Embed Size (px)

Citation preview

Strategic Management Journal, Vol. 11, 153-169 (1990)

MATCHING COMPENSATION ANDORGANIZATIONAL STRATEGIESDAVID B. BALKINCollege of Business and Administration, University of Colorado, Boulder, Colorado,U.S.A.

LUIS R. GOMEZ-MEJIACollege of Business, Arizona State University, Tempe, Arizona, U.S.A.

This study examines the impact of organizational strategies (at both the corporate andbusiness unit level) on pay strategies, and their interactive influence on the effectiveness ofthe compensation system. The empirical findings are based on the survey responses of 192human resource management executives in business units of large manufacturing firms.Corporate strategy was a significant predictor of pay package design, pay level relative tothe market, and pay administration policies. Business unit strategy was a significant predictorof pay package design and pay level relative to the market. The findings are supportive ofcongruency notions which suggest that the effectiveness of the compensation system is partlya function of the fit between pay strategies and organizational strategies.

Issues of variation, interrelation, and fit are welldeveloped in the strategy literature. It containstnany analyses of congruence between strategyand other organizational variables—includingformal organizational structure, technology, mar-ket competence, and environment—(cf. Miller,1986; Tichy, 1983; Prescott, 1986), This body ofresearch suggests that coherent or matchingstrategy types are more effective (e.g. Woo andCooper, 1981; Hambrick, 1983a, 1984),

The concept of fit is based on the notionthat strategies are decomposable (Simon, 1981),consisting of elements (e,g. technology) that areinteresting for their individual importance aswell as their role in overall strategic plans(Venkatraman and Camillus, 1984), If the variouselements are not integrated or congruent withthe overall strategy, the organization has anunclear, or missing, strategic direction leadingto suboptimal or even dysfunctional outcomes(Lawless, 1987), In other words, because strategy'elements' should be mutually determined bya firm, this interrelationship implies that animportant normative test for a firm's strategy isinternal consistency (Porter, 1980; Galbraith and

0143-2095/90/020153-17$08,50© 1990 by John Wiley & Sons, Ltd,

Schendel, 1983). The congruency question hasbeen operationalized by examining the relation-ship between vectors of variables that typicallyfall within the realm of management responsi-bility; that is, controllable variables such aspricing, promotion, and research and develop-ment (e.g. Woo and Cooper, 1981), Becausethey are collections of controllable factors them-selves, it is possible to consider these in termsof functional or subfunctional area strategy,such as marketing strategy, financial strategy,compensation strategy, etc, (Galbriath and Schen-del, 1983),

Following the stream of research noted above,a growing number of writers are advocating astrategic approach to the reward system basedon such notions as 'congruency', 'fit', and'linkages' which call for a close articulationbetween compensation, overall corporate strate-gies, and business unit missions (e,g, Carroll,1987; Lawler, 1981; Balkin and Gomez-Mejia,1987a; Henderson and Risher, 1987), In afuturistic 'environmental scanning' of major com-pensation trends. Hay Management Consultants(1986) concluded that linking pay systems to

Received 4 May 1987Revised 5 July 1989

154 D. B. Balkin and L. R. Gomez-Mejia

overarching organizational strategies will be themajor challenge in compensation as we moveinto the twenty-first century. The underlyingassumption is that, when properly designed, thereward system of an organization can be a keycontributor to the accomplishment of its strategicobjectives (Schuler and MacMillan, 1984), How-ever, for this to occur, careful analysis needs tobe made of the role that reward systems can andshould play in the strategic plan of the firm.The normative implication flowing from thesearguments is that unless pay strategies reinforcethe organization's overall strategy, the return oncompensation dollars (which average about 60percent of total costs in the United States) willbe less than optimal, and even negative in somecases if pay policies induce behaviors that runcounter to the firm's strategic objectives (Lawler,1981),

Perhaps the oldest and most voluminousliterature that specifically addresses strategicconcerns in compensation can be found in theexecutive compensation area (e,g, Roberts, 1959;Kerr and Bettis, 1987; Salter, 1973; Gomez-Mejia, Tosi and Hinkin, 1987; Tosi and Gomez-Mejia, 1989), The major thrust of this researchhas been focused on the relationship betweenpay level, the design of the pay package, andorganization performance. Closely related to thework on executive compensation are some studiesthat have examined the relationship betweencorporate strategy and rewards for middle man-agers. Based on expectancy theory, Guth andMacMillan (1986) provide evidence that middlemanagers are not motivated to implement corpo-rate strategies that conflict with their own self-interest, Kerr's (1985) data, based on 20 largeorganizations, suggest that the process by whicha firm's diversification strategy had been achievedexerts a major influence on the design of themanagerial reward system, Napier and Smith(1987) report that highly diversified firms offerlarger bonuses to their middle managers whencompared to less diversified companies. Someadditional research has examined compensationstrategy in terms of specific industries andemployee groups. For example, Balkin andGomez-Mejia (1987b) found that the effectivenessof pay incentives for scientists and engineers inthe high-technology industry was related to thegrowth stage of the product life cycle andinversely related to company size.

All things considered, however, surprisinglylittle empirical investigation has been conductedthat could serve as a guide in designing rewardsystems that are aligned with corporate andbusiness unit (SBU) strategies. Much workremains to be done if we are to move from aprescriptive to a research-based body of knowl-edge in this area. First, there is a need to studythese issues at a macro level of analysis using abroad conceptualization of compensation strategythat includes pay package design, market position-ing, and pay policy choices. Second, there is alack of multivariate research that examines theunique and additive impact of both corporateand business unit strategies on SBU pay strategies,after partialling out the effect of other correlates(e,g, firm size). Third, the contingency notion ofeffectiveness should be explored so that it ispossible to determine the conditions under whichreliance on particular pay strategies is more likelyto produce desired results. This paper addressesall three of these concerns. The research questionsdriving this study may be summarized as follows:

1, Are there consistent and recurrent patterns ofSBU compensation strategies (in terms of paypackage design, market positioning, and paypolicy choices) that are associated with particu-lar organizational strategies?

2, Do corporate and business unit strategiesexercise an independent as well as a combinedinfluence on various SBU pay strategies? Ifso, are there any discernible patterns?

3, What is the pay effectiveness configurationfor various combinations of pay, corporate,and SBU strategies?

METHODSample

A total of 600 business units from differentmanufacturing companies was selected for thisstudy, SBUs were chosen within manufacturingto assure some comparability of technology,capital intensity and other characteristics amongthem (Hambrick, 1983b), The top humanresource (HRM) executive within the businessunit was selected as an informant because thisindividual is intimately involved in the formulationof organizational pay policies. Also, the HRMexecutive is likely to be the most knowledgeableperson about the SBU compensation strategies.

Matching Compensation and Organizational Strategies 155

The annual membership directory from theAmerican Compensation Association (ACA) wasused to identify the respondents. Many humanresource executives belong to this association tokeep current with trends in the compensationenvironment. Of the 600 HRM executives selectedfor this study, 212 (35,3 percent) agreed toparticipate in exchange for a free copy of atechnical report. All participants were promisedstrict confidentiality of any information providedto the investigators. The organizations thatparticipated in the study had an average salesvolume for 1985 (the latest year available) of$840 million in sales.

The instrument used in the study was developedafter an exhaustive literature review and on-siteinterviews with human resource executives. Thesurvey instrument was pretested with a sampleof 10 executives to ensure it was complete, easyto follow, and that the items were not ambiguous.The survey, conducted through the mail duringsummer 1986, included questions pertaining tocorporate and SBU characteristics, corporate andSBU strategy, and pay strategies. The operationalmeasures are described in greater detail below.

Operational measures

The organizational strategy at both the corporateand business unit level was operationalized fromexisting strategy typologies. The HRM executiveswere asked to identify their firm's strategy fromwritten descriptions in a manner similar to theapproach used by Snow and Hrebiniak (1980),Advantages of this method are (1) it is possibleto obtain standardized and consistent strategymeasures across different organizations; and (2)it is possible to study a larger sample of firms(Snow and Hrebiniak, 1980),

Corporate strategy

The corporate strategy measure used in this studyis the widely known taxonomy developed byRumelt (1974), who operationalized it as thedegree of diversification exhibited by the firm(see the Appendix for description of scale).

Business unit (SBU) strategy

In the present study, a modified version of thetypology developed by Gerstein and Reissman

(1983) was used to measure SBU strategy (seethe Appendix for a description of scale). Thistypology was selected for three main reasons.First, it is a hybrid of most existing typologiesand has wide applicability across a broad cross-section of firms. It provides a simple yet eclecticdescription of each strategy type. Second, it isrelatively free of academic jargon, so that it isintuitively meaningful and more appealing topracticing managers. Obviously, this is a crucialconsideration given the sample used in this study.Finally, a policy capturing study of manufacturingfirms in the PIMS data base by Galbraith andSchendel (1983) produced a SBU typology thatgreatly overlaps with the Gerstein and Reissman(1983) strategy types, providing empirical con-firmation of its validity in a manufacturingenvironment.

Only the 'dynamic growth' and 'rationalization/maintenance' SBU strategy choices generatedenough cases from the respondents to be enteredinto the analysis. The lack of dispersion of therespondents' SBU strategy choices probablyreflects the homogeneity of the ACA member-ship, which is more representative of largerorganizations with full-fledged human resourcemanagement departments that provide resourcesthat support professional association membershipsand travel to meetings. Business units characterizedby entrepreneurial, turnaround or divestiture strat-egies are more likely to rely on external manage-ment consultants instead of hiring their owninternal, specialized human resource staff.

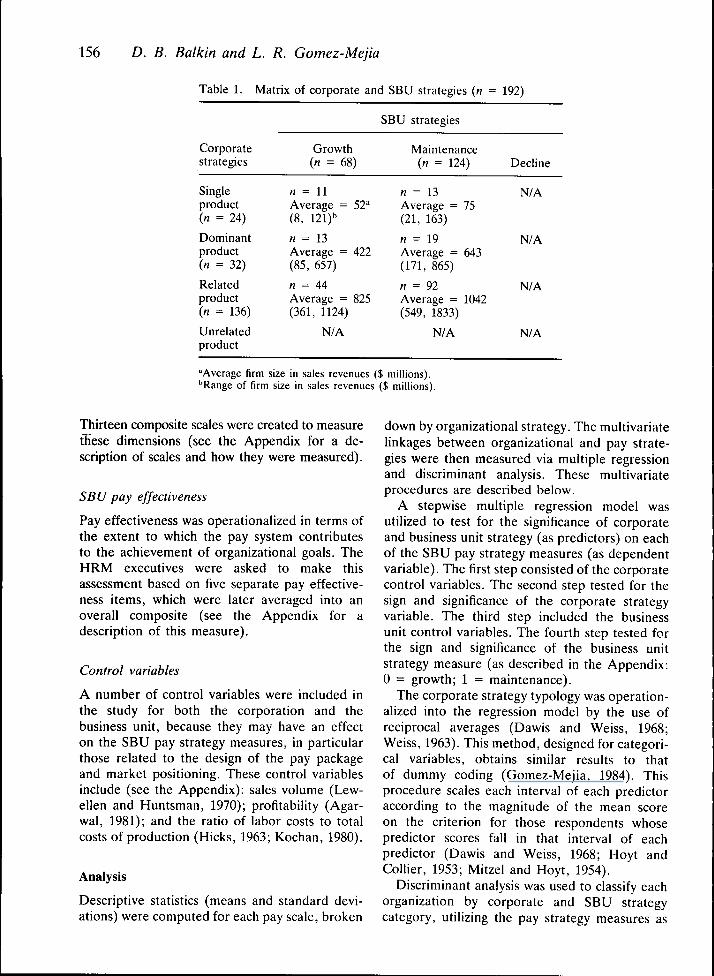

The domain of corporate and SBU strategychoices covered in this study is summarized bythe matrix in Table 1,

Business unit compensation strategies

Compensation strategies were operationalized interms of pay package design, market positioning,and pay policy choices (Milkovich, 1988; Balkinand Gomez-Mejia, 1987a; Lawler, 1981; Gomez-Mejia and Welbourne, 1988), The first dimensionrefers to the relative importance of salary,benefits, .and incentives in the pay mix. Marketpositioning refers to the extent to which theorganization targets its pay level below or aboveits competitors. The last dimension, pay policychoices, consists of the organization's admin-istrative framework, criteria, and proceduralapproaches used to remunerate its employees.

156 D. B. Balkin and L. R. Gomez-Mejia

Table 1, Matrix of corporate and SBU strategies {n = 192)

Corporatestrategies

Singleproduct(n = 24)

Dominantproduct(n = 32)

Relatedproduct(n = 136)

Unrelatedproduct

Growth{n = 68)

n = nAverage = 52"(8, 121)"

n = 13Average = 422(85, 657)

n = 44Average = 825(361, 1124)

N/A

SBU strategies

Maintenance(n = 124)

n = 13Average = 75(21, 163)

« = 19Average = 643(171, 865)

n = 92Average = 1042(549, 1833)

N/A

Decline

N/A

N/A

N/A

N/A

"Average firm size in sales revenues ($ millions),''Range of firm size in sales revenues ($ millions).

Thirteen composite scales were created to measurethese dimensions (see the Appendix for a de-scription of scales and how they were measured),

SBU pay effectiveness

Pay effectiveness was operationalized in terms ofthe extent to which the pay system contributesto the achievement of organizational goals. TheHRM executives were asked to make thisassessment based on five separate pay effective-ness items, which were later averaged into anoverall composite (see the Appendix for adescription of this measure).

Control variables

A number of control variables were included inthe study for both the corporation and thebusiness unit, because they may have an effecton the SBU pay strategy measures, in particularthose related to the design of the pay packageand market positioning. These control variablesinclude (see the Appendix): sales volume (Lew-ellen and Huntsman, 1970); profitability (Agar-wal, 1981); and the ratio of labor costs to totalcosts of production (Hicks, 1963; Kochan, 1980),

Analysis

Descriptive statistics (means and standard devi-ations) were computed for each pay scale, broken

down by organizational strategy. The multivariatelinkages between organizational and pay strate-gies were then measured via multiple regressionand discriminant analysis. These multivariateprocedures are described below,

A stepwise multiple regression model wasutilized to test for the significance of corporateand business unit strategy (as predictors) on eachof the SBU pay strategy measures (as dependentvariable). The first step consisted of the corporatecontrol variables. The second step tested for thesign and significance of the corporate strategyvariable. The third step included the businessunit control variables. The fourth step tested forthe sign and significance of the business unitstrategy measure (as described in the Appendix:0 = growth; 1 = maintenance).

The corporate strategy typology was operation-alized into the regression model by the use ofreciprocal averages (Dawis and Weiss, 1968;Weiss, 1963), This method, designed for categori-cal variables, obtains similar results to thatof dummy coding (Gomez-Mejia, 1984), Thisprocedure scales each interval of each predictoraccording to the magnitude of the mean scoreon the criterion for those respondents whosepredictor scores fall in that interval of eachpredictor (Dawis and Weiss, 1968; Hoyt andCollier, 1953; Mitzel and Hoyt, 1954),

Discriminant analysis was used to classify eachorganization by corporate and SBU strategycategory, utilizing the pay strategy measures as

Matching Compensation and Organizational Strategies 157

discriminating variables. This procedure allowsone to obtain a combined estimate of thesimultaneous effect of all pay strategies indifferentiating across organizational strategies, Aseparate discriminant analysis procedure usingthe direct method (Statistical Package for theSocial Sciences, 1987) was conducted for thecorporate and SBU strategy typology. Theclassification accuracy of this method is assessedby the 'hit rates' or the percentage correspondencebetween actual and estimated group membershipfor each categorical (organizational strategy)variable. Because firms are classified into anestimated group membership for each categorical(organizational strategy) variable, there was noneed to develop a numerical scale for each ofthese variables. Therefore, in addition to theclassification information offered by discriminantanalysis, this method provided a built-in doublecheck on the reliability of the regression pro-cedure.

The last set of analyses was designed to answerthe question: which pay strategies appear to bemost effective under each corporate and SBUstrategy type? A cross-tabulation table wasdeveloped, with each of the pay strategies on thevertical axis and the corporate and SBU strategiesalong the horizontal axis. Each of the paystrategies was dichotomized into 'high' (firm isabove the median) and 'low' (firm is below themedian) groups, A matrix was then created thatshowed the mean effectiveness score for eachcell. So, for example, all firms below the medianin 'internal equity' that are also pursuing a'growth' strategy would have an average payeffectiveness score calculated in that subsample.Statistical tests of significance were then computedfor mean differences. This procedure provides anoverall picture of the effectiveness configurationassociated with various organization/pay strategycombinations.

RESULTS

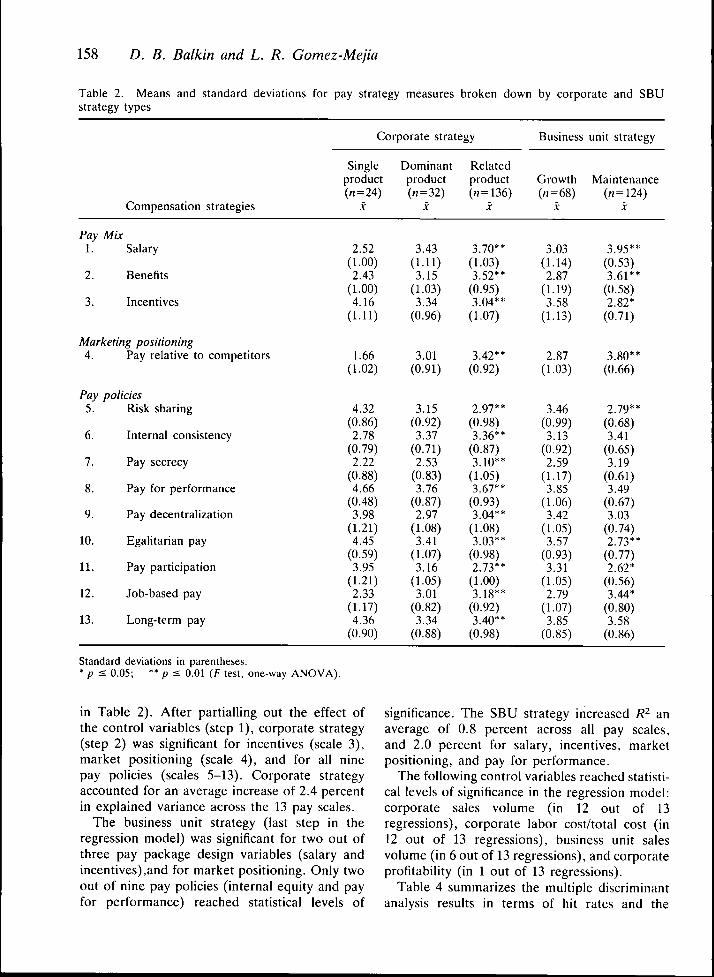

Table 2 presents descriptive statistics (means andstandard deviations) for each of the pay strategiesbroken down by corporate and SBU strategy type.As shown in the table, the overall relationshipbetween corporate strategy and each of the 13SBU pay strategies was statistically significant.The related product strategy (i,e, most diversifiedfirms) is associated with a higher pay level as

compared to the market (market positioning)and greater emphasis on salary and benefits vis-a-vis incentives. It is also associated with themost bureaucratic pay policies. There is a higherdegree of pay secrecy, internal consistency, paycentralization and job-based pay policies and alower degree of pay-for-performance, egali-tarianism, participation in pay decisions and long-term pay policies. The single-product strategy,on the other hand, is associated with lower paylevels relative to the market and a strongeremphasis on incentives in the compensation mix.It is also associated with more flexibile paypolicies: an emphasis on pay for performance,pay participation, decentralized compensationdecisions, egalitarianism, long-term orientationand skill-based pay and lower levels of paysecrecy and internal consistency. The dominant-product category tends to be associated with paystrategies that fell between the mean responsesof the single-product strategy and the related-product strategy.

Table 2 also shows a comparison of paystrategy means for the SBU strategy types. Therelationship between SBU strategy, tjie design ofthe pay package, and market positioning reachedstatistical levels of significance. The maintenancestrategy is associated with a higher pay levelrelative to the market and more emphasis onsalary and benefits vis-a-vis incentives in thecompensation mix. The growth strategy, on theother hand, exhibits a lower market position anda greater reliance on pay incentives. Risk-sharingis also more pronounced under the growthstrategy, with a portion of an employee's earningstied to individual, group or organizational goals.Only three out of eight pay policies are signifi-cantly related to SBU strategy. Under themaintenance category, pay policies are lessegalitarian, less involving employee participationand more job-based (implying a lower tendencytoward skill-based pay). Under the growthstrategy there were higher levels of egalitarianism,participation in pay decisions and skill-based pay.

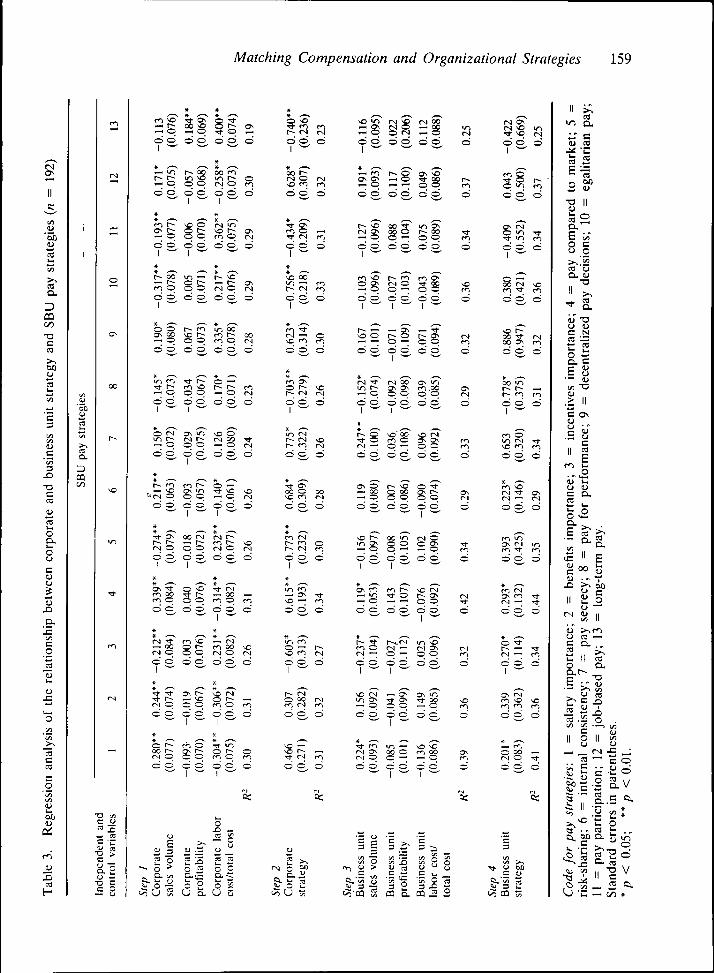

Table 3 summarizes the stepwise regressionfindings. The overall regression model explainedbetween 25 percent (long-term pay) and 44percent (market positioning) of the variance (R^)of the SBU pay strategies, (Note: the directionof the corporate strategy variable in the regressiontable with respect to the reciprocal averagescoding procedure can be discerned by inspectingthe corresponding means for each strategy type

158 D. B. Balkin and L. R. Gomez-Mejia

Table 2, Means and standard deviations for pay strategy measures broken down by corporate and SBUstrategy types

Pay1,

2,

3,

Compensation strategies

MixSalary

Benefits

Incentives

Marketing positioning4,

Pay5,

6,

7,

8,

9,

10,

11,

12,

13,

Pay relative to competitors

policiesRisk sharing

Internal consistency

Pay secrecy

Pay for performance

Pay decentralization

Egalitarian pay

Pay participation

Job-based pay

Long-term pay

Corporate strategy

Singleproduct(«=24)

X

2,52(1,00)2,43

(1,00)4,16

(1,11)

1,66(1,02)

4,32(0,86)2,78

(0,79)2,22

(0,88)4,66

(0,48)3,98

(1,21)4,45

(0,59)3,95

(1,21)2,33

(1,17)4,36

(0,90)

Dominantproduct(«=32)

X

3,43(1,11)3,15

(1,03)3,34

(0,96)

3,01(0,91)

3,15(0,92)3,37

(0,71)2,53

(0,83)3,76

(0,87)2,97

(1,08)3,41

(1,07)3,16

(1,05)3,01

(0,82)3,34

(0,88)

Relatedproduct(« = 136)

X

3,70**(1,03)3,52**(0,95)3,04**(1.07)

3,42**(0,92)

2,97**(0,98)3,36**

(0,87)3,10**

(1,05)3,67**(0,93)3,04**(1,08)3,03**

(0,98)2,73**(1,00)3,18**

(0,92)3,40**(0,98)

Business

Growth(«=68)

X

3,03(1,14)2,87

(1,19)3,58

(1,13)

2,87(1,03)

3,46(0,99)3,13

(0,92)2,59

(117)3,85

(1,06)3,42

(1,05)3,57

(0,93)3,31

(1,05)2,79

(1,07)3,85

(0,85)

unit strategy

Maintenance(rt = 124)

X

3,95**(0,53)3,61**

(0,58)2,82*

(0,71)

3,80**(0,66)

2,79**(0,68)3,41

(0,65)3,19

(0,61)3,49

(0,67)3,03

(0,74)2,73**(0,77)2,62*

(0,56)3,44*

(0,80)3,58

(0,86)

Standard deviations in parentheses.* p < 0,05; *• p £ 0,01 {F test, one-way ANOVA).

in Table 2), After partialling out the effect ofthe control variables (step 1), corporate strategy(step 2) was significant for incentives (scale 3),market positioning (scale 4), and for all ninepay policies (scales 5-13), Corporate strategyaccounted for an average increase of 2,4 percentin explained variance across the 13 pay scales.

The business unit strategy (last step in theregression model) was significant for two out ofthree pay package design variables (salary andincentives),and for market positioning. Only twoout of nine pay policies (internal equity and payfor performance) reached statistical levels of

significance. The SBU strategy increased R? anaverage of 0,8 percent across all pay scales,and 2,0 percent for salary, incentives, marketpositioning, and pay for performance.

The following control variables reached statisti-cal levels of significance in the regression model:corporate sales volume (in 12 out of 13regressions), corporate labor cost/total cost (in12 out of 13 regressions), business unit salesvolume (in 6 out of 13 regressions), and corporateprofitability (in 1 out of 13 regressions).

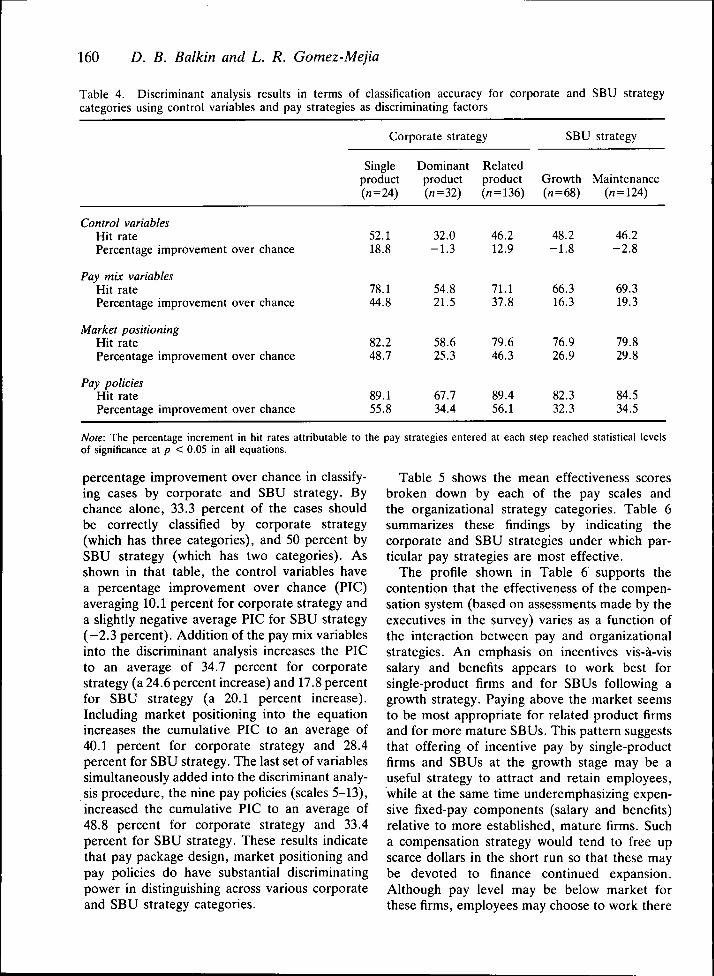

Table 4 summarizes the multiple discriminantanalysis results in terms of hit rates and the

Matching Compensation and Organizational Strategies 159

0 0

raa.D03onT3cra

00<u

3

C

i

1)x>

o

03C03

O

OO

a:

O3

ro NO

" B !§ J r^ O N• O .—I

o1

171*

o

*

,193

'(0

075)

o

,077

)

o

057

o1

,006

(0

(890

o ..0

70)

o

258*

*

o1

«36

2*(0

073)

B

,075

)

o

o

29

.740

o1

.839

,236

307)

rotNd

tNto

o p.

t^ 00 in ^ - r^ NO,— P - O 1 ^ —• I ^ ONro p p P tN p tNd d^ d d^ d d d

-H pd d

t^ fONO t ^o O

00

in Bd d d d

t o

d1

*vO

t—

d1

#rotNNO

ONOtN

d

^00

tN

d• " •

^^ ^

d

d

o

LT) r o , ^ t ^•^ r^ r o NO— o opo o

o —t^ t— to^ - p tN

d d_ d o_ d

O (N ON >/ NO Oin t^ tN r-- tN 00—• o o o ^- o

D0/5

° S-

1^ ro ro t^

o o o

, — ^ o in Tt NO NO••tNO o o ^-"O tNo

274*

*

o1

(007

9)

o1

018

o1

(007

2)

o

o1

232*

*

o

(0.

077)

o

o

NOtN

o

o o o

Ov ' ^ O ^ -^ (Nr-) 00 rj- r -H 00 ^ro p op r*~) p r*^do <z^ ci> c^ d d

fN pd d

en '^ — (Nor - m 00O O r o

( N O O O

t—

d1

**in

d

i n

sd

r-oro

tNrotN

d

to"ON

d

roro

2-

?7ootN

ot o

d

Ttt o

d

tN

d

tNro

o ;

1 o Tt in. r o t; O ro O

o o o : o ;

o o o

ro

d

S2

1.1ora

rs.<ij O

o U

oETO 2 "-5

aio SU D.

OX)J2OJra

g_OU

SOO

01/

oCJ

SS !::8 5Sd d d d d d

t ^ NO 00 •» mtN ON 00 o r— O O " Pd d d

ro NO t^ to ro ON

2 p p ^ p pd d d d d d

t ^ ^ - ,— ON — -^NO O t^ O r^ ON

— — o — o oo

.703

**

o1

.775

'

o

.684

*

o .

.279

)

o .

.322

)

o^

.309

)

d

NOtNd

NOtNd

,28

o15

2*

o1

*

.247

'

o

.119

(0.

.074

).1

00)

o .

,080

)

o1

092

o1

036.

o

,007

s

(860

o

(80 r

o .

.086

)

o

039

o

096

o

.090

(0.

.085

)

(360'

o

,074

)

d

d

rorod

ONtN

— pd d

p^ 00 in tN o

~ - 2 2g• <z> o o

O (N —' OI ON

—; o — o p

d d d d d d d

•* ro in — NO NCtN ON 00 O ro 00(N p p —' —' Pd o_ d d d d

3 I 3 ^

O >o 1/1

-o 2 t/3 ^T t/l O ra

PQ Q, pa _ra O

tN O\tN NO v-iTl; >S tN

d d d

Tt O t^p in rod d d

dTf

d

00 tN NOto " ^ to

d d d

NO 1 ^OC • * t N0 0 ON ro

d d d

00 inr rod d

ro Oin t i "^NO ro rod d d

m NOtN Tl-tN —'

d d

to inON tNtO ^

d d d

m tNON t otN —•

o ^t-- —tN —

ON tNt o NOro ro

O 00 —M O Tt

§ • 1( ^ CQ

ca

• s "a.E -o co o>N!Sra CJD. U

T3

C Nra —

cu

• - I );/! -OU

.>. IIC ON

IsII ra

c ra

1) , - VX I >> 00

CJ ^

2i

ra Ct ! II rao Q.

tilII O II

, , 2 CO2 h c •>= o

>, t oa , ' ra t .„a.. 00 Q. h in, c "-" oO '= ra "S dIT-s !^-o VTa /, II c

160 D. B. Balkin and L. R. Gomez-Mejia

Table 4, Discriminant analysis results in terms of classification accuracy for corporate and SBU strategycategories using control variables and pay strategies as discriminating factors

Corporate strategy SBU strategy

Single Dominant Related

Control variablesHit ratePercentage improvement over chance

Pay mix variablesHit ratePercentage improvement over chance

Market positioningHit ratePercentage improvement over chance

Pay policiesHit ratePercentage improvement over chance

product(/2=24)

52,118,8

78,144,8

82,248,7

89,155,8

product(«=32)

32,0-1,3

54,821,5

58,625,3

61.134,4

product(/I = 136)

46,212,9

71,137,8

79,646,3

89,456,1

Growth(«=68)

48,2-1,8

66,316,3

76,926,9

82,332,3

Mamtenance(/I = 124)

46,2-2,8

69,319,3

79,829,8

84,534,5

Note: The percentage increment in hit rates attributable to the pay strategies entered at eaeh step reached statistical levelsof significance at p < 0,05 in all equations.

percentage improvement over chance in classify-ing cases by corporate and SBU strategy. Bychance alone, 33,3 percent of the cases shouldbe correctly classified by corporate strategy(which has three categories), and 50 percent bySBU strategy (which has two categories). Asshown in that table, the control variables havea percentage improvement over chance (PIC)averaging 10.1 percent for corporate strategy anda slightly negative average PIC for SBU strategy(-2.3 percent). Addition of the pay mix variablesinto the discriminant analysis increases the PICto an average of 34,7 percent for corporatestrategy (a 24.6 percent increase) and 17,8 percentfor SBU strategy (a 20,1 percent increase).Including market positioning into the equationincreases the cumulative PIC to an average of40,1 percent for corporate strategy and 28,4percent for SBU strategy. The last set of variablessimultaneously added into the discriminant analy-sis procedure, the nine pay policies (scales 5-13),increased the cumulative PIC to an average of48,8 percent for corporate strategy and 33,4percent for SBU strategy. These results indicatethat pay package design, market positioning andpay policies do have substantial discriminatingpower in distinguishing across various corporateand SBU strategy categories.

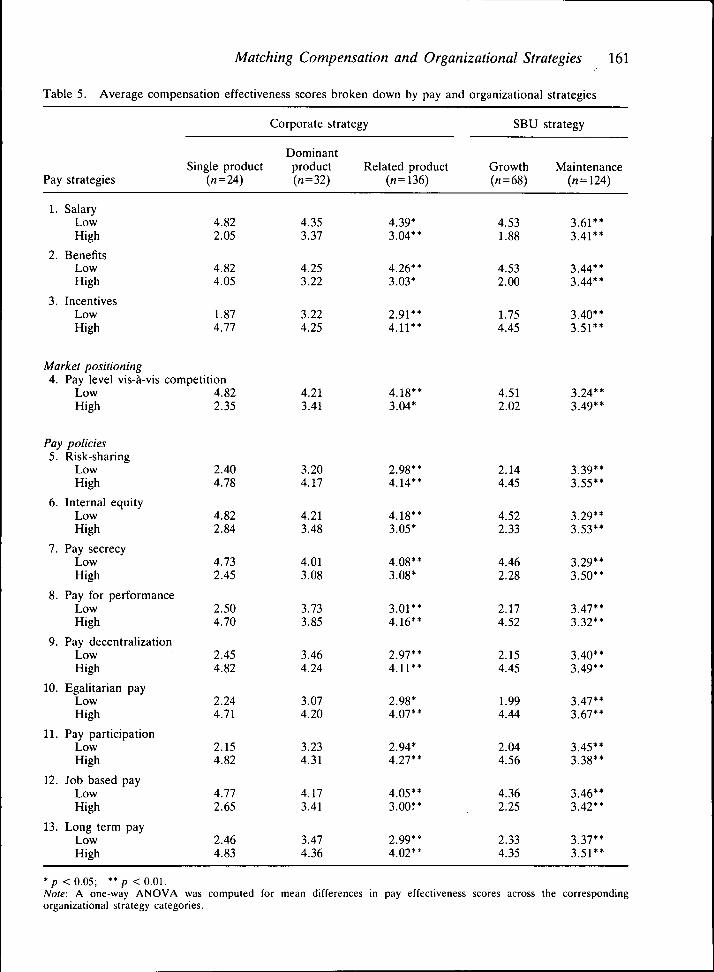

Table 5 shows the mean effectiveness scoresbroken down by each of the pay scales andthe organizational strategy categories. Table 6summarizes these findings by indicating thecorporate and SBU strategies under which par-ticular pay strategies are most effective.

The profile shown in Table 6 supports thecontention that the effectiveness of the compen-sation system (based on assessments made by theexecutives in the survey) varies as a function ofthe interaction between pay and organizationalstrategies. An emphasis on incentives vis-a-vissalary and benefits appears to work best forsingle-product firms and for SBUs following agrowth strategy. Paying above the market seemsto be most appropriate for related product firmsand for more mature SBUs, This pattern suggeststhat offering of incentive pay by single-productfirms and SBUs at the growth stage may be auseful strategy to attract and retain employees,while at the same time underemphasizing expen-sive fixed-pay components (salary and benefits)relative to more established, mature firms. Sucha compensation strategy would tend to free upscarce dollars in the short run so that these maybe devoted to finance continued expansion.Although pay level may be below market forthese firms, employees may choose to work there

Matching Compensation and Organizational Strategies 161

Table 5, Average compensation effectiveness scores broken down by pay and organizational strategies

Pay

1,

2,

3,

strategies

SalaryLowHigh

BenefitsLowHigh

IncentivesLowHigh

Single product(n=24)

4,822,05

4,824,05

1,874,77

Corporate strategy

Dominantproduct(n=32)

4,353,37

4,253,22

3,224,25

Related product(/i=136)

4,39*3,04**

4,26**3,03*

2,91**4,11**

SBU

Growth(n=68)

4,531,88

4,532,00

1,754,45

strategy

Maintenance(n = 124)

3,61**3,41**

3,44**3,44**

3,40**3,51**

Market positioning4, Pay level vis-a-vis competition

Low 4,82High 2,35

4,213,41

4,18*'3,04*

4,512,02

3,24**3,49**

Pay5.

6,

7,

8,

9,

10,

11,

12,

13,

policiesRisk-sharing

LowHigh

Internal equityLowHigh

Pay secrecyLowHigh

Pay for performanceLowHigh

Pay decentralizationLowHigh

Egalitarian payLowHigh

Pay participationLowHigh

Job based payLowHigh

Long term payLowHigh

2,404,78

4,822,84

4,732,45

2,504,70

2,454,82

2,244,71

2,154,82

4,772,65

2,464,83

3,204,17

4,213,48

4,013,08

3,733,85

3,464,24

3,074,20

3,234,31

4,173,41

3,474,36

2,98**4,14**

4,18**3,05*

4,08**3,08*

3,01**4,16**

2,97**4,11**

2,98*4,07**

2,94*4,27**

4,05**3,00?*

2,99**4,02**

2,144,45

4,522,33

4,462,28

2,174,52

2,154,45

1,994,44

2,044,56

4,362,25

2,334,35

3,39**3,55**

3,29**3,53**

3,29**3,50**

3,47**3,32**

3,40**3,49**

3,47**3,67**

3,45**3,38**

3,46**3,42**

3,37**3,51**

*p<0 ,05 ; **p<0 ,01 .Note: A one-way ANOVA was computed for mean differences in pay effectiveness scores across the correspondingorganizational strategy categories.

162 D. B. Balkin and L. R. Gomez-Mejia

Table 6, A profile of most effective pay strategies by corporate and SBU strategies

Pay package designMarket positioningPay policies

Corporate strategy

Singleproduct(«=24)

IncentivesBelow marketRisk-sharingFlexibility

Open paycommunicationPay forperformancePaydecentralizationEgalitarian payEmployeeparticipationSkill-basedpayLong-termorientation

Relatedproduct(« = 136)

Salary and benefitsAbove marketGuaranteed payInternalconsistencyPay secrecy

Seniority

PaycentralizationHierarchical payLow employeeinputJob-based pay

Short-termorientation

SBU

Growth(«=60)

IncentivesBelow marketRisk-sharingExternalorientationOpen paycommunicationPay forperformancePaydecentralizationEgalitarian payEmployeeparticipationSkill-basedpayLong-termorientation

strategy

Maintenance(n = 124)

Salary and benefitsAbove marketGuaranteed payInternalorientationPay secrecy

Seniority

PaycentralizationHierarchical payLow employeeinputJob-based pay

Short-termorientation

Note: For the sake of simplicity, only the two ends of the corporate strategy types (single-product and related-product) areshown in the above table.

in exchange for greater potential returns in thefuture, Balkin and Gomez-Mejia (1987a) foundthat to be the case among smaller high-tech firmsin the New England area, which tend to relyquite heavily on incentive compensation.

The profile shown in Table 6 also suggeststhat more 'freewheeling' pay practices that areresponsive to varying conditions, contingencies,and individual situations seem to be most effectivefor single-product firms and SBUs at the growthstage. Formalized rules and procedures that tendto 'routinize' pay decisions, and that are applieduniformly across the entire organization, appearto work best for related-product firms and SBUsat the maintenance stage. In contrast to single-product firms and SBUs at the growth stage, thefollowing pay policies appear to be most effectivefor the latter group: (1) guaranteed pay vs, risksharing; (2) internal consistency vs, flexibility;(3) pay secrecy vs, open pay communication;(4) seniority vs, performance emphasis; (5)hierarchical vs, egalitarian pay; (6) low employeeinput vs, employee participation; (7) job-based

vs, skill-based pay; and (8) short-term vs, long-term orientation.

DISCUSSION AND CONCLUSIONS

The purpose of this study has been to examinethe relationship between organizational and paystrategies and their interactive impact on theeffectiveness of the compensation system. Theresults reported here indicate that two levels oforganizational strategy, corporate and businessunit, are determinants of several SBU pay strategydimensions. The corporate-level influences paystrategies across a wide domain, including paypackage design, market positioning, and all ninepay policies included in the study. The SBUlevel, on the other hand, seems to have a morefocused effect on pay strategies, primarily thosepertaining to pay package design and marketpositioning.

The data also show that organization size as

Matching Compensation and Organizational Strategies 165

associated with the last category, this strategywas deleted from the analysis.

While it may seem surprising that thereare few 'unrelated-product' firms, the sampleselection procedure of choosing manufacturingfirms for purposes of comparability led to thedeletion of many conglomerates from the sample.Therefore a subset of the full range of diversifi-cation strategies is examined in this study inorder to assure some comparability betweenfirms.

Business unit (SBU) strategy

Executives were asked to identify their SBUstrategy by choosing one of the following catego-ries (see Gerstein and Reissman, 1983): 'entre-preneurial' (five cases), 'dynamic growth' (68cases), 'rationalization/maintenance' (124 cases),'turnaround' (no cases) and 'divestiture' (sevencases). Because of small n sizes, only the secondand third categories were included in the analysis.These two categories are briefly described below,

(a) Dynamic growth strategy. Projects withsignificant financial risks are undertakenfrequently. Firm is making high invest-ments in order to expand market share.There is a constant dilemma betweendoing current work and building supportfor the future, A need is beginning to befelt for more control and structure for anever-expanding operation. This categoryclosely corresponds to the 'growth' strategyin the Galbraith and Schendel (1983)study,

(b) Rationalization/maintenance strategy. Thefirm is interested in minimizing costs whileretaining its position in the market. Thefocus is on maintaining existing profitlevels. Modest cost-cutting and employeeterminations may be occurring. Controlsystems are well developed along with anextensive set of policies/procedures. Thiscategory closely corresponds to the 'main-tenance' strategy in the Galbraith andSchendel (1983) study.

Business unit compensation strategies

The HRM executives were asked to report thepay strategies followed in their business units in

terms of pay mix, their target position vis-a-visthe market, and pay policy choices. To this end,a set of 35 Likert-type items was developed tocover these different aspects. These 35 itemswere then used to construct 13 separate compositescales, A brief description of each scale is providedbelow; Table Al lists the items associated witheach of the scales and the coefficient alphas.

Six items were used to operationalize pay mix,broken down into three separate scales thatmeasure the relative importance of salary, benefitsand incentives (see Table Al), The responseformat for each item consisted of a five-pointLikert scale ranging from 'strongly disagree' to'strongly agree'. As shown in Table Al, thecoefficient alpha exceeded 0,80 for each of thethree scales, indicating high internal reliability.

Two questions in the survey (one for salaryand one for benefits) asked the executive toindicate the SBUs preferred pay level vis-a-visits competitors (see Table Al), The responseformat consisted of a five-point Likert scaleranging from 'substantially below the market' to'substantially above the market'. These two itemswere combined into a single score to measurethe SBU's market positioning. The Crombachalpha for the composite scale was 0,94, indicatinga high degree of homogeneity.

The nine pay policy dimensions used in thisstudy were adapted from Lawler (1981), TableAl shows the items associated with each of thenine pay policy scales and the coefficient alphas.The response format for each item consisted ofa five-point Likert scale ranging from 'stronglydisagree' to 'strongly agree'. The coefficientalphas were all satisfactory, ranging from a lowof 0,83 for 'internal consistency' to a high of 0,92for 'risk-sharing',

SBU pay effectiveness

A five-item scale (see Table Al) was developedto measure pay effectiveness. The responseformat for each item consisted of a 1-5 Likertscale that ranged from (1) 'strongly disagree' to(5) 'strongly agree'. The composite scale wastested for reliability and found to be internallyconsistent with an alpha of 0,94, The compositeeffectiveness score was calculated by averagingthe responses to the five items.

It would be ideal if objective pay effectivenessindices could be used as a way to cross-validate

166 D. B. Balkin and L. R. Gomez-Mejia

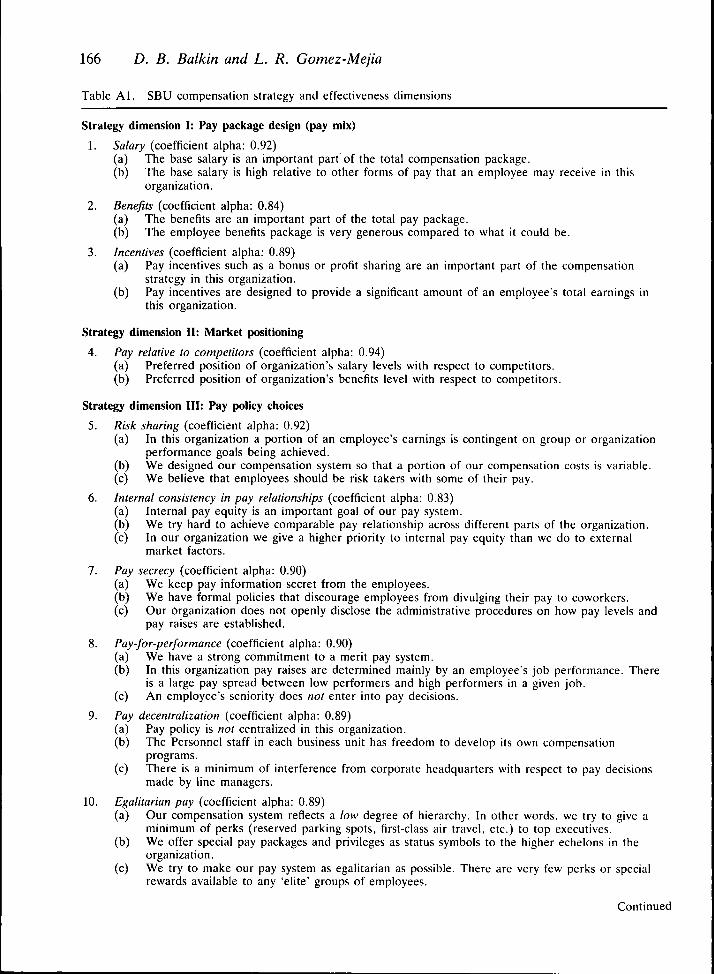

Table Al, SBU compensation strategy and effectiveness dimensions

Strategy dimension I: Pay package design (pay mix)

1, Salary (coefficient alpha: 0,92)(a) The base salary is an important part of the total compensation package,(b) The base salary is high relative to other forms of pay that an employee may receive in this

organization,

2, Benefits (coefficient alpha: 0,84)(a) The benefits are an important part of the total pay package,(b) The employee benefits package is very generous compared to what it could be,

3, Incentives (coefficient alpha: 0,89)(a) Pay incentives such as a bonus or profit sharing are an important part of the compensation

strategy in this organization,(b) Pay incentives are designed to provide a significant amount of an employee's total earnings in

this organization.

Strategy dimension II: Market positioning

4, Pay relative to competitors (coefficient alpha: 0,94)(a) Preferred position of organization's salary levels with respect to competitors,(b) Preferred position of organization's benefits level with respect to competitors.

Strategy dimension III: Pay policy choices

5, Risk sharing (coefficient alpha: 0,92)(a) In this organization a portion of an employee's earnings is contingent on group or organization

performance goals being achieved,(b) We designed our compensation system so that a portion of our compensation costs is variable,(c) We believe that employees should be risk takers with some of their pay,

6, Internal consistency in pay relationships (coefficient alpha: 0,83)(a) Internal pay equity is an important goal of our pay system,(b) We try hard to achieve comparable pay relationship across different parts of the organization,(c) In our organization we give a higher priority to internal pay equity than we do to external

market factors,

7, Pay secrecy (coefficient alpha: 0,90)(a) We keep pay information secret from the employees,(b) We have formal policies that discourage employees from divulging their pay to coworkers,(c) Our Organization does not openly disclose the administrative procedures on how pay levels and

pay raises are established,

8, Pay-for-performance (coefficient alpha: 0,90)(a) We have a strong commitment to a merit pay system,(b) In this organization pay raises are determined mainly by an employee's job performance. There

is a large pay spread between low performers and high performers in a given job,(c) An employee's seniority does not enter into pay decisions,

9, Pay decentralization (coefficient alpha: 0,89)(a) Pay policy is not centralized in this organization,(b) The Personnel staff in each business unit has freedom to develop its own compensation

programs,(c) There is a minimum of interference from corporate headquarters with respect to pay decisions

made by line managers,

10, Egalitarian pay (coefficient alpha: 0,89)(a) Our compensation system reflects a low degree of hierarchy. In other words, we try to give a

minimum of perks (reserved parking spots, first-class air travel, etc) to top executives,(b) We offer special pay packages and privileges as status symbols to the higher echelons in the

organization,(c) We try to make our pay system as egalitarian as possible. There are very few perks or special

rewards available to any 'elite' groups of employees.

Continued

Matching Compensation and Organizational Strategies 167

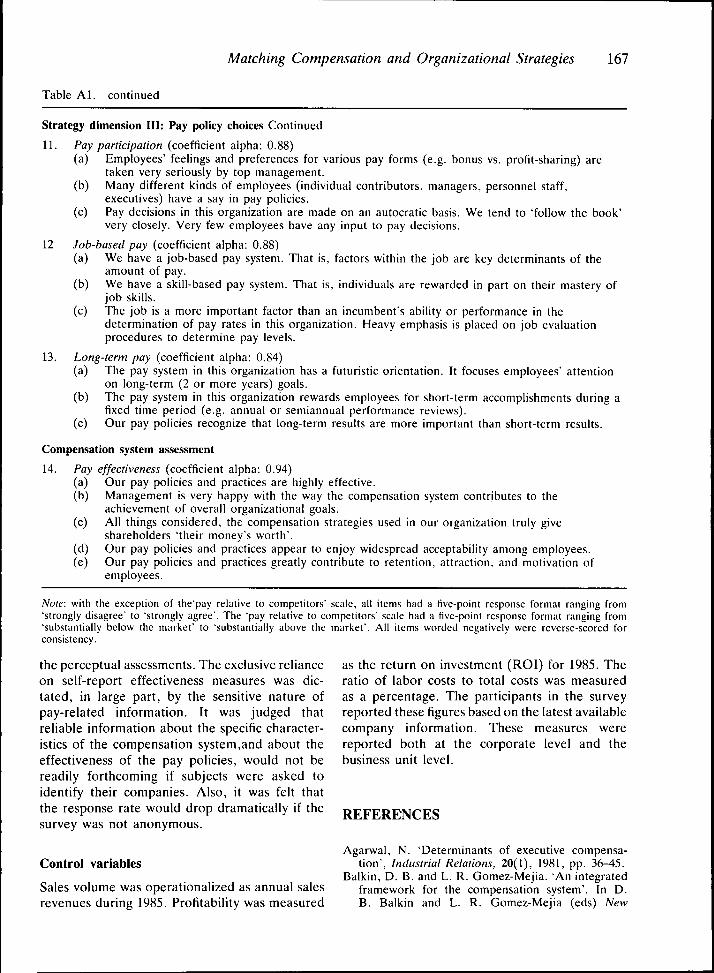

Table Al, continued

Strategy dimension III: Pay policy choices Continued

11, Pay participation (coefficient alpha: 0,88)(a) Employees' feelings and preferences for various pay forms (e,g, bonus vs, profit-sharing) are

taken very seriously by top management,(b) Many different kinds of employees (individual contributors, managers, personnel staff,

executives) have a say in pay policies,(c) Pay decisions in this organization are made on an autocratic basis. We tend to 'follow the book'

very closely. Very few employees have any input to pay decisions,

12 Job-based pay (coefficient alpha: 0,88)(a) We have a job-based pay system. That is, factors within the job arc key determinants of the

amount of pay,(b) We have a skill-based pay system. That is, individuals are rewarded in part on their mastery of

job skills,(c) The job is a more important factor than an incumbent's ability or performance in the

determination of pay rates in this organization. Heavy emphasis is placed on job evaluationprocedures to determine pay levels,

13, Long-term pay (coefficient alpha: 0,84)(a) The pay system in this organization has a futuristic orientation. It focuses employees' attention

on long-term (2 or more years) goals,(b) The pay system in this organization rewards employees for short-term accomplishments during a

fixed time period (e,g, annual or semiannual performance reviews),(c) Our pay policies recognize that long-term results are more important than short-term results.

Compensation system assessment

14, Pay effectiveness (coefficient alpha: 0,94)(a) Our pay policies and practices are highly effective,(b) Management is very happy with the way the compensation system contributes to the

achievement of overall organizational goals,(c) All things considered, the compensation strategies used in our organization truly give

shareholders 'their money's worth',(d) Our pay policies and practices appear to enjoy widespread acceptability among employees,(e) Our pay policies and practices greatly contribute to retention, attraction, and motivation of

employees.

Note: with the exception of the'pay relative to competitors" scale, all items had a five-point response format ranging from'strongly disagree' to "strongly agree". The "pay relative to competitors" scale had a five-point response format ranging from'substantially below the market' to "substantially above the market". All items worded negatively were reverse-scored forconsistency.

the perceptual assessments. The exclusive reliance as the return on investment (ROI) for 1985, Theon self-report effectiveness measures was die- ratio of labor costs to total costs was measuredtated, in large part, by the sensitive nature of as a percentage. The participants in the surveypay-related information. It was judged that reported these figures based on the latest availablereliable information about the specific character- company information. These measures wereistics of the compensation system,and about the reported both at the corporate level and theeffectiveness of the pay policies, would not be business unit level,readily forthcoming if subjects were asked toidentify their companies. Also, it was felt thatthe response rate would drop dramatically if the RFFFRFNCFSsurvey was not anonymous,

Agarwal, N, 'Determinants of executive compensa-Control variables tion'. Industrial Relations, 20(1), 1981, pp, 36-45,

Balkin, D, B, and L, R, Gomez-Mejia, 'An integratedSales volume was operationalized as annual sales framework for the compensation system'. In D,revenues during 1985, Profitability was measured B, Balkin and L, R, Gomez-Mejia (eds) New

168 D. B. Balkin and L. R. Gomez-Mejia

Perspectives on Compensation, Prentice-Hall,Englewood Cliffs, NJ, 1987a,

Balkin, D, B, and L, R, Gomez-Mejia, 'Towarda contingency theory of compensation strategy'.Strategic Management Journal, 8, 1987b, pp,169-182,

Carroll, S, J, 'Business strategies and compensationsystems'. In D, B, Balkin and L, R, Gomez-Mejia(eds), New Perspectives in Compensation, Prentice-Hall, Englewood Cliffs, NJ, 1987,

Carroll, S, J, 'Handling the need for consistency andthe need for contingency in the management ofcompensation'. Human Resource Planning, 11,1988, pp, 191-196,

Dawis, R, and D, Weiss, 'Reciprocal averages predic-tion'. Proceedings of the American PsychologicalAssociation, 1968, pp, 50-54,

Galbraith, C, and D, Schendel, 'An empirical analysisof strategy types'. Strategic Management Journal,4, 1983, pp, 153-173,

Gerstein, M, and H, Reissman, 'Strategic selection:Matching executives to business conditions', SloanManagement Review, Winter (1), 1983, pp, 33-49,

Gomez-Mejia, L, R, 'Effect of occupation on taskrelated, contextual, and job involvement orien-tation: A cross-cultural perspective'. Academy ofManagement Journal, 27, 1984, pp, 706-720,

Gomez-Mejia, L, R, and T, Welbourne, 'Compen-sation strategy: An overview and future steps'.Human Resource Planning, 11, 1988, pp, 173-189,

Gomez-Mejia, L, R,, H, Tosi and T, Hinkin,'Managerial control, performance, and executivecompensation'. Academy of Management Journal,30, 1987, pp, 51-70,

Guth, W, D, and I, C, MacMillan, 'Strategy implemen-tation versus middle management self-interest'.Strategic Management Journal, 1,1986, pp, 313-327,

Hambrick, D, 'High profit strategies in mature capitalgoods industries: A contingency Sipprodxh', Academyof Management Journal, 26, 1983a, pp, 681-701.

Hambrick, D, C, 'Some tests of the effectiveness andfunctional attributes of Miles and Snow's strategictypes', Academy of Management Journal, 26, 1983b,pp, 5-26,

Hambrick, D, 'Taxonomic approaches to studyingstrategy: Some conceptual and methodologicalissues'. Journal of Management, 10, 1984, pp27-41,

Hay Management Consultants, Scanning of Compen-sation Issues for the 1990s. Hay ManagementConsultants, Philadelphia, PA, 1986,

Henderson, R, and H, W, Risher, 'Influencingorganizational strategy through compensation lead-ership'. In D, B, Balkin and L, R, Gomez-Mejia(eds). New Perspectives on Compensation, Prentice-Hall, Englewood Cliffs, NJ, 1987,

Hicks, J, R, The Theory of Wages, Macmillan, NewYork, 1963,

Hoyt, D, J, and R, O, Collier, 'The mathematicalbasis of reciprocal averages'. Readings of thePsychometric Society. Psychometric Society, Cleve-land, OH, 1953,

Kerr, J, L, 'Diversification strategies and managerialrewards: An empirical study'. Academy of Manage-ment Journal, 28, 1985, pp, 155-179,

Kerr, J, and R, A, Bettis, 'Board of directors,top management compensation and shareholderreturns'. Academy of Management Journal, 30,1987, pp, 645-664,

Kochan, T, A, Collective Bargaining and IndustrialRelations. Irwin, Homewood, IL, 1980,

Lawler, E, E,, III, Pay and Organization Development,Addison-Wesley, Reading, MA, 1981,

Lawless, M, W, 'The structure of strategy: A taxonomicstudy of competitive strategy and technology sub-strategy'. Unpublished technical report. Universityof Colorado, Boulder, CO, 1987,

Lewellen, W, G, and B, Huntsman, 'Managerial payand corporate performance', American EconomicReview, 60, 1970, pp, 710-720,

Milkovich, G, T, 'A strategic perspective to compen-sation management'. In K, Rowland and G, Ferris(eds). Research in Personnel and Human ResourcesManagement, JAI Press, Greenwich, CT, 1988,

Miller, D, 'Configurations of strategy and structure:towards a synthesis'. Strategic Management Journal,7, 1986, pp, 233-249,

Mitzel, H, E, and C, J, Hoyt, 'A methodological studyof reciprocal averages applied to an attitude scale'.Journal of Counseling Psychology, 1, 1954, pp,256-259,

Napier, N, K, and M, Smith, 'Product diversification,performance criteria and compensation at thecorporate manager level'. Strategic ManagementJournal, 8, 1987, pp, 195-201,

Newman, J, 'Compensation strategies in decliningindustries'. Human Resource Planning, 11, 1988,pp, 197-206,

Porter, M, E, Competitive Strategy, Free Press, NewYork, 1980,

Prescott, J, 'Environments as moderators of therelationship between strategy and performance'.Academy of Management Journal, 29, 1986, pp,329-346,

Roberts, D, R, 'A general theory of executivecompensation based on statistically tested proposi-tions'. Quarterly Journal of Economics, 70, 1959,pp, 270-294,

Rumelt, R, P, Strategy, Structure and EconomicPerformance, Division of Research, Harvard Busi-ness School, Boston, MA, 1974,

Salter, M, S, 'Tailor incentive compensation tostrategy'. Harvard Business Review, 51(2), 1973,pp, 94-102,

Schuler, R, S, and I, C, MacMillan, 'Gainingcompetitive advantage through human resourcemanagement practices'. Human Resource Manage-ment, 23, 1984, pp, 241-255,

Simon, H, The Sciences of the Artificial. MIT Press,Cambridge, MA, 1981,

Snow, C, C, and L, G, Hrebiniak, 'Strategy, distinctivecompetence, and organizational performance'.Administrative Science Quarterly, 25, 1980, pp,317-336,

Matching Compensation and Organizational Strategies 169

Statistical Package for the Social Sciences, Users Venkatraman, N, and J, C, Camillus, 'Exploring theManual, Northwestern University, Evanston, IL, concept of "fit" in strategic management',/Icadewy1987, of Management Review, 9, 1984, pp, 513-525,

Tichy, N, Managing Strategic Change, Wiley, New Weiss, L, W, 'Technique for multivariate prediction',York, 1983, Unpublished doctoral dissertation. University of

Tosi, H, and L, R, Gomez-Mejia, 'The decoupling of Minnesota, 1963,CEO pay and performance: An agency theory Woo, C, and A, Cooper, 'Strategies for effective lowperspective'. Administrative Science Quarterly, 34, share businesses'. Strategic Management Journal, 2,1989, pp, 169-194, 1981, pp, 301-318,