Embed Size (px)

Citation preview

IFRS UpdateSustainability Reporting

21 September, 2021

IFRS Update – Sustainability Reporting - September 2021 2

Agenda

Lennart NordqvistPartner Risk Advisory - Sustainability

Mattias OverudDirector AFR

• Overview of ESG trends

• EU Taxonomy & CSRD

• Climate & Climate Risk

• Q&A

IFRS Update – Sustainability Reporting - September 2021 33

Significantly increased expectations

Sustainable Finance

Market Society

Regulators/Authorities

IFRS Update – Sustainability Reporting - September 2021 44

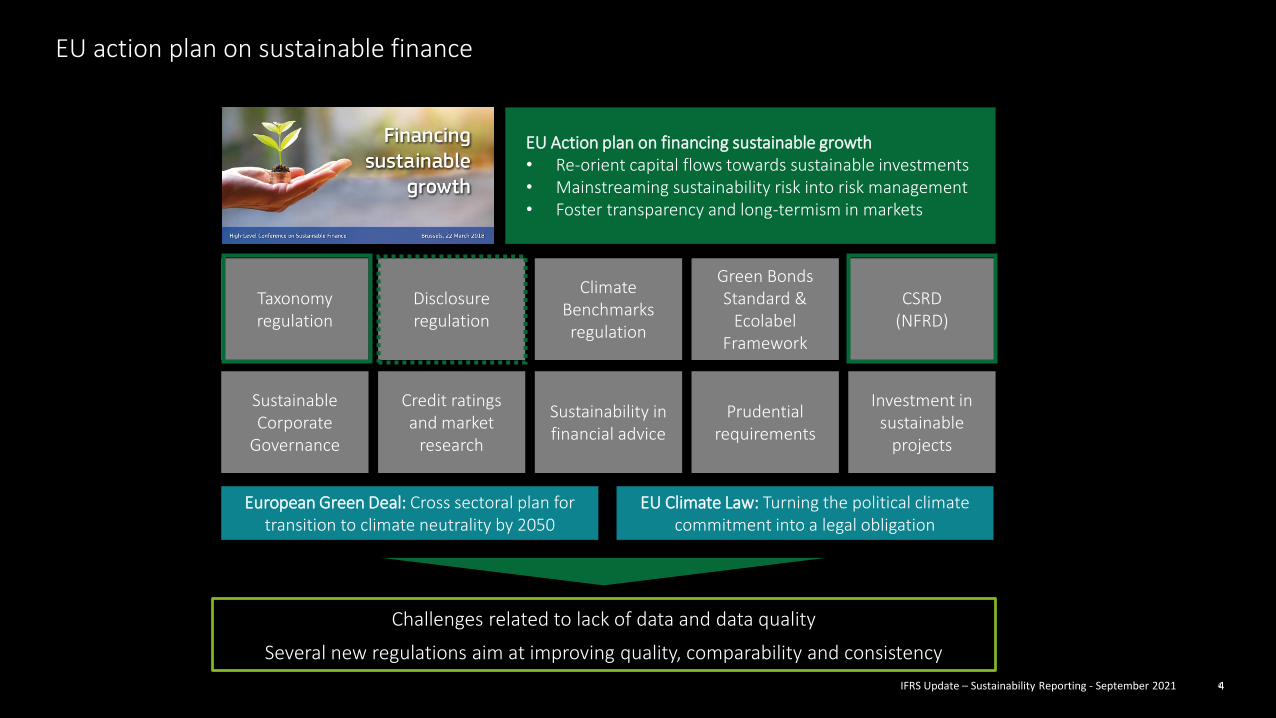

EU action plan on sustainable finance

Taxonomy regulation

Disclosure regulation

Climate Benchmarks regulation

Investment in sustainable

projects

Sustainable Corporate

Governance

Credit ratings and market

research

Sustainability in financial advice

EU Action plan on financing sustainable growth• Re-orient capital flows towards sustainable investments• Mainstreaming sustainability risk into risk management• Foster transparency and long-termism in markets

Green Bonds Standard &

Ecolabel Framework

CSRD(NFRD)

Prudential requirements

European Green Deal: Cross sectoral plan for transition to climate neutrality by 2050

EU Climate Law: Turning the political climate commitment into a legal obligation

Challenges related to lack of data and data quality

Several new regulations aim at improving quality, comparability and consistency

IFRS Update – Sustainability Reporting - September 2021 55

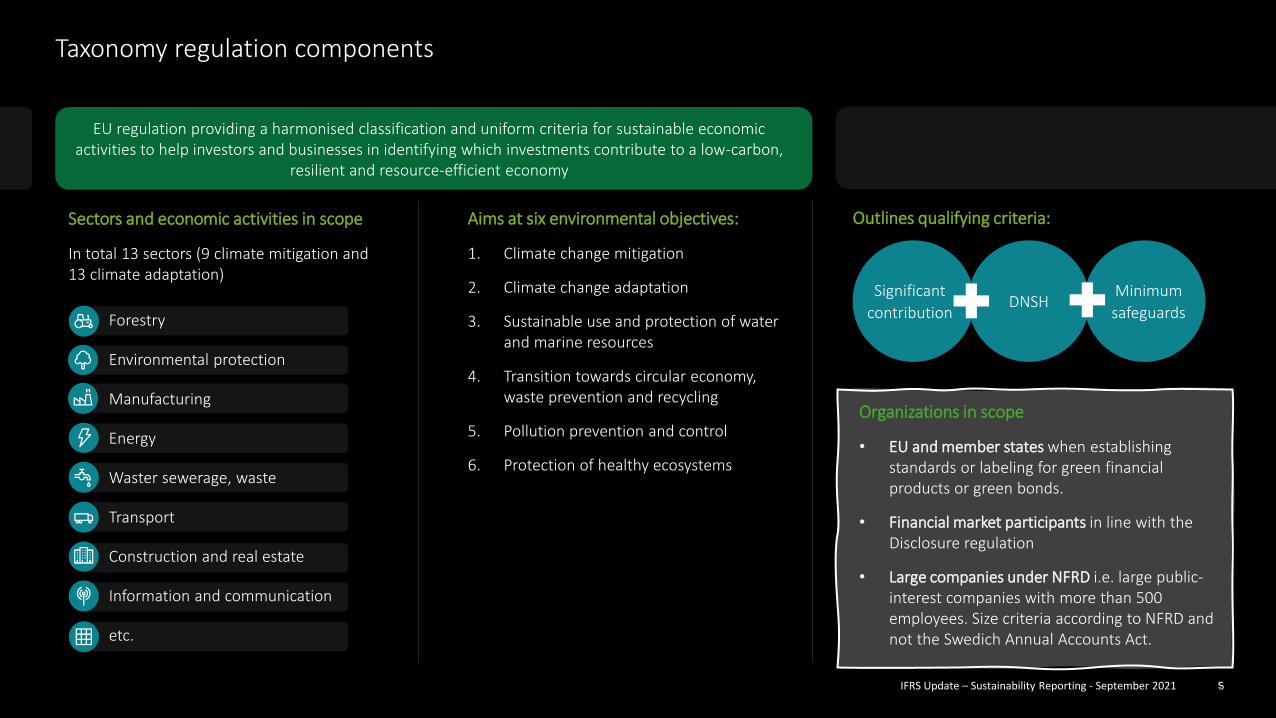

Taxonomy regulation components

EU regulation providing a harmonised classification and uniform criteria for sustainable economic activities to help investors and businesses in identifying which investments contribute to a low-carbon,

resilient and resource-efficient economy

Significant

contributionDNSH

Minimum

safeguards

Outlines qualifying criteria:Aims at six environmental objectives:

1. Climate change mitigation

2. Climate change adaptation

3. Sustainable use and protection of water and marine resources

4. Transition towards circular economy, waste prevention and recycling

5. Pollution prevention and control

6. Protection of healthy ecosystems

Sectors and economic activities in scope

In total 13 sectors (9 climate mitigation and 13 climate adaptation)

Forestry

Environmental protection

Manufacturing

Energy

Waster sewerage, waste

Transport

Construction and real estate

Information and communication

etc.

Organizations in scope

• EU and member states when establishingstandards or labeling for green financialproducts or green bonds.

• Financial market participants in line with the Disclosure regulation

• Large companies under NFRD i.e. large public-interest companies with more than 500 employees. Size criteria according to NFRD and not the Swedich Annual Accounts Act.

IFRS Update – Sustainability Reporting - September 2021 66

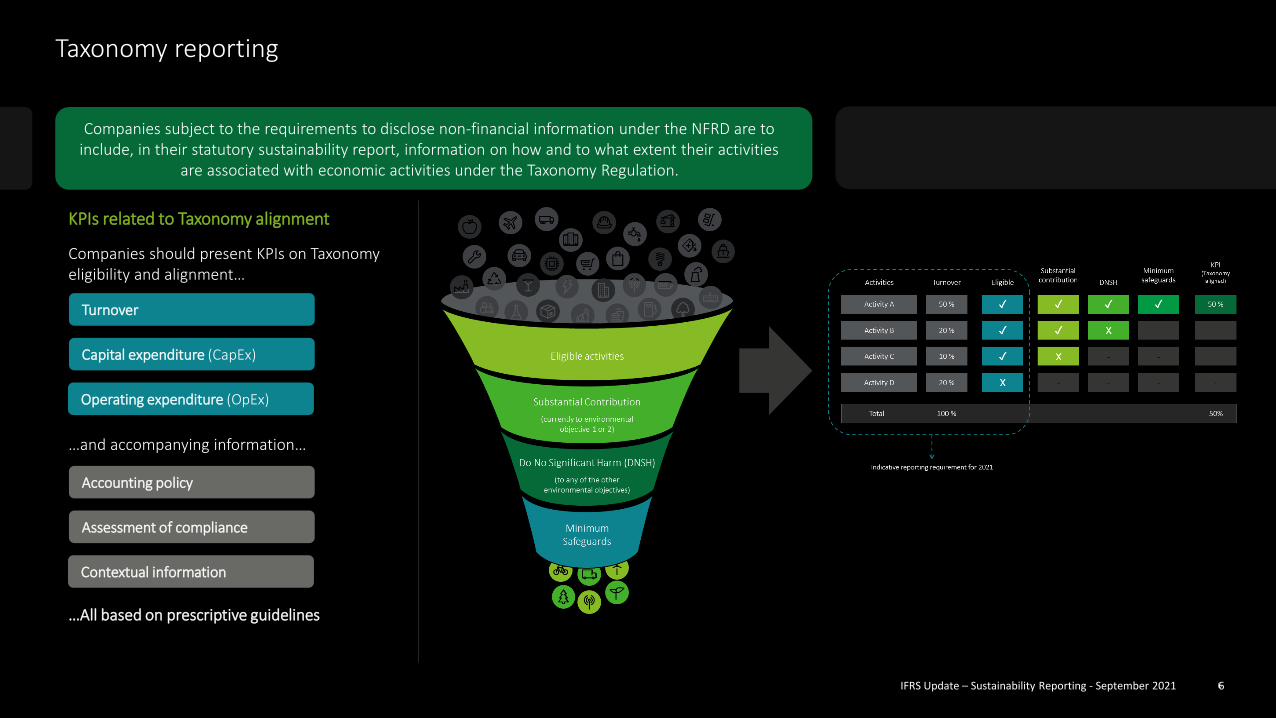

Taxonomy reporting

Companies subject to the requirements to disclose non-financial information under the NFRD are to include, in their statutory sustainability report, information on how and to what extent their activities

are associated with economic activities under the Taxonomy Regulation.

KPIs related to Taxonomy alignment

Companies should present KPIs on Taxonomy eligibility and alignment…

…and accompanying information…

…All based on prescriptive guidelines

Turnover

Capital expenditure (CapEx)

Operating expenditure (OpEx)

Accounting policy

Assessment of compliance

Contextual information

IFRS Update – Sustainability Reporting - September 2021 7

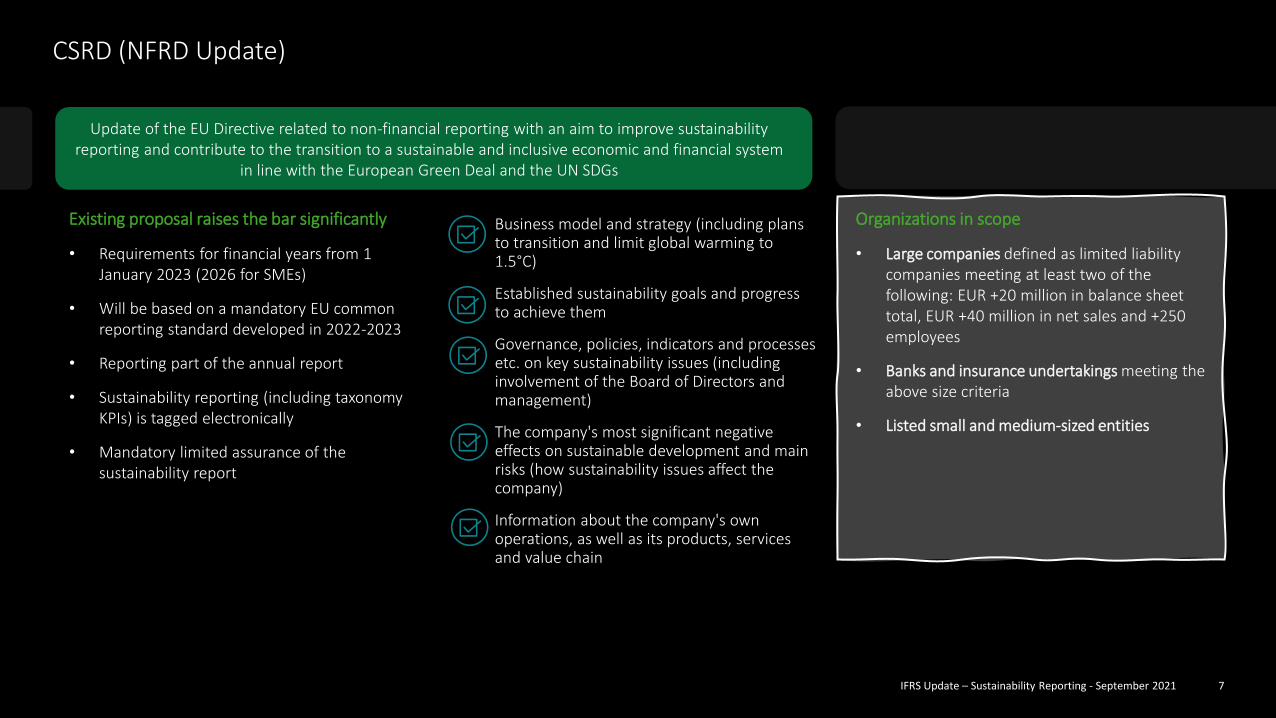

CSRD (NFRD Update)

Organizations in scope

• Large companies defined as limited liability companies meeting at least two of the following: EUR +20 million in balance sheet total, EUR +40 million in net sales and +250 employees

• Banks and insurance undertakings meeting the above size criteria

• Listed small and medium-sized entities

Business model and strategy (including plans to transition and limit global warming to 1.5°C)

Established sustainability goals and progress to achieve them

Governance, policies, indicators and processes etc. on key sustainability issues (including involvement of the Board of Directors and management)

The company's most significant negative effects on sustainable development and main risks (how sustainability issues affect the company)

Information about the company's own operations, as well as its products, services and value chain

Existing proposal raises the bar significantly

• Requirements for financial years from 1 January 2023 (2026 for SMEs)

• Will be based on a mandatory EU common reporting standard developed in 2022-2023

• Reporting part of the annual report

• Sustainability reporting (including taxonomy KPIs) is tagged electronically

• Mandatory limited assurance of the sustainability report

Update of the EU Directive related to non-financial reporting with an aim to improve sustainability reporting and contribute to the transition to a sustainable and inclusive economic and financial system

in line with the European Green Deal and the UN SDGs

IFRS Update – Sustainability Reporting - September 2021 88

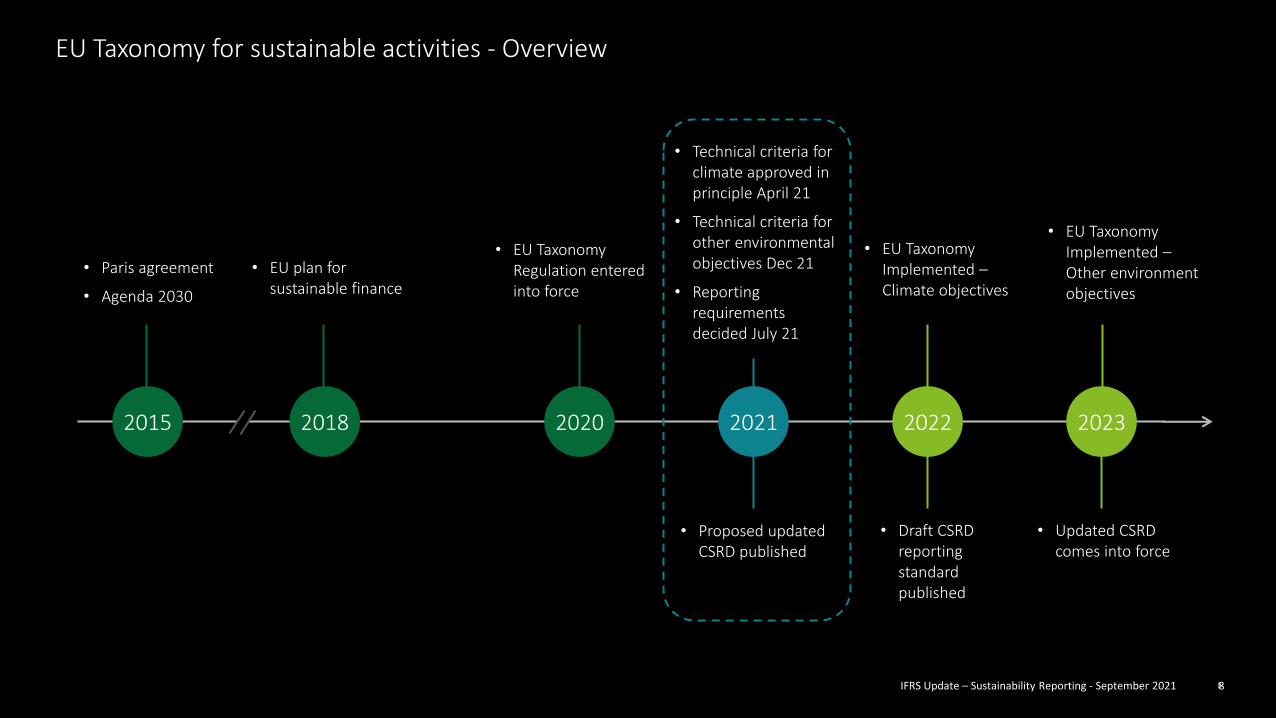

EU Taxonomy for sustainable activities - Overview

2015 2022 20232018 20212020

• Paris agreement

• Agenda 2030

• EU plan for sustainable finance

• EU Taxonomy Regulation entered into force

• Technical criteria for climate approved in principle April 21

• Technical criteria for other environmental objectives Dec 21

• Reporting requirements decided July 21

• Proposed updated CSRD published

• EU Taxonomy Implemented –Climate objectives

• EU Taxonomy Implemented –Other environment objectives

• Updated CSRD comes into force

• Draft CSRD reporting standardpublished

IFRS Update – Sustainability Reporting - September 2021 99

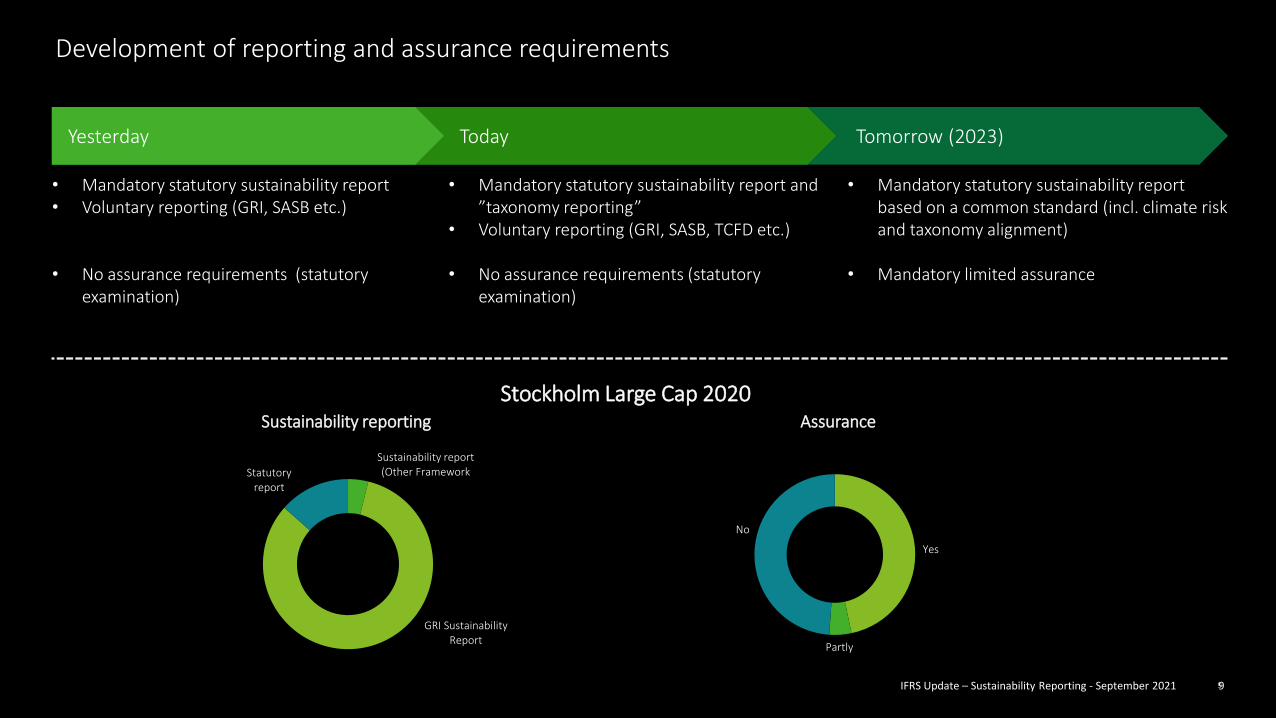

Development of reporting and assurance requirements

Yes

Partly

No

Sustainability report (Other Framework

GRI Sustainability Report

Statutory report

• Mandatory statutory sustainability report• Voluntary reporting (GRI, SASB etc.)

• No assurance requirements (statutory examination)

• Mandatory statutory sustainability report and ”taxonomy reporting”

• Voluntary reporting (GRI, SASB, TCFD etc.)

• No assurance requirements (statutory examination)

• Mandatory statutory sustainability report based on a common standard (incl. climate risk and taxonomy alignment)

• Mandatory limited assurance

Stockholm Large Cap 2020Sustainability reporting Assurance

Today Tomorrow (2023)Yesterday

IFRS Update – Sustainability Reporting - September 2021 1010

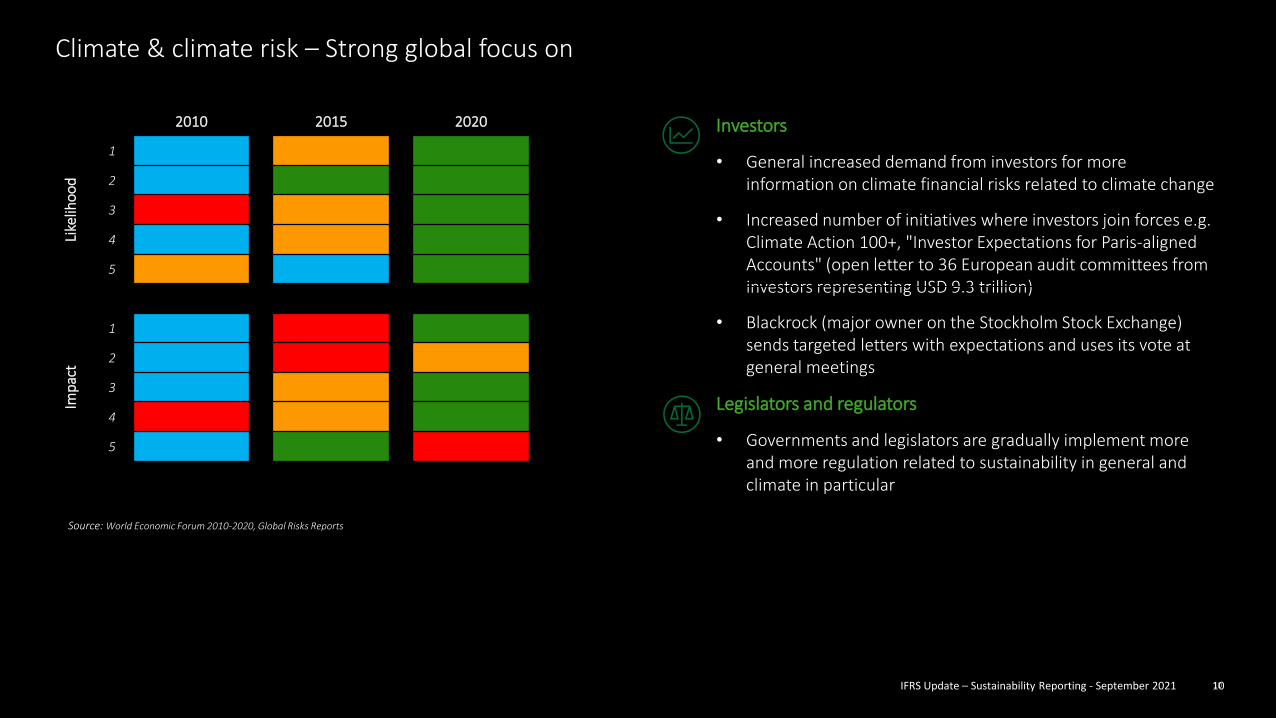

Climate & climate risk – Strong global focus on

Source: World Economic Forum 2010-2020, Global Risks Reports

2010 2015 2020

Like

liho

od

1

2

3

4

5

Imp

act

1

2

3

4

5

Investors

• General increased demand from investors for more information on climate financial risks related to climate change

• Increased number of initiatives where investors join forces e.g. Climate Action 100+, "Investor Expectations for Paris-aligned Accounts" (open letter to 36 European audit committees from investors representing USD 9.3 trillion)

• Blackrock (major owner on the Stockholm Stock Exchange) sends targeted letters with expectations and uses its vote at general meetings

Legislators and regulators

• Governments and legislators are gradually implement more and more regulation related to sustainability in general and climate in particular

IFRS Update – Sustainability Reporting - September 2021 11

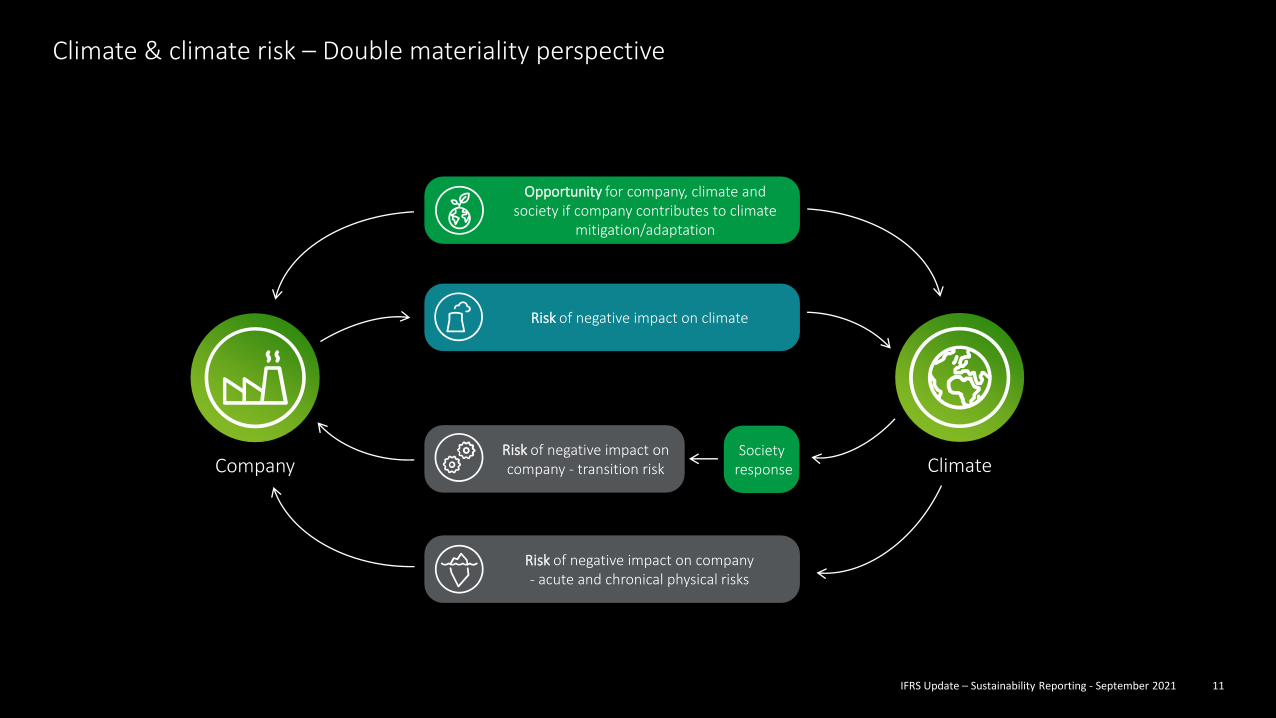

Climate & climate risk – Double materiality perspective

Company Climate

Opportunity for company, climate and society if company contributes to climate

mitigation/adaptation

Risk of negative impact on climate

Risk of negative impact on company - acute and chronical physical risks

Society response

Risk of negative impact on company - transition risk

IFRS Update – Sustainability Reporting - September 2021 12

Does IFRS Standards address issues that relate to climate-change risks today?

• Companies must consider climate-related matters in applying IFRS Standards when the effect of those matters is material in the context of the financial statements taken as a whole.

• IAS 1 Presentation of Financial Statements contains some overarching requirements that could be relevant when considering climate-related matters. For example, a company shall disclose information not specifically required by IFRS Standards and not presented elsewhere in the financial statements but that is relevant to an understanding of any of the financial statements. Also, company´s are required to consider whether any material information is missing from its financial statements— ie a company is required to consider whether to provide additional disclosures when compliance with the specific requirements in IFRS Standards is insufficient to enable investors to understand the impact of particular transactions, other events and conditions on the company’s financial position and financial performance.

• Companies will therefore need to consider whether to provide additional disclosures when compliance with the specific requirements in IFRS Standards is insufficient to enable investors to understand the impact of climate-related matters on the company’s financial position and financial performance. These overarching requirements in IAS 1 may be especially relevant for companies whose financial position or financial performance is particularly affected by climate-related matters.

IFRS Update – Sustainability Reporting - September 2021 13

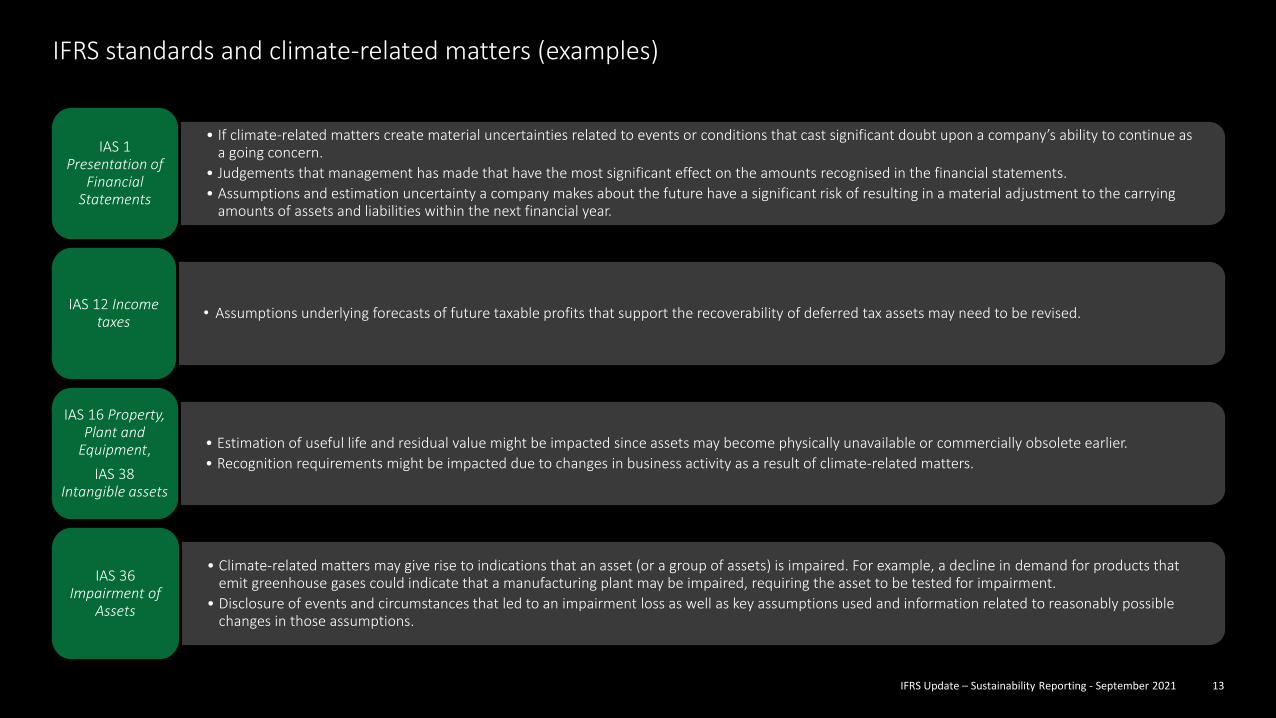

IFRS standards and climate-related matters (examples)

• If climate-related matters create material uncertainties related to events or conditions that cast significant doubt upon a company’s ability to continue as a going concern.

• Judgements that management has made that have the most significant effect on the amounts recognised in the financial statements.

• Assumptions and estimation uncertainty a company makes about the future have a significant risk of resulting in a material adjustment to the carrying amounts of assets and liabilities within the next financial year.

IAS 1 Presentation of

FinancialStatements

• Assumptions underlying forecasts of future taxable profits that support the recoverability of deferred tax assets may need to be revised.IAS 12 Income

taxes

• Estimation of useful life and residual value might be impacted since assets may become physically unavailable or commercially obsolete earlier.

• Recognition requirements might be impacted due to changes in business activity as a result of climate-related matters.

IAS 16 Property, Plant and

Equipment,

IAS 38 Intangible assets

• Climate-related matters may give rise to indications that an asset (or a group of assets) is impaired. For example, a decline in demand for products that emit greenhouse gases could indicate that a manufacturing plant may be impaired, requiring the asset to be tested for impairment.

• Disclosure of events and circumstances that led to an impairment loss as well as key assumptions used and information related to reasonably possiblechanges in those assumptions.

IAS 36 Impairment of

Assets

IFRS Update – Sustainability Reporting - September 2021 14

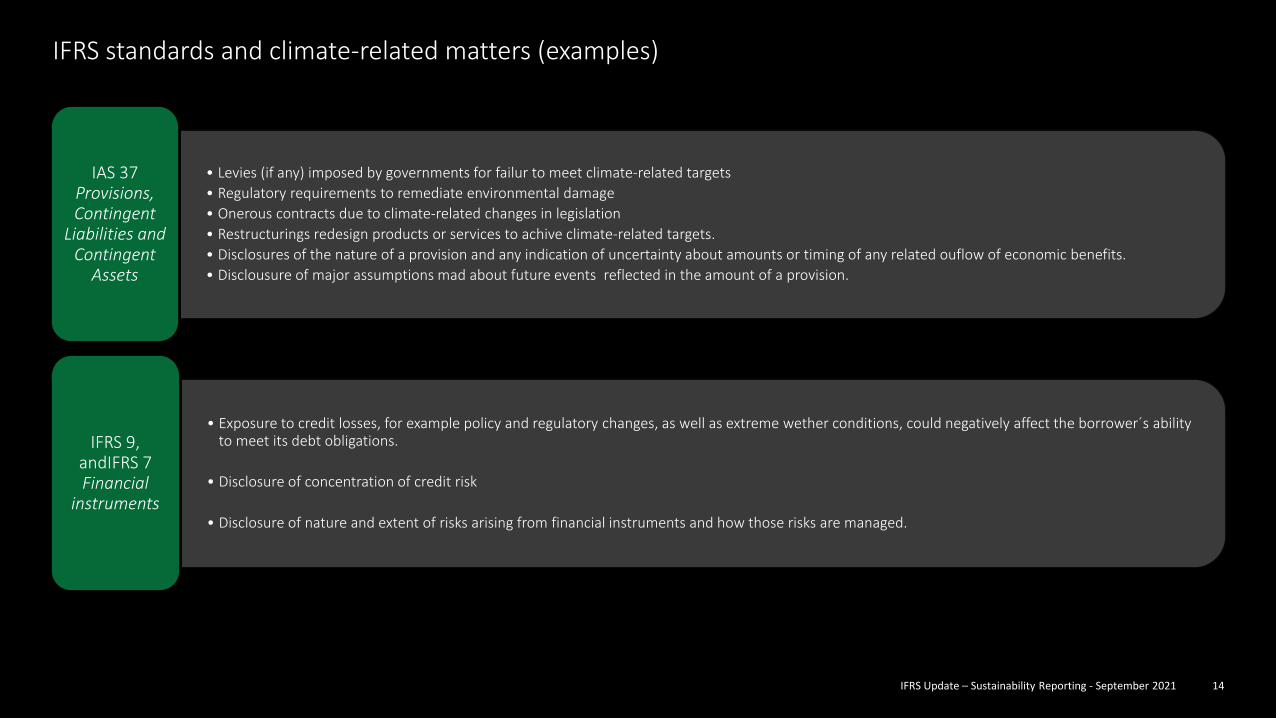

IFRS standards and climate-related matters (examples)

• Levies (if any) imposed by governments for failur to meet climate-related targets

• Regulatory requirements to remediate environmental damage

• Onerous contracts due to climate-related changes in legislation

• Restructurings redesign products or services to achive climate-related targets.

• Disclosures of the nature of a provision and any indication of uncertainty about amounts or timing of any related ouflow of economic benefits.

• Disclousure of major assumptions mad about future events reflected in the amount of a provision.

IAS 37 Provisions, Contingent

Liabilities and Contingent

Assets

• Exposure to credit losses, for example policy and regulatory changes, as well as extreme wether conditions, could negatively affect the borrower´s abilityto meet its debt obligations.

• Disclosure of concentration of credit risk

• Disclosure of nature and extent of risks arising from financial instruments and how those risks are managed.

IFRS 9, andIFRS 7 Financial

instruments

IFRS Update – Sustainability Reporting - September 2021 15

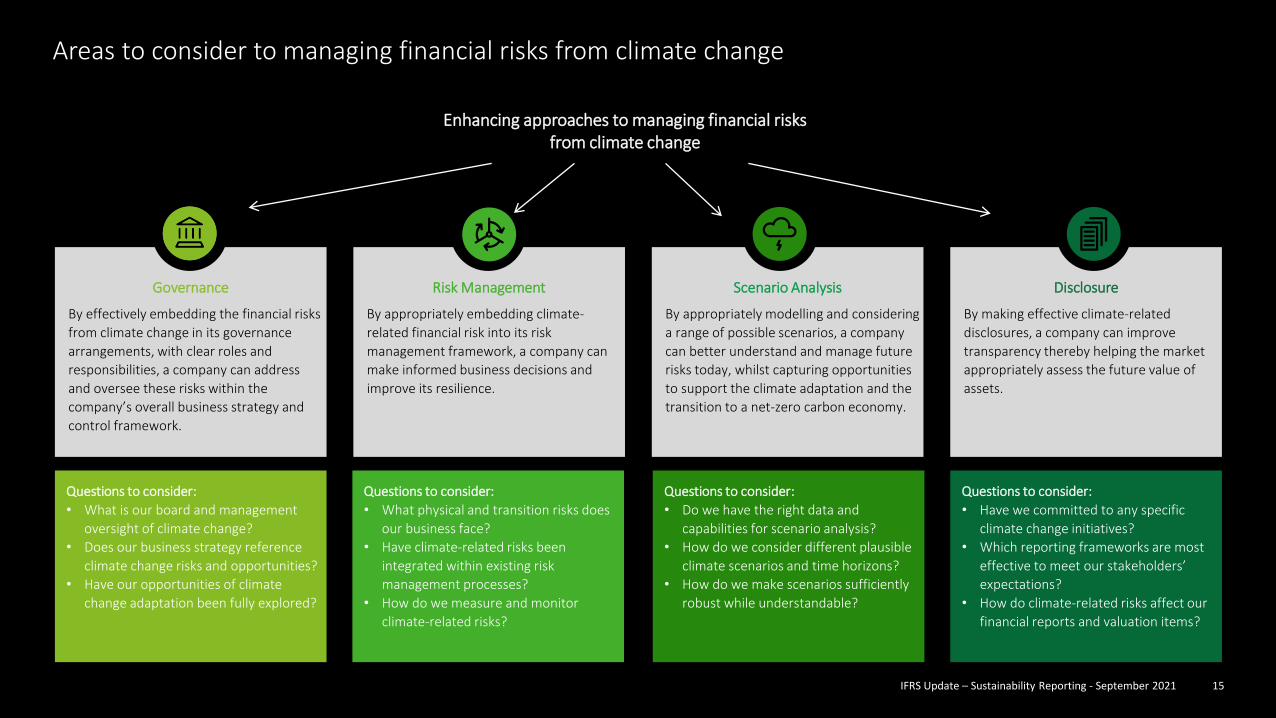

Areas to consider to managing financial risks from climate change

Disclosure

By making effective climate-related

disclosures, a company can improve

transparency thereby helping the market

appropriately assess the future value of

assets.

Scenario Analysis

By appropriately modelling and considering

a range of possible scenarios, a company

can better understand and manage future

risks today, whilst capturing opportunities

to support the climate adaptation and the

transition to a net-zero carbon economy.

Risk Management

By appropriately embedding climate-

related financial risk into its risk

management framework, a company can

make informed business decisions and

improve its resilience.

Governance

By effectively embedding the financial risks

from climate change in its governance

arrangements, with clear roles and

responsibilities, a company can address

and oversee these risks within the

company’s overall business strategy and

control framework.

Enhancing approaches to managing financial risks from climate change

Questions to consider:

• What is our board and management

oversight of climate change?

• Does our business strategy reference

climate change risks and opportunities?

• Have our opportunities of climate

change adaptation been fully explored?

Questions to consider:

• What physical and transition risks does

our business face?

• Have climate-related risks been

integrated within existing risk

management processes?

• How do we measure and monitor

climate-related risks?

Questions to consider:

• Do we have the right data and

capabilities for scenario analysis?

• How do we consider different plausible

climate scenarios and time horizons?

• How do we make scenarios sufficiently

robust while understandable?

Questions to consider:

• Have we committed to any specific

climate change initiatives?

• Which reporting frameworks are most

effective to meet our stakeholders’

expectations?

• How do climate-related risks affect our

financial reports and valuation items?

IFRS Update – Sustainability Reporting - September 2021 1616

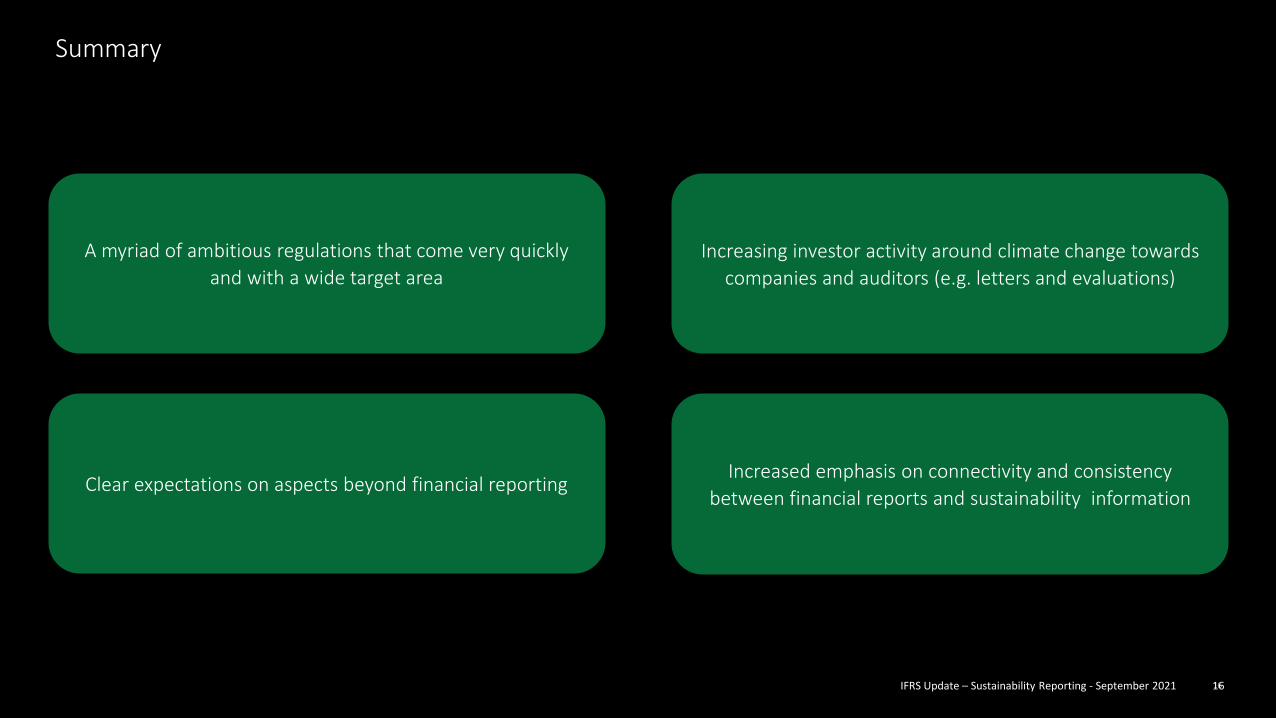

Summary

A myriad of ambitious regulations that come very quickly

and with a wide target area

Increasing investor activity around climate change towards

companies and auditors (e.g. letters and evaluations)

Clear expectations on aspects beyond financial reportingIncreased emphasis on connectivity and consistency

between financial reports and sustainability information

17Strategic Cost Transformation, Webinar June 2020

Q&A

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited (“DTTL”), its global network of member firms, and their related entities (collectively, the “Deloitte organization”). DTTL (also referred to as “Deloitte Global”) and each of its member firms and related entities are legally separate and independent entities, which cannot obligate or bind each other in respect of third parties. DTTL and each DTTL member firm and related entity is liable only for its own acts and omissions, and not those of each other. DTTL does not provide services to clients. Please see www.deloitte.com/about to learn more.

Deloitte is a leading global provider of audit and assurance, consulting, financial advisory, risk advisory, tax and related services. Our global network of member firms and related entities in more than 150 countries and territories (collectively, the “Deloitte organization”) serves four out of five Fortune Global 500® companies. Learn how Deloitte’s approximately 330,000 people make an impact that matters at www.deloitte.com.

Our advice is prepared solely for the use of the client. You may not disclose it or its contents to any other person without our prior written consent. No other person may rely on the advice and we accept no responsibility to any other person.

© 2021 For more information, contact Deloitte AB.