Embed Size (px)

Citation preview

Rajdeep Grewal, Anindita Chakravarty, & Amit Saini

Governance Mechanisms inBusiness-to-Business Electronic

MarketsRather than relying on traditional relational exchanges, recent technological advances have made it feasible forfirms to undertake market-based transactions through information technology–mediated electronic markets. Thesuccess of such business-to-business electronic markets depends on the governance practices of the marketmaker—that is, the firm that manages and administers the electronic market. Market makers use three governancemechanisms to manage electronic markets: (1) monitoring the market participants (i.e., buyers and sellers thatparticipate in the market), (2) building a sense of community among market participants to instill mutual respectand trust, and (3) self-participating in the electronic market to build know-how about how the market functions.Building on transaction cost analysis theory, the authors suggest that the influence of these governancemechanisms on electronic market performance (i.e., meeting strategic and financial objectives) depends onbehavioral and external uncertainty in the market. Survey data from market makers show that (1) monitoring iseffective for reputed market makers and when demand uncertainty is high, (2) community building is beneficialwhen pricing is static rather than dynamic, and (3) self-participation is useful when the market maker is well reputedand when the market relies on dynamic pricing.

Keywords: business-to-business marketing, electronic markets, governance mechanisms, performance,uncertainty

Rajdeep Grewal is Irving & Irene Bard Professor of Marketing, SmealCollege of Business, Pennsylvania State University (e-mail: [email protected]). Anindita Chakravarty is Assistant Professor of Marketing, Terry Col-lege of Business, University of Georgia (e-mail: [email protected]). Amit Saini is Assistant Professor of Marketing, College of BusinessAdministration, University of Nebraska–Lincoln (e-mail: [email protected]). The authors contributed equally and are listed in random order. Thisresearch was supported in part by funds provided by the Institute for theStudy of Business Markets (www.isbm.org), Pennsylvania State Univer-sity. The authors thank Anandhi Bharadwaj, Alok Kumar, and Bill Ross, aswell as the three anonymous JM reviewers, for their helpful feedback.

© 2010, American Marketing AssociationISSN: 0022-2429 (print), 1547-7185 (electronic)

Journal of MarketingVol. 74 (July 2010), 45–6245

Recent advances in communication and informationtechnologies have produced markets based on thesetechnologies for a diverse set of goods and services,

such as Virtual Chip Exchange for electronic componentsand Steel Spider for steel. Transactions that have histori-cally been conducted using relational interfirm exchangescan now be completed through business-to-business (B2B)electronic markets (e.g., Garicano and Kaplan 2001; Gre-wal, Comer, and Mehta 2001). These electronic marketsconsist of a market maker that manages the market and theparticipant firms—namely, buyers and sellers—that transactin it (hereinafter, when we mention electronic markets, wemean B2B electronic markets). The economic significanceof B2B electronic commerce, of which electronic marketsform a substantial portion, has grown far beyond that ofbusiness-to-consumer electronic commerce; U.S. CensusBureau (2009) figures on e-commerce shipments in 2006attribute 92.5% of them to the B2B side.

The significance of electronic markets has promptedresearch (e.g., Bakos 1997; Garicano and Kaplan 2001) pre-dominantly focused on developing typologies of electronicmarkets (e.g., Bakos 1998; Kaplan and Sawhney 2000) andunderstanding the behaviors of market participants in singlemarkets (e.g., Choudhury, Hartzel, and Konsynski 1998;Grewal, Comer, and Mehta 2001). This concentration on asingle market overlooks the role of market makers, whichmanage electronic markets by laying out and implementingthe rules for interactions between buyers and sellers (e.g.,Bakos 1998); we detail the functions of the market maker inTable 1.

The market maker’s role in facilitating interactionsbetween buyers and sellers requires it to emphasize gover-nance mechanisms that can ensure that market participantsare able to participate in a fair manner. The better governedan electronic market is, the higher is the likelihood that itwill attract participants and thus improve market perfor-mance (conceptualized as meeting strategic and financialobjectives). Therefore, we consider two interrelatedresearch questions: (1) What governance mechanisms canthe market maker use to improve the electronic market’sperformance? and (2) How might behavioral uncertaintywithin the electronic market and external uncertainty miti-gate the effectiveness of governance mechanisms?

Research into the effectiveness of governance mecha-nisms mostly addresses interfirm governance (e.g.,Leiblein, Reuer, and Dalsace 2002; Zaheer and Venkatra-man 1995; Zollo and Singh 2002) in diverse contexts,including dyadic marketing channels (Brown, Dev, and Lee

2000), buyer–seller relationships (Wuyts and Geyskens2005), strategic alliances (Ghosh and John 2005), and inter-firm networks (Lorenzoni and Lipparini 1999). We build onthis literature, but the focus is on a market-making firm thatgoverns multiple market participant firms, not on a singlerelationship, such as a buyer trying to manage its seller’sopportunism.

Electronic market making can employ three predomi-nant governance mechanisms. First and foremost, a marketmaker can monitor the behavior of market participants (e.g.,Bergen, Dutta, and Walker 1992). Some market makersdevise mechanisms to authenticate product representations(e.g., AUCNET; Warbelow and Korkuryo 1989) or trackunethical bidding practices (e.g., eBay; Kambil and VanHeck 2002). Second, market makers can build a sense ofcommunity among the market participants and use socializa-tion to build interfirm trust as a governance mechanism (e.g.,Wathne and Heide 2000). For example, ChemConnect, anelectronic market maker for chemicals and plastics, empha-sizes collaboration hubs among market participants (www.chemconnect.com).1 Third, early literature on electronic

46 / Journal of Marketing, July 2010

markets (e.g., Kambil and Van Heck 2002; Malone, Yates,and Benjamin 1994) has noted that a market maker mightself-participate in the market as a buyer and/or seller. Thisself-participation provides a signal that the market makerbelieves in the electronic market and gives the marketmaker experiential knowledge about the inner workings ofthe market, including how direct interactions with partici-pants proceed and how to exert hands-on governance. How-ever, self-participation might offer an unfair advantage tothe market maker, which makes and implements the rulesthat govern the electronic market and therefore must policeitself, thus creating a conflict of interest between the market-making and market participant roles.

To study the effectiveness of the three governancemechanisms (monitoring, community building, and self-participation) in B2B electronic markets, we rely on trans-action cost analysis (e.g., Krishnan, Martin, and Noorder-haven 2006; Rindfleisch and Heide 1997; Williamson 1985)and suggest that the boundary conditions for the effective-ness of these governance mechanisms depend on uncer-tainty, whether related to the behaviors of the market mak-

1Although Wathne and Heide (2000) describe four governancemechanisms, including monitoring and socialization (which wecall community building), in general, scholars study only the gov-ernance mechanisms that are appropriate for the research contextat hand. For example, for their supply chain network context,Wathne and Heide (2004) consider adaptation to uncertainty. Simi-larly, in the context of restaurants, Srinivasan (2006) views vertical

Function Explanation and Examples

Create and managecontent

•Create original content°Agriplace, an electronic market for the agriculture community, provides the services of an agro-nomic expert to participant firms, along with a custom crop planner that enables participant firmsto develop fertilizer schedules.

•Provide and summarize relevant third-party content°MRO.com, an electronic market for streamline supply chain management related to maintenance,repair, and operating materials provides daily news updates and its own analysis of the news.

•Provide links to third-party content.°Spot Metals Online Inc., an electronic market for real-time trading of metals, provides links to theWeb sites of its member companies, such as the National Steel Corporation.

Aggregate demandand match buyersand sellers

•Engage in marketing strategies to attract potential exchange partners to the market.•Provide incentives to participating firms to make the market their regular and primary sales channel.•Design standard forms for requests for information and quotes.•Provide security from hackers and viruses.•Facilitate buyers’ search for sellers and sellers’ search for buyers.•Develop and maintain a payment settlement system.

Manage participantopportunism

•Provide history of the transactions of participant firms.•Rate and evaluate participant firms.•Enforce rules.•Punish rogue participant firms.•Ensure that participant firms comply with legal aspects of contract law.

Price-making process •Establish the rules for the price-making process.•Maintain and regularly upgrade the systems for real-time auctions and price discovery processes.

Provide secondaryservices

•Logistics.•Training to participant firms.•Provide credit.•Provide insurance against malpractice for participant firms.

TABLE 1Functions of Market Makers

integration and market governance as competing mechanisms.Because we examine a market setting with multiple buyers andsellers, the market maker’s use of incentive-alignment systems,such as profit sharing, would not be practical, and selection seemscontrary to the spirit of an open marketplace; although ex post vio-lators can be asked to leave the marketplace, ex ante selection islikely to be impractical.

ers and participants or external to the electronic market. Weuse the market maker’s reputation to gauge uncertaintyrelated to the market maker; a better reputation shouldreduce behavioral uncertainty (e.g., Weigelt and Camerer1988). To identify uncertainty related to participant behav-ior, we use the price-making mechanism of the electronicmarket (i.e., static or dynamic pricing); dynamic pricingrepresents greater participant behavioral uncertainty.Finally, external uncertainty reflects the inability of firms topredict future events (e.g., Milliken 1987), which we theo-rize may manifest as variability in demand conditions ordemand uncertainty (e.g., Dwyer and Welsh 1985). Follow-ing research that suggests that knowledge-based firm com-petencies complement transaction cost considerations (e.g.,Poppo and Zenger 1998; Tippins and Sohi 2003), we alsouse organization learning theory to complement the transac-tion cost analysis when appropriate.

This research makes several important substantive andtheoretical contributions. From a substantive standpoint, weprovide the first investigation of a population of electronicmarkets and offer a generalized understanding of the gover-nance of electronic markets. Because of the economic sig-nificance of B2B electronic commerce and the criticality ofelectronic markets in facilitating this electronic commerce,we cannot overstate the importance of this understanding.Theoretically, we extend the use of transaction cost analysisfrom a dyadic setting to a market setting, in which a marketmaker governs transactions among multiple buyers and sell-ers. We also build on governance literature. Monitoring hasbeen studied extensively in interfirm contexts (e.g.,Dahlstrom and Nygaard 1999), and socializing has beendiscussed in the literature (e.g., Wathne and Heide 2000),though it has not received empirical scrutiny, but self-participation seems to be unique to the electronic marketcontext. We also identify conditions for the effectiveness ofthe governance mechanisms, in the form of behavioral uncer-tainty within the electronic market and external uncertainty.

Theoretical BackgroundElectronic markets comprise several characteristics thatmake their governance unique and challenging. For exam-ple, without face-to-face interactions, electronic marketslack the tangibility and visibility of a physical infrastruc-ture, and the ability for anonymous participation createsquestions about the accurate representation of products andtrades. Consequently, governance challenges might includeestablishing rules, laws, and social principles for transac-tions; ensuring the enforcement of trading commitments;and resolving disputes expeditiously (Kambil and Van Heck2002). A review of emerging academic literature on elec-tronic markets (e.g., Choudhury, Hartzel, and Konsynski1998; Kaplan and Sawhney 2000; Varadarajan, Yadav, andShankar 2008) and marketing literature on governance ininterfirm relationships (e.g., Brown, Dev, and Lee 2000;Ghosh and John 2005; Wathne and Heide 2000) suggeststhree primary governance mechanisms that market makersuse to administer electronic markets: monitoring, commu-nity building, and self-participation. Building on transactioncosts analysis (e.g., Williamson 1985), we also reason that

Governance Mechanisms in Electronic Markets / 47

their effectiveness may depend on manifestations of uncer-tainty about the behaviors of the market maker and marketparticipants (e.g., Rindfleisch and Heide 1997) and uncer-tainty that is external to the electronic market (e.g., Milliken1987).

Uncertainty

Behavioral uncertainty: market maker. The marketmaker’s primary responsibility is to bring buyers and sellerstogether to facilitate their transactions. Because not all of itsactions can be transparent to every participant, considerableuncertainty may arise among market participants aboutthe market maker’s behaviors. We argue that the extent ofthis behavioral uncertainty depends on the market maker’sreputation.

Reputation refers to the extent to which a market makeris held in high esteem, which we can gauge according to therespect and credibility it garners in the industry (e.g.,Weigelt and Camerer 1988; Weiss, Anderson, and MacInnis1999). Reputation signals the market maker’s integrity(Davies and Miles 1998; Dollinger, Golden, and Saxton1997) and ability (Doney and Cannon 1997; Yoon, Guffey,and Kijewski 1993), as well as its reliability, which shouldenable it to reduce behavioral uncertainty (Klein and Leffler1981). Thus, reputation should help a market maker retainthe trust of market participants and sustain the electronicmarket’s performance (e.g., Doney and Cannon 1997;Ganesan 1994).

Behavioral uncertainty: market participants. The price-making mechanism of an electronic market determines thenature of its interaction and, thus, the uncertainty marketparticipants feel about the behavior of other participants.Electronic markets usually contain one of two generic price-making mechanisms: static or dynamic (e.g., Kambil andVan Heck 2002). Static pricing occurs when the marketmaker aggregates the product offerings of multiple vendorsand sells them to buyers at a relatively static (fixed) price(e.g., www.testandmeasurement.com); in lead generatormarkets, in which the market makers derive revenue fromadvertisements, commissions on sales, or fees for generatingqualified sales leads for suppliers (e.g., www.servicemagic.com); and in workflow marketplaces that provide projecttracking or collaboration services for complex, iterative,multiparty projects, for which the provider earns a fee (e.g.,www.isqft.com). In contrast, dynamic pricing is more com-mon in auctions, in which multiple buyers bid competitivelyfor products from a single supplier (e.g., www.stockshifters.com); in reverse auctions, in which buyers post their needsfor products or services and suppliers bid competitively toserve those needs (e.g., www.hedgehog.com); and in two-sided exchanges, in which buyers and sellers interact toexchange information and engage in trade, facilitated bysome negotiated dynamic pricing system, such as a bid-and-ask system (e.g., www.xsag.com).

Behavioral uncertainty about market participants shouldbe higher in a dynamic pricing than a static pricing marketbecause, in the latter, the price does not change in real time(though there can be some periodic change), so market par-ticipants can be reasonably sure of the price. With dynamic

pricing, there is no such pricing guarantee, and the pricechanges in real time, which offers more scope for oppor-tunistic bidding practices. For example, Jap (2007) showsthat buyers use dynamic pricing mechanisms, such as openbidding, to obtain price concessions. Electronic markets,which often allow for anonymity among market partici-pants, enhance this effect; the behavior of other participantsis relatively less transparent and more suspicious indynamic versus static pricing situations.

Demand uncertainty. Demand uncertainty results fromunpredictability and volatility in the environment that sur-rounds the electronic market (e.g., Dwyer and Welsh 1985).This unpredictability and volatility arises as a result of fre-quent changes in market participants’ composition, needs,and behaviors. High turnover of market participants andtrouble understanding or anticipating customer needs createuncertainty for the market maker regarding whether itsstrategies are appropriate for the electronic market.

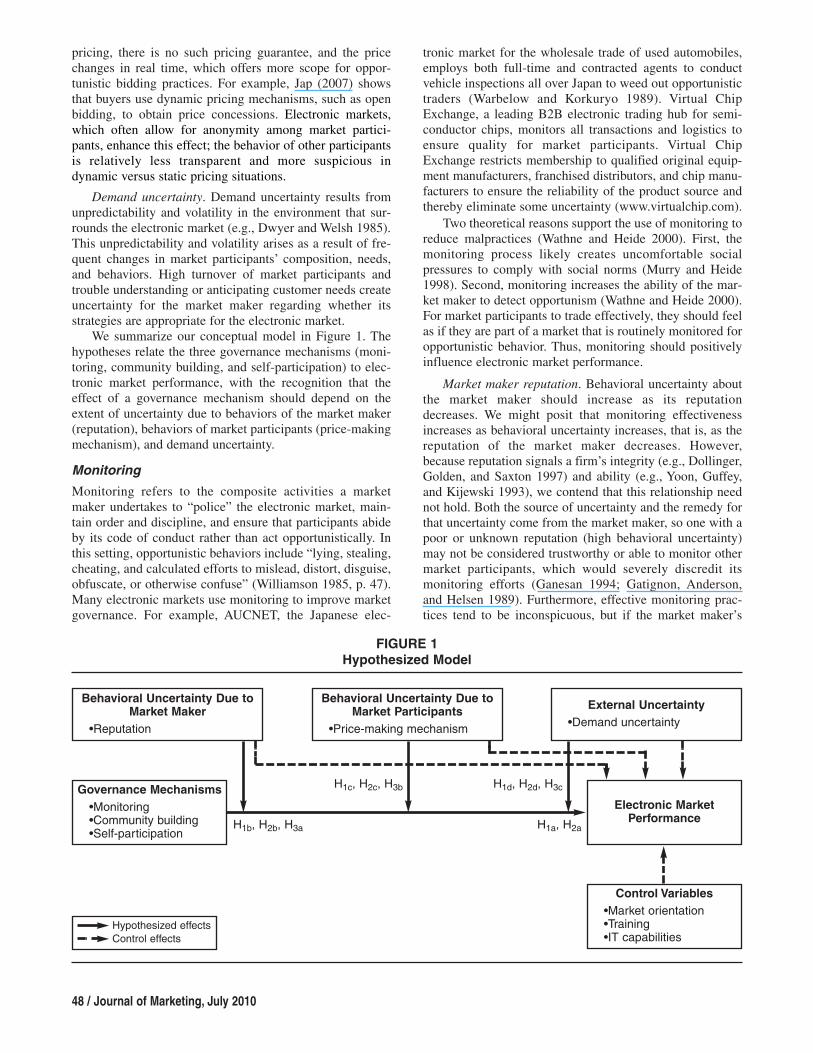

We summarize our conceptual model in Figure 1. Thehypotheses relate the three governance mechanisms (moni-toring, community building, and self-participation) to elec-tronic market performance, with the recognition that theeffect of a governance mechanism should depend on theextent of uncertainty due to behaviors of the market maker(reputation), behaviors of market participants (price-makingmechanism), and demand uncertainty.

Monitoring

Monitoring refers to the composite activities a marketmaker undertakes to “police” the electronic market, main-tain order and discipline, and ensure that participants abideby its code of conduct rather than act opportunistically. Inthis setting, opportunistic behaviors include “lying, stealing,cheating, and calculated efforts to mislead, distort, disguise,obfuscate, or otherwise confuse” (Williamson 1985, p. 47).Many electronic markets use monitoring to improve marketgovernance. For example, AUCNET, the Japanese elec-

48 / Journal of Marketing, July 2010

tronic market for the wholesale trade of used automobiles,employs both full-time and contracted agents to conductvehicle inspections all over Japan to weed out opportunistictraders (Warbelow and Korkuryo 1989). Virtual ChipExchange, a leading B2B electronic trading hub for semi-conductor chips, monitors all transactions and logistics toensure quality for market participants. Virtual ChipExchange restricts membership to qualified original equip-ment manufacturers, franchised distributors, and chip manu-facturers to ensure the reliability of the product source andthereby eliminate some uncertainty (www.virtualchip.com).

Two theoretical reasons support the use of monitoring toreduce malpractices (Wathne and Heide 2000). First, themonitoring process likely creates uncomfortable socialpressures to comply with social norms (Murry and Heide1998). Second, monitoring increases the ability of the mar-ket maker to detect opportunism (Wathne and Heide 2000).For market participants to trade effectively, they should feelas if they are part of a market that is routinely monitored foropportunistic behavior. Thus, monitoring should positivelyinfluence electronic market performance.

Market maker reputation. Behavioral uncertainty aboutthe market maker should increase as its reputationdecreases. We might posit that monitoring effectivenessincreases as behavioral uncertainty increases, that is, as thereputation of the market maker decreases. However,because reputation signals a firm’s integrity (e.g., Dollinger,Golden, and Saxton 1997) and ability (e.g., Yoon, Guffey,and Kijewski 1993), we contend that this relationship neednot hold. Both the source of uncertainty and the remedy forthat uncertainty come from the market maker, so one with apoor or unknown reputation (high behavioral uncertainty)may not be considered trustworthy or able to monitor othermarket participants, which would severely discredit itsmonitoring efforts (Ganesan 1994; Gatignon, Anderson,and Helsen 1989). Furthermore, effective monitoring prac-tices tend to be inconspicuous, but if the market maker’s

FIGURE 1Hypothesized Model

Behavioral Uncertainty Due toMarket Maker

•Reputation

Behavioral Uncertainty Due toMarket Participants

•Price-making mechanism

External Uncertainty•Demand uncertainty

Control Variables•Market orientation•Training•IT capabilities

Governance Mechanisms•Monitoring•Community building•Self-participation

Electronic MarketPerformanceH1b, H2b, H3a H1a, H2a

H1d, H2d, H3cH1c, H2c, H3b

Hypothesized effectsControl effects

reputation is low, its monitoring efforts may be perceived asimpertinent and meddlesome. In summary, we expect theeffectiveness of monitoring for electronic market perfor-mance to increase as the reputation of the market makerincreases.

Price-making mechanism. The effectiveness of monitor-ing efforts also may be greater when the price-makingmechanism is dynamic (high market participant behavioraluncertainty) rather than static (low market participantbehavioral uncertainty). Dynamic pricing induces more par-ticipant opportunism than static pricing because market par-ticipants can resort to problematic practices, such as collu-sion and shilling in dynamic pricing settings (Kambil andVan Heck 2002). For example, in auction markets, buyer-side collusion occurs when two bidders illegally team up toenter a low and a high bid and then later withdraw the highbid so that the sale goes to the low-bid collaborator. Sellersuse shells that enter fake bids to drive the price higher. Withthe static pricing mechanism, participant pricing instead isfixed and transparent, leaving little room for irregularities,so investments in monitoring routines may not add value.The greater probability of unfair and surreptitious biddingactivities in dynamic pricing markets creates higher payoffsfrom monitoring efforts designed to curb such activities.Therefore, monitoring mechanisms should be more effec-tive under dynamic pricing than static pricing because theydiscover, prevent, and correct opportunistic behavior as itoccurs.

Demand uncertainty. The effectiveness of monitoringefforts for electronic market performance should increase asdemand uncertainty increases (e.g., Bergen, Dutta, andWalker 1992). The effects of demand uncertainty are ubiq-uitous, such that firms are rewarded (penalized) for(in)effective and (in)efficient managerial practices indynamic environments (e.g., Aldrich 1979). When demanduncertainty is high, monitoring efforts to accumulate,assimilate, interpret, and use participant information toanticipate changing environmental conditions should yieldhigher rewards (e.g., Jaworski and Kohli 1993). However,when demand uncertainty is low, participant compositionand behavior is predictable, and monitoring does not yieldmuch new information about participants or their behaviors.Therefore, with low demand uncertainty, monitoring effortsmay not add any value to electronic market performance.

H1: Monitoring as a governance mechanism is (a) positivelyassociated with electronic market performance, and itseffectiveness increases (b) as the reputation of the marketmaker increases, (c) in dynamic rather than static price-making mechanisms, and (d) as demand uncertaintyincreases.

Community Building

Community building refers to the totality of effort exerted bythe market maker to create a congenial market environmentfor participants, which consists of high levels of mutualtrust, integrity, and honesty exhibited by participants.Because electronic markets primarily comprise corporateparticipants that trade big-ticket items, such as capitalgoods and industrial services (Malone, Yates, and Benjamin

Governance Mechanisms in Electronic Markets / 49

1994), cultivating trust and integrity may take priority overother community values, such as conviviality (which iscritical in interpersonal online communities; see Miller,Fabian, and Lin 2009). For example, VertMarkets operates58 industry-specific electronic markets (e.g., PlasticsNet,SemiconductorOnline) and encourages membership in itscommunity of buyers and sellers by offering benefits suchas a downloadable library of white papers, access to tradeassociations, and industry event calendars (www.plasticsnet.com; www.semiconductoronline.com). PrintCities, a world-wide electronic market for printing equipment, emphasizesbuilding a community for participants by offering an inde-pendently moderated technology forum that users canaccess at any time (www.printcities.com).

From a theoretical standpoint, community-buildingefforts represent the market maker’s attempt to createembedded social relationships that help mitigate the risksassociated with opportunistic behaviors by market partici-pants (e.g., Granovetter 1985; Kaufman, Jayachandran, andRose 2006). By emphasizing trust among market partici-pants, community building ultimately enables bilateral rela-tionships in an electronic market. Because these effects canhave positive ramifications with regard to greater marketacceptance and usage, we expect community building toinfluence electronic market performance positively.

Market maker reputation. The effectiveness of the mar-ket maker’s community-building efforts should increasewith its reputation. Community-building efforts attempt tofoster trust through informal relationships among marketparticipants, and research among small groups suggests thatfor entities to benefit from informal relationships, they mustbe willing to engage with one another (Caniels and Romijin2003). In addition, social identity research suggests that agroup member’s readiness to participate in new relation-ships depends on whether the group can form a salientsocial identity (Brewer and Gardner 1996). We contend thatcommunity building should be more effective when themarket maker’s reputation is stronger because this strongreputation, unlike a poor reputation, provides a salientsocial identity for market participants: They are a commu-nity managed by a credible, legitimate, and valued entity.Similarly, the characteristics of a prominent entity in smallorganizations create the context for participants to findcommon grounds for their interactions (Tjosvold andWeicker 1993). However, a market maker’s poor reputationshould induce concern about its behaviors, which attenuatesany of its efforts to maintain the community.

Price-making mechanism. Community building shouldbe more effective in dynamic pricing settings than in staticpricing ones. Dynamic pricing creates uncertainty about thefinal price, and some buyers may even be uncertain aboutthe identity of the seller. These inherent uncertainties pro-vide incentives for unfair bidding practices, such as collu-sion and shilling (Kambil and Van Heck 2002). Communitybuilding instead emphasizes fair practices and should lessenmarket participants’ incentives to engage in opportunisticbidding behaviors. In contrast, community building offersno value for static pricing markets, because the supplierinformation, including pricing, is available all the time,

such as in a catalog. The what-you-see-is-what-you-getnature of the market enables participants to assess suppliersin advance and reduces participant apprehension aboutpotential trading partners. Furthermore, the inherent trans-parency of static pricing makes community-building effortsredundant; all relevant market participant behaviors appearin the public domain.

Demand uncertainty. We argue that the effectiveness ofcommunity-building efforts for electronic market perfor-mance should increase as demand uncertainty increases.High demand uncertainty, in contrast with low demanduncertainty, implies that participants join and leave the elec-tronic market frequently and exhibit widely varying needsand behaviors. Podolny (1993) shows that in turbulent envi-ronments, markets develop a social character, in the sensethat organizations search for trading partners with whomthey have interacted or transacted before. In an uncertainmarket context, optimal exchange partners cannot be deter-mined easily, so firms engage in “satisficing”; that is, theysearch for partners who are good enough because their pref-erences are similar (Levitt and March 1988). In this case,the community-building efforts by the market maker pro-vide ideal opportunities for informal interactions, whichfacilitate the search for appropriate transaction partners. Byproviding trade association memberships, invitations toindustry events, or informal networks (Bakos 1997), marketmakers also give participants the tools to search for partnersthey might prefer, facilitate their transactions, and calm themarket. In contrast, the value of community building maybe redundant when demand uncertainty declines, consider-ing the high predictability and stability of the participantcomposition and behavior in such markets.

H2: Community building as a governance mechanism is (a)positively associated with electronic market performance,and its effectiveness increases (b) as the reputation of themarket maker increases, (c) in dynamic rather than staticprice-making mechanisms, and (d) as demand uncertaintyincreases.

Self-Participation

When the market maker participates in the electronic mar-ket, it experiences the impact of its rules on its own trans-action productivity. It also can interact directly with othermarket participants. In essence, self-participation providesthe market maker a unique opportunity to evaluate the mar-ket from both its own perspective and that of a market par-ticipant. Such an opportunity may be valuable to all parties,which is the primary goal of governance in an electronicmarket (Ghosh and John 1999). Therefore, various marketmakers choose to govern through self-participation, includ-ing Converge in electronic component distribution (www.converge.com), Exostar in aerospace (www.exostar.com),and Quadrem in procurement services (www.quadrem.com).

However, the direct impact of self-participation onmarket performance is debatable. On the one hand, self-participation can be an effective governance tool because itencourages tacit learning about the inner workings of themarket and signals the market maker’s confidence in theorderly state of its own market. By participating, the market

50 / Journal of Marketing, July 2010

maker makes transaction-specific investments of its time andinformation (e.g., Ganesan 1994), so it has a high stake inensuring that all other participants play by the rules. On theother hand, self-participation may be less effective as a gov-ernance mechanism if market participants perceive it solelyas an opportunity for the market maker to take advantage ofits dual role as market maker and market participant (e.g.,Malone, Yates, and Benjamin 1994). The market makermight seem to manipulate the market rules to benefit itsown transactions; such concerns among market participantsmay undermine the purpose of self-participation. Therefore,we suggest that the effectiveness of self-participation as agovernance mechanism depends on the prevailing behav-ioral and external uncertainties in the market.

Market maker reputation. The effectiveness of self-participation for electronic market performance shouldincrease as the market maker’s reputation increases. If thegeneral perception of the market maker is of a reputable andhonest entity, its experiential knowledge, ability to under-stand signals of wrongdoing, and style of hands-on gover-nance should induce more credence than the possibility ofthe market maker acting out of self-interest. In contrast, amarket maker with a poor reputation cannot govern effec-tively through self-participation, because participants arelikely to question its intent continually.

Price-making mechanism. Self-participation effective-ness should increase for dynamic versus static pricing.When the price-making mechanism is dynamic, market par-ticipants can take advantage of the flexibility of the pricingprocess to undercut one another and deceive counterparties(Jap 2007). Detecting opportunistic practices in price nego-tiations and bids is difficult because of the anonymity par-ticipants generally retain at the time of trading, as well asthe information asymmetry between the trading entities(Kambil and Van Heck 2002). In the presence of highbehavioral uncertainty about other market participants, eachparticipant necessarily relies on the market maker to main-tain order. As a participant, the market maker signals itscompetence to detect patterns of improper pricing behaviorand to take punitive actions. It also may be harmed itself byopportunistic price-making behavior, so its self-participationmay be construed as a personal incentive to ensure order. Inaddition, in its administrative role, the market maker shouldrealize the general marketplace behavior exhibited by theparticipants. Such information, as a complement of the mar-ket maker’s experience and interactions as a participant, canmake self-participation a powerful tool when behavioraluncertainty about market participants is high because of adynamic price-making mechanism.

Demand uncertainty. The effectiveness of the marketmaker’s self-participation increases as demand uncertaintydecreases. In a context of high versus low demand uncer-tainty, market makers must cope with volatile participantneeds and rapid turnover. Self-participation endows themarket maker with knowledge gained from actual inter-actions with the participants in the electronic market. Webelieve that demand uncertainty determines the extent towhich this acquired knowledge generalizes to all partici-pants, and generalizability should be higher in low-demand-

uncertainty environments than in high-demand-uncertaintyenvironments because the variability in needs across partici-pants is lower. Thus, the market maker’s limited compre-hension and learning about the changing demand character-istics of market participants in a high-demand-uncertaintyenvironment should allow for more opportunities for marketparticipants to engage in unethical transaction behaviorsthan in low-demand-uncertainty environments.2

H3: The effectiveness of self-participation as a governancemechanism for electronic market performance is greater(a) as the reputation of the market maker increases, (b) indynamic rather than static price-making mechanisms, and(c) as demand uncertainty decreases.

MethodSampling Frame

Perhaps because of their relative newness, a comprehensivelist of B2B electronic markets is unavailable, so we createda sampling frame that includes the maximum number ofB2B electronic markets available at the time of data collec-tion. An initial Internet search provided one publicly avail-able mailing list, the knowledge base of the online maga-zine Net Market Makers, which consists of various B2Be-commerce players, including market makers, infrastruc-ture providers, and industry-sponsored markets (listed byJupiter Media Matrix). For this research, the market makersand industry-sponsored markets (e.g., Covisint in the auto-mobile industry) form the initial sampling frame. In addi-tion, we supplement the list of 364 potential respondentswith 168 market makers identified by SG Cowen (1999) inone of the first industry reports, as well as with marketmaker lists obtained through Web searches (primarilyb2b.yahoo.com) and markets noted by popular infrastruc-ture providers (e.g., Ariba, Commerce One, i2). Conse-quently, the list grew to 572 B2B electronic markets.3

Next, we visited the Web sites of each market to qualifythe market makers and obtain and update contact informa-tion. This qualification exercise led to the deletion of firmsthat were not market makers but for some reason appearedon the list (e.g., www.grainger.com). We also attempted to

Governance Mechanisms in Electronic Markets / 51

snowball; that is, during the process of identifying keyrespondents, we asked each potential respondent to nametwo to three electronic markets in his or her industry. Usu-ally, the markets they named already appeared in the sam-pling frame, so this exercise also served as a validationcheck of comprehensiveness. Constructing the samplingframe elucidated the dynamic nature of B2B electronic mar-kets; some markets had gone out of business (e.g., www.chemdex.com), and others were being revised (e.g., www.covisint.com). Some electronic markets even shut downduring the period of data collection (e.g., www.esteel. com).In the end, the sampling frame consisted of 428 B2B elec-tronic markets.

Data Collection Procedure and Key RespondentIdentification

Initially, we contacted market makers by telephone toobtain the name and designation of a key respondent, a topmanager involved in strategic decision making regardingthe electronic market. In most cases, the key respondentswere chief executive officers, founders, or vice presidents.During the telephone call, we attempted to talk with the keyrespondent and, if possible, explain the purpose of thestudy, as well as remind him or her that the questionnairewould arrive in a week’s time. We also queried theserespondents about their ability to answer the questionnaireand stressed the criticality of their responses, with thepromise of an executive summary of the findings as anadded incentive. To snowball and test the extensiveness ofthe sampling frame, we asked about other possible elec-tronic markets. If the key respondent was unavailable dur-ing the first telephone call, we made two more attempts totalk to him or her, usually in the next seven to ten days. Inmost cases, we were able to talk to or obtain the name andtitle of the key respondent.

The survey packet consisted of a cover letter on univer-sity letterhead, the questionnaire, a self-addressed and pre-paid return envelope, and an incentive of $1. The cover let-ter stated that the data were being collected to investigatethe management and efficacy of electronic markets andpromised a copy of the findings as an incentive to partici-pate. Three weeks after mailing the surveys, we mailedreminder letters with another copy of the questionnaire andself-addressed and prepaid return envelopes to nonrespon-dents. In the follow-up letter, we reiterated the criticality ofresponding and again promised a copy of the findings. Thisdata collection exercise resulted in 114 responses (26.6%response rate), 107 of which were complete and usable.

Measures

Consistent with contemporary measurement theory, we usedmultiple items to measure each latent construct. Wheneverpossible, we used established scales (i.e., electronic marketperformance and demand uncertainty), but some constructs(i.e., monitoring, community building, self-participation,reputation, and price-making mechanism) are new measures(see the Appendix). For the new constructs, we generated apool of items through field interviews and then refined themin two steps. First, two doctoral students trained in psycho-

2The learning process we postulated for self-participation underdynamic pricing is unlikely to resolve demand uncertainty. In thecontext of dynamic pricing, a self-participating marker makerlearns about the subtleties of price setting and negotiating, whichhelps improve its knowledge of not only the price-making mecha-nism but also the opportunistic behaviors of market participants.However, demand uncertainty is manifest because of the widerange (beyond pricing behaviors) of expectations across existingand potential participants (who may be involved with a competingelectronic market or not be participating in any electronic market).Thus, learning from self-participation is likely to be of limited util-ity for managing demand uncertainty.

3An electronic market serves as the unit of analysis. In somecases, one firm maintained multiple marketplaces (e.g., Vertical-Net with 58, Ventro with 4), so we asked the market maker to com-plete a questionnaire for each market; however, these market mak-ers agreed to complete only one. Consistent with prior research(e.g., Murry and Heide 1998), we asked the multiple market mak-ers to complete the questionnaire with respect to a typical market.

metric theory filled out the preliminary research instrumentto identify ambiguous items. Second, two e-commerce con-sultants from a leading consulting firm critically evaluatedthe research instrument with regard to the scale items andflow.

To measure monitoring, we assessed the market maker’sefforts to ensure that participants do not take advantage ofother participants, methods for handling complaints aboutopportunistic behavior by market participants, emphasis onpolicing, stress on maintaining order, and emphasis on disci-pline in the market. The community-building measureassessed the market maker’s efforts to create a sense of com-munity among participant firms, to build trust, and to createa congenial atmosphere. The measure of the market maker’sself-participation relied on a dummy variable that took avalue of 1 if the market maker transacted in the electronicmarket, whether as a buyer or a seller, and 0 if otherwise.

The measure for reputation assessed the image of themarket maker in the industry. In addition to a direct mea-sure, the items determined whether the market maker wasperceived as respectful and as possessing integrity, as wellas the extent to which the market maker’s opinions weresought and valued. The price-making mechanism dummyvariable equaled 1 if the electronic market was an auction,reverse auction, or an exchange, which implies a dynamicmarket; otherwise, the pricing mechanism was static andtook a value of 0.

We controlled for the market maker’s market orienta-tion, or the extent to which the firm understands its cus-tomers and competitors (Kirca, Jayachandran, and Bearden2005), which positively influences firm performance (e.g.,Jaworski and Kohli 1993; Narver and Slater 1990). We alsocontrolled for the training capabilities of the market maker.The newness and idiosyncrasies of electronic markets sug-gest that the training the market maker provides about howto participate in the market should influence market perfor-mance. Because the very genesis of electronic marketsrelies on advances in information technology (IT) (e.g.,Grewal, Comer, and Mehta 2001), the extent of IT capabili-ties of the market maker should be important for marketperformance. Thus, we controlled for the IT capabilities ofthe market maker, measured as a second-order construct

52 / Journal of Marketing, July 2010

consisting of IT infrastructure and IT skills (e.g., Bharadwaj2000).

Measure Validation

To validate and purify the measures, we used compositereliability to assess the internal consistency and confirma-tory factor analysis (CFA) models to assess the unidimen-sionality and discriminant validity (e.g., Anderson andGerbing 1988). To maintain a healthy ratio of the samplesize to the number of parameters estimated, similar to previ-ous studies, we estimated three CFA models, in which theconstructs of each are maximally similar to provide a strin-gent test of discriminant validity. In general, each modelshows statistically significant factor loadings (p < .01) andfit indexes close to or above recommended levels (see Table2). For the discriminant validity, we assessed whether theestimated measurement error-corrected correlation parame-ters for each set of constructs are significantly differentfrom 1.0 (Anderson and Gerbing 1988); because none are,we establish discriminant validity. A comparison of earlyand late respondents on all variables indicates that both aresimilar (p > .10), which signals that nonresponse bias is notlikely an issue. We also took two steps to alleviate commonmethod concerns, namely, questionnaire design and statisti-cal testing (Podsakoff et al. 2003). First, in terms of ques-tionnaire design, we employed several subsections, sorespondents needed to pause and read the instructions foreach section of questions. Within and across the sections, wealso used different response formats.4 For example, in addi-tion to seven-point Likert rating scales (“agree/disagree”),we used “unsatisfactory/satisfactory” scales and multiple-choice options (e.g., price-making mechanism). Second, weused Harmon’s single-factor test to assess common methodbias. Using exploratory factor analysis, we estimated amodel with all items for the seven latent constructs (i.e.,monitoring, community building, reputation, demanduncertainty, market orientation, training, and IT capabili-

TABLE 2Results from CFA Models

Range of Standardized Tucker–LewisMeasurement Model Factor Loadings CFA Index Index RMSEA χ2 (d.f., p-Value)

Monitoring, community .59–.87 .96 .95 .06 543.86 (335, p < .01)building, reputation, training,IT skills, and IT infrastructure

Electronic market performance, .57–.85 .96 .95 .06 828.16 (499, p < .01)demand uncertainty, marketorientation, IT skills, and ITinfrastructure

IT capability (second order)a .68–.85 .97 .94 .08b 155.79 (76, p < .01)

aBoth IT skills and IT infrastructure load positively on IT capability (IT infrastructure γ1 = 1.21, t = 13.25, p < .001; IT skills γ2 = 1.19, t = 13.68,p < .001).bThe root mean square error of approximation (RMSEA) values in all three CFAs are less than or equal to .08, which is well within the prescribedrange for a reasonable fit for continuous data items (Schreiber et al. 2006). A more stringent RMSEA cutoff at .05 tends to reject properlyspecified models when sample sizes are close to 100 (Yu 2002).

4We changed the response formats for independent constructsonly. However, changing the response formats between dependentand independent constructs might have better alleviated concernsabout common method variance.

ties). The rotated factor-loading matrix for the seven-factorsolution indicates that the items for the different constructsload on different latent factors (though IT infrastructure andIT skills load on the same factor), which minimizes com-mon method concerns. We averaged the items to createsingle indicators for the latent constructs; we provide thedescriptive statistics in Table 3.

Model Estimation

Because we consider moderating hypotheses, we createdinteraction terms by multiplying the mean-centered explana-tory variables (i.e., governance mechanisms) with the mean-centered moderating variables (i.e., uncertainty variables).The mean-centering increases the interpretability of themain effects of the explanatory variables; the main effectsare the effects of the explanatory variables on the dependentvariables when the moderator is at its mean value of 0.

The continuous dependent variable (electronic marketperformance) prompts us to use an ordinary least squaresregression to test the hypotheses. However, endogenousself-selection could influence the reputation variable. Thatis, market makers with poor reputations could have self-selected themselves out of responding to the survey, inwhich case the close relationship between reputation andelectronic market performance might be an artifact of theexclusion of poorly reputed market makers from the sample(e.g., Ferguson, Deephouse, and Ferguson 2000; Robertsand Dowling 2002).5 To correct for this self-selection bias,we followed the specific steps that Garen (1984) prescribes.First, we regressed reputation on several constructs andobtained the predicted error:

(1) z = ∆x + ϑ,

where z is reputation, which is a continuous construct; X isthe matrix of predictors; ∆ is the matrix of coefficients; andϑ is the standard error term. Second, we used IT capabili-ties, market orientation, training, and dynamic uncertainty

Governance Mechanisms in Electronic Markets / 53

as predictors of reputation.6 Third, we estimated the mainregression model by introducing additional terms to thehypothesized regression models (Garen 1984):

(2) y = Rβ + αϑϑΛ+ αϑzϑ

Λz + ε,

where y is electronic market performance; R is the matrixof independent variables used in the regression models inTable 3; β, αϑ, and αϑz are coefficients to be estimated,with αϑ equal to the coefficient of the estimated error termfrom Equation 1 and αϑz equal to the coefficient for theproduct of the estimated error from Equation 1 and the rep-utation variable; ϑΛ is the estimated error term from Equa-tion 1; and ε is the standard error term. The coefficientsestimated in Equation 2 using ordinary least squares are sta-tistically inefficient because of heteroskedasticity in theerror term, for which we use White’s (1980) correction.

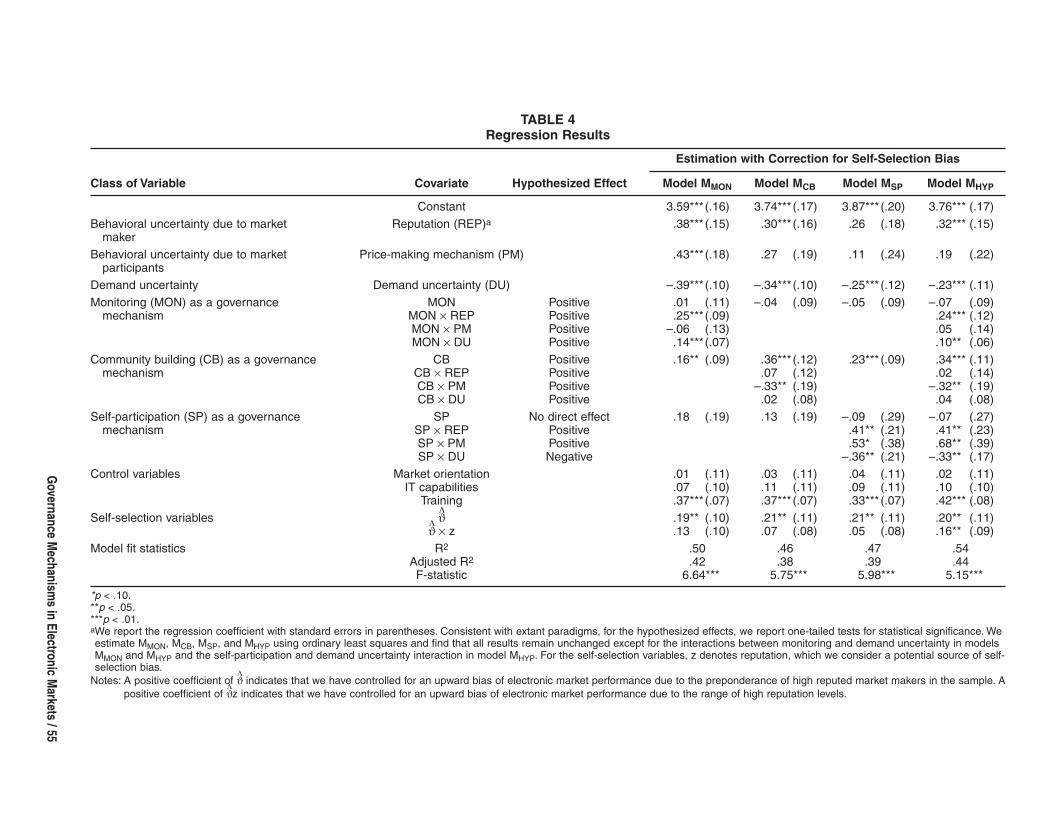

ResultsModel Selection and Robustness Assessment

For the explanatory variables, including the interactionterms, the variance inflation factors (highest value is 6.28,below the recommended cutoff of 10.00) and the conditionindexes (highest value is 8.23, well below the recommendedcutoff of 30.00) indicate that multicollinearity is not anissue (e.g., Mason and Perreault 1991). As we show in Table4, the independent variables together explain a statisticallysignificant amount of variance in market performance (R2 =.54, p < .01). Despite the high R-square value, we attemptto assess the robustness of the results by comparing thehypothesized model (MHYP) with three submodels in which

TABLE 3Descriptive Statistics

PER MON CB SP REP PM DU MO TRN ITC

Electronic market performance (PER)Monitoring (MON) .17aCommunity building (CB) .25** .46**Self-participation (SP) .21* –.06 .00Reputation (REP) .39** .13 .19* .12Price-making mechanism (PM) .14 –.06 .12 .15 .09Demand uncertainty (DU) –.17 .11 .17 –.02 –.01 –.11Market orientation (MO) .35** .31** .39** –.01 .44** .06 .04Training (TRN) .36** .11 .08 .18 .17* .04 –.09 .32**IT capability (ITC) .23* .16* .10 –.07 .32* .00 .09 .21* .16M 4.25 4.12 4.16 .26 5.68 .62 4.42 4.92 4.72 5.44SD 1.36 1.33 1.95 .44 .94 .48 .94 1.12 1.18 .99

*p < .05.**p < .01.aTwo-tailed tests for bivariate correlations.

5We thank an anonymous reviewer for pointing out this issueand the potential solution to us.

6We use several combinations of predictors, as available in thesurvey. The final regression results in Equation 2 remain consis-tent. The correction terms include both the predicted error fromEquation 1 and the product of the predicted error and the reputa-tion variable. Garen (1984) prescribes such an approach becausethe self-selection bias correction is conditional on the value of thereputation variable, so the correction will differ for every value ofthe reputation variable.

only monitoring (MMON), only community building (MCB),or only self-participation (MSP) appears as a single gover-nance construct. The likelihood ratio tests reveal that MHYPoutperforms all three submodels (MMON χ26 = 3.68, p < .01;MCB χ26 = 4.51, p < .01; MSP χ26 = 4.37, p < .01). In terms ofstatistical significance, the results do not change across thefour models.7

Hypotheses Testing

The main effect of monitoring is not statistically significant(bMON = –.07, p > .19). Although we do not find support forH1a, the results indicate support for H1b, which posits thatthe effectiveness of monitoring for electronic market perfor-mance increases with the reputation of the market maker(bMON × REP = .24, p < .01; see Table 4). We conduct a slopeanalysis to investigate this result (see Table 5) and find thatwhen the market maker’s reputation is strong, the effect ofmonitoring on market performance is positive (bMON ×REPhigh = .36, p < .05), but when that reputation is poor, theeffect of monitoring is negative (bMON × REPlow = –.44, p <.05). We must reject H1c because the interaction of monitor-ing with the price-making mechanism is not statisticallysignificant (bMON × PM = .05, p > .92). However, the resultssupport H1d for the interaction between monitoring anddemand uncertainty (bMON × DU = .10, p < .05). A slopeanalysis shows that at low levels of demand uncertainty,monitoring leads to a deterioration of market performance(bMON × DUlow = –.27, p < .01), but monitoring has a positiveeffect when demand uncertainty is high (bMON × DUhigh =.13, p < .05; Table 5).

The results for H2 are similarly mixed. We find supportfor H2a; that is, community building has a positive maineffect on electronic market performance (bCB = .34, p <.01). However, the effect of community building on marketperformance does not increase with the reputation of themarket maker (bCB × REP = .02, p > .29), and the interactionbetween community building and the price-making mecha-nism is opposite the effect we hypothesized. That is, theeffectiveness of community building is greater for staticpricing than for dynamic pricing (bCOM × PM = –.32, p <.05), and the slope analysis confirms that community build-ing has a positive and statistically significant effect only instatic pricing conditions (bCOM × PMstatic = .34, p < .01;bCOM × PMdyn = .02, p > .51). We also do not find support forH2d, because community building is not more effectivein conditions of high rather than low demand uncertainty(bCB × DU = .04, p > .57).

Consistent with H3a, the results suggest that the effect ofself-participation on market performance increases with thereputation of the market maker (bSP × REP = .41, p < .05).The slope analysis reveals that highly reputed market mak-ers can effectively use their self-participation as a gover-nance mechanism (bSP × REPhigh = .42, p < .05), whereasmarket makers with poor reputations cannot (bSP × REPlow =–.89, p < .01). We also find support for H3b; the interaction

54 / Journal of Marketing, July 2010

between self-participation and the price-making mechanismis statistically significant (bSP × PM = .68, p < .05). From theslope analysis for this interaction effect, we determine thatwhen the price-making mechanism is dynamic, the effectof self-participation is positive and statistically significant(bSP × PMdyn = .61, p < .05), but when the pricing mechanismis static, the effect of self-participation is not statisticallysignificant (bSP × PMstat = –.07, p > .67). In support of H3c,the impact of the market maker’s self-participation decreasesas demand uncertainty increases (bSP × DU = –.33, p < .05),and the slope analysis suggests that with high demanduncertainty, self-participation is ineffective as a governancemechanism (bSP × DUhigh = –.69, p < .01), whereas at lowlevels of demand uncertainty, its effect is not statisticallysignificant (bSP × DUlow = .55, p > .19).

DiscussionRecognizing the growing importance of electronic marketsfor consummating B2B transactions, we attempt to advanceextant research on electronic markets by focusing on therole of the market maker as a facilitator of trade. Our spe-cific focus centers on the effectiveness of the governancemechanisms that the market maker might use to govern themarket. We rely on transaction cost analysis and organiza-tional learning theory to suggest that the effectiveness ofthree governance mechanisms should depend on behavioraland external demand uncertainties in the market (e.g.,Williamson 1985).

The results from the survey data demonstrate the bound-ary conditions for the effectiveness of the three governancemechanisms we consider. Monitoring market participantsseems to be effective when the market maker is reputableand demand uncertainty in the external environment is high.However, we find no difference in the effectiveness ofmonitoring in alternative price-making scenarios. Perhapswith dynamic pricing, the range of possible bidding behav-iors makes monitoring too difficult, whereas in a static pric-ing setting, the monitoring efforts are rendered redundantwith the open and transparent fixed pricing system.

In contrast, community building, which is a culturalgovernance mechanism (rather than a bureaucratic gover-nance mechanism such as monitoring; Jaeger and Baliga1985), is effective in most conditions, as the statisticallysignificant main effect suggests. Contrary to the hypothesis,however, the effectiveness of community building is mostpronounced in electronic markets with static pricing. Itseems that the inherent transparency of static pricing makescommunity-building efforts effective because all relevantmarket participant information appears in the public domainand the buyers can select the sellers they prefer, whereasdynamic pricing relies on the price-making process to matchbuyers and sellers. Some static pricing electronic market for-mats, such as workflow marketplaces, bring multiple partiestogether for collaborative projects and thus, by their verynature, may be more amenable to community building.

Furthermore, the effectiveness of community building isnot bound by the market maker’s reputation. We had rea-soned that reputation would boost community-buildingefforts; however, the results seem to suggest that regardless

7For hypothesized effects, we use one-tailed tests of statisticalsignificance. Considering the small sample size (107 electronicmarkets), in addition to tests of significance at p < .01 and .05, wereport tests of statistical significance at p < .10.

Governance

Mechanism

sin

ElectronicM

arkets/55

TABLE 4Regression Results

Estimation with Correction for Self-Selection Bias

Class of Variable Covariate Hypothesized Effect Model MMON Model MCB Model MSP Model MHYP

Constant 3.59*** (.16) 3.74*** (.17) 3.87*** (.20) 3.76*** (.17)Behavioral uncertainty due to market Reputation (REP)a .38*** (.15) .30*** (.16) .26 (.18) .32*** (.15)maker

Behavioral uncertainty due to market Price-making mechanism (PM) .43*** (.18) .27 (.19) .11 (.24) .19 (.22)participants

Demand uncertainty Demand uncertainty (DU) –.39*** (.10) –.34*** (.10) –.25*** (.12) –.23*** (.11)Monitoring (MON) as a governance MON Positive .01 (.11) –.04 (.09) –.05 (.09) –.07 (.09)mechanism MON × REP Positive .25*** (.09) .24*** (.12)

MON × PM Positive –.06 (.13) .05 (.14)MON × DU Positive .14*** (.07) .10** (.06)

Community building (CB) as a governance CB Positive .16** (.09) .36*** (.12) .23*** (.09) .34*** (.11)mechanism CB × REP Positive .07 (.12) .02 (.14)

CB × PM Positive –.33** (.19) –.32** (.19)CB × DU Positive .02 (.08) .04 (.08)

Self-participation (SP) as a governance SP No direct effect .18 (.19) .13 (.19) –.09 (.29) –.07 (.27)mechanism SP × REP Positive .41** (.21) .41** (.23)

SP × PM Positive .53* (.38) .68** (.39)SP × DU Negative –.36** (.21) –.33** (.17)

Control variables Market orientation .01 (.11) .03 (.11) .04 (.11) .02 (.11)IT capabilities .07 (.10) .11 (.11) .09 (.11) .10 (.10)

Training .37*** (.07) .37*** (.07) .33*** (.07) .42*** (.08)Self-selection variables ϑ

Λ.19** (.10) .21** (.11) .21** (.11) .20** (.11)

ϑΛ× z .13 (.10) .07 (.08) .05 (.08) .16** (.09)

Model fit statistics R2 .50 .46 .47 .54Adjusted R2 .42 .38 .39 .44F-statistic 6.64*** 5.75*** 5.98*** 5.15***

*p < .10.**p < .05.***p < .01.aWe report the regression coefficient with standard errors in parentheses. Consistent with extant paradigms, for the hypothesized effects, we report one-tailed tests for statistical significance. Weestimate MMON, MCB, MSP, and MHYP using ordinary least squares and find that all results remain unchanged except for the interactions between monitoring and demand uncertainty in modelsMMON and MHYP and the self-participation and demand uncertainty interaction in model MHYP. For the self-selection variables, z denotes reputation, which we consider a potential source of self-selection bias.Notes: A positive coefficient of ϑ

Λindicates that we have controlled for an upward bias of electronic market performance due to the preponderance of high reputed market makers in the sample. A

positive coefficient of ϑΛz indicates that we have controlled for an upward bias of electronic market performance due to the range of high reputation levels.

of the market maker’s reputation, a community that hasreached a particular level continues to provide returns toparticipants. Nor does demand uncertainty make a differ-ence for the influence of community building on marketperformance. Demand uncertainty may increase the empha-sis on organizational information-processing capabilitiesand, thus, economic-oriented governance mechanismsrather than social mechanisms (i.e., similar to the motivationdichotomy of the differential emphasis on efficiency versuslegitimacy motives; Grewal, Comer, and Mehta 2001).

Finally, self-participation is a unique governance mech-anism for electronic markets that arises from the potentialdual role of the market maker. The findings suggest thatself-participation as a governance mechanism should beemphasized when the market maker enjoys a high reputa-tion and when dynamic pricing mechanisms appear in themarket (Table 5). In contrast, self-participation is not effec-tive when the market maker’s reputation is poor anddemand uncertainty is high (Table 5).

These findings highlight two important recommenda-tions for the governance of electronic markets. First, thethree governance mechanisms are differentially effectiveunder different sources of uncertainty, which implies that theconditions a market maker faces should determine the gover-nance mechanisms it uses. Second, community building hasreceived a great deal of press, but its role in B2B electronicmarkets may be limited. Community building is effectivefor electronic markets with static pricing mechanisms, so itcould be employed effectively by catalog aggregators, leadgenerators, and workflow markets. Furthermore, the maineffect of community building is positive and statisticallysignificant, which means that it is equally beneficial regard-less of whether the market maker is reputable or whetherdemand uncertainty is high or low. Perhaps communitybuilding plays a greater role for business-to-consumer andconsumer-to-consumer electronic markets and for socialinteraction Web sites; this issue demands further research.8

Theoretical Implications

Before discussing the crucial theoretical implications of thisresearch, we acknowledge some limitations. First, we use a

56 / Journal of Marketing, July 2010

cross-sectional survey design, and all the limitations of thisresearch approach are pertinent here. Because of the evolv-ing nature of electronic markets (i.e., technology, marketparticipants, and competing markets), a cross-sectionalsnapshot might mask some important variables and insights.Longitudinal studies could add significantly to the findings.Second, because market makers typically are small entre-preneurial firms, historical data on them remain rather lim-ited. We conceptualize demand uncertainty only from themarket maker’s point of view, but it also may stem fromvariability in demand in the buyer’s or seller’s industry. Theeffects of demand uncertainty from such alternative sourcescould differ. Third, because of the lack of measurementoptions for the performance of electronic markets (most areprivately held), we use only self-reported measures for thedependent variable. Nonetheless, because we rely on impor-tant practitioner and academic literature from strategic mar-keting and transaction cost analysis research to develop thehypotheses, this study provides significant theoretical andpractical insights and represents an important initial steptoward building a theory of electronic market making.

The primary theoretical contribution lies in the explana-tion of electronic market performance across a populationof electronic markets; we take some initial steps towarddetermining how successful market making works. Previousempirical research on electronic markets has concentratedon one market at a time (e.g., Grewal, Comer, and Mehta2001), but it has overlooked the roles and challenges ofmarket makers. We believe that the current research pavesthe way for further research into electronic market makingthat can uncover boundary conditions other than uncer-tainty, such as structural factors (e.g., concentrated versusdispersed markets), participant switching costs, or the pro-portion of revenue derived from the electronic market.These variables capture variance in market participants’dependence on the electronic market for their operations,which may be effective indicators of their asset specificity.Additional research should also address market participantand market maker opportunism as constructs that couldmediate the relationship between governance mechanismsand electronic market performance.9

We contribute to governance literature in marketing(e.g., Wathne and Heide 2000) by theorizing about the rele-

8For example, eBay has successfully created the world’s largestWeb-based community of consumer-to-consumer auctions, whichestablishes high switching costs and enhances user loyalty. TheWeb-based music retailer lala.com has created a community of musiclisteners that complements its pay-per-download business model.

9We thank an anonymous reviewer for suggesting opportunismtesting as a direction for further research.

TABLE 5Slope Analysis of Hypothesized Moderating Effects

Dependent Variable: Electronic Market Performance

Static Dynamic Low HighLow High Price-Making Price-Making Demand Demand

Reputation Reputation Mechanism Mechanism Uncertainty Uncertainty

Slope for monitoring –.44* (.25) .36* (.21) –.07 (.19) –.02 (.03) –.27** (.13) .13* (.07)Slope for community building .34a (.22) .35 (.63) .34** (.17) .02 (.02) .29 (.73) .32 (.29)Slope for self-participation –.89** (.42) .42* (.23) –.07 (.51) .61* (.32) .55 (.59) –.69** (.32)

*p < .05.**p < .01.aConsistent with extant paradigms, for the hypothesized effects, we report one-tailed tests for statistical significance.

vant governance mechanisms for B2B electronic markets.The online electronic market space allows for the use ofmultiple governance mechanisms, whether bureaucratic(monitoring), cultural (community building), or participa-tory (self-participation). In this realm, we identify the ambi-ent conditions that become manifest in response to behav-ioral uncertainty on the part of the market maker andmarket participants and to external demand uncertainty toidentify potential boundary conditions on the effectivenessof the governance mechanisms. To the best of our knowl-edge, this is the only marketing study that empiricallyexamines the effectiveness of community building whilealso considering self-participation as a governance mecha-nism that seems unique to electronic markets.

We also conceptualize new constructs for communitybuilding and self-participation, develop a valid and reliablemeasure for community building, and identify a way tocapture self-participation and price-making mechanismsthrough nominal measurement. The community-buildingconstruct is applicable across different contexts and there-fore could serve to assess efforts to build esprit de corpsamong a dealer network of an industrial organization, forexample.

Managerial Implications

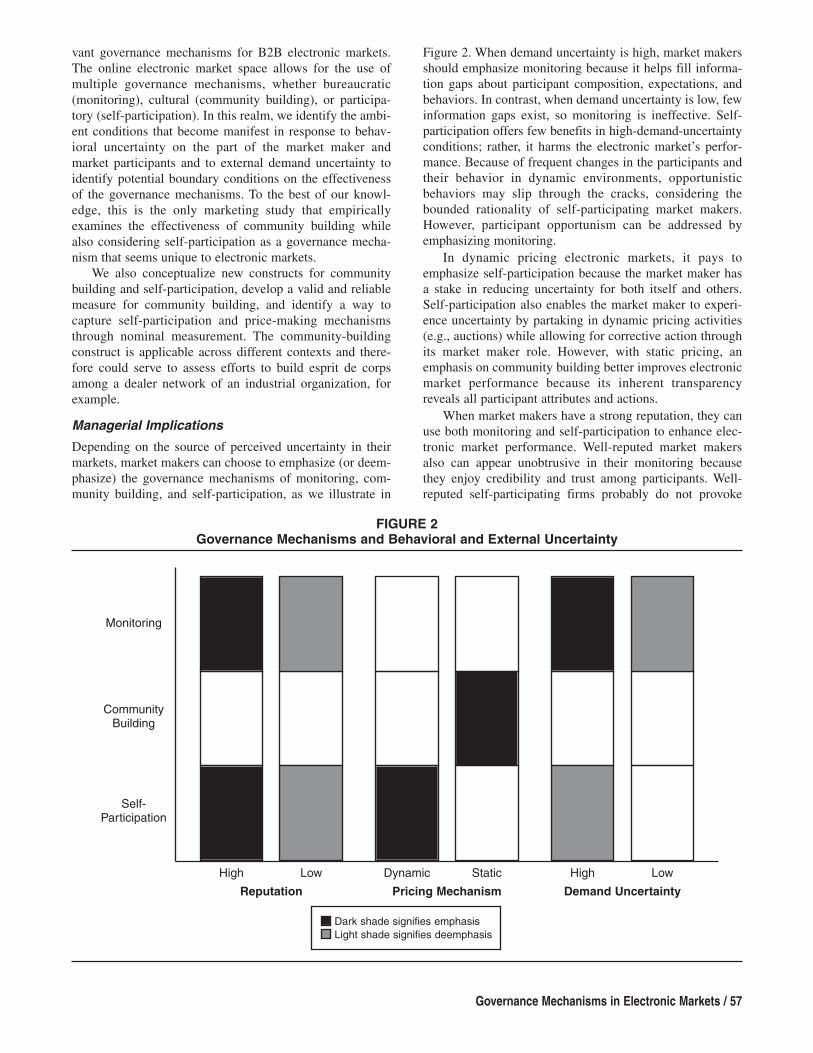

Depending on the source of perceived uncertainty in theirmarkets, market makers can choose to emphasize (or deem-phasize) the governance mechanisms of monitoring, com-munity building, and self-participation, as we illustrate in

Governance Mechanisms in Electronic Markets / 57

Figure 2. When demand uncertainty is high, market makersshould emphasize monitoring because it helps fill informa-tion gaps about participant composition, expectations, andbehaviors. In contrast, when demand uncertainty is low, fewinformation gaps exist, so monitoring is ineffective. Self-participation offers few benefits in high-demand-uncertaintyconditions; rather, it harms the electronic market’s perfor-mance. Because of frequent changes in the participants andtheir behavior in dynamic environments, opportunisticbehaviors may slip through the cracks, considering thebounded rationality of self-participating market makers.However, participant opportunism can be addressed byemphasizing monitoring.

In dynamic pricing electronic markets, it pays toemphasize self-participation because the market maker hasa stake in reducing uncertainty for both itself and others.Self-participation also enables the market maker to experi-ence uncertainty by partaking in dynamic pricing activities(e.g., auctions) while allowing for corrective action throughits market maker role. However, with static pricing, anemphasis on community building better improves electronicmarket performance because its inherent transparencyreveals all participant attributes and actions.

When market makers have a strong reputation, they canuse both monitoring and self-participation to enhance elec-tronic market performance. Well-reputed market makersalso can appear unobtrusive in their monitoring becausethey enjoy credibility and trust among participants. Well-reputed self-participating firms probably do not provoke

FIGURE 2Governance Mechanisms and Behavioral and External Uncertainty

Low

Reputation

High

Dark shade signifies emphasisLight shade signifies deemphasis

Low

Demand Uncertainty

High

Pricing Mechanism

Dynamic Static

Monitoring

Self-Participation

CommunityBuilding

concerns about self-interest-seeking behaviors; monitoringand self-participation are likely to be viewed as legitimatepolicing actions. In contrast, if nonreputable market makersadopt monitoring and self-participation, it hurts the bottomline. Monitoring comes across as overbearing, and self-participation appears ethically questionable. Communitybuilding also may work for reputable market makers; thecoefficients of the slopes of community building acrossreputation conditions are all reasonable (see Table 5).

Because the three governance mechanisms are differen-tially effective under different aspects of behavioral andexternal uncertainty, market makers should recognize howeach can be developed, implemented, and maintained in thecontext of electronic markets. For example, monitoringefforts require investments to develop supervisory routines,as well as technology that can accumulate and analyze par-ticipant behavior data, provide instant reporting of tradinganomalies, and establish a responsive complaint manage-ment system. To build communities, market makers need atleast two channels of communication and feedback: a bilat-eral channel between the market maker and individual par-

58 / Journal of Marketing, July 2010

ticipants and a network channel among participants. Com-munity building also involves the effective communicationof market norms through newsletters, e-mail messages, chatrooms, and message boards. Finally, self-participationrequires the market maker to be able to balance tradingskills and market-making skills and to manage risk. Toavoid surprises, self-participation requires the full disclo-sure of the market maker’s role in the electronic market.

ConclusionMarket making requires an effective infrastructure forexchange, the regulation of participant behavior, and steadygovernance that takes into account the uncertainty in themarket. Electronic markets, the new frontier in market mak-ing, create both governance challenges and opportunitiesfor market makers. The key challenge is to govern underuncertainty in the virtual environment. The opportunity liesin the freedom to create a market for any product or service,global or local, as long as market makers make the rightdecisions about when to monitor, when to build a commu-nity, and when to self-participate.

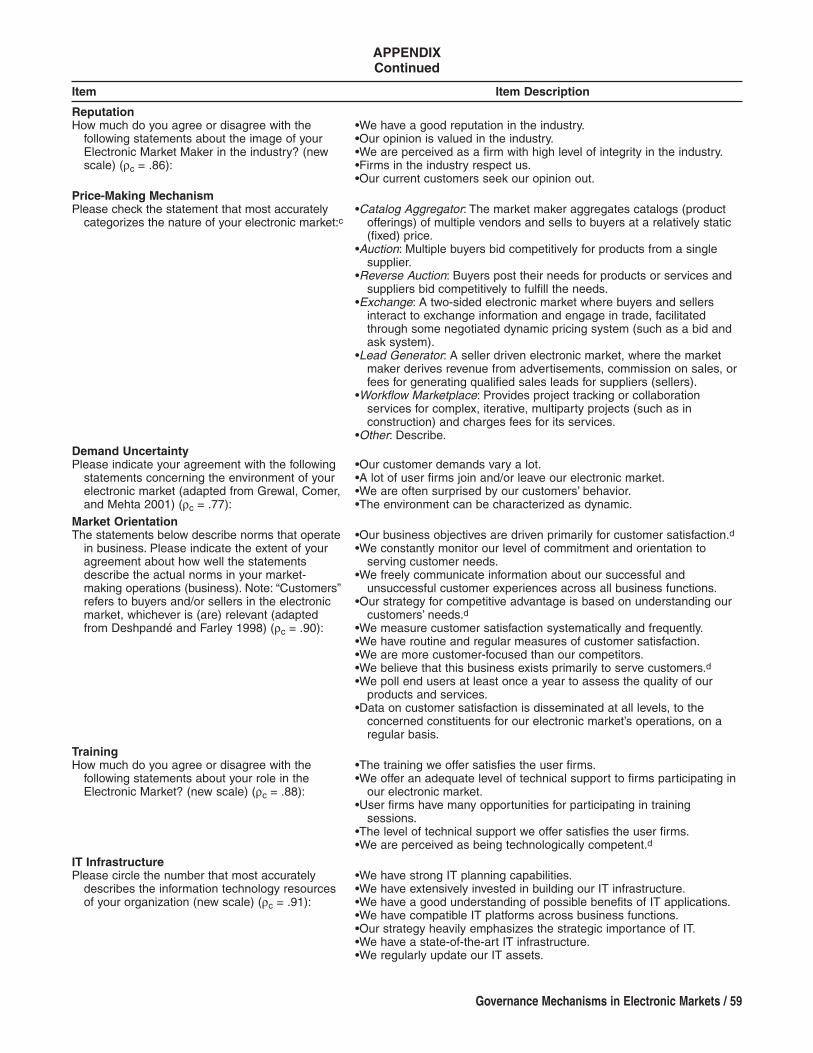

APPENDIXMeasures

Item Item Description

Electronic Market PerformancePlease use the scale below to rate aspects of theperformance of your electronic marketa (ρc =.96):b

•Return on investment relative to objective.•Sales relative to objective.•Profits relative to objective.•Growth relative to objectives.•Market share relative to objective.•Market acceptance.•General success.

MonitoringHow much do you agree or disagree with thefollowing statements in describing themanagement of your Electronic Market? (newscale) (ρc = .87):

•We monitor the electronic market closely to make sure that theparticipating firms do not take advantage of other participating firms.

•We take the complaints of opportunistic behavior on the part of userfirms seriously.

•We believe that one of the primary roles of market makers of anelectronic market is to police the market.

•It is important for market makers to maintain order in their electronicmarkets.

•We lay heavy emphasis on our disciplining role as a market maker.

Community BuildingHow much do you agree or disagree with thefollowing statements in describing themanagement of your Electronic Market? (newscale) (ρc = .72):

•We expend a lot of effort to build trust among firms participating in ourelectronic market.

•Creating a congenial atmosphere in the electronic market is one ofour primary goals.

•Building a sense of community among the firms participating in ourelectronic market is an important goal for us.

Self-ParticipationThe market maker (or firm that owns the electronicmarket) transacts in the market as either a buyeror a seller. For example, Covisint is a self-participating electronic market, as a co-ownerFord participates in the market, whereasESTEEL is an unbiased electronic market.Please check the statement that most accuratelydescribes the OPERATING status of theELECTRONIC MARKET you manage:

_____ The market maker (or one of the firms that owns the electronicmarket) transacts in the market as a buyer or seller.

_____ The market maker maintains neutrality and does not transact inthe electronic market.

Governance Mechanisms in Electronic Markets / 59

APPENDIXContinued

Item Item Description

ReputationHow much do you agree or disagree with thefollowing statements about the image of yourElectronic Market Maker in the industry? (newscale) (ρc = .86):

•We have a good reputation in the industry.•Our opinion is valued in the industry.•We are perceived as a firm with high level of integrity in the industry.•Firms in the industry respect us.•Our current customers seek our opinion out.

Price-Making MechanismPlease check the statement that most accuratelycategorizes the nature of your electronic market:c

•Catalog Aggregator: The market maker aggregates catalogs (productofferings) of multiple vendors and sells to buyers at a relatively static(fixed) price.

•Auction: Multiple buyers bid competitively for products from a singlesupplier.

•Reverse Auction: Buyers post their needs for products or services andsuppliers bid competitively to fulfill the needs.

•Exchange: A two-sided electronic market where buyers and sellersinteract to exchange information and engage in trade, facilitatedthrough some negotiated dynamic pricing system (such as a bid andask system).

•Lead Generator: A seller driven electronic market, where the marketmaker derives revenue from advertisements, commission on sales, orfees for generating qualified sales leads for suppliers (sellers).

•Workflow Marketplace: Provides project tracking or collaborationservices for complex, iterative, multiparty projects (such as inconstruction) and charges fees for its services.

•Other: Describe.Demand UncertaintyPlease indicate your agreement with the followingstatements concerning the environment of yourelectronic market (adapted from Grewal, Comer,and Mehta 2001) (ρc = .77):

•Our customer demands vary a lot.•A lot of user firms join and/or leave our electronic market.•We are often surprised by our customers’ behavior.•The environment can be characterized as dynamic.

Market OrientationThe statements below describe norms that operatein business. Please indicate the extent of youragreement about how well the statementsdescribe the actual norms in your market-making operations (business). Note: “Customers”refers to buyers and/or sellers in the electronicmarket, whichever is (are) relevant (adaptedfrom Deshpandé and Farley 1998) (ρc = .90):

•Our business objectives are driven primarily for customer satisfaction.d•We constantly monitor our level of commitment and orientation toserving customer needs.

•We freely communicate information about our successful andunsuccessful customer experiences across all business functions.

•Our strategy for competitive advantage is based on understanding ourcustomers’ needs.d

•We measure customer satisfaction systematically and frequently.•We have routine and regular measures of customer satisfaction.•We are more customer-focused than our competitors.•We believe that this business exists primarily to serve customers.d•We poll end users at least once a year to assess the quality of ourproducts and services.

•Data on customer satisfaction is disseminated at all levels, to theconcerned constituents for our electronic market’s operations, on aregular basis.

TrainingHow much do you agree or disagree with thefollowing statements about your role in theElectronic Market? (new scale) (ρc = .88):

•The training we offer satisfies the user firms.•We offer an adequate level of technical support to firms participating inour electronic market.

•User firms have many opportunities for participating in trainingsessions.

•The level of technical support we offer satisfies the user firms.•We are perceived as being technologically competent.d

IT InfrastructurePlease circle the number that most accuratelydescribes the information technology resourcesof your organization (new scale) (ρc = .91):

•We have strong IT planning capabilities.•We have extensively invested in building our IT infrastructure.•We have a good understanding of possible benefits of IT applications.•We have compatible IT platforms across business functions.•Our strategy heavily emphasizes the strategic importance of IT.•We have a state-of-the-art IT infrastructure.•We regularly update our IT assets.

60 / Journal of Marketing, July 2010

APPENDIXContinued

Item Item Description

IT SkillsPlease circle the number that most accuratelydescribes human information technologyresources of your organization (new scale)(ρc = .92):

•Is experienced with IT.•We have strong technical IT skills.•We have adequate knowledge about IT.•Our IT skills are comparable with the best in the industry.•We invest heavily in our IT human resources.•We have adequate managerial IT skills.