Embed Size (px)

Citation preview

Apply online

Octopus Inheritance Tax Service

Looking after your family’s future

Octopus Inheritance Tax ServiceJanuary 2022

Before you start, some important information:For UK investors only

• The Octopus Inheritance Tax Service is an investment that places your money at risk. This means you may not get back the full amount you put in.

• The benefit of tax relief depends on individual circumstances. Tax treatment is assumed as per current legislation and interpretation, which may change in the future.

• Qualification for Business Property Relief depends on the portfolio companies maintaining their qualifying status, which is assessed at the point a claim for the relief is made.

• Past performance is not an indicator of future returns.

• The key risks associated with this product are explained in full on page 22 of this brochure. It is important that you read and fully understand the risks involved before deciding whether it is right for you.

• Investors should seek specialist advice to make sure their will is drafted so their estate will benefit from available inheritance reliefs including Business Property Relief.

This document does not constitute advice on investments, legal matters, taxation or anything else. We always recommend you talk to a qualified financial adviser before making any investment decision.

All data and factual information within this document is provided by Octopus Investments and is correct at 30 September 2021, unless stated otherwise.

Issued by Octopus Investments Limited, which is authorised and regulated by the Financial Conduct Authority. Registered office: 33 Holborn, London EC1N 2HT. Registered in England and Wales No. 03942880. We record telephone calls. Issued: January 2022. CAM011607-2201

Three tax solutions,one expert provider.Find out more by visiting octopusinvestments.com

Find it fast

About Octopus 4Over a decade of the Octopus Inheritance Tax Service 6How it works 8A worked example 10Our investment strategy 12An example portfolio company 13Getting started 14After you’ve invested 15The Growth Shield: putting your returns first 16Responsible investing at Octopus 18Our approach to responsible investment 19How the Octopus Inheritance Tax Service is managed responsibly 21Understanding the key risks 22Conflicts of interest 24The charges 26How to invest 27

For more than a decade, the Octopus Inheritance Tax Service has been helping thousands of people to plan for the future. And it could help you, too.

4 Inheritance tax

About Octopus

We invest in the sectors we know inside out. And we’ve built investments that make a real difference to your financial planning.

Seen us before?You may be wondering ‘Is this the same Octopus?’ Octopus Energy is part of the Octopus family, and the UK’s only Which? Recommended energy provider four years running.

Renewable energyWe’re the

largest solar investor in Europe. We also invest in landfill gas sites, wind farms and biomass plants.

Smaller companiesWe turn small businesses into

big ones, driving the economy and

creating jobs.

HealthcareWe help build

state-of-the-art care homes

and retirement communities.

PropertyWe provide

award-winning finance for property

investment and development.

Octopus Inheritance Tax Service 5

We’re ready for your callWe can’t give you financial or tax advice, but we can answer questions about us and our investments. You can call us on 0800 316 2295 or email [email protected].

21 years of OctopusWe launched Octopus in 2000, wanting to create an investment company that put its customers first. We looked at what didn’t work well, and found ways to do things differently.

Along the way, we’ve become the largest manager of venture capital trusts and investments that qualify for relief from inheritance tax. And we’re still looking for new ways to improve people’s financial lives. Today we have more than 750 employees and manage £11.3 billion on behalf of tens of thousands of investors.

Octopus is a Certified B Corporation™. We meet the highest standards of social and environmental consideration, transparency and accountability. Our approach means we can continue to meet the needs of all those that matter to us, from our customers to our communities.

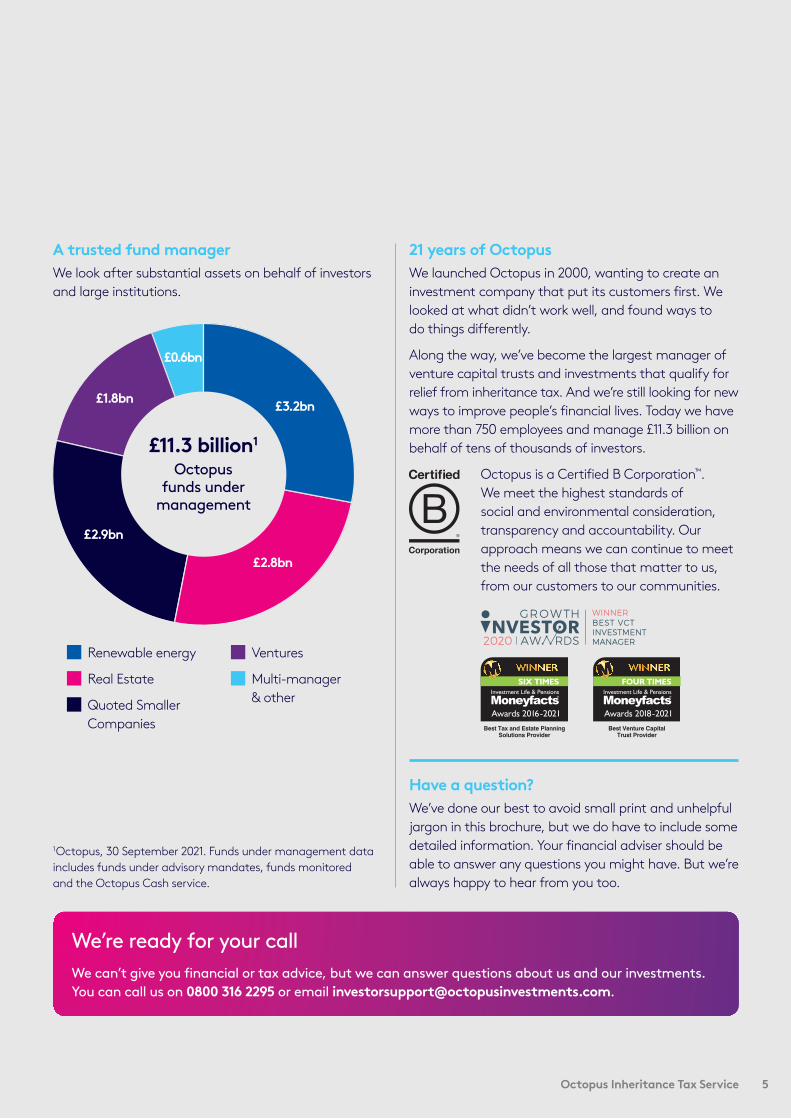

A trusted fund managerWe look after substantial assets on behalf of investors and large institutions.

Renewable energy

Real Estate

Quoted Smaller Companies

Ventures

Multi-manager & other

1 Octopus, 30 September 2021. Funds under management data includes funds under advisory mandates, funds monitored and the Octopus Cash service.

£11.3 billion1

Octopusfunds under

management

£3.2bn

£2.9bn

£1.8bn

£0.6bn

£2.8bn

Have a question?We’ve done our best to avoid small print and unhelpful jargon in this brochure, but we do have to include some detailed information. Your financial adviser should be able to answer any questions you might have. But we’re always happy to hear from you too.

Over a decade of the Octopus Inheritance Tax Service

You don’t have to be particularly wealthy to leave behind a large inheritance tax bill when you die. But our flagship estate planning service could help you to pass on more of your wealth to your family.

If you’ve been carefully building up assets throughout your life, you probably want to pass on as much of your estate as you can to your family when you die. If you don’t plan ahead, the part of your estate that exceeds the inheritance tax threshold of £325,000 could be taxed at 40%. This means that your family may miss out on a significant portion of your wealth.

Traditional estate planning solutions can be inflexible. For example, if you give away your assets to family and friends during your lifetime, these gifts take seven years before they become exempt from inheritance tax.

Similarly, putting assets into a trust also takes seven years before the value of the assets falls outside of your taxable estate. Both of these options result in you no longer being able to access your wealth if you need to. Also, for many people, giving away their hard-earned money and investments can be very unattractive.

How we can helpSince 2007, the Octopus Inheritance Tax Service has given investors the opportunity to invest in the shares of companies making a positive contribution to the UK’s economic growth. The companies are unlisted, which means their shares do not trade on any stock exchange. We select companies that we expect to qualify for Business Property Relief (BPR). This is a government-approved relief from inheritance tax, which we explain on the opposite page.

The service aims to deliver steady investment growth of 3% per year on average over the lifetime of an investment. It can help give your family a better financial future, and is flexible enough to adapt to your needs, should your circumstances change in later life.

Octopus Inheritance Tax Service is a Discretionary Fund Management Service and you should make sure you are comfortable with the risks that come with investing in this type of product. The risks are explained on page 22.

6 Inheritance tax

Inheritance tax: the basicsInheritance tax is paid on the money and possessions that you leave to your beneficiaries when you die. The first £325,000 of your assets are free from inheritance tax (this is often called the ‘nil-rate band’). In 2017, the Government introduced an additional inheritance tax allowance, called the residence nil-rate band. It’s an allowance of £175,000 which applies to the family home in certain circumstances, for example if someone is leaving their main residence to their children or grandchildren. Everything that isn’t covered by these nil-rate bands is taxed at 40%. There are a number of well-established ways to reduce or potentially even eliminate the amount of inheritance tax your loved ones are required to pay. Examples include gifts, trusts and making the most of investments that qualify for Business Property Relief.

Business Property Relief (BPR) is an established form of tax relief that gives people an incentive to invest their money into trading businesses. It was introduced in 1976 as a way to ensure that inheritance tax wasn’t paid on small businesses. Shares in a BPR-qualifying business can be left to beneficiaries free from inheritance tax, provided they have been owned for at least two years at the time of death. You can read more about BPR on the HM Revenue & Customs (HMRC) website at hmrc.gov.uk. To find the relevant pages, just type ‘Business Relief’ in the search box.

Octopus Inheritance Tax Service 7

Want to learn more about inheritance tax and Business Property Relief?There are two simple videos on our website that explain how inheritance tax and BPR work.

octopusinvestments.com/ihtvideooctopusinvestments.com/bprvideo

It’s an investment service that benefits from a government-approved incentive designed to help companies grow.

Portfolio managementWhen you invest in the service, your money is placed in a discretionary portfolio managed by Octopus. This means we use the money to buy shares on your behalf, in companies that we select.

Our experienced Investment Management team is responsible for making sure that capital is invested in ways that are consistent with the aims of the service. We only target companies that we believe are capable of delivering a predictable level of growth over the long term. We explain our investment strategy in more detail on page 12.

The shares we select are expected to qualify for BPR. This means that the investment should become free from inheritance tax after two years, provided the investment is still held at the time of death. They can then be passed on as part of your estate to beneficiaries named by you.

To the best of our knowledge, all investments made in the Octopus Inheritance Tax Service have been able to be passed to beneficiaries free from inheritance tax. We have now passed 4,000 estates that have been entitled to claim Business Property Relief.1

Built-in flexibilityThe service is flexible should your circumstances change. This means you can invest more money, or you can sell part of your investment and have the proceeds returned to you. We describe this in more detail on page 15.

We target annual growth for investors of 3% on the value of the shares, compounded over the lifetime of the investment. This is calculated on the amount invested after initial charges and the initial dealing fee.

Because of the aims of the service, many of our investors remain invested for several years. When investors or their beneficiaries ask us to sell shares, we will calculate whether we have achieved what we set out to. If we haven’t delivered the 3% target return, after taking our annual management charge into account, we will reduce or eliminate the annual management charge we take.

How it works

“We are here to make life easier for you and your family”The Octopus Inheritance Tax Service is intended to be held over the long term. Family members may not be familiar with the investment, or know what their options are in the event of your death. That’s why we have a dedicated Estates and Probate team helping the families and the beneficiaries of our clients, who might need some help with what to do next. Sometimes it’s easier to talk with someone either in person or over the phone and we will do our best to help in any way we can.

1 Octopus Investments, 30 September 2021.

8 Inheritance tax

Ben Charrington Estates and Probate team0800 294 6826

Octopus Inheritance Tax Service 9

Key benefits

More of your wealth can be passed on to your familyThe Octopus Inheritance Tax Service invests in companies that are expected to qualify for relief from inheritance tax.

SpeedYour investment should become free of inheritance tax after two years – as long as you still hold the shares at the time of your death.

A simple processThere are no complicated legal structures (as with a trust) and no medical underwriting (as with an insurance policy).

Access to your investmentYou can ask us to sell some or all of your shares at any time, and we will return the proceeds to you. You can even set up regular withdrawals if you want them.

Long-term sustainable growthThe companies we invest in carry out a range of different trades in order to target 3% growth per annum over the long term for investors.

We won’t take our annual management charge if we don’t deliverWe’ll only take our annual management charge after you or your family ask us to sell shares. And we’ll only take it if we’ve achieved sufficient growth in the value of your portfolio over its lifetime to deliver the annual target return to you. Keeping these charges in your portfolio acts as a cushion so that if the investment returns don’t meet the target, we lose out before you do. Please read page 16 for more details about our ‘Growth Shield’.

See page 22 for more information on the risks to be considered before making this investment.

Key risks

Your capital is at riskWe invest in trading companies that are not listed on a stock exchange. The companies we invest in could fall in value and you may not get back the full amount you invest. Even with our ‘Growth Shield’, there’s no guarantee that the target return for investors will be achieved, and you could lose some or all of your investment.

Tax relief cannot be guaranteedThis brochure is based on current tax legislation and interpretation. There’s no guarantee that the companies we invest in will remain BPR-qualifying. Tax rules could change in the future. The value of tax relief will depend on your personal circumstances.

Your investment could take longer to sell than expectedAlthough one of the aims of the Octopus Inheritance Tax Service is to make sure investors can sell their investment quickly if they want to, it invests in the shares of unquoted companies that are not listed on any stock exchange. This means the shares we invest in may take longer to sell than the shares of companies listed on the main market of the London Stock Exchange. The timing of share sales, and when we can return the proceeds to you, cannot be guaranteed.

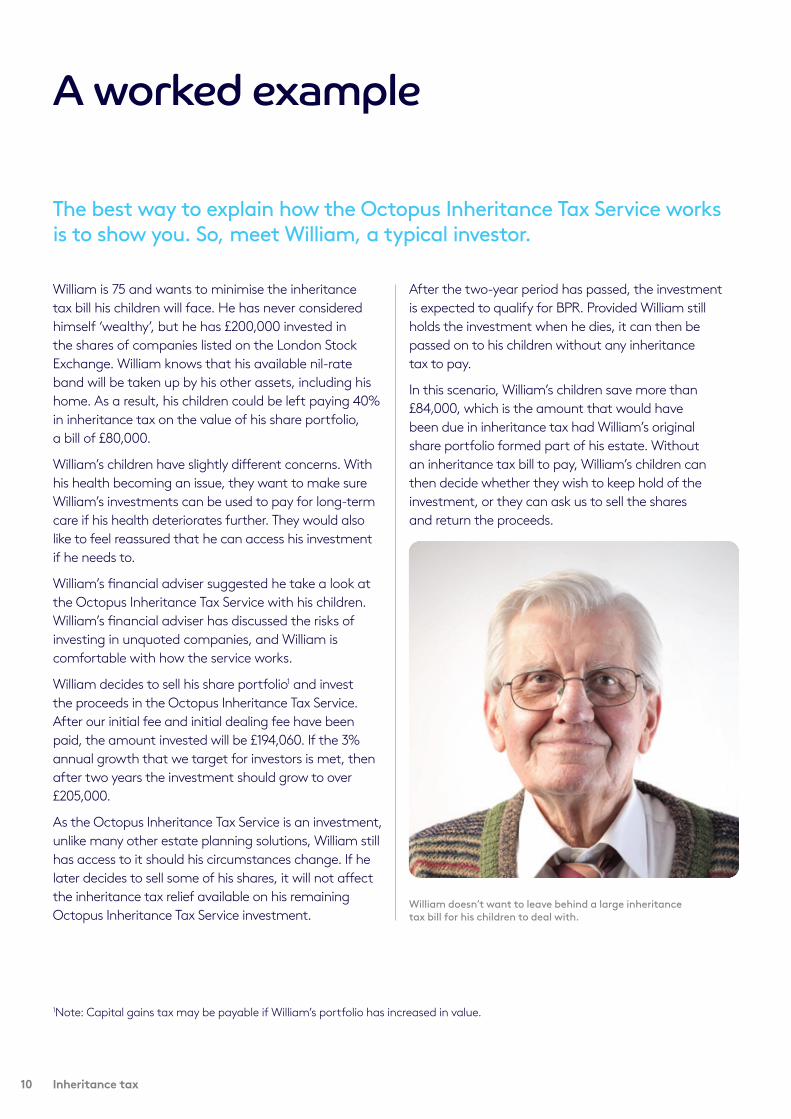

A worked example

The best way to explain how the Octopus Inheritance Tax Service works is to show you. So, meet William, a typical investor.

William is 75 and wants to minimise the inheritance tax bill his children will face. He has never considered himself ‘wealthy’, but he has £200,000 invested in the shares of companies listed on the London Stock Exchange. William knows that his available nil-rate band will be taken up by his other assets, including his home. As a result, his children could be left paying 40% in inheritance tax on the value of his share portfolio, a bill of £80,000.

William’s children have slightly different concerns. With his health becoming an issue, they want to make sure William’s investments can be used to pay for long-term care if his health deteriorates further. They would also like to feel reassured that he can access his investment if he needs to.

William’s financial adviser suggested he take a look at the Octopus Inheritance Tax Service with his children. William’s financial adviser has discussed the risks of investing in unquoted companies, and William is comfortable with how the service works.

William decides to sell his share portfolio1 and invest the proceeds in the Octopus Inheritance Tax Service. After our initial fee and initial dealing fee have been paid, the amount invested will be £194,060. If the 3% annual growth that we target for investors is met, then after two years the investment should grow to over £205,000.

As the Octopus Inheritance Tax Service is an investment, unlike many other estate planning solutions, William still has access to it should his circumstances change. If he later decides to sell some of his shares, it will not affect the inheritance tax relief available on his remaining Octopus Inheritance Tax Service investment.

After the two-year period has passed, the investment is expected to qualify for BPR. Provided William still holds the investment when he dies, it can then be passed on to his children without any inheritance tax to pay.

In this scenario, William’s children save more than £84,000, which is the amount that would have been due in inheritance tax had William’s original share portfolio formed part of his estate. Without an inheritance tax bill to pay, William’s children can then decide whether they wish to keep hold of the investment, or they can ask us to sell the shares and return the proceeds.

William doesn’t want to leave behind a large inheritance tax bill for his children to deal with.

10 Inheritance tax

1Note: Capital gains tax may be payable if William’s portfolio has increased in value.

Octopus Inheritance Tax Service 11

By William investing £200,000 in the Octopus Inheritance Tax Service, his children could save more than £84,000 after just two years.

£123,108

£200,000 £200,000

N/A £194,060

-£86,861 N/A

N/A -£4,000

£217,153 £210,703

-£2,172 -£2,107

N/A -£1,940

-£5,012 -£4,863

£203,733

Gross investment

William keeps his share portfolio

William invests in the Octopus Inheritance Tax Service

Net investment subscribed for shares

Amount lost through 40% inheritance tax on death

2% initial charge

Value of investment after two years assuming growth of 4.2% each year

1% dealing fee

1% dealing fee (inclusive of any stamp duty payable)

Annual Management Charge accrued after 2 years (1%+VAT*)

Cash value to beneficiaries

*Please refer to pages 16 and 17 for further information regarding the Annual Management Charge (AMC).

Octopus targets a 3% a year return (after an annual management charge of up to 1%+VAT has been taken into account) on the amount invested net of initial charges and initial dealing fees. This equates to a 4.2% gross growth target. This diagram assumes that the target return is met (i.e. two years’ compound growth on £194,060, or £194,060 x 1.042 x 1.042). Our diagram also assumes that William’s share portfolio would have generated an equivalent return and has equivalent charges. In reality, a share portfolio may return more or less than what’s assumed here. The risk profile of the share portfolio is likely to be different to the risk profile of the Octopus Inheritance Tax Service. This table only shows an illustration and each investor’s own tax situation may be different. In addition, it assumes the current nil-rate band of £325,000 has been used against other assets. The target return is not guaranteed, capital is at risk and investor’s may get back less than the amount invested.

The example shows the impact of charges paid to Octopus but it does not include any charges paid to an adviser. Please refer to pages 22 and 23 for a full list of charges.

12 Inheritance tax

Our main aims are to achieve inheritance tax exemption for your investment and deliver sustainable growth over the long term.

Your money will be placed in a discretionary portfolio service run by Octopus. This means we use the money to invest in one or more in companies on your behalf. We select companies that we believe will grow at a steady rate, targeting sustainable growth over the long term. We continually monitor the progress of the companies we invest in with these aims in mind.

We invest in privately-held companies The companies we invest in are not listed on a stock exchange. These companies are managed on a day-to-day basis by Octopus. As the only shareholders in these companies are investors in the Octopus Inheritance Tax Service, we can run the companies in a way that is entirely aligned with the interests of those investors. We want you to be confident that your interests are always being looked after as they should be, so the majority of the board of directors of each company are independent of Octopus.

We target annual growth of 3%We target annual growth of 3% for investors (after our annual management charge) over the period you hold the investment. This target growth is based on the amount you invest, after deducting initial charges and the initial dealing fee on the investment. The performance of the Octopus Inheritance Tax Service depends on the growth in value of the company, or companies, we invest your money in.

Returns are not capped, although because we look to deliver sustainable growth in line with our target rather than deliver high returns, you should not expect a return significantly higher than 3% per year over the life of your investment.

Our interests are aligned with yoursWe defer our annual management charge until you or your family ask us to sell shares. We expect to be able to deliver growth of 3% on average each year over the lifetime of the investment, taking into account our annual management charge, and we will not take our full annual management charge if the target isn’t met. For more information on how the deferred annual management charge could act as a barrier against a fall in portfolio value, please see page 16.

Making the service as flexible as possibleWe invest in unlisted companies which have a smaller market for sales and purchases of their shares than companies listed on the main stock exchange. Therefore when we select companies to invest in, we look for shares that can be sold relatively easily when investors ask us to sell their investment. We organise share dealing every week for these companies. Of course, we also select companies that are expected to deliver the target level of growth.

Our investment strategy

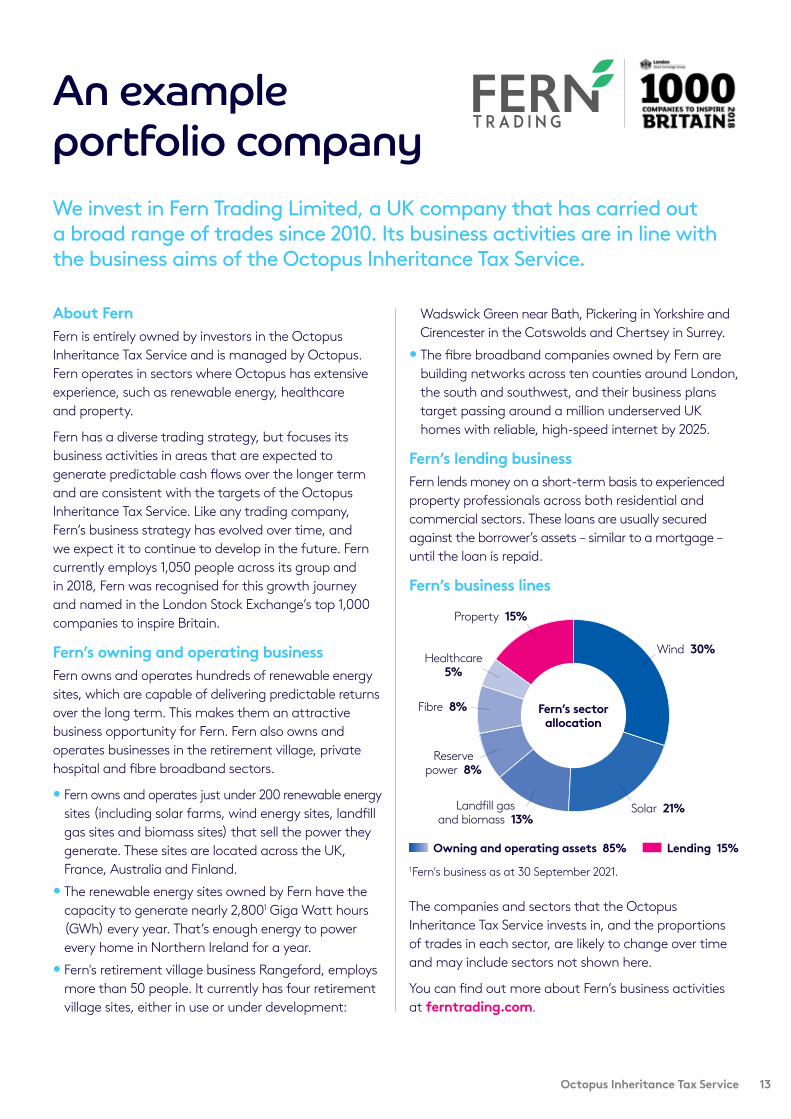

We invest in Fern Trading Limited, a UK company that has carried out a broad range of trades since 2010. Its business activities are in line with the business aims of the Octopus Inheritance Tax Service.

About FernFern is entirely owned by investors in the Octopus Inheritance Tax Service and is managed by Octopus. Fern operates in sectors where Octopus has extensive experience, such as renewable energy, healthcare and property.

Fern has a diverse trading strategy, but focuses its business activities in areas that are expected to generate predictable cash flows over the longer term and are consistent with the targets of the Octopus Inheritance Tax Service. Like any trading company, Fern’s business strategy has evolved over time, and we expect it to continue to develop in the future. Fern currently employs 1,050 people across its group and in 2018, Fern was recognised for this growth journey and named in the London Stock Exchange’s top 1,000 companies to inspire Britain.

Fern’s owning and operating businessFern owns and operates hundreds of renewable energy sites, which are capable of delivering predictable returns over the long term. This makes them an attractive business opportunity for Fern. Fern also owns and operates businesses in the retirement village, private hospital and fibre broadband sectors.

• Fern owns and operates just under 200 renewable energy sites (including solar farms, wind energy sites, landfill gas sites and biomass sites) that sell the power they generate. These sites are located across the UK, France, Australia and Finland.

• The renewable energy sites owned by Fern have the capacity to generate nearly 2,8001 Giga Watt hours (GWh) every year. That’s enough energy to power every home in Northern Ireland for a year.

• Fern's retirement village business Rangeford, employs more than 50 people. It currently has four retirement village sites, either in use or under development:

Wadswick Green near Bath, Pickering in Yorkshire and Cirencester in the Cotswolds and Chertsey in Surrey.

• The fibre broadband companies owned by Fern are building networks across ten counties around London, the south and southwest, and their business plans target passing around a million underserved UK homes with reliable, high-speed internet by 2025.

Fern’s lending businessFern lends money on a short-term basis to experienced property professionals across both residential and commercial sectors. These loans are usually secured against the borrower’s assets – similar to a mortgage – until the loan is repaid.

Fern’s business lines

Fern’s sectorallocation

Healthcare5%

Fibre 8%

Property 15%

Wind 30%

Solar 21%

Reservepower 8%

Landfill gasand biomass 13%

Owning and operating assets 85% Lending 15%1 Fern's business as at 30 September 2021.

The companies and sectors that the Octopus Inheritance Tax Service invests in, and the proportions of trades in each sector, are likely to change over time and may include sectors not shown here.

You can find out more about Fern’s business activities at ferntrading.com.

An example portfolio company

Octopus Inheritance Tax Service 13

Keeping investors happy is a big part of what we do.We try to make the information we give investors as clear and uncomplicated as possible. But if there’s anything our investors don’t understand, they know they can call us. We don’t offer financial advice, but we’ll do whatever we can to help.

14 Inheritance tax

We recommend investors take financial advice before making any investment decisions. Your financial adviser will be able to help you understand if this investment is right for you.

Making an initial applicationYou should complete the application form and send it back to us with your initial investment. The minimum initial investment is £25,000, and you can invest as much as you like.

Setting up your investmentWe place your money in our client bank account after receiving your application, before using it to make your investment. It usually takes no more than a week to purchase shares on your behalf.

Two years after this investment date, your investment should be free from inheritance tax, provided you still hold the shares at the time of your death.

Keeping you informedWe’ll send you valuation reports at quarterly intervals, so you can see the progress of your investment. You can also call our Investor Support team 0800 316 2295 or visit our online secure website at octopusinvestments.com at any time.

Getting started

Octopus Inheritance Tax Service 15

We understand that personal circumstances can change. That’s why the Octopus Inheritance Tax Service has been designed to be flexible enough to adapt to your needs.

You can add to your investment Each additional investment must be at least £10,000. Don’t forget, it will take two years for each separate investment to become eligible for relief from inheritance tax.

We will keep you informedWe’ll keep you updated on your investment with regular reports every quarter.

These will show any activity within the reporting period, along with information on the companies you hold investments in.

You can choose to sell shares We can arrange to sell some, or all, of your shares if you need to. We can usually sell shares within ten days and, since the Octopus Inheritance Tax Service was launched in 2007, share sales have never taken us more than a month. However, in certain circumstances it could take significantly longer. Please read the risks on page 22.• To make regular share sales: just tell us how much

you need, and how often you’d like us to sell shares on your behalf. You can choose from monthly, every three months, twice a year or once a year. You can sell any amount, and you can amend or cancel your instruction any time you like.

• To make a one-off share sale: you need to sell shares worth at least £5,000, and you must have at least £5,000 remaining in your investment.

Some important points on taxAs a reminder, selling shares will reduce the amount that you can expect to become inheritance tax-free. You should also remember that the proceeds of any sale will become part of your taxable estate again, unless you spend it before you die.

After selling shares, you may have to pay tax on any growth achieved on that portion of your investment. This growth will normally be taxed as a capital gain, but it may be subject to income tax if the companies you have invested in buy your shares back from you.

After you dieWe’ll give your loved ones as much help as we can. We have a dedicated Estates and Probate team who are on hand to help executors and beneficiaries with any information they might need. They can be contacted on 0800 294 6826.

Your executors will need to complete the form IHT 412 with details of your Octopus Inheritance Tax Service investment and send it to HMRC as part of the probate process. Executors then have three options:• They could ask us to sell the portfolio and pass the

money to your beneficiaries.• They could keep the portfolio invested for beneficiaries

(if it qualified for BPR on your death, then it will also be outside beneficiaries’ estates for inheritance tax).

• They could ask us to use the portfolio to pay any inheritance tax on your other assets, such as your home, directly to HMRC.

We understand how difficult this time can be, and even though we can’t give financial advice, our team of specialists can help answer any questions your beneficiaries may have.

After you’ve invested

16 Inheritance tax

Our Growth Shield works in your favour if your investment doesn’t meet its target return. However, it doesn’t guarantee the performance of your investment and you may not get back the amount you invested.

What is the Growth Shield?It’s the total annual management charge in your portfolio that builds up over time. It acts as a barrier against any potential fall in the value of your portfolio. Here’s how it works. We invest in companies that we expect to deliver growth in value of 4.2% on average each year. That’s the level of growth that would enable us to take our full annual management charge (1% + VAT) and still deliver the 3% annual target investment growth to you. We then calculate our annual management charge, but we don’t take it. Instead of it being paid to us annually, it remains within your investment portfolio. We only take our annual management charge when you or your beneficiaries ask us to sell shares.

Our aim is to achieve an annual target investment growth of 3% for investors (after our annual management charge) compounded over the time you’ve held the investment. The longer you are invested in the service, the bigger the available Growth Shield created by our annual management charge is likely to be. So, when you ask us to sell your shares, if we haven’t delivered the expected growth in portfolio value, the annual management charge we take will be reduced or eliminated.

When would it be called upon?If your portfolio drops in value, the Growth Shield will absorb this reduction in value first, before the value of your investment falls. If the investment hasn’t achieved the 3% annual target return for investors over its lifetime, when it’s sold, our annual management charge will be reduced to help make up the shortfall. However, if your portfolio fell in value by more than the value of the accrued annual management charge, the Growth Shield would be used up and the value of the investment to you would reduce.

Does this mean returns are capped? We don’t cap investment returns. But because the service targets steady growth, we don’t make investments that are likely to deliver a higher return. This means you should not expect returns significantly higher than 3% on average.

The Growth Shield: putting your returns first

Three things to remember about the Growth ShieldWe only take our annual management charge when you or your beneficiaries ask us to sell shares.

The longer you or your beneficiaries hold the investment, the bigger the Growth Shield is likely to become. We’ll show the value of the Growth Shield every time we send out a valuation.

The Growth Shield is intended to reduce the impact of short-term volatility on your investment, but it doesn’t mean your investment is protected from losses. If the value of your investment falls by more than the value of the Growth Shield, the amount you get back when you sell your shares will be reduced.

1

2

3

Octopus Inheritance Tax Service 17

What if the target growth is achieved?Let’s use Year 6 as an example. If William’s portfolio has grown by 4.2% annually over the holding period, then by the end of Year 6 its value will be £248,394. The Growth Shield value is £15,875, which is the total amount of annual management charges not yet taken. William sees these amounts on his portfolio statements. At the end of Year 6, William asks us to sell his investment. Provided the target 4.2% growth has been achieved, the Growth Shield isn’t needed to cover an investment shortfall. Therefore, Octopus collects its accrued annual management charge in full and William receives £231,718 (less a 1% dealing fee).

What if the target return is not achieved?Alternatively, let’s imagine that at the end of Year 6, William’s portfolio falls in value by £15,000 (around 6%). Because the target 4.2% growth has not been met, the total annual management charge we collect when William asks us to sell shares will be reduced. As a result, the investment will still deliver a 3% return per year on average for William, and he will still receive back £231,718 (less the 1% dealing fee). The annual management charge that we collect is reduced by £15,000.

Remember: If the value of the investment falls by more than the value of the Growth Shield, the amount you get back when you sell your shares will be reduced.

An illustration of how the Growth Shield works, using William’s example portfolio.

The companies we invest in on William’s behalf are expected to grow in value by an average of 4.2% each year. This would deliver the target return of 3% each year after our annual management charge.

Value of portfolio at 3% return

Total portfolio value at target growth (4.2%)

Maximum Growth Shield

Day 1 1 £194,060 £194,060 -

Year 2 £205,878 £210,703 £4,863

Year 4 £218,416 £228,774 £10,143

Year 6 £231,718 £248,394 £15,875

Year 8 £245,829 £269,698 £22,099

Year 10 £260,800 £292,828 £28,857

£100,000

80,000

60,000

40,000

20,000

0Day 1 Year 2 Year 4 Year 6 Year 8 Year 10

£28,857

£66,740Growth in value ofWilliam’s investment

GrowthShield

Illustration: increase in value of William’s investment portfolio at 4.2% annual growth

1Note: Investment amount after the initial charge and dealing charge.

18 Inheritance tax

Responsible investing at Octopus

Firstly, what is the difference between responsible investing and Environmental, Social, and Governance (ESG) integration?Although the two terms are often used interchangeably, there is an important distinction to be made.

ESG integration should be seen as an input into an investment process. It is when fund managers incorporate ESG information into investment decisions to minimise risk and make the most of opportunities. Better returns are expected in the long term from ESG integration because fund managers have an enhanced understanding of whether an investment is exposed to certain threats or opportunities.

Responsible investment, on the other hand, is where managers are actively and intentionally seeking to create a better output for society and the environment. It can be viewed as an umbrella term to describe funds or strategies using investment as a force for positive change, from which stems a spectrum of differing approaches. These range from those that exclude certain sectors or companies, to those that explicitly aim to deliver a positive and measurable impact to the people and the planet.

What does responsible investing mean at Octopus?Increasingly, people want to work for, buy from and invest with companies which understand what it means to make the world a better place. These companies understand that how they behave is just as important as what they do, and ultimately we believe they will generate the best financial returns for investors over the coming decades.

To create value for our investors, we consider environmental, social and governance factors when making investment decisions. We are a specialist asset manager, focused in specific sectors where we have significant and often market-leading investment credentials. Since setting up Octopus in 2000, we’ve invested more than £6.8 billion into building a sustainable planet, empowering people and revitalising healthcare. We believe that business can be, and should be, used

as a force for good. Fundamentally, we want the world to be a better place because of where and how we invest our clients’ money.

As one of only a handful of investment companies in the world to be an accredited B Corporation, we are very proud of the impact that Octopus, and the investments we manage, have on the planet.

How do we make sure that responsibility sits at the heart of everything we do?

Certified B CorporationWe are an accredited B Corporation. These are businesses that meet the highest standards of verified social and environmental performance, public transparency, and legal accountability to balance profit with their impact on the world. Octopus undergoes a B Corp assessment every two years.

UN PRI signatoryWe are a UN PRI signatory, supporting the incorporation of ESG factors in our decision making. We are subject to an annual Principles of Responsible Investing (PRI) assessment.

Responsible Investment CommitteeEach investment team at Octopus reports to our Responsible Investment Committee each quarter on ESG integration, key ESG metrics and performance. The committee is made up of our founders, Chief Investment Officer and Heads of Business.

Octopus Inheritance Tax Service 19

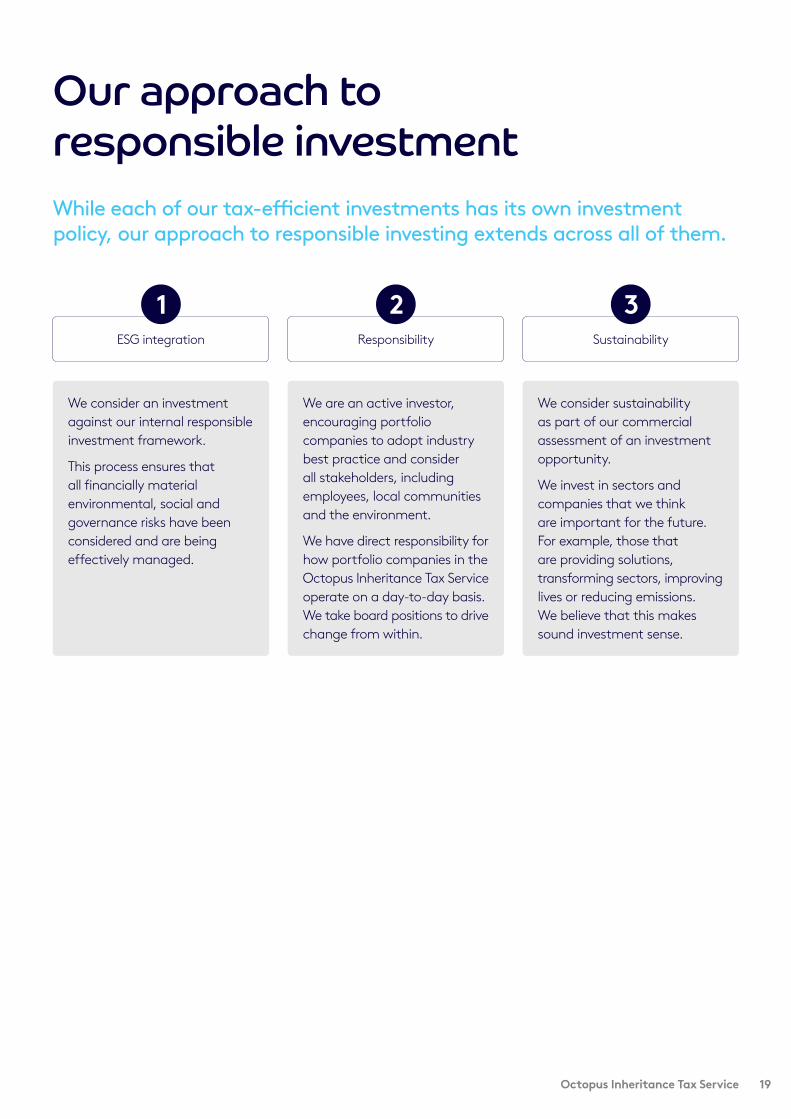

While each of our tax-efficient investments has its own investment policy, our approach to responsible investing extends across all of them.

ESG integration Responsibility Sustainability

We consider an investment against our internal responsible investment framework.

This process ensures that all financially material environmental, social and governance risks have been considered and are being effectively managed.

We are an active investor, encouraging portfolio companies to adopt industry best practice and consider all stakeholders, including employees, local communities and the environment.

We have direct responsibility for how portfolio companies in the Octopus Inheritance Tax Service operate on a day-to-day basis. We take board positions to drive change from within.

We consider sustainability as part of our commercial assessment of an investment opportunity.

We invest in sectors and companies that we think are important for the future. For example, those that are providing solutions, transforming sectors, improving lives or reducing emissions. We believe that this makes sound investment sense.

1 2 3

Our approach to responsible investment

20 Inheritance tax

Octopus Inheritance Tax Service 21

Environmental, Social and Governance integration

Fern Trading Ltd ('Fern'), a portfolio company in the Octopus Inheritance Tax Service, is fully owned by the investors in the Service and is run on a day-to-day basis by Octopus. Established in 2007, Fern is the parent of more than 300 subsidiary companies, between them employing more than 1,000 people and providing many more jobs through the contracts they place.

The Octopus Inheritance Tax Service targets sustainable growth for investors, so it’s no coincidence that it includes assets that are reducing emissions and improving healthcare options. We believe these sectors make sound investment sense.

ESG integrationESG issues are considered within the investment process to mitigate risk and improve the risk return of investments. This approach utilises the Sustainability Accounting Standards Board (SASB) Materiality Map, which helps the investment team identify and mitigate material risk exposure.

As part of the due diligence process for all new acquisitions, we require an ESG questionnaire to be completed for consideration against our ESG criteria for the Service. This process plays a key role in the Investment Committee decision and the framework is paramount in identifying potential ESG risk.

Prospective companies are scored by three key themes against the SASB Materiality Map. Planet evaluates environmental impact, such as energy management. People looks at social impacts such as employee health and safety. Performance covers leadership and governance. Each theme is given a score between 1 and 5. 1 is the lowest, indicating ‘lasting damage’ and 5 the highest, denoting ‘contributes to solutions’.

ResponsibilityWe have direct responsibility for how each portfolio company operates on a day-to-day basis. We drive each company to adopt industry best practice, considering all stakeholders including employees, local communities and the environment.

When a portfolio company acquires a new business, one or more Octopus employees are appointed as non-executive directors on the Board of the company, alongside the management team. This enables Octopus to bring extra rigour to the oversight and management of the business’s practices.

SustainabilityFern is the largest owner and operator of solar energy sites outside of the major energy suppliers in the UK, generating more than 2,300 gigawatt hours a year. The renewable energy Fern generates avoids the production of carbon dioxide that would have the same effect on the atmosphere as planting 3.3 million trees or removing 249,000 cars from the road for a year.

Fern operates a healthcare division, which is paving the way for better retirement choices. It is looking to improve the options for people in later life by building and running three state-of-the-art retirement villages. These allow older people to live in surroundings that suit their needs, for the rest of their life. Fern’s two operational villages are providing accommodation for over 300 residents, and there are a further two villages of a similar size under construction.

Fern’s fibre broadband division is on a mission to provide much-needed internet access and connectivity. It is building and operating fibre networks in some of the most underserved towns and regions in the country. The fibre division is targeting network build across ten counties around London, the South and Southwest, and is targeting a total of 1 million connected properties by 2025. To date, Fern has deployed more than £150 million in developing its networks, providing ultra-fast fibre broadband to customers.

How the Octopus Inheritance Tax Service is managed responsibly

22 Inheritance tax

We want you to feel completely comfortable with how this investment works. Please take time to understand the key risks associated on these pages and discuss them with your financial adviser and loved ones.

You may lose moneyThe Octopus Inheritance Tax Service is a discretionary portfolio service. It invests in unquoted companies that are not listed on a stock exchange. The value of such companies can fall or rise more sharply than shares in larger, listed companies. The shares of unquoted companies can also be more difficult to sell. As with all investments, your shares could fall in value. Also, when it’s time to sell you may not get back the full amount invested.

Target returns are not guaranteedThe target returns of the Octopus Inheritance Tax Service are not guaranteed and you should not consider the past performance of the investment to be a reliable indicator of future results. The performance of the Octopus Inheritance Tax Service is based on the value of the underlying portfolio companies.

Tax rules can changeRates of tax, tax benefits and tax allowances are based on current legislation, interpretation based on case law, and HMRC practice. We can’t guarantee that tax rules won’t change in the future. The value of tax reliefs depend on your own personal circumstances.

Requests to sell shares could take longer than anticipatedSelling shares in the Octopus Inheritance Tax Service is normally achieved by selling the shares you own to other investors, and there is no guarantee that a buyer will be found. If there are unusually large withdrawals, the companies you have invested in may need to carry out a share buyback, a process that could take approximately three months.

In exceptional circumstances (such as a change in tax rules) where the companies do not have sufficient available funds to carry out a share buyback, the process could take much longer, as we would need to sell the assets owned by the portfolio companies in order to return the proceeds of the share sale to you. You should not invest in the Octopus Inheritance Tax Service unless you understand and accept that – in exceptional circumstances – it could take a year or more to access your investment following a withdrawal request.

Your investment may be in only one companyThe Octopus Inheritance Tax Service will only invest in one or a small number of companies conducting trades in one or more sectors. Your investment could have less diversification when compared with a portfolio of investments spread across many different sectors.

Portfolio companies may use different sources of financeInvestors in the Octopus Inheritance Tax Service are the only shareholders of the companies into which the service invests. Like any company, in order to deliver 3% growth per annum to investors, the portfolio companies need to make higher returns to cover their running costs. In order to achieve these returns, and to undertake a wider range of activities, these companies may borrow funds from external lenders, such as banks, to fund part of their trades. However, this activity could increase the risk of your investment falling in value if interest repayments cannot be met by the portfolio companies.

Understanding the key risks

Octopus Inheritance Tax Service 23

BPR is assessed on a case-by-case basisWe cannot guarantee that the investments we make on your behalf will qualify for BPR in every case in the future. HMRC will only conduct a BPR assessment after the death of an investor, to confirm whether the companies invested in qualify for BPR at that time. If you borrow money to invest in the Octopus Inheritance Tax Service, your investment is unlikely to qualify for relief from inheritance tax.

Investment horizonThe Octopus Inheritance Tax Service is not intended to be a short-term investment, and the typical holding period for our investors is more than five years. It will normally take two years for an investment to qualify for BPR. This two-year period will begin once your money is invested in companies within the service. You need to continue holding the investment until you die if you would like your estate to benefit from inheritance tax relief.

It is important to keep your will up to date This is particularly relevant after you’ve made significant changes to your estate, for example after choosing to invest in the Octopus Inheritance Tax Service. Investors should seek specialist advice to make sure their will is drafted to ensure their estate benefits from available inheritance reliefs, such as the nil-rate band, exempt gifts and BPR. For example, where an individual intends to leave exempt gifts in their will, it can be beneficial to bequeath BPR-qualifying investments as a specific gift, rather than as part of the residue of their estate.

Financial Services Compensation SchemeOctopus is part of the Financial Services Compensation Scheme (FSCS). The FSCS is the compensation fund of last resort for customers of financial services organisations. If an organisation goes out of business, investors can make a claim to the FSCS for any losses resulting from the organisation’s bad investment advice, negligence or mis-selling. It is important to understand that the FSCS does not protect against, or compensate for, losses from poor performance, such as when shares in a company have reduced in value.

24 Inheritance tax

Conflicts could arise between our interests and yours, so it’s important that you understand what these conflicts are, and why they exist.

The Octopus Inheritance Tax Service invests in companies that are run by Octopus. While this can be beneficial (as we explain below), it can also potentially create conflicts between the interests of Octopus and those of investors in the service. This section explains the types of conflicts that can arise, as well as the controls we have put in place to prevent or manage these conflicts appropriately.

Portfolio companies outsource many of their day-to-day operations to OctopusWhile the portfolio companies we invest in may have employees or consultants who they pay directly to run their day-to-day operations, they have few employees at a senior or managerial level. Therefore, their managerial activities are outsourced to Octopus, which charges a fee for the services provided. Where managerial staff are employed by Fern, their salaries are recharged to Octopus as part of the service fee.

Fees for the current year have been set at 2.5% (+ VAT) of the value of each company. All fees are agreed with the portfolio companies’ independent directors, who are responsible for safeguarding the interests of shareholders (Octopus Inheritance Tax Service investors). The independent directors must agree the fees are good value for the services provided. Sometimes, when a management team is employed directly by a company Fern owns, they may have a small amount of equity in that company.

Why is this beneficial?Having a greater level of control over how the portfolio companies operate helps to ensure the needs of investors in the Octopus Inheritance Tax Service are met. By operating these companies, we can make sure they:• Target sustainable growth over the long term.• Trade in ways that should qualify for BPR.• Maintain an appropriate level of liquidity.

Portfolio companies may trade with other companies owned or managed by OctopusIf Octopus has an interest in a company that a portfolio company engages with, Octopus may partially benefit from the trade. For example, Octopus may benefit in the following ways: • Octopus could be entitled to a share of profits if a

portfolio company provides finance to a company that Octopus owns an equity stake in, and that company could become more profitable as a result.

• Octopus could be paid management fees by other companies that a portfolio company lends money to. These fees would be paid in the ordinary course of Octopus managing them.

• Octopus may already manage or partially own a company that a portfolio company buys shares in, or purchases assets from.

Why is this beneficial? Taking stakes in businesses allows us to undertake extensive research and gives portfolio companies confidence that they can continue to access quality trading opportunities as they grow. Where Octopus supports another business, it sometimes gets a seat on the board of directors. This can give Octopus more oversight, helping to ensure that the companies operate in ways that help meet the aims of the Octopus Inheritance Tax Service.

Conflicts of interest

Octopus Inheritance Tax Service 25

Managing conflicts of interest

We endeavour to make sure that the interests of our customers are always looked after. So we have a number of controls in place to prevent or manage conflicts of interest.

An appropriate governance structure and committee processOur Investment Committee reviews any new investment opportunities. It’s their job to make sure every investment made on behalf of investors in the Octopus Inheritance Tax Service is in their best interests. Proposals likely to raise a conflict of interest are reviewed by a Conflicts Committee. This committee is independent of the Investment Committee and decides whether, given the risk of conflict, the investment proposal is being handled in an appropriate way.

Keeping relationships at ‘arm’s length’Whenever we’ve identified a potential conflict of interest between businesses managed, owned or controlled by Octopus, we use external benchmarks where available. These benchmarks are taken from similar transactions taking place elsewhere in the wider market and are used to make sure that the terms and prices for each transaction are set independently. We may also use third parties for independent advice.

Independent directorsAs with any company, the board of directors of a company we invest in has ultimate responsibility for ensuring it is managed in the best interests of its shareholders, who are all investors in the Octopus Inheritance Tax Service. These board members are all experienced business professionals and the majority are independent of Octopus.

For more information please refer to our Conflicts of Interest policy, which is available on our website octopusinvestments.com.

Fair and accurate valuationsOctopus calculates the share prices of portfolio companies according to industry standard guidelines. These valuations are part of the services Octopus provides to the companies. Share prices are then approved by the directors, who must confirm that they represent fair value for the companies’ shares. Share prices are updated monthly.

“ We want investors to feel reassured that we prevent or manage potential conflicts in the correct way.”People need to feel comfortable about what they are investing in, and understand how their money is being invested. We want our investors to be clear about what conflicts of interest could arise and reassure them that, where we cannot prevent them, we have controls in place to manage these conflicts appropriately. Conflicts of interest are not a problem in themselves, but they do need to be managed carefully. Each potential conflict is treated on its own merits, but one thing is absolutely clear – we’ll look after your interests and treat you fairly every time.

John Averill Head of Risk and Compliance

26 Inheritance tax

A few points to keep in mind Our target annual return of 3% (after annual management charge) is based on the amount you invest, after deducting the initial charges and the initial 1% dealing fee on investment. We also charge a dealing fee of 1% that applies when you instruct us to sell shares.

When do we take our annual management charges? Our annual management charges will accrue on your invested portfolio on a daily basis. However, they will only be taken when you sell shares. And, most importantly, we’ll only deduct the charges from any growth of your portfolio above 3% a year, calculated over the period you’ve held your investment. So, unless the companies we invest in grow by more than 3% a year (on average) over the period you have held them, we won’t take any of our accrued annual management charge. You can see a worked example on page 10.

Transferring your investment into trustIf you decide to transfer your investment into a trust, we will start collecting our annual management charge each year (in other words, it will no longer be deferred). We will also pay any adviser charges or intermediary commissions on an annual basis. If this is something you’re interested in, please give us a call and we can assist you.

Paying adviser or intermediary charges If you agree to pay an ongoing charge to your financial adviser, or an ongoing commission to your intermediary, we will facilitate this payment for you by selling a proportion of the shares you hold in the Octopus Inheritance Tax Service. Please note, that this will reduce your overall return. We will pay adviser charges on a monthly basis and intermediary commissions twice a year (January and July). If you decide to transfer your investment into a trust both adviser charges and intermediary commissions will switch to be paid annually.

Company running costsThe companies we invest in will pay Octopus to manage their business operations. The level of these fees is agreed for each company by their independent boards of directors. For the current year, these fees have been set at 2.5% (+ VAT) of the value of each company. We describe these costs in further detail in the ‘Conflicts of interest’ section on page 24. Our 3% annual target return for investors is calculated after these fees have been taken into account.

If you are investing through an adviser

Octopus initial charge: 2%

Initial charge to your adviser: Agreed with your adviser

Annual management charge: Up to 1%+ VAT per annum

Ongoing fee to your adviser: Agreed with your adviser

Dealing fee (for investments and withdrawals): 1%

If you are investing through an intermediary who doesn’t give you advice (execution-only)

Octopus initial charge (with up to 1% payable to your intermediary): 3.5%

Annual management charge: Up to 1%+ VAT

Dealing fee (for investments and withdrawals): 1%

Annual fee paid to your intermediary: 0.5% paid by you

We encourage our investors to seek financial advice when making investment decisions. We therefore charge investors who have not taken advice a higher initial fee.

If you are investing through an intermediary, you’ll need to complete a suitability form. This can be found at octopusinvestments.com.

The charges

Giving us feedbackOutstanding customer service is at the heart of everything we do. But that doesn’t mean we get it right every time. If you’re not happy with the service we give you, we’ll listen to your complaint and confirm it in writing, as well as outlining how we plan to resolve it.

Our complaints procedures follow the rules set out by the Financial Conduct Authority, responsible for regulating investment companies like Octopus, and the Financial Ombudsman Service, which has been set up to resolve disputes between consumers and companies.

If you want to make a complaint, email [email protected], call 0800 316 2295 or write to us at: Octopus Investments Limited, 33 Holborn, London EC1N 2HT.

Octopus Inheritance Tax Service 27

How to invest

Talk to a financial adviser in the first instance We recommend you take financial advice prior to deciding to invest. A financial adviser will be able to help you decide whether this investment is suitable for you, and they can also help you to complete your application. If your adviser has any questions, they can call us on 0800 316 2067 or visit octopusinvestments.com.

If you are investing via an intermediaryWe recommend that you speak to the intermediary in the first instance. If you like, you can call our Investor Support team on 0800 316 2295. Please remember that we can’t offer investment or tax advice, but we’ll be happy to talk you through the application process and help you with anything else we can.

Octopus Investments 33 Holborn London EC1N 2HT

0800 316 2295 [email protected] octopusinvestments.com