Embed Size (px)

Citation preview

AKU-T-79-004 C. 3

MARKET STRUCTURE

uf the

ALASKA SEAFOOD PROCESSING INDUSTRY

by

V. L. Orth

3. A. Richardson

S. Mj. Piddle

I! niver~ity of Alack t

gaea ~rant Report 7H - 10

Bee entber 1979

Alaska Sea Grant ProgramUniversity of Alaska

Fairbanks, Alaska 99701

MARKET STRUCTURE

OF THE

ALASKA SEAFOOD PROCESSING INDUSTRY

Volume I

Shellfish

by

Franklin L. Orth

James A. Richardson

Sandra M. Pidde

Sea Grant Report 78-10November 1979

CONTENTS

PAGE

FIGURES vij

TABLES.

ACKNOWLEDGEMENTS. XVi i

CHAPTER I. INTRODUCTION

1 3 5Industry:

7

9

9

13

15

65

Background and Scope of the Study.Data Resources ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Organization.Structural Elements of the UPS. Seafood Processing

A Literature Summary. ~ ~ ~ ~ ~ ~

Alaska Fishing Industry: Regulatory Environment..Federal

State..

CHAPTER II. ECONOMIC STRUCTURE OF THE ALASKA SEAFOOD PROCESSING

SECTOR AND DETAILED SHELLFISH PROCESSING INDUSTRIES. ~

Introduction.

Structural Parameters of the Alaska Seafood ProcessingS ector.. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Geographic Distribution of Production Facilities........Aggregate Concentration..Diversification.

Turnover....

Vertical Integration ~ ~ ~ ~ ~ ~ ~ 4 ~ ~ 0 ~ ~ 4

Other Company-Specific InformationStructural Parameters of Individual Seafood Markets: Shellfish

Market Concentration ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Plant Size Characteristics............

Summary

CHAPTER III. THE HISTORY OF THE KING AND TANNER CRAB FISHERIESIN ALASKA

Development of the Alaska King Crab FisheryThe Foreign Fishery.The U.S. Fishery ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

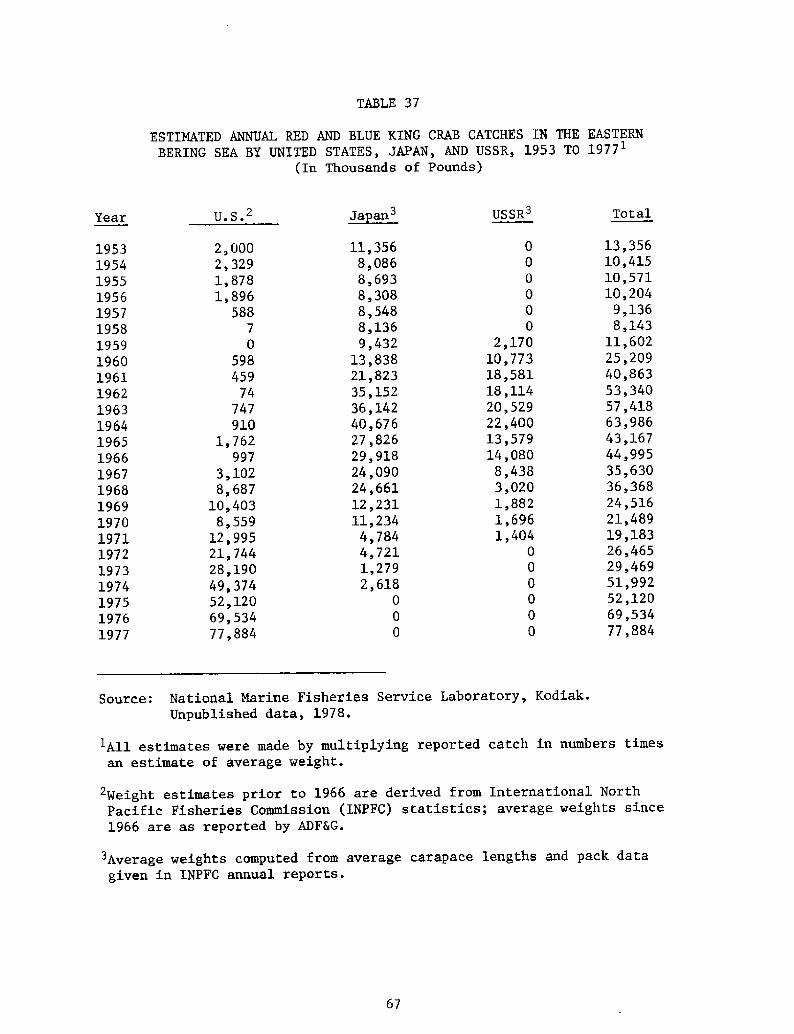

Development. of the Alaska Tanner Crab Fishery.Foreign Fishery: Japan.......Foreign Fishery: USSR... . . ~T he U.S. Fishery

16

16

19

31

36

40

41

45

47

52

56

65

65

72

76

76

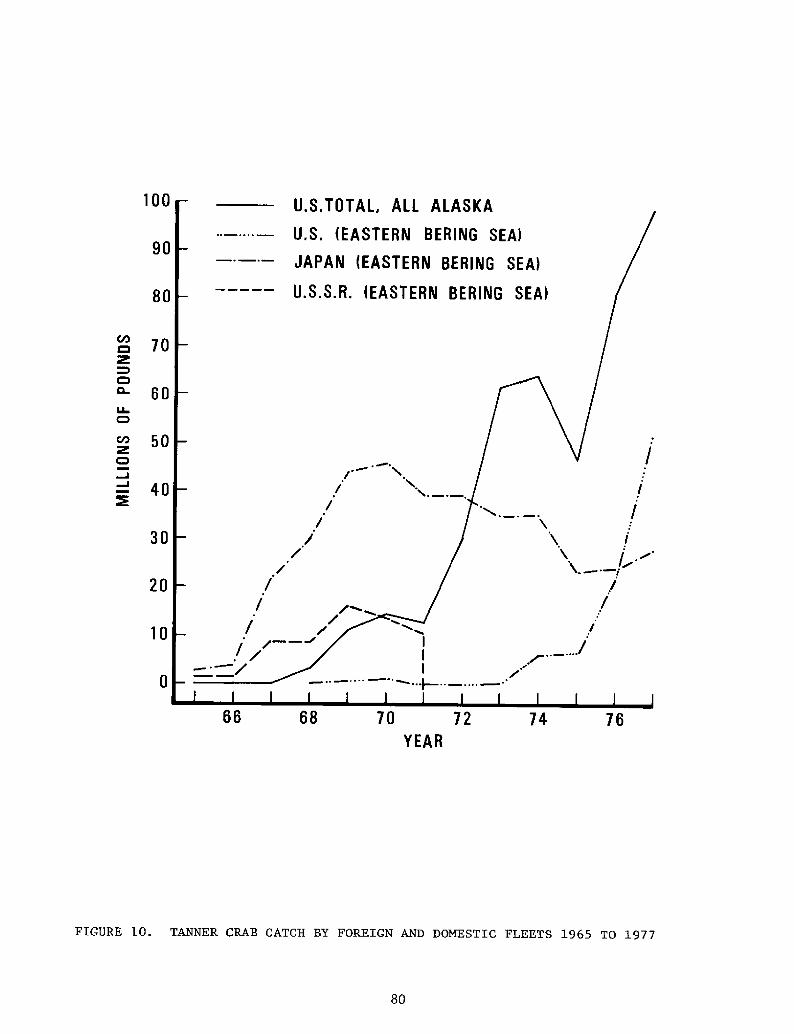

77

81

CONTENTS

continued!

PAGE

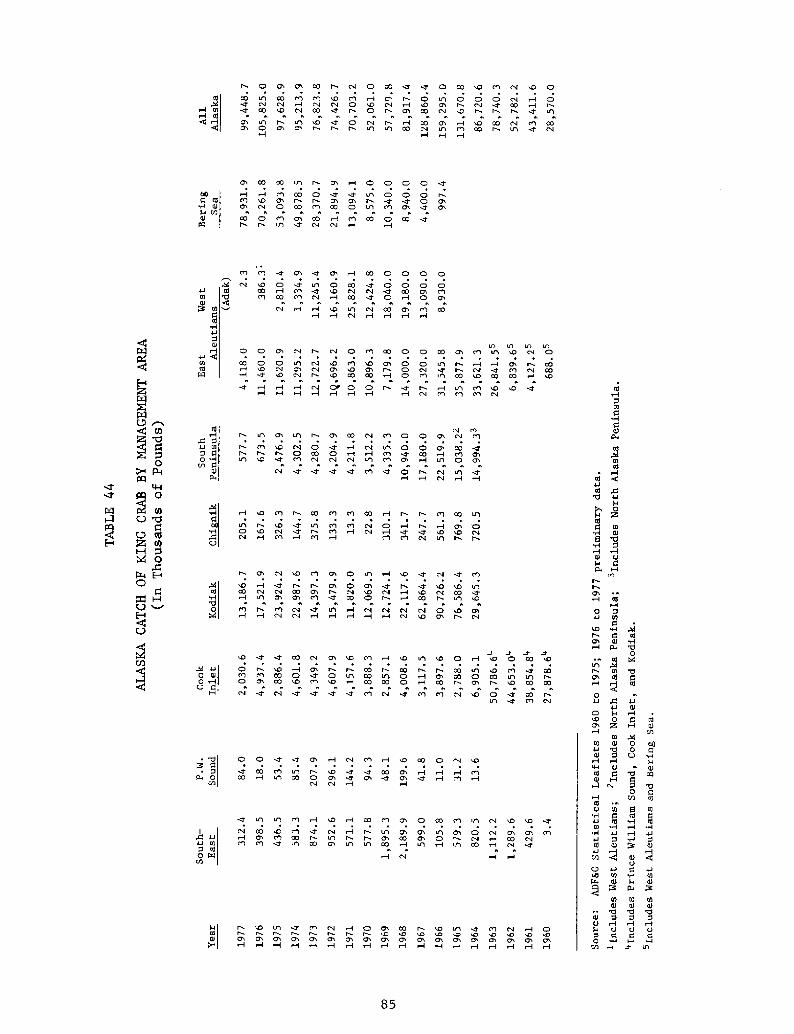

83CHAPTER IV. THE CRAB RESOURCE.

King Crab.World Catch...........

Expansion Potential ofTanner Crab

Catch and Abundance In

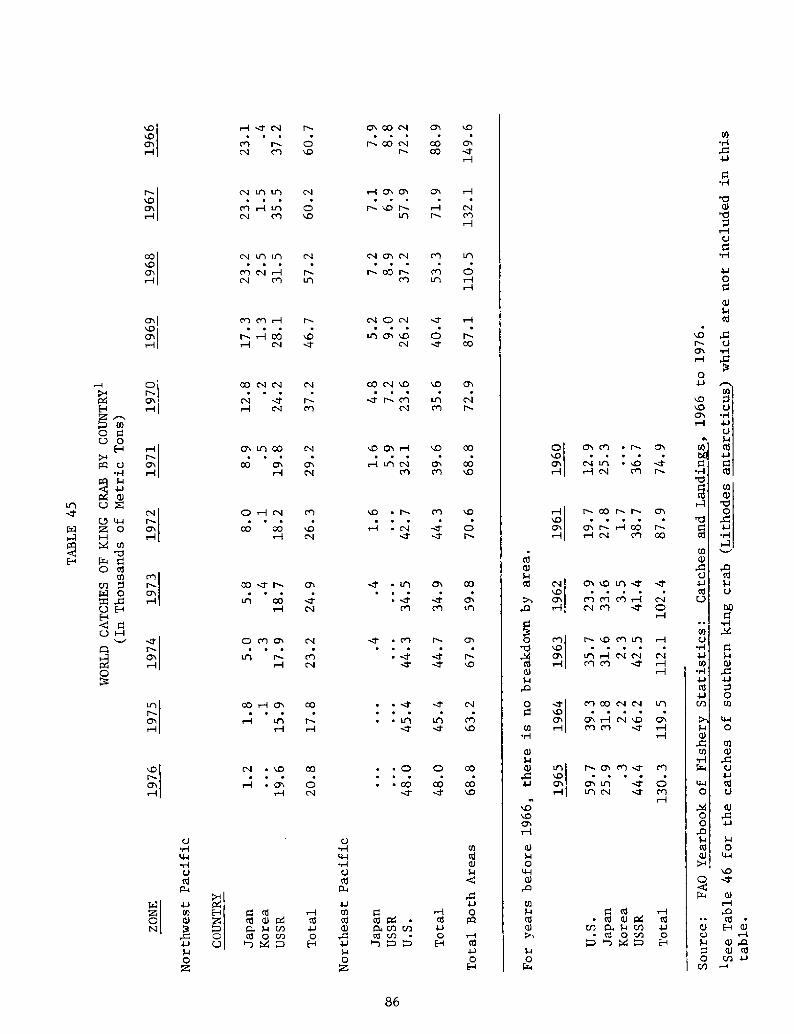

World Catch.

Expansion Potential ofDungeness Crab.

83

83

87

88

88

92

92

92

the King Crab Fishery............

Alaska. ~ ~ ~ ~ ~~ ~ ~ ~ ~ ~ ~

the Tanner Crab Fishery.....

121

121

121

124

125

129

132

132

CHAPTER V. FISHING GEAR AND PROCESSING METHODS FOR KING AND

ANNE R CRAB ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ e ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~T

Crab Fishing Gear.Vessels

Gear on the Vessel.

Pots' ~ ~ ~

Circulating Seawater Tanks..B uoys........... ~ .... ~ ~ ~

B ait 4 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ J 4 ~ ~ ~ ~

Fishing the GearHarvesting Capacity..

Processing ~ ~ ~ ~ ~ ~ ~ ~ ~

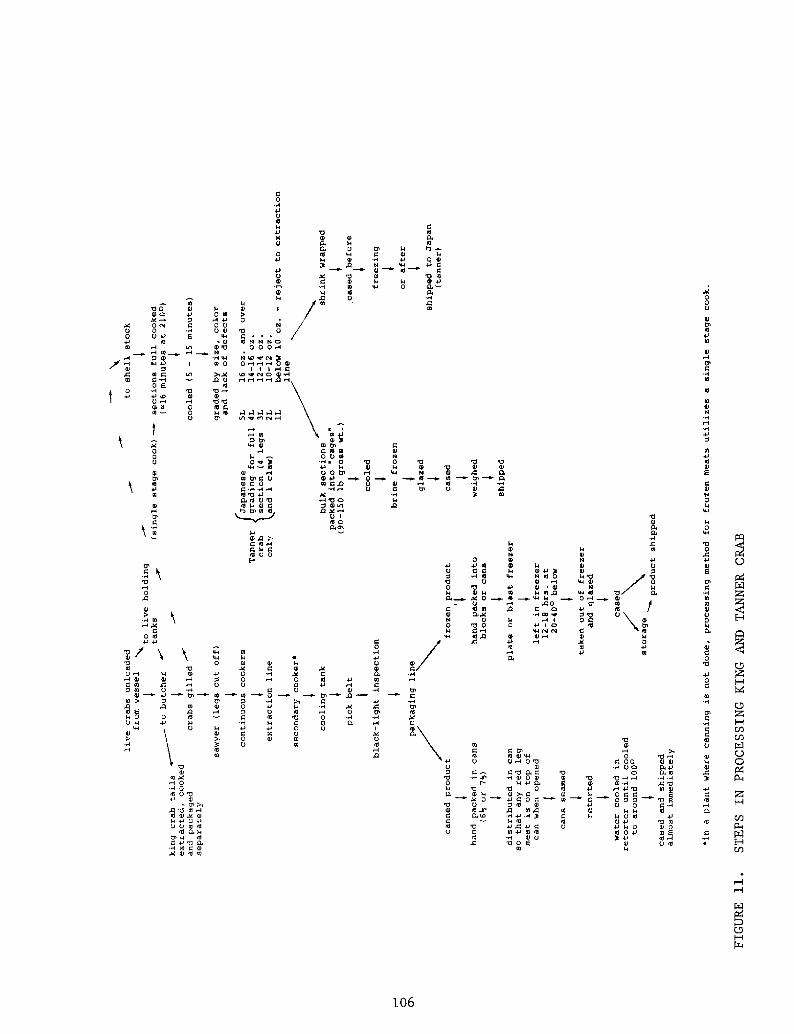

Processing Methods... ~ ~

Processing of Crab MeatsProcessing of Crab Sections Shell Stock!....New Developments in Crab Processing Methods..Processing Capacity and Capacity Utilization.Southeastern Alaska..

Prince William Sound.

Cook Inlet

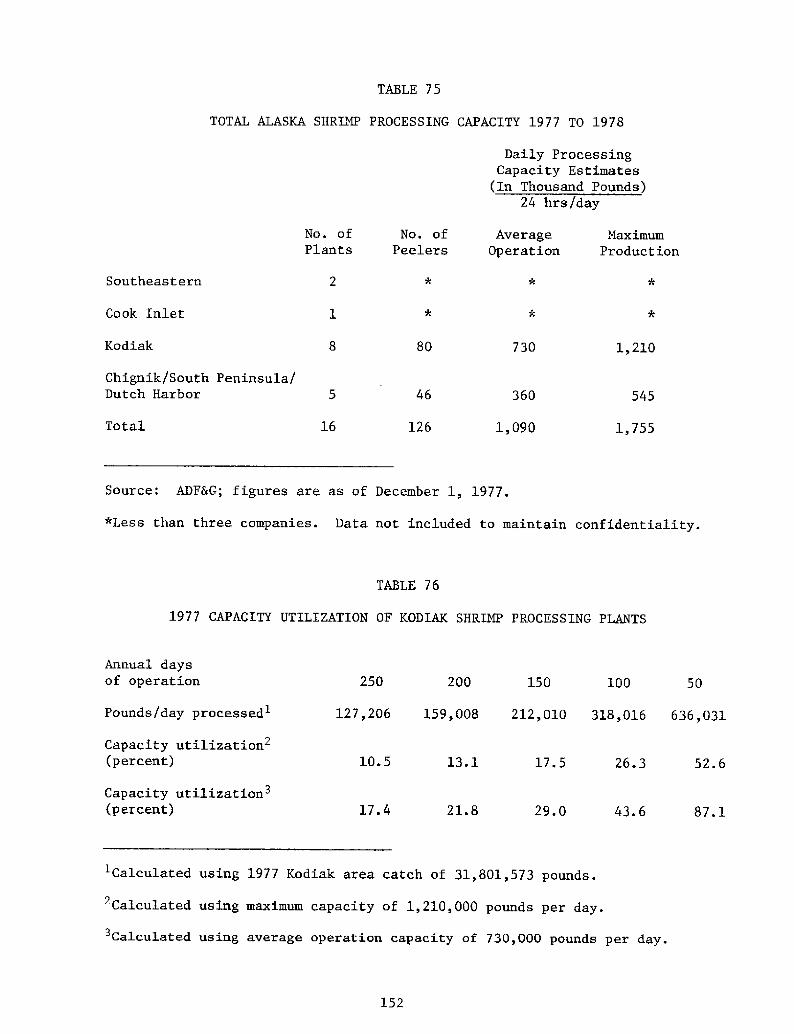

Kodiak. ~ ~

Westward.

CHAPTER VI. THE HISTORY OF THE SHRIMP FISHERY IN ALASKA..........

Foreign Shrimp Fishing in Waters off Alaska.Japanese Shrimp FisherySoviet Shrimp Fishery..................

U.S. Shrimp Fishery in Alaska...............

CHAPTER VII ' THE SHRIMP RESOURCE ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ e ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Pacific Coast Pandalid Shrimp FisheryWorld Supply ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0 ~ ~ ~ 4 ~ ~ ~ ~ ~ ~

95

95

98

98

100

100

101

101

101

104

105

105

107

108

108

111

113

113

115

117

CONTENTS

continued!

PAGE

137

ilization........

155

Crab.

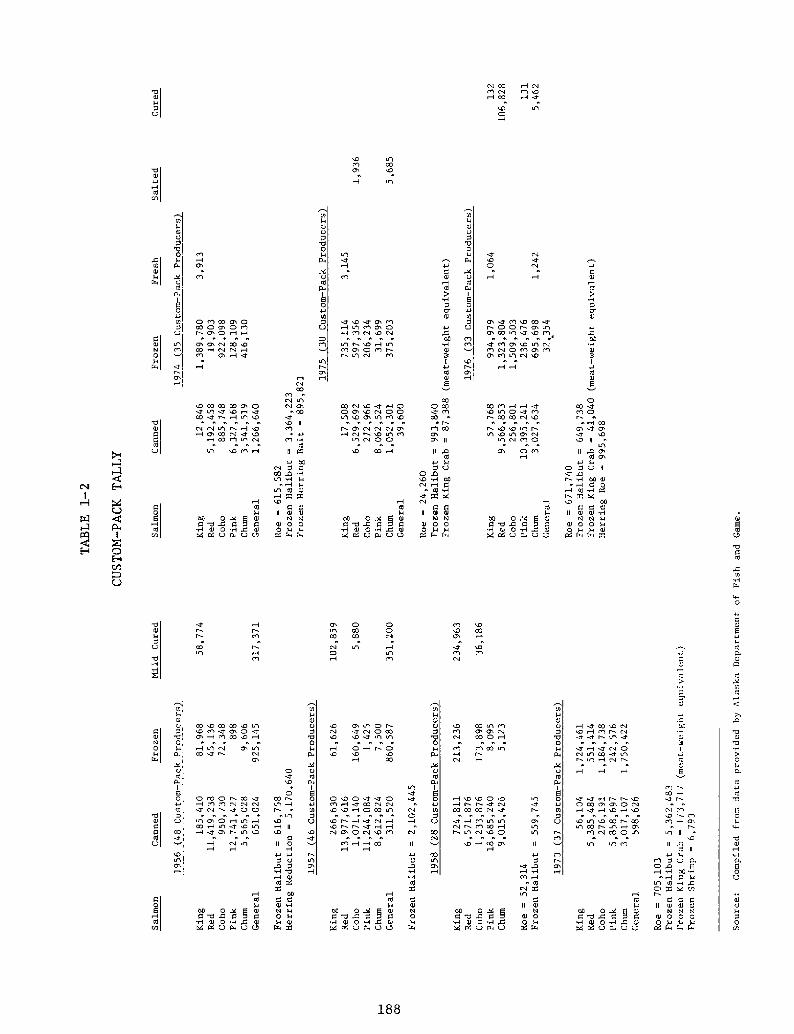

183

184

184

185

185

189

192~ ~ ~ 92 ~ ~ ~ ~File and

193

CHAPTER VIII. FISHING GEAR AND PROCESSING METHODS FOR SHRIMP...

Shrimp Fishing Gear......................Vessels

Types of Gear......... ~ .....On-Board Handling......... ~Electronic Gear.

New Technology............ ~ ..........Harvesting Capacity..................

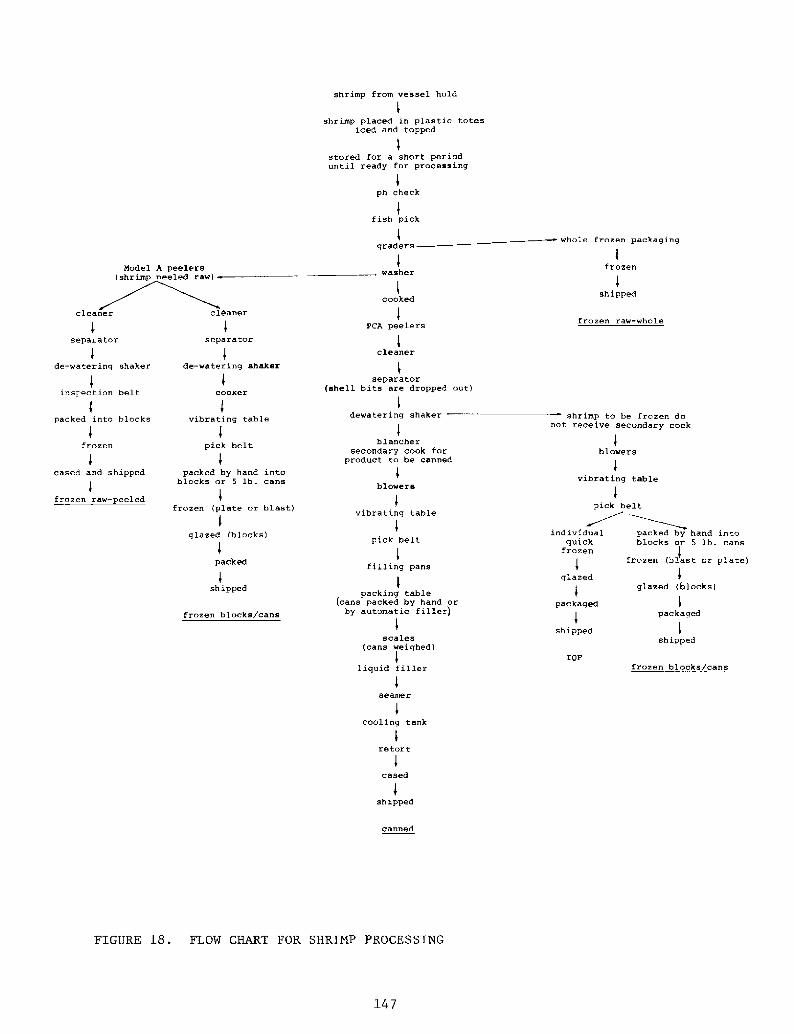

Processing Methods for Shrimp.Frozen Raw-Whole.....................

Frozen Raw-Peeled. ~ .. ~ ....... ~ .......

Frozen Cooked-Blocks/Canned..........Individual Quick Frozen..............Canned.

Shrimp Processing Capacity and Capacity UtSoutheasterne ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0 a ~Cook Inlet.

Kodiak ~ ~ ~ ~

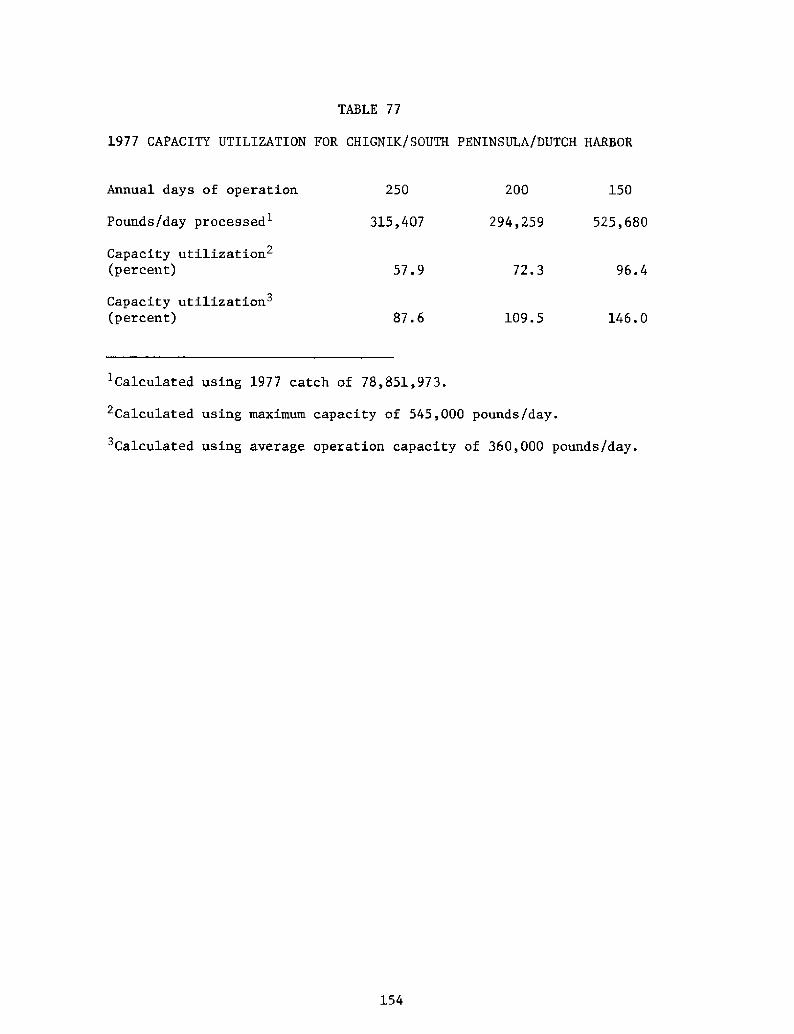

Chignik/South Peninsula/Dutch Harbor.

CHAPTER IX. ~TING OF ALASKA SHELLFISH ~ ............. ~ .... ~

Marketing of King Crab..............Marketing of Tanner Crab............Geographic Distribution..Market Channels for King and Tanner

Product for Export.............Product for the Domestic Market

Import and Export Markets.... ~ .D emand. ~ ~ ~ ~ ~ ~ ' ~ ~ ~ ~ ~ ~ ~Prices. ~ ~ ~ 0 ~ ~

Marketing of Shrimp.................Market Channels..... ~ .......

Geographic Distribution..... ~Import and Export MarketsDemand. ~ ~ ~

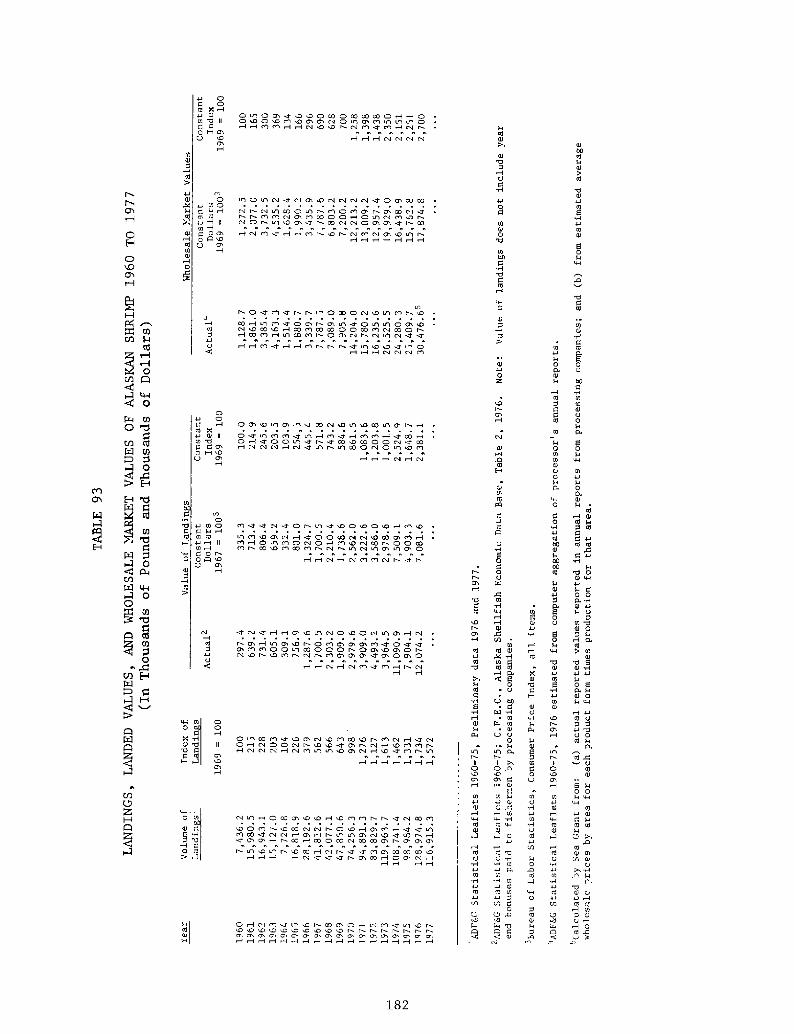

Pl ices ~ ~ ~ ~ ~ ~ ~

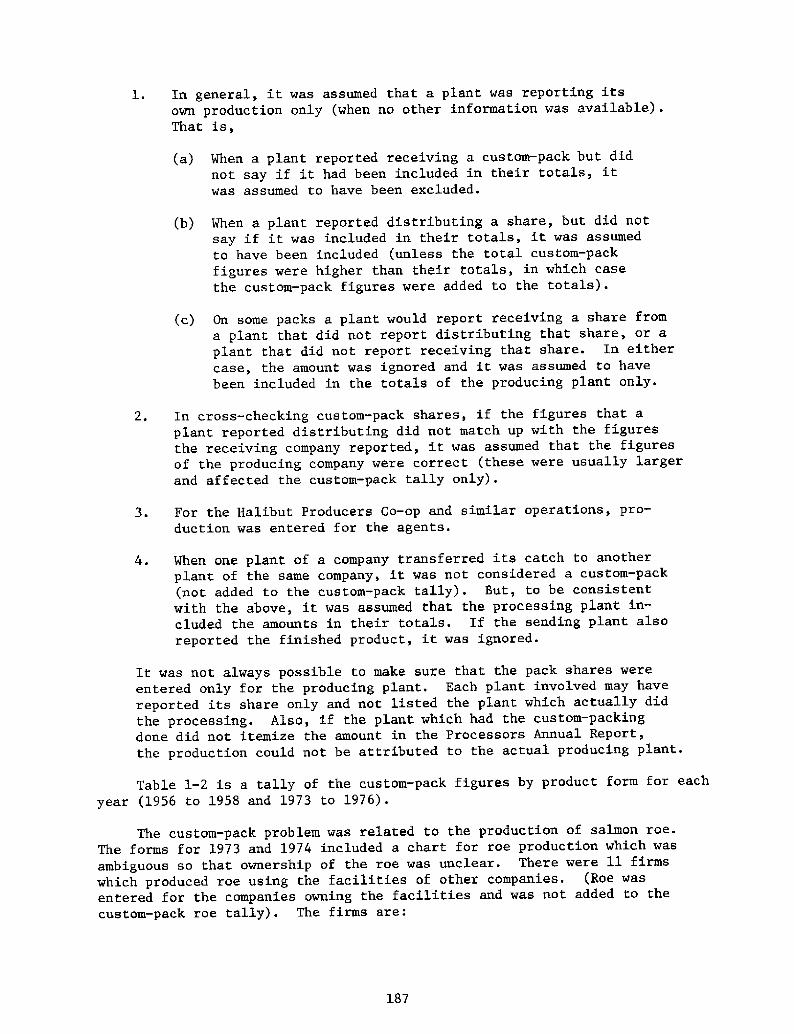

APPENDIX I. REVIE'W OF PROCEDURES FOR DATA FILE REFINEMENTS.....

Part I: Resolution of Problems.......

Classification of Plants..

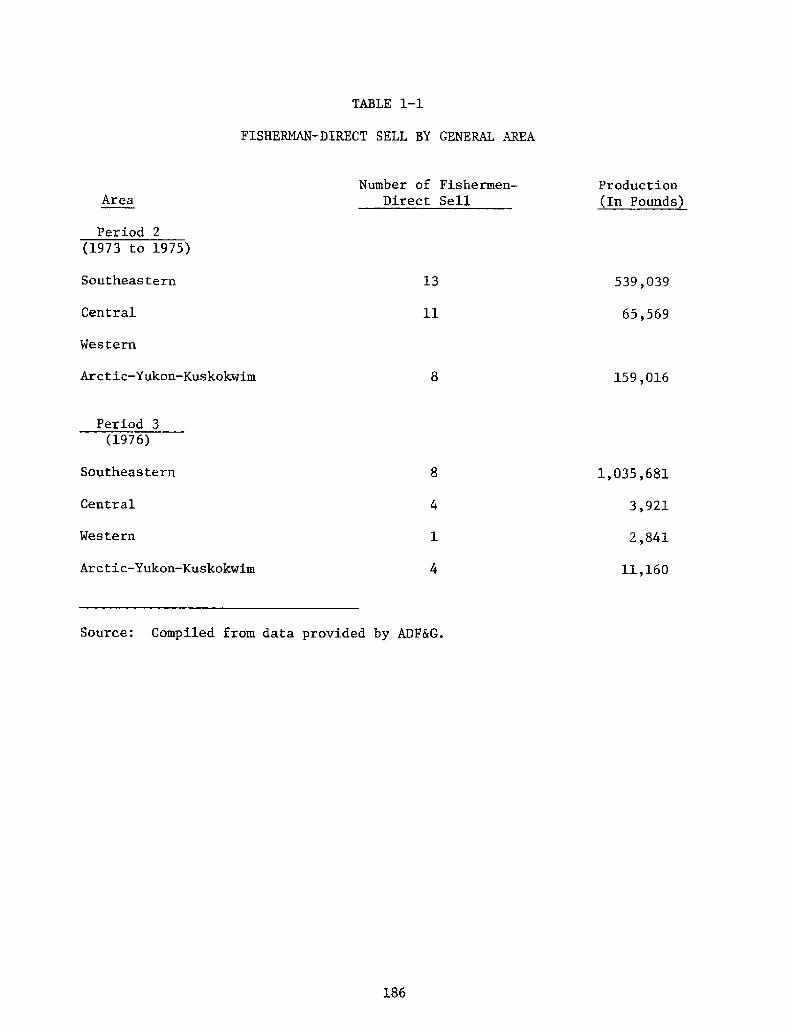

Fisherman-Direct Sell............

Custom-Packing..Recovery and Conversion Factors..Incomplete Data................Apparent Accuracy of Edited Data

Published Statistics...........

137

137

137

141

141

142

142

146

146

148

148

148

148

149

149

149

151

153

155156

158

160

159159

163

166

172

172

177

177

178

178

179

CONTENTS

continued!

PAGE

201

202

Sectors.........

217

221

222

242

259

283

Part II: Recommendations for Improvements in Alaska'sFisheries Data..........

Catch and Landing Data by Species and Area.........Production Data by Species, Product Form and Area..Price Series Data by Species and Area..............Employment Statistics by Area....

APPENDIX II. STRUCTURE OF UNITED STATES SEAFOOD PROCESSINGINDUSTRY ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Part I: Conceptual Framework of Industrial Organization

Part II: A Literature Review..........

In't r o due t ion ~ ~ e ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Economic Structure of Process Form

Overview

Fresh Process Form Sector....

Frozen Process Form Sector...

Canned Process Form Sector...

Cured Process Form Sector

S ummary s ~ ~ ~ ~ ~ i ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

P TT ~art III. Glossarye ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ r ~ ~

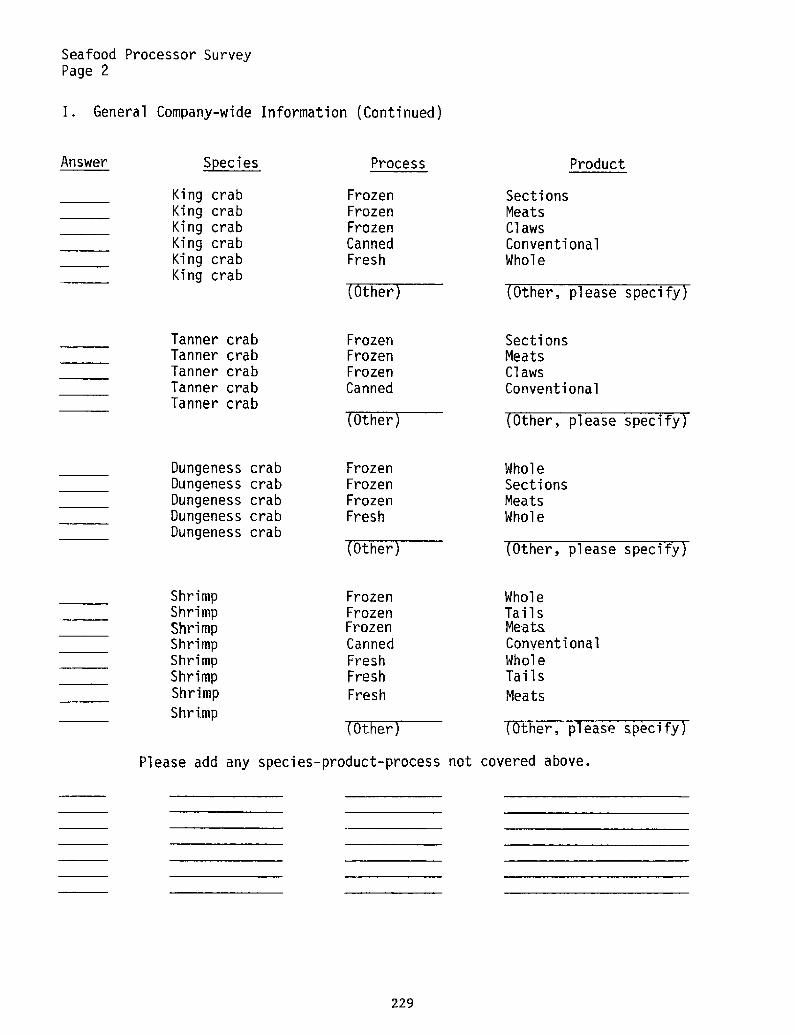

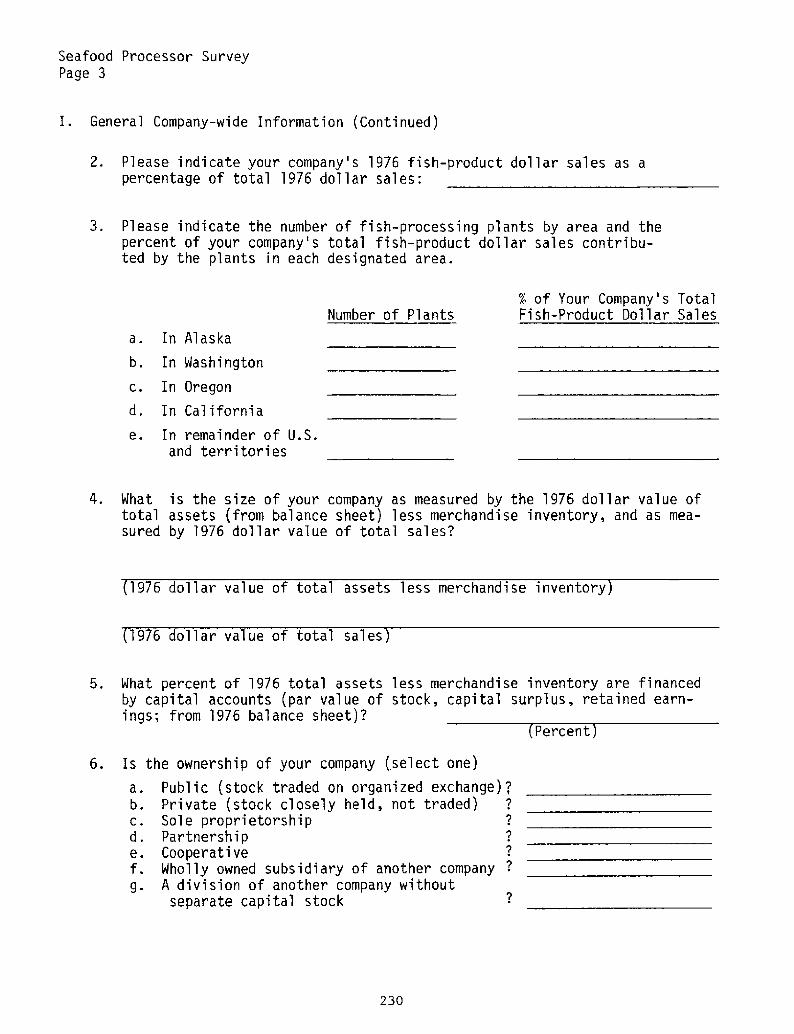

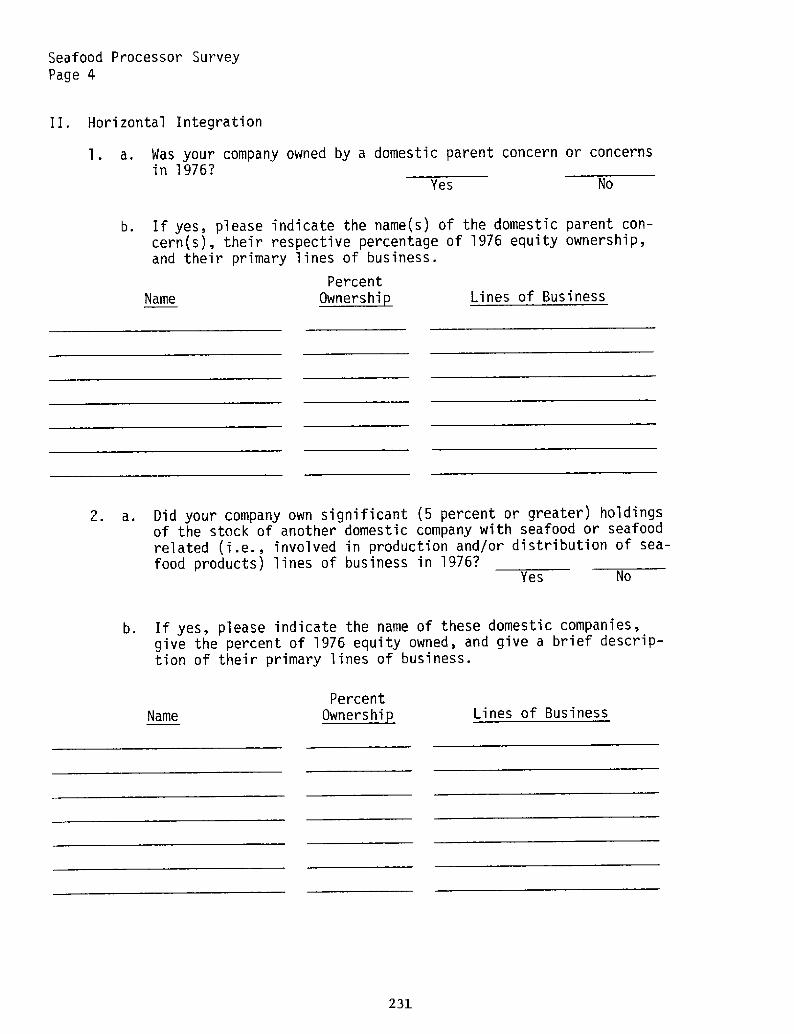

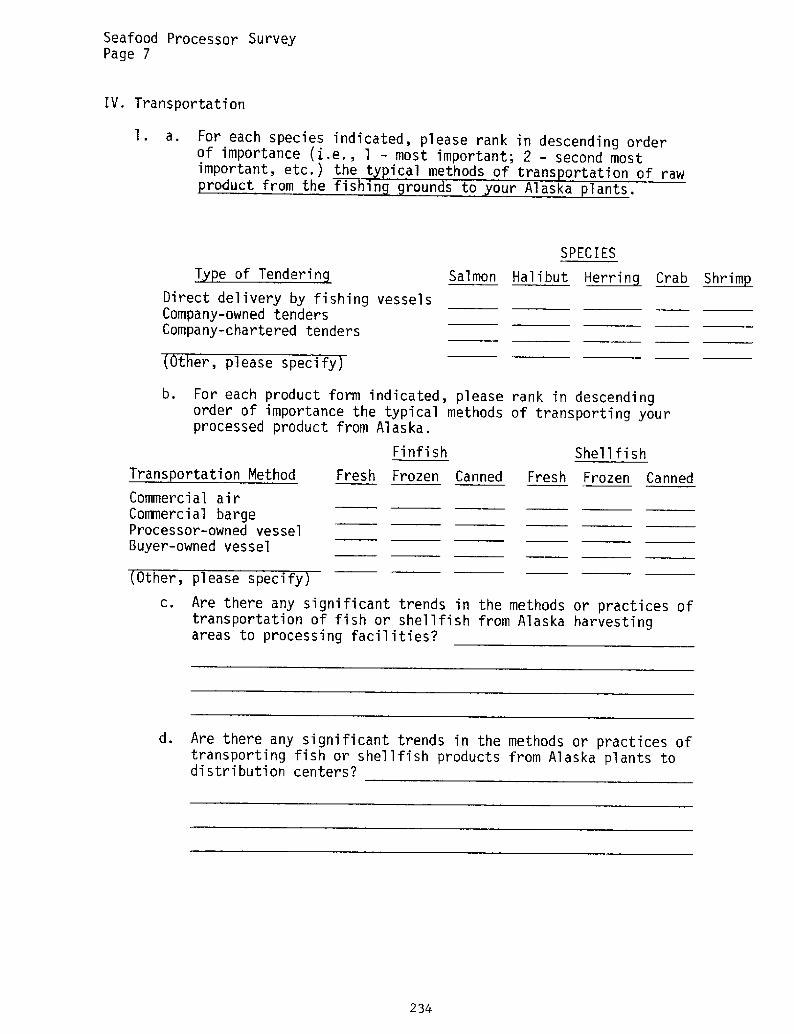

APPENDIX III. INDUSTRY SURVEY: SURVEY FORM AND RESPONSES...

Part I: Survey Form...........

Part II: Survey Responses............. ~ ..........

APPENDIX IV. PERIOD 3 �976! STRUCTURAL PAKVKTERS..... ~ ....

FERENCES ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ t s ~ ~ e ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

197

197

197

198

199

206

206

206

206

207

210

213

215

215

FIGURES

PAGE

FIGURE 3

29

30

FIGURE 7

75

FIGURE 8

78

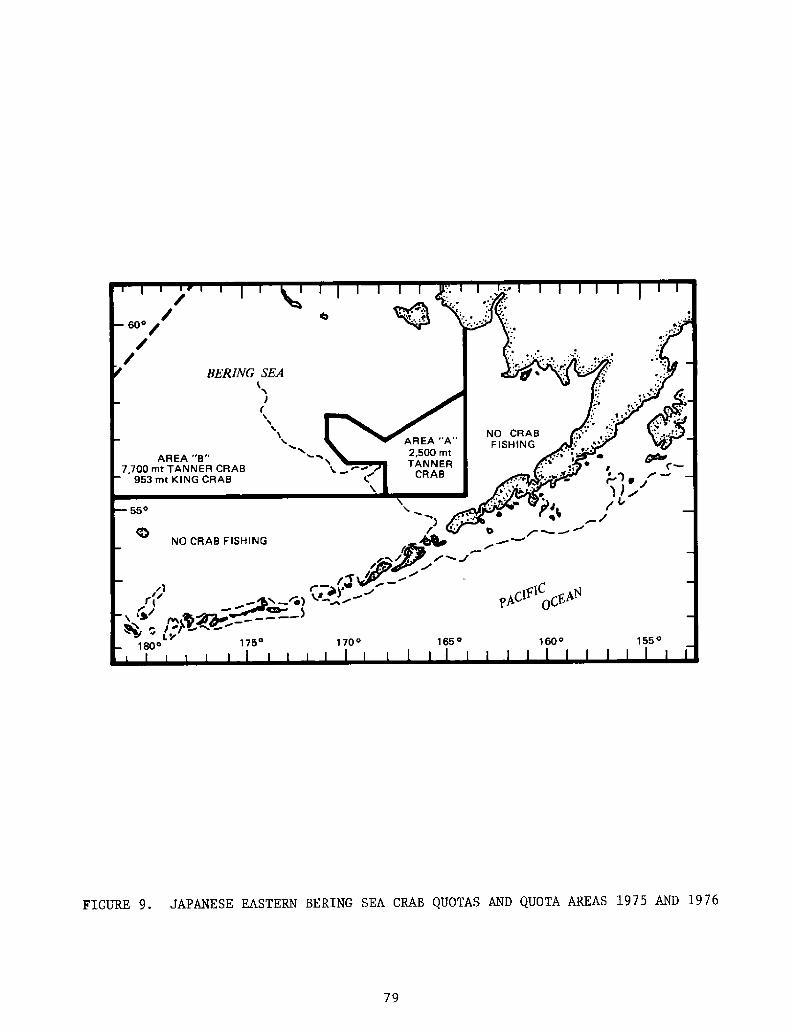

FIGURE 9

79

FIGURE 10

80

106

109

FIGURE 13

110

FIGURE 14

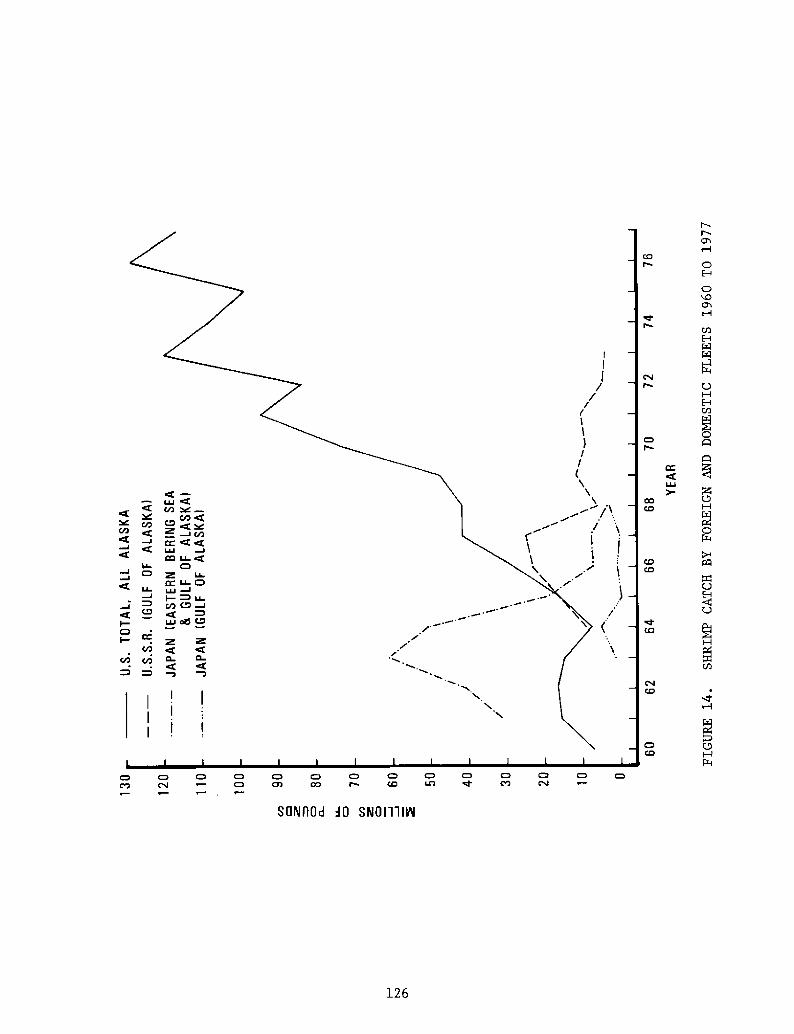

126

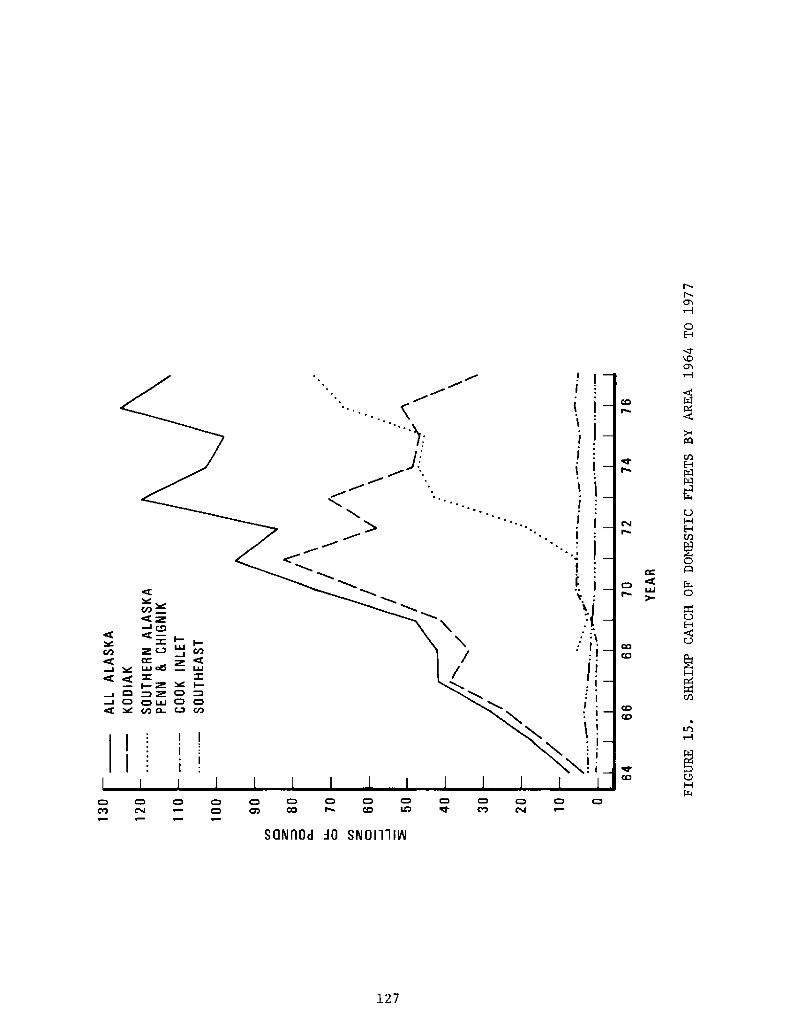

FIGURE 15 Shrimp Catch of Domestic Fleets by Area 1964 to 1977. 127

FIGURE 16 Typical Rigging for a Shrimp Otter Trawl............. 140

FIGURE 1

FIGURE 2

FIGURE 4

FIGURE 5

FIGURE 6

FIGURE ll

FIGURE 12

Conceptualization of Market Structure Study..........

Landed Weight, Ex-vessel Value and WholesaleValue of Alaska Fisheries 1975.................... ~ ..

Agencies and Organizations Affecting AlaskaMarine Resources Development.........................

Lorenz Curves for Alaska Seafood Processing Plants...

Lorenz Curves for Alaska Seafood Processing Companies

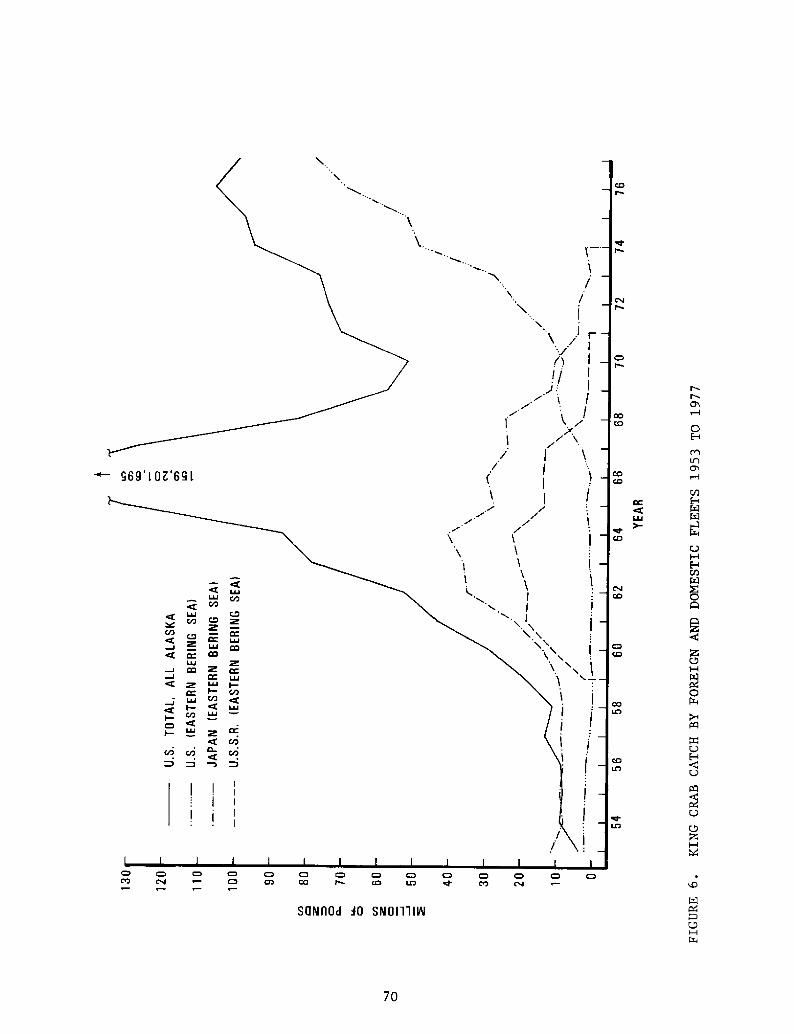

King Crab Catch by Foreign and Domestic Fleets1953 to 1977.

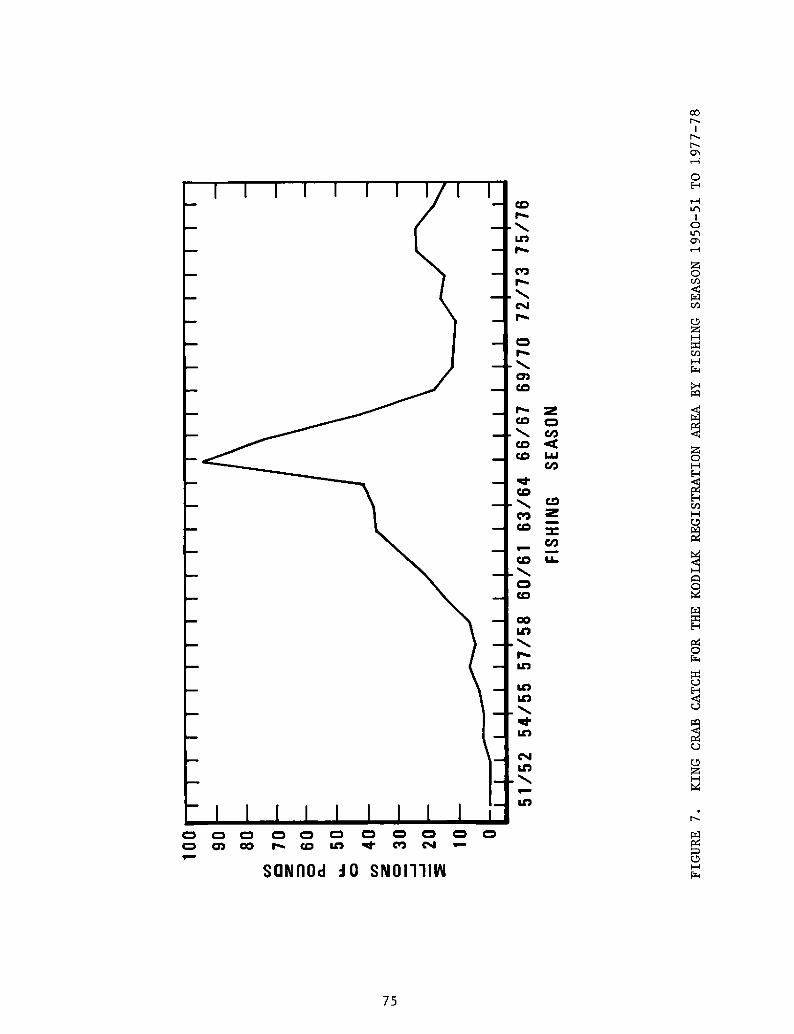

King Crab Catch for the Kodiak Registration Areaby Fishing Season 1950-51 to 1977-78

Areas and Catch Quotas for 1973 and 1974 Establishedfor Japanese King and Tanner Crab Fishing in theEastern Bering Sea by the U.S.-Japan Agreement ofDecember 1972

Japanese Eastern Bering Sea Crab Quotas and QuotaAreas 1975 and 1976.............................

Tanner Crab Catch by Foreign and Domestic Fleets1 965 'to 1977 o ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ t ~ a ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ s ~ ~ ~ ~ ~

Steps in Processing King and Tanner Crab........... ~ ~

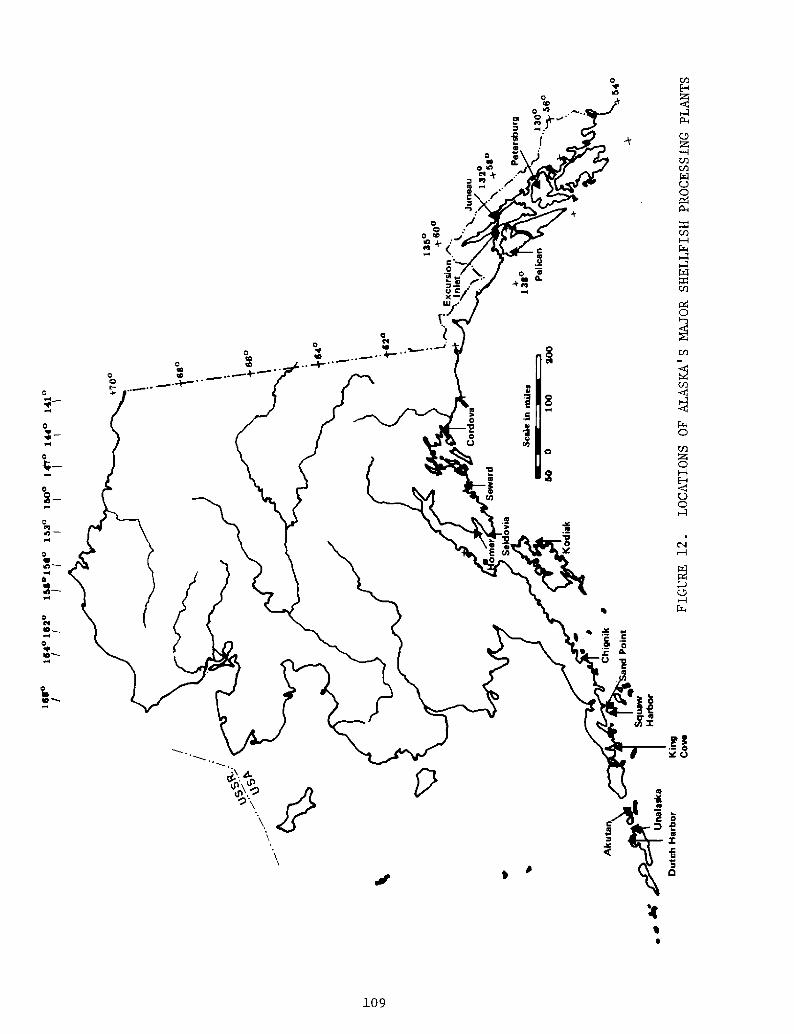

Locations of Alaska's Major Shellfish Processingp lantso ~ ~ ~ ~ t ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ t ~ ~ t ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

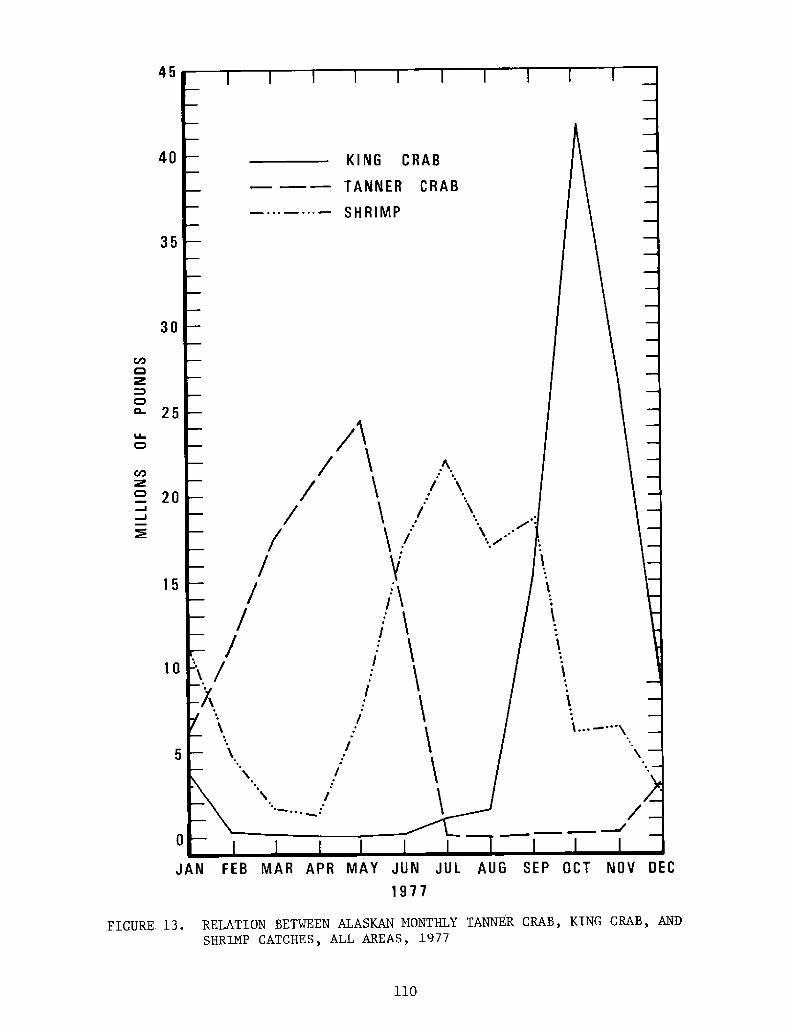

Relation Between Alaskan Monthly Tanner Crab, KingCrab and Shrimp Catches, All Areas, 1977.............

Shrimp Catch by Foreign and Domestic Fleets 1960 to1977 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

FIGURES

continued!

PAGE

140Double-Rigged Shrimp Trawler

147

by Major160

CrabFIGURE 20161

FIGURE 21

162

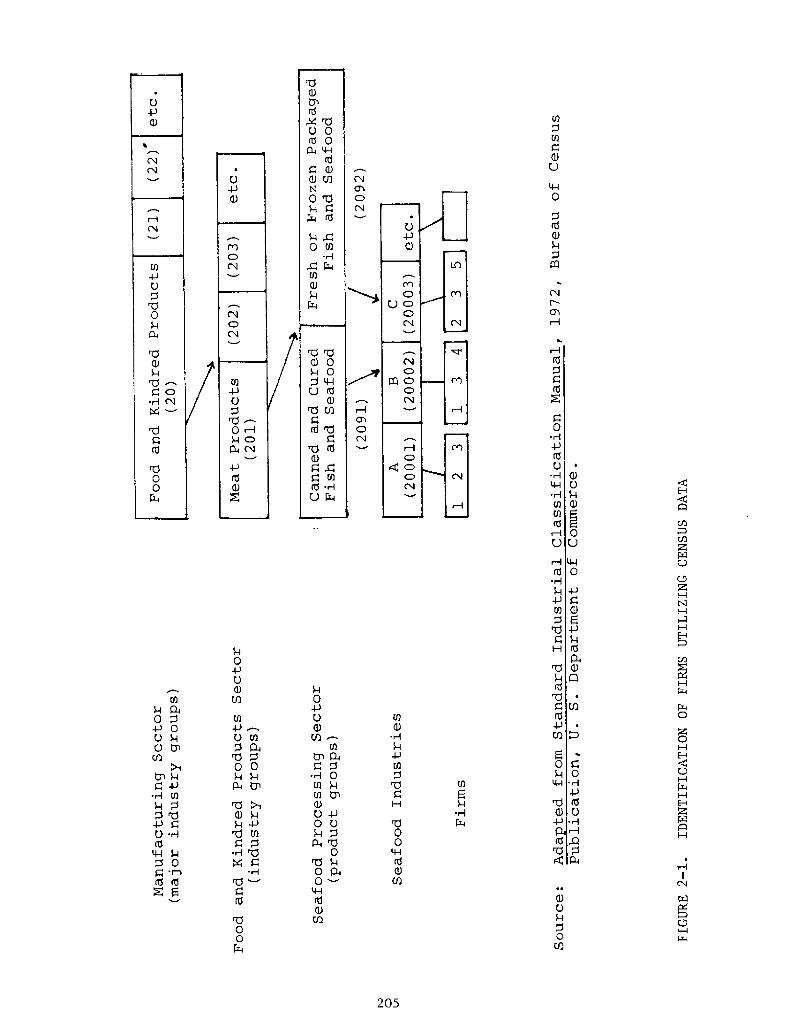

205FIGURE 2-1 Identification of Firms Utilizing Census Data......

FIGURE 17

FIGURE 18

FIGURE 19

Flow Chart for Shrimp Processing...................

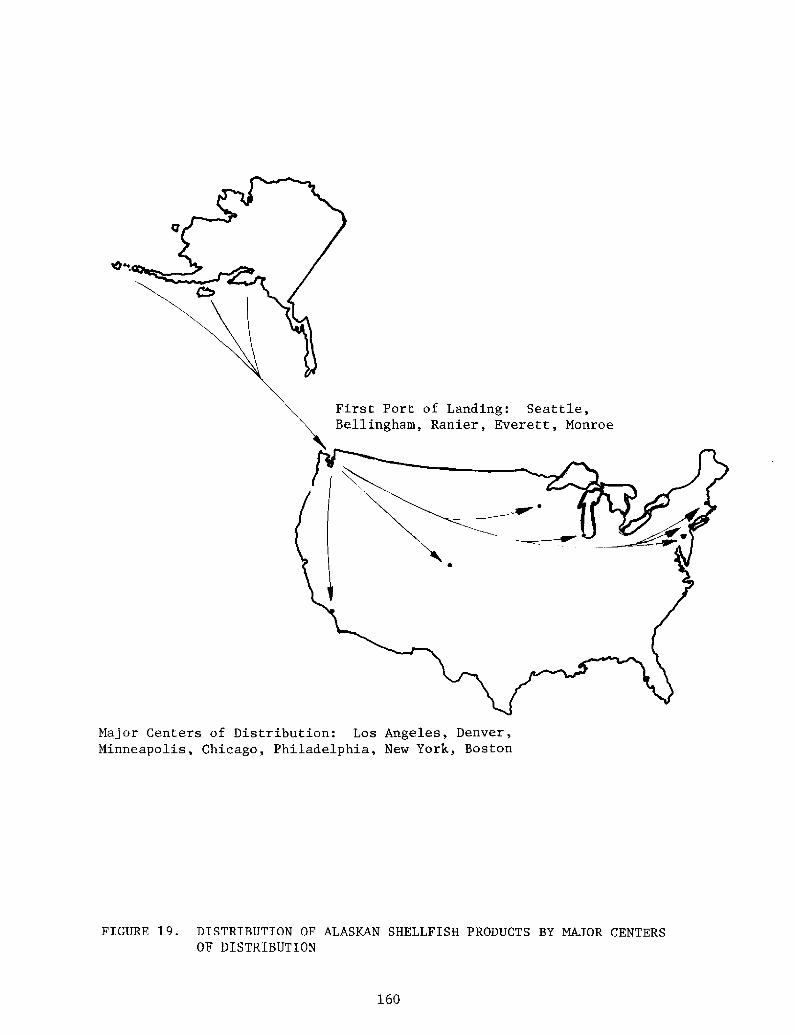

Distribution of Alaskan Shellfish Products

Centers of Distribution..........

Market Channels for Frozen King and TannerProducts ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0 ~ ~ ~ ~

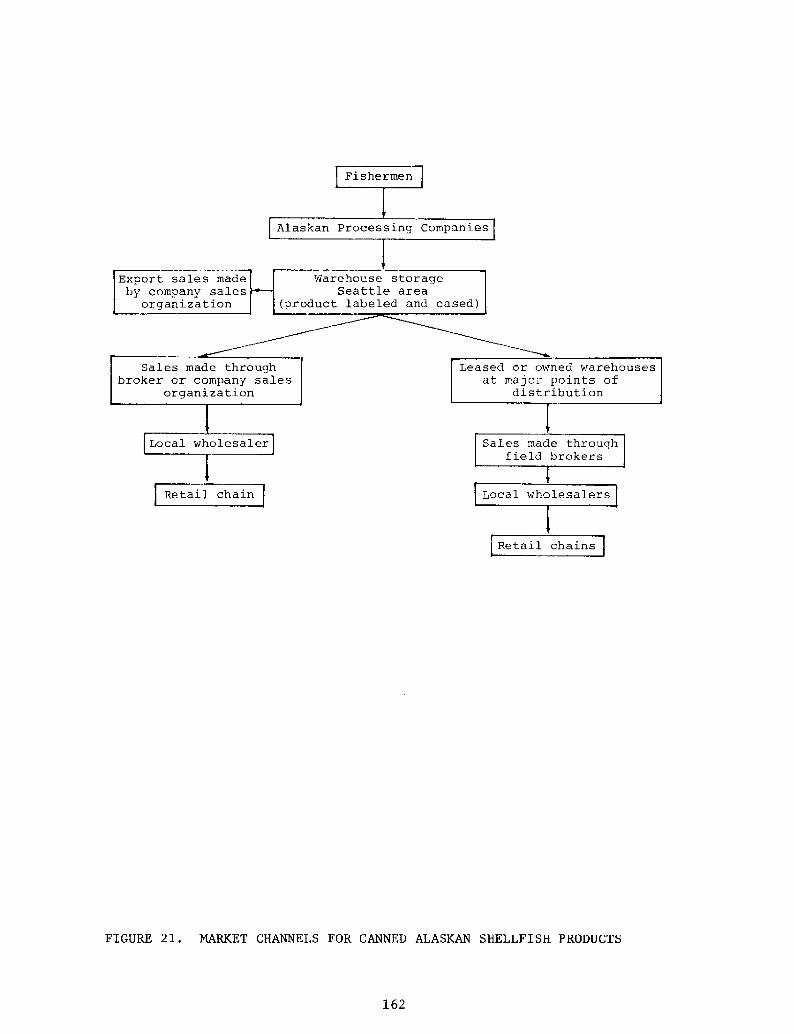

Market Channels for Canned Alaskan Shellfish

p loductse ~ ~ a ~ s.a~~os.~.s.o.~.e.os..see.~o...e~ee..

TABLES

PAGE

TABLE 1

TABLE 417

20

22

23

25

TABLE 1126

TABLE 1227

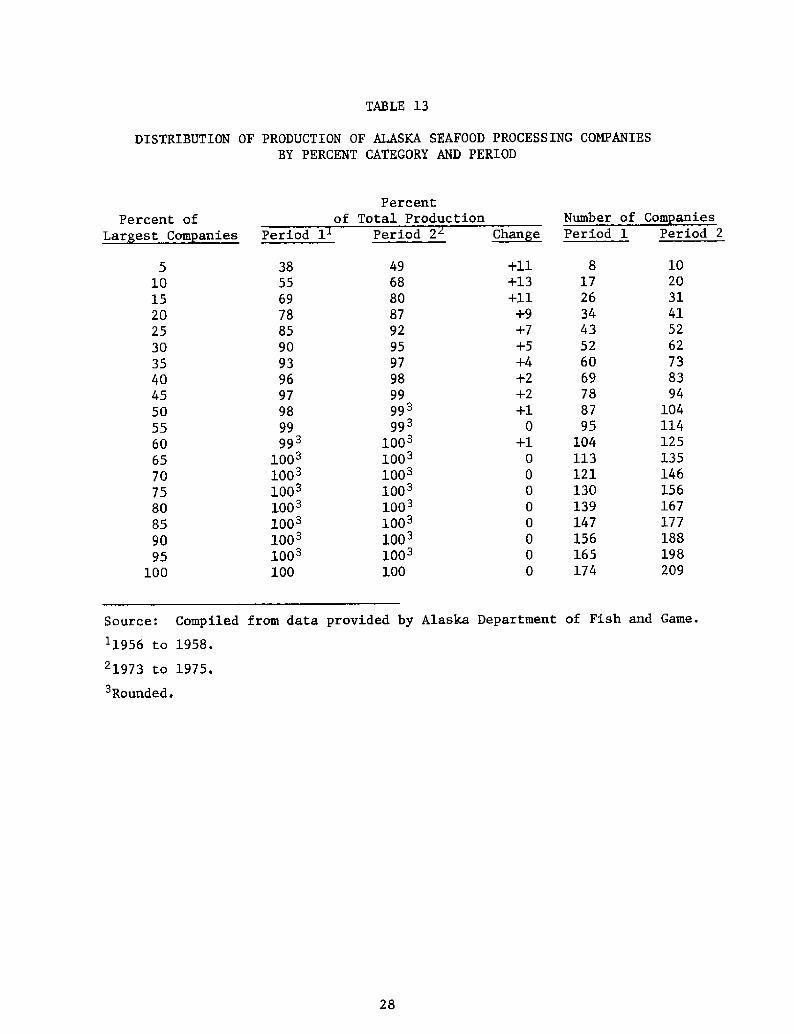

TABLE 13

28

TABLE 14

32

TABLE 15

33

TABLE 2

TABLE 3

TABLE 6

TABLE 7

TABLE 8

TABLE 9

TABLE 10

Seafood Processing Plant Count and Harvests byearl ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 0 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~7

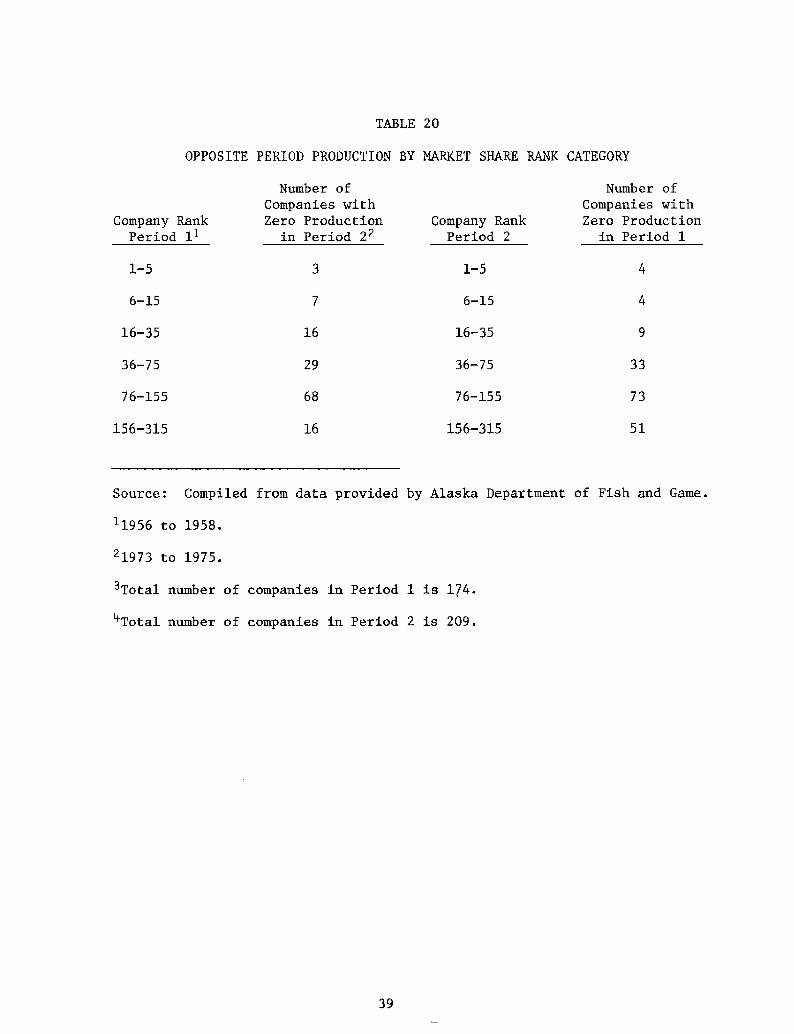

Continuity of Company Operation by Period..........

Summary of Market Structure Elements of U.S. Sea-food Processing Industry by National and RegionalProcess Form Sectors..

Alaska Seafood Processing Production Facilities,Regional Summary by Period.

Geographic Distribution of Seafood ProcessingPlants and Companies by Period..

Harvest of Finfish and Shellfish by Region.........

Company Frequency Distribution by Number ofGeneral Regions and Specific Areas by Period.......

Plant Size Distribution by Region and Period.......

Company Size Distribution by Region and Period.....

Number of Alaska Seafood Plants Operated byCompanies by Period

Size Distribution of Alaska Seafood Plants andCompanies by Period.......

Distribution of Production of Alaska SeafoodProcessing Plants by Percent Category and Period...

Distribution of Production of Alaska SeafoodProcessing Companies by Percent Category andPeriod..

Aggregate Concentration in the Alaska SeafoodProcessing Sector by Plants and Companies andby Period........

Diversification of Alaska Seafood ProcessingPlants and Companies as Measured by the Numberof Species Handled and by Period.

TABLES

continued!

PAGE

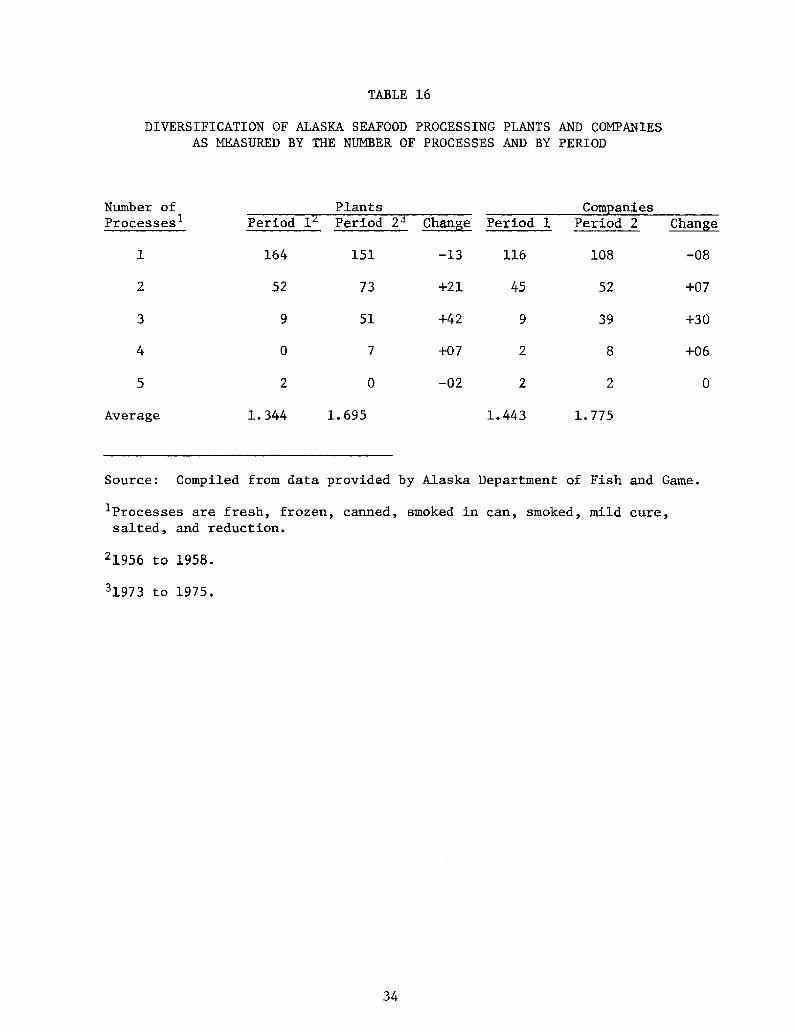

TABLE 16

34

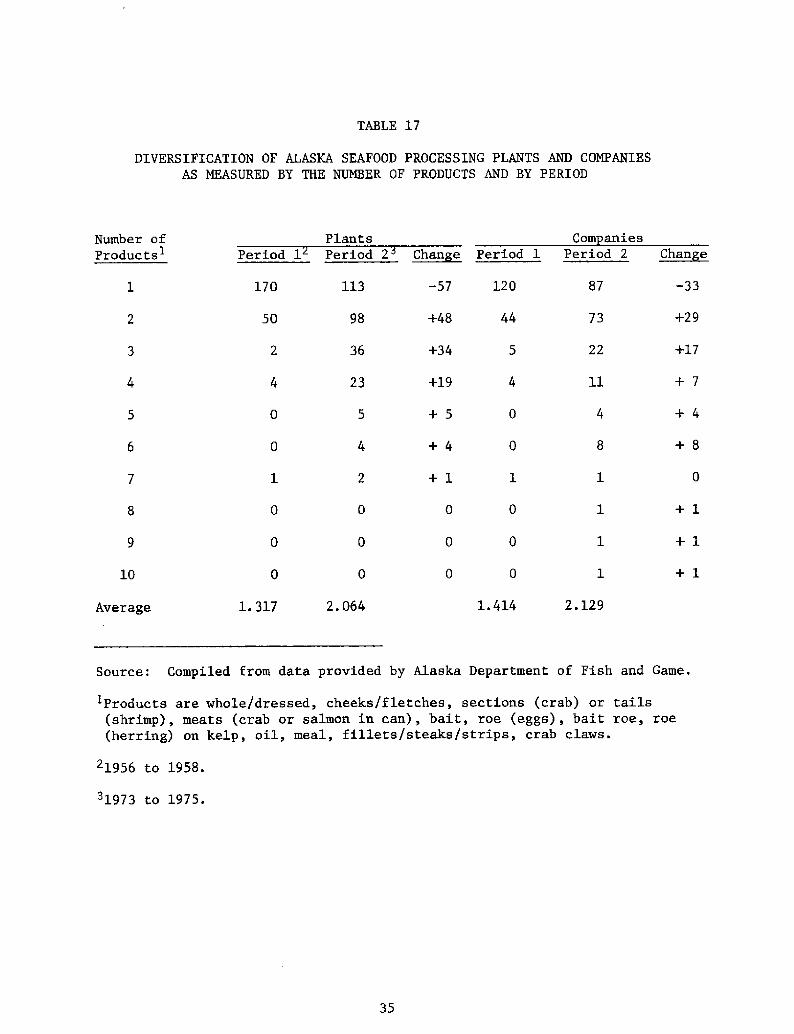

TABLE 17

35

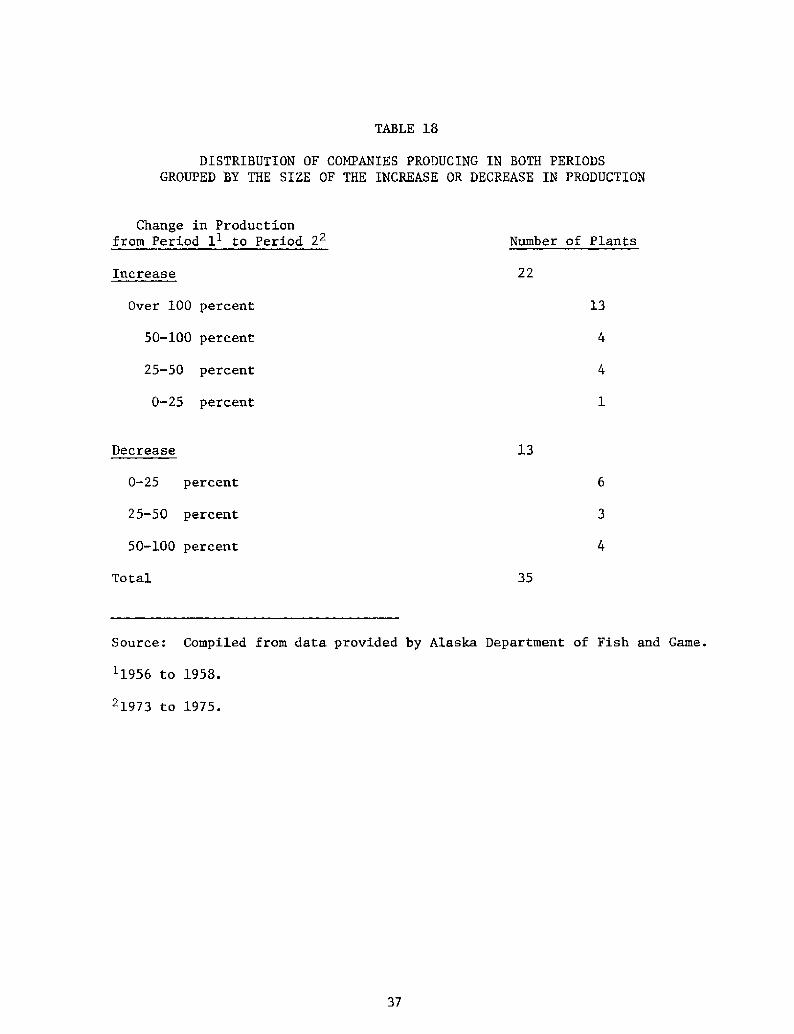

TABLE 18

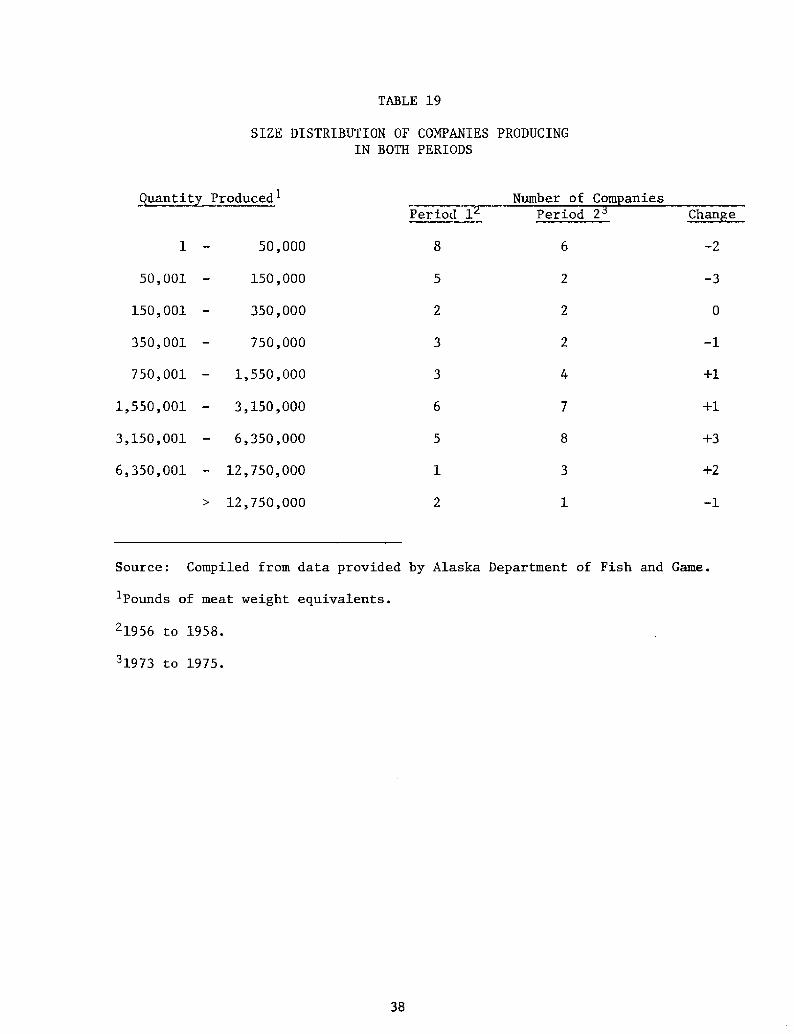

37

TABLE 19

38

TABLE 20

39

46

48

TABLE 24

49

TABLE 25

50

TABLE 26

51

TABLE 27

53

TABLE 28

TABLE 29

55

TABLE 21

TABLE 22

TABLE 23

Diversification of Alaska Seafood ProcessingPlants and Companies as Measured by the Numberof Processes and by Period..

Diversification of Alaska Seafood ProcessingPlants and Companies as Measured by the Numberof Products and by Period

Distribution of Companies Producting in BothPeriods Grouped by the Size of the Increase orDecrease in Production...

Size Distribution of Companies Producing in BothPeriods ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Opposite Period Production by Market Share RankC ategory. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ + ~ ~ ~ ~ ~ ~ ~ ~ ~

Extent of Vessel Ownership by "Yes" Respondents....

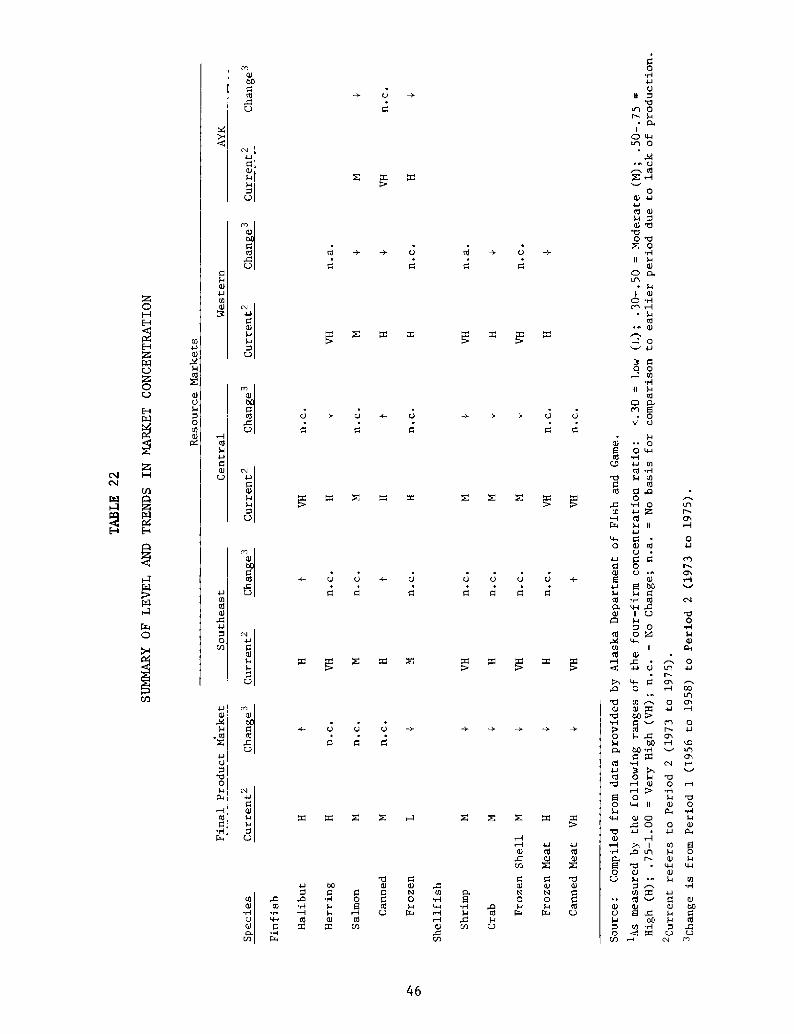

Summary of Level and Trends in Market Concentration

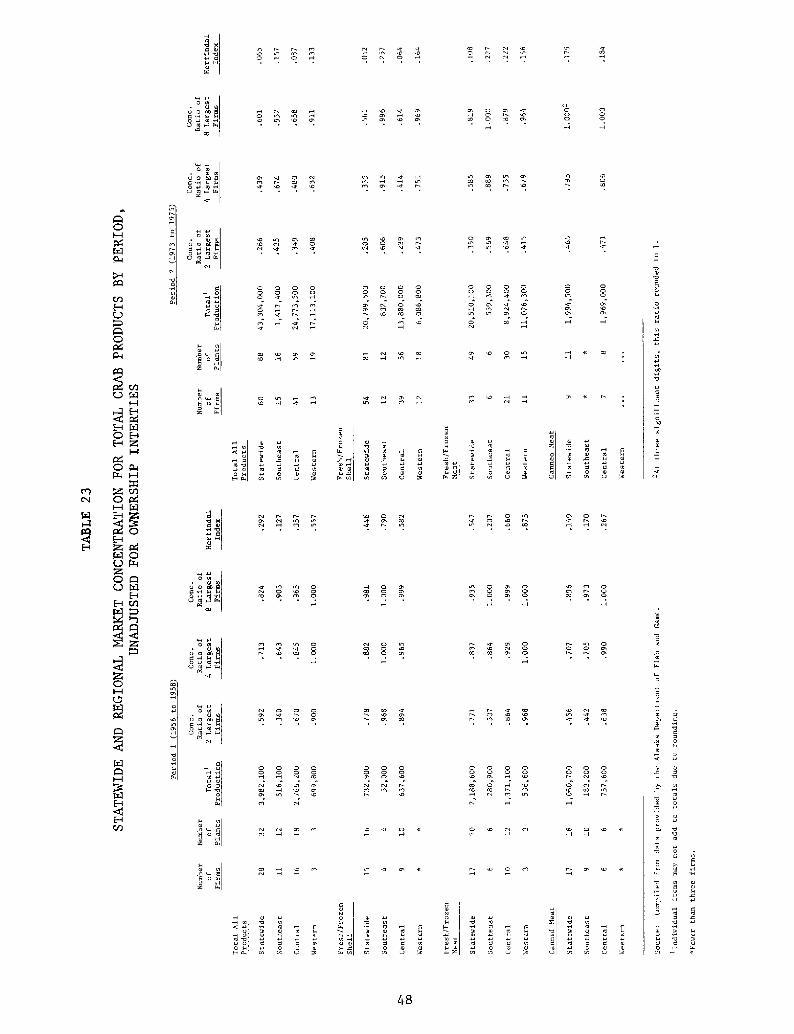

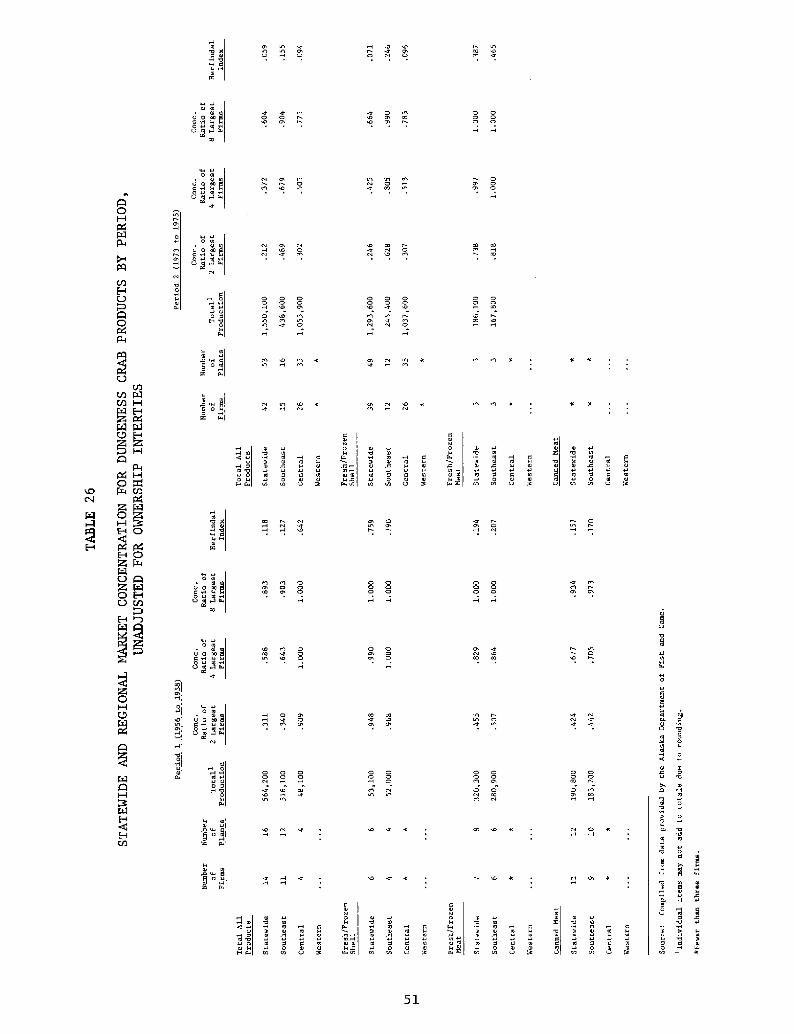

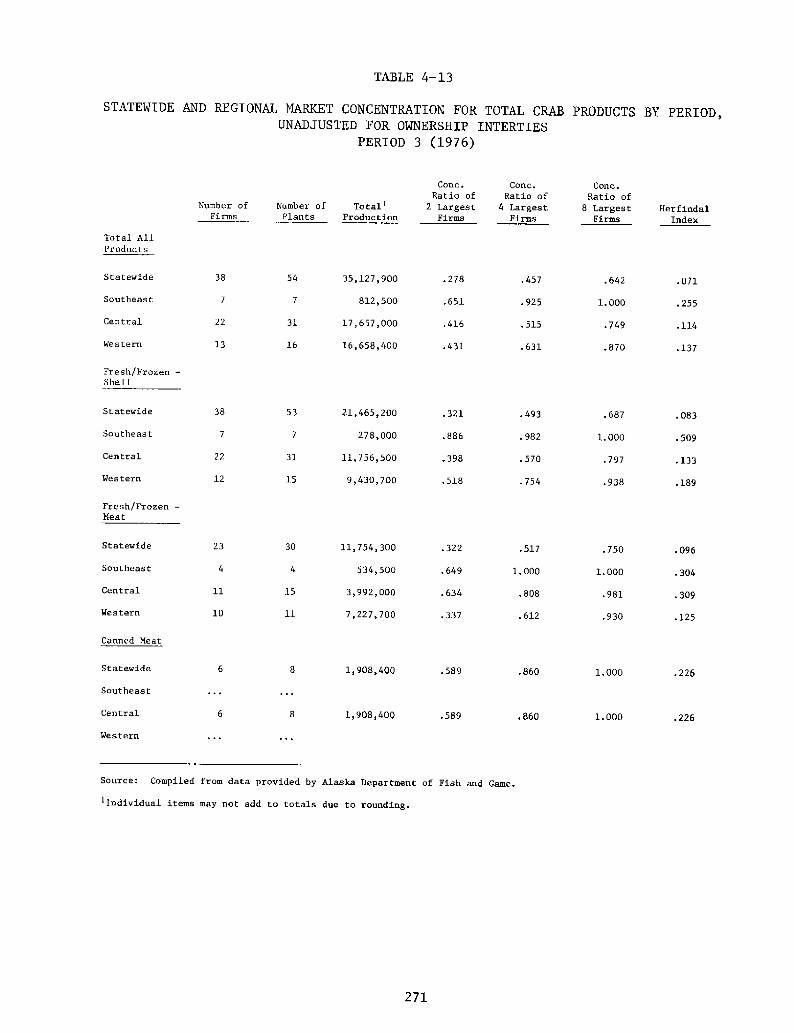

Statewide and Regional Market Concentration forTotal Crab Products by Period, Unadjusted forOwnership Interties

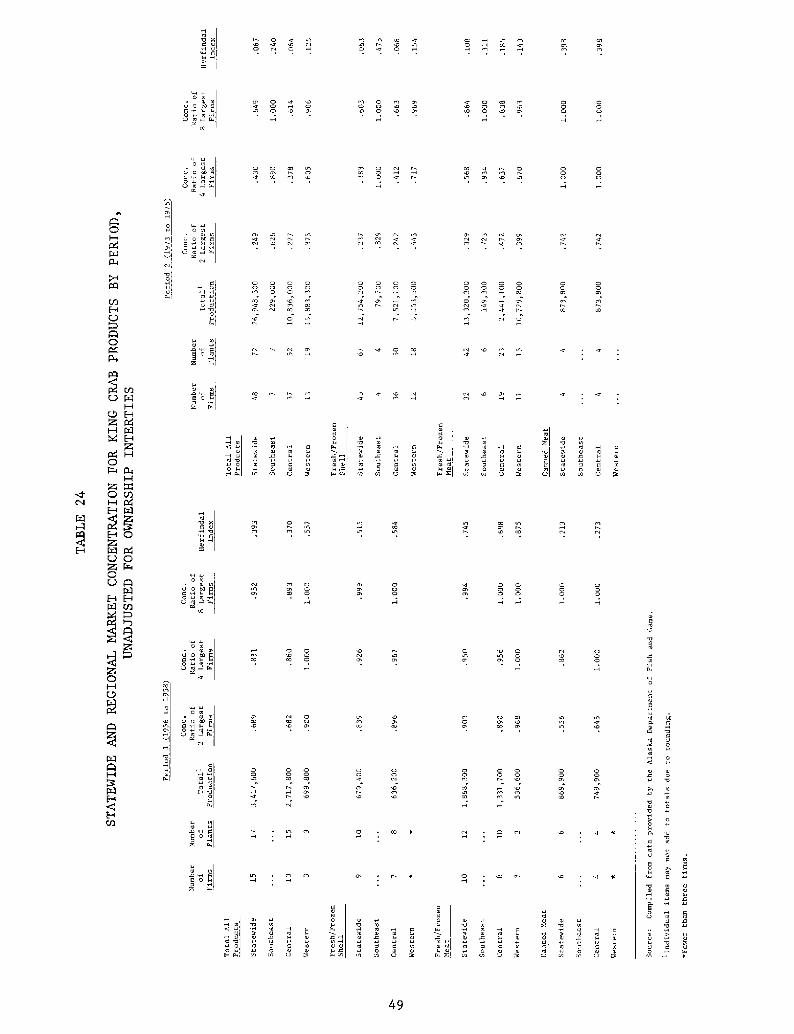

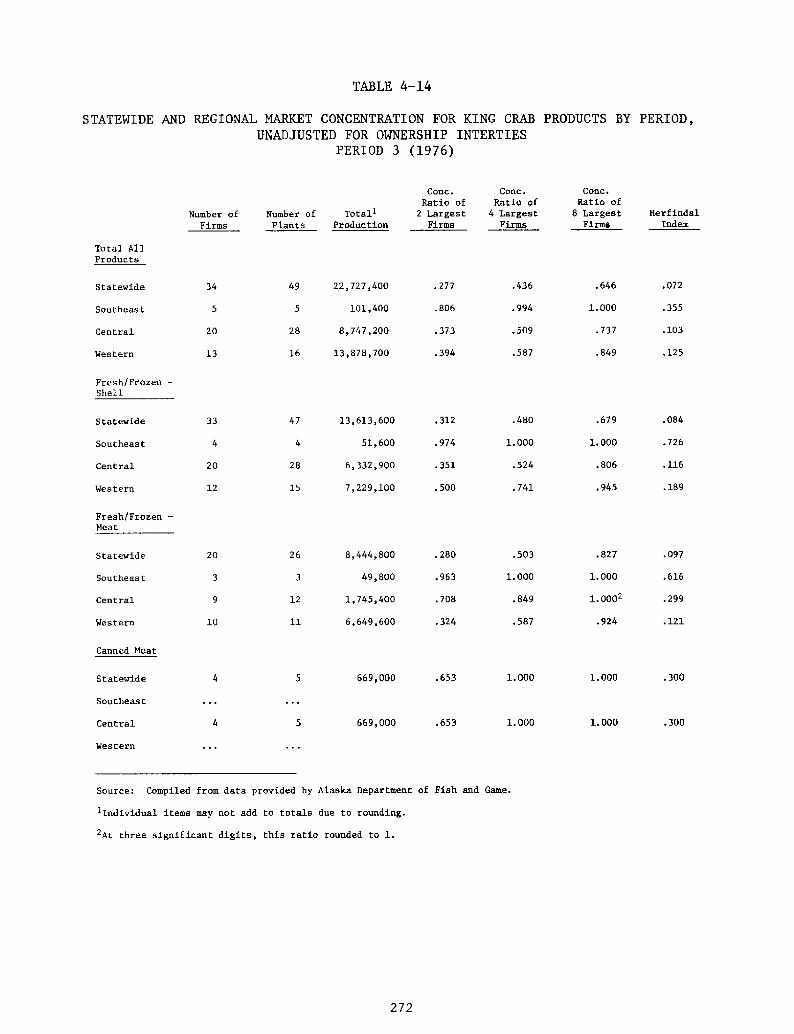

Statewide and Regional Market Concentration forKing Crab Products by Period, Unadjusted forOwnership Interties.

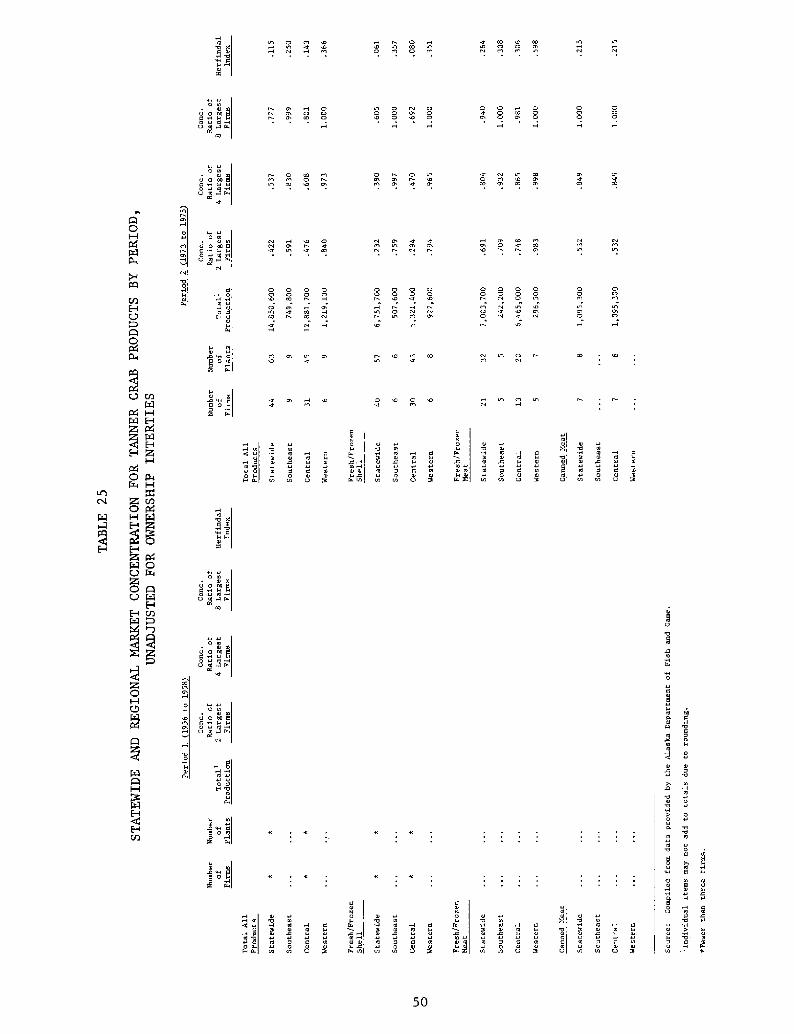

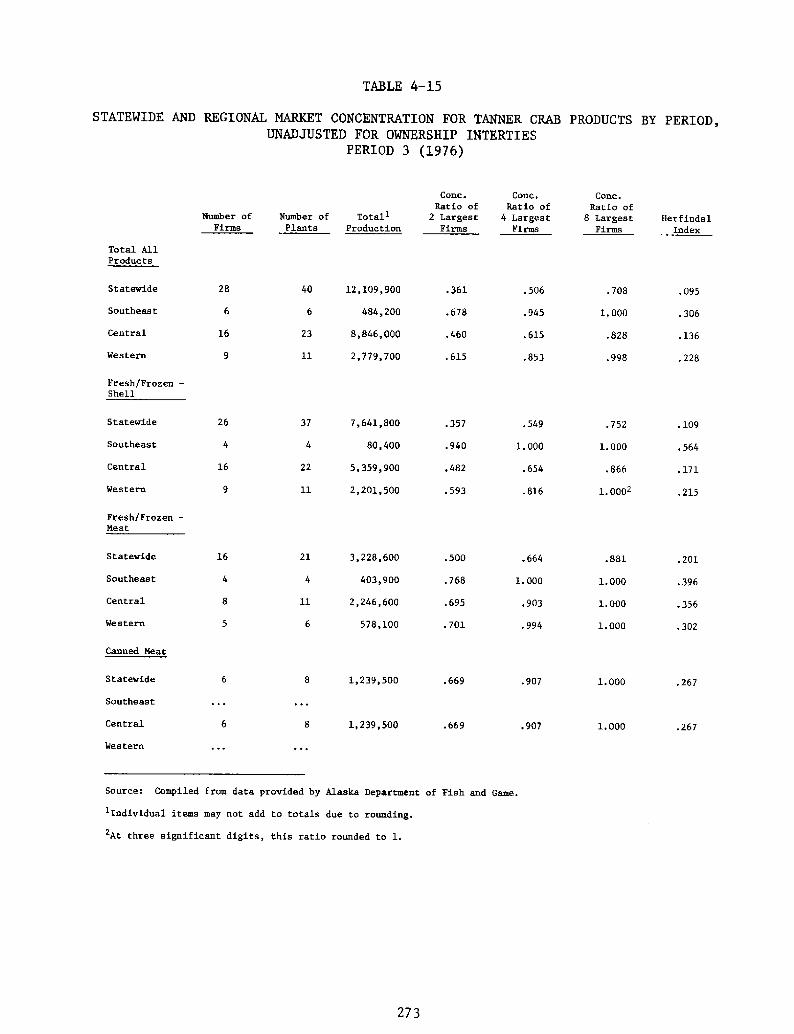

Statewide and Regional Market Concentration forTanner Crab Products by Period, Unadjusted for Owner-ship Interties

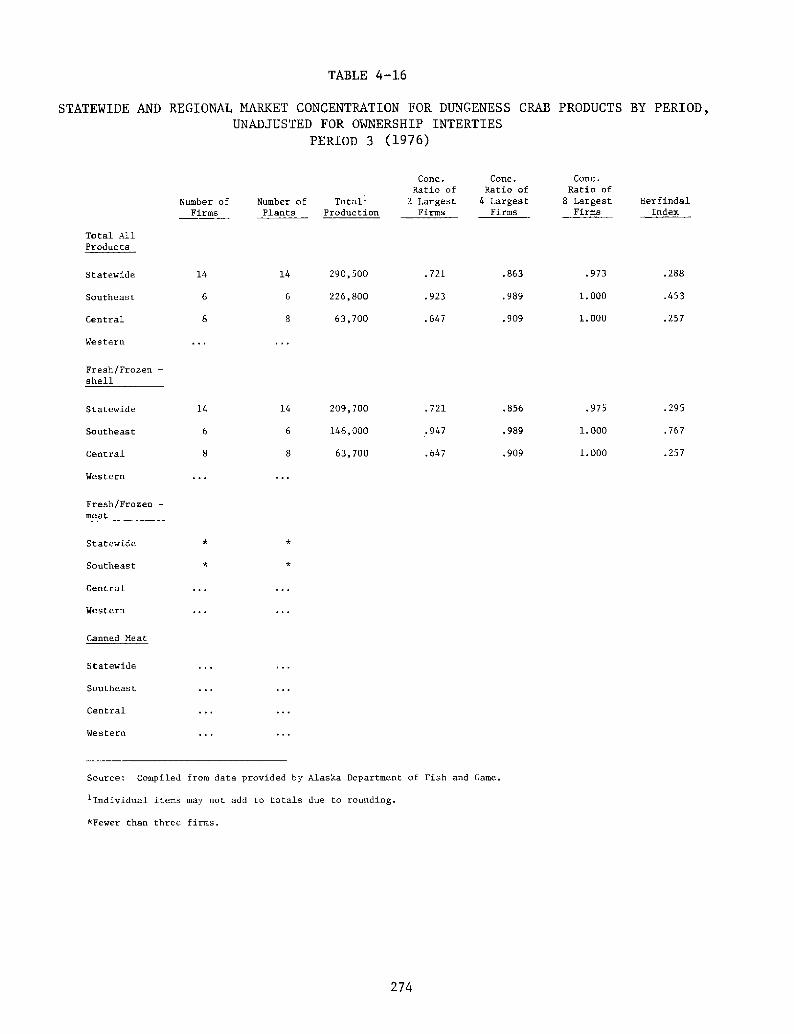

Statewide and Regional Market Concentration forDungeness Crab Products by Period, Unadjusted forOwnership Interties. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

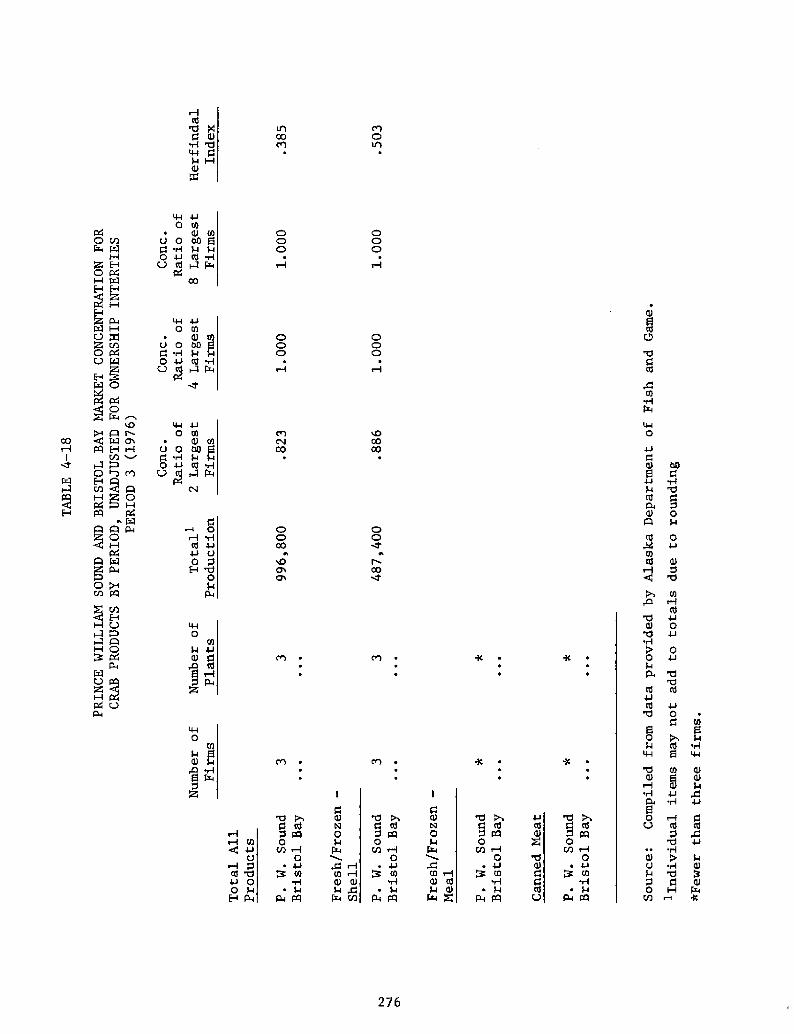

Prince William Sound and Bristol Bay Market Con-centration for Crab Products by Period, Unadjustedfor Ownership Interties........

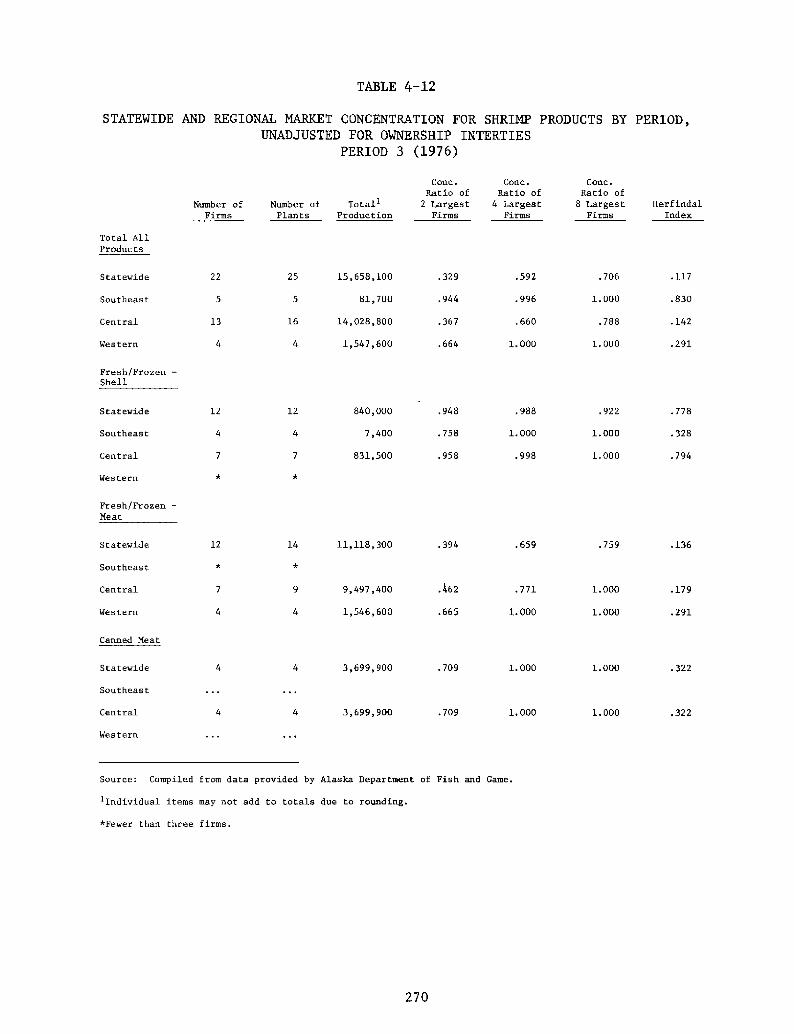

Statewide and Regional Market Concentration forShrimp Products by Period, Unadjusted for Owner-ship Interties.

Prince William Sound and Bristol Bay Market Con-centration for Shrimp Products by Period, Unad-justed for Ownership Interties

TABLES

continued!

PAGE

TABLE 30

57

TABLE 31

58

TABLE 32

59

TABLE 3360

TABLE 3461

TABLE 3562

TABLE 3666

TABLE 37

67

TABLE 3869

TABLE 3971

73

74

TABLE 4282

TABLE 4384

86

89

TABLE 40

TABLE 41

TABLE 44

TABLE 45

TABLE 46

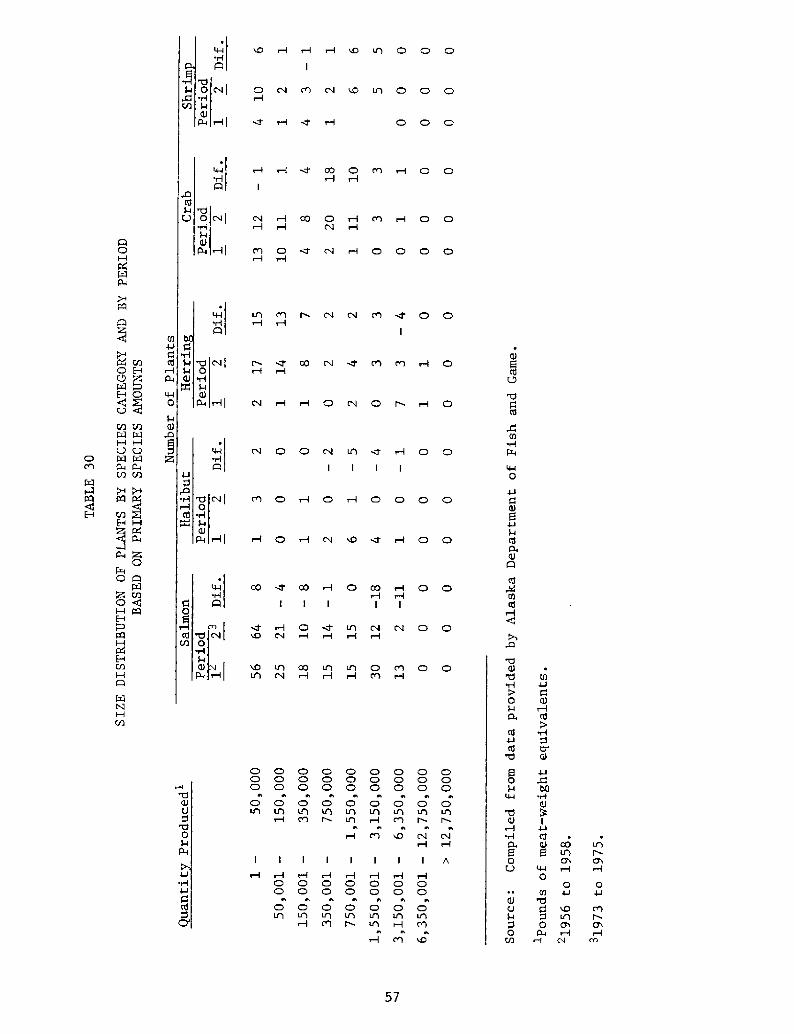

Size Distribution of Plants by Species Categoryand by Period Based on Primary Species Amounts....

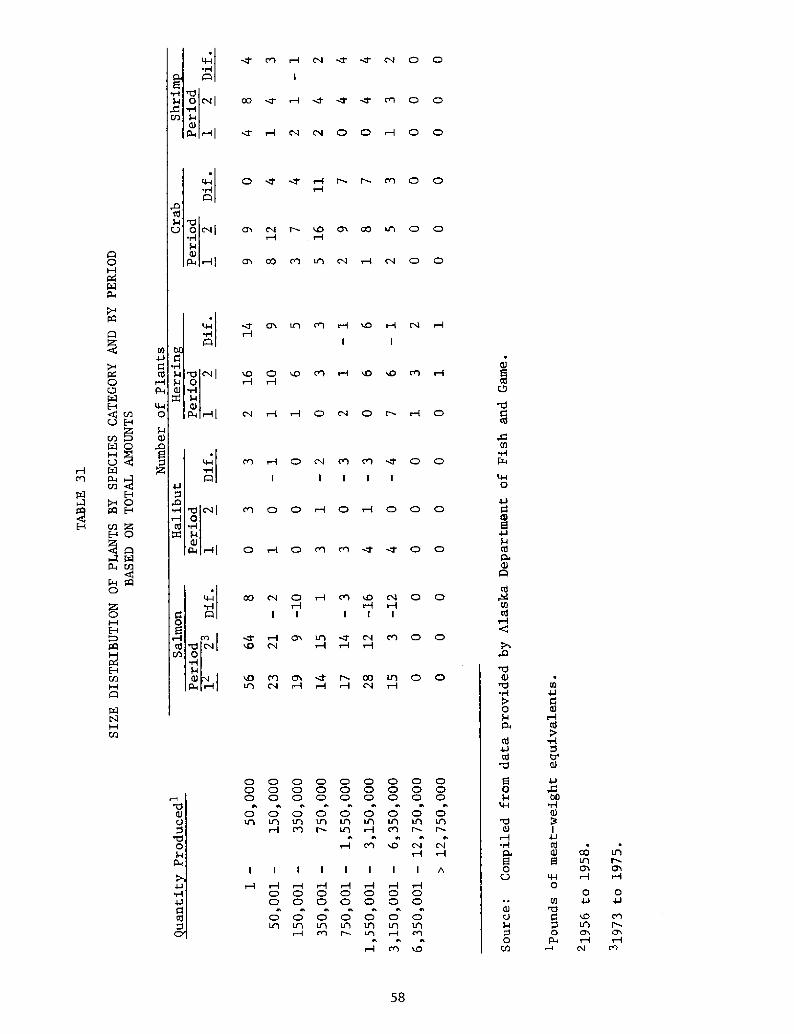

Size Distribution of Plants by Species Categoryand by Period Based on Total Amounts... ~ ......

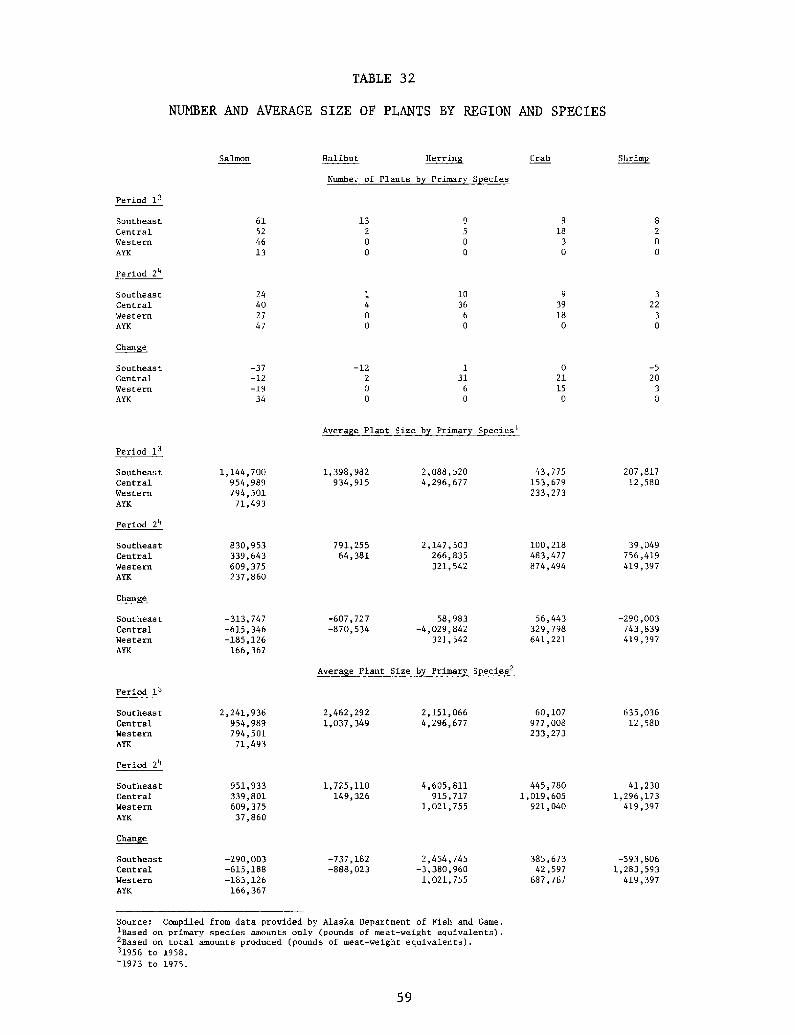

Number and Average Size of Plants by Region andSpecies. ~ ~ t ~ ~

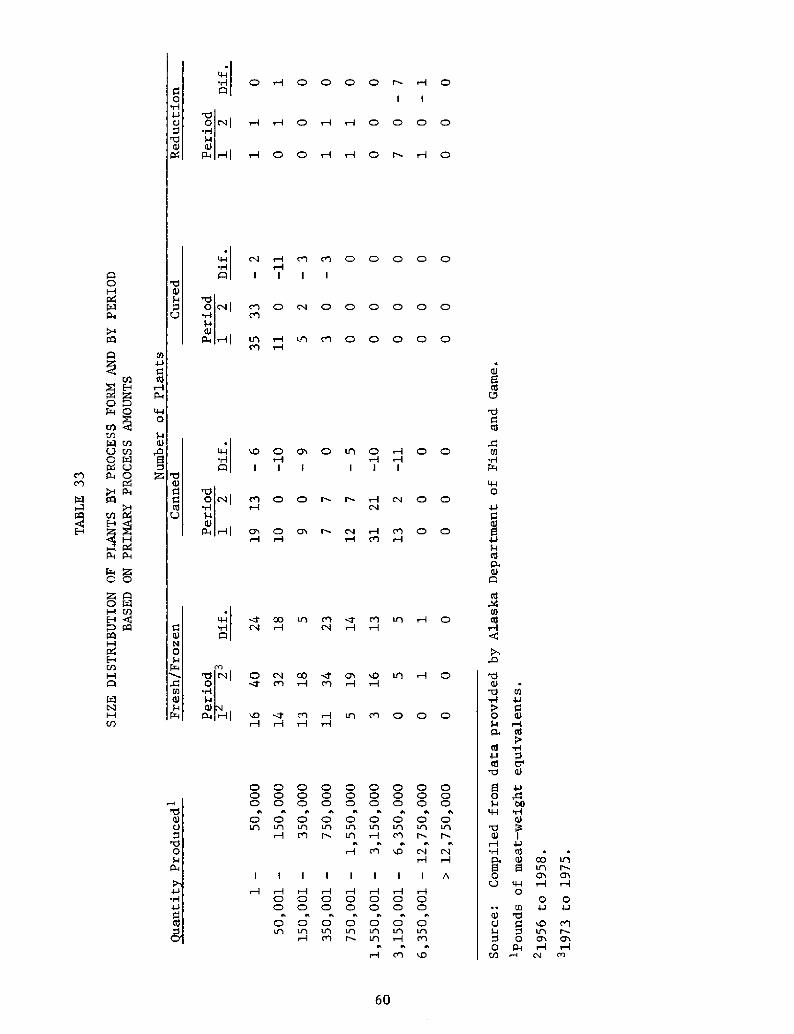

Size Distribution of Plants by Process Form andby Period Based on Primary Process Amounts........

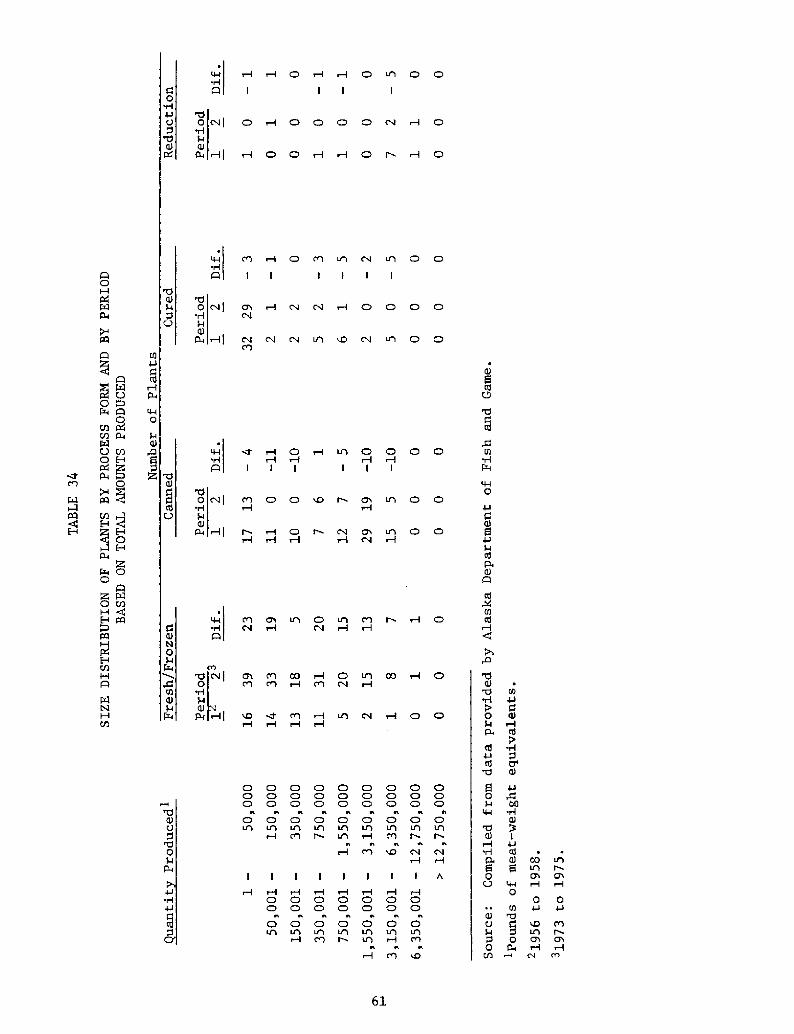

Size Distribution of Plants by Process Form andby Period Based on Total Amounts Produced.........

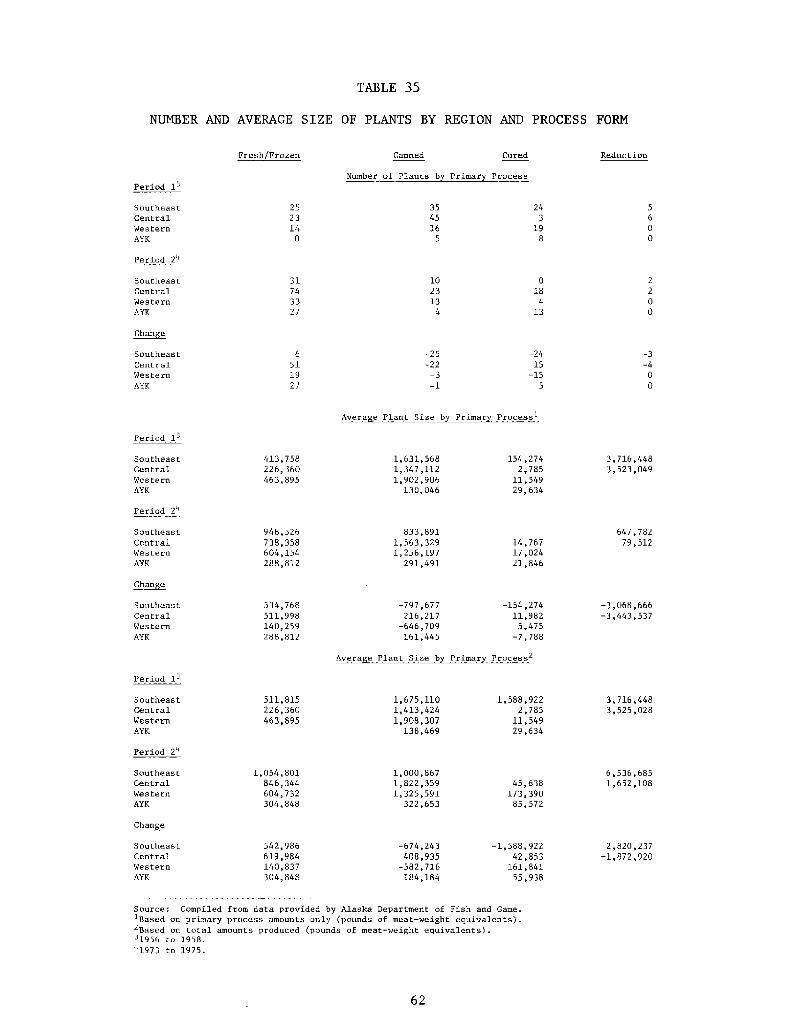

Number and Average Size of Plants by Region andProcess Form. ~ ~ ~

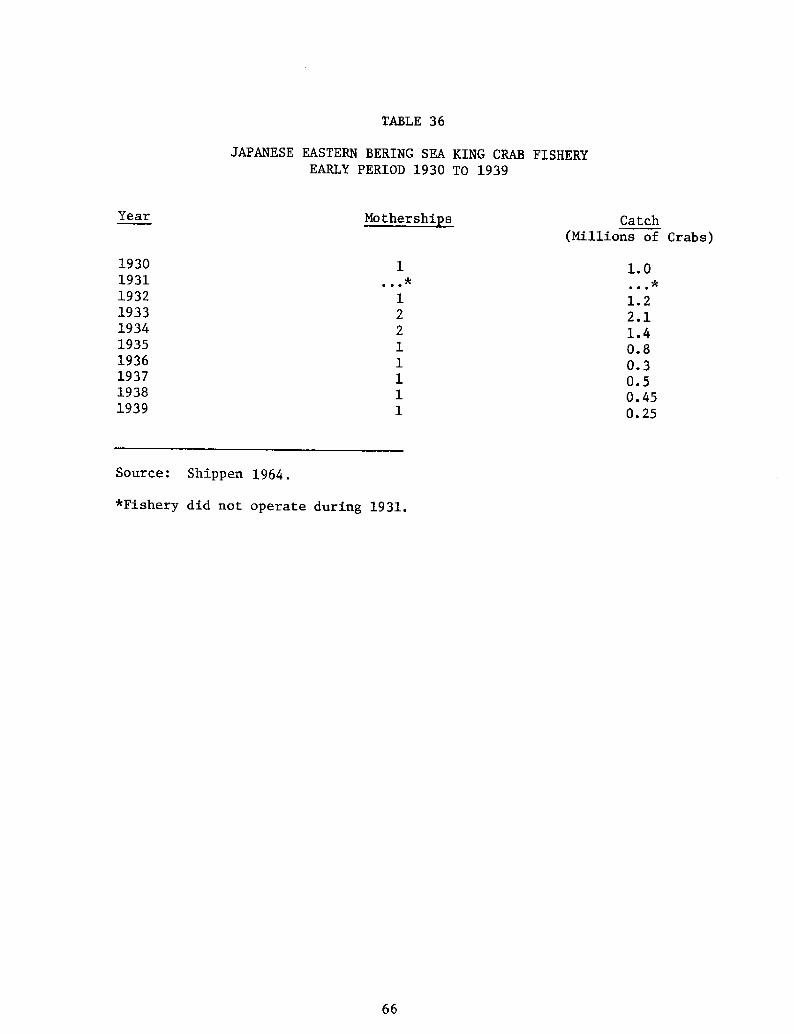

Japanese Eastern Bering Sea King Crab FisheryEarly Period 1930 to 1939 ' ......... ~ ..............

Estimated Annual Red and Blue King Crab Catchesin the Eastern Bering Sea by United States, Japanand USSR 1953 to 1977.. ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Foreign quotas for King and Tanner Crab inEastern Bering Sea ~ ~

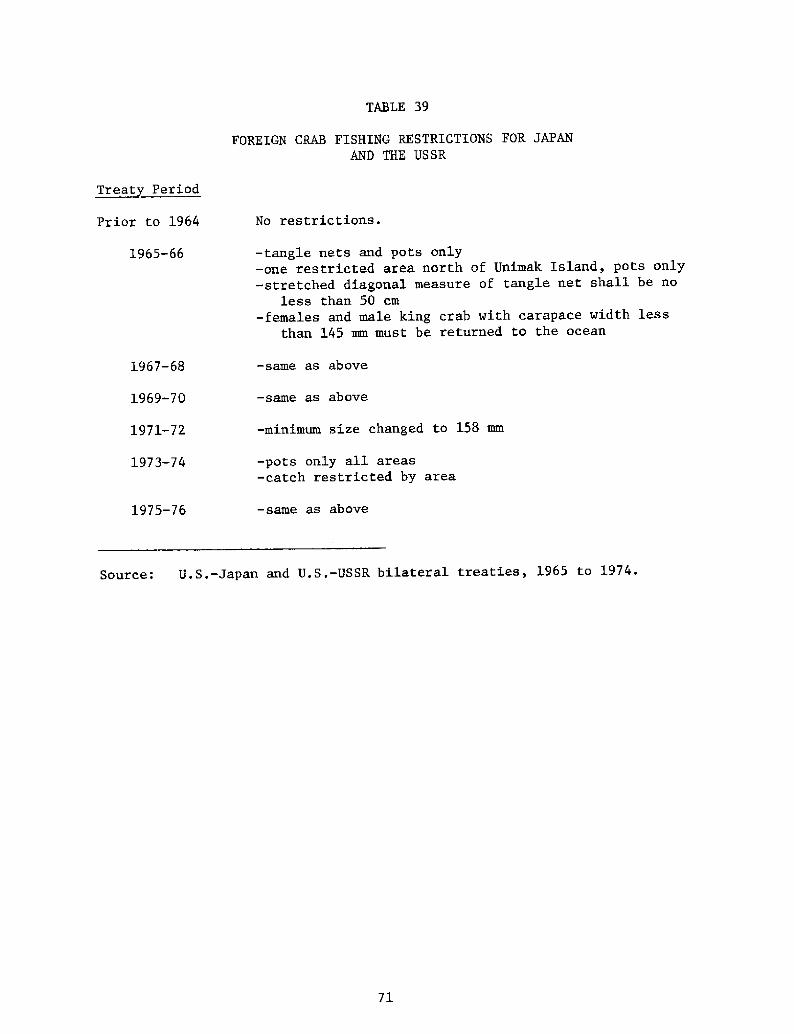

Foreign Crab Fishing Restrictions for Japan andthe VSSRe ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

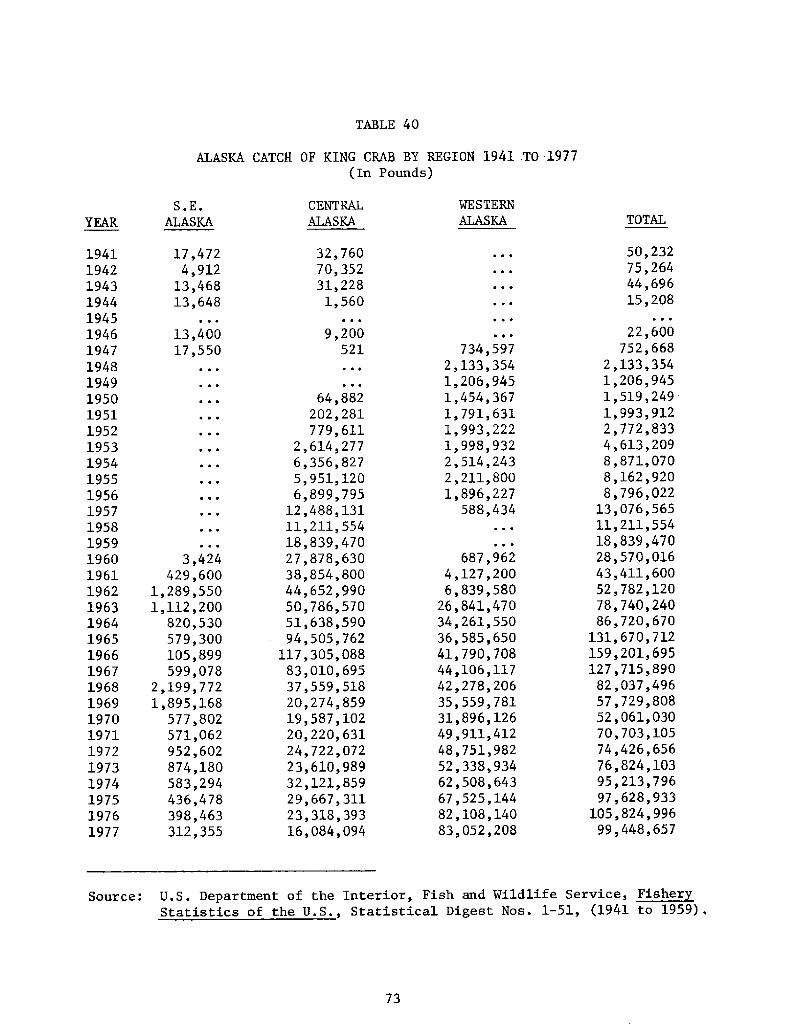

Alaska Catch of King Crab by Region 1941 to 1977..

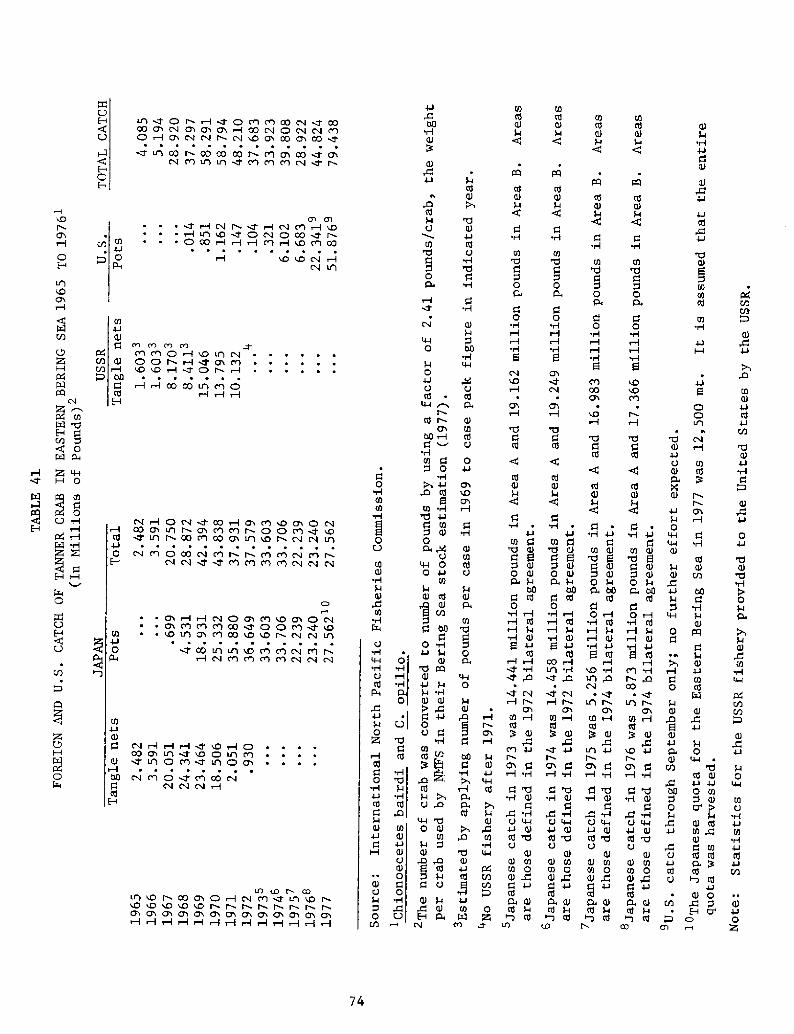

Foreign and U.S. Catch of Tanner Crab in EasternBering Sea 1965 to 1976.. ~ ~ ~ 4 ~ ~ ~ ~ ~ 4 ~ ~ ~ ~ ~ ~ ~

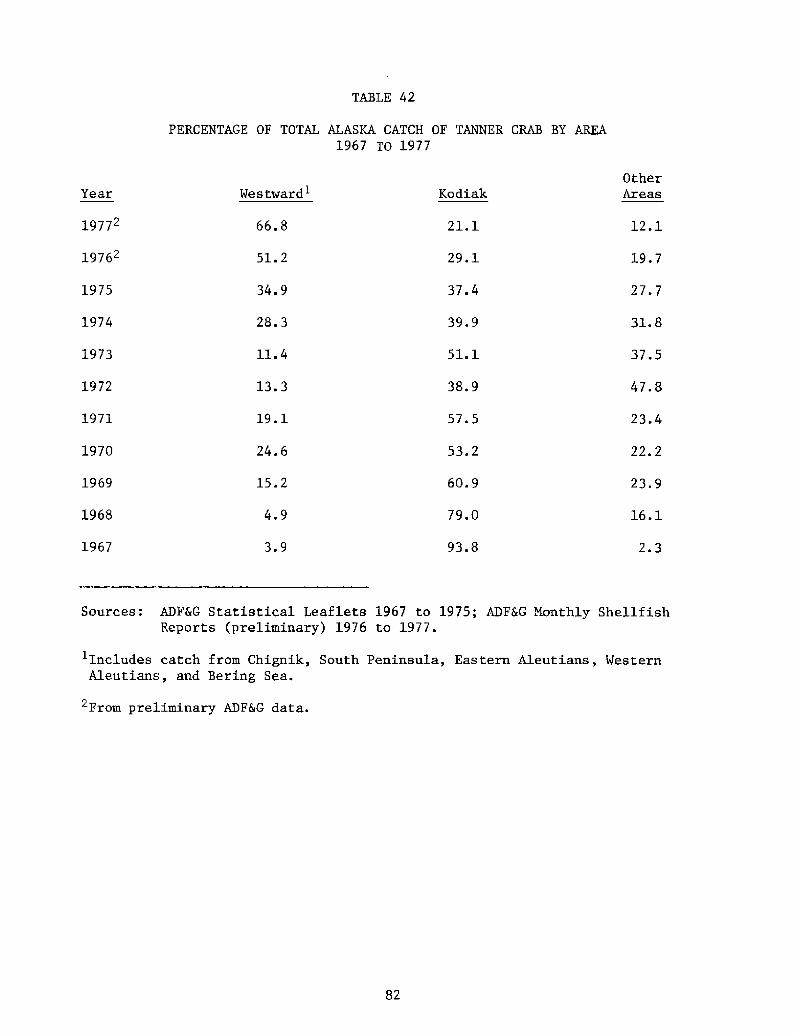

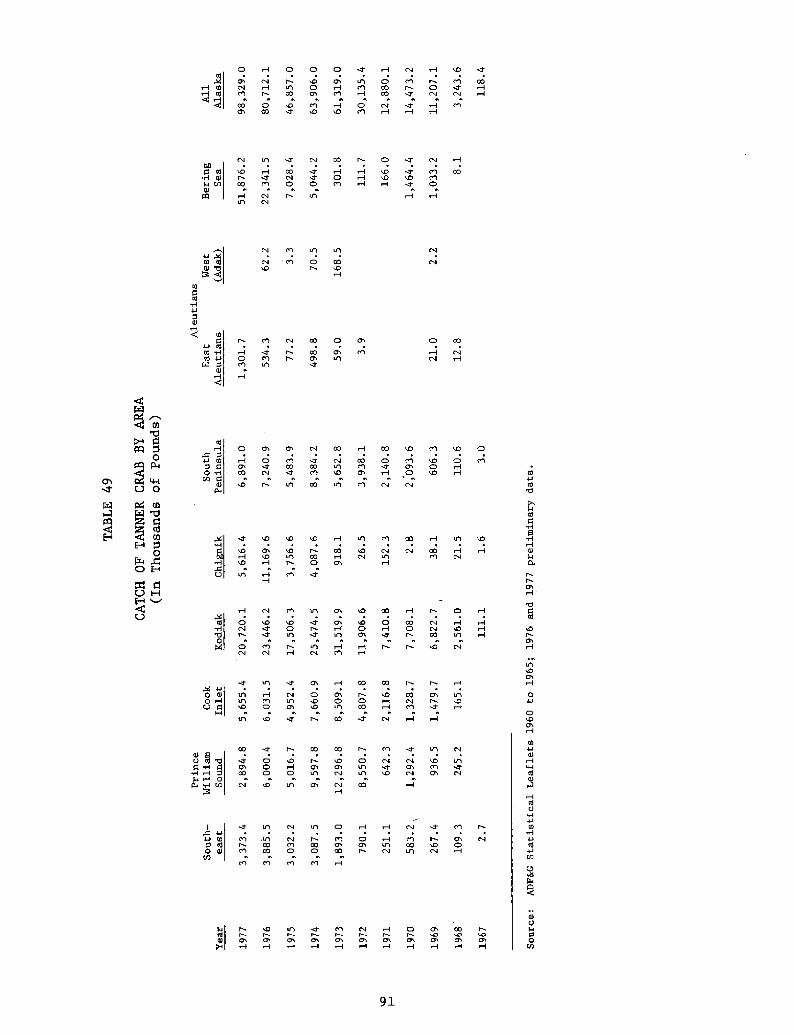

Percentage of Total Alaska Catch of Tanner Crabby Area 1967 to 1977.....

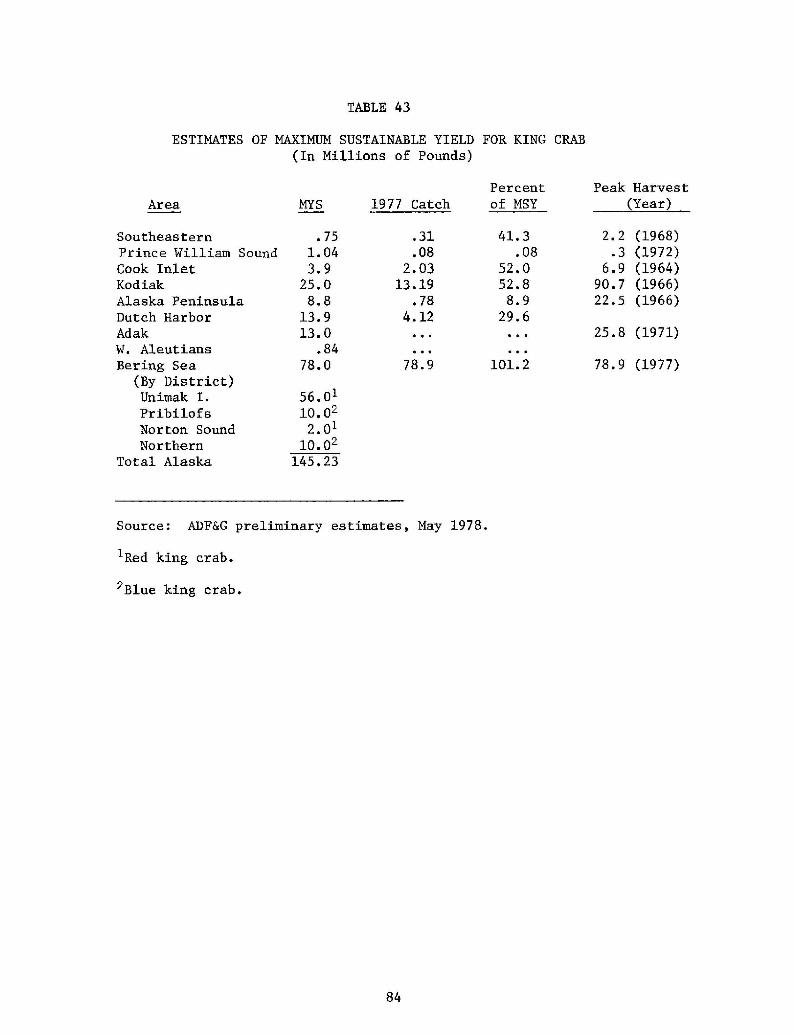

Estimates of Naximum Sustainable Yield for KingCrab. ~ ~ ~

Alaska Catch of King Crab by Management Area......

World Catches of King Crab by Country.............

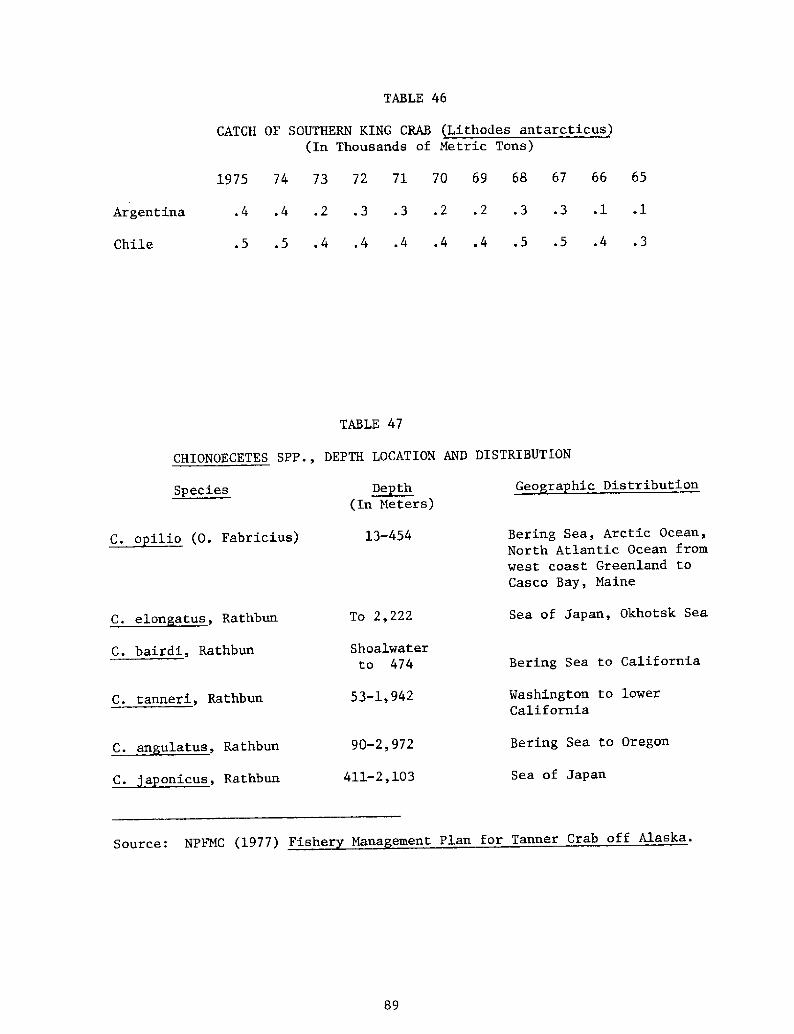

Catch of Southern King Crab Lithodes antarcticus!

TABLES

continued!

PAGE

TABLE 47

TABLE 48

89

90

91

93

96

TABLE 52

97

TABLE 53

99

102

103

112

112

TABLE 58

114

TABLE 59

116

TABLE 60

120

TABLE 61

120

TABLE 62

122

TABLE 63

TABLE 64

TABLE 65

130

Xii

TABLE 49

TABLE 50

TABLE 51

TABLE 54

TABLE 55

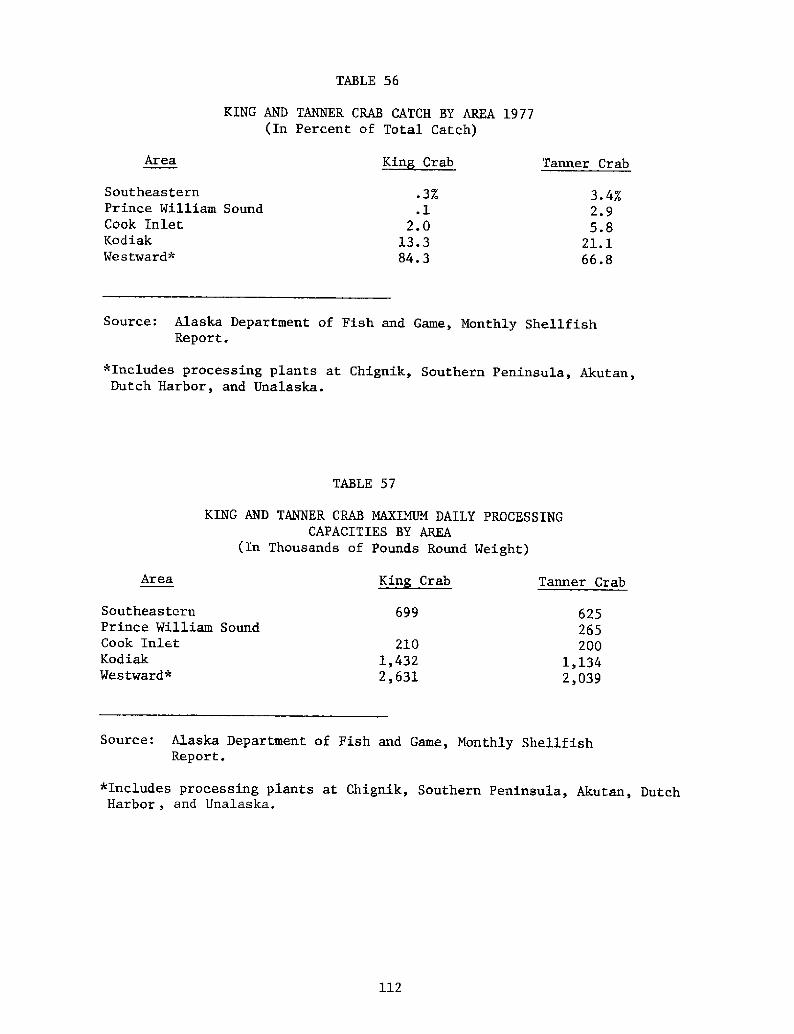

TABLE 56

TABLE 57

Chionoecetes spp., Depth Location and Distribution

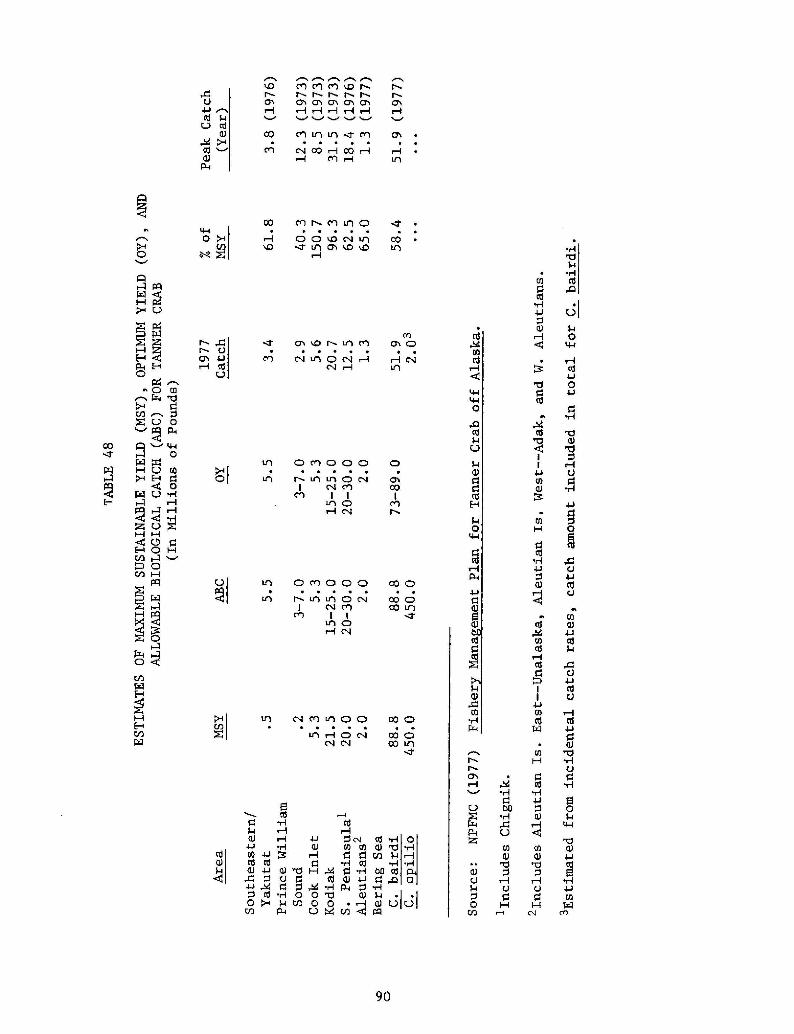

Estimates of Maximum Sustainable Yield MSY!,Optimum Yield OY!, and Allowable Biological Catch ABC! for Tanner Crab....

Catch of Tanner Crab by Area.......................

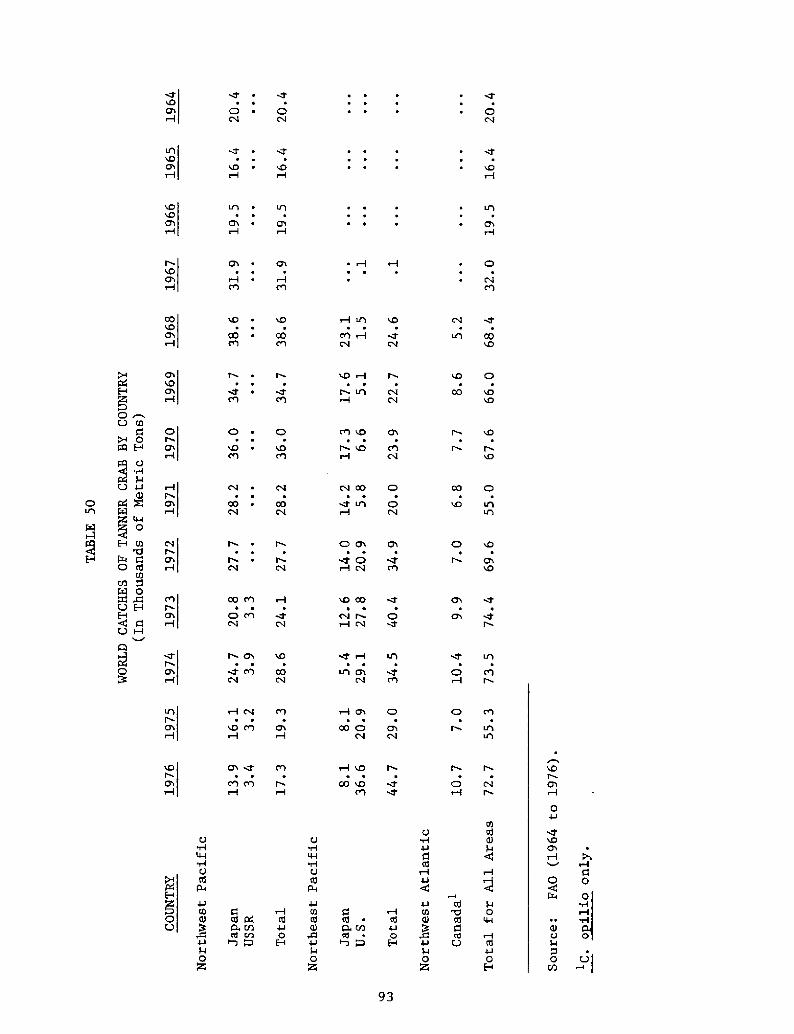

World Catches of Tanner Crab by Country............

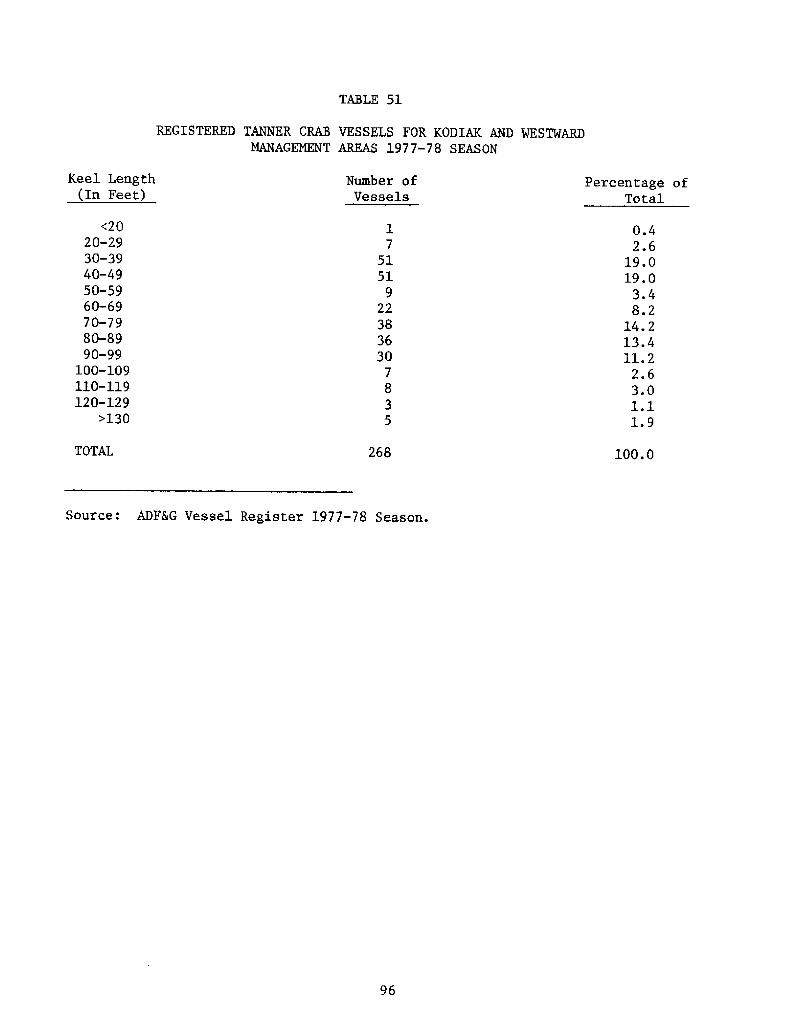

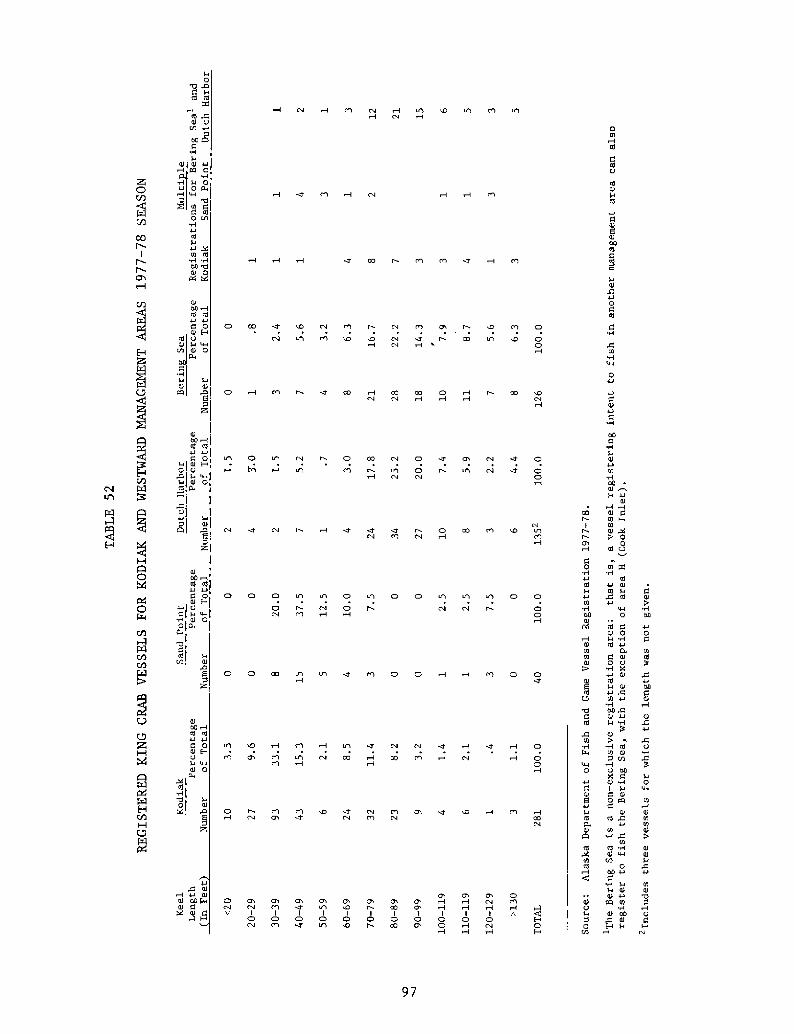

Registered Tanner Crab Vessels for Kodiak andWestward Management Areas 1977-78 Season...........

Registered King Crab Vessels for Kodiak andWestward Management Areas 1977-78 Season...........

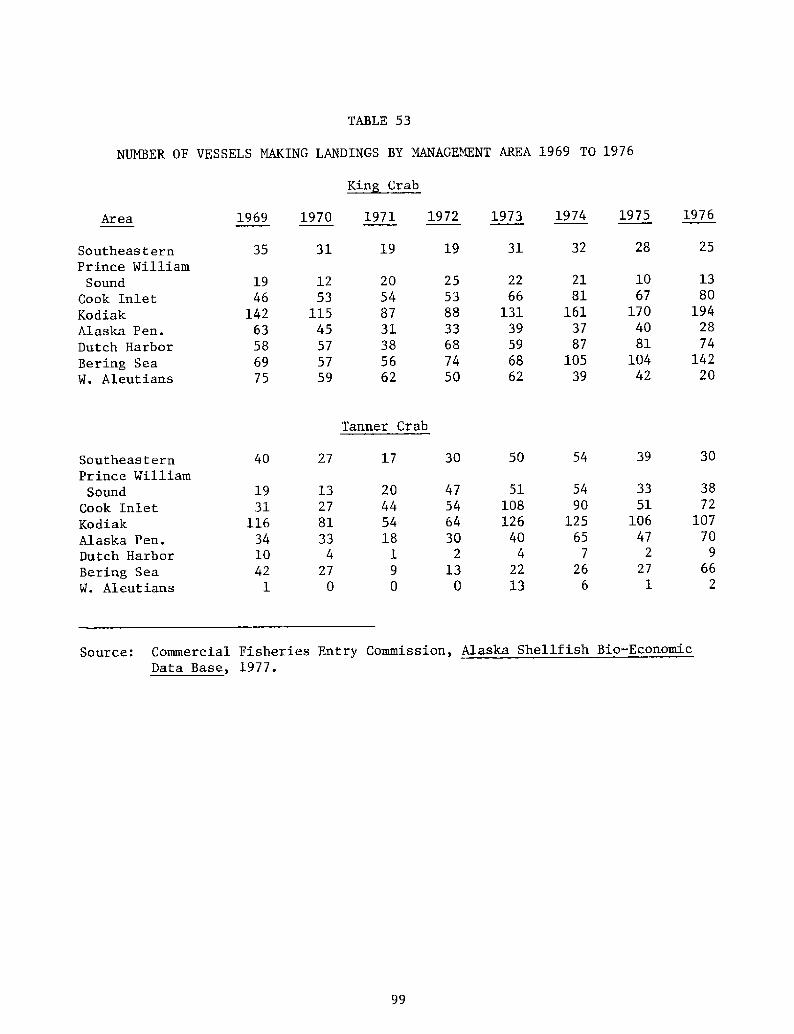

Number of Vessels Making Landings by ManagementArea 1969 to 1976............. ~ . ~ ... ~ ~ ~ ~ ~ - ~ ~ ~ ~ ... ~-

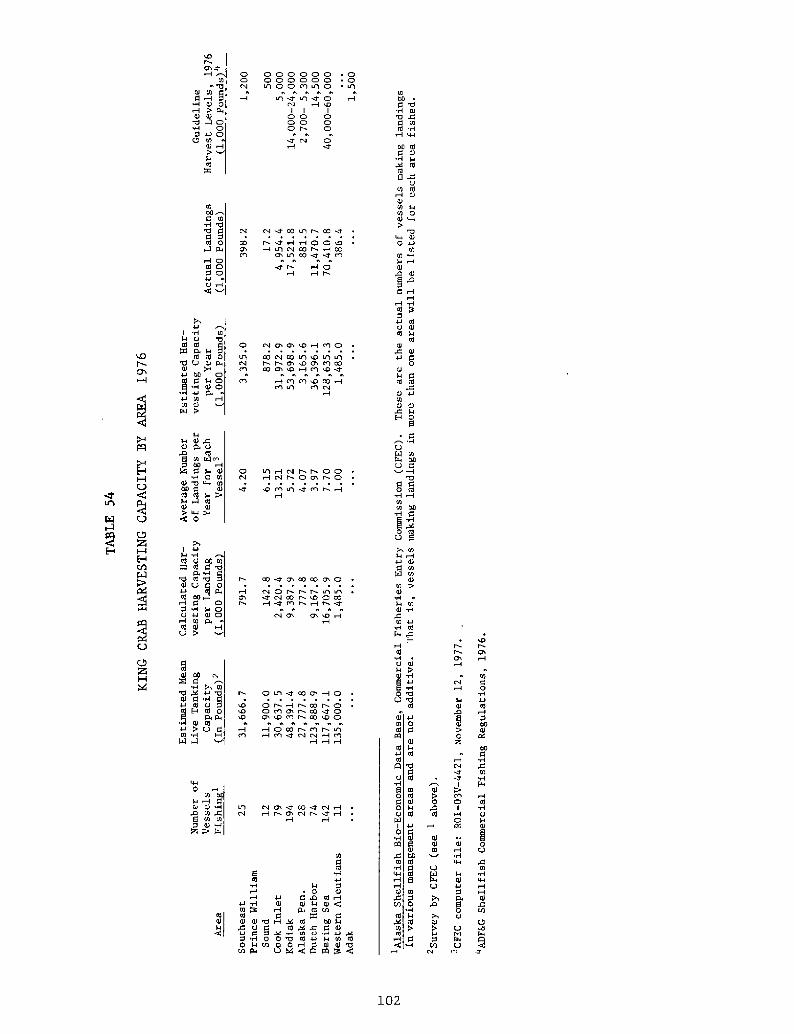

King Crab Harvesting Capacity by Area 1976.........

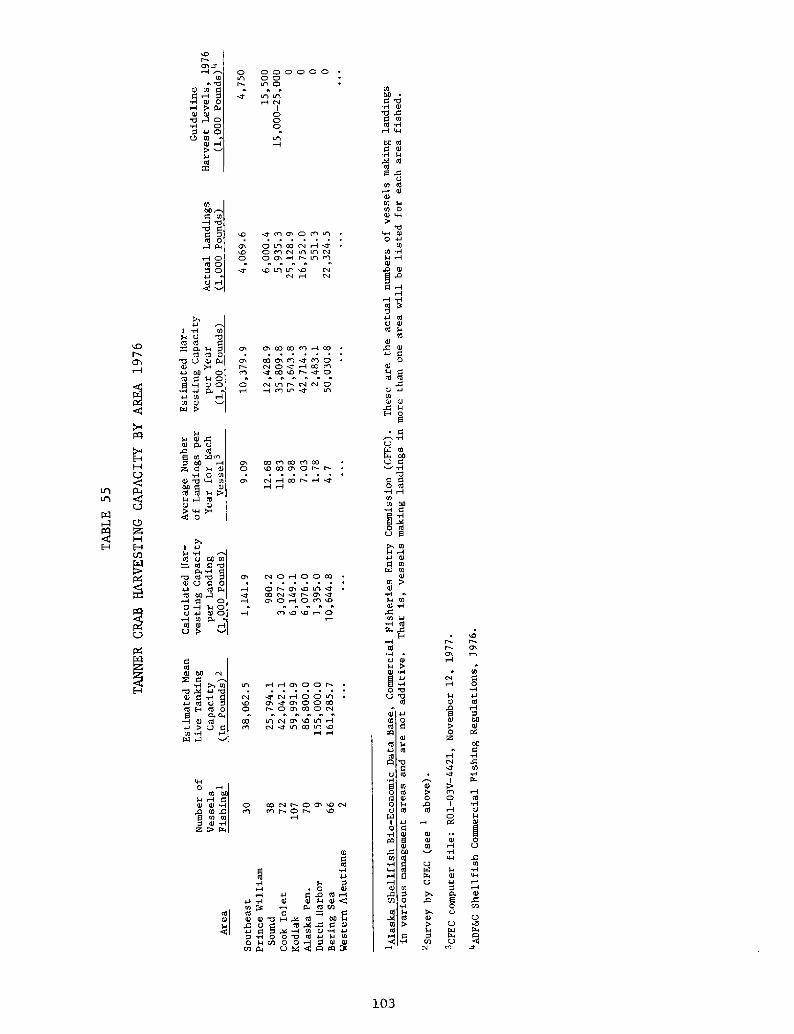

Tanner Crab Harvesting Capacity by Area 1976.......

King and Tanner Crab Catch by Area 1977............

King and Tanner Crab Maximum Daily ProcessingCapacities by Area.........

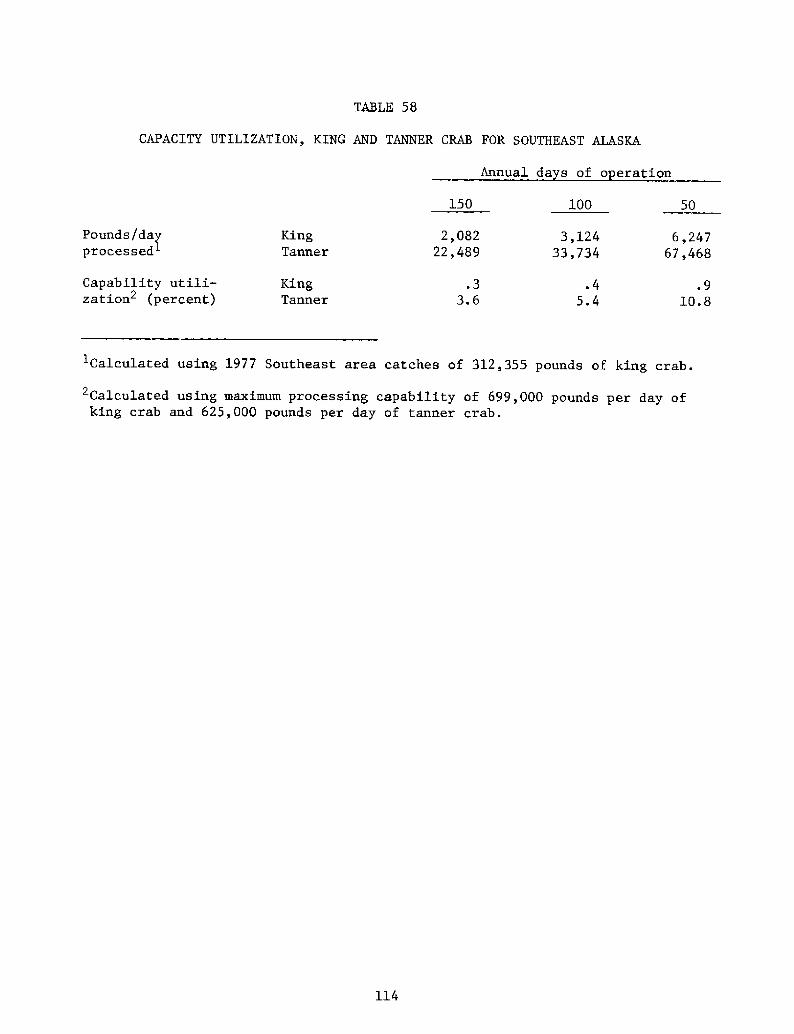

Capacity Utilization, King and Tanner Crab forSoutheast Alaska....................

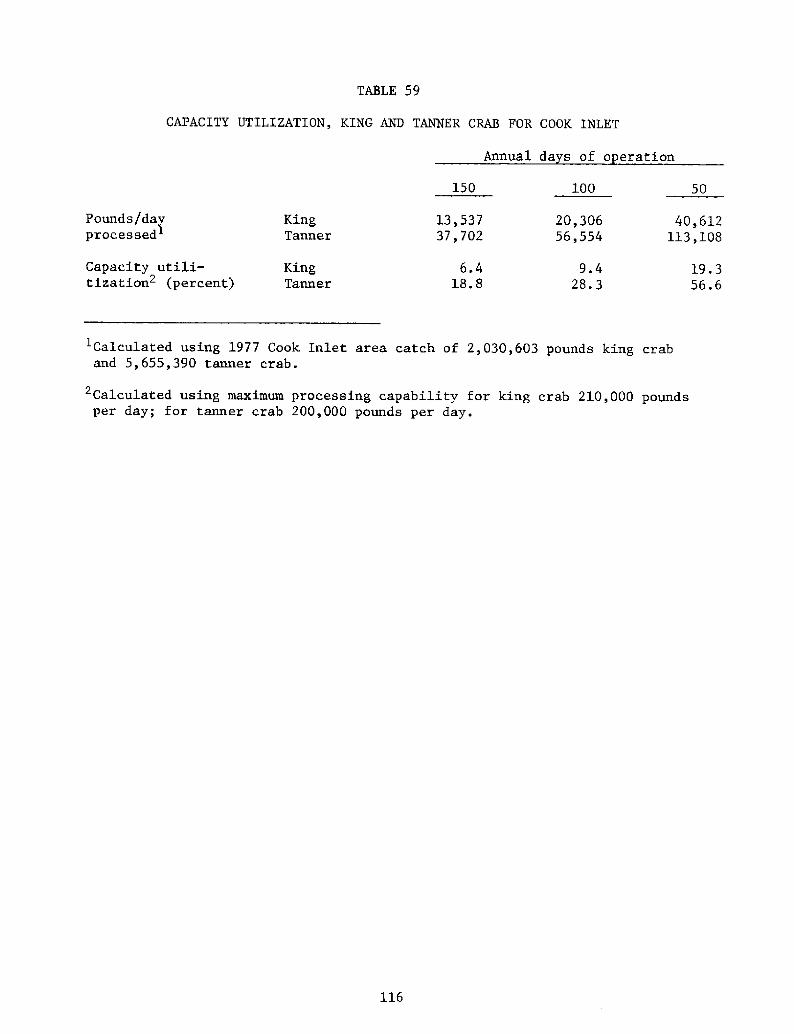

Capacity Utilization, King and Tanner Crab forook Inlet........................... ~ .....C

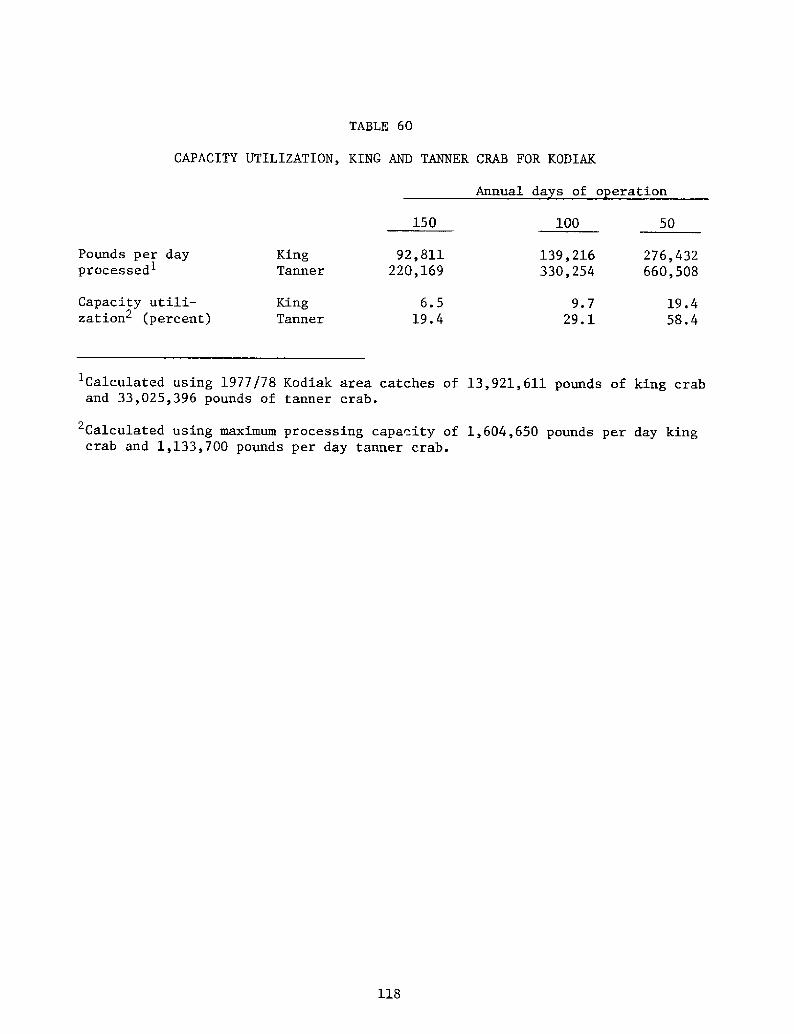

Capacity Utilization, King and Tanner Crab forK odiak ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Capacity Utilization, King and Tanner Crab forWestward Area

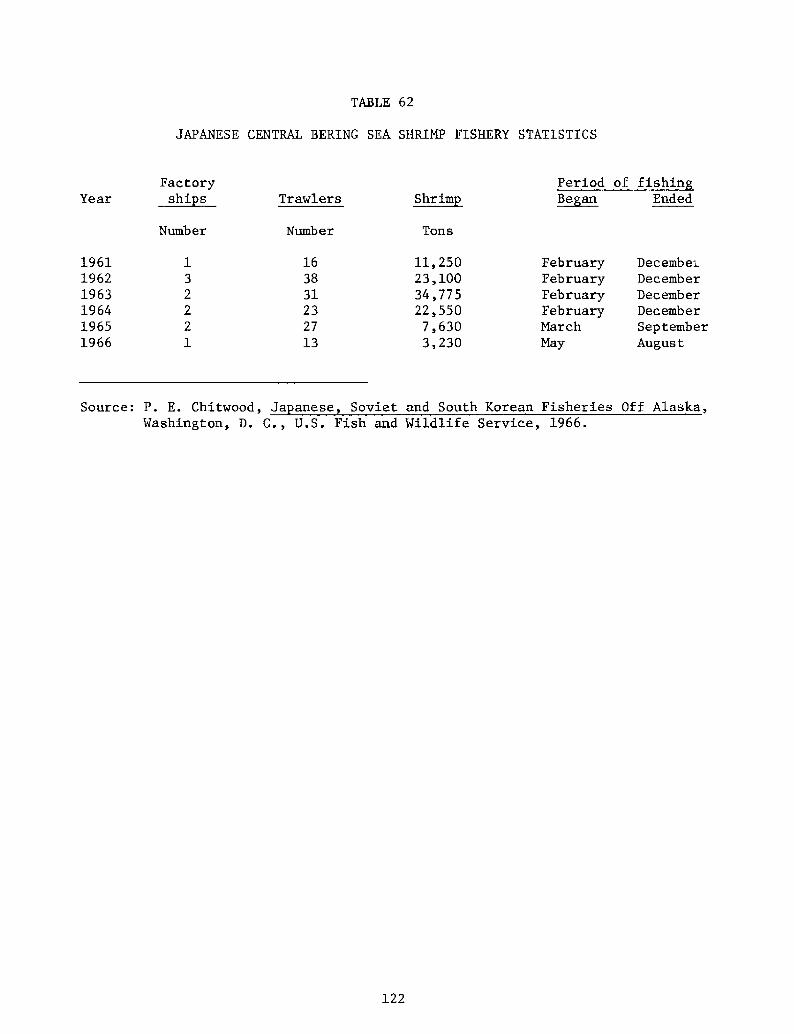

Japanese Central Bering Sea Shrimp FisheryS tatistics.........................

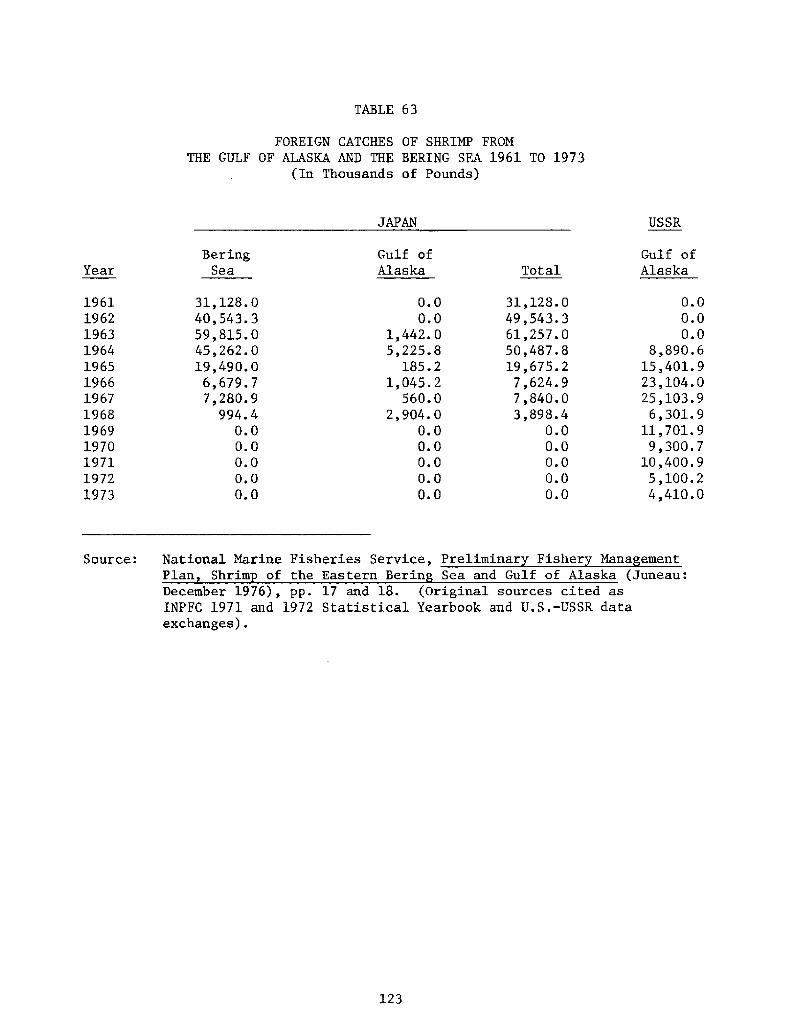

Foreign Catches of Shrimp from the Gulf of Alaskaand the Bering Sea 1961 to 1973.................... 123

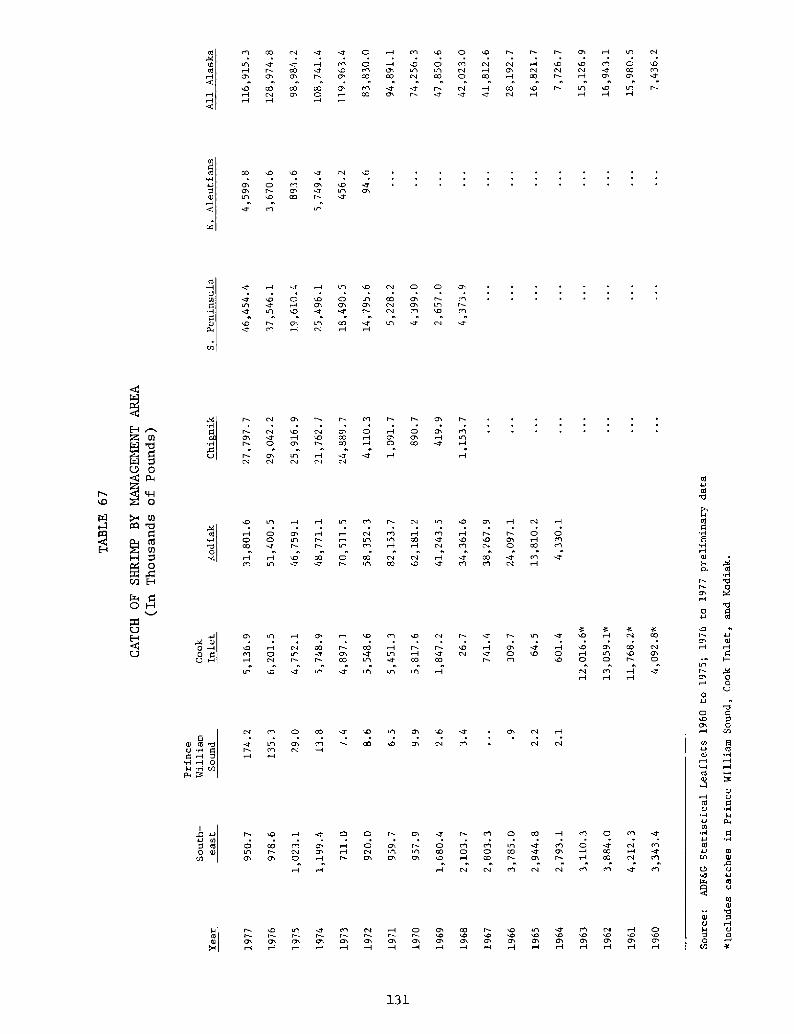

Alaska Shrimp Catch by Management Area 1964 to 1977 128

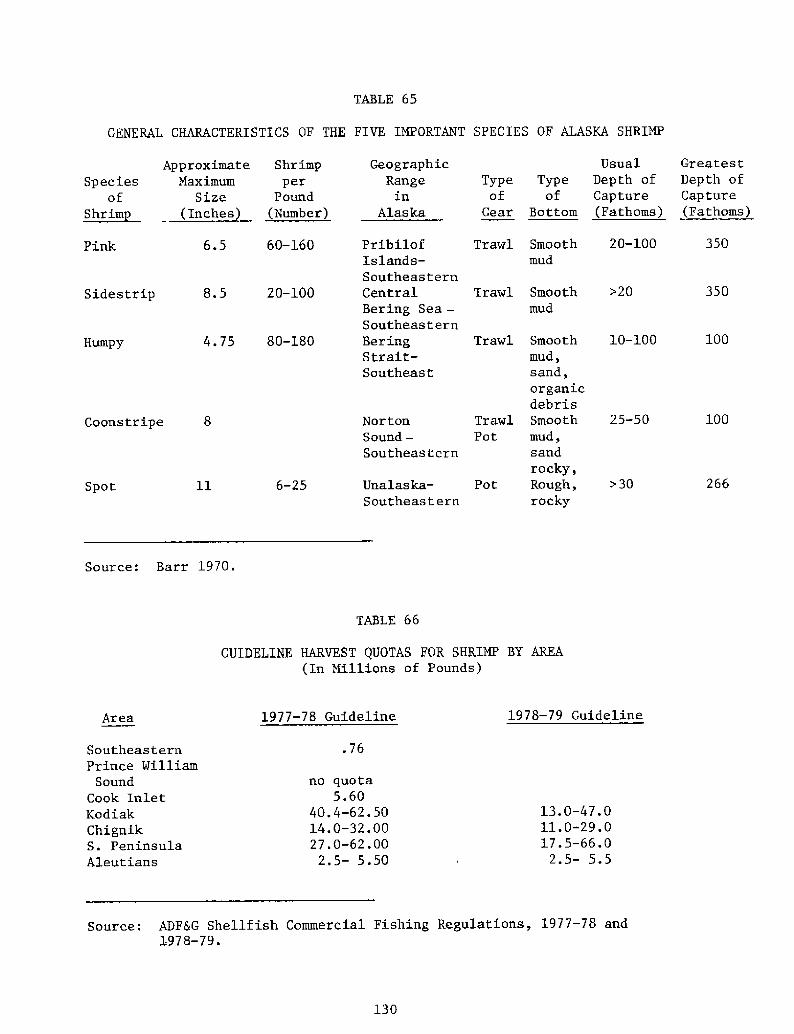

General Characteristics of the Five ImportantSpecies of Alaska Shrimp.......................

TABLES

continued!

PAGE

131

133

135

138

TABLE 72143

145

150

152

TABLE 76152

TABLE 77154

157

164

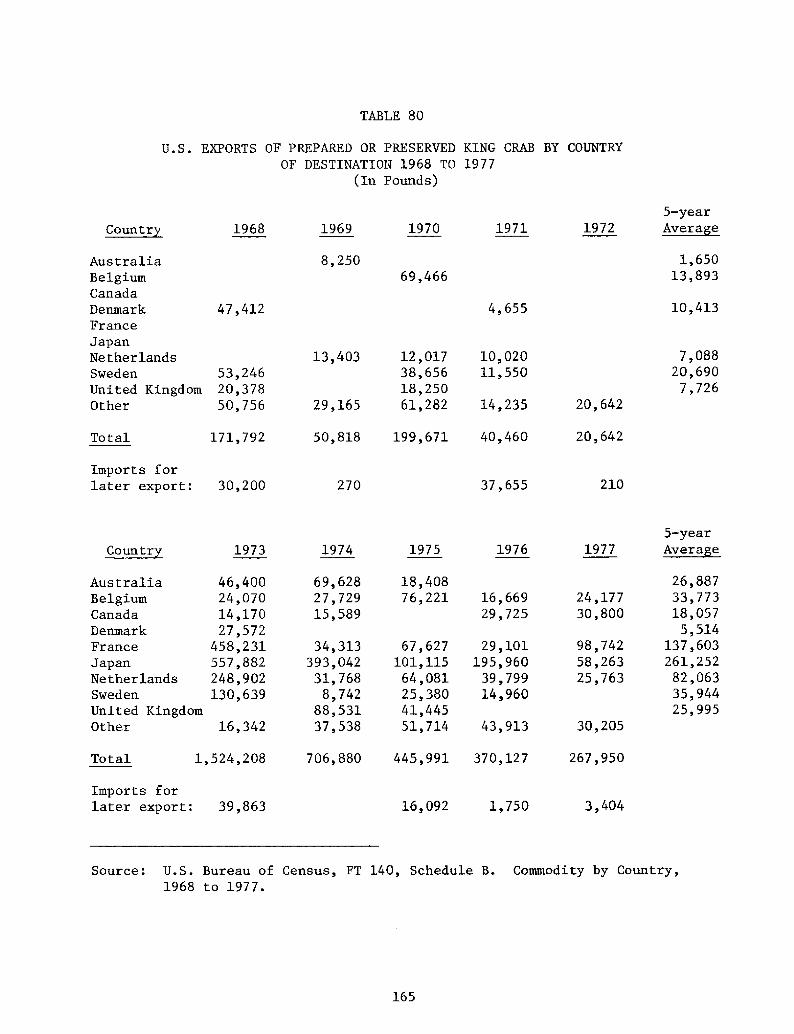

TABLE 80165

TABLE 81167

TABLE 82167

TABLE 83168

169TABLE 84

TABLE 66

TABLE 67

TABLE 68

TABLE 69

TABLE 70

TABLE 71

TABLE 73

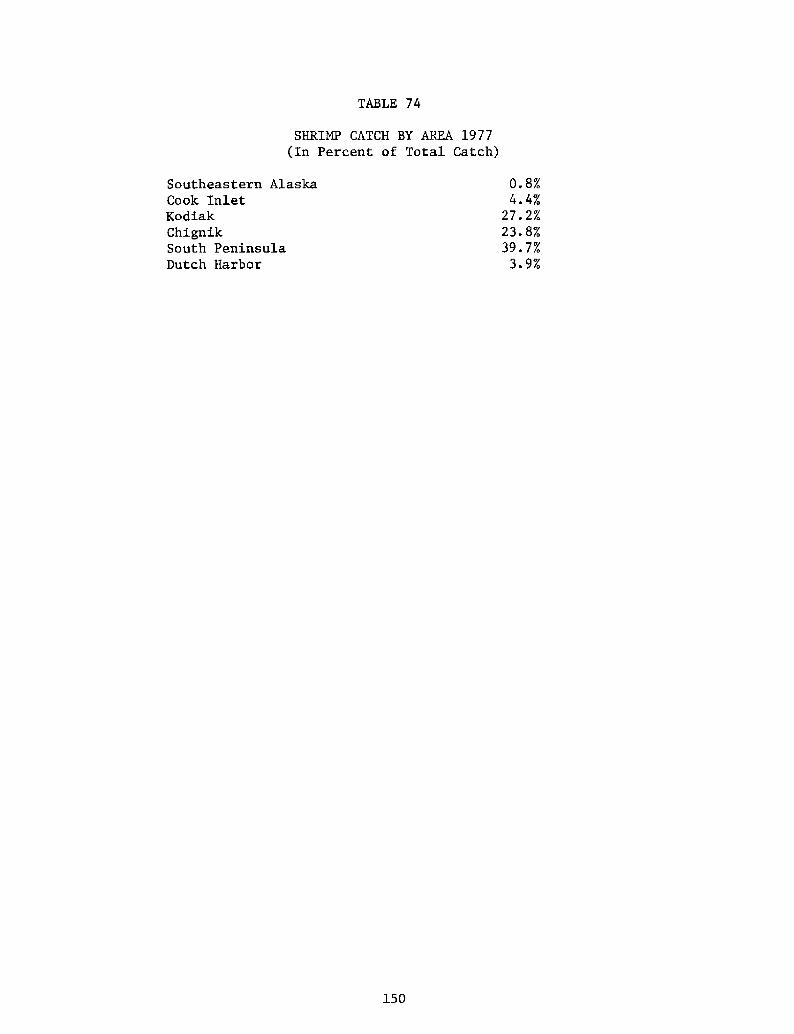

TABLE 74

TABLE 75

TABLE 78

TABLE 79

Guideline Harvest Quotas for Shrimp by Area....... 130

Catch of Shrimp by Management Area

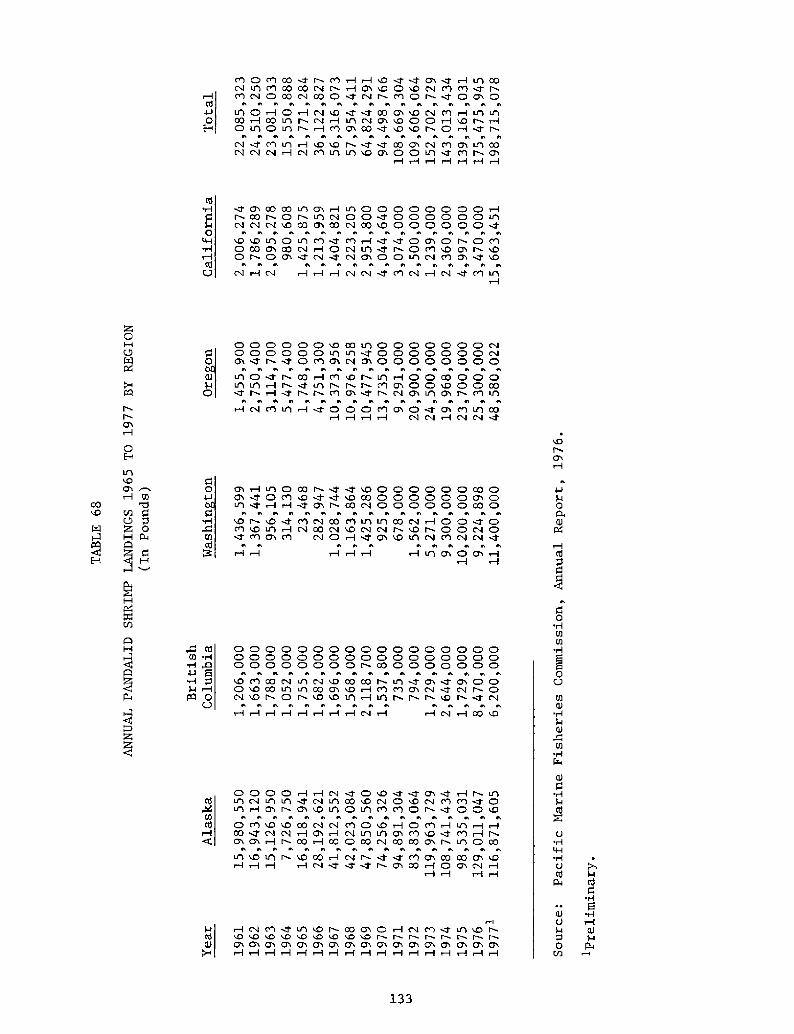

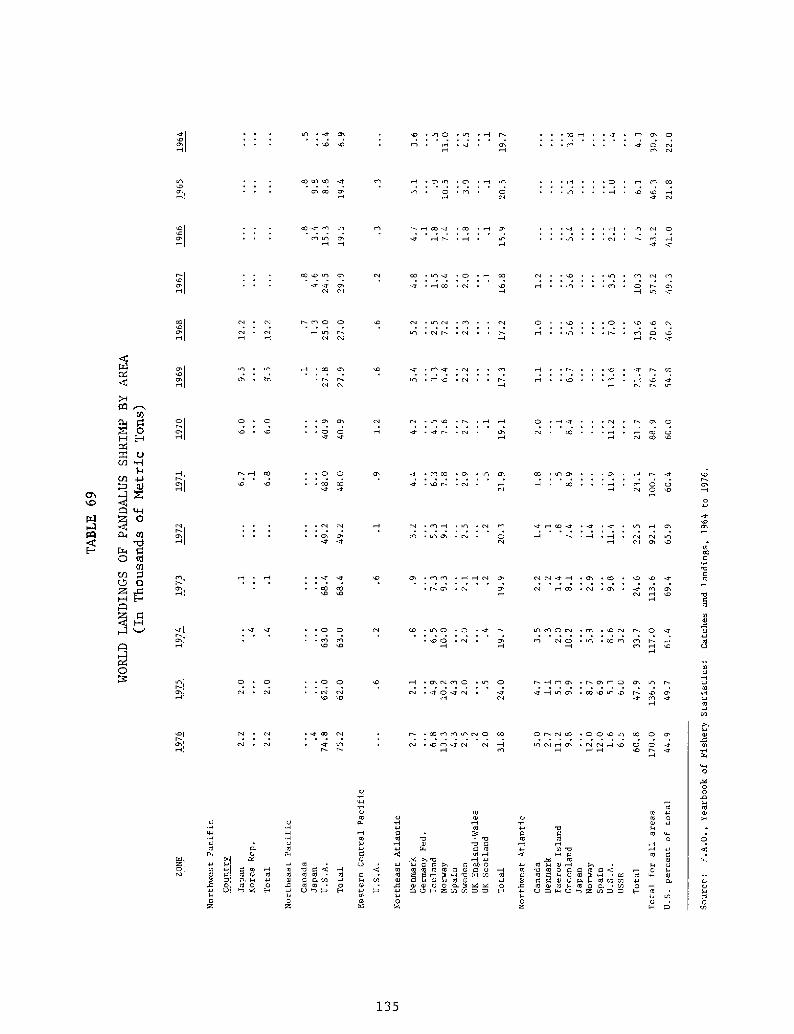

Annual Pandalid Shrimp Landings 1965 to 1977by Region. 4 ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

World Landings of Pandalus Shrimp by Area.........

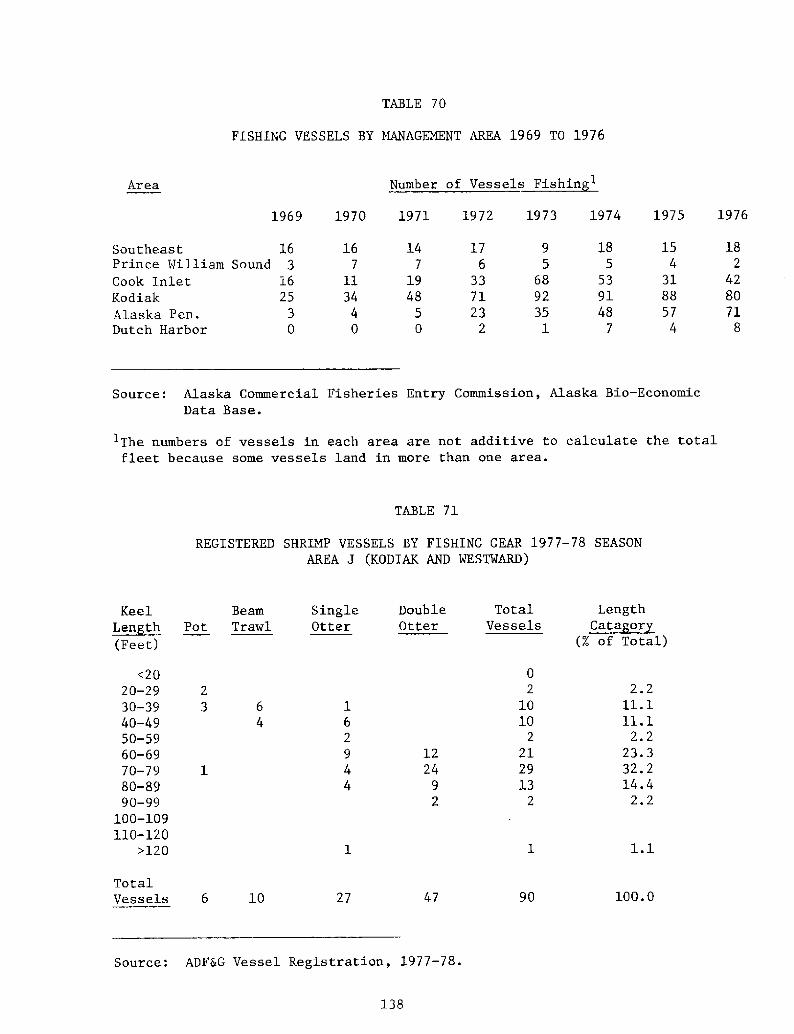

Fishing Vessels by Management Area 1969 to 1976...

Registered Shrimp Vessels by Fishing Gear 1977-78Season Area J Kodiak and Westward! 138

Shrimp Harvesting Capacity Estimate for theSoutheastern Alaska Area 1976-77 Season...........

Shrimp Harvesting Capacity by Area 1976...........

Shrimp Catch by Area 1977...... ~ ............. ~ ....

Total Alaska Shrimp Processing Capacity 1977 to1978.

1977 Capacity Utilization of Kodiak ShrimpProcessing Plants.......

1977 Capacity Utilization for Chignik/SouthPeninsula/Dutch Harbor

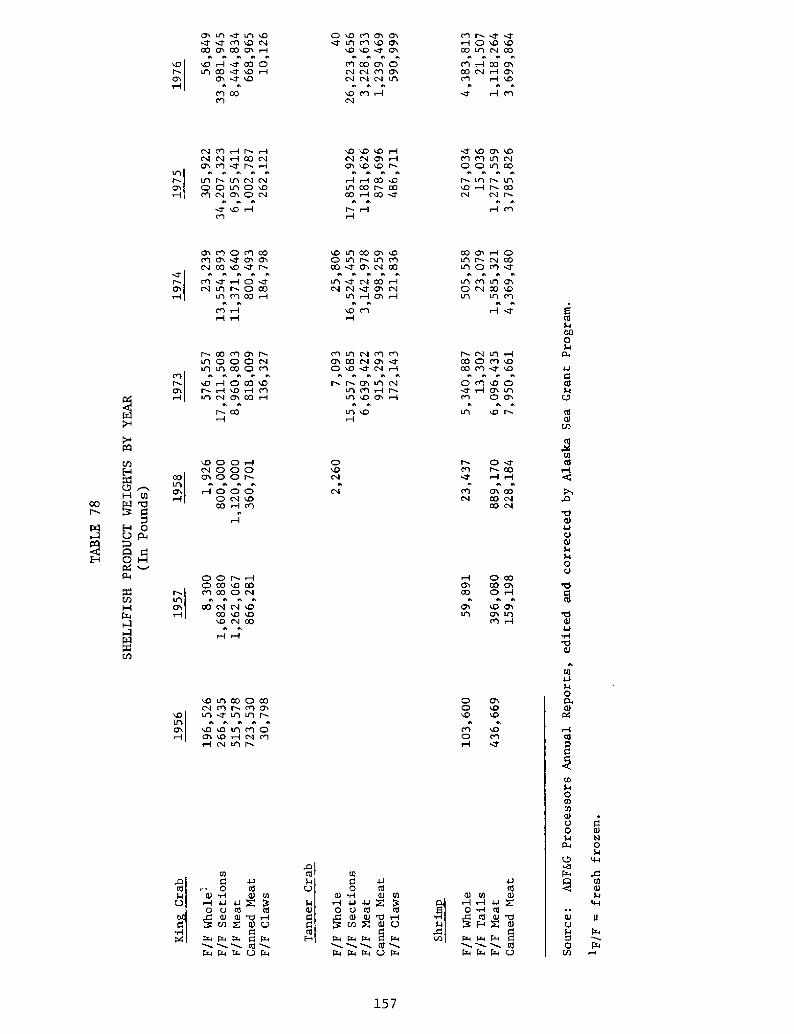

Shellfish Product Weights by Year............. ~ . ~ .

U.S. Exports of Frozen King Crab by Country ofDestination 1968 to 1977...

U.S. Exports of Prepared or Preserved King Crabby Country of Destination 1968 to 1977........ ~ ...

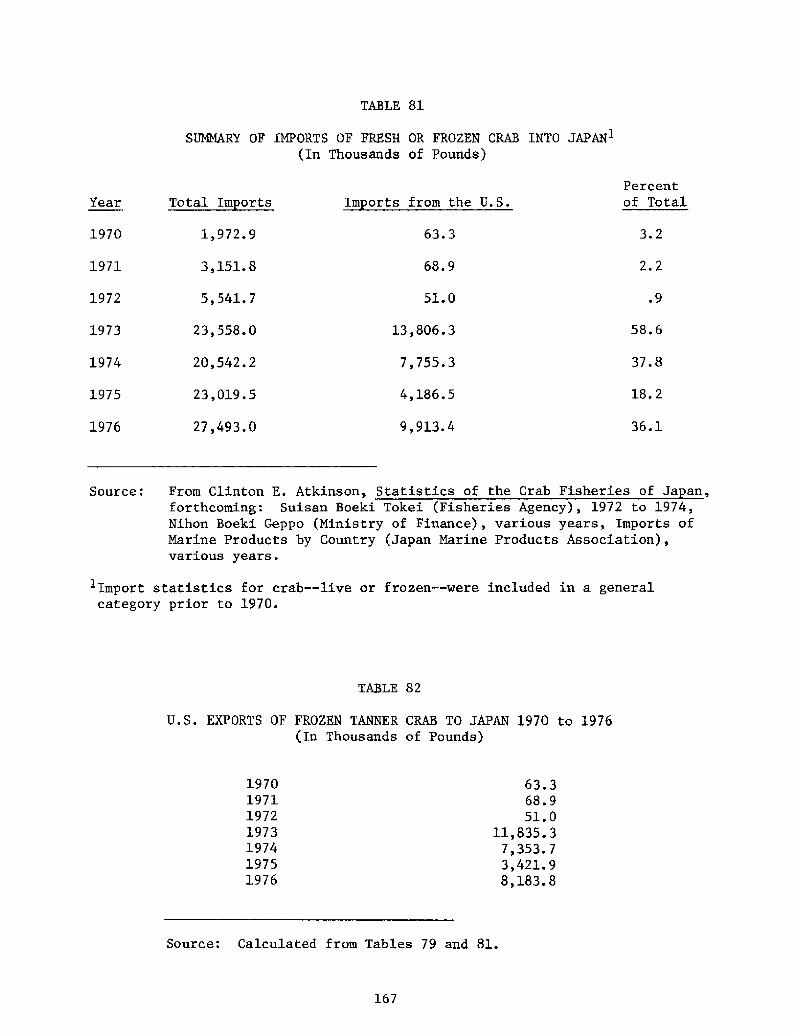

Summary of Imports of Fresh or Frozen Crab intoJapan. ~ ~ ~ ~

U.S. Exports of Frozen Tanner Crab to Japan 1970to 1976 a ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

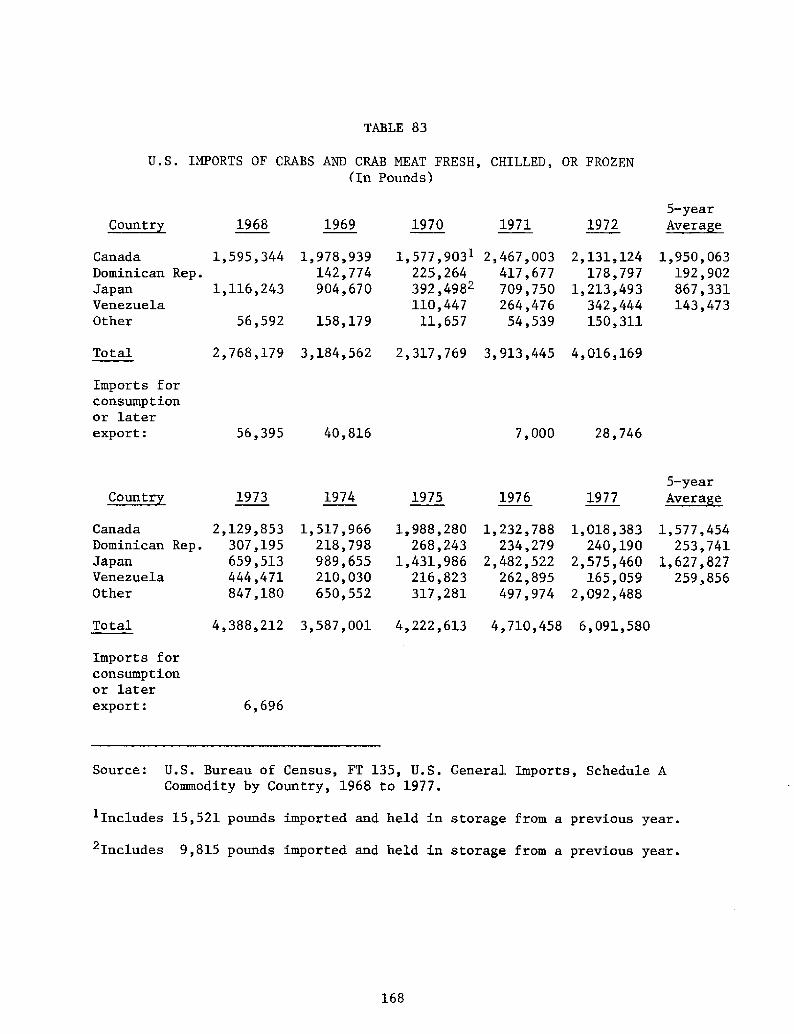

U.S. Imports of Crabs and Crab Meat Fresh,Chilled, or Frozen........... ~ ~ ~ ~ ~ ~

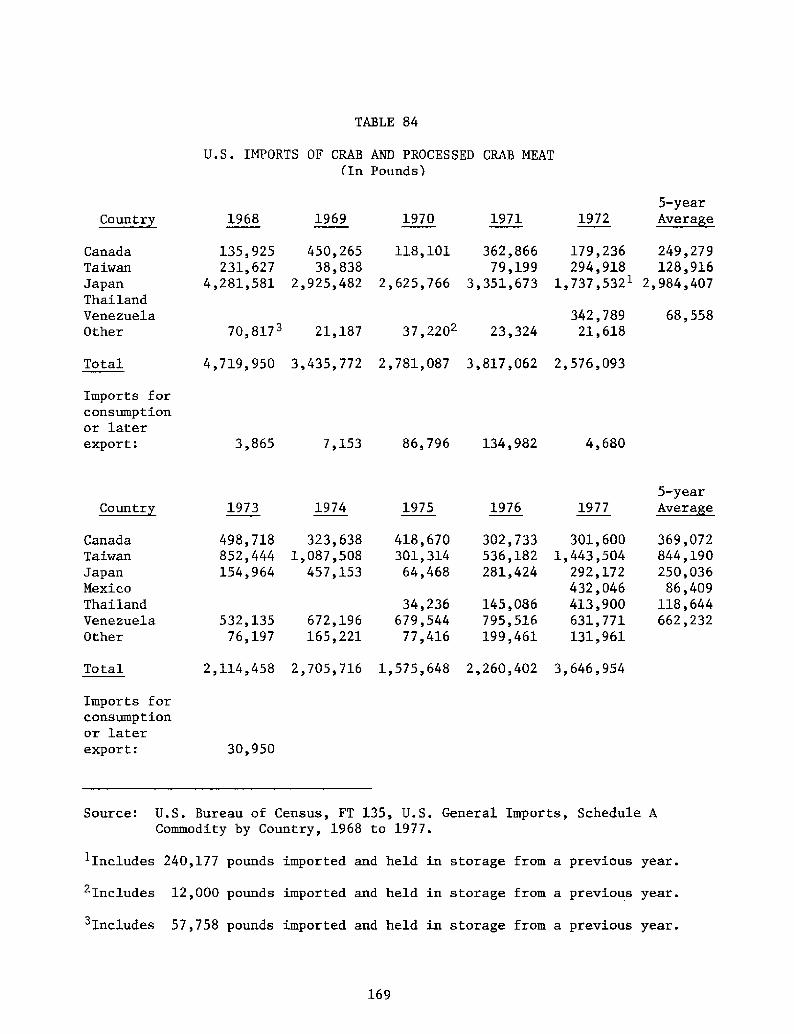

U.S. Imports of Crab and Processed Crab Meat......

TABLES

continued!

PAGE

TABLE 85

170

TABLE 86

170

TABLE 87

TABLE 88

174

TABLE 89

175

TABLE 90

176

180

181

182

186

Custom-Pack Tally 188

190

194

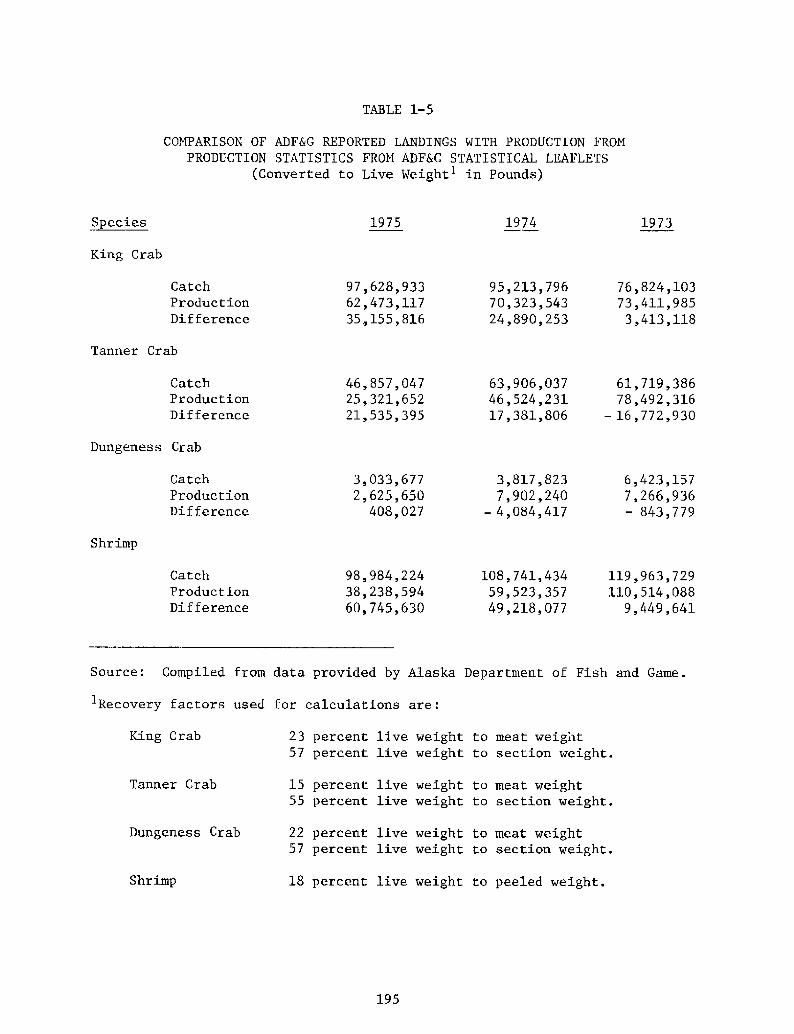

TABLE 1-5

195

APPENDIX II

TABLE 2-1,

203

TABLE 2 � 2

208

xiv

TABLE 91

TABLE 92

TABLE 93

APPENDIX I

TABLE 1-1

TABLE 1-2

TABLE 1-3

TABLE 1-4

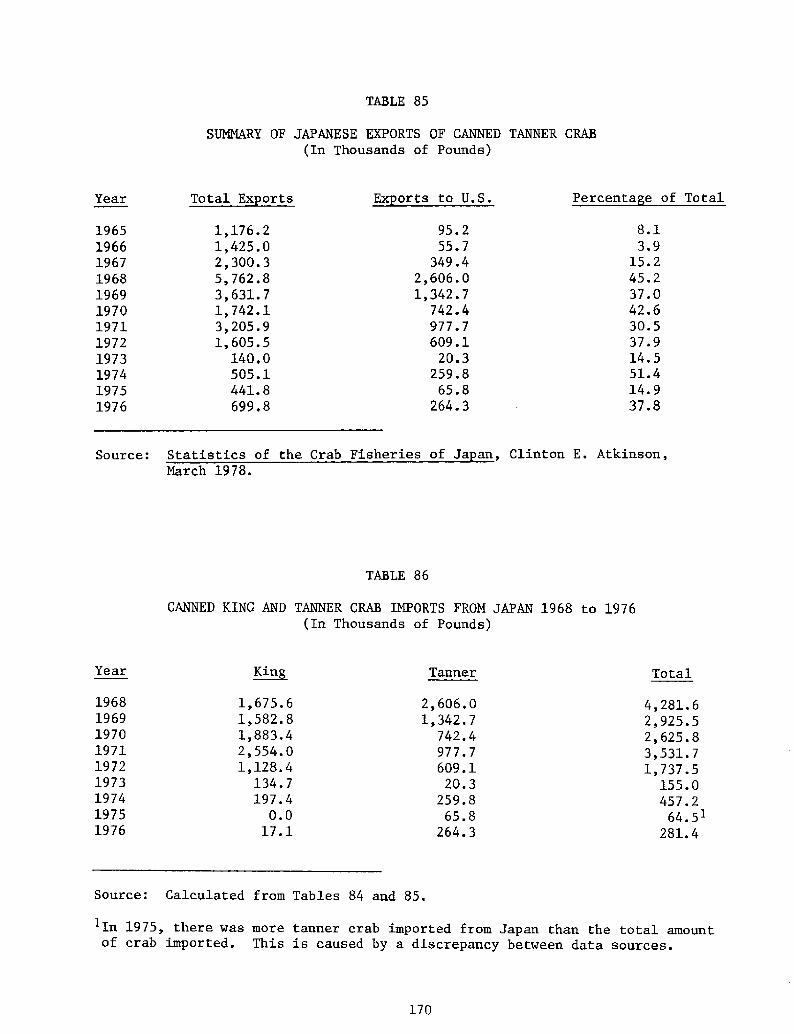

Summary of Japanese Exports of Canned TannerCrab. ~ ~ ~

Canned King and Tanner Crab Imports from Japan1968 to 1976.

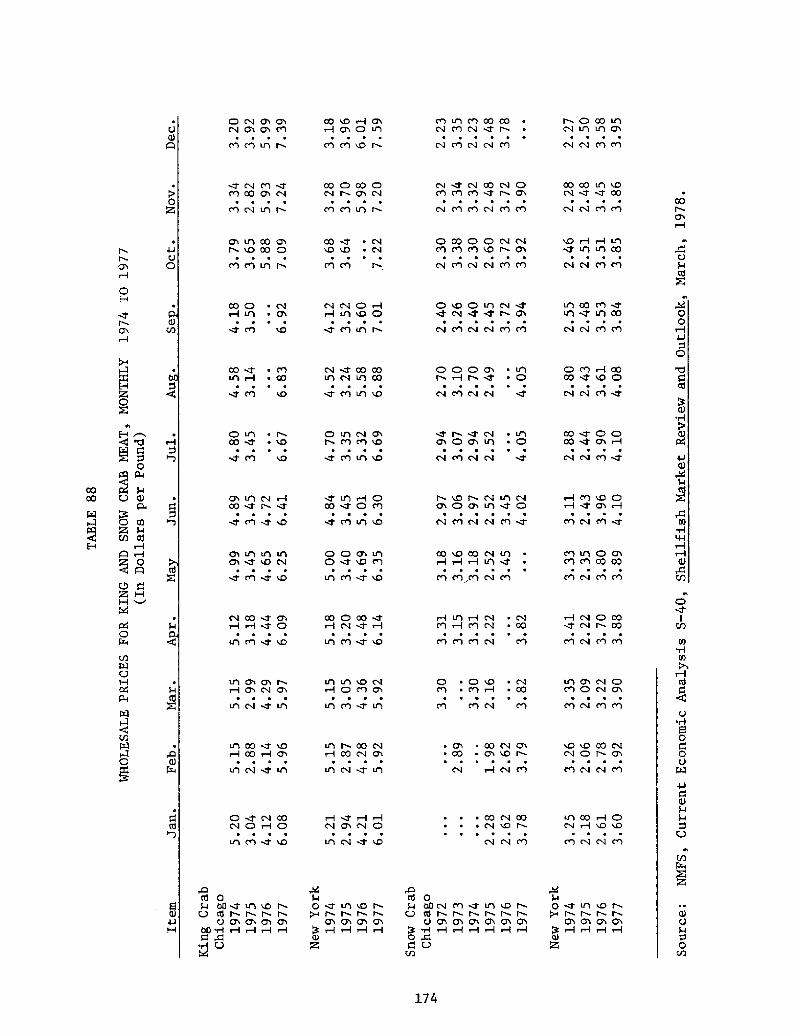

Kodiak Ex-Vessel Prices of King and Tanner Crab1970 to 1977. 173

Wholesale Prices for King and Snow Crab Neat,Nonthly 1974 to 1977.. ~ ............

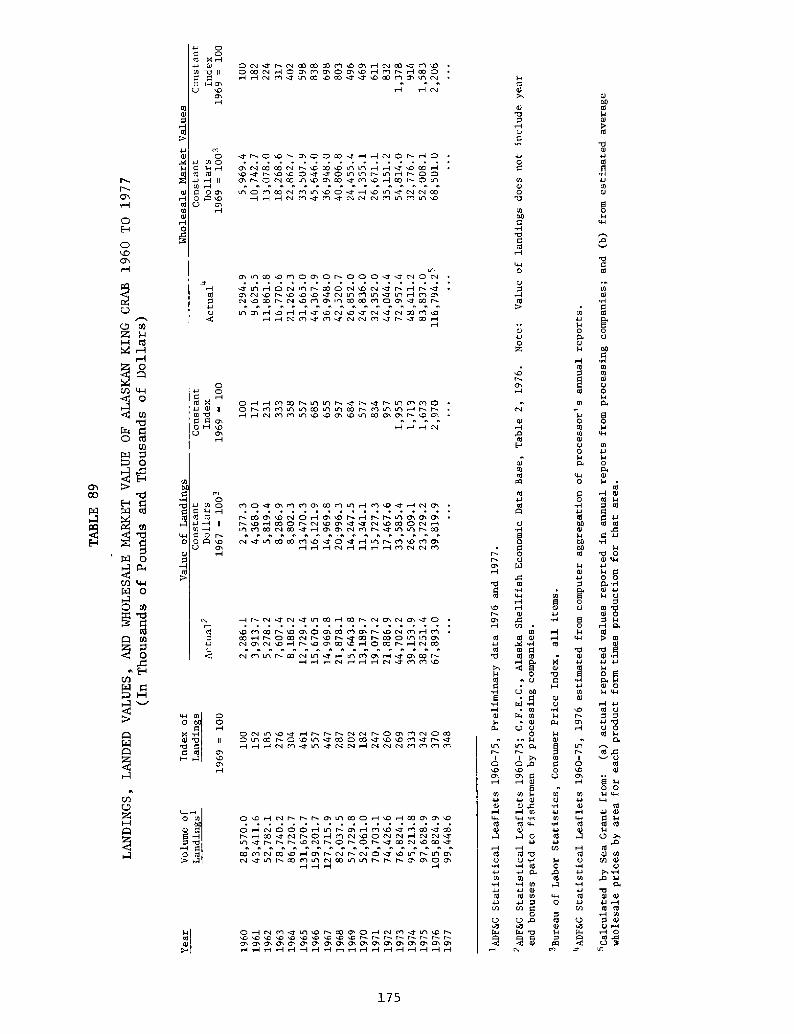

Landings, Landed Values, and Wholesale MarketValue of Alaskan King Crab 1960 to 1977............

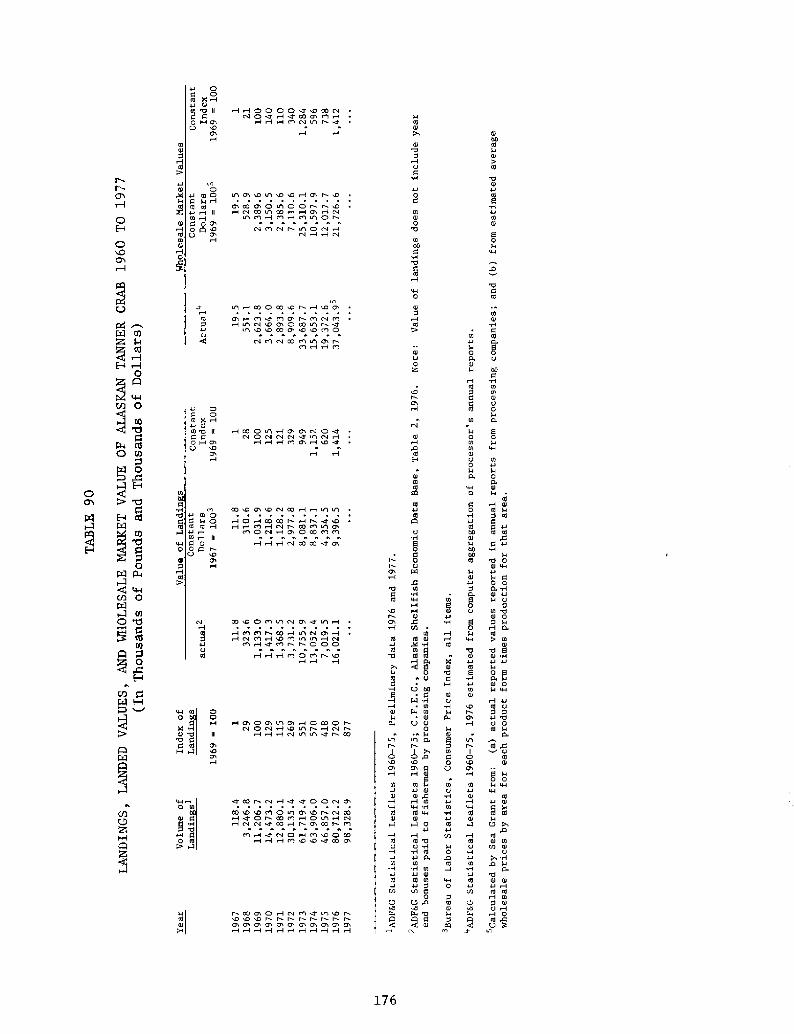

Landings, Landed Values, and Wholesale MarketValue of Alaskan Tanner Crab 1960 to 1977..........

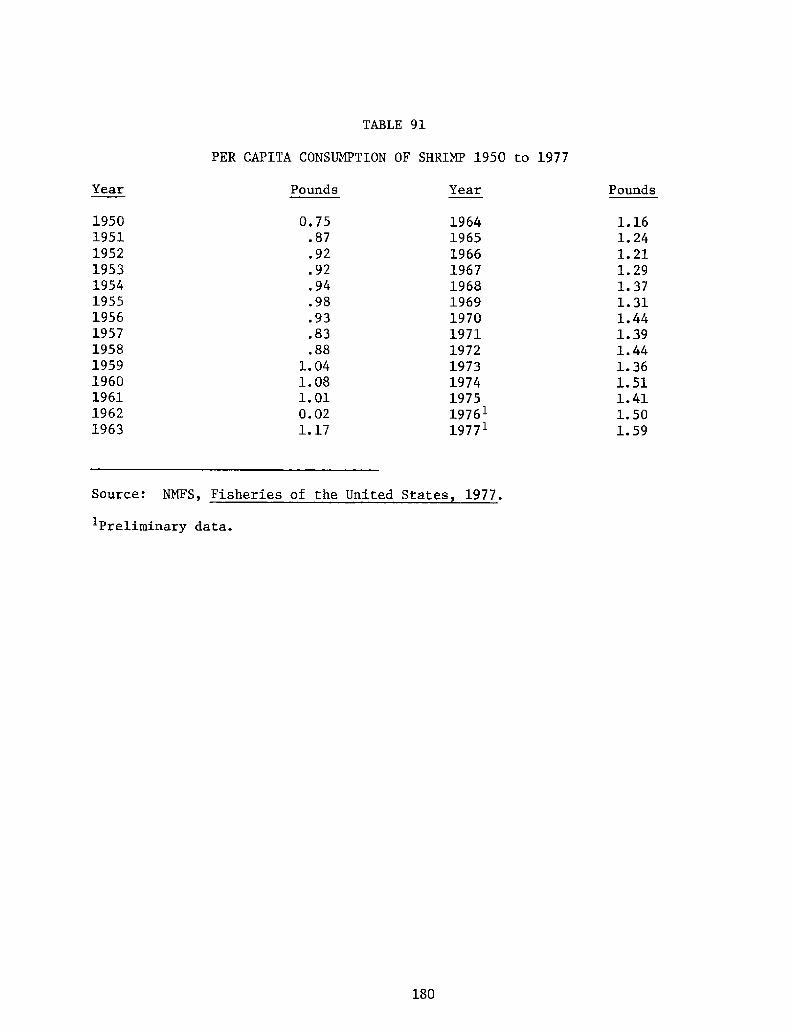

Per Capita Consumption of Shrimp 1950 to 1977......

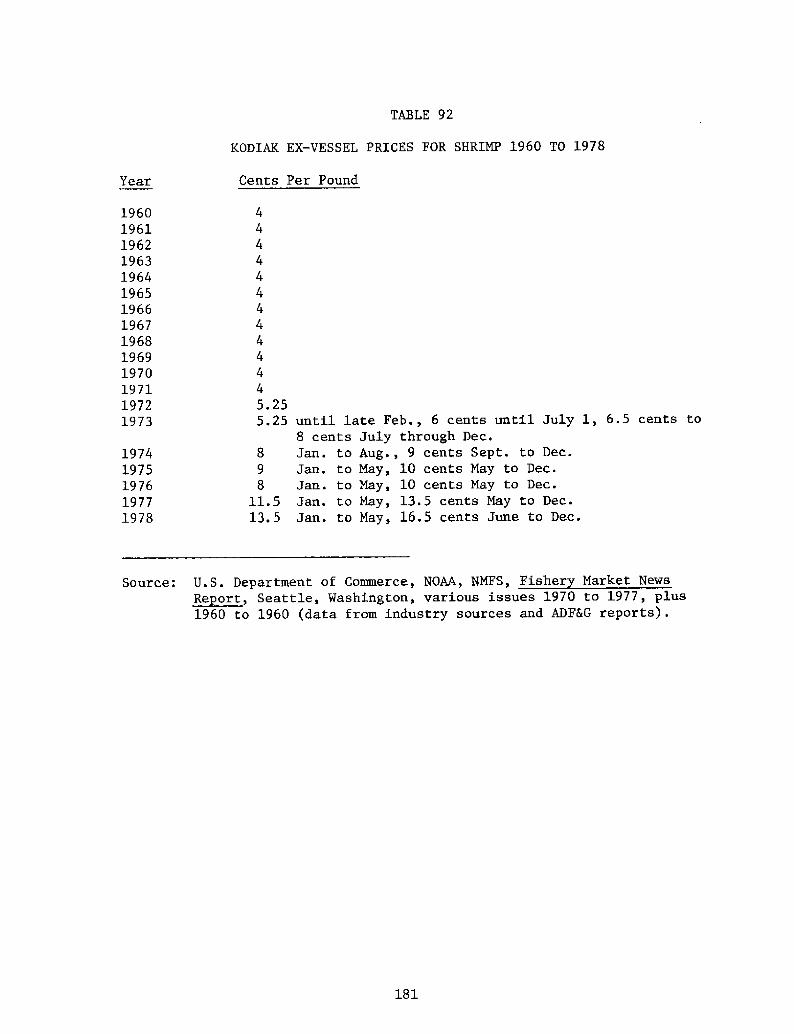

Kodiak Ex-Vessel Prices for Shrimp 1960 to 1978....

Landings, Landed Values, and Wholesale MarketValues of Alaskan Shrimp 1960 to 1977.......

Fisherman-Direct. Sell by General Area..............

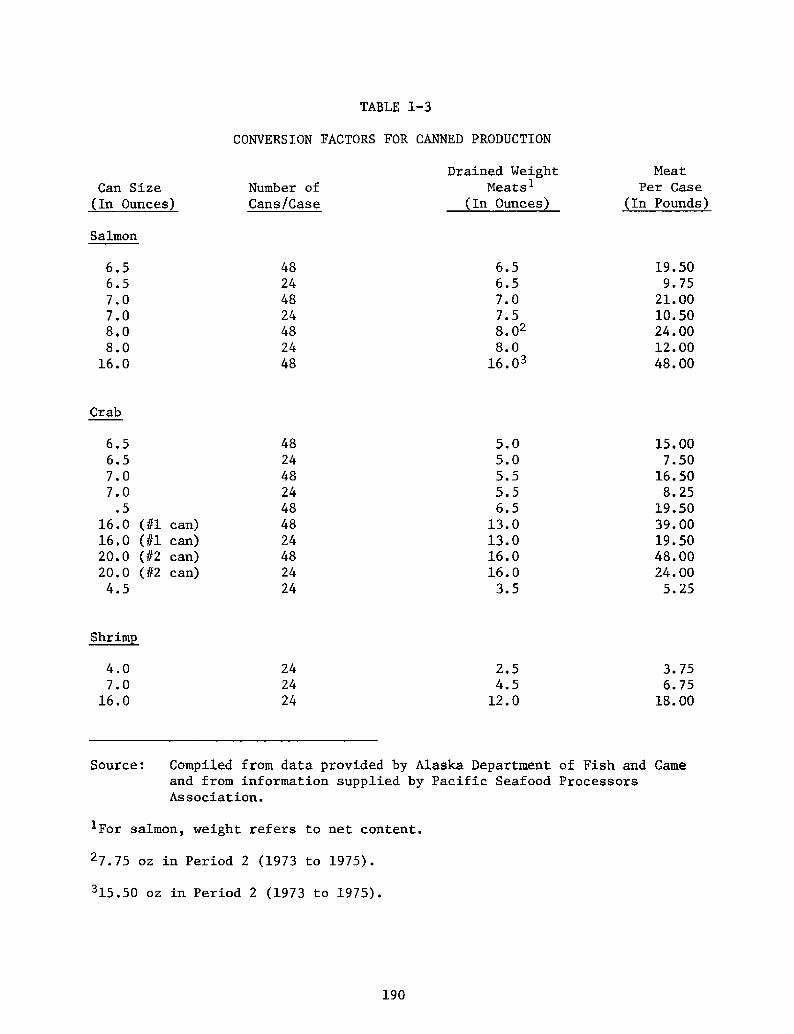

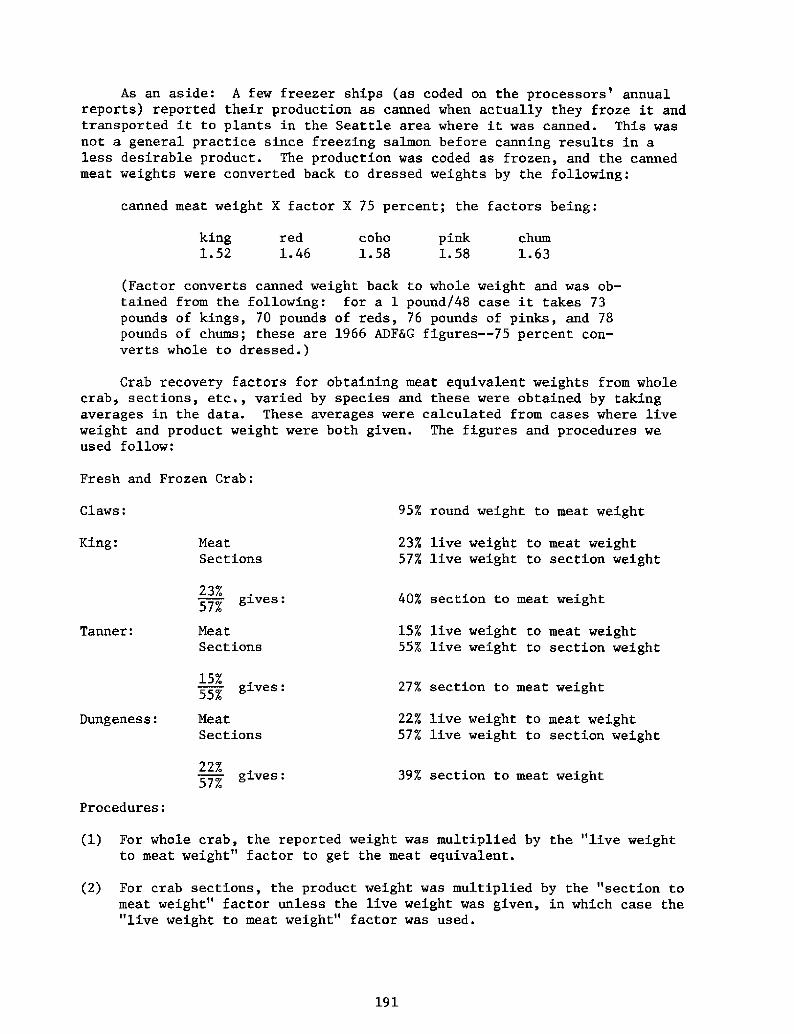

Conversion Factors for Canned Production...........

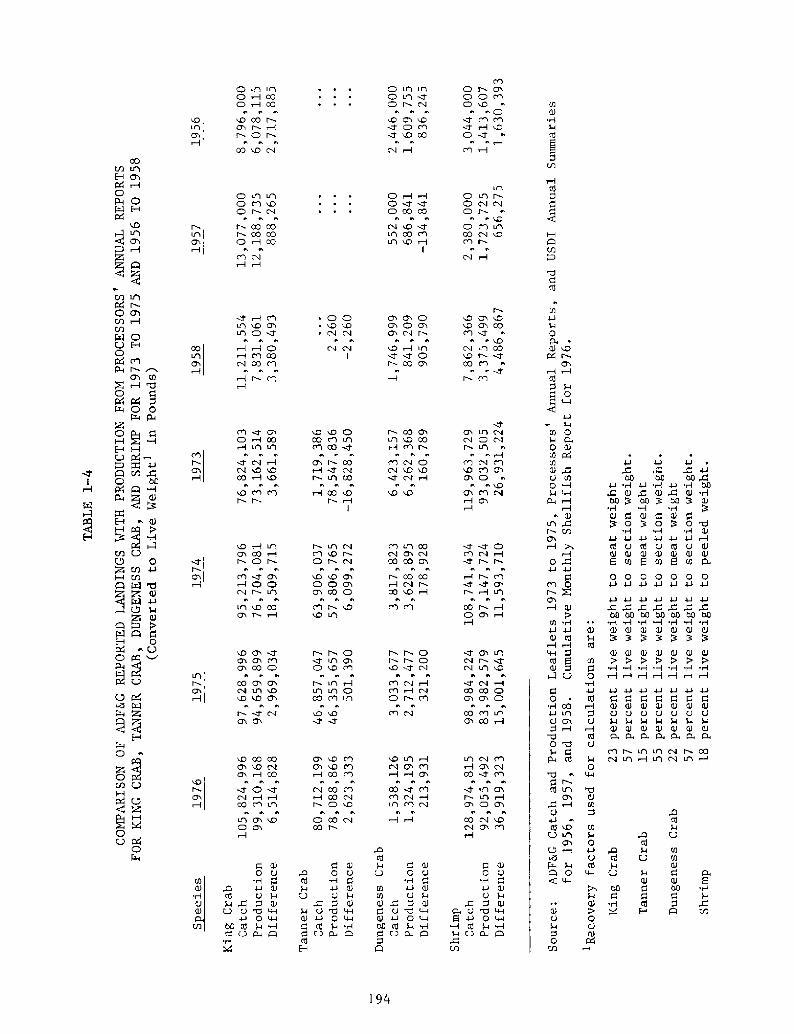

Comparison of ADF&G Reported Landings with Pro-duction from Processors' Annual Reports for KingCrab, Tanner Crab, Dungeness Crab, and Shrimp for1973 to 1975 and 1956 to 1958.

Comparison of ADF&G Reported Landings with Pro-duction from Production Statistics from ADF&G

Statistical Leaflets..........

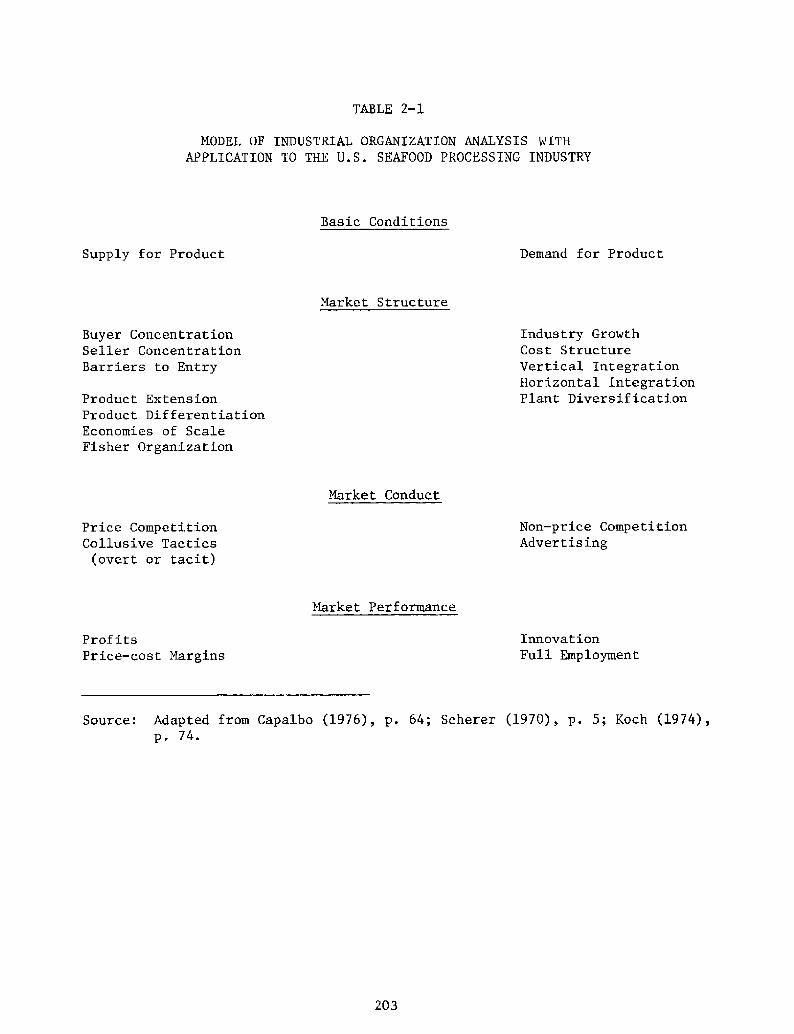

Model of Industrial Organization Analysis withApplication to the U.S. Seafood Processing Industry

States Included in the National Marine Fisheries

Service Regions............... ~ ~ ~

TABLES

continued!

PAGE

TABLE 2-3

209

TABLE 2-4

212

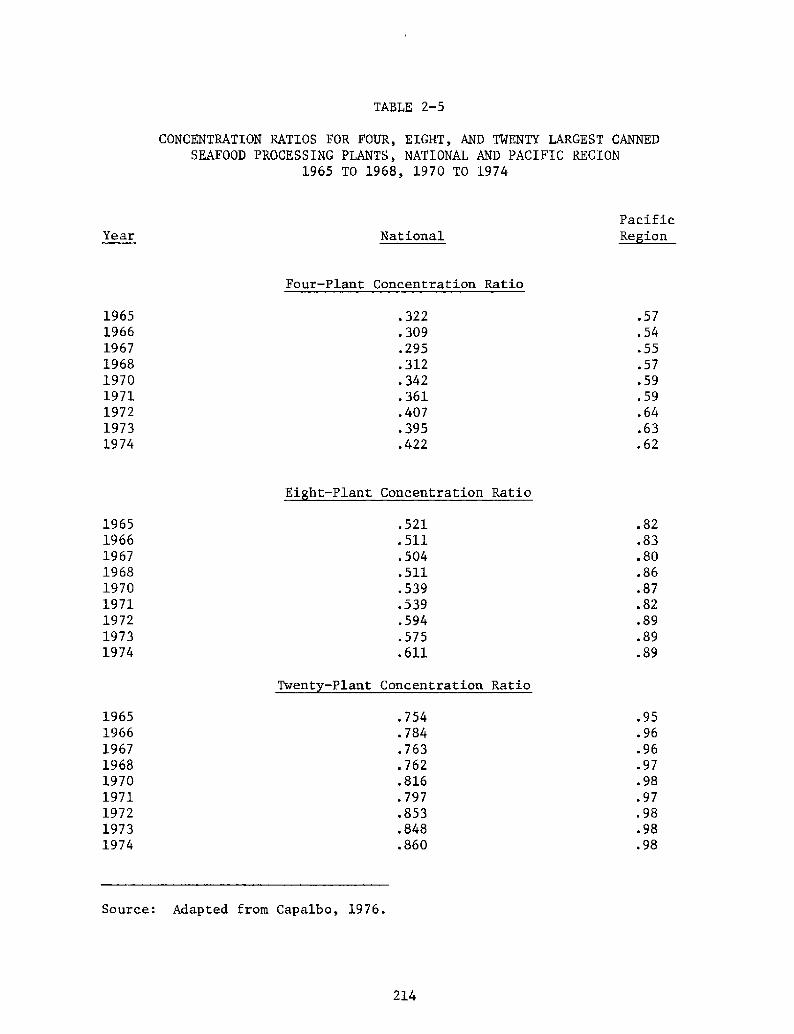

TABLE 2-5

214

TABLE 2 � 6

216

TABLE 4 � 2

TABLE 4-3

262

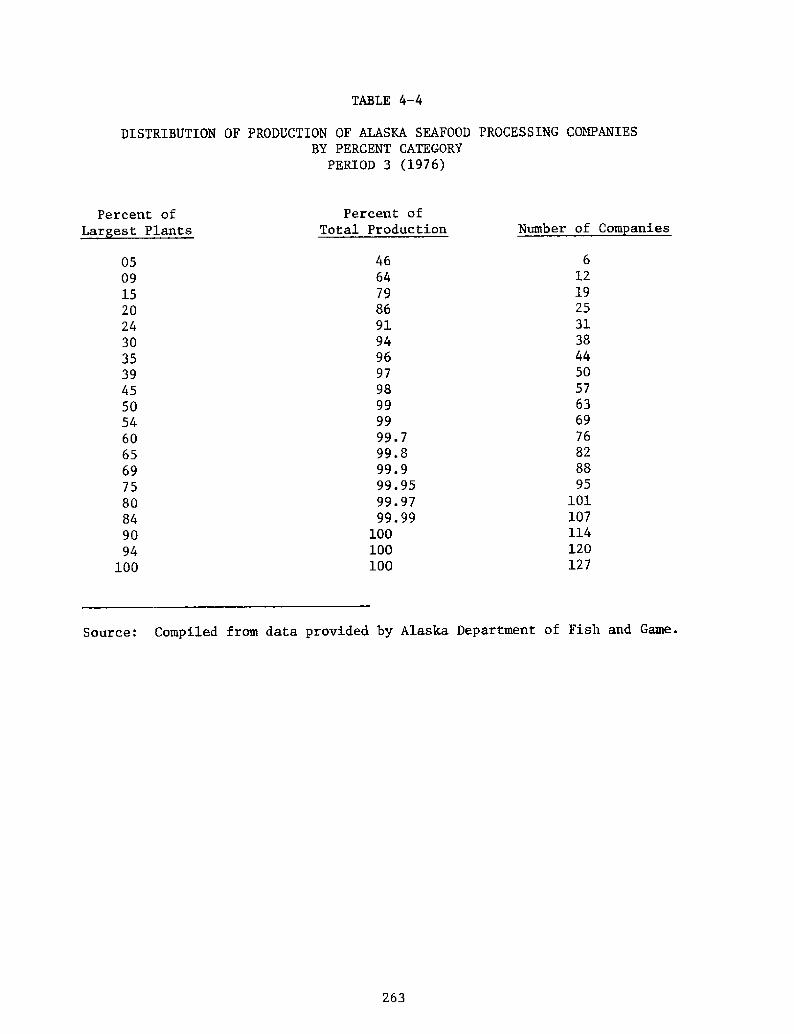

TABLE 4 � 4

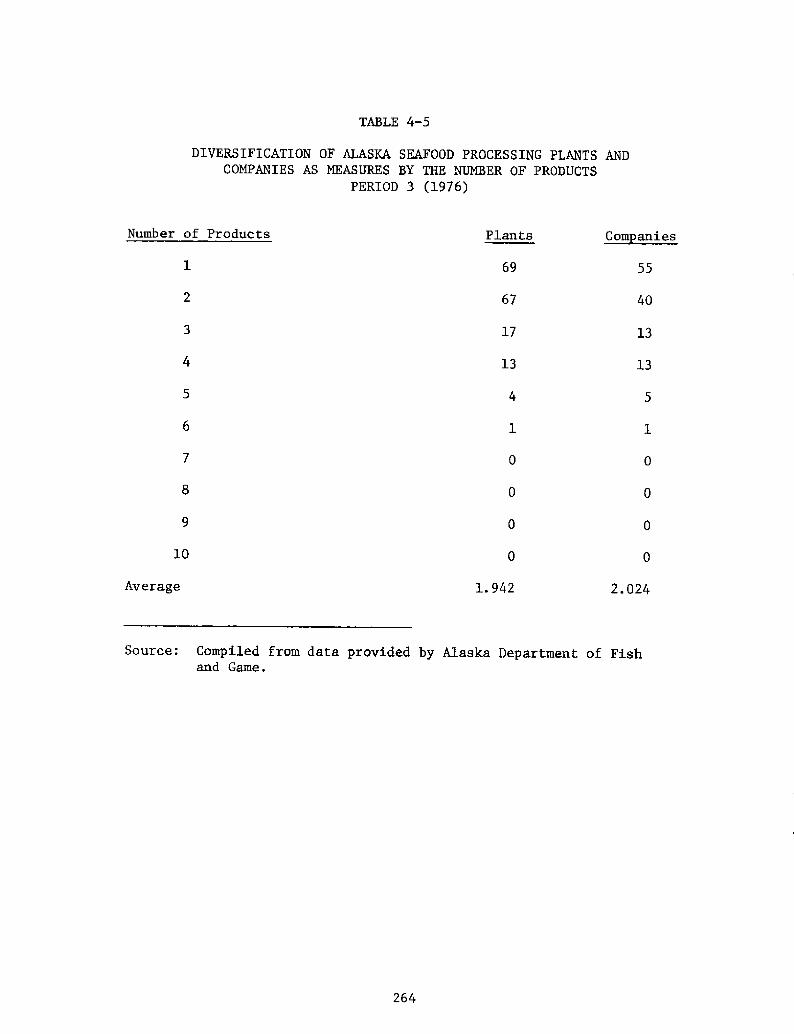

TABLE 4-5

264

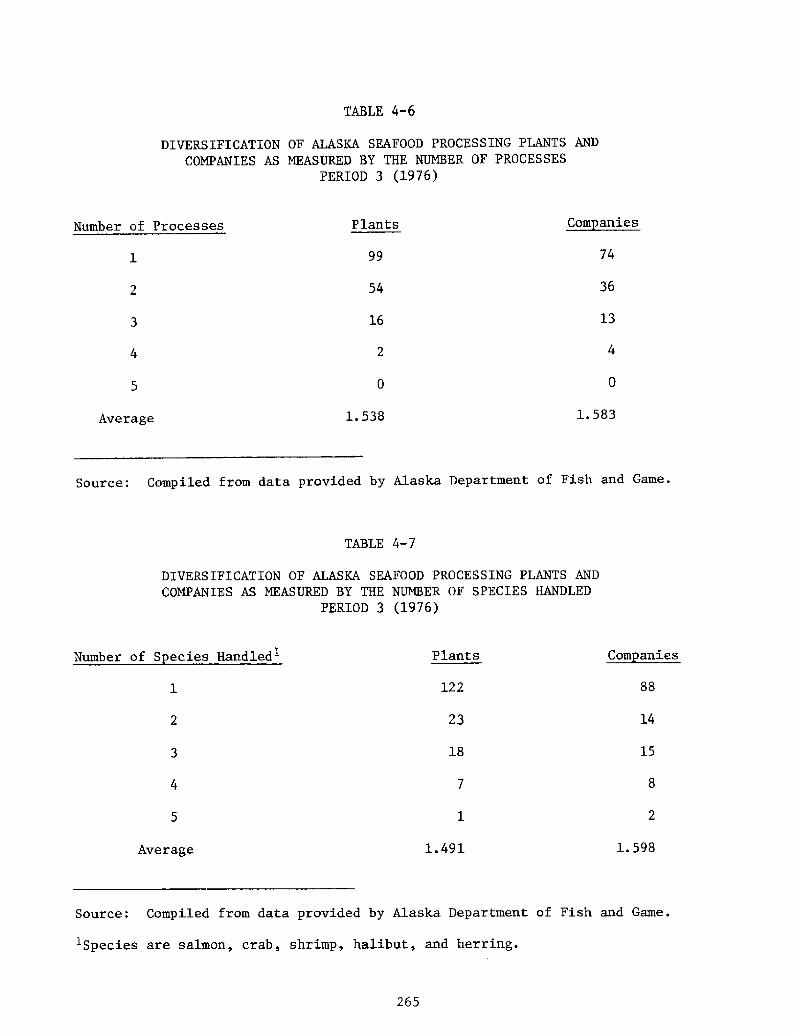

TABLE 4-6

265

TABLE 4-7

265

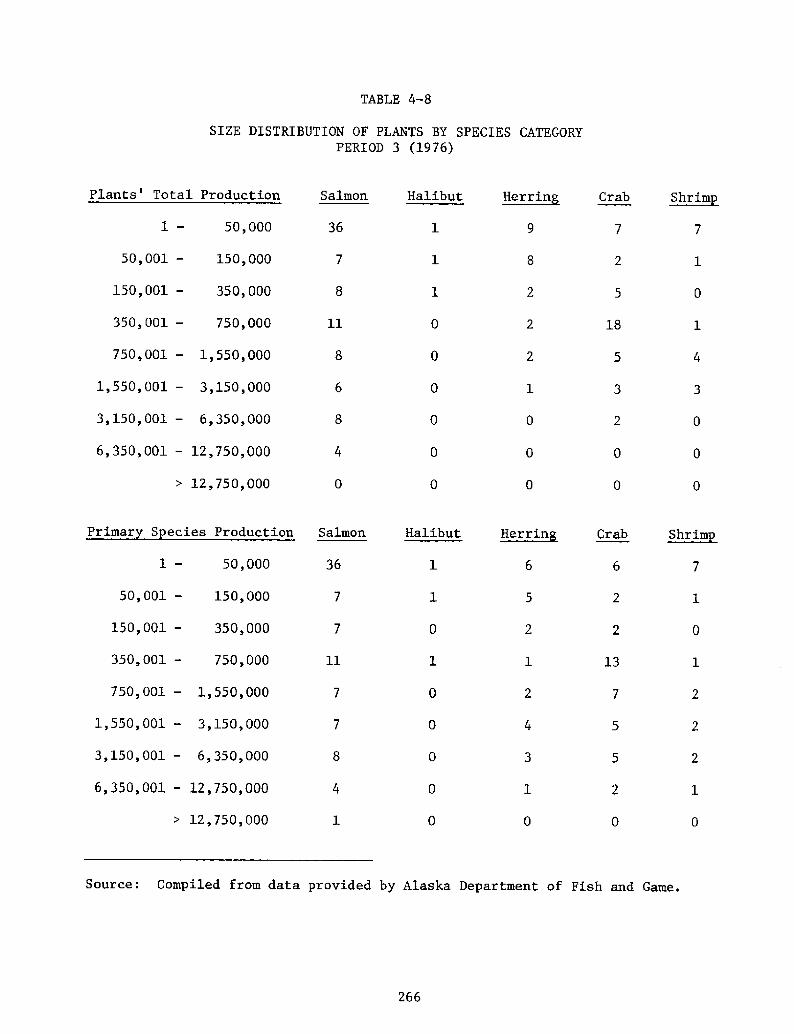

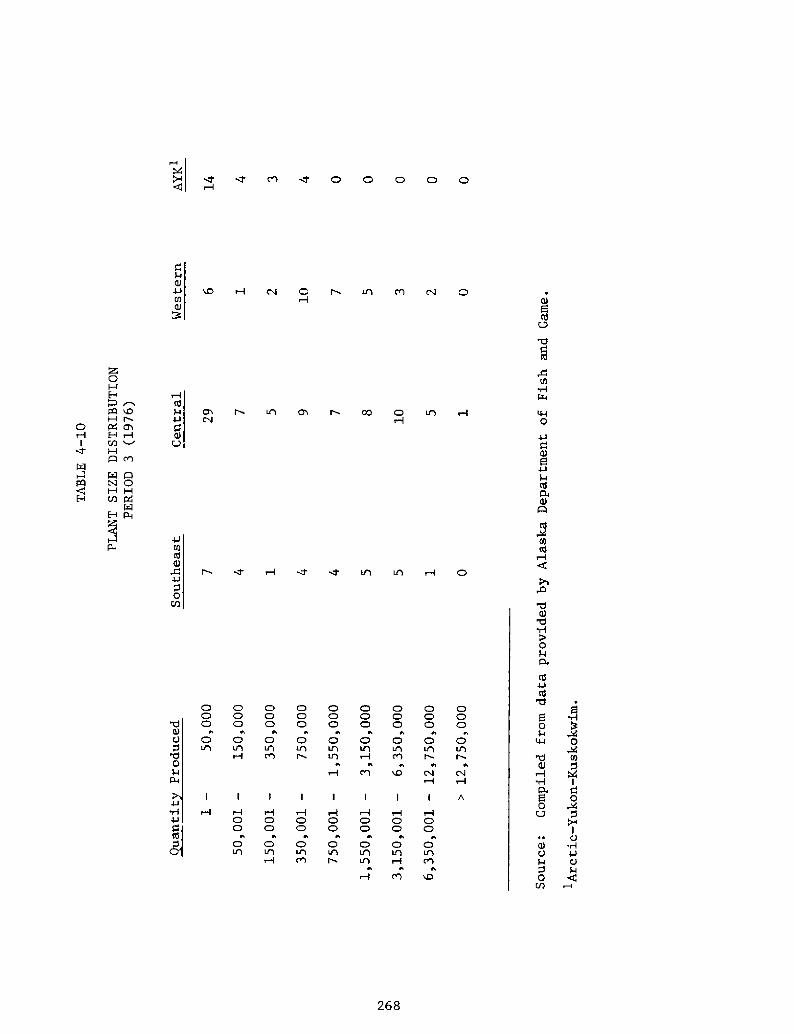

TABLE 4-8 Size Distribution of PlantsPeriod 3 �976!.

by Species Category266

Size Distribution of Plants

Period 3 �976!...........

TABLE 4-9 by Process Form

267

APPENDIX IV

TABLE 4 � 1

Concentration Ratios for Four, Eight, and TwentyLargest Fresh Seafood Processing Plants, National,New England, and Middle Atlantic Region 1965 to1968, 1970 to 1974 '

Concentration Ratios for Four, Eight, and TwentyLargest Frozen Seafood Processing Plants, National,New England, and Middle Atlantic Region 1965 to1968, 1970 to 1974.

Concentration Ratios for Four, Eight, and TwentyLargest Canned Seafood Processing Plants, Nationaland Pacific Region 1965 to 1968, 1970 to 1974......

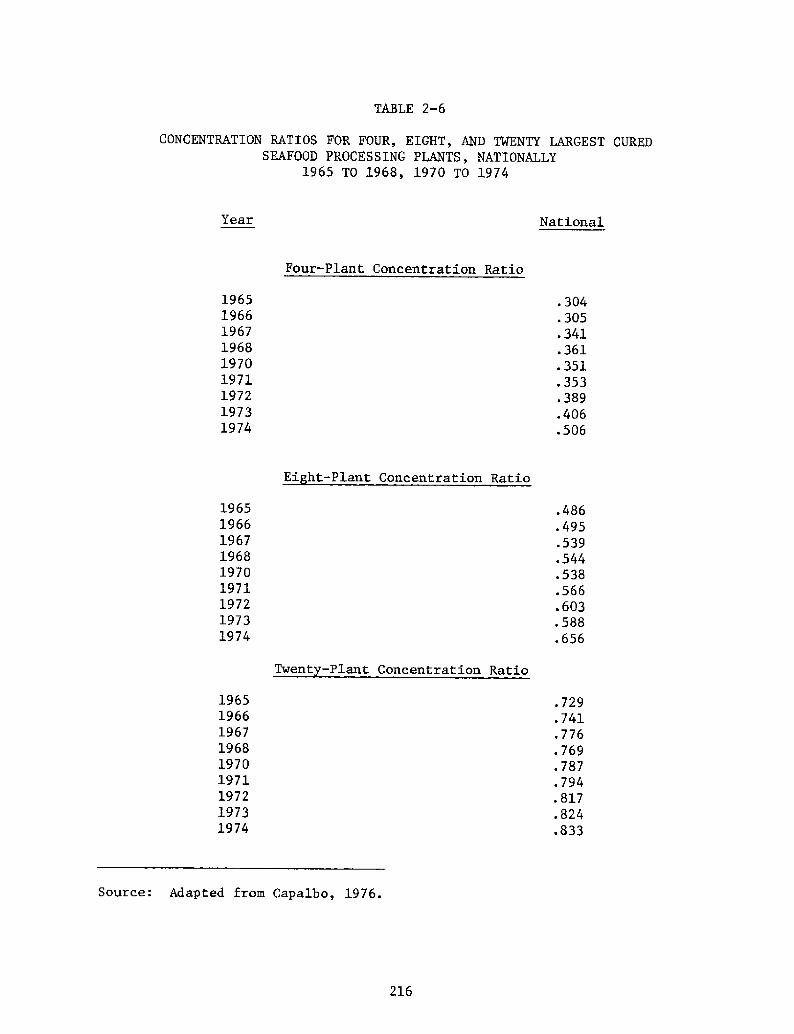

Concentration Ratios for Four, Eight, and TwentyLargest Cured Seafood Processing Plants, Nationally1965 to 1968, 1970 to 1974.

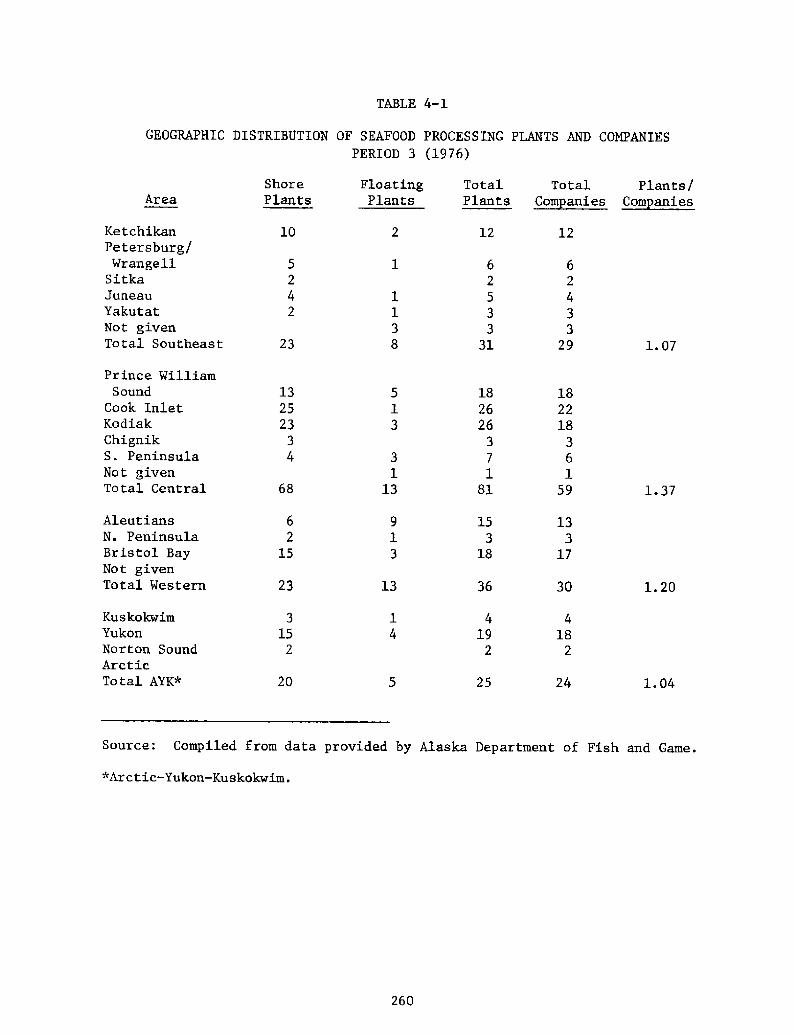

Geographic Distribution of Seafood Processing Plantsand Companies Period 3 �976! . . ... ... 260

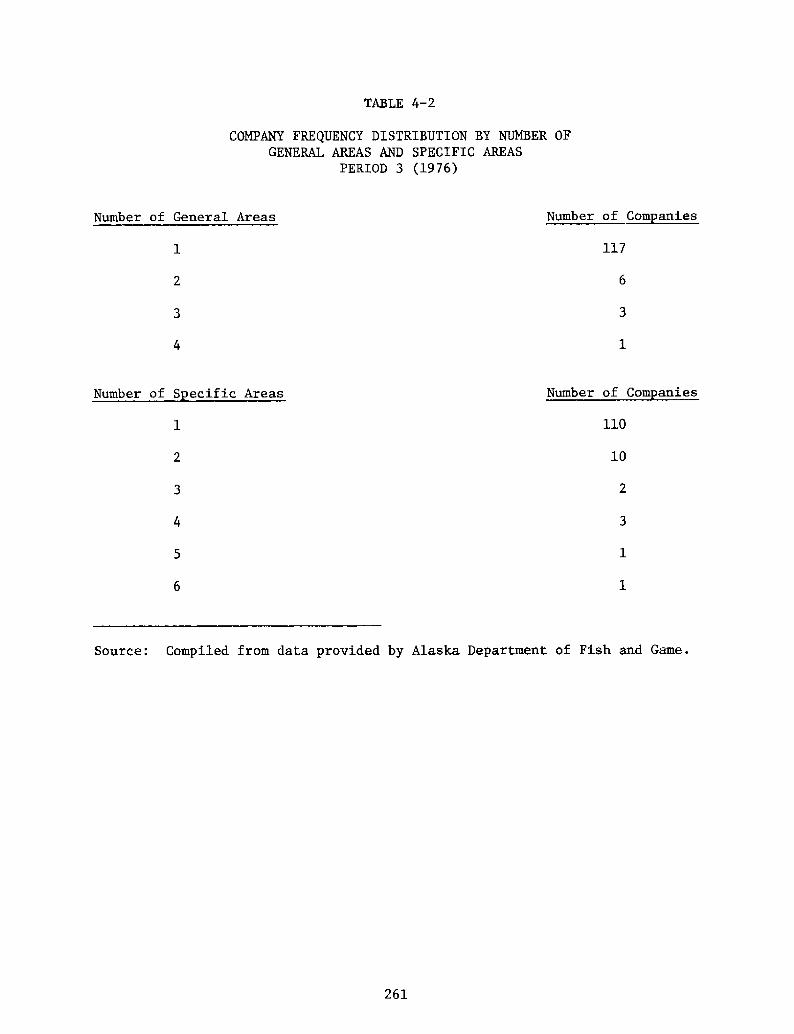

Company Frequency Distribution by Number of GeneralAreas and Specific Areas Period 3 �976!........ ~ .. 261

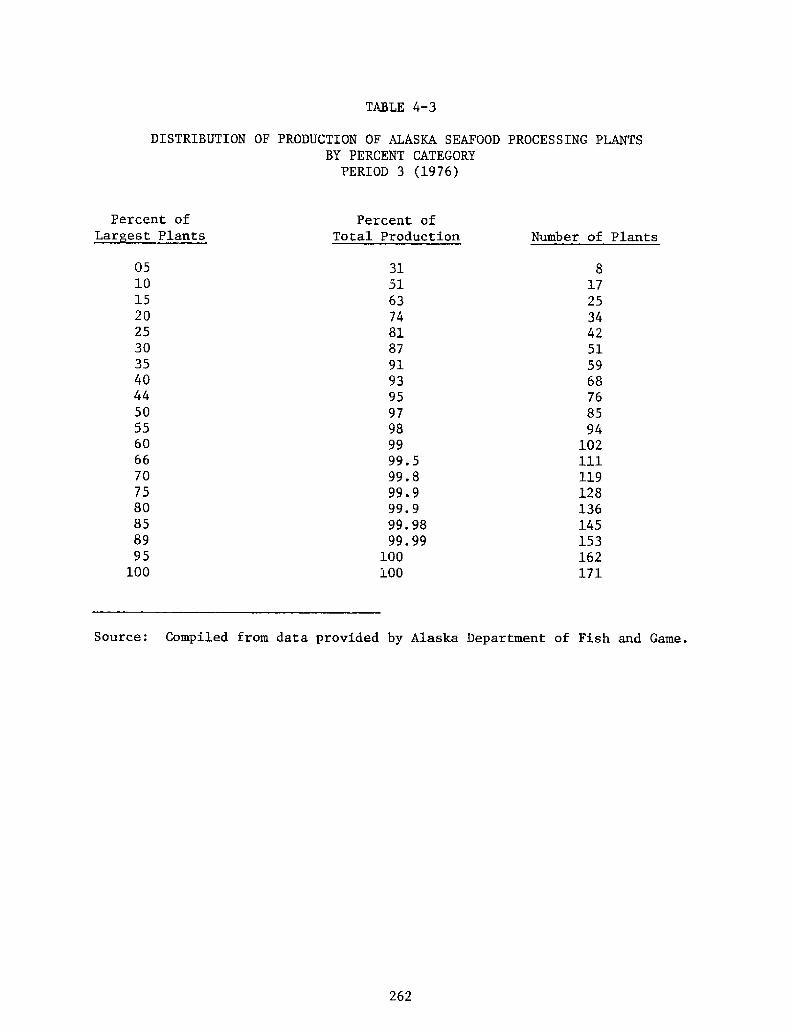

Distribution of Production of Alaska Seafood Pro-cessing Plants by Percent Category Period 3 �976!.

Distribution of Production of Alaska Seafood Pro-cessing Companies by Percent Category Period 3 �976! 263

Diversification of Alaska Seafood Processing Plantsand Companies as Measured by the Number of ProductsPeriod 3 �976!.

Diversification of Alaska Seafood Processing Plantsand Companies as Measured by the Number of ProcessesPeriod 3 �976!.... ~ ... ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Diversification of Alaska Seafood Processing Plantsand Companies as Measured by the Number of SpeciesHandled Period 3 �976!.....

TABLE

continued!

PAGE

268

269

270

TABLE 4-13

271

TABLE 4-14

272

TABLE 4-15

273

TABLE 4 � 16

TABLE 4-17

275

TABLE 4-18

276

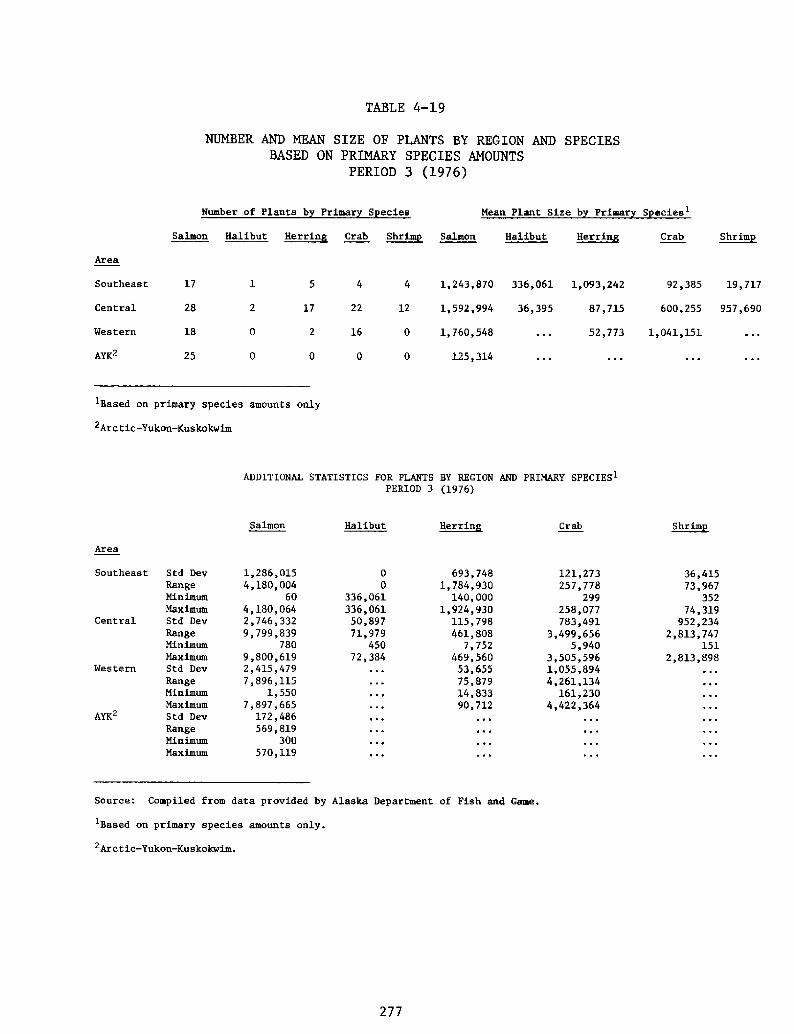

TABLE 4-19

277

TABLE 4-20

278

TABLE 4-21

279

TABLE 4-22

280

xvi

TABLE 4-10

TABLE 4-11

TABLE 4-12

Plant Size Distribution Period 3 �976!.....

Company Size Distribution Period 3 �976!...

Statewide and Regional Market Concentrationfor Shrimp Products by Period, Unadjustedfor Ownership Interties Period 3 �976!.....

State~ide and Regional Market Concentrati,onfor Total Crab Products by Period, Unadjustedfor Ownership Interties Period 3 �976!.....

Statewide and Regional Market Concentrationfor King Crab Products by Period, Unadjustedfor Ownership Interties Period 3 �976!.....

Statewide and Regional Market Concentrationfor Tanner Crab Products by Period, Unadjustedfor Ownership Interties Period 3 �976!.....

Statewide and Regional Market Concentrationfor Dungeness Crab Products by Period, Un-adjusted for Ownership Interties Period 3 1 97 6! ~ ~ ~ o ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ t

Prince William Sound and Bristol Bay MarketConcentration for Shrimp Products by Period,Unadjusted for Ownership Interties Period 3 1 976! ~ ~ ~ ~ ~ ~ ~ o ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~

Prince William Sound and Bristol Bay MarketConcentration for Crab Products by Period,Unadjusted for Ownership Interties Period 3 1976! ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ a s ~ ~ ~ ~ ~ ~ ~ ~ a ~ ~ e ~ o o ~

Number and Mean Size of Plants by Region andSpecies Based on Primary Species AmountsPeriod. 3 �976!......

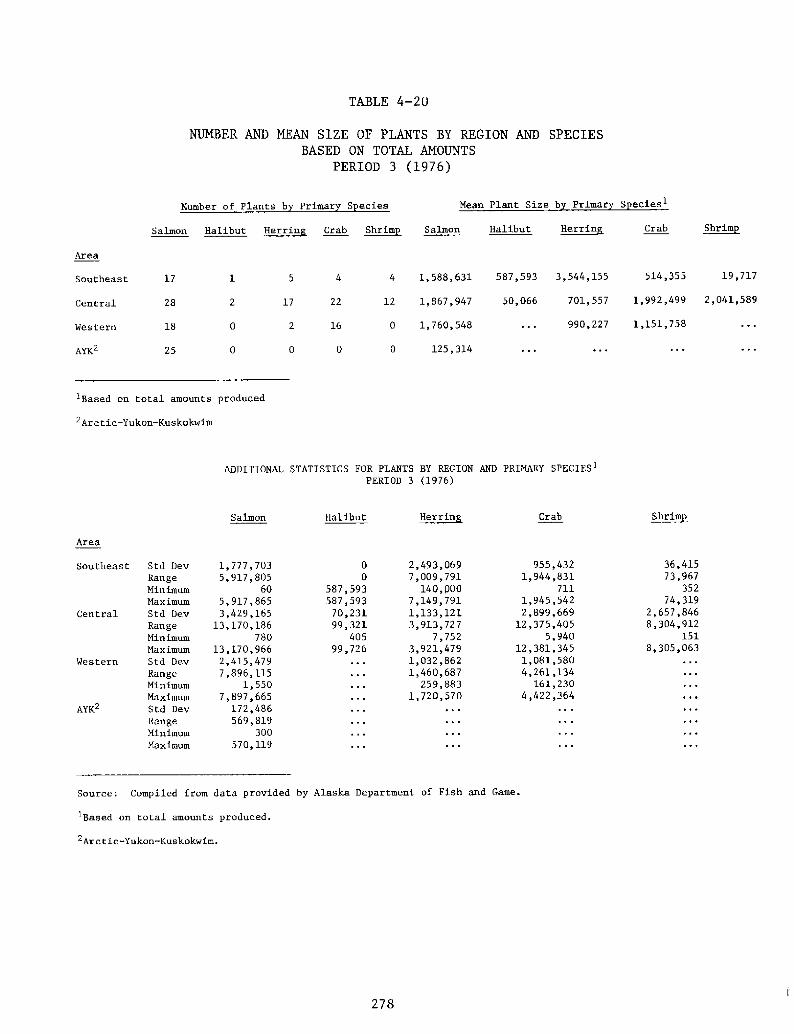

Number and Mean Size of Plants by Region andSpecies Based on Total Amounts Period 3 �976!

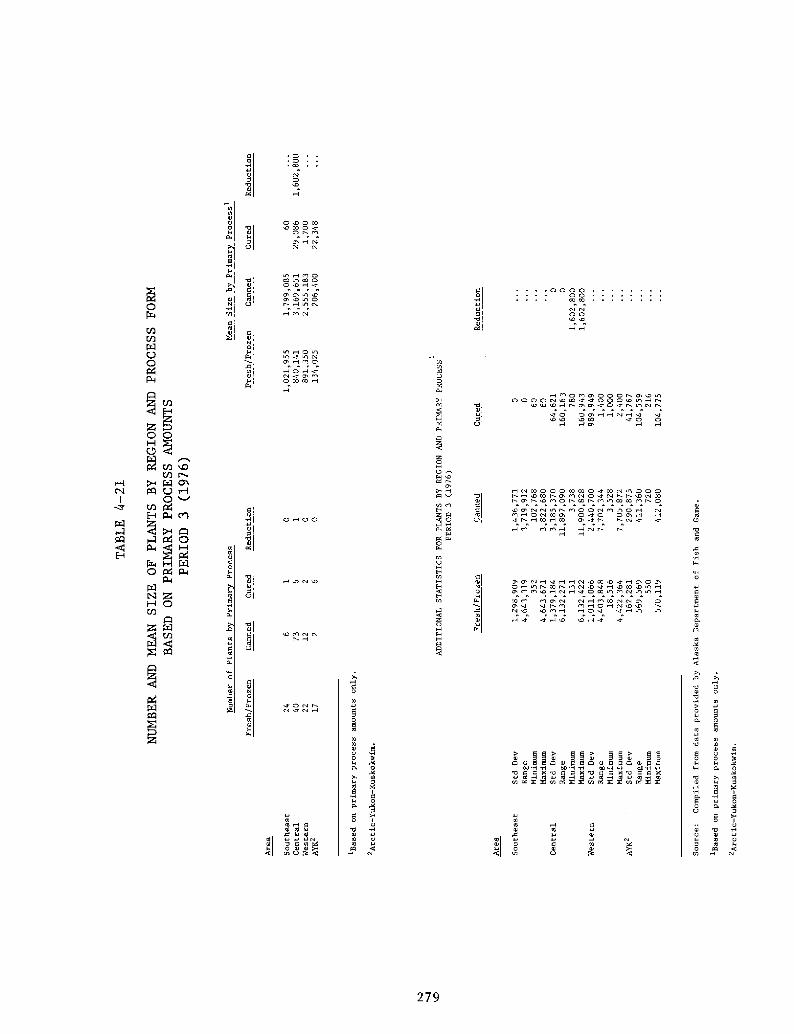

Number and Mean Size of Plants by Region andProcess Form Based on Primary Process AmountsPeriod 3 �976!..........+..................

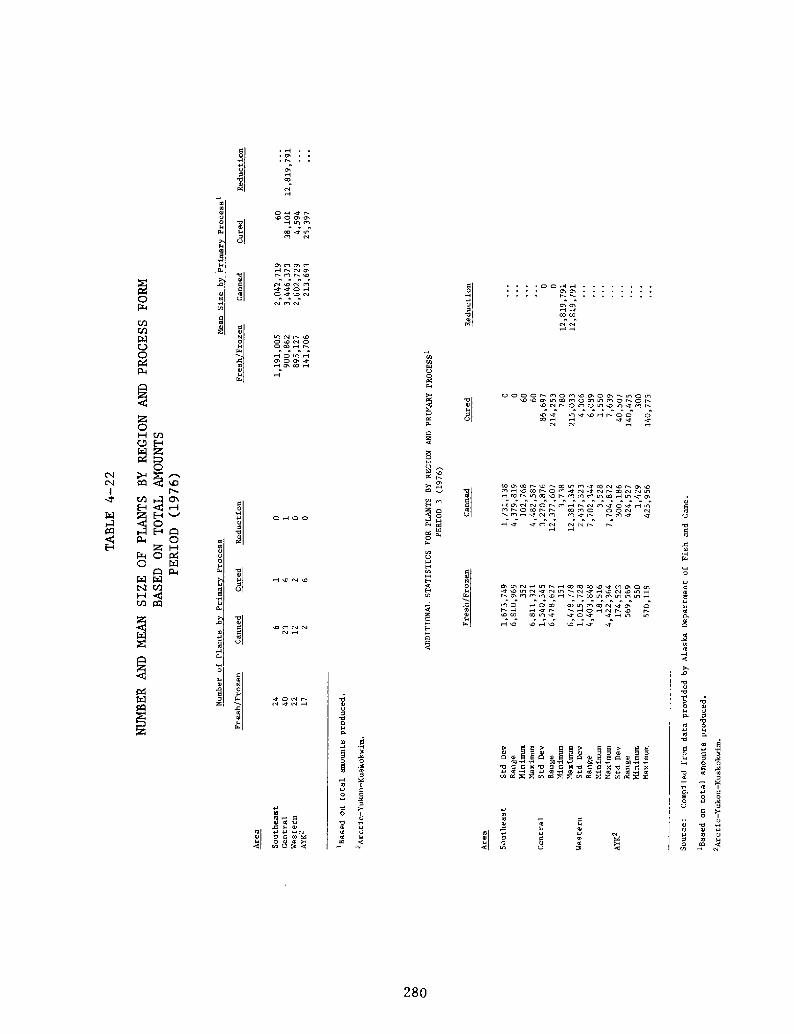

Number and Mean Size of Plants by Region andProcess Form Based on Total Amounts Period3 1 97 6! ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ e ~ ~ ~ a ~ ~ ~ ~ ~ s ~ ~ ~ ~

ACKNOWLEDGMENTS

The authors wish to gratefully acknowledge the assistance they havereceived throughout the course of this project from a large number ofindividuals in the seafood processing industry and in various governmentagencies, in obtaining data necessary to this study. While space con-straints make it impossible to list all those who assisted in providinginformation, mention should be made of a number of people who deserverecognition for their contributions. They are: Judy Brakel, AlaskaCommercial Fisheries Entry Commission; Pete Harris, New England FishCompany; Pat Holmes, Alaska Department of Fish and Game ADF&G!, Kodiak;Chuck Jensen, Pacific Pearl Seafoods, Inc.; Dick Johnston, Oregon StateUniversity; Ralph Jones, Alaska-Shell, Inc.; Blake Kinnear, Pan-AlaskaFisheries; Jack Lind, Peter Pan Seafoods, Inc.; Jim Major, East PointSeafood; Carl Rosier, ADF&G; Fred Smith, Oregon State University; WaltYonker, Pacific Seafood Processors Association, and several of the ADF&Gfield biologists. The information provided by these people was invaluableas it is not available in published form in most cases.

In addition, the assistance of Peter Rogers is acknowledged fordeveloping the literature review section and the appendix information onindustrial organisation concepts. Special thanks are due to MichelleKrog and Helen Greschke for the typing of this report.

Any errors or omissions remain the responsibility of the authors.

This report is the result of research sponsored by the Alaska SeaGrant Program, cooperatively supported by NOAA Office of Sea Grant, U.S.Department of Commerce, under Grant 04-8-M01-187, and by the Universityof Alaska with funds appropriated by the State of Alaska.

The University of Alaska provides equal educational and employmentopportunities for all regardless of race, religion, color, national origin,sex, age, physical handicap, or veteran status.

CHAPTER I

INTRODUCTION

The Fisheries Conservation and Management Act of 1976 formally incor-porated economic analysis into the legal and institutional framework forfisheries management. The implementation of this broadened managementconcept can occur only gradually as economic information needs are definedand as systems for collection, storage, and dissemination are devised. Inthe meantime, it is important to exploit existing data sources, if by doingso, meaningful economic information and insights are provided to those in-dividuals and agencies responsible for implementing the Act.

This report is directed at this near-term goal by providing as indeptha picture of the Alaska seafood processing sector as available institutionaldata and industry sources have allowed. The objective underlying thisresearch effort has been to assess the economic structure of Alaska seafoodprocessing as it has evolved since statehood, in the context of changingregulatory, technological, and biological environments. This "in context"approach is dictated by the fact that economic structure is primarily deter-mined by the dynamic forces that constitute an industry's operating environ-ment. Accordingly, this report contains information on the basic industryconditions corresponding to each major processing industry--historicaloverview, the resource, harvesting and processing methods, and marketing.This information is intended to provide the background for interpretingpresent structural conditions and structural changes that have occurred sincestatehood. Many readers will need to use this background material foroccasional reference only. For those not knowledgeable about a particularfishery, a complete reading should prove to be beneficial.

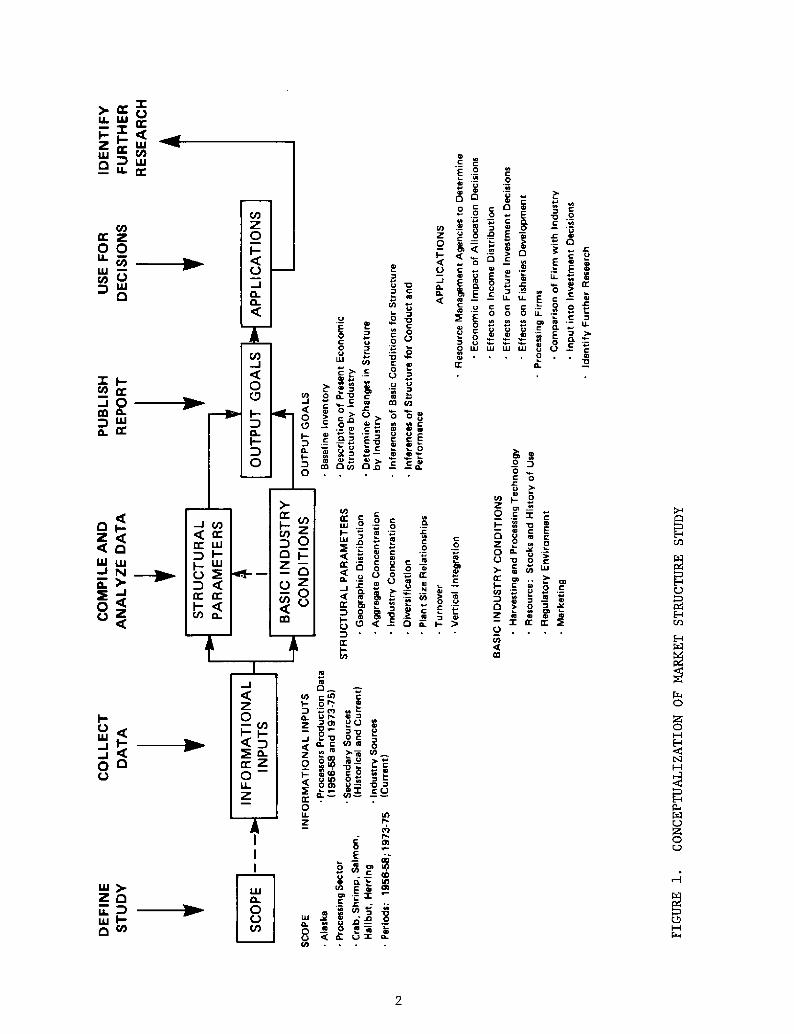

Another objective of this work has been to provide management agenciesand industry executives with a baseline inventory and description of theprimary components of the seafood processing sector. This should provideinformation for current decision making, and build the framework for annualor periodic updating for all or selective segments of the seafood processingsector. Included in the baseline inventory is the geographic distributionof plants and firms and, within regions, the number and size distribution ofplants and firms in total and by major species and process forms. Figure 1shows how this research was conceptualized and conducted.

Back round and Sco e of the Stud

In 1976, a research effort was initiated under funding by the AlaskaSea Grant Program to develop a comprehensive description of the economic

K Z I-CLD

LL

ZUJCI

C6ZI2CO

V IllO

0 crIO

IL C 0 Ug CI

5 0a.

Z CO

IQ

IX:

0 K0 g00c 0V

c2 c ZNS0

Zo~~O a o

Fy coK caC eCrr 'vVl

«oZ ~ ~ I ~K K

Ocaar

c0 co v 0v«m 'v

PC v

o cK'0 c vo O 00

R m

Kca

0 I-Z c CoUJ

N

p 0~ Z

C Cl

E 0cUr

0 CV Va Qa

K 2

0 a h crC

.5v I

I-

g C ~ 0O

8 o 0ca«. VC

IOrrOI

OlIOor

~ OI

UJZ 0g. Dm I-a~

C 0 VIUc +

0 a.'0V

0 c Eo'v E

c 9«

N +vco 0 crr

vIOCICIO Cor evs ls4l«cn UOI<0 0 ca. c err e

ae a

0 v~

cc crr

Epo

o.ID Ec Cvl Crr

UJ ~ IIIse g Cl0 a. Och

a

V V IUrI 0

v 0'v 0O

C ClW IOO ~ 0

crIcl g vcr ~ C

C V'0 c 0

O 0 F V «Lcrr0g CV

04l VIc cra.

E C 0c 0

K cv

0 a.

c C04

oB0v 0

W

I-v 0

O c

a. LEtoClC o

Ecl 0C0V0 UJ

K

c 0

c 0 v

0 EL vv g0 c

E Vc C C0 0V Olv v

vv UJ UJ

V yhlO0

C viiv 0

cCa

U v gv- a K0 Cc0

CW U0E

cO � c4l0

structure of the Alaska seafood processing industry. Two factors pri-marily justified the research, although they by no means exhaust thepossible benefits from increased knowledge. The first was the observationthat Alaska fisheries resource managers could benefit by an improved under-standing of the seafood processing sector. Processing firms make decisionswhich affect the rate and geographic pattern of utilization of stocks undermanagement. Conversely, processors are affected by the decisions of manage-ment agencies. The second justification was that, short of a descriptivestudy of the type reported herein, there were no ready vehicles for providingthe information needed by managers.

The scope of this study is limited in four ways:

First, the study focuses primarily on the processing sector of eachfishery; no indepth treatment of the harvesting and marketing levels wasattempted.

Second, this focus is on Alaska seafood processing to the exclusion ofprocessing activity in Washington, Oregon, California, British Columbia, andthe United States generally. Because these states and regions compete invarying degrees for final-consumption markets, an assessment of economicstructure for only one production region must be interpreted cautiously whenused as data for evaluations of competitive conditions in these markets. Incases where further processing occurs outside Alaska, as is often the case forfroze~ crab sections for example, the assessment of final market-competi.tiveconditi.ons based only on primary-production-area data would be even moretenuous. On the other hand, economic structure in Alaska will be indicativeof competitive conditions on the buying side of the market, that is, in theacquisition of raw fish for processing.

Third, the time periods compared in this study are: �! the three-year periods immediately prior to statehood, and �! the most recent three-year period for which complete data were available. Data were not sufficientto permit coverage of the intervening years.

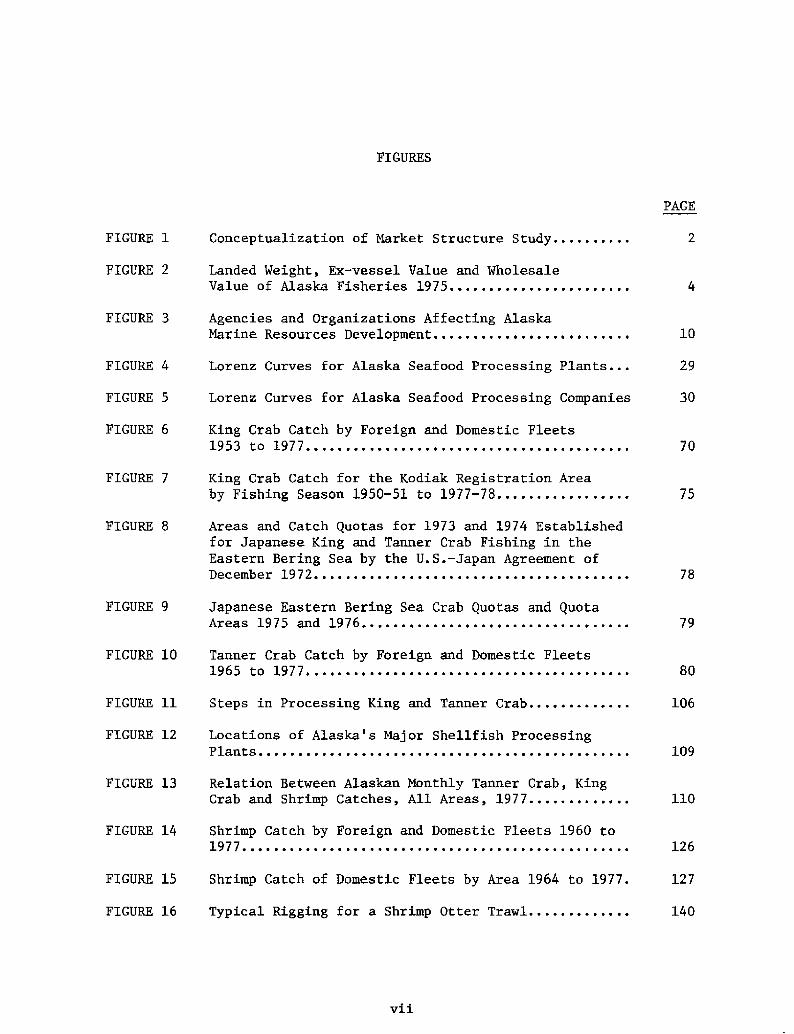

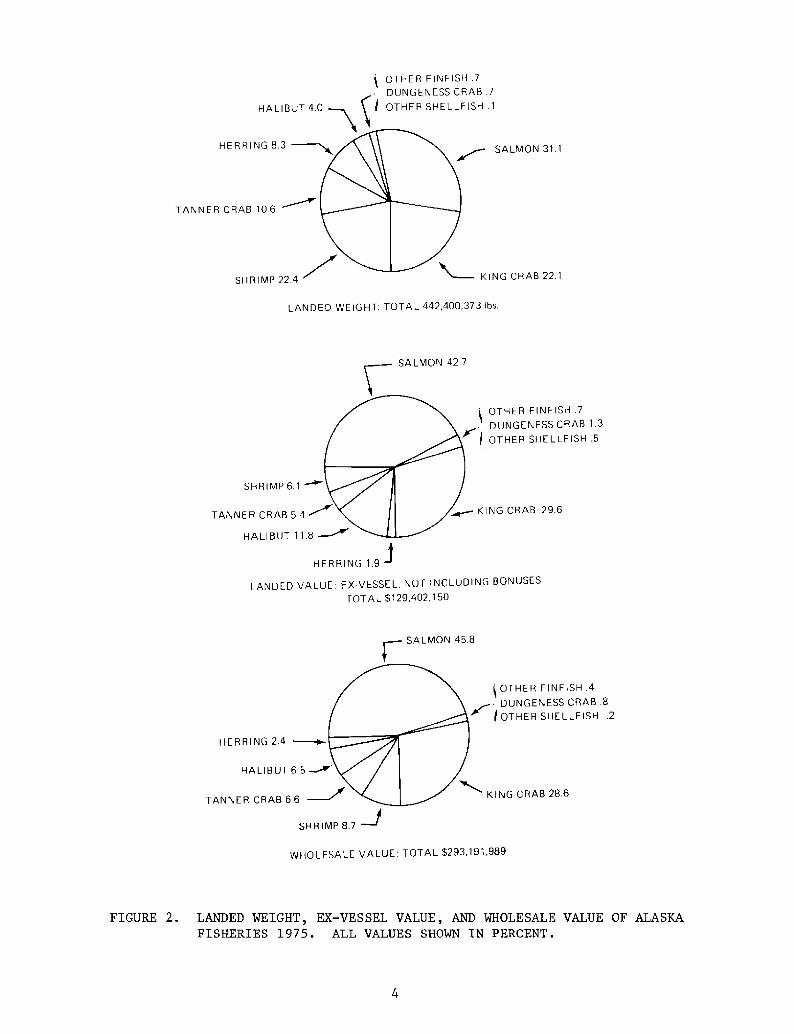

Fourth, the study describes the economic structure of the processingindustry for each of Alaska's major fisheries � salmon, halibut, herring, crab,and shrimp see Figure 2! � but it does not attempt coverage of the othermiscellaneous species.

Data Resources

Nost of the data for measuring structure were obtained through the co-operation of the Division of Commercial Fisheries of the Alaska Department ofFish and Game, and the Alaska Regional Office of the National Marine FisheriesService. These data cover the years 1956 to 1958 and 1973 to 1976. Inaddition, an industry survey was conducted during the spring and earlysummer of 1978 to acquire descriptive information not available frominstitutional sources. On a less formal individual basis, industry execu-tives were approached throughout the period of this study for factual and

OTHER FINFISH .7DUNGE ~ ESS CRABOTHER SHELLF SH 1HA L I 8 LIT 4.0

HERRING 8.3 SALMON 31.1

TANNER CRAB 10.6

KING CRAB 22,1SHRIMP 22 4

LANDED WEIGHT: TOTAL 442,400,373 Ihs.

SALMON 42 7 OTHER FINFISH .7DUNGENESS CRAB 1.3

II OTHER SHELLFISH .5

SHR I MP 6.1

TANNER CRAB 5 4 KING CRAB 29.6

HALIBUT 11.8

HERRING 1.9

LANDED VALUE: FX VESSEL, NOT INCLUDING BONUSESTOTAL 8129,402,150

SALMON 45.8 OTHER FINFISH.4DUNGENESS CRAB .8

! OTHER SHELLFISH .2

HERRING 2.4

HALIBUT 6 5 ~

KING CRAB 28.6TANNE R CRAB 6 6

SHRIMP 8.7 +WHOLESALE VALUE. TOTAL $293,191,989

FIGURE 2. LANDED WEIGHT, EX-VESSEL VALUE, AND WHOLESALE VALUE OF ALASKAFISHERIES 1975. ALL VALUES SHOWN IN PERCENT.

interpretive input. Although experience varied widely, most were verygenerous with their time and knowledge.

While Alaska is not unique in this regard, data on the economic di-mensions of its fisheries are sparse and of poor quality. This, of course,is a reflection of the historical orientation of fisheries management towardbiological research. The best fisheries data, therefore, are at the harvestinglevel, where they were used for stock assessment work. Available data pro-gressively decreases as the fish are processed, transported, and marketed.Since this is a study of the processing sector, it was not surprising to findthat the quality of the basic data are poor. Many judgements, some arbitrary,were required to make use of the raw production quantity! data that wereavailable. Value price! data were found to be so poor that they were notusable in any form in this study. A thorough description of data problemsand how they were handled is provided in Appendix I to Volume I.

The basic data used in this study was plant production data of the pro-cess form, product form, and species detail requested on the CommercialOperators Annual Report form. Plants not reporting production of any one ofthe five major species were excluded from the data base. Incomplete reporting,custom production, and changes in plant ownership each caused special problemsfor this study, as described in Appendix I.

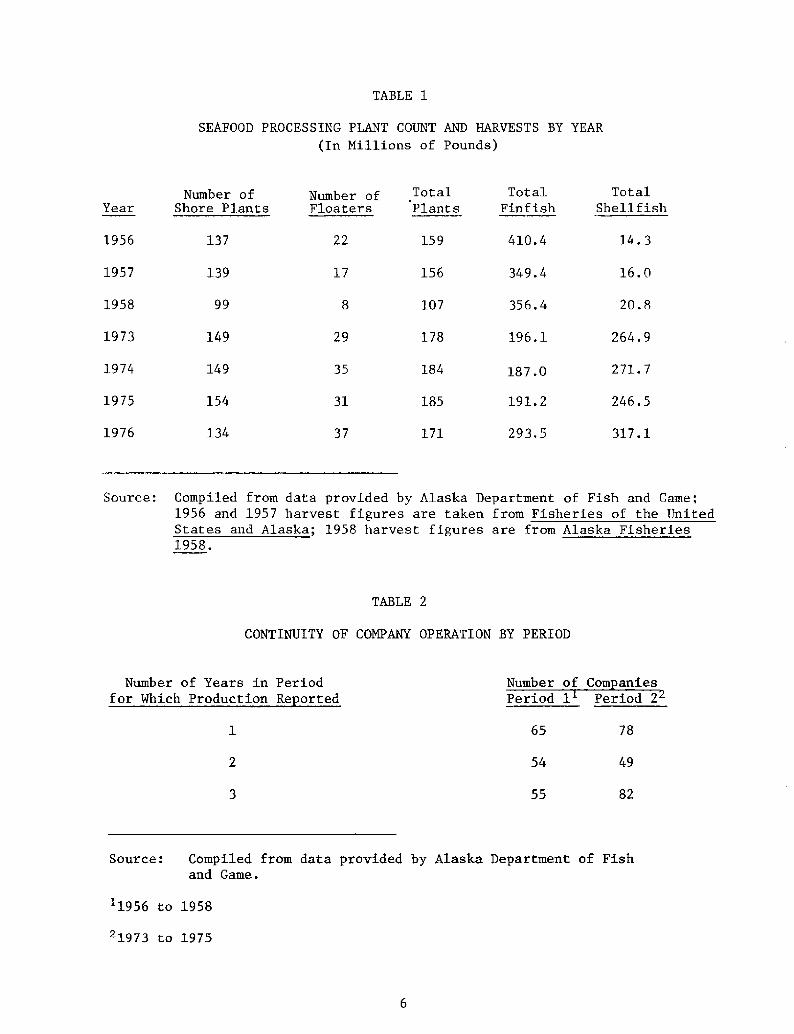

Annual fluctuations in the production of processed fishery products cor-respond to variations in landings. Some means of normalizing for thesevariations is required if economic structure is going to be accurately depicted.For example, in a poor salmon season, some plants might not operate at alleven though in the previous and subsequent seasons they may have been signifi-cant producers. In this case, the size distribution of production over plantsin a region would have been drastically different depending on the year ofmeasurement. Table 1 shows the number of plants reporting production, as wellas total harvest of finfish and shellfish, in each year covered by this study.Table 2 shows how many companies produced in all three years of each period,two of three years, and only one of three years. As can be seen, there isample room for distortion with the use of data for a single year. This isespecially true at the regional level which can be expected to have experiencedgreater variation than revealed by statewide totals. To reduce the distortingeffect of annual variations, three-year average production figures were usedto measure concentration.

Reference to "Period 1" in this study is to the 1956 to 1958 period, and"Period 2", 1973 to 1975. The latest year for which data were available whenthe study was begun was 1975. Data for 1976, "Period 3," were subsequentlyevaluated and are included in Appendix IV. The reader is cautioned that thesesingle-year measurements may not be as representative of the distribution ofproduction across plants and companies as the averages for Period 2, 1973 to1975.

The results of this study are presented in two volumes. Volume 1,Shellfish, includes king crab, tanner crab, and shrimp. Volume II, Finfish,

TABLE 1

SEAFOOD PROCESSING PLANT COUNT AND HARVESTS BY YEAR

In Millions of Pounds!

Number of Number of Total Total TotalYear Shore Plants Floaters Plants Finfish Shellfish

1956 14. 3137

1957 139 156 16. 0

20.81958 99 107

1973 149 178 196.1 264.9

1974 149 271. 718435

1975 154 31 246.5185

1976 134 37 171 317.1

Source: Compiled from data provided by Alaska Department of Fish and Game;1956 and 1957 harvest figures are taken from Fisheries of the UnitedStates and Alaska; 1958 harvest figures are from Alaska Fisheries1958.

Number of Years in Period

for Which Production Re orted.

65 78

54

8255

Source: Compiled from data provided by Alaska Department of Fishand Game.

~1956 to 1958

21973 to 1975

410.4

349.4

356. 4

187.0

191.2

293.5

TABLE 2

CONTINUITY OF COMPANY OPERATION BY PERIOD

covers halibut, herring, and salmon. Volume I is organized as follows:The remainder of this chapter will provide a brief review of other seafoodprocessing structure studies more detailed treatment of this material isprovided in Appendix II!, and a description of the regulatory environmentfacing the seafood processing sector. The review of other studies isintended to allow the reader to place the results of the present study inbroader perspective.

Chapter II describes the structure of the Alaska seafood processingsector and detailed shellfish processing industries. Chapters III, IV, andV present descriptive information on the basic industry conditions history,the resource, harvesting, and processing methods! of the crab processingindustry. Chapters VI through VIII provide the same categories of informationfor the shrimp processing industry. Chapter IX describes the marketing ofAlaska shellfish.

Appendix I provides detailed information on how data problems were treatedin the course of this research. Appendix II provides a conceptual overviewof economic organization structure! in general, a review of literature onseafood processing structure in the United States, and a glossary of terms.Appendi~ III presents the compiled results of the industry survey. AppendixIV includes statistical tables for Period 3 �976 only! comparable to thoseshown in the main body of this report for Period 1 �956 to 1958! and Period2 �973 to 1975!.

Structural Elements of the UPS. Seafood

Processin Industrv: A Literature Summar

Relatively few studies have been conducted on structural aspects of theU.S. seafood processing industries. Those that presently exist assessstructural components on national and regional bases Capalbo 1976! or byparticular fish and shellfish species Alvarez, Andrews, and Prochaska 1976;Jensen 1975; Kolhonen 1976; Orth et al. 1977! ~ The scope of the Capalbo studyis limited in that it does not evaluate structural elements in all regions andbecause such elements, when assessed, are aggregated by process form sector.The latter feature renders interpretation of structural parameters more diffi-cult as process form sectors rarely conform to the concept of an industry ormarket. The specific-species studies, while being free of the above drawbacks,are simply too limited in number or scope; a few species and/or regions arecovered by these works but not enough to characterize adequately the economicstructure of regional or national markets for these or similar fish products.

In general, the particular species studies are consistent with, and thustend to support, the study of Capalbo �976!. For this reason, a summary ofthe Capalbo study is used to describe structural elements of the U.S. pro-cessing industry. The other studies are discussed in Appendix II.

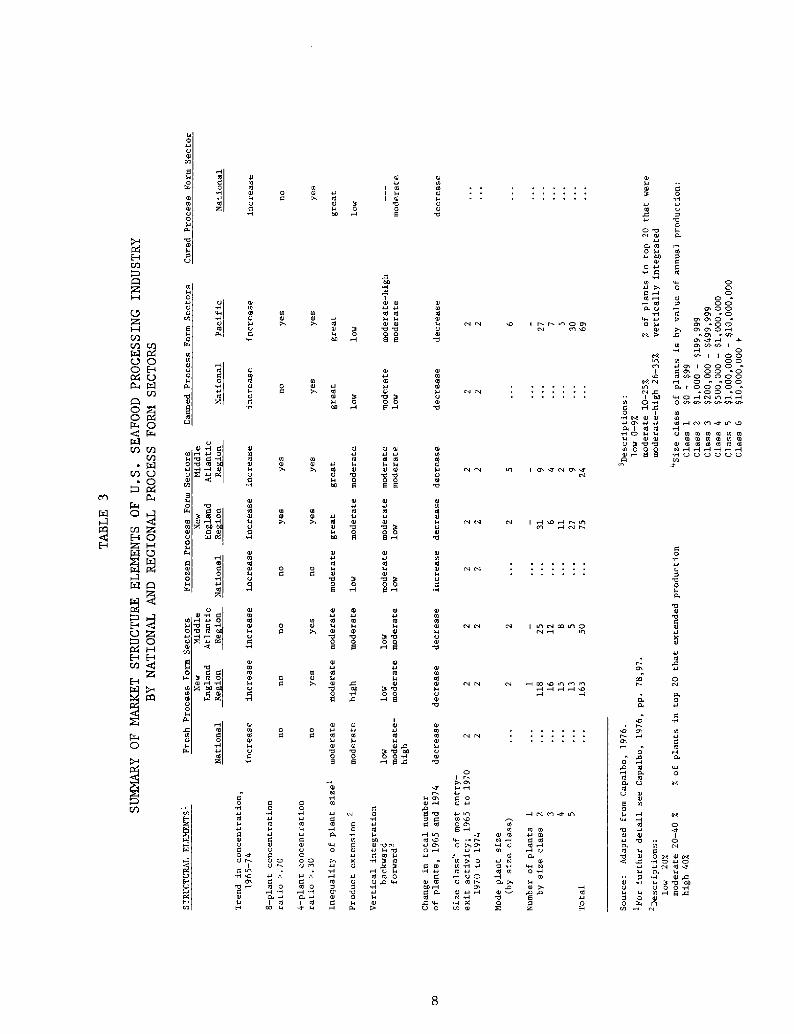

A summary of structural elements is presented in Table 3. Most ofthe structural elements assessed by Capalbo are included in the table; theonly regions for which there was coverage for such elements are the New

0IJ

Ql4J

0e

Ot/6IdQtI 00'0

C 0

Z

0 0

'0 04 0

M IDOlV 06

IJOl

0 ml64 OtJJc4 m0 ODOfC JJ

0 VW 0

Qt

'0 m

4OD

1ol mal of

0 06 6

Ct

0 0 ID0CP

+0 00 00 00 00 00 0

W 0

04 00/04 000mf46. c/7

r r crc 04

mc

IJC 0 00 00 00 00 0 IA

0/4/J OCDI 00

0 m JJIdQl66

64 CO'0 44 00

VJJOj

m ~ Ic6

alldQt0at

attdIU'0 Cl6

JJ6! Ql4al al0 0e 6

Ol0 CD

m m 4Ol

OlOlQI4 IJC

Of44Oj4 IU'006

r t/Ica I

C0

'00 4 0

al

m m UC

OIJJcd

m 0 6C 0 0 0

0 Olrc

Ol

V IC

Ol4JOl

m 0 6

Ol4Jtd4 Ql

60

0 ca 64

IJId~ I4Jtd0'06 0

m IU06

064 640 0IJ

IQl

'Cf 660 6 J-

0 ta0'Cf0

IUIJmm'0 06

ttl4 0IJ

0C M 0 cdCa

0I4JC 0IU 4J4 0cm

6 odCC oj

Oj00JJmCOt tdOD W0 CalW0

0JJal

QtC 0 0V

C 04JttlIJ

C m C 0 0U

C 0IJctlJJ

0 0 0 0V Cl

0JJcdODaf aj4/ 4

rJaj ajV JD

0

4J

W 0

4J

nj0'Cr4

I/IItf 00 06 wr0

WM ! 0I/I fm IJtd JJV 00 It! I0 JJWr6 tU

C

0 QlJJ

m 006

afm~ I Val4/Col at

0 JDm'00Z

IDcdal mVCLQt

4 af6

Cfro 0td4 0

QIO44 td

0 06

ACOl 0C cd

/ICm 00CO 4

0JJ0

a

H

C4O 00 6

O

O

0

CQ O~ 0

C4

0

A

O RD 0C4 HCa mj,'

R

jQ-l

O

4 0

6

0 06 mCJ

QI00 0LI

60

Ural olOl Zal

C alN 0

Ol4 '00 '0

0m Zm 0 064

4

I I

0

0 m CJ 0

4/I 64 CO Mt OCQ 4/I

I

ODrd OC0 IU tUCh 4J JJm al4 '44 0 mU e '00~6'C.

0

00

0,al ol0 Oal IUme rd0W'0Ot QI4 '0

'4J4 IJ0

mV U m0 QI0 tm ID46

ID ID ID Dl M MID ID ID ID I/Im oj m m Q! QjIJ IJ OOOO

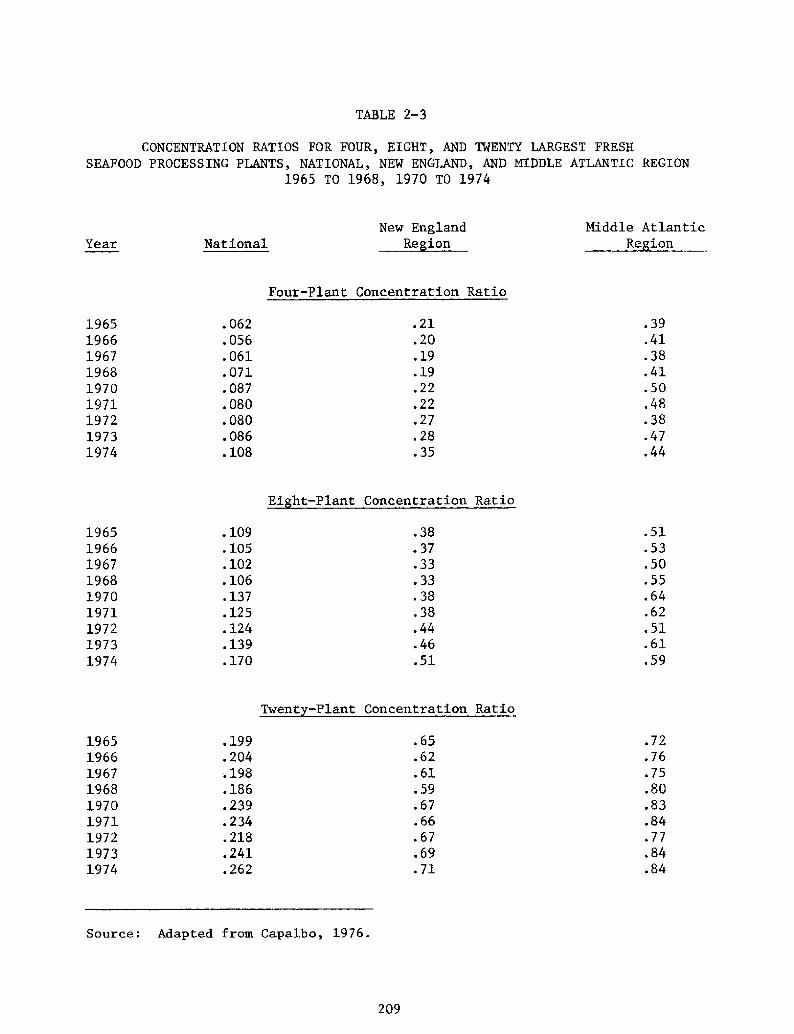

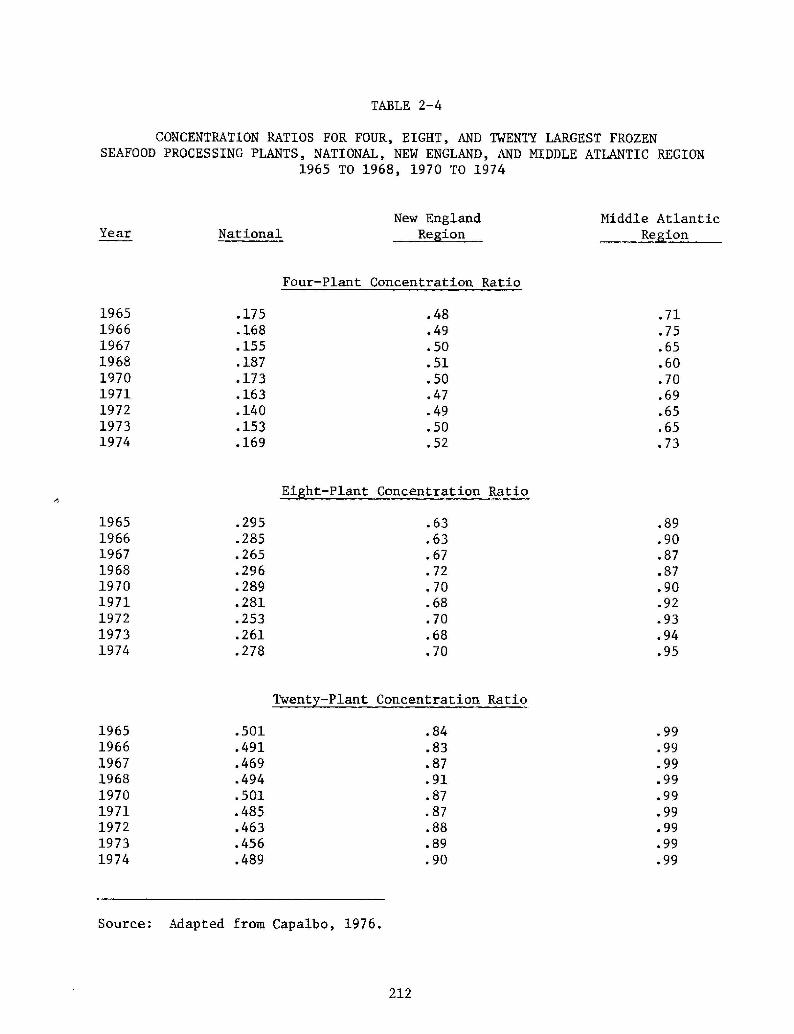

England and Middle Atlantic regions. It can be seen in the table that con-centration increased from 1965 to 1974, at both national and regional levels,in all four process form sectors. The frozen, canned, and cured process formsectors were generally more concentrated than the fresh sector and exhibitedgreater inequality in plant size. Firms in most sectors did not extendproduction diversify! to other process forms, either at the national orregional level. Backward vertical integration appeared to be relatively lowin the fresh sector, moderate in the frozen and cured sectors, and moderateto relatively high in the canned sector. Forward integration was generallylow to moderate in all sectors but the fresh sector at the national level.

All sectors experienced a decline in plant numbers from 1965 to 1974.Most entry and exit activity was accounted for by plants with annual salesin the $1,000 to $199,999 range. The mode plant size in the fresh sectorwas relatively small $1,000 to $199,999! while it was comparatively large $1,000,000 +! in the frozen and canned sectors.

It should be reiterated that the above description of structural elementsis general and not applicable to all species within a process form sector.The information presented is highly aggregated and should be interpretedwith care.

Alaska Fishin Industr : Re ulator Environment

Alaska's fishing industry is subject to direct and indirect regulationby many state and federal agencies and departments. In some cases this com-plex organizational structure leads to overlapping jurisdictions betweenfederal and state government, and contradictory and undefined governmentpolicies and objectives.

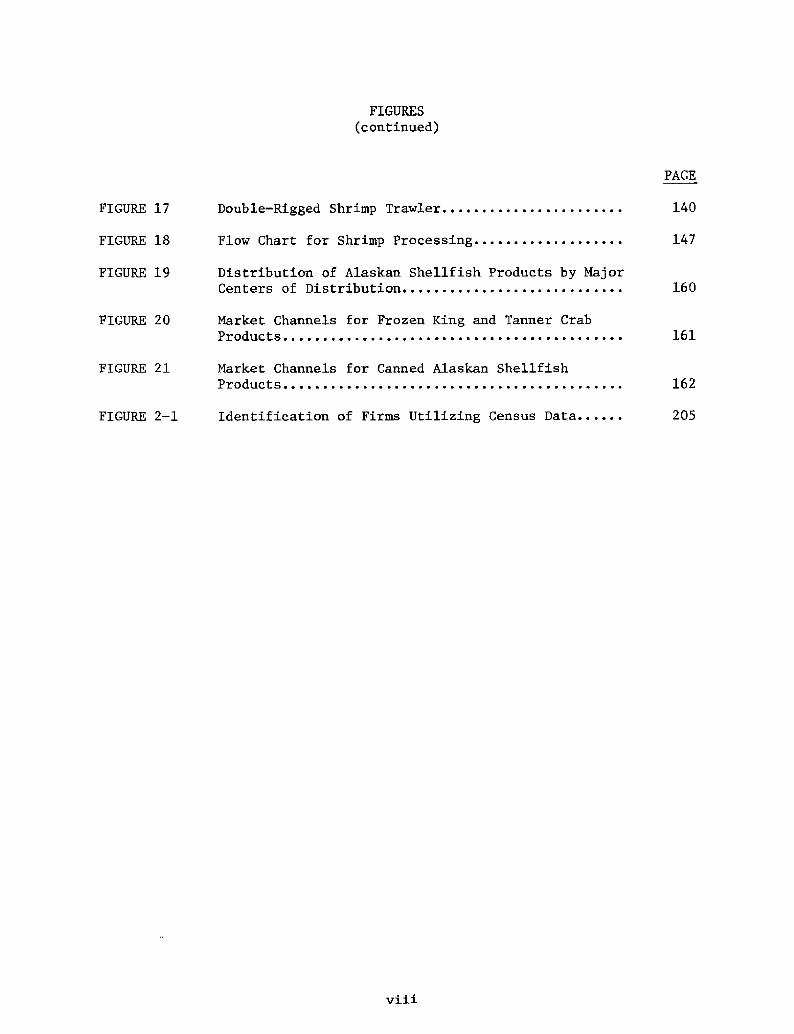

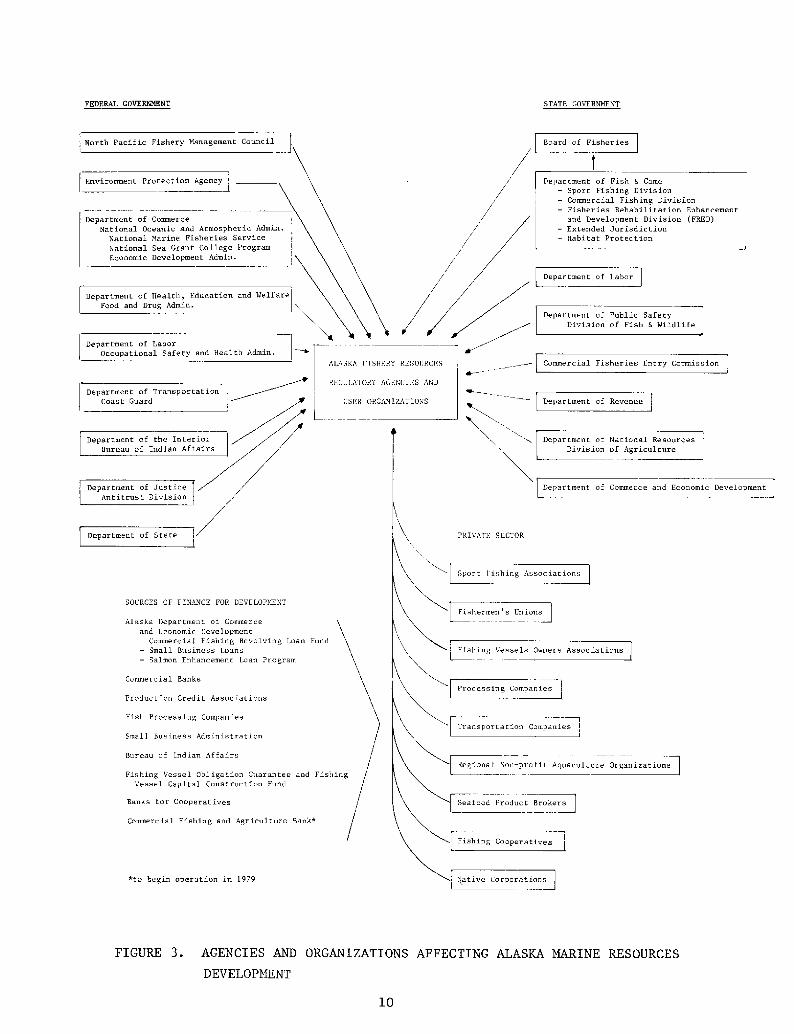

A review of the federal and state regulatory agencies that affect Alaskafisheries is included. This section will briefly discuss the role of eachand point out some of the constraints to the successful management of Alaskafisheries. This review is not intended to be comprehensive, but is intendedonly to illustrate the general responsibilities of each agency. A summaryof these agencies and user groups is shown in Figure 3.

Federal

North Pacific Fisher Mana ement Council NPFMC!. NPFMC is one of theeight regional management councils organized under the Fishery Conservationand Management Act of 1976. The NPFMC has authority over the fisheries of theArctic Ocean, Bering Sea and the Pacific Ocean from three to 200 miles sea-ward of Alaska.

Capalbo did not explicitly consider this structural aspect. The infor-mation for this element was derived primarily from other studies Alvarezet al. 1976; Jensen 1975!.

STATE OVERNHENTFEDERAL GOVERNNENT

Department of LaborOccupational Safety snd Health Admin.

Commercial Fisheries Entry CommissionALASKA I!SHFRY RE!OORCFS

Department of Transportation ces

onomic Development

SOL'RCES OF FINANCE FOR DEVELOPFIENT

Alaska Department. of Commerceand Economic Development

Commercial Fishing Revolving .oan FundSmall Business !.oansSalmon Enhancement Loan Program

Commercial Banks

Production Credit Associations

Fish Processing Companie!

Small Business Administ.ration

Bureau of Indian Affairs

Fishing Vessel Obligation Guarantee and FishiVessel Capital Construction Fund

Banks for Cooperatives

Commercia! Fishing and Agriculture Bank*

*to begin operation in 1979

FIGURE 3. AGENCIES AND ORGANIZATIONS AFFECTING ALASKA MARINE RESOURCES

DEVELOPMENT

10

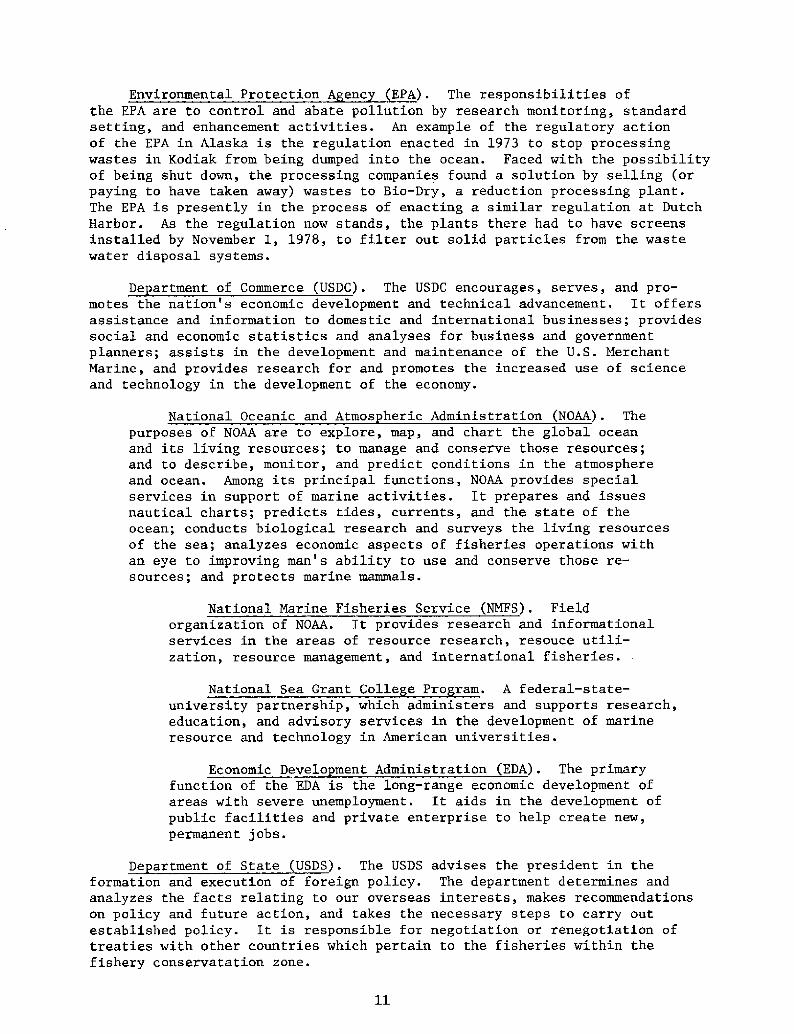

De artment of Commerce USDC!. The USDC encourages, serves, and pro-motes the nation's economic development and technical advancement. It offersassistance and information to domestic and international businesses; providessocial and economic statistics and analyses for business and governmentplanners; assists in the development and maintenance of the U.S. MerchantMarine, and provides research for and promotes the increased use of scienceand technology in the development of the economy.

National Oceanic and Atmos heric Administration NOAA!. Thepurposes of NOAA are to explore, map, and chart the global oceanand its living resources; to manage and conserve those resources;and to describe, monitor, and predict conditions in the atmosphereand ocean. Among its principal functions, NOAA provides specialservices in support of marine activities. It prepares and issuesnautical charts; predicts tides, currents, and the state of theocean; conducts biological research and surveys the living resourcesof the sea; analyzes economic aspects of fisheries operations withan eye to improving man's ability to use and conserve those re-sources; and protects marine mammals.

National Marine Fisheries Service NMFS!. Fieldorganization of NOAA. It provides research and informationalservices in the areas of resource research, resouce utili-zation, resource management, and international fisheries.

Colle e Pro ram. A federal-state-

which administers and supports research,services in the development of marinein American universities.

National Sea Grant

university partnership,education, and advisoryresource and technology

Economic Develo ment Administration EDA!. The primaryfunction of the EDA is the long-range economic development ofareas with severe unemployment. It aids in the development ofpublic facilities and private enterprise to help create new,permanent jobs.

De artment of State USDS!. The USDS advises the president in theformation and execution of foreign policy. The department determines andanalyzes the facts relating to our overseas interests, makes recommendationson policy and future action, and takes the necessary steps to carry outestablished policy. It is responsible for negotiation or renegotiation oftreaties with other countries which pertain to the fisheries within thefishery canservatation zone.

11

Environmental Protection A enc EPA!. The responsibilities ofthe EPA are to control and abate pollution by research monitoring, standardsetting, and enhancement activities. An example of the regulatory actionof the EPA in Alaska is the regulation enacted in 1973 to stop processingwastes in Kodiak from being dumped into the ocean. Faced with the possibilityof being shut down, the processing companies found a solution by selling orpaying to have taken away! wastes to Bio-Dry, a reduction processing plant.The EPA is presently in the process of enacting a similar regulation at DutchHarbor. As the regulation now stands, the plants there had to have screensinstalled by November 1, 1978, to filter out solid. particles from the wastewater disposal systems.

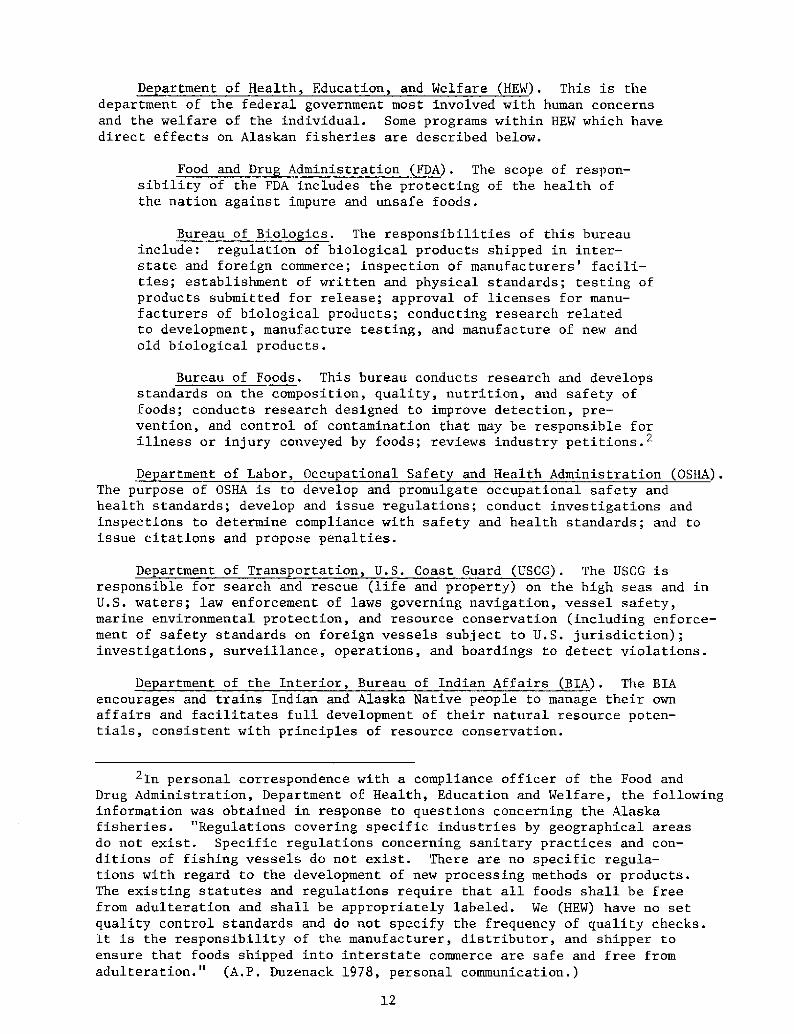

De artment of Health, Education, and Welfare HEW!. This is thedepartment of the federal government most involved with human concernsand the welfare of the individual. Some programs within HEW which havedirect effects on Alaskan fisheries are described below.

Food and Dru Administration FDA!. The scope of respon-sibility of the FDA includes the protecting of the health ofthe nation against impure and unsafe foods.

Bureau of Biolo ics. The responsibilities of this bureauinclude: regulation of biological products shipped in inter-state and foreign commerce; inspection of manufacturers' facili-ties; establishment of written and physical standards; testing ofproducts submitted for release; approval of licenses for manu-facturers of biological products; conducting research relatedto development, manufacture testing, and manufacture of new andold biological products.

Bureau of Foods. This bureau conducts research and developsstandards on the composition, quality, nutrition, and safety offoods; conducts research designed to improve detecti.on, pre-vention, and control of contamination that may be responsible forillness or injury conveyed by foods; reviews industry petitions.~

De artment of Labor, Occu ational Safet and Health Administration OSHA!.The purpose of OSHA is to develop and promulgate occupational safety andhealth standards; develop and issue regulations; conduct investigations andinspections to determine compliance with safety and health standards; and toissue citations and propose penalties.

Department of Transportation, U.S. Coast. Guard USCG!. The USCG isresponsible for search and rescue life and property! on the high seas and inU.S. waters; law enforcement of laws governing navigation, vessel safety,marine environmental protection, and resource conservation including enforce-ment of safety standards on foreign vessels subject. to U.S. jurisdiction!;investigations, surveillance, operations, and boardings to detect violations.

Department of the Interior, Bureau of Indian Affairs BIA!. The BIAencourages and trains Indian and Alaska Native people to manage their ownaffairs and facilitates full development of their natural resource poten-tials, consistent with principles of resource conservation.

In personal correspondence with a compliance officer of the Food andDrug Administration, Department of Health, Education and Welfare, the followinginformation was obtained in response to questions concerning the Alaskafisheries. "Regulations covering specific industries by geographical areasdo not exist. Specific regulations concerning sanitary practices and con-ditions of fishing vessels do not exist. There are no specific regula-tions with regard to the development of new processing methods or products.The existing statutes and regulations require that all foods shall be freefrom adulteration and shall be appropriately labeled. We HEW! have no setquality control standards and do not specify the frequency of quality checks.It is the responsibility of the manufacturer, distributor, and shipper toensure that foods shipped into interstate commerce are safe and free fromadulteration." A.PE Duzenack 1978, personal communication.!

Department of Justice, Antitrust Division. This organization is re-sponsible for enforcement of federal antitrust laws which involves investi-gation of possible violations, preparing and trying antitrust cases, pro-secuting appeals, etc. It also represents the U.S. in judicial proceedingsto review certain orders of the Interstate Commerce Commission, FederalMaritime Commission, etc.

State

Board of Fisheries. This board is responsible for the establishmentand changes to commercial or sport fishing regulations; holding publicmeetings to allow public participation and input on proposed regulationchanges.

De artment of Fish and Game. This department is responsible for themanagement of Alaska's fishery resources.

De artment of Labor. The workmen's compensation division administersthe fishermen's fund which is comprised of 60 percent of the revenuecollected from commercial fishing licenses. Medical and convalescentbenefits are drawn against the fund through claims filed by fishermen in-jured or sustaining an illness while fishing.

De artment of Public Safet , Division of Fish and Wildlife. Thedivision is responsible for enforcement of harvesting regulations.

Commercial Fisheries Entr Commission. This commission was established

in 1973 for the purpose of stabilizing the number of units of gear in thecommercial fisheries at levels consistent with good fisheries management andfair dollar returns to the fishermen. Permanent entry permits were issuedin 1975 on a point system measuring a fisherman's dependence on fishing; thepermits are transferable.

Crab, canned

Crab, other processes

2 percent of raw value

1 percent of raw value if shore-based processor

4 percent of raw value if floatingprocessor

Shrimp, all processes 1 percent of raw value if shore-based processor

4 percent of raw value if floatingprocessor.

13

De artment of Revenue, Taxation DRT!. DRT is responsible for collectingtax revenue from Alaska fisheries operations. Each processing plant mustcomplete an application for an Alaska fish processor license and pay anannual fee of $25. The state receives "fish tax" revenue from the shellfishindustry through processing companies. The schedule of rates at the timeof the writing of this report are:

Department of Revenue definitions are as follows: "Shore-based fishprocessor means cold storage and processing plants that are permanentlyattached to the land or have remained in the same location from January 1through December 31 of the previous calendar year. Cold storage and fishprocessing plants which are not permanently attached to the land or didnot remain in the same location the previous calendar year are classified as'floating fish processors.'" Floating processors which moor in the samelocation every year except for removal for drydock or repairs are apparentlyeligible for the shore-based rate unless they return to a different locationto process according to the following Alaska statutes. "Removal of vesselsf i . Removal of vessels from the state for drydock repairs does notrequire reclassification under the higher rate of taxation. State vs.Wakefield Fisheries, Inc., Sup. Ct. Op. No. 779 File Nos. 1397, 1398!, 495 p.2d 166 �972!. Removal of vessels for periodic repairs and maintenance shouldnot destroy the continuity of the period during which the vessels are deemedto be at fixed locations for one calendar year. State vs. Wakefield Fisheries,Inc., Sup. Ct. Op. No. 779 File Nos. 1397, 1398!, 495 p. 2d 166 �972!.Processor dis uglified from 'shore-based' status. Where, in addition to theyearly trips to Seattle for maintenance, the processors also sailed amongseveral Alaskan communities to conduct their processing operations, theywere disqualified from 'shore-based' status under this section. State vs.Reefer King Co., Sup. Ct. Op. No. 1344 File Nos. 2605, 2606, 2607!, 559 p.2d 56 �976!."3

Discussions with persons at the Department of Revenue show that thereis no clear definition of the amount of time a processor may remain in dry-dock outside the state each year and still retain shore-based status.

The state also obtains tax revenues from all people involved in anyaspect of the fishing industry in Alaska by state tax on personal income.This is true for year-round or part-year residents.

De artment of Natural Resources, Division of A riculture DNR, DA!.The DNR, DA is the state agency for regulatory control of sanitary conditionsof the seafood harvesting and processing industries.

De artment of Commerce and Economic Develo ment. This department isresponsible for government assistance for fisheries development in Alaska andadministers the fisheries revolving loan fund and. other loan programs forwhich fishermen are eligible. Nost ad hoc programs for fisheries developmentare administered by the department.

Alaska Statutes 543.75.060.

CHAPTER II

ECONOMIC STRUCTURE OF THE ALASKA SEAFOOD PROCESSING SECTORAND DETAILED SHELLFISH PROCESSING INDUSTRIES

Introduction

The collection and interpretation of economic information requires theuse of a systematic and consistent definitional framework. IndustrialOrganization, a branch of the discipline of Economics, provides a conceptualframework that is applicable to seafood processing and all other industriesin the private enterprise economy. The purpose of the framework is to pro-vide a means for sorting and categorizing economic informatin in a mannerwhich is useful for assessing the competitive environment in specific markets.

The economic entities with which economic-structure studies are concernedare plants, firms, industries, and markets. In some instances, the interrela-tionship between or among entities is straightforward; in other cases, they areobscured by vertical integration, ownership interties, diversification, jointventures, and custom-production arrangements. All of these complicatingfactors are common in the Alaska seafood processing sector. Further complicatingany description of economic structure is the difficulty of making precise andpractical delineations among geographic markets and product markets.

It will suffice here to define an industry as the basic competitive entitywhich consists of all sellers firms! who produce a close substitute productand sell to a common group of buyers Bain 1968!. The "close substitute pro-duct" constitutes the "relevant product market," and "the common group of buyers"constitutes the "relevant geographic market." An industry, therefore, is allfirms who compete in a particular geographic and product market. 'For example,the relevant product market might be canned king or tanner crab meat, and therelevant geographic market would be nationwide. The canned crab meat kingand tanner! industry would thus be defined as all firms who produce thesespecies of canned crab meat and sell into the nationwide market system.

As an alternative to a long digression in the body of this report,Appendix II has been developed to provide a conceptual background for theinterpretation of information presented in this report, as well as forassisting the reader who wishes to obtain a general understanding of economicorganization. Appendix II also provides an overview of the results of otherstudies of seafood market structure. This information is intended to allowthe reader to place the results of the present study in broader perspective.Finally, Appendix II contains a glossary of technical terms to assist readersas necessary, although an effort has been made to minimize the use of economicj argon.

The relevant market in which the firm competes as a seller is only oneof several competitive environments among processors in the acquisition offish from harvesters. The competitive environment among processors in theacquisition of fish constitutes the most si,gnificant source of public interestin seafood processing market structure. Where buyer concentration exists,whether due to geographic isolation of landing ports or other factors, itconsistently arouses strong opposition among harvesters, particularly justprior to or during the season when ex-vessel prices are determined.

The statistical information gathered for this study is evaluated at twolevels of industry detail. First, data are compiled for the Alaska seafoodprocessing sector as a whole without regard to differences which separate theindividual industries of the sector. The structural parameters for thislevel o detail will be discussed first,. Second, production data are organizedby indiv"'dual industries in order that the economic structure of theseentities can be determined. The later level of detail is the more theroeti-cally correct for assessing competitive conditions, particularly on the buyingside of the market. The individual industry analysis will follow thesectorial analysis.

Structural Parameters of the Alaska Seafood Processin Sector

This section will present measures of market structure which are appli-cable to the entire Alaska seafood processing sector as opposed to the in-dividual industries which together comprise the processing sector!. Theprimary characteristic of this information is that it lacks specificity withregard to species and process forms.

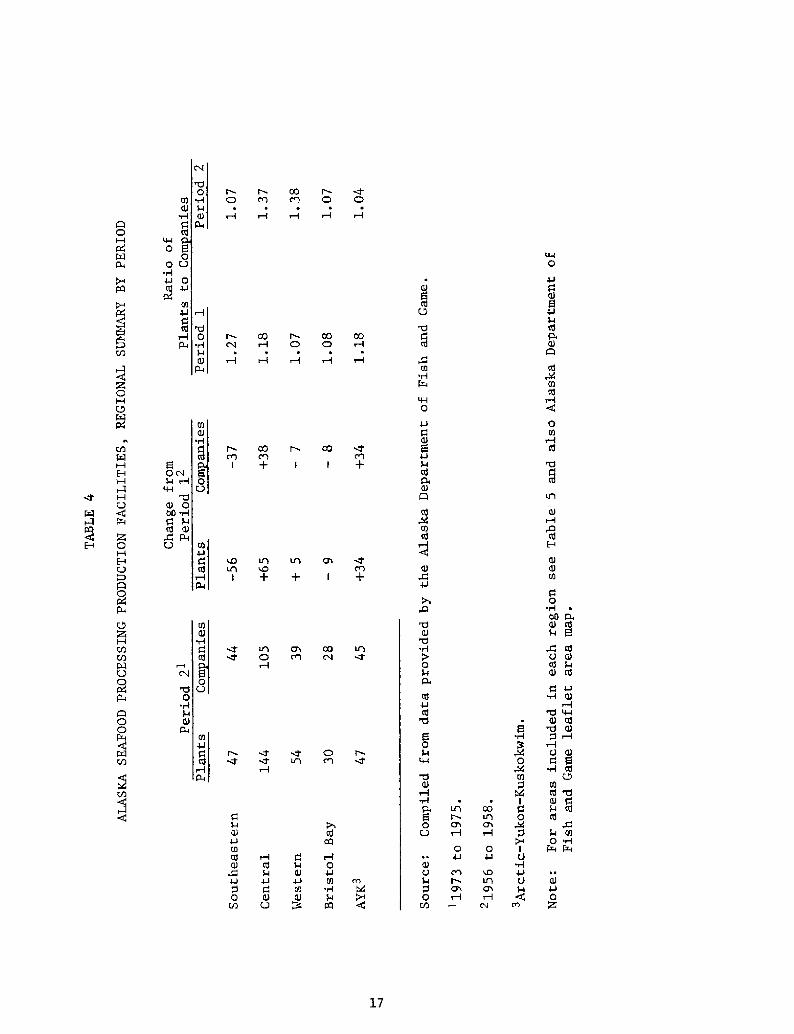

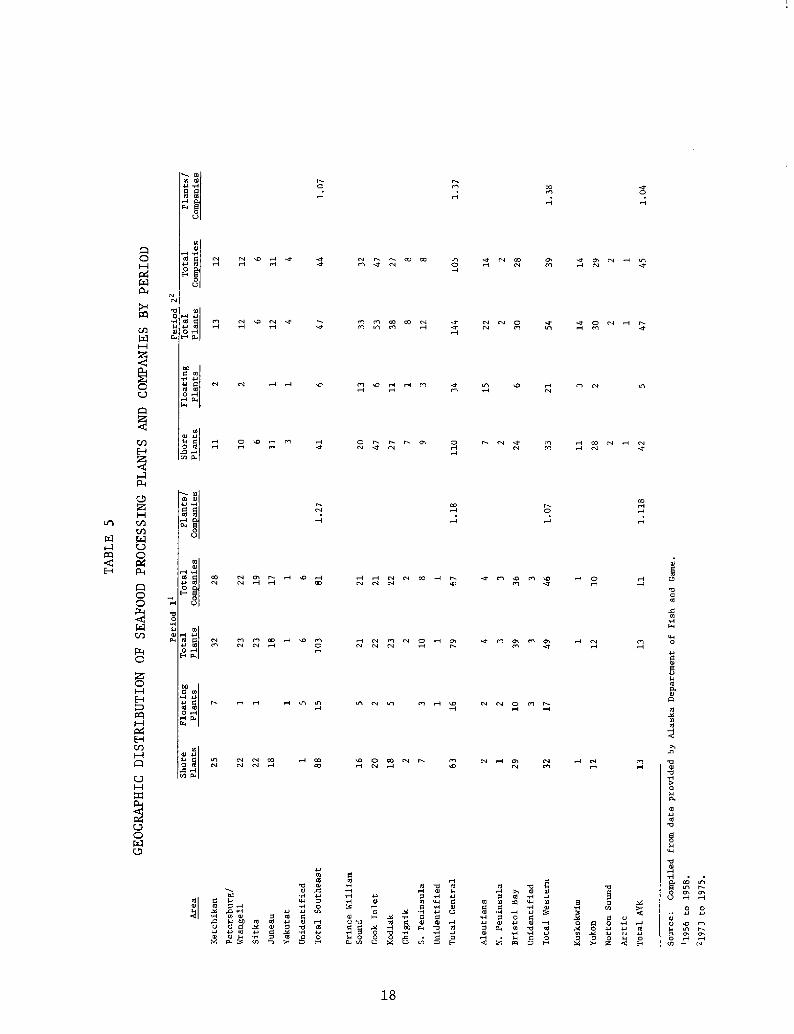

Geo ra hic Distribution of Production Facilities

Coastal Alaska has seafood processing establishments from the extremesoutheast to the Arctic. As shown in Tables 4 and 5, the present day dis-tribution of production facilities has changed significantly since the pre-statehood period. The number of production establishments in Southeast Alaskahas declined to less than half, falling from 103 to 47. The number of companiesdeclined from 81 to 44 and the prevalence of multiplant companies fell as well.Yakutat is the only community experiencing growth in both plants and companiesand all of the latter are single-plant entities. During Period 1 �956 to1958!, six establishments failed to report specific location.

Southcentral Alaska, in contrast, has experienced significant growth sincestatehood in both plants and companies, regionwide and in each community orlanding port!. The greatest growth occurred in Cook Inlet, which gained 31plants and 26 companies. Kodiak gained 15 plants and five companies. Theoccurrence of multiplant companies has increased significantly, especially inCook Inlet and Kodiak. Chignik experienced the greatest proportional growth,a fourfold increase in both the number of plants and companies'

COO O

Ql

cdW 0 e

00 ~

A OH

cd

cUA

'0

0 QI CO COO

O HC3 W 0

QI84J

cd

Qla

80 U

W'0

<U 0CO Wgcd cU

+ +

C 0 Cd IQQI cd

gcd

V QIcdQI cd

A O O

~80C3

cU

V 0cfl

~ ~Ql

0

17

~ 92

H O R O H O I-IO H o

p COO

CO M CO

I + I I +

Ch COC>

Ql cd9'-I

cdQl cd $-I 0

QI4J W W cd

C ro0 cU QIm o

8

A' 0A cd

CO0

0 IV

LA

0 WQI cd

QI

~ A cdC3

cUcd

0

M O

cll4J0 Oc

N N

44

0 W44N NN

4! 4J'40 tdClj I4

N CJ

440N

0 M4J

0W 0N N N CON ccjcO

M 444cICCJ

N CON CO c0N N

CA C4J MJ4 0

nj IC$clj

C0 0M4J0

MIJC0

Mj0 M4J0cll td0N C4

MIC MIJ4J g0 44IM

N N

C

A J- 4 Mj0 0 C4J 4J cdCl lll

'0

W44 4J

CIA C

MM4J0

NN N N

0Cj0'0 M

g J!0 0 OC II! CJ

'0cl IJW CM4J CJC0 Ill

Ill

cd 0IJ Cj

0 Clal

W 4J04J MM 04CM

jj

0A5

N W CCIN

cO Nl R c

CO N 6 N

CCj0IJM 44Cj

7I

0 0C!4Jcl'0 CI84W'0

0 CO CCI60 Cj Oc

0 0CjCJCOCI CI0Clj CV

Western Alaska experienced a net decline in companies from 46 to 39,but gained a net of five producing establishments. This resulted in anincrease in the number of multiplant companies. Within this vast region,the Aleutians gained 18 plants �3 of which are floaters! and ten companies.Bristol. Bay, on the other hand, lost nine plants and eight companies.

The Arctic-Yukon � Kuskokwin AYK! region has enjoyed significant growthsince statehood. This region has gained 34 plants and 34 companies, causingmultiplant companies to decrease slightly in relative importance. Both theYukon and Kuskokwim districts are characterized by small pLants and companies.

As might be expected, the distribution of production facilities hasfollowed the geographic distribution of harvestable surpluses in importantstocks see Table 6!. In particular, Southeastern Alaska with the exceptionof Yakutat! and Bristol Bay have lost production facilities, presumably dueto the decline in salmon stocks. Central Alaska and the Aleutians have grownrapidly as a result of exploitation of previously underutili,zed or unutilizedshellfish stocks.

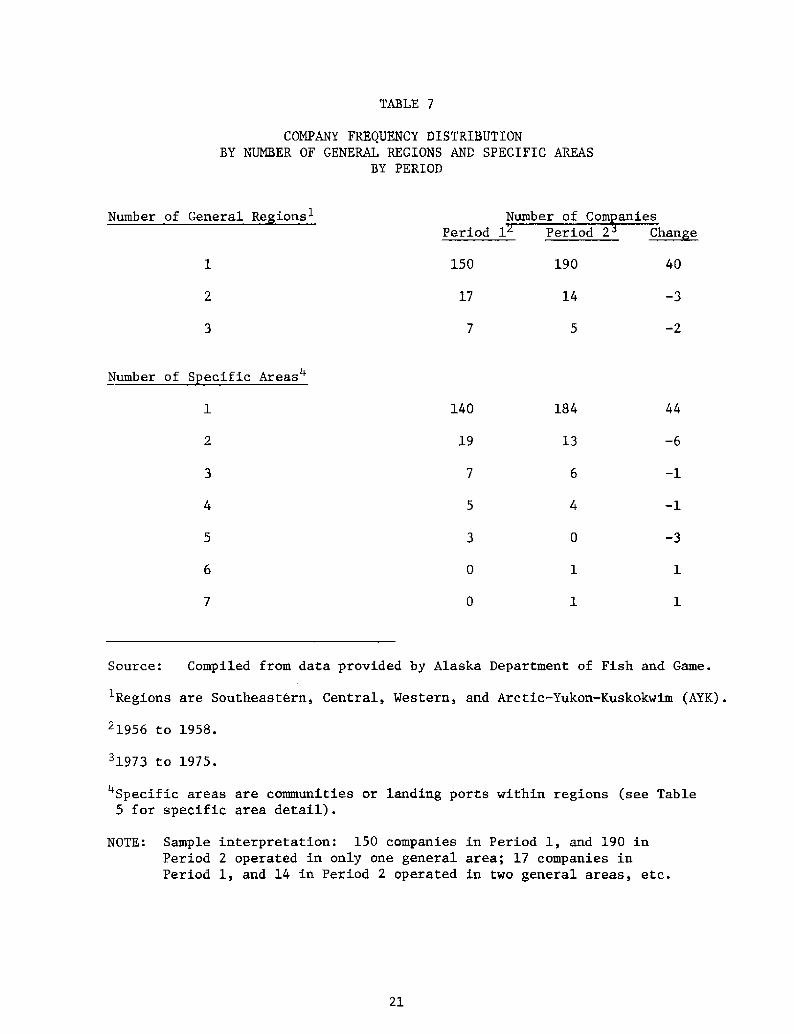

Another relevant aspect of geographic distribution refers to the degreeto which companies specialize geographically and whether this tendency ischanging. As shown in Table 7, geographic specialization is increasing, bothin terms of number of companies producing in multiple regions general areas!and multiple communities specific areas!. The shift in effort to, and thelocation of surplus shellfish stocks in Central and Western Alaska may explainthe increased geographic specializati.on, as these regions are larger andmore remote.

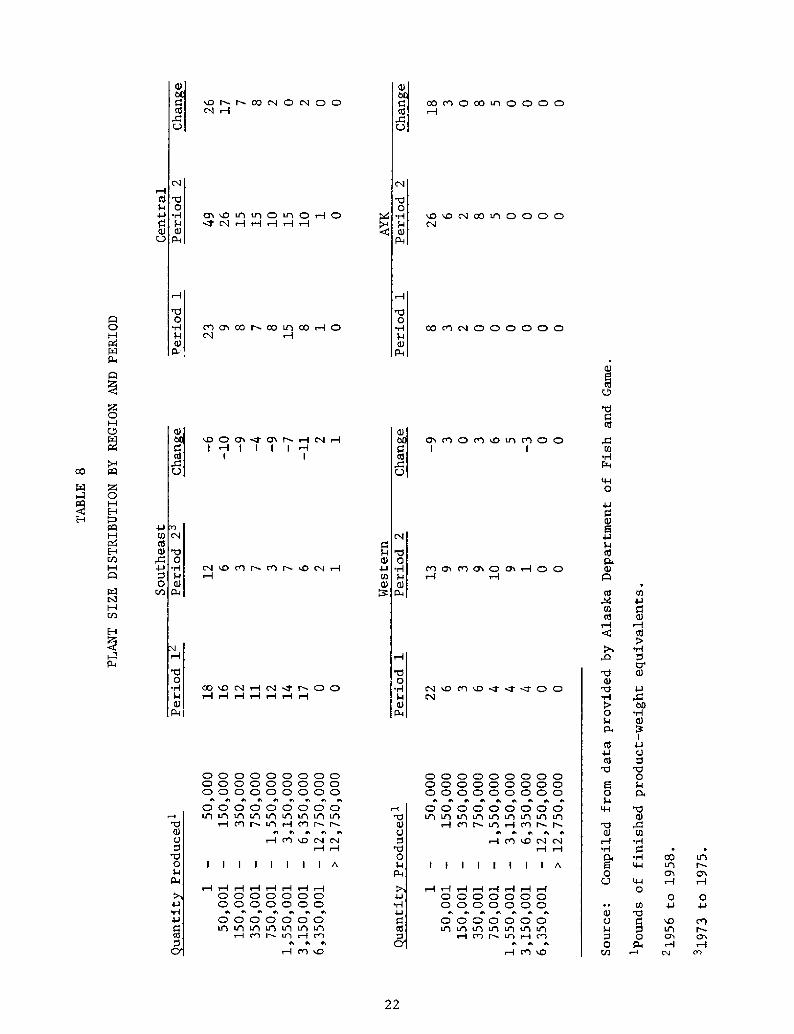

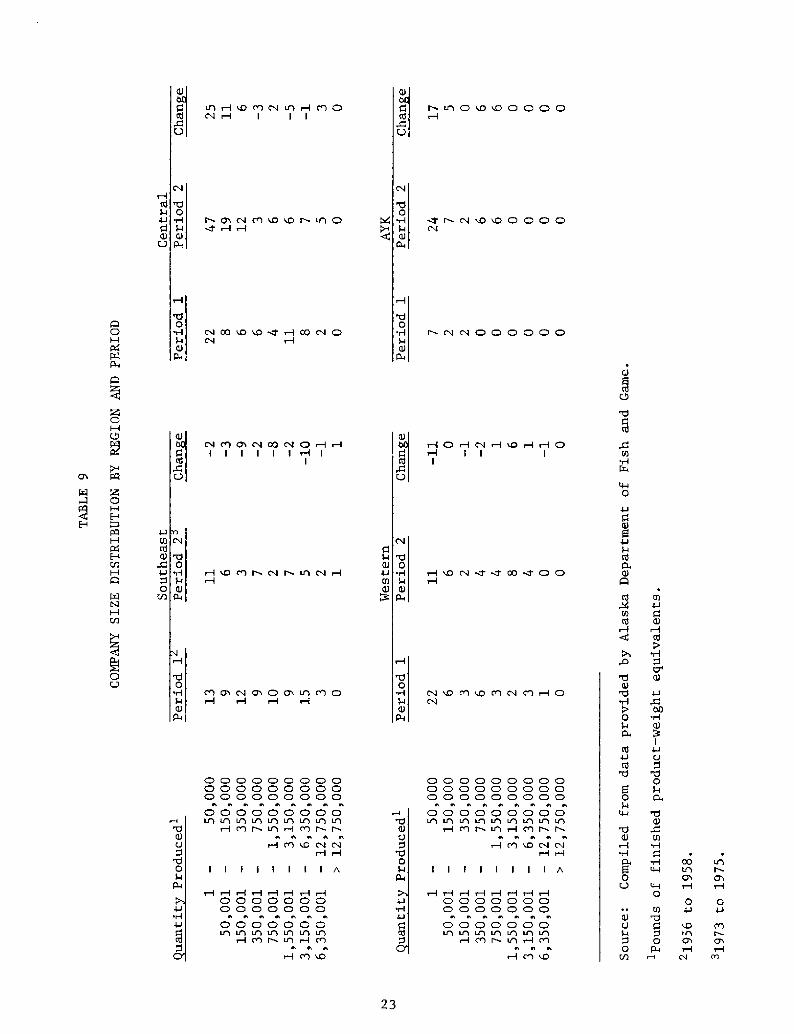

Tables 8 and 9 show the size distribution of plants and companies re-spectively by region and by period. Surprisingly, Southeast Alaska was theonly region gaining plants in the largest size categories though it lostplants overall. Small plants and companies gained in Central and AYK anddeclined in number in Western Alaska.

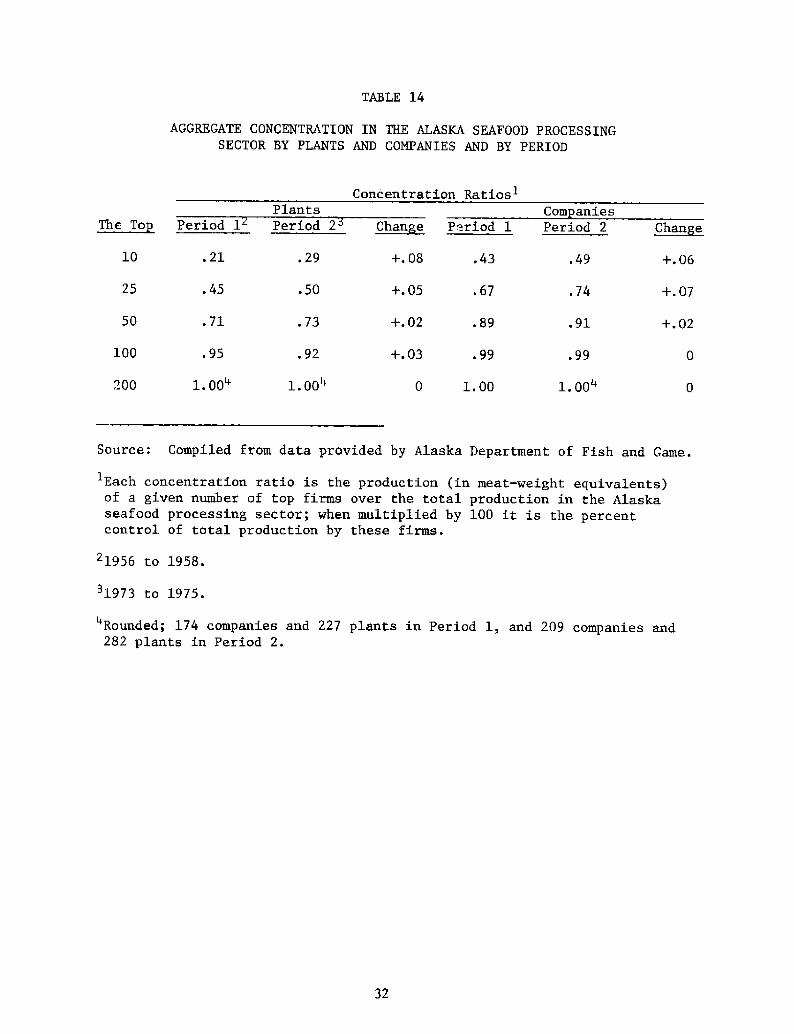

A re ate Concentration

Aggregate concentration refers to the size distribution of all seafoodproduction among companies or plants!, without regard to species or processform categories. The economic implications of high aggregate concentrationare uncertain. First, high aggregate concentration in the economy or majorsectors thereof does not necessarily imply high concentration in individualindustries for example, canned shrimp, crab sections, etc.!. Second, highaggregate concentration tends to be associated with firms that are large inrelation to the individual markets in which they operate; that is it. tends tobe associated with dominant firms Gort 1962!. The latter, in turn, areoften associated with "price-leadership" pricing behavior by firms in oligo-polistically structured industries. Third, high aggregate concentration ispositively associated with large firm size and diversification, both of whichcan be sources of market power Gort 1962; Orth 1970; Scherer 1970!. Fourth,there is evidence suggesting that large firms tend to be more progressivethan smaller firms, making them more dynamic competitors Scherer 1970!.

19

~ l~ 0

~ l

lP!

Oa

CV

a aCO0

0 CVtl

0 00 00 0

~ I tl'LDCO OCQ 0a a

OH%Ch GOO COB

aCh W O

O'4 Lh 0

a a a&Wr

a ~0 0

FlCO Ch

a a

0

O Ch

0a a

aO <

OOCO0 0 CV H0 0 CO Ha a a aC4 h CO

0a a

0 Ch

GOCh W

Cha ~

< OCQ Yl

a a

Ch NCh

~ I a acV+0

a a a

GOr I cv

~ ~ ~~ ~ ~

GI

Ql

QI lI

CO0 nJ

~ l a t tlOWWCQ

cv 0a a a a

Vlr4WW

l1l CQa a

th 0l1l CV

a aCV COM GO

O~ a

cV GV PCO lA

Ch O~ 92 a

0 OH

GON

tl t

~ aGO

GOCV

O < Cha t ~

P 0 ACh O

CQ~ 92 a tl

QI

0

04J

nJCO

v-I W ~ Wa a tl

~ l aCh CO

fl a0 GQCO WO Ch

a a

O GOCV

OGO

a tlCh M CO

GO

CO

20

GO H Ch ClICOORNA

Ch ad'a ~ a tl a

CO

R O rl N Ot t a tl a

CV WWWC4O Ch R O

M MCO WW U1

QI nnnr ~r I

W 0 c5A 0

QJ 0

0g~ +

d QIVJ

�

0 ~0 W Ct

QI QI

0 QI QI

A

QItd

'CIVJ IdQI

0~ Rbd Gd 0QI

M

TABLE 7

COMPANY FREQUENCY DISTRIBUTIONBY NUMBER OF GENERAL REGIONS AND SPECIFIC AREAS

BY PERIOD

Number of General Re ions

Period an e

150 190 40

Number of S ecific Areas"

140 184 44

19

4Specific areas are communities or landing ports within regions see Table5 for specific area detail!.

NOTE: Sample interpretation: 150 companies in Period 1, and 190 inPeriod 2 operated in only one general area; 17 companies inPeriod 1, and 14 in Period 2 operated in two general areas, etc.

21

Source: Compiled from data provided by Alaska Department of Fish and Game.

Regions are Southeastern, Central, Western, and Arctic-Yukon-Kuskokwim AYK!.

21956 to 1958.

31973 to 1975.

cd

Cj

A0 H 0 H

'cj0

Ch

dj

och+OO~ -I

000000000000 0 0 0

~ I tl tI t tI00000

lA~ 92

0 00 00 00 0

~ I tlCII

0 00 00 0a0 0

~ I ~

0 0 0000000

0 00 00 0

~ I tI0 0

~ I

0000OOOOOOOO

~ I ~ tlOOOO 000

~ I tI tl

00~ I0

000000~ I tI tl000

LC!p1

0 00 0t S

0 00 0

0 0cr!

A

0 00 0t0 0

~ I tlLQ

0 0 00 00 0

~ tI0 0

0 000 0

tI ~

22

CO

0

9-IH cc

djcrjMA

0ch

Nr r COAOAOQ

00~ e Ch < W R 0 e 0 M 0

dj

0co wco Lrjco IHO

4dj

MQChWChr HCVHI I I I

I I

0VII % A w A w % II

Gj

'00

CO % & H CII N W 0 0

djCk I

I I I I I I I I A

co ctj 0 co v! 0 0 0 0

00~ tI NIIOCII COulOOOO

CVdj

CO ctj hl 0 0 0 0 0 0

O Y! cO A M 0 0I I

W&MNNNOO

I I I I I I I I A

dj8

djC-I

cdAcd

0 C4cd

cd0

80

<U

60U

t ~cdcj

0

dj

V'dj

COdj

ICj

00

'0dj

COW

ChI I

00 0

cC 4J

0 chCct

P!

CV&HWOI I I

cd4J

dI

cd

0 dl'cd

0 <LIC4A O H 0

0

COCdcddl

«OH

0crt

Q 00 00 0

~ I a0 0

H

000000ODD

0 00 00 0A R0 0

A e

0 00 00 0A0 0

A a

r I &

OOOO00000000

~ ~OOOO

00000DOOOO00000

~ I rh tl ~OQOQO

A A R A AY! % CV

000

CO EC!

000000 A000

00 A0

r I0 00 0

0 0

a ~

W r40 0 0DOOA ~ODD

0 00 0A0 0

lAcCI

0

0 00 00 0

A0 0

0 0

23

ncd0~ 6 N Ch CV & cO % W tel O

dl

«0 cO 4 < + CO hl 0

HHCh&OOAOHHI I I I I W I

I

0CV W c«l CV

dlC4

0O Ch R W O

dl

I I I I I I I I A

P WDcOZOOQOc-I

0Cf 6'44>0000

C4

c ACVOOQQQQ

H 0 H CV H cO H R 0I I I

I

HC>cVWN«ONOD

0rl &KWCI WCVPl&0

dl

I I I I I I I A

8 cdC4dlA

A 'cddl

v 0 Occd

cd

8 0 0U

cd

v dIbd

5 I

V 0'cddI

0

The applicability of these generalizations to the Alaska seafood pro-cessing sector is not necessarily straight-forward. For this reason, andbecause a thorough analysis of these issues is beyond the scope of thisstudy, this report will be devoted to a presentation of the factualmaterial gathered. The latter is of interest because it describes theorganization of plants and companies within the sector and how organi-zation has changed since statehood.

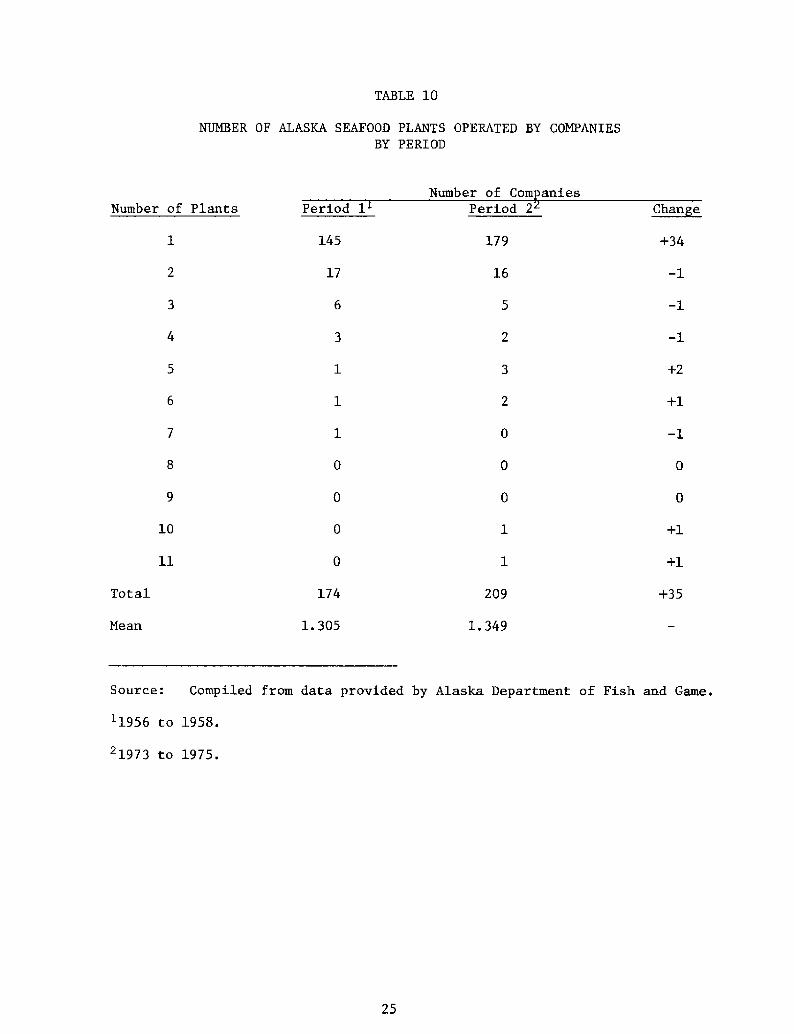

During Period 1 �956 to 1958! there were 227 plants and 174 companiesreporting some production. Of these companies, 145 operated only one plant,17 companies operated two plants, six companies had three plants, three hadfour plants, and one each had five, six, and seven plants. As shown inTable 10, the number of one � plant companies in Period 2 was 179. Period 2is otherwise quite comparable to Period 1 except that there are two companieshaving 10 and 11 plants respectively. The mean number of plants in Period1 was 1.305 and in Period 2 it was 1.349.

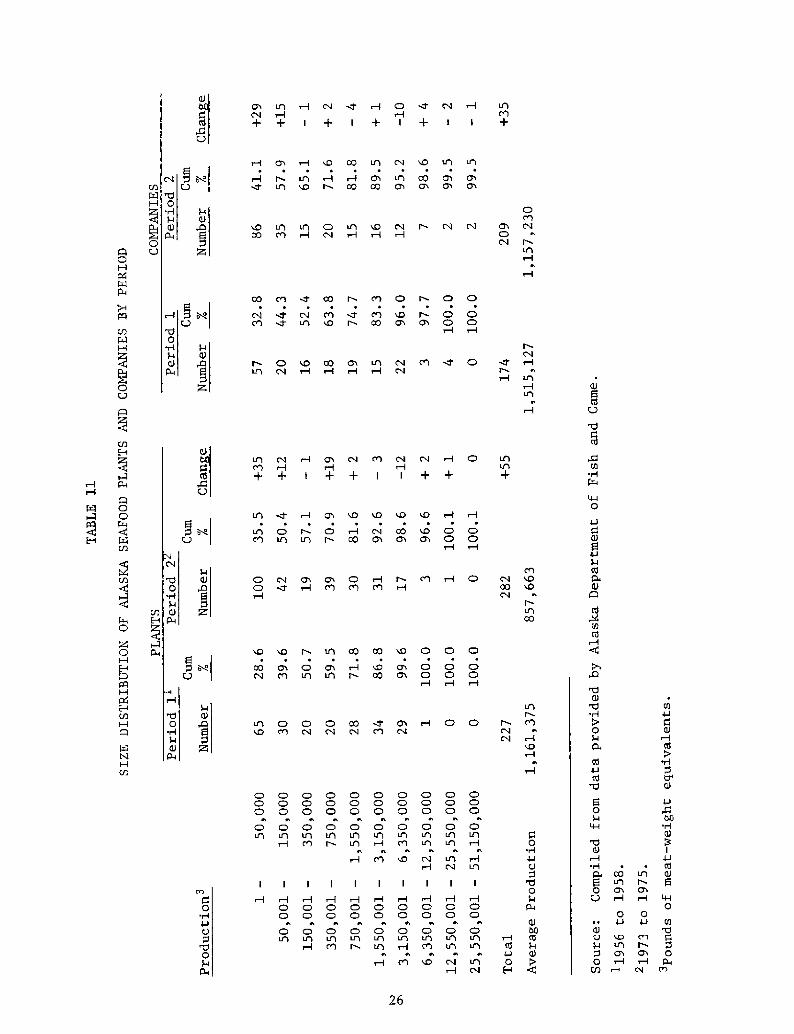

Table ll shows the size distribution of plants and companies for Period 1and Period 2. In Period 1, 28.6 percent of plants produced less than 50,000pounds of product meat weight equivalents! and. 50.7 percent produced lessthan 350,000 pounds. In period 2, 35.5 percent and 57.1 percent of plantsproduced less than 50,000 and 350,000 pounds respectively. In Period 1,28.2 percent of plants produced more than 1.5 million pounds and only 18.4percent of plants produced more than this amount in Period 2. The middlerange, from 350,000 pounds to 1.5 million pounds held 21.1 percent of plantsin Period 1 and 24.5 percent in Period 2. The average production of plantswas approximately 1 ~ 2 million pounds in Period 1 and 0.9 million pounds inPeriod 2.

The distribution of companies by production is similar to that for plants.This is not surprising given that 83 percent of companies in Period 1 and 86percent in Period 2 were single-plant companies. In Period 1, 32.8 percentof companies produced less than 50,000 pounds and 52.4 percent produced lessthan 350,000 pounds. In Period 2, these were 41.1 percent and 65.1 percentrespectively. There were 25.3 percent of all companies producing more than1.5 million pounds in Period 1 and 18.2 percent in Period 2. In Period 1,21.3 percent of the companies produced between 350,000 pounds and 1.5 millionpounds and 16.7 percent fell in this range in Period 2. The average pro-duction of companies was approximately 1.5 and 1.2 million pounds in Periods1 and 2, respectively.

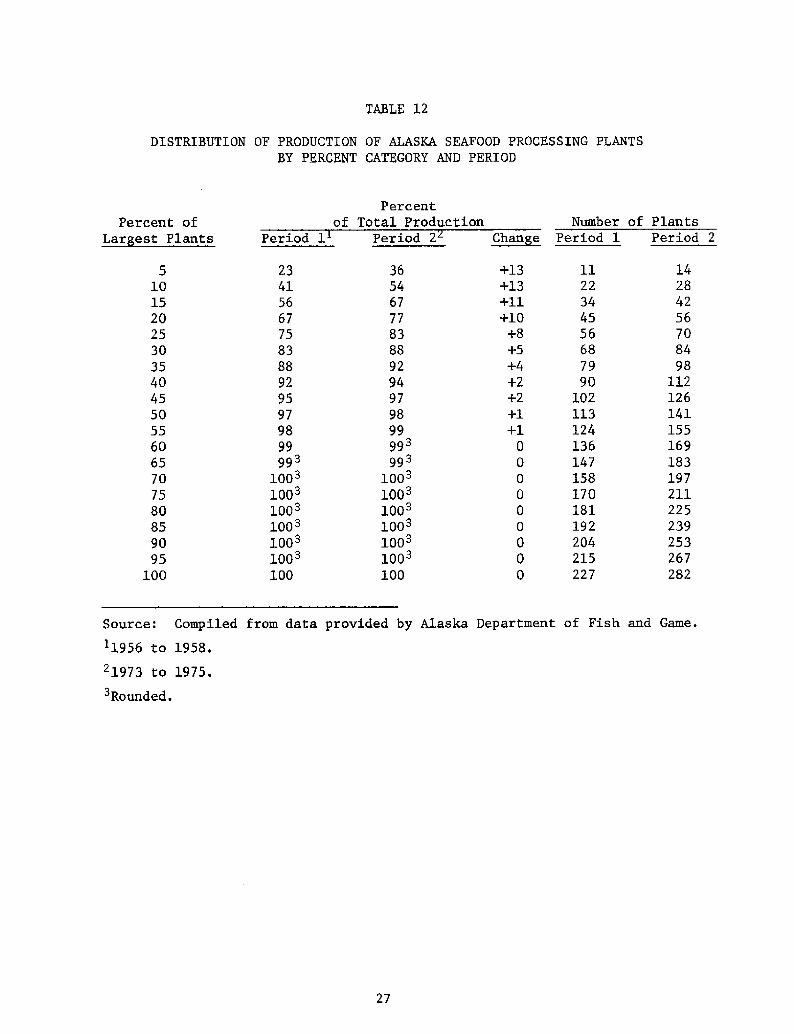

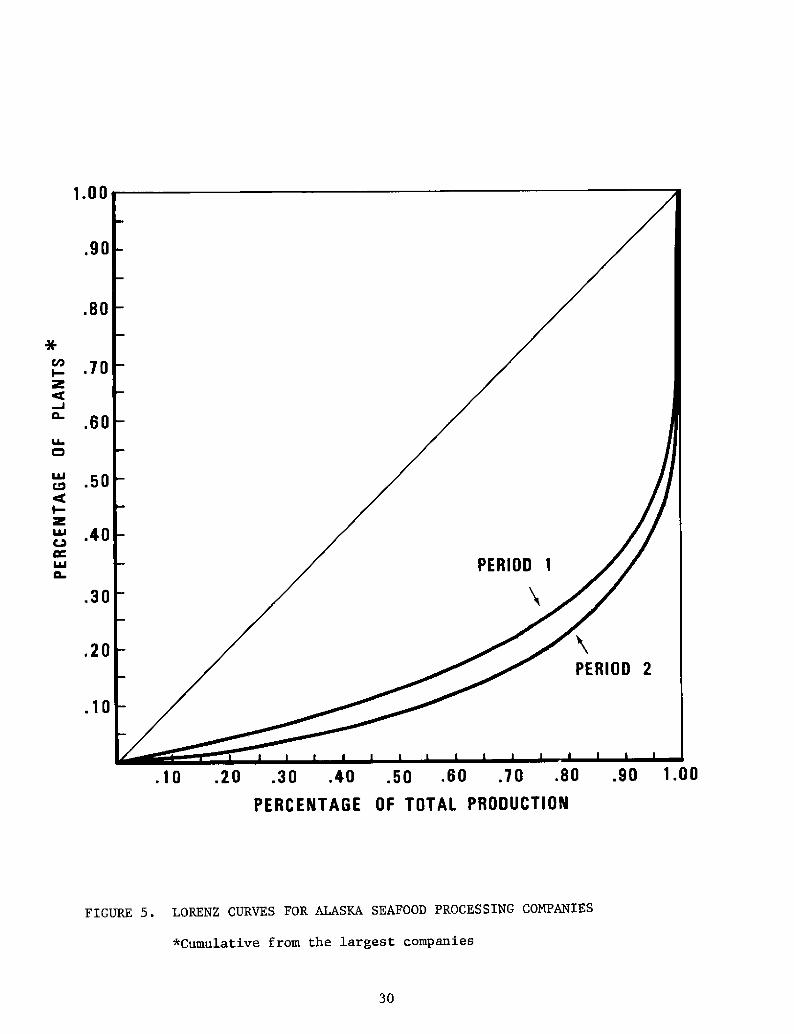

In addition to the number and percent of plants and companies in eachsize category, it is useful to know the cumulative control over productionaccounted for by plants and companies of different sizes. That is, inaddition to knowing the number of companies in a size category, one shouldalso know the percent of total production controlled by those companies.This information is obtained from Tables 12 and 13 and Figures 4 and 5.

Roughly one-half of all plants produced 97 percent of total productionin Period 1 and 98 percent in Period 2. In Period 1, 113 of 227 plantsproduced only three percent of total output, and in Period 2 this fell totwo percent for 141 of 282 plants. The level of aggregate company concentration

24

TABLE 10

NUMBER OF ALASKA SEAFOOD PLANTS OPERATED BY COMPANIES

BY PERIOD

Number of Com aniesPeriod 1 Period 2Number of Plants

145 179

17 16

+1

10 +1

174Total 209 +35

l. 305 l. 349Mean

Source: Compiled from data provided by Alaska Department of Fish and Game.

il956 to 1958.

~1973 to 1975 '

QQ ChCh Ch

QO

QO QO

00

0 H H0 0 0O 0 O

~ h

0

CD0

Vl

O 0 00 H hl COP QO Ol Ch

QO

0 0

0 00 0

O

OCh O

QO & CD ChlA A

QQ QO

8 O'8

0 0 0 00 0 0 00 0 0 0

h0 0 0 0

e1 LCI ECI

IVI

0 0 00 0 00 0 0

0 0 0

LCl

H

0 0 00 0 00 0 0

a0 0 0

80

0

'0 0m 0

'Cl0

H0 0 0 00 0 0 0

~ I 4 a a0 0 0 0

LCl~ A a A

F1 W CV

0 0 00 0 0

0 0 0nfl

LCl

0 00 0

0 0

26

a0 0 0 0 H H H

c-I D W NCV+ + I + I + I +

CD W W M PGO

QO W W CO W & 0

CVQO

I O UD CO Ch A CV W < OcV

CVYl H H+ + I + + I I + +

O N a Ol O H > W H OCD QO

O O O QQ < Ch + O OCV K N

I I I I I I I I I I

QCI

5 IQI

W 00

Cl

Ch 0

c4 m

TABLE 12

DISTRIBUTION OF PRODUCTION OF ALASKA SEAFOOD PROCESSING PLANTS

BY PERCENT CATEGORY AND PERIOD

Percent

of Total Production Number of PlantsPercent of

Period 1 ~Chen e Period 2 Period 2Period 2

Source: Compiled from data provided by Alaska Department of Fish and Game.

il956 to 1958.

21973 to 1975.

3Rounded.

27

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

85

90

95

100

23

41

56

67

75

83

88

92

95

97

98

9999~

10031003100~100310031003100

36

54

67

77

83

88

92

94

97

98

99993993

100310031003100310031003100

+13

+13

+11

+10

+8

+5

+4

+2

+2

+1

+1

0 0 0 0 0 00

0 0

ll

22

34

45

56

68

79

90

102

113

124

136

147

158

170

181

192

204

215

227

14

28

42

56

70

84

98

112

126

141

155

169

183

197

211

225

239

253

267

282

TABLE 13

DISTRIBUTION OF PRODUCTION OF ALASKA SEAFOOD PROCESSING COMPANIESBY PERCENT CATEGORY AND PERIOD

Percent