Embed Size (px)

Citation preview

Analysts who prepared this report are registered as research analysts in Korea but not in any other jurisdiction, including the U.S.

Korea Tech Strategy

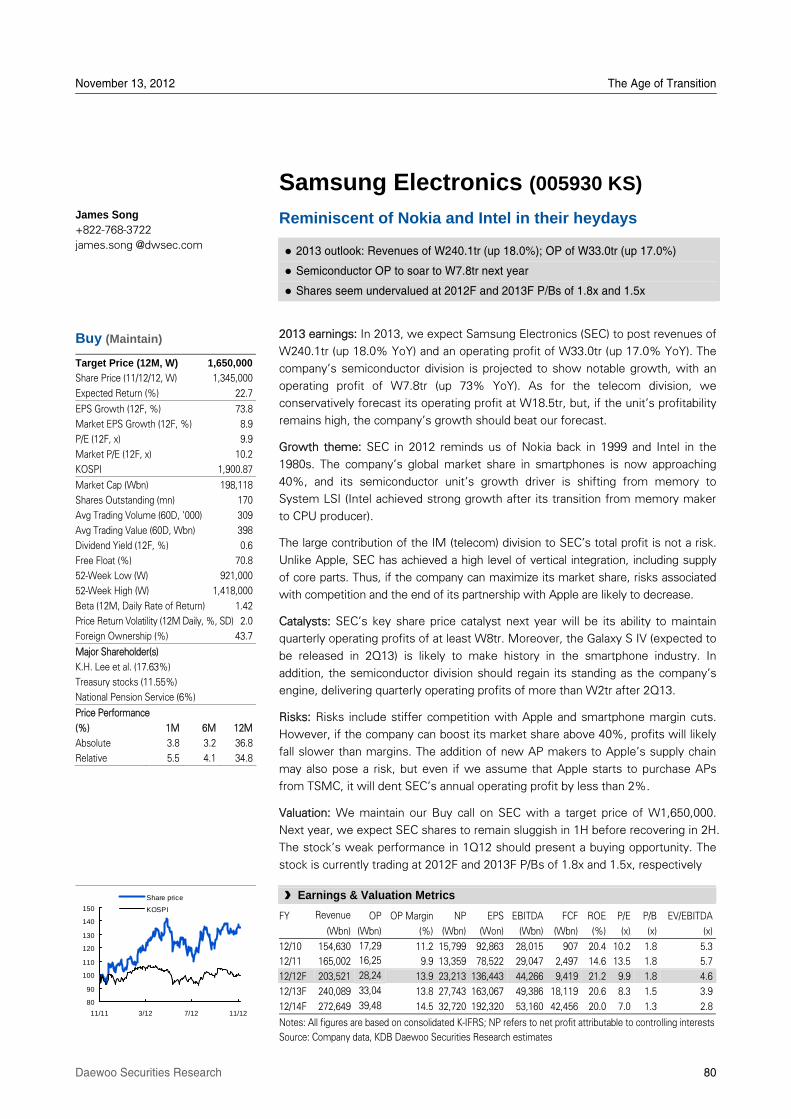

November 13, 2012The Age of Transition

The outlook for IT from a “disruptive innovation” perspective

Mobile revolution: From revolution to evolution

The mobile revolution has been a history of „disruptive innovation.‰ And at the heart of

this remarkable shake-up lie Apple, Samsung Electronics (SEC), Google, and Amazon.

Notably, the global IT industry is currently facing several major shifts and issues,

including: 1) AppleÊs „innovatorÊs dilemma‰; 2) a reshuffling of global supply chains; 3)

the return of Microsoft; and 4) the zero growth of the PC industry. How Korean IT

players approach these issues will create significant implications for the memory,

display, components, and electronic materialsÊ markets in 2013 onwards.

“Apple without SEC” vs. “SEC without Apple”

Apple is now one of the most valuable corporations in the world. However, SEC sells

more smartphones than Apple does. Unsurprisingly, global investors are paying keen

attention to the competition between Apple and SEC, their innovations, and their

potential breakup. Our analysis suggests Apple is increasingly leaning toward

„sustaining innovation‰ while SEC pursues a strategy of differentiation. At the same

time, in reshuffling the global supply chain, we expect Apple could have difficulty

procuring parts supply without SECÊs contributions, while the Korean giant is likely to

see very limited impacts from the absence of demand from Apple.

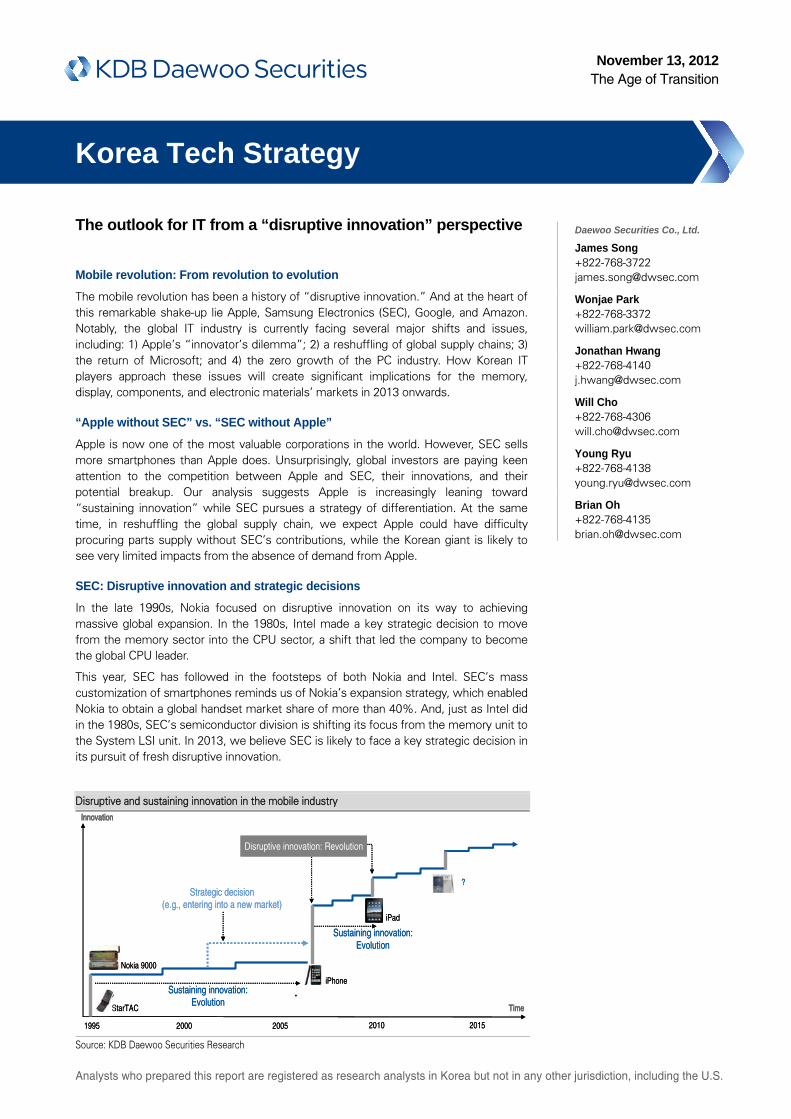

SEC: Disruptive innovation and strategic decisions

In the late 1990s, Nokia focused on disruptive innovation on its way to achieving

massive global expansion. In the 1980s, Intel made a key strategic decision to move

from the memory sector into the CPU sector, a shift that led the company to become

the global CPU leader.

This year, SEC has followed in the footsteps of both Nokia and Intel. SECÊs mass

customization of smartphones reminds us of NokiaÊs expansion strategy, which enabled

Nokia to obtain a global handset market share of more than 40%. And, just as Intel did

in the 1980s, SECÊs semiconductor division is shifting its focus from the memory unit to

the System LSI unit. In 2013, we believe SEC is likely to face a key strategic decision in

its pursuit of fresh disruptive innovation.

Daewoo Securities Co., Ltd.

James Song +822-768-3722

Wonjae Park +822-768-3372

Jonathan Hwang +822-768-4140

Will Cho +822-768-4306

Young Ryu +822-768-4138

Brian Oh +822-768-4135

Disruptive and sustaining innovation in the mobile industry

Strategic decision(e.g., entering into a new market)

Sustaining innovation:Evolution

Sustaining innovation:Evolution

Innovation

2000 201020051995

iPad

iPhone

Nokia 9000

StarTAC

?

2015

Time

Disruptive innovation: Revolution

Strategic decision(e.g., entering into a new market)

Sustaining innovation:Evolution

Sustaining innovation:Evolution

Innovation

2000 201020051995

iPad

iPhone

Nokia 9000

StarTAC

?

2015

Time

Disruptive innovation: Revolution

Source: KDB Daewoo Securities Research

2

[Prologue] Moving from revolution to evolution .........................................................................4

Mobile market: From revolution to evolution.................................................................................4

Mobile revolution: A story of disruptive innovation........................................................................5

Strategic decisions: Lessons from Intel of the 1980s ...................................................................6

Gearing up for the next disruptive innovation ...............................................................................7

IT sector investment strategy for 2013..........................................................................................8

I. Apple: “The innovator’s dilemma”...........................................................................................12

Why the “innovator’s dilemma?”..................................................................................................12

Two issues facing Apple..............................................................................................................13

Growth of new smart devices......................................................................................................14

SEC’s differentiated smartphone lineup......................................................................................15

SEC: “It doesn’t take a genius” ...................................................................................................17

Innovation from content producers .............................................................................................18

II. Global supply chain reshuffle..................................................................................................21

Implications of Apple’s supply chain change ..............................................................................21

Apple without SEC Greater supply chain risk ........................................................................22

Exclusion of SEC from Apple’s supply chain would have a limited impact ................................24

Exclusion from Apple’s AP supplier list to have minimal impact on SEC...................................25

TSMC could begin supplying APs to Apple from late 2013 ........................................................26

Risks and opportunities for SEC’s System LSI unit ....................................................................27

III. Losers’ league: Competition among second-tier makers to intensify...............................29

Second-tiers to continue the fight for survival.............................................................................29

Who will exceed the 40mn threshold? ........................................................................................30

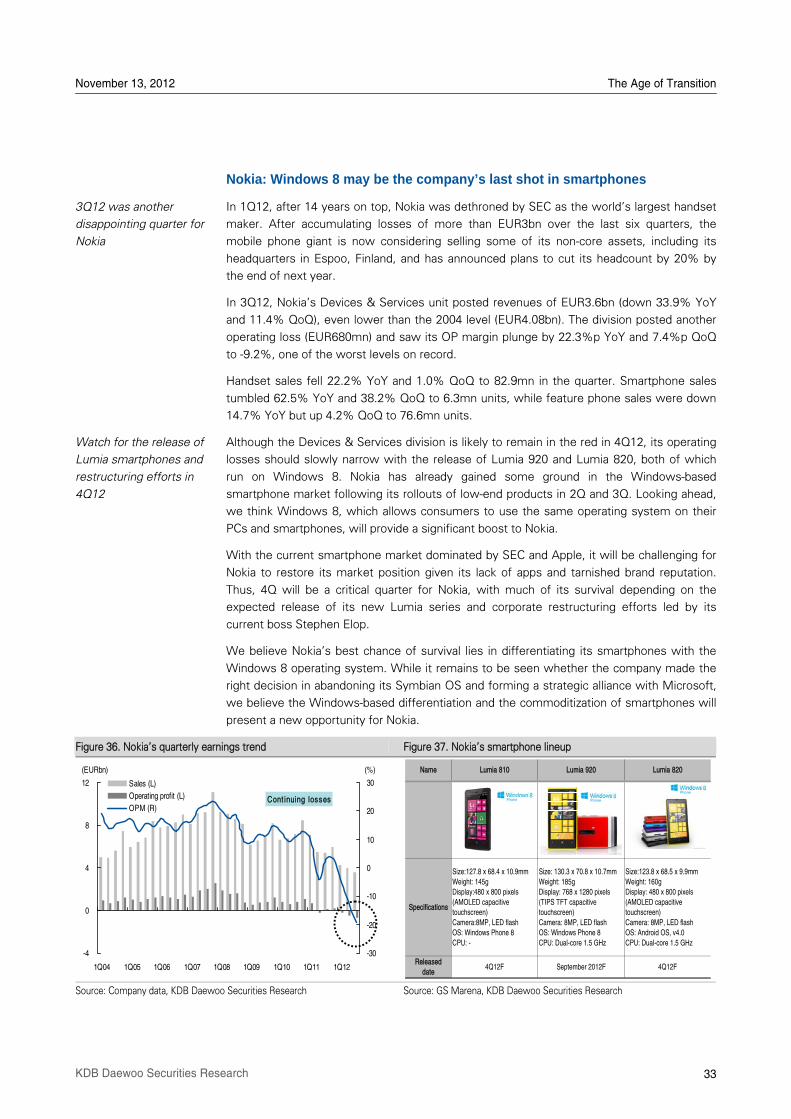

Nokia: Windows 8 may be the company’s last shot in smartphones..........................................33

HTC: Standing out in the low- to mid-end market.......................................................................34

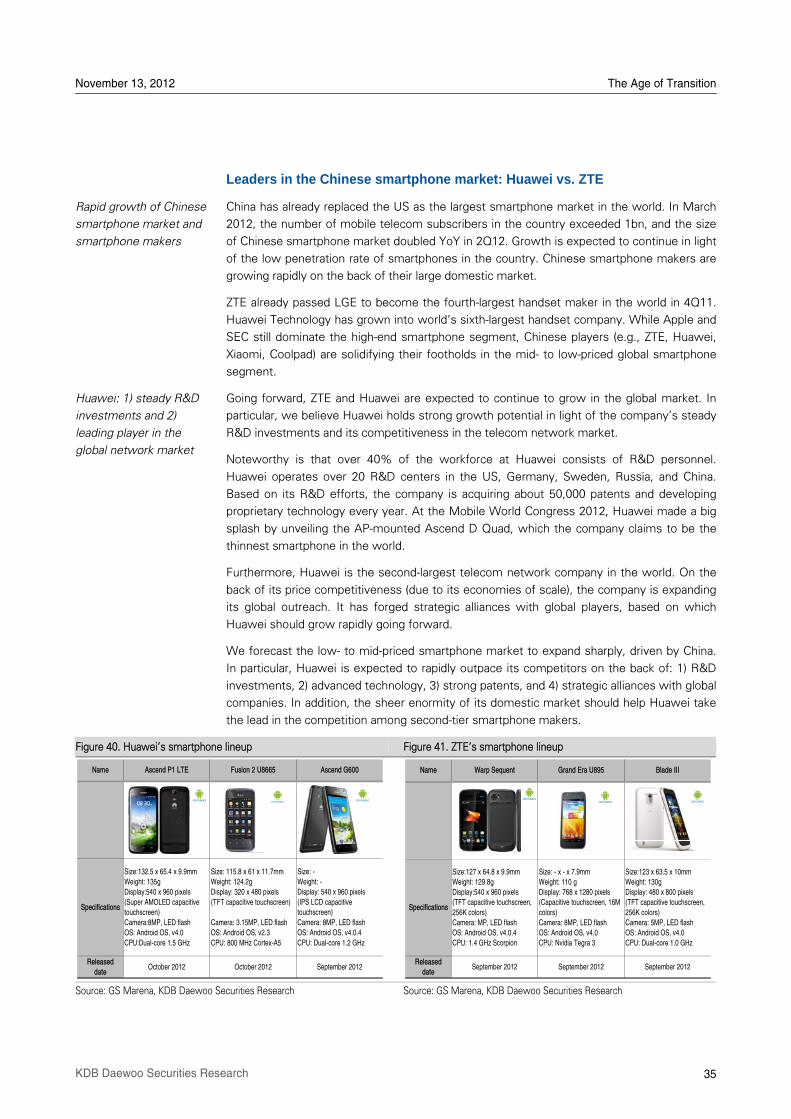

Leaders in the Chinese smartphone market: Huawei vs. ZTE ...................................................35

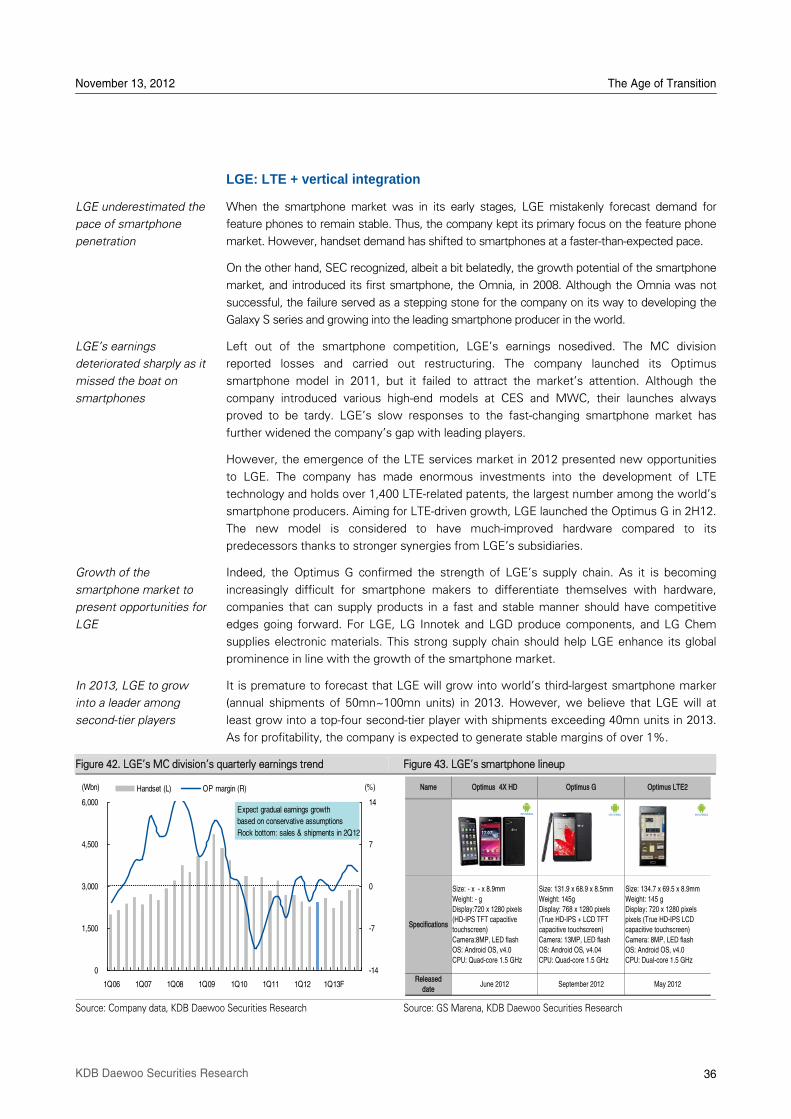

LGE: LTE + vertical integration ...................................................................................................36

IV. Return of Microsoft: Windows 8 and tablet market growth..................................................................38

iOS 6 vs. Jelly Bean ....................................................................................................................38

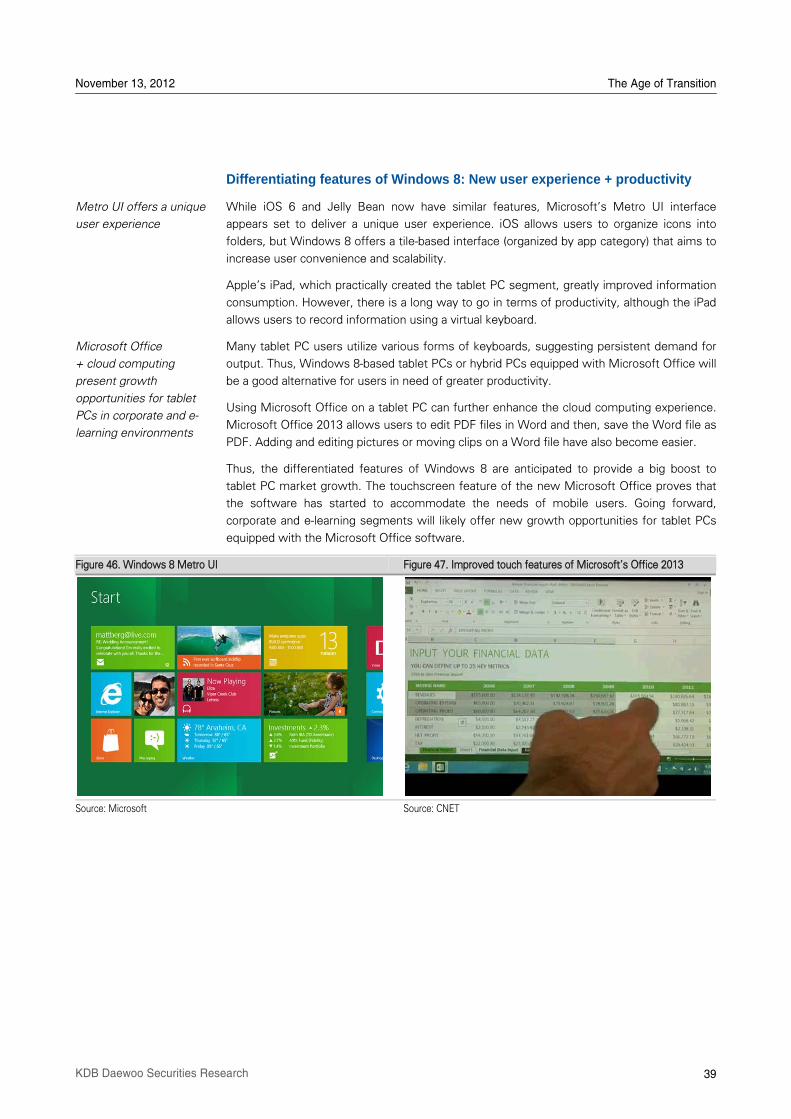

Differentiating features of Windows 8: New user experience + productivity ..............................39

Windows 8: New growth driver for the tablet PC market ............................................................40

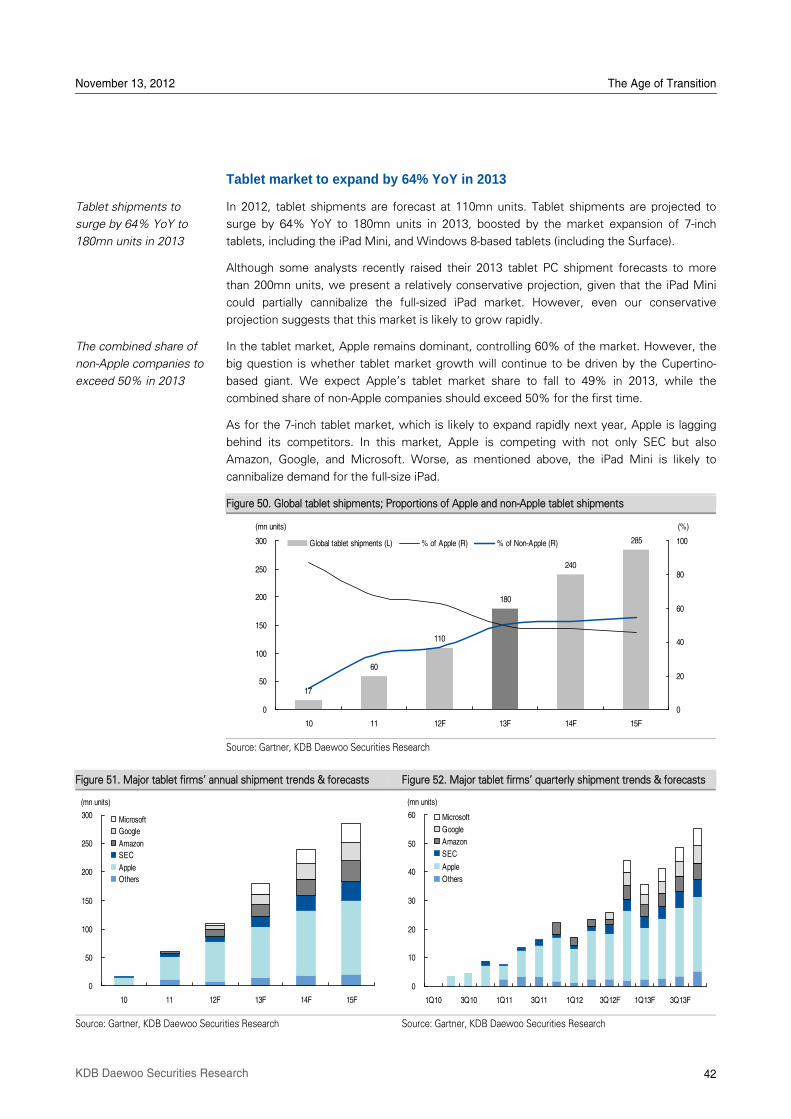

Tablet market to expand by 64% YoY in 2013 ...........................................................................42

Medium- to long-term change in OS market competition ...........................................................43

Beneficiaries of tablet PC market expansion ..............................................................................44

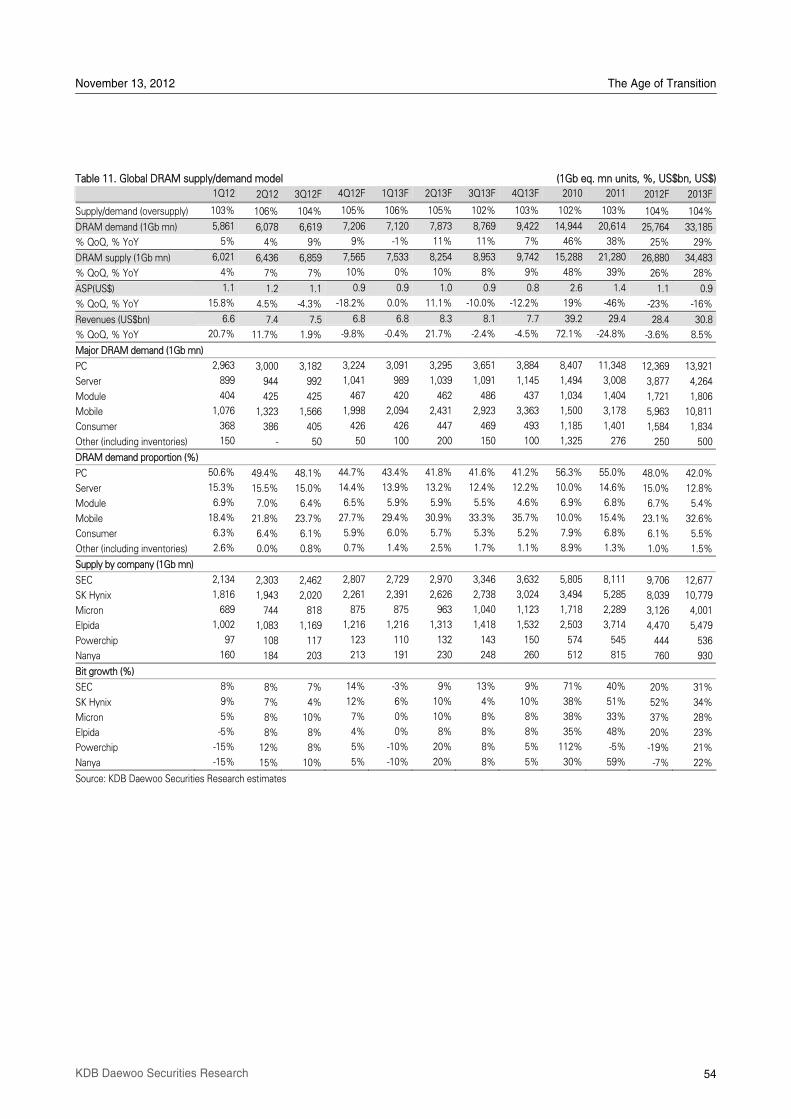

V. Farewell to the PC era!: Zero PC growth and its implications for the memory industry .47

PC industry headed for zero growth ...........................................................................................47

Memory industry’s dynamics have completely changed ............................................................48

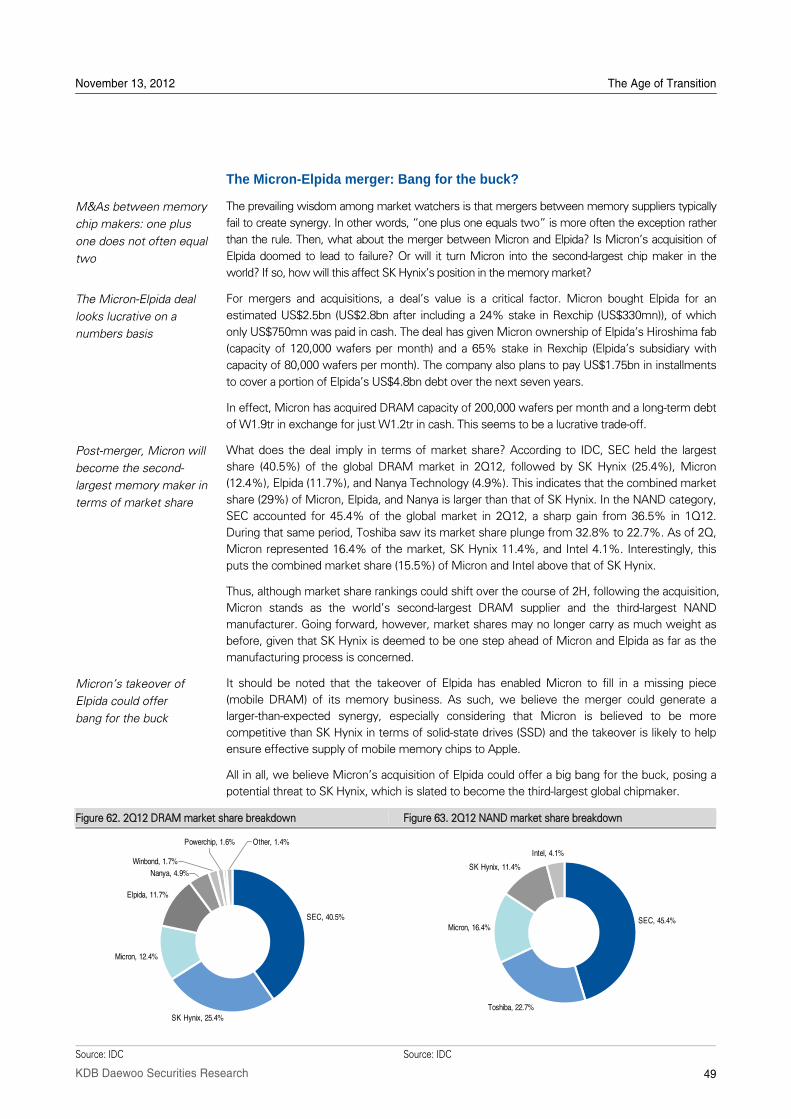

The Micron-Elpida merger: Bang for the buck? ..........................................................................49

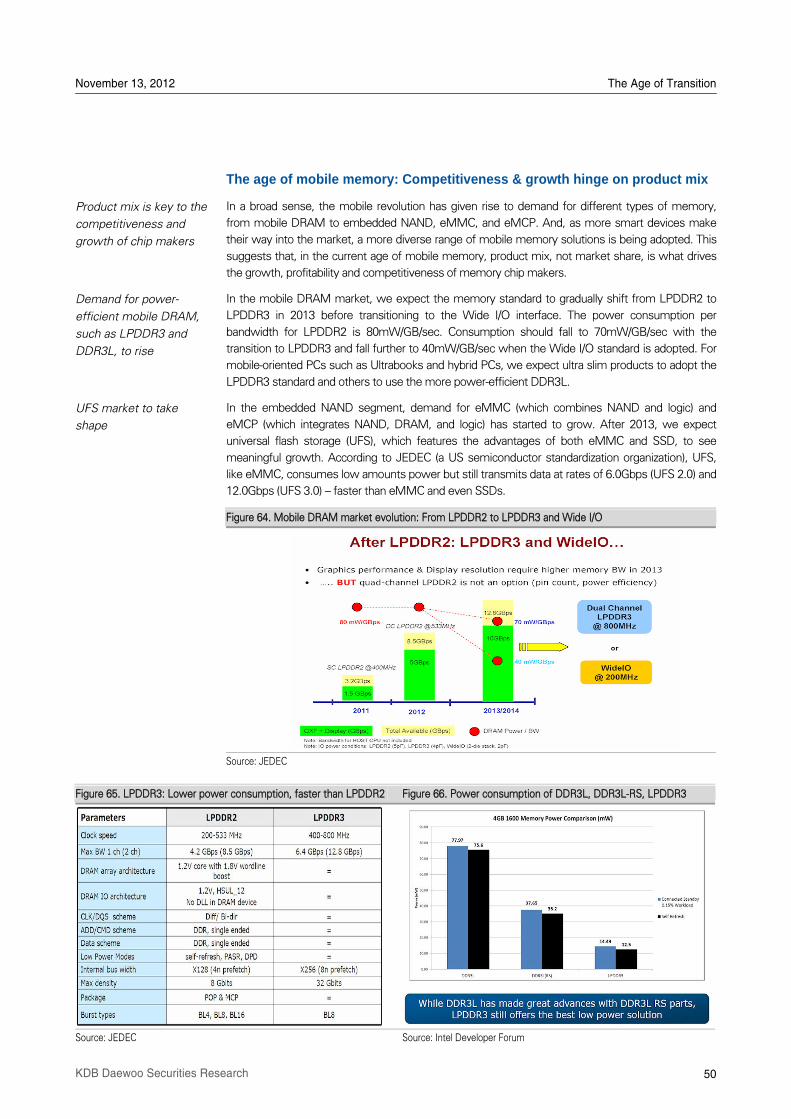

The age of mobile memory: Competitiveness & growth hinge on product mix ..........................50

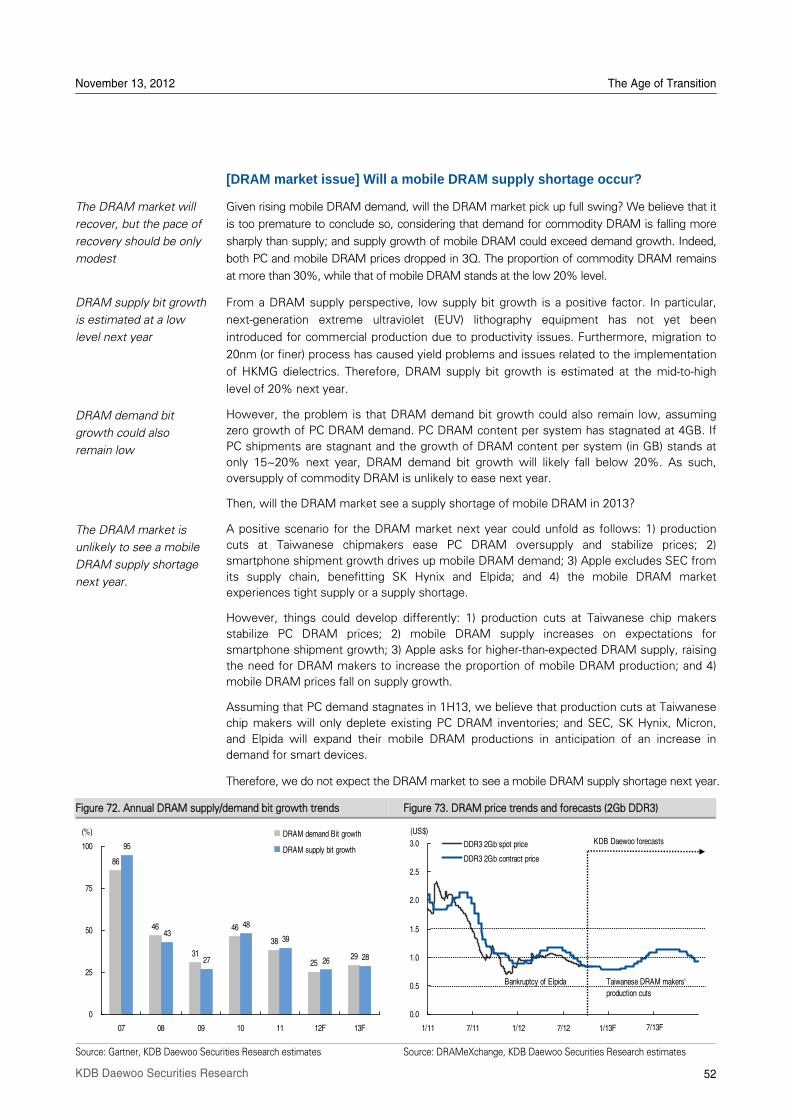

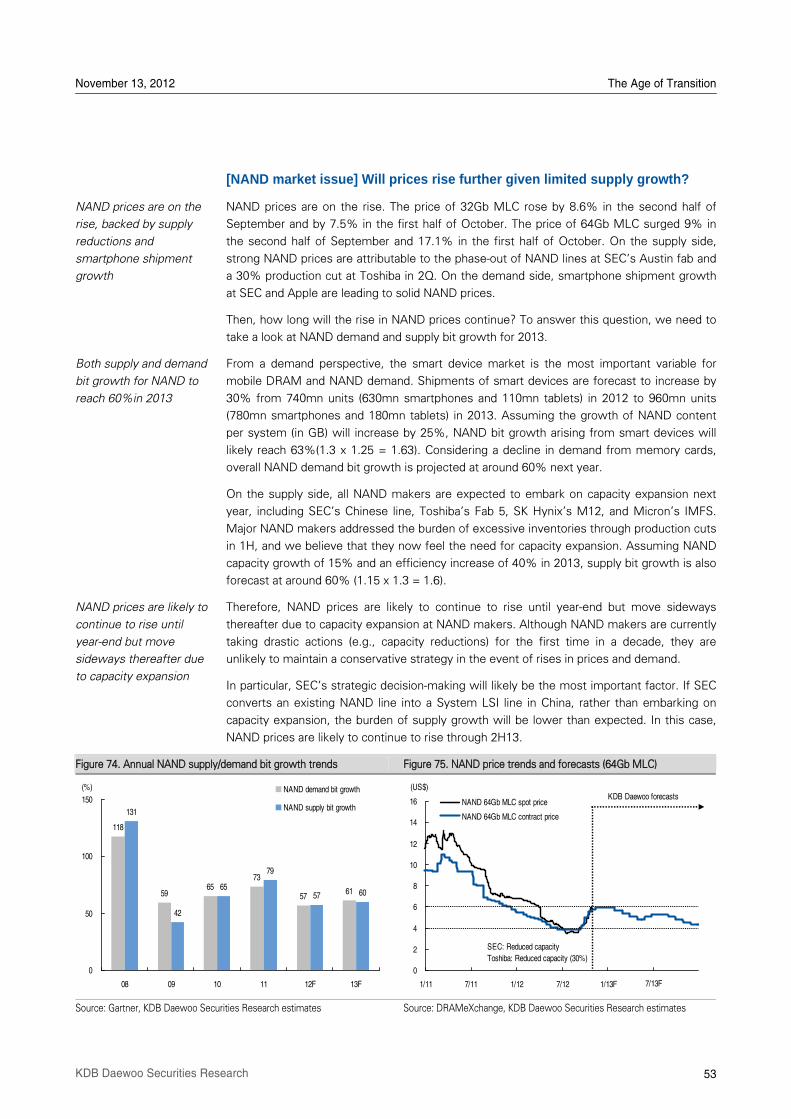

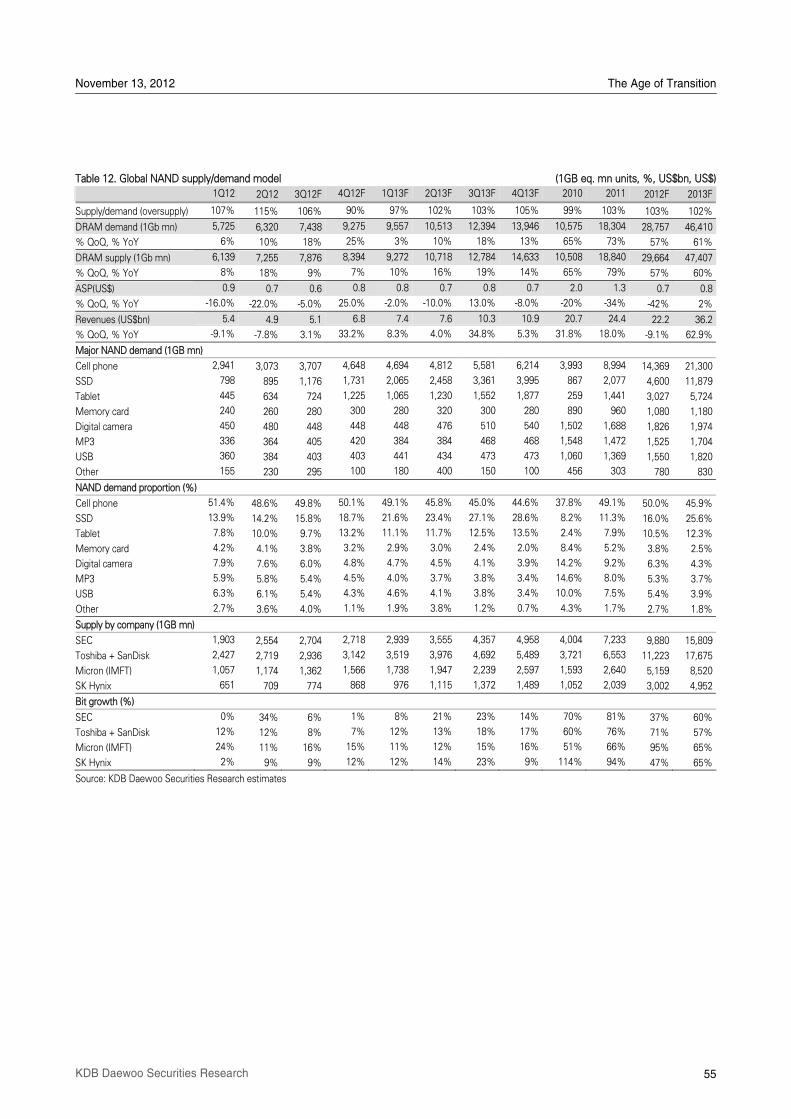

[DRAM market issue] Will a mobile DRAM supply shortage occur? ..........................................52

[NAND market issue] Will prices rise further given limited supply growth?................................53

3 KDB Daewoo Securities Research

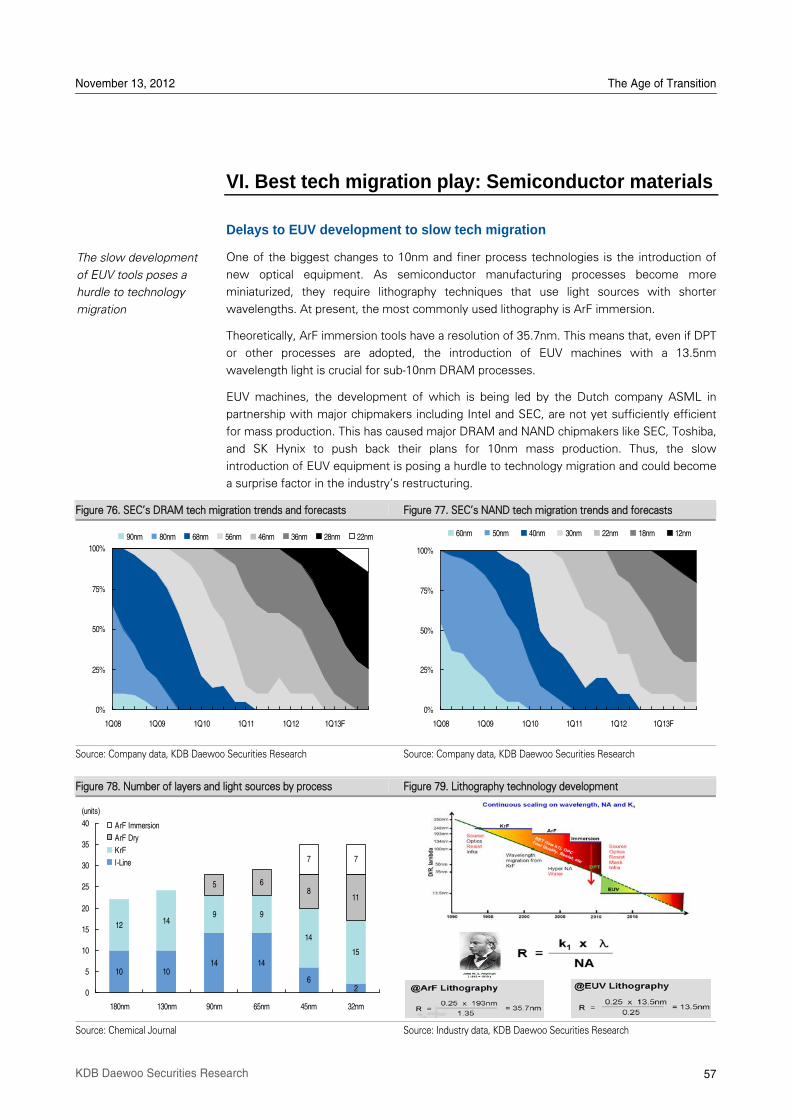

VI. Best tech migration play: Semiconductor materials ...........................................................57

Delays to EUV development to slow tech migration ...................................................................57

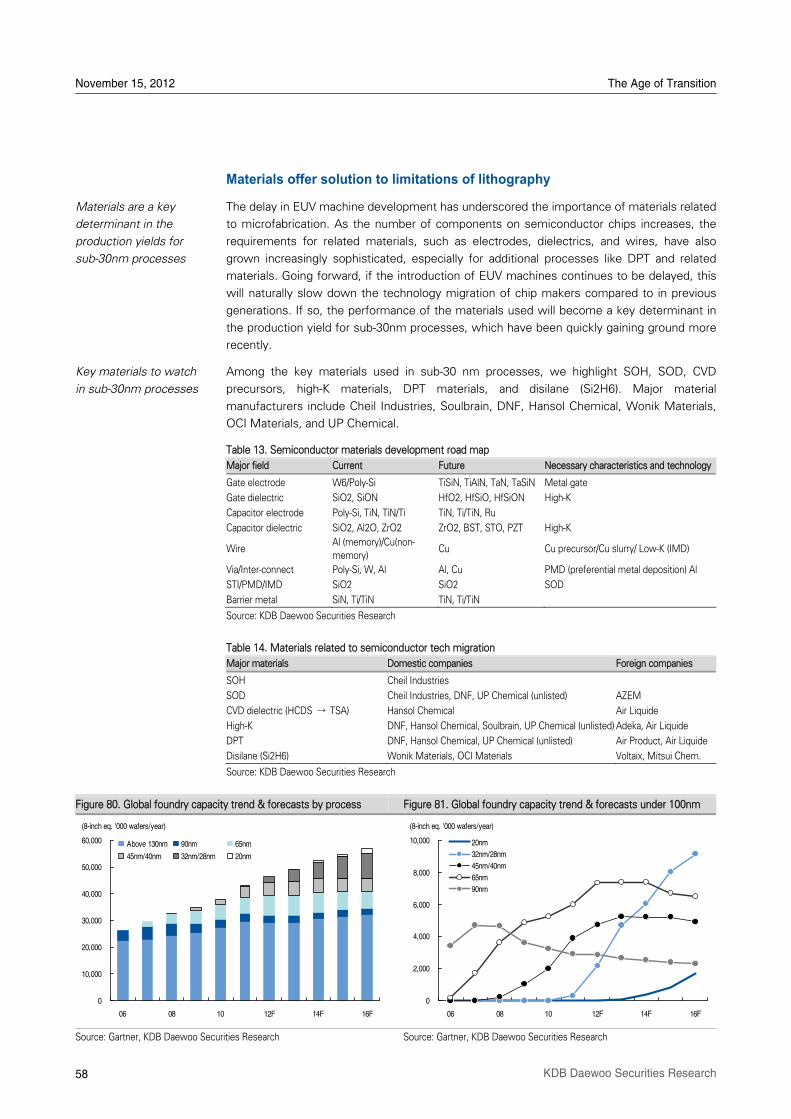

Materials offer solution to limitations of lithography ....................................................................58

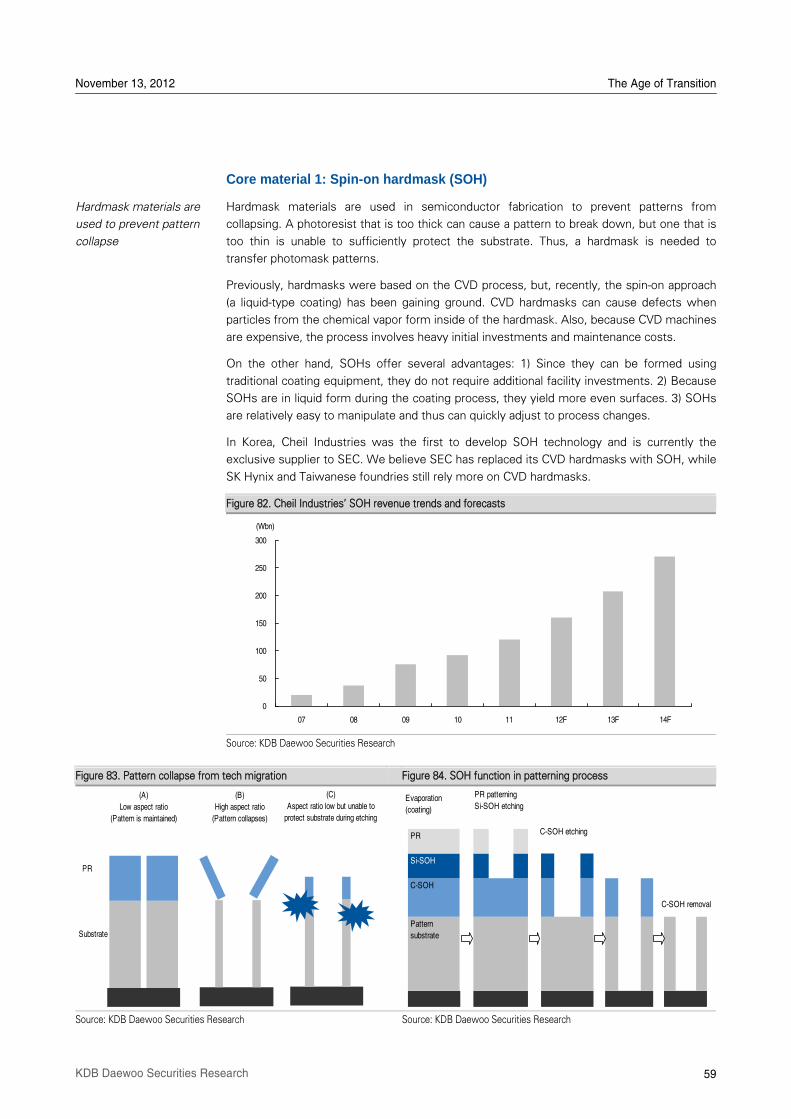

Core material 1: Spin-on hardmask (SOH) .................................................................................59

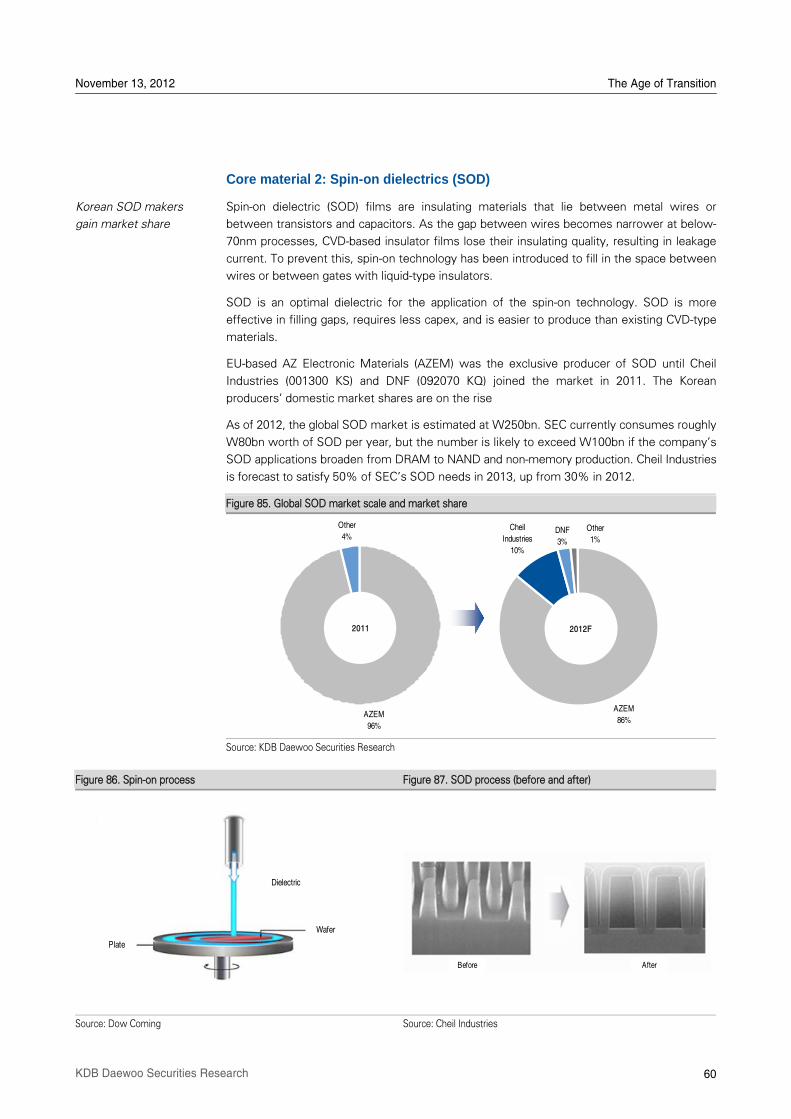

Core material 2: Spin-on dielectrics (SOD).................................................................................60

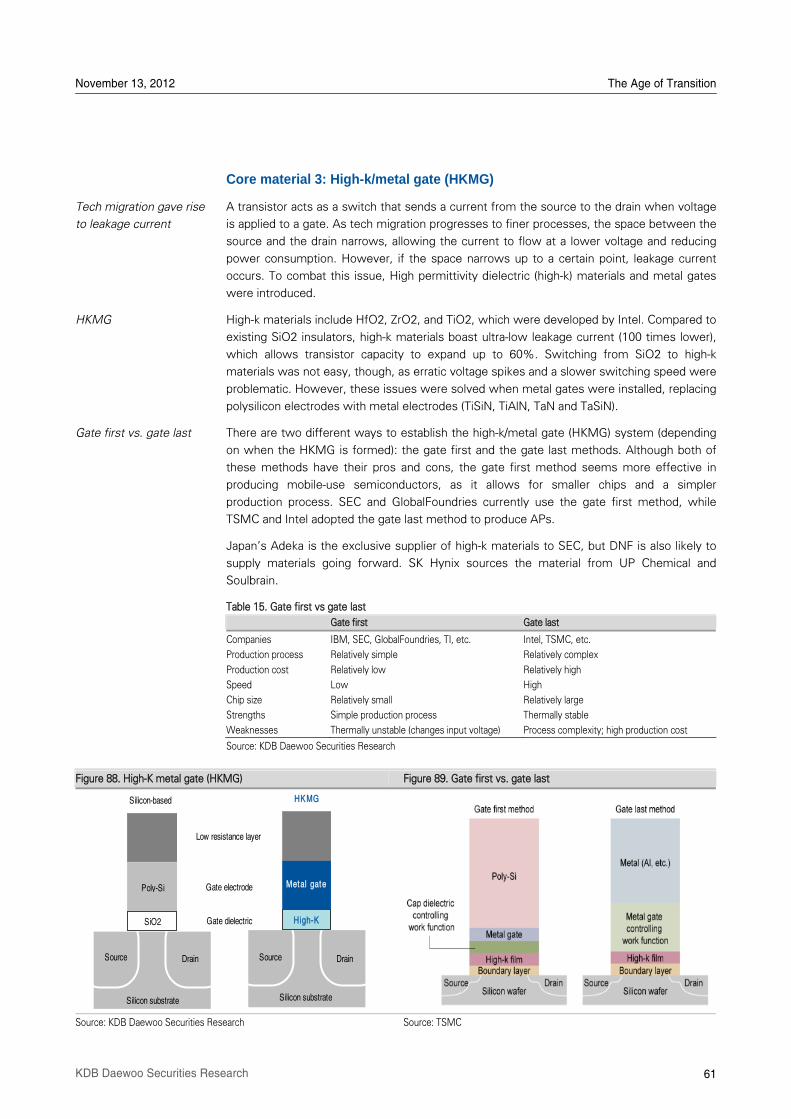

Core material 3: High-k/metal gate (HKMG)...............................................................................61

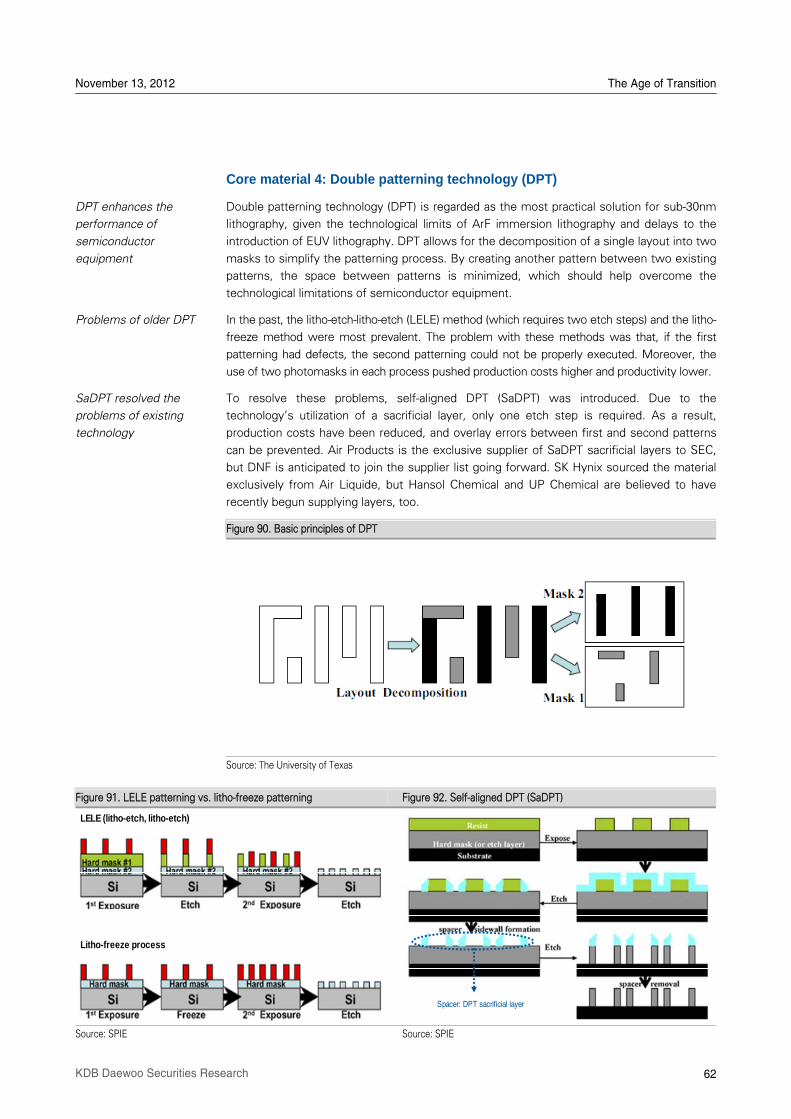

Core material 4: Double patterning technology (DPT)................................................................62

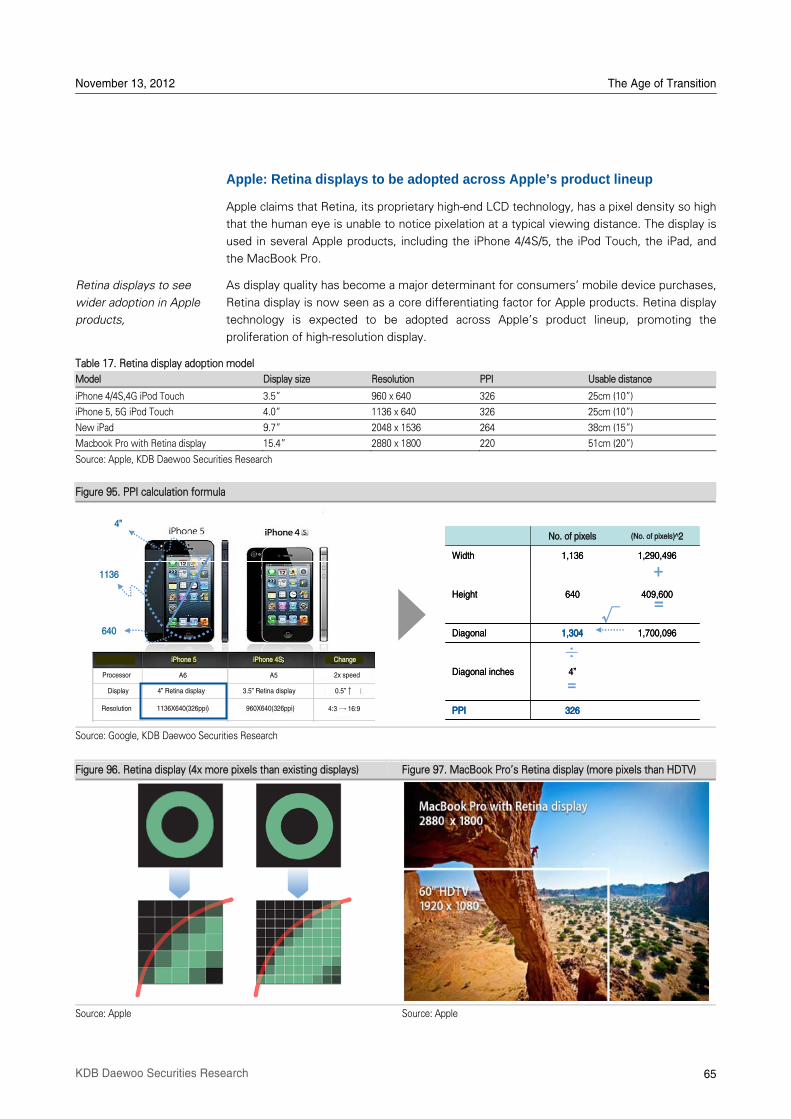

VII. The ongoing innovation of displays: AMOLED vs. Retina display ...................................64

Proliferation of high-resolution displays: Form factor counts!.....................................................64

Apple: Retina displays to be adopted across Apple’s product lineup.........................................65

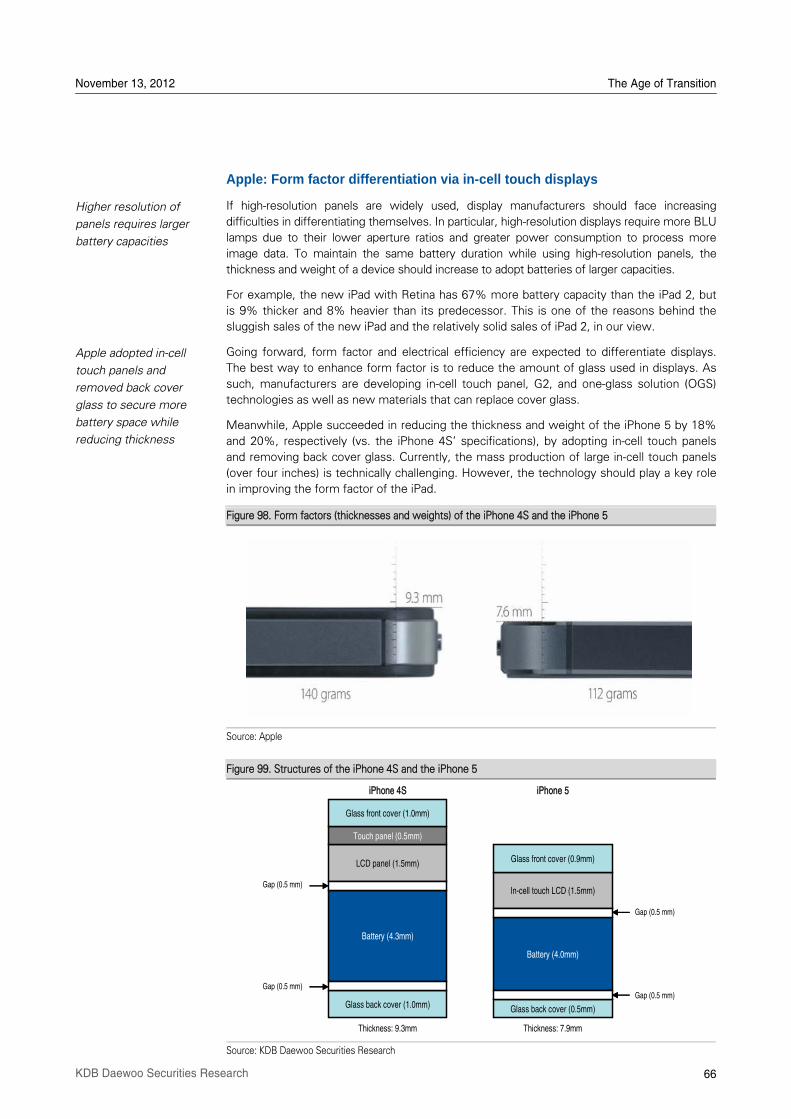

Apple: Form factor differentiation via in-cell touch displays........................................................66

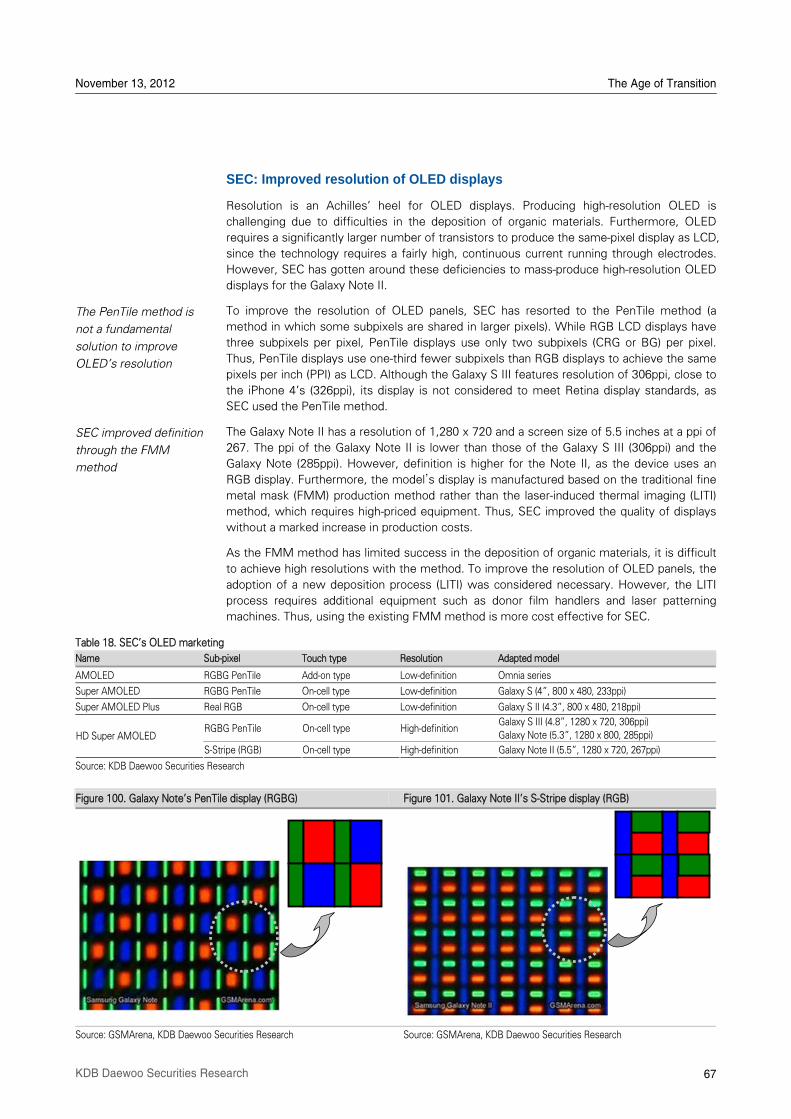

SEC: Improved resolution of OLED displays ..............................................................................67

SEC: Differentiating itself with flexible OLED technology...........................................................68

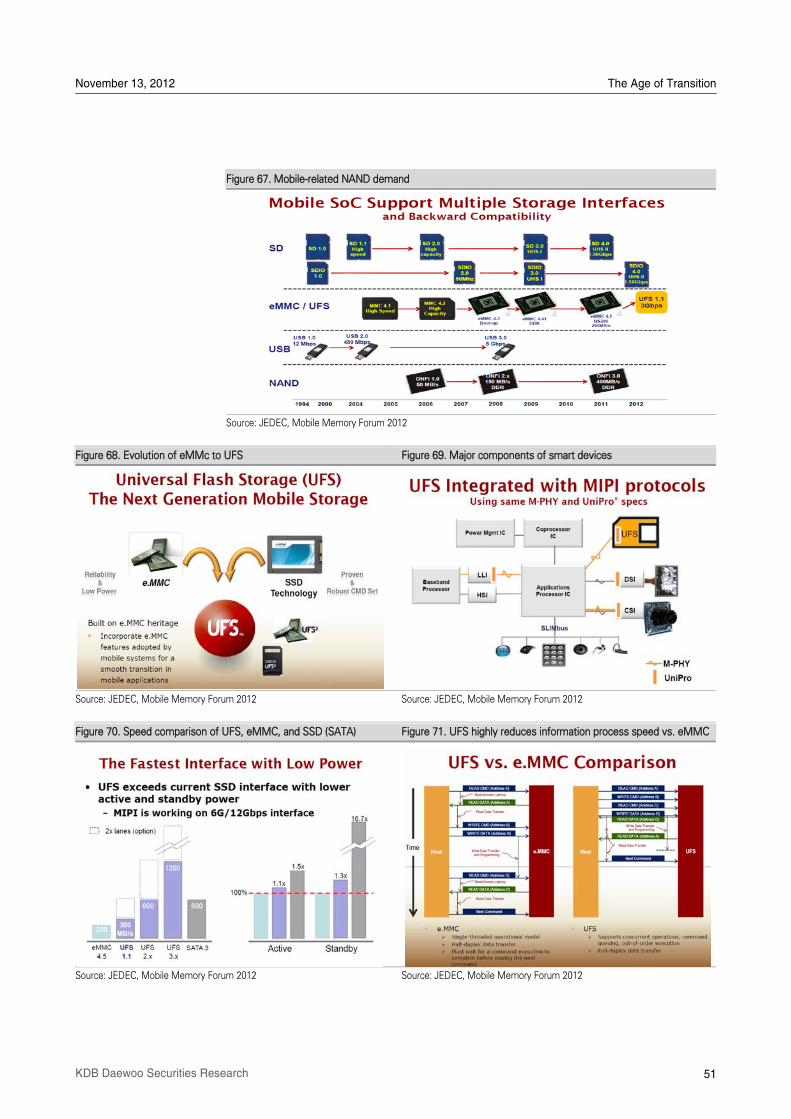

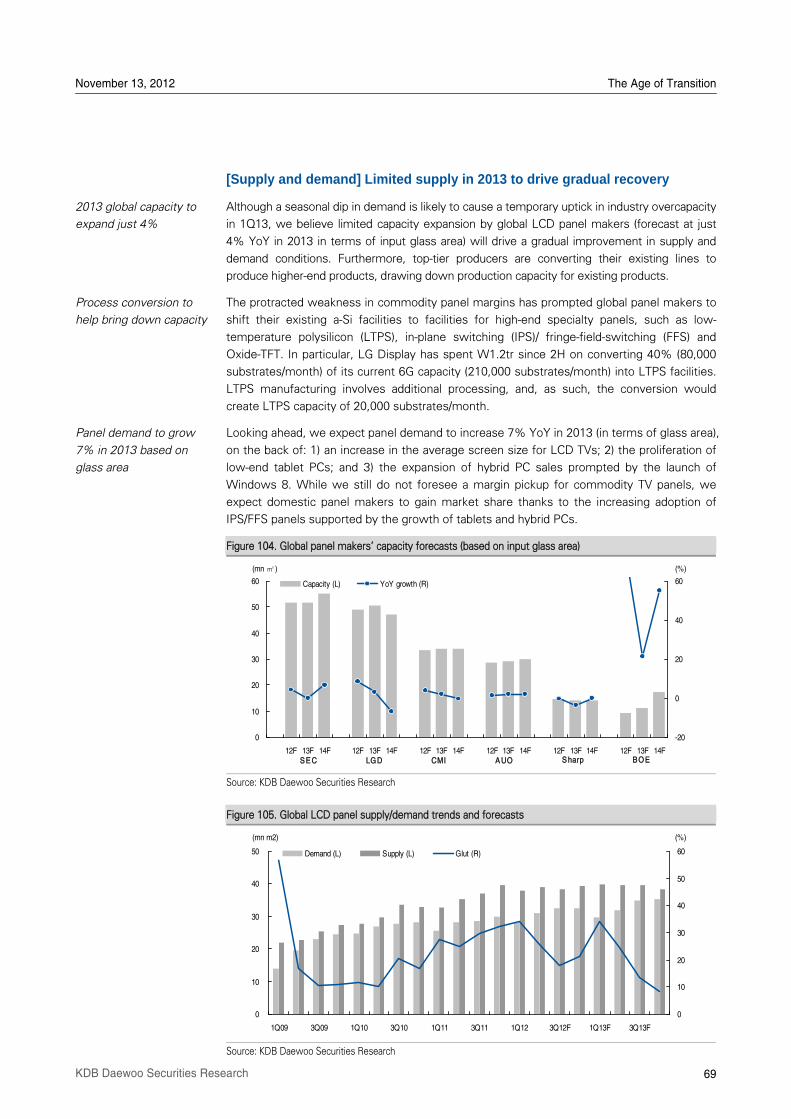

[Supply and demand] Limited supply in 2013 to drive gradual recovery....................................69

VIII. IT sector investment strategy for 2013................................................................................71

[Macroeconomic view] The IT sector in context..........................................................................71

[Global view] Apple vs. SEC .......................................................................................................72

[2013 investment strategy] Weak in 1H, but strong in 2H ..........................................................73

SEC’s supply chain vs. Apple’s supply chain [Top 11 IT stocks] ...............................................74

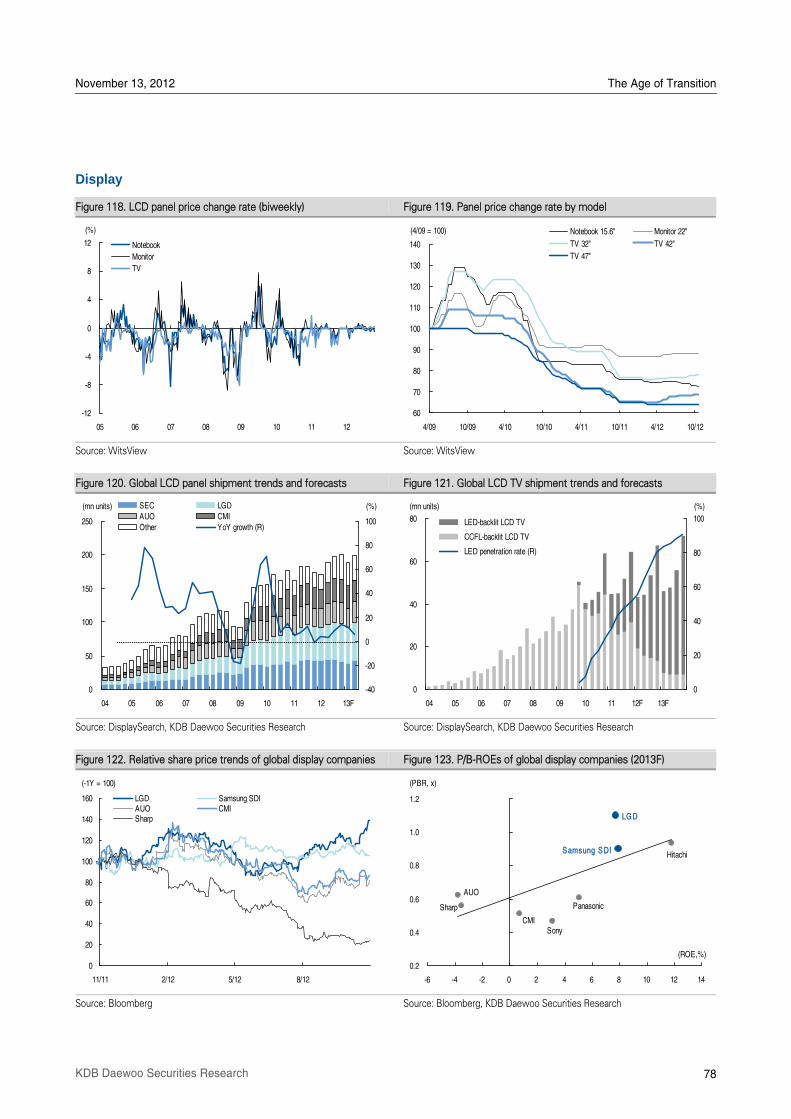

Semiconductor.............................................................................................................................77

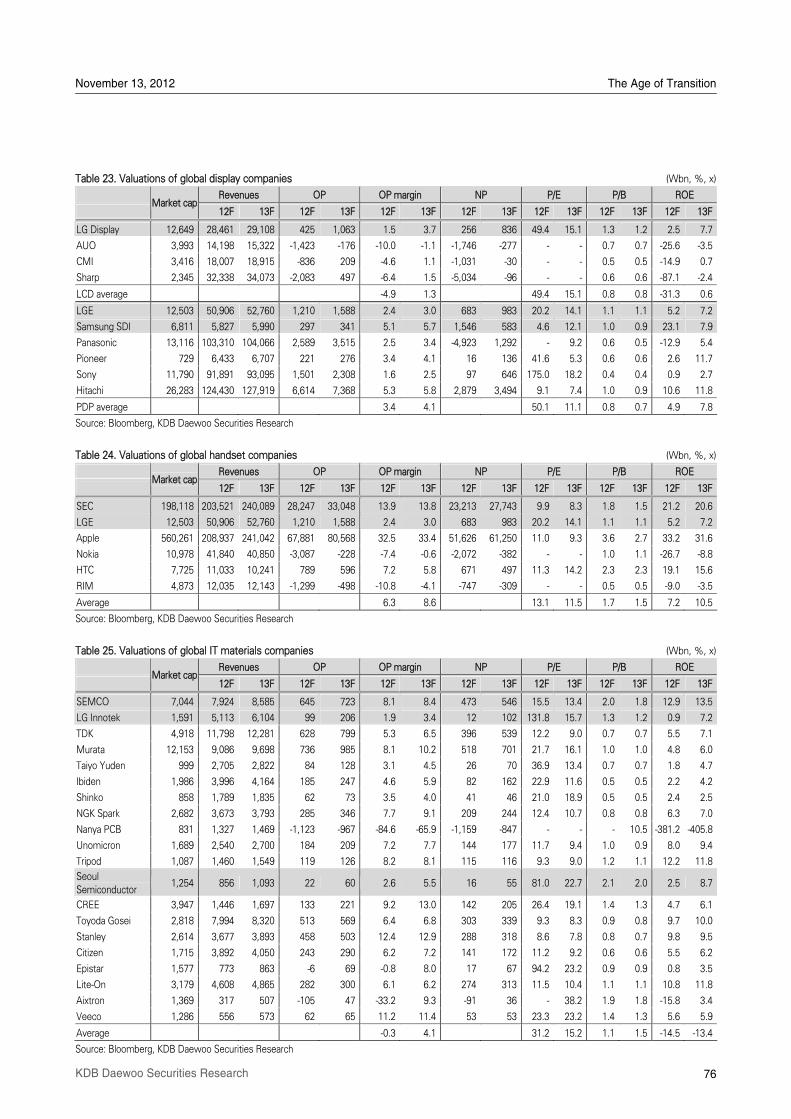

Display .........................................................................................................................................78

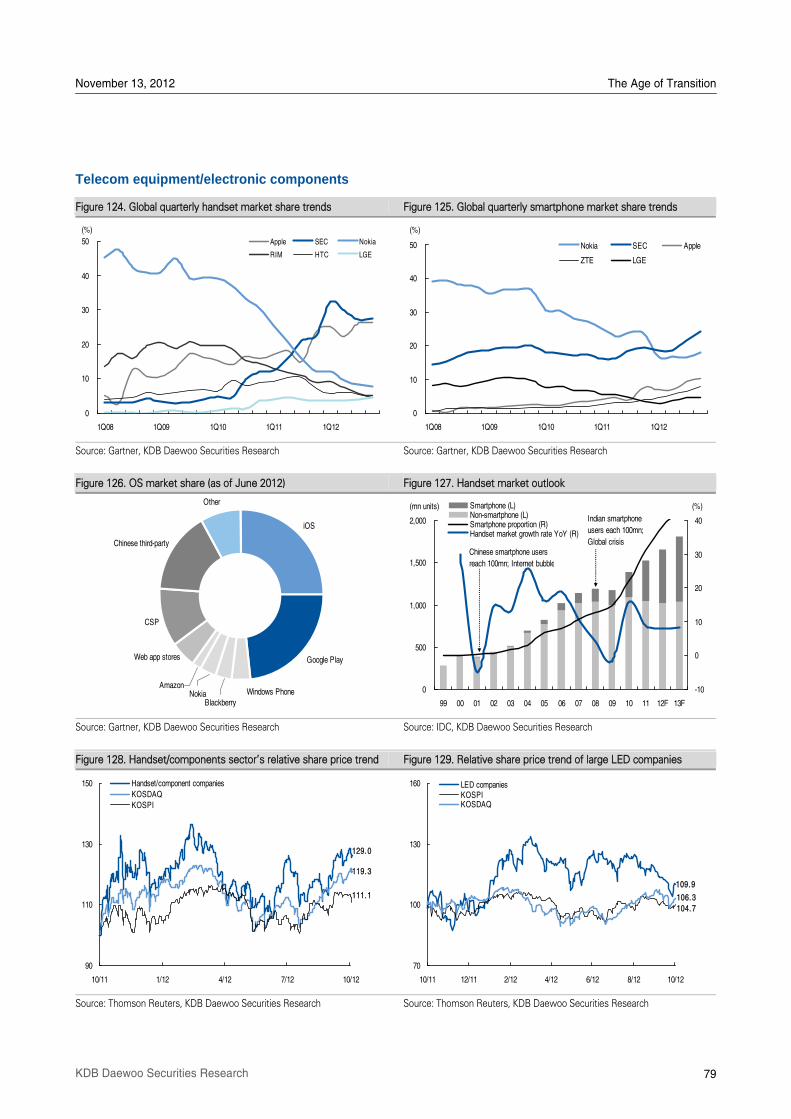

Telecom equipment/electronic components ...............................................................................79

IX. Top picks ................................................................................................................................. 80

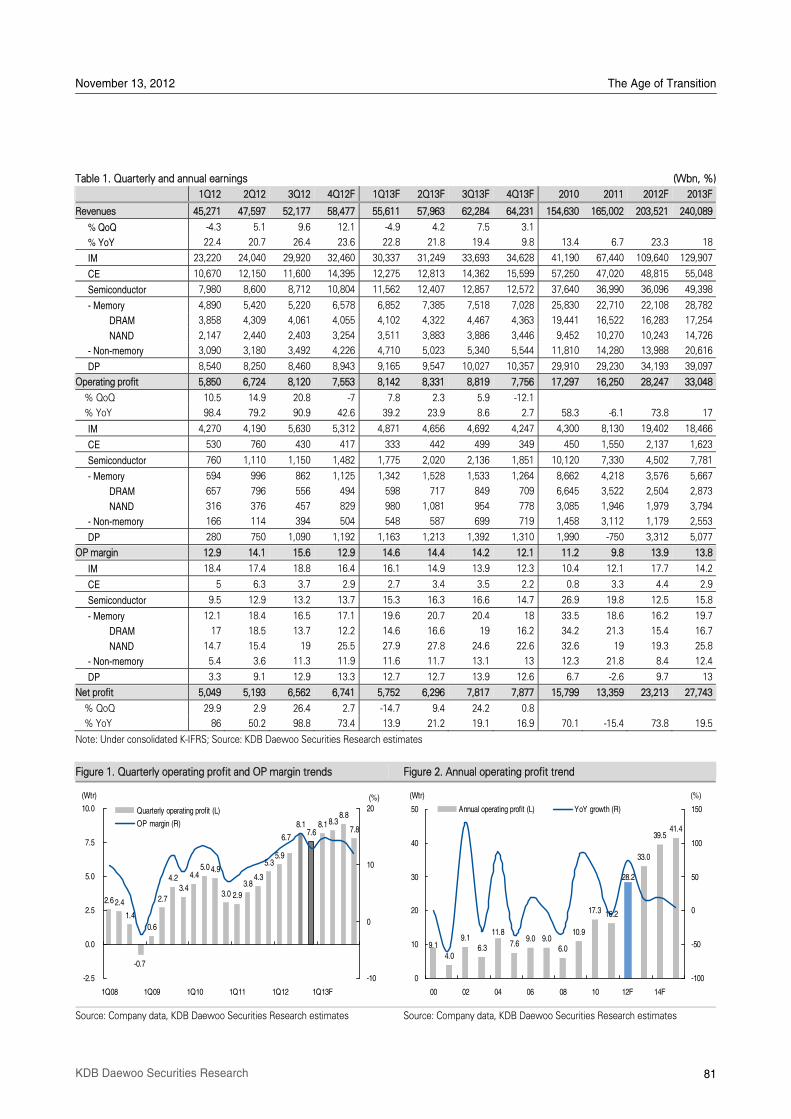

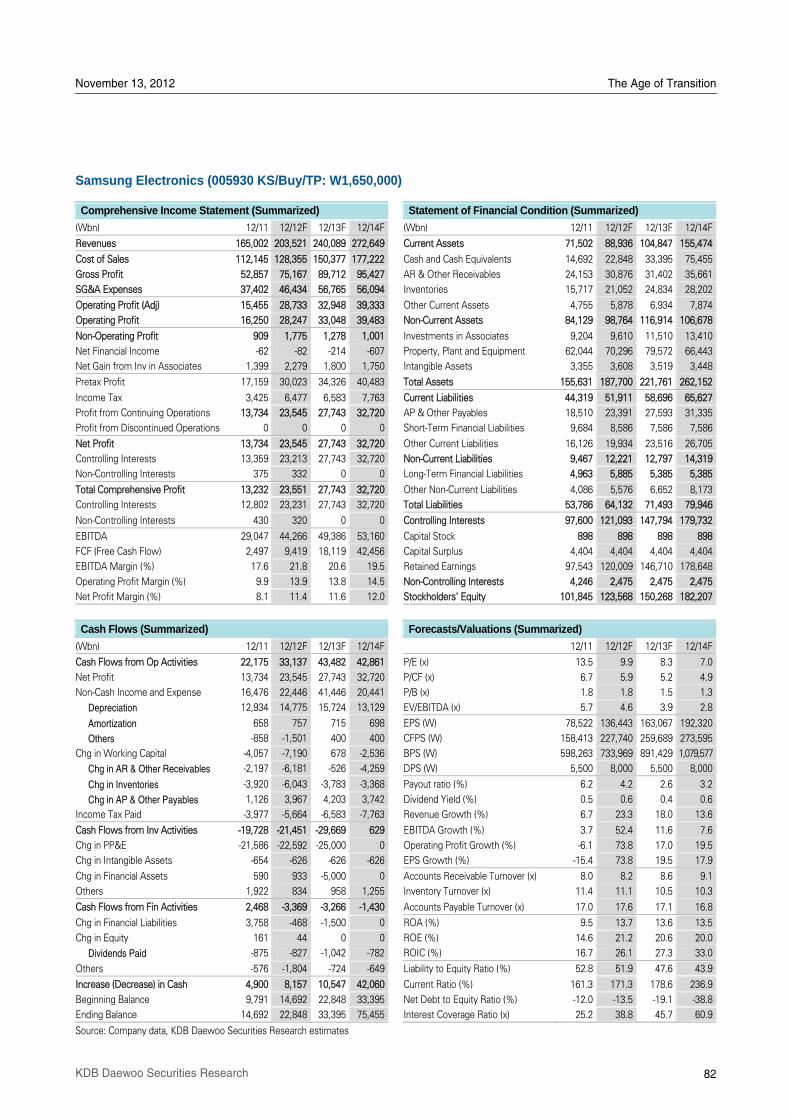

Samsung Electronics (005930 KS/Buy)......................................................................................80

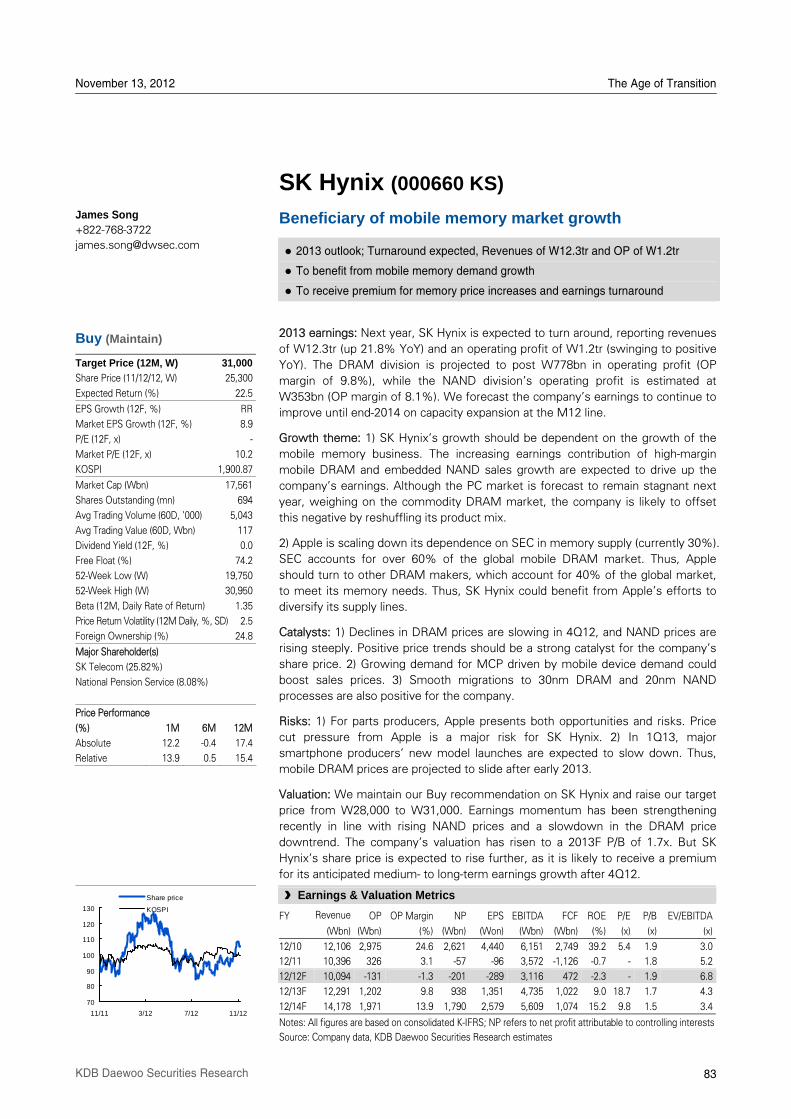

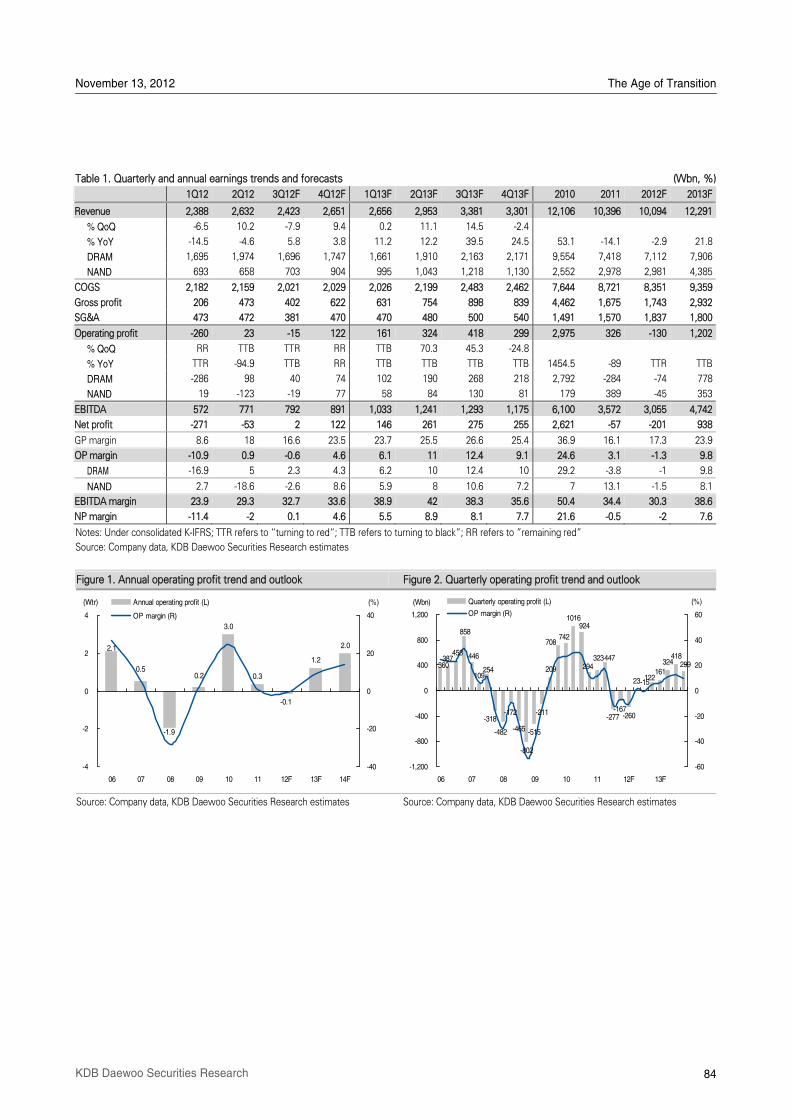

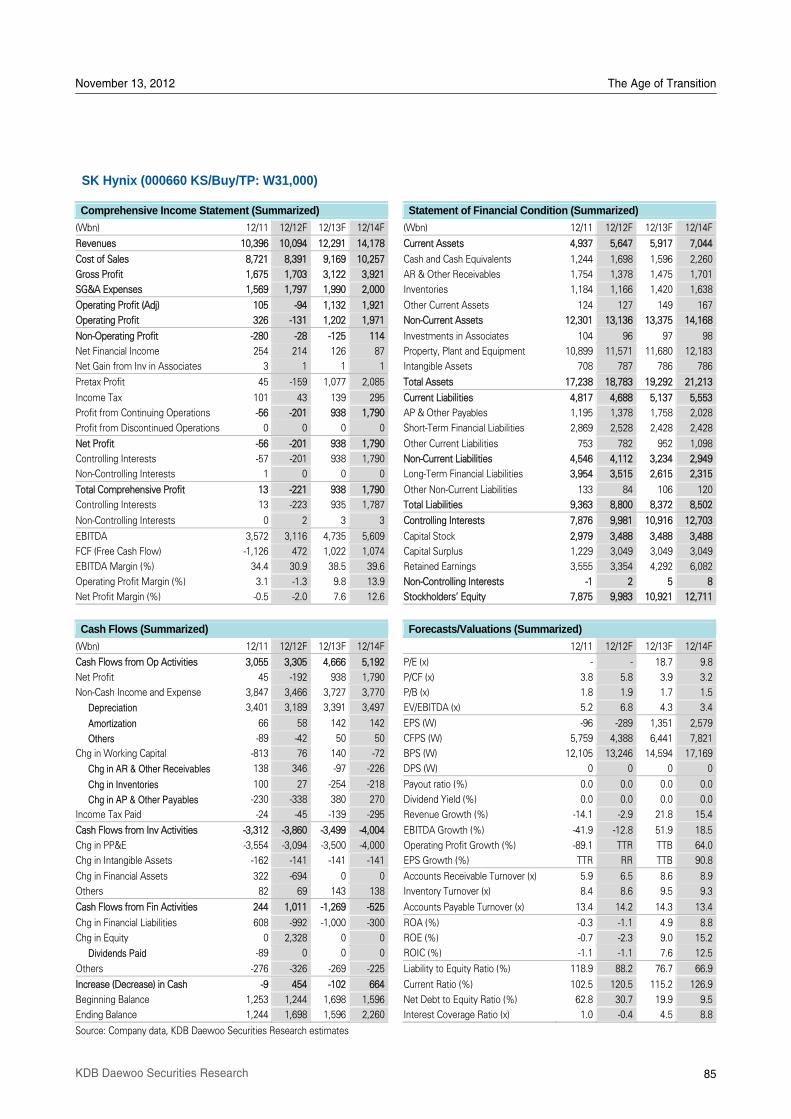

SK Hynix (000660 KS/Buy) .........................................................................................................83

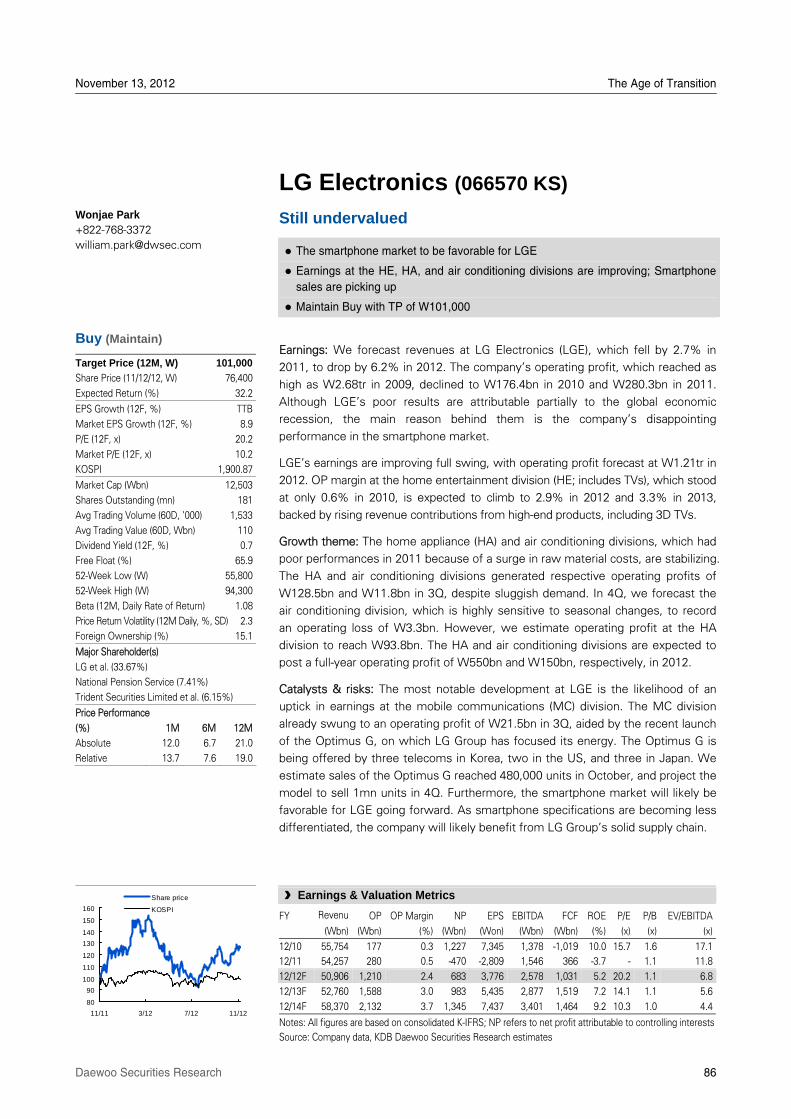

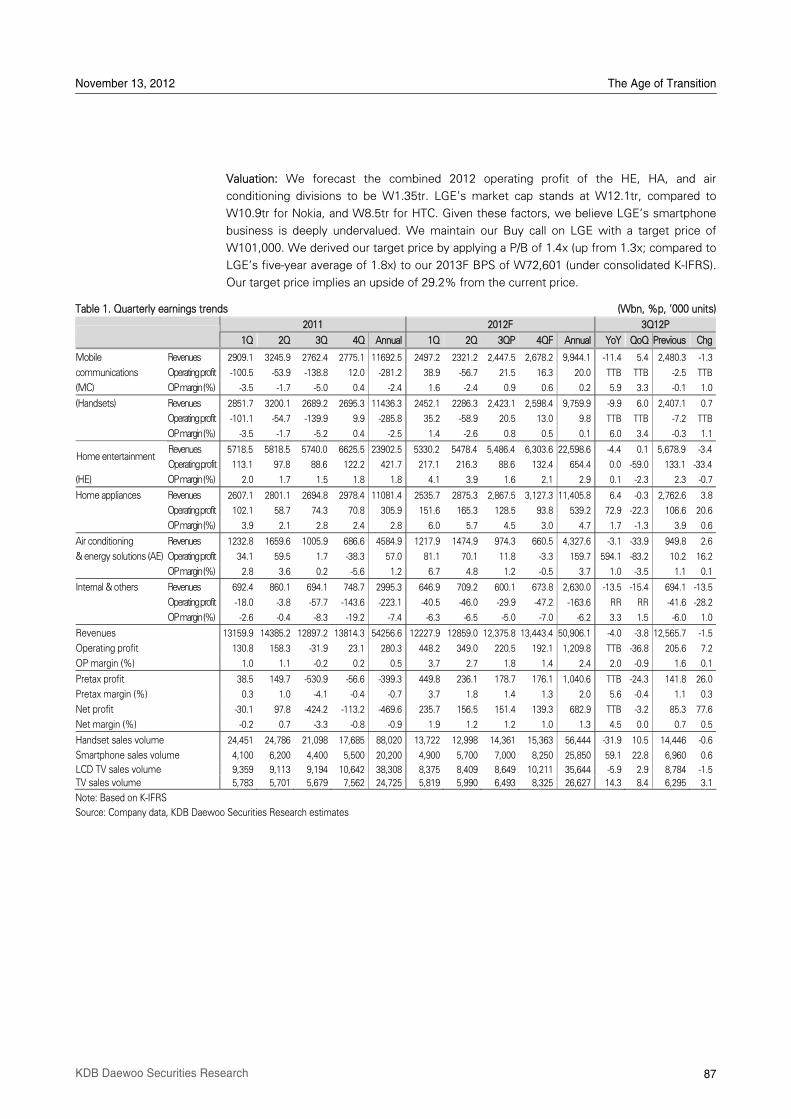

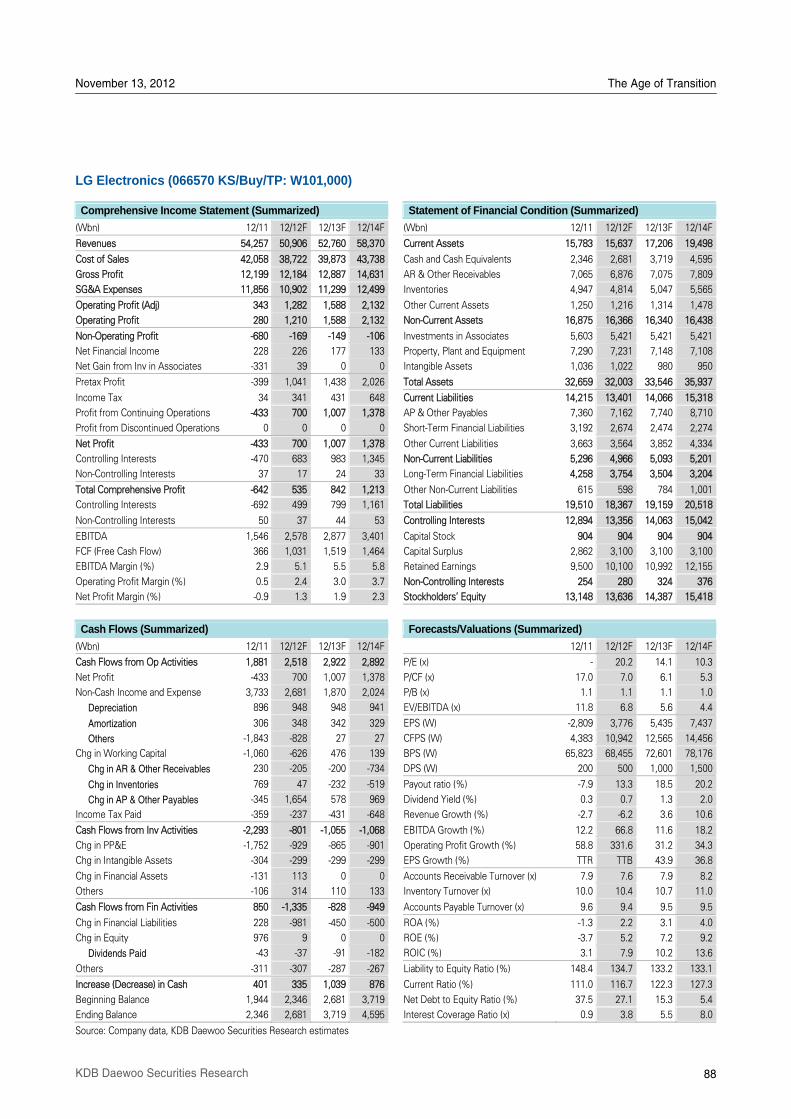

LG Electronics (066570 KS/Buy) ................................................................................................86

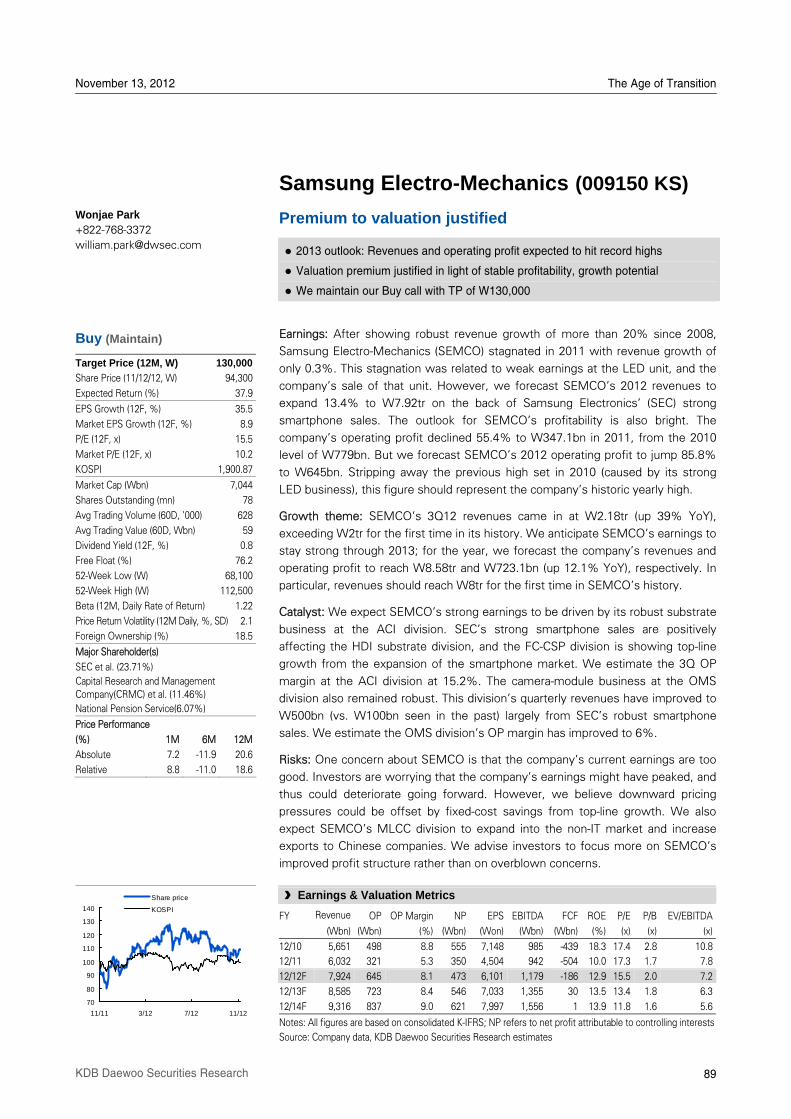

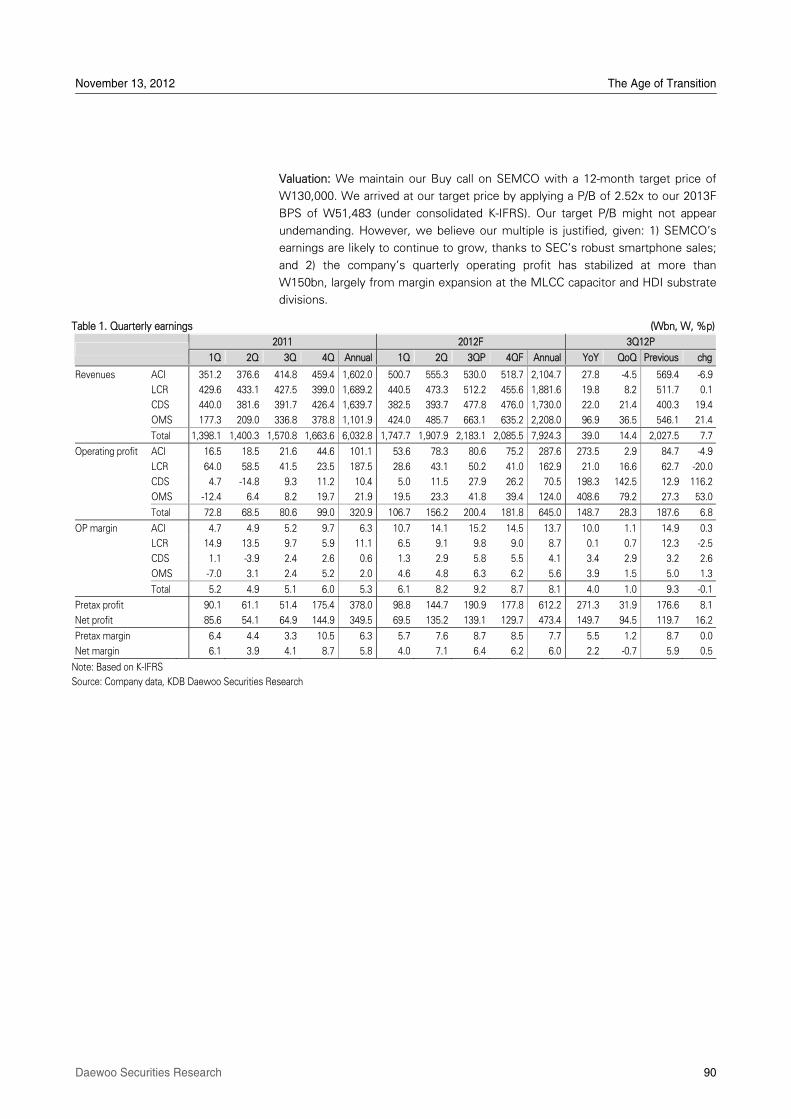

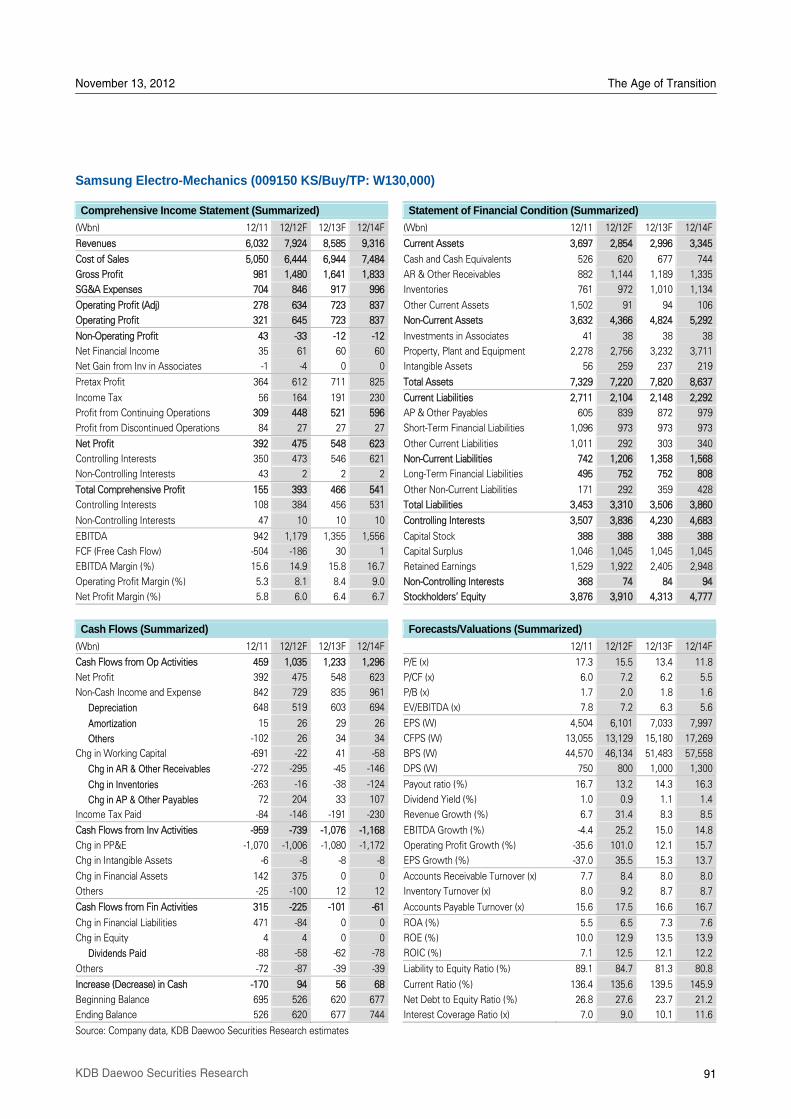

Samsung Electro-Mechanics (009150 KS/Buy)..........................................................................89

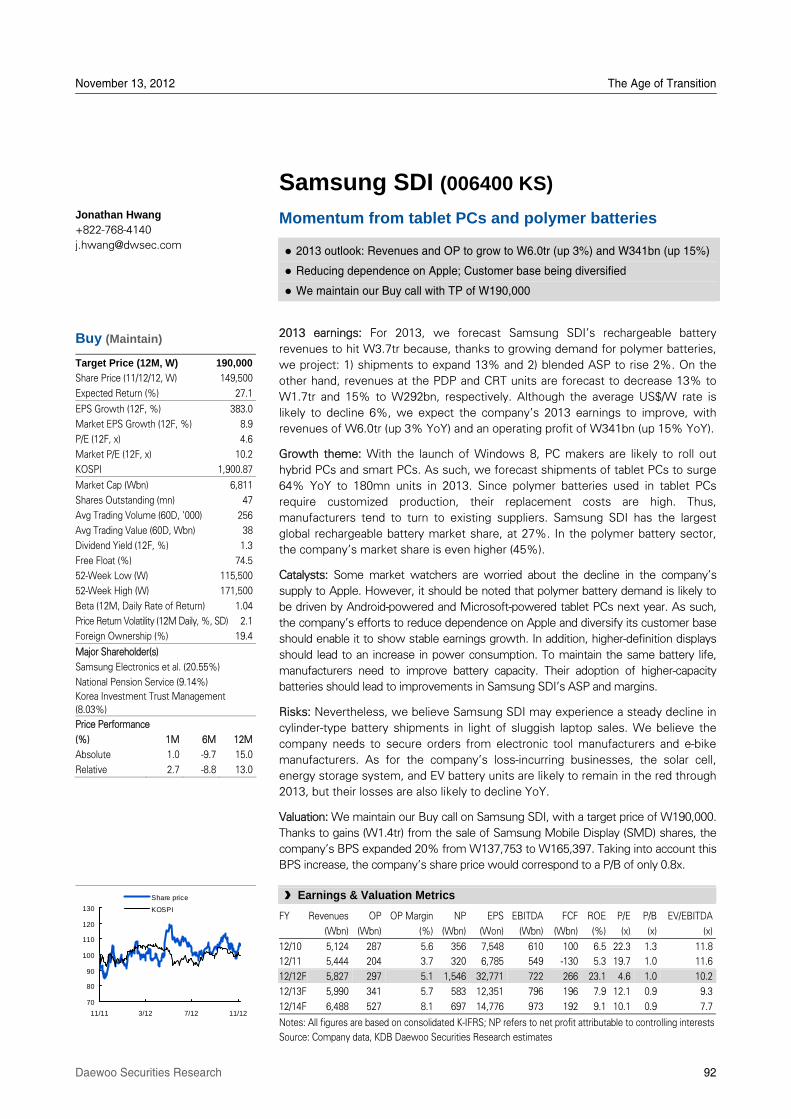

Samsung SDI (006400 KS/Buy)..................................................................................................92

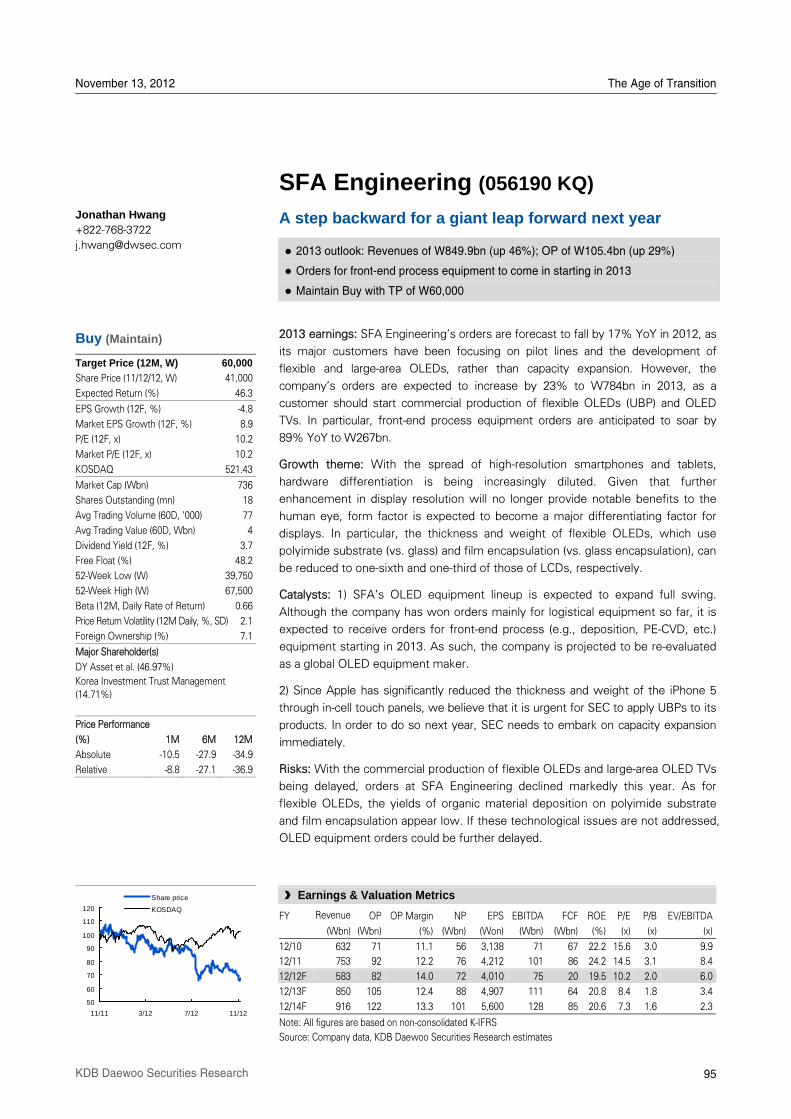

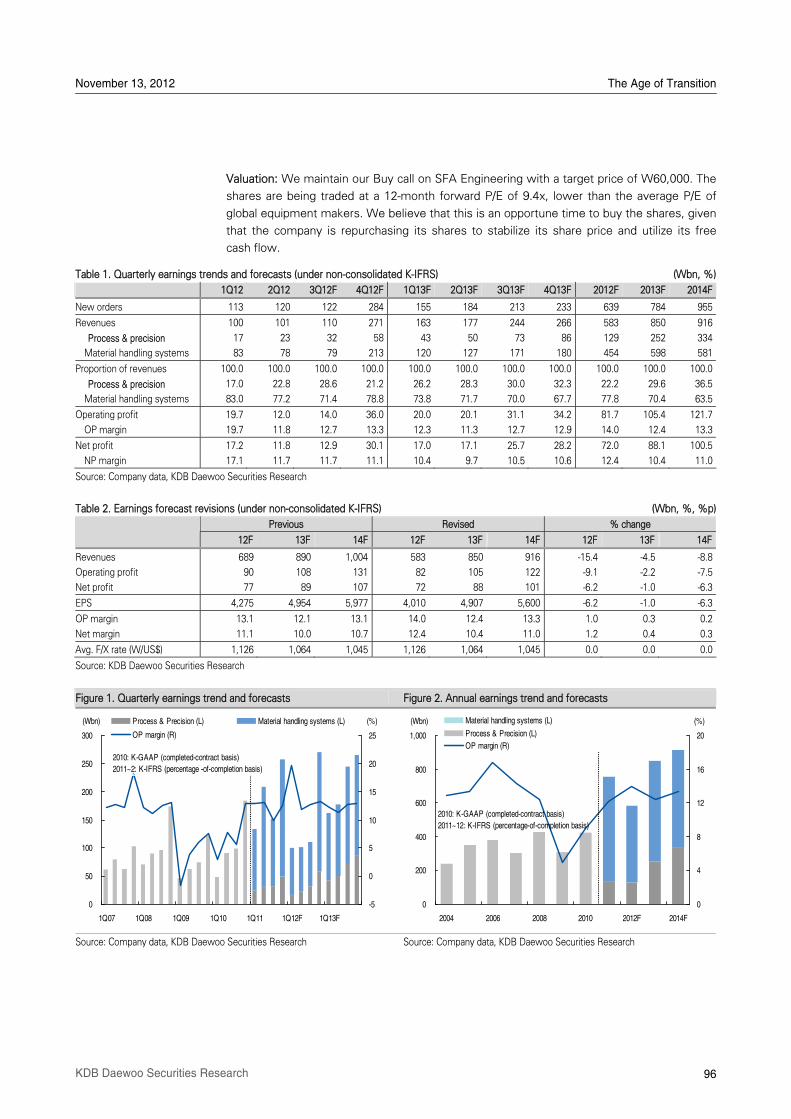

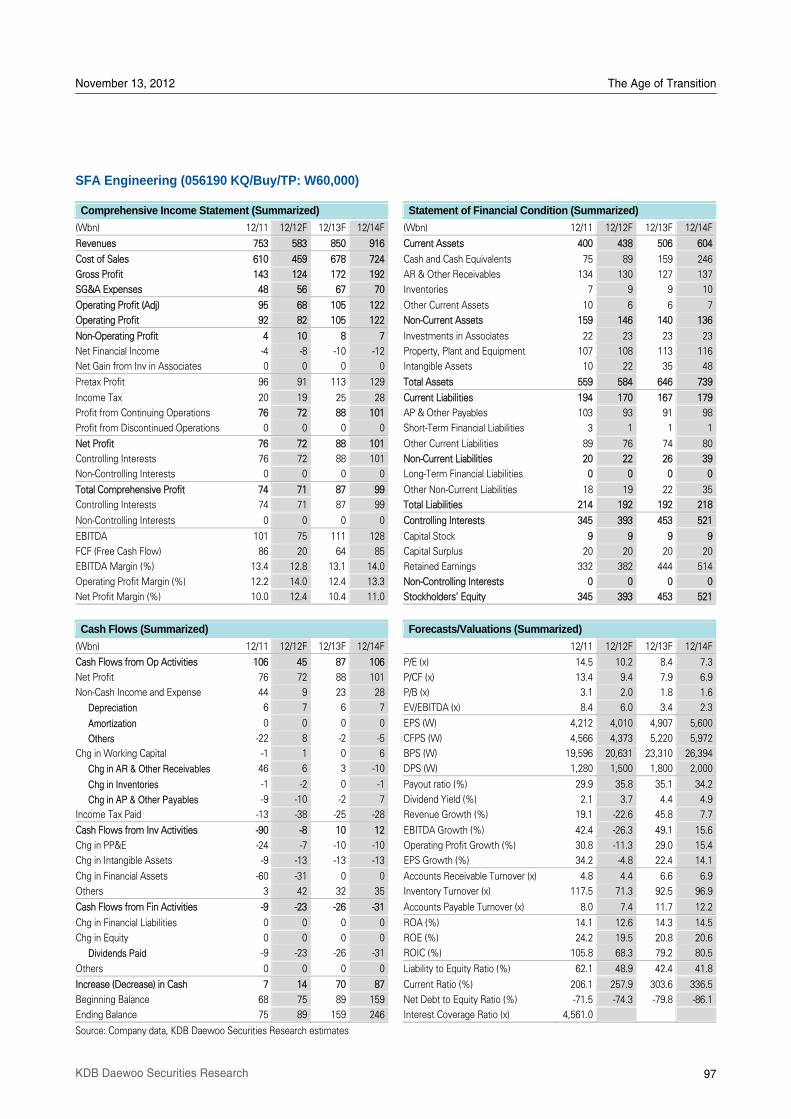

SFA Engineering (056190 KQ/Buy) ............................................................................................95

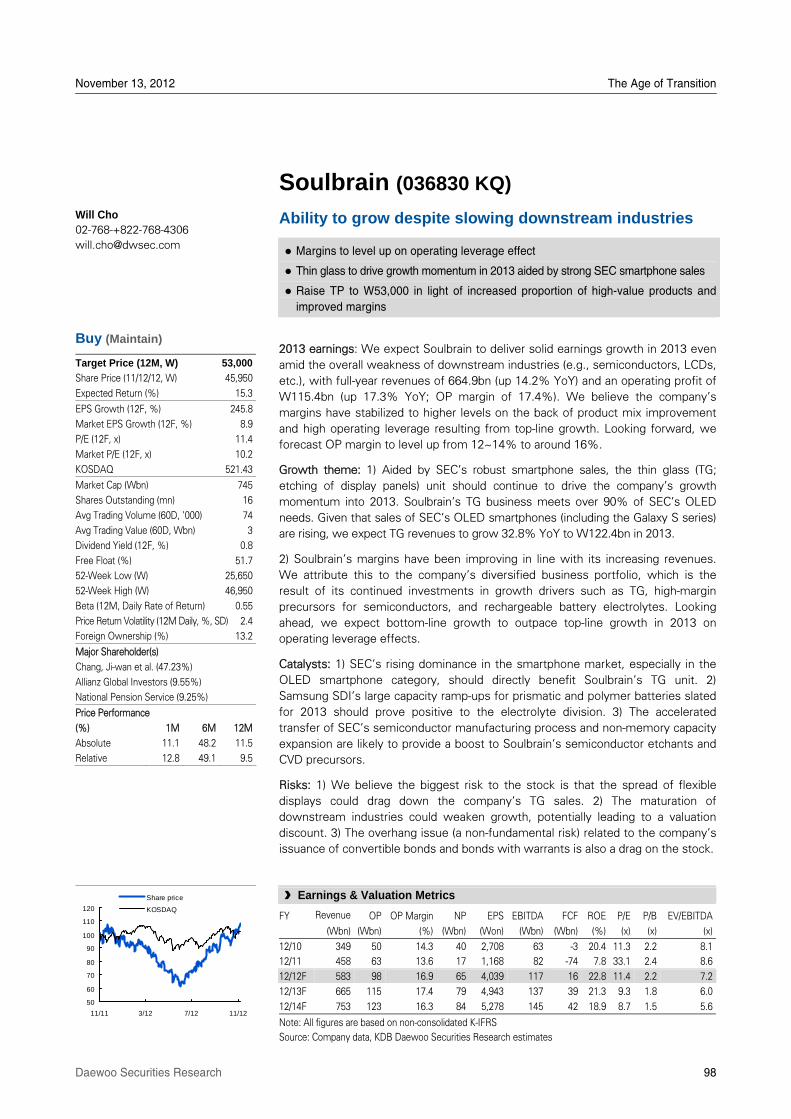

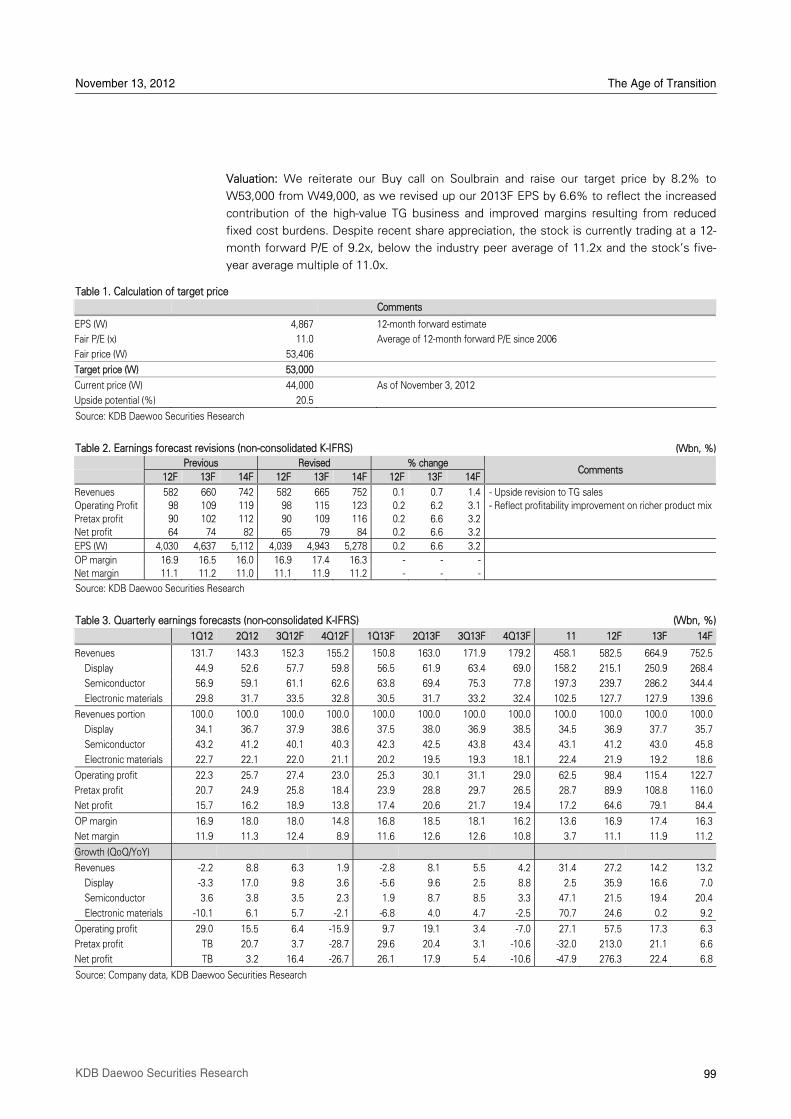

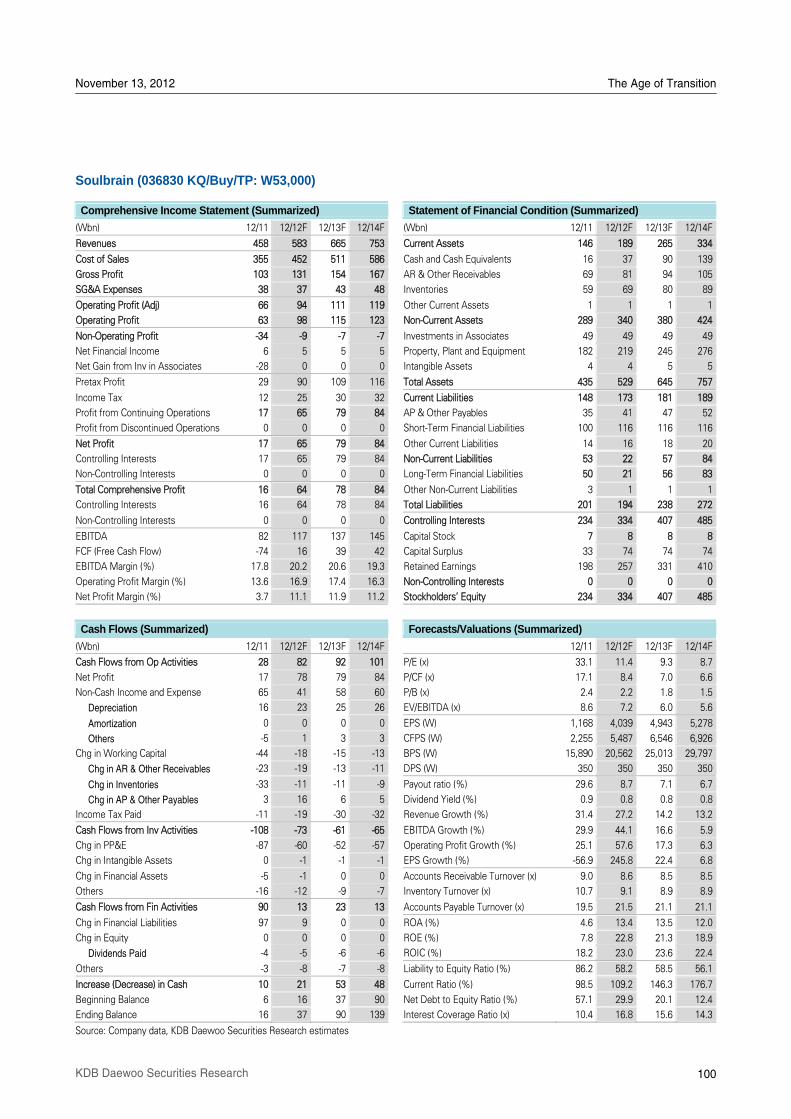

Soulbrain (036830 KQ/Buy) ........................................................................................................98

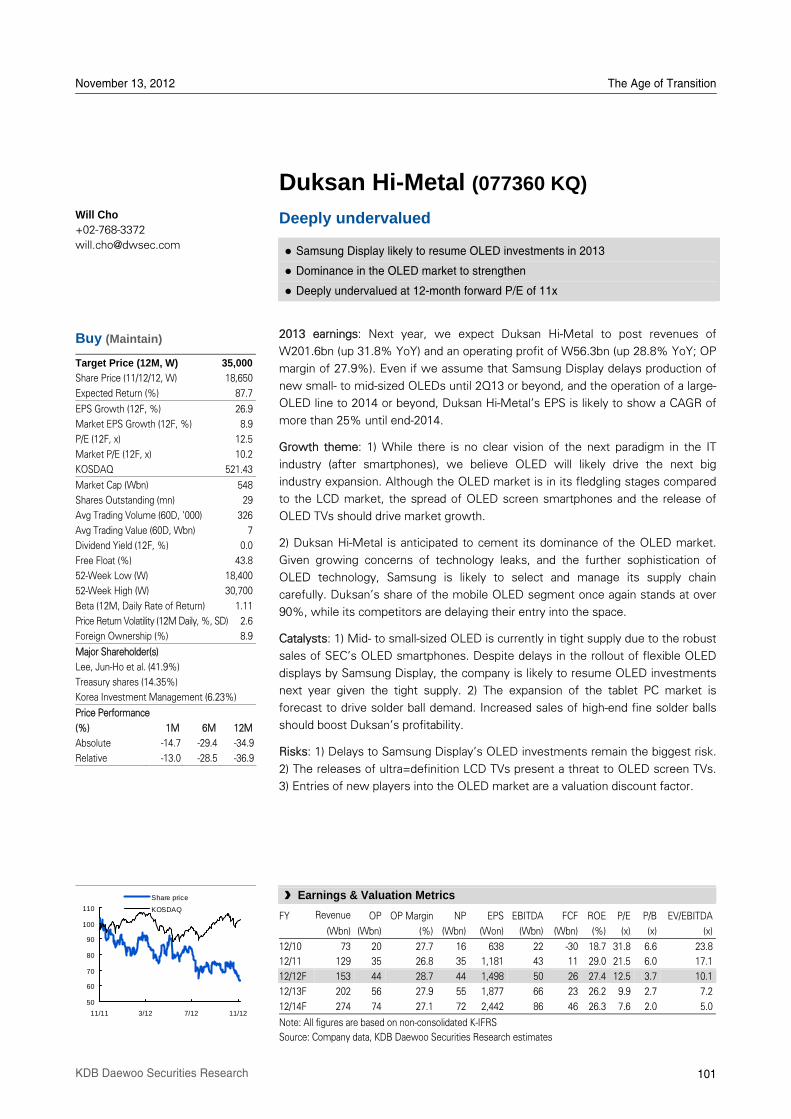

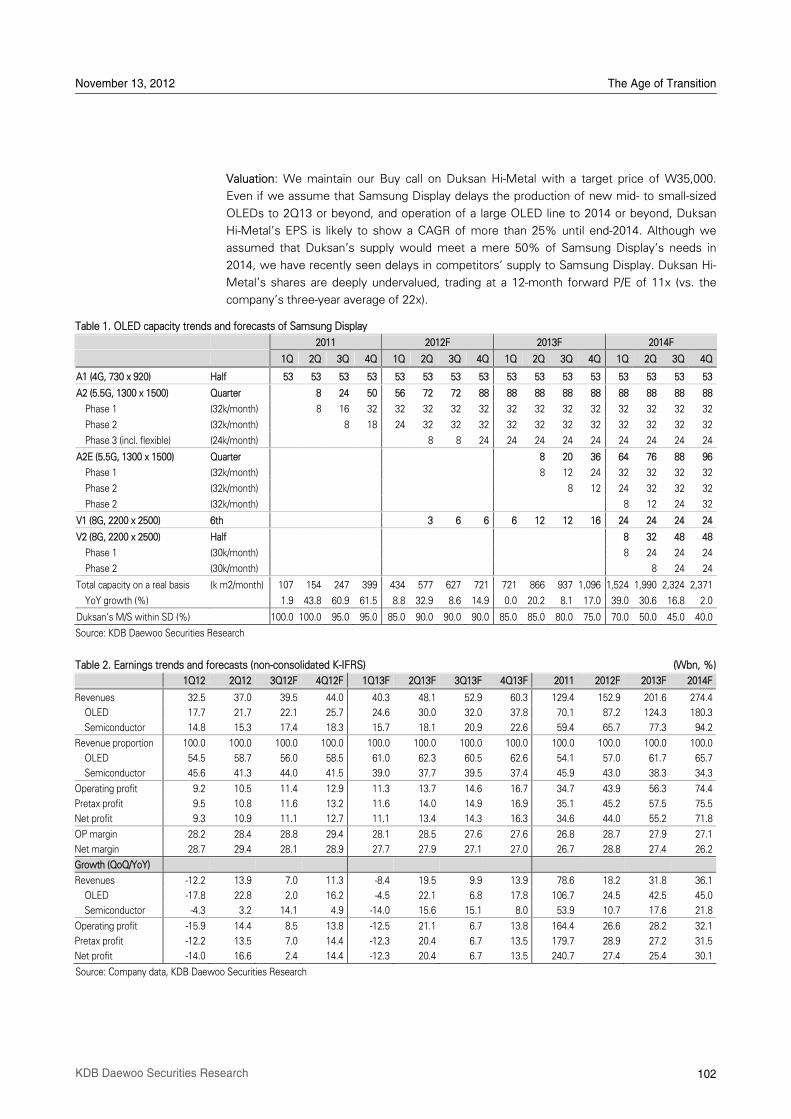

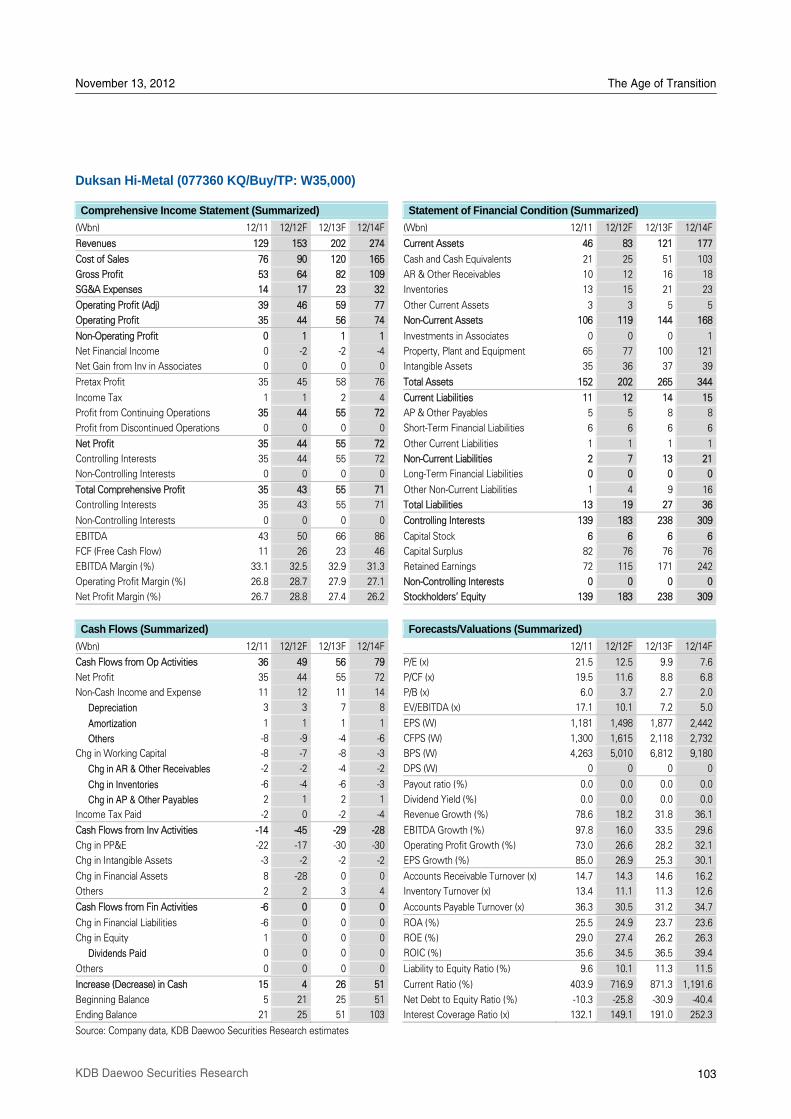

Duksan Hi-Metal (077360 KQ/Buy)...........................................................................................101

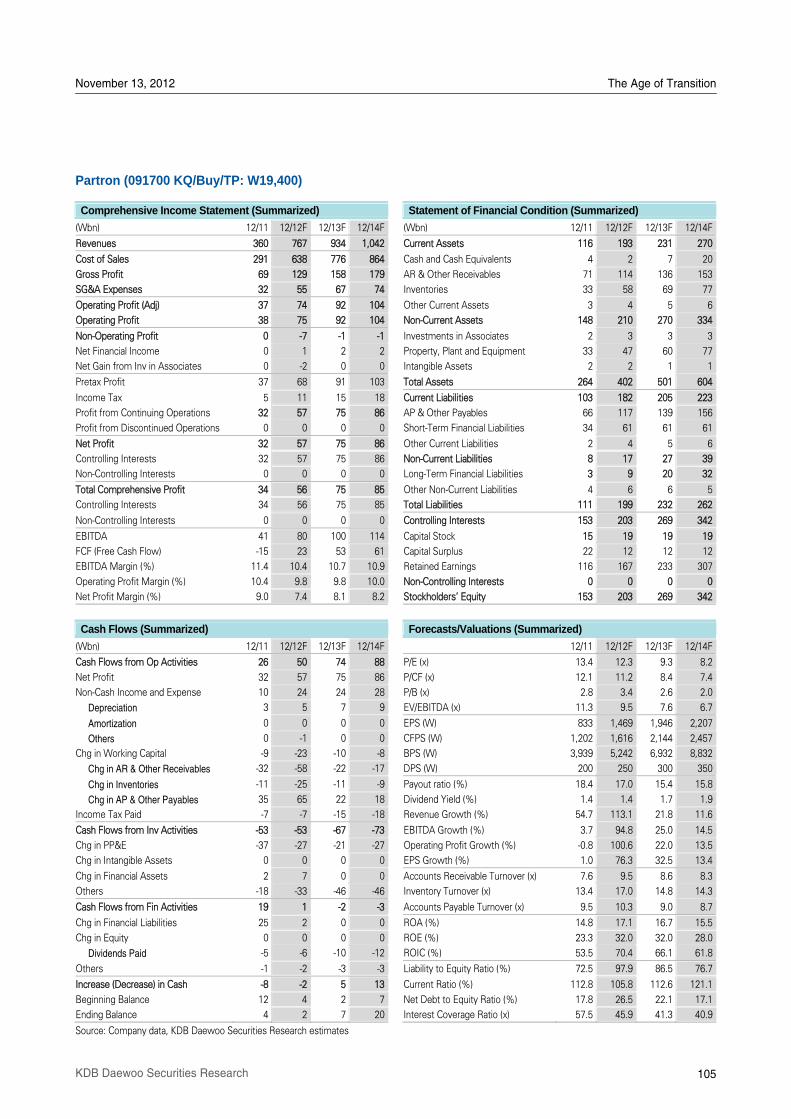

Partron (091700 KQ/Buy)..........................................................................................................104

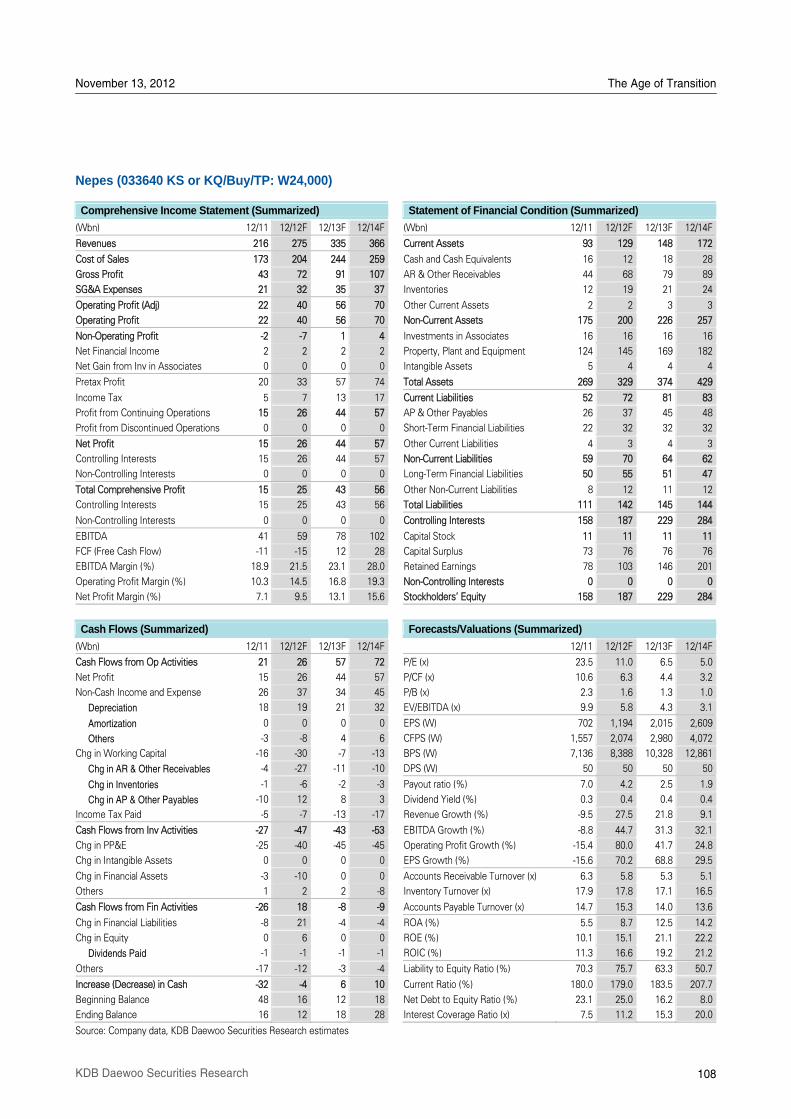

Nepes (033640 KQ/Buy) ...........................................................................................................106

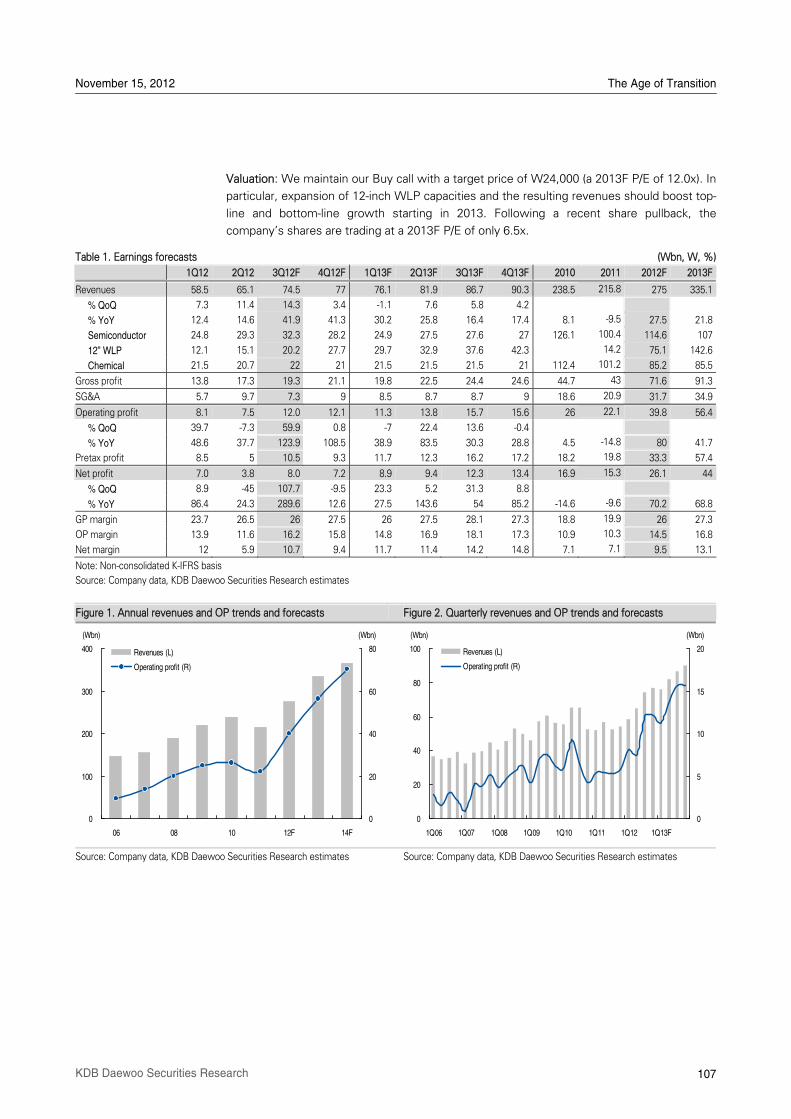

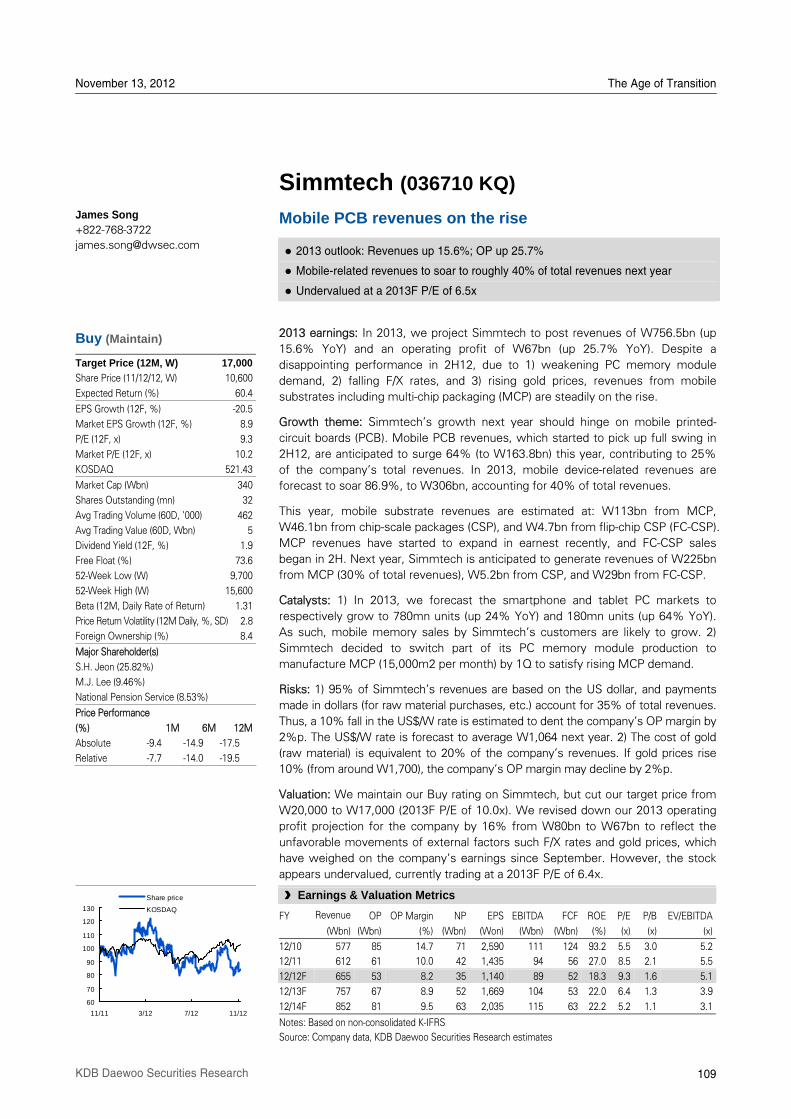

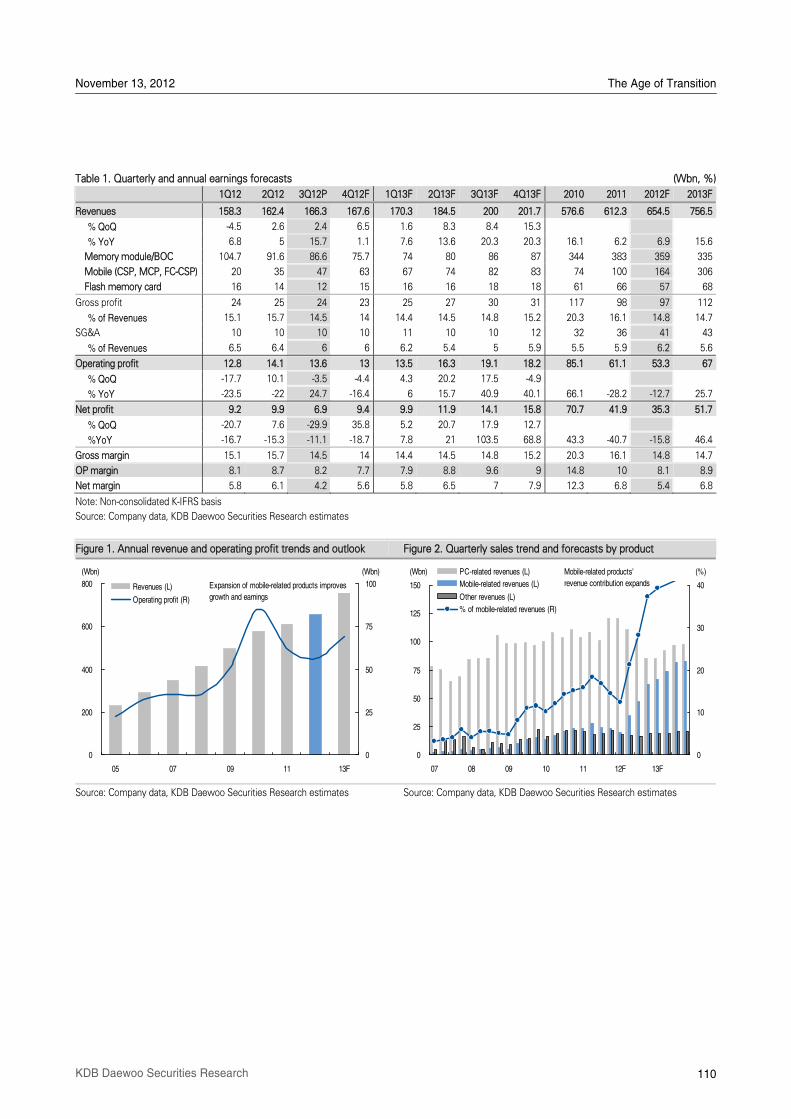

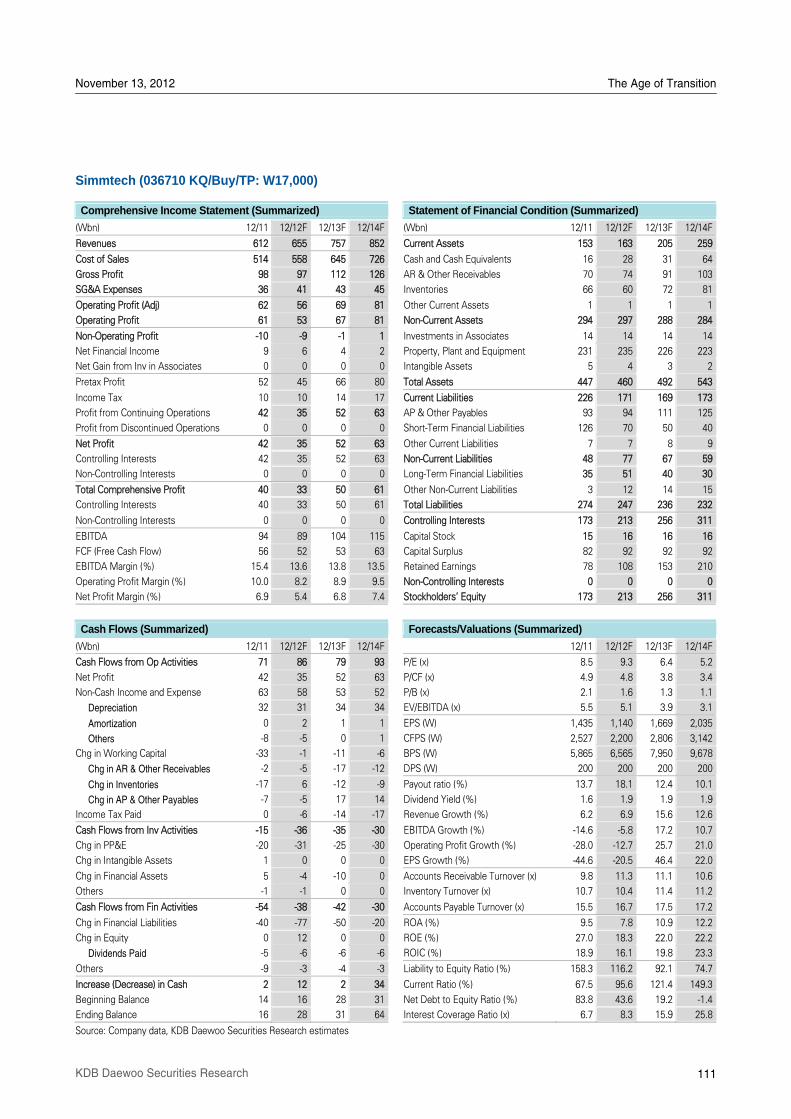

Simmtech (036710 KQ/Buy) .....................................................................................................109

November 13, 2012 The Age of Transition

4 KDB Daewoo Securities Research

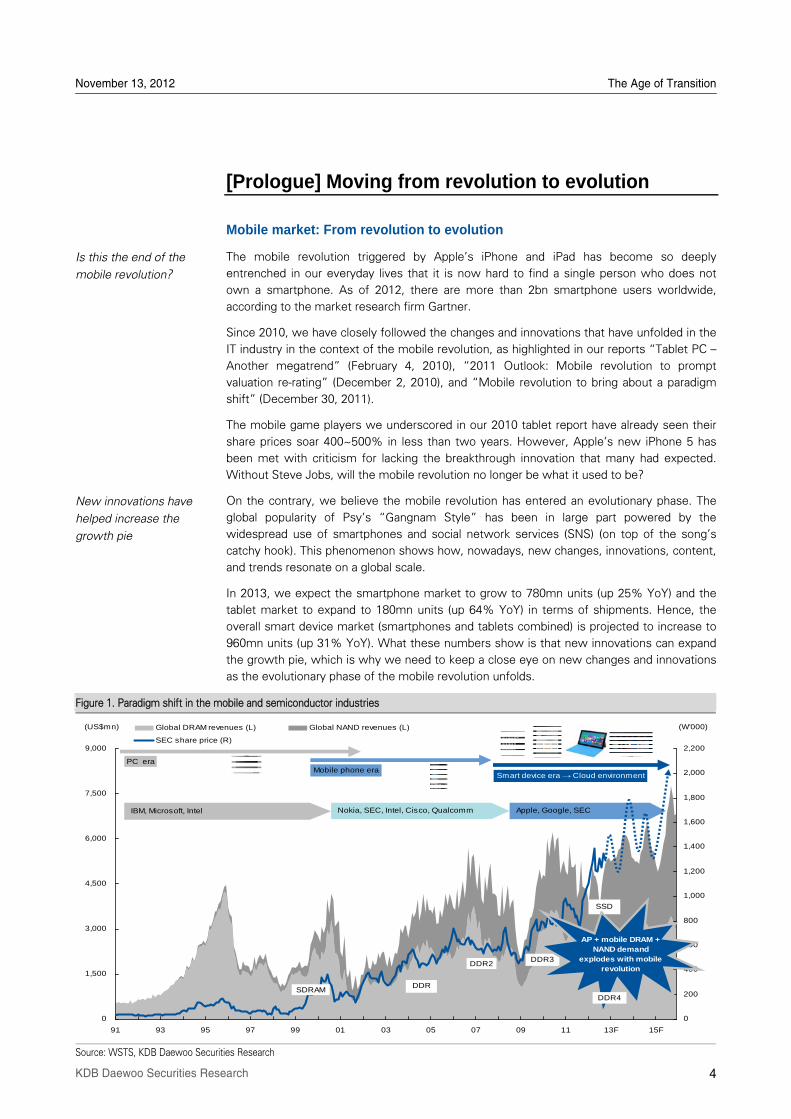

[Prologue] Moving from revolution to evolution

Mobile market: From revolution to evolution

The mobile revolution triggered by AppleÊs iPhone and iPad has become so deeply

entrenched in our everyday lives that it is now hard to find a single person who does not

own a smartphone. As of 2012, there are more than 2bn smartphone users worldwide,

according to the market research firm Gartner.

Since 2010, we have closely followed the changes and innovations that have unfolded in the

IT industry in the context of the mobile revolution, as highlighted in our reports „Tablet PC –

Another megatrend‰ (February 4, 2010), „2011 Outlook: Mobile revolution to prompt

valuation re-rating‰ (December 2, 2010), and „Mobile revolution to bring about a paradigm

shift‰ (December 30, 2011).

The mobile game players we underscored in our 2010 tablet report have already seen their

share prices soar 400~500% in less than two years. However, AppleÊs new iPhone 5 has

been met with criticism for lacking the breakthrough innovation that many had expected.

Without Steve Jobs, will the mobile revolution no longer be what it used to be?

On the contrary, we believe the mobile revolution has entered an evolutionary phase. The

global popularity of PsyÊs „Gangnam Style‰ has been in large part powered by the

widespread use of smartphones and social network services (SNS) (on top of the songÊs

catchy hook). This phenomenon shows how, nowadays, new changes, innovations, content,

and trends resonate on a global scale.

In 2013, we expect the smartphone market to grow to 780mn units (up 25% YoY) and the

tablet market to expand to 180mn units (up 64% YoY) in terms of shipments. Hence, the

overall smart device market (smartphones and tablets combined) is projected to increase to

960mn units (up 31% YoY). What these numbers show is that new innovations can expand

the growth pie, which is why we need to keep a close eye on new changes and innovations

as the evolutionary phase of the mobile revolution unfolds.

Figure 1. Paradigm shift in the mobile and semiconductor industries

Source: WSTS, KDB Daewoo Securities Research

Is this the end of the

mobile revolution?

New innovations have

helped increase the

growth pie

0

1,500

3,000

4,500

6,000

7,500

9,000

91 93 95 97 99 01 03 05 07 09 11 13F 15F

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Global DRAM revenues (L) Global NAND revenues (L)

SEC share price (R)

(US$mn) (W'000)

SDRAMDDR

DDR2DDR3

PC eraMobile phone era

Smart device era → Cloud environment

Apple, Google, SEC IBM, Microsoft, Intel Nokia, SEC, Intel, Cisco, Qualcomm

SSD

AP + mobile DRAM +NAND demand

explodes with mobilerevolution

DDR4

November 13, 2012 The Age of Transition

5 KDB Daewoo Securities Research

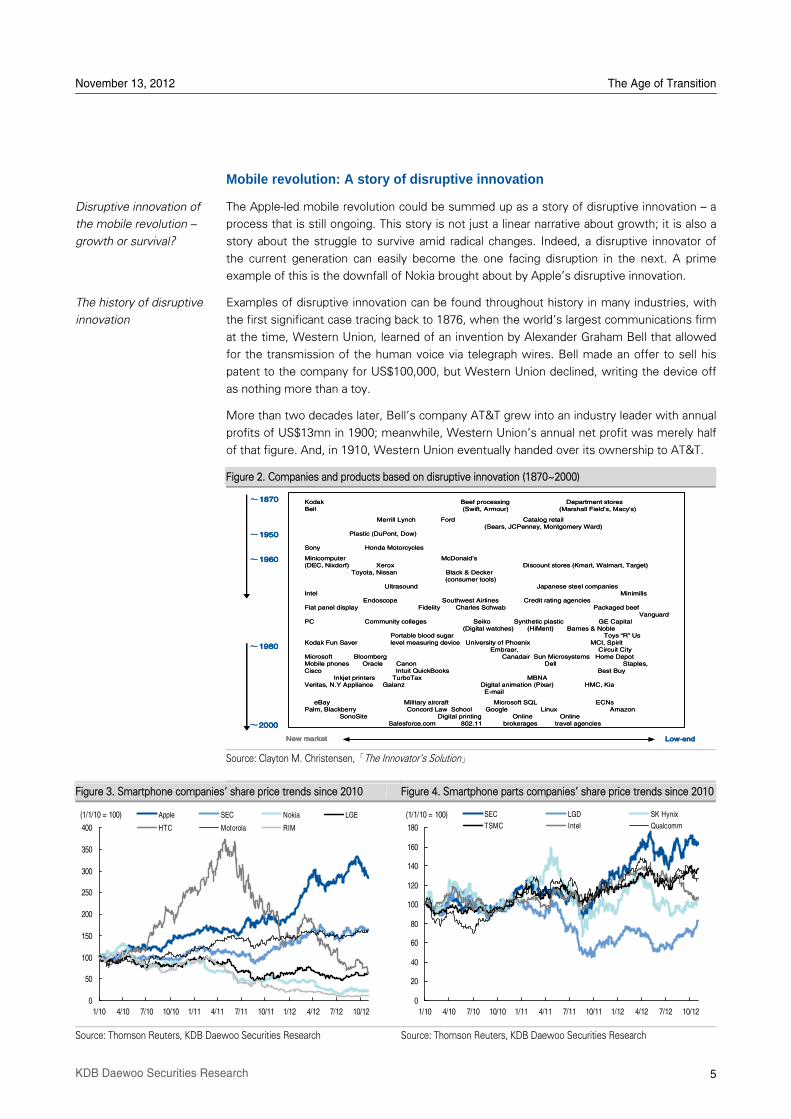

Mobile revolution: A story of disruptive innovation

The Apple-led mobile revolution could be summed up as a story of disruptive innovation – a

process that is still ongoing. This story is not just a linear narrative about growth; it is also a

story about the struggle to survive amid radical changes. Indeed, a disruptive innovator of

the current generation can easily become the one facing disruption in the next. A prime

example of this is the downfall of Nokia brought about by AppleÊs disruptive innovation.

Examples of disruptive innovation can be found throughout history in many industries, with

the first significant case tracing back to 1876, when the worldÊs largest communications firm

at the time, Western Union, learned of an invention by Alexander Graham Bell that allowed

for the transmission of the human voice via telegraph wires. Bell made an offer to sell his

patent to the company for US$100,000, but Western Union declined, writing the device off

as nothing more than a toy.

More than two decades later, BellÊs company AT&T grew into an industry leader with annual

profits of US$13mn in 1900; meanwhile, Western UnionÊs annual net profit was merely half

of that figure. And, in 1910, Western Union eventually handed over its ownership to AT&T.

Figure 2. Companies and products based on disruptive innovation (1870~2000)

Source: Clayton M. Christensen,「The InnovatorÊs Solution」

Figure 3. Smartphone companiesÊ share price trends since 2010 Figure 4. Smartphone parts companiesÊ share price trends since 2010

Source: Thomson Reuters, KDB Daewoo Securities Research Source: Thomson Reuters, KDB Daewoo Securities Research

Disruptive innovation of

the mobile revolution –

growth or survival?

The history of disruptive

innovation

0

50

100

150

200

250

300

350

400

1/10 4/10 7/10 10/10 1/11 4/11 7/11 10/11 1/12 4/12 7/12 10/12

Apple SEC Nokia LGE

HTC Motorola RIM

(1/1/10 = 100)

0

20

40

60

80

100

120

140

160

180

1/10 4/10 7/10 10/10 1/11 4/11 7/11 10/11 1/12 4/12 7/12 10/12

SEC LGD SK Hynix

TSMC Intel Qualcomm

(1/1/10 = 100)

Kodak Beef processing Department storesBell (Swift, Armour) (Marshall FieldÊs, Macy's)

Merrill Lynch Ford Catalog retail(Sears, JCPenney, Montgomery Ward)

Plastic (DuPont, Dow)

Sony Honda Motorcycles

Minicomputer McDonaldÊs (DEC, Nixdorf) Xerox Discount stores (Kmart, Walmart, Target)

Toyota, Nissan Black & Decker(consumer tools)

Ultrasound Japanese steel companiesIntel Minimills

Endoscope Southwest Airlines Credit rating agencies Flat panel display Fidelity Charles Schwab Packaged beef

VanguardPC Community colleges Seiko Synthetic plastic GE Capital

(Digital watches) (HiMent) Barnes & NoblePortable blood sugar Toys „R‰ Us

Kodak Fun Saver level measuring device University of Phoenix MCI, SpiritEmbraer, Circuit City

Microsoft Bloomberg Canadair Sun Microsystems Home DepotMobile phones Oracle Canon Dell Staples,Cisco Intuit QuickBooks Best Buy

Inkjet printers TurboTax MBNAVeritas, N.Y Appliance Galanz Digital animation (Pixar) HMC, Kia

eBay Military aircraft Microsoft SQL ECNsPalm, Blackberry Concord Law School Google Linux Amazon

SonoSite Digital printing Online OnlineSalesforce.com 802.11 brokerages travel agencies

New market Low-end

∼1870

∼1950

∼1960

∼1980

∼2000

Kodak Beef processing Department storesBell (Swift, Armour) (Marshall FieldÊs, Macy's)

Merrill Lynch Ford Catalog retail(Sears, JCPenney, Montgomery Ward)

Plastic (DuPont, Dow)

Sony Honda Motorcycles

Minicomputer McDonaldÊs (DEC, Nixdorf) Xerox Discount stores (Kmart, Walmart, Target)

Toyota, Nissan Black & Decker(consumer tools)

Ultrasound Japanese steel companiesIntel Minimills

Endoscope Southwest Airlines Credit rating agencies Flat panel display Fidelity Charles Schwab Packaged beef

VanguardPC Community colleges Seiko Synthetic plastic GE Capital

(Digital watches) (HiMent) Barnes & NoblePortable blood sugar Toys „R‰ Us

Kodak Fun Saver level measuring device University of Phoenix MCI, SpiritEmbraer, Circuit City

Microsoft Bloomberg Canadair Sun Microsystems Home DepotMobile phones Oracle Canon Dell Staples,Cisco Intuit QuickBooks Best Buy

Inkjet printers TurboTax MBNAVeritas, N.Y Appliance Galanz Digital animation (Pixar) HMC, Kia

eBay Military aircraft Microsoft SQL ECNsPalm, Blackberry Concord Law School Google Linux Amazon

SonoSite Digital printing Online OnlineSalesforce.com 802.11 brokerages travel agencies

New market Low-end

∼1870

∼1950

∼1960

∼1980

∼2000

November 13, 2012 The Age of Transition

6 KDB Daewoo Securities Research

Strategic decisions: Lessons from Intel of the 1980s

For disruptive innovation to be successful, it must be supported by strategic decision-making.

Here, we look at the key takeaways that SEC can learn from: 1) the disruptive innovation

that triggered the collapse of Nokia, which had ruled the global handset market from the late

1990s to the early 21st century; and 2) the strategic decision of Intel to move away from

memory products and into CPUs in the 1980s. We think the situation facing present-day SEC

share similarities to what Nokia went through in 1999 and Intel in 1980.

1) In 1999, Nokia overtook Motorola as the largest global handset supplier in the world. The Nokia

7110 was the first sliding phone the world had ever seen, the 3210 was the first mobile phone

equipped with an antenna, and the 8810 gained wide popularity among celebrities in the fashion

world. Compared to todayÊs smartphones, these models may appear outdated and archaic, but

they were nonetheless considered examples of disruptive innovation during their time.

In order to meet the diverse demand in the handset market, Nokia took both a tailored and

integrated approach, which allowed it to solidify its global expansion strategy. NokiaÊs past approach

has a lot in common with SECÊs present mass customization strategy. We highlight two points with

regard to NokiaÊs story: First, how did it manage to establish a dominant position in the handset

market? And, second, how was AppleÊs disruptive innovation able to bring down the company?

2) IntelÊs entry into the CPU market was a matter of coincidence. In 1970, a Japanese

electronics maker commissioned Intel to build a calculator chip, which eventually led to the

development of the 8080 processor in 1974. Then, IBM decided to outsource its CPU

production to Intel, deeming chip-making a non-core operation. This confluence of events

changed the course of IntelÊs future, as it led the company to decide to focus on CPUs. And

the stage was set for IntelÊs phenomenal growth in the CPU market.

SECÊs story is a lot like IntelÊs. In 1996, SEC embarked on a project with Digital Equipment

Corporation (DEC) to develop a 64bit Alpha chip. But when DEC, which had been bought by

Compaq, was sold again to Intel, the Alpha chip project was at risk of being shut down. In

the end, the technology SEC accumulated from the project made it possible for the company

to design and manufacture the AP for iPhones in 2007, thus setting the stage for its

remarkable success in the AP market.

Strategic decisions are what drive the dynamic evolution of a company. Professor Robert A.

Burgelman of Stanford University, a renowned expert in business strategy, stresses in his book

Strategy is Destiny that IntelÊs strategic decision was not made overnight and was rather the result

of its ability to co-evolve with the changing business environment. This co-evolution enabled Intel to

make the successful strategic decision to shift its business focus from memory to CPUs.

Figure 5. NokiaÊs innovative handset models released in 1999 Figure 6. Intel: Transition from memory to CPU

Source: Nokia Source: Robert A. Burgelman,「Strategy is Destiny」

Nokia became the top

global handset maker on

the back of disruptive

innovation

Intel grew into the

largest global CPU

maker on the back of

strategic decision-

making (and

coincidence)

Strategic decisions are

what drive dynamic

evolution: Now is the

time!

72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88

100

80

60

40

20

% of revenues

Microprocessor makerMemory chip maker

Microprocessor

Memory chips

Memory chip maker Microprocessor maker72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88

100

80

60

40

20

% of revenues

Microprocessor makerMemory chip maker

Microprocessor

Memory chips

Memory chip maker Microprocessor maker

November 13, 2012 The Age of Transition

7 KDB Daewoo Securities Research

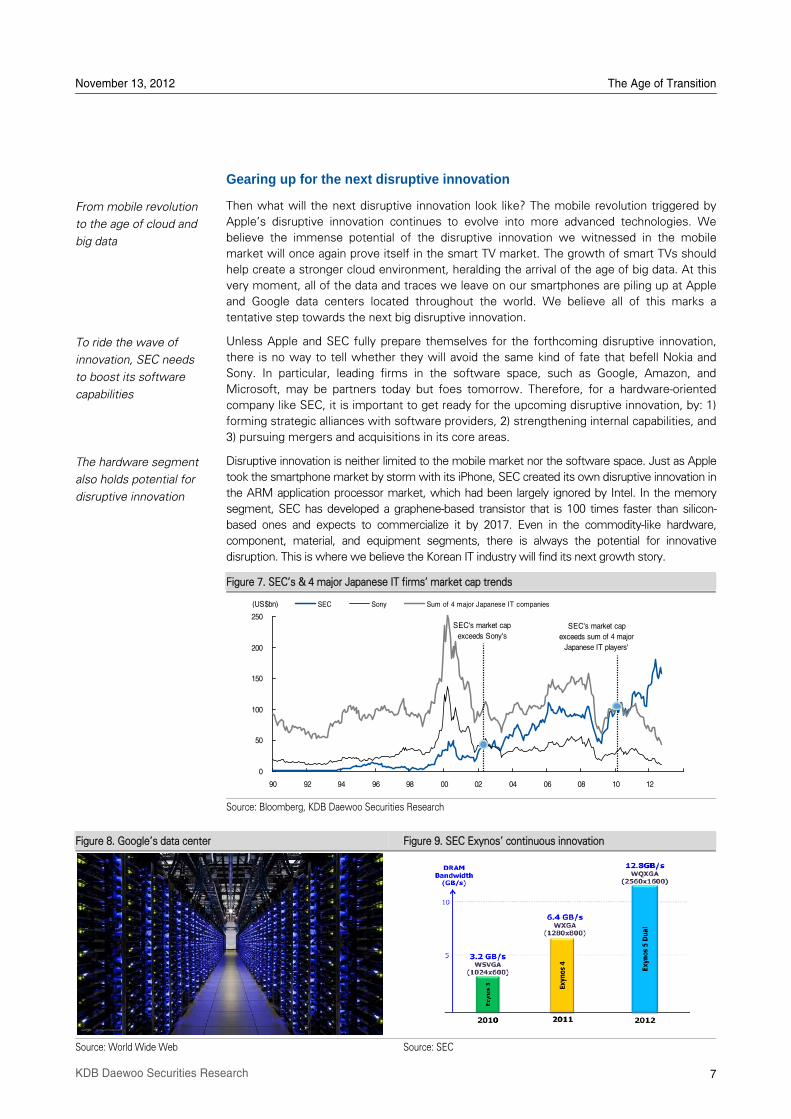

Gearing up for the next disruptive innovation

Then what will the next disruptive innovation look like? The mobile revolution triggered by

AppleÊs disruptive innovation continues to evolve into more advanced technologies. We

believe the immense potential of the disruptive innovation we witnessed in the mobile

market will once again prove itself in the smart TV market. The growth of smart TVs should

help create a stronger cloud environment, heralding the arrival of the age of big data. At this

very moment, all of the data and traces we leave on our smartphones are piling up at Apple

and Google data centers located throughout the world. We believe all of this marks a

tentative step towards the next big disruptive innovation.

Unless Apple and SEC fully prepare themselves for the forthcoming disruptive innovation,

there is no way to tell whether they will avoid the same kind of fate that befell Nokia and

Sony. In particular, leading firms in the software space, such as Google, Amazon, and

Microsoft, may be partners today but foes tomorrow. Therefore, for a hardware-oriented

company like SEC, it is important to get ready for the upcoming disruptive innovation, by: 1)

forming strategic alliances with software providers, 2) strengthening internal capabilities, and

3) pursuing mergers and acquisitions in its core areas.

Disruptive innovation is neither limited to the mobile market nor the software space. Just as Apple

took the smartphone market by storm with its iPhone, SEC created its own disruptive innovation in

the ARM application processor market, which had been largely ignored by Intel. In the memory

segment, SEC has developed a graphene-based transistor that is 100 times faster than silicon-

based ones and expects to commercialize it by 2017. Even in the commodity-like hardware,

component, material, and equipment segments, there is always the potential for innovative

disruption. This is where we believe the Korean IT industry will find its next growth story.

Figure 7. SECÊs & 4 major Japanese IT firmsÊ market cap trends

Source: Bloomberg, KDB Daewoo Securities Research

Figure 8. GoogleÊs data center Figure 9. SEC ExynosÊ continuous innovation

Source: World Wide Web Source: SEC

From mobile revolution

to the age of cloud and

big data

To ride the wave of

innovation, SEC needs

to boost its software

capabilities

The hardware segment

also holds potential for

disruptive innovation

0

50

100

150

200

250

90 92 94 96 98 00 02 04 06 08 10 12

SEC Sony Sum of 4 major Japanese IT companies

SEC's market cap

exceeds Sony's

SEC's market cap

exceeds sum of 4 major

Japanese IT players'

(US$bn)

November 13, 2012 The Age of Transition

8 KDB Daewoo Securities Research

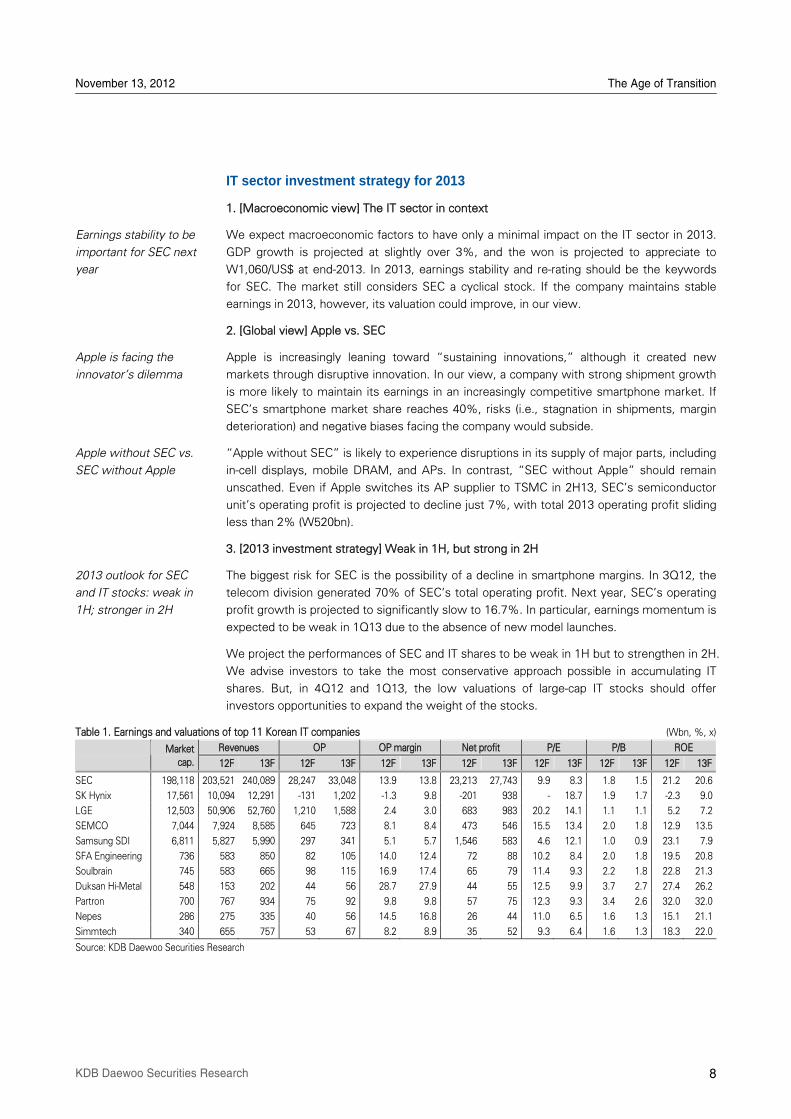

IT sector investment strategy for 2013

1. [Macroeconomic view] The IT sector in context

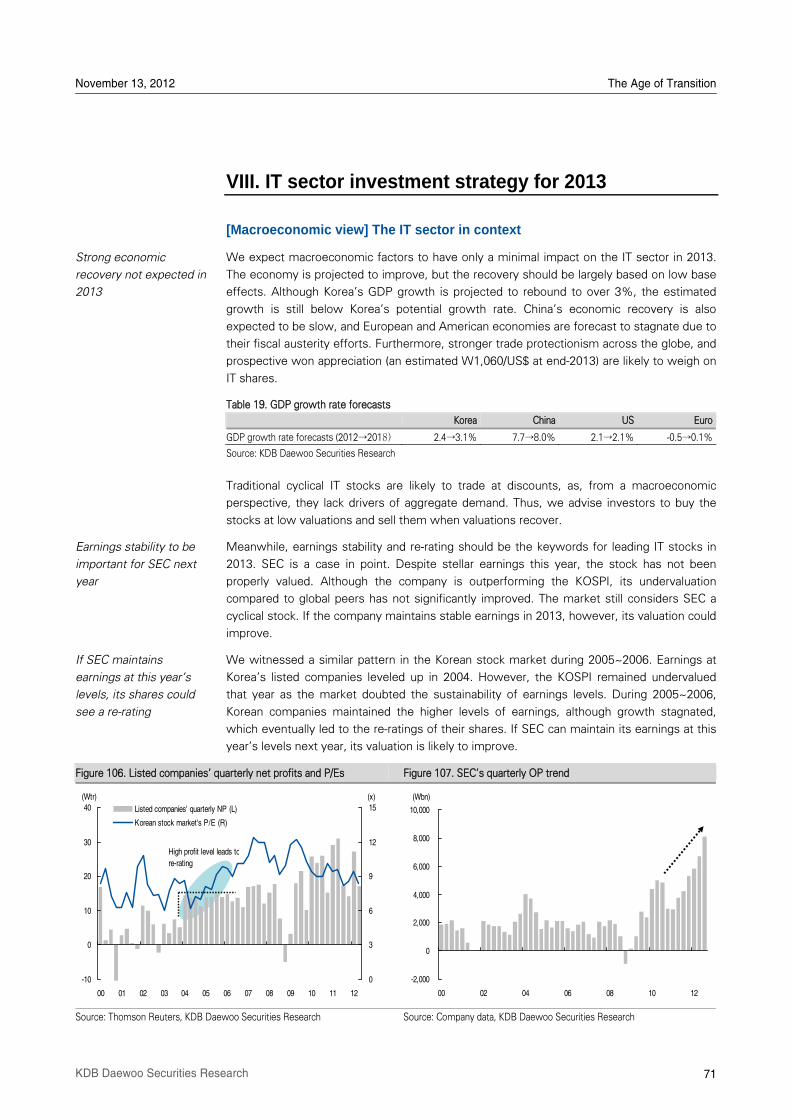

We expect macroeconomic factors to have only a minimal impact on the IT sector in 2013.

GDP growth is projected at slightly over 3%, and the won is projected to appreciate to

W1,060/US$ at end-2013. In 2013, earnings stability and re-rating should be the keywords

for SEC. The market still considers SEC a cyclical stock. If the company maintains stable

earnings in 2013, however, its valuation could improve, in our view.

2. [Global view] Apple vs. SEC

Apple is increasingly leaning toward „sustaining innovations,‰ although it created new

markets through disruptive innovation. In our view, a company with strong shipment growth

is more likely to maintain its earnings in an increasingly competitive smartphone market. If

SECÊs smartphone market share reaches 40%, risks (i.e., stagnation in shipments, margin

deterioration) and negative biases facing the company would subside.

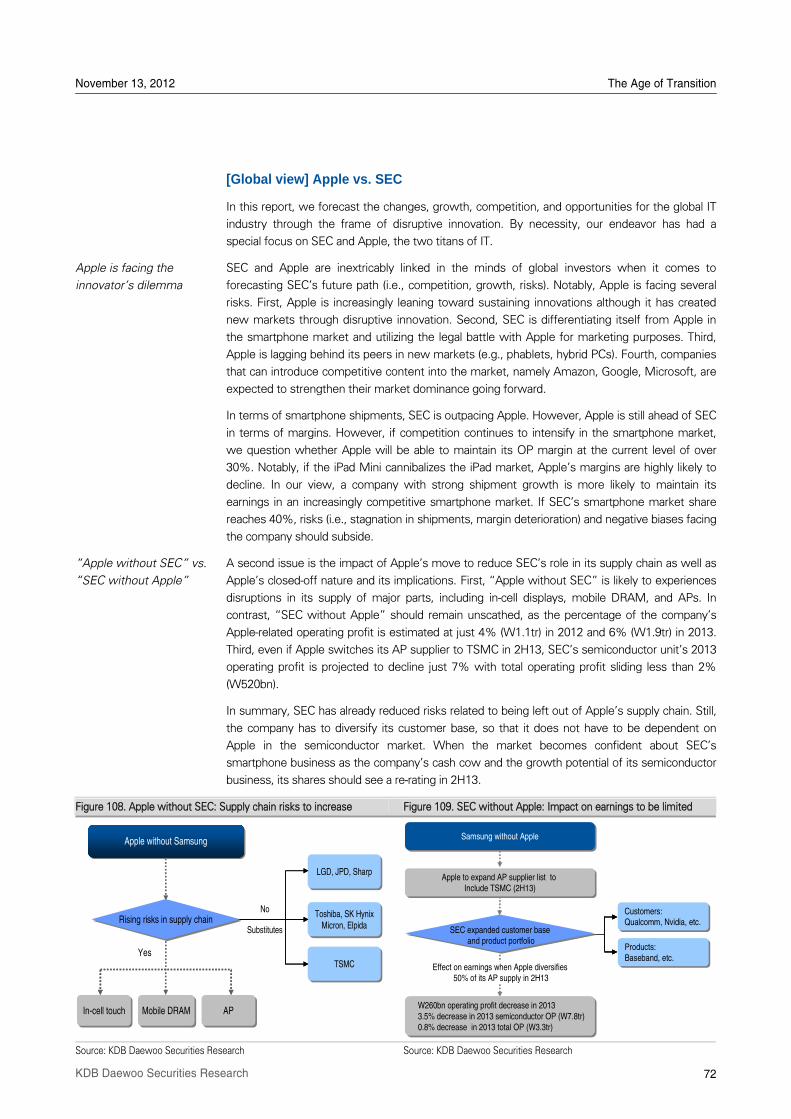

„Apple without SEC‰ is likely to experience disruptions in its supply of major parts, including

in-cell displays, mobile DRAM, and APs. In contrast, „SEC without Apple‰ should remain

unscathed. Even if Apple switches its AP supplier to TSMC in 2H13, SECÊs semiconductor

unitÊs operating profit is projected to decline just 7%, with total 2013 operating profit sliding

less than 2% (W520bn).

3. [2013 investment strategy] Weak in 1H, but strong in 2H

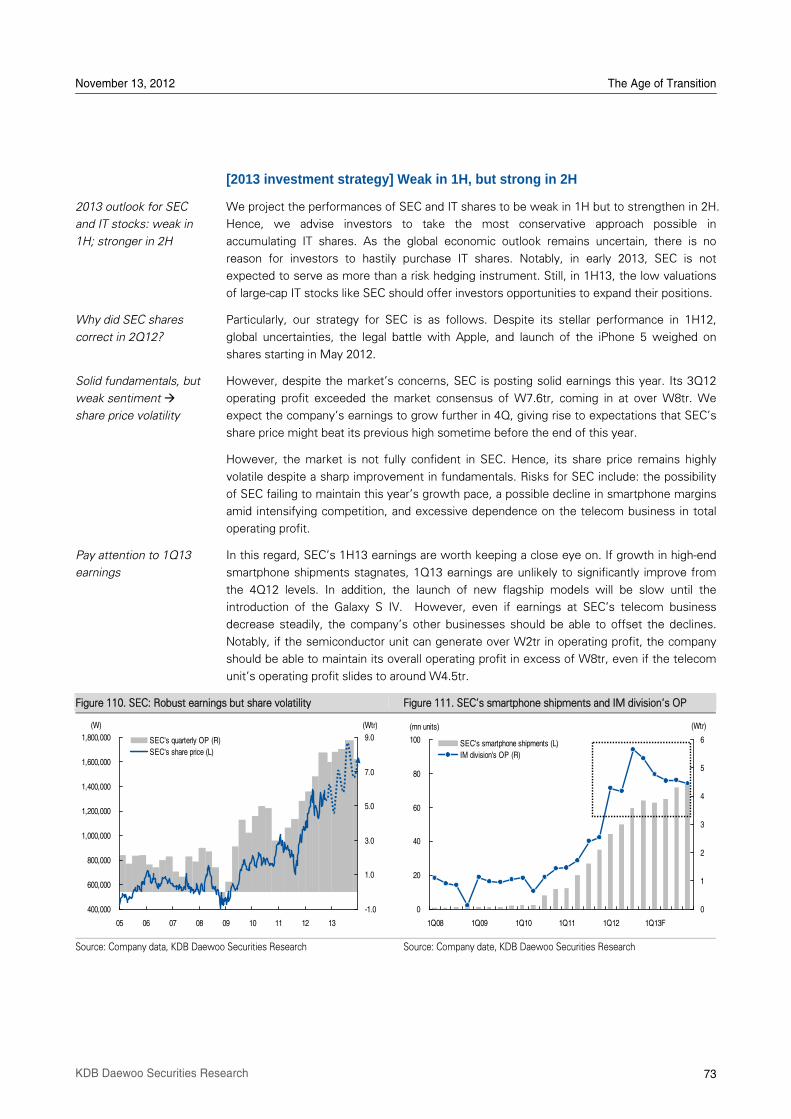

The biggest risk for SEC is the possibility of a decline in smartphone margins. In 3Q12, the

telecom division generated 70% of SECÊs total operating profit. Next year, SECÊs operating

profit growth is projected to significantly slow to 16.7%. In particular, earnings momentum is

expected to be weak in 1Q13 due to the absence of new model launches.

We project the performances of SEC and IT shares to be weak in 1H but to strengthen in 2H.

We advise investors to take the most conservative approach possible in accumulating IT

shares. But, in 4Q12 and 1Q13, the low valuations of large-cap IT stocks should offer

investors opportunities to expand the weight of the stocks.

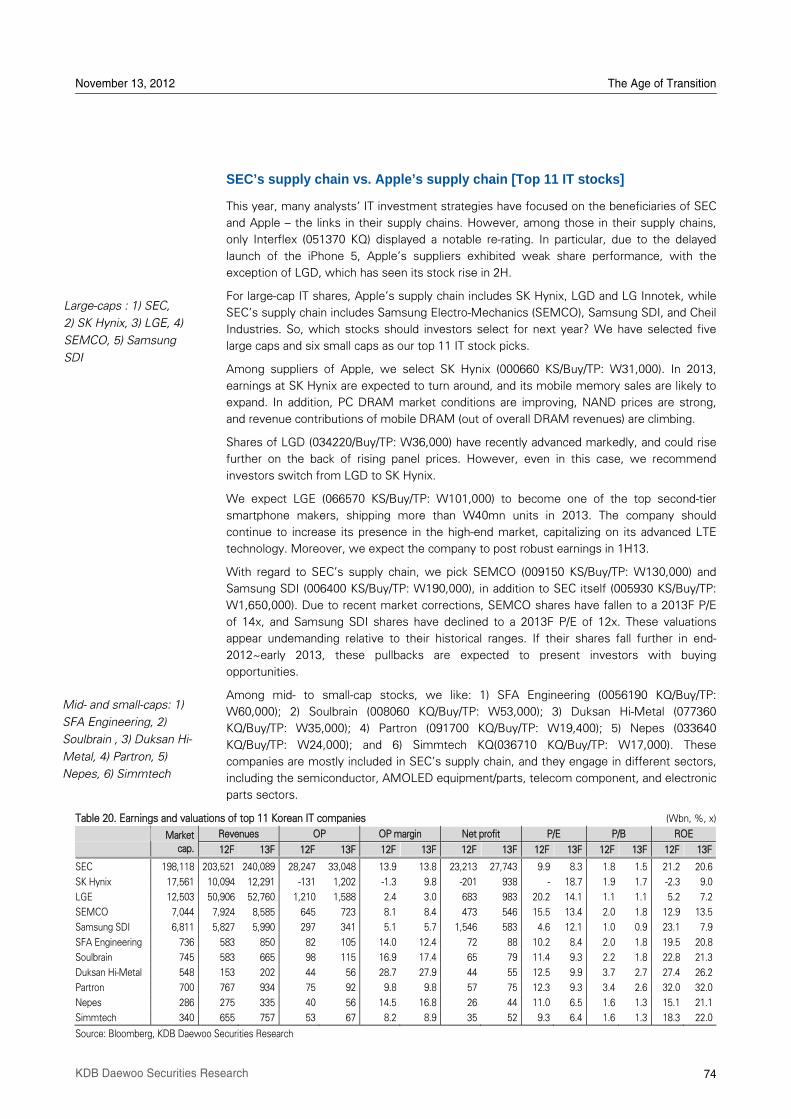

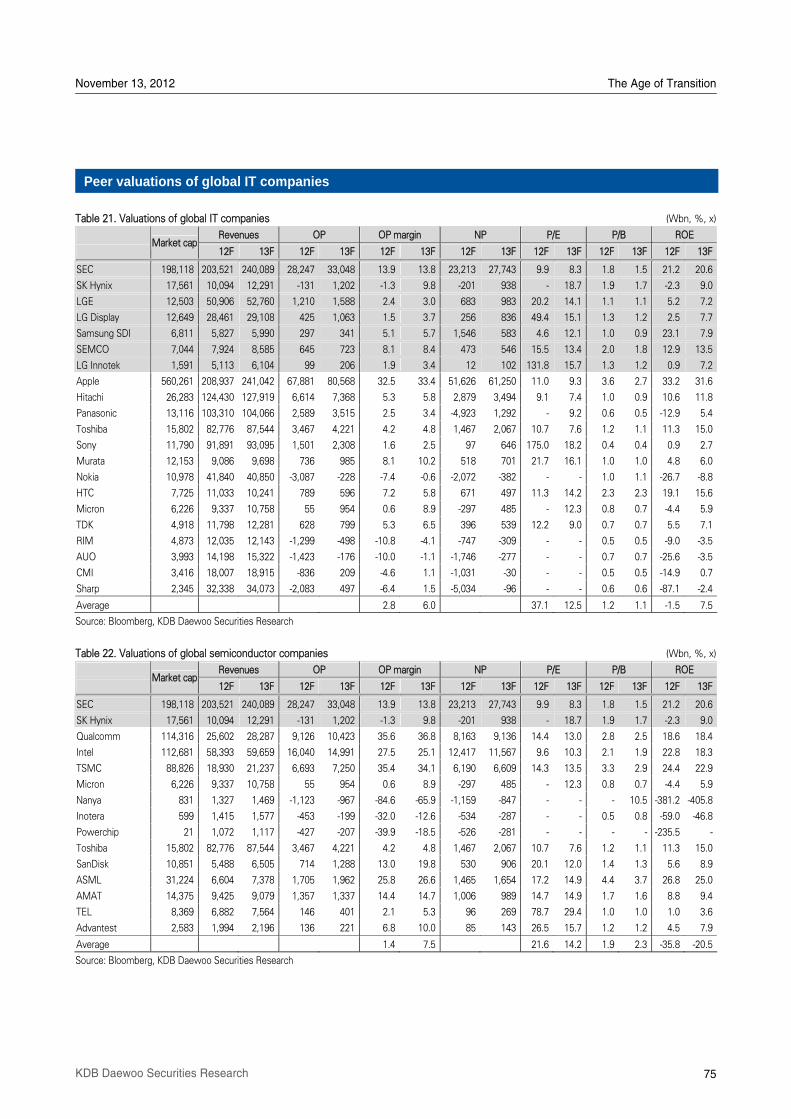

Table 1. Earnings and valuations of top 11 Korean IT companies (Wbn, %, x)

Revenues OP OP margin Net profit P/E P/B ROE

Market

cap. 12F 13F 12F 13F 12F 13F 12F 13F 12F 13F 12F 13F 12F 13F

SEC 198,118 203,521 240,089 28,247 33,048 13.9 13.8 23,213 27,743 9.9 8.3 1.8 1.5 21.2 20.6

SK Hynix 17,561 10,094 12,291 -131 1,202 -1.3 9.8 -201 938 - 18.7 1.9 1.7 -2.3 9.0

LGE 12,503 50,906 52,760 1,210 1,588 2.4 3.0 683 983 20.2 14.1 1.1 1.1 5.2 7.2

SEMCO 7,044 7,924 8,585 645 723 8.1 8.4 473 546 15.5 13.4 2.0 1.8 12.9 13.5

Samsung SDI 6,811 5,827 5,990 297 341 5.1 5.7 1,546 583 4.6 12.1 1.0 0.9 23.1 7.9

SFA Engineering 736 583 850 82 105 14.0 12.4 72 88 10.2 8.4 2.0 1.8 19.5 20.8

Soulbrain 745 583 665 98 115 16.9 17.4 65 79 11.4 9.3 2.2 1.8 22.8 21.3

Duksan Hi-Metal 548 153 202 44 56 28.7 27.9 44 55 12.5 9.9 3.7 2.7 27.4 26.2

Partron 700 767 934 75 92 9.8 9.8 57 75 12.3 9.3 3.4 2.6 32.0 32.0

Nepes 286 275 335 40 56 14.5 16.8 26 44 11.0 6.5 1.6 1.3 15.1 21.1

Simmtech 340 655 757 53 67 8.2 8.9 35 52 9.3 6.4 1.6 1.3 18.3 22.0

Source: KDB Daewoo Securities Research

Earnings stability to be

important for SEC next

year

Apple is facing the

innovatorÊs dilemma

Apple without SEC vs.

SEC without Apple

2013 outlook for SEC

and IT stocks: weak in

1H; stronger in 2H

November 13, 2012 The Age of Transition

9 KDB Daewoo Securities Research

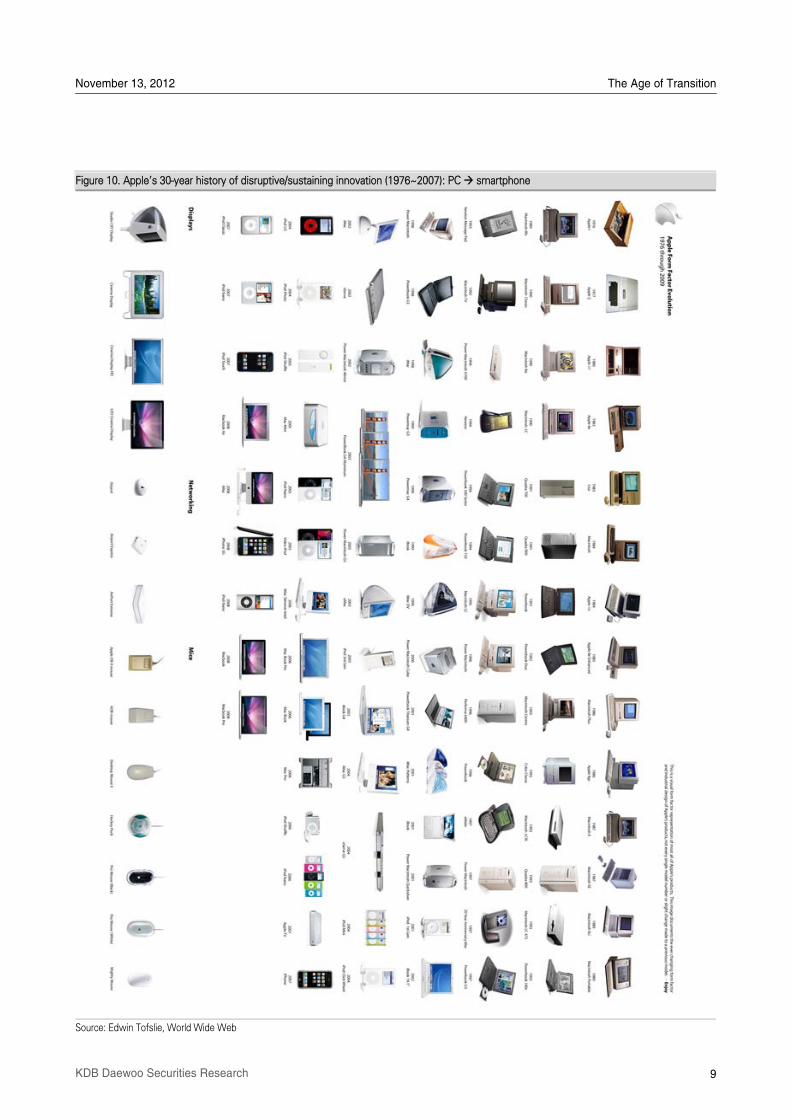

Figure 10. AppleÊs 30-year history of disruptive/sustaining innovation (1976~2007): PC smartphone

Source: Edwin Tofslie, World Wide Web

November 13, 2012 The Age of Transition

10 KDB Daewoo Securities Research

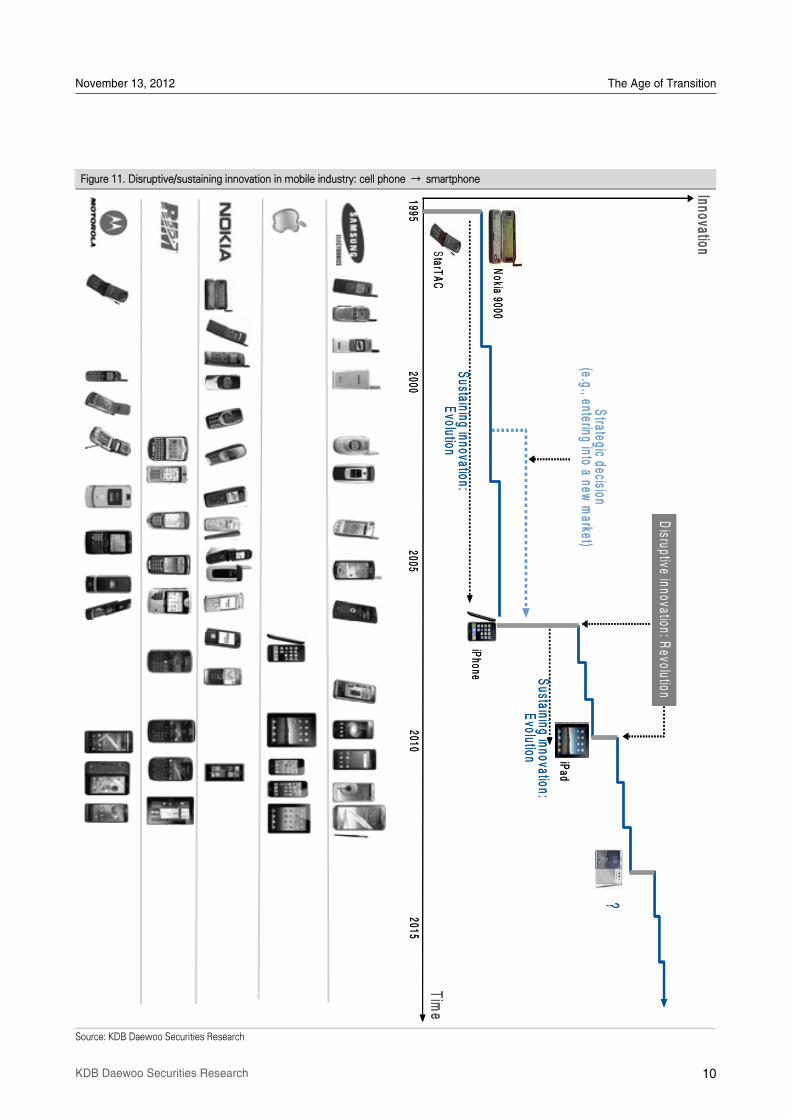

Figure 11. Disruptive/sustaining innovation in mobile industry: cell phone → smartphone

Source: KDB Daewoo Securities Research

Strategic decision

(e.g., entering into a new m

arket)

Sustaining innovation:

Evolution

Sustaining innovation:

Evolution

Innovation

20002010

20051995

iPad

iPhone

Nokia 9000

StarT

AC

?

2015

Time

Disruptive innovation: R

evolution

Strategic decision

(e.g., entering into a new m

arket)

Sustaining innovation:

Evolution

Sustaining innovation:

Evolution

Innovation

20002010

20051995

iPad

iPhone

Nokia 9000

StarT

AC

?

2015

Time

Disruptive innovation: R

evolution

11 KDB Daewoo Securities Research

I Apple: The Innovator’s Dilemma

While Apple has been preoccupied with „sustaining innovations,‰ other new markets have

been gaining ground in the smart device world: namely: 1) 5~7-inch smart devices called

„phablets‰ and 2) smart PCs, otherwise referred to as hybrid PCs. Amazon and Google are

already making their mark in the 7-inch phablet market with the releases of the Kindle Fire

and the Nexus 7. In particular, AmazonÊs robust content offerings have made the company a

serious competitive threat.

While Amazon, Google, and Microsoft are sweeping into the tablet PC market, the new iPad

is increasingly losing its appeal to consumers. Will the iPad Mini be received differently, or

will it just signal AppleÊs fall from market visionary to copycat and/or follower? Although we

do not yet have an answer, one thing seems clear: Apple is facing the innovatorÊs dilemma.

November 13, 2012 The Age of Transition

12 KDB Daewoo Securities Research

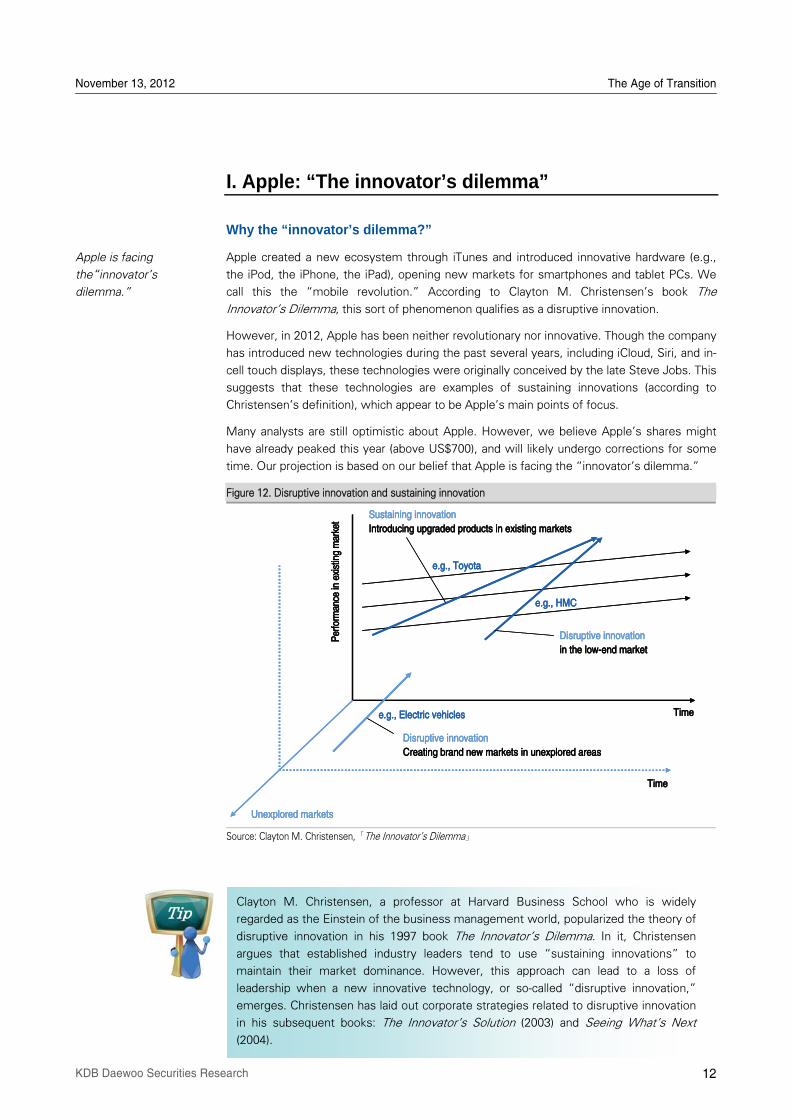

I. Apple: “The innovator’s dilemma”

Why the “innovator’s dilemma?”

Apple created a new ecosystem through iTunes and introduced innovative hardware (e.g.,

the iPod, the iPhone, the iPad), opening new markets for smartphones and tablet PCs. We

call this the „mobile revolution.‰ According to Clayton M. ChristensenÊs book The

InnovatorÊs Dilemma, this sort of phenomenon qualifies as a disruptive innovation.

However, in 2012, Apple has been neither revolutionary nor innovative. Though the company

has introduced new technologies during the past several years, including iCloud, Siri, and in-

cell touch displays, these technologies were originally conceived by the late Steve Jobs. This

suggests that these technologies are examples of sustaining innovations (according to

ChristensenÊs definition), which appear to be AppleÊs main points of focus.

Many analysts are still optimistic about Apple. However, we believe AppleÊs shares might

have already peaked this year (above US$700), and will likely undergo corrections for some

time. Our projection is based on our belief that Apple is facing the „innovatorÊs dilemma.‰

Figure 12. Disruptive innovation and sustaining innovation

Source: Clayton M. Christensen,「The InnovatorÊs Dilemma」

Apple is facing

the„innovatorÊs

dilemma.‰

Clayton M. Christensen, a professor at Harvard Business School who is widely

regarded as the Einstein of the business management world, popularized the theory of

disruptive innovation in his 1997 book The InnovatorÊs Dilemma. In it, Christensen

argues that established industry leaders tend to use „sustaining innovations‰ to

maintain their market dominance. However, this approach can lead to a loss of

leadership when a new innovative technology, or so-called „disruptive innovation,‰

emerges. Christensen has laid out corporate strategies related to disruptive innovation

in his subsequent books: The InnovatorÊs Solution (2003) and Seeing WhatÊs Next

(2004).

Disruptive innovation

Creating brand new markets in unexplored areas

e.g., Electric vehicles

Unexplored markets

Per

form

ance

in e

xist

ing

mar

ket

e.g., Toyota

e.g., HMC

Disruptive innovation

in the low-end market

Time

Time

Sustaining innovation

Introducing upgraded products in existing markets

Disruptive innovation

Creating brand new markets in unexplored areas

e.g., Electric vehicles

Unexplored markets

Per

form

ance

in e

xist

ing

mar

ket

e.g., Toyota

e.g., HMC

Disruptive innovation

in the low-end market

Time

Time

Sustaining innovation

Introducing upgraded products in existing markets

November 13, 2012 The Age of Transition

13 KDB Daewoo Securities Research

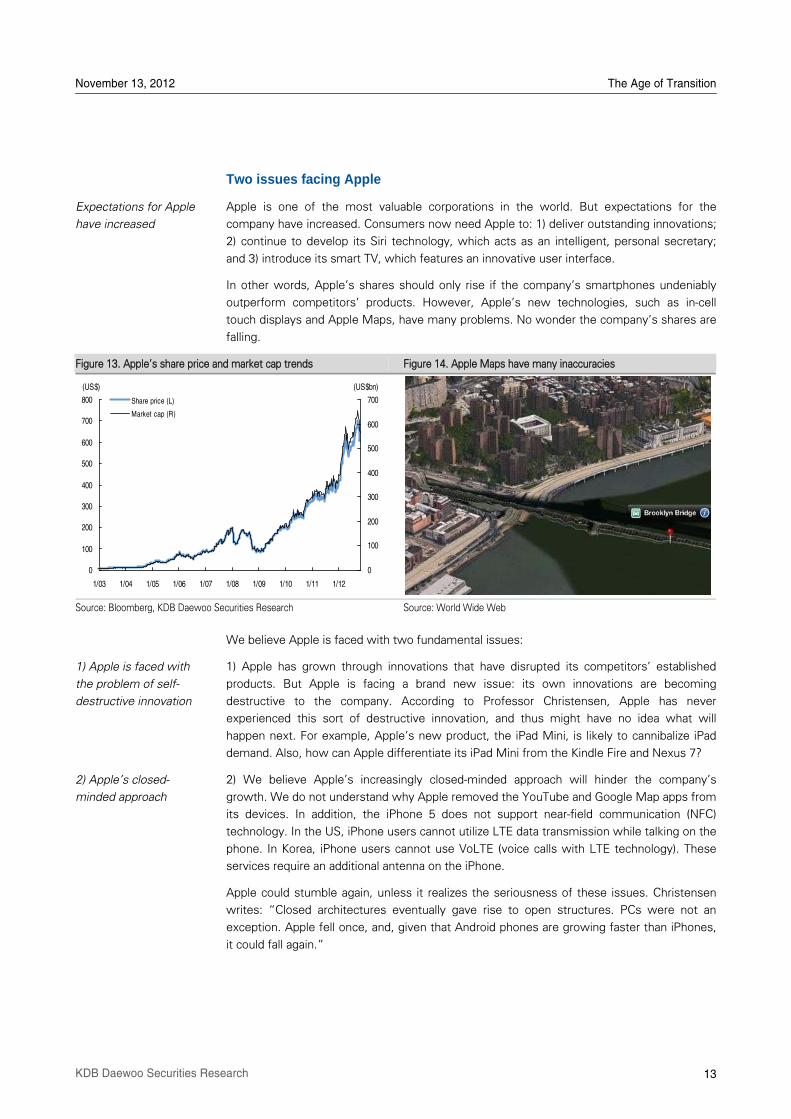

Two issues facing Apple

Apple is one of the most valuable corporations in the world. But expectations for the

company have increased. Consumers now need Apple to: 1) deliver outstanding innovations;

2) continue to develop its Siri technology, which acts as an intelligent, personal secretary;

and 3) introduce its smart TV, which features an innovative user interface.

In other words, AppleÊs shares should only rise if the companyÊs smartphones undeniably

outperform competitorsÊ products. However, AppleÊs new technologies, such as in-cell

touch displays and Apple Maps, have many problems. No wonder the companyÊs shares are

falling.

Figure 13. AppleÊs share price and market cap trends Figure 14. Apple Maps have many inaccuracies

Source: Bloomberg, KDB Daewoo Securities Research Source: World Wide Web

We believe Apple is faced with two fundamental issues:

1) Apple has grown through innovations that have disrupted its competitorsÊ established

products. But Apple is facing a brand new issue: its own innovations are becoming

destructive to the company. According to Professor Christensen, Apple has never

experienced this sort of destructive innovation, and thus might have no idea what will

happen next. For example, AppleÊs new product, the iPad Mini, is likely to cannibalize iPad

demand. Also, how can Apple differentiate its iPad Mini from the Kindle Fire and Nexus 7?

2) We believe AppleÊs increasingly closed-minded approach will hinder the companyÊs

growth. We do not understand why Apple removed the YouTube and Google Map apps from

its devices. In addition, the iPhone 5 does not support near-field communication (NFC)

technology. In the US, iPhone users cannot utilize LTE data transmission while talking on the

phone. In Korea, iPhone users cannot use VoLTE (voice calls with LTE technology). These

services require an additional antenna on the iPhone.

Apple could stumble again, unless it realizes the seriousness of these issues. Christensen

writes: „Closed architectures eventually gave rise to open structures. PCs were not an

exception. Apple fell once, and, given that Android phones are growing faster than iPhones,

it could fall again.‰

Expectations for Apple

have increased

1) Apple is faced with

the problem of self-

destructive innovation

2) AppleÊs closed-

minded approach

0

100

200

300

400

500

600

700

800

1/03 1/04 1/05 1/06 1/07 1/08 1/09 1/10 1/11 1/12

0

100

200

300

400

500

600

700Share price (L)

Market cap (R)

(US$) (US$bn)

November 13, 2012 The Age of Transition

14 KDB Daewoo Securities Research

Growth of new smart devices

While Apple has been preoccupied with sustaining innovations, other new markets have

been gaining ground in the smart device world: namely 1) 5~7-inch smart devices called

phablets and 2) smart PCs, otherwise referred to as hybrid PCs. Amazon and Google are

already making their mark in the 7-inch market with the release of their respective products,

the Kindle Fire and the Nexus 7. In particular, AmazonÊs robust content offerings have made

the company a serious competitive threat.

What is worth noting is that both of the aforementioned markets have effectively

incorporated features that have been largely ignored by Apple: For example, SECÊs

introduction of stylus functionality in its Galaxy Note phablet, and the integration of

keyboards in MicrosoftÊs Surface and SECÊs ATIV hybrid PCs. And, as for operating systems,

Microsoft has been pushing Windows 8 in both markets.

It seems almost as if Apple was predestined to strip away the stylus and the keyboard from its

smart devices in order to launch the multi-touch market. In the words of Steve Jobs, „We have

been very lucky to have brought a few revolutionary user interfaces to the market in our time.

First was the mouse. The second was the click wheel. And, now, we're going to bring multi-

touch to the market. And each of these revolutionary interfaces has made possible a

revolutionary product: the Mac, the iPod and now the iPhone‰

But arenÊt the stylus and the keyboard indispensable parts of our history? In fact, they may

have been more groundbreaking than the multi-touch panel.

Figure 15. The creation of the phablet and smart PC markets

Source: KDB Daewoo Securities Research

Figure 16. Content driving AmazonÊs tablet market share expansion Figure 17. SECÊs ATIV series

Source: World Wide Web Source: World Wide Web

Phablets and smart PCs:

Newly emerging

markets

The stylus and keyboard,

features largely

bypassed by Apple, have

been successfully

introduced

Smartphone3.0~5.0‰

Tablet PC7.0~10.0‰

Notebook PC10.0~15.0‰

Smart/hybrid PC(keyboard)

Phablet5.0~7.0‰(stylus)

Smartphone3.0~5.0‰

Tablet PC7.0~10.0‰

Notebook PC10.0~15.0‰

Smart/hybrid PC(keyboard)

Phablet5.0~7.0‰(stylus)

November 13, 2012 The Age of Transition

15 KDB Daewoo Securities Research

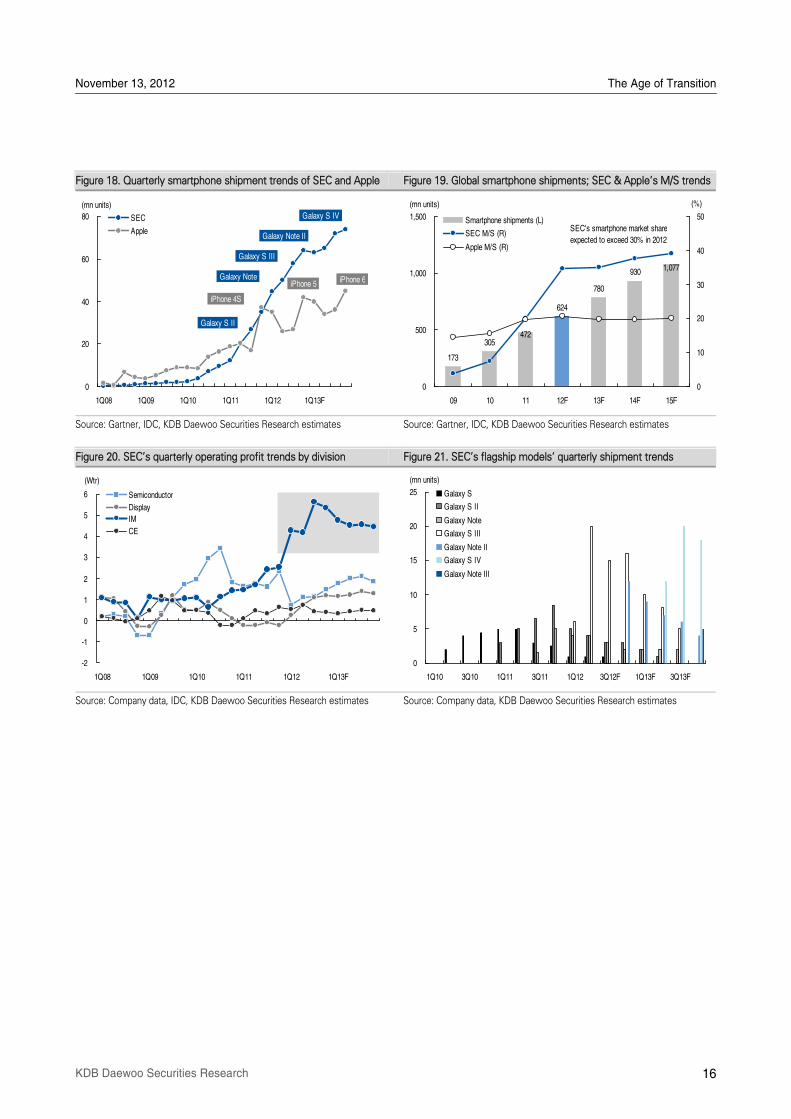

SEC’s differentiated smartphone lineup

The strategic differences between SEC and Apple have become pronounced in 2012. Given

that smartphone demand is projected to increase by 33% YoY this year, SECÊs differentiated

strategy of diversification will likely stand out.

Early this year, we believed that competition between SEC and Apple would be

characterized simply by a battle between the Galaxy S III and the iPhone 5. However, SEC

has moved more quickly than expected following its launch of the Galaxy Note, establishing

a high-end smartphone lineup of the Galaxy Note, Galaxy S III, and Galaxy Note II. If SEC

releases the Galaxy S IV early next year, the company will establish a track record of rolling

out new models every one or two quarters.

In comparison, AppleÊs strategy of launching a new model only once a year seems to be

causing the company to lag behind smartphone demand growth. The launch of the iPhone 5

should be too late despite consumersÊ desire to see a new iPhone model as soon as

possible. This strategic difference has led to SECÊs recent overwhelming edge in

smartphone shipments.

Some Investors believe that the launch of the iPhone 5 will dent Galaxy S III sales. However,

we believe that the sales volume of the Galaxy S III will not plunge on the rollout of the new

iPhone model, as the innovations that the Galaxy S III features are different from those of

the iPhone 5. Consumers who think that a four-inch screen is the greatest downside to the

iPhone are unlikely to buy the iPhone 5.

Diversification: SECÊs

strategic differentiation

AppleÊs new product

launch strategy is not

keeping up with

smartphone demand

growth

The innovations that the

Galaxy S III features are

different from those of

the iPhone 5

November 13, 2012 The Age of Transition

16 KDB Daewoo Securities Research

Figure 18. Quarterly smartphone shipment trends of SEC and Apple Figure 19. Global smartphone shipments; SEC & AppleÊs M/S trends

Source: Gartner, IDC, KDB Daewoo Securities Research estimates Source: Gartner, IDC, KDB Daewoo Securities Research estimates

Figure 20. SECÊs quarterly operating profit trends by division Figure 21. SECÊs flagship modelsÊ quarterly shipment trends

Source: Company data, IDC, KDB Daewoo Securities Research estimates Source: Company data, KDB Daewoo Securities Research estimates

0

5

10

15

20

25

1Q10 3Q10 1Q11 3Q11 1Q12 3Q12F 1Q13F 3Q13F

Galaxy S

Galaxy S II

Galaxy Note

Galaxy S III

Galaxy Note II

Galaxy S IV

Galaxy Note III

(mn units)

0

20

40

60

80

1Q08 1Q09 1Q10 1Q11 1Q12 1Q13F

SEC

Apple

(mn units)

iPhone 4S

Galaxy Note

Galaxy S II

Galaxy S III

iPhone 5

Galaxy Note II

Galaxy S IV

iPhone 6

173

305

780

930

472

624

1,077

0

500

1,000

1,500

09 10 11 12F 13F 14F 15F

0

10

20

30

40

50Smartphone shipments (L)

SEC M/S (R)

Apple M/S (R)

(mn units) (%)

SEC's smartphone market share

expected to exceed 30% in 2012

-2

-1

0

1

2

3

4

5

6

1Q08 1Q09 1Q10 1Q11 1Q12 1Q13F

(Wtr)

Semiconductor

Display

IM

CE

November 13, 2012 The Age of Transition

17 KDB Daewoo Securities Research

SEC: “It doesn’t take a genius”

The patent lawsuit between Apple and SEC resulted in a landslide victory for Apple in San

Jose. The final ruling is expected to be handed down in 4Q, and the fight is likely to continue

in the US Court of Appeals for the Federal Circuit. So, does this mean that SEC will never be

able to catch up to their Cupertino-based rival? Will consumers think that SECÊs products are

copycats and become unwilling to buy them?

This type of lawsuit surely presents a risk for SEC. Still, we need to take a look at the flip

side of the coin, especially in terms of marketing. Furthermore, we could raise the question:

„Is it better to be a copycat or Nokia?‰

In the face of disruptive innovation (driven by Apple), Nokia lost its long-held global

dominance of the handset market to Apple and SEC. Furthermore, SEC not only overtook

Nokia, but also surpassed Apple in terms of shipments. This success proves that SEC made

the right strategic choices, despite risking being called a copycat.

Although Apple won its US patent lawsuit against SEC, its new iPhone model appears to

have fallen short of customer expectations in terms of innovation. So, does this mean that

Apple is doomed without Steve Jobs? Or that a genius has been surpassed by a copycat?

Although SEC lost the patent suit, we believe that the company is turning lemons into

lemonade (in terms of marketing).

Going forward, SEC will be able to use Windows 8 to strengthen its case that it is not a

copycat and use LTE technology to attack Apple.

“It doesn’t take a genius.

The Next Big Thing Is Already Here”

The advertisement to the right, which

SEC started to run in the US market

immediately after losing the

aforementioned patent lawsuit, created a

huge sensation. By emphasizing the

innovative features of the Galaxy S III, the

company is making a strong appeal to

non-Apple users.

Thus, the unfavorable ruling may have a

silver lining, especially with regard to

marketing. By paying W1tr in damages

now, the company may have a chance to

earn W10tr in the future.

Copycat or Nokia?

SEC will use LTE

technology as a weapon

against Apple

November 13, 2012 The Age of Transition

18 KDB Daewoo Securities Research

Innovation from content producers

„Demand is an unusual form of energy that turns many wheels from big to small, from

economies to markets to organizations to our paychecks, here and around the world.

Everything depends on it. Without it, growth slows, economies falter, progress stops.‰

--Adrian J. Slyworzky, Demand

In his book Demand, Adrian J. Slyworzky examined six factors that lead to the creation of

demand: 1) magnetic offers, 2) a hassle map (and its resolution), 3) a back story, 4) a trigger,

5) a trajectory, and 6) variation.

Take Apple, for example. The tablet PC market was spawned by AppleÊs disruptive

innovation, the iPad. Although several tablet PC models had preceded the iPad, it was not

until the release of AppleÊs version that the market, and an accompanying ecosystem,

actually emerged. Based on its ecosystem, Apple could build a differentiated user interface

and hardware. And, importantly, all of the six aforementioned factors necessary for demand

creation were present during the iPadÊs rise.

However, while Apple was resting on its laurels, content providers stepped in and started to

drive innovation.

Jeff Bezos claims that AmazonÊs new Kindle Fire, priced at US$119, is a service, not a

product. AmazonÊs Kindle and GoogleÊs Nexus 7 have: 1) magnetic offers and backstories

(rich content), 2) triggers (reasonable prices), and 3) variation (7-inch screens). MicrosoftÊs

Surface resolved a hassle map problem (e.g., inconveniences arising from the lack of a

keyboard) and also has a trigger (Windows 8) and a backstory (Microsoft Office).

As mentioned earlier, Clayton Christensen warned of the risk of the innovatorÊs dilemma,

saying that a disruptor of one decade could become a disruptee in the following one. Steve

Jobs also emphasized the need to constantly innovate to tackle this issue.

Indeed, while Amazon, Google, and Microsoft are sweeping into the tablet PC market, the

new iPad is increasingly losing its appeal to consumers. Will the iPad Mini become a

variation, or just signal AppleÊs fall from market visionary to copycat and/or follower?

Although we do not yet have an answer, one thing seems clear: Apple is facing the

innovatorÊs dilemma.

Where does demand

come from?

Creating a legend

through disruptive

innovation

Content makers have

emerged as new

innovation drivers

November 13, 2012 The Age of Transition

19 KDB Daewoo Securities Research

Figure 22. How does the creation of new demand begin?

Source: Adrian J. Slyworzky「Demand」

Figure 23. Demand creation by content companies

Source: KDB Daewoo Securities Research

Content provider Google Amazon Microsoft

Product Nexus 7 Kindle Fire Surface

Magnetic: Sensitivity, performance v v v

Hassle map: Solutions for problems v

Backstory: Infrastructure, ecosystem v v v

Trigger: Creation of demand v

Trajectory: Quality improvement v v

Variation: Various needs v v v

DemandDemand

MagneticMagnetic

Hassle mapHassle map

BackstoryBackstory

VariationVariation

TrajectoryTrajectory

TriggerTrigger

Combination of strong performance and sensitivity

CustomerÊs troubles can present attractive opportunities to those who create new demand

External factors that make a product more attractive(e.g., Infrastructure, ecosystem)

Something that turns spectators into customers

(e.g., personal experience, quick delivery)

How quickly the attractiveness of a product improves(e.g., via ontinuous quality improvement)

Breaking the illusion of „the average customer‰ with products that can meet customersÊ needs exactly

20 KDB Daewoo Securities Research

II Global Supply Chain Reshuffle

Although Apple and SEC had been widely anticipated to remain business partners despite

their court battles, the latest change in AppleÊs supply chain (for the iPhone 5) suggests

otherwise. Given their interdependence up to this point, it will be interesting to see how

Apple and SEC operate without the help of one another going forward.

How will this change affect SEC next year? SECÊs semiconductor operating profit is forecast

to expand to W7.8tr in 2013, from W4.5tr in 2012. However, if SEC does not supply APs to

Apple (from 2H13) and fails to find new customers, the 2013 revenues and operating profit

of the System LSI segment should decline 15% YoY and 20% YoY, respectively. Even so, a

20% contraction (W520bn) corresponds to only 7% of the semiconductor divisionÊs 2013

operating profit estimate, and just 1.6% of the companyÊs total operating profit projection of

W33tr.

November 13, 2012 The Age of Transition

21 KDB Daewoo Securities Research

II. Global supply chain reshuffle

Implications of Apple’s supply chain change

Unlike AppleÊs previous smartphone models, the iPhone 5 does not feature SECÊs memory

chips. Given that SEC is the worldÊs largest memory maker, AppleÊs decision not to use

SECÊs chips has given rise to much speculation about the souring relationship between the

two companies. This change in AppleÊs supply chain has caught the attention of global parts

makers as well as investors.

The huge success of AppleÊs iPod, iPhone, and iPad has considerably increased the

companyÊs influence on the global memory market. Indeed, Apple consumes about 30% of

global NAND production, and ToshibaÊs and ElpidaÊs shares of the memory market have

fluctuated widely depending on AppleÊs order volume.

However, AppleÊs large order volume does not appear to have improved the earnings of

memory makers, such as Toshiba, SK Hynix and Elpida, due to low supply prices. Apple

even caused a supply glut in the NAND market after cancelling a large number of orders.

Some memory makers that expanded capacity to supply to Apple suffered severe inventory

buildup.

It is not clear whether it was Apple or SEC that caused the exclusion of SECÊs memory chips

from the iPhone 5. SECÊs basic guideline is that it supplies parts only if a reasonable margin

is guaranteed. Thus, we believe that SEC refused to supply its products to Apple.

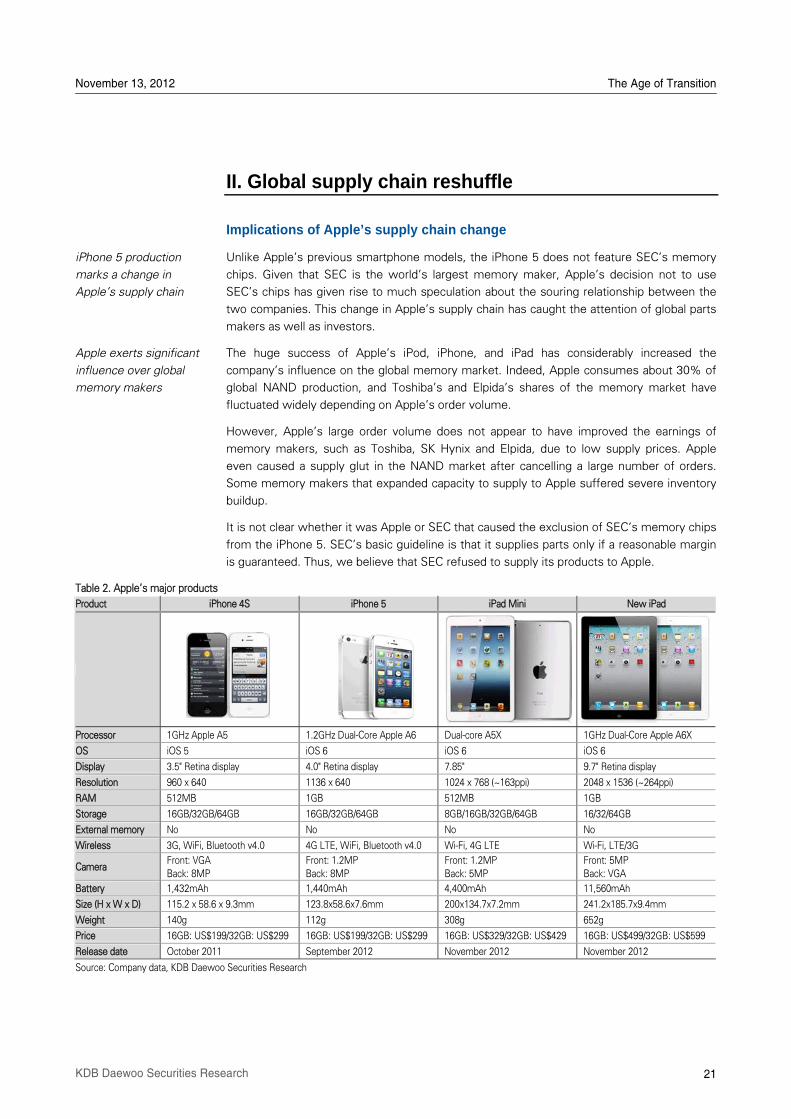

Table 2. AppleÊs major products

Product iPhone 4S iPhone 5 iPad Mini New iPad

Processor 1GHz Apple A5 1.2GHz Dual-Core Apple A6 Dual-core A5X 1GHz Dual-Core Apple A6X

OS iOS 5 iOS 6 iOS 6 iOS 6

Display 3.5" Retina display 4.0" Retina display 7.85" 9.7" Retina display

Resolution 960 x 640 1136 x 640 1024 x 768 (~163ppi) 2048 x 1536 (~264ppi)

RAM 512MB 1GB 512MB 1GB

Storage 16GB/32GB/64GB 16GB/32GB/64GB 8GB/16GB/32GB/64GB 16/32/64GB

External memory No No No No

Wireless 3G, WiFi, Bluetooth v4.0 4G LTE, WiFi, Bluetooth v4.0 Wi-Fi, 4G LTE Wi-Fi, LTE/3G

Camera Front: VGA

Back: 8MP

Front: 1.2MP

Back: 8MP

Front: 1.2MP

Back: 5MP

Front: 5MP

Back: VGA

Battery 1,432mAh 1,440mAh 4,400mAh 11,560mAh

Size (H x W x D) 115.2 x 58.6 x 9.3mm 123.8x58.6x7.6mm 200x134.7x7.2mm 241.2x185.7x9.4mm

Weight 140g 112g 308g 652g

Price 16GB: US$199/32GB: US$299 16GB: US$199/32GB: US$299 16GB: US$329/32GB: US$429 16GB: US$499/32GB: US$599

Release date October 2011 September 2012 November 2012 November 2012

Source: Company data, KDB Daewoo Securities Research

iPhone 5 production

marks a change in

AppleÊs supply chain

Apple exerts significant

influence over global

memory makers

November 13, 2012 The Age of Transition

22 KDB Daewoo Securities Research

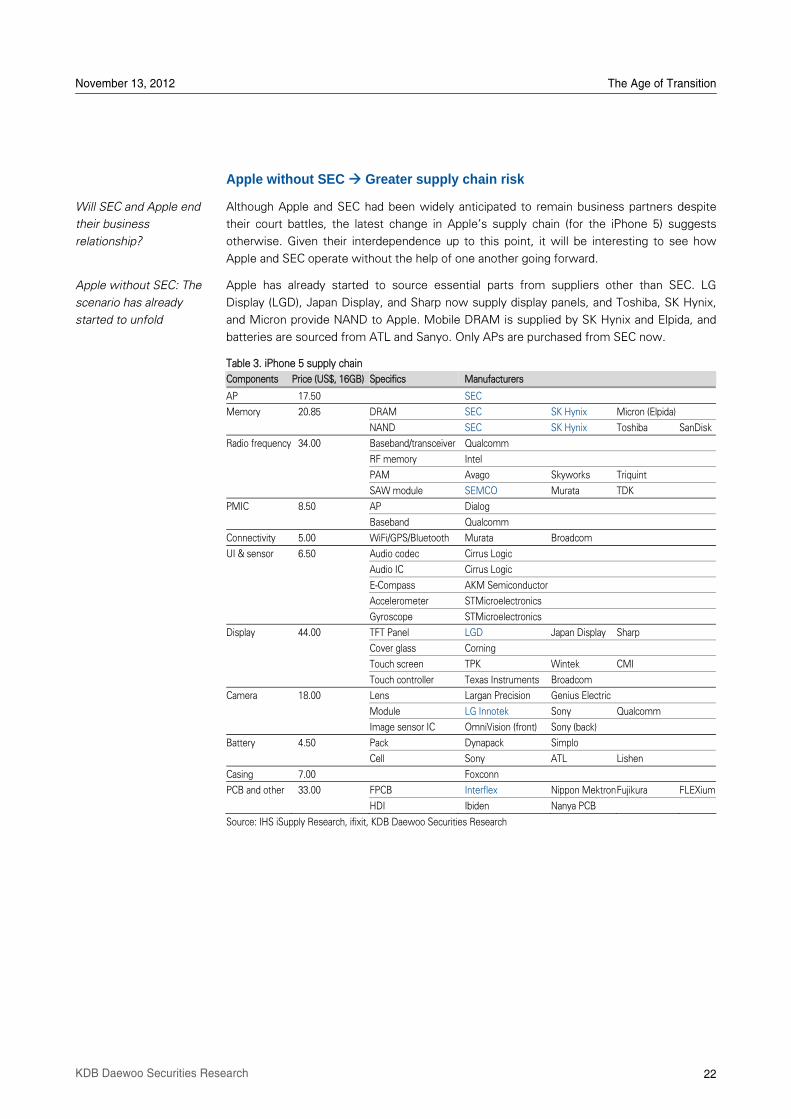

Apple without SEC Greater supply chain risk

Although Apple and SEC had been widely anticipated to remain business partners despite

their court battles, the latest change in AppleÊs supply chain (for the iPhone 5) suggests

otherwise. Given their interdependence up to this point, it will be interesting to see how

Apple and SEC operate without the help of one another going forward.

Apple has already started to source essential parts from suppliers other than SEC. LG

Display (LGD), Japan Display, and Sharp now supply display panels, and Toshiba, SK Hynix,

and Micron provide NAND to Apple. Mobile DRAM is supplied by SK Hynix and Elpida, and

batteries are sourced from ATL and Sanyo. Only APs are purchased from SEC now.

Table 3. iPhone 5 supply chain

Components Price (US$, 16GB) Specifics Manufacturers

AP 17.50 SEC

Memory 20.85 DRAM SEC SK Hynix Micron (Elpida)

NAND SEC SK Hynix Toshiba SanDisk

Radio frequency 34.00 Baseband/transceiver Qualcomm

RF memory Intel

PAM Avago Skyworks Triquint

SAW module SEMCO Murata TDK

PMIC 8.50 AP Dialog

Baseband Qualcomm

Connectivity 5.00 WiFi/GPS/Bluetooth Murata Broadcom

UI & sensor 6.50 Audio codec Cirrus Logic

Audio IC Cirrus Logic

E-Compass AKM Semiconductor

Accelerometer STMicroelectronics

Gyroscope STMicroelectronics

Display 44.00 TFT Panel LGD Japan Display Sharp

Cover glass Corning

Touch screen TPK Wintek CMI

Touch controller Texas Instruments Broadcom

Camera 18.00 Lens Largan Precision Genius Electric

Module LG Innotek Sony Qualcomm

Image sensor IC OmniVision (front) Sony (back)

Battery 4.50 Pack Dynapack Simplo

Cell Sony ATL Lishen

Casing 7.00 Foxconn

PCB and other 33.00 FPCB Interflex Nippon Mektron Fujikura FLEXium

HDI Ibiden Nanya PCB

Source: IHS iSupply Research, ifixit, KDB Daewoo Securities Research

Will SEC and Apple end

their business

relationship?

Apple without SEC: The

scenario has already

started to unfold

November 13, 2012 The Age of Transition

23 KDB Daewoo Securities Research

On the surface, the „Apple without SEC‰ scenario seems perfectly viable, given AppleÊs

strong market power. However, problems have already begun to emerge on three fronts.

In-cell display: The in-cell display significantly improved iPhone 5Ês form factor, but some

users are experiencing screen-related problems. Moreover, insufficient supply is limiting

production. LGD and Japan Display, which each satisfy 50% of AppleÊs in-cell display

needs, can each produce up to 7mn displays per month. This means that 4Q iPhone 5

shipments are likely to fall short of 45mn units.

Mobile DRAM: Apple consumes around 30% of global mobile DRAM production, and SEC

produces 60% of global mobile DRAM. Without SEC, Apple has to fully rely on SK Hynix and

Elpida, which produce the remaining 40% of the global supply. This means a greater risk for

Apple in case of any disruption in mobile DRAM production, especially at Elpida.

AP: SEC is currently AppleÊs exclusive AP supplier. Apple is estimated to need 70mn APs

per quarter, or 50,000 wafers/month based on SECÊs dual-core AP production capacity. SEC

started to produce 28nm chips in 2H, and its customer base (Qualcomm) and product

portfolio (baseband) have begun to diversify. Next year, if SEC cuts its AP production for

Apple to the 30~40,000 wafer/month level, Apple may face a huge problem in making its

products.

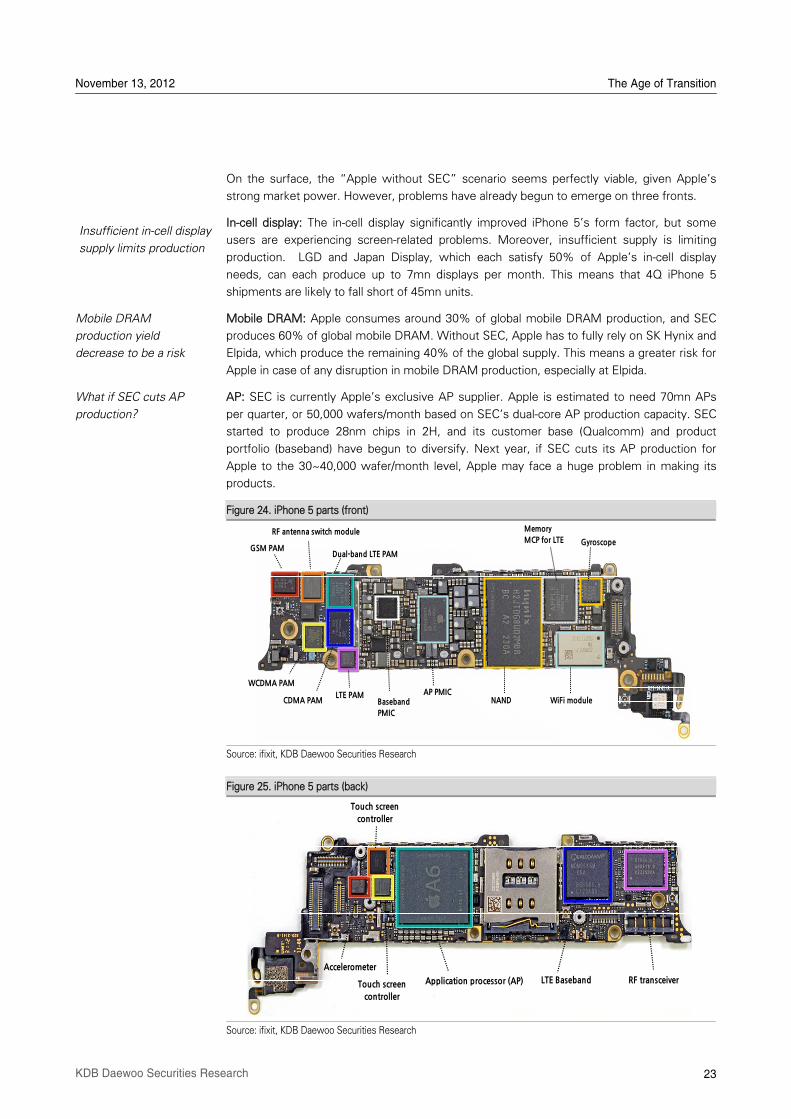

Figure 24. iPhone 5 parts (front)

Source: ifixit, KDB Daewoo Securities Research

Figure 25. iPhone 5 parts (back)

Source: ifixit, KDB Daewoo Securities Research

Insufficient in-cell display

supply limits production

Mobile DRAM

production yield

decrease to be a risk

What if SEC cuts AP

production?

GSM PAM

RF antenna switch module

Dual-band LTE PAM

WCDMA PAM

LTE PAMCDMA PAM Baseband

PMIC

AP PMICNAND WiFi module

Gyroscope

Memory

MCP for LTE

Application processor (AP) LTE Baseband RF transceiver

Touch screen

controller

Accelerometer

Touch screen

controller

November 13, 2012 The Age of Transition

24 KDB Daewoo Securities Research

Exclusion of SEC from Apple’s supply chain would have a limited impact

The likelihood of Apple diversifying its parts suppliers has been seen as the biggest risk

factor for SEC due to AppleÊs firm dominance in the smart device market. If Apple excludes

SEC completely from its supply chain, how much of an impact would it have on SEC?

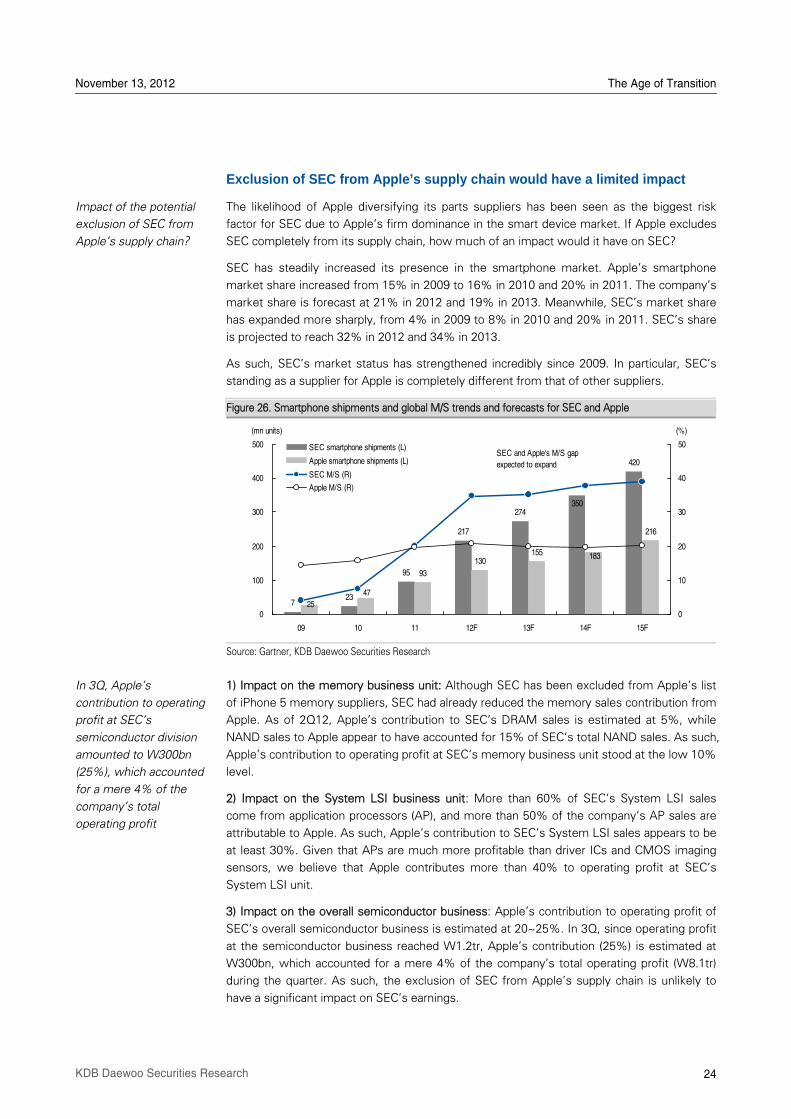

SEC has steadily increased its presence in the smartphone market. AppleÊs smartphone

market share increased from 15% in 2009 to 16% in 2010 and 20% in 2011. The companyÊs

market share is forecast at 21% in 2012 and 19% in 2013. Meanwhile, SECÊs market share

has expanded more sharply, from 4% in 2009 to 8% in 2010 and 20% in 2011. SECÊs share

is projected to reach 32% in 2012 and 34% in 2013.

As such, SECÊs market status has strengthened incredibly since 2009. In particular, SECÊs

standing as a supplier for Apple is completely different from that of other suppliers.

Figure 26. Smartphone shipments and global M/S trends and forecasts for SEC and Apple

Source: Gartner, KDB Daewoo Securities Research

1) Impact on the memory business unit: Although SEC has been excluded from AppleÊs list

of iPhone 5 memory suppliers, SEC had already reduced the memory sales contribution from

Apple. As of 2Q12, AppleÊs contribution to SECÊs DRAM sales is estimated at 5%, while

NAND sales to Apple appear to have accounted for 15% of SECÊs total NAND sales. As such,

AppleÊs contribution to operating profit at SECÊs memory business unit stood at the low 10%

level.

2) Impact on the System LSI business unit: More than 60% of SECÊs System LSI sales

come from application processors (AP), and more than 50% of the companyÊs AP sales are

attributable to Apple. As such, AppleÊs contribution to SECÊs System LSI sales appears to be

at least 30%. Given that APs are much more profitable than driver ICs and CMOS imaging

sensors, we believe that Apple contributes more than 40% to operating profit at SECÊs

System LSI unit.

3) Impact on the overall semiconductor business: AppleÊs contribution to operating profit of

SECÊs overall semiconductor business is estimated at 20~25%. In 3Q, since operating profit

at the semiconductor business reached W1.2tr, AppleÊs contribution (25%) is estimated at

W300bn, which accounted for a mere 4% of the companyÊs total operating profit (W8.1tr)

during the quarter. As such, the exclusion of SEC from AppleÊs supply chain is unlikely to

have a significant impact on SECÊs earnings.

Impact of the potential

exclusion of SEC from

AppleÊs supply chain?

In 3Q, AppleÊs

contribution to operating

profit at SECÊs

semiconductor division

amounted to W300bn

(25%), which accounted

for a mere 4% of the

companyÊs total

operating profit

723

95

217

274

420

93

130155

216

350

183

47

250

100

200

300

400

500

09 10 11 12F 13F 14F 15F

0

10

20

30

40

50SEC smartphone shipments (L)

Apple smartphone shipments (L)

SEC M/S (R)

Apple M/S (R)

(mn units) (%)

SEC and Apple's M/S gap

expected to expand

November 13, 2012 The Age of Transition

25 KDB Daewoo Securities Research

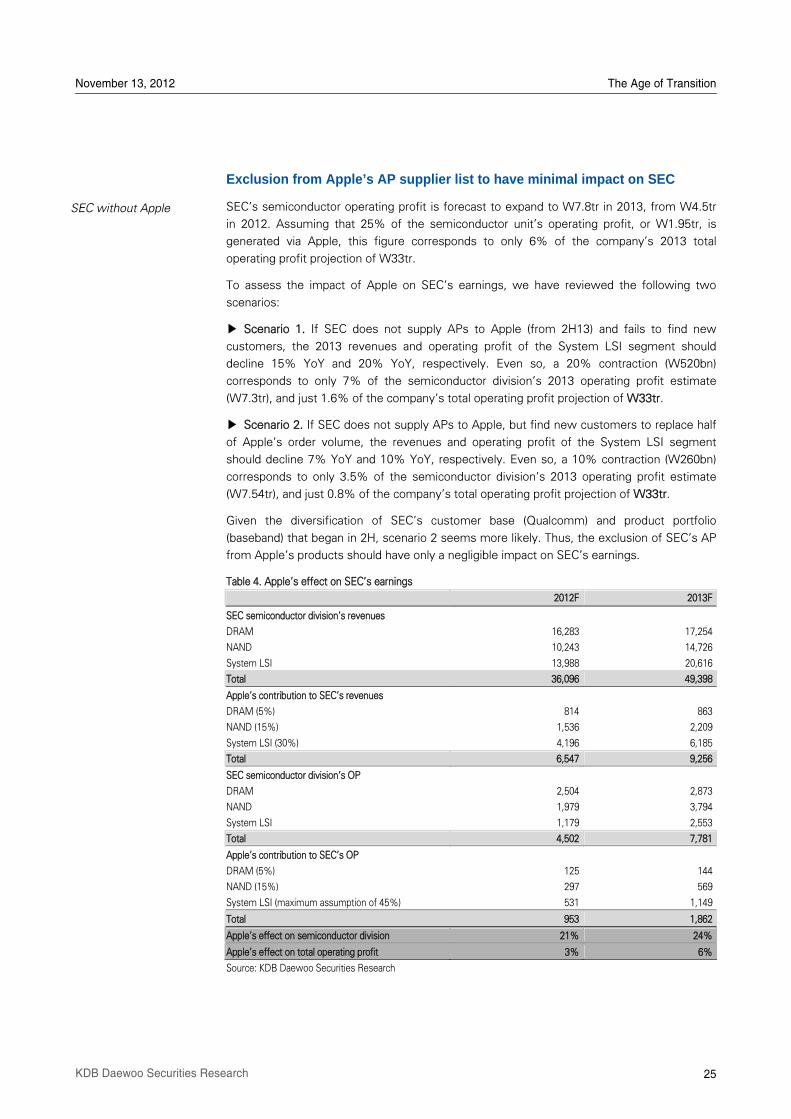

Exclusion from Apple’s AP supplier list to have minimal impact on SEC

SECÊs semiconductor operating profit is forecast to expand to W7.8tr in 2013, from W4.5tr

in 2012. Assuming that 25% of the semiconductor unitÊs operating profit, or W1.95tr, is

generated via Apple, this figure corresponds to only 6% of the companyÊs 2013 total

operating profit projection of W33tr.

To assess the impact of Apple on SECÊs earnings, we have reviewed the following two

scenarios:

▶ Scenario 1. If SEC does not supply APs to Apple (from 2H13) and fails to find new

customers, the 2013 revenues and operating profit of the System LSI segment should

decline 15% YoY and 20% YoY, respectively. Even so, a 20% contraction (W520bn)

corresponds to only 7% of the semiconductor divisionÊs 2013 operating profit estimate

(W7.3tr), and just 1.6% of the companyÊs total operating profit projection of W33tr.

▶ Scenario 2. If SEC does not supply APs to Apple, but find new customers to replace half

of AppleÊs order volume, the revenues and operating profit of the System LSI segment

should decline 7% YoY and 10% YoY, respectively. Even so, a 10% contraction (W260bn)

corresponds to only 3.5% of the semiconductor divisionÊs 2013 operating profit estimate

(W7.54tr), and just 0.8% of the companyÊs total operating profit projection of W33tr.

Given the diversification of SECÊs customer base (Qualcomm) and product portfolio

(baseband) that began in 2H, scenario 2 seems more likely. Thus, the exclusion of SECÊs AP

from AppleÊs products should have only a negligible impact on SECÊs earnings.

Table 4. AppleÊs effect on SECÊs earnings

2012F 2013F

SEC semiconductor divisionÊs revenues

DRAM 16,283 17,254

NAND 10,243 14,726

System LSI 13,988 20,616

Total 36,096 49,398

AppleÊs contribution to SECÊs revenues

DRAM (5%) 814 863

NAND (15%) 1,536 2,209

System LSI (30%) 4,196 6,185

Total 6,547 9,256

SEC semiconductor divisionÊs OP

DRAM 2,504 2,873

NAND 1,979 3,794

System LSI 1,179 2,553

Total 4,502 7,781

AppleÊs contribution to SECÊs OP

DRAM (5%) 125 144

NAND (15%) 297 569

System LSI (maximum assumption of 45%) 531 1,149

Total 953 1,862

AppleÊs effect on semiconductor division 21% 24%

AppleÊs effect on total operating profit 3% 6%

Source: KDB Daewoo Securities Research

SEC without Apple

November 13, 2012 The Age of Transition

26 KDB Daewoo Securities Research

TSMC could begin supplying APs to Apple from late 2013

Why has Apple kept SEC as an AP supplier while removing it from its list of memory

suppliers? Probably because it has no other viable options. For now, it is next to impossible

for Apple to make its tablets and smartphones without SECÊs AP supply. The most viable

alternative would be the Taiwanese firm TSMC, but we believe the company does not yet

have the production yield and capacity to meet AppleÊs needs.

Then, at what point will TSMC have the yield and capacity to begin supplying Apple?

The A6 chip that powers the new iPhone 5 is a dual-core processor manufactured on a 32nm

high-k metal gate (HKMG) process. Even though TSMC was one step ahead of SEC in

offering a 28nm HKMG process (SEC followed after 3Q12), the fact that Apple still relies on

SECÊs 32nm process instead indicates that TSMCÊs 28nm process lags behind in terms of

both capacity and efficiency.

TSMC is the worldÊs largest foundry, and its fabs and processes are as diverse as its client

base. The company owns 15 fabs, of which only three are 12 inch-based. In 2Q12, 65nm or

larger processes accounted for 65% of its revenues, while production on the 28nm process

made up only 7% (estimated at around 20,000 wafers per month). Therefore, it would be

natural to assume that SEC has a much larger capacity than TSMC for APs using 30nm or

finer processes.

TSMC already has a number of clients that opt for the 28nm process, including Qualcomm,

AMD, and Nvidia. Recently, TSMC has been experiencing yield problems on its 28nm

process node, causing a production shortage for QualcommÊs MSM 8960 (one-chip solution).

The situation is not that different for Nvidia and AMD, suggesting manufacturing is having

difficulty keeping up with design. Thus, although Apple represents an enormous opportunity

for TSMC, prioritizing Apple over its existing clients may be a risky move for the foundry

given its limited capacity.

Assuming AppleÊs 4Q12 shipments of smartphones and tablets at around 70mn units, its AP

requirements would be roughly 23mn units per month, or based on dual-core capacity, a

monthly supply of 48,000 wafers (23mn/480 per month). This means TSMC would have to

ramp up its 28nm capacity to 100,000 wafers per month in order to meet AppleÊs demand.

Thus, while we do see risks of TSMC supplying APs to Apple as early as 2H13, we do not

expect any meaningful supply before 2014.

Figure 27. TSMCÊs process breakdown in 2Q12 Figure 28. TSMCÊs sub-65nm revenue trend

Source: TSMC Source: TSMC

Apple still faces

limitations in diversifying

its AP supplier base

TSMC lags behind SEC

in terms of both yield

and capacity

Full-fledged supply could

become possible from

2014

0.15/0.18um, 15%

90nm, 10%

28nm, 7%40/45nm, 28%

65nm, 26%

025/0.35um, 6%

0.5um+, 2%

0.11/0.13um, 6%

November 13, 2012 The Age of Transition

27 KDB Daewoo Securities Research

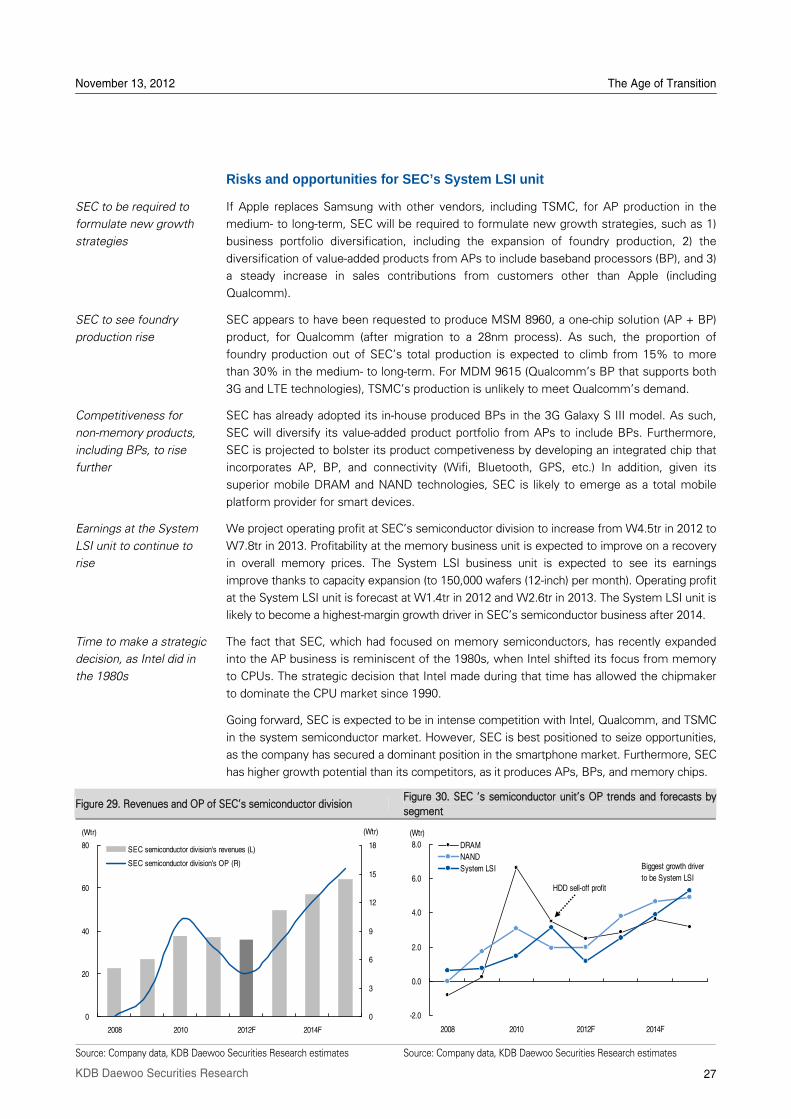

Risks and opportunities for SEC’s System LSI unit

If Apple replaces Samsung with other vendors, including TSMC, for AP production in the

medium- to long-term, SEC will be required to formulate new growth strategies, such as 1)

business portfolio diversification, including the expansion of foundry production, 2) the

diversification of value-added products from APs to include baseband processors (BP), and 3)

a steady increase in sales contributions from customers other than Apple (including

Qualcomm).

SEC appears to have been requested to produce MSM 8960, a one-chip solution (AP + BP)

product, for Qualcomm (after migration to a 28nm process). As such, the proportion of

foundry production out of SECÊs total production is expected to climb from 15% to more

than 30% in the medium- to long-term. For MDM 9615 (QualcommÊs BP that supports both

3G and LTE technologies), TSMCÊs production is unlikely to meet QualcommÊs demand.

SEC has already adopted its in-house produced BPs in the 3G Galaxy S III model. As such,

SEC will diversify its value-added product portfolio from APs to include BPs. Furthermore,

SEC is projected to bolster its product competiveness by developing an integrated chip that

incorporates AP, BP, and connectivity (Wifi, Bluetooth, GPS, etc.) In addition, given its

superior mobile DRAM and NAND technologies, SEC is likely to emerge as a total mobile

platform provider for smart devices.

We project operating profit at SECÊs semiconductor division to increase from W4.5tr in 2012 to

W7.8tr in 2013. Profitability at the memory business unit is expected to improve on a recovery

in overall memory prices. The System LSI business unit is expected to see its earnings

improve thanks to capacity expansion (to 150,000 wafers (12-inch) per month). Operating profit

at the System LSI unit is forecast at W1.4tr in 2012 and W2.6tr in 2013. The System LSI unit is

likely to become a highest-margin growth driver in SECÊs semiconductor business after 2014.

The fact that SEC, which had focused on memory semiconductors, has recently expanded

into the AP business is reminiscent of the 1980s, when Intel shifted its focus from memory

to CPUs. The strategic decision that Intel made during that time has allowed the chipmaker

to dominate the CPU market since 1990.

Going forward, SEC is expected to be in intense competition with Intel, Qualcomm, and TSMC

in the system semiconductor market. However, SEC is best positioned to seize opportunities,

as the company has secured a dominant position in the smartphone market. Furthermore, SEC

has higher growth potential than its competitors, as it produces APs, BPs, and memory chips.

Figure 29. Revenues and OP of SECÊs semiconductor division Figure 30. SEC Âs semiconductor unitÊs OP trends and forecasts by

segment

Source: Company data, KDB Daewoo Securities Research estimates Source: Company data, KDB Daewoo Securities Research estimates

SEC to be required to

formulate new growth

strategies

SEC to see foundry

production rise

Competitiveness for

non-memory products,

including BPs, to rise

further

Earnings at the System

LSI unit to continue to

rise

Time to make a strategic

decision, as Intel did in

the 1980s

-2.0

0.0

2.0

4.0

6.0

8.0

2008 2010 2012F 2014F

(Wtr)

DRAM

NAND

System LSI Biggest growth driver

to be System LSIHDD sell-off profit

0

20

40

60

80

2008 2010 2012F 2014F

(Wtr)

0

3

6

9

12

15

18SEC semiconductor division's revenues (L)

SEC semiconductor division's OP (R)

(Wtr)

28 KDB Daewoo Securities Research

III Losers’ League

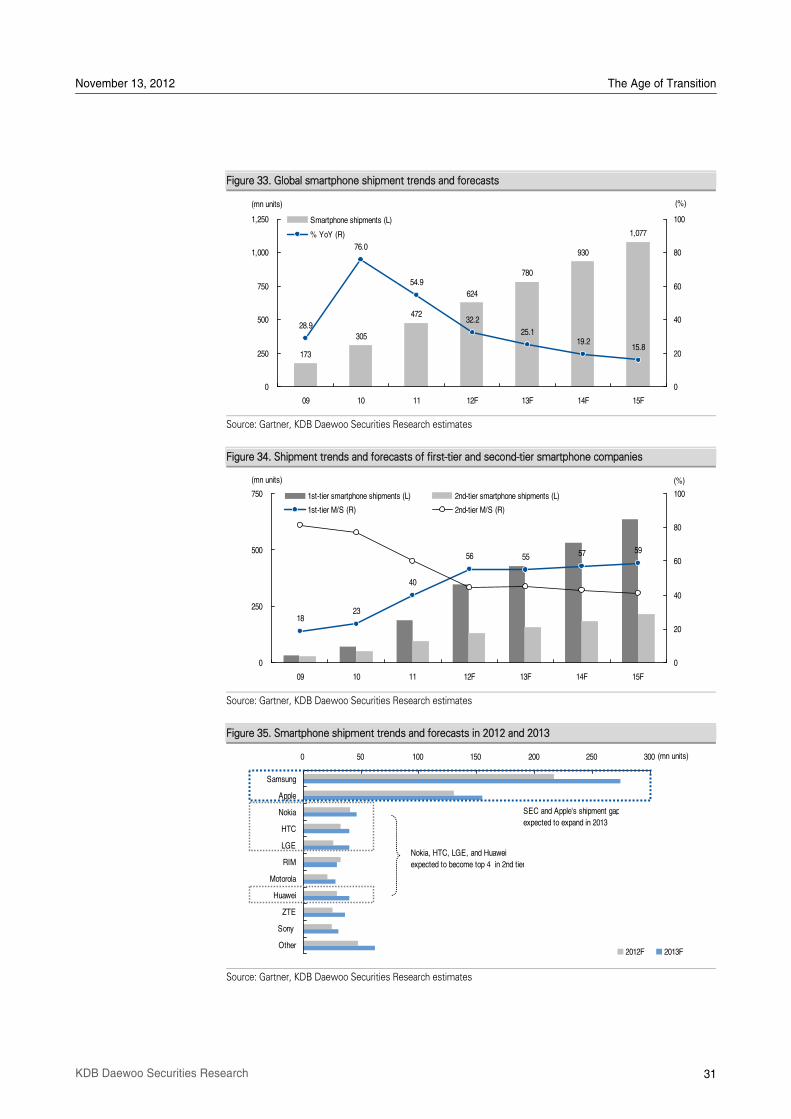

With the global smartphone market being dominated by only two makers, we do not expect

a third player (that is able to churn out over 50mn smartphones per year) to join the

competition anytime soon. Second-tier smartphone makers have yet to differentiate

themselves in terms of: 1) hardware, 2) software/content, and 3) marketing strategies.

In 2013, we expect second-tier smartphone makers to compete within their own league.

Among the eight second-tier makers, we believe that four (Nokia, HTC, LG Electronics (LGE)

and Huawei) will take loftier positions (40mn shipments per year). The rest are anticipated to

ship around 20~30mn smartphones per year.

November 13, 2012 The Age of Transition

29 KDB Daewoo Securities Research

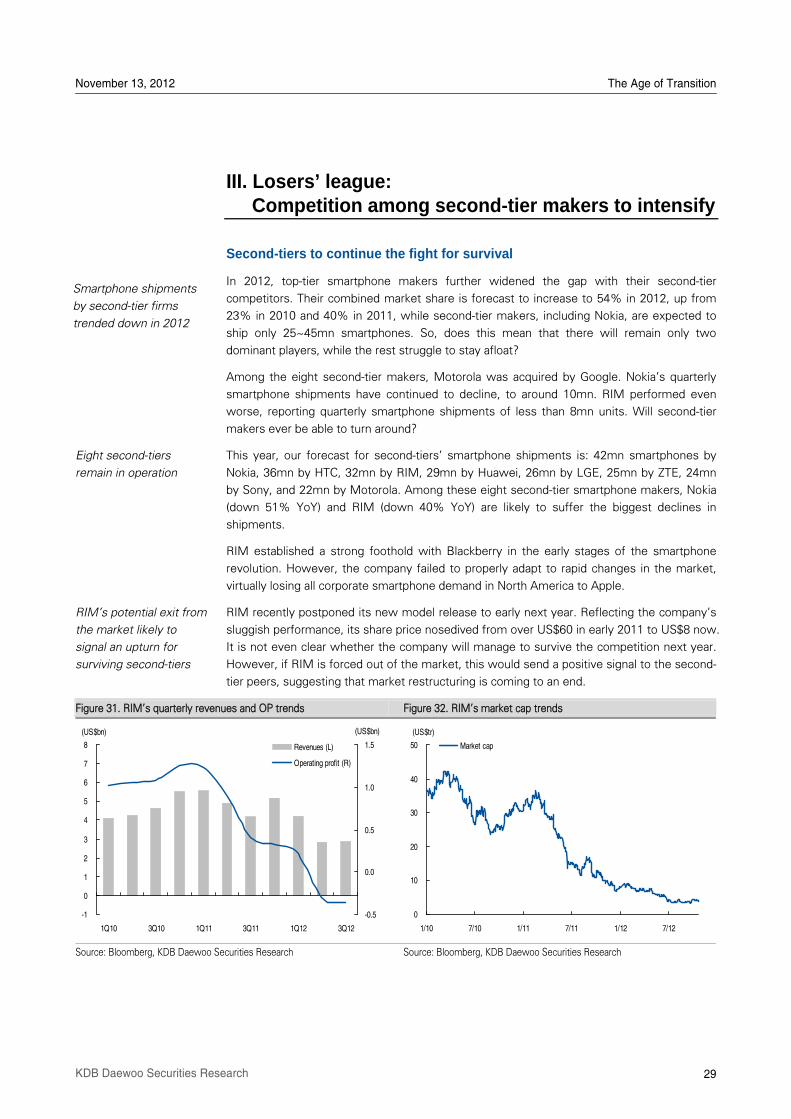

III. Losers’ league: Competition among second-tier makers to intensify

Second-tiers to continue the fight for survival

In 2012, top-tier smartphone makers further widened the gap with their second-tier

competitors. Their combined market share is forecast to increase to 54% in 2012, up from

23% in 2010 and 40% in 2011, while second-tier makers, including Nokia, are expected to

ship only 25~45mn smartphones. So, does this mean that there will remain only two

dominant players, while the rest struggle to stay afloat?

Among the eight second-tier makers, Motorola was acquired by Google. NokiaÊs quarterly

smartphone shipments have continued to decline, to around 10mn. RIM performed even

worse, reporting quarterly smartphone shipments of less than 8mn units. Will second-tier

makers ever be able to turn around?

This year, our forecast for second-tiersÊ smartphone shipments is: 42mn smartphones by

Nokia, 36mn by HTC, 32mn by RIM, 29mn by Huawei, 26mn by LGE, 25mn by ZTE, 24mn

by Sony, and 22mn by Motorola. Among these eight second-tier smartphone makers, Nokia

(down 51% YoY) and RIM (down 40% YoY) are likely to suffer the biggest declines in

shipments.

RIM established a strong foothold with Blackberry in the early stages of the smartphone

revolution. However, the company failed to properly adapt to rapid changes in the market,

virtually losing all corporate smartphone demand in North America to Apple.

RIM recently postponed its new model release to early next year. Reflecting the companyÊs

sluggish performance, its share price nosedived from over US$60 in early 2011 to US$8 now.

It is not even clear whether the company will manage to survive the competition next year.

However, if RIM is forced out of the market, this would send a positive signal to the second-

tier peers, suggesting that market restructuring is coming to an end.

Figure 31. RIMÊs quarterly revenues and OP trends Figure 32. RIMÊs market cap trends

Source: Bloomberg, KDB Daewoo Securities Research Source: Bloomberg, KDB Daewoo Securities Research

Smartphone shipments

by second-tier firms

trended down in 2012

Eight second-tiers

remain in operation

RIMÊs potential exit from

the market likely to

signal an upturn for

surviving second-tiers

-1

0

1

2

3

4

5

6

7

8

1Q10 3Q10 1Q11 3Q11 1Q12 3Q12

(US$bn)

-0.5

0.0

0.5

1.0

1.5Revenues (L)

Operating profit (R)

(US$bn)

0

10

20

30

40

50

1/10 7/10 1/11 7/11 1/12 7/12

(US$tr)

Market cap

November 13, 2012 The Age of Transition

30 KDB Daewoo Securities Research

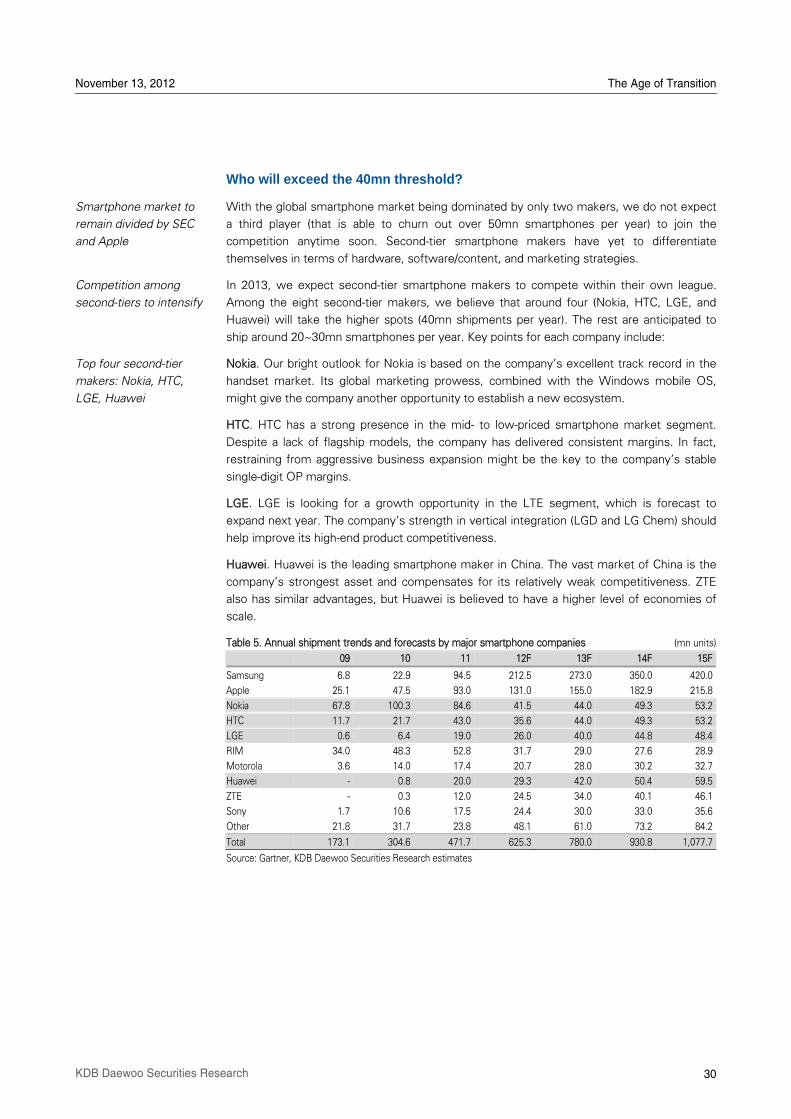

Who will exceed the 40mn threshold?

With the global smartphone market being dominated by only two makers, we do not expect

a third player (that is able to churn out over 50mn smartphones per year) to join the

competition anytime soon. Second-tier smartphone makers have yet to differentiate

themselves in terms of hardware, software/content, and marketing strategies.

In 2013, we expect second-tier smartphone makers to compete within their own league.

Among the eight second-tier makers, we believe that around four (Nokia, HTC, LGE, and

Huawei) will take the higher spots (40mn shipments per year). The rest are anticipated to

ship around 20~30mn smartphones per year. Key points for each company include:

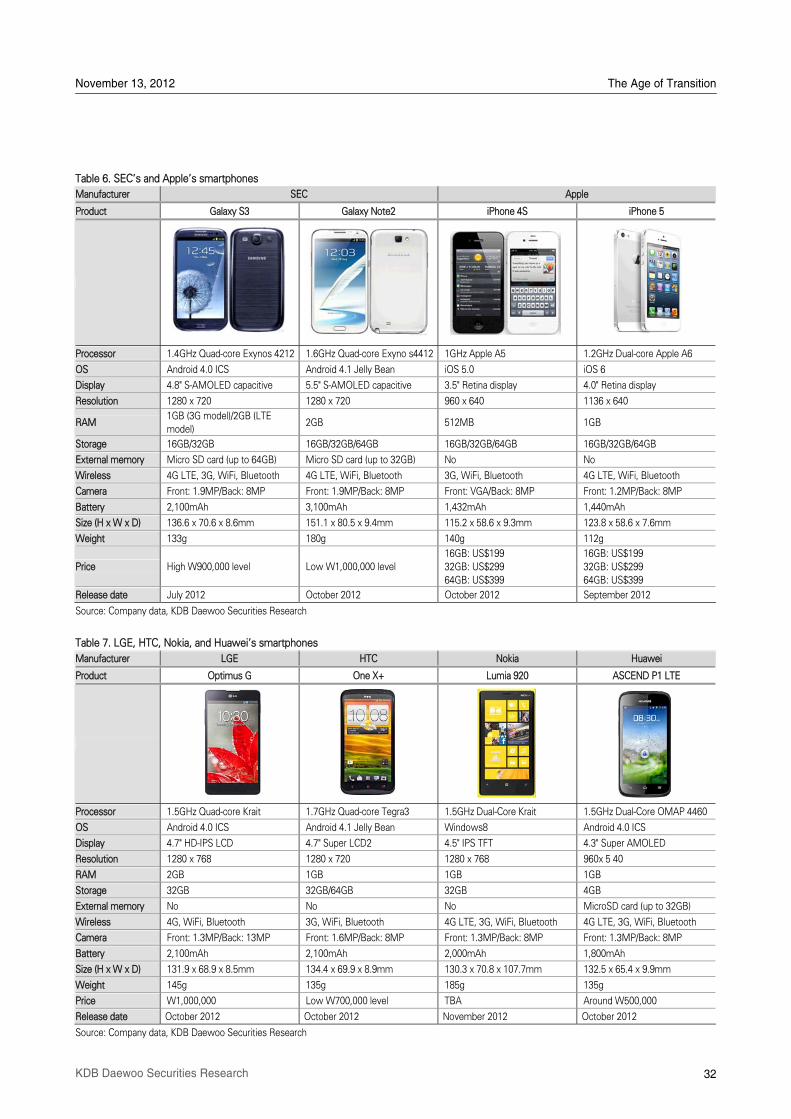

Nokia. Our bright outlook for Nokia is based on the companyÊs excellent track record in the

handset market. Its global marketing prowess, combined with the Windows mobile OS,

might give the company another opportunity to establish a new ecosystem.