Embed Size (px)

Citation preview

Electronic copy available at: http://ssrn.com/abstract=1719562

1

Angelou, G.N. and Economides, A.A. (2009) "Telecommunication Investments Analysis: An

integration of various decision approaches in a multi-criteria perspective," Chapter in Handbook

of Research on Telecommunications Planning and Management for Business.

Title:

TTEELLEECCOOMMMMUUNNIICCAATTIIOONN IINNVVEESSTTMMEENNTTSS AANNAALLYYSSIISS:: AA MMUULLTTII--CCRRIITTEERRIIAA MMOODDEELL

Georgios N. Angelou & Anastasios A. Economides UNIVERSITY OF MACEDONIA Information Systems Department

Egnatia 156 Thessaloniki 54006, GREECE

1. Corresponding author: Prof. Anastasios A. Economides UNIVERSITY OF MACEDONIA Information Systems Department Egnatia 156 Thessaloniki 54006, GREECE Tel: +30-2310-891799 Fax: +30-2310-891750 email: [email protected] http://conta.uom.gr 2. Georgios Angelou Phd Candidate UNIVERSITY OF MACEDONIA Information Systems Department Egnatia 156 Thessaloniki 54006, GREECE email: [email protected]

Electronic copy available at: http://ssrn.com/abstract=1719562

2

TTEELLEECCOOMMMMUUNNIICCAATTIIOONN IINNVVEESSTTMMEENNTTSS AANNAALLYYSSIISS:: AA MMUULLTTII--CCRRIITTEERRIIAA MMOODDEELL

Georgios Angelou, Anastasios Economides

University of Macedonia, Thessaloniki, Greece

Abstract Recognizing the inadequacy of traditional quantitative cost-benefits analysis for evaluating telecommunications investments, researchers suggest real options (ROs) for controlling and valuating telecommunications business activities. However, ROs are based on the concept to delay investment for collecting more information and learning more about business conditions and during this delay another competitor may act gaining significant competition advantage. In addition, RO models are strictly quantitative and very often telecommunications investments may contain qualitative factors, which cannot be quantified in monetary terms. In addition, ROs analysis results in some factors that can be treated more efficiently when taken qualitatively. This work deals with quantitative and qualitative analysis and integrates ROs and Analytic Hierarchy Process (AHP) into a common decision analysis framework providing a multi-criteria model, for analyzing telecommunication investments in the deregulated business field. Introduction Telecommunications markets all over the world recently have been, and still are, undergoing drastic changes, fuelled my market reforms and technological progress. State-owned monopolists have been privatized and markets have been liberalized. These transformed markets have attracted entrants in many varieties. Some entrants roll out complete networks, while other build only partial networks or perhaps offer services without having infrastructure themselves but having access to the networks of incumbent operators.

The valuation of telecommunication business activities is a challenging task because it is characterized by high-level uncertainty. In addition, these business activities are not possessed exclusively by a single firm but rather are shared by many competitors. The main challenge for a potential provider (investor) is to roll out its business activity at the right time and the right scale. The time and scale depend on telecommunication services penetration, network infrastructure cost, area characteristics, applications offered, expected tariff evolution, customers’ willingness to pay, demand forecasts, evolution of expected market shares and investor’s technical skills.

Although the traditional cost-benefit analysis expressed in money terms such as investment cost, revenues, and Net Present Value (NPV) are significant factors to be

3

taken into account in the analysis process, it is by no means sufficient for capturing the complexity of the problem in its entire. It is not able to accommodate the flexibility, for example, to defer and to abandon an investment plan at certain discrete pre-specified points in time.

Real Options (ROs) address this inadequacy and offers management the flexibility to take actions, which can change aspects of the business activity over time. ROs have been proposed for business analysis and risk management (Trigeorgis, 1996).

ROs applications to risk management and investment evaluation of telecommunication business field have mainly focused on a single and a-priori known option. However, these options are not inherent in any telecommunication investment. Actually, they must be carefully planned and intentionally embedded in the telecommunication investments in order to mitigate its risks and increase its return. Moreover, when a telecommunication investment involves multiple risks, by adopting different series of cascading options we may achieve risk mitigation and enhance investment performance. Given the investment’s requirements, assumptions and risks, the goal is to maximize the investment’s value by identifying a good way to structure it using carefully chosen real options (Benaroch, 2002).

However, ROs application in telecommunication business field raise some issues that require attention. ROs models are strictly quantitative, while telecommunication analysis may also involve qualitative factors. In addition, ROs analysis itself brings to the “surface” a number of factors that cannot be quantified, at least easily, by existing ROs models and methodologies.

In this work we discuss all these issues and include them in a multi-criteria perspective providing specific decision analysis models. We consider that a holistic methodology is required in order to assist executives and decision makers in formulating problem parameters, understanding their interactions, estimating their contribution to the overall business value and so valuating effectively new telecommunication business activities.

We discuss limitations of the quantitative analysis, in the specific field proposing qualitative factors that can be combined in a multi-criteria analysis. For integrating quantitative and qualitative factors in one utility function we adopt Analytic Hierarchy Process (AHP). The proposed analysis provides a better understanding of the telecommunication risks and the various qualitative factors inherent in such investments, enabling these investments to be deployed more optimum and valued with higher accuracy. Our main contributions are the following:

We integrate financial quantitative, qualitative and risk factors as provided by the ROs and competition threat in an Analytic Hierarchy Process (AHP) structure.

We provide a risk management framework for telecommunication investments based on ROs thinking.

Our aim is to find the business deployment that achieves a balance between risk control and performance maximization under competition.

4

The rest of the paper is organized as follows. In Section 2, we provide background for the involved techniques. In Section 3, we provide the proposed methodology and model. In Section 4, we apply the proposed decision analysis framework to a real life case study. In Sections 5 and 6 we conclude and suggest possible future research.

Background ROs background material An option gives its holder the right, but not the obligation, to buy (call option) or sell (put option) an underlying asset in the future. Financial options are options on financial assets (e.g. an option to buy 100 shares of Nokia at the pre-agreed price 90€ per share on January 2008). ROs approach is the extension of the options concept to real assets (Trigeorgis, 1996). For example, a telecommunication investment can be viewed as an option to exchange the cost of the specific investment for the benefits resulting from this investment. An investment embeds a RO when it offers to the management the opportunity to take some future action (such as abandoning, deferring or expanding the investment) in response to events occurring within the firm and its business environment (Trigeorgis, 1996). Telecommunication research on ROs recognizes that such investments can embed various types of ROs, including: defer, stage, explore, alter operating scale, abandon, lease, outsource, and growth. Trigeorgis (1996) provided an in-depth review and examples on different real options. For more practical issues the reader is referred to Mun (2002). Especially, for the telecommunication business field Iatropoulos et. al. (2004) applied ROs analysis for analyzing broadband technology investments. Finally, Angelou and Economides (2005) provided an extended survey of ROs applications in real life telecommunication investments.

Real options limitations and need for qualitative perspective integration

In business practice, several conceptual and practical issues emerge when trying to use options theory as proposed in the current information communication technology (ICT) literature. It is accepted that all ROs models provide approximate valuations of ROs values (Renkema, 1999).

Even the so-called accurate ROs models such as the Black-Scholes formula require some assumptions whose validity is still under criticism in the field of telecommunication investments. In particular, while ROs analysis is widely proposed for evaluating such investments, it is still accepted that ROs applicability is limited by the fact that ICT investments assets are not traded. The non-tradability of ICT assets cannot reveal the investor’s risk attitudes to estimate the correct discount factor of ICT investments. The theoretical foundation of the ROs analysis and its relevance to ICT investments has been discussed and applied in practice by Benaroch and Kauffman (1999, 2000) as far as the real asset non-tradability issue and risk-neutrality of the investor are concerned. However, its limitation is still under discussion.

Existing models for ROs valuation assume a certain distribution of the resulting cash flows, based on an efficient market. However, this is rarely the case in the context of investments in the ICT business field, which is known for its uncertain and unpredictable

5

conditions. It has also been recognized that finance-oriented option valuation models are too complex for managerial decision-making practice, when real life business conditions are considered Fichman et. al. (2005). In particular, after the liberalization of the telecommunication market, the required competition modeling has increased the complexity of existing options models. It is very difficult for senior managers to accurately estimate the parameters of a statistical distribution of outcomes and mainly volatility since they do not really have a “gut feel” for the estimation of the volatility, even though they understand its technical definition as a statistic. Options theory in its present state does provide a conceptual decision framework to evaluate technology investments but, in many cases, cannot be considered as a fully operational tool for management. If it is expected that practitioners and senior managers will resist the use of formal options pricing models, then the qualitative option valuation can be an alternative analysis process. This is based more on the intuition of decision makers and forecasting for risks profiles, and less on sharply quantified prediction for parameters used in the formal options models.

Overall, these issues suggest that even quantified ROs analysis could produce only approximate valuations, which in some cases can cause serious mistakes in investment decisions Fichman et. al. (2005). For these reasons, we may adopt typical DCF techniques such as NPV instead of ENPV value and combine tangible factors with qualitative ROs thinking. Hence, our multi-criteria decision analysis framework can be extended including typical tangible factors from financial perspective and intangible ones from qualitative ROs thinking.

A brief AHP presentation and literature review AHP is a multi-criteria decision analysis technique. It aims at choosing from a number of alternatives based on how well these alternatives rate against a chosen set of qualitative as well as quantitative criteria Saaty and Vargas (1994), (Schniederjans,2005). Using AHP, it is possible to structure the decision problem into a hierarchy that reflects the values, goals, objectives, and desires of the decision-makers. Thus, AHP fits the strategic investments problems and the framework of this study. The main advantage of the AHP approach is that different criteria with different measures can be easily transformed into a single utility measure. As input, AHP uses the judgments of the decision makers about the alternatives, evaluation criteria, relationships between the criteria (importance), and the relationships between the alternatives (preference). In the evaluation process, subjective values, personal knowledge, and objective information can be linked together. As an output, the goal hierarchy, the priorities of alternatives and their sensitivities are reached. Concerning, examples of AHP application in information, communication technology literature, Bodin et al. (2005) proposed the AHP method to determine the optimal allocation of a budget for maintaining and enhancing the security of an organization’s information system. Hallikainen et al. (2002) proposed an AHP-based framework for the evaluation of strategic IT investments. They applied the principles of AHP to compare a number of Information Technology investment alternatives. Tam and Tummala (2002) formulated and applied an AHP-based model for selecting a vendor for a telecommunications system. Lai et al. (1999) applied the AHP to the selection of a

6

multimedia authoring system. Finally, Kim (1998) used the AHP to measure the relative importance of Intranet functions for a virtual organization.

The proposed model-methodology Next, we present a methodology that helps to address the question: How can we control firm, market and competition risks so as to configure a specific telecommunication business activity in a way to minimize risk and increase performance? The proposed model contains three perspectives, financial tangible factors (FTF) perspective, risk mitigation factors (RMF) perspective, and intangible factors (IF) perspective (Figure 1).

Figure 1. The proposed model – three perspectives

Financial Tangible Factors Perspective

The financial perspective evaluates how a company is meeting though financial measures. For the valuation of financial perspective we may adopt traditional accounting techniques such as Net Present Value (NPV), Return on Investment (ROI) and Internal Rate of Return (IIR). We also include the Expanded Net Present Value (ENPV), which is the business value as estimated by ROs analysis. As mentioned before in the deregulated business field typical ROs models do not sufficiently model the competition threat. We propose the model of Angelou and Economides (2007B) for estimating the business value with ROs under competitive conditions in a business environment with may players. They adopt exogenous competition modeling considering that competitors arrival rate and competition impact from each entry in to the market follow a joint-diffusion process with business revenues.

Intangible Factors (IF) perspective

Intangible factors are difficult, if not impossible, to quantify in absolute monetary terms, but are still important to the decision making process. Particularly, ROs analysis itself brings to the “surface” a number of factors that cannot be quantified, at least easily, by

Financial Tangible Factors

Perspective

Risk Mitigation Factors

Perspective

Intangible Factors

Perspective

Company Business Planning

7

existing ROs models and methodologies. Fichman et al. (2005) called them potential pitfalls of option thinking for risk management and investment evaluation. We integrated some of them, in our analysis, in order to achieve a balance between risk control achieved by options adoption and other issues influencing the overall investment’s deployment strategy and limit the options thinking applicability.

Among others, not all investments can be divided into stages implementing stage and expand options. Sometimes a firm should consider an investment as a whole entity, such as when external funds must be raised or when co-investment from other parties is required. Another issue is that stakeholders may prefer all at once funding to obtain maximum control of the investment and have so more time to get a troubled investment back on track before facing a next track of justification. We introduce this possibility in our analysis by considering the intangible factor “Capability-Interest of staging the investment” (CSI).

In ROs literature investment opportunities, known in advance, based on initial infrastructure investments are treated as growth options, while for the estimation of their values compound option models are utilized. However, telecommunication growth investment opportunities in reality can be hardly defined during decision phase (Benaroch, 2002). For this reason, we model qualitatively the existence of growth investment opportunities, which are based on investments in previous phases of a firm’s business activity and cannot be defined quantitatively in advance.

Concerning growth options, the main challenge is the difficulty of estimating their values (due to ambiguity of future cash flows) and uncertainty about the appropriate value for option model parameters. We name this intangible option factor as “no clarified growth options” (NCO). Also, building in option to abandon or contract operation may concern intangible costs related to credibility and morale. We model this possibility by the intangible factor “cost of scaling down operation” (CSO). Finally, a potential pitfall of switch-use option is that it can add extra time and expense to the development of the initial information communication technology platform in order to change from shadow to real option. Creating this option (making it real) usually involves making the ICT platform more generic and modular for obtaining higher flexibility, experiencing however higher cost. We model this issue as intangible factor named “cost of systems flexibility-modularity” (CSF).

Another factor that can be integrated in a future work is the higher uncertainty clearness-control (UC) during waiting period. In our model, we consider the amount and type of uncertainty control achieved by each of the portfolio’s projects. We do not want to substitute the UC, achieved by the ROs analysis and quantified by the volatility of the stochastic parameters, such as investment revenues V and one time investment cost C (σv, σc). However, the overall uncertainty of an investment opportunity cannot be easily quantified. For example, the uncertainty of customers’ demand may be quantified by estimating its contribution in the overall investment’s volatility, while the contribution of technology and the firm’s uncertain capability to optimally exploit investment benefits may not. By adopting qualitative analysis, we can model some of the uncertainties inherent in the investment opportunity that cannot be quantitatively estimated and included in the overall investment’s volatility.

8

Benaroch (2002) provided a method for estimating the overall investment’s uncertainty (volatility), which can be broken down into its components (e.g., customers’ demand uncertainty, competition’s uncertainty and technology’s uncertainty). However, the estimation of each component of the uncertainty may be impossible. We may extend this work by considering that some of the overall components of the uncertainty may be treated as qualitative factors, while the sources of uncertainty that can be quantified and included in the estimation of the overall volatility can be integrated into the typical ROs models. Angelou and Economides (2007 C) provide an extensive discussion of these subjects.

Risk Mitigation Factors Perspective Risk management strategies are oriented towards identifying different types of risks, assessing their relative importance for the project, and implementing strategies for managing risks (Kumar, 2002). Risk management actions can be viewed as being of two types. The first is oriented towards reducing the degree of risk; for example, a major source of uncertainty in IT projects is uncertainty regarding the scope or specifications of the project. This can be partially resolved by interviewing multiple stakeholders. However, since risk cannot be completely eliminated, a second type of strategy, oriented towards hedging risks is important. Risk hedging strategies are insurance-like ones oriented towards minimizing the negative impact of risk, when the associated uncertainty is resolved over time. For example, specification uncertainty in IT projects may be due to uncertain business conditions that may be resolved as the project progresses (Kumar, 2002). Telecommunication risks can be placed into three categories (Benaroch, 2002; Bräutigam and Esche, 2002).

Firm-specific risks are due to uncertain endogenous factors (endogenous or technical uncertainty). They could be the result of uncertainty about the ability of the firm to fully fund a long-term capital-intensive investment, the adequacy of the firm's development capabilities to a target investment, the fit of the target application with various organizational units, etc. These factors affect the ability of the investing firm to successfully realize an investment opportunity.

Competition risks are the result of uncertainty about whether a competitor will make a preemptive move, or simply copy the investment and improve on it. These risks give rise to the possibility that the investing firm might loss part or all of the investment opportunity.

Market risks are due to uncertain exogenous factors that affect every firm considering the same investment (exogenous or market-related uncertainty). These risks could be the result of uncertainty about customer demand and prices for the products or services, a target investment yields, potential regulatory changes, unproven capabilities of a target technology, the emergence of a cheaper or superior substitute technology, and so on. These factors can affect the ability of the investing firm to obtain the payoffs expected from a realized investment opportunity.

Research on technology investment’s evaluation and risk management recognizes that ROs thinking emphasizes the sources of risks inherent in such investments and contributes to risk control.

9

Life-cycle of investment opportunity real options The lifecycle of an investment starts at the inception stage. During this period the investment exists as an implicit opportunity for the firm that can be facilitated by a prerequisite investment (Figure 2). The firm posses a shadow option. During the recognition stage, call “Wait-and-See” (WaS) period, the investment is seen to be a viable opportunity. The opportunity can be treated as a RO. The building stage follows upon a decision to undertake the investment opportunity. In the operation stage, the investment produces direct and measurable payoffs. Upon retirement, the investment continues to produce indirect payoffs, in the form of spawned investment opportunities that build on the technological assets and capabilities it has yielded. When these assets and capabilities no longer can be reused, the investment reaches the obsoleteness stage. Each stage of the investment opportunity is relevant to a number of operating and growth ROs, such as option to defer, stage, lease, expand (Benaroch, 2002). The reason is that each type of RO essentially enables the deployment of specific responses to threats and/or enhancement steps. In addition, each stage of the investment is also experiencing a variety of risks.

Figure 2. Types of risks and ROs arising at different stages in the investment lifecycle

For controlling these risks we can adopt a number of investment modes

Defer investment to learn about risk in the investment recognition stage. If we don't know how serious some risk is, the option to defer investment permits learning about the risk by acquiring information passively (observe competitor moves, review emerging ITs, monitor regulatory actions, etc.) or actively (conduct market surveys, lobby for regulatory changes, etc.). Such learning-by-waiting helps to resolve market risk, competition risk, and organizational risk. Apparently, the greater the risk, the more learning can take place, and the more valuable is the deferral option.

Partial investment with active risk exploration in the building stage. If we don't know how serious some risk is, investing on a smaller scale permits to actively explore it. Three options facilitate learning-by-doing, that is, enable gathering information about the firm’s technological

Types of risks

Competition Market

Competition, Market, Organizational

Competition, Market, Organizational

Competition, Market

Existence form

Shadow investment opportunity

Real investment opportunity

Opportunity realization

Operation of implemented opportunity

Source of value

Shadow option Strategic Growth /Operating option

Operating Option Operating option

Type of RO

Option to Defer investment

Stage, pilot, lease and outsource options

Contract, expand, outsource, abandon operations options

Inception stage

Recognition stage

Building stage

Operation stage

Retirement stage

Obsoleteness stage

Prerequisite investments Future (spawned) investment opportunities

10

and organizational ability to realize the investment successfully. The option to stage investment supports learning via a sequential development effort, and the options to pilot and prototype support learning through the production of a scaled down operational investment. The last two options compress the investment lifecycle, thus allowing to learn early how competitors, customers, regulatory bodies and internal parties will react to the investment initiative. Put another way, these options permit market risk, development risk and organizational risk to be transferred to earlier parts of the full scaled investment lifecycle. Similarly, the stage option divides the investment realization effort into parts, thus permitting to transfer risk across parts within the building stage. For example, implementing the riskiest parts of the realization effort as early as possible helps to reveal up-front whether the entire realization effort can be completed successfully (e.g., within schedule and budget).

Full investment with reduction of the expected monetary impact of risk in the building and operation stages. Here, options help to lower the value consequences of risk and/or the probability of its occurrence. An example of the former is the option to lease development resources, which protects against development and market risks by allowing to kill an investment in midstream and save the residual cost of investment resources. A way to lower the probability of risk occurrence is the option to outsource development. This option lowers the risk of development failure by subcontracting (part or all of) the realization effort to a third party that has the necessary development capabilities and experience. In essence, both these options permit transferring risk (partially or fully) to a third party.

Dis-investment/Re-investment with risk avoidance in the operation stage. If we accept the fact that some risk cannot be actively controlled, two options offer contingency plans for the case it will occur. The option to abandon operations allows redirecting resources if competition, market or organizational risks materialize. The option to alter scale allows contracting (partially disinvest) or expanding (reinvest) the operational investment in response to unfolding market and organizational uncertainties.

Based on the logic of these investment modes, the mapping of specific risks to specific options that control them can be refined to fit any class of IT investments. Examples of ROs thinking in the basis of the aforementioned investment modes are provided by Benaroch (2002) and Angelou and Economides (2007 A). Particularly, they apply ROs thinking based on the aforementioned investment modes for analyzing information technology investment opportunities. ROs analysis can control different sources of risks existing in the various stages of the investment life-cycle. We use a classification for analytical definition of telecommunication risks based on Benaroch (2002) and (Bräutigam & Esche 2002) proposals. Table 1 shows the main sources of telecommunication risks as well as their mapping to the specific ROs that can control them.

11

Table 1. Risk factors inherent in telecommunication investments and options that can control them

In the following we propose an AHP structure in order to combine all the aforementioned factors into one utility function.

Integrating qualitative Real Options with AHP model The structure of the decision analysis framework contains four levels: i) the content of the specific investment opportunity, which can be deployed in various ways, ii) the life-cycle stages of the investment opportunity, iii) the options level that is embedded in each of these stages and mapped to specific types of risks, iv) the multi-criteria level that contains financial tangible, risk and intangible analysis (Figure 3). The overall utility of AHP structure is composed by these criteria (factors), which may be further decomposed into their applicable sub-criteria. We apply the pair-wise comparisons for each of these sub-criteria. The final result of the analysis, at the top, is the prioritization of the various deployment scenarios according to the overall firm business utility.

Recognition

Defer Stage Explore/Pilot Outsource Developmen

t

Lease Abandon Contract Expand

Outsource

F1 firm cannot afford the project (unacceptable financial exposure) + + + +

F2 costs may not remain in line with projected benefits + + + + + + +

P1 staff lacks needed technical skills + + + + +

P2 project is too large or too complex + + + +

P3 inadequate infrastructure for implementation + + + +

P4 the project is not on Time + + + +

F1 wrong design (eg, analysis failed to assess correct requirements) + + + +

F2 problematic requirements (stability, completeness, etc.) + + +

O1 uncooperative internal parties + + + +

O2 parties slow to adopt the application + + + +

C1 competition's response eliminates the firm's advantage + + + + + +

C2 competition acts before the firm + +

E1 low customer demand, with inability to pull out of market + + + + + + + +

E2 demand exceeds expectations (follow-up opportunities exist) + + +

E3 too high customer response may overwhelm the application + + + + + + +

E4 customers may (bypass) develop their own solutions + + + +

E5 unanticipated action of regulatory bodies + + +

E6 Price uncertainty + +

E7 environment changed requirements (expected benefits vanish) + + +

E8 Other factors such as Legal issues, Natural Phenomena, Social issues, Armed conflicts, Taxation. + +

T1 application may be infeasible with the technologies considered + + + + + +

T2 the introduction of a new superior implementation technology may render the application obsolete + + + +

T3 the implementation technologies considered may be immature + + + +

OperationBuildingRisk Opportunity

12

Figure 3. Analytical view of the decision analysis framework

The analytical view of the Risk Mitigation sub-module is deeply analyzed in Figure 4. The criteria used in our structure are coming from Table 1 and indicate the risk inherent in telecommunication investments. Analytically, we perform pair-wise comparisons of the deployment scenarios for each of the risk factors focusing on the risk control that each scenario can provide. The pair-wise comparisons concern the amount of risk that is resolved and controlled, depending on the option(s) existence in each scenario. Our target is to select the deployment scenario that provides the highest value for the risk mitigation utility.

Risk Mitigation Factors -

Intangible Factors

NCO

CSI

Financial Tangible Factors

Net Present Value

ENPV

Payback Period

…It is analyzed extensively... in figure 4

CSO

Business Utility

Investment Costs

Recognition Building

Operation

Deployment Scenario 1

Deployment Scenario 2

Deployment Scenario N

Deployment Scenario …

Defer Stage

Explore/ Pilot

Outsou rce

development

Abandon Contract

Expand Outsource

Operation

CSF

13

Figure 4. The risk mitigation sub-module of the proposed framework

Summary

The proposed methodology involves four main steps that must be repeated over time as more information is collected concerning the overall business environment. These steps help to optimally configure the investment under the information set available initially, but as time passes they must be re-applied in case that some risks get resolved or new risks surface. In the following we present these steps.

Risk Mitigation Utility

Market Risks Competition Risks

Firm Specific Risks

F 1

F2

P1

P2

P1

P3

P4

F1

F2

O1

O2

F1

F2

E1

E2

E3

E4

E5

E6

E7

E8

T1

T2

T3

Recognition Building

Operation

Deployment Scenario 1

Deployment Scenario 2

Deployment Scenario N

Deployment Scenario …

Defer Stage

Explore/ Pilot

Outsource

development

Abandon Co ntract

Expand Outsource

Operation

14

Define the content of the overall business activity and its risk profile. State the investment goals, requirements and assumptions (technological, organizational, economic, etc.), and then identify the risks inherent in the investment.

Recognize the options mapped to specific risks and use them to adopt investment modes to be examined.

Evaluate investment-structuring alternatives and find a subset of the recognized options that maximally contributes to the investment value. For the evaluation of the structuring alternatives we use AHP analysis and perform pair-wise comparison among the alternatives. For the AHP implementation we adopt the commercial tool Expert Choice.

Perform sensitivity analysis in order to understand the contribution of each criterion in the overall business utility.

A case illustration To illustrate the proposed methodology we apply it to an ICT investment decision for a growing Water Supply & Sewerage Company, which we refer to as WSSC to protect its identity and its projects. We focus on the risk mitigation factors. The Company’s principal business is the supply of water and sewerage services to over 1.5 million people.

The WSSC is challenged on several areas. First, there is an opportunity for the WSSC to offer advanced water management services to its existing customers. This results to enhanced service quality and efficient control of its operating expenses. In addition, its service area is going to significantly increase attracting new customers. In order to achieve all these WSSC management is focusing on the significance of the ICT applications that could transform the company’s relationships with customers, suppliers, other partners and environment regulators.

WSSC is interested in proceeding on implementation of a ICT platform in order to improve automation aspects of its operations, decision taken methods, customer services as well as new strategic opportunities in long-term perspective. A. Define the content of the overall ICT business activity and its risk profile

Analytically, the investment opportunity under examination includes.

Telemetry-ICT (TICT) infrastructure to enable WSSC to perform more efficiently water network management as well as Asset Management.

WSSC also examines the possibility of integrating two extra tools into the ICT platform for improving the decision support processes:

ArcInfo, a Geographical Information System (GIS), that allows users to create, view, access and analyze map (geo-referenced) data.

StruMap, a Hydraulic Analysis simulation tool, which helps the Water Network Modeling and therefore the Water Management.

15

Finally, based on the information collected and manipulated by the afore mentioned platform and its sub-modules a web-based customers support tool will be implemented providing also on line question and answer service to WSSC customers.

Of course, the system integration with the functional internal processes of the company requires re-engineering of the company’s internal processes and especially these that are related to the customer support and information.

In our analysis we consider the aforementioned investment opportunity as an overall entity. We focus on Risk Mitigation Factors Perspective.

The investment goals, requirements, assumptions and risks are summarized below.

Risks presentation

Concerning the specific investment opportunity for the WSSC there are some risks that can influence negatively its performance. In our case, there are mainly company-specific risks, environmental and technological risk since the Company does not experience any customers demand uncertainty or any competition threat. In particular, many of the ICT investments projects either completely fail, or deliver reduced functionality. ICT platform may experience lack of users acceptance, but also lack of companies personnel technical expertise. Also, risk factors may concern unrealistic implementation schedule and environmental complexities such as installation of complex equipment in a large scale that can cause inconvenience to the customers. Risks modeling included in our analysis is given in gray cell in Table 1. Finally, there is uncertainty about the firm’s capability to integrate efficiently the initially planned scale of the ICT infrastructure with the required applications as well as with the content of them.

B. Recognize the options mapped to specific risks and use them to adopt investment modes to be examined. In this step recognize the options that the investments could embed, based on the identified investment risks. The overall investment deployment strategy in its most complex strategy can include all the options that can control partially or fully the specific investment’s risks, Figure 5. In our analysis we consider the options to defer, stage, expand, contract and outsource operations.

Defer

0 1

Outsource

2

Expand 1

1 5

Stage 1

In

6

t i m e Stage 2

3

Expand 2

5

Contract

Recognition stage Defer investment

mode

Building stage Partial or Full investment

mode

Operation stage Re-investment or/and Dis-investment mode

16

Figure 5. A configuration of options taken into account in our analysis Defer: To defer (up to Td=2years) the base scale TICT platform that contains the Telemetry-ICT system for water management monitoring system including the asset management module (D). Stage: To build ICTP base scale platform in two stages at Ts1=Td and Ts2=Td+1 option to stage 1 (S1) and option to stage 2 (S2). The option to stage S1 concerns the pure telemetry system while the options to stage S2 concerns the asset management sub-module. Expand: We consider the option to expand (E1) operation at Te1= Td+2 as well as the option to expand (E2) at Te2=Td+3. The first option to expand concerns the GIS and HM sub-modules integration with the Telemetry-ICT base scale system, while the second option the development of a new web-based customers support tool that is based on the technical information retrieved by the already installed and operated sub modules of the ICTP system. Contract: The company’s management may also decide to contract operation for investment stage (E1) instead of expanding them to E2 web-based customer support tool if business conditions become unfavorable. Outsource: The company’s management examines the possibility of outsourcing the base scale operation and maintenance of the T-ICT system after 4 years of operation (i.e. at To=Td+4)

The investment’s deployment scenarios to be examined are given below, Figure 6. We are looking for the optimum ranking of these scenarios.

Figure 6. Scenarios examined (options combinations – investment content) The different boxes indicate different investment stages

( --- recognition and building stages, operation stages )

T-ICT+AM+GIS+HM+WB Stage 1 at t=0

D-S1: T-ICT Stage 1 at t=Td

S2: T-ICT+AM Stage 2 at t=Td+1

E1: T-ICT+AM+GIS+HM Stage 3 at t=Td+2

E2: T-ICT+AM+GIS+HM+WB Stage 4 at t=Td+3

O: T-ICT Stage 5 at t=Td+4

E1: T-ICT+AM+GIS+HM Stage 2 at t=Td+1

E2: T-ICT+AM+GIS+HM+WB Stage 3 at t=Td+2

D-S1-S2: T-ICT+AM Stage 1 at t=Td

D: T-ICT+AM+GIS+HM+WB Stage 1 at t=Td

E1-E2: T-ICT+AM+GIS+HM+WB Stage 2 at t=Td+1

D-S1-S2: T-ICT+AM Stage 1 at t=Td

Scenario 1 – Full investment/Dis-investment mode

Scenario 3 – Defer investment / Dis-investment mode

Scenario 6 – Defer investment / Partial investment / Re-investment/Dis-investment mode

Scenario 5 – Defer investment / Re-investment/Dis-investment mode

Scenario 4 – Defer investment / Re-investment/Dis-investment mode

O: WB or C:WB Stage 2 at t=2

O: T-ICT Stage 3 at t=3

O: T-ICT and/or C:WB Stage 2 at t=Td+2

O: T-ICT Stage 4 at t=Td+3

O: T-ICT Stage 3 at t=Td+2

S1: T-ICT Stage 1 at t=0

S2: T-ICT+AM Stage 2 at t=1

E1-E2: T-ICT+AM+GIS+HM+WB Stage 3 at t= 2

Scenario 2 –Partial investment / Re-investment/Dis-investment mode

O: T-ICT and/or C:WB Stage 4 at t=3

17

C. Evaluate investment-structuring alternatives (investment modes) and find a subset of the recognized options that maximally contributes to the investment value

We have identified the alternative ways to configure the ICT investment using different subsets of the recognized options. For the evaluation of the investment alternatives we do not adopt the quantitative analysis and existing ROs models such as Black-Scholes formula or binomial model. Our intentions was also supported by the interview process with the company’s management, which revealed the degree of uncertainty for the various phases of the investment. The company’s management expressed the uncertainties level for each investment phase in qualitative way, since it had difficulties in expressing the volatility of the expected value of investments benefits.

Applying the proposed AHP methodology, the pair wise comparison matrices are derived and the relative performance measures are computed for intangible risk factors.

We use the nine-point scale as suggested by Saaty et. el. (1994) however, modified in order to incorporate with our analysis. In particular, we judge our projects portfolio as extreme risk control (E), very strong risk control (VS), strong risk control (S), moderate risk control (M) and equal risk control (E) including intermediate values between the main characterization types. By using the Expert Choice and making judgments according the aforementioned nine-point scale we derive the pair wise comparison matrixes.

Our example is for intuition purpose only and hence we do the scoring alone. Roper-Lowe and Sharp (1990) comment that since it is sometimes difficult to find technical people who can compare options it is necessary for the analyst to learn in detail about each option and do the scoring alone. We play here the analyst role. We select the consistency ratio level, as according to AHP method a consistency ratio must be less than 0.10 to be acceptable (Saaty, 1994).

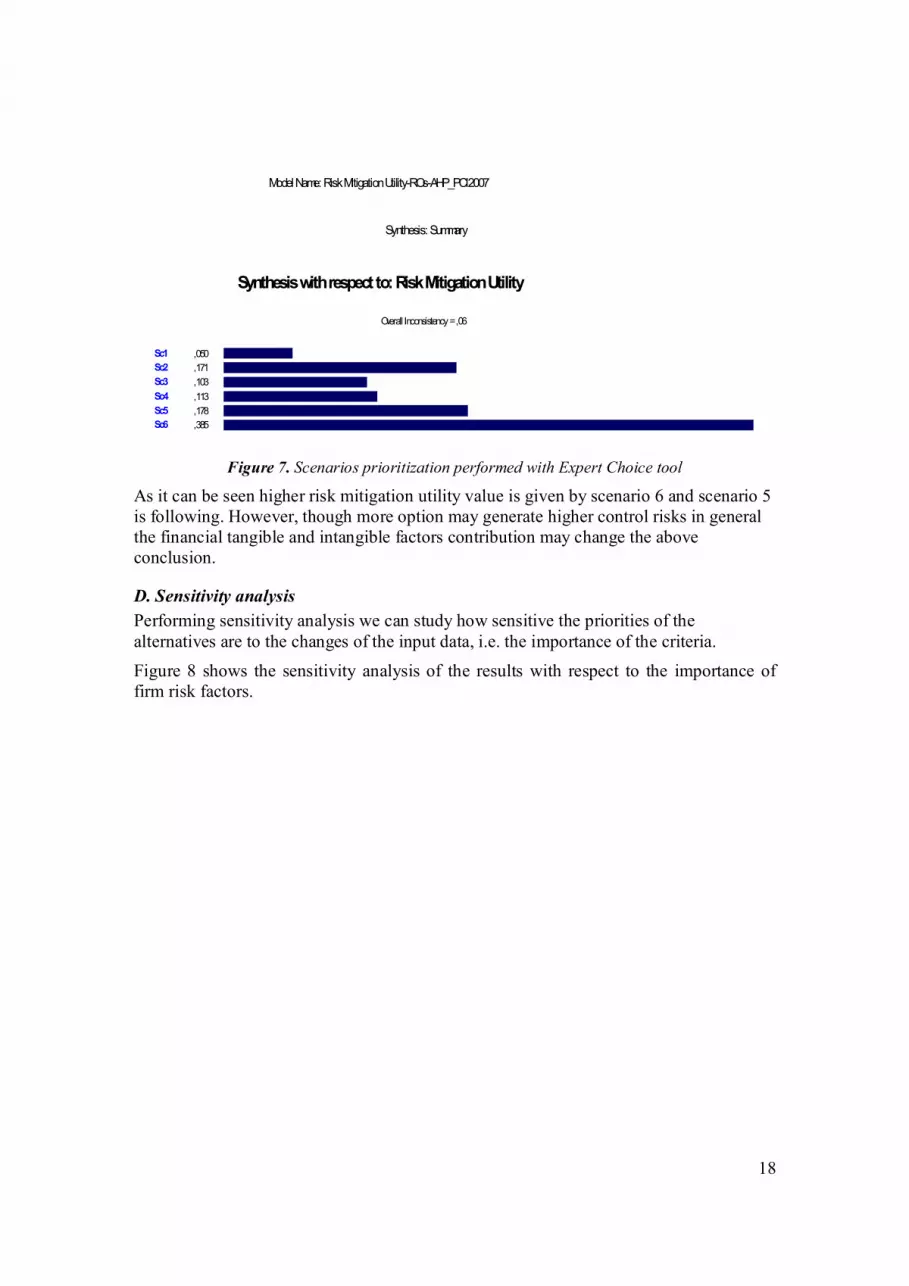

After making all paired comparisons, for all alternatives, according to the principles of the AHP with respect to all criteria defined in the proposed framework, we compute the total priorities for the alternatives using the known commercial tool Expert Choice. The prioritization results are given below, Figure 7.

18

Model Name: Risk Mitigation Utility-ROs-AHP_PCI2007 Synthesis: Summary

Synthesis with respect to: Risk Mitigation Utility Overall Inconsistency = ,06

Sc1 ,050 Sc2 ,171 Sc3 ,103 Sc4 ,113 Sc5 ,178 Sc6 ,385

Figure 7. Scenarios prioritization performed with Expert Choice tool

As it can be seen higher risk mitigation utility value is given by scenario 6 and scenario 5 is following. However, though more option may generate higher control risks in general the financial tangible and intangible factors contribution may change the above conclusion.

D. Sensitivity analysis Performing sensitivity analysis we can study how sensitive the priorities of the alternatives are to the changes of the input data, i.e. the importance of the criteria.

Figure 8 shows the sensitivity analysis of the results with respect to the importance of firm risk factors.

19

Gradient Sensitivity for nodes below: Risk Mitigation Utility

,00

,10

,20

,30

,40Alt%

0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1Firm Risks

Sc1

Sc4

Sc3

Sc5

Sc2

Sc6

Figure 8. Sensitivity analysis for firm specific risks

The figure shows that scenario 6 experiences the highest utility value. Also, for firm risk factors weights from 0 up to 0,75 scenario 5 presents the second priority, while from 0,75 to 1 scenario 2 becomes the second best. The input data are quite subjective, especially the intangible ones. For this reason, it is important to study the dynamics of the sensitivities carefully. For example, if the importance of one criterion changes significantly, the priorities of between scenarios may change due to space limitations we do not present these results while they are available to the interest reader. 5. Discussion and Future Trends There is empirical evidence to support the fact that managers who are aware of some options-like ideas do a better job of evaluating and managing risky telecommunication investments.. Also, senior finance executives are becoming increasingly aware of the need to view major risky capital investments as options.

ROs have already applied in the literature for risk management and evaluation of telecommunication investments. In practice managers identify risks and formulate strategies that can control these risks in the most efficient way. These strategies may contain option analysis and the target is to map options to risks and find the optimum combination of them in order to achieve the optimal value for the investment opportunity. However, the option analysis experiences criticism concerning the need for the parameters quantification of the option models. The issue becomes even more complicated in telecommunication markets. Particularly, after the markets liberalization competition intensity has been increased dramatically and the players are usually so many that oligopoly models are becoming very complicated to be used in practice. Hence, the quantitative analysis of competition influence in telecom investment opportunities is a very difficult task that requires high-level of mathematical modeling and high number of

20

assumptions while managers and practisians quite often do not “feel comfortable” to adopt it.

Instead, we provide qualitative option thinking. Our analysis requires from the management and business analysts to recognize qualitatively the options, during the lifecycle of an investment opportunity that can at least partially control specific risks. Sometimes deferring an investment may be optimum, while some other times the immediate implementation is the best solution adopting afterwards a step-wise deployment strategy during building and operation period. We propose a decision analysis framework where we compare the various types of adopted options and investment modes for a telecommunication opportunity by adopting AHP analysis. In our analysis, we are not only based on qualitative option thinking but also integrate financial tangible and intangible factors coming by both the nature of the telecommunication investments and the options analysis itself.

Our framework of analysis can be also applied in information technology (IT) service management (e.g. ITIL) and IT governance (e.g. Cobit). Particularly, they deal with issues such as how to provide a good service at the good price. People combine these approaches to the maturity concept. For example, risks P1 to P4 mainly depend on the maturity of the firm on the technologies used in the project, on its current infrastructure which indicates how the project will be integrated. IT service management and IT Governance frameworks are not mutually exclusive and could be combined to provide a powerful IT governance, control and best-practice in IT service management, (Mingay and Bittinger, 2002). Indeed, one can map ITIL process onto the perspective of the standard IT Balanced Scorecard (BSC) as presented below. IT BSC Business Contribution o Financial Management IT BSC User Orientation o Service Level Management o Availability Management o Continuity Management o Incident Management o Financial Management IT BSC Operational Excellence o Problem Management o Service Level Management o Change Management o Service Level Management IT BSC Future Orientation o Service Level Management o Capacity Management o Change Management o Financial Management

21

A similar mapping exists for the CobiT processes. For instance, in the delivery and support domain such as define and manage service levels, manage performance and capacity, ensure continuous service, etc. maps well onto one or more ITIL processes such as service level, configuration, capacity, availability management etc. (Salle, 2004). Similar to this analysis the aforementioned perspective can be applied to our model considering an AHP hierarchical structure.

6. Conclusion In this work we provide a decision analysis framework for prioritizing telecommunication investment deployment strategies adopting qualitative option thinking. In our analysis, we take into account financial tangible and intangible factors and quantify managerial flexibility in the projects’ implementation strategy. So far in the literature, ROs models employ only a quantitative factors analysis for both benefits and costs. However, very often a telecom ICT project also owns a number of qualitative factors that should be taken into account in parallel with the quantitative ones. In addition, the ROs analysis itself in existing models requires input parameters that very often are difficult to be fully quantified. For this reason, we adopt the AHP in order to structure risk profile for telecommunication investments and recognize options that can optimally control them as well as combine tangible and intangible factors into one utility function. It is the first time in the literature where ROs and AHP are combined in a common framework of analysis offering a multi-criteria prioritization model that contains risk, intangible and tangible factors related to telecom business activities. A limitation of our work is the lack of competition modeling especially focusing on oligopoly cases. In this case, some one could adopt game theory and integrate it with our analysis. In particular, we can consider two players where each of them has to configure its investment in a way that is optimum for him taking also into account the decisions of the competitor. References Angelou, G.N. & Economides, A.A. (2007A) E-learning investment risk management.

Information Resource Management Journal, Vol. 20, No. 4, pp. 80-104, October – December.

Angelou, G.N. & Economides, A.A (2007B). A Real Options approach for prioritizing ICT business alternatives: A case study from Broadband Technology business field. Journal of the Operational Research Society. Forthcoming.

22

Angelou, G.N. & Economides, A.A. (2007C) "A decision analysis framework for prioritizing a portfolio of ICT infrastructure projects". IEEE Transactions on Engineering Management – Forthcoming.

Angelou G. & Economides A., (2005). Flexible ICT investements analysis using real options. International Journal of Technology, Policy and Management, 5(2):146–166.

Benaroch M., (2002). Managing information technology investment risk: a real options perspective. Journal of Management Information Systems, 19(2): 43-84.

Benaroch, M. & Kauffman, R. J., (2000). Justifying electronic banking network expansion using real options analysis. MIS Quarterly, 24(2), pp. 197–225.

Benaroch, M. & Kauffman, R. J., (1999). A case for using real options pricing analysis to evaluate information technology project investments. Information Systems Research, 10(1), pp. 70-86.

Bodin L., Gordon L. and Loeb M., (2005). Evaluating information security investments using the analytic hierarchy process. Communications of the ACM, 48(2):78 - 83

Bräutigam, J. and C. Esche, c (2003) Uncertainty as a key value driver of real options. 7th Annual Real Options Conference.

Expert Choice, (1995). Expert Choice for windows based on Analytic Hierarchy Process, Version 9, User Manual, Pittsburgh, PA.

Fichman, R., Keil, M. & Tiwans, A., (2005). Beyond Valuation: “Option Thinking” in IT Project Management. California Management Review. 47 (2), 2005, pp. 74-95.

Hallikainen P., Kivijarvi H. and Nurmimaki K., (2002). Evaluating strategic IT investments: An assesment of investment alternatives for a web content management system. Proceedings of the 35th Hawaii International Conference on Systems Sciences.

Gunasekaran A., Love E., Rahimi F. and Miele R., (2001). A model for investment justification in information technology projects. International Journal of Information Management, 21: 349-364.

Iatropoulos A., Economides A. and Angelou G., (2004). Broadband investments analysis using real options methodology: A case study for Egnatia Odos S.A. Communications and Strategies, 55(3): 45-76.

Kim J., (1998). Hierachical structure of intranet functions and their relative importance: Using the analytic hierarchy process for virtual organizations. Decision Support Systems, 23:59-74.

Lai S., Trueblood P. and Wong K., (19990. Software Selection: a case study of the application of the analytic hierarchy process to the selection of multimedia authoring system. Information & Management, 36: 221-232.

Mingay S. and Bittinger S., "Combine CobiT and ITIL for Powerful IT Governance", in Research Note, TG-16-1849, Gartner, 2002.

Mun J., (2002). Real Options Analysis: Tools and techniques for valuing strategic investments and decisions, Wiley Finance.

23

Renkema, T., (1999) The IT value quest: how to capture the business value of IT-based infrastructure, Jhon Wiley & Sons, Ltd.

Roper-Lowe G, and Sharp J., (1990). Analytic hierarchy process and its application to an information technology decision. Journal of Operational Research Society, 42(1): 49-59.

Saaty T.L and Vargas L.G., (1994). Decision making in economic, political, social, and technological environments with the analytic hierarchy process. Pittsburgh: RWS Publications.

Sallé M., IT Service Management and IT Governance: Review, Comparative Analysis and their Impact on Utility Computing, Trusted Systems Laboratory, HP Laboratories Palo Alto, 2004

Schniederjans M., Hamaker J. and Schniederjans A, (2005). Information technology investment – decision-making methodology. Singapore: World Scientific Publishing.

Tam M. and Tummala R., (2001). An application of the AHP in vendor selection of a telecommunications system. Omega, 29: 171-182.

Trigeorgis L., (1996), Real options: managerial flexibility and strategy in resource allocation. The MIT Press. Cambridge MA.

Key Terms and Their Definitions Risk management The process of identifying different types of risks, assessing their relative importance for the project, and implementing strategies for managing risk

Real Option It is the extension of financial options concept to real assets.

Expanded Net Present Value It is the total value of a project that owns one or more options. It is given by: Expanded (Strategic) NPV = Static (Passive) NPV + Value of Options from Active Management

Real Option under competition threat The value of ROs when during waiting period before exercising it there is the threat that a competitor may preempt the owner of the ROs and “steal” or abstract its value.

Investment Cost The amount of money spent for the investment, investment expenditure required to exercise the option (cost of converting the investment opportunity into the option's underlying asset, i.e. the operational project)

Deployment Scenario The way the investment is deployed in terms of time and scale implementation.

24

Business Utility It is the overall utility of the under investigation business activity for the company. It contains both quantitative and qualitative factors.

Analytic Hierarchy Process (AHP) A process that deals in a hierarchical structure a number of quantitative and qualitative criteria in one utility function.