal of Business Venturing 7(1),

9–27.

Sapienza, H.J., Autio, E., George, G., Zahra, S.A., 2006. A capabilities perspective on the effects

of early internationalization on firm survival and growth. Academy of Management

Review 31(4), 914-933.

Sapienza, H.J., Manigart, S., Vermeir, W., 1996. Venture capitalist governance and value added

in four countries. Journal of Business Venturing 11(6), 439-469.

Schwens, C., Kabst, R., 2009. How early opposed to late internationalizers learn: Experience of

others and paradigms of interpretation. International Business Review 18(5), 509–522.

Sharma, D.D., Blomstermo, A., 2003. The internationalization process of born globals: a

network view. International Business Review 12(6), 739–753.

33

Sharman, M., Gray, B., Yan, A., 1991. The context of organizational collaboration in the

garment industry: an institutional perspective. Journal of Applied Behavioral Science 27,

181-208.

Shi, Y.N., Sia, C.L., Banerjee, P., Luo, C., Tan, B.C.Y., Chen, H., 2009. Choice of knowledge

source in situations of equivocality: Impact of cultural traits. Pacific Asia Conference on

Information Systems. Proceedings, 2009. City University Hongkong.

Simsek, Z., Heavey, C.B., Veiga, J.F., Souder, D., 2009. A typology for aligning organizational

ambidexterity's conceptualizations, antecedents, and outcomes. Journal of Management

Studies 46(5), 864–894.

Smith, G., 2001. How early stage entrepreneurs evaluate venture capitalists. The Journal of

Private Equity 4(2), 33-45.

Stevenson, H.H, Jarillo, J.C., 1990. A paradigm of entrepreneurship: Entrepreneurial

management. Strategic Management Journal 11(4), 17-27.

Stinchcombe, A.L., 1965. Social structure and organizations, in: Marsh, J.G. (Eds.), Handbook

of Organizations. Rand McNally, Chicago, pp. 142–193.

Tallman, S., Fladmore-Lindquist, K., 2002. Effects of international diversity and product

diversity on the performance of multinational firms. Academy of Management Journal

39, 179-196.

Uzzi, B., 2000. The sources and consequences of embeddedness for the economic performance

of organizations. American Sociological Review 61, 674-698.

Vermeulen, F., Barkema, H., 2002. Pace, rhythm, and scope: Process dependence in building a

profitable multinational corporation. Strategic Management Journal 23, 637–653.

34

Wright, M., Pruthi, S., Lockett, A., 2005. International venture capital research: From cross-

country comparisons to crossing borders. International Journal of Management Reviews

7(3), 135-165.

Yli-Renko, H., Autio, E., Tontti, V., 2002. Social capital, knowledge, and the international

growth of technology-based new firms. International Business Review 11(3), 279–304.

Zaheer, S., 1995. Overcoming the liability of foreignness. The Academy of Management

Journal 38(2), 341–363.

Zahra, S., 2005. A theory of international new ventures: A decade of research. Journal of

International Business Studies 36(1), 20–29.

Zahra, S., Hayton, J., 2008. The effect of international venturing on firm performance: The mod-

erating influence of absorptive capacity. Journal of Business Venturing 23(2), 195–220.

Zahra, S., Matherne, B., Carleton, J., 2003. Technological resource leveraging and the inter-

nationalisation of new ventures. Journal of International Entrepreneurship 1(2), 163–186.

Zahra, S., Ucbasaran, D., Newey, L., 2009. Social knowledge and SMEs innovative gains from

internationalization. European Management Review 6(2), 81–93.

Zhou, L., 2007. The effects of entrepreneurial proclivity and foreign market knowledge on early

internationalization. Journal of World Business 42(3), 281–293.

Zook, M.A., 2004. The knowledge brokers: Venture capitalists, tacit knowledge and regional

development. International Journal of Urban and Regional Research 28(3), 621-41.

Zott, C., 2003. Dynamic capabilities and the emergence of intraindustry differential firm per-

formance. Insights from a simulation study. Strategic Management Journal, 24, 97-125.

35

FIGURE 1

Interaction between VC and Entrepreneur Knowledge Sources

Venture Capitalist

Entrepreneur

cu

mu

lative k

no

wle

dg

e

ba

lan

ced k

no

wle

dge

high

high

low

low

KH KW

KH KW

KA KY

KA KY

KH = know how KW = know who KA = know what KY = know why

KH

KH

KW

KW

KA

KA

KY

KY

Dis

en

tang

led

kn

ow

ledge

KH

KH

KW

KW

KA

KA

KY

KY

KHKH

KW

KW

KA

KY

KY

KY

TABLE 1

Literature Related to Knowledge and Internationalization, Annotated with Knowledge Type

Author(s) Research Objective VC’s or Entrepreneurs’ Knowledge

Type of Knowledge

Conceptual / Empirical Knowledge-Related Major Findings

Kuemmerle (2002)

Examine effects of early stage venture’s international activities on knowledge management and firm survival

Entrepreneurs’ knowledge

Founder’s professional or academic international experience

Founder’s knowledge from cross-border activities

Know-what Know-how

Empirical (case)

Founder’s professional or academic international experience increases international entrepreneurship activity

Founder’s cross-border activities in the early stages increase venture’s knowledge base

Yli-Renko, Autio & Tontti (2002)

Examine impact of social capital on knowledge and internationalization

Entrepreneurs’ knowledge

Internal social capital

External social capital of founders, management, employees

Know-who Know-how

Empirical No statistically significant relationship between internal social capital and the level of foreign market knowledge.

External social capital of founders, management, and employees is positively related to the level of foreign market knowledge

Foreign market knowledge is positively related to internationalization

Sharma & Blomstermo (2003)

Propose knowledge and network based models of Born Global (BG) internationalization process

Entrepreneurs’ knowledge

Experience based knowledge of BG employees

Know-what Know-how

Empirical (case)

Experience-based knowledge codified and shared among employees with similar technical knowledge drives BG internationalization process

Internationalization knowledge is procedural

BGs’ internationalization knowledge influences foreign market choice/entry mode

Johnson (2004)

Examine why small technology ventures often internationalize at/near inception

Entrepreneurs’ knowledge

Founders’ prior international experience

International contacts

Know-why Know-what Know-who

Empirical High technology products/services may require entrepreneurs to adopt early to foreign market entry/ expansion

International contacts lead to early internationalization

Makela & Maula (2005)

Propose theory of how cross-border VC influences new venture internationalization

VC’s knowledge

Business and legal knowledge of international target market

International social capital

Know-what Know-how Know-who

Empirical Cross-border VCs reduce ventures’ liabilities of foreignness; increase legitimacy

Cross-border VCs provide business/legal knowledge of target international market

Cross-border VCs provide international social capital

Zhou (2007) Examine entrepreneurial proclivity related to market knowledge and internationalization

Entrepreneurs’ knowledge

Foreign market knowledge

Know-what Empirical Foreign market knowledge leads to early/rapid internationalization

Brennan & Garvey (2008)

Review internationalization models; examine applicability to BGs

Entrepreneurs’ knowledge

Knowledge based on prior international experience of founders; recruited employees

Know-what Know-how

Conceptual Knowledge as “driver of accelerated internationalization process,” not a “barrier” in BGs

Intensity and amount of international knowledge accumulated by international experience of founders and other recruited employees influence internationalization process/ pattern

Lockett, Wright, Burrows, Scholes, &Paton (2008)

Suggest resource-based view of VC influence on venture export behaviours

VC’s knowledge

Value-added resources and internationalization expertise

Know-what Know-how

Empirical Value-added resources of VCs increase export intensity

VCs may provide assistance with foreign market entry and marketing strategies.

Positive impact of value-added VC resources on export intensity is greater for early-stage ventures,

Casillas, Moreno, Acedo,

Suggest integrative model of knowledge in internationalization

Entrepreneurs’ knowledge

Founders’ international experience

Know-what Know-how

Conceptual Founders’ and TMT’s international experience and education, acquired both prior to company creation and within the company, help recognize internationalization as opportunity to improve performance

37

Author(s) Research Objective VC’s or Entrepreneurs’ Knowledge

Type of Knowledge

Conceptual / Empirical Knowledge-Related Major Findings

Gallego &Ramos (2009)

behaviour Company-level knowledge generated from individual-level knowledge

Degree to which new knowledge is compatible with prior knowledge is positively related to speed of foreign market entry

Firm’s degree of internationalization positively related to rate of international learning and to speed of its internationalization process

Fernandez-Ortiz &Lombardo (2009)

Examine how TMT characteristics influence SME internationalizations

Entrepreneurs’ knowledge

Knowledge based on TMT prior international experience and foreign language ability

Know-what Know-how

Empirical SME TMT’s prior international experience positively influences level of international diversification

TMT’s foreign language knowledge positively influences level of international diversification

Fernhaber &McDougall-Covin (2009)

Examine role of VC as catalyst to new venture internationalization

VC’s knowledge

VC’s prior international experience

Know-what Know-how

Empirical VCs’ international knowledge positively influences new venture internationalization

The positive impact of VC international knowledge on new venture internationalization is greater when VC is reputable

“Vicariously exploited” VC knowledge by new ventures adds to venture’s resource base

Fernhaber, McDougall-Covin, &Shepherd (2009)

Examine sources and impact of internal and external sources of international knowledge for new ventures

VC’s knowledge

Prior international investments

Networking and human resources

Entrepreneur’s knowledge

TMT international experience

Know-what Know-how

Empirical Higher international knowledge of VCs is associated with more internationalization of ventures

The positive influence of VCs’ international knowledge on new venture internationalization is less for ventures with TMT with greater international knowledge

Freeman, Hutchings Lazaris, &Zyngier (2009)

Provides model for rapid knowledge development which better explains accelerated internationalization

Entrepreneurs’ knowledge

Social networks

Know-who

Conceptual BG managers can use both pre-existing and newly formed relationships to proactively develop new knowledge

Trust and time are required to build networks which facilitate tacit knowledge sharing and development of new knowledge

Javernick-Will (2009)

Suggest how firms acquire international knowledge using different sources and methods

Entrepreneurs’ knowledge

International regulative, normative, cultural-cognitive knowledge from pioneering, new hires, outside sources

Know-what Empirical International real estate developers, contractors, engineering firms acquire knowledge necessary for new international environment via pioneering, external relationships, local consultants

For acquiring regulative knowledge, local consultants are more important

For acquiring normative and cultural cognitive knowledge, pioneering and local hires are more important

Schwens &Kabst (2009)

Examine firm’s asset, TMT prior experience, and network as determinants of early internationalization

Entrepreneurs’ knowledge

Knowledge based on international experience of founders or key management

Know-what Know-how Know-who

Empirical Prior international experience of founders or key management positively influences early internationalization and decreases liability of foreignness

International network contacts of founders or key management positively influences early internationalization by reducing risk of opportunism and eases learning