Embed Size (px)

Citation preview

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

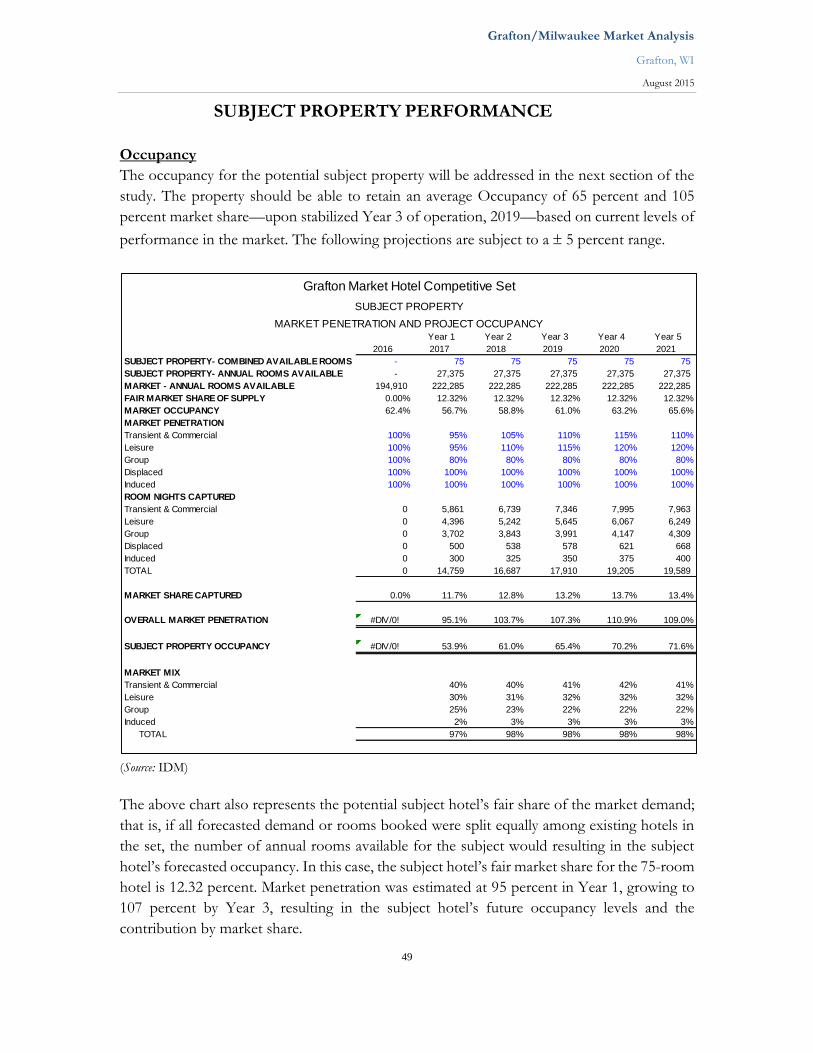

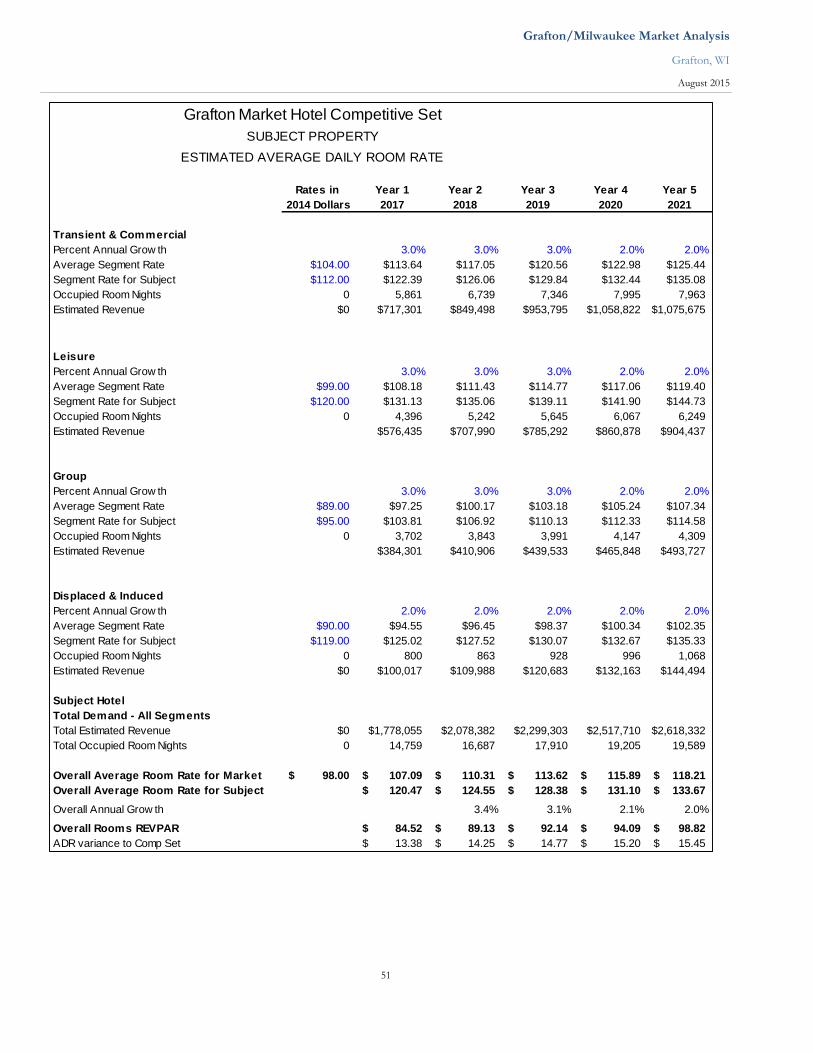

Hotel Market Analysis Project Feasibility

Grafton, WI

Prepared by: Sean Skellie Vice President of Business Analysis IDM Group, LLC Hospitality Consultants (262) 442-4720

Submitted to: Darrell Hofland Village Administrator Village of Grafton PO Box 125 Grafton, WI 53024 (262) 375-5300

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

ii

Market Analysis & Project Feasibility Study Grafton/Milwaukee, WI

Section 1—Executive Summary ........................................................................................................................ 1 Engagement Scope ..................................................................................... 2 Assignment Location—Grafton, WI ........................................................... 5 Subject Site Analysis .................................................................................. 11 Section 3—Regional Economic Investigation .............................................................14 County Economic Overview ......................................................................21 Regional Economic Profile ....................................................................... 22 Economic Conclusions ............................................................................. 27 Section 4—Regional Hotel Market & Competitive Set Analysis ................................ 28 Subject Market Competitive Set ............................................................... 30 STR Historical Trend of the Competitive Set .......................................... 36 Competitive Set Performance Analysis ..................................................... 37 Subject Hotel Competitiveness Factor ..................................................... 39 Seasonal Market Trends of the Competitive Set ...................................... 39 Section 5—Lodging Demand & Segment Penetration Investigation ..........................41 Growth in Lodging Demand..................................................................... 42 Commercial, Group, Transient & Leisure ................................................ 44 Growth in Lodging Demand Projections ................................................. 46 Market Segment Projections ....................................................................................................... Unaccommodated Lodging Demand ....................................................... 47 Section 6—Subject Property Performance .................................................................. 49 Market Segmentation ADR Projections .................................................... 51 Section 7—Lodging Facility Recommendations ........................................................ 52 Property Description and Recommendations .......................................... 54 Section 8—Summary Conclusions............................................................................... 55 Section 9—Conclusions: Feasibility Study Review ..................................................... 56 Property Financial Projections ................................................................. 58 Section 10—Regional Economic Impact .................................................................... 59 Section 11—Certification, Assumptions, and Limiting Conditions Statement ........... 60 Section 12—Glossary of Hospitality Terms ................................................................. 62

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

iii

Addenda

3—Geographical Subject Locations ........................................................................ 3

Location of Milwaukee, WI, in the United States .........................................

Geographic Location of the Grafton/Milwaukee, WI, Area ..........................

Subject Market Within the Village of Grafton, WI ........................................

Competitive Set Within the Region ...............................................................

4—Subject Operating Pro Forma ............................................................................ 4 5— Market Projections & STR Reports .................................................................. 5 6— Room Tax Collection Reports ....................................................................... 6 7— Let Blank 8—IDM 2008 Market Study Financials ................................................................... 8

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

1

EXECUTIVE SUMMARY

The Village of Grafton engaged IDM Group, LLC to produce the following report for the

potential development of an upscale, select-service hotel with meeting and conference facilities

in Grafton, Wisconsin, located in Ozaukee County. The purpose of the study is to analyze the

surrounding community and cities to determine the feasibility of the market and understand

the risks associated with a development. The study is an update to the original study completed

by IDM in 2008 and updated in 2011.

Given the size and pace of the economic activity in Grafton and its surrounding area—the

nearby communities of Mequon and Cedarburg, the location of the subject site and its

proximity to the greater Milwaukee market—it seems apparent that there is a base demand for

a hotel and possible meeting facilities. There was new guest room supply recently added to the

Village of Grafton and competitive subject market. The potential for development in the area

is promising, and IDM is engaged to verify market demand and overall market observation.

This study includes a preliminary Economic Analysis Section that will further verify the

potential of building a hotel in Grafton and Ozaukee County.

Initially, IDM is engaged to provide a Competitive Market Overview, a Comprehensive

Statistical Market Study, and all project economics from operations to development. This

includes operational speculations providing an overview of market, potential development

information concerning the Grafton market area, and market factors that would affect the

possible development of a hotel at this location. The goal is to provide a Competitive Market

Overview, a Comprehensive Statistical Market Study, and all Project Economics—from

operations to development—on operational speculations.

Given the consultants’ development experience, existing hotel management, and knowledge

of the hospitality industry, they are fully aligned to develop first-class hotels and qualified to

offer market analyses. All parties remain confident that an independent review of this report

would support our findings.

This report may or may not be acceptable for external investing and/or lending purposes and

may depend upon this market’s ability to support this hotel, additional requirements, and the

desire for more specific information.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

2

ENGAGEMENT SCOPE

This study presents the current and potential demand for hotel accommodations and analysis

of existing facilities in the Grafton market and the greater surrounding competitive market. It

recommends the scope and general characteristics of the hotel and other project amenities to

complement the development. These characteristics will be driven by architectural site

limitations, functionality of the operation, and the market’s ability to sustain the business.

Process Overview and Scope

For market analysis, the consultants interviewed area businesses and data from the Convention

and Visitors Bureau, regional developers, major franchise chains, and independent hotel

facilities regarding the status of their businesses and future plans for each market addressed in

the analysis. Forecasts were made based on the market’s historic performance, the growth in

demand, and anticipated supply. The proposed hotel’s accommodation occupancy levels

through the first several years of operation are based on those historical trends.

The market analysis determines the current and potential market for hotel accommodations

and amenities, including the necessary components, and further determines the appropriate

size, positioning, and scope of facilities to best serve the market, including market share and

competitive advantages and disadvantages. These recommendations will be presented in a

narrative and tables that set forth the hotel description, meeting space, breakout rooms, largest

room, potential mix and type of guest rooms, recommended facilities and amenities, and other

commentary on the development of a conferencing facility. The consultants will also identify

recommended price points and estimated levels of utilization.

Based on recommendations regarding project design, the consultants will prepare a

consolidated statement of estimated annual operating results for the proposed facility,

complete with sources and level of revenues, related and unallocated expenses for the property

through available cash flow for debt service and return on equity. The estimate will address a

typical year in the property’s operation in current value dollars and set forth the anticipated

first several years of operating results in inflationary dollars.

The first step of this process involved an extensive market visit and tour. We identified the

site location and existing facility conditions, reviewed site goals, possibilities, objectives, and

the competitive markets to be analyzed.

To be competitive and successful within a subject market is of major importance. We provide

factors important to this hotel’s success and address factors necessary for the hotel’s site. The

factors that we address in the market study are:

Project site and its accessibility.

Visibility from various points.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

3

Regional demand generators and their impact.

Benefit of support amenities and services, once expanded.

Facility amenities and design enhancements to the existing product.

General economics of the proposed market and operating hotel.

Comparison to competitive hotels’ characteristics.

Continuity with your overall development strategy or Master Plan.

Lodging demand within the subject market and property market share.

Competitive set investigation and comparison.

The conclusion of this analysis includes:

A review of the statistical history of competitive hotels within the market.

Forecast of occupancy, ADR, and revenue trends for the subject market and potential

subject property.

Detailed operational projections for sales and expenses for guest rooms, and food and

beverage such as banquet and catering departments. We will also review past and

current trends to industry averages.

Market segment contribution projections to determine hotel amenities.

Ten-year operational profit & loss and sales projections, evaluated in today’s dollar.

Economic impact within the region.

Research This report focuses on the supply and demand in hotel accommodations within the subject

market. To best understand the current market dynamics and relative positioning of potential

development, we looked at current demographics, market analysis from independent

resources, and a physical inspection of the most competitive and comparable hotels, meeting,

and banquet facilities. Our research identified the historic and projected occupancy, Average

Daily Rate (ADR), market segmentation mix, and operational positioning of the project. Our

research leads to the review of the facilities, amenities, services, and general condition of the

competition to position the hotel.

Similar trends affect the economics of hotel operations and the demand for hotel

accommodations. To forecast these operational projections, we used industry standards,

relevant data from managed properties, area demographics, and industry statistics. To

determine if the business environment could sustain the added hotel supply, we gathered and

analyzed relevant data such as current and proposed demand generators, population growth

and demographics, and employment growth. This information is found in the Hotel Lodging

Demand section.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

4

Market Performance and Facilities Recommendations

The consultants utilized independent statistical data to project both the supply of and the

demand for hotel lodging and meeting facilities in the competitive set or potential market. The

consultants looked at the market history and considered the viability of a subject facility based

on market trends.

Next, in detailed fashion, we project the occupancy, average rate, and revenues for the first 10

years of operation based on historical trends within the subject market. We used those

projections to recommend the size, type, and characteristics of the hotel and the amenities

offered. We will meet with you to discuss the feasibility and align various interests of the

developer and operator.

Development Costs & Operational Costs: Economic Analysis

The Economic Analysis was not part of the original proposal in the market study but could

be expanded to show development and construction estimates based on our experience and

industry-supplied data (such as industry averages) to complement the revenue and expense

pro forma analysis for this hotel project. These figures will be compared with the estimated

development costs for a full understanding of risk level. Whole debt service assumptions and

equity return are not modeled or directly addressed.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

5

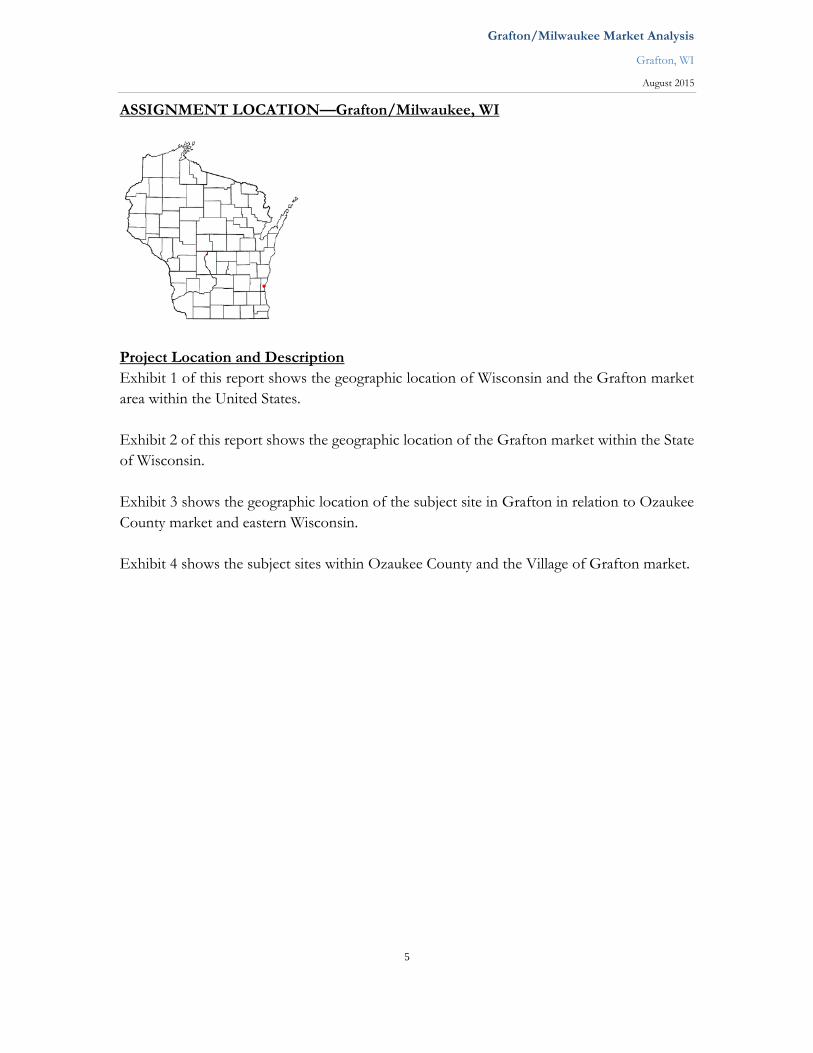

ASSIGNMENT LOCATION—Grafton/Milwaukee, WI

Project Location and Description

Exhibit 1 of this report shows the geographic location of Wisconsin and the Grafton market

area within the United States.

Exhibit 2 of this report shows the geographic location of the Grafton market within the State

of Wisconsin.

Exhibit 3 shows the geographic location of the subject site in Grafton in relation to Ozaukee

County market and eastern Wisconsin.

Exhibit 4 shows the subject sites within Ozaukee County and the Village of Grafton market.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

6

Grafton, Wisconsin, Overview

Grafton is a village in Ozaukee County, WI, United States. The last census reported the

population at 11,467. The village is adjacent to the Town of Grafton and the City of

Cedarburg. Grafton is situated at the eastern end of the state at the intersection of Highway 60

and Interstate 43, the main north/south corridor for the region, and offers a high quality of

personal and economic lifestyle that draws people and businesses alike to this community.

Grafton offers a diverse array of stores, shops, restaurants, and industrial enterprises along

with a variety of recreational activities. This popular suburb, just 20 miles north of Milwaukee,

has experienced a great deal of development over the last 10 years.

The Village is 4.53 square miles in size and was incorporated in 1896.

1900s to the Present

Grafton has developed into a community of varied industries, including fabricated metal and

plastic products, machinery, printing and publishing, electric and electronic equipment, and

various other manufacturing concerns.

Grafton Today

Grafton is a desirable community of relative wealth and small-town charm. Located an easy

commute north of Milwaukee, a hub of economic activity in Wisconsin, this Village is a great

place to live, work, and play. The community tagline is “Quality Life. Naturally.”

Ozaukee County History In the early 1800s, the only residents of Ozaukee County were Potawatomi and Menominee

Indians. The land comprising Ozaukee County was part of Milwaukee County, Michigan

Territory. In 1835, Michigan Territory was in the midst of petitioning Congress to become a

state. One of the requirements was that Michigan assist Wisconsin in becoming a separate

territory. The U.S. government moved the process along by advertising land for public sale in

Wisconsin, prompting thousands of New Englanders to come to Wisconsin. People traveled

by way of the Great Lakes on ships to Wisconsin where they found cheap land at $1.25 per

acre.

Rich deposits of limestone and excellent fishing led to early development of quarries and

harbors. Early settlers formed trails through Ozaukee County, which became major

transportation routes to other areas of the state. Two Indian trails met in an area that grew to

become the Village of Saukville. The old Green Bay Road served as the primary pathway

between Milwaukee and Green Bay. Numerous small communities grew along the original

trail to support the travelers, including an unincorporated area known as Hamilton in the

Town of Cedarburg.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

7

Fertile ground, moderate temperatures, and numerous small creeks and streams prompted

development of agriculture and dairy farming. Octagonal stone barns were commonplace

throughout the county, several of which remain standing today as evidence of this cultural

heritage. Larger, modern farm buildings in use today dwarf these historic smaller buildings.

Today

Ozaukee County’s 2010 census population was 86,395. Its county seat is Port Washington.

Ozaukee County has the smallest land mass of any county in the State of Wisconsin. The

county covers 235 square miles of land area. Located on 25 miles of the western shore of Lake

Michigan, the county encompasses approximately 900 square miles of Lake Michigan waters.

The greater community, as listed below, has a varied industry base that includes fabricated

metal, plastic products, machinery, printing, and various other manufacturing.

As of the 2000 Census, Ozaukee County had the second-lowest poverty rate of any county in

the United States, at 2.6 percent. In terms of per capita income, it is the 25th wealthiest county

in the country, as determined by the U.S. Census Bureau. Bolstered by low crime rates and

school districts with high graduation rates, Forbes Magazine ranked Ozaukee County No. 2 on

its list of “America's Best Places to Raise a Family” in June 2008.

Milwaukee, WI, Overview Milwaukee, Grafton’s neighboring city to the south, is a community where history celebrates

life. From its obscure beginnings as an Indian settlement and its hopeful days as a booming

Great Lakes port, Milwaukee has emerged as a stronghold of industries and immigrants,

displaying bold experiments in municipal government and a gradual immersion in national and

global affairs.

By the early twentieth century, Milwaukee had developed a national reputation based on three

related hallmarks: Germanism, Socialism, and beer. Today, all three have faded in

importance—but, as the new century began, the Milwaukee Idea retains a thoroughly

distinctive sense of place. Choice and circumstance have combined to produce a unique

community, one whose character reflects influences as diverse as Harley-Davidson and Pabst

Blue Ribbon, Golda Meir and Father Groppi, the German revolutionaries of 1848 and the

Milwaukee Braves of 1957. (Source: Historian John Gurda from his book The Making of Milwaukee.)

History of the City of Milwaukee

Milwaukee is the largest city within the State of Wisconsin and 26th largest in the United States

based on population. Located on the southwestern shore of Lake Michigan, the city is the

county seat of Milwaukee County. As of the 2010 U.S. Census estimate, Milwaukee County

had a population of 947,735. Milwaukee is the main cultural and economic center of the

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

8

Milwaukee–Racine–Waukesha Metropolitan Area with a population of 1,533,034 as of the

2010 census. Milwaukee is also the regional center of the seven counties that comprise the

Greater Milwaukee Area, with an estimated population of 2,014,032 as of 2008.

The first Europeans to pass through were French missionaries and fur traders. In 1818,

Frenchman Solomon Juneau settled in the area, and in 1846, Juneau’s town combined with

two neighboring towns to incorporate as the City of Milwaukee. Large numbers of German

and other nationalities’ immigrants helped increase the city’s population during the 1840s and

the following decades.

Milwaukee residents are known as Milwaukeeans. Milwaukee is known as “The City of

Festivals” for its great number of ethnic and musical festivals, the largest of which is

Summerfest. It has also been called “Brew City” due to Milwaukee having been home to

several major breweries throughout its history.

1960 to the Present

Milwaukee, like many northern industrial cities, continued to grow vigorously until the late

1950s. Milwaukee was home to immigrants from Ireland, Germany, Hungary, Poland, and

other Central European nations. There was also great northward migration of African

Americans from the Southern United States. With the large influx of immigrants, Milwaukee

became one of the 15 largest cities in the nation, and by the mid-1960s, its population reached

nearly 750,000. Starting in the late 1960s, like many cities in the Great Lakes “rust belt,”

Milwaukee saw its population start to decline due to various factors, including the loss of blue-

collar jobs and the phenomenon of “white flight.”

In recent years, the city began to make strides in improving its economy, neighborhoods, and

image, resulting in the revitalization of neighborhoods such as the Historic Third Ward, the

East Side and, more recently, Bay View, along with attracting new businesses to its downtown

area. The city continues to make plans for increasing its revitalization through various projects.

In 2006—largely due to its efforts to preserve its history—Milwaukee was named one of the

“Dozen Distinctive Destinations” by the National Trust for Historic Preservation. The city is

also home to the Milwaukee Bar Association, the fourth oldest of such organization in the

United States. Founded in 1858, it now has more than 2,600 members.

Like other historically industrial northern cities, Milwaukee has taken steps over the past few

years to reshape its image, in large part by reviving its downtown. In the past decade, new

additions to downtown have included the Riverwalk, the Frontier Airlines Center (formally

the Midwest Airlines Center), Miller Park, an internationally renowned addition to the

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

9

Milwaukee Art Museum, and Pier Wisconsin, as well as the major renovations to the

Milwaukee Auditorium and U.S. Cellular Arena.

Businesses in Milwaukee

Once known almost exclusively as a brewing and manufacturing powerhouse, Milwaukee has

taken steps in recent years to reshape its image. In addition to the major venues mentioned,

the city has many new skyscrapers, condos, lofts, and apartments, all constructed in

neighborhoods on and near the lakefront and riverbanks.

Greater Milwaukee markets nationally and internationally to tourists and to convention and

meeting planners, dedicated to ensuring its guests are warmly welcomed and enjoy an enriching

experience in this jewel of the Great Lakes. VISIT (the GMCVB-Greater Milwaukee

Convention and Visitors Bureau) has nearly 700 members, including hotels/motels,

restaurants, attractions, services, and other area businesses. Tourism generated $2.3 billion in

spending in Greater Milwaukee in 2009 and supported more than 57,813 local jobs. The Spirit

of Milwaukee and Potawatomi Bingo Casino are strategic partners with VISIT Milwaukee,

providing funding support for conventions and tourism programs.

Major Industries and Commercial Activity

As a commercial and industrial hub for the Great Lakes region, Milwaukee is home to six

Fortune 1000 manufacturers—including Harley-Davidson, Inc., Rockwell Automation, and

Johnson Controls—banks, and diversified service companies as well as one of the nation’s 10

largest insurance firms. The metropolitan area places among the top manufacturing centers in

the United States, ranking second among major metropolitan areas in the percentage of its

workforce in manufacturing. The economy is dominated by small- to medium-size firms with

representatives in nearly every industrial classification.

Metropolitan area firms are engaged primarily in the manufacture of machinery. Contrary to

Milwaukee’s reputation as a brewery capital, less than 1 percent of the city’s industrial output

is related to brewing. In recent years, the metro region has earned a reputation as a center for

precision manufacturing. It leads the nation in the production of industrial controls, X-ray

equipment, steel foundry parts, and mining machinery. The area is also considered a printing

and publishing center, housing more than 11 percent of the top 70 printing companies in

North America. Publishers and printers combined employ more than 21,000 people, about

2.5 percent of the workforce.

Professional and managerial positions are the fastest-growing occupations in Milwaukee,

accounting for almost 27 percent of the workforce. Service businesses constitute the largest

sector of the local economy, and healthcare positions account for about 27 percent of service

sector jobs. The area is home to four major multi-hospital health systems. Other major areas

of service employment include business services (27 percent), educational services (7 percent),

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

10

and social services (10 percent).

Nearly a quarter of Wisconsin’s high-tech firms, employing more than one-third of the state’s

technology industry staff, are located in Milwaukee County. Between 1990 and 1999,

Milwaukee led Wisconsin in the creation of high-tech jobs, adding 10,000 positions.

Milwaukee’s healthcare industry includes several health systems. The Milwaukee Regional

Medical Complex, located between 8700–9200 West Wisconsin Avenue, is on the former

Milwaukee County Fairgrounds. This area includes the Children’s Hospital of Wisconsin,

Froedtert Hospital, Blood Center of Wisconsin, the Ronald McDonald House, Curative

Rehabilitation, and the Medical College of Wisconsin. Children’s Hospital of Wisconsin was

ranked in the top three children’s hospitals in the United States in 2006. Aurora Health Care

includes St. Luke’s Medical Center, Aurora Sinai Medical Center, West Allis Memorial, and St.

Luke’s South Shore. Wheaton Franciscan Healthcare includes St. Joseph’s Hospital, Elmbrook

Memorial (Brookfield), and others in the Milwaukee area. Columbia St. Mary’s Hospital is on

Milwaukee’s lakeshore and has established affiliations with Froedtert Hospital and the Medical

College of Wisconsin. The Medical College of Wisconsin is one of two medical schools in

Wisconsin and the only one in Milwaukee.

Tourism is also a major contributor to the local economy. Milwaukee hosts many festivals and

parades throughout the year and is home to nationally recognized museums, a zoo,

professional sports teams, and entertainment venues. All together, these attractions bring more

than 5 million tourists and generate $1.9 billion annually.

Items and goods produced: automobile frames and parts, heavy pumping machinery, gas

engines, heavy lubricating and agricultural equipment, large mining shovels, dredges, sawmill

and cement machinery, malt drinks and products, packaged meat, boots, shoes, leather

products, knit goods, women’s sportswear, gloves, children’s clothes, diesel engines,

motorcycles, outboard motors, electrical equipment, products of iron and steel foundries, and

metal fabricators.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

11

SUBJECT SITE ANALYSIS

The market being studied in this analysis is the Village of Grafton, WI. The area started as a

lumber town. Grafton is located at the crossroads of two major highways. The downtown area

of Grafton is located on the Milwaukee River.

Safety The area is regarded as a safe community. Surrounding residents in this area are mostly families

and professionals. Crime rate in the Grafton Market has an index average of 72 compared to

the average index in the US at 323.2, as reported by the FBI Crime Index in 2006. There has

been no violent crime recently committed and most reported were 150+ incidences of

property crimes. According to MOVOTO a website that uses statistics and the 2012 FBI

Uniform Crime Report to compare crime data; the Village of Grafton was rated the 6th safest

in the state.

The downtown Milwaukee market is regarded as a borderline area and an area of concern.

Violent crime in Milwaukee has declined substantially since the late 1990s. For several years,

Milwaukee ranked among the 10 most dangerous large cities in the United States, although in

recent years, it no longer appears even among the 25 most dangerous cities. However, despite

its improvements, Milwaukee still fares worse than average when comparing specific crime

types to the national average (e.g., homicide, rape, robbery); only aggravated assaults occur less

frequently in Milwaukee than the national average. In 2008, Milwaukee’s homicide rate fell to

a 23-year low, according to the Milwaukee Journal Sentinel, which credits targeted policing,

cooperation among law enforcement agencies, and a focus on gang violence as main reasons

for the decline.

Safety in the City Center has driven residents, retail, jobs, and development to neighboring

suburbs such as Grafton.

Visibility In the 2008 study performed by IDM, two sites were considered regarding site visibility. The

first site, occupying a downtown geographical area, has less visibility from one of the region’s

busiest interstates, Interstate 43. The secondary development site considered is positioned

parallel to the Interstate 43 corridor. This area has seen significant retail, medical, and office

development in the past few years. Traffic counts indicate over 25,000+ vehicles travel pass

the site daily. The idea of a downtown hotel seems intriguing and yet not practical. The

Interstate 43 interchange has grown significantly and its visibility and access to traveler support

services lends a higher degree of compatibility than a downtown location. The village has

multiple sites and it is our opinion that visibility will be important to the hotel’s success.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

12

Accessibility

The Village of Grafton is located off Interstate 43, a major state throughway in the State of

Wisconsin, and is easily accessible by automobile or air travel. Below is a list of major regional

cities, their distances, and approximate drive times to Grafton:

Milwaukee—24 miles (½ hour)

Chicago—112 miles (2 hours)

Minneapolis—356 miles (5¾ hours)

Madison—97 miles (1¾ hours)

Green Bay—95 miles (1½ hours)

Indianapolis—273 miles (4½ hours)

Air Transportation

The closest major international airport that grants access to the Grafton market is the

Milwaukee airport, General Mitchell. Milwaukee is home to two airports: General Mitchell

International Airport on the southern edge of the city, and the smaller Timmerman Field on

the north side. Mitchell is served by a dozen airlines that offer roughly 250 daily departures

and 245 daily arrivals. Approximately 115 cities are served nonstop or direct from Mitchell

International, which is the largest airport in Wisconsin. The airport terminal is open 24 hours

a day.

In August of 2010, the airport had the largest average airfare decline (cost of tickets) in the

country’s top 100 airports in the first quarter of the year. This was related to the aggressive

expansion of Air Tran and Frontier Airlines, combined with the entrance of Southwest

Airlines into the market. Fares are so reasonable, the airport is finding an increase of region

travelers to the airport, making it a regional choice (regarding accessibility and affordability)

over Chicago’s airports.

Milwaukee County executives announced that an all-time one-month high number of

passengers traveled through General Mitchell International Airport in June 2010. It was the

first month in which the airport served more than 900,000 passengers, with a count of 922,984,

an increase of 212,197 (+29.86 percent) over last June’s 710,767 passengers. The June total

marks 10 straight months of record passenger growth and beats the previous one-month high

of 896,598 passengers in March 2010.

In the first half of 2010, the airport served 1,225,221 more passengers than over the same

period in 2009, a 34.41 percent increase from the 3,560,224 passengers. The increase of

travelers has a direct effect on tourism spending in the Greater Milwaukee area.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

13

In October 2008, a Condé Nast Traveler poll ranked Milwaukee County’s General Mitchell

International Airport fourth in the nation in the categories of Location and Access, Design,

Customs and Baggage, Perceived Safety and Security, as well as Food, Shops and Amenities.

Train and Bus Transportation

The Milwaukee Intermodal Station

Milwaukee’s Amtrak station was renovated in 2007 to create the Intermodal Transportation

Station near downtown Milwaukee and the Third Ward. The renovated station hosts Amtrak,

Greyhound Lines, and Jefferson Lines intercity bus transportation. Milwaukee is served by the

Hiawatha Amtrak express service up to seven times daily between downtown Milwaukee and

downtown Chicago, including a stop at the Milwaukee Airport Rail Station, Sturtevant (near

Racine), and Glenview, IL. Amtrak operates its Empire Builder passenger train daily between

Chicago and the Pacific Northwest, with stops near Madison, Wisconsin Dells, and

Minneapolis.

The Badger Bus and station in downtown Milwaukee provides bus service between Milwaukee

and Madison. Stops include the UW-Madison Memorial Union, Madison Bus Depot, Johnson

Creek, Goerkes Corners, Milwaukee 84th St., Milwaukee Bus Depot (downtown Milwaukee),

and Milwaukee Airport.

Education

Higher Education

Milwaukee has one of the highest per capita student populations, ranking sixth among U.S.

and Canadian cities in number of college students per 100 residents, according to a January

2000 study from McGill University.

Primary and Secondary Education

Milwaukee maintains Milwaukee Public Schools (MPS), the largest school district in Wisconsin

and fifth in the nation. As of 2007, it had an enrollment of 392,395 students and as of 2006,

employed 11,100 full-time and substitute teachers in 323 schools. Milwaukee Public Schools

operate as magnet schools, with individualized specialty areas for interests in academics or the

arts. (Source: Wikipedia.com)

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

14

WISCONSIN REGIONAL ECONOMIC INVESTIGATION

Tourism and Demand Generators

It is our intent to measure the strength of regional tourism the Greater Milwaukee market.

Tourism is the region’s primary source of revenue and is represented by the local

accommodations. Later in the report we document the trends of occupancy in the area and

greater region. The area has long been a tourist market and popular destination for seasonal

travel and vacation homes.

Tourism plays a vital role in the county, and businesses that cater to tourism—such as resorts,

hotels, campgrounds, bed & breakfasts, and retail stores—complement the hundred miles of

biking trails as well as the many parks, golf courses, historic sites, and area attractions.

Wisconsin’s Tourism Investment

In this section of the market study, we will define the current level of tourism-related business

within the state as provided in the Wisconsin Economic Impact Industry Report 2015

completed by according to research conducted by Tourism Economics and Longwood’s

International.

In 2014, Wisconsin’s $18 billion tourism industry remained one of the core strengths of the

state’s economy. The rise in visitor spending and overall travelers was up significantly, based

on the state’s impact report delivered in April 2015. The report published the following

statistics:

Tourism activity in the state was up $1 billion, from $17.5 billion in 2013 to $18.5

billion in 2014. This 5.5% growth was prompted by increases in both visits and

spending per trip.

The past four years have been outstanding for Wisconsin’s tourism industry. Since

2010, tourism activity is up by $3.7 billion, a 25% increase. This is the first time in

four years that all 72 counties posted a positive increase in visitor spending.

Visitor growth in 2014 topped 102 million, an increase of 7 million visits since 2010.

Other positive industry indicators included a 5.3% increase in per trip spending led by

recreation and entertainment (7.8%), lodging (7.2%), and food and beverage (6.4%).

Wisconsin’s lodging sector had their strongest year since 2011, with room demand

growing by 3.5% and average room rates increasing by 3.7%.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

15

Traveler spending is a significant source of employment and taxes. Largely comprised

of small businesses, travel and hospitality jobs can’t be outsourced or exported.

Tourism supported 187,643 jobs with a total personal income of $4.8 billion. The

tourism industry added over 6,200 jobs to Wisconsin’s total employment since 2011.

Visitors generated $1.4 billion in state and local revenue, saving Wisconsin taxpayers

$620 per household.

Tourism plays a vital role in Wisconsin. Travel and tourism is a revenue-generating machine

for state and local governments. It is the main employer in many communities throughout the

state, providing stability and diversity, and complementing manufacturing, agriculture, and the

state’s knowledge-based sectors.

Marketing Wisconsin

For every $1 the Department spent on summer and fall advertising in 2012, $6 was

returned to the state in additional tax revenue.

Tourism generates a positive impression of the state’s image, which is critical for

economic development.

Longwood’s International conducted research to measure how tourism advertising

and visitation influences consumers’ perception of the state. Travelers who have

visited Wisconsin in the past two years rate the state much higher in attributes such as

a good place to live, start a business, attend college, or purchase a retirement home

than those who have not visited the state.

The Department markets the state as the premier destination for fun, whether it’s

leveraging the power of celebrities with Wisconsin ties in ad campaigns, bringing in

the nation’s top travel writers to experience our destinations, providing reliable and

inspiring travel information to potential visitors, or attracting lucrative sporting events,

meetings and conventions.

The most recent TV ad starring UW Madison basketball coach Bo Ryan aired during

the Big Ten and NCAA Championships and received over 6 million impressions. In

addition, it has been viewed online over 526,000 times, a record for any ad in the

Department’s history.

Last year’s public relations efforts generated over $114 million in earned media with

coverage in The New York Times, Chicago Tribune, Singapore Times, the Miami

Herald, the Japan Times, the Washington Post and the LA Times. Over the last four

years, earned media topped $284 million.

A record 5 million users visited TravelWisconsin.com, an increase of 146%.

The Department’s public relations, social media and marketing efforts have garnered

65 state, regional, national and international awards and recognitions since May 2011.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

16

The Tourism Outlook for 2015

U.S. travel is returning to high levels of optimism with positive travel intentions for

2015. In fact, 32% of U.S. leisure travelers plan to increase their travel spending in

2015 and 57% indicate they plan to spend about the same according to the “State of

the American Traveler” survey.

Lower gas prices have produced a positive impact on consumers’ discretionary

incomes and travel habits.

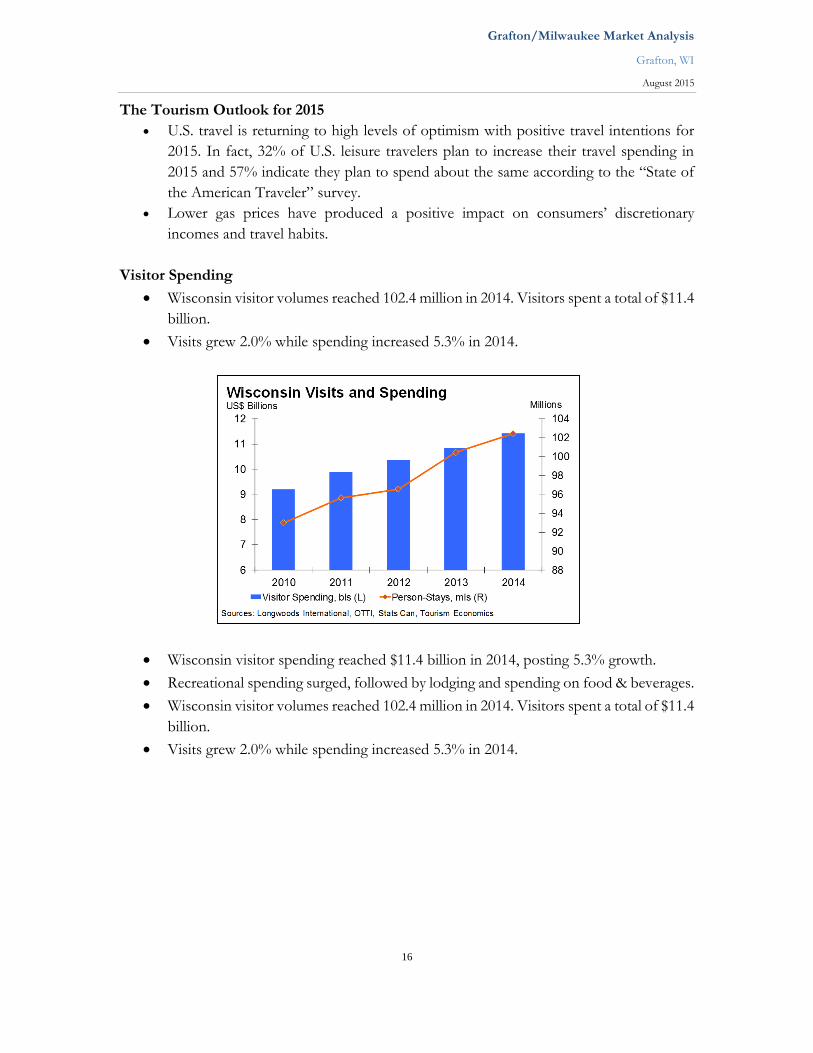

Visitor Spending

Wisconsin visitor volumes reached 102.4 million in 2014. Visitors spent a total of $11.4

billion.

Visits grew 2.0% while spending increased 5.3% in 2014.

Wisconsin visitor spending reached $11.4 billion in 2014, posting 5.3% growth.

Recreational spending surged, followed by lodging and spending on food & beverages.

Wisconsin visitor volumes reached 102.4 million in 2014. Visitors spent a total of $11.4

billion.

Visits grew 2.0% while spending increased 5.3% in 2014.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

17

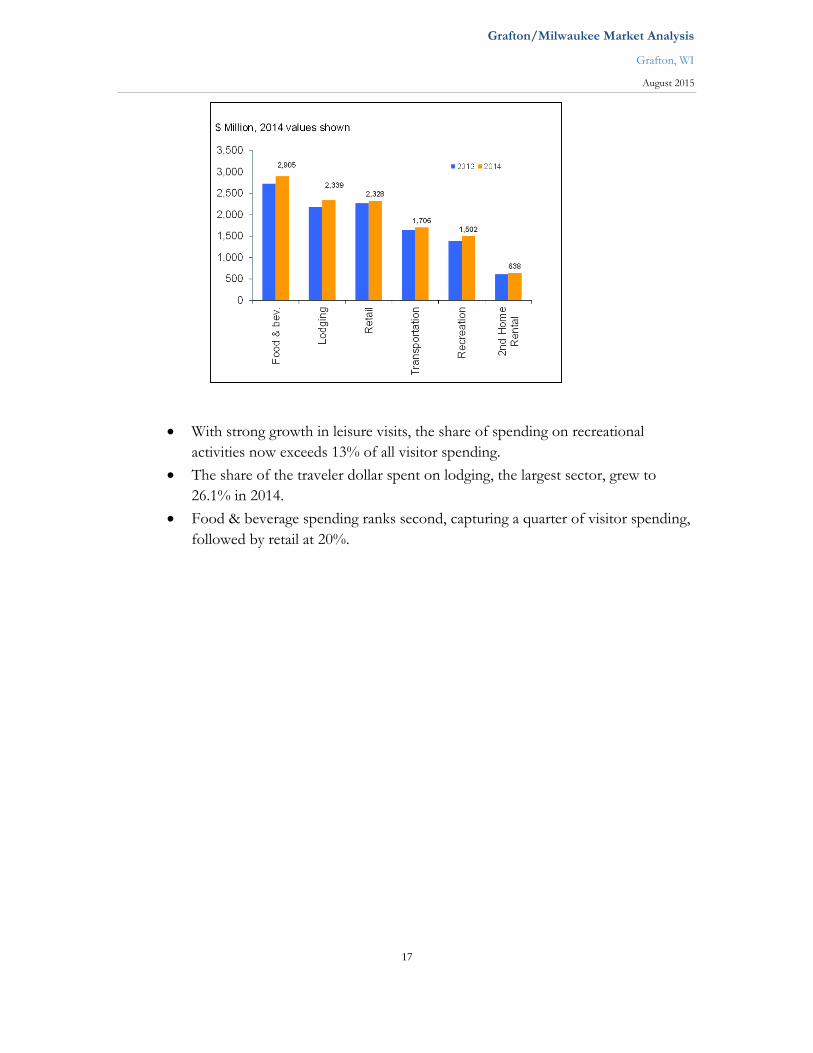

With strong growth in leisure visits, the share of spending on recreational

activities now exceeds 13% of all visitor spending.

The share of the traveler dollar spent on lodging, the largest sector, grew to

26.1% in 2014.

Food & beverage spending ranks second, capturing a quarter of visitor spending,

followed by retail at 20%.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

18

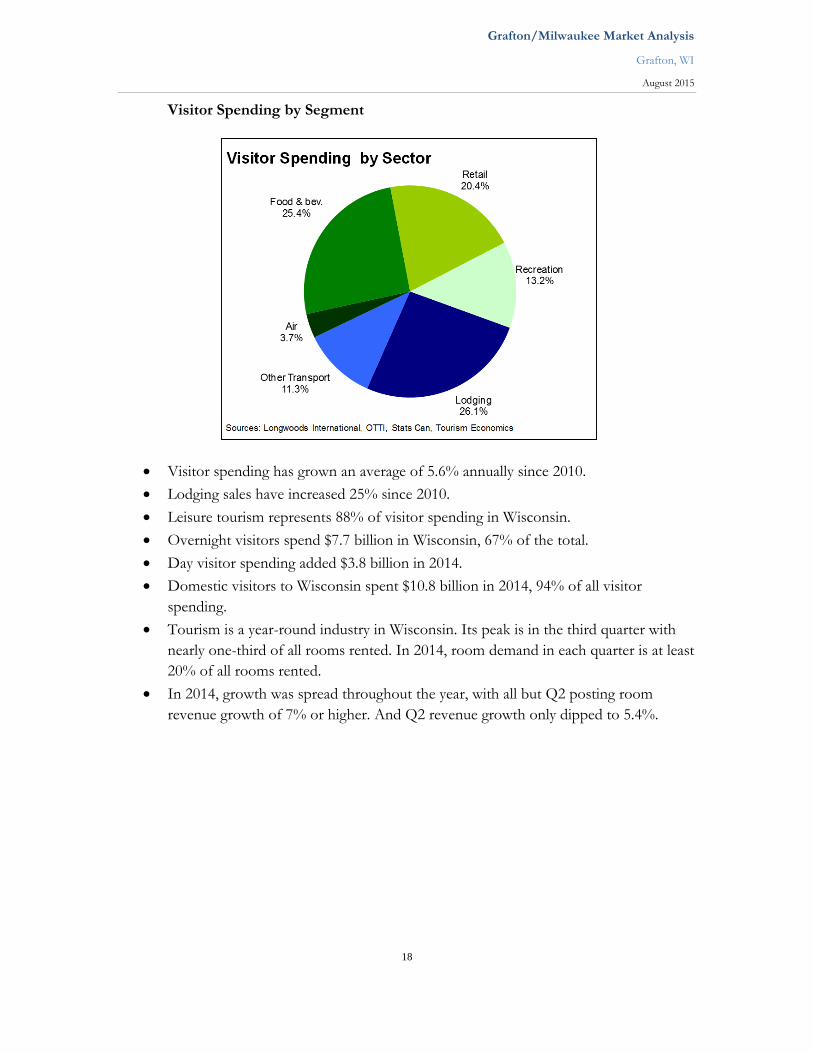

Visitor Spending by Segment

Visitor spending has grown an average of 5.6% annually since 2010.

Lodging sales have increased 25% since 2010.

Leisure tourism represents 88% of visitor spending in Wisconsin.

Overnight visitors spend $7.7 billion in Wisconsin, 67% of the total.

Day visitor spending added $3.8 billion in 2014.

Domestic visitors to Wisconsin spent $10.8 billion in 2014, 94% of all visitor

spending.

Tourism is a year-round industry in Wisconsin. Its peak is in the third quarter with

nearly one-third of all rooms rented. In 2014, room demand in each quarter is at least

20% of all rooms rented.

In 2014, growth was spread throughout the year, with all but Q2 posting room

revenue growth of 7% or higher. And Q2 revenue growth only dipped to 5.4%.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

19

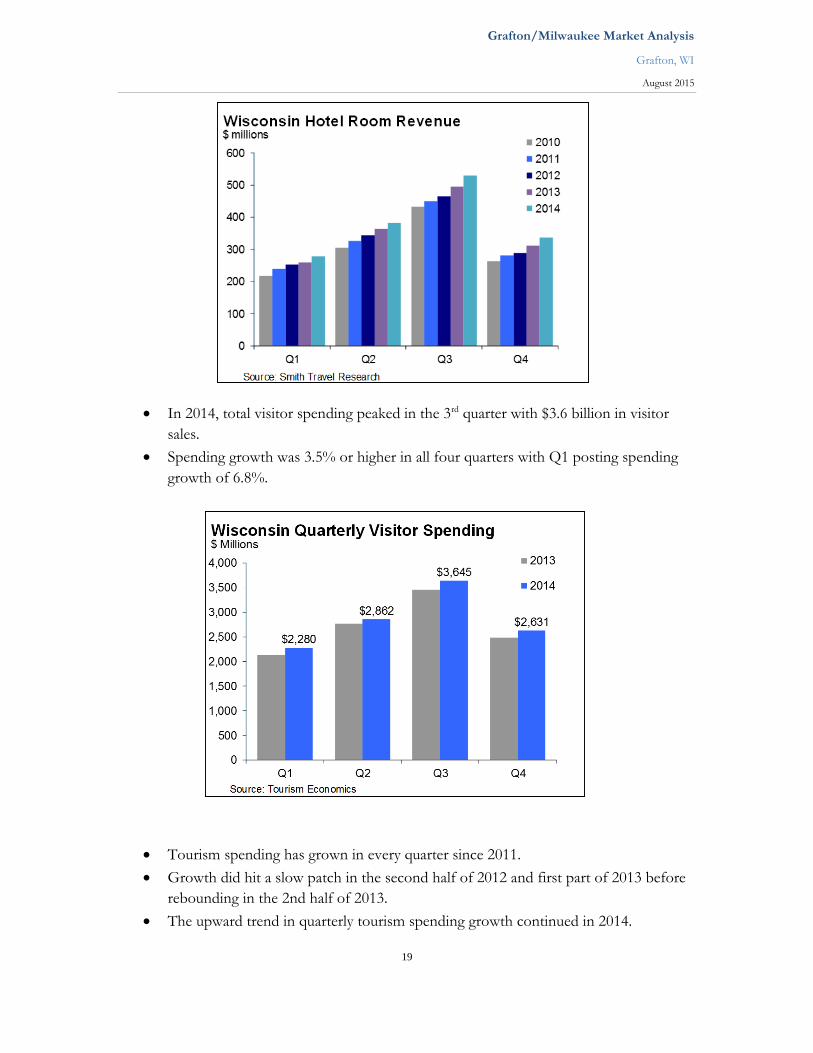

In 2014, total visitor spending peaked in the 3rd quarter with $3.6 billion in visitor

sales.

Spending growth was 3.5% or higher in all four quarters with Q1 posting spending

growth of 6.8%.

Tourism spending has grown in every quarter since 2011.

Growth did hit a slow patch in the second half of 2012 and first part of 2013 before

rebounding in the 2nd half of 2013.

The upward trend in quarterly tourism spending growth continued in 2014.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

20

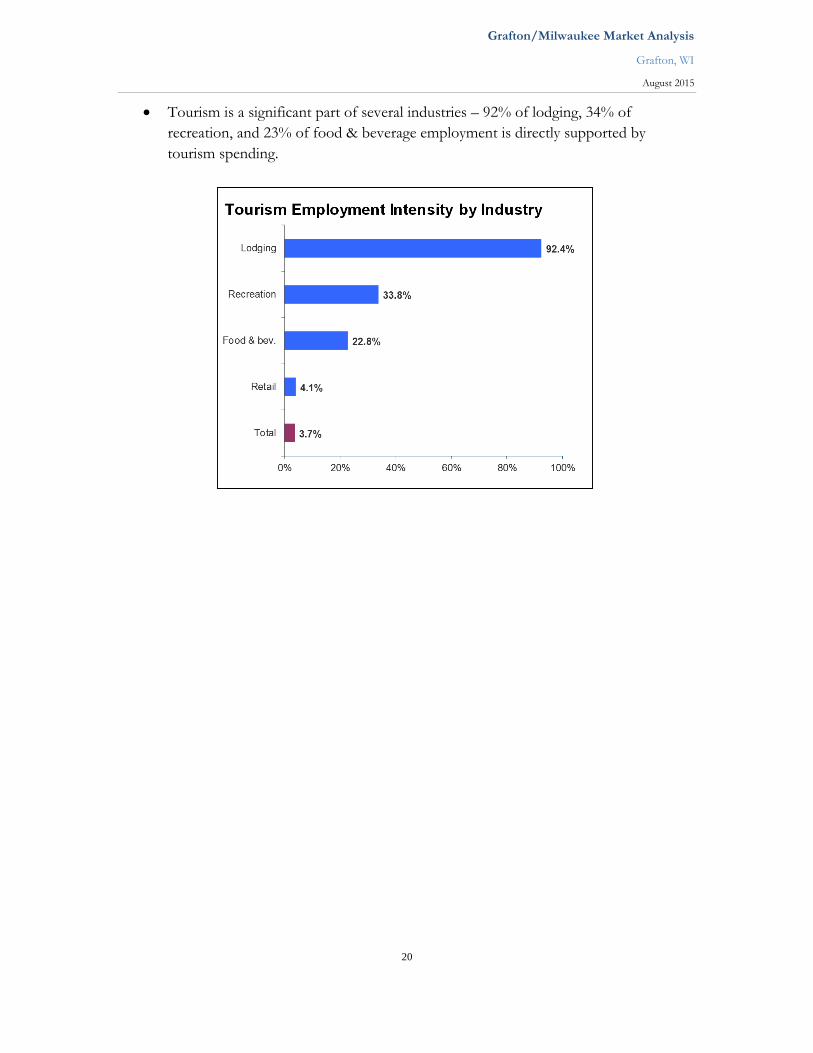

Tourism is a significant part of several industries – 92% of lodging, 34% of

recreation, and 23% of food & beverage employment is directly supported by

tourism spending.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

21

Ozaukee County Tourism Overview

The following information is specific to the subject market in county regional markets, as

reported in the Annual 2015 Wisconsin Tourism’s Economic Impact Study published in

May 2014.

Tourism spending in Ozaukee County as it relates to direct visitor spending was up 3.49%

to $87.6 million in 2014 compared to a 5.34% increase in the State of Wisconsin to $11.4

billion.

Tourism spending in Ozaukee as it relates to total business sales was up 4.58% to $177

million in 2014 compared to a 5.47% increase in the State of Wisconsin to $18.4 billion.

Of Wisconsin’s 72 counties, Milwaukee County ranks No. 28 in the state for traveler

spending and total tourism revenues.

The tourism industry provides work across the spectrum of employment, from entry-level

and part-time jobs to management and executive-level positions. In fact, traveler spending

in 2014 supported nearly 2,000 full-time equivalent jobs in the county, an report relatively

no increase from 2013. Ozaukee County paid more than $52.7 million in wages and

salaries.

Travel spending in Ozaukee County generated a total impact of $11.4 million in state and

local taxes, an increase of 2.54%.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

22

Village of Grafton Economic Profile

Population

Of the households, 34.5 percent have children under the age of 18; 61.4 percent are married

couples living together; 7.2 percent have a female householder with no husband present; and

28.9 percent are non-families. Of all households, 24.2 percent are made up of individuals, and

8.4 percent are someone living alone who is 65 years of age or older. The average household

size is 2.54, and the average family size is 3.06.

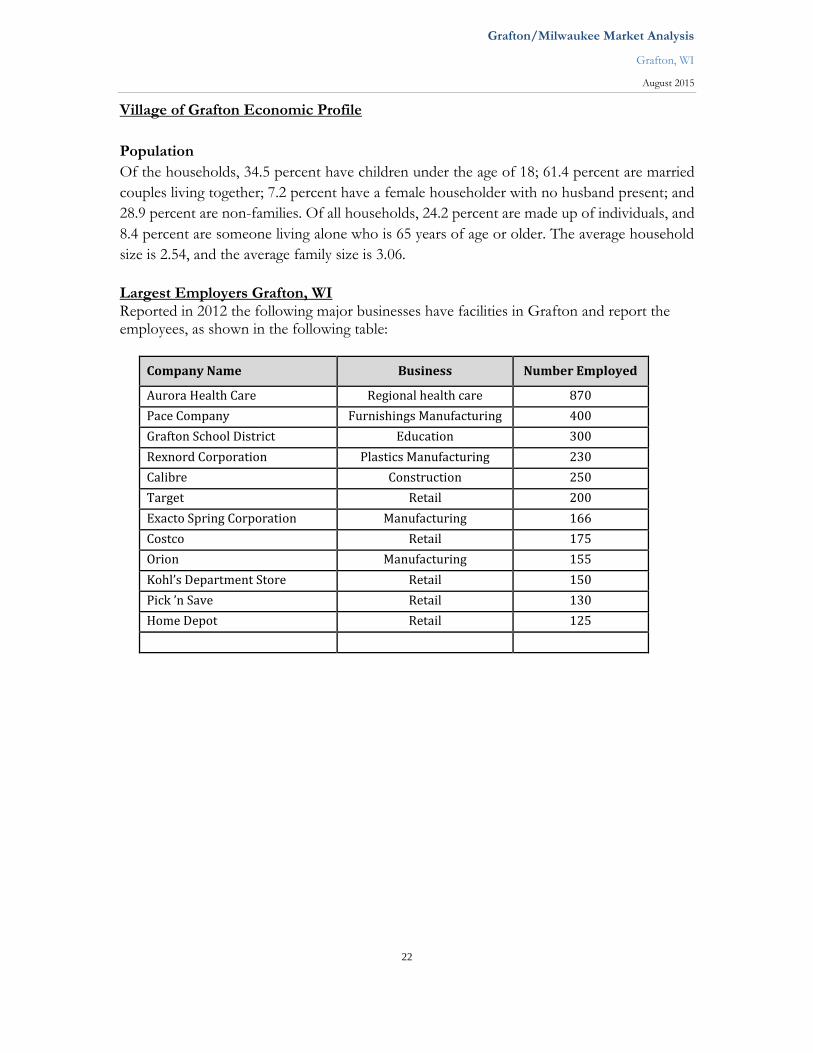

Largest Employers Grafton, WI Reported in 2012 the following major businesses have facilities in Grafton and report the employees, as shown in the following table:

Company Name Business Number Employed

Aurora Health Care Regional health care 870

Pace Company Furnishings Manufacturing 400

Grafton School District Education 300

Rexnord Corporation Plastics Manufacturing 230

Calibre Construction 250

Target Retail 200

Exacto Spring Corporation Manufacturing 166

Costco Retail 175

Orion Manufacturing 155

Kohl’s Department Store Retail 150

Pick ’n Save Retail 130

Home Depot Retail 125

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

23

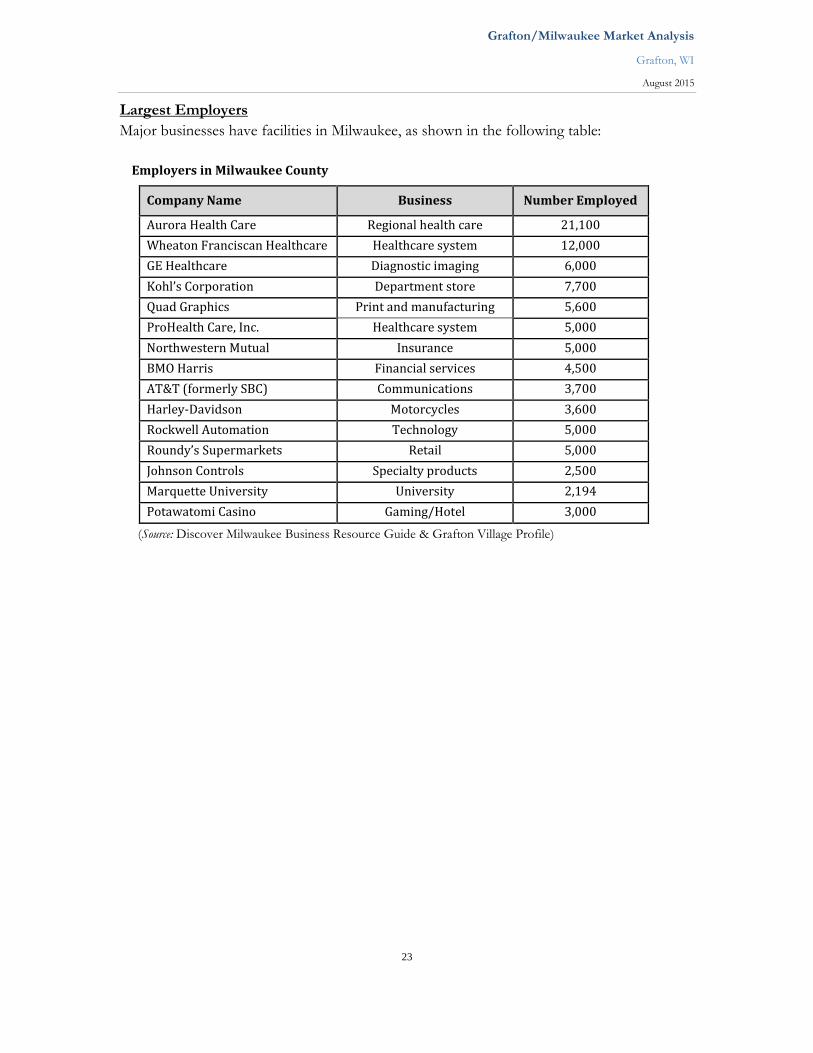

Largest Employers

Major businesses have facilities in Milwaukee, as shown in the following table:

Employers in Milwaukee County

Company Name Business Number Employed

Aurora Health Care Regional health care 21,100

Wheaton Franciscan Healthcare Healthcare system 12,000

GE Healthcare Diagnostic imaging 6,000

Kohl’s Corporation Department store 7,700

Quad Graphics Print and manufacturing 5,600

ProHealth Care, Inc. Healthcare system 5,000

Northwestern Mutual Insurance 5,000

BMO Harris Financial services 4,500

AT&T (formerly SBC) Communications 3,700

Harley-Davidson Motorcycles 3,600

Rockwell Automation Technology 5,000

Roundy’s Supermarkets Retail 5,000

Johnson Controls Specialty products 2,500

Marquette University University 2,194

Potawatomi Casino Gaming/Hotel 3,000

(Source: Discover Milwaukee Business Resource Guide & Grafton Village Profile)

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

24

Subject Site Regional Tourism Demand Generators

The Grafton market, as a suburb of the greater Milwaukee area, is centrally located among

many of the area’s largest businesses. Following, we have identified a few of those core

businesses that drive regional demand and cause market compression and overflow of guest

room demand outside the immediate Milwaukee market. This demand is both seasonally and

business generated. This is not an extensive list of all area businesses or demand generators.

The 2008 Market Analysis has a through list of regional business and demand generating

businesses.

Major Tourism Demand-Generating Businesses

Harley Davidson Museum

400 Canal St.

Milwaukee, WI 53203

Harley-Davidson is an American motorcycle manufacturer founded in Milwaukee during the

first decade of the twentieth century. It is one of two major American motorcycle

manufacturers to survive the Great Depression. Harley-Davidson also survived a period of

poor quality control and competition from Japanese manufacturers.

The company sells heavyweight (over 750 cc) motorcycles designed for cruising on the

highway. Harley-Davidson motorcycles (popularly known as “Harleys”) have a distinctive

design, exhaust note, and the tradition of heavy customization that gave rise to the chopper-

style motorcycle.

Harley has two significant sources of demand sites that drive business to the area hotels. The

Wauwatosa and Menomonee Falls Powertrain Operation Plants are operational factories that

produce engines for bikes; they sell merchandise and offer two types of tours to the public.

The Harley-Davidson Museum in downtown Milwaukee is an archive of Harleys, offering

exhibits of people, products, and culture. The museum draws an estimated 300,000 visitors

annually. The Harley-Davidson Museum includes 130,000 square feet of display space. The

culture of Harley-Davidson shown in various exhibits that tell stories of the people and history.

There is an extensive collection of Harley-Davidson motorcycles, photographs, videos, and

clothing. A portion of the Harley-Davidson archives that has previously been closed to the

public is now on display.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

25

MillerCoors

Visitor Center

4251 West State St.

Milwaukee, WI 53208

Miller Brewing Company merged with Coors Brewing Company on July 1, 2008, to become

MillerCoors. Prior to the joint venture, Miller Brewing was the second-largest brewing

company in the United States behind Anheuser-Busch and was based in Milwaukee. Miller

Brewing Company was founded in 1855 by Frederick Miller when he purchased the small

Plank-Road Brewery. The brewery’s location in the Menomonee Valley provided easy access

to raw materials produced on nearby farms.

Miller Park

201 South 46th St.

Milwaukee, WI 53214

Miller Park is a baseball park located in Milwaukee and home to the National League’s

Milwaukee Brewers. The stadium was built in 2001 as a replacement for Milwaukee County

Stadium. The park is located just southwest of the intersection of I-94, US-41, and Miller Park

Way, 2.4 miles from the subject hotel. The title sponsor is MillerCoors. Miller’s contract with

the stadium was for $40 million and runs until 2020.

The park, completed in 2001, features North America’s only fan-shaped convertible roof,

which can open and close in less than 10 minutes. Large panes of glass allow natural grass to

grow. In 2005, Sports Illustrated conducted fan surveys that rated Miller Park the best ballpark

based on value per dollar spent.

Although attendance dropped after the 2001 opening season to a low of 20,993 per game in

2003, attendance rebounded in subsequent seasons. In 2008, the Brewers set a franchise record

for attendance with more than 3 million. This was ninth among the 30 major league teams,

despite Milwaukee being one of the smallest markets in baseball.

Summerfest

Henry Maier Park

200 N. Harbor Dr.

Milwaukee, WI 53202

“Summerfest (also known as “The Big Gig”) is a yearly music festival held at the 75-acre Henry

Maier Festival Park along the lakefront in Milwaukee. The festival lasts for 11 days, and since

the mid-1970s, has run from late June through early July—always including the Fourth of July

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

26

holiday. Summerfest attracts almost 1 million people each year. Summerfest promotes itself as

“The World’s Largest Music Festival,” a title certified by the Guinness World Records in 1999.

Summerfest is run by the non-profit Milwaukee World Festival, Inc.

Summerfest features both local and nationally known music talent from a variety of music

genres. The event also provides the opportunity to sample a wide variety of food from many

Milwaukee restaurants. Other Summerfest attractions include comedy acts, shopping booths,

fireworks (including “The Big Bang” by Bartolotta Fireworks on opening night), karaoke,

children’s activities, and more.

Live musical acts are offered on 12 stages throughout the grounds, including the 23,000-seat

Marcus Amphitheater. With the exception of headlining acts at the Marcus Amphitheater, all

shows are free with a Summerfest admission ticket. Admission tickets cost between $10 and

$20, depending on the time of day; there are numerous promotions for discounted or free

tickets.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

27

Economic Conclusions

This section identified a wide variety of economic indicators that are pertinent to the market

area. In review, the tourism economy has been stable over the past 10 years and is growing

and remaining somewhat stable in this economic recession. The diversity of the business and

economy are above average. Workforce, population, redevelopment, and growth in the market

are projected to be in recovery, and growth is slow for the village, city, and county. The tourism

industry is stable and somewhat seasonal. The outlook for the area is generally favorable, and

growth should recover through the near term, although some recession indicators are present.

Subject site strengths include:

Excellent, easy access from the region’s corridors. Milwaukee seems to be the most

influential white-collar city amongst the Wisconsin Region, having both a vibrant

tourism and arts following and a business-minded community.

The subject market is competitively priced at a value to the other downtown hotels

and easily accessible. The area offers comparable services and amenities at a reasonable

price.

Tourism is a significant regional industry, and travelers are driven based on location,

price, and amenities. The combined tourism impact on Greater Milwaukee County is

estimated at $18.5 billion in Wisconsin and Milwaukee County leads the overall market

impact.

Of Wisconsin’s 72 counties, Milwaukee County ranks first in the state for traveler

spending, accounting for $3.1 billion in revenues collected up about 6 percent over

2014. The Milwaukee market drives compression to the surrounding markets, and the

subject market is in close proximity.

Easily accessible to largest market businesses, demand generators, and corporate

businesses. The area has increased traveler support services for dining and retail

options within a walkable distance, and retail in the area continues to expand.

Subject site weaknesses include:

The subject market has seen a recent increase in rooms available, as discussed later.

Competition is growing, and most branded hotels drive demand to the chain.

The current existing hotels are well established within the market given their age, and

travelers and companies have strong relationships with those properties.

The site is more than 20 miles north of the core of City Center hotels in downtown

Milwaukee. There is significant supply in the core, and the subject market may be a

destination market hotel is a destination site of its own, yet easily accessible to that

core market.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

28

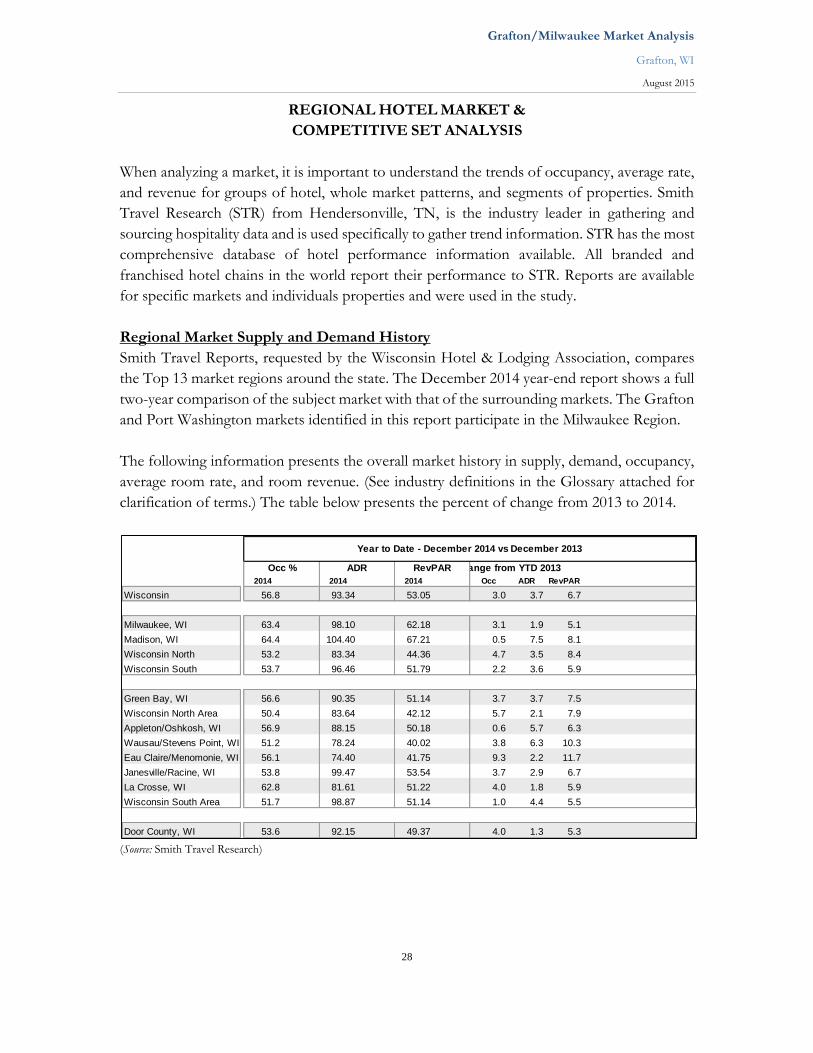

REGIONAL HOTEL MARKET &

COMPETITIVE SET ANALYSIS

When analyzing a market, it is important to understand the trends of occupancy, average rate,

and revenue for groups of hotel, whole market patterns, and segments of properties. Smith

Travel Research (STR) from Hendersonville, TN, is the industry leader in gathering and

sourcing hospitality data and is used specifically to gather trend information. STR has the most

comprehensive database of hotel performance information available. All branded and

franchised hotel chains in the world report their performance to STR. Reports are available

for specific markets and individuals properties and were used in the study.

Regional Market Supply and Demand History

Smith Travel Reports, requested by the Wisconsin Hotel & Lodging Association, compares

the Top 13 market regions around the state. The December 2014 year-end report shows a full

two-year comparison of the subject market with that of the surrounding markets. The Grafton

and Port Washington markets identified in this report participate in the Milwaukee Region.

The following information presents the overall market history in supply, demand, occupancy,

average room rate, and room revenue. (See industry definitions in the Glossary attached for

clarification of terms.) The table below presents the percent of change from 2013 to 2014.

(Source: Smith Travel Research)

Percent Change from YTD 2013

2014 2014 2014 Occ ADR RevPAR

Wisconsin 56.8 93.34 53.05 3.0 3.7 6.7

Milwaukee, WI 63.4 98.10 62.18 3.1 1.9 5.1

Madison, WI 64.4 104.40 67.21 0.5 7.5 8.1

Wisconsin North 53.2 83.34 44.36 4.7 3.5 8.4

Wisconsin South 53.7 96.46 51.79 2.2 3.6 5.9

Green Bay, WI 56.6 90.35 51.14 3.7 3.7 7.5

Wisconsin North Area 50.4 83.64 42.12 5.7 2.1 7.9

Appleton/Oshkosh, WI 56.9 88.15 50.18 0.6 5.7 6.3

Wausau/Stevens Point, WI 51.2 78.24 40.02 3.8 6.3 10.3

Eau Claire/Menomonie, WI 56.1 74.40 41.75 9.3 2.2 11.7

Janesville/Racine, WI 53.8 99.47 53.54 3.7 2.9 6.7

La Crosse, WI 62.8 81.61 51.22 4.0 1.8 5.9

Wisconsin South Area 51.7 98.87 51.14 1.0 4.4 5.5

Door County, WI 53.6 92.15 49.37 4.0 1.3 5.3

RevPARADROcc %

Year to Date - December 2014 vs December 2013

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

29

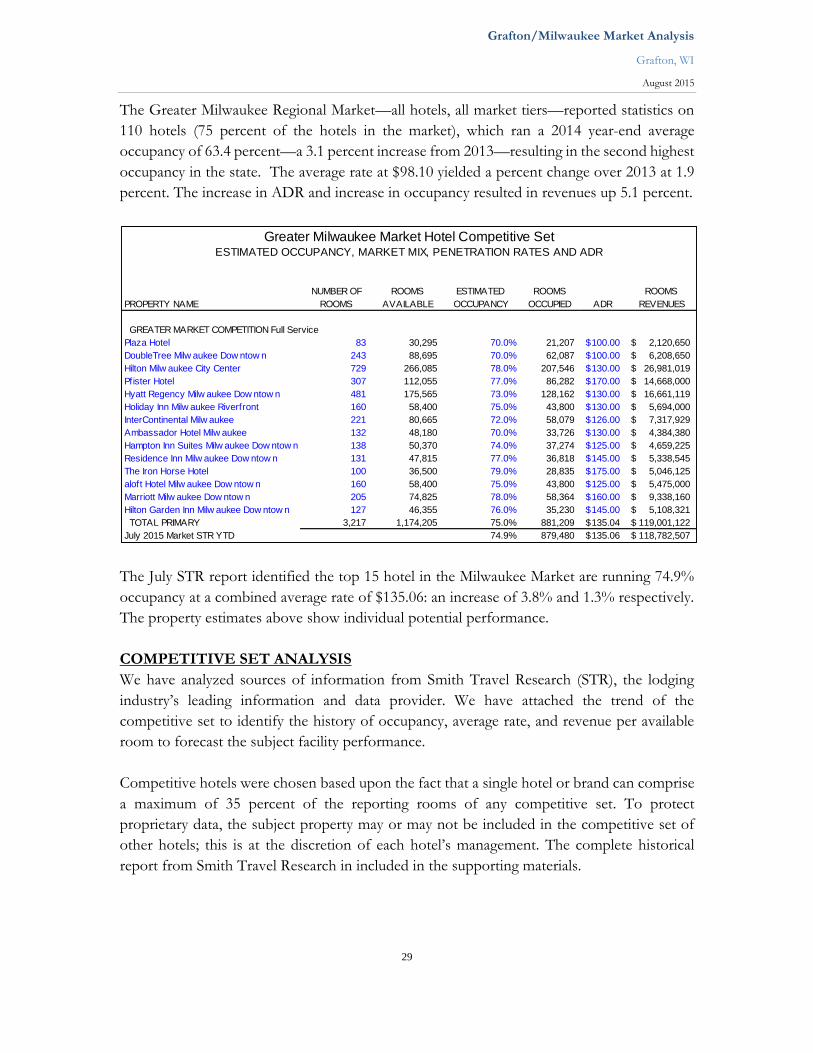

The Greater Milwaukee Regional Market—all hotels, all market tiers—reported statistics on

110 hotels (75 percent of the hotels in the market), which ran a 2014 year-end average

occupancy of 63.4 percent—a 3.1 percent increase from 2013—resulting in the second highest

occupancy in the state. The average rate at $98.10 yielded a percent change over 2013 at 1.9

percent. The increase in ADR and increase in occupancy resulted in revenues up 5.1 percent.

The July STR report identified the top 15 hotel in the Milwaukee Market are running 74.9%

occupancy at a combined average rate of $135.06: an increase of 3.8% and 1.3% respectively.

The property estimates above show individual potential performance.

COMPETITIVE SET ANALYSIS

We have analyzed sources of information from Smith Travel Research (STR), the lodging

industry’s leading information and data provider. We have attached the trend of the

competitive set to identify the history of occupancy, average rate, and revenue per available

room to forecast the subject facility performance.

Competitive hotels were chosen based upon the fact that a single hotel or brand can comprise

a maximum of 35 percent of the reporting rooms of any competitive set. To protect

proprietary data, the subject property may or may not be included in the competitive set of

other hotels; this is at the discretion of each hotel’s management. The complete historical

report from Smith Travel Research in included in the supporting materials.

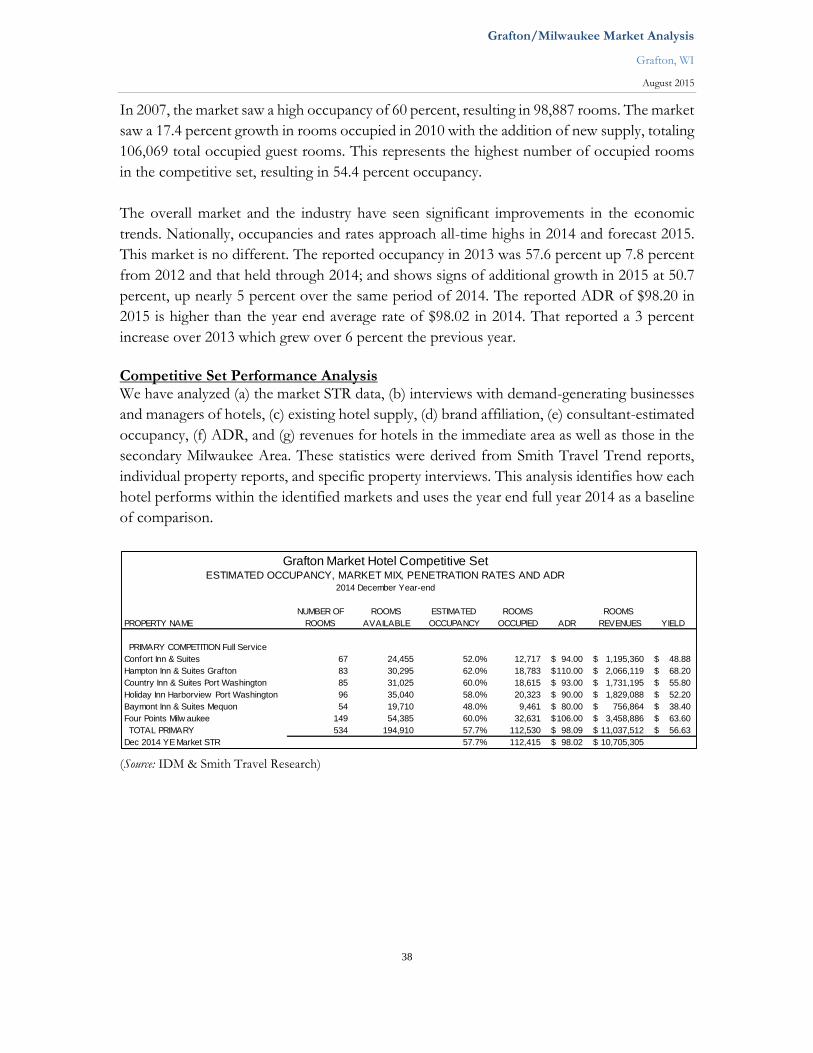

Greater Milwaukee Market Hotel Competitive SetESTIMATED OCCUPANCY, MARKET MIX, PENETRATION RATES AND ADR

NUMBER OF ROOMS ESTIMATED ROOMS ROOMS

PROPERTY NAME ROOMS AVAILABLE OCCUPANCY OCCUPIED ADR REVENUES

GREATER MARKET COMPETITION Full Service

Plaza Hotel 83 30,295 70.0% 21,207 100.00$ 2,120,650$

DoubleTree Milw aukee Dow ntow n 243 88,695 70.0% 62,087 100.00$ 6,208,650$

Hilton Milw aukee City Center 729 266,085 78.0% 207,546 130.00$ 26,981,019$

Pfister Hotel 307 112,055 77.0% 86,282 170.00$ 14,668,000$

Hyatt Regency Milw aukee Dow ntow n 481 175,565 73.0% 128,162 130.00$ 16,661,119$

Holiday Inn Milw aukee Riverfront 160 58,400 75.0% 43,800 130.00$ 5,694,000$

InterContinental Milw aukee 221 80,665 72.0% 58,079 126.00$ 7,317,929$

Ambassador Hotel Milw aukee 132 48,180 70.0% 33,726 130.00$ 4,384,380$

Hampton Inn Suites Milw aukee Dow ntow n 138 50,370 74.0% 37,274 125.00$ 4,659,225$

Residence Inn Milw aukee Dow ntow n 131 47,815 77.0% 36,818 145.00$ 5,338,545$

The Iron Horse Hotel 100 36,500 79.0% 28,835 175.00$ 5,046,125$

aloft Hotel Milw aukee Dow ntow n 160 58,400 75.0% 43,800 125.00$ 5,475,000$

Marriott Milw aukee Dow ntow n 205 74,825 78.0% 58,364 160.00$ 9,338,160$

Hilton Garden Inn Milw aukee Dow ntow n 127 46,355 76.0% 35,230 145.00$ 5,108,321$

TOTAL PRIMARY 3,217 1,174,205 75.0% 881,209 135.04$ 119,001,122$

July 2015 Market STR YTD 74.9% 879,480 135.06$ 118,782,507$

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

30

Grafton Competitive Sets: Defined for Subject Property

A competitive set consists of a group of hotel properties that directly compete for room nights

due to proximity and similarity of product. A competitive set enables individuals to compare

property performance with the aggregate performance of their direct competition.

We have identified properties that would be competitive with the proposed hotel project for

room accommodations, banquets/meetings, and food & beverage. This competitive set was

determined through consideration of factors such as location, size, consumer attraction,

amenities offered, rate structure, management, and demand generators. It includes properties

within a five-mile radius of the subject hotel. We have excluded hotels within the local market

that we view as uncompetitive due to their size, location, facility, or focus market.

In the Grafton area, there are six competitive hotels totaling 534 rooms. These hotels range

from full-service facilities to limited-service properties, some with full suites. The average-

sized hotel in the market is 89 rooms, the largest at 149 rooms, and the smallest at 54 rooms.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

31

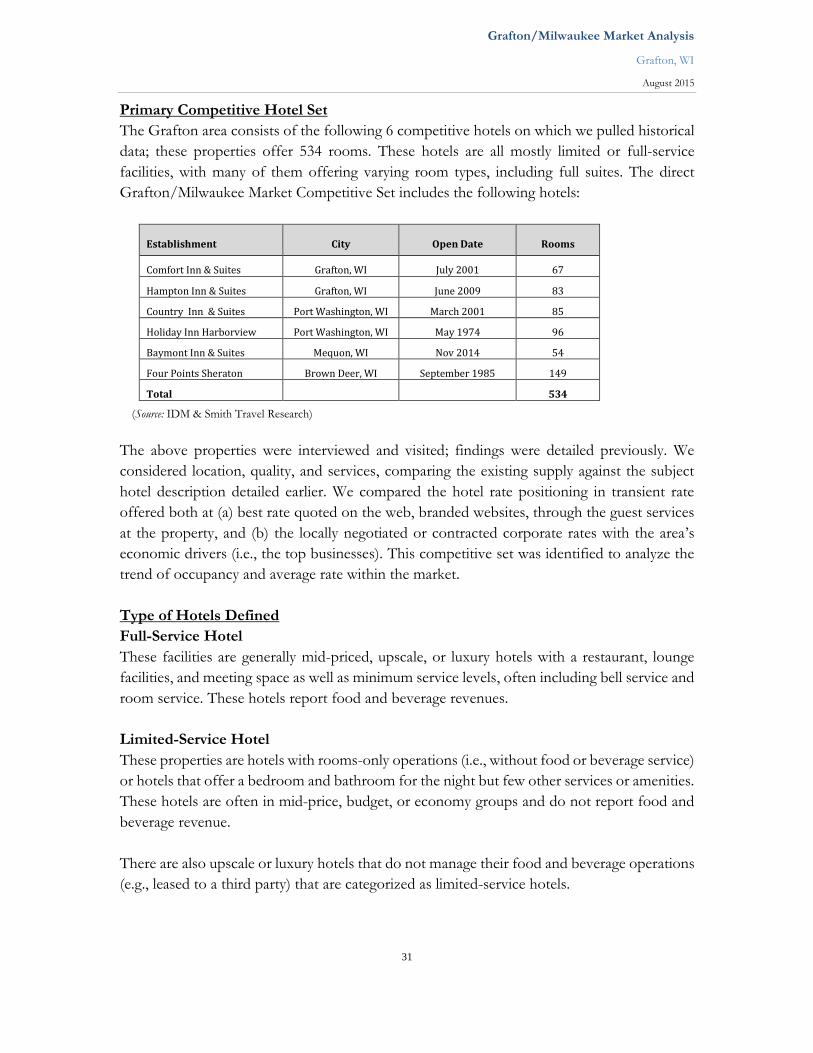

Primary Competitive Hotel Set

The Grafton area consists of the following 6 competitive hotels on which we pulled historical

data; these properties offer 534 rooms. These hotels are all mostly limited or full-service

facilities, with many of them offering varying room types, including full suites. The direct

Grafton/Milwaukee Market Competitive Set includes the following hotels:

Establishment City Open Date Rooms

Comfort Inn & Suites Grafton, WI July 2001 67

Hampton Inn & Suites Grafton, WI June 2009 83

Country Inn & Suites Port Washington, WI March 2001 85

Holiday Inn Harborview Port Washington, WI May 1974 96

Baymont Inn & Suites Mequon, WI Nov 2014 54

Four Points Sheraton Brown Deer, WI September 1985 149

Total 534

(Source: IDM & Smith Travel Research)

The above properties were interviewed and visited; findings were detailed previously. We

considered location, quality, and services, comparing the existing supply against the subject

hotel description detailed earlier. We compared the hotel rate positioning in transient rate

offered both at (a) best rate quoted on the web, branded websites, through the guest services

at the property, and (b) the locally negotiated or contracted corporate rates with the area’s

economic drivers (i.e., the top businesses). This competitive set was identified to analyze the

trend of occupancy and average rate within the market.

Type of Hotels Defined

Full-Service Hotel

These facilities are generally mid-priced, upscale, or luxury hotels with a restaurant, lounge

facilities, and meeting space as well as minimum service levels, often including bell service and

room service. These hotels report food and beverage revenues.

Limited-Service Hotel

These properties are hotels with rooms-only operations (i.e., without food or beverage service)

or hotels that offer a bedroom and bathroom for the night but few other services or amenities.

These hotels are often in mid-price, budget, or economy groups and do not report food and

beverage revenue.

There are also upscale or luxury hotels that do not manage their food and beverage operations

(e.g., leased to a third party) that are categorized as limited-service hotels.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

32

Subject Market Competitive Set

The primary set of competitive hotels were the properties that leveraged location and

amenities to complement the transient nature of their businesses and offer guests a place to

meet, celebrate, and spent more money.

The primary competitive set of hotels was evaluated and information gathered through various

online travel agents or OTAs. The star ratings and rates were taken from current peer

evaluation sites, such as Trip Advisor, and industry evaluation organizations. The competitive

hotels are comprised of the following properties. These hotels are:

Comfort Inn & Suites (formally Baymont Inn & Suites)

1415 Port Washington Road

Grafton, WI 53024

(262) 387-1180

www.Choicehotels.com

Nightly rates recently viewed: $99.00–$119.00

AAA Rating: 3 Diamonds

Trip Advisor: 2½ Stars

The hotel opened in July of 2001. It offers 67 rooms and suites with the typical amenities of a

limited-service hotel that includes a heated indoor swimming pool, business center, fitness

center, and free wireless Internet in all guest rooms. All stays include a complimentary

breakfast and free USA Today in the lobby. In-room, there is a coffee maker with coffee, iron

and ironing board, and 25-inch TV with HBO or Showtime, Lodgenet pay-per-view movies,

and Nintendo. Pets are also allowed.

The hotel is part of the Choice International guest loyalty program which offers travel rewards

program where you can earn points redeemable for multiple brand locations.

The hotel offers one 575-square-foot meeting room that accommodates 40 people. There are

no catering services available onsite, and AV is limited. Local companies use this room

frequently because there are few meeting rooms in the market and its location within the

market.

The rate positioning for the hotel offers midweek rates starting at $99.00 and locally negotiated

rates with businesses at $89. This is a 15 percent discount off the transient rate. The hotel also

has direct-billing privileges, which implies they have a large volume of business at the property.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

33

Hampton Inn & Suites

2633 Washington Street

Grafton, WI 53024

(262) 474-1000

www.hilton.com

Nightly rates recently viewed: $139.00–$159.00

AAA Rating: 3 Diamonds

Trip Advisor: 3 Stars

The Hampton Inn and Suites is the latest hotel to be built in the immediate market, opening

in June 2009 with 83 rooms and suites. The hotel is part of the Hilton family of hotels.

Hampton Inn is a leading chain of quality, value-priced hotels. It offers comfortable rooms

standard with coffee maker, iron and ironing board, and free in-room movie channels. Free

local calls and complimentary high-speed Internet access, complimentary On the House hot

breakfast, complimentary copies of USA Today (Monday through Friday), free coffee and tea

in the lobby 24 hours a day, and 24-hour front desk message and fax service. The property

also features microwaves and refrigerators available in all rooms, an indoor pool, hot tub, and

fitness center.

The property offers 944 square feet of flexible meeting and banquet space for up to 25−40

people with audio/visual equipment and a business center. The hotel offers in-house

audio/visual services and local vendor catering.

The Hampton is likely the strongest and closest competitor in the market in close proximity

to Grafton. The Hampton brand has a strong history of the transient market segment,

following in the industry through the Hilton brand affiliation and Honors Points Program;

that, coupled with the small meeting facility, allows the property to attract social functions.

The offerings at the Hampton should be similar to the offerings of the subject hotel, with the

subject hotel’s extension of evening dining options and a superior product.

The rate positioning for the hotel offers midweek rates starting a $139.00 and locally

negotiated rates or corporate rates for area businesses over $90.00. This is a 30 percent

discount off the transient rate.

Country Inn & Suites

350 East Seven Hills Road

Port Washington, WI 53074

(262) 284-2100

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

34

www.countryinns.com

Nightly rates recently viewed: $94.00–$134.00

AAA Rating: 3 Diamonds

Trip Advisor: 2½ Stars

This hotel, opened in March of 2001, offers 85 rooms and suites and is a typical Country Inns

& Suites hotel. It offers value along with services and amenities within a smaller, informal

setting. With charming décor and comfortable amenities, the Port Washington hotel caters to

business and leisure travelers.

All of the guest rooms offer a country-style décor that seems a bit dated and not upscale by

any means. Guest rooms offer free high-speed Internet access and continental breakfast, cable

TV with HBO, coffee makers, hair dryers and irons with ironing boards. Some suites also

include whirlpools and fireplaces.

The hotel has a heated indoor swimming pool, whirlpool, and fitness center. Other amenities

include guest laundry facilities, complimentary USA Today newspaper, and complimentary

local telephone calls. The meeting space offers 8,500 square feet of flexible space.

The chain is part of Minneapolis-based Carlson Hotels Worldwide, which also includes

Regent Hotels & Resorts, Radisson Hotels & Resorts, Park Plaza Hotels & Resorts, and Park

Inn.

This hotel offers 8,500+ square feet of meeting space with theatre-style seating capacity for

400 people. The hotel offers onsite catering and bar service through Saz’s Catering. There is

a 450-square-foot meeting room and a board-style room. AV is available.

The rate positioning for the hotel offers midweek rates range from $94.00−$109.00 and locally

negotiated rates with business or corporate rate are $84.00−$94.00; this is a 15- to 20-percent

discount off the transient rate.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

35

Holiday Inn Harborview

135 East Grand Avenue

Port Washington, WI 53074

(262) 284-9461

www.ichotelsgroup.com

Nightly rates recently viewed: $109.00–$147.00

AAA Rating: 3 Diamonds

Trip Advisor: 3 Stars

This hotel is the oldest in the competitive set, opening in May of 1974. The hotel offers

96 rooms of which 32 are suites. This typical aging Holiday Inn offers value along with a

unique waterside location. On the shores of Lake Michigan, this hotel is popular with leisure

travelers in the summer and business travelers through the year. Some of the services and

amenities offered include an onsite restaurant serving breakfast and dinner, small meeting

space, small fitness facility, indoor pool, sauna, and whirlpool.

The rate positioning for the hotel offers midweek rates starting a $109.00 and locally

negotiated rates with businesses at $89; this is a 20 percent discount off the transient rate.

Baymont Inn & Suites Mequon

10330 N. Port Washington Road

Mequon, WI 53092

(262) 241-3677

www.quiethouse.com

Nightly rates recently viewed: $109.00–$139.00

AAA Rating: 3 Diamonds

Trip Advisor: 2½ Stars

This hotel formally the Best Western hotel opened in May of 1995 and offers 54 rooms, all

which include a spacious living room area. All rooms have a microwave and refrigerator, hair

dryer, iron and ironing board, coffee maker, free high-speed Internet, indoor swimming pool

and whirlpool, as well as other expected amenities.

The Baymont Inn is a two property regional ownership with properties in Mequon and

Dodgeville, Wisconsin. Meeting rooms are not available, and this hotel is uncompetitive for

group or small meetings.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

36

Sheraton Four Points Milwaukee North

8900 North Kildeer Court

Brown Deer, WI 53209

(414) 355-8585

www.sheraton.com

Nightly rates recently viewed: $129.00–$144.00

AAA Rating: 3 Diamonds

Trip Advisor: 3 Stars

This hotel opened in November of 2000 and offers 149 guest rooms plus 6 meeting and

function rooms. This is the most direct competition for a full-service facility in the market.

The hotel restaurant, 8900 Bar & Bistro, has full menu and bar options.

The Sheraton Four Points is part of the Starwood Hotel & Resorts Collection, and it focuses

on the value-minded traveler, offering no extra charges for the basics such as high-speed

Internet access and in-room bottled water. The indoor and outdoor pool, whirlpool, sauna,

local shuttle, and fitness room are all free for guests as well.

With more than 7,000 square feet of flexible meeting space, the hotel can accommodate

various groups of up to 385 people. All-day meeting packages and wedding packages are

available.

This Starwood Hotel has full-service meeting and catering accommodations, with attractive

and flexible meeting space to accommodate corporate meetings and banquet up to 250 people.

This property offers all the necessary services, professional staff, and menu choices to plan a

quality event.

The rate positioning for the hotel offers midweek rates starting a $119.00 and locally

negotiated rates with business under $89.00; this is a 25 percent discount off the transient rate.

Grafton/Milwaukee Market Analysis

Grafton, WI

August 2015

37

STR Historical Trend of the Primary Competitive Set

The first step in the process of forecasting the potential rate and occupancy of the subject

hotel is to understand the historical trends of the competitive set or the region in which the

subject hotel resides, as well as the position in which the subject hotel will contend. These

factors will help in estimating future demand levels. We have based estimated growth on the

historical changes in occupancy and the average rate of the competitive set from the historical

performance, as seen in the following chart.

(Source: IDM & Smith Travel Research)

The table above quantifies the past ten plus years’ trends for room occupancy, Average Daily

Rate (ADR), and the ratio of rooms available to rooms’ revenue (RevPAR) for the Grafton

market. Overall, this competitive set has seen stable and consistent growth with a combined

8-year average of 2.1 percent in rooms available, 2.0 percent growth in rooms occupied, and

1.7 percent change in ADR. The last five years have proven to show more aggressive trends

with rooms occupied growing at nearly 5 percent and ADR at 3.6 percent with RevPAR at 6.9

percent.

The market has seen few changes in overall room count or rooms available since 2002,

although most hotels have gone through renovations. The competitive set absorbed supply

addition in 2009−2010 with the opening of The Hampton Inn & Suites; new additions to the

greater market resulted in an occupancy decline by -7.7 percent from 2008 and 2009, given the

supply changes and economic impact of reduced travel in the recession.

ROOMS ROOMS

AVAILABLE OCCUPIED

ROOMS PERCENT ROOMS PERCENT PERCENT PERCENT REGIONAL

AVAILABLE CHANGE OCCUPIED OCCUPANCY CHANGE ADR CHANGE REVPAR CHANGE ROOM REVENUE

2002 164,615 84,697 51.5% $84.15 $43.30 7,127,253$

2003 164,615 0.0% 83,106 50.5% -1.9% $85.14 1.2% $42.98 -0.7% 7,075,645$

2004 164,615 0.0% 91,898 55.8% 10.6% $82.02 -3.7% $45.79 6.5% 7,537,474$

2005 164,615 0.0% 94,250 57.3% 2.6% $82.57 0.7% $47.27 3.2% 7,782,138$