Embed Size (px)

Citation preview

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page i�

� �

�

Luxury Retailand Digital Management

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page ii�

� �

�

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page iii�

� �

�

Luxury Retailand Digital

ManagementDeveloping Customer Experience

in a Digital World

SECOND EDITION

Michel ChevalierMichel Gutsatz

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page iv�

� �

�

Copyright © 2020 by John Wiley & Sons Singapore Pte. Ltd.

Published by John Wiley & Sons Singapore Pte. Ltd.1 Fusionopolis Walk, #07-01, Solaris South Tower, Singapore 138628

All rights reserved.

Edition HistoryJohn Wiley & Sons Singapore Pte. Ltd. (1e, 2012)

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any formor by any means, electronic, mechanical, photocopying, recording, scanning, or otherwise, except asexpressly permitted by law, without either the prior written permission of the Publisher, orauthorization through payment of the appropriate photocopy fee to the Copyright Clearance Center.Requests for permission should be addressed to the Publisher, John Wiley & Sons Singapore Pte. Ltd.,1 Fusionopolis Walk, #07-01, Solaris South Tower, Singapore 138628, tel: 65–6643–8000, fax:65–6643–8008, e-mail: [email protected].

Limit of Liability/Disclaimer of Warranty: While the publisher and author have used their best effortsin preparing this book, they make no representations or warranties with respect to the accuracy orcompleteness of the contents of this book and specifically disclaim any implied warranties ofmerchantability or fitness for a particular purpose. No warranty may be created or extended by salesrepresentatives or written sales materials. The advice and strategies contained herein may not besuitable for your situation. You should consult with a professional where appropriate. Neither thepublisher nor the author shall be liable for any damages arising herefrom.

Other Wiley Editorial Offices

John Wiley & Sons, 111 River Street, Hoboken, NJ 07030, USAJohn Wiley & Sons, The Atrium, Southern Gate, Chichester, West Sussex, P019 8SQ, UnitedKingdomJohn Wiley & Sons (Canada) Ltd., 5353 Dundas Street West, Suite 400, Toronto, Ontario, M9B 6HB,CanadaJohn Wiley & Sons Australia Ltd., 42 McDougall Street, Milton, Queensland 4064, AustraliaWiley-VCH, Boschstrasse 12, D-69469 Weinheim, Germany

Library of Congress Cataloging-in-Publication Data

Names: Chevalier, Michel, author. | Gutsatz, Michel, author.Title: Luxury retail and digital management : developing customer

experience in a digital world / Michel Chevalier, Michel Gutsatz.Other titles: Luxury retail managementDescription: Second edition. | Solaris South Tower, Singapore : Wiley,

[2020] | Includes bibliographical references and index.Identifiers: LCCN 2019048771 (print) | LCCN 2019048772 (ebook) | ISBN

9781119542339 (hardback) | ISBN 9781119542346 (adobe pdf) | ISBN9781119542353 (epub)

Subjects: LCSH: Luxury goods industry—Management. | Retailtrade—Management.

Classification: LCC HD9999.L852 C34 2020 (print) | LCC HD9999.L852(ebook) | DDC 658.8/7—dc23

LC record available at https://lccn.loc.gov/2019048771LC ebook record available at https://lccn.loc.gov/2019048772

Cover Design: WileyCover Image: © jcarroll-images/Getty Images

Typeset in 11.5/14pt, BemboStd by SPi Global, Chennai, India.

Printed in Singapore by Markono Print Media SINGAPORE

10 9 8 7 6 5 4 3 2 1

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page v�

� �

�

You can have the best strategy in the world, the differencebetween the excellent and the incompetent is execution,execution, execution.

–Domenico deSole, former CEO Gucci

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ffirs01.tex V1 - 01/16/2020 8:02 A.M. Page vi�

� �

�

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ftoc.tex V1 - 01/16/2020 8:02 A.M. Page vii�

� �

�

Contents

Foreword ixby Luca Solca

Introduction xiii

PART I: IMPORTANT CHOICES IN LUXURYDISTRIBUTION 1

Chapter 1: The Various Models in Luxury Distribution 3

Chapter 2: Do Luxury Products Still Sell in Stores? 21

Chapter 3: Concept and Design of a Luxury Boutique 39

Chapter 4: Online, Offline or O2O? 67

PART II: KNOW AND UNDERSTAND THECLIENT 87

Chapter 5: Putting the Customer Back in the Centre 89

Chapter 6: Customer Identification and CRM 107

vii

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 ftoc.tex V1 - 01/16/2020 8:02 A.M. Page viii�

� �

�

viii C O N T E N T S

Chapter 7: The Challenges of Offline and OnlineIntegration 121

Chapter 8: Logistics Adapted to a Digital Culture 135

PART III: MAKING CLIENT RELATIONSHIPSMORE MEANINGFUL 151

Chapter 9: Customer Behaviour in the Store or Online 153

Chapter 10: The Importance of Stores for BuildingCustomer Relationships 163

Chapter 11: Customer Experience and Building Loyalty 177

Chapter 12: How the Internet Has Shattered theTraditional Sales Model 203

PART IV: MANAGEMENT TOOLS FOR LUXURYSTORES 219

Chapter 13: Location of Sales Points 221

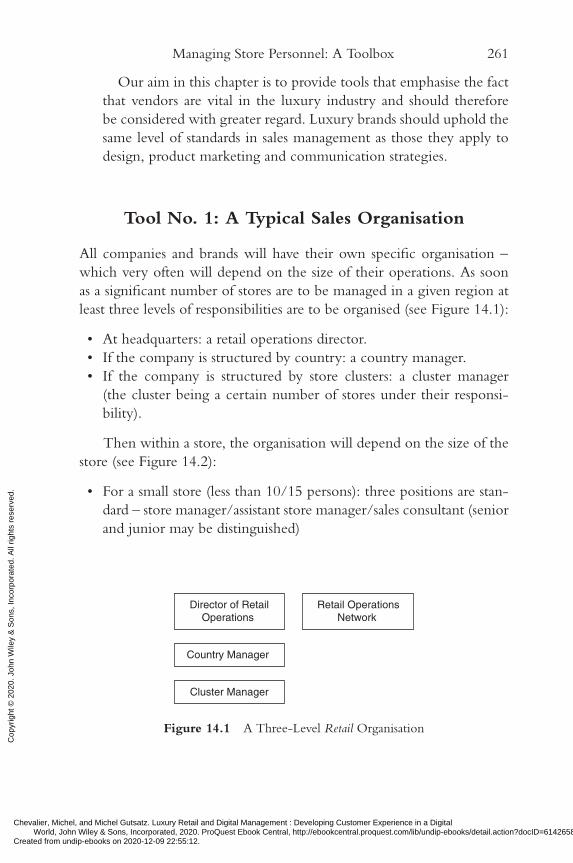

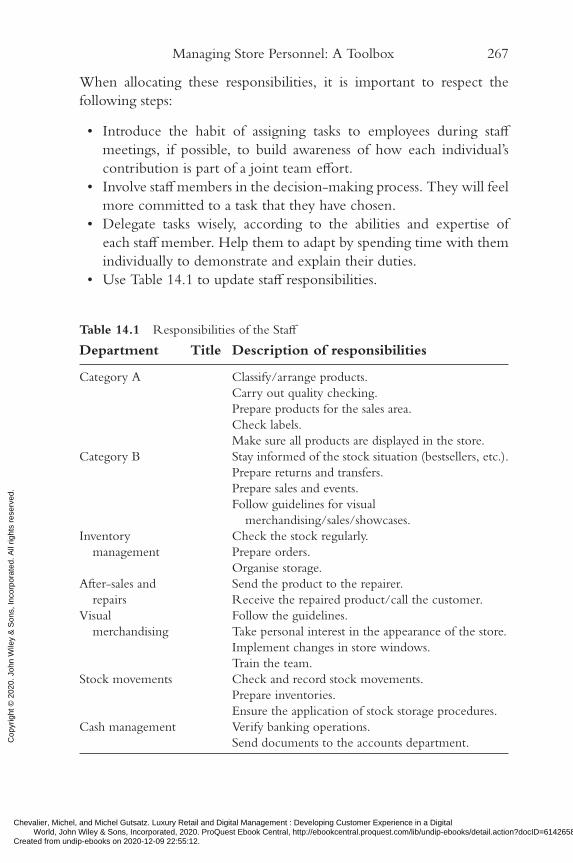

Chapter 14: Managing Store Personnel: A Toolbox 259

Chapter 15: At What Price Should Products Be Sold? 297

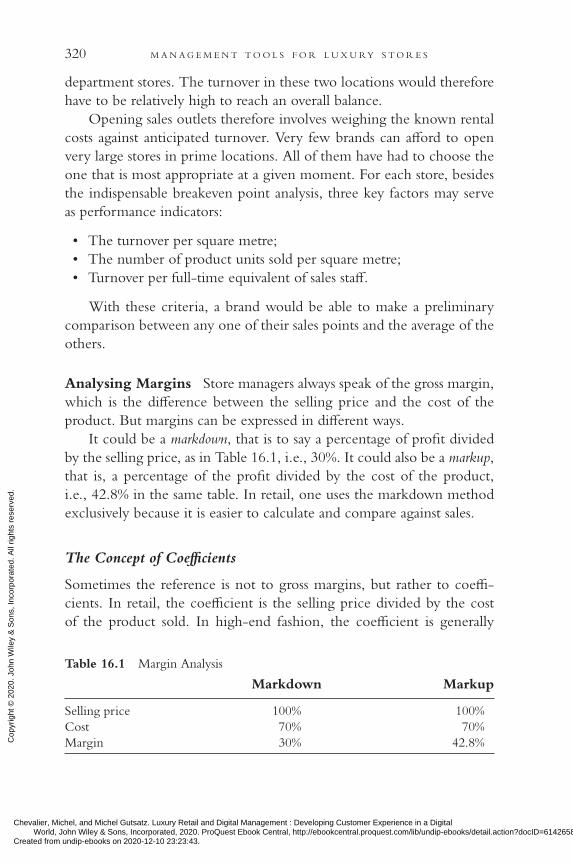

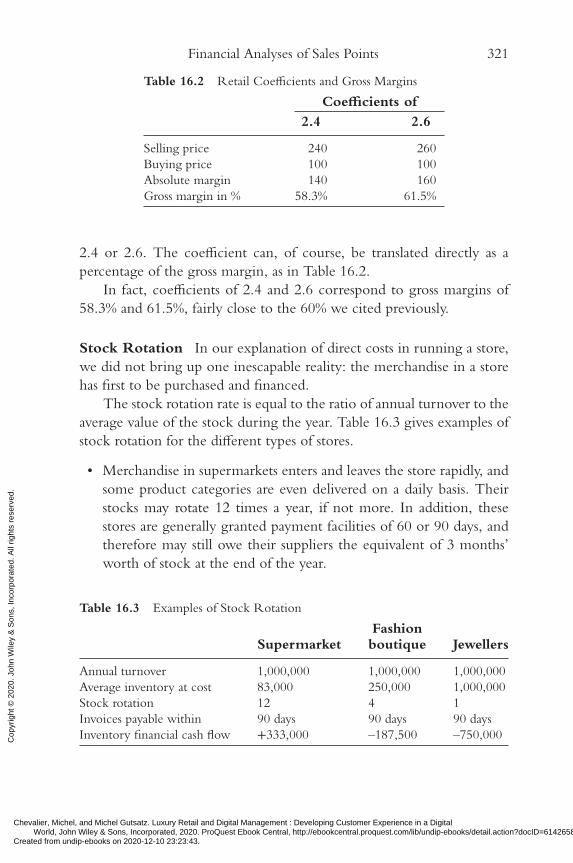

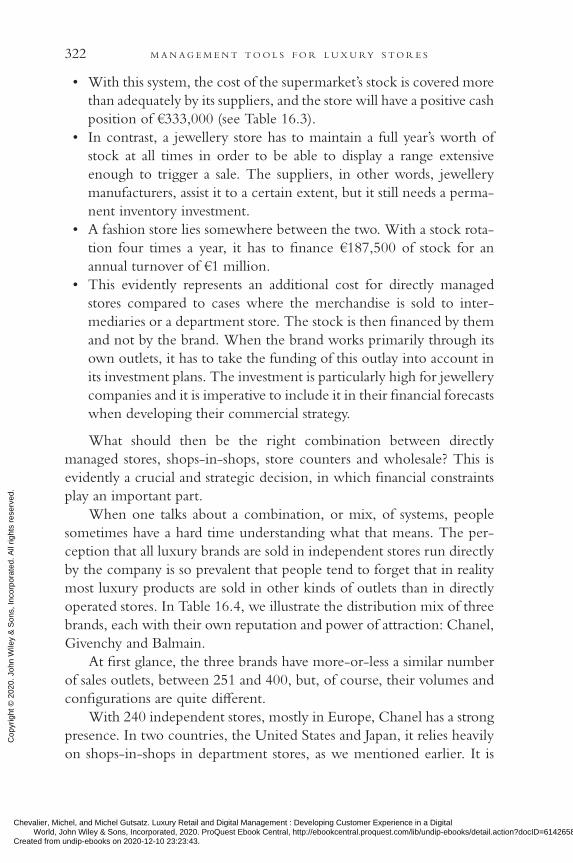

Chapter 16: Financial Analyses of Sales Points 315

Conclusion 339Bibliography 345About the Authors 351Index 353

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page ix�

� �

�

Foreword

I am convinced Michel Gusatz and Michel Chevalier are very right inwriting a second edition of their comprehensive book on the retailmanagement of luxury goods.

I see three major forces converge and reshape this area:First, as the title of the new book suggests, digital has taken the luxury

goods industry by storm – including its retail side. Ten years ago, you couldfind the vast majority of luxury brands still pushing back on digital(frequently, I heard comments like: ‘the Internet is not for us’, ‘we wantour customers to come to our stores to experience the brand and theproduct’, ‘e-commerce is for CDs and books’, ‘I have better things to dothan setting up a website – I need to open more stores in China’). Today,everyone is bending over backwards to convince the market they haveset ‘digital’ as their number one priority. The mere notion of luxury retailwithout m-commerce, e-commerce and a fully integrated digital servicein-store (buy online, pick-up in-store; buy online, return in-store; orderin-store for home/hotel delivery) is tantamount to the idea we shouldcommute to the office every day on horseback. It is not just yester-day’s story; it is utterly and completely obsolete. Either you have a fully

ix

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

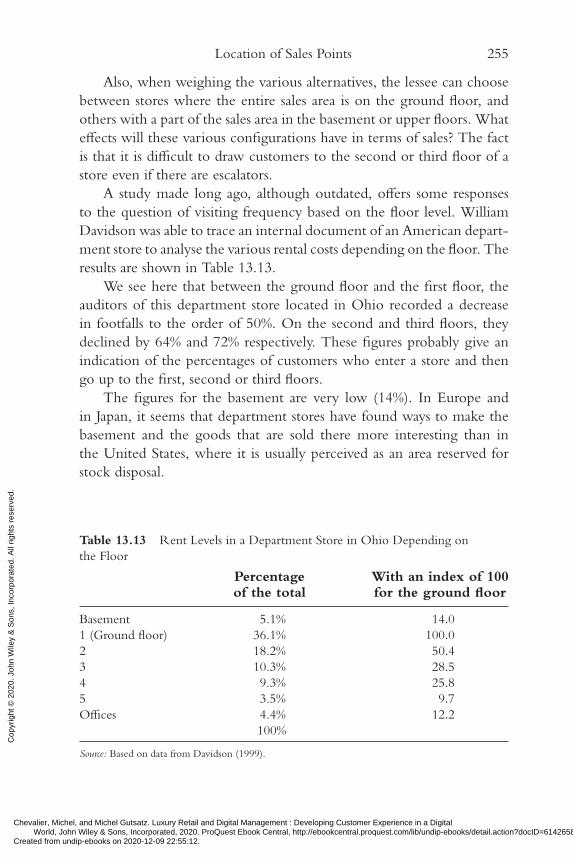

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page x�

� �

�

x F O R E W O R D

developed digital retail strategy and activity, or you are not in a conditionto play. Hence, the need to think through what the right digital strategyand the right digital activity should mean for the specifics of your brandand your business.

Second – and linked to the point above – physical retail networkdevelopment in luxury goods is virtually done, at least for the foreseeablefuture. We have seen for a number of years that the largest luxurybrands haven’t added any stores to their total. Actually, most have beenin ‘trimming mode’, reducing one or two stores here and there. A casein point is the network consolidation that has been going on in China,hand in hand with a Darwinian fight among luxury shopping malls,which has led to a shake-out and ‘survival of the fittest’. When welook at who has been leading store openings in the past five years,we find two kinds: (a) up-and-coming smaller brands that have beenable to ‘strike gold’ (Moncler, Saint Laurent, Celine, Balenciaga);(b) accessible luxury brands that have built their networks worldwide (acase in point, Michael Kors). The point here is that everyone else hasbeen confronted with a relatively static store base and a completely newset of challenges versus the previous expansion era.

In fact, during the expansion phase, most brands were concerned aboutattaining comparable standards all across the world. Store appearance andin-store service was supposed to be of a similar level, anywhere in theworld. So much so, that store blueprints and ‘selling ceremony hand-books’ were created. One could say, most brands used a cookie-cutterapproach to store expansion. The advantage, of course, was consistency.The disadvantage – and this is becoming all too obvious today – wasa risk of boring customers and failing to drive in-store traffic. Whyon earth should I go and visit a store in Milan, New York or L.A.,when it is virtually identical – and actually a tad smaller – than the oneI have close to me in Shanghai? And why should I go to a store in thefirst place, when I can buy what I need online, and when I can touchand see the products while I go through the airport in their airsidelocations?

Brands today are confronted with a new task: how to make their storesunique and interesting enough so that customers continue to be keen to visitthem – both in their hometown and when they travel. This will requirea completely new approach: standardisation is out. It is time for brands

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xi�

� �

�

Foreword xi

to go back to the drawingboard and answer two questions. For starters:How can I make my stores different from my competitors’, other thanfor the colour of the marble on the floor and their size? How can thenew stores ‘speak’ about the DNA of my brand, and plastically embodyit? We have seen a few brands stand out on this front – Tiffany openinga cafe in its NYC flagship with a view of Central Park is a best-in-classexample of uniquely reconnecting store and brand equity. And then ofcourse, the other question is how to make each store in my chain slightlydifferent and interesting enough to deserve a visit. This, I believe, willdemand more ‘localisation’ and less ‘globalisation’. Striking the right bal-ance alone demands a whole new handbook on how to manage luxurygoods retail.

Third, luxury brands face today more demanding consumers. Goneare the days of lines in front of luxury flagships, and hordes of new con-sumers all clamouring to buy the well-known luxury icons. Today, manyconsumers have seen it all and bought it all. This means innovation hasbecome essential, if brands want to continue to stay relevant to them. Prod-uct innovation, first and foremost. But in-store innovation too. As wellas innovation in communication and client engagement. We have calledthis the need to ‘surprise’ consumers. For luxury retail, this means that storesneed to change frequently and host a whole new array of activities. Mostly, brandshave tackled this need with pop-ups. Far from being a ‘side act’, pop-upshave become a major cost line in the overall retail budget. This opensup a completely new management front: how to best locate pop-ups vsflagships, what to do in them which can be meaningful for the brand,how to create synergies with the rest of the network, whether to locateoutside or inside flagships themselves. Here too is a whole new worldfor managers to tackle.

Luca SolcaManaging Director, Luxury Goods, Sanford C. Bernstein (Schweiz)

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xii�

� �

�

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xiii�

� �

�

Introduction

What Is the Reason for This Revision?

January 2012 saw the publication of the English version of our bookLuxury Retail Management that we had written in 2010 and 2011. Sevenyears later, as close observers and players in the luxury industry,1 werealised that the industry had undergone such upheavals since then thatwe had to revise our book so that it remained relevant in the con-text of these evolutions. During this rereading, we also realised that the2012 edition was premonitory in many respects (especially the chaptersreferring to the Internet and China) but it did need to be completelyrevamped if we wanted it to preserve its role as a reference book to beread by every specialist of luxury distribution in its English, French orChinese versions.

We therefore decided to rewrite most of this book, structuring itaround the new luxury business model – omnichannel – where the cus-tomer is placed at the core of communication and distribution channels,

1 The authors are – independently of one another – involved in the perfume industry.

xiii

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xiv�

� �

�

xiv I N T RO D U C T I O N

and of organisations. Is, or should be? As we will see while reading throughthese pages, this will be the major challenge for luxury brands over thenext 5 years: placing the customer at the heart and building the organi-sation and information systems that will allow it around the customer.

It is therefore necessary to start with the client, and to do so oneneeds to understand the major changes that have taken place in recentyears.

Change Is Accelerating: The Luxury Customer IsNo Longer the Same

In their 2017 annual study on luxury, Bain & Co. showed that all thestructuring trends for the industry are linked to the rise of the millenni-als – or Generation Y, that is, those born between 1980 and 2000 (Straussand Howe 2000). Two figures explain the impact of this generation:

• They currently represent 38% of luxury buyers and 30% of the mar-ket (in value).

• 85% of the growth in the luxury market in 2017 was generated bythem.

Their tastes, behaviour and expectations are therefore shaping themarket and influencing other generations. We have identified threebehaviour traits that we believe essential:

• The quest for experiences: One no longer consumes a product butlives an experience. Giving a meaning to life is an important goal andcustomers will look for brands that can bring them these elementsof meaning. For example, customers have their own passions and arelooking for brands that know how to construct a relationship aroundthose passions.

• Involvement: The closer a brand is to these customers, the morelikely they are to become its ambassadors. They want to ‘live thestory’ of the brand and not consume it, which in turn allows themto share it – on the Internet.

• Affirming one’s own identity: By choosing a personal style, luxuryis a means of self-expression.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xv�

� �

�

Introduction xv

Therefore, the bricks-and-mortar and Internet boutique duo couldbe considered the sole epicentre of the brand, a place where the customerwill live the story. All the skill of the brand would involve linking theexperiences of the customer’s life (their passions, communities, personalstyle) to the experience of the brand (services, transactions, values, thecommunity around the brand).

For this reason, Bain urges leaders of luxury brands to make thecustomer their ‘obsession’ and to soak in the spirit of the millennials – insix steps that should be on the agenda of every head of the industry:

1. Make the history of the brand come to life through inspiring dia-logues and experiences.

2. Build personalised relationships with customers.3. Rethink the customer’s itinerary by adopting a holistic view of dis-

tribution – what we hereafter call the omnichannel.4. Understand (and decode) customers’ aspirations so that they become

relevant to them – which inversely means that any brand that movesfurther away from customer (and particularly millennial) expecta-tions would become obsolete.

5. Develop the individualising of the product, services and messages allthrough the customer’s life.

6. Invest in talents and skills to achieve all these goals (Gutsatz andAuguste 2015) and maintain a product-marketing approach.

In short, luxury brands – which have been developing over thelast 20 years, partly through the opening of boutiques (that requireconsiderable investment and result in an increase in turnover) – arefaced with the challenge of changing their models and rebuilding onmarketing and customer relations. This will lead to increasing yearlyoperational expenses for public relations and promotions, which willconsequently weigh down their operating accounts. Luxury brandsare thus at a historic turning point: they have to reinvent themselves.The 2017 figures put forward by Bain are disturbing in this respect:whereas, at the time when the luxury sector was flourishing, whetherduring the period of democratisation (1994/2007) or that of Chinesebulimia (2010/2014), 85 to 95% of the brands showed positive results.Since 2016, only 65% of them are profitable (and only 35% have

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xvi�

� �

�

xvi I N T RO D U C T I O N

succeeded in increasing their profitability!). The current period thatone can consider the ‘New Normal’ will engender winners and losers.

This book is therefore our contribution towards understanding thesenew challenges that luxury brands have to face.

Case Study: A Striking Example: ‘See Now /Buy Now’

On 4 February 2016, Burberry announced that they wereimplementing what proved to be a revolution in the world offashion: a synchronisation of the dates of the fashion shows and theavailability of the new collection in their boutiques (Amed and Abnet2016). From September 2016 onwards, the collections werereduced to two per year, the women’s and men’s fashion showswere merged and products were made available in boutiquesat the same time. In the wake of this change, other brandsannounced their intention to follow Burberry’s example:Tommy Hilfiger, Tom Ford, Rebecca Minkoff, Vêtements,Mulberry, etc.

Fast forward to 24 February 2017 – Ralph Toledano, Chair-man of the French Federation of Ready-to-Wear Dressmakersand Fashion Designers announced that they would not make anychanges to the existing schedule, followed in quick successionby Gucci and all the Kering brands.

Christopher Bailey, then CEO and Creative Director ofBurberry, justified this choice, citing the desire to draw closerto his customers: in his opinion, he did not see why productsshould not be available immediately or why fashion shouldcontinue to make distinctions between fall and winter andspring and summer when fashion is distributed worldwide (andconcerns both hemispheres). For him, at the end of the day, allit required was only an optimisation of the processes of supplyand production:

When you break it all down, it’s just a shift in your supplychain – that’s the crunch. (Amed and Abnett 2016)

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xvii�

� �

�

Introduction xvii

He could also have evoked the lower costs that such a deci-sion implied, especially at a time when Burberry’s results werepoor (for the first six months of 2015 sales and profits were stable;revenue on licences declined by 13%).

But, of course, the story lies elsewhere: the big comebackof luxury and a new episode in the conflict between France andItaly on the one side and the English and Americans on theother.

‘Several people, including designers and retailers, are com-plaining about the shows. Something is not functioning becauseof social media, people are lost’, said Diane Von Furstenberg,Chairperson of the Council of Fashion Designers of America(CFDA), announcing that they were looking into the possibilityof a ‘See Now, Buy Now’ Fashion Week (Lockwood 2015).It was, of course, an American initiative, presented as thoughit was done under the pressure of social media and consumers.This point is important. One may recall, for example, thatduring his last fashion show, Tommy Hilfiger delineated a spacededicated to ‘instagrammers’, to allow them to photograph theshow under the best conditions possible and to publish their‘live’ snapshots by Instagram (Le Luxe est Vivant 2016) and thatAmerican fashion shows are now open to the public (againstan entrance fee). American fashion shows have thus become‘democratised’ entertainment.

The reaction of luxury brands (showing in Paris and Milan)was immediate. They reasserted they were luxury brandspractising real scarcity management. They projected themselvesas ‘creation driven’ – thus consigning the American brands totheir ‘marketing-driven’ image. By doing so, they categoricallydifferentiated themselves from the American brands (andBurberry), often presented as being accessible luxury. We thuswitnessed on that occasion a general repositioning of brandswithin the luxury industry itself.

(continued)

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xviii�

� �

�

xviii I N T RO D U C T I O N

(Continued)

But it was not a rigid position confronting an immov-able model on the part of the French and the Italians. Pradaimmediately made available two models of its bags that werepresented during its fashion shows in its boutiques. And KarlLagerfeld admitted that Chanel’s organisation was much smarterthan previously thought:

Chanel creates six collections a year, but I just createdone more – the ‘capsule’ collection – that we presentneither to the press nor to anyone else; it only surfaceswhen our stores receive the presentation leaflet. ButI would like to do something else – it may be too earlyto talk about it – a special Internet collection: 15 modelsthat will be displayed on the Web: You see it, you ordera model and you receive it immediately. (Amed 2015)

A vision much more refined than ‘See Now, Buy Now’.

The Definition of Luxury

It is impossible to speak about luxury without attempting to define theconcept. Many experts debate what the word means, apparently withouthaving reached a consensus.

The first distinction one has to make is between luxury and fashion.For some, a brand in the textile or accessories sector starts out merelyas a ‘fashion’ brand and becomes a ‘luxury’ brand only if it has achieveda certain consistency in its concept and timelessness in its collections.According to that theory, a fashion brand has to be creative and come upwith new ideas, new concepts, and new products every season in orderto arouse the interest of the consumer. If it creates classic models thatsell year in, year out and become bestsellers that endure, its status thenevolves from ‘fashion’ to ‘luxury’. But although this distinction betweena fashion brand and a luxury brand is a valid one, it is nonetheless mis-leading because even a fashion brand that has achieved luxury status,

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xix�

� �

�

Introduction xix

such as Chanel or Dior, has to come up with new models each seasonand present them in new ways in order to retain consumer interest.

Why Is It So Difficult to Find a Definition? The concept of luxuryhas varied over time. In the Middle Ages, people saw luxury as unneces-sary and therefore superfluous. A luxury item was more intricate than anordinary item used to accomplish the same function. The most strikinghistorical example is that of Christophle, which sold tableware accessi-ble to the petite bourgeoisie at the beginning of the nineteenth centuryby replacing the noble solid silver with plated silver. Up until the nine-teenth century, luxury items were intended only for the ‘gentry’ andwere a means to set themselves apart from the crowd.

Today, the term luxury carries a connotation that is far less negative.It is no longer considered superfluous or reserved for a small group ofindividuals. A new concept has emerged – the brand concept – wherebya luxury item has become an object that carries a known, credible andrespected brand name. The introduction of the signature, that is, of thebrand, pushes back the concept of exclusion (‘It is not for everyone’)and shifts the focus to the quality of the product.

Another element that may have contributed to this more positiveview of the concept of luxury is the emergence of what one maycall ‘accessible luxury’ that, in practical terms, means luxury meantfor everyone. Hence, the impression that the consumer retains is thatluxury products are sophisticated and expensive, of a quality clearlyabove average, and signed by a brand bearing a name with a strongpower of attraction.

The Many Approaches to Luxury Another way to differentiate thedefinitions of luxury is to look at the criteria that different people mayapply to distinguish one luxury product from another.

• In terms of perception, the consumer decides what is or is not a lux-ury product. Today, one would not speak of ‘conspicuous waste’as Thorstein Veblen would have, but of the quality of service in asophisticated environment.

• In terms of production, manufacturers decide whether or not theywant their products to be part of the luxury sector. Accordingly, they

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xx�

� �

�

xx I N T RO D U C T I O N

ensure that the luxury item is the product of the work of a meticulousartisan, that it is sold in a sophisticated environment and that it ispromoted in a unique way, placing the focus on the brand and its ownvalues. However, manufacturers and consumers do not necessarilyagree: the management of Hugo Boss, for example, doubtlessly doeseverything it can to associate their brand with high-quality productssold in a relatively sophisticated environment. And taking a differentapproach, from the point of view of Zara’s management, the focuson its exclusive network of outlets situated in the best locations inevery city, and the constant flow of new models in each store, theirbusiness is akin to that of the luxury industry.

• In terms of social and individual comportment, sociologists woulddescribe a luxury product as an object that allows its user to standout from the crowd. Customers would probably speak in hedonisticterms and describe how the possession of that particular luxuryitem gives them personal satisfaction and genuine pleasure, perhapsreflecting the refinement of the objects they own or plan to acquire.

There is one constant underlying these various definitions: the branditself and its own values. A product, of course, has its own technicaland aesthetic characteristics – but it also carries a brand name. Thisbrand identity should be consistent with what the product representsand should deliver added value so that its coherence is evident.

A Set of Values that Define Luxury Another approach to defin-ing luxury is to identify the various qualities that a luxury item shouldinclude.

• The notion of exclusivity underlies the concept of luxury. A luxuryproduct should be rare and not easy to acquire. It should be acces-sible, of course, but purchasers should have the impression that theyset themselves apart by using it, that they are capable of distinguish-ing what makes this product so different from others or other brands,and that it reflects remarkable sophistication and taste.

• An obvious characteristic of a luxury product is, of course, its qual-ity. It has to be more beautiful than another. Its guarantee shouldbe clearly defined and generous. The packaging has to be elegant

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xxi�

� �

�

Introduction xxi

and the object expensive, in any case more expensive than a similarmass-market product.

• Another aspect: a certain form of hedonism. The product should bea pleasure to own and use; it should give the owner a very personalfeeling of satisfaction.

• The brand image is undoubtedly the crowning touch. It has to bereputed, but also unique, and different, but with features everyonerecognises.

Ultimately, luxury simply boils down to a question of status. A pro-fessional in the luxury business should never forget their real job: to makecustomers feel they have a special status, directly or indirectly, throughwhatever form it takes.

In short, customers are willing to pay higher prices because, withall its features, the luxury item satisfies all their desires, emotional orsymbolic, and offers them a memorable experience. That is what exclu-siveness, quality, hedonism and brand image are all about.

The Various Types of Luxury Instead of embarking on a long debateto find one common concept of luxury, it may be more practical todistinguish the different types of luxury.

• Authentic luxury would refer to objects that quite clearly differ frommass-market products in that they are the handiwork of skilledcraftsmen. They conceivably last longer, are probably simpler to useand have a brand identity that is gratifying. A true luxury productwill be timeless to some extent and the user will find pleasure inoperating or using it because of the endless number of refined andcarefully crafted details it has. It will definitely not be cheap, and itsname will represent a great deal more than just its monetary value.It will not be so much a question of price as an object endowedwith aesthetic components that will bring added emotional value toits owner.

• Intermediate luxury (one of the authors of this book has coinedthe expression ‘Luxe Populi’ in his other book, see Gutsatz 2002)refers to products that have the traditional attributes of luxury interms of creativity, statement and coherence where brand identity

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xxii�

� �

�

xxii I N T RO D U C T I O N

is concerned, but are merely an upgraded version of traditionalconsumer products. They are not the product of individualcraftsmanship. They position themselves in the upper-middle rangeon the price scale and are produced in relatively large quantities inautomated factories, but their brand image is carefully cultivatedand controlled.

• Offbeat luxury refers to products that are in fact exclusive creationsthat stand out very clearly from the ordinary. Ferrari is a goodexample: a Porsche would be an authentic luxury product; a Ferrariadds another dimension, more off-the-wall. Ferraris are produced invery limited numbers (for years Ferrari capped its annual productionat 7,000 cars) and seem to assert the right to the freedom andcreativity typical of Ferrari. The company does not manufactureautomobiles but exclusive collectors’ items, some of which willnever see an ordinary country road.

As Jean-Louis Dumas, the former Chairman of Hermès, oncesaid: ‘A luxury brand must respect three conditions: produce beau-tiful objects, select clients who will become individual agents of itsown promotion, and decide freely and without any constraint whatit wishes to do’ (personal communication). There is probably nobetter definition of luxury.

• Affordable luxury may not be luxury at all, or perhaps it may justbe a special category of intermediate luxury. Zara is an example ofthis segment: creative products that rotate very quickly, and con-sumers who find a psychological satisfaction in buying and usingthese quick-moving products. The prices are very reasonable and thebrand image is carefully managed and promoted, with a well-definedlong-term vision. As we will see, Zara’s business model is very effec-tive. Although, from the manufacturer’s viewpoint, it employs manytools derived from the luxury sector, it is perhaps merely a formof intermediate luxury – or even simply a sophisticated and skilfulmass-market brand. Zara is perhaps a poor example because mostreaders would say that the brand has nothing to do with the lux-ury sector. We do understand this point of view, but in our opinionmany tools used in luxury could be used for mass-market brands.Besides, we can no doubt discern a continuum with Zara at one endand Gucci and Chanel at the other.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xxiii�

� �

�

Introduction xxiii

The Contents of This New Edition

The difference between this edition and the first one, which contained13 descriptive chapters, is that in this one we wished to emphasise fouressential factors that come into play in the management of sales outlets.We could be in fact discussing not only the luxury sector, but also allother market sectors for which stores are often the primary source ofincome.

It is a fact that, compared to more traditional sectors, the luxuryindustry has some specificities that are noteworthy: the possibility ofbeing able to identify customers whose contact information is relativelyeasy to obtain and to track their purchases over several years. The samecustomer may also purchase products sometimes near their home or placeof work, and at other times at the other end of the world while travellingfor work or pleasure.

In the first part, we will be describing the main choices facing luxurybrands in terms of distribution:

• Which distribution model should it adopt? (Chapter 1)• Do we still need stores? (Chapter 2)• What store concept should it adopt? (Chapter 3)• How can it integrate its offline and online businesses? (Chapter 4)

In the second part, the customer will take centre stage. Luxurycustomers expect seamless service. They wish to be able to changefrom an online approach to an offline approach at any time and expectthe brand to be organised enough to allow them to switch seamlesslyfrom one method to another at any given time. There is no universallyaccepted term that describes this today: the term most often used inFrance is omnichannel; in the USA it is called ROPO (‘ResearchOnline, Purchase Offline’), i.e. search for information online (on theInternet), purchase offline (in a store), or the contrary: search forinformation offline (in a store), purchase online (on the Internet). InChina, the term O2O (‘Offline to Online’) is used. In this book, we willuse the term O2O – which is interchangeable (Offline to online/Onlineto offline/Offline to online to offline, etc.). However, O2O, whichhas to continuously adapt to customers switching from one system toanother, requires very astute management, logistics and control systems.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 flast.tex V1 - 01/16/2020 8:03 A.M. Page xxiv�

� �

�

xxiv I N T RO D U C T I O N

We will therefore examine successively:

• How brands can place the customer at the centre of their approachand their organisation (Chapter 5).

• How brands can identify the customer and the issues around CRM(Chapter 6).

• How brands can coordinate marketing campaigns in an O2O world(Chapter 7).

• The war of the platforms (Chapter 8).

In the third part, we will delve deeper into the type of service tobe provided to customers, how to build loyalty and how to ensure thequality and meticulousness of service.

This will bring us to four essential elements:

• Understanding customer behaviour (Chapter 9).• Building customer relationships (Chapter 10).• How to ensure customer loyalty (Chapter 11).• Understanding how the Internet has shattered the traditional sales

model (Chapter 12).

In the fourth part, we will present the more traditional and moretypical elements of sales point management.

• Location of sales points (Chapter 13).• Management of sales point staff (Chapter 14).• The financial analysis of sales points (Chapter 15).• Managing sales prices in global markets (Chapter 16).

In Chapter 14, we have also compiled all the information that couldbe useful to a luxury sales point manager or a business or sales pointdevelopment manager.

In this book we have sought to answer all the questions that luxurybrands have today with regard to physical distribution and to offer someideas for reflection and a projection of what could happen in the nextfew years.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2021-10-26 07:35:23.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 p01.tex V1 - 01/16/2020 8:03 A.M. Page 1�

� �

�

Part I

Important Choices inLuxury Distribution

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 p01.tex V1 - 01/16/2020 8:03 A.M. Page 2�

� �

�

.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 3�

� �

�

Chapter 1

The Various Models inLuxury Distribution

Luxury today no longer sells because of rarity but on a feeling ofexclusivity, which depends primarily upon the selectivity of itsdistribution, both physical and digital.

–Jean-Noël Kapferer1

F rom the outside, observers may believe that all luxury brands aredistributed in the same way – through exclusive stores owned bythe brand – and that they are able to manage them from their

head offices. In fact, the reality is much more complex.

1 Kapferer (2017).

3

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 4�

� �

�

4 I M P O RT A N T C H O I C E S I N L U X U RY D I S T R I B U T I O N

Some luxury products, such as perfumes and watches, are sold forthe most part in multi-brand stores that do not belong to them. Thesestores generally do what they think is most efficient for their multi-brandbusinesses and they are never easy to motivate or mobilise.

In some countries (e.g. Thailand and Vietnam) a foreign companythat imports and distributes products manufactured abroad is notallowed to be a majority owner of its local subsidiary (it is only possiblein China since 2018). It has to associate with a majority-holding partnerthat is a national of the country. So, no luxury group can, even if itinitially wanted to, become the owner of all its sales outlets in the world.

Building a global network of outlets demands an enormous amountof time and money. Indeed, for a large luxury brand, having its ownstore in Ulaanbaatar would be wonderful, but how can it ensure thatcustomers will find the same service there (hospitality, advice, prices andafter-sales service, for example) as they receive in Paris or Milan?

Also, although Gucci or Chanel might have the means to invest inopening a store in New York, a small brand that is already struggling tomake profits in its Paris store would find it much more difficult to do so.

A discussion on the sales points of luxury brands all over the worldtherefore involves describing all models, physical or digital, that can orshould be used to present the products to customers the world over.

Direct and Indirect Distribution

Luxury brands did not start out with exclusive stores in every cityin the world. Their distribution systems grew. They often opened asingle store in one city (the city of origin) and then used a network ofmulti-brand outlets that afforded them initial exposure and internationalturnover. The business environment has also evolved over the last150 years; the main store categories have changed and found their raisond’être and their stability.

A Historical Perspective

Retail trade is doubtlessly one of the oldest professions in the world.From the dawn of history, when people realised that they could not

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 5�

� �

�

The Various Models in Luxury Distribution 5

obtain everything they required for their own survival by themselves,they had to turn to others who were capable of searching for andgathering together the various commodities they required, and whoexchanged these items for a monetary consideration. This act ofselecting and gathering various goods that would be subsequently soldto others saw the emergence of the trader and retail trade.

Later, during the Middle Ages, as trade developed, merchants fromthe same domain often tended to cluster together in the same street.They seemed to believe that it was better to place themselves in proxim-ity to their competitors, assuming that customers would be more likely toenter their shops, and those of their competitors as well when they wentaround all the shops on the street. Those that set up shop elsewhere,resolutely isolated from their peers, found themselves away from theshopping circuits and missed out on sales opportunities. Being locatedfar away from other shops but close to residential areas was neverthe-less an advantage for everyday services such as food – in other words, asconvenience stores.

This distinction between proximity purchases and others has alwaysexisted and explains the differences in localising strategy. The factthat merchants from the same sector wished to group together andconcentrate their pulling power is not very different from what we seetoday in big cities with the concentration of luxury stores in the sameneighbourhood.

The foundational event worth mentioning here is the creation in1851 of the world’s first department store, Le Bon Marché, in Paris.The idea behind it was that, for the first time, ready-to-wear clothesfor men and women, shoes, kitchen utensils and suchlike would all besold together in the same store. As always, when an idea is good, itis quickly emulated and in 1856 the first American department store,Macy’s, opened in New York, where it still stands now.

As time went on, the appearance and the system of presentation ofthe products in department stores were strongly influenced by technicalinnovation. In 1869, the first elevator was installed in a Parisian store,making it easy for customers to go from one floor to another, and alsomaking it possible to present products on four or five different levels.

Yet another innovation, which dates back to 1892, influenced thecadence in all department stores in the world: the escalator. This allowedcustomers to go from one floor to another at their own pace, without

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 6�

� �

�

6 I M P O RT A N T C H O I C E S I N L U X U RY D I S T R I B U T I O N

having to wait for a lift. Escalators have thus defined the space of almostevery department store today: a central well in the middle of a hall aslarge and impressive as possible, sometimes crowned with a dome; theescalators moving through this well, allowing customers to go from onefloor to another as and when they wish. The first escalators were installedin Harrods in London in 1895.

Mitsukoshi Nihonbashi, the first Japanese department store, wasopened in Tokyo in 1915.

The year 1919 is also another very important date: the first air con-ditioning system was installed at Abraham & Strauss in New York. Sincethen, department stores no longer need windows. Air conditioning doesaway with the need for windows for ventilation and, in some cases, fordoors that open onto the street: stores could be integrated into a galleryor mall. Boutiques therefore do not need windows anymore, except, ofcourse, as showcases for presenting products. The appearance of depart-ment store buildings remained more or less unchanged after that, muchlike we know them today.

In 1922, the first shopping centre, the Country Club Plaza, wasopened in Kansas City and the appearance of these centres has remainedvirtually unchanged for the past 95 years, with very little innovation,except for the first duty-free store that opened in 1957 in ShannonAirport, Ireland.

On another plane, we should mention the appearance of the firstelectronic cash register in 1970 and the first optical reading device in1975. Before these dates, it would have been difficult to imagine thatevery product sold in the world would one day have its own code easilydecipherable by a machine.

Today’s department stores, shopping malls, shopping arcades andduty-free outlets are in fact the end products of 150 years of innovationand development in distribution.

The Various Types of Sales Outlets

Wholesale and Retail Sales There are in fact two methods topresent products to the consumer: having one’s own store, to fullycontrol customer relations (retail), or selling to stores that will presentthe products to their customers themselves (wholesale). This distinction

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 7�

� �

�

The Various Models in Luxury Distribution 7

applies, of course, to brick-and-mortar stores. The same difference alsoexists in the digital domain. Celine, for example, sells its shoes throughtheir own website (retail) but also sells them on the ‘Net-a-Porter’website (wholesale). In both cases, the selling price to the consumeris the same (same retail price) but in the second case (throughNet-a-Porter) Celine has to pay a retail margin to the platform.

At first glance one might think that the wholesale option (throughindependent multi-brand outlets or online sites other than that of thebrand) is simpler, because the brand would have practically nothingto do and it would not have to tie up its capital in store ownershipsand stocks. But, of course, it would have to share its margin with therespective stores.

On the contrary, one might think that it is easier to sell exclusivelythrough directly operated stores and save the entire margin. But is thebrand reputed enough to attract customers and persuade them to entertheir own stores? Also, is the purchase important enough to a customerto motivate him to go and buy the product directly? An example maymake the issue clear: would Hermès sell more bottles of its cologne,Eau d’Orange Verte, if it sold this product in all the perfumeries in Parisor by reserving it exclusively for its own boutiques in Paris?

Directly Operated Stores Directly operated or independent storesseem to have priority among many brand managers.

Of course, when a brand acquires a strong power of attraction, and itdisposes of sufficient financial means, it could be tempted by this system,which enables it to determine consumer reaction to a new collectionor a new product early in the game. But developing a large network ofdirectly operated stores somewhat changes the manner of functioningof a brand that creates exceptional products: it would have to become amanager of these sales points, and the priorities of the brand, its organi-sation and the use of its financial resources may be affected. Selling, as wewill see later, is a real profession. Most luxury brands – structured aroundcreation – did not have ‘retail’ skills and acquired them over time.

Partner Stores To a customer, partner stores (or TPOS – Third-Party-Operated Stores) are outwardly similar to a directly operated store: they

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 8�

� �

�

8 I M P O RT A N T C H O I C E S I N L U X U RY D I S T R I B U T I O N

use the same concept, the same decor and the same layout as a directlyoperated store and the client would not be able to tell them apart. Theydisplay the brand’s products in exactly the same way as the original storein Paris or Milan, but they are managed, financed and developed by anintermediary.

The intermediary is sometimes a ‘franchisee’ who is interested ina particular brand that is not found in his chosen territory (Toulouse,for example, for a French brand, or why not in Astana in Kazakhstan?).The franchisee undertakes to open a store, fully respect the concept ofthe brand, buy a minimum quantity of the brand’s products from eachcollection, and pay the brand a percentage of its turnover in the formof royalties (in general, 2–5%). In exchange it will be granted territorialexclusivity for the duration of the contract.

This system is widely used by national fashion brands with a‘premium’ price category. They use several franchisees in the samecountry, each having exclusivity over a city or part of a city.

For luxury brands, the intermediary is more often an exclusivedistributor in a particular country (for example, China, Japan orRussia). It will be granted territorial exclusivity and will choose, withthe brand, the cities where it will be installed in priority. The exclusivedistributor invests directly in the building of a network of exclusiveboutiques and will be granted a long-term contract (sometimes morethan 20 or 25 years). In such cases, the distributor would have to ensurethe advertising and digital media presence of the brand and its publicrelations in the country.

Lastly, there exists a specific type of exclusive distribution, wherethe luxury brand operates in a country where foreigners do not havethe permission to hold majority stakes in a subsidiary. The brand’s man-agement therefore decides on an exclusive distributor who will becomethe majority shareholder of the local distribution subsidiary. This major-ity shareholder also has to respect the guidelines of the brand in thedesign and decor of sales outlets, and will ensure the logistics of thebrand in a particular territory. As mentioned above, in certain countriessuch as Kuwait, Qatar, Thailand, Vietnam and many others, a foreignshareholder cannot hold majority shares in a distribution subsidiary.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 9�

� �

�

The Various Models in Luxury Distribution 9

Department Stores Traditionally, department stores were created toobtain supplies of various kinds of products, purchase them, and havethe specialised staff to present them to customers at suitable counters.Department stores have therefore to accomplish a range of tasks:

• Finding and selecting products.• Purchasing, receiving and storing of the products.• Paying for the products, sometimes before they are received.• Display on a counter.• Presenting the product to customers.• Selling and other activities by sales staff.• Collecting the proceeds.

These, therefore, are a combination of financial, logistics, merchan-dising and commercial services.

Today the major luxury brands are sold in shops-in-shops. Here thedepartment store provides the space (almost like a real estate agent), theluxury brand decorates it at its own expense, hires and trains the salesstaff, provides them with a uniform and remunerates them. It selects theproducts that will be most suitable for that particular sales point and, inmany cases, retains property rights until the day of the sale. The depart-ment store merely collects the sale proceeds, retains the retail marginand transfers the wholesale amount to its ‘supplier’. Its function simplyconsists of:

• Providing a space• Collecting the sales proceeds

Its role is thus relatively simpler as compared to the initial responsi-bility of a department store – and resembles that of a lessor of a buildingspace.

Between these two methods of working with a department store(the new one and the traditional), there exists a third type of agreement:a ‘corner’ contract obtained by the brand where it disposes of a cornerspace, opening out to the other departments but still identifiable andconvertible, with vendors paid by the brand and merchandise that is theproperty of the department store.

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 10�

� �

�

10 I M P O RT A N T C H O I C E S I N L U X U RY D I S T R I B U T I O N

Evolution and Perspectives of theVarious Types of Sales Outlets

Evolution since 1950

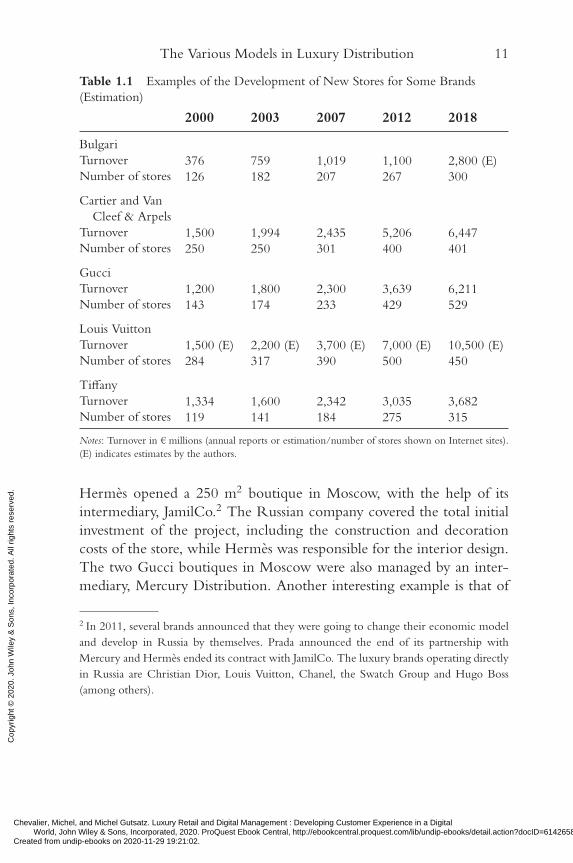

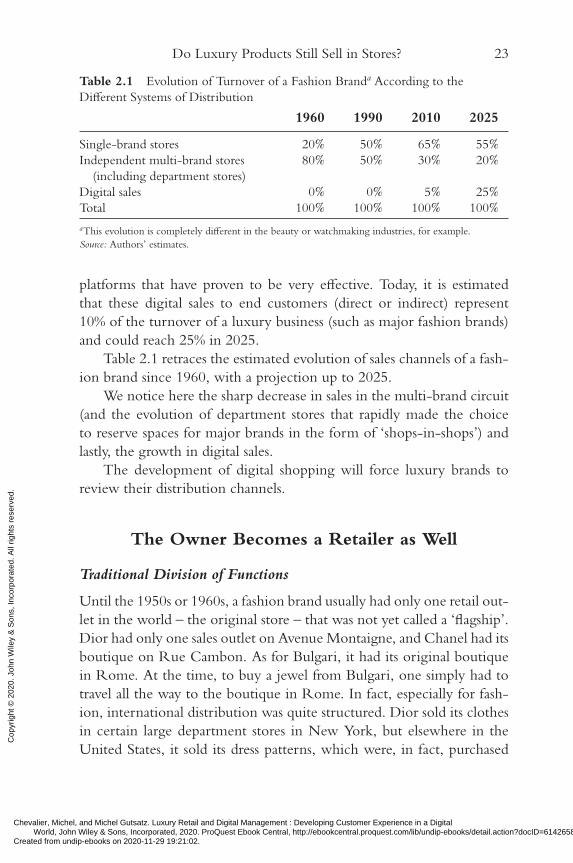

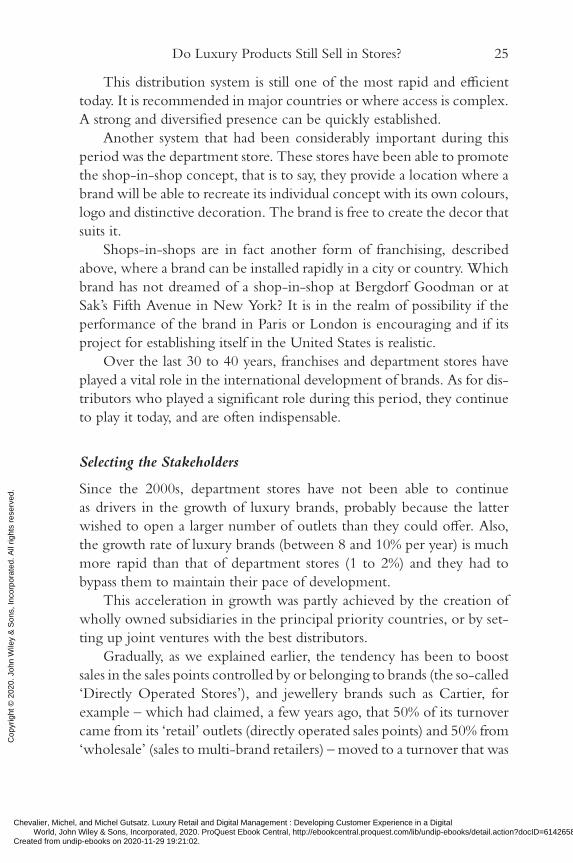

In Table 1.1 we show the number of outlets and the turnover of certainluxury brands over the past 18 years. The brands chosen are: Bulgari,Cartier, Van Cleef and Arpels, Gucci, Louis Vuitton and Tiffany.

The table clearly illustrates the following facts:

• The increase of direct sales points has clearly been a major occupationand strategic issue for luxury over the last 20 years.

• Among these six brands given as examples, the total number ofsingle-label stores increased from 922 to 1995. The management,control and human resources relating to these outlets have thusbecome important aspects for the management of a luxury brand.

In fact, in this progression, we see both the general evolution of themarket and the emergence of big brands that are becoming increasinglystronger.

Well-known brands find it quite easy to pay very high lease rightsto acquire a privileged location in a big city like Tokyo or Paris and beappealing enough to attract a very large number of clients right from theoutset – the break-even point is easily attained.

For a small brand, the situation is more complex. At the beginningof its development cycle, the brand usually starts with a directly operatedstore and distributes its products through selected retailers, in particular,multi-brand outlets. To enter a new market, it will do so through localagents or a distribution agreement. For example, Bluebell and DicksonPoon are distributors that European brands often have recourse to whenthey wish to enter the Asian market.

When the brand grows, it establishes its own stores and, at the sametime, switches from distribution agreements to franchises or joint ven-tures with its local partners. In nascent markets, like the Russian mar-ket, franchises would be the solution. For example, in December 2000,

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 11�

� �

�

The Various Models in Luxury Distribution 11

Table 1.1 Examples of the Development of New Stores for Some Brands(Estimation)

2000 2003 2007 2012 2018

BulgariTurnoverNumber of stores

376126

759182

1,019207

1,100267

2,800 (E)300

Cartier and VanCleef & Arpels

TurnoverNumber of stores

1,500250

1,994250

2,435301

5,206400

6,447401

GucciTurnoverNumber of stores

1,200143

1,800174

2,300233

3,639429

6,211529

Louis VuittonTurnoverNumber of stores

1,500 (E)284

2,200 (E)317

3,700 (E)390

7,000 (E)500

10,500 (E)450

TiffanyTurnoverNumber of stores

1,334119

1,600141

2,342184

3,035275

3,682315

Notes: Turnover in € millions (annual reports or estimation/number of stores shown on Internet sites).(E) indicates estimates by the authors.

Hermès opened a 250 m2 boutique in Moscow, with the help of itsintermediary, JamilCo.2 The Russian company covered the total initialinvestment of the project, including the construction and decorationcosts of the store, while Hermès was responsible for the interior design.The two Gucci boutiques in Moscow were also managed by an inter-mediary, Mercury Distribution. Another interesting example is that of

2 In 2011, several brands announced that they were going to change their economic modeland develop in Russia by themselves. Prada announced the end of its partnership withMercury and Hermès ended its contract with JamilCo. The luxury brands operating directlyin Russia are Christian Dior, Louis Vuitton, Chanel, the Swatch Group and Hugo Boss(among others).

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 12�

� �

�

12 I M P O RT A N T C H O I C E S I N L U X U RY D I S T R I B U T I O N

Club 213 from Singapore, distributor for Armani in the UK, the US, andAsia (Singapore, Malaysia, Thailand, Hong Kong and Australia) throughfranchise agreements.

Eventually, when a brand considers that it is sufficiently robust andthe market is mature enough, it will buy back these franchises or itsdistribution joint ventures and create a wholly owned subsidiary. Thishas been a major trend in recent years for global brands like Gucciand Hermès, as mentioned above, and Louis Vuitton and Armani.We see here an emblematic model with Gucci – the brand that hadactually initiated this business model 20 years ago under the initiative ofDomenico De Sole.4

At the end of the day, controlling distribution relies on managingfive major channels:

• Directly operated stores in the major markets (in foreign countries:through subsidiaries).

• Distributors or franchises in developing and foreign countries.• Shops-in-shops in department stores, so as to retain full control

over visual merchandising, sales and customer relations. Only verywell-established brands can operate in department stores exclusivelywith large shops-in-shops. Other brands would have to settle forcounters that would be strongly influenced by the department storeitself.

3 Christina Ong, the wife of the Singapore oil magnate, Ong Beng Sing, can be creditedfor having given London a fashion capital label in the 1990s. Club 21, her business empire,had franchises from some of the most coveted fashion brands: Giorgio Armani, EmporioArmani, Prada, Donna Karan, DKNY and Guess. Not only owner of a substantial part ofLondon’s most coveted commercial real estate, Ong had been able to intelligently attract,by other means, the modern London visitor who was eager for culture and had money tospend. She owned two of the most distinguished hotels of the capital – the Halkin opened in1991 in Belgravia, with staff dressed by Giorgio Armani, and the trendy Metropolitan Hotelon Old Park Lane, where the staff wore navy-blue uniforms created by DKNY (InternationalHerald Tribune, 15 March 1997).4 In this context, Gucci had a far-ranging plan: July 2001: It bought back the remaining35% of its joint-venture with FJ Benjamin Holdings Limited in Australia. February 2001:It bought back its operations in Spain (three stores) from its intermediary. May 1998: Itbought back nine stores and nine tax-free sales points from its Korean intermediary SungJoo International Limited. April 1998: It bought back 51% of Shiatos Taiwan Co. Ltd, itsintermediary in Taiwan (nine stores and one tax-free sales point).

Chevalier, Michel, and Michel Gutsatz. Luxury Retail and Digital Management : Developing Customer Experience in a Digital World, John Wiley & Sons, Incorporated, 2020. ProQuest Ebook Central, http://ebookcentral.proquest.com/lib/undip-ebooks/detail.action?docID=6142658.Created from undip-ebooks on 2020-11-29 19:21:02.

Cop

yrig

ht ©

202

0. J

ohn

Wile

y &

Son

s, In

corp

orat

ed. A

ll rig

hts

rese

rved

.

Trim Size: 152mm x 229mm Chevalier542339 c01.tex V1 - 01/16/2020 8:03 A.M. Page 13�

� �

�

The Various Models in Luxury Distribution 13

• Travel retail sales outlets, because even if operating costs and mar-gins demanded by duty-free operators are high, sales volumes aresignificant. However, the image of the brand and the impression ofexclusivity and quality of the products may deteriorate over time ifthe company does not maintain sufficient control over these oper-ations. For this reason, Gucci established its first duty-free outletoutside Italy, in Heathrow in 1999 – and extended those in Romeand Milan by 100 m2; Chanel opened its first duty-free outlets in1999 in several terminals in Heathrow (100 m2 each), but Prada, forexample, took a longer time to open there.

• For watches, jewellery, perfumes, cosmetics and eyewear, more andmore brands are selecting the top multi-brand stores, those that arecompatible with their brand image.

Type of Distribution and Robustness of the Brand As explainedabove, there is no single made-to-measure system for the distribution ofluxury goods, but opportunities resulting from the level of attractivenessof a brand and its sales volumes.

Professionals easily compare brands based on the turnover per squaremetre generated at their sales points. When this figure is very high (saybetween €50,000 to €100,000 per square metre a year), opening newstores and paying their rent is not an issue. When this figure is 10 or 20times less, it is better to work with multi-brand outlets.

That is why there is no one optimum solution for the distributionof luxury goods. It would depend on the sales volumes that can be gen-erated at a sales outlet: