Embed Size (px)

Citation preview

Resolving systemic financial crises efficiently

Edward J. Kane*

Department of Finance, Boston College, Fulton Hall 330A, Chestnut Hill, MA 02467, USA

Abstract

Systemic crises occur when governmental strategies for preventing and resolving financial-insti-

tution insolvencies fail massively. This paper outlines market-mimicking strategies for preventing and

managing financial crises. Efficient prevention focuses on enforcing adequate levels of bank capital

and being prepared to resolve institutional insolvencies expeditiously when they arise. Efficient crisis

management requires officials to develop, staff, rehearse, update, promulgate, and commit themselves

irrevocably to a market-mimicking plan for managing systemic banking disasters. By adopting these

strategies, a government would make itself accountable for preventing, identifying, and resolving

bank insolvencies at miminum long-run social cost.D 2002 Elsevier Science B.V. All rights reserved.

JEL classification: G21; K23

Keywords: Bank runs; Financial crisis; Insolvency resolution

A systemic financial crisis occurs when widespread depositor runs reveal that most or

all of the accounting capital in a country’s banking system is illusory. To resolve a

systemic crisis efficiently without outside help, a national government needs the three A’s:

adequate tax-collecting capacity, accurate policy advice, and appropriately skilled person-

nel. A country’s top regulators must not only know what sequence of policy actions would

be optimal, they must also be confident that the personnel and financial resources they

command have the capacity to perform these actions in timely fashion.

During the 1990s, most crisis governments lacked the prerequisites for undertaking

optimal action. What these governments did possess was ready access to external

assistance. Like most offers of help, crisis assistance came with strings attached. Multi-

lateral and bilateral assistance brought with it suboptimal policy advice that protected the

interests of foreign creditors by directing recipient governments to play for time, without

stopping to measure or adjust the depth of the inadequacies in their fiscal capacity and

supervisory systems that brought the crisis about.

0927-538X/02/$ - see front matter D 2002 Elsevier Science B.V. All rights reserved.

PII: S0927 -538X(02 )00044 -6

* Tel.: +1-617-552-3986; fax: +1-617-552-0431.

E-mail address: [email protected] (E.J. Kane).

www.elsevier.com/locate/econbase

Pacific-Basin Finance Journal 10 (2002) 217–226

External lenders espoused the rosy view that, in the midst of crisis, the urgent

macroeconomic problem of reliquifying domestic bank deposits could be addressed

separately from the microeconomic problem of measuring and distributing the losses that

the official balance sheets of insolvent banks still concealed (Fischer, 2001). Fiscally

underpowered governments were urged to guarantee the liabilities of insolvent and solvent

banks alike. While the credibility of these indiscriminate guarantees turned in the short run

on well-publicized lines of credit from supranational institutions, foreign banks, and

foreign governments, in the long run a crisis government’s ability to fulfill its commit-

ments depended on its ability to carry out a series of unlikely reforms in monetary, fiscal,

and trade policies and in the quality of bank supervision.

Recipient governments were persuaded to put aside, until crisis pressures passed, the

task of controlling bank risk-taking to concentrate on curtailing disruptive depositor runs.

However, this policy sequence embodies a time-inconsistent strategy that successor

governments are bound to regret. Blanket guarantees reduce incentives for depositors to

monitor insolvent and undercapitalized banks, and backing up these guarantees imposes

substantial deferred costs on taxpayers. In the absence of a fair distribution of preexisting

losses, indiscriminate guarantees fail to correct whatever combination of corrupt and risk-

taking behavior drove the country’s banking system to its knees in the first place.

Insurance theory refers to the conflict between the objectives of insureds and the

insurers as the problem of moral hazard. Crisis countries should not be advised to ignore

the dangers posed by moral hazard. To prevent depositor discipline from being under-

mined by government guarantees, it is critical to simultaneously adopt guarantee structures

and insolvency resolution strategies that promise to make contractual bank stakeholders

bear their fair share of accrued losses. When a government’s capacity to observe and

resolve bank insolvencies is inadequate, the more sweeping its guarantees of bank debt

and the longer crisis pressures persist, the more unbooked debt moral hazard loads onto the

ordinary taxpayer’s economic balance sheet.

Creditor institutions have not advised crisis governments to calculate the costs of moral

hazard, nor have they urged these governments to track the opportunity cost of the fiscal

resources that would be required to make good on blanket guarantees. The result is that

crisis governments have not made themselves accountable for assuring that the benefits of

quickly halting depositor runs equaled or exceeded the costs that playing for time has on

the country’s unbooked fiscal deficits and increased exposure to future crises.

The next two sections of this paper outline market-mimicking strategies for preventing

and managing financial crisis. The final section summarizes how governments that

promulgate and adhere to these twinned strategies will render themselves accountable–

in crisis and out of crisis–for preventing, identifying, and resolving bank insolvencies in

an economically efficient manner.

1. A market-mimicking strategy for crisis prevention1

Institutions become economically insolvent when their tangible and intangible assets

can no longer generate enough income to fully service their obligations to creditors.

1 This section and the next draw heavily on Kane (2001a,b,c).

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226218

Insolvency resolution is the process of recognizing and assigning shortfalls in corporate

capital. Resolution entails formally writing down the claims of owners and creditors to

values that add up to the reduced market value of corporate assets (MVA).

Corporations may be said to fall into ‘‘financial distress’’ well before the market value of

stockholders’ stake in the firm (MVNW) reaches zero. Because the probability of financial

distress is a function of endogenous decisions about leverage and earnings volatility, lenders

typically insist that borrowers accept a package of disclosure and risk-control obligations as

part of the debt contract. For creditors and guarantors, these covenanted obligations increase

the transparency of borrowers’ affairs by requiring borrowers to conduct and report the

outcomes of a series of periodic tests of their current financial strength and evolving

vulnerability to future loss. Covenant violations that appear to have no material effect on

lenders’ position are waived. However, whenever one or more violations seem material,

creditors can insist that the borrower remedies the violation or enters into negotiations to

reprice the loan or otherwise mitigate the damage inflicted on the lender.

Covenant violations may be thought of as windows that throw light on areas of

corporate loss exposure that standard accounting reports do not. Covenants increase the

chance that insolvency resolution negotiations can begin before the market value of

borrower net worth has been fully exhausted. Borrowers and lenders have a strong

incentive to work out minor violations. Lenders that are dissatisfied with the ‘‘quid’’ a

borrower offers in exchange for waiving a material violation typically have the right to

demand immediate repayment of their debt. Because enforcing this right would reveal the

borrower’s still-concealed weakness to third parties, a breakdown in negotiations is apt to

intensify a borrowing firm’s distress and possibly force it to seek formal bankruptcy

protection.

To assure that bank capital requirements are truly risk-sensitive, government regulators

must put themselves into a lender’s mind-set. They must impose covenant-like reporting

and loss-control obligations on each bank they supervise. To control moral hazard, banks

must be made to regularly measure how well their capital can support their current risk

exposures and convey to regulators market-mimicking rights to demand that apparent

shortfalls in capital be alleviated in rapid order. In the United States and many other

countries, a bank’s incentives to report truthfully are enhanced by on-site examinations and

civil and criminal penalties for fraudulent and negligent misrepresentation. The more

strongly self-reporting obligations are enforced, the more effectively regulators can

monitor and police individual bank insolvency on behalf of depositors. Policing entails

the power to order stops to unacceptable administrative practices or behavior and to

impose escalating penalties on any nonconforming firm. Escalation may take the form of

progressively higher deposit insurance premiums and/or progressively tighter surveillance.

Regulators must recognize that deterrent regulatory discipline cannot always stop a

distressed bank’s slide into economic insolvency. To follow market-mimicking principles

of insolvency resolution, officials must prepare themselves to take control of a bank more or

less as its insolvency emerges (Kaufman and Scott, 2000). After takeover, officials would

proceed to make two further decisions: what to do with the bank, and how to restructure

preexisting creditor, stockholder, and government claims on its assets (Hart, 2000). If

officials determine that it is more efficient for society to keep the bank in operation, the

second decision results in a plan to recapitalize and perhaps to restaff the institution. If

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226 219

officials decide to shut down the bank, the second decision entails liquidating the bank’s

assets and distributing liquidation proceeds among government and private stakeholders

more or less in accordance with the bank’s contractual obligations to each party.

Efficient crisis prevention policies entail a series of cost-efficient expenditures on

monitoring and enforcing the adequacy of bank capital and on preparing to resolve

individual bank insolvencies promptly when they arise. Adopting such market-mimicking

principles of insolvency prevention and resolution is a necessary condition for crisis

prevention expenditures to be cost-efficient. The next section describes market-mimicking

requirements that should govern expenditures incurred in crisis management.

2. A market-mimicking strategy for crisis management

Banking crises occur when a government’s day-to-day policies for preventing and

resolving individual bank insolvencies have been circumvented on a massive scale (Todd,

1994). Some degree of circumvention is likely because accounting records are imperfectly

informative, and government officials face different incentives in monitoring and dis-

ciplining distressed banks than private creditors would (Kane, 2000). Officials’ reluctance

to acknowledge their incentive conflicts compromises crisis prevention activities and

supports an underinvestment in disaster planning. This underinvestment harms taxpayers,

in that it justifies a time-inconsistent approach to crisis management and increases the

ability of stakeholders in insolvent banks to extract implicit and explicit subsidies when

and as the threat of an actual crisis intensifies.

Politically, a banking crisis is a nasty struggle about which sectors’ wealth is to be forced

to absorb the capital shortfalls that insolvent banks have amassed. Without ready access to

reliable information and a reasoned plan of crisis management, inexperienced authorities

are apt to see little alternative to the 1990s protocol of indiscriminately guaranteeing the

liabilities of insolvent institutions and leaving the problem of subsequently scaling back the

blanket guarantees to an unspecified later (and quieter) time. Although blanket guarantees

provide a quick way to stabilize aggregate liquidity, they surrender longer-run incentive

benefits that would be generated by promptly marking down devalued assets and allocating

the opportunity losses these markdowns convey to bank stakeholders who can be identified

as having voluntarily agreed to finance the now-troubled assets.

Regulators’ efforts to convince taxpayers that financial crises are unthinkable cata-

strophes look suspiciously like disinformational attempts to avoid accountability for

unduly lenient strategies of insolvency resolution. Systemic and near-systemic crises are

not uncommon. Looking at the two decades ending in 1999, Caprio and Klingebiel (1999)

enumerate 112 instances of systemic crises in 93 countries and 51 borderline episodes in

46 countries. Additional crises have occurred in several other countries since. In fact, the

threat of disruptive exits looms in any industry where competition is intense. Being

allowed to frame the emergence of exit pressure in the banking industry as an unfore-

castable and uncontrollable disaster allows supervisory officials to shirk their duty to

observe and resolve exit pressure in timely fashion.

When suppressed evidence of widespread banking weakness surfaces suddenly, it is

tempting for officials to minimize their embarrassment by arguing that bank runs are

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226220

destructive and that their spread must be halted at all costs. Because a crisis intensifies the

tenuousness of incumbents’ hold on their office, exaggerating the odds of triggering a

contagious loss of depositor confidence is a reputationally and politically convenient

strategy. It allows officials to turn a blind eye to the depth of particular insolvencies and to

defer loss distribution to a later date. Such a policy extracts risk capital from taxpayers and

invests it inefficiently. The investment is inefficient for two reasons. First, even if a

subsequent turnaround in the macroeconomy restores the value of a troubled bank’s assets,

private stakeholders rather than taxpayers reap the bulk of the benefit. Second, banks that

are permitted to operate with free capital are attracted to inappropriately risky loans.

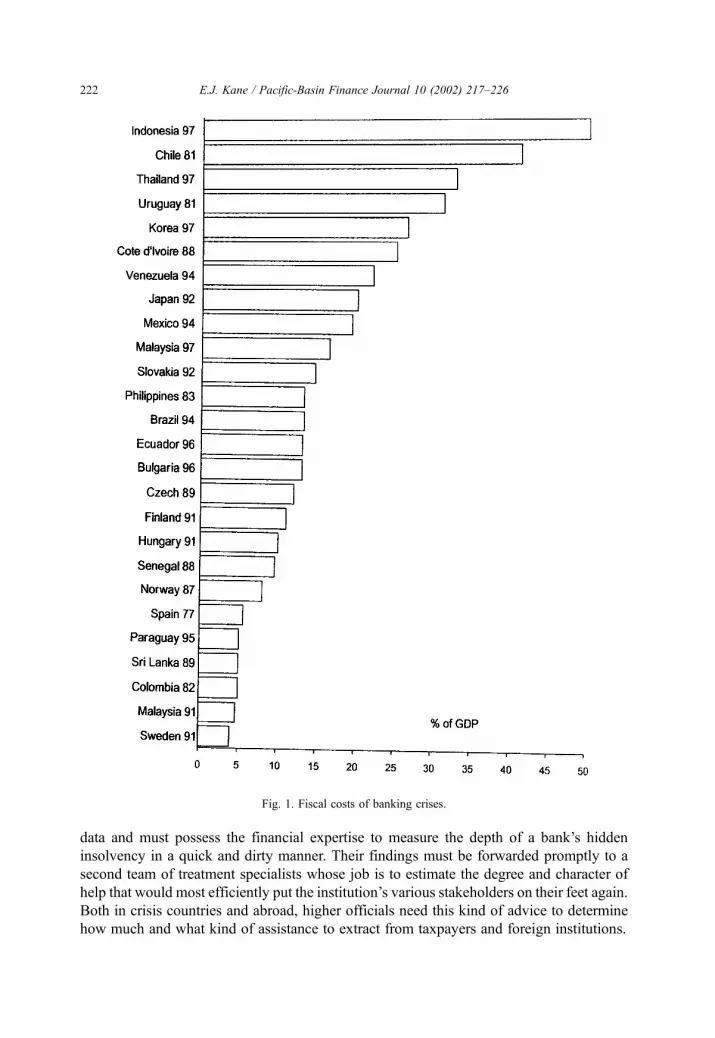

As summarized in Fig. 1, Honohan and Klingebiel (in press) establish that in settling

recent crises, the burden placed on taxpayers has typically exceeded 10% of GDP. Using

regression analysis, these same authors show that taxpayers’ burden proved higher in

countries that adopted indiscriminate guarantees than in countries that employed a sterner

crisis management strategy.

To position bank regulators to make time-consistent choices, taxpayers must formally

oblige officials to develop, staff, rehearse, and update regularly a well-publicized strategic

plan for managing a systemic banking disaster and must also oblige their government to

follow this plan when a crisis ensues. In most practical endeavors, the quality of one’s

performance is a function of one’s talent, knowledge, and experience. Even the most gifted

musicians, surgeons, and athletes have to regularly practice their skills and be encouraged to

search unstintingly for new and better ways of doing things. By likening a systemic financial

breakdown to a building collapse, it is easy to see that a complete disaster management plan

must address three problems: (1) rescue and triage, (2) panic control, and (3) cleanup. The

next three subsections outline efficient procedures for addressing each problem in turn.

2.1. Rescue and triage

When a tall building collapses, appropriate actions and decisions must be taken

expeditiously. Rescue and medical personnel and equipment must be moved onto the

scene and put to work as soon as possible. Survivors must be promptly diagnosed and

queued for treatment. Ambulances and other vehicles must be commandeered to shuttle to

clinics and hospitals whatever wounded parties can be safely moved. To the extent that it is

feasible, survivors must be interviewed for information about the identities and potential

locations of missing persons. Body-sniffing dogs may be used to further pinpoint salvage

efforts. Barriers must be erected to keep gawkers from interfering with operations.

When a banking system collapses, governments must execute parallel actions and

decisions. The casualties that need to be found and treated are the stockholders, employ-

ees, depositors, and nondeposit creditors of a nation’s banks. Regulators cannot expect to

uncover individual casualties efficiently unless they have previously formulated an

integrated disaster plan, hired appropriate personnel, and drilled staff members under

simulated crisis conditions in plan execution. In an emerging crisis, staff members must be

able to visit and diagnose the condition of institutions undergoing depositor runs without

having to hang back to await detailed instructions to flow down from on high.

The first team of officials dispatched to a troubled bank should be forensic bank

examiners. These officials must have the authority to take immediate possession of relevant

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226 221

data and must possess the financial expertise to measure the depth of a bank’s hidden

insolvency in a quick and dirty manner. Their findings must be forwarded promptly to a

second team of treatment specialists whose job is to estimate the degree and character of

help that would most efficiently put the institution’s various stakeholders on their feet again.

Both in crisis countries and abroad, higher officials need this kind of advice to determine

how much and what kind of assistance to extract from taxpayers and foreign institutions.

Fig. 1. Fiscal costs of banking crises.

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226222

In exchange for whatever financial assistance that domestic and foreign officials decide

to ask taxpayers and foreign banks to supply, a crisis government must be empowered to

levy enforceable claims on the future profits of each troubled bank it keeps in operation. In

a demonstrably insolvent institution, the new claims should either greatly diminish or

completely extinguish the rights of former shareholders. At a minimum, authorities should

carve out a warrant position large enough to compensate suppliers of public risk capital for

the administrative and risk-bearing costs of contributing to a rescued bank’s recapital-

ization. In all cases, governments and supragovernmental institutions that receive equity

positions would do well to commit themselves to offer their claims to private parties once

reliable information on asset values emerges.

During an emergency, the autonomy of information collection teams must be supported

at every level of government. Although accountability requires that staff judgments be

reviewed and criticized later, triage assessments cannot be postponed to wait for formal

ratification by incentive-conflicted and less-informed higher-ups. Government officials

must condition one another and the press to respect the proposition that, in dealing with

hopelessly insolvent institutions, it is inappropriate to devote public funds either to

preserving the positions of stockholders and subordinated creditors or to paying lofty

salaries to discredited managers.

In the aftermath of a building collapse, emergency personnel cannot divert their limited

surgical resources to sewing up the wounds or setting the broken bones of dying

individuals. To neutralize the plaintive pleas for mercy that wounded bank stakeholders

are bound to emit, supervisors and the public must be taught in advance why it is efficient

in deeply insolvent institutions to annihilate stockholders’ position and to cut back

management salaries. Basic corporate finance theory clarifies that the economic value

of stakeholders’ aggregate claims against a corporation can never exceed the fair market

value of its assets. Hence, whenever a bank’s assets lose a substantial portion of their

value, the total value of the bank’s obligations decline to the same degree. Adverse

information about borrower prospects or about hidden bank frauds or trading losses that

destroys asset values destroys realizable liability values in tandem.

2.2. Panic control

Panic refers to hysterical behavior that spreads through a group when its members are

exposed to a horrific vision or event. The triggering event in a banking panic is the

surfacing of adverse information that destroys public confidence in the repayment capacity

of several of a nation’s banks. This loss of confidence may be based on either rational

calculation or (far more rarely) wholly irrational fears. The trigger can take the form of

general information about the consequences of major economic events or information that

is specific to individual banks or to a class of assets they are known to hold.

A banking panic combines the phenomenon of simultaneous runs on multiple banks

with a seizing up of opportunities for interbank borrowing and for sales of usually liquid

securities. In a panic, bank runs and fears of runs become so widespread that individual

banks can no longer raise funds quickly by selling portfolio assets to other parties at fair

prices. Institutions not experiencing runs back away from lending funds to affected banks

so as to support more firmly the convertibility of their own deposits into cash.

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226 223

Panic control turns on keeping the nation’s money supply from shrinking. The central

bank and foreign officials can offset the negative effects of regulators’ triage efforts by

standing ready both to purchase good assets they are offered for sale and to lend

vigorously to demonstrably solvent or near-solvent banks.

As Kaufman and Seelig (2000) emphasize, how depositors are treated at failed banks

can greatly assist the central bank’s liquidity maintenance efforts. Insured depositors

should be granted access to their funds as soon as this becomes administratively feasible

and uninsured depositors should be accorded a just degree of immediate fractional access

to their balances. Determining the fraction of an insolvent bank’s uninsured deposit

balances that can be immediately withdrawn should be founded on the conservative

valuation techniques that the teams of forensic examiners and treatment specialists are

required to rehearse at frequent intervals. Each emergency examination would estimate the

percentage of uninsured deposits that liquidators could reasonably expect to recover if the

bank’s tangible portfolio were to be liquidated at a later date in an orderly fashion. To

reflect the margin for error inherent in the rough-and-ready loss assessments the

emergency examination teams produce, the percentage haircut applied to uninsured

balances should be somewhat lower than this figure. Bank employees would be directed

to set the frozen part of each uninsured balance aside and stand ready to unfreeze it in

stages as it proves possible to assess more accurately the value of intangible positions and

the depth of each bank’s insolvency.

Summarizing, a panic ends when aggregate liquidity is restored. To do avert a panic, a

country’s central bank must maintain aggregate liquidity. It can do this efficiently by open-

market operations, even while allowing supervisory personnel to assess a financial

institution’s wounds before paying out deposit insurance claims or granting banks and

their formally uninsured creditors irreversible access to liquid government funds. Injec-

tions of liquidity from domestic and external sources must be directed as exclusively as

possible toward insured depositors, recoverable portions of uninsured balances, and

putatively solvent institutions. Hopelessly insolvent institutions must be identified and

control over them transferred smoothly into socially responsible hands.

It should be understood that, even during forensic examiners’ brief insolvency assess-

ment timeout period, urgent private transactions can and will still take place. Would-be

transactors would have strong private incentives to use standard and innovative forms of

credit to prevent transactions from grinding to a halt. For example, credit cards and checks

can be accepted–especially if supplemented by ad hoc documents or collateral– to

establish evidence of personal indebtedness. Claims to the amounts on the instruments’

paylines would become collectable in part from other sources if authorities place into

liquidation the bank on which they are drawn.

2.3. Cleanup

Unlike triage and panic control, the cleanup tasks of reprivatizing problem assets and

banking franchises and collecting payments from problem borrowers require careful rather

than quick decisions. In most crises, the information that lowers bank asset values is

broadly accurate. This means that liabilities supported by the lost asset value become

‘‘junk’’. Regulators should promptly remove junky liabilities from bank balance sheets.

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226224

The market-mimicking standard of policy response asks bank supervisors to operate the

economic equivalent of a junkyard.

The junkyard’s job is to identify and gather near-worthless assets and liabilities and to

dispose of them quickly and efficiently. Officials are asked to do this–not to punish

anyone–but to restore healthy incentives for subsequent investment and economic growth

by clearing bank balance sheets of unsupportable claims on future returns that would

generate new losses by dangerously distorting future lending incentives.

Market-mimicking cleanup procedures center on surgically separating diseased assets

from the healthy parts of troubled bank portfolios. In practice, this involves either selling

troubled assets at market value to a preexisting workout specialist or specifically chartering

a new public or private entity to extract maximum value from the problem borrowers. This

good bank/bad bank surgical model was pioneered in the 1990s by US regulators and has

been copied with some degree of success in several other countries since.

The expectation that ownership claims and uninsured liabilities will expire when they

become valueless is necessary for lending and deposit markets to function appropriately.

Writing down the realizable value of unsupportable assets and liabilities in bad states of

the world is a crucial part of the evolutionary process of economic renewal that

Schumpeter brilliantly characterized as ‘‘creative destruction’’.

Despite the temporary disruption bank runs invoke, in the long run, depositor runs

assist society by forcing sleepy authorities to repair, rehabilitate, or eliminate troubled

banks and problem industries in a more timely fashion. The desire to end a panic quickly

must not override the need to identify hopelessly insolvent enterprises and to wind up their

insolvency in an efficient manner. Issuing blanket government loans and guarantees to

solvent and insolvent banks alike is time-inconsistent because it greatly reduces sub-

sequent political and economic pressure for cleanup. Guarantees release managers,

stockholders, and creditors of troubled institutions from the spur of bearing due

responsibility for loss-making decisions they directly or indirectly ratify. Indiscriminate

guarantees reinforce perverse lending and investment incentives and promise to expand

rather than reduce the number of negative present-value investments a country undertakes.

3. Summary discussion

In many countries, government plans for recovering from a financial disaster amount to

expecting to call frantically on supragovernmental institutions, foreign governments, and

foreign banks for help. Moreover, these potential rescuers often plan in turn to extract their

help from the country’s taxpayers in hidden ways.

Public choice theory clarifies that authorities’ reliance on self-serving rather than

market-mimicking strategies of crisis management is evidence of weaknesses in public

sector governance. Poor governance creates accountability resistance and fosters conflicts

of interest between taxpayers and financial regulators in individual countries and also in

cross-country relationships. To be economically efficient, regulatory strategies must

enforce market-mimicking concepts of insolvency, insolvency prevention, and insolvency

resolution. Supervisory standards must not focus merely on averting depositor runs.

Efficiency requires that regulators in different countries and in supranational organizations

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226 225

credibly commit themselves and their successors to fair and efficient policies of insolvency

resolution and crisis management as well.

Optimal supervision minimizes the depositor discipline that safety-net guarantees

displace. Depositor disciplinary activity is displaced by government guarantees because

guarantees directly undermine depositors’ incentives to look out for themselves by

gathering, analyzing, and reacting to news about changes in their banks’ financial

condition and risk exposures (Demirguc�-Kunt and Detragiache, in press; Demirguc�-Kuntand Sobaci, 2001; Laeven, 2000). Other things equal, the more supervisory responsibility

a government accepts, the more effectively large depositors and foreign-bank creditors can

exploit an unstructured crisis situation. They can lobby for a government bailout by using

the media to blame the government for whatever losses triage officials propose to allocate

to them. On the other hand, depositor discipline may be expected to increase with

strategies of prompt insolvency resolution and with crisis planning. The market-mimicking

strategies proposed here lay down a baseline pattern of responding to bank insolvency that

curtails officials’ discretion. This curtailment lessens the extent to which owners and other

formally uninsured stakeholders can expect to extract important regulatory benefits or

highly subsidized loans if their bank becomes insolvent.

References

Caprio, G., Klingebiel, D., 1999. Episodes of systemic and borderline financial crises. World Bank Working

Paper, Washington, DC.

Demirguc� -Kunt, A., Detragiache, E., 2002. Does deposit insurance increase banking system stability? An

empirical investigation. Journal of Monetary Economics (in press).

Demirguc�-Kunt, A., Sobaci, T., 2001. Deposit insurance around the world: a database. World Bank Economic

Review 15 (3), 481–490.

Fischer, S., 2001. International Economic Policy Under the Clinton Administration, Speech delivered at Harvard

University (June 27) and published on the International Monetary Fund website (http://www.imf.org.).

Hart, O., 2000. Different approaches to bankruptcy. Harvard University Discussion Paper No. 1903, Cambridge,

MA (September).

Honohan, P., Klingebiel, D., 2002. The fiscal cost implications of an accommodating approach to banking crises.

Journal of Banking and Finance (in press).

Kane, E.J., 2000. Designing financial safety nets to fit country circumstances. Boston College, Boston, MA (May).

Kane, E.J., 2001a. Dynamic inconsistency of capital forbearance: Long-run vs. short-run effects of too-big-to-fail

policymaking. Pacific Basin Finance Journal 9, 281–299 (August).

Kane, E.J., 2001b. Relevance and need for international regulatory standards. Brookings–Wharton Papers on

Financial Services, vol. 4. The Brookings Institution, Washington, DC, pp. 87–116.

Kane, E.J., 2001c. Using disaster planning to optimize expenditures on financial safety nets. Atlantic Economic

Journal 29, 243–253 (September).

Kaufman, G., Scott, K., 2000. Does bank regulation retard or contribute to systemic risk? Loyola University

working paper, Chicago (Nov. 29).

Kaufman, G., Seelig, S.A., 2000. Treatment of depositors at failed banks, etc. Loyola University, Chicago

(November 27).

Laeven, L., 2000. Banking risks around the World: The implicit safety net subsidy approach. World Bank

working paper, Washington, DC (November).

Todd, W.F., 1994. Lessons from the collapse of three state-chartered private deposit insurance funds. Economic

Commentary. Federal Reserve Bank of Cleveland, Cleveland, OH (May 1).

E.J. Kane / Pacific-Basin Finance Journal 10 (2002) 217–226226