Embed Size (px)

Citation preview

INTERNSHIP REPORT ON

NEPAL BANK LIMITED

Submitted To:

Apex College, Internship Management Team

In the partial fulfillment of the requirement for the degree of

Bachelors of Business Administration in Banking and

Insurance

Submitted By:

Saman Rijal

PU Roll No: 13450569

PU Reg. No: 2012-2-45-0180

December, 2015

Kathmandu

DECLARATION

I hereby declare that this submission is my own work and that, to the best of my

knowledge and belief, it contains no material previously published or written by

another person nor material which to a substantial extent has been accepted for

the award of any other degree of a university or other institution of higher

learning, expect where due acknowledgements.

Further I would like to declare that the report prepared by me is only for the

academic purpose. The contents included by me are taken from the observations,

secondary data, and internet sources.

Thank you

…………………..

SamanRijal

ACKNOWLEDGEMENT

It had been a great experience working in Nepal Bank Limited (NBL), Branch

Office-Dillibazar and making a project under the heading of CSD of NBL. This

project is dedicated to all the people who have helped directly or indirectly to

complete this project.

Firstly I would like to thank Apex College for providing me an opportunity to use

the theoretical knowledge in the practical field in course of my internship program

of 6th semester, under Pokhara University.

I am heartily thankful to Manager for providing me the opportunity to be an

internee in NBL and gain the practical knowledge of the banking area.

Also, I am equally grateful to all of the Nepal Bank Limited who provided the

valuable information during my internship period.

SamanRijal

BBA-BI

Apex College

ABBREVIATIONS

BBA-BI: Bachelors of Business Administration in Banking & Insurance

NRB: Nepal Rastra Bank

ABBS: Any Branch Banking Service

CSD: Customer Service Department

NBL: Nepal Bank Limited

IME: International Money Exchange

ATM: Automatic Teller Machine

KYC: Know Your Customer

LC: Letter of Credit

SMS: Short Message Service

CEO: Chief Executive Officer

BOD: Board of Director

PU: Pokhara University

ABSTRACT

As per the requirement of Pokhara University course under BBA-BI program this

report is designed according to the knowledge gained on field base experiences.

The main aim of the 8 weeks internship program is to provide internee an

opportunity to implement their theoretical knowledge practically. Out of the

various area or sector for internship, I choose banking sector, more specifically

customer service department of Nepal Bank Ltd, Dillibazar branch. This is the

world of economy, competitive service oriented product. The world is getting

smaller an smaller in terms of globalization due to the development of technology.

Among the various business firms banking plays very important role in an

economy by providing various services like: payment system, deposit, loan etc.

but it is not easy to cope and function in the changing globalized environment.

This is only possible with the help of sound planning. Also Nepal Band Ltd. is the

pioneer of banking in Nepalese history as well as one of the leading banks in

Nepalese environment with many branches all over the country.

Customers are the important element of any kind of business and it is important in

banking too. Banking service is for the customer so customer service department

plays an important role for day to day operations of bank. Main objectives of this

report, is to understand various aspects of customer service, NRB reporting and

overall operations of Customer Service Department of NBL.

Although this report is the outcome of 8 weeks experiences in CSD of NBL, I

have mentioned all the important information as far as possible. This report is

basically based on secondary data; also it’s an outcome of various experience,

interaction and analysis during internship periods. Finally this report is the short

and sweet outcome of continuous effort of 8 weeks program which will be

beneficial for the understanding mechanism of planning.

TABLE OF CONTENTS

CHAPTER I.............................................................................................................1

INTRODUCTION...................................................................................................1

1.1 Background of the Study...........................................................................1

1.2 Objectives..................................................................................................3

1.3 Methodology.............................................................................................4

1.4 Sources of Data.........................................................................................4

1.5 Selection of the Organization....................................................................5

1.6 Duration....................................................................................................5

1.7 Activities...................................................................................................5

1.8 Limitation..................................................................................................6

1.9 Introduction of Banking Industry..............................................................7

1.9.1 Meaning of Bank.....................................................................................7

1.9.2 Origin of Bank.........................................................................................7

1.9.3 Modern Banking......................................................................................8

1.9.4 Functions Offered by Bank.....................................................................8

1.9.5 Role of Bank..........................................................................................11

1.9.6 Meaning of Commercial Bank..............................................................11

1.9.7 Functions of Commercial Bank.............................................................13

1.9.8 History and Development of commercial banks in Nepal....................13

1.10 Introduction of Nepal Bank Limited.......................................................15

1.10.1 History.................................................................................................15

1.10.2 Introduction.........................................................................................16

1.10.3 Shareholding Composition..................................................................18

1.10.4 NBL Network Overview.....................................................................18

1.10.5 Objectives............................................................................................18

1.10.6 Vision...............................................................................................19

1.10.7 Mission................................................................................................19

1.10.8 SWOT Analysis...................................................................................19

CHAPTER II.........................................................................................................21

REPORT ABOUT INTERNSHIP EXPERIENCE................................................21

2.1 Activities Performed in the Organization.....................................................21

2.1.1 Customer Service Department...............................................................21

2.1.2 Remittance Department.........................................................................23

2.1.3 Clearing Department.............................................................................23

2.2 Problem Faced During Internship................................................................27

CHAPTER III........................................................................................................29

SUMMARY, CONCLUSION AND RECOMMENDATION...............................29

3.1 Summary......................................................................................................29

3.2 Conclusion...................................................................................................29

3.3 Recommendations........................................................................................30

BIBLIOGRAPHY..................................................................................................32

CHAPTER I

INTRODUCTION

1.1 Backgroundof the Study

An internship is a study program for the students which are carried out in an

organization to meet the requirement of the study in colleges or universities. This

report is submitted to fulfill the requirements for the completion of the degree of

“Bachelor of Business Administration in Banking and Insurance (BBA-BI)” under

faculty of management, Pokhara University. BBA-BI is a four year undergraduate

program in which emphasizes on managerial skill required for the middle level

manager. Apart from management and its allied courses, BBA-BI gives thrust on

information technology also.

Interns are usually college or university students to gain various skills, knowledge

and learning experiences on different aspect of organization’s environment.

Internship also helps students to know how different activities in the organization

are coordinated so that the synergistic effects are achieved and how

communication takes place in corporate world. Students are involved as non-paid

authentic employees receiving academic credits for work experiences. This will

support the students to acquire social, technical and communications skills to

work effectively in industry. Today, many organizations are cooperating with the

educational institutions to provide the internship service with the specific benefits

to their students.

An internship provides the student with a greater understanding of organization’s

work environment with educational qualifications. Hence in this frenetic

financialenvironment, the roles of commercial banks are unavoidable. The report

focuses on over all banking activities concerned with its major functioning

1

departments ofNepal Bank Limited.

Through internship an individual can explore the working process of an

organization being a part of the actual working environment. Here every students

receives practical knowledge through observation and develops academic credit

for the work experiences as well. An internship will help the individual to expose

to the interpersonal relationship, which is the demand of every job, both with the

boss, co-workers, supervisors and the other lower level staff members who are the

first basic things for a bank to obtain successful and contented career. It assists the

students to identify potentiality and area of interest. Internship is the necessary

medium for enabling employers to persist students to work in up to date

competitive business environment. Internship is seen as the major way to enhance

and support the internee’s banking careers well.

As we know that, an internship is the way of learning managerial activities by

practically doing it, therefore it provides an opportunity for learning as well as

developing the managerial skills. It gives a direction and provides ideologies for

the practical problems. Every single activity that takes places daily is

simultaneously observed and analyzed. Any usual problems and the underlying

causes or drawbacks are closely monitored, understood .The potential solutions

can be determined that certainly enhances the effectiveness and the strength,

minimizes the weaknesses that helps to maximize the profit and the growth rate.

An internship acts as a medium that ables an individual’s to work in group,

manage work pressure and analyze the lessons learnt in class and on the field. It

can be remarkable way of determining if the industry and the banking career is

best suited or not for him or her. It makes an individual more concerned about the

options and opportunities one can get both physically and mentally. A successful

internship student has developed characteristics, which are the essentials of the

Modern commercial world. This whole internship process ables a student to

experience and gives exposure to the working pressure that a internee is likely to

2

face in the futureby making them familiar with the corporate cultures and also by

understanding the primitive knowledge of the business settings of the

international standards. It also helps to develop the professional working habits

and creates a platform to create differences in the work style. Thus, it makes the

internee’s mind pre-prepared to pursue the career in the banking field in the

future.

Pokhara University offers a course for the BBA-BI faculty, which is the best way

to learn and gain the knowledge regarding the corporate environment and culture.

This way any individual can obtain the maximum knowledge from a business

world. They have the right to learn and make the things more transparent. This

internship was carried on in the branch office of the Nepal Bank Limited at

Dillibazar. The internship program was for six weeks, which started from…….

and ended on…….. in which the internee was placed in different departments like

Remittance Department, Customer service department (CSD), Bills Department,

clearing.

1.2 Objectives

During the internship period, the main aim is to gain and explain about the

knowledge experienced during the banking operations through observation,

interaction. Likewise, the other specific objectives are as follows:

a) To have a work experience on the bank.

b) To be familiar with the principles, manuals, provision, guidelines,

regulations of the operational activities.

c) To perceive broader knowledge by involving own self in the situation and

work environment.

d) To observe the policies and the regulations in the financial sector.

3

1.3 Methodology

Methodology is the description of the procedure followed while collecting the

necessary data and information needed for research work and report preparation.

Various data were collected by observation, making inquiries with concerned

staffs, quantitative data collected from the past records. The following

methodologies are used in this study.

1.4 Sources of Data

For the information of the various departments, personal interviews were taken

and inquiries were made. Information was collected by observation and formal

group discussions with every related member of the organization. Regular

communication and consults were made with the staffs and the costumers for the

reliability of the data. The books, magazines, newspapers, journals and the past

records obtained all the formal and the quantitative data. There were formal group

discussions, observation, personal inquiries as the source of the primary data, and

for other secondary data past records were referred. Consulting with the staff

members and costumers were the other source of reliable information. Data was

collected by various means and mediums such as direct interviewing, enquiring

with the staffs.The previous bank records were referred for the relative data and

information.

Information were collection from the official website www.NBL.com.np

Different books of journals and magazines, newspapers, bank profiles,

regular manuals of the departments, annual reports were gathered for the

preparation of the report.

Information gathered from the related staff members were thoroughly

studied and hence recorded for creating better understandings with the

bank and the banking transactions.

4

1.5 Selection of the Organization

I choose bank as organization for internship with regarding bank as one of the

service industry where I can gain various knowledge about general management

concepts. With the aim of implementing my knowledge that I gained in college by

doing internship in the organization that is related to management field, I chose

NBL as organization for internship program. Due to the support of my college I

was able to join Nepal Bank Limited for internship.

1.6 Duration

The duration of the prolonged internship was of 6 weeks, started from …. to the

date……. In the course of the internship period, the intern worked on the different

departments, performed activities. All the factors such as discipline, attendance,

regularity, interest towards the work, sincerity, behavior, and the efforts that she

made to understand the banking functions were closely monitored.

1.7Activities

During the entire internship period of eight weeks, the intern had a time to visit

the four different departments like Remittance, Customer Service Department,

loan Department and clearance. In the course of the internship, I spent equal

number of days in every department. The activities performed on these

departments are as given below in table.

5

S. No. Department Activities performed

1 Customer service department Preparing balance certificate, opening

and closing accounts, cheque printing,

statement printing, handling telephones

2 Remittance Department Preparing IDT, IBT, cheque deposits,

data entry

3 Letter of credit Studied the different types of loans and

loan files of the customers.

1.8 Limitation

There are several limitations that hindered the proper analysis of this study. These

are:

Difficult in analyzing the information obtained from respondent due to the

qualitative nature of information.

Another limitation to this study is the lack of statistical data. Report is

mainly based on the secondary data.

The experience obtained is limited.

The deep comprehensive analysis and study couldn’t be done due to time

constraints.

Time limitation and busy schedule of the staffs also prevented internee

from learning time to time.

6

1.9 Introduction of Banking Industry

1.9.1 Meaning of Bank

A bank is a type of financial institutions that are established under a certain act to

perform monetary and credit transactions. The bank accepts the deposits in the

form of capital and collateral, formulates, and implements monetary and foreign

exchange policy to maintain price and balance payment stability for a sustainable

development of the country. It provides necessary liquidity for promoting the

stability of the financial sectors.It raises funds by collecting deposits from

business and consumers through saving gio sits, time deposits. Besides this, it

gives facilities to business like giving loans to business, housing, saving deposited

money, buying and selling of bonds etc.

It also helps to develop a safe, sound, and efficient payment system. Bank helps in

making regulations, inspection, supervision, and maintaining the sound

development of the banking system.

According to the American Law bank has been defined as “Any Kind of

institution offering deposit subject to withdrawal on demand and making loans of

a commercial or business nature is a Bank"

The bank regulation of India defines it as a means of accepting for the purpose of

leading or investment of deposit of money from the public repayable on demand

or otherwise able by cheque, draft or otherwise.

1.9.2 Origin of Bank

Actually, the word “Bank” has been originated from the Latin word “bancus”;

Italian word “Banca” and a French word banque; which all refers to the Bench.

Jews, the early bankers, in Lombardy, used to transact their business at benches in

the market place. In the history of origin of banking in the world, “The Bank of

Venice”, was the first, which was originated in Venice of Italy in the year 1157

A.D. In addition, the first central bank which was established in 1844 A.D. was

7

“The Bank of England”.

Bank is a financial intermediary accepting deposits and granting loans and also

offers the variety of services like conversion foreign currency into domestic

currency and vice versa, lending money, saving deposits etc. Even if we look at

the past, banking concept is found. In the ancient period, this concept existed,

when goldsmiths and the rich people used to give money to the common people

against the promise of safekeeping their valuable items on the presentation of the

receipt, the depositors would get back their gold and valuables of the paying a

small amount for safekeeping and saving.

1.9.3 Modern Banking

Merchants, Goldsmiths, moneylenders are known as the ancient bankers.

Development of modern banking in the 15th, 16th and 17th centuries gradually

shifted the Centre of the world commerce from the Mediterranean region towards

Europe and the British isles, where banking became a leading industry. During

third initial phase of modern banking development Industrial Revolution was

developed, which demanded a well-developed financial system. Modern banking

was developed to provide new methods of making payments and credit available,

which were required as economy of various countries adopted mass production.

At previous times, banks functions were limited. They only accepted deposits of

money or valuables for safekeeping and verifying coinage or exchanging one

jurisdiction’s coins for another’s. Various banks were developed as modern banks

such as Medici Bank of Italy and Hochstetler Bank in Germany.

Now bank has become a known place for every people and it also offers wide

variety of services than before.

1.9.4 Functions Offered by Bank

There are various functions provided by the bank. They are as follows:

8

Deposit function

Accepting deposits is the primary function of the bank. The most important fund

of the banks is deposits. Without deposits, it would be difficult for the bank to

invest high return sectors. The main objective of the bank is to collect deposits in

as lowest cost of fund possible. If the bank is able to collect deposits at the lowest

cost it leads the bank to earn a huge amount of fortune.

Providing loans

This is the other function of a bank. It provides loan to a customer, company or

institution. Bank is able to gain benefit by giving loans and charging them with

some amount of interest rate to a customer as per the law and banking policies,

terms and conditions. It provides loans by accepting the security of a debtor.

Credit function

Bank provides credit to the deficit customers such as hire purchase loan, real

estate loan, leasing of the fixed assets, working capital loan and other long term

loans. The interest rate charged to the loan amount and the interest provided to the

depositor’s difference leads to the profit of the bank.

Payment function

The bank provides various payment facilities to the costumers to make the

economy efficient and effective. If the payment facilities were not developed it

would be difficult for the costumers to transfer the money from one place to

another. Some of the payment instrument is as cheques, bank overdraft, online

various banks also provide payments.

Trust function

The most important function of the modern bank is to maintain credibility towards

the depositors as well as towards investors. If the bank fails to maintain the

9

credibility, it becomes difficult for the bank to attract depositors as well as

investors to purchase their security.

Investment function

Bank uses the surplus amount of money at the profitable area where the return on

investments is high. Bank also invests a huge amount of money in government

securities and bonds, as it is a 0% risk free investment.

Cash management function

It is necessary for the bank to manage the cash collection and cash disbursement

to retain its position in the markets well as credibility. If the cash management

leads to deficit rather than surplus it would be difficult for the bank to manage its

environment effectively.

Insurance function

Another important function the modern banks play is insurance function. Bank

provides loans and advances to various sectors as a result of the assets or the loan

amount should be insured and various collateral must also b taken under bank’

eye. In case of providing loans to purchase a car, it is necessary that the vehicle is

insured so that the risk of not recovering the money is low.

Underwriting function

It is necessary for each bank to issue public shares in the marketplace. Banks has

the right to under right the various securities such as common stock, preferred

stock, or debentures. It is necessary that legal bank be listed in the stock market o

that the interested investors can invest a huge amount of money in the bank by

purchasing various securities.

Brokerage function

A modern bank also plays an important role as a broker for the necessary clients.

Banks earns a non-operating income acting as a broker. as a broker banks helps

10

the client to purchase and sale various securities of the banks as well of different

banks. Banks may charge some percentage of commission or may even some

amount of rupees with difference between the selling and purchasing price.

1.9.5 Role of Bank

The various roles played by the banks are as follows:

Intermediation Role

It transforms saving received primarily from households into credit

(loans) for business firms and others in order to make investments in new

building, equipment’s, and other goods.

Payment Role

It carries out payments for goods and services on behalf of their customers

such as issuing cheques, wiring funds, providing a conduit for electronic

payment and dispensing currency and coins.

Guarantor Role

Bank Stands behind their costumer to pay off costumers debts when those

customers are unable to pay such an issuing letter of credit.

Agency Role

Bank acts as an agency on behalf of the costumer to manage and protect

their property or issue and redeem their securities usually providing

through the bank trust department.

Policy Role

It also serves as a conduit for the government policy in attempting to

regulate the growth of the economy and pursue social goals.

1.9.6 Meaning of Commercial Bank

Commercial Bank is the major sector for upgrading country economy. It is the

oldest form of the bank. It is defined as "A commercial Bank is the one which

exchanges money, accepts deposits, grant loans and performs commercial

function and which is not a bank meant for cooperative, agriculture, industries or

11

for such purpose" according to the commercial Bank Act.

In general, bank that performs all kinds of banking business and generally

finances trade and commerce is called commercial bank. Commercial banks are

financial intermediaries that accept deposits from the members of the public who

do not have intermediates use foe funds (savers) and lending such funds to those

requiring funds for investment (borrowers). It also transfers fund from one

costumer to another and provides other services such as offering advice on a wide

range of matters relating to finance.

It has also been defined as “Commercial bank is a financial institution that

operates currency exchange, money transactions, accepts deposits, advances loans

and performs other commercial transactions which is not specifically established

with the objective of cooperative, agricultural, industrial or any other such kind of

specified purpose.” according to the Commercial Bank Act 2031, section 2(a).

They are those banks, which gathers altogether the scattered savings of the

community and arrange for their productive use and generate profit. They accept

deposits from the public and use the money to help the community by making

loans to individuals, organizations, governments and business. Commercial banks,

acquire funds from group of surplus spending units and making these funds

available to the deficit units facilitating the effective mobilization of resources,

which in return leads to sound economic growth of the country.

The main aim of the commercial bank is to earn profit like any other business

entity. It lends a certain percentage of the cash lying in deposits on higher interest

rate than it pays on such deposits. The difference on interest on deposit received

and loans advanced are the main source of its income. Thus, commercial banks

are merely a business firm engaged in financial intermediation as well as perform

additional functions under strict supervision and control of the central bank.

12

1.9.7 Functions of Commercial Bank

a) To accept deposits

b) To provide loan and advances

c) To provide general utility functions

d) To provide overseas trading services

e) To provide information and other services

f) To provide investment facilities

g) To provide remittance facilities

1.9.8 History and Development of commercial banks in Nepal

At the early stage, zamindars were known as banks, the focus was more on

lending money against securities like land and ornaments, which could be

redeemed if the loan wad defaulted. TejarathAdda, established in 1933B.S at the

time of Prime Minister Ranoddip Singh, is taken as the first step for the

development of institutional banking system.

Nepal Bank Limited Came in Nepal as the first ever-commercial bank of Nepal.

The government incorporated Nepal Rastra Bank (central Bank) along with

RastraBanijya Bank and Agricultural Development Banking 2024 B.S. FDI in the

banking sector, through joint venture banks, the first being Nepal Arab Bank

Limited now NABIL Bank. Nepal Bank Limited was established on 30 Kartik

1994 B.S., the first bank of Nepal. Banking terms started in two senses, with its

establishment. It conducts dual function of both commercial and central bank. In

order to allow Nepal Bank Limited to concentrate on commercial features, on 14

Baishakh 2013 B.S., Nepal Rastra Bank was set up under Nepal Rastra Bank at

2012 B.S. as the central bank of Nepal. This act has been repealed and Nepal

Rastra Bank act 2058 has been in an act by the parliament. It is regarded as the

apex body of the monetary and the banking structure. RastriyaBanijya bank was

set up as the fully government owned commercial bank in 2022 B.S. with its

establishment banking services spread to both urban and rural areas. Agricultural

13

development bank was established in 2024 B.S. for the upliftment of the

agricultural sector.

Government formulated liberal economic policy to accelerate countries growth

and development. Government encouraged foreign investment and participation

of private sector in the banking sector. The government then applied the policy of

“Joint Venture Banking”. This was a great significant event. Healthy competition

prevailed and people were offered valuable services and national as a whole

begun to take benefit.

Commercial banks should operate under the Commercial Bank Act 2031, Nepal

Rastra Bank Act 2058. Company Act 2053 and Contract Act 2056. Nepal Arab

Bank Limited (NABIL) is the first bank established in joint investment in Nepal

in 2041 B.S. A year later Nepal Indosuez Bank Limited currently renamed as

Nepal Investment Bank Limited was set up, with passage of time several other

joint venture and private bank has been established.

After the restoration of democracy in Nepal, there has been tremendous

development in banking sector. Rural development banks are formed for all

development banks under the control and supervision of Nepal Rastra Bank.

These banks includes

a) Eastern Rural Development Bank

b) Central Rural Development Bank

c) Western Rural Development Bank

d) Mid-western Rural Development Bank

e) Far-western Rural Development Bank

Nepal Industrial Development Corporation (NIDC) and Agricultural Development

Bank (ADB) were only two development banks to be established before the

enactment of Nepal Development Bank Act 2052 B.S. After the introduction of

Nepal Development Act 2052 B.S., many development banks were set up.

14

Nowadays it has also been one of the attractive places for employment, investors

etc.

1.10 Introduction of Nepal Bank Limited

1.10.1 History

NepalBank Limited, The first bank of Nepal was established in November 15,

1937 A.D (Kartik, 30, 1994). It was formed under the principle of Joint venture

(Joint venture between govt. & general public). NBL's authorized capital was Rs.

10 million & issued capital Rs. 2.5 million of which paid-up capital was Rs. 842

thousand with 10 shareholders. The bank has been providing banking through its

branch offices in the different geographical locations of the country.

The history of Nepal Bank ltd is very old. It is the first bank of Nepal. His

Majesty King Tribhuvan inaugurated Nepal Bank Limited on Kartik 30,1994

Bikram Sambat. This maarked the beginning of an era of formal banking in

Nepal. Until then all monetary tractions were carried out by private dealers and

trading center.

Then Prime Minister Maharaja JuddhaShumsher J.B.R. speaking on the occasion

with the kind permission of His Majesty the King stated this work which is being

done in the larger interest of the nation is a great moment for me. Until today a

bank could not be opened in Nepal. Therefore this bank, which is being

established under the name of Nepal Bank Limited to fill that, need and to be

inaugurated by His Majesty the King, is a moment of great joy and happiness.

The Bank's objectives to render service to the people whether rich or poor and to

contribute to the nation's development will also need the support and best wishes

of all, which I am confident, will be coming. In that era, very few understood or

15

had confidence in this new concept of formal banking. Rising equity shares were

not easy and mobilization of deposits even more difficult. This was evident when

the bank floated equity shares worth NRs. 2,500,000, but was successful only in

raising NRs. 842,000.

"In the absence of any bank in Nepal the economic progress of the country was

being hampered and causing inconvenience to the people and therefore with the

objective of fulfilling that need by providing service to the people and for the

betterment of the country, this law in hereby promulgated for the establishment of

the Bank and its operation"

The total deposits for the first year was NRs. 17,02,025 where current deposits

was about NRs. 12,98,898 fixed was about NRs. 3,88,964 and saving was NRs.

14,163. Loan disbursed and outstanding at the end of the first year was NRs.

1,985,000.

From the very conception and its creation, Nepal Bank Ltd, was as joint venture

between the government and the private sector. Out of 2500 equity shares of NRs.

100 face value, 40% was subscribed by the government and the balanced i.e. 60%

was offered for the sale to private sector. There were only 10 shareholders when

the bank first started.

1.10.2 Introduction

Nepal Bank Limited, The first bank of Nepal was established in November 15,

1937 A.D (Kartik, 30, 1994). It was formed under the principle of Joint venture

(Joint venture between govt. & general public). NBL's authorized capital was Rs.

10 million & issued capital Rs. 2.5 million of which paid-up capital was Rs. 842

thousand with 10 shareholders. The bank has been providing banking through its

branch offices in the different geographical locations of the country.

16

Network for inclusion: Use bank's network to increase its reach all over the

country from urban areas to rural areas and help in improving the lifestyle of rural

population and in turn become the bank of choice of corporate, medium

businesses and rural market.

Enhancing the value: To employees, shareholders, government and customers

World class banking services: Provide world class banking services by achieving

excellence in customer service and adopting high level technology standards.

Segmented business approach: For risk management and enhancement of

efficiency.

Partnership: With all stakeholders including the Government, employees,

shareholders and customer.

Innovation: Of business areas and processes for providing Advanced banking

services, and enhance competitiveness.

Responsiveness: responding to the changing need of the market/society/business

on timely basis.

Integrity: Uphold trustworthiness and business ethics in the business processs.

Total banking solutions: To cater the need of all sections of society.

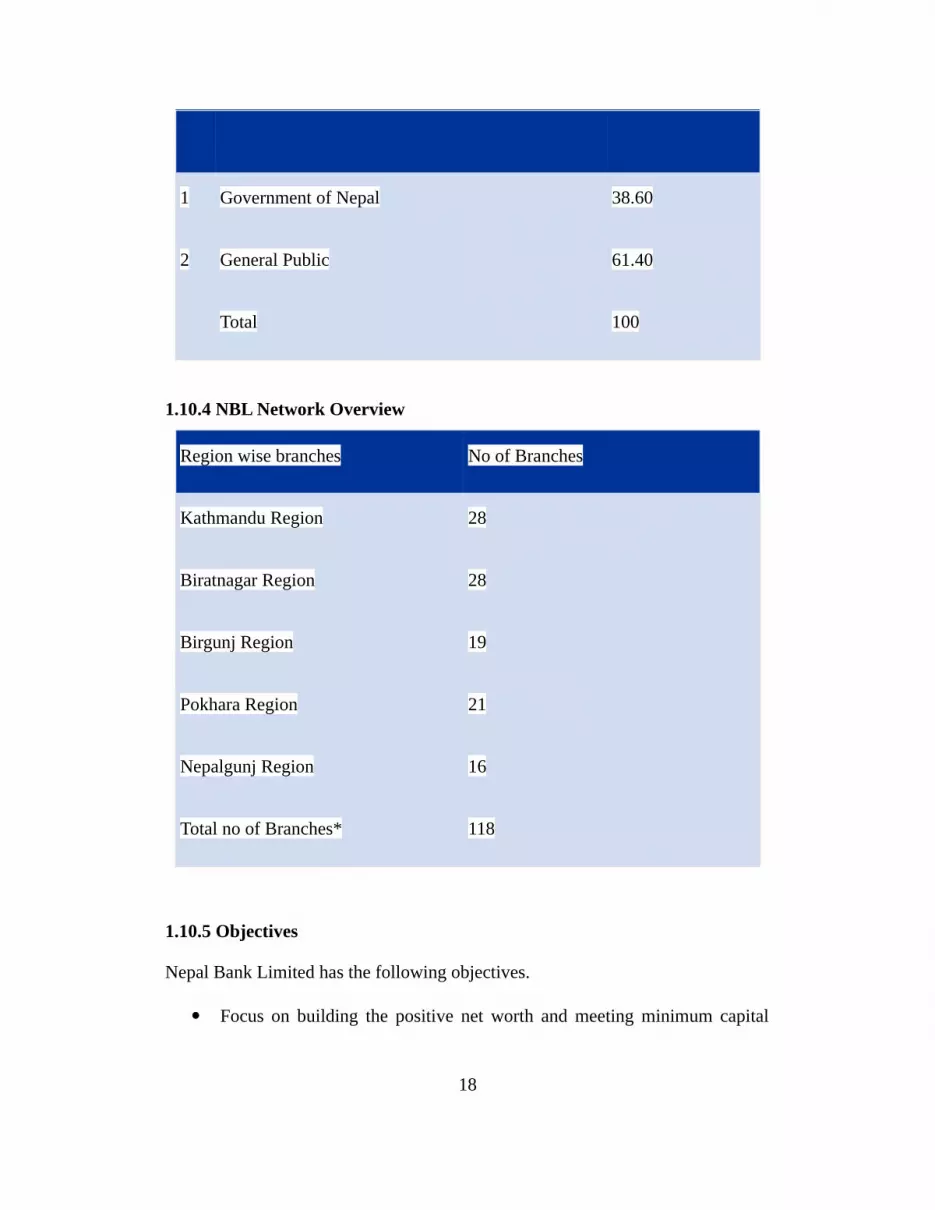

1.10.3 Shareholding Composition

S.N Ownership Percent

17

1 Government of Nepal 38.60

2 General Public 61.40

Total 100

1.10.4 NBL Network Overview

Region wise branches No of Branches

Kathmandu Region 28

Biratnagar Region 28

Birgunj Region 19

Pokhara Region 21

Nepalgunj Region 16

Total no of Branches* 118

1.10.5 Objectives

Nepal Bank Limited has the following objectives.

Focus on building the positive net worth and meeting minimum capital

18

requirement over the coming five years.

Focus on increasing the customer base and market share.

Maximize the potential/efficiency of bank's staff.

Focus on minimizing the risk associated with the business.

Focus on providing the world class business solutions.

Focus on increasing the sustainable profit.

1.10.6 Vision

“Pioneer bank with complete banking solution” Nepal Bank Limited holds of a

vision to become a Leading Bank of the countryby providing premium products

and services to the customers. It ensures attractive and substantial returns to the

stakeholders of the Bank.

1.10.7 Mission

Nepal Bank Limited seeks to provide an environment within which the bank can

bring unique financial value and services to all customers. It will be a sound

institution where depositors continue to have faith in the security of their funds

and receive reasonable returns; borrowers are assured of appropriate credit

facilities at reasonable prices; other service- seekers receive prompt and attentive

service at reasonable cost; employees are paid adequate compensation with

professional career growth opportunities and stockholders receive satisfactory

return for their investment.

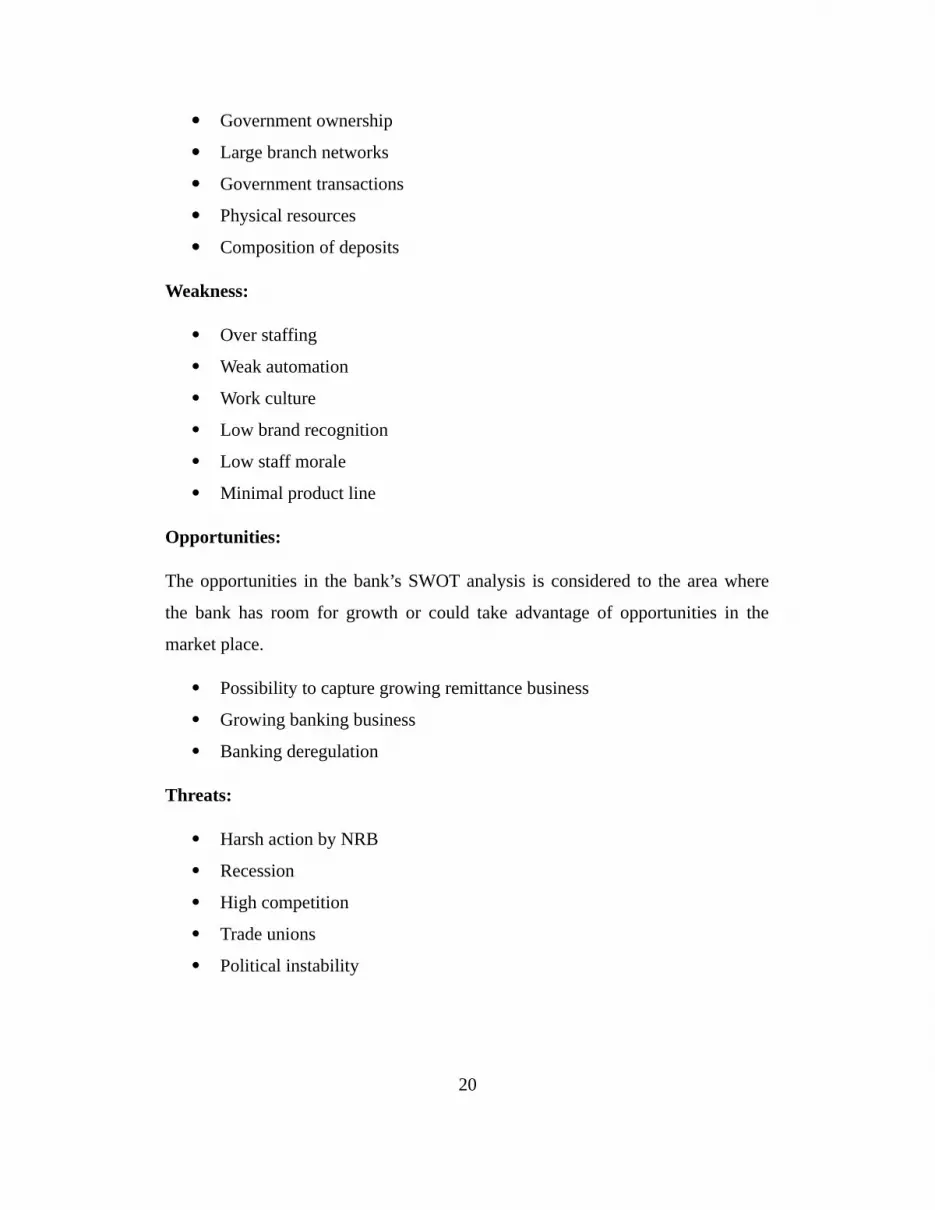

1.10.8 SWOT Analysis

SWOT analysis of the bank is to evaluate the Strength Weakness Opportunities

and Threats involved in its business operation and identifying the internal and

external factors that are favorable and unfavorable to achieve bank’s objectives.

Further major weakness of the bank where bank has to work on for the

improvement to increase the operational efficiency and hence increase

profitability has also been analyzed.

Strength:

19

Government ownership

Large branch networks

Government transactions

Physical resources

Composition of deposits

Weakness:

Over staffing

Weak automation

Work culture

Low brand recognition

Low staff morale

Minimal product line

Opportunities:

The opportunities in the bank’s SWOT analysis is considered to the area where

the bank has room for growth or could take advantage of opportunities in the

market place.

Possibility to capture growing remittance business

Growing banking business

Banking deregulation

Threats:

Harsh action by NRB

Recession

High competition

Trade unions

Political instability

20

CHAPTER II

REPORT ABOUT INTERNSHIP EXPERIENCE

As prescribed by the faculty of management Apex College, the duration of

internship has been 6 weeks. Most of the time internship period has been spent in

loan and customer service department and also have been placed in pension and

remittance department.

2.1 Activities Performed in the Organization

2.1.1 Customer Service Department

For any banks are valuable assets .keeping this in mind, NBL tries to give best to

its customers. This department is the sensitive part of a bank as it interacts directly

with the customers. People come for various enquiries about banks, its new

services. Thus it should be efficient, clean and effectively handled by the

employees of the bank. This department creates an impression of the bank

towards its customers, better services, they will come for the services again and

we are a part of the bank.Here the internee carried out the following activities:

a) Counseling the customers

b) Interacting and communicating with existing and new clients

c) Opening of new account for the new clients

d) Making of chequebook and issue of chequebook to existing and new

clients.

e) Printing of financial statement for clients

f) Scanning of account holders photos and signatures

g) Checking account holders customer balance

h) Checking account holders photos signatures

21

i) Handling telephones and use photocopy machine for customers’ ease.

Analysis of the Activities in Customer Service Department:

Customer counseling

As we know that a bank performs well when their customers are satisfied. So, in

this department an internee tries provided by the bank to its new and existing

customers. They try to solve enquiries, questions and doubts the customers are

having.

Account opening

There are various kind of account opening facilities given by the bank like, saving

a/c , current a/c , Mahilabachatkhata, Sajilobachatkhata, fixed saving, diamond

saving, nepallaxmibachat etc.

Here, an internee helps the customer by explaining about the types of services

they need like various types of service they need like various types of account

opening facility, advantage behind the particulars account, fill up their forms who

are unable to do so.

Statement printing and issuance

Statement includes the information like day to day transaction amount, balance,

interest charge etc. it is free of cost. It is a frequent and regular activity done in the

bank with the help of software given by the authority. Statement issuing is done in

the concerned bank only where an account holder has opened an account. For that

customer should provide their related account number.

Balance checking, scanning and photocopy

An internee was also allowed to check the balance asked by the customer under

the supervisor’s authority. An internee also learned to scan the forms before

keeping the records of new account holder or filing them along with some other

important documents. Similarly, photo copy was to be done frequently in the

22

department, to provide ease to the customer. Internee also learned how to contact

with the customers through telephone.

2.1.2 Remittance Department

Remittance can be defined as the transfer of money from one place to another that

may be from bank to bank or from country to country. The department of

remittance deals with the management of the remitted money, which is sent by the

migrant workers from abroad or within the country as well. Nepal Bank receives

remittance through swift code. NBL is the pioneer in the field of retail money

transfer business with over 11years of customized services delivery experience in

the field. It has the largest network covering all major cities, towns and villages of

the country and is capable of paying at more than 200 locations across Nepal. The

bank enjoys the strategic with the lending remittance companies like Xpress

Money, MoneyGram etc. In this department, the internee learned the following

task:

a) Helped in remittance payment by using the concerned software according

the RAD digit.

b) Helped in Account enquiry and preparing the statement.

c) Observed in preparing demand draft and fund transfer.

d) Observed foreign currency exchange(purchase and sell)

e) Learned to keep records of various drafts.

2.1.3 Clearing Department

In this department customers bring checks of different bank and they fill a

voucher to credit their account by the amount specified in the check and by

debiting the amount in the check of the specific bank. After receiving different

checks they are given the specific OBC number and recorded in the register and

later they are recorded in the computers as well and after all the checks are

recorded the final print out is printed, 3 pages of each banks are printed and

vouchers are attached with single page of the specific bank and 2 pages are

23

attached with the checks and the checks are passed to the next step where they are

checked that all the checks and vouchers are in order or not and then again they

are entered in the excel sheet in the next step and final print out is made. The

printed papers of all the checks along with all checks are taken to Nepal Rastra

Bank the very next working day for the clearance.

In NRB, there are different counters of different commercial banks and they are

given their checks and Nepal Bank receives its check and then the advice is

prepared by debiting and crediting the amount and the balance of different banks

at NRB are debited and credited on the basis of advice. If the checks are

dishonored then they are returned to the NRB by 3:00 PM in the evening of same

day and again advice is prepared and balance of Dr. and Cr. should be same and

informed to NRB.

Outward Bills for Collections

There are some cheques that are drawn by a Non NBL account that is outside the

city area in favor of NBL account holders and thus are treated as OBC’s. The

process for clearing of the OBC’s is as follows:

a) Cheques receives by NBL.

b) The officer affixes the OBC stamp on the cheques and writes its individual

number from the OBC register.

c) Entries of all OBC cheques are written in an OBC register.

d) An OBC letter is printed, which shows the cheque numbers, the branch

drawn on and amount.

e) Original Cheques are attached to these letter and sent to the main NBL

branch in that area by courier

f) When that area branch clears the amount from the Non-NBL branch, it

sends an Inter Branch Credit Advice (IBCA) to NBL and the officer at the

branch credits the customer account with that amount.

24

Inward Clearing

Inward clearing takes place when a KBO account holder draw’s a cheque in favor

of a Non- NBL account holder. The process for inward clearing is as follows:

Cheques are received by the operations department.

The bank officer verifies all particulars from the instruments and the

system for sufficient balance etc. If any fault is found, then the officer will

mark the cheques as a return, stating the reasons with them.

If no fault is found, then the officer will post these cheques in the system

by debiting the customer account.

The particular of the returned cheques are entered in the ‘O/W return of

inward clearing’ register and returned.

Letter of credit:

Letter of Credit means a party of a country wants to do trade with the other party

or organization of the other country and they cannot trust each other that one party

will pay the amount for the goods and the other party will send the appropriate

goods after receiving the advance payment for the goods. So both the parties

contact the Banks of their own country and both the Banks guarantee for their

party. Beneficiary party sends the Performa invoice to the applicant party and by

taking the invoice the applicant goes to the Bank and on behalf of the invoice the

Bank opens the L/C for the applicant party. L/C can be opened of Import or of

Export by the company.L/C can be opened under Limit or can be opened by

paying the 100% amount mentioned in the Performa Invoice to the Bank. After

opening L/C the insurance of the goods should be done and the insurance can be

done by the applicant or by the beneficiary under mutual understanding of both

parties. Insurance should be done 110% of the goods so that in case of any

damage the 100% return is gained against the goods. Whereas 10% is used to

compete the other charges while inspectinggoods.

25

Parties under L/C are given below:

Applicant: The person or party who wants to import the goods from the

other country.

Beneficiary: The party which sends the goods to the Applicant and

receives money for it.

Issue Bank: The Bank which opens the L/C on behalf of the Applicant.

Advisory Bank: The Bank which sends the documents to the Issue Bank

that goods have been send from here and receives payment from the Issue

Bank.

Reimbursing Bank: Bank which have the Issue Banks Dollar account.

Conforming Bank: Bank which works as a mediator between the

beneficiary and Issue Bank in case if the beneficiary does not trust the

Issue Bank.

Generally L/C is opened at Sight or at Usance. If the applicant party does pay the

money within 5 working days of receiving the documents then it is at sight L/C

and in case of Usance L/C the applicant is provided maximum of 180 days of

credit limit. Bank deals with the documents send by the beneficiary bank rather

than the goods send by the party to the applicant party. If the commercial invoice

send by the beneficiary party does not match with the Performa Invoice which

was send in the opening of L/C by the beneficiary party then the Issue bank is not

liable to pay the amount to the beneficiary bank. But if the Applicant and

Beneficiary party wants then the amendment can be done by the bank. Now days

L/C is of irrevocable nature means if and only if both parties agree to discontinue

or close the L/C then only it can be closed otherwise by the single party either by

Applicant or by Beneficiary party it cannot be closed.Documentations required

are given below.

a) Covering

b) Commercial Invoice

26

c) Bill of Lading, Airway or Transport Bill

d) Quality Certificate

e) Insurance Document

If the documents are not acceptable then it is returned to the beneficiary bank by

the issue bank and if the documents are fulfilled then Applicant is provided the

documents and Applicant party can clear the goods from custom with the help of

those documents. And on the basis of documents the issue bank swifts the amount

to the beneficiary bank and the beneficiary gets the money for its goods.

2.2 Problem Faced During Internship

While carrying out the task assigned by the supervisor, the internee faced different

types of problems. They are as follows:

a) Some of the customer disagrees to accept the charges for account closing

and make argument on this matter for long time. So, it becomes difficult to

convince them about the bank’s charges.

b) Though the instructions and required documents are clearly explained in

the account opening form, even then customers ask those for time to time

and reasons for extra documents that are already sated in back side of the

form. So, it is tough to give them each and every guideline on filling

different types of form as well.

c) The accountholder’s relation asks for the chequebook without bringing the

letter of authority and citizenship with accountholder’s valid signature and

account number.

d) When the customers lost their chequebook and request for new one, in this

case it is difficult to find out all the used and unused cheque, valid

signature and account number from their record on the computer carefully.

e) Failure to remember the reference number on the remittance services such

27

as Money gram or Express money or Cash instant as the customer

presented the form of different reference number.

f) Sometime customer came to take the money but bank unable to give the

payment due delay of information in the bank website.

g) Quite confusion in inward and outward clearing bills while keeping the

record in the computer.

28

CHAPTER III

SUMMARY, CONCLUSION AND

RECOMMENDATION

3.1 Summary

Internship done under the requirement of PU to complete BBA has been proved as

an effective way of studying. It helps to get broader knowledge about the

working as well as banking environment .This report is based on the banking

operation of Nepal Bank .Internee selected this particular bank as it is one among

many reputed Organization. As we know that bank is place where financial

activities are carried out. NBL was established in November 1937. It offers

various services like remittance, loan, deposit products etc. The main thing was

that interne was able to learn about the various activities carried out in different

department. In remittance department internee learned to make demand drafts ,

balance certificates .In clearing department internee learned about dealing with

customers, counseling them, balance checking , statement printing and so

on .During these period of internship many problems were faced by the internship

and they were also solved . Thus internee now can really understand about the

banking scenario in general.

3.2 Conclusion

Nepal Bank limited culture is built on a set of core values: client focus, teamwork,

meritocracy, ethic & integrity, pioneering. The company is committed to its

clients' best interests as well as preserving a good relationship by defining

realistic objectives.

29

Since the establishment of Nepal Bank Limited, it has aimed to become the

leading bank of Nepal by that provides outstanding services to its customers.

The services that Nepal Bank Limited provides have a great market penetration

not only because of their features but also the profit and markup rates that they

charge. Also the products that Nepal Bank Limited provides cater to sector of the

economy.

Furthermore, as the bank is growing, new and more energetic employees are

entering which is sure to invigorate the performance of the bank.

Lastly, to become the leading bank of Nepal, Nepal Bank Limited has to

benchmark its services to its major competitors in the industry or the market

leader in the industry and provide a continuous mean of improvement in its

existing products and services, while introducing new ones to the industry.

3.3 Recommendations

NBL should concentrate on better logistics like better maintenance of

printer, good paper quality for cheques, good UPS and the like.

Information should be timely conveyed to customers regarding any change

in regulations.

Training needs to be provided to employees regarding use of the system

and computer skills also needs to be brushed upon.

Try to do better in giving services like instant ATM cards, etc. It will be

better if the bank follows new network that will also be used outside the

country.

The good communication flow between bottom to top as well as top to

bottom level, staffs etc.

New products are necessary as there is growing competitive market.

More number of computers are needed in the customer service department

30

so that there will be no rush inside the department

Sometimes refreshment programs for the employees can be carried out to

motivate the employees.

The provision of job rotation has to be made to make the employees

familiar with the works and to make the work done if anyone is absent.

Nepal Bank has been giving its best services toward its customers .It always

thinks of new and better way of serving its customers. Its hard work and banking

facilities has able the bank to survive as one of the leading banks of the nation

despite of rapid increase of number of banks and tough competition in the

Nepalese banking environment.

31

BIBLIOGRAPHY

Annual report of Nepal Bank Limited

Shrestha, M.K. &Bhandari, B.D (2008).Financial Markets and Institutions

Kathmandu, Asmita Publication

Nepal Bank Limited. Available <http://www.nbl.com.np//

Website: Available <http://www.google.com// [online]

Website: Available <http://www.wikipedia.com// [online]

32