Embed Size (px)

Citation preview

This report must be read with the disclaimer on the last page and forms part of it

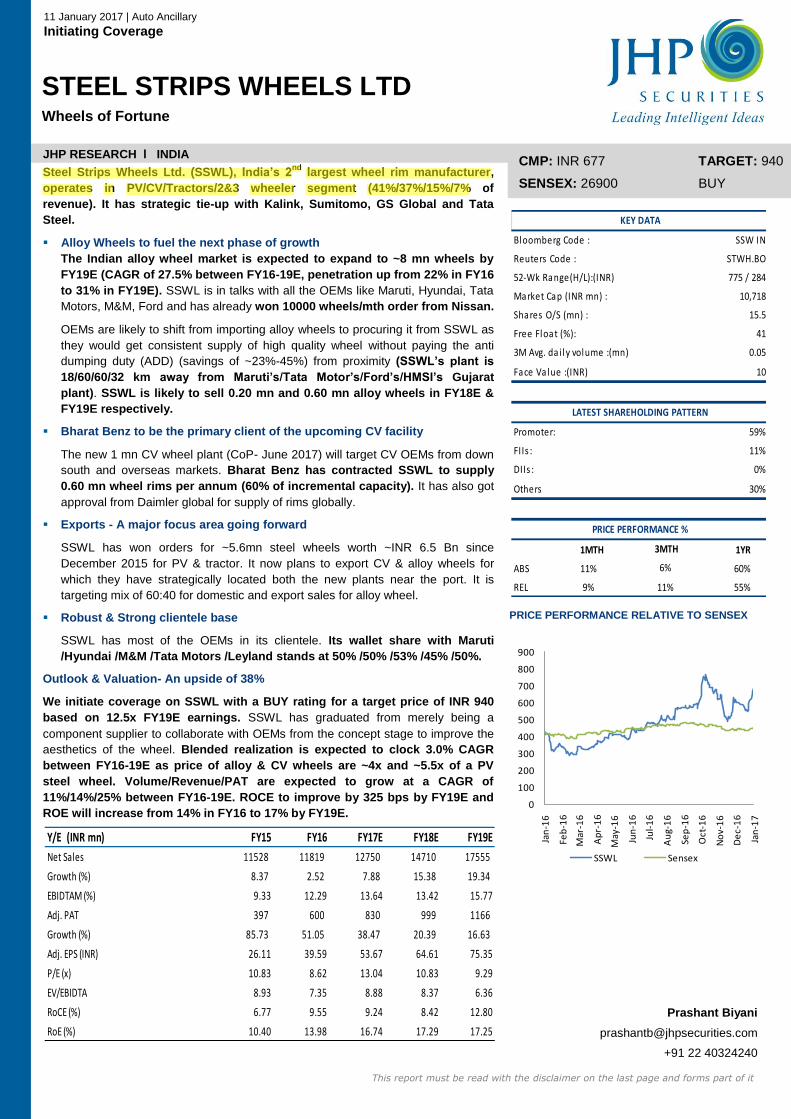

s CMP: INR 677 TARGET: 940

SENSEX: 26900 BUY Steel Strips Wheels Ltd. (SSWL), India’s 2

nd largest wheel rim manufacturer,

operates in PV/CV/Tractors/2&3 wheeler segment (41%/37%/15%/7% of

revenue). It has strategic tie-up with Kalink, Sumitomo, GS Global and Tata

Steel.

Alloy Wheels to fuel the next phase of growth

The Indian alloy wheel market is expected to expand to ~8 mn wheels by

FY19E (CAGR of 27.5% between FY16-19E, penetration up from 22% in FY16

to 31% in FY19E). SSWL is in talks with all the OEMs like Maruti, Hyundai, Tata

Motors, M&M, Ford and has already won 10000 wheels/mth order from Nissan.

OEMs are likely to shift from importing alloy wheels to procuring it from SSWL as

they would get consistent supply of high quality wheel without paying the anti

dumping duty (ADD) (savings of ~23%-45%) from proximity (SSWL’s plant is

18/60/60/32 km away from Maruti’s/Tata Motor’s/Ford’s/HMSI’s Gujarat

plant). SSWL is likely to sell 0.20 mn and 0.60 mn alloy wheels in FY18E &

FY19E respectively.

Bharat Benz to be the primary client of the upcoming CV facility

The new 1 mn CV wheel plant (CoP- June 2017) will target CV OEMs from down

south and overseas markets. Bharat Benz has contracted SSWL to supply

0.60 mn wheel rims per annum (60% of incremental capacity). It has also got

approval from Daimler global for supply of rims globally.

Exports - A major focus area going forward

SSWL has won orders for ~5.6mn steel wheels worth ~INR 6.5 Bn since

December 2015 for PV & tractor. It now plans to export CV & alloy wheels for

which they have strategically located both the new plants near the port. It is

targeting mix of 60:40 for domestic and export sales for alloy wheel.

Robust & Strong clientele base

SSWL has most of the OEMs in its clientele. Its wallet share with Maruti

/Hyundai /M&M /Tata Motors /Leyland stands at 50% /50% /53% /45% /50%.

Outlook & Valuation- An upside of 38%

We initiate coverage on SSWL with a BUY rating for a target price of INR 940

based on 12.5x FY19E earnings. SSWL has graduated from merely being a

component supplier to collaborate with OEMs from the concept stage to improve the

aesthetics of the wheel. Blended realization is expected to clock 3.0% CAGR

between FY16-19E as price of alloy & CV wheels are ~4x and ~5.5x of a PV

steel wheel. Volume/Revenue/PAT are expected to grow at a CAGR of

11%/14%/25% between FY16-19E. ROCE to improve by 325 bps by FY19E and

ROE will increase from 14% in FY16 to 17% by FY19E.

Y/E (INR mn) FY15 FY16 FY17E FY18E FY19E

Net Sales 11528 11819 12750 14710 17555

Growth (%) 8.37 2.52 7.88 15.38 19.34

EBIDTAM (%) 9.33 12.29 13.64 13.42 15.77

Adj. PAT 397 600 830 999 1166

Growth (%) 85.73 51.05 38.47 20.39 16.63

Adj. EPS (INR) 26.11 39.59 53.67 64.61 75.35

P/E (x) 10.83 8.62 13.04 10.83 9.29

EV/EBIDTA 8.93 7.35 8.88 8.37 6.36

RoCE (%) 6.77 9.55 9.24 8.42 12.80

RoE (%) 10.40 13.98 16.74 17.29 17.25

STEEL STRIPS WHEELS LTD Wheels of Fortune

Prashant Biyani

+91 22 40324240

JHP RESEARCH l INDIA

11 January 2017 | Auto Ancillary

Initiating Coverage

PRICE PERFORMANCE RELATIVE TO SENSEX

1MTH 1YR

ABS 11% 60%

REL 9% 55%11%

FIIs : 11%

DIIs : 0%

Others 30%

PRICE PERFORMANCE %

3MTH

6%

Promoter: 59%

Shares O/S (mn) : 15.5

Free Float (%): 41

3M Avg. da i ly volume :(mn) 0.05

Face Value :(INR) 10

LATEST SHAREHOLDING PATTERN

Reuters Code : STWH.BO

52-Wk Range(H/L):(INR) 775 / 284

Market Cap (INR mn) : 10,718

Bloomberg Code : SSW IN

KEY DATA

0

100

200

300

400

500

600

700

800

900

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

De

c-1

6

Jan

-17

SSWL Sensex

INITIATING COVERAGE 2

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

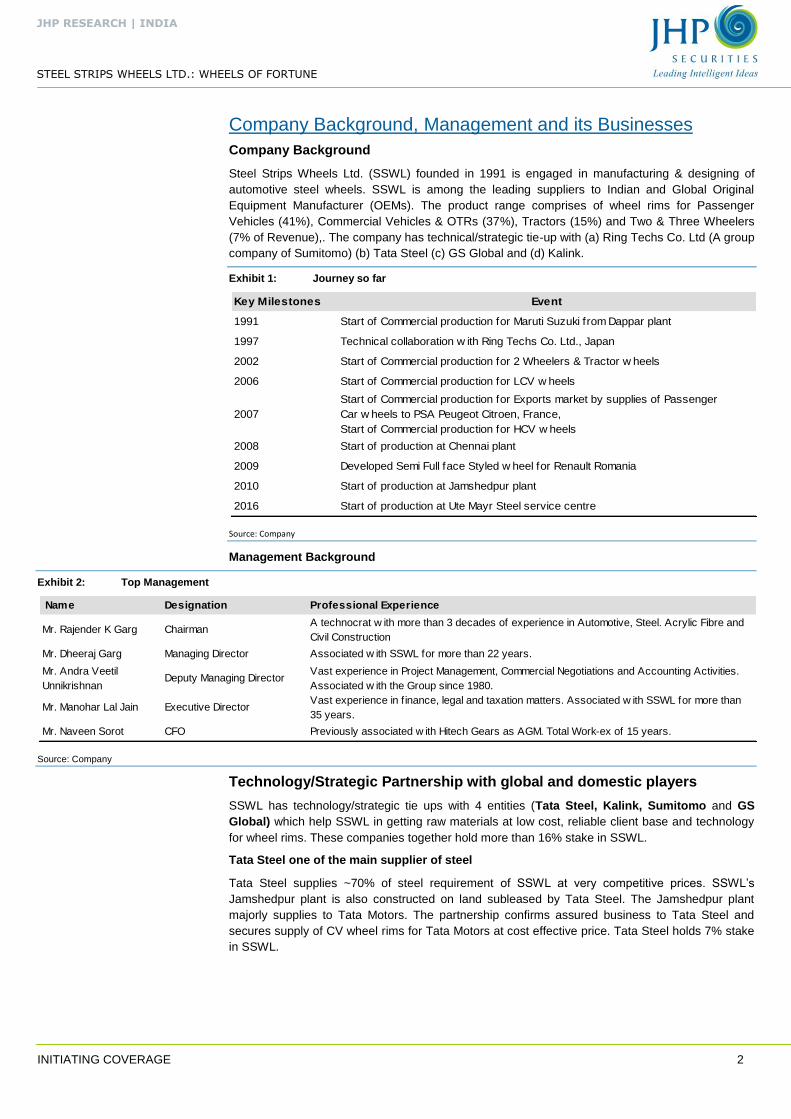

Company Background, Management and its Businesses

Company Background

Steel Strips Wheels Ltd. (SSWL) founded in 1991 is engaged in manufacturing & designing of

automotive steel wheels. SSWL is among the leading suppliers to Indian and Global Original

Equipment Manufacturer (OEMs). The product range comprises of wheel rims for Passenger

Vehicles (41%), Commercial Vehicles & OTRs (37%), Tractors (15%) and Two & Three Wheelers

(7% of Revenue),. The company has technical/strategic tie-up with (a) Ring Techs Co. Ltd (A group

company of Sumitomo) (b) Tata Steel (c) GS Global and (d) Kalink.

Exhibit 1: Journey so far

Source: Company

Management Background

Exhibit 2: Top Management

Source: Company

Technology/Strategic Partnership with global and domestic players

SSWL has technology/strategic tie ups with 4 entities (Tata Steel, Kalink, Sumitomo and GS

Global) which help SSWL in getting raw materials at low cost, reliable client base and technology

for wheel rims. These companies together hold more than 16% stake in SSWL.

Tata Steel one of the main supplier of steel

Tata Steel supplies ~70% of steel requirement of SSWL at very competitive prices. SSWL’s

Jamshedpur plant is also constructed on land subleased by Tata Steel. The Jamshedpur plant

majorly supplies to Tata Motors. The partnership confirms assured business to Tata Steel and

secures supply of CV wheel rims for Tata Motors at cost effective price. Tata Steel holds 7% stake

in SSWL.

Key Milestones Event

1991 Start of Commercial production for Maruti Suzuki from Dappar plant

1997 Technical collaboration w ith Ring Techs Co. Ltd., Japan

2002 Start of Commercial production for 2 Wheelers & Tractor w heels

2006 Start of Commercial production for LCV w heels

2007

Start of Commercial production for Exports market by supplies of Passenger

Car w heels to PSA Peugeot Citroen, France,

Start of Commercial production for HCV w heels

2008 Start of production at Chennai plant

2009 Developed Semi Full face Styled w heel for Renault Romania

2010 Start of production at Jamshedpur plant

2016 Start of production at Ute Mayr Steel service centre

Name Designation Professional Experience

Mr. Rajender K Garg ChairmanA technocrat w ith more than 3 decades of experience in Automotive, Steel. Acrylic Fibre and

Civil Construction

Mr. Dheeraj Garg Managing Director Associated w ith SSWL for more than 22 years.

Mr. Andra Veetil

UnnikrishnanDeputy Managing Director

Vast experience in Project Management, Commercial Negotiations and Accounting Activities.

Associated w ith the Group since 1980.

Mr. Manohar Lal Jain Executive DirectorVast experience in f inance, legal and taxation matters. Associated w ith SSWL for more than

35 years.

Mr. Naveen Sorot CFO Previously associated w ith Hitech Gears as AGM. Total Work-ex of 15 years.

INITIATING COVERAGE 3

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Technological tie-up with Kalink, a leading South Korean wheel rim manufacturer

Kalink, which is a leading South Korean wheel rim manufacturer with manufacturing facilities in

South Korea and China (total capacity- 4.5 mn wheel rims) has entered into a technical

collaboration with SSWL to provide technology for the Alloy wheel plant in Gujarat. Kalink supplies

to OEMs based in USA, Europe and Japan. Kalink had recently bought 1.35% stake in SSWL

@INR 640/share and it intends to increase the stake to 10%-15%in SSWL over the next 3-4 years.

Ring Tech, part of the Sumitomo Group has been its technological partner for 15 years

Ring Tech, a wholly owned subsidiary of Sumitomo has been a technology partner of SSWL for the

last 15 years. Ring Tech assist SSWL in (a) achieving benchmark productivity levels (b) procuring

equipments and (3) Increase exports to Japan, among others. Sumitomo holds 5.5% stake in the

company.

Steel Strips has 3 Manufacturing Units, in process to set up 4th unit in Gujarat

SSWL has 3 manufacturing units located at Dappar (Punjab), Chennai (Tamil Nadu) and

Jamshedpur (Jharkhand). It is setting up fourth unit in Gujarat and undergoing expansion at the

Chennai plant. While the Gujarat plant will be a 2.5 mn alloy wheel plant, the Chennai unit will

be a 1 mn CV wheels plant. Both the Gujarat plant and the CV plant will focus more on exports.

Exhibit 3: Segment-wise Capacity

Source: Company

Location Segment Capacity

2 & 3 Wheelers, PV 7.25 Mn

CV, Tractors & OTRs 1.75 Mn

PV 6.00 Mn

CV (Under Construction) 1.00 Mn

Jamshedpur CV 1.60 Mn

Gujarat PV (Under Construction) 2.50 Mn

Chandigarh

Chennai

INITIATING COVERAGE 4

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

India’s 2nd largest wheel rim manufacturer

Well established player in the Steel Wheel Rims space

SSWL is one of the largest automotive wheel rim manufacturer in India with a combined capacity of

16.6 Mn wheels. SSWL is in the process of additional capacity of 3.5 Mn wheels by H1FY18E. PV,

CV and Tractors account for 93% of its revenue. SSWL primarily caters to domestic OEMs which

are its major clients.

Steady Growth in Volumes: Clocked a 6.6% CAGR between FY12-16 and 11.6% YTD

SSWL’s volume recorded a 6.6% CAGR during FY12-16, surpassing the automobile industry

volume growth of 4.4% over the same period. Segment wise, 2&3 wheeler/CV segments grew @

24%/17% whereas PV segment grew at 3%. Tractor segment volumes declined by 4.3% during the

same period.

Exhibit 4: Total volume and Sales mix trend over the years

Source: Company

Exports growth have outpaced Domestic sales volume growth

Exports accounts for 12% of revenue) and has presence in more than 20 geographies across

continents. During FY11 – FY16, Export volume recorded a 10.4% CAGR while domestic sales

volume recorded 6.1% CAGR. However, in FY16, sales volume growth for both domestic and

exports market were at 5.6% Y-o-Y.

Exhibit 5: Wheel volume mix over the years

Source: Company

12% 18%23% 25% 22% 22% 22% 20%

71% 65%60% 60% 62% 62% 61% 63%

7% 12% 6% 7% 10% 10% 10% 11%10% 9% 11% 8% 7% 7% 8% 6%

10 1011

1213

14 1618

0

2

4

6

8

10

12

14

16

18

20

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

2 & 3 Wheelers PV CV Tractor Total Volume (Mn Wheels) (RHS)

Volume in Mn (nos) FY11 FY12 FY13 FY14 FY15 FY16

Exports 0.92 1.21 1.29 1.53 1.43 1.51

Domestic 8.67 8.98 8.82 9.51 11.04 11.66

Total Volumes 9.59 10.19 10.11 11.04 12.47 13.17

INITIATING COVERAGE 5

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

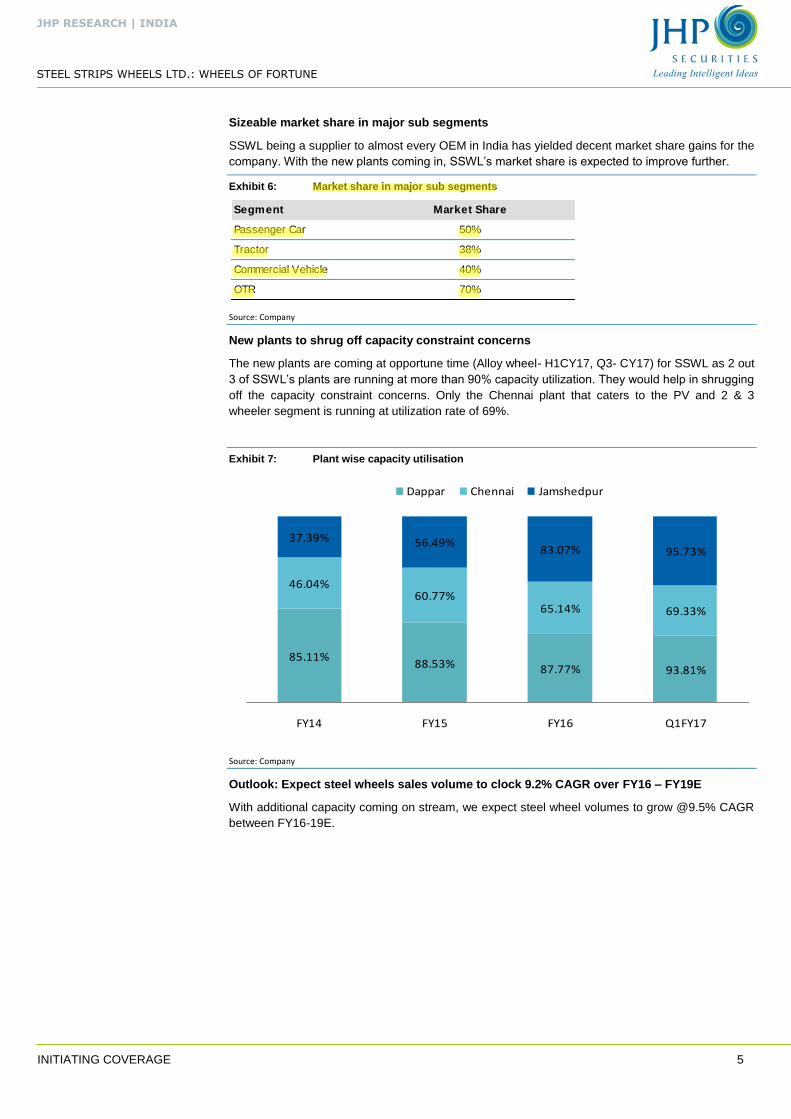

Sizeable market share in major sub segments

SSWL being a supplier to almost every OEM in India has yielded decent market share gains for the

company. With the new plants coming in, SSWL’s market share is expected to improve further.

Exhibit 6: Market share in major sub segments

Source: Company

New plants to shrug off capacity constraint concerns

The new plants are coming at opportune time (Alloy wheel- H1CY17, Q3- CY17) for SSWL as 2 out

3 of SSWL’s plants are running at more than 90% capacity utilization. They would help in shrugging

off the capacity constraint concerns. Only the Chennai plant that caters to the PV and 2 & 3

wheeler segment is running at utilization rate of 69%.

Exhibit 7: Plant wise capacity utilisation

Source: Company

Outlook: Expect steel wheels sales volume to clock 9.2% CAGR over FY16 – FY19E

With additional capacity coming on stream, we expect steel wheel volumes to grow @9.5% CAGR

between FY16-19E.

Segment Market Share

Passenger Car 50%

Tractor 38%

Commercial Vehicle 40%

OTR 70%

85.11%88.53% 87.77% 93.81%

46.04%60.77%

65.14% 69.33%

37.39% 56.49%83.07% 95.73%

FY14 FY15 FY16 Q1FY17

Dappar Chennai Jamshedpur

INITIATING COVERAGE 6

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

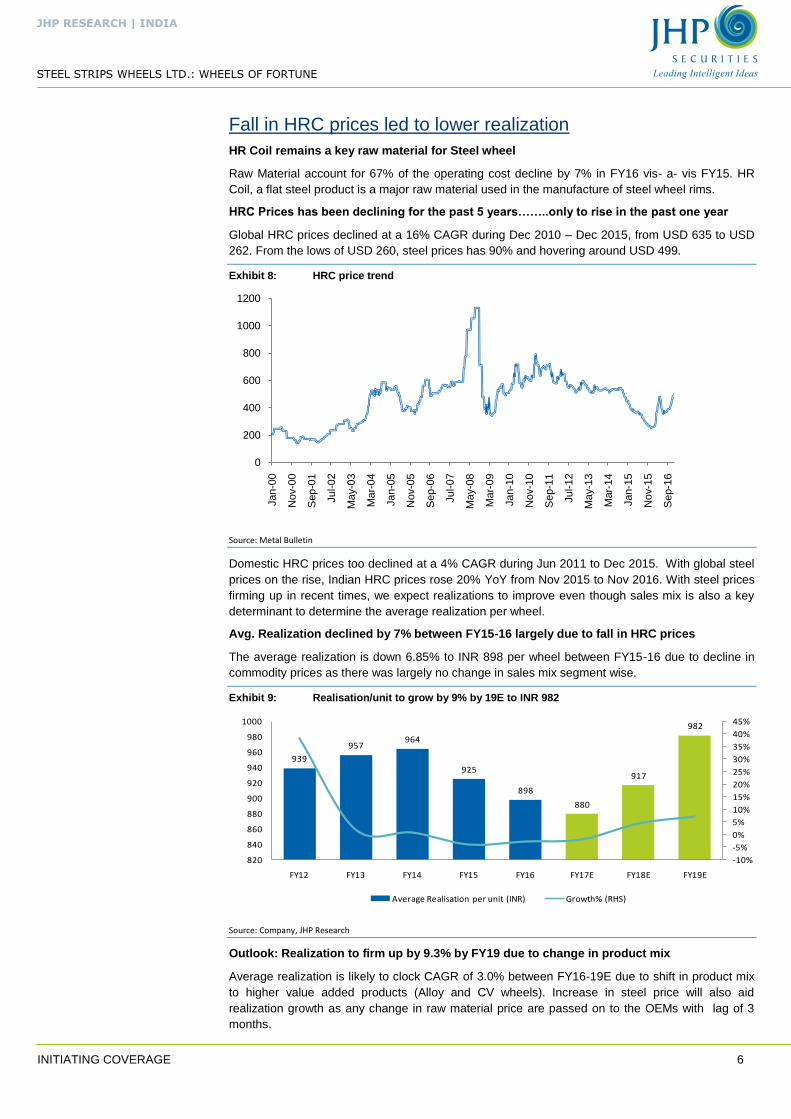

Fall in HRC prices led to lower realization

HR Coil remains a key raw material for Steel wheel

Raw Material account for 67% of the operating cost decline by 7% in FY16 vis- a- vis FY15. HR

Coil, a flat steel product is a major raw material used in the manufacture of steel wheel rims.

HRC Prices has been declining for the past 5 years……..only to rise in the past one year

Global HRC prices declined at a 16% CAGR during Dec 2010 – Dec 2015, from USD 635 to USD

262. From the lows of USD 260, steel prices has 90% and hovering around USD 499.

Exhibit 8: HRC price trend

Source: Metal Bulletin

Domestic HRC prices too declined at a 4% CAGR during Jun 2011 to Dec 2015. With global steel

prices on the rise, Indian HRC prices rose 20% YoY from Nov 2015 to Nov 2016. With steel prices

firming up in recent times, we expect realizations to improve even though sales mix is also a key

determinant to determine the average realization per wheel.

Avg. Realization declined by 7% between FY15-16 largely due to fall in HRC prices

The average realization is down 6.85% to INR 898 per wheel between FY15-16 due to decline in

commodity prices as there was largely no change in sales mix segment wise.

Exhibit 9: Realisation/unit to grow by 9% by 19E to INR 982

Source: Company, JHP Research

Outlook: Realization to firm up by 9.3% by FY19 due to change in product mix

Average realization is likely to clock CAGR of 3.0% between FY16-19E due to shift in product mix

to higher value added products (Alloy and CV wheels). Increase in steel price will also aid

realization growth as any change in raw material price are passed on to the OEMs with lag of 3

months.

0

200

400

600

800

1000

1200

Jan-0

0

Nov-0

0

Sep-0

1

Jul-

02

May-0

3

Mar-

04

Jan-0

5

Nov-0

5

Sep-0

6

Jul-

07

May-0

8

Mar-

09

Jan-1

0

Nov-1

0

Sep-1

1

Jul-

12

May-1

3

Mar-

14

Jan-1

5

Nov-1

5

Sep-1

6

939

957964

925

898

880

917

982

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

820

840

860

880

900

920

940

960

980

1000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Average Realisation per unit (INR) Growth% (RHS)

INITIATING COVERAGE 7

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

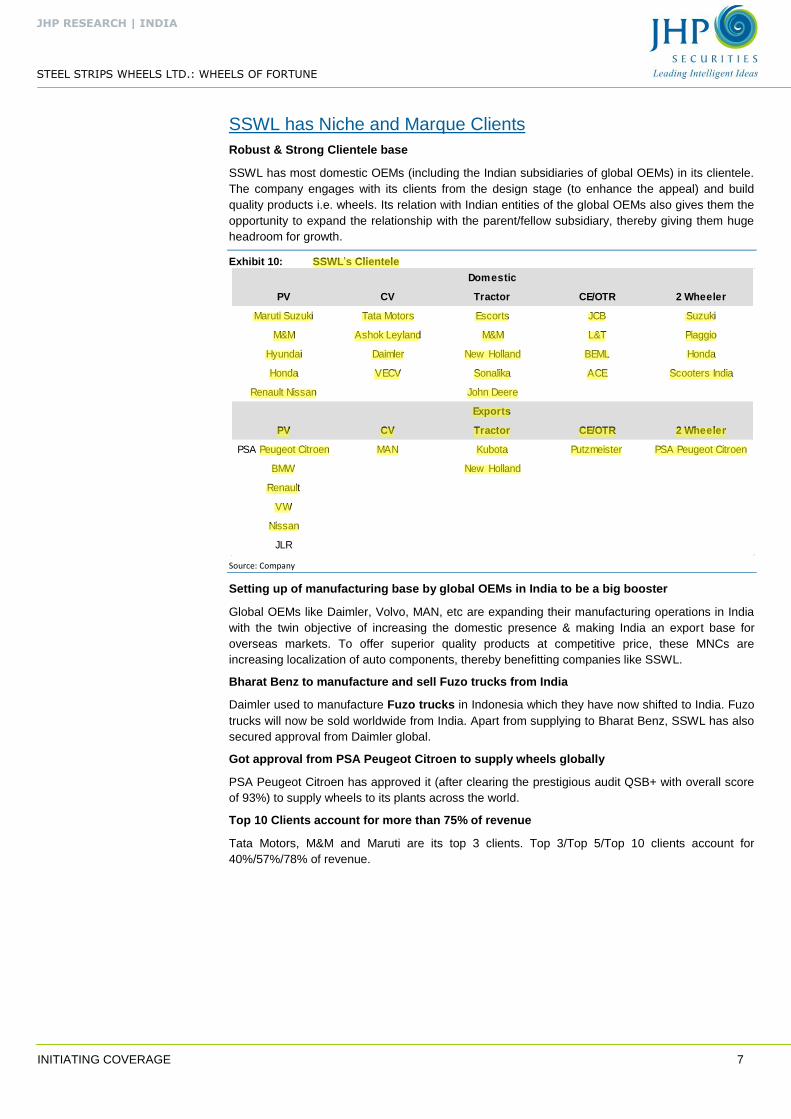

SSWL has Niche and Marque Clients

Robust & Strong Clientele base

SSWL has most domestic OEMs (including the Indian subsidiaries of global OEMs) in its clientele.

The company engages with its clients from the design stage (to enhance the appeal) and build

quality products i.e. wheels. Its relation with Indian entities of the global OEMs also gives them the

opportunity to expand the relationship with the parent/fellow subsidiary, thereby giving them huge

headroom for growth.

Exhibit 10: SSWL’s Clientele

Source: Company

Setting up of manufacturing base by global OEMs in India to be a big booster

Global OEMs like Daimler, Volvo, MAN, etc are expanding their manufacturing operations in India

with the twin objective of increasing the domestic presence & making India an export base for

overseas markets. To offer superior quality products at competitive price, these MNCs are

increasing localization of auto components, thereby benefitting companies like SSWL.

Bharat Benz to manufacture and sell Fuzo trucks from India

Daimler used to manufacture Fuzo trucks in Indonesia which they have now shifted to India. Fuzo

trucks will now be sold worldwide from India. Apart from supplying to Bharat Benz, SSWL has also

secured approval from Daimler global.

Got approval from PSA Peugeot Citroen to supply wheels globally

PSA Peugeot Citroen has approved it (after clearing the prestigious audit QSB+ with overall score

of 93%) to supply wheels to its plants across the world.

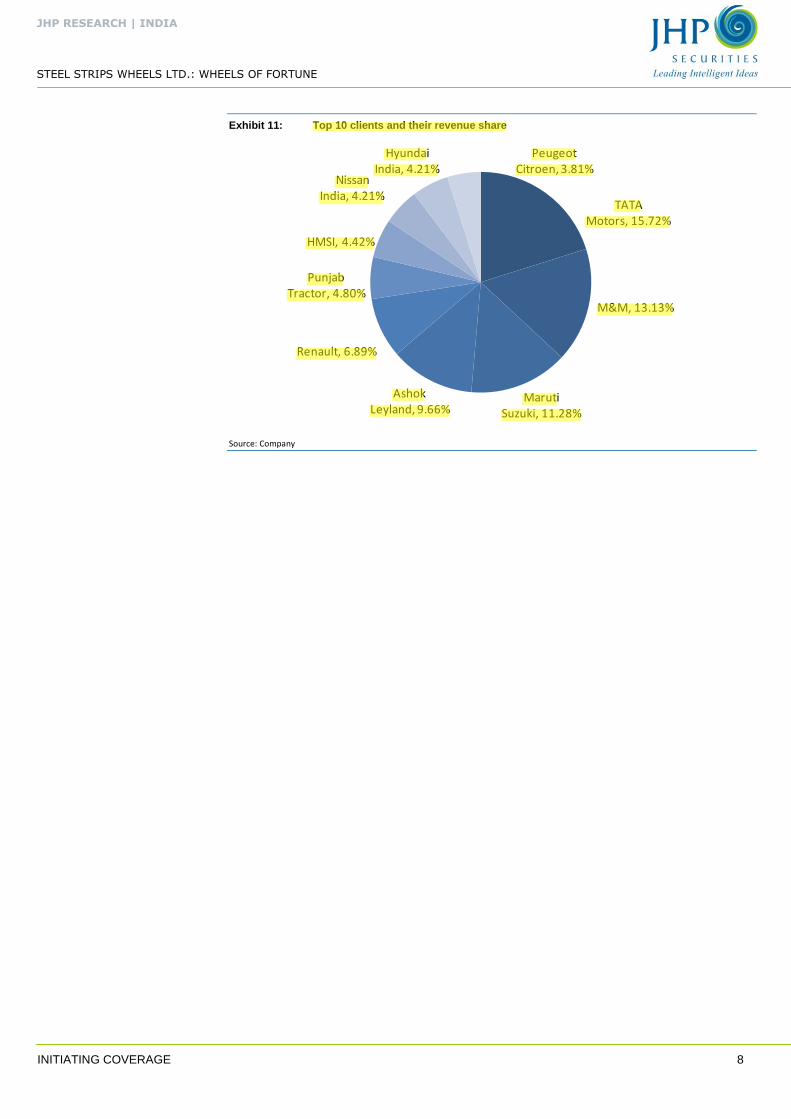

Top 10 Clients account for more than 75% of revenue

Tata Motors, M&M and Maruti are its top 3 clients. Top 3/Top 5/Top 10 clients account for

40%/57%/78% of revenue.

PV CV Tractor CE/OTR 2 Wheeler

Maruti Suzuki Tata Motors Escorts JCB Suzuki

M&M Ashok Leyland M&M L&T Piaggio

Hyundai Daimler New Holland BEML Honda

Honda VECV Sonalika ACE Scooters India

Renault Nissan John Deere

PV CV Tractor CE/OTR 2 Wheeler

PSA Peugeot Citroen MAN Kubota Putzmeister PSA Peugeot Citroen

BMW New Holland

Renault

VW

Nissan

JLR

Domestic

Exports

INITIATING COVERAGE 8

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Exhibit 11: Top 10 clients and their revenue share

Source: Company

TATA Motors, 15.72%

M&M, 13.13%

Maruti Suzuki, 11.28%

Ashok Leyland, 9.66%

Renault, 6.89%

Punjab Tractor, 4.80%

HMSI, 4.42%

Nissan India, 4.21%

Hyundai India, 4.21%

Peugeot Citroen, 3.81%

INITIATING COVERAGE 9

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

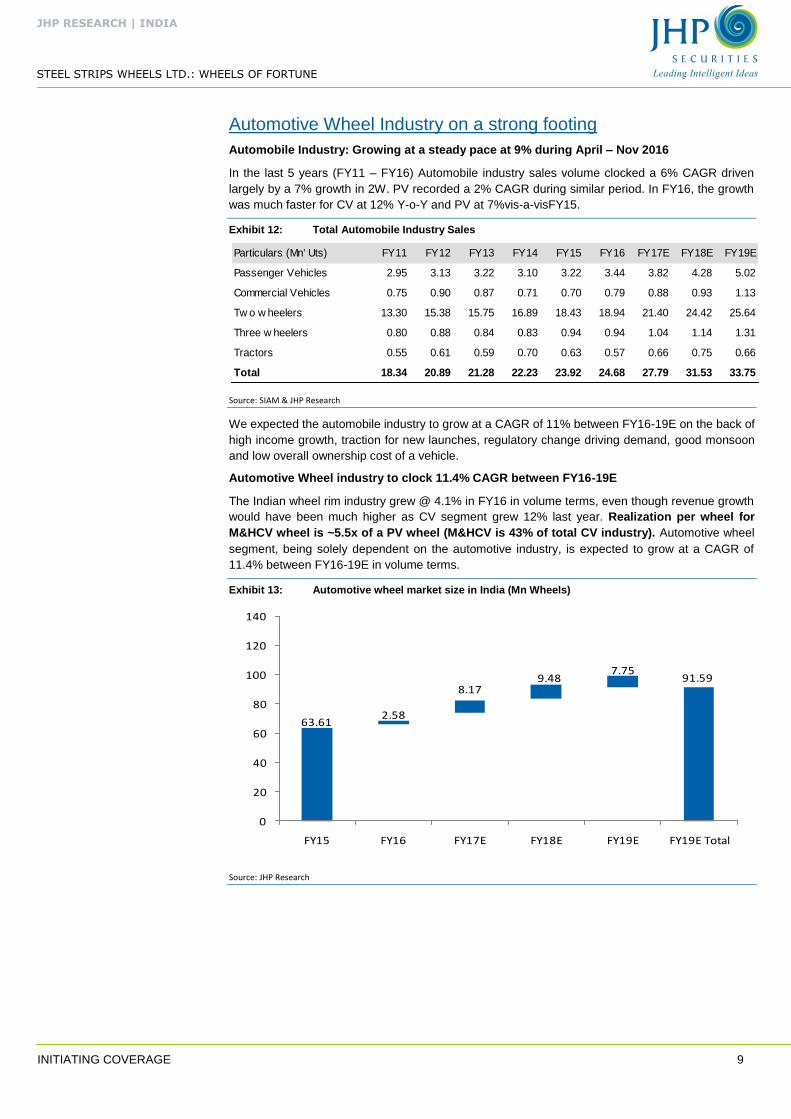

Automotive Wheel Industry on a strong footing

Automobile Industry: Growing at a steady pace at 9% during April – Nov 2016

In the last 5 years (FY11 – FY16) Automobile industry sales volume clocked a 6% CAGR driven

largely by a 7% growth in 2W. PV recorded a 2% CAGR during similar period. In FY16, the growth

was much faster for CV at 12% Y-o-Y and PV at 7%vis-a-visFY15.

Exhibit 12: Total Automobile Industry Sales

Source: SIAM & JHP Research

We expected the automobile industry to grow at a CAGR of 11% between FY16-19E on the back of

high income growth, traction for new launches, regulatory change driving demand, good monsoon

and low overall ownership cost of a vehicle.

Automotive Wheel industry to clock 11.4% CAGR between FY16-19E

The Indian wheel rim industry grew @ 4.1% in FY16 in volume terms, even though revenue growth

would have been much higher as CV segment grew 12% last year. Realization per wheel for

M&HCV wheel is ~5.5x of a PV wheel (M&HCV is 43% of total CV industry). Automotive wheel

segment, being solely dependent on the automotive industry, is expected to grow at a CAGR of

11.4% between FY16-19E in volume terms.

Exhibit 13: Automotive wheel market size in India (Mn Wheels)

Source: JHP Research

Particulars (Mn' Uts) FY11 FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Passenger Vehicles 2.95 3.13 3.22 3.10 3.22 3.44 3.82 4.28 5.02

Commercial Vehicles 0.75 0.90 0.87 0.71 0.70 0.79 0.88 0.93 1.13

Tw o w heelers 13.30 15.38 15.75 16.89 18.43 18.94 21.40 24.42 25.64

Three w heelers 0.80 0.88 0.84 0.83 0.94 0.94 1.04 1.14 1.31

Tractors 0.55 0.61 0.59 0.70 0.63 0.57 0.66 0.75 0.66

Total 18.34 20.89 21.28 22.23 23.92 24.68 27.79 31.53 33.75

63.612.58

8.179.48

7.7591.59

0

20

40

60

80

100

120

140

FY15 FY16 FY17E FY18E FY19E FY19E Total

INITIATING COVERAGE 10

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Exhibit 14: Automotive Wheels Volume Mix Segment-wise

Source: JHP Research

Alloy wheel market to clock a 27.5% CAGR between FY16-19E

The alloy wheel market in the passenger vehicle industry is currently in high growth phase,

recording a 27% CAGR between FY14-16. The scorching pace of growth is expected to continue

as consumers have turned aspirational and is willing to pay higher price for better products. The

conversion rate could have been high had there been adequate availability of reliable and

consistent supply of alloy wheels in India. Currently alloy wheels are in short supply in India

due to lack of domestic production, the same in imported from various countries including

China, Korea and Thailand. In May 2015 the government had levied anti-dumping duty on alloy

wheels being imported from China, Korea and Thailand. We expect the alloy wheel industry in

India to record a 27.5% CAGR between FY16-19E, achieving a market size of 7.8 mn wheels.

13.5% 14.0% 13.8% 13.6% 14.9%2.9% 3.2% 3.2% 3.0% 3.3%

77.3% 77.0% 77.2% 77.6% 76.2%

3.9% 3.8% 3.7% 3.6% 3.9%2.3% 2.0% 2.1% 2.1% 1.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FY15 FY16 FY17E FY18E FY19E

PV CV 2 Wheelers 3 Wheelers Tractors

INITIATING COVERAGE 11

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

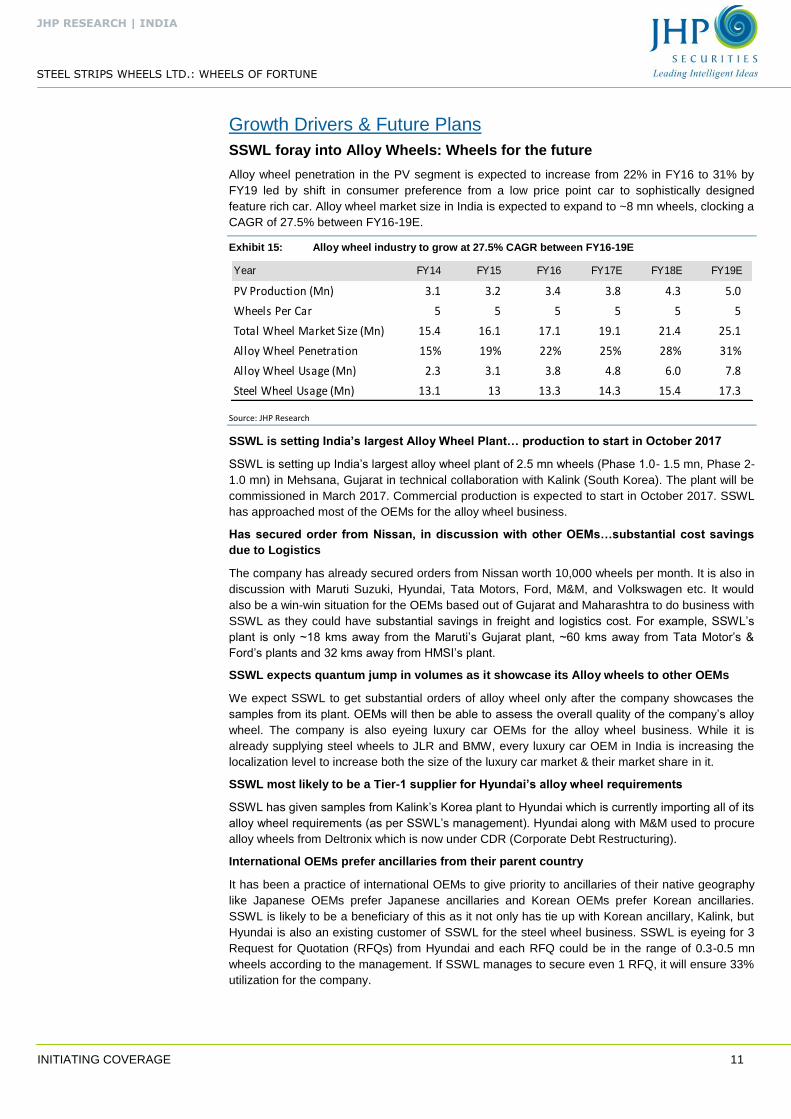

Growth Drivers & Future Plans

SSWL foray into Alloy Wheels: Wheels for the future

Alloy wheel penetration in the PV segment is expected to increase from 22% in FY16 to 31% by

FY19 led by shift in consumer preference from a low price point car to sophistically designed

feature rich car. Alloy wheel market size in India is expected to expand to ~8 mn wheels, clocking a

CAGR of 27.5% between FY16-19E.

Exhibit 15: Alloy wheel industry to grow at 27.5% CAGR between FY16-19E

Source: JHP Research

SSWL is setting India’s largest Alloy Wheel Plant… production to start in October 2017

SSWL is setting up India’s largest alloy wheel plant of 2.5 mn wheels (Phase 1.0- 1.5 mn, Phase 2-

1.0 mn) in Mehsana, Gujarat in technical collaboration with Kalink (South Korea). The plant will be

commissioned in March 2017. Commercial production is expected to start in October 2017. SSWL

has approached most of the OEMs for the alloy wheel business.

Has secured order from Nissan, in discussion with other OEMs…substantial cost savings

due to Logistics

The company has already secured orders from Nissan worth 10,000 wheels per month. It is also in

discussion with Maruti Suzuki, Hyundai, Tata Motors, Ford, M&M, and Volkswagen etc. It would

also be a win-win situation for the OEMs based out of Gujarat and Maharashtra to do business with

SSWL as they could have substantial savings in freight and logistics cost. For example, SSWL’s

plant is only ~18 kms away from the Maruti’s Gujarat plant, ~60 kms away from Tata Motor’s &

Ford’s plants and 32 kms away from HMSI’s plant.

SSWL expects quantum jump in volumes as it showcase its Alloy wheels to other OEMs

We expect SSWL to get substantial orders of alloy wheel only after the company showcases the

samples from its plant. OEMs will then be able to assess the overall quality of the company’s alloy

wheel. The company is also eyeing luxury car OEMs for the alloy wheel business. While it is

already supplying steel wheels to JLR and BMW, every luxury car OEM in India is increasing the

localization level to increase both the size of the luxury car market & their market share in it.

SSWL most likely to be a Tier-1 supplier for Hyundai’s alloy wheel requirements

SSWL has given samples from Kalink’s Korea plant to Hyundai which is currently importing all of its

alloy wheel requirements (as per SSWL’s management). Hyundai along with M&M used to procure

alloy wheels from Deltronix which is now under CDR (Corporate Debt Restructuring).

International OEMs prefer ancillaries from their parent country

It has been a practice of international OEMs to give priority to ancillaries of their native geography

like Japanese OEMs prefer Japanese ancillaries and Korean OEMs prefer Korean ancillaries.

SSWL is likely to be a beneficiary of this as it not only has tie up with Korean ancillary, Kalink, but

Hyundai is also an existing customer of SSWL for the steel wheel business. SSWL is eyeing for 3

Request for Quotation (RFQs) from Hyundai and each RFQ could be in the range of 0.3-0.5 mn

wheels according to the management. If SSWL manages to secure even 1 RFQ, it will ensure 33%

utilization for the company.

Year FY14 FY15 FY16 FY17E FY18E FY19E

PV Production (Mn) 3.1 3.2 3.4 3.8 4.3 5.0

Wheels Per Car 5 5 5 5 5 5

Total Wheel Market Size (Mn) 15.4 16.1 17.1 19.1 21.4 25.1

Alloy Wheel Penetration 15% 19% 22% 25% 28% 31%

Alloy Wheel Usage (Mn) 2.3 3.1 3.8 4.8 6.0 7.8

Steel Wheel Usage (Mn) 13.1 13 13.3 14.3 15.4 17.3

INITIATING COVERAGE 12

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

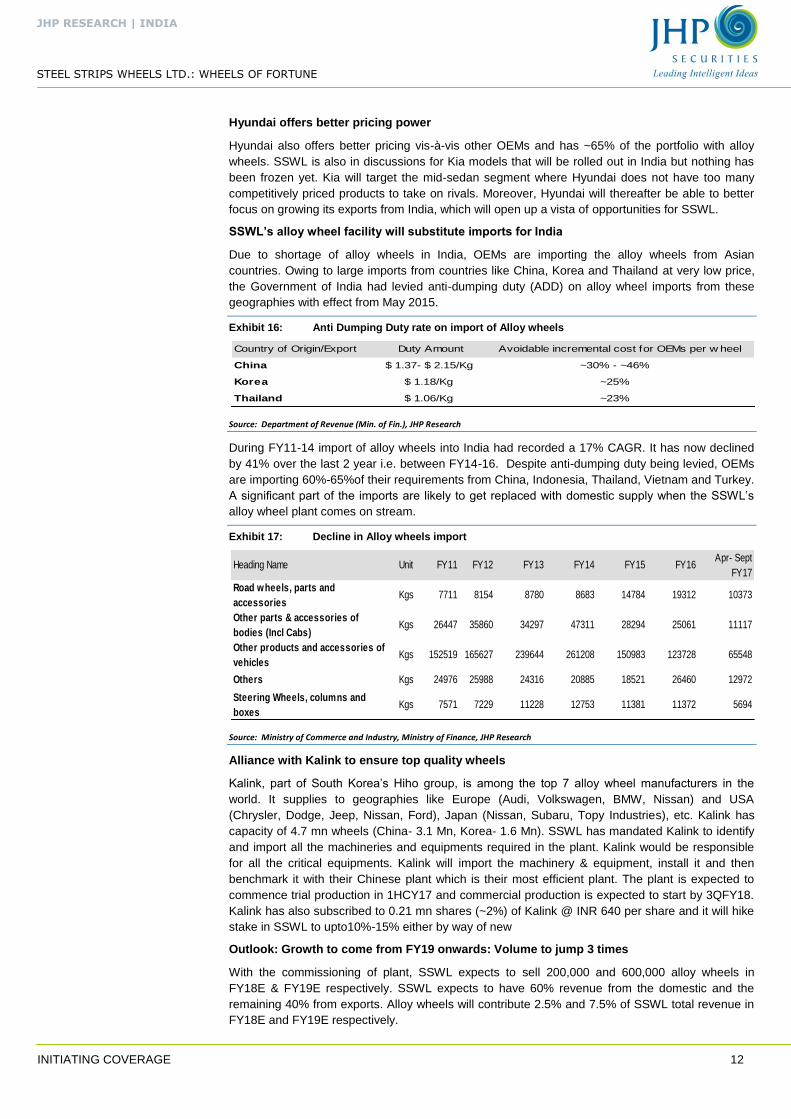

Hyundai offers better pricing power

Hyundai also offers better pricing vis-à-vis other OEMs and has ~65% of the portfolio with alloy

wheels. SSWL is also in discussions for Kia models that will be rolled out in India but nothing has

been frozen yet. Kia will target the mid-sedan segment where Hyundai does not have too many

competitively priced products to take on rivals. Moreover, Hyundai will thereafter be able to better

focus on growing its exports from India, which will open up a vista of opportunities for SSWL.

SSWL’s alloy wheel facility will substitute imports for India

Due to shortage of alloy wheels in India, OEMs are importing the alloy wheels from Asian

countries. Owing to large imports from countries like China, Korea and Thailand at very low price,

the Government of India had levied anti-dumping duty (ADD) on alloy wheel imports from these

geographies with effect from May 2015.

Exhibit 16: Anti Dumping Duty rate on import of Alloy wheels

Source: Department of Revenue (Min. of Fin.), JHP Research

During FY11-14 import of alloy wheels into India had recorded a 17% CAGR. It has now declined

by 41% over the last 2 year i.e. between FY14-16. Despite anti-dumping duty being levied, OEMs

are importing 60%-65%of their requirements from China, Indonesia, Thailand, Vietnam and Turkey.

A significant part of the imports are likely to get replaced with domestic supply when the SSWL’s

alloy wheel plant comes on stream.

Exhibit 17: Decline in Alloy wheels import

Source: Ministry of Commerce and Industry, Ministry of Finance, JHP Research

Alliance with Kalink to ensure top quality wheels

Kalink, part of South Korea’s Hiho group, is among the top 7 alloy wheel manufacturers in the

world. It supplies to geographies like Europe (Audi, Volkswagen, BMW, Nissan) and USA

(Chrysler, Dodge, Jeep, Nissan, Ford), Japan (Nissan, Subaru, Topy Industries), etc. Kalink has

capacity of 4.7 mn wheels (China- 3.1 Mn, Korea- 1.6 Mn). SSWL has mandated Kalink to identify

and import all the machineries and equipments required in the plant. Kalink would be responsible

for all the critical equipments. Kalink will import the machinery & equipment, install it and then

benchmark it with their Chinese plant which is their most efficient plant. The plant is expected to

commence trial production in 1HCY17 and commercial production is expected to start by 3QFY18.

Kalink has also subscribed to 0.21 mn shares (~2%) of Kalink @ INR 640 per share and it will hike

stake in SSWL to upto10%-15% either by way of new

Outlook: Growth to come from FY19 onwards: Volume to jump 3 times

With the commissioning of plant, SSWL expects to sell 200,000 and 600,000 alloy wheels in

FY18E & FY19E respectively. SSWL expects to have 60% revenue from the domestic and the

remaining 40% from exports. Alloy wheels will contribute 2.5% and 7.5% of SSWL total revenue in

FY18E and FY19E respectively.

Country of Origin/Export Duty Amount Avoidable incremental cost for OEMs per w heel

China $ 1.37- $ 2.15/Kg ~30% - ~46%

Korea $ 1.18/Kg ~25%

Thailand $ 1.06/Kg ~23%

Heading Name Unit FY11 FY12 FY13 FY14 FY15 FY16Apr- Sept

FY17

Road wheels, parts and

accessoriesKgs 7711 8154 8780 8683 14784 19312 10373

Other parts & accessories of

bodies (Incl Cabs)Kgs 26447 35860 34297 47311 28294 25061 11117

Other products and accessories of

vehicles Kgs 152519 165627 239644 261208 150983 123728 65548

Others Kgs 24976 25988 24316 20885 18521 26460 12972

Steering Wheels, columns and

boxesKgs 7571 7229 11228 12753 11381 11372 5694

INITIATING COVERAGE 13

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Bharat Benz to be the primary client of the upcoming CV facility in Chennai

The new 1 mn CV wheel facility which is likely to start from June 2017 will target growing demand

from CV OEMs in south and overseas markets. With M&HCV industry recording a 23% CAGR

between FY14-16, the utilization for SSWL’s Jamshedpur plant had increased from 37% in FY14 to

83% in FY16 and 96% by the end of Q1FY17. Due to capacity constraints, neither the company

has been able to tap the southern markets to its full potential nor has it been able to export CV

wheels. Now with Chennai facility coming in we expect steady demand for its CV wheels from both

the South Indian and overseas markets. SSWL will supply ~50000 wheel rims per month (60%

of total capacity) to Bharat Benz. Once the plant starts commercial production, deliveries are

likely to commence after the quality audit from Daimler.

Exports - A major growth driver going forward

SSWL is keen to increase the penetration in export markets aggressively with the start of its

Chennai plant. Chennai plant is strategically located near the port to reduce the logistics cost of

transporting the wheels to port.

Huge potential for CV wheel rims (tubeless tyres) in the global market

There is also a huge potential for export of CV wheel rims for tubeless tyres for the European and

South American market which the company would tap once the Chennai plant comes on stream.

The proposed facility is well equipped with modern technology to meet the international quality

standard.

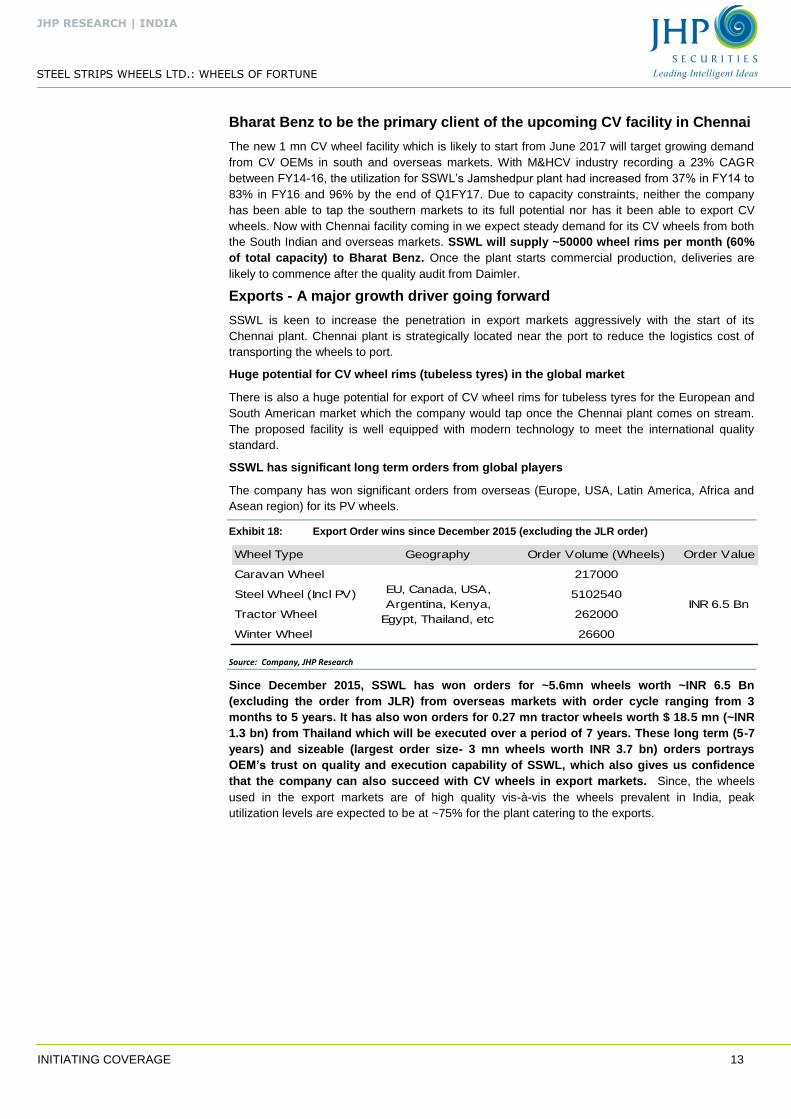

SSWL has significant long term orders from global players

The company has won significant orders from overseas (Europe, USA, Latin America, Africa and

Asean region) for its PV wheels.

Exhibit 18: Export Order wins since December 2015 (excluding the JLR order)

Source: Company, JHP Research

Since December 2015, SSWL has won orders for ~5.6mn wheels worth ~INR 6.5 Bn

(excluding the order from JLR) from overseas markets with order cycle ranging from 3

months to 5 years. It has also won orders for 0.27 mn tractor wheels worth $ 18.5 mn (~INR

1.3 bn) from Thailand which will be executed over a period of 7 years. These long term (5-7

years) and sizeable (largest order size- 3 mn wheels worth INR 3.7 bn) orders portrays

OEM’s trust on quality and execution capability of SSWL, which also gives us confidence

that the company can also succeed with CV wheels in export markets. Since, the wheels

used in the export markets are of high quality vis-à-vis the wheels prevalent in India, peak

utilization levels are expected to be at ~75% for the plant catering to the exports.

Wheel Type Geography Order Volume (Wheels) Order Value

Caravan Wheel 217000

Steel Wheel (Incl PV) 5102540

Tractor Wheel 262000

Winter Wheel 26600

EU, Canada, USA,

Argentina, Kenya,

Egypt, Thailand, etc

INR 6.5 Bn

INITIATING COVERAGE 14

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

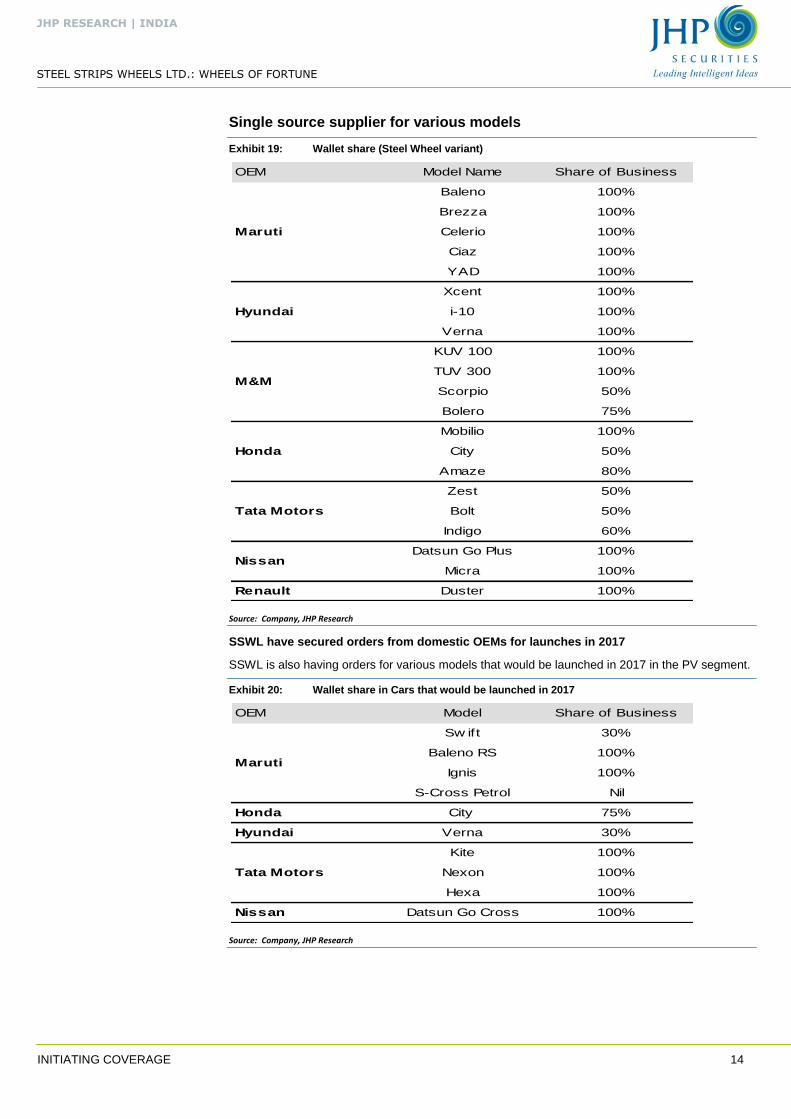

Single source supplier for various models

Exhibit 19: Wallet share (Steel Wheel variant)

Source: Company, JHP Research

SSWL have secured orders from domestic OEMs for launches in 2017

SSWL is also having orders for various models that would be launched in 2017 in the PV segment.

Exhibit 20: Wallet share in Cars that would be launched in 2017

Source: Company, JHP Research

OEM Model Name Share of Business

Baleno 100%

Brezza 100%

Celerio 100%

Ciaz 100%

YAD 100%

Xcent 100%

i-10 100%

Verna 100%

KUV 100 100%

TUV 300 100%

Scorpio 50%

Bolero 75%

Mobilio 100%

City 50%

Amaze 80%

Zest 50%

Bolt 50%

Indigo 60%

Datsun Go Plus 100%

Micra 100%

Renault Duster 100%

Nissan

Maruti

Hyundai

M&M

Honda

Tata Motors

OEM Model Share of Business

Sw ift 30%

Baleno RS 100%

Ignis 100%

S-Cross Petrol Nil

Honda City 75%

Hyundai Verna 30%

Kite 100%

Nexon 100%

Hexa 100%

Nissan Datsun Go Cross 100%

Maruti

Tata Motors

INITIATING COVERAGE 15

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Results Improving but rising Debt a Concern

Revenue clocked a 5.4% CAGR between FY12-16……

SSWL had reported 5.4%/11.8%/19.8% growth in Top-line / EBITDA / Bottom-line between FY12-

16. The company had shown improvement in financial metrics despite the automobile industry

growing by a meager 4% during the said period. The company reported volume growth of 6.6%

whereas realizations stood largely constant @ INR 900 per wheel. EBITDA margin increased from

9.7% in FY12 to 12.3% in FY16 largely due to reduction in raw material cost. PBT grew 24.3% and

PBT margin expanded by 323 bps over the same period. On the leverage side, even though

absolute level of debt has increased, net debt to equity has reduced from 1.56 to 1.20. ROCE and

ROE has improved from 6.64%/9.84% in FY12 to 9.55%/13.98% in FY16.

…….. Is expected to improve to 14.1% CAGR between FY16-19E

Top-line growth is expected to accelerate to 14.1% CAGR between FY16-19E. Wheel rim

volumes are expected to grow by 10.8% CAGR over the same period driven by decent

demand growth for the alloy wheels and CV wheels. SSWL is expected to touch volume of 18

mn wheels and revenue of INR 17.5 bn by FY19E. Blended realization is expected to surge to INR

982/wheel (CAGR of 3.0% between FY16-19E) as the share of CV and alloy wheels will increase in

total volume. Realization for alloy wheel is 4x of a steel wheel whereas realization for a truck

wheel is 5.5x of a PV wheel. Also the thrust on higher exports will also aid realization. EBITDA is

expected to nearly double between FY16-19E (CAGR- 24%) and margins are likely to expand

by 348 bps to 15.8% by FY19E. Higher depreciation, interest cost & tax rate is likely to

restrict the profit CAGR to 24.8% over the same period. SSWL is likely to report PAT & EPS

of INR 1166 mn and INR 75.35 in FY19E.

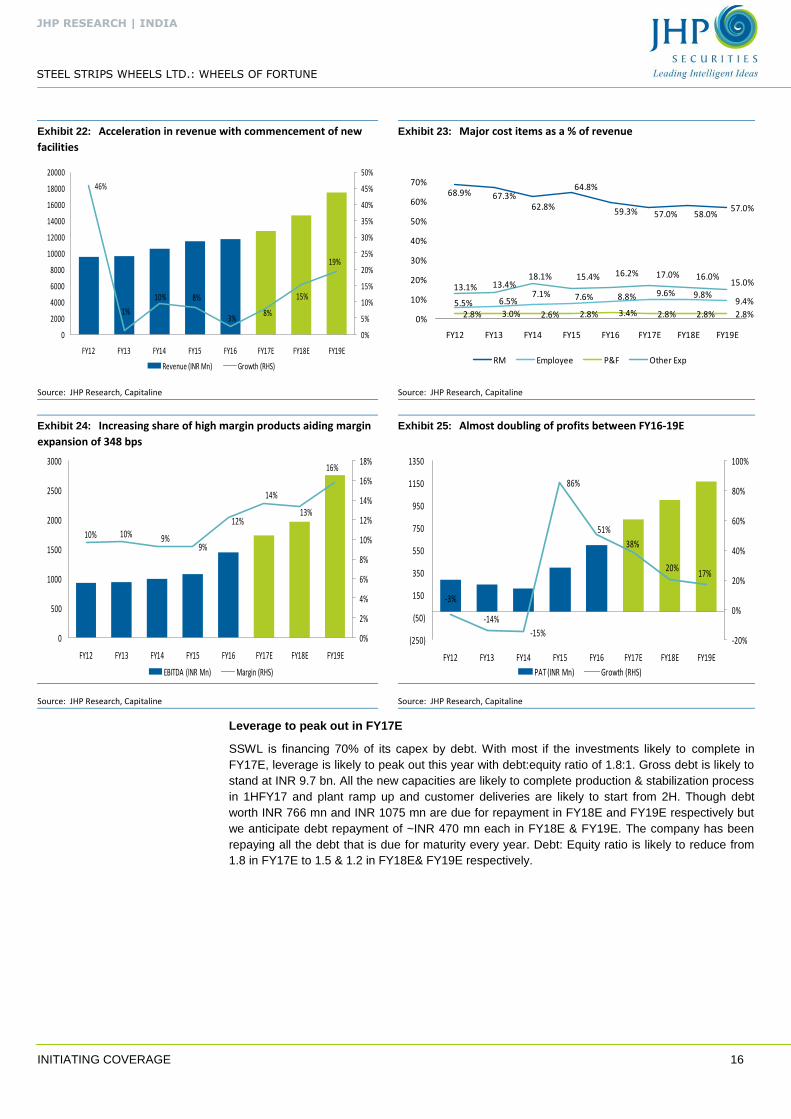

Exhibit 21: Acceleration in revenue with commencement of new facilities

Source: JHP Research, Company

46%

1%10% 8%

3% 8%

15%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Revenue (INR Mn) Growth (RHS)

INITIATING COVERAGE 16

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Exhibit 22: Acceleration in revenue with commencement of new

facilities

Exhibit 23: Major cost items as a % of revenue

Source: JHP Research, Capitaline Source: JHP Research, Capitaline

Exhibit 24: Increasing share of high margin products aiding margin

expansion of 348 bps

Exhibit 25: Almost doubling of profits between FY16-19E

Source: JHP Research, Capitaline Source: JHP Research, Capitaline

Leverage to peak out in FY17E

SSWL is financing 70% of its capex by debt. With most if the investments likely to complete in

FY17E, leverage is likely to peak out this year with debt:equity ratio of 1.8:1. Gross debt is likely to

stand at INR 9.7 bn. All the new capacities are likely to complete production & stabilization process

in 1HFY17 and plant ramp up and customer deliveries are likely to start from 2H. Though debt

worth INR 766 mn and INR 1075 mn are due for repayment in FY18E and FY19E respectively but

we anticipate debt repayment of ~INR 470 mn each in FY18E & FY19E. The company has been

repaying all the debt that is due for maturity every year. Debt: Equity ratio is likely to reduce from

1.8 in FY17E to 1.5 & 1.2 in FY18E& FY19E respectively.

46%

1%

10% 8%

3%8%

15%

19%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

20000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Revenue (INR Mn) Growth (RHS)

68.9% 67.3%62.8%

64.8%

59.3% 57.0% 58.0%57.0%

5.5% 6.5%7.1% 7.6% 8.8% 9.6% 9.8%

9.4%

2.8% 3.0% 2.6% 2.8% 3.4% 2.8% 2.8% 2.8%

13.1% 13.4%18.1% 15.4% 16.2% 17.0% 16.0%

15.0%

0%

10%

20%

30%

40%

50%

60%

70%

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

RM Employee P&F Other Exp

10% 10% 9%9%

12%

14%

13%

16%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

500

1000

1500

2000

2500

3000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

EBITDA (INR Mn) Margin (RHS)

-3%

-14%

-15%

86%

51%

38%

20%17%

-20%

0%

20%

40%

60%

80%

100%

(250)

(50)

150

350

550

750

950

1150

1350

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

PAT (INR Mn) Growth (RHS)

INITIATING COVERAGE 17

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

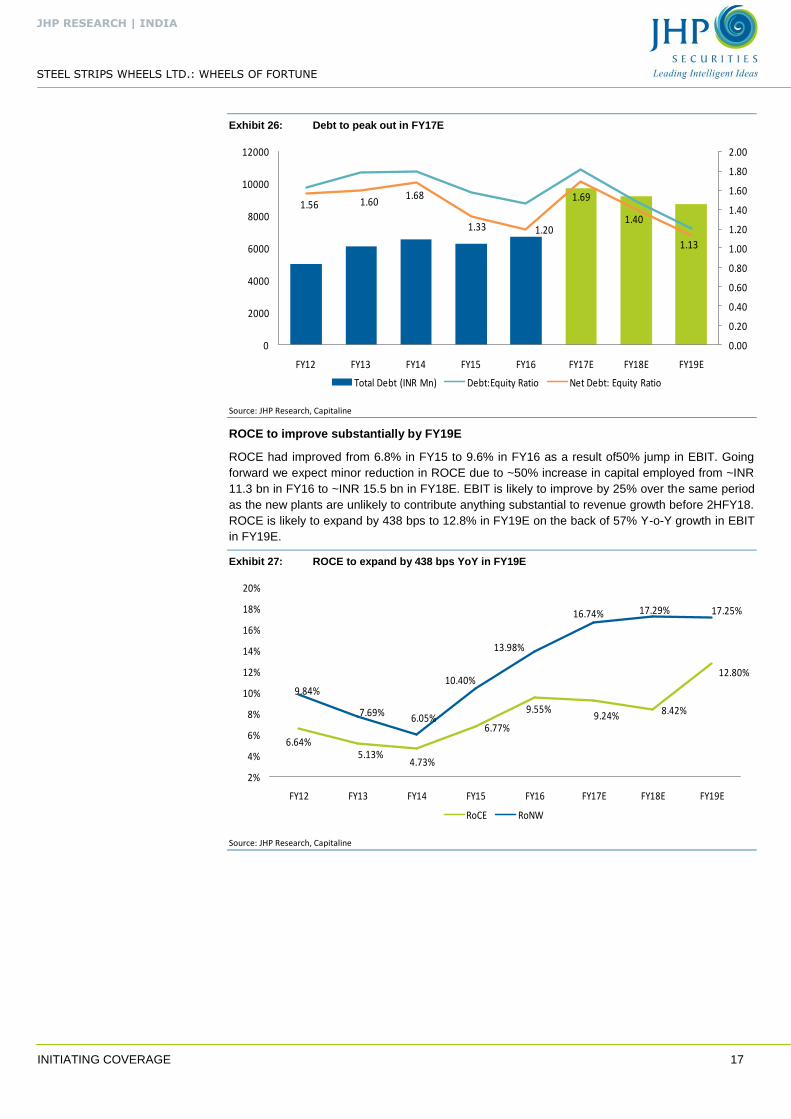

Exhibit 26: Debt to peak out in FY17E

Source: JHP Research, Capitaline

ROCE to improve substantially by FY19E

ROCE had improved from 6.8% in FY15 to 9.6% in FY16 as a result of50% jump in EBIT. Going

forward we expect minor reduction in ROCE due to ~50% increase in capital employed from ~INR

11.3 bn in FY16 to ~INR 15.5 bn in FY18E. EBIT is likely to improve by 25% over the same period

as the new plants are unlikely to contribute anything substantial to revenue growth before 2HFY18.

ROCE is likely to expand by 438 bps to 12.8% in FY19E on the back of 57% Y-o-Y growth in EBIT

in FY19E.

Exhibit 27: ROCE to expand by 438 bps YoY in FY19E

Source: JHP Research, Capitaline

1.56 1.601.68

1.33 1.20

1.69

1.40

1.13

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

2.00

0

2000

4000

6000

8000

10000

12000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

Total Debt (INR Mn) Debt:Equity Ratio Net Debt: Equity Ratio

6.64%5.13%

4.73%

6.77%

9.55%9.24% 8.42%

12.80%

9.84%

7.69% 6.05%

10.40%

13.98%

16.74% 17.29% 17.25%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

RoCE RoNW

INITIATING COVERAGE 18

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

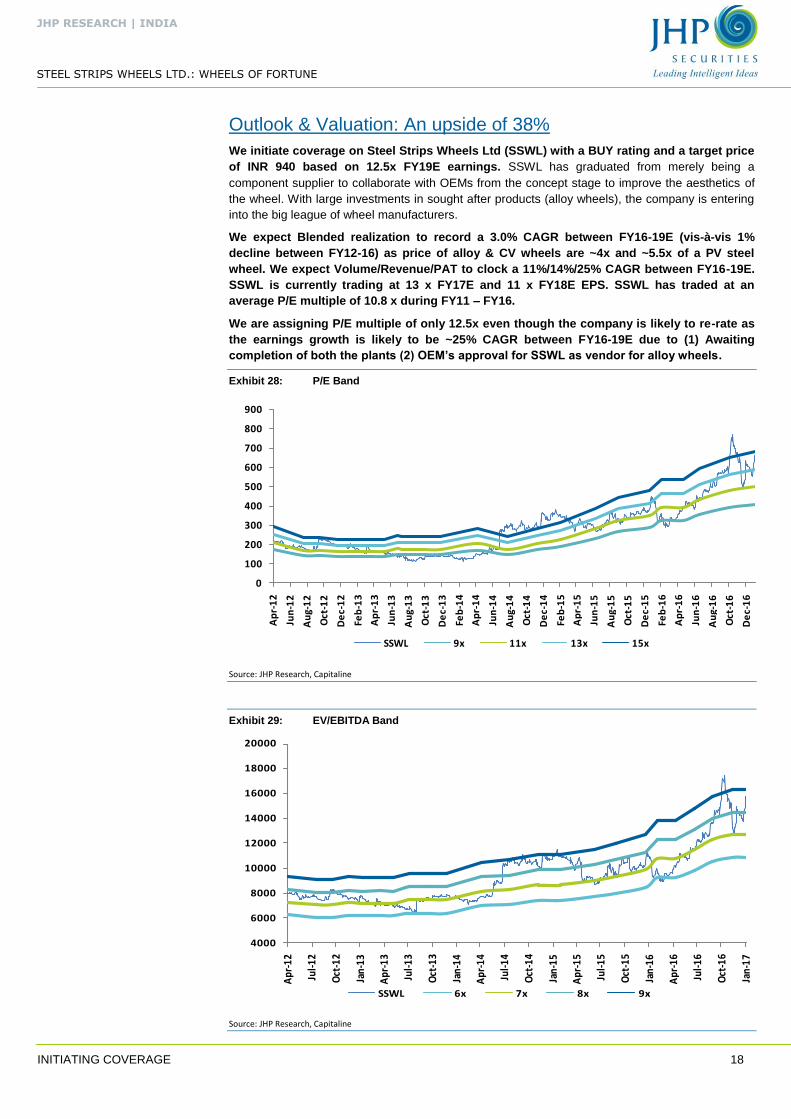

Outlook & Valuation: An upside of 38%

We initiate coverage on Steel Strips Wheels Ltd (SSWL) with a BUY rating and a target price

of INR 940 based on 12.5x FY19E earnings. SSWL has graduated from merely being a

component supplier to collaborate with OEMs from the concept stage to improve the aesthetics of

the wheel. With large investments in sought after products (alloy wheels), the company is entering

into the big league of wheel manufacturers.

We expect Blended realization to record a 3.0% CAGR between FY16-19E (vis-à-vis 1%

decline between FY12-16) as price of alloy & CV wheels are ~4x and ~5.5x of a PV steel

wheel. We expect Volume/Revenue/PAT to clock a 11%/14%/25% CAGR between FY16-19E.

SSWL is currently trading at 13 x FY17E and 11 x FY18E EPS. SSWL has traded at an

average P/E multiple of 10.8 x during FY11 – FY16.

We are assigning P/E multiple of only 12.5x even though the company is likely to re-rate as

the earnings growth is likely to be ~25% CAGR between FY16-19E due to (1) Awaiting

completion of both the plants (2) OEM’s approval for SSWL as vendor for alloy wheels.

Exhibit 28: P/E Band

Source: JHP Research, Capitaline

Exhibit 29: EV/EBITDA Band

Source: JHP Research, Capitaline

0

100

200

300

400

500

600

700

800

900

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

De

c-1

3

Feb

-14

Ap

r-1

4

Jun

-14

Au

g-1

4

Oct

-14

De

c-1

4

Feb

-15

Ap

r-1

5

Jun

-15

Au

g-1

5

Oct

-15

De

c-1

5

Feb

-16

Ap

r-1

6

Jun

-16

Au

g-1

6

Oct

-16

De

c-1

6

SSWL 9x 11x 13x 15x

4000

6000

8000

10000

12000

14000

16000

18000

20000

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Apr

-16

Jul-1

6

Oct

-16

Jan-

17

SSWL 6x 7x 8x 9x

INITIATING COVERAGE 19

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

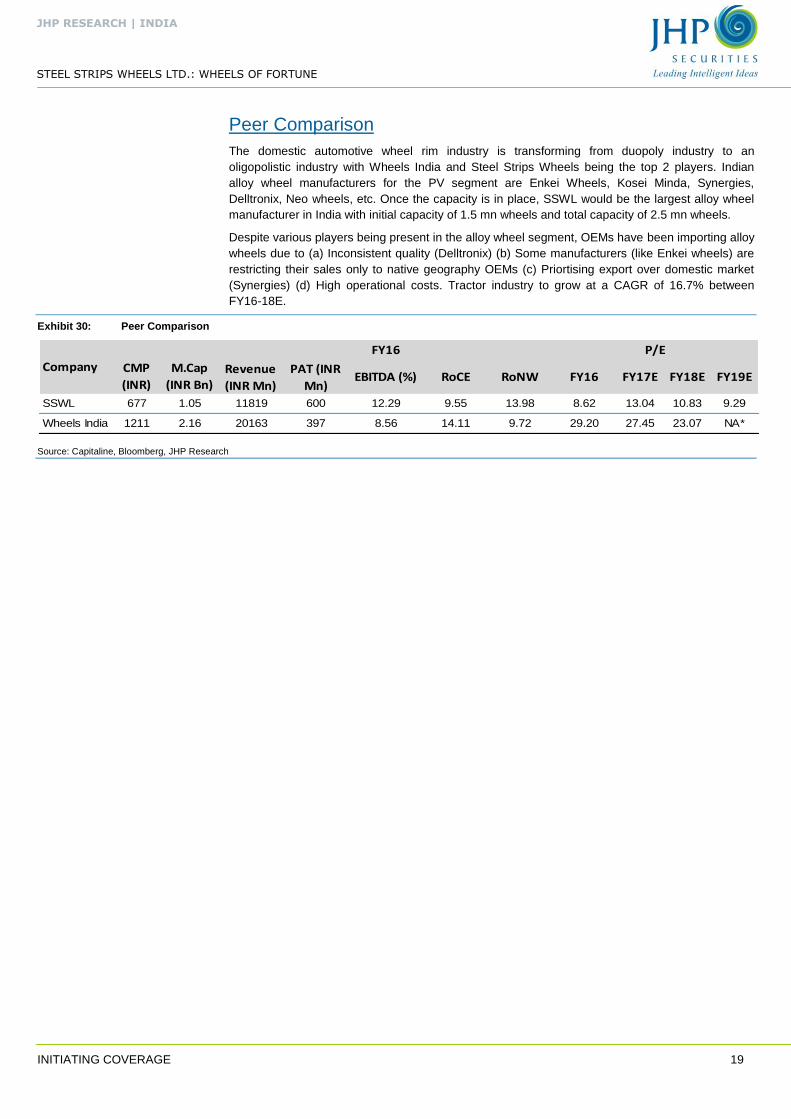

Peer Comparison

The domestic automotive wheel rim industry is transforming from duopoly industry to an

oligopolistic industry with Wheels India and Steel Strips Wheels being the top 2 players. Indian

alloy wheel manufacturers for the PV segment are Enkei Wheels, Kosei Minda, Synergies,

Delltronix, Neo wheels, etc. Once the capacity is in place, SSWL would be the largest alloy wheel

manufacturer in India with initial capacity of 1.5 mn wheels and total capacity of 2.5 mn wheels.

Despite various players being present in the alloy wheel segment, OEMs have been importing alloy

wheels due to (a) Inconsistent quality (Delltronix) (b) Some manufacturers (like Enkei wheels) are

restricting their sales only to native geography OEMs (c) Priortising export over domestic market

(Synergies) (d) High operational costs. Tractor industry to grow at a CAGR of 16.7% between

FY16-18E.

Exhibit 30: Peer Comparison

Source: Capitaline, Bloomberg, JHP Research

Revenue

(INR Mn)

PAT (INR

Mn)EBITDA (%) RoCE RoNW FY16 FY17E FY18E FY19E

SSWL 677 1.05 11819 600 12.29 9.55 13.98 8.62 13.04 10.83 9.29

Wheels India 1211 2.16 20163 397 8.56 14.11 9.72 29.20 27.45 23.07 NA*

Company CMP

(INR)

M.Cap

(INR Bn)

P/EFY16

INITIATING COVERAGE 20

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Risk & Concern

High Leverage

SSWL has funded 70% of its capex requirement via debt. Debt equity ratio is expected to swell to

1.82 by the end of FY17E and may gradually decline from there on. High leverage is a key risk for

the company as incase of a slowdown, elevated debt levels may compound the problem for the

company.

Delay in commercial production of new capacities

The alloy wheel plant and the new CV plant are expected to start commercial production from

Q4FY17 and H1FY18 respectively. Delay in commissioning of new capacities might impact the

delivery schedules to the OEMs resulting in losses for the company and potential loss of clients as

well.

Prolonged slowdown in the automobile segment

Demonetisation has negatively impacted the general economy which has resulted in slowdown in

CV sales. Being a discretionary item, Passenger vehicles and 2 wheelers have also seen sharp

decline in sales as consumers have deferred the purchases. Prolonged slowdown in the

automobile segment can limit SSWL’s growth potential.

INITIATING COVERAGE 21

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Appendix: Wheels: An indispensable part of an Automobile

Wheels play a major role in improving the aesthetics of a car

The primary purpose of wheel rim manufacturer is to provide a firm base to fit the tyre. The

dimension and shape should be suitable to adequately accommodate the particular tyre required

for the vehicle. But the role of wheel manufacturer has progressed from being merely a component

supplier to collaborate with OEMs from the concept stage & work as a team. Auto components like

light lamps (Head lights, tail lights), grille and wheel rims, etc are now playing significant role in

overall exterior design and appeal of a vehicle. The challenge before a wheel manufacturer is to

make continuous design changes to improve the aesthetics of the wheel without

compromising on the strength of the wheel. The look of a car can dramatically change with

perfectly designed wheels. In a bid to make low-end models more stylish, we may see high-end-

models-like wheel design in the lower segment cars as a standard feature going forward. For all

these factors continuous investments in R&D and manufacturing facilities have to be made. Further

aggressive adoption of alloy wheels by OEMs offers an opportunity to automotive wheel suppliers

like SSWL to expand its customer base.

Alloy Wheels v/s Steel Wheels: Beauty and the Beast

Passenger Vehicles (PV) wheels are divided into two main groups i.e. steel wheels and alloy

wheels. Alloy wheels are made of alloy of light metals like aluminium, magnesium or a mix of both.

Alloy wheels weights less than steel wheels and offers quicker acceleration, higher fuel efficiency

and less tension to suspension components. Since alloy wheel can be cast and worked in many

different designs they are more conducive to complex designing.

Steel wheels are heavier and can thus take greater load

Steel wheels are heavier and stronger than alloy wheels and can bear greater load. They are also

better suited for off-road applications. Steel wheels are also more easily repaired than alloy wheels,

as steel can often be hammered back into place when bent.

Alloy wheels enjoys pricing power: Are 3 x the price of Steel wheel

Alloy wheels are more than 3x the price of steel wheels (till date) because of the difference in the

production techniques. They tend to bend easier than steel wheel under the road impact and have

a tendency to crack if bent too far. They are also vulnerable to impacts of curb scrapes, saltwater

corrosion and exposure to acidic products. Steel wheels also offer better pothole resistance.

Wheel Manufacturing Process

Steel wheels are made up of two pressed components, a rim and a wheel disc which is joined

(welded) together. A rim is produced by first cutting large steel sheets to required width and length

specifications. These steel sections are rolled and welded to form a circular rim, which is flared and

formed in the roll form operation. The majority of discs are manufactured using presses that both

blank and form the center to specifications in multiple stage operations. It is then painted through a

multi-step coating process.

Large earthmoving/construction steel wheels are manufactured from hot and cold-rolled steel. Hot-

rolled steel are generally used to increase cross section thickness in high stress areas of large

diameter wheels. A special cold forming process for certain wheels is used to increase cross

section thickness while reducing the number of wheel components. Rims are built from a series of

hoops that are welded together to form a rim base. The rims are then tested extensively for fatigue,

impact and durability.

INITIATING COVERAGE 22

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

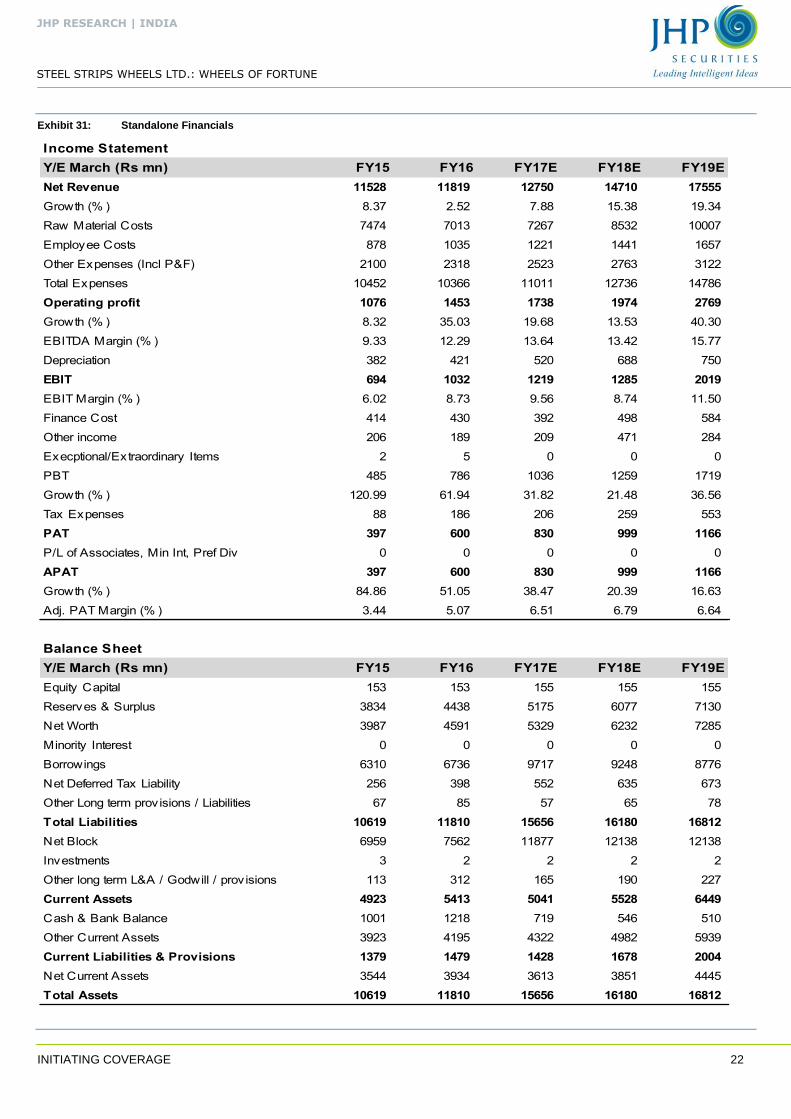

Exhibit 31: Standalone Financials

Y/E March (Rs mn) FY15 FY16 FY17E FY18E FY19E

Net Revenue 11528 11819 12750 14710 17555

Growth (% ) 8.37 2.52 7.88 15.38 19.34

Raw Material Costs 7474 7013 7267 8532 10007

Employee Costs 878 1035 1221 1441 1657

Other Expenses (Incl P&F) 2100 2318 2523 2763 3122

Total Expenses 10452 10366 11011 12736 14786

Operating profit 1076 1453 1738 1974 2769

Growth (% ) 8.32 35.03 19.68 13.53 40.30

EBITDA Margin (% ) 9.33 12.29 13.64 13.42 15.77

Depreciation 382 421 520 688 750

EBIT 694 1032 1219 1285 2019

EBIT Margin (% ) 6.02 8.73 9.56 8.74 11.50

Finance Cost 414 430 392 498 584

Other income 206 189 209 471 284

Execptional/Extraordinary Items 2 5 0 0 0

PBT 485 786 1036 1259 1719

Growth (% ) 120.99 61.94 31.82 21.48 36.56

Tax Expenses 88 186 206 259 553

PAT 397 600 830 999 1166

P/L of Associates, Min Int, Pref Div 0 0 0 0 0

APAT 397 600 830 999 1166

Growth (% ) 84.86 51.05 38.47 20.39 16.63

Adj. PAT Margin (% ) 3.44 5.07 6.51 6.79 6.64

Y/E March (Rs mn) FY15 FY16 FY17E FY18E FY19E

Equity Capital 153 153 155 155 155

Reserves & Surplus 3834 4438 5175 6077 7130

Net Worth 3987 4591 5329 6232 7285

Minority Interest 0 0 0 0 0

Borrowings 6310 6736 9717 9248 8776

Net Deferred Tax Liability 256 398 552 635 673

Other Long term prov isions / Liabilities 67 85 57 65 78

Total Liabilities 10619 11810 15656 16180 16812

Net Block 6959 7562 11877 12138 12138

Investments 3 2 2 2 2

Other long term L&A / Godwill / prov isions 113 312 165 190 227

Current Assets 4923 5413 5041 5528 6449

Cash & Bank Balance 1001 1218 719 546 510

Other Current Assets 3923 4195 4322 4982 5939

Current Liabilities & Provisions 1379 1479 1428 1678 2004

Net Current Assets 3544 3934 3613 3851 4445

Total Assets 10619 11810 15656 16180 16812

Income Statement

Balance Sheet

INITIATING COVERAGE 23

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

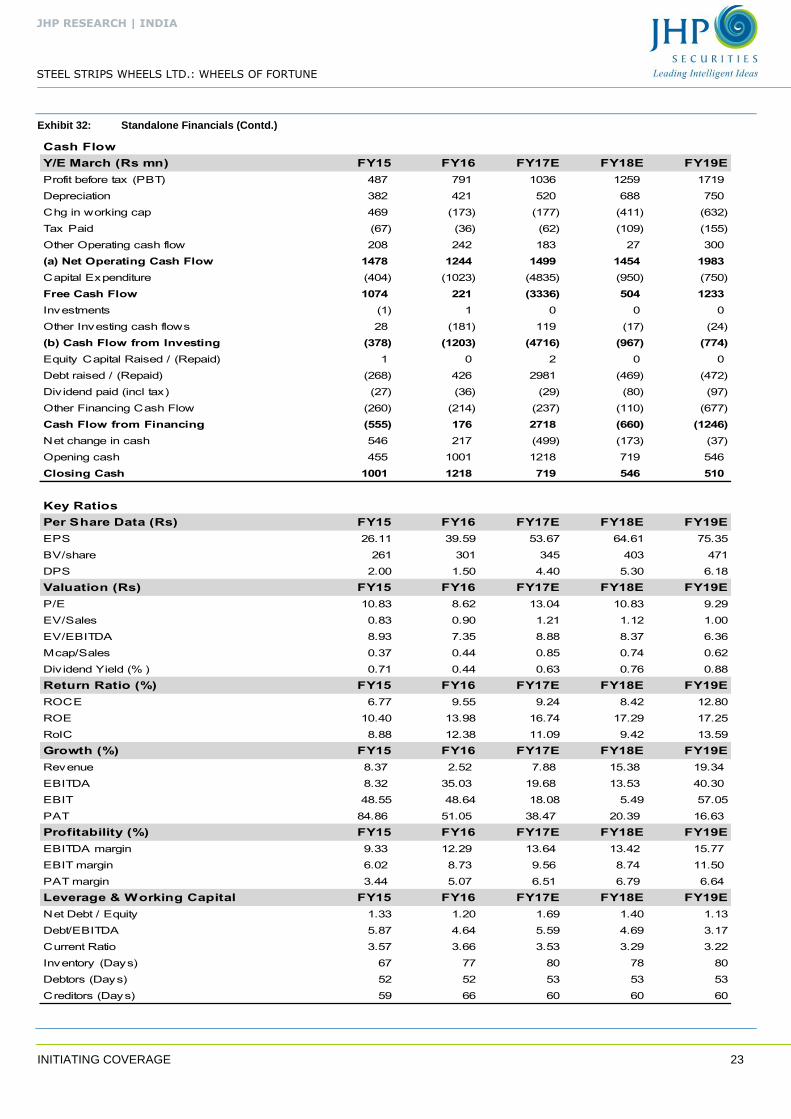

Exhibit 32: Standalone Financials (Contd.)

Y/E March (Rs mn) FY15 FY16 FY17E FY18E FY19E

Profit before tax (PBT) 487 791 1036 1259 1719

Depreciation 382 421 520 688 750

Chg in working cap 469 (173) (177) (411) (632)

Tax Paid (67) (36) (62) (109) (155)

Other Operating cash flow 208 242 183 27 300

(a) Net Operating Cash Flow 1478 1244 1499 1454 1983

Capital Expenditure (404) (1023) (4835) (950) (750)

Free Cash Flow 1074 221 (3336) 504 1233

Investments (1) 1 0 0 0

Other Investing cash flows 28 (181) 119 (17) (24)

(b) Cash Flow from Investing (378) (1203) (4716) (967) (774)

Equity Capital Raised / (Repaid) 1 0 2 0 0

Debt raised / (Repaid) (268) 426 2981 (469) (472)

Div idend paid (incl tax) (27) (36) (29) (80) (97)

Other Financing Cash Flow (260) (214) (237) (110) (677)

Cash Flow from Financing (555) 176 2718 (660) (1246)

Net change in cash 546 217 (499) (173) (37)

Opening cash 455 1001 1218 719 546

Closing Cash 1001 1218 719 546 510

Per Share Data (Rs) FY15 FY16 FY17E FY18E FY19E

EPS 26.11 39.59 53.67 64.61 75.35

BV/share 261 301 345 403 471

DPS 2.00 1.50 4.40 5.30 6.18

Valuation (Rs) FY15 FY16 FY17E FY18E FY19E

P/E 10.83 8.62 13.04 10.83 9.29

EV/Sales 0.83 0.90 1.21 1.12 1.00

EV/EBITDA 8.93 7.35 8.88 8.37 6.36

Mcap/Sales 0.37 0.44 0.85 0.74 0.62

Div idend Yield (% ) 0.71 0.44 0.63 0.76 0.88

Return Ratio (%) FY15 FY16 FY17E FY18E FY19E

ROCE 6.77 9.55 9.24 8.42 12.80

ROE 10.40 13.98 16.74 17.29 17.25

RoIC 8.88 12.38 11.09 9.42 13.59

Growth (%) FY15 FY16 FY17E FY18E FY19E

Revenue 8.37 2.52 7.88 15.38 19.34

EBITDA 8.32 35.03 19.68 13.53 40.30

EBIT 48.55 48.64 18.08 5.49 57.05

PAT 84.86 51.05 38.47 20.39 16.63

Profitability (%) FY15 FY16 FY17E FY18E FY19E

EBITDA margin 9.33 12.29 13.64 13.42 15.77

EBIT margin 6.02 8.73 9.56 8.74 11.50

PAT margin 3.44 5.07 6.51 6.79 6.64

Leverage & Working Capital FY15 FY16 FY17E FY18E FY19E

Net Debt / Equity 1.33 1.20 1.69 1.40 1.13

Debt/EBITDA 5.87 4.64 5.59 4.69 3.17

Current Ratio 3.57 3.66 3.53 3.29 3.22

Inventory (Days) 67 77 80 78 80

Debtors (Days) 52 52 53 53 53

Creditors (Days) 59 66 60 60 60

Cash Flow

Key Ratios

INITIATING COVERAGE 24

JHP RESEARCH | INDIA

STEEL STRIPS WHEELS LTD.: WHEELS OF FORTUNE

Registered office

201, Dev Neo Vikram, Sahakar Nagar C.H.S., New Link Road, Andheri (W), Mumbai - 400 053 Tel. +91 22 4082 4242.

Disclaimer / disclosures, analyst certification

I, PrashantBiyani, research analyst, hereby certify that all of the views expressed in this research report accurately reflect our views about the

subject issuer(s) of securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific

recommendation(s) or view(s) in this report.

JHP Securities Private Limited Mumbai, India (hereinafter referred to as “JHP”) is engaged in the business of Stock Broking, Portfolio Manager,

and Depository Participant.

This document has been prepared by the Research Division of JHP and is meant for use by the recipient only as information and is not for

circulation. This document is not to be reported or copied or made available to others without prior permission of JHP. It should not be

considered or taken as an offer to sell or a solicitation to buy or sell any security.

The information contained in this report has been obtained from sources that are considered to be reliable. However, JHP has not independently

verified the accuracy or completeness of the same. Neither JHP nor any of its affiliates, its directors or its employees accepts any responsibility

of whatsoever nature for the information, statements and opinion given, made available or expressed herein or for any omission therein.

Recipients of this report should be aware that past performance is not necessarily a guide to future performance and value of investments can go

down as well. The suitability or otherwise of any investments will depend upon the recipient's particular circumstances and, in case of doubt,

advice should be sought from an independent expert/advisor.

Either JHP or its affiliates or its directors or its employees or its representatives or its clients or their relatives may have position(s), make market,

act as principal or engage in transactions of securities of companies referred to in this report and they may have used the research material prior

to publication.

JHP submits that no material disciplinary action has been taken on us by any Regulatory Authority impacting equity research analysis activities.

JHP or its research analysts including their associates may have any financial interest in the subject company.

JHP or its research analysts including their associates may have actual/beneficial ownership of one per cent or more securities of the subject

company at the end of the month immediately preceding the date of publication of the research report.

JHP or its research analysts including their associates may have any material conflict of interest at the time of publication of the research report.

JHP or its research analysts have not received compensation from the subject company in the past twelve months.

It is confirmed that PrashantBiyani, research analyst of this report has not received any compensation from the companies mentioned in the

report in the preceding twelve months. The research analyst for this report certifies that all of the views expressed in this report accurately reflect

his or her personal views about the subject company or companies and its or their securities, and no part of his or her compensation was, is or

will be, directly or indirectly related to specific recommendations or views expressed in this report. The research analyst for this report has not

served as an officer, director or employee of the subject company. JHP or its research analysts have not engaged in market making activity for

the subject company

Our sales people, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients

that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make

investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that

any or all o the foregoing, among other things, may give rise to real or potential conflicts of interest.

JHP and their directors and employees may,

(a) from time to time, have a long or short position in, and buy or sell the securities of the subject company or

(b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the

financial instruments of the subject company or act as an advisor or lender/borrower to the subject company or may have any other potential

conflict of interests with respect to any recommendation and other related information and opinions.