Embed Size (px)

Citation preview

UNIT 9: MANAGEMENT ACCOUNTING: COSTING AND BUDGETING

LECTURER: JUDITH ROBB-WALTERS

UNIT 9: MANAGEMENT ACCOUNTING: COSTING AND BUDGETING

LEARNING OBJECTIVE3:Be able to prepare forecasts and budgets for a business

THE BASIC SYLLABUS

1. Be able to analyse cost information within a business.

2.Be able to propose methods to reduce costs and

enhance value within a business.

3. Be able to prepare forecasts and budgets for a

business.

4. Be able to monitor performance against budgets

within a business.

LEARINGING OUTCOMES

Be able to monitor performance against budgets within a business

At the end of the class the students should be able to:

4.2 Prepare an operating statement reconciling budgeted and actual results

OVERVIEW

The purpose of calculating variances

is to identify the different effects of

each item of cost/income on profit

compared to the expected profit.

These variances are summarised in a

reconciliation statement or operating

statement.

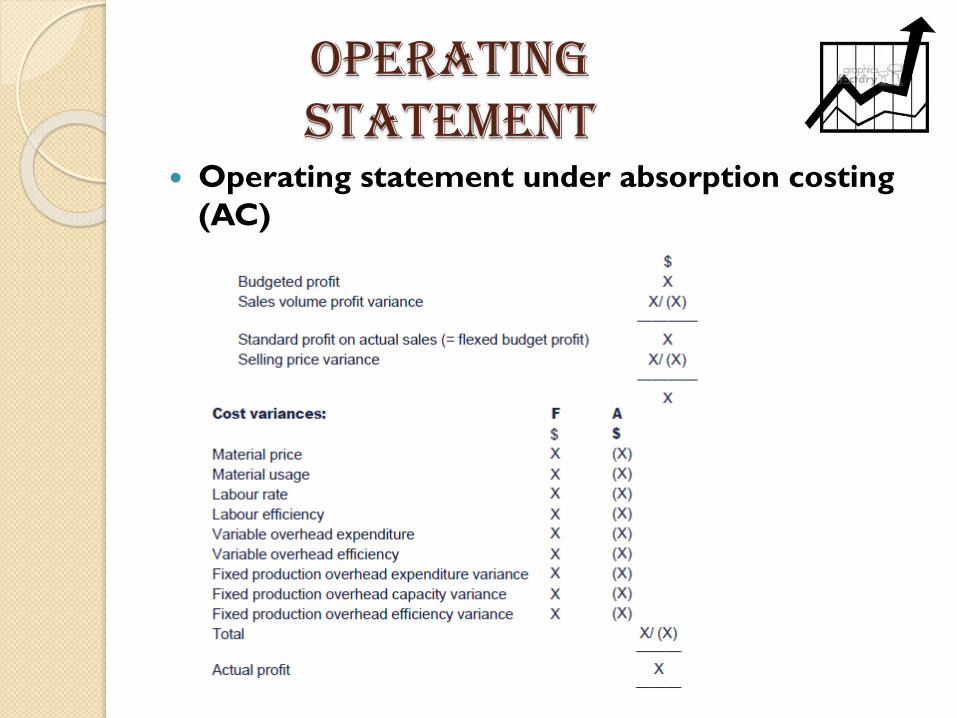

operating statement

Operating statement under absorption costing

(AC)

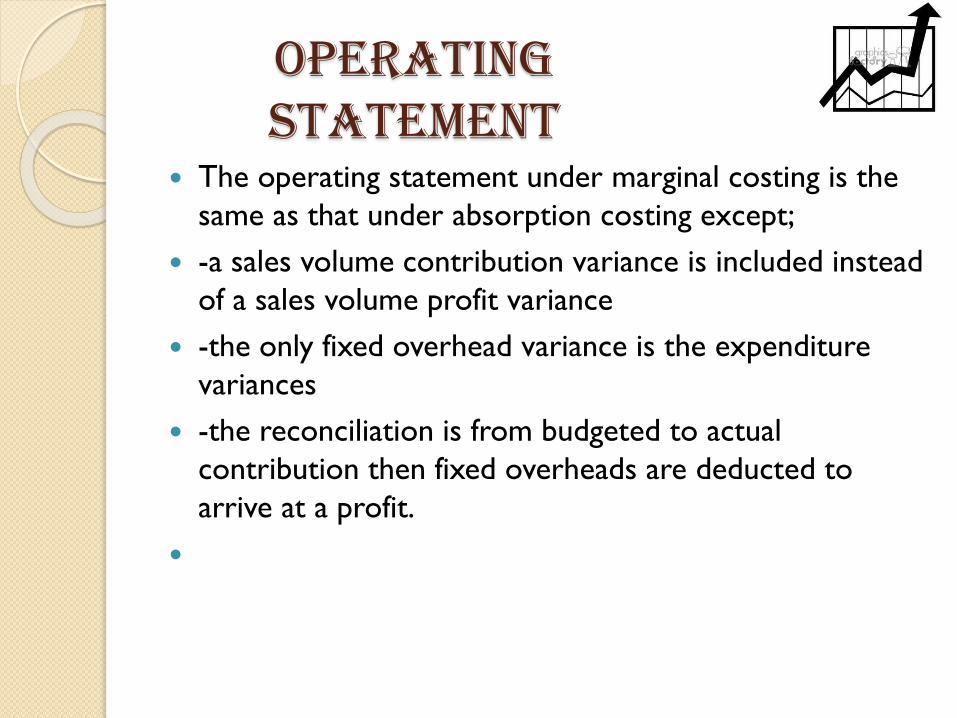

operating statement

The operating statement under marginal costing is the

same as that under absorption costing except;

-a sales volume contribution variance is included instead

of a sales volume profit variance

-the only fixed overhead variance is the expenditure

variances

-the reconciliation is from budgeted to actual

contribution then fixed overheads are deducted to

arrive at a profit.

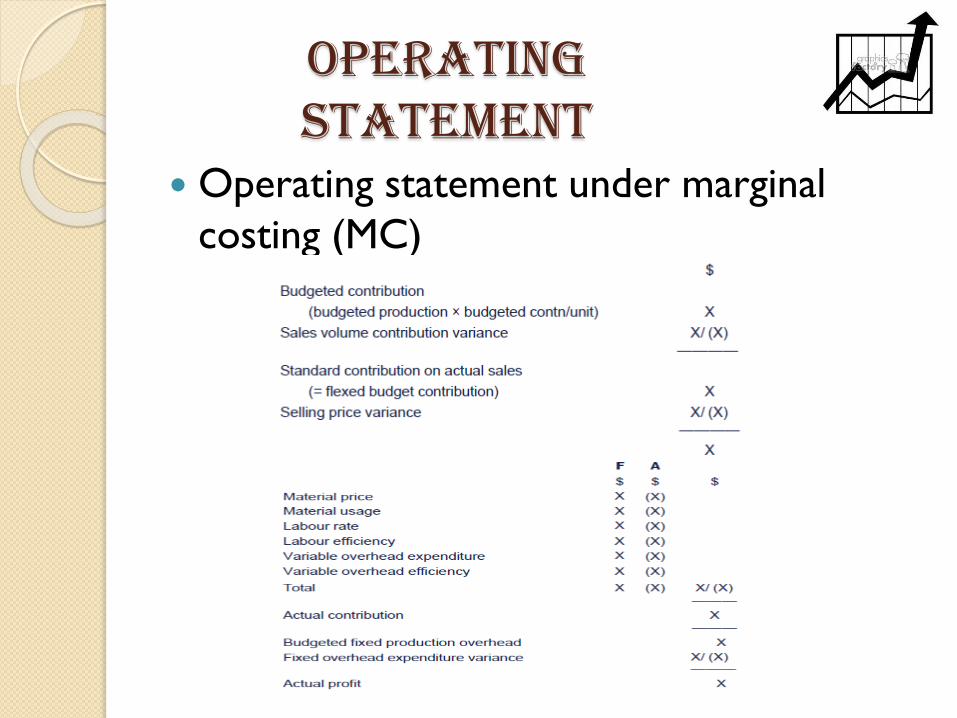

operating statement

Operating statement under marginal

costing (MC)

Reconciliation of budgeted and actual resultsDefinition: Budget reconciliation is the process of reviewing transactions and supporting documentation, and resolving any discrepancies that are discovered.

The process encompasses two different activities or roles:

Detailed review of transactions and supporting documentation (department staff)

High level budget review and analysis by a person accountable for the budget (budget reviewer).

Reconciliation of budgeted and actual results

Budget Reconciliation is not the same as ProCardreconciliation or any other transaction verification process required by a specific system or overseeing authority (e.g. a granting agency).

Your departmental reconciliation process should cover these requirements as well as the general budget reconciliation guidelines outlined here.

Purpose: Regular reconciliation should be done in your department to provide reasonable assurance that transactions are authorized, reasonable, allowable, and correct.

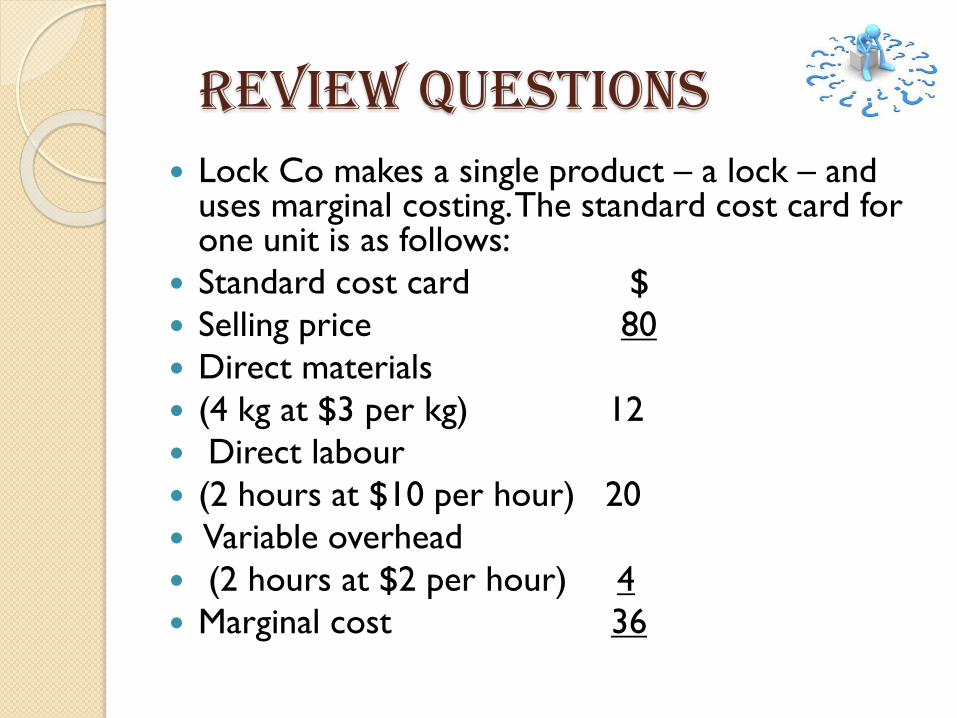

Review questions Lock Co makes a single product – a lock – and

uses marginal costing. The standard cost card for one unit is as follows:

Standard cost card $

Selling price 80

Direct materials

(4 kg at $3 per kg) 12

Direct labour

(2 hours at $10 per hour) 20

Variable overhead

(2 hours at $2 per hour) 4

Marginal cost 36

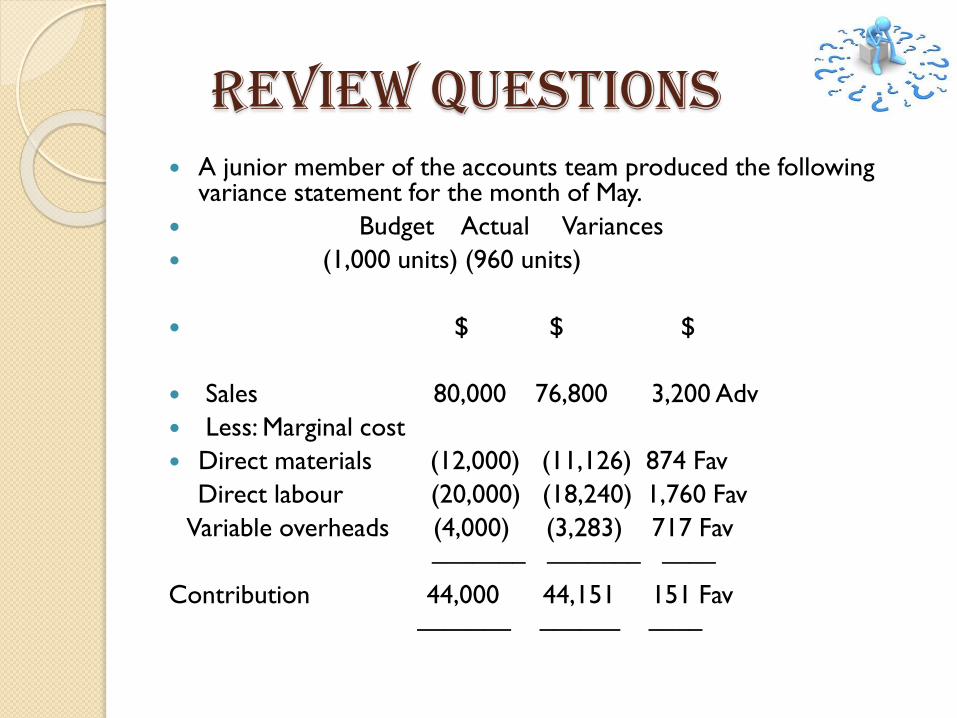

Review questions A junior member of the accounts team produced the following

variance statement for the month of May.

Budget Actual Variances

(1,000 units) (960 units)

$ $ $

Sales 80,000 76,800 3,200 Adv

Less: Marginal cost

Direct materials (12,000) (11,126) 874 Fav

Direct labour (20,000) (18,240) 1,760 Fav

Variable overheads (4,000) (3,283) 717 Fav

––––––– ––––––– ––––

Contribution 44,000 44,151 151 Fav

––––––– –––––– ––––

Review questions Lock Co used 3,648 kg of materials in the period and

the labour force worked – and was paid for – 1,824 hours.

Until now, Lock Co has had a market share of 25%. In the month of May, however, the market faced an unexpected

10% decline in the demand for locks.

Required:

(a) Prepare a statement which reconciles budgeted contribution to actual contribution in as much detail as possible. Do not calculate the sales price and the labourrate variances, since both of these have a value of nil.

BIBLIOGRAPHY

F2.washington.edu, (2015). GL & Budget Reconciliation | Financial

Accounting. [online] Available at: http://f2.washington.edu/fm/fa/gl-budget-

reconciliation [Accessed 30 Sep. 2015].

Anon, (2015). [online] Available at:

http://www.cimaglobal.com/Documents/Student%20docs/2011_CBA/C01_

variances_jan04.pdf [Accessed 30 Sep. 2015].

Acca global .com. N.p., 2015. Web. 7 Oct. 2015.

Kfknowledgebank.kaplan.co.uk, (2015). [online] Available at:

http://kfknowledgebank.kaplan.co.uk/KFKB/Wiki%20Pages/Variance%20

Analysis.aspx [Accessed 29 Sep. 2015].