Embed Size (px)

Citation preview

SAVING THE EURO: EU’S LEGAL SOLUTIONS

Simona Catană, PhD student in Public Law, Université Paris 8, France

(Abstract): Fighting the economic crisis which begun in the United States of America, with the fall ofLehman Brothers, was a tough challenge for the Member States of the European Union. Once thecrisis crossed the Atlantic, it became a real “euro zone crisis”, with the sovereign debts issue. The highdisparities between the strength of the European economies became apparent, and the weakerMember States came to be easy targets for the financial markets. Nevertheless, the Treatiesprohibited the direct purchase of sovereign debt of Member States by the European Central Bank, orby national banks, as well as EU or its Member States assuming commitments of central governmentsor other public authorities. With this legal framework and the risk of the disappearance of the euro atstake, the European leaders had to improvise a series of legal solution to contain the crisis. From theStability and Growth Pact, the so called “six-pack” and “two-pack” to the Treaty on Stability,Coordination and Governance in the Economic and Monetary Union, EU’s legal solutions in responseto the crisis did stop the euro from exploding. But these legal solutions also changed the balance ofpower instituted by the Treaties between the European institutions and the Member States.

Key words: Euro Zone, European Union, European integration, Europeaneconomic governance

Although a much disputed concept among the legal experts,the existence of an economic constitution of the EuropeanUnion can be revealed even within the treaties. Moreover, whenthe founding European countries decided to build a commoncurrency, the treaty of Maastricht gave even more economicrules for the states which wanted to join the euro. Andbecause the Maastricht criteria applied only to the countrieswanting to enter the euro zone, it was set in place theStability and Growth Pact, for the states already in the eurozone. All these rules, based on economic indicators, formed alegal framework meant to protect the euro countries fromcrisis (I). However, when the financial crisis broke out, andthe European banking system found itself severely affected andbasically froze the interbank lending market, the European

states had to step in, at the price of deepening their publicdeficits and public debts. The financial markets then suddenlyperceived the asymmetries between the European countries andstarted charging more the weaker states. It soon became clearthat the legal framework build over the last decades hadbecome not only inefficient, but its relative inflexibilitywas part of the problem. A new set of rules was set in place,using both European law and international law, and alsochanging the balance of power between the European institutionand the member states (II).

I. The economic constitution of the European UnionThe “economic constitution” of the European Union imposes

itself like undisputable evidence among the jurists. From itsvery beginning, the European Communities, which later mergedinto the European Union, were designed as a “community oflaw”, heavily inspired by the ordoliberal doctrine, developedin Germany. Ordoliberalism, although not well known outsideGermany, inspired the rules of the founding treaties relatedto the economy. Basically, the ordoliberal theories privilegea dual form of comprehension of the role of the state, usingat the same time legal and economic notions. According to theordoliberals, the so called “Freiburg school”, an “economicconstitution” includes all rules that are essential forestablishing the preferred economic system1. And despite thefact that further discussion can dispute the “liberal”orientation of an “economic constitution”, stating that, forexample, the rules set in place after the Soviet revolutionalso represent an economic constitution, but relying on adifferent economic model2, the ordoliberalism forged theconcept of “social market economy” as being at the heart oftheir understanding of the best “economic constitution”. Thus,the competition represents an essential and integral part ofthe welfare state, but in order to guarantee the undistortedcompetition, the state has to be strong enough to impose the

1 DREXL Josef, « La Constitution économique européenne - L'actualité du modèle ordolibéral »,Revue internationale de droit économique, 2011/4 t.XXV, p. 419-454. DOI : 10.3917/ride.254.04192 RABAULT Hugues, “La theorie de la constitution économique: notion et disctinction”, Conférence « L’avènement de la constitution économique. Comparaisons française, allemande et italienne », Metz, France, 9 – 10 October 2014

rules of the game and the respect for these rules3. Hence, therule of law has an essential role in defining the economicframework, and the public authorities have a responsibility inregulating the economy.

As about the European economic constitution, it lies inthe core of the establishing Treaty of Rome, 1957. Later, theMaastricht Treaty launches the economic and monetary union(EMU), making thus concrete steps towards a real politicalunion – the declared goal of the treaties4. In order to pursuethe integration of the single market, the Member states mustcoordinate their economic policies, as their national policiesare a matter of common concern5. Moreover, in order to assurethe convergence of the economic policies, the Member States,acting by qualified majority within the Council, formulate thebroad guidelines of the economic policies of the MemberStates, based on the recommendations of the Commission6. TheTreaty also institutes the multilateral surveillance, statingthat the Member States shall forward information to theCommission about “important measures” taken at national levelin the field of economic policies. The Commission formulates areport based on the information received from the Memberstates, and informs the Council. If the Commission considersthat a Member State’s economic policies are not consistentwith the broad guidelines formulated by the Council and thatthere is a risk of jeopardizing the functioning of theeconomic and monetary union, it can present the case in frontof the Council. The Council, stating on qualified majority,can then “make the necessary recommendations to the MemberState concerned”7. Obviously, these provisions lack any legalpower, so that there were practically no means of making arecommendation formulated by the Council legally binding forthe concerned Member State.

According to the treaty, the Member States Establishingthe euro as a single common currency and the powers of theEuropean Central Bank, the Maastricht Treaty strives tocomplete the single market. The establishment of the singlecurrency was made in three successive stages: first,3 DREXL Josef, op. cit. p. 4544 Maastricht Treaty – Treaty on European Union (1992), http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:11992M/TXT&rid=5 5 Maastricht Treaty, art. 103, paragraph 1 6 Maastricht Treaty, art. 103, paragraph 27 Maastricht Treaty, art. 103, paragraph 4

liberating the movement of capitals, began in 1 January 1990;the second stage, began in 1 January 1994, provided theconvergence of the economic policies; the third, set to beginat the latest on 1 January 1999, set the creation of thesingle currency and the establishment of the European CentralBank (ECB)8. But entrusting exclusively a European institutionwith the monetary policies also means for the Member Statesgiving up an important part of their sovereignty and of theirmeans of conducting their economic policies. Moreover, thestructure in charge with the monetary policy is the EuropeanSystem of Central Banks, consisting of the ECB and thenational central banks9. And as the ordoliberal doctrinesuggested, the ECB and the national central banks are grantedwith full independence of the national or European politicalinfluences. Thus, the Treaty specifies that when exercisingthe powers and duties conferred by the Treaty, neither the ECBnor national bank nor any other member of their decision-making bodies shall receive instructions from any governmentor European institutions10. And when analysing the historicalcontext of a unified Germany, fact that prompted Frenchpresident François Mitterrand to ask in counterpart Germany togive up its strong Deutsch Mark, that Germany, in its turn,asked for the independence of the European Central Bank11.Fearing the dangers of an irresponsible Keynesian monetarypolicy, Germany, still under the shock of the hyperinflationlived under the Weimar Republic, also asked for theprohibition of financial assistance of the Member States.Overdraft facilities or any other type of credit facility withthe ECB or the central banks of the Member States were alsoprohibited12.

In order to join the common currency, a Member State ofthe European Union has to fulfill certain economic and legalconditions, designed to ensure that the Member State’s economyis sufficiently prepared to enter the euro zone and that itscentral bank legislation is compatible with euro zonerequirements, notably the independence of its central bank. As8 Europa – Legislation Summaries, Treaty of Maastricht on European Union, http://europa.eu/legislation_summaries/institutional_affairs/treaties/treaties_maastricht_en.htm 9 Maastricht Treaty, art. 4a10 Maastricht Treaty, art. 10711 BONIFACE Pascal, Comprendre le monde, Armand Collin, Paris, 2011, p. 10012 Maastricht Treaty, art. 104

part of the preparations for the introduction of the euro, theMember States agreed in 1991 on some “convergence criteria”,also known as “Maastricht criteria”, defined as a set ofmacroeconomic indicators. Thus, among the requirements are:price stability – to show that inflation is controlled, theinflation has to be not more than 1.5% above the rate of thethree best performing Member States of the euro area; soundand stable public finances – limiting the government borrowingand the national debt, in order to avoid excessive deficits,the public deficit has to be under 3% of the country’s GDP,whilst the public debt has to be under 60% of the GDP;exchange rate stability, through participation in the ExchangeRate Mechanism (ERM II) for at least two years, without strongdeviations from the ERM II central rate; and the durability ofconvergence, meaning that the long term interest rates haveto be not more than 2% above the rate of the three bestperforming Member States in terms of price stability13. Onceevery two years, or at the request of the Member State, theCommission and the ECB assess the progress made by thecandidate countries.

However, since the tougher control of the convergenceconditions was possible only in the case of the candidatestates, the Member States also wanted to ensure some kind ofcoordination of national fiscal policies for the countriesalready in the euro zone. As a consequence, in 1997 theStability and Growth Pact (SGP) was established as a rule-based framework, to safeguard sound public finances, as theeconomic policies were considered a matter of common concernfor the entire euro zone. SGP’s implementation started on 1January 1999, to make sure that the euro zone Member Statesmaintained fiscal discipline after the introduction of thecommon currency. As fiscal criteria, the countries had tomaintain the general government budget deficit under 3% of itsGDP, and the public debt under the threshold of 60%.Technically, the SGP was formed by two Council regulations,one on the strengthening of the surveillance of budgetarypositions and the surveillance and coordination of economicpolicies14 and the other one on speeding up and clarifying the

13 European Commission, « Adopting the euro », Economic and Financial Affairs, http://ec.europa.eu/economy_finance/euro/adoption/who_can_join/index_en.htm14 Official Journal of the European Union, Council Regulation (CE) no 1466/97 of 7 July1997 on strengthening of the surveillance of budgetary positions and the surveillance and

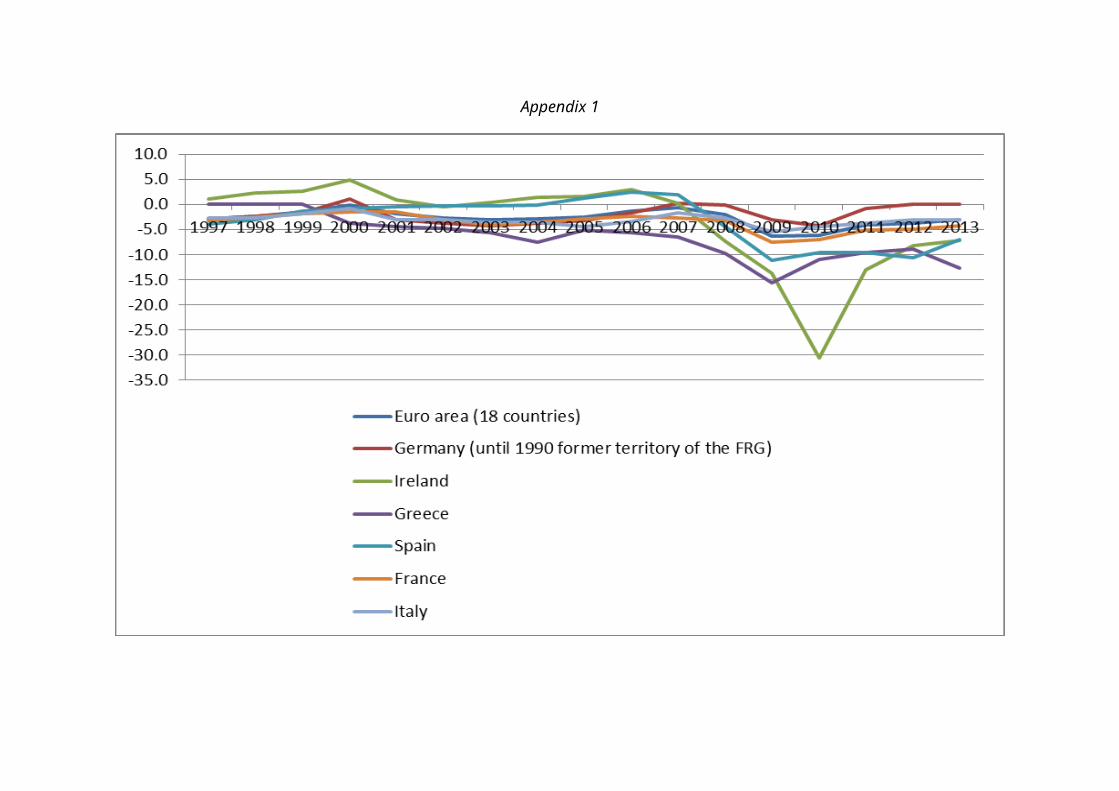

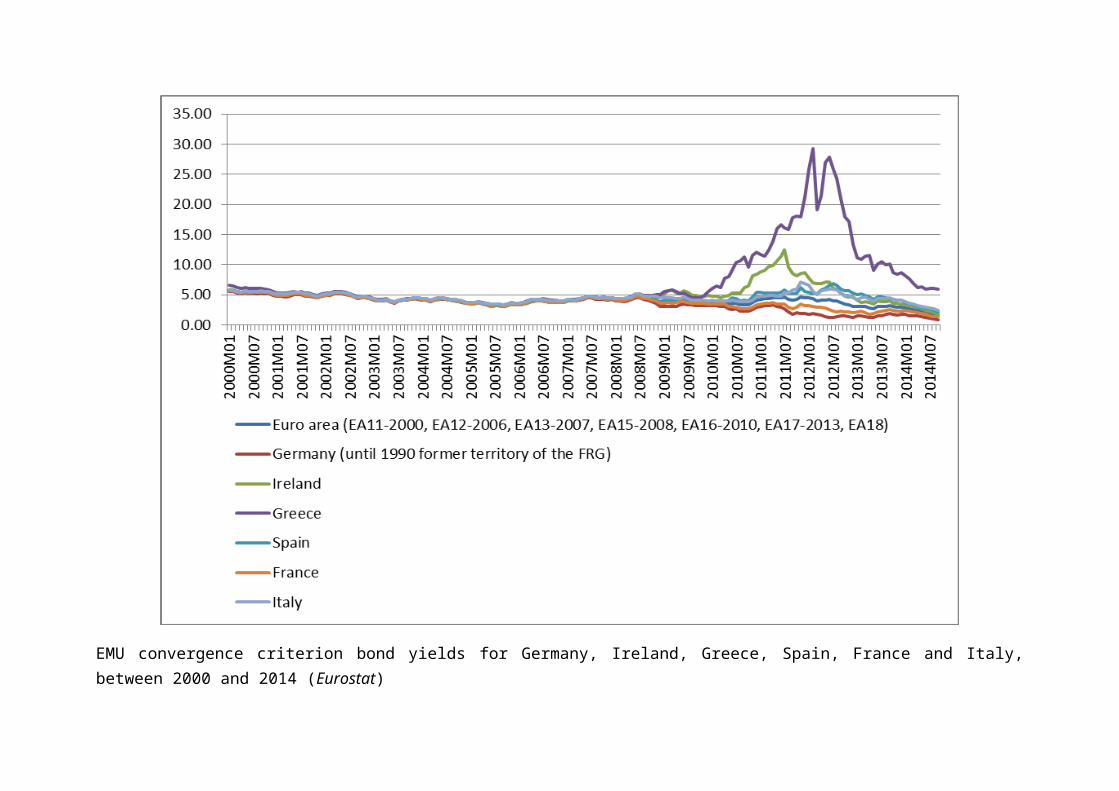

implementation of the excessive deficit procedure15. Theadhering Member States committed themselves to push for themedium term objective for budgetary position of close tobalance or surplus, and take corrective actions if needed.Nevertheless, the Member States remained responsible for theirnational budgets, and the Commission didn’t have thecompetence to intervene in the elaboration of the budget plan,even if budgetary discipline was considered necessary tosafeguard price stability in the whole euro zone. However, ifthe Commission considers that an excessive deficit exists, itcould, under the Regulation 1467/97, address an opinion and arecommendation to the Council. But the decision ofrecommending the concerned Member State the correction of theexcessive deficit was left to the Council, acting on qualifiedmajority. Immediately after the “implementation” of the SGP,the biggest European countries deepened their budgetarydeficit (Appendix 1), triggering a series of recommendationsfrom the Commission. The SGP ultimately failed, when theCouncil, dominated by the big countries, rejected the proposalof the Commission of sanctioning France and Germany forexcessive deficit in 200316.

The failure of the SGP was one of the first signs of theflaws in the European economic policy coordination framework.Moreover, despite the asymmetries between their economies, theEuropean states were treated by the financial markets as beingsimilarly reliable and charged them with converging yields fortheir government bonds (Appendix 2). Nevertheless, when Greekcrisis broke out, and when this country revealed its realdeficit of 12.7% of its GDP17 and when the contract withGoldman Sachs, which permitted Greek public debt to seemsmaller as it wanted to fulfill the Maastricht criteria andjoin the common currency, thanks to some swaps made at a

coordination of economic policies, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:31997R1466&rid=2 15 Official Journal of the European Union, Council Regulation (CE) no 1467/97 of 7 July1997 on speeding up and clarifying the implementation of the excessive deficit procedure, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:31997R1467&rid=3 16 KESNER-SKREB Marina, “Stability and Growth Pact”, Financial Theory and Practice 32 (1), 2008 17 The Economist, A very European Crisis: Greece’s sovereign-debt crunch, February 4th 2010, http://www.economist.com/node/15452594

historical exchange rate18, the euro zone suddenly became thetarget of the financial markets. Yields rose at historicalhigh levels for the so called “peripheral” countries, and soonenough not only Greece, but also Ireland and Portugal neededto be bail out. The credit ranking agencies took their tolland started downgrading the Eurozone countries19, even if theywere blind enough not to see the risks of the mortgage backedsecurities including subprimes, which they rated AAA and thushelped propagate the financial crisis20.

II. Core problem: preserving the euroThe “black swan” theory developed by Nassim Nicholas

Taleb21 can very well be applied in the case of the financialcrisis of 2007-2008: neither the states, nor the financialmarkets saw it coming, even if there were signs for it. Andwhen the “toxic assets” held by the European banks froze, theinterbank lending froze, as a result of the lack of theconfidence. In order to contain the crisis, the Europeangovernments intervened by giving state aids22, but, at the sametime, deepened their deficit and their public debt (Appendix 1and 3). Besides exposing the absence of a European bankingresolution authority, the banking crisis lived by the Europeanstates also showed the limits of a non-centralized Europeanframework, with responsibility remaining purely at nationallevel23, especially since the European banking market goesbeyond the borders of the Member States. “Toxic banks” led to

18 DUNBAR Nicholas, MARTINUZZI Elisa, Goldman Secret Greece Loan Shows Two Sinners asClient Unravels, Bloomberg, March 6th, 2012, http://www.bloomberg.com/news/2012-03-06/goldman-secret-greece-loan-shows-two-sinners-as-client-unravels.html 19 GEORGIOPOULOS George and BRANDIMARTE Walter, « Greece falls to S&P’s lowest rated, default warned», Reuters, June 13th 2011, http://www.reuters.com/article/2011/06/13/us-greece-ratings-sandp-idUSN131268592011061320 GOURGUECHON Gérard, « Les agences de notation », blogue de Jean Gadrey Alternatives économiques, p. 3, le 17 janvier 2012, http://alternatives-economiques.fr/blogs/gadrey/files/agences-de-notation26p.pdf21 TALEB Nassim Nicholas, The Black Swan: the Impact of the Highly Improbable, 2007, Penguin Books Ltd, London22 Nicolas de Sadeleer, “La gouvernance économique européenne: Léviathan ou colosse aux pieds d’argile?” Revue Europe, number 4, April 2012, etude 523 DEWATRIPONT Mathias, NGUYEN Gregory, PRAET Peter and SAPIR Andre, Working Paper The role of state aid control in improving bank resolution in Europe, Bruegel Policy Contribution no. 2010/04

the explosion of the debt in Ireland24 or Spain25, and even ifit took some time before touching the real economy, the crisisshook the foundation of the common currency.

What soon became the “European debt crisis” touched allthe member states, and one of the best indicators is thegovernment bonds yields spread (Appendix 2). And while therumours about Greece leaving the common currency spread,Italy, the third economic power in the euro zone, also becomesa target for the financial markets, causing the resignation ofits prime minister, Silvio Berlusconi26. The crisis deepened,and it became clear that Europe needed new solutions, not justthe promise of reforms coming from fragile Member States.

In a first move, to avoid the systemic risk triggered bya Greek bankruptcy, the Member States of the euro zone agreedon a financial assistance accorded to Greece, via a complexstructure of bilateral loans. Since Greece was no longer ableto fund itself on the free markets, the Member Statesactivated a “stability support” to Greece, pooled by theEuropean Commission and under strong policy conditionality.Basically, Greece agreed to implement a programme ofstructural reforms and fiscal adjustments in exchange for afinancial package worth 110 billion euros. The conditionalityfor this financial aid was negotiated by the Greek authoritieswith the Commission, the ECB and the International MonetaryFund – the so called “troika”27.

The Greek rescue package was soon followed by otherfinancial assistance programmes, requested by Ireland andPortugal. The (temporary) solution implemented by the MemberStates was the creation in May 2010 of the European Financial

24 Le Monde, Explosion de la dette de du déficit irlandais, 30th September 2010, http://www.lemonde.fr/europe/article/2010/09/30/l-irlande-s-attend-a-une-explosion-de-son-deficit-public-en-raison-du-sauvetage-de-l-anglo-irish-bank_1417990_3214.html?xtmc=crise_euro&xtcr=14025 DONCEL L., ABELLAN L., La deuda espanola desciende un peldano, El Pais, le 29 avril 2010, http://elpais.com/diario/2010/04/29/economia/1272492002_850215.html26 TYMKIW Catherine, Italian bond yields back in the danger zone, CNN Money, le 25 novembre 2011, http://money.cnn.com/2011/11/25/markets/bondcenter/italian_bond_yields/index.htm27 Council of the European Union, Statement by the Eurogroup, 2nd May 2010, Brussels, http://www.consilium.europa.eu/uedocs/cmsUpload/100502-%20Eurogroup_statement-sn02492.en10.pdf

Stability Facility (EFSF)28, initially charged with managing440 billion euros in Member State guarantees. The legal basefor instituting EFSF was the article 122 (2) TFEU, allowingthe financial assistance to a Member State “in difficulties orseriously threatened with severe difficulties by naturaldisasters or exceptional occurrences beyond its control”29. Theargumentation of the Council relied on the fact that “suchdifficulties may be caused by a serious deterioration in theinternational economic and financial environment”30. In tryingto stop the contagion of the crisis, a temporary mechanism wasnot enough, so the Member States decided the creation of apermanent European Stability Mechanism (ESM)31, provided withan initial maximum lending volume of 500 billion euros.Designed as an international financial institution, the ESM isset to be a kind of European IMF and provide “stabilitysupport” to any of its members, when “its regular access tomarket financing is impaired or is at risk of beingimpaired”32. Just like the IMF loans, the financial assistanceaccorded by the ESM to one of its Member States is subject toa strict conditionality. Thus, the beneficiary Member Statenegotiates with the European Commission and the ECB a“memorandum of understanding” detailing the conditionalityattached to the financial assistance33. Later on, the EuropeanCommission and the ECB are entrusted with monitoringcompliance with the conditionality attached to the loan34. TheCourt of Justice of the European Union (CJEU) is given thejurisdiction over the disputes concerning the interpretationand the application of the ESM treaty35. As the ESM treaty isan intergovernmental treaty, signed as an internationalagreement and not as a legal act under the EU law, the use ofthe European institutions – Commission, ECB and Court ofJustice – by this organism became problematic. The case even28 Official Journal of the European Union, Council Regulation (EU) no 407/2010 of 11 May 2010 establishing a European Financial Stabilisation Mechanism, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2010:118:0001:0004:en:PDF29 TFEU art. 122 paragraph 230 Council Regulation (EU) no 407/2010, (1)31 Treaty establishing the European Stability Mechanism (2012), http://www.european-council.europa.eu/media/582311/05-tesm2.en12.pdf 32 Treaty establishing the European Stability Mechanism, Preamble (13)

33 Treaty establishing the European Stability Mechanism, art. 13 paragraph 334 Treaty establishing the European Stability Mechanism, art. 13 paragraph 735 Treaty establishing the European Stability Mechanism, art. 37 paragraph 3

came to the CJEU36, which declared itself competent tointerpret the provisions of the ESM treaty, since this treatyis based directly on the TFEU, the Union’s primary law. Thus,a dispute linked to the interpretation of the ESM treaty fallsin the jurisdiction of the CJEU, as such a dispute would bebetween the Member States of the EU and would relate to thesubject-matter of the Treaties37.

Nevertheless, according financial assistance to theMember States in difficulties was not enough to preserve thestability of the entire euro zone. The macroeconomicimbalances had to be taken care of by also by other means,before a Member State getting too deep into trouble. Thelegislative framework for the economic union – including thenot-so-functional SGP – was amended in 2011 by the famous“six-pack”. In fact, five regulations and one directive aimedto redefine the fiscal surveillance, to prevent macroeconomicimbalances and set a new Macroeconomic imbalance procedure.The “six-pack” was set to strengthen the SGP’s so calledpreventive arm – stating that the Member States’ budgetarybalance shall converge towards the country-specific medium-term objective (MTO), with a government deficit not exceeding3% of the GDP, and the debt under 60% of GDP. The “correctivearm” of the SGP was also strengthened, with the possibility ofimposing sanctions on the Member States whose debt is notdiminishing at a “satisfactory pace”38. A Member State whosecurrency is the euro can be subject of a sanction, if theCouncil decides that it failed to take action in response to aprevious Council recommendation39 in the context of the

36 Court of Justice of the European Union, The Court of Justice approves the Europeanstability mechanism, Press release no. 154/12 Judgment in Case C-370/12, le 27Novembre 2012, Luxembourg,http://curia.europa.eu/jcms/upload/docs/application/pdf/2012-11/cp120154en.pdf37 Court of Justice of the European Union, Judgment of the Court (FullCourt) 27 November 2012,http://curia.europa.eu/juris/document/document.jsf?text=&docid=130381&pageIndex=0&doclang=EN&mode=lst&dir=&occ=first&part=1&cid=2599932 38 European Commission, Six-pack? Two-pack? Fiscal Compact? A short guide to the new EU fiscal governance, le 14 mars 2012, http://ec.europa.eu/economy_finance/articles/governance/2012-03-14_six_pack_en.htm39 Official Journal of the European Union, Regulation (EU) no 1173/2011 of the European Parliament and of the Council of 16 November 2011 on the effective enforcement of

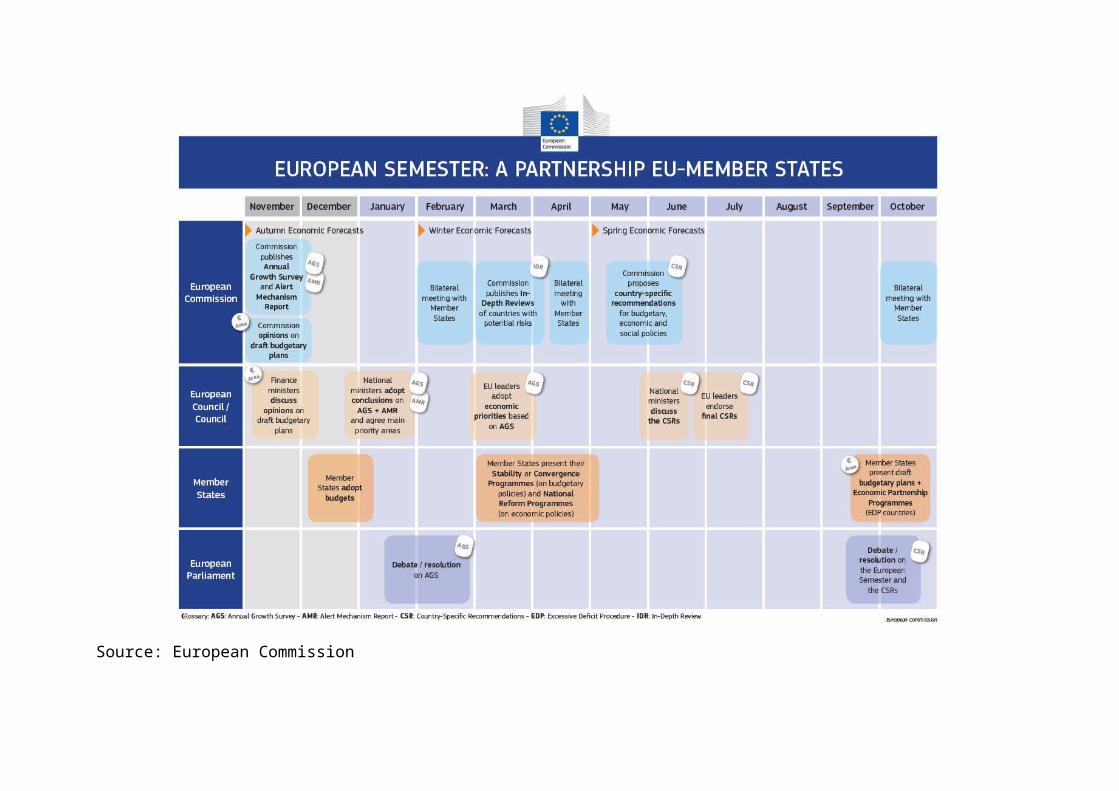

multilateral surveillance system. The “six-pack” enforces themeasures to correct excessive macroeconomic imbalances40. Italso strengthens the surveillance of budgetary positions andthe surveillance of economic policies by instituting theEuropean Semester, a cycle of policy surveillance andcoordination procedures, which starts in March with an overallmacroeconomic evaluation made by the European Council. TheMember States present in April their plans for sound publicfinances and their reforms. These National Reform Programmesare assessed by the Commission in May-June. The Commission,mandated with a stronger role in the enhanced surveillance,can make specific country recommendations and warnings.Moreover, the Commission can undertake on-site missions in theMember States which are the subject of recommendations.Finally, end of June or early July, the Council formallyadopts the country-specific recommendations (Appendix 4)41. The“six-pack” also implements an “alert mechanism” to facilitatethe early identification and the monitoring of imbalances,giving again to the Commission the role of assessing theevolution of imbalances, based on a list of indicators set toidentify the internal imbalances (including those that canarise from public and private indebtedness, financial andasset market developments, including housing, evolution ofprivate sector credit flow or the evolution of unemployment)and the external imbalances (current account and netinvestment positions of Member States, real effective exchangerates, export market shares, changes in price and costdevelopments and non-price competitiveness)42.

budgetary surveillance in the euro area, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0001:0007:en:PDF40 Official Journal of the European Union, Regulation (EU) no 1174/2011 of the European Parliament and of the Council of 16 November 2011 on enforcement measures to correct excessive macroeconomic imbalances in the euro area, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0008:0011:en:PDF41 Official Journal of the European Union, Regulation (EU) no 1175/2011 of the European Parliament and of the Council of 16 November 2011 on amending Council Regulation (EC) no 1466/97 on the strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0012:0024:en:PDF42 Official Journal of the European Union, Regulation (EU) no 1176/2011 of the European Parliament and of the Council of 16 November 2011 on prevention and correction of

The greatest change “six-pack” brings in 2011 in thelegislative framework is that a recommendation formulation bythe Commission to the Council is set to be adopted by theCouncil, if there isn’t a blocking qualified majority43. Inother words, the inverse qualified majority gives more powersthe Commission, whose recommendations are now less likely tobe rejected by the Council, like it was the case in 2003, whenthe SGP was proven inefficient.

The euro crisis, precipitated by a never-ending Greekcrisis (as the country needed its second bailout) was notcontained by these measures. The governmental bond marketcontinued to charge ever-higher rates of interest for Italyand Spain, now also severely hit by the debt crisis (see alsoAppendix 2). In this context, the European Council summit inDecember 2011 was held under the heavy pressure of urgency.The EU’s leaders wanted to show calm and confidence, trying tosend the message that they have the situation under control.The proposal for a revision of the Treaty of Lisbon, in orderto incorporate new rules strengthening EU’s oversight overMember States’ economic policies was rejected by the UnitedKingdom’s threat with using its veto. The rest of the MemberStates chose then the path of an intergovernmental treaty.Later, the Czech Republic joined the UK and the Treaty onStability, Coordination and Governance in the Economic andMonetary Union (TSCG) was finally signed on 2 March 2012 onlyby 25 Member State, including all the 17 countries using thecommon currency44. TSCG requires contracting parties to respectand ensure the convergence towards the country-specificmedium-term objective, lowering the limit of the structuraldeficit (corrected from the cyclical effects) to 0.5% of GDP.It also asks from the contracting states the implementation,at national level, of a correction mechanism, which shouldensure the implementation of measures to correct thedeviations45. The compliance to those rules is to be monitoredby national level independent institutions. And just like theESM treaty, the TSCG – an intergovernmental agreement, thus

macroeconomic imbalances, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0025:0032:en:PDF43 Regulation (EU) no 1173/2011 art. 4 paragraph 344 Treaty on Stability, Coordination and Governance in the Economic and Monetary Union (2012), http://european-council.europa.eu/media/639235/st00tscg26_en12.pdf45 TSCG art. 3

not EU law – gives the CJEU the jurisdiction over theimplementation of the treaty, and even the power of imposingfinancial sanctions if a country does not properly implementthe new budget rules46.

The “six-pack” – EU secondary law – and the TSCG –intergovernmental agreement – run in parallel, with TSCGincluding concepts from the “six-pack”: medium termobjectives, significant deviation, and exceptionalcircumstances. However, the TSCG goes a bit further andimposes more stringent provisions than the “six-pack”: thestructural deficit is differently calculated, and the TSCGasks the contracting Member States to enshrine in theirnational law the country-specific medium-term objectives.

Considering that the shortcomings in economic governanceand budgetary surveillance at the EU level are not yetsufficiently addressed by the SGP, the “six-pack” and theTSCG, the Commission proposed in November 2011 two furtherRegulations to strengthen euro area budgetary surveillance. InMay 2013, these two Regulations were adopted by the legislator(the Council and the European Parliament) and entered intoforce on 30th May 2013. The reason for the “two-pack” is thatbudgetary spill-over effects are higher in a common currencyarea, and whilst in good times, this interdependence bringsmore prosperity, in harder times risks are shared at a greaterextent, the Commission argues47. The “Two-pack” focuses more oncoordination than on implementing new fiscal rules,introducing a common budgetary timeline for the Member Statesof the euro area, as budgetary decisions of each country, evenif a matter of national sovereignty, also are a matter ofcommon concern. The major innovation of the “two-pack” is thatthe Member States have to publish their draft budgets for thefollowing year by 15 October, and that the Commission examinesand gives an opinion on each draft budget by 30 November. Andif the Commission detects non-compliances with the obligationsunder SGP, it asks the Member State to revise its budgetplan48. In the case of the countries experiencing or threatened46 TSCG art. 847 European Commission, Two-pack enters into force, competing budgetary surveillance cycle and further improving economic governance for the euro area, http://europa.eu/rapid/press-release_MEMO-13-457_en.htm 48 Official Journal of the European Union, Regulation (EU) no 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States

with serious difficulties with respect to their financialstability, the Commission can decide to enhance thesurveillance of the concerned state. The concerned MemberState has to adopt measures aimed at addressing the sources ofits difficulties, in cooperation with the Commission and theECB, taking into account any recommendations addressed to itunder the SGP. The fiscal situation is closer monitored inthis case, and the concerned member state has to communicateto the ECB, in its supervisory capacity, disaggregatedinformation on developments in its financial system. It alsohas to submit to regular assessments of its supervisorycapacities over the financial sector, and has to carry out,under the supervision of the ECT, stress test exercises orother sensitivity analysis.

Conclusion: “More Europe” – a solution for the crisis?In the midst of the crisis, and in a context not so

favourable to more integration, the leaders of the EuropeanUnion made a call for “More Europe”. Starting with the memosand the green papers presented by Barroso Commission and thedeclaration of the chief of governments and of states at theend of each “crisis summit”, the EU’s legal solutions went inthe direction of a deeper fiscal and budgetary integration,even if the word the most often used was “coordination”. AsLuuk van Middelaar remarked, it could be that the MemberStates have a growing conscience of sharing a common interestand the need of playing in the same team, since their nationalinterests are transcended by their European identity49.

The legal solutions implemented were, at the time, highlycriticised, for a couple of reasons. First of all, they brokethe “no bailout clause” set in the treaties (art. 125 TFEU)50.The flexibility or inflexibility of this clause is subject tointerpretation, with some authors arguing that there never wasa “no assistance principle”, but only a “no co-responsibility”principle for public debts51, and others considering the

in the euro area, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013R0473&from=EN 49 MIDDELAAR Luuk van, Le passage à l’Europe: Histoire d’un commencement, EditionsGallimard, Paris, Janvier 201250 Official Journal of the European Union, Consolidated versions of the Treaty on European Union and the Treaty on the Functioning of the European Union, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:C:2010:083:FULL&from=FR 51 PISANI-FERRY, Jean : Euro-area governance: what went wrong? How

interdiction clause as being extremely clear and explicit52. M.Ruffert questioned the financial assistance given to Greece,because such a decision is in breach of European Union law.Moreover, the author questions the “emergency clause”53 invokedby the rescuers, stating that the difficulties med by Greeceare not “caused by exceptional occurrences beyond itscontrol”54. The same argument is also used in the Irishbailout: “though the extent of the financial crisis wasexceptional, its effects were by no means unusual given theIrish government’s failure to adequately supervise and tax thefinancial sector”55. The second counter-argument was thedemocratic legitimacy for the “troika” to impose structuralreforms, involving huge social effects, to the rescuedcountries. The second debate still goes on, raising questionmarks and fuelling the emotions, especially in the rescuedMember States.

Nevertheless, the euro was saved, and we no longer assistat endless debates about the reversibility of the euro areaintegration, even if technically the possibility for a stateto leave the common currency still exists. In the process ofsaving the euro, the Member States gave more powers toEuropean institutions, like the Commission, the ECB or theCJEU. And in order to do so, they used all kind of legal meansat their disposal, from EU primary and secondary law tointergovernmental agreements. The social and political costshowever are high: with unemployment at unacceptable highlevels, the now social crisis questions the very fundament ofthe European Union – the trust of its citizens. With the riseof anti-European parties and euro-sceptical wave acrossEurope, the Union faces now another challenge: saving itself,as a common political project for the peoples of Europe.

to repair it?, Bruegel policy contribution, No. 2010/05,http://hdl.handle.net/10419/4551552 RUFFERT Matthias, “The European debt crisis and European Union law”(2011) 48 Common Market Law Review, Issue 6, pp. 1777–180553 TFEU art. 122 paragraph 254 RUFFERT Matthias, op. cit. p. 178655 RUFFERT Matthias, op. cit. p. 1787

References:

AGLIETTA Michel, « Europe and the world economy at the tipping point », Economie internationale, 2012/2 n° 130, p. 5-31.BARBERIS Nicholas, Psychology and the Financial Crisis of 2007-2008, August 2011, Yale School of Economics, http://faculty.som.yale.edu/nicholasbarberis/cp10.pdf BONIFACE Pascal, Comprendre le monde, Armand Collin, Paris, 2011Council of the European Union, Statement by the Eurogroup, 2nd May 2010, Brussels, http://www.consilium.europa.eu/uedocs/cmsUpload/100502-%20Eurogroup_statement-sn02492.en10.pdfCourt of Justice of the European Union, Judgment of the Court (Full Court)27 November 2012, http://curia.europa.eu/juris/document/document.jsf?text=&docid=130381&pageIndex=0&doclang=EN&mode=lst&dir=&occ=first&part=1&cid=2599932 Court of Justice of the European Union, The Court of Justice approves the Europeanstability mechanism, Press release no. 154/12 Judgment in Case C-370/12, le 27Novembre 2012, Luxembourg,http://curia.europa.eu/jcms/upload/docs/application/pdf/2012-11/cp120154en.pdfDEWATRIPONT Mathias, NGUYEN Gregory, PRAET Peter and SAPIR Andre, Working Paper The role of state aid control in improving bank resolution in Europe, Bruegel Policy Contribution no. 2010/04 DONCEL L., ABELLAN L., La deuda espanola desciende un peldano, El Pais, le 29 avril 2010, http://elpais.com/diario/2010/04/29/economia/1272492002_850215.htmlDREXL Josef, « La Constitution économique européenne - L'actualité du modèle ordolibéral »,Revue internationale de droit économique, 2011/4 t.XXV, p. 419-454. DOI : 10.3917/ride.254.0419DUNBAR Nicholas, MARTINUZZI Elisa, Goldman Secret Greece Loan Shows Two Sinners as Client Unravels, Bloomberg, March 6th, 2012, http://www.bloomberg.com/news/2012-03-06/goldman-secret-greece-loan-shows-two-sinners-as-client-unravels.html Europa – Legislation Summaries, Treaty of Maastricht on European Union, http://europa.eu/legislation_summaries/institutional_affairs/treaties/treaties_maastricht_en.htm European Commission, « Adopting the euro », Economic and Financial Affairs, http://ec.europa.eu/economy_finance/euro/adoption/who_can_join/index_en.htmEuropean Commission, Six-pack? Two-pack? Fiscal Compact? A short guide to the new EU fiscal governance, le 14 mars 2012, http://ec.europa.eu/economy_finance/articles/governance/2012-03-14_six_pack_en.htmEuropean Commission, « European Stability Mecanism », Economic and Financial Affairs, http://ec.europa.eu/economy_finance/european_stabilisation_actions/esm/index_en.htmEuropean Commission, Two-pack enters into force, competing budgetary surveillance cycle and further improving economic governance for the euro area, http://europa.eu/rapid/press-release_MEMO-13-457_en.htm European Stability Mechanism, http://www.esm.europa.eu/about/index.htmGEORGIOPOULOS George and BRANDIMARTE Walter, « Greece falls to S&P’s lowest rated, default warned», Reuters, June 13th 2011,

http://www.reuters.com/article/2011/06/13/us-greece-ratings-sandp-idUSN1312685920110613GOURGUECHON Gérard, « Les agences de notation », blogue de Jean Gadrey Alternatives économiques, p. 3, le 17 janvier 2012, http://alternatives-economiques.fr/blogs/gadrey/files/agences-de-notation26p.pdfKESNER-SKREB Marina, “Stability and Growth Pact”, Financial Theory and Practice 32 (1), 2008Le Monde, Explosion de la dette de du déficit irlandais, 30th September 2010, http://www.lemonde.fr/europe/article/2010/09/30/l-irlande-s-attend-a-une-explosion-de-son-deficit-public-en-raison-du-sauvetage-de-l-anglo-irish-bank_1417990_3214.html?xtmc=crise_euro&xtcr=140Le Monde, S&P menace de baisser la note de l’Italie, 24th May 2011 http://www.lemonde.fr/web/recherche_breve/1,13-0,37-1158833,0.html?xtmc=agence_de_notation&xtcr=59Maastricht Treaty – Treaty on European Union (1992), http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:11992M/TXT&rid=5 MASSON Paul R., « Fiscal asymmetries and the survival of the euro zone », Economie internationale, 2012/1 n° 129, p. 5-29MIDDELAAR Luuk van, Le passage à l’Europe: Histoire d’un commencement, EditionsGallimard, Paris, Janvier 2012Official Journal of the European Union, Consolidated versions of the Treaty on European Union and the Treaty on the Functioning of the European Union, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=OJ:C:2010:083:FULL&from=FR Official Journal of the European Union, Council Regulation (EU) no 407/2010 of 11 May2010 establishing a European Financial Stabilisation Mechanism, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2010:118:0001:0004:en:PDFOfficial Journal of the European Union, Council Directive 2011/85/EU of 8 November 2011 on requirements for budgetary frameworks of the Member States, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0041:0047:en:PDFOfficial Journal of the European Union, Regulation (EU) no 1173/2011 of the European Parliament and of the Council of 16 November 2011 on the effective enforcement of budgetary surveillance in the euro area, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0001:0007:en:PDFOfficial Journal of the European Union, Regulation (EU) no 1174/2011 of the European Parliament and of the Council of 16 November 2011 on enforcement measures to correct excessive macroeconomic imbalances in the euro area, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0008:0011:en:PDFOfficial Journal of the European Union, Regulation (EU) no 1175/2011 of the European Parliament and of the Council of 16 November 2011 on amending Council Regulation (EC) no 1466/97on the strengthening of the surveillance of budgetary positions and the surveillance and coordinationof economic policies, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0012:0024:en:PDFOfficial Journal of the European Union, Regulation (EU) no 1176/2011 of the European Parliament and of the Council of 16 November 2011 on prevention and correction of macroeconomic imbalances, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0025:0032:en:PDFOfficial Journal of the European Union, Regulation (EU) no 1177/2011 of the European Parliament and of the Council of 8 November 2011amending Regulation (EC) no 1467/97 on speeding

up and clarifying the implementation of the excessive deficit procedure, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:306:0033:0040:en:PDF Official Journal of the European Union, Council Regulation (CE) no 1466/97 of 7 July1997 on strengthening of the surveillance of budgetary positions and the surveillance and coordination of economic policies, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:31997R1466&rid=2 Official Journal of the European Union, Council Regulation (CE) no 1467/97 of 7 July1997 on speeding up and clarifying the implementation of the excessive deficit procedure, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:31997R1467&rid=3 Official Journal of the European Union, Regulation (EU) no 472/2013 of the European Parliament and of the Council of 21 May 2013 on the strengthening of economic and budgetary surveillance of Member States in the euro area experiencing or threatened with serious difficulties with respect to their financial stability, http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:140:0001:0010:EN:PDF Official Journal of the European Union, Regulation (EU) no 473/2013 of the European Parliament and of the Council of 21 May 2013 on common provisions for monitoring and assessing draft budgetary plans and ensuring the correction of excessive deficit of the Member States in the euro area, http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32013R0473&from=EN PISANI-FERRY, Jean : Euro-area governance: what went wrong? Howto repair it?, Bruegel policy contribution, No. 2010/05,http://hdl.handle.net/10419/45515RABAULT Hugues, “La theorie de la constitution économique: notion et disctinction”,Conférence « L’avènement de la constitution économique. Comparaisonsfrançaise, allemande et italienne », Metz, France, 9 – 10 October 2014RUFFERT Matthias, “The European debt crisis and European Union law” (2011)48 Common Market Law Review, Issue 6, pp. 1777–1805TALEB Nassim Nicholas, The Black Swan: the Impact of the Highly Improbable, 2007, Penguin Books Ltd, LondonSADELEER Nicolas de, “La gouvernance économique européenne: Léviathan oucolosse aux pieds d’argile?” Revue Europe, numéro 4, avril 2012, etude 5SCHOUTHEETE Philippe, « La crise et la gouvernance européenne », Politique étrangère, 2009/1 Printemps, p. 33-46. DOI : 10.3917/pe.091.0033TYMKIW Catherine, Italian bond yields back in the danger zone, CNN Money, le 25 novembre 2011, http://money.cnn.com/2011/11/25/markets/bondcenter/italian_bond_yields/index.htmThe Financial Crisis Inquiry Commission, Financial Crisis Inquiry Report. Final report of the National Commission on the causes of the financial and economic crisis in the United States, January 2011, http://fcic-static.law.stanford.edu/cdn_media/fcic-reports/fcic_final_report_full.pdf The Economist, A very European Crisis: Greece’s sovereign-debt crunch, February 4th 2010,http://www.economist.com/node/15452594Treaty establishing the European Stability Mechanism (2012), http://www.european-council.europa.eu/media/582311/05-tesm2.en12.pdf

Treaty on Stability, Coordination and Governance in the Economic and Monetary Union (2012), http://european-council.europa.eu/media/639235/st00tscg26_en12.pdf

Appendix 1

Government deficit/surplus for Euro area, Germany, Ireland, Greece, Spain, France and Italy (Eurostat)

Appendix 2

EMU convergence criterion bond yields for Germany, Ireland, Greece, Spain, France and Italy,between 2000 and 2014 (Eurostat)

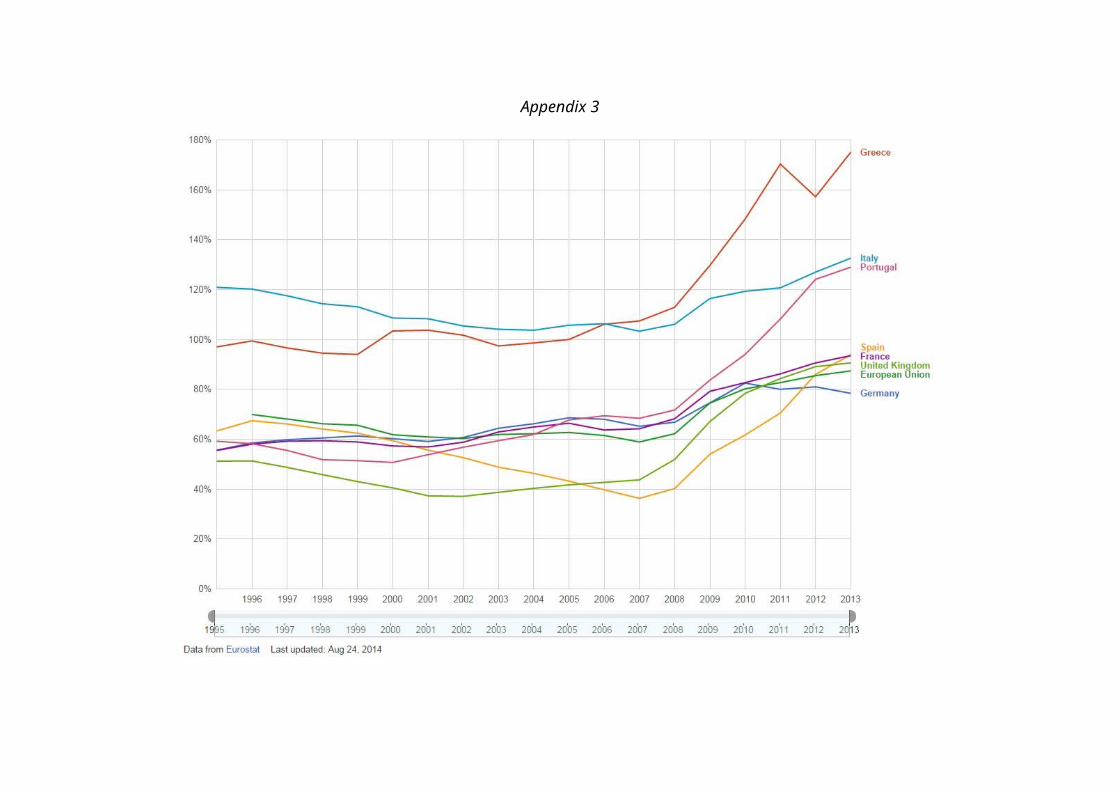

Appendix 3

Government debt as percentage of GDP for Greece, Italy, Portugal, Spain, France, United Kingdom,Germany and the EU

Appendix 4

Source: European Commission