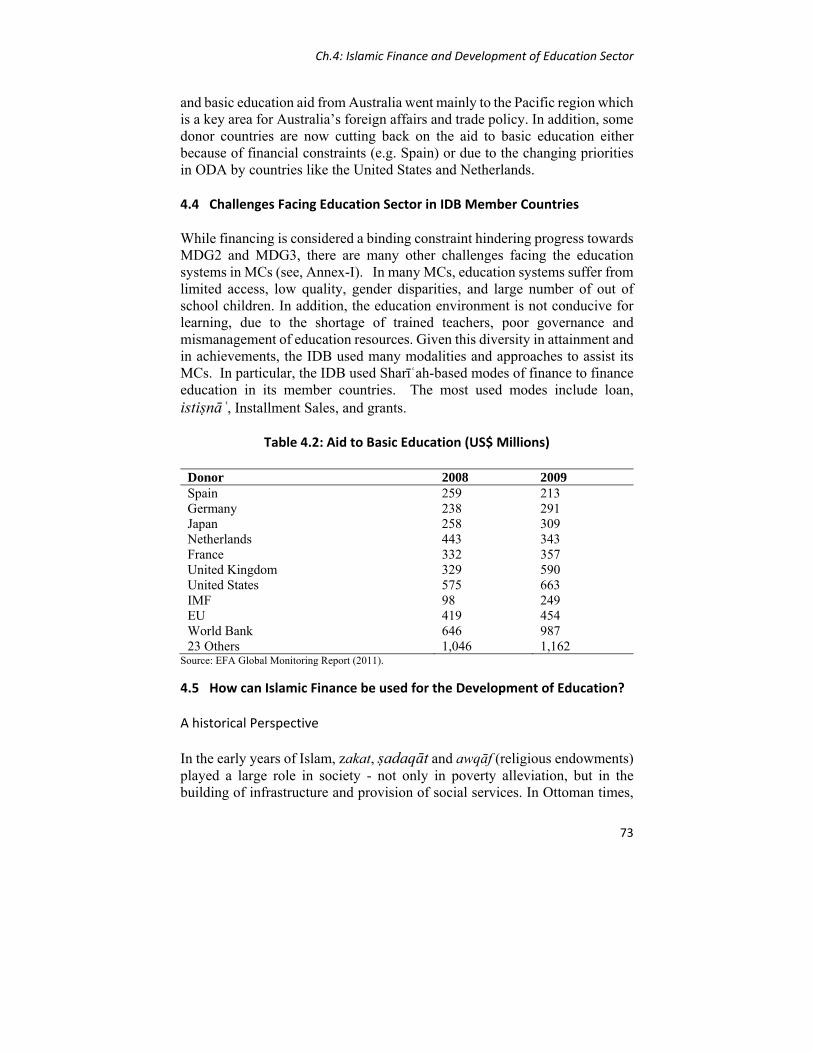

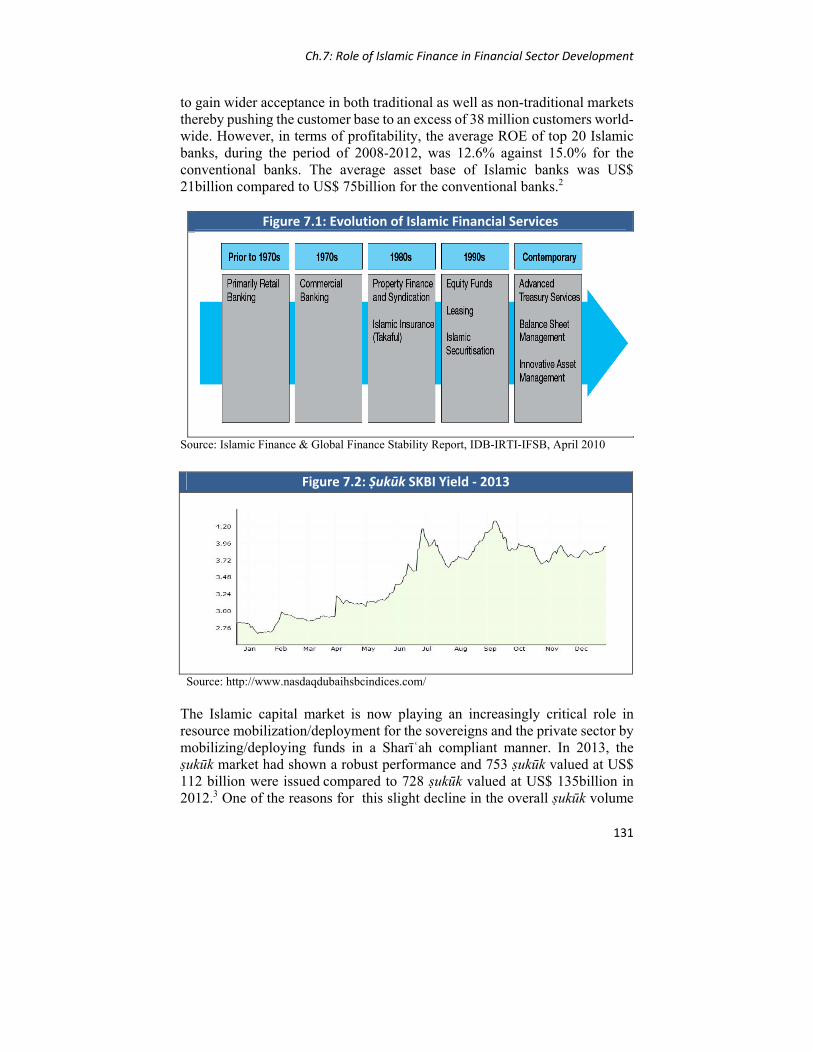

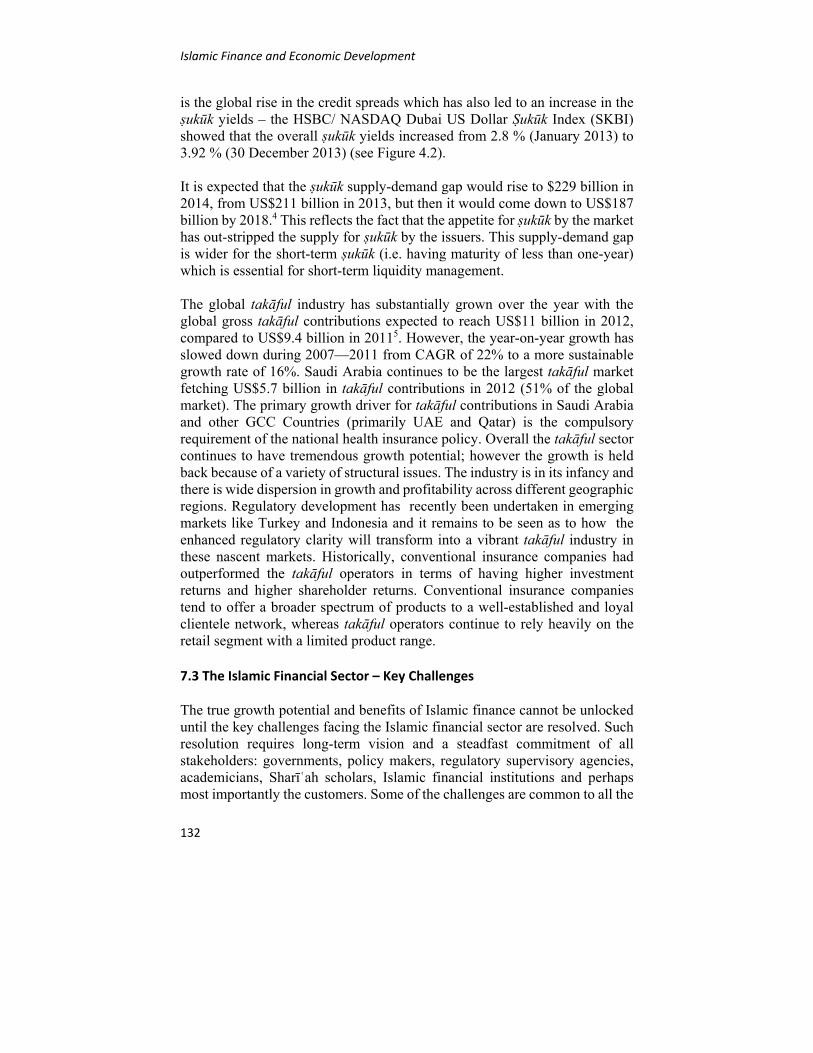

Embed Size (px)

Citation preview

Islam

Ic FIn

an

ce a

nd

eco

no

mIc

dev

elopm

ent lesso

ns Fro

m th

e past a

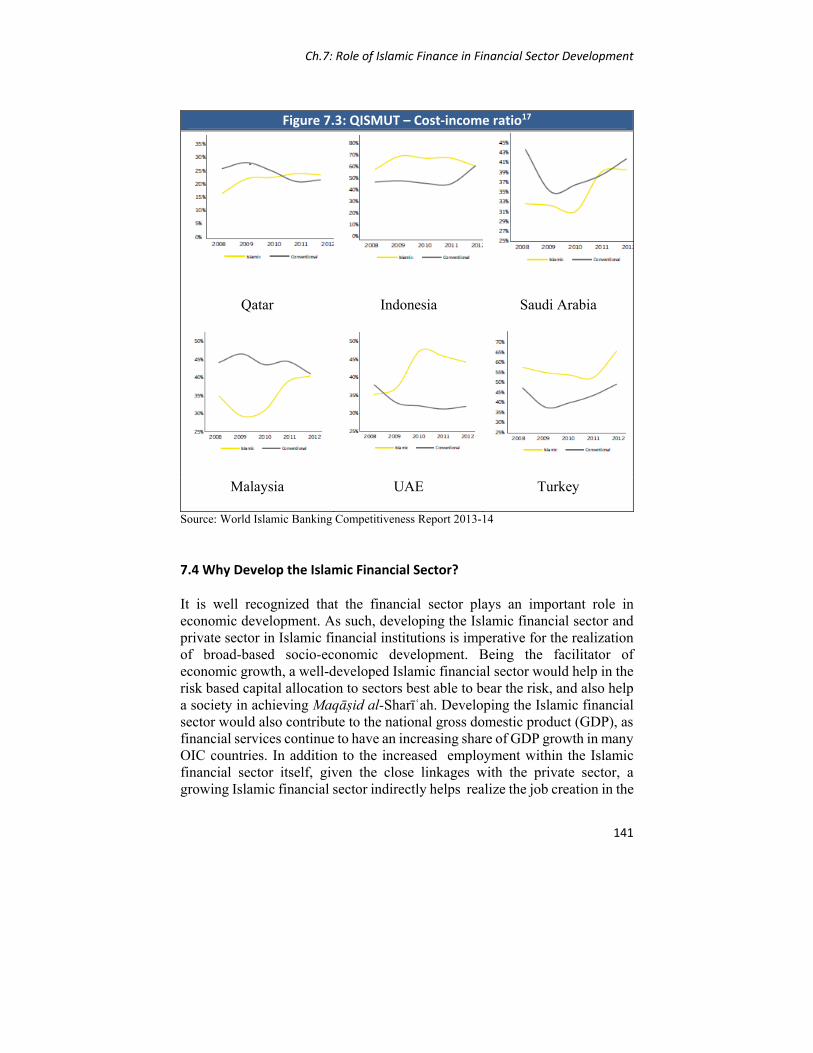

nd

prospec

ts For th

e Futu

re

IslamIcFInanceand Economic dEvElopmEntlEssons from thE past andprospEcts for thE futurE

IslamIcFInanceand Economic dEvElopmEntlEssons from thE past andprospEcts for thE futurE

De

sign

ed

By

: Mo

ha

ma

d A

li A

siri ©

201

4

P.O. Box 9201, Jeddah 21413Kingdom of Saudi Arabia Tel: (00966-2) 636 1400Fax: (00966-2) 637 8927

Email: [email protected]

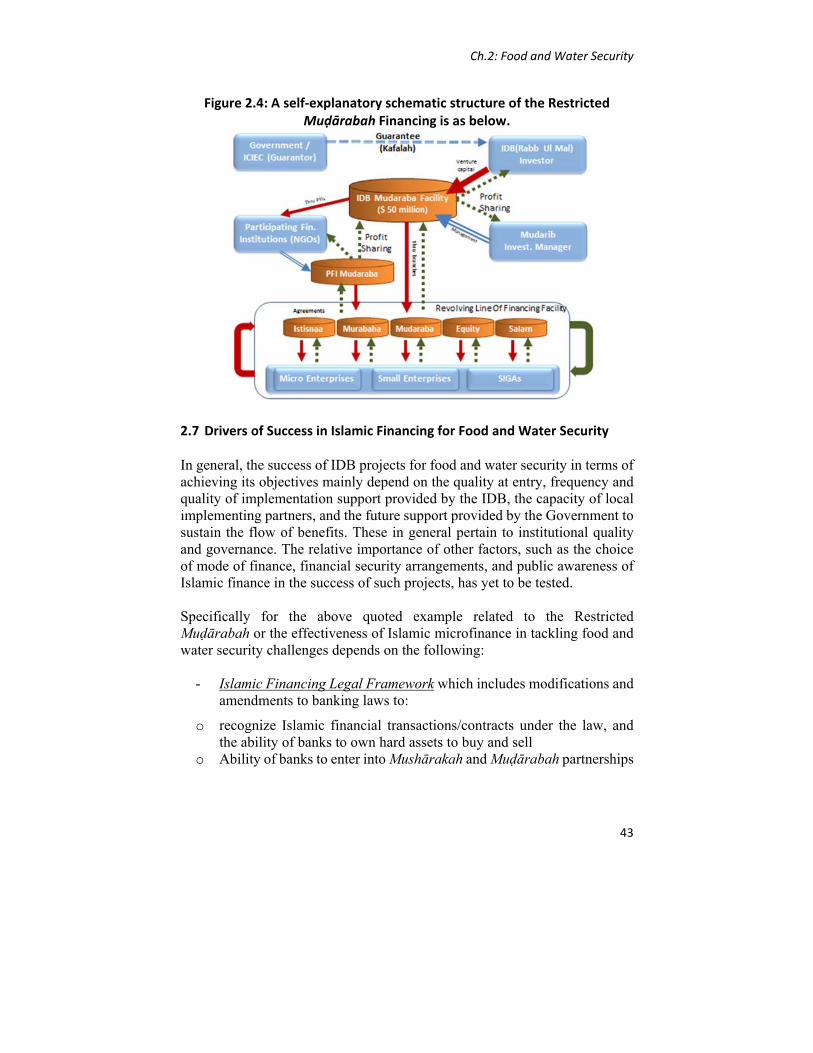

Islamic Development Bank (IDB)EstablishmentThe Islamic Development Bank is an international financial institution established in pursuance of the Declaration of Intent issued by the Conference of Finance Ministers of Muslim Countries held in Jeddah in Dhul Qa’dah 1393H (December, 1973). The inaugural Meeting of the Board of Governors took place in Rajab 1395H (July 1975) and the Bank was formally opened on 15 Shawwal 1395H (20 October, 1975).

VisionBy the year 1440H Hijrah, IDB shall have become a world-class development bank, inspired by Islamic principles that have helped significantly transform the landscape of comprehensive human development in the Muslim world and help restore its dignity.

MissionThe mission of IDB is to promote comprehensive human development, with a focus on the priority areas of alleviating poverty, improving health, promoting education, improving governance and prospering the people.

MembershipThe present membership of the Bank consists of 56 countries. The basic condition for membership is that the prospective member country should be a member of the Organization of Islamic Cooperation (OIC), pay its contribution to the capital of the Bank and be willing to accept such terms and conditions as may be decided upon by the IDB Board of Governors.

CapitalAs of the month of Rajab 1431H, the Authorized Capital of the Bank was ID 30 Billion, and the Issued Capital was ID 18 Billion, of which ID 17.474 Billion was subscribed with ID 4.031 Billion Paid-Up.

GroupAt present the IDB Group is made up of Islamic Research and Training Institute (IRTI), International Islamic Trade Finance Corporation (ITFC), The Islamic Corporation for Insurance of Investments and Export Credit (ICIEC) and The Islamic Corporation for the Development of the Private Sector (ICD).

Headquarters and Regional OfficesThe Bank’s headquarters is in Jeddah in the Kingdom of Saudi Arabia. Four regional offices were opened in Rabat, Morocco (1994), Kuala Lumpur, Malaysia (1994), Almaty, Kazakhstan (1997) and Dakar, Senegal (2008).

Financial YearThe Bank’s financial year is the lunar Hijra year.

Accounting UnitThe accounting unit of the IDB is the Islamic Dinar (ID), which is equivalent to one SDR – Special Drawing Right of the International Monetary Fund.

LanguagesThe official language of the Bank is Arabic, but English and French are also used as working languages.

Islamic Research & Training Institute (IRTI)

EstablishmentThe Islamic Research and Training Institute (IRTI) was established by the Board of Executive Directors (BED) of the Islamic Development Bank (IDB) in conformity with paragraph (a) of the Resolution No. BG/14-99 of the Board of Governors adopted at its Third Annual Meeting held on 10th Rabi-ul-Thani, 1399H corresponding to 14th March, 1979. The Institute became operational in 1403H corresponding to 1983. The Statute of the IRTI was modified in accordance with the resolutions of the IDB BED No.247 held on 27/08/1428H.

PurposeThe Institute undertakes research for enabling the economic, financial and banking activities in Muslim countries to conform to Sharah, and to extend training facilities for personnel engaged in development activities in the Bank’s member countries.

FunctionsThe functions of the institute are to:

A. Develop dynamic and innovative Islamic Financial Services Industry (IFSI).B. Develop and coordinate basic and applied research for the application of Shariah in economics, banking

and finance.C. Conduct policy dialogue with member countries.D. Provide advisory services in Islamic economics, banking and finance.E. Disseminate IFSI related knowledge through conference, seminars, workshops, apprenticeships, and

policy & research papers.F. Provide learning and training opportunities for personnel engaged in socio-economic development

activities in member countries.G. Collect and systematize information and disseminate knowledge.H. Collaborate to provide policy advice and advisory services on the development and stability of Islamic

Finance and on the role of Islamic institutions in economic development to member government, private sector and the NGO sector.

I. Develop partnership with research and academic institutions at OIC and international levels.

OrganizationThe President of the IDB is the President and the Legal Representative of the Institute. The Board of Executive Directors of the IDB acts as the supreme body of the institute responsible for determining its policy. The Institute’s management is entrusted to a Director General selected by the IDB President in consultation with the Board of Executive Directors. The Institute has a Board of Trustees that function as an Advisory body to the Board of Executive Directors. The Institute consists of two Departments, each with two Divisions:

Training & Information Services DepartmentResearch & Advisory Services Department

Training DivisionIslamic Economics & Finance Research Division

Information & Knowledge Services DivisionAdvisory Services in Islamic Economics & Finance Division

HeadquartersThe Institute is located at the headquarters of the Islamic Development Bank in Jeddah, Saudi Arabia.P.O. Box 9201, Jeddah 21413Kingdom of Saudi ArabiaTel: (00966-2) 636 1400 Fax: (00966-2) 637 8927Home page: http://www.irti.org Email: [email protected]

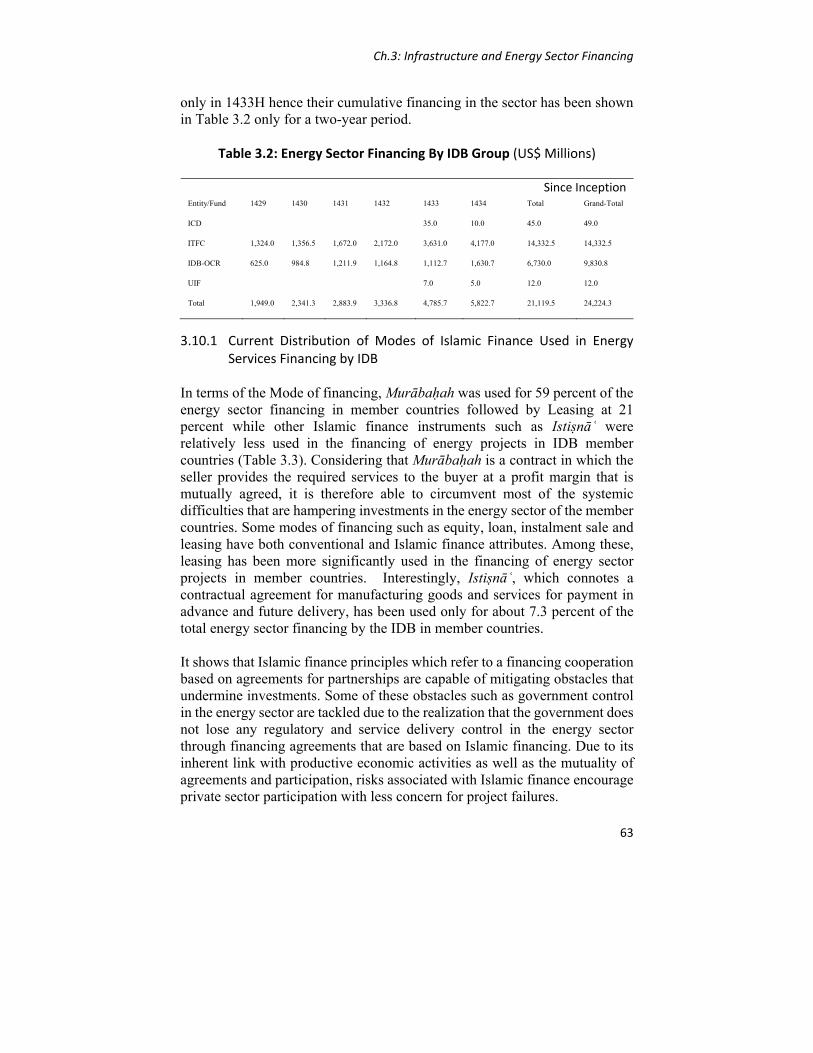

ISLAMIC FINANCE AND ECONOMIC DEVELOPMENT LESSONS FROM THE PAST AND PROSPECTS FOR THE FUTURE

ii

iii

iv

v

ISLAMIC FINANCE AND ECONOMIC DEVELOPMENT LESSONS FROM THE PAST AND PROSPECTS FOR THE FUTURE

Salman Syed Ali

IRTI Occasional Paper No.15

vi

© 2014 Islamic Research & Training Institute, a member of the Islamic Development Bank Group. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopied, recorded, or otherwise without the prior written permission of the copyright holder, except for reference and citation, with proper acknowledgement. The views expressed in this publication are those of the authors and do not necessarily reflect the views of the Islamic Research and Training Institute or of the Islamic Development Bank Group.

Cover Design by Mohammad Ali Asiri 2014 First Published 1435H (2014) Islamic Research and Training Institute P.O. Box 9201, Jeddah 21413, Saudi Arabia King Fahad National Library Cataloguing-in-Publication Data Ali, Salman Syed

Islamic Finance and Economic Development: Lessons from the Past and Prospects for the Future. / Salman Syed Ali 222 p+ (xviii); 24x17 cm Includes references, appendices and glossary ISBN 9789960322834 1. Development 2. Islamic Finance 3. Sectorial Financing I. Ali, Salman II. Title III. Occasional Paper 332 – dc HG3691

vii

Table of Contents

List of Abbreviations Glossary Foreword Acknowledgements and Credits

CHAPTER‐1 ...................................................................................... Islamic Finance and Economic Development: An Introduction and Overview 1

CHAPTER‐2 ......................................................................................

Food and Water Security 23

CHAPTER‐3 ......................................................................................

Infrastructure and Energy Sector Financing 53 CHAPTER‐4 ......................................................................................

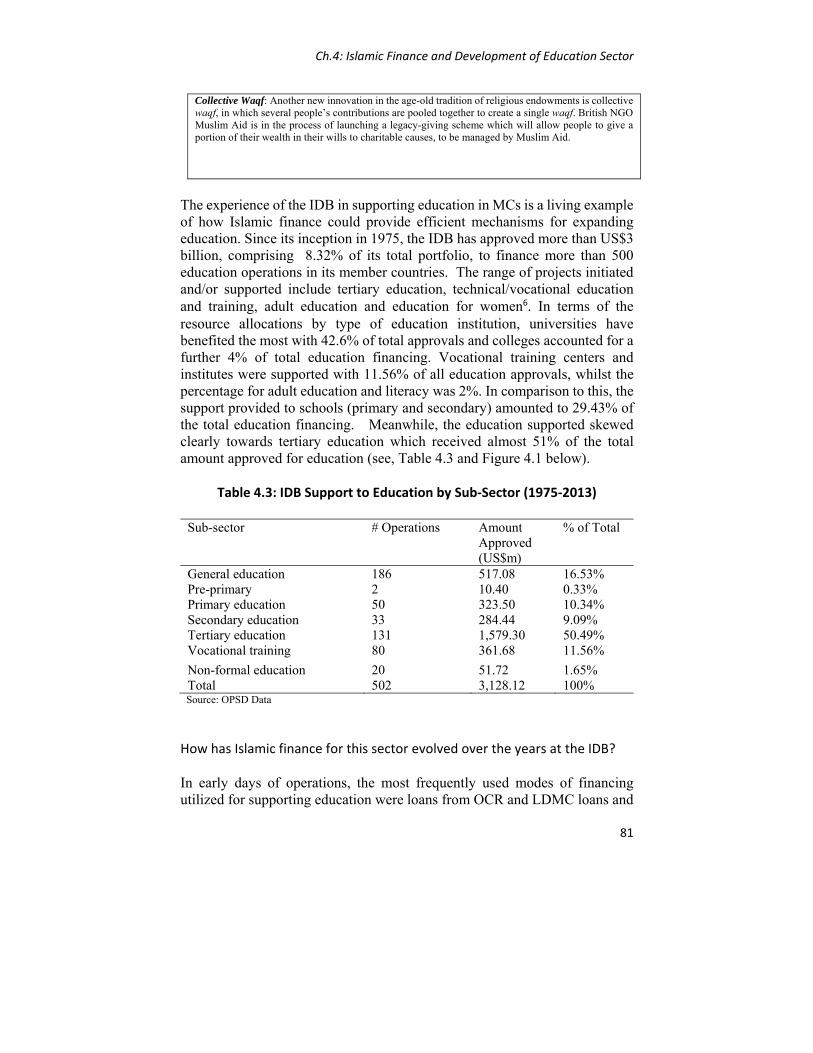

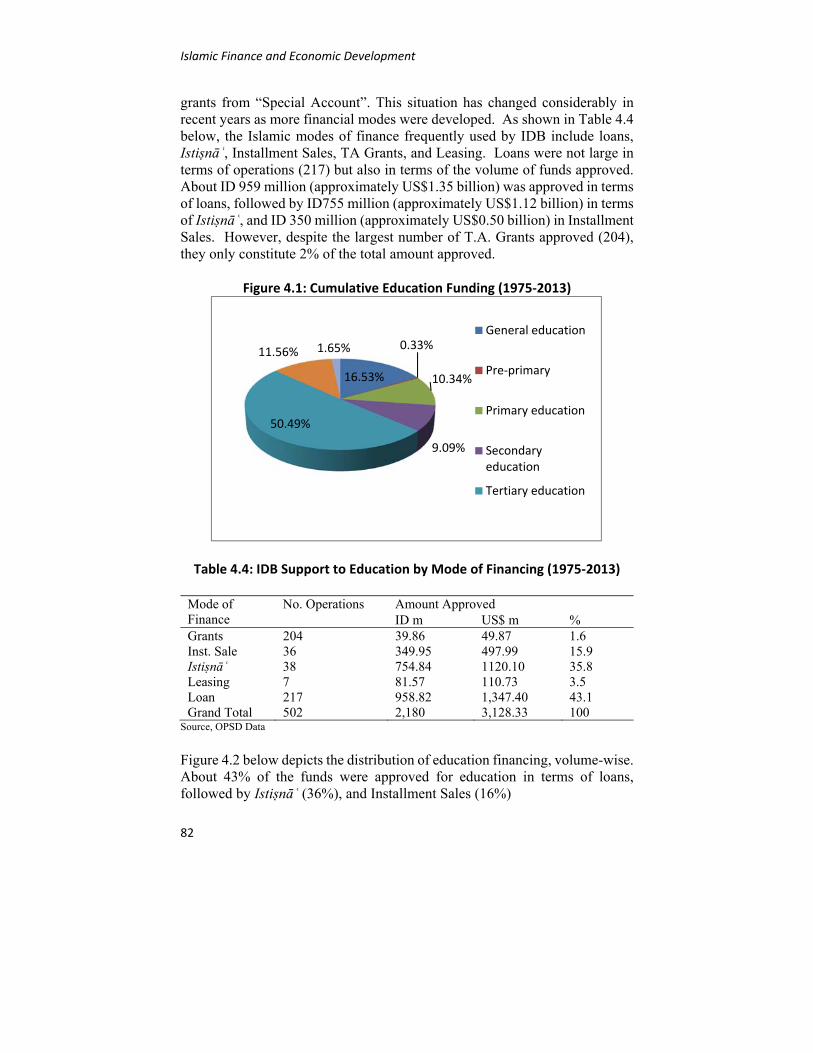

Islamic Finance and Development of Education Sector 69

CHAPTER‐5 ......................................................................................

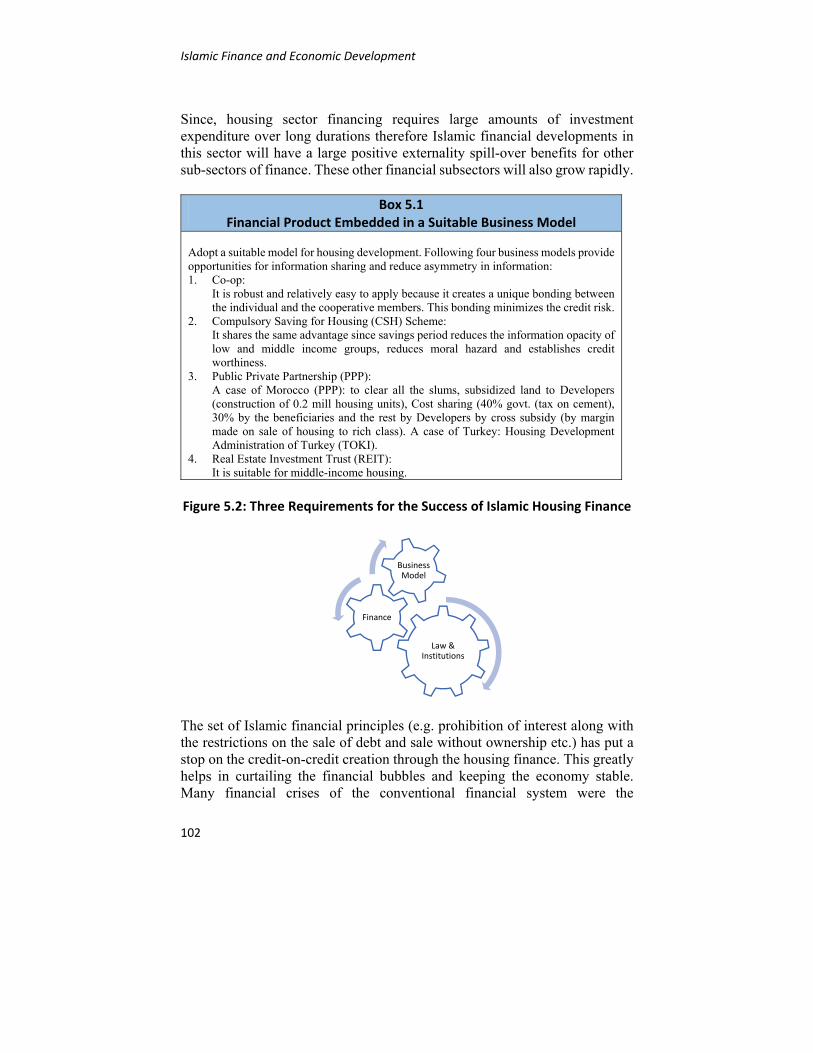

Islamic Finance and Development of Housing Sector 93 CHAPTER‐6 ......................................................................................

Role of Islamic Finance in Development of International Trade 107 CHAPTER‐7 ......................................................................................

Role of Islamic Finance in Financial Sector Development 129 CHAPTER‐8 ......................................................................................

Funding for Development Finance 171 CHAPTER‐9 ......................................................................................

Conclusions: Challenges, Lessons and Prospects 197

viii

ix

List of Abbreviations AAOIFI Accounting and Auditing Organization for Islamic

Financial Institutions ADB Asian Development Bank AfDB African Development Bank APIF Awqaf Properties Investment Fund AsDF Asian Development Fund BADEA Arab Bank for Economic Development in Africa BCBS Basel Committee on Banking Supervision BOT Build Operate and Transfer BOOT Build Own Operate and Transfer CDD Community Driven Development CGAP Consultative Group to Assist the Poor CIBAFI Council of Islamic Banks and Financial Institutions CIS Commonwealth of Independent States CIT Countries in Transition ECAs Export Credit Agencies EFA Education for All FDI Foreign Direct Investment GCC Gulf Cooperation Council GDP Gross Domestic Product GNI Gross National Income HDR Human Development Report HQLA High Quality Liquid Assets IAIS International Association of Insurance Supervisors ICD Islamic Corporation for Development of Private Sector ICIEC The Islamic Corporation for Insurance of Investments

and Export Credits ICR Irrevocable Commitment to Reimburse IDA International Development Assistance IDB Islamic Development Bank IFIs Islamic Financial Institutions IFIIs Islamic Financial Infrastructure Institutions iFSAP Islamic Financial Sector Assessment Program IFSB Islamic Financial Services Board IFSI Islamic Financial Services Industry IICRA International Islamic Centre for Reconciliation and

Arbitration IIF IDB Infrastructure Fund IIFM International Islamic Financial Markets IIRA Islamic International Rating Agency ILO International Labour Organization IMF International Monetary Fund IMFIs Islamic Microfinance Institutions IOSCO International Organization of Securities Commissions

x

IRTI Islamic Research and Training Institute IsDB Islamic Development Bank ISFD Islamic Solidarity Fund for Development ITFC International Islamic Trade Finance Corporation IWAH International Waqf Advisory House L/C Letter of Credit LDMCs Least Developed Member Countries MCs Member Countries MCPS Member Country Partnership Strategy MDBs Multilateral Development Banks MDFIs Multilateral Development Finance Institutions MDGs Millennium Development Goals MDP Microfinance Development Program MENA Middle East and North Africa MFIs Microfinance Institutions NGOs Non-Government Organizations MTN Medium Term Note OCR Ordinary Capital Resources ODA Official Development Assistance OECD Organisation for Economic Co-operation and

Development OFID OPEC Fund for International Development OIC Organization of Islamic Cooperation PPP Public Private Partnership REITs Real Estate Investment Trusts SMEs Small and Medium Enterprises SPV Special Purpose Vehicle SSA Sub-Saharan Africa TA Technical Assistance UIF Unit Investment Fund UN United Nations UNDP United Nations Development Program UNESCO United Nations Educational, Scientific and Cultural

Organization UNICEF United Nations Children's Fund WB World Bank WEF World Economic Forum WWF World Waqf Foundation

xi

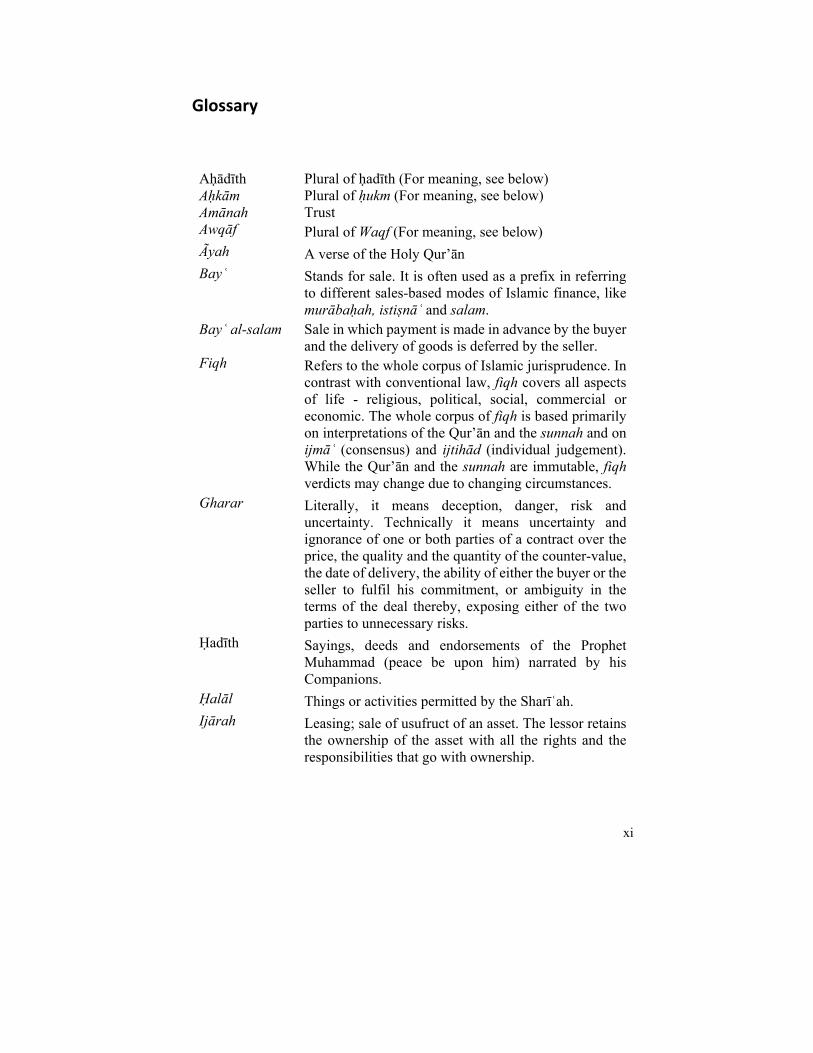

Glossary Aḥādīth Plural of ḥadīth (For meaning, see below) Aḥkām Plural of ḥukm (For meaning, see below) Amānah Trust Awqāf Plural of Waqf (For meaning, see below) Ãyah A verse of the Holy Qur’ān Bayʿ Stands for sale. It is often used as a prefix in referring

to different sales-based modes of Islamic finance, like murābaḥah, istiṣnāʿ and salam.

Bayʿ al-salam Sale in which payment is made in advance by the buyer and the delivery of goods is deferred by the seller.

Fiqh Refers to the whole corpus of Islamic jurisprudence. In contrast with conventional law, fiqh covers all aspects of life - religious, political, social, commercial or economic. The whole corpus of fiqh is based primarily on interpretations of the Qur’ān and the sunnah and on ijmāʿ (consensus) and ijtihād (individual judgement). While the Qur’ān and the sunnah are immutable, fiqh verdicts may change due to changing circumstances.

Gharar Literally, it means deception, danger, risk and uncertainty. Technically it means uncertainty and ignorance of one or both parties of a contract over the price, the quality and the quantity of the counter-value, the date of delivery, the ability of either the buyer or the seller to fulfil his commitment, or ambiguity in the terms of the deal thereby, exposing either of the two parties to unnecessary risks.

Ḥadīth Sayings, deeds and endorsements of the Prophet Muhammad (peace be upon him) narrated by his Companions.

Ḥalāl Things or activities permitted by the Sharīʿah. Ijārah Leasing; sale of usufruct of an asset. The lessor retains

the ownership of the asset with all the rights and the responsibilities that go with ownership.

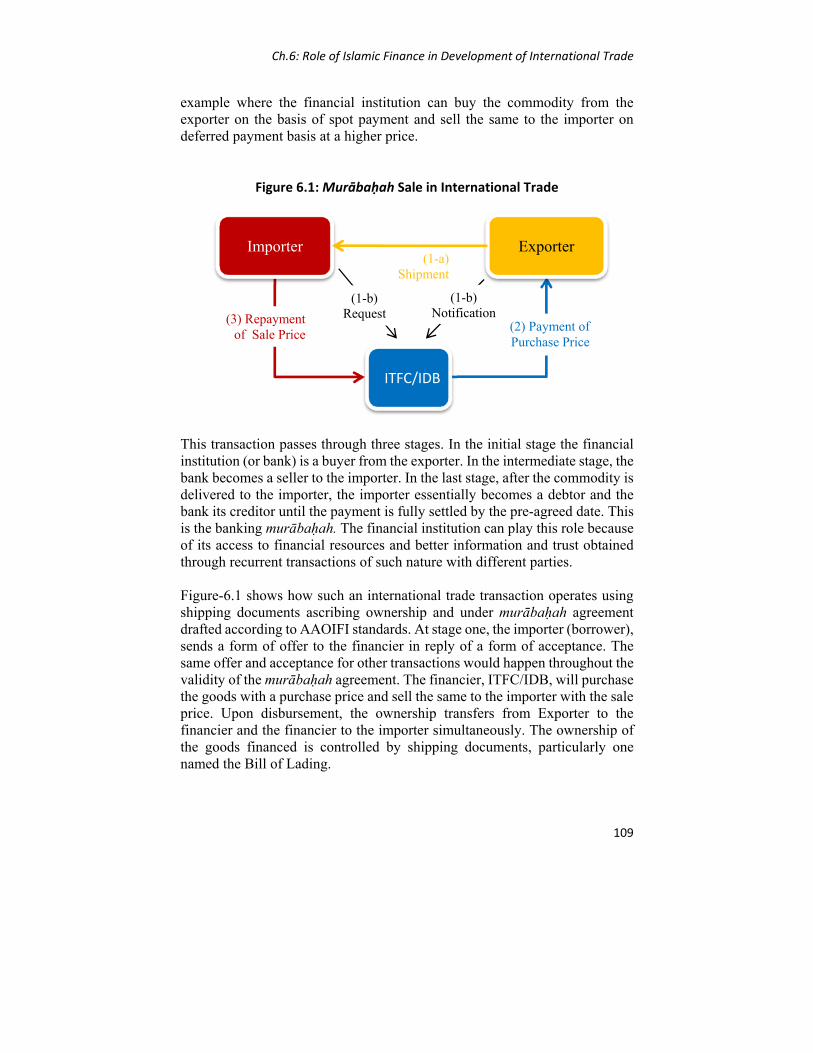

xii

Istiṣnāʿ (used as a short form for bayʿ al- Istiṣnāʿ)

Refers to a contract whereby a manufacturer (contractor) agrees to produce (build) and deliver a well-described good (or premise) at a given price on a given date in the future. As against salam, in Istiṣnāʿ, the price need not be paid in advance. It may be paid in instalments with the preferences of the parties or partly at the front end and the balance later on as agreed.

Muḍārabah A contract between two parties, capital owner(s) or financiers (called rabb al-māl) and an investment manager (called muḍārib). Profit is distributed between the two parties in accordance with the ratio upon which they agree at the time of the contract. Financial loss is borne only by the financier(s). The entrepreneur’s loss lies in not getting any reward for his services.

Murābaḥah Sale at a specified profit margin. The term, however, is now used to refer to a sale agreement whereby the seller purchases the goods desired by the buyer and sells them at an agreed marked-up price, the payment being settled within an agreed time frame, either in instalments or in a lump sum. The seller bears the risk for the goods until they have been delivered to the buyer. Murābaḥah is also referred to as bayʿmu’ajjal.

Mushārakah Partnership. A mushārakah contract is similar to a muḍārabah contract, the difference being that in the former, both the partners participate in the management and provision of the capital and share in the profit and loss. Profits are distributed between the partners in accordance with the ratios initially set, whereas loss is distributed in proportion to each one’s share in the capital.

Ribā Literally, it means increase or addition or growth. Technically it refers to the ‘premium’ that must be paid by the borrower to the lender along with the principal amount as a condition for the loan or an extension in its maturity. Interest, as commonly known today is regarded by fuqahā’ to be equivalent to ribā.

Salam The short form of bayʿal salam.

xiii

Sharīʿah Refers to the corpus of Islamic law based on Divine guidance as given by the Qur’ān and the sunnah and embodies all aspects of the Islamic faith, including beliefs and practices.

Ṣukūk al- Ijārah

A negotiable financial instrument issued on the basis of an asset to be leased. The investors provide funds to a lessor (say an Islamic bank). The lessor acquires an asset (either existing or to be created in the future) and leases it out if it is not already leased out. The ṣukūk al- ijārah are issued by the lessor in favour of the investors, who become owners of the leased asset in proportion to their investment. These ṣukūk entitle the holders to collect rental payments from the lessee directly. These ṣukūk can also be made tradable in the stock exchange.

Takāful An insurance structure compatible with Islamic law, an alternative for the contemporary insurance contract based on mutual assistance. A group of persons agree to share certain risk (for example, damage by fire) by collecting a specified sum from each. In case of loss to anyone of the group, the loss is met from the collected funds.

Ummah The nation of Muslims ʿUshr A tax on agricultural produce (one tenth) Wakālah Contract of agency. In this contract, one person

appoints someone else to perform a certain task on his behalf, usually against a fixed fee.

Waqf Appropriation or tying up a property in perpetuity for specific purposes. No property rights can be exercised over the corpus. Only the usufruct is applied towards the objectives (usually charitable) of the Waqf.

Zakāt The amount payable by a Muslim on his net worth as a part of his religious obligations; mainly for the benefit of the poor and the needy.

xiv

xv

Foreword Islamic Finance is playing a role in socio-economic development of countries and societies through public, private and voluntary sectors. This role can be significantly enhanced by providing enabling environment and promoting efforts to put it into practice in ideal form. This is an uphill task which will take some time but intention and action in this direction is a noble endeavour.

IDB since its inception as a development finance institution for the OIC member countries and for the Muslim communities in non-member countries has been using Islamic financial modes to provide development assistance. It has also endeavoured to revive the concept of waqf and its effectiveness for social causes. Over the last forty years it has grown from a single Bank to IDB Group comprising of the Bank and four affiliated entities: Islamic Research and Training Institute (IRTI), Islamic Corporation for Insurance of Investment and Export Credit (ICIEC), Islamic Corporation for the Development of the Private Sector (ICD), International Islamic Trade Finance Corporation (ITFC), and more recently Islamic Solidarity Fund for Development (ISFD). The year 1435H (2014) is the 40th anniversary of IDB’s inception and operation. Taking this into account, this year’s Occasional Paper focuses on “Islamic Finance and Economic Development: Lessons from the Past and Prospects for the Future.” In drawing these lessons the paper banks on the development financing experience of IDB and discusses what works and what does not in the use of Islamic finance for development assistance. This is done by analysing the constraints in financing and development of some key economic and social sectors, and giving examples of practices adopted as solutions to overcome those constraints. It also highlights the efforts of IDB in the development of Islamic financial sector in its member countries and at global level. Development assistance and financing also requires fund sourcing. The funding model of IDB has been changing and evolving towards a market based and waqf based funding. The paper also discusses this transformation and the issues involved.

xvi

The analysis of the role of Islamic finance in socio-economic development in this paper is general enough to be accessible to a wide range of readers. At the same time drawing on the financing experiences of IDB Group it is specific enough to attract policy makers and researchers to gain some new insights and devise institutions and policies suitable to local circumstances to increase the developmental impact of Islamic finance.

This Occasional Paper is an effort of IRTI towards its mandate to provide knowledge to help enable policy makers and practitioners implement Islamic financial system and practices for the socio-economic development of the Ummah. It has been competed with the help of a number of colleagues from various departments and entities of IDB Group. The authors of the paper and other colleagues from various departments of the IDB Group who directly and indirectly contributed to the preparation of this paper are highly appreciated and acknowledged.

Dr. Mohamed Azmi Omar Director General, IRTI

xvii

Credits and Acknowledgements Salman Syed Ali served as the principal author and coordinator for this occasional paper. Individual chapters were contributed by various co-authors whose names appear on the respective chapters: Salman Syed Ali (for Chapter 1); Ali Muhammad Khan, Zafar Iqbal, Sohail Malik and Aamir Ghani Mir (for Chapter 2); Musa Jega Ibrahim and Noman Siddiqui (for Chapter 3); Abdel-Hameed Bashir (for Chapter 4); Ahmet Suayb Gundogdu (for Chapter 6); Muhammad Umair Husain, Salman Syed Ali, Azfar Qarni, and Haseebullah Siddiqui (for Chapter 7); Mustafa Omar, Salman Syed Ali, Muhammad Obaidullah, and Turkhan Abdul Manap, (for Chapter 8); and Salman Syed Ali (for Chapter 9). The paper has also greatly benefited from the discussions and comments of Irfan Aleem from the Country Department who acted as official reviewer. Sajjad Qurban served as typesetter and provided excellent secretarial assistance. Mohammed Salat, Mohammad Asiri, and others managed the printing and publication process. The principal author and co-authors are grateful to the members of the IRTI Academic Committee and the members of the Management Committee for their insightful guidance and constructive suggestions from the inception to the completion of the occasional paper. We express our profound gratitude to a number of people who provided help and directly or indirectly contributed with information or clarification, these include: Farid Alam, Farid Khan, Intizar Husain, Nasim Shirazi, Sami Al-Suwailem, and Zakky Bantan. Thanks are also due to IRTI professionals and to the participants of the in-house seminar presentations of the occasional paper for their comments and suggestions.

xviii

We are also thankful to various departments and entities of the IDB Group for their cooperation. These include (alphabetically): Agriculture and Rural Development Department, Awqaf Properties Investment Fund (APIF), Country Programs Department, Group Operations Evaluation Department, Infrastructure Department, Islamic Corporation for the Development of Private Sector (ICD), Islamic Corporation for Insurance of Investment and Export Credit (ICIEC), Islamic Financial Services Department, International Islamic Trade Finance Cooperation (ITFC), Islamic Solidarity Fund for Development, Operations Policy and Services Department, Treasury Department, and World Waqf Foundation.

1

How can Islamic finance significantly contribute to socio-economic development? And why the present system of interest-based financing has not been consistent in contributing to socio-economic development in a systematic, sustainable and stable way? These are important questions in themselves but the recent events such as the global financial crisis, the European sovereign debt crises, and the Arab Spring have made these questions more relevant and urgent. Looking at economic history in retrospect we can assert that finance matters, and it matters both in the rise and in the fall of economies. Finance that is innovative, diverse, multichannel, morally guided, and linked with real economic activity is the type of finance we need for economic development. It can result in stable, inclusive, broad-based and sustainable growth. This study starts by asking some fundamental questions as to what role Islamic finance can play in socio-economic development, how similar or different it is from the conventional finance, and how its effectiveness can further be enhanced. The study analyzes the channels of impact of Islamic finance on real economic activities and, using the experiences of the Islamic Development Bank Group in development financing, highlights the success factors and challenges in using Islamic finance in various sub-sectors of the economy. The study also covers aspects of resource mobilization and sound development of Islamic financial sector that has its own importance for effective use of Islamic finance in socio-economic progress. The mission and objectives of the IDB Group are noble. The study highlights the ways in which the IDB provides development assistance and sets out a framework to draw lessons in using Islamic finance for economic development. The first part of Chapter-1 of this study describes the theoretical link between Islamic finance and socio-economic development. It highlights how Islamic finance is conducive for socio-economic development due to its emphasis on

CHAPTER 1

Islamic Finance and Economic Development: An Introduction and Overview

Salman Syed Ali

Islamic Finance and Economic Development

2

moral values, internal design, and diversity of financial products and multiplicity of operational channels. This type of finance can potentially serve the real economic sector very well, avoid system-wide excessive debt accumulation, and enhance stability. The second part of the chapter provides an overview of the subsequent chapters of the study where potential role of Islamic finance is discussed in the context of the IDB’s intervention in various economic sub-sectors. It also discusses the IDB’s efforts for Islamic financial sector development in its member countries and across the world. This effort towards Islamic financial sector development is important not only to provide a much needed stable financial system in the member-countries but it is also important for the enhanced impact of the IDB’s financing and development assistance in other sectors. As such, existence of Islamic financial institutions along with proper legal and regulatory framework can help the IDB in extending its development financing in Sharīʿah-compliant manner. Development financing requires resources and funding. It is noteworthy that the IDB’s own funding model is undergoing significant changes in the wake of increased demand for financing by its member-countries. The study is timely in its coverage of the IDB’s efforts in resource mobilization for its development operations. The Link between Islamic Finance and Economic Development Islamic finance is only a part of Islamic socio-economic system that is based on oneness and supremacy of Allah. This way of life is defined by a purpose, a freedom of choice and the associated accountability. The purpose is the willful obedience to Allah; the freedom is in the form of Allah’s granted choice given to the humans to obey or disobey Him; and the accountability is facing the consequences of this choice in this world as well as in the hereafter. With this world view, the Islamic principles of finance obligate the zakāt which is a monetary contribution taken from the rich and given to the poor; encourage cooperation, fair dealings, transparency and spending on others. These principles also remind that in addition to zakat, there are other rights of the poor in the wealth of the rich. Another set of Islamic principles prohibit the charging and paying of interest, indulging in gambling as well as gambling-like transactions, and usurping (eating unlawfully) other people’s wealth. Similarly, there are principles that discourage miserliness, profiteering and other behavioral ills of financial dealings. The concept of Islamic finance is based on the core tenants of Islam that define the rights of Allah and the rights of the other humans and creatures in relation

Ch.1: An Introduction and Overview

3

to man. It emphasizes respect of property rights, social and economic justice, observance of the rights pertaining to earnings and distribution of wealth, governance, mutual agreements etc. Islamic principles give rise to a system in which loans are not interest-bearing and not tradable hence pure debt-securities are eliminated. Debt would however be there through interest-free loans or through sale of goods and services at deferred but marked-up price. Sale-based, fee-based and profit-and-loss sharing contracts will be promoted. Sanctity of contracts and ethics in business conduct would be inculcated and enforced. Cooperation for the good and re-distribution to the poor and destitute would be promoted. These principles give rise to financial designs and institutional setups that become more conducive, in many ways, to social and economic development of human societies. We will argue that this system can restore and maintain a strong link between economy and finance, provide stability, and ensure social justice. While the emphasis on Islamic principles can generate financial instruments and institutional setups very different from the conventional financial products and institutions that are predominantly composed of interest-based debt, many similarities are also expected to exist between an Islamic and a conventional financial system. These similarities are due to the common objectives of financial systems with regard to the facilitation of economic transactions, resource mobilization, and resource allocation to alternate uses. Likewise, both systems face the problems of incomplete and imperfect information as their common challenges. The Objectives of Financial Systems The above mentioned objectives of financial system and the importance of finance for economic development are well recognized today and they were also known in the past. For example, in recent years Levine (2005 and 2007) has forcefully shown the long-run connection between economic growth and finance. However, hundreds of years earlier Ibn Khaldun (1377) had also identified the relationship between finance and economic growth and also argued that this bidirectional relationship depends on many auxiliary and catalytic factors such as the security of life and property, low tax rates, healthy physical environment, division of labour, specialization and sedentary culture. The modern economic thinking argues for similar aspects, emphasizing the role of information and transaction costs, taxation system, contract enforcement, and the legal and regulatory environment in the emergence and

Islamic Finance and Economic Development

4

evolution of different financial contracts and financial institutions across countries and work as the moderating factors in this relationship. With regard to the above mentioned three key roles of finance, namely, facilitation of transactions, resource mobilization, and its allocation; the relative importance of these roles change with time and with the institutional setup of the financial system. Rousseau (2003) has argued, that during the past few centuries, it had been the financial resource mobilization and the developments and innovations in it that had played more important role in spurring economic development. For example, the resource mobilization made possible by muḍārabah contracts that were used in Muslim territories during 7th, 8th and 9th centuries; and its later adaptation and transformation as commenda in Europe during the Medieval ages promoted long-distance trade (Goitein;1967) and contributed to socio-economic development. Similarly, the creation of joint stock and the concept of limited liability companies in the sixteenth and seventeenth centuries in Europe promoted large-scale resource mobilization and made possible the pooling of financial resources for furthering the trade as well as the manufacturing sectors. The limited liability provided the necessary indemnity and risk tolerance for the investors in joint-stock companies, while the legal entity of corporate firm provided the exit opportunity without necessarily winding-up the business.

Figure 1.1: Key Purposes of the Financial Sector

Nevertheless, the other two roles of the financial sector i.e., facilitating economic transactions and optimal allocation of funds are the main objectives of mobilizing resources. Recently, particularly the frequent occurrences of several financial crises and the consequent adverse effects on economic

Roles of the Financial Sector

Fund Mobilization

Resource Allocation

Facilitating Economic Activities

Ch.1: An Introduction and Overview

5

development testify to the importance of these other two roles of finance and what happens if these roles are not managed properly. By providing a moral and legal set of institutions, rules and norms, an Islamic financial system links the financial and the real economy in stronger ways to provide economic growth with stability. Development economists recognize these other two important roles of the financial sector that go beyond its fund mobilization role. For example, it is recognized that the development of financial sector provides information to enhance resource allocation, improves the corporate governance, helps in the trading and diversification of risks, and facilitates the exchange of goods and services. These functions in turn influence various sub-sectors of the economy. They contribute towards the private sector development through productivity enhancement and capital accumulation, increase in competition and innovation, and improvement in payments system; towards achieving macroeconomic stability through a better shock absorption capacity, investment in long-term projects, and less fragile financial system; towards public sector development through moral responsibility and the development of the third-sector, less crowding out of private investment; and towards stimulating household sector through human capital accumulation and increase in consumption (Figure 1.2). All these ultimately increase human well-being per capita at sustainable rates. Going beyond GDP per capita, the effects of the financial sector development can also be measured in terms of poverty reduction, and rise in wellbeing. The channels through which the financial sector development can reduce poverty can be ‘direct’ as well as ‘indirect’. Financial sector development can enhance the GDP growth as discussed above and hence indirectly influence poverty situation through the trickle-down effect. The direct channel is through an improved access to financial services by the poor and underprivileged. The improved access to finance helps in the job creation, expansion of micro, small and medium enterprises as well as of the informal sector. It also helps in the consumption smoothing for the poor. All these factors can potentially contribute to greater welfare and development of the society.

Islamic Finance and Economic Development

6

Figure 1.2: Financial Development and Impact on Wellbeing and GDP Per Capita Growth

The Disappointments of the Conventional Finance However, these potential advantages have not been materialized to benefit everyone. There is a growing concern that the conventional finance may have failed in alleviating poverty, reducing unemployment and accomplishing social justice. Instead, the financial sector has acquired a life of its own independent of its serving nature for the economy. For example, the financial sector now grows independent of the real economic activity and survives on rampant speculative activities that constitute wealth transfer rather than the wealth creation in the society. This has given rise to disappointments and a strong need to search for solutions. This is further elaborated below. Unemployment, poverty and inequality: While the financial sector has been growing fast, its benefits have not been reflected in some key aspects of economic development such as in the job

Financial Sector Development implies

• Increased Mobilization of Savings

• Efficient Resouce Allocation

• Facilitating Exchange of Goods and Services

• Improved transparency and Timely Dessimination of Information

• Imroved Corporate Governance

• Facilitating Risk Management

Influenced Sectors

• Private Sector Development

• Macroeconomic Stability

• Public Sector Development

• Third sector Development

• Household Sector

Specific Impact Areas

• Productivity Increase and Capital Accumulation

• Increased Competition and Innovation

• Better Payment System

• Shock Absorption

• Investment in Long‐term Projects

• Less (Costly) Financial Crises

• Investment in Key Infrastructure

• Less Crowdingout of Private Investment

• Human Capital Development

• Increase in Consumption

Increased Well‐being

Increased Per Capita Income

Ch.1: An Introduction and Overview

7

creation, poverty reduction and in achieving social justice. In the wake of a fast growing financial sector and with the existence of the above mentioned potential link between finance and economy it would not have been unreasonable to expect significant reduction in unemployment. However, unemployment remains a major unresolved problem in many developed countries with developed and growing financial sectors. According to ILO data,1 in 2011, unemployment in USA remained high at 8.9 percent, in UK at 7.8 percent, in Spain at 21.6 percent, in Italy at 8.4 percent and in France at 9.3 percent. If one looks at youth unemployment it is much higher (close to 30% and above, see Clements et al., 2012). Similarly, the growth of finance, despite its strong connection with economic growth, has not been inclusive and has benefited only a small group causing increased inequalities of income, wealth and opportunities. For example, in OECD countries the inequality of income has increased since 1980s in a way that the average income of the richest 10 percent of population became nearly nine times that of the poorest 10 percent in 2005.2 The Gini coefficient in the same period also increased from 0.29 to 0.316 and subsequently remained high. The realization of this failure is getting stronger among some economists. Stiglitz (in his book, Price of Inequality, 2013) has therefore commented that “the power of markets is enormous, but they have no inherent moral character. We have to decide how to manage them…. For all these reasons, it is plain that markets must be tamed and tempered to make sure they work to the benefit of most citizens. And that has to be done repeatedly, to ensure that they continue to do so.” Debt Burden: Another consequence of conventional finance is unsustainable debt burden both in private and public sectors. The debt grows at contractual rate and it grows persistently without any effort, while the payback capacity through production of new goods and services not only fluctuates but also requires considerable efforts and good decision making on the part of the borrower. As the conventional finance promotes debt over all other forms of financing, the external indebtedness of developing countries has been increasing persistently. It increased from USD 2,338 billion in 2005 to USD 4,829 billion in 2012.3 On average, this debt was 71.9 percent of their exports and 22.1 percent of their Gross National Income in 2012.4 This average hides the high variation across countries where some were burdened significantly more than the others. This high indebtedness is alarming for the economic stability and economic freedom of future generations in these developing countries. Interestingly, a large portion (51.8 percent) of the long-term debt was public and publically guaranteed (USD 1,765.6 billion out of USD 3,406.3 billion

Islamic Finance and Economic Development

8

long-term external debt) indicating that it was presumably obtained not for profit but for development and for meeting social needs. Instability: Even in the most developed economies the direct value addition by the financial sector to the GDP is small in comparison with value-added contributions of other sectors (for example, value-added by financial sector in the USA was 8.3 percent in 2007 and 4.9 percent in 1980.5 While value-added by industrial sector6 constituted 22.0 percent of GDP and the services sector7 constituted about 76.9 percent of the GDP of the USA in 2007). The indirect productive contribution of the financial sector to the real economy is its supply of intermediate services that are used as inputs in the real economic sectors, which are: financial resources that are actually used in productive activity, its allocation and information and risk management services that are required to execute this optimal allocation of financial resources among the competing customers.8 However, due to the legal and social acceptance of interest-based lending, sale of debt as well as sale without ownership as the essential liberal features of conventional finance, the financial sector has been able to create a sideshow or life of its own. In this sideshow it takes risks, creates new risks, transfer those risks, and then tries to manage them as well. This inflates the size of the financial sector which helps it survive and extends its artificial life and increases its book-earnings in the form of fee, commission and windfall capital gains. This is the realm of speculative financial markets, including those for financial derivatives, promotion of borrowing culture by the financial intermediation institutions and their unchecked extension of credit. Financial sector thus gets a life of its own rather than remaining a servant of the real economic activity. This domain of finance is expandable by the financial sector itself by choosing to supply certain kinds of activities and hence the financial sector volume grows tremendously. In financial markets it is reflected in terms of high market capitalization, outstanding amount of debt, trading volume, volume of derivatives outstanding, etc. In financial intermediation services it is reflected in high growth of credit or equivalently in high indebtedness. In short, the direct and indirect value-added in GNP by the financial sector is small but volume and size of financial sector in nominal value is enormous, the associated risks are high, and the productive resources and human capital that it has diverted to itself are large. This makes financial sector’s size and its volatility much more important factors towards creating instability that can be transmitted to the real sector than the positive contribution through the size of direct value added share of the financial sector in the GDP. In short, financial turmoil and fluctuations can cause value destruction in many subsectors of the real economy resulting in much greater cost than the simple diversion of productive resources to a low value added

Ch.1: An Introduction and Overview

9

activity. These costs remain unaccounted in the present method of calculations. Social Effects: The real cost of the debt-based system gets hidden from the private parties who do not internalize it but have passed it to the society as negative externalities. The negative externalities of interest-based finance come in many forms: from the inculcation of greed, moral degeneration, suppression of cooperative spirit, and promotion of self interest in the society to the distortion of incentives, the promotion of a culture of risk shifting, and a culture of preponing enjoyment and postponing the burden to the future. Can Islamic Finance Overcome these Problems? Islamic finance in principle can contribute to economic development through the same ‘direct’ and ‘indirect channels identified above. However, because of its design principles and emphasis on moral behaviour it has the potential to avoid the problems of disconnection between the financial and the real economic sectors. A disconnect which has resulted in financial growth without employment growth, increased inequalities, excessive indebtedness and instability. Islam promotes markets that are based on moral principles: seeking mutual gain and win-win outcomes that make the two parties of trade better-off. The same principle prevents gambling and interest-based finance that tends to be win-lose situation and thus morally damaging. There is also a financial inclusion side through which Islamic finance can positively contribute to economic development. By integrating zakāt, charity and philanthropic activities in the financial system, the poor have better access to finance and therefore are better able to contribute to economic development. In addition to the above universal advantages of Islamic finance there is also a pro-financial inclusion argument for Muslim societies in the present times. Muslims, comprise a large segment of world population and want to avoid interest due to it’s religious prohibition. Offering Islamic financing can bring them to the formal financial sector thus improving financial inclusion and impact on economic growth. Given this condition, Islamic finance can have greater impact on economic development both due to its design principles and due to enhanced financial inclusion.

Islamic Finance and Economic Development

10

Advantage of Design Principles of Islamic Finance: On the design side it may be noted that Islamic finance is not money-for-money finance. It is money-for-goods & services; and goods & services-for-money finance. This means that Islamic financing will always have real effects due to its constant link with economic activity. This is in contrast to the conventional finance where a large portion of finance comprises of money-for-money transactions. Such money-for-money financial transactions where goods and services do not directly come into the picture at the transaction level, may or may not contribute to the real economic activity. This detachment of conventional finance from the real economic activity help create an accumulated increase of divergence of the two sectors resulting in financial crisis. These frequent financial crises can be seen as abrupt re-adjustments due to the absence of any endogenous mechanism to keep the financial and the real sectors of the economy linked together. The private sector finance is more prone to this disconnect than the public sector finance because self-interest can lead to private gain transactions utilized for pure financial speculation, such as those offered by derivative trade and pure speculative trading (sale and purchase) of shares in the secondary stock markets. Governments usually do not indulge in these speculative transactions except for their financial hedging needs. However, the use of ordinary loan on interest in private or public transactions also breaks the link between finance and the real economic sectors creating an adverse impact on economic development. The amount of interest on a loan can grow at the contractual rate for an indefinite period until the interest and the principal is fully paid. Whereas, the economic projects in which the fund was invested, if not wasted, do not grow by any contract. The project’s return can grow faster or slower and do not remain the same in all periods. It is affected by numerous factors where many of them are not in control of the beneficiary of the loan. This can easily result in more borrowing, higher indebtedness and higher interest obligation to service the existing loan without any benefit accruing to the project. The possibility of this happening is more in case of borrowings for public projects. Over the course of time the increase in the indebtedness can be more than the increase in the value of the project. The observed high and persistent indebtedness of many developing countries, as mentioned above, coupled with their low economic growth and underperforming real economic sectors point to the problem that the link between finance and economy has been broken and that finance is not necessarily helping development. Additionally, when it does impact growth, it is not promoting equitable growth and it fails in reducing poverty, unemployment and achieving social justice.9

Ch.1: An Introduction and Overview

11

From the lenders’ perspective, as long as a collateral is available that can be liquidated in case of default, the lender has no incentive to help the borrower sort out the problems encountered in case of the underperformance of the project or to help the borrower in overcoming those management, governance and other problems. The collateral is sometimes not in the form of a tangible asset belonging to the borrower but it is a government guarantee put in place to encourage lending to certain sectors or prioritized social needs or simply for political leverage. Again the result is the same that is, over-lending by the lenders and the indebtedness of the borrowers beyond their capacity to repay.10 Moreover, with weak regulations and weak bankruptcy regimes the loans do not close and the debt hangover perpetuate for long. The Islamic finance principle of profit and loss sharing automatically adjusts the cost of finance according to the payback capacity of the project. It increases when the project returns are high and decreases when the returns are low. The principle of no trading in debt puts up such restrictions that the ballooning of debt is stopped. Whereas, financing by the credit sale creates a debt obligation on the buyer, this debt cannot grow by refinancing and rollover of the receivables. Similarly, the prohibition of selling what is not owned and regulations against gharar restricts the possibilities of undue financial speculation and keeps financial sector growth to stay in line with the growth of the real sector. Islamic finance, thus, ‘improves the incentives’11 of all economic agents (direct parties to the contracts, auxiliary parties, as well as their regulators) to keep them aligned to the real needs of the society. Since in reality the behavior of economic agents is not exclusively governed by economic motives and incentives alone, therefore, for further enhancement of this aspect, Islamic finance uses both the moral (internalized values) and legal (external enforcement) mechanisms. Diversity of Products and Financial Inclusion: Islamic finance provides a more diversified set of financial products compared to the conventional finance. The seemingly large variety of modes and products available under the conventional finance gives a wrong impression of its diversity. While many different kinds of financial products for satisfying the needs of economic agents can potentially exist, the reliance of the conventional finance on interest has resulted in the strange phenomenon of narrowing its options in products. Almost all financing under the conventional financial system is now based on only one mode, i.e., interest-based debt instruments. The seemingly large variety of financial products is nothing but debt with various repayment options and variations of the collateral. Zero coupon bonds, fixed coupon bonds, variable interest mortgage, fixed rate

Islamic Finance and Economic Development

12

mortgage, debt with balloon repayment near the end of maturity period, interest rate futures and options, interest rate swaps, saving deposits, wealth protected funds, CDOs, and CDS are just some examples of the above fact. This is referred to by an astute observer of the scene as potato kitchen of the conventional finance where only potato is available in various forms: boiled potato, mashed potato, curried potato, backed potato, fried potato, potato chips, French fried potato, etc. This is not a real diversity of dishes.12 As a result, conventional finance finds itself in a difficult position for its application to a wide range of uses. It thus moved to become simply an act of trading in, and renting of, money-for-money. Therefore it had to devise some long-winded and indirect methods to make finance applicable to the economic and social needs of the society. This, often results in inadvertent and unwelcome outcomes creating negative externalities for the society at large. For its control, therefore, heavy reliance on external supervision and regulation is sought. The system invariably results in benefiting one party at the cost of other. The winning party is the one that has a greater bargaining power, mostly the lender but sometimes the borrower also has the upper hand when there is a competition in lending among the lenders. Another disadvantage is that external supervision and regulation cannot keep pace with the changing market conditions due to the usual information and decision gaps and often result in distorting the incentives of the parties. This is not to claim that regulation and supervision will not be needed for the smooth functioning of Islamic finance but only to point out the fact that Islamic system relies on principles-based regulation; and by making available a suitably diverse set of financial products which address the specific actual needs of the customers, it avoids many distortions and excesses that otherwise invite more regulation and supervision which often fail.13 It would be interesting to analyze how and why the conventional finance became restricted to loans only. Again the key culprits are ribā (interest-based debt) and gharar (gambling and wagering) that the conventional finance gradually accepted as indispensable. Once this was accepted, no room was left for tying finance with real economic needs because pure money-for-money transactions could be carried out for wealth transfer, but are devoid of wealth creation. That is, gains and losses could be made simply from risk transfers without necessarily contributing to wealth creation or welfare improvement.14 Meanwhile, wealth creation and gains from trade, are the hallmarks of a real exchange of goods and services. Indeed, pure financial deals cannot perpetually generate income out of thin air, there has to be a functioning real sector to generate some value addition, albeit small, without which the speculative finance cannot provide credible betting

Ch.1: An Introduction and Overview

13

opportunities. However, real activities are little more costly than money-for-money speculation and pure risk transfer activities; but collectively they are more rewarding and generate better stability. Money-for-money in contrast generates individual returns at the expense of the society. It thus becomes a kind of Prisoner’s Dilemma Game: The real economy requires cooperation among agents to produce the common good. Money-for-money is a Defection strategy that generates private returns but is self-defeating in the medium term. As opposed to this, Islamic finance has a variety of modes of finance that can be combined in various ways to produce a larger variety of financial products to suit the needs in a wider range of applications. These modes evolve from, and are based on, real economic needs, not from money-for-money transactions. Historically, human societies had relied only on four basic contractual ways of exchange and transfering goods and services between people. These are: sale, lease, loan, and gift in various forms. Societies have also used four basic ways of working together, with mutual consent, for economic gains. These are: partnership or joint venture, agency, hiring, and social cooperation. Islamic finance uses all these separately as well as in various combinations to function. A point to note is that all these modes of finance that are made available under the Islamic financial system are also available to conventional finance. However, these modes are not being practiced on a significant scale due to the dominance of the interest-based debt finance which is easy to implement and seemingly advantageous to the contracting parties. The real cost of the interest bearing debt-based system remains hidden, as the contracting parties do not internalize the costs but pass it to the society as negative externalities. As mentioned before, the negative externalities of interest come in many forms: from the inculcation of greed, moral degeneration, suppression of cooperative spirit, and promotion of self interest in the society to the distortion of incentives, promotion of a culture of risk shifting, and a culture of preponing enjoyment and postponing the burden to the future. This gives rise to excessive debt accumulation in the economy, run-away financial sector, and frequent crashes. Diversity of Application and Multiplicity of Channels: The coverage of Islamic finance is very broad in supporting and creating assets and in facilitating exchange of goods and services. It can cover all economic sectors, private and public, of commercial and development nature. Moreover, it is not a single-mode finance but uses multiple modes and their combinations to create a wide variety of ways to finance any sector that can have a role in

Islamic Finance and Economic Development

14

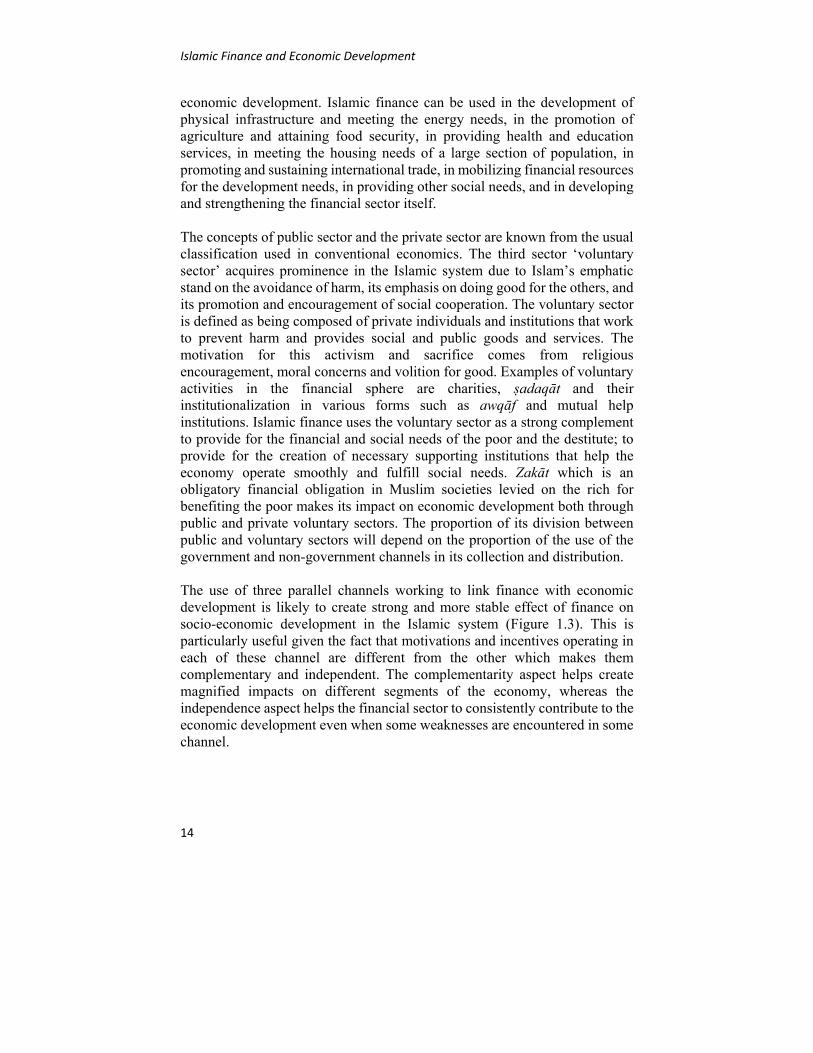

economic development. Islamic finance can be used in the development of physical infrastructure and meeting the energy needs, in the promotion of agriculture and attaining food security, in providing health and education services, in meeting the housing needs of a large section of population, in promoting and sustaining international trade, in mobilizing financial resources for the development needs, in providing other social needs, and in developing and strengthening the financial sector itself. The concepts of public sector and the private sector are known from the usual classification used in conventional economics. The third sector ‘voluntary sector’ acquires prominence in the Islamic system due to Islam’s emphatic stand on the avoidance of harm, its emphasis on doing good for the others, and its promotion and encouragement of social cooperation. The voluntary sector is defined as being composed of private individuals and institutions that work to prevent harm and provides social and public goods and services. The motivation for this activism and sacrifice comes from religious encouragement, moral concerns and volition for good. Examples of voluntary activities in the financial sphere are charities, ṣadaqāt and their institutionalization in various forms such as awqāf and mutual help institutions. Islamic finance uses the voluntary sector as a strong complement to provide for the financial and social needs of the poor and the destitute; to provide for the creation of necessary supporting institutions that help the economy operate smoothly and fulfill social needs. Zakāt which is an obligatory financial obligation in Muslim societies levied on the rich for benefiting the poor makes its impact on economic development both through public and private voluntary sectors. The proportion of its division between public and voluntary sectors will depend on the proportion of the use of the government and non-government channels in its collection and distribution. The use of three parallel channels working to link finance with economic development is likely to create strong and more stable effect of finance on socio-economic development in the Islamic system (Figure 1.3). This is particularly useful given the fact that motivations and incentives operating in each of these channel are different from the other which makes them complementary and independent. The complementarity aspect helps create magnified impacts on different segments of the economy, whereas the independence aspect helps the financial sector to consistently contribute to the economic development even when some weaknesses are encountered in some channel.

Ch.1: An Introduction and Overview

15

Figure 1.3: Islamic Finance – Multiplicity in Channels of Operation

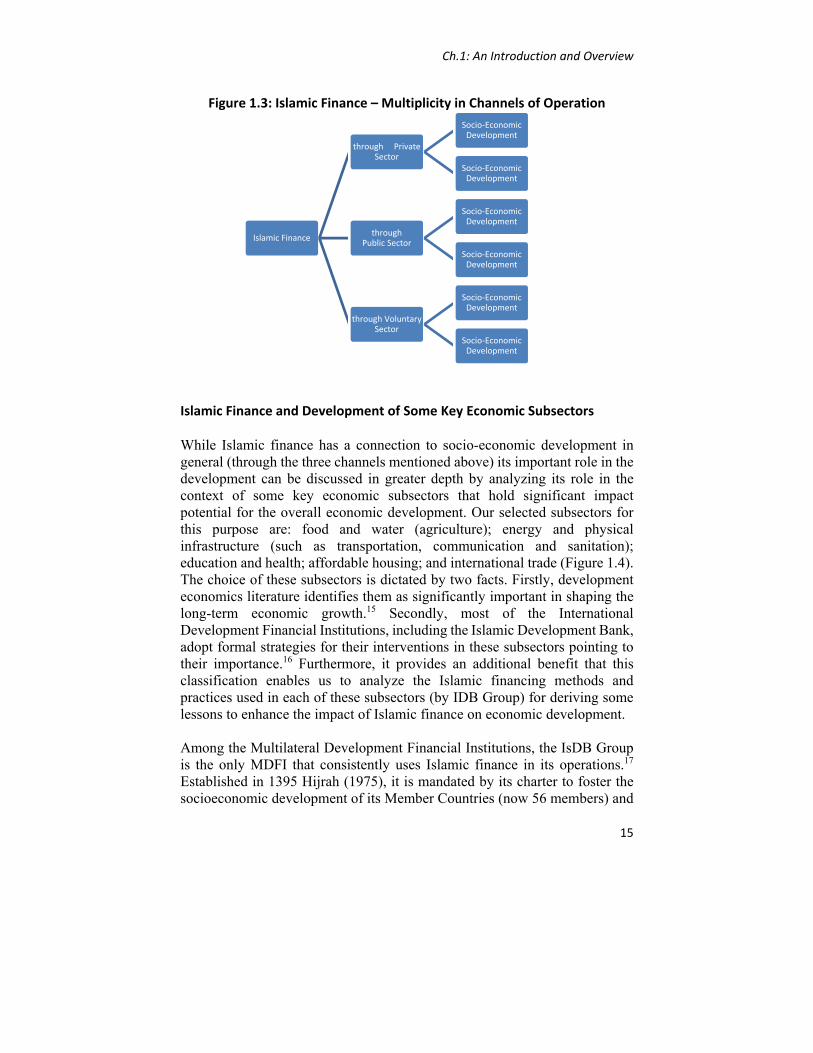

Islamic Finance and Development of Some Key Economic Subsectors While Islamic finance has a connection to socio-economic development in general (through the three channels mentioned above) its important role in the development can be discussed in greater depth by analyzing its role in the context of some key economic subsectors that hold significant impact potential for the overall economic development. Our selected subsectors for this purpose are: food and water (agriculture); energy and physical infrastructure (such as transportation, communication and sanitation); education and health; affordable housing; and international trade (Figure 1.4). The choice of these subsectors is dictated by two facts. Firstly, development economics literature identifies them as significantly important in shaping the long-term economic growth.15 Secondly, most of the International Development Financial Institutions, including the Islamic Development Bank, adopt formal strategies for their interventions in these subsectors pointing to their importance.16 Furthermore, it provides an additional benefit that this classification enables us to analyze the Islamic financing methods and practices used in each of these subsectors (by IDB Group) for deriving some lessons to enhance the impact of Islamic finance on economic development. Among the Multilateral Development Financial Institutions, the IsDB Group is the only MDFI that consistently uses Islamic finance in its operations.17 Established in 1395 Hijrah (1975), it is mandated by its charter to foster the socioeconomic development of its Member Countries (now 56 members) and

Islamic Finance

through Private Sector

Socio‐Economic Development

Socio‐Economic Development

throughPublic Sector

Socio‐Economic Development

Socio‐Economic Development

through Voluntary Sector

Socio‐Economic Development

Socio‐Economic Development

Islamic Finance and Economic Development

16

Muslim communities in non-Member Countries, in accordance with the principles of Sharīʿah (Islamic Law).18

Figure 1.4: Islamic Finance: Possible Applications in Economic Development

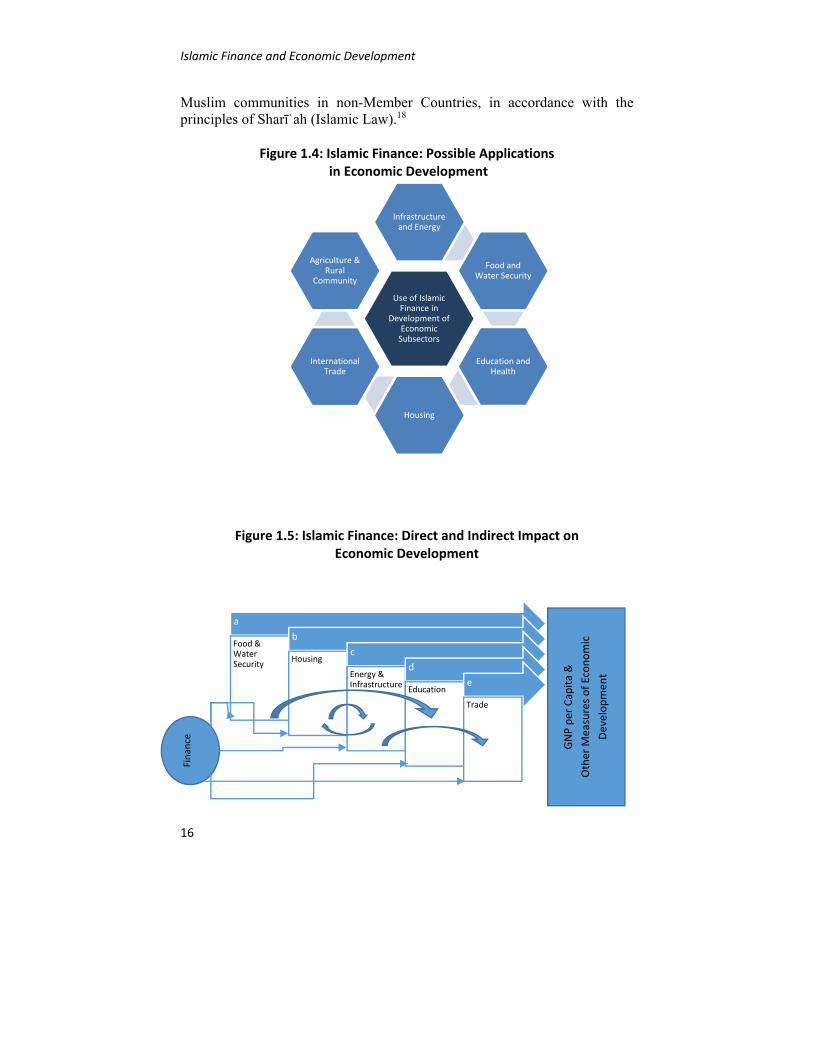

Figure 1.5: Islamic Finance: Direct and Indirect Impact on Economic Development

GNP per Capita &

Other M

easures of Economic

Developmen

t

a

Food & Water Security

b

Housingc

Energy & Infrastructure

d

Educatione

Trade

Finance

Use of Islamic Finance in

Development of Economic Subsectors

Infrastructure and Energy

Food and Water Security

Education and Health

Housing

International Trade

Agriculture & Rural

Community

Ch.1: An Introduction and Overview

17

It may be noted that the development of these subsectors not only make a direct impact on the overall socio-economic development, but growth in one can affect the growth of the others and hence also indirectly impact the overall socio-economic progress (Figure 1.5). For example, food and water security makes a population better off that large number of people can have the mental opportunity to consider seeking more education. This increases both the demand and supply of education in the society and subsequently increasing the level and rate of socio-economic development. Similarly, the development of housing sector can have an impact upon the energy and infrastructure sector; and in reverse manner, the availability of road and energy infrastructure in certain locality can give rise to faster development of housing projects in that area and hence, leave an impact upon the overall socio-economic development. In short, Islamic finance is conducive for socio-economic development due to its emphasis on moral values, internal design, and diversity of financial products and multiplicity of operational channels. This finance can potentially serve the real economic sector very well, avoid system-wide excessive debt accumulation, and enhance stability. The Overview of the Subsequent Chapters of the Study In the subsequent chapters (Chapter 2 to 6) the study will discuss how Islamic finance can be usefully applied for the development of (i) food and water security; (ii) energy and physical infrastructure; (iii) education and health; (iv) affordable housing; and (v) international trade. In each case and where available, examples will be drawn from Islamic financing activities of the IDB Group. It will then attempt to analyze the factors that contribute to the success or failure of Islamic finance in those projects and activities. For each of these subsectors the following questions are explored:

1. What is the existing level of the development of the subsector in IDB Member Countries and what is its impact on the overall economic development?

2. What is the importance of finance in the development of this sector?

3. What are the challenging issues in financing this sector?

4. How can Islamic finance be usefully applied for the development of this sector and why is it expected to make an impact?

Islamic Finance and Economic Development

18

5. What is the current state and modes of IDB Group’s financing to this subsector; can its scope and scale be increased and what are the associated challenges?

6. What are the success factors and their relative importance?

7. What lessons can be drawn for enhancing the use and impact of Islamic finance on this subsector through the public sector, private sector and voluntary sector financing channels?

Other important dimensions in using Islamic finance for socio-economic development are resource mobilization (Chapter 7) and the development of Islamic financial sector itself (Chapter 8). In this regard, a well-developed Islamic financial sector is not only important for resource mobilization by private and voluntary sectors but it is also important for the cost efficiency and enhanced development impact of the IDB Group’s operations in its member countries. This study will address these important aspects, highlighting the challenges and achievements that have been made so far. It concludes with (Chapter 9), drawing lessons for future directions.

Notes 1 ILO Data website. 2 OECD (2011) and Salman et al. (2013b) citing from OECD (2011). 3 World Bank (2014), International Debt Statistics 2014, p.35. 4 Ibid. 5 Greenwood and Scharfstein (2003). 6 In World Bank data ‘Industry’ corresponds to the ISIC divisions 10-45 and includes manufacturing (ISIC divisions 15-37). It comprises value-added in mining, manufacturing, construction, electricity, water, and gas. 7 In World Bank data ‘services’ correspond to ISIC divisions 50-99 and they include value-added in wholesale and retail trade (including hotels and restaurants), transport, and government, financial, professional, and personal services such as education, health care, and real estate services. Also included are imputed bank service charges, import duties, and any statistical discrepancies. 8 Haldane (2009) also recognizes two roles of financial sector: risk management and risk taking. According to him risk management is a type of productive activity while risk taking is not. The nominal size of the financial sector reflects both together without distinguishing former from the later. 9 See note xx. For a more detailed discussion and literature survey on these aspects see Chapters 3 and 4 of Ali, Shirazi, and Nabi (2013b), Ali (2013a), and Chapter 1 of Ali (forthcoming 2014). 10 Experience of Fannie Mae and Freddie Mac shows clearly that sovereign guarantee and mandated increase in credit to minority borrowers and underserved locations resulted in the declining underwriting standards and over lending. Rajan (2010) among others put it as a key explanation behind the precipitation of the global financial crisis.

Ch.1: An Introduction and Overview

19

11 For a discussion on the regulatory response to the global financial crisis and the need for improved incentives see Claessens and Kodres (2014). 12 Al-Jarhi (2013) writes in his blog: “Conventional finance has only one ingredient to use in structuring its financial products, viz., the conventional loan contract. Like a potato kitchen, it is a matter of how you would like your potatoes: boiled, baked, fried, mashed, curried, etc. Islamic finance in contrast has several modes of finance to use in product structuring. The room for financial innovation is almost limitless. With numerous modes of finance, Islamic finance is haute cuisine. Therefore, while you can eat almost anything in an Islamic finance kitchen, except for potatoes (which refers here to lending money at interest), the conventional finance kitchen serves only the potatoes of your choice.” [Spelling of the word finance has been corrected in this quotation]. (Blog date June 9, 2013) from http://maljarhi.blogspot.com/2013/06/institutional-tawarruq-product-of-ill.html 13 For a similar idea that complexity cannot be regulated by more complexity see Haldane (2012). 14 Conventional finance may or may not create assets depending on the nature of finance and the end-use of loan. For example, if the nature of finance is money-for-money financial transactions such as derivatives there is no real asset creation. It is pure transfer to some at the cost of others. Even a simple loan that is based on interest does not necessarily create real-assets in the society until the loan is used properly for productive purposes. However, it does creates a clear liability on the borrower which has to be met by the depletion of some real assets or transfer of the real asset from the borrower to the lender. Islamic finance when practiced correctly is necessarily real-asset creating. 15 See for example, http://web.worldbank.org/WBSITE/EXTERNAL /TOPICS/EXTINFRA/0,,contentMDK:23154473~pagePK:64168445~piPK:64168309~theSitePK:8430730,00.html See also Calderón, César; Enrique Moral-Benito and Luis Servén (2011), “Is Infrastructure Capital Productive? A Dynamic Heterogeneous Approach”, Working Paper N.º 1103, Banco De España, Madrid. As an extension to this, Loayza and Odawara (2010) found in the case of Egypt that an increase in infrastructure expenditures from 5 to 6 percent of Gross Domestic Product would raise the annual GDP per capita growth rate by half a percent in a decade’s time and one percent by the third decade which is a substantial impact. Loayza, Norman V. and Rei Odawara (2010), “Infrastructure and Economic Growth in Egypt”, Policy Research Working Paper No. 5177, World Bank. 16 Recent research shows that every 10 percent increase in the infrastructure provision increases the output by approximately 1 percent in the long term and that improved infrastructure quality accounted for 30 percent of growth attributed to the infrastructure in developing countries. It may be noted that the approved financing of IDB Group to infrastructure sectors such as energy, transportation, water, sanitation and urban services amounted to US$12,595.8 million, allocated to 308 projects, and constituted 67 percent of the total IDB Group financing during the 2006 to 2011 period. Therefore, it is expected that the economic impact of the IDB’s development financing would be manifold. 17 Other MDFIs have rarely used Islamic finance: International Finance Corporation (IFC) issued one sukuk to mobilize resources; African Development Bank (AfDB) and Asian Development Bank (ADB) are contemplating to use Islamic finance in resource mobilization and project financing. 18 The stated mission of IDB Group is “to promote comprehensive human development, with a focus on priority areas of alleviating poverty, improving health, promoting education, improving governance and prospering the people.”

Islamic Finance and Economic Development

20

References

Ali, Salman Syed (2013a). “Financial Stability and Economic Development: An Islamic Perspective” in Valentino Cattelan (edited), Islamic Finance in Europe: Towards a Plural Financial System, Cheltenham, UK: Edward Elgar Publishing Ltd.

Ali, Salman Syed, Nasim Shah Shirazi, and Sami Nabi (2013b). The Role of Islamic Finance in The Development of The IDB Member Countries: A Case Study of The Kyrgyz Republic and Tajikistan, IRTI Occasional Paper No. 13, Jeddah: Islamic Research and Training Institute, IDB.

Ali, Salman Syed (2014). “Islamic Capital Markets: Objectives and the Way Forward” in Salman Syed Ali (edited), Towards Competitive and Resilient Islamic Capital Markets, Jeddah: Islamic Research and Training Institute, IDB.

Clements, B., de Mooij, R., and Schwartz, G. (2012), "Confronting the jobs crisis under tight fiscal constraints", http://www.voxeu.org/article/confronting-jobs-crisis-under-tight-fiscal-constraints.

Claessens, Stijn and Laura Kodres (2014), The Regulatory Response to the Global Financial Crisis: Some Uncomfortable Questions, IMF Working Paper WP/14/46 (March).

Goitein S. D. (1967), “A Mediterranean Society” Volume 1: Economic Foundations. University of California Press

Greenwood, Robin and David Scharfstein (2013), “The Growth of Finance”, Journal of Economic Perspectives, Vol. 27, No. 2, Spring, pp. 3-28.

Haldane, Andrew; Simon Brennan and Vasileios Madouros (2010), “What is the contribution of the financial sector: Miracle or mirage?” in Adair Turner and others edited, The Future of Finance: The LSE Report, London School of Economics and Political Science.

Haldane, Andrew G and Vasileios Madouros (2011), “What is the contribution of the financial sector?” VOX column, 22 November, http://www.voxeu.org/article/what-contribution-financial-sector

Haldane, Andrew and Vasileios Madouros (2012), “The dog and the Frisbee” Speech given at the Federal Reserve Bank of Kansas City’s 366th Economic Policy Symposium, “The Changing Policy Landscape”, Jackson Hole, Wyoming, 31 August 2012. Available at http://www.bis.org/review/r120905a.pdf?frames=0

Ch.1: An Introduction and Overview

21

Levine, Ross (1997), “Financial Development and Economic Growth: Views and Agenda”, Journal of Economic Literature, volume 35, pp. 688-726.

Levine, Ross (2005), “Finance and Growth: Theory and Evidence”, in Philippe Aghion and Steven Durlauf (ed.), Handbook of Economic Growth, edition 1, volume 1, chapter 12, pp. 865-935, Elsevier.

McKinnon, R. I. (1973), “Money and Capital in Economic Development”, The Brookings Institute, Washington D.C.

OECD (2011), “An Overview of Growing Income Inequalities in OECD Countries: Main Findings” in Divided We Stand. Available at http://www.oecd.org/social/soc/49499779.pdf

Rajan, Raghuram G. (2010), Fault Lines: How Hidden Fractures Still Threaten the World Economy. Princeton, NJ: Princeton University Press.

Rousseau, Peter L. (2003), “Historical Perspectives on Financial Development and Economic Growth” Review, Federal Reserve Bank of Saint Louis (July / August), pp. 81-106. Available at: http://research.stlouisfed.org/publications/review/03/07/Rousseau.pdf

Stiglitz, Joseph (2013), The Price of Inequality: How Today’s Divided Society Endangers Our Future. UK: Penguin Books Ltd.

UN Food Agriculture Organization (FAO) (2012), The State of Food Insecurity in the World 2012.

World Bank (2014), International Debt Statistics 2014. Washington D.C: World Bank.

Islamic Finance and Economic Development

22

Blank Page

23

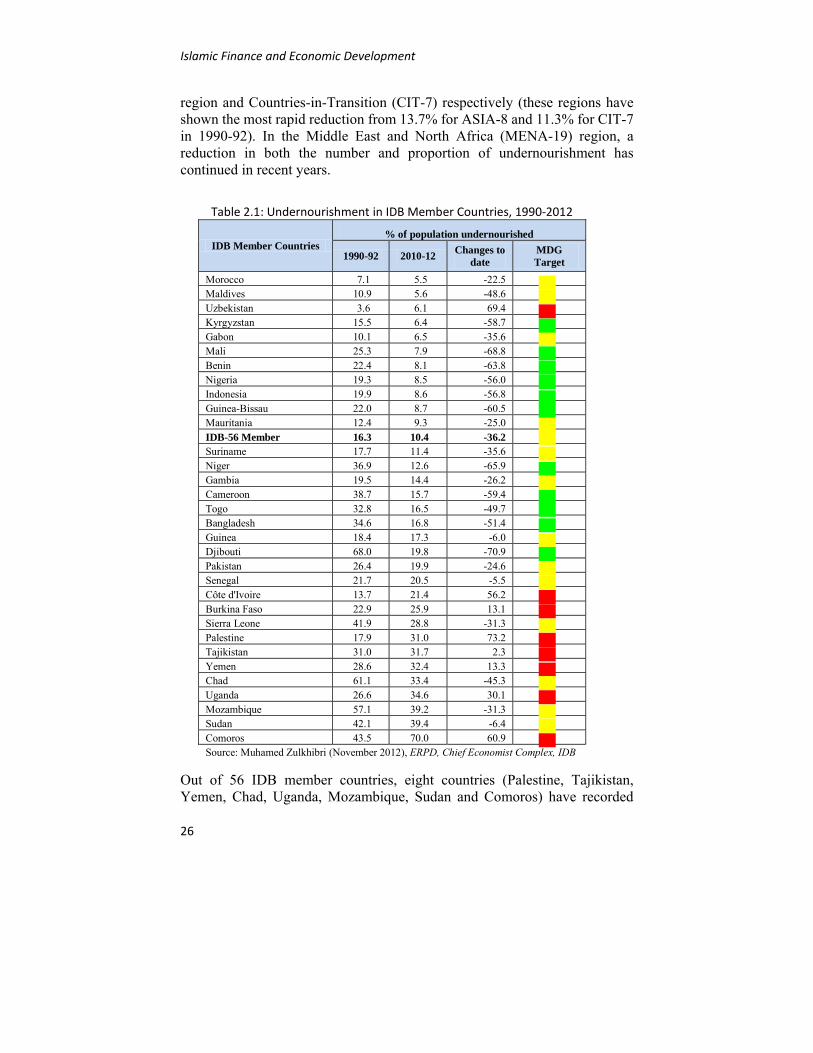

2.1 Setting the Context Food and Water Security and Economic Development Food and water security is vital for achieving sustainable development and inclusive growth. However, food and water insecurity is appearing as a major global threat, mainly due to the increasing population, increased food purchasing power and demand in emerging economies, climate change, land degradation, and price volatility. Food and water security is a complex sustainable development issue, linked to health through malnutrition, but also to sustainable economic development, environment, and trade. Over the next decade, the world is expected to face a great challenge of food and water security, therefore, the world needs to be food and water-secure. It is also critical that the post-2015 development agenda must include an explicit goal on long-term food and water security with sustainability targets and indicators. With this objective, the agriculture will need a considerable level of financing to contribute to inclusive socio-economic development in the coming years. In recent years, food and water security has emerged as an important development challenge which spans over multiple sectors and themes. The importance of these issues has come to the forefront in the wake of two successive global crises in 2008 and 2011. During the peak of the crises, the FAO Food Price Index (FFPI) was reportedly at its highest in the last few decades, reaching 170 points, pushing a significant number of people below the poverty line. This renewed the debate on the importance of food and water security to the socio-economic development of the country. The issues of food and water security are highly interrelated. Farming accounts for around 70% of the total water resource use in the world and agriculture contributes significantly to water pollution and sustainability of water

CHAPTER 2

Food and Water Security

Ali Muhammad Khan Zafar Iqbal Sohail Malik

Aamir Ghani Mir

Islamic Finance and Economic Development

24