Embed Size (px)

Citation preview

Technical Report No. 03-4/06

BETTER IRRIGATION BETTER ENVIRONMENT BETTER FUTURE

The Sustainability Challenge

Performance reporting by the North Burdekin Water Boardand sustainability: Foundations for the future

Mark Shepheard, John Wolfenden and Steve Attard

June 2006

CRC for Irrigation Futures i

The Sustainability Challenge Performance reporting by the North Burdekin Water Board and sustainability: foundations for the future Mark Shepheard, John Wolfenden and Steve Attard CRC for Irrigation Futures CRC for Irrigation Futures Technical Report No. 03-4/06 June 2006

ii CRC for Irrigation Futures

Copyright and Disclaimer © 2006 IF Technologies Pty Ltd. This work is copyright. It may be reproduced subject to the inclusion of an acknowledgement of the source.

Important Disclaimer The Cooperative Research Centre for Irrigation Futures advises that the information contained in this publication comprises general statements based on scientific research. The reader is advised and needs to be aware that such information may be incomplete or unable to be used in any specific situation. No reliance or actions must therefore be made on that information without seeking prior expert professional, scientific and technical advice. To the extent permitted by law, the Cooperative Research Centre for Irrigation Futures (including its employees and consultants) excludes all liability to any person for any consequences, including but not limited to all losses, damages, costs, expenses and any other compensation, arising directly or indirectly from using this publication (in part or in whole) and any information or material contained in it.

Acknowledgements The ability of this project to commence working in the Lower Burdekin is largely due to the rapport established by others in CSIRO, SunWater and the Queensland Department of Natural Resources and Mines, who have worked on irrigation and natural resource management issues in the region. We thank all those involved for this groundwork developed over a much longer period of time than the period of this project. The ability of the project to move forward over the last 18 months has been very much a result of the good will shown to us by the members of the North Burdekin Water Board TBL project working group, namely: • Graham Laidlow, Manager of the North Burdekin Water Board • George Nielson, previous Chairman of North Burdekin Water Board • Daniel Ellis, Board member • Mark Castelanelli, Board member • Bill Lowis, Manager of the South Burdekin Water Board • Mal Johnston, Department of Natural Resources and Mines (The project team

would like to offer condolences to Mal’s family following his passing in December 2005).

CRC for Irrigation Futures iii

Reports in this series The guidelines provided in Report 1 (No. 03-1/06) are the main focus of the sustainability challenge project. The guidelines are supported by Reports 2 to 6 in the series, providing the background to triple bottom line reporting and the experience of working with a variety of organisations to apply the approach within the irrigation industry.

1. A Guide to using Triple Bottom Line reporting as a framework to promote the sustainability of rural and urban irrigation in Australia. E.W. Christen, M.L. Shepheard, N.S. Jayawardane, P. Davidson, M. Mitchell, B. Maheshwari, D. Atkins, H. Fairweather, J. Wolfenden and B. Simmons.

2. The Principles and Benefits of Triple Bottom Line Performance Reporting for the Australian Irrigation Sector. M.L. Shepheard, E.W. Christen, N.S. Jayawardane, P. Davidson, M. Mitchell, B. Maheshwari, D. Atkins, H. Fairweather, J. Wolfenden and B. Simmons.

3. Use of reporting systems to improve the sustainable use of water for urban and peri-urban irrigation. Deborah Atkins, Basant Maheshwari, Bruce Simmons and Paul Mulley.

4. Performance reporting by the North Burdekin Water Board and sustainability, foundations for the future. Mark Shepheard, John Wolfenden and Steve Attard.

5. The development of sustainability reporting by a rural irrigation water provider, the Murray Irrigation Limited experience. Alex Marshall, Mark Shepheard, Demelza Brand, Catherine Norwood and Evan Christen.

6. Embarking on a triple bottom line reporting process with Murrumbidgee Irrigation Pty Ltd. Michael Mitchell, Evan Christen, Penny Davidson, Nihal Jayawardane and Mark Shepheard.

iv CRC for Irrigation Futures

Foreword The triple bottom line (TBL) concept provides both a model for understanding sustainability and a system of performance measurement, accounting, auditing and reporting. TBL reporting is also part of a broader framework of change management for integrating sustainability into business management decisions. It is generally accepted that the TBL refers to the economic, social and environmental aspects of business performance. As such the various aspects should not be viewed in isolation from each other, but as an integrated suite for sustainability assessment. The CRC for Irrigation Futures with its partners under took the “Sustainability Challenge” project (CRCIF 2.08) with the vision that the research would lead to “An irrigation industry that applies TBL reporting for continuous improvement and enhanced sustainability”. The research was a collaborative effort between the CRC for Irrigation Futures partners and organisations in case study regions in both rural and urban settings. The study regions were the Lower Burdekin of north Queensland, Western Sydney council areas and the irrigation areas in the Murrumbidgee and Murray river basins of southern NSW. The project researchers have worked with the case study organisations to develop a joint vision of sustainability, an Irrigation Sustainability Assessment Framework and then to integrate these with sustainability reporting by the organisations. It is hoped that this report and the accompanying report series will assist those businesses and organisations in the irrigation sector to undertake more thorough sustainability reporting, and that this will lead to a process of continuous improvement, resulting in better outcomes across the social, economic and environmental spectrum for all associated with or affected by irrigation in Australia. Dr. Evan Christen and Prof. Basant Maheshwari Leaders, Sustainability Challenge CRC for Irrigation Futures

CRC for Irrigation Futures 1

Table of Contents Acknowledgements......................................................................................................... ii Foreword.........................................................................................................................iv Table of Contents ........................................................................................................... 1 1. Introduction ................................................................................................................. 2 2. Burdekin Catchment Characteristics .......................................................................... 2 3. Operations of the North Burdekin Water Board in the Lower Burdekin Region.......... 4 4. Identifying a Triple-Bottom-Line Approach ................................................................. 5 5. Visioning ..................................................................................................................... 7 6. Stakeholder Identification ........................................................................................... 9 7. Triple-Bottom-Line Reporting and the NBWB............................................................. 9 8. Conclusions .............................................................................................................. 15 9. References ............................................................................................................... 16

2 CRC for Irrigation Futures

1. Introduction The Lower Burdekin case study sets out to work with the North Burdekin Water Board (NBWB or the Board) in its understanding of the triple bottom line (TBL) concept, and whether it meets their performance management and reporting needs. The Board is facing community pressure to improve its environmental management and wants to respond by managing waterways in a way that is compatible with a range of stakeholder expectations while also meeting statutory requirements. Water reform pressure from Government is also impacting on the Board as it positions itself to become a broader natural resource manger for its area, rather than the narrower role of being a water resource provider/manager. Under these pressures the Board anticipates that improved performance reporting following a triple-bottom-line approach can help to accurately communicate performance with more of its stakeholders. The Board has identified its most pressing sustainability issues as; • Uncertainty on institutional responsibilities associated with water reform • Uncontrolled groundwater extraction • Perceptions that water trading may lead to unsustainable water management • Unknown safe groundwater yield • Lack of funds for sustainable management of land and water resources • Inadequate surface water delivery network to allow replenishment of pumped

groundwater. The project aims to provide the Board with an opportunity to evaluate its business management approach through evaluating how it demonstrates its performance, to build a vision for the future and work in closer contact with its stakeholders. Specific objectives to achieve this aim are to; 1. Undertake visioning with the Board. Explore what the Board now does and what it

ought to aspire to do better or differently in the future. Assess how this relates to sustainability (through ISA High Level objectives).

2. Identify stakeholders. The triple bottom line report as such is not the only outcome, as shared learning and stakeholder engagement should also occur as part of the process as this will yield higher benefits than the report on its own.

3. Evaluate current reporting and agree on a TBL-style report table of contents for future reporting.

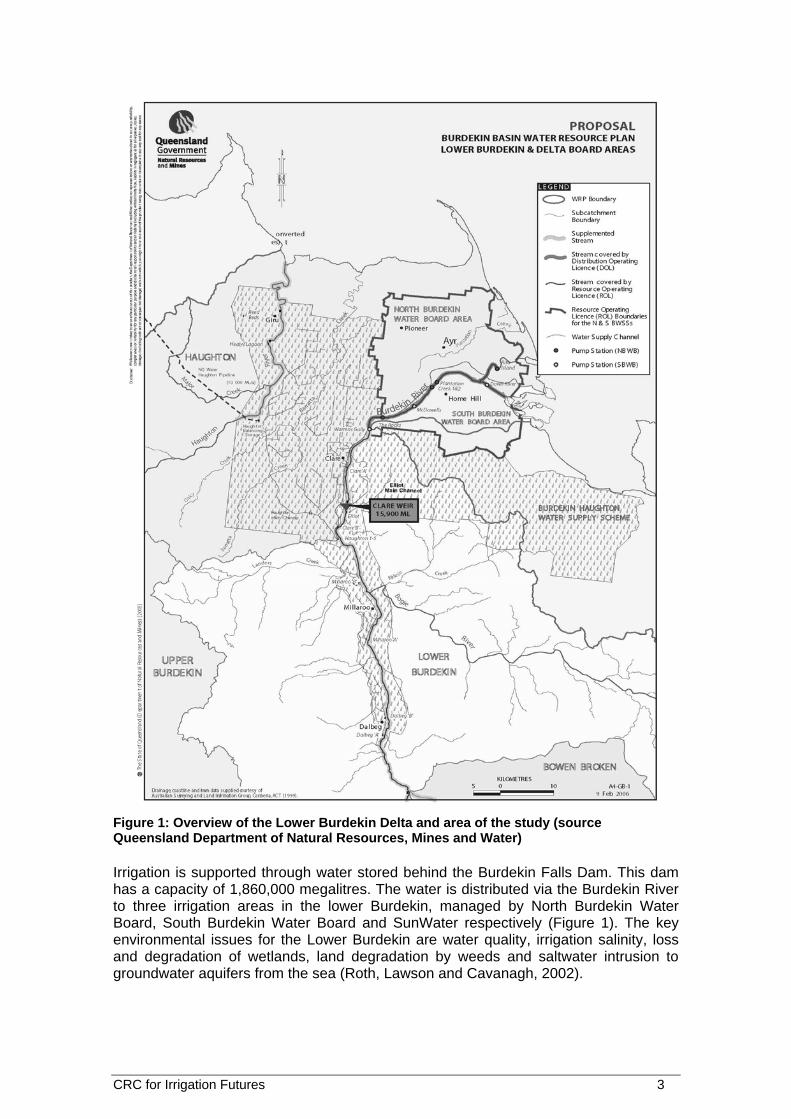

2. Burdekin Catchment Characteristics The Burdekin catchment is located in the dry tropics on the north eastern coast of Queensland, to the south and west of the regional city of Townsville. The focus for this study is defined by the area shown as North Burdekin Water Board Area, within the Lower Burdekin Delta (Figure 1). The major town in the area is Ayr, where the North Burdekin Water Board office is located.

CRC for Irrigation Futures 3

Figure 1: Overview of the Lower Burdekin Delta and area of the study (source Queensland Department of Natural Resources, Mines and Water) Irrigation is supported through water stored behind the Burdekin Falls Dam. This dam has a capacity of 1,860,000 megalitres. The water is distributed via the Burdekin River to three irrigation areas in the lower Burdekin, managed by North Burdekin Water Board, South Burdekin Water Board and SunWater respectively (Figure 1). The key environmental issues for the Lower Burdekin are water quality, irrigation salinity, loss and degradation of wetlands, land degradation by weeds and saltwater intrusion to groundwater aquifers from the sea (Roth, Lawson and Cavanagh, 2002).

4 CRC for Irrigation Futures

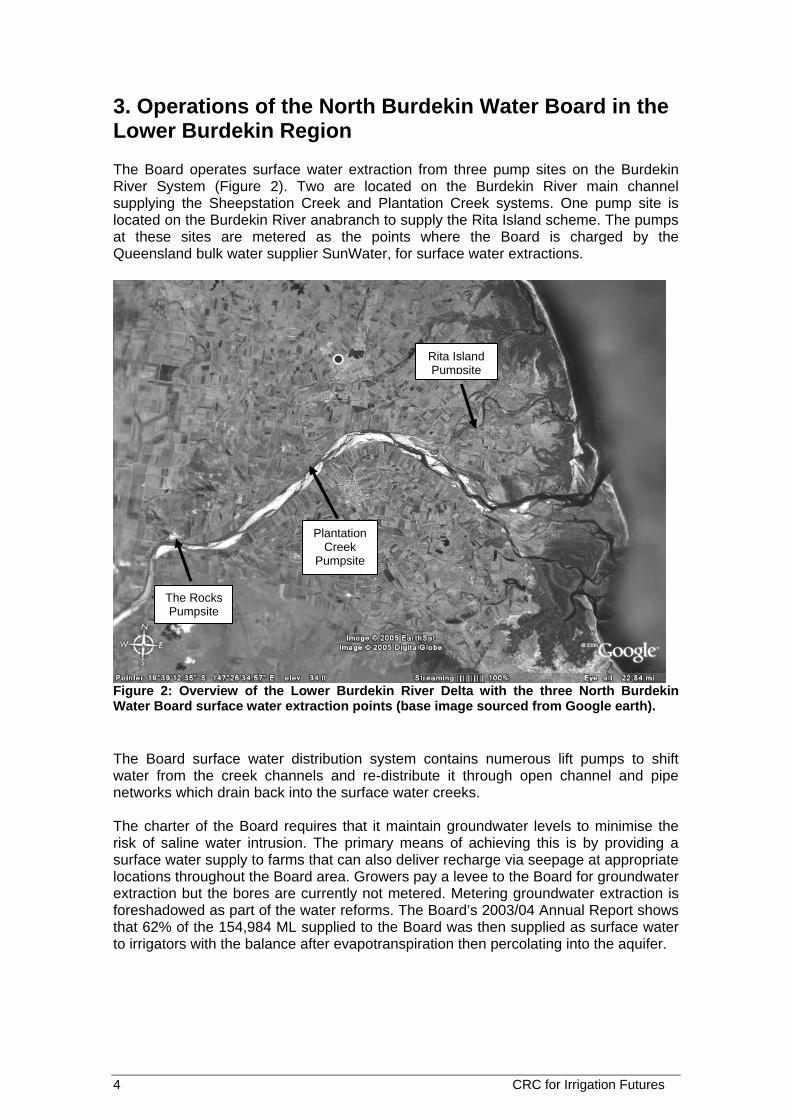

3. Operations of the North Burdekin Water Board in the Lower Burdekin Region The Board operates surface water extraction from three pump sites on the Burdekin River System (Figure 2). Two are located on the Burdekin River main channel supplying the Sheepstation Creek and Plantation Creek systems. One pump site is located on the Burdekin River anabranch to supply the Rita Island scheme. The pumps at these sites are metered as the points where the Board is charged by the Queensland bulk water supplier SunWater, for surface water extractions.

Figure 2: Overview of the Lower Burdekin River Delta with the three North Burdekin Water Board surface water extraction points (base image sourced from Google earth). The Board surface water distribution system contains numerous lift pumps to shift water from the creek channels and re-distribute it through open channel and pipe networks which drain back into the surface water creeks. The charter of the Board requires that it maintain groundwater levels to minimise the risk of saline water intrusion. The primary means of achieving this is by providing a surface water supply to farms that can also deliver recharge via seepage at appropriate locations throughout the Board area. Growers pay a levee to the Board for groundwater extraction but the bores are currently not metered. Metering groundwater extraction is foreshadowed as part of the water reforms. The Board’s 2003/04 Annual Report shows that 62% of the 154,984 ML supplied to the Board was then supplied as surface water to irrigators with the balance after evapotranspiration then percolating into the aquifer.

The Rocks Pumpsite

Plantation Creek

Pumpsite

Rita Island Pumpsite

CRC for Irrigation Futures 5

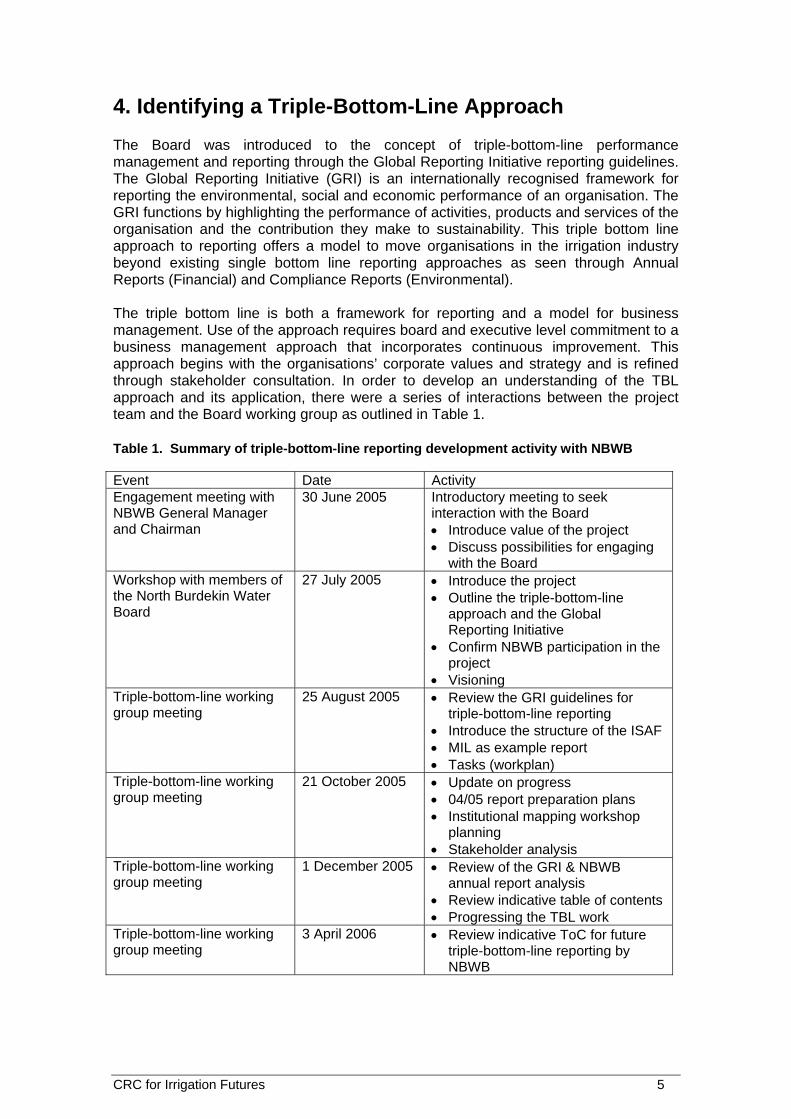

4. Identifying a Triple-Bottom-Line Approach The Board was introduced to the concept of triple-bottom-line performance management and reporting through the Global Reporting Initiative reporting guidelines. The Global Reporting Initiative (GRI) is an internationally recognised framework for reporting the environmental, social and economic performance of an organisation. The GRI functions by highlighting the performance of activities, products and services of the organisation and the contribution they make to sustainability. This triple bottom line approach to reporting offers a model to move organisations in the irrigation industry beyond existing single bottom line reporting approaches as seen through Annual Reports (Financial) and Compliance Reports (Environmental). The triple bottom line is both a framework for reporting and a model for business management. Use of the approach requires board and executive level commitment to a business management approach that incorporates continuous improvement. This approach begins with the organisations’ corporate values and strategy and is refined through stakeholder consultation. In order to develop an understanding of the TBL approach and its application, there were a series of interactions between the project team and the Board working group as outlined in Table 1. Table 1. Summary of triple-bottom-line reporting development activity with NBWB Event Date Activity Engagement meeting with NBWB General Manager and Chairman

30 June 2005 Introductory meeting to seek interaction with the Board • Introduce value of the project • Discuss possibilities for engaging

with the Board Workshop with members of the North Burdekin Water Board

27 July 2005 • Introduce the project • Outline the triple-bottom-line

approach and the Global Reporting Initiative

• Confirm NBWB participation in the project

• Visioning Triple-bottom-line working group meeting

25 August 2005 • Review the GRI guidelines for triple-bottom-line reporting

• Introduce the structure of the ISAF • MIL as example report • Tasks (workplan)

Triple-bottom-line working group meeting

21 October 2005 • Update on progress • 04/05 report preparation plans • Institutional mapping workshop

planning • Stakeholder analysis

Triple-bottom-line working group meeting

1 December 2005 • Review of the GRI & NBWB annual report analysis

• Review indicative table of contents • Progressing the TBL work

Triple-bottom-line working group meeting

3 April 2006 • Review indicative ToC for future triple-bottom-line reporting by NBWB

6 CRC for Irrigation Futures

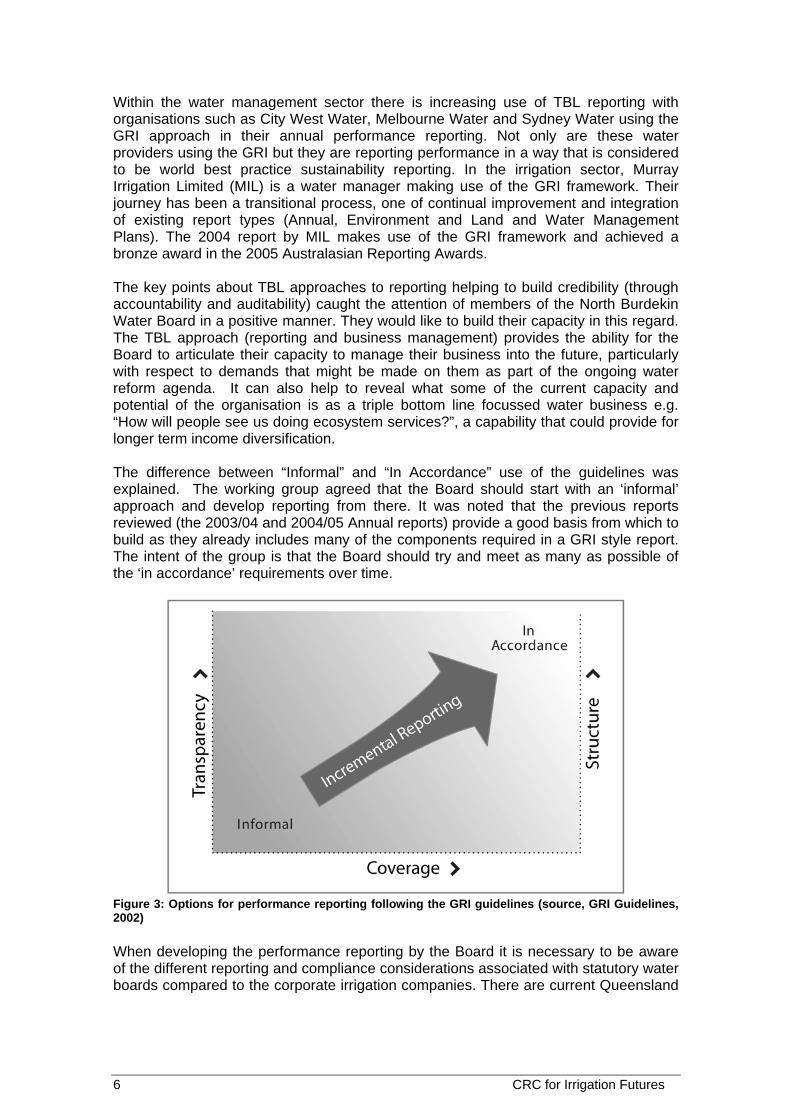

Within the water management sector there is increasing use of TBL reporting with organisations such as City West Water, Melbourne Water and Sydney Water using the GRI approach in their annual performance reporting. Not only are these water providers using the GRI but they are reporting performance in a way that is considered to be world best practice sustainability reporting. In the irrigation sector, Murray Irrigation Limited (MIL) is a water manager making use of the GRI framework. Their journey has been a transitional process, one of continual improvement and integration of existing report types (Annual, Environment and Land and Water Management Plans). The 2004 report by MIL makes use of the GRI framework and achieved a bronze award in the 2005 Australasian Reporting Awards. The key points about TBL approaches to reporting helping to build credibility (through accountability and auditability) caught the attention of members of the North Burdekin Water Board in a positive manner. They would like to build their capacity in this regard. The TBL approach (reporting and business management) provides the ability for the Board to articulate their capacity to manage their business into the future, particularly with respect to demands that might be made on them as part of the ongoing water reform agenda. It can also help to reveal what some of the current capacity and potential of the organisation is as a triple bottom line focussed water business e.g. “How will people see us doing ecosystem services?”, a capability that could provide for longer term income diversification. The difference between “Informal” and “In Accordance” use of the guidelines was explained. The working group agreed that the Board should start with an ‘informal’ approach and develop reporting from there. It was noted that the previous reports reviewed (the 2003/04 and 2004/05 Annual reports) provide a good basis from which to build as they already includes many of the components required in a GRI style report. The intent of the group is that the Board should try and meet as many as possible of the ‘in accordance’ requirements over time.

Figure 3: Options for performance reporting following the GRI guidelines (source, GRI Guidelines, 2002) When developing the performance reporting by the Board it is necessary to be aware of the different reporting and compliance considerations associated with statutory water boards compared to the corporate irrigation companies. There are current Queensland

CRC for Irrigation Futures 7

Government reporting requirements for water boards as well as proposed requirements under future bulk water licensing arrangements (Table 2). Table 2: Preferred Format for Category 2 Water Authorities Annual Reporting, in accordance with the requirements of the Queensland Financial Administration and Audit Act 1977 and Water Act 2000.

Report format requirements Purpose 1. Constitution and Function To provide background on the Board’s

establishment and its main functions in the community

2. Access To provide details on how the community can contact the Board

3. Management To outline who the key decision makers are and give an indication of their experience and knowledge of water authority matters

4. Review of operations a. Key achievements b. Capital works c. Administration d. Staff e. Finances f. General

To provide an overview and historical record of the Board’s achievements and operations for the year

5. Preview of forward operations To provide a very broad overview of the Board’s strategic direction for the future, i.e. where it is headed.

6. Submission of report To advise if the report was prepared and submitted in accordance with the Act

5. Visioning The triple-bottom-line approach can support enhanced strategic management, but to do this it is important to consider the directions the organisation might take (i.e. strategic vision). This can be worked through by addressing the questions (1) What does the organisation do well now? (2) What would you like the organisation to do more of? and (3) What other things might the organisation aspire to do better or differently in the future? In response to the first question, the core business of the North Burdekin Water Board was identified as replenishment of the aquifer through taking surface water from the Burdekin River and causing infiltration (through various means). The Board also seeks to manage extractions from the aquifer mainly through provision of surface water as an alternative to groundwater extraction for irrigators. A properly replenished and functioning aquifer was noted as the foundation of economic activity in the Burdekin delta. In order to undertake its core business, the Board has various physical assets and needs to manage these. There are infrastructure assets such as pumps, channels, pipelines, sand dams and recharge pits. Other assets include waterways (creeks and streams) which provide for residual drainage, and wetlands. The Board undertakes a de-facto water resources management function as it manages its various assets, and

8 CRC for Irrigation Futures

also provides some research coordination for the delta, for example through its involvement in the Lower Burdekin Initiative. Following this brief review of the Board’s current activities, participants were invited to consider possible future activity. A couple of ‘rules’ were suggested for this exercise: 1) assume that there will still be irrigation in the area – and/or that water is sold from the area to support a million people in Townsville (for instance); and 2) assume that no individual in the room would be involved in the future management organisation in any way. The following ideas were proposed. • There would be one Board (or other institutional structure) for management of

water in the Lower Burdekin region (i.e. the area below the dam). • This organisation would be the recognised ‘voice’ for water management in the

delta. • There will be unified groundwater management. • Making money from water/assets in new ways (e.g. ecosystem services provision,

Redclaw freshwater crayfish in the recharge pits). • Conjunctive use approach, with improved science to support it. • Waterways managed to full potential (e.g. ecotourism, fish breeding, Redclaw

freshwater crayfish farming). • Augmented income stream (increased rate base, payments for NRM management

e.g. reduced impacts on GBR lagoon, reduced water use, increased productivity). • Could instigate research into better technology. • Continual process of environmental monitoring, evaluation and action (includes

anticipation and pro-active management). Taken together, the review of current activity and the visioning of what could be happening in the future provide a guide to the appropriate strategic sustainability objectives for the NBWB. The strategic objectives help to determine the scope of TBL reporting by guiding organisational management in the formation of Board level operational objectives that can be measured and monitored for performance reporting in the future. Possible strategic sustainability objectives for the North Burdekin Water Board arising out of the visioning process are; 1. The region is recognised and paid for its ecosystem service provision role. 2. Alternative uses of water and assets implemented in parallel with water supply and

groundwater recharge (e.g. aquaculture, ecotourism, ecosystem service provision) 3. One organisation responsible for natural resource management and at the forefront

of integrated surface and groundwater management in the Lower Burdekin region. (Note, this is strictly not something that the North Board can deliver on its own. It will require collaborative activity with the South Board and Sunwater, as well as a potential complete rethink by the Queensland Government on local institutional arrangements.)

A related CRC for Irrigation Futures’ project looking at locally driven institutional reform for irrigation in the Lower Burdekin Region is linked to the visioning exercise outlined above and the stakeholder identification exercise outlined in the following section. These are reported in detail in that report (Wolfenden and Attard 2006).

CRC for Irrigation Futures 9

6. Stakeholder Identification The triple-bottom-line working group undertook a discussion about stakeholders considered to be influencing reporting in the Lower Burdekin Region. A map of the region was used as the basis for discussion about the range of stakeholders considered to be important by the working group. The area of focus was the dam to the delta, generally the North Burdekin Water Board Area, the South Burdekin Water Board Area and the Burdekin-Haughton Water Supply Scheme as indicated in Figure 1. Geographical features and irrigation infrastructure were used to trigger thinking on who the stakeholders were. This exercise resulted in the following list of stakeholders; • Entities such as the Water Boards themselves (North and South Burdekin),

SunWater and the River Trust • Government organisations such as the Department of Natural Resources, Mines

and Water, Environment Protection Authority, Department of Primary Industries and Fisheries, the Beach Protection Authority, Great Barrier Reef Marine Park Authority

• Graziers • Australian Institute of Marine Science • Australian Centre for Tropical Freshwater Research • Burdekin Shire Council • Burdekin Dry Tropics Board and Burdekin Bowen Integrated Floodplain

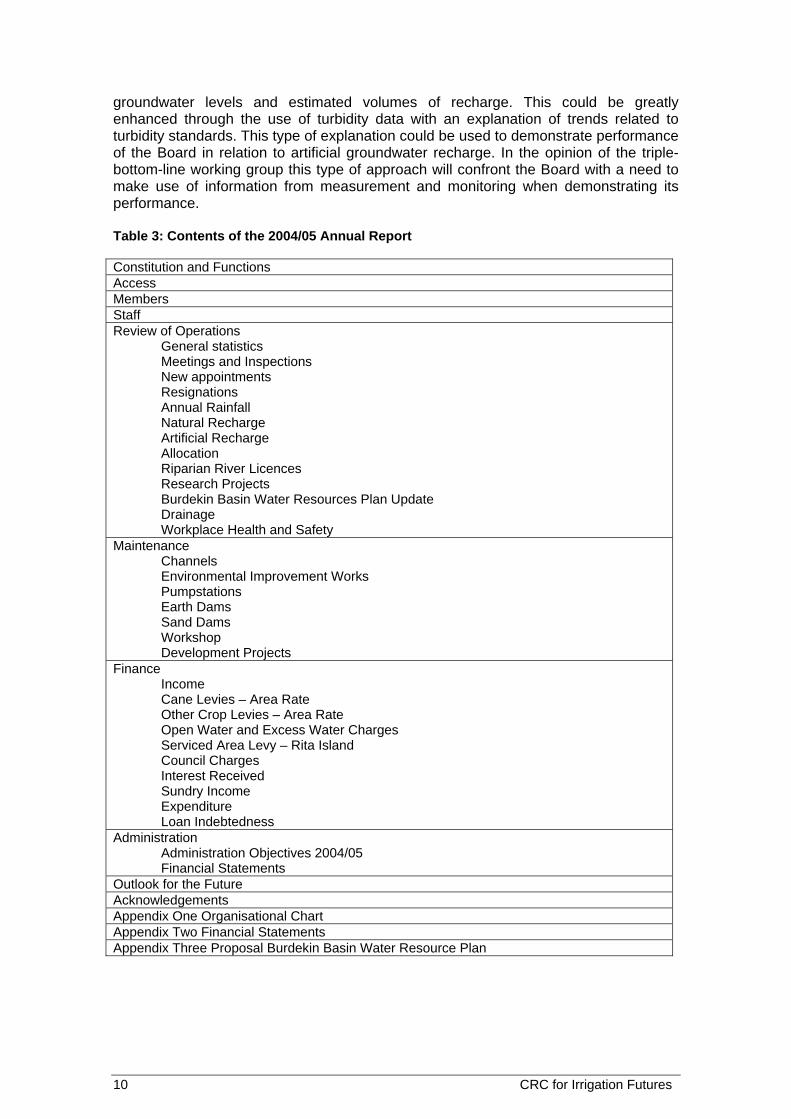

Management Advisory Committee • Sand extractors • Aquaculture and fisheries (commercial and recreational) • Bird watching • Mining • Tourism • Sugar Mills • Communities of Ayr and Home Hill • Indigenous groups • Conservation groups (See Wolfenden and Attard 2006 for more detail on this.) 7. Triple-Bottom-Line Reporting and the NBWB The triple-bottom-line concept and its application have been introduced to the Board using the GRI approach complemented by the Irrigation Sustainability Assessment Framework (ISAF). The application of GRI guidelines to an irrigation context was highlighted by the example of Murray Irrigation Limited and its use of the GRI as a basis for performance reporting. The working group recognises that a comparison of annual reporting by the Board with the GRI based approach highlights shortcomings with the amount of data presented and the adequacy of information presented to provide an accurate picture of performance, such as appears in the 2004/05 NBWB annual report (Table 3). The group appreciates that a TBL approach offers the opportunity to be confronted with elements of performance where data is not used or not available. An example of how additional data can be used to add value to reporting is the reporting of surface water turbidity and aquifer recharge. Turbidity of surface water is a significant water quality parameter that impacts on the ability of the Board to undertake artificial groundwater aquifer recharge. The current annual reporting only reports on

10 CRC for Irrigation Futures

groundwater levels and estimated volumes of recharge. This could be greatly enhanced through the use of turbidity data with an explanation of trends related to turbidity standards. This type of explanation could be used to demonstrate performance of the Board in relation to artificial groundwater recharge. In the opinion of the triple-bottom-line working group this type of approach will confront the Board with a need to make use of information from measurement and monitoring when demonstrating its performance. Table 3: Contents of the 2004/05 Annual Report Constitution and Functions Access Members Staff Review of Operations

General statistics Meetings and Inspections New appointments Resignations Annual Rainfall Natural Recharge Artificial Recharge Allocation Riparian River Licences Research Projects Burdekin Basin Water Resources Plan Update Drainage Workplace Health and Safety

Maintenance Channels Environmental Improvement Works Pumpstations Earth Dams Sand Dams Workshop Development Projects

Finance Income Cane Levies – Area Rate Other Crop Levies – Area Rate Open Water and Excess Water Charges Serviced Area Levy – Rita Island Council Charges Interest Received Sundry Income Expenditure Loan Indebtedness

Administration Administration Objectives 2004/05 Financial Statements

Outlook for the Future Acknowledgements Appendix One Organisational Chart Appendix Two Financial Statements Appendix Three Proposal Burdekin Basin Water Resource Plan

CRC for Irrigation Futures 11

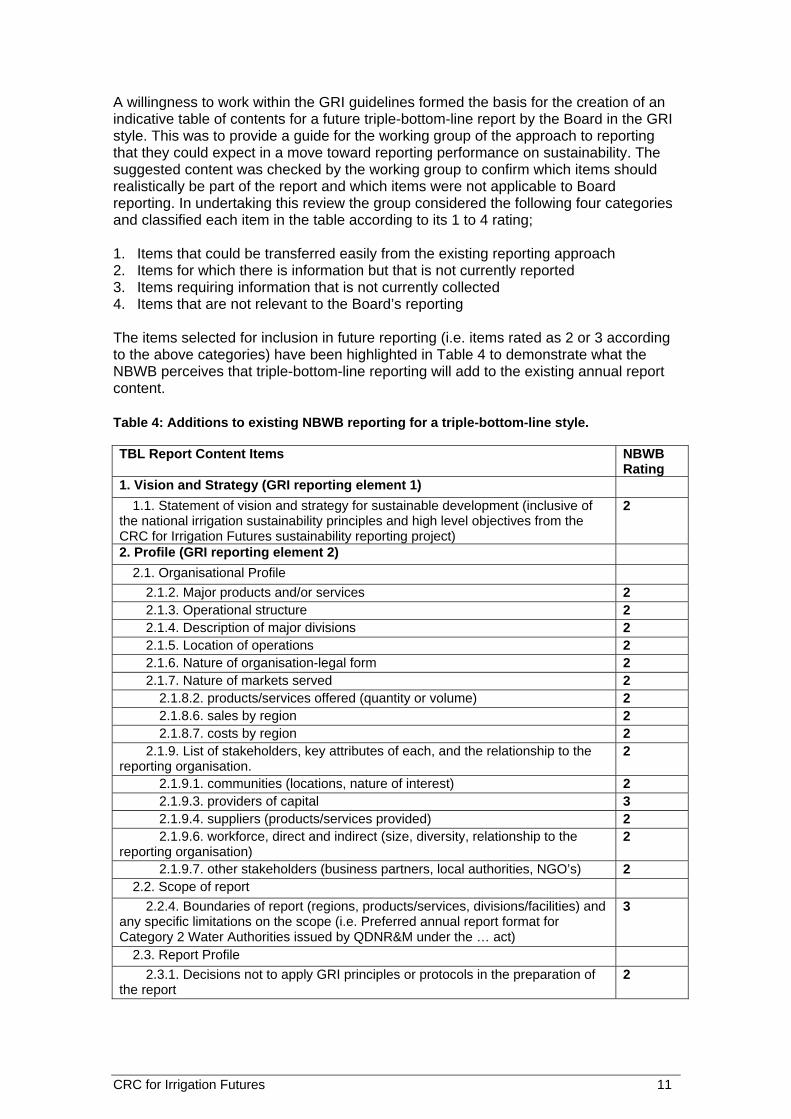

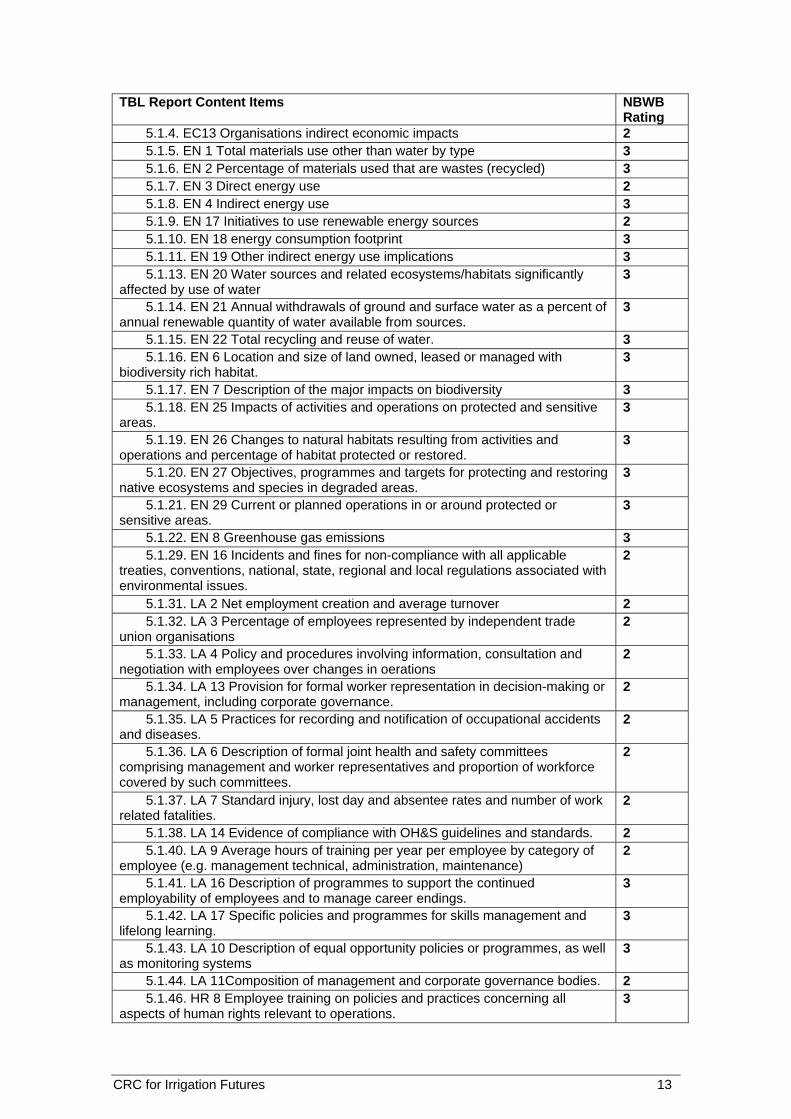

A willingness to work within the GRI guidelines formed the basis for the creation of an indicative table of contents for a future triple-bottom-line report by the Board in the GRI style. This was to provide a guide for the working group of the approach to reporting that they could expect in a move toward reporting performance on sustainability. The suggested content was checked by the working group to confirm which items should realistically be part of the report and which items were not applicable to Board reporting. In undertaking this review the group considered the following four categories and classified each item in the table according to its 1 to 4 rating; 1. Items that could be transferred easily from the existing reporting approach 2. Items for which there is information but that is not currently reported 3. Items requiring information that is not currently collected 4. Items that are not relevant to the Board’s reporting The items selected for inclusion in future reporting (i.e. items rated as 2 or 3 according to the above categories) have been highlighted in Table 4 to demonstrate what the NBWB perceives that triple-bottom-line reporting will add to the existing annual report content. Table 4: Additions to existing NBWB reporting for a triple-bottom-line style. TBL Report Content Items NBWB

Rating 1. Vision and Strategy (GRI reporting element 1)

1.1. Statement of vision and strategy for sustainable development (inclusive of the national irrigation sustainability principles and high level objectives from the CRC for Irrigation Futures sustainability reporting project)

2

2. Profile (GRI reporting element 2) 2.1. Organisational Profile

2.1.2. Major products and/or services 2 2.1.3. Operational structure 2 2.1.4. Description of major divisions 2 2.1.5. Location of operations 2 2.1.6. Nature of organisation-legal form 2 2.1.7. Nature of markets served 2

2.1.8.2. products/services offered (quantity or volume) 2 2.1.8.6. sales by region 2 2.1.8.7. costs by region 2

2.1.9. List of stakeholders, key attributes of each, and the relationship to the reporting organisation.

2

2.1.9.1. communities (locations, nature of interest) 2 2.1.9.3. providers of capital 3 2.1.9.4. suppliers (products/services provided) 2 2.1.9.6. workforce, direct and indirect (size, diversity, relationship to the

reporting organisation) 2

2.1.9.7. other stakeholders (business partners, local authorities, NGO’s) 2 2.2. Scope of report

2.2.4. Boundaries of report (regions, products/services, divisions/facilities) and any specific limitations on the scope (i.e. Preferred annual report format for Category 2 Water Authorities issued by QDNR&M under the … act)

3

2.3. Report Profile 2.3.1. Decisions not to apply GRI principles or protocols in the preparation of

the report 2

12 CRC for Irrigation Futures

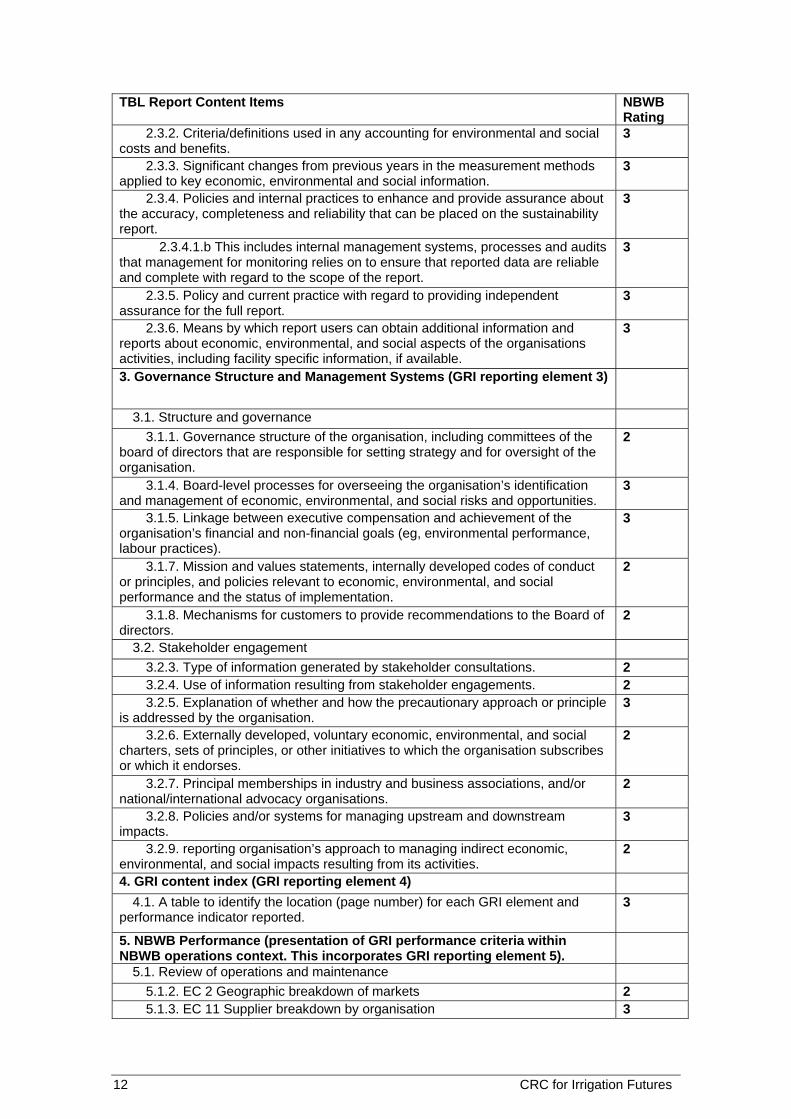

TBL Report Content Items NBWB Rating

2.3.2. Criteria/definitions used in any accounting for environmental and social costs and benefits.

3

2.3.3. Significant changes from previous years in the measurement methods applied to key economic, environmental and social information.

3

2.3.4. Policies and internal practices to enhance and provide assurance about the accuracy, completeness and reliability that can be placed on the sustainability report.

3

2.3.4.1.b This includes internal management systems, processes and audits that management for monitoring relies on to ensure that reported data are reliable and complete with regard to the scope of the report.

3

2.3.5. Policy and current practice with regard to providing independent assurance for the full report.

3

2.3.6. Means by which report users can obtain additional information and reports about economic, environmental, and social aspects of the organisations activities, including facility specific information, if available.

3

3. Governance Structure and Management Systems (GRI reporting element 3)

3.1. Structure and governance 3.1.1. Governance structure of the organisation, including committees of the

board of directors that are responsible for setting strategy and for oversight of the organisation.

2

3.1.4. Board-level processes for overseeing the organisation’s identification and management of economic, environmental, and social risks and opportunities.

3

3.1.5. Linkage between executive compensation and achievement of the organisation’s financial and non-financial goals (eg, environmental performance, labour practices).

3

3.1.7. Mission and values statements, internally developed codes of conduct or principles, and policies relevant to economic, environmental, and social performance and the status of implementation.

2

3.1.8. Mechanisms for customers to provide recommendations to the Board of directors.

2

3.2. Stakeholder engagement 3.2.3. Type of information generated by stakeholder consultations. 2 3.2.4. Use of information resulting from stakeholder engagements. 2 3.2.5. Explanation of whether and how the precautionary approach or principle

is addressed by the organisation. 3

3.2.6. Externally developed, voluntary economic, environmental, and social charters, sets of principles, or other initiatives to which the organisation subscribes or which it endorses.

2

3.2.7. Principal memberships in industry and business associations, and/or national/international advocacy organisations.

2

3.2.8. Policies and/or systems for managing upstream and downstream impacts.

3

3.2.9. reporting organisation’s approach to managing indirect economic, environmental, and social impacts resulting from its activities.

2

4. GRI content index (GRI reporting element 4) 4.1. A table to identify the location (page number) for each GRI element and

performance indicator reported. 3

5. NBWB Performance (presentation of GRI performance criteria within NBWB operations context. This incorporates GRI reporting element 5).

5.1. Review of operations and maintenance 5.1.2. EC 2 Geographic breakdown of markets 2 5.1.3. EC 11 Supplier breakdown by organisation 3

CRC for Irrigation Futures 13

TBL Report Content Items NBWB Rating

5.1.4. EC13 Organisations indirect economic impacts 2 5.1.5. EN 1 Total materials use other than water by type 3 5.1.6. EN 2 Percentage of materials used that are wastes (recycled) 3 5.1.7. EN 3 Direct energy use 2 5.1.8. EN 4 Indirect energy use 3 5.1.9. EN 17 Initiatives to use renewable energy sources 2 5.1.10. EN 18 energy consumption footprint 3 5.1.11. EN 19 Other indirect energy use implications 3 5.1.13. EN 20 Water sources and related ecosystems/habitats significantly

affected by use of water 3

5.1.14. EN 21 Annual withdrawals of ground and surface water as a percent of annual renewable quantity of water available from sources.

3

5.1.15. EN 22 Total recycling and reuse of water. 3 5.1.16. EN 6 Location and size of land owned, leased or managed with

biodiversity rich habitat. 3

5.1.17. EN 7 Description of the major impacts on biodiversity 3 5.1.18. EN 25 Impacts of activities and operations on protected and sensitive

areas. 3

5.1.19. EN 26 Changes to natural habitats resulting from activities and operations and percentage of habitat protected or restored.

3

5.1.20. EN 27 Objectives, programmes and targets for protecting and restoring native ecosystems and species in degraded areas.

3

5.1.21. EN 29 Current or planned operations in or around protected or sensitive areas.

3

5.1.22. EN 8 Greenhouse gas emissions 3 5.1.29. EN 16 Incidents and fines for non-compliance with all applicable

treaties, conventions, national, state, regional and local regulations associated with environmental issues.

2

5.1.31. LA 2 Net employment creation and average turnover 2 5.1.32. LA 3 Percentage of employees represented by independent trade

union organisations 2

5.1.33. LA 4 Policy and procedures involving information, consultation and negotiation with employees over changes in oerations

2

5.1.34. LA 13 Provision for formal worker representation in decision-making or management, including corporate governance.

2

5.1.35. LA 5 Practices for recording and notification of occupational accidents and diseases.

2

5.1.36. LA 6 Description of formal joint health and safety committees comprising management and worker representatives and proportion of workforce covered by such committees.

2

5.1.37. LA 7 Standard injury, lost day and absentee rates and number of work related fatalities.

2

5.1.38. LA 14 Evidence of compliance with OH&S guidelines and standards. 2 5.1.40. LA 9 Average hours of training per year per employee by category of

employee (e.g. management technical, administration, maintenance) 2

5.1.41. LA 16 Description of programmes to support the continued employability of employees and to manage career endings.

3

5.1.42. LA 17 Specific policies and programmes for skills management and lifelong learning.

3

5.1.43. LA 10 Description of equal opportunity policies or programmes, as well as monitoring systems

3

5.1.44. LA 11Composition of management and corporate governance bodies. 2 5.1.46. HR 8 Employee training on policies and practices concerning all

aspects of human rights relevant to operations. 3

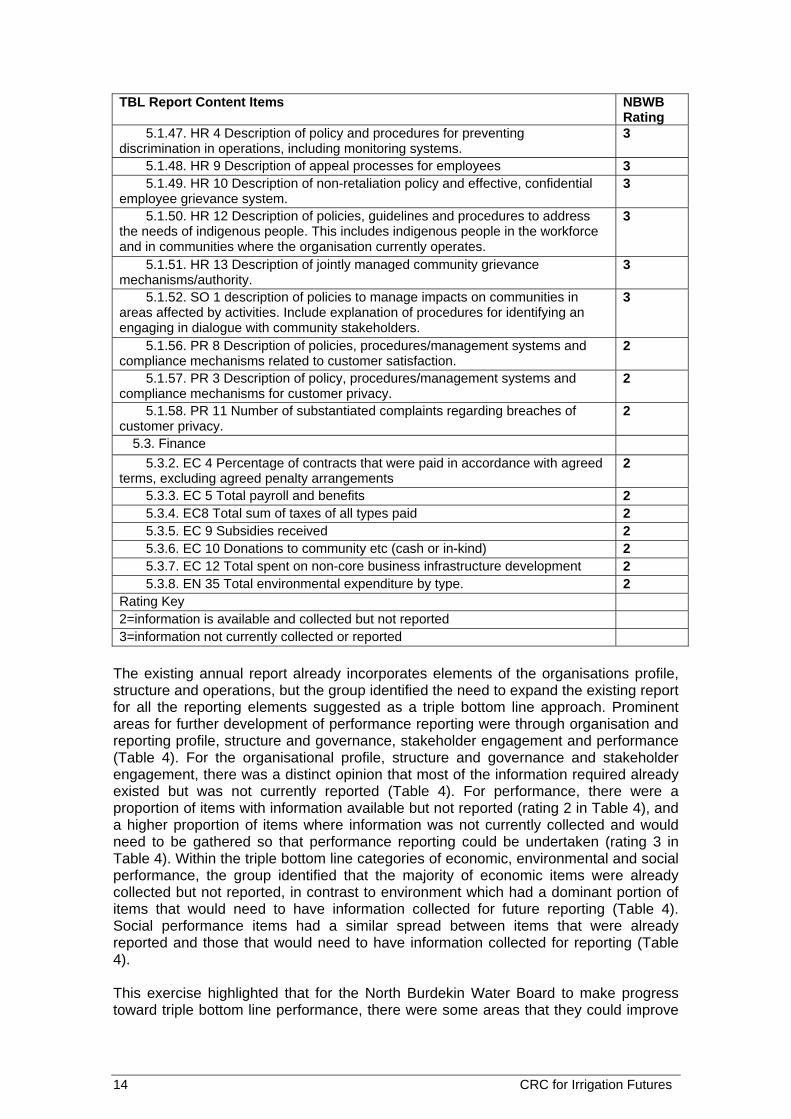

14 CRC for Irrigation Futures

TBL Report Content Items NBWB Rating

5.1.47. HR 4 Description of policy and procedures for preventing discrimination in operations, including monitoring systems.

3

5.1.48. HR 9 Description of appeal processes for employees 3 5.1.49. HR 10 Description of non-retaliation policy and effective, confidential

employee grievance system. 3

5.1.50. HR 12 Description of policies, guidelines and procedures to address the needs of indigenous people. This includes indigenous people in the workforce and in communities where the organisation currently operates.

3

5.1.51. HR 13 Description of jointly managed community grievance mechanisms/authority.

3

5.1.52. SO 1 description of policies to manage impacts on communities in areas affected by activities. Include explanation of procedures for identifying an engaging in dialogue with community stakeholders.

3

5.1.56. PR 8 Description of policies, procedures/management systems and compliance mechanisms related to customer satisfaction.

2

5.1.57. PR 3 Description of policy, procedures/management systems and compliance mechanisms for customer privacy.

2

5.1.58. PR 11 Number of substantiated complaints regarding breaches of customer privacy.

2

5.3. Finance 5.3.2. EC 4 Percentage of contracts that were paid in accordance with agreed

terms, excluding agreed penalty arrangements 2

5.3.3. EC 5 Total payroll and benefits 2 5.3.4. EC8 Total sum of taxes of all types paid 2 5.3.5. EC 9 Subsidies received 2 5.3.6. EC 10 Donations to community etc (cash or in-kind) 2 5.3.7. EC 12 Total spent on non-core business infrastructure development 2 5.3.8. EN 35 Total environmental expenditure by type. 2

Rating Key 2=information is available and collected but not reported 3=information not currently collected or reported

The existing annual report already incorporates elements of the organisations profile, structure and operations, but the group identified the need to expand the existing report for all the reporting elements suggested as a triple bottom line approach. Prominent areas for further development of performance reporting were through organisation and reporting profile, structure and governance, stakeholder engagement and performance (Table 4). For the organisational profile, structure and governance and stakeholder engagement, there was a distinct opinion that most of the information required already existed but was not currently reported (Table 4). For performance, there were a proportion of items with information available but not reported (rating 2 in Table 4), and a higher proportion of items where information was not currently collected and would need to be gathered so that performance reporting could be undertaken (rating 3 in Table 4). Within the triple bottom line categories of economic, environmental and social performance, the group identified that the majority of economic items were already collected but not reported, in contrast to environment which had a dominant portion of items that would need to have information collected for future reporting (Table 4). Social performance items had a similar spread between items that were already reported and those that would need to have information collected for reporting (Table 4). This exercise highlighted that for the North Burdekin Water Board to make progress toward triple bottom line performance, there were some areas that they could improve

CRC for Irrigation Futures 15

on by reporting more openly on the information they already have about their operations, but there is also a number of performance aspects that will require additional information to be collected by the Board or sourced from other organisations (e.g. State agencies or research institutions) so that a more accurate account of performance can be presented by the Board. The prerogative is now with the Board to take this concept further. The various discussions held with Board members and staff during the course of this project and the related Planning for Change project reported elsewhere (Wolfenden and Attard 2006) suggest to the authors that it would most definitely be in the strategic interest of the Board to invest resources in progressing towards annual reporting that is increasingly in alignment with the GRI reporting framework. However, this will necessarily involve the Board having to decide whether the benefits to be obtained in doing so justify the costs involved. At time of writing, this issue has not been clearly resolved. The authors also note that a new idea for TBL reporting has been spawned by this and the Planning for Change project. Among other things, it follows from the strategic purpose identified above that there would be one organisation responsible for natural resource management and at the forefront of integrated surface and groundwater management in the Lower Burdekin region. In the short term, this is not likely to eventuate. However, it may be possible to manage as though such an organisation existed, through adopting a cross-organisational adaptive management approach based upon integrated TBL reporting for the Lower Burdekin. This would involve SunWater along with the North and South Burdekin Water Boards. A preliminary proposal for a project to initiate this has been included in the Planning for Change report (Wolfenden and Attard 2006). A working group has been formed to pursue this objective. Whether TBL reporting is taken forward by NBWB only, or as in integrated exercise for the Lower Burdekin, there is an information gap that is presently limiting the effectiveness of sustainability reporting. There is a general lack of monitoring of key environmental indicator variables that could be used within the reporting structure. At time of writing, the Integrated Reporting Project Working Group is undertaking an audit of what is available, and what additional monitoring needs to be implemented. Once this situation is clarified, the intent is to move ahead with the integrated reporting project. 8. Conclusions The project has established a knowledge base about the triple-bottom-line approach in relation to the strategic management and future performance reporting of the NBWB as part of the Lower Burdekin region. This has included: • Comprehending the strategic management value of the TBL reporting process, as

well as the general communication benefit of the report it produces. This is in the context of the North Burdekin Water Board viewing itself as a steward of natural resources rather than only as a water manager.

• Visioning to inform the development of management strategy within the North Burdekin Water Board.

• Stakeholder identification for consultation in relation to strategic management and performance reporting.

16 CRC for Irrigation Futures

• A comprehension of the scope of existing information that can be better used, and additional information required, for the Board to progress toward a triple bottom line type of report.

• A connection between the need for the Board to resource efforts to make appropriate use and obtain additional information on its performance for its strategic future.

• The intent for the North Burdekin Water Board to work with the South Burdekin Water Board and SunWater to develop an integrated TBL report for the Lower Burdekin system.

• Agreement about the need for some National aspirations for irrigation sustainability that should be converted into action at the local level through the operations of local organisations. This is consistent with the project’s Irrigation Sustainability Assessment Framework approach (see Report 2 of this series ‘A Guide to using Triple Bottom Line reporting as a framework to promote the sustainability of rural and urban irrigation in Australia’ as listed on page iii of this report).

9. References Global Reporting Initiative (GRI). 2002. Sustainability Reporting Guidelines. Roth, C.H., Lawson, G. and Cavanagh, D. 2002. Overview of Key Natural Resource

Management Issues in the Burdekin Catchment, with particular reference to Water Quality and Salinity: Burdekin Catchment Condition Study Phase I, CSIRO Land and Water. Accessed 10 Feb from http://ww.clw.csiro.au/ publications/consultancy

Wolfenden, J. and Attard, S. 2006. Analysis of Formal and Informal Institutional

Arrangements and Processes – Lower Burdekin Irrigation Region Case Study. CRCIF Sub-project 1.07a Report.

PO Box 56, Darling Heights Qld 4350 | Phone: 07 4631 2046 | Fax: 07 4631 1870 | Web: www.irrigationfutures.org.au

Partner Organisations