Embed Size (px)

Citation preview

The impact of IFRS 8 ondisclosure practices of Jordanian

listed companiesGhassan H. Mardini, Louise Crawford and David M. Power

School of Business, University of Dundee, Dundee, UK

Abstract

Purpose – The purpose of this paper is to compare the segmental information disclosures ofJordanian companies under IFRS 8 for 2009 with disclosures under IAS 14R for 2008.Design/methodology/approach – A sample of 109 Jordanian companies is used in this research. Adisclosure index checklist was constructed to assess the segmental information provided by thesample companies. In particular, the checklist collected information about: the number of segmentsreported; the number and type of segmental items published; the geographic segment definitions(areas) used; and the identity of the chief operating decision maker (CODM).Findings – The results suggest that segmental disclosures under IFRS 8 have increased compared tothe information published under IAS 14R. There is an increase in the number of companies disclosingsegmental information while the number of business and geographic segments for which informationis provided rose under IFRS 8. Items required under the previous standard (IAS 14R) are still beingprovided in 2009, and the new segmental information required (if reviewed by the CODM) underIFRS 8 is also disclosed. As a result, the total number of segmental items disclosed increased.Moreover, a majority of companies identified the CODM as the chief executive officer.Research limitations/implications – This research highlights that the introduction of IFRS 8 hasbeen associated with more Jordanian companies now disclosing segmental information. However,factors other than IFRS 8 may have contributed to the increased disclosure; these are not considered inthe current paper.Originality/value – This research shows that IFRS 8 compliance amongst Jordanian first marketcompanies has resulted in an increase in the number of segments and items per segment disclosed.

Keywords Jordan, Disclosure, International standards, Financial reporting, IFRS 8,Segmental information

Paper type Research paper

1. IntroductionAs part of its convergence programme with the US Financial Accounting StandardBoard, the International Accounting Standards Board (IASB) issued InternationalFinancial Reporting Standard No. 8 (IFRS 8) “Operating Segments” in November 2006;this became effective for periods beginning on or after 1 January 2009 (IASB, 2006a).IFRS 8 converges with its US counterpart, Statement of Financial Accounting Standard(SFAS) No. 131[1], except for minor differences of interpretation and terminology toconform with other International Accounting Standards (IASs).

IFRS 8 supersedes the previous IAS: IAS 14 Revised (IAS 14R) “SegmentReporting” (IASB, 1997). IAS 14R defined reportable segments according to a two-tierapproach as described by Street and Nichols (2002). Companies had to select eitherbusiness class or geographic activities as their primary segments; the segment typenot selected for the primary segments was then used to identify the secondarysegments. Identifying segments required preparers to consider “the predominantsource and nature of risks and differing rates of return facing the entity” (IAS 14R,para 27). By contrast, the new standard (IFRS 8) requires segments to be identifiedin accordance with the management approach. Operating segments are to be identified

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2042-1168.htm

Journal of Accounting in Emerging

Economies

Vol. 2 No. 1, 2012

pp. 67-90

r Emerald Group Publishing Limited

2042-1168

DOI 10.1108/20421161211196139

67

Jordanian listedcompanies

on the basis of internal reports that are “regularly reviewed by the Chief OperatingDecision Maker (CODM) to make decisions about resources to be allocated to thesegment and assess its performance” (IFRS 8, para 5)[2]; there is no distinction betweenprimary and secondary segments under IFRS 8.

The core principle of IFRS 8 requires an entity to: “[y] disclose information toenable users of its financial statements to evaluate the nature and financial effectsof the business activities in which it engages and the economic environments in whichit operates” (IFRS 8, para 1). At the time of its adoption, a number of commentatorsin the UK expressed concerns about the possible reduction in the quality and quantityof segmental information that would be published under IFRS 8 (Financial ReportingReview Panel (FRRP), 2010; Crawford et al., 2010). In addition, concerns were alsoraised that the identity of the CODM was not specified, disclosure of geographicsegments was not mandated, and non-IFRS measurements were permitted forsegmental information (IASB, 2006b).

Jordan has adopted IASs since 1997; this long time span makes Jordan anappropriate country for researching the implementation of IFRS 8 since preparers andusers will already be familiar with other IASs[3]. Further, Jordan is an open economywith experience of international exports to many countries in different business areas;thus the issue of segmental reporting and compliance with IFRS 8 should beinteresting to examine from Jordanian companies financial statements. Finally, moststudies on the introduction of IFRS 8 have so far been conducted on the UK (Crawfordet al., 2010); investigating how companies in another country have implementedIFRS 8 should help determine if initial UK findings apply more generally in countrieswith different business environment.

The objective of this study is to assess the impact of IFRS 8 on the disclosures ofJordanian listed firms, and ascertain the extent to which segmental informationprovided under IFRS 8 in 2009 differs from segmental disclosures under IAS 14R in2008. Specifically, the empirical investigation compares the annual reports for a sampleof first-market companies[4] in 2009 prepared under IFRS 8 with the annual reportsfor the same sample in 2008 prepared under IAS 14R; a disclosure index approach isused to analyse segmental information in the financial statements of 109 Jordaniancompanies. In addition, this study examines the extent to which Jordanian listed firmshave specified the identity of the CODM in their annual reports.

2. The Jordanian financial reporting frameworkThe legal framework underpinning financial reporting within Jordan is based on anumber of company laws that date back to the 1960s as well as stock exchange listingrequirements. For example, in 1966 the Jordanian Ministry of Industry and Trade(MIT) issued a Commercial Law (Trade Law No. 12) mandating companies to keeprecords of their financial activities. This law required all companies to keep three mainbooks: a general journal, inventory records, and a correspondence register. However,the law was not specific about the content and format of information to be containedin these books (Al-Akra et al., 2009, 2010a). A number of additional laws weresubsequently issued by the MIT in order to assist with the development of theJordan economy. These included the Encouragement of Investment Law of 1972; theRegistration of Foreign Companies Law of 1975; and the Control of Foreign BusinessActivities Defence Regulations of 1978. As a result of these laws, many foreigncompanies and businesses shifted their operations to Jordan and relocated theirregional headquarters to the capital city – Amman (Haddad, 2005). This in turn,

68

JAEE2,1

prompted the Central Bank of Jordan to set up the Amman Financial Market in1978. The only disclosure requirement at that time was that listed public companiesshould provide the Amman Financial Market with audited financial statements(Piro, 1998).

Under the Auditing Profession Practice Law No. 32 of 1985[5], the JordanianAssociation of Certified Public Accountants ( JACPA) was established as a localprofessional accounting body. However, no local accounting standards were createdfor them to apply. Therefore, JACPA played an important role in facilitating theadoption of IASs and recommended that all Jordanian companies voluntarily adoptIAS/IFRS effective from January 1990. Nevertheless, JACPA were unable to force alllisted companies to comply with IAS. Indeed, they could not even get all of theirmembers to employ IASs (Suwaidan, 1997). The absence of any legal or professionalrequirement to implement IASs until 1997 allowed firms to choose which ever (GAAP)they wanted to adopt[6].

In the late 1990s, the government implemented a reform programme, whichpromoted privatisation procedures[7] and developed a new Jordanian CapitalMarket[8]. After 1997, legislation was enacted which stated that entities supervisedby the Jordanian Securities Commission (JSC) were required to apply IASs in thepreparation of their financial statements (balance sheet, income statement, statement ofcash flows, statement of shareholders equity, and notes to the financial statements).The JSC law required all listed companies to present interim financial statements forthe first six months of the fiscal year within a maximum period of one month after theirmid-year end and audited financial statements annually within a maximum periodof three months after the fiscal year-end date. Further, this law clearly defined theGAAP to be employed compared to the wide range of choices that had previouslybeen afforded.

In 2002, the Securities Law of 1997 was updated. Again, the new law required allentities to comply fully with IASs in the preparation of their annual reports and tosubmit an annual audited report to the JSC; there was no opt out where IASs conflictedwith local GAAP. The law stated that “the international accounting standards issuedby the Board of International Accounting Standards are hereby adopted wherebyall the parties subject to the Commission’s monitoring shall prepare their financialstatements consistently therewith” (Article 14). Therefore, since 1997, IASs have beenmandated within Jordan; the country provides an interesting research site to studythe adoption of IFRS 8 by the IASB for implementation in accounting periods onor after 2009; the implementation of what was initially seen and arguably stillis a controversial standard should yield interesting insights (FRRP, 2010; Crawfordet al., 2010).

3. IFRS 8 and literature review on segmental reportingSegmental reporting has long been a problematic issue for standard setters(Rennie and Emmanuel, 1992; Emmanuel et al., 1999; Edwards and Smith, 1996). Forinstance, under IAS 14R, concerns were raised about the disclosures which companieswere required to make ( Jermakowicz and Gornik-Tomaszewski, 2006). Yet, thesubstantive literature suggests that segmental reporting provides importantinformation for the decisions of financial statement users including analysts(Herrmann and Thomas, 2000a). For example, Street and Nichols (2002) argue thatsegmental information supplies disaggregated information for analysts and otherusers of financial statements to examine. Ettredge et al. (2005) state that segmental

69

Jordanian listedcompanies

information helps investors better understands an entity’s performance by allowingthem to estimate future cash flows more accurately. Balakrishnan et al. (1990) andBehn et al. (2002) find that analysts’ forecasts of income and turnover are moreaccurate when geographic segmental data are employed.

To date, the only study about segmental reporting in Jordan has been conducted bySuwaidan et al. (2007). They investigated the segmental information disclosed underIAS 14R by 67 Jordanian industrial companies listed on the Amman Stock Exchange(ASE) from annual reports published in 2002. Applying their own disclosure indexchecklist, the authors found that the average disclosure of segmental items by thesample companies was only 15 per cent of the information, which should have beenpublished under IAS 14R. They suggested that this poor level of disclosure meant thatsegmental information provided by Jordanian industrial companies was less usefulthan it might otherwise have been. The current research builds upon this study fromSuwaidan et al. (2007) by investigating whether the introduction of IFRS 8 hasincreased compliance with segmental reporting requirements; it examines whether theintroduction of IFRS 8 has raised awareness about segmental disclosure requirementsamong Jordanian listed companies and increased compliance since Suwaidan et al.’sanalysis was undertaken.

Literature about the likely impact of IFRS 8 on disclosure practices of companies isrelatively scarce; papers by European Commission (2007), Veron (2007), and Crawfordet al. (2010) are the main exceptions to this generalisation. Veron (2007) highlightedthe potential problems, which firms might face when adopting IFRS 8. Crawford et al.(2010) extended this analysis by seeking the views of a small sample of preparers,auditors, regulators, and users in 2008-2009 about the likely consequences ofimplementing IFRS 8 in Europe. They found that most interviewees considered thatthe absence of mandatory geographical operating segments was uncontroversial;interview responses indicated that companies would continue to publish geographicsegmental information because this data would be provided to the CODM. In addition,a majority of those interviewed suggested that the introduction of the managementapproach for the identification of operating segments was “unproblematic”. However,a couple of concerns were noted; analysts who included segmental information intheir equity valuation models were concerned about the possible size of any differencebetween non-GAAP segmental disclosures and the figures reported in the financialstatements. In addition, preparers indicated that information reported internally to theCODM might change as a result of companies complying with the managementapproach[9]. However, the European Commission (2007) concluded that the benefits ofadopting IFRS 8 for European listed companies outweighed concerns raised bycommentators.

Unfortunately, the early UK evidence about the implementation of IFRS 8 was notencouraging (FRRP, 2010). On 4 January 2010, the UK regulation authorities expressed“concern about how companies are reporting the performance of key parts of theirbusiness in the light of the introduction of IFRS 8”. Specifically, following a review of asample of interim financial statements for 2009 and the annual reports of “earlyadopters” for 2008, several companies were asked to supply additional informationabout their segments.

Despite these concerns, prior US studies on the impact of a standard similar toIFRS 8 (SFAS 131), have shown that the total number of segments reported and thetotal number of segmental items increased significantly under SFAS 131[10](Herrmann and Thomas, 2000b)[11]; the segmental items required by the previous

70

JAEE2,1

US standard continued to be published under SFAS 131 and there was an increase innew disclosures required by SFAS 131 (if reported internally to the CODM), such as theincome tax expense, interest expense, interest revenue, and other non-cash expenses.In addition, Street et al. (2000) found that consistency of segment information withother parts of the annual report improved when the management approach wasadopted by the US standard setter. Since IFRS 8 requirements are similar to thedisclosures mandated under SFAS 131, the current study examines whether theexperience of Jordanian companies with the new standard on segmental reporting(IFRS 8) mirrors the experiences in the US when SFAS 131 was introduced in 1998.Specifically, it considers whether the quantity and quality of disclosures changed as aresult of IFRS 8 being mandated for Jordanian listed companies[12].

4. Method4.1 Sample selectionThe ASE official web site was used to determine the number of companies listed ontwo main stock markets in Jordan for 2009. According to this web site, companies onthe ASE are grouped into three main sectors: financial, services, and industrial. Thefinancial sector is divided into three sub-sectors: banks, insurance, and financialservices. Table I shows that there were 119 first market and 154 second market listedcompanies across the three sectors at the time of this study.

Prior studies have argued that the size of the company can have a significant impacton the extent to which segmental information is disclosed in developed (Rennie andEmmanuel, 1992; Ettredge et al., 2005; Tsakumis et al., 2006) and developing countries(Talha et al., 2006; Talha et al., 2007; Suwaidan et al., 2007). These investigations havedocumented that large companies disclose more segmental information than theirsmall- and medium-sized counterparts. In this research, second market companies(154 (56.4 per cent)) are excluded from the sample to avoid companies which do notdisclose a great deal of segmental information; the possible bias from includingsuch companies is therefore avoided[13].

In addition, ten companies from the insurance sector of the first market are excludedfrom the sample for two reasons. First, a review of their financial statements showedthat none of the insurance companies disclosed any business class or geographicsegmental information. Second, the Insurance Regulatory Commission (IRC) wasestablished in 1999, as a financially independent entity that issues instructions for thesector as regards the implementation of IAS/IFRS (Report on the Observance ofStandards and Codes (ROSC), 2004; United Insurance Company, 2008; The Holy Land

Company sector First market (%) Second market (%) Total (%)

FinancialBanks 14 93.3 1 6.7 15 5.5Insurance 10 35.7 18 64.3 28 10.3Financial services 36 48.6 38 51.4 74 27.1Services 25 40.3 37 59.7 62 22.7Industrial 34 36.2 60 63.8 94 34.4Total 119 43.6 154 56.4 273 100

Note: This table shows the ASE listed companies based on the ASE web site http://194.165.154.66/markets.php (accessed 21 December 2009)

Table I.Companies listed in theAmman stock exchange

71

Jordanian listedcompanies

Insurance Company, 2009). Hence, the financial statements of insurance companies inJordan are prepared in accordance with formats that are determined by the IRC andtend to differ from their non-insurance counterparts[14] (ROSC, 2004). Thus, a finalsample of 109 first market companies, excluding the insurance industry is used in thisresearch. The annual reports of the sample companies were downloaded from the websites of the company, the ASE, or the JSC; all reports were published in Arabic.

4.2 Disclosure index approachA spreadsheet[15] was constructed to capture the extent to which segmentalinformation is disclosed by the sample of Jordanian companies, before and after theintroduction of IFRS 8. In particular, the spreadsheet collected information about: first,the number of segments reported on; second, the number and type of segmental itemspublished; three, the geographic segment definitions (areas) used; and fourth, theidentity of the CODM.

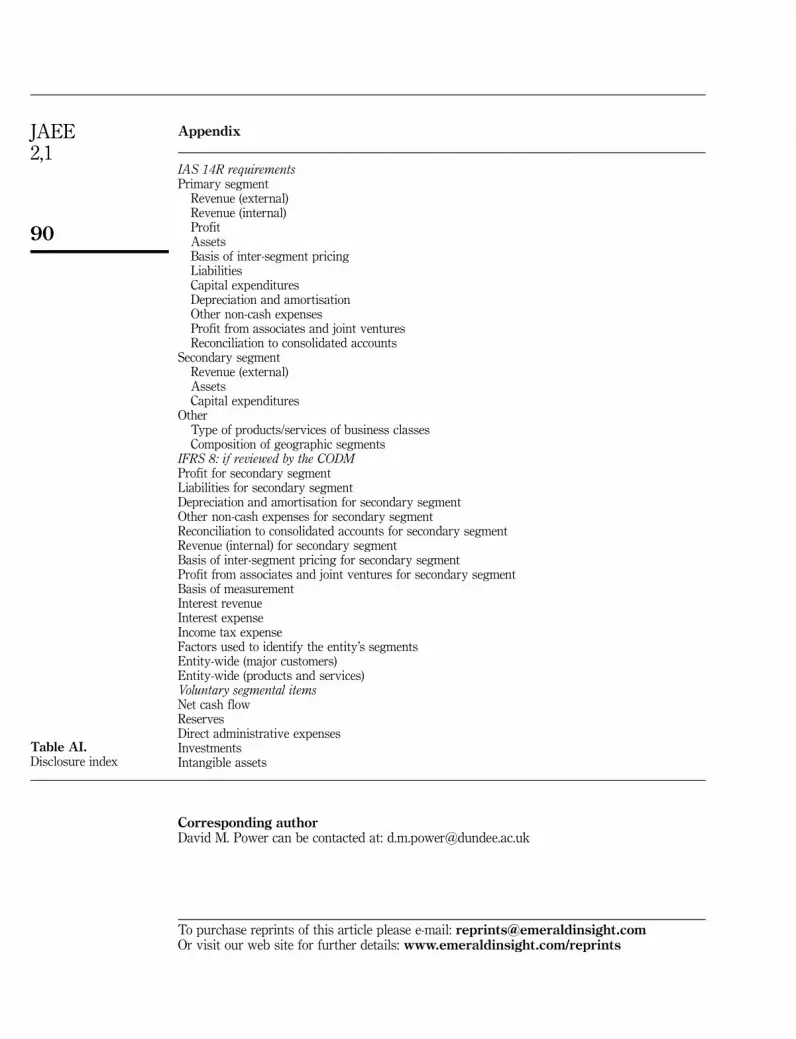

This spreadsheet incorporated information about 36 items which were included inthe disclosure index. Sixteen items were based on IAS 14R mandated disclosures(IASC, 1997)[16], and a further five voluntary items were identified from a pilotreview[17] of 46 annual reports of Jordanian companies reporting in 2008 (net cashflows for primary segments and reserves for primary segments) and 2009 (directadministrative expenses, investments, and intangible assets for operating segments).The remaining 15 items were drawn from those required by IFRS 8 to be disclosed ifthe item is included in information that is regularly reviewed by the CODM (IASB,2006a, b). The disclosure index checklist is reproduced in the Appendix.

The disclosure index described above was used to extract descriptive statisticsabout the quantity of individual segment items disclosed before and after IFRS 8. Inaddition, the disclosure index enabled calculation of a total disclosure score for eachcompany. An un-weighted disclosure index approach was employed which treats allfinancial reporting items as equally important in order to avoid any subjectivity in theanalysis (Cooke and Wallace, 1989; Marston and Shrives, 1991; Gray et al., 2007). Thus,if an item was disclosed in the financial statements of a company, a value of 1 wasrecorded; if an item was not disclosed, it was given a value of 0. The total disclosurescore of mandatory and voluntary segmental items (TD) for a company was calculatedby adding the individual scores for the different items and then divided by the totalitems included in the disclosure index checklist:

TD ¼Xm

i¼1

di=m ð1Þ

where d¼ 1 if the item is disclosed and 0 otherwise.The main problem with this approach is that each item included in the index may

not necessarily be relevant for all companies. For instance, in the disclosure index forthe study, all companies have external revenues, but they may not necessarily haveinter-segment sales. Thus, this segmental item and the basis of inter-segment pricingmay not be relevant for a particular company. Moreover, not all companies have jointventures or associate companies, so the segmental item for “profit from associates andjoint ventures” as required under IAS 14R and IFRS 8 (if reviewed by the CODM) mayalso be not relevant. To solve this problem the annual reports were read to confirm thetotal possible disclosure score for each individual company, and this company-specifictotal was used to calculate a company-specific disclosure score. Thus, the disclosure

72

JAEE2,1

score was tailored to differentiate between non-disclosure of a relevant item, scored as0, from non-disclosure of an irrelevant item, noted as not applicable (n/a) (Cooke, 1989).

To increase the reliability of the index used in the current research, the annualreports for the financial periods 2008 and 2009 were each read twice. In addition, asample was read by more than one researcher to check on the reliability of the codingused. This strategy was employed to ensure that the scoring was consistent and toavoid any mistakes with the coding before the index results were analysed and thefindings examined; an item was considered relevant for a company if it wasappropriate to its operations; non-applicable items were removed from the index.

5. Results and discussion5.1 Definition of segments disclosed under IAS 14R (2008) and IFRS 8 (2009)For this study, the sample of Jordanian companies was categorised into three groups:first, companies that did not disclose any segmental information and for whom thedisclosure index had a value of 0 (“NS” companies hereafter); second, companies thatdid disclose segmental information and had a non-zero disclosure index value butwhich did not identify segments (as primary/secondary or operating/entity-wide) asrequired under the effective standard (“UD” companies hereafter); and third, companiesthat disclosed segmental information and had a disclosure index value 40, andidentified the segments (as primary/secondary under IAS 14R or operating/entity-wideunder IFRS 8) according to the effective standard (“DF” companies hereafter).Specifically, the distinction between the DF and UD categories was employed todistinguish between the companies that complied fully or partially with the relevantstandard (IAS 14R and IFRS 8), respectively, in terms of segment identification. Thiscategorisation was based on whether a company had a segmental informationnote in their annual reports and whether any segmental information provided inthe note to the annual report distinguished between primary and secondary segmentsunder IAS 14R and between operating segment and entity-wide disclosures (EWDs)under IFRS 8. The number of sample companies for each of these three categories(NS, UD, and DF) is detailed in Table II. Panel A of this table provides a summaryof the number of companies for each category in the sample for 2008 (IAS 14R) whilepanel B displays similar information for 2009 (IFRS 8).

As inspection of Table II, panel A reveals that only one-third of the samplecompanies defined their segments in accordance with the IAS 14R approach in 2008(DF category); some 21 companies (19.3 per cent) were in the UD category while afurther 52 (47.7 per cent) provided no segmental information whatsoever in theirfinancial statements for that year. A more detailed analysis of the table reveals that thenumbers complying with IAS 14R were not equally distributed across the differentsectors. All the banks in the sample (14 banks) complied fully with the standard inrelation to identifying primary and secondary segments. However, only eight (32 percent) of the service sector companies were in the DF category. Indeed, a majority ofthe financial services firms (66.7 per cent) and service companies (52.0 per cent) were inthe NS category suggesting that more than half of the firms in these industriesclassified themselves as single-activity entities which only operated in one geographicregion. The highest number (and percentage) of firms in the UD category operatedin the industrial sector; some 11 (33 per cent) of industrial companies were allocatedto this group. There is no obvious reason why industrial companies should havepublished disaggregated information as mandated by IAS 14R and not identifiedthe business activity or geographic disclosures as either their primary or secondary

73

Jordanian listedcompanies

segmental data[18]. Perhaps, the firms in this sector followed a reporting formatproduced by an industry leader, which adopted such an approach[19]. Interestingly,nine out of 11 of these companies were audited by the same audit firm, which did notpick up on this error[20].

One of the most striking findings to emerge from panel B of Table II is that after theintroduction of IFRS 8 the number of companies identifying operating segments inaccordance with the management approach increased to 47 compared with only 36identifying primary and secondary segments under IAS 14R. In 2009, this DF groupdisclosed disaggregated information for business operating segments. Ten of theseDF companies also disclosed geographic operating segments, whilst the remaining37 companies reported geographic information as EWDs. None of the companies in theDF category disclosed entity-wide, business-related information.

Again, the distribution of companies across the different disclosure categories,varied according to the sector to which they belonged. A sizeable minority of 42(38.5 per cent) companies (NS) did not disclose any segmental information (Table II,panel B). Only nine (25 per cent) of the financial services sector companies were inthe DF category, while all banks complied fully with IFRS 8 when identifying theirsegments. In fact, most of the increase in the compliance with accounting requirementsfor identifying segments came from companies in the financial services and industrial

Company sector NS (%) UD (%) DF (%) Total

Panel A: 2008 (IAS 14R)FinancialBanks 0 0.0 0 0.0 14 100 14Financial services 24 66.7 6 16.7 6 16.7 36

Services 13 52.0 4 16.0 8 32.0 25Industrial 15 44.1 11 32.4 8 23.5 34Total 52 47.7 21 19.3 36 33.0 109Panel B: 2009 (IFRS 8)FinancialBanks 0 0.0 0 0.0 14 100 14Financial services 18 50.0 9 25.0 9 25.0 36

Services 14 56.0 0 0.0 11 44.0 25Industrial 10 29.4 11 32.4 13 38.2 34Total 42 38.5 20 18.3 47 43.1 109

Notes: This table shows sample details for different segmental disclosure categories. NS, firms withno segmental information provided; UD, firms which disclosed segmental information withoutcategorising the segments as either primary or secondary as required under IAS 14R for 2008 or asoperating segments as required under IFRS 8 for 2009; DF, firms which disclosed segmentalinformation and identified segments as either primary or secondary under IAS 14R for 2008 or asoperating segments under IFRS 8 for 2009. Thirteen companies disclose segmental information in2009 but not in 2008; nine out of 13 companies are in the DF category while four are in the UD group.Three services companies that disclose segmental information in 2008, provide no segmentalinformation in 2009; two out of three were UD companies in 2008 and one company were categorisedunder DF in 2008. Three services companies, which were in UD category in 2008 changed to theDF category in 2009. The w2 test shows that the proportions in each category are different acrossthe sectors (p-value o0.0005); specifically, the financial banking sector is significantly differentfrom other sectors

Table II.Company sectors andsegmental disclosurecategory for 2008and 2009

74

JAEE2,1

sectors since the numbers in the NS category for these sectors fell by 15 per cent.However, a sizeable minority in these sectors still did not fully comply with IFRS 8when identifying their segments; nine (25 per cent) financial services companiesand 11 industrial companies were classified in the UD group for 2009[21].

For the remainder of the analysis, only 70 Jordanian companies were investigatedsince they disclosed segmental information in 2008 and/or 2009; the 39 companies thatdid not provide segmental information in both 2008 and 2009 were dropped from theanalysis.

5.2 Number of segments disclosedThe number of business segments under IFRS 8 was not significantly different fromthat disclosed under IAS 14R. Specifically, information for 187 business segments wasdisclosed in 2009 compared to 170 in 2008 (Table III). Panel A of this table shows thatthe mean (median) number of business segments disclosed under IFRS 8 was 2.7 (2.0)per firm compared to 2.4 (2.0) per firm under IAS 14R. This finding is similar to theresult from Crawford et al. (2010) where the authors found that the introduction ofIFRS 8 in the UK was associated with an increase in the number of businesssegments[22].

According to Table III, the median number of business segments remained thesame for the Jordanian companies in the current research suggesting that the highermean under IFRS 8 was possibly due to a large increase by a small number of firms(panel B). Panel B shows there was an increase in firms reporting data for 1, 2, 4, and 5business segments under IFRS 8, and a decrease (from 13 to 3) in the number of firms

2008 (IAS 14R) 2009 (IFRS 8)

Panel A: average number of business segments disclosedTotal of segments 170 187Mean 2.4 2.7Median 2.0 2.0Panel B: distribution of the number of business segments disclosedNo. of business segments0 13 31 4 82 19 263 17 144 10 115 5 76 2 1Total 70 70Panel C: change in number of business segments disclosedNumber of companies which increased the business segments disclosed 18Number of companies which decreased the business segments disclosed 9Number of companies which had no change to the business segments disclosed 43Total 70

Note: This table shows descriptive information about the number of business segments reported bythe sample of 70 Jordanian companies in 2008 and/or 2009. Information for 170 business segments wasdisclosed in 2008, and while details for 187 business operating segments were disclosed in 2009. Thedifferences from 2008 to 2009 were significant at the 10 per cent level

Table III.Number of business

segments reported for2008 and 2009 for the

same firm

75

Jordanian listedcompanies

reporting zero business segments. The combination of these two changes resulted inthe increase in the mean values. However, panel C confirms that the change in the meanin panel A arose from additional disclosures by a minority of firms following theadoption IFRS 8: 18 firms increased the number of business segments reported;nine firms reduced the number of business segments reported; and 43 firms disclosedthe same number of business segments in both 2008 and 2009[23].

Geographic segmental information is not mandated under IFRS 8, although EWDsabout geographic areas is required if the necessary information is available.Despite this relaxation in the requirements to supply geographic information, Table IVshows that the number of geographic segments or EWDs actually increased to127 under IFRS 8 compared with 107 under IAS 14R. Panel A of this table highlightsthat the mean number of geographic segments/EWDs for which information wasdisclosed under IFRS 8 rose to 1.8 from 1.5[24]. Crawford et al. (2010) documentedsimilar results for their UK sample of 65 firms[25]. For the current study, the reasonfor this finding relates to the number of firms providing data for 1, 3, and 6 distinctgeographic segments/EWDs increasing under IFRS 8 (panel B). Also, 13 firmswhich did not disclose any geographic information in 2008 published such informationin 2009.

In fact the number of companies increasing their geographic segment/EWDsinformation was even higher than those increasing their business segments disclosureunder IFRS 8. Panel C of Table IV shows that 24 companies disclosed details about

2008 (IAS 14R) 2009 (IFRS 8)

Panel A: average number of geographic segments disclosedTotal of segments/EWDs 107 127Mean 1.5 1.8Median 1.0 1.0Panel B: distribution of the number of geographic segments/EWDs disclosedNo. of geographic segments/EWDs0 13 31 25 332 26 243 0 44 2 15 3 16 0 37 1 1Total 70 70Panel C: change in number of geographic segments/EWDs disclosedNumber of companies which increased the geographic segments/EWDs disclosed 24Number of companies which decreased the geographic segments/EWDs disclosed 6Number of companies which had no change to the geographic segments/EWDsdisclosed

40

Total 70

Note: This table illustrated descriptive information about the number of geographic segmentsentity-wide reported by the sample of 70 Jordanian companies in 2008 and/or 2009. Informationfor 107 geographic segments was disclosed in 2008, and details for 127 geographic operatingsegments and EWDs were disclosed in 2009. The differences from 2008 to 2009 were significantat the 10 per cent level

Table IV.Number of geographicsegments and entity-widedisclosures (EWDs)reported for 2008 and 2009for the same firm

76

JAEE2,1

more geographic segments/EWDs in 2009, while only six companies reduced thenumber of geographic segments/EWDs; 40 companies did not change their reportingpattern for geographic data. For instance, Jordan National Bank reported twogeographic secondary segments in 2008, but disclosed information about fourgeographic segments as EWDs in 2009. Moreover, an industrial company Dar Al-DawaDevelopment and Investment, reported on four geographic secondary segments in2008, but increased this to six geographic areas under EWDs in 2009. These resultsprovide some evidence that the requirements to provide entity-wide geographicdisclosures under IFRS 8 may have resulted in an increase in the geographicinformation supplied, even though this geographic segmental information was notexplicitly mandated in the new standard.

The six Jordanian companies that reduced the quantity of disclosed geographicinformation comprised: two financial services companies, one industrial company, andthree services companies sector. The three services companies did disclosed segmentalinformation under IAS 14R, but did not disclose any segmental information underIFRS 8. The industrial company in its annual report for 2009 argued that in the lastquarter of 2009, new companies entered the mining and extraction sector, and thisnegatively affected their performance; the reduction in the industrial company’sgeographic disclosures was one possible response to this apparent competitivepressure. However, this response is interesting since IFRS 8 does not allow an opt-outfrom disclosures on the grounds of competitive sensitivity (IASB, 2006a, b). Becauseof the financial crisis, the two financial services companies witnessed a reduction intheir total assets and thus, a decrease in their total activities; in response to thisreduction, they only disclosed data for “Jordan” or “inside Jordan” geographic areasin 2009 compared to information for the “Free Zones” and the “Aqaba regions” in 2008;presumably, the reduction in total assets meant that disaggregated information forthese companies within Jordan was not material and not reviewed regularly by theCODM.

5.3 Items reported for each segmentIAS 14R required the disclosure of external revenue, internal revenue, profit, assets, thebasis of inter-segment pricing, liabilities, capital expenditures, depreciation andamortisation, other non-cash expenses, the profit of joint ventures, and a reconciliationto consolidated accounts for primary segment items as well as a smaller number ofitems for secondary segments (external revenue, assets, and capital expenditures). Inaddition, it specified that companies should disclose the type of products or servicesprovided by business classes and the composition of geographic segments (IASC,1997). These other disclosures were also mandated by the Jordanian regulators ( JSC,Instructions of Issuing Companies Disclosure, Accounting and Auditing Standardsfor the Year 2004, Article 4-B). By contrast, IFRS 8 only requires, for each operatingsegment, that the basis of measurement for profit and total assets (as well as liabilitiesif regularly reviewed by the CODM) and reconciliations to the consolidated accountsbe disclosed. Moreover, external revenue, internal revenue, interest revenue, interestexpense, depreciation and amortisations, profits of associates and joint ventures,income tax expense, and other non-cash expenses should be disclosed if these itemswere regularly reviewed by the CODM. In addition to operating segment information,IFRS 8 also requires EWDs for: product or service, geographical areas and informationabout major clients. This entity-wide information should be disclosed if it is availableand if it is judged to be material. It also specifies that those factors used to identify

77

Jordanian listedcompanies

the entity’s reportable segments and the types of products and services should beclassified as general information. Hence, the firm’s CODM plays a significant role indetermining the segmental information to be disclosed for a particular financial yearunder IFRS 8 (Herrmann and Thomas, 2000b; Ettredge et al., 2002; Ettredge et al.,2005).

The mean number of items disclosed for each type of segment increased under IFRS8 (panel A of Table V) to 10.4 (10.0) for all firms compared to 6.4 (6.0) under IAS 14R.Panel B reveals that the mean (median) disclosure index total score for all segmentalitems was 30.6 per cent (29.0 per cent) under IFRS 8 compared to 18.6 per cent(17.7 per cent) under IAS 14R; this increase was spread across a wide variety ofitems[26]. Panel C shows the number of companies, which disclosed individual itemsas a percentage of the total number of firms in the sample[27].

A number of points emerge from an inspection of this table. First, the introduction ofIFRS 8 lead to sizeable increases in the percentage of firms disclosing informationabout business classes which had been required under IAS 14R. For profit, assets,and liabilities, the increases were 21.2, 28.5, and 27.1 per cent, respectively. In fact, over75 per cent of the sample disclosed details of revenue, assets, and liabilities for businessclass segments under IFRS 8; no item had been disclosed by such a high percentageof the sample firms under IAS 14R. Second, for two items (other non-cash expensesand reconciliation to consolidated accounts) the percentage of firms supplyinginformation fell under IFRS 8. In both instances, the percentages had been low underIAS 14R and fell slightly (�1.4 and �2.9 per cent) when the new standard wasintroduced. One possible explanation for this decline is that such information wasnot viewed by the CODM for business class segments. In addition, the low level ofcompliance with requirements to disclose these two items under IAS 14R may suggestthat such information was not thought to be relevant to reporting segmentperformance.

Third, there was an increase in firms making non-mandated disclosures forbusiness class segments under IFRS 8. Such a finding is not surprising since thenew standard was less prescriptive about the items that companies had to disclose;instead, under the management approach, the information made available to theCODM had to be supplied. What is apparent from Table V is that different CODMsappear to see a wide range of items about their business segments. For 12 of thevoluntary items listed in Table V[28], the percentage of firms supplying informationabout business class segments increased. In two of these cases, the changes weresizeable. In particular, 61.4 per cent of firms disclosed the “basis of measurement”under IFRS 8 while none had provided this information previously. In addition,28.6 per cent of firms included details about their “income tax expenses” for businessclass segments in their 2009 financial statements whereas none had supplied thisinformation in 2008.

Fourth, the items that were required under IAS 14R as secondary segments forgeographic areas were still disclosed under IFRS 8. However, there were significantchanges in the percentage of firms providing such information. In particular, thepercentage for assets increased from 37.1 per cent under IAS 14R to 80.0 per cent underIFRS 8. The percentage for revenue (external) also increased under IFRS 8 from 70.0 to92.9 per cent. This increase in geographic disclosure may be due to the requirementof IFRS 8 for EWDs; it may also reflect the fact that the new standard offers moreflexibility for disclosing geographic information (Herrmann and Thomas, 2000b; Streetet al., 2000). However, companies did not use this flexibility to disclose more detail

78

JAEE2,1

2008 (IAS 14R) 2009 (IFRS 8)

Panel A: average number of segmental items disclosed

Mean 6.4 10.4

Median 6.0 10.0

Panel B: average disclosure index score for segmental items disclosed (%)

Mean 18.6 30.6

Median 17.7 29.0

Panel C: segmental items disclosed (%)

2008 2009

Requirements (IAS 14R) Business Geographic Other Business Geographic Other

Revenue (external) 72.9 70.0 – 85.7 92.9 –

Revenue (internal) (BS) 55.6 N/R – 55.6 N/R –

Profit (BS) 47.4 N/R – 68.6 N/R –

Assets 52.9 37.1 – 81.4 80.0 –

Basis of inter-segment pricing (BS) 44.4 N/R – 44.4 N/R –

Liabilities (BS) 50.0 N/R – 77.1 N/R –

Capital expenditures 35.7 24.3 – 35.7 21.4 –

Depreciation and amortisation (BS) 40.0 N/R – 57.1 N/R –

Other non-cash expenses (BS) 15.7 N/R – 14.3 N/R –

Profit from associates and joint ventures (BS) 31.7 N/R – 43.9 N/R –

Reconciliation to consolidated accounts (BS) 28.6 N/R – 25.7 N/R –

Type of products/services of business classes – – 70.0 – – 88.6

Composition of geographic segments – – 54.3 – – 65.7

Voluntary (added items)

Profit (GS) – 0.0 – – 8.6 –

Liabilities (GS) – 5.4 – – 8.6 –

Depreciation and amortisation (GS) – 0.0 – – 7.1 –

Other non-cash expenses (GS) – 0.0 – – 1.4 –

Reconciliation to consolidated accounts (GS) – 0.0 – – 2.8 –

Revenue (internal) (GS) – 0.0 – – 0.0 –

Basis of inter-segment pricing (GS) – 0.0 – – 0.0 –

Profit from associates and joint ventures (GS) – 0.0 – – 2.4 –

Net cash flow 1.4 – – 1.4 – –

Reserves 1.4 – – 1.4 – –

Basis of measurement 0.0 0.0 – 61.4 12.9 –

Interest revenue 0.0 0.0 – 10.0 4.2 –

Interest expense 0.0 0.0 – 7.1 2.8 –

Income tax expense 0.0 0.0 – 28.6 7.1 –

Direct administrative expenses 0.0 – – 4.2 – –

Investments 0.0 – – 1.4 – –

Intangible assets 0.0 – – 1.4 – –

Factors used to identify the entity’s segments – – 0.0 – – 28.6

Entity-wide (major customers) – – 0.0 – – 54.3

Entity-wide (products and services) – – 0.0 – – 0.0

Notes: For 2009 geographic items included operating segments and entity-wide disclosures. For comparison

purposes, the list of items in 2009 is based on IAS 14R requirements; as a result, the entity-wide revenue and

assets disclosures were divided into two as “revenue (external)” and “assets” items. Total possible disclosure

for internal revenue and the basis of inter-segment pricing items was only nine out of the 70 companies in the

sample. Total possible disclosure for the profit from associates and joint ventures item was only 41 out of 70

companies. N/R, not required; BS, business segments; GS, geographic segments. The differences from 2008 to

2009 were significant at the 5 per cent level

Table V.Segmental items disclosedfor 2008 and 2009 basedon IAS 14R requirements

79

Jordanian listedcompanies

about capital expenditure in different geographic areas. Such information may beperceived as commercially sensitive since the percentage of firms disclosing it fell from24.3 to 21.4 per cent.

Fifth, voluntary disclosures of geographic information for profit, liabilities,depreciation and amortisation, other non-cash expenses, and reconciliation toconsolidated accounts increased under IFRS 8 (by 8.6, 8.6, 7.1, 1.4 and 2.8 per cent,respectively); these items were disclosed by the ten companies classified in the DFgroup that identified their geographic segmental information as operating segments.However, these items were the main difference between the ten companies thatidentified their geographic information as operating segments and the other 37companies that disclosed their geographic information as EWDs. In other words, bothgroups provided their external revenue and assets as requested for EWDs with moreitems disclosed (profit, liabilities, depreciation and amortisation, other non-cashexpenses, and reconciliation to consolidated accounts) for the ten companies thatidentified their geographic information as operating segments.

Finally, an interesting finding from a study of the disclosures behind Table V is that43 of the 47 companies in the DF group for operating business segments and ten of theten companies that defined their geographic information as operating segments usedthe accruals basis to calculate their segmental profit. The only exception was anindustrial company (The Jordan Cement Factories). However, this firm did not outlinewhy the basis of measurement for segmental data was different from that used in itsconsolidated financial statements. It simply informed the users of its financialstatements that the segmental profit was different with no information about the actualbasis that they had adopted:

Segmental performance is evaluated based on operating profit or loss which in certainrespects, is measured differently from operating profit or loss in the consolidated financialstatements (Annual Report, 2009, p. 55).

Further, the DF group measured their segmental assets (and liabilities if reviewedby the CODM) on a historical cost basis. Thus, the majority of the Jordanian firstmarket companies that identified their segments as required under IFRS 8 (the DFgroup) did not employ non-IFRS measurements for segmental information in their2009 annual reports.

The information in Table VI builds upon the details contained in Table V. Forexample, panel A of Table VI illustrates that 12 companies disclosed 17 or more itemsunder IFRS 8, compared to the maximum number of items under IAS 14R (16 items, seeAppendix). It also highlights why the mean and median segmental disclosuresbetween 2008 and 2009 changed according to Table V; the distribution was spreadmore evenly in 2009 with a greater tendency to disclose additional items under the newsegmental standard. For instance, while only two companies published more than 13items of segmental information in 2008, 18 companies did so in 2009. According topanel B, just over half of the sample companies increased the number of segmentalitems disclosed under IFRS 8, while a small minority of nine companies reducedthe number of segmental items published under the new standard. Some 23companies disclosed the same number of segmental items in both 2008 and 2009.Overall, the items that were required under IAS 14R were still published in 2009with new items added following the introduction of IFRS 8. This indicates that theinformation regularly reviewed by the CODM goes beyond that previously required byIAS 14R.

80

JAEE2,1

5.4 Geographic area definitionsThe overall distribution of the number of geographic areas increased slightly upon theadoption of IFRS 8 (Table IV). It is therefore hardly surprising that the geographic areadefinitions changed under IFRS 8. Table VII[29], highlights that the number ofindividual country disclosures was higher (five companies had finer definitions) underIFRS 8 as well as the number of broader geographic locations (three companieshad broader definitions). All companies disclosed “Jordan” or “inside Jordan” as ageographic area except one service and one industrial company in both 2008 and 2009.This table included companies that changed the level of their segmental disclosures;the 13 companies, which did not disclose segmental information in 2008 (Table IV),but disclosed it in 2009 plus the three services companies, which did not reportsegmental information in 2009 but had reported it in 2008. This explains the differenceof ten companies for the “Jordan” or “inside Jordan” category (65-55) for 2009. In otherwords, companies that disclosed segmental information for the first time upon the

Number of companiesNumber of items disclosed 2008 (IAS 14R) 2009 (IFRS 8)

Panel A: distribution of the items disclosed0 13 32 2 13 10 04 6 55 3 86 5 37 0 28 3 79 3 510 6 511 7 412 5 513 5 414 1 115 0 316 1 217 0 318 0 219 0 120 0 221 0 326 0 1Total 70 70Panel B: changes in the distribution of the items disclosed from 2008 to 2009Number of companies which increased the segmental items disclosed 38Number of companies which decreased the segmental items disclosed 9Number of companies which had no change to the segmental items disclosed 23Total 70

Note: This table shows the distribution of the number of segmental items disclosed, and changes inthe number of companies, which disclosed segmental information

Table VI.The distribution of thenumber of segmentalitems disclosed for

2008 and 2009

81

Jordanian listedcompanies

introduction of IFRS 8 in 2009 employed this categorisation and operated withinJordan only; these companies were included in the “new information under IFRS 8”group in panel B of this table.

From Table VII, 17 companies disclosed “outside Jordan” as a geographic area withno further disaggregation or information about specific locations under IFRS 8 downfrom 22 companies under IAS 14R. All the bank companies employed this level ofdisclosure in 2008 but some changed their practices in 2009; five banks disclosed

2008 (IAS 14R) 2009 (IFRS 8)

Panel A: geographic areasGeneralJordan/inside Jordan 55 65Outside Jordan 22 17ContinentsEurope 2 4America 1 2Asia 2 4Africa 2 3Other 2 4RegionsEastern Arabic 1 1Arabic Gulf 4 4Middle East 3 3Free Zones 1 0Associated companies, Jordan 1 1Aqaba – Jordan 4 2Foreign countryEriteria 1 0Sudan 1 0Saudi Arabia 1 0Palestine 2 7Syria 1 1Lebanon 0 1Cyprus 0 2Morocco 0 1Egypt 0 1Iraq 1 4Panel B: geographic segment definitionsNew information under IFRS 8 13Finer under IFRS 8 6Broader under IFRS 8 5Same 40Less fine under IFRS 8 1Less broad under IFRS 8 2No information under IFRS 8 3Total 70

Note: This table shows the geographic area definitions for 2008 and 2009. The “outside Jordan”category refers to companies, which disclosed information under this heading without providingfurther more disaggregation details. Finer refer to individual country disclosures. Broader refers togeographic continent or regionSource: Herrmann and Thomas (2000b)

Table VII.Geographic areadefinitions for2008 and 2009

82

JAEE2,1

“finer” definitions under IFRS 8. The decrease in the use of this “outside Jordan”category when identifying geographic areas provides some indication that more of thesample companies disclosed additional disaggregated geographic locations.

An analysis of panel B of this table shows that identifying geographic segments bycontinent and by individual country increased under IFRS 8. The data showscompanies disclosed either the same or “finer” geographic locations when reportingunder the new standard; the only exception to this generalisation is an industrialcompany that did not provide data for Eriteria, Sudan, and Saudi Arabia in 2009whereas it had done so in 2008 (The Jordan Cement Factories). In fact, six companies(five banks and one industrial firm) provided geographic data for Palestine, Lebanon,Cyprus, Morocco, Egypt, and Iraq for the first time in 2009. Some four companiesprovided data for continents which was double the number disclosing suchinformation in 2008, whilst the regional disclosures dropped in 2009 mainly due to theactions of two financial services companies; one of these financial services companiesdid not disclose Free Zones and Aqaba as regions in 2009, while the another companydid not disclose Aqaba as a region. However, some firms improved their geographicsegment disclosures upon the adoption of IFRS 8. For instance, three industrialcompanies disclosed “outside Jordan” under IAS 14R, but based the definition of theirgeographic segments on the country level upon the introduction of IFRS 8.

5.5 The identity of the CODM for DF firmsAccording to IFRS 8 “An operating segment is a component of an entity that(i) engages in business activities from which it may earn revenues and incur expenses(ii) whose operating results are regularly reviewed by the entity’s chief operatingdecision maker to make decision about the segments and (iii) for which discretefinancial information is available” (IASB, 2006a). IFRS 8 does not specify the identity ofthe “CODM”; it simply states that “it is not necessarily a manager with a specific title.However, it may be the chief executive officer (CEO) or chief operating officer but, forexample, it [also] may be a group of executive directors or other” (IASB, 2006a).

Table VIII shows that over 60 per cent of the DF group[30] identified theCODM in their financial statements for 2009. From these, the majority (51.1 per cent)assigned the role of the CODM to the company’s CEO. This was especially true forfinancial services (77.8 per cent) and industrial (61.5 per cent) companies whereas only35.7 per cent of banks and 36.4 per cent of services companies stated that the CEO was

Company sector CEO (%) MGT (%) CFO (%) BoD (%) NP (%) Total

FinancialBanks 5 35.7 1 7.1 1 7.1 0 0.0 7 50.0 14Financial services 7 77.8 0 0.0 0 0.0 1 11.1 1 11.1 9Services 4 36.4 1 9.1 0 0.0 0 0.0 6 54.5 11Industrial 8 61.5 1 7.7 0 0.0 0 0.0 4 30.8 13Total 24 51.1 3 6.4 1 2.1 1 2.1 18 38.3 47

Notes: This table provides details about the identity of the CODM for the sample of 47 companies,which identified the CODM when providing details about operating segments in their financialstatements for 2009. CEO, chief executive officer; MGT, management; CFO, chief financial officer;BoD, Board of Directors; NP, not provided

Table VIII.Details about the identityof the CODM for the DF

group under IFRS 8

83

Jordanian listedcompanies

the CODM. For instance, in the financial statements of Middle East Complex forEngineering, Electronics and Heavy Industries, the industrial company stated that“the company (group) has organized its segments and measured [performance]according to the reports that are used by the chief executive officer who is the maindecision maker” (Annual Report, 2009, p. 56).

In only a small number of instances were an individual or group other than the CEOidentified the CODM. For example, three companies (Arab Banking Corporation,Jordan Petroleum Refinery, and Salam International Transport and Trading)highlighted that the CODM was “Management” without giving any details aboutwhether this was a person or a committee, while the service company SalamInternational Transport and Trading stated that “for administrative purposes,the company organized its segments and measured its performance according tothe reports that are used by the Management of the company through these segments”(Annual Report, 2009, p. 53). One company stated that the CODM was the chieffinancial officer while one other company (United Arab investors) stated that the“Board of Directors” fulfilled this function within their organisation: “the grouporganized its segments and measured performance according to the reports that areused by the Board of Directors” (Annual Report, 2009, p. 28).

One of the surprising results to emerge from Table VIII is that 18 (38.3 per cent)companies did not provide any information about the CODM. This will arguablyimpact on the usefulness of the information disclosed as users will not be able tounderstand which management perspective is being portrayed in the segmentaldisclosure note.

6. ConclusionsUnder IFRS 8, entities are now required to disclose segmental information, which isconsistent with how management views the entity based on its internal reports. Thefindings show that over one-third of the sample companies that disclose segmentalinformation in 2008 and/or 2009 changed their definition of segments upon theadoption of the new segmental reporting standard. The new definition of segmentsemployed with the implementation of IFRS 8 has resulted in several improvements inthe level of segmental disclosures for the Jordanian listed companies. The introductionof IFRS 8 saw about 10.0 per cent of the sample companies disclosing segmentalinformation for the first time. Some 13 out of 109 companies studied disclosedsegmental information for the first time under IFRS 8, whilst three services companiesstopped providing segmental information when the new standard was introduced.Apparently, the remaining companies previously defined their segments under IAS14R in a manner consistent with the internal organisation of the company and inaccordance with management approach under IFRS 8. Thus, the IFRS 8 reporting ruleshave had some impact.

Moreover, IFRS 8 has had a significant impact on the manner of which entitiesdisclosed segmental information. For example, companies disclosed more items foreach operating segment on average. The disclosures mandated by IAS 14R continuedunder IFRS 8 with an increase of new disclosures required by IFRS 8, such as the basisof measurement, factors used to identify the entity’s segments and EWDs (majorcustomers details). Also, new items were disclosed if recognised by the CODM suchas interest revenue, interest expense, and income tax expense. Further, the number ofbusiness classes and geographic segments for which information was providedincreased. Finally, the geographic locations that were employed were finer for

84

JAEE2,1

individual country disclosures and broader for continents under IFRS 8; the entity-wide geographic disclosures seemed to improve the flexibility to disclose moregeographic segments with finer and broader disaggregation of geographic locations. Ingeneral, the disclosure of segmental information under the IFRS 8 managementapproach increased.

The principle underpinning IFRS 8 is to enable users to interpret a company’sposition and performance based on internal reports that are regularly reviewed by theCODM. This study’s findings show that many Jordanian listed companies did notidentify who the CODM was or which internal function it related to. Of the remainingcompanies, there was variation in the identity of the CODM, but the function waspredominantly associated with the entity’s CEO. This is an interesting result asinterpretation of company performance and position “through the eyes ofmanagement” must depend on user appreciation of who or what the CODM is andtherefore which management perspective is being presented. Certainly, in the UK,the FRRP (2010) has expressed concerns that preparers of financial information needto be clear on who the CODM is to ensure that information which is communicated tousers can be understood and interpreted appropriately.

There are several limitations to the current paper. For example, the results of thisstudy relate to companies from only one country – Jordan; investigations need to beconducted in other countries to see if similar findings emerge. In addition, the currentstudy only looks at the impact of IFRS 8 in its first year of operation for the financialstatements of Jordanian companies; analysis of data from subsequent years are neededbefore any trend in the findings can be confirmed. Moreover, the disclosure indexmethod used involved some element of judgment about the items mandated by the twostandards on segmental disclosure. In addition, other factors (beyond the introductionof IFRS 8) may have influenced changes in disclosure practices but are not consideredhere. Nevertheless, despite these limitations, the current paper provides someinteresting insights upon which others can build.

Indeed, a number of possible future avenues for future research emerge from thefindings of the current study: first, investigating the usefulness of operating segmentinformation reviewed internally by the CODM relative to the data supplied underIAS 14R could be undertaken; second, examining the level of competitive disadvantagederived from segmental information published under IFRS 8 needs to be investigated;and third, a longitudinal study of compliance with the new standard of segmentalreporting would be helpful to see if the disclosure trends identified in this papercontinue into the future. These future avenues of research could build on the researchresults that are reported for Jordanian companies in the current paper.

Notes

1. SFAS 131 was issued in 1997 and superseded SFAS 14.

2. Although IFRS 8 requires segments to be identified according to reports that are regularlyreviewed by the CODM, it does not specify who the CODM should be. Clearly, this term wasborrowed from the US standard – SFAS 131.

3. The Securities Law of 2002 penalised non-compliance with IASs by imprisonment for aterm of one to three years, and by a fine of between 1,000-10,000 JD for any person thatprepared and published financial statements which did not provide a true and fair viewof the company’s financial position, conveyed incorrect information, incorporatedincorrect statements in the report of the board of directors or in the report of its auditors,

85

Jordanian listedcompanies

or concealed information and clarifications which should be declared according to the law(Article 278).

4. The ASE groups listed companies into the first market and the second market. The formerare larger and more established entities (Haddad, 2005).

5. This Law was updated in 2002; there are two major amendments for the AccountancyProfession under Law 2002. Under this legislation, JACPA became a self-funded andadministratively independent organization (Article 7). JACPAwas also attached to the HighCouncil of the Accounting Profession which gave it new powers such as responsibility todraft its regulations, disciplinary authority over its own members, and the right to inspect itsmembers’ working papers (Abdullatif and Al-Khadash, 2010).

6. According to the Companies Act 1989, the financial statements had to be prepared inaccordance with GAAP; however, the Act did not mention which specific GAAP was to befollowed.

7. Al-Akra et al. (2010b) found that foreign investments accompanying privatisation had asignificant impact on the levels of accounting disclosure in Jordan. Specifically, they foundthat the privatisation programme conducted by the government increased the level ofvoluntary disclosure by Jordanian listed companies.

8. This JCM contains three institutions, the Jordanian Securities Commission, the ASE and theSecurities Depository Centre, in order to improve the investment climate within Jordan.

9. It should be noted that Crawford et al. (2010) findings relate to interviews which took placeprior to the introduction of IFRS 8.

10. However, there is some evidence that problems emerged when SFAS 131 was adopted; Hopeand Thomas (2008) found that geographic disclosures decreased following the introductionof SFAS 131, and managers become “more willing to expand international operations eventhough it lead to lower profitability” (p. 623).

11. Herrmann and Thomas (2000b) purpose was to compare the segment reporting disclosuresunder SFAS No. 131 (1998) with those reported the previous year (1997) under SFAS No.14.

12. Of course, the experience of Jordan might be different from the experience in the USAbecause compliance among US firms with segmental disclosure requirements was higherprior to the new standard being introduced relative to the practice which existed in Jordan.

13. The second market companies are mostly family-owned small local firms which tend tofocus on one business activity and operate in one geographic area; thus, they have fewersegmental disclosures than their first market counterparts (Haddad, 2005; Hutaibat, 2005;Suwaidan et al., 2007). Moreover, a pilot study of 50 companies that listed in the secondmarket revealed that none disclosed any segmental information.

14. The banks sub-sector is regulated by CBJ. However, the banks do disclose segmentalinformation in their annual reports and accounts. Further, results based on a pilot study of 46annual reports for 2008 accounts performed before selecting companies for inclusion in thesample of this study found that the financial statements of banks were similar to those ofother non-insurance firms listed in the first market.

15. The spreadsheet contained a checklist of segmental items determined from an analysis of therequirements of both IAS 14R and IFRS 8.

16. Some of the primary segment items which had to be published under IAS 14R were alsorequired disclosures for operating segments under IFRS 8 such as segmental profit, assets,and liabilities.

17. To ensure that the index included all of the segmental items which the Jordanian companiesin this study provided, a pilot study of 46 annual reports from first market companies

86

JAEE2,1

was undertaken for 2008 and 2009. This step also ensured that the final index wasappropriate for the companies listed in different sectors of the ASE (i.e. banking, industrial,services).

18. These firms were not single segment firms as they published details about more than onebusiness activity/geographic area under IAS 14R. However, they did not specify whichdisclosures related to their primary or secondary segments.

19. This is an issue which is not explored in the current research but could be examined in anyfollow-up investigation.

20. This audit company was not one of the Big 4 firm of auditors.

21. The w2 test shows that there are differences between sectors in 2008 (w2¼ 38.432, p-value

o0.0005) and 2009 (w2¼ 34.433, p-valueo0.0005). Specifically, most of the difference relatesto the financial sector especially for banking where disclosure increases were differentfrom others.

22. The mean number of business segments for UK companies was 4.28 under IFRS 8 comparedto 3.91 under IAS 14R (Crawford et al., 2010).

23. AWilcoxon signed-rank test shows that the difference in the number of business segmentsdisclosed was significant at the 10 per cent level (p-value 0.077).

24. A Wilcoxon signed-rank revealed that difference in the number of geographic segmentsdisclosed was significant at the 10 per cent level (p-value 0.083). Most of this differencerelated to companies in the financial sector (p-value 0.023).

25. The mean number of geographic segments for UK companies was 4.40 under IFRS 8compared to 3.89 under IAS 14R (Crawford et al., 2010).

26. A Wilcoxon signed-rank test shows that the difference in the number of segmental itemsdisclosed was significant at the 5 per cent level (p-value o0.0005). Most of this significantdifference related to firms in the financial and industrial sectors (p-value 0.002 and 0.001,respectively).

27. The list in panel C of Table V is in a slightly different order from the list in the Appendix toaid the display of the results. In particular, the list in panel C of Table V has two headings:first, requirements of IAS 14R and second, voluntary items that includes IFRS 8 items ifreviewed by the CODM and voluntary segmental items from the Appendix list.

28. By voluntary, we mean items where disclosure was contingent on whether or not they werereported to the CODM.

29. The definition of locations and names of geographic areas in the Table VII are those usedby the sample companies in their annual reports of 2008 and 2009.

30. Disclosure of the identity of the CODMwas only investigated in the DF group of firms as thisgroup complies with IFRS 8. However, it should be noted that the annual reports for the 20firms in the UD group during 2009 were also examined, but none of these companiesdisclosed information about the identity of the CODM. This finding is in accordance with therequirements of IFRS 8 since the CODM only be identified where information aboutoperating segments is disclosed; there is no need to identify the CODM when no operatingsegments are identified.

References

Abdullatif, M. and Al-Khadash, H.A. (2010), “Putting audit approaches in context: the caseof business risk audits in Jordan”, International Journal of Auditing, Vol. 14 No. 1,pp. 1-24.

87

Jordanian listedcompanies

Al-Akra, M., Eddie, I.A. and Jahangir, A.M. (2010a), “The influence of the introduction ofaccounting disclosure regulation on mandatory disclosure compliance: evidence fromJordan”, The British Accounting Review, Vol. 42 No. 3, pp. 170-86.

Al-Akra, M., Eddie, I.A. and Jahangir, A.M. (2010b), “The association between privatisation andvoluntary disclosure: evidence from Jordan”, Accounting and Business Research, Vol. 40No. 1, pp. 55-74.

Al-Akra, M., Jahangir, A.M. and Marashdeh, O. (2009), “Development of accounting regulation inJordan”, International Journal of Accounting, Vol. 44 No. 2, pp. 163-86.

Balakrishnan, R., Harris, T.S. and Sen, P.K. (1990), “The predictive ability of geographic segmentdisclosures”, Journal of Accounting Research, Vol. 28 No. 2, pp. 305-25.

Behn, B.K., Nichols, N.B. and Street, D.L. (2002), “The predictive ability of geographic segmentdisclosures by US companies: SFAS No. 131 vs SFAS No. 14”, Journal of InternationalAccounting Research, Vol. 1 No. 1, pp. 31-44.

Cooke, T.E. (1989), “Voluntary corporate disclosure by Swedish companies”, Journal ofInternational Financial Management & Accounting, Vol. 1 No. 2, pp. 171-95.

Cooke, T.E. and Wallace, R.S.O. (1989), “Global surveys of corporate disclosure practices andaudit firms: a review essay”, Accounting and Business Research, Vol. 20 No. 77, pp. 47-57.

Crawford, L., Extance, H., Heillar, C.V. and Power, D.M. (2010), “IFRS 8 adoption linked tochanges in the number of segments reported”, CA Magazine, ICAS, Edinburgh, pp. 56-7.

Edwards, P. and Smith, R.A. (1996), “Competitive disadvantage and voluntary disclosures: thecase of segmental reporting”, British Accounting Review, Vol. 28 No. 2, pp. 155-72.

Emmanuel, C.R., Garrod, N.W., Mccallum, C. and Rennie, E.D. (1999), “The impact of SSAP 25and the 10%materiality rule on segment disclosure in the UK”, British Accounting Review,Vol. 31 No. 2, pp. 127-49.

Ettredge, M., Richardson, V.J. and Scholz, S. (2002), “Dissemination of information for investorsat corporate web sites”, Journal of Accounting and Public Policy, Vol. 21 Nos 4-5, pp. 357-69.

Ettredge, M.L., Soo Young, K., Smith, D.B. and Zarowin, P.A. (2005), “The impact of SFAS No. 131business segment data on the market’s ability to anticipate future earnings”, AccountingReview, Vol. 80 No. 3, pp. 773-804.

European Commission (2007), Endorsement of IFRS 8 Operating Segments, Analysis of PotentialEffects, European Commission, Brussels.

Financial Reporting Review Panel (FRRP) (2010), “FRRP highlights the challenge ofimplementing new segmental reporting requirements”, PN 124, available at:www.frc.org.uk/frrp/press/pub2203.html (accessed 11 November 2010).

Gray, P.S., Williamson, J.B., Karp, D.A. and Dalphin, J.R. (2007), The Research Imagination: AnIntroduction to Qualitative and Quantitative Methods, Cambridge University Press, NewYork, NY.

Haddad, A. (2005), “The impact of voluntary disclosure level on the cost of equity capital in anemerging capital market: the case of the Amman stock exchange”, unpublished thesis,School of Management, University of East Anglia, Anglia.

Herrmann, D. and Thomas, W. (2000a), “A model of forecast precision using segment disclosures:implications for SFAS no. 131”, Journal of International Accounting, Auditing andTaxation, Vol. 9 No. 1, pp. 1-18.

Herrmann, D. and Thomas, W. (2000b), “An analysis of segment disclosures under SFAS No. 131and SFAS No. 14”, Accounting Horizons, Vol. 14 No. 3, pp. 287-302.

The Holy Land Insurance Company (2009), “Annual Report of 2009”, The Holy Land InsuranceCompany, Amman.

Hope, O.K. and Thomas, W.B. (2008), “Managerial empire building and firm disclosure”, Journalof Accounting Research, Vol. 46 No. 3, pp. 591-626.

88

JAEE2,1

Hutaibat, K. (2005), “Management accounting practices in Jordan – a contingency approach”,unpublished thesis, School of Economics, Finance and Management, University of Bristol,Bristol.

International Accounting Standards Committee (IASC) (1997), “International AccountingStandard No. 14 (revised) segment reporting”, IASC, London.

International Accounting Standards Board (IASB) (2006a), available at: www.iasb.co.uk/current-projects/IASBProjects/SegmentReporting/CommentLetters (accessed 12 November 2010).

International Accounting Standards Board (IASB) (2006b), “International Financial ReportingStandard No. 8, operating segments”.

Jermakowicz, E.K. and Gornik-Tomaszewski, S. (2006), “Implementing IFRS from theperspective of EU publicly traded companies”, Journal of International Accounting,Auditing and Taxation, Vol. 15 No. 2, pp. 170-96.

Marston, C.L. and Shrives, P.J. (1991), “The use of disclosure indices in accounting research: areview article”, The British Accounting Review, Vol. 23 No. 3, pp. 195-210.

Piro, T. (1998), The Political Economy of Market Reform in Jordan, Rowman & LittlefieldPublishers Inc, Oxford.

Rennie, E.D. and Emmanuel, C.R. (1992), “Segmental disclosure practice: thirteen years on”,Accounting and Business Research, Vol. 22 No. 86, pp. 151-60.

Report on the Observance of Standards and Codes (ROSC) (2004), “Hashemite kingdom of Jordan( Jordan) accounting and auditing”, ROSA, 10 June.

Street, D.L. and Nichols, N.B. (2002), “LOB and geographic segment disclosures: an analysis ofthe impact of IAS 14 revised”, Journal of International Accounting, Auditing and Taxation,Vol. 11 No. 2, pp. 91-113.

Street, D.L., Nichols, N.B. and Gray, S.J. (2000), “Segment disclosures under SFAS No. 131: hasbusiness segment reporting improved?”, Accounting Horizons, Vol. 14 No. 3, pp. 259-85.

Suwaidan, M. (1997), “Voluntary disclosure of accounting information: the case of Jordan”,unpublished thesis, Department of Accountancy, University of Aberdeen, Aberdeen.

Suwaidan, M., Omari, A. and Abed, S. (2007), “The segmental information disclosures in theannual reports of the Jordanian industrial companies: a filed study”, Commercial Collegefor Scientific Research: Alexandria University, Vol. 2 No. 44, pp. 1-48.

Talha, M., Sallehhuddin, A. and Mohammad, J. (2006), “Changing pattern of competitivedisadvantage from disclosing financial information: a case study of segmental reportingpractice in Malaysia”, Managerial Auditing Journal, Vol. 21 No. 3, pp. 265-74.

Talha, M., Sallehhudin, A. and Mohammad, J. (2007), “Competitive disadvantage and segmentdisclosure: evidence fromMalaysian listed companies”, International Journal of Commerceand Management, Vol. 17 Nos 1/2, pp. 105-24.

Tsakumis, G.T., Doupnik, T.S. and Sesse, L.P. (2006), “Competitive harm and geographic areadisclosure under SFAS 131”, Journal of International Accounting, Auditing and Taxation,Vol. 15 No. 1, pp. 32-47.

United Insurance Company (2008), “Annual Report of 2008”, United Insurance Company, Amman.

Veron, N. (2007), “EU adoption of the IFRS 8 standard on operating segments”, Note for theECON Committee of the European Parliament, Bruegel Institute, Bruegel, 21 September.

Further reading

Jordanian Securities Commission ( JSC) (1997), “The securities law No. 23”, Amended later bySecurities Law of 2002, JSC, Amman.

Jordanian Securities Commission ( JSC) (2002), “The securities law No. 76”, JSC, Amman.

Jordanian Securities Commission ( JSC) (2004), Instructions of Issuing Companies Disclosure,Accounting and Auditing Standards for the Year 2004, The Board of Commissioners,Amman.

89

Jordanian listedcompanies

Appendix

Corresponding authorDavid M. Power can be contacted at: [email protected]

IAS 14R requirementsPrimary segmentRevenue (external)Revenue (internal)ProfitAssetsBasis of inter-segment pricingLiabilitiesCapital expendituresDepreciation and amortisationOther non-cash expensesProfit from associates and joint venturesReconciliation to consolidated accounts

Secondary segmentRevenue (external)AssetsCapital expenditures

OtherType of products/services of business classesComposition of geographic segments

IFRS 8: if reviewed by the CODMProfit for secondary segmentLiabilities for secondary segmentDepreciation and amortisation for secondary segmentOther non-cash expenses for secondary segmentReconciliation to consolidated accounts for secondary segmentRevenue (internal) for secondary segmentBasis of inter-segment pricing for secondary segmentProfit from associates and joint ventures for secondary segmentBasis of measurementInterest revenueInterest expenseIncome tax expenseFactors used to identify the entity’s segmentsEntity-wide (major customers)Entity-wide (products and services)Voluntary segmental itemsNet cash flowReservesDirect administrative expensesInvestmentsIntangible assets

Table AI.Disclosure index

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

90

JAEE2,1