Embed Size (px)

Citation preview

Page 1 of 31

6 Dec 2017

Wilfred Yuen

(852) 2235 7131

Trading data

52-Week Range (HK$)

3 Mth Avg Daily Vol (m)

No of Shares (m)

Market Cap (HK$m)

Major Shareholders (%)

Auditors

Result Due

3.95/5.80

19.5

3,321

16,506

LIU Dian Bo (45.7%)

CITIC PE (5.9%)

E&Y

FY17: Mar

Company description

Founded in 1994, Luye Pharmaceutical engaged in

development, production, marketing and selling of

pharmaceutical products in oncology,

cardiovascular system, metabolism and CNS. The

company is headquartered in Yantai (Shandong

province, China) and was listed on Hong Kong

Stock Exchange in Jul 2014.

Price chart

Source: Bloomberg

0.0

2.0

4.0

6.0

8.0

10.0

Oct-15 Apr-16 Oct-16 Apr-17 Oct-17

Improved pipeline story + business development

Rating Buy Initiation

Target Price HK$6.10

Current price

HK$4.97 Upside +23%

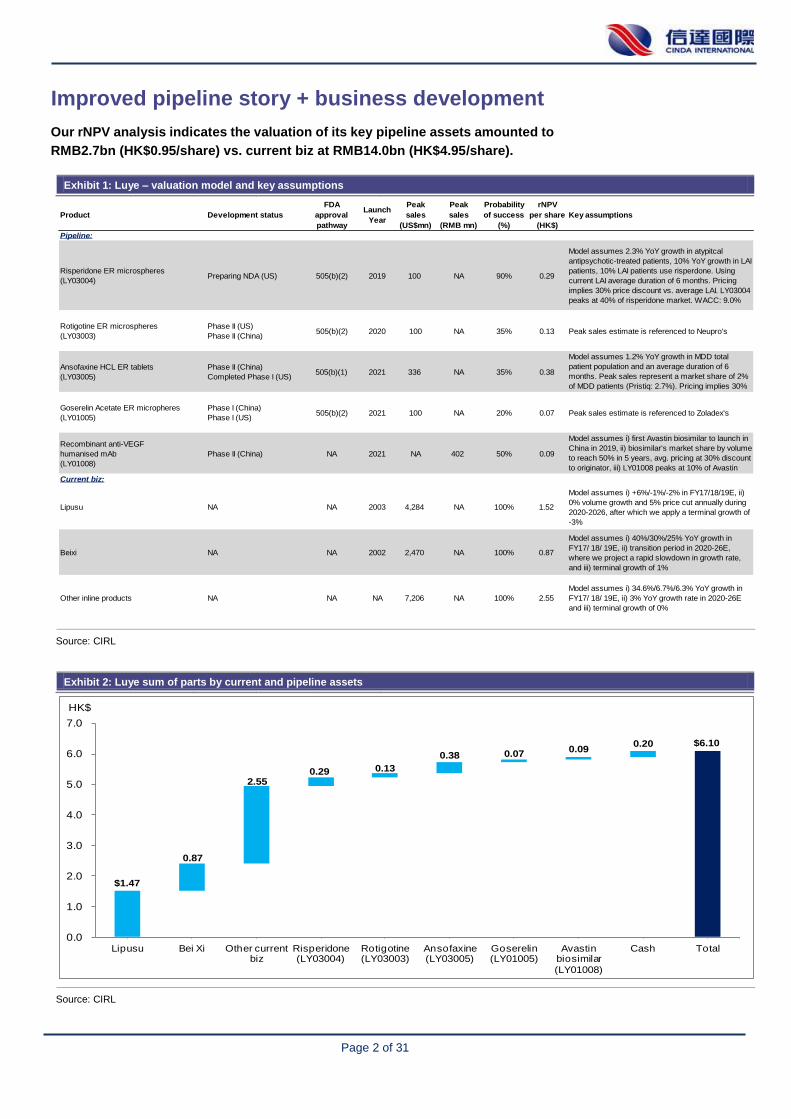

Improved pipeline story + business development We initiate coverage on Luye with a Buy rating and target price of HK$6.10. The stock is currently trading at 14x FY18E P/E, representing a discount of 35% vs. peers’ average of 21x. While near-term revenues/earnings headwinds are reflected in the large discount from a P/E multiple perspective, we believe this view under-appreciates Luye’s pipeline optionality and business development, which provides a strong valuation argument. Our rNPV analysis indicates the valuation of its key pipeline assets amounted to RMB2.7bn (HK$0.95/share) vs. current biz at RMB14.0bn (HK$4.95/share). Moreover, Luye has been active in the business development front with recent acquisitions of Acino and rights to LY01008 and LY06006, which represent a mix of accretive and R&D deals. We expect the company to further diversifying its reliance on its key asset, Lipusu (paclitaxel liposome) and remain active in exploring acquisitions with a focus on commercial-stage CNS assets or R&D assets in oncology.

Pipeline events in 2018 are critical We believe the following two pipeline events are critical for Luye, i) Phase II readouts for LY03005 (Ansofaxine) in 2Q18, ii) NDA submission for LY03004 (Risperidone microsphere) in 3Q18, in the sense that any positive progress could have a meaningful implication for Luye P&L in FY18/19E. For LY03005, the company expects positive results from Phase II study in 2Q18 and is in talks with some pharma MNCs to license out its global rights (ex-China). For LY03004, the company expects to complete stability test for the first production facility (M1) by year-end, and is currently undergoing trial production for another production facility (M2), after which consistency tests between M1 and M2 will be conducted. NDA submission is expected in 3Q18. The annual production capacities for M1 and M2 are 50,000 vials and 0.8 million vials, respectively.

We model Lipusu to peak at RMB1.4bn in 2017 We have taken a more cautious approach (vs. mgmt and street consensus) to forecasting Lipusu franchise (which represents ~40% of FY17E revenues): We assume Lipusu to peak at RMB1.4bn in FY17E, after which we model a declining trajectory due to i) policy risk (the company exited NDRL price negotiation for Lipusu in Jul 2017), ii) increasing competition from Abraxane (protein-bound paclitaxel) and its generics, and iii) patent expiration in 2020.

Valuation and Risks Luye is trading at 15.7x/13.9x FY17E/FY18E P/E. Our NPV-based target price of HK$6.10 implies 17.1x FY18E P/E. Risks include i) higher than expected policy and competition risks on Lipusu, ii) pipeline risk, and iii) integration risk.

RMB mn FY15A FY16A FY17E FY18E FY19E

Revenue 2,563 2,918 3,559 3,765 3,972

Net profit 755 892 896 996 1,038

EPS (RMB) 0.23 0.27 0.27 0.30 0.32

P/E (x) 18.6 15.7 15.7 13.9 13.4

Sources: Company, CIRL estimates

Luye Pharma (2186 HK)

China Puti

Page 2 of 31

Improved pipeline story + business development

Our rNPV analysis indicates the valuation of its key pipeline assets amounted to

RMB2.7bn (HK$0.95/share) vs. current biz at RMB14.0bn (HK$4.95/share).

Exhibit 1: Luye – valuation model and key assumptions

Source: CIRL

Exhibit 2: Luye sum of parts by current and pipeline assets

Source: CIRL

Product Development status

FDA

approval

pathway

Launch

Year

Peak

sales

(US$mn)

Peak

sales

(RMB mn)

Probability

of success

(%)

rNPV

per share

(HK$)

Key assumptions

Pipeline:

Risperidone ER microspheres

(LY03004)Preparing NDA (US) 505(b)(2) 2019 100 NA 90% 0.29

Model assumes 2.3% YoY growth in atypitcal

antipsychotic-treated patients, 10% YoY growth in LAI

patients, 10% LAI patients use risperdone. Using

current LAI average duration of 6 months. Pricing

implies 30% price discount vs. average LAI. LY03004

peaks at 40% of risperidone market. WACC: 9.0%

Rotigotine ER microspheres

(LY03003)

Phase II (US)

Phase II (China)505(b)(2) 2020 100 NA 35% 0.13 Peak sales estimate is referenced to Neupro's

Ansofaxine HCL ER tablets

(LY03005)

Phase II (China)

Completed Phase I (US)505(b)(1) 2021 336 NA 35% 0.38

Model assumes 1.2% YoY growth in MDD total

patient population and an average duration of 6

months. Peak sales represent a market share of 2%

of MDD patients (Pristiq: 2.7%). Pricing implies 30%

discount to Pristiq

Goserelin Acetate ER micropheres

(LY01005)

Phase I (China)

Phase I (US)505(b)(2) 2021 100 NA 20% 0.07 Peak sales estimate is referenced to Zoladex's

Recombinant anti-VEGF

humanised mAb

(LY01008)

Phase II (China) NA 2021 NA 402 50% 0.09

Model assumes i) first Avastin biosimilar to launch in

China in 2019, ii) biosimilar's market share by volume

to reach 50% in 5 years, avg. pricing at 30% discount

to originator, iii) LY01008 peaks at 10% of Avastin

biosimilar marketCurrent biz:

Lipusu NA NA 2003 4,284 NA 100% 1.52

Model assumes i) +6%/-1%/-2% in FY17/18/19E, ii)

0% volume growth and 5% price cut annually during

2020-2026, after which we apply a terminal growth of

-3%

Beixi NA NA 2002 2,470 NA 100% 0.87

Model assumes i) 40%/30%/25% YoY growth in

FY17/ 18/ 19E, ii) transition period in 2020-26E,

where we project a rapid slowdown in growth rate,

and iii) terminal growth of 1%

Other inline products NA NA NA 7,206 NA 100% 2.55

Model assumes i) 34.6%/6.7%/6.3% YoY growth in

FY17/ 18/ 19E, ii) 3% YoY growth rate in 2020-26E

and iii) terminal growth of 0%

$6.10

$1.47

0.87

2.55 0.29 0.13

0.38 0.07 0.09

0.20

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Lipusu Bei Xi Other current biz

Risperidone (LY03004)

Rotigotine (LY03003)

Ansofaxine (LY03005)

Goserelin (LY01005)

Avastin biosimilar

(LY01008)

Cash Total

HK$

Page 3 of 31

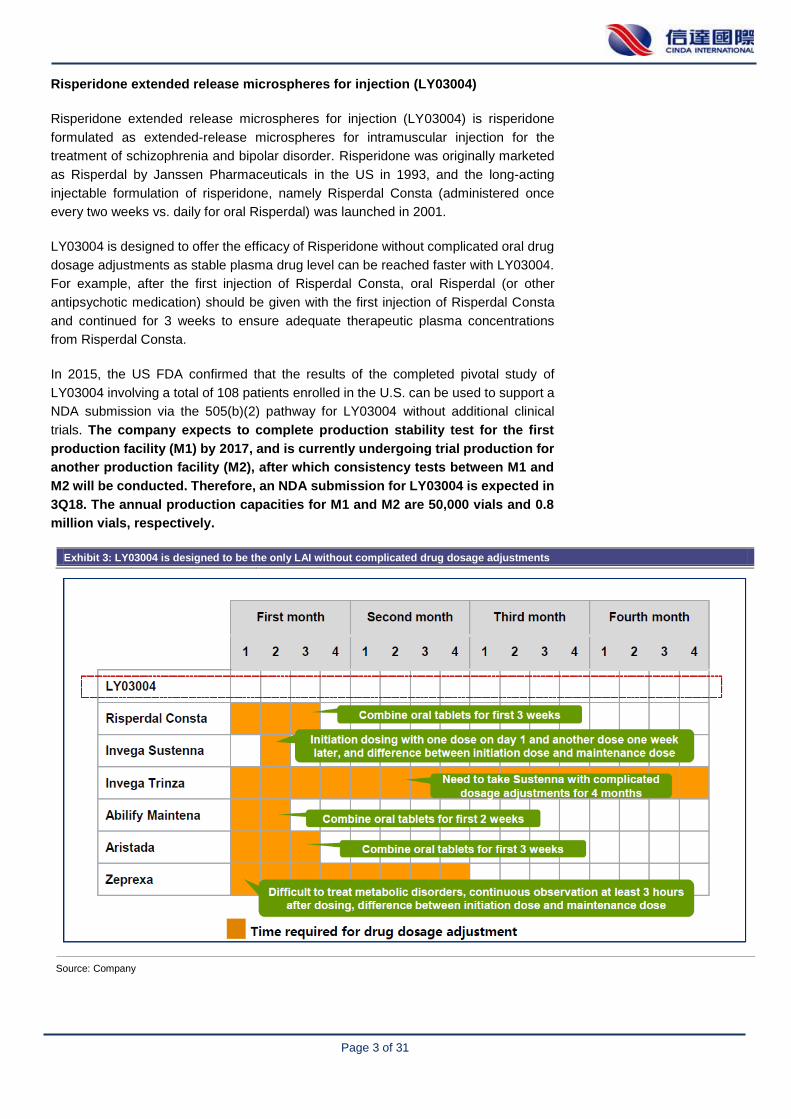

Risperidone extended release microspheres for injection (LY03004)

Risperidone extended release microspheres for injection (LY03004) is risperidone

formulated as extended-release microspheres for intramuscular injection for the

treatment of schizophrenia and bipolar disorder. Risperidone was originally marketed

as Risperdal by Janssen Pharmaceuticals in the US in 1993, and the long-acting

injectable formulation of risperidone, namely Risperdal Consta (administered once

every two weeks vs. daily for oral Risperdal) was launched in 2001.

LY03004 is designed to offer the efficacy of Risperidone without complicated oral drug

dosage adjustments as stable plasma drug level can be reached faster with LY03004.

For example, after the first injection of Risperdal Consta, oral Risperdal (or other

antipsychotic medication) should be given with the first injection of Risperdal Consta

and continued for 3 weeks to ensure adequate therapeutic plasma concentrations

from Risperdal Consta.

In 2015, the US FDA confirmed that the results of the completed pivotal study of

LY03004 involving a total of 108 patients enrolled in the U.S. can be used to support a

NDA submission via the 505(b)(2) pathway for LY03004 without additional clinical

trials. The company expects to complete production stability test for the first

production facility (M1) by 2017, and is currently undergoing trial production for

another production facility (M2), after which consistency tests between M1 and

M2 will be conducted. Therefore, an NDA submission for LY03004 is expected in

3Q18. The annual production capacities for M1 and M2 are 50,000 vials and 0.8

million vials, respectively.

Exhibit 3: LY03004 is designed to be the only LAI without complicated drug dosage adjustments

Source: Company

Page 4 of 31

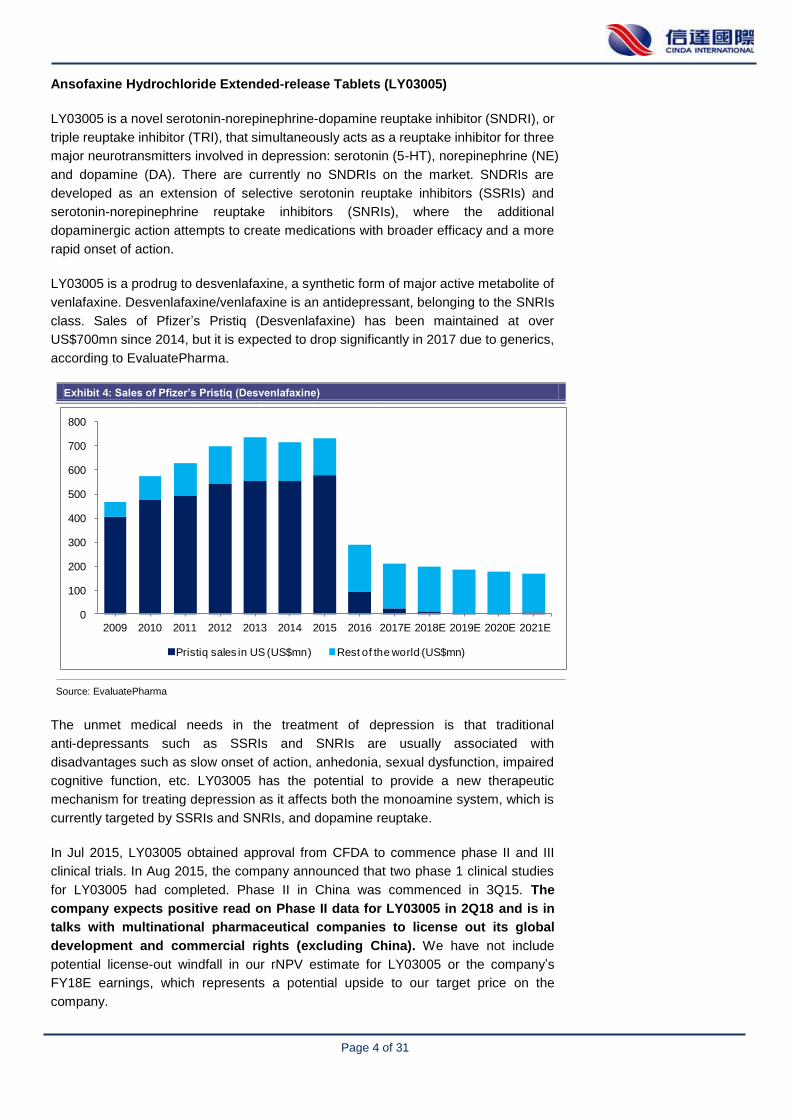

Ansofaxine Hydrochloride Extended-release Tablets (LY03005)

LY03005 is a novel serotonin-norepinephrine-dopamine reuptake inhibitor (SNDRI), or

triple reuptake inhibitor (TRI), that simultaneously acts as a reuptake inhibitor for three

major neurotransmitters involved in depression: serotonin (5-HT), norepinephrine (NE)

and dopamine (DA). There are currently no SNDRIs on the market. SNDRIs are

developed as an extension of selective serotonin reuptake inhibitors (SSRIs) and

serotonin-norepinephrine reuptake inhibitors (SNRIs), where the additional

dopaminergic action attempts to create medications with broader efficacy and a more

rapid onset of action.

LY03005 is a prodrug to desvenlafaxine, a synthetic form of major active metabolite of

venlafaxine. Desvenlafaxine/venlafaxine is an antidepressant, belonging to the SNRIs

class. Sales of Pfizer’s Pristiq (Desvenlafaxine) has been maintained at over

US$700mn since 2014, but it is expected to drop significantly in 2017 due to generics,

according to EvaluatePharma.

Exhibit 4: Sales of Pfizer’s Pristiq (Desvenlafaxine)

Source: EvaluatePharma

The unmet medical needs in the treatment of depression is that traditional

anti-depressants such as SSRIs and SNRIs are usually associated with

disadvantages such as slow onset of action, anhedonia, sexual dysfunction, impaired

cognitive function, etc. LY03005 has the potential to provide a new therapeutic

mechanism for treating depression as it affects both the monoamine system, which is

currently targeted by SSRIs and SNRIs, and dopamine reuptake.

In Jul 2015, LY03005 obtained approval from CFDA to commence phase II and III

clinical trials. In Aug 2015, the company announced that two phase 1 clinical studies

for LY03005 had completed. Phase II in China was commenced in 3Q15. The

company expects positive read on Phase II data for LY03005 in 2Q18 and is in

talks with multinational pharmaceutical companies to license out its global

development and commercial rights (excluding China). We have not include

potential license-out windfall in our rNPV estimate for LY03005 or the company’s

FY18E earnings, which represents a potential upside to our target price on the

company.

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E

Pristiq sales in US (US$mn) Rest of the world (US$mn)

Page 5 of 31

Rotigotine ER microspheres depot for injection (LY03003)

LY03003 is an extended-release microsphere formulation of rotigotine (a dopamine

agonist) that is designed to produce long-term continuous dopamine stimulation for

the treatment of Parkinson’s. It is designed to be administered once-weekly to improve

patient compliance vs. UCB’s once-daily Rotigotine Transdermal Patch System,

namely Neupro.

In Dec 2015, the company announced that the phase 1 clinical studies in US for

LY03003 were completed, which demonstrated that LY03003 was well tolerated and

produced good pharmacokinetic profile after a single injection and multiple injections

within a diversified dose range.

Neupro was initially approved by the FDA in 2007, but it was withdrawn from the US

market in 2008 because there were crystals developed in some patches. UCB

re-launched a new refrigeration-free formulation of Neupro in US market in 2012.

Sales of Neupro was US$390mn (of which US$92mn was in US market) in 2016, with

an expected peak sales of US$481mn by 2020, according to EvaluatePharma.

Exhibit 5: Sales of Neupro (Rotigotine Patch)

Source: EvaluatePharma

0

100

200

300

400

500

2012 2013 2014 2015 2016 2017E 2018E 2019E 2020E 2021E 2022E

Sales of Neupro in US market (US$mn) Rest of the world (US$mn)

Page 6 of 31

Goserelin Acetate Extended-release Microspheres for Injection (LY01005)

LY01005 is a monthly extended release microspheres for intramuscular formulation of

goserelin acetate, a gonadotropin-releasing hormone (GnRH) agonist. Goserelin

acetate was first approved in the US in 1989 and was commercialised by AstraZeneca

under the brand name of Zoladex. There are two other molecules in this class, namely

Decapeptyl (triptorelin) and Lupron (leuproelin), and a related product, GnRH

antagonist Firmagon (degarelix). Zoladex was once the biggest-selling oncology

therapy for AstraZenea. In 2016, sales of Zoladex were US$35mn in US, and

US$821mn globally, according to EvaluatePharma. In Feb 2017, Zoladex’s rights in

Canada and the US was sold to TerSera Therapeutics for US$320mn (upfront

payment of US$250mn).

In 2016, LY01005 obtained the approvals from the FDA and CFDA to initiate clinical

trials for the treatment of carcinoma of the prostate. Like the company’s CNS pipeline,

LY01005 is being registered via a 505(b)(2) pathway in the US. LY01005 is designed

to offer a similar bioavailability comparable to goserelin implant (given subcutaneously,

where a large bore needle is required) while the administration of LY01005 via

intramuscular injection should help improve patient convenience and compliance.

According to Cancer Statistics in 2015, prostate cancer ranked the first incidence

cancer in males in the US. There were total 220,800 new prostate cancer cases

diagnosed in 2015 in the US, which accounted for 26% of all new cancer cases in men.

According to IMS, the market size for gonadotropin-releasing hormone agonist

products in China in 2015 was RMB2.8bn, registering a CAGR of 21.6% from

2013-15.

Exhibit 6: Sales of Zoladex (Goserelin implant)

Source: EvaluatePharma

0

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013 2014 2015 2016 2017E2018E2019E2020E2021E2022E

Zoladex sales in US (US$mn) Rest of the world (US$mn)

Page 7 of 31

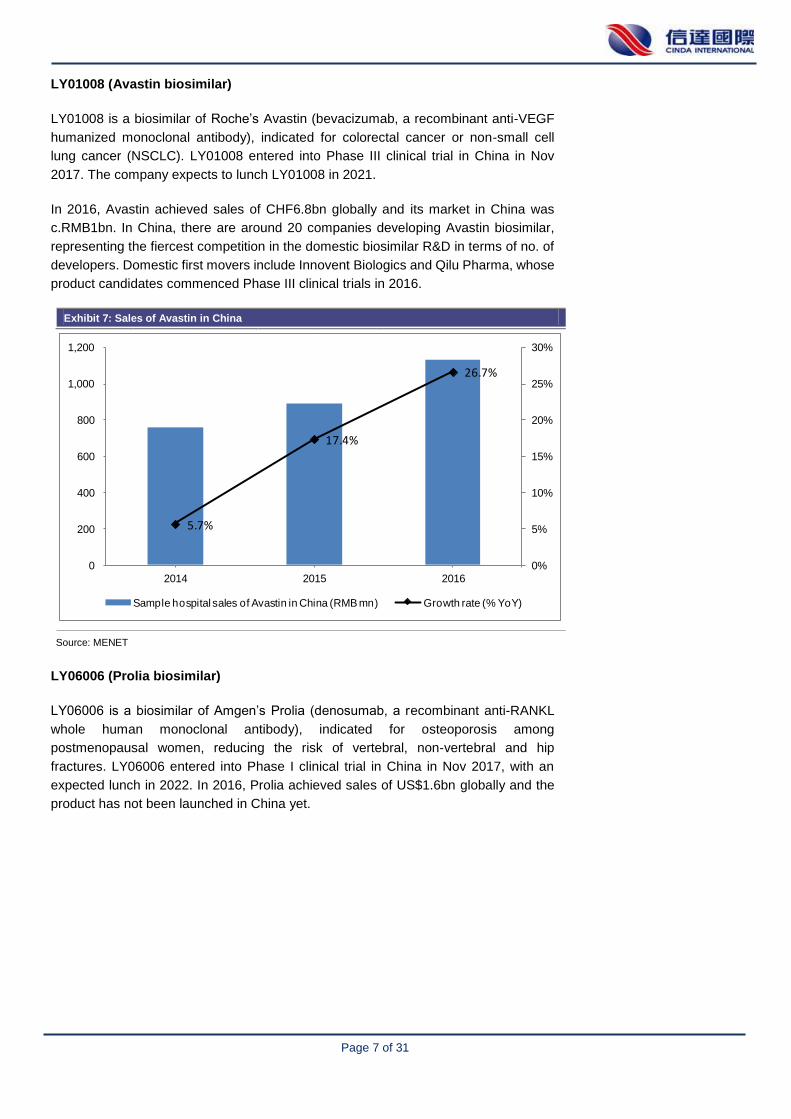

LY01008 (Avastin biosimilar)

LY01008 is a biosimilar of Roche’s Avastin (bevacizumab, a recombinant anti-VEGF

humanized monoclonal antibody), indicated for colorectal cancer or non-small cell

lung cancer (NSCLC). LY01008 entered into Phase III clinical trial in China in Nov

2017. The company expects to lunch LY01008 in 2021.

In 2016, Avastin achieved sales of CHF6.8bn globally and its market in China was

c.RMB1bn. In China, there are around 20 companies developing Avastin biosimilar,

representing the fiercest competition in the domestic biosimilar R&D in terms of no. of

developers. Domestic first movers include Innovent Biologics and Qilu Pharma, whose

product candidates commenced Phase III clinical trials in 2016.

Exhibit 7: Sales of Avastin in China

Source: MENET

LY06006 (Prolia biosimilar)

LY06006 is a biosimilar of Amgen’s Prolia (denosumab, a recombinant anti-RANKL

whole human monoclonal antibody), indicated for osteoporosis among

postmenopausal women, reducing the risk of vertebral, non-vertebral and hip

fractures. LY06006 entered into Phase I clinical trial in China in Nov 2017, with an

expected lunch in 2022. In 2016, Prolia achieved sales of US$1.6bn globally and the

product has not been launched in China yet.

5.7%

17.4%

26.7%

0%

5%

10%

15%

20%

25%

30%

0

200

400

600

800

1,000

1,200

2014 2015 2016

Sample hospital sales of Avastin in China (RMB mn) Growth rate (% YoY)

Page 8 of 31

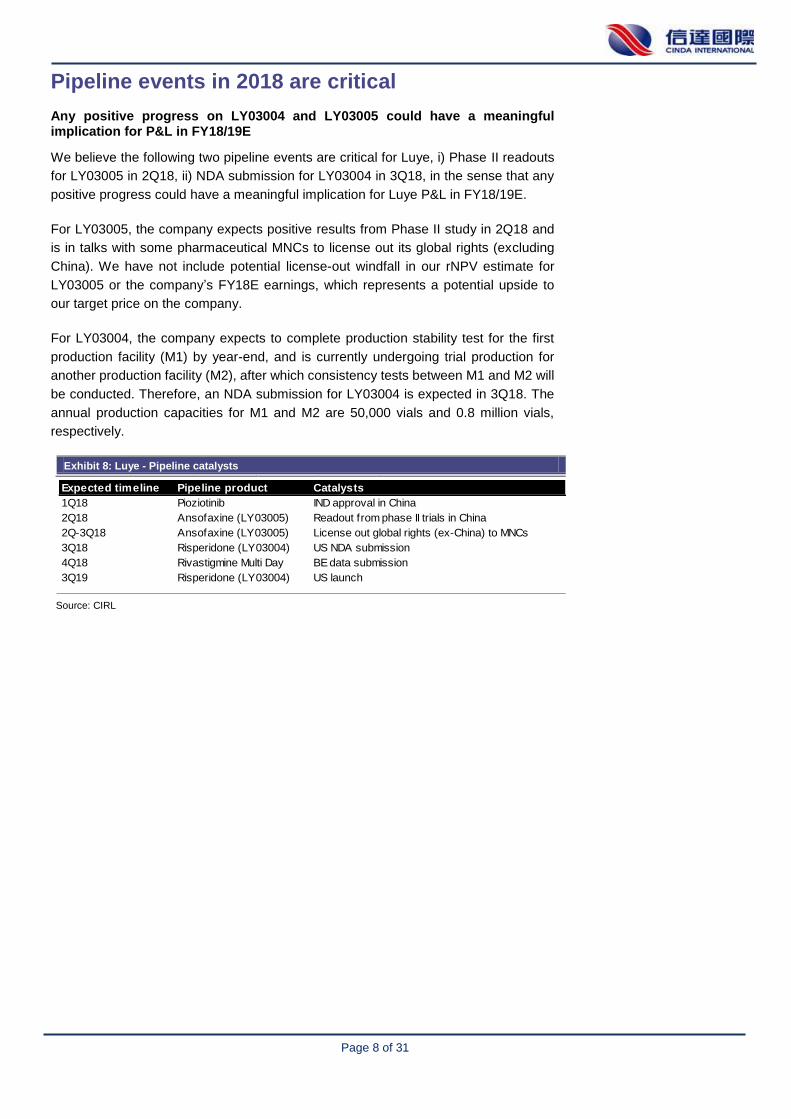

Pipeline events in 2018 are critical

Any positive progress on LY03004 and LY03005 could have a meaningful implication for P&L in FY18/19E

We believe the following two pipeline events are critical for Luye, i) Phase II readouts

for LY03005 in 2Q18, ii) NDA submission for LY03004 in 3Q18, in the sense that any

positive progress could have a meaningful implication for Luye P&L in FY18/19E.

For LY03005, the company expects positive results from Phase II study in 2Q18 and

is in talks with some pharmaceutical MNCs to license out its global rights (excluding

China). We have not include potential license-out windfall in our rNPV estimate for

LY03005 or the company’s FY18E earnings, which represents a potential upside to

our target price on the company.

For LY03004, the company expects to complete production stability test for the first

production facility (M1) by year-end, and is currently undergoing trial production for

another production facility (M2), after which consistency tests between M1 and M2 will

be conducted. Therefore, an NDA submission for LY03004 is expected in 3Q18. The

annual production capacities for M1 and M2 are 50,000 vials and 0.8 million vials,

respectively.

Exhibit 8: Luye - Pipeline catalysts

Source: CIRL

Expected timeline Pipeline product Catalysts

1Q18 Pioziotinib IND approval in China

2Q18 Ansofaxine (LY03005) Readout from phase II trials in China

2Q-3Q18 Ansofaxine (LY03005) License out global rights (ex-China) to MNCs

3Q18 Risperidone (LY03004) US NDA submission

4Q18 Rivastigmine Multi Day BE data submission

3Q19 Risperidone (LY03004) US launch

Page 9 of 31

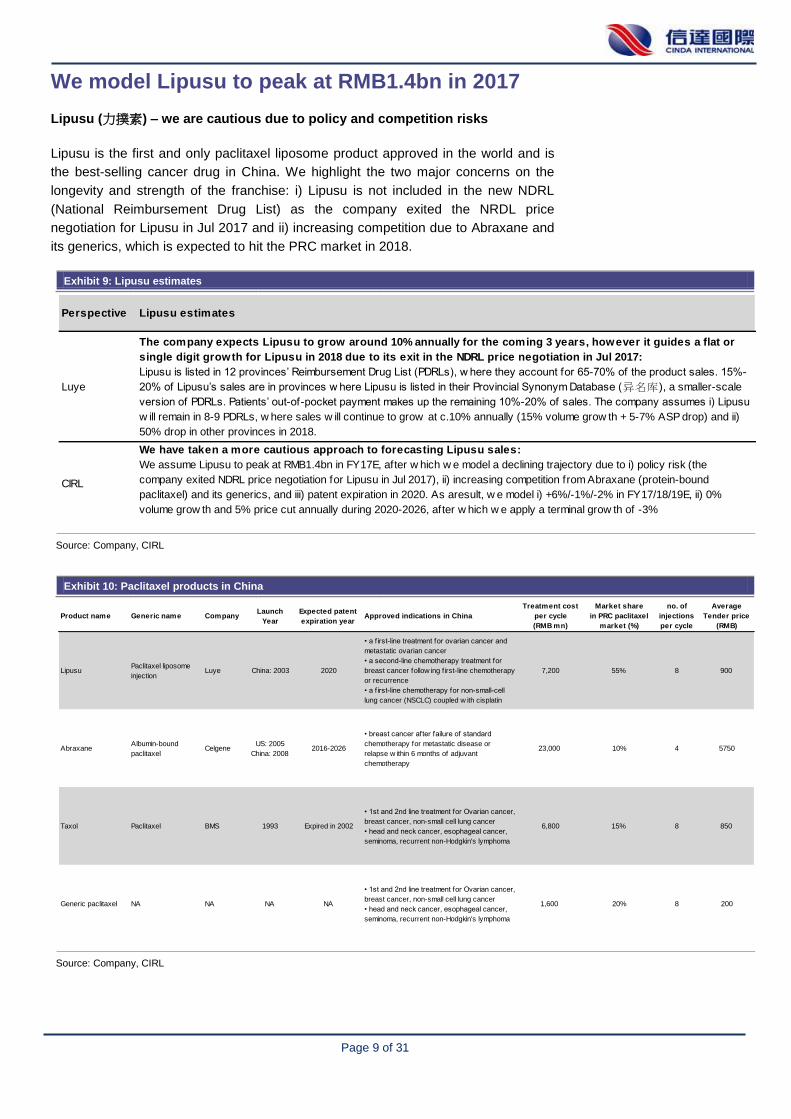

We model Lipusu to peak at RMB1.4bn in 2017

Lipusu (力撲素) – we are cautious due to policy and competition risks

Lipusu is the first and only paclitaxel liposome product approved in the world and is

the best-selling cancer drug in China. We highlight the two major concerns on the

longevity and strength of the franchise: i) Lipusu is not included in the new NDRL

(National Reimbursement Drug List) as the company exited the NRDL price

negotiation for Lipusu in Jul 2017 and ii) increasing competition due to Abraxane and

its generics, which is expected to hit the PRC market in 2018.

Exhibit 9: Lipusu estimates

Source: Company, CIRL

Exhibit 10: Paclitaxel products in China

Source: Company, CIRL

Perspective Lipusu estimates

Luye

The company expects Lipusu to grow around 10% annually for the coming 3 years, however it guides a flat or

single digit growth for Lipusu in 2018 due to its exit in the NDRL price negotiation in Jul 2017:

Lipusu is listed in 12 provinces’ Reimbursement Drug List (PDRLs), w here they account for 65-70% of the product sales. 15%-

20% of Lipusu’s sales are in provinces w here Lipusu is listed in their Provincial Synonym Database (异名库), a smaller-scale

version of PDRLs. Patients’ out-of-pocket payment makes up the remaining 10%-20% of sales. The company assumes i) Lipusu

w ill remain in 8-9 PDRLs, w here sales w ill continue to grow at c.10% annually (15% volume grow th + 5-7% ASP drop) and ii)

50% drop in other provinces in 2018.

CIRL

We have taken a more cautious approach to forecasting Lipusu sales:

We assume Lipusu to peak at RMB1.4bn in FY17E, after w hich w e model a declining trajectory due to i) policy risk (the

company exited NDRL price negotiation for Lipusu in Jul 2017), ii) increasing competition from Abraxane (protein-bound

paclitaxel) and its generics, and iii) patent expiration in 2020. As aresult, w e model i) +6%/-1%/-2% in FY17/18/19E, ii) 0%

volume grow th and 5% price cut annually during 2020-2026, after w hich w e apply a terminal grow th of -3%

Product name Generic name CompanyLaunch

Year

Expected patent

expiration yearApproved indications in China

Treatment cost

per cycle

(RMB mn)

Market share

in PRC paclitaxel

market (%)

no. of

injections

per cycle

Average

Tender price

(RMB)

LipusuPaclitaxel liposome

injectionLuye China: 2003 2020

• a f irst-line treatment for ovarian cancer and

metastatic ovarian cancer

• a second-line chemotherapy treatment for

breast cancer follow ing f irst-line chemotherapy

or recurrence

• a f irst-line chemotherapy for non-small-cell

lung cancer (NSCLC) coupled w ith cisplatin

7,200 55% 8 900

AbraxaneAlbumin-bound

paclitaxelCelgene

US: 2005

China: 20082016-2026

• breast cancer after failure of standard

chemotherapy for metastatic disease or

relapse w ithin 6 months of adjuvant

chemotherapy

23,000 10% 4 5750

Taxol Paclitaxel BMS 1993 Expired in 2002

• 1st and 2nd line treatment for Ovarian cancer,

breast cancer, non-small cell lung cancer

• head and neck cancer, esophageal cancer,

seminoma, recurrent non-Hodgkin's lymphoma

6,800 15% 8 850

Generic paclitaxel NA NA NA NA

• 1st and 2nd line treatment for Ovarian cancer,

breast cancer, non-small cell lung cancer

• head and neck cancer, esophageal cancer,

seminoma, recurrent non-Hodgkin's lymphoma

1,600 20% 8 200

Page 10 of 31

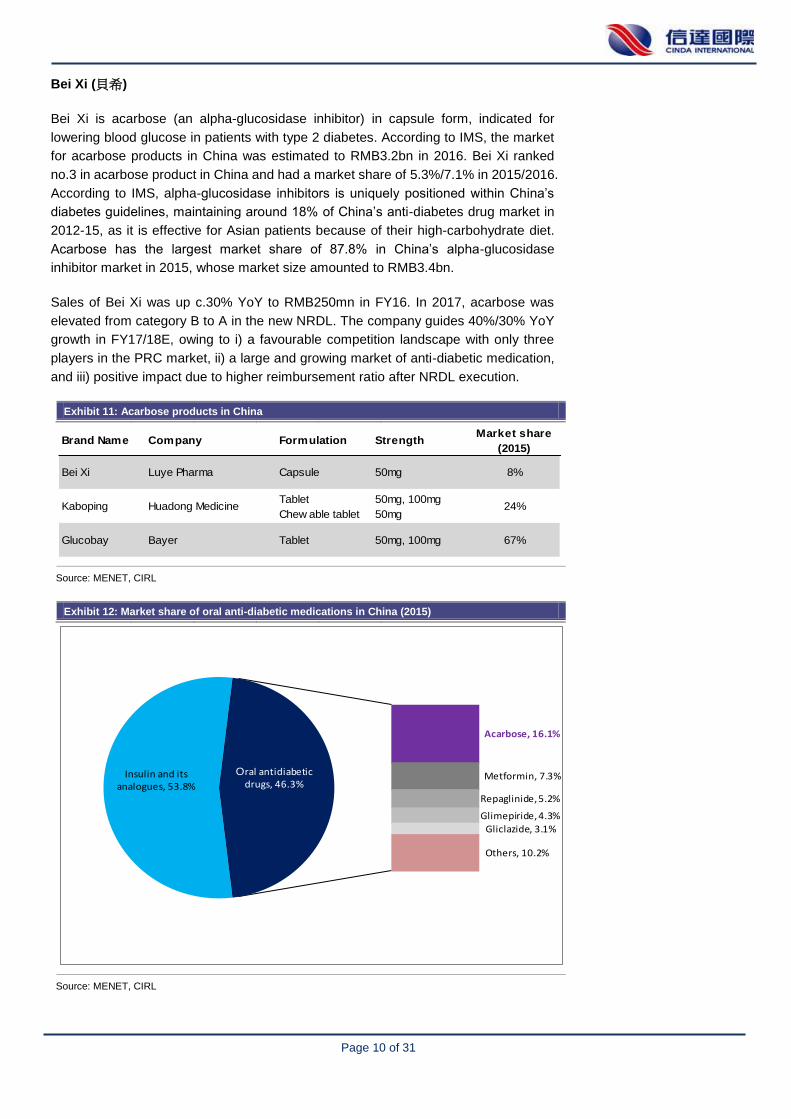

Bei Xi (貝希)

Bei Xi is acarbose (an alpha-glucosidase inhibitor) in capsule form, indicated for

lowering blood glucose in patients with type 2 diabetes. According to IMS, the market

for acarbose products in China was estimated to RMB3.2bn in 2016. Bei Xi ranked

no.3 in acarbose product in China and had a market share of 5.3%/7.1% in 2015/2016.

According to IMS, alpha-glucosidase inhibitors is uniquely positioned within China’s

diabetes guidelines, maintaining around 18% of China’s anti-diabetes drug market in

2012-15, as it is effective for Asian patients because of their high-carbohydrate diet.

Acarbose has the largest market share of 87.8% in China’s alpha-glucosidase

inhibitor market in 2015, whose market size amounted to RMB3.4bn.

Sales of Bei Xi was up c.30% YoY to RMB250mn in FY16. In 2017, acarbose was

elevated from category B to A in the new NRDL. The company guides 40%/30% YoY

growth in FY17/18E, owing to i) a favourable competition landscape with only three

players in the PRC market, ii) a large and growing market of anti-diabetic medication,

and iii) positive impact due to higher reimbursement ratio after NRDL execution.

Exhibit 11: Acarbose products in China

Source: MENET, CIRL

Exhibit 12: Market share of oral anti-diabetic medications in China (2015)

Source: MENET, CIRL

Brand Name Company Formulation StrengthMarket share

(2015)

Bei Xi Luye Pharma Capsule 50mg 8%

Kaboping Huadong MedicineTablet

Chew able tablet

50mg, 100mg

50mg24%

Glucobay Bayer Tablet 50mg, 100mg 67%

Insulin and its analogues, 53.8%

Acarbose, 16.1%

Metformin, 7.3%

Repaglinide, 5.2%

Glimepiride, 4.3%

Gliclazide, 3.1%

Others, 10.2%

Oral antidiabetic drugs, 46.3%

Page 11 of 31

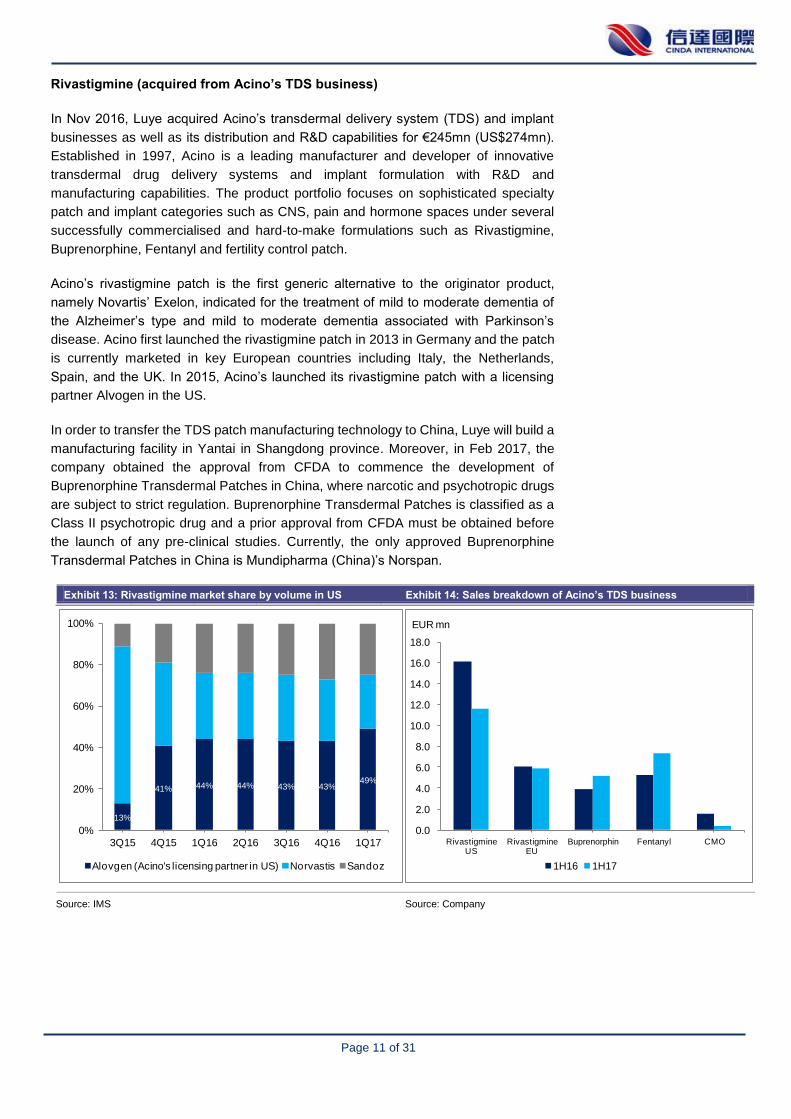

Rivastigmine (acquired from Acino’s TDS business)

In Nov 2016, Luye acquired Acino’s transdermal delivery system (TDS) and implant

businesses as well as its distribution and R&D capabilities for €245mn (US$274mn).

Established in 1997, Acino is a leading manufacturer and developer of innovative

transdermal drug delivery systems and implant formulation with R&D and

manufacturing capabilities. The product portfolio focuses on sophisticated specialty

patch and implant categories such as CNS, pain and hormone spaces under several

successfully commercialised and hard-to-make formulations such as Rivastigmine,

Buprenorphine, Fentanyl and fertility control patch.

Acino’s rivastigmine patch is the first generic alternative to the originator product,

namely Novartis’ Exelon, indicated for the treatment of mild to moderate dementia of

the Alzheimer’s type and mild to moderate dementia associated with Parkinson’s

disease. Acino first launched the rivastigmine patch in 2013 in Germany and the patch

is currently marketed in key European countries including Italy, the Netherlands,

Spain, and the UK. In 2015, Acino’s launched its rivastigmine patch with a licensing

partner Alvogen in the US.

In order to transfer the TDS patch manufacturing technology to China, Luye will build a

manufacturing facility in Yantai in Shangdong province. Moreover, in Feb 2017, the

company obtained the approval from CFDA to commence the development of

Buprenorphine Transdermal Patches in China, where narcotic and psychotropic drugs

are subject to strict regulation. Buprenorphine Transdermal Patches is classified as a

Class II psychotropic drug and a prior approval from CFDA must be obtained before

the launch of any pre-clinical studies. Currently, the only approved Buprenorphine

Transdermal Patches in China is Mundipharma (China)’s Norspan.

Exhibit 13: Rivastigmine market share by volume in US Exhibit 14: Sales breakdown of Acino’s TDS business

Source: IMS Source: Company

13%

41% 44% 44% 43% 43%49%

0%

20%

40%

60%

80%

100%

3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

Alovgen (Acino's licensing partner in US) Norvastis Sandoz

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Rivastigmine US

Rivastigmine EU

Buprenorphin Fentanyl CMO

EUR mn

1H16 1H17

Page 12 of 31

Valuation

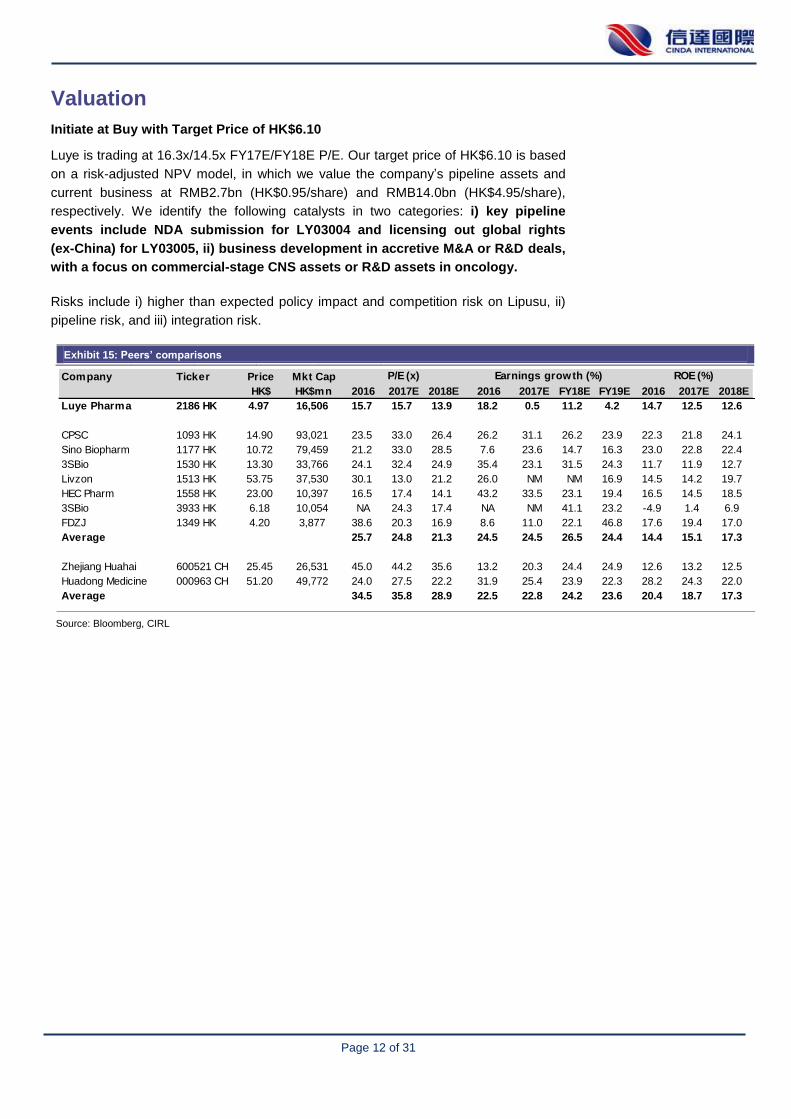

Initiate at Buy with Target Price of HK$6.10

Luye is trading at 16.3x/14.5x FY17E/FY18E P/E. Our target price of HK$6.10 is based

on a risk-adjusted NPV model, in which we value the company’s pipeline assets and

current business at RMB2.7bn (HK$0.95/share) and RMB14.0bn (HK$4.95/share),

respectively. We identify the following catalysts in two categories: i) key pipeline

events include NDA submission for LY03004 and licensing out global rights

(ex-China) for LY03005, ii) business development in accretive M&A or R&D deals,

with a focus on commercial-stage CNS assets or R&D assets in oncology.

Risks include i) higher than expected policy impact and competition risk on Lipusu, ii)

pipeline risk, and iii) integration risk.

Exhibit 15: Peers’ comparisons

Exhibit 1:

Source: Bloomberg, CIRL

Company Ticker Price Mkt Cap

HK$ HK$mn 2016 2017E 2018E 2016 2017E FY18E FY19E 2016 2017E 2018E

Luye Pharma 2186 HK 4.97 16,506 15.7 15.7 13.9 18.2 0.5 11.2 4.2 14.7 12.5 12.6

CPSC 1093 HK 14.90 93,021 23.5 33.0 26.4 26.2 31.1 26.2 23.9 22.3 21.8 24.1

Sino Biopharm 1177 HK 10.72 79,459 21.2 33.0 28.5 7.6 23.6 14.7 16.3 23.0 22.8 22.4

3SBio 1530 HK 13.30 33,766 24.1 32.4 24.9 35.4 23.1 31.5 24.3 11.7 11.9 12.7

Livzon 1513 HK 53.75 37,530 30.1 13.0 21.2 26.0 NM NM 16.9 14.5 14.2 19.7

HEC Pharm 1558 HK 23.00 10,397 16.5 17.4 14.1 43.2 33.5 23.1 19.4 16.5 14.5 18.5

3SBio 3933 HK 6.18 10,054 NA 24.3 17.4 NA NM 41.1 23.2 -4.9 1.4 6.9

FDZJ 1349 HK 4.20 3,877 38.6 20.3 16.9 8.6 11.0 22.1 46.8 17.6 19.4 17.0

Average 25.7 24.8 21.3 24.5 24.5 26.5 24.4 14.4 15.1 17.3

Zhejiang Huahai 600521 CH 25.45 26,531 45.0 44.2 35.6 13.2 20.3 24.4 24.9 12.6 13.2 12.5

Huadong Medicine 000963 CH 51.20 49,772 24.0 27.5 22.2 31.9 25.4 23.9 22.3 28.2 24.3 22.0

Average 34.5 35.8 28.9 22.5 22.8 24.2 23.6 20.4 18.7 17.3

P/E (x) Earnings growth (%) ROE (%)

Page 13 of 31

Financials

Revenue

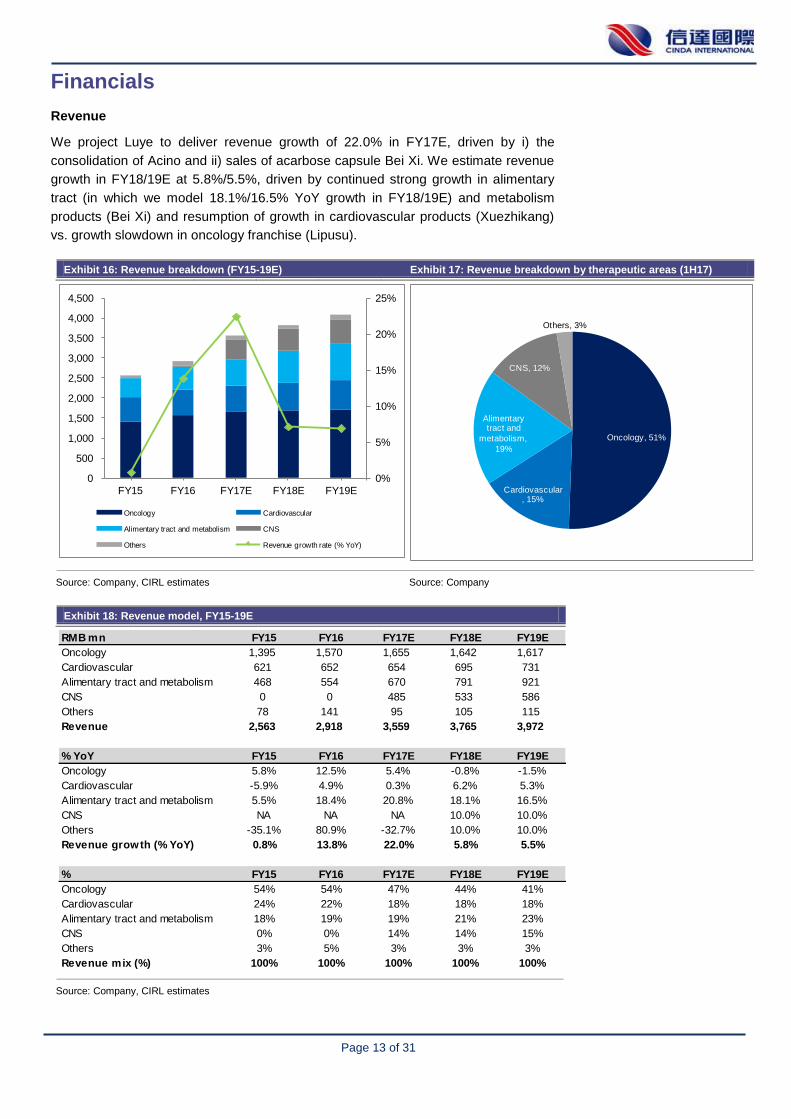

We project Luye to deliver revenue growth of 22.0% in FY17E, driven by i) the

consolidation of Acino and ii) sales of acarbose capsule Bei Xi. We estimate revenue

growth in FY18/19E at 5.8%/5.5%, driven by continued strong growth in alimentary

tract (in which we model 18.1%/16.5% YoY growth in FY18/19E) and metabolism

products (Bei Xi) and resumption of growth in cardiovascular products (Xuezhikang)

vs. growth slowdown in oncology franchise (Lipusu).

Exhibit 16: Revenue breakdown (FY15-19E) Exhibit 17: Revenue breakdown by therapeutic areas (1H17)

Source: Company, CIRL estimates Source: Company

Exhibit 18: Revenue model, FY15-19E

Source: Company, CIRL estimates

0%

5%

10%

15%

20%

25%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY15 FY16 FY17E FY18E FY19E

Oncology Cardiovascular

Alimentary tract and metabolism CNS

Others Revenue growth rate (% YoY)

Oncology, 51%

Cardiovascular , 15%

Alimentary tract and

metabolism,

19%

CNS, 12%

Others, 3%

RMB mn FY15 FY16 FY17E FY18E FY19E

Oncology 1,395 1,570 1,655 1,642 1,617

Cardiovascular 621 652 654 695 731

Alimentary tract and metabolism 468 554 670 791 921

CNS 0 0 485 533 586

Others 78 141 95 105 115

Revenue 2,563 2,918 3,559 3,765 3,972

% YoY FY15 FY16 FY17E FY18E FY19E

Oncology 5.8% 12.5% 5.4% -0.8% -1.5%

Cardiovascular -5.9% 4.9% 0.3% 6.2% 5.3%

Alimentary tract and metabolism 5.5% 18.4% 20.8% 18.1% 16.5%

CNS NA NA NA 10.0% 10.0%

Others -35.1% 80.9% -32.7% 10.0% 10.0%

Revenue growth (% YoY) 0.8% 13.8% 22.0% 5.8% 5.5%

% FY15 FY16 FY17E FY18E FY19E

Oncology 54% 54% 47% 44% 41%

Cardiovascular 24% 22% 18% 18% 18%

Alimentary tract and metabolism 18% 19% 19% 21% 23%

CNS 0% 0% 14% 14% 15%

Others 3% 5% 3% 3% 3%

Revenue mix (%) 100% 100% 100% 100% 100%

Page 14 of 31

Margin analysis, SG&A ratio, R&D expenses

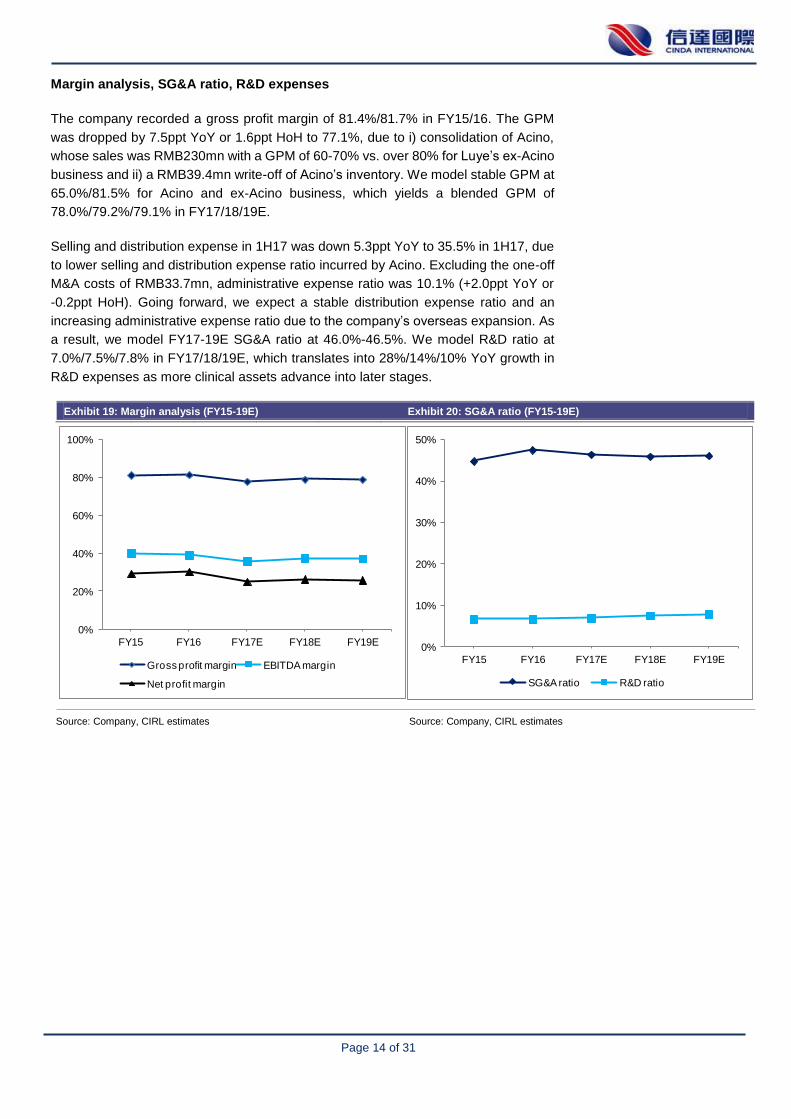

The company recorded a gross profit margin of 81.4%/81.7% in FY15/16. The GPM

was dropped by 7.5ppt YoY or 1.6ppt HoH to 77.1%, due to i) consolidation of Acino,

whose sales was RMB230mn with a GPM of 60-70% vs. over 80% for Luye’s ex-Acino

business and ii) a RMB39.4mn write-off of Acino’s inventory. We model stable GPM at

65.0%/81.5% for Acino and ex-Acino business, which yields a blended GPM of

78.0%/79.2%/79.1% in FY17/18/19E.

Selling and distribution expense in 1H17 was down 5.3ppt YoY to 35.5% in 1H17, due

to lower selling and distribution expense ratio incurred by Acino. Excluding the one-off

M&A costs of RMB33.7mn, administrative expense ratio was 10.1% (+2.0ppt YoY or

-0.2ppt HoH). Going forward, we expect a stable distribution expense ratio and an

increasing administrative expense ratio due to the company’s overseas expansion. As

a result, we model FY17-19E SG&A ratio at 46.0%-46.5%. We model R&D ratio at

7.0%/7.5%/7.8% in FY17/18/19E, which translates into 28%/14%/10% YoY growth in

R&D expenses as more clinical assets advance into later stages.

Exhibit 19: Margin analysis (FY15-19E) Exhibit 20: SG&A ratio (FY15-19E)

Exhibit 2:

Source: Company, CIRL estimates Source: Company, CIRL estimates

0%

20%

40%

60%

80%

100%

FY15 FY16 FY17E FY18E FY19E

Gross profit margin EBITDA margin

Net profit margin

0%

10%

20%

30%

40%

50%

FY15 FY16 FY17E FY18E FY19E

SG&A ratio R&D ratio

Page 15 of 31

Exhibit 21: Net profit growth, 2014-18E

Source: Company, CIRL estimates

0%

5%

10%

15%

20%

25%

30%

35%

0

200

400

600

800

1,000

1,200

FY15 FY16 FY17E FY18E FY19E

RMB mn

Net profit Growth rate (% YoY) net profit margin (%)

Page 16 of 31

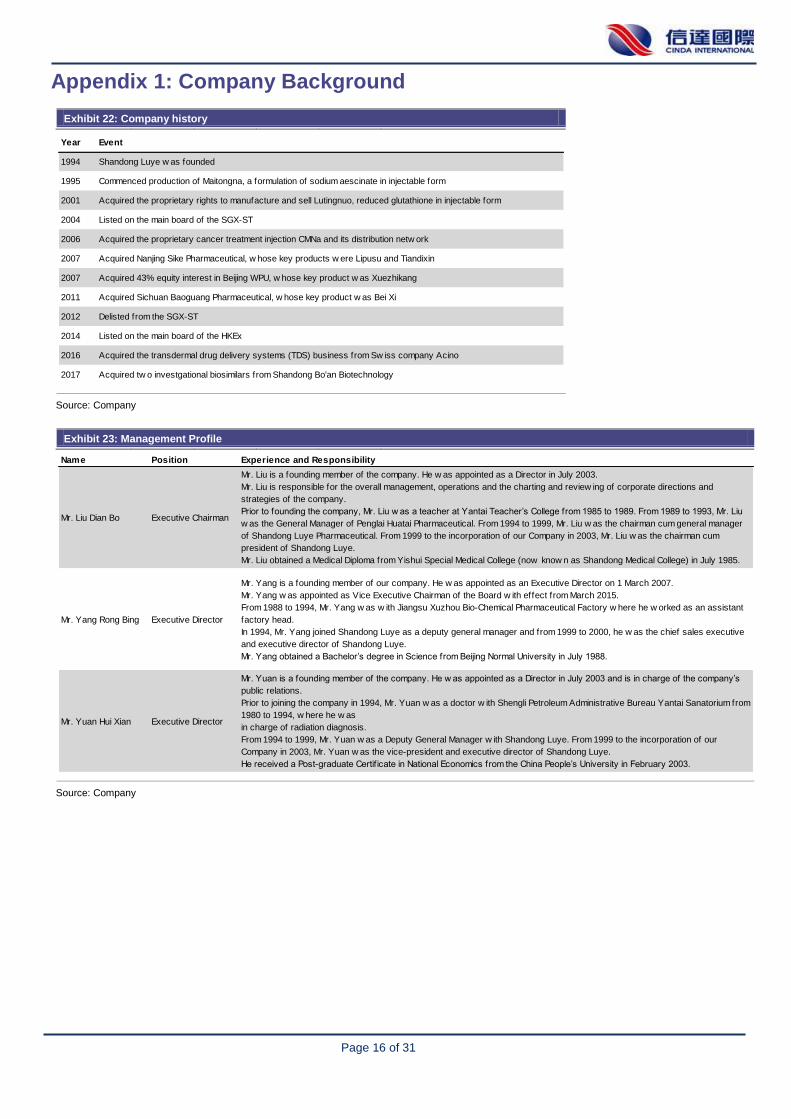

Appendix 1: Company Background

Exhibit 22: Company history

Source: Company

Exhibit 23: Management Profile

Source: Company

Year Event

1994 Shandong Luye w as founded

1995 Commenced production of Maitongna, a formulation of sodium aescinate in injectable form

2001 Acquired the proprietary rights to manufacture and sell Lutingnuo, reduced glutathione in injectable form

2004 Listed on the main board of the SGX-ST

2006 Acquired the proprietary cancer treatment injection CMNa and its distribution netw ork

2007 Acquired Nanjing Sike Pharmaceutical, w hose key products w ere Lipusu and Tiandixin

2007 Acquired 43% equity interest in Beijing WPU, w hose key product w as Xuezhikang

2011 Acquired Sichuan Baoguang Pharmaceutical, w hose key product w as Bei Xi

2012 Delisted from the SGX-ST

2014 Listed on the main board of the HKEx

2016 Acquired the transdermal drug delivery systems (TDS) business from Sw iss company Acino

2017 Acquired tw o investgational biosimilars from Shandong Bo'an Biotechnology

Name Position Experience and Responsibility

Mr. Liu Dian Bo Executive Chairman

Mr. Liu is a founding member of the company. He w as appointed as a Director in July 2003.

Mr. Liu is responsible for the overall management, operations and the charting and review ing of corporate directions and

strategies of the company.

Prior to founding the company, Mr. Liu w as a teacher at Yantai Teacher’s College from 1985 to 1989. From 1989 to 1993, Mr. Liu

w as the General Manager of Penglai Huatai Pharmaceutical. From 1994 to 1999, Mr. Liu w as the chairman cum general manager

of Shandong Luye Pharmaceutical. From 1999 to the incorporation of our Company in 2003, Mr. Liu w as the chairman cum

president of Shandong Luye.

Mr. Liu obtained a Medical Diploma from Yishui Special Medical College (now know n as Shandong Medical College) in July 1985.

Mr. Yang Rong Bing Executive Director

Mr. Yang is a founding member of our company. He w as appointed as an Executive Director on 1 March 2007.

Mr. Yang w as appointed as Vice Executive Chairman of the Board w ith effect from March 2015.

From 1988 to 1994, Mr. Yang w as w ith Jiangsu Xuzhou Bio-Chemical Pharmaceutical Factory w here he w orked as an assistant

factory head.

In 1994, Mr. Yang joined Shandong Luye as a deputy general manager and from 1999 to 2000, he w as the chief sales executive

and executive director of Shandong Luye.

Mr. Yang obtained a Bachelor’s degree in Science from Beijing Normal University in July 1988.

Mr. Yuan Hui Xian Executive Director

Mr. Yuan is a founding member of the company. He w as appointed as a Director in July 2003 and is in charge of the company’s

public relations.

Prior to joining the company in 1994, Mr. Yuan w as a doctor w ith Shengli Petroleum Administrative Bureau Yantai Sanatorium from

1980 to 1994, w here he w as

in charge of radiation diagnosis.

From 1994 to 1999, Mr. Yuan w as a Deputy General Manager w ith Shandong Luye. From 1999 to the incorporation of our

Company in 2003, Mr. Yuan w as the vice-president and executive director of Shandong Luye.

He received a Post-graduate Certif icate in National Economics from the China People’s University in February 2003.

Page 17 of 31

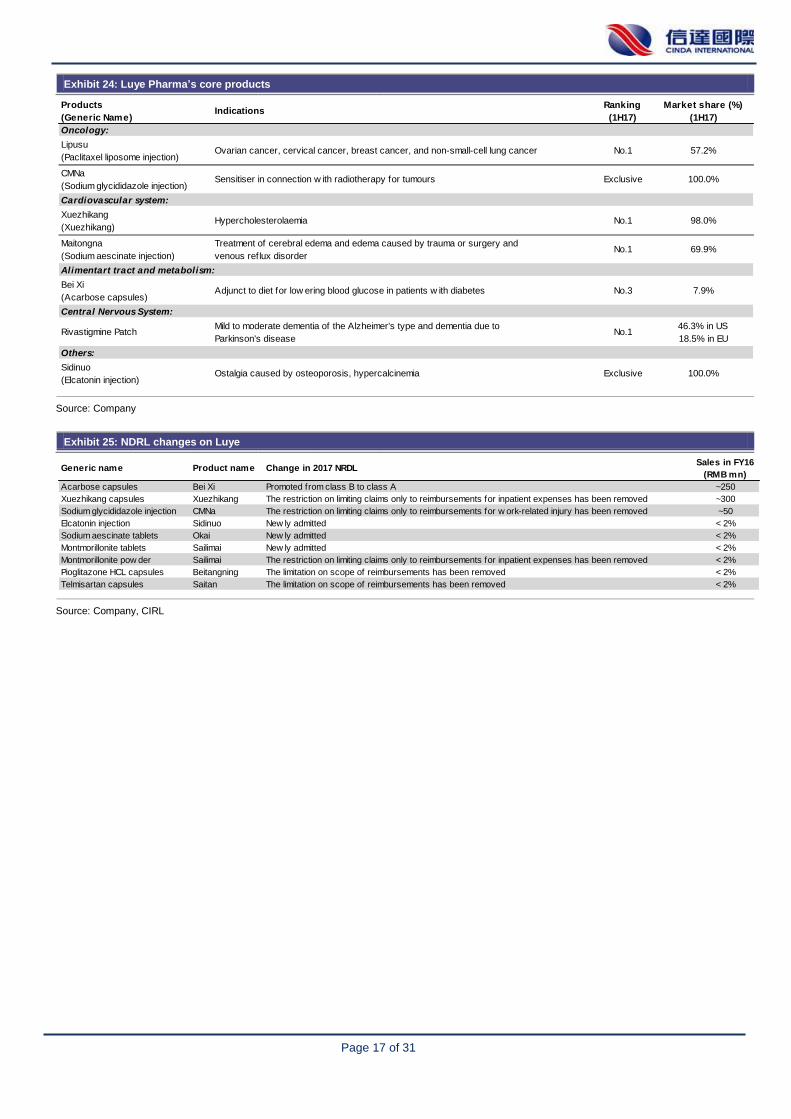

Exhibit 24: Luye Pharma’s core products

Source: Company

Exhibit 25: NDRL changes on Luye

Source: Company, CIRL

Products

(Generic Name)Indications

Ranking

(1H17)

Market share (%)

(1H17)

Oncology:

Lipusu

(Paclitaxel liposome injection)Ovarian cancer, cervical cancer, breast cancer, and non-small-cell lung cancer No.1 57.2%

CMNa

(Sodium glycididazole injection)Sensitiser in connection w ith radiotherapy for tumours Exclusive 100.0%

Cardiovascular system:

Xuezhikang

(Xuezhikang)Hypercholesterolaemia No.1 98.0%

Maitongna

(Sodium aescinate injection)

Treatment of cerebral edema and edema caused by trauma or surgery and

venous reflux disorderNo.1 69.9%

Alimentart tract and metabolism:

Bei Xi

(Acarbose capsules)Adjunct to diet for low ering blood glucose in patients w ith diabetes No.3 7.9%

Central Nervous System:

Rivastigmine PatchMild to moderate dementia of the Alzheimer's type and dementia due to

Parkinson's diseaseNo.1

46.3% in US

18.5% in EU

Others:

Sidinuo

(Elcatonin injection)Ostalgia caused by osteoporosis, hypercalcinemia Exclusive 100.0%

Generic name Product name Change in 2017 NRDLSales in FY16

(RMB mn)

Acarbose capsules Bei Xi Promoted from class B to class A ~250

Xuezhikang capsules Xuezhikang The restriction on limiting claims only to reimbursements for inpatient expenses has been removed ~300

Sodium glycididazole injection CMNa The restriction on limiting claims only to reimbursements for w ork-related injury has been removed ~50

Elcatonin injection Sidinuo New ly admitted < 2%

Sodium aescinate tablets Okai New ly admitted < 2%

Montmorillonite tablets Sailimai New ly admitted < 2%

Montmorillonite pow der Sailimai The restriction on limiting claims only to reimbursements for inpatient expenses has been removed < 2%

Pioglitazone HCL capsules Beitangning The limitation on scope of reimbursements has been removed < 2%

Telmisartan capsules Saitan The limitation on scope of reimbursements has been removed < 2%

Page 18 of 31

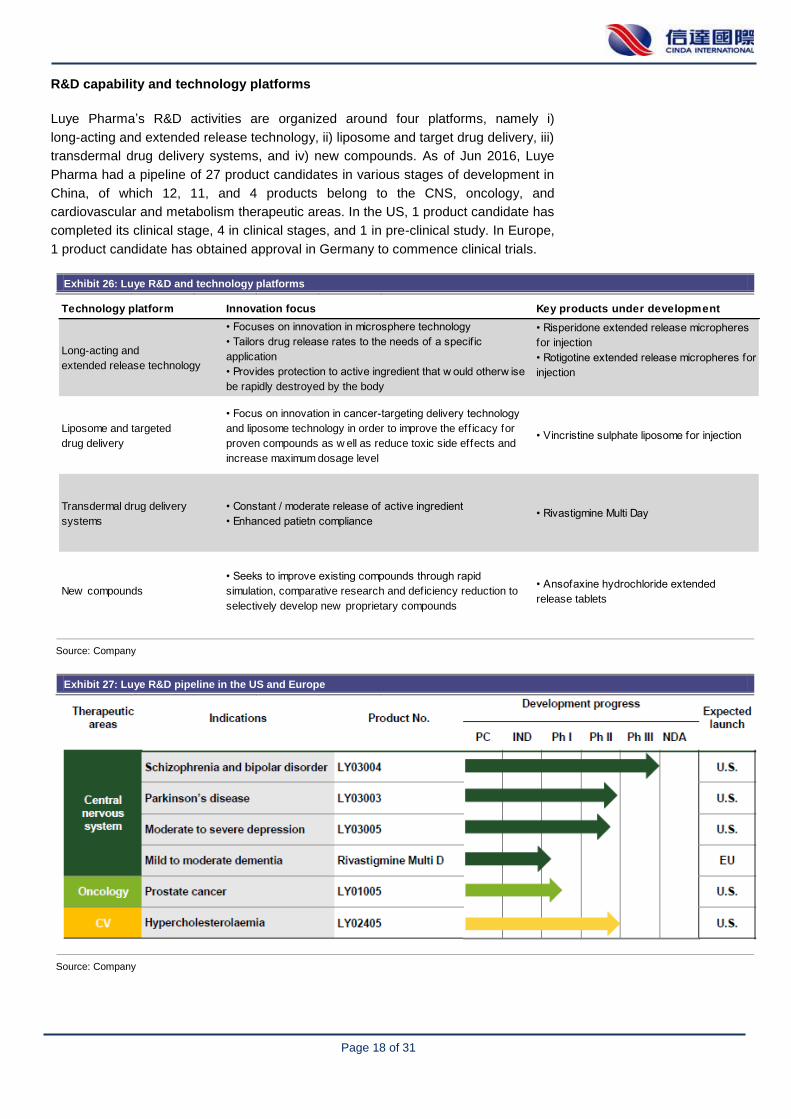

R&D capability and technology platforms

Luye Pharma’s R&D activities are organized around four platforms, namely i)

long-acting and extended release technology, ii) liposome and target drug delivery, iii)

transdermal drug delivery systems, and iv) new compounds. As of Jun 2016, Luye

Pharma had a pipeline of 27 product candidates in various stages of development in

China, of which 12, 11, and 4 products belong to the CNS, oncology, and

cardiovascular and metabolism therapeutic areas. In the US, 1 product candidate has

completed its clinical stage, 4 in clinical stages, and 1 in pre-clinical study. In Europe,

1 product candidate has obtained approval in Germany to commence clinical trials.

Exhibit 26: Luye R&D and technology platforms

Source: Company

Exhibit 27: Luye R&D pipeline in the US and Europe

Source: Company

Technology platform Innovation focus Key products under development

Long-acting and

extended release technology

• Focuses on innovation in microsphere technology

• Tailors drug release rates to the needs of a specif ic

application

• Provides protection to active ingredient that w ould otherw ise

be rapidly destroyed by the body

• Reduces the frequency of administration

• Risperidone extended release micropheres

for injection

• Rotigotine extended release micropheres for

injection

Liposome and targeted

drug delivery

• Focus on innovation in cancer-targeting delivery technology

and liposome technology in order to improve the eff icacy for

proven compounds as w ell as reduce toxic side effects and

increase maximum dosage level

• Vincristine sulphate liposome for injection

Transdermal drug delivery

systems

• Constant / moderate release of active ingredient

• Enhanced patietn compliance• Rivastigmine Multi Day

New compounds

• Seeks to improve existing compounds through rapid

simulation, comparative research and deficiency reduction to

selectively develop new proprietary compounds

• Ansofaxine hydrochloride extended

release tablets

Page 19 of 31

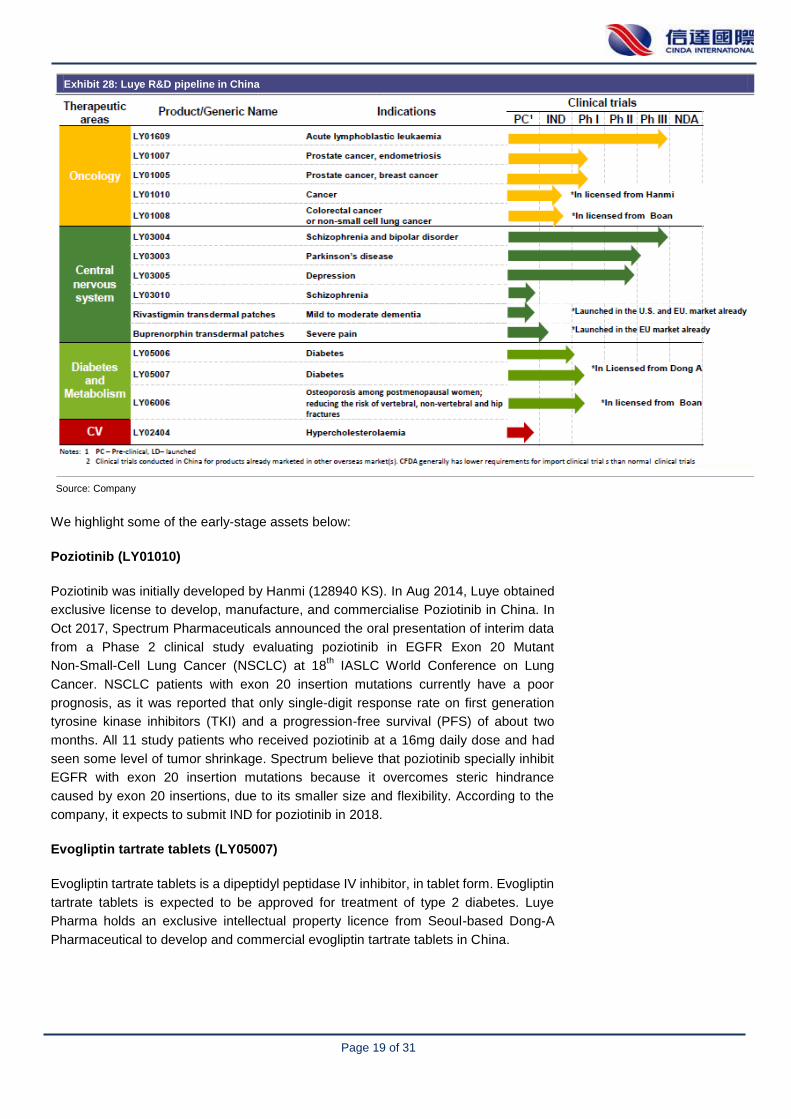

Exhibit 28: Luye R&D pipeline in China

Source: Company

We highlight some of the early-stage assets below:

Poziotinib (LY01010)

Poziotinib was initially developed by Hanmi (128940 KS). In Aug 2014, Luye obtained

exclusive license to develop, manufacture, and commercialise Poziotinib in China. In

Oct 2017, Spectrum Pharmaceuticals announced the oral presentation of interim data

from a Phase 2 clinical study evaluating poziotinib in EGFR Exon 20 Mutant

Non-Small-Cell Lung Cancer (NSCLC) at 18th IASLC World Conference on Lung

Cancer. NSCLC patients with exon 20 insertion mutations currently have a poor

prognosis, as it was reported that only single-digit response rate on first generation

tyrosine kinase inhibitors (TKI) and a progression-free survival (PFS) of about two

months. All 11 study patients who received poziotinib at a 16mg daily dose and had

seen some level of tumor shrinkage. Spectrum believe that poziotinib specially inhibit

EGFR with exon 20 insertion mutations because it overcomes steric hindrance

caused by exon 20 insertions, due to its smaller size and flexibility. According to the

company, it expects to submit IND for poziotinib in 2018.

Evogliptin tartrate tablets (LY05007)

Evogliptin tartrate tablets is a dipeptidyl peptidase IV inhibitor, in tablet form. Evogliptin

tartrate tablets is expected to be approved for treatment of type 2 diabetes. Luye

Pharma holds an exclusive intellectual property licence from Seoul-based Dong-A

Pharmaceutical to develop and commercial evogliptin tartrate tablets in China.

Page 20 of 31

Levetiracetam extended release tablet

In Sep 2011, Luye Pharma obtained an exclusive agency and distribution rights from

Lotus Pharma (1795 TT) to sell levetiracetam extended release tablet in PRC.

Levetiracetam extended release tablet is applicable to epilepsy patients who are over

sixteen as an adjunctive therapy for their partial seizures. In Oct 2011, Lotus Pharma

obtained regulatory approval for launching levetiracetam extended release tablet in

Taiwan. Currently, no products of levetiracetam extended release tablet have been

launched in China.

According to ‘‘Clinical Practice Guidelines: Epilepsy Volume’’ (2007), the lifetime

prevalence of epilepsy is between 0.4% and 0.7% in China. Active epilepsy

prevalence is 0.46% with an annual incidence rate of approximately 30 per 100,000

patients. Accordingly, there are approximately 6 million active epilepsy patients in

China with approximately 0.4 million new epilepsy patients each year. According to

IMS Health Incorporated, the market size for epilepsy treatment products in China was

approximately RMB1.8 billion in 2014, and grew at a compound annual growth rate of

24.5% from 2011 to 2014.

Page 21 of 31

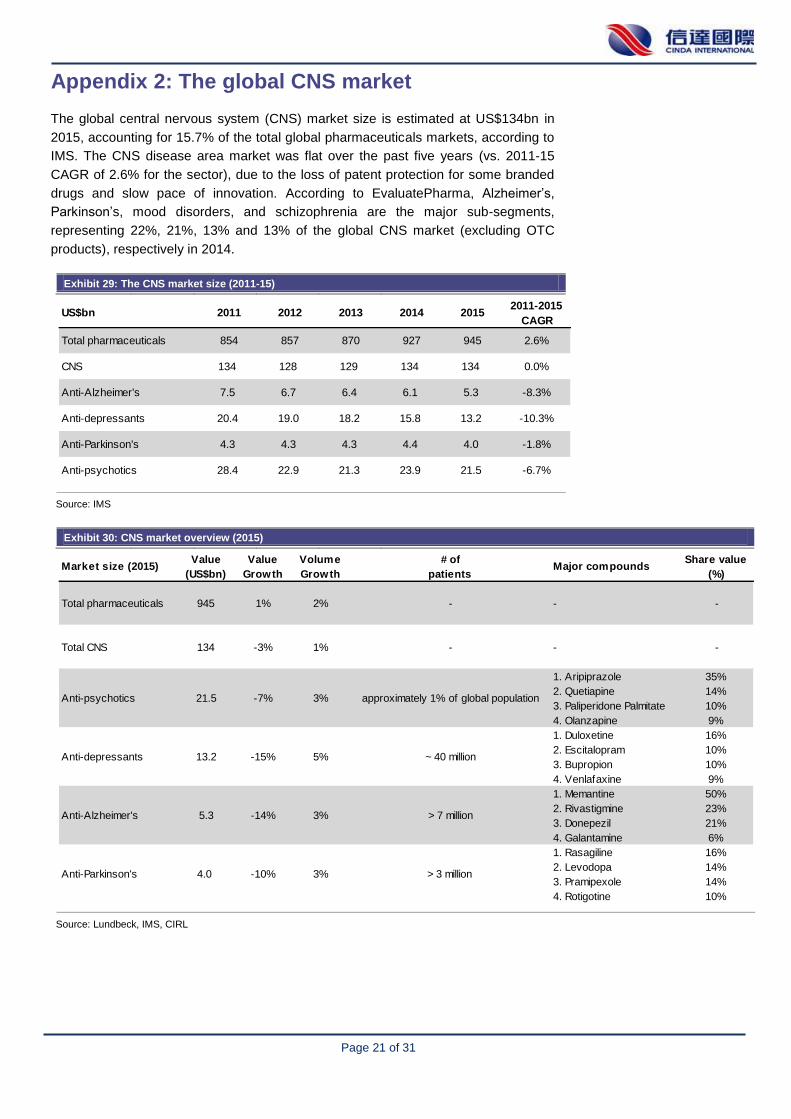

Appendix 2: The global CNS market

The global central nervous system (CNS) market size is estimated at US$134bn in

2015, accounting for 15.7% of the total global pharmaceuticals markets, according to

IMS. The CNS disease area market was flat over the past five years (vs. 2011-15

CAGR of 2.6% for the sector), due to the loss of patent protection for some branded

drugs and slow pace of innovation. According to EvaluatePharma, Alzheimer’s,

Parkinson’s, mood disorders, and schizophrenia are the major sub-segments,

representing 22%, 21%, 13% and 13% of the global CNS market (excluding OTC

products), respectively in 2014.

Exhibit 29: The CNS market size (2011-15)

Source: IMS

Exhibit 30: CNS market overview (2015)

Exhibit 3:

Source: Lundbeck, IMS, CIRL

US$bn 2011 2012 2013 2014 20152011-2015

CAGR

Total pharmaceuticals 854 857 870 927 945 2.6%

CNS 134 128 129 134 134 0.0%

Anti-Alzheimer's 7.5 6.7 6.4 6.1 5.3 -8.3%

Anti-depressants 20.4 19.0 18.2 15.8 13.2 -10.3%

Anti-Parkinson's 4.3 4.3 4.3 4.4 4.0 -1.8%

Anti-psychotics 28.4 22.9 21.3 23.9 21.5 -6.7%

Market size (2015)Value

(US$bn)

Value

Growth

Volume

Growth

# of

patientsMajor compounds

Share value

(%)

Total pharmaceuticals 945 1% 2% - - -

Total CNS 134 -3% 1% - - -

Anti-psychotics 21.5 -7% 3% approximately 1% of global population

1. Aripiprazole

2. Quetiapine

3. Paliperidone Palmitate

4. Olanzapine

35%

14%

10%

9%

Anti-depressants 13.2 -15% 5% ~ 40 million

1. Duloxetine

2. Escitalopram

3. Bupropion

4. Venlafaxine

16%

10%

10%

9%

Anti-Alzheimer's 5.3 -14% 3% > 7 million

1. Memantine

2. Rivastigmine

3. Donepezil

4. Galantamine

50%

23%

21%

6%

Anti-Parkinson's 4.0 -10% 3% > 3 million

1. Rasagiline

2. Levodopa

3. Pramipexole

4. Rotigotine

16%

14%

14%

10%

Page 22 of 31

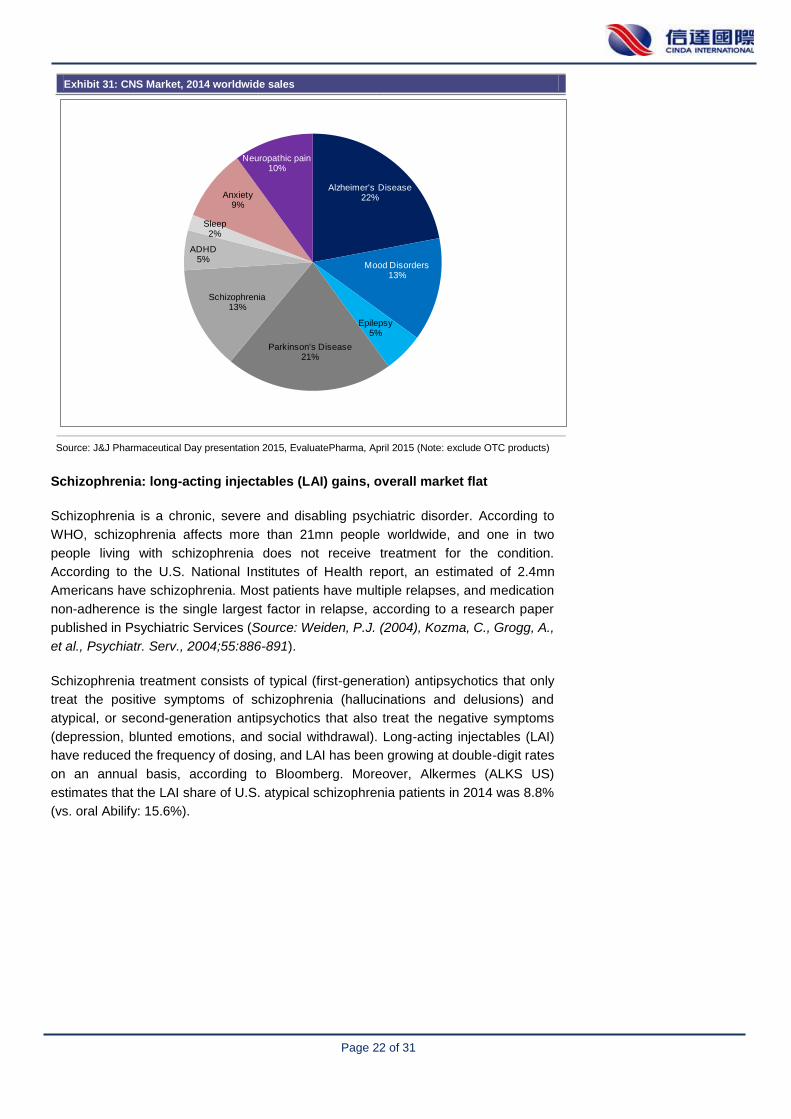

Exhibit 31: CNS Market, 2014 worldwide sales

Source: J&J Pharmaceutical Day presentation 2015, EvaluatePharma, April 2015 (Note: exclude OTC products)

Schizophrenia: long-acting injectables (LAI) gains, overall market flat

Schizophrenia is a chronic, severe and disabling psychiatric disorder. According to

WHO, schizophrenia affects more than 21mn people worldwide, and one in two

people living with schizophrenia does not receive treatment for the condition.

According to the U.S. National Institutes of Health report, an estimated of 2.4mn

Americans have schizophrenia. Most patients have multiple relapses, and medication

non-adherence is the single largest factor in relapse, according to a research paper

published in Psychiatric Services (Source: Weiden, P.J. (2004), Kozma, C., Grogg, A.,

et al., Psychiatr. Serv., 2004;55:886-891).

Schizophrenia treatment consists of typical (first-generation) antipsychotics that only

treat the positive symptoms of schizophrenia (hallucinations and delusions) and

atypical, or second-generation antipsychotics that also treat the negative symptoms

(depression, blunted emotions, and social withdrawal). Long-acting injectables (LAI)

have reduced the frequency of dosing, and LAI has been growing at double-digit rates

on an annual basis, according to Bloomberg. Moreover, Alkermes (ALKS US)

estimates that the LAI share of U.S. atypical schizophrenia patients in 2014 was 8.8%

(vs. oral Abilify: 15.6%).

Alzheimer's Disease22%

Mood Disorders13%

Epilepsy5%

Parkinson's Disease21%

Schizophrenia13%

ADHD5%

Sleep2%

Anxiety9%

Neuropathic pain10%

Page 23 of 31

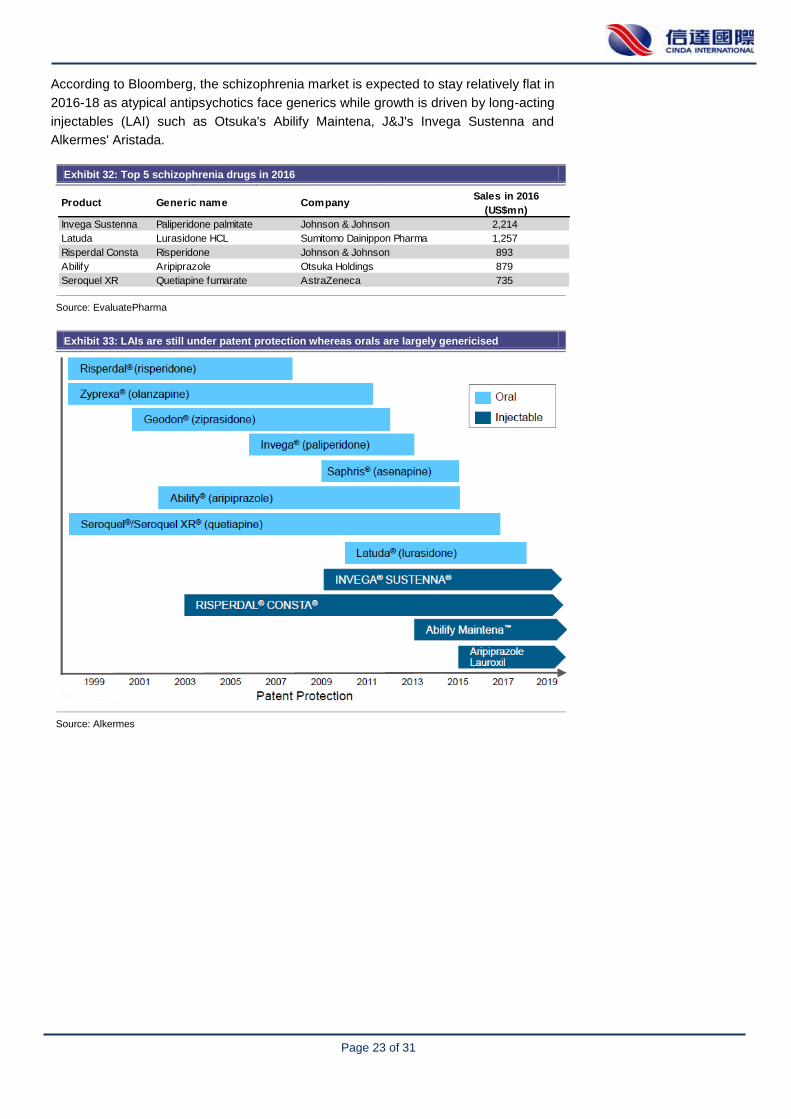

According to Bloomberg, the schizophrenia market is expected to stay relatively flat in

2016-18 as atypical antipsychotics face generics while growth is driven by long-acting

injectables (LAI) such as Otsuka's Abilify Maintena, J&J's Invega Sustenna and

Alkermes' Aristada.

Exhibit 32: Top 5 schizophrenia drugs in 2016

Source: EvaluatePharma

Exhibit 33: LAIs are still under patent protection whereas orals are largely genericised

Source: Alkermes

Product Generic name CompanySales in 2016

(US$mn)

Invega Sustenna Paliperidone palmitate Johnson & Johnson 2,214

Latuda Lurasidone HCL Sumitomo Dainippon Pharma 1,257

Risperdal Consta Risperidone Johnson & Johnson 893

Abilify Aripiprazole Otsuka Holdings 879

Seroquel XR Quetiapine fumarate AstraZeneca 735

Page 24 of 31

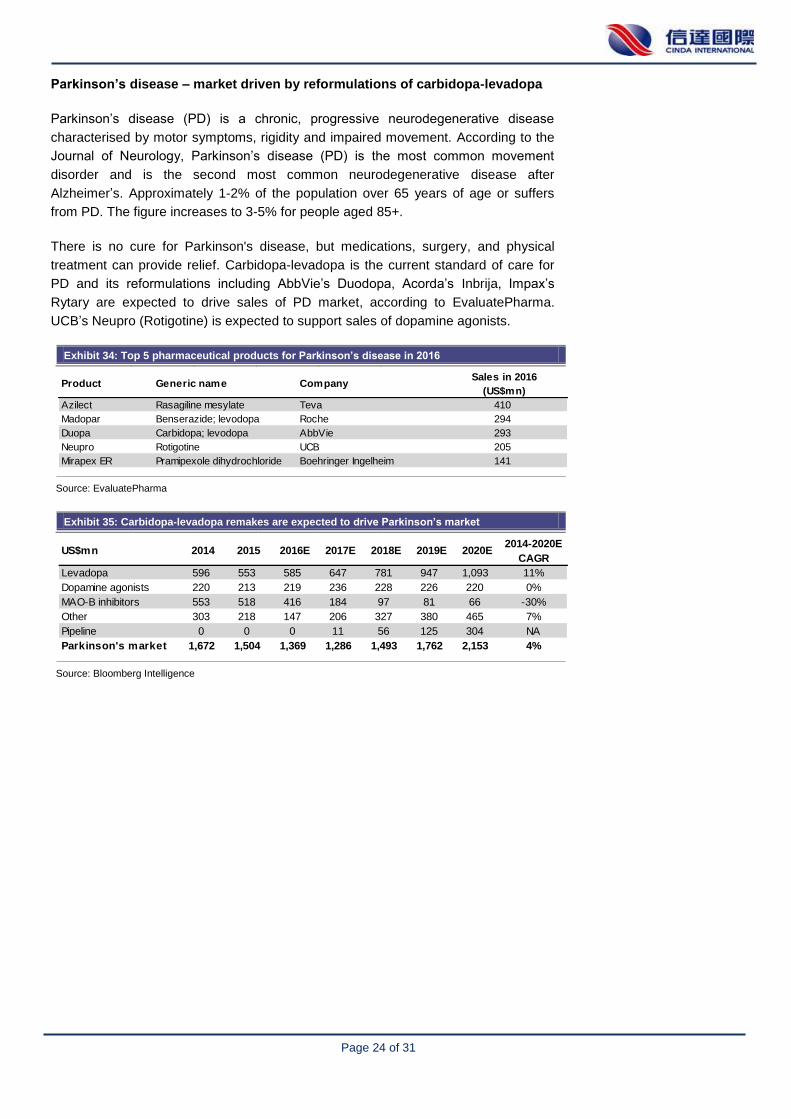

Parkinson’s disease – market driven by reformulations of carbidopa-levadopa

Parkinson’s disease (PD) is a chronic, progressive neurodegenerative disease

characterised by motor symptoms, rigidity and impaired movement. According to the

Journal of Neurology, Parkinson’s disease (PD) is the most common movement

disorder and is the second most common neurodegenerative disease after

Alzheimer’s. Approximately 1-2% of the population over 65 years of age or suffers

from PD. The figure increases to 3-5% for people aged 85+.

There is no cure for Parkinson's disease, but medications, surgery, and physical

treatment can provide relief. Carbidopa-levadopa is the current standard of care for

PD and its reformulations including AbbVie’s Duodopa, Acorda’s Inbrija, Impax’s

Rytary are expected to drive sales of PD market, according to EvaluatePharma.

UCB’s Neupro (Rotigotine) is expected to support sales of dopamine agonists.

Exhibit 34: Top 5 pharmaceutical products for Parkinson’s disease in 2016

Source: EvaluatePharma

Exhibit 35: Carbidopa-levadopa remakes are expected to drive Parkinson’s market

Source: Bloomberg Intelligence

Product Generic name CompanySales in 2016

(US$mn)

Azilect Rasagiline mesylate Teva 410

Madopar Benserazide; levodopa Roche 294

Duopa Carbidopa; levodopa AbbVie 293

Neupro Rotigotine UCB 205

Mirapex ER Pramipexole dihydrochloride Boehringer Ingelheim 141

US$mn 2014 2015 2016E 2017E 2018E 2019E 2020E2014-2020E

CAGR

Levadopa 596 553 585 647 781 947 1,093 11%

Dopamine agonists 220 213 219 236 228 226 220 0%

MAO-B inhibitors 553 518 416 184 97 81 66 -30%

Other 303 218 147 206 327 380 465 7%

Pipeline 0 0 0 11 56 125 304 NA

Parkinson's market 1,672 1,504 1,369 1,286 1,493 1,762 2,153 4%

Page 25 of 31

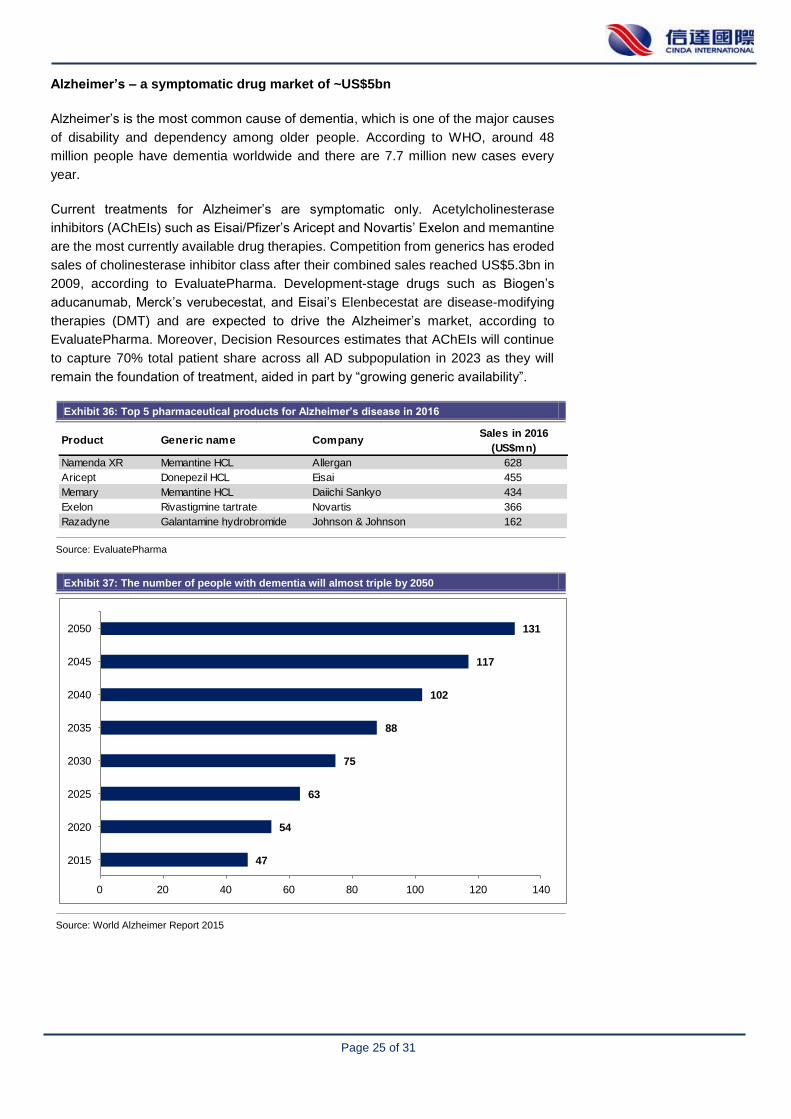

Alzheimer’s – a symptomatic drug market of ~US$5bn

Alzheimer’s is the most common cause of dementia, which is one of the major causes

of disability and dependency among older people. According to WHO, around 48

million people have dementia worldwide and there are 7.7 million new cases every

year.

Current treatments for Alzheimer’s are symptomatic only. Acetylcholinesterase

inhibitors (AChEIs) such as Eisai/Pfizer’s Aricept and Novartis’ Exelon and memantine

are the most currently available drug therapies. Competition from generics has eroded

sales of cholinesterase inhibitor class after their combined sales reached US$5.3bn in

2009, according to EvaluatePharma. Development-stage drugs such as Biogen’s

aducanumab, Merck’s verubecestat, and Eisai’s Elenbecestat are disease-modifying

therapies (DMT) and are expected to drive the Alzheimer’s market, according to

EvaluatePharma. Moreover, Decision Resources estimates that AChEIs will continue

to capture 70% total patient share across all AD subpopulation in 2023 as they will

remain the foundation of treatment, aided in part by “growing generic availability”.

Exhibit 36: Top 5 pharmaceutical products for Alzheimer’s disease in 2016

Source: EvaluatePharma

Exhibit 37: The number of people with dementia will almost triple by 2050

Source: World Alzheimer Report 2015

Product Generic name CompanySales in 2016

(US$mn)

Namenda XR Memantine HCL Allergan 628

Aricept Donepezil HCL Eisai 455

Memary Memantine HCL Daiichi Sankyo 434

Exelon Rivastigmine tartrate Novartis 366

Razadyne Galantamine hydrobromide Johnson & Johnson 162

47

54

63

75

88

102

117

131

0 20 40 60 80 100 120 140

2015

2020

2025

2030

2035

2040

2045

2050

Page 26 of 31

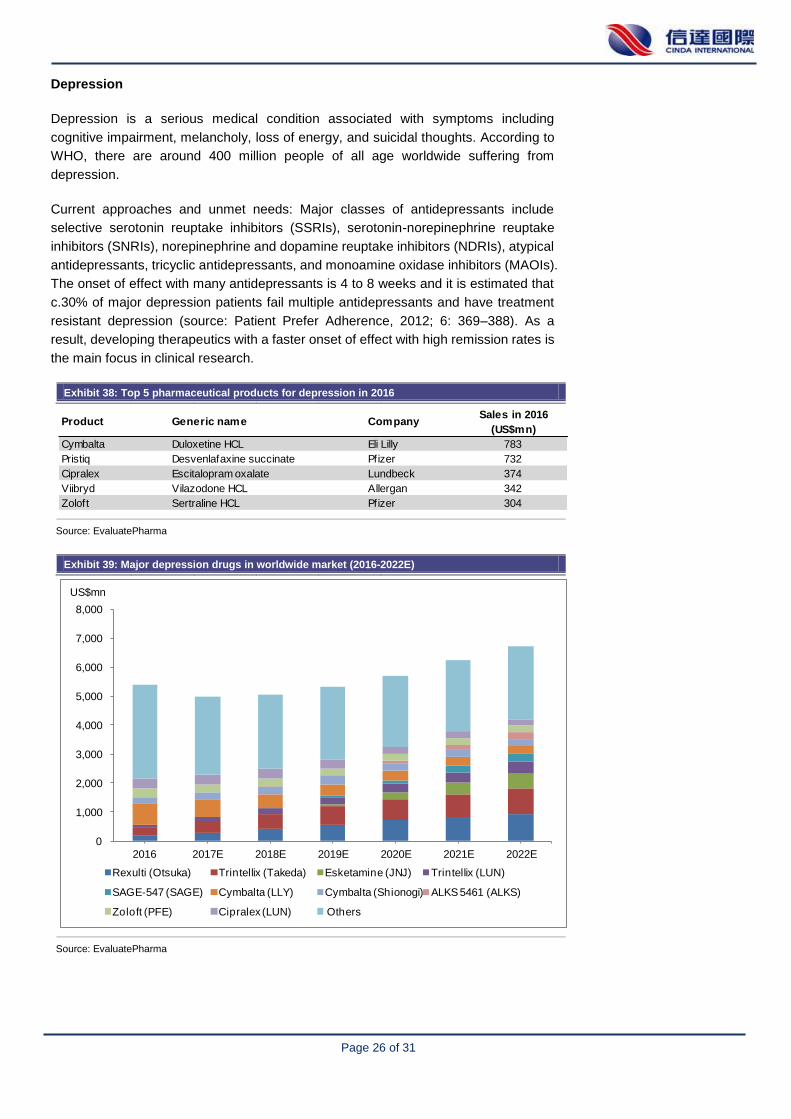

Depression

Depression is a serious medical condition associated with symptoms including

cognitive impairment, melancholy, loss of energy, and suicidal thoughts. According to

WHO, there are around 400 million people of all age worldwide suffering from

depression.

Current approaches and unmet needs: Major classes of antidepressants include

selective serotonin reuptake inhibitors (SSRIs), serotonin-norepinephrine reuptake

inhibitors (SNRIs), norepinephrine and dopamine reuptake inhibitors (NDRIs), atypical

antidepressants, tricyclic antidepressants, and monoamine oxidase inhibitors (MAOIs).

The onset of effect with many antidepressants is 4 to 8 weeks and it is estimated that

c.30% of major depression patients fail multiple antidepressants and have treatment

resistant depression (source: Patient Prefer Adherence, 2012; 6: 369–388). As a

result, developing therapeutics with a faster onset of effect with high remission rates is

the main focus in clinical research.

Exhibit 38: Top 5 pharmaceutical products for depression in 2016

Source: EvaluatePharma

Exhibit 39: Major depression drugs in worldwide market (2016-2022E)

Source: EvaluatePharma

Product Generic name CompanySales in 2016

(US$mn)

Cymbalta Duloxetine HCL Eli Lilly 783

Pristiq Desvenlafaxine succinate Pfizer 732

Cipralex Escitalopram oxalate Lundbeck 374

Viibryd Vilazodone HCL Allergan 342

Zoloft Sertraline HCL Pfizer 304

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2016 2017E 2018E 2019E 2020E 2021E 2022E

US$mn

Rexulti (Otsuka) Trintellix (Takeda) Esketamine (JNJ) Trintellix (LUN)

SAGE-547 (SAGE) Cymbalta (LLY) Cymbalta (Shionogi) ALKS 5461 (ALKS)

Zoloft (PFE) Cipralex (LUN) Others

Page 27 of 31

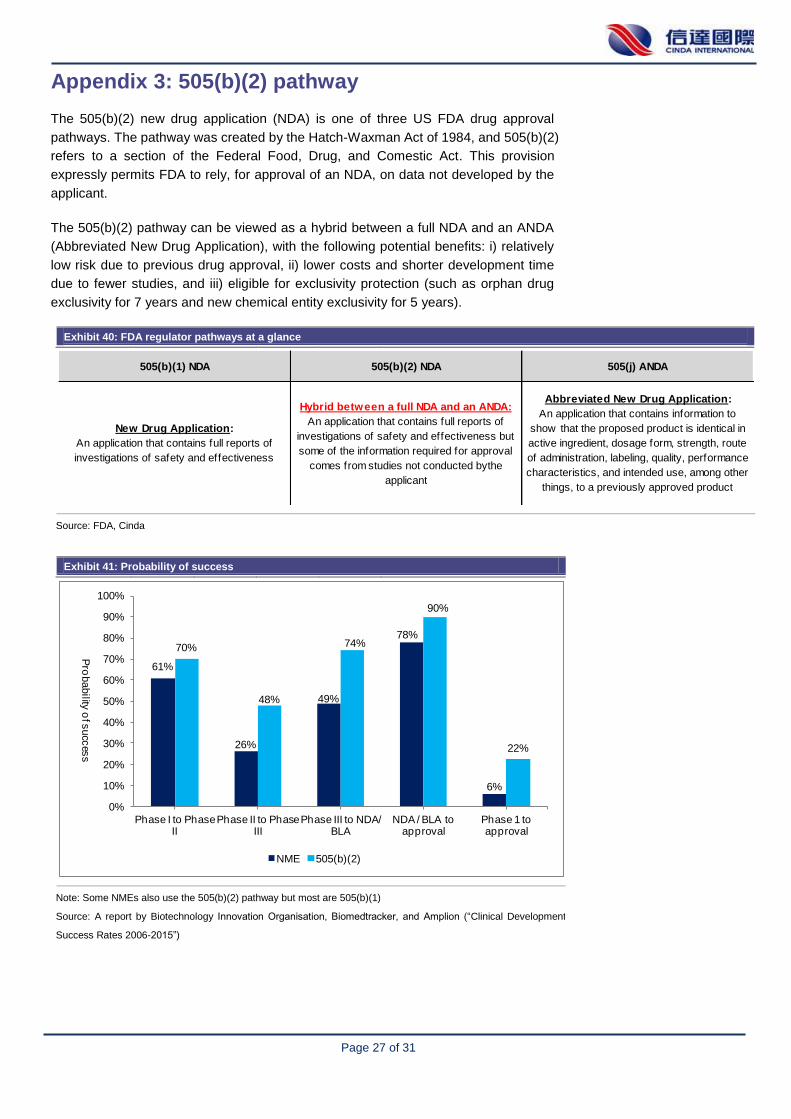

Appendix 3: 505(b)(2) pathway

The 505(b)(2) new drug application (NDA) is one of three US FDA drug approval

pathways. The pathway was created by the Hatch-Waxman Act of 1984, and 505(b)(2)

refers to a section of the Federal Food, Drug, and Comestic Act. This provision

expressly permits FDA to rely, for approval of an NDA, on data not developed by the

applicant.

The 505(b)(2) pathway can be viewed as a hybrid between a full NDA and an ANDA

(Abbreviated New Drug Application), with the following potential benefits: i) relatively

low risk due to previous drug approval, ii) lower costs and shorter development time

due to fewer studies, and iii) eligible for exclusivity protection (such as orphan drug

exclusivity for 7 years and new chemical entity exclusivity for 5 years).

Exhibit 40: FDA regulator pathways at a glance

Exhibit 4:

Source: FDA, Cinda

Exhibit 41: Probability of success

Note: Some NMEs also use the 505(b)(2) pathway but most are 505(b)(1)

Source: A report by Biotechnology Innovation Organisation, Biomedtracker, and Amplion (“Clinical Development

Success Rates 2006-2015”)

505(b)(1) NDA 505(b)(2) NDA 505(j) ANDA

New Drug Application:

An application that contains full reports of

investigations of safety and effectiveness

Hybrid between a full NDA and an ANDA:

An application that contains full reports of

investigations of safety and effectiveness but

some of the information required for approval

comes from studies not conducted bythe

applicant

Abbreviated New Drug Application:

An application that contains information to

show that the proposed product is identical in

active ingredient, dosage form, strength, route

of administration, labeling, quality, performance

characteristics, and intended use, among other

things, to a previously approved product

61%

26%

49%

78%

6%

70%

48%

74%

90%

22%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Phase I to Phase II

Phase II to Phase III

Phase III to NDA/ BLA

NDA / BLA to approval

Phase 1 to approval

NME 505(b)(2)

Pro

bability

of s

ucc

ess

Page 28 of 31

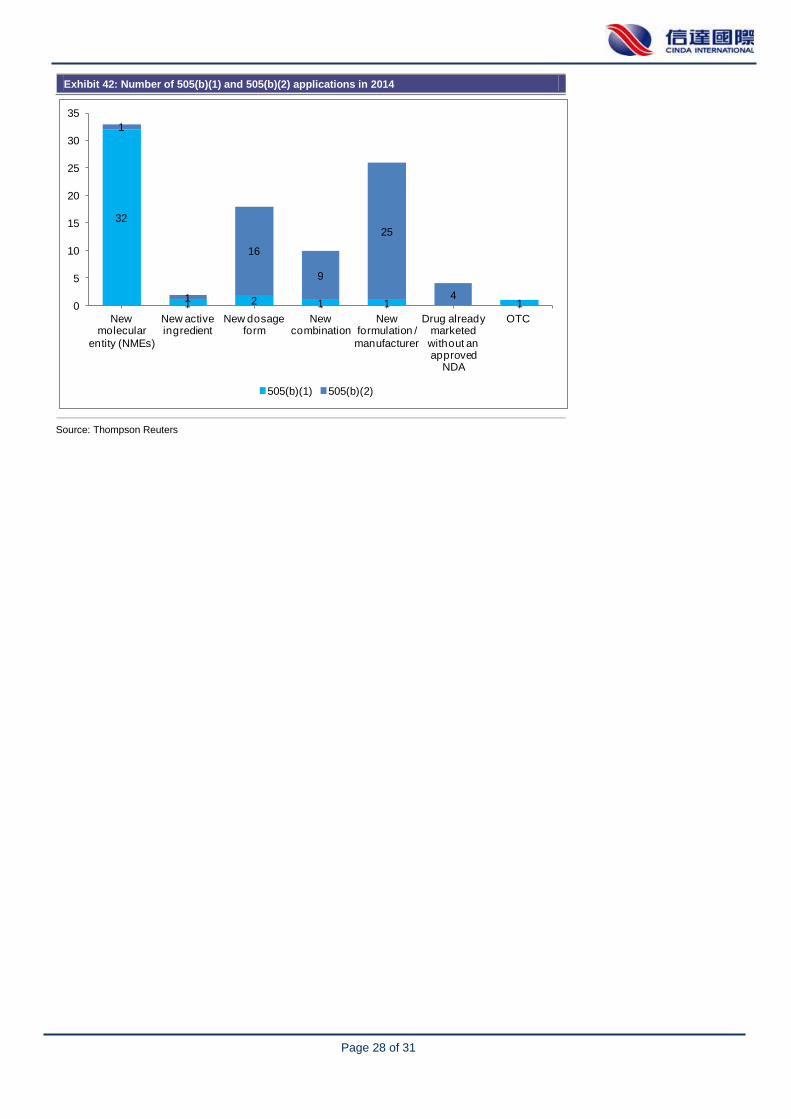

Exhibit 42: Number of 505(b)(1) and 505(b)(2) applications in 2014

Source: Thompson Reuters

32

1 2 1 1 1

1

1

16

9

25

40

5

10

15

20

25

30

35

New molecular

entity (NMEs)

New active ingredient

New dosage form

New combination

New formulation /

manufacturer

Drug already marketed

without an approved

NDA

OTC

505(b)(1) 505(b)(2)

Page 29 of 31

Risk Factors

Policy and competition risk on Lipusu

Lipusu accounted for c.45% of the company’s total revenue in 2015 and 2016,

respectively. There are two major concerns on the product’s sales: i) Lipusu is not

included in the new NDRL (National Reimbursement Drug List) as the company exited

the NRDL price negotiation in Jul 2017 and ii) increasing competition due to generic

Abraxane, which is expected to be launched in China in 2018. We have taken a more

conservative approach (vs. management and street consensus) in our forecast and

model. Higher than expected policy impact and competitions from Abraxane generics

may cause the company’s revenue and profitability to decline.

Pipeline risks

The long-term competitiveness hinges on a company’s pipeline and its ability to

develop and commercialise new biotechnology and other pharmaceutical products.

There are risks of failure to meet safety, efficacy or other standards during the R&D

process, or the failure to obtain necessary regulatory approvals, including CFDA and

FDA on time or at all. Competition risks and rapidly changing market demand would

make commercialisation efforts more complex and less certain.

Integration risks relating to recent M&As

There are integration risks that the company may not be able to integrate acquired

subsidiaries such as Acino to achieve expected synergies and to fulfill the purposes of

acquisitions.

Page 30 of 31

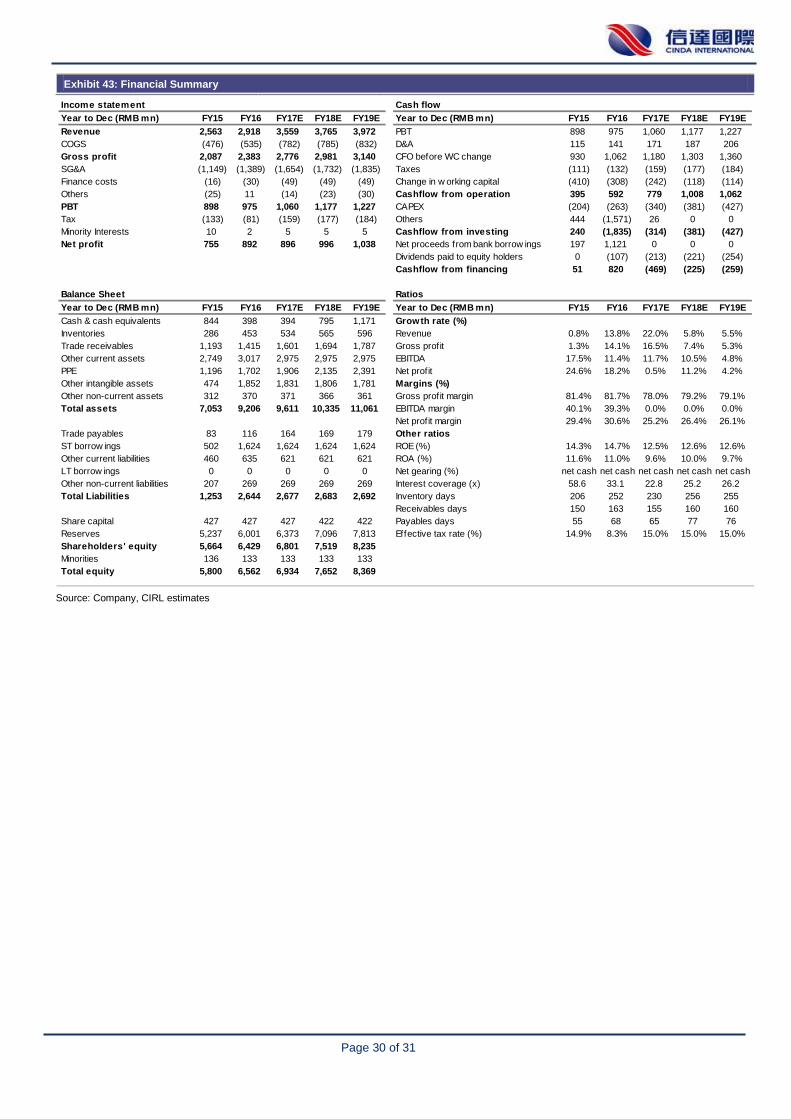

Exhibit 43: Financial Summary

Source: Company, CIRL estimates

Income statement Cash flow

Year to Dec (RMB mn) FY15 FY16 FY17E FY18E FY19E Year to Dec (RMB mn) FY15 FY16 FY17E FY18E FY19E

Revenue 2,563 2,918 3,559 3,765 3,972 PBT 898 975 1,060 1,177 1,227

COGS (476) (535) (782) (785) (832) D&A 115 141 171 187 206

Gross profit 2,087 2,383 2,776 2,981 3,140 CFO before WC change 930 1,062 1,180 1,303 1,360

SG&A (1,149) (1,389) (1,654) (1,732) (1,835) Taxes (111) (132) (159) (177) (184)

Finance costs (16) (30) (49) (49) (49) Change in w orking capital (410) (308) (242) (118) (114)

Others (25) 11 (14) (23) (30) Cashflow from operation 395 592 779 1,008 1,062

PBT 898 975 1,060 1,177 1,227 CAPEX (204) (263) (340) (381) (427)

Tax (133) (81) (159) (177) (184) Others 444 (1,571) 26 0 0

Minority Interests 10 2 5 5 5 Cashflow from investing 240 (1,835) (314) (381) (427)

Net profit 755 892 896 996 1,038 Net proceeds from bank borrow ings 197 1,121 0 0 0

Dividends paid to equity holders 0 (107) (213) (221) (254)

Cashflow from financing 51 820 (469) (225) (259)

Balance Sheet Ratios

Year to Dec (RMB mn) FY15 FY16 FY17E FY18E FY19E Year to Dec (RMB mn) FY15 FY16 FY17E FY18E FY19E

Cash & cash equivalents 844 398 394 795 1,171 Growth rate (%)

Inventories 286 453 534 565 596 Revenue 0.8% 13.8% 22.0% 5.8% 5.5%

Trade receivables 1,193 1,415 1,601 1,694 1,787 Gross profit 1.3% 14.1% 16.5% 7.4% 5.3%

Other current assets 2,749 3,017 2,975 2,975 2,975 EBITDA 17.5% 11.4% 11.7% 10.5% 4.8%

PPE 1,196 1,702 1,906 2,135 2,391 Net profit 24.6% 18.2% 0.5% 11.2% 4.2%

Other intangible assets 474 1,852 1,831 1,806 1,781 Margins (%)

Other non-current assets 312 370 371 366 361 Gross profit margin 81.4% 81.7% 78.0% 79.2% 79.1%

Total assets 7,053 9,206 9,611 10,335 11,061 EBITDA margin 40.1% 39.3% 0.0% 0.0% 0.0%

Net profit margin 29.4% 30.6% 25.2% 26.4% 26.1%

Trade payables 83 116 164 169 179 Other ratios

ST borrow ings 502 1,624 1,624 1,624 1,624 ROE (%) 14.3% 14.7% 12.5% 12.6% 12.6%

Other current liabilities 460 635 621 621 621 ROA (%) 11.6% 11.0% 9.6% 10.0% 9.7%

LT borrow ings 0 0 0 0 0 Net gearing (%) net cash net cash net cash net cash net cash

Other non-current liabilities 207 269 269 269 269 Interest coverage (x) 58.6 33.1 22.8 25.2 26.2

Total Liabilities 1,253 2,644 2,677 2,683 2,692 Inventory days 206 252 230 256 255

Receivables days 150 163 155 160 160

Share capital 427 427 427 422 422 Payables days 55 68 65 77 76

Reserves 5,237 6,001 6,373 7,096 7,813 Effective tax rate (%) 14.9% 8.3% 15.0% 15.0% 15.0%

Shareholders' equity 5,664 6,429 6,801 7,519 8,235

Minorities 136 133 133 133 133

Total equity 5,800 6,562 6,934 7,652 8,369

Page 31 of 31

Rating Policy

Rating Definition

Stock Rating Buy Outperform HSI by 15%

Neutral Between -15% ~ 15% of the HSI

Sell Underperform HSI by -15%

Sector Rating Accumulate Outperform HSI by 10%

Neutral Between -10% ~ 10% of the HSI

Reduce Underperform HSI by -10%

Analysts List

Hayman Chiu Research Director (852) 2235 7677 [email protected]

Kenneth Li Senior Research Analyst (852) 2235 7619 [email protected]

Lewis Pang Senior Research Analyst (852) 2235 7847 [email protected]

Wilfred Yuen Research Analyst (852) 2235 7131 [email protected]

Chloe Chan Research Analyst (852) 2235 7170 [email protected]

Johnny Yum Research Assistant (852) 2235 7617 [email protected]

Analyst Certification

I, Wilfred Yuen hereby certify that all of the views expressed in this report accurately reflect my personal views about

the subject company or companies and its or their securities. I also certify that no part of my compensation was / were,

is / are or will be directly or indirectly, related to the specific recommendations or views expressed in this report / note.

Disclaimer

This report has been prepared by the Cinda International Research Limited. Although the information and opinions

contained in this report have been compiled or arrived at from sources believed to be reliable, Cinda International

cannot and does not warrant the accuracy or completeness of any such information and analysis. The report should not

be regarded by recipients as a substitute for the exercise of their own judgment. Recipients should understand and

comprehend the investment objectives and its related risks, and where necessary consult their own financial advisers

prior to any investment decision. The report may contain some forward-looking estimates and forecasts derived from

the assumptions of the future political and economic conditions with inherently unpredictable and mutable situation, so

uncertainty may contain. Any opinions expressed in this report are subject to change without notice. The report is

published solely for information purposes, it does not constitute any advertisement and should not be construed as an

offer to buy or sell securities. Cinda International will not accept any liability whatsoever for any direct or consequential

loss arising from any use of the materials contained in this report. This document is for the use of intended recipients

only, the whole or a part of this report should not be reproduced to others.