Embed Size (px)

Citation preview

Contents lists available at ScienceDirect

Telecommunications Policy

Telecommunications Policy ] (]]]]) ]]]–]]]

http://d0308-59

n CorrE-m1 ⟨h2 In

patents

Pleasdesig

URL: www.elsevier.com/locate/telpol

Innovation and competition in the smartphone industry:Is there a dominant design?

Grazia Cecere a, Nicoletta Corrocher b,n, Riccardo David Battaglia c

a Institut Mines Télécom, Télécom Ecole de Management, 9 rue Charles Fourier, 91011 Évry, France and Université Paris Sud 11, RITM, 54Bouleveard Desgranges, 92260 Sceaux, Franceb CRIOS, Bocconi University, Via Sarfatti 25, 20136 Milan, Italyc MEDAlics Research Center for Mediterranean Relations, Via del Torrione 95, 89125 Reggio Calabria, Italy

a r t i c l e i n f o

Keywords:SmartphonesDominant designProduct differentiation

x.doi.org/10.1016/j.telpol.2014.07.00261/& 2014 Elsevier Ltd. All rights reserved.

esponding author. Tel.: þ39 02 58363396; fail address: [email protected]://www.ft.com/cms/s/0/eb8ed76e-0500-1August 2012, the court obliges Samsung to p.

e cite this article as: Cecere, G., et an? Telecommunications Policy (2014)

a b s t r a c t

The mobile phone industry is a very innovative segment within the ICT sector and thesmartphone is becoming the standard configuration among the different types of mobiledevices. Technical change and new product proliferation have made this industryextremely dynamic, even if market shares are highly concentrated in the hands of veryfew companies. The present article investigates whether a dominant design has emergedin the smartphone industry. In particular, it studies the evolution in hardware componentsrelying upon an original dataset of product characteristics including all smartphoneslaunched in the market between 2004 and 2013. Results show that, despite someconvergence in the introduction of vertical innovations, product differentiation stillcharacterizes the competition among manufacturers and a dominant design has not yetemerged.

& 2014 Elsevier Ltd. All rights reserved.

1. Introduction

Smartphones have emerged in the market as the standard configuration for mobile devices and currently represent thefastest growing market segment in the telecoms industry. For the first time, in 2013 sales of internet-connectedsmartphones exceeded those for more basic handsets.1 Global mobile phone sales grew by 3.6% to 435 million units inthe second quarter of 2013, for the first time smartphones accounted for more than half of the market. Although devicesoffering telephony and computing features were developed in the 1970s, it was not until the end of 2006, when theBlackberry was introduced onto the market by RIM, that the smartphone became a commercially successful product.In 2007 Apple entered the market by developing the first model of iPhone and soon after (June 2008), Samsung released theSamsung Instinct, a direct iPhone competitor. Since then competition in the market has been quite harsh among incumbentsand between incumbents and new entrants. The recent legal battle over patents and designs between Apple and Samsung isa clear signal that smartphone vendors are fiercely competing for leadership in the market, even if Samsung is consolidatingits leadership also thanks to the diffusion of Android operating system.2 Despite the success of the iPhone design in the

ax: þ39 02 58363399.t (N. Corrocher).1e3-9ffd-00144feab7de.html#ixzz2id9vhg8y⟩.ay Apple just over $1 billion in damages for infringing six of the American firm's software and design

l. Innovation and competition in the smartphone industry: Is there a dominant, http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]2

market, innovation activity among firms continued and many different versions of smartphones currently exist in the sector.This contrasts with the conventional wisdom concerning the emergence of a dominant industry design, which predicts thatimitators tend to follow innovators and, if an innovation is commercially successful and widely adopted, it will become thedominant design because all products in the market will use that specific technology and design features.

The aim of this article is to discuss whether a dominant design has emerged in the market for smartphones by examiningthe innovation strategies of companies. In light of this, the paper will also investigate the relationship between innovativeactivity and industrial dynamics. In doing so, we will answer two research questions. First, has a dominant design insmartphone (hardware) characteristics emerged over time? Second, what are the implications of firms' innovation strategiesfor industrial dynamics? The empirical analysis relies upon the contribution of Koski and Kretschmer (2007) who discussproduct innovation strategies of firms in the mobile phone industry, looking at the evolution of handset characteristics.Accordingly, we will distinguish among two types of innovation strategies, i.e., horizontal product innovation and verticalproduct innovation. Furthermore, even if our investigation mostly focuses on the hardware side, given the peculiarities ofsmartphones, we will also make some consideration on the evolution of software characteristics (operating system) overtime. The remainder of the article is organized as follows. Section 2 reviews the literature on dominant design underliningthe implications for the mobile industry. Section 3 provides evidence on performance of competitors in the market, whileSection 4 investigates whether a dominant design has emerged or instead different smartphone configurations arecontinuing to proliferate, and discusses the implications of firms' innovation strategies for industrial dynamics. Section 5concludes the discussion.

2. The emergence of a dominant design in the market: a review of the literature

The seminal article by Utterback and Abernathy (1975) refers to dominant design as a single architecture3 that establishesdominance in a product category. In the early stages of market evolution, high technical and market uncertainty results in adiversity of product designs (Abernathy & Utterback, 1978; Dosi, 1982; Lee, Neal, Pruett, & Thomas 1995; Smith, 1997;Utterback, 1994). A product category evolves due to the processes of variation, selection, and retention (e.g., Anderson &Tushman, 1990; Tushman, Anderson, & Murmann, 1998). Technological breakthroughs create rivalry among alternativedesigns, resulting in a period of design variation or ferment. The emergence of a dominant design is the transition pointbetween the periods of variation and selection. The article of David and Greenstein (1990) details the different processesthat lead to the creation of standards, underlying the importance of compatibility in the standardization process.

The definition of dominant design is a specific path along an industry's design architecture, which establishes dominanceamong competing design paths. A dominant design usually takes the form of a new product (or novel set of features)synthesized from individual technological innovations introduced independently in prior product variants (Utterback andSuaréz, 1993). A dominant design is a product within a product category that gains general acceptance as the standard fortechnical features that other market players must follow if they want to acquire significant market share (Utterback, 1994).Christensen, Suaréz, and Utterback (1998) explain a dominant design as emerging in a product category when one product'sdesign specifications (consisting of a single feature or a complement of design features) define the product category'sarchitecture. In this respect, it is possible to argue that in complex products such as computers or smartphones, dominantdesigns might emerge in relation to a sub-set of characteristics that are the result of either vertical or horizontal innovations.Srinivasan, Lilien, and Rangaswamy (2006) add that a particular product design architecture can define the specifications forthe entire product category. Argyres, Bigelow and Nickerson (2013) propose an innovative characterization, according towhich a dominant design appears per se, in the form of a breakthrough that can resist market “shakes” and comprises onlyslight and not radical improvements. They define this type of a breakthrough as a “composition desiderata”, because itrepresents a collection of desirable features, and they consider the iPhone to be an example of a composition desiderata.

A large strand of empirical studies documents the emergence of dominant designs in various product categories,including typewriters, televisions, electronic calculators, automobiles (Utterback, 1994), VCRs (Cusumano, Mylonadis, &Rosenbloom, 1992), cochlear implants (Van de Ven and Garud, 1993), fax machines (Baum, Korn, & Kotha, 1995), cement,glass, and minicomputers (Anderson & Tushman, 1990). Koski and Kretschmer (2007) used dominant design theoreticalframework to study innovation in the mobile phone design. Van de Kaa, Van den Ende, De Vries, and Van Heck (2011)reviewed the literature on the topic and identified how format dominances can emerge using five categories: characteristicsof the format supporter, characteristics of the format, format support strategy, other stakeholders, and marketcharacteristics.

Dominant design is satisfying as long as its technical possibilities are driven by the commercial interests of suppliers,users, and competitors (Srinivasan et al., 2006; Tushman & Rosenkopf, 1992; Wade, 1995). However, the literature showsthat the dominant design is not always the design that incorporates the best features and performance. Gallagher (2007)underlines the distinction between dominant designs and industry standards. In particular, standards are driven by therelative importance of network effects, while dominant designs are architectures with recognized implications forindustries. This implies that standards are often important elements of dominant designs.

3 According to Ulrich (1995), a product architecture is the scheme by which the function of the product is allocated to physical components.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 3

An interesting issue in the context of this article is the relationship between standards and dominant design (Katz &Shapiro, 1986; Schilling, 1998). In particular, while de jure standards correspond to legal standards, established by publicentities, producers consortia, or cooperating firms, de facto standards coincide with the dominant design, and depend onmarket acceptance (Koski and Kretschmer (2007)). The literature shows that several standards can coexist and compete foryears without an individual technology emerging as the dominant design (Schilling, 2002, 2005). Indeed, in some sectorsthere are valid examples of this non-emergence, for example, camcorders, supercomputers, video games consoles(Srinivasan et al., 2006).

The evolution of a technology towards a dominant design is explained by Abernathy and Utterback (1975, 1978) throughthe product life cycle model, which discusses the dynamics of product and process innovation within industries, and alsolooks at the competitive scenario and the implications for the companies involved. The model identifies three phases in aproduct's life: fluid phase (introduction), transition phase and specific phase. At the earliest stage, the market is populatedby a large number of competitors struggling to increase their market share by focusing on technical improvements anddeveloping new product features while process innovation is negligible or absent. Innovation is stimulated by informationon potential customer needs, and results in different designs coexisting in the market. The transitional phase ischaracterized by the emergence of a large variety of products and companies working to improve their internal innovationand production capacities. The number of competing firms decreases over time because only the best performers are able tosurvive, which results in decreasing variety and rivalry shifting to price competition – mostly in the mass market althoughsome companies will prefer to focus on market niches. The industry becomes more concentrated and the lowest performingfirms are pushed out of the market. Product innovation slows as particular product features are recognized and assumed tobe dominant in the eyes of both the innovators and early imitators (Henderson & Clark, 1990). At this stage, a widelyaccepted product line can become the dominant design based on consumers' acceptance of its features: this is theconfiguration that will be most imitated and improved on by competitors. As the industry reaches maturity, competition isabout price, and the market becomes concentrated since only a few actors will be able to leverage the economies of scale tomaintain a significant and positive margin. The competitive emphasis is on cost reduction, and as firms try to reduce costs,the predominant form of innovation is incremental and process innovation rather than product. During this phase, productdesigns become standardized and the differences among competing versions of the product are so small as not to constitutea source of competitive advantage.

The emergence of a dominant design affects the market shares (e.g., Anderson & Tushman, 1990) and survival (e.g., Baumet al., 1995; Christensen et al., 1998; Suaréz & Utterback, 1995; Tegarden, Hatfield, & Echols, 1999) of firms. Once a dominantdesign has emerged in the market, large companies generally compete on price and smaller competitors focus on marketniches. In the specific phase, the number of companies naturally decreases due to exits and acquisition processes, and largecompanies are able to maintain their margins through economies of scale and scope. Small companies keen to survive in themarket implement niche strategies and provide target customers with clearly measurable advantages.

In high tech sectors, the emergence of a dominant design (and of a standard) is often caused by the existence of networkeffects (Farrell & Saloner, 1985; Katz and Shapiro 1985, 1986, 1994). Network effects occur when the value of adopting agood/technology increases with the number of other users that join the network. The presence of network effects oftenleads to the emergence of lock-in and to the creation of de facto standards, because of technical interrelatedness(complementarity/modularity) among hardware and software components, system scale economies and quasi irreversibilityof the investments because of high switching costs (David, 1985). Most markets in which network effects exist are “multi-sided”, as they consist of complementary goods and are mediated by platforms – e.g., operating systems (e.g., Evans, 2003;Hagiu, 2005). In markets characterized by network effects, there is a bandwagon effect both in the demand and in thesupply sides, as users and producers imitate each other in the adoption of a specific technology because of informationadvantages, scale effects, and the availability of complementary goods (Schilling, 2002; Van de Kaa et al., 2011). In terms ofindustrial dynamics, the most important implication is that the technology/platform that has an initial advantage overothers tends to increase its advantage, resulting in a winner-takes-all situation. More recently a series of empirical studieshave challenged this conclusion, showing that competition among platforms not necessarily results in a winner-takes-alltype of market, because of issues related to the varying magnitude of network effects, the quality of the competingplatforms and complementary goods, the congestion and the strategic choices and competencies of firms involved (Suaréz,2005; Afuah, 2013).

If we look at the evolution of mobile phone industry over time, it is possible to claim that in the early stages of theindustry, companies engaged in infrastructural innovations related to the development of mobile communication systems(from analogue to digital technologies; from 2G to 3G, etc.) (Fuentelsaz, Maicas, & Polo, 2008), which paved the way forrapid innovation in devices, enabling more user-friendly product characteristics such as lighter weight and longer talk time.Subsequent innovations were related both to the introduction of a set of additional features (e.g., games, ringtones) by themajor players in the industry, and, more recently, to the development of mobile data services, which have been directlyconnected with the development of 3G standards (West and Mace, 2010).

Koski and Kretschmer (2007) look at innovation – i.e., the introduction of new product features – and productdifferentiation – i.e., the extent to which existing products differ along a set of characteristics – in the mobile phone sectorbefore the appearance of smartphones. In particular, they identify two product development strategies used by firms, that is,vertical (product) innovation and horizontal (product) innovation. The first represents improvements to the product'stechnical characteristics and establishes a clear quality ranking for customers. The second entails development of new

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]4

product characteristics, which results in a significant improvement only for those users with a higher willingness to pay.Vertical and horizontal innovations do not necessarily become dominant designs. In particular, before the development ofsmartphones, vertical innovations in the mobile telephony industry did not lead to a dominant design although some weresignificant differentiation attempts (namely, handset talk time, standby time). However, some horizontal innovations havebecome part of a dominant design (e.g., weight, speed dialing, vibration alert, SMS, clock and games), while some haverepresented attempts to differentiate a product (i.e., PC synchronization, WWW capability, number of ringtones, colours,alarm clock, calculator, handset size) (Koski & Kretschmer, 2007).

Notably, the role of entrants as the primary source of product innovation does not seem to be confirmed in the mobilephone sector if innovation is measured merely by the number of new products. As shown by Koski and Kretschmer (2007)almost 40% of the new handset models launched between 1992 and 2003 were produced by the five biggest cellular phonemanufacturers.

3. The emergence of smartphones and its impact on the mobile communication industry

The emergence of smartphones in the mobile communication sector has been characterized by the introduction of aseries of changes in the technology that has been both intangible – the operating system – and tangible – the hardwarecharacteristics. In both cases, we have witnessed the emergence of vertical and horizontal innovations, but whileconvergence tends to occur in vertical innovations – e.g., wi-fi connectivity, USB, touch screen – product differentiationstill remains quite substantial because of the introduction of different horizontal innovations.

The development of mobile Internet services represents an important milestone in the history of smartphones, as itconstituted the main trigger for the introduction of devices that allowed a full convergence between computing andcommunications. Handset producers and system developers in different countries adopted very different strategies toachieve this goal. In particular, while companies in Europe and in the US concentrated their efforts on the high-end of themarket, commercializing high-price multimedia services over mobile networks, NTT DoCoMo in Japan developed thei-mode standard, which achieved widespread adoption thanks to the creation of specific content and to the relatively lowcommission it took on all mobile transaction (Funk, 2001; West & Mace, 2010).

As soon as more advanced mobile data networks (3G) were also developed in the European countries, handsetmanufacturers started experimenting with new devices that could fully exploit the opportunities provided by the mobileInternet. The first step towards this accomplishment was the development of devices merging personal digital assistants(PDAs) and mobile phones, which embedded advanced computer capabilities. This was stimulated by the need to sell valueadded services through high-priced and high-margin products in order to offset the decreasing revenues from voiceservices.

The first attempt to combine telephony, computing, and personalization features was prototyped in 1992 by IBM withthe Angler. An improved version of the Angler – Simon Personal Communicator – was developed in 1993 as the result of apartnership between IBM and BellSouth Cellular Corp and it was officially launched on 16 August 1994. Simon did notachieve the predicted success: only 50 000 units were sold. The first smartphone developed in Europe was Nokia 9000, evenif the description “smartphone” was first used by Ericsson in 1997 to explain the revolutionary features of its GS88, alsoknown as Penelope.4 An important milestone in the evolution of the smartphones was the development of the Symbian jointventure among Nokia, Psion, Motorola and Ericsson, which aimed at creating an operating system (OS) for mobile phones.The development of OS has since constituted an essential feature of smarthphones as it manages the hardware and softwareresources of the smartphones, allowing the exploitation of value added services by users, which are strictly to Internetconnection.

Since the end of the 1990s, most companies in the market embraced the smartphone concept – Nokia with itsCommunicator Line, Motorola with the MPX line, Ericsson with its T series, and later Samsung with its I series. Theseinnovations were imitated by newcomers such as HTC, RIM, MiTAC International Corp. (under the brands Mio Technologyand Navman) and Kyocera, whose 6035 is considered to be the first commercially successful smartphone. The turning pointin the smartphone industry occurred between 2006 and 2007. At the end of 2006, RIM launched a device for the businessworld based on the BlackBerry, which enabled email and instant messaging, and HTML browsing. This was the Curve 8100,which was aimed exclusively at business people. Apple entered this market segment in the beginning of 2007, when the firstiPhone was officially announced to the world by Steve Jobs. The iPhone disrupted the traditional market concept byintegrating the new phone with the OS, and the browser – Safari – and the iTunes Store for downloading audio and videocontent.5 Furthermore, it used a touch screen (instead of a keyboard) with a software-based virtual keyboard (West & Mace,2010). Even if it was not the first model of smartphone in the market, it soon became a point of reference for all producers inthe coming years in terms of design and user interface. On July 11, 2008, the iPhone 3G was launched, with the simultaneousopening of the Apple's App Store, which offered more than 500 applications.

While European companies did not immediately respond to Apple's challenge and continued to produce Symbiansmartphones, other competitors started imitating and improving the iPhone concept, Samsung and LG had accumulated

4 ⟨http://www.techinfo2.com/smartphones-history-reveiew-over-20-years.html⟩.5 Notably, the first iPhone did not allow the development of third-party applications.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 5

competencies in touch screen phones, and of RIM and they had introduced the first touch screen device in 2008. From 2009on however, competition increased substantially, following the introduction of many devices, which used the Android opensource OS developed by the homonymous company that in 2005 had been bought by Google. The widespread adoption ofthis open OS by different mobile device manufacturers – Samsung, HTC, Sony Ericsson – and the development of Google Playapplication store allowed this platform to achieve market leadership against its rival iOS. The combined number of apps onIOS and Android nearly doubled between the end of 2011 (850 000 units) and 2012 (1 400 040 units) (OECD, 2013). Theecosystem initiated around the iPhone spread quickly across the industry, first in the United States then worldwide. Thedevelopment of Android and, later, Windows Mobile further allowed increase of competition between device manufacturersfor smartphones. Since then, manufacturers had greater flexibility as they could use readily available operating systems fortheir devices which permit them to focus on specific product and market segment. The development of different OSseliminates further barriers to entry and encouraged new players into the market. For example, chipset manufacturersreacted by developing systems on a chip combined with reference designs which eliminated an important part of researchand development from designing smartphones. This trend has stimulated the entry of new manufacturers and in particularChinese firms, such as Huawei, Gionee, Oppo and ZTE, who have gained substantial market shares with low-pricedsmartphones, especially in non-OECD economies (OECD, 2013).

The smartphone industry has witnessed substantial growth, driven mostly by the emergence of new actors in the field –

Apple, Samsung – and by technological developments in the hardware and software components. In OECD countries in thefirst quarter of 2012, the share of people having a smartphone ranged from 20% (Japan) to 54% (Norway) of individuals. Theshare reached more than 50% in Australia, Norway, Sweden and the United Kingdom. On average in the EU15 the share ofindividuals equipped with a smartphone increased from 22% in 2009 to 44% at the end of 2011. In 2012, in most OECDselected countries, Apple (iOS) and Google (Android) were the most used OS. However, other OSs registered a wide presencein other markets: Symbian (Nokia) has a share in Finland (43%), China (32%), Italy (25%) and Spain (21%). Meanwhile,Blackberry (RIM), has markets shares in Mexico (25%) and Canada and the United Kingdom (23%) (OECD, 2013).

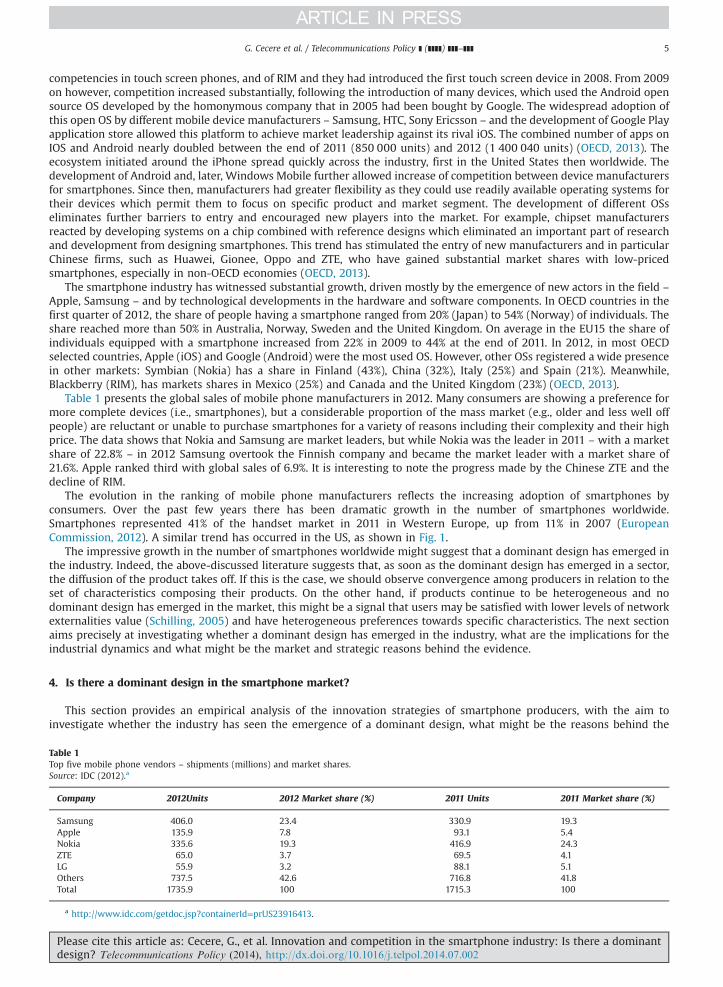

Table 1 presents the global sales of mobile phone manufacturers in 2012. Many consumers are showing a preference formore complete devices (i.e., smartphones), but a considerable proportion of the mass market (e.g., older and less well offpeople) are reluctant or unable to purchase smartphones for a variety of reasons including their complexity and their highprice. The data shows that Nokia and Samsung are market leaders, but while Nokia was the leader in 2011 – with a marketshare of 22.8% – in 2012 Samsung overtook the Finnish company and became the market leader with a market share of21.6%. Apple ranked third with global sales of 6.9%. It is interesting to note the progress made by the Chinese ZTE and thedecline of RIM.

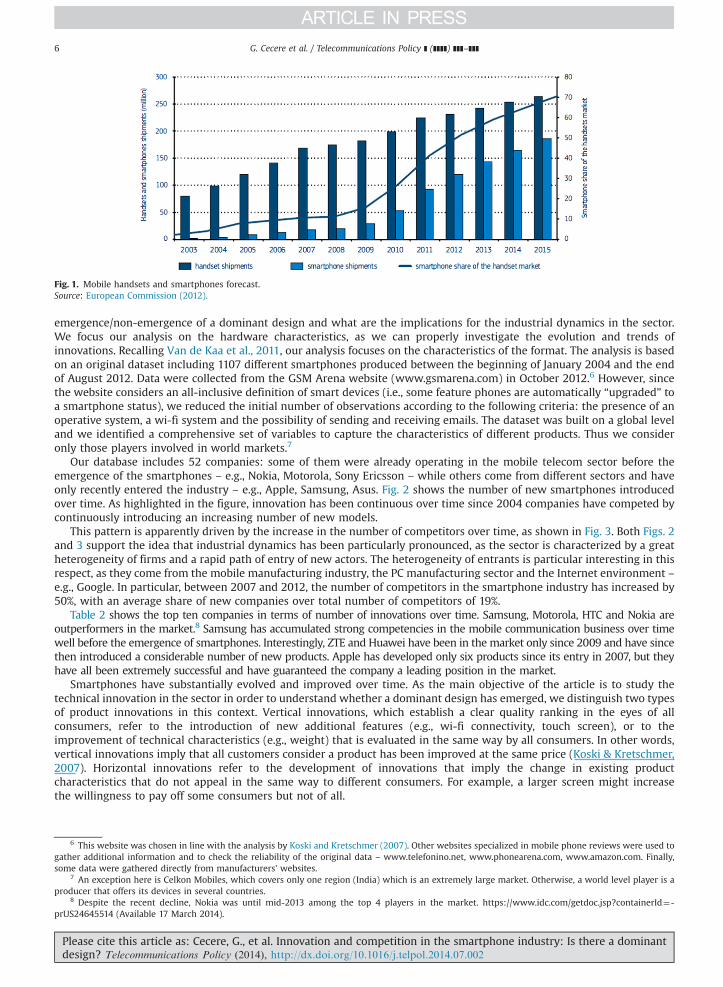

The evolution in the ranking of mobile phone manufacturers reflects the increasing adoption of smartphones byconsumers. Over the past few years there has been dramatic growth in the number of smartphones worldwide.Smartphones represented 41% of the handset market in 2011 in Western Europe, up from 11% in 2007 (EuropeanCommission, 2012). A similar trend has occurred in the US, as shown in Fig. 1.

The impressive growth in the number of smartphones worldwide might suggest that a dominant design has emerged inthe industry. Indeed, the above-discussed literature suggests that, as soon as the dominant design has emerged in a sector,the diffusion of the product takes off. If this is the case, we should observe convergence among producers in relation to theset of characteristics composing their products. On the other hand, if products continue to be heterogeneous and nodominant design has emerged in the market, this might be a signal that users may be satisfied with lower levels of networkexternalities value (Schilling, 2005) and have heterogeneous preferences towards specific characteristics. The next sectionaims precisely at investigating whether a dominant design has emerged in the industry, what are the implications for theindustrial dynamics and what might be the market and strategic reasons behind the evidence.

4. Is there a dominant design in the smartphone market?

This section provides an empirical analysis of the innovation strategies of smartphone producers, with the aim toinvestigate whether the industry has seen the emergence of a dominant design, what might be the reasons behind the

Table 1Top five mobile phone vendors – shipments (millions) and market shares.Source: IDC (2012).a

Company 2012Units 2012 Market share (%) 2011 Units 2011 Market share (%)

Samsung 406.0 23.4 330.9 19.3Apple 135.9 7.8 93.1 5.4Nokia 335.6 19.3 416.9 24.3ZTE 65.0 3.7 69.5 4.1LG 55.9 3.2 88.1 5.1Others 737.5 42.6 716.8 41.8Total 1735.9 100 1715.3 100

a http://www.idc.com/getdoc.jsp?containerId=prUS23916413.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

Fig. 1. Mobile handsets and smartphones forecast.Source: European Commission (2012).

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]6

emergence/non-emergence of a dominant design and what are the implications for the industrial dynamics in the sector.We focus our analysis on the hardware characteristics, as we can properly investigate the evolution and trends ofinnovations. Recalling Van de Kaa et al., 2011, our analysis focuses on the characteristics of the format. The analysis is basedon an original dataset including 1107 different smartphones produced between the beginning of January 2004 and the endof August 2012. Data were collected from the GSM Arena website (www.gsmarena.com) in October 2012.6 However, sincethe website considers an all-inclusive definition of smart devices (i.e., some feature phones are automatically “upgraded” toa smartphone status), we reduced the initial number of observations according to the following criteria: the presence of anoperative system, a wi-fi system and the possibility of sending and receiving emails. The dataset was built on a global leveland we identified a comprehensive set of variables to capture the characteristics of different products. Thus we consideronly those players involved in world markets.7

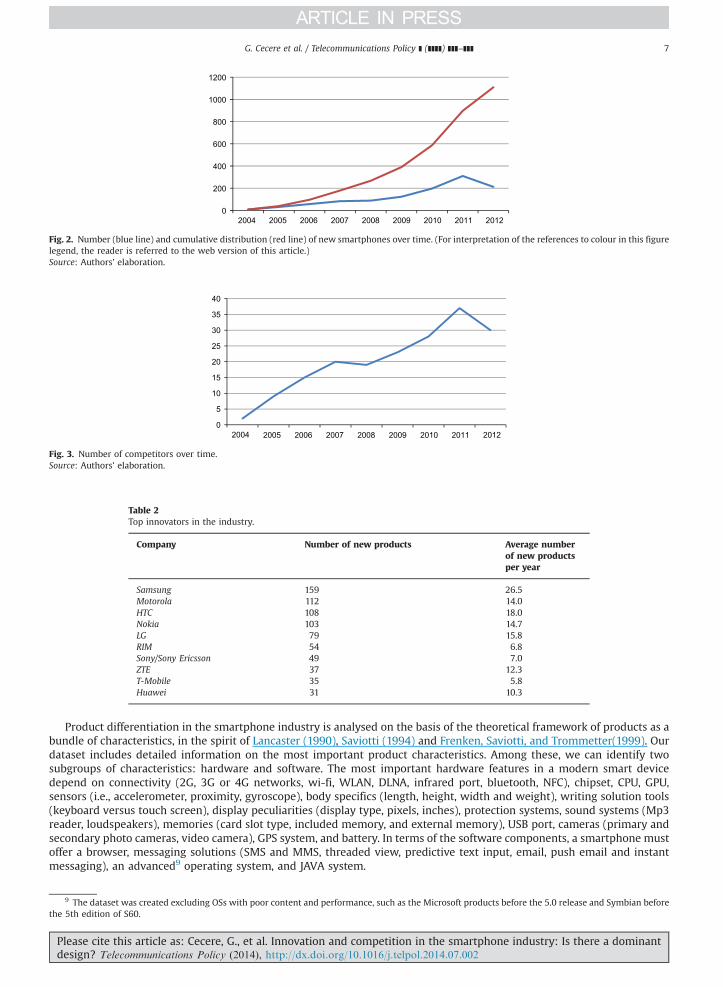

Our database includes 52 companies: some of them were already operating in the mobile telecom sector before theemergence of the smartphones – e.g., Nokia, Motorola, Sony Ericsson – while others come from different sectors and haveonly recently entered the industry – e.g., Apple, Samsung, Asus. Fig. 2 shows the number of new smartphones introducedover time. As highlighted in the figure, innovation has been continuous over time since 2004 companies have competed bycontinuously introducing an increasing number of new models.

This pattern is apparently driven by the increase in the number of competitors over time, as shown in Fig. 3. Both Figs. 2and 3 support the idea that industrial dynamics has been particularly pronounced, as the sector is characterized by a greatheterogeneity of firms and a rapid path of entry of new actors. The heterogeneity of entrants is particular interesting in thisrespect, as they come from the mobile manufacturing industry, the PC manufacturing sector and the Internet environment –e.g., Google. In particular, between 2007 and 2012, the number of competitors in the smartphone industry has increased by50%, with an average share of new companies over total number of competitors of 19%.

Table 2 shows the top ten companies in terms of number of innovations over time. Samsung, Motorola, HTC and Nokia areoutperformers in the market.8 Samsung has accumulated strong competencies in the mobile communication business over timewell before the emergence of smartphones. Interestingly, ZTE and Huawei have been in the market only since 2009 and have sincethen introduced a considerable number of new products. Apple has developed only six products since its entry in 2007, but theyhave all been extremely successful and have guaranteed the company a leading position in the market.

Smartphones have substantially evolved and improved over time. As the main objective of the article is to study thetechnical innovation in the sector in order to understand whether a dominant design has emerged, we distinguish two typesof product innovations in this context. Vertical innovations, which establish a clear quality ranking in the eyes of allconsumers, refer to the introduction of new additional features (e.g., wi-fi connectivity, touch screen), or to theimprovement of technical characteristics (e.g., weight) that is evaluated in the same way by all consumers. In other words,vertical innovations imply that all customers consider a product has been improved at the same price (Koski & Kretschmer,2007). Horizontal innovations refer to the development of innovations that imply the change in existing productcharacteristics that do not appeal in the same way to different consumers. For example, a larger screen might increasethe willingness to pay off some consumers but not of all.

6 This website was chosen in line with the analysis by Koski and Kretschmer (2007). Other websites specialized in mobile phone reviews were used togather additional information and to check the reliability of the original data – www.telefonino.net, www.phonearena.com, www.amazon.com. Finally,some data were gathered directly from manufacturers' websites.

7 An exception here is Celkon Mobiles, which covers only one region (India) which is an extremely large market. Otherwise, a world level player is aproducer that offers its devices in several countries.

8 Despite the recent decline, Nokia was until mid-2013 among the top 4 players in the market. https://www.idc.com/getdoc.jsp?containerId¼-prUS24645514 (Available 17 March 2014).

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

0

200

400

600

800

1000

1200

2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig. 2. Number (blue line) and cumulative distribution (red line) of new smartphones over time. (For interpretation of the references to colour in this figurelegend, the reader is referred to the web version of this article.)Source: Authors' elaboration.

Table 2Top innovators in the industry.

Company Number of new products Average numberof new productsper year

Samsung 159 26.5Motorola 112 14.0HTC 108 18.0Nokia 103 14.7LG 79 15.8RIM 54 6.8Sony/Sony Ericsson 49 7.0ZTE 37 12.3T-Mobile 35 5.8Huawei 31 10.3

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig. 3. Number of competitors over time.Source: Authors' elaboration.

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 7

Product differentiation in the smartphone industry is analysed on the basis of the theoretical framework of products as abundle of characteristics, in the spirit of Lancaster (1990), Saviotti (1994) and Frenken, Saviotti, and Trommetter(1999). Ourdataset includes detailed information on the most important product characteristics. Among these, we can identify twosubgroups of characteristics: hardware and software. The most important hardware features in a modern smart devicedepend on connectivity (2G, 3G or 4G networks, wi-fi, WLAN, DLNA, infrared port, bluetooth, NFC), chipset, CPU, GPU,sensors (i.e., accelerometer, proximity, gyroscope), body specifics (length, height, width and weight), writing solution tools(keyboard versus touch screen), display peculiarities (display type, pixels, inches), protection systems, sound systems (Mp3reader, loudspeakers), memories (card slot type, included memory, and external memory), USB port, cameras (primary andsecondary photo cameras, video camera), GPS system, and battery. In terms of the software components, a smartphone mustoffer a browser, messaging solutions (SMS and MMS, threaded view, predictive text input, email, push email and instantmessaging), an advanced9 operating system, and JAVA system.

9 The dataset was created excluding OSs with poor content and performance, such as the Microsoft products before the 5.0 release and Symbian beforethe 5th edition of S60.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

Table 3Examples of vertical and horizontal innovations in smartphones.

Hardware components Software components

Horizontal innovations Screen size Games; number of ringtonesVertical innovations Weight; wi-fi connectivity; multitouch screen, secondary camera Internet browser

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]8

Table 3 provides a list of examples of vertical and horizontal innovations that occurred in the smartphone industry. Inorder to illustrate the pattern of innovation in the smartphones, we select nine components that refer to the most relevanthardware characteristics and illustrate at best the development of mobile handset, and examine their evolution over time.Seven of these features refer to vertical product innovations, while the remaining two refer to horizontal productinnovations.

As far as vertical innovation is concerned, the seven selected features are WEIGHT, WIFI, 3G, MULTITOUCH, MICROUSB,SECONDARY_CAMERA, 3.5 MM JACK.

First, the weight of the mobile handset has always been extremely important for consumers. We created a continuousvariable WEIGHT whose value ranges from 113 g to 165 g. Second, wireless LAN (local area network, represented by thevariable wi-fi) was evaluated as fundamental for connectivity.10 This feature is present in most products (88.38% of thesample). We built a dummy variable WIFI that takes the value 1 if the smartphone has a wi-fi connection, and 0 otherwise.

Third, staying connected means that users are able to exploit the online capabilities of their devices when they are faraway from a LAN. For this reason producers are embedding global system networks (i.e., 2G networks, 3G networks and 4Gnetworks) into their phones. As a proxy of innovativeness in relation to this characteristic we chose the presence of a 3Gnetwork,11 and built a dummy variable 3G that takes the value 1 if the smartphone has 3G connectivity, and 0 otherwise.

Fourth, most smartphones are designed with a touch screen (65.24% of the sample, 91.98% of devices in 2012); fewer andfewer operate using keyboards only (10.46% of the overall sample and only 1.42% of devices in 2012), while hybrid solutions(products with keyboard and touch screen) have increased over time. The presence of touch screen is measured through adummy variable MULTITOUCH that takes value 1 if this technology is available, and 0 otherwise. This is a key characteristic ofsmartphones: in particular Samsung has been accused of copying different types of touch options such as tap to zoom andmultitouch gesture (respectively, patents US7864163 and US7844195).

Fifth, a smartphone is a pocket-hardware which can be connected to a personal computer or other hardware sets totransfer files. The variable for this feature is USB_type, which indicates the presence of a USB port in the device and the typeof USB port (i.e., miniUSB port, or microUSB port, which is the most innovative). We created a dummy variable MICROUSB thattakes the value 1 if the device has a MICROUSB port,12 and 0 otherwise.

Sixth, the growth of social networking (e.g., Facebook, Twitter) has generated interest among smartphone users ininformation and content sharing, including pictures.13 The availability of a camera as a dummy for innovativeness would notbe informative because all the smartphones in the dataset have a camera. However, the availability of a secondary camera isa meaningful proxy for innovativeness in this aspect: 45.04% of the models in our sample have a secondary camera. Thediffusion of secondary cameras has grown significantly since 2010 (e.g., in 2010 they were only 25.38% of the total, in thefirst half of 2012 they represented 66.04% of the total). The dummy variable SECONDARY_CAMERA takes the value 1 if thesmartphone has a secondary camera, and 0 otherwise.

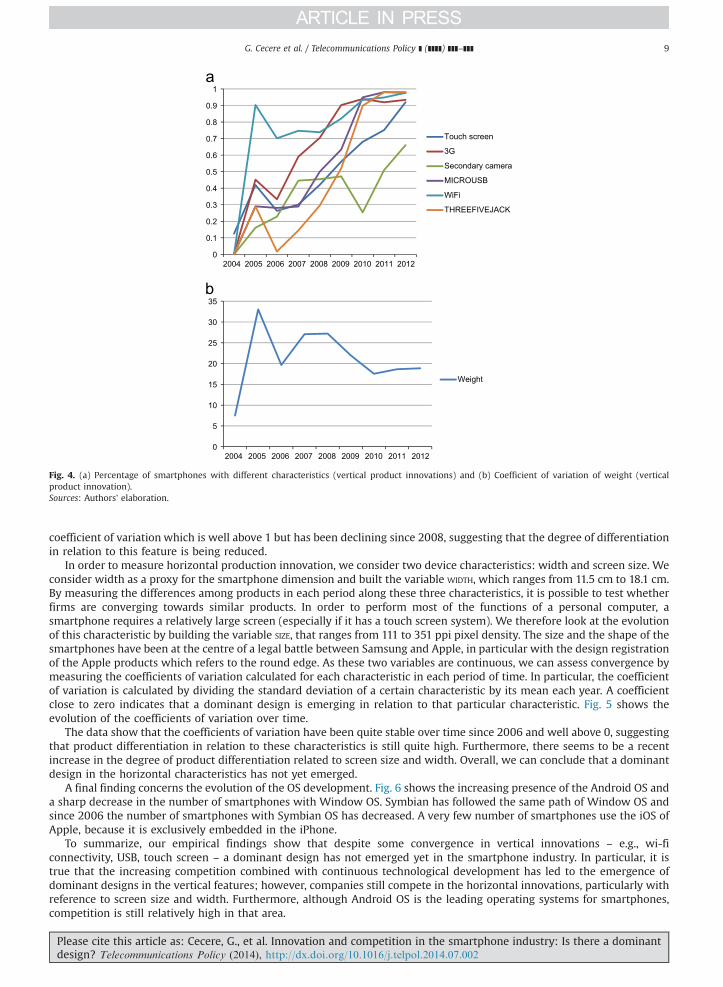

Finally, smart devices allow people to listen to music. They are successful portable music players because they can readMP3 files. As a proxy for innovativeness, we chose the availability of a 3.5 mm jack,14 measured by the dummy variableTHREEFIVEJACK that takes the value 1 if the feature is present, and 0 otherwise. As these characteristics are defined by dummyvariables, in order to understand whether a dominant design has emerged, we compute the percentage of smartphonesembedding each characteristic over time (see Fig. 4a and b).

The empirical evidence shows that there has been an increase in the number of smartphones which have similarcharacteristics, which suggest the emergence of a dominant design in relation to vertical product innovations. In particular,the percentage of smartphones with touch screen rapidly increased from about 30% in 2007 to about 95% in 2012. As far asthe 3G connection is concerned, in 2006 about 35% of smartphones had this feature, but this percentage rose to 90% in 2012.The most rapid standardization occurred in relation to the 3.5 mm jack option which characterized less than 10% ofsmartphones in 2006 and appeared to be in about 95% in 2012. As far as the variable weight is concerned, we observe a

10 We assume here that each mobile phone enables connectivity with the mobile network.11 4G network is becoming more widespread and is likely to become a standard. However, our analysis sample includes very few 4G models (5.81% of

the total devices considered) and therefore we decided to evaluate the connectivity with the degree of innovativeness by looking at the existence of 3Gnetwork connectivity.

12 78.37% of the models considered are equipped with microUSB, a superior technology in terms of dimension (it is smaller) and performance. It is theonly USB type between the two types considered that can be used to charge the device; in August 2012, 207 had a microUSB port (i.e., 97.64% of 2012models).

13 Sharing pictures has become an everyday activity resulting in continuous improvement to the quality and performance of smartphone cameras.14 A 3.5 mm jack is a connector used to plug in headphones such as those found on music players, computers and most other electronic devices with

audio outputs. It can support stereo and/or microphone, depending on the number of separate connector rings on the jack.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2004 2005 2006 2007 2008 2009 2010 2011 2012

Touch screen

3G

Secondary camera

MICROUSB

WiFi

THREEFIVEJACK

0

5

10

15

20

25

30

35

2004 2005 2006 2007 2008 2009 2010 2011 2012

Weight

Fig. 4. (a) Percentage of smartphones with different characteristics (vertical product innovations) and (b) Coefficient of variation of weight (verticalproduct innovation).Sources: Authors' elaboration.

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 9

coefficient of variation which is well above 1 but has been declining since 2008, suggesting that the degree of differentiationin relation to this feature is being reduced.

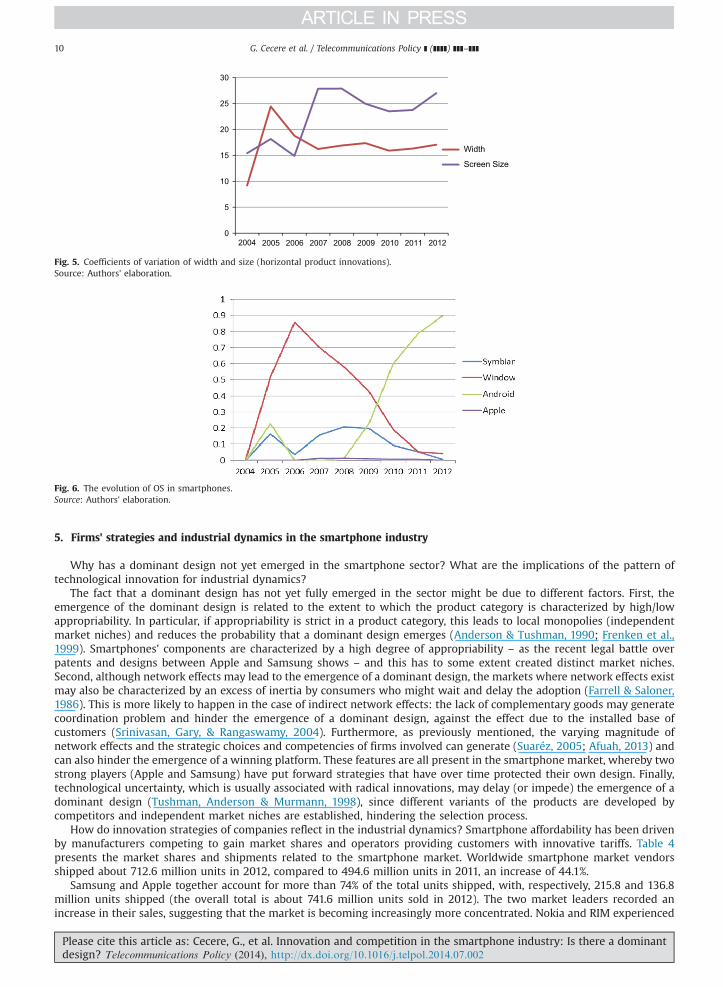

In order to measure horizontal production innovation, we consider two device characteristics: width and screen size. Weconsider width as a proxy for the smartphone dimension and built the variable WIDTH, which ranges from 11.5 cm to 18.1 cm.By measuring the differences among products in each period along these three characteristics, it is possible to test whetherfirms are converging towards similar products. In order to perform most of the functions of a personal computer, asmartphone requires a relatively large screen (especially if it has a touch screen system). We therefore look at the evolutionof this characteristic by building the variable SIZE, that ranges from 111 to 351 ppi pixel density. The size and the shape of thesmartphones have been at the centre of a legal battle between Samsung and Apple, in particular with the design registrationof the Apple products which refers to the round edge. As these two variables are continuous, we can assess convergence bymeasuring the coefficients of variation calculated for each characteristic in each period of time. In particular, the coefficientof variation is calculated by dividing the standard deviation of a certain characteristic by its mean each year. A coefficientclose to zero indicates that a dominant design is emerging in relation to that particular characteristic. Fig. 5 shows theevolution of the coefficients of variation over time.

The data show that the coefficients of variation have been quite stable over time since 2006 and well above 0, suggestingthat product differentiation in relation to these characteristics is still quite high. Furthermore, there seems to be a recentincrease in the degree of product differentiation related to screen size and width. Overall, we can conclude that a dominantdesign in the horizontal characteristics has not yet emerged.

A final finding concerns the evolution of the OS development. Fig. 6 shows the increasing presence of the Android OS anda sharp decrease in the number of smartphones with Window OS. Symbian has followed the same path of Window OS andsince 2006 the number of smartphones with Symbian OS has decreased. A very few number of smartphones use the iOS ofApple, because it is exclusively embedded in the iPhone.

To summarize, our empirical findings show that despite some convergence in vertical innovations – e.g., wi-ficonnectivity, USB, touch screen – a dominant design has not emerged yet in the smartphone industry. In particular, it istrue that the increasing competition combined with continuous technological development has led to the emergence ofdominant designs in the vertical features; however, companies still compete in the horizontal innovations, particularly withreference to screen size and width. Furthermore, although Android OS is the leading operating systems for smartphones,competition is still relatively high in that area.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012

Width

Screen Size

Fig. 5. Coefficients of variation of width and size (horizontal product innovations).Source: Authors' elaboration.

Fig. 6. The evolution of OS in smartphones.Source: Authors' elaboration.

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]10

5. Firms' strategies and industrial dynamics in the smartphone industry

Why has a dominant design not yet emerged in the smartphone sector? What are the implications of the pattern oftechnological innovation for industrial dynamics?

The fact that a dominant design has not yet fully emerged in the sector might be due to different factors. First, theemergence of the dominant design is related to the extent to which the product category is characterized by high/lowappropriability. In particular, if appropriability is strict in a product category, this leads to local monopolies (independentmarket niches) and reduces the probability that a dominant design emerges (Anderson & Tushman, 1990; Frenken et al.,1999). Smartphones' components are characterized by a high degree of appropriability – as the recent legal battle overpatents and designs between Apple and Samsung shows – and this has to some extent created distinct market niches.Second, although network effects may lead to the emergence of a dominant design, the markets where network effects existmay also be characterized by an excess of inertia by consumers who might wait and delay the adoption (Farrell & Saloner,1986). This is more likely to happen in the case of indirect network effects: the lack of complementary goods may generatecoordination problem and hinder the emergence of a dominant design, against the effect due to the installed base ofcustomers (Srinivasan, Gary, & Rangaswamy, 2004). Furthermore, as previously mentioned, the varying magnitude ofnetwork effects and the strategic choices and competencies of firms involved can generate (Suaréz, 2005; Afuah, 2013) andcan also hinder the emergence of a winning platform. These features are all present in the smartphone market, whereby twostrong players (Apple and Samsung) have put forward strategies that have over time protected their own design. Finally,technological uncertainty, which is usually associated with radical innovations, may delay (or impede) the emergence of adominant design (Tushman, Anderson & Murmann, 1998), since different variants of the products are developed bycompetitors and independent market niches are established, hindering the selection process.

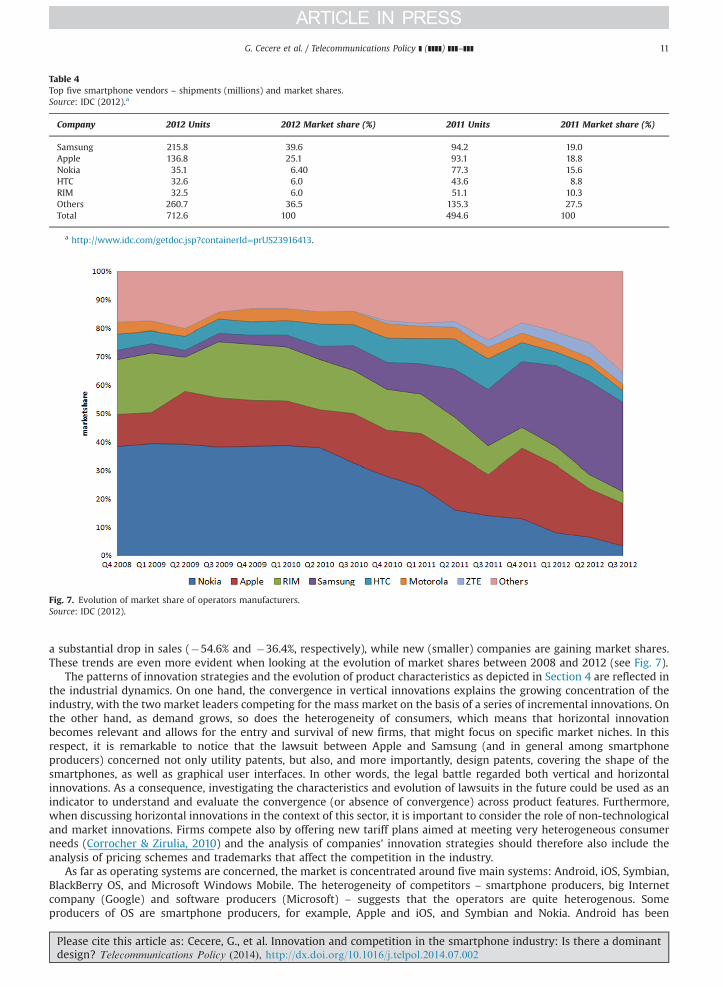

How do innovation strategies of companies reflect in the industrial dynamics? Smartphone affordability has been drivenby manufacturers competing to gain market shares and operators providing customers with innovative tariffs. Table 4presents the market shares and shipments related to the smartphone market. Worldwide smartphone market vendorsshipped about 712.6 million units in 2012, compared to 494.6 million units in 2011, an increase of 44.1%.

Samsung and Apple together account for more than 74% of the total units shipped, with, respectively, 215.8 and 136.8million units shipped (the overall total is about 741.6 million units sold in 2012). The two market leaders recorded anincrease in their sales, suggesting that the market is becoming increasingly more concentrated. Nokia and RIM experienced

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

Table 4Top five smartphone vendors – shipments (millions) and market shares.Source: IDC (2012).a

Company 2012 Units 2012 Market share (%) 2011 Units 2011 Market share (%)

Samsung 215.8 39.6 94.2 19.0Apple 136.8 25.1 93.1 18.8Nokia 35.1 6.40 77.3 15.6HTC 32.6 6.0 43.6 8.8RIM 32.5 6.0 51.1 10.3Others 260.7 36.5 135.3 27.5Total 712.6 100 494.6 100

a http://www.idc.com/getdoc.jsp?containerId=prUS23916413.

Fig. 7. Evolution of market share of operators manufacturers.Source: IDC (2012).

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 11

a substantial drop in sales (�54.6% and �36.4%, respectively), while new (smaller) companies are gaining market shares.These trends are even more evident when looking at the evolution of market shares between 2008 and 2012 (see Fig. 7).

The patterns of innovation strategies and the evolution of product characteristics as depicted in Section 4 are reflected inthe industrial dynamics. On one hand, the convergence in vertical innovations explains the growing concentration of theindustry, with the two market leaders competing for the mass market on the basis of a series of incremental innovations. Onthe other hand, as demand grows, so does the heterogeneity of consumers, which means that horizontal innovationbecomes relevant and allows for the entry and survival of new firms, that might focus on specific market niches. In thisrespect, it is remarkable to notice that the lawsuit between Apple and Samsung (and in general among smartphoneproducers) concerned not only utility patents, but also, and more importantly, design patents, covering the shape of thesmartphones, as well as graphical user interfaces. In other words, the legal battle regarded both vertical and horizontalinnovations. As a consequence, investigating the characteristics and evolution of lawsuits in the future could be used as anindicator to understand and evaluate the convergence (or absence of convergence) across product features. Furthermore,when discussing horizontal innovations in the context of this sector, it is important to consider the role of non-technologicaland market innovations. Firms compete also by offering new tariff plans aimed at meeting very heterogeneous consumerneeds (Corrocher & Zirulia, 2010) and the analysis of companies' innovation strategies should therefore also include theanalysis of pricing schemes and trademarks that affect the competition in the industry.

As far as operating systems are concerned, the market is concentrated around five main systems: Android, iOS, Symbian,BlackBerry OS, and Microsoft Windows Mobile. The heterogeneity of competitors – smartphone producers, big Internetcompany (Google) and software producers (Microsoft) – suggests that the operators are quite heterogenous. Someproducers of OS are smartphone producers, for example, Apple and iOS, and Symbian and Nokia. Android has been

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

0102030405060708090

100

Nor

way

Aus

tralia

Uni

ted

Kin

gdom

Sw

eden

Den

mar

kS

pain

New

Zea

land

Uni

ted

Sta

tes

Net

herla

nds

Sw

itzer

land

Irela

ndFr

ance

Finl

and

Aus

tria

Can

ada

Ger

man

yIta

lyB

elgi

umM

exic

oJa

pan

Chi

naE

gypt

Bra

zil

Don't Know

Other

Microsoft Windows MobileSymbian (Nokia)

Blackberry OS

iOS (iPhone)

Android

smartphone penetration

(%)

Fig. 8. Smartphone and operating systems' penetration in selected countries.Source: OECD (2013).

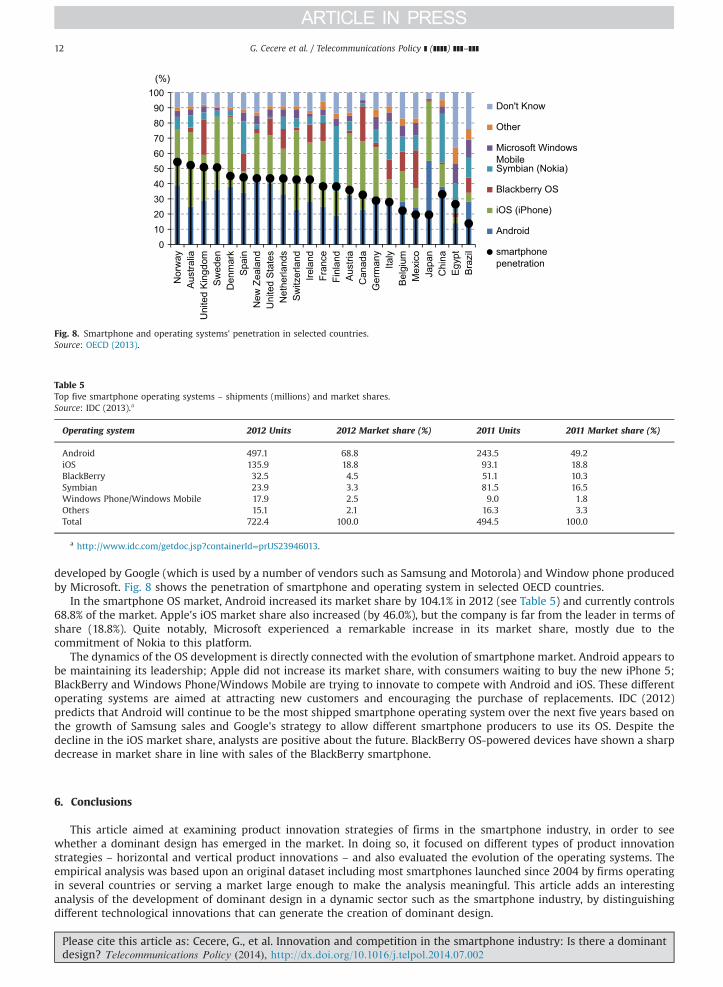

Table 5Top five smartphone operating systems – shipments (millions) and market shares.Source: IDC (2013).a

Operating system 2012 Units 2012 Market share (%) 2011 Units 2011 Market share (%)

Android 497.1 68.8 243.5 49.2iOS 135.9 18.8 93.1 18.8BlackBerry 32.5 4.5 51.1 10.3Symbian 23.9 3.3 81.5 16.5Windows Phone/Windows Mobile 17.9 2.5 9.0 1.8Others 15.1 2.1 16.3 3.3Total 722.4 100.0 494.5 100.0

a http://www.idc.com/getdoc.jsp?containerId=prUS23946013.

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]12

developed by Google (which is used by a number of vendors such as Samsung and Motorola) and Window phone producedby Microsoft. Fig. 8 shows the penetration of smartphone and operating system in selected OECD countries.

In the smartphone OS market, Android increased its market share by 104.1% in 2012 (see Table 5) and currently controls68.8% of the market. Apple's iOS market share also increased (by 46.0%), but the company is far from the leader in terms ofshare (18.8%). Quite notably, Microsoft experienced a remarkable increase in its market share, mostly due to thecommitment of Nokia to this platform.

The dynamics of the OS development is directly connected with the evolution of smartphone market. Android appears tobe maintaining its leadership; Apple did not increase its market share, with consumers waiting to buy the new iPhone 5;BlackBerry and Windows Phone/Windows Mobile are trying to innovate to compete with Android and iOS. These differentoperating systems are aimed at attracting new customers and encouraging the purchase of replacements. IDC (2012)predicts that Android will continue to be the most shipped smartphone operating system over the next five years based onthe growth of Samsung sales and Google's strategy to allow different smartphone producers to use its OS. Despite thedecline in the iOS market share, analysts are positive about the future. BlackBerry OS-powered devices have shown a sharpdecrease in market share in line with sales of the BlackBerry smartphone.

6. Conclusions

This article aimed at examining product innovation strategies of firms in the smartphone industry, in order to seewhether a dominant design has emerged in the market. In doing so, it focused on different types of product innovationstrategies – horizontal and vertical product innovations – and also evaluated the evolution of the operating systems. Theempirical analysis was based upon an original dataset including most smartphones launched since 2004 by firms operatingin several countries or serving a market large enough to make the analysis meaningful. This article adds an interestinganalysis of the development of dominant design in a dynamic sector such as the smartphone industry, by distinguishingdifferent technological innovations that can generate the creation of dominant design.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]] 13

The emergence of smartphones has represented an important change in the mobile phone industry, both in terms oftechnological innovations and in terms of industrial dynamics. In particular, the most successful companies in thedevelopment of smartphones – Apple and Samsung – were not in the mobile phone industry initially and have takenadvantage of the convergence among mobile communication and information technologies. We investigated the evolutionof smartphones along two dimensions: horizontal and vertical product innovation.

Our empirical analysis shows that the number of new products has remarkably increased over time, also due to the entry ofnew companies coming from outside the telecom sector. In terms of technical features, smartphones have considerably improvedover time, with the continuous introduction of new functionalities both on the hardware and on the software side. Looking at theinnovation activity, however, it is quite remarkable to notice that the two market leaders have followed a very differentinnovation strategy, with Samsung being the most prolific company in terms of new products launched on the market and Applehaving introduced only six new products. The latter has, however, developed a proprietary OS which has increased the networkeffects of adoption over time, creating lock-into the platform for consumers. Therefore, the lack of a clear dominant design in thesector is driven not only by evolution in the technical characteristics, but more prominently by firms' strategies and conducts.

Our results have important implications for competition (and regulation) in this segment of telecom industry, also inlight of the recent legal battle between the market leaders. Despite the high levels of market concentration and the almostundisputable leadership of Samsung in the industry, empirical evidence suggests that the smartphone sector is largelyinnovative in terms of new product introduction and variety of designs. This pattern is related not only to the evolution inthe technical characteristics of the devices, but also to the changes in the operating systems. In this respect, the existence ofproduct variety is important for two reasons. First, it allows to maintain competition among heterogeneous manufacturersin the market that have different innovation strategies and, at the same time, to stimulate collaboration between hardwaremanufacturers and software developers with the co-existence of few platforms. Second, it allows to address differentmarket segments and attract different types of users worldwide. In this respect, also marketing and non-technologicalinnovations are crucial for firms, as they allow them to create new features and differentiate their products. The evolution ofthese devices has important impacts on the recent development of the telecommunication sector which is witnessing anincreasing volume of data and voice traffic going from fixed to mobile networks. As the diffusion of smarthphones (andtablets) is an important factor driving this shift, analysing the emergence of innovation and product variety in this marketsegment is particularly important to understand the future trends of mobile communications.

References

Abernathy, W. J., & Utterback, J. M. (1978). Patterns of industrial innovation. Technology Review, 8, 40–47.Afuah, A. (2013). Are network effects really all about size? The role of structure and conduct. Strategic Management Journal, 34, 257–273.Anderson, P., & Tushman, M. L. (1990). Technological discontinuities and dominant designs: A cyclical model of technological change. Administrative Science

Quarterly, 35(4), 604–633.Argyres, N., Bigelow, L., & Nickerson, J. (2013). Dominant designs, innovation shocks and the follower's dilemma. Strategic Management Journalhttp://dx.doi.

org/10.1002/smj.2207.Baum, J. A. C., Korn, H. J., & Kotha, S. (1995). Dominant designs and population dynamics in telecommunications services: Founding and failure of facsimile

transmission service organizations, 1965–1992. Social Science Research, 24(2), 97–135.Christensen, C. M., Suaréz, F. F., & Utterback, J. M. (1998). Strategies for survival in fast-changing industries. Management Science, 44, 207–220.Corrocher, N., & Zirulia, L. (2010). Demand and innovation in services: The case of mobile communications. Research Policy, 39, 945–955.Cusumano, M., Mylonadis, Y., & Rosenbloom, R. (1992). Strategic maneuvering and mass-market dynamics: The triumph of VHS over betamax. Business

History Review, 66(1), 51–94.David, P. A. (1985). Clio and the economics of QWERTY. American Economic Review, 75(2), 332–337.David, P. A., & Greenstein, S. (1990). The economics of compatibility standards: An introduction to recent research. Economics of Innovation & New

Technologies, 1(1, 2), 3–41.Dosi, G. (1982). Technological paradigms and technological trajectories. Research Policy, 11(3), 147–162.European Commission (2012). Digital Agenda for Europe – Scoreboard 2012. European Commission, Directorate-General for Communication Networks,

Content and Technology (CONNECT).Evans, D. S. (2003). Some empirical aspects of multi-sided platform industries. Review of Network Economics, 2, 191–209.Farrell, J., & Saloner, G. (1985). Standardization, compatibility and innovation. Rand Journal of Economics, 16, 70–83.Farrell, J., & Saloner, G. (1986). Standardization and variety. Economics Letters, 20, 71–74.Frenken, K., Saviotti, P. P., & Trommetter, M. (1999). Variety and niche creation in aircraft, helicopters, motorcycles, and microcomputers. Research Policy, 28,

469–488.Fuentelsaz, L., Maicas, J. P., & Polo, Y. (2008). The evolution of mobile communications in Europe: The transition from the second to the third generation.

Telecommunications Policy, 32, 436–449.Funk, J. L. (2001). The mobile Internet: How Japan dialled up and the West disconnected. Hong Kong: ISI Publications.Gallagher, S. (2007). The complementary role of dominant designs and industry standards. IEEE Transactions on Engineering Management, 54(2), 371–388.Hagiu, A. (2005). Pricing and commitment by two-sided platforms. The Rand Journal of Economics, 37, 720–737.Henderson, R. M., & Clark, K. B. (1990). Architectural innovation: There configuration of existing product technologies and the failure of established firms.

Administrative Science Quarterly, 35, 9–30.Katz, M., & Shapiro, C. (1986). Technology adoption in the presence of network externalities. Journal of Political Economy, 94(4), 822–841.Katz, M. L., & Shapiro, C. (1985). Network externalities, competition and compatibility. American Economic Review, 75, 424–440.Katz, M. L., & Shapiro, C. (1994). System competition and network effects. Journal of Economic Perspectives, 8, 93–115.Koski, H., & Kretschmer, T. (2007). Innovation and dominant design in mobile telephony. Industry and Innovation, 14(3), 305–324.Lancaster, K. J. (1990). The economics of product variety: A survey. Marketing Science, 9(3), 189–206.Lee, J. P., Neal, D. E., Pruett, M. W., & Thomas, H. (1995). Planning for dominance: A strategic perspective on the emergence of a dominant design. R&D

Management, 25(1), 3–15.OECD (2013). Communications outlook. Paris: OECD.Saviotti, P. P. (1994). Variety, economic and technological development. In A. F. J. Van Raan (Ed.), Handbook of quantitative studies of science and technology.

Amsterdam: North-Holland.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i

G. Cecere et al. / Telecommunications Policy ] (]]]]) ]]]–]]]14

Schilling, M. A. (1998). Technological lockout: An integrative model of the economic and strategic factors driving technology success and failure. Academy ofManagement Review, 23(2), 267–284.

Schilling, M. A. (2002). Technology success and failure in winner-take-all markets: The impact of learning orientation, timing, and network externalities.Academy of Management Journal, 45(2), 387–398.

Schilling, M. A. (2005). Strategic management of technological innovation. New York, USA: Mc Graw Hill.Smith, C. G. (1997). Design competition in young industries: An integrative perspective. Journal of High Technology Management Research, 7(2), 227–243.Srinivasan, R., Gary, L. L., & Rangaswamy, A. (2004). First in, first out? Effect of network externalities on pioneer survival. Journal of Marketing, 68(1), 41–57.Srinivasan, R., Lilien., G., & Rangaswamy, A. (2006). The emergence of dominant designs. Journal of Marketing, 70(2), 1–17.Suaréz, F. F. (2005). Network effects revisited: The role of strong ties in technology selection. Academy of Management Journal, 48(4), 710–720.Suaréz, F. F., & Utterback, J. M. (1995). Dominant designs and the survival of firms. Strategic Management Journal, 16(6), 415–430.Tegarden, L. F., Hatfield, D. E., & Echols, A. E. (1999). Doomed from the start: What is the value of selecting a future dominant design?. Strategic Management

Journal, 20(6), 495–518.Tushman, M. L., Anderson, P., & Murmann, J. P. (1998). Dominant designs, technology cycles, and organizational outcomes. Research in Organizational

Behavior, 20, 231–266.Tushman, M. L., & Rosenkopf, L. (1992). Organizational determinants of technological change: Toward a sociology of technological evolution. Research in

Organizational Behavior, 14, 311–347.Ulrich, K. (1995). The role of product architecture in manufacturing firm. Research Policy, 24(3), 419–440.Utterback, J., & Suaréz, F. F. (1993). Innovation, competition, and industry structure. Research Policy, 22, 1–21.Utterback, J. M. (1994). Mastering the dynamics of innovation: How companies can seize opportunities in the face of technological change. Boston: Harvard

Business School Press.Utterback, J. M., & Abernathy, W. J. (1975). A dynamic model of process and product innovation. Omega, 3(6), 639–656.Van de Kaa, G., Van den Ende, J., De Vries, H. J., & Van Heck, E. (2011). Factors for winning interface format battles: A review and synthesis of the literature.

Technological Forecasting & Social Change, 78, 1397–1411.Van de Ven, A., & Garud, R. (1993). Innovation and industry development: The case of cochlear implants. In R. Burgelman, & R. Rosenbloom (Eds.), Research

on technological innovation, management and policy, Vol. 5 (pp. 1–46). CT: JAI Press.Wade, J. (1995). Dynamics of organizational communities and technological bandwagons: An empirical investigation of community evolution in the

microprocessor market. Strategic Management Journal, 16(5), 111–133.West, J., & Mace, M. (2010). Browsing as the killer app: Explaining the rapid success of Apple's iPhone. Telecommunications Policy, 34, 270–286.

Please cite this article as: Cecere, G., et al. Innovation and competition in the smartphone industry: Is there a dominantdesign? Telecommunications Policy (2014), http://dx.doi.org/10.1016/j.telpol.2014.07.002i