Embed Size (px)

Citation preview

MANAGEMENT ACCOUNTING SYSTEMS AND INSTITUTIONALIZATION IN MEDIUM-SIZED AND LARGE FAMILY BUSINESSES - EMPIRICAL EVIDENCE FROM GERMANY AND AUSTRIA

Herbert Neubauer, Vienna University of Economics and Business, Vienna, Austria Stefan Mayr, Johannes Keppler University Linz, Austria

Birgit Feldbauer-Durstmüller, Johannes Keppler University, Linz, Austria Christine Duller, Johannes Keppler University, Linz, Austria

ABSTRACT This article examines differences between family and non-family businesses with regard to the manifestation of management accounting systems and addresses the question of whether business size or the differentiation of family vs. non-family businesses is the dominant influencing factor in the formalization of management accounting and the use of the corresponding tools. The findings of the empirical study presented in the article show that the size of the business is the main factor in the implementation of management accounting and the use of the corresponding tools. The difference in business structure (family or non-family business) represents an additional influencing factor. Based on its multi-country perspective (Germany and Austria) as well as the integration of differing reference theories (contingency and systems theory as well as principal-agent and stewardship theory), the article presents well-grounded insights which enhance our understanding of management accounting in medium-sized family businesses. Keywords: Management Accounting, Family Business, Resource-Based View of the Firm Theory 1. INTRODUCTION Medium-sized enterprises and family businesses constitute a highly important economic factor in Germany and Austria. In both countries, more than 99% of all businesses can be classified as medium-sized enterprises. In Austria, 70 to 80 percent of all enterprises are family businesses (Fröhlich, 1995; Hasch et al., 2000), and the corresponding figure for Germany is approximately 95 percent (Haunschild et al., 2007; Klein, 2000). These medium-sized enterprises (MEs) are characterized by limited resources in terms of capital, personnel (including management) and time. It is specifically those resource deficits which limit these companies in terms of management. While the term “business management system” refers to all tools, policies/rules, institutions and processes with which leadership tasks (e.g. definition of objectives, planning, decision-making, control and monitoring) are performed, management accounting is understood as a subsystem of business management which serves the purpose of coordinating information provision, planning and monitoring in an enterprise. Family businesses (FBs) are a very special type of enterprise in which the “family” system exercises a strong socioeconomic influence on business policy. Although a certain body of empirical research on business management in FBs has emerged at the international level (Dyer, 2003; Sharma, Chrisman and Chua, 2003; Sharma, 2004; Casillas, Acedo and Moreno, 2007), the topic of management accounting in FBs has only seen marginal attention in empirical research (Salvato and Moores, 2010). With regard to controlling (the term coined to denote the rough equivalent to management accounting in German-speaking countries), we have observed an increasing number of empirical studies on the topic in large enterprises (LEs) as well as medium-sized enterprises (e.g. Ossadnik, Barklage and Lengerich, 2004; Weber et al., 2006; Wagenhofer, 2006), but aspects related to FBs have seen only little attention in research (Schachner, Speckbacher and Wentges, 2006; Feldbauer-Durstmüller, Wimmer and Duller, 2007). No multi-country empirical studies, e.g. on the manifestations of controlling, have been carried out to date. In this context, the question arises whether there are major differences between FBs and non-family businesses (NFBs) with regard to the formalization of controlling, which manifests itself in the establishment of a separate controlling unit. The relevant literature has proposed the hypothesis (which

has not yet been verified empirically by a comprehensive multi-country study) that FBs have substantially less formalized controlling systems compared to NFBs ( Morris et al., 1997; Picot, 2008). In addition, it is not known whether the institutionalization of a controlling system is influenced more by business size or the differentiation between FBs and NFBs. The discussion above gives rise to the research questions addressed in this article: 1. Are there significant differences between FBs and NFBs with regard to the manifestation of controlling

systems? 2. Are there significant differences between FBs and NFBs with regard to the use of controlling tools? 3. Which influence dominates in the formalization of controlling and in the use of controlling tools:

business size or the differentiation between FBs and NFBs? In an attempt to find answers to the questions above, an empirical study was conducted among German and Austrian enterprises. The remainder of this article is structured as follows: Section 2 presents the reference theories used as a basis of the article, which are essentially systems and contingency theory as well as principal-agent and stewardship theory. In addition, Section 2 provides definitions of the terms “medium-sized enterprise” and “family business”. The measurement and assessment of the question whether an enterprise is a family or non-family business is carried out on the basis of (and by applying) the theoretical concept of substantial family influence (SFI). Based on the theoretical background and previous empirical findings. Section 3 starts by discussing the state of the art in controlling research among medium-sized FBs. Section 4 then presents the development of hypotheses for the multi-country study. Section 5 describes the study methods used, the responses received, demographic data on the respondent businesses as well as the findings of the study, including an evaluation of the hypotheses. The final section summarizes the key results and provides an outlook with questions and avenues for further research. 2. THEORETICAL BACKGROUND 2.1 Systems and contingency theory The first reference theories underlying the study are systems theory and contingency theory. As defined by Ulrich (1970), a system refers to the “ordered totality of all elements between which any relat ionships exist or may be established.” The ideas underlying systems theory are closely interrelated with cybernetics, meaning that one can speak of systems theory-based, cybernetic systems of statements. Interpreted under systems theory, controlling mainly takes on a coupling (and thus coordinating) function for the individual subsystems within an enterprise (Horváth, 2009). Contingency theory, which examines the influence of environmental factors on the manifestation of a target variable was also used by Gordon and Miller (1976) and Khandwalla (1977) as an explanatory theory in management accounting and controlling research (see also Lawrence and Lorsch, 1967). Contingency theory attempts to generate empirically grounded statements about relationships between situational conditions, organizational structures, the behavior of organization members as well as the degree to which an individual organization attains its objectives (Kieser and Walgenbach, 2007), and it is therefore frequently used as a theoretical basis in accounting and controlling research (Luft and Shields, 2003; Chenhall, 2007; Byrne and Pierce, 2007). In this context, empirical studies on the link between various contextual variables and controlling as a dependent variable were also conducted in German-speaking countries at a very early stage, for example in the study by Uebele (1981). However, current international research on contingency theory, including Chenhall (2007), is based on the assumption that contingency theory holds only limited explanatory potential in questions related to management accounting and controlling, thus calling for an integration of theories. Taken individually, the two theoretical constructs – systems theory and contingency theory – each exhibit certain disadvantages, which is why it appears necessary to integrate the theories in empirical research on controlling. 2.2 Principal-agent and stewardship theory Principal-agent theory has been used in both theoretical and empirical works to explain the differing manifestations of ownership, control and management structures as well as the differences in performance between FBs and NFBs (Hack, 2009). In general, principal-agent theory (Jensen and Meckling, 1976; Arrow, 1985; Eisenhardt, 1989) describes possible conflicts of interest between at least

two parties to an agreement, specifically the principal and the agent. A typical example of the principal-agent problem in FBs is the relationship between a shareholder and a manager who assumes responsibility for managing the business on behalf of the principal. Under this theory, the conflict of interest is analyzed within the framework of a contractual relationship which is characterized by asymmetric levels of information, bounded rationality, opportunistic behavior and incomplete contracts. The fundamental assumption in principal-agent theory is that the principal has an information disadvantage in relation to the agent and cannot monitor the agent’s activities comprehensively and without incurring costs (Jacobides and Croson, 2001). This means that the provision of information throughout the performance process constitutes a crucial element in the principal’s process of monitoring the agent. The installation of a separate controlling unit and the implementation of formal controlling tools can therefore represent a suitable approach for the establishment of formalized control and monitoring systems. Stewardship theory and the concept of altruism are especially important in the context of FBs (Dyer, 2003; Corbetta and Salvato, 2004; Songini, 2006; Witt, 2008; Le Breton-Miller and Miller, 2009; Vallejo, 2009). While principal-agent theory assumes opportunism on the part of the agent, stewardship theory postulates that agents will act in accordance with social principles and devote their efforts to the common good (Davis, Schoorman and Donaldson, 1997). Cooperative, selfless behavior is assumed among members of families in particular (cf. Schulze, Lubatkin and Dino, 2003). Altruism among family members and the reduction of transaction costs are supported by the case study in Karra, Tracey and Philips (2006) as well as additional empirical findings (Chrisman, Chua and Litz, 2004). Formalized corporate governance mechanisms are considered dysfunctional in this context because they precipitate a loss of trust and may demotivate stewards, who are primarily motivated intrinsically (Davis, Schoorman and Donaldson, 1997). These arguments warrant the conclusion that FBs do not require control and monitoring systems to the same extent as NFBs. 2.3 Controlling: Conceptions and definition As a praxeological phenomenon, controlling did not arise from scientific theory, but from practice. While management accounting research in Anglo-American countries has advanced rapidly in both theoretical and empirical terms (e.g. Chenhall, 2003; Luft and Shields, 2003), controlling research in German-speaking countries is still in the midst of a debate on various possible conceptions of the discipline. Although controlling and management accounting are not exactly the same thing, it is considered permissible to include findings from management accounting research in this article due to the close proximity of the two fields (Hoffjan, 2008). In general, various theoretical foundations can be identified in controlling research (Amshoff, 1993; Luft and Shields, 2003). As the relevant German-language literature provides many different conceptions of controlling (e.g. Horváth, 2009; Weber and Schäffer, 2008), there is still no uniform understanding of the term. In this context, a “conception of controlling” is understood as the entirety of statements describing the parameters of its manifestation, such as the objectives, functions, tools and organization or controlling (Schweitzer and Friedl, 1992; Küpper, 2008). The remainder of this article does not refer to a specific conception of controlling; instead, the following definition of the term is used with regard to the research questions discussed above: Controlling is defined as a subsystem of business management which provides support for the latter through information provision as well as planning and monitoring. As a process or way of thinking, controlling arises from the cooperation of managers and controllers in a team. The institutional manifestation of controlling is made visible by the establishment of controlling units; alternatively, controlling tasks may also be handled by other departments. In order to achieve its ends, controlling makes use of various operational and strategic tools. 2.4 Medium-sized family businesses In economics, politics and society, the terms “family business” (FB), “medium-sized business” and “small and medium-sized enterprise” (SME) are often used synonymously. Although there are vast areas of overlap between SMEs and FBs, the terms are nonetheless defined differently. The definitions of SMEs are generally based on specific size categories: The number of employees and/or revenues, total assets, value added and equity capital are conceivable size indicators. These values are used as distinguishing features in order to underscore the differences between businesses of different sizes. According to the

European Commission (Recommendation 2003/361/EC), medium-sized enterprises (which represent the upper limit within the SME category) are defined as undertakings which have no more than 249 employees and annual revenues of less than EUR 50 million or total assets of less than EUR 43 million, and which are (largely) independent. In this study, the number of employees was used as the criterion for size categories. In line with the hypotheses, medium-sized enterprises (50 to 249 employees) should be compared with large enterprises (LEs), which have 250 or more employees. Such a delimitation based on business size was also chosen because in the specific research field under examination (controlling tools), a certain minimum business size must be reached in order for the presumed mutual effects to be observable in the utilization of tools. In addition to quantitative criteria, qualitative features are also used for the purpose of distinguishing SMEs (Pfohl, 1997). These features reveal the specific character of this type of enterprise, which lies in the lacking deployment of specialists (Belz and Travella, 1999), in the heavier orientation of the business person’s knowledge toward production than toward management, in the limited time available for management tasks, in the lacking deployment of sophisticated planning and business management tools, in the neglect of strategic business management, and in decision-making behavior geared toward day-to-day problem-solving and determined by current human resources and priorities. In addition to the quantitative components (size category), qualitative characteristics such as ownership and management rights frequently shape the definition of medium-sized businesses in the literature. In contrast, FBs are less amenable to quantitative differentiation as they are largely defined in qualitative terms and are not subject to specific size limits. Accordingly, the analysis in this article focuses on qualitative dimensions such as ownership and management rights, experience, culture and the will to continue the business. As this research deals with FBs and their specific characteristics in business management, it is necessary to examine the most essential criteria and features of FBs more closely. Over many decades, the family business as an organizational form of economic activity with its own specific characteristics has proven to be a stable component of free economic systems. It is thus all the more surprising that economic research has only begun to examine this construct and its special characteristics more closely in the last two decades (Neubauer and Lank, 1998; Heck and Scannel Trent, 1999; Quermann, 2004 ). One of the key reasons for this late development is probably the fact that no uniform definition of FBs has emerged, meaning that the basis for substantiated, theory-driven and empirical research has rested on rather weak foundations (Berthold, 2010). The least common denominator among all proposed definitions of an FB is probably the insight that that such businesses are characterized by a close relationship between the family and business organization (Berthold, 2010). The systems approach is very well suited as a means of capturing the character of FBs in a theoretically grounded manner. Under this approach, FBs are characterized by a structural coupling of the family and enterprise as institutions which are each organized according to a different logic. On the basis of systems theory, it is possible to create a conceptual framework which allows a holistic (Schmidt, 1997) examination of the distinguishing features of FBs. Strictly speaking, FBs are not defined here; instead, the individual systems are described. The key features which emerge in this context are the influence of the family and the will to maintain the business (e.g. Litz, 1995; Hennerkes, 1998; Chua, Chrisman and Sharma, 1999). While such subjectively abstract features capture the essence of FBs most effectively, operationalization relies on objectively verifiable elements of the family’s presence in the business. In the literature, this has yielded the insight that the efforts to draw as clear a dividing line as possible between FBs and NFBs should give way to a description of various FB configurations according to the nature and scope of the family’s involvement in the business organization (Habbershon and Williams, 1999; Heck and Scannel Trent, 1999; Uhlaner, 2002; Astrachan and Shanker, 2003). In line with this idea, Astrachan, Klein and Smyrnios developed a modular construct with which the degree of family influence on the business is determined using a cardinal scale ( Astrachan, Klein and Smyrnios, 2002; Klein, Astrachan and Smyrnios, 2003; Klein, Astrachan and Smyrnios, 2005). The F-PEC scale thus makes it possible to calculate an index for the influence of the family using three dimensions: power, experience and culture. The first component includes characteristic feature-based variables. The family possesses “power” to the extent that it makes equity available or recruits members of management or supervisory bodies from within the family (or deploys such members at its own discretion). The relative shares attributable to a family in this component are added up to yield an indicator value. A low level of influence in one factor will thus be

offset by dominance in another area (Klein, 2000). The “experience” component focuses on the significance of the family’s business experience, which is documented by intra-family transfers of power in the business. In quantitative terms, power is captured by assigning exponentially declining weights to the number of successfully completed succession processes, with the contribution of all directly and indirectly involved family members included in the calculation. The “culture” component adds subjective dimensions to this highly objective basis by including cultural aspects. This component is intended to account for the degree to which the values of the family and the business overlap, and whether the family has a positive commitment to its business mission (which can be projected onto the future). Similar considerations can be found in Habig and Berninghaus (2004). What all of these definitions have in common is the effort to capture manifestations of the family’s influence on the business in theoretical and/or operational terms (Klein, 2004; Zahra, Hayton and Salvato, 2004; Chrisman, Chua and Litz, 2004; Moog, Mirabella and Schlepphorst, 2010). Given the objective of this article – to analyze the development of strategic approaches which contribute to ensuring the continued operation of family businesses – it is necessary to develop not only a fundamental understanding but also an operational perspective on this type of business organization, especially as the article deals with the comparability of FBs and NFBs. In this study, the power dimension as defined in the F-PEC scale, i.e. the family’s exercise of substantial influence on the business, is also used as a delimiting criterion between FBs and NFBs (SFI concept: substantial family influence). Based on the minimum requirement that the family holds a share (> 0) of the undertaking’s equity, an FB is defined as a business where the following condition is fulfilled (Klein, 2004). Where Fam EQ is greater than 0, the following applies: Fam EQ MoSB Fam MoMB Fam FB = (Total EQ ) + (Total MoSB ) + (Total MOMB ) ≥ 1 The core statement of such an SFI concept is that substantial family influence (SFI) on a business can be exercised by way of an equity share (EQ), through members of a supervisory body (MoSB) and through members of the management board (MoMB). In this context, the values describing SFI (Fam) are placed in relation to total equity (Total EQ), to the total number of members in the supervisory body (Total MoSB), and to the total number of members in the management board (Total MoSB). Finally, as in any empirical research (on medium-sized enterprises), the question of a practicable and operationalizable applied definition arises. In particular, this definition has to be “manageable”, that is, it should enable as objective and transparent a delimitation of FBs as possible based on the available data. As discussed above, the distinction between FBs and NFBs in this study is based on the SFI concept, while the definition of MEs is based on the number of employees in the organization. 3. STATE OF THE ART IN CONTROLLING RESEARCH ON MEDIUM – SIZED FAMILY

ENTERPRISES Despite increased research efforts in recent years, the current state of research on controlling in medium-sized businesses can still be described as fragmented; a clear need for further research, including praxeological efforts, can be observed. In his study on the factors influencing the use of controlling in medium-sized enterprises, Flacke (2007) states that there are only few studies which refer exclusively to this size category. In addition, Flacke notes that the methods applied and the definitions operationalized for medium-sized businesses in previous descriptive studies are so heterogeneous that the findings are hardly or not at all comparable (Flacke, 2007). Table 1 provides an overview of the studies on controlling in MEs published in German-speaking countries over the last 30 years. Overall, the results of the descriptive studies closely reflect the progress of controlling implementation, especially with regard to controlling tools. The use of tools focuses heavily on operational planning and monitoring instruments, whereas strategically oriented tools are used to a substantially lower extent.

Table 1: Overview of controlling research in German-speaking countries

Source Year of survey

Respondents

Number of employees

Region Form of publication

Bussiek (1981) n/a 208 <1,000 n/a Monograph

Kropfberger (1986) 1982, 1983

394 259

67.1% with ≤ 500

Austria Monograph

Pohl/Rehkugler (1986)

1984 217 20-1,000 Bremen/ Stade Monograph

Haake (1987) n/a 1,132 <500 Switzerland/ Western Europe

Dissertation

Lachnit/Dey (1989) 1986 24 <500 Oldenburg Chamber of Commerce and Industry (IHK)

Article in collected edition

Lanz (1990) 1986 420 <500 Switzerland Dissertation

Kosmider (1994) 1988 440 20 to >500 Koblenz Chamber of Commerce and Industry (IHK)

Monograph

Niedermayr (1994) 1992 292 70.2% with ≤ 500

Austria Dissertation

Kropfberger/Mödritscher (1999)

1994, 1995

354 159

77.7% with ≤ 499

Austria Article in collected edition

Legenhausen (1998) 1992 139 <500 Bremen Chamber of Commerce and Industry (IHK)

Dissertation

Dintner/Schorcht (1999)

1994, 1996

152 <500 Thuringia Article in collected edition

Schadenhofer (2000) 1997 363 >100 Austria Diploma thesis

Leitner (2001) 1996 100 <500 Austria Dissertation

Zimmermann (2001) 2000 84 50-1,000 Former FRG Dissertation

Keßler/Frank (2003) 2000 63 84.1% with ≤ 249

Austria IGA

Ossadnik/Barklage/ Lengerich (2004)

2002 155 <500 Osnabrück-Emsland

Controlling

Bischof/Benz/Maier (2004)

n/a 34 <750 Vorarlberg (Austria)

ControllerNews

Wimmer (2004) 2004 482 48.3% with ≤ 250

Austria Dissertation

Berens/Püthe/Siemes (2005)

2004 213 n/a Germany ZfCM

Kummert (2005) 2003 44 10-150 Austria Dissertation

Rautenstrauch/Müller (2005, 2006)

2003 188 20-500 Eastern Westphalia

ZP, ZfCM

Schachner/Speckbacher/ Wentges (2006)

2003 205 50-500 Southern Germany / Austria

ZfB

Günther/Gonschorek (2008)

2006 307 n/a Germany Article in collected edition

Deimel/Kraus (2007) 2005 101 5-500 Germany, Austria, Switzerland

Article in collected edition

Flacke (2007) 2004 211 <500 Münster Region Dissertation

Schiller/Keimer/Egle/ Keune (2007)

2006 539 n/a Switzerland Controlling

Feldbauer-Durstmüller/ Wimmer/Duller (2007)

2007 236 >50 Upper Austria ZP

Heidenbauer (2008) 2007 244 86.6% with ≤ 499

Austria Dissertation

Becker/Ulrich (2009) 2007 45 73.3% with ≤ 300

Germany ZfCM

Feldbauer/Haas (2009)

2007 236 >50 Upper Austria Article in collected edition

Becker/Staffel/Ulrich (2010)

2008 63 >30 Germany Controlling

In addition to descriptive studies on the progress of controlling implementation in MEs, German-language controlling research as well as international research on controlling and management accounting (e.g. Matthews and Scott, 1992; Reid and Smith, 2000; Gibson and Cassar, 2002) has also produced studies on contingency factors in controlling (Austria: Kropfberger, 1986; Niedermayr, 1994; Kropfberger and Mödritscher, 1999; Feldbauer-Durstmüller/Wimmer/Duller, 2007; Germany: Ossadnik, Barklage and Lengerich, 2004; Berens, Püthe and Siemes, 2005; Becker and Ulrich, 2009; Becker, Staffel and Ulrich, 2010; Austria and Germany: Schachner, Speckbacher and Wentges, 2006). Empirical, contingency-based controlling research mainly examines the effects of contextual factors on controlling as a dependent variable. In both German-language and international literature on SMEs, medium-sized enterprises and FBs, the two contingency factors “business size” and “business type” (ME vs. LE or FB vs. NFB) have been identified as the most important contingency factors (Flacke, 2007). Research on controlling in medium-sized enterprises has generally focused on instrumental perspectives. For example, a number of studies point to a positive correlation between increasing business size and management by executives on the one hand and the use of controlling tools on the other (e.g. Niedermayr, 1994 for German-speaking countries). Matthews and Scott (1995) find significant positive and negative correlations between uncertainty and business size as influencing factors and strategic and operational planning as dependent variables. In a survey of 3,554 Australian businesses, Gibson and Cassar (2002) identify a significant positive relationship between business size and planning as a dependent variable. Schachner, Speckbacher and Wentges (2006) show that exclusively owner-run businesses – relatively independently of business size – are more centrally organized and use formalized control systems (e.g. balanced scorecards) far less frequently. However, as soon as external executives are involved in management, more formalized control systems are used. In partly owner-run businesses, the authors find that business size has a considerable influence: The larger the number of employees, the more decentralized structures are used and the more frequently the balanced scorecard is deployed. Several articles and empirical studies on the units responsible for controlling show that its institutionalization gains significance as business size increases. The main reasons cited for this development are increasing complexity and the accompanying need for specialization (Flacke, 2007). There is also reason to assume that owner- or family-run businesses rely less on institutionalized controlling staff than manager-run businesses do (Niedermayr, 1994; Davila, 2005; Flacke, 2007). As for methodological grounding, it can be observed that previous studies make reference to theory, but that reference theories such as systems and contingency theory as well as principal-agent and stewardship theory have not been integrated to this extent in the past. 4. DEVELOPMENT OF HYPOTHESES 4.1 Overview The hypotheses below are derived on the basis of the reference theories presented in Section 1 and the field of research discussed in Section 2. Upon initial examination, the objectives and functions of controlling do not differ in MEs and LEs or in FBs and NFBs. However, differences can be identified in the manner in which these functions are translated into tasks and tools, and the manner in which the performance of these tasks is anchored in the organization. For example, with regard to the presumed

special characteristics of controlling in FBs, one can assert that the strategy process in FBs and NFBs is identical in terms of steps in the process. Likewise, success or failure will be similar in all businesses, as it should be measured on the basis of the defined objectives in all cases (Sharma, Chrisman and Chua, 1997). Instead, the differences between FBs and NFBs are far more likely to be identified in the way in which the strategy process is executed instrumentally and in the persons involved in the process. This study broadens the horizon of observation to include a multi-country perspective. This is intended to fill a significant gap in the research, as no studies on country-specific differences in the implementation of controlling have been carried out in German-speaking countries to date. By examining the contingency variables of size and business structure, this study employs a method commonly used in contingency theory-based research. 4.2 Hypotheses on the influence of business size In explaining the influence of business size on the institutionalization of controlling, the extant literature largely relies on the differentiation-integration paradigm (Amshoff, 1993; Niedermayr, 1994), which asserts that increasing business size will be accompanied by increasing differentiation in the business organization as well as an increasing degree of specialization in controlling tools and organization. In MEs, an accumulation of tasks among decision-makers can be observed, especially in the management board. Based on these considerations and on classic contingency theory, which implies a correlation between business size and organizational differentiation, one can assume that LEs are more likely than MEs to establish separate controlling units. A similar relationship is postulated for the degree to which strategic and operational controlling tools are utilized. H1a: Large enterprises are more likely to establish separate controlling units than are medium-sized enterprises. H2a: Large enterprises are more likely to use strategic controlling tools than are medium-sized enterprises. H3a: Large enterprises are more likely to use operational controlling tools than are medium-sized enterprises. 4.3 Hypotheses on family influence As in MEs, it can be observed in FBs that structures are geared toward the individual family business person and not defined independently of specific persons, as is the case in anonymous joint-stock companies and LEs (Hennerkes, 1998). Nevertheless, the low deployment of business administration tools is a shortcoming very frequently identified in FBs. The resistance to tools which can be observed in FBs may be rooted in the inability to adapt the tools to the individual needs of the business people (Rüttler, 1998) and in a strong focus on day-to-day operations (Schröder, 1998). In addition to these assumptions derived from practice-oriented literature on FBs, it is also necessary to develop an explanation based on theory. To this end, principal-agent theory is especially well suited to NFBs, while stewardship theory is particularly appropriate for FBs. Due to the divergence of interests and asymmetry of information between NFB shareholders and management, the former are forced to protect themselves from damaging behavior on the part of the management by implementing the corresponding monitoring tools and incentive systems. The professional provision of information is therefore a very important element in the principal’s process of monitoring the agent. With reference to principal-agent theory, one can assume that controlling will be more formalized in NFBs than in FBs. At the same time, the literature on stewardship theory (cf. Vallejo, 2009) emphasizes the high importance of trust and non-formalized coordination systems in FBs. Therefore, FBs will make less use of controlling tools, which are associated with the mistrust-based approach under principal-agent theory. Based on the studies cited above as well as stewardship theory, it is assumed that management – and thus also controlling – in FBs will exhibit a lower degree of formalization than management in NFBs. H1b: Non-family businesses are more likely to establish separate controlling units than are family businesses. H2b: Non-family businesses are more likely to use strategic controlling tools than are family businesses.

H3b: Non-family businesses are more likely to use operational controlling tools than are family businesses. 5. METHODS AND FINDINGS 5.1 Study design In order the verify hypotheses developed in the previous section, a total of 5,406 Austrian enterprises with at least 50 employees were surveyed in July and August 2009. The survey was then carried out among 7,550 businesses in North Rhine-Westphalia and Lower Saxony between November 2009 and January 2010, and among 5,000 enterprises in Bavaria and Baden-Württemberg in February and March 2010. The survey tool used was a standardized and pre-tested online questionnaire. The management of each business was contacted by e-mail and asked to take part in the study (with a hyperlink to the questionnaire). The questionnaire was completed by a total of 1,658 businesses (return rate: 9.2%), of which 1,169 returned valid data. An additional 117 questionnaires had to be eliminated because the enterprises could not be assigned to the desired size category or to the selected federal state or province. As a result, the analysis below is based on a total of 1,052 completed questionnaires. In order to determine whether the sample is representative, the answers provided by the first third of respondents (early respondents) were compared with those of the last third (late respondents; Leslie, 1972). As no significant differences between those groups were identified, it can be assumed that representativeness is not affected by non-response bias (Bortz and Döring, 2006; Creswell, 2009; Fowler, 2009). In order to meet the high conceptual requirements of the SFI concept, 102 enterprises were eliminated from the business structure-based analysis due to missing data. Of the 950 businesses which could be classified under the SFI concept, 55.6% can be considered FBs. With regard to business size, 65.7% were categorized as LEs with more than 249 employees.

The hypotheses were verified using the appropriate

statistical tests at a significance level of alpha = 0.05; the respective p-values are indicated along with the results. The individual hypotheses were tested using the following methods: chi-squared test of independence and Fisher’s exact test, Kolmogorov-Smirnov adaptation test, and the Mann-Whitney U test. The specific requirements for the application of individual tests (e.g. for the chi-squared test) were observed in each case. Finally, logistic regression enabled a simultaneous analysis of the size and structure factors, which should provide information as to whether it is primarily the business structure or size that plays a decisive role in this context. 5.2 Findings In the first step, the hypotheses are tested individually and grouped by theme for the sake of a clear overview. Country-specific peculiarities are indicated separately for each hypothesis.

H1a: Large enterprises are more likely to establish separate controlling units than are medium-sized enterprises.

Table 2: Organization of controlling in medium-sized and large enterprises (deviations in case numbers [indicated by n] result from missing responses to individual questions

The chi-squared test shows a significant result (p = 0.000), thus supporting Hypothesis 1a. One-third of MEs have established a separate controlling unit, while approximately three-quarters of LEs have set up such a unit. The share of MEs as well as LEs with independent controlling units observed in Austria is significantly higher than in Germany. While controlling tasks are handled to a greater extent by the management in German MEs, businesses in Austria primarily establish independent controlling departments or assign controlling tasks to the (financial) accounting department. In comparison to previous studies, it can again be observed in this study (in a multi-country perspective) that controlling tasks in MEs are primarily handled by separate units, although the degree of institutionalization in MEs lags far behind that of LEs (Ossadnik, Barklage and Lengerich, 2004).

H1b: Non-family businesses are more likely to establish separate controlling units than are family businesses.

Table 3: Organization of controlling in FBs and NFBs

Approximately 60% of NFBs have established a separate controlling department; this figure is substantially lower among FBs (37.6%), meaning that the data also confirm Hypothesis 1b. This result validates the insights from earlier studies by Kosmider (1994), Niedermayr (1994), and Schachner, Speckbacher and Wentges (2006), which show that FBs – relatively independently of their size – are significantly more centrally organized and less likely to establish independent controlling units. While the difference between German and Austrian businesses with regard to the establishment of separate controlling units in FBs is not significant, a significantly larger share of NFBs in Austria have established

A D A D

Separate controlling department 37.6% 59.9% 40.8% 35.7% 66.5% 52.2%

Management board 28.2% 15.0% 22.5% 31.7% 10.4% 20.3%

(Financial) Accounting dept. 25.5% 21.6% 28.8% 23.5% 20.3% 23.1%

External 5.7% 2.0% 6.8% 5.0% 1.9% 2.1%

Other organizational forms 0.4% 0.8% 0.0% 0.6% 0.5% 1.1%

No active controlling 2.5% 0.8% 1.0% 3.4% 0.5% 1.1%

Number of cases (n) 510 394 191 319 212 182

NFB Organization of controlling FB NFB

FB

A D A D

Separate controlling department 33.2% 76.5% 39.8% 28.2% 81.7% 71.8%

Management board 28.5% 10.1% 21.4% 33.9% 7.0% 12.8%

(Financial) Accounting dept. 30.0% 10.7% 31.6% 28.7% 9.9% 11.5%

External 5.4% 1.3% 6.0% 4.9% 0.7% 1.9%

Other organizational forms 0.7% 0.7% 0.0% 1.1% 0.7% 0.6%

No active controlling 2.3% 0.7% 1.1% 3.2% 0.0% 1.3%

Number of cases (n) 614 298 266 348 142 156

ME LE Organization of controlling ME LE

separate controlling departments than in Germany. Within the FB category, it is also striking that Austrian FBs which do not have separate controlling units tend to rely more on the (financial) accounting department for controlling tasks, while these duties are more often performed by the management in German enterprises.

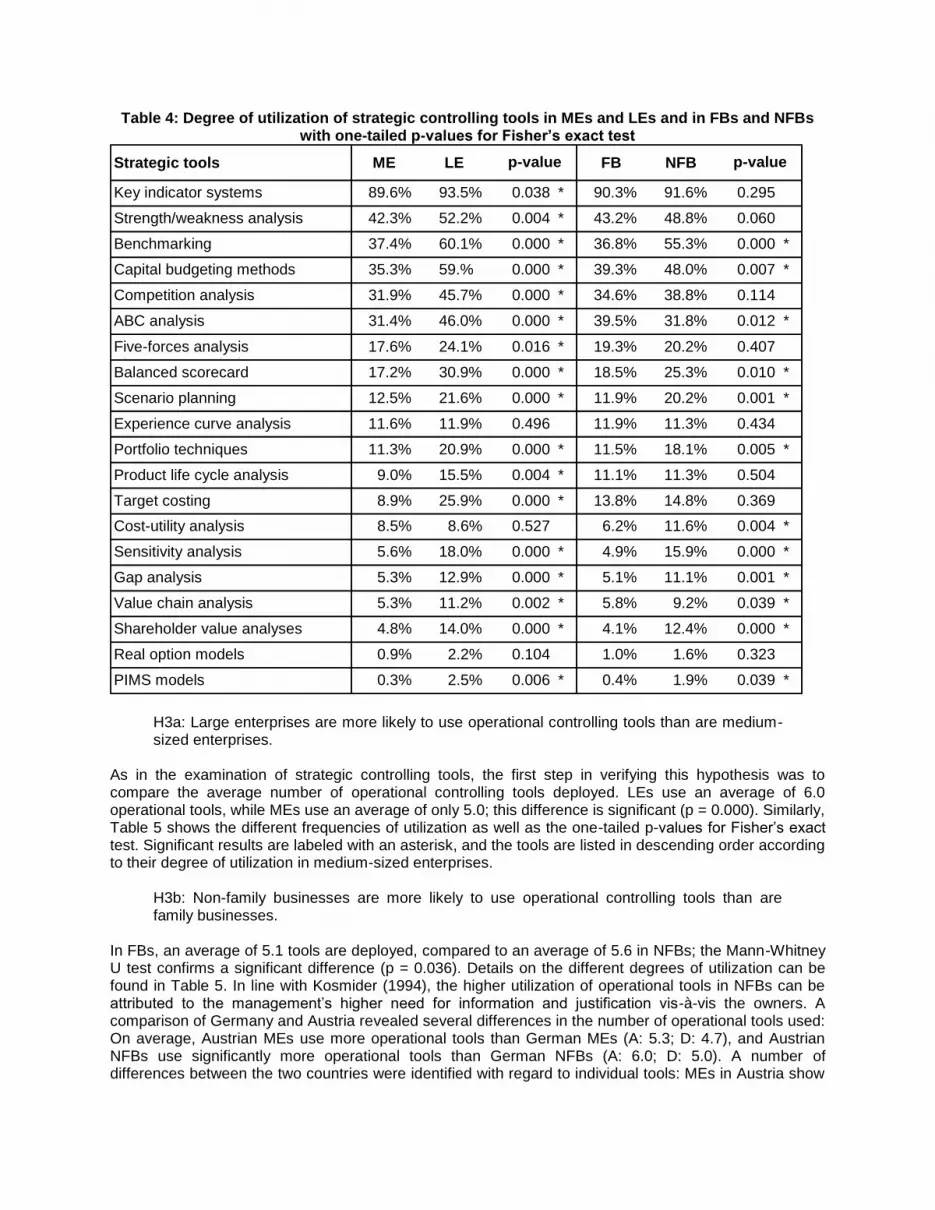

H2a: Large enterprises are more likely to use strategic controlling tools than are medium-sized enterprises.

In order to verify this hypothesis, the first step was to compare the average number of strategic controlling tools deployed. In LEs, an average of 5.7 strategic tools are used, while MEs showed an average of only 3.9. This difference is significant (p = 0.000), thus confirming Hypothesis H2a. In the next step, each individual tool was examined for significant differences in terms of the degree of utilization in MEs and LEs (cf. Table 4). For this purpose, Fisher’s exact test was used. Table 4 shows the different degrees of utilization and the one-tailed p-values for the Fisher test. Significant results are labeled with an asterisk, and the tools are listed in descending order according to their degree of utilization in medium-sized enterprises. The results of the study by Kropfberger (1999) can therefore be confirmed: LEs require substantially more organizational measures in order to integrate their differentiated organizational areas. This requires the deployment of strategic tools such as strength/weakness analyses or benchmarking.

H2b: Non-family businesses are more likely to use strategic controlling tools than are family businesses.

In analogy to the verification of H2a, the Mann-Whitney U test was used to compare the average numbers in this context. FBs use an average of 4.1 strategic tools, while NFBs use an average of 5.0; this difference is also significant (p = 0.000). In order to examine the individual tools, Fisher’s exact test was used once again (see Table 4 for details). The results confirm the findings of previous studies: For example, Schachner, Speckbacher and Wentges (2006) find that FBs use the balanced scorecard significantly less than NFBs. Similarly, Becker and Ulrich (2009) come to the conclusion that NFUs carry out substantially more strategically oriented tasks. A comparison of Germany and Austria yielded only few differences in terms of the average number of strategic tools used, with the only marked difference being that Austrian NFBs use significantly more strategic tools than their German counterparts (A: 5.4; D: 4.6). A number of differences between the two countries were identified with regard to individual tools: In Austrian MEs, the use of benchmarking (A: 43.9%; D: 32.2%), balanced scorecards (A: 22.7%; D: 13.0%), gap analyses (A: 9.0%; D: 2.4%) and sensitivity analyses (A: 7.8%; D: 3.9%) is significantly higher than in Germany, while Austrian LEs make heavier use of scenario planning (A: 26.9%; D: 16.7%) but deploy five-forces analysis less often (A: 17.9%; D: 29.9%). Within the FB category, the only significant difference between Germany and Austria was identified in the use of the balanced scorecard (A: 23.1%; D: 15.7%); among NFBs, the use of benchmarking (A: 60.3%; D: 49.4%), scenario planning (A: 25.6%; D: 14.0%) and gap analysis (A: 15.1%; D: 6.4%) differed significantly.

Table 4: Degree of utilization of strategic controlling tools in MEs and LEs and in FBs and NFBs with one-tailed p-values for Fisher’s exact test

H3a: Large enterprises are more likely to use operational controlling tools than are medium-sized enterprises.

As in the examination of strategic controlling tools, the first step in verifying this hypothesis was to compare the average number of operational controlling tools deployed. LEs use an average of 6.0 operational tools, while MEs use an average of only 5.0; this difference is significant (p = 0.000). Similarly, Table 5 shows the different frequencies of utilization as well as the one-tailed p-values for Fisher’s exact test. Significant results are labeled with an asterisk, and the tools are listed in descending order according to their degree of utilization in medium-sized enterprises.

H3b: Non-family businesses are more likely to use operational controlling tools than are family businesses.

In FBs, an average of 5.1 tools are deployed, compared to an average of 5.6 in NFBs; the Mann-Whitney U test confirms a significant difference (p = 0.036). Details on the different degrees of utilization can be found in Table 5. In line with Kosmider (1994), the higher utilization of operational tools in NFBs can be attributed to the management’s higher need for information and justification vis-à-vis the owners. A comparison of Germany and Austria revealed several differences in the number of operational tools used: On average, Austrian MEs use more operational tools than German MEs (A: 5.3; D: 4.7), and Austrian NFBs use significantly more operational tools than German NFBs (A: 6.0; D: 5.0). A number of differences between the two countries were identified with regard to individual tools: MEs in Austria show

Strategic tools ME LE FB NFB

Key indicator systems 89.6% 93.5% 0.038 * 90.3% 91.6% 0.295

Strength/weakness analysis 42.3% 52.2% 0.004 * 43.2% 48.8% 0.060

Benchmarking 37.4% 60.1% 0.000 * 36.8% 55.3% 0.000 *

Capital budgeting methods 35.3% 59.% 0.000 * 39.3% 48.0% 0.007 *

Competition analysis 31.9% 45.7% 0.000 * 34.6% 38.8% 0.114

ABC analysis 31.4% 46.0% 0.000 * 39.5% 31.8% 0.012 *

Five-forces analysis Five-forces analysis

17.6% 24.1% 0.016 * 19.3% 20.2% 0.407

Balanced scorecard 17.2% 30.9% 0.000 * 18.5% 25.3% 0.010 *

Scenario planning 12.5% 21.6% 0.000 * 11.9% 20.2% 0.001 *

Experience curve analysis 11.6% 11.9% 0.496 11.9% 11.3% 0.434

Portfolio techniques 11.3% 20.9% 0.000 * 11.5% 18.1% 0.005 *

Product life cycle analysis 9.0% 15.5% 0.004 * 11.1% 11.3% 0.504

Target costing 8.9% 25.9% 0.000 * 13.8% 14.8% 0.369

Cost-utility analysis 8.5% 8.6% 0.527 6.2% 11.6% 0.004 *

Sensitivity analysis 5.6% 18.0% 0.000 * 4.9% 15.9% 0.000 *

Gap analysis 5.3% 12.9% 0.000 * 5.1% 11.1% 0.001 *

Value chain analysis 5.3% 11.2% 0.002 * 5.8% 9.2% 0.039 *

Shareholder value analyses 4.8% 14.0% 0.000 * 4.1% 12.4% 0.000 *

Real option models 0.9% 2.2% 0.104 1.0% 1.6% 0.323

PIMS models 0.3% 2.5% 0.006 * 0.4% 1.9% 0.039 *

p-value p-value

a significantly higher utilization of procurement planning tools (A: 39.5%; D: 30.5%), financial profit and tax planning tools (A: 59.7%, D: 48.7%) and budgeted balance sheets (A: 56.7%; D: 38.9%) than in Germany, while Austrian LEs make heavier use of product program planning tools (A: 49.2%; D: 30.3%) and budgeted balance sheets (A: 62.7%; D: 50.0%) than their German counterparts. Within the FB category, no significant differences were identified between the two countries. Among NFBs, on the other hand, Austrian businesses made heavier use of financial profit and tax planning tools (A: 63.4%; D: 50.3%), budgeted balance sheets (A: 72.0%; D: 48.4%), inventory planning tools (A: 30.1%; D: 18.5%) and HR planning tools (A: 75.3%; D: 64.3%). This study confirms the findings of Weber et al. (2006), who assert that financial controlling – which is presented under liquidity planning in this study – is considered a high priority regardless of business size.

Table 5: Degree of utilization of operational controlling tools in MEs and LEs and in FBs and NFBs

with one-tailed p-values for Fisher’s exact test

Both the overall institutionalization of controlling and individual strategic and operational tools exhibit significant differences between businesses of differing size and structure. In the next step, a logistic regression was modeled for institutionalization and for the individual tools. The dependent variable in the regression equation is the outcome of interest in dichotomized form (separate unit vs. integrated unit; tools used vs. not used), or more strictly speaking, the probability that the outcome of interest will arise (i.e. that a separate controlling unit will exist or a certain tool will be used in a business). The possible influencing factors or independent variables are business structure (FB, NFB) and business size (ME, LE), with MEs and FBs serving as reference categories. For the selection of variables, the stepwise method was chosen; the resulting regression coefficients, their odds and p-values as well as the sequence of variable selection are reported in Table 6.

Operational tools ME LE FB NFB

Revenue/sales planning 81.0% 86.4% 0.000 * 82.7% 83.1% 0.481

Liquidity planning 75.2% 79.8% 0.085 75.1% 79.0% 0.111

HR planning 60.4% 69.8% 0.006 * 58.2% 70.3% 0.000 *

Financial profit and tax planning 53.5% 59.3% 0.073 53.9% 57.4% 0.182

Budgeted balance sheet 46.8% 56.2% 0.008 * 41.3% 61.2% 0.000 *

Imputed profit planning 38.6% 42.6% 0.157 37.3% 43.4% 0.048 *

Procurement planning 34.5% 42.6% 0.016 * 36.4% 37.9% 0.360

Production planning 33.0% 44.2% 0.002 * 40.9% 30.9% 0.002 *

Inventory planning 25.9% 34.9% 0.006 * 31.7% 24.8% 0.020 *

Product program planning 23.3% 39.5% 0.000 * 29.0% 27.7% 0.375

R&D planning 15.9% 29.8% 0.000 * 18.4% 22.7% 0.081

Other sub-plans 11.2% 17.1% 0.016 * 9.0% 18.4% 0.000 *

p-value p-value

Table 6: Results of logistic regression (regression coefficients and variable selection)

The “Influence” column shows the sequence of variable selection in the model. “Si St” thus means that business size (Si) was first taken as the explanatory variable, then business structure (St). Thus structure does have an additional effect along with business size, but the latter makes a more important contribution. In the case of balanced scorecards, for example, only business size was included in the model, which means that business structure has no additional influence on the question of whether the business uses a balanced scorecard or not. Instead of the regression coefficient (B) itself, the odds of the regression coefficient are usually used for interpretation; these odds have a functional relationship to the regression coefficient (Odds = exp (B)). In the case of business size, MEs are used as the reference category, i.e. the odds that an LE will have a separate controlling unit are 6.48 times higher than in the case of MEs. NFBs are more than twice as likely to have a separate controlling unit compared to FBs. In this context, it is also clear that ABC analysis is used more heavily in FBs, as the odds of the analysis being used in NFBs are only two-thirds of those shown for FBs. Only in the case of operational tools does business structure play a more important role (HR plan and budgeted balance sheet) or represent the only significant influencing factor in the regression model (Other sub-plans). The corresponding model tests are significant, meaning that the probability of the outcome (separate department / deployment of a tool) can be estimated more accurately with the variables than without them. However, Nagelkerke’s coefficients of determination (Backhaus et al., 2006) point to poor quality levels. However, this does not come as a surprise, as the main focus in this context was the sequence of variable selection and the objective of the logistic regression was not to develop a model for the purpose of predicting an outcome. To that end, it would be necessary to examine other influencing factors in addition to the variables used

B exp(B) p B exp(B) p

1 Separate department 1.869 6.48 0.000 0.840 2.32 0.000 Si St

ABC analysis 0.662 1.94 0.000 -0.420 0.66 0.005 Si St

Balanced scorecard 0.722 2.06 0.000 Si

Benchmarking 0.851 2.34 0.000 0.685 1.98 0.000 Si St

GAP analysis 0.871 2.39 0,001 0.736 2.09 0.006 Si St

Capital budgeting 0.954 2.60 0,000 Si

PIMS models 2.025 7.58 0.012 Si

Portfolio technique 0.663 1.94 0.001 0.455 1.58 0.022 Si St

Sensitivity analysis 1.204 3.33 0.000 1.187 3.28 0.000 Si St

Shareholder value a. 1.047 2.85 0.000 1.090 2.97 0.000 Si St

Scenario planning 0.603 1.83 0.002 0.563 1.76 0.003 Si St

Value chain analysis 0.815 2.26 0.002 Si

Inventory planning 0.411 1.51 0.013 -0.386 0.68 0.018 Si St

HR planning 0.372 1.45 0.024 0.529 1.70 0.001 Si St

Budgeted balance sheet 0.320 1.38 0.041 0.806 2.24 0.000 Si St

Production planning 0.463 1.59 0.003 -0.489 0.61 0.001 Si St

Other sub-plans 0.823 2.28 0.000 St

H

2

3

Influence Dependent variable

Independent variables

Size Structure

and to model possible interactions. This would provide an interesting point of departure for further statistical analyses of the data set. 5.3 Discussion of results Controlling is far more developed in LEs and NFBs, as shown in both the significantly higher number of separate controlling units established and in the heavier usage of strategic and operational controlling tools (confirmation of Hypotheses 1a and 1b, 2a and 2b, as well as 3a and 3b). As regards stewardship theory, the results of the study confirm the assumption that family-centered behavior dominates in FBs, meaning that the institutionalization of controlling is far less pronounced. From a principal-agent theory perspective, the results confirm the assumption that planning and monitoring tools are deployed in order to mitigate the principal’s information disadvantages in NFBs. In the comparison of German and Austrian businesses, this article has demonstrated for the first time that one country (Austria) has significantly more independent controlling units than the other (Germany). These national differences may be attributed to cultural, competition-related, legal and educational factors, or to industry-specific characteristics. The fact that controlling duties are more frequently performed by the management board in Germany can probably be attributed to the fact that German executives are subject to more stringent reporting and controlling obligations imposed by their banks. Further qualitative research would be required in order to explain these differences more accurately, for example by means of in-depth interviews. Despite the differing implementation of controlling units in Germany and Austria, no differences ultimately appear in the hierarchical manifestation of controlling. In both countries, separate controlling departments are established at the highest or second-highest level of the business hierarchy in approximately 92% of all cases. As in Weber at al. (2006), the results of this study show that a vast majority – some 85% of controllers – work at the highest or second-highest hierarchical level. In the case of strategic instruments, Austrian MEs tend to make heavier use of these tools compared to their German counterparts. However, as the extent and frequency of usage are not known, additional research would also be warranted in this context. In this context, questions remain unresolved with regard to the quality of usage and the frequency with which these tools are used. Another important area for future research would be whether the differing deployment of strategic tools brings about differences in business performance. A general tendency can be observed in which newer and more sophisticated tools (such as the balanced scorecard) are used more frequently in NFBs than in FBs. This could be directly related to the persons responsible for controlling and their qualifications. As for the deployment of operational controlling tools, the results of this study demonstrate that LEs use more operational instruments than MEs. The lower use of these tools in German businesses compared to their Austrian counterparts might be explained by the parties responsible for controlling: In German MEs, far more executives are responsible for controlling tasks in addition to their management duties. This accumulation of tasks might be a reason for the use of simpler tools. As a possible explanation for the significant difference between FBs and NFBs in the usage of HR planning tools, one might conjecture that intuition and trust tend to substitute for more formalized planning with specific regard to the “soft” factor of human resources (Moog, Mirabella and Schlepphorst, 2010). The significantly different degrees to which budgeted balance sheets are used in FBs and NFBs might be attributed to higher corporate governance requirements in NFBs. 6. SUMMARY In summary, it can be stated that business size is the key factor in the manifestation of controlling and the deployment of controlling tools. In addition, the differentiation based on business structure (FB or NFB) represents an additional influencing factor. From an empirical perspective, this multi-country study – which also presents country-specific characteristics – has substantially expanded the horizon of extant research. Significant differences in the organization of controlling in Germany and Austria have been identified. Whereas FBs were previously described in sweeping terms as having less formalized control systems, this study offers a more differentiated view by identifying individual instruments which are used more frequently in NFBs. In general, however, one can state that operational instruments – probably also due to Basel II – are generally used in FBs, while the tools used for strategic purposes in FBs tend to be more easily manageable tools such as key indicator systems, strength/weakness analysis or ABC

analysis. NFBs, on the other hand, tend to use newer and more sophisticated (strategic) tools. This appears to be directly linked to the institutionalization of controlling in each category. FBs clearly lag behind in terms of institutionalization, and the resources made available are insufficient to deal with strategic issues. What is truly striking is that in far more than 50% of the MEs and FBs surveyed, controlling is either handled by the management board or the (financial) accounting department (compared to some 21% in LEs and approximately 37% in NFBs). This clearly indicates a need to professionalize controlling in medium-sized family businesses. Additional research questions might focus on the reasons for establishing a separate controlling department and for the degree to which these strategic and operational tools are used. This article has thus filled a gap in the research by broadening the observation horizon from previous studies with a multi-country perspective and by integrating different theoretical foundations through the comprehensive use of reference theories. REFERENCES

Amshoff, B., Controlling in deutschen Unternehmungen, 2

nd ed., Gabler, Wiesbaden, 1993.

Arrow, K.J., “The Economics of the Agency”, in: Pratt, J.W. and Zeckhauser, R.J., editor, “Principals and Agents, The Structure of Business”, Harvard Business School Press, Boston, 1985. Astrachan. J., Klein. S. and Smyrnios, K., “The F-Pec Scale of Family Influence, A Proposal for Solving the Family Business Definition Problem”, Family Business Review, Volume 15, Number 1, Pages 45-58, 2002. Astrachan, J.and Shanker, M., “Family Business Contribution to the US Economy, A Closer Look”, Family Business Review, Volume 16, Number 3, Pages 211-219, 2003. Backhaus, K., Erichson, B., Plinke, W. and Weiber, R., Multivariate Analysemethode. Eine anwendungsorientierte Einführung, 11

th ed., Springer, Heidelberg, 2006.

Becker, W., Staffel, M. and Ulrich, P., „Elemente von Controllingsystemen im Mittelstand – Empirische Analyse und Ableitung von Handlungsempfehlungen“, Controlling, Volume 21, Number 3, Pages 195-203, 2010. Becker, W. and Ulrich, P., „Spezifika des Controllings im Mittelstand – Ergebnisse einer Interviewaktion“, Zeitschrift für Controlling & Management, Volume 53, Number 5, Pages 308-316, 2009. Belz, Ch. and Travella, R., Marketingfähigkeiten von mittelständischen Unternehmen – Studie Deutschland. Universität St. Gallen, One Marketing Services, St.Gallen, 1999. Berens, W., Püthe, T. and Siemes, A., „Ausgestaltung der Controlling-Systeme im Mittelstand – Ergebnisse einer Untersuchung“, Zeitschrift für Controlling & Management, Volume 49, Number 3, Pages 186-191, 2005. Bertalanffy, L., General System Theory, George Braziller, New York, 1968. Berthold, F., Familienunternehmen im Spannungsfeld zwischen Wachstum und Finanzierung, Köln, 2010. Bischof, J., Benz, C. and Maier, E., „Controlling in mittelständischen Betrieben: Ergebnisse einer Untersuchung in Vorarlberg“, Controller News, Volume 7, Number 5, Pages 154-158, 2004. Bortz, J. and Döring, N., Forschungsmethoden und Evaluation für Human- und Sozialwissenschaftler, 4

th

edn., Springer, Heidelberg, 2006. Bussiek, J., Erfolgsorientierte Steuerung mittelständischer Unternehmen, Beck, München, 1981. Byrne, S. and Pierce, B., “Towards a More Comprehensive Understanding of the Roles of Management Accountants”, European Accounting Review, Volume 16, Number 3, Pages 469 – 498, 2007. Casillas, J.C., Acedo, F.C. and Moreno, A.M., International entrepreneurship in family businesses. Elgar, Cheltenham, 2007. Chenhall, R.H., “Management control systems design with its organizational context: findings from contingency-based research and directions for the future”, Accounting, Organizations and Society, Volume 28, Number 2 and 3, Pages 127-168, 2003. Chenhall, R. H., “Theorizing Contingencies in Management Control Systems Research”, in: Chapmann, C. S. and Hopwood, A.G. and Shield, M.D., (Eds.), Handbook of Management Accounting Research, Volume 1, Pages 163 – 205, 2007. Chrisman, J.J., Chua, J.H. and Litz, R.A., “Comparing the Agency Costs of Family and Non-Family Firms: Conceptual Issues and Exploratory Evidence”, Entrepreneurship Theory & Practice, Volume 28, Number 4, Pages 335-354, 2004.

Chua, J., Chrisman, J. and Sharma, P., “Defining the Family Business by Behavior”, Entrepeneurship Theory & Practice, Volume 23, Number 4, Pages 19-39, 1999. Corbetta, G. and Salvato, C., “Self-Serving or Self-Actualizing? Models of Man and Agency Costs in different Types of Family Firms: A Commentary on Comparing the Agency Costs of Family and Non-family Firms: Conceptual Issues and Exploratory Evidence”, Entrepreneurship Theory & Practice, Volume 28, Number 4, Pages 355-362, 2004. Creswell, J. W., Research design: Qualitative, quantitative, and mixed methods approaches, 3

rd ed.,

2009. Davila, T., “An exploratory study on the emergence of management control systems: formalizing human resources in small growing firms”, Accounting, Organizations and Society, Volume 30, Number 3, Pages 222-249, 2005. Davis, J.H., Schoorman, F.K. and Donaldson, L., “Toward a Stewardship Theory of Management”, Academy of Management Review, Volume 22, Number 1, Pages 20-47, 1997. Deimel, K. and Kraus, S., Strategisches Management in kleinen und mittleren Unternehmen – Eine empirische Bestandaufnahme, in: Letmathe, P., (Ed.), Management kleiner und mittlerer Unternehmen, Stand und Perspektiven der KMU-Forschung, Deutscher Universitäts-Verlag, Wiesbaden, 2007. Dintner, R. and Schorcht, H., Stand der Voraussetzungen für das Controlling und Entwicklungstendenzen in KMU, in: Dintner, R., (Ed.), Controlling in kleinen und mittleren Unternehmen, Klassifikation, Stand und Entwicklung, Lang, Frankfurt am Main, 1999. Dyer, W.G., “The Family: The Missing Variable in Organizational Research”, Entrepreneurship Theory & Practice, Volume 27, Number 4, Pages 401-416, 2003. Eisenhardt, K.M., “Agency Theory: An Assessment and Review”, Academy of Management Review, Volume 14, Number 1, Pages 57-74, 1989. Feldbauer-Durstmüller, B. and Haas, T., Controlling im oberösterreichischen Mittelstand – Theorie und Empirie? in: Mussnig, W., Mödritscher, G. and Heidenbauer, M., (Ed.), Erfolgsstrategien mittelständischer Unternehmen, Festschrift für Dietrich Kropfberger, Linde, Wien, 2009. Feldbauer-Durstmüller, B., Wimmer, B. and Duller, C., „Controlling in österreichischen Familienunternehmen – dargestellt am Bundesland Oberösterreich“, Zeitschrift für Planung & Unternehmenssteuerung, Volume 18, Number 4, Pages 427-443, 2007. Flacke, K., Controlling in mittelständischen Unternehmen – Ausgestaltung, Einflussfaktoren der Instrumentennutzung und Einfluss auf die Bankkommunikation, Dissertation, Westfälische Wilhelms-Universität Münster, 2007. Fowler, F.J., Survey Research Methods, 4

th edn., 2009.

Fröhlich, E., Familie als Erfolgspotential im Gewerbe und Handwerk, in: Kemmetmüller, W., Kotek, H., Petermandl, M. and Stiegler, H., (Ed.), Erfolgspotentiale für Klein- und Mittelbetriebe, Trauner Linz, 1995. Gibson, B. and Cassar, G., “ Planning Behavior Variables in Small Firms”, Journal of Small Business Management, Volume 40, Number 3, Pages 171-186, 2000. Gordon, L.A. and Miller, D., “A contingency framework for the design of accounting information systems”, Accounting, Organizations and Society, Volume 1, Number 1, Pages 59-69, 1976. Günter. T. and Gonschorek, T., Wert(e)orientierte Unternehmensführung im Mittelstand, Ausgewählte Ergebnisse einer empirischen Untersuchung, in: Lingnau, V., (Ed.), Die Rolle des Controllers im Mittelstand, Funktionale, instititutionale und instrumentale Ausgestaltung, Eul, Lohmar, 2008. Haake, K., Strategisches Verhalten in europäischen Klein- und Mittelunternehmen, Duncker & Humblot, Berlin, 1987. Habbershon, T. and Williams, M., “A Resource-Based Framework for Assessing the Strategic Advantages of Family Firms”, Family Business Review, Volume 12, Number 1, Pages 1-25, 1999. Habig, H. and Berninghaus, J., Die Nachfolge im Familienunternehmen ganzheitlich regeln, 2

nd ed.,

Springer, Berlin, 2004. Hack, A., „Sind Familienunternehmen anders? Eine kritische Bestandsaufnahme des aktuellen Forschungsstands“, ZfB Special Issue, Volume 2, Pages 1-29, 2009. Hasch, A., et al., Praxishandbuch der Unternehmensnachfolge, Überreuter, Wien, 2000. Haunschild, L., Wallau, F., Hauser, H.E. and Wolter, H.J., Die volkswirtschaftliche Bedeutung der Familienunternehmen, Gutachten im Auftrag der Stiftung Familienunternehmen, in: IfM Bonn, (Ed.), IfM-Materialien Nr. 172, Bonn, 2007. Heck, R. and Scannel,T.E., “Prevalence of Family Business from a Household Sample”, Family Business Review, Volume 12, Number 3, Pages 209-224, 1999.

Heidenbauer, M., Erfolgsfaktoren in KMU: Der Einfluss des Controllingsystems auf den Erfolg von KMU, Eine vergleichende empirische Studie, Dissertation, Alpen-Adria Universität Klagenfurt, 2008. Hennerkes, B.H., Das Familienunternehmen – eine Einführung in die Problemfelder, in: Hennerkes, B.H. and Kirchdörfer, R., (Ed.), Unternehmenshandbuch Familiengesellschaften, 2

nd ed., Heymann, Köln,

1998. Hoffjan, A., „Comparative Management Accounting – Vergleich des anglo-amerikanischen Management Accountings und des deutschen Controllings“, Controlling, Volume 20, Number 12, Pages 655-661, 2008. Horváth, P., Controlling, 11

th ed., Vahlen, München, 2009.

Jacobides, M. and Croson, D.C., “ Information Policy and Shaping the Value of Agency Relationships”, Academy of Management Review, Volume 36, Number 2, Pages 202-223, 2001. Jensen, M.C. and Meckling, W.H., “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure”, Journal of Financial Economics, Volume 3, Number 4, Pages 305-360, 1976. Karra, N., Tracey, P. and Phillips, N., “ Altruism and Agency in the Family Firm: Exploring the Role of Family, Kinship and Ethnicity”, Entrepreneurship Theory & Practice, Volume 30, Number 6, Pages 861-877, 2006. Keßler, A. and Frank, H., „Strategische Planung und Controlling in österreichischen KMU der Industrie – empirische Bestandsaufnahme und Reflexion“, Internationales Gewerbearchiv, Volume 51, Number 4, Pages 237-253, 2003. Khandwalla, P.N., Design of organizations, arcourt Brace Jovanovich, New York, 1977. Kieser, A. and Walgenbach, P., Organisation, 5

th ed., Schäffer-Poeschel, Stuttgart, 2007.

Klein, S., “Family Businesses in Germany: Significance and Structure”, Family Business Review, Volume 13, Number 3, Pages 157-181, 2000. Klein, S., Familienunternehmen. Theoretische und empirische Grundlagen, 2

nd ed., Gabler, Wiesbaden,

2004. Klein, S., Astrachan, J. and Smyrnios, K., Towards the Validation of the F-PEC Scale of Family Influence, in: Poutziouris, P. and Steier, L., (Ed.), New Frontiers in Family Business Research, the Leadership Challenge, IFERA Publications, Lausanne, 2003. Klein, S., Astrachan, J. and Smyrnios, K., “The F-PEC Sale of Family Influence: Construction, Validation and Further Implication for Theory”, Entrepreneurship Theory & Practice, Volume 29, Number 3, Pages 321-339, 2005. Koeberle-Schmid, A., Brockhoff, K. and Witt, P., „Performanceimplikationen von Aufsichtsgremien in deutschen Familienunternehmen“, ZfB Special Issue, Volume 2, Pages 83-109, 2009. Kosmider, A., Controlling im Mittelstand, Eine Untersuchung der Gestaltung und Anwendung des Controllings in mittelständischen Industrieunternehmen, 2

nd edn., Schäffer-Poeschel, Stuttgart, 1994.

Kropfberger, D., Erfolgsmanagement statt Krisenmanagement, Strategisches Management in Mittelbetrieben, Trauner, Linz, 1986. Kropfberger, D. and Mödritscher, G., Diffusionsprozesse von Managementmethoden und ihre Einflußfaktoren, Theoretische Konzepte und empirische Überprüfung am Beispiel der Unternehmensplanung in Österreichs Industrie und Gewerbe, in: Egger, A. and Grün, O. and Moser, R., (Ed.), Managementinstrumente und –konzepte, Entstehung, Verbreitung und Bedeutung für die Betriebswirtschaftslehre, Schäffer-Poeschel, Stuttgart, 1999. Küpper, H.U., Controlling, Konzeption, Aufgaben, Instrumente, 5

th ed., Schäffer-Poeschel, Stuttgart, 2008.

Kummert, B., Controlling in kleinen und mittleren Unternehmen, Vom Geschäftsprozessmodell zum Controller-Profil, Deutscher Universitäts-Verlag, Wiesbaden, 2005. Lachnit, L. and Dey, G., Stand der in Klein- und Mittelbetrieben angewendeten Führungs-Informationssysteme: eine empirische Untersuchung, in: Lachnit, L., (Ed.), EDV-gestützte Unternehmensführung in Mittelständischen Betrieben: Controllingsysteme zur integrierten Erfolgs- und Finanzlenkung auf operativer und strategischer Basis, Vahlen, München, 1989. Lanz, R., Controlling in kleinen und mittleren Unternehmen, 2

nd ed., Haupt, Bern, 1990.

Lawrence, P. and Lorsch, J., Organization and Environment, Homewood, 1967. Le Breton-Miller, I. and Miller, D., “ Agency vs. Stewardship in Public Family Firms, A Social Embeddedness Reconciliation”, Entrepreneurship Theory & Practice, Volume 33, Number 6, Pages 1069-1091, 2009. Legenhausen, C., Controllinginstrumente für den Mittelstand, Gabler, Wiesbaden, 1998.

Leitner, K.H., Strategisches Verhalten von kleinen und mittleren Unternehmungen, Eine empirische Untersuchung an österreichischen Industrieunternehmen vor einem industrieökonomischen und organisationstheoretischen Hintergrund, Dissertation, Universität Wien, 2001. Leslie, L.L., “Are high response rates essential to valid surveys?”, Social Science Research, Volume 1, Number 3, Pages 323-334, 1972. Litz, R., “ The Family Business: Toward Definitional Clarity”, Family Business Review, Volume 8, Number 2, Pages 71-81, 1995. Luft, J. and Shields, M.D., “Mapping management accounting: graphics and guidelines for theory-consistent empirical research”, Accounting, Organizations and Society, Volume 28, Number 2 and 3, Pages 169-250, 2003. Matthews, C.H. and Scott, S.G., “Uncertainty and planning in small and entrepreneurial firms: an empirical assessment”, Journal of Small Business Management, Volume 33, Number 4, Pages 34-52, 1995. Moog, P., Mirabella, D. and Schlepphorst, S., “Owner orientations and strategies and their impact on family business”, International Journal of Entrepreneurship and Innovation Management, (in print), 2010. Morris, M.H., Williams, R.O., Allen, J.A. and Avila, R.A., “Correlates of Success in Family Business Transitions”. Journal of Business Venturing, Volume 12, Number 5, Pages 385-401, 1997. Neubauer, F. and Lank, A., The Family Business, Its Governance for Sustainability, Macmillan, Basingstoke, 1998. Niedermayr, R., Entwicklungsstand des Controlling, System, Kontext und Effizienz, Deutscher Universitäts-Verlag, Wiesbaden, 1994. Ossadnik, W., Barklage, D. and van Lengerich, E., „Controlling im Mittelstand, Ergebnisse einer empirischen Untersuchung“, Controlling, Volume 16, Number 11, Pages 621-630, 2004. Pfohl, H.C., (Ed.), Betriebswirtschaftslehre der Mittel- und Kleinbetriebe, Größenspezifische Probleme und Möglichkeiten zu ihrer Lösung, 3

rd edn., Schmidt, Berlin, 1997.

Picot, G., Familien- und Mittelstandsunternehmen im globalen Wandel von Wirtschaft und Gesellschaft, in: Picot, G., (Ed.), Handbuch für Familien- und Mittelstandsunternehmen, Strategie, Gestaltung, Zukunftssicherung, Schäffer-Poeschel, Stuttgart, 2008. Pohl, H.J. and Rehkugler, H., Mittelständische Unternehmen: durch qualifiziertes Management zum Erfolg, Schriftenreihe des Fachbereichs Wirtschaft der Hochschule Bremen Nr. 33, Bremen, 1986. Quermann, D., Führungsorganisation in Familienunternehmungen, Eul, Lohmar, 2004. Rautenstrauch, T. and Müller, C., „Verständnis und Organisation des Controlling in kleinen und mittleren Unternehmen“, Zeitschrift für Planung & Unternehmenssteuerung, Volume 16, Number 2, Pages 189-209, 2005. Rautenstrauch, T. and Müller, C., „Investitionscontrolling in kleinen und mittleren Unternehmen (KMU)“, Zeitschrift für Controlling & Management, Volume 50, Number 2, Pages 100-105, 2006. Reid, G.C. and Smith, J.A., “The impact of contingencies on management accounting system development”, Journal of Management Accounting Research, Volume 11, Number 4, Pages 427-450, 2000. Rüttler, M., Führung des Familienunternehmens – Betriebswirtschaftliche Defizite in Familienunternehmen, in: Hennerkes, B. and Kirchdörfler, R., (Ed.), Unternehmenshandbuch Familiengesellschaft – Sicherung von Unternehmen, Vermögen und Familie, 2

nd ed., Heymann, Köln,

1998. Salvato, C. and Moores, K., “Research on Accounting in Family Firms: Past Accomplishments and Future Challenges”, Family Business Review, Volume 23, Number 3, Pages 193-215, 2010. Schachner, M., Speckbacher, G. and Wentges, P., „Steuerung mittelständischer Unternehmen: Größeneffekte und Einfluss der Eigentums- und Führungsstruktur“ Zeitschrift für Betriebswirtschaft, Volume 76, Number 6, Pages 589-614, 2006. Schadenhofer, M., Neuausrichtung des Controlling, Mit der Balanced Scorecard zum Balanced Controlling, Service-Fachverlag, Wien, 2000. Schiller, U., Keimer, I., Egle, U. and Keune, H., „Kostenmanagement in der Schweiz, Eine empirische Studie“, Controlling, Volume 19, Number 6, Pages 301-307, 2007. Schmidt, J., Eigentum und strategisches Management, Deutscher Universitäts-Verlag, Wiesbaden, 1997. Schröder, E., Controlling – Unternehmenssteuerung im Familienunternehmen, in: Hennerkes, B. and Kirchdörfler, R., (Ed.), Unternehmenshandbuch Familiengesellschaft – Sicherung von Unternehmen, Vermögen und Familie, 2nd ed., Heymann, Köln, 1998.

Schulze, W.S., Lubatkin, M.H. and Dino, R.N., “Toward a theory of agency and altruism in family firms”, Journal of Business Venturing, Volume 18, Number 4, Pages 473-490, 2003. Schweitzer, M. and Friedl, B., Beitrag zu einer umfassenden Controlling-Konzeption, in: Spreman, K. and Aeberhard, K., (Ed.), Controlling: Grundlagen - Informationssysteme – Anwendungen, Wiesbaden, Pages 141-167, 1992. Sharma, P., Chrisman, J. and Chua, J., “Strategic Management of the Family Business: Past Research and Future Challenges”, Family Business Review, Volume 10, Number 1, Pages 1-35, 1997. Sharma, P., “Overview of the Field of Family Business Studies: Current Status and Directions for the Future”, Family Business Review, Volume 17, Number 1, Pages 1-36, 2004. Sharma, P., Chrisman, J. and Chua, J., “Predictors of satisfaction with the succession process in family firms”, Journal of Business Venturing, Volume 18, Numbers 5, Pages 667-687, 2003. Songini, L., The Professionalization of Family Firms: Theory and Practice, in : Poutziouris, P.Z. and Smyrnios, K.X. and Klein, S.B., (Ed.), Handbook of Research on Family Business, Pages 269-297, 2006. Uebele, H., Verbreitungsgrad und Entwicklungsstand des Controllings in deutschen Industrieunternehmen, Poeschel, Stuttgart, 1981. Uhlaner, L., The Use of the Guttman Scale in Development of a Family Business Index, EIM, Zoetermeer, 2002. Ulrich, H., Die Unternehmung als produktives soziales System, Grundlagen einer allgemeinen Unternehmungslehre, 2

nd ed., Haupt, Bern, 1970.

Vallejo, M.C., “The Effect of Committement of Non-Family Employees of Family Firms from the Perspective of Stewardship Theory”, Journal of Business Ethics, Volume 87, Number 3, Pages 379-390, 2009. Wagenhofer, A., “Management Accounting Research in German-Speaking Countries”, Journal of Management Accounting Research, Volume 18, Pages 1-19, 2006. Weber, J., Hirsch, B., Rambusch, R., Schlüter, H., Sill, F. and Spatz, A., Controlling 2006 – Stand und Perspektiven, ICV, Berlin. 2006. Weber, J. and Schäffer, U., Einführung in das Controlling, Schäffer-Pöschl, Stuttgart, 2008. Wimmer, B., Unternehmensplanung und –kontrolle, Integrative Konzepte und Stand der Praxis unter besonderer Berücksichtigung von Wertorientierung und informatorischer Gestaltungsmöglichkeit, Dissertation, Johannes Kepler Universität Linz, 2004. Witt, P., “Corporate Governance in Familienunternehmen”, ZfB Special Issue, Volume 2, Pages 1-19, 2008. Zahra, S., Hayton, J. and Salvato, C., “Entrepreneurship in Family vs. Non-Family Firms: A Resource-based Analysis of the effect of Organizational Culture”, Entrepreneurship Theory & Practice, Volume 28, Number 4, Pages 363-381, 2004. Zimmermann, C., Controlling in international tätigen mittelständischen Unternehmen, Deutscher Universitäts-Verlag, Wiesbaden, 2001. Author Profiles: Dr. Herbert Neubauer earned his PH.D. at the Vienna University of Economics and Business. Currently he is professor of entrepreneurship and Small Business Management at Department of Cross-Border Business Vienna University of Economics and Business. Dr. Stefan Mayr earned his PH.D. at the Johannes Keppler University Linz. Currently he is associateprofessor in the Institute of Controlling and Consulting at the Johannes Keppler University Linz. Dr. Birgit Feldbauer-Durstmüller earned her PH.D. at the Johannes Keppler University Linz. Currently she is professor of Controlling and Consulting at Faculty of Social Sciences, Economics and Business Institute of Controlling and Consulting at the Johannes Keppler University Linz. Dr. Christine Duller earned her PH.D. at the Johann Keppler University Linz. Currently she is assistant professor of Data Analysis and Econometrics at the Institute of Applied Statistics at the Johannes Keppler University Linz.