Embed Size (px)

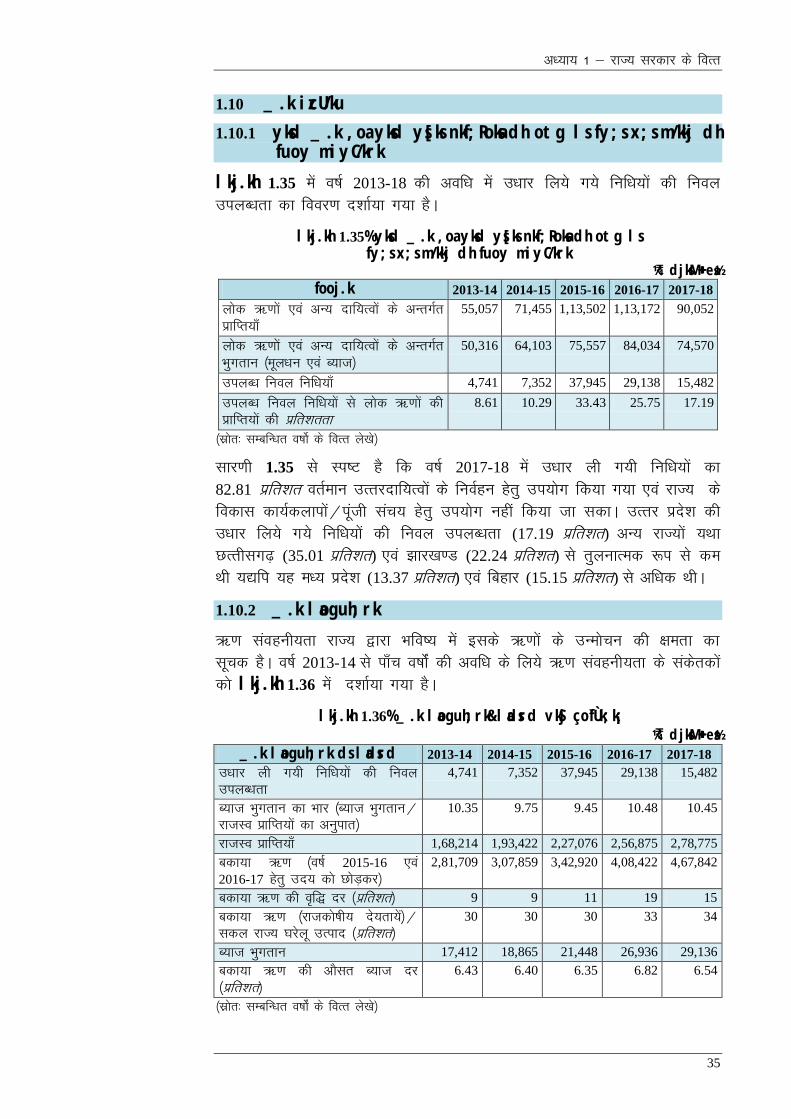

Citation preview

Hkkjr ds fu;a=d&egkys[kkijh{kd dk

jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy,

mÙkj izns'k ljdkj izfrosnu la[;k 3 & o"kZ 2019

i

vuqØef.kdk

fooj.k lanHkZ

çLrj i`"B la[;k

çkDdFku - v

dk;Zdkjh lkj - vii

v/;k; 1

jkT; ljdkj ds foRr

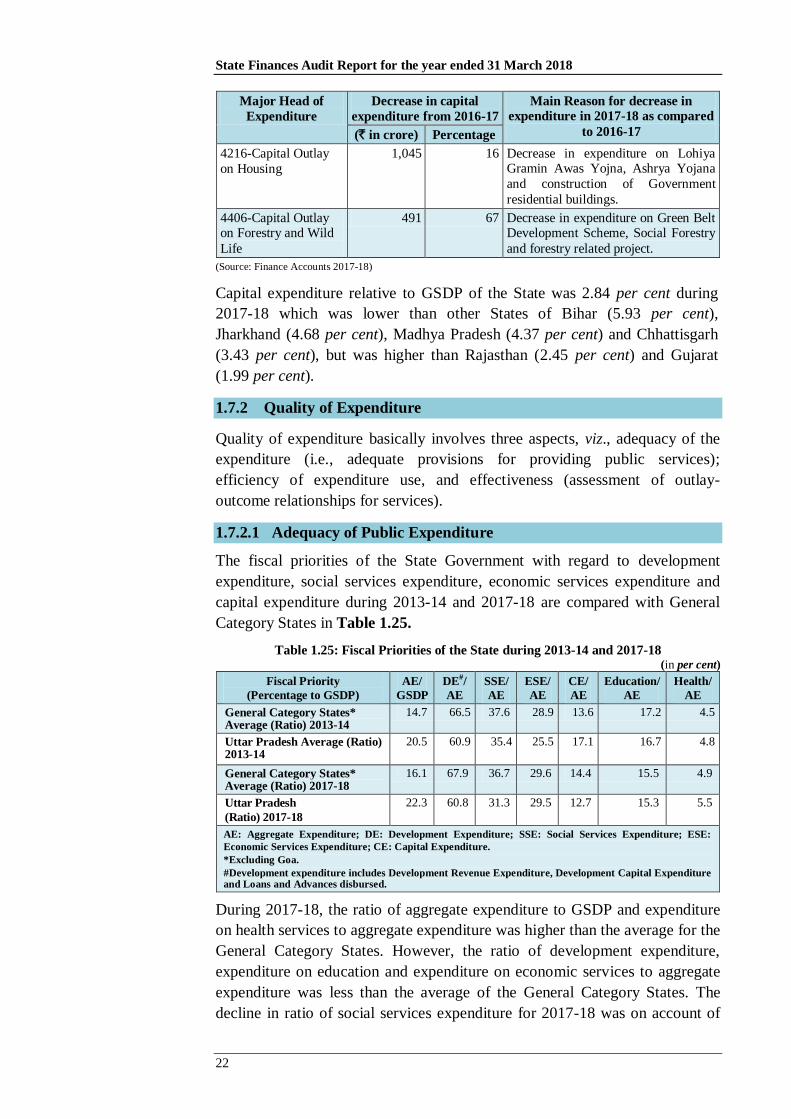

ldy jkT; ?kjsyw mRikn 1.1 1

jktdks’kh; ysu&nsuksa dk lkjka'k 1.2 2

jktdks"kh; fLFkfr dh leh{kk 1.3 5

jkT; ds foRrh; lalk/ku 1.4 8

jktLo cdk;k 1.5 17

laxzg dh ykxr 1.6 17

lalk/kuksa ds vuqiz;ksx 1.7 18

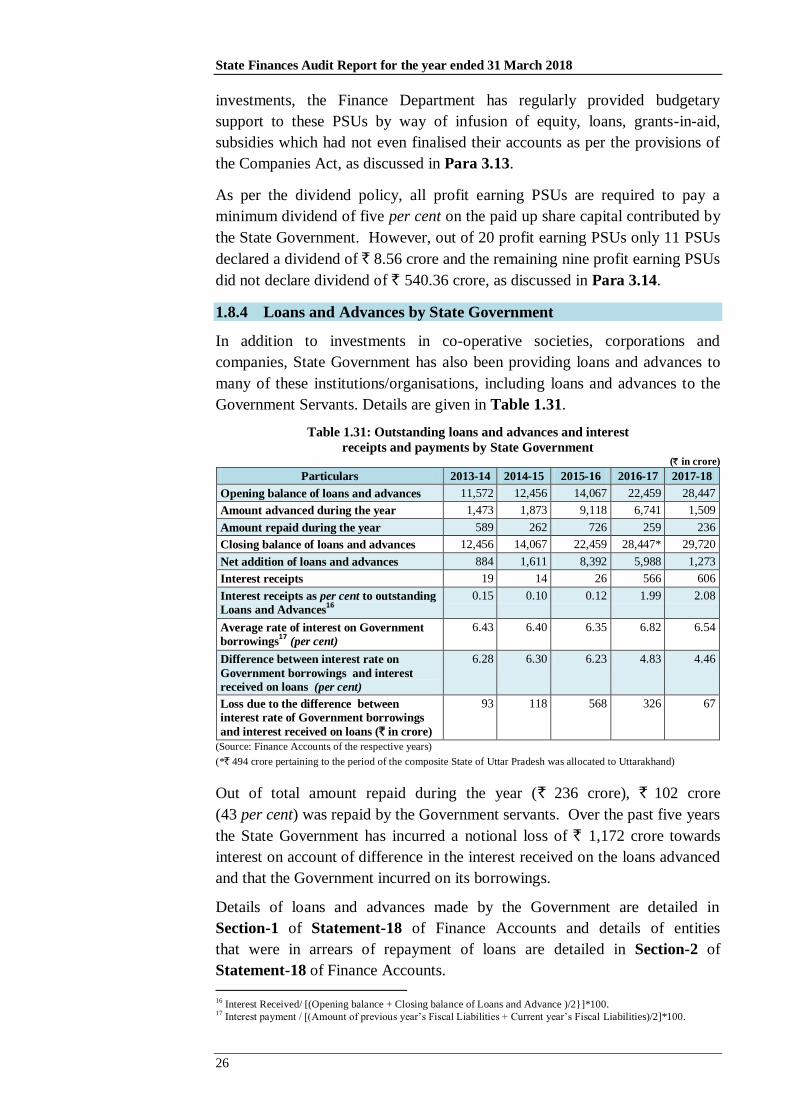

“kkldh; O;; ,oa fuos'k 1.8 25

ifjlEifRr;k¡ ,oa ns;rk;sa 1.9 29

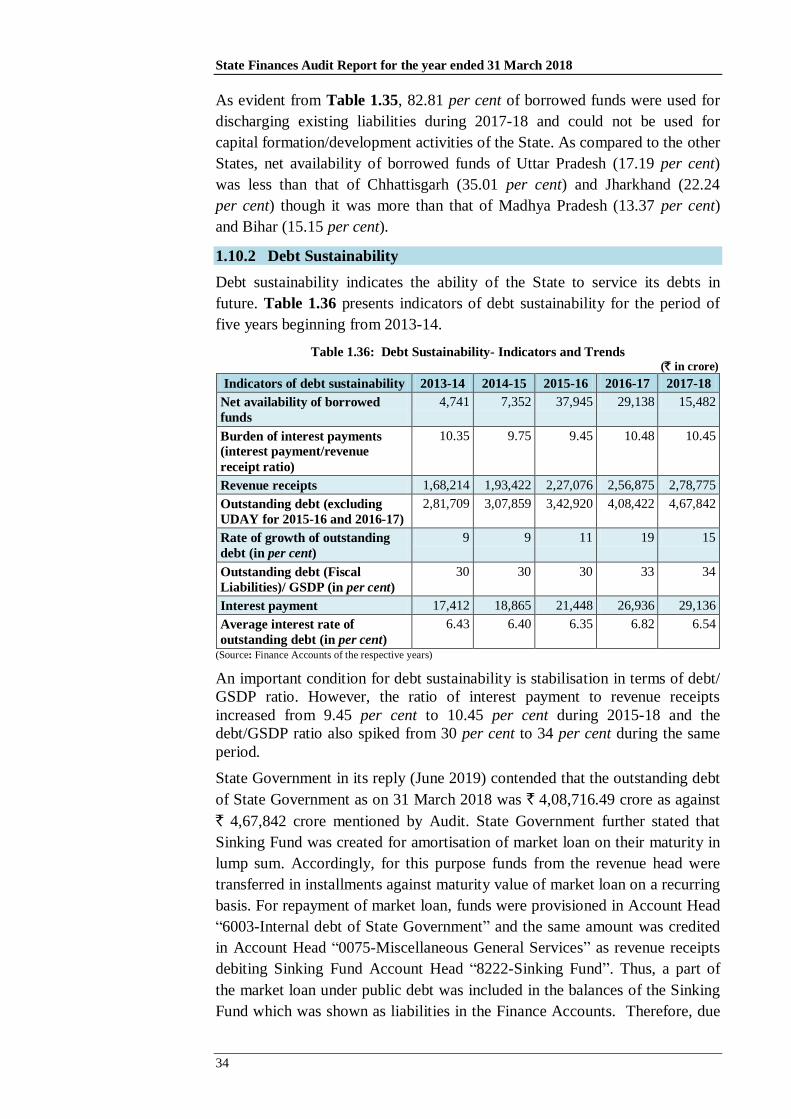

_.k izcU/ku 1.10 35

vuqorhZ dk;Zokgh 1.11 36

v/;k; 2

foRrh; çcU/ku ,oa ctVh; fu;U=.k

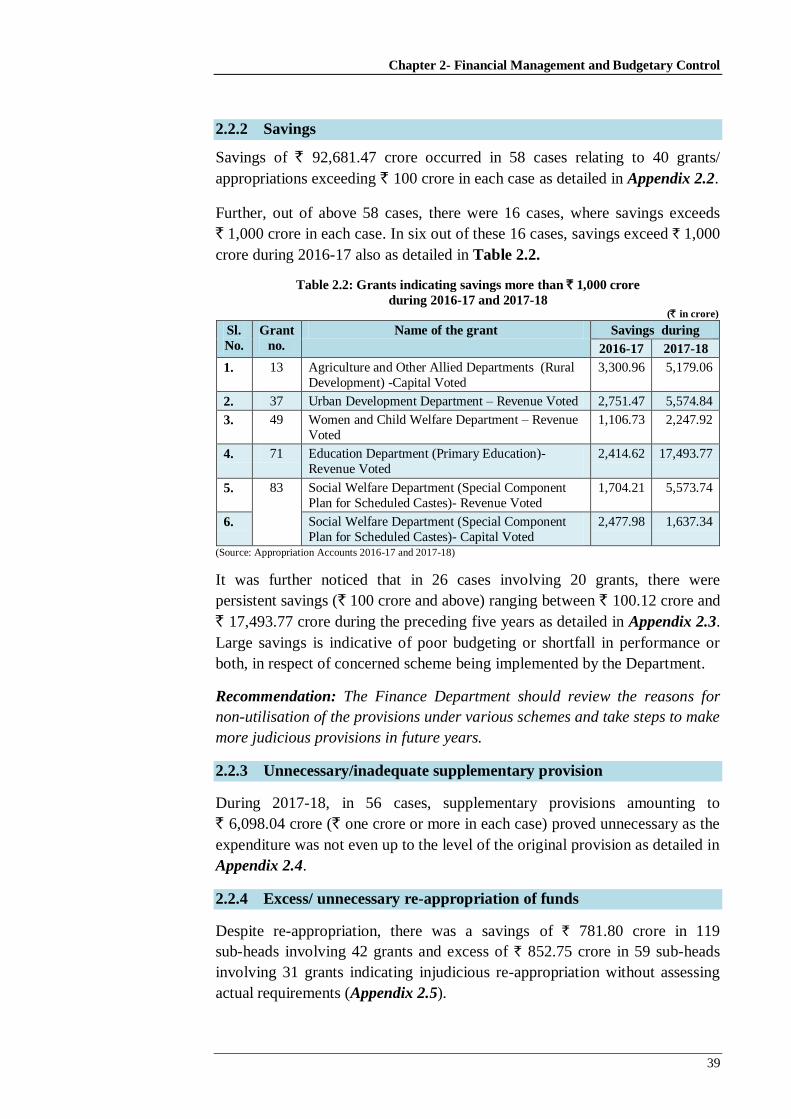

fofu;ksx ys[ks dk laf{kIr fooj.k 2.1 37

foRrh; mRrjnkf;Ro rFkk ctV çcU/ku 2.2 38

v/;k; 3

foRrh; fjiksfVZax ,oa ys[kkvksa ij fVIi.kh

oS;fDrd tek [kkrk 3.1 43

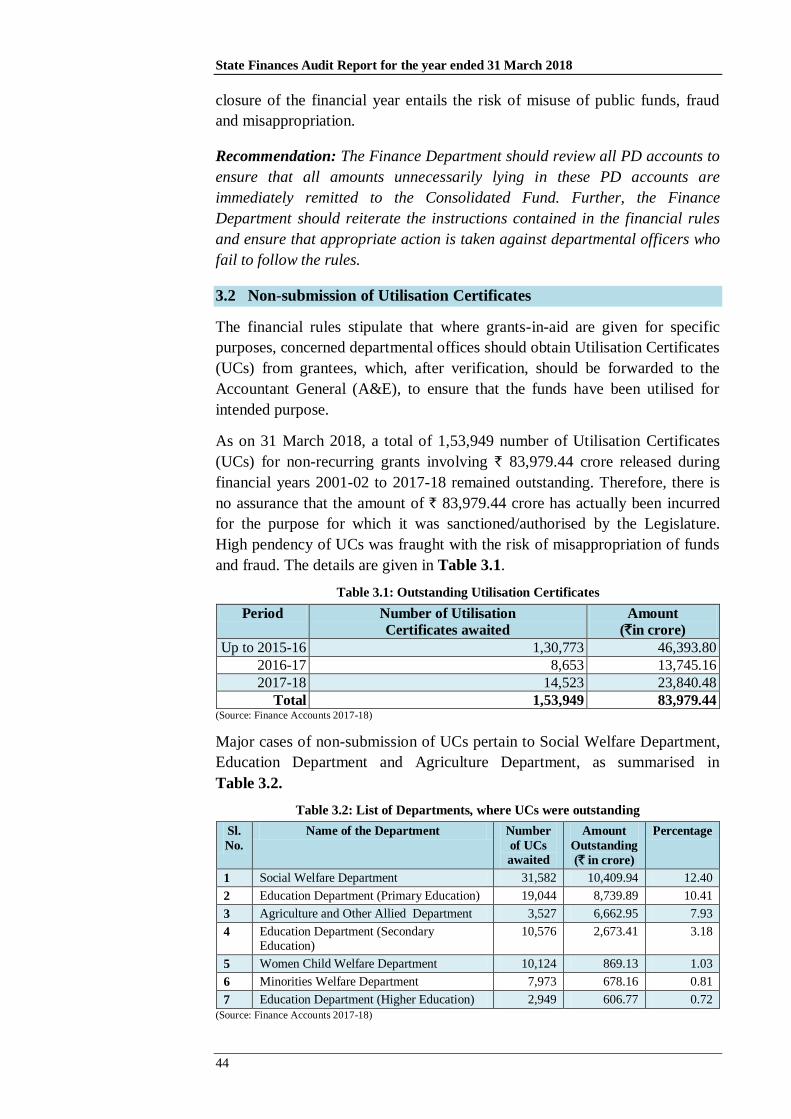

miHkksx izek.ki=ksa dks izsf’kr u fd;k tkuk 3.2 44

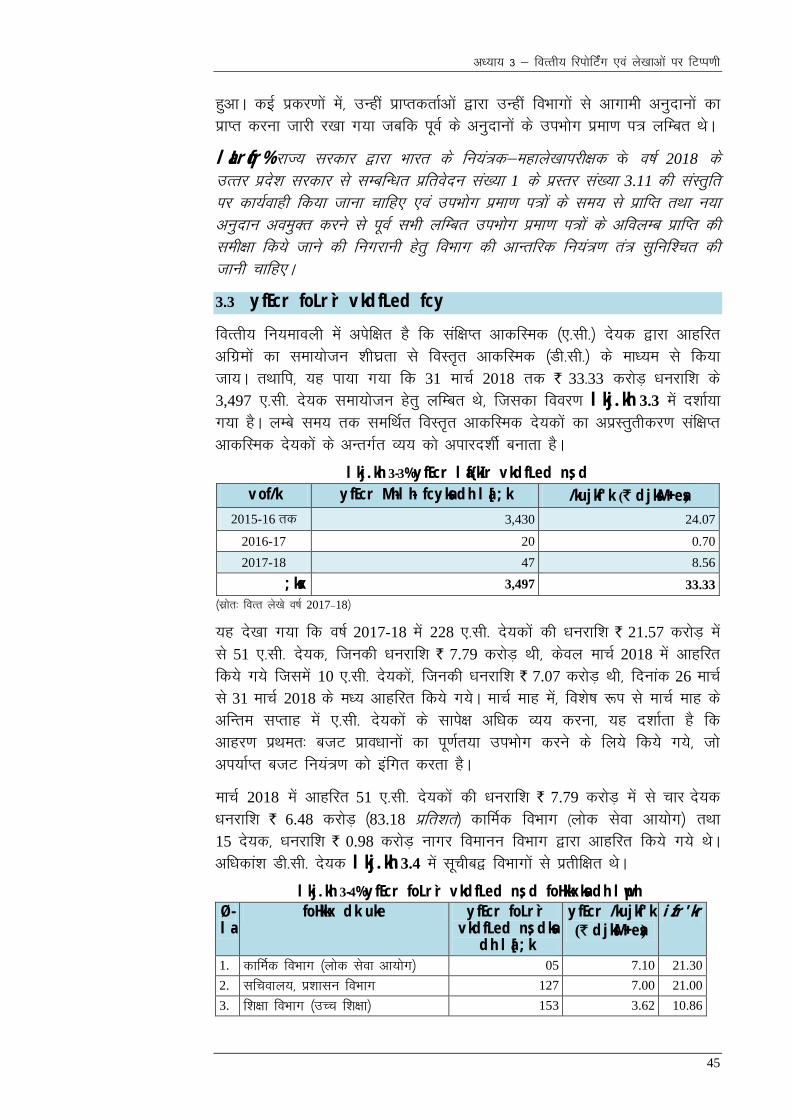

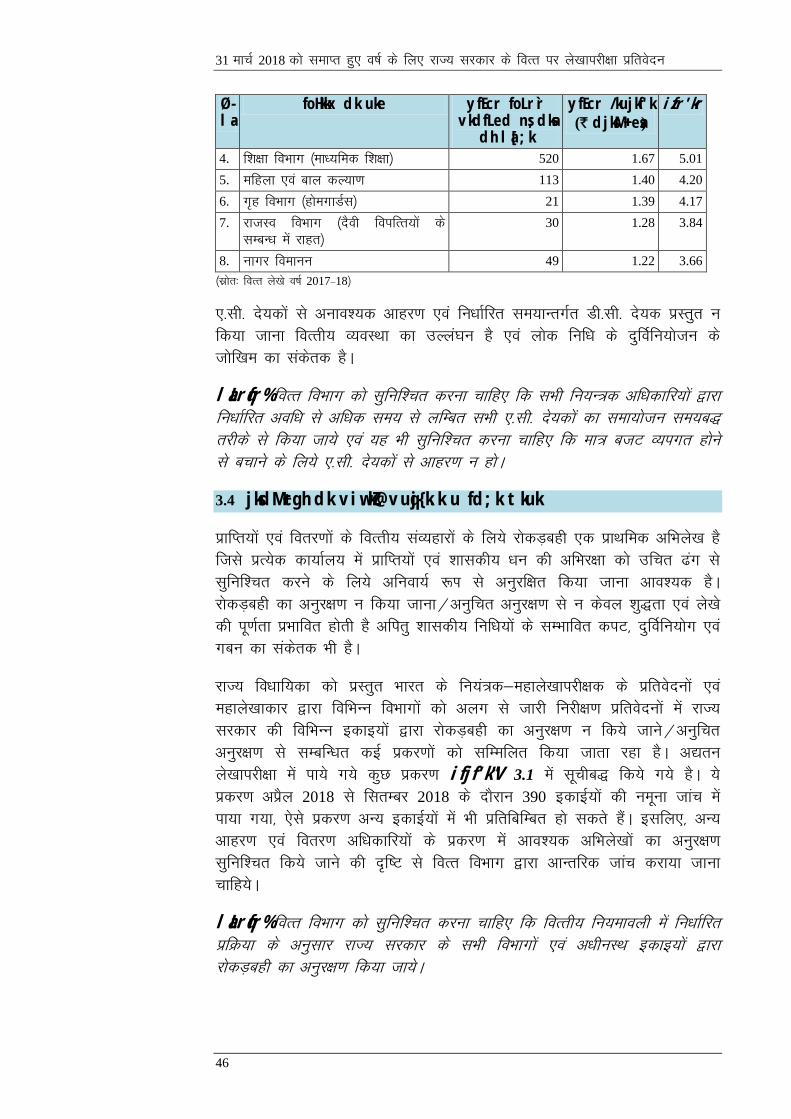

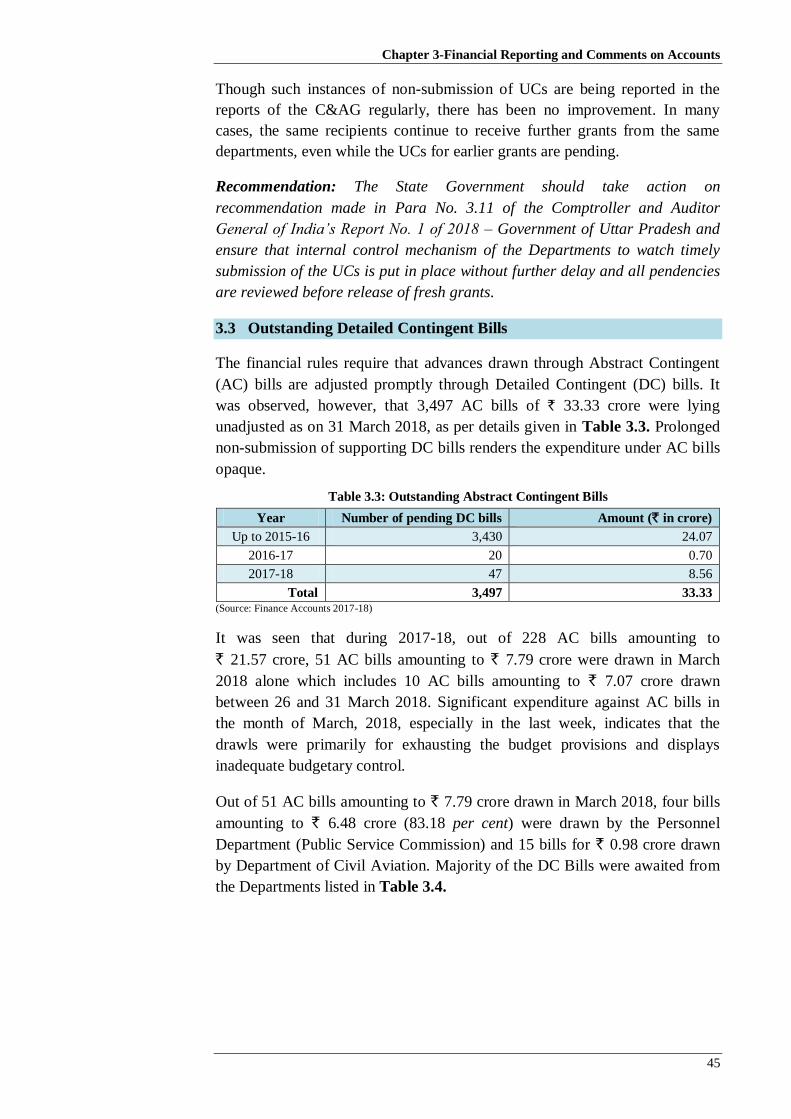

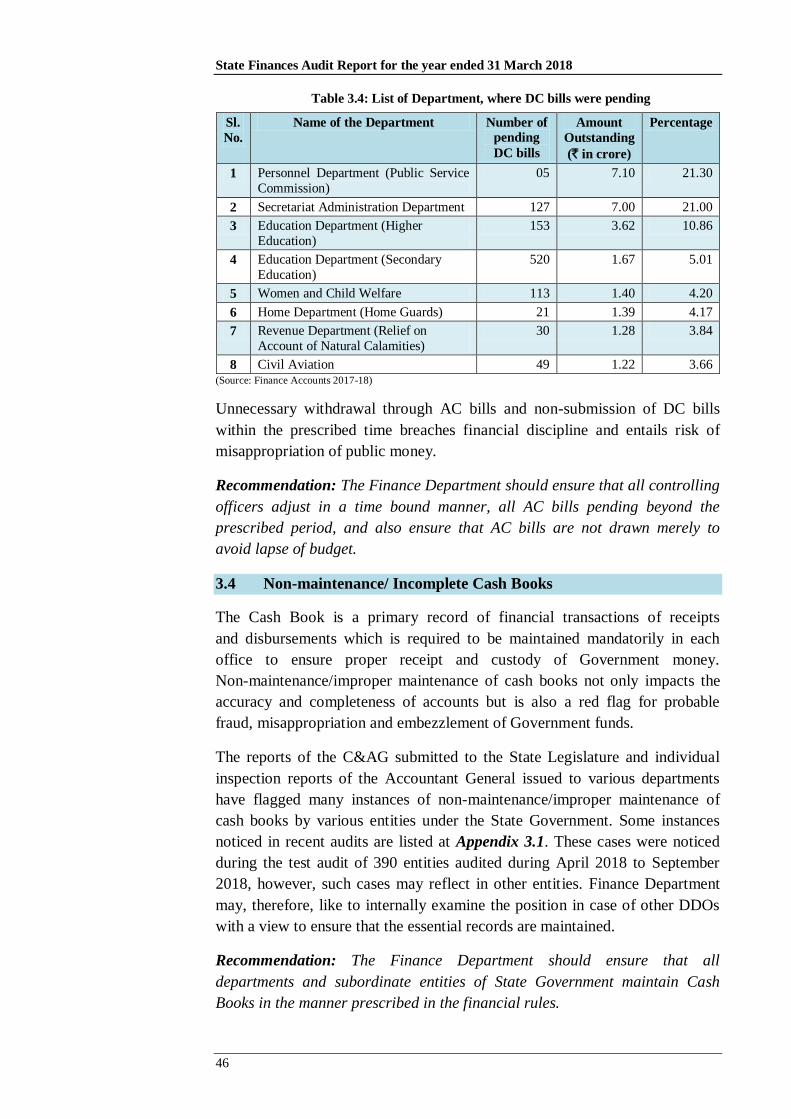

yfEcr foLr`r vkdfLed fcy 3.3 45

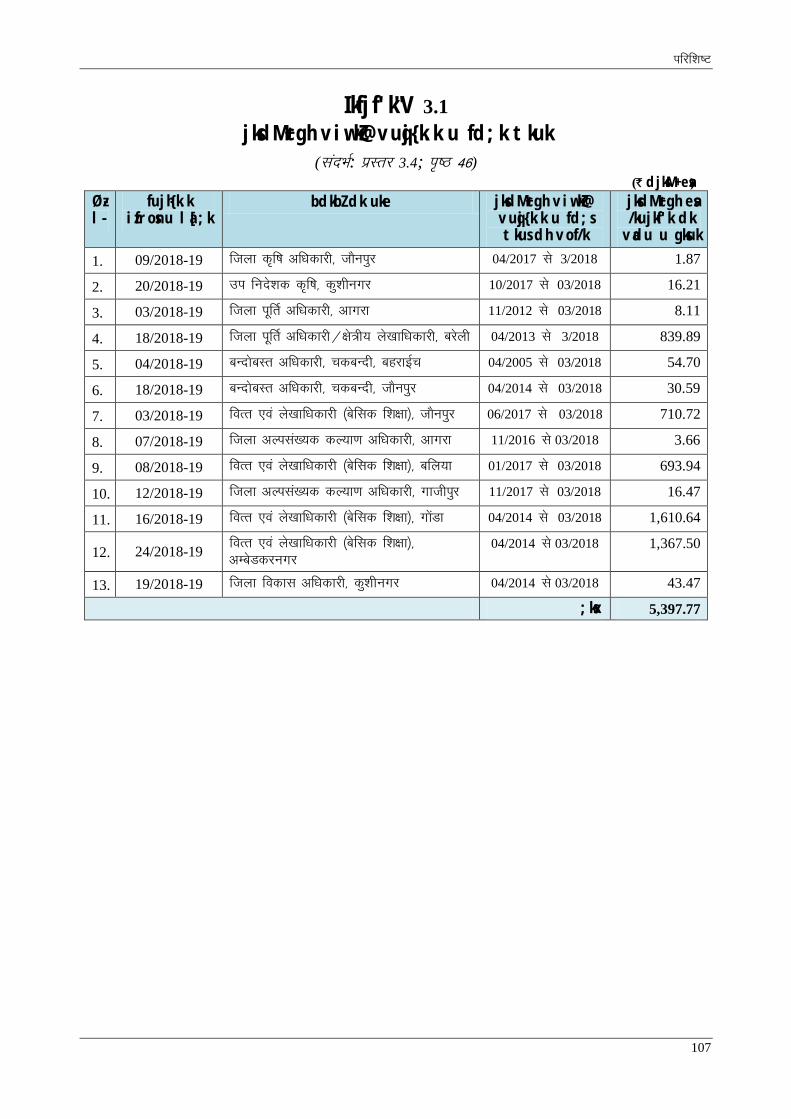

jksdM+ cgh dk viw.kZ@vuqj{k.k u fd;k tkuk 3.4 46

jksdM+ vo'ks’k esa fHkUurk 3.5 47

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

ii

/kujkf'k;ksa dk dsUnzh; lM+d fuf/k esa gLrkarj.k u fd;k tkuk 3.6 47

C;kt dk lek;kstu 3.7 47

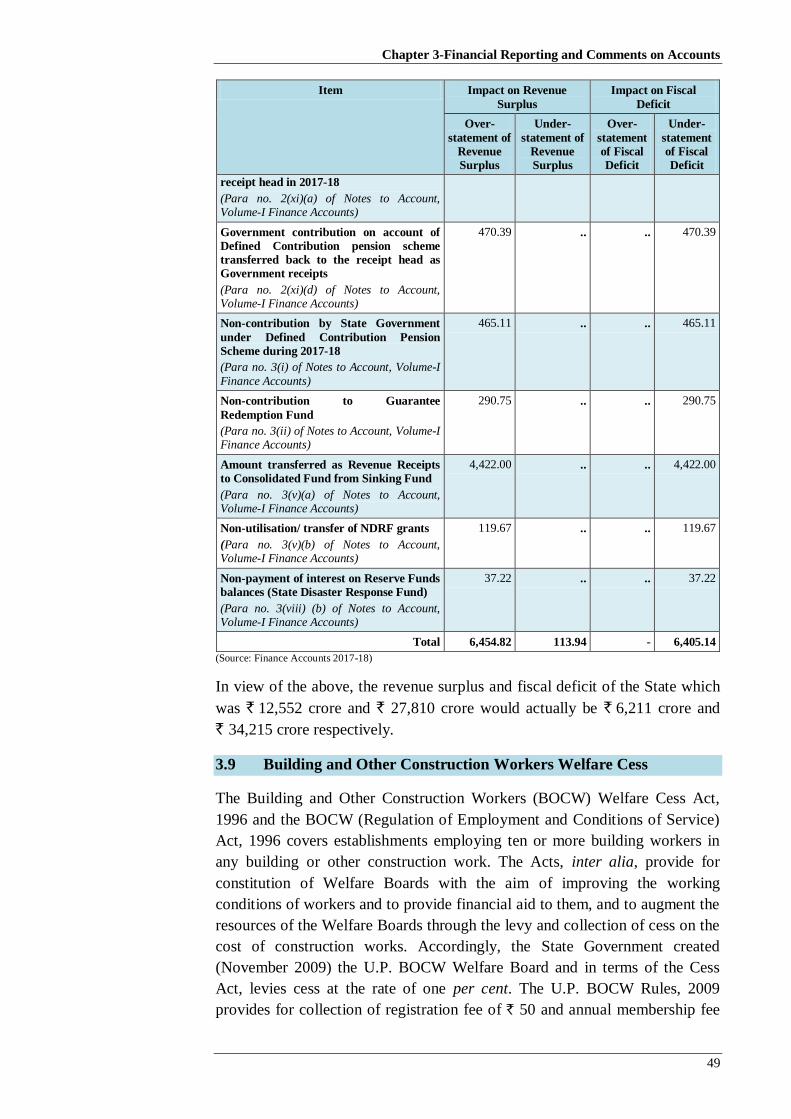

jktLo vkf/kD; ,oa jktdks’kh; ?kkVs ij izHkko 3.8 48

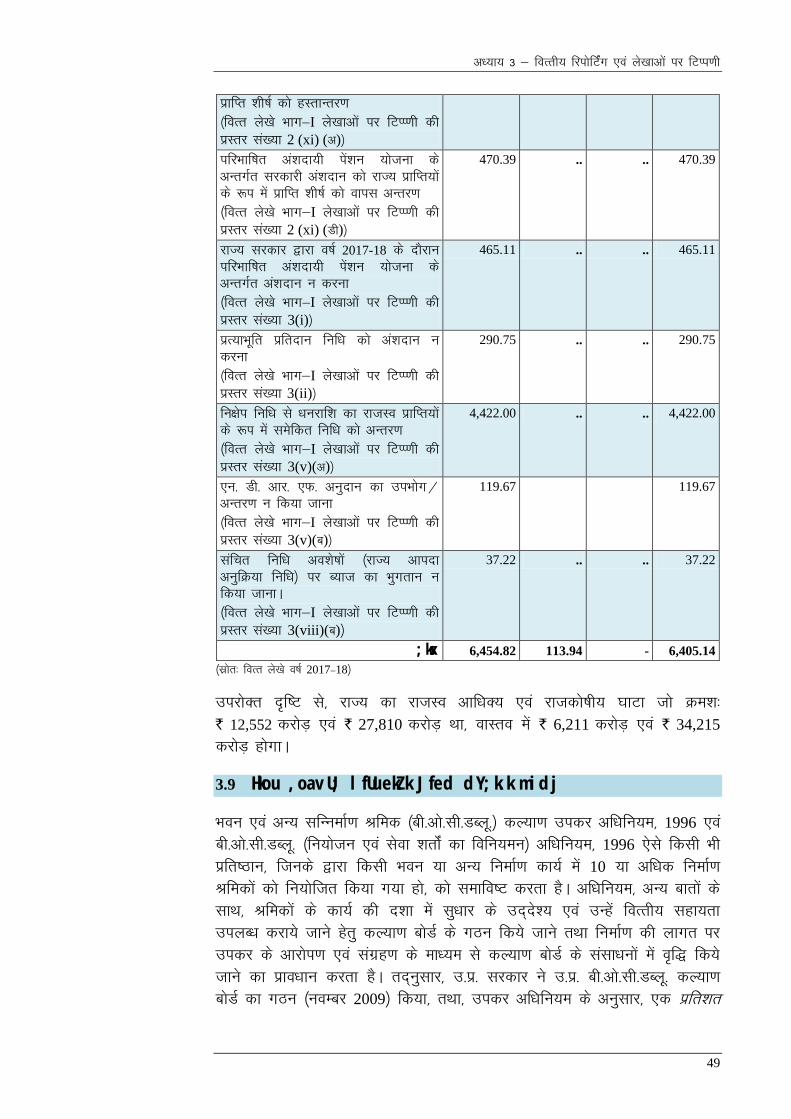

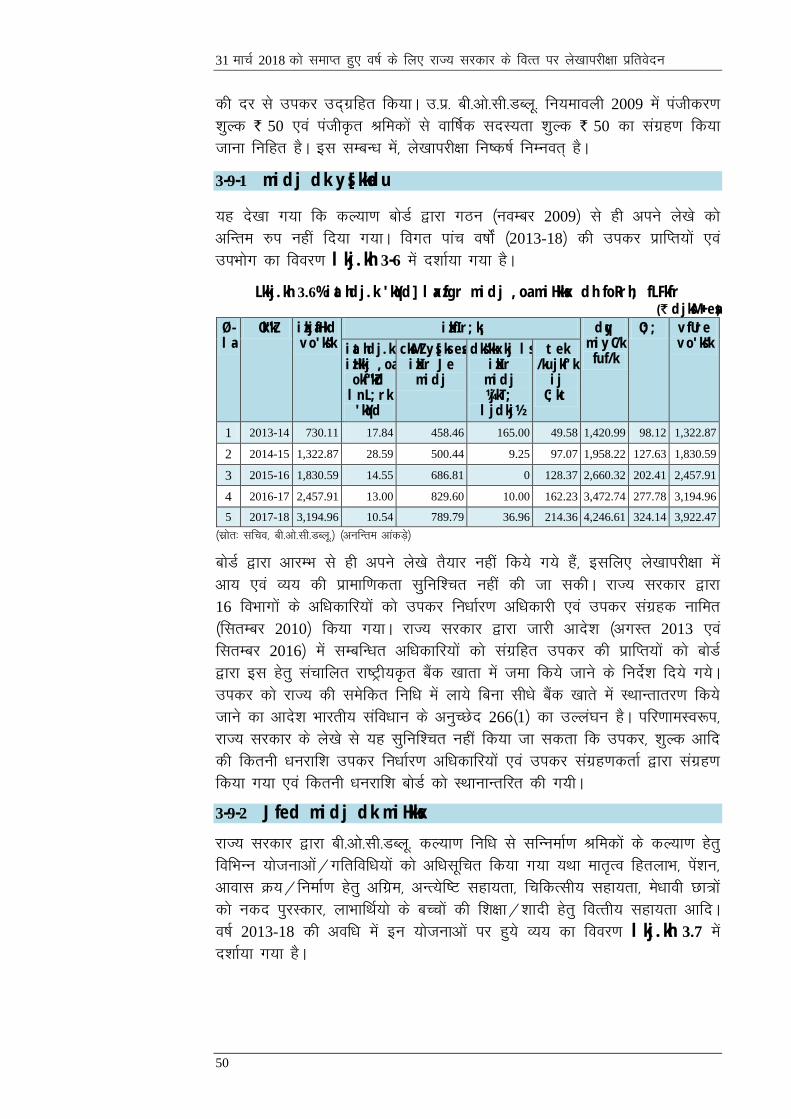

Hkou ,oa vU; lfUUkekZ.k Jfed dY;k.k midj 3.9 49

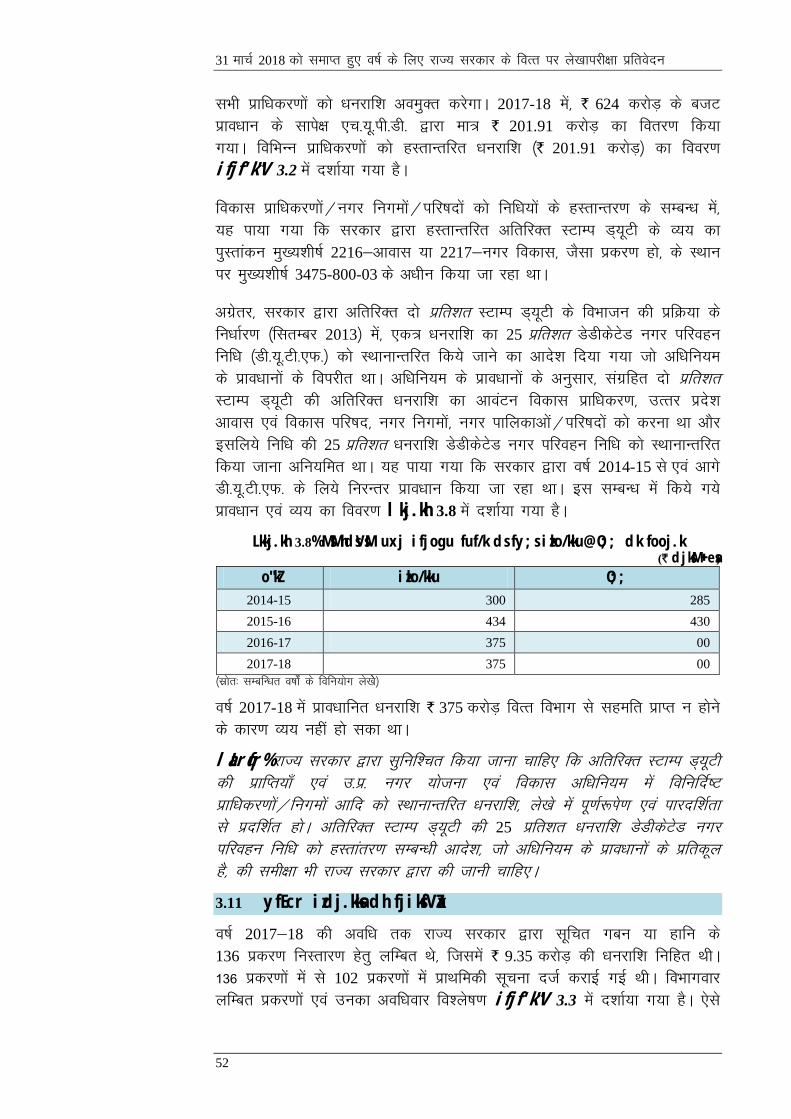

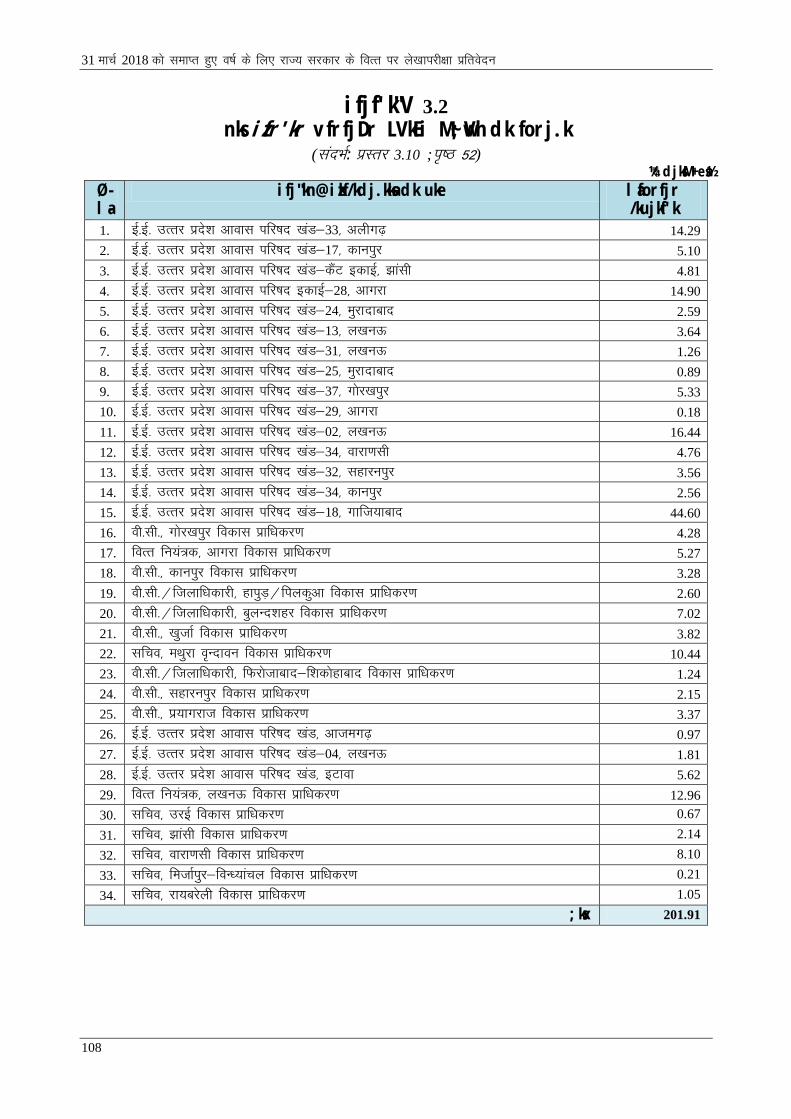

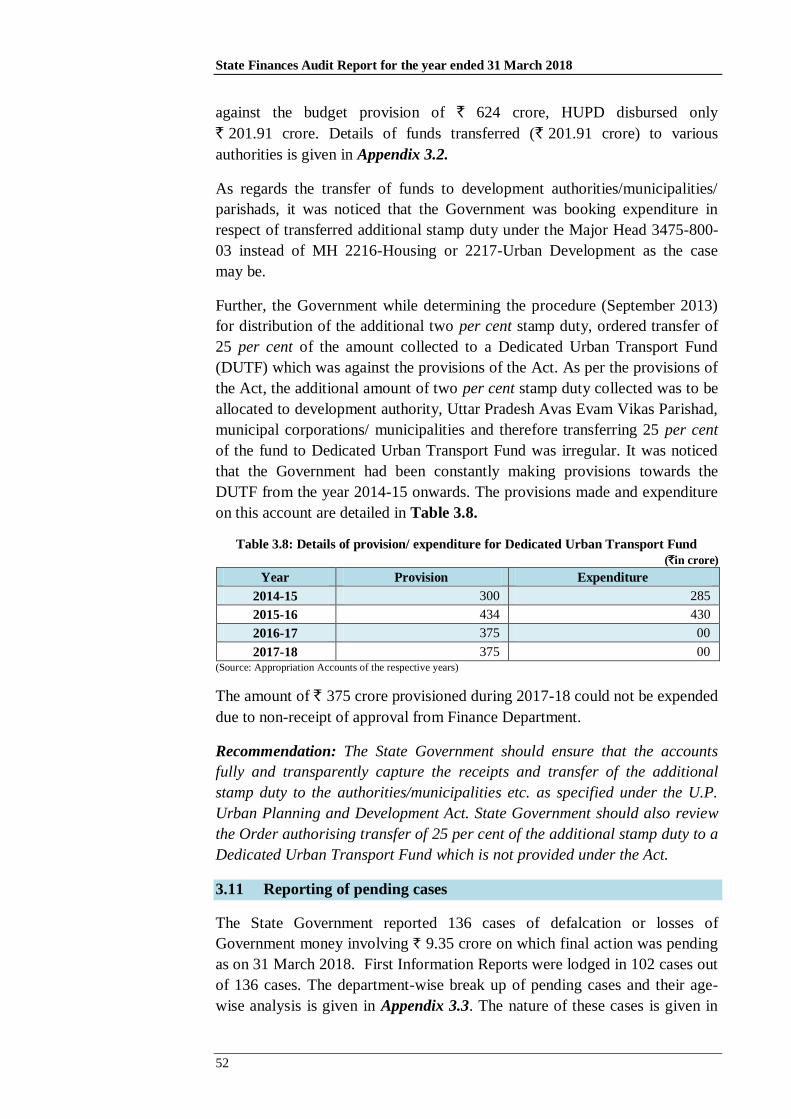

fodkl izkf/kdj.kksa dks vfrfjDr LVkEi M~;wVh dk vUrj.k 3.10 51

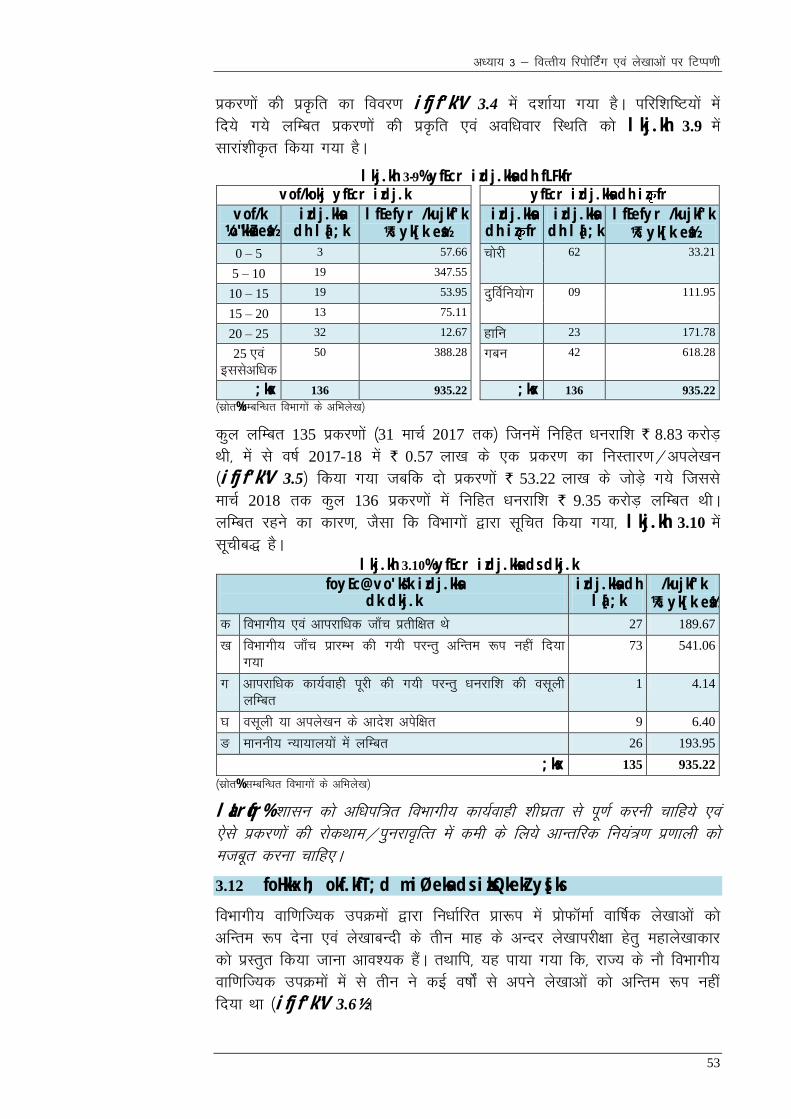

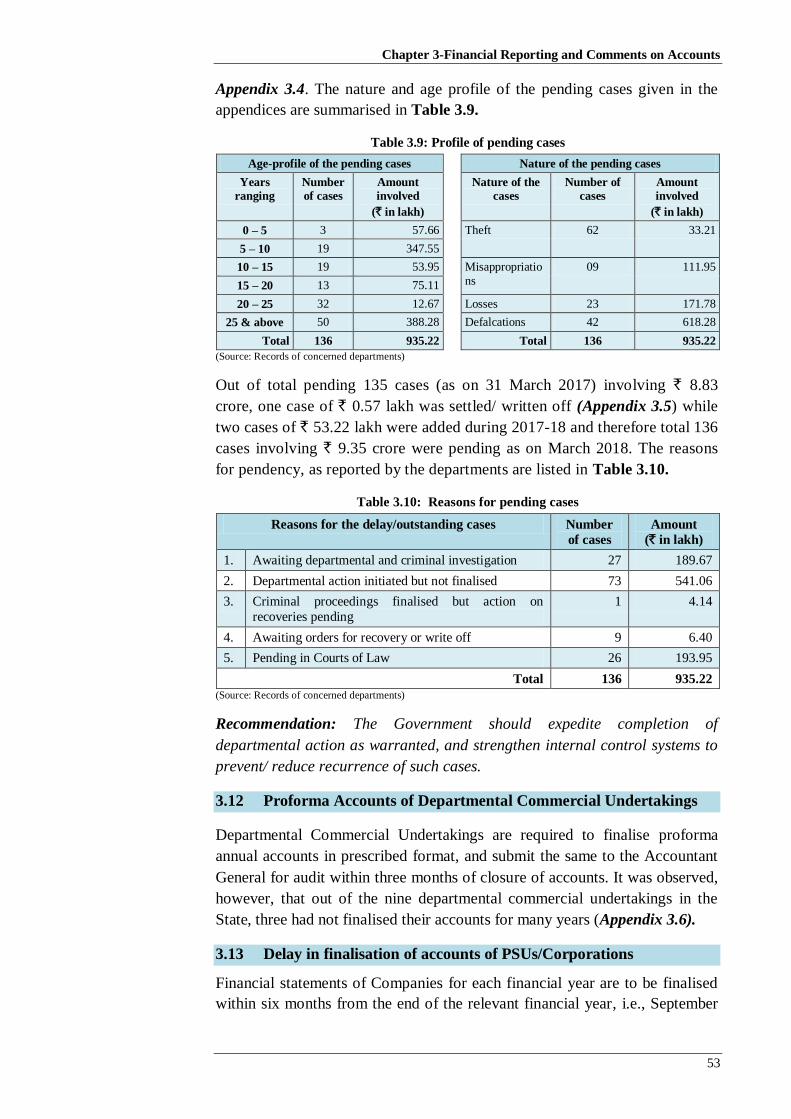

yfEcr izdj.kksa dh fjiksfVZax 3.11 52

foHkkxh; okf.kfT;d miØeksa ds izksQkekZ ys[ks 3.12 53

lkoZtfud {ks= ds miØeksa@fuxeksa ds ys[kkvksa ds vfUrehdj.k esa

foyEc

3.13 54

ykHkka'k ?kksf’kr u fd;k tkuk 3.14 55

bfDoVh@_.kksa dk feyku u fd;k tkuk 3.15 56

ys[kkvksa esa vikjnf'kZrk 3.16 56

jkT;ksa ds iquxZBu ij vo'ks’kksa dk foHkktu 3.17 57

ifjf'kf"V;k¡

ifjf'k"V 1.1 jkT; dk ifjn'; 59

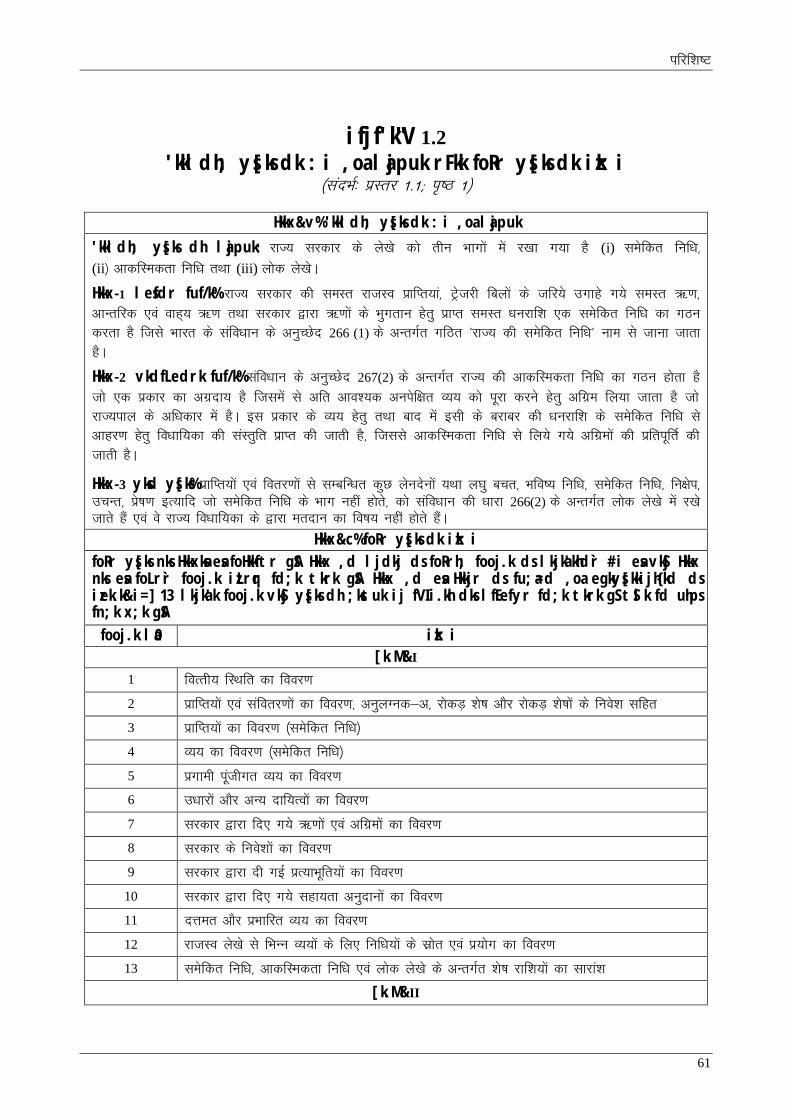

ifjf'k"V 1.2 'kkldh; ys[ks dk :i ,oa lajpuk rFkk foRr ys[ks dk izk:i 61

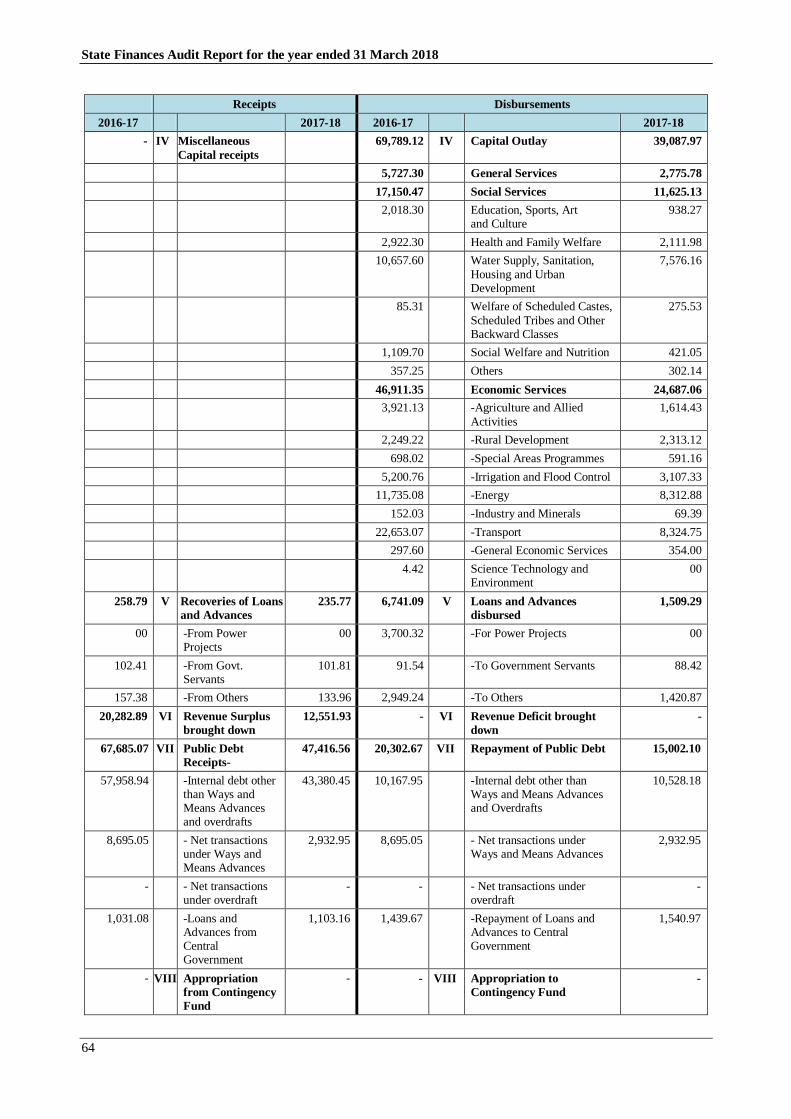

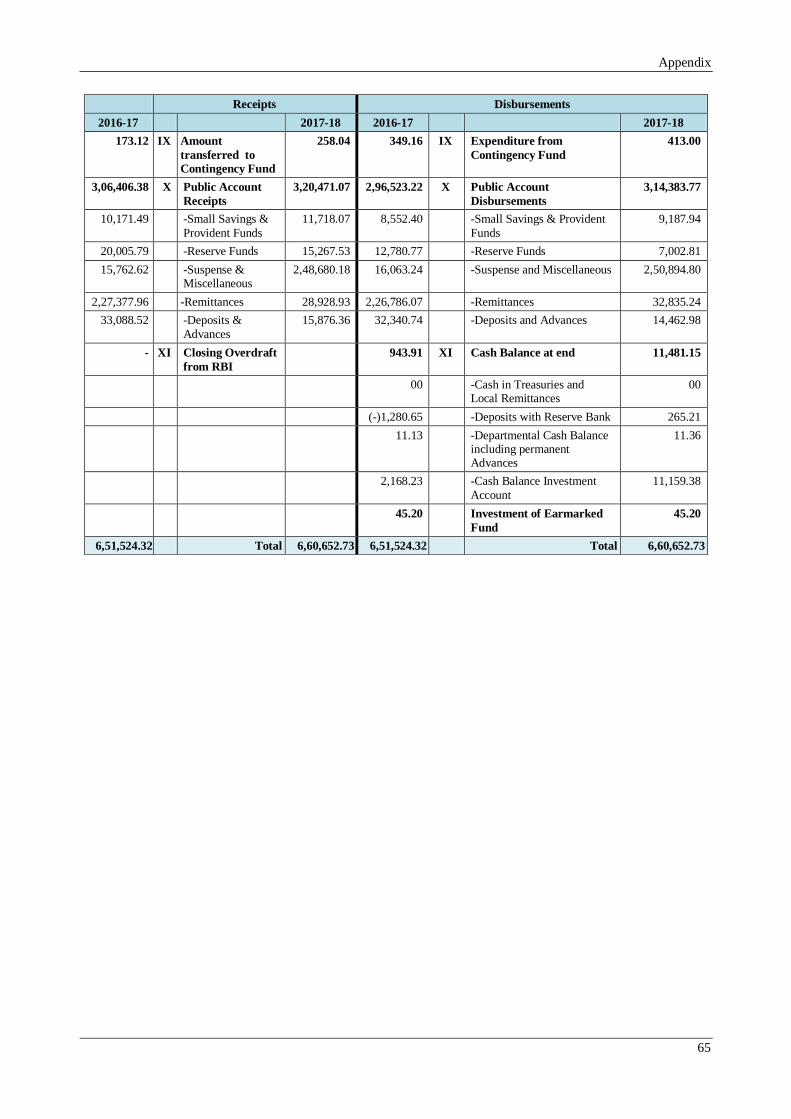

ifjf'k"V 1.3 o’kZ 2017-18 ds fy, izkfIr;kas ,oa laforj.kksa dk lkj 63

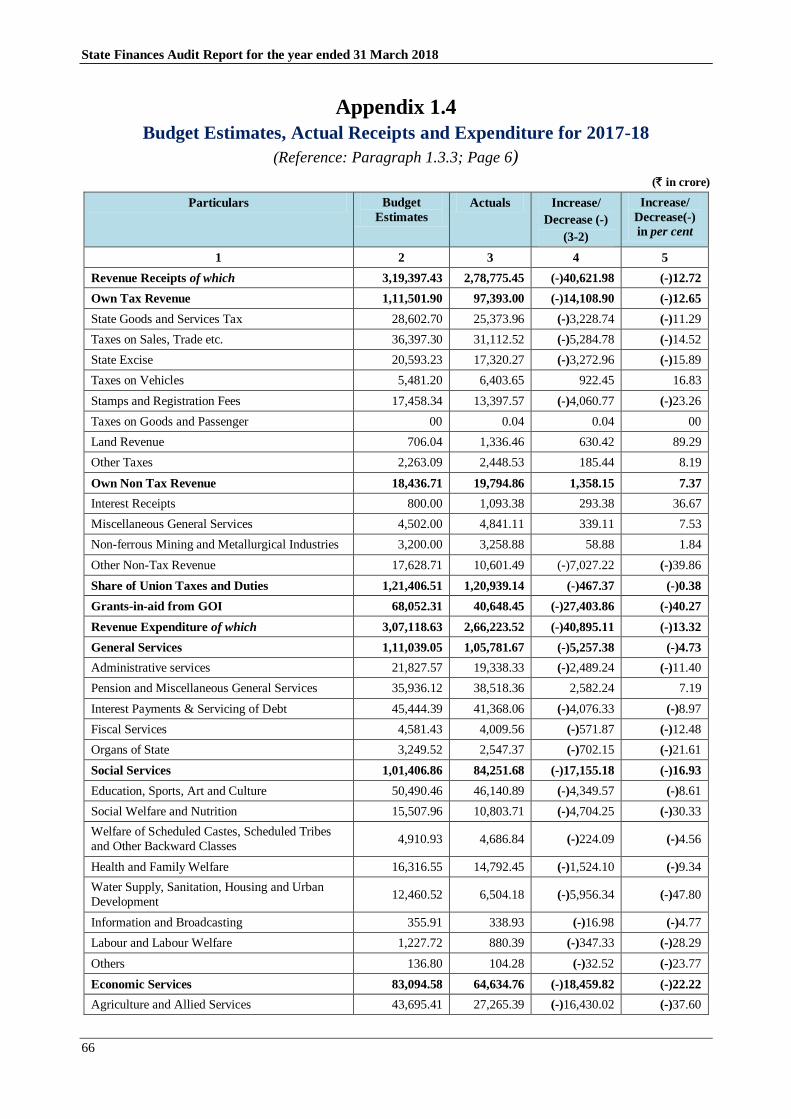

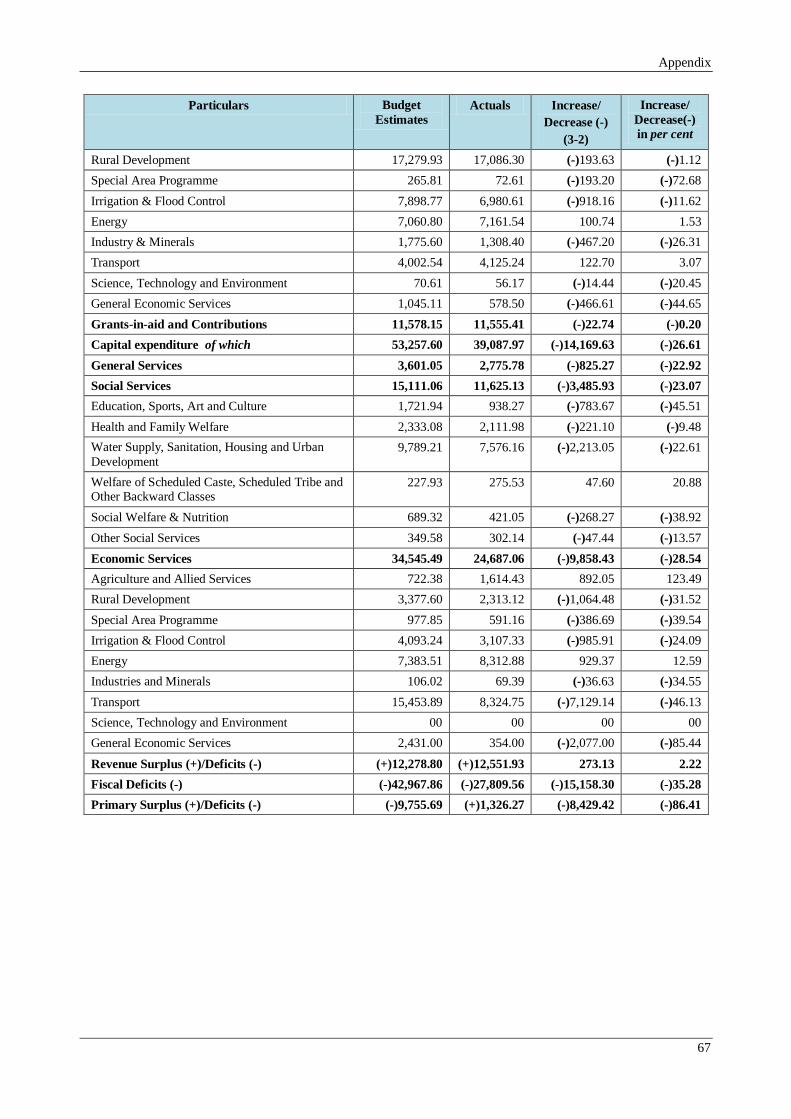

ifjf'k"V 1.4 o’kZ 2017-18 ds fy, ctV vuqeku] okLrfod izkfIr;ka ,oa O;; 66

ifjf'k"V 1.5 jkT; ljdkj ds foRr ds le;c) vk¡dM+s 68

ifjf'k"V 1.6 ¼v½ o’kZ 2013-18 dh vof/k esa Lo;a dk dj jktLo

¼c½ o’kZ 2013-18 dh vof/k esa Lo;a dk djsrj jktLo

71

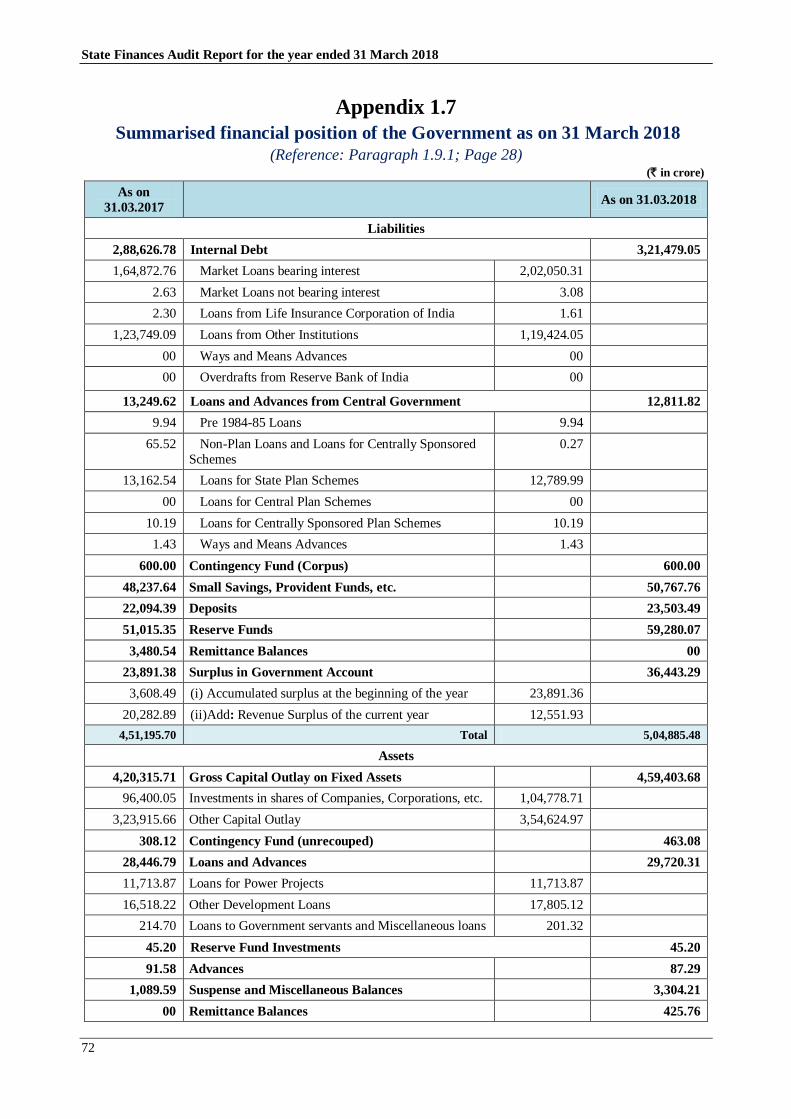

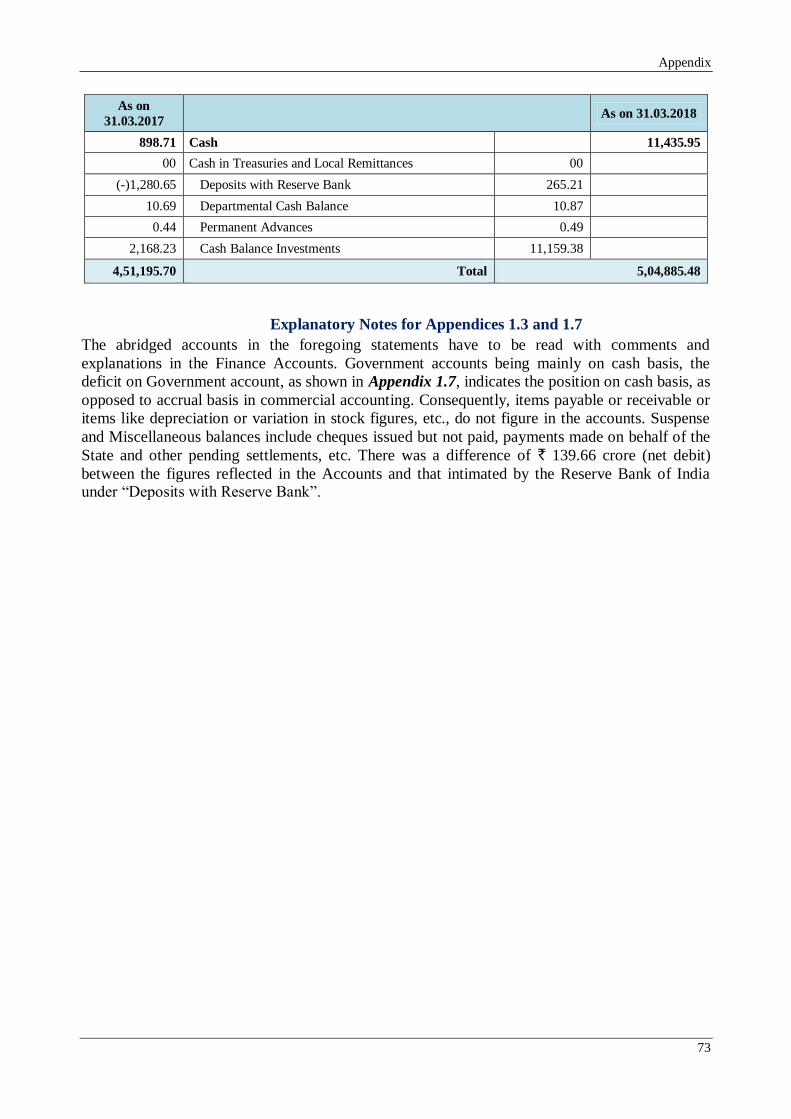

ifjf'k"V 1.7 31 ekpZ 2018 dks ljdkj dh foRrh; fLFkfr dk laf{kIr lkj 72

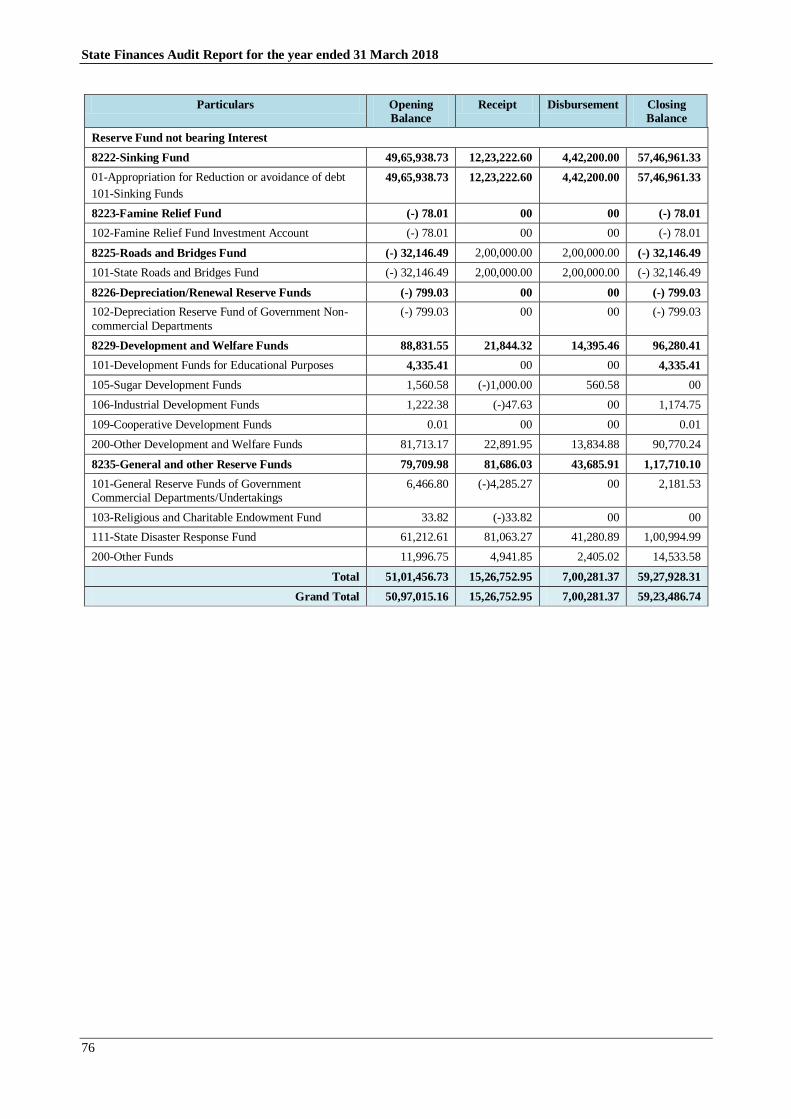

ifjf'k"V 1.8 vkjf{kr fuf/k;ksa dk fooj.k 74

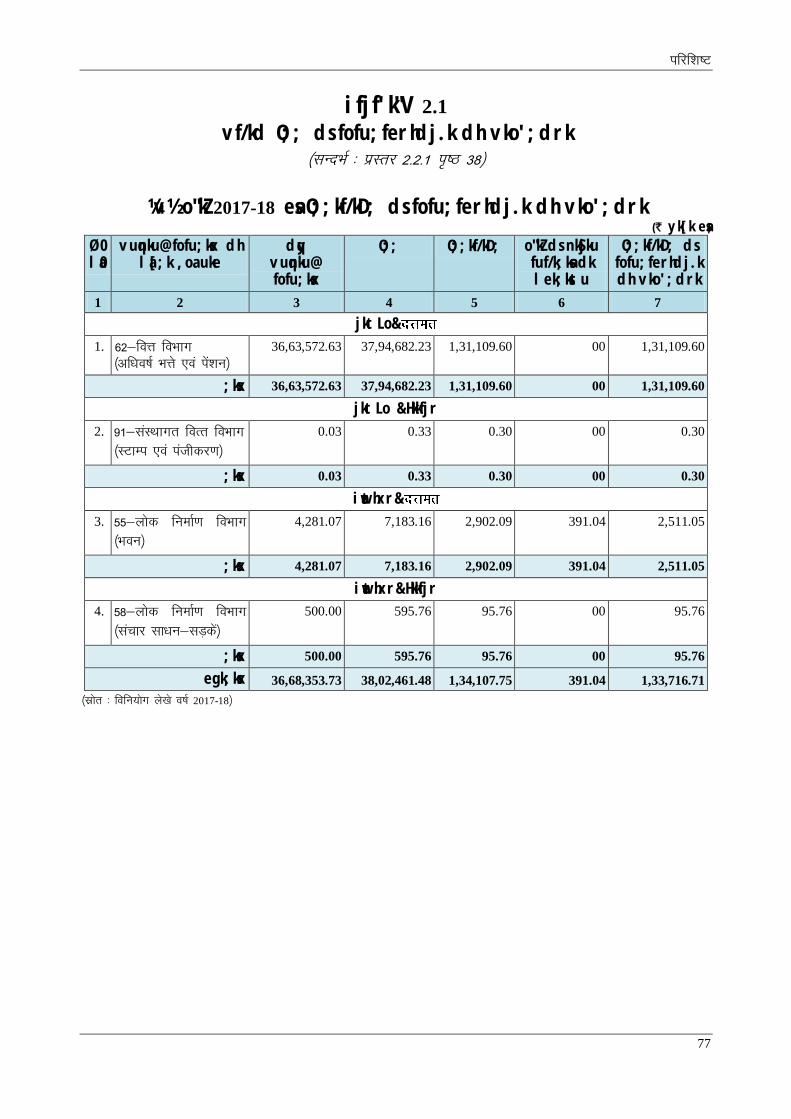

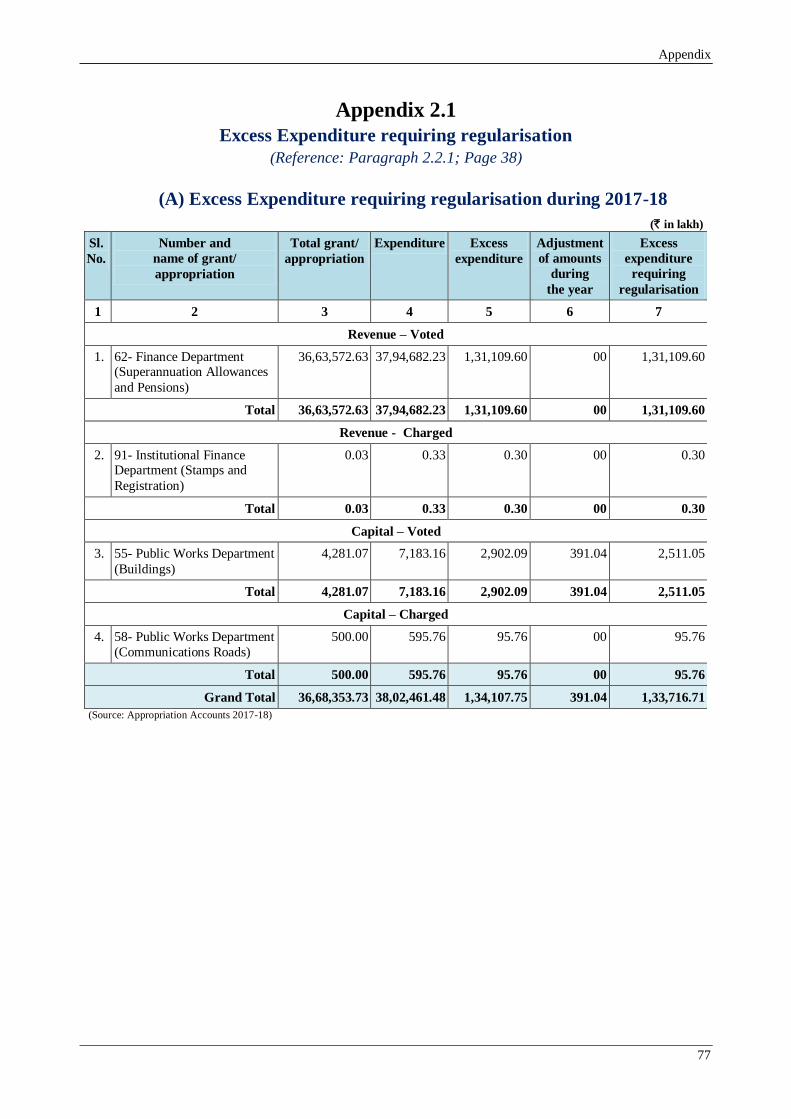

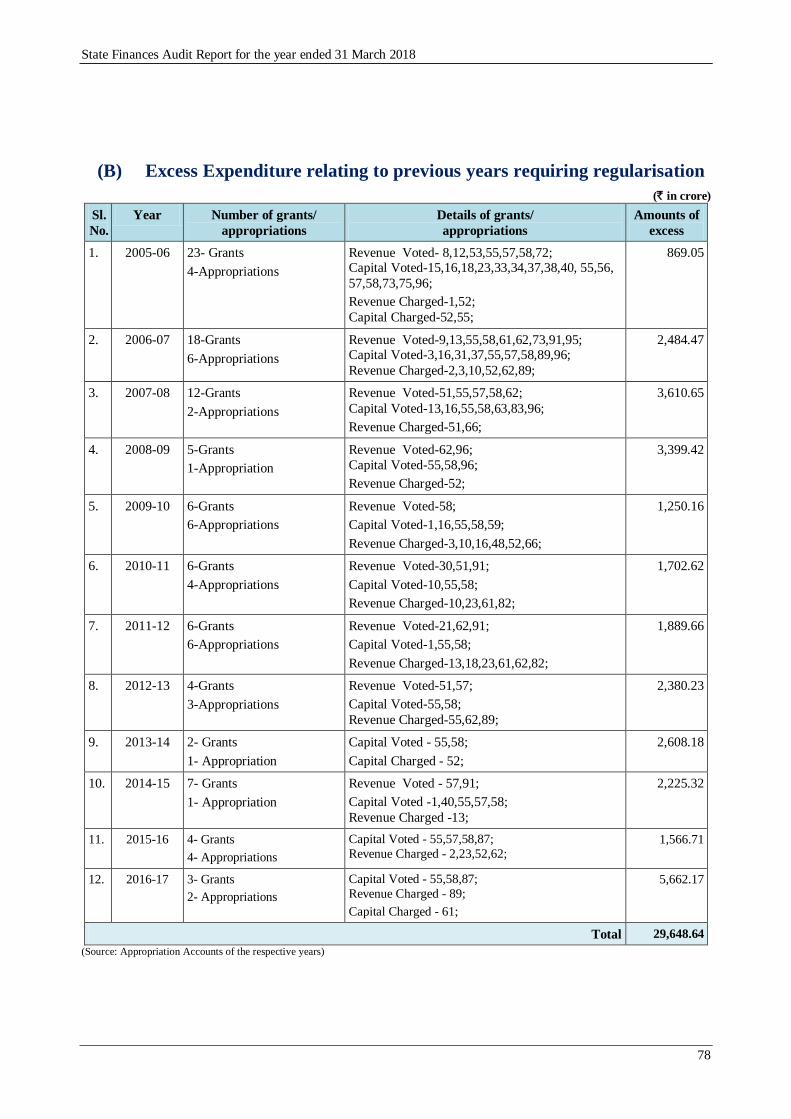

ifjf'k"V 2.1 ¼v½ o’kZ 2017-18 ds O;;kf/kD; ds fofu;ferhdj.k dh vko';drk

¼c½ foxr o’kksZa ds O;;kf/kD; ds fofu;ferhdj.k dh vko';drk

77

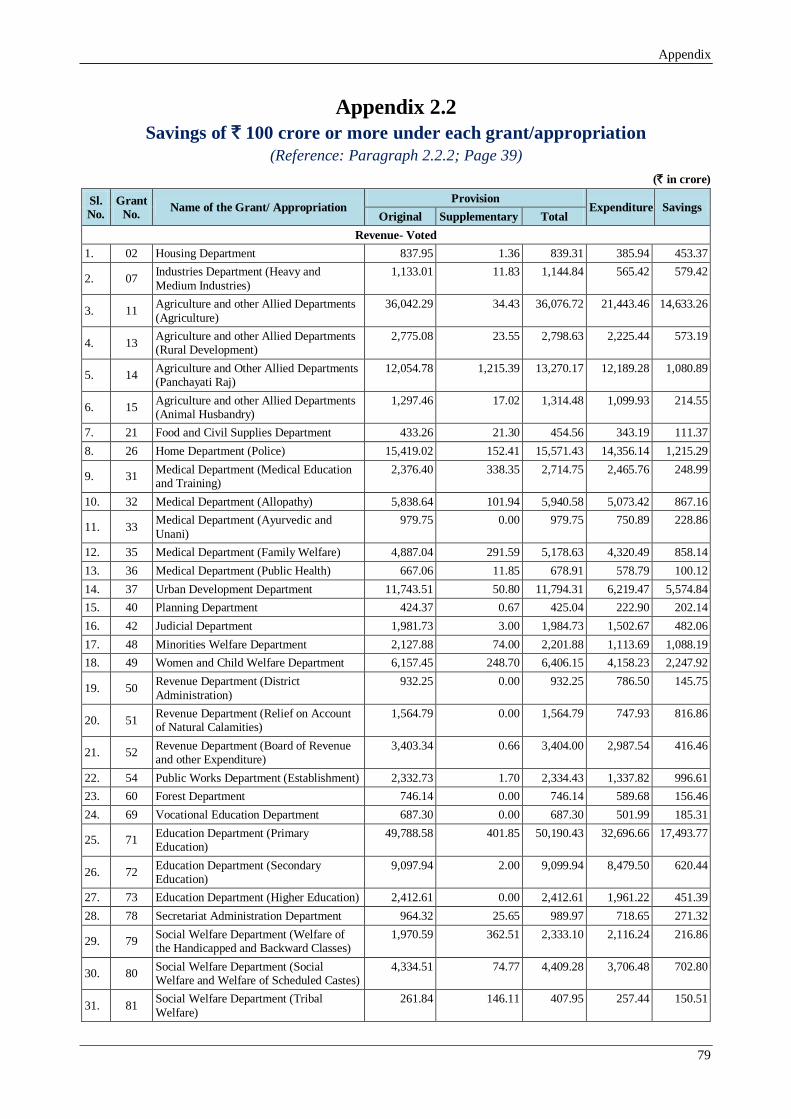

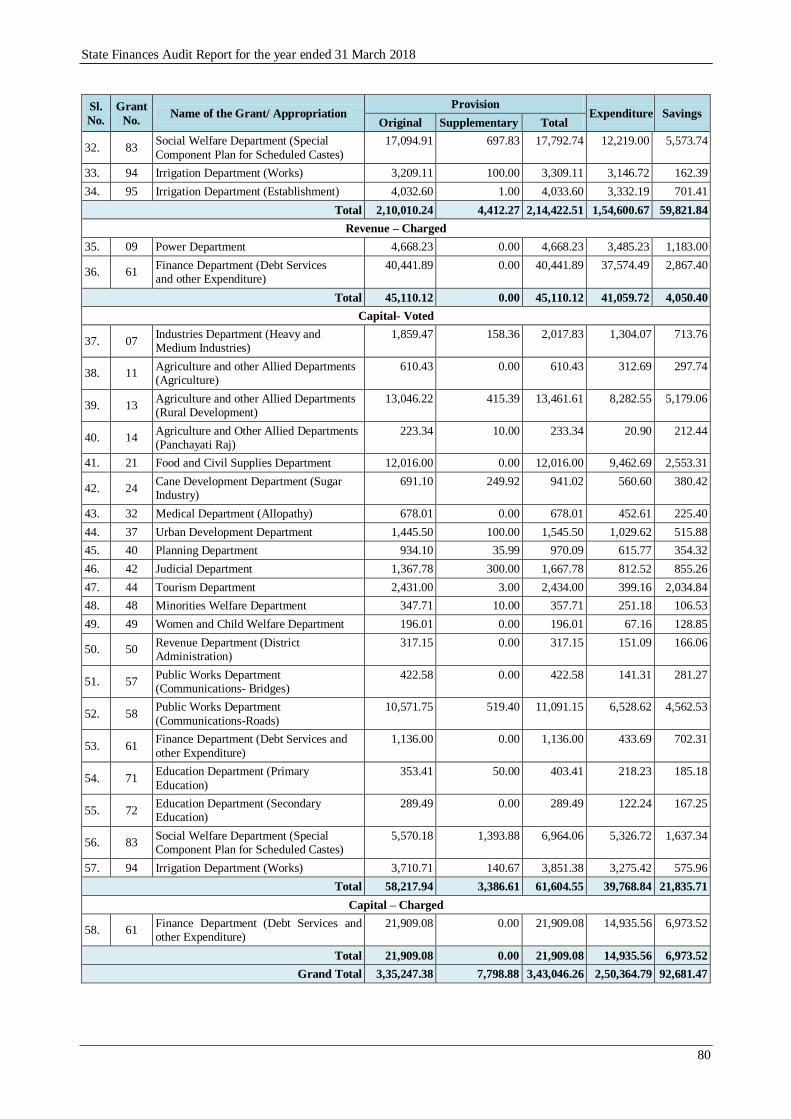

ifjf'k"V 2.2 ` 100 djksM++ ;k mlls vf/kd dh cpr okys vuqnku@fofu;ksx 79

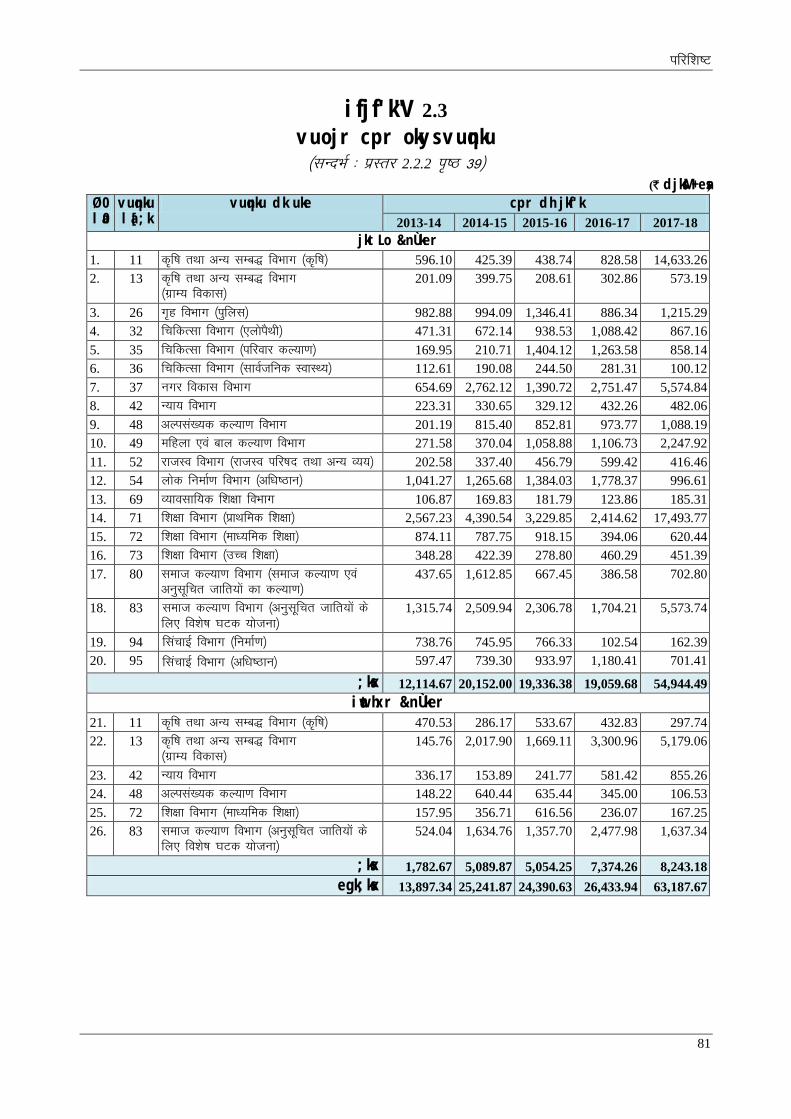

ifjf'k"V 2.3 vuojr cpr okys vuqnku 81

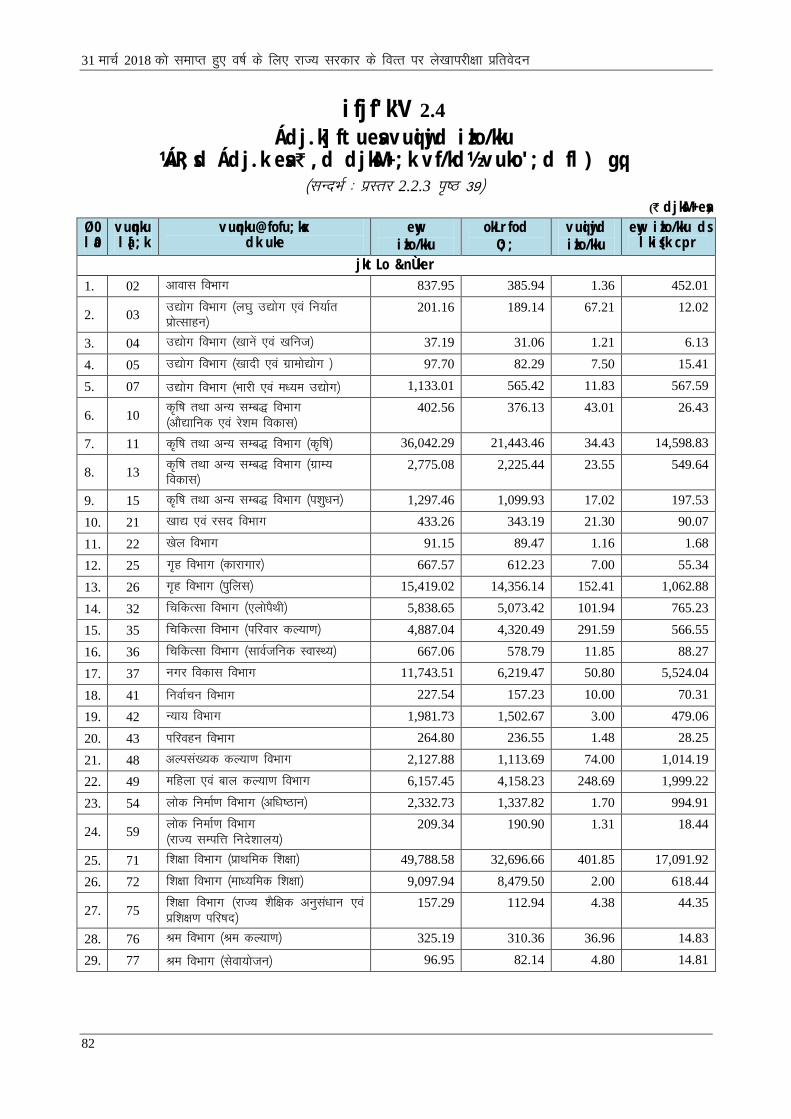

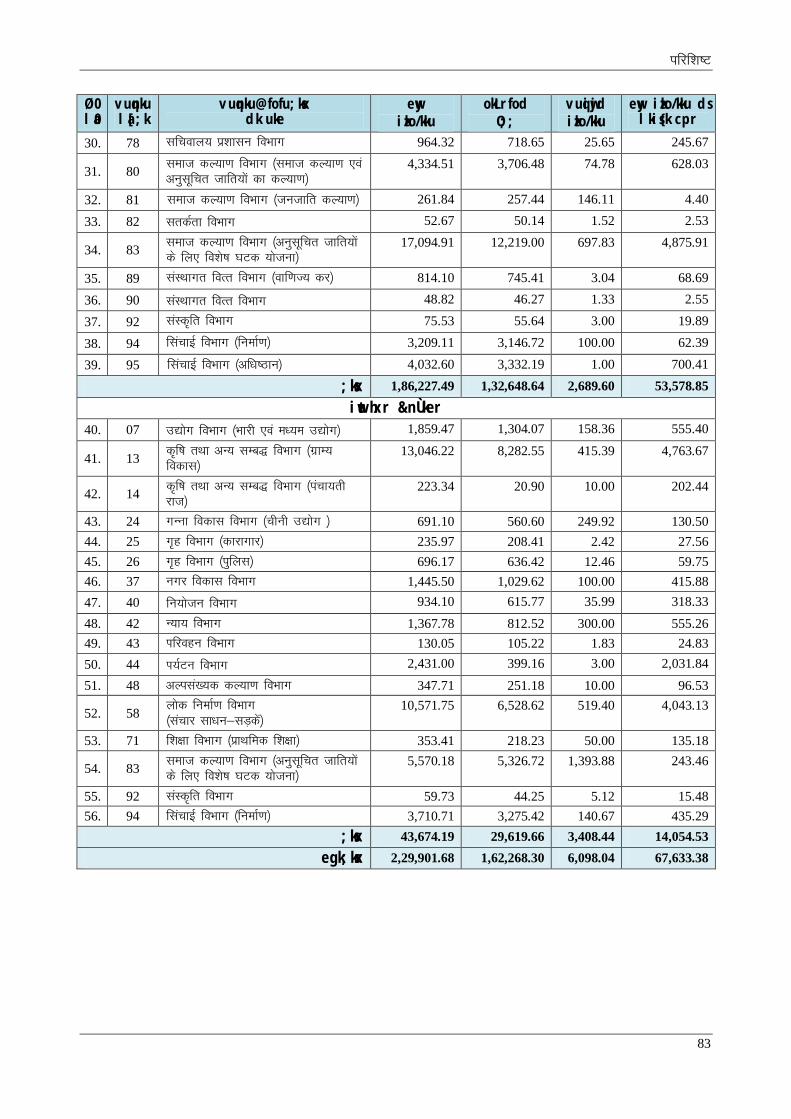

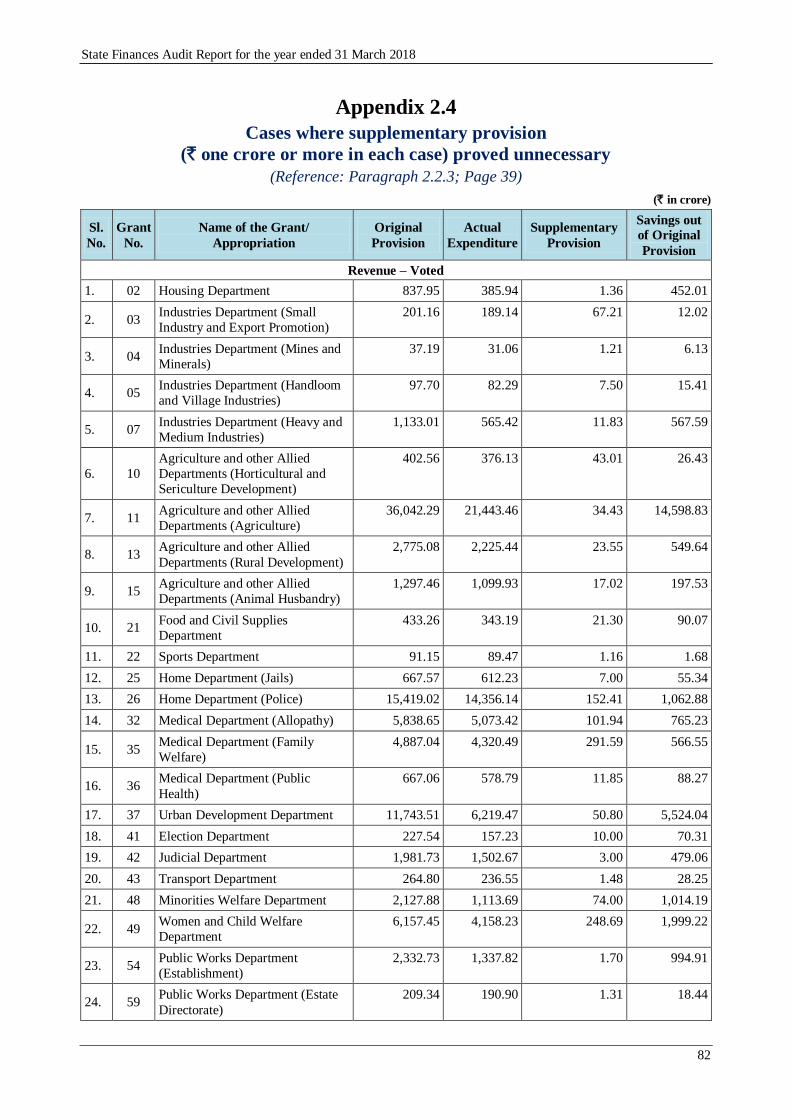

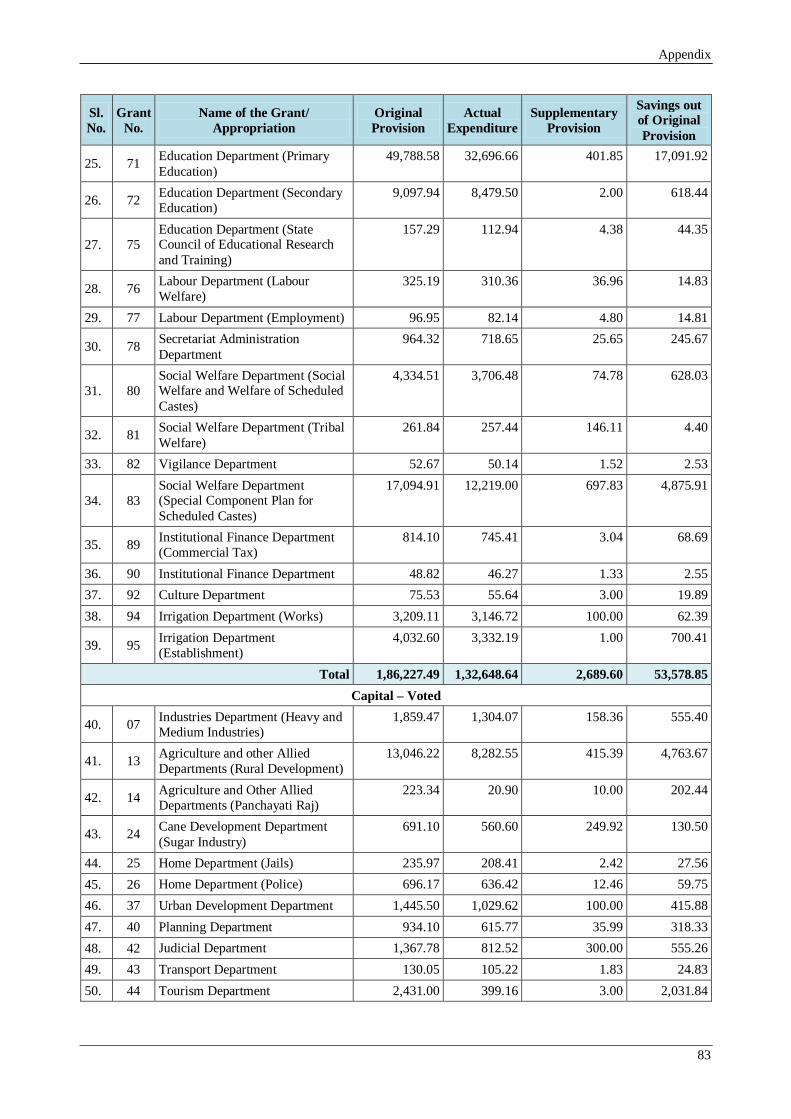

ifjf'k"V 2.4 izdj.k] ftuesa vuqiwjd izko/kku ¼izR;sd izdj.k esa ` ,d djksM+ ;k

vf/kd½ vuko';d fl) gq,

82

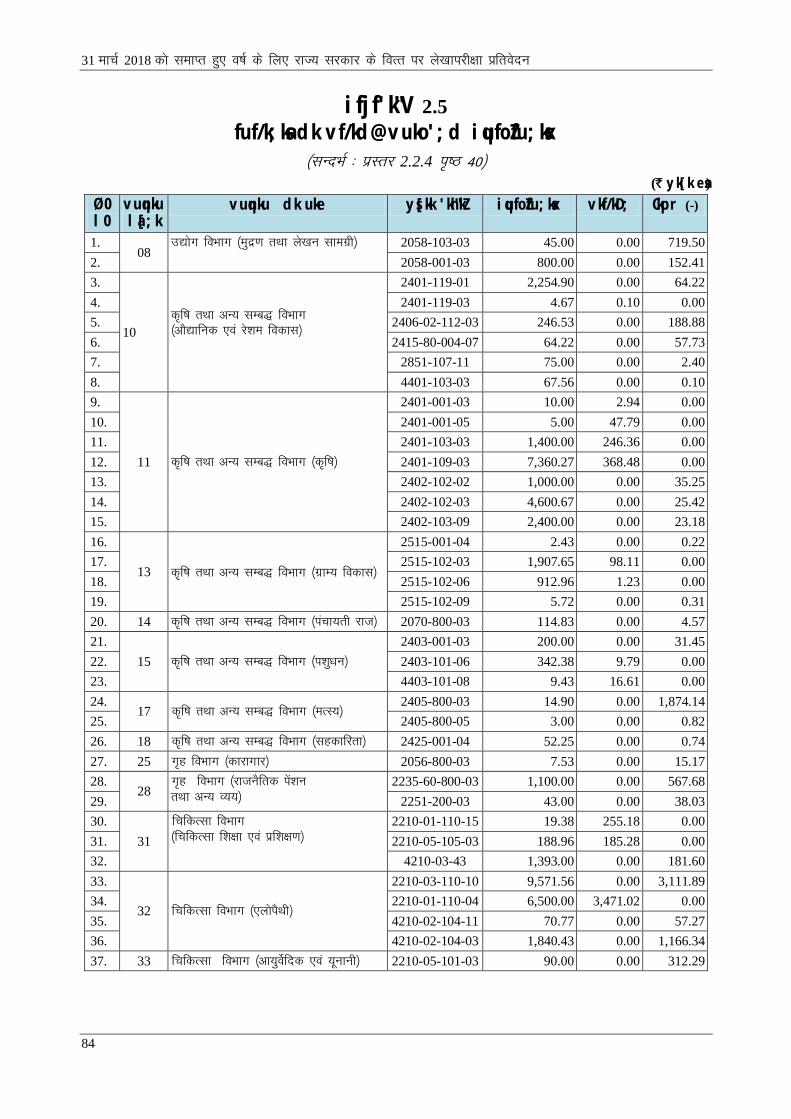

ifjf'k"V 2.5 fuf/k;ksa dk vf/kd@vuko';d iqufoZfu;ksx 84

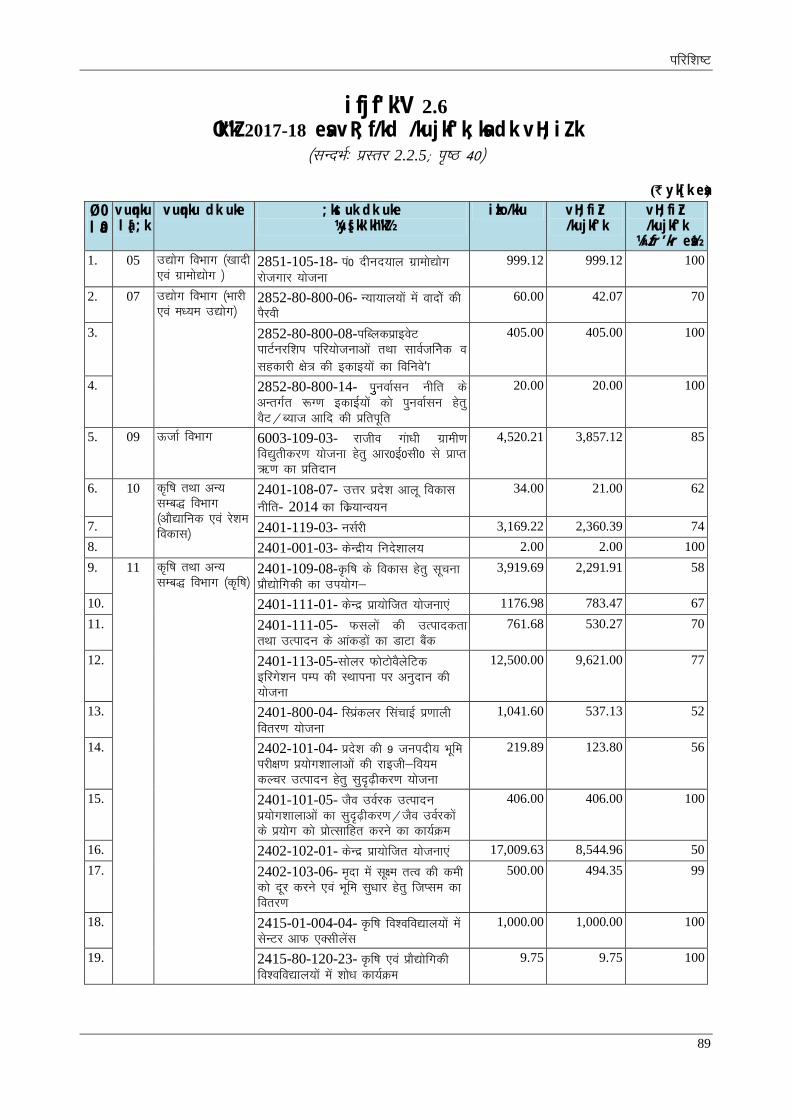

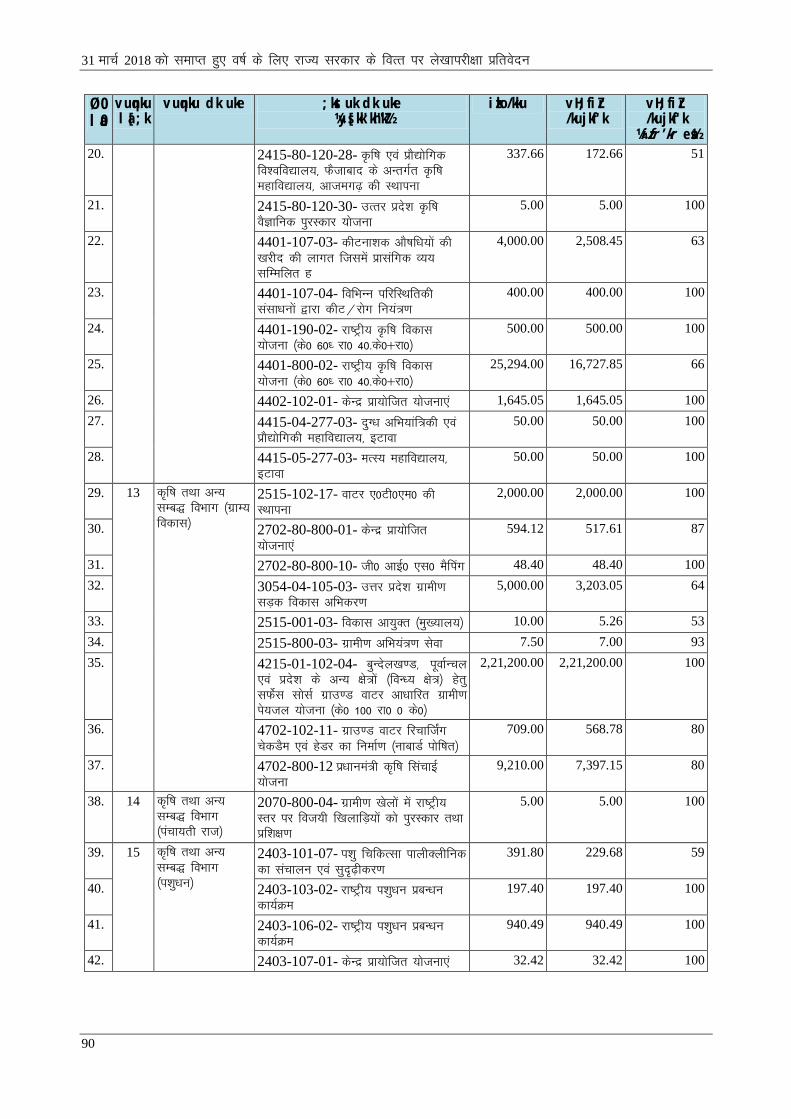

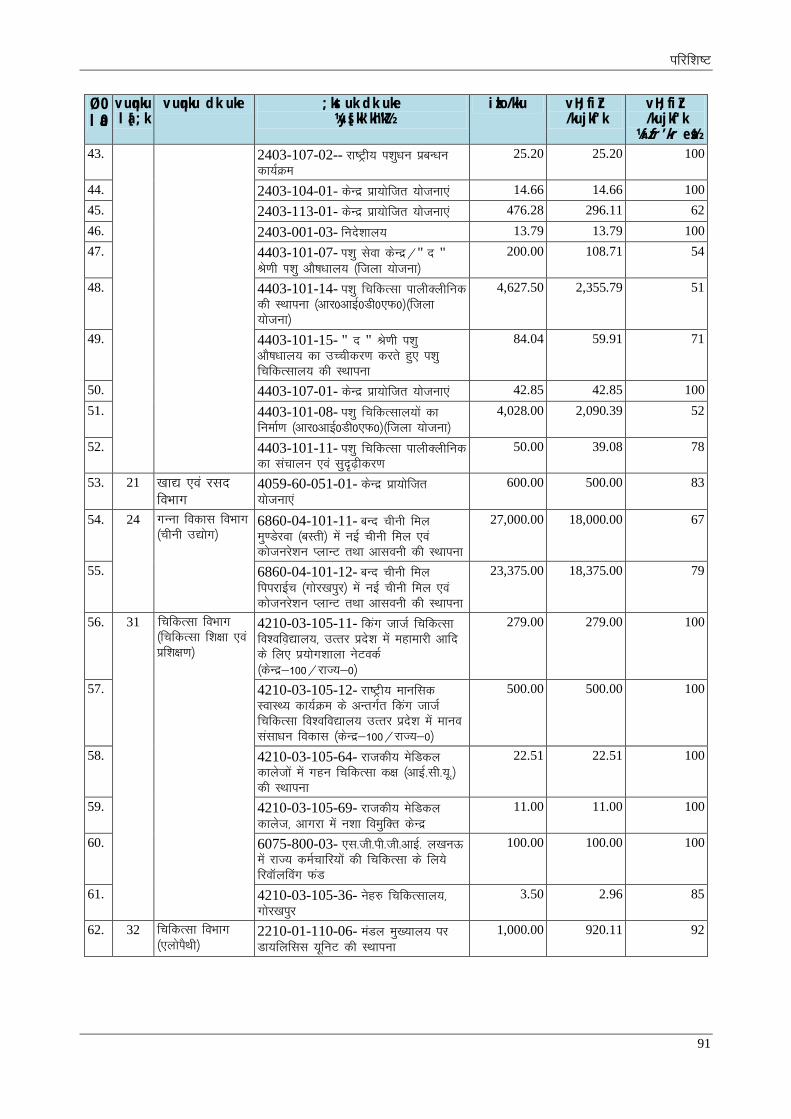

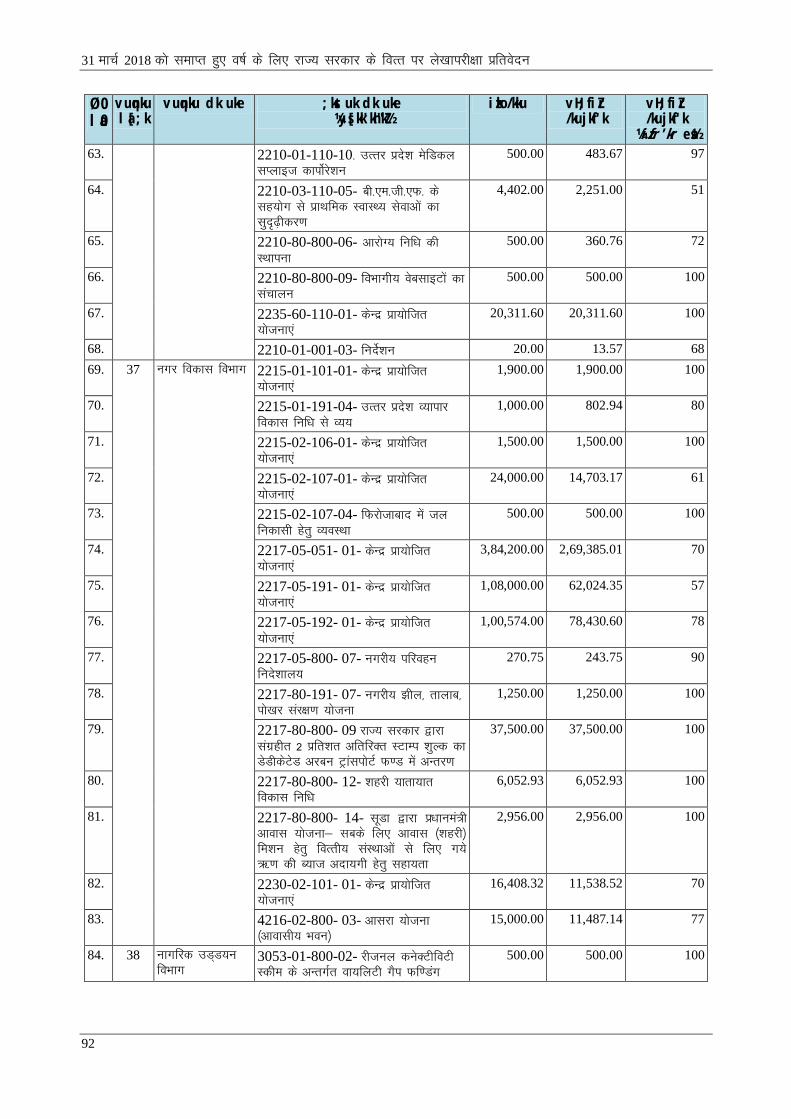

ifjf'k"V 2.6 o’kZ 2017-18 esa vR;f/kd /kujkf'k;ksa dk vH;iZ.k 89

ifjf'k"V 2.7 okLrfod cpr ls vf/kd vH;iZ.k ¼` 50 yk[k ;k vf/kd½ 99

vuqØef.kdk

iii

ifjf'k"V 2.8 vuqnkuksa@fofu;ksxksa dk fooj.k] ftuesa cpr gqbZ ijUrq mldk dksbZ

Hkkx vH;fiZr ugha fd;k x;k

100

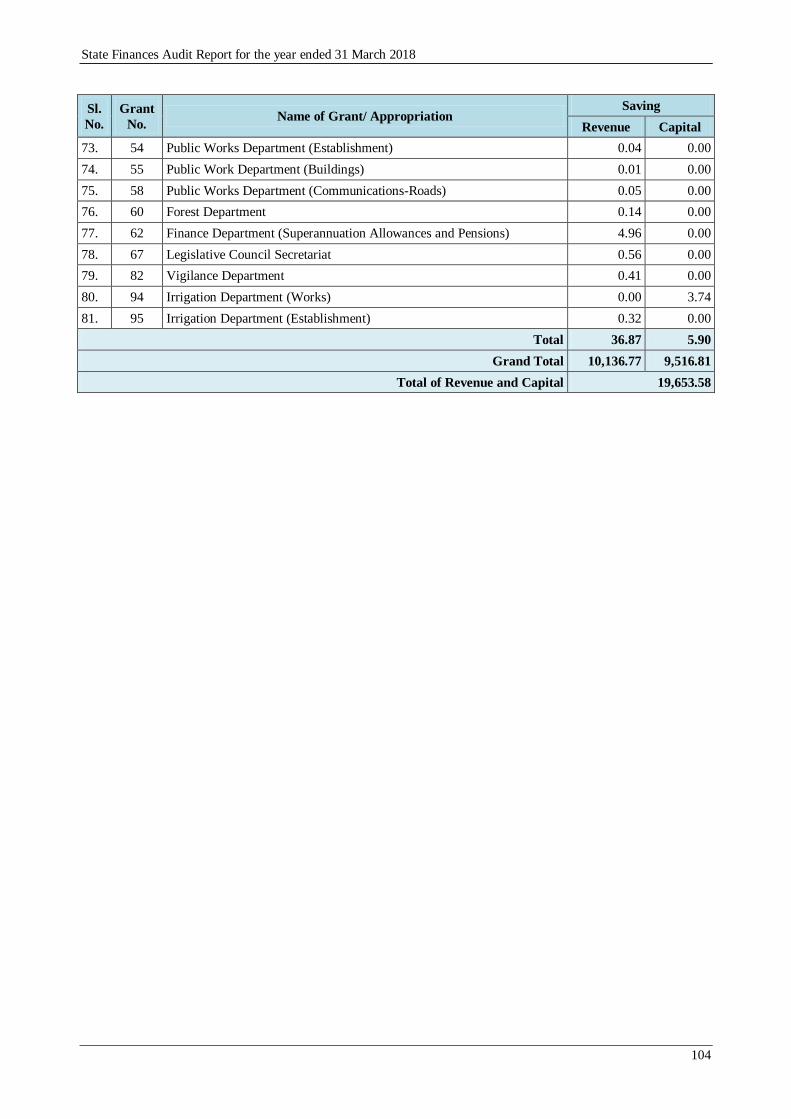

ifjf'k"V 2.9 vH;fiZr u dh x;h ` ,d djksM+ ,oa mlls vf/kd dh

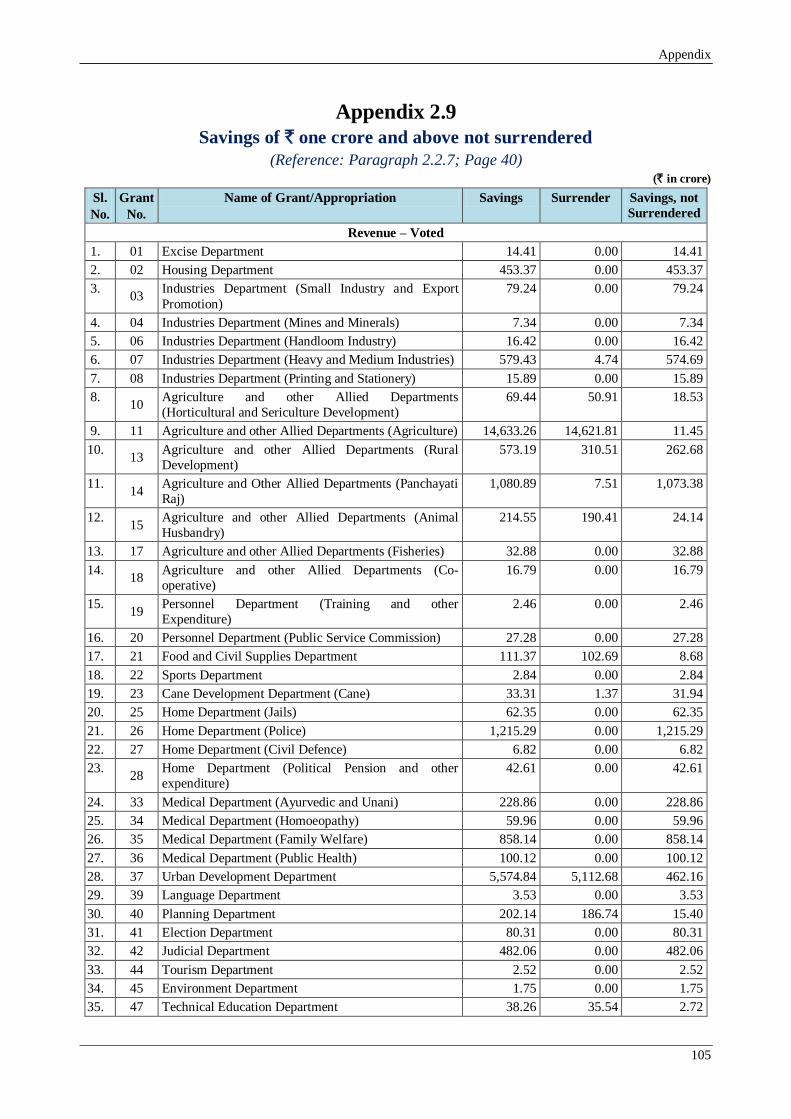

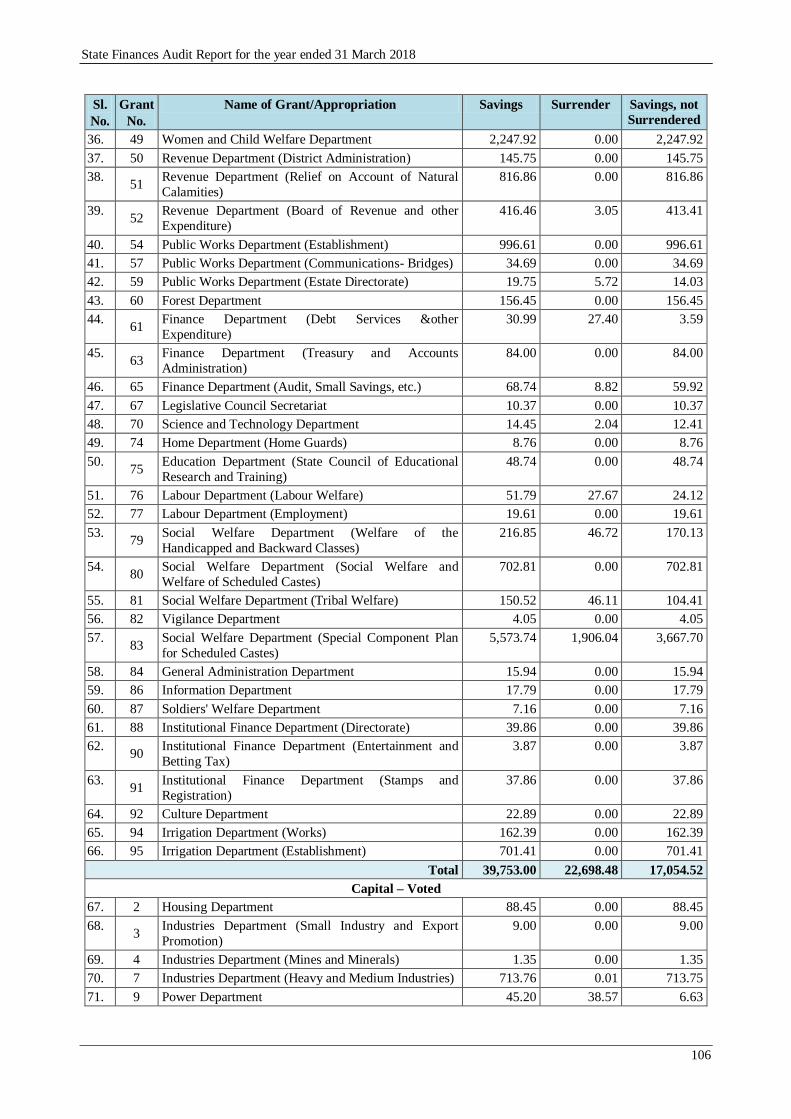

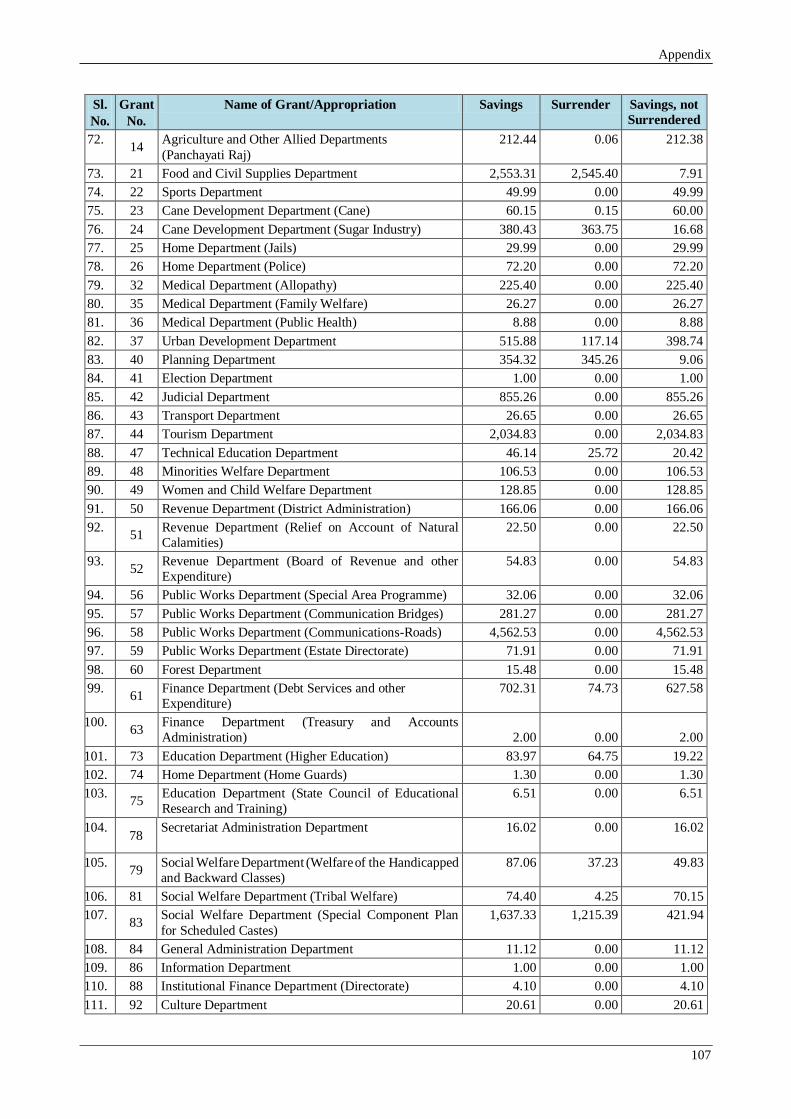

cprsa

103

ifjf'k"V 3.1 jksdM+ cgh viw.kZ@vuqj{k.k u fd;k tkuk 107

ifjf'k"V 3.2 nks izfr'kr vfrfjDr LVkEi M~;wVh dk forj.k 108

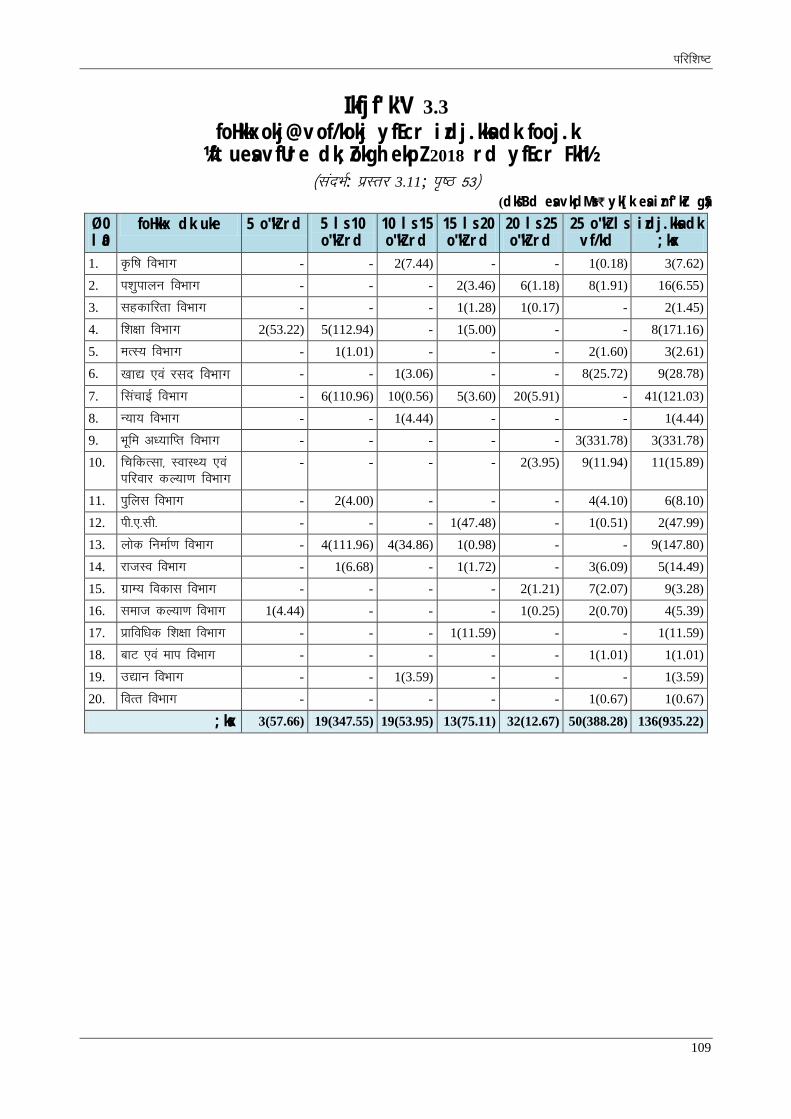

ifjf'k"V 3.3 foHkkxokj@vof/kokj yfEcr izdj.kksa dk fooj.k ¼ftuesa vfUre

dk;Zokgh ekpZ 2018 rd yfEcr Fkh½

109

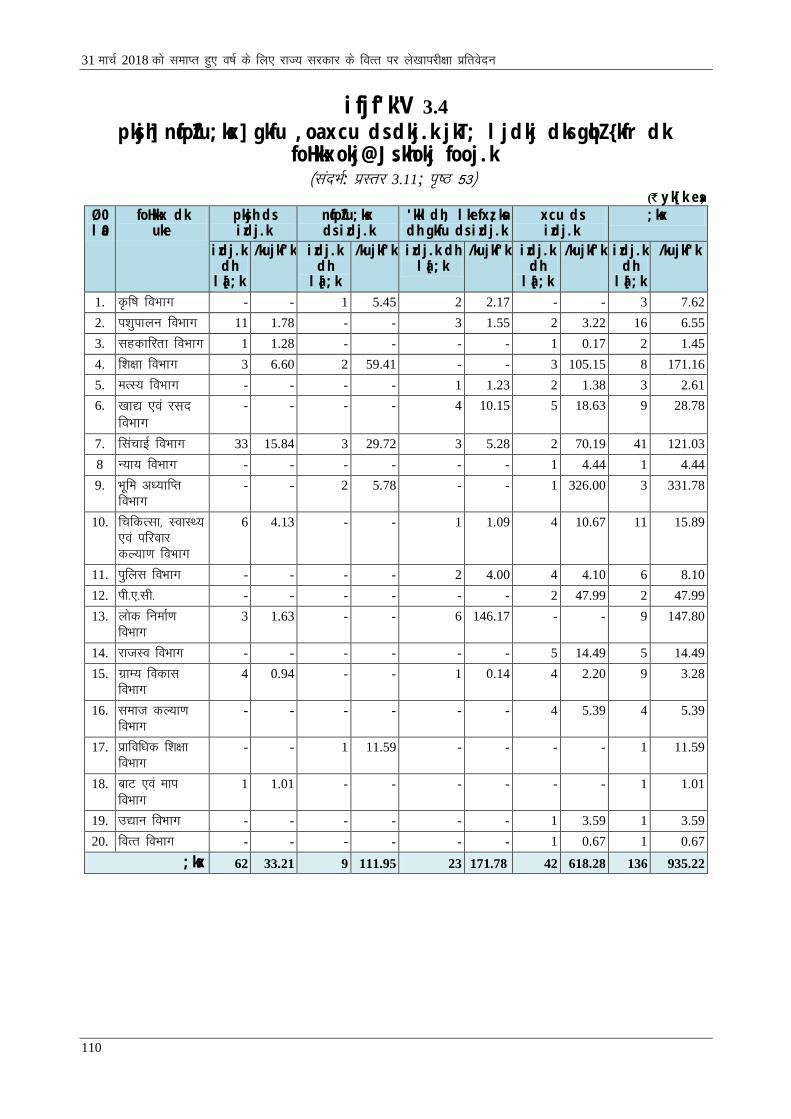

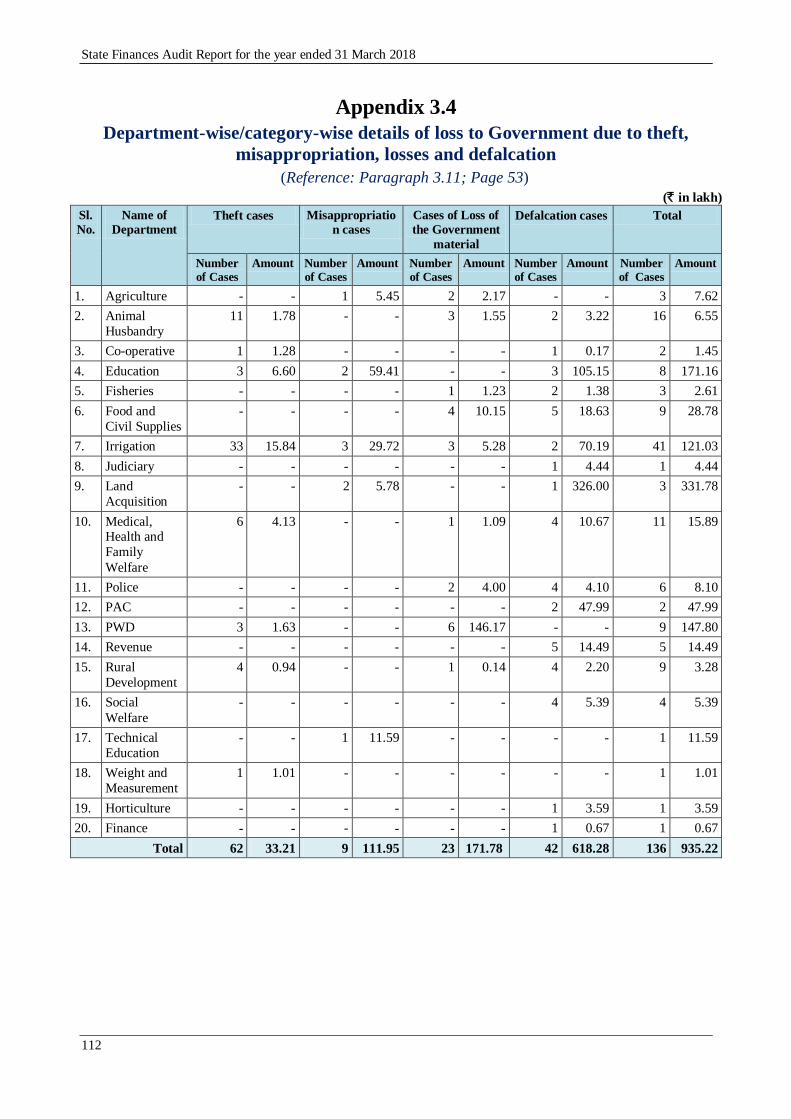

ifjf'k"V 3.4 pksjh] nqfoZfu;ksx] gkfu ,oa xcu ds dkj.k jkT; ljdkj dks gqbZ

{kfr dk [email protected] fooj.k

110

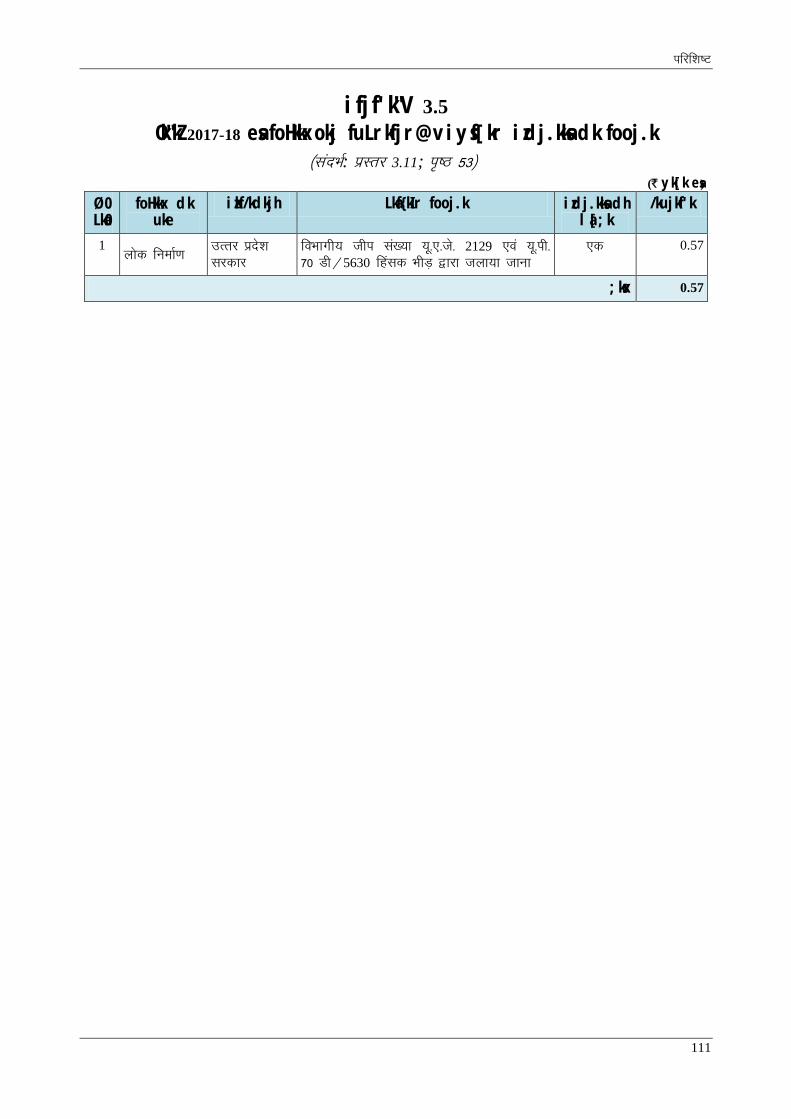

ifjf'k"V 3.5 o’kZ 2017-18 esa foHkkxokj fuLrkfjr@viysf[kr izdj.kksa dk

fooj.k

111

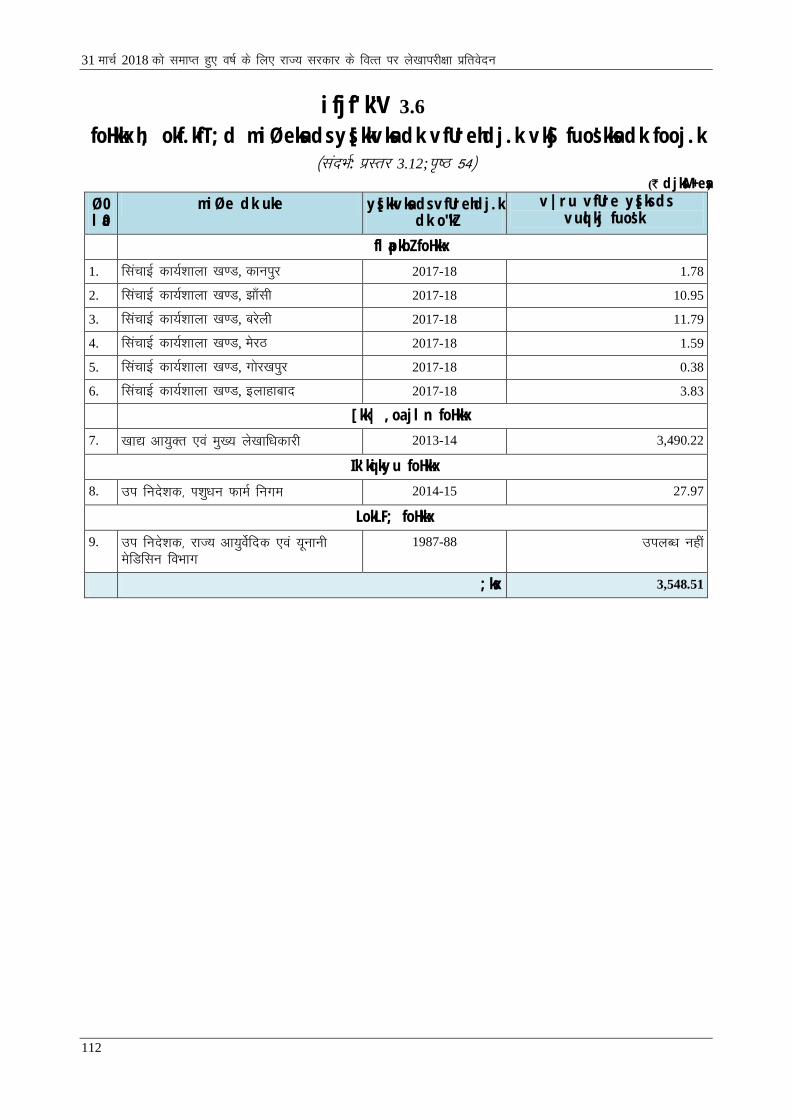

ifjf'k"V 3.6 foHkkxh; okf.kfT;d miØeksa ds ys[kkvksa dk vfUrehdj.k vkSj

fuos'kksa dk fooj.k

112

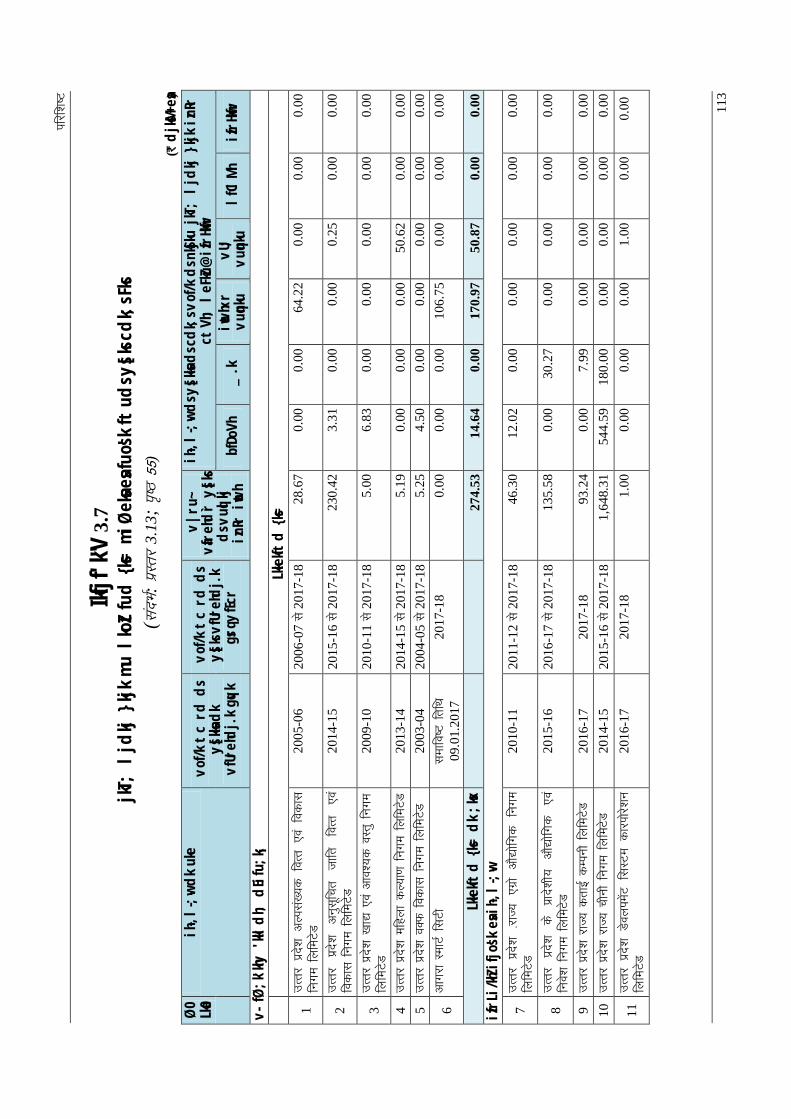

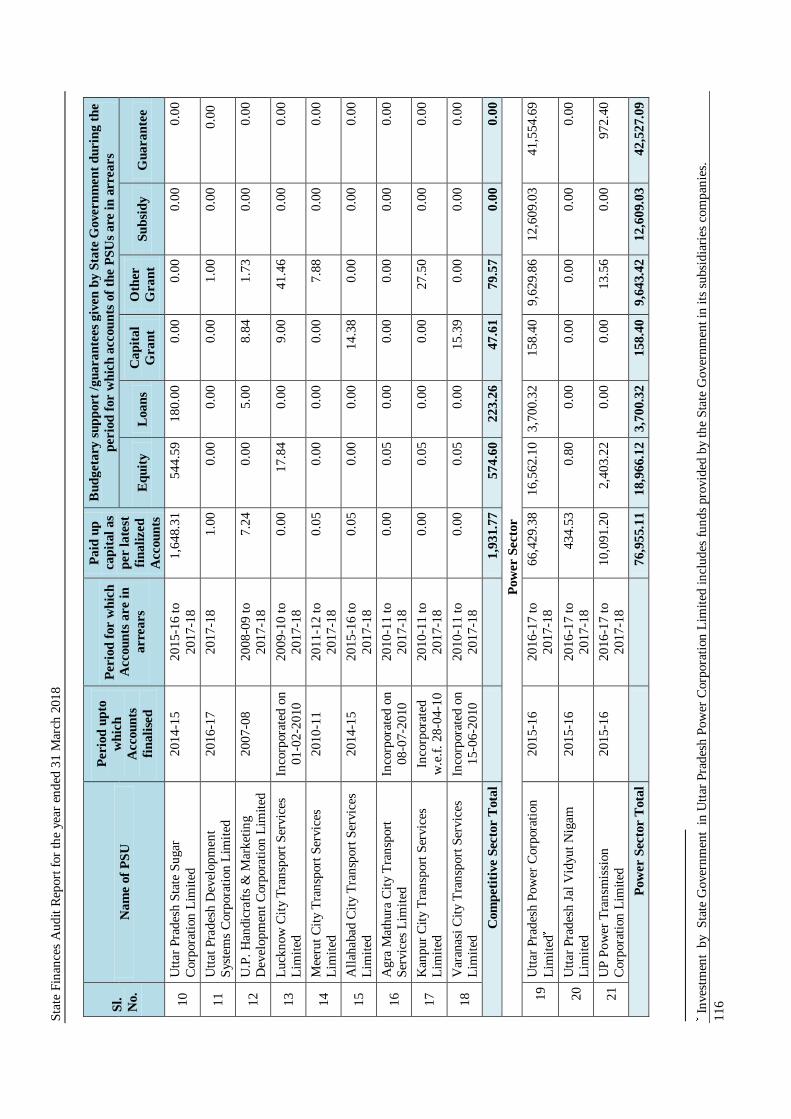

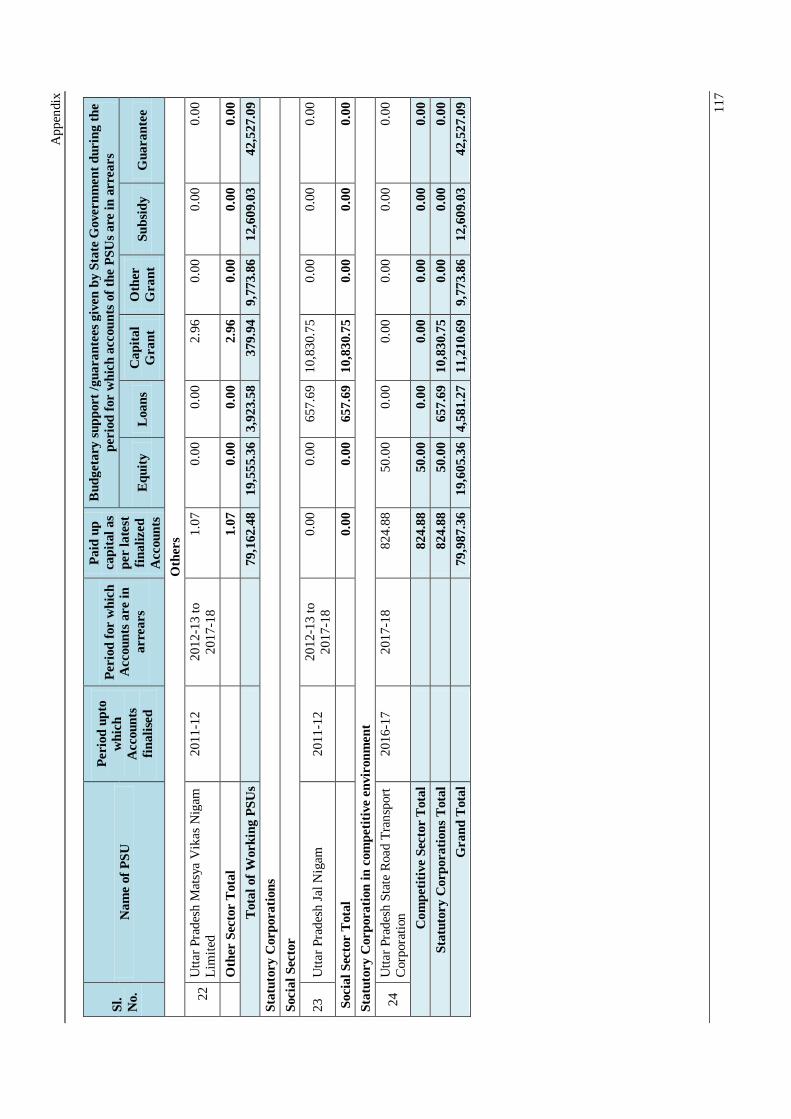

ifjf'k"V 3.7 jkT; ljdkj }kjk mu lkoZtfud {ks= miØeksa esa fuos'k ftuds

ys[ks cdk;s Fks

113

ifjf'k"V 3.8 ykHk vftZr djus okys lkoZtfud {ks= miØe ls ykHkka'k 116

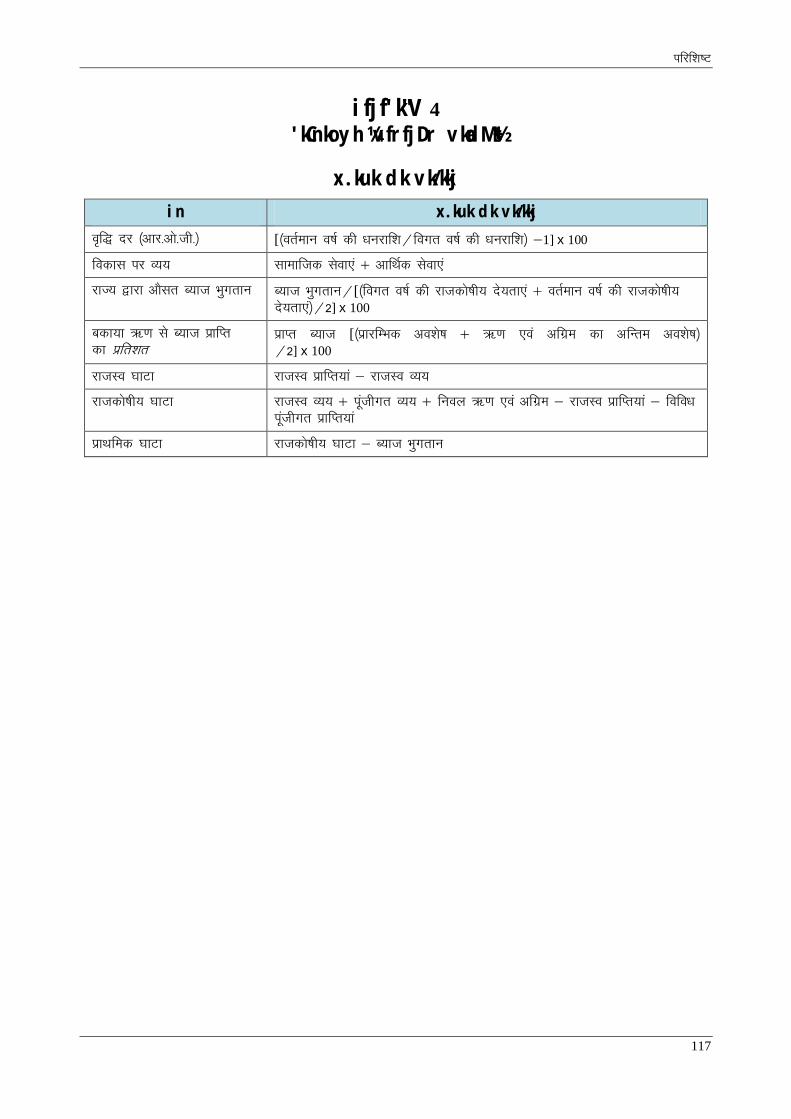

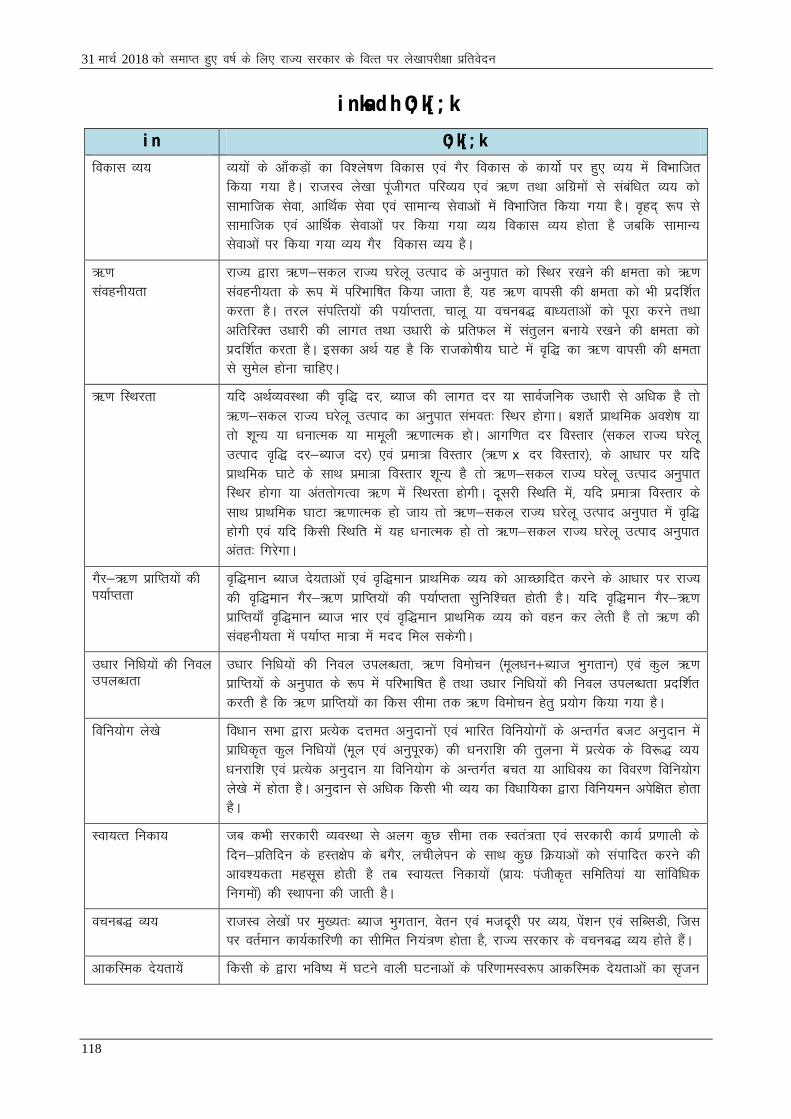

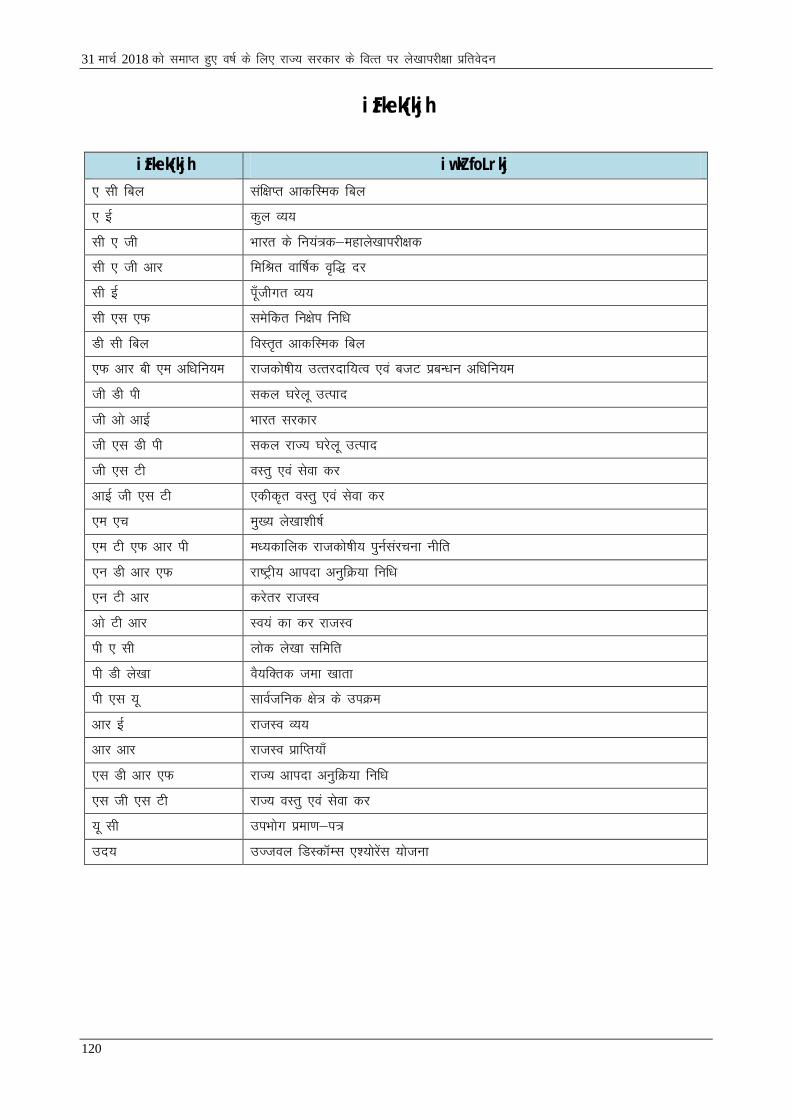

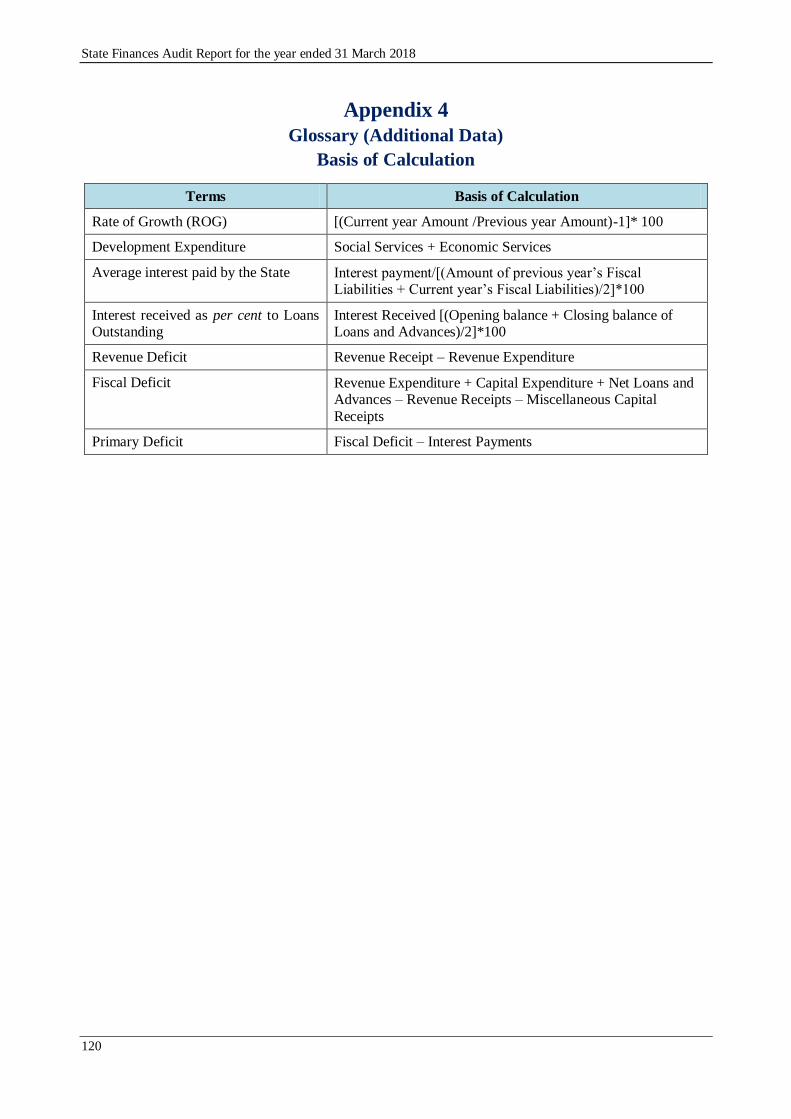

ifjf'k"V 4 'kCnkoyh ¼vfrfjDr vk¡dM+s½

x.kuk dk vk/kkj 117

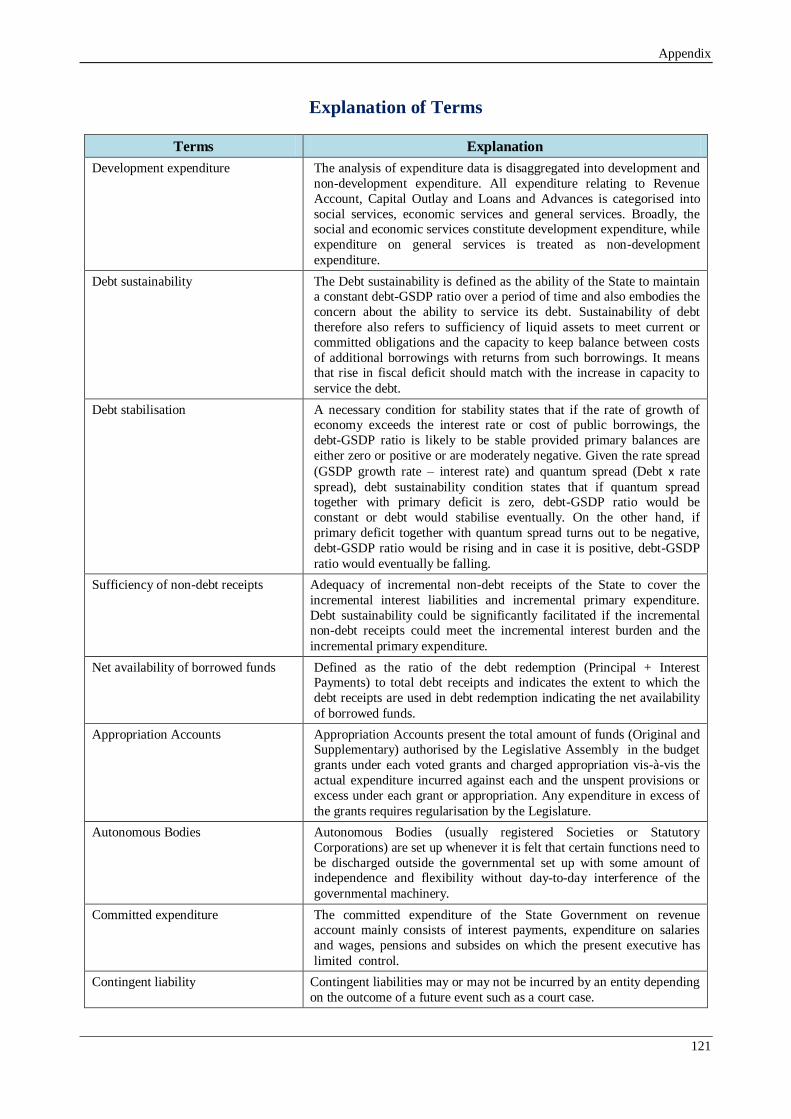

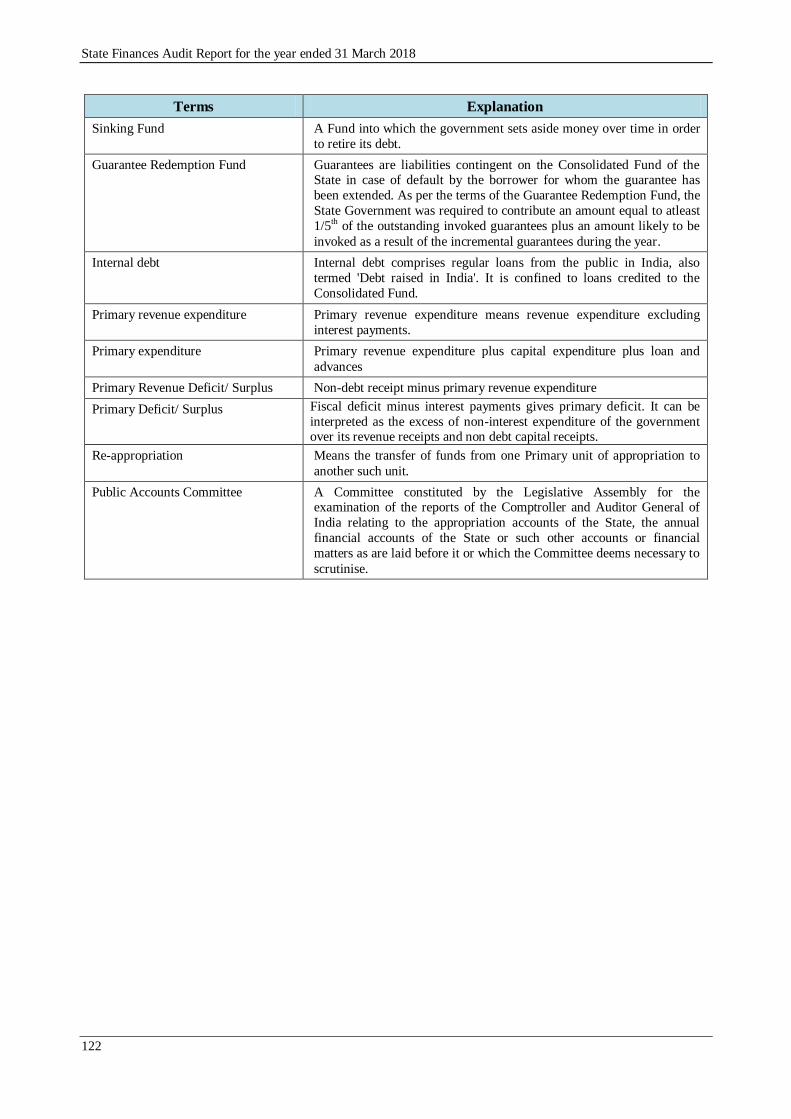

inksa dh O;k[;k 118

izFkek{kjh 119

v

izkDdFku

;g izfrosnu lafo/kku ds vuqPNsn 151 ds vUrxZr mRrj izns'k ds

jkT;iky dks izLrqr djus gsrq rS;kj fd;k x;k gSA

mRrj izns'k ljdkj ds foRr ij vk/kkfjr ;g izfrosnu o"kZ 2017-18 esa

jkT; ds foRrh; izn'kZu dk vkdyu djrk gS ,oa jkT; fo/kkf;dk ds

le{k foRrh; vkadM+ksa dk ys[kkijh{kk fo'ys’k.k izLrqr djrk gSA bl

izfrosnu esa mRrj izns'k jktdks’kh; mRrjnkf;Ro ,oa ctV izcU/ku

¼la'kks/ku½ vf/kfu;e] 2016] pkSngosa foRr vk;ksx dh fjiksVZ ,oa ctV

vuqeku 2017-18 }kjk ifjdfYir y{;ksa ds lkis{k foRrh; izn'kZu dk

fo'ys’k.k djus dk iz;kl fd;k x;k gSA ;g izfrosnu rhu v/;k;ksa esa

lajfpr gSA

v/;k; 1 foRr ys[ks dh ys[kkijh{kk ij vk/kkfjr gS ,oa 31 ekpZ 2018

dks mRrj izns'k ljdkj dh jktdks’kh; fLFkfr dk ewY;kadu djrk gSA ;g

C;kt Hkqxrku] osru ,oa etnwjh] isa'ku] _.kksa ds Hkqxrku ,oa m/kkj ij

O;; dh izofRr ij izdk'k Mkyrk gSA

v/;k; 2 fofu;ksx ys[ks dh ys[kkijh{kk ij vk/kkfjr gS ,oa blesa

vuqnkuokj fofu;ksxksa rFkk lsoknk;h foHkkxksa }kjk fdl izdkj vkoafVr

lalk/kuksa dk izcU/ku fd;k x;k gS] dk fooj.k gSA

v/;k; 3 mRrj izns'k ljdkj }kjk fofHkUUk fjiksfVZax vko';drkvksa ,oa

foRrh; fu;eksa ds vuqikyu dk ys[kk&tks[kk gSA

ys[kkijh{kk dk fu"iknu Hkkjr ds fu;a=d&egkys[kkijh{kd }kjk fuxZr

ys[kkijh{kk ekudksa ds vuq:i fd;k x;k gSA

vii

dk;Zdkjh lkj

jktdks"kh; fLFkfr dh leh{kk

o’kZ 2013-14 ls o’kZ 2017-18 dh vof/k esa eqnzkLQhfr dks x.kuk esa ysus ds ckn Hkh jktLo

izkfIr;ksa ,oa jktLo O;; esa of) gqbZA o’kZ 2013-14 ls o’kZ 2016-17 dh vof/k esa iwathxr O;;

esa Hkh of) gqbZ ijUrq o’kZ 2016-17 dh rqyuk esa o’kZ 2017-18 esa blesa 44 izfr'kr dh fxjkoV

ntZ dh xbZA

(izLrj 1.2)

jkT; }kjk o’kZ 2017-18 esa ` 12,552 djksM+ dk jkTkLo vkf/kD; izkIr fd;k x;k tSlk fd ctV

vuqeku ,oa e/;dkfyd jktdks’kh; iqu%lajpuk uhfr ¼,e-Vh-,Q-vkj-ih-½ 2017 }kjk yf{kr FkkA

Ok’kZ 2017-18 esa l-jk-?k-m- ds lkis{k jktdks’kh; ?kkVs dk vuqikr ctV vuqeku] ,e-Vh-,Q-vkj-ih-

,oa pkSngosa foRr vk;ksx }kjk fu/kkZfjr y{; ds vUnj jgkA vxzsrj] jkT; ds jktdks’kh; ?kkVs

¼` 27,810 djksM+½ esa o’kZ 2016-17 ¼2016-17 esa mn; ds izHkko dks gVkus ds Ik'pkr~½ dh rqyuk

esa 32 izfr'kr dh deh gqbZA ;|fi ;g iwathxr O;; esa deh ds vkuq’kafxd Fkk ftlesa o’kZ dh

rqyuk eas 44 izfr'kr dh deh gqbZA

vxzsrj] jkT; }kjk l-jk-?k-m- ds lkis{k dqy cdk;k _.k ds vuqikr ds lEcU/k esa ctV vuqeku]

,e-Vh-,Q-vkj-ih- ,oa pkSngosa foRr vk;ksx }kjk fu/kkZfjr y{; izkIr ugah fd;k tk ldkA

(izLrj 1.3 ,oa 1.3.1)

lalk/kuksa dk laxzg.k

o’kZ 2016-17 ds lkis{k jktLo izkfIr;ksa esa ` 21,900 djksM+ ¼ukS izfr'kr½ dh of) gqbZ tks ctV

vuqekuksa ds lkis{k de ¼` 40,622 djksM+½ FkhA

o’kZ 2016-17 ds lkis{k jktLo O;; esa ` 29,632 djksM+ ¼13 izfr'kr½ dh of) gqbZ tks ctV

vuqekuksa ds lkis{k de ¼` 40,895 djksM+½ FkhA

o’kZ 2016-17 ds lkis{k iwathxr O;; esa ` 30,701 djksM+ ¼44 izfr'kr½ dh deh gqbZ tks ctV

vuqekuksa ds lkis{k de ¼` 14,170 djksM+½ FkhA o’kZ 2017-18 esa y?kq ,oa lhekar d`’kdksa dks

Qlyh +_.k ekQh ds fy;s jktLo O;; ds ctV izkOk/kku esa ` 36,000 djksM+ dh vR;f/kd

of) ds dkj.k iwathxr O;; ds o’kZ 2016-17 ds ctV izko/kku ¼` 71,878 djksM+½ ds lkis{k

o’kZ 2017-18 esa ctV izko/kku esa ¼` 53,258 djksM+½ esa 26 izfr'kr dh deh gqbZA

laLrqfr: foRr foHkkx dks ctV rS;kj djus dh izfØ;k dks rdZlaxr cukuk pkfg, ftlls ctV

vuqeku rFkk okLrfodrkvksa esa yxkrkj c<+rs vUrj dks de fd;k tk ldsA

(izLrj 1.3.3, 1.4 ,oa 1.7.1)

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

viii

ifjHkkf"kr va'knk;h isa'ku ;kstuk

1 vçSy 2005 dks ;k mlds ckn HkrhZ fd, x, jkT; ljdkj ds deZpkjh ifjHkkf"kr va'knk;h

isa'ku ;kstuk ds rgr vkPNkfnr gSaA jkT; ljdkj us vius oS/kkfud nkf;Ro dk fuoZgu ugha

fd;k D;ksafd og foRrh; o"kZ 2017-18 esa ljdkjh lgk;rk çkIr laLFkkuksa vkSj Lok;Rr fudk;ksa

ds deZpkfj;ksa ds laca/k esa ifjHkkf"kr va'knk;h isa'ku ;kstuk ds vUrxZr jkT; ljdkj }kjk leku

eSfpax “ks;j ds :Ik esa ` 465.10 djksM+ dk ;ksxnku djus esa foQy jghA foxr foRrh; o"kksa Z

2008-09 ls 2016-17 dh vof/k esa jkT; ljdkj us ljdkjh deZpkfj;ksa] ljdkjh lgk;rk çkIr

laLFkkuksa vkSj Lok;Ùk fudk;ksa ds deZpkfj;ksa ds laca/k esa ifjHkkf"kr va'knk;h isa'ku ;kstuk ds rgr

blds eSfpax “ks;j ds :i esa ` 211.69 djksM+ dk va'knku ugha fd;kA

vxzsrj] jkT; ljdkj us o"kZ 2008-09 ls o"kZ 2017-18 dh vof/k esa ifjHkkf’kr va'knk;h isa'ku

;kstuk ds vUrxZr ljdkjh deZpkfj;ksa] ljdkjh lgk;rk çkIr laLFkkuksa vkSj Lok;Ùk fudk;ksa ds

deZpkfj;ksa ,oa jkT; ljdkj ds va'knku ds :i esa ` 8,205.66 djksM+ #i;s ,d= fd,] ysfdu

;kstuk ds çko/kkuksa ds vuqlkj vkxs fuos'k ds fy, ukfer çkf/kdkjh dks ` 703.16 djksM+ tek

ugha fd,A bl çdkj] 31 ekpZ 2018 dks] ukfer çkf/kdkjh dks ` 1,379.95 djksM+ ¼`465.10

djksM+ $ `211.69 djksM+$`703.16 djksM+½ dk de gLrkUrj.k fd;k x;k vkSj orZeku ns;rk

dks Hkfo"; ds o"kZ ¼vksa½ ds fy, vkLFkfxr fd;k x;kA blds vykok] jkT; ljdkj us Hkfo"; esa

deZpkfj;ksa dks ns; ykHk ds laca/k esa vfuf'prrk iSnk dh@ljdkj ds fy, Hkfo’; esa ifjgk;Z

foÙkh; ns;rk lftr dh vkSj bl çdkj Lo;a gh ;kstuk dks laHkkfor foQyrk dh vksj vxzlj

fd;kA

laLrqfr% jkT; ljdkj dks ;g lqfuf'pr djus ds fy, rqjUr dkjZokgh izkjEHk djuh pkfg, fd

1 vçSy 2005 dks ;k mlds ckn HkrhZ gksus okys deZpkfj;ksa dks mudh HkrhZ dh frfFk ls

va'knk;h isa'ku ;kstuk ds vUrxZr iw.kZ :Ik ls vkPNkfnr fd;k tk;sA ;g bl izdkj lqfuf'pr

fd;k tkuk pkfg, fd deZpkfj;ksa ds osru ls dVkSrh iwjh rjg ls dh tk,] ljdkj }kjk viuk

iw.kZ ;ksxnku nsrs gq, le;c) rjhds ls ,u-,l-Mh-,y- ds ek/;e ls ukfer Q.M eSustj dks

lEiw.kZ :Ik ls LFkkukUrfjr dj fn;k tk,A

(izLrj 1.7.1.3)

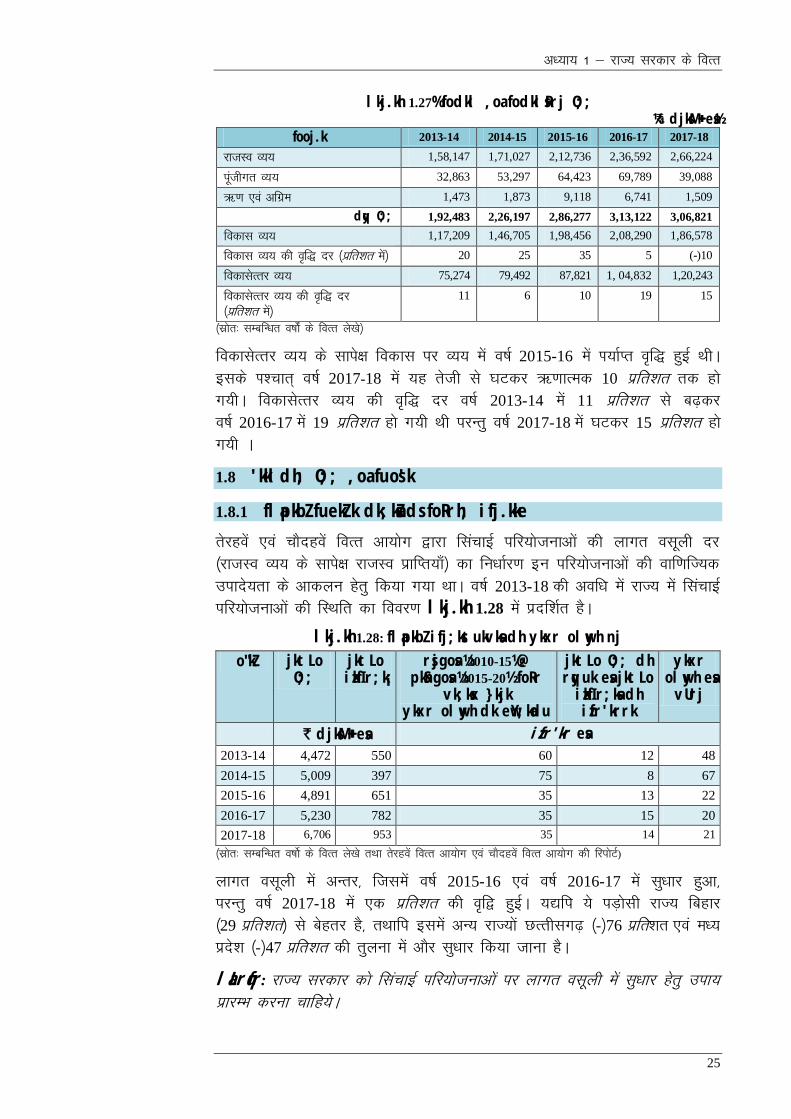

yksd O;; dh i;kZIrrk

Ok’kZ 2017-18 esa] fodkl ij O;;] vkfFkZd lsokvksa ij O;; ,oa f'k{kk ij O;; dk dqy O;; ls

vuqikr lkekU; Js.kh ds jkT;ksa ls de FkkA

(izLrj 1.7.2.1)

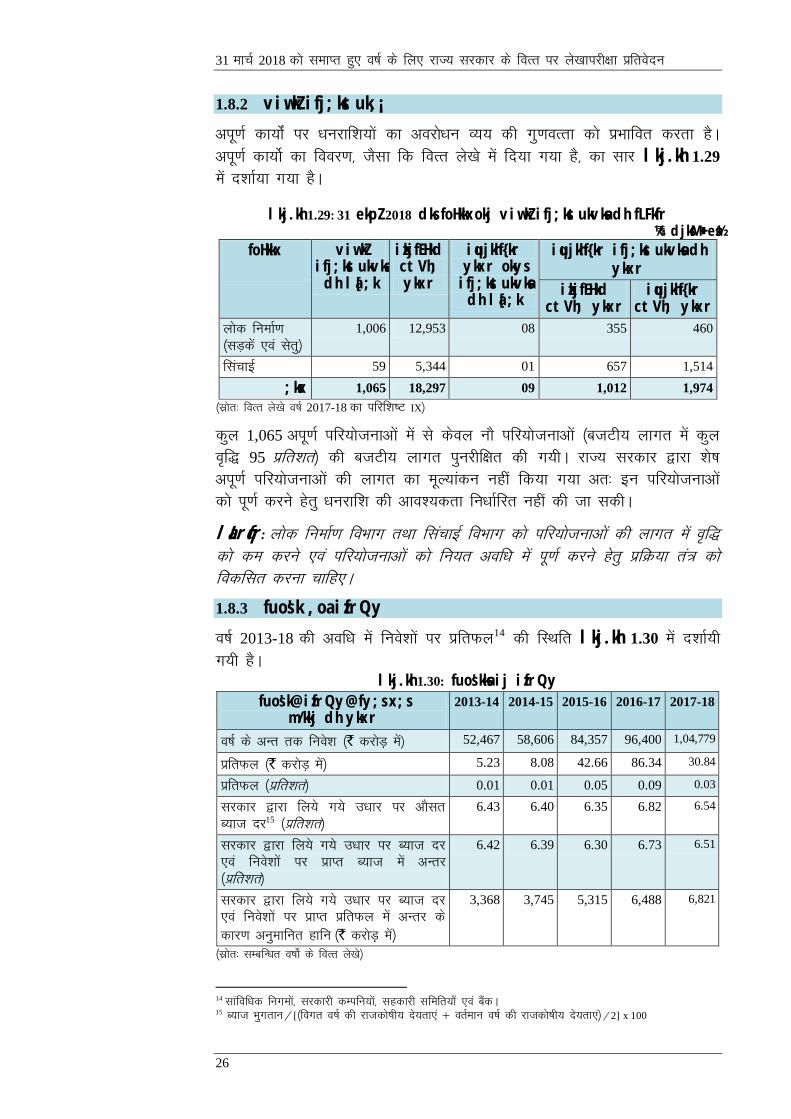

flapkbZ fuekZ.k dk;ksZa ds foRrh; ifj.kke

rsjgosa ,oa pkSngosa foRr vk;ksx }kjk flapkbZ ifj;kstukvksa dh ykxr olwyh nj ¼jktLo O;; ds

lkis{k jkTkLo izkfIr;k¡½ dk fu/kkZj.k bu ifj;kstukvksa dh okf.kfT;d mikns;rk ds vkdyu gsrq

fd;k x;k FkkA ykxr olwyh esa vUrj] ftlesa o’kZ 2015-16 ,oa o’kZ 2016-17 esa lq/kkj gqvk]

ijUrq o’kZ 2017-18 esa ,d izfr'kr dh of} gqbZA rFkkfi blesa vU; jkT;ksa NRrhlx<+ ,oa e/;

izns'k dh rqyuk esa vkSj lq/kkj fd;k tkuk gSA

laLrqfr: jkT; ljdkj dks flapkbZ ifj;kstukvksa ij ykxr olwyh esa lq/kkj gsrq mik; izkjEHk

djuk pkfg;sA (izLrj 1.8.1)

dk;Zdkjh lkj

ix

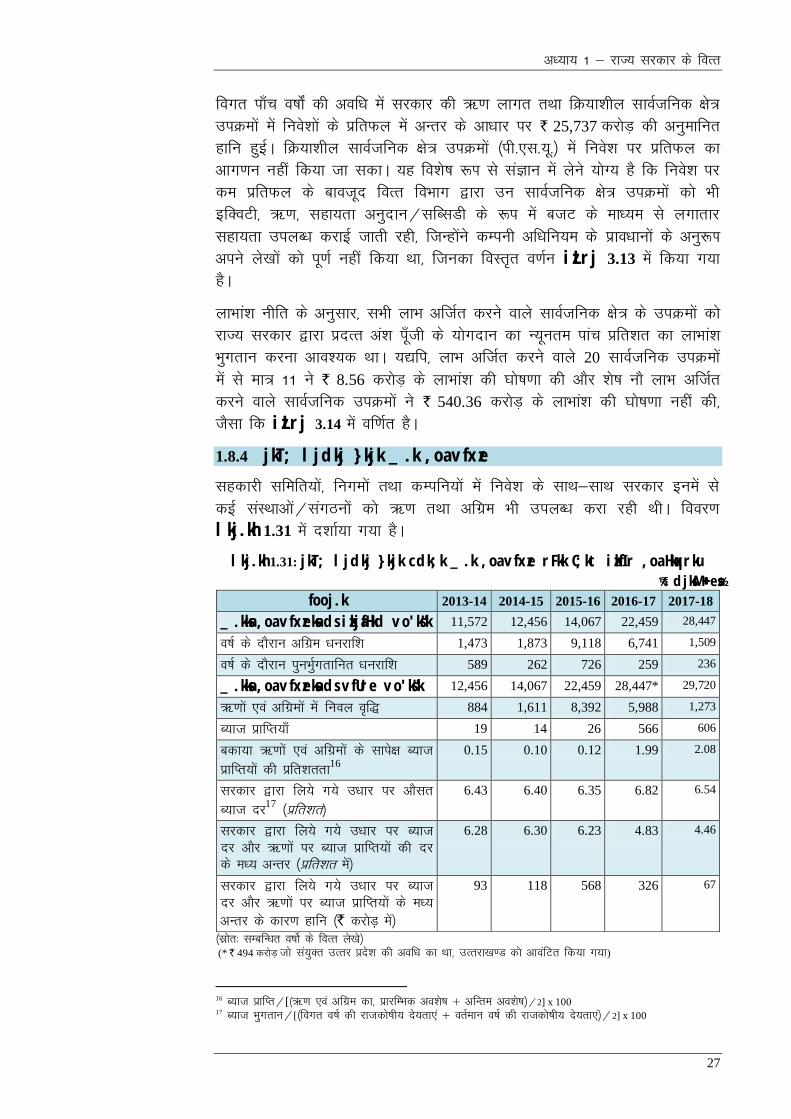

fuos'k ,oa izfrQy rFkk _.k ,oa vfxze

o’kZ 2013-18 dh vof/k esa ljdkj dh _.k ykxr rFkk fØ;k'khy lkoZtfud {ks= miØeksa esa

fuos'kksa ds izfrQy esa vUrj ds vk/kkj ij ` 25,737 djksM+ dh vuqekfur gkfu gqbZA blds

vfrfjDr] ljdkj }kjk fn;s x;s _.kksa ls izkIr C;kt rFkk fy;s x;s m/kkj ij Hkqxrkfur C;kt

dh /kujkf'k esa vUrj ds vk/kkj ij ljdkj dks ` 1,172 djksM+ dh vuqekfur gkfu gqbZA

laLrqfr: jkT; ljdkj dks vius fuos'k RkFkk fofHkUu bdkb;ksa dks fn;s x;s _.k dks bl izdkj

rdZlaxr cukuk pkfg, ftlls fuos'k rFkk _.k ij izfrQy de ls de ljdkj dh _.k ykxr

ls esy [kk;sA (izLrj 1.8.3 ,oa 1.8.4)

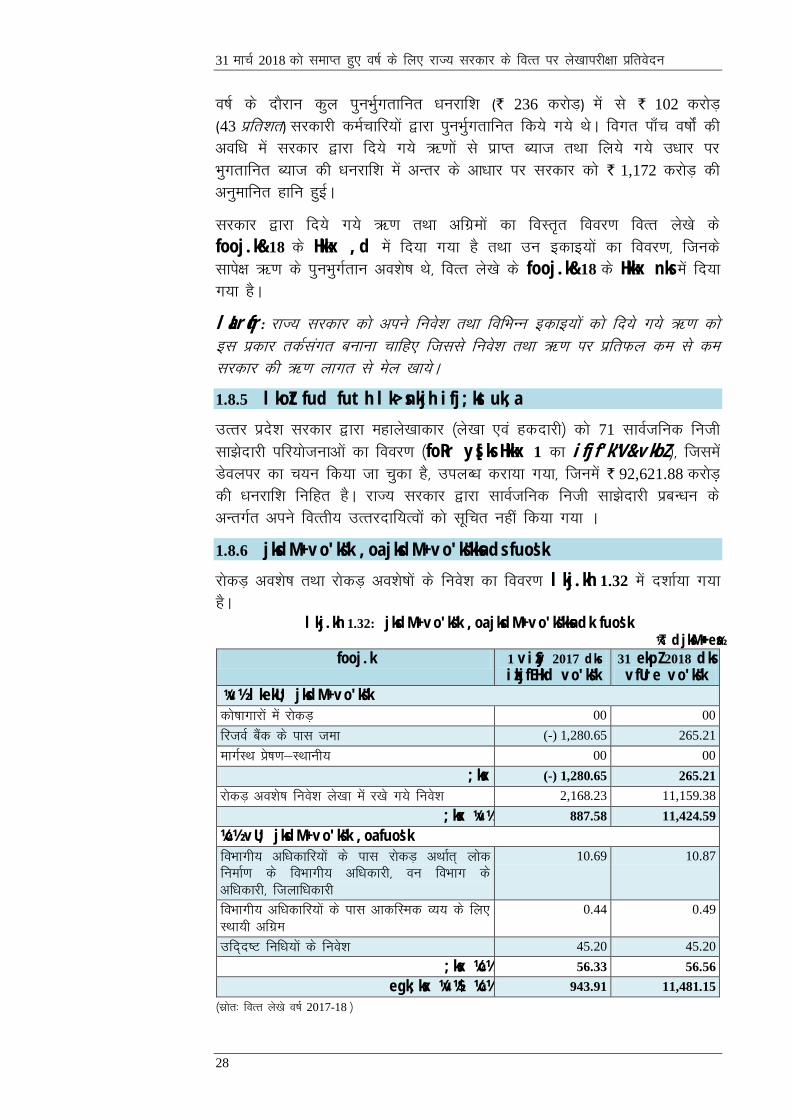

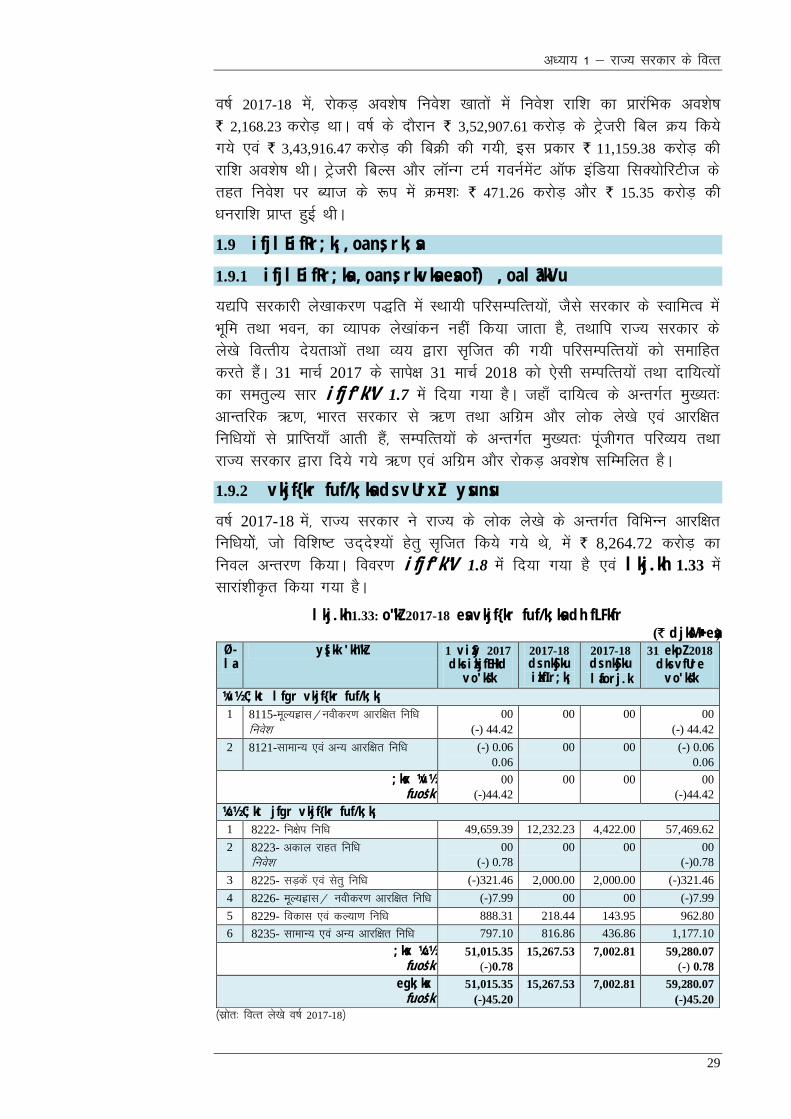

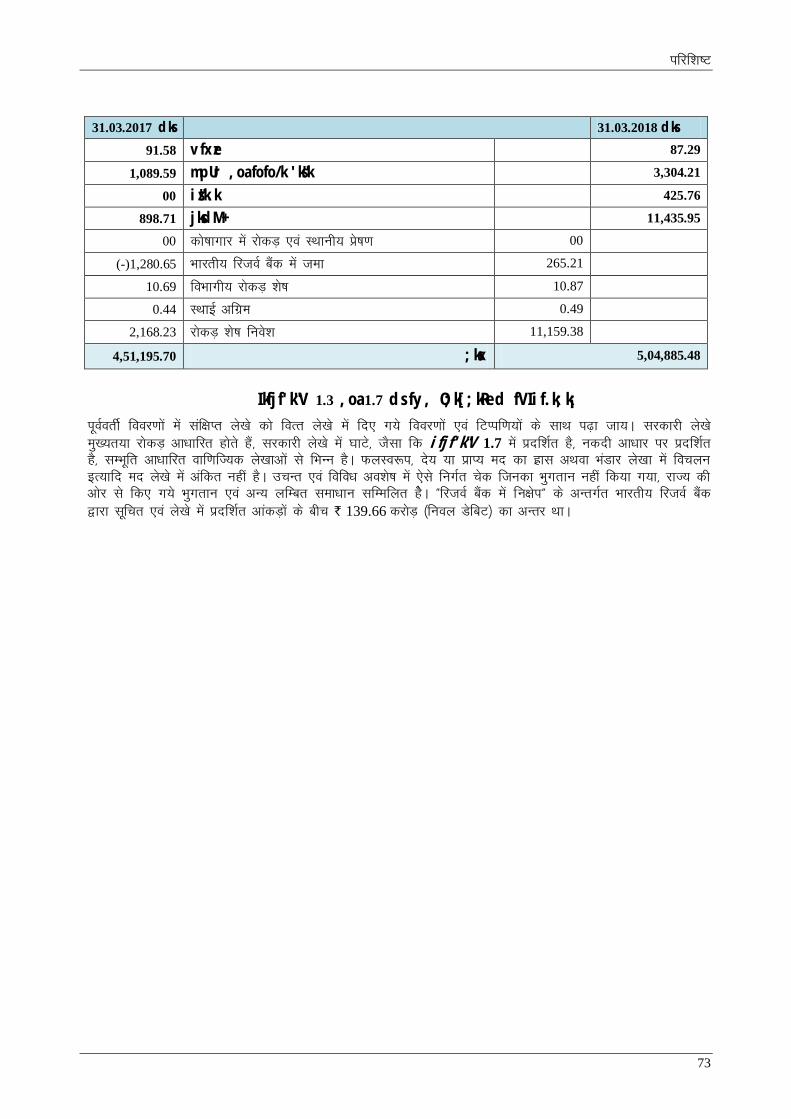

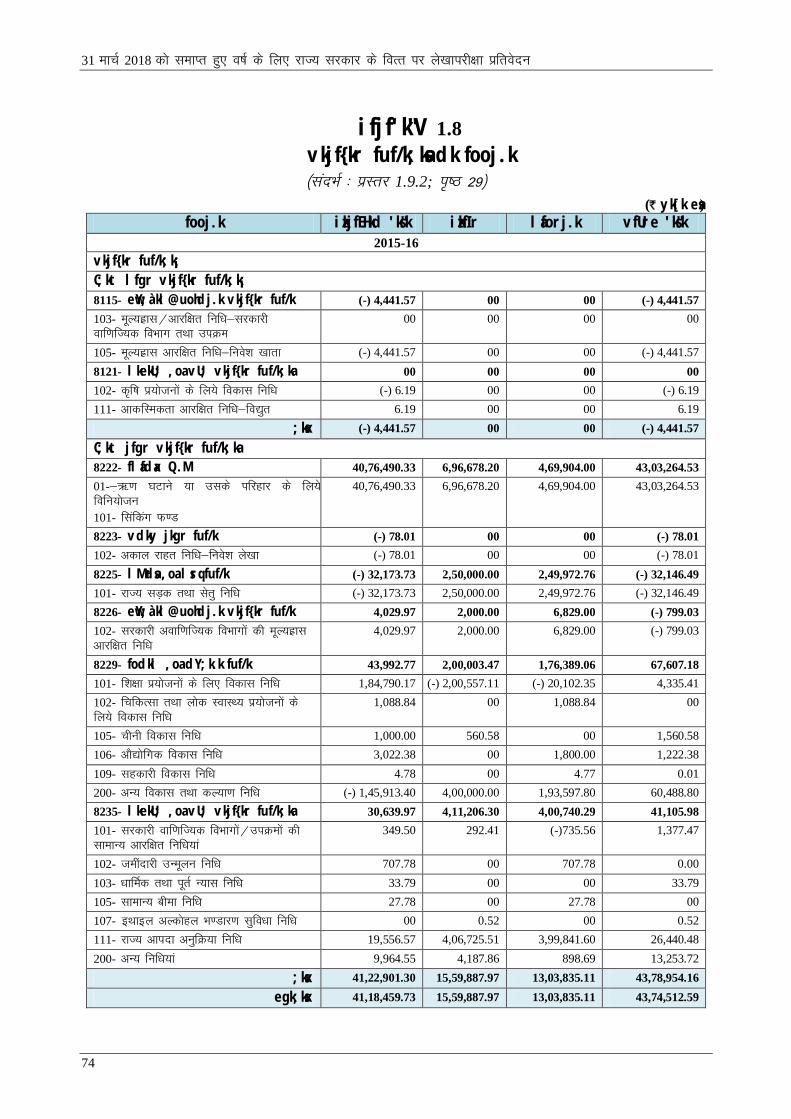

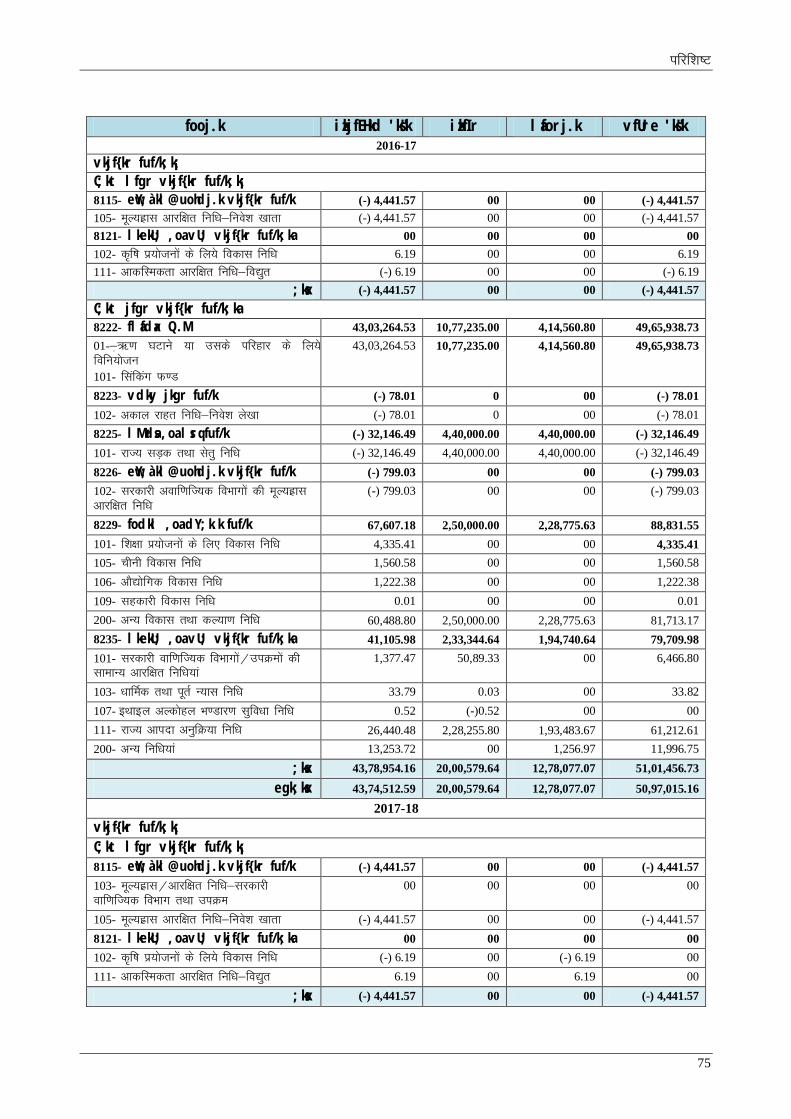

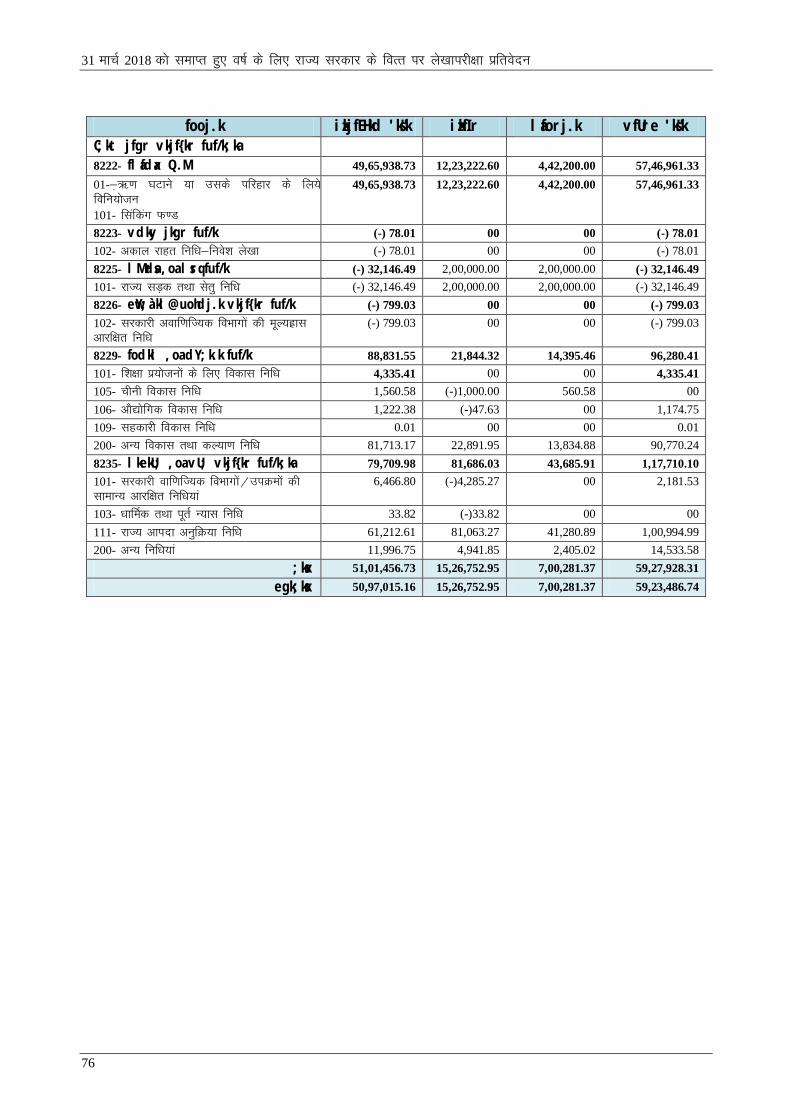

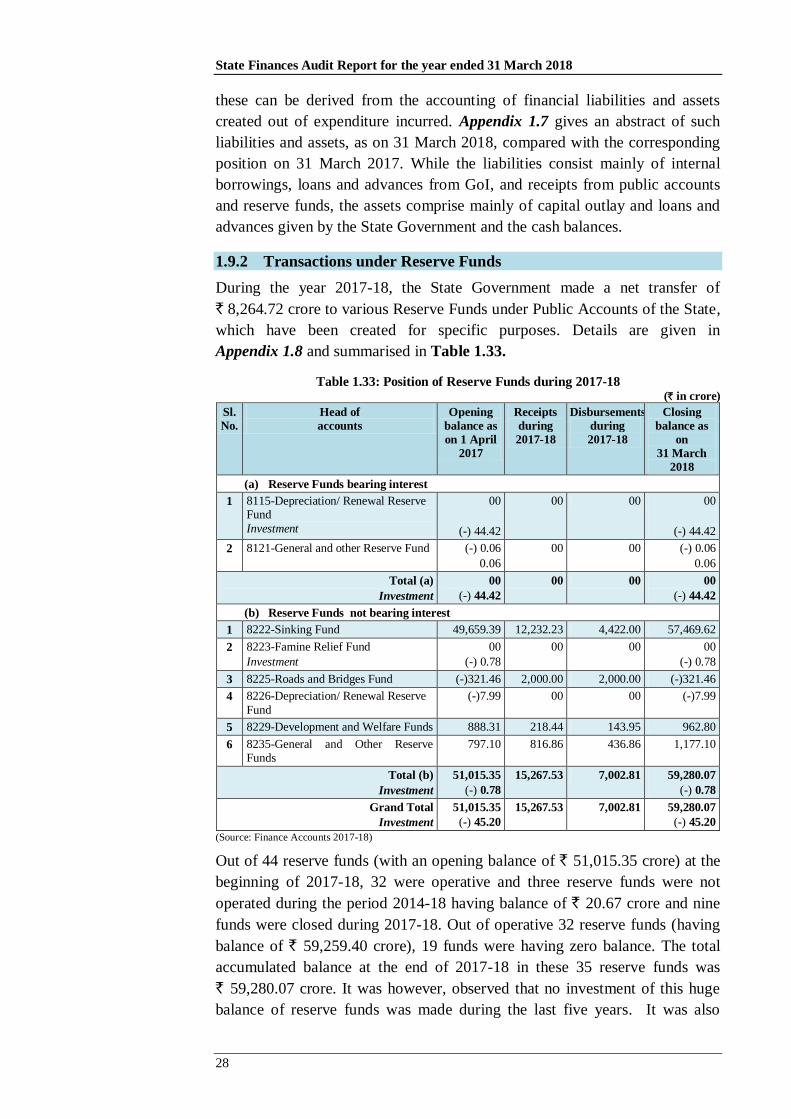

vkjf{kr fuf/k;ksa ds vUrxZr ysunsu

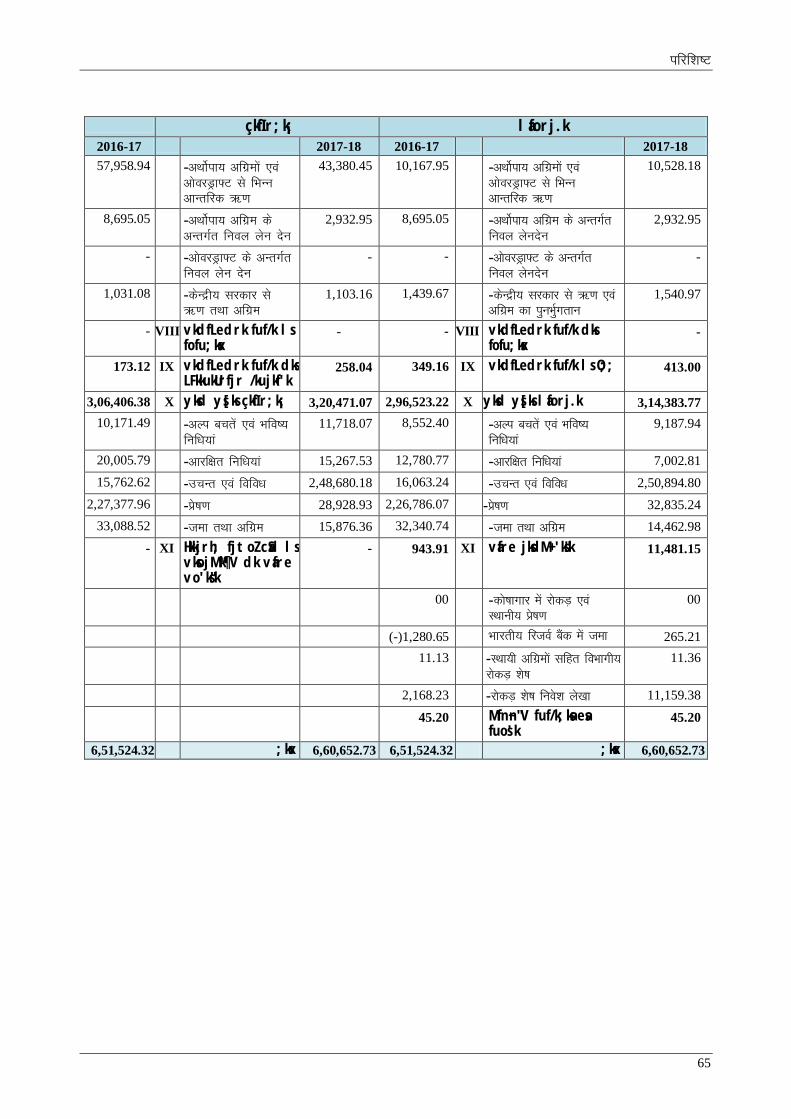

o’kZ 2017-18 ds vUr esa 35 vkjf{kr fuf/k;ksa esa dqy ` 59,280.07 djksM+ dk lafpr vo'ks’k FkkA

;|fi] jkT; ljdkj }kjk vkjf{kr fuf/k;ksa ds lkis{k iznf'kZr ysu nsu dsoy iqLrd izfof’V;k¡ gh

Fkha] tks vkjf{kr fuf/k;ksa ds ltu ,oa lapkyu ds ewyHkwr fopkj/kkjk dk mYya?ku djrh gSaA nks

vlapkfyr vkjf{kr fuf/k;ksa ds vfrfjDr] ftuesa ` 45.20 djksM+ dk fuos'k n'kdksa iwoZ fd;k x;k

Fkk] bu vkjf{kr fuf/k;ksa ds bl vR;f/kd vo'ks’k dk dksbZ fuos'k ugha fd;k x;kA fof'k’V

vkjf{kr fuf/k;ksa ds lkis{k _.kkRed rFkk MsfcV vo'ks’kksa dks lesfdr fuf/k ls fofu;ksx }kjk

fofu;ferhdj.k djk;s tkus dh vko';drk gSA

laLrqfr% foRr foHkkx dks vkjf{kr fuf/k;ksa ds vUrxZr ysunsu ,oa vo'ks’kksa dk

j[k& j[kko iqLrd izfof’V;ksa ds ek/;e ls fd;s tkus dh leh{kk djuh pkfg;s rFkk udn

ys[kkadu ds fl)karksa dk ikyu Hkkjrh; fjtoZ cSad ds lkFk vo'ks’kksa ds okLrfod fuos'k ds

ek/;e ls djuk pkfg,A

(izLrj 1.9.2)

fu{ksi fuf/k

ckjgosa foRr vk;ksx dh laLrqfr;ksa ds vuqlkj jkT; ljdkj dks cdk;k nkf;Roksa ds ifjgkj gsr q

lesfdr fu{ksi fuf/k ¼l-fu-fu-½ dk ltu djuk pkfg,A Hkkjrh; fjtoZ cSad] tks buds lapkyu

ds fy, mRrjnk;h gS] ds fn'kk&funsZ'kkssa ds vuqlkj fiNys foRrh; o’kZ ds vUr esa cdk;k nkf;Roksa

ds 0.5 izfr'kr dk U;wure okf’kZd va'knku fd;k tkuk pkfg, FkkA rnuqlkj] jkT; ljdkj }kjk

o’kZ 2017-18 esa bl fuf/k esa ` 2,116.12 djksM+ dh jkf'k ¼fnukad 31 ekpZ 2017 dks cdk;k

nkf;Ro ` 4,23,223.78 djksM+ dk 0.5 izfr'kr ½ dk va'knku fd;k tkuk visf{kr FkkA rFkkfi]

jkT; ljdkj us bu fn'kkfunsZ'kksa ds lanHkZ esa l-fu-fu- ¼ekStwnk fuf/k dks lfEefyr djrs gq;s½ dh

LFkkiuk ds fy, dksbZ dk;Zokgh ugha dhA

o"kZ 2017-18 esa jkT; ljdkj us ` 12,232.23 djksM+ dk çko/kku fd;k vkSj iqLrdh;

gLrkUrj.k ds }kjk fu{ksi fuf/k esa gLrkarfjr fd;kA fu{ksi fuf/k esa ls] fcuk fdlh udn cfgiZzokg

ds] cktkj _.k ds iquHkqZxrku ds lerqY; ` 4,422 djksM+ dh jkf'k dks lesfdr fuf/k ds vUrxZr

jktLo çkfIr;ksa ds vUrxZr vUrfjr fd;k x;kA fu{ksi fuf/k ls jktLo [kkrs esa vUrfjr

/kujkf'k ¼` 4,422 djksM+½ ls o’kZ ds jktLo vkf/kD; esa vfr'k;rk gqbZA vxzsrj] 31.03.2018 dks

fu{ksi fuf/k ds vfUre vo“ks’k ` 57,469.61 djksM+ dk fuos'k ugha fd;k x;kA blds vfrfjDr]

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

x

fu{ksi fuf/k esa ` 7,810 djksM+ ds fuoy of) ds ifj.kkeLo:i jkT; dh cdk;k nsunkfj;ksa esa

mruh gh jkf'k ds leku of) gqbZA

laLrqfr% jkT; ljdkj }kjk ckjgosa foRr vk;ksx dh laLrqfr;ksa dks Lohdkj djrs gq;s vkj-ch-vkbZ-

}kjk fuos'k fd, tkus okys lesfdr fu{ksi fuf/k dk xBu fd;k tkuk pkfg;sA blds vfrfjDr]

fuf/k ls LFkkukUrfjr /kujkf'k dks jktLo çkfIr ugha ekuk tkuk pkfg,A fdlh Hkh fLFkfr esa]

jkT; ljdkj dks ;g lqfuf'pr djuk pkfg, fd fuf/k dh 'ks"k jkf'k okLro esa fuos'k dh tk;s

vkSj og ek= iqLrd çfof"V u gksA

(izLrj 1.9.2.1)

jkT; vkink vuqfØ;k fuf/k (jk-vk-v-fu-)

Hkkjr ljdkj ds fn'kkfunsZ'kksa ds fo:) fd jk-vk-v-fu- dks ^^C;kt lfgr vkjf{kr fuf/k^^ ds

vUrxZr lapkfyr djuk pkfg;s] jkT; ljdkj jk-vk-v-fu- dks ^^C;kt jfgr vkjf{kr fuf/k^^ ds

vUrxZr lapkfyr dj jgh gSA vxzsrj] fuf/k ds vo“ks’k ek= iqLrdh; izfof’V;ka gS ftudk

jk-vk-v-fu- ds fu/kkZfjr fn'kkfunsZ'kksa ds vuqlkj] fuos'k ugha fd;k x;kA jkT; ljdkj }kjk

o’kZ 2017-18 ds fy;s ` 37.22 djksM+ ds C;kt dk Hkqxrku ugha fd;k x;kA

vxzsrj] o"kZ 2017-18 esa jkT; ljdkj us `119.67 djksM+ dh jkf'k jk"Vªh; vkink vuqfØ;k fuf/k

ls izkIr dh] ftls eq[; “kh’kZ 1601& Hkkjr ljdkj ls lgk;rk vuqnku ds vUrxZr iqLrkafdr

fd;k x;k ,oa izkfIr ds :i esa ekuk x;kA rFkkfi] o"kZ 2017-18 esa jk"Vªh; vkink vuqfØ;k

fuf/k ls izkIr ` 119.67 djksM+ dk vuqnku jkT; vkink vuqfØ;k fuf/k esa LFkkukUrfjr ugha dh

xbZA ifj.kkeLo:i] ` 119.67 djksM+ ls jkT; ljdkj ds jktLo vkf/kD; esa vfr'k;rk ,oa

jktdks’kh; ?kkVs esa U;wurk gqbZ gSA

laLrqfr% jkT; ljdkj }kjk jk-vk-v-fu- dh “ks’k jkf'k dks eq[; “kh’kZ 8121&lkekU; rFkk vU;

vkjf{kr fuf/k ^^C;kt lfgr vkjf{kr fuf/k** dh Js.kh esa LFkkukUrfjr fd;k tkuk pkfg, ,oa jk-

vk-v-fu- ds fn'kkfunsZ'kksa vuqlkj vftZr C;kt fuf/k esa tek fd;k tkuk pkfg,A jkT; ljdkj

dks fn'kkfunsZ'k esa fu/kkZfjr “kSyh esa fuf/k ds vo'ks"kksa dk fuos'k djus dh Hkh vko';drk gSA

(izLrj 1.9.2.3)

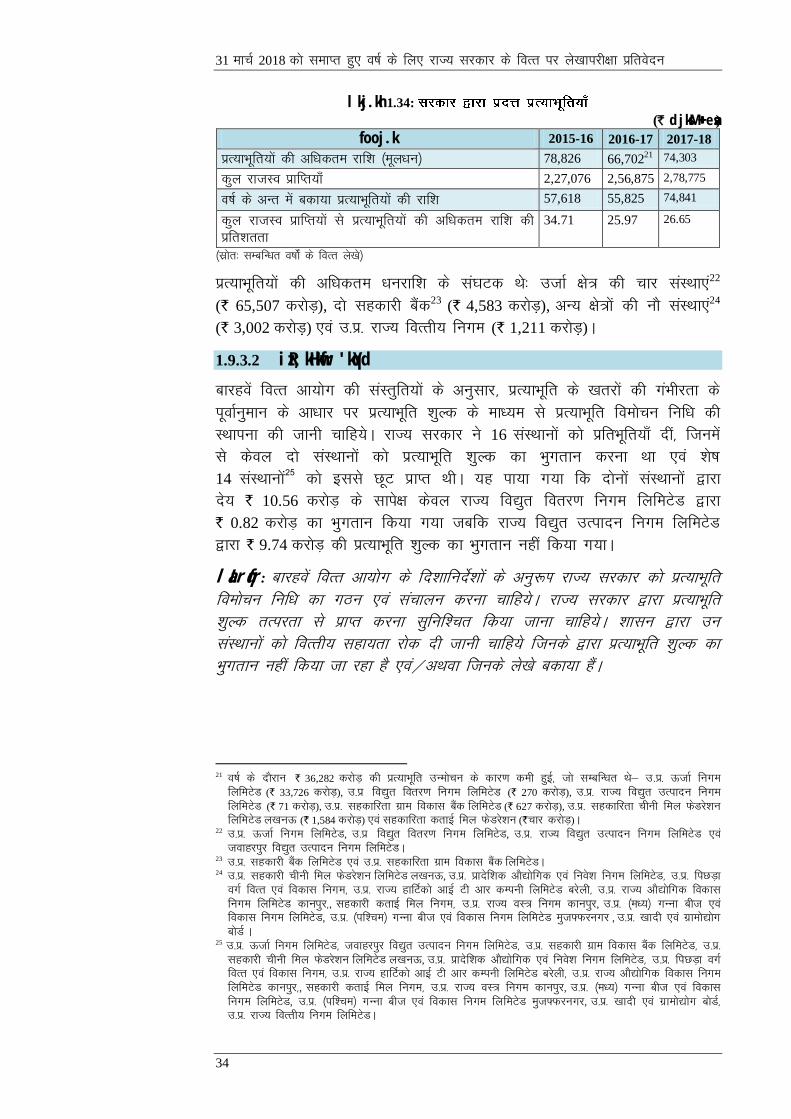

vkdfLed ns;rk,a&izR;kHkwfr;ksa dh fLFkfr

ckjgosa foRr vk;ksx dh laLrqfr;ks ds vk/kkj ij jkT; ljdkj }kjk izR;kHkwfr foekspu fuf/k dk

ltu ugha fd;k x;kA jkT; ljdkj }kjk ` 290.75 djksM+ dk U;wure okf"kZd vfHknku ¼o"kZ

2017-18 ds izkjEHk dh cdk;k izR;kHkwfr ` 58,149.03 djksM dk 0.5 izfr'kr½ fd;k tkuk

visf{kr Fkk] tks ugha fd;k x;kA blds dkj.k ` 290.75 djksM+ lss jktLo vkf/kD; esa vfr'k;rk

rFkk jktdks’kh; ?kkVs esa U;wurk gqbZ gSA

jkT; ljdkj us 16 laLFkkuksa dks izfrHkwfr;k¡ nha] ftuesa ls dsoy nks laLFkkuksa dks izR;kHkwfr “kqYd

dk Hkqxrku djuk Fkk ,oa “ks’k 14 laLFkkuksa dks blls NwV izkIr FkhA ;g ik;k x;k fd

nksuksa laLFkkuksa }kjk ns; ` 10.56 djksM+ ds lkis{k jkT; fo|qr mRiknu fuxe fyfeVsM us

` 9.74 djksM+ dh izR;kHkwfr “kqYd dk Hkqxrku ugha fd;kA

laLrqfr: ckjgosa foRr vk;ksx ds fn'kk&funsZ'kksaa ds vuq:Ik jkT; ljdkj dks izR;kHkwfr foekspu

fuf/k dk xBu ,oa lapkyu djuk pkfg;sA jkT; ljdkj }kjk izR;kHkwfr “kqYd rRijrk ls izkIr

dk;Zdkjh lkj

xi

djuk lqfuf'pr fd;k tkuk pkfg;sA “kklu }kjk mu laLFkkuksa dks foRrh; lgk;rk jksd nh

tkuh pkfg;s ftuds }kjk izR;kHkwfr “kqYd dk Hkqxrku ugha fd;k tk jgk gS ,oa@vFkok ftuds

ys[ks cdk;k gSaA

(izLrj 1.9.3)

vf/kd gq, O;;ksa ds fofu;ferhdj.k dh vko';drk

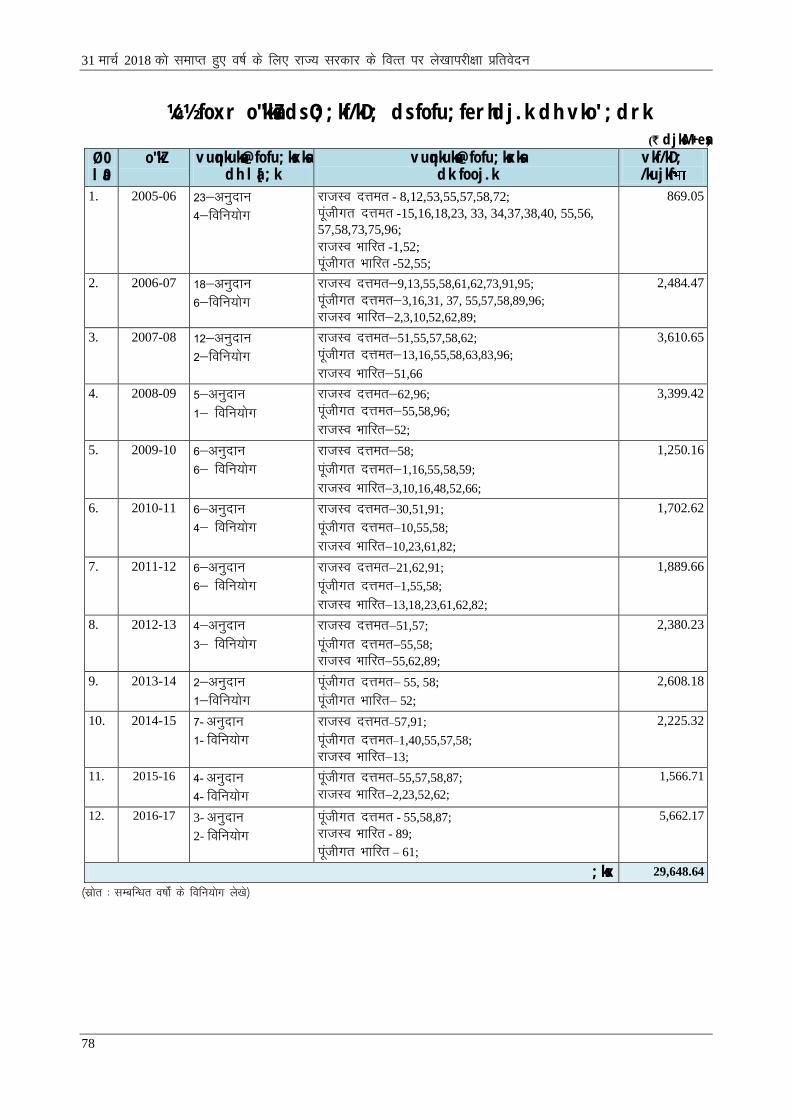

foRrh; o’kZ 2017-18 ds nkSjku] nks vuqnkuksa rFkk nks fofu;ksxksa ds vUrxZr jkT; fo/kkf;dk }kjk

izkf/k—r /kujkf'k ls ` 1,337.17 djksM+ dk O;;kf/kD; gqvkA o’kZ 2005-06 ls 2016-17 ls

lEcfU/kr 96 vuqnkuksa ,oa 40 fofu;ksxksa ds vUrxZr O;;kf/kD; ` 29,648.64 djksM+ dk

fofu;ferhdj.k jkT; fo/kkf;dk }kjk vHkh Hkh fd;k tkuk “ks’k gSA ;g lafo/kku ds vuqPNsn 204

rFkk 205 dk mYya?ku gS] tks izko/kkfur djrk gS fd jkT; fo/kkf;dk }kjk cuk;h x;h fof/k }kjk

fd;s x;s fofu;kstu ds vfrfjDr lesfdr fuf/k ls dksbZ Hkh /kujkf/k vkgfjr ugha dh tk

ldsxhA ;g ctVh; rFkk foRRkh; fu;a=.k iz.kkyh dks fu’izHkkfor djrk gS rFkk yksd lalk/kuksa ds

izcU/ku esa foRrh; vuq'kklughurk dks izksRlkfgr djrk gSA

laLrqfr% jkT; ljdkj }kjk ;g lqfu'fpr djuk pkfg;s fd O;;kf/kD; ds lHkh orZeku izdj.kksa

dks fofu;fer djus gsrq jkT; fo/kf;dk ds le{k rRdky izLrqr fd;k tk;A jkT; ljdkj }kjk

O;;kf/kD; ds dkj.kksa dh tk¡p dh tkuh pkfg;s ,oa mRrjnkf;Ro fu/kkZfjr fd;k tkuk pkfg;sA

iqu% dks’kkf/kdkfj;ksa dks funsZf'kr fd;k tkuk pkfg;s fd os ctV izko/kkuksa ls vf/kd O;; djus

dh vuqefr u nsa ,oa Hkfo’; esa ,sls O;;kf/kD; iw.kZr% lekIr fd;k tkuk pkfg;sA

(izLrj 2.2.1)

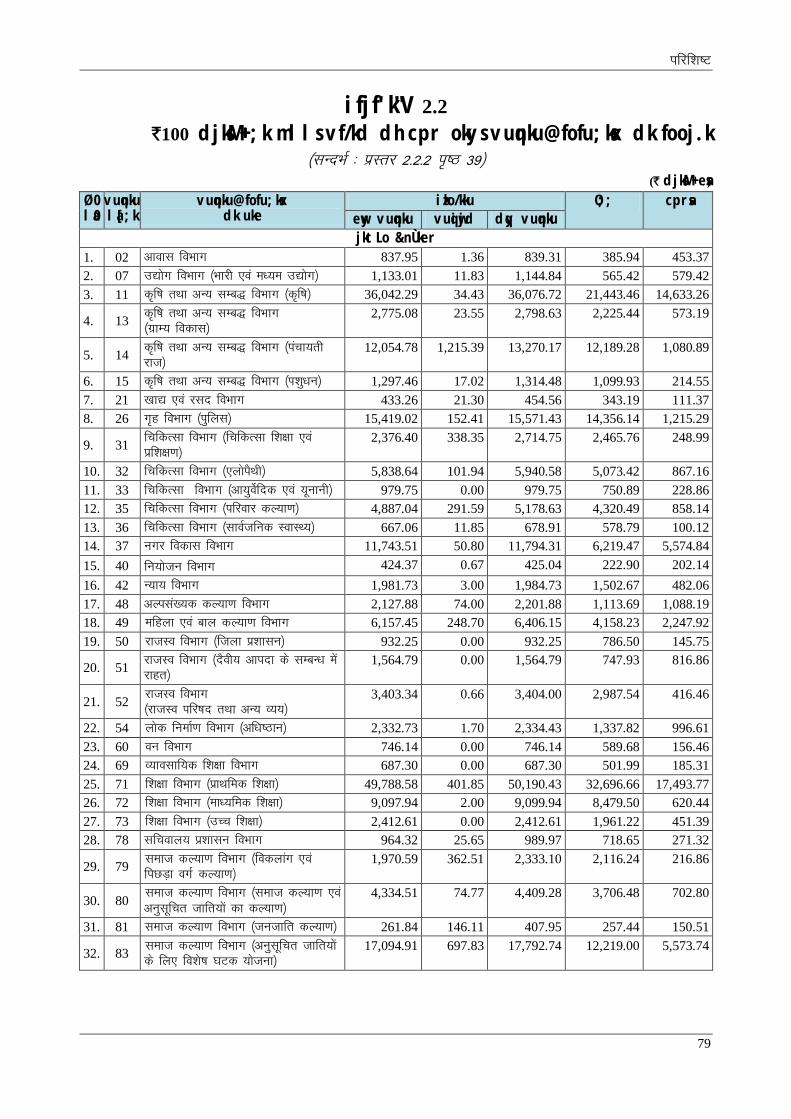

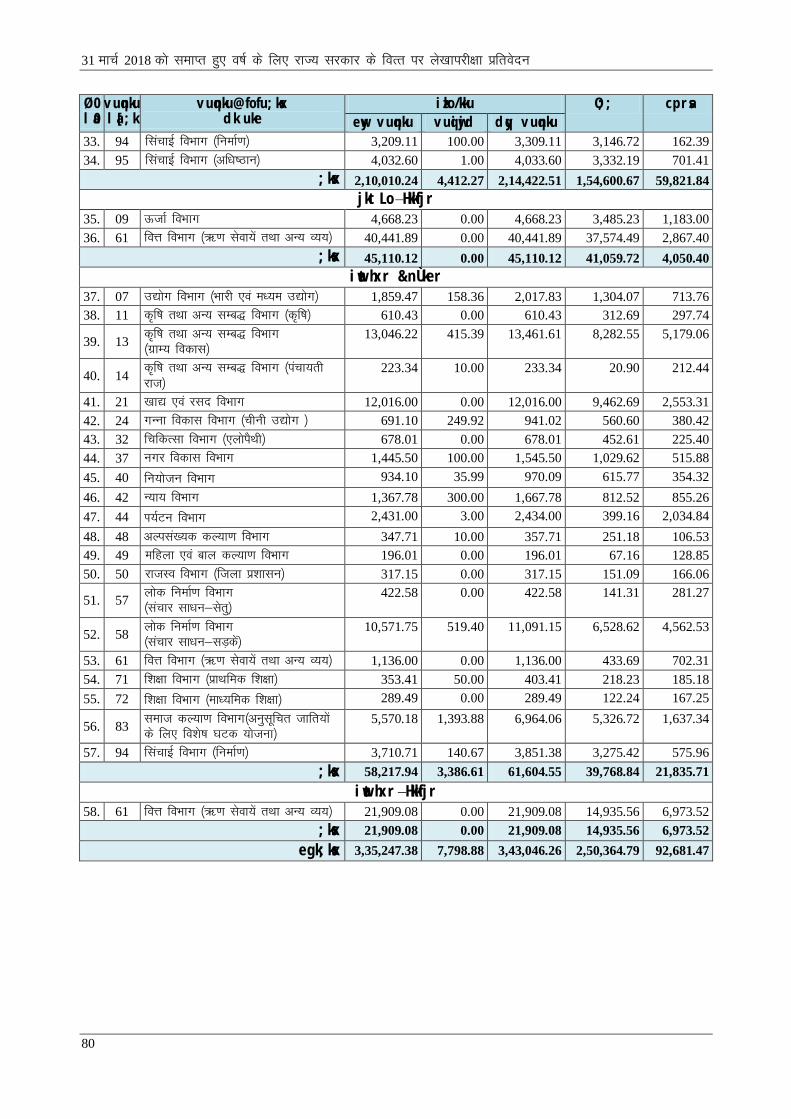

cprsa

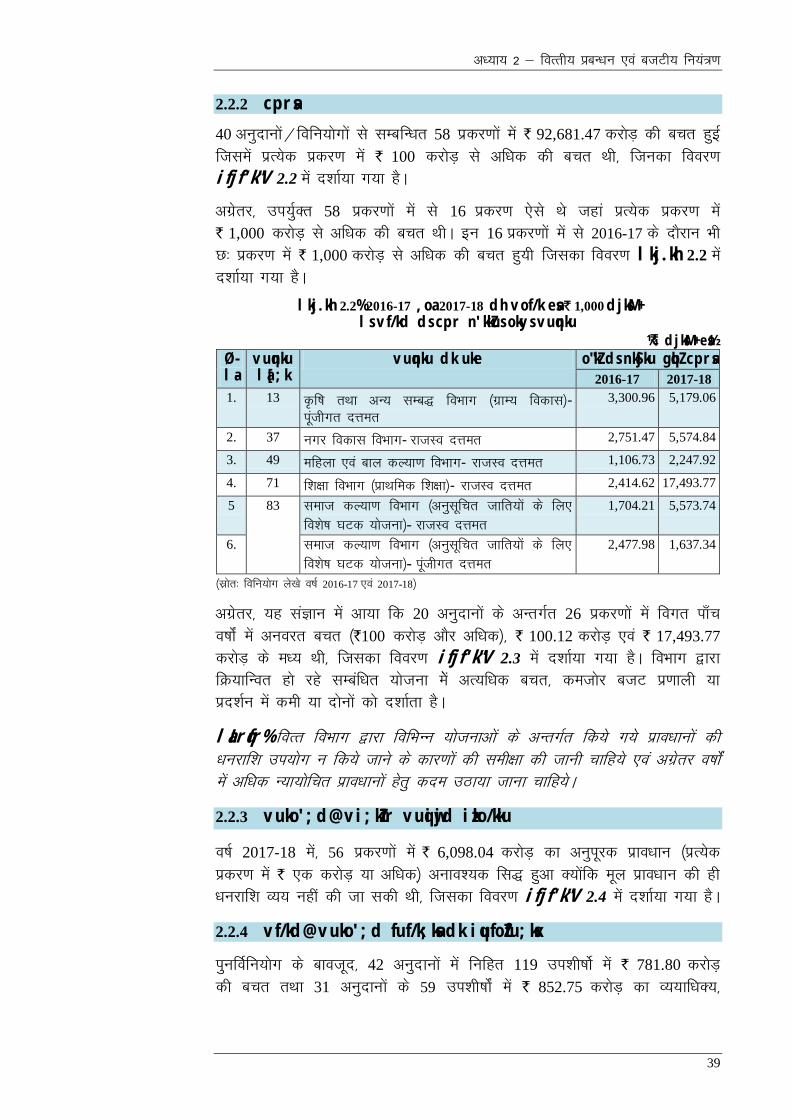

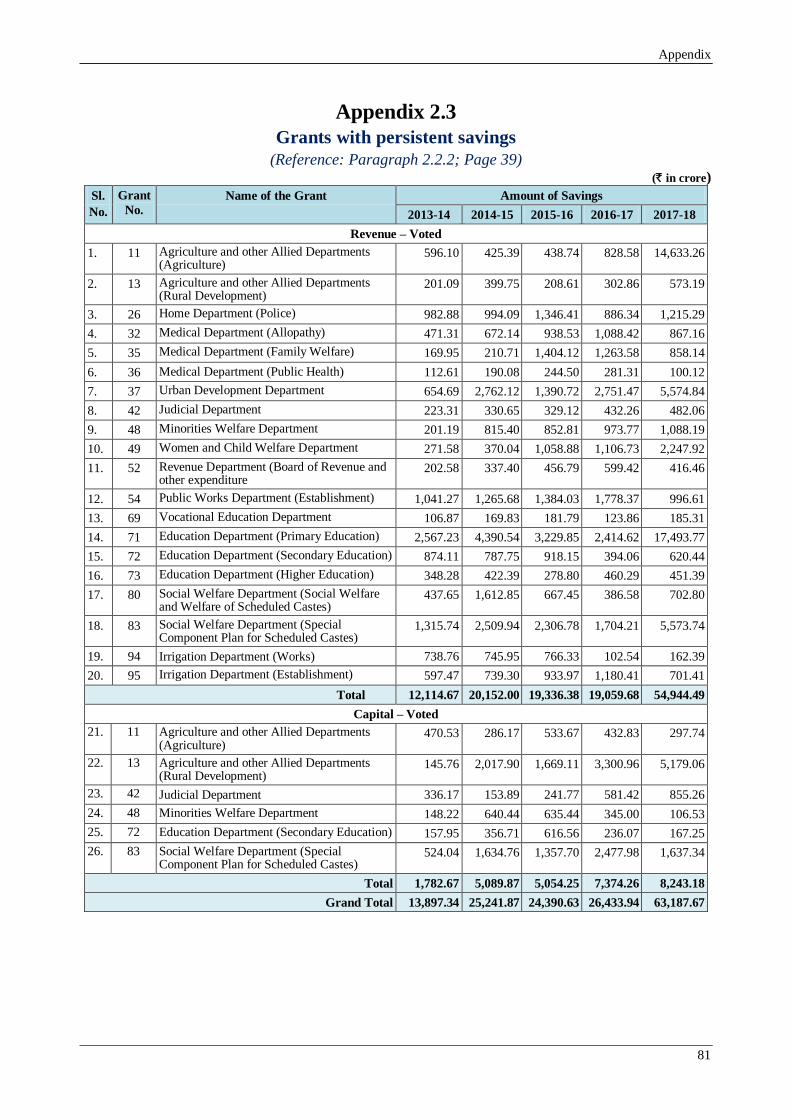

40 vuqnkuksa@fofu;ksxksa ls lEcfU/kr 58 izdj.kksa esa ` 92,681.47 djksM+ dh cpr gqbZ ftlesa

izR;sd izdj.k esa ` 100 djksM++ ls vf/kd dh cpr FkhA vxzsrj] mi;ZqDr 58 izdj.kksa esa ls

16 izdj.k ,sls Fks tgka izR;sd izdj.k esa ` 1,000 djksM++ ls vf/kd dh cpr FkhA 20 vuqnkuksa

ds vUrxZr 26 izdj.kksa esa foxr ik¡p o"kksZa ls vuojr cpr ¼`100 djksM+ vkSj vf/kd½]

` 100.12 djksM++ ,oa ` 17,493.77 djksM+ ds e/; FkhA

laLrqfr% foRr foHkkx dks fofHkUu ;kstukvksa ds vUrxZr fd;s x;s izko/kkuksa dh /kujkf'k mi;ksx

u fd;s tkus ds dkj.kksa dh leh{kk dh tkuh pkfg;s ,oa vxzsrj o’kksZa esa vf/kd U;k;ksfpr

izko/kkuksa gsrq dne mBk;k tkuk pkfg;sA

(izLrj 2.2.2)

vkdfLedrk fuf/k ls vfxze &izfriwfrZ ugha dh x;h

31 ekpZ 2018 rd vkdfLedrk fuf/k ls ` 463.08 djksM+ dh /kujkf'k vkgfjr dh x;h ftldh

izfriwfrZ ugha dh x;h] ftlesa iwoZ o’kZ dk ` 300 djksM+ dk vo'ks’k izfriwfrZ lfEefyr gSA

o’kZ 2017-18 esa ` 413 djksM+ dh /kujkf'k dk forj.k fd;k x;k ftlesa ls ` 125 djksM+

o’kZ 2017-18 esa m-iz-lgdkjh phuh feYl la?k fyfeVsM dks _.k gsrq vkgfjr fd;k x;k ftldh

izfriwfrZ 2018-19 ds vuqiwjd vuqnku ls dh tkuh FkhA o’kZ 2017-18 esa vkgfjr vo'ks’k cdk;k

vfxze ` 288 djksM+ ds lkis{k ` 249.92 djksM+ dh /kujkf'k dh izfriwfrZ 31 ekpZ 2018 rd dh

x;hA

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

xii

laLrqfr% jkT; ljdkj dks ;g lqfuf'pr djuk Pkkfg;s fd vkdfLedrk fuf/k ls fy;s x;s vfxze

dh izfriwfrZ le; ls dh tk;A

(izLrj 2.2.9)

oS;fDrd tek ¼ih-Mh-½ [kkrk

jkT; ljdkj }kjk foRrh; o’kZ 2017-18 esa oS;fDrd tek ¼ih-Mh-½ [kkrksa esa tek ,oa laforj.kksa

dk fooj.k miyC/k ugha djk;k x;kA 31 ekpZ 2018 dks 1,328 ih-Mh- [kkrksa esa vo'ks’k

` 4,688.14 djksM+ esa ls ` 2,460.82 djksM+ dh jkf'k 31 ih-Mh- [kkrs eq[; 'kh’kZ 8342&vU;

tek&120&fofo/k tek ls lEcfU/kr Fkh] tks ih-Mh- [kkrksa ds fy, fufnZ’V ys[kk'kh’kZ ugha gSA

vxzsrj] lkafgfrd izko/kkuksa ds foijhr] ` 108.70 djksM+ dh jkf'k 641 ih-Mh- [kkrksa esa vfu;fer

:i ls tek Fkh] tcfd ;s ih-Mh- [kkrs rhu o’kksZa ls vf/kd le; ls vlapkfyr FksA ;g izFkk

fo/kkf;dk ds vfHkizk; dk mYya?ku djrh gS ftldk mn~ns'; ;g lqfuf'pr djuk gS fd mlds

}kjk foRrh; o’kZ gsrq vuqeksfnr /kujkf'k dk O;; mlh foRrh; o’kZ esa dj fy;k tk;sA iqu%'p]

ih-Mh- [kkrksa esa vo'ks’k jkf'k;ksa dk feyku u djk;k tkuk rFkk bu ih-Mh- [kkrksa esa vO;f;r

vo'ks’kksa dks jkT; ds lesfdr fuf/k esa foRrh; o’kZ dh lekfIr ds igys varfjr u fd;k tkuk

yksd fuf/k ds nq:i;ksx] diV ,oa xcu dks izoRr djrk gSA

laLrqfr% foRr foHkkx }kjk lHkh ih-Mh- [kkrksa dh leh{kk ;g lqfuf'pr djus ds fy;s dh tkuh

pkfg, fd bu ih-Mh- [kkrksa esa vuko';d iM+h lHkh /kujkf'k;ksa dks rRdky lesfdr fuf/k esa

izsf’kr fd;k tk;A vxzsRkj] foRrh; fu;ekoyh esa fufgr funsZ'kksZa dks foRr foHkkx }kjk nksgjkrs gq;s

;g lqfuf'pr fd;k tkuk pkfg, fd fu;eksa ds vuqlj.k djus esa vlQy jgs foHkkxh;

vf/kdkfj;ksa ds fo:) mfpr dk;Zokgh dh tk;A

(izLrj 3.1)

miHkksx izek.k&i=ksa dks izsf"kr u fd;k tkuk

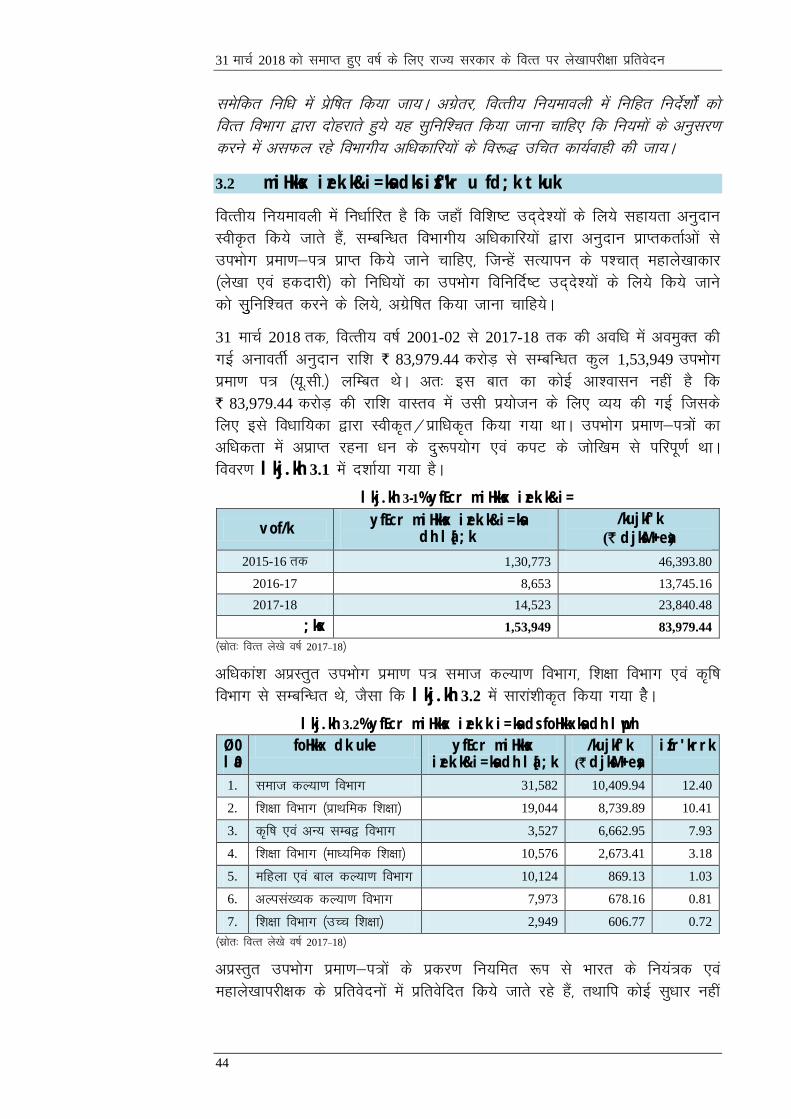

31 ekpZ 2018 rd foRrh; o’kZ 2001-02 ls 2017-18 rd dh vof/k esa voeqDr dh xbZ

vukorhZ vuqnku jkf'k ` 83,979.44 djksM+ ls lEcfU/kr dqy 1,53,949 miHkksx izek.k&i=

¼;w-lh-½ yfEcr FksA vr% bl ckr dk dksbZ vk'oklu ugha gS fd ` 83,979.44 djksM+ dh jkf'k

okLro esa mlh iz;kstu ds fy, O;; dh xbZ ftlds fy, bls fo/kkf;dk }kjk Lohd`r@izkf/kdr

fd;k x;k FkkA miHkksx izek.k&i=ksa dk vf/kdrk esa vizkIr jguk /ku ds nq:Ik;ksx ,oa diV ds

tksf[ke ls ifjiw.kZ FkkA

laLrqfr% jkT; ljdkj }kjk Hkkjr ds fu;a=d&egkys[kkijh{kd ds o’kZ 2018 ds mRrj izns'k

ljdkj ls lEcfU/kr izfrosnu la[;k 1 ds izLrj la[;k 3.11 dh laLrqfr ij dk;Zokgh fd;k

tkuk pkfg, ,oa miHkksx izek.k&i=ksa ds le; ls izkfIr rFkk u;k vuqnku voeqDr djus ls iwoZ

lHkh yfEcr miHkksx izek.k i=ksa ds vfoyEc izkfIr dh leh{kk fd;s tkus dh fuxjkuh gsrq foHkkx

dh vkUrfjd fu;a=.k ra= lqfuf'pr dh tkuh pkfg,A

(izLrj 3.2)

dk;Zdkjh lkj

xiii

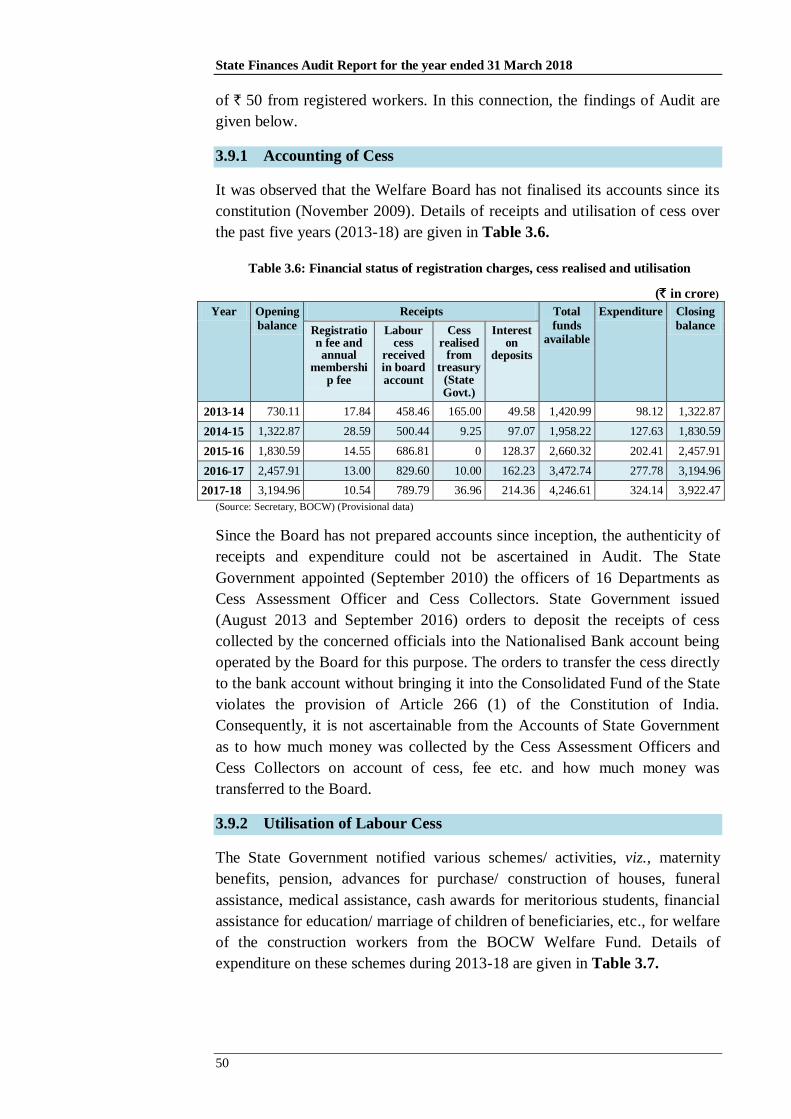

Hkou ,oa vU; lfUuekZ.k Jfed ¼ch-vks-lh-MCyw-½ dY;k.k midj

ch-vks-lh-MCyw- cksMZ }kjk xBu ¼uoEcj 2009½ ls gh vius ys[ks dks vfUre #i ugha fn;k x;k]

blfy, ys[kkijh{kk esa vk; ,oa O;; dh izkekf.kdrk lqfuf'pr ugha dh tk ldhA

ljdkj }kjk tkjh vkns'k ¼vxLr 2013 ,oa flrEcj 2016½] midj dks jkT; dh lesfdr fuf/k

esa yk;s fcuk lh/ks cSad [kkrs esa LFkkURkkrj.k fd;k tkuk Hkkjrh; lafo/kku ds vuqPNsn 266¼1½ dk

mYya?ku gSA ifj.kkeLo:i] jkT; ljdkj ds ys[ks ls ;g lqfuf'pr ugha fd;k tk ldrk gS fd

midj] “kqYd vkfn dh fdruh /kujkf'k midj fu/kkZj.k vf/kdkfj;ksa ,oa midj laxzg.kdrkZ }kjk

laxzg.k fd;k x;k ,oa fdruh /kujkf'k cksMZ dks LFkkukUrfjr dh x;hA

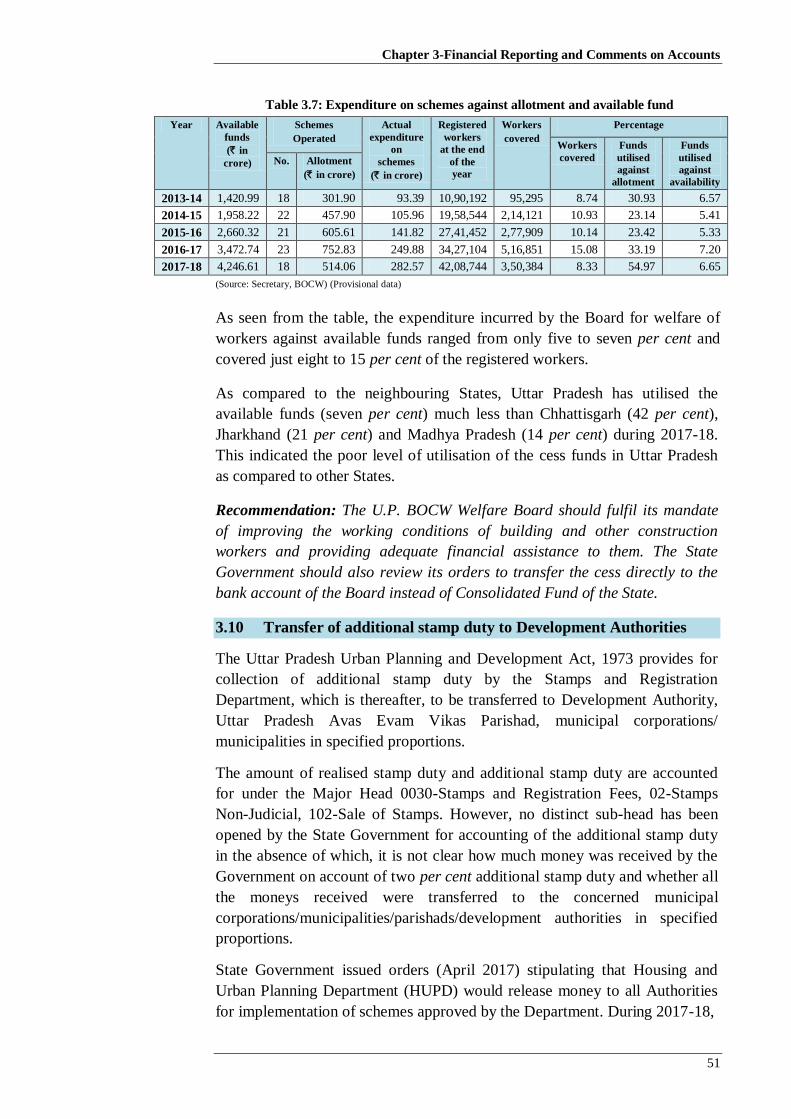

cksMZ }kjk miyC/k djk;s x;s vufUre vkadM+s ds vuqlkj] CkksMZ }kjk Jfedksa ds dY;k.k ds fy;s

miyC/k /kujkf'k ds lkis{k ikap ls lkr izfr'kr O;; fd;k x;k ,oa vkB ls 15 izfr'kr

iathd`r Jfedksa dks vkPNkfnr fd;k x;kA

laLrqfr% m-iz- ch-vks-lh-MCyw- dY;k.k cksMZ }kjk Hkou ,oa lfUuekZ.k Jfedksa dh dk;Z dh n'kk esa

lq/kkj ,oa mUgsa Ik;kZIr foRrh; lgk;rk fn;s tkus ds vf/kns'k dh iwfrZ fd;k tkuk pkfg,A

midj dks] lesfdr fuf/k ds ek/;e ls] ds LFkku ij cksMZ ds cSad [kkrs esa lh/ks LFkkukUrj.k fd;s

tkus ds vius vkns'kksa dh jkT; ljdkj }kjk leh{kk Hkh dh tkuh pkfg,A

(izLrj 3.9)

fodkl izkf/kdj.kksa dks vfrfjDr LVkEi M~;wVh dk vUrj.k

jkT; ljdkj }kjk vfrfjDr LVkEi M~;wVh ds ys[kkadu ds fy, vyx ls mi “kh’kZ ugha [kksyk

x;k gS ftlds vHkko esa ;g Li’V ugha gS fd ljdkj }kjk nks izfr'kr vfrfjDr LVkEi M~;wVh ds

:Ik esa fdruh /kujkf'k izkIr dh x;h gS rFkk D;k izkIr leLr /kujkf'k;ksa dks lEcfU/kr uxj

fuxeksa@uxj ikfydkvksa@ifj’knksa@fodkl izkf/kdj.kksa dks fofuZfn’V vuqikr esa LFkkukUrfjr dj

fn;k x;kA

ljdkj }kjk fuxZr vkns'k ¼flrEcj 2013½ esa] vfrfjDr LVkEi M~;wVh dk 25 izfr'kr MsMhdsVsM

uxj ifjogu fuf/k ¼Mh-;w-Vh-,Q-½ dks vUrj.k fd;k tkuk izkf/kd`r fd;k x;kA ;g mRrj izns'k

uxj ;kstuk ,oa fodkl vf/kfu;e] 1973 ds izko/kkuksa ds foijhr Fkk ftlesa bl rjg ds

foHkktu dk izko/kku ugha FkkA

laLrqfr% jkT; ljdkj }kjk lqfuf'pr fd;k tkuk pkfg, fd vfrfjDr LVkEi M~;wVh dh izkfIr;k¡

,oa m-iz- uxj ;kstuk ,oa fodkl vf/kfu;e esa fofufnZ’V izkf/kdj.kksa@fuxeksa vkfn dks

LFkkukUrfjr /kujkf'k] ys[ks esa iw.kZ:Iks.k ,oa ikjnf'kZrk ls iznf'kZr gksA vfrfjDr LVkEi M~;wVh dh

25 izfr'kr /kujkf'k MsMhdsVsM uxj ifjogu fuf/k dks gLrkarj.k lEcU/kh vkns'k] tks vf/kfu;e

ds izko/kkuksa ds izfrdwy gS] dh leh{kk Hkh jkT; ljdkj }kjk dh tkuh pkfg,A

(izLrj 3.10)

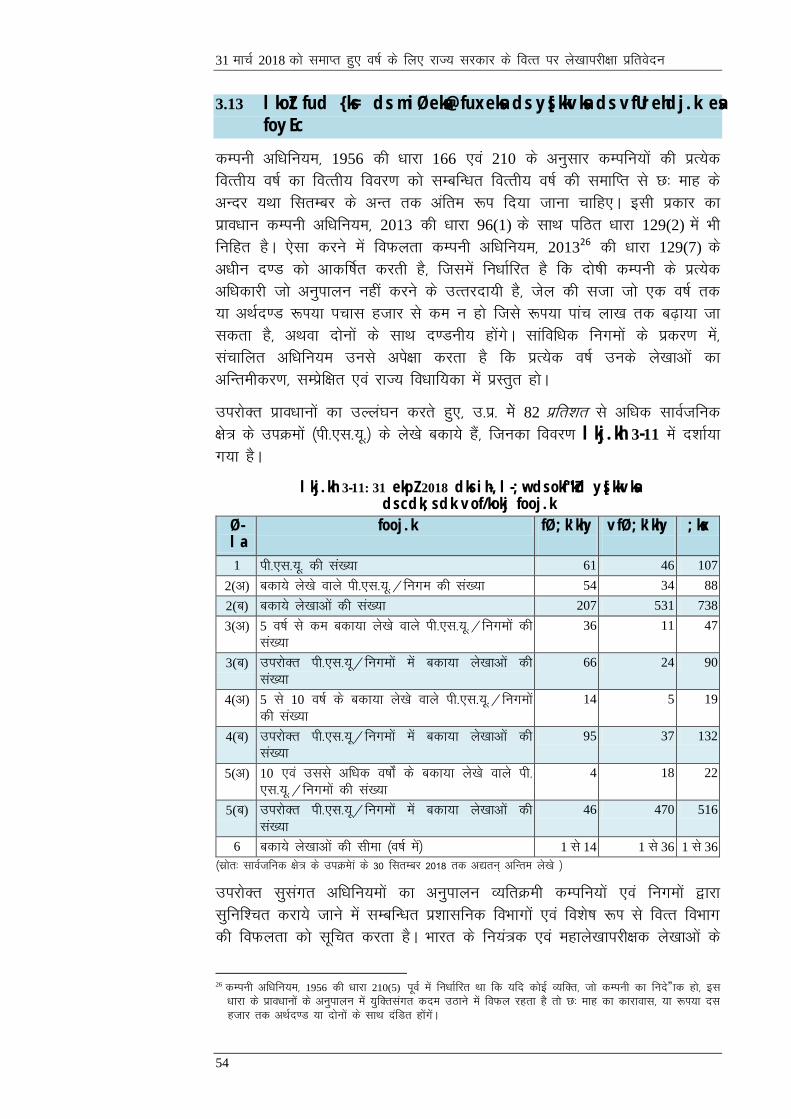

lkoZtfud {ks= ds miØeksa@fuxeksa ds ys[kkvksa ds vfUrehdj.k esa foyEc

54 fØ;k'khy ih-,l-;w-@fuxeksa ¼207 ys[ks½ ,oa 34 vfØ;k'khy ih-,l-;w-@fuxeksa ¼531 ys[ks½ ds

ys[ks ,d ls 36 o’kksZa ls cdk;s esa FksA jkT; ljdkj }kjk ctVh; lgk;rk ` 57,780-21 djksM+

¼bfDoVh% ` 19,605-36 djksM+] _.k% ` 4,581-27 djksM+] iwathxr vuqnku ` 11,210-69 djksM+]

vU; vuqnku% ` 9,773-86 djksM+ ,oa lfClMh% ` 12,609-03 djksM+½ rFkk izfrHkwfr ` 42,527-09

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

xiv

djksM+ 24 fØ;k'khy dEifu;ksa@lkafof/kd fuxeksa dks ys[kkvksa ds cdk;k vof/k ds nkSjku fn;k

x;kA bl izdkj bu ih-,l-;w- }kjk foRrh; lgk;rk ds fy;s dh x;h ekax dh okLrfodrk dk

fu.kZ; djus ds fy;s ys[kkvksa ds vHkko esas Hkh] foRr foHkkx }kjk bu ih-,l-;w- dks ctVh;

lgk;rk fu;fer :Ik ls miyC/k djk;k x;kA jkT; ljdkj dks O;; dh mi;ksfxrk ns[kus dh

vko';drk gSA

laLrqfr% foRr foHkkx dks mu lHkh ih-,l-;w-ds izdj.kksa dh leh{kk djuh pkfg, ftuds ys[ks

cdk;k gSa ,oa lqfuf'pr djuk pkfg, fd mfpr le;kUrxZr ys[ks orZekudkfyd cus ,oa mu

LkHkh izdj.kksa esa foRrh; lgk;rk dh leh{kk djuh pkfg, tgka ys[ks fujUrj cdk;k gSaA

(izLrj 3.13)

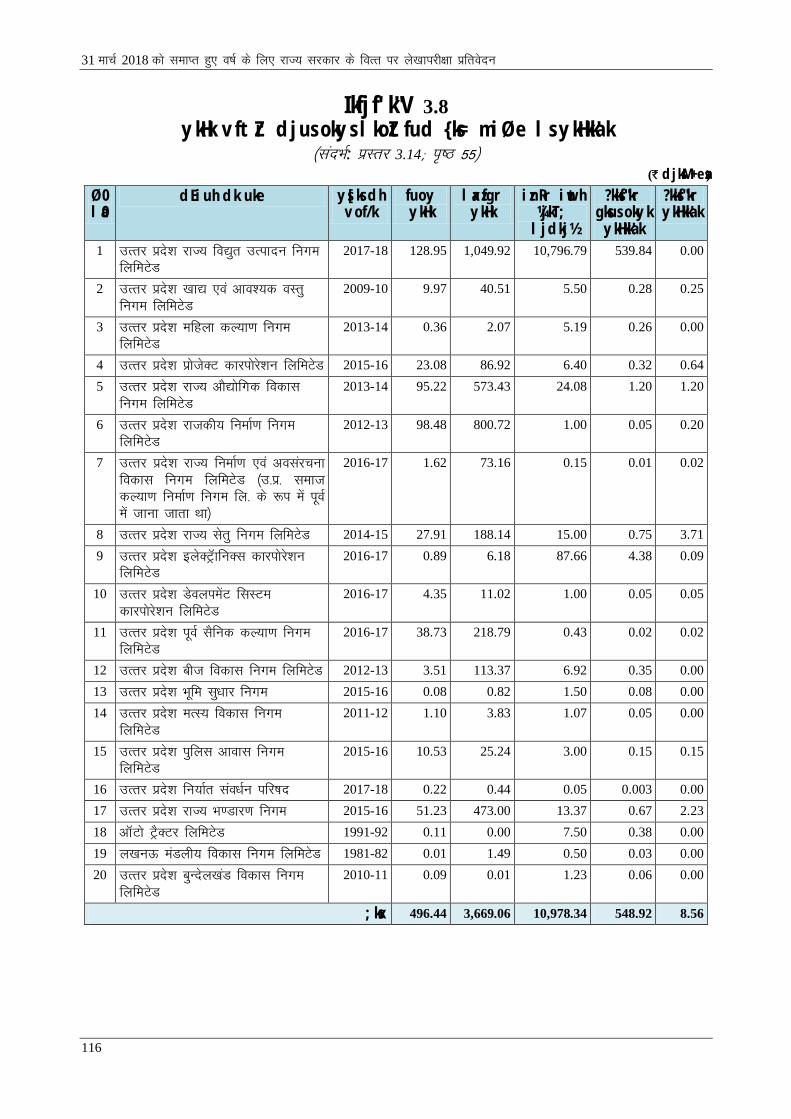

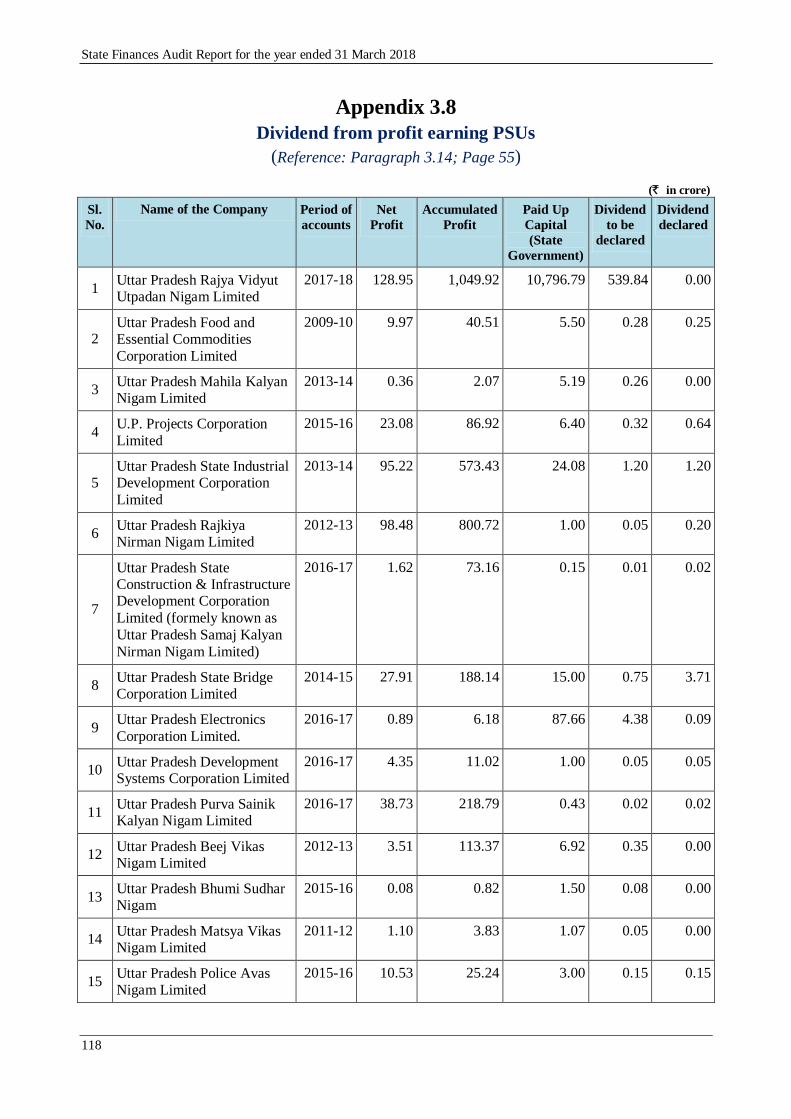

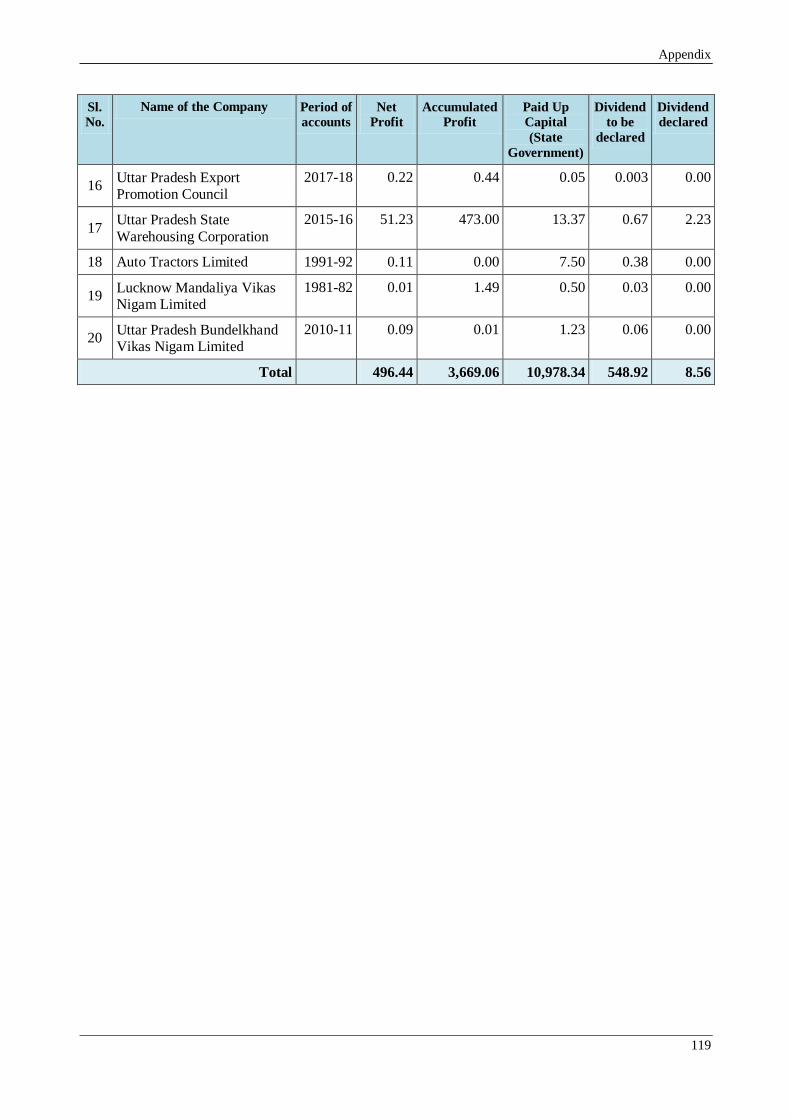

ykHkka'k ?kksf"kr u fd;k tkuk

jkT; ljdkj }kjk ,d ykHkka'k uhfr ftlds vUrxZr lHkh ykHk vftZr djus okyh lkoZtfud

{ks= ds miØeksa dks jkT; ljdkj }kjk iznRr va'kiwath ds ;ksxnku dk U;wure ikap izfr'kr

ykHkka'k Hkqxrku djuk pkfg,] ds foijhr ukS ih-,l-;w- us ` 540-36 djksM+ dk ykHkka'k ?kksf’kr ugha

fd;kA

laLrqfr% jkT; ljdkj }kjk lqfuf'pr fd;k tkuk pkfg, fd ykHk vftZr djus okys ih-,l-;w-

}kjk o’kZ ds vUr rd fofufnZ’V ykHkka'k dks fuf'pr :Ik ls “kkldh; ys[ks esa tek fd;k tk;A

(izLrj 3.14)

ys[kkvksa esa vikjnf'kZrk

jkT; ljdkj ds foHkkxksa }kjk y?kq “kh’kZ 800 dk fu;fer :i ls ifjpkyu fd;k tk jgk gS]

ftls tc ys[ks esa mfpr y?kq “kh’kZ ugh fn;k x;k gks rHkh ifjpkfyr fd;k tkuk vHkh’V

gSA o’kZ 2017&18 esa izkfIr;ksa ds vUrxZr ` 18,383.80 djksM+ ,oa O;; ds vUrxZr

` 27,162.32 djksM+ y?kq 'kh’kZ 800 esa iqLrkafdr fd;k x;k ftlds ifj.kkeLo:i ysunsuksa eas

vikjnf'kZrk jghA

laLrqfr% foRr foHkkx }kjk y?kq 'kh’kZ 800 ds v/khu orZeku esa nf'kZr gks jgs lHkh enksa dh

foLrr leh{kk egkys[kkdkj ¼ys[kk ,oa gdnkjh½ ds ijke'kZ ls lapkfyr djuh pkfg, ,oa

lqfuf'pr djuk pkfg, fd Hkfo’; esa ,sls lHkh izkfIr;ksa ,oa O;;ksa dks ys[ks ds leqfpr “kh’kZ ds

v/khu iqLrkafdr fd;k tk;A

(izLrj 3.16)

jkT; ds iquxZBu ij vo'ks"kksa dk foHkktu

jkT; ljdkj }kjk vHkh Hkh ¼uoEcj 2000 ls) mRrjkf/kdkjh jkT;ksa mRrj izns'k ,oa mRrjk[k.M ds

e/; tek vkSj vfxze ds vUrxZr vo'ks’k /kujkf'k ¼` 8,757.37 djksM+½ foHkktu gsrq vo'ks’k FkkA

laLrqfr% jkT; ljdkj }kjk tek vkSj vfxze ¼` 8,757.37 djksM+½ ds vo'ks’kksa dk foHkktu nksuksa

mRrjkf/kdkjh jkT;ksa ds e/; “kh?kz fd;k tkuk pkfg;sA

(izLrj 3.17)

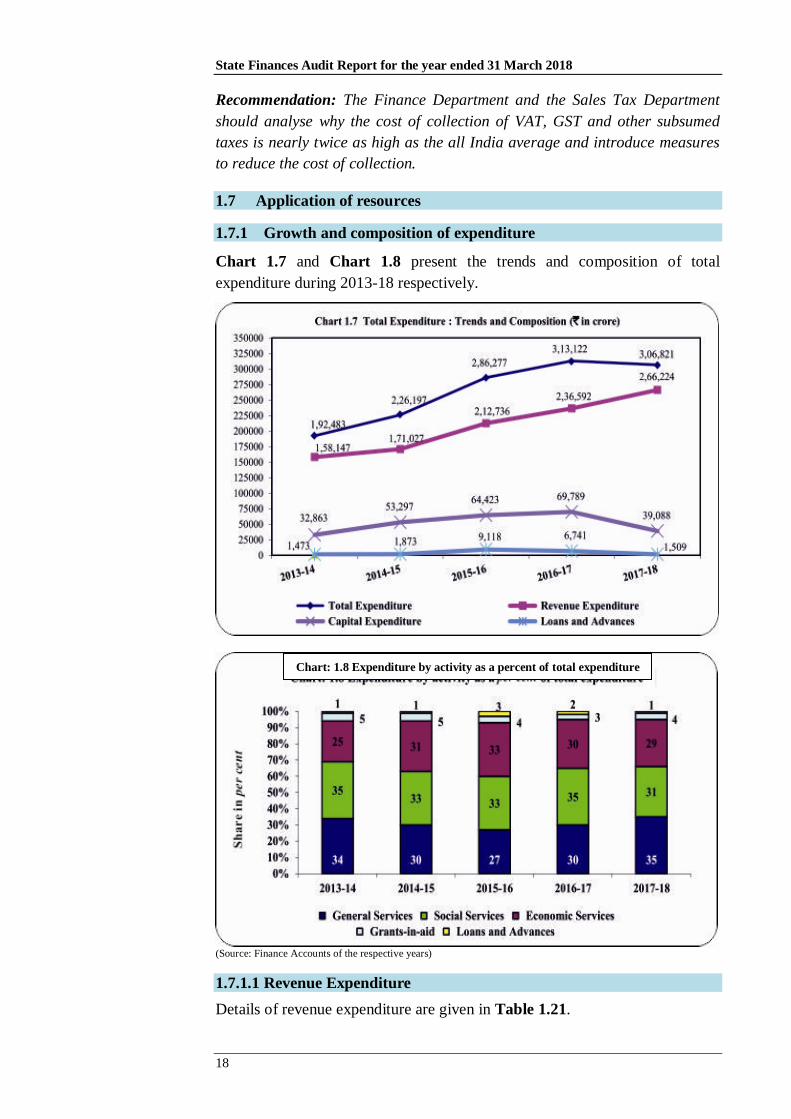

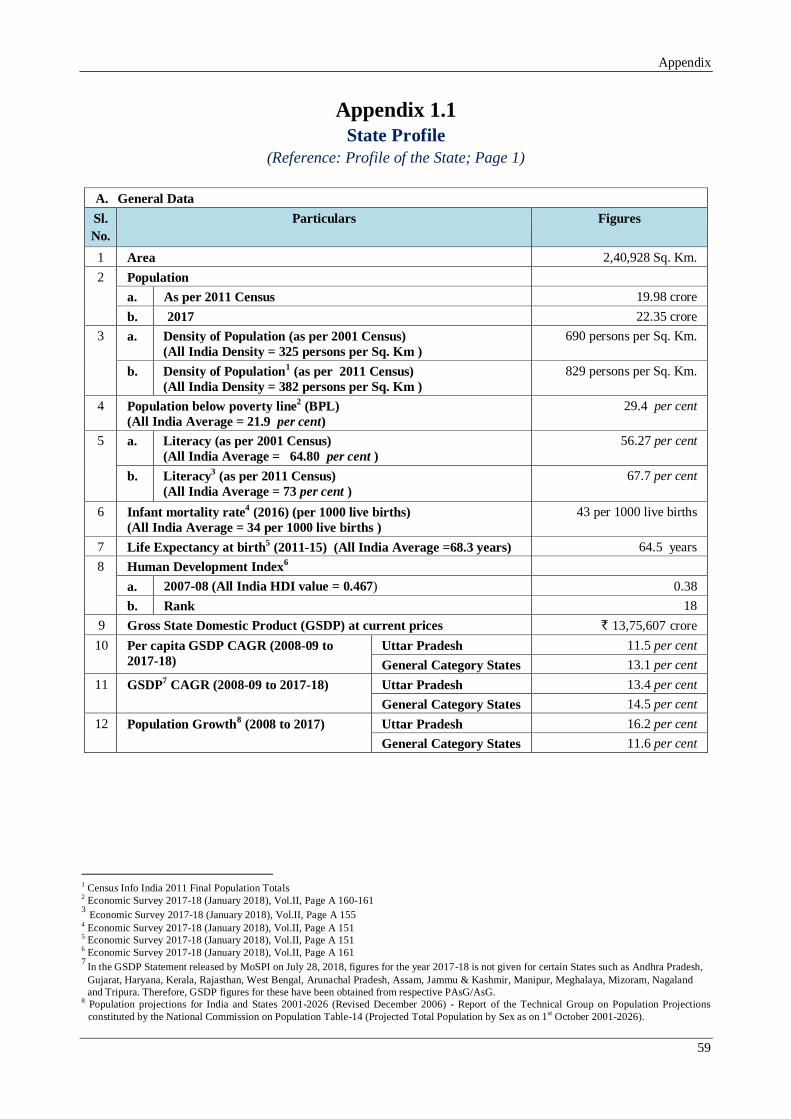

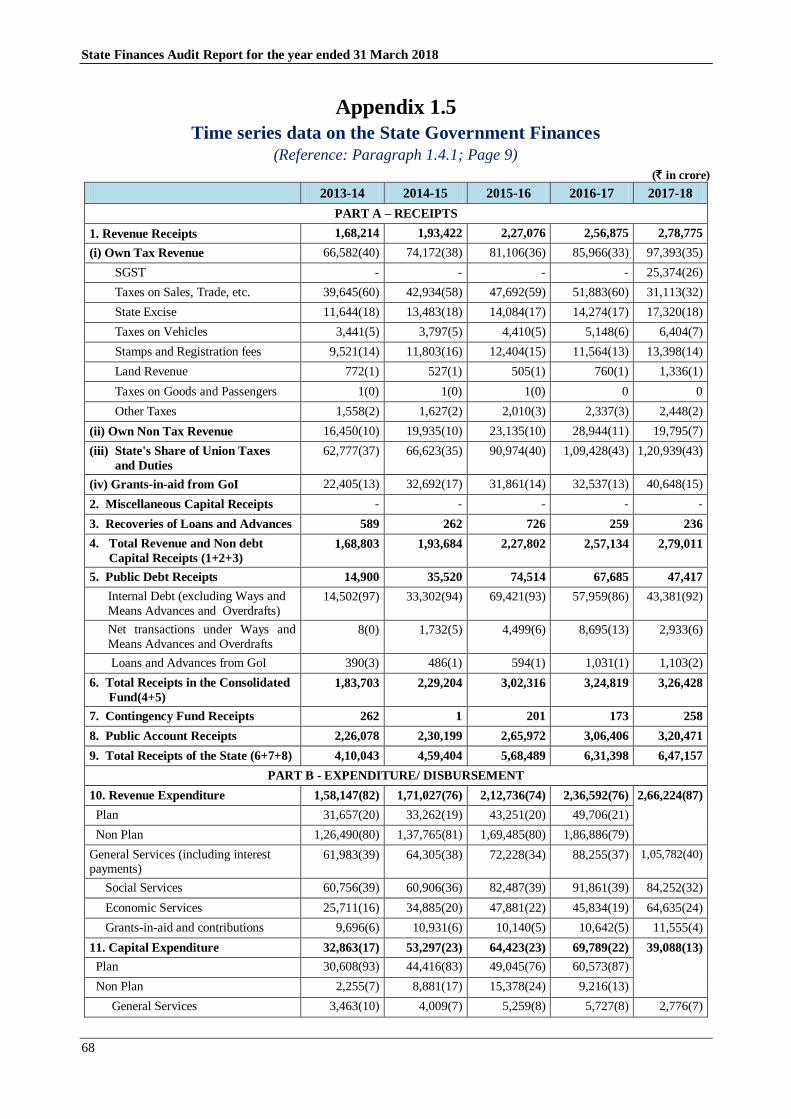

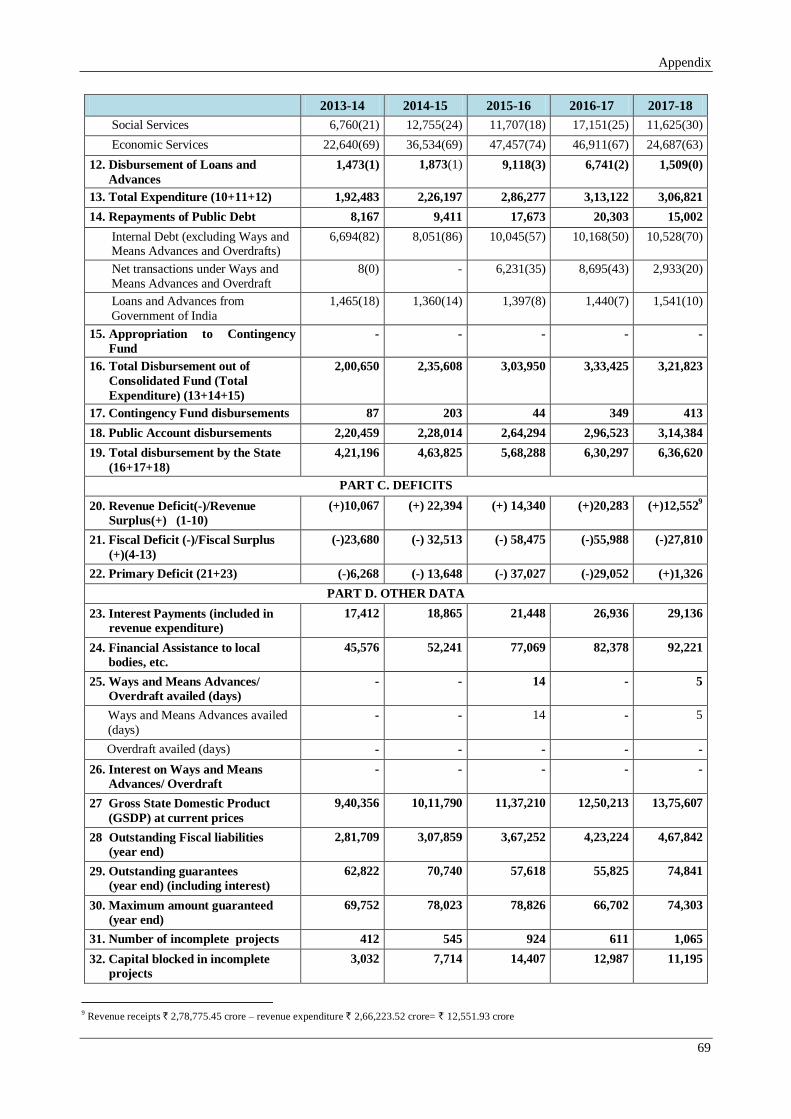

1

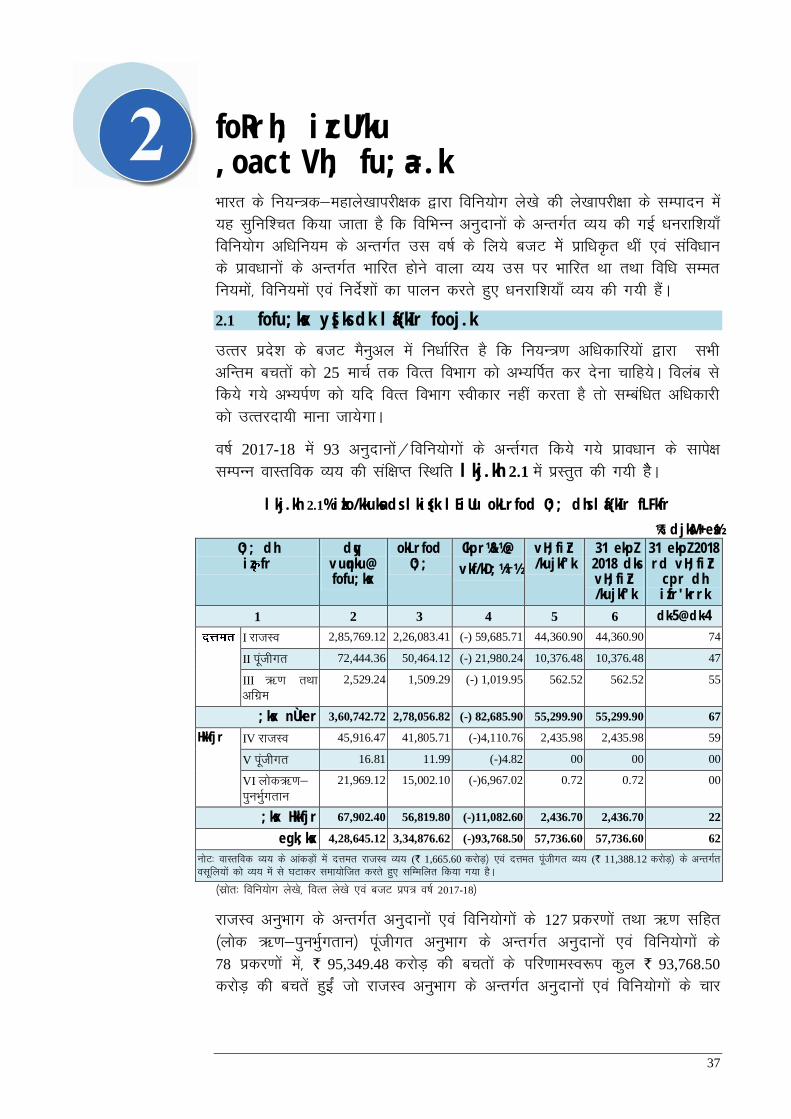

jkT; ljdkj ds foRr ;g v/;k; jkT; ljdkj ds o’kZ 2017-18 ds foRr dk ys[kkijhf{kr ifjn'; izLrqr

djrk gS ,oa foxr ik¡p o’kksZa dh vof/k esa lexz la?kVdksa dks /;ku esa j[krs gq, eq[;

jktdks’kh; lewgksa dk o’kZ 2016-17 dh rqyuk esas ifjorZuksa dk leh{kkRed fo'ys’k.k

djrk gSA

;g leh{kk mRrj izns'k ¼jkT; ljdkj½ jkT; ds foRr ys[ks esa lfEefyr vkadM+ksa ij

vk/kkfjr gSA jkT; dk ifjn'; ifjf'k"V 1.1 esa n'kkZ;k x;k gSA

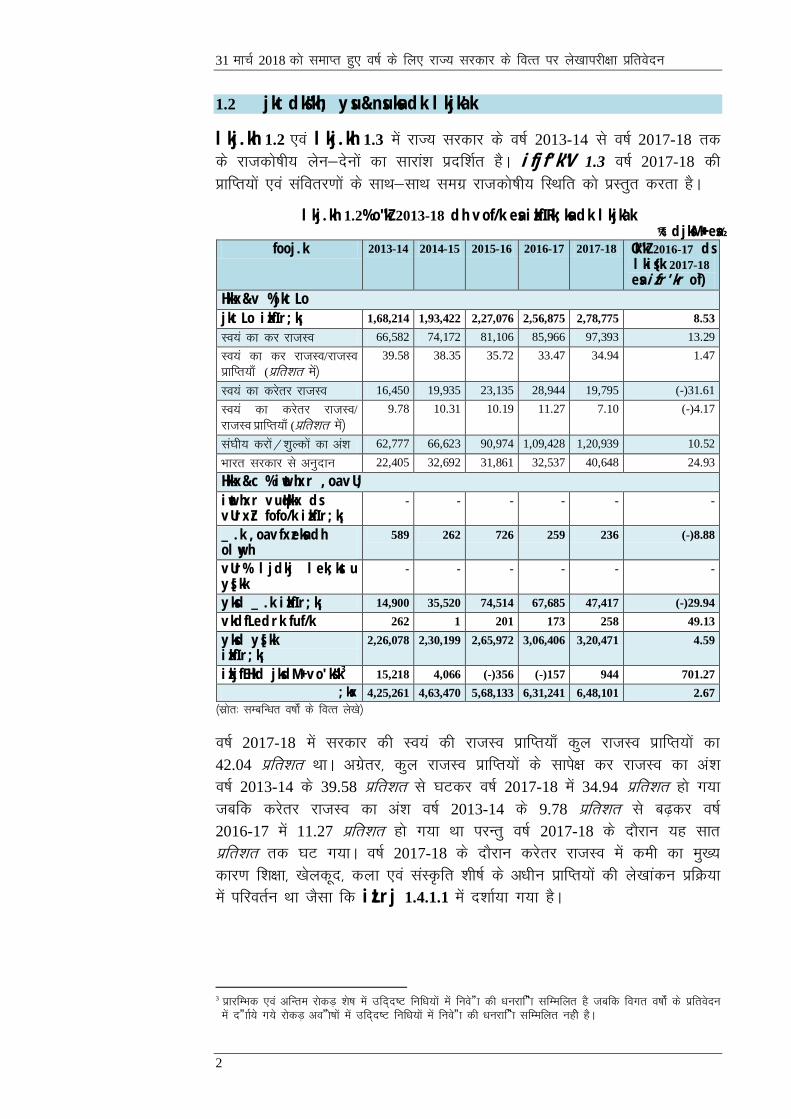

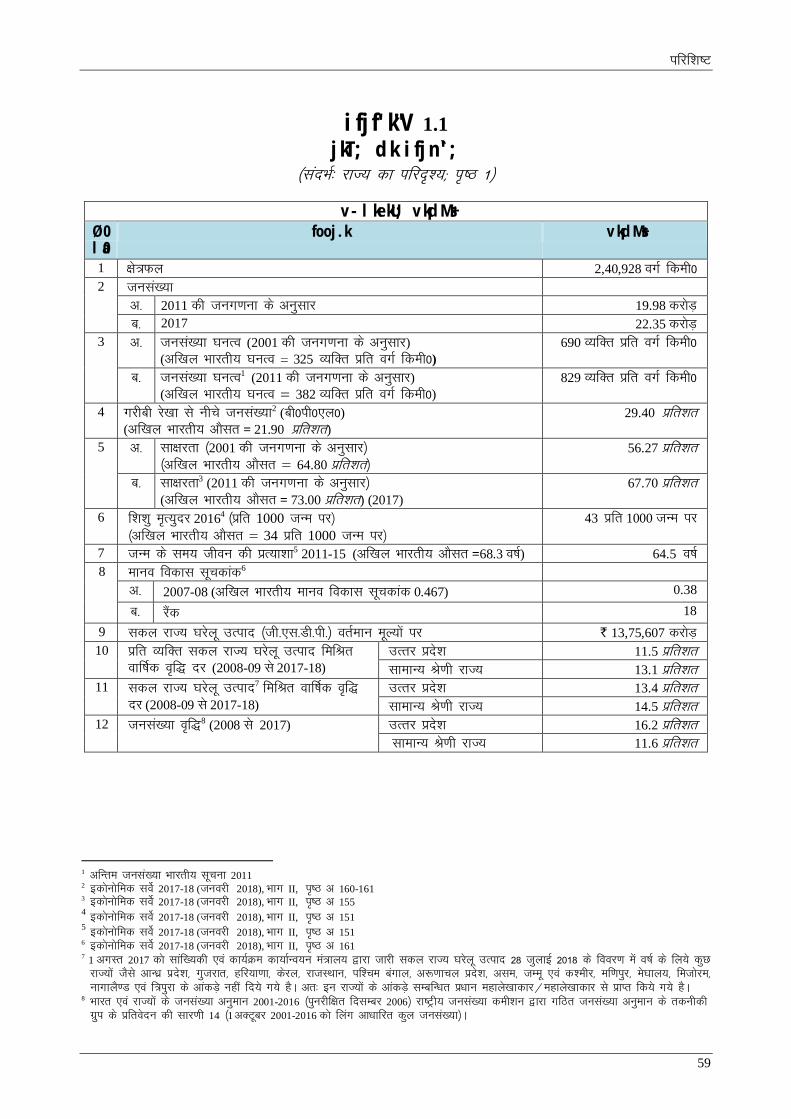

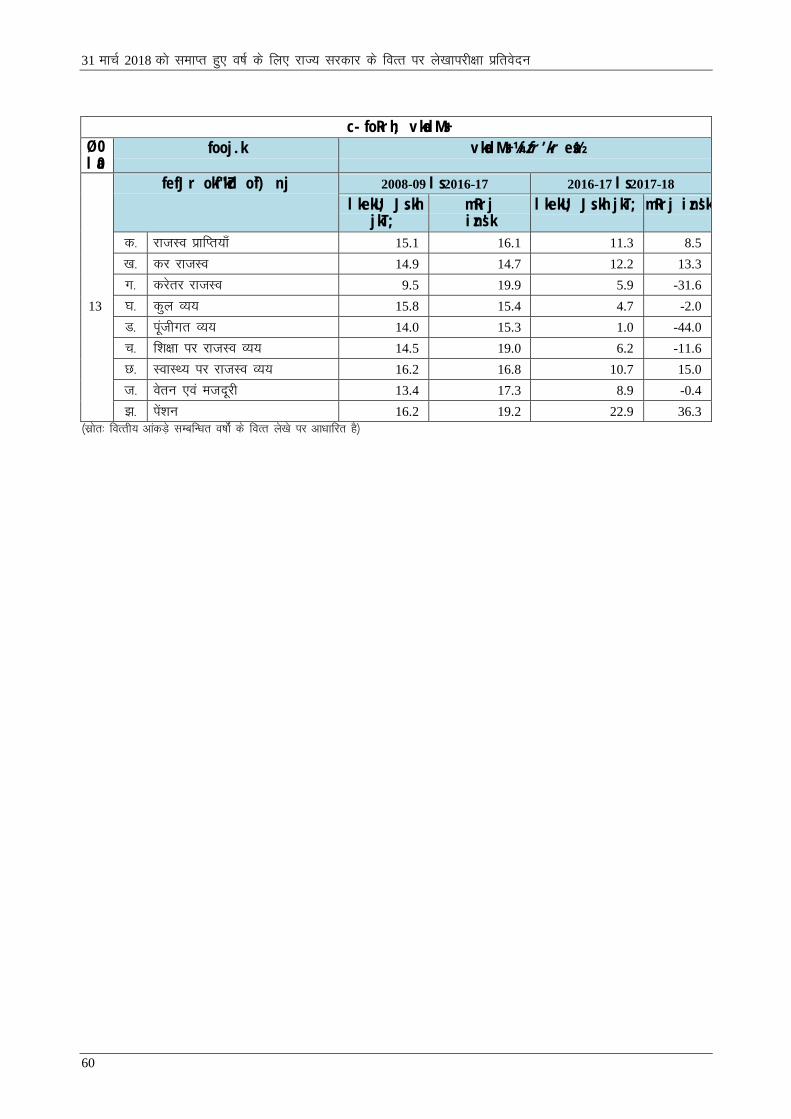

1.1 ldy jkT; ?kjsyw mRikn (l-jk-?k-m-)1

orZeku rFkk fLFkj ewY; ¼vk/kkj o’kZ 2011-12½ ij Hkkjr ds ldy ?kjsyw mRikn

¼l-?k-m-½ rFkk jkT; ds ldy jkT; ?kjsyw mRikn ¼l-jk-?k-m-½ dh okf’kZd izofÙk;ksa dks

lkj.kh 1.1 esa n'kkZ;k x;k gSA

lkj.kh 1-1% Hkkjr dk ldy ?kjsyw mRikn ,oa jkT; dk ldy jkT; ?kjsyw mRikn

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

Hkkjr dk orZeku ewY; ij

ldy ?kjsyw mRikn ¼` djksM+++++ esa½ 1,12,33,522 1,24,67,959 1,37,64,037 1,52,53,714 1,67,73,145

ldy ?kjsyw mRikn dh of) nj

¼izfr'kr esa½ 12.97 10.99 10.40 10.82 9.96

jkT; dk orZeku ewY; ij

ldy jkT; ?kjsyw mRikn

¼` djksM+++++ esa½

9,40,356 10,11,790 11,37,210 12,50,213 13,75,6072

orZeku ewY; ij ldy jkT;

?kjsyw mRikn dh of) nj

¼izfr'kr esa½

14.3 7.6 12.4 9.9 10.0

jkT; dk fLFkj ewY; ij ldy

jkT; ?kjsyw mRikn ¼` djksM+++++ esa½ 8,02,070 8,34,432 9,07,700 9,74,120 10,36,149

fLFkj ewY; ij ldy jkT;

?kjsyw mRikn dh of) nj

¼izfr'kr esa½

5.8 4.0 8.8 7.3 6.4

¼lzksr% ldy ?kjsyw mRikn@ldy jkT; ?kjsyw mRikn ds vkadM+s fnukad 28.08.2018 dks Hkkjr ljdkj ds lkaf[;dh

,oa dk;ZØe dk;kZUo;u ea=ky; }kjk tkjh fd;s x;s½

“kkldh; ys[ks dh lajpuk ifjf'k"V 1.2 ds Hkkx&v vkSj foRr ys[ks dk izk:i

Hkkx&c esa n'kkZ;k x;k gSA

1 ldy ?kjsyw mRikn ,oa ldy jkT; ?kjsyw mRikn fn;s x;s le;kof/k esa ns'k ,oa jkT; esa mRikfnr lHkh vkf/kdkfjd

:i ls ekU; vfUre lkefxz;ksa ,oa lsokvksa dk cktkj ewY; gksrk gS rFkk ns'k ,oa jkT; dh vFkZO;oLFkk dk egRoiw.kZ

ladsrd gSA 2 jkT; ljdkj }kjk lwfpr fd;k x;k ¼twu 2019½ fd o’kZ 2017-18 gsrq jkT; ds iz{ksfir ¼01-08-2017½ ldy jkT;

?kjsyw mRikn dk vuqeku ` 13,78,643 djksM+ gSA rFkkfi Hkkjr ljdkj ds lkaf[;dh ,oa dk;ZØe dk;kZUo;u ea=ky;

}kjk fnukad 28.08.2018 dks tkjh fd;s x;s iqujhf{kr vkadM+s bl izfrosnu esa lfEefyr fd;s x;s gSA

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

2

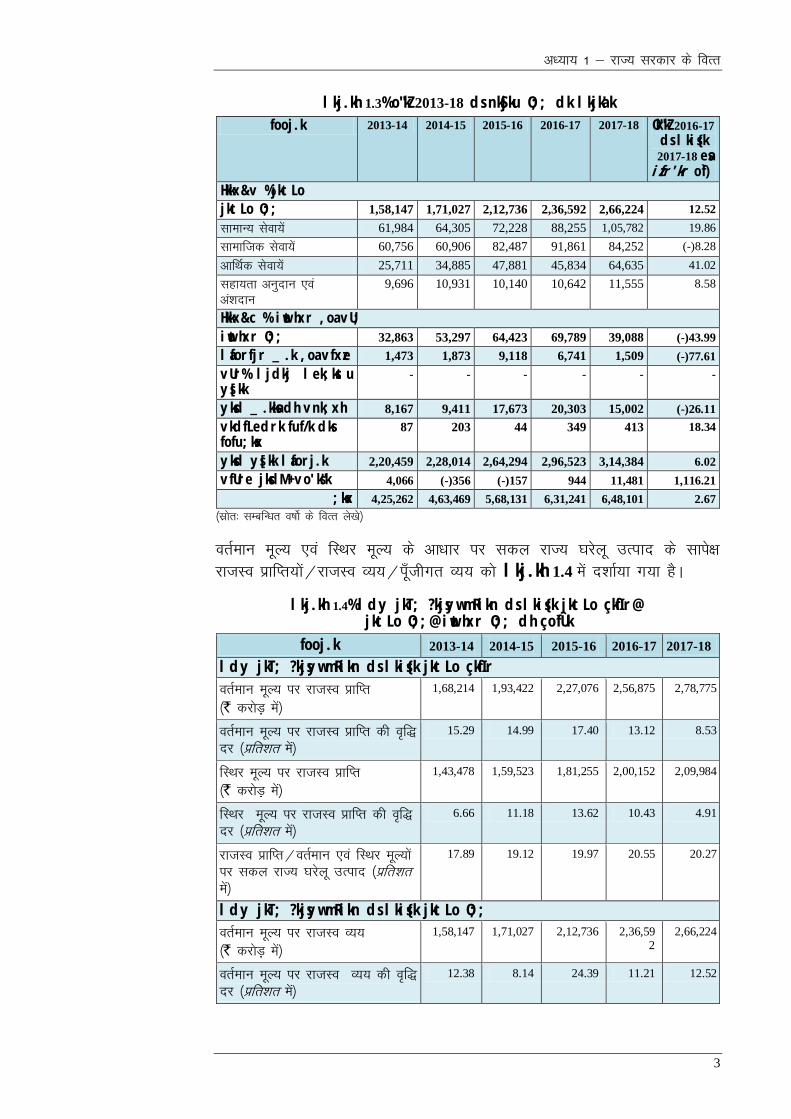

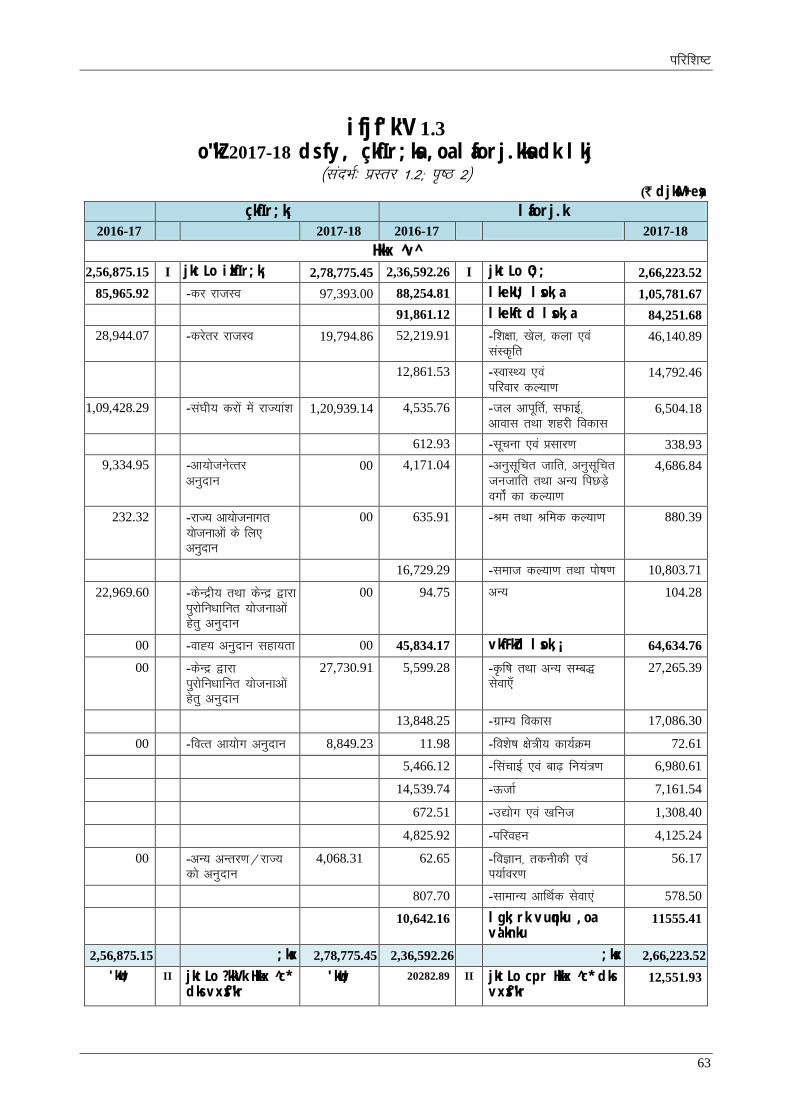

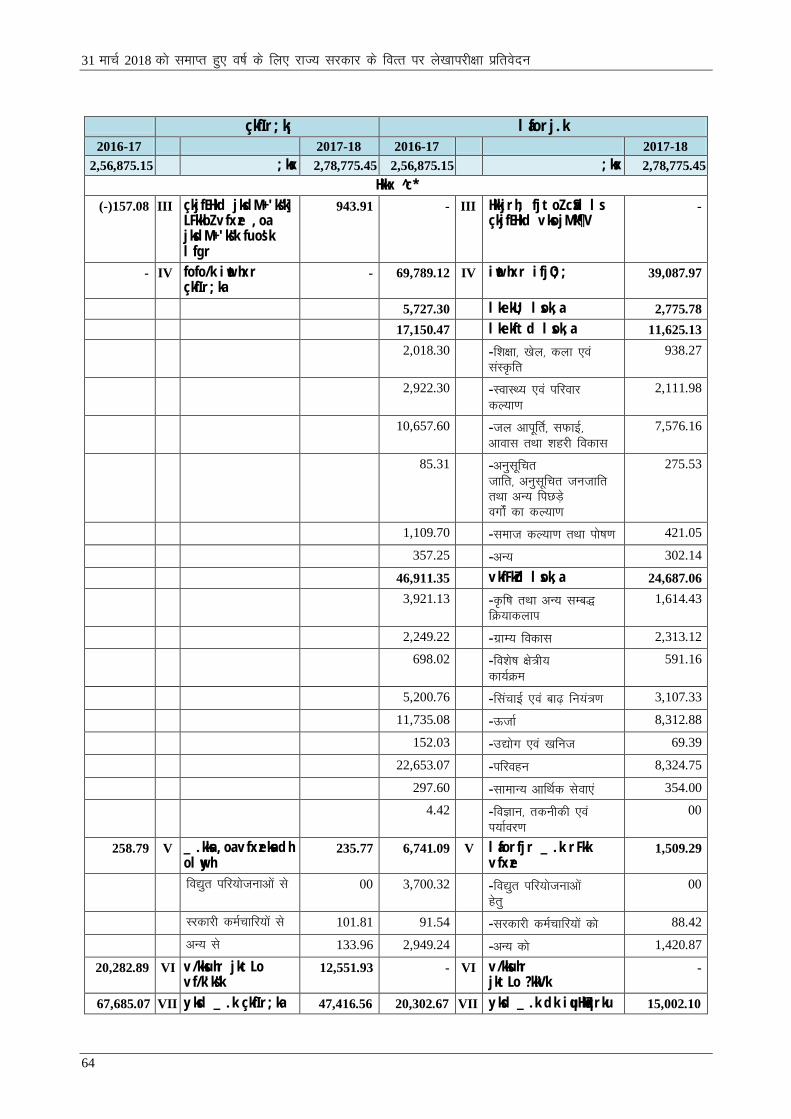

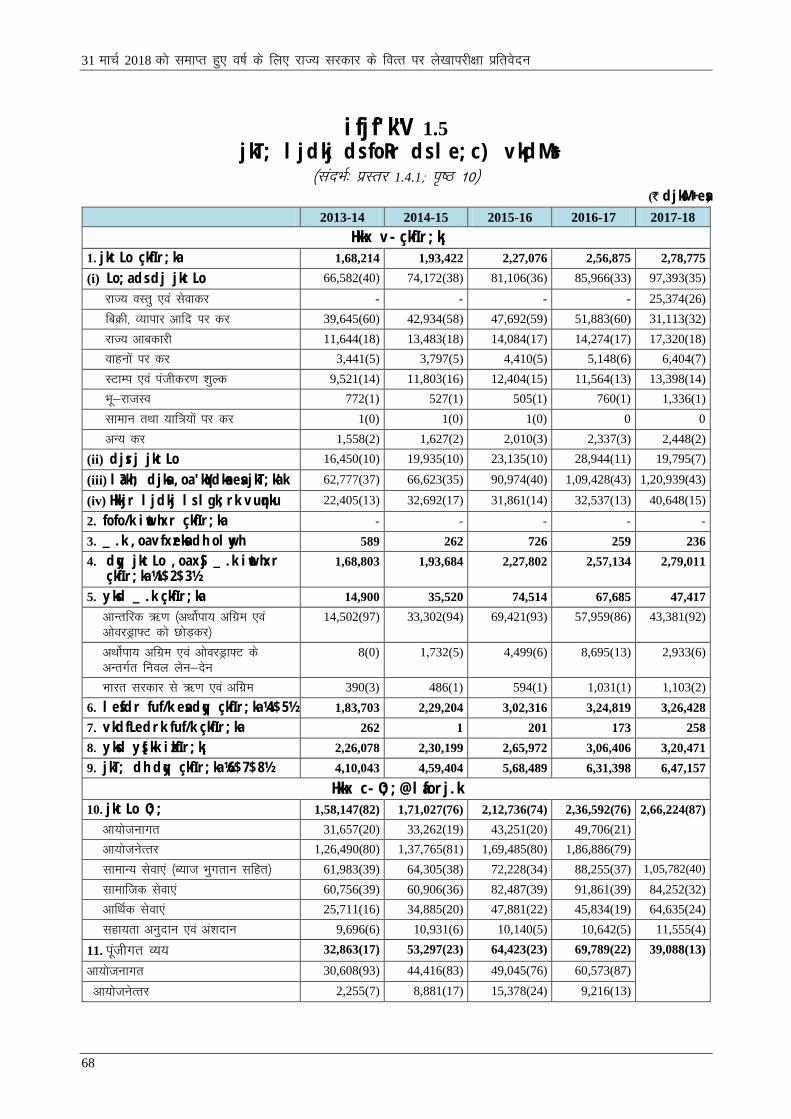

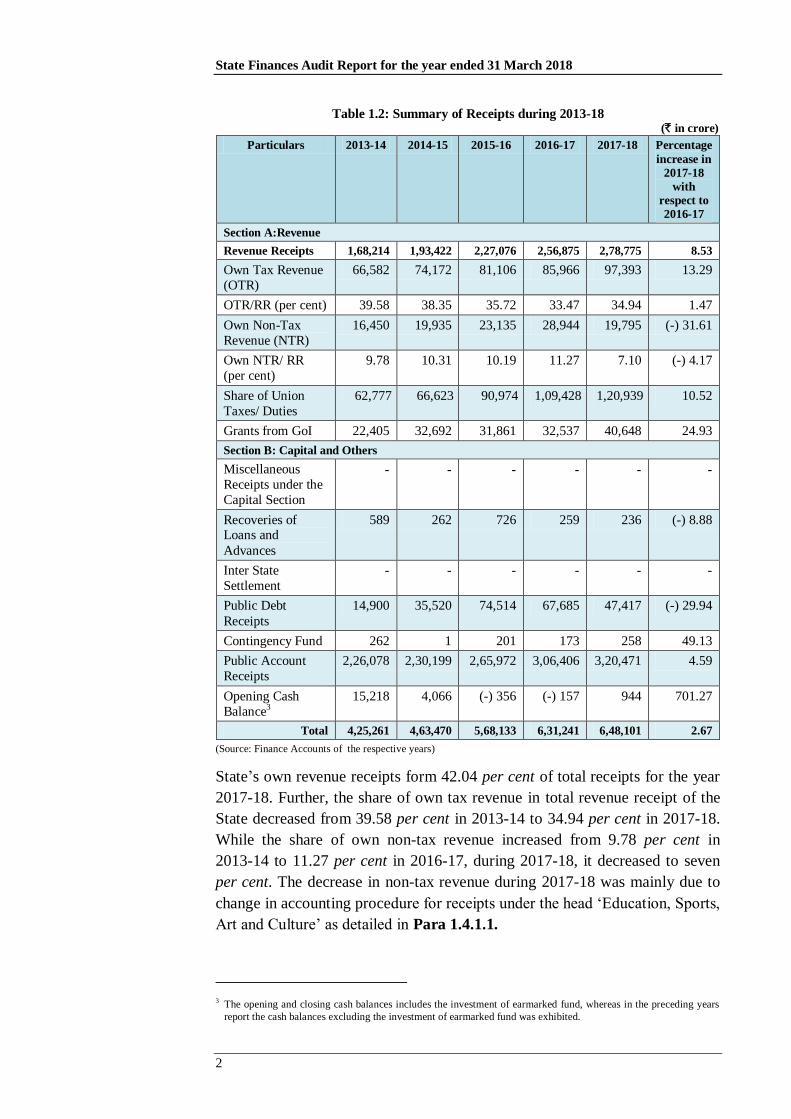

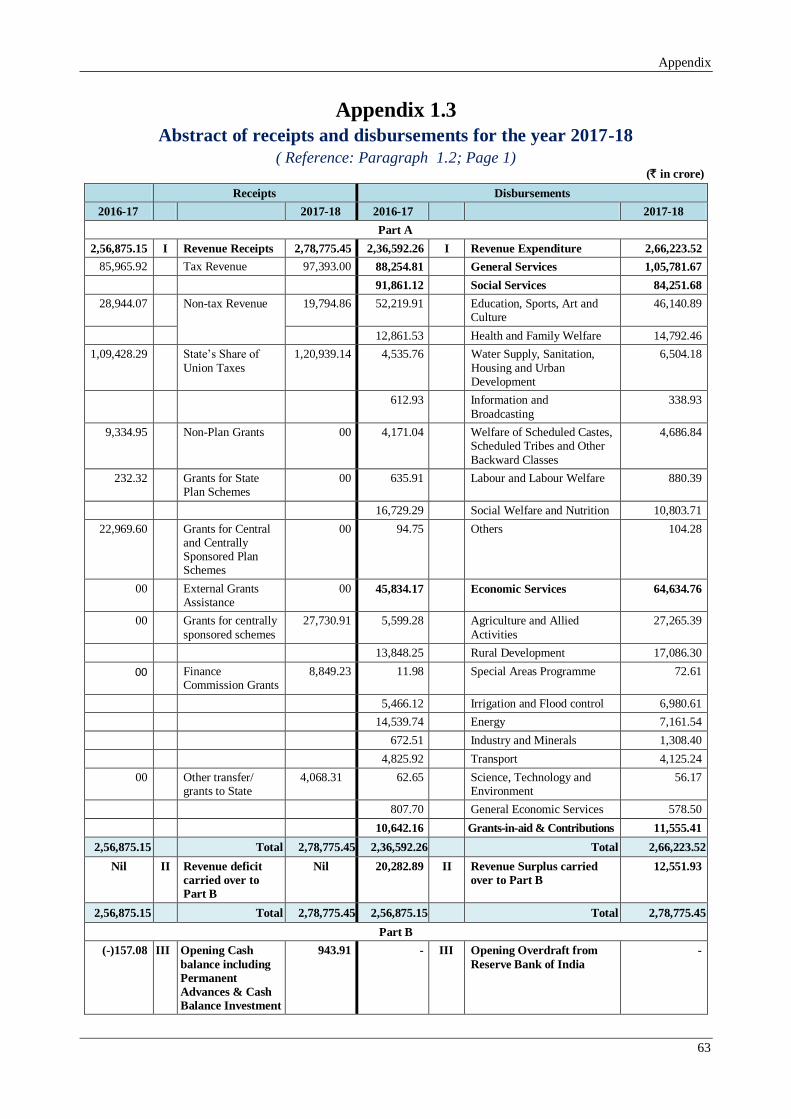

1.2 jktdks"kh; ysu&nsuksa dk lkjka'k

lkj.kh 1.2 ,oa lkj.kh 1.3 esa jkT; ljdkj ds o"kZ 2013-14 ls o"kZ 2017-18 rd

ds jktdks"kh; ysu&nsuksa dk lkjka'k iznf'kZr gSA ifjf'k"V 1.3 o"kZ 2017-18 dh

çkfIr;ksa ,oa laforj.kksa ds lkFk&lkFk lexz jktdks"kh; fLFkfr dks izLrqr djrk gSA

lkj.kh 1.2% o"kZ 2013-18 dh vof/k esa izkfIRk;ksa dk lkjka'k ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18 Ok"kZ 2016-17 ds lkis{k 2017-18

esa izfr'kr o`f)

Hkkx&v % jktLo

jktLo izkfIr;k¡ 1,68,214 1,93,422 2,27,076 2,56,875 2,78,775 8.53

Lo;a dk dj jktLo 66,582 74,172 81,106 85,966 97,393 13.29

Lo;a dk dj jktLo/jktLo

izkfIr;k¡ (izfr'kr esa½

39.58 38.35 35.72 33.47 34.94 1.47

Lo;a dk djsrj jktLo 16,450 19,935 23,135 28,944 19,795 (-)31.61

Lo;a dk djsrj jktLo/

jktLo izkfIr;k¡ (izfr'kr esa½

9.78 10.31 10.19 11.27 7.10 (-)4.17

la?kh; djksa@'kqYdksa dk va'k 62,777 66,623 90,974 1,09,428 1,20,939 10.52

Hkkjr ljdkj ls vuqnku 22,405 32,692 31,861 32,537 40,648 24.93

Hkkx&c % iwathxr ,oa vU;

iwathxr vuqHkkx ds vUrxZr fofo/k izkfIr;k¡

- - - - - -

_.k ,oa vfxzeksa dh olwyh

589 262 726 259 236 (-)8.88

vUr% ljdkj lek;kstu ys[kk

- - - - - -

yksd _.k izkfIr;k¡ 14,900 35,520 74,514 67,685 47,417 (-)29.94

vkdfLedrk fuf/k 262 1 201 173 258 49.13

yksd ys[kk izkfIr;k¡

2,26,078 2,30,199 2,65,972 3,06,406 3,20,471 4.59

izkjfEHkd jksdM+ vo'ks"k3 15,218 4,066 (-)356 (-)157 944 701.27

;ksx 4,25,261 4,63,470 5,68,133 6,31,241 6,48,101 2.67

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

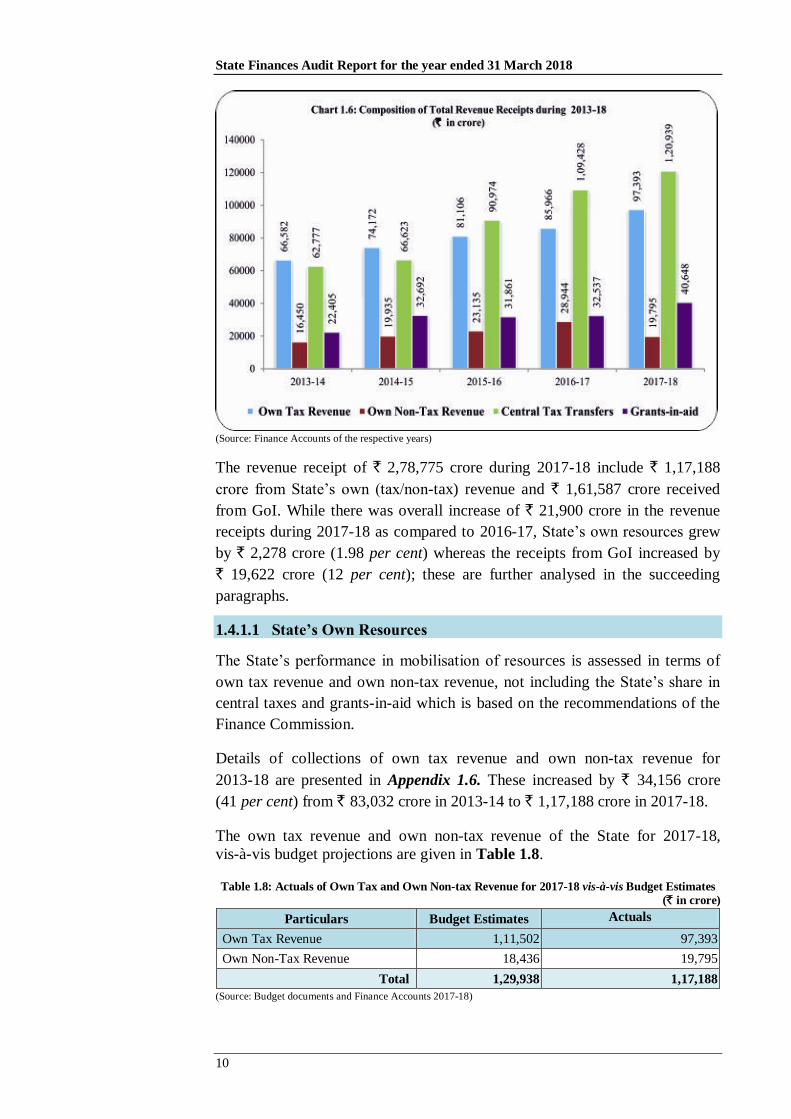

o’kZ 2017-18 esa ljdkj dh Lo;a dh jktLo izkfIr;k¡ dqy jktLo izkfIr;ksa dk

42.04 izfr'kr FkkA vxzsrj] dqy jktLo izkfIr;ksa ds lkis{k dj jktLo dk va'k

o’kZ 2013-14 ds 39.58 izfr'kr ls ?kVdj o’kZ 2017-18 esa 34.94 izfr'kr gks x;k

tcfd djsrj jktLo dk va'k o’kZ 2013-14 ds 9.78 izfr'kr ls c<+dj o’kZ

2016-17 esa 11.27 izfr'kr gks x;k Fkk ijUrq o’kZ 2017-18 ds nkSjku ;g lkr

izfr'kr rd ?kV x;kA o’kZ 2017-18 ds nkSjku djsrj jktLo esa deh dk eq[;

dkj.k f'k{kk] [ksydwn] dyk ,oa laLÑfr “kh’kZ ds v/khu izkfIr;ksa dh ys[kk adu izfØ;k

esa ifjorZu Fkk tSlk fd izLrj 1.4.1.1 esa n'kkZ;k x;k gSA

3 izkjfEHkd ,oa vfUre jksdM+ “ks’k esa mfn~n’V fuf/k;ksa esa fuos”k dh /kujkf”k lfEefyr gS tcfd foxr o’kksZa ds izfrosnu

esa n”kkZ;s x;s jksdM+ vo”ks’kksa esa mfn~n’V fuf/k;ksa esa fuos”k dh /kujkf”k lfEefyr ughs gSA

v/;k; 1 & jkT; ljdkj ds foRr

3

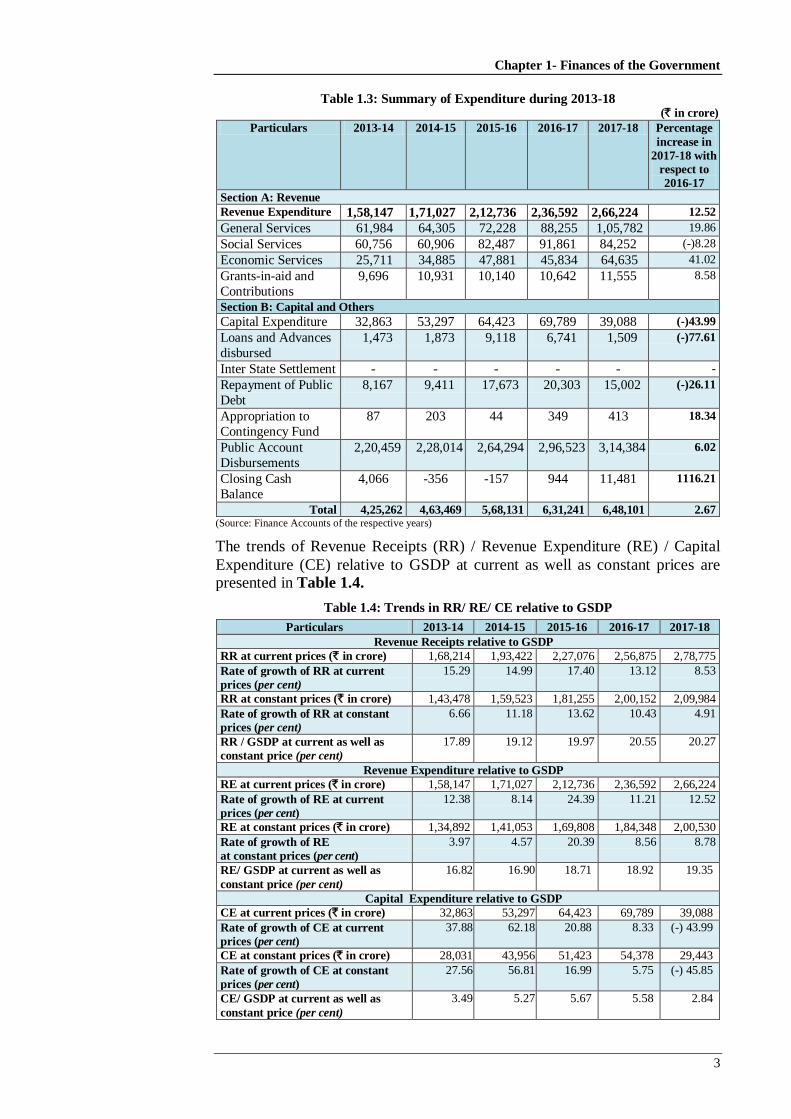

lkj.kh 1.3% o"kZ 2013-18 ds nkSjku O;; dk lkjka'k

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18 Ok"kZ 2016-17 ds lkis{k 2017-18 esa izfr'kr o`f)

Hkkx&v % jktLo

jktLo O;; 1,58,147 1,71,027 2,12,736 2,36,592 2,66,224 12.52

lkekU; lsok;sa 61,984 64,305 72,228 88,255 1,05,782 19.86

lkekftd lsok;sa 60,756 60,906 82,487 91,861 84,252 (-)8.28

vkfFkZd lsok;sa 25,711 34,885 47,881 45,834 64,635 41.02

lgk;rk vuqnku ,oa

va'knku 9,696 10,931 10,140 10,642 11,555 8.58

Hkkx&c % iwathxr ,oa vU;

iwathxr O;; 32,863 53,297 64,423 69,789 39,088 (-)43.99

laforfjr _.k ,oa vfxze 1,473 1,873 9,118 6,741 1,509 (-)77.61

vUr% ljdkj lek;kstu ys[kk

- - - - - -

yksd _.kksa dh vnk;xh 8,167 9,411 17,673 20,303 15,002 (-)26.11

vkdfLedrk fuf/k dks fofu;ksx

87 203 44 349 413 18.34

yksd ys[kk laforj.k 2,20,459 2,28,014 2,64,294 2,96,523 3,14,384 6.02

vfUre jksdM+ vo'ks"k 4,066 (-)356 (-)157 944 11,481 1,116.21

;ksx 4,25,262 4,63,469 5,68,131 6,31,241 6,48,101 2.67

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

orZeku ewY; ,oa fLFkj ewY; ds vk/kkj ij ldy jkT; ?kjsyw mRikn ds lkis{k

jkTkLo izkfIr;ksa@jkTkLo O;;@iw¡thxr O;; dks lkj.kh 1.4 esa n'kkZ;k x;k gSA

lkj.kh 1.4% ldy jkT; ?kjsyw mRikn ds lkis{k jktLo çkfIr@ jktLo O;;@iwathxr O;; dh ço`fÙk

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

ldy jkT; ?kjsyw mRikn ds lkis{k jktLo çkfIr

orZeku ewY; ij jktLo çkfIr

¼` djksM++++ esa½

1,68,214 1,93,422 2,27,076 2,56,875 2,78,775

orZeku ewY; ij jktLo çkfIr dh of)

nj ¼çfr'kr esa½

15.29 14.99 17.40 13.12 8.53

fLFkj ewY; ij jktLo çkfIr

¼` djksM++++ esa½

1,43,478 1,59,523 1,81,255 2,00,152 2,09,984

fLFkj ewY; ij jktLo çkfIr dh of)

nj ¼çfr'kr esa½

6.66 11.18 13.62 10.43 4.91

jktLo çkfIr@orZeku ,oa fLFkj ewY;ksa

ij ldy jkT; ?kjsyw mRikn ¼izfr'kr

esa½

17.89 19.12 19.97 20.55 20.27

ldy jkT; ?kjsyw mRikn ds lkis{k jktLo O;;

orZeku ewY; ij jktLo O;;

¼` djksM++++ esa½

1,58,147 1,71,027 2,12,736 2,36,592

2,66,224

orZeku ewY; ij jktLo O;; dh of)

nj ¼çfr'kr esa½

12.38 8.14 24.39 11.21 12.52

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

4

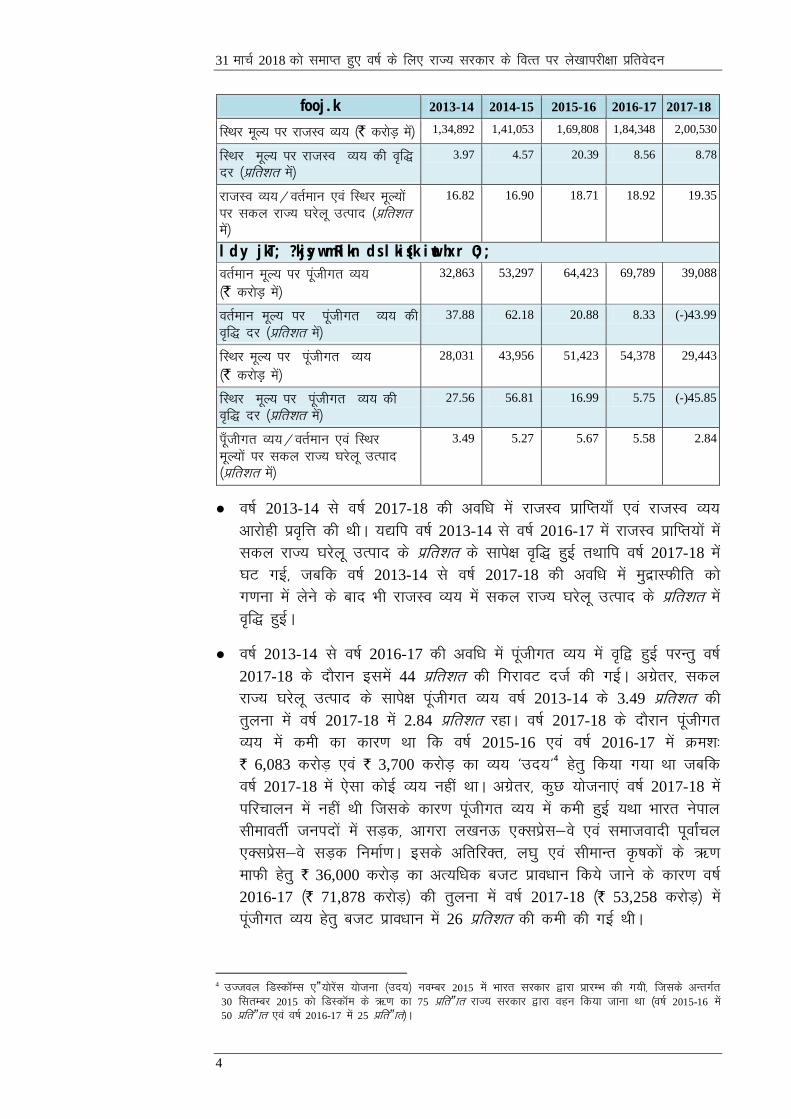

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

fLFkj ewY; ij jktLo O;; ¼` djksM++++ esa½ 1,34,892 1,41,053 1,69,808 1,84,348 2,00,530

fLFkj ewY; ij jktLo O;; dh of)

nj ¼çfr'kr esa½

3.97 4.57 20.39 8.56 8.78

jktLo O;;@orZeku ,oa fLFkj ewY;ksa

ij ldy jkT; ?kjsyw mRikn ¼çfr'kr

esa½

16.82 16.90 18.71 18.92 19.35

ldy jkT; ?kjsyw mRikn ds lkis{k iwathxr O;;

orZeku ewY; ij iwathxr O;;

¼` djksM++++ esa½

32,863 53,297 64,423 69,789 39,088

orZeku ewY; ij iwathxr O;; dh

of) nj ¼çfr'kr esa½

37.88 62.18 20.88 8.33 (-)43.99

fLFkj ewY; ij iwathxr O;;

¼` djksM++++ esa½

28,031 43,956 51,423 54,378 29,443

fLFkj ewY; ij iwathxr O;; dh

of) nj ¼çfr'kr esa½

27.56 56.81 16.99 5.75 (-)45.85

iw¡thxr O;;@orZeku ,oa fLFkj

ewY;ksa ij ldy jkT; ?kjsyw mRikn

¼çfr'kr esa½

3.49 5.27 5.67 5.58 2.84

● o’kZ 2013-14 ls o"kZ 2017-18 dh vof/k esa jktLo izkfIr;k¡ ,oa jktLo O;;

vkjksgh izofŸk dh FkhA ;|fi o’kZ 2013-14 ls o"kZ 2016-17 esa jktLo izkfIr;ksa esa

ldy jkT; ?kjsyw mRikn ds izfr'kr ds lkis{k of) gqbZ rFkkfi o"kZ 2017-18 esa

?kV xbZ] tcfd o’kZ 2013-14 ls o"kZ 2017-18 dh vof/k esa eqnzkLQhfr dks

x.kuk esa ysus ds ckn Hkh jktLo O;; esa ldy jkT; ?kjsyw mRikn ds izfr'kr esa

of) gqbZA

● o’kZ 2013-14 ls o"kZ 2016-17 dh vof/k esa iwathxr O;; esa of} gqbZ ijUrq o’kZ

2017-18 ds nkSjku blesa 44 izfr'kr dh fxjkoV ntZ dh xbZA vxzsrj] ldy

jkT; ?kjsyw mRikn ds lkis{k iwathxr O;; o’kZ 2013-14 ds 3.49 izfr'kr dh

rqyuk esa o’kZ 2017-18 esa 2.84 izfr'kr jgkA o’kZ 2017-18 ds nkSjku iwathxr

O;; esa deh dk dkj.k Fkk fd o’kZ 2015-16 ,oa o"kZ 2016-17 esa Øe'k%

` 6,083 djksM+ ,oa ` 3,700 djksM++ dk O;; ^mn;^4 gsrq fd;k x;k Fkk tcfd

o’kZ 2017-18 esa ,slk dksbZ O;; ugha FkkA vxzsrj] dqN ;kstuk,a o’kZ 2017-18 esa

ifjpkyu esa ugha Fkh ftlds dkj.k iwathxr O;; esa deh gqbZ ;Fkk Hkkjr usiky

lhekorhZ tuinksa esa lM+d] vkxjk y[kuÅ ,Dlizsl&os ,oa lektoknh iwokZapy

,Dlizsl&os lM+d fuekZ.kA blds vfrfjDr] y?kq ,oa lhekUr —’kdksa ds _.k

ekQh gsrq ` 36,000 djksM+ dk vR;f/kd ctV izko/kku fd;s tkus ds dkj.k o’kZ

2016-17 ¼` 71,878 djksM+½ dh rqyuk esa o’kZ 2017-18 ¼` 53,258 djksM+½ esa

iwathxr O;; gsrq ctV izko/kku esa 26 izfr'kr dh deh dh xbZ FkhA

4 mTtoy fMLdkWEl ,”;ksjsal ;kstuk ¼mn;½ uoEcj 2015 esa Hkkjr ljdkj }kjk izkjEHk dh x;h] ftlds vUrxZr

30 flrEcj 2015 dks fMLdkWe ds _.k dk 75 izfr”kr jkT; ljdkj }kjk ogu fd;k tkuk Fkk ¼o’kZ 2015-16 esa

50 izfr”kr ,oa o"kZ 2016-17 esa 25 izfr”kr½A

v/;k; 1 & jkT; ljdkj ds foRr

5

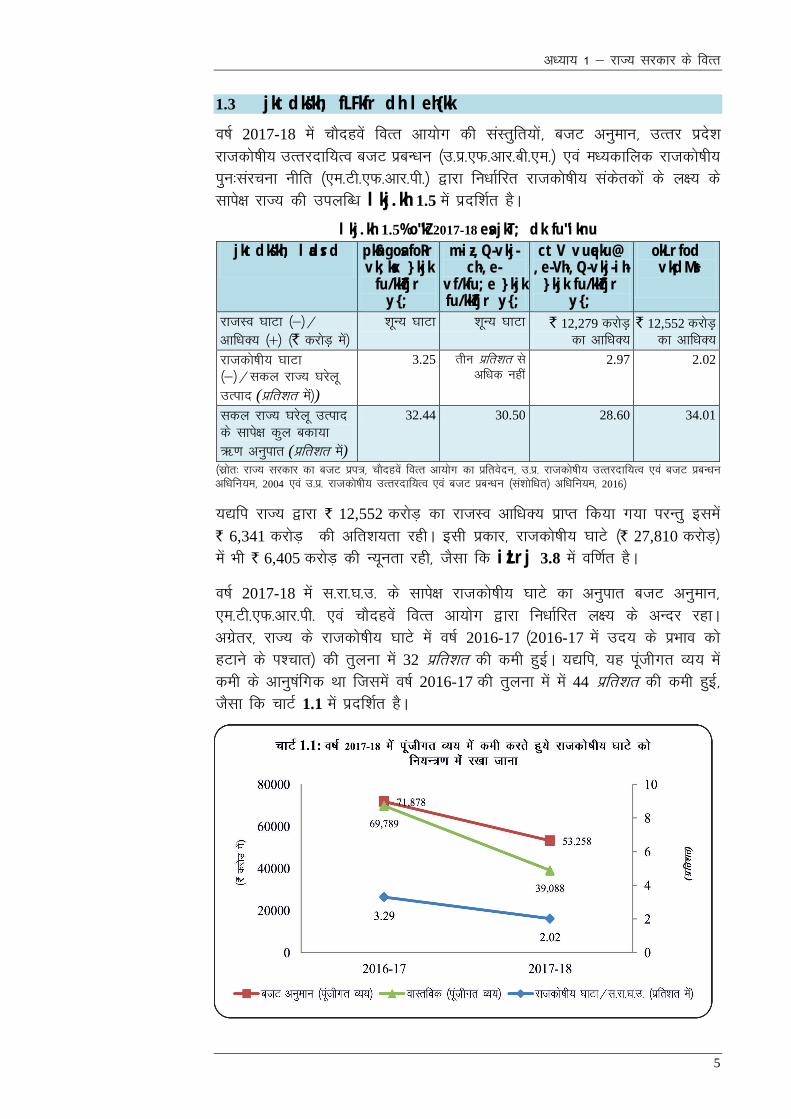

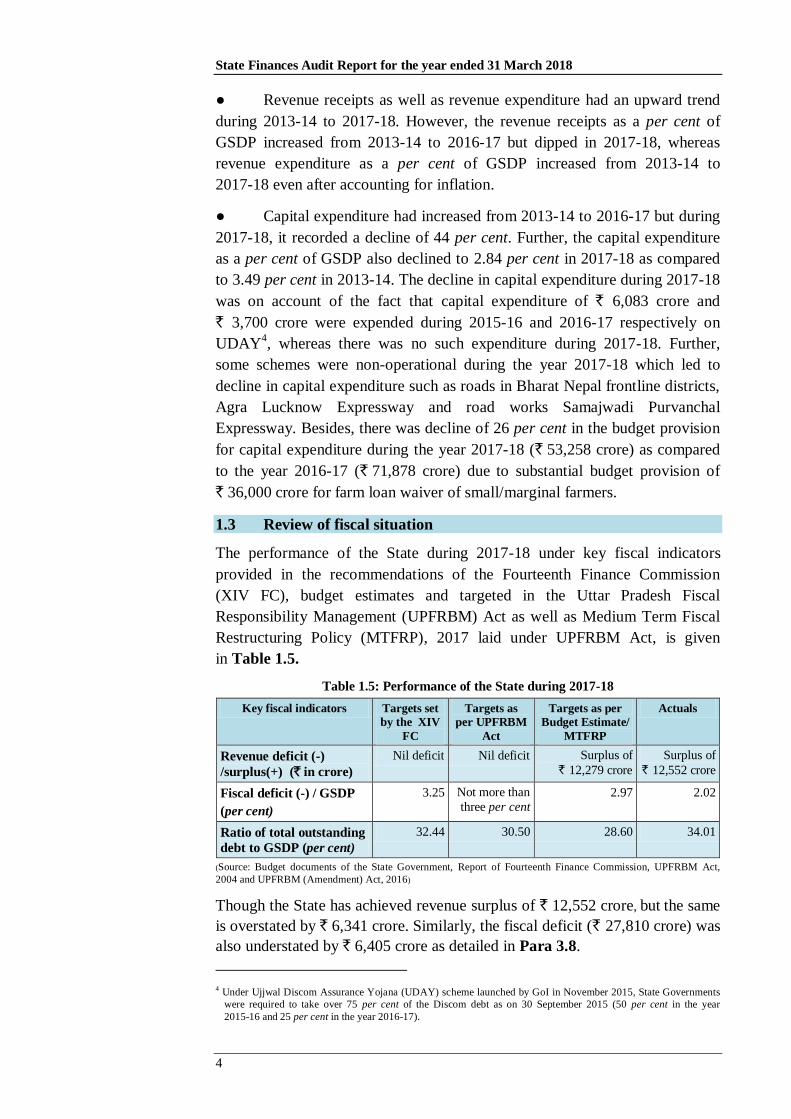

1.3 jktdks"kh; fLFkfr dh leh{kk

o’kZ 2017-18 esa pkSngosa foRr vk;ksx dh laLrqfr;ksa] ctV vuqeku] mRrj izns'k

jktdks’kh; mRrjnkf;Ro ctV izcU/ku ¼m-iz-,Q-vkj-ch-,e-½ ,oa e/;dkfyd jktdks’kh;

iqu%lajpuk uhfr ¼,e-Vh-,Q-vkj-ih-½ }kjk fu/kkZfjr jktdks"kh; ladsrdksa ds y{; ds

lkis{k jkT; dh miyfC/k lkj.kh 1.5 esa iznf'kZr gSA

lkj.kh 1.5% o"kZ 2017-18 esa jkT; dk fu"iknu

jktdks"kh; ladsrd

pkSngosa foRr vk;ksx }kjk fu/kkZfjr y{;

m-iz-,Q-vkj-ch-,e-

vf/kfu;e }kjk fu/kkZfjr y{;

ctV vuqeku@ ,e-Vh-,Q-vkj-ih- }kjk fu/kkZfjr

y{;

okLrfod vk¡dM+s

jktLo ?kkVk ¼&½@

vkf/kD; ¼$½ ¼` djksM++++ esa½

'kwU; ?kkVk 'kwU; ?kkVk ` 12,279 djksM++++

dk vkf/kD; ` 12,552 djksM++++

dk vkf/kD;

jktdks’kh; ?kkVk

¼&½@ldy jkT; ?kjsyw

mRikn (çfr'kr esa½)

3.25 Rkhu izfr'kr ls

vf/kd ugha

2.97 2.02

ldy jkT; ?kjsyw mRikn

ds lkis{k dqy cdk;k

_.k vuqikr (çfr'kr esa)

32.44 30.50 28.60 34.01

¼lzksr% jkT; ljdkj dk ctV izi=] pkSngosa foRr vk;ksx dk izfrosnu] m-iz- jktdks’kh; mRrjnkf;Ro ,oa ctV izcU/ku

vf/kfu;e] 2004 ,oa m-iz- jktdks’kh; mRrjnkf;Ro ,oa ctV izcU/ku ¼la'kksf/kr½ vf/kfu;e] 2016½

;|fi jkT; }kjk ` 12,552 djksM+ dk jkTkLo vkf/kD; izkIr fd;k x;k ijUrq blesa

` 6,341 djksM+ dh vfr'k;rk jghA blh izdkj] jkTkdks’kh; ?kkVs ¼` 27,810 djksM+½

esa Hkh ` 6,405 djksM+ dh U;wurk jgh] tSlk fd izLrj 3.8 esa of.kZr gSA

Ok’kZ 2017-18 esa l-jk-?k-m- ds lkis{k jktdks’kh; ?kkVs dk vuqikr ctV vuqeku]

,e-Vh-,Q-vkj-ih- ,oa pkSngosa foRr vk;ksx }kjk fu/kkZfjr y{; ds vUnj jgkA

vxzsrj] jkT; ds jktdks’kh; ?kkVs esa o’kZ 2016-17 ¼2016-17 esa mn; ds izHkko dks

gVkus ds Ik'pkr½ dh rqyuk esa 32 izfr'kr dh deh gqbZA ;|fi] ;g iwathxr O;; esa

deh ds vkuq’kafxd Fkk ftlesa o’kZ 2016-17 dh rqyuk eas esa 44 izfr'kr dh deh gqbZ]

tSlk fd pkVZ 1.1 eas iznf'kZr gSA

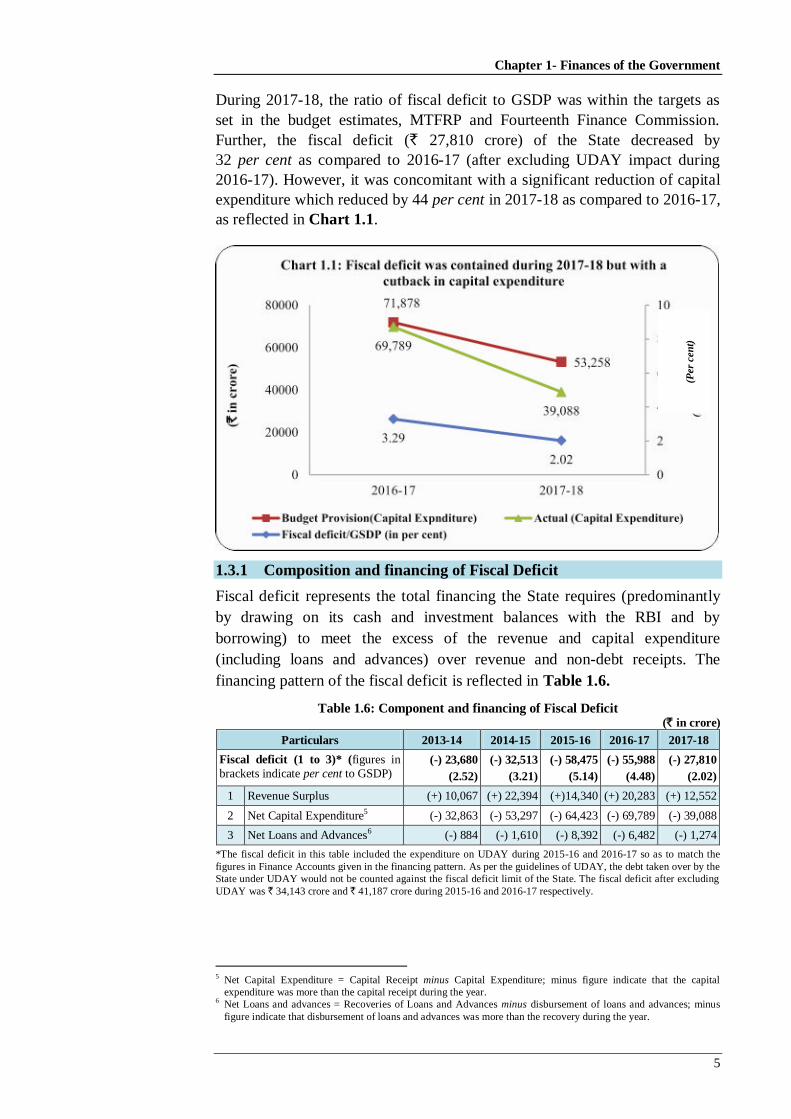

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

6

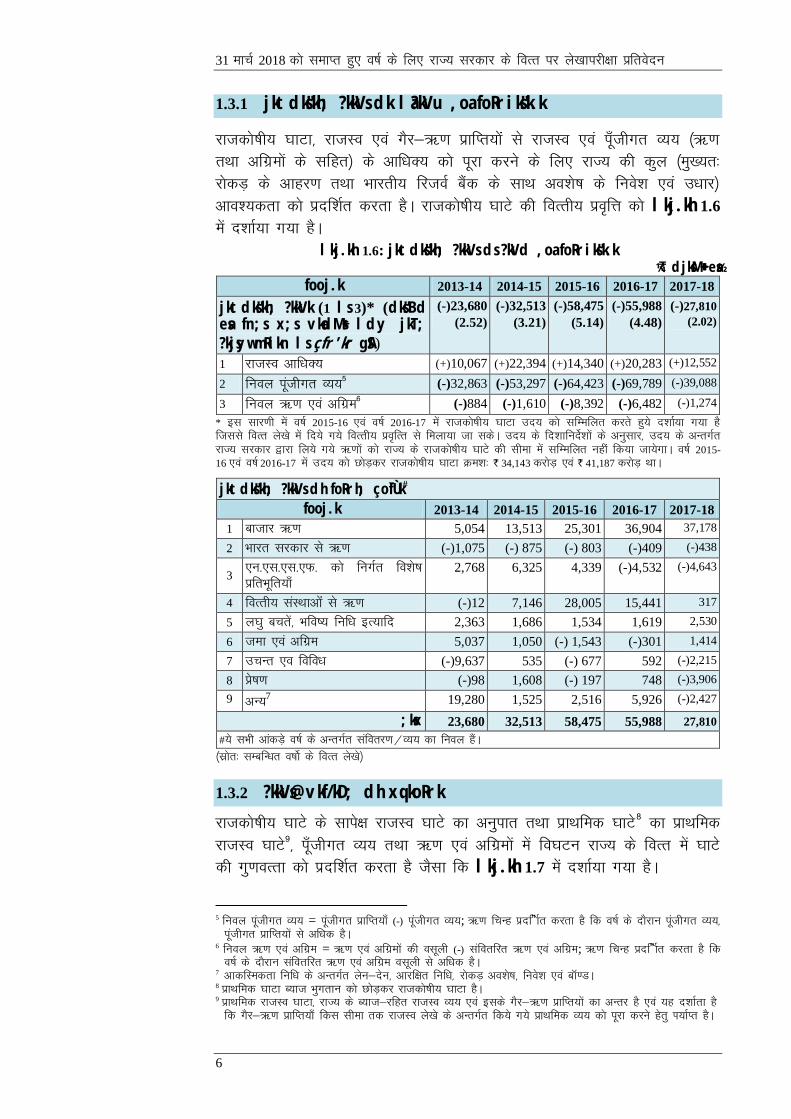

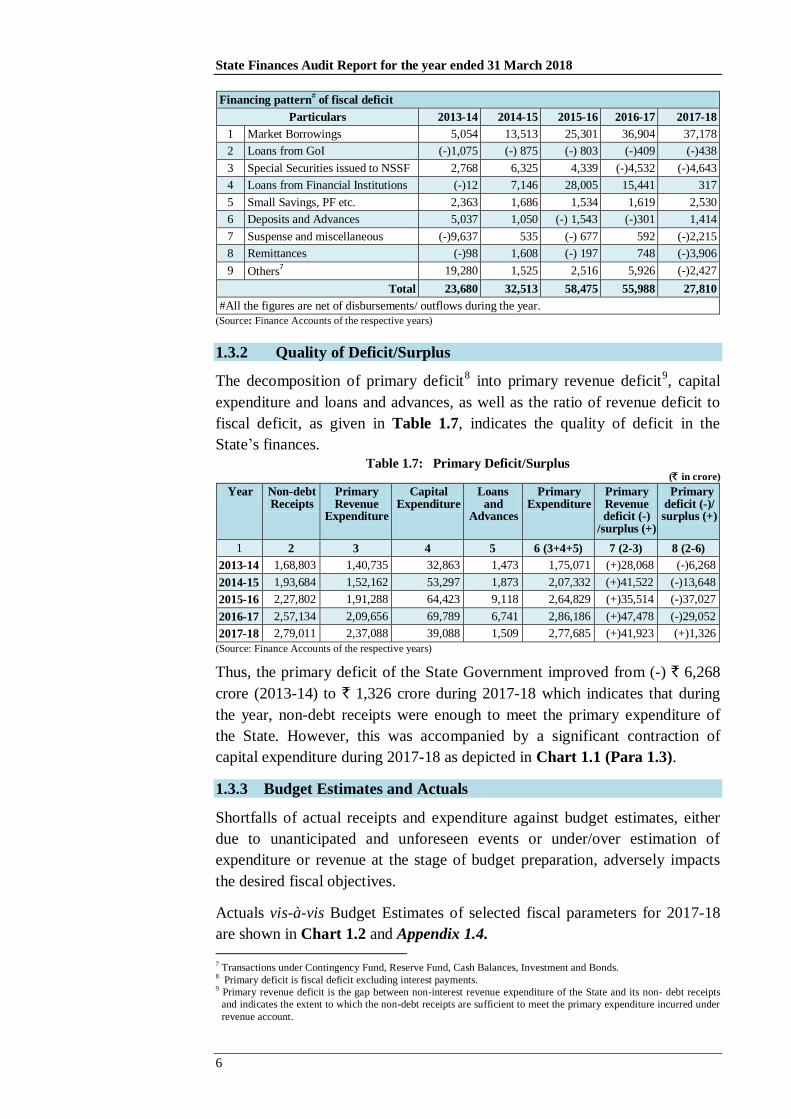

1.3.1 jktdks"kh; ?kkVs dk la?kVu ,oa foRriks"k.k

jktdks’kh; ?kkVk] jktLo ,oa xSj&_.k izkfIr;ksaa ls jkTkLo ,oa iw¡thxr O;; ¼_.k

rFkk vfxzeksa ds lfgr½ ds vkf/kD; dks iwjk djus ds fy, jkT; dh dqy ¼eq[;r%

jksdM+ ds vkgj.k rFkk Hkkjrh; fjtoZ caSd ds lkFk vo'ks’k ds fuos'k ,oa m/kkj½

vko';drk dks iznf'kZr djrk gSA jktdks’kh; ?kkVs dh foRrh; izofÙk dks lkj.kh 1.6

esa n'kkZ;k x;k gSA

lkj.kh 1.6: jktdks"kh; ?kkVs ds ?kVd ,oa foRriks"k.k ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

jktdks"kh; ?kkVk (1 ls 3)* (dks"Bd esa fn;s x;s vkadM+s ldy jkT; ?kjsyw mRikn ls çfr'kr gSA)

(-)23,680

(2.52)

(-)32,513

(3.21)

(-)58,475

(5.14)

(-)55,988

(4.48)

(-)27,810

(2.02)

1 jktLo vkf/kD; (+)10,067 (+)22,394 (+)14,340 (+)20,283 (+)12,552

2 fuoy iwathxr O;;5 (-)32,863 (-)53,297 (-)64,423 (-)69,789 (-)39,088

3 fuoy _.k ,oa vfxze6 (-)884 (-)1,610 (-)8,392 (-)6,482 (-)1,274

* bl lkj.kh esa o’kZ 2015-16 ,oa o"kZ 2016-17 esa jktdks’kh; ?kkVk mn; dks lfEefyr djrs gq;s n'kkZ;k x;k gS

ftlls foRr ys[ks esa fn;s x;s foRrh; izofRr ls feyk;k tk ldsA mn; ds fn'kkfunsZ'kksa ds vuqlkj] mn; ds vUrxZr

jkT; ljdkj }kjk fy;s x;s _.kksa dks jkT; ds jktdks’kh; ?kkVs dh lhek esa lfEefyr ugha fd;k tk;sxkA o’kZ 2015-

16 ,oa o"kZ 2016-17 esa mn; dks NksM+dj jktdks’kh; ?kkVk Øe'k% ` 34,143 djksM+ ,oa ` 41,187 djksM+ FkkA

jktdks"kh; ?kkVs dh foRrh; ço`fÙk#

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

1 cktkj _.k 5,054 13,513 25,301 36,904 37,178

2 Hkkjr ljdkj ls _.k (-)1,075 (-) 875 (-) 803 (-)409 (-)438

3 ,u-,l-,l-,Q- dks fuxZr fo'ks"k

izfrHkwfr;k¡ 2,768 6,325 4,339 (-)4,532 (-)4,643

4 foRrh; laLFkkvksaa ls _.k (-)12 7,146 28,005 15,441 317

5 y?kq cprsa] Hkfo"; fuf/k bR;kfn 2,363 1,686 1,534 1,619 2,530

6 tek ,oa vfxze 5,037 1,050 (-) 1,543 (-)301 1,414

7 mpUr ,o fofo/k (-)9,637 535 (-) 677 592 (-)2,215

8 çs"k.k (-)98 1,608 (-) 197 748 (-)3,906

9 vU;7 19,280 1,525 2,516 5,926 (-)2,427

;ksx 23,680 32,513 58,475 55,988 27,810

#;s lHkh vkadMs+ o"kZ ds vUrxZr laforj.k@O;; dk fuoy gSaA

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

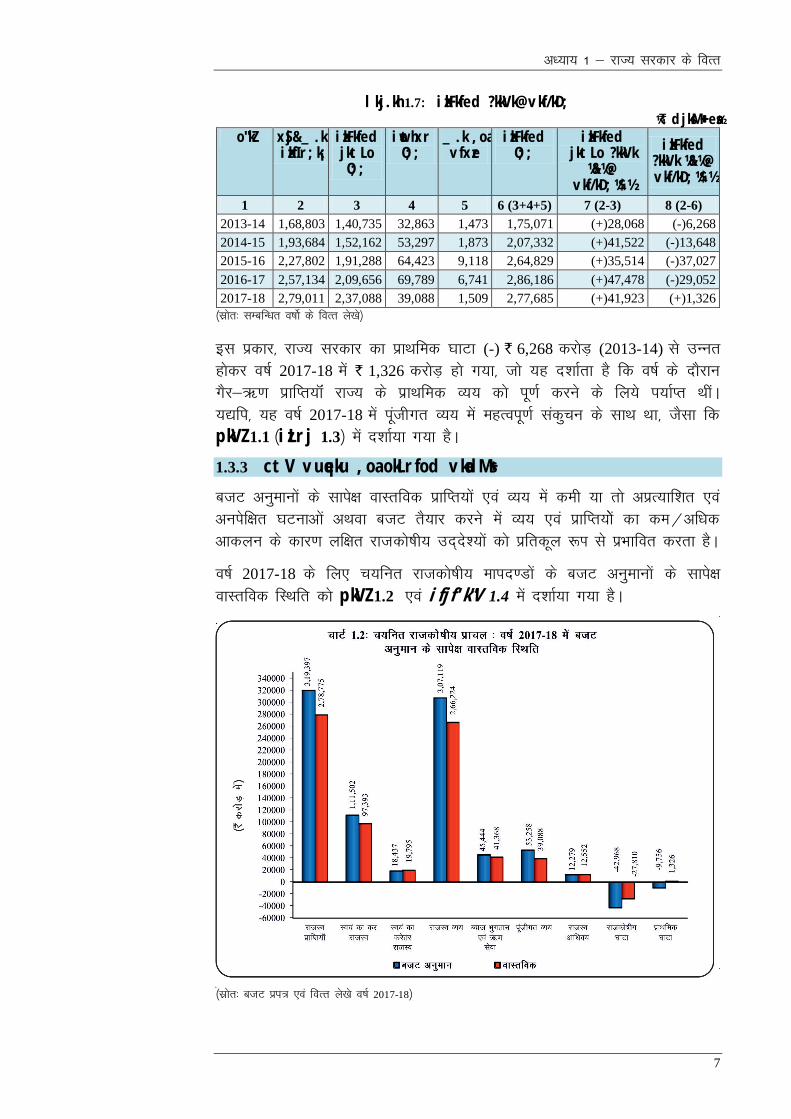

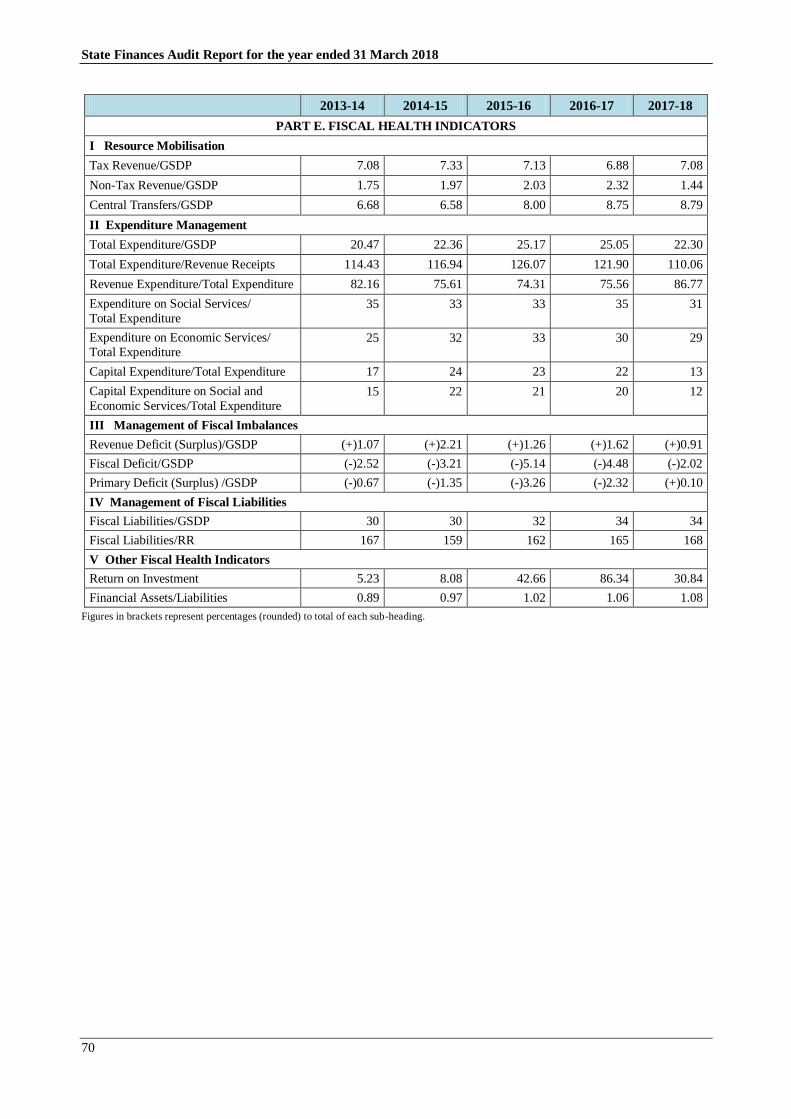

1.3.2 ?kkVs@vkf/kD; dh xq.koRrk

jktdks’kh; ?kkVs ds lkis{k jktLo ?kkVs dk vuqikr rFkk izkFkfed ?kkVs8 dk izkFkfed

jktLo ?kkVs9] iw¡thxr O;; rFkk _.k ,oa vfxzeksa esa fo?kVu jkT; ds foRr esa ?kkVs

dh xq.koRrk dks iznf'kZr djrk gS tSlk fd lkj.kh 1.7 esa n'kkZ;k x;k gSA

5 fuoy iwathxr O;; = iwathxr izkfIr;k¡ (-) iwathxr O;;; _.k fpUg iznf”kZr djrk gS fd o’kZ ds nkSjku iwathxr O;;]

iwathxr izkfIr;ksa ls vf/kd gSA

6 fuoy _.k ,oa vfxze = _.k ,oa vfxzeksa dh olwyh (-) laforfjr _.k ,oa vfxze; _.k fpUg iznf”kZr djrk gS fd

o’kZ ds nkSjku laforfjr _.k ,oa vfxze olwyh ls vf/kd gSA 7 vkdfLedrk fuf/k ds vUrxZr ysu&nsu] vkjf{kr fuf/k] jksdM+ vo'ks"k] fuos'k ,oa ckW.MA

8 izkFkfed ?kkVk C;kt Hkqxrku dks NksM+dj jktdks’kh; ?kkVk gSA

9 izkFkfed jktLo ?kkVk] jkT; ds C;kt&jfgr jktLo O;; ,oa blds xSj&_.k izkfIr;ksa dk vUrj gS ,oa ;g n'kkZrk gS

fd xSj&_.k izkfIr;k¡ fdl lhek rd jktLo ys[ks ds vUrxZr fd;s x;s izkFkfed O;; dks iwjk djus gsrq Ik;kZIr gSA

v/;k; 1 & jkT; ljdkj ds foRr

7

lkj.kh 1.7: izkFkfed ?kkVk@vkf/kD; ¼` djksM++++ esa½

o"kZ xSj&_.k izkfIr;k¡

izkFkfed jktLo O;;

iwathxr O;;

_.k ,oa vfxze

izkFkfed O;;

izkFkfed jktLo ?kkVk

¼&½@ vkf/kD;¼$½

izkFkfed ?kkVk ¼&½@ vkf/kD;¼$½

1 2 3 4 5 6 (3+4+5) 7 (2-3) 8 (2-6)

2013-14 1,68,803 1,40,735 32,863 1,473 1,75,071 (+)28,068 (-)6,268

2014-15 1,93,684 1,52,162 53,297 1,873 2,07,332 (+)41,522 (-)13,648

2015-16 2,27,802 1,91,288 64,423 9,118 2,64,829 (+)35,514 (-)37,027

2016-17 2,57,134 2,09,656 69,789 6,741 2,86,186 (+)47,478 (-)29,052

2017-18 2,79,011 2,37,088 39,088 1,509 2,77,685 (+)41,923 (+)1,326

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

bl izdkj] jkT; ljdkj dk izkFkfed ?kkVk (-) ` 6,268 djksM+ (2013-14) ls mUur

gksdj o’kZ 2017-18 esa ` 1,326 djksM+ gks x;k] tks ;g n'kkZrk gS fd o’kZ ds nkSjku

xSj&_.k izkfIr;kWa jkT; ds izkFkfed O;; dks iw.kZ djus ds fy;s i;kZIr FkhaA

;|fi] ;g o’kZ 2017-18 esa iwathxr O;; esa egRoiw.kZ ladqpu ds lkFk Fkk] tSlk fd

pkVZ 1.1 ¼izLrj 1.3½ esa n'kkZ;k x;k gSA

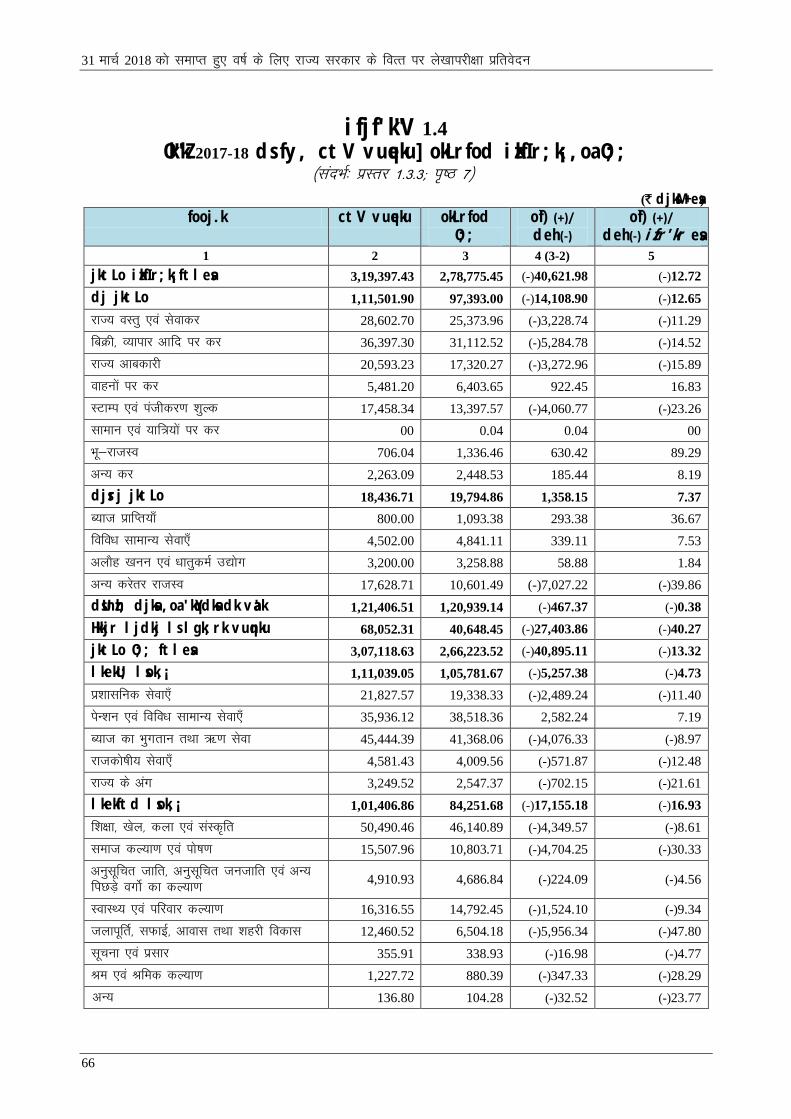

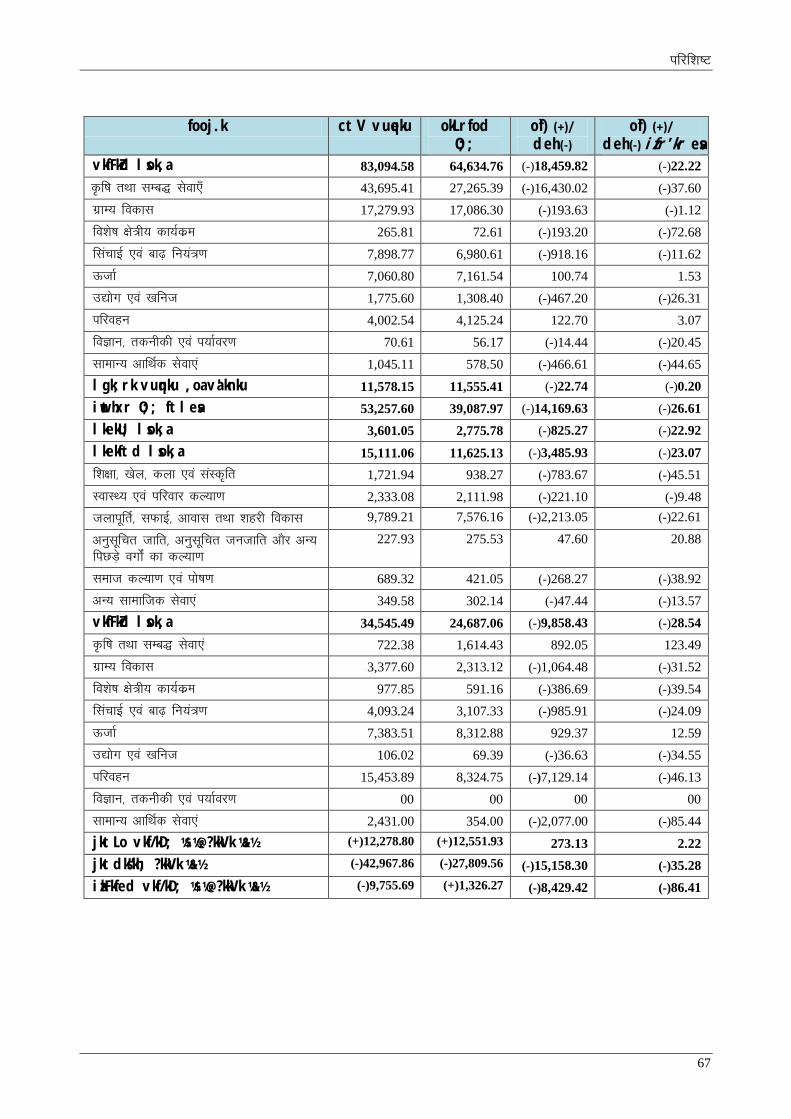

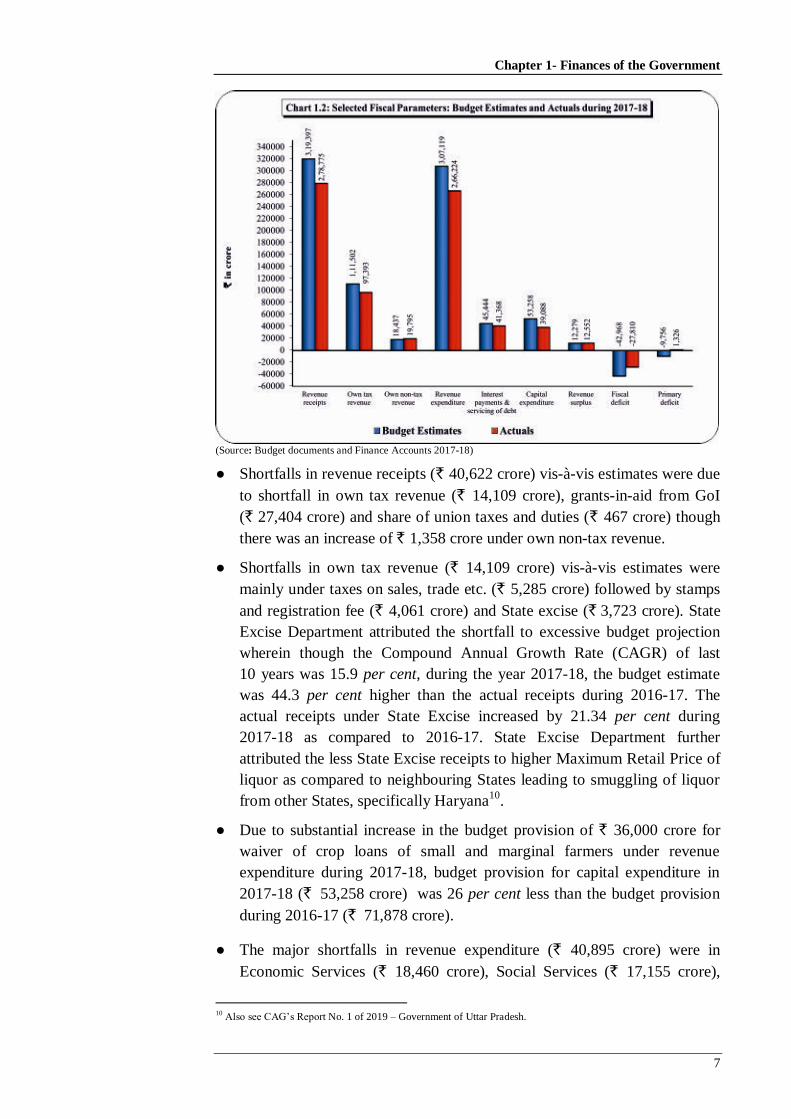

1.3.3 ctV vuqeku ,oa okLrfod vkadM+s

ctV vuqekukas ds lkis{k okLrfod izkfIr;ksa ,oa O;; esa deh ;k rks vizR;kf'kr ,oa

vuisf{kr ?kVukvksa vFkok ctV rS;kj djus esa O;; ,oa izkfIr;kssa dk de@vf/kd

vkdyu ds dkj.k yf{kr jktdks’kh; mn~ns';ksa dks izfrdwy :Ik ls izHkkfor djrk gSA

o’kZ 2017-18 ds fy, p;fur jktdks’kh; ekin.Mksa ds ctV vuqekuksa ds lkis{k

okLrfod fLFkfr dks pkVZ 1.2 ,oa ifjf'k"V 1.4 esa n'kkZ;k x;k gSA

¼lzksr% ctV izi= ,oa foRr ys[ks o’kZ 2017-18½

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

8

● jktLo izkfIr;ksa esa ctV vuqekuksa ds lkis{k deh ¼` 40,622 djksM+½ Lo;a ds

dj jktLo ¼` 14,109 djksM+½] Hkkjr ljdkj ls lgk;rk vuqnku ¼` 27,404

djksM+½ ,oa la?kh; djksa rFkk “kqYdksa esa jkT;ka'k ¼` 467 djksM+½ dh deh ds

dkj.k gqbZ tcfd Lo;a ds djsrj jktLo ds vUrxZr ` 1,358 djksM+ dh of}

gqbZA

● Lo;a ds dj jktLo esa ctV vuqekuksa ds lkis{k deh ¼` 14,109 djksM+½

eq[;r% fcØh] O;kikj vkfn ij dj ¼` 5,285 djksM+½] LVkEi ,oa iathdj.k

“kqYd ¼` 4,061 djksM+½ ,oa jkT; vkcdkjh ¼` 3,723 djksM+½ ds vUrxZr gqbZA

jkT; vkcdkjh foHkkx us deh dk dkj.k vR;f/kd ctV izko/kku gksuk

crk;k D;ksafd tgk¡ foxr 10 o’kksaZ esa la;qDr okf’kZd of} nj ¼lh-,-th-vkj-½

15.9 izfr'kr Fkh] o’kZ 2017-18 ds fy;s ctV izko/kku o’kZ 2016-17 dh

okLrfod izkfIr;ksa ds lkis{k 44.3 izfr'kr vf/kd fd;k x;k FkkA jkT;

vkcdkjh ds vUrxZr okLrfod izkfIr;ksa esa o’kZ 2016-17 dh rqyuk esa o’kZ

2017-18 esa 21.34 izfr'kr dh of) gqbZA jkT; vkcdkjh foHkkx us vxzsRkj

crk;k fd jkT; vkcdkjh izkfIr;ksa esa deh dk dkj.k iM+kslh jkT;ksa dh rqyuk

esa “kjkc dk vf/kdre [kqnjk ewY; T;knk gksus ds dkj.k vU; jkT;ksa eq[;r%

gfj;k.kk10 ls rLdjh fd;k tkuk gSA

● o’kZ 2017-18 ds ctV izkOk/kku esa y?kq ,oa lhekar d`’kdksa dks Qlyh _.k

ekQh ds fy;s jktLo O;; esa ` 36,000 djksM+ dh vR;f/kd of) ds dkj.k

iwathxr O;; ds o’kZ 2016-17 ds ctV izko/kku ¼` 71,878 djksM+½ ds lkis{k

o’kZ 2017-18 esa ctV izko/kku esa ¼` 53,258 djksM+½ esa 26 izfr'kr dh deh

gqbZA

● jktLo O;; esa eq[; deh ¼` 40,895 djksM+½ vkfFkZd lsok;sa ¼` 18,460 djksM+½]

lkekftd lsok;sa ¼` 17,155 djksM+½] lkekU; lsok;sa ¼` 5,257 djksM+½ rFkk

lgk;rk vuqnku ,oa va'knku ¼` 23 djksM+½ ds vUrxZr gqbZA iwathxr O;; esa

deh ¼` 14,170 djksM+½ vkfFkZd lsok;sa ¼` 9,859 djksM+½] lkekftd lsok;sa

¼` 3,486 djksM+½ rFkk lkekU; lsok;sa ¼` 825 djksM+½ ds vUrxZr deh ds

dkj.k gqbZA jktLo ,oa iwathxr O;; esa deh tSlk fd jkT; ljdkj ds

fofu;ksx ys[ks 2017-18 esa n'kkZ;k x;k gS] vR;f/kd ctV izko/kku] foRrh;

Lohd`fr fuxZr u gksuk] fuf/k;ksa dk voeqDr u gksuk] ;kstuk dh Lohdfr u

gksuk] fjDr inksa vkfn ds dkj.k gqbZA

laLrqfr: foRr foHkkx dks ctV rS;kj djus dh izfØ;k dks rdZlaxr cukuk pkfg,

ftlls ctV vuqeku rFkk okLrfodrkvksa esa yxkrkj c<+rs vUrj dks de fd;k tk

ldsA

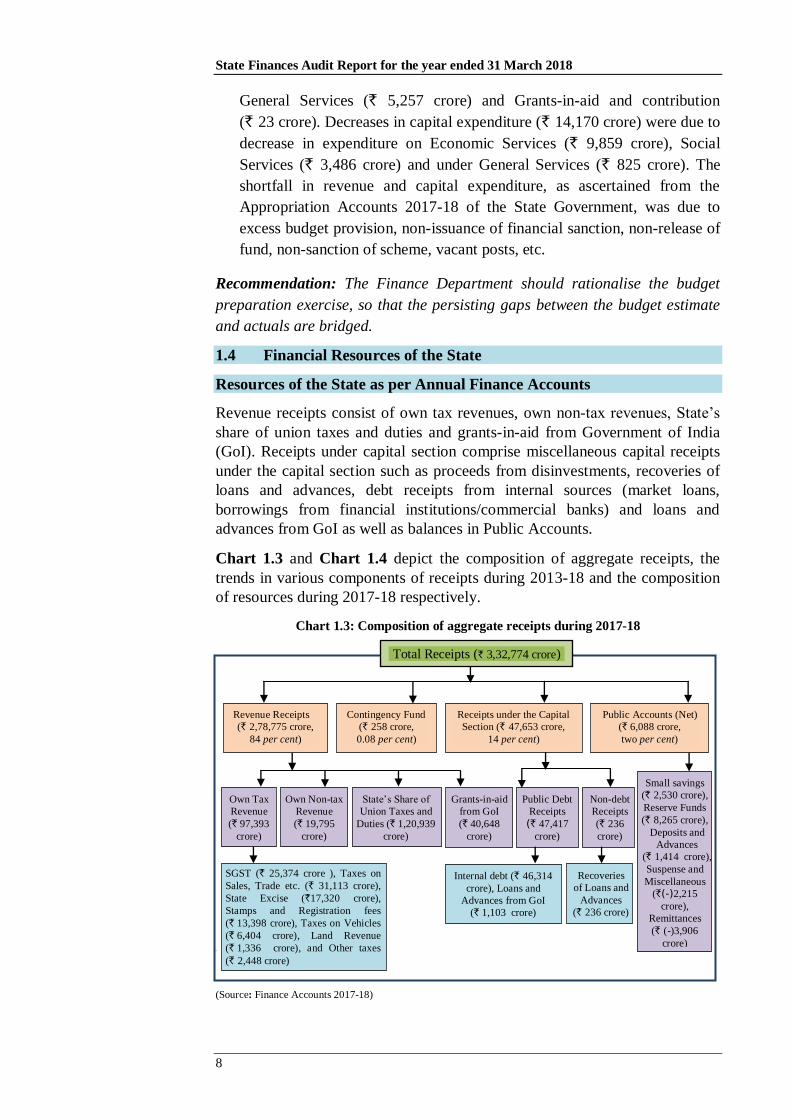

1.4 jkT; ds foRrh; lalk/ku

okf"kZd foRr ys[ks ds vuqlkj jkT; ds lalk/ku

jktLo izkfIr;ksa ds vUrxZr Lo;a dk dj jktLo] Lo;a dk djsrj jktLo] dsUnzh;

djksa rFkk “kqYdksa esa jkT;ka'k rFkk Hkkjr ljdkj ls izkIr lgk;rk vuqnku lfEefyr

10

fu;a=d&egkys[kk ijh{kd dh m-iz- ljdkj dh izfrosnu la[;k 1 ¼2019½ Hkh ns[ksaA

v/;k; 1 & jkT; ljdkj ds foRr

9

gSA iw¡thxr vuqHkkx ds vUrxZr izkfIr;k¡] fofo/k izkfIr;k¡ tSls fofuos'k ls izkfIr;k¡ ,oa

_.k vfxzeksa dh olwyh] vkUrfjd lzksrksa ¼cktkj _.k] foRrh; [email protected];d

cSadksa ls _.k½ RkFkk Hkkjr ljdkj ls izkIr _.k ,oa vfxze ds lkFk&lkFk yksd ys[ks

ds vo'ks’k lfEefyr gS aA

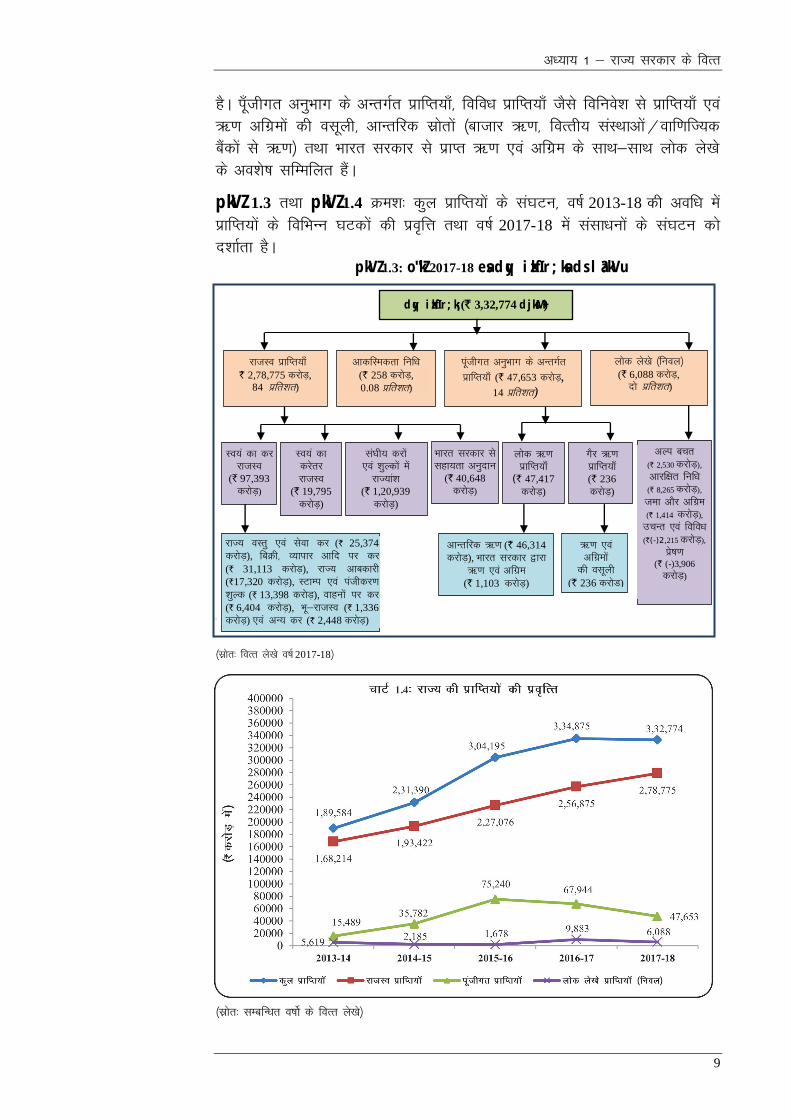

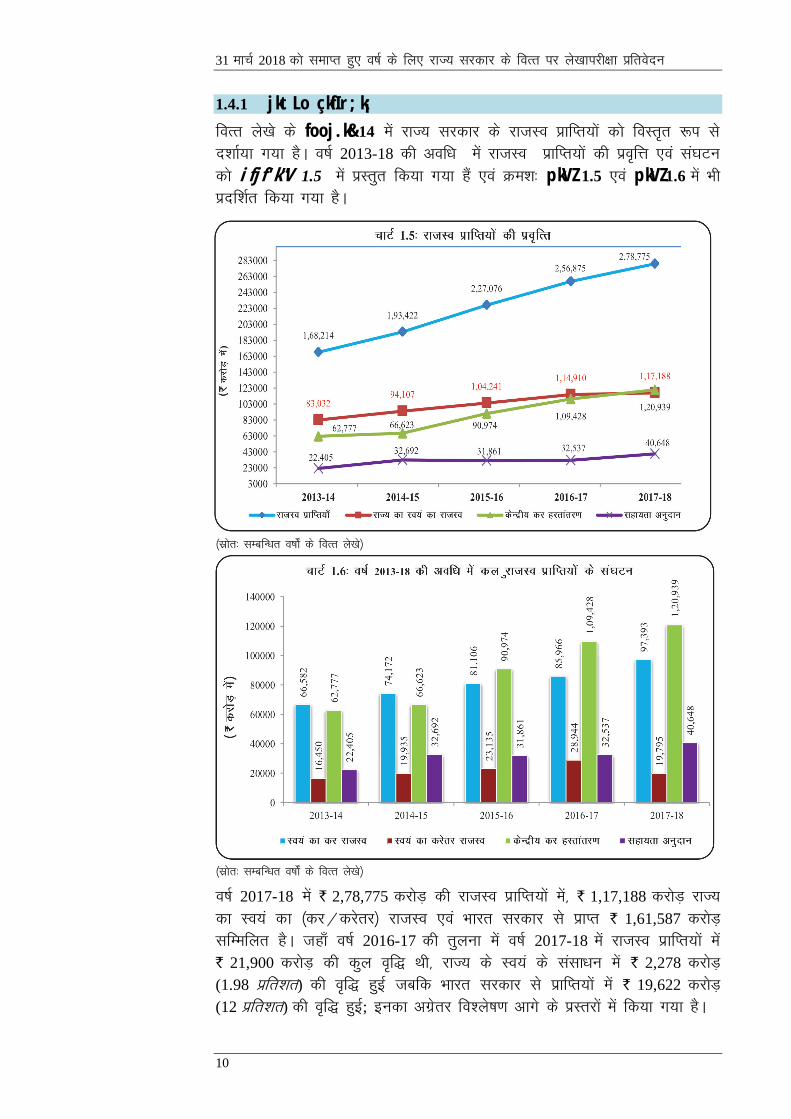

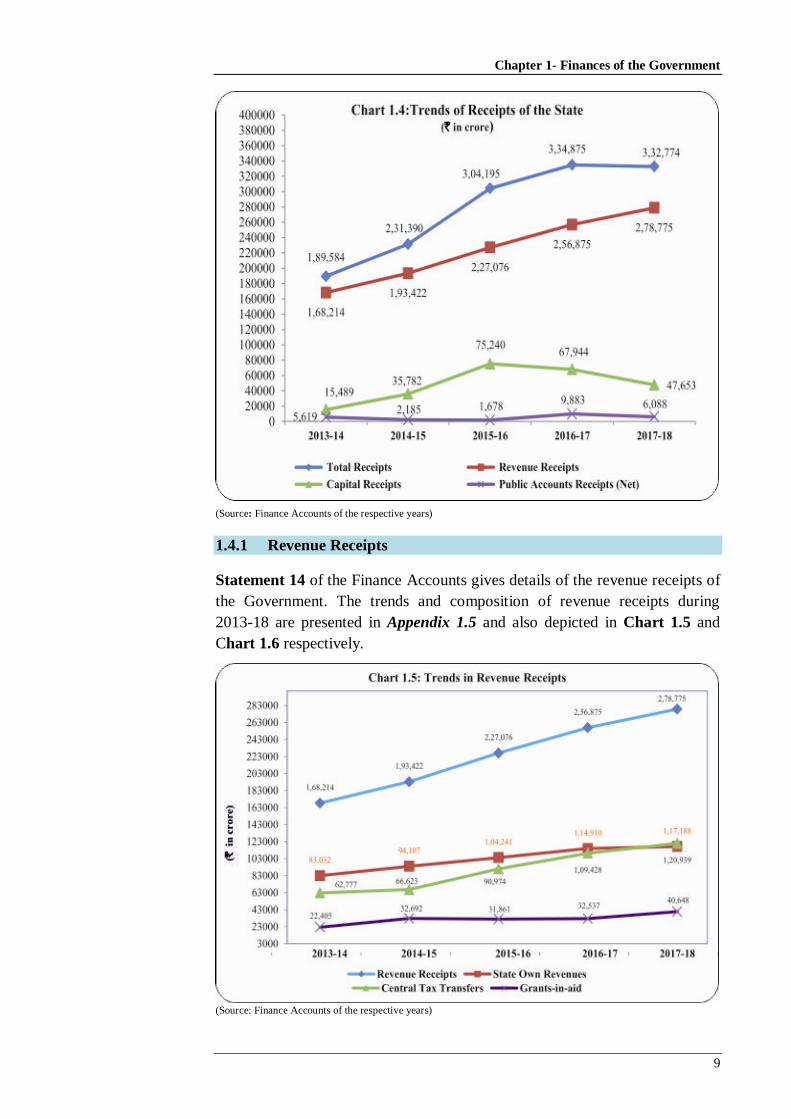

pkVZ 1.3 rFkk pkVZ 1.4 Øe'k% dqy izkfIr;ksa ds la?kVu] o’kZ 2013-18 dh vof/k esa

izkfIr;ksa ds fofHkUu ?kVdksa dh izofÙk rFkk o’kZ 2017-18 esa lalk/kuksa ds la?kVu dks

n'kkZrk gSA

pkVZ 1.3: o"kZ 2017-18 esa dqy izkfIr;ksa ds la?kVu

9(

¼lzksr% foRr ys[ks o’kZ 2017-18½

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

dqy izkfIr;k¡ (` 3,32,774 djksM+)

Lo;a dk dj

jktLo (` 97,393

djksM++)

Lo;a dk

djsrj

jktLo

(` 19,795

djksM++)

la?kh; djksa

,oa 'kqYdksa esa

jkT;ka'k

(` 1,20,939

djksM+++)

Hkkjr ljdkj ls

lgk;rk vuqnku

(` 40,648

djksM+)

yksd _.k

izkfIr;k¡

(` 47,417

djksM+)

xSj _.k

izkfIr;k¡

(` 236

djksM+)

yksd ys[ks ¼fuoy½

(` 6,088 djksM+,

nks izfr'kr)

vYi cpr

(` 2,530 djksM+),

vkjf{kr fuf/k

(` 8,265 djksM+),

tek vkSj vfxze

(` 1,414 djksM+),

mpUr ,oa fofo/k

(`(-)2,215 djksM+),

izs"k.k

(` (-)3,906

djksM+)

_.k ,oa

vfxzeksa

dh olwyh

(` 236 djksM+)

vkdfLedrk fuf/k

(` 258 djksM+,

0.08 izfr'kr)

iwathxr vuqHkkx ds vUrxZr

izkfIr;k¡ (` 47,653 djksM+,

14 izfr'kr)

jktLo izkfIr;k¡

` 2,78,775 djksM+,

84 izfr'kr)

vkUrfjd _.k (` 46,314

djksM+), Hkkjr ljdkj }kjk

_.k ,oa vfxze

(` 1,103 djksM+)

jkT; oLrq ,oa lsok dj (` 25,374

djksM+), fcØh] O;kikj vkfn ij dj

(` 31,113 djksM+), jkT; vkcdkjh

(`17,320 djksM+), LVkEi ,oa iathdj.k

'kqYd (` 13,398 djksM+), okguksa ij dj

(` 6,404 djksM+), Hkw&jktLo (` 1,336

djksM+) ,oa vU; dj (` 2,448 djksM+)

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

10

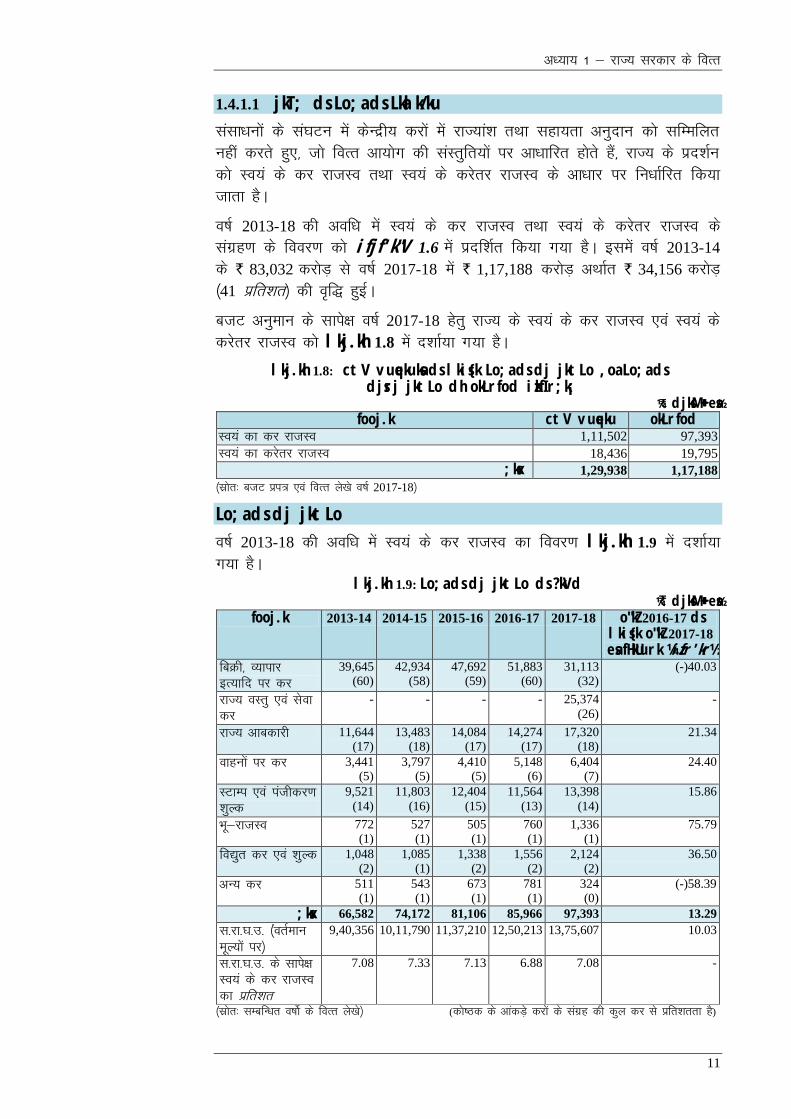

1.4.1 jktLo çkfIr;k¡

foRr ys[ks ds fooj.k&14 esa jkT; ljdkj ds jktLo çkfIr;ksa dks foLrr :i ls

n'kkZ;k x;k gSA o"kZ 2013-18 dh vof/k esa jktLo izkfIr;ksa dh izofŸk ,oa la?kVu

dks ifjf'k"V 1.5 esa izLrqr fd;k x;k gSa ,oa Øe'k% pkVZ 1.5 ,oa pkVZ 1.6 esa Hkh

iznf'kZr fd;k x;k gSA

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

¼lzksr% lEcfU/kr o’kksZ a ds foRr ys[ks½

o’kZ 2017-18 esa ` 2,78,775 djksM+ dh jktLo izkfIr;ksa esa] ` 1,17,188 djksM+ jkT;

dk Lo;a dk ¼dj@djsrj½ jktLo ,oa Hkkjr ljdkj ls izkIr ` 1,61,587 djksM+

lfEefyr gSA tgk¡ o’kZ 2016-17 dh rqyuk esa o’kZ 2017-18 esa jkTkLo izkfIr;ksa esa

` 21,900 djksM+ dh dqy of) Fkh] jkT; ds Lo;a ds lalk/ku esa ` 2,278 djksM+

(1.98 izfr'kr) dh of) gqbZ tcfd Hkkjr ljdkj ls izkfIr;ksa esa ` 19,622 djksM+

(12 izfr'kr) dh of) gqbZ; budk vxzsrj fo'ys’k.k vkxs ds izLrjksa esa fd;k x;k gSA

v/;k; 1 & jkT; ljdkj ds foRr

11

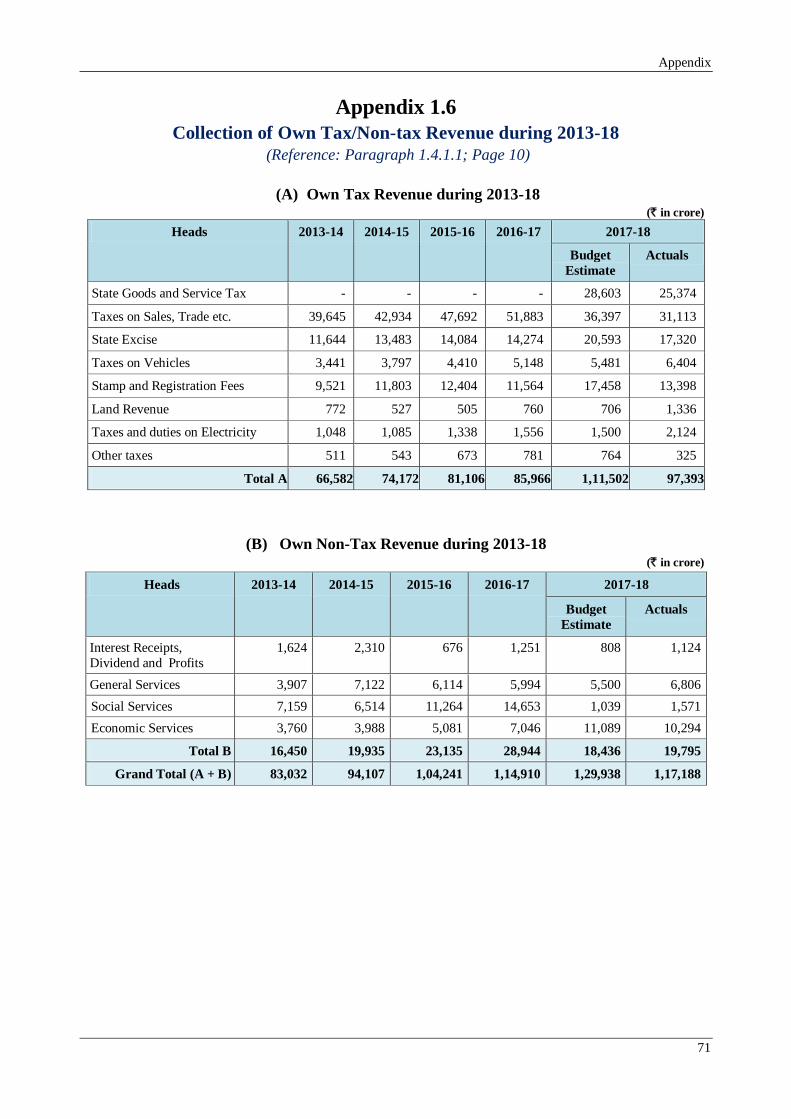

1.4.1.1 jkT; ds Lo;a ds Lkalk/ku

lalk/kuksa ds la?kVu esa dsUnzh; djksa esa jkT;ka'k rFkk lgk;rk vuqnku dks lfEefyr

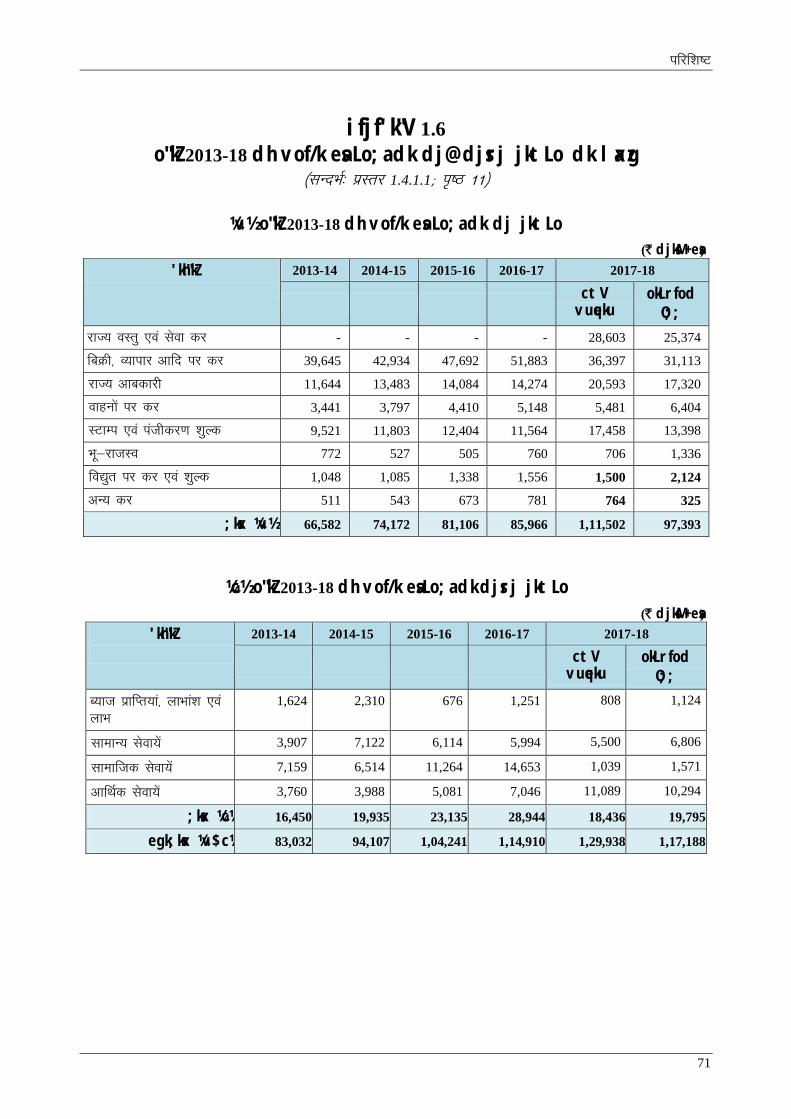

ugha djrs gq,] tks foRr vk;ksx dh laLrqfr;ksa ij vk/kkfjr gksrs gSa] jkT; ds izn'kZu

dks LOk;a ds dj jktLo rFkk Lo;a ds djsrj jktLo ds vk/kkj ij fu/kkZfjr fd;k

tkrk gSA

o’kZ 2013-18 dh vof/k esa Lo;a ds dj jktLo rFkk Lo;a ds djsrj jktLo ds

laxzg.k ds fooj.k dks ifjf'k"V 1.6 esa iznf'kZr fd;k x;k gSA blesa o’kZ 2013-14

ds ` 83,032 djksM+ ls o’kZ 2017-18 esa ` 1,17,188 djksM+ vFkkZr ` 34,156 djksM+

¼41 izfr'kr½ dh of) gqbZA

ctV vuqeku ds lkis{k o’kZ 2017-18 gsrq jkT; ds Lo;a ds dj jktLo ,oa Lo;a ds

djsrj jktLo dks lkj.kh 1.8 esa n'kkZ;k x;k gSA

lkj.kh 1.8: ctV vuqekuksa ds lkis{k Lo;a ds dj jktLo ,oa Lo;a ds djsrj jktLo dh okLrfod izkfIr;k¡

¼` djksM++++ esa½ fooj.k ctV vuqeku okLrfod

Lo;a dk dj jktLo 1,11,502 97,393

Lo;a dk djsrj jktLo 18,436 19,795

;ksx 1,29,938 1,17,188

¼lzksr% ctV izi= ,oa foRr ys[ks o’kZ 2017-18½

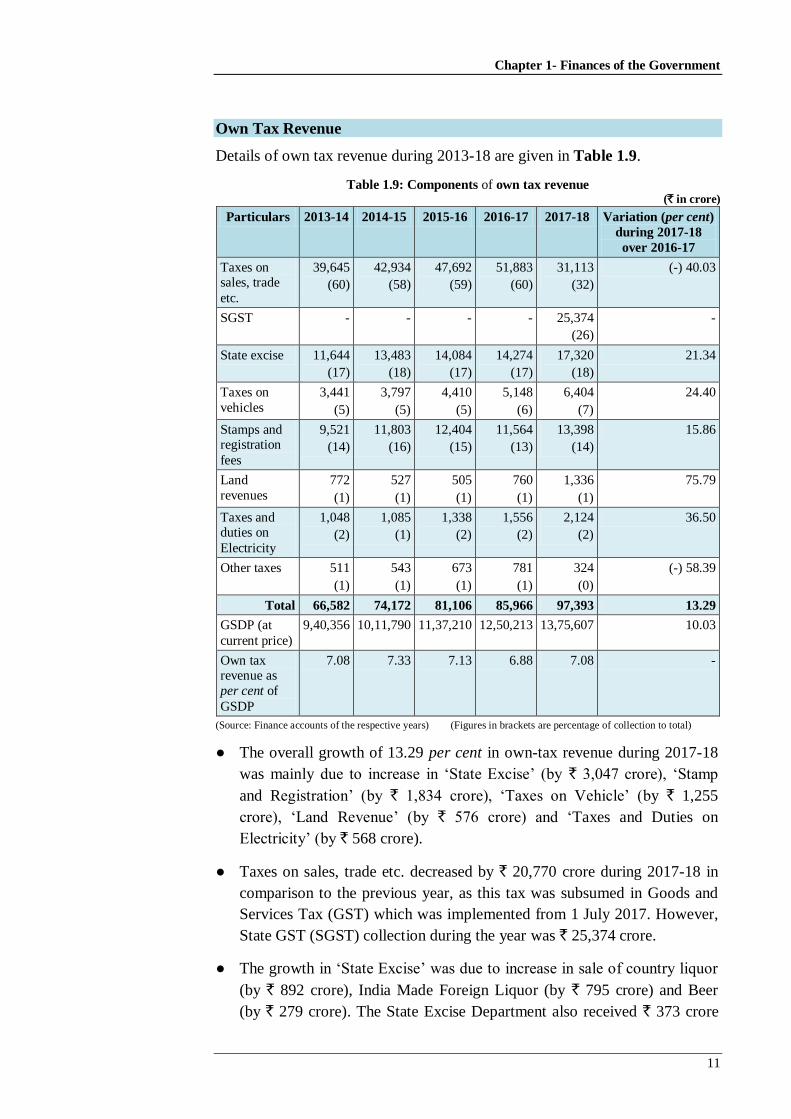

Lo;a ds dj jktLo

o"kZ 2013-18 dh vof/k esa Lo;a ds dj jktLo dk fooj.k lkj.kh 1.9 esa n'kkZ;k

x;k gSA

lkj.kh 1.9: Lo;a ds dj jktLo ds ?kVd ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18 o"kZ 2016-17 ds lkis{k o"kZ 2017-18

esa fHkUurk ¼izfr'kr½ fcØh] O;kikj

bR;kfn ij dj 39,645

(60) 42,934

(58) 47,692

(59) 51,883

(60) 31,113

(32) (-)40.03

jkT; oLrq ,oa lsok

dj - - - - 25,374

(26)

-

jkT; vkcdkjh 11,644 (17)

13,483 (18)

14,084 (17)

14,274 (17)

17,320 (18)

21.34

okguksa ij dj 3,441 (5)

3,797 (5)

4,410 (5)

5,148 (6)

6,404 (7)

24.40

LVkEi ,oa iathdj.k

'kqYd 9,521

(14)

11,803

(16)

12,404

(15)

11,564

(13)

13,398

(14)

15.86

Hkw&jktLo 772 (1)

527 (1)

505 (1)

760 (1)

1,336 (1)

75.79

fo|qr dj ,oa “kqYd 1,048 (2)

1,085 (1)

1,338 (2)

1,556 (2)

2,124 (2)

36.50

vU; dj 511 (1)

543 (1)

673 (1)

781 (1)

324 (0)

(-)58.39

;ksx 66,582 74,172 81,106 85,966 97,393 13.29

l-jk-?k-m- ¼aorZeku

ewY;ksa ij½ 9,40,356 10,11,790 11,37,210 12,50,213 13,75,607 10.03

l-jk-?k-m- ds lkis{k

Lo;a ds dj jktLo

dk izfr'kr

7.08 7.33 7.13 6.88 7.08 -

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½ (dks’Bd ds vkadM+s djksa ds laxzg dh dqy dj ls izfr'krrk gS)

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

12

● o’kZ 2017-18 esa Lo;a ds dj jktLo esa dqy 13.29 izfr'kr dh of} eq[;r%

^jkT; vkcdkjh^ ¼` 3,047 djksM+½] ^LVkEi ,oa iathdj.k^ ¼` 1,834 djksM+½]

^okguksa ij dj^ ¼` 1,255 djksM+½] ^Hkw&jktLOk^ ¼` 576 djksM+½ rFkk ^fo|qr dj

,oa “kqYd^ ¼` 568 djksM+½ esa of} ds dkj.k gqbZA

● foxr o’kZ dh rqyuk esa o’kZ 2017-18 esa fcØh] O;kikj bR;kfn ij dj esa

` 20,770 djksM+ dh deh gqbZ D;ksafd ;g dj oLrq ,oa lsok dj ¼th-,l-Vh-½ esa

lekfgr fd;k x;k tks fd 1 tqykbZ 2017 ls fØ;kfUor fd;k x;k x;kA

;|fi] o’kZ ds nkSjku jkT; oLrq ,oa lsok dj ¼,l-th-,l-Vh-½ ds vUrxZr

` 25,374 djksM+ dk laxzg.k gqvkA

● jkT; vkcdkjh esa of} ns'kh “kjkc ¼` 892 djksM+½] Hkkjr esa fufeZr fons'kh “kjkc

¼` 795 djksM+½ ,o ach;j ¼` 279 djksM+½ dh fcØh esa of} ds dkj.k gqbZA jkT;

vkcdkjh foHkkx dks o’kZ ds nkSjku ` 373 djksM+ dh izkfIr o’kZ 2018-19 esa

nqdkuksa ds fy;s bZ&ykVjh Vs.Mj izfØ;k viukus ds dkj.k Hkh izkIr gqvkA

● *LVkEi ,oa iathdj.k* ds vUrxZr izkfIr;ksa esa of} eq[;r% Hkwfe ds okf’kZd

iqujhf{kr lfdZy jsV] jftLVªh izi=ksa ds “kqYd ls vf/kd izkfIr;ksa ¼58 izfr'kr½

rFkk U;kf;d ,oa U;kf;dsRrj LVSEIl dh fcØh ¼23 izfr'kr½ ds dkj.k gqbZA

*fo|qr dj ,oa “kqYd* dh izkfIr;ksa esa of} fo|qr dk miHkksx ,oa fcØh ij

vf/kd dj laxzg.k ¼41 izfr'kr½ ds dkj.k gqbZA

● o’kZ 2017-18 esa jkT; ds l-jk-?k-m- ds lkis{k Lo;a dk dj jktLo

7.08 izfr'kr Fkk tks vU; jkT;ksa tSls NÙkhlx<+ ¼6.82 izfr'kr½] e/; izns'k

¼6.34 izfr'kr½] jktLFkku ¼6.02 izfr'kr½] xqtjkr ¼5.42 izfr'kr½] >kj[k.M

¼4.84 izfr'kr½ ,oa fcgkj ¼4.74 izfr'kr½ dh rqyuk esa vf/kd FkkA

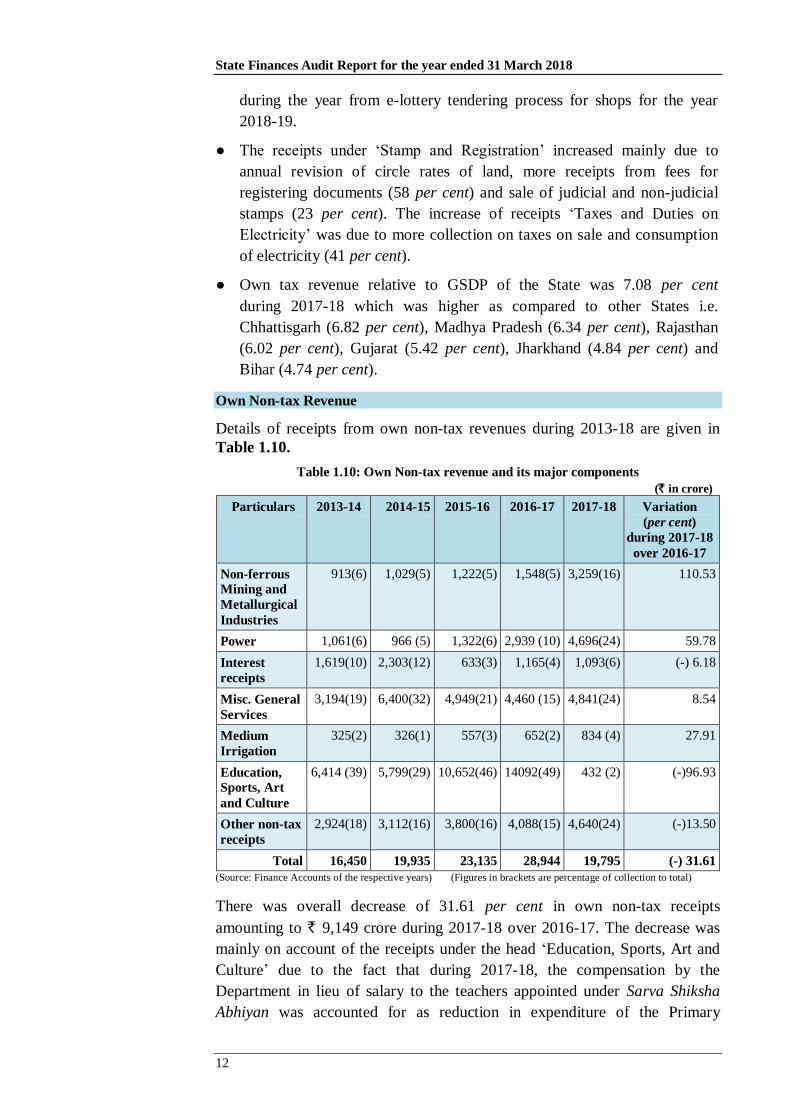

Lo;a dk djsrj jktLo

o"kZ 2013-18 dh vof/k esa djsrj jktLo dh izkfIr;ksa dk fooj.k lkj.kh 1.10 esa

n'kkZ;k x;k gSA

lkj.kh 1.10: LOk;a ds djsrj jktLo ,oa blds eq[; ?kVd

¼` djksM++++ esa½ fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18 o"kZ 2016-17 ds

lkis{k o"kZ 2017-18

esa fHkUurk ¼izfr'kr½ vykSg [kuu ,oa

/kkrqdeZ m|ksx

913

(6)

1,029

(5)

1,222

(5)

1,548

(5)

3,259

(16)

110.53

ÅtkZ 1,061(6) 966 (5) 1,322(6) 2,939 (10) 4,696(24) 59.78

C;kt izkfIr;k¡ 1,619

(10)

2,303

(12)

633

(3)

1,165

(4)

1,093

(6)

(-) 6.18

fofo/k lkekU;

lsok;sa

3,194

(19)

6,400

(32)

4,949

(21)

4,460

(15)

4,841

(24)

8.54

e/;e flapkbZ 325

(2)

326

(1)

557

(3)

652

(2)

834

(4)

27.91

f'k{kk] [ksydwn]

dyk ,oa laL—fr

6,414

(39) 5,799

(29)

10,652

(46)

14,092

(49)

432

(2)

(-)96.93

vU; djsrj

izkfIr;k¡

2,924

(18)

3,112

(16)

3,800

(16)

4,088

(15)

4,640

(24)

(-)13.50

;ksx 16,450 19,935 23,135 28,944 19,795 (-) 31.61

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½ (dks’Bd ds vkadM+s djksa ds laxzg dh dqy dj ls izfr'krrk gS)

v/;k; 1 & jkT; ljdkj ds foRr

13

o’kZ 2016-17 ds lkis{k o’kZ 2017-18 esa Lo;a ds djsrj izkfIr;ksa esa 31.61 izfr'kr

/kujkf'k ` 9,149 djksM+ dh deh gqbZA ;g eq[;r% ^f'k{kk] [ksy] dyk ,oa laLd`fr^

“kh’kZ ds vUrxZr izkfIr;ksa d s de gksus ds dkj.k Fkk] ftldk okLrfod dkj.k ;g Fkk

fd o’kZ 2017-18 esa loZ f'k{kk vfHk;ku ds vUrxZr fu;qDr f'k{kdksa dkss osru ds fy;s

dh tkus okyh izfriwfrZ dks izkFkfed f'k{kk foHkkx ds O;; esa deh ds :Ik esa

ys[kkafdr fd;k x;k tcfd iwoZ esa ;g jkT; ds djsrj izkfIr;ksa ds :i esa n'kkZ;k

tkrk FkkA vxzsrj] vykSg [kuu rFkk /kkrq deZ m|ksx ds vUrxZr [kfut fj;k;rh

“kqYd] fdjk;k ,oa jkW;YVh ¼186 izfr'kr½ esa vf/kd izkfIr;k¡ eq[;r% fofHkUu [kfutksa

ds jkW;YVh@fLFkj fdjk;s dh nj ds iqujhf{kr gksus ds dkj.k FkkA

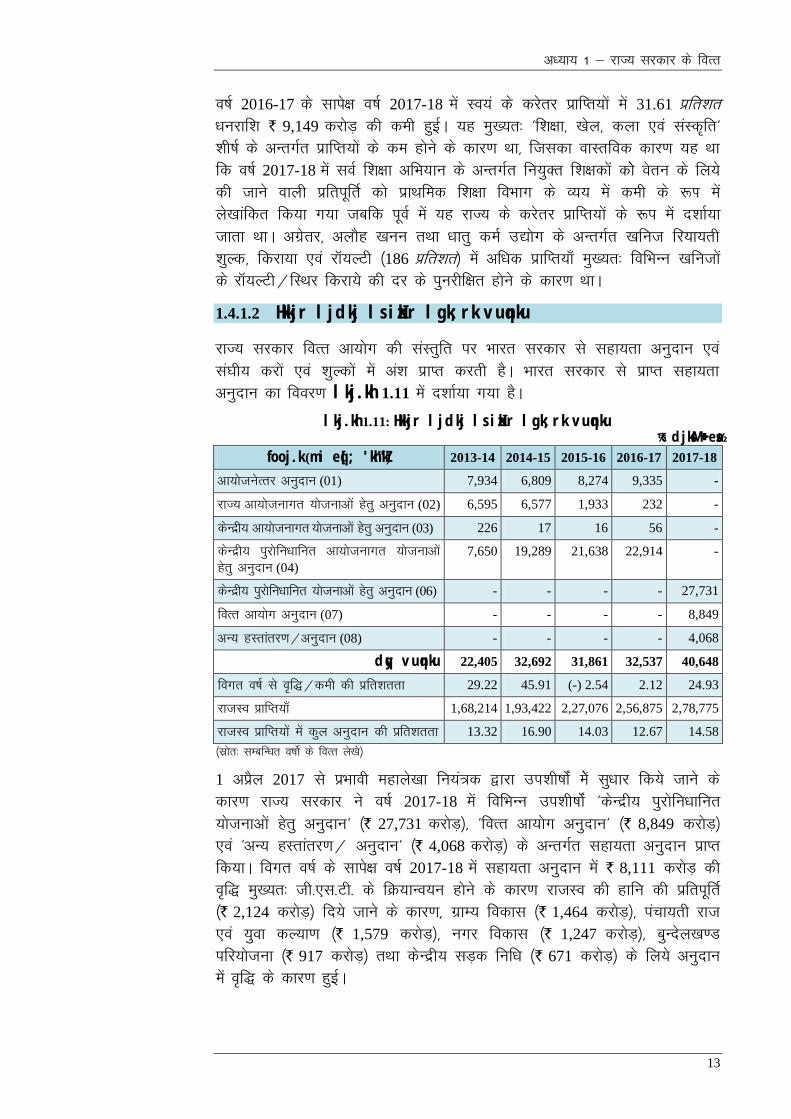

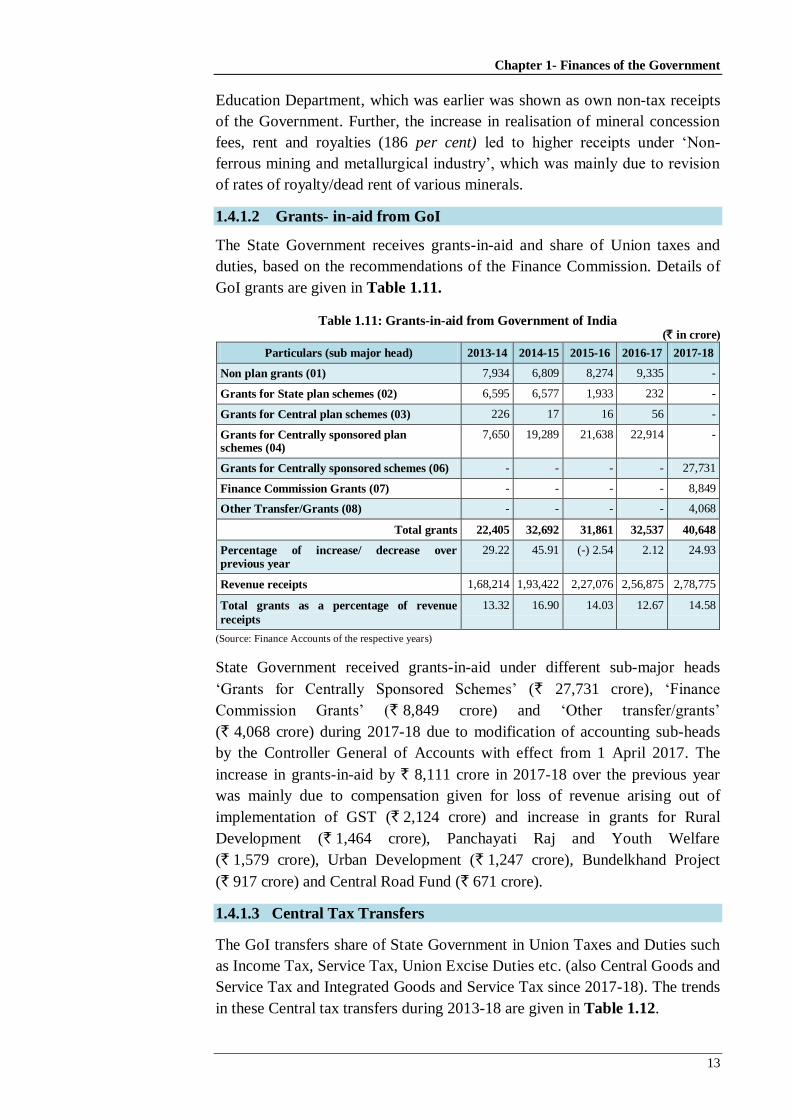

1.4.1.2 Hkkjr ljdkj ls izkIr lgk;rk vuqnku

jkT; ljdkj foRr vk;ksx dh laLrqfr ij Hkkjr ljdkj ls lgk;rk vuqnku ,oa

la?kh; djksa ,oa “kqYdksa esa va'k izkIr djrh gSA Hkkjr ljdkj ls izkIr lgk;rk

vuqnku dk fooj.k lkj.kh 1.11 esa n'kkZ;k x;k gSA

lkj.kh 1.11: Hkkjr ljdkj ls izkIr lgk;rk vuqnku

¼` djksM++++ esa½

fooj.k (mi eq[; 'kh"kZ) 2013-14 2014-15 2015-16 2016-17 2017-18

vk;kstusRrj vuqnku (01) 7,934 6,809 8,274 9,335 -

jkT; vk;kstukxr ;kstukvksa gsrq vuqnku (02) 6,595 6,577 1,933 232 -

dsUnzh; vk;kstukxr ;kstukvksa gsrq vuqnku (03) 226 17 16 56 -

dsUnzh; iqjksfu/kkfur vk;kstukxr ;kstukvksa

gsrq vuqnku (04)

7,650 19,289 21,638 22,914 -

dsUnzh; iqjksfu/kkfur ;kstukvksa gsrq vuqnku (06) - - - - 27,731

foRr vk;ksx vuqnku (07) - - - - 8,849

vU; gLrkarj.k@vuqnku (08) - - - - 4,068

dqy vuqnku 22,405 32,692 31,861 32,537 40,648

foxr o"kZ ls of)@deh dh izfr'krrk 29.22 45.91 (-) 2.54 2.12 24.93

jktLo izkfIr;k¡ 1,68,214 1,93,422 2,27,076 2,56,875 2,78,775

jktLo izkfIr;ksa esa dqy vuqnku dh izfr'krrk 13.32 16.90 14.03 12.67 14.58

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

1 vizSy 2017 ls izHkkoh egkys[kk fu;a=d }kjk mi'kh’kksZa esas lq/kkj fd;s tkus ds

dkj.k jkT; ljdkj us o’kZ 2017-18 esa fofHkUu mi'kh’kksZa ^dsUnzh; iqjksfu/kkfur

;kstukvksa gsrq vuqnku^ ¼` 27,731 djksM+½] ^foRr vk;ksx vuqnku^ ¼` 8,849 djksM+½

,oa ^vU; gLrkarj.k@ vuqnku^ ¼` 4,068 djksM+½ ds vUrxZr lgk;rk vuqnku izkIr

fd;kA foxr o’kZ ds lkis{k o’kZ 2017-18 esa lgk;rk vuqnku esa ` 8,111 djksM+ dh

of) eq[;r% th-,l-Vh- ds fØ;kUo;u gksus ds dkj.k jktLo dh gkfu dh izfriwfrZ

¼` 2,124 djksM+½ fn;s tkus ds dkj.k] xzkE; fodkl ¼` 1,464 djksM+½] iapk;rh jkt

,oa ;qok dY;k.k ¼` 1,579 djksM+½] uxj fodkl ¼` 1,247 djksM+½] cqUnsy[k.M

ifj;kstuk ¼` 917 djksM+½ rFkk dsUnzh; lM+d fuf/k ¼` 671 djksM+½ ds fy;s vuqnku

esa of) ds dkj.k gqbZA

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

14

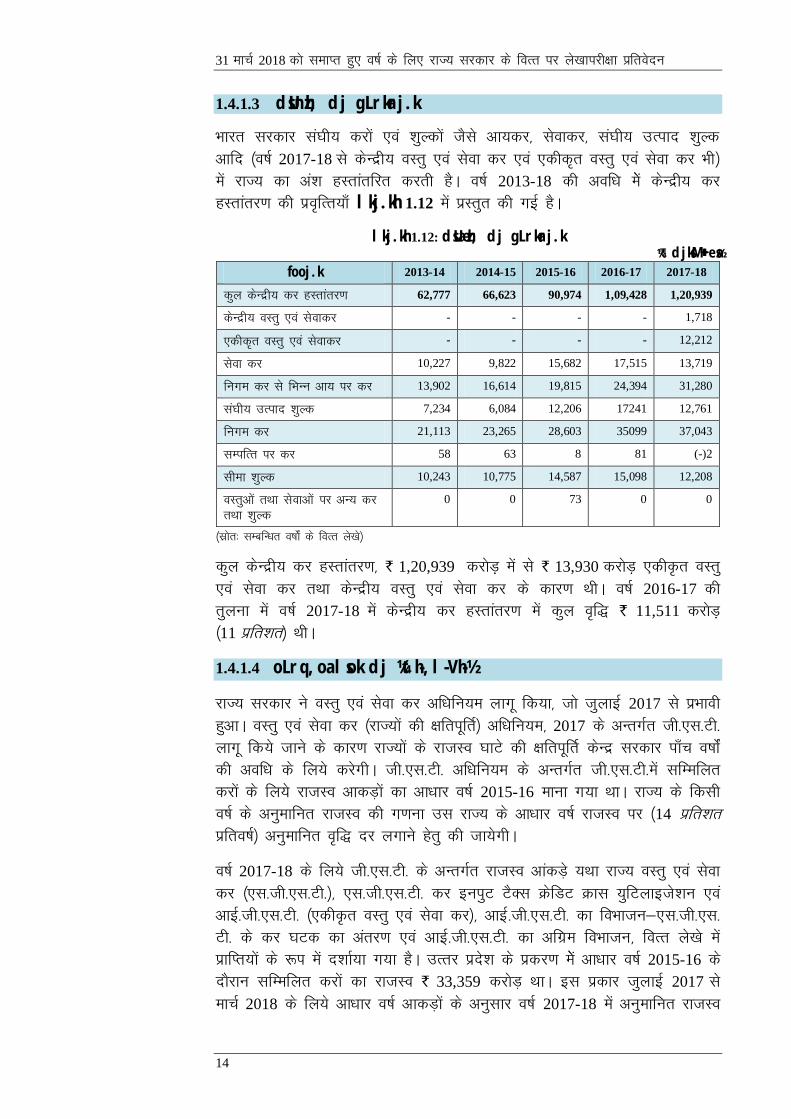

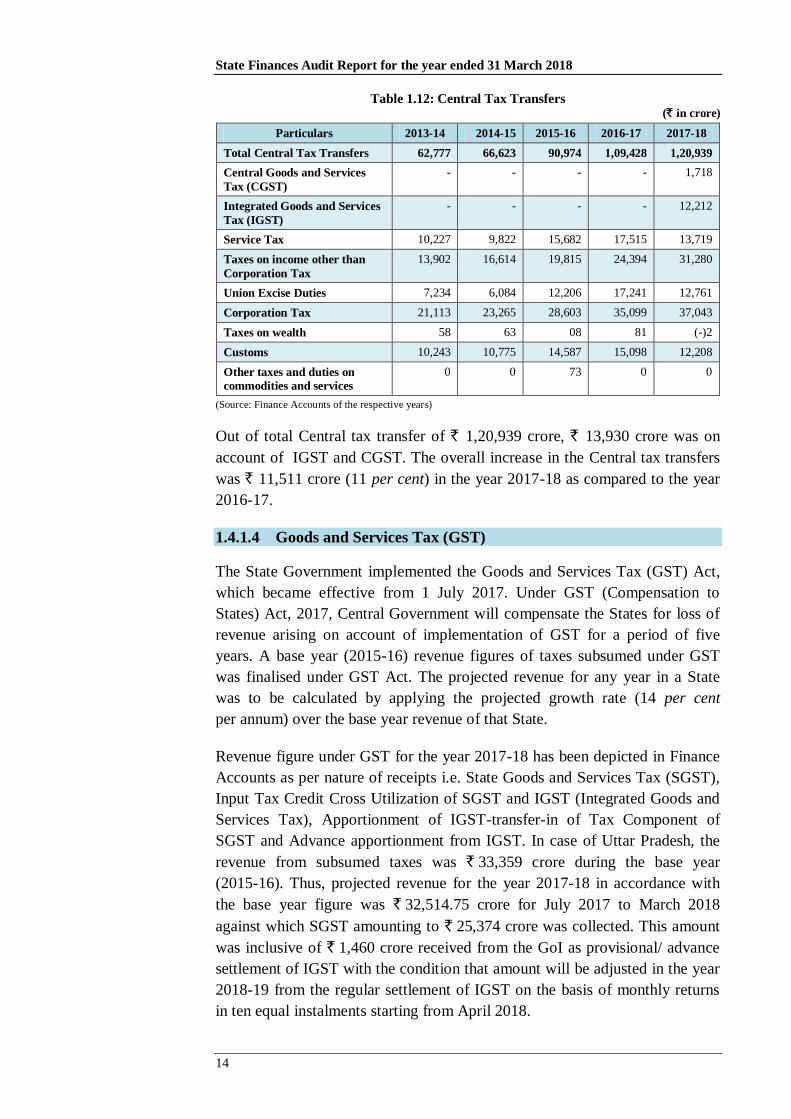

1.4.1.3 dsUnzh; dj gLrkarj.k

Hkkjr ljdkj la?kh; djksa ,oa 'kqYdksa tSls vk;dj] lsokdj] la?kh; mRikn 'kqYd

vkfn ¼o’kZ 2017-18 ls dsUnzh; oLrq ,oa lsok dj ,oa ,dhd`r oLrq ,oa lsok dj Hkh½

esa jkT; dk va'k gLrkarfjr djrh gSA o"kZ 2013-18 dh vof/k esas dsUnzh; dj

gLrkarj.k dh izofRr;k¡ lkj.kh 1.12 esa izLrqr dh xbZ gSA

lkj.kh 1.12: dsUæzh; dj gLrkarj.k ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

dqy dsUnzh; dj gLrkarj.k 62,777 66,623 90,974 1,09,428 1,20,939

dsUnzh; oLrq ,oa lsokdj - - - - 1,718

,dhdr oLrq ,oa lsokdj - - - - 12,212

lsok dj 10,227 9,822 15,682 17,515 13,719

fuxe dj ls fHkUu vk; ij dj 13,902 16,614 19,815 24,394 31,280

la?kh; mRikn 'kqYd 7,234 6,084 12,206 17241 12,761

fuxe dj 21,113 23,265 28,603 35099 37,043

lEifRr ij dj 58 63 8 81 (-)2

lhek 'kqYd 10,243 10,775 14,587 15,098 12,208

oLrqvksa rFkk lsokvksa ij vU; dj

rFkk 'kqYd

0 0 73 0 0

¼lzksr% lEcfU/kr o"kksZa ds foRr ys[ks½

dqy dsUnzh; dj gLrkarj.k] ` 1,20,939 djksM+++ esa ls ` 13,930 djksM+++ ,dh—r oLrq

,oa lsok dj rFkk dsUnzh; oLrq ,oa lsok dj ds dkj.k FkhA o’kZ 2016-17 dh

rqyuk esa o’kZ 2017-18 esa dsUnzh; dj gLrkarj.k esa dqy of) ` 11,511 djksM+++

¼11 izfr'kr½ FkhA

1.4.1.4 oLrq ,oa lsok dj ¼th-,l-Vh-½

jkT; ljdkj us oLrq ,oa lsok dj vf/kfu;e ykxw fd;k] tks tqykbZ 2017 ls izHkkoh

gqvkA oLrq ,oa lsok dj ¼jkT;ksa dh {kfriwfrZ½ vf/kfu;e] 2017 ds vUrxZr th-,l-Vh-

ykxw fd;s tkus ds dkj.k jkT;ksa ds jktLo ?kkVs dh {kfriwfrZ dsUnz ljdkj ik¡p o’kksZ a

dh vof/k ds fy;s djsxhA th-,l-Vh- vf/kfu;e ds vUrxZr th-,l-Vh-esa lfEefyr

djksa ds fy;s jktLo vkdM+ksa dk vk/kkj o’kZ 2015-16 ekuk x;k FkkA jkT; ds fdlh

o’kZ ds vuqekfur jktLo dh x.kuk ml jkT; ds vk/kkj o’kZ jktLo ij ¼14 izfr'kr

izfro’kZ½ vuqekfur of) nj yxkus gsrq dh tk;sxhA

o’kZ 2017-18 ds fy;s th-,l-Vh- ds vUrxZr jktLo vkadM+s ;Fkk jkT; oLrq ,oa lsok

dj ¼,l-th-,l-Vh-½] ,l-th-,l-Vh- dj buiqV VSDl ØsfMV Økl ;qfVykbts'ku ,oa

vkbZ-th-,l-Vh- ¼,dhÑr oLrq ,oa lsok dj½] vkbZ-th-,l-Vh- dk foHkktu&,l-th-,l-

Vh- ds dj ?kVd dk varj.k ,oa vkbZ-th-,l-Vh- dk vfxze foHkktu] foRr ys[ks esa

izkfIr;ksa ds :i esa n'kkZ;k x;k gSA mRrj izns'k ds izdj.k esas vk/kkj o’kZ 2015-16 ds

nkSjku lfEefyr djksa dk jktLo ` 33,359 djksM+ FkkA bl izdkj tqykbZ 2017 ls

ekpZ 2018 ds fy;s vk/kkj o’kZ vkdM+ksa ds vuqlkj o’kZ 2017-18 esa vuqekfur jktLo

v/;k; 1 & jkT; ljdkj ds foRr

15

` 32,514.75 djksM+ Fkk] ftlds lkis{k ,l-th-,l-Vh- ds :Ik esa ` 25,374 djksM+

laxzg gqvk FkkA bl /kujkf'k esa Hkkjr ljdkj ls vkbZ-th-,l-Vh- vufUre@vfxze

lek/kku ds :Ik esa izkIr ` 1,460 djksM+ lfEefyr FkkA ;g bl “krZ ds lkFk Fkk fd

mDr /kujkf'k dk lek;kstu o"kZ 2018-19 esa ekg vizSy 2018 ls nl leku ekfld

fd'rkas esa vkbZ-th-,l-Vh- ds fu;fer lek/kku ls fd;k tk;sxkA

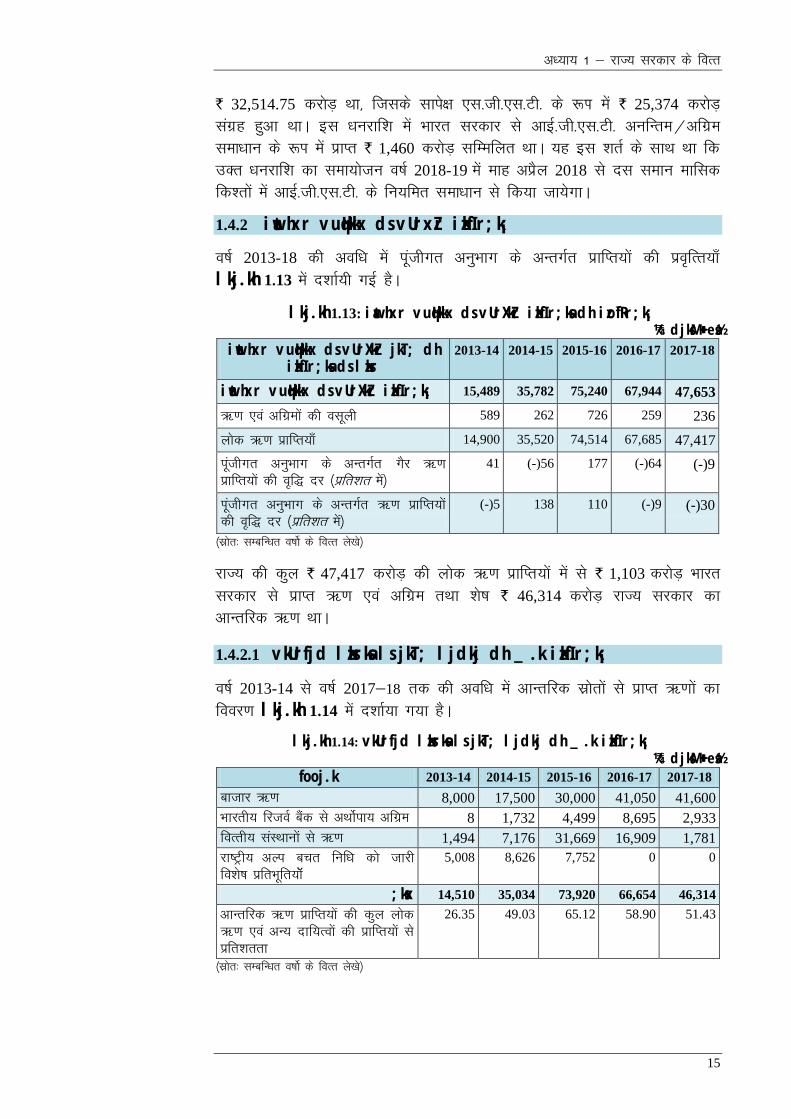

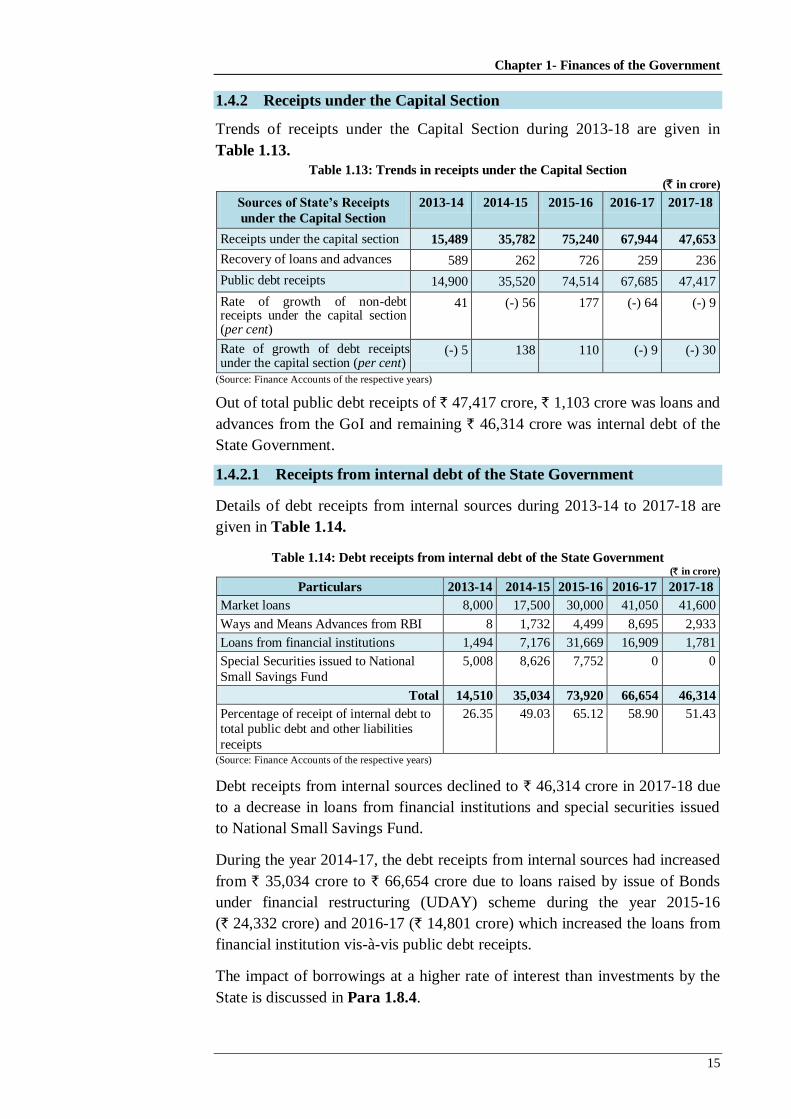

1.4.2 iwathxr vuqHkkx ds vUrxZr izkfIr;k¡

o’kZ 2013-18 dh vof/k esa iwathxr vuqHkkx ds vUrxZr izkfIr;ksa dh izofRr;k¡

lkj.kh 1.13 esa n'kkZ;h xbZ gSA

lkj.kh 1.13: iawthxr vuqHkkx ds vUrXkZr izkfIr;ksa dh izo `fRr;k¡ ¼` djksM++++ esa½

iwathxr vuqHkkx ds vUrXkZr jkT; dh izkfIr;ksa ds lzksr

2013-14 2014-15 2015-16 2016-17 2017-18

iwathxr vuqHkkx ds vUrXkZr izkfIr;k¡ 15,489 35,782 75,240 67,944 47,653

_.k ,oa vfxzeksa dh olwyh 589 262 726 259 236

yksd _.k izkfIr;k¡ 14,900 35,520 74,514 67,685 47,417

iwathxr vuqHkkx ds vUrXkZr xSj _.k

izkfIr;ksa dh of+) nj ¼izfr'kr esa½

41 (-)56 177 (-)64 (-)9

Ikwathxr vuqHkkx ds vUrXkZr _.k izkfIr;ksa

dh of+) nj ¼izfr'kr esa½

(-)5 138 110 (-)9 (-)30

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

jkT; dh dqy ` 47,417 djksM+ dh yksd _.k izkfIr;ksa esa ls ` 1,103 djksM+ Hkkjr

ljdkj ls izkIr _.k ,oa vfxze rFkk “ks’k ` 46,314 djksM+ jkT; ljdkj dk

vkUrfjd _.k FkkA

1.4.2.1 vkUrfjd lzksrksa ls jkT; ljdkj dh _.k izkfIr;k¡

o’kZ 2013-14 ls o’kZ 2017&18 rd dh vof/k esa vkUrfjd lzksrksa ls izkIr _.kksa dk

fooj.k lkj.kh 1.14 esa n'kkZ;k x;k gSA

lkj.kh 1.14: vkUrfjd lzksrksa ls jkT; ljdkj dh _.k izkfIr;k¡ ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

cktkj _.k 8,000 17,500 30,000 41,050 41,600

Hkkjrh; fjtoZ cSad ls vFkksZik; vfxze 8 1,732 4,499 8,695 2,933

foRrh; laLFkkuksa ls _.k 1,494 7,176 31,669 16,909 1,781

jk’Vªh; vYi cpr fuf/k dks tkjh

fo'ks’k izfrHkwfr;ksWa

5,008 8,626 7,752 0 0

;ksx 14,510 35,034 73,920 66,654 46,314

vkUrfjd _.k izkfIr;ksa dh dqy yksd

_.k ,oa vU; nkf;Roksa dh izkfIr;ksa ls

izfr'krrk

26.35 49.03 65.12 58.90 51.43

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks½

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

16

o"kZ 2017-18 esa foRrh; laLFkkuksa ls _.k ,oa jk’Vªh; vYi cpr fuf/k;ksa dks tkjh

fo'ks’k izfrHkwfr;ksa esa deh gksus ds dkj.k vkUrfjd L=ksrksa ls _.k izkfIr;kWaa de gksdj

` 46,314 djksM+ gks x;hA

o"kZ 2014-17 dh vof/k esa foRrh; iqulaZjpuk ;kstuk ¼mn;½ ds vUrxZr o’kZ

2015-16 (` 24,332 djksM+) ,oa o’kZ 2016-17 (` 14,801 djksM+) ds ckW.M tkjh djds

fy;s x;s _.kksa ds dkj.k vkURkfjd L=ksrksa ls =.k izkfIr;ksa esa of) gksdj ` 35,034

djksM+ ls ` 66,654 djksM+ gks x;h ftlds dkj.k foRrh; laLFkkuksa ls _.k ds

lkFk&lkFk yksd _.k izkfIr;ksa esa Hkh of) gqbZA

jkT; }kjk fuos'kksa ij izkIr C;kt ls vf/kd nj ij m/kkj ysus ds izHkko dk o.kZu

izLrj 1.8.4 esa fd;k x;k gSA

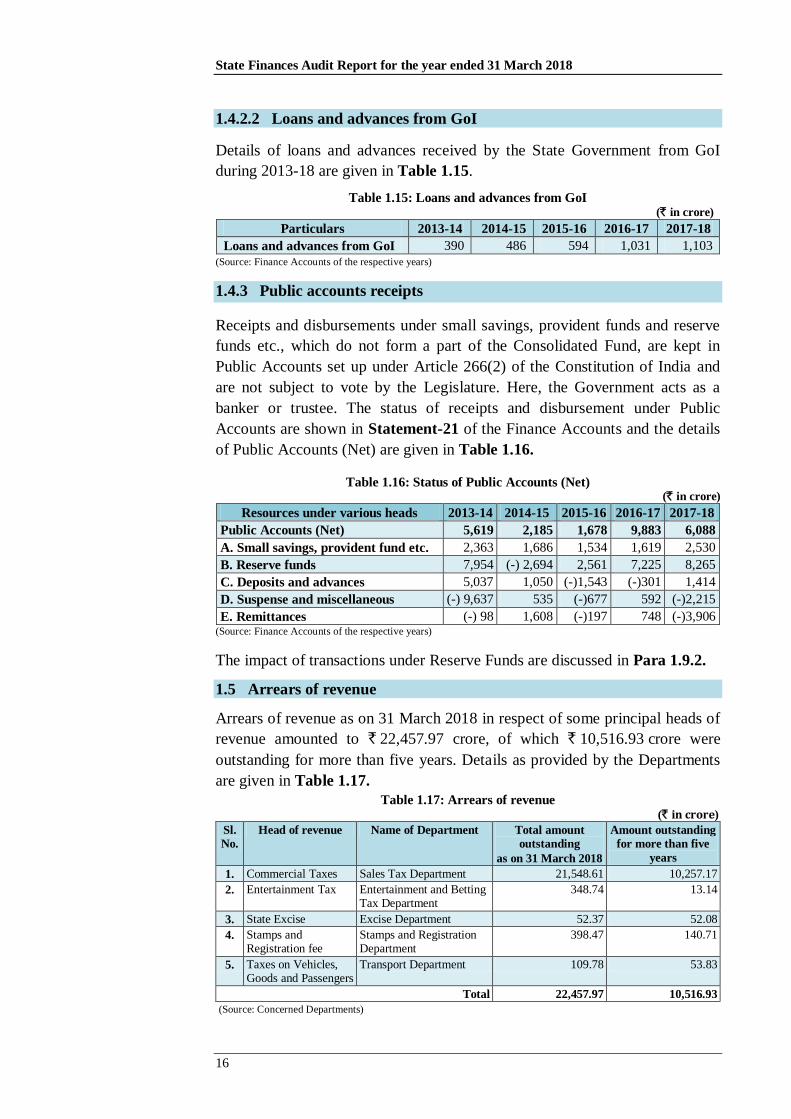

1.4.2.2 Hkkjr ljdkj ls izkIr _.k ,oa vfxze

o"kZ 2013-18 dh vof/k esa jkT; ljdkj }kjk Hkkjr ljdkj ls izkIr _.kksa ,oa

vfxzekas dk fooj.k lkj.kh 1.15 esa n'kkZ;k x;k gSA

lkj.kh 1.15: Hkkjr ljdkj ls izkIr _.k ,oa vfxze ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

Hkkjr ljdkj ls izkIr _.k ,oa vfxze 390 486 594 1,031 1,103

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

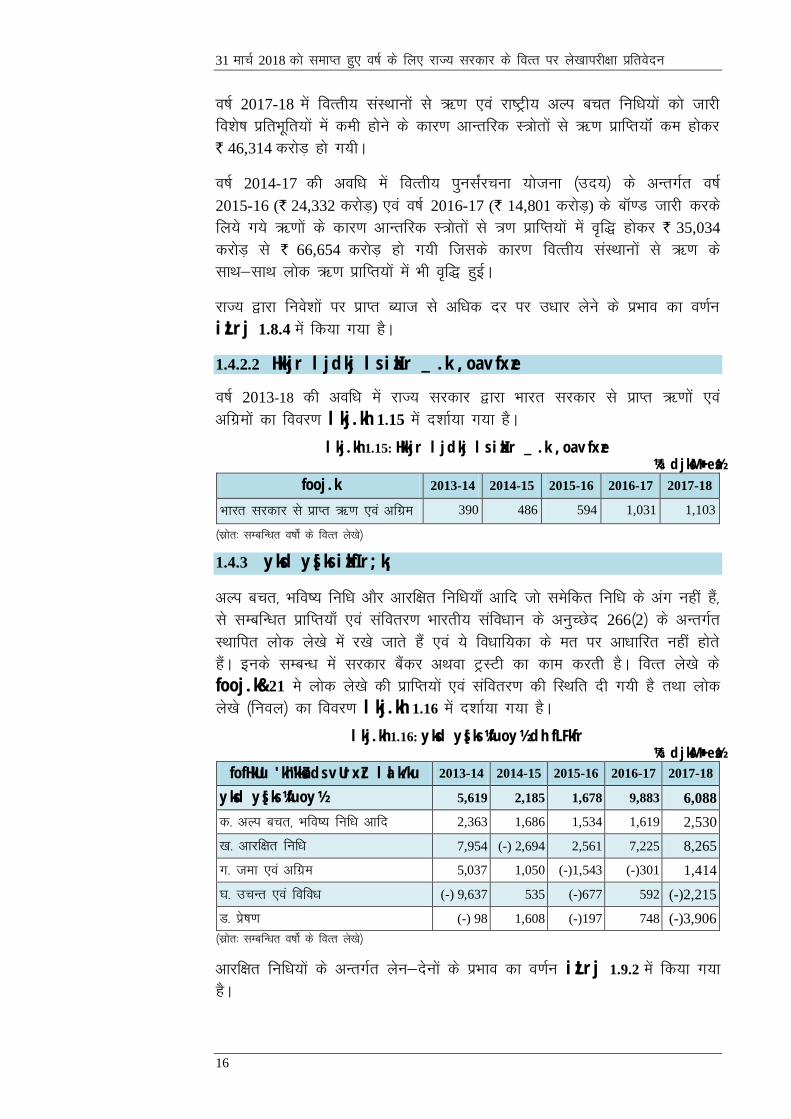

1.4.3 yksd ys[ks izkfIr;k¡

vYi cpr] Hkfo’; fuf/k vkSj vkjf{kr fuf/k;k¡ vkfn tks lesfdr fuf/k ds vax ugha gSa]

ls lEcfU/kr izkfIr;k¡ ,oa laforj.k Hkkjrh; lafo/kku ds vuqPNsn 266¼2½ ds vUrxZr

LFkkfir yksd ys[ks esa j[ks tkrs gSa ,oa ;s fo/kkf;dk ds er ij vk/kkfjr ugha gksrs

gSaA buds lEcU/k esa ljdkj cSadj vFkok VªLVh dk dke djrh gSA foRr ys[ks ds

fooj.k&21 es yksd ys[ks dh izkfIr;ksa ,oa laforj.k dh fLFkfr nh x;h gS rFkk yksd

ys[ks ¼fuoy½ dk fooj.k lkj.kh 1.16 esa n'kkZ;k x;k gSA

lkj.kh 1.16: yksd ys[ks ¼fuoy½ dh fLFkfr ¼` djksM++++ esa½

fofHkUu 'kh"kksZa ds vUrxZr lalk/ku 2013-14 2014-15 2015-16 2016-17 2017-18

yksd ys[ks ¼fuoy½ 5,619 2,185 1,678 9,883 6,088

d- vYi cpr] Hkfo’; fuf/k vkfn 2,363 1,686 1,534 1,619 2,530

[k- vkjf{kr fuf/k 7,954 (-) 2,694 2,561 7,225 8,265

x- tek ,oa vfxze 5,037 1,050 (-)1,543 (-)301 1,414

?k- mpUr ,oa fofo/k (-) 9,637 535 (-)677 592 (-)2,215

M- isz’k.k (-) 98 1,608 (-)197 748 (-)3,906

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

vkjf{kr fuf/k;ksa ds vUrxZr ysu&nsuksa ds izHkko dk o.kZu izLrj 1.9.2 esa fd;k x;k

gSA

v/;k; 1 & jkT; ljdkj ds foRr

17

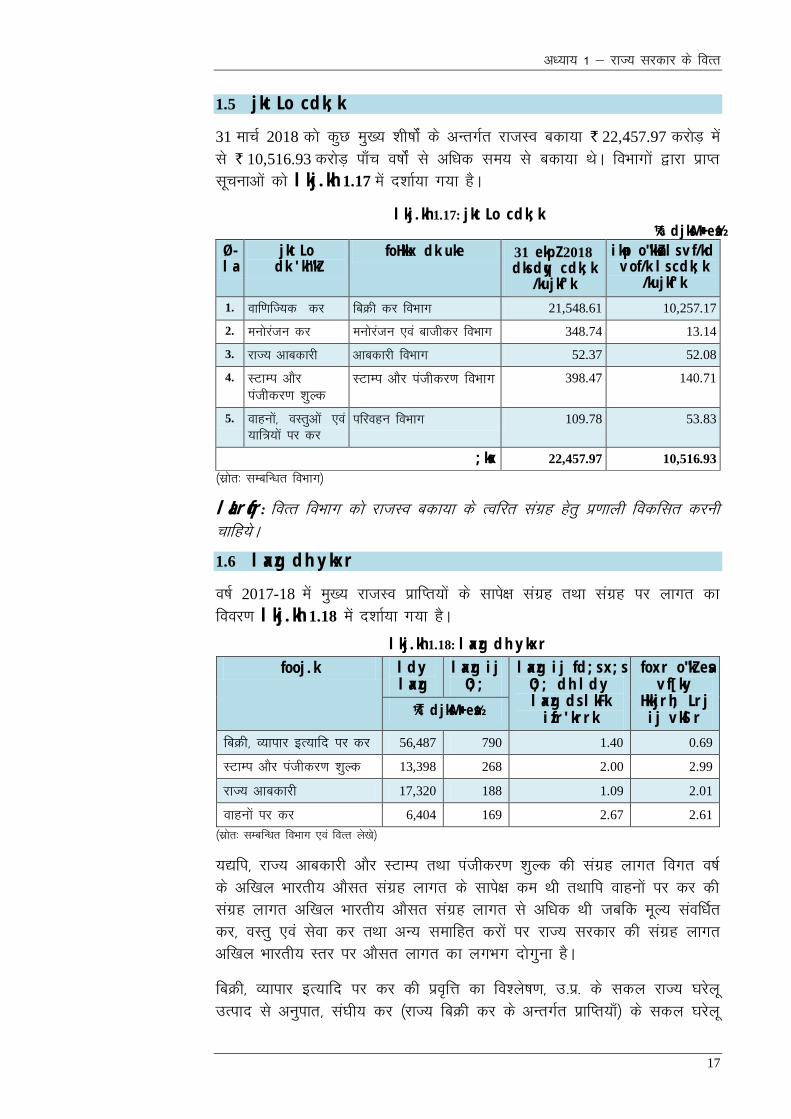

1.5 jktLo cdk;k

31 ekpZ 2018 dks dqN eq[; “kh’kksZa ds vUrxZr jktLo cdk;k ` 22,457.97 djksM+ esa

ls ` 10,516.93 djksM+ ik¡p o’kksaZ ls vf/kd le; ls cdk;k FksA foHkkxksa }kjk izkIr

lwpukvksa dks lkj.kh 1.17 esa n'kkZ;k x;k gSA

lkj.kh 1.17: jktLo cdk;k ¼` djksM++++ esa½

Ø- la-

jktLo dk 'kh"kZ

foHkkx dk uke 31 ekpZ 2018 dks dqy cdk;k

/kujkf'k

ikap o"kksZa ls vf/kd vof/k ls cdk;k

/kujkf'k

1. Okkf.kfT;d dj fcØh dj foHkkx 21,548.61 10,257.17

2. euksjatu dj euksjatu ,oa ckthdj foHkkx 348.74 13.14

3. jkT; vkcdkjh vkcdkjh foHkkx 52.37 52.08

4. LVkEi vkSj

iathdj.k 'kqYd

LVkEi vkSj iathdj.k foHkkx 398.47 140.71

5. okguksa] oLrqvksa ,oa

;kf=;ksa ij dj

ifjogu foHkkx 109.78 53.83

;ksx 22,457.97 10,516.93

¼lzksr% lEcfU/kr foHkkx½

laLrqfr: foRr foHkkx dks jkTkLo cdk;k ds Rofjr laxzg gsrq iz.kkyh fodflr djuh

pkfg;sA

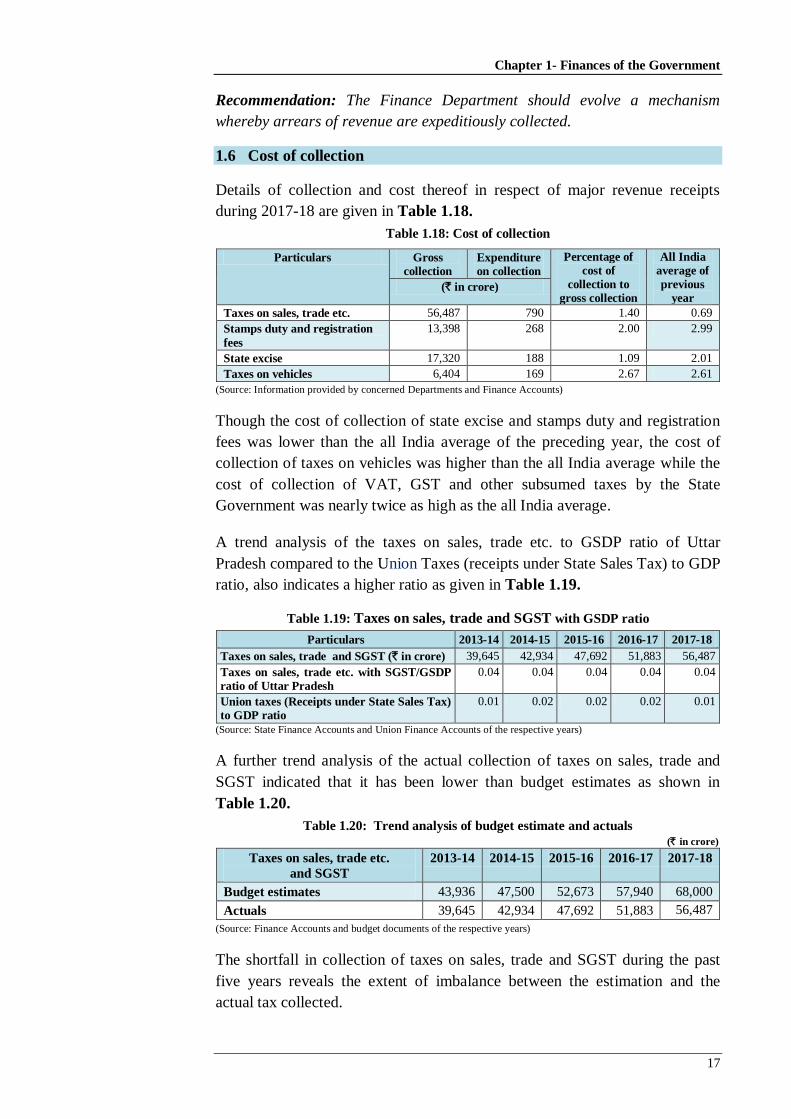

1.6 laxzg dh ykxr

o’kZ 2017-18 esa eq[; jktLo izkfIr;ksa ds lkis{k laxzg rFkk laxzg ij ykxr dk

fooj.k lkj.kh 1.18 esa n'kkZ;k x;k gSA

lkj.kh 1.18: laxzg dh ykxr

fooj.k ldy laxzg

laxzg ij O;;

laxzg ij fd;s x;s O;; dh ldy laxzg ds lkFk izfr'krrk

foxr o"kZ esa vf[ky

Hkkjrh; Lrj ij vkSlr

¼` djksM+++ esa½

fcØh] O;kikj bR;kfn ij dj 56,487 790 1.40 0.69

LVkEi vkSj iathdj.k 'kqYd 13,398 268 2.00 2.99

jkT; vkcdkjh 17,320 188 1.09 2.01

okguksa ij dj 6,404 169 2.67 2.61

¼lzksr% lEcfU/kr foHkkx ,oa foRr ys[ks½

;|fi] jkT; vkcdkjh vkSj LVkEi rFkk iathdj.k “kqYd dh laxzg ykxr foxr o’kZ

ds vf[ky Hkkjrh; vkSlr laxzg ykxr ds lkis{k de Fkh rFkkfi okguksa ij dj dh

laxzg ykxr vf[ky Hkkjrh; vkSlr laxzg ykxr ls vf/kd Fkh tcfd ewY; laof/kZr

dj] oLrq ,oa lsok dj rFkk vU; lekfgr djksa ij jkT; ljdkj dh laxzg ykxr

vf[ky Hkkjrh; Lrj ij vkSlr ykxr dk yxHkx nksxquk gSA

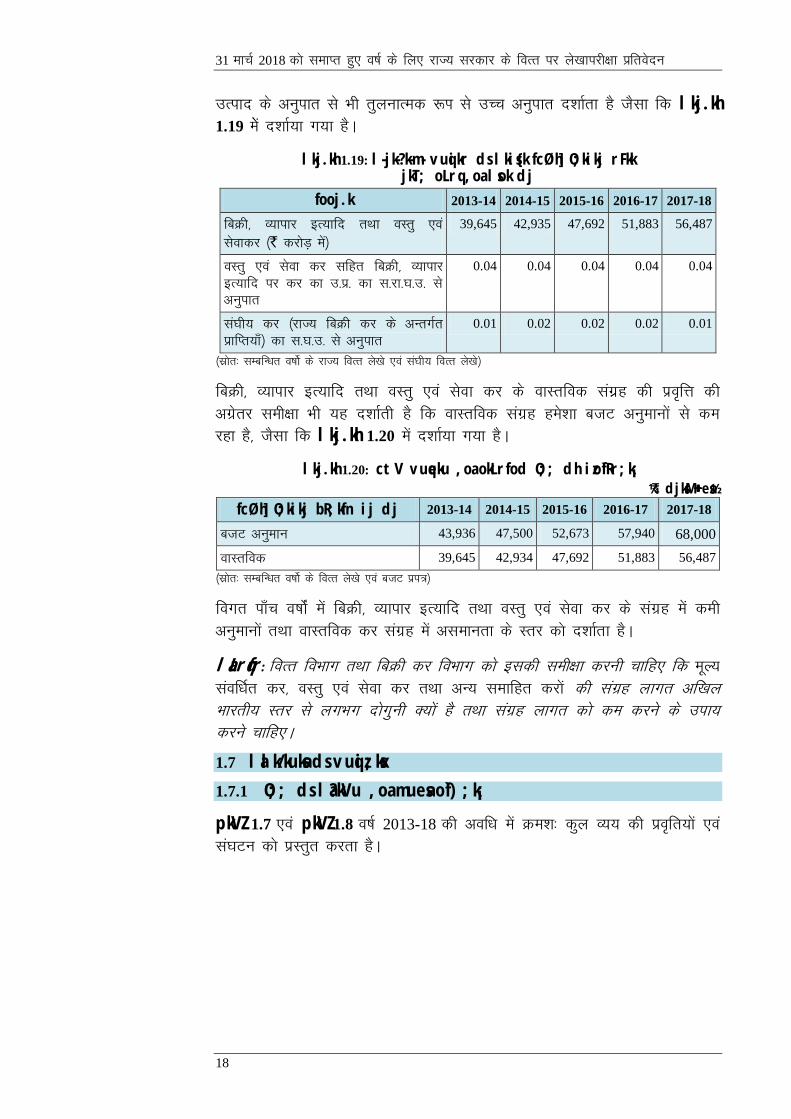

fcØh] O;kikj bR;kfn ij dj dh izofÙk dk fo'ys’k.k] m-iz- ds ldy jkT; ?kjsyw

mRikn ls vuqikr] la?kh; dj ¼jkT; fcØh dj ds vUrxZr izkfIr;k¡½ ds ldy ?kjsyw

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

18

mRikn ds vuqikr ls Hkh rqyukRed :Ik ls mPp vuqikr n'kkZrk gS tSlk fd lkj.kh 1.19 essa n'kkZ;k x;k gSA

lkj.kh 1.19: l-jk-?k-m- vuqikr ds lkis{k fcØh] O;kikj rFkk jkT; oLrq ,oa lsok dj

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

fcØh] O;kikj bR;kfn rFkk oLrq ,oa

lsokdj ¼` djksM++++ esa½

39,645 42,935 47,692 51,883 56,487

oLrq ,oa lsok dj lfgr fcØh] O;kikj

bR;kfn ij dj dk m-iz- dk l-jk-?k-m- ls

vuqikr

0.04 0.04 0.04 0.04 0.04

la?kh; dj ¼jkT; fcØh dj ds vUrxZr

izkfIr;k¡½ dk l-?k-m- ls vuqikr 0.01 0.02 0.02 0.02 0.01

¼lzksr% lEcfU/kr o’kksZ ds jkT; foRr ys[ks ,oa la?kh; foRr ys[ks½

fcØh] O;kikj bR;kfn rFkk oLrq ,oa lsok dj ds okLrfod laxzzg dh izofÙk dh

vxzsrj leh{kk Hkh ;g n'kkZrh gS fd okLrfod laxzg ges'kk ctV vuqekuksa ls de

jgk gS] tSlk fd lkj.kh 1.20 esa n'kkZ;k x;k gSA

lkj.kh 1.20: ctV vuqeku ,oa okLrfod O;; dh izo`fRr;k¡ ¼` djksM++++ esa½

fcØh] O;kikj bR;kfn ij dj 2013-14 2014-15 2015-16 2016-17 2017-18

ctV vuqeku 43,936 47,500 52,673 57,940 68,000

okLrfod 39,645 42,934 47,692 51,883 56,487

¼lzksr% lEcfU/kr o’kksZ ds foRr ys[ks ,oa ctV izi=½

foxr ik¡p o’kksZa esa fcØh] O;kikj bR;kfn rFkk oLrq ,oa lsok dj ds laxzg esa deh

vuqekuksa rFkk okLrfod dj laxzg esa vlekurk ds Lrj dks n'kkZrk gSA

laLrqfr: foRr foHkkx rFkk fcØh dj foHkkx dks bldh leh{kk djuh pkfg, fd ewY;

laof/kZr dj] oLrq ,oa lsok dj rFkk vU; lekfgr djksa dh laxzg ykxr vf[ky

Hkkjrh; Lrj ls yxHkx nksxquh D;ksa gS rFkk laxzg ykxr dks de djus ds mik;

djus pkfg,A

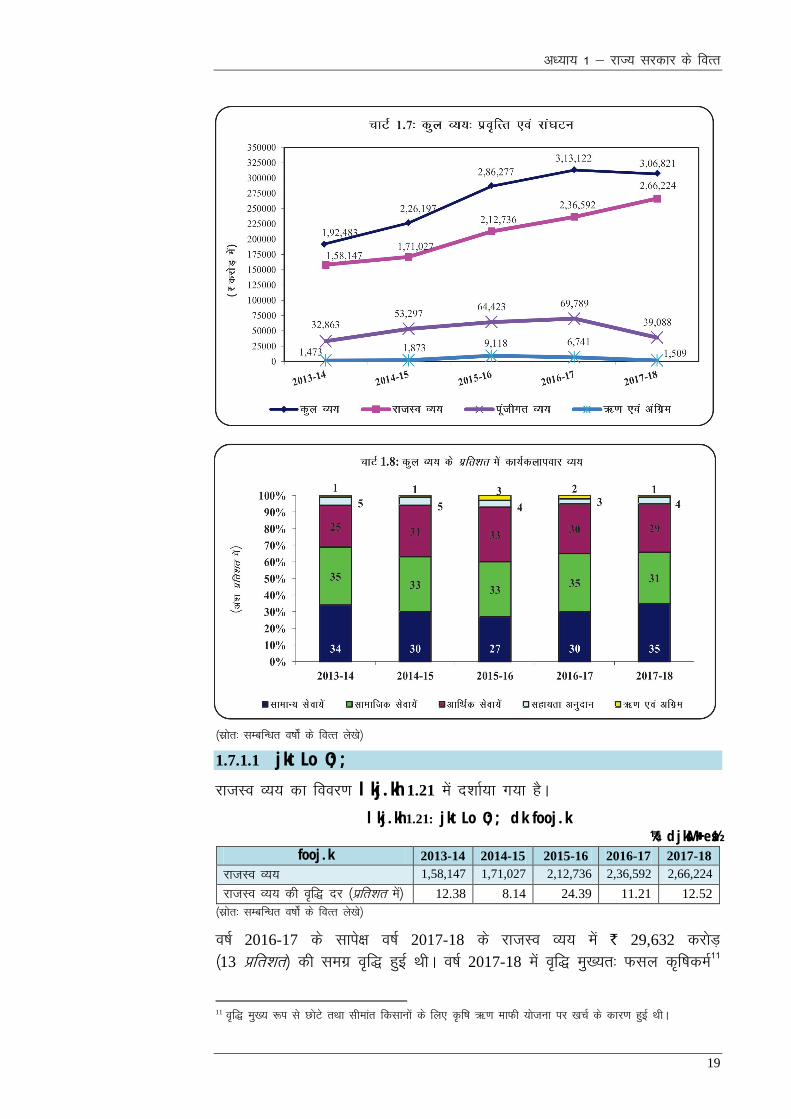

1.7 lalk/kuksa ds vuqiz;ksx

1.7.1 O;; ds la?kVu ,oa muesa o`f);k¡

pkVZ 1.7 ,oa pkVZ 1.8 o’kZ 2013-18 dh vof/k esa Øe'k% dqy O;; dh izofRk;ksa ,oa

la?kVu dks izLrqr djrk gSA

v/;k; 1 & jkT; ljdkj ds foRr

19

¼lzksr% lEcfU/kr o’kksZ a ds foRr ys[ks½

1.7.1.1 jktLo O;;

jktLo O;; dk fooj.k lkj.kh 1.21 esa n'kkZ;k x;k gSA

lkj.kh 1.21: jktLo O;; dk fooj.k ¼` djksM++++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

jktLo O;; 1,58,147 1,71,027 2,12,736 2,36,592 2,66,224

jktLo O;; dh of) nj ¼izfr'kr esa½ 12.38 8.14 24.39 11.21 12.52

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

o’kZ 2016-17 ds lkis{k o’kZ 2017-18 ds jktLo O;; esa ` 29,632 djksM+

¼13 çfr'kr½ dh lexz of) gqbZ FkhA o’kZ 2017-18 esa of) eq[;r% Qly d`f’kdeZ11

11 of) eq[; :i ls NksVs rFkk lhekar fdlkuksa ds fy, —f"k _.k ekQh ;kstuk ij [kpZ ds dkj.k gqbZ FkhA

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

20

¼` 21,500 djksM+½] isa'ku ,oa vU; lsokfuofRr fgrykkHk ¼` 10,250 djksM+½] C;kt

Hkqxrku ¼` 2,200 djksM+½] iqfyl ¼` 1,767 djksM+½] fpfdRlk ,oa yksd LokLF;

¼` 1,600 djksM+½] “kgjh fodkl ¼` 1,216 djksM+½] yksd fuekZ.k ¼` 942 djksM+½ ,oa

y?kq flapkbZ ¼` 740 djksM+½ ds vUrxZr gqbZ FkhA foxr o’kZ ds lkis{k deh eq[;r%

ÅtkZ12 ¼52 çfr'kr½ RkFkk lkekftd lqj{kk ,oa dY;k.k

13 ¼28 çfr'kr½ ds vUrxZr

FkhA

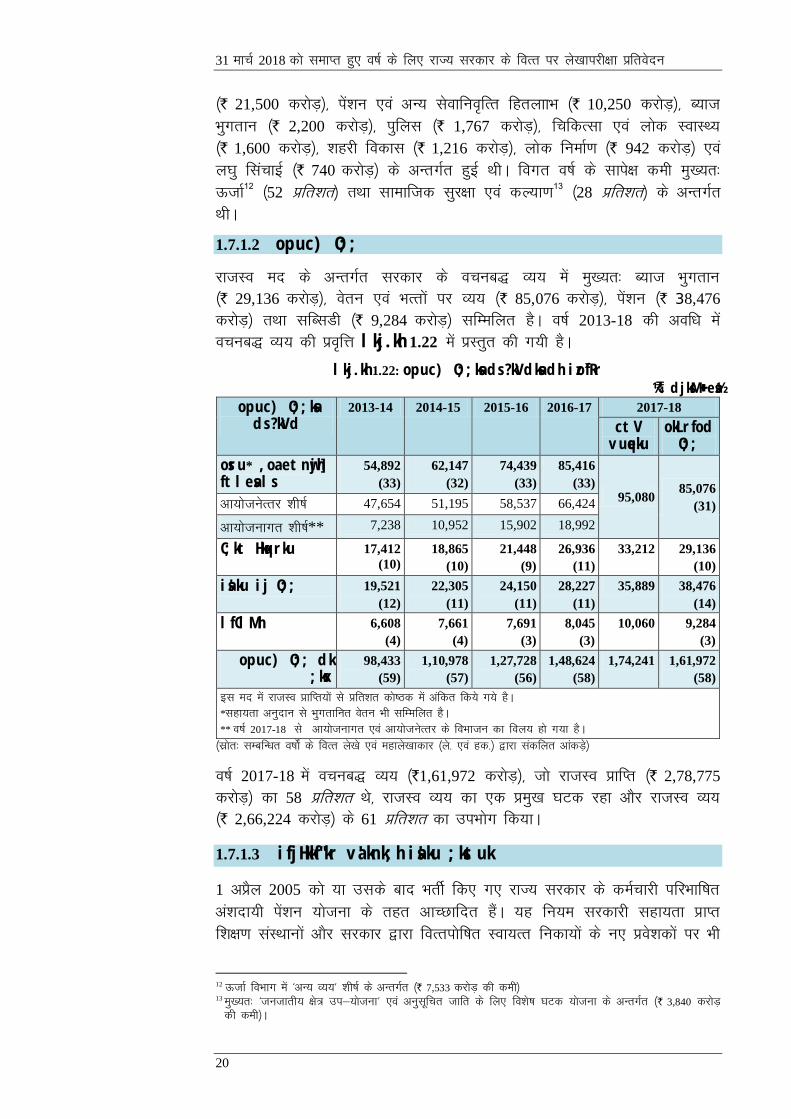

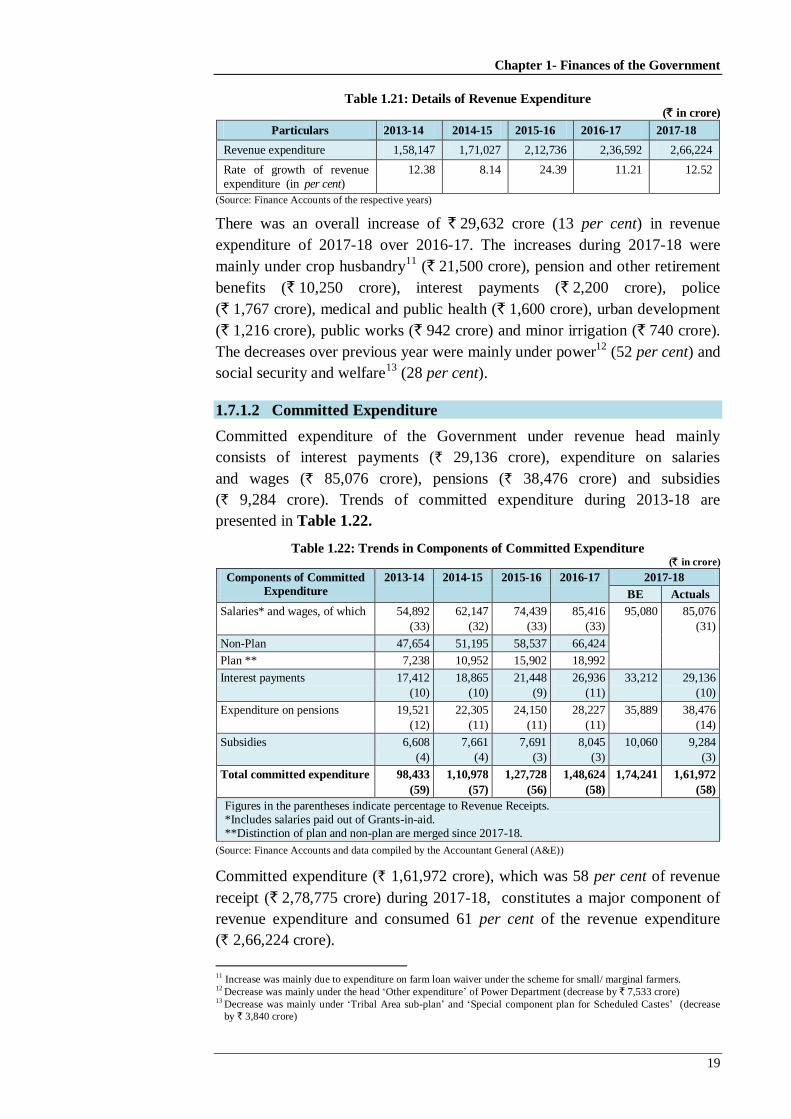

1.7.1.2 opuc) O;;

jktLo en ds vUrxZr ljdkj ds opuc) O;; esa eq[;r% C;kt Hkqxrku

¼` 29,136 djksM+½] osru ,oa HkRrksa ij O;; ¼` 85,076 djksM+½] isa'ku ¼` 38,476

djksM+½ RkFkk lfClMh ¼` 9,284 djksM+½ lfEefyr gSA o’kZ 2013-18 dh vof/k esa

opuc) O;; dh izofÙk lkj.kh 1.22 esa izLrqr dh x;h gSA

lkj.kh 1.22: opuc) O;;ksa ds ?kVdksa dh izo`fRr

¼` djksM++++ esa½ opuc) O;;ksa

ds ?kVd 2013-14 2014-15 2015-16 2016-17 2017-18

ctV vuqeku

okLrfod O;;

osru* ,oa etnwjh] ftlesa ls

54,892

(33)

62,147

(32)

74,439

(33)

85,416

(33) 95,080

85,076

(31) vk;kstusRrj 'kh"kZ 47,654 51,195 58,537 66,424

vk;kstukxr 'kh"kZ** 7,238 10,952 15,902 18,992

C;kt Hkqxrku 17,412

(10)

18,865

(10)

21,448

(9)

26,936

(11)

33,212 29,136

(10)

isa'ku ij O;; 19,521

(12)

22,305

(11)

24,150

(11)

28,227

(11)

35,889 38,476

(14)

lfClMh 6,608

(4)

7,661

(4)

7,691

(3)

8,045

(3)

10,060 9,284

(3)

opuc) O;; dk ;ksx

98,433

(59)

1,10,978

(57)

1,27,728

(56)

1,48,624

(58)

1,74,241 1,61,972

(58)

bl en esa jktLo çkfIr;ksa ls çfr'kr dks’Bd esa vafdr fd;s x;s gSA

*lgk;rk vuqnku ls Hkqxrkfur osru Hkh lfEefyr gSA

** o"kZ 2017-18 ls vk;kstukxr ,oa vk;kstusRrj ds foHkktu dk foy; gks x;k gSA

¼lzksr% lEcfU/kr o"kksZa ds foRr ys[ks ,oa egkys[kkdkj ¼ys- ,oa gd-½ }kjk ladfyr vkadM+s½

o’kZ 2017-18 esa opuc) O;; ¼`1,61,972 djksM+½] tks jktLo çkfIr ¼` 2,78,775

djksM+½ dk 58 çfr'kr Fks] jktLo O;; dk ,d çeq[k ?kVd jgk vkSj jktLo O;;

¼` 2,66,224 djksM+½ ds 61 çfr'kr dk miHkksx fd;kA

1.7.1.3 ifjHkkf"kr va'knk;h isa'ku ;kstuk

1 vçSy 2005 dks ;k mlds ckn HkrhZ fd, x, jkT; ljdkj ds deZpkjh ifjHkkf"kr

va'knk;h isa'ku ;kstuk ds rgr vkPNkfnr gSaA ;g fu;e ljdkjh lgk;rk çkIr

f'k{k.k laLFkkuksa vkSj ljdkj }kjk foRriksf"kr Lok;Rr fudk;ksa ds u, ços'kdksa ij Hkh

12

ÅtkZ foHkkx esa ^vU; O;;* “kh’kZ ds vUrxZr ¼` 7,533 djksM+ dh deh½ 13 eq[;r% ^tutkrh; {ks= mi&;kstuk* ,oa vuqlwfpr tkfr ds fy, fo'ks"k ?kVd ;kstuk ds vUrxZr ¼` 3,840 djksM+

dh deh½A

v/;k; 1 & jkT; ljdkj ds foRr

21

ykxw gksrk gSA ;kstuk ds lanHkZ esa] ljdkjh deZpkjh ewy osru vkSj egaxkbZ HkRrs dk

10 çfr'kr ;ksxnku djrs gSa] ftlesa jkT; ljdkj }kjk leku eSfpax “ks;j

feyk;k tkrk gS vkSj lEiw.kZ /kujkf'k us'kuy flD;ksfjVht fMi�ftVjh fyfeVsM

¼,u,lMh,y½@VªLVh cSad ds ek/;e ls ukfer fuf/k izca/kd dks gLrkarfjr dh tkrh

gSA

jkT; ljdkj us vius oS/kkfud nkf;Ro dk fuoZgu ugha fd;k D;ksafd og foRrh; o"kZ

2017-18 esa ljdkjh lgk;rk çkIr laLFkkuksa vkSj Lok;Rr fudk;ksa ds deZpkfj;ksa ds

laca/k esa ifjHkkf"kr va'knk;h isa'ku ;kstuk ds vUrxZr jkT; ljdkj }kjk leku

eSfpax “ks;j ds :Ik esa ` 465.10 djksM+ dk ;ksxnku djus esa foQy jghA foxr

foRrh; o"kksZsa 2008-09 ls 2016-17 dh vof/k esa jkT; ljdkj us ljdkjh

deZpkfj;ksa] ljdkjh lgk;rk çkIr laLFkkuksa vkSj Lok;Rr fudk;ksa ds deZpkfj;ksa ds

laca/k esa ifjHkkf"kr va'knk;h isa'ku ;kstuk ds rgr blds eSfpax “ks;j ds :i esa

` 211.69 djksM+ dk va'knku ugha fd;k A

vxzsrj] jkT; ljdkj us o"kZ 2008-09 ls o"kZ 2017-18 dh vof/k esa ifjHkkf’kr

va'knk;h isa'ku ;kstuk ds vUrxZr ljdkjh deZpkfj;ksa] ljdkjh lgk;rk çkIr

laLFkkuksa vkSj Lok;Rr fudk;ksa ds deZpkfj;ksa ds ,oa jkT; ljdkj ds va'knku ds :i

esa ` 8,205.66 djksM+ #i;s ,d= fd,] ysfdu ;kstuk ds çko/kkuksa ds vuqlkj vkxs

fuos'k ds fy, ukfer çkf/kdkjh dks ` 703.16 djksM+ tek ugha fd,A bl çdkj]

31 ekpZ 2018 dks] fufnZ"V çkf/kdkjh dks ` 1,379.95 djksM+ ¼`465.10 djksM+$

` 211.69 djksM+ $ `703.16 djksM+½ dk de gLrkUrj.k fd;k x;k vkSj orZeku

ns;rk dks Hkfo"; ds o"kZ ¼vksa½ ds fy, vkLFkfxr fd;k x;kA blds vykok] jkT;

ljdkj us Hkfo"; esa deZpkfj;ksa dks ns; ykHk ds laca/k esa vfuf'prrk iSnk

dh@ljdkj ds fy, Hkfo’; esa ifjgk;Z foÙkh; ns;rk lftr dh vkSj bl çdkj Lo;a

gh ;kstuk dks laHkkfor foQyrk dh vksj vxzlj fd;kA

o"kZ 2017-18 ds izkjaHk esa fu/kkZfjr va'knk;h isa'ku ;kstuk ds lkis{k ` 545.68

djksM]+ C;kt lfgr tek [kkrs esa vo'ks’k Fkk ftlds fy, jkT; ljdkj us ljdkjh

deZpkfj;ksa ds th-ih-,Q- dh C;kt nj ij ykxw okf"kZd C;kt nj ds vk/kkj ij

vkxf.kr ` 25.78 djksM+ C;kt dk Hkqxrku fd;k FkkA ;|fi] vo'ks’k jkf'k ij

Hkqxrku fd, x, C;kt dh i;kZIrrk dks tk¡pk ugha tk ldk] D;ksafd isa'ku

funs'kky; us ys[kkijh{kk tkWap ds fy, lacaf/kr x.kuk izi= çnku ugha fd;kA

laLrqfr% jkT; ljdkj dks ;g lqfuf'pr djus ds fy, rqjUr dk;Zokgh izkjEHk djuh

pkfg, fd 1 vçSy 2005 dks ;k mlds ckn HkrhZ gksus okys deZpkfj;ksa dks mudh

HkrhZ dh frfFk ls va'knk;h isa'ku ;kstuk ds vUrxZr iw.kZ :Ik ls vkPNkfnr fd;k

tk;sA ;g bl izdkj lqfuf'pr fd;k tkuk pkfg, fd deZpkfj;ksa ds osru ls dVkSrh

iwjh rjg ls dh tk,] ljdkj }kjk viuk iw.kZ ;ksxnku nsrs gq, le;c) rjhds ls

,u-,l-Mh-,y- ds ek/;e ls ukfer Q.M eSustj dks lEiw.kZ :Ik ls LFkkukUrfjr dj

fn;k tk,A

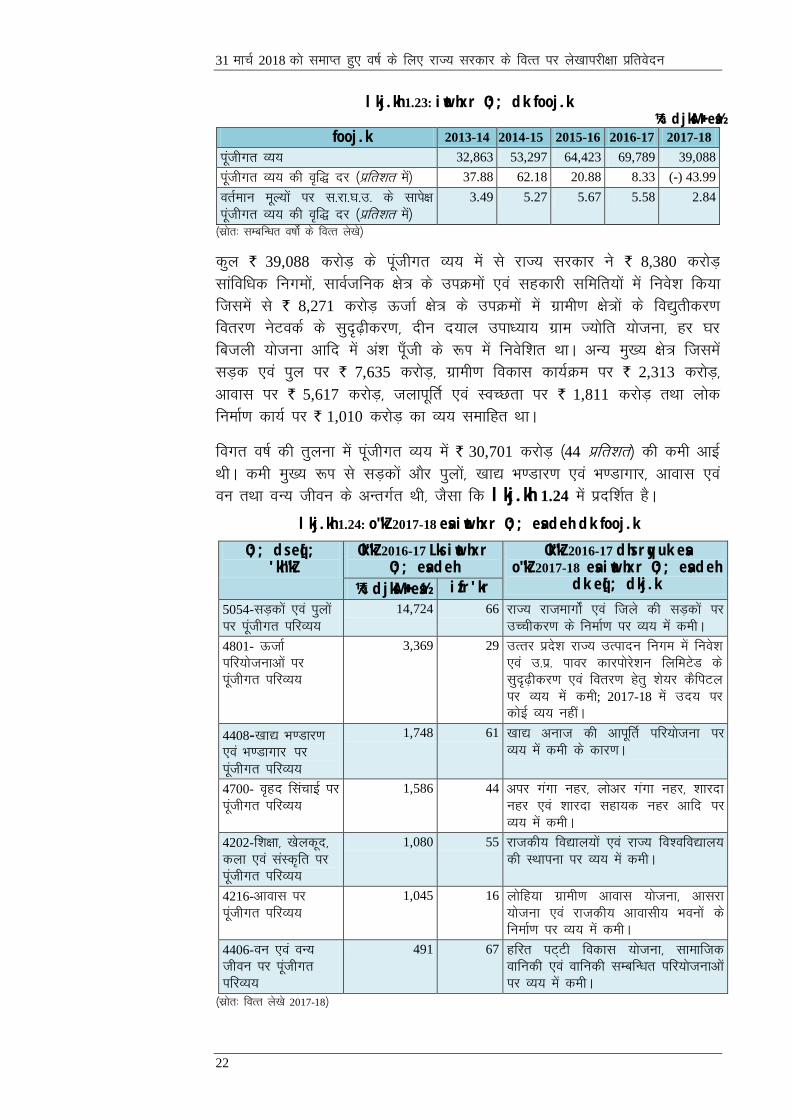

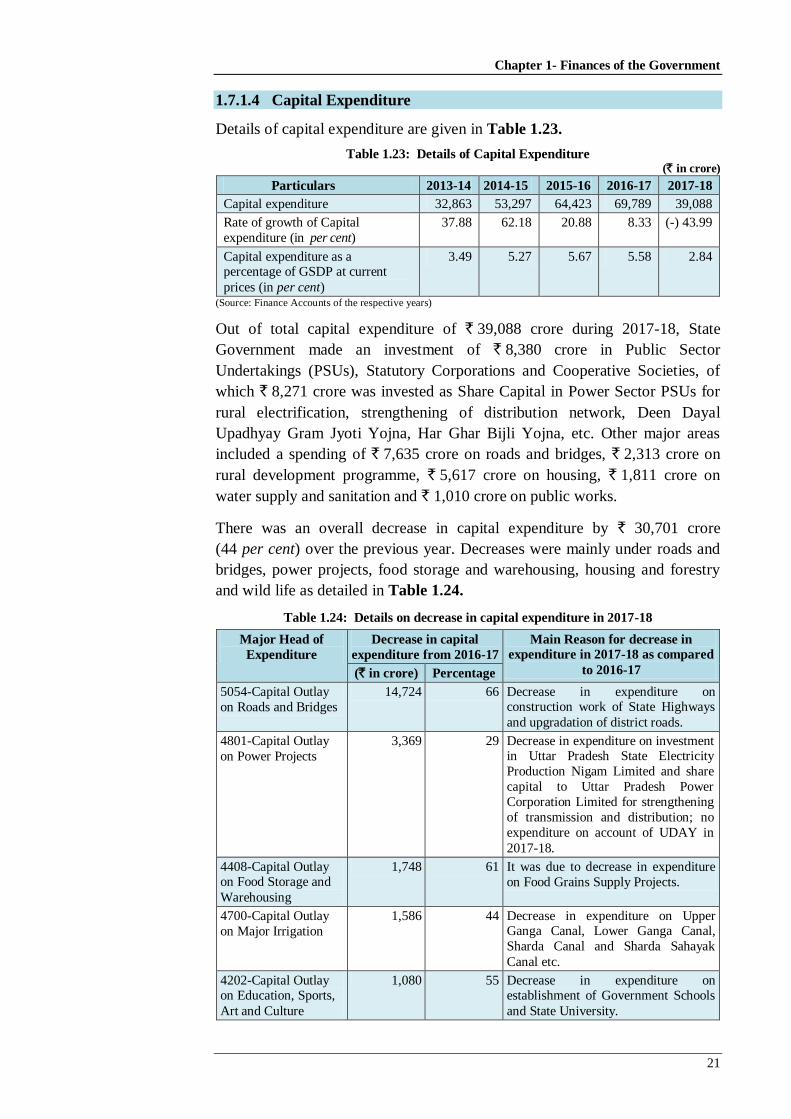

1.7.1.4 iwathxr O;;

iwathxr O;; dk fooj.k lkj.kh 1.23 esa izLrqr fd;k x;k gSA

31 ekpZ 2018 dks lekIr gq, o"kZ ds fy, jkT; ljdkj ds foRr ij ys[kkijh{kk izfrosnu

22

lkj.kh 1.23: iwathxr O;; dk fooj.k ¼` djksM++ esa½

fooj.k 2013-14 2014-15 2015-16 2016-17 2017-18

iwathxr O;; 32,863 53,297 64,423 69,789 39,088

iwathxr O;; dh of) nj ¼izfr'kr esa½ 37.88 62.18 20.88 8.33 (-) 43.99

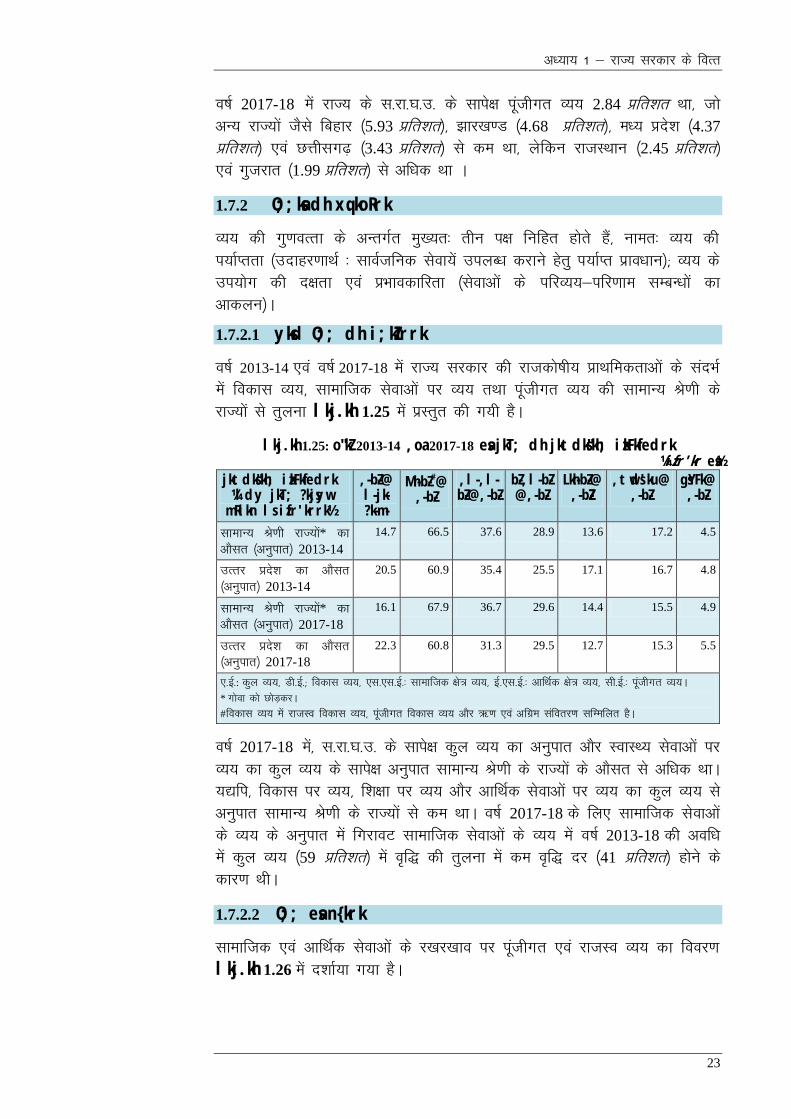

orZeku ewY;ksa ij l-jk-?k-m- ds lkis{k

iwathxr O;; dh of) nj ¼izfr'kr esa½

3.49 5.27 5.67 5.58 2.84

¼lzksr% lEcfU/kr o’kksZa ds foRr ys[ks½

dqy ` 39,088 djksM+ ds iwathxr O;; esa ls jkT; ljdkj us ` 8,380 djksM+

lkafof/kd fuxeksa] lkoZtfud {ks= ds miØeksa ,oa lgdkjh lfefr;ksa esa fuos'k fd;k

ftlesa ls ` 8,271 djksM+ ÅtkZ {ks= ds miØeksa esa xzkeh.k {ks=ksa ds fo|qrhdj.k

forj.k usVodZ ds lqn<+hdj.k] nhu n;ky mik/;k; xzke T;ksfr ;kstuk] gj ?kj

fctyh ;kstuk vkfn esa va'k iw¡th ds :Ik esa fuosf'kr FkkA vU; eq[; {ks= ftlesa

lM+d ,oa iqy ij ` 7,635 djksM+] xzkeh.k fodkl dk;ZØe ij ` 2,313 djksM+]

vkokl ij ` 5,617 djksM+] tykiwfrZ ,oa LoPNrk ij ` 1,811 djksM+ rFkk yksd

fuekZ.k dk;Z ij ` 1,010 djksM+ dk O;; lekfgr FkkA

foxr o"kZ dh rqyuk esa iwathxr O;; esa ` 30,701 djksM+ ¼44 çfr'kr½ dh deh vkbZ

FkhA deh eq[; :Ik ls lM+dksa vkSj iqyksa] [kk| Hk.Mkj.k ,oa Hk.Mkxkj] vkokl ,oa

oUk rFkk oU; thou ds vUrxZr Fkh] tSlk fd lkj.kh 1.24 eas iznf'kZr gSA

lkj.kh 1.24: o"kZ 2017-18 esa iwathxr O;; esa deh dk fooj.k

O;; ds eq[; 'kh"kZ

Ok"kZ 2016-17 Lks iwathxr O;; esa deh

Ok"kZ 2016-17 dhs rqyuk esa o"kZ 2017-18 esa iwathxr O;; esa deh

dk eq[; dkj.k ¼` djksM++++ esa½ izfr'kr

5054-lM+dksa ,oa iqyksa

ij iwathxr ifjO;;

14,724 66 jkT; jktekxksZa ,oa ftys dh lM+dksa ij

mPphdj.k ds fuekZ.k ij O;; esa dehA

4801- ÅtkZ

ifj;kstukvksa ij

iwathxr ifjO;;

3,369 29 mRrj izns'k jkT; mRiknu fuxe esa fuos'k

,oa m-iz- ikoj dkjiksjs'ku fyfeVsM ds

lqn<+hdj.k ,oa forj.k gsrq “ks;j dSfiVy

ij O;; esa deh; 2017-18 esa mn; ij

dksbZ O;; ughaA

4408-[kk| Hk.Mkj.k

,oa Hk.Mkxkj ij

iwathxr ifjO;;