Embed Size (px)

Citation preview

Multiple-criteria decision-aiding framework to analyzeand assess the governance of sustainability

Myriam Merad • Nicolas Dechy • Frederic Marcel •

Igor Linkov

Published online: 22 May 2013

� Springer Science+Business Media New York 2013

Abstract Past and present disasters and scandals, such as

the BP Deepwater Horizon oil disaster in the Gulf of Mexico

in 2010, the Servier Mediator (Benfluorex) scandal in 2009

and the Enron collapse in 2001, have uncovered weaknesses

in governance issues. The authors argue that there is a need to

develop methods and tools to diagnose and assess the gov-

ernance of organizations with respect to Sustainable

Development (SD). However, this task remains difficult due

to the fact that it is difficult to appraise the quality of gov-

ernance. The authors propose a protocol to diagnose and

analyze the governance of SD and explore the use of multi-

ple-criteria decision-aiding methods to achieve this task.

Two aggregation methods to assess the global governance

are proposed: (1) The identification of a final governance

index for an Organization. This method helps in establishing

a global diagnosis of the quality of the governance of an

Organization with respect to SD challenges. The governance

index is based on the calculation of three indexes: the partial

opportunity index, the partial risk index and the partial

equilibrium index. (2) The ranking of a set of Organizations

according to their governance of SD. This method aims at

assessing a set of Organizations based on a pairwise com-

parison according to a set of criteria that represents the seven

domains of the ISO 26000 norm (ISO 26000—Guidance on

social responsibility, 2010). This method is based on the

outranking aggregation approach ELECTRE III. A practical

example is used to illustrate two methods of governance

assessment.

Keywords Governance � Corporate Social Responsibility �Sustainable Development � Indicators � Aggregation

procedures

1 Introduction

Sustainable Development (SD) is a key issue for both

private and public sector organizations. Corporate Social

Responsibility (CSR) is one way for organizations to

achieve Sustainable Development; CSR has received

attention recently after environmental, health and financial

scandals and disasters such as the Deepwater Horizon oil

disaster in the Gulf of Mexico in 2010, Servier Mediator

(Benfluorex) scandal in 2009 and Enron affair and collapse

in 2001. Indeed, weaknesses in governance issues seem to

be the core problem. The lack of investments in safety and

lack of risk prevention culture within British Petroleum

(BP), deficiencies in Enron’s Risk assessment and Control

department, ethical transgression of the external auditor

(Arthur Anderson) of Enron and of the French Medicine

Agency AFSSAPS in the case of French ‘‘Mediator scan-

dal,’’ and deficiencies in the organization of the Board of

Directors of Enron and BP are examples of these issues

(Vincent et al. 2011; Benston 2006; Goodman et al. 2011;

Grappi et al. 2013; Chevis and Stuebs 2012). It is possible

to continue to enumerate the examples, but the list of

weaknesses in governance is too significant.

Scholarly advisement (Abdel-khalik 2002; Jones 2003;

Bhimani and Soonawalla 2005; Brown and Caylor 2006;

Brown and Lee 2010; Balmer et al. 2011) has contributed

M. Merad (&) � F. Marcel

INERIS, Parc technologique ALATA, BP 2,

60550 Verneuil en Halatte, France

e-mail: [email protected]

N. Dechy

IRSN, BP 17, 92262 Fontenay-aux-Roses Cedex, France

I. Linkov

Risk and Decision Science Focus Area Lead, US Army Engineer

Research and Development Center, Concord, MA, USA

123

Environ Syst Decis (2013) 33:305–321

DOI 10.1007/s10669-013-9447-4

to delimit, according to theory and/or based on experience,

what is understood by the governance of organization with

respect to SD. Merad and Marcel (2012a) have suggested

that looking at the governance of an organization in the

perspective of reaching SD consists of considering the

system by which decisions are taken and applied to reach

the objectives of SD. It is indeed necessary to identify the

values advocated by the organization and how they are

concretely and operationally applied; to focus the attention

on the decisional process that is used to reach SD (e.g.,

autocratic, participative, deliberative) considering the

actors’ and stakeholders’ needs and constraints; and to

consider the way the organization fixes its progress and

innovation perspectives and reduce risks. According to

these contributions, it is possible to determine a set of

aspects that can help the characterization of weaknesses in

organizational governance. Theses aspects are related to

functions and domains of the organization. The function of

the Board of Directors, the organization’s project imple-

mentation, the risk management and risk management

policies, relationships with stakeholders and the reporting

of CSR and SD all fall under the category of functions.

Ethical and deontological principles, such as the account-

ability and transparency of the organization; respect for

stakeholders’ interests and respect for the rule of law,

international norms and human rights, fall under the cate-

gory of domains.

For marketing, many organizations claim to have an

ethical identity and good governance (Balmer et al.

2011). It is difficult to define what is ‘‘good governance’’

due to the fact that the governance of sustainability is

‘‘context-specific’’ and ‘‘values-infused.’’ However, it is

possible to provide elements of information of what

is context-adapted sustainability governance. There is also

a need for methods and tools to diagnose, analyze, assess

and rate governance. Due to the fact that it is hard to

make the distinction between green-washing and facts as

well as to fix an absolute and definitive judgment about

the quality of the governance, the authors have proposed a

set of governance indicators that can help establish a

framework for diagnosing the state of an organization’s

governance system. (Merad and Marcel 2012a). The

authors have considered that organizations have different

juridical structures, missions and objectives and cultures.

Indeed, the qualitative value of SD governance depends

on the respect of a set of seven basic values and princi-

ples that are proposed and summarized in the ISO 26000

norm (ISO 2010) on Corporate Social Responsibility. It is

necessary and crucial to involve different stakeholders

and actors in the process of fixing and defining a common

and shared vision of what is the qualitative value of

governance. This last point should be done in a partici-

pative and/or deliberative process.

This last decade brought an increased interest in assessing

governance (see for example Brown and Caylor 2006; Fryd-

man et al. 2007; GRI 2006; OCDE 2004; UNECE/OECD/

Eurostat Working Group on Statistics for Sustainable Devel-

opment 2008; ISIS 2009a, b). These initiatives show a large

diversity in scoring and aggregating information on gover-

nance. Merad and Marcel (2012a) have suggested that the

issues surrounding the assessment of sustainable organiza-

tional governance have lead to the need for discussing the

direct and indirect effects of assessments. In fact, it is almost

clear that this assessment process of SD governance can and

will be used in different ways and for different perspectives:

• Establish a diagnosis of how organizations have

adapted their governance to take up the SD challenges.

This is done in general for the internal use of the

organization and to inform the General Director, the

Board of Directors and other internal staff, by listing

the strengths and weaknesses in terms of self-adapta-

tion to SD challenges in the perspective of a continuous

evolution (Deming wheel).

• Report progress and exemplary actions (for transparency

and accountability reasons) taken in governance prac-

tices to take up the SD challenges (Green or Corporate

social Responsibility governance reporting). This report-

ing can be added to the one done, in the French public

organizations, to the central authorities (e.g., Ministries)

and/or for both private and public sector organizations to

different stakeholders (e.g., non-governmental organi-

zations—NGO, citizens).

If this reporting is integrated/aggregated to assess the

general governance of the organization facing SD

challenges, it can be used by external stakeholders to:

(1) assess the risks and the opportunities and/or (2) assess

performance. This is generally done by including or

expelling the more viable, sustainable, less risky or the

more exemplary organizations in one domain of activity.

The assessment of organizational governance consider-

ing SD challenges can be done, methodologically speaking,

in five different ways depending on the final user of the

assessment initiative Merad and Marcel (2012a):

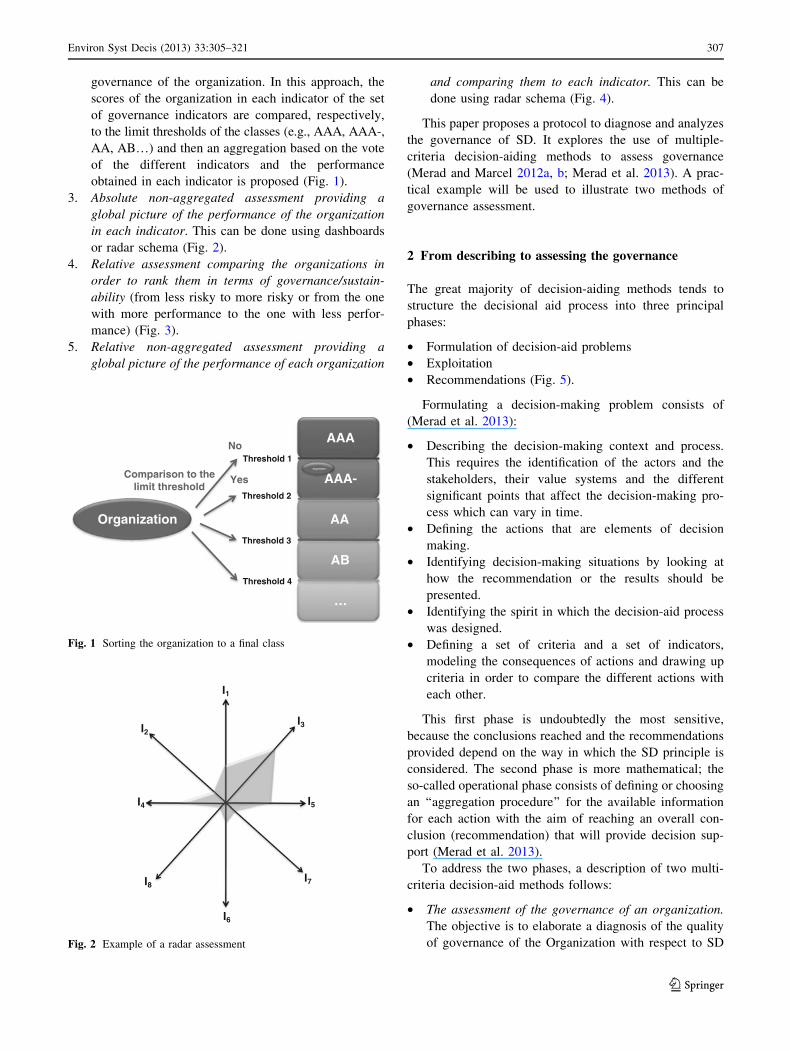

1. Absolute assessment that consists of giving a finale

score (e.g., a value between 1 and 10) to the

governance of the organization. In this approach, the

scores, of the organization in each indicator of the set

of governance indicators, are aggregated into one

single final score.

Final scoreSustainable governance

¼ Aggregation Function Score on Indicatorið Þ

2. Absolute assessment that consists of giving a final

classification (e.g., AAA, AAA-, AA, AB…) to the

306 Environ Syst Decis (2013) 33:305–321

123

governance of the organization. In this approach, the

scores of the organization in each indicator of the set

of governance indicators are compared, respectively,

to the limit thresholds of the classes (e.g., AAA, AAA-,

AA, AB…) and then an aggregation based on the vote

of the different indicators and the performance

obtained in each indicator is proposed (Fig. 1).

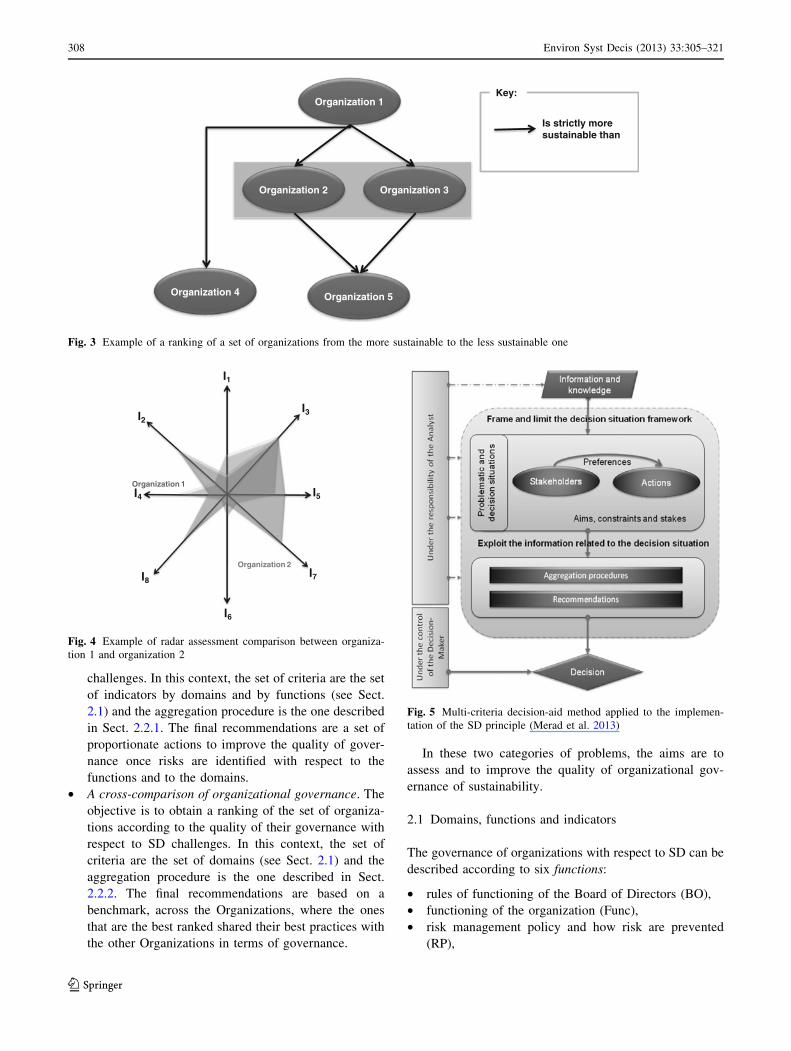

3. Absolute non-aggregated assessment providing a

global picture of the performance of the organization

in each indicator. This can be done using dashboards

or radar schema (Fig. 2).

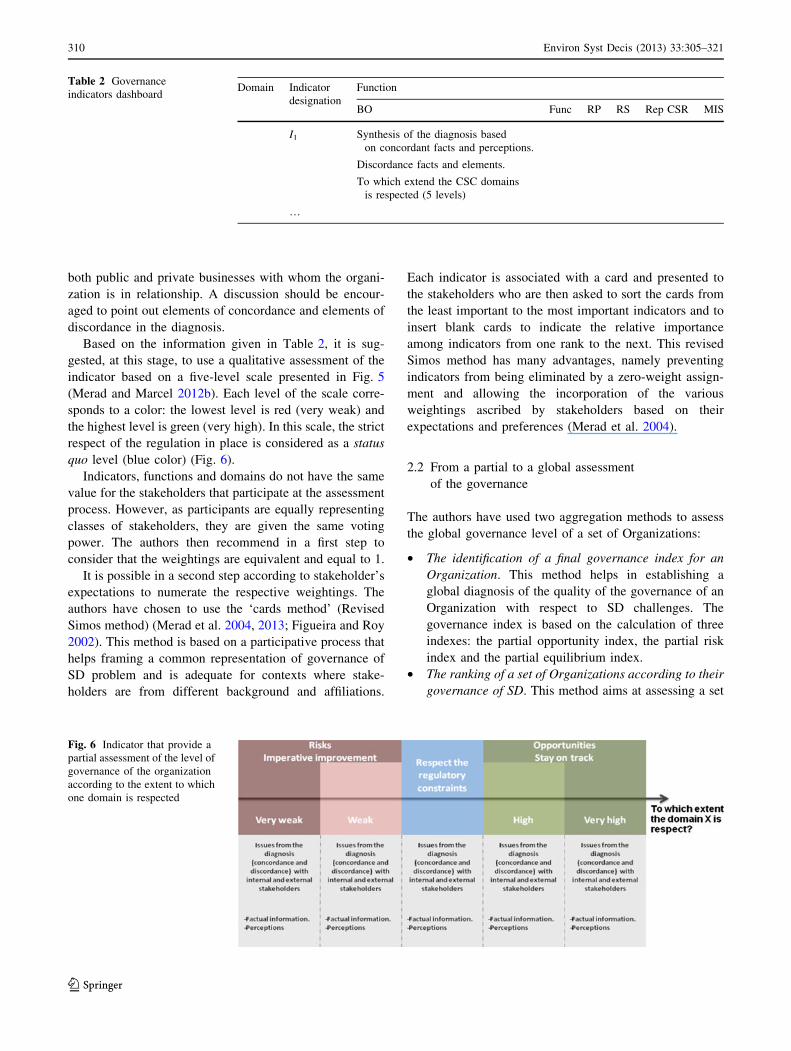

4. Relative assessment comparing the organizations in

order to rank them in terms of governance/sustain-

ability (from less risky to more risky or from the one

with more performance to the one with less perfor-

mance) (Fig. 3).

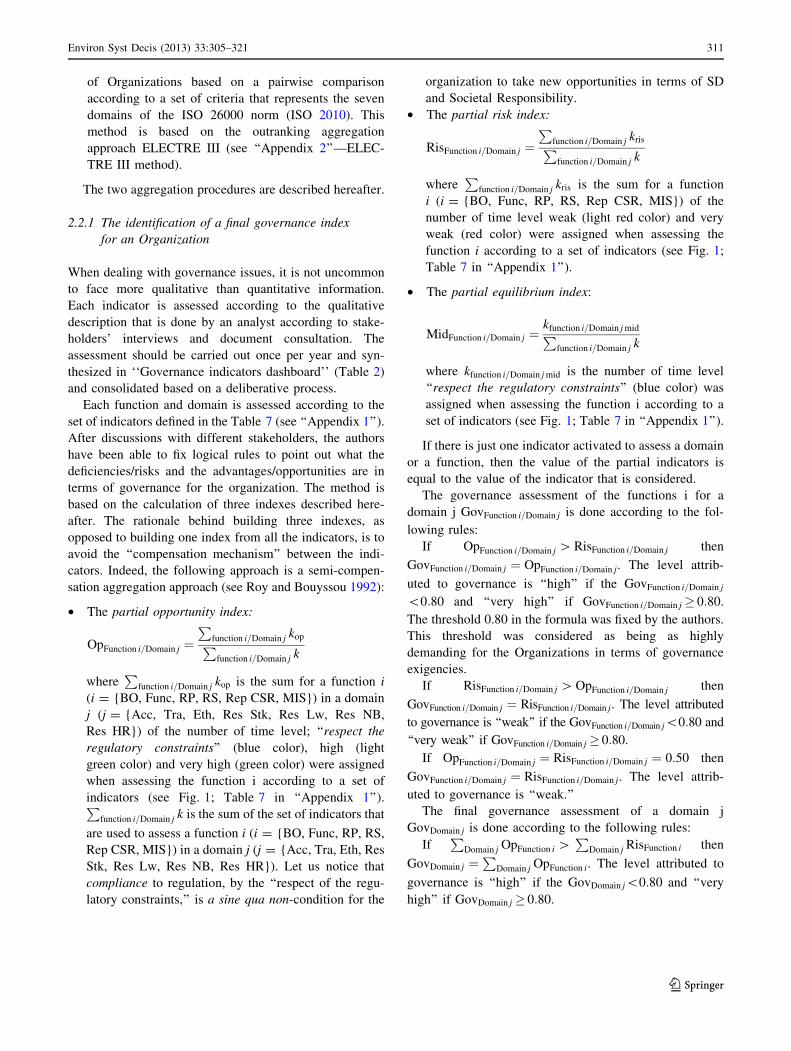

5. Relative non-aggregated assessment providing a

global picture of the performance of each organization

and comparing them to each indicator. This can be

done using radar schema (Fig. 4).

This paper proposes a protocol to diagnose and analyzes

the governance of SD. It explores the use of multiple-

criteria decision-aiding methods to assess governance

(Merad and Marcel 2012a, b; Merad et al. 2013). A prac-

tical example will be used to illustrate two methods of

governance assessment.

2 From describing to assessing the governance

The great majority of decision-aiding methods tends to

structure the decisional aid process into three principal

phases:

• Formulation of decision-aid problems

• Exploitation

• Recommendations (Fig. 5).

Formulating a decision-making problem consists of

(Merad et al. 2013):

• Describing the decision-making context and process.

This requires the identification of the actors and the

stakeholders, their value systems and the different

significant points that affect the decision-making pro-

cess which can vary in time.

• Defining the actions that are elements of decision

making.

• Identifying decision-making situations by looking at

how the recommendation or the results should be

presented.

• Identifying the spirit in which the decision-aid process

was designed.

• Defining a set of criteria and a set of indicators,

modeling the consequences of actions and drawing up

criteria in order to compare the different actions with

each other.

This first phase is undoubtedly the most sensitive,

because the conclusions reached and the recommendations

provided depend on the way in which the SD principle is

considered. The second phase is more mathematical; the

so-called operational phase consists of defining or choosing

an ‘‘aggregation procedure’’ for the available information

for each action with the aim of reaching an overall con-

clusion (recommendation) that will provide decision sup-

port (Merad et al. 2013).

To address the two phases, a description of two multi-

criteria decision-aid methods follows:

• The assessment of the governance of an organization.

The objective is to elaborate a diagnosis of the quality

of governance of the Organization with respect to SD

AAA

AAA-

AA

AB

…

Threshold 1

Threshold 2

Threshold 3

Threshold 4

Organization

Comparison to the limit threshold

No

Yes Organization

Fig. 1 Sorting the organization to a final class

I1

I2I3

I4 I5

I6

I7I8

Fig. 2 Example of a radar assessment

Environ Syst Decis (2013) 33:305–321 307

123

challenges. In this context, the set of criteria are the set

of indicators by domains and by functions (see Sect.

2.1) and the aggregation procedure is the one described

in Sect. 2.2.1. The final recommendations are a set of

proportionate actions to improve the quality of gover-

nance once risks are identified with respect to the

functions and to the domains.

• A cross-comparison of organizational governance. The

objective is to obtain a ranking of the set of organiza-

tions according to the quality of their governance with

respect to SD challenges. In this context, the set of

criteria are the set of domains (see Sect. 2.1) and the

aggregation procedure is the one described in Sect.

2.2.2. The final recommendations are based on a

benchmark, across the Organizations, where the ones

that are the best ranked shared their best practices with

the other Organizations in terms of governance.

In these two categories of problems, the aims are to

assess and to improve the quality of organizational gov-

ernance of sustainability.

2.1 Domains, functions and indicators

The governance of organizations with respect to SD can be

described according to six functions:

• rules of functioning of the Board of Directors (BO),

• functioning of the organization (Func),

• risk management policy and how risk are prevented

(RP),

Organization 1

Organization 2 Organization 3

Organization 5Organization 4

Is strictly more sustainable than

Key:

Fig. 3 Example of a ranking of a set of organizations from the more sustainable to the less sustainable one

I1

I2I3

I4 I5

I6

I7I8

Organization 1

Organization 2

Fig. 4 Example of radar assessment comparison between organiza-

tion 1 and organization 2

Fig. 5 Multi-criteria decision-aid method applied to the implemen-

tation of the SD principle (Merad et al. 2013)

308 Environ Syst Decis (2013) 33:305–321

123

• relationship with stakeholders (RS),

• communication and reporting on CSR and SD (Rep

CSR) and

• the way missions and projects of the organization are

conducted (MIS).

These functions are assessed according to the seven

values of the ISO 26000 norm (ISO 2010): accountability

(Acc), transparency (Tra), ethical behaviors (Eth), respect

for stakeholders’ interests (Res Stk), respect of the rule of

law (Res Lw), respect for international norms of behaviors

(Res NB) and respect for human rights (Res HR). These

values are denoted hereafter as ‘‘domains.’’

Each domain is assessed according to a set of indicators.

The set of indicators was identified after a 3-year research

project coordinate by INERIS based on the consultation of

different stakeholders in different organizations. The con-

clusions of the project were published, by the French

Ministry in charge of the Environment and the Sustainable

Development in 2013, as a national guideline (see MEDDE

and INERIS 2013). Early conclusions of the research

projects were published in Merad and Marcel (2012a). The

authors have proposed a set of indicators that provide

insight about domains and functions (see Table 1;

‘‘Appendix 1’’—Table 7). These indicators are generic and

were designed in a way that applies to different organiza-

tions. Indicators are informed based on interviews that

lasted 1–3 h, on documents and reports and also on

investigations within and outside the organization. For

every indicator, qualitative and quantitative information

based on facts and perception must be provided when

possible. Information must be robust (coherent, stable

during the period of investigation) and actionable (based on

facts and elements that can be mobilized and to which can

be refer to). The final assessment of the indicator must be

done in a participative process in order to consider the

difference between stakeholders perception.

Each function and each domain are assessed neither

according to the same indicators nor to the same number of

indicators (see ‘‘Appendix 1’’—Table 7). When the num-

ber of indicators to assess a function or a domain is high,

there are a high number of exigencies that are needed and

advocated to qualify a global level of risk or a global level

of opportunity in terms of governance. This is the case for

domains such as ‘‘Transparency’’ and ‘‘Accountability’’ or

for functions such as ‘‘Board of Directors’’ and ‘‘Func-

tioning of the Organization.’’ This high level of exigencies

is also due to the fact that the large majority of research in

governance in the field of Corporate Social Responsibility

and Sustainable Development were dedicated to these

aspects (see ISIS 2009a, b; Merad et al. 2013). For domains

and functions, few indicators were used; the assessment of

the global level of risk or a global level of opportunity in

terms of governance is submitted to a quasi veto mecha-

nism effect. If one indicator presents a high, or a low level

of risk, then the level of the global governance will be

correlated and will follow the same direction.

To fulfill the dashboard (Table 2), it is recommended to

respect a protocol during the diagnosis that consists of

providing the opportunity to stakeholders within and out-

side the organization to give their opinion without cen-

sorship. The interviewed stakeholders should be composed

a minima of the highest level of management, workers

representatives, health, safety and environment (HSE)

representative, non-governmental organizations (NGO) and

Table 1 Partial assessment of the governance of SD for an organization for the domains and the functions

Functions

Rules of

functioning of

the Board of

Directors (BO)

Functioning

of the

organization

(Func)

Risk management

policy and how

risk are prevented

(RP)

Relationship

with

stakeholders

(RS)

Communication

and reporting on

CSR and SD

(Rep CSR)

Way missions and

projects of the

organization are

conducted (MIS)

Domains

Accountability Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Transparency Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Ethical behaviors Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Respect for

stakeholders’ interests

Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Respect of the rule of law Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Respect for international

norms of behaviors

Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Respect for human rights Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators Set of indicators

Environ Syst Decis (2013) 33:305–321 309

123

both public and private businesses with whom the organi-

zation is in relationship. A discussion should be encour-

aged to point out elements of concordance and elements of

discordance in the diagnosis.

Based on the information given in Table 2, it is sug-

gested, at this stage, to use a qualitative assessment of the

indicator based on a five-level scale presented in Fig. 5

(Merad and Marcel 2012b). Each level of the scale corre-

sponds to a color: the lowest level is red (very weak) and

the highest level is green (very high). In this scale, the strict

respect of the regulation in place is considered as a status

quo level (blue color) (Fig. 6).

Indicators, functions and domains do not have the same

value for the stakeholders that participate at the assessment

process. However, as participants are equally representing

classes of stakeholders, they are given the same voting

power. The authors then recommend in a first step to

consider that the weightings are equivalent and equal to 1.

It is possible in a second step according to stakeholder’s

expectations to numerate the respective weightings. The

authors have chosen to use the ‘cards method’ (Revised

Simos method) (Merad et al. 2004, 2013; Figueira and Roy

2002). This method is based on a participative process that

helps framing a common representation of governance of

SD problem and is adequate for contexts where stake-

holders are from different background and affiliations.

Each indicator is associated with a card and presented to

the stakeholders who are then asked to sort the cards from

the least important to the most important indicators and to

insert blank cards to indicate the relative importance

among indicators from one rank to the next. This revised

Simos method has many advantages, namely preventing

indicators from being eliminated by a zero-weight assign-

ment and allowing the incorporation of the various

weightings ascribed by stakeholders based on their

expectations and preferences (Merad et al. 2004).

2.2 From a partial to a global assessment

of the governance

The authors have used two aggregation methods to assess

the global governance level of a set of Organizations:

• The identification of a final governance index for an

Organization. This method helps in establishing a

global diagnosis of the quality of the governance of an

Organization with respect to SD challenges. The

governance index is based on the calculation of three

indexes: the partial opportunity index, the partial risk

index and the partial equilibrium index.

• The ranking of a set of Organizations according to their

governance of SD. This method aims at assessing a set

Table 2 Governance

indicators dashboardDomain Indicator

designation

Function

BO Func RP RS Rep CSR MIS

I1 Synthesis of the diagnosis based

on concordant facts and perceptions.

Discordance facts and elements.

To which extend the CSC domains

is respected (5 levels)

…

Fig. 6 Indicator that provide a

partial assessment of the level of

governance of the organization

according to the extent to which

one domain is respected

310 Environ Syst Decis (2013) 33:305–321

123

of Organizations based on a pairwise comparison

according to a set of criteria that represents the seven

domains of the ISO 26000 norm (ISO 2010). This

method is based on the outranking aggregation

approach ELECTRE III (see ‘‘Appendix 2’’—ELEC-

TRE III method).

The two aggregation procedures are described hereafter.

2.2.1 The identification of a final governance index

for an Organization

When dealing with governance issues, it is not uncommon

to face more qualitative than quantitative information.

Each indicator is assessed according to the qualitative

description that is done by an analyst according to stake-

holders’ interviews and document consultation. The

assessment should be carried out once per year and syn-

thesized in ‘‘Governance indicators dashboard’’ (Table 2)

and consolidated based on a deliberative process.

Each function and domain is assessed according to the

set of indicators defined in the Table 7 (see ‘‘Appendix 1’’).

After discussions with different stakeholders, the authors

have been able to fix logical rules to point out what the

deficiencies/risks and the advantages/opportunities are in

terms of governance for the organization. The method is

based on the calculation of three indexes described here-

after. The rationale behind building three indexes, as

opposed to building one index from all the indicators, is to

avoid the ‘‘compensation mechanism’’ between the indi-

cators. Indeed, the following approach is a semi-compen-

sation aggregation approach (see Roy and Bouyssou 1992):

• The partial opportunity index:

OpFunction i=Domain j ¼P

function i=Domain j kopP

function i=Domain j k

whereP

function i=Domain j kop is the sum for a function i

(i = {BO, Func, RP, RS, Rep CSR, MIS}) in a domain

j (j = {Acc, Tra, Eth, Res Stk, Res Lw, Res NB,

Res HR}) of the number of time level; ‘‘respect the

regulatory constraints’’ (blue color), high (light

green color) and very high (green color) were assigned

when assessing the function i according to a set of

indicators (see Fig. 1; Table 7 in ‘‘Appendix 1’’).P

function i=Domain j k is the sum of the set of indicators that

are used to assess a function i (i = {BO, Func, RP, RS,

Rep CSR, MIS}) in a domain j (j = {Acc, Tra, Eth, Res

Stk, Res Lw, Res NB, Res HR}). Let us notice that

compliance to regulation, by the ‘‘respect of the regu-

latory constraints,’’ is a sine qua non-condition for the

organization to take new opportunities in terms of SD

and Societal Responsibility.

• The partial risk index:

RisFunction i=Domain j ¼P

function i=Domain j krisP

function i=Domain j k

whereP

function i=Domain j kris is the sum for a function

i (i = {BO, Func, RP, RS, Rep CSR, MIS}) of the

number of time level weak (light red color) and very

weak (red color) were assigned when assessing the

function i according to a set of indicators (see Fig. 1;

Table 7 in ‘‘Appendix 1’’).

• The partial equilibrium index:

MidFunction i=Domain j ¼kfunction i=Domain j midP

function i=Domain j k

where kfunction i=Domain j mid is the number of time level

‘‘respect the regulatory constraints’’ (blue color) was

assigned when assessing the function i according to a

set of indicators (see Fig. 1; Table 7 in ‘‘Appendix 1’’).

If there is just one indicator activated to assess a domain

or a function, then the value of the partial indicators is

equal to the value of the indicator that is considered.

The governance assessment of the functions i for a

domain j GovFunction i=Domain j is done according to the fol-

lowing rules:

If OpFunction i=Domain j [ RisFunction i=Domain j then

GovFunction i=Domain j ¼ OpFunction i=Domain j. The level attrib-

uted to governance is ‘‘high’’ if the GovFunction i=Domain j

\0:80 and ‘‘very high’’ if GovFunction i=Domain j� 0:80.

The threshold 0.80 in the formula was fixed by the authors.

This threshold was considered as being as highly

demanding for the Organizations in terms of governance

exigencies.

If RisFunction i=Domain j [ OpFunction i=Domain j then

GovFunction i=Domain j ¼ RisFunction i=Domain j. The level attributed

to governance is ‘‘weak’’ if the GovFunction i=Domain j\0:80 and

‘‘very weak’’ if GovFunction i=Domain j� 0:80.

If OpFunction i=Domain j ¼ RisFunction i=Domain j ¼ 0:50 then

GovFunction i=Domain j ¼ RisFunction i=Domain j. The level attrib-

uted to governance is ‘‘weak.’’

The final governance assessment of a domain j

GovDomain j is done according to the following rules:

IfP

Domain j OpFunction i [P

Domain j RisFunction i then

GovDomain j ¼P

Domain j OpFunction i. The level attributed to

governance is ‘‘high’’ if the GovDomain j\0:80 and ‘‘very

high’’ if GovDomain j� 0:80.

Environ Syst Decis (2013) 33:305–321 311

123

IfP

Domain j RisFunction i [P

Domain j OpFunction i then

GovDomain j ¼P

Domain j RisFunction i. The level attributed to

governance is ‘‘weak’’ if the GovDomain j\0:80 and ‘‘very

weak’’ if GovDomain j� 0:80.

IfP

Domain j OpFunction i ¼P

Domain j RisFunction i ¼ 0:5

then GovDomain j ¼P

Domain j RisFunction i. The level attrib-

uted to governance is ‘‘weak.’’

There will be indexes for where there are no or very few

indicators and indexes for where there are a large number

of indicators that are activated (Table 7 in ‘‘Appendix 1’’).

The question that arises is: Isn’t there a possibility of bias

for assessing governance due to the large differences in the

number of indicators in each function and at each domain?

In fact, each aggregation method presents a set of limits

and biases. In the method presented above, the biases are

the quasi veto mechanism effects when the number of

indicators is low, and the high level of requirement to

achieve a high quality in terms of global governance when

the number of indicators is high.

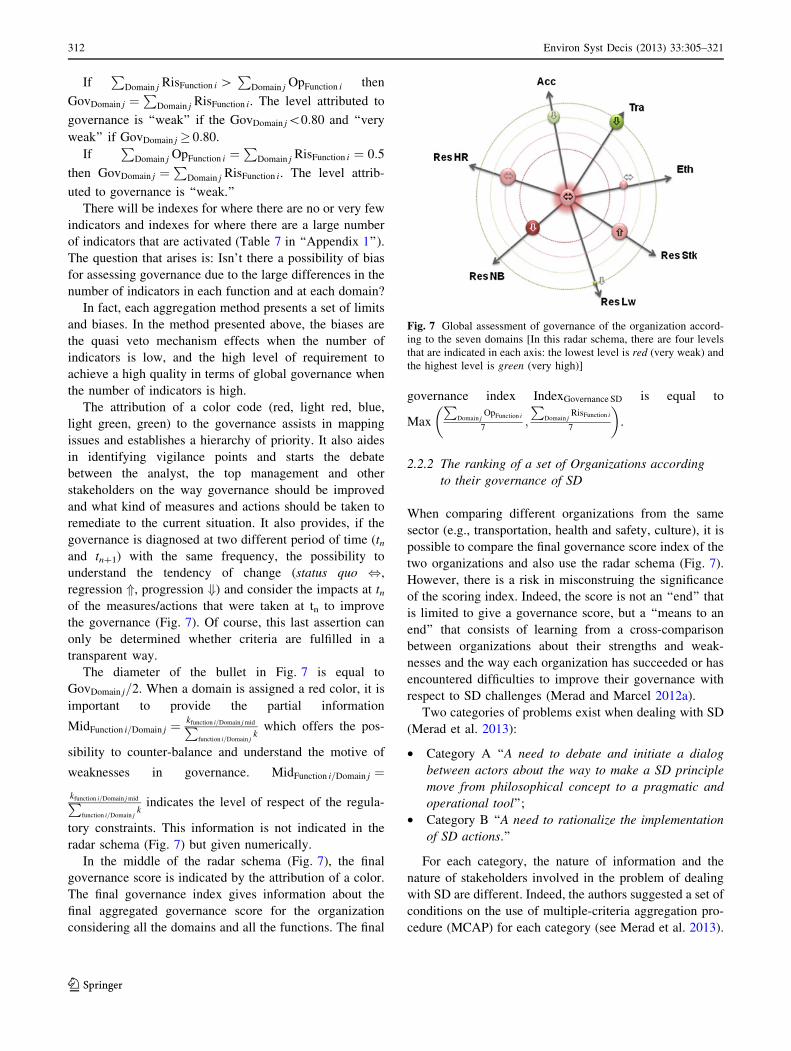

The attribution of a color code (red, light red, blue,

light green, green) to the governance assists in mapping

issues and establishes a hierarchy of priority. It also aides

in identifying vigilance points and starts the debate

between the analyst, the top management and other

stakeholders on the way governance should be improved

and what kind of measures and actions should be taken to

remediate to the current situation. It also provides, if the

governance is diagnosed at two different period of time (tnand tn?1) with the same frequency, the possibility to

understand the tendency of change (status quo ,,

regression *, progression +) and consider the impacts at tnof the measures/actions that were taken at tn to improve

the governance (Fig. 7). Of course, this last assertion can

only be determined whether criteria are fulfilled in a

transparent way.

The diameter of the bullet in Fig. 7 is equal to

GovDomain j=2. When a domain is assigned a red color, it is

important to provide the partial information

MidFunction i=Domain j ¼kfunction i=Domain j midP

function i=Domain jk

which offers the pos-

sibility to counter-balance and understand the motive of

weaknesses in governance. MidFunction i=Domain j ¼kfunction i=Domain j midP

function i=Domain jk

indicates the level of respect of the regula-

tory constraints. This information is not indicated in the

radar schema (Fig. 7) but given numerically.

In the middle of the radar schema (Fig. 7), the final

governance score is indicated by the attribution of a color.

The final governance index gives information about the

final aggregated governance score for the organization

considering all the domains and all the functions. The final

governance index IndexGovernance SD is equal to

Max

PDomain j

OpFunction i

7;

PDomain j

RisFunction i

7

� �

.

2.2.2 The ranking of a set of Organizations according

to their governance of SD

When comparing different organizations from the same

sector (e.g., transportation, health and safety, culture), it is

possible to compare the final governance score index of the

two organizations and also use the radar schema (Fig. 7).

However, there is a risk in misconstruing the significance

of the scoring index. Indeed, the score is not an ‘‘end’’ that

is limited to give a governance score, but a ‘‘means to an

end’’ that consists of learning from a cross-comparison

between organizations about their strengths and weak-

nesses and the way each organization has succeeded or has

encountered difficulties to improve their governance with

respect to SD challenges (Merad and Marcel 2012a).

Two categories of problems exist when dealing with SD

(Merad et al. 2013):

• Category A ‘‘A need to debate and initiate a dialog

between actors about the way to make a SD principle

move from philosophical concept to a pragmatic and

operational tool’’;

• Category B ‘‘A need to rationalize the implementation

of SD actions.’’

For each category, the nature of information and the

nature of stakeholders involved in the problem of dealing

with SD are different. Indeed, the authors suggested a set of

conditions on the use of multiple-criteria aggregation pro-

cedure (MCAP) for each category (see Merad et al. 2013).

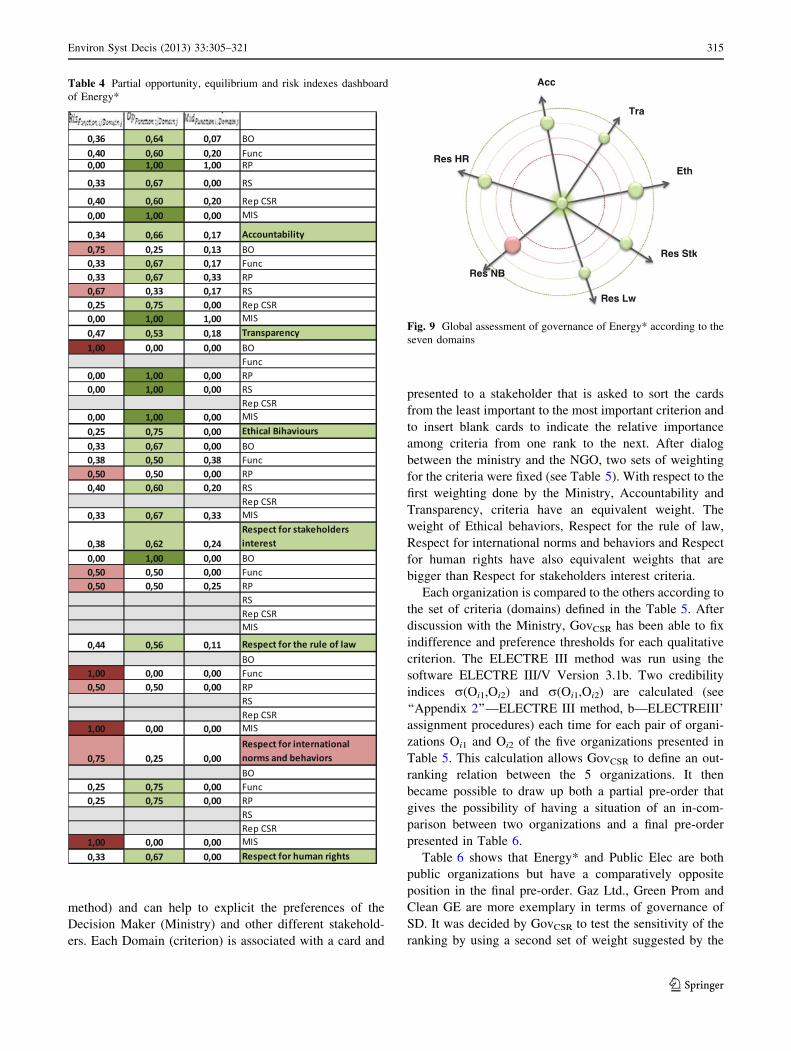

Fig. 7 Global assessment of governance of the organization accord-

ing to the seven domains [In this radar schema, there are four levels

that are indicated in each axis: the lowest level is red (very weak) and

the highest level is green (very high)]

312 Environ Syst Decis (2013) 33:305–321

123

Governance diagnosis and assessment is ‘‘a category A’’

problem where the large majority of information is quali-

tative and where a large number of stakeholders should be

consulted and involved. Therefore, the authors suggest

ELECTRE III method (see the ‘‘Appendix 2’’—ELETRE

III method and the reference Roy and Bouyssou 1992) to

rank organizations from the more exemplary and sustain-

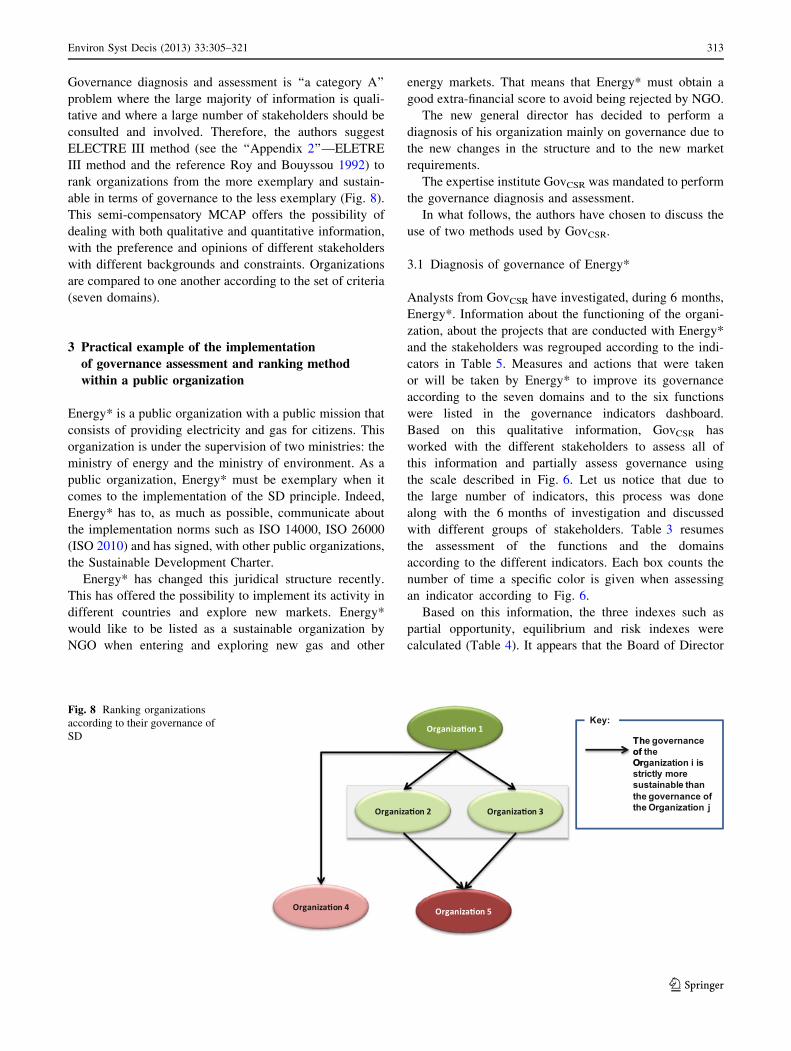

able in terms of governance to the less exemplary (Fig. 8).

This semi-compensatory MCAP offers the possibility of

dealing with both qualitative and quantitative information,

with the preference and opinions of different stakeholders

with different backgrounds and constraints. Organizations

are compared to one another according to the set of criteria

(seven domains).

3 Practical example of the implementation

of governance assessment and ranking method

within a public organization

Energy* is a public organization with a public mission that

consists of providing electricity and gas for citizens. This

organization is under the supervision of two ministries: the

ministry of energy and the ministry of environment. As a

public organization, Energy* must be exemplary when it

comes to the implementation of the SD principle. Indeed,

Energy* has to, as much as possible, communicate about

the implementation norms such as ISO 14000, ISO 26000

(ISO 2010) and has signed, with other public organizations,

the Sustainable Development Charter.

Energy* has changed this juridical structure recently.

This has offered the possibility to implement its activity in

different countries and explore new markets. Energy*

would like to be listed as a sustainable organization by

NGO when entering and exploring new gas and other

energy markets. That means that Energy* must obtain a

good extra-financial score to avoid being rejected by NGO.

The new general director has decided to perform a

diagnosis of his organization mainly on governance due to

the new changes in the structure and to the new market

requirements.

The expertise institute GovCSR was mandated to perform

the governance diagnosis and assessment.

In what follows, the authors have chosen to discuss the

use of two methods used by GovCSR.

3.1 Diagnosis of governance of Energy*

Analysts from GovCSR have investigated, during 6 months,

Energy*. Information about the functioning of the organi-

zation, about the projects that are conducted with Energy*

and the stakeholders was regrouped according to the indi-

cators in Table 5. Measures and actions that were taken

or will be taken by Energy* to improve its governance

according to the seven domains and to the six functions

were listed in the governance indicators dashboard.

Based on this qualitative information, GovCSR has

worked with the different stakeholders to assess all of

this information and partially assess governance using

the scale described in Fig. 6. Let us notice that due to

the large number of indicators, this process was done

along with the 6 months of investigation and discussed

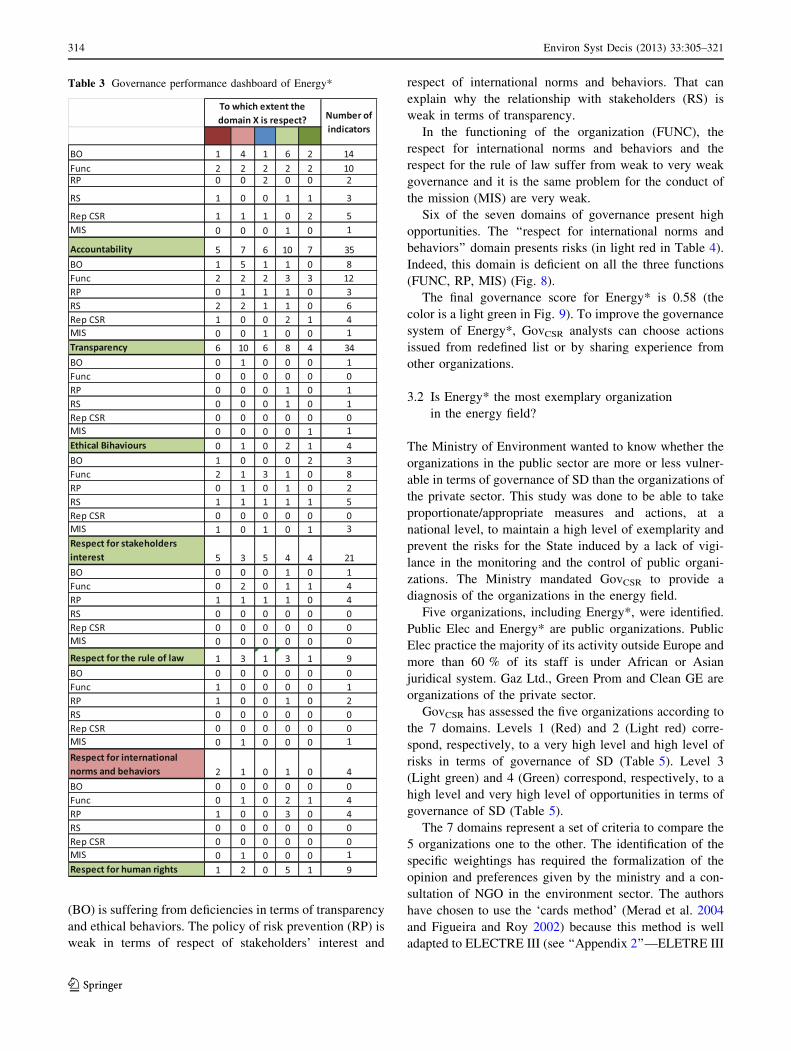

with different groups of stakeholders. Table 3 resumes

the assessment of the functions and the domains

according to the different indicators. Each box counts the

number of time a specific color is given when assessing

an indicator according to Fig. 6.

Based on this information, the three indexes such as

partial opportunity, equilibrium and risk indexes were

calculated (Table 4). It appears that the Board of Director

Fig. 8 Ranking organizations

according to their governance of

SD

Environ Syst Decis (2013) 33:305–321 313

123

(BO) is suffering from deficiencies in terms of transparency

and ethical behaviors. The policy of risk prevention (RP) is

weak in terms of respect of stakeholders’ interest and

respect of international norms and behaviors. That can

explain why the relationship with stakeholders (RS) is

weak in terms of transparency.

In the functioning of the organization (FUNC), the

respect for international norms and behaviors and the

respect for the rule of law suffer from weak to very weak

governance and it is the same problem for the conduct of

the mission (MIS) are very weak.

Six of the seven domains of governance present high

opportunities. The ‘‘respect for international norms and

behaviors’’ domain presents risks (in light red in Table 4).

Indeed, this domain is deficient on all the three functions

(FUNC, RP, MIS) (Fig. 8).

The final governance score for Energy* is 0.58 (the

color is a light green in Fig. 9). To improve the governance

system of Energy*, GovCSR analysts can choose actions

issued from redefined list or by sharing experience from

other organizations.

3.2 Is Energy* the most exemplary organization

in the energy field?

The Ministry of Environment wanted to know whether the

organizations in the public sector are more or less vulner-

able in terms of governance of SD than the organizations of

the private sector. This study was done to be able to take

proportionate/appropriate measures and actions, at a

national level, to maintain a high level of exemplarity and

prevent the risks for the State induced by a lack of vigi-

lance in the monitoring and the control of public organi-

zations. The Ministry mandated GovCSR to provide a

diagnosis of the organizations in the energy field.

Five organizations, including Energy*, were identified.

Public Elec and Energy* are public organizations. Public

Elec practice the majority of its activity outside Europe and

more than 60 % of its staff is under African or Asian

juridical system. Gaz Ltd., Green Prom and Clean GE are

organizations of the private sector.

GovCSR has assessed the five organizations according to

the 7 domains. Levels 1 (Red) and 2 (Light red) corre-

spond, respectively, to a very high level and high level of

risks in terms of governance of SD (Table 5). Level 3

(Light green) and 4 (Green) correspond, respectively, to a

high level and very high level of opportunities in terms of

governance of SD (Table 5).

The 7 domains represent a set of criteria to compare the

5 organizations one to the other. The identification of the

specific weightings has required the formalization of the

opinion and preferences given by the ministry and a con-

sultation of NGO in the environment sector. The authors

have chosen to use the ‘cards method’ (Merad et al. 2004

and Figueira and Roy 2002) because this method is well

adapted to ELECTRE III (see ‘‘Appendix 2’’—ELETRE III

Table 3 Governance performance dashboard of Energy*

314 Environ Syst Decis (2013) 33:305–321

123

method) and can help to explicit the preferences of the

Decision Maker (Ministry) and other different stakehold-

ers. Each Domain (criterion) is associated with a card and

presented to a stakeholder that is asked to sort the cards

from the least important to the most important criterion and

to insert blank cards to indicate the relative importance

among criteria from one rank to the next. After dialog

between the ministry and the NGO, two sets of weighting

for the criteria were fixed (see Table 5). With respect to the

first weighting done by the Ministry, Accountability and

Transparency, criteria have an equivalent weight. The

weight of Ethical behaviors, Respect for the rule of law,

Respect for international norms and behaviors and Respect

for human rights have also equivalent weights that are

bigger than Respect for stakeholders interest criteria.

Each organization is compared to the others according to

the set of criteria (domains) defined in the Table 5. After

discussion with the Ministry, GovCSR has been able to fix

indifference and preference thresholds for each qualitative

criterion. The ELECTRE III method was run using the

software ELECTRE III/V Version 3.1b. Two credibility

indices r(Oi1,Oi2) and r(Oi1,Oi2) are calculated (see

‘‘Appendix 2’’—ELECTRE III method, b—ELECTREIII’

assignment procedures) each time for each pair of organi-

zations Oi1 and Oi2 of the five organizations presented in

Table 5. This calculation allows GovCSR to define an out-

ranking relation between the 5 organizations. It then

became possible to draw up both a partial pre-order that

gives the possibility of having a situation of an in-com-

parison between two organizations and a final pre-order

presented in Table 6.

Table 6 shows that Energy* and Public Elec are both

public organizations but have a comparatively opposite

position in the final pre-order. Gaz Ltd., Green Prom and

Clean GE are more exemplary in terms of governance of

SD. It was decided by GovCSR to test the sensitivity of the

ranking by using a second set of weight suggested by the

Table 4 Partial opportunity, equilibrium and risk indexes dashboard

of Energy*

Eth

Acc

Tra

Res NB

Res Lw

Res Stk

Res HR

Fig. 9 Global assessment of governance of Energy* according to the

seven domains

Environ Syst Decis (2013) 33:305–321 315

123

NGO (weights 2 in Table 5). The ranking of the five

organizations stays the same. No score is given to the

organizations. This helps to focus the debate on the mea-

sures to improve the vulnerabilities noticed in Public Elec

and learn from what have been done in the organizations

that are better ranked (see Table 6).

4 Conclusion

Corporate Social Responsibility (CSR) guidelines for

public and private sectors show that governance issues are

more than optional issues of reporting for organizations.

Governance issues cannot be limited to corporate gover-

nance aspects. In addition to the rules of functioning of the

Board of Directors, aspects such as functioning of the

organization, risk management policy and how risk are

prevented, relationship with stakeholders, communication

and reporting on Corporate Social Responsibility and

Sustainable Development and the way missions and

projects of the organization are conducted (MIS) must be

considered.

In this paper, the authors have argued that there is a need

to neatly diagnose the governance of organizations

according to accepted and effective indicators before

assessing the governance according to its compliance and

performance. The authors have then proposed a multiple-

criteria decision-aiding approach to diagnose and assess the

governance of an organization with respect to Sustainable

Development (SD) and CSR.

Two methods and tools for both qualitative assessment

and aggregation of stakeholders’ judgments and prefer-

ences on governance were proposed. Two aggregation

procedures were used. The first aggregation procedure was

calibrated to allow dealing with qualitative information and

establishing a diagnosis of one organization. The second

aggregation procedure is based on an outranking approach

ELECTRE III to compare one organization to another

based on seven qualitative criteria.

The implementation of these aggregation procedures on

practical examples shows that these methods are easy to

understand and communicate and allow engaging a dis-

cussion on the measures to improve the governance of the

organization rather than focusing the attention of the

stakeholders on a final score.

Acknowledgments The authors are grateful to Elisa Tatham and to

the anonymous reviews for their useful comments and suggestions to

improve the paper.

Appendix 1

See Table 7.

Table 5 Governance performance dashboard of in the energy field

Table 6 Ranking of the five organizations according to the seven

domains of CSR

Rank Final pre-order: exemplarity

order in terms of governance

of SD on organizations according

to the 7 criteria (domains)

1 Energy*

Gaz Ltd

2 Green Prom

Clean GE

Public Elec

316 Environ Syst Decis (2013) 33:305–321

123

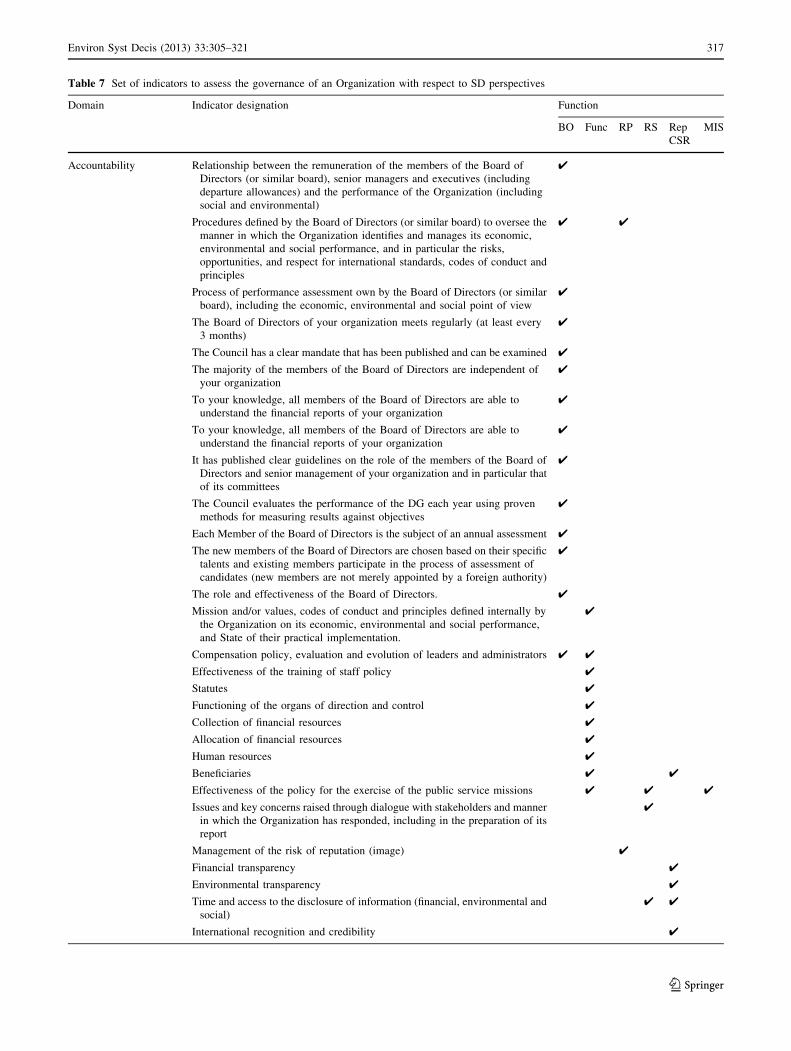

Table 7 Set of indicators to assess the governance of an Organization with respect to SD perspectives

Domain Indicator designation Function

BO Func RP RS Rep

CSR

MIS

Accountability Relationship between the remuneration of the members of the Board of

Directors (or similar board), senior managers and executives (including

departure allowances) and the performance of the Organization (including

social and environmental)

4

Procedures defined by the Board of Directors (or similar board) to oversee the

manner in which the Organization identifies and manages its economic,

environmental and social performance, and in particular the risks,

opportunities, and respect for international standards, codes of conduct and

principles

4 4

Process of performance assessment own by the Board of Directors (or similar

board), including the economic, environmental and social point of view

4

The Board of Directors of your organization meets regularly (at least every

3 months)

4

The Council has a clear mandate that has been published and can be examined 4

The majority of the members of the Board of Directors are independent of

your organization

4

To your knowledge, all members of the Board of Directors are able to

understand the financial reports of your organization

4

To your knowledge, all members of the Board of Directors are able to

understand the financial reports of your organization

4

It has published clear guidelines on the role of the members of the Board of

Directors and senior management of your organization and in particular that

of its committees

4

The Council evaluates the performance of the DG each year using proven

methods for measuring results against objectives

4

Each Member of the Board of Directors is the subject of an annual assessment 4

The new members of the Board of Directors are chosen based on their specific

talents and existing members participate in the process of assessment of

candidates (new members are not merely appointed by a foreign authority)

4

The role and effectiveness of the Board of Directors. 4

Mission and/or values, codes of conduct and principles defined internally by

the Organization on its economic, environmental and social performance,

and State of their practical implementation.

4

Compensation policy, evaluation and evolution of leaders and administrators 4 4

Effectiveness of the training of staff policy 4

Statutes 4

Functioning of the organs of direction and control 4

Collection of financial resources 4

Allocation of financial resources 4

Human resources 4

Beneficiaries 4 4

Effectiveness of the policy for the exercise of the public service missions 4 4 4

Issues and key concerns raised through dialogue with stakeholders and manner

in which the Organization has responded, including in the preparation of its

report

4

Management of the risk of reputation (image) 4

Financial transparency 4

Environmental transparency 4

Time and access to the disclosure of information (financial, environmental and

social)

4 4

International recognition and credibility 4

Environ Syst Decis (2013) 33:305–321 317

123

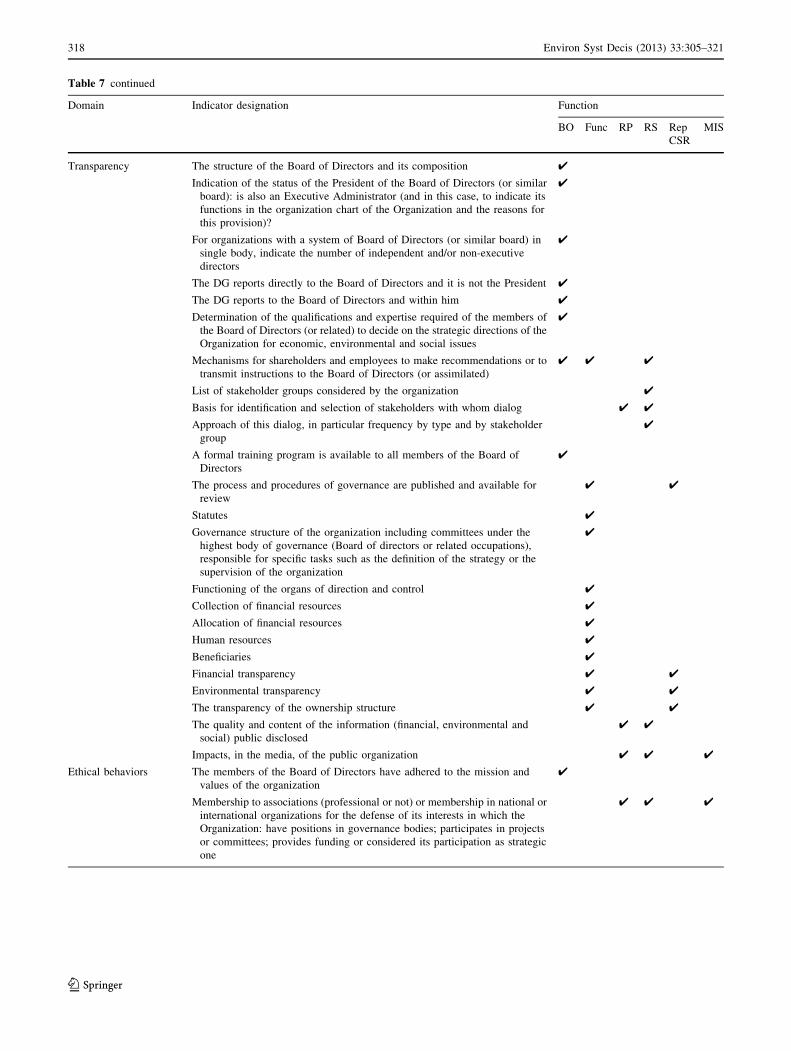

Table 7 continued

Domain Indicator designation Function

BO Func RP RS Rep

CSR

MIS

Transparency The structure of the Board of Directors and its composition 4

Indication of the status of the President of the Board of Directors (or similar

board): is also an Executive Administrator (and in this case, to indicate its

functions in the organization chart of the Organization and the reasons for

this provision)?

4

For organizations with a system of Board of Directors (or similar board) in

single body, indicate the number of independent and/or non-executive

directors

4

The DG reports directly to the Board of Directors and it is not the President 4

The DG reports to the Board of Directors and within him 4

Determination of the qualifications and expertise required of the members of

the Board of Directors (or related) to decide on the strategic directions of the

Organization for economic, environmental and social issues

4

Mechanisms for shareholders and employees to make recommendations or to

transmit instructions to the Board of Directors (or assimilated)

4 4 4

List of stakeholder groups considered by the organization 4

Basis for identification and selection of stakeholders with whom dialog 4 4

Approach of this dialog, in particular frequency by type and by stakeholder

group

4

A formal training program is available to all members of the Board of

Directors

4

The process and procedures of governance are published and available for

review

4 4

Statutes 4

Governance structure of the organization including committees under the

highest body of governance (Board of directors or related occupations),

responsible for specific tasks such as the definition of the strategy or the

supervision of the organization

4

Functioning of the organs of direction and control 4

Collection of financial resources 4

Allocation of financial resources 4

Human resources 4

Beneficiaries 4

Financial transparency 4 4

Environmental transparency 4 4

The transparency of the ownership structure 4 4

The quality and content of the information (financial, environmental and

social) public disclosed

4 4

Impacts, in the media, of the public organization 4 4 4

Ethical behaviors The members of the Board of Directors have adhered to the mission and

values of the organization

4

Membership to associations (professional or not) or membership in national or

international organizations for the defense of its interests in which the

Organization: have positions in governance bodies; participates in projects

or committees; provides funding or considered its participation as strategic

one

4 4 4

318 Environ Syst Decis (2013) 33:305–321

123

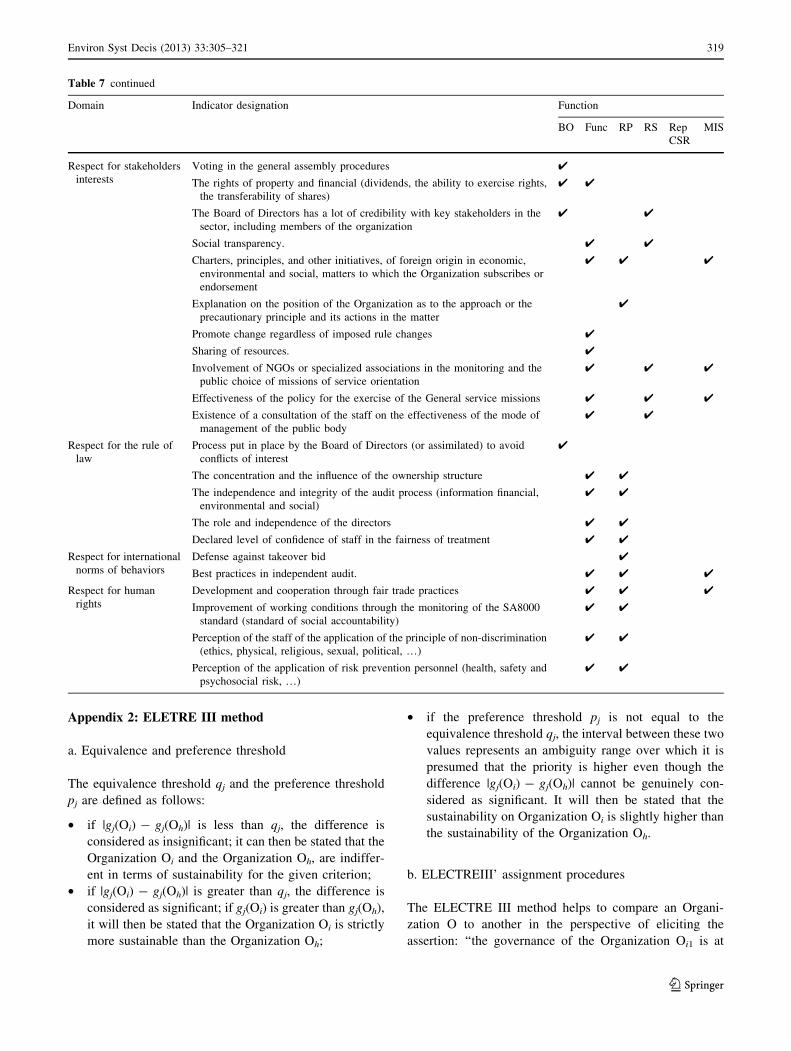

Appendix 2: ELETRE III method

a. Equivalence and preference threshold

The equivalence threshold qj and the preference threshold

pj are defined as follows:

• if |gj(Oi) - gj(Oh)| is less than qj, the difference is

considered as insignificant; it can then be stated that the

Organization Oi and the Organization Oh, are indiffer-

ent in terms of sustainability for the given criterion;

• if |gj(Oi) - gj(Oh)| is greater than qj, the difference is

considered as significant; if gj(Oi) is greater than gj(Oh),

it will then be stated that the Organization Oi is strictly

more sustainable than the Organization Oh;

• if the preference threshold pj is not equal to the

equivalence threshold qj, the interval between these two

values represents an ambiguity range over which it is

presumed that the priority is higher even though the

difference |gj(Oi) - gj(Oh)| cannot be genuinely con-

sidered as significant. It will then be stated that the

sustainability on Organization Oi is slightly higher than

the sustainability of the Organization Oh.

b. ELECTREIII’ assignment procedures

The ELECTRE III method helps to compare an Organi-

zation O to another in the perspective of eliciting the

assertion: ‘‘the governance of the Organization Oi1 is at

Table 7 continued

Domain Indicator designation Function

BO Func RP RS Rep

CSR

MIS

Respect for stakeholders

interests

Voting in the general assembly procedures 4

The rights of property and financial (dividends, the ability to exercise rights,

the transferability of shares)

4 4

The Board of Directors has a lot of credibility with key stakeholders in the

sector, including members of the organization

4 4

Social transparency. 4 4

Charters, principles, and other initiatives, of foreign origin in economic,

environmental and social, matters to which the Organization subscribes or

endorsement

4 4 4

Explanation on the position of the Organization as to the approach or the

precautionary principle and its actions in the matter

4

Promote change regardless of imposed rule changes 4

Sharing of resources. 4

Involvement of NGOs or specialized associations in the monitoring and the

public choice of missions of service orientation

4 4 4

Effectiveness of the policy for the exercise of the General service missions 4 4 4

Existence of a consultation of the staff on the effectiveness of the mode of

management of the public body

4 4

Respect for the rule of

law

Process put in place by the Board of Directors (or assimilated) to avoid

conflicts of interest

4

The concentration and the influence of the ownership structure 4 4

The independence and integrity of the audit process (information financial,

environmental and social)

4 4

The role and independence of the directors 4 4

Declared level of confidence of staff in the fairness of treatment 4 4

Respect for international

norms of behaviors

Defense against takeover bid 4

Best practices in independent audit. 4 4 4

Respect for human

rights

Development and cooperation through fair trade practices 4 4 4

Improvement of working conditions through the monitoring of the SA8000

standard (standard of social accountability)

4 4

Perception of the staff of the application of the principle of non-discrimination

(ethics, physical, religious, sexual, political, …)

4 4

Perception of the application of risk prevention personnel (health, safety and

psychosocial risk, …)

4 4

Environ Syst Decis (2013) 33:305–321 319

123

least as sustainable as the governance of the Organization

Oi2.’’ This assertion is denoted ‘‘Oi1 outranks Oi2’’ or ‘‘Oi1

S Oi2.’’

The following situations should be considered: [Oi1 S

Oi2 and Oi2 S Oi1] or [no Oi1 S Oi2 and no Oi2 S Oi1]. The

first possibility corresponds to an equivalence situation (Oi1

I Oi2) between the two organizations where the two orga-

nizations are considered of equal importance. The second

situation corresponds to incomparability (Oi1 R Oi2)

between the two organizations.

We use the index r(Oi1, Oi2) to calculate the credibility

of the assertion ‘‘the governance of the Organization Oi1 is

at least as sustainable as the governance of the Organi-

zation Oi2.’’ This index takes values in the interval [0, 1]: is

equal to 0 if the assertion ‘‘Oi1 S Oi2’’ is rejected and 1 if

the assertion is validated. Between 0 and 1, the credibility

index is calculated using two other indices:

• Concordance index C(Oi1, Oi2). This index considers

the concordant criteria with the assertion ‘‘Oi1 S Oi2’’

taking into account their relative importance (weight of

the criteria).

• Partial discordance index dj(Oi1, Oi2). This index

considers the discordant criteria, expressed individu-

ally, with the assertion ‘‘Oi1 S Oi2.’’ When the gap on

one criterion gj is bigger than vj, the discordance

indexes take the value 1 and can help to reconsider the

credibility of the assertion ‘‘Oi1 S Oi2’’ (r(Oi1,

Oi2) = 0). vj is the veto threshold.

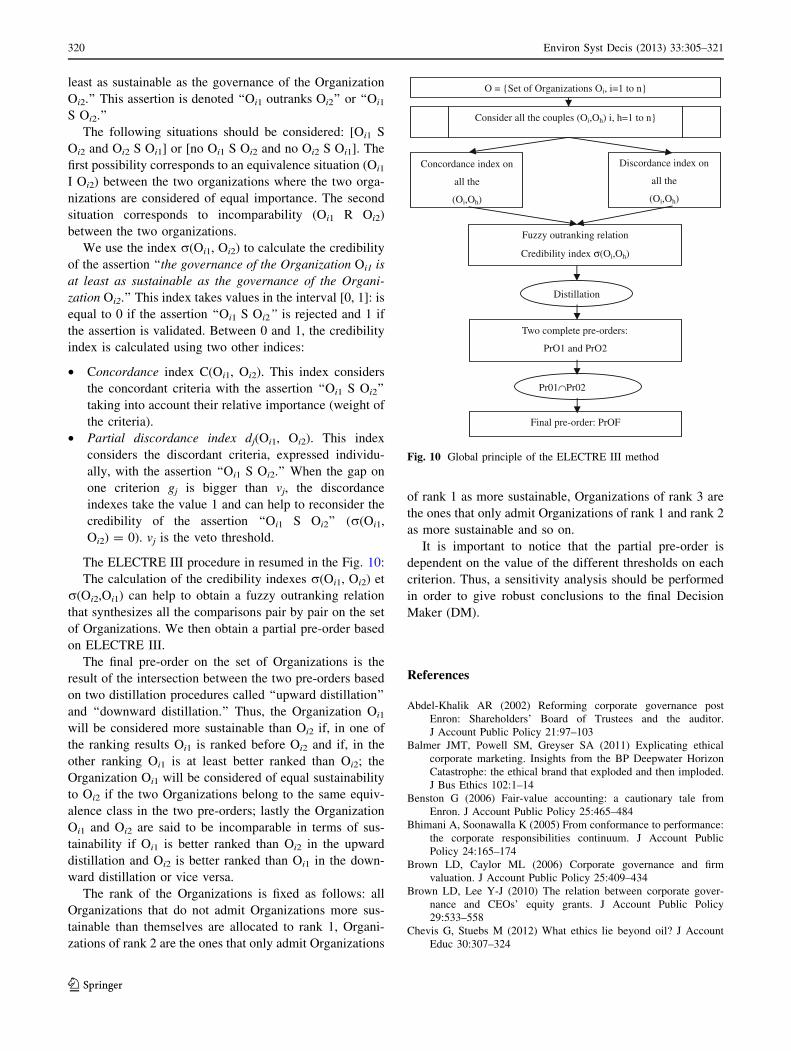

The ELECTRE III procedure in resumed in the Fig. 10:

The calculation of the credibility indexes r(Oi1, Oi2) et

r(Oi2,Oi1) can help to obtain a fuzzy outranking relation

that synthesizes all the comparisons pair by pair on the set

of Organizations. We then obtain a partial pre-order based

on ELECTRE III.

The final pre-order on the set of Organizations is the

result of the intersection between the two pre-orders based

on two distillation procedures called ‘‘upward distillation’’

and ‘‘downward distillation.’’ Thus, the Organization Oi1

will be considered more sustainable than Oi2 if, in one of

the ranking results Oi1 is ranked before Oi2 and if, in the

other ranking Oi1 is at least better ranked than Oi2; the

Organization Oi1 will be considered of equal sustainability

to Oi2 if the two Organizations belong to the same equiv-

alence class in the two pre-orders; lastly the Organization

Oi1 and Oi2 are said to be incomparable in terms of sus-

tainability if Oi1 is better ranked than Oi2 in the upward

distillation and Oi2 is better ranked than Oi1 in the down-

ward distillation or vice versa.

The rank of the Organizations is fixed as follows: all

Organizations that do not admit Organizations more sus-

tainable than themselves are allocated to rank 1, Organi-

zations of rank 2 are the ones that only admit Organizations

of rank 1 as more sustainable, Organizations of rank 3 are

the ones that only admit Organizations of rank 1 and rank 2

as more sustainable and so on.

It is important to notice that the partial pre-order is

dependent on the value of the different thresholds on each

criterion. Thus, a sensitivity analysis should be performed

in order to give robust conclusions to the final Decision

Maker (DM).

References

Abdel-Khalik AR (2002) Reforming corporate governance post

Enron: Shareholders’ Board of Trustees and the auditor.

J Account Public Policy 21:97–103

Balmer JMT, Powell SM, Greyser SA (2011) Explicating ethical

corporate marketing. Insights from the BP Deepwater Horizon

Catastrophe: the ethical brand that exploded and then imploded.

J Bus Ethics 102:1–14

Benston G (2006) Fair-value accounting: a cautionary tale from

Enron. J Account Public Policy 25:465–484

Bhimani A, Soonawalla K (2005) From conformance to performance:

the corporate responsibilities continuum. J Account Public

Policy 24:165–174

Brown LD, Caylor ML (2006) Corporate governance and firm

valuation. J Account Public Policy 25:409–434

Brown LD, Lee Y-J (2010) The relation between corporate gover-

nance and CEOs’ equity grants. J Account Public Policy

29:533–558

Chevis G, Stuebs M (2012) What ethics lie beyond oil? J Account

Educ 30:307–324

O = {Set of Organizations Oi, i=1 to n}

Consider all the couples (Oi,Oh) i, h=1 to n}

Concordance index on

all the

(Oi,Oh)

Discordance index on

all the

(Oi,Oh)

Fuzzy outranking relation

Credibility index σ(Oi,Oh)

Distillation

Two complete pre-orders:

PrO1 and PrO2

Pr01∩Pr02

Final pre-order: PrOF

Fig. 10 Global principle of the ELECTRE III method

320 Environ Syst Decis (2013) 33:305–321

123

Figueira J, Roy B (2002) Determining the weights of criteria in the

ELECTRE type methods with a revised Simos’ procedure. Eur J

Oper Res 139(2):317–326

Frydman B, Hennebel L, Lewkowicz G, di Pascale A, Amado J-C,

Faure N (2007) Self-regulation and co-regulation of corporate

social responsibility in Europe ent/map/05/3.3. Final report

Goodman PS, Ramanujam R, Carroll JS, Edmondson AC, Hofmann

DA, Sutcliffe KM (2011) Organizational errors: directions for

future research. Res Organ Behav 31:151–176

Grappi S, Romani S, Bagozzi R (2013) Consumer response to

corporate irresponsible behavior: moral emotions and virtues.

J Bus Res. doi:10.1016/j.jbusres.2013.02.002

GRI (2000–2006) RG—sustainability reporting guidelines. Version

3.0

ISIS (2009a) PASSO—Deliverable 2.1—Participatory assessment of

sustainable development indicators on good governance from the

Civil Society perspective

ISIS (2009b) PASSO—Deliverables 2.2 et 2.3—Participatory assess-

ment of sustainable development indicators on good governance

from the Civil Society—Report on the protocol for the selection

of indicators and Report on the development of a new list of

indicators perspective

ISO (2010) ISO 26000—Guidance on social responsibility

Jones AM (2003) Managing the gap: evolutionary science, work/life

integration, and corporate responsibility. Organ Dyn 32(1):

17–31

MEDDE and INERIS (2013) Governance guidelines—Governance

indicators « Les guides Gouvernance du Club DDEP—Les

indicateurs de gouvernance des organismes publics en reponse

aux enjeux du developpement durable ». 56 pp. www.develop

pement-durable.gouv.fr/spip.php?page=searchSalleLecture&

query=Gouvernance&motclesaisi=Gouvernance&x=0&y=0&

sort=date?desc&start=

Merad M, Marcel F (2012a) Assessing the governance of the

organizations: risks, resiliencies and sustainable development.

PSAM 11/ESREL 2012. 25–29 June 2012, Helsinki, Finland

Merad M, Marcel F (2012b) The governance of organizations: dealing

with complexity and sustainability demands. Lambda-Mu 18—

La maıtrise des risques des systemes complexes. Tours, 16–18

Oct 2012

Merad M, Verdel T, Roy B, Kouniali S (2004) Use of multi-criteria

decision-aids for risk zoning and management of large area

subjected to mining-induced hazards. Tunnel Underground

Space Technol 19(2):125–138

Merad M, Dechy N, Serir L, Grabisch M, Marcel F (2013) Using a

multi-criteria decision aid methodology to implement sustain-

able development principles within an organization. Eur J Oper

Res 224(3):603–613

OCDE (2004) OECD principles of corporate governance. OECD

Publications Service, Paris

Roy B, Bouyssou D (1992) Aide multicritere a la decision.

Economica, Paris, pp 415–434

UNECE/OECD/Eurostat Working Group on Statistics for Sustainable

Development (2008) Measuring sustainable development. Uni-

ted Nations, New York

Vincent L, Guardiola B, Tsouderos Y, Canet E (2011) Mediator:

who’s to blame? The Lancet 377(9782):11–17

Environ Syst Decis (2013) 33:305–321 321

123