Embed Size (px)

Citation preview

Report No. 5906-MA

Malaysia:Industrializing a Primary ProducerOn Two Volumes) Volume I

June, 19%6

East Asia and Pacific Programs Department

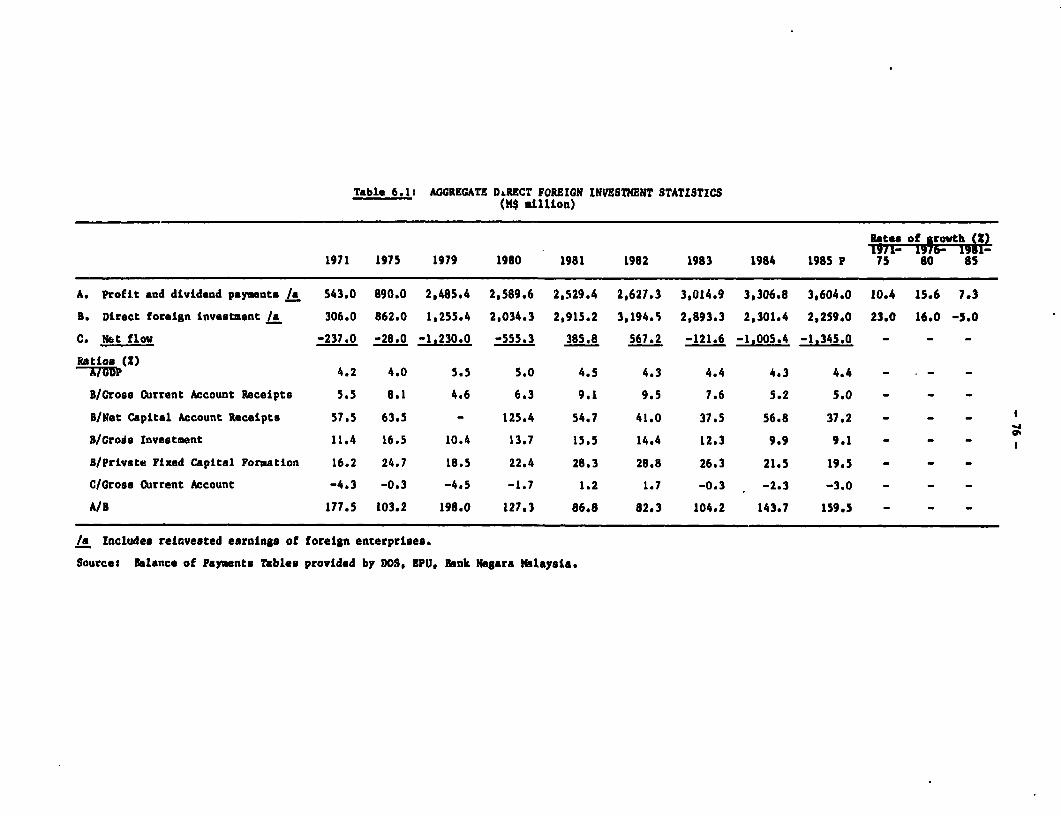

FOR OFFICIAL USE ONLY

Docunent-of the World Bank

This report has a restficted distribution and may be used by recipientsonly in th performance of ther official duties. Its contents may not otherwisebe disdosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit - Ringgit (M$)

1985 March 1986US$1 = M$2.48 M$2.53M$1 = US$0.40 US$0.40

FISCAL YEAR

January 1 - December 31

ABBREVIATIONS

2MP - Second Malaysia Plan (1971-75)3MP - Third Malaysia Plan (1976-80)4MP - Fourth Malaysia Plan (1981-85)5MP - Fifth Malaysia Plan (1986-90)ACI - Action Com,ictee for IncentivesEPF - Employees Provident FundFAMA - Federal Agricultural Marketing AuthorityFAS - United States Dept. of Agriculture Foreign

Agriculture ServiceFELCRA - Federal Land Consolidation and Rehabilitation

AuthorityFELDA - Federal Land Development AuthorityFTZ - Free Trade ZoneICA - Industrial Coordination ActLMW - Licensed Manufacturing WarehouseLPN - National Paddy and Rice AuthorityMADA - Muda Agricultural Development AuthorityMAS - Malaysia Airlines SystemMIDA - Malaysian Industrial Development AuthorityMIPS - Malaysian Industrial Policy StudiesMOA - Ministry of AgricultureMOPGC - Malaysian Oil Palm Growers' CouncilNEP - New Economic PolicyNFPE - Nonfinancial Public EnterprisePERNAS - Perbadanan Nasional BerhadPETRONAS - Petroleum Nasional BerhadPNB - Permodalan Nasional BerhadRISDA - Rubber Industry Smallholder Development AuthorityUSDA - United States Department of Agriculture

FOI eFmCI USE ONLY

This report was prepared by a team that visited Malaysia in July1985. The mission consisted of S. Yusuf (mission chief), D. Bhattasali,W. Cuddihy, S. Faruqi, and R. K. Peters, Jr. The Institute of Strategic andInternational Studies in Kuala Lumpur prepared reviews on four industrialsubsectors. Ms. Helen Callaghan provided assistance in Washington. Thereport was discussed with the authorities in January 1986 and the finalversicn reflects the comments received and is updated on the basis of freshstatistics provided in April 1986. Mr. Vikraz Nehru contributed to therevision.

Ths dowument hu a timed dinrbuio and may be ued by rcipien ondy in te pefonneof their oiidudteL. Its ctent may not odrwe be dicked withut Word hnkauthoriatdon.

ABSTRACT

The report examines Malaysia's prospects for developing export-oriented manufacturing industries on the economic base provided by its primarysectors while persevering with the adjustment program begun in 198S. Malaysiahas an efficient tree crop sector and substantial petroleum resources, but oilproduction is approaching its peak, rubber output is on a declining trend andearnings from palm oil and cocoa, the two most lucrative agricultural exportsof recent years, will take time to recover from the price slump that hasafflicted commodity markets. During the remainder of the eightiea, thecontribution of these subsectors to the growth of the GDP is likely to bemodest. The cut in energy and raw material prices in 1985-86 has also erodedgovernment revenues and the economy's potential for saving. Achievingbalance-of-payments equilibrium and containing the increase in external debtmake a further spell of fiscal austerity unavoidable, and this is underlinedby the restrained investment program outlined in the Fifth Five-Year Plan. Asneither government spending nor the primary sector will contribute signifi-cantly to growth, the report emphasizes the importance of broadening theindustrial base and promoting manufactured exports through major institutionalchanges and a reform of incentives as a way of regaining growth momentum.

MALAYSIA

INDUSTRIALTZING A PRIMARY PRODUCER

Table of ContentsPage No.

SUN ARY AND CONCLUSIONSe.e e...................... e e.............. i

I. TRENDS AND PROSPECTS..RS....C TS..1....e....................

A Changed Environent ........... 1Malaysia's Economy: Recent Developmnts...o............. 2Sources of Growth: Demand Factors....................... 5Sources of Growth: Sectoral Contributiono............... 7Decomposition of Gro w th.... 8Approach to Industrialization......... ............ o...o. 11

II. RESOURCE BALANCES AND THE PUBLIC SECTOR...................... 14

Deficits and Their Fiin .. .. . 15Revenue Generation Through the Tax Systemostem......... 20Spending Cuts...us.................. .... ..... o.......... 23

III. THE ROLE OF LABOR AND EXCHANCE RATES IN EXPORT-ORIENTEDDEVELOPfEfTessoooooeeeooooeeooooo.oo.ooooo.Esoo.o.ooe Tsoooose 28

Labor Markets in East Asia... sia....00............... 28Population and Industrial Progress..........og r e... ... 28Sectoral Labor Suppliesp....0..0... . .. .... 0.. ...... * ..... 29

~~~ 'ages ~~~~~~~~~~~30Wage Competitiveness .... .. 0. 00........0..... 35Exchange Rate Policyo.....y 38

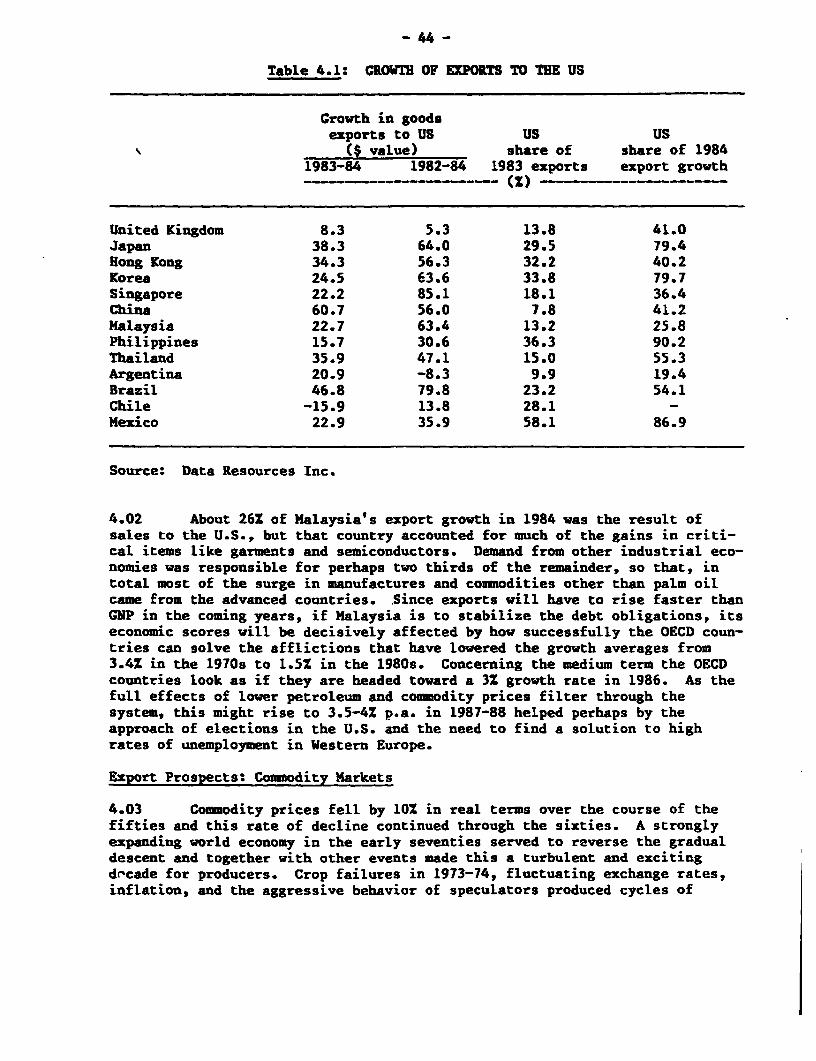

IV. THE FUTURE OF EXPORTS e. ..................................... 43

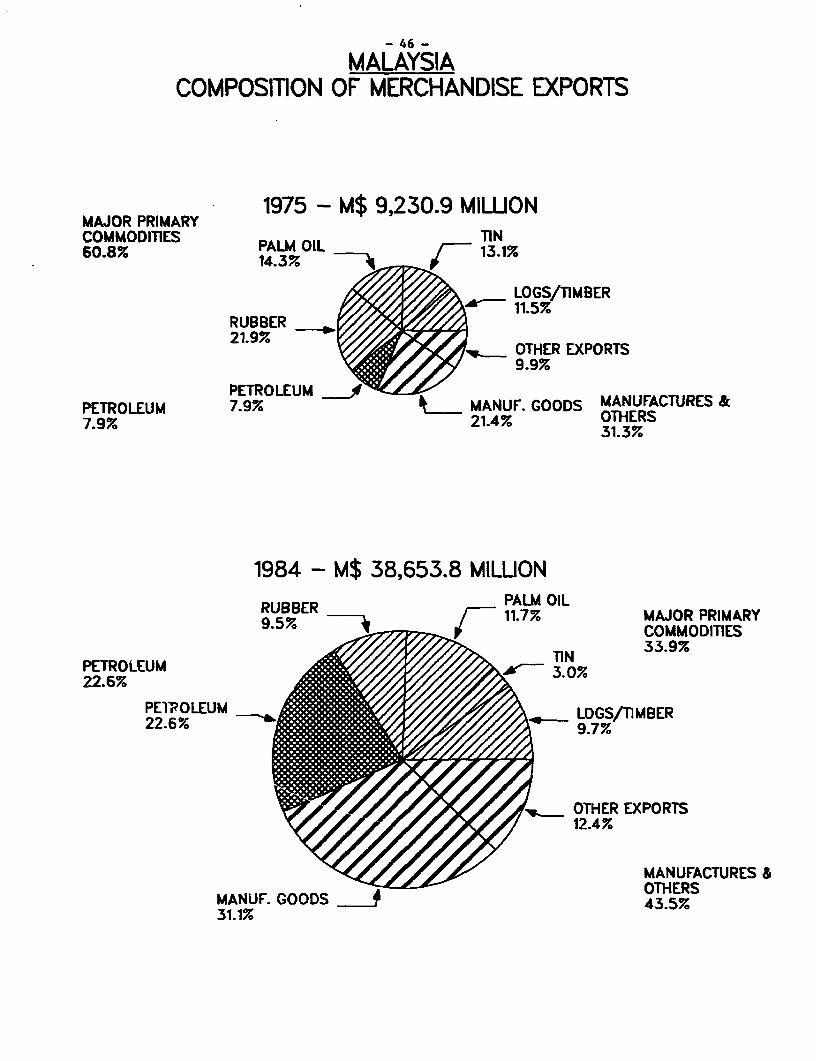

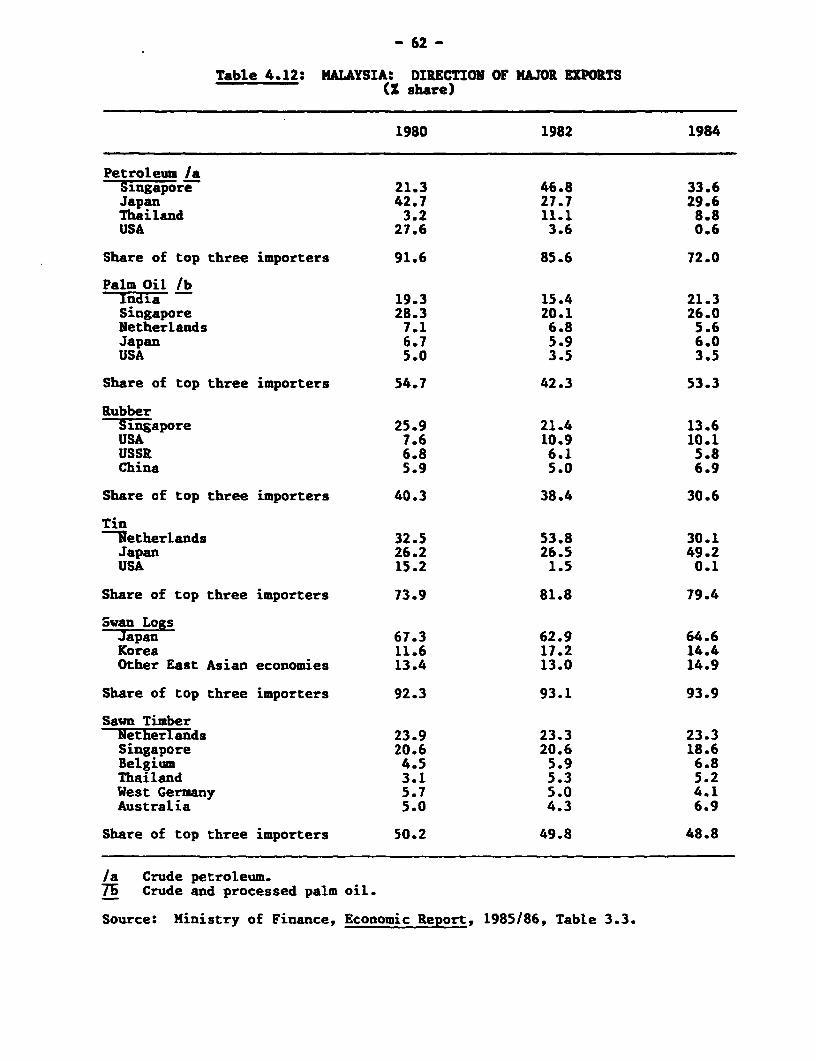

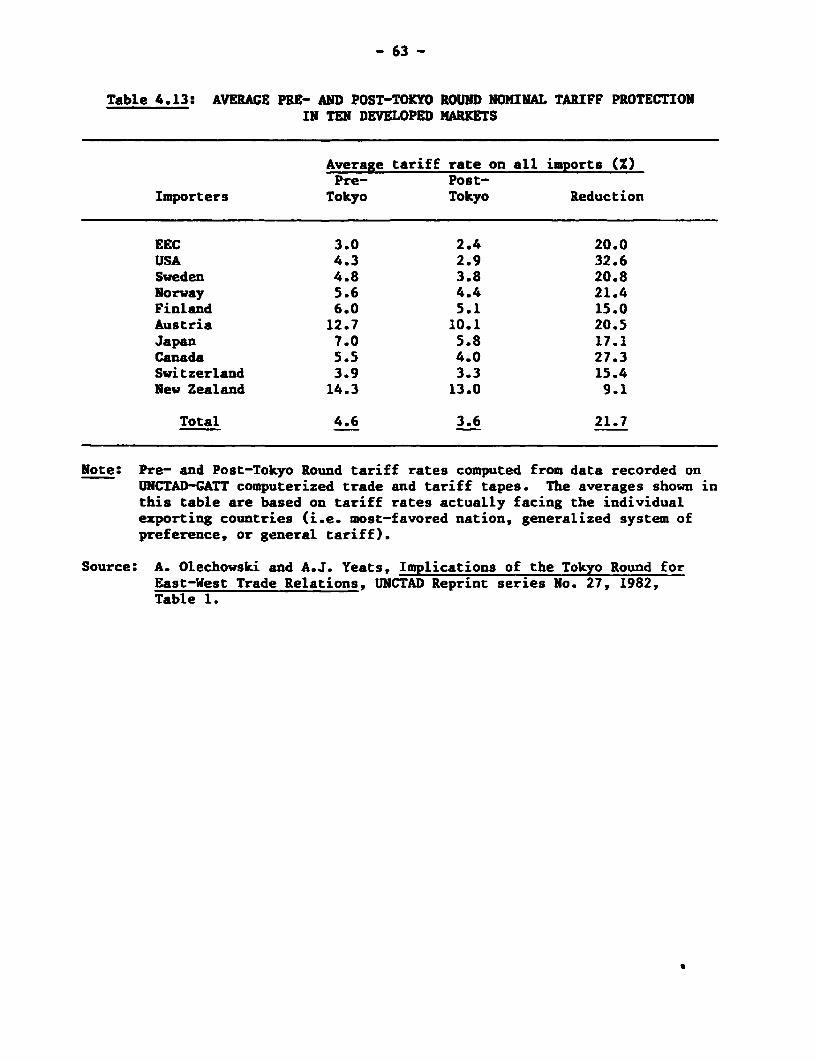

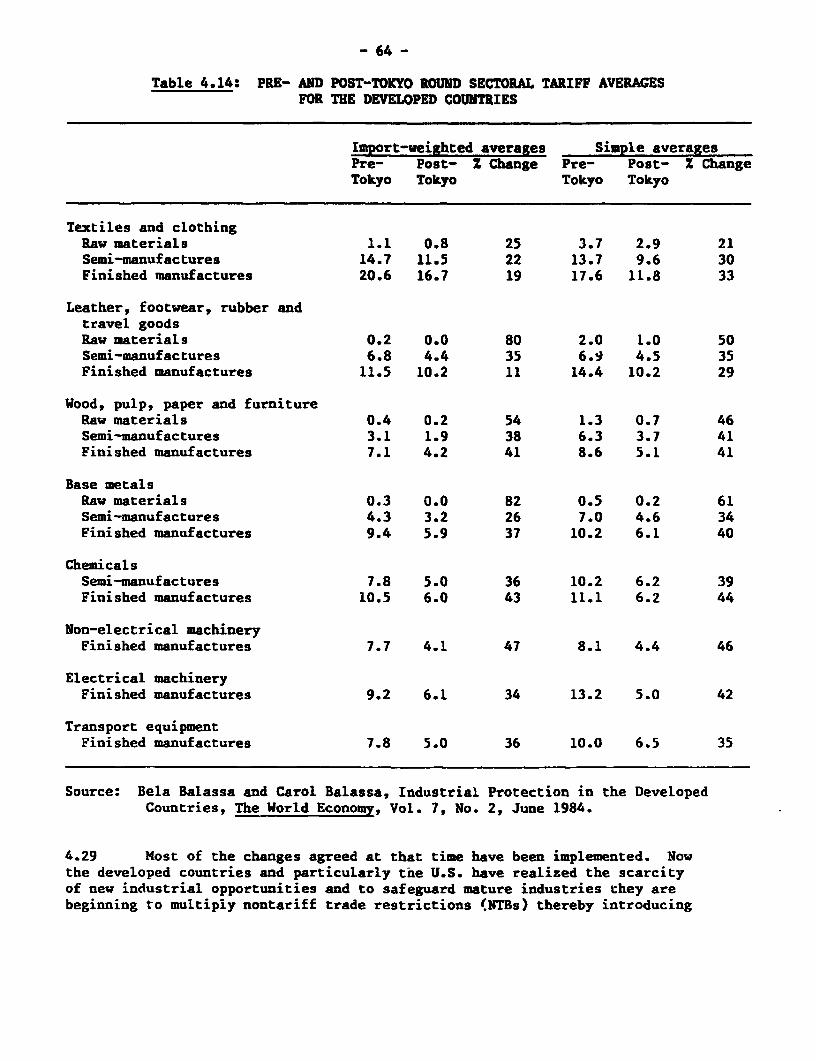

Export Prospects: Commodity Marketsr.k.e..et.s...... 44Export Prospects: Petroleum............................. 51Export Prospects: Manufactures............00O....... . 53Malaysia's Export Trader.................................. 59International Trading Environment ...... ................. 61

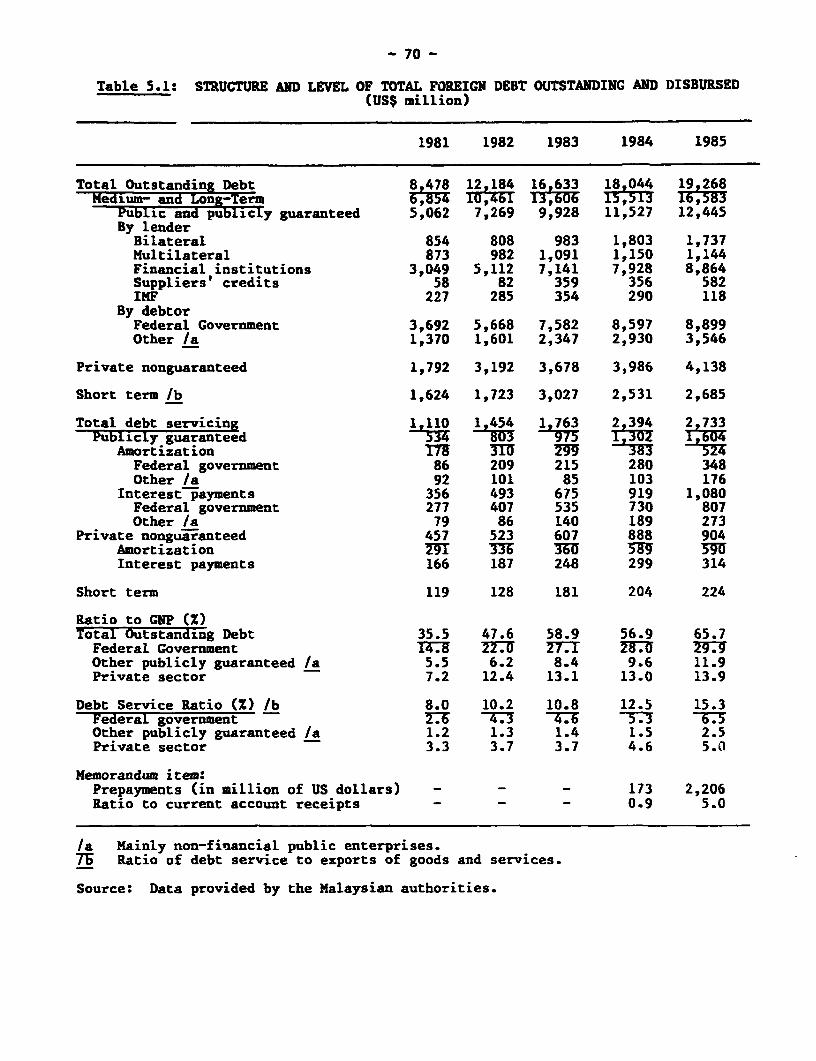

V. EXTERNAL BOnROWING AND CAPITAL FLS......................... 69

International Financial Markets ........... 0 . 71Equity Purchases and Capital Flows 71Regulating Capital Movementsv.... ....... 72

- ii -

Page No.

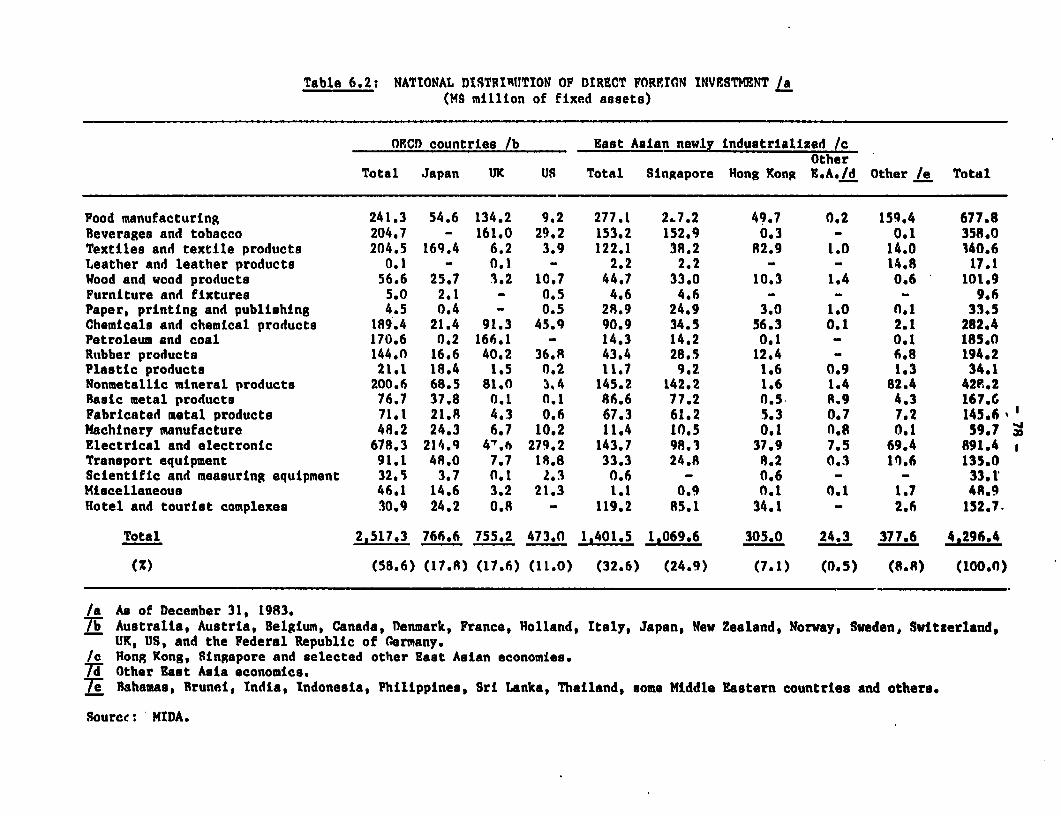

VI. DIRECT FOREIGN INVESTMENT AND ECONOMIC MODERNIZAIION ......... 74

Direct Foreign Investment in Malaysia.......o.o..oo ..... 74MNC Strategy and the Future of DFI....................... 77

VII. INDUSTRIAL STRATEGY AND DEVELOPMENT ...... .............. ..... o 82

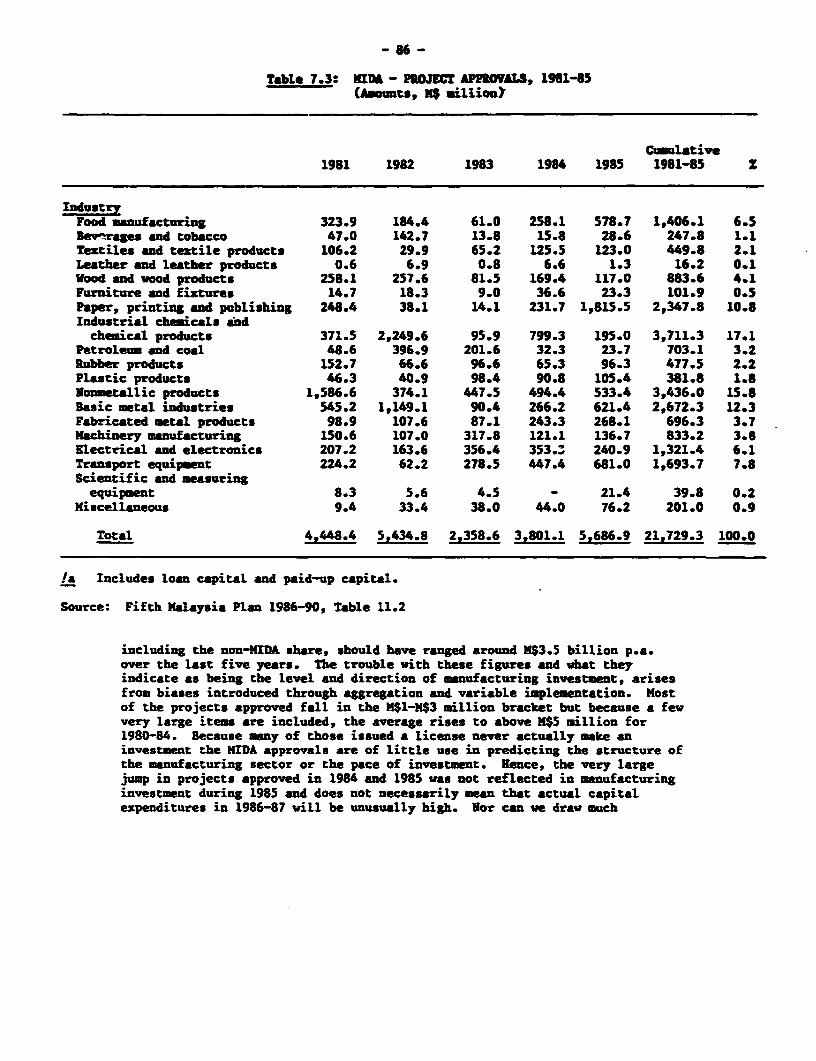

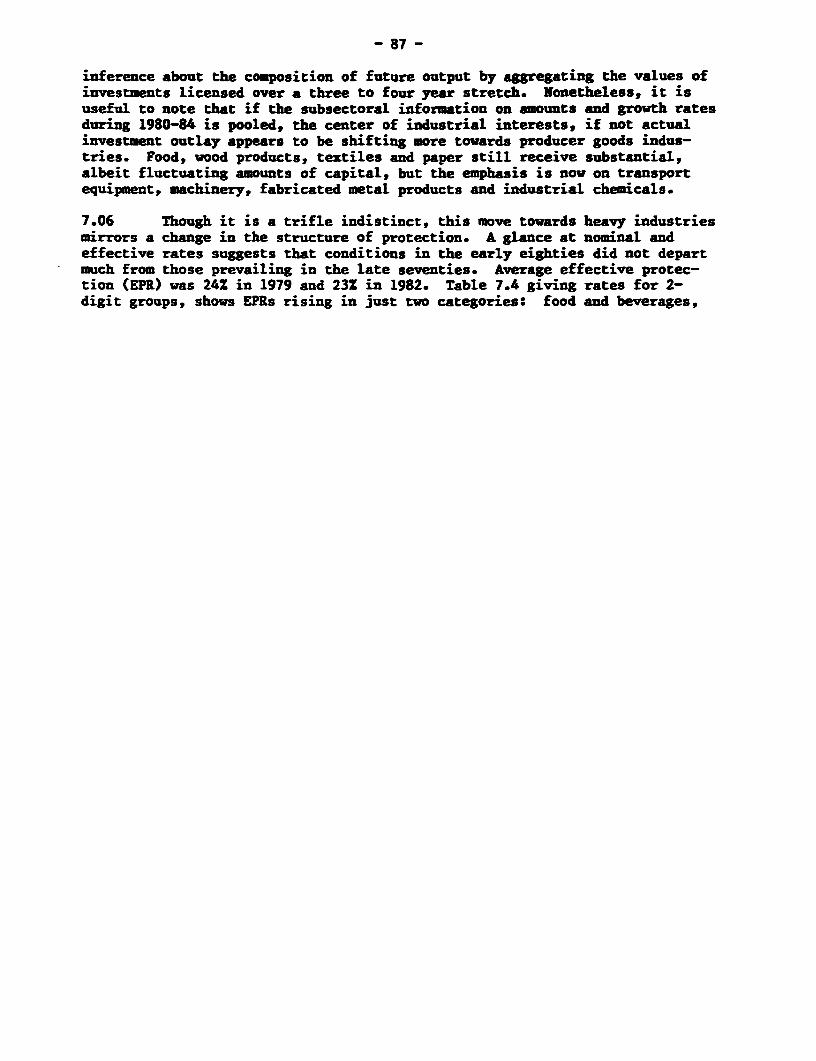

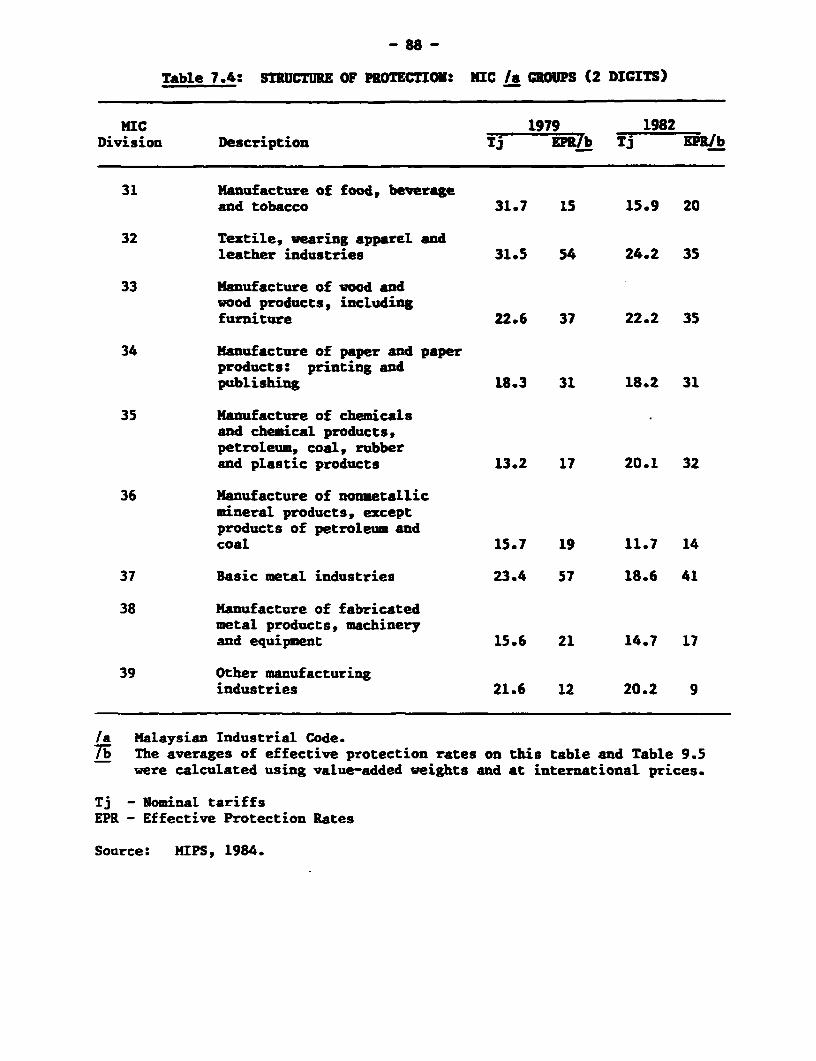

Strategy ........................... ................. 89Market Efficiency ........................................ 90Regulation ................... ............................ 93Industrial Deepening.....4 ......... ... 95Sectoral Constraints and Policies ...........ii..e....s 98Textiles and Clothing........... ........ .98Electrical Machinery and Applianceso.....oo 101Agricultural Machinery ..... ....... o**o . .0.. .. .... * 103Electronics...... 104Wooden Furniture ...... o ............ oG6....o6......... 108Rubber Products .... o... ..... ................... 109

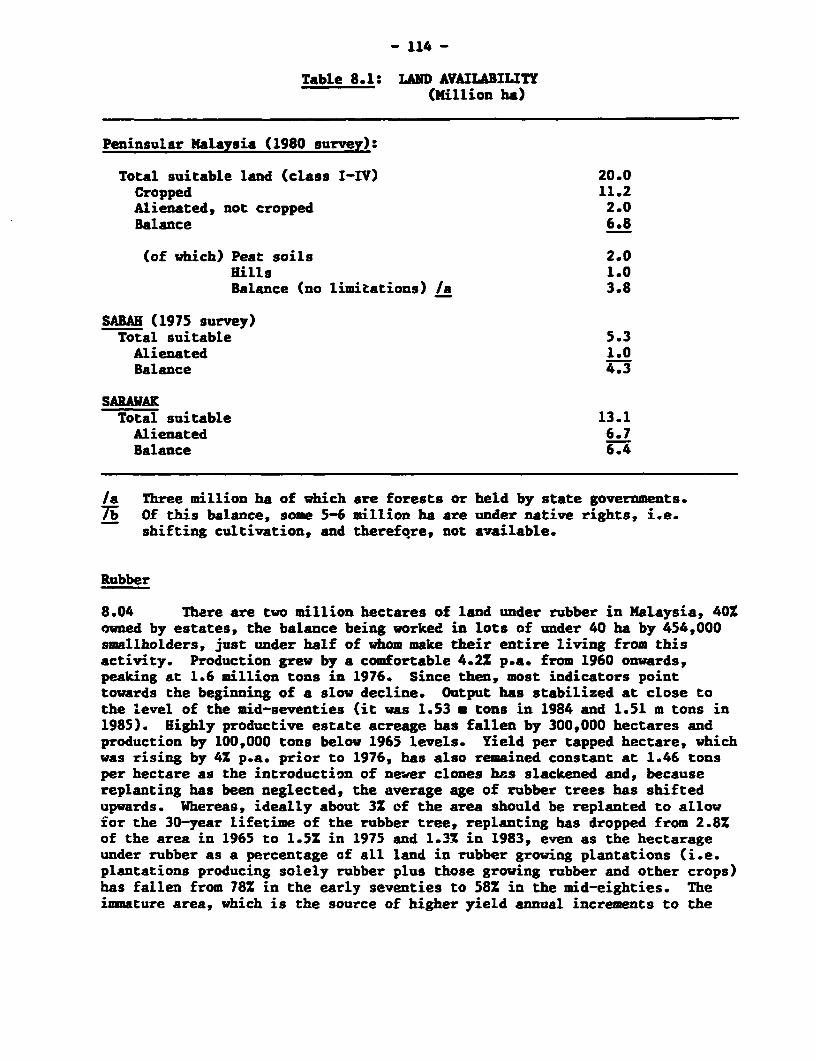

VIII. THE FUTURE OF AGRICULTURE. .... -o ............. .ooee............ 113

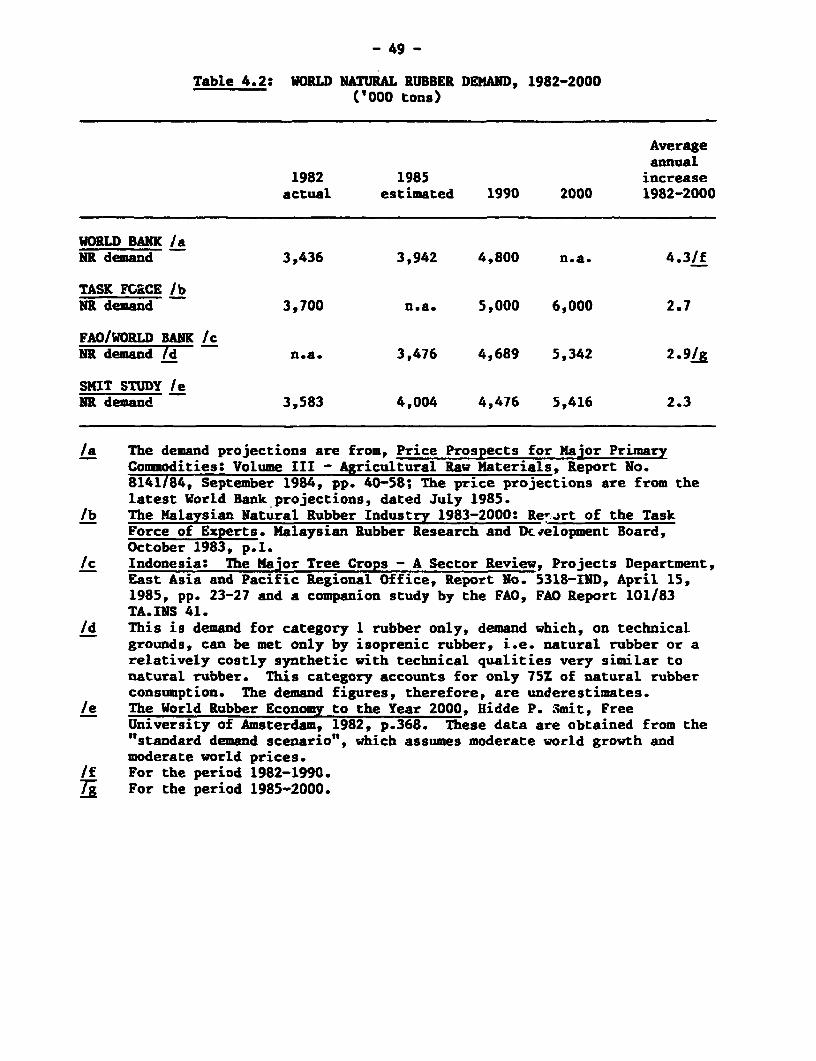

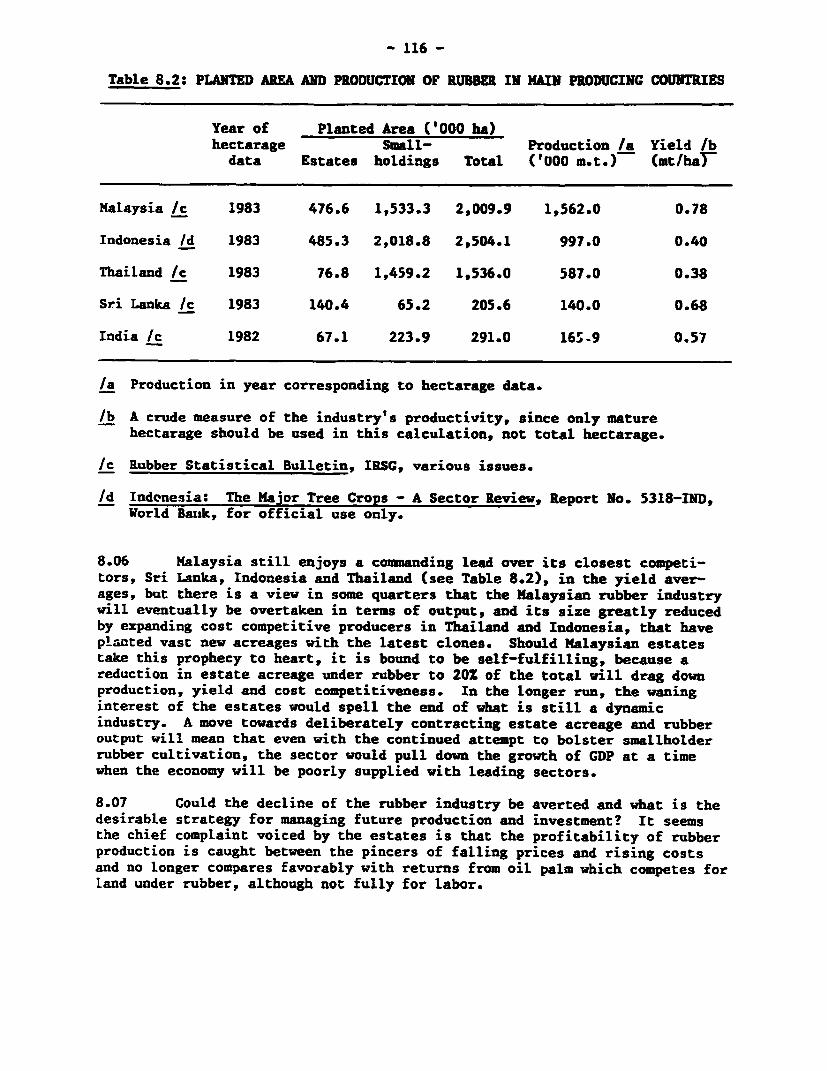

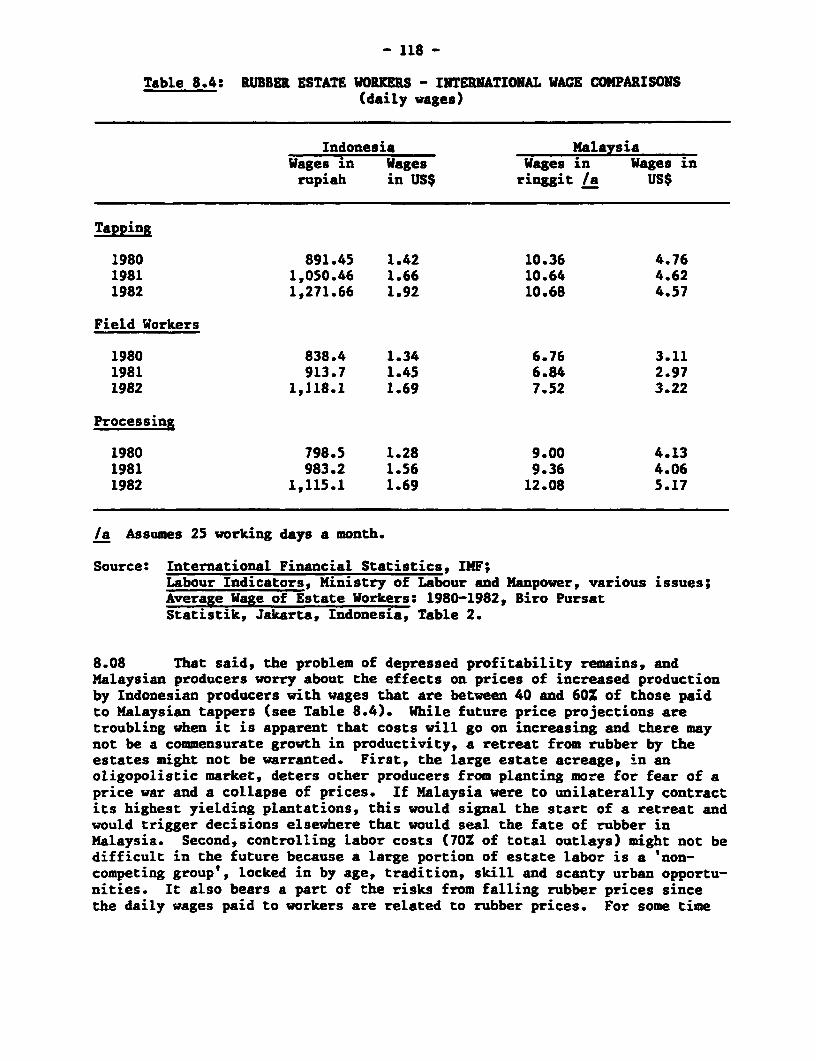

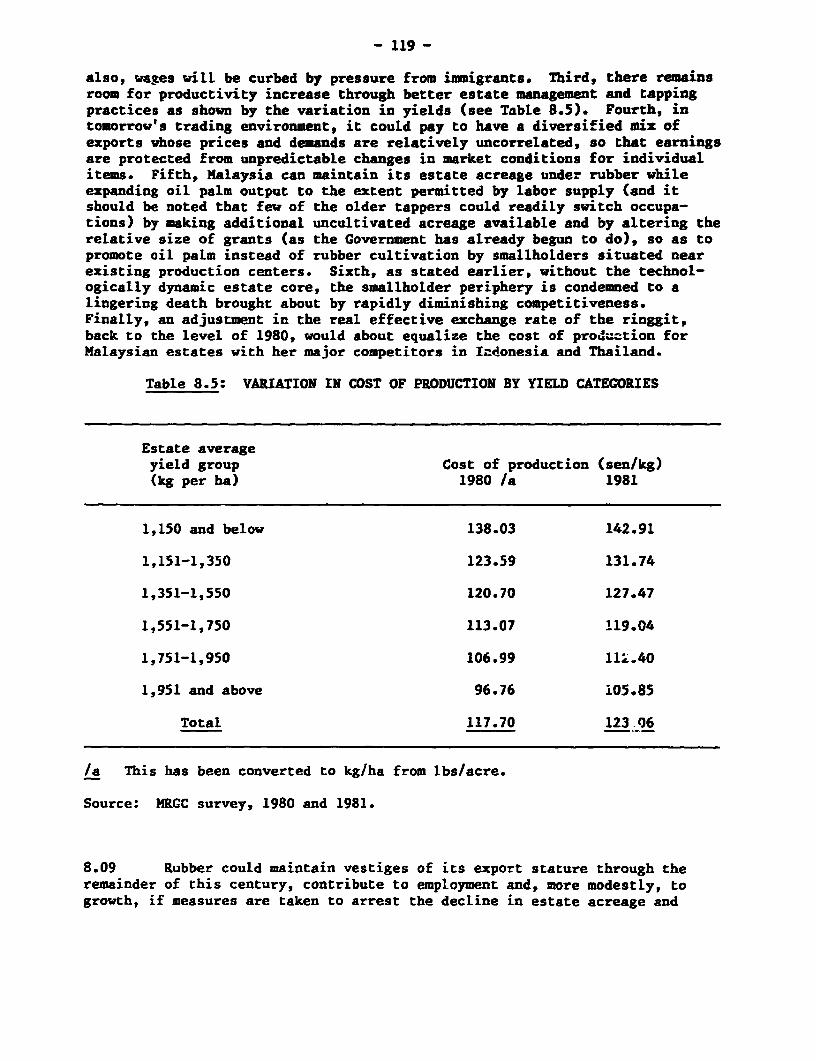

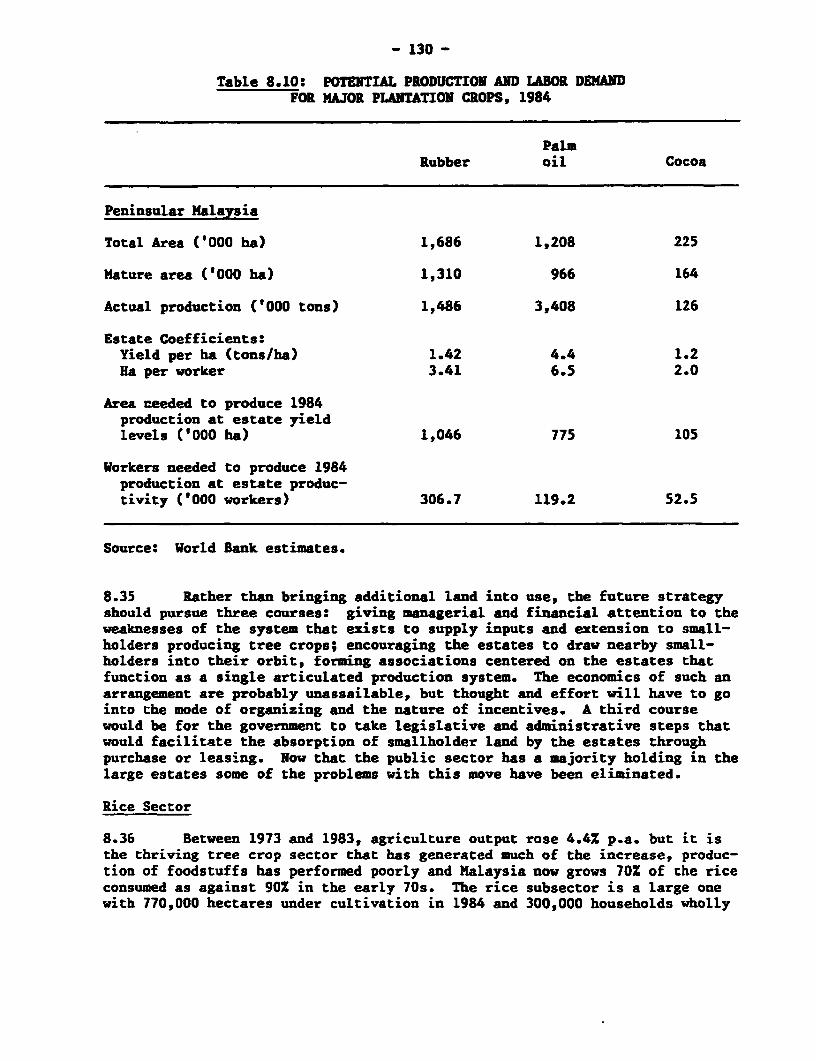

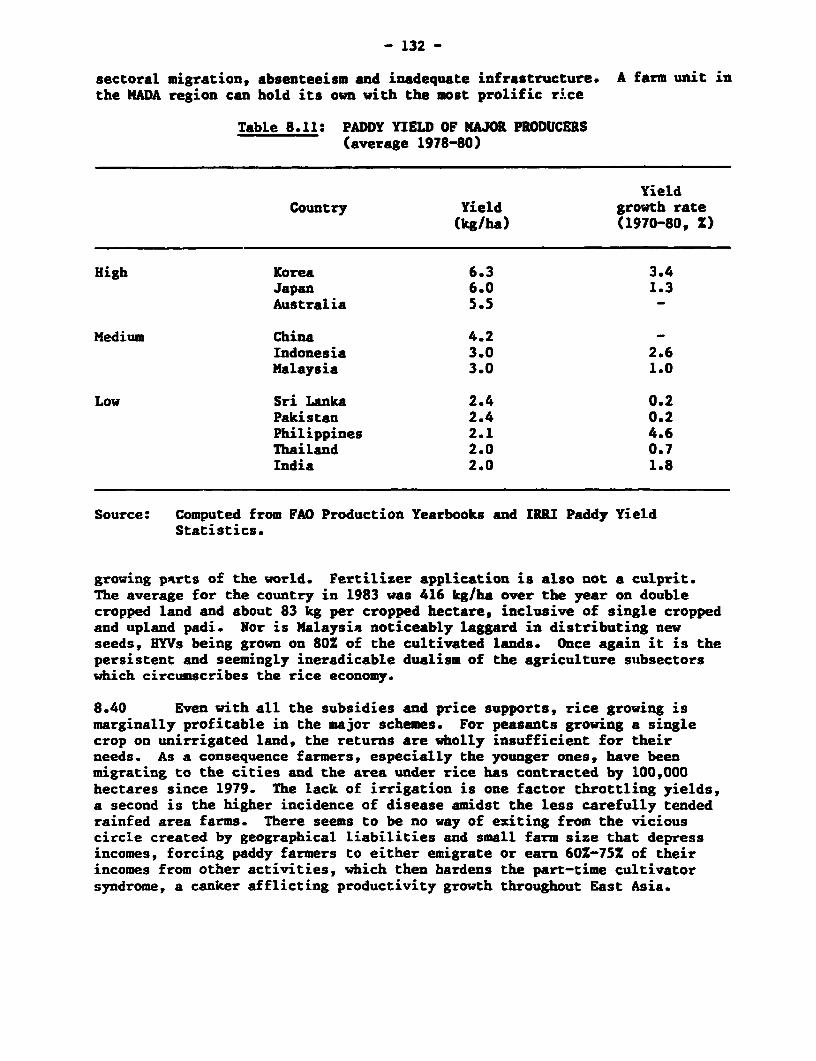

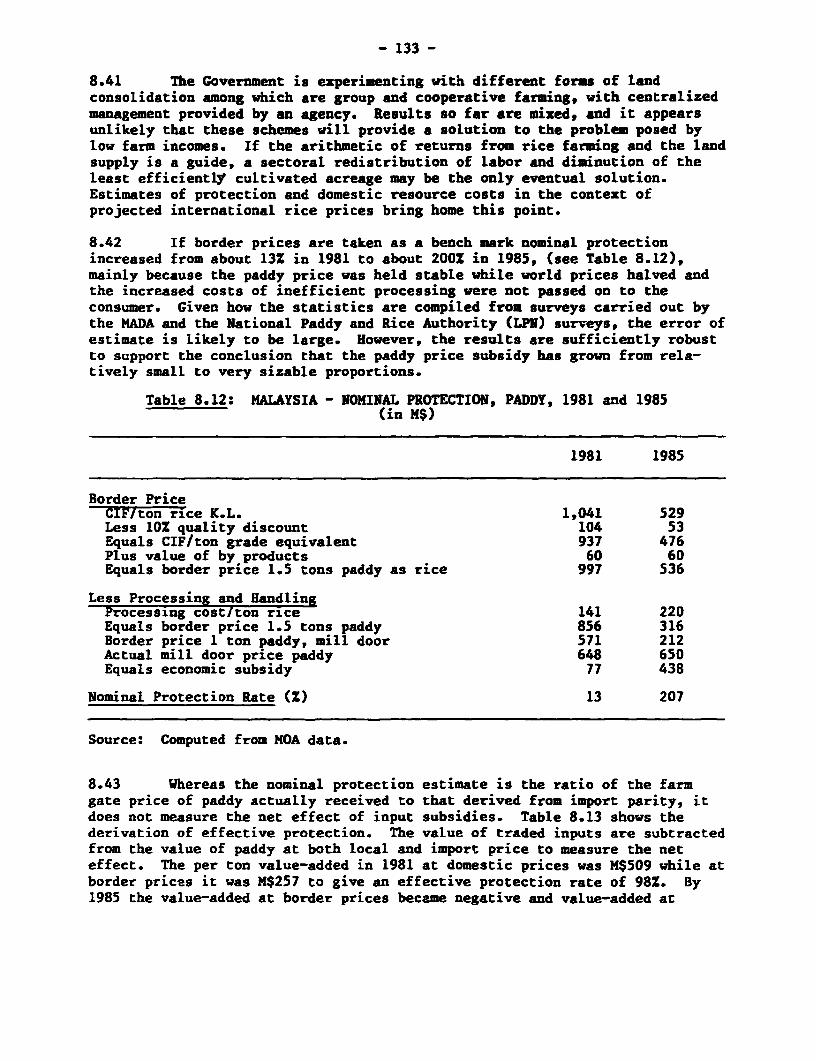

Rubber... .... .... o...... -...... 00.........e......00 .... 114Palm Oil ..... o........o............... ..... 122Cocoa ..........o.................................oo ... ....oe.woo.ooe.. 126Tree Crop Sector Summary ........... . .... .. ........-... 129Rice Sectoro............ oo............ ..... 60-000 ........ 130Overview .............. ..............- 13............. . ...... 136

IX. SIMULATINC THE FUT... .......... o.......................... 141

TABLES IN TEXT

l.1 Malaysia: Principal Macro In dicators ... 3 ...... .... 31.2 Malaysia: Demand Decomposition, Sources of Growth ........ oo 61.3 Malaysia: Sectoral Decomposition, Sources of Growth ......... 81.4 Malaysia: Factor Decomposition, Sources of Gro wth 9....- .... g1.5 Malaysia: Allocation of Credit by Sector............... 12

2.1 The Evolution of Resource Balances in the Economy...*......... 152.2 Public Sector Rescurce Balance ............. .................. 162.3 Nonbank Sources of Budget Finance ............... ................... 172.4 Savings Performance of the Federal Government...............O.. 192.5 Public Enterprise Statistics..................... 192.6 Structure of Public Sector Revenues ..... ........................ 202.7 Tax Revenue Buoyancies, 1960-85.................. .............. ... 212.8 Economic Classification of Federal Operating Expenditures ..... 242.9 Federal Subsidy Expenditures ........ ............... ..... *...... 252.10 Federal Government Development Expenditures by Sector..o....... 27

-iii -

Page No.

3.1 Malaysia: Real Average Monthly Earnings in Manufacturing31

3.2 Malaysia: Employment and Productivity by Sector.....ctor..... 323.3 Trend in Employment by Major Occupational Groups, Peninsular

Malaysia, 1962-70 .......- .......................... 343.4 Occupational Structure of Public Sector Employment and All

Urban Employment in Peninsular Malysia yi.a...e9oee*.*9e 343.5 Nominal Average Monthly Earnings in Manufacturing.....o....... 363.6 Value-Added per Worker ...... 373.7 Malaysia: Female Participation in Employment by Sectors,

1 9 5 7 -79oee.*oee**.a..ooooo... es.9 . 383.8 Malaysia: Index of Nominal and Real Effective Exchange

41

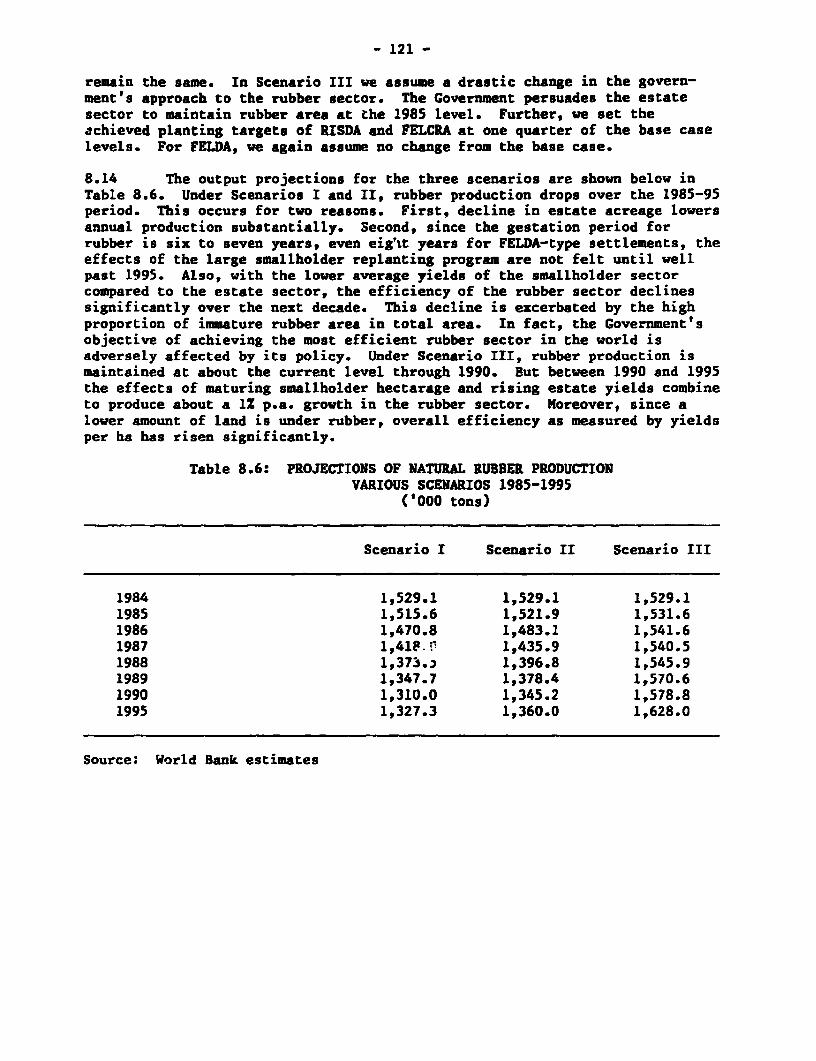

4.1 Growth of Exports to the USA.............. ...... ....... 444.2 World Natural Rubber Demand, 1982-2000..........8 494.3 World Production of Major Oils and Fats....................... 504.4 Annual Growth Rates of LDCs' Manufactured Exports............. 544.5 Share of Manufactured Exports in Total Exports................ 544.6 Share of Developed Market Economies in Manufactured Exports

of LDCD.......C.......s. ........... 554.7 Largest Manufactured Exports from Selected Asian Countries

to Major OECD Economies .................. .56

4.8 Fastest-Crowing Manufactured Exports from Selected AsianCountries to Major OECD Economies.... ..... 57

4.9 Malaysia: Merchandise Es p os............................... 594.10 Malaysia: Exports by Destination............................. 604.11 Malaysia: Largest Manufactured Exports to Major OECD

E c o n o m i es-ooo .... o.e.ooee..e ...... ee..000 .... 0-900.04-.. 604.12 Malaysia: Direction of Major Exports.... 624.13 Average Pre- and Post-Tokyo Round Nominal Tariff Protection

in the Developed Markets................ ......... ...... .... 634.14 Pre- and Post-Tokyo Round Sectoral Tariff Averages for the

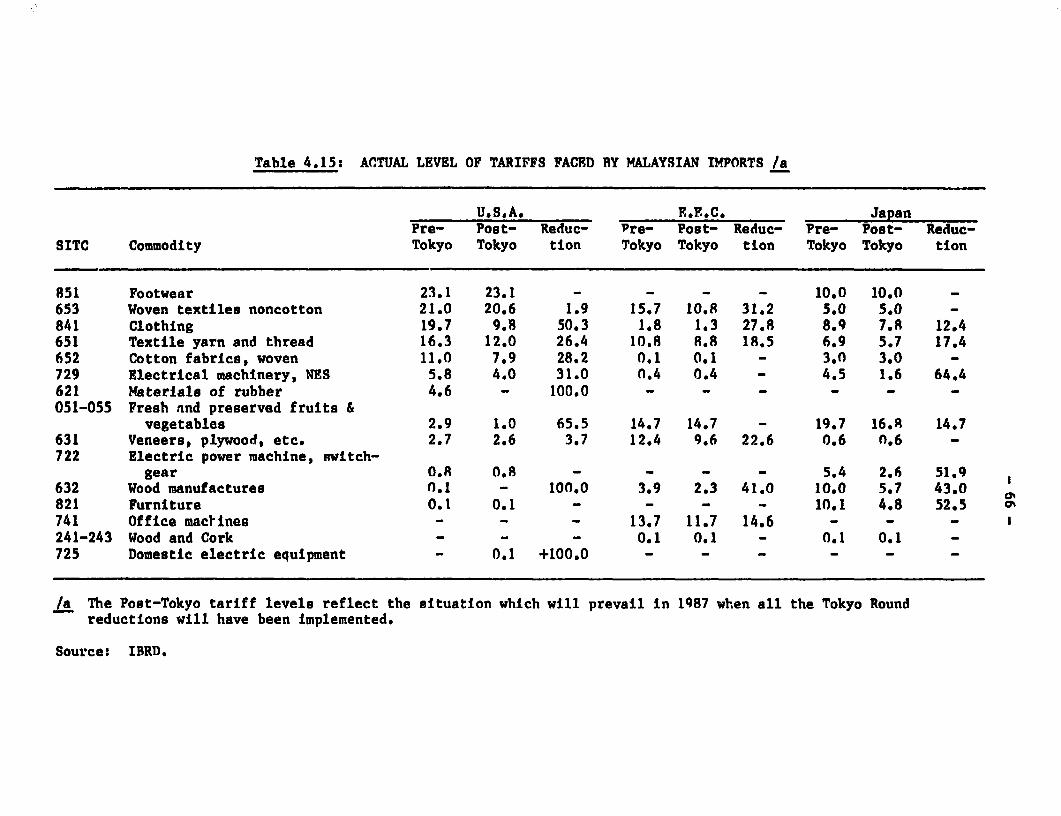

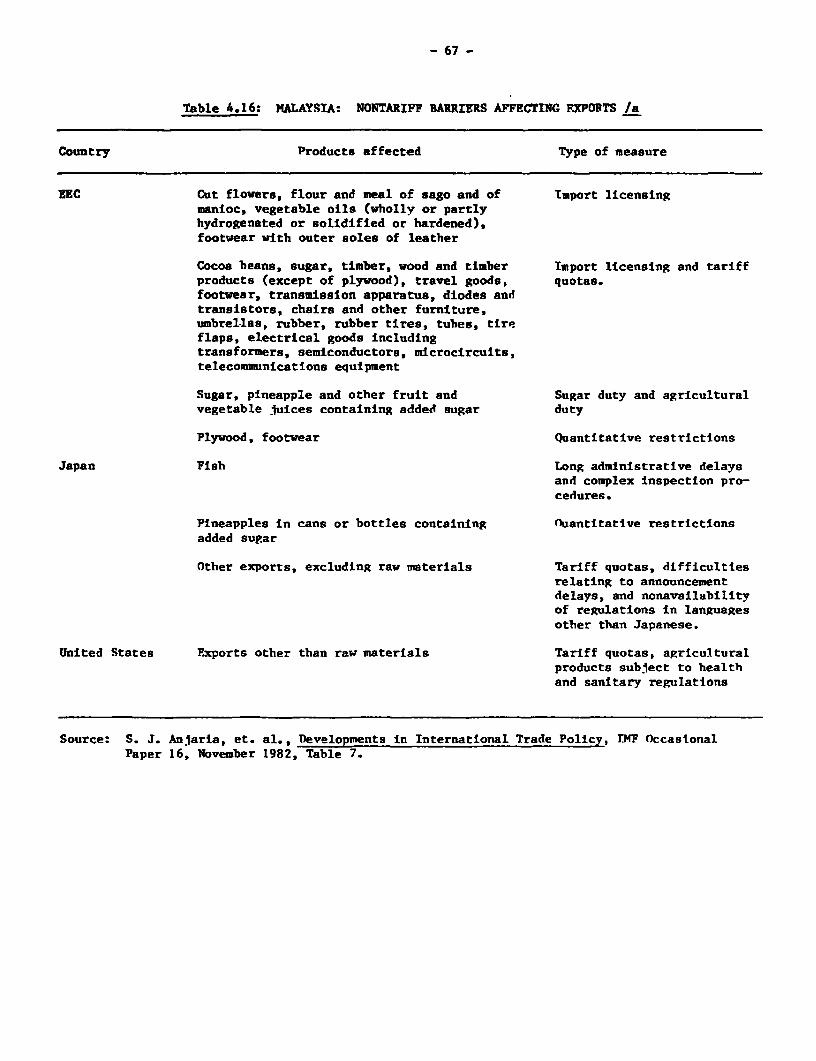

Developed Countries.....ou.n............... r ............... 644.15 Actual Level of Tariffs Faced by Malaysian Imports .664.16 Malaysia: Nontariff Barriers Affecting Exports............... 67

5.1 Structure and Level of Total Foreign Debt Outstanding andDisbursed ........ ........ ......... * ............ ....... 70

5.2 Ownership or Corporate Assets in Malaysia .725.3 Errors and Omissions in the Balance of Payments 73

6.1 Aggregate Direct Foreign Investment Statistics.............. 766.2 Malaysia: National Distribution of Direct Foreign Investment 78

7.1 Industrial Sector - Basic Data............. t..... ........ .. 847.2 MIDA - Project Approvals, 1981-85 (No. of Projects)........... 857.3 MIDA - Project Approvals, 1981-85 (Amounts). u.n..o............ 867.4 Structure of Protection: MIC Groups (2 Digits) ........ o.... &... 887.5 Structure of Protection: End-Use Groups.......... ...... &... 897.6 Characteristics of the Asian Electronics Industryu............ 1057.7 Composition of Electronic Sector Output....................... 107

-iv-

Page No.

8.1 Land Availabiity ............. ..... ......... ... e** 1148.2 Planted Area and Production of Rubber in Main Producing

8.3 Malaysia: Cost of Production for Rubber Estates.............. 1178.4 Rubber Estate Workers - International Wage Comparisons ........ 1188.5 Variation in Cost of Production by Yield Category.............. 1198.6 Projections of Natural Rubber Production - Various

Scenarios, 1985-95 ... oooeooeoeeeomasoeo..... .............................. 1218.7 Malaysia: Basic Statistics on Palm Oil..o ..... ........... . 1238.8 Estimated Economic Performance of Estates and Smallholdings,

Malaysia, 1984 o e o ms o o oe e o e eo o o..................oo.................... . 1248.9 Malaysia: Comparison of Tree Crop Coefficients ........... o 1288.10 Potential Production and Labor Demand for Major Plantation

Crops, 1984 ooooo.ooo*oeoo.s ... on.o.o ... oo............................ 130

8.11 Paddy Yield of Major Producers.o.o..o......................... 1328.12 Malaysia: Nominal Protection, Paddy, 1981 and 1985............. 1338.13 Malaysia: Effective Protection, Paddy, 1981 and 1985......... 1348.14 Malaysia: Domestic Resource Cost, Paddy...................... 1358.15 Malaysia: Grain Production, Import, Consumption.............. 139

9.1 Selected Macroeconomic Indicators - Base Case and Low Case.... 143

CHARTS AND GRAPHS

Malaysia - Nominal and Real Effective Exchange Rates. ........... o 42Malaysia - Composition of Merchandise Exports...... o.............. 46

MAP

IBRD 19374

Page 1 of 2

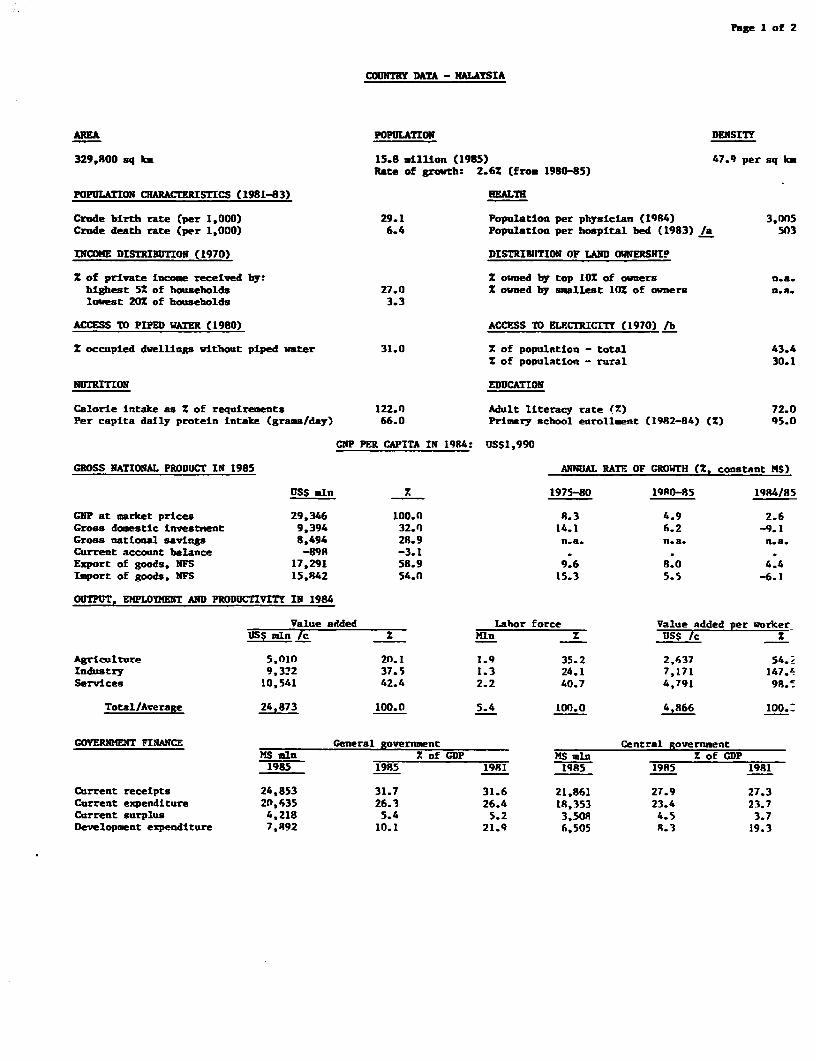

COUNTRY DATA - MALAYSIA

AREA POPULATION DENSITY

329,800 sq km 15.8 million (1985) 47.9 per sq kmRate of growth: 2.62 (from 1980-85)

POPULATION CHARACTERISTICS (1981-83) HEALTH

Crude birth rate (per 1,000) 29.1 Population per physician (1984) 3,005Crude death rate (per 1.000) 6.4 Population per hospital bed (1983) /a 503

INCOME DISTRIRUTION (1970) DISTRIRUTION OF LAND OWNERSHIP

2 of private income received by: Z owned by top 10X of owners n.a.highest 52 of households 27.0 Z owned by smallest 101 of owners n.a.lowest 20X of households 3.3

ACCESS TO PIPED WATER (1980) ACCESS TO ELFCTRICITY (1970) lb

Z occupied dwellings without piped water 31.0 X of population - total 43.42 of population - rural 30.1

NUTRITION EDUCATION

Calorie intake as 2 of requirements 122.0 Adult literacy rate (2) 72.0Per capita daily protein intake (grass/day) 66.0 Primary school enrollment (1982-84) (2) 95.0

GNP PER CAPITA IN 1984: US$1,990

GROSS NATIONAL PRODUCr IN 1985 ANNUAL RATE OF GROWTH (2, constant MS)

USS mln X 1975-80 19R0-85 1984/85

GUP at market prices 29,346 100.0 8.3 4.9 2.6Gross domestic investnent 9,394 32.0 14.1 6.2 -9.1Gross national savings 8,494 28.9 n.a. n.a. n.a.Current account balance -898 -3.1Export of goods. NFS 17,291 58.9 9.6 8.0 4.4Ioport of goods, NFS 15,842 54.n 15.3 5.5 -6.1

OUTPUT, EMPLOYMENT AND PRODUCTIVITY IN 1984

Value added Labor force Value added per workerUs$ min /c Z Mln 2 US5 /c Z

Agriculture 5,01n 20.1 1.9 35.2 2,637 54.;Industry 9.322 37.5 1.3 24.1 7,171 147.4Services 10,541 42.4 2.2 40.7 4,791 9S.'

Total/Average 24,873 100.0 5.4 100.0 4,866 100._

GOVENMMENT FINANCE General government Central governmentMS mln Z of GOP MS =In Z of CDP1985 1985 1981 1985 1985 1981

Current receipts 24,853 31.7 31.6 21,861 27.9 27.3Current expenditure 20,635 26.3 26.4 18,353 23.4 23.7Current surplus 4,218 5.4 5.2 3,50S 4.5 3.7Development expenditure 7,892 10.1 21.9 6,505 8.3 19.3

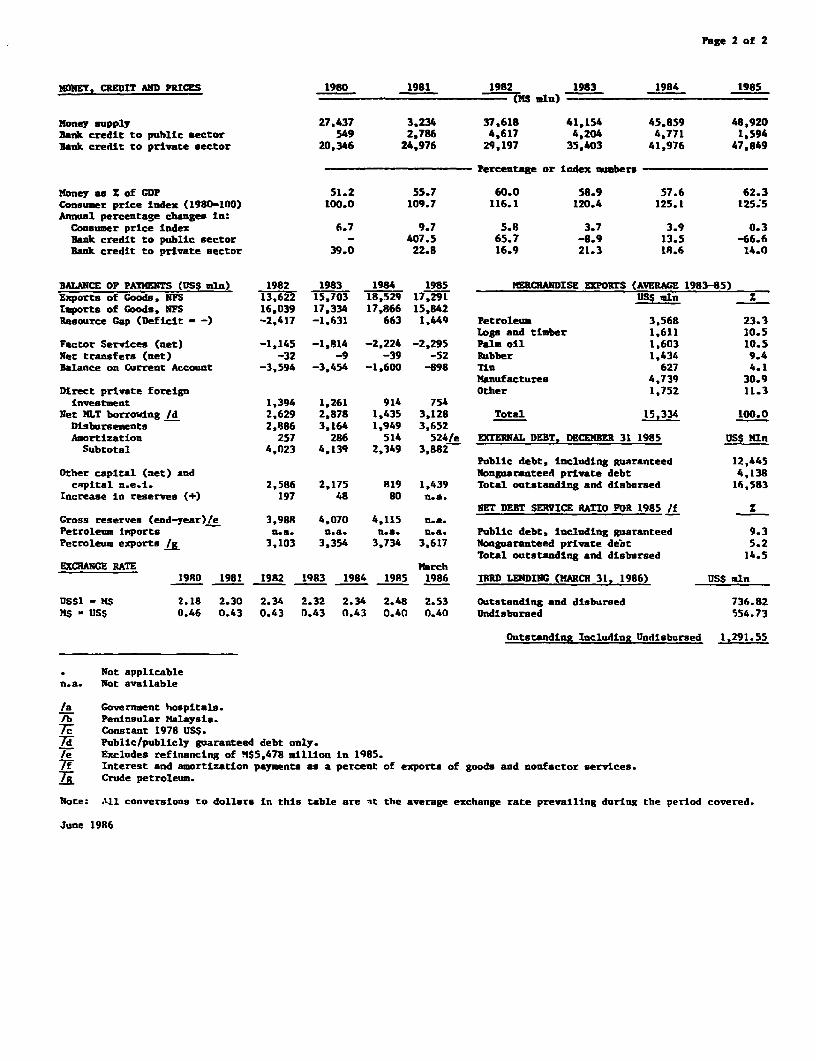

Page 2 of 2

MDNEY, CREDIT AND PRICZS 1980 1981 1982 1983 1984 1985

money supply 27,437 3.234 37,618 41.154 45.859 48,920Bank credit to public sector 549 2,786 4,617 4,204 4,771 1,594Bank credit to private sector 20,346 24,976 29,197 35,403 41,976 47.849

Percentage or Index numbers -

Honey as 2 of GDP 51.2 55.7 60.0 58.9 57.6 62.3Consumer price index (1980-100) 100.0 109.7 116.1 120.4 125.1 125.5Annual percentaSe changes In:

Consumer price lndex 6.7 9.7 5.8 3.7 3.9 0.3Bank credit to public sector - 407.5 65.7 -8.9 13.5 -66.6Bank credit to private sector 39.0 22.8 16.9 21.3 18.6 14.0

BALANCE OP PAYMENTS (US$ aln) 1982 1983 1984 1985 MERCNANDISE EXPORTS (AVERAGE 1983-85)Exports of Goods, NFS 13.622 15.703 18.529 17,291 US$ mln I

Imports of Goods, NFS 16.039 17,334 17.866 15,842Resource Gap (Deficit - -) -2,417 -1.631 663 1.449 Petroleum 3.568 23.3

Logs and timber 1,611 10.5Factor Services (net) -1,145 -1.814 -2.224 -2.295 Palm oil 1,603 10.5Net transfers (net) -32 -9 -39 -52 Ruibber 1,434 9.4Balance on Current Account -3,594 -3,454 -1.600 -898 Tin 627 4.1

Manufactures 4,739 30.9Direct private foreign Other 1,752 11.3

investment 1,394 1,261 914 754Net HLT borrowing /d 2.629 2,878 1,435 3,128 Total 15,334 100.0Disbursements 2,886 3,164 1,949 3,652Amortization 257 286 514 524/e EXTERNAL DEBT, DECEMBER 31 1985 US$ Mln

Subtotal 4,023 4,139 2.349 3,882Public debt, including guaranteed 12,445

Other capital (net) and Nonguaranteed private debt 4,138capital n.e.i. 2,586 2,175 819 1,439 Total outstanding and disbursed 16,583

Increase in reserves (+) 197 48 80 n.a.NET DEBT SERVICE RATIO FOR 1985 /f 1

Gross reserves (end-year)/e 3,98R 4.070 4,115 n.a.Petroleum livports n.a. n.a. n.a. n.a. Public debt, including guaranteed 9.3Petroleun exports /g 3,103 3.354 3,734 3.617 Nonguaranteed private deot 5.2

ETotal outstanding and disbursed 14.5EXCHANGE RATE March

1980 1981 1982 1983 1984 1985 1986 IRRD LENDING (MARCH 31, 1986) USS nln

USSi - MS 2.18 2.30 2.34 2.32 2.34 2.48 2.53 Outstanding and disbursed 736.82MS - USS 0.46 0.43 0.43 0.43 0.43 0.40 0.40 Undisbursed 554.73

Outstanding Including Undisbursed 1,291.55

Not applicablen.a. Not available

/a Government hospitals./b Peninsular Malaysia.7W Constant 1978 US$.T7- Public/publicly guaranteed debt only./e Excludes refinancing of HS5,478 million in 1985.W( Interest and amortization payments as a percent of exports of goods and nonfactor services.2j Crude petroleum.

Note: All conversions to dollars in this table are aet the average exchange rate prevailing during the period covered.

June 1986

- iii -

a result of cuts in oil and commodity prices. Aside from the diminished flowof revenues attributable to levies on petroleum, the scope for savings by theGovernment has been reduced by revenue losses arising from changes in thestructure of income taxes. The upward drift in the operating expenses ofpublic enterprises, meanwhile, has been yet another force serving to bringdown savings. A turnaround in private savings might occur if growth accele-rates in the late eighties, but it would be only prudent to guard against thepossibility of a shortfall by buttressing the revenue earning and savingspotential of the government through appropriate tax changes. The task ofrationalizing and simplifying the tax system must continue, but together withthis, it is necessary to restore, at least partially, the revenue earningpotential of direct and indirect taxes.

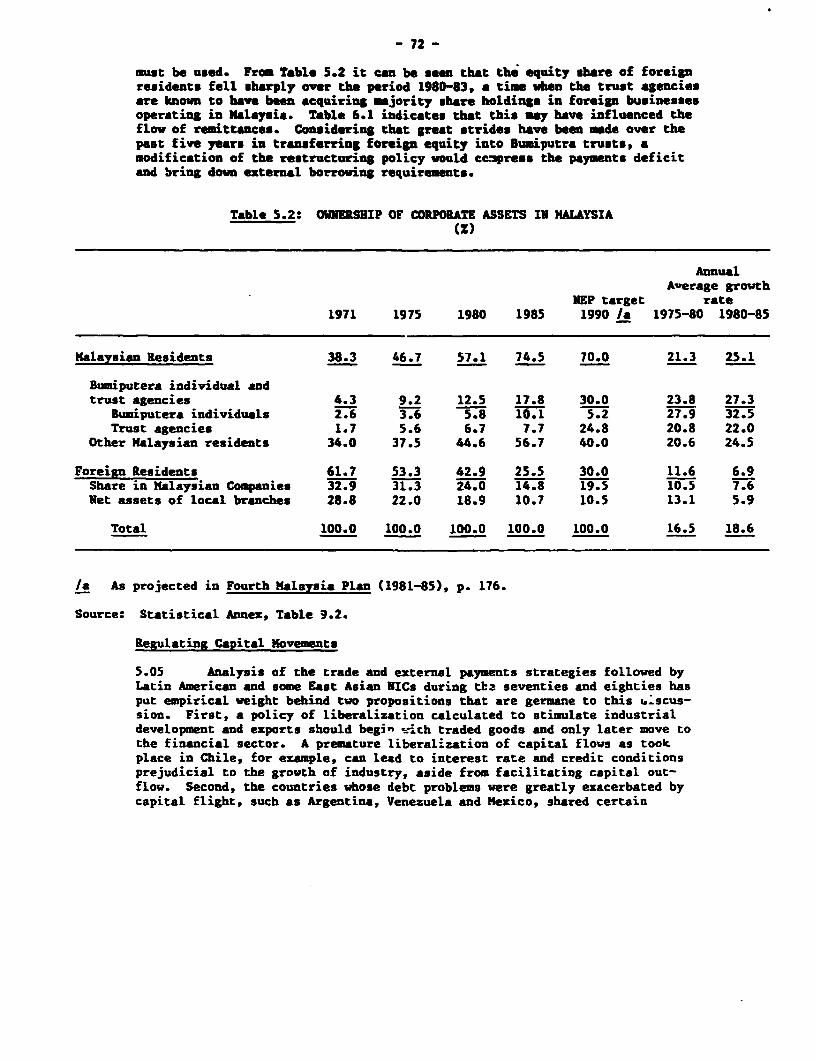

8. Domestic resource availability might also be enhanced if the annualloss in gross domestic savings through dividends, fees, repatriated profitsand capital flight, could be diminished. There are limits to how far an openeconomy, that is anxious to attract direct foreign investment and cement link-ages with world financial markets, can monitor or regulate capital flows, butpolicymakers might reflect on two possibilities. The last few years have wit-nessed a sizeable drop in the percentage of corporate equity held by foreign-ers. Many factors have been at work, but probably the one most important isthe deliberate campaign by public trust agencies to acquire corporate shares,which is central to the New Economic Policy (NEP). This may have inducedforeign shareholders to sell some of their Malaysian assets and move the fundsrealized out of the country. Adjustment goals, the progress made towards theNEP targets and the dimensions already attained by the public sector wouldrecoamend a partial suspension of this policy which is a drain on resources ata difficult time for the economy and may be undermining if not in fact coun-teracting Malaysia's policies to attract direct foreign investment.

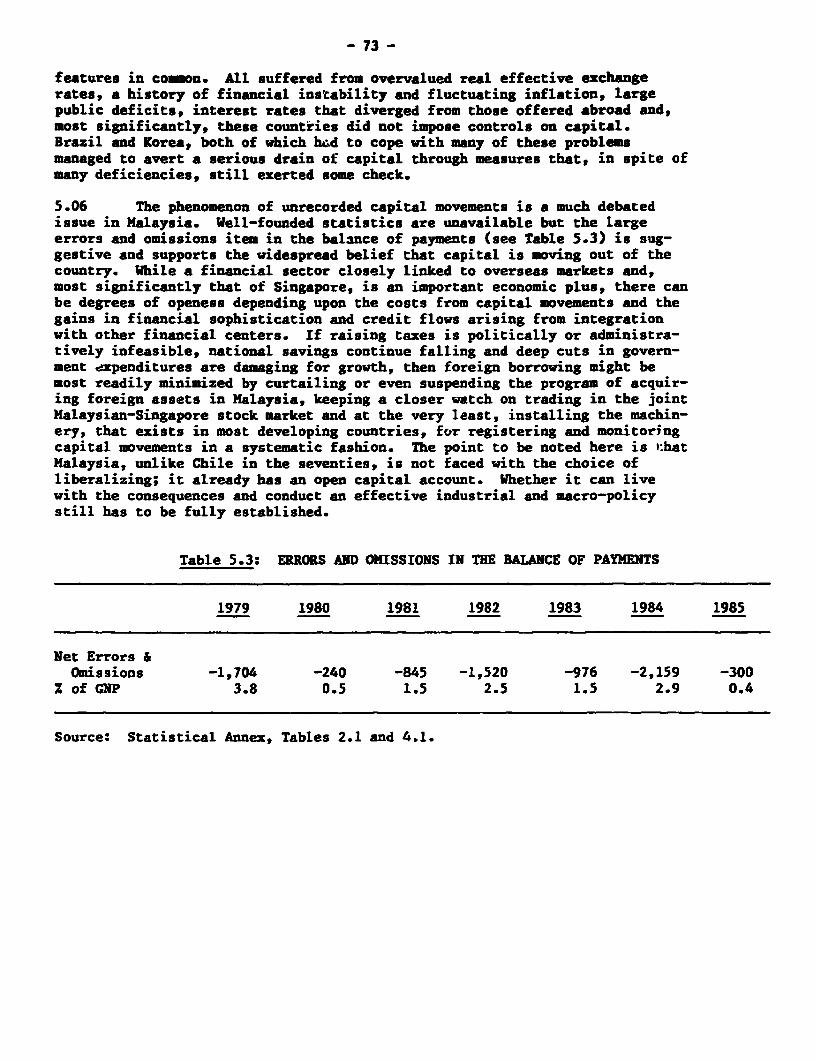

9. In these crisis-ridden years, unrecorded capital movements have beena thorn in the side of several debtor nations and have severely constrainedthe enterprise of economic management under adversity. An analysis of thefactors influencing such movements of funds has identified: fluctuatinginflation, overvalued exchange rates, interest differentials and politicalhappenings. But it has also indicated that the two countries with largeexternal debts - Brazil and Korea -- who were able to minimize the volume ofcapital outflow, may have derived substantial benefit from regulating capitalflows in a systematic fashion. For a variety of good historical and economicreasons, Malaysia allows unimpeded capital flows in and out of the country andthis policy cannot be lightly abandoned because the implications would be farreaching, but if the measures to balance investment needs against the supplyof national savings run afoul of institutional, political or behavioralobstacles, and unrecorded capital movements continue, the Korean and Brazilianexperience might serve as a guide on how the problem might be checked.

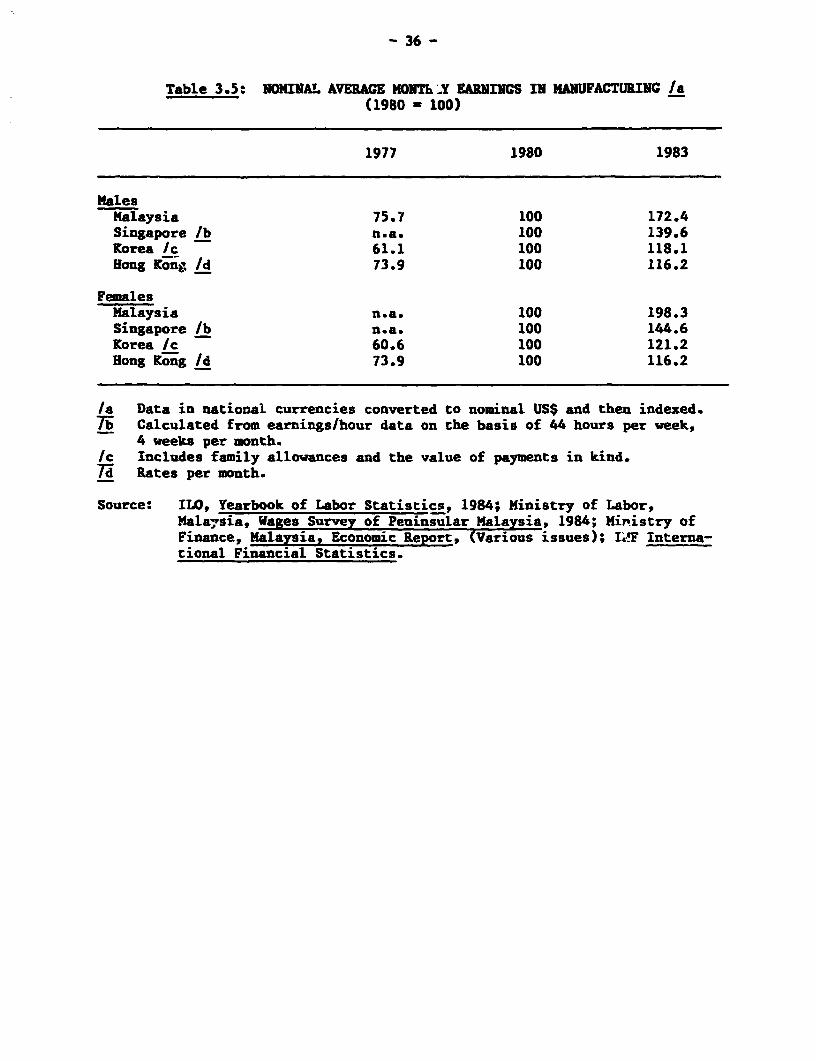

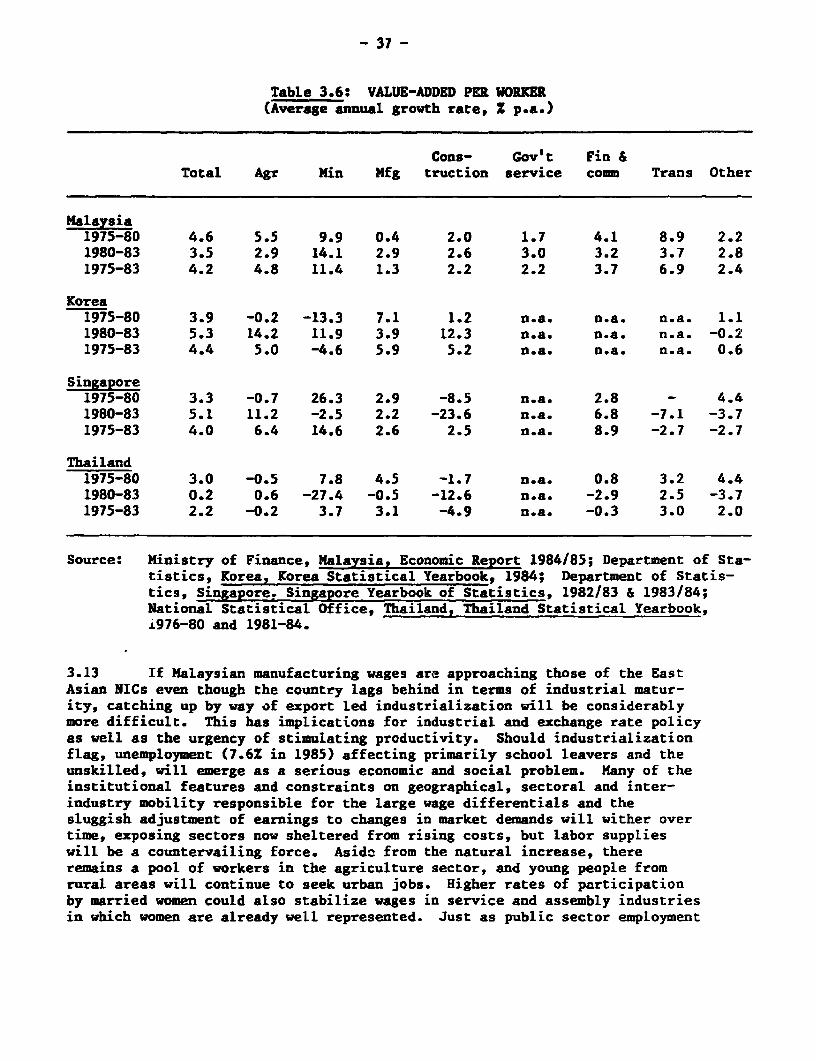

Labor Markets and Export Competitiveness

10. A;though in a narrow sense adjustment is tied to resource balances,it does eventually join forces with measures designed to engender manufacturedexports. Savings facilitate adjustment, but it is the ability to export thatultimately closes the payments gap. If a country can develop efficient and

- iv -

competitive exportables., there need not be much tension between the goals ofadjustment and growth. It was stated earlier that the aggregate labor supplysituation in Malaysia is comfortable and wage pressures have been quiterestrained. On closer examination the picture is not without blemishes.

11. The production of tree crops seems headed towards tro-uble. Migra-tion to urban areas is denuding the rural labor force of its younger elements,those who will determine whether the sector thrives in the late nineties andbeyond. Spot labor shortages are being experienced by rubber, oil palm andcocoa estates, and it is evident that once the aging pool of workers retires,rubber production which is difficult to mechanize, may not have a long future.Recruiting young men to harvest oil palm is also becoming harder and longbefore the sector feels the edge of a land constraint, it might have beenbrought to an halt by labor scarcities. A faster increase in wages mightmoderate the exodus. However, the rubber industry is in no position to paymore for its labor, as falling international prices and profitability alreadyputs it at a disadvantage to oil palm cultivation. Wages in the oil palm andcocoa estates have kept pace with productivity and the earnings of harvestershave risen more quickly, but even these industries are hostages of interna-tional price movements and forced to take anxious note of their competitors'cost structures.

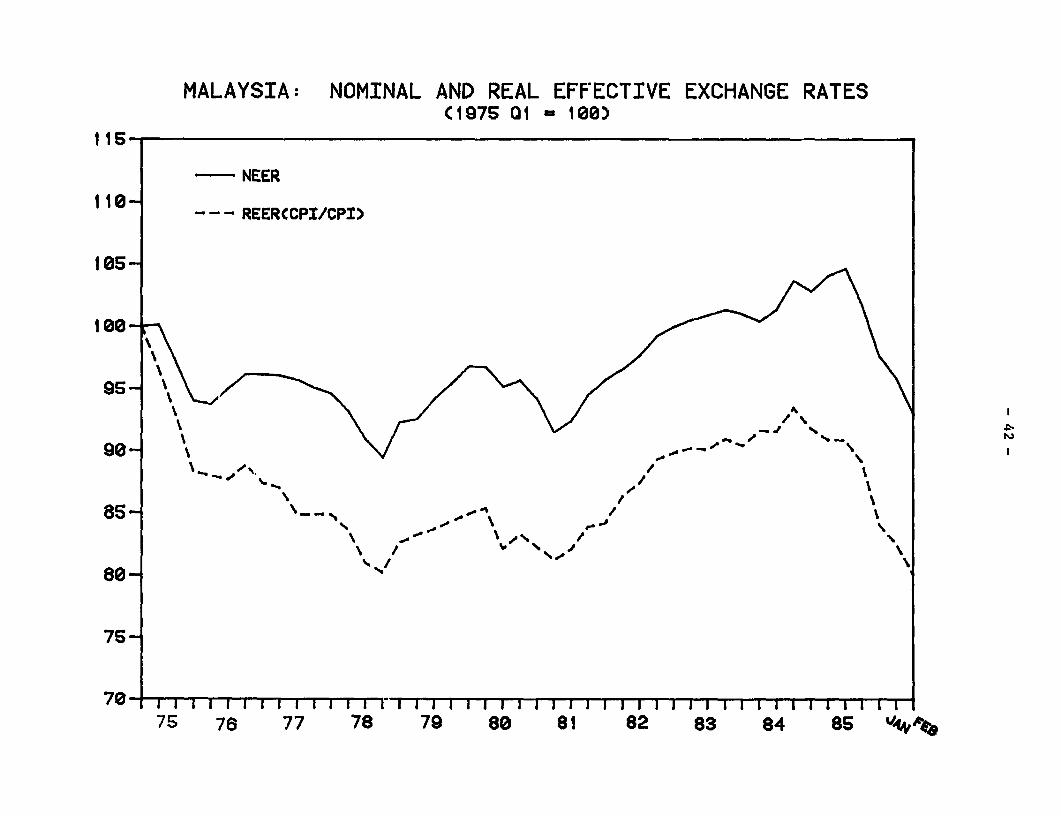

12. Agriculture's loss is industry's gain. The labor migration that iscondemning the primary sector to slow growth will ensure that industry bene-fits from elastic supplies. All through the seventies the increase in realwages could, more or less, be paid out of the increments in productivity, butin the early eighties, the impetus provided by public expenditures and highpublic wage scales, resulted in a marked acceleration in the growth of wagesin certain industria' subsectors. Where once Malaysian wages trailed those ofthe East Asian NICs by a wide margin, they have now moved much closer, eventhough, in terms of industrial activity and productivity, Malaysia is not onan equal footing with its industrializing neighbors. The suspicion thatrising costs may be eroding the competitiveness of the manufacturing sectorwas reinforced by the trend in real effective exchange rates. Flexibleexchange rate policies jpted in late 1984 have improved competitiveness andfalling commodity prices in early 1986, combined with the depreciation of theUS dollar, have contributed to this trend.

13. Wage movements have retreated to the trends followed in the seven-ties with the recent interim settlement for public employees allowing only a3.5% p.a. increase. Further, falling raw material prices and expenditures onconstruction and real estate will reduce pressures on relative prices thatbias the scales against tradables. But it may still be necessary to followexchange rate policies that (a) remove any cost disadvantages Malaysian treecrop producers and industrial exporters face vis-a-vis their East Asian compe-titors; and (b) ensure that this equilibrium is sustained by compensating fordifferences in productivity, wage rates and expenditure patterns betweenMalaysia and its neighbors.

Trade Patterns and Comparative Advantage

14. Labor and exchange rate issues bring us to the vezed questionconcerning the size and composition of future trade flows. For a number ofwell-known reasons the OECD countries may grow at a lover average rate in thefuture even after the benefits from lower oil prices are factored in.Combined with protectionism and changing consumer preferences, it suggeststhat export-oriented LDCs such as Malaysia should search for trade and indus-trial policies that might prevail in the face of slowly growing world demandfor traditional items. International trade in the sixties and seventiesappears to have favored the products of chemical, transport and engineeringindustries. The latter two have held their ground in the eighties. A surveyof the most successful exports from the East Asian NICs shows that electro-nics, electrical equipment, office machines, metal products and precisionequipment, have now joined the list. If we extrapolate this pattern into thefuture, it offers some very rough guidelines as to which industries might bestserve export goals in the medium term. Some of these products are tooresearch and capital intensive for a developing economy but certain types ofmachinery, metal products, petrochemicals and the supply of parts for electri-cal, electronic and automotive industries should be within the capabilities ofan industrial newcomer.

Direct Foreign Investment

15. Manufacturing industry in Malaysia has attracted much attention fromforeign investors. Firms producing semiconductors, conrumer electronics,telecommunications equipment, and garments in the Free Trade Zones (FTZs) orthe Licensed Manufacturing Warehouses (LHWs) that account for close to twothirds of manufactured exports, are either foreign-owned or have substantialforeign shareholding. But domestically oriented companies in lines such asfood, beverages, tobacco, automobiles, chemicals and rubber products have alsoserved as conduits for brand names, capital aud technology from abroad.Direct foreign investment (DFI) in all of these subsectors is likely to con-tinue but the available evidence suggests, at least tentatively, that neitherthe skills nor the funds brought in by foreign corporations will do much toadvance Malaysia's industrial ambitions or ease her entry into new exportmarkets.

16. In net terms, that is after subtracting profits and dividends repat-riated from annual DFI, Malaysia has incurred large deficits for well over adecade. Further, foreign companies that have established assembly type opera-tions either to derive cost advantages from using Malaysian labor or to uti-lize the country's textile quotas, have transferred few skills, limited tech-nology and done virtually nothing for industrial deepening. Malaysian firmsare in no better position to establish an independent presence in the inter-national markets for garments and electronic products today than they werefive years ago.

17. If trade barriers continue to hedge the flow of textiles and othercountries seem to offer superior wage bargains, spinning, weaving and garmentmaking operations in Malaysia will not be attracting much new foreign invest-ment. And should the electronics industry find it economically efficient and

- vi -

politically desirable to put up factories in the industrialized countries, thedevelopment of the electronics subsector in Southeast Asian economies mightalso stabilize.

18. A country seeking to deepen its industrial sector, increase manufac-turing value-added and widen its export possibilities cannot rely upon DFI todo the entire job. The objectives of multinational corporations and indus-trializing economies are not always congruent. One is searching for marketsand a means of reducing production costs through efficient sourcing andobtaining the maximum return from its financial options. The other wants todevelop its own independent industrial capacities and appropriate as many ofthe benefits in terms of profits, employment, technology and linkages as ispossible, benefits that the involvement of MNCs often transfers overseas.Malaysia must continue to try and attract DFI because of its effects onemployment generation, the need for foreign borrowing and on technology trans-fer, but increasingly, this will have to be complemented by domestic effortsoriented towards industrial deepening and the assimilation of technology.

Industrial Strategy

19. A declining role for overseas investors means that Malaysi: mustfind an industrial strategy that will harness domestic capital and skills, andgive a direction to the development of the manufacturing sector that is fruit-ful in terms of future exports. From the discussion of international tradingpatterns, the recent history of the manufacturing sector, the state of theincentives system and the projected supply of technical and engineeringskills, the report identifies a three pronged industrial sLrategy comprisedof: privatization that will stabilize, if not reverse, the tendency of thepublic sector to enlarge its industrial role and induce it to concentratecapital and managerial resources in areas where its presence can contributecritically to the development process; a rationalization of incentives andlicensing procedures to minimize distortions introduced by the wide dispersalof tax and tariff rates and regulations governing entry; and support for themanufacture of producer and intermediate goods that will lead to a deepeningof the industrial sector and provide the basis f-- future export growth. Thereport concludes that:

(a) although the average level of effective protection in Malaysia (23Zin 1982) compares favorably with that of other developing economies,the wide dispersion of rates and the frequent recourse to quotasincreases the likelihood of distortions and inefficiencies inresource use. A move towards greater uniformity in rates of effec-tive protection through the adjustment of tariffs at the extremeends, together with the substitution of tariffs for quotas couldadvance the cause of allocative efficiency without compromising thegrowth of current infant industries or the possibility of creatingnew ones.

(b) a diversified industrial system made up of many amaller sized firmswill not be possible without vigorous entrepreneurial activity. Oflate this has been conspicuously absent. It is widely believed inbusiness circles that the strict regulation of business investment

- vii -

by the Government as a part of the Industrial Coordination Act(ICA), might be to blame for the low level of private interest. InDecember 1985, the-Government responded by raising the industriallicensing threshold from N$250,000 to M$l million and therebystrongly reaffirmed its commitment to development led by privateindustry. This is a major step but it may not be enough to crackattitudes towards investment and risk that have hardened after tenyears under the ICA. A move to a M$5 million exemption limit whichwould remove four fifths of industrial projects from the purview ofthe licensing body merits consideration for the medium run. Nowthat a different situation prevails and industrial initiative ratherthan rent-earning primary products must underwrite economic advance,the rules governing the actions of the various players have to bedrafted afresh. Small changes in the architecture of the ICA, whichopen a few windows in the system while retaining much of the struc-ture, may not bring about the decisive shift in business psychologycalled for at this juncture. To the extent allowable by thenation's politics, the Government might wish to divorce the goals ofequity and enlarging the Bumiputra share of the national wealth fromthe pursuit of industrial development and rely upon fiscal and wel-fare policies to achieve the former. Malaysian businessmen arecompeting in an unusually tough envi.1 nment and the greater theburden of licensing, the larger are the social claims on theirearnings, and the smaller their flexibility in allocating resourcesand using available skills, the more likely it is that the race toindustrialize sweeping the eastern margins of the Pacific will bewon by countries where business endeavor is not too rigidly circum-scribed by social obligations.

(c) events in the world market argue against specializing in a narrowrange of products. Amongst the East Asian NICs, those with highlydiversified exports produced by energetic small- and mediumrsizedfirms have taken less of a bruising from protectionism and theswings in trade;

(d) in the early eighties, Malaysian industry has been moving intotransport, machinery, metal and chemical industries. Past trendsindicate that these subsectors, along with electronics, continue tohave high export potential. Excluding some areas in electronics andautomobile production, they also present a new entrant with rela-tively moderate technology, scale and marketing barriers. That isto say, the opportunities for finding and widening export nichesappear to be greater than elsewhere.

Industrial Micro Issues

20. Going beyond broad sectoral strategy, the Report looks at the stateof six manufacturing subsectors and assesses their prospects. They are: tex-tiles, electronics, rubber products, wooden furniture, electrical machineryand equipment, and farm machinery. With the exception of electronics, theproblems of these industries are not dissimilar, although each confronts quitedifferent learning curves and export possibilities. Electronics remain an

- viii -

enclave in the industrial system with a future that is tied to the productionstrategies of foreign firms. If the economics of assembly in offshore plat-forms turns sour, the enclave will shrink; there is only a small chance ofgrowth rivalling the expansion of the seventies and early eighties. Linkagesmay continue to sprout but they will remain sparse, as technology, brand namesand marketing ability are more serious entry barriers than in other subsec-tors.

21. Textiles, and the two resource based industries are likely to behamstrung by slowly growing world demand, and complications introduced bytrade restrictions (textiles) and low profitability (rubber tires). Themachinery subsectors are far better placed as regards both market trends andassimilating technology. But all five subsectors will need much help toloosen a number of constraints.

22. Technical, engineering and design skills are scarce throughout themanufacturing sector and their effects are felt in the mastering of tech-nology, innovation, quality of product, the ability to fully utilize equip-ment, and repair and rebuild machinery. Smaller firms that have limitedcollateral frequently cannot raise sufficient credit and are forced to make dowith old machines, which further detracts from the standards of quality andfinish. Companies that are without foreign partners show scant understandingof marketing techniques that are as important as innovativeness, design,quality and price competitiveness in achieving export success. Finally,Malaysia still has to build the network of channels that will provide manufac-turers the volume of detailed information necessary to detect a market openingand design a product that will fit the market's specifications.

23. Industrial policy must act upon many facets of industrial life. Itmust create the right atmosphere so that entrepreneurs will be stimulated toact; tariff, taxes and subsidies must be fashioned to effectively supportfirms populating the sector; it must ensure that education and training poli-cies generate an adequate supply of skills; R&D activities must be cateredfor. In addition, industrial policy must alleviate some of the micro-problemsthat the average firm encounters on a daily basis, problems associated withcredit sapply, the use of facilities, obtaining raw materials and intermediategoods, and gaining access to market information.

24. The report identifies four areas where active government supportwill be required:

(a) industrial credit, possibly through existing development banks or byway of commercial institutions;

(b) centers for design and research where higher-level skills could beimparted;

(c) vocational training, possibly supplemented by subsidized apprentice-ship programs to meet the needs of modern industry; and

(d) a system for gathering market intelligence from overseas.

- is -

The Agriculture Sector

25. In the simplest terms the future of Malaysian agriculture will bedecided by international market conditions and rural labor supply. Four sub-sectors are covered in the Report: rubber, oil palm, cocoa and rice. Theyall share certain features: in each there is an efficient wing where yieldsare among the highest in the world and the latest technologies are in use, aswell as a backward segment where the smallholders derive low returns from theuse of labor and land. All agricultural activities are threatened to varyingdegrees by the withdrawal of labor, but their fate is likely to be one ofgradual decline rather than a sudden precipitous drop in output.

26. Rubber production is the one area where the large-scale switch tooil palm planned by the estates could have far-reaching effects on productionin the medium run. Rubber has fallen from grace because at prevailing andanticipated prices its profitability does not compare favorably with that ofpalm oil and cocoa. Since the estates cannot readily increase their totalarea, they are cutting rubber trees so as to make room for oil palm. Mean-while, the government is attempting to enlarge the size and productivity ofthe smallholder hectarage by providing replanting subsidies, extension ser-vices and assistance in establishing mini estates. The conclusion of theReport is that with the prices of commodities subject to wide oscillations,and demand being somewhat difficult to predict, it is advisable to maintainefficient and diversified coummodity production. If the estates continuemoving out of rubber, output will diminish and technological change slacken asestates take the lead in planting new clones. Foreign producers will see thisas evidence of a retreat by the world's leading supplier and move to expandtheir own area. Once the rubber industry is left to the smallholders, it willbe of minor significance, and Malaysia's agricultural commodity basket will bereduced to one major export, palm oil and two minor ones, rubber and cocoa.

27. Palm oil's trade prospects are superior to those of rubber, competi-tion from other suppliers is weaker and even at the depressed prices prevail-ing in 1986, it gives higher returns. Malaysia's strategy should encourageestates not to reduce their rubber acreage below 1984 levels and urge small-holders currently growing rubber to plant oil palm instead. Efficient rubberproduction would be retained. Some of the poverty stricken rubber small-holders would be able to raise their earnings by shifting to a new tree crop.Palm oil output would expand and since the differential between smallholdersand estate yields is less for palm oil than that for rubber, the final produc-tion outcome would not depart too far from the scenario where the estatesconvert 70Z of their land to oil palm.

28. The collapse of palm oil prices from about US$730 per ton in 1984 toUS$290 per ton in the first quarter of 1986 should be warning enough as to therisks of increasing supplies at a rate which the market cannot digest and thehazards of specializing in a single comuodity.

The Rice Economy

29. After attempting for several years to meet over 80Z of its needsfrom the domestic production of rice, Malaysia is prepared to settle for amuch lower target. The decision was motivated by low international riceprices that are projected well into the future and the failure of costly pricesupport and subsidy programs to reverse the stagnation in output. Irrigatedareas in four major schemes that are the source of 60Z of the rice producedare productive enough and will flourish so long as no major changes are intro-duced in the incentive system. The problems are in the rainfed areas wheresmallholders achieve low yields and cannot earn enough from rice farming torise above the poverty line. Many farmers in these regions have sought supp-lementary off-farm occupations, and others have given up trying to make endsmeet and migrated to the cities.

30. Policymakers have three options: the high domestic resource costs ofrice production can be used as a justification for scaling down incentives, amove that would swell the numbers seeking urban jobs; over the medium term theGovernment could hold the line on incentives and accept the slow attrition ofthe farm economy; or it could pour funds into developing irrigation facilitiesand infrastructure in the rainfed areas in an attempt to bolster yields, thereturns from rice cultivation and the total production of rice in the country.Concerns arising from food security and uncertainty about the availability ofenough employment in the urban sector limit the palatability of the firstoption. Past experience with small-scale irrigation and the high opportunitycost of capital, suggest that such an approach will not stem migration andcould tie up resources in projects with low returns. On these grounds, thesecond option seems most appropriate for the balance of the eighties. It willprobably result in stagnant or slowly falling levels of production but willminimize dislocation in the rice economy and argue against any costly newexpenditures for developing rice land.

Projecting Growth

31. Malaysia possesses the resources to join the ranks of the NICs, butit will require a steadfast industrial strategy and the benefit of fair inter-national trading weather. The process will take time because new industriesrequire a minimum number of years to mature into seasoned exporters. If theFifth Plan is successful at quickening the tempo of manufacturing activity,the transition from primary producer to an emerging industrial nation would bewell advanced by the beginning of the nineties. The slump in oil and commo-dity prices by depressing public revenues and foreign exchange earnings will,in the short-term, magnify the adjustment problem. To minimize net brorowingsome growth may need to be sacrificed in order that the balance of paymentsdifficulties can be resolved more quickly. Our base scenario assumes there-fore that the economy will gather momentum gradually, with growth remaining inthe 1.52 - 2.5Z range during 1986-87 but picking up in the later years (4.0Z -4.5Z) as the economy moves towards a resource equilibrium by way of fiscalmeasures that restore government savings and the strong check on public expen-ditures proposed in the Fifth Plan. Over this entire period, agriculture andmineral production will contribute very moderately to the expansion of thenational product. The manufacturing sector and the continuing development of

- xi -

social overhead capital will be supplying most of the push, and manufacturedexports will determine whether or not trading goals are met. Should progressin the manufacturing sphere falter, it will be very hard to do justice eitherto the growth objective or that of adjustment.

CHAPTER I: TRENDS AND PROSPECTS

A Changed Environment

1.01 Small open economies lead a vulnerable existence on the interna-tional stage. Where larger countries can find a degree of seclusion from thebustle of the world market to pursue their own domestic designs, an economythe size of Malaysia cannot afford to neglect the activities beyond itsshores. The entire effort of development must be cued to signals arrivingfrom its major trading partners. Ever since the second round of oil priceadjustments in 1979, the tempo of economic activity worldwide has been weaker,in part because of technological, institutional and demand-related develop-ments in the industrial nations; partly also as a result of strains bred bythe rise of many new aspirants to the status of industrial maturity, who haveprofoundly affected the pattern of trade and capital flows.

1.02 The meager productivity gains emanating from the electronics revolu-tion suggest that the time may have passed when the advanced economies couldexpect substantial annual bonuses from the increased efficiency of resourceuse. Aa aging population and institutions canted towards distributive justiceand generous welfare benefits are likely to limit the scale of capital accumu-lation as well as the market directed flexibility in the pricing and the real-locating of resources. Finally, for many basic consumer goods and durables,saturated wants might dislodge the growth in demand from past trends. All ofthese presage a smaller appetite in the markets of the industrial countriesfor the goods produced in the developing world. International trade, theforce behind the widespread surge in postwar living standards, could increasemore fitfully under the weight of restrictions sparked by political concernsand the fears of deindustrialization. With trade and growth slowing, capitalflows that have been so consequential in putting the surplus savings of theadvanced economies behind the industrial ambitions of the LDCs, would alsobegin to falter, especially if debt crises continue to fan the apprehensionsof bankers.

1.03 From the standpoint of the developing market economies, such asMalaysia, the earlier industrial strategy which assumed relatively unimpededaccess to growing markets in the affluent West, might have to be refashionedin important ways. The path revealed by comparative advantage and exportopportunities exploited in the past may have to be reconsidered to allow forthe political limits to the expansion of trade in products favored by newdevelopers, the likely persistence of international capital scarcities, andthe spreading influence of multinational companies (MNCs) in the spheres ofinvestment, trade, technology transfer and product development. Increasingintracompany trade and market sharing by major international industries aresome of the more significant features of the current economic environment. Sofar, at least, policymakers searching for a way around the multiplying com-plexities have leaned upon the themes of trade liberalization, comparativeadvantage and distortion minimizing, policy and price reforms. The challengeis ensuring the fruition of industrial initiatives begun in the recent pastand devising policies that will deliver economic results in the face of muchgreater odds.

- 2-

Malaysia's Economy: Recent Developments

1.04 Five yeers ago it became clear that Malaysia would have to concen-trate on building an industrial system using the resources transferred ou ofthe plantation sector and revenues earned through petroleum imports. With thevitality ebbing from mining and parts of the plantation economy because ofrising costs and weak demand, concentrating investible resources on manufac-turing development using the example of the East Asian NICs, was the mostattractive route. But export led growth must now be managed in a far harsherenvironment and while it might still be the strategy promising the largestrewards, the risks have increased and small countries with limited bargainingpower are very much at the mercy of major trading partners and large multina-tional producers. Over the course of the Fifth Plan period (1986-90) a numberof decisions will have to be taken which will determine the long-run sectoralcomposition and potentialities of the Malaysian economy. It is important thatthese be fully informed not just by the experience of the NICs in the seven-ties and early eighties, but also by the knowledge of how international econo-mic relations are likely to be shaped.

1.05 The speed and direction of Malaysian economic progress in theeighties reflects the interplay of certain policy decisions with internationalmarket developments. Rising commodity prices in 1975-77 and the tripling ofoil prices in 1979-80 provided an infusion of rental earnings which enrichedthe economy and elevated the country's credit standing. Its attractiveness asa base for assembly-type textile and electronics industries, stimulated a sub-stantial volume of foreign investment. MNCs looking for a blend of politicalstability, cheap labor, adequate infrastructure, unfilled export quotas andfiscal incentives, flocked to Malaysia. The factories they helped to estab-lish within and outside Free Trade Zones (FTZs), allowed Malaysia to capital-ize on the enormous growth in the market for semiconductors during 1980-84 aswell as the steady expansion in the demand for cheaper Asian-made garments inthe USA and to a lesser extent the EEC. Intertwined with these was the Gov-ernment's decision to move at all possible speed towards modernizing infra-structure and creating the base for future industrial advance through invest-ments in automobiles, machinery, petrochemicals, ferrous metals and cement. Asecond key decision, motivated by Malaysia's comfortable debt service ratio,the expectation of low or negative real interest rates on foreign loans (aswas the case after the first oil shock) and the desire to cushion the economyagainst externally transmitted recession, was the willingness to borrow heav-ily to finance domestic, primarily public, investment. A third move relatedto the public sector's development push, was the parceling of responsibilitiesto nonfinancial public enterprises (NFPEs) created during 1976-81 without atthe same time erecting a monitoring and control apparatus equal to the task ofsupervising the activities of many agencies and keeping track of the totalfinancial implications of dispersed investment decisions.

1.06 The effects of these are visible in the macro indicators trackingthe economy's movements in the first half of the eighties (see Table 1.1).First, growth, though lower than the average for the seventies (7.7%) wasfairly stable because of the strong impetus from capital spending. Second,investment outlays rose far above the country's substantial gross nationalsavings, resulting in very large current account deficits that had then to be

- 3 -

financed through commercial borrowing. External debt registered a threefoldincrease between 1980 and 1984. Following a pattern observed in several ofthe Latin American NICs but also in Korea, the sudden disequilibrium inresource balances and the reliance on foreign savings which it entailed, arosesquarely from the actions of the public sector. Spending by public agenciesand especially the NFPEs, rose with alarming swiftness as is shown by thebehavior of public sector deficits.

Table 1.1: MALAYSIA: PRINCIPAL MACRO INDICATORS

1979 1980 1981 1982 1983 1984 1985

GNP growth (Z p.a.) /a 9.1 9.2 7.5 4.2 3.9 6.6 2.6GDP growth (Z p.a.) 7T 9.3 7.9 6.9 5.6 6.3 7.6 2.8

GDI/GNP (Z) 30.3 31.9 36.5 39.2 38.7 35.9 32.0

GNS/GDP (Z) 33.3 29.6 25.5 24.0 24.8 28.8 26.8

Merchandise tradebalance (M$ mln) 6,908 5,238 -243 -1,758 1,093 6,913 8,628

Current account balance(M$ mlin) 2,033 -620 -5,633 -8,409 -8,026 -3,743 -2,230as Z of GNP 4.7 -1.2 -10.4 -14.4 -12.1 -5.8 -3.1

Public sector overall balance /b(M$ mln) -1,890 -6,150 -9,464 -10,711 -8,510 -7,491 -4,930as Z of GNP -4.3 -11.9 -17.0 -17.9 -13.0 -10.1 -6.8

Total debt/GYP (Z) /c 24.3 25.5 35.5 47.6 58.9 56.9 65.7

Debt service ratio /d 5.9 4.3 8.0 10.2 10.8 12.5 15.3

la At constant prices.T7 1979 data refer to Federal Government, 13 State Governments, 4 Local Govern-

ments and 10 Public Enterprises. Since 1980, 26 additional public enterpriseshave been included.

/c Total debt = Public and publicly guaranteed, nonguaranteed private, and shortterm debt.

/d Ratio of total debt service to exports of goods and services.

Source: Statistical Appendix Tables 2.1, 3.1, 4.1 and text Table 5.1.

1.07 Finally, the fruits of building capacity in electronics and tex-tiles, but also the benefits of enlarging the dimensions of the palm oilindustry, are apparent in the export statistics, especially for 1983/84, whenMalaysia's growth and balance of payments were buoyed by a real increase of

- 4 -

14X in exports of goods and nonfactor services. But the economic gains thatso heartened policymakers in 1984 also stemmed from the Government regainingits grip over the spending of independent agencies, which served to narrow thepublic deficit. To ensure that spending by the NFPEs remains harnessed to theobjective of reducing the public sector's deficit, monitoring committees havebeen established in both the Treasury and the Economic Planning Unit (EPU).Backing them up with more detailed surveillance of planned expenditures andaccounts is a newly created monitoring and control unit (CICU).

1.08 The economy entered 1985 in a spirit of considerable optimism butevents during the course of the year belied the earlier expectations. Growthin the US slipped to little over 2% and as this was not counterbalanced bystronger performance in other large industrial nations, world trade quicklyfelt the chill and increased by only 3% as compared to the 9% rate registeredin 1984. This was damaging for Malaysia's manufactured exports and sales ofboth textiles and electronics, the two principal items declined. It may alsohave brought added pressure to bear on the markets for petroleum, palm oil andtin, three of Malaysia's largest commodity exports, that were already feelingthe effects of oversupply. Petroleum prices began to retreat in mid-1985,followed shortly thereafter by palm oil and the market for tin collapsed inlate October. In 1984, Malaysia exported 343,800 bpd of crude at an averageprice per barrel of US$29.87. Sales rose in 1985 to about 354,500 bpd but theweighted price was US$27.50 per barrel. Palm oil did substantially worse.Export earnings from palm oil and products (stearin, olein, kernel oil andcake) dropped by 1lZ from M$5.71 billion in 1984 to M$5.09 billion in 1985.Since tin accounts for less than 3Z of Malaysia's merchandise exports, thesuspension of trading on the London Metal Exchange on October 24 and thecollapse of the price barely dented overall export earnings but the rippleeffects of mine closures and loss of employment were damaging on a regionalscale, the economy of Perak being especially hard hit.

1.09 Overall the deterioration in the terms of trade during 1985 amountedto 5.6%. Combined with the reduction in certain commodity and manufacturedexports as well as the decline in private investment, this resulted in theworst economic performance in a decade. Higher production of petroleum, palmoil and timber helped raise the real GDP by 2.8%, but in nominal terms thedomestic product was 2.1Z less than in 1984. As the economy generated fewerjobs, the unemployment rate climbed to 7.6%. But a slowing economy and fall-ing commodity prices had certain beneficial consequences as well: inflationwas a negligible 0.3% (CPI); and a larger merchandise surplus served to narrowthe current account deficit to 3.3% of GDP. Hence, medium- and long-term(MLT) debt grew 6.9Z to US$16,583 million as against US$15,513 million in 1984.

1.10 Starting in 1986, Malaysia will be charting an economic course thatwill be defined in the Fifth Five Year Plan. For sound political and economicreasons, the Government would like to set its sights as high as possible.During the Second and Third Plan periods, growth rates of GNP averaged 7.1%and 8.6%, respectively. In the first half of the 1980s, growth slowed to 5%p.a. and it appears from the trends projected in the markets for Malaysia'scommodity exports that traditional sectors will need to be strongly abetted byothers sources of growth if the country is to sustain an acceptable pace ofeconomic advance.

-5-

1.11 Lessons learned over the course of the Fourth Plan period have beenchastening. External demand is undependable and traditional exports of commo-dities as well as light manufactures are having to struggle in buyers' marketsor scale ever higher nontariff barriers. At the same time, an aggressiveattempt at generating growth through public investment in both infjastructureand industry may have been a costly way of propelling the economy.- Averageinvestment levels exceeding 36X (1981-83) of CUP added little more than 5%p.a. to the national product but saddled the country with a sizeable debt.

1.12 If growth is to move hand in hand with external adjustment, asmaller quantum of investment must be made to yield larger returns and more ofthe domestic value-added must find its way into exports. What this implies,first of all, is greater factor productivity. Second, Malaysia must enlargethe value-added in important export categories, for example, light manufac-tures, machinery, metal and wood products. Many other changes will also berequired, calling for a very different constellation of policies and a tiltingof initiatives away from the public and towards the private sector. Perhapsthe most effective way of tracing the feasible economic perimeter is to assessthe economy's supply potential from the macro plane and again at the subsec-toral level. Then to juxtapose this with the demand possibilities that we seegerminating internationally in the world of the late eighties.

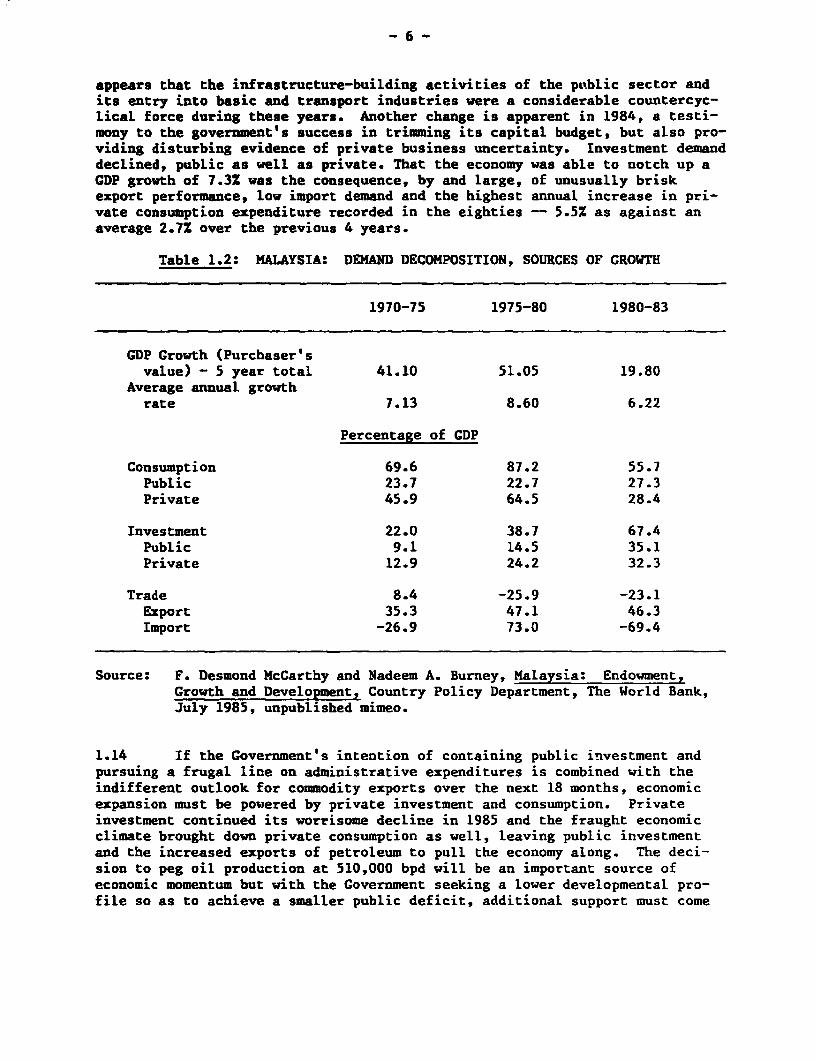

Sources of Growth: Demand Factors

1.13 An economy's sinews are moved by demand. How rapidly it advancesultimately rests on the strength of demand from expenditures on consumption,investment and exports. Except in certain stages of growth, it is consumptionthat leads the way with capital spending some way behind and trade often adistant third. In Malaysia, the pull of consumption rose significantly fromthe first half of the seventies to the second, because of a major surge inprivate outlays (see Table 1.2). As foreign purchases of import intensiveconsumption and development expenditures outpaced the growth of exports, theexternal account turned from being a small net contributor to growth to asignificant drag on the economy's expansion. In addition, Malaysia's manufac-tured exports that began rising in the late seventies, were based on the pro-cessing of imported intermediate goods. The weight of both private and publicinvestment was greater in the second period when Malaysia, benefiting from theprimary commodity boom and heightened world business activity, was racingahead of the Third Plan's growth targets. A decisive shift in sectoral con-tributions is evident after 1980, with changed external circumstances anddevelopment policies. Most significant was the reduced pull by private con-sumption. Larger public consumption spending, some of it on administration,the rest on welfare and subsidies, compensated only marginally for the halvingof the private sector's contribution to GDP growth. What sustained growth wasthe vast increase in public investment and to a lesser extent private capitaloutlay. As the net demand impetus from trade remained negative and at aboutthe same level as in the late seventies, GDP grew more slowly but it certainly

1/ See Malaysia: Development Strategies and Their Financing, World Bank,Report No. 5560-MA, September 1985.

-6-

appears that the infrastructure-building activities of the public sector andits entry into basic and transport industries were a considerable countercyc-lical force during these years. Another change is apparent in 1984, a testi-mony to the government's success in trimming its capital budget, but also pro-viding disturbing evidence of private business uncertainty. Investment demanddeclined, public as well as private. That the economy was able to notch up aGDP growth of 7.3% was the consequence, by and large, of unusually briskexport performance, low import demand and the highest annual increase in pri-vate consumption expenditure recorded in the eighties -- 5.5% as against anaverage 2.7% over the previous 4 years.

Table 1.2: MALAYSIA: DEMAND DECOMPOSITION, SOURCES OF GROWTH

1970-75 1975-80 1980-83

GDP Growth (Purchaser'svalue) - 5 year total 41.10 51.05 19.80

Average annual growthrate 7.13 8.60 6.22

Percentage of GDP

Consumption 69.6 87.2 55.7Public 23.7 22.7 27.3Private 45.9 64.5 28.4

Investment 22.0 38.7 67.4Public 9.1 14.5 35.1Private 12.9 24.2 32.3

Trade 8.4 -25.9 -23.1Export 35.3 47.1 46.3Import -26.9 73.0 -69.4

Source: F. Desmond McCarthy and Nadeem A. Burney, Malaysia: Endowment,Growth and Development, Country Policy Department, The World Bank,July 1985, unpublished mimeo.

1.14 If the Government's intention of containing public investment andpursuing a frugal line on administrative expenditures is combined with theindifferent outlook for commodity exports over the next 18 months, economicexpansion must be powered by private investment and consumption. Privateinvestment continued its worrisome decline in 1985 and the fraught economicclimate brought down private consumption as well, leaving public investmentand the increased exports of petroleum to pull the economy along. The deci-sion to peg oil production at 510,000 bpd will be an important source ofeconomic momentum but with the Government seeking a lower developmental pro-file so as to achieve a smaller public deficit, additional support must come

- 7 -

from a revival of private investment. The Government has introduced a numberof measures, which are discussed later in the report, to spur business activ-ity. Entrepreneurial response to these recent moves will determine not justthe scale of economic gains over the short run but also the longer-term pros-pects of the economy that rest very much on the extent and efficiency ofdiversification into tradable manufacturing and tertiary activities. Even ifinternational business activity recovers under the influence of reduced oilprices and inflation rates, the next 12 to 18 months are freighted with muchuncertainty for the Malaysian economy. There has been a significant narrowingof the bases for growth, the reflationary potential of the public sector isseverely constrained, and it is private investment initiatives in what areadmittedly difficult times that will spell the difference between stagnationand a growth rate of 2.5-3.5% which is consonant with continued adjustment.

Sources of Growth: Sectoral Contribution

1.15 In the first half of the seventies, a little over one fifth of theincrease in GDP came from agriculture, nearly 30Z from manufacturing, govern-ment services accounted for 17% and construction and commerce for another 15%(see Table 1.3). Both the major productive sectors, agriculture and industryhave sunk in importance in the course of this decade. Agriculture's share nowhovers around 12% while industry is close to 16%. The sectors that havegained in stature are construction, commerce, transport and government ser-vices. This reflects the resilience of services and the lure of real estatewhen other business activity is slow, it also indicates that Malaysia isadjusting towards an economic structure on par with its income level. Theadvance of services and construction attests, moreover, to the permeation ofthe economy by the public sector, the great increase in public employment, theproliferation of agencies offering diverse services and the large injection ofpublic funds into various types of construction activity.

1.16 The expansion of services and of the government sector is a normaland perhaps inevitable process, and multicountry research suggests that in thearly stages, government size has a positive effect on economic performance.2Beyond a point, it can divert resources from the directly productive activi-ties and tilt the economic balance too far in the direction of nontradables,generating cost pressures and export supply constraints deleterious to thelong term development of a highly open economy. There are few signs that thediminishing sectoral contribution of agriculture will be reversed. The briefspurt by industry in 1984 was not repeated in 1985, but unless industry canreestablish itself as the principal sectoral player, Malaysia's developmentprogram will lack a dynamic center and without industry providing the "spreadeffects" which serve as the underpinning for the prosperity of other sectors,the economy could quickly run out of momentum. Rents from primary exportswould continue to underwrite some of the bills, but the battle to escape frommiddle income status into more comfortable circumstances would have been lost.

2/ R. Ram, "'Government Size and Economic Growth: A New Framework and SomeEvidence from Cross-Section and Time Series Data," American EconomicReview, Vol. 76, No. 1, March 1986.

-8-

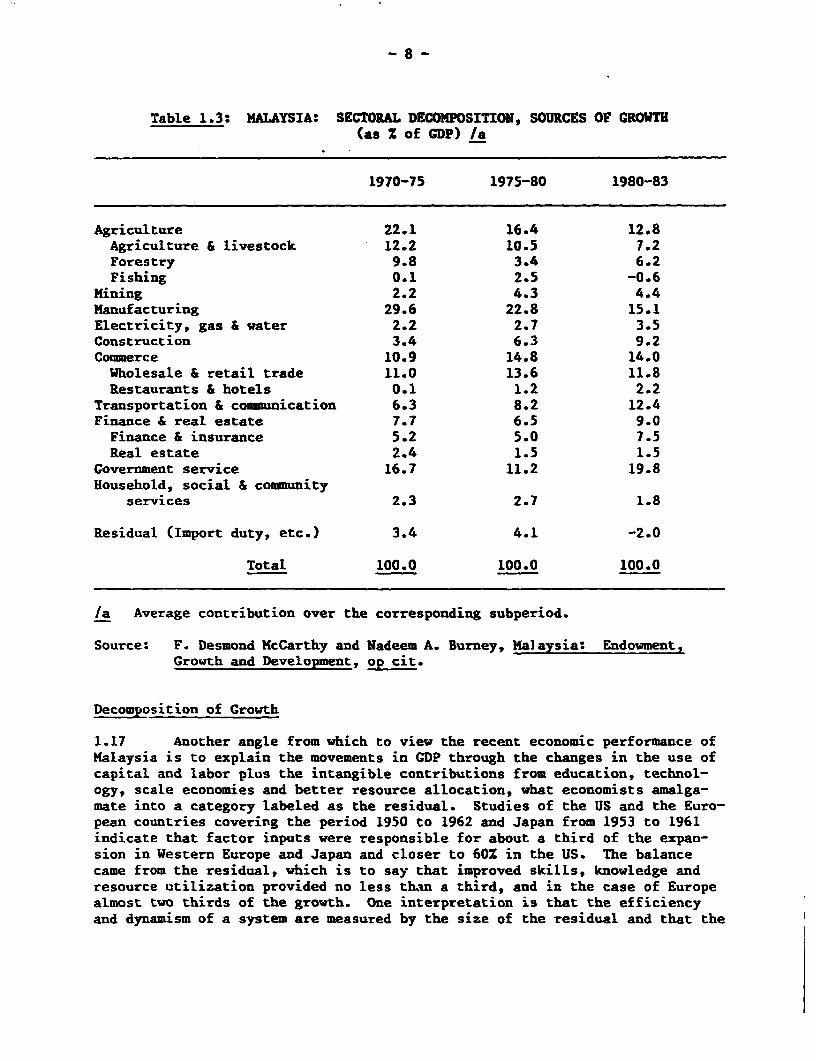

Table 1.3: MALAYSIA: SECTORAL DECOMPOSITION, SOURCES OF GROWTH(as S of GDP) /a

1970-75 1975-80 1980-83

Agriculture 22.1 16.4 12.8Agriculture & livestock 12.2 10.5 7.2Forestry 9.8 3.4 6.2Fishing 0.1 2.5 -0.6

Mining 2.2 4.3 4.4Manufacturing 29.6 22.8 15.1Electricity, gas & water 2.2 2.7 3.5Construction 3.4 6.3 9.2Commerce 10.9 14.8 14.0Wholesale & retail trade 11.0 13.6 11.8Restaurants & hotels 0.1 1.2 2.2

Transportation & communication 6.3 8.2 12.4Finance & real estate 7.7 6.5 9.0Finance & insurance 5.2 5.0 7.5Real estate 2.4 1.5 1.5

Government service 16.7 11.2 19.8Household, social & community

services 2.3 2.7 1.8

Residual (Import duty, etc.) 3.4 4.1 -2.0

Total 100.0 100.0 100.0

/a Average contribution over the corresponding subperiod.

Source: F. Desmond McCarthy and Nadeem A. Burney, Malaysia: Endowment,Growth and Development, op cit.

Decomposition of Growth

1.17 Another angle from which to view the recent economic performance ofMalaysia is to explain the movements in GDP through the changes in the use ofcapital and labor plus the intangible contributions from education, technol-ogy, scale economies and better resource allocation, what economists amalga-mate into a category labeled as the residual. Studies of the US and the Euro-pean countries covering the period 1950 to 1962 and Japan from 1953 to 1961indicate that factor inputs were responsible for about a third of the expan-sion in Western Europe and Japan and closer to 60Z in the US. The balancecame from the residual, which is to say that improved skills, knowledge andresource utilization provided no less than a third, and in the case of Europealmost two thirds of the growth. One interpretation is that the efficiencyand dynamism of a system are measured by the size of the residual and that the

-9-

maturity of an industrial economy rspresented by its technological orienta-tion, its reserves of human capital and its sophisticated market mechanismshould be captured by increases in the residual.

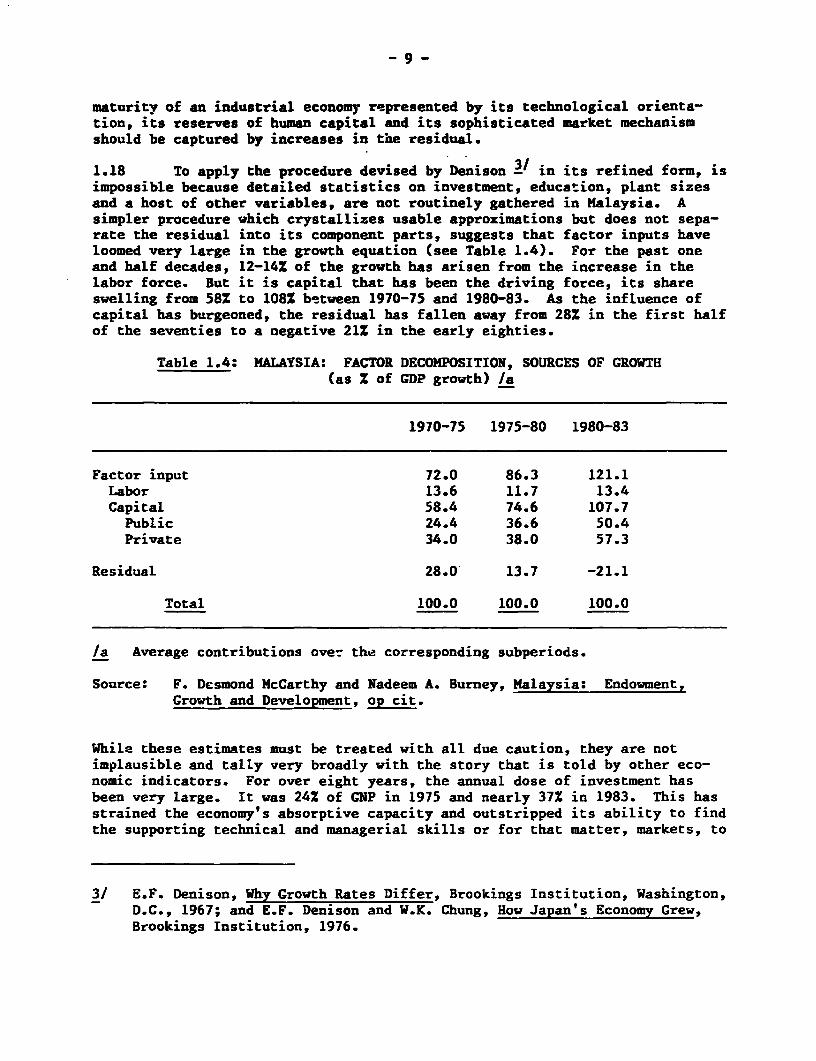

1.18 To apply the procedure devised by Denison 31 in its refined form, isimpossible because detailed statistics on investment, education, plant sizesand a host of other variables, are not routinely gathered in Malaysia. Asimpler procedure which crystallizes usable approximations but does not sepa-rate the residual into its component parts, suggests that factor inputs haveloomed very large in the growth equation (see Table 1.4). For the past oneand half decades, 12-14X of the growth has arisen from the increase in thelabor force. But it is capital that has been the driving force, its shareswelling from 58% to 1081 between 1970-75 and 1980-83. As the influence ofcapital has burgeoned, the residual has fallen away from 28% in the first halfof the seventies to a negative 21Z in the early eighties.

Table 1.4: MALAYSIA: FACTOR DECOMPOSITION, SOURCES OF GROWTH(as X of GDP growth) /a

1970-75 1975-80 1980-83

Factor input 72.0 86.3 121.1Labor 13.6 11.7 13.4Capital 58.4 74.6 107.7Public 24.4 36.6 50.4Private 34.0 38.0 57.3

Residual 28.0 13.7 -21.1

Total 100.0 100.0 100.0

/a Average contributions ove- the corresponding subperiods.

Source: F. Desmond McCarthy and Nadeem A. Burney, Malaysia: Endowment,Growth and Development, op cit.

While these estimates must be treated with all due caution, they are notimplausible and tally very broadly with the story that is told by other eco-nomic indicators. For over eight years, the annual dose of investment hasbeen very large. It was 242 of GNP in 1975 and nearly 37% in 1983. This hasstrained the economy's absorptive capacity and outstripped its ability to findthe supporting technical and managerial skills or for that matter, markets, to

3/ E.F. Denison, Why Growth Rates Differ, Brookings Institution, Washington,D.C., 1967; and E.F. Denison and W.K. Chung, How Japan's Economy Grew,Brookings Institution, 1976.

- 10 -

do justice to the services and goods for which production capacity exists. Sorapidly has the capital base been expanded that new industries have been slowto move up their learning curves and few have made a start at serious appliedresearch or process innovation directly affecting the residual. One implica-tion is that the residual could contribute importantly to future growth, espe-cially since significant additions to the stock of skilled manpower can beexpected in the next few years. A smaller increase in the stock of capitalwould not, therefore, dampen GDP growth, on the contrary it might provide forsorely needed rationalization. A second and less reassuring message can alsobe drawn. If a sizeable proportion of the capital accumulated is in the formof capital intensive projects with very long payback periods or has gone intomanufacturing operations which will have to battle long and hard to find mar-kets for their products, efficiency and learning related gains will accruevery 1,owly. In this connection, the experience of Singapore may be instruc-tive.- Although the growth of manufacturing industries between 1970 and 1979was very rapid, it can be asc:ibed almost entirely to the increase in inputs-- total factor productivity contributed less than than 10Z to the change inproduction. Three reasons have been advanced to explain this phenomenon whichdiffers markedly from total factor productivity trends in Korea and other EastAsian NICs: because Singapore's industry is dominated by foreign firms,little effort has gone into adapting imported technology to the local environ-ment and there has been less room for the learning which is responsible forminor innovations; until recently the emphasis was on labor-intensive assemblyoperations and as Singapore wages were fairly stable in the latter half of theseventies, incentives for raising labor productivity were diluted; andSingapore's financial and commercial expertise does not find an echo in theindustrial sector. As a result, the entrepreneurial efforts at enhancingproductivity have been weak or nonexistent. Each of these causative factorsstraddles the Malaysian experience and should be taken note of in the framingof industrial policies.

1.19 Each of these glances into the past is suggestive i;. its own way.All of them reveal an economy that showed great promise in the seventies,weathered the early eighties with far fewer scars than most others andthroughout this period, has been near the forefront in its propensity toinvest. However, unlike the East Asian NICs who have derived rich export andgrowth dividends from accumulated capital, Malaysia has attained the status ofa middle income country but fallen well short of becoming an industrialnation. It is worth noting why this has transpired, and the reasons for thesurprisingly evanescent nature of the recovery in 1984, as they are the step-ping stones towards an understanding of Malaysia's strategic options.

4/ Y. Tsao, "Growth Without Productivity, Singapore Manufacturing in the1970s," Journal of Development E:onomics, Vol. 18, 1985, pp. 25-38.

- 11 -

Approach to Industrialization

1.20 Lacking natural resources, tbe investment and energies of the EastAsian NICs were directed more forcefully and single-mindedly towards indus-trial advancement. Malaysia put much money into petroleum, palm oil, rubber,tin, timber and cocoa, which has paid handsomely but detracted from the diffi-cult task of laying a secure industrial foundation. Second, from the verystart the public sector has been active in providing infrastructure and ser-vices. As it had access to the earnings from primary production channeledthrough the Government, an increasing amount of investment has found its wayinto office construction, housing, transport facilities and overhead capitalfor agriculture. Because the attention of planners and indigenous businessmenalike was drawn towards the unfolding opportunities in the primary productsector and construction, certain critical aspects of manufacturing develop-ment, relating to technology transfer, securing backward and forward linkages,conscious efforts at grooming import substituting industries for eventualentry into the export market, were given insufficient attention. Exportindustries were left largely in foreign hands instead of becoming a preserveof Malaysian entrepreneurs and the focal center of the economy. In Korea,Hong Kong, and elsewhere in East Asia, the entry of MNCs was followed, after aspell, by competing local investments and the aggressive expansion of inputsuppliers. In Malaysia, the foreign owned assembly operations have long beenseen as providers of employment, some training and a small suite of linkages.

1.21 The narrow dimensions of industrial development were very evident in1984, the best year enjoyed by the economy in the eighties, but one from whichthe economy derived scant long term gains. Manufactured exports, especiallytextiles and electronics which constitute two thirds of the total, rose by 27%pushing the sector's growth to 11%, more than twice the average for thepreceding 3 years. Palm oil production climbed 23X over 1983 and overseassales of crude and processed palm oil were 50Z higher than the year before.But it was housing, real estate and construction that continued to occupy thecenter of the economic stage. Over 35Z of all bank and finance company creditand 44% of total loans were channeled into these subsectors, a continuation ofa trend visible for several years (see Table 1.5). This was significant for anumber of reasons. First, the inclinations of the banking community, lowerconstruction prices, housing programs and the preoccupation of the NFPEs withsuitable office facilities, all continued to draw funds into these activitieseven thoulh signs of an impending glut are widespread. In Kuala Lumpur836,000 m of office space lie unused, rents have dropped precipitously andworse will follow as 65 buildings under construction will add 1.1 million m2

to the rental market by 1987.

- 12 -

Table 1.5: MALAYSIA: ALLOCATION OF CREDIT BY SECTOR /a

Share of total credit Share of GDP(Z) (Z)

1975 1980 1983 1984 1975 1980 1984

Agriculture 8.2 8.3 6.8 4.6 27.7 23.8 21.1Mining and quar-rying 1.7 1.1 1.6 1.1 4.6 4.5 5.0

Manufacturing 17.8 19.8 17.8 16.1 16.4 18.6 18.6Building andconstruction 7.7 7.1 7.0 7.5 3.8 4.6 5.4

Utilities /b 0.0 1.1 0.2 0.1 2.1 2.3 2.6/cGeneral commerce /d 24.0 19.7 17.3 16.7 12.8 13.5 13.5Real estate - 5.0 8.8 13.3 15.1 n.a. n.a. n.a.Transport, storageand commuunica-tions 1.8 2.5 2.5 2.3 6.2 6.9 7.9

Finance, insuranceand business ser-vices 5.9 5.7 9.9 10.8 8.5 7.8 8.0/e

Housing 8.7 11.6 12.4 12.7 n.a. n.a. n.a.Miscellaneous /f 19.2 14.2 11.2 13." 18.1 18.1 17.9/&

Total 100.0 100.0 100.0 100.0 100.0 100.0 100.0

Memo:1. Total housing,real estate andconstructionsectors 21.4 27.5 32.7 35.3 n.a. n.a. n.a.

2. Finance,insurance,business ser-vices, real estatehousing 19.6 26.1 35.6 38.6 8.5 7.8 8.0

3. (1) and (2)plus Construction 27.3 33.2 42.6 46.1 12.3 12.4 13.4

/a Includes only credit from commercial banks and finance companies.71 Electricity.7E Electricity and water.7T Data up to December 1979 include bills discounted or purchased and bills

receivable for foreign trade. Since December 1980 such bills have beenclassified according to borrowers and included in the data for the appropriategroup.

/e Includes real estate and ownership of dwellings as well as finance, insurance andbusiness services.

/f Includes restaurants, hotels and boarding houses, purchase of stocks and shares,consumption credit, and other unidentified credit. Data in this group up toDecember 1979 includes loans to the Federal and State Governments. SinceDecember 1980, such loans have been classified according to borrowers.

/g Government and other services.7h Wholesale and retail trade.

Source: Statistical Appendix Tables 2.2 and 5.2.

- 13 -

1.22 Construction has three negative strikes against it. It has furtherswollen the country's large investment budget at a time when adjustment moti-vated austerities are desirable. It has tightened the financial market forindustrial entrepreneurs, with some deterrent effects on investment in primaryand secondary sectors. But most importantly from the perspective of medium-term investment, the support volunteered by the banks for real estate develop-ment has saddled financial institutions with a large portfolio of doubtfulasbets, some of which are currently nonperforming and many others threatenedby the after-effects of a continuing slump in the market. Such a portfoliowill eat into bank profits, will sharpen their aversion to risks and willweaken their willingness to support an investment drive by the productivesectors.

1.23 Two other developments with a bearing on industrialization must alsobe considered. One is the persistent unresponsiveness of the stock marketboth to the strong economic performance of 1984 and the financial inducementsprovided by the Government in the first half of 1985, which included the open-ing of credit lines for banks lending to investors, lengthening scrip deliverytimes, a halt on new listings and the proposal to establish a M$1 billion fundfor industrial entrepreneurs. The state of the stock market places anotherhurdle in the way of businesses seeking equity financing, but beyond that, italso points towards an undertow of doubt regarding Malaysia's economic futurethat is seemingly impervious to the good economic tidings of 1984 and theGovernment's attempts at sweetening industrial incentives in 1985.